Chapter 10: Accounting for a Merchandising Business

39

1 Chapter 10: Accounting for a Merchandising Business

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Chapter 10: Accounting for a Merchandising Business

1

Chapter 10: Accounting for a

Merchandising Business

2

merchandising business a business that buys goods and sells them at a profit.

10.1 The Merchandising Business Pages 396 402

Different categories of merchandising businesses:1. wholesaler buys goods from a manufacturer and sells them to a retailer.

2. retailer buys goods from wholesalers and/or manufactures and sells them to the public.

3

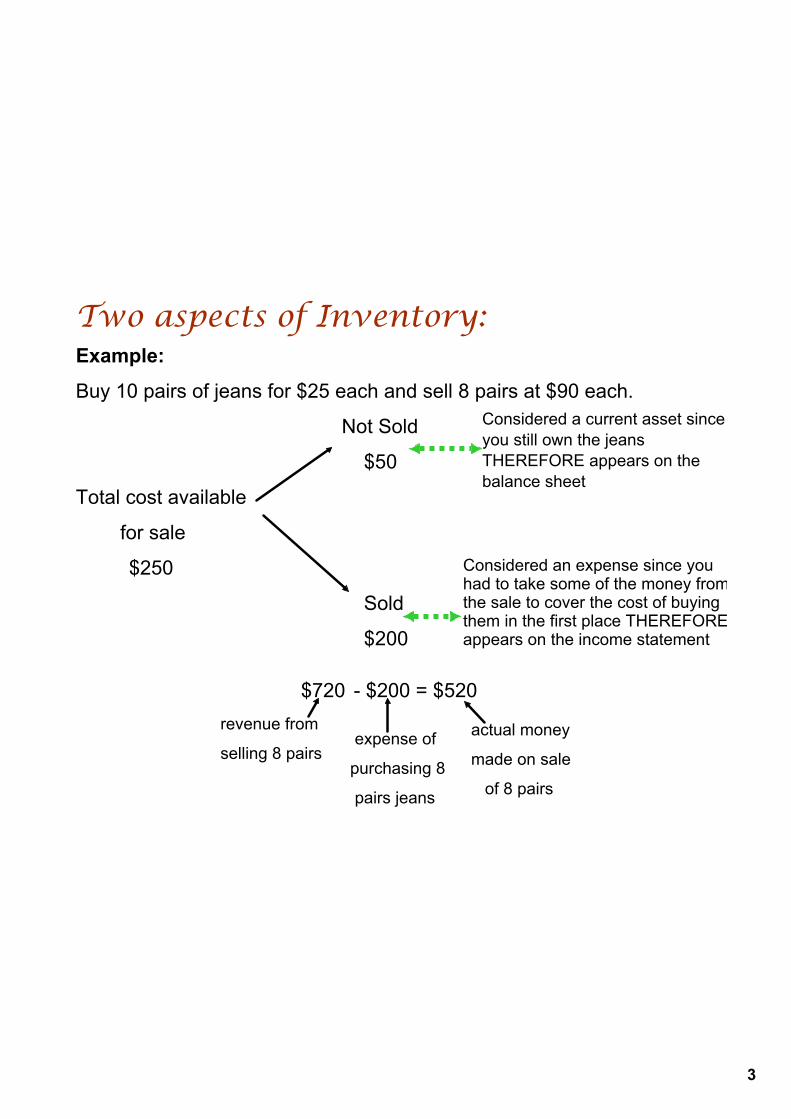

Two aspects of Inventory:Example:

Buy 10 pairs of jeans for $25 each and sell 8 pairs at $90 each.

Not Sold

$50

Total cost available

for sale

$250

Sold

$200

Considered a current asset since you still own the jeans THEREFORE appears on the balance sheet

Considered an expense since you had to take some of the money from the sale to cover the cost of buying them in the first place THEREFORE appears on the income statement

$720 $200 = $520revenue from

selling 8 pairs expense of

purchasing 8

pairs jeans

actual money

made on sale

of 8 pairs

4

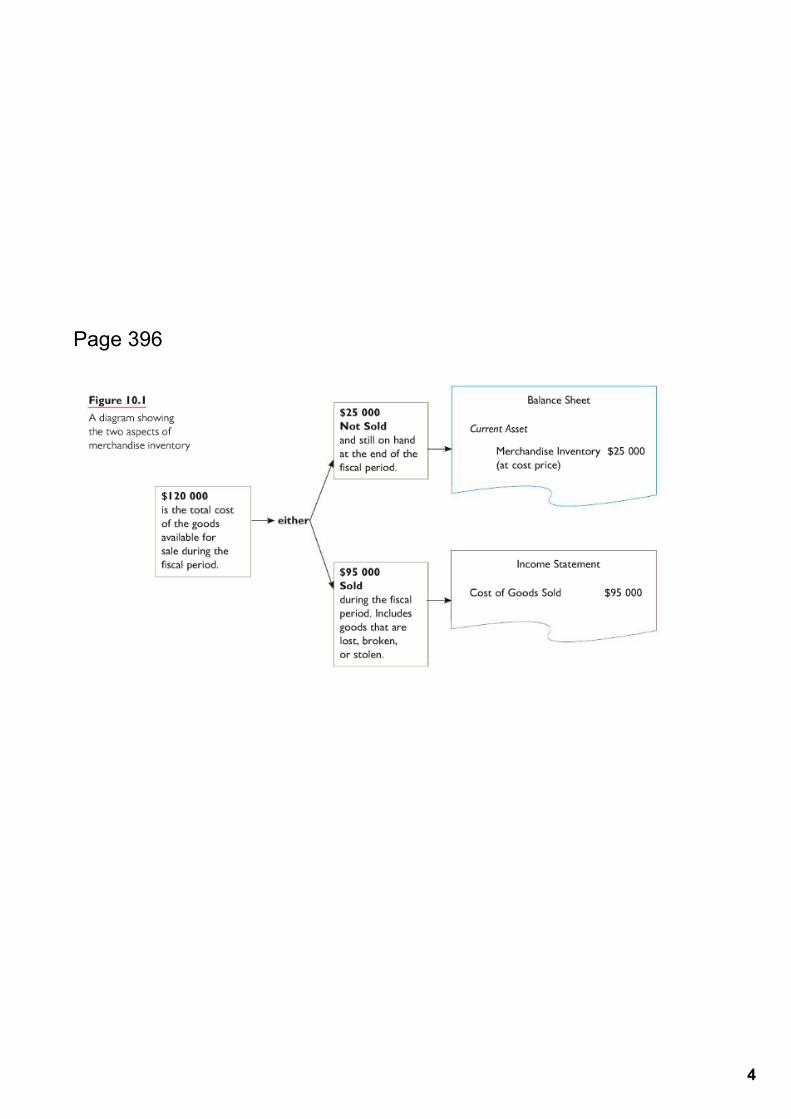

Page 396

5

merchandise inventory (stockintrade) the quantity of merchandise on hand available for sale.

Two methods of calculating inventory:1. periodic cost of inventory sold is determined at the end of the fiscal period by means of a physical inventory.

physical inventory a procedure in which the unsold goods of a merchandising business are counted and valued (at cost price).

2. perpetual cost of inventory sold determined after each sale by means of a computerized system

6

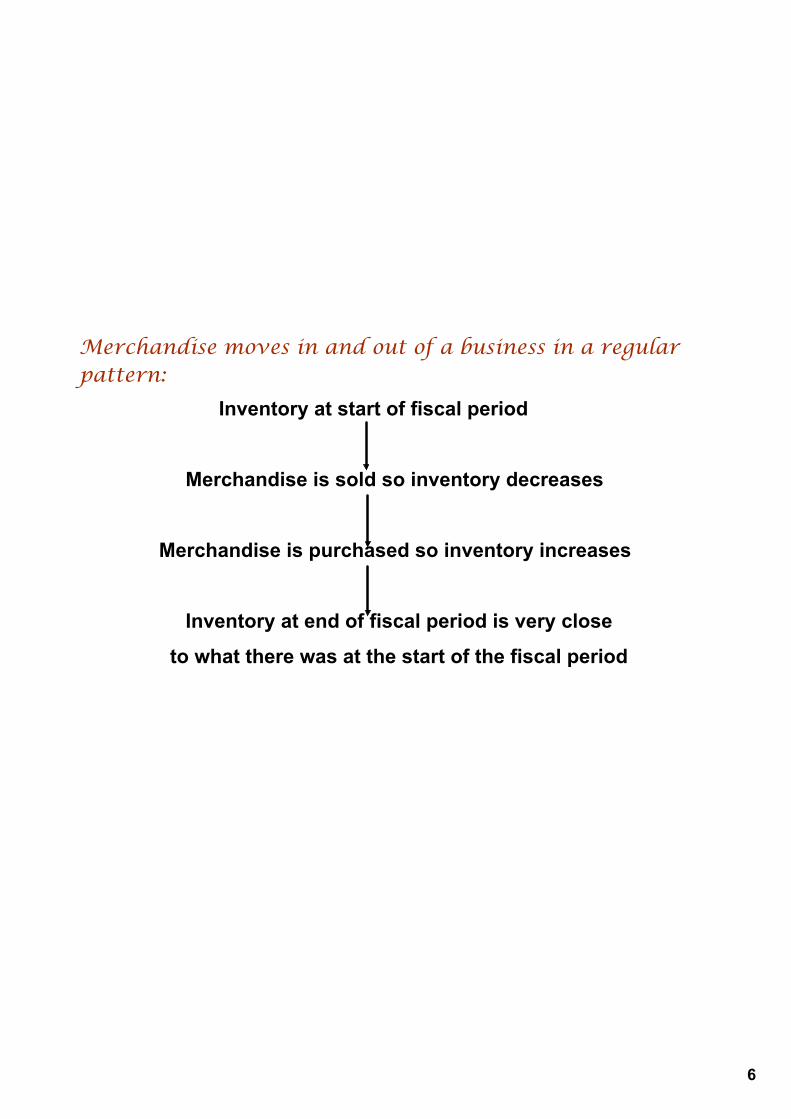

Merchandise moves in and out of a business in a regular pattern:

Inventory at start of fiscal period

Merchandise is sold so inventory decreases

Merchandise is purchased so inventory increases

Inventory at end of fiscal period is very close

to what there was at the start of the fiscal period

7

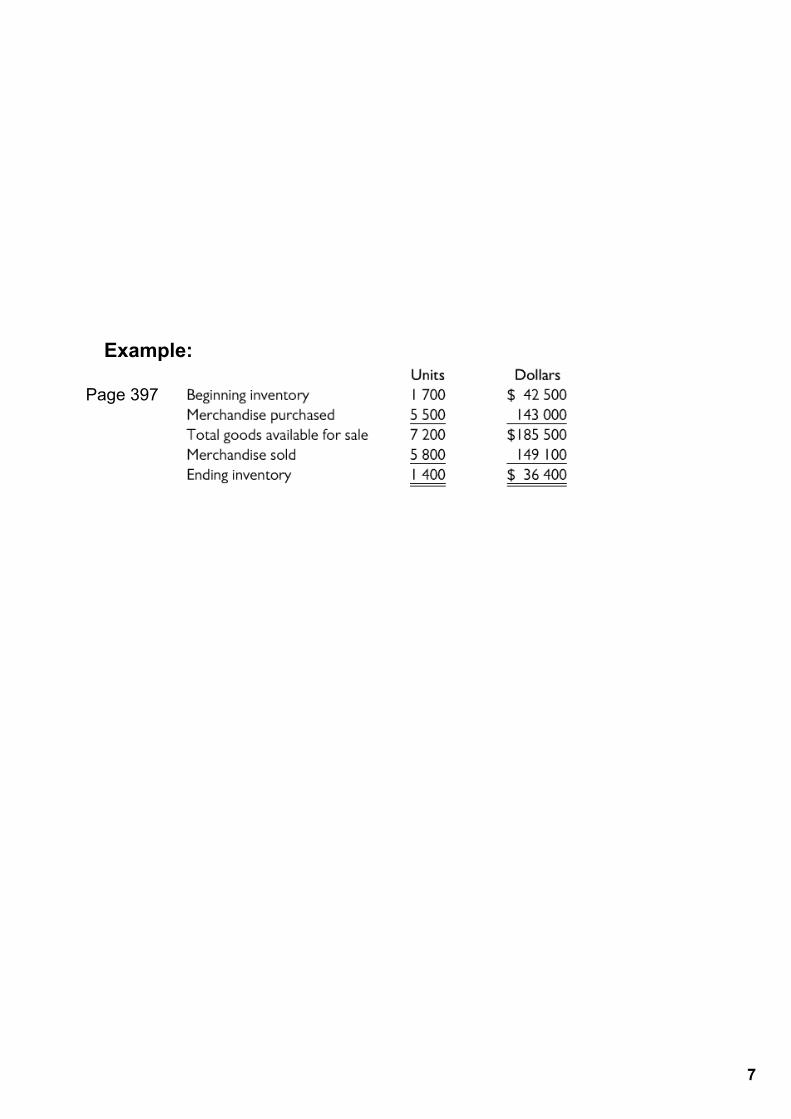

Example:

Page 397

8

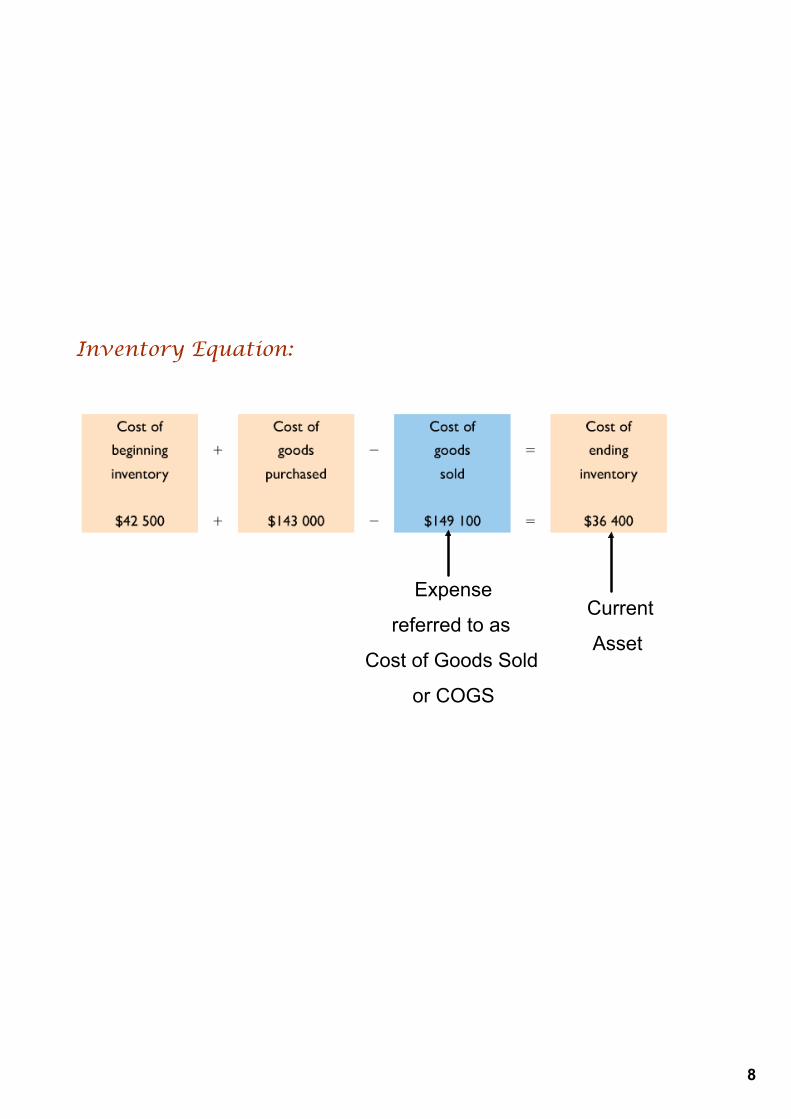

Inventory Equation:

Current

Asset

Expense

referred to as

Cost of Goods Sold

or COGS

9

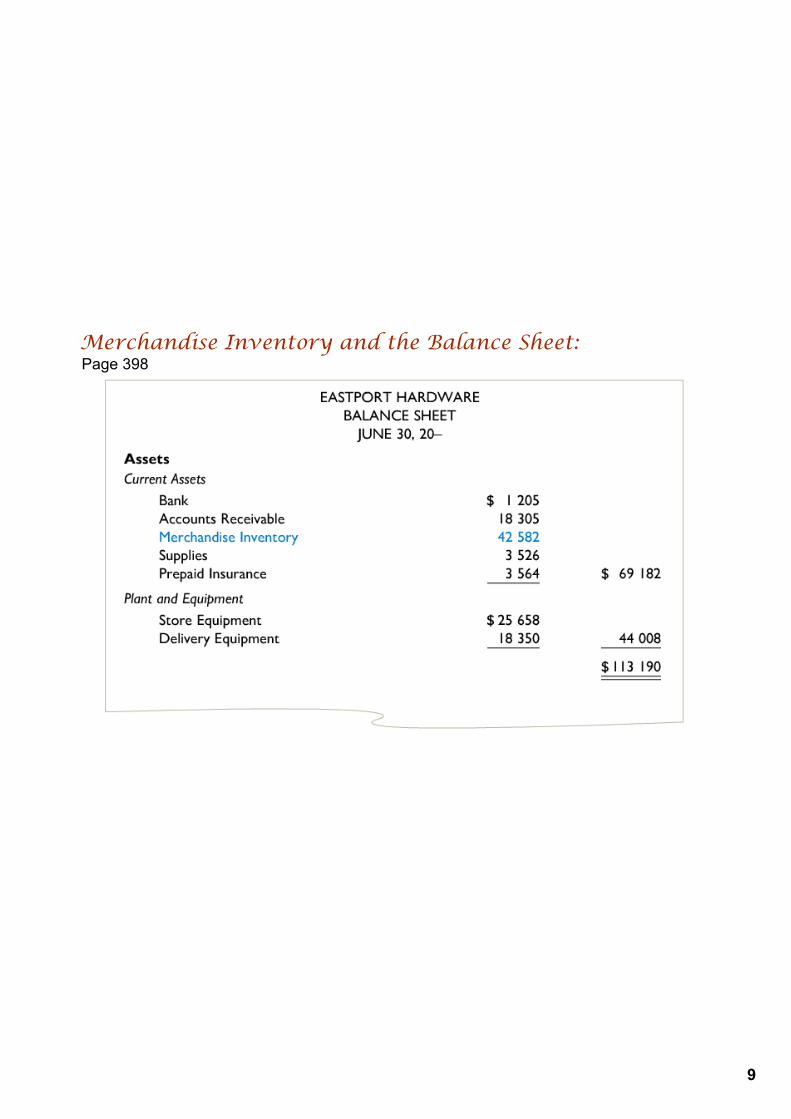

Merchandise Inventory and the Balance Sheet:

Page 398

10

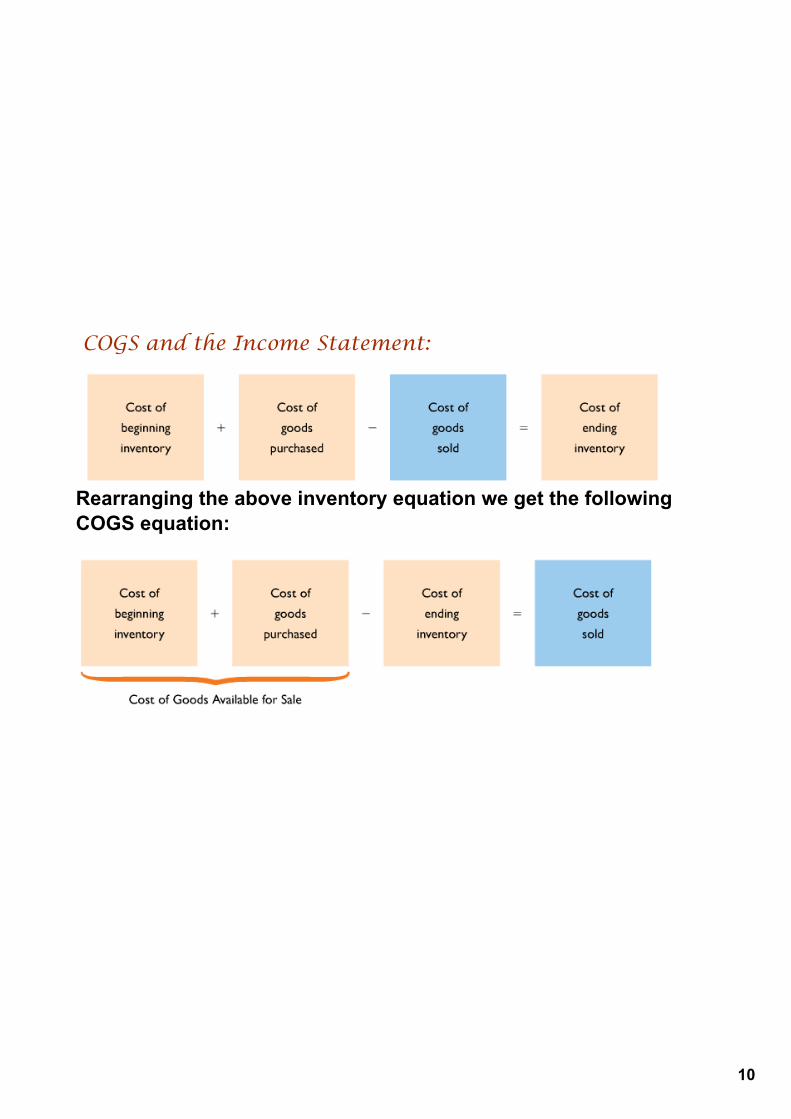

COGS and the Income Statement:

Rearranging the above inventory equation we get the following COGS equation:

11

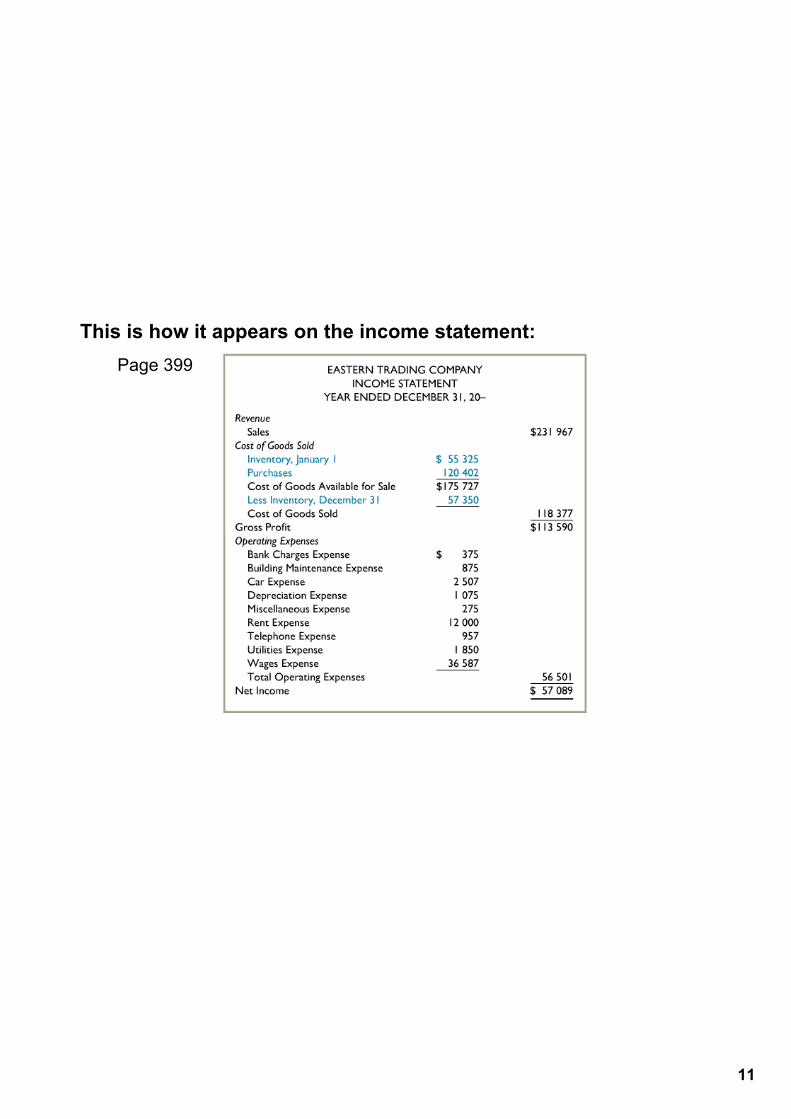

This is how it appears on the income statement: Page 399

12

Gross Profit = Selling Price COGS

(Revenue)

13

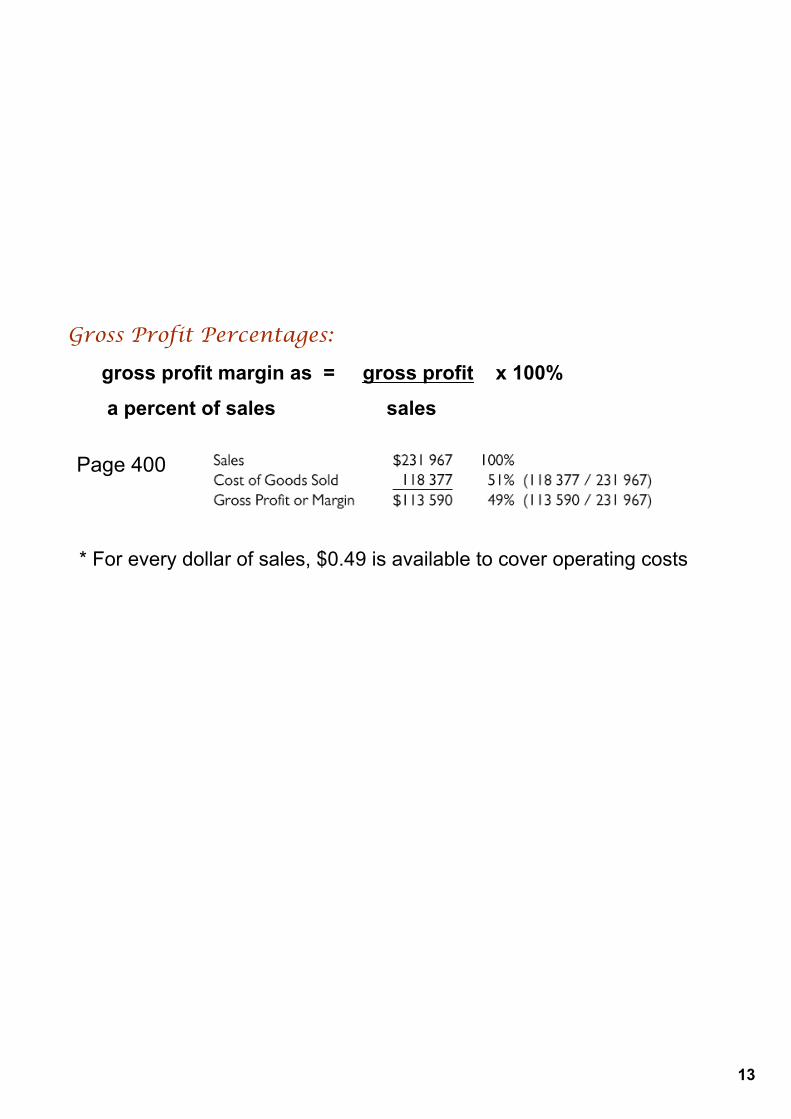

Gross Profit Percentages:

Page 400

gross profit margin as = gross profit x 100%

a percent of sales sales

* For every dollar of sales, $0.49 is available to cover operating costs

14

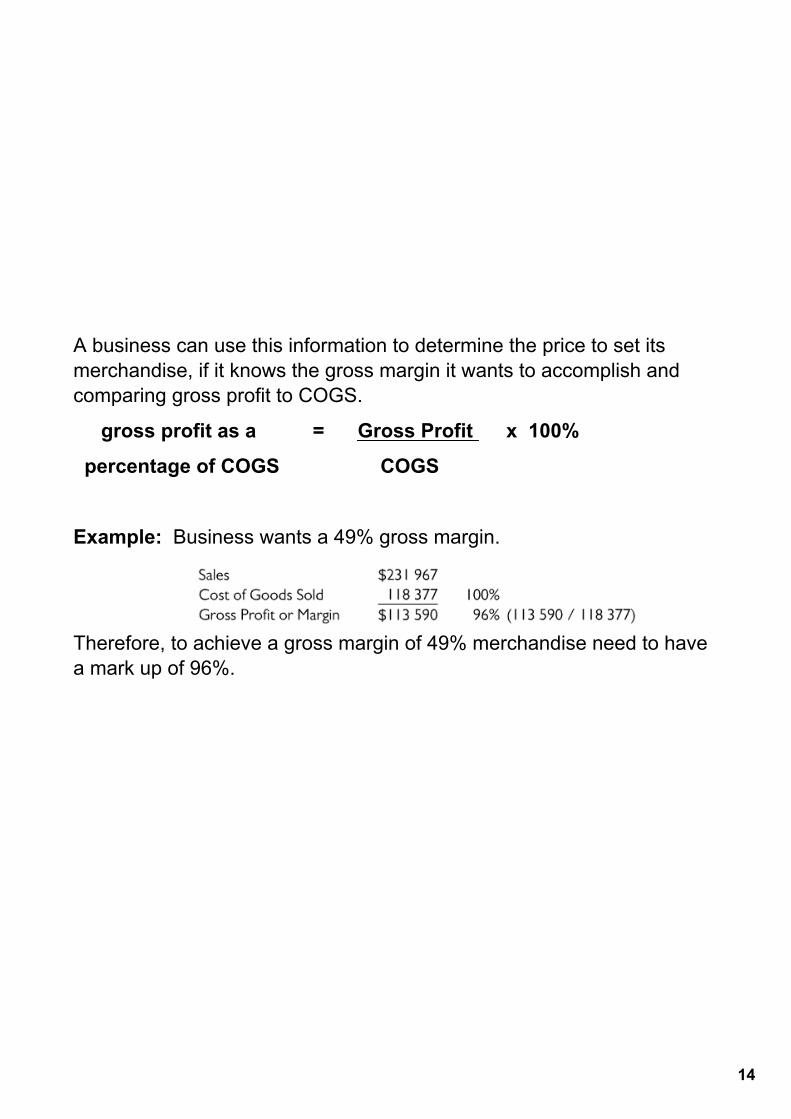

A business can use this information to determine the price to set its merchandise, if it knows the gross margin it wants to accomplish and comparing gross profit to COGS.

gross profit as a = Gross Profit x 100%

percentage of COGS COGS

Example: Business wants a 49% gross margin.

Therefore, to achieve a gross margin of 49% merchandise need to have a mark up of 96%.

15

markup the amount that a merchandising business increases the cost of a good to arrive at a selling price.

16

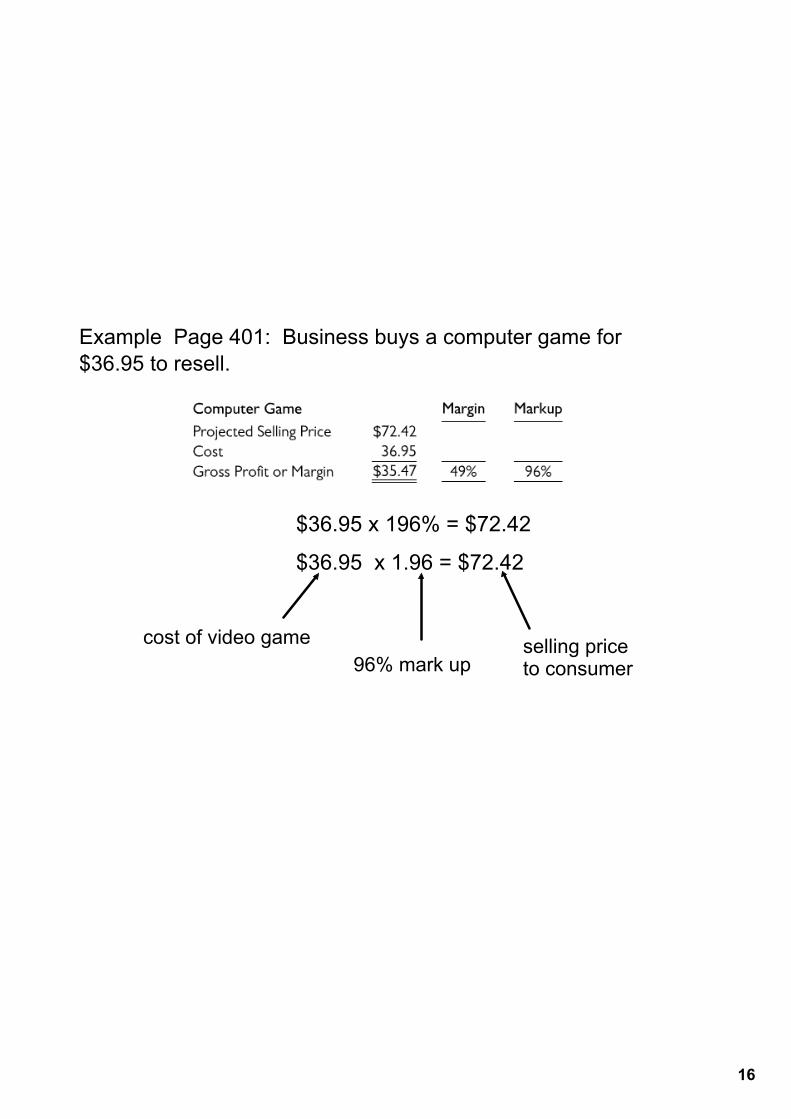

Example Page 401: Business buys a computer game for $36.95 to resell.

$36.95 x 196% = $72.42

$36.95 x 1.96 = $72.42

cost of video game96% mark up

selling price to consumer

17

Limitations of the Periodic Inventory:

Accurate financial statements cannot be prepared until a physical inventory is done.

Physical inventories are inconvenient and timeconsuming often requiring a business to shut down for a couple of days.

18

Advantage of the Periodic Inventory:

- Relatively easy to manage which is important for small businesses. However, improvements in quality and cost of technology are making it more attractive for a business to adopt a perpetual system.

19

10.2 Accounting Procedures for Pages 404 408 Merchandising Business

Accounts used in a Merchandising Business:

1. Merchandise Inventory Account used in a periodic inventory method. shows inventory figure at the beginning of the fiscal period. only entry made is the inventory adjustment at the end of the fiscal period.

20

2. Purchases Account keeps track of merchandise purchased.

accounting entry made when merchandise is purchased:

Purchases DRHST Recoverable DR

A/P OR Bank CR

21

3. Sales Account name of the revenue account for a merchandising business.

Accounting entry when a sale is made: A/R OR Bank DR

Sales CRHST Payable CR

22

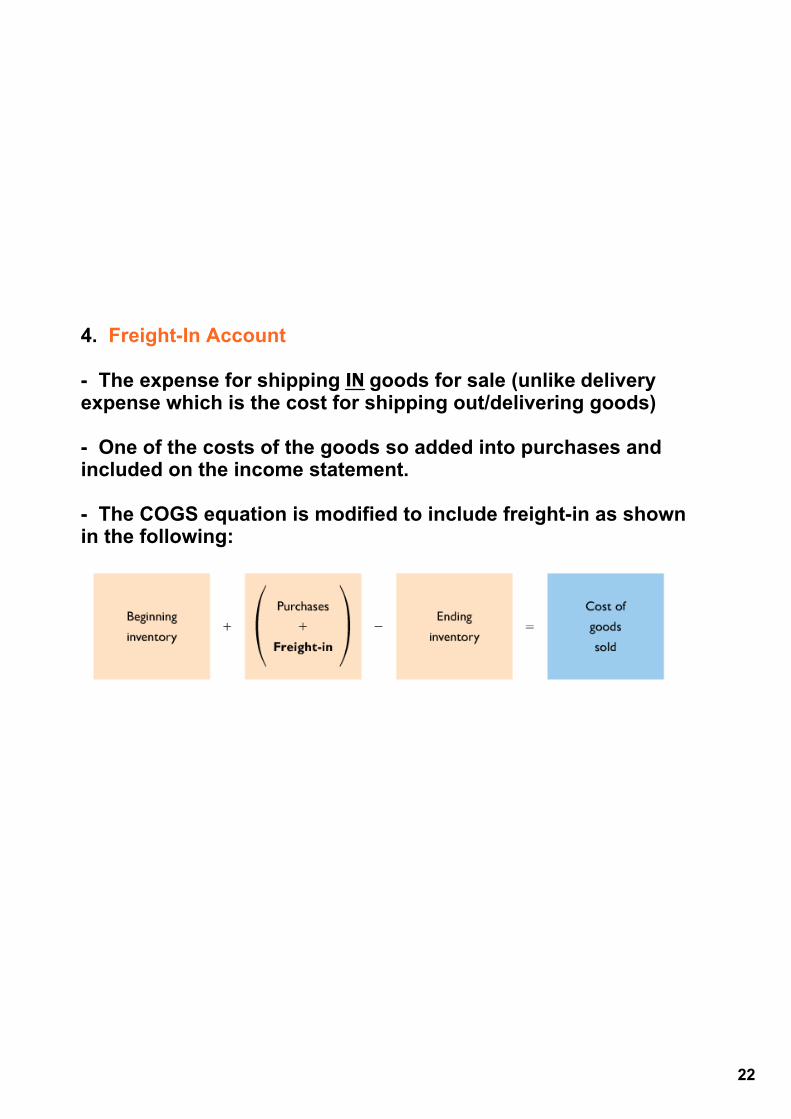

4. FreightIn Account

The expense for shipping IN goods for sale (unlike delivery expense which is the cost for shipping out/delivering goods)

One of the costs of the goods so added into purchases and included on the income statement.

The COGS equation is modified to include freightin as shown in the following:

23

10.3 Worksheet for a Merchandising Pages 435 443 Business

Most of the procedures used to complete the worksheet for a merchandising business are the same as before with the following additional steps:• The beginning inventory figure needs to be removed from and the ending inventory must be added to the merchandise inventory account.

• Figures need to be organized to calculate COGS figure for the IS.

24

3 step procedure for treating merchandise inventory, freight-in, and purchases on the worksheet:#1. Beginning inventory is transferred to the IS Dr column.

#2 Ending inventory is transferred to both IS Cr and BS Drcolumns.

#3 Purchases and freightin are transferred to the IS Dr columns.

25

Page 408

26

Inventory figures have to be treated this way in order to calculate COGS properly on the income statement as shown in the following diagram:

Page 409

27

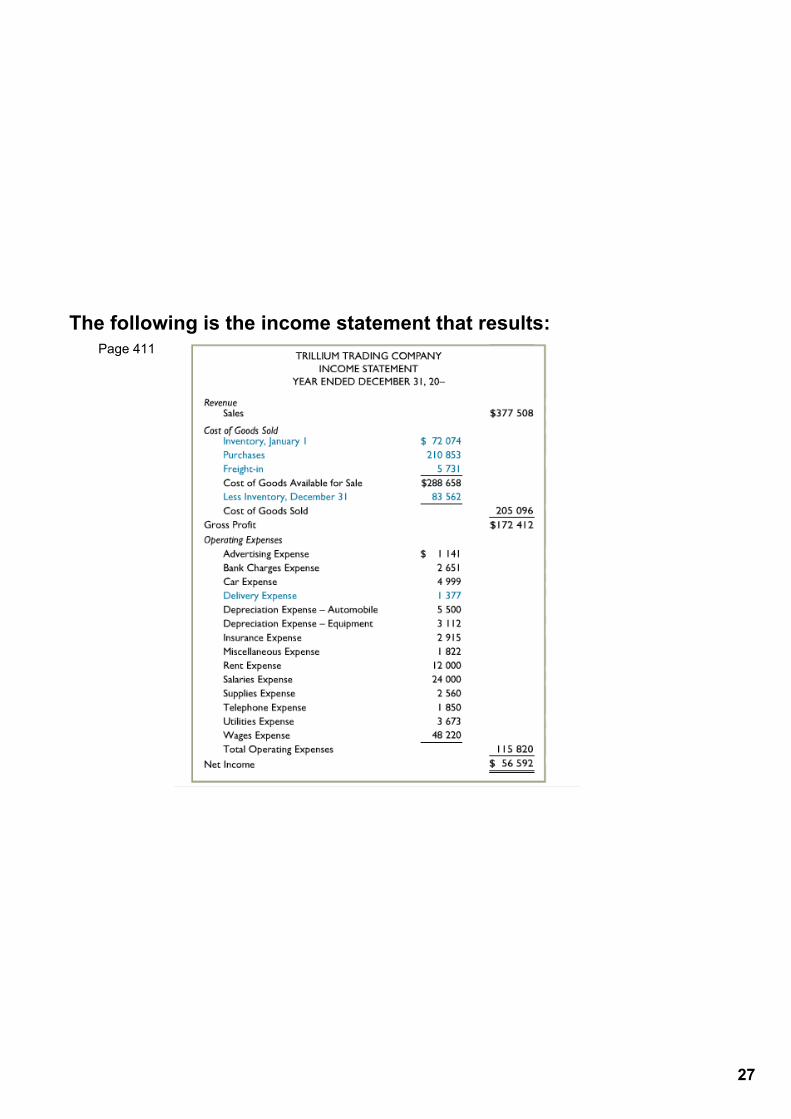

The following is the income statement that results:Page 411

28

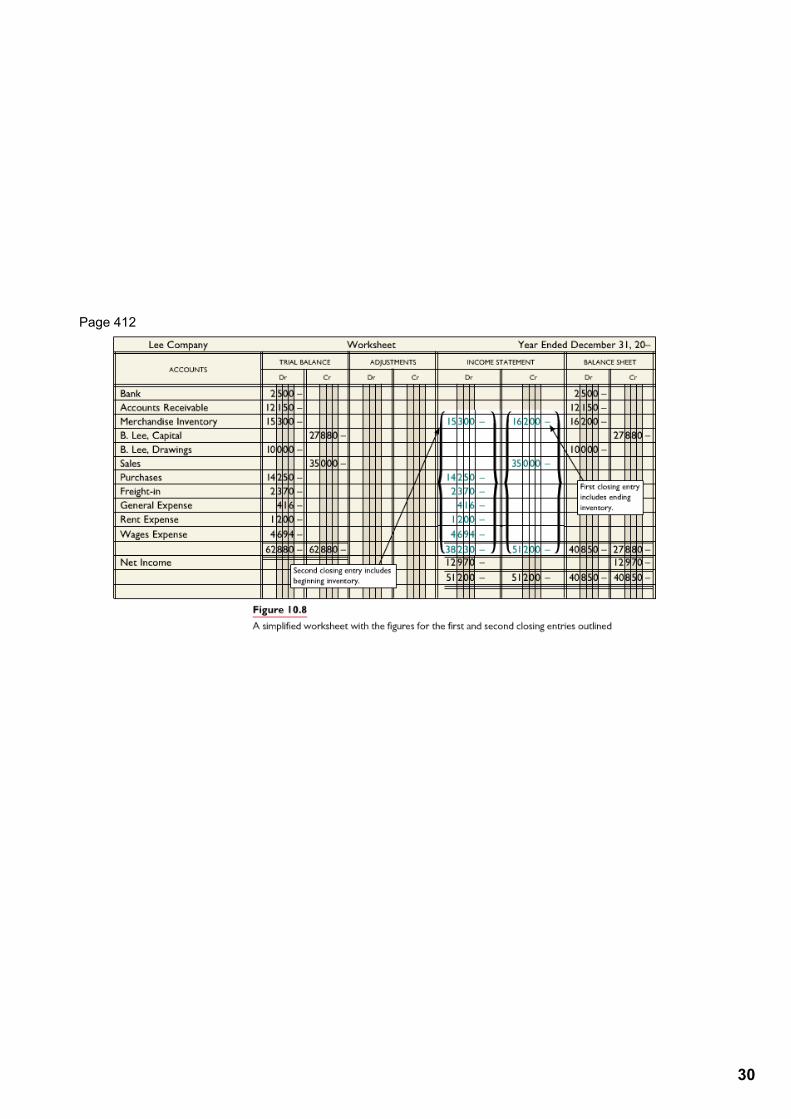

Closing Entries for a Merchandising Business: Closes out old inventory and adds new one. When closing the Sales account, also debit the new inventory figure. When closing expenses, also credit the old inventory figure. When closing expenses, also close the Purchases and Freightin accounts.

29

Generally:• The IS Cr column indicates the figures that must be debited when closing the accounts.

• The IS Dr column indicates the figures that must be credited to close the accounts.

30

Page 412

31

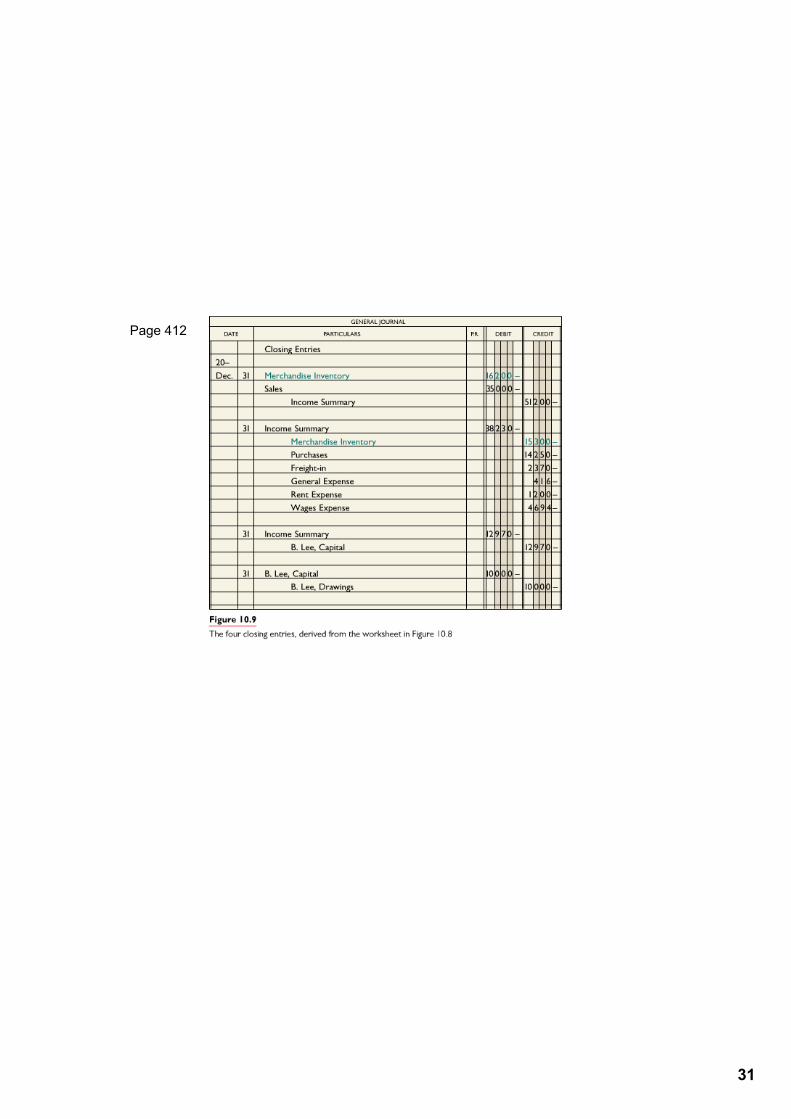

Page 412

32

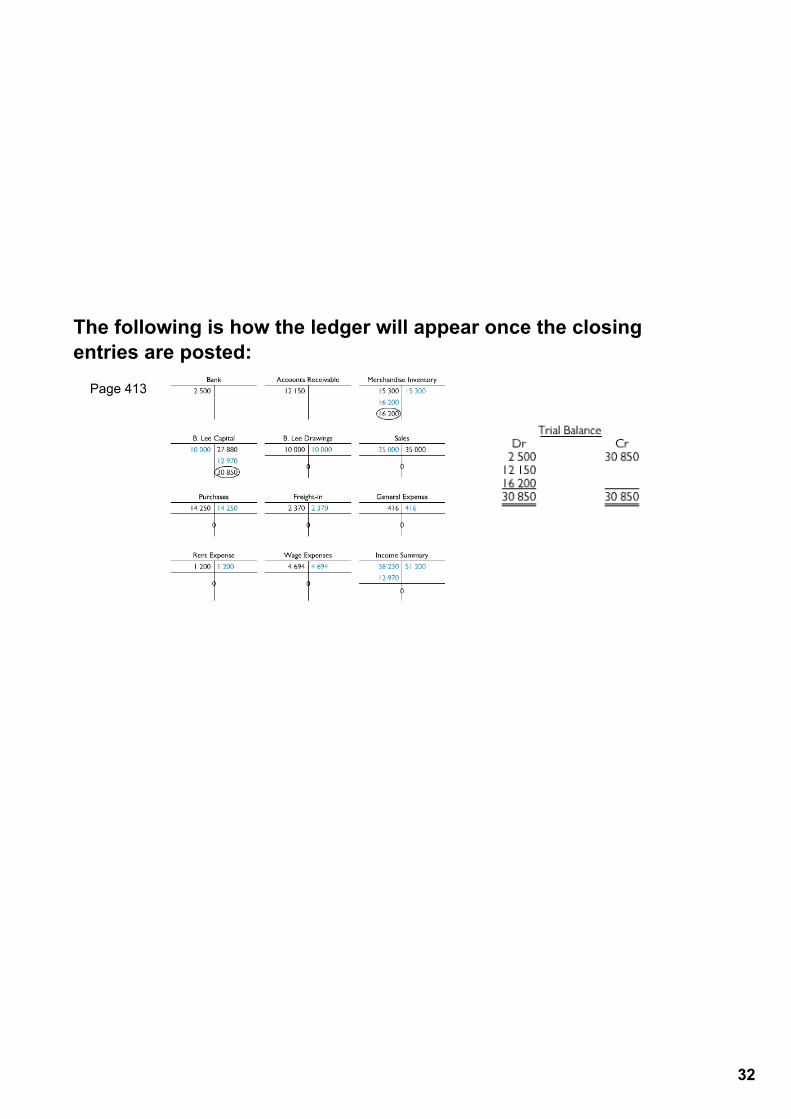

The following is how the ledger will appear once the closing entries are posted:

Page 413

33

perpetual inventory system an inventory system in which a detailed record of items in stock is kept up to date on an ongoing basis.

Provides uptotheminute information about a company's stock.

10.7 Perpetual Inventory Pages 441 445

34

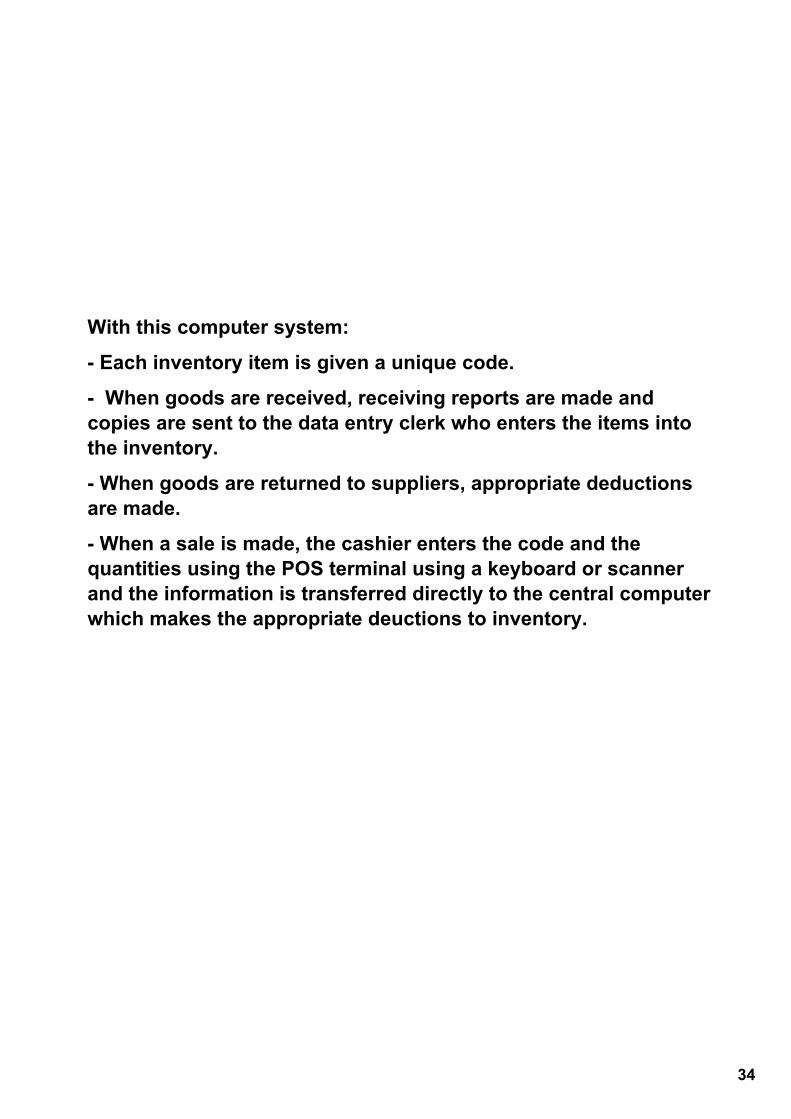

With this computer system:

Each inventory item is given a unique code.

When goods are received, receiving reports are made and copies are sent to the data entry clerk who enters the items into the inventory.

When goods are returned to suppliers, appropriate deductions are made.

When a sale is made, the cashier enters the code and the quantities using the POS terminal using a keyboard or scanner and the information is transferred directly to the central computer which makes the appropriate deuctions to inventory.

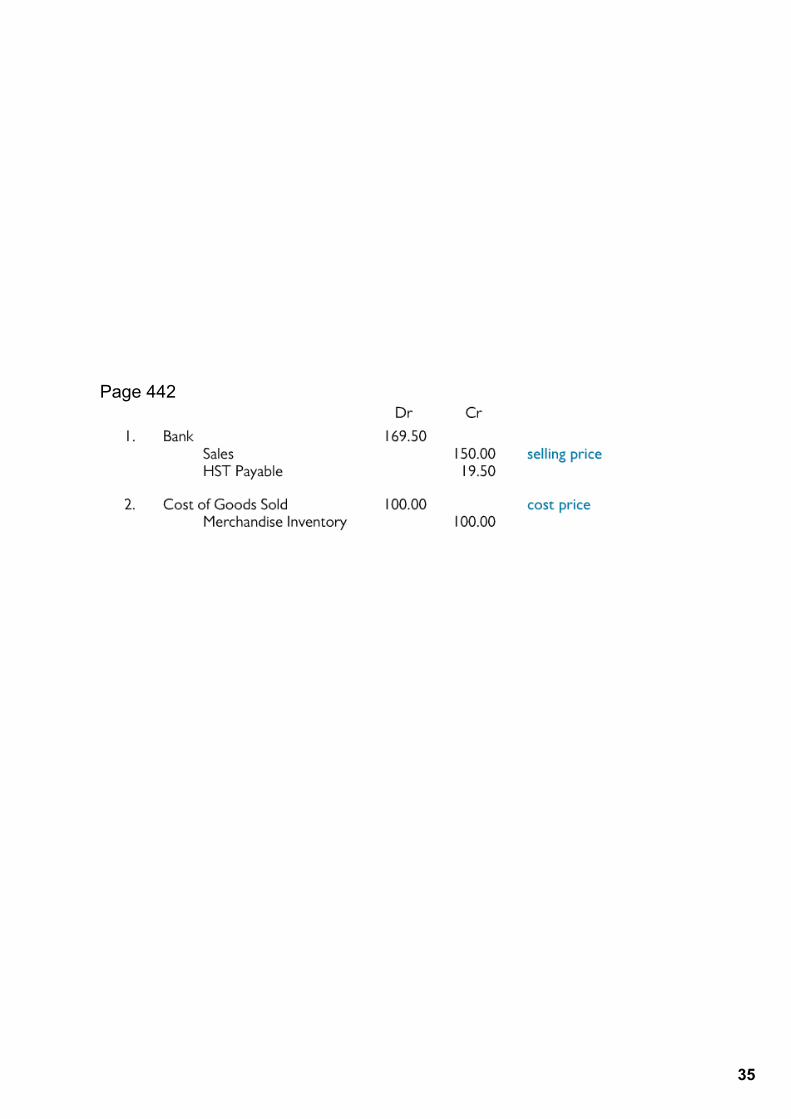

35

Page 442

36

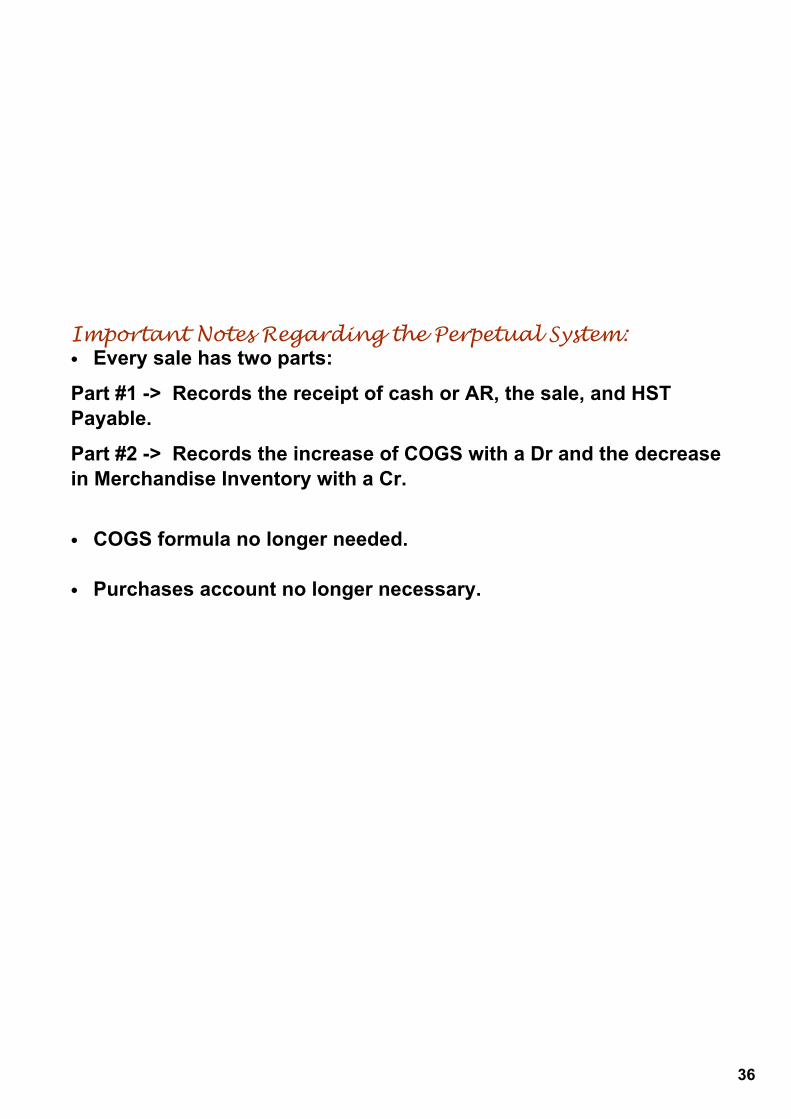

Important Notes Regarding the Perpetual System:• Every sale has two parts:

Part #1 > Records the receipt of cash or AR, the sale, and HST Payable.

Part #2 > Records the increase of COGS with a Dr and the decrease in Merchandise Inventory with a Cr.

• COGS formula no longer needed.

• Purchases account no longer necessary.

37

Transactions Compared Under Periodic and Perpetual Inventory Systems:

38

39

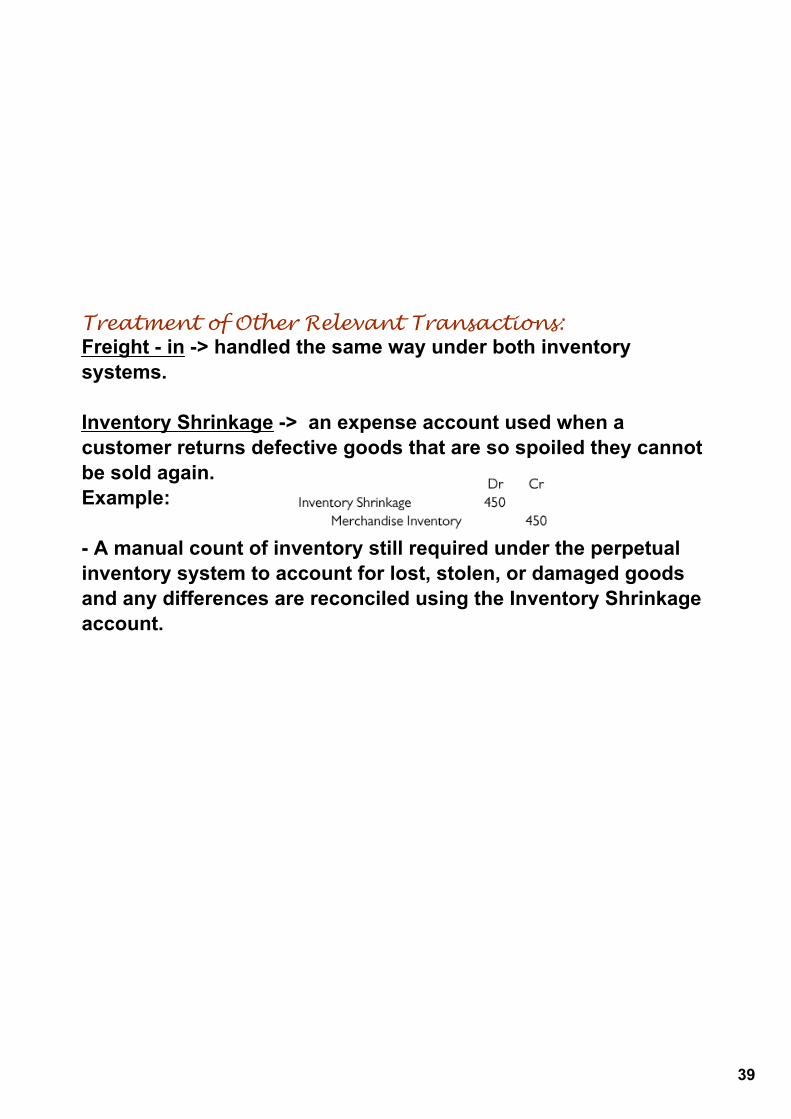

Treatment of Other Relevant Transactions:Freight in > handled the same way under both inventory systems.

Inventory Shrinkage > an expense account used when a customer returns defective goods that are so spoiled they cannot be sold again.Example:

A manual count of inventory still required under the perpetual inventory system to account for lost, stolen, or damaged goods and any differences are reconciled using the Inventory Shrinkage account.