MY PROJECT WORK

105

UNIVERSITY OF PROFESSIONAL STUDIES EVALUATING THE RELATIONSHIP BETWEEN INTERNAL CONTROL MEASURES AND PERFORMANCE IN THE TRANSPORTATION SECTOR IN GHANA: A CASE STUDY OF METRO MASS TRANSIT LIMITED BY GROUP 67 NAMES ID DONKOR GODWIN 10BAW203 ISSAH YAHAYA 10BAW210 OWUSU GORDON MENSAH 10BAW201 A DISSERTATION PRESENTED TO THE DEPARTMENT OF ACCOUNTING OF FACULTY OF ACCOUNTING AND FINANCE, UNIVERSITY OF PROFESSIONAL

-

Upload

koforiduapolytechnic -

Category

Documents

-

view

0 -

download

0

Transcript of MY PROJECT WORK

UNIVERSITY OF PROFESSIONAL STUDIES

EVALUATING THE RELATIONSHIP BETWEENINTERNAL CONTROL MEASURES AND PERFORMANCEIN THE TRANSPORTATION SECTOR IN GHANA: ACASE STUDY OF METRO MASS TRANSIT LIMITED

BY

GROUP 67

NAMES ID

DONKOR GODWIN 10BAW203

ISSAH YAHAYA 10BAW210

OWUSU GORDON MENSAH 10BAW201

A DISSERTATION PRESENTED TO THE DEPARTMENT OF ACCOUNTING OF

FACULTY OF ACCOUNTING AND FINANCE, UNIVERSITY OF PROFESSIONAL

STUDIES, ACCRA, IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR

THE AWARD OF BACHELOR OF SCIENCE (BSC) DEGREE IN ACCOUNTING

JUNE 2013

CANDIDATE’S DECLARATION

We, the undersigned do hereby declare that this Dissertation is

the result of our own original research and that no part of it

has been presented for another degree in any university. However,

all sources of borrowed materials have been duly acknowledged.

NAMES SIGN

DATE

DONKOR GODWIN ………………….

……………

ISSAH YAHAYA ………………….

……………

OWUSU GORDON MENSAH ………………….

……………

I

SUPERVISOR’S DECLARATION

I declare that the preparation and the presentation of this

Dissertation were in accordance with the guidelines on

supervision of Dissertation laid by the University of

Professional Studies.

Sign……………………………………………….

Name……………………………………………..

Date……………………………………………….

II

DEDICATION

To our families and friends for their love, support and

encouragement throughout our academic studies in the university.

We humbly dedicate this work to all of them.

III

ACKNOWLEDGEMENT

The research team wishes to express their sincerest gratitude

first to God Almighty for His grace and mercies and good health

that He has shown to us throughout our stay in the University of

Professional Studies.

We would like to express thanks for the many useful comments and

suggestions provided by our supervisor, Mr. Timothy King Avordey,

and colleagues who reviewed all or portions of this project work

during its development.

Our appreciation also goes to the management of Metro Mass

Transit Limited who assisted the research team in their data

collection efforts especially Mr. Kwame Obeng the assistant

managing director.

IV

ABSTRACT

The study analysed internal control measures and its performance

in the transportation industry; a case of Metro Mass Transit

Limited (MMT), Accra. The study specifically, found out the

internal control system put in place by the MMT, ascertained the

level of effectiveness of the internal control system in place,

assessed the challenges facing the MMT in its attempt to

implement existing controls, and to determine the level of

performance given its controls. Although examples of successful

BRT systems abound, the same cannot be said in Ghana’s case. The

research design was a case study. The target population of 5000

from which a sample frame of 200 was drawn comprising employees

and passengers of MMT at the Kaneshie terminal, Accra. Sampling

method used was simple random sampling whilst the research

instrument used was a closed-ended questionnaire. Data collected

was analysed with SPSS. Even though the MMT had lots of controls

in place; it had serious challenges implementing them.

Nonetheless, passengers rated their performance high in exception

of a few areas begging for improvement. The MMT might improve

further, if it is to widen its portfolio of controls, work on

motivation and commitment and finally benchmark or adopt proven

innovative ways of loading.

V

LIST OF TABLES

Table 1:4.1: Gender of Respondents ………………………………………………………….37

Table 2:4.2: Age of Respondents ……………………………………………………………..38

Table 3:4.3. Marital Status of Respondents

…………………………………………………..38

Table 4:4.4: Educational Level of Respondents ………………………………………………

39

Table 5:4.5: Period of Service of

Respondents………………………………………………..40

Table 6:4.6: Transportation Qualification of

Respondents…………………………………….40

Table 7:4.7: Are Internal Ccontrols in place in Metro Mass

Transit Limited? ..........................41

Table 8:4.8: Challenges Facing MMT in implementing its internal

controls………………….43

Table 9:4.9: The Level of Effectiveness of the Internal Control

System………………………45

Table 10:4.10 Determination of the Level of

Performance……………………………………48

VI

LIST OF ACRONYM

COSO : Committee of Sponsoring Organisation

COBIT: Control Objectives for Information and Related

Technology

CO2: Carbon Dioxide

BRT: Bus Rapid Transit

INTOSAI: International Organisation of Supreme Auditing

Institutions

IT: Information Technology

JCI: Johannesburg Consolidated

Investment

MMT: Metro Mass Transit

MDG: Millennium Development goals

MFI; Monetary Financial Institution

MIS: Management Information System

OSA: Omnibus Service Authority

SOX: Sarbanes-Oxley

STC: State Transport Corporation

VII

TABLE OF CONTENTS

CONTENT PAGE

CANDIDATES’ DECLARATION……………………………………………………. I

SUPERVISOR’S DECLARATION…………………………………………………....II

DEDICATION…………………………………………………………………………...III

ACKNOWLEDGEMENT………………………………………………………………IV

ABSTRACT………………………………………………………………………………V

LIST OF TABLES……………………………………………………………………….VI

LIST OF ACRONYMS…………………………………………………………………VII

CHAPTER ONE: INTRODUCTION……………………………………………………. 1

1.1 Background of the Study……………………………………………………………….. 1

1.2 Statement of the Problem……………………………………………………………….. 7

1.3 Objectives of the Research……………………………………………………………… 8

1.4 Research Questions……………………………………………………………………... 8

1.5 Significance of the Research……………………………………………………………. 9

1.6 Scope and Organisation of the Study…………………………………………………… 9

CHAPTER TWO: INTRODUCTION………………………………………………….11

2.0 Literature review………………………………………………………………………11

2.1 Theoretical Literature…………………………………………………………………..11

2.1.1 Concept of Internal Control…………………………………………………………... 12

2.1.2 Components of Internal Control Systems……………………………………………..

13

2.1.3 Objectives of Internal Control………………………………………………………… 17

2.1.4 The Need for Internal Control………………………………………………………… 17

2.1.5 Limitations on Internal Control

Effectiveness……………………………………….. 18

2.1.6 Processes and Models in Mass Transportation…………………………………………

20

2.1.7 Organisation Performance………………………………………………………….......24

2.2.0 Empirical Literature………………………………………………………………….. 26

2.2.1 Successful Bus Rapid Transit Systems around the

World……………………………..27

2.2.2 Relationship between internal control and organizational

performance……………….29

2.3 Operational Definition of Terms and

Constructs………………………………………...31

CHAPTER THREE: INTRODUCTION…………………………………………………32

3.0 Methodology……………………………………………………………………...........32

3.1 Research Design…………………………………………………………………………32

3.2 Population and Sampling……………………………………………………………… 33

3.2.1 Target Population……………………………………………………………………... 33

3.2.2 Sample Frame………………………………………………………………………. 33

3.2.3 Sampling……………………………………………………………………………. 33

3.3 Primary Source of Data Collection…………………………………………………

34

3.4 Research Instruments………………………………………………………………. 34

3.5 Data Analysis…………………………………………………………………………35

3.6 Validation of Research Instruments……………………………………………………35

3.6.1 Reliability of the Research

Instruments……………………………………………….36

CHAPTER FOUR: INTRODUCTION………………………………………………….. 37

4.0 Results and Discussions…………………………………………………………………37

4.1 Demographic Profile of Respondents…………………………………………………..37

4.2 Are Internal Ccontrols in place in Metro Mass Transit

Limited? ...................................41

4.3 Assessment of the Challenges facing Metro Mass Transit in

implementing its Internal

Controls………………………………………………………………………………………43

4.4 The Level of Effectiveness of the Internal Control

System at Metro Mass Transit

Limited..........................................................

.............................................................45

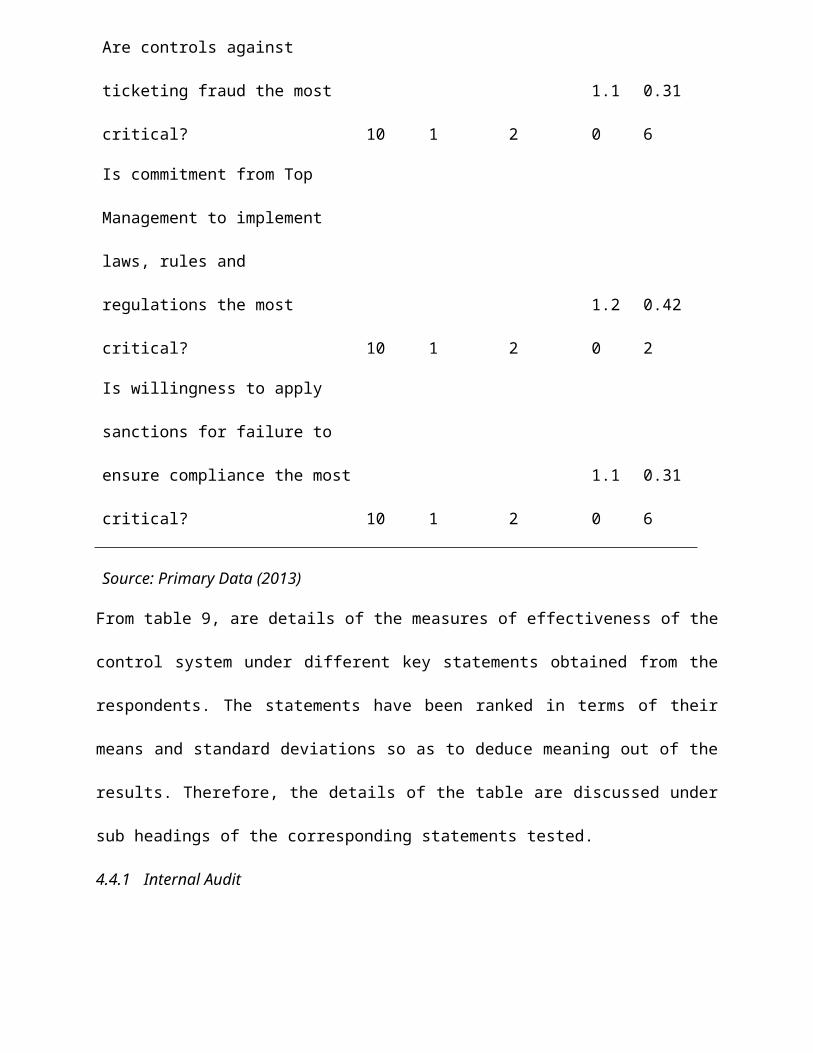

4.4.1 Internal Audit……………………………………………………………………….46

4.4.2 Human Resource Controls…………………………………………………………..46

4.4.3 Controls Against Asset Loss………………………………………………………..46

4.4.4 Controls Against Ticketing Fraud…………………………………………………..47

4.4.5 Commitment from Top Management to implement Laws and

Regulations………..47

4.4.6 Willingness to Apply Sanctions for Failure to Ensure

Compliance…………………47

4.5 Determination of the Level of Performance in Metro Mass

Transit Limited……….48

4.5.1 Performance in Customer Service…………………………………………………...49

4.5.1 Ticketing…………………………………………………………………………….49

4.5.3 Fleet Maintenance……………………………………………………………………50

4.5.4 General Performance…………………………………………………………………50

4.5.5 Effectiveness in Solving Ghana’s Road Transport

Problems…………………………50

4.5.6 Departure and Arrival Times…………………………………………………………..51

4.5.7 Overloading……………………………………………………………………………51

CHAPTER FIVE INTRODUCTION

…................................................................

...........53

5.0 Conclusions and recommendations…………………………………………………….53

5.1 Summary of Results…………………………………………………………………… 54

5.2 Recommendations…………………………………………………………………… 54

5.3 Limitations of the Study……………………………………………………………….. 55

5.4 Further Studies………………………………………………………………………… 56

REFERENCES

APPENDIX A: QUESTIONNAIRE

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

In the past, people used to walk or use animals for

mobility. Transportation development came after European

colonization to Africa. They came to Africa in the 1400s for

the first time (George, 1958). There were well aligned and

extensively networked roads during the 1600s. These roads

were also used to transport slaves in the trans-Atlantic

slave era (Fage, 1969). Horse-drawn carts or ox-drawn carts

were used to transport slaves (Muhammad, 2003). In the

colonial era of Africa, there was a decline in interest in

road construction due to the Europeans interest to develop

rail transport for their raw material mobility. They focused

on rail transport due to the huge cost of investment needed

in creating road facilities (Thomas, 1973). They invested in

railways because it would return them highest profits of

their investments. So the road transport was neglected

When transport systems are deficient in terms of capacity or

reliability, they can have an economic cost such as reduced or

missed opportunities. Efficient transportation reduces costs,

while inefficient transportation increases costs. The impacts of

transportation are not always intended, and can have unforeseen

or unintended consequences such as congestion. Transport also

carries an important social and environmental load, which cannot

be neglected. (Rodrigue & Notteboom, 1998). Man, nations, regions

and the world would be severely limited in development without

transportation, which is a key factor for physical and economic

growth (Oyesiku, 2002). According to Bailey et al (2008),

transportation route is part of distinct development pattern or

road network and mostly described by regular street patterns as

an indispensable factor of human existence, development and

civilization. The route network coupled with increased transport

investment result in changed levels of accessibility reflected

through Cost Benefit Analysis, savings in travel time, and other

benefits. These benefits are noticeable in increased catchment

areas for services and facilities like shops, schools, offices,

banks, and leisure activities.

According to Oyesiku (2002), urbanization in Nigeria has a long

history in its growth and development. Extensive development

being a feature of the 19th and 20th centuries, with concentration

of economic and administrative decision-making in Lagos, Ibadan,

Kaduna, Jos, and Enugu, and high degree of specialization and

larger population associated with greater specialization of goods

and services. Wyatt (1997) states that urban areas have tendency

to develop at nodal points in transport network and places with

good road network will possess relative advantage over locations

having poor network. Urban locations with such relative advantage

are found where different transport routes converge with high

degree of compactness,

connectivity, density, length and accessibility exhibited within

the intra- and inter- urban road networks.

According to the United Nations Economic and Social Council,

Economic Commission for Africa (2009) sustainable economic growth

and poverty reduction address a complex set of issues that call

for the development of all sectors of the economy to meet the

needs of the current generation without compromising the long-

term needs of future generations. Transport is one of the key

sectors that play crucial roles in achieving the goals of poverty

eradication and sustainable development. The transport sector is

very much linked and influences developments in other sectors of

the economy. Indeed, it affects attainment of all eight

Millennium Development Goals (MDGs).

Most African countries face huge costs associated with

transportation. In accessing foreign markets, on average,

Africa’s transport and insurance costs represent 30 per cent of

the total value of exports, which compares unfavourably with 8.6

per cent for all developing countries. Although most share the

problem of high transport costs, landlocked countries face the

most excessive transport costs recorded on the continent, United

Nations Economic and Social Council, Economic Commission for

Africa (2009).

The first Bus Rapid Transit (BRT) system was the Rede Integrada

de Transporte in Curitiba, Brazil (translated as 'Integrated

Transportation Network') which entered service in 1974, which

inspired the respected TransMilenio in Bogota, Colombia (opened

2000) and subsequently many other systems around the world.

In 1927, the Accra Town Council operated bus services in Accra,

Kumasi, Sekondi–Takoradi and Obuasi. Governments over the years

have established bus service companies such as the Omnibus

Services Authority (OSA), State Transport company (STC), City

Express Services (CES), and lately Metro Mass Transit (MMT)

Limited for various reasons including government

social obligations, environmental factors, energy considerations

and the promotion of efficient public transportation to increase

productivity and economic growth. Notable among the transport

operators in the informal sector in the 1980s was King of Kings

Limited. Its bus operation, which was heavily patronized, was

concentrated mainly on the Odorkor–Accra corridor.

The introduction of Metro Mass Transit Limited buses to the

existing ones has somehow eased passenger congestion during rush

hours along the roads across both the urban cities and rural

areas. Metro Mass Transit Limited has its headquarters at

Kaneshie, a suburb of Accra, and the various other terminals

across the regions. Metro Mass Transit (MMT) Limited was

introduced between 2001 and 2004 by the then government in place

who thought of strengthening the inadequate bus transportation

system already in place in the country. The Metro Mass Transit

Limited was officially incorporated in March 2003, as a limited

liability company under the Companies Act 1963, Act 179 to

provide safe, affordable, efficient and reliable movement of

commuters within the metropolitan and municipal areas. The

shareholders include State Insurance Company (SIC), National

Investment Bank (NIB), Ghana Oil Company Limited (GOIL),

Agriculture Development Bank (ADB), Prudential Bank (PB) and

Social Security and National Insurance Trust (SSNIT). These

together have 55% shareholding. The Government of Ghana holds the

remaining 45% shares.

In general, Metro Mass Transit Limited wants to set up a public

transport system, an integrated network of scheduled buses. A

public transport system interlinking residential areas, business

districts, Central bus terminals, suburbs and villages in a

reliable, efficient, safe and affordable way. The focus of Metro

Mass Transit Limited is presently on the short and medium

distances, i.e. intra-city transport (Metro Mass Transit Limited,

2012). Metro Mass Transit Limited aims to co-operate with the

Government to ensure that the pilot Bus Rapid Transit System

(BRTS)

succeeds. A Bus Rapid Transit System is the solution for heavily

congested areas in the regional capitals of Ghana and that is why

the proposed system will be copied to other relevant areas.

However, Metro Mass Transit Limited has not been without

problems. Some of which as reported by Gariba, C. A (2011) are;

(i) They have relatively reliable departure times but there are

instances where one can get delayed for an hour or two.

(ii) Some management practices being adopted by the officials of

the Metro Mass Transit buses are defeating the purpose of the

buses thus making life very uncomfortable for travelers.

(iii) Passengers travelling on the Metro Mass buses have always

been frustrated regarding the period of time they have to spend

joining long queues in anticipation of getting a ticket to buy.

Internal controls are put in place to keep organizations on

course towards profitability goals and achievement of its mission

and to minimize surprise along the way. They enable management to

deal with rapidly changing economic and competitive environment,

shifting customer demands and priorities and restructuring for

future growth. Internal controls promote efficiency, reduce risks

of asset loss and help to ensure the reliability of financial

statements and compliance with laws and regulations (COSO, 1992).

At the end of the research, the researcher intend to identify

additional internal controls to enable Metro Mass Transit Limited

curtail some of the problems enumerated.

As a result of injecting a reasonable level of efficiency into

the subject matter, Ghana can become one of the forerunners in

Africa combining fantastic bus infrastructure with a frequent bus

service.

Metro Mass Transit Limited has grown to be one of the major

employers in Ghana considering that it has operations in almost

all the ten regions of Ghana. In addition, it outsources indirect

jobs to third parties in the areas of security, bus washing and

cleaning services (Metro Mass Transit Limited, 2012). Moreover,

the operations of Metro Mass Transit Limited has empowered the

Ghanaian community by making jobs, markets, schools and

healthcare centers better accessible.

Organizational performance is measured in terms of customer

satisfaction, through reduced customer complaints (Kloot, 1999).

In order to be able to perform, organizations should critically

look at customers and all stakeholders in business and know how

best they are satisfying their needs. Kloot adds that

organizations should continuously improve their services through

assets accumulation, value creation, improved quality services

and flexibility of internal control system is intertwined with

organizations’ operating activities; it is most effective when

controls are built into the organizations infrastructure becoming

part of the very essence of the organization’s success, in terms

of continued improvement on performance standards as part of the

competitive advantage of the organization.

1.2 Statement of the Problem

The first Bus Rapid Transit (BRT) system was the Rede Integrada

de Transporte in Curitiba, Brazil (translated as 'Integrated

Transportation Network') which entered service in 1974, which

inspired the respected TransMilenio in Bogota, Colombia (opened

2000) and subsequently many other systems around the world. In

all of the above cases cited, the respective systems have been

successful due to particular regard for prioritization (dedicated

bus lanes), quality stations, high-frequency all day services

(for all income ranges), high capacity buses ( bi-articulated

buses, double-decker buses, or guided buses) and prominent brands

or identities.

However, in Ghana, the national transport system has

characterized by deficient customer services, poor maintenance

culture, poor ticketing administration and inadequate use of

spare tyres (Gariba, 2011).

The problem is to analyse and evaluate the internal control

structures that has brought about Metro Mass Transit Limited’s

uninspiring internal control structures that has brought about

adverse effects on the Ghanaian citizenry and ultimately the

economy, the complain of low productivity by both the private and

the government sectors of which are due to delayed departure

times, low profits leading to low tax revenues to the government,

free movement of people hampered and many other knock-on effects.

The benefit of administering good internal control measures in

the country’s transport industry will help to improve all the

above effects.

1.3 General Objective

The study sought to analyse the effects of internal control

measures and its performance in Metro Mass Transit Limited in

Ghana.

Specific Objectives

Specific objectives for the research are:

To find out the control systems in Metro Mass Transit Limited.

To ascertain the level of effectiveness of the internal

control system at Metro Mass Transit Limited.

To assess the challenges facing the Metro Mass Transit limited

in its attempt to implement these controls.

To determine the level of performance in Metro Mass Transit

Limited.

1.4 Research Questions

The research questions are:

1. What kinds of control systems are put in place by the Metro

Mass Transit Limited?

2. What are the challenges confronting Metro Mass Transit

Limited in the implementation of its internal control measures.

3. What is the most critical internal control measure that would

fundamentally help to improve Metro Mass Transit Limited’s

performance?

4. What is the level of performance in Metro Mass Transit

Limited?

1.5 Significance of the Study

The results of the study will help identify new control measures

and ways of strengthening the already existing ones in Metro Mass

Transit limited. It is also the researcher’s belief that the

study will bring invaluable benefits to management and those

charged with governance, thus ultimately helping to solve a

country’s age-old problem. The study will also add to the

existing knowledge bank regarding internal control measures and

performance in general. Also the study will assist in creating

awareness within the staff with regard to the importance of

putting in place internal controls in Metro Mass Transit Limited

as well as strict adherence to such internal control mechanisms.

1.6 Scope and Organisation of the Study

This study is limited to Metro Mass Transit Limited only. It is

also limited to the kinds of internal controls put in place by

Metro Mass Transit Limited, the extent of implementation of the

controls, their effectiveness, and the challenges hampering their

smooth implementation. The study is organised into five chapters

as outlined below:

Chapter one constitutes the introduction which includes an

overview of the background of the study, statement of the

problem, purpose of the study, objectives of study, research

questions and the scope and organisation of the study and how the

results of this work could be used.

Chapter two discusses the literature review which highlights both

the theoretical and the empirical literature of the study. It

ended with the operational definition of certain technical terms

and phrases used in the study.

Chapter three considers the methodology used in the study. This

chapter includes the research design, population and sampling

method used and the research instrument. How the data was

analysed as well as the statistical instrument used in analysing

the data is all included in this chapter. The fourth chapter

dealt with the presentation and discussions of the findings. This

Chapter discussed and presented the findings of the study by

using descriptive statistics, frequency tables and percentages.

Chapter five summarized the major findings of the research, the

conclusions reached and ended by making relevant recommendations,

limitations of the study not forgetting the recommendations for

further studies.

CHAPTER TWO

2.0 LITERATURE REVIEW

Introduction

This second chapter reviewed both theoretical and empirical

literature on the topic. The chapter reviewed available theories

relating to the concept, components, objectives of performance.

The review of literature, in addition, aims at providing detailed

account of earlier studies in internal control measures,

processes and models in the transport industry and related them

in order to identify the gap that exists in the literature, which

the study attempted to fill. The empirical literature however,

cited similar works by other researchers in discussing the topic

to help enrich the discussion further. It also discussed the link

between the variables of this study.

2.1 Theoretical Literature

When companies suddenly collapse, the often-resounding question

is, “what went wrong?” A breakdown in the internal control system

is the usual cause. Internal control is a process that guides an

organization towards achieving its objectives. These objectives

include operational efficiency and effectiveness, reliability of

financial reporting, and compliance with relevant laws and

regulations (COSO 1992). The COSO framework has, as of 14 May,

2013, been updated to comply with Sarbanes-Oxley Act of 2002

(SOX) and to review, refresh and modernize the original framework

ensuring it remains relevant. Absence of these variables often

results in organizational failure. The findings of the Treadway

Commission Report of 1987 in the United States (USA) confirmed

absence of, or weak, internal controls as the primary cause of

many cases of fraudulent company financial reporting. The

widespread global corporate accounting scandals that assumes near

epidemic proportions in recent years inform this study. Notable

cases include Enron and WorldCom in the USA, Parmalat in Europe,

and ChuoAoyama in Asia. In

South Africa, cases of accounting scandals have been recorded in

JCI and Randgold and Exploration companies. In Nigeria, the

Managing Director and Chief Financial Officer of Cadbury Nigeria

plc were dismissed in 2006 for inflating the profits of the

company for some years before the company’s foreign partner

acquired controlling interest. These scandals emphasize the need

to evaluate, scrutinize, and formulate systems of checks and

balances to guide corporate executives in decision-making. These

executives are legally and morally obliged to produce honest,

reliable, accurate and informative corporate financial reports

periodically.

2.1.1 Concepts of Internal Control

According to COSO (2011) Internal Control is a process effected

by an entity’s board of directors, management and other

personnel, designed to provide reasonable assurance regarding the

achievement of objectives in the following categories:

• Effectiveness and efficiency of operations.

• Reliability of reporting

• Compliance with applicable laws and regulations.

This definition emphasizes that internal control is:

• A process consisting of ongoing tasks and activities. It is a

means to an end, not an end in itself.

• Effected by people. It is not merely about policy manuals,

systems and forms, but about people at every level of an

organisation that impact internal control.

• Able to provide reasonable assurance, not absolute assurance,

to an entity’s senior management and board.

• Geared to the achievement of one or more separate but

overlapping categories.

• Adaptable to the entity structure.

An organisation establishes a mission, sets strategies,

establishes the objectives it wants to achieve, and formulates

plans for achieving them. Objectives may be set for an entity as

a whole, or be targeted to specific activities within the entity.

Though many objectives are specific to a particular entity, some

are widely shared. For example, objectives common to most

entities are sustaining organizational success, providing

reliable reporting to stakeholders, recruiting and retaining

motivated and competent employees, achieving and maintaining a

positive reputation within the business and consumer communities,

and complying with laws and regulations.

2.1.2 Components of Internal Control Systems

Supporting the organisation to achieve its objectives are five

components of internal control, COSO (2011):

Control Environment- is the foundation for all other components

of internal control. The board and senior management establish

the tone from the top regarding the importance of internal

control and expected standards of conduct. It provides

discipline, process and structure.

Risk Assessment-involves a dynamic and iterative process for

identifying and analyzing risks to achieving the entity’s

objectives, forming a basis for determining how risks should be

managed. Management considers possible changes in the external

environment and within its own business model that may impede its

ability to achieve its objectives.

Control Activities-are the actions established by policies and

procedures to help ensure that management’s directives to

mitigate risks to the achievement of objectives are carried out.

Information and Communication-provides the organisation with the

information needed to carry out internal control

responsibilities. It also enables personnel to understand their

internal control responsibilities and their importance.

Monitoring Activities-ongoing evaluations, separate evaluations,

or some combination of the two are used to ascertain whether each

of the five components of internal control are present and

functioning.

The framework above relates to the aggregate control system of

the organisation, which is composed of many individual control

procedures. According to Amudo & Inanga (2009), the COSO

framework may be relevant to larger organisations, but

inappropriate for smaller ones due to costs and operational

complexity. Management of small entities may not need formal

internal controls for the reliability of the records and other

information, because of their personal involvement in the

operations of the organisation. This raises a question of whether

the controls of small companies should be as complex as those of

large companies for them to be effective.

Amudo & Inanga (2009) also note that COSO framework did not

recognize and capture the delicate balance between formal and

informal controls in smaller organisations. More so, can small

companies’ internal controls be effective when only few of the

components recommended by COSO are present and yet the controls

could still be effective? COSO did not address this question.

The final weakness of the COSO mechanism is failure to recognize

Information Technology (IT) as one of the major control

components. IT is crucial to an internal control framework. In

contemporary times, organisations use IT for initiation,

authorization, recording and processing of transactions. IT

ensures effectiveness of internal controls. However, COSO’s

failure to recognize IT as a control component motivated other

bodies to design and develop frameworks to remedy the omission.

One such framework is the Control Objectives for Information and

Related Technology (COBIT 1996, 1998, 2000, 2005, 2007).

In 2001, the International Organisation of Supreme Auditing

Institution (INTOSAI) decided to update the 1992 guidelines on

internal control standards to take into account all relevant and

recent evolutions in internal control and to incorporate the

concept of the COSO report titled Internal Control – Integrated

Framework in the INTOSAI document.

According to INTOSAI (2001), Internal Control is an integral

process that is effected by an entity’s management and personnel

and is designed to address risks and to provide reasonable

assurance that in pursuit of the entity’s mission, the following

general objectives are being achieved:

• executing orderly, ethical, economical, efficient and effective

operations;

• fulfilling accountability obligations;

• complying with applicable laws and regulations;

• safeguarding resources against loss, misuse and damage.

Internal control is a dynamic integral process that is

continuously adapting to the changes an organisation is facing.

Internal control should be built in rather than built on. People

are what make internal control work. It is accomplished by

individuals within an

organisation by what they do and say. Achievement of an

organisation’s mission is basically the reason for internal

controls measures. After identifying the risks that faces an

organization, internal controls are put in place to reduce such

risks.

Provides reasonable assurance

No matter how well designed and operated, internal controls

cannot provide management absolute assurance regarding the

achievement of the general objectives. Instead, the guidelines

acknowledge that only a “reasonable” level of assurance is

attainable. Reasonable assurance equates to a satisfactory level

of confidence under given considerations of costs, benefits, and

risks. Determining how much assurance is reasonable requires

judgment. In exercising that judgment, managers should identify

the risks inherent in their operations and the acceptable levels

of risk under varying circumstances, and assess risk both

quantitatively and qualitatively.

Reasonable assurance reflects the notion that uncertainty and

risk relate to the future, which no one can predict with

certainty. Also factors outside the control or influence of the

organisation can affect the ability to achieve its objectives.

Achievement of objectives

Internal control is geared to the achievement of a separate but

interrelated series of general objectives. These general

objectives are implemented through numerous specific sub-

objectives, functions, processes, and activities.

2.1.3 Objectives of Internal Control

According to INTOSAI (2001), the objectives of internal controls

are:

Executing orderly, ethical, economical, efficient and

effective operations:

The entity’s operations should be orderly, ethical, economical,

efficient and effective. They have to be consistent with the

organisation’s mission. “Orderly” means in a well-organized way

or methodical. Ethical relates to moral principles. General

expectations are that public servants should serve the public

interest with fairness and manage public resources properly.

Citizens should receive impartial treatments in the basis of

legality and justice. Economical means not wasteful or extravagant.

It means getting the right amount of resources, of the right

quality, delivered at the right time and place and at lowest

cost. Efficient refers to the relationship between the resources

used and the outputs produced to achieve the objectives. It means

the minimum resources input to achieve the given quantity and

quality of output, or a maximum output with a given quantity and

quality of resource inputs. Effective refers to the accomplishment

of objectives or to the extent to which the outcomes of an

activity match the objective or the intended effects of that

activity.

2.1.4 The need for Internal Control

Internal Control is designed to ensure that an organisation

carries out its required functions effectively and efficiently so

that its financial reporting is reliable, and that it complies

with the relevant laws and regulations. For most organisations,

such internal controls are focused on controlling allocation of

spending, accounting procedures and financial statements to avoid

theft or fraud. Employee fraud or organizational fraud is defined

as a form of employee dishonesty that causes losses to the

organisation. All forms of occupational fraud are clandestine,

violate the employee’s fiduciary duties to the organisation, and

are committed for the purpose of direct or indirect financial

benefit to the perpetrator, and costs the employing organisation

assets, revenues or reserves (Holtfreter, 2004). Holtfreter

further argues that employee fraud causes extensive costs related

to societal outcomes such as diminished trust in governmental and

corporate institutions and reduces public confidence.

Therefore, internal control is a tool used by management and

directly related to the entity’s objectives. As such, management

is an important element of internal control. However, all

personnel in the organisation play important roles in making it

happen (Aucoin et al., 2004).

2.1.5 Limitations on Internal Control Effectiveness

The limitations on internal control effectiveness need to be

stressed to avoid exaggerated expectations due to a

misunderstanding of its effective scope. Internal control cannot

by itself ensure the achievement of the general objectives

defined earlier. An effective internal control system, no matter

how well conceived and operated can provide only reasonable – not

absolute – assurance to management about the achievement of an

entity’s objectives or its survival. It can give management

information about the entity’s progress, or lack of it, toward

achievement of the objectives. But internal control cannot change

an inherently poor manager into a good one.

Moreover, shifts in government policy or programs, demographic or

economic conditions are typically beyond management’s control and

may require managers to redesign controls or adjust the level of

acceptable risk.

An effective system of internal control reduces the probability

of not achieving the objectives. However, there will always be

the risk that internal control will be poorly designed or fail to

operate as intended. Because internal control depends on the

human factor, it is subject to flaws in design, errors or

judgment or interpretation, misunderstanding, carelessness,

fatigue, distraction, collusion, abuse or override.

Another limiting factor is that the design of an internal control

system faces resource constraints. The benefits of controls must

consequently be considered in relation to their costs.

Maintaining an internal control system that eliminates the risk

of loss is not realistic and would probably cost more than is

warranted by the benefit derived. In determining whether a

particular control should be established, the likelihood of the

risk occurring and the potential effect on the entity are

considered along with the related costs of establishing a new

control.

Organizational changes and management attitude can have a

profound impact on the effectiveness of internal control and the

personnel operating the system. Thus, management needs to

continually review and update controls, communicate changes to

personnel, and set an example by adhering to those controls.

The large number of accounting scandals during the early part of

the 21 century resulted in the Sarbanes-Oxley Act of 2002.

Sections 302 and 404 of this Act require companies to maintain,

assess, and disclose internal control over financial reporting.

The disclosures of internal controls were intended to provide

financial statement users with an early warning about potential

future problems that could result from deficiencies in internal

controls (Nicolaisen, 2004). The broader objectives of internal

controls are not limited to the reliability of financial

reporting as required

by SOX alone. A number of key internal control frameworks, such

as COSO’s (1992) and Turnbull’s Guidance on Internal Control

(1999) have been developed prior to the high profile accounting

scandals at the turn of the century.

Thus, management needs to continually review and update controls,

communicate changes to personnel and set example by adhering to

those controls.

2.1.6 Processes and Models in Mass Transportation

The Bus Rapid Transit Model

The “bus rapid transit” system (BRT) is a mobility concept for

rapidly growing cities. Urban buses travel in dedicated bus

lanes with a high service frequency and separate traffic lights.

Buses are given priority, enabling them to travel at high speeds.

This means fast and comfortable travel, even at peak traffic

times. Daimler is committed to BRT solutions as only a reliable

and safe public transport system can incentivise people to make

the switch from private transport. This is particularly important

in larger cities to take the strain off the transport system and

therefore to ensure permanent mobility for all sections of the

population into the future. Deploying state-of-the-art engine

technology and ensuring that bus traffic flows smoothly without

stop-and-go also contributes to reducing CO2 emissions. A further

advantage for municipal operators is that BRT is cheaper in terms

of procurement and maintenance than rail-based concepts and can

be integrated into existing infrastructures more easily. This

makes BRT a sustainable, future-proof concept that Daimler has

already successfully implemented from planning through to

introduction and provision with buses in cities including

Istanbul, Nantes, Mexico City and Bogota. About 17,000 buses by

Mercedes-Benz are operating for more than 20 BRT systems around

the world - from minibuses to articulated uses. BRT systems are

characterised by separate bus lanes and priority over other road

users, barrier-free entrance via

bus-stop platforms, optimised vehicles in terms of size and

design, ticket purchase and access control outside the vehicle,

integration of all modes of transport, control via ITS

(Intelligent Transport System) and organisation of the system

into main and feeder routes, The mobility concepts of Daimler.

(n.d.).

The DHV route optimization model

The DHV route optimization model (or in short DHV-model) was

developed by the Dutch consulting engineering firm DHV

Consultants BV. Initially the model was developed for the urban

bus company “De Lijn” operating in Brussels, the capital of

Belgium. The aim of the bus company was to improve the quality of

their services with the current resources in terms of budget,

vehicles and drivers. The model was subsequently applied for the

public transport route optimization of the cities of Rotterdam

and Denhaag in the Netherlands on mainframe computers. The

application of the DHV model was boosted following the further

development of the model on a personal computer platform.

Following this development, the model was successfully applied in

various cities in the formal Soviet Union, as well as central

Europe and Asia. The model was used to identify new profitable

routes which will meet the demand of the public transport

passengers. The model was applied through close co-operation

between the transport authority and the operators. The following

input information is required to apply the route optimization

model:

A reliable origin-destination (O-D) matrix for public

transport trips (train, taxi and bus);

The road and rail networks available for the use of public

transport vehicles;

The available resources for public transport operations

(budget, vehicles, drivers).

Apart from the information on the resources, all other

information is normally available from conventional transport

modelling studies.

To determine an optimised network it is not necessary to have

knowledge of the current route structure, but this is useful in

order to simulate the existing situation to determine the

improvement achieved by the optimised network. The DHV model

makes use of operational research techniques to identify the

optimal set of routes and frequencies to meet the demand for

public transport, subject to resource constraints such as the

operating budget and vehicle fleet. In the DHV model the

optimization is primary approach from the interest of the public

user. The main aim of model is to satisfy the needs of the

passenger in terms of the reduction in the travelling time (more

direct routes, higher frequency and less meeting time, etc.) and

the reduction in the number of transfers. The DHV model consists

of two main components: a simulation sub-model and an

optimization sub-model. The simulation model is traditional step

transport model which can be used for matrix estimation,

assignment and evaluation similar to the EMME/2 model which is

normally used for transport planning in South Africa. The

optimization sub-model generates the optimal route network in

view of the specified demand. After the assignment of the

existing trip matrix to the existing route network (the reference

situation) the first step in the process is the calculation of

the concentrated network. The concentrated network represents the

shortest paths for all public transport users, ensuring a

specified minimum number of passengers per road link. The

concentrated network represents the demand for bus and taxi

routes. In the line generation a large number of lines are

generated between each pair of existing and potential public

transport terminals in the study area subjects to user supplied

restrictions. In the generation process, routes are identified

following the concentrated paths. In this process the potential

supply of routes is calculated. The final step in the route

optimization process is line selection. In this step the most

attractive lines are selected from the list of generated and

existing routes. The concentrated network is used in the

selection of attractive lines. The final result of the

optimization process is a complete set of public

transport routes (bus or taxi), the required frequency of each

individual routes and the identification of the locations where

transfer terminals are needed. It is important to state that the

optimised set of routes, as proposed by the computer model, is

not the final answer. The result of the optimization process

needs to be verified by the modeller and the public transport

operators. The verification by the modeller is needed to both

check and improve the result of the model. After the assignment

of the optimised route the modeller may have to:

change some 2-way routes into 1-way route (the model suggests

defaults 2-way routes)

change some of the frequencies if the occupancies shown in

the assignment are too high

Combine two short routes into one longer route

Exchange some taxi and bus routes based on the loading and

frequency of the vehicle.

The impact of these changes of the individual routes as well as

the total network performance can be determined with the help of

assignment statistics (Zyl, V. et al 1999, August).

2.1.7 Organisation Performance

Brown (1996) argues that performance measures in organizations

must focus attention on what makes, identifies and communicates

the drivers of success, support organizations learning and

provide a basis for assessment and reward. Dixion (1990) adds

that appropriate performance measures are those which enable

organizations to direct their actions towards achieving their

strategic objectives. This is because according to him, a firm’s

performance is central to the future well-being and prosperity of

any enterprise.

Study by Whyte (1991), shows that performance can be measured at

both organizational and individual levels. This measurement is

sometimes referred to as performance appraisal. Whyte argues that

organizations have desired potentials in terms of capacity,

attraction, manual share and financial strength and performance

is the difference between those potentials and those that

have been achieved. Whyte argues that human capital asset

accumulation has significant impact on the organization’s ability

to introduce new products, compete within markets thus

influencing the level of performance. It increases knowledge base

within the organization’s success and performance.

Rumelt (1994), assert that availability and level of resources

can also be used to analyse the performance of an organization.

Rumelt contend that resources which may include assets, finances,

employee skills and organizational processes are key indicators

of the organization’s performance at one time. In agreement with

this, Barney (1991) suggested that resources could be grouped

into physical, human and capital resources and that a firm can

increase its performance only when other firms are unable to

imitate its resources. Rhyne (1994) argues that although a strong

financial performance indicates a strong institution, qualitative

indicators like the nature of management and educational level of

labour force must supplement the quantitative indicators in order

to enable the enterprise’s ability to meet its focus and

objectives.

Palmer (1993) emphasizes that performance in organizations is

looked at in terms of economy, efficiency and effectiveness.

Economy and efficiency are usually measured in financial terms

and data such as costs, volume of sales and productivity are

used. Economy is defined as acquiring resources in appropriate

quantities and at the least cost.

Drucker (1999) defines efficiency as maximizing inputs for a

required output. On the other hand Drucker defines effectiveness

as the extent to which the defined task has been accomplished and

is consistent with notions of non-financial accountability.

Effectiveness may partly be measured in terms of quality service,

customer satisfaction and achievement of goals.

Morton (1992) is also in agreement with Drucker’s (1999)

contention that performance should be measured in terms of

customer satisfaction. Morton argues that in order to be able to

perform, organizations should critically look at their customers

and know how best they are satisfying

their needs. He adds that organizations should continuously

improve on their services through innovations and great value.

Kloot (1999) adds that in order to assess performance,

organizations should be examined in terms of quality of services,

flexibility, utilization and innovations.

2.2 Empirical Literature

The introduction of the Metro Mass Transit buses in Ghana is

probably one of the best policy interventions in the transport

sector in the last decade. Everyday these buses transport

thousands of Ghanaians and their goods to various destinations in

the country.

However, the apparent neglect and subsequent decay of some of the

Metro Mass Transit buses in recent times leaves much to be

desired. The focus of this study is to analyse the effects of

internal control measures and its performance in the

transportation industry and try to link it with the case of Metro

Mass Transit Limited. In doing this, references were made

throughout the work to previous research works.

Previous research have focused on studying certain control

elements such as communication which was handled by Hooks et al

(1994), risk management Mills (1997) and human resource practices

done by Carey and Stringer, (1995). The study on village banks in

Uganda, Kenya and Tanzania by German Technical Cooperation

assistance (GTZ) and Africa Rural Agriculture and Credit

Association (AFRICA) (2002) revealed that most of the MFIs were

operating without documented policies and procedures and lacked

operational manuals. It identified the necessity to provide

support to the MFIs so that they can come up with operational

manuals and to improve on the existing systems. Information

system is a set of interrelated components all of which should be

present and work together for a common purpose. Internal control

mechanisms must have well documented processes that are

understood by everyone involved. There is immense need for MFIs

to set aside resources such as time, money and personnel to

develop or

improve a MIS that can match its information requirement (The

Center for Micro Enterprise Development Project, 1999). An

organization which lacks information will be unable to attain its

potential performance even if it may have capable and motivated

staff (CGAP, 1998).

2.2.1 Successful Bus Rapid Transit Systems around the World

The China Bus Rapid Transit System

Among the facilities provided by the Bus Rapid Transit (BRT), E-

card charge stations scored the highest, followed by BRT ticket

machines. In relation to the rush hour congestion, measures such

as the capacity to add departure frequency and vehicle are highly

praised. In the meantime, the city of Guangzhou, China, won the

2011 Sustainable Transport Award for its new world-class Bus

Rapid Transit system that integrates with bike lanes, bike share

and metro stations into a collective transport system. This

award, presented by the Institute for Transportation Development

Policy (ITDP) on 24 January 2011, goes to a city that made the

most progress over the year to increase mobility, while reducing

transportation greenhouse and CO2 emissions, and improving road

safety. Today the Guangzhou BRT services over 800,000 riders

daily and was built for about one-tenth the cost of the metro,

with an average of one bus passing every 10 seconds in peak

hours, it carries more passengers in a single direction than just

about every metro lines in all of China, and more than triple any

other BRT system in Asia. The system has resulted in 30 percent

higher bus speeds, and reduced congestion along the corridor at

the same time as vehicle volumes have increased, primarily due to

the solving of severe problems of congestion at bus stops, and

intersection signal improvements. explained ITDP director of

marketing and communications, Dani Simons The Guangzhou BRT was

able to eliminate 50,000 tons of carbon dioxide in its first

year, mostly due in part to residents choosing BRT over private

vehicles, in addition to help cut congestion and improve traffic

flow, Bus & Coach (n.d.).

The Argentina Bus Rapid Transit System

Argentina’s first Bus Rapid Transit system was inaugurated by

Mauricio Macri, the mayor of Buenos Aires, on 2nd June, marking

its first day of operation. Government officials and the public

speak of the tremendous impact this transit system will have in

improving people’s lives. The new BRT system, called “Metrobus”

has 21 stations and physically separated lanes that run in the

middle of the street. As an extra safety measure, the Metrobus

has elevated station platforms and features countdown clocks that

notify riders of the next arriving bus on each platform to keep

riders informed. The BRT will connect to two commuter rail

stations on opposite sides of the city, forming a trip that takes

40% less time than before, ITDP reports. With the addition of the

BRT to the city’s transport network, city officials expect the

line to grow to an anticipated 100,000 daily riders, a 15 percent

increase in ridership. City officials also expect the system to

reduce fuel use by buses in the city by 30 percent, and therefore

cut carbon emissions and improve air quality. The implementation

of Metrobus in Buenos Aires, the first BRT corridor in Argentina,

represents significant progress in the development of urban

transportation, allowing for an increased quality of life of more

than 100,000 people, said Macri. Our main goal, as those

responsible for urban planning, is to restore the quality of

public transportation, for which the support of the W.J. Clinton

Foundation and ITDP has been crucial in the process of

development and implementation of a world-class BRT system. In

the coming years, based on the success of this first phase, we

plan to continue the expansion of the BRT network in the City of

Buenos Aires. Road transportation accounts for 90% of all

transportation emissions in Latin America, half of which are

produced by passenger traffic, said Stephen Crolius, director of

the Transportation Program at the Clinton Climate Initiative.

“Bus rapid transit systems play an important role in addressing

those emissions as they create dedicated bus lanes across cities,

providing millions of people with a more cost and time efficient

solution to using cars—resulting

in fewer emissions and improved air quality. The system was built

in just seven months, showing the huge savings that BRT provides

in construction time, cost and logistics when compared to a fixed

rail system, ITDP explains. The BRT comes as only one component

of Buenos Aires’s efforts in creating a comprehensive transit

network to its residents and visitors. In a remarkably short

amount of time the City has helped improve conditions for walking

downtown, dramatically increased the availability of high quality

bike lanes, and provided a public bicycle system, said Andres

Fingeret, director of ITDP’s Argentina office. And now Metrobus

will add another high quality transportation option that will get

residents where they need to go, quickly, with less pollution and

without getting stuck in traffic. Bus & Coach (n.d.).

2.2. Relationship between internal control and organizational

performance

COSO (1992) provided criteria against which effectiveness of

internal controls can be assessed. Internal control can be judged

effective, if the entity’s operational objectives are being

achieved; published financial statements are being prepared,

reliable and applicable laws and regulations are being complied

with. While internal control is a process, its effectiveness is a

state at a point in time. Accordingly, the effective functioning

of components of internal control provides a reasonable assurance

regarding achievement of one or more of the stated categories of

objectives to ensure high levels of organizational performance.

Efficiency and effectiveness of operations have been taken to

mean efficiencies and effective use of its resources including

personnel, accurate information for decision making and

safeguarding of assets and records (Aren and Lwebbecke, 1994).

One of the five interrelated components of an internal control

system is the control environment. It refers to the integrity,

ethical values and competence of personnel (COSO, 1994). Internal

control should be viewed in a broader context, for example, it

should as well be reorganized as a

function of people’s ethical values as it is of standards and

compliant mechanisms (COCO, 1995). Wells (2001), illustrate

practical fraud occurrences discovered by competent accountants

within organizations and what the accountants say about how they

detect fraudulent transactions. Internal control system helps an

organization to achieve its objectives such as its efficiency and

effectiveness, reliable financial reporting and compliance with

regulations COSO (1994). Controls serve the system goals, they

interact with the system and its environment thus directing the

energy of the system toward fulfillment, in the same way changes

in the environment are easily noticed and adapted to (COCO,

1995). ACMAD (1994) recognizes that internal controls can enhance

the productivity and competitiveness of organizations.

In conclusion, internal control serves as a major mechanism that

every organisation must have to enhance its performance and

achievement of objectives.

2.3 Operational Definitions of Term and Constructs

For the purpose of this dissertation, the following terms were

defined:

Effectiveness

The degree to which objectives are achieved and the extent to

which targeted problems are solved. In contrast to efficiency,

effectiveness is determined without reference to costs and,

whereas efficiency means "doing the thing right," effectiveness

means "doing the right thing."

Efficient refers to the relationship between the resources used

and the outputs produced to achieve the objectives. It means

the minimum resources input to achieve the given quantity and

quality of output, or a maximum output with a given quantity

and quality of resource inputs.

CHAPTER THREE

3.0 METHODOLOGY

Introduction

This chapter provides an account on how this study was conducted.

3.1 Research Design

The study sought to analyse the effects of internal control

measures and its performance in Metro Mass Transit Limited in

Ghana. In order to achieve the purpose, the researcher sought to

find out control measures put in place, challenges confronting

their implementation, the most critical of the measures to attain

performance targets and most importantly determine the level of

performance given controls in place at Metro Mass Transit

Limited.

The study is a case study. A case study offers an opportunity to

study a particular subject in depth, for instance an organization

and usually involves gathering and analyzing information that may

be both qualitative and quantitative. Consequently the researcher

used explanatory research to look out for explanations of the

nature of the internal control measures and its effects on

performance of the transportation industry. The main advantage of

explanatory research is that, it helps the researcher to

understand the relationship that exists between variables as a

result of hypothesis testing. It however has some downsides. The

main disadvantage is that, it is less useful for observational

research since several other factors come into play.

The target population comprised employees and passengers of Metro

Mass Transit buses at the Kaneshie terminal, Accra. Sampling

method used was simple random sampling whilst the research

instrument used was a closed-ended self-administered

questionnaire.

3.2 Population and Sample

3.2.1 The Target population:

A research population is a well-defined collection of individuals

or objects known to have similar characteristics. All individuals

or objects within a certain population usually have a common,

binding characteristic or trait (Castillo, 2009).

The target population comprised employees and passengers of Metro

Mass Transit buses at the Kaneshie terminal, Accra. The total

number is estimated to be around five thousand (5000) within the

main Kaneshie terminal.

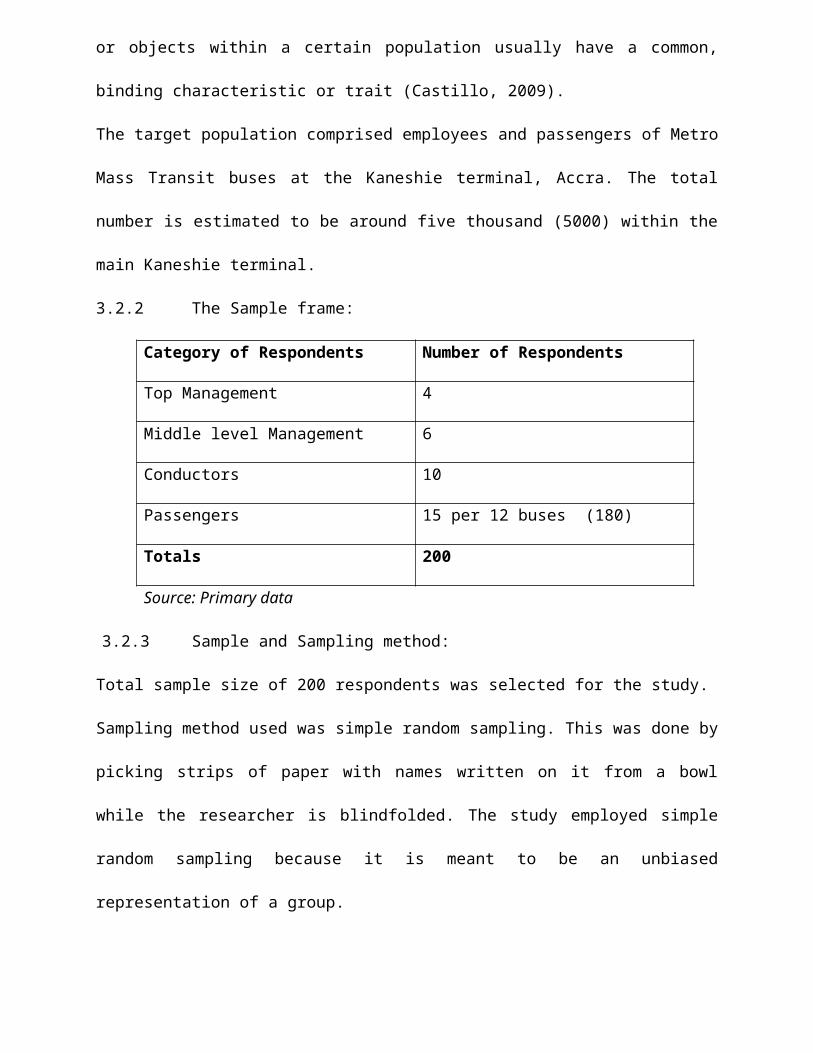

3.2.2 The Sample frame:

Category of Respondents Number of Respondents

Top Management 4

Middle level Management 6

Conductors 10

Passengers 15 per 12 buses (180)

Totals 200

Source: Primary data

3.2.3 Sample and Sampling method:

Total sample size of 200 respondents was selected for the study.

Sampling method used was simple random sampling. This was done by

picking strips of paper with names written on it from a bowl

while the researcher is blindfolded. The study employed simple

random sampling because it is meant to be an unbiased

representation of a group.

3.3 Data Collection Method

The main instrument that was used during data collection was a

self-administered questionnaire. It is closed-ended and made use

of a four-point and a two-point likert-scales respectively

(A=Excellent, B=Satisfactory, C=Above Average, D=Poor), (A=Yes,

B=No). There were four sets (for top management, middle

management, conductors and passengers) of questionnaires each of

which had two sections made up of background information and the

main questions. The questionnaires were delivered personally by

the researcher.

Both management and conductors were able to answer their

questionnaire without any assistance. However, questionnaires

issued to passengers were done by self- administration. This was

largely because the researcher was called upon to repeatedly

explain questions in our local Ghanaian dialect.

3.4 Research Instruments

In this study, a structured questionnaire was used as the primary

research instrument and can be found at appendix A.

The questionnaires were closed-ended questions of simple “Yes and

No” and “Excellent, Satisfactory, Above Average and Poor” where

respondents were asked to choose from a list of answer choices.

This plan is designed to give a researcher a sense of direction

and focus in undertaking the study within a specific time frame.

Primary data is data observed or collected directly from first-

hand experience. Published data and data collected in the past

are called secondary data.

3.5 Data Analysis

The researcher attempted to analyse the relationship between

internal control measures and its performance.

Data collected was analysed by way of Statistical Package for

Social Sciences (SPSS Version 16.0). SPSS Statistics is a

software package used for statistical analysis. It is now

officially named "IBM SPSS Statistics". It allows for in-depth

data access and preparation, analytical reporting, graphics and

modeling.

3.6 Validation of Research Instrument

The research instrument was validated both internally and

externally. The following

internal validations were used.

For face validity, the researcher thought that it was logical to

measure internal control effectiveness using a questionnaire-base

survey.

To achieve content validity, the questionnaire for this study

was given to the research fellow (supervisor) for review.

For criterion validity, the questionnaire developed was

matched up with other similar validated instruments that have

been developed and used in several studies.

Construct validity were ensured by deriving the component and

objectives of internal control system from COSO (1992),

INTOSAI (2001) frameworks and others.

To ensure external validity, the findings and results were

generalized to Metro Mass Transit Limited only.

3.6.1 Reliability of the Research Instrument

To test the reliability of the instrument, the researcher

administered the same questionnaire twice at both the Kaneshie

and Accra terminals of Metro Mass Transit Limited.

CHAPTER FOUR

4.0 RESULTS AND DISCUSSIONS

Introduction

This chapter presents empirical findings in reference to research

objectives in chapter one. These findings were obtained from only

primary sources. They were presented and analysed using

descriptive statistics, frequency tables and percentages. The

first section summarizes the averages of the demographic profiles

of top management, middle-level management operational level and

passengers. The second section finds out the control systems in

Metro Mass Transit Limited. The third section ascertains the

level of effectiveness of the internal control system in Metro

Mass Transit Limited. The fourth section assesses the challenges

facing Metro Mass Transit Limited in its attempt to implement

these controls. The fifth section tries to determine the level of

performance in Metro Mass Transit Limited.

4.1 Findings of Demographic Profile of Respondents

Source: Primary Data, 2013

Of the 200 sampled, 140 representing 70% of the respondents were

males, while 60 representing 30% were females.

Table 2.Age of Respondents

Frequency Percentage (%)

Less than 20 years 0 0

20-34 years 180 90

35-49 years 20 10

50 years and above 0 0

Total 200 100

Source: Primary Data (2013)

Table 1. Gender of Respondents

Frequency

Percentage

(%)

Male 140 70

Female 60 30

Total 200 100

With regard to table 2 above, there were no respondents less than

21 years and 50 years and above whilst there were 180 (90%) and

20 (10%) of respondents between the ages of 20-34 years and 35-49

years respectively. Findings indicate that majority were in the

age group of 20-34 years. Since majority of the respondents were

in the maturity group, it can be said that they can answered the

questionnaires in a matured way.

Table 3. Marital Status

Frequency Percentage (%)

Never Married 160 80

Married 40 20

Divorced 0 0

Widow/Widower 0 0

Total 200 100

Source: PrimaryData (2013)

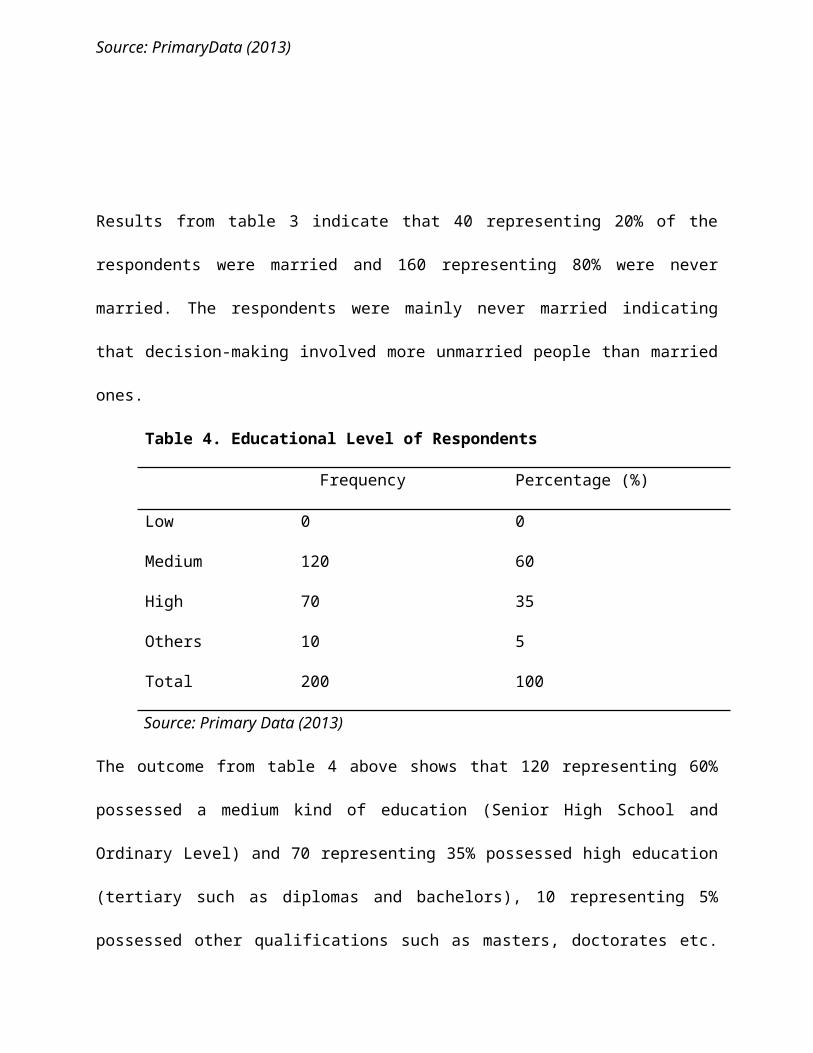

Results from table 3 indicate that 40 representing 20% of the

respondents were married and 160 representing 80% were never

married. The respondents were mainly never married indicating

that decision-making involved more unmarried people than married

ones.

Table 4. Educational Level of Respondents

Frequency Percentage (%)

Low 0 0

Medium 120 60

High 70 35

Others 10 5

Total 200 100

Source: Primary Data (2013)

The outcome from table 4 above shows that 120 representing 60%

possessed a medium kind of education (Senior High School and

Ordinary Level) and 70 representing 35% possessed high education

(tertiary such as diplomas and bachelors), 10 representing 5%

possessed other qualifications such as masters, doctorates etc.

the educational levels of the respondents were on the higher side

and helped to enhance the reliability of the data.

Source: Primary Data (2013)

Findings in table 5 above show that 140 (70%) of the respondents

served between 1-5 years and 60 (30%) served between 6-10 years.

It appeared there was fair balances as far as the ages were

concerned making the respondents fairly aware of the day-to-day

operations of the organisation.

Table 6. Transportation Qualification of Respondents

Frequency Percentage (%)

Degree 80 40

Diploma 20 10

Certificate 80 40

Table 5. Period of Service of Respondents

Frequency

Percentage

(%)

1-5 years 140 70

6-10 years 60 30

11-15 years 0 0

16 years and above 0 0

Total 200 100

Others 20 10

Total 200 100

Source: Primary Data (2013)

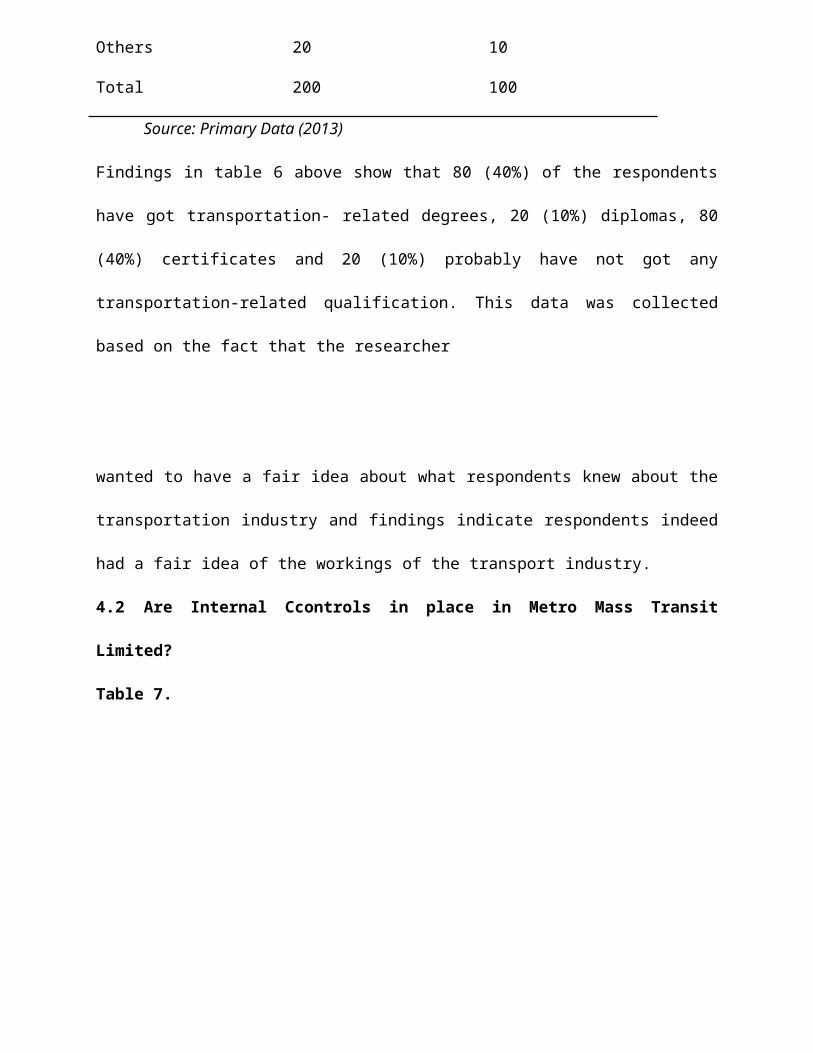

Findings in table 6 above show that 80 (40%) of the respondents

have got transportation- related degrees, 20 (10%) diplomas, 80

(40%) certificates and 20 (10%) probably have not got any

transportation-related qualification. This data was collected

based on the fact that the researcher

wanted to have a fair idea about what respondents knew about the

transportation industry and findings indicate respondents indeed

had a fair idea of the workings of the transport industry.

4.2 Are Internal Ccontrols in place in Metro Mass Transit

Limited?

Table 7.

Source: Primary Data (2013)

Are Internal Controls put in

place in MMT

Yes No

Has MMT established internal

control system? √

Do you have controls to ensure

good financial statements? √

Are controls in place to ensure

employment of competent

personnel? √

Are controls in place to secure

against asset loss? √

Are controls put in place to

prevent and detect fraud and

error? √

Are controls put in place to

ensure general compliance with

laws and regulations? √

√=Yes X=No

Clearly, all respondents were of the view that internal controls

are in place. Upon further interrogation the researcher

discovered that the finance staff record all sales, promptly bank

all monies for the day, not one individual handles all accounting

processes and then payment vouchers are properly approved before

monies are paid out.

More so, information obtained during the data gathering process

indicates that, to be employed, one has to formally apply, go

through an interview process, gets hired and trained, put through

a probation process and then finally maintained or rejected

depending on performance exhibited. There are also structures in

place for already employed personnel to continually develop

themselves. In addition, all buses were parked within the

terminals everyday after work under tight security to secure

against asset loss. The researcher realised that unless a genuine

need for spare parts arises, requisitions are not approved. To

check against fraud and error within the organisation,

transactions must be approved by the appropriate staff at all

departmental levels. For instance, some contracts to purchase

buses cannot be approved by the managing director alone without

consulting the board. All units within the organisation have

operating manuals and policies which must be followed religiously

in performing their day-to-day duties.

4.3 Challenges Facing MMT in implementing its internal controls

Table 8.

Yes No

Is internal audit function

effective? √

Are workers generally satisfied

with conditions of service? X

Are workers motivated to work? X

Is the HR unit effective in its

employment decisions? √

Is there any likelihood of

collusion to steal company

assets? √

Is the maintenance culture

effective? √

Is the asset replacement policy

of MMT effective? √

Are controls against ticketing

fraud effective? √

Is top management committed to √

implementing policies, laws and

regulations?

Is top management willing to

apply sanctions for failure to

ensure compliance? √

√=Yes X=No

Source: Primary Data, (2013)

It is clear from the findings that the organisation faced few