1994-10-Management-Accounting-v76-n4.pdf - Strategic ...

76

11 1 i1MM1 4w ,,

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 1994-10-Management-Accounting-v76-n4.pdf - Strategic ...

1 1 � 1

i1MM1

4w

,,

AnnouncingThe

cii

ent/SepvepFinancialWith

softwapeEven ilh ng The

Competition Has.

(And MOIng TheY DOWL)

One click connects you to Theonly financial software withproven client server technology.

Y

We provide business software to more than seof the Fortune 500. How's that for references?

Masterpiece is mulll-currency, mulll- languageand multi - company. So Itlets you consolidate finan-cials from around the world.

M R

OMPUTERSSOCIATEs

Software superior by design.

Before choosing financial solfware gelan expert's opinion. Free when you call,

Query and reporting tools that can betailored for the needs of your business.

V. it's about the benefits that technologydes. Real -time data access. Advanced decision -ort tools. Global capabilities. More timely andate data. And increased work force productiv-gether, it all adds up to greatly lower costs forasiness.

For More Inlormation, can1- 600-225 -5224, Dept. 51562

We'll show you why, in client /server financial>ftware, we're everything the competition isri t.

Client/Server Financial Softwam� f,�Computer�Associates�Imemational.�I . Islarulia, NY 1178&7000, AU other pnxWa nwn,, refemiml hetein are trademarks of their rnpe¢he companies

Circle No. 2

MANAGEMENTACCOUNTINGEPUBLISHED BY INSTITUTE OF MANAGEMENT ACCOUNTANTS

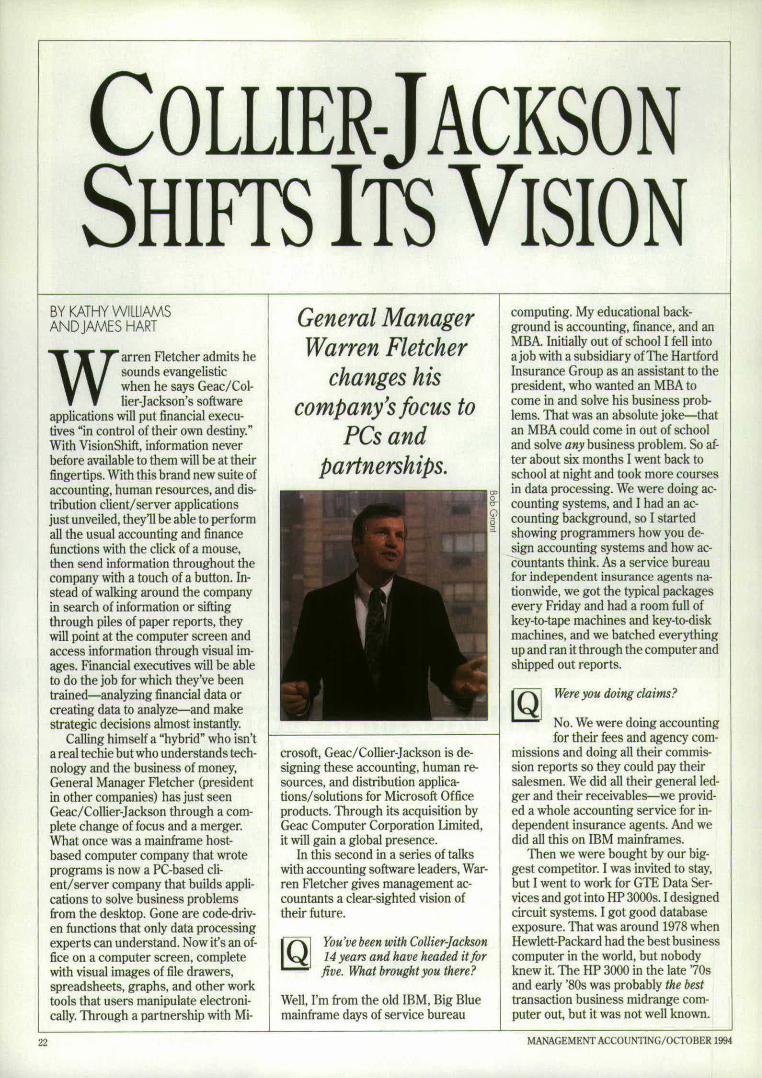

22COLLIER-JACKSONSHIFTS ITS VISIONBY KATHY WILLIAMSAND JAMES HARTWarren D. Fletcher,general manager ofGeac /Collier - Jackson, tellshow his company refocusedfrom a mainframehost -based computercompany to a PC -basedclient/server company. Hesays the shift will putfinancial executives incontrol of their own destiny.

29SHEDDING THE BEANCOUNTER IMAGEBY WILLIAM M. BAKER,CMAABC, scorecards, andexecutive informationsystems have changedaccountants' daily routine,but it is still bean counting.This article exploresshedding the traditionalrole through participation insystem design.

32ATLANTIC DRYDOCK'S UNIQUE COSTESTIMATION SYSTEMBY THOMAS L. BARTON,CPA, AND FREDERICK M.COLE, CPAThe bid for the job is thesame as the budget at aJacksonvile, Fla., drydockcompany. The integrationof the estimating systemwith the budgeting processis made more efficient bycomputerization.

41WHO'S IN CHARGE:CIO OR CFO?BY SHELDON R.GAWISERChief information officersand chief financial officersneed to forge a newworking relationship —cooperation. Financialexecutives should be on theteam that decides whattechnology their companieswant to pursue.

OCTOBER 1994 /VOL. LXXVI No. 4

45OUTSMARTING THEBANDITSBY JAMES L. LOOMISUnless a company can show"due diligence" inprevention or correctiveaction in determining checkfraud, it can incur hugecosts once borne only bybanks. Here are severaltried and true strategiesthat financial managers canuse to combat check fraud.

MANAGEMENTACCOUNTING /OCTOBER 1994

Y .

C O

, J

Wa n t t o g i v e s a l e s a r e a l p u s h ?

Now you ca n, w ith . . .

In the uphill battle for more sales, the winnerisn't always the biggest, but the most resourceful.

Which is why Sprint Business is introducingReal Solutions- a new program designed toboost productivity. With special em- r ,

personally work with you to identi fy newways of improving your bot tom l ine.

Real Solutions also gives you:• flat -rate pricing to take the guess-work out of your monthly expenses;

phasis on the insurance industry. � ! • one simplified bill combiningIt all starts with a free compre-

u„ both voice and data services;

hensive action plan that will analyze f0 CW ~ • free software that allows for

where you stand in relation to other billi' n o i t A. ' kinsurance providers. And show you whatadvanced communications can do for you.

A, a Real Solutions customer, you willhave unlimited access to all the resources of theReal Solutions Business Center and our staff ofprofessional business consultants . They will

g n a convenen ,• t h e o p p o r t u n i t y t o e a r n

credits for valuable p roducts and services.

So call today. And get Real Soluti ons from Sprint

Business . Becaus e it 's a lot easie r to give sa les a

push when you 've got the right team behind you.

- � Sprint.Business

[C a l l 1 - 50 0- 5 1 6 -R EAL

01994 Sprint Communications Company L.P. Monthly minimum and term plan apply.

MANAGEMENTACCOUNTING%PUBLISHED BY INSTITUTE OF MANAGEMENT ACCOUNTANTS

49BACKUP ANDRECOVERYBY JACK M. CATHEY,CPA, AND ROBERT H.PHILLIPS, JR.Hard drives often fail, so itis important to back up dataproperly. Here is a practicalguide to backup andrecovery strategies andsoftware systems withvendor phone numbers.

SSTOOLING UPBY NEIL R STEWART'As reengineering movesthrough American industry,eliminating thousands ofjobs, managementaccountants mustreengineer their ownrole to survive.

OCTOBER 1994 /VOL. LXXVI No. 4

60 COLUMNS DEPARTMENTS1993.94 ANNUALREPORT SUMMARY PERSPECTIVES LETTERS 81993 -94 President Leo M.Loiselle reports on IMA's Continuing professional

NEWS 20fiscal year just ended. educeducation—a bridge to thefuture.

IMA NEWS 5912WASHINGTON COMPUTERS&

REPORT ACCOUNTING 62Banking agencies andFASB reach agreement-

OFFICE14 TECHNOLOGY 64MANAGING YOURCAREER TRENDS IN`How can I survive a new MANAGEMENTCEO's cut ?'

ACCOUNTING 6616FINANCIAL MANAGER TRENDS INIPOs aren't the buyer's pot EDUCATION 69of gold.

18 CLASSIFIED 70TAXESThe IRS nonfiler initiative. ADVERTISERS'INDEX 7168ETHICS IN THE LIBRARY 72

Views expressed herein are authors' and do not represent Institute policy unless so stated. Publicationof paid advertising and new product and service in-formation does not constitute an endorsement by theInstitute of the advertiser or the product or service.

MANAGEMENT ACCOUNTING(g) is indexed in the Ac-countants' Indexand also in the on -line database ofthe same name. This publication is available in otherforms of media through Information Access Compa-ny and through University Microfilms. Inc., andABI /INFORM (313)761 -4700. For more information

Ethics cases from academe.

call (800)227.8431. The full text of MANAGEMENTACCOUNTING* is also available in the electronic ver-sions of the Business PeriodicalsIndex.

Permission is granted to reproduce any of the con-tents of this issue for use in courses of instruction,so long as the source and Institute of ManagementAccountants' copyright are indicated in any such re-productions. Written application must be made to theEditor for permission to reproduce any of the con-tents of this issue for use in other than courses ofinstruction —e.g., textbooks and books of readings

or cases. Except as otherwise noted, the copyrighthas been transferred to the Institute of ManagementAccountants for all items appearing in this magazine.For those items for which the copyright has not beentransferred, permission to reproduce must be ob-tained directly from the author or from the personor organization given at the end of the article.

(quantity reprbtts of any article in MANAGEMENTAC-COUNMNG% or back issues (subject to availability)may be obtained from Special Order Department,IMA, 10 Paragon Drive, Montvale, NJ 07645 -1760.

MANAGEA11:NT ACCO 17NTI NG/OCTOBER 1994

CCH Tax Ass I*stant helpsyou do it all. Fast.

O Z E r jyFco,�

A

� � f2 Urrirn

Qp� t� TIFIESBEY puES

Revolutionary interactive softwareautomates the way you work.

CCH Tax Assistant can cut time - consuming tasks by 50% or more, accordingto independent market research.

It helps identify key issues quickly. Then sorts through CCH's broad base of taxinformation and selects pertinent points of law. You don't get side - tracked. You don'twaste time. Tax Assistant guides you through a focused, comprehensive analysis.You make all the decisions. And arrive at them faster.

You wind up with documents ranging from completed IRS - approved forms tocustomized worksheets and research memos. Tax Assistant can even link to full -textlaws and regulations on CD -ROM (sold separately).

The new Federal Elections product helps you quickly determine whether yourclient is qualified for an election and create fileable election documents in a flash.

The new Multistate Corporate Income product provides quick research acrossmultiple states and covers all states with corporate income tax.

Let�CCH�Tax�Assistant�give�you�a�hand.�•�Business�Deductions�•�Federal�Elections•�Multistate�Corporate�Income�•�S�Corporations

To order or get a FREE demonstration disk, call 1 800 228 8353.

CCHCircle No. 4

O 19 94 CCH INCORPORA TED MA ID 9 4

PERSPECTIVESCONTINUING PROFESSIONALEDUCATION -A BRIDGE TO THE FUTURE

Last month's column was devoted to "A Bridge to the Ac-ademic Community." There will be considerable activity onthis topic in the coming year. In September, we hosted anAccounting Education Summit meeting, which was attend-ed by representatives of the appropriate stakeholdergroups. We will work together to make the changes neededin education for careers in management accounting.

This month, I want to talk about the critical importanceof Continuing Professional Education (CPE) in "BuildingBridges" to our future.

The professor who taught my first accounting coursewas one of the best teachers I had in college. He constantlytold us that we should view education not as an objectiveor goal to be attained but as a way of life. He stressed that

the most we can expect to take from a class is a basic foundation of current knowl-edge at a point in time. The world of business and the field of accounting are con-stantly evolving beyond that point. If we do not continuously add to and modifyour knowledge and skill base, we quickly become obsolete as the world and thefield of accounting rapidly move ahead. There is no such thing as standing still;we either more forward or we are left behind.

The pace of change today is much faster than it was just a decade ago. Thethings we do and the ways we do them are evolving so rapidly that accountantswho do not view education as a way of life are increasingly less valuable in themarketplace. It is a fact that we are entering an era in which employers are fre-quently asking if we add enough value to justify our cost. Transaction handlingrequires fewer people each year as organizations reengineer their accounting pro-cesses. We face a future job market that demands fewer but much more highlyskilled accountants than today.

The IMA leadership sincerely cares about your professional future and the pro-fessional image of our organization in the business community. This is why yourBoard of Directors recently adopted Bylaw provisions which established CPE stan-dards for most members. This CPE standard is 10 hours per year for regular mem-bers starting January 1, 1996. The standard rises to 20 hours per year on January1, 1998. Leaders should set a good example, so there is a 20- hour - per -year standardeffective January 1, 1994, for members serving at the national level. The require-ment of 30 hours per year for CMAs is not changed. When employers were askedtheir opinions of IMA's newest CPE requirement, they expressed unanimous sup-port, indicating that it will add significant value to an IMA membership. We nowcan proudly say that we are an organization whose members are committed tocontinuous professional improvement.

We have not done a good job of communicating the important benefits of thenew CPE standards. There is speculation that some of our members will resignfrom the IMA rather than accept the new standards. I do not accept such a positionand firmly believe that every regular member of IMA expects to do, and will do,whatever is needed to remain a `value- adding" professional. We will move acrossthe "CPE Bridge to the Future" together because we know education must be a"way of life" for the IMA and its members.

K iG.t...1./ t

KEITH BRYANT,JR, CMAPresident, 199495

MANAGEMENTACCOt1NTING■

(USPS 327 -160)

VOL LXXVI NO.4 OCTOBER 1994

EDITOR / Robert F. Randall

MANAGING EDITOR / Kathy Williams

TECHNICAL EDITOR / Karen S. Bell

SENIOR EDITOR / Claire Barth

PRODUC'nON / Lisa NasutaPatricia L. Keeley

EDITORIAL ASSISTANT / Gloria Discini

CIRCULATION / Alice Schulman

EDITORIAL ADVISORY BOARDLouis Bisgay, CPA; Germain Boer; Robert Boyle,CMA, CPA; James Bulloch, CMA; Joseph V,Carcello, CMA, CPA; Anthony Joseph Cataldo,CMA, CPA; Anthony Curatola; Robert A Czekanski,CMA; Rebecca Dillard, CMA, CPA;- Julian Freedman,CMA, CPA, CPIM; Bridgette Hobart, CPA; SusanJayson, CFP; Thomas J. Jordan, CMA; Siraj Khan,CPA. Alfred M. King, CMA; Edward J. McCracken;C. Mike Metz, CMA, CPA; John G. Mezquita, CPA:J.T. Marty O'Malley, CMA, CPA; Michael D. Osher-off, William L. Paladin; Susan P ierce, CMA, CPA;William C . Rogers , CMA, CPA; Patrick Ro mano,CMA, CPA; Annette West, CMA.

official publication of the

INSTITUTE of

MANAGEMENTACCOUNTANTSI'CIRIP1rD 11AINA4CMi71T ACCULT7A Mr M((1GHAM

10 Paragon Drive, Montvale, NJ 07645

PUBLISHERGary M. Scopes, CAE

ADVERTISING REPRESENTATIVES

I.P.C. Enterprises, New York, NYPeter Mc Grath, Senior Partner

Jim Hart, Senio r PartnerTel: (212) 575.3100

Midwest Representatives: SIR Publications213 West Institute Place, Suite 311

Chicago. IL 60610

Southwest Representative: Richard KuhlmanKuhlman & Associates Publishers Representatives

2000 East Lamar Blvd., 6th FloorArlington, TX 76006

Tel: (817) 361 -2913 Fax (817) 261 -0118

Alice Schulman, Advertising CoordinatorTel: (800) 638 -0427 Ext. 280: Fax # (201) 573 -0639

Authorization to photocopy items for intemal or per-sonal use, or the internal or personal use of specificclients, is granted by the IMA to libraries and otherusers registered with the Cop yright Clearance Cen-ter (CCC) Transactional Reporting Service, providedthat the base fee of S2.00 per copy, plus 20C per page,is paid directly to CCC, 222 Rosewood Drive, Dan.vers, MA 01923. 00'25 - 1690/90 S2.00 + 2M.

Copyright 0— 1994 bythe Institute of Management Accountants

MANAGEMENTACCOUNTING /OCTOBER 1994

"Searching for cost - reduction opportunities islike drilling for oiL 1&u know the payoffs there sornewbere, but

you're not sure wben, to start. In

our case, we were usinga stan-

dard rostiq systern fOr all I I ofour domestic plants. Capturink

aril analyzing that data was an

enormoustask,arid weknew wr

weren't seeing actual costs.

"That's why we cbose ABC

Technologies. ABC's activity -

based management tools let us

idenqfy and analyze true costs

across allofour plants. We looked

at inventory, materials handling,

manufacturing, packaging, and

traf fuc.

"And we struck it big. We

discovered a surprising 20%

variation in manufacturing costs among our plants. ABC helped identify

problems in setups and changeovers and mike corresponding cost - saving

modifications.

"In fact, we're well on our way to seeing a I0% reduction in costs

domestically. We plan to extend these savings enterprise -wide by usingABC's

software and support in our international phurts in Canada, Australia, and

The Netherlands.

"ABC helpedusfind actual costs arid reduce them. The result is a bottom

linetbat's anything but crude."

Want to know more aboutThe ValvolineCompany/ABCTechnologies

Call 1-800-882-3141study.for the free case

Circle No. I I

Refine Your Bottom Line — EnterpriseWide —With ABC Technologies

Knowledge is power,At ABC,

we put knowledge into your

hands with software that makes it

easyto track and measure activity

costs and increase profitability

departmentally or corporate wide.

ABC Technologies' solutions

range from stand -alone education

and pilot products to enterprise-

wide, activity-based management

solutions —fully integrated across

ABC'sproducts give you infor-

mation about quality, processes,

and costing that helps you make

faster, better decisions. The kind

of decisions that pump up the

EasyABC (left).The standardfor powerful,stand -aloneABMsolutions,Easy ABC helpsdrivecompanies tonewlevels ofprofitand performance.

Oros (right). For corporate -wide solutions, Oros deliversrobust tightly integrated activity -based management fornet -workedenvironments.

The leader in activity -basedmanagement 3ABC Technologies Incorporated5075 S.W.Griffith Drive • Beaverton,OR 97005

503/ 626-4895.503/ 626-4003 (fax)

LETTERSTO THE EDITOR

ROBERT F. RANDALL, EDITOR

A REBUTTAL TO 5 MYTHS

ermain Boer's recent article,"Five Modern Management Ac-counting Myths," January 1994,

raises serious questions concerningthe foundations on which activity-based costing and management(ABCM) has been developed. Due tothe rapid spread of ABCM systemadoptions throughout industry,' it iscrucial that a balanced view of thesesystems be maintained. Exaggeratedpositions (on either side of the debate)will only serve to confuse the debatefurther.

Rebuttal 1: Labor costs have been rel-atively significant in the past and over-head costs have increased dramaticallyin recent years. Dr. Boer argues that"the notion that at some time in thepast labor was relatively significant"and that the idea of a dramatic in-crease in overhead costs during re-cent years are just myths. Rather, hestates that his overhead data "indicatea tremendous diversity in overheadcosts across industries in 1987 and a

steady rise in overhead across all in-dustries going back to the 1920s. How-ever, this analysis does not properlyemphasize the importance of the rela-tive relationship between labor andoverhead costs. When discussingwhether or not labor was ever a signif-icant cost factor, it is important that thequestion be placed in context. A morepowerful question might be: "Have therelationships between, and relative siz-es of, labor and overhead changed sig-nificantly over time ?" Early researchby Jeffrey Miller and Thomas Voll-mann2 also indicates that while directlabor as a percentage of value addedhas decreased dramatically, overheadas a percentage of value added has in-creased correspondingly. The authorsargue that, as a result, overhead rateshave exploded. Using Dr. Boer's data,we can perform an analogous compar-ison of the change in overhead rates.

The chart below shows a compari-son of the overhead and production la-bor costs that were given for 1849 and1987. Using the fact that "material costhas remained at approximately 55% ofsales for all manufacturing firms from1849 through 1987," we can calculatethe rough effect of therelative shift be-tween production labor and overheadcosts. Unfortunately, neither we norDr. Boer have data to separate over-head and profit, so the calculations areperformed on the combined figures.Cost Categories 1849 1987 % change fromas a%d Sales 1849

Production labor 23% 10% 57% decease(direct & Indirect)

mat" Costs 55% 55% —

NorA -abor 2296 35% 59% increaseOverhead & Profit

Overhead & Profit 96% 350% 26s%rcreaseRate (as a % ofProduction Labor)

MANAGEMENT ACCOUNTING IS SEEKING ARTICLES!The impact of the expanding global economy on accounting and reporting issues is asubject that MANAGEMENT ACCOUNTING® would like to explore in depth. We arelooking for articles pertaining to U.S. companies' growth in international markets, move-ment of international companies to the U.S., the EEC, NAFTA, and other trade agree-ments impacting U.S. companies, or any idea dealing with the dynamic of the interna-tional exchange of accounting trends and practices.

MANAGEMENT ACCOUNTING® also is seeking manuscripts covering the changing ac-counting environment. Specifically, we would like to explore the concerns raised bythe IMA /FEI survey pertaining to what Corporate America wants in entry level accoun-tants published in the September issue. The decrease in hiring of accounting graduatesat the Big b and the issues uncovered in the survey are areas for coverage.

The deadline for submissions is December 31, 1994. Please send all submissions toKaren S. Bell, technical editor.

Dr. Boer argues that production la-bor has never been relatively signifi-cant However, when we consider thatproduction labor was 23% of sales in1849, we believe that the significanceof production labor is a subjective judg-ment. When production labor is (1) ofthe same magnitude as the combinedtotal of overhead and profit and (2) rep-resents almost one - quarter of totalcost, we view it as a relatively signifi-cant cost.

The table shows that while Produc-tion Labor has decreased during theperiod, overhead has increased. Addi-tionally, in 1849, it is crucial to note thatProduction Labor was only slightlylarger than the combined total of Over-head and Profit. This relationship isdramatically different in 1987, whenProduction Labor represents less than30% of the combined total of Overheadand Profit. This shift of cost from Pro-duction Labor to Overhead has also re-sulted in a tremendous increase in theaverage overhead rate from 96% to350% of Production Labor!

The shift in overhead rates (as a per-cent of labor) is also recognized by Dr.Boer, who states that "[t] hese writersargue (rightfully, I might add) thatoverhead is now so much larger thandirect labor cost that managers shouldfocus more attention on managingoverhead instead of on managing laborcost." However, he goes on to arguethat the increase in overhead is char-acterized as "a steady rise in overheadacross all industries going back to the1920s" and that the "big bang" in over-head costs is just another managementaccounting myth. This statement ismade based upon a Computed TrendLine of Overhead as a Percent of Salesover a 40 -year period (1947 -1987) ...

We would suggest that the shape ofthe datacurveindicatesa very strong in-creasein overhead as a percent of salesfrom 1980 through 1990. However, byreviewing the slope of the actual dataover various periods of time, we cansee that the last decade shows an ex-tremely sharp increase in the overheadrate as compared to previous periods.The data, therefore, may actually indi-cate that a tremendous increase or "bigbang" in overhead costs has takenplace in recent years.

Rebuttal 2: Product cost does influ-ence product price.There are manyways that we can view the relationshipbetween product cost and productprice. Generally, the cost of a productis viewed as the "floor" or bottom priceat which a firm could price its productin the long run. Obviously, if the mar-

MANAGEMENT ACCOUNTING /OCTOBER 1994

To ®A AP M

P 7 t e T - WHILE YOU WEFIE OU

M J�of ea

Q IG8

em. aO n a M . L,O.

PLEASE CALLYOU WILL CALL AGAIN

„ URGENT

Me863L oo

O a t s Hey. re - . _ t I P M

PENDANT/

VOTRE A88ENCEM c u

T d l p h p n e i - 1r r • . nw.A TELEPHONE PRI RE D'ADPELER

EST VENU VOW VM RAPPEL LER

VEUT voUS VOIR URGENTFRTD AT YOM APPEL

P

F@0)7f ffi 6

111l0M0ISRlEUI I

nlol oml I

retie l uai ttflt

nfeaecM tAMM'11*IMvfIV.2 AaNTIM*s ! 0 " M f e e - ] i

nmcm.

a G

Ar.oeu.T, zeltw / j l w e H A 9 W

P a r e A

F e c n e Ho r e P M

M 8 j8T UV 0 FUE p'

S.-(S)( ):(e)f ):_

de t

Ta W a n a r _ , I -I •CM In,

LLAMO

VINO A VERLO!A1

DESEA VERLEDEVOLVI6 SU tlA

R e c e d a

La

(— _J.ulieL I

W V . : l . l i JL. t { I . 4 r +

,t j } t ,u , , r , } r 4

. t r i l l s I„ . t l . 1 J .

L i t- 1910 f t !_ Y

Only SunSystems Version 4.1 accounting softwaredel ive rs wha t J eff needs f rom 20 languages ,51 currencies and 100 tax codes in 160 countries.SunSystems1m supports Client /Server, DOS, Windows, Unix, Novell, plus platforms youdon't even know you're using. In fact, it 's the only package you can put into every S M

country right now. That's why it's used by over 200 international Fortune 500 companies. �G � �' P O "u—

A t m w f i W S a f t u a u U n i m

Call 1-800 - 542-5420 for a copy of our technology white paper or the name of your local SunSystems representative in the US, Canada or Latin America,

Circ le No. 10

ket price exceeds the bottom -price, arational manager would price a prod-uct at the market price. This does notimply, however, that prices and costsare unrelated in the long run; rather,it implies that the relationship is acomplicated and multifaceted one.

Dr. Boer presents two months ofdata regarding the price of corn andthe price of feeder steers to demon-strate that "product cost does not in-fluence product price." This may betrue in the short run;however, manag-ers strategically price products pri-marily in the long run, and those pric-es reflect multiple factors (includingbut not limited to cost) ...

The author is right: pricing is acomplex issue. However, it is crucialto realize that pricing depends onproduct cost, but not necessarily in aconstant way over time. Corn cost isnot the only factor in the pricing offeeder cattle futures contracts. Theprices of these contracts depend on(to name a few of the more importantfactors): future contract prices for livecattle, seasonal effects concerningfeed and the cattle themselves, weath-er, disease, substitutes for beef...

We have examined the complex offeeder cattle future contract prices andthe complex of corn futures contractprices for the past 15 years. It is possi-ble to find for a two-month period (ora three -month period or a four -monthperiod) virtually any pattern that wemay desire. The period of time and theparticular series chosen by the authorjust happen to be consistent with thepoint argued for.

While Dr. Boer's analysis is mis-leading and technically incorrect,there is much merit in the discussion.The relationship between productcosts and product price may varythrough time, possibly with ever -changing structure, in such a way thata satisfying accounting relationshipcannot be obtained...

This does not however, [imply]that cost is irrelevant in price determi-nation, but rather that a simple linearrelationship between cost and pricedoes not usually exist either over timeor at a single point in time.Albert S. PaulsonKatherine J. SilvesterRensselaer Polytechnic InstituteTroy, N.Y.

Northwestern UniversityJ. L. Kellogg Graduate School of Management

Business Process Reengineering:A Strategy for BreakthroughPerformance

December 4 -7, 1994

Faced with mature markets, intense competition, rapid technologicalchange, and demanding yet price - sensitive customers, organizationstoday are constantly seeking new tools and concepts to help themreverse chronically poor profits or sustain historical profit growth rates.This executive program is designed to help organizations that areconsidering BPR (or that have tried it on a limited trial basis) developclear expectations of what BPR can and cannot achieve, and to addressorganizational problems that must be overcome if BPR is to achievebreakthrough levels of profit and growth improvement.

For a brochure, please contactExec u tive P ro g ramsKello gg Grad uate S c h o o l

of ManagementJames L. Allen CenterNorthwes tern UniversityEvanston, IL 60208 -2800Phone 708. 467 -7000Fax 708 - 491 -4323

Kefloggt i w y

NO HARD AND FAST RULESFOR SOFTWAREThe article "Software —The Unrecord-ed Cost" in your August 1994 issue wastimely. In a recent informal search, Icame away empty handed in an at-tempt to find uniform practices amonglarge firms on how they account forsoftware. Hence I recognize the voidthat the authors have identified.

However, I disagree with some oftheir conclusions and wonder aboutthe relevance of the population used intheir sample. The investment and con-trol arguments cited in the article maysupport capitalizing software costs.But the other reasons — product cost-ing and performance evaluation —aresomewhat more tenuous.

Sunk software costs have littlebearing on product decisions. Suchdecisions will be based on whetheror not the market will pay a highenough price to cover the costs of theproduct. The relevant costs, exceptfor a few lucky monopolies, are incre-mental costs and a return require-ment to compensate for risk and lostopportunities.

Contrary to the assumptions in thearticle, performance measurementcalls for expensing, not capitalizing,software costs. To future employeesand shareholders, who did not makethe original decision to acquire soft-ware, capitalization and amortizationresembles taxation without represen-tation, unless the software also has fu-ture benefits. There is less certaintywith software than with buildings (theexample in the article) that these fu-ture benefits truly exist.

Ironically, accounting firms, whichthe authors chose to survey, havegood reasons for not capitalizing soft-ware. Tax software, for instance, is on-ly as good as the next few changes inthe tax code. Consulting software hasto be modified with every manage-ment fad. And all software becomesobsolete at the same dizzying rate ashardware (8088, 80286 all the way toPentiums) and systems (DOS ver-sions, Windows, OS /2, and, soon,Chicago).

And finally, it is not such a bad ideathat the FASB has not produced anyclearer guidance than in SFAS 86. Giv-en that software lives are dependent ontype of industry—short for accountingfirms, but long for more stable manu-facturing industries —any FASB pro-nouncement will be at best arbitrary.Newton L Owi, CMAChicago Chapter

10 MANAGEMENT ACCOUNTING /OcTOBER 1994

� P

0C, JSP.

P JPV̀P

9

Of Alki 30

!JW1

There's only one activity -based management system

powerful enough to take you from data capture through to

report ing, without compromise.

Hyper ABC f rom Armstrong Laing.

Designed to make your job easier, it will unlock data

wherever irs stored without rekeying or re- formatting.

Once captured, its built -in controls validate everything, so

1

you only ever view the correct results. And it's self maintaining

- automatically incorporating any changes you make.

As for reporting, Hyper ABC lets you view the data you

want in the format you need via familiar spreadsheets.

To find out about the activi ty-based

management with more muscle, telephone M M

800 883 41 11 now for our free brochure.

C 1993 Armstrong Laing Inc 7 Piedmont Center, Suite 500, 3525 Piedmont Road, Atlanta, Georgia, 30305 Telephone 404 364 1836 Facsimile 404 233 4883

Circle No. 24

WASHINGTON REPORT

STEPHEN BARLAS, EDITOR

BANKINGAGENCIES ANDFASB REACHAGREEMENT

our of the five federal financialagencies represented in theFederal Financial Institutions

Examination Council have sent out amemorandum to chief executives ofU.S. banks clarifying the handling ofnonhigh -risk mortgage securities in fi-nancial statements. The operative lan-guage in that statement says: "Themere existence of examiners' divesti-ture authority for high -risk mortgagesecurities should not preclude an insti-tution from concluding it has the intentand ability to hold to maturity those se-curities that were nonhigh -risk whenacquired." The agencies are the Comp-troller of the Currency, Federal Depos-it Insurance Corp., Office of Thrift Su-pervision, and Federal Reserve Board.These agencies adopted a policy on ac-counting for so- called collateralizedmortgage obligations (CMO) early in1992. That policy basically said thatwhen a security failed any of threestress tests, it could not be considered"held to maturity." But when the FASBcame out with Statement 115, "Ac-counting for Certain Investments inDebt and Equity Securities," in May1993, it made the policy statementadopted by the FFIEC untenable. Inmid -April 1994, the FFIEC came upwith a draft revision of its policy andpresented it to FASB. The EmergingIssues Task Force of FASB refused tosign off on the FFIEC revision. Addi-tional changes were made by theFFIEC, and, finally, at an EITF meetingon July 21, FASB gave its approv-al —with a small reservation —to thestatement the four FFIEC agencieswanted to send to bank executives.

James A. Kaitz

BUSINESS GROUPSUNHAPPY WITHPENSION REFORMBILLA bill tightening corporate responsibil-ities toward pension funds (H.R. 3396)is heading toward congressional ap-proval despite the objections of groupssuch as the Financial Executives Insti-tute (FED. The bill passed the Ways &Means Committee on July 22 and thenthe House Education and Labor Com-mittee on August 11. There has beenno action in the Senate. But becausethe bill would raise nearly $1 billion viacorporate fee increases and tax chang-es, the Clinton administration wants totack it onto the GATT trade bill, which,because of its elimination of tariffs, willcost the federal government about $12billion over five years. The pension billwould help recoup those federal reve-nue losses. If the pension bill is at-tached to the GATT bill, the Senate

would not have to approve H.R. 3396.Jim Kaitz, FEI vice president, govern-ment relations, says H.R. 3396 hasthree major weaknesses, including itsprovisions on interest rate corridors,mortality tables, and mergers and ac-quisitions. "Phis bill gives the PensionBenefit Guaranty Corporation (PBGC)new, unprecedented authority to stopa merger or acquisition," Kaitz ex-plains. The PBGC could ostensiblystop a merger or acquisition when ag-gregate underfunded pension liabil-ities for both companies exceeded $50million. Lisa Winton of the AmericanInstitute of CPAs, which expressed nu-merous concerns during hearings inWays & Means, says her group doesnot have a position on H.R. 3396.

SEC /EPANEGOTIATINGAGREEMENTThe Securities & Exchange Commis-sion (SEC) and Environmental Protec-tion Agency (EPA) are negotiating amemorandum that would formalizeand expand their existing relationship.That relationship involves the EPA'spassing information on prospective Su-perfund enforcement actions andsome EPA rule makings, such as CleanAir technology improvement orders,to the SEC. The SEC checks to seewhether a company has mentioned aSuperfund enforcement action in itsMD&A and, if not, writes a letter ask-ing the company to explain that omis-sion. Sometimes the SEC sends thatletter to the EPA to check the reason-ing in the letter. Rick Roberts, one ofthe SEC commissioners, has beenmeeting with officials in an effort toagree on a Memorandum of Under-standing. Mike Northridge, an officialin the EPA office of enforcement, sayshe hopes a memorandum will besigned this fall. In speeches, Robertshas said that Arthur Levitt, Jr., the SECchairman, has put a high priority onEPA/SEC cooperation. Some coopera-tion goes on now, but it is informal.Northridge says he hopes the memo-randum will expand the current areasof cooperation but declines to specifywhat new areas might be covered. TheEPA has been increasingly interestedin encouraging corporations to adopttotal cost accounting. ■

Stephen Barlas is a journalist with morethan 15 years of experience reportingfrom Washington, D.C.

12 MANAGEMENT ACCOUNTING /OCTOBER 1994

T Weabook Techntiopies, Inc. 1994

Last year a major banking firm established over 485,000 loan portfoliosaas.and this was the only paper they handled.

Paper. It's the curse of the modern workplace. You stack it, sort it, shuffle it, file it ... and eventually lose it.

And the whole time you mutter, "there's got to be a better way."

There is: File Magic Plus. It's the award - winning* Windows -based document management system that lets

you conduct business without handling paper. At last.

June 14,19e4� File Magic Plus works by scanning and storing any document, with text and graphics, so that you can findFlo 11411c Plus forW.-groups.78

it or fax it in a snap with simple keywords or phrases.

Call 1 -BOO- WHY -FILE (800- 949 -3453) to find out how you can end the paper curse. •

Then, like PC Magazine,you'll believe in magic, too.

A " t

KUS1 - MUspanro,June 14,1991, "Deparu mmel Image Management'

Ci r c l e N o . 1 2 Nl brand and product names are tradamerks or registered uademaks Mdrelt respective canpames

MANAGING YOUR CAREERH̀OW CAN I SURVIVE A NEW CEO'S CUT?'

ROBERT HALF, EDITOR

Ourcompany hired a new president three months ago, and last month he asked for

my resignation. I wasn't the only one to go. I was close with the previous president,who fell into disfavor with the boardofdirectors, so 1 suppose 1 shouldn't have beensurprised. However, I thought —still think —I was doing a great job. The worst partwas that the new president asked me to leave the same day, asif 1had mishandledfunds or might try to damage the company before my departure. I'm still shell- shockedand keep wondering what I should have done to keep from losing my job. The newpresident was impossible to read —he had no expression on his face —and every time1 tried to reach him, he was out of the office. I know it's not productive to stew aboutit, but 1'd appreciate your advice so 1 can keep this from happening again should 1find myself in a similar position.

is always difficult when newleadership takes over a com-pany. Inevitably, people arelet go as new presidents de-velop their own staffs in theimage of what they think isneeded. Often, as you have

learned, good people are asked toleave, sometimes simply because theydon't fit that image. And, in many cas-es, corporate lawyers insist that de-parting employees leave right away, es-pecially if they have access to companyfunds, sensitive information, or aredeemed likely to be a disruptive forceif allowed to linger on the job.

The reengineering of America'scorporations has put a lot of people inyour position. New presidents or chair-men are hired by boards of directorsto come in and "turn the companyaround." That often means that theycome in with a mandate from the boardto reduce expenses wherever possible.

Nevertheless, the quickest way tomake an impact on the bottomline —and prove to the board that im-mediate action is being taken— unfor-tunately is to cut the staff.

Your new boss gave you some cluesthat this was in the works. He was non-committal in his reactions to you andkept himself unavailable. By keepingstaff at a distance, he avoided develop-ing a personal relationship with any-one. In this way, not only could hejudge performance objectively, it madeit easier to fire people he hadn't gottento know and like.

In addition, your new presidentspent a lot of time out of the office.

While his absence could be explainedby meetings with colleagues as he fa-miliarized himself with his new compa-ny, it also could mean—and probablydid —that he was being circumspectabout interviewing job candidates.

A friend of mine, who took over ascontroller at a food division of a largemultinational, spent half her time dur-ing her first few months conducting in-terviews at her university club. Shetold me that if she talked with prospec-tive employees back in her office, itwould have had a negative impact onthe productivity of her staff. "I'd end upgetting the rumor mill going," shesaid. "People don't work well whenthey're absorbed in worrying whereand when the ax is going to fall."

Of course, when new superiorskeep their distance to maintain objec-tivity, and are out of the office a lot,

Unplanned obsolescence.

they also lose the advantage of beingable to observe the fine work the cur-rent staff is doing, and would continueto do if motivated by job security.

Here are some things to do the nexttime a new leader takes over:

Don't be modest. Seek proper cred-it when you and /or your departmentaccomplish something important, andmake sure everyone hears about it.Consider it as personal public rela-tions. All effective public relations iscumulative. Personal PR will pay offwhen word of your success expandsbeyond your fellow employees andreaches your boss, perhaps even theboard of directors.

When a new administration comesin, write up your job description. Thisact will help you to organize yourthoughts and be prepared when you'reasked to explain your responsibilities.Such a written description will giveyour new supervisor a concise pictureof everything you do. At the same time,it gives you a chance to review whatyou've written to ensure you haven'tforgotten anything significant.

Get out of your office, walk around,make your own copies, get your owncoffee. You may meet the new boss inthe hall. If so, use it as an opportunityto get points across and to impresswith your efficiency.

Be a team player. It's harder to dis-miss an employee who has establishedstrong, productive relationships withother departments.

Invite your new president for a tourof your department. Offer to walk himor her around and introduce others inyour department to their new leader.

Above all, keep in mind that achange of administration often meansa change of staff as well. Good peoplelike yourself might be asked to leavethrough no fault of your own.

Do your best to impress a new boss.If it doesn't work, don't take your dis-missal personally. Instead, understandthat there were dynamics at work thatwere beyond your control, put yourjob - seeking house in order, and mar -shall your energies toward finding andkeeping anew and even better job. ■

Robert Half, CPA, is the founder of Rob-ert Half International, Inc., the world'sfirst and largest staffing serviee firm spe-cializing in the accounting, finance, andinformation systems fields. There aremore than 160 Robert Half and Aceoun-temps offices on three continents. His lat-est book is Finding, Hiring and Keepingthe Best Employees (John Wiley &Sons).

14 MANAGEMENTACCOUNTING /OCTOBER 1994

ABC grows upTrue, ABC can give you more reliable productcosts. But then what? With NetProphet software,you can improve the underlying processes todosomething about those costs. Only NetProphetcombines the best of all worlds: ABC, ABM,process -view analysis, capacity planning,constraint checking, and BPR — all in one easy -to -use, integrated package.

Process vs. productsThrough its Windows interface, NetProphetallows you to look at your business in a common-sense, graphical process view. Columns and rowsof numbers may be fine for the accountants, butwhat about the rest of your organization?NetProphet gives everyone a picture that theycan understand and use.

What -if analysisOnly NetProphet provides quick and flexible"what -if" analysis. You — and anyone you des-ignate on the network —can project differentbusiness possibilities. Just point to the process,change the variable, and the results are displayedinstantly.There's no need to build multiple modelsand wait for lengthy reallocations.

Generate your reports,not ours

NetProphet includes an integrated report writer,so you can produce custom reports with theinformation, range, and look that you want. Or,you can easily export data and results fromNetProphet into other applications.

Unlimited network accessMultiple users across a network can access theNetProphet model simultaneously, to testdifferent scenarios and generate their ownreports — all without affecting the integrity ofthe "master" model. And, the economic benefitsare compelling: for 10 users, the cost is half thatof the leading competitor's software.

Your industry,your experience

With hundreds of active installations, we andour international network of value -addedconsultants can help you design the rightmodel for your business. And, only Saplingoffers industry- specific training classes, frombeginner to advanced to expert. Plus, you getunlimited technical support and softwareupgrades for six months – free!

SOFTWARE)FEATURES

NETWOAAVERSIQV

PAKESSVIEW

WHAT -IFSCENARIOS

REPORTWRITER

ADVANCEDTRAINING

NETFROPHETII YES YES YES YES YES

PRODUCT A NO NO No YES No

PRODUCT C YES NO No No No

PRODUCT E No No No No No

S ki P L I N GS O F T W A R E A J O E o P L A N N I N G

Sapling Inc, U.S.A Toll -Free 14MD -335 -5050Tel: (201) 592 -5012 Fax: (201) 592 -4765

Sapling Corporation, CanadaTel: (905) 678.1661 Fax: (905) 678 -1667

Sapling Corporation, EuropeTel: 081 9951331 Fax: 081 742 7301

Circle No. 6

FINANCIAL MANAGER

T. CARTER HAGAMAN, EDITOR

IPOS AREN'TTHE BUYER'S POTOF GOLD

ince 1960, more than10,000 IPOs— initialpublic offerings— haveraised more than $140billion, a small but criti-cal niche in capital fi-nancing. Most compa-

nies get their start by raising equityprivately from a few investors who takea large risk, hoping the company willsucceed. If it fails, there's no liquidityfor their investment. If the companydoes succeed, it's likely to need stillmore capital, which it can get in twoways: sale of the business or throughan IPO. IPOs provide a powerful in-ducement to bring risk capital intobusinesses from a broad array of addi-tional investors.

Only a minority of private compa-nies qualify as IPOs because there hasto be enough promise to attract an in-vestment banker and interest stock-brokers. Frequently this means a"growth company" or a company withexotic potential. The fees for a success-ful IPO are high — sometimes as muchas 10% of the offering. A major studyby Ibbotson, Sindelar, and Ritter'makes three points: First -day returnsfrom IPOs typically are high; the op-portunity to bring an IPO to market ishighly cyclical; and average long -terminvestment performance of IPOs lagsother securities of comparable risk.

Pricing the IPO is an educatedguess based on market performance ofcomparable companies, the receptiongiven other recent IPOs, market con-ditions, and, above all, indications ofbuying interest (the "book ") built bythe army of brokers in the sellinggroup. A successful offering is defined

16

as one in which the market price staysabove the offering price at least for atime. The underwriter tries to set aprice that will assure this outcome.Pricing is a negotiation between theunderwriter and the company, butmost of the bargaining power and allof the market information is in thehands of the underwriter. If the com-pany walks, it may not get another un-derwriter and the money it needs.IPOs are priced with the intention ofsecuring a market gain for the initial in-vestor. Success, however, also dependson the "aftermarket" or subsequenttrading, which depends on a continuityof market interest in the stock.

Greed during bull markets and fear

I I V A %

FF Powerful, flexible 11accounting software for

dynamic asset manageme• Rapidly calculate depreciation using

any method for unlimited assetsplus:

• Automatically post all transactions toproper General Ledger accounts

• Fully account for leased assets and allphysical asset activity

• Provide key data for Activity BasedCosting and for minimizing taxes

For the full story on this completely open,100% ORAC1.0 based answer to your fixed

asset needs, call Axtell today:

1 -800- 678 -6535Axtell Development Corporation

360 N. Hayden Road, Scottsdale, AZ85257Tel. (602) 255 -0508Fax (602) 970 -6355

Circle No. 22

during bear markets explain the cycli-cality of IPOs. Volume varies dramati-cally from year to year —for example,only nine offerings in all of 1974 versusnearly 1,000 in 1985. In hot markets,judgment vanishes, and both initialpricing and subsequent market activitycan bear little relationship to invest-ment fundamentals. The market forIPOs thus parallels the market for highP/E growth stocks and little -knowncompanies already in the marketplace.Research has shown that few investorsin IPOs do any security analysis. In onesurvey, only a quarter of the respon-dents claimed that they looked at therelationship between the stock priceand the firm's underlying value.

The hope of quick gains and the ab-sence of analysis help to explain whyIPOs perform poorly over the longhaul. Because most 1POs are sold inhot markets, they are sold at an aver-age price higher than the long -term av-erage including both bull and bearmarkets. But the return to investors isbased on the price the investor paid.Therefore, total return will be lowerthan what could be obtained from asimilar portfolio acquired at the aver-age price.

IPOs are likely to be a good deal on-ly if you can get on the gravy train anddon't ride too long, which means youneed to qualify for initial allocations of"hot issues" and avoid the others. Im-portant customers of the selling firmsand some politicians are in this posi-tion; most ordinary folk are not. Thereare many chances to buy into question-able deals, but the good ones are high-ly rationed. If you buy after the initialoffering, as many people must for amarket to exist, you need to be both as-tute and lucky. You won't get advice ofthis sort from stockbrokers becausethey make extra money selling newstocks. Further, if you hold the stocksfor the long pull, the statistical odds areagainst your receiving a return as highas you could get with other stocks ofsimilar risk. Thus, success with IPOsdepends on initial preference, skillfulreading of market psychology, and adollop of luck. ■

T. Carter Hagaman is an independentinvestment analyst. He teaches at KeanCollege oflVew jersey and can be reachedat (201) 762 -6378.

tIbbotson, Sindelar, and Ritter,'Me Market's Prob-lems with the Pricing of Initial Public Offerings,"Journal ofAppiied Corporate Finance,Spring 1994.

MANAGEMENT ACCOUNTING /OCTOBER 1994

Some things weren't meant for a wild ride.

Your savings, for example.Move your dollars to a secure investment with provenperformance— Institute of Management Accountants (1MA)-sponsored GoldPortfolio® FDIC - insured deposit accountswith higher interest rates than the average market rates.

You may have already seen GoldPortfoho* deposit accountslisted in nationally recognized financial publications. Formore than four years, GoldSavers* Money Market rateshave exceeded the national average rates calculated by BankRate Monitor. And at least one GoldCertificate* CD term hasbeen ranked in 100 HighestYields for more than 80 weeks'.

Unlike a mutual fund, GoldPortfolio accounts feature theadded safety of FDIC insurance —up to $100,000 perdepositor. And because GoldPortfolio is offered byMBNA America, your money is in the care of the nation's"top- ranked" bank in 1993, as determined by FinancialWorld magazine*

Rely on GoldPortfolio for performance, security, andCustomer satisfaction— because when it comes to yoursavings, the last thing you want is a wild ride.

Control your financial future with FDIC - insured GoldPortfoho.Call 1 -800- 345 -0397, Extension 6058

Investor Service Representatives are at your serviceMonday —Friday 8 am -8 pm, Saturday 8 am —5 pm, Eastern time.

INSTITUTE of

MANAGEMENTACCO UN'Q'ANTS'eamrnOt .Rlf uu t�� C4'd xnM�r l pf ,.AM IMBNA*December 7, 1993 issue.

A M E R I C A®

MBNA America! GoldPortfolio" GoldSavers*and GoldCxnificate• arefederally registered service marks of MBNA America Bank, NA.

Member FDIC

Circle No. 28

INSTITUTE ofMANAGEMENTACCOUNTANTScunt�un�W�em� 2.rrn�ar� nr�wx�� w

TSubstantial penalty for early withdrawal of certificate of deposit funds.® t994 MBNA America Bank, NA AD 6-1731 -94A

TAXESTHE IRS NONFILERINITIATIVE

ANTHONY P. CURATOIA, EDITOR

W. RICHARD SHERMAN, CPA,AND WAQAR I. GHANI

And He said to them, "Render untoCaesar that which is Caesar's... "Luke 20.22 -25.

hile almost all in-dividuals knowthat if their in-come level ex-ceeds specifiedthresholds theyare legally re-

quired to file a tax return and pay tax-es, an estimated 10 million taxpayers(7.2 million individuals) fail to file.These nonfilers represent a large por-tion of the 19% noncompliance rate andthe estimated $20 billion of legalsource income that goes unreportedannually. (Estimates for total unreport-ed income, illegal as well as legal,range as high as $176 billion per year.)

Since October 1992, as part of itsCompliance 2000 Program, the IRS hasbeen doing its best to bring delinquenttaxpayers back into the fold. Althoughnot intended as a tax amnesty pro-gram, the "voluntary disclosure" prac-tice allows delinquent taxpayers to for-go criminal prosecution and, in somecases, the civil penalties normally con-nected with not filing. There are con-ditions, however, that must be met.

First of all, the taxpayer (or, moreaccurately, nontaxpayer) must initiatecontact with the IRS.' This action isboth a condition and an incentive. If theindividual continues to evade the taxsystem, and the IRS makes the firstcontact, all bets are off. The Servicewill proceed to impose all availablepenalties —civil and criminal.

A second condition is that the tax-payer must have only legal source in-come to report. Compliance 2000 is in-tended for individuals who, despite

their noncompliance with the tax laws,are law- abiding citizens. IRS studieshave found that often a traumatic eventsuch as divorce, the death of a lovedone, or other personal or economicproblems precipitate nonfiling.

A third requirement, as would beexpected, is that the individual mustfile a "true and correct" tax return ormust cooperate with the IRS in at-tempting to determine his or her cor-rect liability. In short, the program re-quires the nonfiler to become a filer.Furthermore, the IRS has been requir-ing that nonfilers go back and file re-turns for the previous six years if theyalready have not done so. This condi-tion may require a taxpayer to try andreconstruct income and deductions foryears in which record keeping was atbest spotty and maybe even nonexis-tent. Nonetheless, the nonfiler mustmake a good faith, "best efforts" at-tempt to complete an accurate tax re-turn for those years.

Finally, the individual must make afull payment of all the taxes, interest,and penalties due or must arrange anacceptable payment schedule with theIRS. In the latter instance, the IRS hasauthorized revenue agents to enter in-to installment agreements if the tax li-ability is less than $10,000. If the defi-ciency exceeds $10,000, the IRS hassimplified its procedures for extendedinstallment agreements between thetaxpayer and the HZS Collections Divi-sion. If either the collectability or theexistence of the tax liability is doubtful,the Service may be willing to accept an"offer in compromise." Such an offersettles the taxpayer's account forsomething less than the balance due asoriginally determined by the IRS. Toapply for an offer in compromise, thetaxpayer must file Form 656 (Offer inCompromise) and Form 433-A or 433 -B (Collection Information Statement).

Nonfilers who participate in the vol-untary disclosure program do not in-crease the chance of an income tax au-dit. The IRS has stated publicly that thereturns filed under this program arenot audited automatically. The returnswill be subject to the normal reviewand selection criteria as all other re-turns, but because they are usuallyoutof syncwith the usual IRS examinationcycle there is a lower probability thedelinquent returns will be selected forexamination.

The IRS intends to prosecute themore abusive nonfiler cases aggres-sively, with close coordination be-tween its Criminal Investigation Divi-sion and the Department of Justice.

The IRS has been using computers tomatch more rigorously W2 and 1099information with filed returns, a pro-cess that easily identifies nonfilers. Inaddition, because an estimated 64% ofnonfilers are self - employed individualswho are not subject to withholding tax,the IRS has been targeting specific oc-cupations for closer examination. TheChicago IRS office has been siftingthrough the list of Illinois - licensedCPAs in order to identify nonfilers.A similar tactic is being pursued inPennsylvania for all state - licensed at-torneys.

At the state level (but not yet in ev-ery state), programs encourage nonfil-ers to come clean with the govern-ment. Pennsylvania, for example, hasadopted a policy of accepting threeyears of taxes and interest without pen-alties for those who comply voluntarily.Furthermore, these taxpayers cancome forward on an unnamed basisuntil a settlement with the state hasbeen reached. The state offers a de-ferred payment plan for taxpayers thatqualify.

In many ways, the nonfiler programis nothing more than a continuation ofprior IRS policy. Since 1952, before rec-ommending criminal prosecution theIRS has taken into consideration thatthe taxpayer has come forward volun-tarily. Compliance 2000, however, rep-resents a closer cooperative effort bythe Examination and Collection Divi-sion with increased support by thePublic Affairs Office, Criminal Investi-gation, and Taxpayer Service to makethe program more visible and more ac-cessible. A more equitable system willbe promoted if nonfilers assume re-sponsibility and render unto Caesarthat which is Caesar's. ■

W. Richard Sherman, a member ofIMA's Philadelphia Chapter, is asso-ciate professor, Department ofAccount-ing,Saint Joseph's University, Philadel-phia, Pa. He can be reached at (610)660 -1662.

Waqar L Ghani, Ph.D., is assistantProfessor, Department of Accounting,Saintjoseph's University. He can be con-tacted at (610) 660-1661.

Anthony P. Curatola, Ph.D., is theJo-seph F. Ford Professor, Drexel University,Philadelphia, Pa. He can be reached at(215) 895 -1453.

'Who initiated contact is so critical that it is in thetaxpayers best interest to keep careful records ofall contacts with the IRS. A formal meeting is notnecessary for establishing the initial contact. Thetelephone, electronic, or written communicationswill suffice.

18 MANAGEMENT ACCOUNTING/OCTOBER 1994

CCH introduces ahigher state of intelligence.

r

i

Z

Two new CD -ROMs for the hottest areas in StateTax:Sales & Use and Corporate Income.

Sales& Use Tax-For the first time ever, you get comprehensive information on everystate that has a sales or use tax ... on one CD -ROM! No longer will you have to thumb througha lot of different books looking up a lot of different states. You get answers quickly and easily.

Multistate Corporate Income Tax-For the first time ever, you can search full -text lawsand regulations on corporate income taxacross multiple statesin a matter of seconds!

With more state audits on the horizon, you should investigate both the new CCH SalesTax Guide and the new CCH Multistate Corporate lncomeTax Guide on CD -ROM.

They're out of this world. To order, or for more information, call 1800 TELL CCH.

rccn'

0,994 CM NiCORPOPA$D MA 1094

Circle No. 30

NEWS

KATHY WILLIAMS, EDITOR

IHLANFELDT NAMED TO FASAC

illiam J. Ihlanfeldt, CPA, re-tired assistant controller ofShell Oil Company and presi-

dent -elect of IMA, has been named tothe Financial Accounting StandardsAdvisory Council. FASAC's members,who are broadly representative of theFinancial Accounting StandardsBoard's constituency, offer advice tothe FASB regarding what issues to puton its agenda and comment on the sta-tus of its current projects.

Mr. Ihlanfeldt, a member of theHouston Chapter, was IMA vice presi-dent, professional relations, in 1993 -94.He also has served as chairman of theManagement Accounting PracticesCommittee and has been a member ofthe Executive Committee, NationalBoard, Planning Committee, and Bud-get Committee.

CD -ROM USE IS ON THE RISE

ccording to the results of the faxsurvey in the August issue ofMANAGEMENT ACCOUNT -

ING@, members' use of CD -ROM tech-nology is on the upswing. Of those in-dividuals using the CD -ROM, most useit at home for entertainment/encyclo-pedia applications. The second great-est use is at work for accounting /taxtopics. (We won't include any percent-ages as this survey was not a randomsample.)

Both at home and at work, most re-spondents use at least an IBM or com-patible 386 with Windows and /orDOS. About a third are on networks atthe office. Extras: Respondents have aCD -ROM drive, a 2400 bps or highermodem, and a fax /modem in both plac-es. Not many are online yet, but ofthose who are, most use CompuServeat work and CompuServe and America

20

Online at home.When asked what services IMA

might provide on CD -ROM, the great-est number of respondents requestededucation /training and "best prac-tices" information to use at the office.For home, it was education /training.

IMA thanks readers for their inputand will keep them posted on the sta-tus of the CD-ROM project.

FINANCIAL HIRINGWILLREMAIN STEADY, CFOS SAY

he hiring of finance and account-ing professionals will remain sta-ble in the fourth quarter, CFOs

who responded to Robert Half's latestsurvey said. Ten percent of the respon-dents said their companies plan to addstaff, 81% anticipated no change, and4% expected to decrease staff. One no-table change has occurred: The Moun-tain region (Montana, Idaho, Wyo-ming, Colorado, Arizona, Utah, NewMexico, Nevada) anticipates a 17% in-crease in financial hiring, which is up10 percentage points from last quar-ter's projections. The Mid - Atlantic re-gion also will see a small increase.

The construction industry is show-ing the most growth, with 13% of therespondents expecting to hire. Sevenpercent of the CFOs in the retail andprofessional and business services al-so expect a hiring increase.

Robert Half International surveyed1,000 of the nation's CFOs in compa-nies with 20 or more employees. Forinformation about the entire survey,

William J. Ihlanfeldt

contact Steve Pehanich at (415) 8549700 or Marc Silbert at (516) 767 -3700.

WORKPLACE SUBSTANCEABUSE INFORMATION KITSARE AVAILABLE

t has been estimated that sub-stance abuse in the workplacecosts American businesses be-

tween $44 and $200 billion a year in lostproductivity, increased health carecosts, absenteeism, and accidents. Inaddition, the federal government hasfound that nearly 66% of all drug usersare employed, most of them full -time.

Although many larger corporationsconduct their own programs on sub-stance abuse, smaller companies with100 or fewer employees may not haveadequate information or resources toaddress the problem. In an effort tohelp small businesses cover this issue,the U.S. Department of Labor, througha private and public sector initiativecalled Working Partners, is makingworkplace substance abuse informa-tion kits available. For details, callKaren Herson at (703) 267 -3547.

TEMP WORK A BENEFIT

eventy-eight percent of execu-tives polled by OfficeTeam sayconsistent temporary employ-

ment is comparable to full-time work,so having temporary positions on a re-sume doesn't seem like a gap in em-ployment. This takes the pressures offjob seekers who have felt they musttake any full-time job –maven the wrongone—to have a consistent record.

WHAT WOULD YOU DO IF YOUWERE LET GO TOMORROW?

orty -nine percent of Americanworkers who responded to an Ac-countants On Call poll said they

would look for a job in the same field.Fourteen percent said they would takesome time off temporarily to think orrest, 13% would start their own busi-ness, 9% would look for a job in anotherfield, 7% would go back to school, 4%said they would retire or never workagain, and 4% couldn't decide.

The survey was the next in the"Profile of the American Worker" se-ries conducted by Accountants OnCall. For complete survey details,contact Debbie Buchsbaum at(201) 843 -0006. ■

MANAGEMENT ACCOUNTING /OCTOBER 1994

REACH ONLY FOR THE BEST INCOST MANAGEMENT PUBLICATIONS.

From today's leadingpublisher for corporate publications in this fast- growing field give you theaccounting and financial professionals. kind of timely, practical guidance and comprehensive

analysis you need to maximize your company'sWhenever you have a problem in any area financial performance.

of accounting or financial management, turn to So give us a call. And find out why the mostWarren, Gorham & Lamont for practical solutions useful publications for corporate accounting andyou can apply right away financial professionals come only from Warren,

Take cost management, for example. Our leading Gorham & Lamont.

Call toll free today for more information.1 -800- 950 -1213

WC;WARREN, GORHAM & LAMONT • 31 St. James Avenue • Boston, Massachusetts 02116

Circle No. 18

COLLIER=JACKSONSHIFTS ITS VISION

BY KATHY WILLIAMSAND JAMES HART

arren Fletcher admits hesounds evangelisticwhen he says Geac /Col-lier- Jackson's software

applications will put financial execu-tives "in control of their own destiny."With VisconShift, information neverbefore available to them will be at theirfingertips. With this brand new suite ofaccounting, human resources, and dis-tribution client /server applicationsjust unveiled, they'll be able to performall the usual accounting and financefunctions with the click of a mouse,then send information throughout thecompany with a touch of a button. In-stead of walking around the companyin search of information or siftingthrough piles of paper reports, theywill point at the computer screen andaccess information through visual im-ages. Financial executives will be ableto do the job for which they've beentrained — analyzing financial data orcreating data to analyze —and makestrategic decisions almost instantly.

Calling himself a "hybrid" who isn'ta real techie but who understands tech-nology and the business of money,General Manager Fletcher (presidentin other companies) has just seenGeac /Collier- Jackson through a com-plete change of focus and a merger.What once was a mainframe host -based computer company that wroteprograms is now a PC -based cli-ent /server company that builds appli-cations to solve business problemsfrom the desktop. Gone are code-driv-en functions that only data processingexperts can understand. Now it's an of-fice on a computer screen, completewith visual images of file drawers,spreadsheets, graphs, and other worktools that users manipulate electroni-cally. Through a partnership with Mi-

22

General ManagerWarren Fletcher

changes hiscompany'sfocus to

PCs andpartnerships.

crosoft, Geac /Collier- Jackson is de-signing these accounting, human re-sources, and distribution applica-tions /solutions for Microsoft Officeproducts. Through its acquisition byGeac Computer Corporation Limited,it will gain a global presence.

In this second in a series of talkswith accounting software leaders, War-ren Fletcher gives management ac-countants a clear- sighted vision oftheir future.

You've been with Collier Jackson14 years and have headed it forfive. What brought you there?

Well, I'm from the old IBM, Big Bluemainframe days of service bureau

computing. My educational back-ground is accounting, finance, and anMBA. Initially out of school I fell intoa job with a subsidiary of The HartfordInsurance Group as an assistant to thepresident, who wanted an MBA tocome in and solve his business prob-lems. That was an absolute joke —thatan MBA could come in out of schooland solve any business problem. So af-ter about six months I went back toschool at night and took more coursesin data processing. We were doing ac-counting systems, and I had an ac-counting background, so I startedshowing programmers how you de-sign accounting systems and how ac-countants think. As a service bureaufor independent insurance agents na-tionwide, we got the typical packagesevery Friday and had a room full ofkey - to-tape machines and key - to-diskmachines, and we batched everythingup and ran it through the computer andshipped out reports.

IQQWere you doing claims?

No. We were doing accountingfor their fees and agency com-

missions and doing all their commis-sion reports so they could pay theirsalesmen. We did all their general led-ger and their receivables —we provid-ed a whole accounting service for in-dependent insurance agents. And wedid all this on IBM mainframes.

Then we were bought by our big-gest competitor. I was invited to stay,but I went to work for GTE Data Ser-vices and got into HP 3000s. I designedcircuit systems. I got good databaseexposure. That was around 1978 whenHewlett- Packard had the best businesscomputer in the world, but nobodyknew it. The HP 3000 in the late '70sand early '80s was probably the besttransaction business midrange com-puter out, but it was not well known.

MANAGEMENT ACCOUNTING /OCTOBER 1994

Target Your Career

t \

pC.

If you are an accounting and finance professional in business,public, or government accounting who measures success in terms ofopportunity, recognition, and reward, then target your career today!

Become aCertified Management Accountant

1 -800- 638 -4427 -- - Institute of Management Accountants

10 Paragon DriveMontvale, NJ 07645 -1760 '

In late 1978 I got an offer from Col-Her-Jackson to design a circulation sys-tem for Knight-Ridder newspapers,which were using HP 3000 computers.That was a successful project for Col-lier- Jackson. Then I got an offer fromData General Corp. to be a systems en-gineer for the Southeast. I wanted toget technically educated, and I thoughtthe best place to do it was in a mid-range computer business. During thetwo years I worked there I spent a yearand a half in school —at Data Generalschool, studying operating systems,communications, file manage-ment —all the basics about computersand computer hardware. Then I wentback into application development.

Collier Jackson rehired me to de-sign an advertising system for Knight-Ridder. It was a unique system fornewspapers that included order entry,accounting, receivables, the contractmanagement area, statistical report-ing —the whole back end of a newspa-per environment integrated with thegeneral ledger, payables, human re-sources— systems that are critical tothe business. I've been there since1980, designing and managing, really,almost all the implementation and allthe systems we've ever built. I ve beengeneral manager of Collier Jackson(now Geac /Collier Jackson) since1989.

Q�̀ C What has been the secret of yoursuccess at Collier Jackson?

Understanding the business. Ithink that understanding the technol-ogy and understanding what peopleare doing is important. If you don't un-derstand their problems or the issuesthey are facing, you are going to getsnowed by a technical person wantingto invent something for which there isno market.

FQDoes that happen quite a bit?

Probably more than any soft-ware company would like, but

we try very hard not to. In today's mar-ket, you can't afford to make too manymistakes. We're flying one or two mis-takes high most of the time. Equate itto a pilot —one mistake you may getaway with. Two and you may end updinging the plane. It doesn't meanyou're going out of business, but itmeans you have to be careful becauseyou have limited resources. Things arechanging rapidly. If you've made a mis-take, you'd better cut your losses andget on to something that is profitable

or —look out you're going to be introuble.

I think a lot of companies today arein trouble because of rapidchange —not just because they madesuch bad decisions. But how do youturn a ship quickly? That's one of thebig issues. Technical people likethings that are neat. They like thingsthat interest them. I guess I'm guilty ofthat like everybody else, but, at thesame time, responsibility says, "Thatmay be neat, but can you sell it? Doesit solve a business need ?" Those arethe two critical questions.

IQQSo, then, at Collier-Jackson youhave structured your softwareand your programs to solvebusi-ness needs?

That's right, and it's why our new ac-counting software suite runs on thedesktop. We want to leverage the in-vestments corporations are making inclient /server technology and allowthem to take advantage of networksand distributive software.

F What is Collier Jackson doing inthe accounting realm?

About 65% of our business is inaccounting systems. We've been a VAR

Bob Gront

(value -added reseller) for Hewlett -Packard since 1978, selling and resell-ing their equipment and working withthem as a software partner. In the early1980s, DEC (Digital Equipment Corpo-ration) asked us to move our softwareto the DEC environment, and we be-came a VAR for them as well.

Throughout the '80s we were suc-cessful where HP and DEC were suc-cessful— manufacturing, distribution,and newspapers. (Today our customerbase is largely the same, and we sell tocompanies doing $50 million and up.)In the late '80s we moved our softwareto the HP and DEC versions of UNIX,and IBM approached us to port oursoftware to their UNIX box as an indus-try remarketer. This was the advent ofclient /server and open computing. Iwatched the technology closely. It be-came clear that we needed to engineerour new products from scratch and notport our existing systems. If we weregoing to have true third- generation cli-ent /server products, we needed towrite our systems on the client side,where processing takes place, and takeadvantage of the power of the PC. Thatchanged Collier - Jackson's culture.

That's called learning from your ex-periences and learning how to dothings faster and cheaper so you canstay in business. We decided to be in-dependent. We view ourselves as appli-cations providers. We do not invent anytechnology; we do not want to inventany technology; we want to partnerwith people that have technology. Thelast thing we ever do is try to writesomething new and unique. We want touse tools that are available to the gen-eral marketplace to provide solutions.Period.

We took a pretty bold step in decid-ing not to do host -based computinganymore but to concentrate every dol-lar of R&D on client /server, desktopcomputing —the way we think peoplewant to compute. If we didn't changethe focus of our business, we wouldn'tbe in business in three to four years.We saw a couple of key things happen-ing in the industry. One was the pro-liferation of PCs. Within the next fiveyears, every profitable business willreautomate. Period. They will reauto-mate because they have to to be com-petitive— because the level of serviceand productivity they are going to gainwill be such that they have to. Thetechnology has moved so rapidly inthe last 36 months that what you'veseen in the last 36 is nothing com-pared to what you'll see in the next 36.Price - performance curves will contin-

24 MANAGEMENT ACCOUNTING /OCTOBER 1994

ue to be in that realm of 50% to 100%per year. What you buy next year willcost the same price for twice the per-formance of what you just bought.That's going to continue and maybeeven accelerate.

People want personal computing,whether it's enterprise wide or wheth-er it really is just desktop. But the rev-olution that's taking place is the one ofPC and the price performance curveand acceleration of the price perfor-mance curve. With the introduction ofthe 486, the price performance curvetook a dramatic leap. It also was thefirst time we had enough power on edesktopdesktop to write commercial applica-tions: not CAD /CAM but the 1/0 in-tensive, the interface intensive, thetransactional nature of applications forbusiness. So we took a quantum leapand went with Microsoft.

What will this partnership withMicrosoft mean forthe end user,forour readers?

It means our accounting software —general ledger, accounts payable, andaccounts receivable —are integratedwith the Microsoft Office and will havethe same look and feel as MicrosoftWord, Excel, Mail, and Project. Ifyou're buying an accounting systemfor the '90s and beyond, you're goingto want it to integrate with all the desk-top enablers — )-mail, word process-ing, spreadsheet, and project soft-ware—to increase productivity. Whatif, sitting at your desk and pointing toyour computer screen, you could bringup a mail form, request an expensecheck, send it off and get it approved,with nobody ever touching it exceptyou see your check show up? Wouldthat make you more productive? Whatmakes you productive? Your word pro-cessor, your scheduling system? Yourlife, basically, is on that computer. Whynot integrate your life —and your per-sonal manager and your tools —withyour financial systems? That's produc-tivity. That's what we're doing with ourproducts — integrating them with thedesktop — making them more than justclient /server.

101 Will everybody have access to theI same data, then?

According to how we secure it.Obviously, there will be security re-strictions on who can see what. In ad-dition, think about general ledger. Howmany general ledgers are there in theworld? Some unique things about our

general ledger are that it's completelyconfigurable, it has unlimited numberof segments, unlimited number of seg-ment sizes, so you can roll your owngeneral ledger. We've built a tool tobuild your general ledger. We can giveyou a standard set, but you, as a cus-tomer, can look at that general ledgerand with a little consulting help canbuild one and actually customize thatgeneral ledger for your environment,and we never change the code. We'reactually taking a tool and building atool so you can build a general ledger.

IQQ In your literature, you talkabout automatically devised seg-ments. What is it that you'rereally talking about?

Let's translate segments into account-ing terminology: companies, divisions,products, departments, regions, terri-tories —all the things you would put in-to an account number so that you canreport, summarize, and analyze the da-ta. We ask, "How do you structure yourbusiness ?" We don't say, "Here is ourstructure; see if you can fit in it." That'sthe old way of doing things. The newway of doing things is: "How do yourun your business, customer ?" Webuild to suit. Then your ability is unlim-ited. Once you've done your accountstructure —how you're going to runyour business —you punch a buttonand it generates all the screens andforms for you, customized to your en-vironment.

Our competitive ad-vantage is: You want tocustomize it? It doesn'tcost you a dime to do allthe things you want to do,to build the structure youwant. We think we're go-ing to eliminate tremen-dous amounts of custom-ization, especially on the basicbusiness setup. This general ledgerwill look different everywhere it runsif you have a different way of lookingat your business.

Fol Is this the VisionShift line?

Yes, this is all the VisionShiftline. Now, what happens if your