City of Altoona WI

296

ZOOM instructions >> Review Minutes >> Summary + Materials >>

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of City of Altoona WI

ZOOM instructions >>

Review Minutes >>

Summary + Materials >>

Summary + Materials >>

Summary + Materials >>

Summary + Materials >

Summary + Materials >>

Summary + Materials >>

Summary + Materials >>

Summary + Materials >>

ZOOM INSTRUCTION GUIDE

WEBSITE and TELEPHONE

DUE TO CORONAVIRUS COVID-19 RESIDENTS ARE ENCOURAGED TO ATTEND THE FINANCE COMMITTEE AND CITY COUNCIL MEETING VIA THE

APPLICATION, ZOOM UNTIL FURTHER NOTICE.

ZOOM MEETING INFORMATION: WEBSITE: https://zoom.us/join

CALL IN PHONE NUMBER: 1-312-626-6799

IMPORTANT INFORMATION

ZOOM can be accessed by telephone or computer. You must have a computer or mobile phone app to see the PowerPoint slides.

For those participating by computer only, you must have a microphone enabled computer to communicate verbally. Otherwise you will have to call in via the telephone as well.

MEETING ID: 857 2284 0147 Webinar Password: 824341

RETURN to Agenda >>

TO ACCESS VIA TELEPHONE:

1. Call phone number: 1-312-626-6799

2. Enter Meeting ID: 857 2284 0147

3. Enter webinar password: 824341# to confirm you are a participant and enter the meeting

4. To state a public comment, “raise hand”: *9(You will be called on in order received)

TO ACCESS VIA WEBSITE: 1. Access website at: https://zoom.us/join

2. A set of dialogue boxes will appear (as seen below)

Enter Meeting ID: 857 2284 0147

CLICK HERE

1

2

Enter meeting ID: 857 2284 0147

CLICK HERE

Enter Your Name to be displayed in Zoom meeting for public viewing

3

4 857 2284 0147

5. Enter webinar password on the next screen: 824341

CLICK HERE

5a

5b

Computer Audio

Phone Call

Call 1-312-626-6799 1-312-626-6799

Meeting ID: 857 2284 0147

Meeting Password: 824341

3. Use icon RAISE HAND to provide Public Comments. You will be unmuted andcalled upon on in the order received.

SEE WEBSITE LINKS BELOW FOR MORE TUTORIALS

https://support.zoom.us/hc/en-us/articles/201362193

https://support.zoom.us/hc/en-us

https://www.youtube.com/embed/vFhAEoCF7jg?rel=0&autoplay=1&cc_load_policy=1

Click here to PUBLIC COMMENT

6

Draft Minutes

City of Altoona, WI Council Meeting Minutes August 12, 2021 Page 1 of 4

CITY OF ALTOONA, WI

REGULAR COUNCIL MEETING MINUTES

August 12, 2021

(I) Call Meeting to Order

Mayor Brendan Pratt called the meeting to order at 6:00 p.m. The Regular Council Meeting was held in

the Council Chambers at Altoona City Hall, 1303 Lynn Avenue, Altoona, WI.

(II) Pledge of Allegiance

Mayor Pratt led the Common Council and others in attendance in the Pledge of Allegiance.

(III) Roll Call

City Clerk Cindy Bauer called the roll. Mayor Brendan Pratt, Council Members Timothy Lima,

Matthew Biren, Tim Sexton, and Susan Rowe were present. Dale Stuber was present via phone.

Also Present: City Attorney John Behling, City Engineer/Director of Public Works (CE/DPW) Dave Walter,

City Planner Joshua Clements, Finance Director Tina Nelson, and City Clerk Cindy Bauer.

Absent: Council Member Maria Guzman

City Administrator Michael Golat.

(IV) Citizen Participation Period

Motion by Biren/Lima to close the Citizen Participation Period. Motion carried.

(V) Approval of minutes.

Motion by Biren/Rowe to approve the minutes of the July 22, 2021, Regular Council Meeting. Motion

carried.

(VI) City Officers/Department Heads Report

Management Analyst Roy Atkinson updated the Council on the Smoking Cessation Project with the

Smoking Cessation Group.

CE/DPW David Walter update the Council on the Bradwood Avenue Reconstruction Project.

City Planner Clements updated the Council on the Comprehensive Plan Community Planning

Workshops.

City Committee Reports – None.

(VII) Consent Agenda –

(1) Discuss/consider approval of Resolution 8A-21, a resolution authorizing the City Engineer/Public Works

Director and/or their designee to submit an application on behalf of the City of Altoona, WI for the WI DNR

Urban Forestry Grant and/or Urban Forestry Catastrophic Storm Grant Programs.

(2) Discuss/consider amending the premise description on the “Class B” Combination Liquor and Beer

License issued to Somewhere Pub, LLC, DBA Somewhere Pub, located at 1485 Front Porch Place, to include

Storage Room A to the premise description.

Motion by Rowe/Lima to approve Consent Agenda Items 1 and 2. Motion carried.

(VIII) Unfinished Business – None.

(IX) New Business

(1) Updated PreSale Report for 2021 Financing & Refinancing by Financial Advisor Sean Lentz.

Sean Lentz, Financial Advisor for Ehlers was present to give an updated Presale Report for the 2020B

Bond Issues. The new report includes financing the 2021 Capital Projects and also adds the refinancing of debt

that results in a restructure of debt and allows for interest savings. No action is required. The sales

Return to Agenda >>

Draft Minutes

City of Altoona, WI Council Meeting Minutes August 12, 2021 Page 2 of 4

results/approval will be presented at the August 26, 2021 Council Meeting.

(IX)(2) Quarterly Tourism Report Presented by Visit Eau Claire.

As you are aware, Visit Eau Claire is Altoona’s contracted tourism promotion agency. In order to detail

tourism marketing efforts in Altoona, Visit Eau Claire will continue providing quarterly updates to the council.

Benny Anderson, Executive Director of Visit Eau Claire, was present at the meeting to discuss tourism marketing

in Altoona and gave a quarterly report on Tourism.

(IX)(3) Presentation by Eagle Scout regarding Gaga Ball Pit project in River Prairie Park and Altoona City

Park. Possible action to follow.

Management Analyst Atkinson explained that over the last several years City staff has partnered with local

Eagle Scouts to complete several projects within Altoona City Parks. Recently, Scout Isaac Holzinger contacted

the City regarding a potential project in which he would fundraise and build Gaga Ball Pits within Altoona (10th

Street) and River Prairie Parks. Staff has met with Isaac on multiple occasions to discuss/vision the project and to

determine the definite sizes of the pits within the park spaces. Isaac is proposing to complete his project by the

end of August - early September.

Eagle Scout Isaac Holzinger was in attendance to present his project to the City Council and answer any

questions they had regarding Gaga Ball Pit.

Motion by Rowe/Lima to approve construction of two Gaga Ball Pits subject to review/approval by the

Parks and Recreation Committee. Motion carried.

(IX)(4) Public hearing at 6:00 p.m. or as soon thereafter as possible regarding proposed modifications to

Altoona Municipal Code 19.52 Parking and Loading Spaces regarding residential driveway widths.

Mayor Pratt opened the public hearing at 6:35 p.m.

City Planner Josh Clements explained Ordinance 8A-21. Clements said that newer homes that are

proposed and under construction feature garages with total width of openings are approximately 30 feet. The

current ordinance permits driveways up to 30 feet in width, leaving no additional pavement beyond the width of

the opening. This creates a functional challenge for people entering or exiting the vehicles with little to no

pavement in the egress area. Adding two feet on each side of the garage creates such an area.

City Planner Clements said the current ordinance does include a provision whereby the “Zoning

Administrator may grant minor deviations from the standards under this Section wherein site constraints

reasonably necessitate flexibility (...)”. However, deviations of greater than ten percent are typically not considered

to be minor. The proposed amendment to the zoning title provides for a small adjustment to fit current functional

conditions.

Motion by Lima/Rowe to close the public hearing at 6:37 p.m. Motion carried.

(IX)(5) Discuss/consider approval of Ordinance 8A-21, an Ordinance amending Section 19.52.080 of the

Altoona Municipal Code 19.52 Parking and Loading Spaces regarding residential driveway widths.

City Planner noted that the Plan Commission voted unanimously to recommend approval on July 20th.

Motion by Rowe/Lima to approve Ordinance 8A-21, an Ordinance amending Section 19.52.080 regarding

residential driveway widths. Motion carried.

(IX)(6) Discuss/consider approval of a Retail Class “B” Beer license to sell fermented malt beverages and

a Retail “Class C” wine license to sell wine in the City of Altoona to Xavier Artisan, DBA Xavier Artisan,

Robert DeFatta, Agt, 1470 River’s Edge Trail, Altoona, WI.

City Clerk Bauer explained that the City received an Alcohol Beverage Retail License Application from

Robert DeFatta, who will be operating a Bistro under the name of Xavier Artisan, located in the River Prairie

Wellness Center, 1470 River’s Edge Trail, located in the northeast quadrant of River Prairie. They are requesting

a Retail Class “B” Beer license to sell fermented malt beverages and a Retail “Class C” Wine License to sell wine

in their establishment. They plan to be open for business by November 1, 2021. The licensing period will be

effective September 1, 2021 through June 30, 2022. Police Chief Kelly Bakken has reviewed the application and

recommends approval.

Draft Minutes

City of Altoona, WI Council Meeting Minutes August 12, 2021 Page 3 of 4

Robert DeFatta was present to ask for an amendment on the Premise Description to include a fenced in

outside patio.

Motion by Biren/Rowe to approve a Retail Class “B” Beer license and “Class C” wine license in the City

of Altoona to Xavier Artisan. Motion carried.

(IX)(7) Discuss/consider awarding the bid for the 2021 Lake Road Pavement Replacement project.

CE/DPW Walter explained that the city held a bid opening for the 2021 Lake Road Pavement Replacement

project at 2:00 p.m. on August 10, 2021. The bid tabulation was distributed to Council members prior to the

meeting. The project includes pulverizing the existing pavement and base, shaping of the base course, repaving

with asphaltic concrete pavement, shoulder improvements, and lawn restoration. CE/DPW Walter said that the

city received one bid from Haas Sons, Inc, Thorp, WI.

Motion by Lima/Biren to approve awarding the bid for the Lake Road Pavement Replacement project to

Haas Sons for $208,098.08. Motion carried.

(IX)(8) Discuss/consider approval of Resolution 8B-21, a final resolution of the Common Council of the City

of Altoona exercising its police powers pursuant to Section 66.0703 of Wisconsin Statutes to specially assess

for the 2021 Lake Road Pavement Replacement project.

CE/DPW Walter explained that a public hearing was held on July 22, 2021 to consider input from

interested parties and affected property owners regarding the Lake Road Pavement Replacement project. Affected

property owners as listed in the Eau Claire County tax roll were notified and were provided a copy of their

estimated assessments. The scope of the project includes pavement replacement on Lake Road from 100 feet east

of the Union Pacific driveway to Park Road. Walter noted that items included in the project consist of pulverization

of the existing pavement and base, shaping of the base course, repaving with asphaltic concrete pavement, shoulder

improvements, and lawn restoration.

CE/DPW Walter noted that Council just approved awarding the bid to Haas Sons, Inc. Walter noted that

paragraph 3 in the final resolution was amended to include the following:

Payment, in part, for the improvements shall be made by assessing $52,492.89 of the estimated total

project cost of $208,098.08 to property benefited.

Motion by Rowe/Lima to approve Resolution 8B-21, a final resolution exercising its police powers

pursuant to Section 66.0703 of Wisconsin Statutes to levy special assessments against benefited property for the

2021 Lake Road pavement Replacement Project as amended under paragraph 3 of the Final Resolution. Motion

carried.

(IX)(9) Discuss/consider transfer of ownership of outlots within the High Point Estates Subdivision.

City Attorney John Behling explained that there are three Outlots platted within the High Point Estates

subdivision still owned by the original Developer (Sirius Development, LLC), each serving a different purpose.

One lot was set aside for a subdivision entrance sign, one for a storm water pond and another to provide access to

School District of Altoona property to the north.

The covenants for High Point stipulate that ownership of the outlots will be conveyed from the Developer

to a homeowner’s association (HOA) made up of all the owners of lots in the subdivision. However, while perhaps

implied, the covenants do not stipulate that responsibility for maintenance of the outlots transfers to the HOA.

Complicating matters is that the HOA is not active, and I understand there is no desire by the affected property

owners to activate the HOA. Given the complicated nature of the situation, Sirius approached the City to request

guidance on how to move forward with disposition of the outlots.

City Attorney Behling mentioned that Staff consulted with legal counsel to come up with a solution to

address the outlot issue. Staff and legal counsel are suggesting that ownership of the subject outlots be conveyed

to three different parties as follows:

1. Lot 1: The subdivision entrance sign, to the residential neighbor to the south located at 1212 Thompson Drive.

2. Outlot 2: The storm water pond outlot, to the City.

3. Outlot 3: The lot providing access to the school property, to the School District of Altoona.

City Attorney Behling noted that each of the prospective property recipients have been approached and

each has expressed interest in owning the respective outlots. Before moving forward, legal counsel is suggesting

Draft Minutes

City of Altoona, WI Council Meeting Minutes August 12, 2021 Page 4 of 4

that the City contact each owner of a lot in High Point Estates to determine whether any owner objects to the

transfer of the outlots as noted. Following approval, Legal Counsel will prepare Quit Claim Deeds to all three

outlots.

Motion by Lima/Biren to approve transfer of ownership of outlots within the High Point Estates

Subdivision as described. Motion carried.

(X) Miscellaneous Business and Communication.

Mayor Pratt asked for Council input regarding going back to Council Meetings via Zoom. Consensus was

to go back with Zoom Meetings starting with the August 26, 2021 Council Meeting.

(XI) Adjournment.

Motion by Lima/Rowe to adjourn at 7:16 p.m. Motion carried.

Minutes submitted by Cindy Bauer, City Clerk

City of Altoona, WI, Regular Council Meeting Summary, August 26, 2021 Page 1 of 4

MEMORANDUM

TO: Altoona City Council

FROM: Michael Golat, City Administrator

SUBJECT: Summary of THURSDAY, AUGUST 26, 2021 Council Meeting Items

Provided below for your consideration is a summary of the THURSDAY, AUGUST 26, 2021 Council

Meeting agenda items.

(VII) CONSENT AGENDA

(VIII) UNFINISHED BUSINESS

(IX) NEW BUSINESS

ITEM 1 - Discuss/consider approval of Resolution 8C-21, a resolution authorizing the closing of books

of account for the year ended December 31, 2020 and to accept the Comprehensive Annual Financial

Report for 2020. (Discussed at the August 26, 2021 Finance Committee Meeting).

Following completion of the Auditor’s presentation, given at the August 26, 2021 Finance Committee

meeting, staff recommends Council approve a motion to authorize closing the books of account for 2020

and to accept the City’s 2020 Comprehensive Annual Financial Report as presented.

Attached are the 2020 Financial Statement and Communication Letters. Also attached is a summary of the

Financials prepared by CLA (CliftonLarsonAllen LLP).

Suggested motion: I move to approve/not approve Resolution 8C-21, a resolution authorizing the closing

of books of account for the year ended December 31, 2020 and to accept the Comprehensive Annual

Financial Report for 2020.

ITEM 2 - Discuss/consider approval of Resolution 8D-21 Authorizing the Issuance and Sale of

$6,680,000 General Obligation Promissory Notes, Series 2021B.

This resolution accepts the best bid for the G.O. Promissory Notes, Series 2021B and secures the

proposed term for a closing on the notes. The Notes are being issued to provide financing for 2021

General Fund and Water, Sewer and Stormwater Utilities 2021 Capital Projects and refund certain

obligations of the City that will allow the City to save on interest cost. Sean Lentz, from Ehlers will be

present and go over the Sale Day Report. The resolution is being prepared by our Bond Council Quarles

and Brady LLP. and will be forthcoming. Also forthcoming will be the Preliminary Official Statement.

This document is used for the purpose of disclosing information regarding the Notes to prospective

underwriters in the interest of receiving competitive proposals.

RETURN to Agenda >>

City of Altoona, WI, Regular Council Meeting Summary, August 26, 2021 Page 2 of 4

Suggested motion: I move to approve/not approve Resolution 8D-21, a resolution providing for the

approval of the $6,680,000 General Obligation Promissory Notes, Series 2021B.

ITEM 3 - Public Hearing at 6:00 or as soon thereafter as possible regarding a proposed Certified

Survey Map to divide parcel 201100209060 located between Woodman Drive and River Prairie

Drive (Discussed at the August 17 Plan Commission).

See Enclosed:

- Proposed CSM

The proposed Certified Survey Map subdivides the 2.101-acre parcel into a 1.12-acre and 0.981-acre parcel.

The easterly parcel, 1.12-acres, is subject to a proposed Specific Implementation Plan to be considered later

on the agenda.

Suggested motion: I move to close the public hearing.

ITEM 4 - Discuss/consider approval of a Certified Survey Map to subdivide parcel 201100209060.

See ITEM 3 for summary and materials. The Plan Commission recommended approval on August 17th.

Suggested Motion: I move to approve the Certified Survey Map.

ITEM 5 - Discuss/consider approval of a Specific Implementation Plan for a multi-tenant building

occupying the eastern half of parcel number 201100209060 located between Woodman Drive and

River Prairie Drive in the River Prairie Mixed Use District. (Discussed at the 8/17/2021 Plan

Commission meeting).

See Enclosed:

- Staff Report 21-08B

- Proposed Specific Implementation Plan

The proposed Specific Implementation Plan (SIP) for a 6,200 ft2 commercial multi-tenant building

architecture and site design elements for property located between Woodman Drive and River Prairie

Drive, east of Bluestem Boulevard. This site is part of the Woodman’s Crossing General

Implementation Plan in the River Prairie Mixed Use District zoning. The property is a prepared “pad

ready” site.

The 2.101-acre site is proposed to be subdivided via CSM to create two parcels. This proposed SIP

applies to the easterly 1.12 acres. The vehicle ingress/egress is taken from Woodman Drive, a private

road.

See the enclosed Staff Report and proposed Specific Implementation Plan for further analysis and

detail.

City of Altoona, WI, Regular Council Meeting Summary, August 26, 2021 Page 3 of 4

Staff recommends approval of the Specific Implementation Plan as being in substantial compliance

with the River Prairie Design Guidelines and Standards with the following modifications:

A. Access, Circulation & Parking (RPDG IX. 1)

1. Walkways shall be a minimum of six feet in width [IX. 1. (C)(5)].

B. Building and Architectural Standards [RPDG IX 7]

1. The Council recognizes that the proposed site arrangement does not meet the design

guidelines insofar as allowing automobile circulation and parking between the building and the

primary street [RPDG IX 7.3 (B)(2)], and greater setback than otherwise permitted, due to the

proposed uses that include vehicle drive-through facilities [RPDG IX 7.3 (B)].

2. Any/all mechanical equipment, including roof-mounted units, shall be appropriately

screened by building-compatible materials or landscaping [RPDG, IX 7 H].

3. Sign permits will be required for all building and ground signs and meet design

requirements outlined in the River Prairie Design Guidelines, IX 5.

4. All exterior lighting on the site shall be of full cut-off design and be shielded to prevent

spillover of direct light onto adjacent properties [Altoona Municipal Code 19.59.030 (H)].

C. Utilities

1. If the building features a sprinkler system, the Fire Department Connection (FDC) shall be

4” STORTZ with final placement reviewed and approved by Altoona Fire Department.

2. Submittal and successful review of final storm water plan and civil site plan by City

Engineer as described in the Altoona Municipal Code Chapter 14.

The SIP was recommended for approval, with the above modifications, by the Plan Commission on August

17th.

Suggested motion: I move to approve/not approve the proposed Specific Implementation Plan as being in

substantial compliance with the River Prairie Design Guidelines & Standards with staff-recommended

modifications.

ITEM 6 - Discuss/consider approval of a Development Agreement for Prairie View Ridge II.

See Enclosed:

- Proposed Development Agreement

The proposed Development Agreement for Prairie View Ridge provides for the terms and conditions for

the private development of public facilities and related conditions of land subdivision. Much of the

agreement is standard development agreement terms.

City of Altoona, WI, Regular Council Meeting Summary, August 26, 2021 Page 4 of 4

Section 3, “Special Conditions” includes particular provisions unique to this development, including the

location and sizing of specific utility elements. The Agreement also includes a provision to preserve the

proposed woodland preservation “no cut” easement area throughout the development process and measures

to communicate the presence of the easement to future owners.

The Agreement includes the required parkland dedication fee which is modified from the Development

Agreement for Prairie View Ridge due to a change in the number of lots, and the planned acquisition of

two lots by the City for a future well location.

The City Attorney is working on a restrictive covenant to record with the plat to include management and

enforcement provisions of the “no cut” easement. A draft of this document will be provided as far in

advance of the meeting as possible. Final revisions may be required prior to recording.

Suggested motion: I move to approve/not approve the proposed Development Agreement and authorize

the Mayor to sign upon completion of the restrictive covenant regarding the woodland preservation,

provision of the performance guarantee, and approval of the Civil Plan.

ITEM 7 - Discuss/consider approval of the Final Plat for Prairie View Ridge II. (Discussed at the

8/17/2021 Plan Commission Meeting).

See Enclosed:

- Final Plat, Prairie View Ridge II

The Preliminary Plat for Prairie View Ridge II was conditionally approved by the City Council on May 13,

2021. As you may recall, a portion of the subject area was also rezoned from R1 to TH during that same

meeting.

The proposed Final Plat is substantially consistent with the approved preliminary plat. The Final Plat was

recommended for approval by the Plan Commission on August 17th.

Suggested motion: I move to approve/not approve the Final Plat for Prairie View Ridge II.

ITEM 8 - Discuss/consider approval of Ordinance 8B-21, an Ordinance amending Chapter 10.20 of

the Altoona Municipal Code “Stopping, Standing and Parking” to add a parking prohibited section

along the west side of North 10th Street West north of Spooner Avenue.

Eau Claire Transit contacted City Staff with a request to add a parking prohibition along the west side of

North 10th Street West, north of Spooner Avenue. Transit drivers have experienced difficulties in loading

and unloading passengers at the bus stop due to parked cars adjacent to Golden Acres I. The proposed

parking prohibition would extend northerly from Spooner Avenue a distance of 150 feet as can be seen in

the attached drawing.

Suggested motion: I move to approve/not approve Ordinance 8B-21, an Ordinance amending Chapter

10.20 of the Altoona Municipal Code adding parking restrictions on North 10th Street West.

City of Altoona, WI, Regular Council Meeting Summary, August 26, 2021 Page 1 of 1

MEMORANDUM

TO: Altoona City Council

FROM: Michael Golat, City Administrator

SUBJECT: Summary of THURSDAY, AUGUST 26, 2021 Council Meeting Items

Provided below for your consideration is a summary of the THURSDAY, AUGUST 26, 2021 Council

Meeting agenda items.

(VII) CONSENT AGENDA

(VIII) UNFINISHED BUSINESS

(IX) NEW BUSINESS

ITEM 1 - Discuss/consider approval of Resolution 8C-21, a resolution authorizing the closing of books

of account for the year ended December 31, 2020 and to accept the Comprehensive Annual Financial

Report for 2020. (Discussed at the August 26, 2021 Finance Committee Meeting).

Following completion of the Auditor’s presentation, given at the August 26, 2021 Finance Committee

meeting, staff recommends Council approve a motion to authorize closing the books of account for 2020

and to accept the City’s 2020 Comprehensive Annual Financial Report as presented.

Attached are the 2020 Financial Statement and Communication Letters. Also attached is a summary of the

Financials prepared by CLA (CliftonLarsonAllen LLP).

Suggested motion: I move to approve/not approve Resolution 8C-21, a resolution authorizing the closing

of books of account for the year ended December 31, 2020 and to accept the Comprehensive Annual

Financial Report for 2020.

City Council | August 26, 2021New Business | Item 1 | Page 1 of 91

Return to Agenda >>

RESOLUTION NO. 8C-21

RESOLUTION TO AUTHORIZE CLOSING OF BOOKS OF ACCOUNT FOR THE

YEAR ENDED DECEMBER 31, 2020 AND TO ACCEPT THE COMPREHENSIVE

ANNUAL FINANCIAL REPORT FOR 2020.

WHEREAS action on all claims for the year ended December 31, 2020, have been finalized and,

WHEREAS appropriate designations of ending fund balances have been made and are reported

within the Comprehensive Annual Financial Report, and

WHEREAS an annual detailed audit of the city's financial transactions and accounts has been

accomplished by an independent certified public accountant in accordance with Section

66.0609(3) of the Wisconsin Statutes and the audit opinion has been discussed and reviewed

with the Mayor and members of the City Council,

NOW THEREFORE BE IT RESOLVED, to authorize the closing of the books of account for the

year ended December 31, 2020, and to accept the Comprehensive Annual Financial Report for

the City of Altoona for the year ended December 31, 2020, as prepared by the Finance Director

and reviewed by the independent accounting firm of CliftonLarsenAllen LLP

BE IT FURTHER RESOLVED, that a copy of the Comprehensive Annual Financial Report for

the year ended December 31, 2020, attached hereto is incorporated into and made a part of this

resolution.

Dated this 26th day of August , 2021

Brendan Pratt, Mayor

Cindy Bauer, City Clerk

Approved

Published:

City Council | August 26, 2021 New Business | Item 1 | Page 2 of 91

City of Altoona

Item1 Reports Issued:

Auditor's Report (Opinion):- The financial statements are fairly stated. We will issue what is known as an "unmodified" audit opinion.- Additional paragraph to explain a prior period adjustment.

Management Letter:Our report on internal control included the following deficiencies in internal control over financial reporting.

Material Weaknesses:Annual Financial Reporting Under Generally Accepted Accounting Principals (GAAP)Material Audit AdjustmentsLack of Segregation of Duties

2 Other Assistance and Observations:Regulatory Filing Assistance:

Public Service Commission Annual ReportFinancial Report Form CTax Incremental District On-line Reporting

3 General Fund: The General Fund is the general operating fund of the City. It is used to account for all financial resources which are not required to be accounted for in another fund.

12/31/2020 12/31/2019 12/31/2018 12/31/2017 General Fund Balance Sheet Summary:

Cash and Investments 7,600,667$ 7,802,940$ 8,855,111$ 6,506,923$ Taxes & Special Assessments Receivable 2,808,546 2,534,183 2,344,807 2,180,584 Advances to Other Funds 2,016,951 2,862,466 756,707 1,216,622 Other Assets 618,105 176,441 167,690 173,722 Total Assets 13,044,269$ 13,376,030$ 12,124,315$ 10,077,851$

Liabilities 317,109$ 362,590$ 336,229$ 247,891$ Deferred Inflows of Resources 2,725,336 2,449,466 2,277,547 2,106,353 Total Liabilities & Deferred Inflows 3,042,445 2,812,056 2,613,776 2,354,244 Fund Balance:

Nonspendable 2,033,017 2,876,428 771,090 12,083 Restricted - - 30,721 89,850 Committed 3,928,085 4,737,436 4,393,800 3,473,632 Assigned 225 21,140 - - Unassigned 4,040,497 2,928,970 4,314,928 4,148,042

Total Fund Balance 10,001,824 10,563,974 9,510,539 7,723,607 13,044,269$ 13,376,030$ 12,124,315$ 10,077,851$

General Fund Operations Summary:Revenues 6,374,219$ 5,740,431$ 5,168,446$ 4,530,545$ Expenditures (5,677,070) (5,576,712) (5,323,981) (4,717,106) Net Other Financing Sources/Uses (1,608,853) 889,716 1,942,467 61,185

(911,704)$ 1,053,435$ 1,786,932$ (125,376)$

% of Unassigned Fund Balanceto General Fund Expenditures 71.2% 52.5% 81.0% 87.9%

Financial Statement Notations

City Council | August 26, 2021 New Business | Item 1 | Page 3 of 91

City of Altoona

4 Special Revenue Funds: Special Revenue Funds are used to account for the proceeds of specific revenues sourcesthat are restricted to expenditures for specified purposes.

12/31/2020 12/31/2019 12/31/2018 12/31/2017Special Revenue Funds Balances:

Public Library 187,756$ 164,121$ 148,843$ 133,378$ CDBG/Residential Loan Fund 225,627 233,276 231,602 241,527

413,383$ 397,397$ 380,445$ 374,905$

5 Debt Service Funds: Debt Service Funds are used to account for the accumulation of resources for, and the payment of,certain general long-term debt principal, interest and related charges.

12/31/2020 12/31/2019 12/31/2018 12/31/2017Debt Service Fund Balances:

General Debt Service Fund 743,412$ 581,875$ 585,260$ 557,687$

6 Capital Project Funds: Capital Project funds are used to account for financial resources to be used for the acquisitionor construction of major capital facilities other than those financed from proprietary funds.

12/31/2020 12/31/2019 12/31/2018 12/31/2017Capital Project Fund Balances:

Tax Incremental District #2 (426,815)$ (647,549)$ -$ -$ Tax Incremental District #3 (1,402,486) (2,296,418) (152,493) 896,352 Tax Incremental District #4 813,133 708,209 478,240 492,189 Capital Projects Fund 1,619,478 301,079 (862,311) (1,354,167)

603,310$ (1,934,679)$ (536,564)$ 34,374$

7 Enterprise Funds: Enterprise Funds are used to account for operations that are financed and operated in a mannersimilar to private business enterprises-- where the intent of the governing body is that the costs of providing the servicesis to be recovered from those using the services.

12/31/2020 12/31/2019 12/31/2018 12/31/2017Water Utility

Cash and Investments 1,803,316$ 1,563,903$ 1,284,642$ 528,268$ Other Current Assets 395,793 384,931 418,906 378,264 WRS Asset and Deferred Outflows 111,849 96,077 31,876 53,673 Capital Assets 10,131,027 9,265,228 8,789,348 8,888,869 Other Long-term Assets 301,808 226,849 265,273 256,796

Total Assets and Deferred Outflows 12,743,793$ 11,536,988$ 10,790,045$ 10,105,870$

Current Liabilities 300,428$ 233,709$ 234,578$ 183,261$ Long-term Obligations 1,170,868 1,440,002 1,268,925 1,093,389 Deferred Inflows 143,738 106,656 93,866 108,019

Total Liabilities and Deferred Inflows 1,615,034 1,780,367 1,597,369 1,384,669 Net Position:

Net Investment in Capital Assets 8,727,979 7,657,912 7,377,273 7,541,319 Restricted 33,537 - 11,158 - Unrestricted 2,367,243 2,098,709 1,804,245 1,179,882 Total Net Position 11,128,759 9,756,621 9,192,676 8,721,201

12,743,793$ 11,536,988$ 10,790,045$ 10,105,870$

Current Ratio (1+ Desired) 7.32 8.34 7.26 4.95 Change in Net Position 1,372,138$ 563,945$ 471,475$ 460,734$ Rate of Return 7.14% 6.39% 9.10% 5.35%Date of Last Rate Adjustment April 20, 2015

Financial Statement Notations

City Council | August 26, 2021 New Business | Item 1 | Page 4 of 91

City of Altoona

7 Enterprise Funds: (Continued)

12/31/2020 12/31/2019 12/31/2018 12/31/2017Sewer Utility

Cash and Investments 2,847,968$ 2,562,250$ 2,115,160$ 1,561,271$ Other Current Assets 468,295 475,044 492,073 500,905 WRS Asset and Deferred Outflows 43,020 14,781 12,144 28,751 Capital Assets 5,673,344 5,006,044 4,724,043 4,465,977 Other Long-term Assets 143,773 74,584 94,272 65,917

Total Assets and Deferred Outflows 9,176,400$ 8,132,703$ 7,437,692$ 6,622,821$

Current Liabilities 348,561$ 317,944$ 312,186$ 267,546$ Long-term Obligations 682,509 804,847 397,308 278,319 Deferred Inflows 38,765 7,599 8,489 12,066

Total Liabilities and Deferred Inflows 1,069,835 1,130,390 717,983 557,931 Net Position:

Net Investment in Capital Assets 4,874,835 4,118,635 4,271,735 4,140,977 Restricted 12,899 - 4,251 - Unrestricted 3,218,831 2,883,678 2,443,723 1,923,913 Total Net Position 8,106,565 7,002,313 6,719,709 6,064,890

9,176,400$ 8,132,703$ 7,437,692$ 6,622,821$

Current Ratio (1+ Desired) 9.51 9.55 8.35 7.71 Change in Net Position 1,104,252$ 282,604$ 654,819$ 299,969$

12/31/2020 12/31/2019 12/31/2018 12/31/2017Storm Water Fund

Cash and Investments 1,687,136$ 1,710,037$ 1,631,249$ 1,367,562$ Other Current Assets 104,973 67,511 106,768 103,574 WRS Asset and Deferred Outflows 10,755 5,543 4,554 26,132 Capital Assets 2,912,067 2,425,146 2,182,015 2,339,812 Other Long-term Assets - - - -

Total Assets and Deferred Outflows 4,714,931$ 4,208,237$ 3,924,586$ 3,837,080$

Current Liabilities 149,786$ 137,261$ 119,230$ 108,129$ Long-term Obligations 661,137 807,319 804,918 797,030 Deferred Inflows 9,691 2,849 3,183 9,987

Total Liabilities and Deferred Inflows 820,614 947,429 927,331 915,146 Net Position:

Net Investment in Capital Assets 2,107,423 1,488,863 1,261,583 1,439,507 Restricted 3,225 - 1,594 - Unrestricted 1,783,669 1,771,945 1,734,078 1,482,427 Total Net Position 3,894,317 3,260,808 2,997,255 2,921,934

4,714,931$ 4,208,237$ 3,924,586$ 3,837,080$

Current Ratio (1+ Desired) 11.96 12.95 14.58 13.61 Change in Net Position 633,509$ 263,553$ 75,321$ 112,856$

Financial Statement Notations

City Council | August 26, 2021 New Business | Item 1 | Page 5 of 91

City of Altoona

8 Long-term Obligations 12/31/2020 12/31/2019 12/31/2018 12/31/2017

Governmental Activities:General Obligation Notes 14,846,000$ 14,843,000$ 14,365,000$ 15,235,000$ State Trust Fund Loans 6,392,832 6,972,545 7,528,116 8,059,763 Developer Incentives 135,000 135,000 354,584 470,683 Landfill Post-Closure Liability 32,040 32,040 32,040 112,000 Compensated Absences 638,997 555,535 577,591 466,184 WRS Pension (Asset)/Liability (595,276) 679,706 (531,328) 138,868 OPEB Liability 1,700,231 1,427,380 1,270,054 999,429 Life Insurance OPEB Liability 197,312 105,611 120,202 - Unamortized Premium 198,974 164,012 191,001 167,623

Business Type Activities:General Obligation Notes 2,551,000 2,933,000 2,245,000 1,935,000 Mortgage Revenue Bonds 435,941 475,603 514,266 551,957 Unamortized Premium 19,260 22,405 25,549 -

26,552,311$ 28,345,837$ 26,692,075$ 28,136,507$

Equalized Valuation 806,015,500$ 741,668,900$ 682,442,800$ 655,395,200$

General Obligation Debt Limit 40,300,775$ 37,083,445$ 34,122,140$ 32,769,760$

Debt Subject to Limit 17,397,000$ 17,776,000$ 16,610,000$ 17,170,000$

General Obligation Debt asPercent of Debt Limitation 43.2% 47.9% 48.7% 52.4%

Financial Statement Notations

City Council | August 26, 2021 New Business | Item 1 | Page 6 of 91

CITY OF ALTOONA, WISCONSIN

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

YEAR ENDED DECEMBER 31, 2020

City Council | August 26, 2021 New Business | Item 1 | Page 7 of 91

CITY OF ALTOONA, WISCONSIN TABLE OF CONTENTS

YEAR ENDED DECEMBER 31, 2020

INDEPENDENT AUDITORS’ REPORT 1

MANAGEMENT’S DISCUSSION AND ANALYSIS 4

BASIC FINANCIAL STATEMENTS

STATEMENT OF NET POSITION 15

STATEMENT OF ACTIVITIES 16

BALANCE SHEET – GOVERNMENTAL FUNDS 17

RECONCILIATION OF TOTAL GOVERNMENTAL FUND BALANCES TO NET POSITION OF GOVERNMENTAL ACTIVITIES 18

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES – GOVERNMENTAL FUNDS 19

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES 20

STATEMENT OF NET POSTION – PROPRIETARY FUNDS 21

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET POSITION – PROPRIETARY FUNDS 23

STATEMENT OF CASH FLOWS – PROPRIETARY FUNDS 24

STATEMENT OF NET POSITION - FIDUCIARY FUNDS 26

STATEMENT OF CHANGES IN NET POSITION - FIDUCIARY FUNDS 27

NOTES TO BASIC FINANCIAL STATEMENTS 28

REQUIRED SUPPLEMENTARY INFORMATION

1 – BUDGETARY COMPARISON SCHEDULE – GENERAL FUND 66

2 – SCHEDULE OF PROPORTIONATE SHARE OF WISCONSIN RETIREMENT SYSTEM NET PENSION PLAN (ASSET) LIABILITY – LAST TEN MEASUREMENT PERIODS 67

3 – SCHEDULE OF CONTRIBUTIONS TO WISCONSIN RETIREMENT SYSTEM PENSION PLAN – LAST TEN FISCAL YEARS 68

4 – SCHEDULE OF CITY’S PROPORTIONATE SHARE OF THE NET OPEB LIABILITY WISCONSIN LOCAL RETIREE LIFE INSURANCE FUND MULTI-EMPLOYER OPEB PLAN – LAST TEN MEASUREMENT PERIODS 69

5 – SCHEDULE OF CITY’S CONTRIBUTIONS TO WISCONSIN LOCAL RETIREE LIFE INSURANCE FUND MULTI-EMPLOYER OPEB PLAN – LAST TEN FISCAL YEARS 70

6 - SCHEDULE OF CHANGES IN THE CITY’S OPEB LIABILITY, RELATED RATIOS AND ACTUARIAL ASSUMPTIONS – LAST TEN MEASUREMENT PERIODS 71

NOTES TO REQUIRED SUPPLEMENTARY INFORMATION 72

SUPPLEMENTARY INFORMATION

COMBINING BALANCE SHEET – NONMAJOR GOVERNMENTAL FUNDS 73

COMBINING STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES – NONMAJOR GOVERNMENTAL FUNDS 74

City Council | August 26, 2021 New Business | Item 1 | Page 8 of 91

(1)

INDEPENDENT AUDITORS' REPORT To the City Council City of Altoona Altoona, Wisconsin

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Altoona, Wisconsin (City) as of and for the year ended December 31, 2020, and the related notes to the financial statements, which collectively comprise the City’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

City Council | August 26, 2021 New Business | Item 1 | Page 9 of 91

The City Council City of Altoona

(2)

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Altoona, Wisconsin as of December 31, 2020, and the respective changes in the financial position and, where applicable, cash flows, thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Emphasis-of-Matter Regarding a Correction of an Error

As described in Note 11 to the financial statements, the City is making a prior year adjustment to record Land Held for Resale on the governmental fund statements. Our opinion is not modified with respect to that matter.

Other Matters

Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis, budgetary comparison information, pension and other postemployment benefit schedules as referenced in the table of contents, be presented to supplement the basic financial statements. Such information, although not part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

City Council | August 26, 2021 New Business | Item 1 | Page 10 of 91

The City Council City of Altoona

(3)

Supplementary Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City’s basic financial statements. The individual fund statements are presented for purposes of additional analysis and are not a required part of the basic financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. The information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the basic financial statements as a whole.

CliftonLarsonAllen LLP

Eau Claire, Wisconsin July 29, 2021

City Council | August 26, 2021 New Business | Item 1 | Page 11 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(4)

As management of the City of Altoona, Wisconsin (City), we offer the readers of the City's financial statements this narrative overview and analysis of financial activities of the City for the fiscal year ending December 31, 2020. Please consider this information in conjunction with the City’s financial statements, which begin on page 15 following this narrative. FINANCIAL HIGHLIGHTS

Key financial highlights for the year ended December 31, 2020 include the following:

The assets and deferred outflows of resources of the City exceeded its liabilities and deferred inflows at the close of the most recent fiscal year by $52,647,765 (net position). Of this amount, $35,460,164 represented the City’s net investment in capital assets, $3,490,931 was held for restricted purposes, and $13,696,670 was unrestricted. The unrestricted net position may be used to meet the City’s ongoing obligations to citizens and creditors.

During the fiscal year, the City’s total net position increased by $5,970,977 or approximately

12.8 percent. Net position related to the business-type activities of the City increased $3,109,899 while net position related to governmental activities increased $2,861,078.

At the close of the fiscal year, the City’s governmental funds reported combined ending fund balance of $11,761,929, an increase of $1,803,808 from the previous year.

At the end of 2020, the unassigned general fund balance totaled $4,040,497, or 53.8 percent of

the general fund expenditures.

The City’s total long-term general obligation notes decreased by $379,000 during the current fiscal year.

OVERVIEW OF THE FINANCIAL STATEMENTS

This discussion and analysis is intended to serve as an introduction to the City’s basic financial statements. The City’s basic financial statements are comprised of three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Government-Wide Financial Statements The two government-wide financial statements are designed to provide readers with a broad overview of the City’s finances, in a manner similar to a private-sector business. The Statement of Net Position presents information on all of the City’s assets, liabilities and deferred inflows/outflows, with the difference reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the City is improving or deteriorating.

City Council | August 26, 2021 New Business | Item 1 | Page 12 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(5)

The Statement of Activities presents information showing how the City’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of the related cash flows. Thus, revenues and expenses are reported in this statement for some items that will result in cash flows in future fiscal periods (e.g., uncollected taxes). Both of the government-wide financial statements distinguish those functions of the City that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and service charges (business-type activities). The governmental activities of the City include general government, public safety, public works, health and human services, culture, recreation and education, and conservation and development. The business-type activities of the City include a water, sewer and storm water utilities. The government-wide financial statements can be found beginning on page 15 of this report. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like other governmental entities, uses fund accounting to ensure and demonstrate compliance with various finance-related legal requirements. All of the funds of the City can be divided into three categories: governmental funds, proprietary funds and fiduciary funds. Governmental funds – Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures and changes in fund balances for the general fund, debt service fund, capital projects fund and the River Prairie Tax Incremental District #3 fund, which are considered to be major funds. Data from the other governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements in the supplementary information section. The governmental fund financial statements can be found beginning on page 17 of this report.

City Council | August 26, 2021 New Business | Item 1 | Page 13 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(6)

Proprietary Funds – The City maintains one type of proprietary funds - enterprise funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The City uses enterprise funds to account for its water, sewer and storm sewer utilities. Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for each of the enterprise funds, each of which is considered to be major funds of the City. The basic proprietary fund financial statements can be found beginning on page 21 of this report. Fiduciary Funds – Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statement because the resources of those funds are not available to support the City’s own programs. The accounting used for fiduciary funds is similar to that used for proprietary funds. The basic fiduciary fund financial statements can be found on page 26 of this report. Notes to Financial Statements The notes to basic financial statements provide additional detail that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the basic financial statements can be found beginning on page 28 of this report. Supplementary Information In addition to the basic financial statement and accompanying notes, this report presents certain required supplementary information on the City’s operating budget and the pension and other postemployment benefit plans. Required supplementary information can be found beginning on page 66 of this report. Following the basic government-wide and fund financial statements, accompanying notes, and required supplementary information, additional supplementary information has been provided as part of this report. The supplementary information includes combining statements for the nonmajor governmental funds. This supplementary information section of the report begins on page 73.

City Council | August 26, 2021 New Business | Item 1 | Page 14 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(7)

FINANCIAL ANALYSIS OF THE CITY AS A WHOLE

As noted earlier, net position may serve over time as a useful indicator of a government’s financial position. The City’s assets and deferred outflows exceeded liabilities and deferred inflows by $52,647,765 at the close of 2020. The largest portion of net position (67.4%) reflect the City’s investment in capital assets, including land, land improvements, buildings, machinery and equipment, and plant in service, net of related outstanding debt used to acquire the assets. These capital assets are used to provide services to citizens and are not available for future spending. Although the City’s investment in capital assets is reported net of related debt, it should be noted that the resources needed to repay debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. The following is a summary of the City’s statement of net position:

Condensed Statement of Net Position December 31, 2020 and 2019

2020 2019 2020 2019 2020 2019

Current and Other Assets 20,454,910$ 18,342,513$ 7,356,806$ 6,763,340$ 27,811,716$ 25,105,853$ Capital Assets 41,187,733 40,638,226 18,716,438 16,696,418 59,904,171 57,334,644 Other Noncurrent Assets 2,228,894 839,669 445,581 301,433 2,674,475 1,141,102

Total Assets 63,871,537 59,820,408 26,518,825 23,761,191 90,390,362 83,581,599

Deferred Outflows of Resources 1,902,299 1,900,955 115,963 116,401 2,018,262 2,017,356

Current Liabilities 984,452 1,150,389 306,752 266,916 1,291,204 1,417,305 Long-Term Liabilities 24,141,386 24,872,007 3,006,201 3,473,830 27,147,587 28,345,837

Total Liabilities 25,125,838 26,022,396 3,312,953 3,740,746 28,438,791 29,763,142

Deferred Inflows of Resources 11,129,874 9,041,921 192,194 117,104 11,322,068 9,159,025

Net Position:Net Investment in

Capital Assets 19,749,927 18,537,264 15,710,237 13,265,410 35,460,164 31,802,674 Restricted 3,441,270 1,406,685 49,661 - 3,490,931 1,406,685 Unrestricted 6,326,927 6,713,097 7,369,743 6,754,332 13,696,670 13,467,429

Total Net Position 29,518,124$ 26,657,046$ 23,129,641$ 20,019,742$ 52,647,765$ 46,676,788$

Governmental Activities Business-Type Activities Totals

An additional portion of the City’s net position (6.6%) represents resources that are subject to other restrictions as to how they may be used. The remaining $13,467,429 of total net position (26.0%) may be used to meet the City’s ongoing obligations to its citizens and creditors. It is important to note that $7,369,743 of unrestricted net position is related to the City’s business-type activities. Consequently, it generally may not be used to fund governmental activities. The condensed statement of changes in net position shown on the following page shows that total net position of the City increased $5,970,977 or approximately 12.8 percent. The change consisted of an increase in net position related to governmental activities in the amount of $2,861,078 and an increase in net position related to business-type activities in the amount of $3,109,899.

City Council | August 26, 2021 New Business | Item 1 | Page 15 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(8)

The following is a summary of the changes in the City’s net position for the years ended December 31, 2020 and 2019:

Condensed Statement of Changes in Net Position Years Ended December 31, 2020 and 2019

2020 2019 2020 2019 2020 2019REVENUESProgram Revenues

Charges for Services 675,266$ 772,609$ 3,277,268$ 3,140,692$ 3,952,534$ 3,913,301$ Operating Grants and Contributions 1,501,531 1,573,111 - - 1,501,531 1,573,111 Capital Grants and Contributions - 231,559 - - - 231,559

General RevenuesProperty Taxes 8,072,258 7,738,144 - - 8,072,258 7,738,144 Other Taxes 263,281 267,988 - - 263,281 267,988 Grants and Contributions not

Restricted for a Particular Purpose 181,530 289,284 - - 181,530 289,284 Other 2,002,100 1,935,430 148,019 225,576 2,150,119 2,161,006

Total Revenues 12,695,966 12,808,125 3,425,287 3,366,268 16,121,253 16,174,393

EXPENSESGeneral Government 599,184 1,109,879 - - 599,184 1,109,879 Public Safety 3,127,061 2,827,383 - - 3,127,061 2,827,383 Public Works 280,731 3,260,024 - - 280,731 3,260,024 Health and Human Services 1,750 1,398 - - 1,750 1,398 Culture and Recreation 2,547,697 1,813,303 - - 2,547,697 1,813,303 Conservation and Development 287,120 334,823 - - 287,120 334,823 Interest and Fiscal Charges 439,089 242,194 - - 439,089 242,194 Water - - 990,196 819,256 990,196 819,256 Sewer - - 1,468,723 1,431,126 1,468,723 1,431,126 Storm Water - - 408,725 414,565 408,725 414,565

Total Expenses 7,282,632 9,589,004 2,867,644 2,664,947 10,150,276 12,253,951

TRANSFERS (2,552,256) (408,781) 2,552,256 408,781 - -

CHANGE IN NET POSITION 2,861,078 2,810,340 3,109,899 1,110,102 5,970,977 3,920,442 Net Position - Beginning of Year 26,657,046 23,846,706 20,019,742 18,909,640 46,676,788 42,756,346 NET POSITION - END OF YEAR 29,518,124$ 26,657,046$ 23,129,641$ 20,019,742$ 52,647,765$ 46,676,788$

Governmental Activities Business-Type Activities Totals

A review of statement of activities can provide a concise picture of how the various functions/programs of the City are funded. The following charts draw data from the statement of activities. For governmental services the City is primarily dependent on property taxes (63.7%), general revenues (23.1% which include land sales) and state and federal operating grants (13.2%).

City Council | August 26, 2021 New Business | Item 1 | Page 16 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(9)

Fees, Charges, and Other5.3%

Operating Grants and Contributions

11.8%Capital Grants and

Contributions0.0%

Grants and Contributions not Restricted for a Particular Purpose

1.4%

Property Taxes63.7%

Other Taxes2.1%

Other General Revenue15.7%

Governmental Activities Revenues by Source

General Government8.1%

Public Safety42.9%

Public Works3.9%Health and Human

Services0.0%

Culture, Recreation, and Education

35.0%

Conservation and Development

3.9%

Interest and Fiscal Charges

6.1%

Governmental Activities Expenditures by Function

City Council | August 26, 2021 New Business | Item 1 | Page 17 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(10)

In the case of business-type activities charges for services (95.7%) is the primary revenue source.

$-

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

$1,500,000

$1,750,000

$2,000,000

Water Sewer Storm Water

Expenses and Program Revenues - Business-Type Activities

Expenses

Program Revenues

Charges for Services95.7%

Other4.3%

Revenue by Source - Business-Type Activities

`

City Council | August 26, 2021 New Business | Item 1 | Page 18 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(11)

FINANCIAL ANALYSIS OF THE CITY’S MAJOR FUNDS

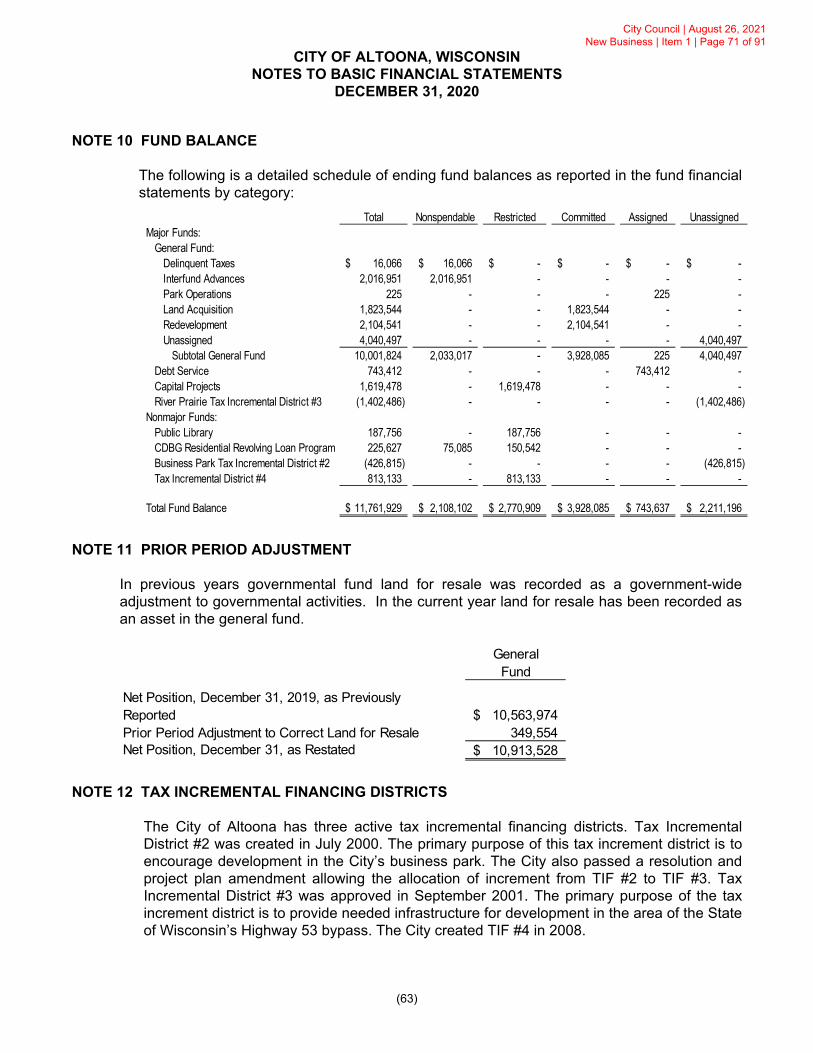

As noted earlier, the City uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental Funds The focus of the City’s governmental funds is to provide information regarding near-term inflows, outflows and balances of spendable resources. Such information can be useful in assessing the City’s financing requirements. In particular, the level of unassigned fund balances may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. As of December 31, 2020, the City’s governmental funds reported combined ending fund balances of $11,761,929, an increase of $2,153,362 from the previous year. The governmental funds comprising this balance are shown below:

Current YearNonspendable Restricted Committed Assigned Unassigned Total Change

Major Funds:General Fund 2,033,017$ -$ 3,928,085$ 225$ 4,040,497$ 10,001,824$ (562,150)$ Debt Service - - - 743,412 - 743,412 161,537 Capital Projects - 1,619,478 - - - 1,619,478 1,318,399 River Prairie Tax Incremental District #3 - - - - (1,402,486) (1,402,486) 893,932

Nonmajor Funds:Public Library - 187,756 - - - 187,756 23,635 CDBG Residential Revolving Loan Program 75,085 150,542 - - - 225,627 (7,649) Business Park Tax Incremental District #2 - - - - (426,815) (426,815) 220,734 Tax Incremental District #4 - 813,133 - - - 813,133 104,924

2,108,102$ 2,770,909$ 3,928,085$ 743,637$ 2,211,196$ 11,761,929$ 2,153,362$

Fund Balances at December 31, 2020

Restrictions of fund balances represent amounts that are not subject to appropriation or are legally restricted by outside parties for use for a specific purpose. Assignments of fund balance represent tentative management plans that are subject to change. The balance of the unassigned fund balance is not for any specific purposes. The general fund is the primary operating fund used to account for the governmental operations of the City. As a measure of the general fund’s liquidity, it may be useful to compare both total fund balance and unassigned fund balance to measures of operating volume such as fund expenditures or fund revenues. The total year-end general fund balance represented 133.3 percent of total general fund expenditures reported on the statement of revenues, expenditures and changes in fund balances while the unassigned balance represented 53.8 percent of the same amount. The general fund’s total fund balance decreased $911,704 during the year. The debt service fund had a total fund balance of $743,412, all of which was assigned for the payment of debt service. This balance has accumulated over time for the payment of future, scheduled long-term indebtedness. The balance in this fund decreased $161,537 during 2020. The balance in the capital projects fund, increased $1,318,399 during the year and had a balance of $1,619,478 at year-end.

City Council | August 26, 2021 New Business | Item 1 | Page 19 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(12)

The balance in River Prairie Tax Incremental District #3 fund, a capital projects fund, increased $893,932 during the year. The fund had a deficit balance of $1,402,486 at year-end. The aggregated other governmental funds column includes two special revenue funds used to account for the proceeds of specific revenue sources that are restricted to expenditures for specific purposes and two tax incremental financing capital projects funds. The accumulated fund balances of these funds increased $341,644 during 2020. Transactions of these funds are individually detailed in the supplementary information section of this report. Proprietary Funds The City’s proprietary funds provide the same type of information found in the government-wide financial statements, but in greater detail. The net position of the enterprise-type proprietary funds at the end of 2020 totaled $23,129,641, up $3,109,899 from the previous year as shown below.

Condensed Statement of Changes in Net Position for Enterprise Funds Years Ended December 31, 2020 and 2019

2020 2019 2020 2019 2020 2019 2020 2019

Operating Revenues 1,418,351$ 1,305,306$ 1,507,188$ 1,486,722$ 351,729$ 348,664$ 3,277,268$ 3,140,692$ Operating Expenses

Depreciation 332,408 307,442 178,220 161,798 231,616 197,102 742,244 666,342 Other 625,919 468,899 1,275,045 1,242,723 155,935 191,921 2,056,899 1,903,543

Operating Income (Loss) 460,024 528,965 53,923 82,201 (35,822) (40,359) 478,125 570,807 Nonoperating Income and

Nonoperating Expenses 3,458 (1,853) 76,211 95,044 (151) 37,323 79,518 130,514 Net Income (Loss) before

Contributions & Transfers 463,482 527,112 130,134 177,245 (35,973) (3,036) 557,643 701,321 Capital Contributions

Developers/Customers 660,566 - - - 327,919 - 988,485 - Capital Transferred from City 462,152 238,646 974,118 105,359 341,563 266,589 1,777,833 610,594

Transfers (214,062) (201,813) - - - - (214,062) (201,813) Change in Net Position 1,372,138$ 563,945$ 1,104,252$ 282,604$ 633,509$ 263,553$ 3,109,899$ 1,110,102$

TotalsWater Utility Sewer Utility Storm Water Utility

City Council | August 26, 2021 New Business | Item 1 | Page 20 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(13)

GENERAL FUND BUDGETARY HIGHLIGHTS

As shown in the Budgetary Comparison Schedule for the general fund (in required supplementary information), the City ended the year with a net negative budget variance of $911,704. Revenues and other financing sources were $158,595 more than the budgeted amounts and expenditures and other financing uses were $1,070,299 more than amounts budgeted. CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets The City’s investment in capital assets for its governmental and business-type activities as of December 31, 2020 and 2019, net of accumulated depreciation, is shown below:

Capital Assets, Net of Accumulated Depreciation December 31, 2020 and 2019

2020 2019 2020 2019 2020 2019Not Subject to Depreciation:

Land and Land Rights 1,266,326$ 1,266,326$ 126,676$ 126,676$ 1,393,002$ 1,393,002$ Construction Work in Progress 663,352 1,936,460 84,569 13,275 747,921 1,949,735

Subject to Depreciation:Buildings and Improvements 10,432,026 10,381,298 - - 10,432,026 10,381,298 Improvements other than Building 2,109,722 1,637,349 - - 2,109,722 1,637,349 Equipment 2,666,924 2,649,717 - - 2,666,924 2,649,717 Vehicles 2,777,289 2,526,273 - - 2,777,289 2,526,273 Infrastructure 47,778,200 44,424,997 - - 47,778,200 44,424,997 Water System Plant - - 14,222,181 13,173,188 14,222,181 13,173,188 Wastewater System Plant - - 8,679,531 7,848,729 8,679,531 7,848,729 Storm Water System Plant - - 4,279,059 3,560,522 4,279,059 3,560,522

Subtotal 67,693,839 64,822,420 27,392,016 24,722,390 95,085,855 89,544,810 Accumulated Depreciation 26,506,106 24,184,194 8,675,578 8,025,972 35,181,684 32,210,166

Total 41,187,733$ 40,638,226$ 18,716,438$ 16,696,418$ 59,904,171$ 57,334,644$

Governmental Activities Business-Type Activities Totals

Additional information related to the City’s capital assets is reported in Note 4 following the financial statements.

City Council | August 26, 2021 New Business | Item 1 | Page 21 of 91

CITY OF ALTOONA, WISCONSIN MANAGEMENT’S DISCUSSION AND ANALYSIS

YEAR ENDED DECEMBER 31, 2020

(14)

Long-Term Obligations At December 31, 2020, the City had outstanding $25,250,044 of long-term debt and other long-term obligations. A summary detail of this amount, together with the net change from the previous year, is shown below:

Outstanding Long-Term Obligations December 31, 2020 and 2019

%

LONG-TERM OBLIGATIONS 2020 2019 2020 2019 2020 2019 ChangeLong-Term Debt

General Obligation Notes 14,846,000$ 14,843,000$ 2,551,000$ 2,933,000$ 17,397,000$ 17,776,000$ -2.1%State Trust Fund Loans 6,392,832 6,972,545 - - 6,392,832 6,972,545 -8.3%

Other Long-Term ObligationsMortgage Revenue Bonds - - 435,941 475,603 435,941 475,603 -8.3%Developer Incentives 135,000 135,000 - - 135,000 135,000 0.0%Landfill Post-Closure Liability 32,040 32,040 - - 32,040 32,040 0.0%Compensated Absences 638,997 555,535 - - 638,997 555,535 15.0%Net Unamortized Debt Premium 198,974 164,012 19,260 22,405 218,234 186,417 17.1%

Total 22,243,843$ 22,702,132$ 3,006,201$ 3,431,008$ 25,250,044$ 26,133,140$ -3.4%

Governmental Activities Business-Type Activities Totals

Under Wisconsin State Statutes, the outstanding general obligation long-term debt of a municipality may not exceed 5 percent of the equalized property value of all taxable property within the jurisdiction. The applicable debt of the City outstanding at December 31, 2020 totaled $17,397,000, approximate 43.2 percent of the maximum legal limit of $40,300,775. Additional information related to the City’s long-term debt is reported in Note 5 following the financial statements. CURRENTLY KNOWN FACTS

The State of Wisconsin has imposed limits on the City’s property tax levy beginning with the 2006 budget year levy. Essentially, the legislation restricts the growth in the City’s property taxes (except for debt service and tax increments) to the percentage increase in the City’s equalized value due to new construction. The City approved a levy of $3,360,650 for its 2021 balanced budget, an increase of $98,850 (or 3.03%) from the 2020 budget levy of $3,261,800. REQUESTS FOR INFORMATION

This financial report is designed to provide a general overview of the City of Altoona’s finances for all those with an interest in the government’s finances. Questions concerning any of the information provided in this report or requests for additional information should be addressed to the office of the City Administrator, 1303 Lynn Avenue, Altoona, Wisconsin 54720. The City can be contacted by phone at (715) 839-6092.

City Council | August 26, 2021 New Business | Item 1 | Page 22 of 91

CITY OF ALTOONA, WISCONSIN STATEMENT OF NET POSITION

DECEMBER 31, 2020

See accompanying Notes to Basic Financial Statements. (15)

Governmental Business-Type

Activities Activities TotalsASSETS

Current Assets:Cash and Investments 10,186,394$ 6,338,420$ 16,524,814$ Taxes Receivable 9,104,140 - 9,104,140 Other Receivables 384,922 949,117 1,334,039 Inventories - 19,608 19,608 Restricted Assets:

Cash and Investments 184,178 - 184,178 Net Wisconsin Retirement System Pension Asset 595,276 49,661 644,937

Total Current Assets 20,454,910 7,356,806 27,811,716

Noncurrent Assets:Solar Investment, Net 58,012 165,751 223,763 Special Assessments Receivable 525,273 279,830 805,103 Loan Receivable 75,085 - 75,085 Land Held for Resale 1,570,524 - 1,570,524 Capital Assets:

Capital Assets Not Being Depreciated 1,929,678 126,676 2,056,354 Capital Assets Being Depreciated 65,764,161 27,265,340 93,029,501 Less: Accumulated Depreciation (26,506,106) (8,675,578) (35,181,684)

Total Noncurrent Assets 43,416,627 19,162,019 62,578,646

Total Assets 63,871,537 26,518,825 90,390,362

DEFERRED OUTFLOWS OF RESOURCESWisconsin Retirement System Pension Related 1,390,053 115,963 1,506,016 Single-Employer Other Post-Employment Benefits Related 415,644 - 415,644 Multiple-Employer Life Insurance Other Post-Employment Benefits Related 96,602 - 96,602

Total Deferred Outflows of Resources 1,902,299 115,963 2,018,262

LIABILITIESCurrent Liabilities:

Accounts Payable 635,075 240,523 875,598 Accrued Interest Payable 262,068 10,577 272,645 Other Accrued Expenses 87,309 55,652 142,961 Total Current Liabilities 984,452 306,752 1,291,204

Noncurrent Liabilities:Amounts Due Within One Year 2,940,996 491,687 3,432,683 Amounts Due in More than One Year 19,302,847 2,514,514 21,817,361 Single-Employer Other Post-Employment Benefits

Amounts Due Within One Year 78,019 - 78,019 Amounts Due in More than One Year 1,622,212 - 1,622,212

Multiple-Employer Life Insurance Other Post-Employment Benefits Liability 197,312 - 197,312 Total Noncurrent liabilities 24,141,386 3,006,201 27,147,587

Total Liabilities 25,125,838 3,312,953 28,438,791

DEFERRED INFLOWS OF RESOURCESSubsequent Years Taxes 9,020,930 - 9,020,930 Wisconsin Retirement System Pension Related 1,789,021 149,245 1,938,266 Single-Employer Other Post-Employment Benefit Related 289,381 - 289,381 Multiple-Employer Life Insurance Other Post-Employment Benefits Related 30,542 - 30,542 PSC Regulatory Credit - 42,949 42,949 Total Deferred Inflows of Resources 11,129,874 192,194 11,322,068

NET POSITIONNet Investment in Capital Assets 19,749,927 15,710,237 35,460,164 Restricted for:

Capital Projects 2,432,611 - 2,432,611 Library Operations 187,756 - 187,756 Loan Programs 225,627 - 225,627 Net Wisconsin Retirement System Pension Asset 595,276 49,661 644,937

Unrestricted 6,326,927 7,369,743 13,696,670 Total Net Position 29,518,124$ 23,129,641$ 52,647,765$

City Council | August 26, 2021 New Business | Item 1 | Page 23 of 91

CITY OF ALTOONA, WISCONSIN STATEMENT OF ACTIVITIES

YEAR ENDED DECEMBER 31, 2020

See accompanying Notes to Basic Financial Statements. (16)

Charges Operating CapitalFor Grants and Grants and Governmental Business-Type

FUNCTIONS/PROGRAMS Expenses Services Contributions Contributions Activities Activities TotalGOVERNMENTAL ACTIVITIES

General Government 599,184$ -$ 59,502$ -$ (539,682)$ -$ (539,682)$ Public Safety 3,127,061 80,354 34,730 - (3,011,977) - (3,011,977) Public Works 280,731 10,119 935,922 - 665,310 - 665,310 Health and Human Services 1,750 - - - (1,750) - (1,750) Culture, Recreation, and Education 2,547,697 287,984 216,203 - (2,043,510) - (2,043,510) Conservation and Development 287,120 296,809 255,174 - 264,863 - 264,863 Interest and Fiscal Charges 439,089 - - - (439,089) - (439,089)

Total Governmental Activities 7,282,632 675,266 1,501,531 - (5,105,835) - (5,105,835)

BUSINESS-TYPE ACTIVITIESWater Utility 990,196 1,418,351 - - - 428,155 428,155 Sewer Utility 1,468,723 1,507,188 - - - 38,465 38,465 Storm Water 408,725 351,729 - - - (56,996) (56,996)

Total Business-Type Activities 2,867,644 3,277,268 - - - 409,624 409,624

Total Primary Government 10,150,276$ 3,952,534$ 1,501,531$ -$ (5,105,835) 409,624 (4,696,211)

GENERAL REVENUESProperty Taxes, Levied for General Purposes 7,269,370 - 7,269,370 Property Taxes, Levied for Debt Service 802,888 - 802,888 Mobile Home Taxes 104,382 - 104,382 Room Taxes 158,899 - 158,899 Grants and contributions not restricted for a particular purpose 181,530 - 181,530 Unrestricted Investment Earnings 1,302,036 57,384 1,359,420 Miscellaneous 151,016 90,635 241,651 Gain on Sale of Capital Assets 549,048 - 549,048

TRANSFERS (2,552,256) 2,552,256 - Total General Revenues and Transfers 7,966,913 2,700,275 10,667,188

CHANGE IN NET POSITION 2,861,078 3,109,899 5,970,977

Net Position - Beginning of Year 26,657,046 20,019,742 46,676,788

NET POSITION - END OF YEAR 29,518,124$ 23,129,641$ 52,647,765$

Program Revenues Net (Expense) Revenueand Changes in Net Position

City Council | August 26, 2021 New Business | Item 1 | Page 24 of 91

CITY OF ALTOONA, WISCONSIN BALANCE SHEET

GOVERNMENTAL FUNDS DECEMBER 31, 2020

See accompanying Notes to Basic Financial Statements. (17)

River TotalGeneral Debt Capital Prairie Nonmajor Governmental

Fund Service Projects TIF #3 Funds FundsASSETS

Cash and Cash Equivalents 7,600,667$ 743,412$ 948,464$ -$ 893,851$ 10,186,394$ Taxes Receivable 2,267,207 827,190 - 5,240,235 753,442 9,088,074 Delinquent Personal Property Taxes 16,066 - - - - 16,066 Special Assessments Receivable 525,273 - - - - 525,273 Loans Receivable - - - - 75,085 75,085 Other Receivable 146,454 - - 238,468 - 384,922 Advances to Other Funds 2,016,951 - - - - 2,016,951 Land for Resale 471,651 - 1,008,660 - 90,213 1,570,524 Restricted Cash and Investments - - - - 184,178 184,178

Total Assets 13,044,269$ 1,570,602$ 1,957,124$ 5,478,703$ 1,996,769$ 24,047,467$

LIABILITIES, DEFERRED INFLOWS OFRESOURCES AND FUND BALANCES

Liabilities:Accounts Payable 231,977$ -$ 337,646$ 43,888$ 20,945$ 634,456$ Accrued Liabilities 84,524 - - - 2,785 87,309 Due to Other Governments 608 - - - 11 619 Advance from Other Funds - - - 1,597,066 419,885 2,016,951

Total Liabilities 317,109 - 337,646 1,640,954 443,626 2,739,335