Year 8 summer project Science Fiction writing - Rastrick High ...

Upload

independentCategory

view

0download

0

CHAPTER-1

INTRODUCTION

1.1 Meaning of banking

The word “Bank” is derived from Italian word

“Banco” which means a bench. In the past, the

ancestor of modern banking system that were

merchants, goldsmith and money lenders used to

perform the monetary task sitting on the bench

not in the market. So, “Banco” was used to denote

monetary transactions.

Generally the bank refers to those

institutions which are established under law for

dealing with monetary transactions. It means

those institutions are treated as banks which

accept the deposit of public and grant loan to

the needy person or businessmen or industrialists

against security deposits. A bank can generate

revenue in a variety of different ways including

interest, transaction fees and financial advice.

The main method is via charging interest on

capital it lends out to customers. The bank

profits from the difference between level of

interest it pays for deposits and other sources

of fund and level of interest it charges in its1

lending activities. Besides this, bank is engaged

in different types of activities such as exchange

currency, joint venture, underwriting, bank

guarantee, discounting bills etc.

Different economists have given definitions

of bank. Definitions given by popular economists

are given below:

According to Dr. H.L. Hart, ”A bank is one

who, in the ordinary course of his business,

receives money which he pays by honoring cheque

of persons from whom or whose account receives.”

According to Kinsley, “Bank is an

establishment to individuals, such advances of

money as may be required and safely made and to

which individuals entrust money when not required

by them for use.”

According to US law, “Any institution

offering deposits subject to withdrawal on demand

and making loans of a commercial or business

nature is a bank.”

Therefore, bank can be defined as a

institution which deals with monetary

transactions for the mobilization of idle money2

or deposits in productive sector which is

essential for development of whole nation.

History of banking:

In the banking history of Nepal, Nepal Bank

Ltd. is the first bank of Nepal which was

established in 1994 B.S where only metallic coins

were used as medium of exchange. After that,

Nepal Rastra Bank was established in 2012 B.S

with the objective of issuing paper currency,

maintaining stability in exchange rate,

mobilizing capital and developing banking sector

in country. Accordingly, Rastriya Banijya Bank,

Agriculture Development Bank and Nepal Industrial

Development Bank were established. After the

restoration of multiparty democracy in Nepal,

government took liberal policy in the banking

sector. As a result, a large number of commercial

banks established in Nepal with the joint venture

with foreign commercial banks. Nepal Arab Bank

Ltd, Himalayan Bank, Bank of Kathmandu are some

examples of such banks. As per the provision of

liberal policy adopted in Nepal, bank can be

established easily. On the permission of central

bank, such bank can established at any time3

anywhere. At present there are 32 commercial

banks in Nepal.

4

Table No. 1

Commercial banks in Nepal

Nepal Bank LimitedRastriya Banijya BankNabil Bank LimitedNepal Investment Bank LtdStandard Chartered BankHimalayan Bank LtdNepal SBI Bank LtdNepal Bangladesh Bank LtdEverest Bank LtdBank Of Kathmandu LtdNCC Bank LtdLumbini Bank LtdNIC Bank LtdMachhapuchre Bank LtdSiddhartha Bank LtdAgriculture Bank LtdGlobal Bank LtdCitizen Bank InternationalPrime Commercial Bank LtdBank Of Asia Nepal LtdSunrise Bank LtdGrand Bank Nepal LimitedNMB Bank Ltd

5

Kist Bank LtdJanata Bank Nepal LtdMega Bank Nepal LtdCommerz and Trust Bank Nepal Ltd Civil Bank LtdCentury Commercial Bank LimitedSanima Bank LimitedKumari Bank LtdLaxmi Bank Ltd

Basically basic functions of commercial

banks are collecting various types of deposit

facility, exchange of money, lending of money,

remittance of money, letter of credit, guarantee,

loans, foreign exchange etc. Commercial banks are

profit oriented financial institution having

certain rate of interest given to the depositors

and also charged certain interest rate to the

loan burrowers.

1.2.1 Background of EBL

Everest Bank Limited (EBL), one of the

leading bank of Nepal commenced its operation in

6

1994.Its head office is situated in Lazimpat,

Kathmandu Nepal which regulates all its branches.

The bank has 45 branches, 55 ATM counters and 21

Revenue collection counters across the country.

It has objective of extending professionalized

and banking services through the country. EBL has

joint venture partner with Punjab National Bank

that is holding 20% equity in the bank and turned

it around to a highly profitable bank .Punjab

National Bank (PNB) is third largest bank in

India which offers a wide variety of banking

services.

This bank has been steadily growing in its

size and operations. For its excellence in

banking service, the bank has been confirmed with

“Bank of the year 2006, Nepal” by the banker, a

publication of financial times, London.

Similarly, the bank bestowed with the “NICCI

Excellence award” by Nepal India chamber of

commerce for its spectacular performance under

finance sector.

EBL has been expanding range of services to

the customers .It has pioneered in extending

various customer friendly products such as Home7

loan, Education Loan, equity loan, Vehicle loan,

Loan Against Share, Loan Against Life Insurance

Policy and Loan for professionals.EBL was one of

the first bank to introduce ABBS in Nepal.EBL is

also providing Remittance facility through which

EBL customer can remit fund from Nepal to CBS

branches of PNB India.

Drawing its strength from its joint venture

partner, EBL has been steadily growing its size

and operations. The bank is providing customer

friendly services through a network of 27

branches across the nation. The main branch of

EBL is situated in Baneshwor, Kathmandu.

Furthermore, the bank has branches in Teku,

pulchowk, Balaju, Lazimpat, Pokhara, Janakpur,

Biratnagar amongst several other places/cities.

1.2.2 Objectives of EBL

EBL has the following objectives:

To evolve and position the bank as a

progressive, cost effective & customer

friendly bank providing comprehensive

financial and other related services.

8

To be committed to excellence in servicing

the public and also excelling in corporate

values.

To provide excellent professional services

& improve its position as a leader in the

field of financial related services.

To build & maintain a team of motivated

and committed workforce with high work

ethics.

To use the latest technology aimed at

customer satisfaction & act as an

effective catalyst for socio-economic

developments in the country.

1.2.3 Capital structure

Capital structure refers to the way a

corporations finances its assets through

combination of equity, debt, or hybrid

securities. A firm’s capital structure is then

composition or structure of its liabilities.

EBL’s capital structure consists of following

capital structure in the year 2068:-

Table no 3

9

Capital Structure of EBL

Particulars Amount % of total

capitalAuthorized

capital

1250000000 37.53

Issued

capital

1050000000 31.53

Paid up

Capital

1030467300 30.94

Total 3330467300

Source: Annual Report 2010/2011

10

Figure no 1

Capital Structure of EBL

38%

32%

31%

capital structureAuthorized capitalIssued capitalpaid up capital

The above figure shows that the authorized

capital is highest than others. It is 37.53% of

total capital. Second is issued capital that is

31.53% of total capital. And third is paid of

capital that is 30.94% of total capital.

1.3 Introduction of deposit mix

A deposit refers to an amount of money in

cash or checks form or sent via wire transfer

that is placed into bank account. It is main

source of resources to meet the growing demand of

the financial assistance. Higher the volume of

deposits, higher will be the volume of investment

which gives higher profit. The existence of

11

commercial banks basically depends upon

mobilization at deposit.

Types of deposit:-

1) Current Deposit:

In this account any amount can be deposited

and withdrawn any time. No interest is given by

the bank to accountholder under this account. So,

this account is non interest bearing account.EBL

offers various flexible payment methods to allow

customers to distribute money directly to others.

It also provide internet user login for this

account in case of single signatory. EBL’s

Current account offers the following benefits to

the accountholder:

Free monthly statement

Unlimited Withdrawal

Extended banking Hour

All branches of EBL are connected through

ABBS which enables to withdraw and deposit

cash from any of the branches

2) Saving deposit:-

12

This account can be opened with nominal

amount. Limited amount can be deposited and

withdrawn from the bank in the specified time.

This account is held at an EBL bank maintained by

a customer for the purpose of accumulating funds

over a period of time while earning an interest.

Interest rate is calculated on Daily Closing

balance and payable on quarterly basis.EBL

provides nominal rate of interest.EBL Saving

Account provides following benefits:

Free Cheque books

Minimum Balance of NPR 500/- to open

saving account in any branches

Free Statement on demand.

Unlimited withdrawal

13

3) Fixed deposit:

This account is managed to accept the deposit

for fixed period of time providing higher rate of

interest. The amount can be withdrawn from bank

only after the expiry of time. If account holder

needs amount before expiry of time, s/he can take

loan against security deposit.

Benefits:

Attractive interest rate i.e. 10% or 2%

above the deposit rate on actual usage.

Loan/Overdraft facility against FD allowed

up to 90% of deposit amount.

1.4 Objective of the study

The main purpose of the study is to analyze,

examine and interpret the deposit mix of EBL with

the help of financial and non financial

indicators .Some other major objectives are:-

To find the composition of deposit in EBL.

To find out share of fixed current and

saving deposit out of the total deposit.

14

To identify the total deposit trend of

public.

To provide conceptual framework of

different deposit.

To provide suggestion and guideline to

improve problems regarding deposit.

To know whether different kinds of deposit

are in increasing or decreasing trends.

1.5 Limitation of the study

This study mainly focuses on only the

deposit of Everest Bank Ltd. Therefore,

overall position of EBL cannot be judged

by this report.

This study has covered only 4 financial

years from 2065 to 2068 B.S.

Due to time and cost constraints, it

cannot cover all the dimension of the

subject matter.

Validity of report fully depends on the

information provided by concerned

authorities.

15

Some of the data uses are of secondary

type, which is available from bank and

other sources of books.

Research Methodology

It is the heart of the project that provides the

work plan and describes the activities undertaken

for the completion of project. This project uses

both financial and stastical tool for detail

analyses on the project and it includes:-

a) Research design

b) Data collection procedure

c) Data analysis tools

16

2.1 Research DesignResearch design is a master plan specifying

the methods and procedures for collecting and

analyzing the needed information. This serves as

a framework for the study, guiding the collection

and analysis of data, the research instruments to

be utilized, and the sampling plan to be

followed.

Here, this study is concerned on deposit mix

of Everest Bank Limited. For the study,

descriptive and analytical research methodology

is used. Those methodologies involve gathering

data that describes events and then organizes,

tabulates, depicts and describes the data

collection that reduce the data to manageable

form.

2.2 Data collection Procedure

No matter what the basic design of a research

study, it is necessary to collect accurate data

to achieve useful results. For this reason, it is

helpful to consider various sources of collecting

data and the quality of information they produce.

So, two sources of data collection techniques

have been used them are:-

17

2.2.1 Primary data:

Primary data is original data collected for

the first time. I have used primary sources i.e.

interviews, questionnaires and observation to

collect the primary data on EBL.

2.2.2 Secondary data:

Secondary data refers to the data that has

been already gathered by others. I have used

secondary sources too i.e. books, periodicals,

published reports, data services through which

data were collected. Besides them data were

collected from Publication of NEPSE, financial

statements of EBL and annual reports which were

collected from Everest Bank’s website, NEPSE and

from SEBO.

CHAPTER 3

Data Analysis and Presentation

Data analysis is the process of developing

answers to questions through the examination and

interpretation of data. Its purpose is to change

the data from an unprocessed form to an

understandable presentation.

18

In this chapter, total deposit, deposit

composition, saving to total deposit ratio,

current deposit to total deposit ratio, fixed

deposit to total deposit ratio and cash balance

to total deposit ratio are presented to evaluate

deposit mix of EBL. This chapter first explains

methods of organizing data by tabulation and then

placing that data in presentable form by using

figures and tables.

3.1 Total deposit trend

Total deposit refers to total amount of

deposit of public collected by bank under

different accounts. It is essential to evaluate

the overall performance of bank.

Table No.4Total deposits of Everest Bank

(Rs in Crores)Fiscal

year

Total deposit of

Everest Bank

Change

in %

2065

2398

-

2066

3332 38.

95% 3693 10.8

19

2067 3%

2068

4113 11.3

7%

2069

5000 21.5

7%(Source: Annual report of Everest2065-2069)

Figure No 2

Total deposits of Everest Bank

2065 2066 2067 2068 206690

1000

2000

3000

4000

5000

6000Total deposits

Total deposits

In the above table, pie chart and trend, we

see that the total deposits are in increasing

order. In 2065 there were only 2398 crores of

deposits. In 2066 the amount of total deposit is

increased by 38.95%, which is Rs 3332 crores.

Then, the deposit in 2067 was 3693 which shows20

that it was increased by 10.83%. After that, the

deposit in 2068 reached 4113 which means an

increase by 11.37%.Finally, in 2069 the deposit

is 5000 i.e21.57%increase than previous year. It

shows the consistent progress of the bank.

3.2 Deposit Composition of Everest Bank

Deposit composition of EBL comprises of

current, margin, saving, fixed, call and other

deposits. It has been presented in the following

table:-

21

Table no 8

Deposit composition of Everest Bank

(Rs in lakh)

Types of

deposit

2065 2066 2067 2068 2069

Current 24923 48599 41733 47912 60982Margin 2214 2920 3759 4100 4517Saving 11883

9

14782

3

133600 130391 172693

Fixed 64462 70500 104403 150619 130075Call 27807 62940 84128 75501 129522Other 1518 447 1699 2756 2272Total 23976

3

33322

9

369323 411279 500061

(Source: Annual report of Everest Bank 2065-2069)

Figure no 3

Deposit composition of Everest Bank

22

2065 2066 2067 2068 20690

100000

200000

300000

400000

500000

600000

OtherCallFixedSavingMargincurrent

From the above table and graph we can see the

position of different deposits of EBL. We can

clearly see that the saving deposit is in

increasing trend in 2065 and 2066 but it has been

decreased in 2067 & 2068 and again increased in

2069.Current deposit and fixed deposit on other

hand is in increasing trend in every year from

2065 to 2069.The other deposits that are margin,

call and other deposits are also in increasing

trend every year.

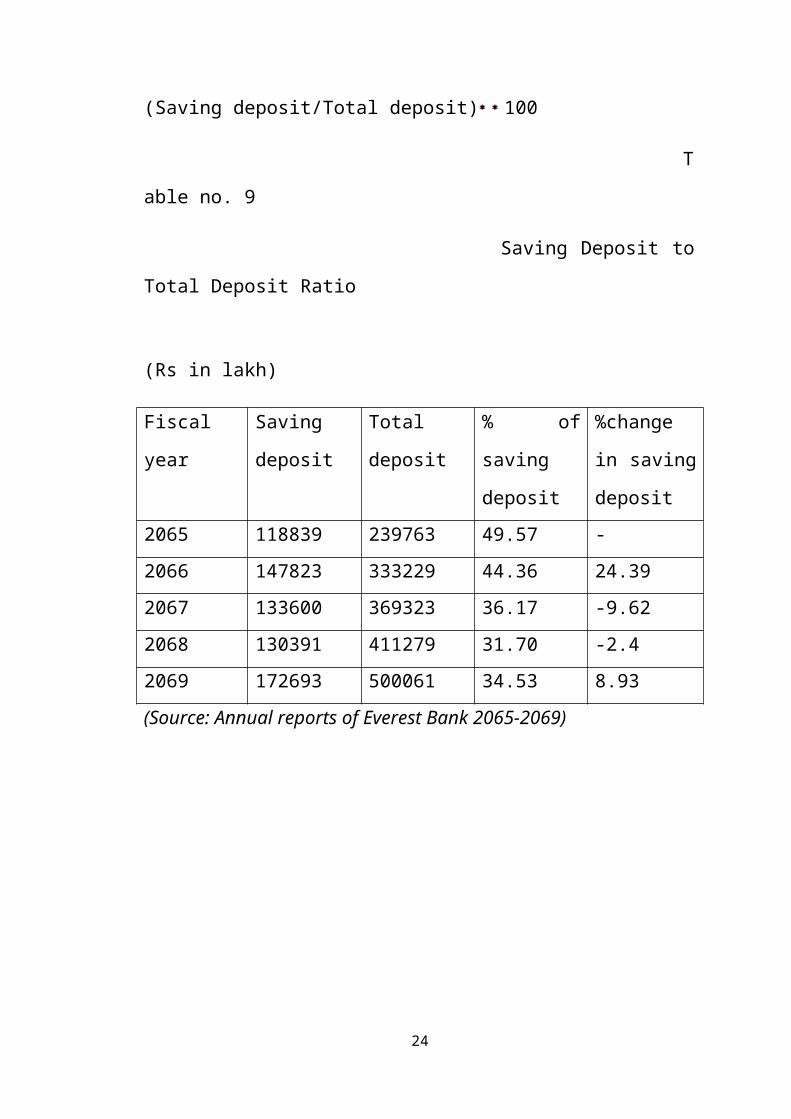

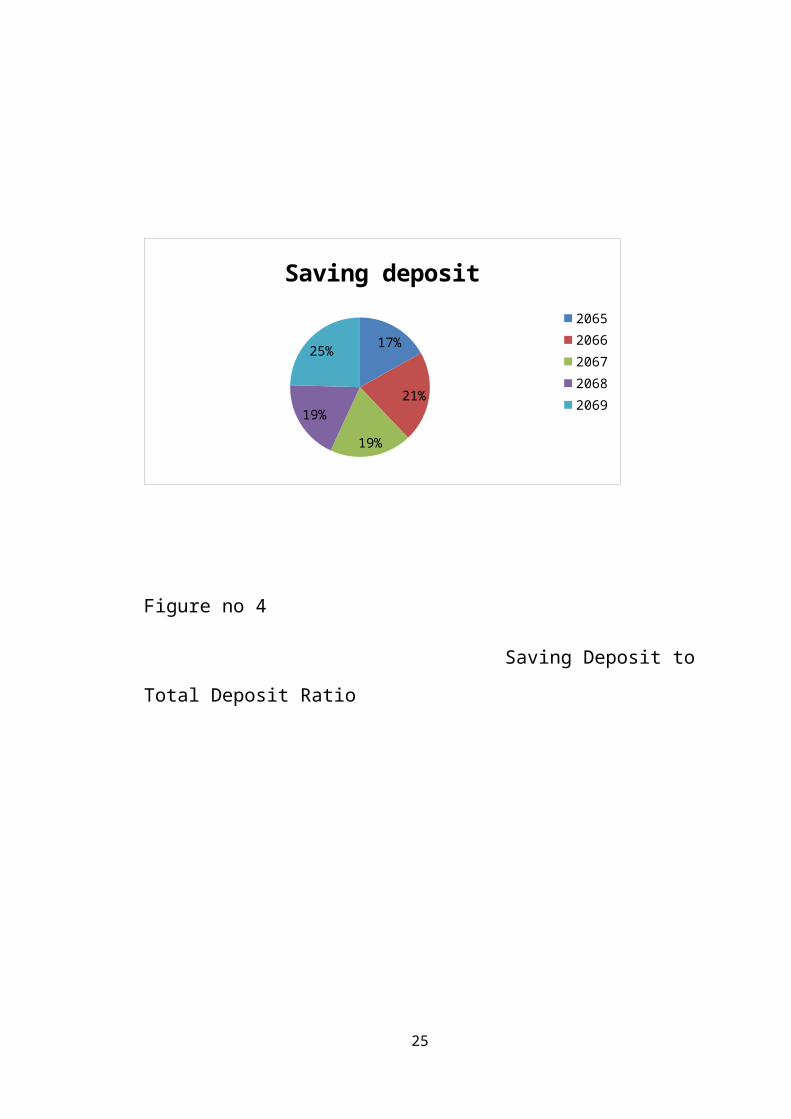

3.3 Saving Deposit to Total Deposit Ratio

It is calculated to find out the proportion

of saving deposit with respect to total deposit.

It can be calculated by the following formula:

23

(Saving deposit/Total deposit) 100

T

able no. 9

Saving Deposit to

Total Deposit Ratio

(Rs in lakh)

Fiscal

year

Saving

deposit

Total

deposit

% of

saving

deposit

%change

in saving

deposit2065 118839 239763 49.57 -2066 147823 333229 44.36 24.392067 133600 369323 36.17 -9.622068 130391 411279 31.70 -2.42069 172693 500061 34.53 8.93(Source: Annual reports of Everest Bank 2065-2069)

24

17%

21%

19%

19%

25%

Saving deposit20652066206720682069

Figure no 4

Saving Deposit to

Total Deposit Ratio

25

2065 2066 2067 2068 20690

100000

200000

300000

400000

500000

600000

saving deposittatal deposit

The above table, chart and graph show the

composition of saving deposits to total deposits.

It shows the decreasing trend of saving deposit

in 2067, 2068 and increasing trend in 2066

&2069.In the year 2066 the saving deposit was Rs

147823 which was 44.36% of total deposits and it

was increased by 24.39%in comparison to 2065.

After that, it got declined. In 2067 it was

decreased by 9.62% which was 36.17% of total

deposit and in 2068 it was decreased by 2.4%

which was 31.70% of total deposit. But in 2069 it

26

was increased by 8.93%and this deposit reached to

172693.

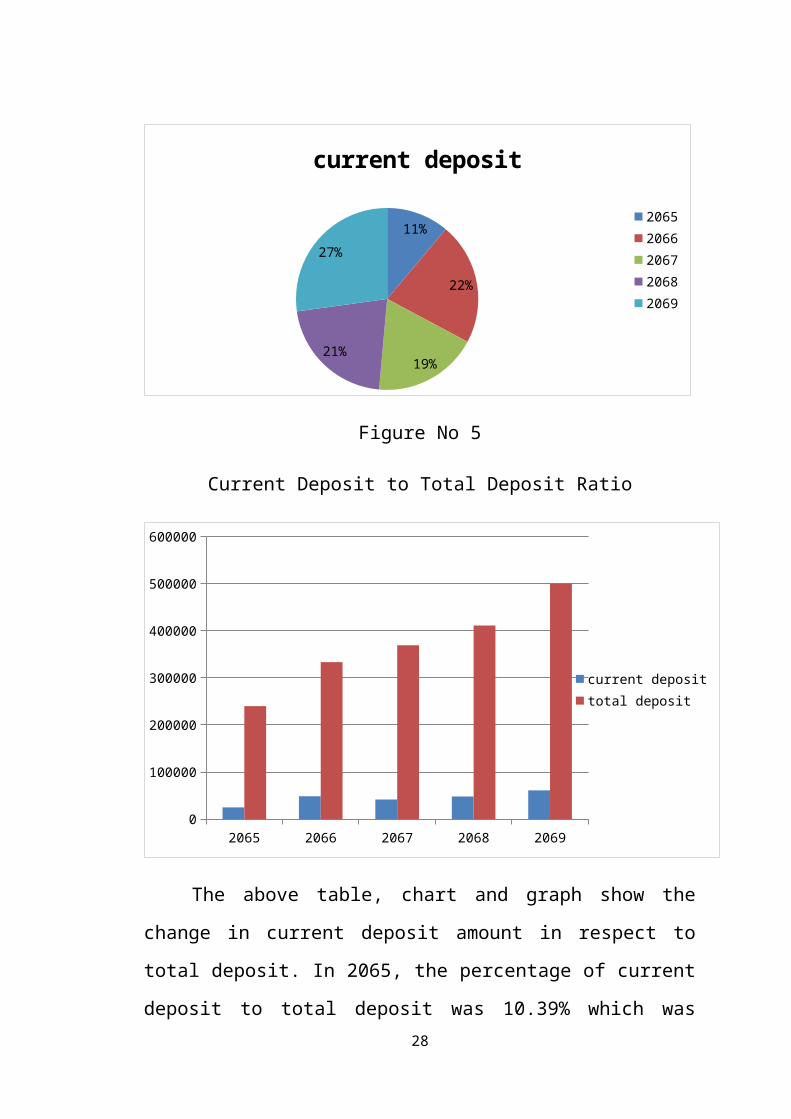

3.4 Current Deposit to Total Deposit Ratio

It is calculated to find out the proportion

of current deposit with respect to total

deposits. It can be calculated by the following

formula:-

(Current Deposit/Total Deposit) 100

Table no 10

Current Deposit to Total Deposit Ratio

(Rs in lakh)

Year Current

Deposit

Total

Deposit

percentage%

2065 24923 239763 10.392066 48599 333229 14.582067 41733 369323 11.302068 47912 411279 11.652069 60982 500061 12.19%(Source: Annual reports of Everest Bank 2065-2069)

27

11%

22%

19%21%

27%

current deposit

20652066206720682069

Figure No 5

Current Deposit to Total Deposit Ratio

2065 2066 2067 2068 20690

100000

200000

300000

400000

500000

600000

current deposittotal deposit

The above table, chart and graph show the

change in current deposit amount in respect to

total deposit. In 2065, the percentage of current

deposit to total deposit was 10.39% which was28

increased to 14.58 in 2066 but it was decreased

in 2067 & 2068 i.e.to 11.30% and 11.65%. Again,

it got increased in 2069 and reached to 60982

lakhs.Current deposits have been steadily

decreasing due to the diversion of current

accounts to the other accounts.

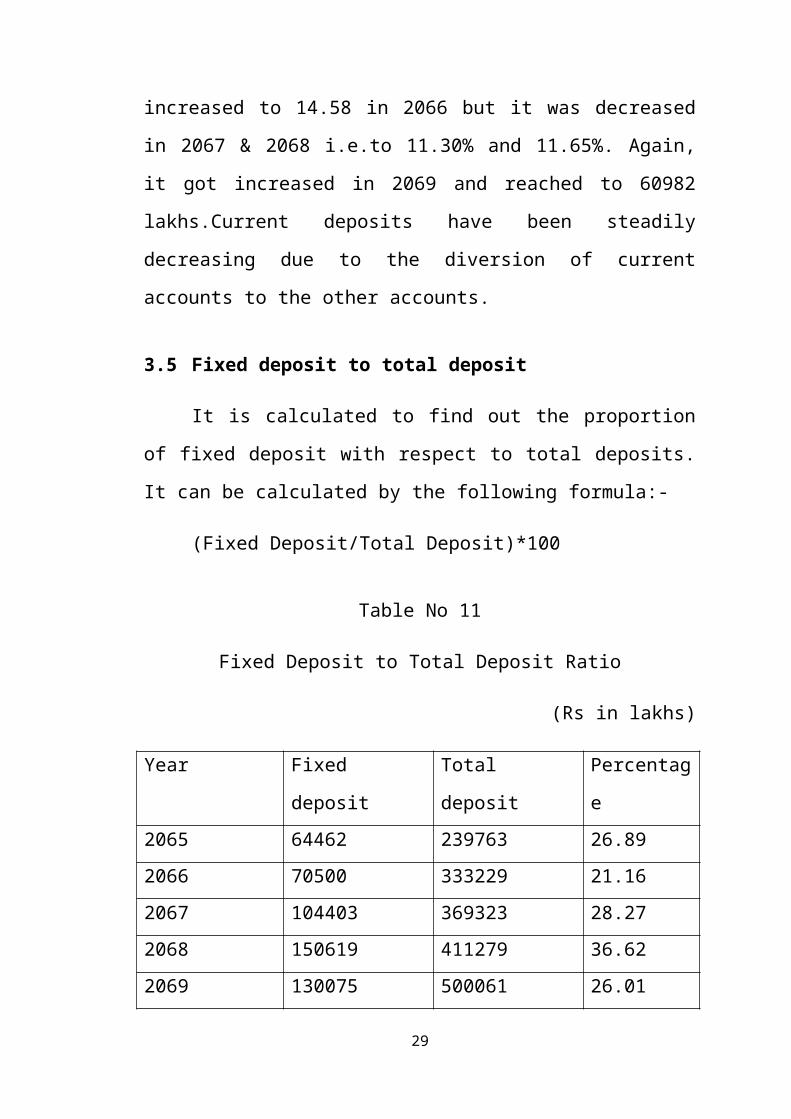

3.5 Fixed deposit to total deposit

It is calculated to find out the proportion

of fixed deposit with respect to total deposits.

It can be calculated by the following formula:-

(Fixed Deposit/Total Deposit)*100

Table No 11

Fixed Deposit to Total Deposit Ratio

(Rs in lakhs)

Year Fixed

deposit

Total

deposit

Percentag

e2065 64462 239763 26.892066 70500 333229 21.162067 104403 369323 28.272068 150619 411279 36.622069 130075 500061 26.01

29

(Source: Annual reports of Everest Bank 2065-2069)

30

Figure No 6

Fixed Deposit to Total Deposit Ratio

12%

14%

20%29%

25%

Fixed deposit

20652066206720682069

2065 2066 2067 2068 20690

100000

200000

300000

400000

500000

600000

Fixed depositTotal deposit

31

In the above table and chart we can see the

percentage of fixed deposit to the total deposit

was 26.89% & 21.16% in 2065 and 2066 which

increased to 28.27% & 36.62% in 2067 and 2068

respectively. But it was decreased in 2069 which

was 26.01%of total deposit .It shows the

increasing volume of fixed deposit during last

fiscal year’s which is due to the increase in

interest rate.

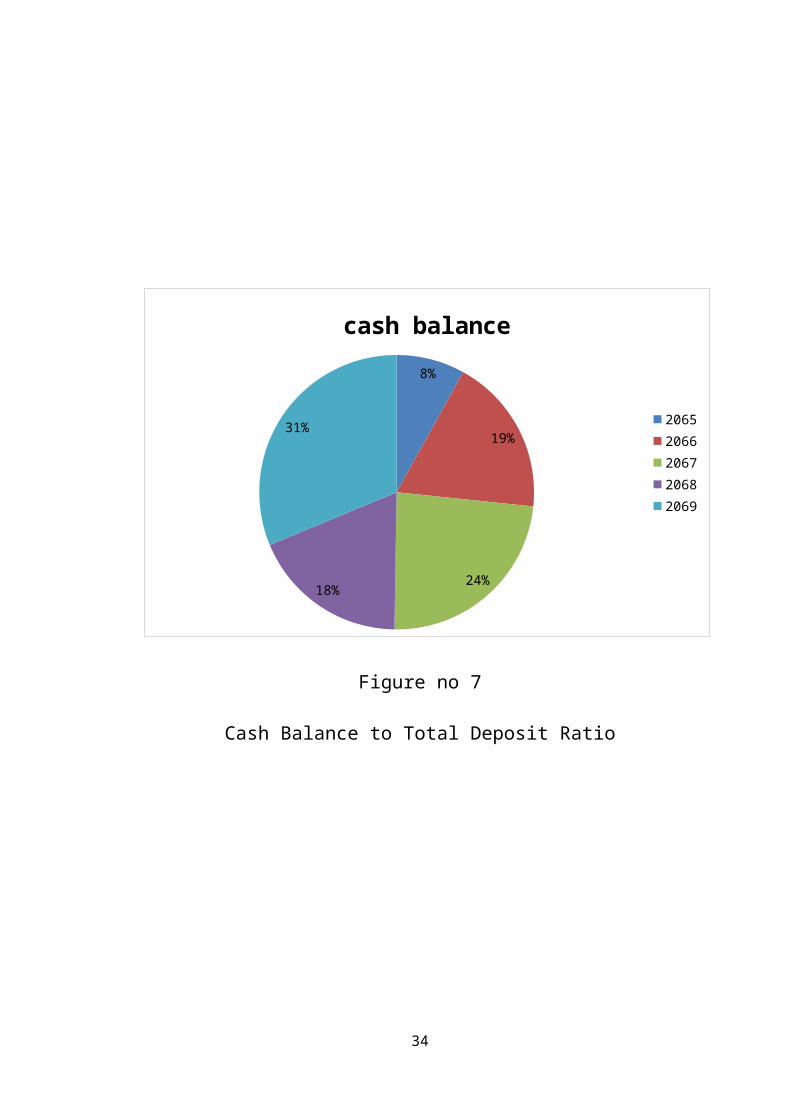

3.6 Cash Balance to Total Deposit Ratio

Cash balance consists of cash on hand,

foreign cash on hand, cheques and other cash

items which represents the greater ability to

meet the deposits. This ratio can be calculated

by the following formula:

Cash Balance/Total

Deposit * 100

Tabl

e no 12

Cash Balance to

Total Deposit Ratio

32

(Rs. In lakh)

Year Cash

balance

Total

deposit

Percentag

e %2065 26679 239763 11.13

2066 61644 333229 18.50

2067 78188 369323 21.17

2068 61228 411279 14.89

2069 103633 500061 20.72

(Source: Annual reports of Everest

Bank 2065-2069)

33

8%

19%

24%18%

31%

cash balance

20652066206720682069

Figure no 7

Cash Balance to Total Deposit Ratio

34

2065 2066 2067 2068 20690

100000

200000

300000

400000

500000

600000

cash balanceTotal deposit

From the above table chart and graph, we can

see cash and bank balance on 2065,2066

and2067were increasing in trend which were

11.13%,18.50% and 21.17% of total deposit but in

2068 it got declined and reached to 14.89% of

total deposit. Again in 2069 it was increased

which was 20.72% of total deposit. From this

analysis it can be concluded that cash and bank

position of Everest bank is in declining state.

For further increasement, EBL can invest in

productive sectors like short term marketable

security, treasury bills etc to improve its

situation.

35

Mathematical analysis

In this report various accounting, financial

and statistical tools have been used to analyze

the collected data and interpret the results

obtained. The various tools used are:-

a) Arithmetic mean

b) Standard deviation

c) Coefficient of variation

3.7 Arithmetic mean

This statistical tool is used in this study

to find the arithmetic average of the variable.

Arithmetic mean is the figure we get when the

total of all the values in a distribution is

divided by the number of values in the

distribution. It is used in this study to

calculate the average value of current, saving

and fixed deposit and interpret it.

36

Mathematically, = ∑ XN

Where, =Mean

∑X = Sum

total of all observations

N=Total number of

observations

3.8 Standard deviation

Standard deviation is often powerful and

helpful measure of dispersion. It is positive

square root of the average of the deviations of

the measurement from their means. It is denoted

by It is used in this study to measure the

size of deviations of current, fixed and saving

deposit from the average.

Mathematically, = √∑ (X−X )2

N

Where N = no. of observation

(X−X ) =Deviation from exact arithmetic

mean

37

3.9 Coefficient of Variation

It is a relative measure of dispersion based

on the standard deviation. In order to compare

the variability between two sets of data,

coefficient of variation can be used as a useful

method. In this study, it is used to find the

variation of the current, fixed and saving

deposits.

Mathematically, C.V= σX

×100

Where, =standard deviation

=Mean

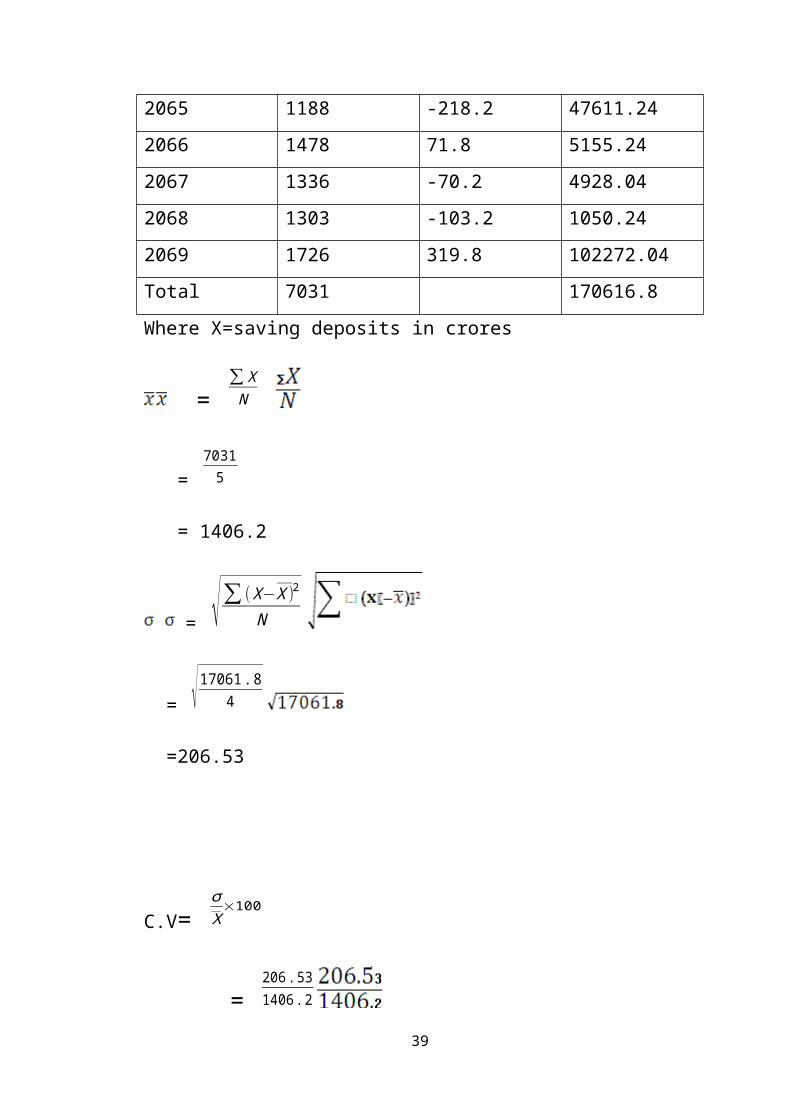

Table no

Calculation of mean, S.D & C.V. of the saving

deposit

Year x (x

38

2065 1188 -218.2 47611.242066 1478 71.8 5155.242067 1336 -70.2 4928.042068 1303 -103.2 1050.242069 1726 319.8 102272.04Total 7031 170616.8Where X=saving deposits in crores

= ∑ XN

= 70315

= 1406.2

= √∑ (X−X )2

N

= √17061.84

=206.53

C.V= σX

×100

= 206.531406.2

39

=14.69%

Table no

Calculation of mean, S.D & C.V Of fixed deposit

Year X (x

2065 644 -395.8 156657.642066 705 -334.8 112091.042067 1044 4.2 17.642068 1506 466.2 217342.442069 1300 260.2 67704.04Total 5199 553812.8Where X= fixed deposit in crores

= ∑ XN

= 51995

= 1039.8

= √∑ (X−X )2

N

= /4

= 372.09

40

C.V= σX

×100

= 372.091059.8

=35.11%

Table no

Calculation of mean, SD & C.V of current deposit

Year X (x

2065 249 -198.8 39521.442066 485 37.2 1383.842067 417 -30.8 948.642068 479 31.2 973.442069 609 161.2 25985.44Total 2239 68812.8

Where X=current deposits in crores

= ∑ XN

= 22395

41

= 447.8

= √∑ (X−X )2

N

= /4

=131.16

C.V= σX

×100

=

=29.29%

3.10Major findings

The major findings of the study which covers

a period of 5 years (2065 to 2069) are as

follows:-

The average deposit of saving, fixed and

current account from 2065 to 2069 are

14062, 1039.8 and 447.8 respectively. It

shows in an average, deposit in saving

account is higher than in other accounts.

42

The standard deviation of saving, current

and fixed accounts from 2065 to 2069 are

206.53, 372.09 and 131.1 respectively. It

shows that there is higher deviation in

the current account.

The coefficient of variation of saving,

current and fixed account from 2065 to

2069 is 14.69%, 35.11% and 29.29%. It

shows that there is greater variation in

current account and less variation in

saving account.

Therefore, here is uniform and consistent

deposit in the saving account.

43

CHAPTER-4

SUMMARY, CONCLUSION AND RECOMMENDATION

4.1 Summary

Financial sector in Nepal comprises of

commercial banks and other financial institutions

like development banks, finance companies,

cooperatives etc. Everest Bank LTD (EBL)

established in 1994 is one of the commercial bank

which started its operation with an objective of

providing excellent professional services and

improves its position as a leader in the field of

financial related services. This bank is a joint

venture partner with Punjab National Bank (PNB)

of India. As the bank has just completed sixteen

years of operation, it has achieved so many

successes in the way of its operation.

Everest Bank mainly collects the deposit

under the account of fixed, saving, current and

others. They are the main source of raising

capital for bank. According to the latest data of

2069 of EBL, the total deposit is 500061 lakh.

Among the total deposit the current deposit is

44

60982 lakh i.e. 12.19% of total deposit whereas

saving deposit is 172693 lakh i.e. 34.53% of

total deposit. But fixed deposit is 130075 lakh

i.e. 26.01% of total deposit. This shows that

saving deposit occupies the larger portion.

EBL is at consistent progress over the five

years which can be known by the increase in

deposits every year. Due to its improvement, it

is gradually expanding its branches. In the same

way, the bank has been facing various challenges

that has arised in the market and has been able

to give best performance in the market.

45

4.2 Conclusion

The trend analysis shows that the deposit of EBL is in increasing trend.This shows that there is consistent progress of the bank.

The share of saving deposits is more

than of fixed, current, margin, call and

other deposits in EBL.

The saving deposit was increased in 2066

by 24.39% and it gradually decreased in

2067 and 2068 by 9.62% and 2.4%.But in

2069, it was increased by 8.93%.So,

saving deposit is in increasing trend.

The current deposit was increased in

2066 by 94.99% but it was decreased in

2067 by 14.13%. After that, it gradually

increased in 2068 and 2069by 14.81% and

27.28% respectively. So, current deposit

is in increasing trend.

The fixed deposit was increased in 2066,

2067 and 2068 by 9.37%, 48.08% and

44.27% respectively. But in 2069 it was

decreased by 13.64%.So, fixed deposit is

in decreasing trend.46

The cash balance was increased in 2066

and 2067 by 38.93% and 10.83%

respectively. But in 2069 it was

decreased by 21.69% and again in 2069 it

was increased by 69.26%.So, cash balance

is in increasing trend.

By the analysis of deposit we can

conclude that bank is able to utilize

its deposit a great extent.

47

4.3 Recommendation

With reference with finding and analysis,

following recommendation are suggested to

overcome the weakness of the organization. They

are:

Bank should invest deposits in various

sectors and provide loan and advances to

its customers so as to increase

deposits, as it is the major sources of

fund.

The bank may increase its deposits by

introducing a number of attractive

deposit mobilizing schemes.

The formalities should be simplified so

that the client feels easy in the

process of cash deposit.

The situation of motivation should be

created to the depositors to encourage

them for depositing under different

accounts.

The interest rate plays an important

role in controlling the fluctuation of

48

deposits; therefore bank should be

careful while determining the interest

rate.

The members of EBL should co ordinate

and make good understanding with the

customers. That is the best way of

deposit collection.

49

Copyright © 2022 FDOKUMEN