Game theory model for European government bonds market stabilization: a saving-State proposal

Upload

khangminh22Category

view

0download

0

ST. PETERSBURG UNIVERSITYGraduate School of Management

Faculty of Applied Mathematics & Control ProcessesTHE INTERNATIONAL SOCIETY OF DYNAMIC GAMES

(Russian Chapter)

CONTRIBUTIONS TO GAME THEORY

AND MANAGEMENT

Volume IV

The Fourth International ConferenceGame Theory and Management

June 28-30, 2010, St. Petersburg, Russia

Collected papersEdited by Leon A. Petrosyan and Nikolay A. Zenkevich

Graduate School of ManagementSt. Petersburg University

St. Petersburg2011

УДК 518.9, 517.9, 681.3.07

Contributions to game theory and management. Vol. IV. Collected paperspresented on the Fourth International Conference Game Theory and Management /Editors Leon A. Petrosyan, Nikolay A. Zenkevich. – SPb.: Graduate School of Man-agement SPbU, 2011. – 514 p.

The collection contains papers accepted for the Fourth International Confer-ence Game Theory and Management (June 28–30, 2010, St. Petersburg University,St. Petersburg, Russia). The presented papers belong to the field of game theoryand its applications to management.

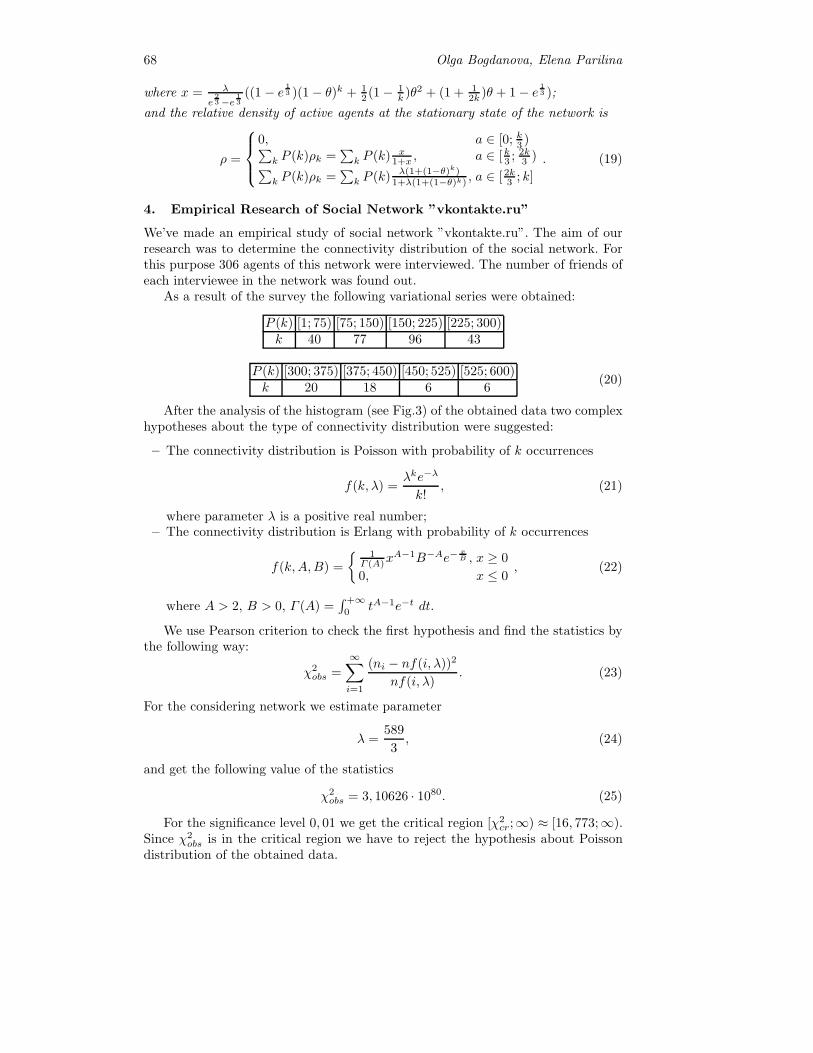

The volume may be recommended for researches and post-graduate students ofmanagement, economic and applied mathematics departments.

c© Copyright of the authors, 2011c© Graduate School of Management, SPbU, 2011

ISBN 978-5-9924-0069-4

Успехи теории игр и менеджмента. Вып. 4. Сб. статей четвертой меж-дународной конференции по теории игр и менеджменту / Под ред. Л.А. Пет-росяна, Н.А. Зенкевича. – СПб.: Высшая школа менеджмента СПбГУ, 2011. –514 с.

Сборник статей содержит работы участников четвертой международнойконференции «Теория игр и менеджмент» (28–30 июня 2010 года, Высшая шко-ла менеджмента, Санкт-Петербургский государственный университет,Санкт-Петербург, Россия). Представленные статьи относятся к теории игр иее приложениям в менеджменте.

Издание представляет интерес для научных работников, аспирантов и сту-дентов старших курсов университетов, специализирующихся по менеджменту,экономике и прикладной математике.

c© Коллектив авторов, 2011c© Высшая школа менеджмента СПбГУ, 2011

Contents

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Graph Searching Games with a Radius of Capture . . . . . . . . . . . . . . . . . . 8Tatiana V. Abramovskaya, Nikolai N. Petrov

Non-Cooperative Games with Chained Confirmed Proposals . . . . . . . . 19G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

The Π-strategy: Analogies and Applications . . . . . . . . . . . . . . . . . . . . . . . 33A. A. Azamov, B. T. Samatov

About Some Non-Stationary Problems of Group Pursuitwith the Simple Matrix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Alexander Bannikov, Nikolay Petrov

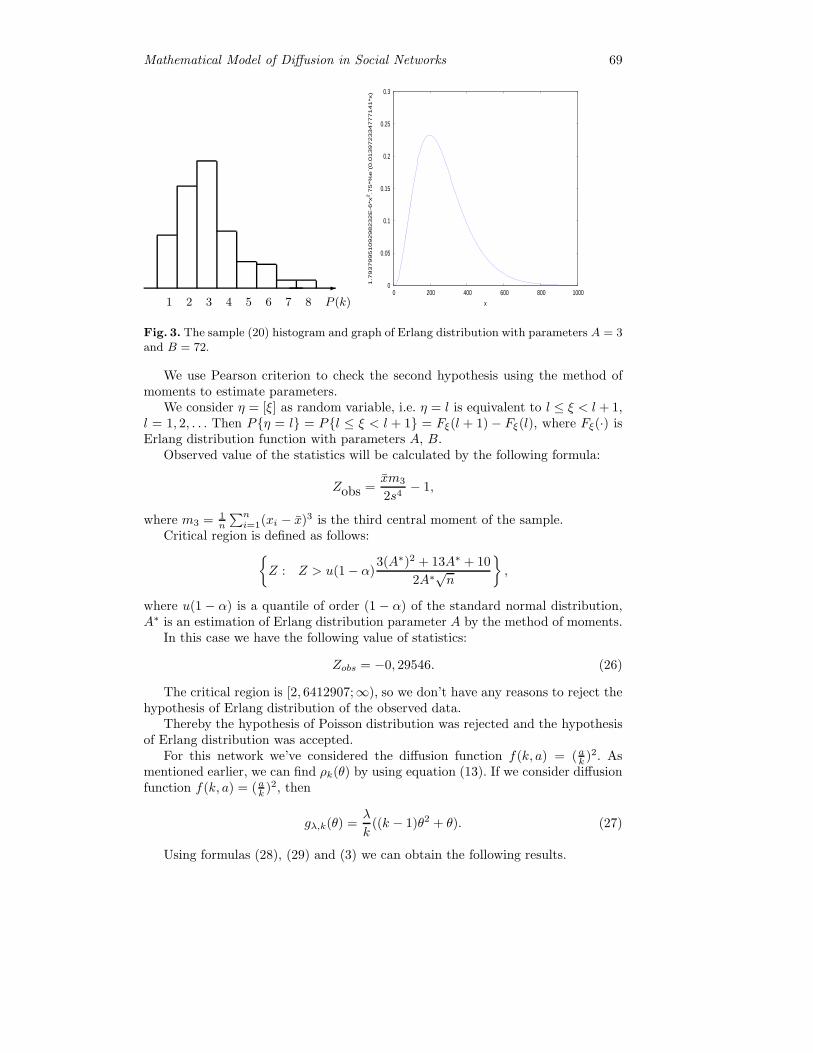

Mathematical Model of Diffusion in Social Networks . . . . . . . . . . . . . . . 63Olga Bogdanova, Elena Parilina

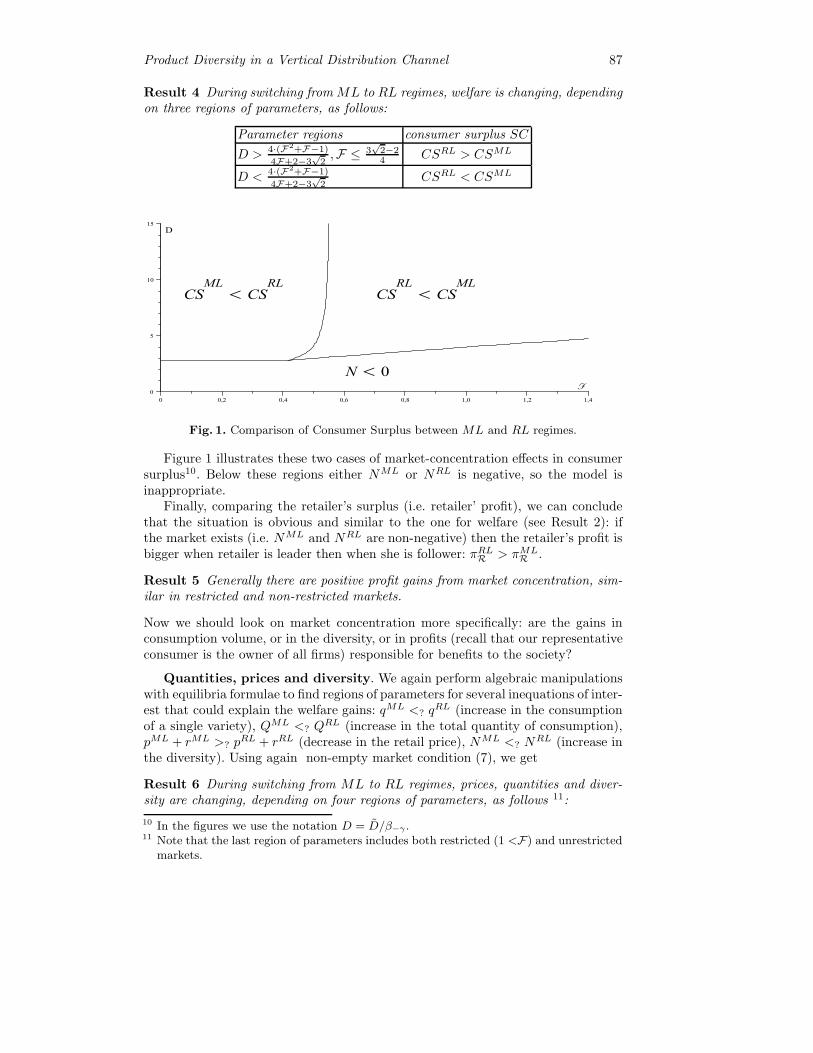

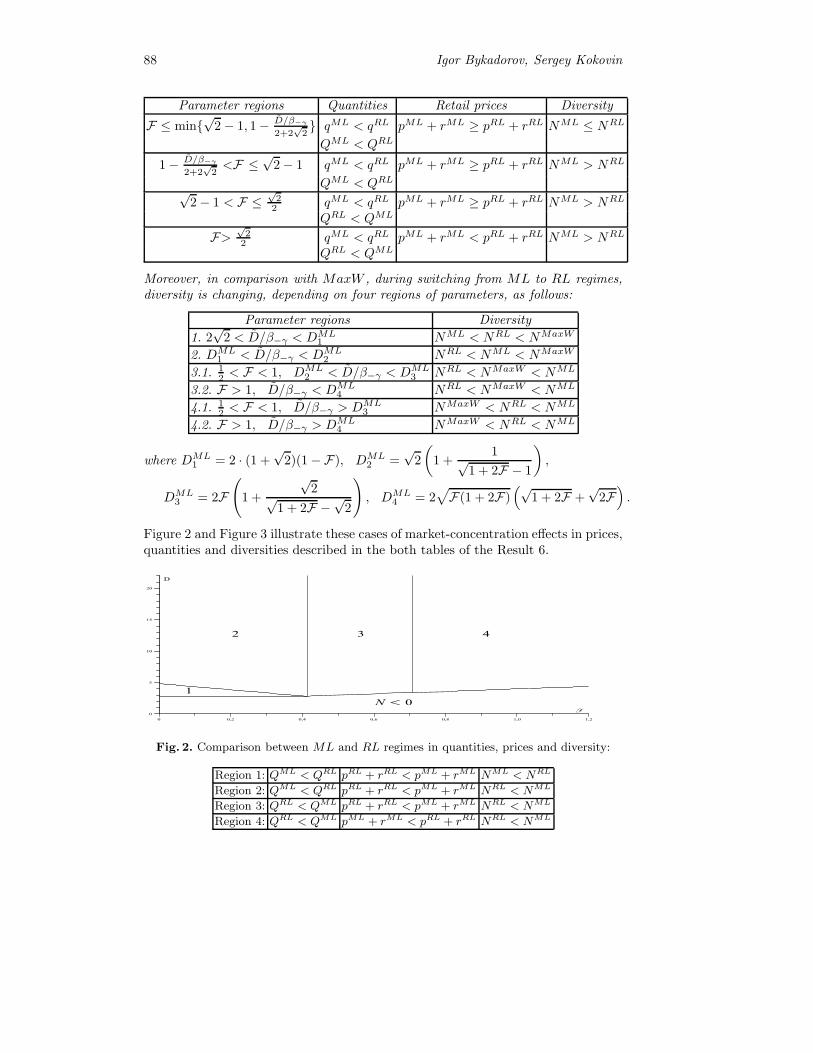

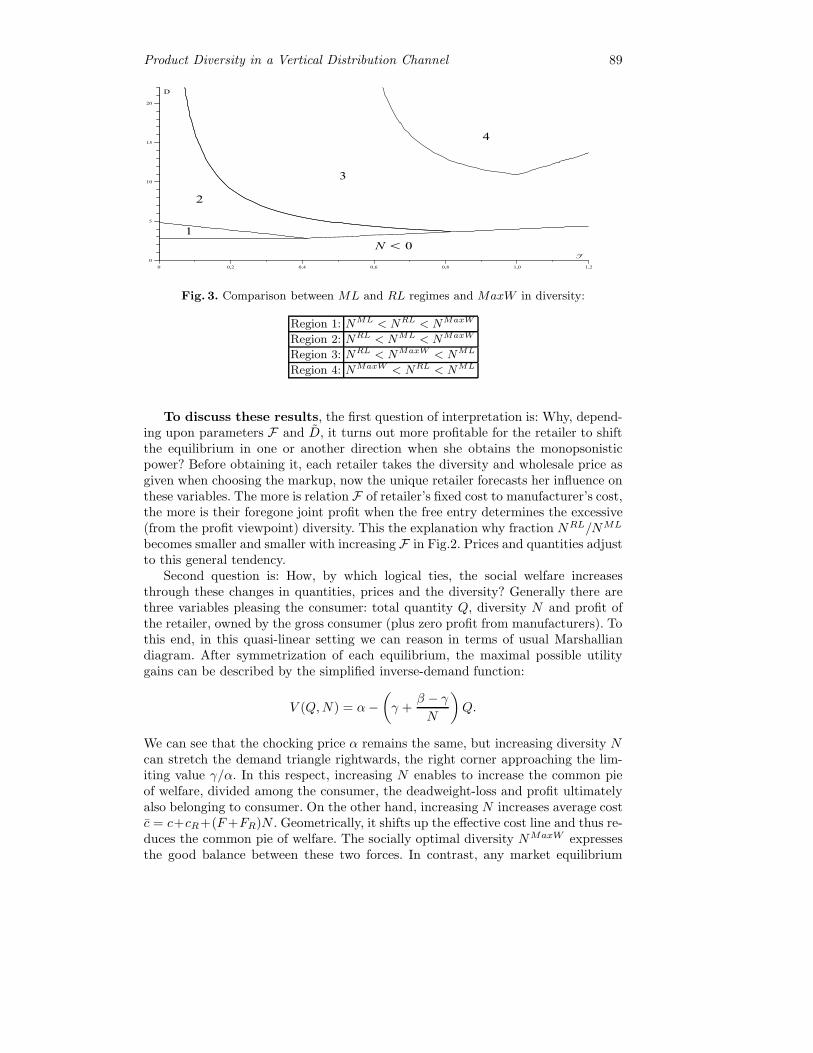

Product Diversity in a Vertical Distribution Channelunder Monopolistic Competition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Igor Bykadorov, Sergey Kokovin, Evgeny Zhelobodko

Strong Strategic Support of Cooperative Solutionsin Differential Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

Sergey Chistyakov, Leon Petrosyan

Strategic Bargaining and Full Efficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112Xianhua Dai, Hong Li†, Xing Tong

Socially Acceptable Values for Cooperative TU Games . . . . . . . . . . . . . 117Theo Driessen, Tadeusz Radzik

Auctioning Big Facilities under Financial Constraints . . . . . . . . . . . . . . . 132Marıa Angeles de Frutos, Marıa Paz Espinosa

Numerical Study of a Linear Differential Gamewith Two Pursuers and One Evader . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Sergey S. Ganebny, Sergey S. Kumkov, Stephane Le Menec, Valerii S. Patsko

The Dynamic Procedure of Information Flow Network . . . . . . . . . . . . . 172Hongwei GAO, Zuoyi LIU, Yeming DAI

Game Theory Approach for Supply Chains Optimization . . . . . . . . . . . 188Mansur G. Gasratov, Victor V. Zakharov

Stochastic Coalitional Games with Constant Matrixof Transition Probabilties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 199

Xeniya Grigorieva

4

Cash Flow Optimization in ATM Network Model . . . . . . . . . . . . . . . . . . 213

Elena Gubar, Maria Zubareva, Julia Merzljakova

Stable Families of Coalitions for Network ResourceAllocation Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223

Vladimir Gurvich, Sergei Schreider

Signaling Managerial Objectives to Elicit Volunteer Effort . . . . . . . . . . 231

Gert Huybrechts, Jurgen Willems, Marc Jegers, Jemima Bidee, Tim Van-tilborgh, Roland Pepermans

Two Solution Concepts for TU Gameswith Cycle-Free Directed Cooperation Structures . . . . . . . . . . . . . . . . . . . 241

Anna Khmelnitskaya, Dolf Talman

Tax Auditing Models with the Application of Theory of Search . . . . . 266

Suriya Sh. Kumacheva

Bargaining Powers, a Surface of Weights, and Implementationof the Nash Bargaining Solution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 274

Vladimir D. Matveenko

On Games with Constant Nash Sum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294

Pierre von Mouche

Claim Problems with Coalition Demands . . . . . . . . . . . . . . . . . . . . . . . . . . . 311

Natalia I. Naumova

Games with Differently Directed Interestsand Their Application to the Environmental Management . . . . . . . . . 327

Guennady A.Ougolnitsky

Memento Ludi: Information Retrievalfrom a Game-Theoretic Perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 339

George Parfionov, Roman Zapatrin

The Fixed Point Method Versus the KKM Method . . . . . . . . . . . . . . . . . 347

Sehie Park

Proportionality in NTU Games:on a Proportional Excess Invariant Solution . . . . . . . . . . . . . . . . . . . . . . . . 361

Sergei L. Pechersky

On a Multistage Link Formation Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 368

Leon Petrosyan, Artem Sedakov

Best Response Digraphs for Two Location Games on Graphs . . . . . . . 378

Erich Prisner

Uncertainty Aversion and Equilibrium in Extensive Games . . . . . . . . . 389

Jorn Rothe

5

Nash Equilibrium in Games with Ordered Outcomes . . . . . . . . . . . . . . . 407Victor V. Rozen

Cooperative Optimality Conceptsfor Games with Preference Relations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 421

Tatiana F. Savina

A Fuzzy Cooperative Game Model for ConfigurationManagement of Open Supply Networks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 433

Leonid B. Sheremetov, Alexander V. Smirnov

Modeling of Environmental Projects under Conditionof a Random Time Horizon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 447

Ekaterina Shevkoplyas, Sergey Kostyunin

A Data Transmission Game in OFDM Wireless NetworksTaking into Account Power Unit Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 460

Anton Toritsyn, Rimma Salakhieva, Andrey Garnaev

Strict Proportional Power and Fair Voting Rules in Committees . . . . 473Frantisek Turnovec

Subgame Consistent Solution for Random-HorizonCooperative Dynamic Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 489

David W.K. Yeung, Leon A. Petrosyan

Efficient CS-Values Based on Consensus and Shapley Values . . . . . . . . 502Alexandra B. Zinchenko, Polina P. Provotorova and George V. Mironenko

Preface

This edited volume contains a selection of papers that are an outgrowth ofthe Fourth International Conference on Game Theory and Management with afew additional contributed papers. These papers present an outlook of the currentdevelopment of the theory of games and its applications to management and variousdomains, in particular, energy, the environment and economics.

The International Conference on Game Theory and Management, a three dayconference, was held in St. Petersburg, Russia in June 28-30, 2010. It was the initia-tive of St. Petersburg University carried out by the Graduate School of ManagementSPbU and the Department of Applied Mathematics Control Processes SPbU in col-laboration with The International Society of Dynamic Games (Russian Chapter).More than 100 participants from 25 countries had an opportunity to hear state-of-the-art presentations on a wide range of game-theoretic models, both theory andmanagement applications.

Plenary lectures covered different areas of games and management applica-tions. They had been delivered by Professor Alain Haurie, University of Geneva(Switzerland); Professor Arkady Kryazhimskiy International Institute for AppliedSystems Analysis (Austria) and Steklov Mathematical Institute RAS (Russia; Pro-fessor Herve Moulin, Rice University (USA) and Professor Ralph Tyrrell Rockafellar,University of Washington (USA).

The importance of strategic behavior in the human and social world is increas-ingly recognized in theory and practice. As a result, game theory has emerged as afundamental instrument in pure and applied research. The discipline of game theorystudies decision making in an interactive environment. It draws on mathematics,statistics, operations research, engineering, biology, economics, political science andother subjects. In canonical form, a game obtains when an individual pursues anobjective(s) in a situation in which other individuals concurrently pursue other(possibly conflicting, possibly overlapping) objectives and in the same time the ob-jectives cannot be reached by individual actions of one decision maker. The problemis then to determine each individual’s optimal decision, how these decisions inter-act to produce equilibria, and the properties of such outcomes. The foundations ofgame theory were laid more than sixty years ago by von Neumann and Morgenstern(1944).

Theoretical research and applications in games are proceeding apace, in areasranging from aircraft and missile control to inventory management, market devel-opment, natural resources extraction, competition policy, negotiation techniques,macroeconomic and environmental planning, capital accumulation and investment.

In all these areas, game theory is perhaps the most sophisticated and fertileparadigm applied mathematics can offer to study and analyze decision making underreal world conditions. The papers presented at this Fourth International Conferenceon Game Theory and Management certainly reflect both the maturity and thevitality of modern day game theory and management science in general, and of

7

dynamic games, in particular. The maturity can be seen from the sophistication ofthe theorems, proofs, methods and numerical algorithms contained in the most ofthe papers in these contributions. The vitality is manifested by the range of newideas, new applications, the growing number of young researchers and the expandingworld wide coverage of research centers and institutes from whence the contributionsoriginated.

The contributions demonstrate that GTM2010 offers an interactive program onwide range of latest developments in game theory and management. It includesrecent advances in topics with high future potential and exiting developments inclassical fields.

We thank Anna Tur from the Faculty of Applied Mathematics (SPbU) for dis-playing extreme patience and typesetting the manuscript.

Editors, Leon A. Petrosyan and Nikolay A. Zenkevich

Graph Searching Games with a Radius of Capture �

Tatiana V. Abramovskaya and Nikolai N. Petrov

St.Petersburg State University,Faculty of Mathematics and Mechanics,

Universitetsky prospekt, 28, 198504, Peterhof, St. Petersburg, Russia.E-mail: [email protected]

Abstract. The problem of guaranteed search on graphs, the so–called ε–search problem, is considered. The properties of the Golovach function whichis the ε–search number as the function of the radius of capture ε are studied.In the present work, we show that the jumps of the Golovach function fortrees may have an arbitrarily large height. We describe some classes of treeswith the non–degenerate Golovach function, and construct the minimal treewith a non–unit jump.

Keywords: guaranteed search, team of pursuers, evader, ε–capture, searchnumbers, Golovach function, unit jumps.

1. Introduction

Here, we deal with a problem of guaranteed search on graphs ”with a radius ofcapture”. As was mentioned by Parsons (1976) — one of the pioneers of the theoryof the guaranteed search — the main features of the guaranteed search in generalcan be studied from the article (Breisch, 1967) by speleologist Richard Breisch.Breisch considered the following problem. A person is lost in a cave, which is intotal darkness, and wandering aimlessly. We are looking for an efficient way forrescue party to search the lost person: what is the minimum number of searchersrequired to explore a cave so that it is impossible to miss finding the victim if he isin the cave. The article of Breisch doesn’t contain strict statements of this problembut provides a lot of examples.

Now, let the cave be represented by the finite connected graph G so that therooms are described by vertices and the passages — by edges. We may assume that Gis embedded in IR3 so that its vertices are points in IR3 and its edges are representedby closed line segments which intersect only at vertices of G. The searchers mustproceed according to a predetermined plan which will find the lost man even if hewas that sort of victim who knows the searcher’s every move, is arbitrarily fast andinvisible for rescuers, and tries to avoid meeting doing his best (in such assumptionit is more correct to call the lost man as evader and the searchers as pursuers). Afamily Π = {x1, . . . , xn} of continuous functions is called a search plan (program).A search plan Π is called winning if for every continuous function there exist i ∈ 1, nand t ∈ [0, T ] such that xi(t) = y(t) holds. The search number of the graph G isthe minimum cardinality of all winning search plans for G.

In this way the problem was posed by Parsons (1976). Later but independentlyand in slightly different terms the similar problem of guaranteed search was posed

� This work was supported by the Federal Targeted Program ”Scientific and EducationalHuman Resources for Innovation-Driven Russia” under grant No.2010-1.1-111-128-033

Graph Searching Games with a Radius of Capture 9

by the second author of the present work (Petrov, 1982). As was proven by Golovachboth problems are equivalent to a certain discrete one (Golovach, 1989).

Later many other ”search numbers” appear in different variations of the de-scribed problem depending on the possible behavior of the players and other con-straints. So that it becomes necessary to distinguish corresponding search numbersfrom each other. Thus search number which is considered in the Parsons-Petrovproblem is called the edge–search number.

There are different connections and applications of the guaranteed graph search-ing. Search numbers are closely connected with some parameters of linear layouts(cut–width, topological bandwidth), which play significant role in extra-large-scaleintegrated circuits (ELSI). There are notable relations between the graph searchingproblems and the theory of graph minors by Robertson and Seymour. Also searchnumbers appear in pebble games, which model the rational computer memory us-age. There are connections between the graph searching problem and different topicsof Information Security, Biology, Linguistics, Robotics and chess composition (see(Fomin and Thilikos, 2008) for more details).

2. The search problem with a radius of capture and the Golovachfunction

The problem of guaranteed search on graphs with a radius of capture was posed byGolovach (1990).

Let a topological graph G be embedded in three dimensional Euclidean spaceso as it was described in Introduction. From this time only finite connected graphswithout loops and multiple edges are considered. And for further simplicity, we shallassume that the edges of the graph are polygonal lines with finite number of linesegments. By ρ we denote the inner metric of the graph, i.e. ρ(x, y) is the shortestpath (in the Euclidean norm) with ends in x and y and contained entirely in G.

A team of pursuers P = (P1, . . . , Pk) and an evader E are bounded within thegraph and possess the simple motions:

(Pi) : xi = ui, ‖ui‖ ≤ 1, i ∈ 1, k,(E) : y = u0,

where the ‖ . . . ‖ is the Euclidean norm and admissible controls are piecewise con-stant functions defined on arbitrary closed ”time” segments. The trajectories of theplayers are piecewise affine vector–functions with values in G. The team of pursuerstries to catch the invisible evader. It is supposed that the evader is caught by thepursuer if they are on distance less than or equal to a given non–negative numberε which is a radius of capture.

The ε–search number, denoted by sG(ε), is the minimum number of pursuerswhich can catch the evader with the radius of capture equal to ε. The problem isto find the ε–search number for each topological graph and given radius of captureε. The given problem is also called the ε–search problem or the Golovach problem.

The function assigning the ε–search number to each ε ≥ 0 is called the Golovachfunction. Let us notice the Golovach function is piecewise constant non-increasingright continuous function.

The rest of this article deals with the problem mentioned above for the case oftrees.

10 Tatiana V. Abramovskaya, Nikolai N. Petrov

2.1. Some properties of the Golovach function for trees

Let us remind that the program of the team of pursuers is the collection Π ofthe trajectories {x1(t), . . . , xk(t), t ∈ [0, T ]}. The program is winning if for everytrajectory y of the evader defined on [0, T ] there are t ∈ [0, T ] and i ∈ 1, k such thatρ(xi(t), y(t)) ≤ ε.

The minimum number of pursuers required for zero–radius capture on G isdenoted by s(G).

Given a positive integer k ≤ s(G), let εG(k) denote the minimum capture radiusfor which k pursuers surely catch the evader on G (it exists in virtue of the rightcontinuity of the Golovach function).

If v is the vertex of tree T , a branch of T at v is a maximal subtree B of Tsubject to the condition that v be of degree 1 in B.

We say that a pursuer P is ε–close to (ε–far from) a point a of the tree at somemoment t if ρ(a, x(t)) ≤ ε (respectively, ρ(a, x(t)) > ε).

The next two lemmas and the theorem were proved in (Abramovskaya andPetrov, 2010).

Lemma 1. For any subtree T ′ of an arbitrary tree T , εT ′(k) ≤ εT (k).

Lemma 2. Let B1, B2 and B3 are distinct branches of T at a. Suppose that foreach branch Bi with i = 1, 2, 3 the following condition holds: for any program ofa team P winning in the ε–capture problem on Bi, there exists a moment of timeat which all of the pursuers are ε–far from a. Then, team P cannot successfullycomplete the ε–search on T .

For any ε > 0, let T (ε) denote the set of all trees T in which a distance betweenarbitrary vertices of degree at least 3 is not equal to 2ε.

Theorem 1. Suppose that T ∈ T (ε) and k pursuers catch an evader with captureradius ε on T . Then, the group of k + 1 pursuers can surely perform the δ–captureon T for some δ < ε.

According to the hypothesis of Theorem 1, the Golovach function for a tree Thas unit jump (or is continuous) at ε subject to the condition that T ∈ T (ε). (Notethat this condition is sufficient but is not necessary.) Thus if for each ε at which theGolovach function for tree T may have a jump it is known that T ∈ T (ε), one canconclude that the Golovach function for T has only unit jumps. Then the followingassertion holds: let a team P can catch the evader on T with a capture radius ε > 0,then the team with more number of pursuers than in P can catch the evader on Twith the capture radius less than ε.

Let us consider the following problem. Suppose that a number k of the pursuersis fixed. The problem is for each topological graph G to find the minimum radiusof capture ε ≥ 0 so that the team of k pursuers can catch the evader on G withcapture radius ε.

For the case of trees and one pursuer this problem was solved in (Abramovskaya,2010). Let T be a tree. Let Z = (a1, . . . , an) is a chain of maximal length in T ,subtrees A1, . . . , Am are branches of T at the vertices of Z subject to the conditionthat each Ai, i = 1, . . . ,m, contains only one vertex of Z. By li, i = 1, . . . ,m, wedenote the maximal length of a chain in Ai that starts at the vertex of Z.

Graph Searching Games with a Radius of Capture 11

Lemma 3. The following equality holds:

εT (1) =1

2mini∈1,m

li.

This assertion has a simple corollary.

Corollary 1. Let T be a tree, if s(T ) > 1, then εT (2) < εT (1).

Further, we study the problem of the existence of non–unit jumps of the Golovachfunction for trees. It was proved in (Golovach et al., 2000) that non–unit jumpsappear in the case of the complete graphs for which the jump may have an arbitrarilylarge height. The case of trees seems greatly simpler but has the same degeneration(the existence of the non–unit jumps) of the Golovach function.

2.2. The main results

In the rest of the present article we denote by T the tree which contains one edgeof length 3 and two edges of length 1, and one vertex of degree 3.

The tree T0 is constructed using three copies of tree T . For each such copy thependant vertex which is incident to the edge of length 3 identified with a certainvertex c0 (see Fig.1, the digits indicate edge lengths).

T

3

1

T1

T2

T0

1

3

c0

3

1

1

c1

1

1

1

3

c2

Fig. 1.

If a tree Tn−1, n ≥ 1, has been defined, let Tn be constructed as follows. Let’sconsider three disjoint copies of tree Tn−1 and a new vertex cn. Let’s connect thevertex cn with the vertex of each branch which is respective with cn−1 by edges oflength 1.

Theorem 2. For each n ≥ 0 and 0 ≤ ε < 0.5 the equality sTn(ε) = n + 3 holds.

Proof. Let’s consider an arbitrary 0 ≤ ε < 0.5 and prove the statement by induction.Let n = 0, three pursuers capture the evader on T0 by means of the following

program with zero radius of capture. P1 is standing in vertex c0 during the wholeprogram. Other two pursuers are searching on the branches of T0 at c0. Further, eachbranch of T0 at c0 coincides with T and requires at least 2 ε–far from c0 pursuers to

12 Tatiana V. Abramovskaya, Nikolai N. Petrov

succeed in ε–capture. Thus, two pursuers can’t catch the evader on T0 with captureradius ε.

The winning program on T1 for the team of four pursuers with zero radius ofcapture is as follows. P1 occupies c1 and stays there in what follows. Sequentiallyfor each branch of T1 at c1, pursuers P2, P3, P4 slide along the edge incident to c1into a vertex c′ respective with c0 in T0. While P2 stays at vertex c′, pursuers P3

and P4 are searching on the remained branches at c′. Further, three pursuers can’tcatch the evader on T1 with capture radius ε in virtue of Lemma 2, because eachbranch of T1 at c1 requires at least 3 ε–far from c1 pursuers to succeed in ε–capture.

Let n− 1 > 1, suppose that the team of n + 2 pursuers can catch the evader onTn−1 with zero radius of capture, and a certain winning program of n + 2 pursuerson Tn−1 allows that a single pursuer is motionless in the vertex cn−1 during thewhole program. Furthermore, suppose that the team of n+ 1 pursuers has failed inpointwise capturing on T .

Let’s proceed by induction from n − 1 to n. The winning program of n + 3pursuers on Tn is as follows. Pursuer P1 occupies vertex cn and stays there in whatfollows. Sequentially for each branch of Tn at cn, pursuers P2, . . . , Pn+3 slide alongthe edge incident to cn to the other endpoint of the edge, say, c′, and then, whileP2 stays at vertex c′, pursuers P3, . . . , Pn+3 are searching on the remained branchesat c′.

To finish the proof it is sufficient to show that the team of n + 2 pursuers areunable to catch the evader on Tn with capture radius ε. Indeed, by the inductionhypothesis it is necessary to put at least n + 2 pursuers on tree Tn−1 to catch theevader with capture radius ε. According to the construction of Tn, the three copiesof Tn−1 connect to vertex cn by the unit length edge. As 2ε is less than 1, theε–catching on each branch of Tn at cn requires n + 2 pursuers ε–far from cn, andLemma 2 takes effect. ��

Theorem 3. Let n ≥ 1, the Golovach function for tree Tn has the jump of height⌈n2

⌉+ 1.

Proof. First we prove that n + 2 −⌈n2

⌉pursuers can catch the evader on Tn with

capture radius 0.5. We consider separately the cases of odd and even n.Let us consider an arbitrary path in Tn from cn to the vertex incident to the edge

of length 3. Let us denote the vertices of this path so that the vertex incident tocn is denoted by cn−1, the vertex incident to ci is denoted by ci−1, i = 1, . . . , n− 1(see Fig.2).

Let n = 2l + 1, thus we deal with the team of l + 2 pursuers. Initially allpursuers are located in cn. Then sequentially for each branch of Tn at cn and foreach path from cn to the vertex incident to the edge of length 3, the pursuers moveas follows. We will explain the common behavior of the pursuers by the example ofpath (cn, cn−1, . . . , c0). First P1 slides from cn to the midpoint of edge (cn, cn−1).Then P2 slides from cn to the midpoint of edge (cn−2, cn−3), e.t.c. Pl+1 slides fromcn to the midpoint of edge (c1, c0). Thus pursuers P1, . . . , Pl+1 control the wholepath since they possess the capture radius 0.5. The branches at c0 which contain theedges of length 3 coincide with the tree T . So the single pursuer Pl+2 can check thisbranches with capture radius 0.5. Then Pl+1 slides via vertex c1 to the midpoint ofthe another edge incident to c1 and adjacent to the edge of length 3. Thus, a newpath from cn is under control of pursuers P1, . . . , Pl+1, and so on.

Graph Searching Games with a Radius of Capture 13

c0

c1

cn

cn-1 c

n-2c

2

Fig. 2.

Let n = 2l, we deal with the team of l + 2 pursuers again. Unlike the evenn case, pursuer P1 stays in cn during the whole program, P2 slides from cn tothe midpoint of edge (cn−1, cn−2). Then P3 slides from cn to the midpoint of edge(cn−3, cn−4), e.t.c. Pl+1 slides from cn to the midpoint of edge (c1, c0). The wholepath (cn, cn−1, . . . , c0) is under control of pursuers P1, . . . , Pl+1, thus the rest ofmovements is similar to the previous case.

Now, let us show that the team of n + 1 −⌈n2

⌉pursuers can’t catch the evader

on Tn with capture radius 0.5.Let us prove this statement by induction. The base is trivial: single pursuer can’t

succeed in 0.5–catching either on T0 or on T1. Let n ≥ 1, suppose that the requiredstatement holds for n − 1 so that the team of (n − 1) + 1 −

⌈n−12

⌉pursuers can’t

succeed in 0.5–catching on tree Tn−1. Consider separately the cases of odd and evenn again.

Let n = 2l, thus to succeed in 0.5–catching on Tn−1 we have to put at least(2l−

⌈2l− 1

2

⌉)+ 1 = l + 1

pursuers on it. Tree Tn has three branches at cn. By the induction hypothesis, tosucceed in 0.5–catching on each branch we need at least l + 1 pursuers. Supposethat the team of l + 1 pursuers can catch the evader on at least one branch, say, Bwithout loosing the control over vertex cn (otherwise, the statement is obvious byLemma 2). Denote the vertex adjacent with cn in B by cn−1, the length of (cn, cn−1)equals to 1, so one of the pursuers has to stay in the midpoint of edge (cn, cn−1).Three branches of B at cn−1 contain the subtrees which coincide with tree Tn−2,and by the induction hypothesis we have to put at least(

(2l− 2) + 1−⌈

2l− 2

2

⌉)+ 1 = l + 1

pursuers on each branch, but we have only l moving pursuers.Let n = 2l + 1, then(

(n− 1) + 1−⌈n− 1

2

⌉)+ 1 =

(2l + 1 +

⌈2l

2

⌉)+ 1 = l + 2

14 Tatiana V. Abramovskaya, Nikolai N. Petrov

pursuers are required to succeed in 0.5-catching on Tn−1, but

n + 1−⌈n

2

⌉= l + 1,

and the statement has been proven by Lemma 1.Thus, in virtue of Theorem 2,

εTn(k)

⎧⎪⎨⎪⎩= 0, k = n + 3,

= 0.5, k = n + 2−⌈n2

⌉, . . . , n + 2,

> 0.5, k ≤ n + 1−⌈n2

⌉that was to be proved. ��

3. The minimal trees with the degenerate Golovach function

Consider tree B in Fig.3. We prove that it is the minimal (with respect to thenumber of the edges) tree with the degenerate Golovach function. It is rather clearthat the Golovach function for B has the following form.

sB(ε) =

⎧⎪⎨⎪⎩4, 0 ≤ ε < 0.5,

2, 0.5 ≤ ε < 2.5,

1, 2.5 ≤ ε.

Let us prove only the fact of the jump of height 2 at point 0.5.

Fig. 3.

The winning program on B for two pursuers with capture radius 0.5 looks asfollows. Pursuer P1 occupies vertex b1, and P2 clears two branches of B at b1 whichcoincide with tree T (see Fig.1). Then P1 moves to the midpoint of the edge ofunit length incident to c1. After that P1 moves to the midpoint of edge (a, b2), andP2 clears three branches of B at b2 which coincide with tree T . Next, P1 moves tothe midpoint of the edge of unit length incident to c2, then to the vertex b3, and

Graph Searching Games with a Radius of Capture 15

P2 clears the branches at b3 which match up with tree T . After that, the searchprocedure ends.

Suppose 0 < ε′ < 0.5, then three pursuers can’t catch the evader on B withcapture radius ε. Indeed, in virtue of Theorem 2, the three pursuers are necessaryto succeed in capturing on T0 with capture radius ε′.

Consider a tree T , a ∈ T , and δ > 0, let Nδ(a) = {x ∈ T |ρ(a, x) ≤ 2δ} — a setof all 2δ–close to a points of T .

Then trees K1 and K3 (which contain vertices b1 and b3 respectively) obtainedby the closure of set B\N0.5(a) have form T0. Further, the subtree K2 obtained byremoval edge (a, b2) of the branch of B at a which contains vertex b2 has form T0,too. It is clear now that we have to put at least three ε′–far from a pursuers on eachsubtree Ki, i ∈ 1, n to success in ε′–catching on Ki. According to the hypothesis ofLemma 2, three pursuers can’n catch the evader on B with capture radius less than0.5.

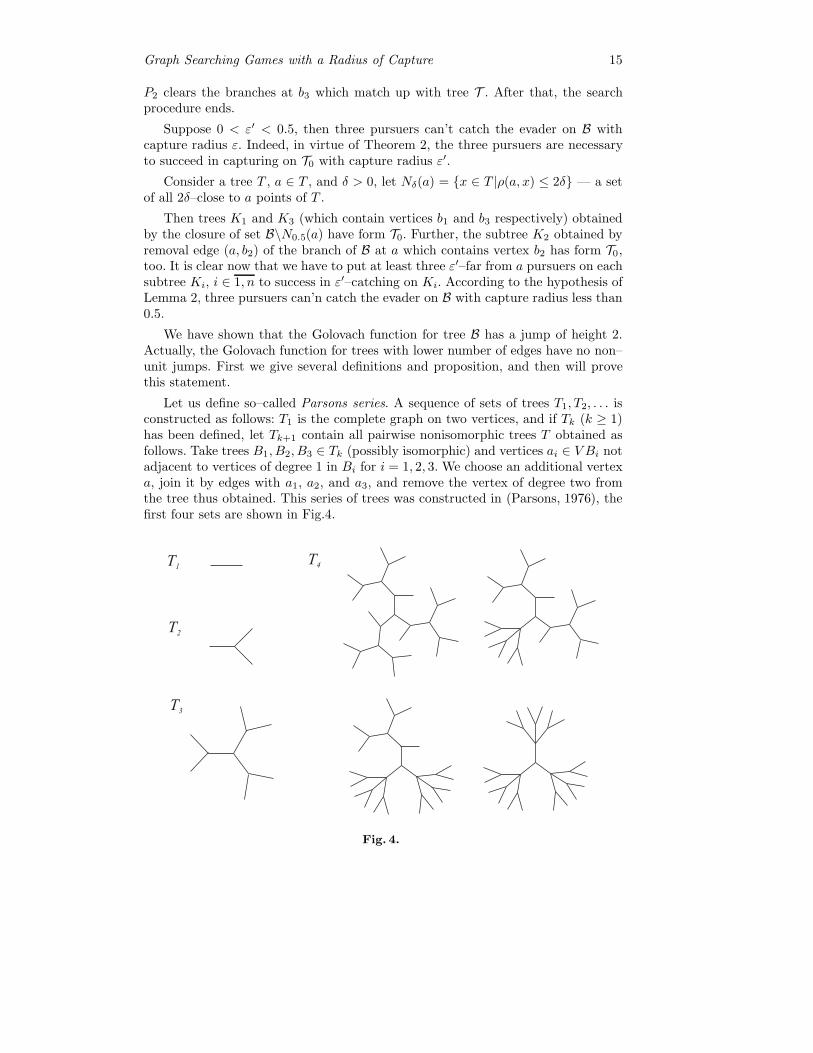

We have shown that the Golovach function for tree B has a jump of height 2.Actually, the Golovach function for trees with lower number of edges have no non–unit jumps. First we give several definitions and proposition, and then will provethis statement.

Let us define so–called Parsons series. A sequence of sets of trees T1, T2, . . . isconstructed as follows: T1 is the complete graph on two vertices, and if Tk (k ≥ 1)has been defined, let Tk+1 contain all pairwise nonisomorphic trees T obtained asfollows. Take trees B1, B2, B3 ∈ Tk (possibly isomorphic) and vertices ai ∈ V Bi notadjacent to vertices of degree 1 in Bi for i = 1, 2, 3. We choose an additional vertexa, join it by edges with a1, a2, and a3, and remove the vertex of degree two fromthe tree thus obtained. This series of trees was constructed in (Parsons, 1976), thefirst four sets are shown in Fig.4.

Fig. 4.

16 Tatiana V. Abramovskaya, Nikolai N. Petrov

The contraction of an edge (a, b) in a graph G is the procedure for obtaininga new graph G′ from graph G. Vertices a and b and edge (a, b) are removed, anadditional vertex c is inserted so that the edges incident to c in graph G′ eachcorrespond to an edge incident to either a or b except edge (a, b).

We say that a graph H is contained in a graph G if G has a subgraph G′ suchthat either this subgraph is isomorphic to H or a graph isomorphic to H can beobtained from G′ by contracting some of its edges. A tree T is called a minimal treewith search number k if s(T ) = k and s(T ′) < k for any tree T ′ not isomorphic toT and contained in T .

As was proven in (Golovach, 1992) the Parsons series represent the minimal treeswith the given search number.

Proposition 1. For a tree T , s(T ) = k if and only if there exists a T ′ ∈ Tkcontained in T and any T ′′ ∈ Tk+1 is not contained in T .

We are ready to prove the main result of this section.

Theorem 4. If a tree T has at most 27 edges, then the Golovach function for Thas only unit jumps.

Proof. If s(T ) = 1, then the Golovach function for tree T is constant. If s(T ) = 2,then, by definition, εT (1) > 0, whereas εT (2) = 0. It follows that the Golovachfunction has one unit jump. If s(T ) = 3, then εT (3) = 0, εT (2) > εT (3), andεT (1) > 0. By Corollary 1, εT (2) < εT (1). Thus, 0 = εT (3) < εT (2) < εT (1).

There is the only tree, say, T 14 from the set T4 with 27 edges, thus if s(T ) = 4

then T is isomorphic to T 14 . As above, the following inequalities are obvious:

εT (4) = 0, εT (4) < εT (3), εT (2) < εT (1), εT (1) > 0.

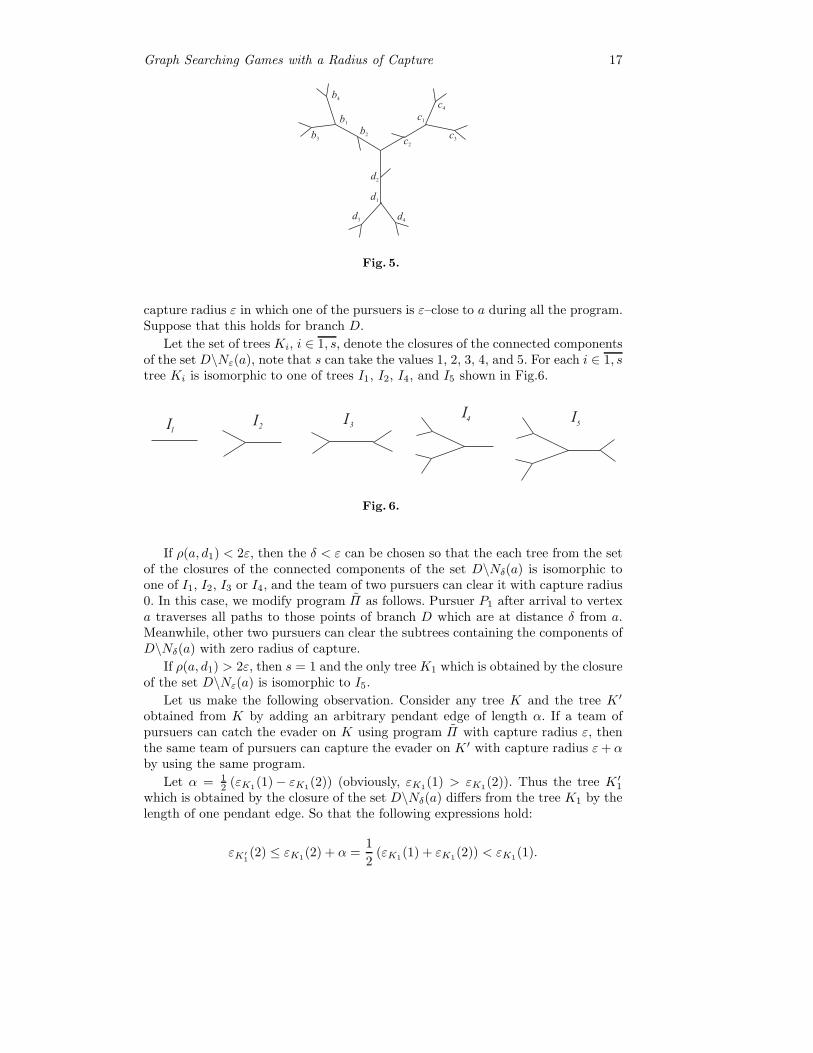

Now we have to check the jump at the point εT (2) is unit.We denote the vertices of tree T as in Fig.5. Let B, C, and D denote the branches

of T at a and containing the vertices b1, c1, and d1, respectively. By Lemma 1, theinequality

εT (2) ≥ max {εB(2), εC(2), εD(2)} (1)

holds. Letε := max {εB(2), εC(2), εD(2)} .

Suppose that the inequality (1) is strict, then we can instantly construct the winningprogram for the team of tree pursuers with capture radius ε: one pursuer occupiesvertex a, and other two pursuers check branches B, C, and D.

Suppose that the inequality (1) is an equality. If the numbers εB(2), εC(2), εD(2)are different, say, εB(2) ≥ εC(2) > εD(2), then we can again specify a program Πon T for three pursuers with capture radius εD(2). This program looks as follows.Pursuer P1 occupies vertex b1, and other two pursuers check the branches at b1 andcontaining b3 and b4 (two pursuers can clear them with zero capture radius). ThenP1 slides to vertex b2, and P2 clears the pendant edge incident to b2. After that, P1

moves to a, and other two pursuers clear tree D. Then P1 moves to c2, P2 clearsthe pendant edge incident to c2, P1 moves to c1, and other two pursuers clear thebranches at c1 which containing c3 and c4. After this step, the program ends.

Consider the case εT (2) = εB(2) = εC(2) = εD(2) = ε. By Lemma 2, for atleast one of branches B, C, D there exists a winning program for two pursuers with

Graph Searching Games with a Radius of Capture 17

c1

c2

c3

c4

b1

b2b

3

b4

d1

d4

d3

d2

Fig. 5.

capture radius ε in which one of the pursuers is ε–close to a during all the program.Suppose that this holds for branch D.

Let the set of trees Ki, i ∈ 1, s, denote the closures of the connected componentsof the set D\Nε(a), note that s can take the values 1, 2, 3, 4, and 5. For each i ∈ 1, stree Ki is isomorphic to one of trees I1, I2, I4, and I5 shown in Fig.6.

I1

2 34I I

I I5

Fig. 6.

If ρ(a, d1) < 2ε, then the δ < ε can be chosen so that the each tree from the setof the closures of the connected components of the set D\Nδ(a) is isomorphic toone of I1, I2, I3 or I4, and the team of two pursuers can clear it with capture radius0. In this case, we modify program Π as follows. Pursuer P1 after arrival to vertexa traverses all paths to those points of branch D which are at distance δ from a.Meanwhile, other two pursuers can clear the subtrees containing the components ofD\Nδ(a) with zero radius of capture.

If ρ(a, d1) > 2ε, then s = 1 and the only tree K1 which is obtained by the closureof the set D\Nε(a) is isomorphic to I5.

Let us make the following observation. Consider any tree K and the tree K ′

obtained from K by adding an arbitrary pendant edge of length α. If a team ofpursuers can catch the evader on K using program Π with capture radius ε, thenthe same team of pursuers can capture the evader on K ′ with capture radius ε + αby using the same program.

Let α = 12 (εK1(1)− εK1(2)) (obviously, εK1(1) > εK1(2)). Thus the tree K ′

1

which is obtained by the closure of the set D\Nδ(a) differs from the tree K1 by thelength of one pendant edge. So that the following expressions hold:

εK′1(2) ≤ εK1(2) + α =

1

2(εK1(1) + εK1(2)) < εK1(1).

18 Tatiana V. Abramovskaya, Nikolai N. Petrov

As was mentioned, there exists a winning program for the team of two pursuers withcapture radius ε on D such that one of the pursuers is ε–close to a during the wholeprogram, which means that εK1(1) ≤ ε. Let us modify program Π again. PursuerP1 after arrival to vertex a moves toward vertex d1 for a distance δ = ε− 1

2α. Othertwo pursuers are able to clear tree K ′

1 with capture radius εK′1(2) < ε. The rest of

the program repeats Π .If ρ(a, d1) = 2ε, then s = 2, let δ = ε

2 . In this case pursuer P1 after arrival to thevertex a passes distant δ toward the vertex d1. Pursuers P2 and P3 act as follows: P2

occupies d3 and P3 clears the pendant edges incident to d3; then P2 and P3 occupyd4, P3 goes to vertex d1, passes distance δ from d1 along the edge (a, d1), returns tod1, clears the pendant edge incident to d1, and returns to d4; next, P2 and P3 moveto d5, and at the final step, P3 clears the pendant edge incident to d5. Program Πthus modified is winning for three pursuers on T with capture radius δ.

If s(T ) ≥ 5, then T contains a tree from T5, while the minimum number of edgesfor a tree from the set T5 is 81. ��

References

Abramovskaya, T. V. (2010). Nontrivial discontinuities of the Golovach functions for trees.Vestnik St. Petersburg Univ. Math., 43(3), 123-130.

Abramovskaya, T. V. and N. N. Petrov (2010). On some problems of guaranteed search ongraphs. Vestnik St. Petersburg Univ. Math., 43(2), 68-73.

Breisch, R. (1967). An intuitive approach to speleotopology. Southwestern Cavers, VI, 72-78.

Golovach, P. A. (1989). Equivalence of two formalizations of a search problem on a graph.Vestnik Leningrad Univ. Math., 22(1), 13-19.

Golovach, P. A. (1990). An extremal search problem on graphs. Vestnik Leningrad Univ.Math., 23(3), 19-25.

Golovach, P. A. (1992). Minimal trees of a given search number. Cybernetics and SystemsAnalysis, 28(4), 509–513.

Golovach, P. A., N. N. Petrov and F. V. Fomin (2000). Search in graphs. Proc. Steklov Inst.Math., 1, S90-S103.

Fomin, F. V. and D. M. Thilikos (2008). An annotated bibliography on guaranteed graphsearching. Theoret. Comp. Science, 399(3), 236-245.

Parsons, T. D. (1976). Pursuit–evasion in a graph. In: Theory and Applications of Graphs(Alavi, Y. and D. R. Lick, eds), Vol. 642, pp. 426-441. Springer: Berlin.

Petrov, N. N. (1982) A problem of pursuit in the absence of information on the pursued.Differ. Uravn., 18(8), 1345–1352 (in Russian).

Non-Cooperative Games with Chained Confirmed Proposals�

G. Attanasi1, A. Garcıa-Gallego2, N. Georgantzıs3 and A. Montesano4

1 LERNA, Toulouse School of Economics2 GLOBE, U. of Granada & LEE, U. Jaume I of Castellon

3 GLOBE, U. of Granada & LEE, U. Jaume I of Castellon & BELIS, U. of Istambul4 Bocconi University, Milan (Italy)

Abstract. We propose a bargaining process with alternating proposals asa way of solving non-cooperative games, giving rise to Pareto efficient agree-ments which will, in general, differ from the Nash equilibrium of the originalgames.

Keywords: Bargaining; Confirmed Proposals; Confirmed Agreement.

JEL classification: C72; C73; C78.

1. Introduction

Since the seminal contributions by Nash (1950, 1953), bargaining models play acentral role in the analysis of situations in which economic agents try to reach anagreement on the split of a certain asset. A plethora of approaches has resulted in avariety of bargaining mechanisms1 keeping fixed the objective of splitting the pie. Ina parallel and mostly independent effort, non-cooperative game theory undertookthe task of determining the actions of individual agents in interactive strategicsituations. While the efficiency of outcomes has been a central issue in both gametheoretic paradigms2, the role of bargaining as a determinant of individual actionsin non-cooperative games has not been systematically explored.

In this paper, we illustrate the consequences of applying alternating proposalprotocols as a way of solving non-cooperative games. From a technical point of view,the basic difference between our framework and that of bargaining over the split of apie is that, in ours, two agents bargain about which strategy profile they will play in anon-cooperative game. Apart from the obvious departure from Rubinstein’s (1982)model in that the set of possible agreements is finite,3 in our setup a confirmedagreement between bargaining agents concerns the pair of strategies that will beactually played in the original non-cooperative game. This fact increases by one thedegrees of freedom and, thus, the dimension of the outcome space, allowing the use

� G. Attanasi gratefully acknowledges financial support by the Chair “Georges Meyer”in Mathematical Economics at Jean-Jacques Laffont Foundation (TSE) and theFrench National Research Agency (ANR) through the project on “Fair Environmen-tal Policies”. N. Georgantzıs and A. Garcıa-Gallego acknowledge financial supportby Bancaixa (P1 1B2007-14) and the Spanish Ministry of Science and Innovation(SEJ2008/04636/ECON). N. Georgantzıs gratefully acknowledges financial support bythe Junta de Andalucıa (P07-SEJ-03155) and hospitality at LEM of University Paris II.

1 While an exhaustive list of the relevant references is beyond the scope of this paper, itis worth mentioning Harsanyi (1956, 1962), Sutton (1986) and Binmore (1987).

2 Relevant references are Harsanyi (1961), Friedman (1971), Smale (1980), and Cubittand Sugden (1994).

3 For a formal treatment of this issue, see the insightful analysis by Muthoo (1991).

20 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

of bargaining with alternating proposals as a method of solving non-cooperativegames.

Assume that two players bargain over the strategy profile to play, given thateach player knows the opponent’s set of possible strategies. Then, there is a non-cooperative game whose execution leads to the two players’ final payoffs and asupergame whose actions in each bargaining period are proposals of strategies forthe original non-cooperative game. Games with confirmed proposals are interac-tive strategic situations in which a player, in order to give official acceptance of acontract, must confirm his/her proposed strategy combined with the strategy cho-sen by his/her opponent.4 Here we focus on non-cooperative games with completeinformation and finite strategy spaces. The bargaining supergame built on themis an infinite horizon game with perfect information. We show that the equilib-rium outcome of the supergame can be unique even though each player’s strategyspace in the supergame and its number of stages are infinite. We call equilibriumconfirmed agreement the corresponding equilibrium contract between players in thesupergame, leading to a strategy profile to be played in the original non-cooperativegame.

2. The Bargaining Supergame

Throughout the paper, we consider only two-players non-cooperative games; thetwo players alternate proposals in the bargaining supergame. The supergame endswhen a player confirms the proposal he/she made the previous stage in which he/shewas active. In modelling the supergame, we focus on a specific family of gameswith confirmed proposals, those with chained proposals. That is, in the case of noconfirmation by one player, the non confirmed strategy profile is taken as the newstarting point for the subsequent negotiation. Except for the selection of the firstmover at the beginning of the supergame, the rules of the game are symmetric.

Let us denote by Sh the finite strategy space for player h (with h = i, j) in theoriginal non-cooperative game. The (super-)game with confirmed proposals is builtsuch that the set of possible proposals of player h in the supergame coincides withthe set of his/her strategies Sh in the original game. The set of possible agreementsof the game with confirmed proposals coincides with the set of outcomes of theoriginal game, i.e. the product set S i × Sj contains all possible agreements of thegame with confirmed proposals built on the original game.

Denote by sth the strategy proposed by player h in stage t of the supergame, witht = 1, 2, ...,+∞. Suppose that player i (“she”) starts the supergame with player j(“he”).

The sequence of alternating proposals is as follows:Stage 1. Player i proposes a certain strategy s1i ∈ Si to player j. Player i would

actually play s1i if (and only if) she would confirm this strategy after the counter-proposal of player j.

Stage 2. Player j proposes strategy s2j ∈ Sj to player i. This strategy would

actually be played if (and only if) either i will confirm her previous strategy s1i orj will confirm his proposal s2j after the counterproposal of player i.

4 The original non-cooperative game can be a game with perfect or imperfect informa-tion and/or with complete or incomplete information. When information is incomplete,players can exploit the bargaining process to extract information on their opponent’stype through their proposals.

Non-Cooperative Games with Chained Confirmed Proposals 21

Stage 3. Player i chooses whether or not to confirm her previous strategy s1i . Ifshe confirms s1i , i.e. s3i = s1i , then the bargaining process ends, through the sequence(s1i , s

2j , s

1i ), with the confirmed agreement (s1i , s

2j) and the two players receive the

payoffs corresponding to the strategy profile (s1i , s2j) in the original game. If she

does not confirm, i.e. she proposes a new strategy s3i = s1i , the bargaining processcontinues with s2j being player j’s proposal and s3i being player i’s counterproposalto j’s proposal.

Stage 4. Player j chooses whether or not to confirm his previous strategy s2j . If

he confirms s2j , i.e. s4j = s2j , then the bargaining process ends, through the sequence

(s2j , s3i , s

2j), with the confirmed agreement (s2j , s

3i ) and the two players receive the

payoffs corresponding to the strategy profile (s3i , s2j) in the original game. If he

does not confirm, i.e. he proposes a new strategy s4j = s2j , the bargaining process

continues with s3i being player i’s proposal and s4j being player j’s counterproposalto i’s proposal.

And so on and so forth.If no strategy profile is ever confirmed by either player, then the outcome is

the disagreement event Ω. Define with f(st−2h , st−1

−h ) the outcome of the game with

confirmed proposals in case the agreement (st−2h , st−1

−h ) would be confirmed in staget, with t = 3, ...,+∞. We assume that each player h’s preference relation �h satisfiesthe following conditions:5

(a) Disagreement is not better than any agreement :Ω �h f(st−2

h ,st−1−h ) for all (st−2

h , st−1−h ) ∈ Sh × S−h and for all t = 3, ...,+∞.

(b) Patience, i.e. the time of the agreement is irrelevant: if st−2h = st

′−2h and st−1

−h =

st′−1−h , then f(st−2

h , st−1−h )∼hf(st

′−2h , st

′−1−h ) for all t = t′, with t, t′ = 3, ...,+∞.

(c) Stationarity, i.e. the preference between two agreements does not depend on

time: if st−2h = st

′−2h , st−1

−h = st′−1−h , st−2

h = st′−2h and st−1

−h = st′−1−h , then

f(st−2h , st−1

−h ) �h f(st−2h , st−1

−h ) if and only if f(st′−2h , st

′−1−h ) �h f(st

′−2h , st

′−1−h ),

for all t = t′, with t, t′ = 3, ...,+∞.

We refer to the extensive (super-)game with perfect information thus defined asthe game with chained confirmed proposals (henceforth GCCP).

In the next section, we analyze the GCCP version of some well-known inter-active strategic situations, extensively studied both in the theoretical and in theexperimental literature. First, we analyze two examples in which the original gameis a 2x2 static game. Then, by maintaining the assumption of two players only, weconcentrate on three cases where the original game is a two-stage dynamic gamewith perfect information.

In each of the GCCP discussed in the paper, we basically look for the set of sub-game perfect equilibrium outcomes (equilibrium confirmed agreements). Now, thebackward induction solution procedure is well-defined for all generic finite gameswith perfect information. Games with confirmed proposals are games with perfectinformation if the non-cooperative game on which they rely is with perfect infor-mation (as in the cases we analyze here). However, they are by construction neitherfinite nor generic, given that different terminal histories can yield the same payoff

5 Conditions (a) and (c) characterize also Rubinstein (1982), while in Rubinstein’s modeltime is valuable and a discount factor is introduced accordingly.

22 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

vector. In fact, the same agreement can be obtained through different combinationsof proposals and counterproposals. Nonetheless, the backward induction procedurecan be easily applied to some non-generic games of perfect information, specificallyto those with no-relevant ties.6 Games with confirmed proposals do belong to thiscategory, if the non-cooperative game on which they rely is static and with no rel-evant ties (as in the two examples in section 3.1). If the original game is dynamic(as in the three examples in section 3.2), the fact that it has no relevant ties isnot enough: given that the payoff function of the game with confirmed proposals isdefined over the strategic form of this game, at least one player 7 each time wherehe/she active, he/she will have at his/her disposal (at least) two proposals (corre-sponding to payoff-equivalent strategies in the original game) leading to (at least)two payoff-equivalent confirmed agreements.

In all the games with confirmed proposals analyzed in the paper, we obtain theequilibrium outcome(s) through iterated weak dominance, that in generic gamesof perfect information yields the backward induction outcome. In section 3.1 weanalyze the GCCP version of the Prisoner’s Dilemma and of the Battle of Sexes.In section 3.2 we focus on the Trust Game, the Entry Game and the UltimatumGame. Here we show that iterated weak dominance yields the backward inductionoutcome also for the GCCP built on these specific dynamic games with no relevantties.

3. Confirmed Agreements in Standard Two-Player Games

3.1. Bargaining over Static Games

Consider the GCCP version of the Prisoner ’s Dilemma (PD). The original gameis a standard static PD, and the bargaining supergame built on it is an infinitehorizon game with perfect and complete information. The sets of players’ feasibleproposals in the GCCP coincide with their sets of actions in the original game: Si =Sj = {Cooperate,Defect}, henceforth {C,D} . Figure 1, with a > c > d > z showsthe simultaneous-move original game and all possible agreements of the bargainingsupergame with chained confirmed proposals built on it.

Fig. 1. Payoff matrix of the PD game

6 A game with perfect information has no relevant ties if, for every pair of distinct terminalhistories, the player who is decisive for one vs the other (i.e. the player who is activeat the last common predecessor of the two terminal histories) is not indifferent betweenthem.

7 This applies to all players having the possibility to observe their opponent’s action inthe constituent game. Only a first mover who is active once does not belong to thiscategory.

Non-Cooperative Games with Chained Confirmed Proposals 23

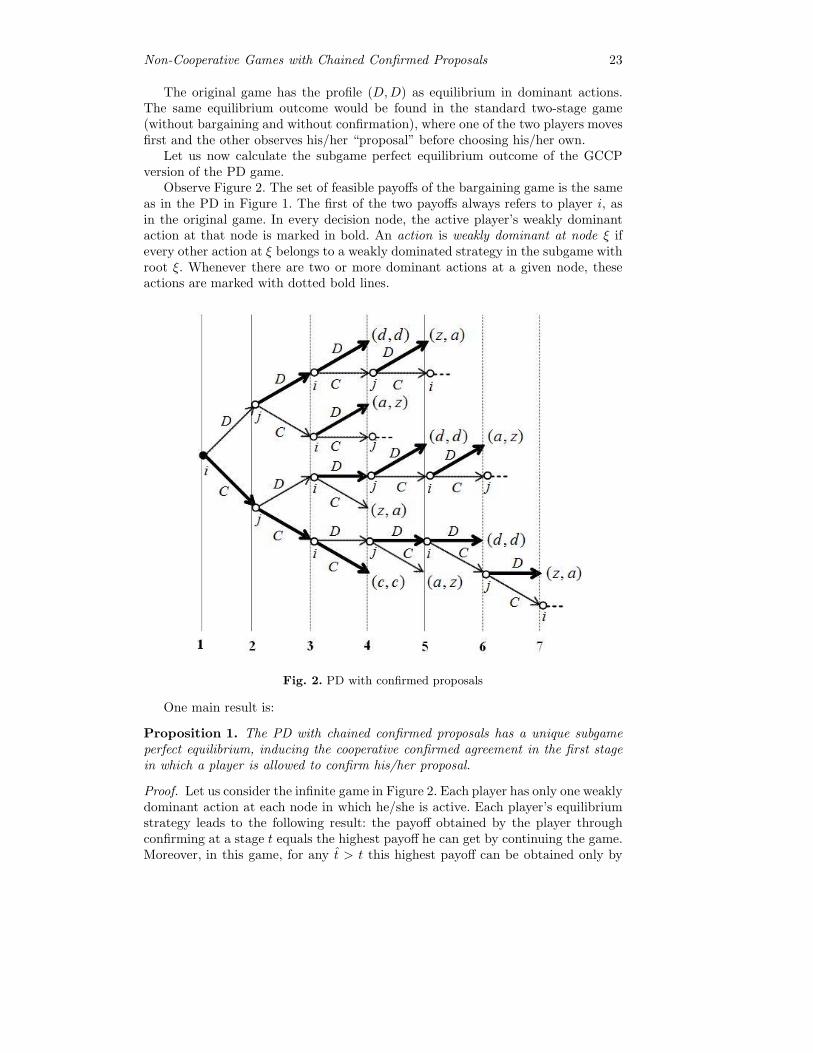

The original game has the profile (D,D) as equilibrium in dominant actions.The same equilibrium outcome would be found in the standard two-stage game(without bargaining and without confirmation), where one of the two players movesfirst and the other observes his/her “proposal” before choosing his/her own.

Let us now calculate the subgame perfect equilibrium outcome of the GCCPversion of the PD game.

Observe Figure 2. The set of feasible payoffs of the bargaining game is the sameas in the PD in Figure 1. The first of the two payoffs always refers to player i, asin the original game. In every decision node, the active player’s weakly dominantaction at that node is marked in bold. An action is weakly dominant at node ξ ifevery other action at ξ belongs to a weakly dominated strategy in the subgame withroot ξ. Whenever there are two or more dominant actions at a given node, theseactions are marked with dotted bold lines.

Fig. 2. PD with confirmed proposals

One main result is:

Proposition 1. The PD with chained confirmed proposals has a unique subgameperfect equilibrium, inducing the cooperative confirmed agreement in the first stagein which a player is allowed to confirm his/her proposal.

Proof. Let us consider the infinite game in Figure 2. Each player has only one weaklydominant action at each node in which he/she is active. Each player’s equilibriumstrategy leads to the following result: the payoff obtained by the player throughconfirming at a stage t equals the highest payoff he can get by continuing the game.Moreover, in this game, for any t > t this highest payoff can be obtained only by

24 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

confirming the same agreement confirmed at t. The subgame perfect equilibriumis found through iterated weakly dominance in three steps. Observe that in Figure2 (first 7 stages of the game) there are four decision nodes where a player canconfirm the agreement yielding him/her a, his/her highest payoff possible. At staget=4, after the non-terminal history (D,D,C), player j can get a by choosing D,hence confirming his most preferred agreement. If, instead of confirming, playerj chooses to continue the game, he can get, in any subgame in the continuationgame, at most a payoff of a, by confirming the same agreement he could alreadyconfirm at stage t=4. Therefore, for player j confirming (D,C) at stage t=4 weaklydominates continuing the game. The same holds for player i at stage t=3, afterhistory (D,C), and at stage t=5 after history (C,D,D,C); and for player j at staget=6 after history (C,C,D,D,C). Therefore, at the first step the action prescribingnot to confirm the favourable asymmetric agreement is eliminated at each node inwhich it is available. Given that, in order to prevent the opponent from confirminghis/her favorable asymmetric agreement, the agreement (D,D) should be confirmedwhenever possible. Therefore, it is weakly dominant to propose D in each stage twhen at least one of the two players has proposed D in at least a t < t and topropose C otherwise. By eliminating all other actions at the second step, we areleft with the two terminal histories (C,C,C) and (D,D,D). At the third step, theaction D in t=1 is eliminated. ��

Thus, in the unique subgame perfect equilibrium of the game, player i starts byproposing strategy C to player j, who counter-proposes strategy C. Then, player iconfirms her strategy C, such that the original game strategy profile (C,C) is the(unique) confirmed agreement. This is reached already in stage t = 3, after the firstinteraction among players takes place.

Consider now the GCCP version of the Battle of Sexes (BS). The set of players’feasible proposals, which coincides with the set of players’ actions in the originalgame, is Si = Sj = {Opera, Football}, henceforth {O,F} . Figure 3 shows theone-shot original game and, also, all possible agreements of the GCCP built on it.Parameters are such that a > b > max {c1, c2, c3, c4}.

Fig. 3. Payoff matrix of the BS game

The original game has two Nash equilibria in pure strategies: (O,O) and (F, F ).In the standard two-stage dynamic version of the game, the player moving first8

has an advantage. Consider now the BS with confirmed proposals for the case inwhich player i is the first mover (Figure 4). Observe that, surprisingly, there isa first-mover disadvantage: the unique equilibrium confirmed agreement coincideswith the Nash equilibrium of the original game which is preferred by player j.

8 In fact, this is equivalent to a commitment.

Non-Cooperative Games with Chained Confirmed Proposals 25

Fig. 4. BS with confirmed proposals

Proposition 2. The BS with chained confirmed proposals has a unique equilibriumconfirmed agreement, involving players’ coordination on the constituent game equi-librium favourable to the second mover.

Proof. The game ends with the confirmation of the strategy profile (F , F ), whateveris player i’s initial proposal. In each of the two subgame perfect equilibria in purestrategies, j replies to i’s first proposal by indicating the opposite proposal (F if Oand O if F ). By doing that, j obliges player i to propose the same action alreadyproposed by him (otherwise, i would confirm her initial action and would get c1 < bor c3 < b). If this action is F , then j confirms F and gets his highest payoff possible.If instead this action is O, then j proposes F and i finds convenient to propose F,since, otherwise, she would get c1 < b; then j confirms F and gets his highest payoffpossible. Therefore, in the first stage player i is indifferent between her two possibleproposals. ��

Thus, in the BS with chained confirmed proposals the second mover is able toconfirm the coordinating equilibrium outcome of the original game more favorableto him.

3.2. Bargaining over Dynamic Games

Let us now focus on the case where the bargaining supergame concerns a dynamicoriginal game. Here the confirmed proposals structure is built on the strategic formof the original game. Therefore, a player’s set of possible proposals in the GCCPcorresponds to his/her set of strategies in the original game.

Let us begin by considering as original game the Trust Game (TG). In theoriginal game, player i (the truster) chooses whether to Trust (T ) or to Not trust(N) player j (the trustee). In case i trusts j, total profits are higher. In that case, jwould decide whether to Grab (G) or to Share (S) the higher profits. The strategicform of the game in Figure 5, where x :=“x if T ”, with x = G,S, and ci > di >

26 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

z ≥ 0, a > cj > dj > 0, a + z = ci + cj , represents all possible agreements of theGCCP built on this dynamic game.9

Fig. 5. Payoff matrix of the TG

In the unique subgame perfect equilibrium of the original game, i does not trustj, while the latter would choose to grab if i had trusted him in the first place.

Given players’ role asymmetries in the original game, the resulting GCCP in-volves two possible versions: one in which the truster in the original game (i) is thefirst mover of the bargaining sequence, and one in which the trustee in the originalgame (j) is the first mover of the bargaining sequence. In the latter case, j beginsthe GCCP by announcing his intention to grab or to share the higher total profitsin case i would trust him. The two versions of the TG with chained confirmed pro-posals are represented in Figure 6.a and 6.b respectively. Recall that the first of thetwo payoffs always refers to player i, as in the original game.

Fig. 6. TG with confirmed proposals, with i (Figure 6.a) or j (Figure 6.b) as first mover

For the two GCCP in Figure 6, the following result holds.

9 Notice that, in order for j to confirm an agreement, he has to re-propose the samestrategy in two subsequent stages in which he is active. According to this rule, forexample (S,N,G) is not a terminal history of the GCCP, even though both strategyprofiles (N,S) and (N,G) induce the same terminal history in the original game.

Non-Cooperative Games with Chained Confirmed Proposals 27

Proposition 3. The TG with chained confirmed proposals has a unique equilibriumconfirmed agreement, the cooperative one. This agreement is immediately confirmedby the first mover in the GCCP.

Proof. We impose that when a player is active at a decision node, he/she plays aweakly dominant action at that node. Because of that, in both GCCP in Figure6, at each stage t each player would: (1) confirm his/her most preferred agreementif he/she is given the possibility in that stage; (2) confirm agreements other thanhis/her most preferred if: (2.1) in some stage t > t (with t < ∞) of the equilib-rium continuation path, his/her opponent would confirm an agreement not betterfor him/her than the one he/she could confirm in t; (2.2) by not confirming in t,neither (1) nor (2.1) applies to any stage t+k, with k = 1, ...,+∞, and the bestagreement he/she could confirm when he/she is active in the continuation subgameis payoff-equivalent to the one he/she could confirm in stage t. When the first moveris player i, in stage 3 she would confirm (T, S) because of (1). She would confirmalso (N,G) because of (2.1), and (N,S) because of (2.2). Instead, she would notconfirm (T,G), given that none of the above mentioned cases applies. Hence, shewould propose N after history (T,G). In stage 4, after (T,G,N), player j is in-different between confirming the agreement (N,G) and proposing S. In both casesthe payoffs are (di, dj), since, if he proposes S, in the subsequent stage, player iwould confirm (N,S) because of (2.2) (as we have previously seen after history(N,S)). Thus, the subgame perfect equilibrium path is (T, S, T ), with i confirmingthe agreement (T, S) in stage 3. When the first mover is player j, in equilibrium heconfirms the same agreement in stage 3. This follows from the fact that in stage 3 hewould confirm the agreement (T,G) because of (1), (T, S) because of (2.1) and heis indifferent between confirming or not the agreements (N,G) and (N,S) becauseof (2.2) (as we have already seen when the first mover is the player i, after history(T,G,N)). ��

Notice that, as in the example of the BS, in both versions of the TG withchained confirmed proposals, the second mover reciprocates in stage 2 the first-mover’s proposal: he/she cooperates if the first-mover’s proposal is cooperative (Sif T and T if S, respectively) and does not cooperate otherwise (G if N and N ifG, respectively).

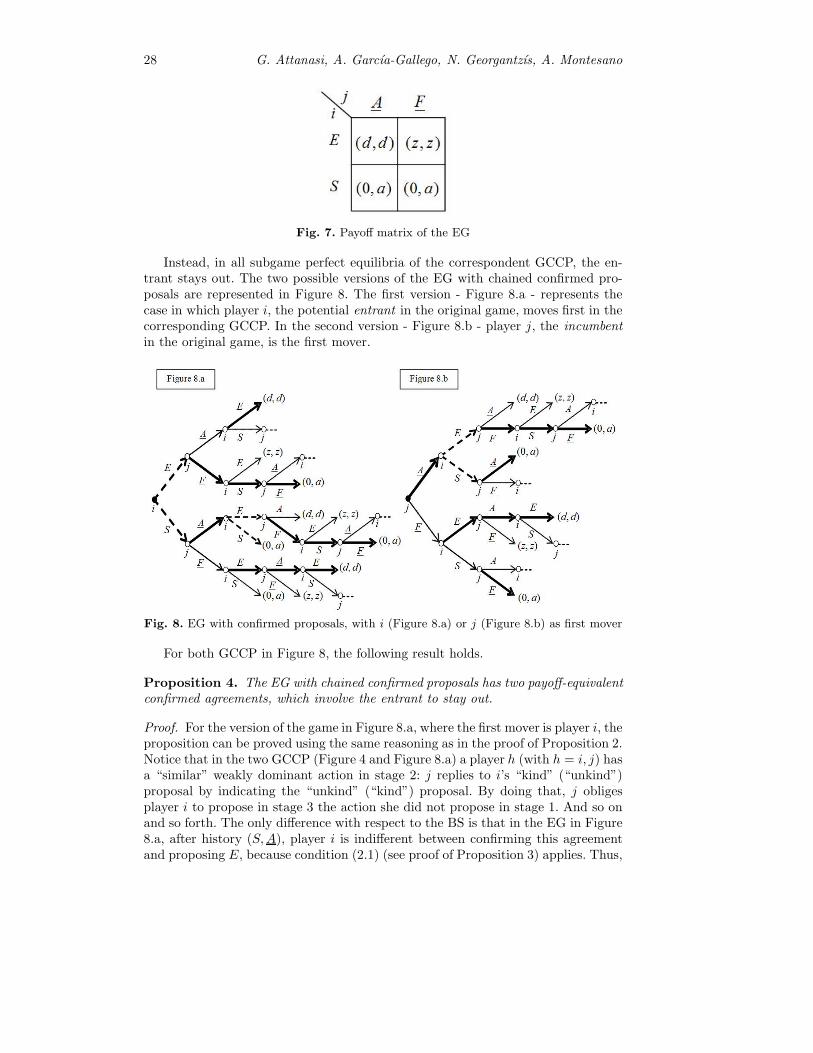

Consider now as original game the dynamic Entry Game (EG). In the originalgame i (the potential entrant) chooses whether to Enter (E) or to Stay Out (S) ofthe market, with j (the incumbent) deciding whether to Accommodate (A) or Fight(F ) if the entrant decides to enter. The strategic form of the game in Figure 7, wherex :=“x if E”, with x = A,F , and a > d > 0 > z, represents all possible agreementsof the bargaining GCCP built on this dynamic game. In the unique subgame perfectequilibrium of the original game, i’s entry takes place, with j accommodating it.

28 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

Fig. 7. Payoff matrix of the EG

Instead, in all subgame perfect equilibria of the correspondent GCCP, the en-trant stays out. The two possible versions of the EG with chained confirmed pro-posals are represented in Figure 8. The first version - Figure 8.a - represents thecase in which player i, the potential entrant in the original game, moves first in thecorresponding GCCP. In the second version - Figure 8.b - player j, the incumbentin the original game, is the first mover.

Fig. 8. EG with confirmed proposals, with i (Figure 8.a) or j (Figure 8.b) as first mover

For both GCCP in Figure 8, the following result holds.

Proposition 4. The EG with chained confirmed proposals has two payoff-equivalentconfirmed agreements, which involve the entrant to stay out.

Proof. For the version of the game in Figure 8.a, where the first mover is player i, theproposition can be proved using the same reasoning as in the proof of Proposition 2.Notice that in the two GCCP (Figure 4 and Figure 8.a) a player h (with h = i, j) hasa “similar” weakly dominant action in stage 2: j replies to i’s “kind” (“unkind”)proposal by indicating the “unkind” (“kind”) proposal. By doing that, j obligesplayer i to propose in stage 3 the action she did not propose in stage 1. And so onand so forth. The only difference with respect to the BS is that in the EG in Figure8.a, after history (S,A), player i is indifferent between confirming this agreementand proposing E, because condition (2.1) (see proof of Proposition 3) applies. Thus,

Non-Cooperative Games with Chained Confirmed Proposals 29

besides the agreement (S, F ), also (S,A) is an equilibrium agreement, equivalent inpayoff to (S, F ). More precisely, if player i starts the bargaining process, there arethree equilibrium terminal histories: (E,F , S, F ), (S,A,E, F , S, F ) and (S,A, S).When the first mover is player j (Figure 8.b), there are two equilibrium terminalhistories: (A,E, F , S, F ) and (A,S,A). This follows from the fact that: each playeralways confirms agreements leading to his/her highest payoff possible, i.e. (d, d) forplayer i and (0, a) for player j; players’ optimal behavior after history (S,A,E) inFigure 8.b is the same as after history (A,E) in Figure 8.a; after history (A), playeri is indifferent between E and S because condition (2.1) (see proof of Proposition3) applies. ��

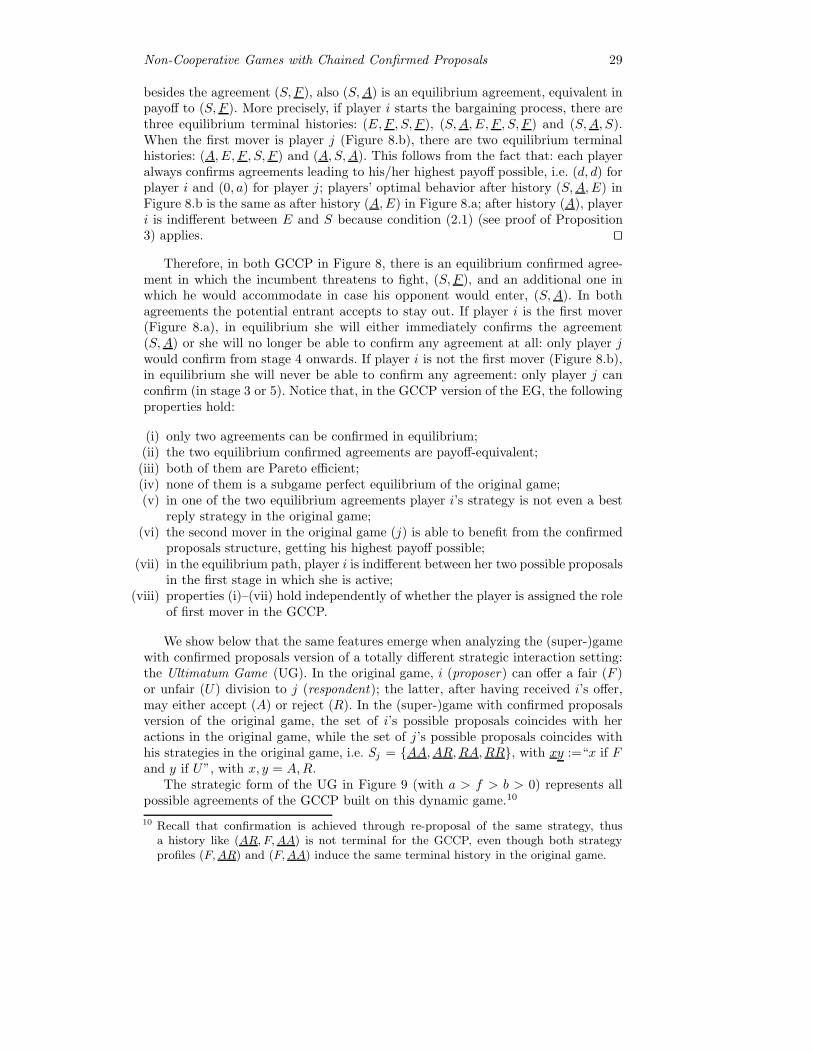

Therefore, in both GCCP in Figure 8, there is an equilibrium confirmed agree-ment in which the incumbent threatens to fight, (S, F ), and an additional one inwhich he would accommodate in case his opponent would enter, (S,A). In bothagreements the potential entrant accepts to stay out. If player i is the first mover(Figure 8.a), in equilibrium she will either immediately confirms the agreement(S,A) or she will no longer be able to confirm any agreement at all: only player jwould confirm from stage 4 onwards. If player i is not the first mover (Figure 8.b),in equilibrium she will never be able to confirm any agreement: only player j canconfirm (in stage 3 or 5). Notice that, in the GCCP version of the EG, the followingproperties hold:

(i) only two agreements can be confirmed in equilibrium;(ii) the two equilibrium confirmed agreements are payoff-equivalent;

(iii) both of them are Pareto efficient;(iv) none of them is a subgame perfect equilibrium of the original game;(v) in one of the two equilibrium agreements player i’s strategy is not even a best

reply strategy in the original game;(vi) the second mover in the original game (j) is able to benefit from the confirmed

proposals structure, getting his highest payoff possible;(vii) in the equilibrium path, player i is indifferent between her two possible proposals

in the first stage in which she is active;(viii) properties (i)–(vii) hold independently of whether the player is assigned the role

of first mover in the GCCP.

We show below that the same features emerge when analyzing the (super-)gamewith confirmed proposals version of a totally different strategic interaction setting:the Ultimatum Game (UG). In the original game, i (proposer) can offer a fair (F )or unfair (U) division to j (respondent); the latter, after having received i’s offer,may either accept (A) or reject (R). In the (super-)game with confirmed proposalsversion of the original game, the set of i’s possible proposals coincides with heractions in the original game, while the set of j’s possible proposals coincides withhis strategies in the original game, i.e. Sj = {AA,AR,RA,RR}, with xy :=“x if Fand y if U”, with x, y = A,R.

The strategic form of the UG in Figure 9 (with a > f > b > 0) represents allpossible agreements of the GCCP built on this dynamic game.10

10 Recall that confirmation is achieved through re-proposal of the same strategy, thusa history like (AR, F,AA) is not terminal for the GCCP, even though both strategyprofiles (F,AR) and (F,AA) induce the same terminal history in the original game.

30 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

Fig. 9. Payoff matrix of the UG

In the unique subgame perfect equilibrium of the original game, unfair divisiontakes place, with j accepting both i’s offers.

Figure 10 shows the two possible versions of the UG with chained confirmedproposals. Figures 10.a refers to the case in which the proposer in the original gamemoves first in the supergame. Figure 10.b shows the version with the responder inthe original game being the first mover in the supergame.

Fig. 10. UG with confirmed proposals, with i (Figure 10.a) or j (Figure 10.b) as firstmover

For both GCCP in Figure 10, the following result holds.

Proposition 5. The UG with chained confirmed proposals has an infinite numberof subgame perfect equilibria, all leading to two payoff-equivalent confirmed agree-ments, which involve the egalitarian outcome.

Proof. The proof is similar for the two versions of the GCCP. Consider the firstversion of the game, where i is the first mover (Figure 10.a). By imposing that eachplayer chooses a weakly dominant action at each node where he/she is active, playeri is never able to confirm her most preferred agreement (U,AA) or (U,RA). In fact,if she proposed an unfair offer, j would reply with a proposal not incorporating

Non-Cooperative Games with Chained Confirmed Proposals 31

the acceptance of U (AR or RR), otherwise i would confirm U in the subsequentstage. Therefore, in every subgame after i has proposed U , j would never proposeAA or RA. Then, both after each history of the type (..., stj , U,AR) with stj = ARand after each (..., stj , U,RR) with stj = RR , i would propose F , otherwise shewould confirm j’s rejection of her unfair offer, hence getting 0. Then, after each(..., stj , U,AR, F ) with stj = AR, j would propose AR, thus confirming his mostpreferred agreement (F,AR); after each (..., stj , U,RR, F ) with stj = RR, j wouldnever propose RR, because that would lead to confirm an agreement involvingthe rejection of i’s fair offer, hence getting 0. Moreover, player j is always able toavoid confirming the agreements (U,RR) and (U,AR). In fact, after each history(..., RR,U), he would propose the strategy AR, thus avoiding to confirm the zero-payoff agreement (U,RR) or to give player i the possibility to confirm (U,AA) or(U,RA) in the subsequent stage; after each history (..., AR,U), he would proposeRR, thus avoiding to confirm the zero-payoff agreement (U,AR), or to give player ithe possibility to confirm (U,AA) or (U,RA) in the subsequent stage. This explainswhy whenever an agreement is confirmed by j in a stage t > 3, this agreement is(F,AR) and each terminal history is of the type (..., U,AR, F,AR). All previousconsiderations about player j’s weakly dominant proposals in stage t conditionalon i’s possible proposals in stage t − 1 explain why player i could never obtainthe confirmation of an agreement which would impose player j to accept an unfairoffer. Therefore, whenever in a stage t > 3 she has to choose between confirmingan agreement (F,Ax), with x = A,R and entering a subgame leading to a terminalsub-history of the type (U,AR,F,AR), she is indifferent according to condition (2.2)(see proof of Proposition 3): both choices allow player i to get her second highestpayoff possible and player j to get his highest payoff possible. Moreover, given thati would always propose F in each decision node where she could confirm (U,RR),then, after every sequence of proposals (F, stj , U,RR) with stj = AA,AR,RA, someequilibrium loops could emerge, thus leading to an infinite number of equilibriumterminal histories, all ending with player j’s confirmation of the agreement (F,AR),or with player i’s confirmation of the agreement (F,Ax), with x = A,R. The onlycase in which player j can confirm, in equilibrium, an agreement different from(F,AR) is in stage 3 of the GCP (Figure 10.b), where he confirms the payoff-equivalent agreement (F,AA). ��

Therefore, in every subgame perfect equilibrium of the UG with chained con-firmed proposals, i offers a fair division to j, and j accepts. In each GCCP inFigure 10 we indicated the unique equilibrium terminal history leading to confirmthe agreement (F,AA) in stage 3, and two among the infinite possible equilibriumterminal histories leading to confirm the agreement (F,AR) in a stage t > 3. Bothkind of agreements lead to a fair division.

Quite surprisingly, the equilibrium agreements of the chained confirmed propos-als version of the UG satisfy the same features (i)–(viii) characterizing the equilibriain the EG with chained confirmed proposals. In this regard, note also the strongsimilarity between the subgame perfect equilibrium paths of TG with chained con-firmed proposals in Figure 6.a and those of the PD with chained confirmed proposalsin Figure 2. The same holds for the EG with chained confirmed proposals in Figure8.a and the BS with chained confirmed proposals in Figure 4. Finally, for the threeGCCP in Figure 4 (BS), 8.a (EG) and 10.a (UG) it is common that a first-mover

32 G. Attanasi, A. Garcıa-Gallego, N. Georgantzıs, A. Montesano

disadvantage exists, while instead the relative original games are all characterizedby a first-mover advantage.

All these results suggest that the bargaining mechanism proposed in this paperas a supergame works in the same way for original games with different strategicstructures.

4. Conclusions

Throughout the paper, we have defined games with confirmed proposals as a wayof representing bargaining over the strategies of a non-cooperative game. We haveshown the effect of this mechanism on players’ ability to coordinate on Pareto ef-ficient outcomes even in cases in which they are not equilibrium outcomes of theoriginal non-cooperative game. Our focus was on a confirmed proposal mechanismwith a chain, requiring that in the bargaining supergame each non-confirmed strat-egy profile becomes the starting point for the next negotiation round. One coulddiscuss the implications of breaking this chain on the main features of the confirmedproposal mechanism. We leave this for future research.

References

Binmore, K. (1987). Perfect equilibria in bargaining models. In: Economics of Bargaining(Binmore, K. and P. Dasgupta, eds), Cambridge University Press, Cambridge.

Cubitt, R. and R. Sugden (1994). Rationally justifiable play and the theory of non-cooperative games. Economic Journal, 104, 798-803.

Friedman, J. W. (1971). A non-cooperative equilibrium for supergames. Review of EconomicStudies, 38, 1-12.

Harsanyi, J. (1956). Approaches to the bargaining problem before and after the theory ofgames: A critical discussion of Zeuthen’s, Hicks’, and Nash’s theories. Econometrica,24, 144-157.

Harsanyi, J. (1961). On the rationality postulates underlying the theory of cooperativegames. Journal of Conflict Resolution, 5, 179-196.

Harsanyi, J. (1962). Bargaining in ignorance of the opponent’s utility function. Journal ofConflict Resolution, 6, 29-38.

Muthoo, A. (1991). A note on bargaining over a finite number of feasible agreements.Economic Theory, 1, 290-292.

Nash, J. (1950). The bargaining problem. Econometrica, 18, 155-162.Nash, J. (1953). Two-person cooperative games. Econometrica, 21, 128-140.Rubinstein, A. (1982). Perfect equilibrium in a bargaining model. Econometrica, 50, 97-

109.Smale, S. (1980). The Prisoner’s Dilemma and Dynamical Systems Associated to Non-

cooperative Games. Econometrica, 48, 1617-1634.Sutton, J. (1986). Non-cooperative bargaining theory: An introduction. Review of Economic

Studies, 53, 709-724.

The Π-strategy: Analogiesand Applications

A.A. Azamov1 and B.T. Samatov2

1 Institute of Mathematics and Informational Technologiesof Academy of Sciences of UzbekistanE-mail: [email protected]

2 Namangan State University, UzbekistanE-mail: [email protected]

Abstract. The notion of the strategy of parallel pursuit (brieflyΠ-strategy)was introduced and used to solve the quality problem in ”the game with asurvival zone” by L.A.Petrosyan. Further it was found other applications ofΠ-strategy. In the present work Π-strategy will be constructed in the caseswhen 1) a control function of Pursuer should be chosen from the space L2

and that for Evader should be chosen from L∞; 2) control functions bothof players should be chosen from the space L2; 3) a control function of Pur-suer should be chosen from intersection of spaces L2 and L∞ while that forEvader should belong to L∞.

Keywords: differential game, Pursuer, Evader, strategy, parallel pursuit,domain of attainability, survival zone

AMS classification numbers: 91A23, 49N70

1. Formulation of the problem

Consider the differential game when Pursuer P and Evader E having radius vectorsx and y correspondingly move in the space Rn. If their velocity vectors are u and vthen the game will be described by the equations:

x = u, x(0) = x0,y = v, y(0) = y0,

(1)

where x, y, u, v ∈ Rn, n > 1, x0 and y0 are initial points of x and y correspondingly.The family of all measurable functions u(·) : R+ → Rn (controls of P ) satisfying

the following condition∞∫0

|u(t)|2dt ≤ ρ2, ρ ≥ 0, (2)

is denoted by Uρ, Uρ ⊂ L2[0,∞). The family of all measurable functions u(·) :R+ → Rn satisfying the next condition

|u(t)| ≤ α almost everywhere (a.e.) t ≥ 0, (3)

is denoted by Uα, Uα ⊂ L∞[0,∞). Further the family of all measurable functionssatisfying both of conditions (2) and (3) will be denoted Uρ

α.Analogously the family of all measurable functions v(·) : R+ → Rn satisfying

∞∫0

|v(t)|2dt ≤ σ2, σ ≥ 0, (4)

34 A. A. Azamov, B. T. Samatov

is denoted by V σ, V σ ⊂ L2[0,∞) and satisfying the following condition

|v(t)| ≤ α a. e. t ≥ 0 (5)

is denoted by Vβ , Vβ ⊂ L∞[0,∞). Besides the family of all measurable functionssatisfying both of conditions (4) and (5) also will be denoted V σ

β .In the theory of Differential Games an inequality of the forms (2) and (4) is

usually called an integral constraint for control function (we will briefly say I-constraint). Analogously an inequality of the forms (3) and (5) is called a geometricconstraint (briefly G-constraint).