Chibuzor Project work

138

CHAPTER ONE 1.0 INTRODUCTION Insurance brokers prefer to have special skill and knowledge about insurance and are therefore, liable for damages for failure to exercise due care and skill on the discharge of their duties. Ojukwu (2011:2012) Insurance play very important role on the economic development of the nation. By the nature of insurance business, insurers accumulate vast sums of money which are invested in the various facets of the Nigerian economy. According to Ojukwu (2011:190) the law of Agency is an important subject on the study of insurance law and practice the importance of Agency is attributed to the fact that most of the insurance transactions are carried on through insurance intermediaries either as ordinary insurance agents or insurance brokers which is based on fiduciary duties. 1

Transcript of Chibuzor Project work

CHAPTER ONE

1.0 INTRODUCTION

Insurance brokers prefer to have special skill and

knowledge about insurance and are therefore, liable for

damages for failure to exercise due care and skill on

the discharge of their duties. Ojukwu (2011:2012)

Insurance play very important role on the economic

development of the nation. By the nature of insurance

business, insurers accumulate vast sums of money which

are invested in the various facets of the Nigerian

economy. According to Ojukwu (2011:190) the law of

Agency is an important subject on the study of

insurance law and practice the importance of Agency is

attributed to the fact that most of the insurance

transactions are carried on through insurance

intermediaries either as ordinary insurance agents or

insurance brokers which is based on fiduciary duties.

1

1.2 BACKGROUND OF STUDY

Industrial and General Insurance Plc (IGI) was

incorporated as a limited liability company on 31st

October, 1991 and commenced operation on January 1992,

bringing with it fresh beneath of dynamism and

innovation on to the Nigerian Insurance Industry. IGI

group is the largest underwriter on West Africa,

Insurance and remains in the flagship of the 19 group

which has shareholders finds on excess of N31 billion

and assets base an excess of N45 billion with

subsidence and strategic investment on other diverse

sectors and Washington D.C. the company achieved N9.394

billion on gross premium in 2009 from N8.4 increase of

11% or N966 million. Arising from the increase in gross

premium session also lose by 12% for N2.355 million. In

2008 to 2.631 in 2009. The company recorded a 28%

decrease an acquisition cost from N13 billion as a

result of increase in premium generated from direct

2

business. This is as a result of reduction in the total

amount paid as commission. Investment and other income

decrease by 48% to 1.08 billion in 2009 from 2008 due

on part to the reduction on investment income under

life business occasionally placement with banks. I.G.I

Company made a loss of N2.72 billion during the year

under review as recorded in 2008. This made the

shareholders fund to decline from N28.8 2009. However,

total assets remained stable at N37.895 billion.

ORGANIZATION STRUCTURE OF I.G.I

3

Oil and GasClaim

Marine and AviationRe-Insurance

Motor

Fire & AccidentContractors Lega

lPersona

l

BOARD OF DIRECTORS

MANAGING DIRECTOR

Marketing Technical Finance Administration

BOARD OF DIRECTOR

General Dr. Yakubu Gowon

GCER, Ph.D, PSC, JSSC

Chairman

He has been the chairman of the board of IGI since

its inception and currently leads a board of members

that lends its skills and years of experience to

directing the strategy of the company. He was the

Nigerian head of state and commander-in-chief of the

Armed Forces from 1966 to 1975.

4

Apostle Hayfoxo I. Alile

OFR, BA, MBA (Hon) DSC

Director

As well as being a director in the IGI board, he

was director of the Central Bank of Nigeria (1995-

2005). Since has retirement as the Director

General/Chief Executive Office of the Nigeria stock

exchange, he still serves in the governing council of

the exchange as well as on the board of the Nigeria

Security Printing and Minting Company Plc. A former

president of the Harvard Business School Association of

Nigeria, Apostle Alile is a fellow of each of the

institute of directors. The Nigeria institute of

management as well as the Charter Institute of Stock

Brokers.

Chief Gaffer & Animashawum

LLB (London) B.L

Director

5

Holds an LLB degree from the University of London

and is a Barrister of the middle temple. He has his own

Law practice successfully for several decades. His

business interest include insurance and construction

services amongst others.

Mr. Ola Vincent

CRF, B.com (Hons) DSC

Director

Served as the governor of the Central Bank of

Nigeria between 1977 and 1982. He performed the

national duty meritoriously setting exemplary standards

in accountability probity and efficiency.

Dr. Lateef Adegbite

Com, Ph.D (London)

He is a highly respected legal practitioner,

businessman as well as a social and religious leader. A

former attorney general of the Western state of

Nigeria, he is the Secretary-General of Nigeria Supreme

6

Council of Islamic Affairs, he is the principal partner

of Lateef Adegbite & Co. a leading Law firm which

specializes in commercial Law practice. His wealth of

knowledge and experience to the I.G.I board.

Mrs. Olubunmi Olowude

AILMT

Director

She is a laboratory scientist by profession and

has a distinguished career at the Nigeria National

Petroleum Corporation (NNPC) from which she retired as

head of Medical Laboratory Department.

Management Team Of Industrial And General Insurance

(IGI)

Remi Olowide OON - Executive Vice Chairman

Rotimi Fashiola - Deputy Managing Director

Sina Elusakimi - Executive Director

(Specialized)

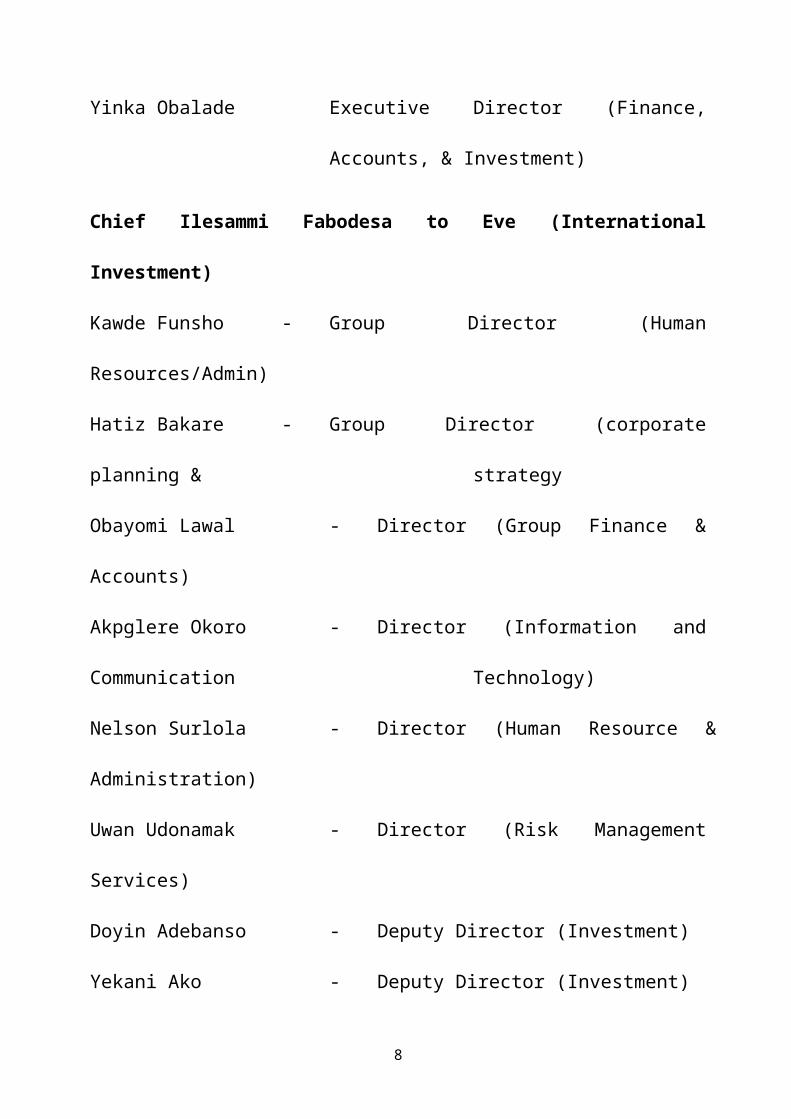

7

Yinka Obalade Executive Director (Finance,

Accounts, & Investment)

Chief Ilesammi Fabodesa to Eve (International

Investment)

Kawde Funsho - Group Director (Human

Resources/Admin)

Hatiz Bakare - Group Director (corporate

planning & strategy

Obayomi Lawal - Director (Group Finance &

Accounts)

Akpglere Okoro - Director (Information and

Communication Technology)

Nelson Surlola - Director (Human Resource &

Administration)

Uwan Udonamak - Director (Risk Management

Services)

Doyin Adebanso - Deputy Director (Investment)

Yekani Ako - Deputy Director (Investment)

8

Reuben A. Gbiyah - Deputy Director/Co-ordinator

(North East Operations)

Doann Adekanmbor - Deputy Director cooperate

communicating

Leke Ogunbanbo - Deputy Director (legal)

Nhamo Manadea - Deputy Director (Life

Operations)

Chiyioke Ezikpe - Deputy Director (Private

sector marketing)

AMERICAN INSURANCE INTERNATIONAL COMPANY (AIICO)

AIICO Insurance Plc, commenced operations in 1963,

and became a public liability company in 1989; in 1990

AIICO got listed on the Nigeria Stock Exchange. AIICO

stability, strength, security and trust over the years

have placed AIICO Insurance Plc at a better advantage

in all classes of life Assurance, AIICO global

affiliation have also enable them to provide the widest

range of Non-life Insurance solutions to his clients.

9

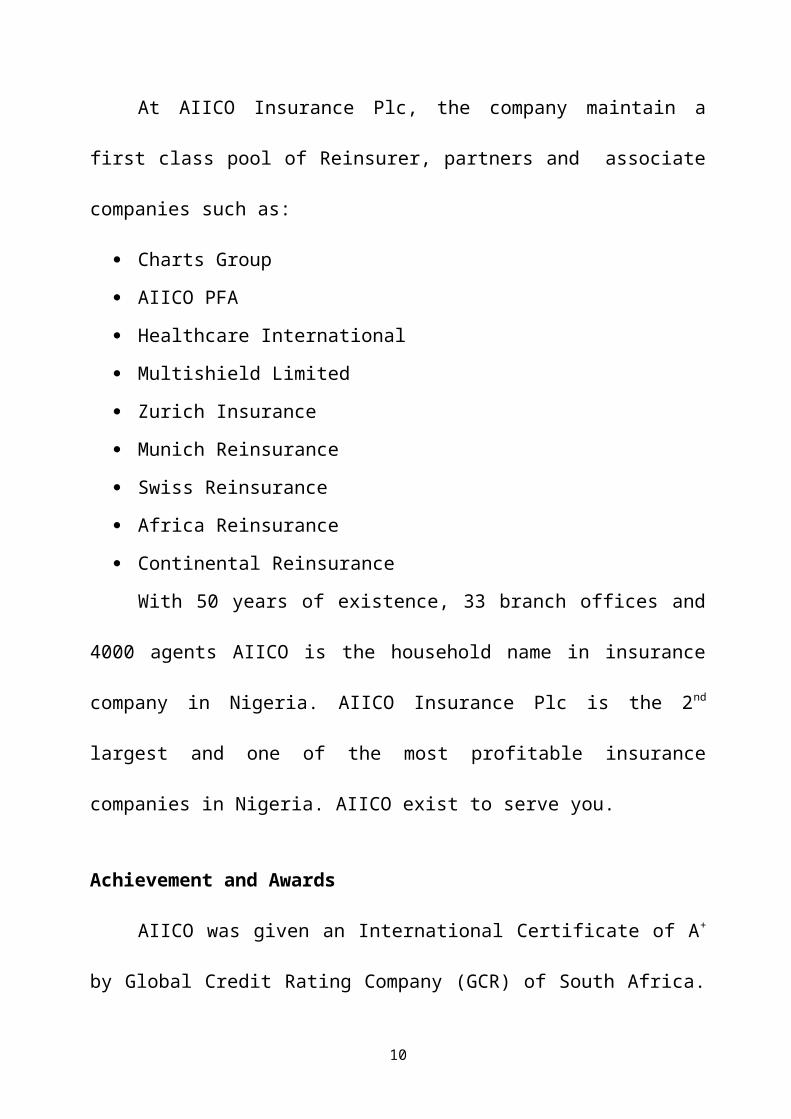

At AIICO Insurance Plc, the company maintain a

first class pool of Reinsurer, partners and associate

companies such as:

Charts Group

AIICO PFA

Healthcare International

Multishield Limited

Zurich Insurance

Munich Reinsurance

Swiss Reinsurance

Africa Reinsurance

Continental Reinsurance

With 50 years of existence, 33 branch offices and

4000 agents AIICO is the household name in insurance

company in Nigeria. AIICO Insurance Plc is the 2nd

largest and one of the most profitable insurance

companies in Nigeria. AIICO exist to serve you.

Achievement and Awards

AIICO was given an International Certificate of A+

by Global Credit Rating Company (GCR) of South Africa.

10

AIICO is a socially aware and responsible corporate

entity. The company believe in impacting positively

within the environment, he operates and contributing

his quota to the nations development as a good

corporate citizen.

To this end AIICO is currently a:

Supporter of the United Nation International

Children Education Funds (UNICEF) Card Initiative.

Donor to the motherless babies home, Isolo Lagos.

Donor to the Pricelli School for the Blind,

Surulere, Lagos.

AIICO’s furniture donation to school and offices

in Iru-Victoria Island Local Government

Development Area as part of his relations policy.

Cash donation to Evaron Nursery and Primary school

Surulere.

AIICO is a financial services company supported by

a team of experienced professionals and risk management

11

specialist who design bespoke solutions that cater to

the versatility of his client individual needs.

AIICO services include:

General insurance and special risks

Life insurance

AIICO insurance is the largest life insurer in

Nigeria and major underwriter for General Insurance

business. AIICO is a key player in Oil and Gas rated on

the top three for General Insurance business in

Nigeria. AIICO travel insurance unit is currently the

market leader in the industry AIICO offer a wide range

of products and services in General insurance for

retail and institutional customer. These include, but

are not limited to:

Fire and special perils

Health Insurance

Motor

Burglary and House breaking

12

Group personal accident

Goods-in-transit public liability

Professional indemnity

Fidelity guarantee

Marine

Travels

Personal liability

Oil and Gas

Aviation

Engineering

Bendo

Director and office liability

CORPORATE MISSION AND VISION

AIICO Mission

AIICO exist to create and protect wealth for his

clients.

AIICO Vision

To become the indisputable leader in all markets he

chose to play in AIICO core values

13

Service Excellence

Trust

Team spirit

Entrepreneurship

Professionalism

Management Profile

Mr. S.D.A. Sobanyo, GMD/CEO - B.Sc, MSC, MBA, FCH

Mr. Onolabi Salami, Chief Client Officer - UB, BL

Mr. Jide Orimolade, Executive Director - B.Sc,

MSC, ACIN

Mr. F.I. Olabiyi, General Manager – MBA, FCII

Mr. Dipo Oguntuga, General Manager – B.Sc, MBA

Mr. Lekan Otusanya, Chief Finance Officer – BA,

FCA

Mr. Moruf Apampo, General Manager – MBA, ACIIN

Mr. Babatunde Fayemirokun, General Manager – B.Sc,

MSC

Mr. Sola Ayayi Deputy, General Manager – B.Sc

14

Mr.s Phil Maduagwu, Deputy General Manager – BA,

MA, MSC, ACIM

Mr. S.A. Oduroye, Deputy General Manager/Company

Secretary – LLB, LLM

Mr. S.A Lawal, Deputy General Manager – MBA, ACLL,

ACLLN, FLLN

1.2 MARKET ENVIRONMENT

According to www.efina.org.ng, the Nigeria

Insurance market like that of other countries around

the world has a long way to go in serving the needs of

the ordinary people. Indeed insurance in Nigeria is

still for the elite and the formally employed. However,

insurance apex body NAICON under the leadership of Mr.

Fola Daniel has introduced Micro insurance products to

be accessed by the low income earners, as takaful

insurance products was alongside introduced to the

insuring public to cut – through religious impediments

on insurance products as well as to deepen the

15

awareness. Conversely the Chartered Insurance Institute

of Nigeria (CIIN) lunched books for the study of

insurance at secondary school level to prepare students

writing insurance at INAEC LEVEL. However, the industry

is not immuned from myriad of challenges such as

complying to the (IFKS) international financial

recording system which 60% insurers are yet to comply

with. As ware acquisition of insurance companies is

also witnessed. The claims payment of Nigeria Insurance

companies without any element of doubt is been

skyrocketed as hundreds of vehicles are damaged and at

level 5000 lives lost due to the nefarious activities

of the Boko Haram insurgent. Thereby depleting the

motor insurance portfolio reserves and group life

assurance portfolio reserves of Nigeria Insurance

Companies.

1.3 STATEMENT OF THE PROBLEM

16

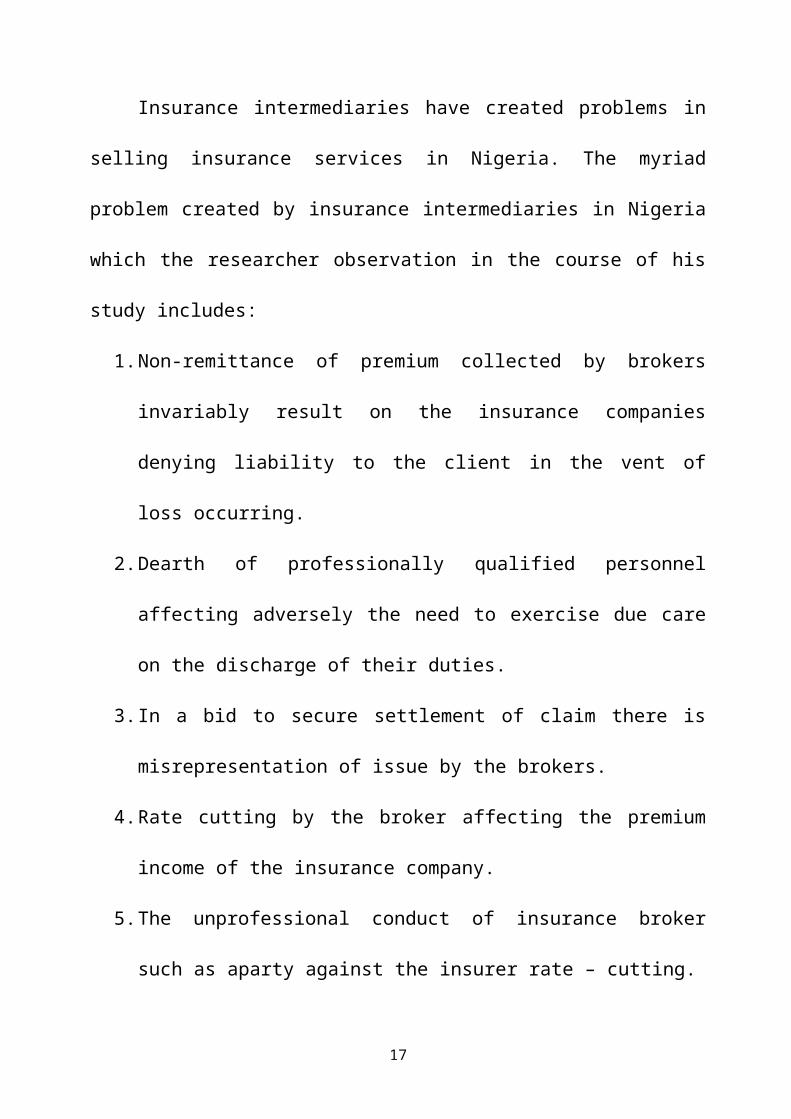

Insurance intermediaries have created problems in

selling insurance services in Nigeria. The myriad

problem created by insurance intermediaries in Nigeria

which the researcher observation in the course of his

study includes:

1.Non-remittance of premium collected by brokers

invariably result on the insurance companies

denying liability to the client in the vent of

loss occurring.

2.Dearth of professionally qualified personnel

affecting adversely the need to exercise due care

on the discharge of their duties.

3.In a bid to secure settlement of claim there is

misrepresentation of issue by the brokers.

4.Rate cutting by the broker affecting the premium

income of the insurance company.

5.The unprofessional conduct of insurance broker

such as aparty against the insurer rate – cutting.

17

1.4 OBJECTIVE OF THE STUDY

The researcher has the following objective to

pursue:

To determine whether insurance brokers have

performed their duty by exercising due care on the

discharge of their duty.

To examine whether insurance intermediaries are

performing up to expectation in their role to assist

the insuring public.

To find out whether intermediaries assist in

claims settlement procedure.

Determining whether insurance intermediaries in Nigeria

have contributed toward the distribution of insurance

services in Nigeria.

1.5 SCOPE OF THE STUDY

This research work will focus on an examination of

the contribution of insurance intermediaries to the

18

insurance industry. The researcher will use Industrial

and General Insurance Plc (IGI) and American Insurance

International Company (AIICO) as a case study.

1.6 SIGNIFICANCE OF THE STUDY

In view of extensive research carried out, it is

expected that this study will help intermediaries and

insurers in packaging their services in a way that will

contribute to the growth of the insurance industryss.

This study also placed a special importance. The

contributions of insurance intermediaries in selling

insurance services in Nigeria. It is expected that the

study will help insurance intermediaries in overcoming

or portraying the constraint which the intermediaries

create in displaying their duties to the insurer and

the insuring public. The study will as vital

information to potential new entrance into the industry

as they will avoid or improve on such constraint. It

19

will equally aid the existing intermediaries in

overcoming such problems in future.

1.7 STATEMENT OF HYPOTHESIS

The researcher formulated the following hypothesis

from the problem identified.

HYPOTHESIS I

H0: Non-remittance of premium collected by brokers

does not result in the insurance companies denying

liability to the insured in the event of loss

occurring.

H1: Non-remittance of premium collected by broker

results in the insurance companies denying

liability to the insured in the event of loss.

HYPOTHESIS II

H0: Rate-cutting by the broker does not affect the

premium income of the insurance company.

H1: Rate-cutting by the brokers affects the premium

income of the insurance company.

20

1.8 DEFINITION OF TERM

1.Indemnity: Placing the insured, subject to the

policy terms in the same financial position after

a loss as the insured occupied immediately before

the happening of an insured event Ojukwu

(2011:127).

2.Insurance Broker: Insurance broker profess to have

special skill and knowledge about insurance and

therefore liable for damages for failure to

exercise due care and skill in the discharge of

their duties Ojukwu (2011:193).

3.Utmost Good Faith: It is the duty of the assured,

the man who desires to have a policy to make a

full disclosure to the underwriter without being

asked of all material circumstance because the

underwriter known nothing and the assured knows

everything, Lord Justice Scrutton in Rozanes V.

Bowen 1928.

21

4.Proximate Cause: This is active efficient cause

that set in motion a train of events which brings

about a result without the intervention of any

force started and working actually from new and

independent source. Ojukwu (2011:155).

5.Insurance Intermediaries: These are middlemen who

are in Business to sell insurance covers on behalf

of the insurance companies to the buyers of

insurance.

6.Remittance: A sum of money that is sent to

somebody in order to pay for something.

7.Agent: A person whose job is to act for or manage

the affairs of other people in business.

8.Premium: The consideration given by the insured in

return for the insurers undertaking to cover the

risk against in the policy of assurance. Lewish V

Norwich Union Fire Insurance Co. Ltd 1916.

9.Ostensible Authority: A legal relationship between

the principal and contract or created by a

22

representation made by the principal to the

contractor, intended to be and infact acted on by

the contractor that the agent have authority to

enter on behalf of the principal into a contract

of a kind within the scope of the “apparent”

authority, so as to render the principal liable to

perform any obligation improved on him by such

contract. Ojukwu (2011:203).

10. Avalanche, Mass or plenty of something.

23

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

In this chapter the researcher will analyse the

avalanche of various literary works such as textbook,

newspapers, presented papers as well as various

legislations. The review of these literary work will

enable the researcher establish their relevance to the

project work. The study of the contributions of

insurance intermediaries to the insurance industry,

insurance plays a major role on the economic

development of Nigeria through the investment of the

economic development of Nigeria through the investment

of the vast sum of fund at their disposal. According to

Ojukwu (2011:190) most of the insurance transactions

are carried on through insurance intermediaries either

as ordinary insurance agents or insurance brokers.

24

2.1 THE DEVELOPMENT OF INSURANCE IN NIGERIA

Prior to the colonization of Nigeria, there was no

organized insurance business as we know it today.

Instead, there existed some traditional system of risk

sharing. Each ethnic group given it’s culture used the

social institutions it had to spread risk amongst them.

A look at the Igbo ethnic group would prove so. The

institution for risk sharing in the Igbo ethnic group

involved the extended family system. Polygamous family

system, age-grade associations, claim union, masquerade

groups, isusu association, trade or craft union, etc.

These institution offered mutual insurance like schemes

for strong benevolence to their members who has

suffered some misfortunes such as death,ill health,

fore ranges or court cases.

The coming of the early British traders who

established trading post on the west coast of Africa

25

raised the need for modern insurance. It started with

the appointment of operate agents to render insurance

services as representative of their mother insurance

companies based on Britain. In 1918, the Royal exchange

Assurance company started operation in Nigeria and was

represented by Barclay back DCO, until February 1921,

when it was converted to a full branch of the parent

company. It operated alone until 1949 when three other

British companies entered the scene. There were tobacco

insurance company limited, the legal and general

assurance society limited and the Norwich Union fire

insurance limited, Dr. Kingsley O. Mbadiwe in 1950

established the first indigenous insurance company, by

1960, there was as many as 25 insurance companies in

Nigeria, out of which 4 were indigenous insurers. As at

1970 the number of registered insurance companies in

Nigeria grew to 66, a lot of operations were moving in

to their share of what was perceived to be a goldmine.

26

The surge contain with its attendant problem such that

there was the need for legislatives to streamline the

insurance business in Nigeria.

2.2 INCORPORATION AND REGISTRATION OF INSURANCE

COMPANIES

Before persons may commence to carry on insurance

business in Nigeria, he will first have to incorporate

and register the company under companies and allied

matters Acts 1990 under section 4 of 2003 Act provides

that subject to the provision of his Act no insurer is

registered by the commission under this Act.

Registration of insurance under section 5 Act states

that an application for registration as an insurer

shall be made to the commission in the prescribed form

and such other document or information as the

commission may from time to time or require.

27

In insurance no person shall commence or carry on

any class of business in Nigeria except

(a) A company duly incorporated on a limited

liability company under the company and allied

matter Act 1990

(b) A body duly established by or pursuant to any

other enactment to transact the business on

insurance or reinsurance section 34.

In respect of insurance brokerage company section

36 of insurance Act 2003 provides that no person shall

transact business in Nigeria as an insurer broker

unless he is registered under this Act section 36(2)

states that a person who transact business as an

insurance broker without having being registered on

that behalf under this Act commits an offence on is

liable to conviction. Moreso in respect of the

operating as an insurance Act 2003 provides that no

28

person shall transact business as an insurance agent

unless

a) He possesses a certificate proving the individual

application by the chartered insurance application

institute of Nigeria referred to this Act as the

institute is duly appointed by our insurer and censed

in that halt under this Act section 34 (2) state that

an application for a license as an insurance agent

shall be made to the commission in the prescribed form

and be accompanied by the prescribed fee and such other

document as prescribed from time to time.

2.3 REGULATION OF INSURANCE COMPANIES IN NIGERIA

According to Ojukwu (2006:36) he propounded that

the Federal government has through various legislations

been very active on the development of insurance

company. The motor vehicle (third party insurance) Act

1945 was the earliest legislation on insurance in

29

Nigeria. Federal government of Nigeria intervention was

necessary in order to guarantee future development of

insurance business and also to ensure that insurance

companies honour their obligation to members of the

public. In order to achieve establishment of a vehicle

insurance industry, parliament set up Obade commission

whose report formed the books of insurance companies

Act 1961 Ojukwu(2011:64).

2.3.1 INSURANCE COMPANIES ACT 1961 AND 1964

The insurance companies Act 1961 laid the

foundation for registration and development of

insurance companies in Nigeria. The Act provides for

registration and development of insurance companies and

prescribed a statutory minimum capital of £25,000 for

and general insurance £50,000.00 for composite

insurance company. The insurance companies Act was

closely followed by the insurance (miscellaneous

30

provision) Act which required all insurance companies

operating in Nigeria to be incorporated locally. The

act further required that insurance companies invest

40% of it’s net premium in Nigeria. The insurance

companies Act and insurance miscellaneous provisions

Act did not provide for effective supervision of

insurance companies and had to be replaced by insurance

Decree of 1976. Ojukwu (2011:64).

2.3.2 Classification of Insurance Business in

Nigeria

Statutorily insurance business is divided into two

main classes insurance Act 2003 provides as follows;

a.Life assurance business

b.Non-life insurance (General) Business

Section 2 in the case of life assurance; the shall be 3

categories;

31

a. Individual life Assurance

b. Group life assurance and person business

c. Health insurance business

In the case of general insurance, there shall be 8

categories

a.Fire insurance business

b.General accident insurance business

c.Motor vehicle insurance business

d.Marine and aviation insurance business

e.Oil and gas insurance

f.Engineering insurance business

g.Bonds credit guarantee and surety insurance

business and

h.Miscellaneous insurance business.

DIAGRAMMATIC CLASSIFICATION OF INSURANCE SECTION 2 (1)

INSURANCE ACT 2003

32

CLASSIFICATION OF INSURANCE

Life Insurance Business

General Insurance Business

Health Insurance

Oil & Gas

Group and

Person

Motor

Engineering

Marine & Aviation

Bonds & credit Guarantee

Fire Individual

Life

Gene

ral

Acci

dent

Miscellaneous

2.3.3 Nature of Insurance

The nature of insurance is that the good fortunes

of the many are used to compensate the misfortune of

the few. The community makes contributions into a

common fund of which those of their members who suffer

33

losses are compensated. This community of people

contributing into the common fund is described as

policy holders. The policy holders know that

misfortunes such as death, personal accident, burglary

auto accident, failed credit as in banks and other

financial institute, losses and stopping of income etc

befall humanity, they have seen it to their members

they have heard of it happen to others and they know

for sure that these can happen at their own time, the

only uncertainty being when, how and to whom it will

happen. By insurance arrangement the policy holder

(contributions) has transferred those risks to the

central managers of the funds (Insurance companies)

with the aim that should any fall victim of any

casualty they will compensate them with the central

fund in order words, insurance is all about risk

transfer.

2.4 PRINCIPLE OF INSURANCE

34

Insurance is governed by well defined principles,

the research will discuss the under mentioned

principles

a) Indemnity

b) Utmost good faith

c) Insurance interest

d) Proximate cause

2.4.1 Indemnity

According to Ojukwu (2011:923), the principle of

indemnity requires that insured cannot recover more

than the actual less. The definition of indemnity was

propounded by Lord Justice Bret Castilian v Preston

1883, they very foundation in my opinion on every rule

which has been applied to insurance law is this namely

that the contract of indemnity and indemnify only and

this contract means that the insured, in case of a loss

against which the policy has been made shall be full

35

indemnified, that is the fundamental principle of

insurance law and of ever a proposition is brought

forward which is at variance with of that is to say,

which either will prevent the insured from obtaining a

full indemnity or which will give the insured more than

a full indemnity that proposition must certainly be

wrong. Insurers indemnity fear insured in the event of

loss in the following ways,

1.Case payment: Minor losses are settled by means of

cash payment to the insured who is obliged to

support his claim with necessary, purchase of

document where the loss is extensive, has

adjuster will be engaged to establish the amount

of his and the insurers will effect settlement of

the amount in practice insurers settle claims by

cheque.

2.Repairs; repair the vehicle is a means in which

the insurer provide indemnity where a vehicle is

36

involved in an accident, the insurers usually

authorize or motor garage to effect repairs. In

Oshevire Ltd V. Tripoh motor, the insurers

authorized Tripoli motors to effect repairs of an

accidental vehicle on the understanding that the

insurer would pay the bill. The insurers refused

to pay the bill on the grounds that the vehicle

was not satisfactory repaired and argued that the

auto engineer want not a party to the contract of

insurance. The court of Appeal held that the

agreement was a tripartite content and bondly by

three parties to it namely; She Insurer the

insured and the property instead of paying cash.

Replacement is usually applied in respect the high

value such as Jewelleries fares, or works of art.

Also on glass insurance the window and doors are

replaced by glazing forms who are paid by She

Insurer. Replacement is also new motor vehicle is

37

destroyed insurers can indemnity the insured by

replacing the damage vehicle with a similar model.

3.Reinstatement: in property insurance the policy

expressly gives the insures she option to pay

cash, replace repair or reinstate on the event of

any loss or damage. Once the insurer elect to

reinstate the building, they cannot with draw

because reinstatement has become onerous, insurer

are bound to reinstate to it; original condition.

Ojukwu J. C. (2011:129).

2.4.2 Utmost Good Faith

According to Ojukwu (2006:78) the definition of

utmost good faith was postulated by mainisfield in

carter v Bohm 176 insurance is contract of speculation.

The specific fact upon which the contingent choice to

be computed lie must commonly in the knowledge of the

insured only; the underwriter trust to his

38

representation and proceeds upon confidence that he

does not keep back any circumstance is his knowledge to

mislead the underwriter into a belief that circumstance

does not trust other proposition of utmost good faith

was provided by Lord Justice Scrutons in Rosance v

Bromean 1928.. It is the duty of the assured, the man

who desires to have a policy to make a pill disclosure

to the underwriter without being asked of all material

circumstances because the underwriter knows nothing and

the assured knows everything. That is expressed by

saying that is a contrast of utmost good faith

“uberemar” fide.

2.4.3 Insurable Interest

The existence of insurance interest is an

essential ingredient in any insurance contract. The

general rule is that the insured must has an insurable

interest in the subject matter of insurance, otherwise

39

the contract is void and destitute of legal effect,

simply put, the insured must have a legal relationship

with the subject matter of insurance. Irrespective of

the class of insurance be it life or non-life business.

It is important to note the legal maximize the non

action other, that is to say legal rights arrive from

illegal cause Ojukwu 2006.

Macura “Northern Assurance co. Macura owned most

of the shares of the company he had transferred his

business (timber) to the company, macura took out fire

insurance policy on his name and not in the name of the

company. The timber was destroyed by therefore. The

insurers, Northern Assurance company denied liability;

the insurers argued that mac

ura having transferred his business to the company has

no insurable interest on the timber. Lord summer said,

though macaura “owned almost all the shares in the

company and the company owned him a good deal of money

40

but neither as creditor nor as shareholder could be

insurer the company’s assets”. The concept of separate

legal entity which is central to company law,

established that the property of the company belongs to

the company not to the shareholders. Possession of

property only is not enough by itself to fund insurable

interest Ojukwu (2011L18).

2.4.4 Proximate Cause

Prompt settlement of claims is the mainstay of

insurance companies however, in order that the insured

can recover from the insurers under a policy, the

insured must establish that the loss was caused peril.

The need for a direct relationship between the cause

and effect informed the causa proxima rule, that is to

say, the proximate cause rule. The cause must be

proximate in efficiency not in time and the onus of

proofs lies with the insured. The insurer on the other

41

hand have the responsibility of establishing that the

loss is not covered because of operation an expected

peril. The classic definition of proximate cause was in

Pawsey V Scottish union and National insurance co 1908

propounded by Lumb J as the “active efficient cause

that set in motion on train of events which brings

about a result without the intervention of any force

started and working actively from a new and independent

source. It was afforded that insurers have the

responsibility of showing that the circumstances which

constitute an exercise for non-payment of the claim

have infact arisen. To use common language, she onus of

proof so far as the exeuse goes, is an onus which rests

upon the insurer”. Ojukwu (2011:51)

2.5 THE NEW PRODUCT

A new product is a set of tangible and intangible

attributes for want satisfaction which the buyer or

42

consumer perceive as new or significantly different

from the existing and/or competing products that are

being replaced. A company’s assortment of the products

must be planned. Product planning is the art of adding

and/or dropping products and modifying products

according to what the changing market requires. The

non-service product may change on size, colours,

styles, quality, fact and quantities. The insurance

product may only change in enrichment, packaging, price

and assortments, a new product must adjust it self to

the market. New product development is a significant

aspect of product planning. It is concerned with

reliably replicating successful business patterns on

the basis of the definition of a new product, three

basic types of new product can be identified;

1.Truly innovative products: These are truly unique

products of which no similar products has ever

existed, examples are the cure for acquired immune

43

deficiency syndrome (AIDS) or cancer. The category

also includes products that are completely

different from existing product but satisfy the

same needs, such as broad casting and films shows,

solar energy on relation to other existing energy

sources, plastics also serve the same purposes as

metals and woods. A unique new product should

generate profit or benefits by identifying the

customers wants and needs and translating them

into products and/or services specification that

provide the denied market share within each market

segment.

2.Replacement products: There are products that are

only significantly different from the existing

ones. Station (1981:162) noted that instant coffee

replaced ground coffee and coffee beans and that

frees-dired instant coffee replaced instant

coffee” group life insurance can replaced

44

industrial life insurance if suitably enhanced or

enriched.

Imitative products

These are products that are new to a particular

organization but not new to the market. It is a “me

too” attitude of capturing part of an existing market.

2.6 INSURANCE INTERMEDIARIES

These are the insurance middlemen who are in

business to sell insurance covers on behalf of the

insurance companies to the buyers of insurance. The

basic different between a broker and an agent is that a

broker is an insurance professional or an insurance

expert where as the agent is generally a non insurance

man whose only interest is to sell insurance in return

for his commission.

2.7 CLASSIFICATION OF INSURANCE INTERMEDIARIES

45

Insurance intermediaries can be classified as

follows;

Agents

Broker

Loss Adjusters

Agents: Legally an agent is one who is employed to

perform an act on behalf of his principal within a

specified guidance. A duly appointed agents, acting

within scope of this authority bonds his principals by

his actions just as though the principal has performed

them personally. There are full time and part time

agents. The full agents are employed on full time basis

by the insurance companies and are remunerated by way

of salary (allowance) commission or an some cases both

salary and commission. The part time agents, are

remunerated only by part time commission, because the

insurance agent is not an expert and usually not an

insurance professional, he is not required or expected

46

to posses a sound technical knowledge of the insurance

business, and he cannot be sued for professional

negligence. In insurance Act 2003, section 35,

subsection 4 it is provided that, “A person who

transacts business as an insurance agent without having

been duly appointed commits an offence and is liable on

consideration to a fine of 100,000 or to imprisonment

for a term of 3 years or to both such fine and

imprisonment and in addition, the court may make an

order requiring the person to refund any sums collected

by him, while so transacting the business, to the

rightful owners of other persons entitled there to”.

Broker: The broker is a full time special of

professional standing, or at least, the law expectation

to be, because the broker undertakes the responsibility

of advising, recommending and arranging insurance

cover, he is presumed in law to have the necessary

professional and technical knowledge of the relevant

47

class of insurance business. His primary aim is to act

for the insured in the handling of all his insurance

problems including assisting in claims settlement and

using his position and connection in the market to get

the best bargain to the insured.

In insurance Act 2003, section 36 provides that,

No person shall transact business in Nigeria as an

insurance broker unless he is registered under this

Act.

b) Application for registration as an insurance broker

shall be made to the commission in the prescribed form

and accompanied by the prescribed fee and such other

document as may be prescribed from time to time

c) If the commission is satisfied that the applicant;

i. Has the prescribed qualifications and

ii. Is a partnership or a company with limited

liability duly registered under the companies and

48

allied Matters Act, 1990, it shall register the

applicant as an insurance broker by issuing the

applicant with a certificate of registration.

4) No form or company shall be registered under this

section unless each partner, chief executive and

executive director is registered as an insurance broker

by the institute.

Low Adjuster; A loss adjuster is a professional

intermediary whose primary function is to investigate

insurance claims with the ultimate view of making

impartial recommendation to the insurer regarding the

extent of their liability under the terms of the

policies. Where liability is established the loss

adjuster has the task of adjusting the claim

appropriately, within bias, and this will be contained

in his report to the insurer. He plays the role of an

49

independent arbiter. To be able to accomplish his

functions adequately, the loss adjuster should be

thorough in his investigation, be transparent honest,

just and fair. His integrity should not be in doubt by

the insurance industry since insurers are expected to

rely on his advice. Also he is expected to be vastly

knowledgeable and experience in several disciplines to

be able to cope with the diversities and complexities

of some claims situation. In essence the adjuster will

be required to make an inspection at the scene and to

discuss the claim, often at length with the insured and

witness with a view to preparing a written report which

for example, in the case of fire would necessitate

giving exact details of the premises, their

construction and occupation, an accurate account of the

event surrounding the fire, a precise description of

the damages, an opinion as to the cause of the fire, if

necessary a well argued opinion as to the possibility

50

of obtaining a recovery against any third party and

finally recommendation as to the amount to be paid on

settlement of the claims reference being made to the

cost of reinstatement or repairs together with comments

concerning adjustments made for depreciation or

appreciation salvage, application of policy limits,

excess and average conditions, and occasionally

recommendations for the improvement of risk.

2.7.1 Classification Of Insurance A Gents

The following are the classification of insurance

agents

Ordinary insurance agent

Insurance brokers

Lloyds broker

51

AGENT

Ordinary Insurance Agents

Full Time Agent

Staff Agent Independent Agent

Non-Insurance Agent

Estate Agent

De Credere Agent

Factor Agent

InsuranceBroker

Lloyd’s Broker

Brokers

2.7.2 Ordinary Insurance Agent

Ordinary Insurance Agent as intermediaries are not

required to possess professional knowledge of the

technicalities of the insurance they arrange, however,

a reasonable degree of proficiency insurance is

mandatory. Section 34 (1) insurance Act provides that

no person shall transact business as an insurance agent

unless he possess a certificate of proficiency issued

in the name of the individual applicant by the

chartered insurance institute of Nigeria. A licence

52

issued to an insurance agent shall entitle the holder

to act as an insurance agent to the insurer. Ordinary

insurance agents are further categorized into the

following groups

i. Full Time Agents: These are agents employed by an

insurer to concern for insurance business

exclusively for the particular insurance company

that engaged them.

ii. Independent agents: these are insurance agents not

lied to any particular insurer and include

Bankers, motor dealer, Accountants retired

insurance practitioners

iii. Staff Agents. Staff agents are usually authorized

by their employers to act as agents to the

company. Such staff agents are paid commission in

respect of business introduced. Ojukwu (2011:194).

2.7.3 Insurance Brokers

53

Insurance brokers typically work for the policy

holders in the insurance process and act independently

or relation to insurer. Brokers assist clients on the

choice of their insurance by presenting them with

alternatives in terms of insurer and products. Acting

as “agent” for the buyer brokers usually work with

multiple companies to place coverage of clients.

Brokers obtain quotes from various insurers and guide

clients in determining the adequate policy from a range

of product. Insurance brokers profess to have special

skill and knowledge about insurance and for damages for

failure to exercise due care and skill on the discharge

of their duties. By virtue of section 36 (1) insurance

Act –no person shall transact business in Nigeria as an

insurance broker unless he is registered under the Act.

The applicant must be a company with limited liability

and registered under the companies and allied Matters

Acts. Section 36 (3) (b).

54

2.7.4 Lloyds Brokers

Lloyd’s underwriters has its origin from the

activities of merchants who gathered at the coffee

house in the city of London owned by a proprietor

called Edward Lloyds. Merchants seeking insurance cover

for various risks namely ship, voyage and cargo will

pass round a slop containing the details of the risk.

Each participating member will accept proportion of the

risk according to his financial ability. The contract

was fully executed when the total value at risk is full

underwritten. This practice led to the use of the term

underwriter. Ojukwu (2011:195).

2.7.5 Non-Insurance Agents

It is important to note that there are

intermediaries who are non insurance agents and these

include the following;

55

1.Estate Agents; An estate agent is a person who us

engaged to find a buyer for a property, and has

implied authority to make representation on the

property whether or not estate agents is paid will

depend on terms of engagement.

2.Del Credere Agent: De credere agent is an agent

engaged to sell goods and for extra remuneration he

undertakes that the purchaser he finds will pay, for

the goods he buys. He does not guarantee any other

liability of the purchaser, for instance if the

purchaser refuses to take delivery. Ojukwu

(2011:198).

3.Factor Agents: A factor agent is a mercantile agents

who has authority over goods consigned to him, to

sell the goods in his name and has a general

discretion over the goods. The agent can refuse money

on the security of the goods. See Factors Act section

1889 section (1). Folks v king 1923, in folk case,

56

the owner of a car delivered it to mercantile agent

Hudson for sale for the equivalent of N150,000.00.

Hudson sold the car for the equivalent of N90,000.00

to king who bought in good faith without notice of

fraud. Hudson misappropriated the M90,000.00 and

folks sued King for the recovery of the car. It was

held that King acquired good title. Scrutton L. J

said that it is enough to show that the true owner

did internationally deposit in the hands of the

mercantile agent the goods in question Ojukwu

(2011:198).

4.Agent of Insured: a general rule, only the agent

under the direct control of the insurer is the agent

of insurer, all other agents are deemed to be the

agent of the insured. It was noted that insurer are

required to print conspicuously on the front page of

the proposal form that an insurance agent who assist

57

an applicant to complete a proposal form is the agent

of the applicant section 54 (2) of insurance 2003.

i) If an agent is expressly appointed by the insured

to place his insurance with insurers he is agent

of the insured.

ii) If the only recognition the insurer gives to the

agent is the payment of his commission, the agent

is the agent of the insured.

iii) An agent who advises the insured where to

place his business is the agent of the insured.

The agents is liable for damages if the insured

acts on his advice and suffers a loss.

In Osman v. J Ralph Moss Ltd, the brokers

recommended to the plaintiff Osman for the purpose of

insuring his vehicle to an insurer already known in the

insurance circles to be financially weak. When the

58

company was wound up the plaintiff was involved in an

accident for which he was liable and was also fined for

driving without insurance. The broker was held liable

for the amount then insured was fined and also the

amount of damages paid to third party.

Agent of the insurer: the agent is regarded as the

agent of the insurer in the following circumstances

i) The agent is the agent of the insurer if the

insurer gives the agent proposal forms and cover

notes to execute on behalf of the insurer. See

Ngillri v NICON 1998.

ii) If the agent has express or implied authority to

collect premium on behalf of the insurer, section

41 (1) provides that where an insurance business

is transacted through an insurance broker, the

insurance broker shall not later than 30 days of

collecting the premium pay to the insurer premium

collected by him.

59

iii) If agent acted without express authority and

in the past the insurers has ratified his actions

the agent is the agent of the insurer. In Murfitt

v Royal Insurance Ltd 1992, the plaintiff secured

a fire insurance cover from the agent of the

insurer who informed him that the risk will be

held covered pending the decision of the insurers.

The insurers declined the risk before they knew

that fire had occurred. The insurer refused to

honour the risk on the ground that the agent has

no authority to grant the cover. The plaintiff

argued that the agent had in the past granted

cover, which the insurers ratified the court

decided that the fact that the agent had for two

years granted the insured cover with the knowledge

and consent of the insurer was a special factor,

the insurer were liable as the agent has implied

authority. Ojukwu (2011:201).

60

2.8 CREATION OF AGENCY AND ACCOMPANYING AUTHORITY

Agency can be created in the following way:

2.8.1 Express Creation

An agent maybe expressly appointed either verbally

or on writing. By appointment in writing specifically

for a purpose for example, where an insured appoint a

broker to his insurance. The appointment can also be

made verbally in freeman & Lockyer V. Buckhurst park

properties (mangal) ltd 1964 Lord Diplock s aid that,

“an actual” authority is a legal relationship between

principal and agent created by a consensual agreement

to which they alone are parties. It’s scope is to be

ascertained by applying ordinary principle of

construction or contracts, including and proper

implication from express words used and on the course

of business between the parties.

61

2.8.2 Creation by Estoppel

Where agency is created by estoppel, it gives rise

to an apparent or ostensible authority. The meaning of

apparent or ostensible authority was stated by Lord

Justice Diplock in freeman and lockyer v Buckhurst park

properties (Mangal Ltd 1964, the facts of the case are

that, kapoor acted as managing director of the

defendant company although there has been no

appointment of kapoor to that office. The company’s

articles of association that is, the rules regulating

the internal operations of the company, provided that

the board should appoint a managing director, the

minutes of the meeting of the company did not reflect

any such appointment. Kapoor engaged the services of

the plaintiff a form of architects and surveyors. The

company refused to pay for the services of the

plaintiff on the ground that kapoor has no authority to

engage them. It was held that the company was bound by

62

the contract. Lord Diplock stated that “an apparent” or

“ostensible authority is a legal relationship between

the principal and the contractor created by a

representation, made by the principal to the

contractor, intended to be and infact acted on by the

contractor, that agent has authority to enter on behalf

of the principal into a contract of a kind within the

scope of the “apparent” authority, so as to render the

principal liable to perform any obligations imposed on

him by such contract.

2.8.3 Implied Authority

The meaning of implied authority was given by Lord

Denning in Hely-Hutchison v Bray head Ltd 1968. The

facts of the case are that Richards the second

defendant was the chairman and chief executive or de

facto managing director of Brayhead Ltd. He often

concluded contracts on his own initiative and later

63

informed the board who acquired in Richard’s mode of

operation. The plaintiff was the managing director of

Perdio Ltd another company that planned to merge or be

acquired by the defendant company. As part of the

agreement the plaintiff became a director on Brayhead

Ltd. Mr. Richards and Hutchison agreed that the

plaintiff should invest more money in pediro ltd on

Richard signing document on behalf of Bray head to

indemnify the plaintiff. When sued on these transaction

the defendant held that Mr. Richards has no authority

to make the contracts the judge held Richard had

apparent authority to bind the decision but on the

grounds that he had actual authority. In the court of

Appeal lord Denning said that in freeman & Lockyer case

at was shown that actual authority might be expressed

or implied. It is express when it given by express

words, such as when a board of directors passes a

resolution which authorize two of their members to sign

64

cheque. It is inferred from the conduct of the parties

and the circumstances of the case, such as, when the

board of directors appoint one of their members to be

managing director. They thereby impliedly authorized

has to do such things as fall within the usual scope of

that office. Actual authority, express or implied is

binding as between the company and the agent, and also

as between the company and others whether they are

written the company or outside it.

2.8.4 Creation By Ratification

Though the initial act was unauthorized a

principal may acquire rights and subject himself to

liabilities by retrospectively approving the act of an

agent. However, there are a number of conditions that

must be satisfied before an unauthorized act of agent

can be ratified namely;

65

i. The agent must have made the contract as an agent in

the first place. In Keighley, Mazsted & Co. v Durant

1901. Keighley authorized an agent a corn merchant

to bay at a certain price; the agent exceeded his

authority and bought the can in his own name instead

of in the name of the principal. However, Keighley

agreed with the agent to take wheat at the price the

agent has agreed, but he failed to take delivery.

Durant resold at loss and sued the agent and

Keighley. The house of the lords held that the

contract cannot be ratified, as agent contracted for

himself his undisclosed intention is not enough to

warrant ratification. This is supported by an old

saying of brain CJ that it is common learning that

the thought of a man is not friable for the devil

has not knowledge of a man’s thought”.

ii. The principal must have been in existence at the

time of contract. In Kelner v Baxter 1806. The

66

Gravesend Royal Alexandra Hotel company Ltd. Was

being formed and Kelner agreed to sell wine to the

promotes of the uniformed company namely John

Baxter, n caster and J. dales. All concerned knew

that the company was being form. However, a written

agreement was signed between Kelner and the promotes

for the purchase of wine for the equivalent of

N240,000,00. The wine was delivered to Gravesend

Royal Alexandra Hotel company ltd and was consumed.

Before payment could be made the company went into

liquidation. Kelner sued the promotes who claims

that liability has passed, by ratification to the

company and no liability attached to them the

promoters were held liable. Eric C. J said that

“where a contract is signed by one who professes to

be signing an agent but who has no principal

existing at the tame, and the contract would be

altogether on the person who signed it, he is bound

67

thereby, and a stranger cannot by a subsequent

ratification receive him from responsibility.

iii. The principal must have capacity at the time of

ratification. In Grover and Grover Ltd V Mathew

1910. At the expiry of a policy the broker wrote to

the underwriters for renewal of the policy, without

the knowledge of the plaintiff. A fire occurred

after the broker requested for renewal but before

broker’s action. When the plaintiff knew about the

transaction they purport to ratify the action of the

broker. It was held that the insurers were not

liable. It should be noted that in respect of marine

insurance ratification is possible after a loss in

marine cases.

Effect of ratification: The effect of ratification is

that the principal in deemed to have made the contract

at the time when the agent did infact make it. In other

words, ratification is retrospective. In Boton partners

68

v Lambert 1888 an offer was accepted by an unauthorized

agent. This acceptance was after ratified by the

principal but before the time of ratification, the

offer or has attempted to revoke it. It was held that

by ratification the principal has become party to the

contract as from the time the agent accepted the offer.

Ojukwu (2011:201-208).

2.9 REGULATORY BODIES OF BROKERS

These are institutions and organization set up

either by government or private bodies to facilitate

insurance operation in Nigeria. These are so many

bodies representing various interest and sectors of the

Nigeria insurance market but for the study we will view

the following

The Nigeria council of Registered Insurance Brokers

(NCRIB)

69

The Nigerian Corporation of Insurance broken, the

precursor of the council was established in 1952 to

provide a central organization for the regulation of

all practising insurance brokers in Nigeria. This body

got it’s first legal recognition in 1991 when the

insurance decree no 58 of 1991 made it compulsory for

all practising insurance brokers to be members of this

body before being registered by the commissioner of

insurance. However, the brokers quest for full legal

recognition through the acquisition of a charter did

not materialize until 2033. When the National Assembly

passed the NCRIB bill and the president chief Olusegun

Obasanjo gave his assent on 4th July 2003. The name of

the body was therefore changed from “The Nigeria

corporation of insurance Broker” to “The Nigeria

council of registered insurance Brokers (NCRIB) with

the signing into law of the NCRIB Act, the insurance

broking profession received full legal powers to be

70

able to regulate the practice as reputable profession

that is an integral arm of the Nigeria insurance

industry. Section 13 of the Act confers on his body

exclusive power to regulate the conduct at all

registered insurance brokers in Nigeria (both

individual and corporate members).

2.9.1 Role Of Insurance Brokers

The brokers play a crucial role to the insurance

industry. The influence of brokers remain very high on

the industry, there is no substitute for the brokers in

the insurance market. According to chief J Akin George

(Nov. 23rd 2001 Journal) the brokers and agent serve as

link between the insured and the insurer, they are the

first contract with the insured who is being introduced

to the business perhaps for the first time. As the

English say, “The first experience lasts long” the way

and manner the broker comes across to the insured will

71

therefore determine whether a successful business deal

can be struck or not. The role of the broker has been

discussed under the following heads.

Insured

Insurer

General

Insured

The role of the broker to the insured cannot be

neglected. The broker is presumed to hold himself out

of the proposer as a person who poses a sound technical

knowledge of insurance and therefore is prepared to

give sound professional advice and arrange insurance

cover in the most favourable manner for all those who

instruct him to act for them. Therefore the duties of

the broker to the insured or proposer cannot be

underrated and so are examined here.

72

i. Use of proper skill and care: The duty of the broker

to use proper skill and care in carrying out his

broking responsibility is very important because

failure to do so amount to negligence of the duty or

breach of contract. The need to exercise due care was

illustrated in Osman V. J Ralph Moss. The broker as

an agent appointed by the principal contract on his

behalf has a legal duty to carry out the instructions

of his client, even when the client has not given any

specific instruction, the broker in under obligation

to act as a bonafide in the best interest of his

client without prejudice. The insured is legally

entitled to relay on the broker to carry out his

instruction faithfully.

ii. Renewal and changes in the policy: where new

insurance products are introduced to the insurance

market, it is the duty of the brokers to bring these

to the doorstep of the insuring public. A part from

73

being busy on policy issues and administration it

then becomes the function of the agents to liaise

more directly and regularly with the insuring public

to ensure that the time and accurate message gets to

the doorstep of the grass roots.

iii. Processing of claim: when claims occur, it is the

duty/brokers to pursue such claims in the interest of

the clients. The broker knows where to go and what to

do such that claim face little or no difficulties.

All these comes under service industry to the

insurance business when efficiently carried out you

can be sure of effective insurance delivery. The

insurance broker as a professional with legal

standing is duty bound to respect the confidence of

his client and must not disclosed, abuse or misuse

any confidential information received about the

proposer with the permission of the insured.

74

Insurer: although the broker is the agent of the

insured for purposes of affecting the insurance, he

becomes the agent of the insurer for the purpose of

collecting premium is a consideration for insurance

contract is usually paid in cash before the insurance

contract comes into force insurance Act 2003 section 41

stats that the broker must pay all premium collected by

him on behalf of any business transacted through him to

the insurer within 30days of collecting such premiums

otherwise the bro ker will be guilty of an offence and

liable on conviction to in June of 25,000 for the third

offence together with the cancellation of the

certificate at the registration of such broker. The

duties of the broker to the insurer are examined below

1) Imputation of brokers knowledge to the insurer; the

agent of the insurer acting with actual or ostensible

authority acting on course of his official duties any

knowledge lee acquires will be imputed to the insurers

75

who cannot claim non-disclosure from the insured in

Blackely V National Mutual life association, before the

completion of a life assurance contract the agent knew

that the proposer has a brain tumor which has just been

operation upon. It was held that the knowledge of the

agent in imputed to the insurer. Ojukwu (2006:104).

General: The broker play a vital role in the creating

of awareness of insurance policies to the public, the

manner of the broker to the public determines the rate

of success of the insurance company. Chief J Akin

George (Journal Nov. 23rd 2001) Continued by saying that

the broker or agent lake a public relations agent, an

image maker for the industry and how he/she carries out

this function will determine the extent to which an

effective insurance delivery is achieved. The general

role of brokers is headed below,

1.Creating Awareness of insurance products; as

brokers, the insurance intermediaries are in a

76

position to ensure improved knowledge of insurance

as well as creating appropriate awareness of the

insurance industry among the public. In a society

where less than 10 percent of possible insurance

business is taking place, you use see the importance

of this particular function of the broker is

ensuring that the public adequately appreciate the

importance of risk insurance in their day to day

living.

2.Economic Development: The broker as well as

insurance companies contributes vehemently to the

economic development of Nigeria. According to miss

Lalla Ben Barka (daily champion Tues 1 June 2010)

“Insurance industry performs several key traditional

functions but particularly relevant is the role of

facilitating and promoting investment which

increases capital formation that consequently

stimulates the promotion of goods and services”. She

77

continued by saying that it also creates employment

opportunities, generates wealth and income and also

reduces poverty all of which are important roles of

economic development. The Nigerian content Act 2010

became operational effective from 2nd April 2010. The

Act is generally accepted is a significant Landmark

in the development of the oil and gas industry in

Nigeria. The main plank of the act is the

prescription of minimum threshold for employment of

local facilities. The fundamental objective being

the development of local capacity through increased

indigenous participation.

2.10 POSITION OF INTERMEDIARIES IN STRUCTURE OF

DISTRIBUTION OF INSURANCE IN NIGERIA

From the point of production to end-usage an

insurance policy is usually moved between several

persons. When a proposal (offer) is made to an

insurer, it is considered for acceptance or rejection

78

based on it characteristics. Where the underwriter

accept it a counter offer is made to the prospective

insured outliving the terms of the contract as to be

contained in the policy. The proposal forwarded to an

insurer can be initiated an agent, broker or

prospective client on his or her own. Transactions can

be direct between any of the members on the channel.

Structure of different forms of position occupied by on

intermediary during insurance transactions are outlined

below;

1) Insurance company – Agent – prospective client

2) Insurance company – Broker – prospective client

3) Insurance company – Agent – Broker –Prospective

client.

The insurance company represents the production source,

agent and broker are intermediaries or middlemen while

prospective clients are consumer or customers.

79

2.10.1 Role Of The Intermediaries On Business

Performance Of Insurance Companies In Nigeria

1.Intermediaries extend the distance between customers

and insurers this gap makes insurer to be alien to

customers, thus making it easier for public

perception of insurers to be lopsided due to low

close relation. When negative occurrences take place

it become easy to generate an after effect on

insurers.

2.Intermediaries provides insurer with a good source of

market research information. This window insurer to

know direction of wants and needs of their respective

target markets. With such background knowledge

insurers are able to create better products to serve

the desires of the market.

3.There is a relationship between intermediaries and

insurance policy research by customers. Given their

closer look with the general public intermediaries

80

are able to encourage customers to renew their

policies. It creates more premium revenue for

insurers.

4.Intermediaries increase the business cost of

insurance companies they have to be paid for their

efforts towards buying and renewing of policy. The

lest comes mostly as commission for a sale of

policies. There other incenteres but all aimed at

encouraging intermediaries to generate more business.

2.10.2 Services Been Marketed By Intermediaries

Services been marketed by intermediaries include

all classes of insurance. Both life and general

insurance business they include;

1.Motor Insurance: Motor vehicles are either insured as

private cars and commercial vehicles depending on

their uses.

81

2.Fire and Special Perils Insurance; thus policy

promises to pay the insured for losses or damages

resulting from fire, lightening, bush fire,

explosion, aircraft, earthquake, wind hurricane,

cyclone etc.

3.Loss of profit (consequential loss); apart from the

direct loss of physical property during fore there is

also the risk of other indirect losses that often

occur. Such loss include; loss of profit and other

fixed charges like pre-paid rent, cost of finding new

accommodation, auditor’s fees and salaries of

employees that have to be paid etc.

4.Burglary and House Breaking Insurance: covers loss or

damage by burglary and house breaking following

forcible and violent entry into or out of the insured

premises. The interest covered are your office

furniture, fixtures, fitting and utensils, printed

books etc.

82

5.Machinery Breakdown Insurance: under this policy,

insured is indemnified against loss or damage to

machinery whether at work, rest on dismantled for the

purpose of serving or inspection. Also covered in

liability to third point resulting from the use of

the named machinery bodily injury, death, or damage

to property

Public liability insurance: in the course of your

claims, you may stand the risk of being liable top a

third party who may have suffered accidental death

bodily injury illness to third party including legal

cost. This could result from the use of plants, lefts

and hosts etc.

Bond: a bond simply means a guarantee given by one

party (the guarantor) to another (the principal)

(employer) on behalf of another (the contractor) to the

effect that contractor shall fulfill certain obligation

under contract or statute as the case may be and

83

whereby the guarantor agrees in the event of default by

the contractor to make good the loss of the principal.

Group Life Assurance: The principle of this act is that

if a collective terms (or temporary) assurance under

which insurance company pays the chosen lumps sum

benefit to the benefit of the beneficiaries of the

company (scheme) members who die from any the of cause

while still in force. The total premium in respect of

all staff members is a year at the commencement of the

policy and subsequent renewal dates.

2.11 CONTRIBUTIONS OF INSURANCE INTERMEDIARIES IN

INSURANCE BUSINESS

Intermediary activity benefits the overall economy

on the national levels. The role of insurance the

overall health of the economy is well understood. There

are several factors that intermediaries bring to the

84

insurance market place that help to increase the

availability of insurance generally.

2.11.1 Innovative Marketing

Insurance intermediaries bring innovative

marketing practices to the insurance market place. This

deepens and boarders insurance markets by increasing

consumers awareness of the protections offered by

insurance, their awareness of the multitude of

insurance options, and their understanding as to how to

purchase the insurance they need.

2.11.2 Dissemination Of Information To Consumers

Intermediaries provide customers with the

necessary information required to make educated

purchase/informed decision. Intermediaries can explain

what a consumer need and what the options are in terms

of insurers, policies and prices. Faced with a

knowledgeable client base that has multiple choices,

85

insurers will offer policies that fit their customers

needs at competitive prices.

2.11.3 Dissemination Of Information To The Market

Place:

Intermediaries gather and evaluate information

regarding placements, premiums and claims experience.

When such knowledge is combined with a intermediaries

understanding of the needs of it’s clients, the

intermediary is well-positioned to encourage and assist

in the development of new and innovative insurance

products and to create markets where none have existed.

In addition dissemination of knowledge and expansion of

markets within a country can help to attract more

direct investment for the insurance sector and related

industries.

2.11.4 Sound Competition

86

Increased consumer knowledge ultimately helps

increase the demand for insurance and improve insurance

take-up rates. Increased utilization of insurance

allows producers or advantage of a more competitive

financial climate, boasting economic growth.

2.11.5 Spread Insurer’s Risk

Quality of business is important to all insurers

for a number of reasons including profitability,

regulatory compliance and ultimately, financial

survival, insurance need to make sure the risk they

cover are insurable-and spread these risks

appropriately so they are not susceptible to

catastrophic losses. Intermediaries help insurers in

the difficult task of spreading the risk in their

portfolio. Intermediaries work with multiple insurers,

variety of clients, and in many cases in a broad

geographical spread. They help carriers spread the risk

on their portfolios according to industry, geography,

87

volume lane of insurance and other factors. This helps

insurers from becoming over exposed on a particular

region or a particular type or risk thus freeing

precious resource for use elsewhere.

2.11.6 Reducing Cost

By helping to reduce cost for insurer, broker

services also reduce the insurance costs of all

undertakings in a country or economy, because insurance

is an essential expense for all business, a reduction

in prices can have a large impact on the general

economy, improving the overall competitive position of

the particular market (www.clab.com//role of inint.pdf.

2.12 PROBLEMS CREATED BY INTERMEDIARIES IN SELLING

INSURANCE SERVICES.

Insurance intermediaries create problems on the

process of selling insurance services, the problem

include;