CEMENT SECTOR - Nirmal Bang

85

IMBALANCE LIKELY TO CONTINUE DEMAND-SUPPLY CEMENT SECTOR

-

Upload

khangminh22 -

Category

Documents

-

view

7 -

download

0

Transcript of CEMENT SECTOR - Nirmal Bang

IMBALANCE LIKELYTO CONTINUE

DEMAND-SUPPLY

CEMENT SECTOR

Institutional Equities

This page has been intentionally left blank

Institutional Equities

Cement Sector

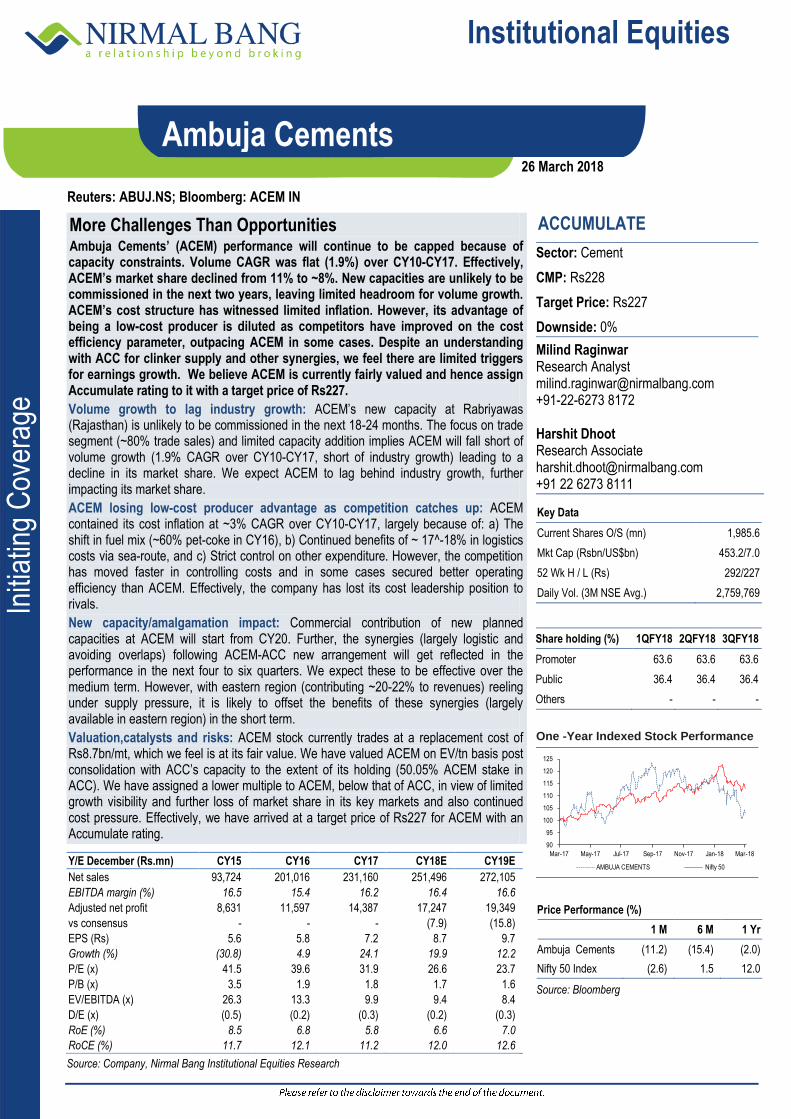

Unfavourable Demand-supply Dynamics; Stretched Valuations The demand-supply balance essentially drives cement pricing, like in any other commodities. However, this (demand-supply relationship) had little to do to drive cement prices in the past five years as supply discipline was the key driving factor for prices, keeping them above the normal price discovery trend. Given that demand-supply gap will continue in the range of ~100mt-140mt for the next two to three years, overall capacity utilisation will hover ~70-75%. This is despite early signs of strong cement demand revival as the contribution in 2HFY18 was largely from the infrastructure segment, although demand lull in real estate segment continued in most parts of India. Hence, we believe that genuine pricing power is unlikely to come back in a hurry. Moreover, cement companies’ ability to maintain/improve operating margin will be tested, which can be attributed to: a) Demand shift towards the infrastructure sector from the remunerative real estate sector. b) Hardening of key raw materials (including inflated cost of limestone and fly-ash). c) Fuel inflation impacting energy cost. Hence, we expect EBITDAM to be flat or under pressure (except in cases of companies undergoing EBITDA correction) and effectively lack of strong earnings growth for large-cap companies. Further, the current premium valuations largely factor in the expected strong demand revival in the initial phase of recovery, leaving limited scope for a further rerating of cement stocks barring a few exceptions. We re-initiate the coverage on the cement sector with our negative view (because of stretched valuation). We have recommended Sell rating on Shree Cement, Dalmia Cement, J K Lakshmi Cement, India Cements and Heidelberg Cement. However we remain positive on select cement stocks such as The Ramco Cements and JK Cement in the mid-cap space, and Sagar Cements in the small-cap space. We believe large-cap companies (ACC, Ambuja and Ultratech) are currently fairly valued and leave little headroom for incremental gains.

Demand growth aided by government-driven infrastructure capex and rural housing: During the past five years, cement demand growth remained subdued because of a) Slow housing demand. b) Limited infrastructure spending (only public spending). c) Weak private sector contribution. Post recovery from the short-term impact of demonetisation and implementation of Goods and Services Tax or GST, we expect cement demand to grow 7%-8% YoY in FY19E/FY20E aided by robust government measures providing a fillip to the infrastructure sector, and rural housing offsetting continuing weakness in commercial/industrial capex and urban housing.

Demand supply gap to continue as supply addition persists: While we expect demand to grow 7%-8% YoY in FY18E-FY20E, we forecast supply CAGR of 3.5% over the same period. However this is on the back of strong 130mt addition in past 5 years (FY12-FY17). Though the pace of supply growth will moderate, demand-supply gap will continue in the range of 100mt-140mt. We expect supply in the range of 460mt-480mt (rated capacity) with effective available supply in the range of 455mt-460mt (based on stabilisation period and available clinker capacity). Given the higher demand-supply gap hovering ~100mt-140mt, we expect no real return of pricing power in the cement sector. We have done sensitivity analysis with expectations of demand swinging faster (~15% YoY) than expected in the next two years as in the previous peak cycle of FY06-FY09. Despite this aggressive assumption the capacity utilization hovers ~ 75% and the demand-supply gap still persists in excess of 100 mt.

Effective capacity utilisation will be sub-optimal: Effective capacity utilisation is likely to be 70%-75% during the next two years, implying that genuine pricing power to cement companies will be still at a fair distance. As cement is a regional play, capacity utilisation in southern region is expected to languish at ~60%-68%, while northern region is likely to show relatively healthier utilisation level (~ 75%-80% in FY19E/FY20E).

Prefer select fundamentally sound companuies in the cement space: At current valuations, we prefer The Ramco Cements (new region expansion, focus on cost control and expected demand revival in strong home market) and JK Cement (better earnings guard from white cement segment) in the mid-cap space, and Sagar Cements (presence in reviving markets like AP/Telangana with timely capacity addition and discounted valuations) in the small-cap space. We believe large-cap cement companies are currently fairly valued and leave limited headroom for gains. We have assigned Sell rating to Shree Cement, Dalmia Bharat, The India Cements, JK Lakshmi Cement and Heidelberg Cement.

View: Negative

Milind Raginwar Research Analyst [email protected] +91-22-6273 8172 Harshit Dhoot Research Associate [email protected] +91-22-6273 8111

Company Rating Market cap.

CMP (Rs)

Target price

(Rs)

Up/ Down

(%)

EV/EBITDA (x) EV/Tonne (mnt) P/E (x)

Rsbn US$mn FY18E FY19E FY20E FY18E FY19E FY20E FY18E FY19E FY20E

ACC Accumulate 2,912 4,485 1,549 1,582 2.1 13.8 12.9 11.4 117 120 117 35.0 28.1 24.0 Acmbuja Cement Accumulate 4,527 6,973 228 227 (0.4) 9.7 9.2 8.2 195 204 199 31.5 26.2 23.4 Dalmia Bharat Sell 2,528 3,894 2,847 2,592 (9.0) 14.5 12.1 11.2 207 206 206 46.0 35.7 31.5 Heidelberg Cement Sell 338 520 149 126 (15.4) 12.2 10.6 9.3 116 116 115 33.2 24.5 20.2 The India Cements Sell 435 669 141 126 (10.6) 9.5 8.6 7.8 68 68 70 39.4 25.4 19.3 JK Cement Buy 709 1,092 1,014 1,179 16.3 10.9 9.3 8.6 130 126 125 21.3 16.0 13.5 JK Lakshmi Cement Sell 523 805 444 389 (12.4) 17.1 14.8 12.4 97 96 95 54.1 36.6 22.7 Sagar Cement Buy 180 276 880 1,058 20.2 13.6 8.4 5.6 72 67 54 76.0 24.3 15.2 Sanghi Industries Accumulate 289 445 115 116 0.9 14.8 12.9 12.2 134 146 161 25.1 20.1 18.3 Shree Cement Sell 5,697 8,774 16,354 15,207 (7.0) 21.7 18.0 15.9 259 259 257 41.2 33.2 28.7 The Ramco Cement Buy 1,743 2,685 736 887 20.5 16.8 14.3 12.3 168 166 167 27.2 21.7 17.6 UltraTech Accumulate 10,770 16,587 3,925 4,302 9.6 21.0 17.3 15.0 207 207 203 46.4 38.6 30.0

Source: Nirmal Bang Institutional Equities Research

26 March 2018

Institutional Equities

4 Cement Sector

Table of Content

Healthy demand from government’s infrastructure capex and rural housing………………………..………….….06

Cement demand expected to grow ~ 7%-8%YoYover the next two years……………………………………….…07

Demand Driver 1: Housing segment’s growth will be aided by rural market, other realty segments to remain weak……………………………………………………………………………………………………………………..….08

Organised urban housing segment will see extended weakness…………………………………………………….10

Commercial property story is no different from organised housing………………………………………………..…11

Demand Driver 2: Government-driven infrastructure creation is a bright spot in an anaemic private capex envirornment……………………………………………………………………………………………………………..…12

Strong government initiatives towards new schemes……………………………………………………………….…14

What do we expect in the next two years?...........................................................................................................16

Incremental supply unabated, demand-supply gap expected to stay in the range of 100mt-140mt……….……..17

Region-wise capacity addition- Focus shifts to eastern region………………………………………………….……18

Key raw materials available in abundance………………………………………………………………….…….….…20

Pricing power remains elusive…………………………………………………………………………………..…….….21

Regional cement prices remain volatile and under pressure…………………………………………………….…...24

Cost inflation is key challenge in the next two years……………………………………………………………….….26

Valuation at a premium………………………………………………………………………………………………...….29

Annexure:…………………………………………………………………………………………………………….…..…32

Companies

ACC ............................................................................................................................................. ……………….37

Ambuja Cements ............................................................................................................................................... 41

Dalmia Bharat ......................................................................................................................................... ………45

HeidelbergCement India ................................................................................................................................... 49

India Cements .................................................................................................................................................... 53

JK Cement ......................................................................................................................................................... 57

JK Lakshmi Cement ........................................................................................................................................... 61

Sagar Cements …………………………………..………..…………………………………………..…..……….…… 65

Sanghi Industries ............................................................................................................................................... 69

Shree Cements .................................................................................................................................................. 73

The Ramco Cements ......................................................................................................................................... 77

UltraTech Cement ................................................................................................................................. 81

Institutional Equities

5 Cement Sector

Key charts and tables

Exhibit 1: P/E and RoE movement in divergent path Exhibit 2:Valuation and EBITDAM moving in opposite direction

Source: Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

Exhibit 3: Earnings-focused companies high on valuation Chart

Source: Nirmal Bang Institutional Equities Research

0

7

14

21

28

0

20

40

60

80

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

P/E (LHS) ROE (RHS)

(x) (%)

0

4

8

12

16

0

9

18

27

36

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

Operating Profit Margin (LHS) EV/EBITDA (RHS)

(%) (x)

0

2

4

6

8

10

12

14

16

18

20

0 5 10 15 20 25

EV

/ E

BIT

DA

(x)

RoE (%)

Bubble Size:EBITDA/tn

ACC Ambuja Cements UltraTech Cement Shree Cement

Dalmia Bharat JK Lakhmi India Cement Heidelberg Cement

Sanghi Industries JK Cement Ramco Cement Sagar Cement

Institutional Equities

6 Cement Sector

Healthy demand from government’s infrastructure capex and rural housing

During the past five years, cement demand growth remained subdued because of: a) Slow housing demand. b) Limited infrastructure spending (only public spending). c) Weak industrial capex and private sector contribution. However, reversing the short-term impact of demonetisation and early phase of GST implementation, we expect cement demand to grow 7%-8 YoY in FY19E/FY20E aided by robust government measures providing a fillip to the infrastructure sector, and rural housing offsetting sustained weakness in urban housing and commercial/industrial capex.

Pan-India cement demand under pressure since the past five years

During the past five years, cement demand growth remained subdued, defying the GDP multiplier link (~1.2x in stable market expanding to 1.3x during the economic recovery). However, cement demand picked up during 3QFY18 YoY, recovering from the demonetisation impact and initial phase of GST implementation, growing by a strong 11.1% YoY although on a weak base (versus ~-1%YoY in 3QFY17 and 2.7%YoY in 9MFY18). Strong infrastructure push is the key factor in driving current growth and is expected to continue in the near future barring unforeseen events.

During the past five years, central and eastern region grew faster compared to other regions with a CAGR of 6.6%/3.6% over FY12-FY17 aided by: a) Focus on infrastructure. b) Low-cost housing, while traditionally strong markets such as northern and western regions reported disappointing growth rate of ~2.6%/3.6%, respectively, during the same period. Southern region reported virtually flat growth.

Region-wise demand

Exhibit 4: Demand in southern region disappoints Exhibit 5: Slow demand in weste rn region because of weak urban housing demand

Source: Nirmal Bang Institutional Equities Research, Industry, Crisil Source: Nirmal Bang Institutional Equities Research, Industry, Crisil

Exhibit 6: Northern region weighed down by weak rural and urban demand

Exhibit 7: Central region relatively a bright spot

Source: Nirmal Bang Institutional Equities Research, Industry, Crisil Source: Nirmal Bang Institutional Equities Research, Industry, Crisil

50

53

56

59

62

65

FY12-13 FY13-14 FY14-15 FY15-16 FY16-17

(MT

)

44

48

52

56

60

FY12-13 FY13-14 FY14-15 FY15-16 FY16-17

(MT

)

38

42

46

50

54

FY12-13 FY13-14 FY14-15 FY15-16 FY16-17

(MT

)

0

14

28

42

56

FY12-13 FY13-14 FY14-15 FY15-16 FY16-17

(MT

)

Institutional Equities

7 Cement Sector

Exhibit 8: Eastern region playing catch-up in government-driven low-cost housing & infrastructure space

Source: Nirmal Bang Institutional Equities Research, Industry, Crisil

Cement demand expected to grow ~ 7%-8%YoYover the next two years

According to industry sources, housing accounts for ~60% of total demand whereas infrastructure contributes ~20% and the rest is accounted for by commercial and industrial establishments. However, this is likely to undergo a change with strong infrastructure demand replacing housing demand in early signs of demand revival since 3QFY18. We have analysed the underlying demand sources in detail and tried to forecast demand growth for the sector over FY19-FY20.

Housing accounts for a significant portion (~60%) of total cement domestic demand in India.

Rising urbanisation, an increasing number of households and higher employment are primarily driving the demand for housing, accounting for ~60% of total cement consumption.

Initiatives undertaken by the government are expected to provide an impetus to construction activity in rural and semi-urban areas through large infrastructure and housing development projects, respectively.

The affordable housing segment has been in focus with two major schemes providing a fillip to growth, including Pradhan Mantri Awas Yojana-Urban (PMAY-U) and Pradhan Mantri Awas Yojana-Gramin (PMAY-G).

Exhibit 9: India cement demand – Key constituents (% in total demand, current and estimated)

Source: Industry, Nirmal Bang Institutional Equities Research Source: Industry, Nirmal Bang Institutional Equities Research

0

13

25

38

50

FY12-13 FY13-14 FY14-15 FY15-16 FY16-17

(MT

)

Infrastructure,20%

Commercial / Industrial, 20%

Housing, 60%

Rural Housing (20%)

Urban Housing (Tier 1) (15%)

Urban Housing (Tier 2) (25%)

Infrastructure, 25.0%

Commercial / Industrial,

20.0%

Housing, 55.0%

Institutional Equities

8 Cement Sector

Demand Driver 1: Housing segment’s growth will be aided by rural market, other realty segments to remain weak

Rural housing is likely to gain momentum aided by a good monsoon and PMAY-G

The government, in the President's address to the joint session of Parliament in May 2014, had announced that before the nation celebrates its 75th year of Independence (i.e., 2022), every family should have a pucca house with water connection, toilet facilities and other basic amenities. As part of the Pradhan Mantri Gramin Awas Yojana-Gramin (PMGAY-G) the government is targeting to build 30mn homes by 2022. It has allocated Rs150bn in the FY17 budget and increased the allocation to Rs230bn in FY18 (Rs202bn spent till 9MFY18). The current budget (FY19) had allocated Rs210bn for PMAY-G. Thus, funding for flagship programmes is not a constraint as it will be tied with budgetary support and borrowing from NABARD. As per the Ministry of Rural Development (MoRD), about 1.0mn houses have been constructed in rural areas under PMAY-G till November 2017.

With a normal monsoon forecast for FY18-FY19 (early prediction), rural demand is expected to be strong and outpace urban demand. The India Meteorology Department’s (IMD) monsoon mission climate forecast system (MMCFS) predicts signals of moderate La Nina condition that will be favourable for Indian monsoon. However, even if it weakens, the monsoon will still be normal. .

Exhibit 10: In the past two years gap between sanctioned and completed houses is narrowing

Source: iay.nic.in

Urban housing: Affordable housing is strong while the organised segment continues to see headwinds

Pradhan Mantri Awas Yojana-Urban (PMAY-U) to drive 3.9mn urban homes: PMAY-U aims to provide ‘Housing for All’ by 2022 with the implementation between FY15-FY22 and will provide central assistance to urban local bodies (ULBs) and other implementation agencies through States/Union Territories. Currently, 1.56mn houses are at various stages of construction and ~ 0.41mn houses have been constructed since the launch of PMAY-U, according to the MHUPA (ministry of housing and urban affairs). However, the total number of affordable homes sanctioned under PMAY-U is 3.74mn for the urban poor. The total budgetary allocation by the central government in FY19 for the PMAY (U) is Rs275.0bn (budgetary allocation in the previous year’s FY16/FY17/FY18 was Rs116bn/Rs209.5bn/Rs290bn.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

Houses Completed Houses Sanctioned

(Houses)

Institutional Equities

9 Cement Sector

Exhibit 11: Implementation methodology

Source: Ministry of Housing and Urban Poverty Alleviation

The credit-linked subsidy scheme is used as a demand-side intervention to expand institutional credit flow to meet the housing needs of urban poor. India’s urban housing shortage is estimated to be 18.78mn. The shortage is acute across economically weaker sections (EWS) and lower income groups (LIGs), which together constitute 95% of the total housing shortage.

Exhibit 12: Credit-linked subsidy scheme details

Particulars Middle Income

Group 1 Middle Income

Group 2

Annual Income (Rs mn) 0.6 to 1.2 1.2 to 1.8

Interest Subsidy (% p.a.) 4% 3%

Max Loan Tenure( in years) 20 20

Eligible Housing Loan Amount for Interest Subsidy (Rs mn) 0.9 1.2

Dwelling Unit Carpet Area 90 Sq.m 110 Sq.m

Discount Rate for Net Present Value (NPV) calculation of interest subsidy (%) 9% 9%

Source: Ministry of Housing and Urban Poverty Alleviation

Adding to that, the major benefactors of PMAY-U have been states with major cement production which include Madhya Pradesh, Rajasthan, Andhra Pradesh and Telangana which augurs well for the cement industry.

Exhibit 13: Government spending on housing is on the rise

Source: CMIE, Industry, Nirmal Bang Institutional Equities

-4%

-2%

0%

2%

4%

6%

-40%

-20%

0%

20%

40%

60%

19

90

-91

19

91

-92

19

92

-93

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

Growth in Central Government's capital expenditure for housing

Capital expenditure for Housing as % of Central Government's total capital expense

Institutional Equities

10 Cement Sector

Organised urban housing segment will see extended weakness

A confluence of high urban real estate prices, lower affordability, sluggish wage growth (particularly in the private sector), and an overall lethargic economic environment have affected demand for real estate in the urban segment. This can be seen from the exhibits below where inventory level continues to remain high and absorption level has declined to FY09 level. Understandably, new housing launches are below the lows witnessed in FY09.

Exhibit 14: Absorption numbers sliding down sharply Exhibit 15: Pan-India inventory level is high

Source: Industry Source: Industry

Exhibit 16: New launches have dried up significantly

Source: Industry

We believe urban housing will see sustained weakness in absorption and new launches in the medium term will be based on the pointers from the data on major cities given below. These are representative of the mood in the organised real estate sector in India as a whole.

Exhibit 17: Lull in residential launch in FY18 continues

Source: Colliers International

0

150

300

450

600

0

120

240

360

480

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

*

(mn sq ft)('000 no of units)

Units(LHS) Area(RHS) *Till Feb'17

0

4,000

8,000

12,000

16,000

0

2,500

5,000

7,500

10,000

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

*

(mn sq ft)('000 no of units)

Units(LHS) Area(RHS) *Till Feb'17

0

900

1,800

2,700

3,600

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

*

(Available Suppy)

*Till Feb'17

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

0

5,000

10,000

15,000

20,000

25,000

NC

R

Ah

me

da

ba

d

Mu

mb

ai

Pu

ne

Be

ng

alu

ru

Hyd

era

ba

d

Ch

en

na

i

Ko

lka

ta

Launch Launch Growth YoY

Institutional Equities

11 Cement Sector

Commercial property story is no different from organised housing

The commercial property segment is also currently undergoing a slowdown in line with the relatively slow economic revival.

All-India medium term trend indicates that the pace of transactions in the commercial property segment has lacked pace. Prompted by the slower pace of transaction, completion of commercial projects has slowed down in the past couple of years. Effectively, with slower completion of projects, the vacancy level declined from ~ 20% in the past couple of years to ~ 15% in 9MFY18.

Exhibit 18: Absorption rate shows a mixed trend in major Indian cities

Source: Colliers International

Exhibit 19: Commercial transactions are flat in top six cities of India

Note: The top six cities are Mumbai, NCR, Bengaluru, Pune, Chennai and Hyderabad

Source: Knight Frank Research, India Real Estate

Exhibit 20: Vacancy trend in major cities hints towards only a marginal change

Source: Colliers International

0123456789101112131415

0123456789

1011121314151617

Bengaluru Chennai Delhi-NCR Hyderabad Kolkata Mumbai Pune

CY2017 CY2018E

12%

15%

17%

20%

22%

0

12

24

36

48

2010 2011 2012 2013 2014 2015 2016 H12017

(mn sq ft)

New Completion Transactions Vacancy

0%

5%

10%

15%

20%

25%

30%

35%

0%

5%

10%

15%

20%

25%

30%

35%

Ben

galu

ru

Che

nnai

Del

hi-N

CR

Hyd

erab

ad

Kol

kata

Mum

bai

Pun

e

CY17 CY18E

Institutional Equities

12 Cement Sector

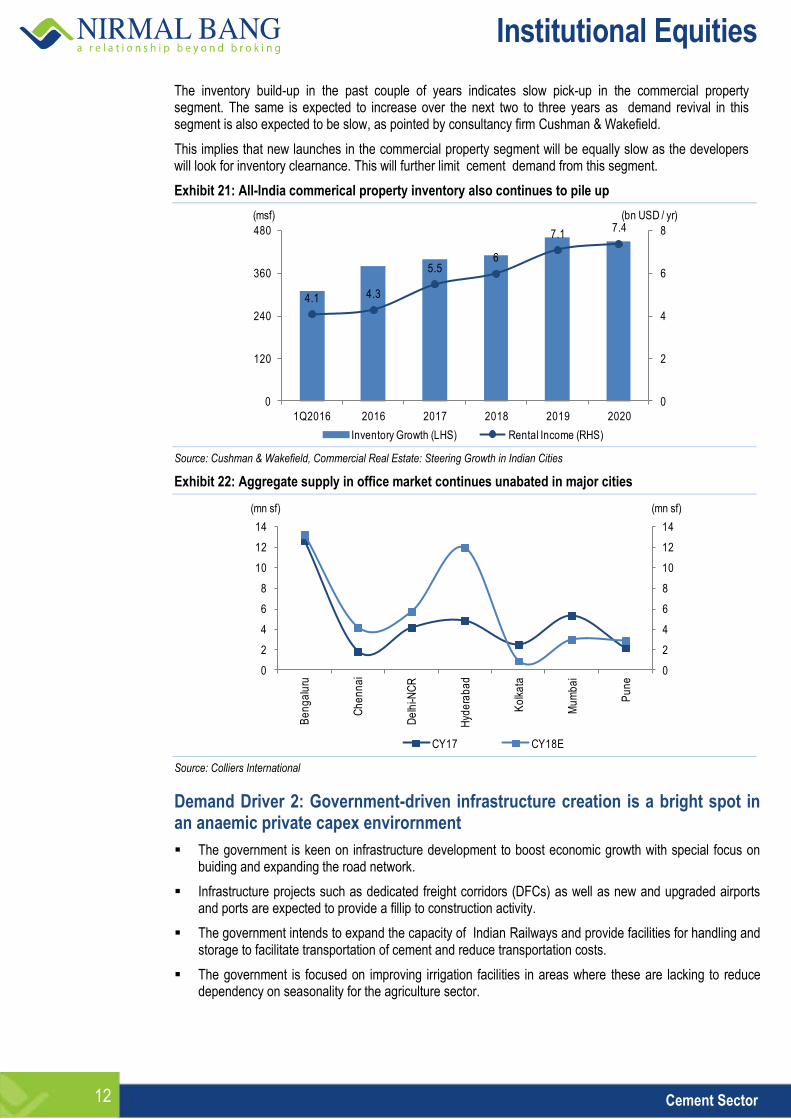

The inventory build-up in the past couple of years indicates slow pick-up in the commercial property segment. The same is expected to increase over the next two to three years as demand revival in this segment is also expected to be slow, as pointed by consultancy firm Cushman & Wakefield.

This implies that new launches in the commercial property segment will be equally slow as the developers will look for inventory clearnance. This will further limit cement demand from this segment.

Exhibit 21: All-India commerical property inventory also continues to pile up

Source: Cushman & Wakefield, Commercial Real Estate: Steering Growth in Indian Cities

Exhibit 22: Aggregate supply in office market continues unabated in major cities

Source: Colliers International

Demand Driver 2: Government-driven infrastructure creation is a bright spot in an anaemic private capex envirornment

The government is keen on infrastructure development to boost economic growth with special focus on buiding and expanding the road network.

Infrastructure projects such as dedicated freight corridors (DFCs) as well as new and upgraded airports and ports are expected to provide a fillip to construction activity.

The government intends to expand the capacity of Indian Railways and provide facilities for handling and storage to facilitate transportation of cement and reduce transportation costs.

The government is focused on improving irrigation facilities in areas where these are lacking to reduce dependency on seasonality for the agriculture sector.

4.1 4.3

5.56

7.17.4

0

2

4

6

8

0

120

240

360

480

1Q2016 2016 2017 2018 2019 2020

(bn USD / yr)(msf)

Inventory Growth (LHS) Rental Income (RHS)

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

Be

ng

alu

ru

Ch

en

na

i

De

lhi-N

CR

Hyd

era

ba

d

Ko

lka

ta

Mu

mb

ai

Pu

ne

CY17 CY18E

(mn sf) (mn sf)

Institutional Equities

13 Cement Sector

Exhibit 23: Central government’s focus on roads and bridges spending is indicates a strong reversal

Source: CMIE, Industry

Exhibit 24: Increased public investment in irrigation

Source: CMIE, Industry

Exhibit 25: NHAI – Total projects under implementation show an improving trend Exhibit

26: Slow pick-up in project recommended by PPPAC*

Source: Department of Economic Affairs Source: Industry ; * PPPAC is public private partnership appraisal committee

-100%

-50%

0%

50%

100%

150%

200%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

2017

-18

2018

-19

Capital expenditure for roads & bridges as % of Central Government's total capital expense

Growth in Central Government's Capital expenditure for Roads & bridges (%)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

(Rsmn)

Investment Projects Outstanding Investment Projects Under implementation

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

1Q

FY

18

(Km)

0

150

300

450

600

20

06

-20

07

20

07

-20

08

20

08

-20

09

20

09

-20

10

20

10

-20

11

20

11

-20

12

20

12

-20

13

20

13

-20

14

20

14

-20

15

20

15

-20

16

20

16

-20

17

20

17

-20

18*

(Rsbn)

*Till 17th May,2017

Institutional Equities

14 Cement Sector

Strong government initiatives towards new schemes

Initiatives by the new government, such as Housing For All, smart cities, Swachh Bharat campaign, infrastructure spending, concrete roads initiative and increase in allocation of funds to states are likely to have a positive impact on the industry in FY19 and FY20.

The government’s recent focus on road projects and increase in state allocations are likely to drive infrastructure and housing demand, thereby drive the demand for cement.

Projects such as smart cities and Atal Mission for Rejuvenation and Urban Transformation (AMRUT) are expected to lead a surge in demand for cement.

The infrastructure segment comprising roads, irrigation and urban infrastructure is expected to witness pointed growth in the next five years which augurs well for the cement sector

Exhibit 27: Increased public investment in irrigation

Source: Industry, Nirmal Bang Institutional Equities

Exhibit 28: The government has fast forwarded the completion of roads under PMGSY in the past three years

Note: Length completed is of new connectivity and upgradation and of both PMGSY-1 and PMGSY-2 schemes

Source: http://omms.nic.in

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY08-FY11 FY13- FY17 FY18 - FY22P

Infrastructure spending

Roads Power Irrigation urban infrastructure Others

0%

50%

100%

150%

200%

15,000

30,000

45,000

60,000

75,000

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

*

(Km)

Target length (km) Completed length (km) Completed length as % of target length

Institutional Equities

15 Cement Sector

Development of metro railway, roads, airports

Metro rail projects in Mumbai, Bengaluru and Hyderabad and the expansion phase in Delhi are likely to drive cement demand.

Airport modernisation across major cities is likely to expand the demand for cement industry

The latest development in the Ahmedabad Metro Rail Project has driven cement demand to a large extent.

Demand Driver 3: Private sector revival another key factor for demand pick-up

The private sector’s capital expenditure has been indicating flat growth since the past five to six years. This is because of the lack of proper policy framework (labour and land acquisition still in abeyance), overall dull economic activity and lack of smooth capital avenues (limited liquidity). This segment accounts for~15-%20% of demand in the cement sector. Importantly, the revival in this sector keeps liquidity momentum in the system, thus contributing to consistent new demand for cement. Currently, this segment is going through a lull phase, thereby keeping the demand momentum limited for the cement sector. We expect private sector capital expenditure to gather momentum in the next two to three years following easing liquidity, typically an extended hand from the banking sector, clarity emerging in government policy on business and the overall revival in economic activity.

Exhibit 29: Private sector projects show flat growth in the past five years

Source: CMIE, Industry

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

(Rsbn)

New investment projects announced Investment projects completed Investment projects dropped (Total)

Investment projects dropped : Abandoned Investment projects dropped:Shelved Investment projects dropped : Stalled

Investment projects dropped : For lack of information Investment projects revived Investment Projects Outstanding : (Total)

Investment Projects Outstanding : Under implementation

Institutional Equities

16 Cement Sector

What do we expect in the next two years?

We expect cement demand to recover healthily from the impact of the government’s demonetisation policy and the early impact of Good and Services Tax (GST) implementation over the next couple of quarters. Rural housing and infrastructure demand is likely to recover strongly and compensate for weak demand from the organised urban housing sector.

We expect cement demand parity to the GDP multiplier (1.2x) to have a lag effect, despite strong initiatives by the government in the infrastructure and housing (low-cost) segment. This is because of the lag in private capital expenditure. This lag is likely to be offset in the medium term and we therefore expect cement demand to grow with a 1.0/1.1x multiplier to GDP growth. We have assumed GDP to grow 7.7%/7.8% in FY19/FY20 (contributed by our economy team), respectively.

We therefore expect cement demand in FY19/FY20 to grow 7%-8% (with an upward bias). The upward bias is to factor in the pent-up demand at the tail-end of 9MFY18 (impacted because of GST implementation and demonetisation) spilling over in FY19 (cement demand is largely deferred, not cancelled). However, we expect demand growth to gain momentum in FY19 because of a relatively steady base and parliamentary elections leading to announcement of new infrastructure projects and the rush for completion of existing projects to showcase them during the elections.

Exhibit 30: Summary of main demand drivers and growth rates

Source: Industry

5-6% 5-6% 10.5-12.5%

Housing 55% Industrial Commercial 20%

Infrastructure 25%

Institutional Equities

17 Cement Sector

Incremental supply unabated, demand-supply gap expected to stay

in the range of 100mt-140mt

Supply addition to continue, southern and eastern regions to lead the pack

Our detailed analysis of demand drivers and supply addition by manufacturers leads us to believe that the pan-India effective utilisation level will continue to hover ~ 70-75% over FY18E-FY20E. While we expect demand to post 8% CAGR over FY18E-FY20E, we forecast supply CAGR of ~3.2% over the same period. It may be noted that supply growth, although it is slow, is on the back of an unprecedented expansion of ~ 240mt (over FY07-FY16). Hence, we expect no real return of pricing power in this sector as the demand-supply gap will continue to be ~ 100mt-140mt in FY20E. As cement is a regional play, the capacity utilisation of players in southern region is expected to be at a lower level of ~65%-70% (improving from a low base) in the next two to three years, while northern region is likely to show relatively healthier utilisation level of ~80%-82% in the same period. We have done sensitivity analysis with expectations of demand swinging faster (~15% YoY) than expected in the next two years as in the previous peak cycle of FY06-FY09. Despite this aggressive assumption the capacity utilization hovers ~ 75% and the demand-supply gap still persists in excess of 100 mt.

In the next two years, we expect capacity addition growth to likely taper off with a CAGR of 3.9% over FY16-FY20E and expect the capacity to top 480mt by FY20E.

The appetite for capacity addition surprises despite the likely lower rate of supply growth during the next two to three years, especially given the fact that capacity utilisation rate hovers in a sub-optimal range (of ~75%). We expect the demand-supply gap to continue for the next two years and the utilisation rate is unlikely to increase substantially, despite the pointers of strong demand in the next two years (relative to the previous trend).

Exhibit 31: All India demand-supply model

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Total Capacity (mt) 313.4 347.5 361.6 392.0 415.8 441.3 454.6 467.3 484.1

Total Effective Capacity (mt) 300.1 329.4 355.5 371.6 403.7 425.5 444.5 457.5 472.5

Total dispatches (mt) 225 248 255.8 270 282.6 272.0 291.0 314.3 339.5

Capacity Utilisation (CU) (%) 71.8 71.4 70.7 68.9 68.0 64.9 64.0 67.3 70.1

Effective CU (%) 74.9 75.3 72.0 72.7 70.0 65.8 65.5 68.7 71.8

Demand growth (%) 7.8 10.3 3.1 5.6 4.7 -1.0 7.0 8.0 8.0

Source: Industry, Nirmal Bang Institutional Equities Research

Exhibit 32: Northern and central regions have better operating ratios which are expected to continue for the next couple of years

Source: Industry, Crisil

0%

25%

50%

75%

100%

North East West South Central Pan -India

Average over last 5 years

Institutional Equities

18 Cement Sector

Region-wise capacity addition- Focus shifts to eastern region

The southern region will continue to add capacity, although the pace of new addition is likely to taper at ~2.4% CAGR over FY16-FY20E. However, with a strong base we expect the demand-supply gap to be significant for any real strong pricing momentum despite the recent strong pick up in the demand. Strong demand revival from the region driven by twin state development of Andhra Pradesh and Telangana since 3QFY18 will keep the demand momentum continuing. However, South India has been maintaining higher prices following the strict supply discipline, defying the demand-supply mechanics.

We like the eastern region as the demand triggers from eastern and north-east regions (given the strong government initiatives) remain robust. However, strong capacity addition by the presence of new cement manufacturers (Emami and Nirma) and cement companies like Shree Cement entering the market, capacity addition is expected to post a CAGR of 8% (FY16-20E) over a high 13% base of FY12-FY16. This is expected to weigh on the capacity utilisation rate.

We expect central region to be the key beneficiary with minimal capacity addition (except for UltraTech Cement) in the next two to three years. With demand gaining momentum, we expect this region to benefit from significant revival in the economy, and consequently provide a fillip to demand. However, post UTCEM’s acquisition of JPA cement assets supply will be unabated from the erstwhile under-utilized capacities in the region.

Exhibit 33: Cement supply

North India cement supply expected to be limited South India continues to add capacity despite DD SS gap of ~70mt

Source: Industry, Crisil, Nirmal Bang Institutional Equities Research Source: Industry, Crisil, Nirmal Bang Institutional Equities Research

East India crowded with supply exerting pressure on prices Limited supply to be added in western region in the next two years

Source: Industry, Crisil, Nirmal Bang Institutional Equities Research Source: Industry, Crisil, Nirmal Bang Institutional Equities Research

0

30

60

90

120

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

P

20

18

-19

P

20

19

-20

P

(MT)

0

45

90

135

180

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

P

20

18

-19

P

20

19

-20

P

(MT)

0

20

40

60

80

100

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

P

20

18

-19

P

20

19

-20

P

(MT)

0

20

40

60

80

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

P

20

18

-19

P

20

19

-20

P(MT)

Institutional Equities

19 Cement Sector

Minimal capacity addition in central region likely given the limited resources

Source: Industry, Crisil, Nirmal Bang Institutional Equities Research

0

15

30

45

60

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

P

20

18

-19

P

20

19

-20

P

(MT)

Institutional Equities

20 Cement Sector

Key raw materials available in abundance

Our analysis of limestone reserves data published by the Indian Bureau of Mines reveals that barring the central region, limestone reserves are available in abundance in key pockets of northern region (Rajasthan), southern region (Andhra Pradesh & Telangana, Karnataka), and western region (Maharashtra). Cement makers are increasingly setting up capacities in Karnataka and Chhattisgarh, shifting the focus from central region (confirmed through our interaction with cement manufacturers). Karnataka is preferred over the traditional limestone base of Andhra Pradesh because of access to lucrative Maharashtra market. Presence in Chattisgarh (CTG) helps access to the eastern region (backward states) where the central government’s focus is on infrastructure and development. Rajasthan continues to be the hot-spot for cement manufacturers.

Exhibit 34: Limestone resources (proven) skewed towards North and South India

Source: Indian Bureau of Mines

North, 37%

South, 26%

East, 16%

West, 12%

Central, 9%

Institutional Equities

21 Cement Sector

Pricing power remains elusive

Cement demand has indicated green shoots from 2HFY18, as indicated by our industry interactions (notwithstanding the weak base). The push to rural demand and government initiatives undertaken to provide a fillip to the infrastructure sector is likely to compensate for weakness in urban housing demand and will help to continue the momentum. Our estimates indicate FY19/FY20 demand is likely to be in high single digits (~7%-8%), as explained in key demand drivers section. However, supply surplus in key pockets such as South and East India will contain the pricing as incremental demand is likely to undershoot excess supply (we do not subscribe to the theory of demand growth exceeding supply growth). Hence, pricing power is likely to be limited as capacity utilisation is far from reaching ~85% in the next two years.

Cement prices likely to be under pressure

Pan-India, the over-supply situation is expected to continue in FY19/FY20. In South India, the demand-supply gap is expected to stay upwards of at least 70mt-80mt in the next two years. In eastern region, supply outpaced demand in the past and this trend is likely to continue for the next two years. Our estimates indicate that central region will be the key beneficiary in the next two years with limited supply addition and healthy demand pick-up in the Madhya Pradesh/Uttar Pradesh belt.

Though we structurally expect cement demand to overcome weakness of the past five years (2012-17), pushed largely by the central government’s infrastructure initiatives and rural housing (as discussed in cement demand section in detail), we expect demand growth of ~ 7-8%YoY. With the demand-supply gap likely to be maintained at ~100mt-120mt, we expect the capacity utilisation rate to hover ~ 73%-75% in FY18E-FY20E which will keep pricing pressure on cement companies.

Effective capacity utilisation rate likely to remain at ~75%

We expect cement capacity utilisation rate to remain at ~75%, even if the rate tends to vary regionally. We expect the rate to touch ~ 80% in western and central regions, while southern region will continue to lag behind (albeit relatively better than the past five years).

With the utilisation rate remaining in mid-70s, we expect the pricing power to change in certain pockets rather than a structural pan-India change in pricing scenario.

Inter-regional movement to improve with GST

Historically, cement movement has remained robust from surplus regions to scarce regions, thereby keeping in the prices under check. The data last available suggests ~8% movement from southern to western region. This, in turn, is likely to move the stock from western region to central region (Madhya Pradesh) from Vidarbha and northern region (Rajasthan) from Gujarat. Thus, the overall pricing will deviate from the secular uptrend that was observed in the last upcycle.

With the introduction of GST, we believe the inter-regional movement (especially in state clusters like the NCR region) will only improve. However, it is early to measure the change in movement.

Cement prices structurally will thus increase only if pan-India cement utilisation rate moves towards ~85% wherein the gains can be measured across regions which is unlikely in the next two years.

Exhibit 35: Inter-regional movement

% Consumption

Supply North East South West Central Total

North 84.4 0.1 0.0 1.5 14.0 100.0

East 0.1 92.5 0.9 3.5 3.0 100.0

South 0.1 1.4 87.5 11.0 0.0 100.0

West 2.1 2.0 10.9 84.0 1.0 100.0

Central 13.4 4.2 0.0 0.4 82.0 100.0

Source: Industry, Nirmal Bang Institutional Equities Research

Institutional Equities

22 Cement Sector

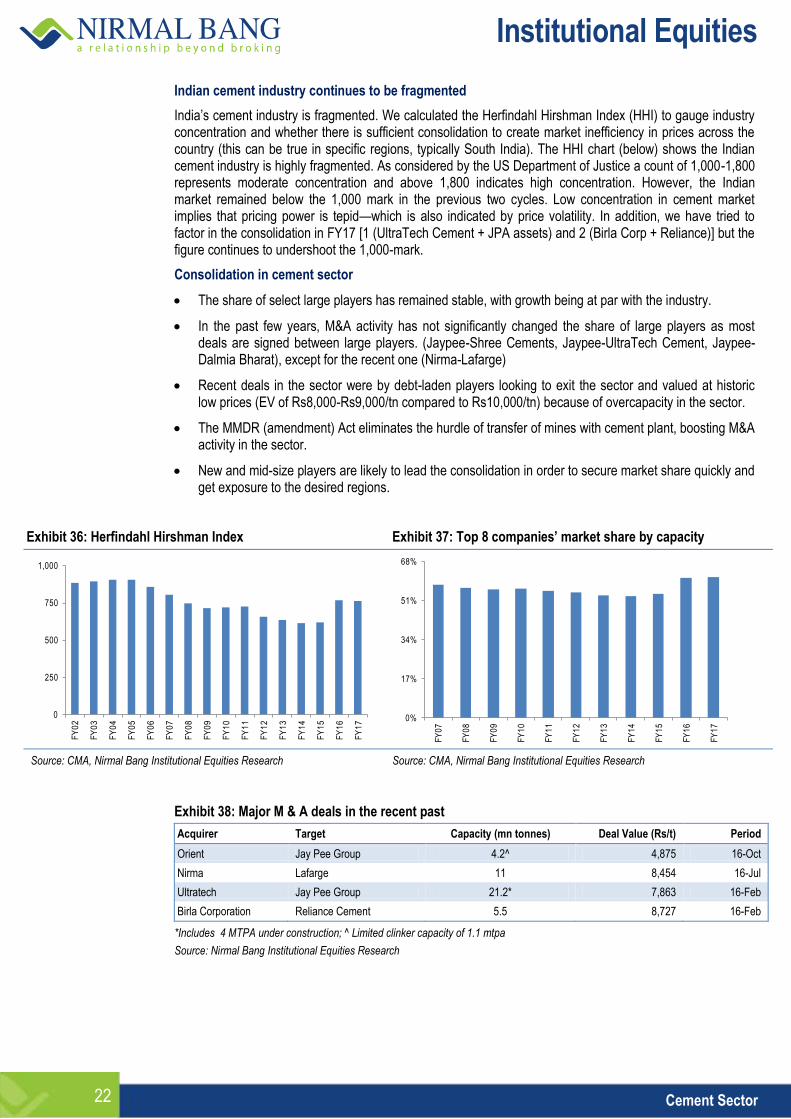

Indian cement industry continues to be fragmented

India’s cement industry is fragmented. We calculated the Herfindahl Hirshman Index (HHI) to gauge industry concentration and whether there is sufficient consolidation to create market inefficiency in prices across the country (this can be true in specific regions, typically South India). The HHI chart (below) shows the Indian cement industry is highly fragmented. As considered by the US Department of Justice a count of 1,000-1,800 represents moderate concentration and above 1,800 indicates high concentration. However, the Indian market remained below the 1,000 mark in the previous two cycles. Low concentration in cement market implies that pricing power is tepid—which is also indicated by price volatility. In addition, we have tried to factor in the consolidation in FY17 [1 (UltraTech Cement + JPA assets) and 2 (Birla Corp + Reliance)] but the figure continues to undershoot the 1,000-mark.

Consolidation in cement sector

The share of select large players has remained stable, with growth being at par with the industry.

In the past few years, M&A activity has not significantly changed the share of large players as most deals are signed between large players. (Jaypee-Shree Cements, Jaypee-UltraTech Cement, Jaypee-Dalmia Bharat), except for the recent one (Nirma-Lafarge)

Recent deals in the sector were by debt-laden players looking to exit the sector and valued at historic low prices (EV of Rs8,000-Rs9,000/tn compared to Rs10,000/tn) because of overcapacity in the sector.

The MMDR (amendment) Act eliminates the hurdle of transfer of mines with cement plant, boosting M&A activity in the sector.

New and mid-size players are likely to lead the consolidation in order to secure market share quickly and get exposure to the desired regions.

Exhibit 36: Herfindahl Hirshman Index Exhibit 37: Top 8 companies’ market share by capacity

Source: CMA, Nirmal Bang Institutional Equities Research Source: CMA, Nirmal Bang Institutional Equities Research

Exhibit 38: Major M & A deals in the recent past

Acquirer Target Capacity (mn tonnes) Deal Value (Rs/t) Period

Orient Jay Pee Group 4.2^ 4,875 16-Oct

Nirma Lafarge 11 8,454 16-Jul

Ultratech Jay Pee Group 21.2* 7,863 16-Feb

Birla Corporation Reliance Cement 5.5 8,727 16-Feb

*Includes 4 MTPA under construction; ^ Limited clinker capacity of 1.1 mtpa

Source: Nirmal Bang Institutional Equities Research

0

250

500

750

1,000

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17 0%

17%

34%

51%

68%

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

Institutional Equities

23 Cement Sector

GST likely to ease inter-regional movement impacting prices

With the introduction of GST, cement movement is likely to be relatively easy across states. Typically, for pan-India cement companies, this is likely to benefit and thus the reach of these companies across states will be higher. Their managements have indicated that the material impact of the benefits will emerge post four to six quarters. The GST rate is 28% which is close to the earlier tax outgo of ~ 28%-30%. Hence, there is no direct impact of GST which replaced the earlier tax regime.

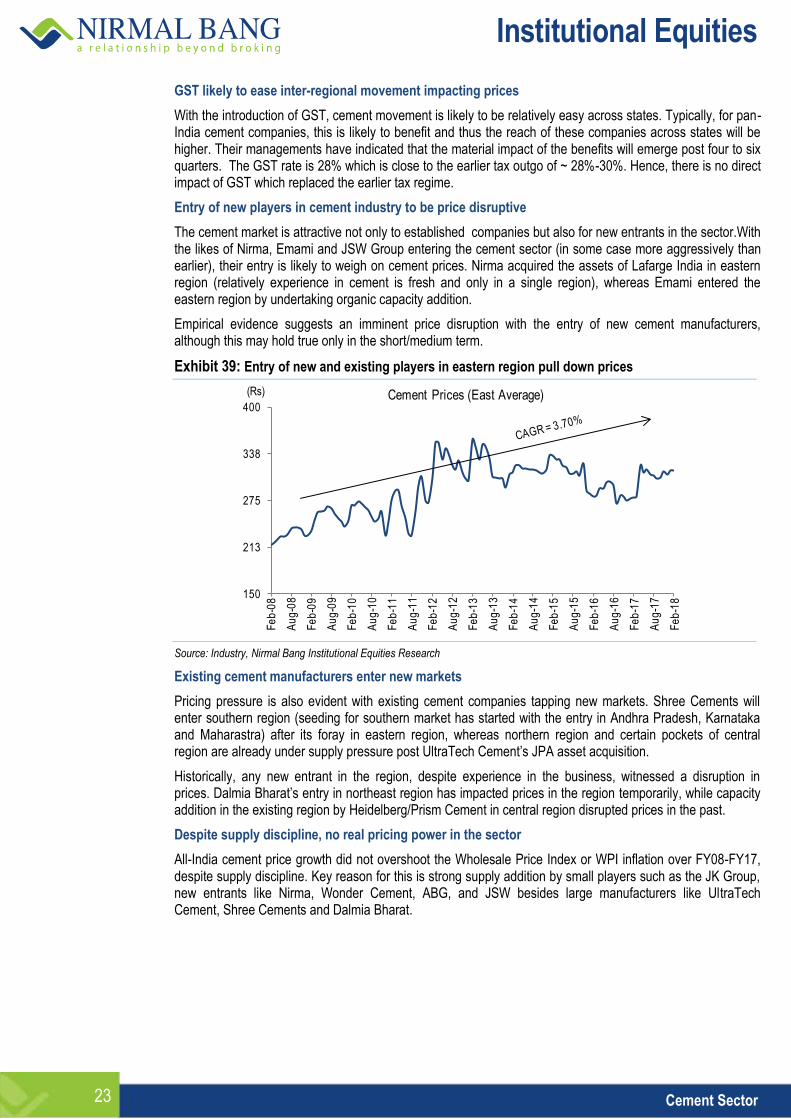

Entry of new players in cement industry to be price disruptive

The cement market is attractive not only to established companies but also for new entrants in the sector.With the likes of Nirma, Emami and JSW Group entering the cement sector (in some case more aggressively than earlier), their entry is likely to weigh on cement prices. Nirma acquired the assets of Lafarge India in eastern region (relatively experience in cement is fresh and only in a single region), whereas Emami entered the eastern region by undertaking organic capacity addition.

Empirical evidence suggests an imminent price disruption with the entry of new cement manufacturers, although this may hold true only in the short/medium term.

Exhibit 39: Entry of new and existing players in eastern region pull down prices

Source: Industry, Nirmal Bang Institutional Equities Research

Existing cement manufacturers enter new markets

Pricing pressure is also evident with existing cement companies tapping new markets. Shree Cements will enter southern region (seeding for southern market has started with the entry in Andhra Pradesh, Karnataka and Maharastra) after its foray in eastern region, whereas northern region and certain pockets of central region are already under supply pressure post UltraTech Cement’s JPA asset acquisition.

Historically, any new entrant in the region, despite experience in the business, witnessed a disruption in prices. Dalmia Bharat’s entry in northeast region has impacted prices in the region temporarily, while capacity addition in the existing region by Heidelberg/Prism Cement in central region disrupted prices in the past.

Despite supply discipline, no real pricing power in the sector

All-India cement price growth did not overshoot the Wholesale Price Index or WPI inflation over FY08-FY17, despite supply discipline. Key reason for this is strong supply addition by small players such as the JK Group, new entrants like Nirma, Wonder Cement, ABG, and JSW besides large manufacturers like UltraTech Cement, Shree Cements and Dalmia Bharat.

150

213

275

338

400

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (East Average)

Institutional Equities

24 Cement Sector

Exhibit 40: Al-India cement price movement vis-à-vis inflation

Source: Nirmal Bang Institutional Equities Research, Industry

Regional cement prices remain volatile and under pressure

Exhibit 41: Fragmented market adds further price volatility in northern region

Exhibit 42: Supply discipline help prices stay elevated amid volatility in southern region

Source: Nirmal Bang Institutional Equities Research, Industry Source: Nirmal Bang Institutional Equities Research, Industry

Exhibit 43: Central region to benefit from demand-supply parity

Exhibit 44: Prices under pressure in western region due to supply pressure from South India

Source: Nirmal Bang Institutional Equities Research, Industry Source: Nirmal Bang Institutional Equities Research, Industry

50

88

125

163

200

Jan

-08

Jun

-08

No

v-0

8

Ap

r-0

9

Se

p-0

9

Fe

b-1

0

Jul-1

0

De

c-1

0

Ma

y-1

1

Oct

-11

Ma

r-1

2

Au

g-1

2

Jan

-13

Jun

-13

No

v-1

3

Ap

r-1

4

Se

p-1

4

Fe

b-1

5

Jul-1

5

De

c-1

5

Ma

y-1

6

Oct

-16

Ma

r-1

7

Au

g-1

7

Jan

-18

(Rs) Cement prices and WPI

India Avg WPI *base 100

150

200

250

300

350

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (North Average)

150

213

275

338

400

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (South Average)

150

200

250

300

350

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (Central Average)

150

200

250

300

350

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (West Average)

Institutional Equities

25 Cement Sector

Exhibit 45: All India cement prices stayed volaltile, is expected to continue the trend

Source: Nirmal Bang Institutional Equities Research, Industry

150

200

250

300

350

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Au

g-1

6

Fe

b-1

7

Au

g-1

7

Fe

b-1

8

(Rs) Cement Prices (India Avg)

Institutional Equities

26 Cement Sector

Cost inflation is key challenge in the next two years

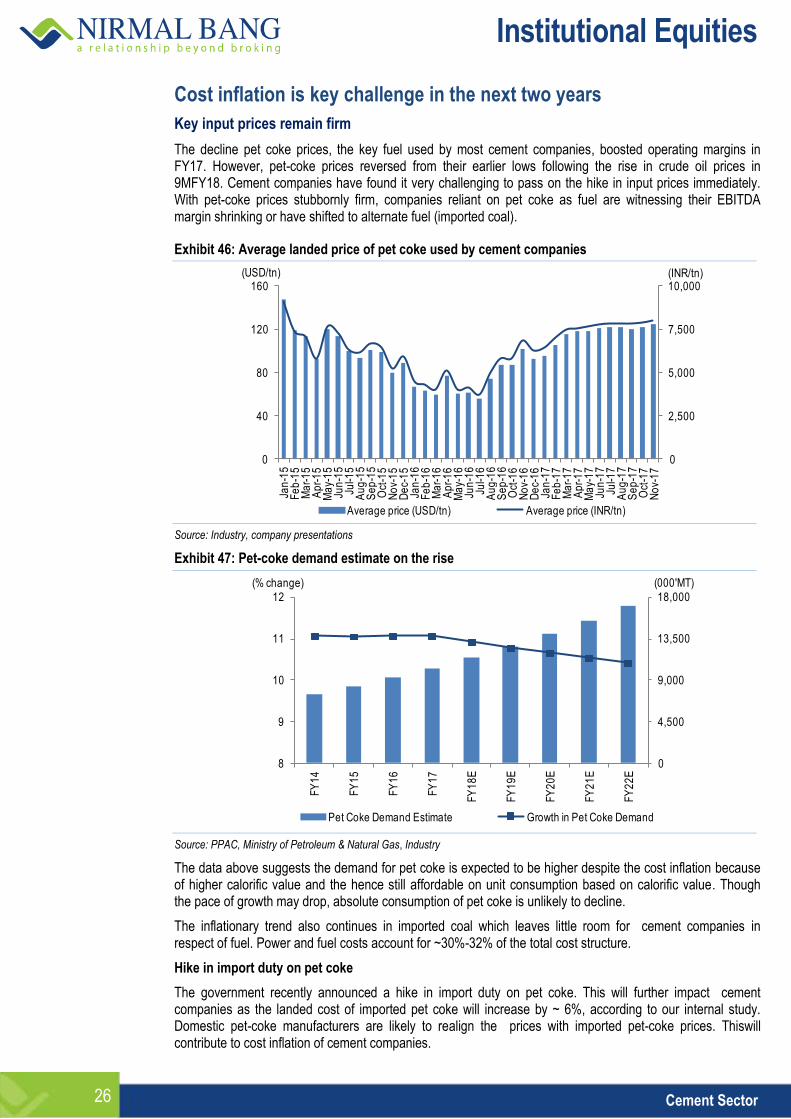

Key input prices remain firm

The decline pet coke prices, the key fuel used by most cement companies, boosted operating margins in FY17. However, pet-coke prices reversed from their earlier lows following the rise in crude oil prices in 9MFY18. Cement companies have found it very challenging to pass on the hike in input prices immediately. With pet-coke prices stubbornly firm, companies reliant on pet coke as fuel are witnessing their EBITDA margin shrinking or have shifted to alternate fuel (imported coal).

Exhibit 46: Average landed price of pet coke used by cement companies

Source: Industry, company presentations

Exhibit 47: Pet-coke demand estimate on the rise

Source: PPAC, Ministry of Petroleum & Natural Gas, Industry

The data above suggests the demand for pet coke is expected to be higher despite the cost inflation because of higher calorific value and the hence still affordable on unit consumption based on calorific value. Though the pace of growth may drop, absolute consumption of pet coke is unlikely to decline.

The inflationary trend also continues in imported coal which leaves little room for cement companies in respect of fuel. Power and fuel costs account for ~30%-32% of the total cost structure.

Hike in import duty on pet coke

The government recently announced a hike in import duty on pet coke. This will further impact cement companies as the landed cost of imported pet coke will increase by ~ 6%, according to our internal study. Domestic pet-coke manufacturers are likely to realign the prices with imported pet-coke prices. Thiswill contribute to cost inflation of cement companies.

0

2,500

5,000

7,500

10,000

0

40

80

120

160Ja

n-1

5F

eb

-15

Ma

r-1

5A

pr-

15

Ma

y-1

5Ju

n-1

5Ju

l-15

Au

g-1

5S

ep

-15

Oct

-15

No

v-1

5D

ec-

15

Jan

-16

Fe

b-1

6M

ar-

16

Ap

r-1

6M

ay-

16

Jun

-16

Jul-1

6A

ug

-16

Se

p-1

6O

ct-1

6N

ov-

16

De

c-1

6Ja

n-1

7F

eb

-17

Ma

r-1

7A

pr-

17

Ma

y-1

7Ju

n-1

7Ju

l-17

Au

g-1

7S

ep

-17

Oct

-17

No

v-1

7

(INR/tn)(USD/tn)

Average price (USD/tn) Average price (INR/tn)

0

4,500

9,000

13,500

18,000

8

9

10

11

12

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

FY

21

E

FY

22

E

(000'MT)(% change)

Pet Coke Demand Estimate Growth in Pet Coke Demand

Institutional Equities

27 Cement Sector

Exhibit 48: Impact on pet-coke prices following the hike in import duty

Particulars Earlier, when import

duty was 2.5% Now, when import

duty is 10%

Buyiing price (US$/tn) 95.0 95.0

Import duty 2.4 9.5

Port handling charges (US$/tn) 3.0 3.0

Price at port (US$) 100.4 107.5

Exchange rate 65.0 65.0

Price at port (Rs/tn) 6,524.4 6,987.5

Freight cost (Rs/tn) 1,786.2 1,786.2

Landed cost (Itn) 8,310.6 8,773.7

Increase in pet-coke prices because of the increase in import duty (%)

5.6

Source: Industry

Cost of limestone – a key raw material -- likely to be challenging

The royalty rates for limestone have been reversed and are expected to be addressed on an ongoing basis— likely to bear another costing impact on cement companies. This will weigh on margins under weak demand circumstances.

Further, the recent bidding for limestone reserves indicates aggression by new/existing companies, thereby inflating the cost of limestone, the basic raw material, for cement manufacture. We have provided here a snapshot of the bidding and its impact on raw material cost for the industry.

The working details of limestone bids by the companies and the cost/tn that will be paid by two companies to the government is disclosed below:

Bidding at Nagaur by Emami Cement

Average price for the past 12 months of auction (pan India) as set by the IBM: Rs500/tn

Reserve price (5%*of average price = Rs500): Rs25/tn.

Final bidding for Nagaur limestone mine auction (64.48%* of average price by Emami): Rs322.4/tonne.

*Two blocks at Nagaur received bids at 67.94% and 60.09% and the weighted average rate was @ 64.48%

Royalty to be paid/tn: Rs80

Contribution to National Mineral Exploration Trust: 2% of royalty

District Magistrate Fund: 10% of royalty

Bidding at Chittorgarh by Dalmia Cement:

Average price for the past 12 months of auction (pan-India) as set by IBM: Rs500/tn

Reserve price (14%*of average price = Rs500): Rs70/tn

Final bidding for Chittorgarh limestone mine auction (48.94%* of average price): Rs244.7

Royalty to be paid/t: Rs80/tonne

Contribution to National Mineral Exploration Trust/t: 2% of royalty

DMF: 10% of royalty.

Institutional Equities

28 Cement Sector

Exhibit 49: Total cost/tn for these two companies following the bidding of limestone mines at Nagaur and Chittorgarh

Details Emami Dalmia

Reserve price (Rs/tn) 322.4 244.7

Royalty (Rs/tn) 80.0 80.0

Contribution to National Mineral Exploration Trust (Rs/tn) 1.6 1.6

DMF (Rs/tn) 8.0 8.0

Total (Rs/tn) (limestone cost/t for companies) 412.0 334.3

Source: Department of Mines & Geology, State of Rajasthan

Institutional Equities

29 Cement Sector

Valuation at a premium

We expect continued volatility in earnings of cement companies, given the persistent over-supply situation. We feel genuine pricing power will not return to cement manufacturers in FY19-FY20. This is despite the demand pick-up (from a weak base) expected in the next two years following the government’s thrust on infrastructure and low- cost housing. However, pricing spike with high volatility is likely because of supply discipline followed by cement companies. Strong predatory pricing may also contribute for the price increase, albeit for a short term.

Though the cement sector is likely to benefit from the government’s thrust on infrastructure, we feel the steep valuation premiums have factored in the same, leaving limited head room for surprises.

Industry RoE is under pressure and has eased from its peak. This is despite the fact that earnings are related largely to supply discipline leading to pricing defying demand-supply dynamics. Hence, we feel the valuations (earnings-based or asset-based) are unjustifiably higher.

Exhibit 50: P/E and RoE movement in divergent paths Exhibit 51: Valuation and EBITDAM moving in opposite directions

Source: Industry Source: Industry

With the realistic pricing power still away for the next two to three years, current cement pricing is clearly driven by supply discipline with supply matching demand. This implies that price discovery is far from demand-supply dynamics and driven by external factors (limited supply). However, with limited genuine pricing power, cement pricing will be erratic and non-sustainable as it will lack structural strength.

With limited pricing power and continued input cost pricing pressure, we expect high EBITDAM-based companies to shed margins or at best stay range-bound. Though earnings growth will be contributed by companies with capacity addition, margins will be under pressure (few companies on correction mode and with lower EBITDAM in the past will witness some improvement in margins). Effectively, we feel RoEs in mid/high-teens will be extremely difficult without supply discipline that is currently followed by cement manufacturers, given the demand-supply gap existing in the country.

Hence, we feel the valuations are higher as with capacity utilsiation hovering ~72% and expected to touch ~75% in the next two years, price discovery (pricing power) will continue to be artificial. Therefore, on premium product pricing (artificial), valuing the stocks at a premium will be clearly a double count.

There is no commodity space where commodities following supply discipline have been commanding higher valuations. Hence, we feel the Indian cement sector is in an unique position where:

Existing supply is higher than demand and is expected to remain that way for at least the next two years.

Despite the same, all companies are operating income positive.

Equity valuation of cement companies are at much higher multiples than what the replacement cost justifies.

Expensive from regional considerations too:

The table below points the gap between valuation of Indian companies and their Asian peers widening to double. Fundamentally, its Asian peers are on a better footing in terms of demand-supply fundamentals and valuations.

0

7

14

21

28

0

20

40

60

80

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

P/E (LHS) ROE (RHS)

(x) (%)

0

4

8

12

16

0

9

18

27

36

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

Operating Profit Margin (LHS) EV/EBITDA (RHS)

(%) (x)

Institutional Equities

30 Cement Sector

Exhibit 52: Peer group comparison in Asian region

Mkt. cap. (US$mn)

Share price (LC)

P/E (x) EPS CAGR (%) FY18E-

FY20E

EV/EBITDA(x) EBITDA CAGR (%)

FY18E-FY20E

P/BV(x) FY20E

RoE % FY20E FY19E FY20E FY19E FY20E

China

Anhui Conch Cement 26,978 32.2 9.8 9.2 16.5 6.1 6.0 25.7 1.5 16.3

China Resources Cement 4,711 5.6 8.9 8.9 18.8 6.5 6.6 53.6 1.1 12.7

West China Cement 895 1.3 7.1 6.4 9.6 4.1 4.0 279.5 0.7 10.6

ASEAN

Indocement Tunggal Prakarsa 5,414 20,250.0 29.7 24.4 -0.8 17.5 14.8 -7.6 2.6 10.7

Lafarge Malaysia 1,104 5.1 338.0 51.7 5.9 19.9 13.3 -2.3 1.5 3.2

Holcim Indonesia 459 825.0

49.9 8.4 11.4 8.1 0.0 0.8 1.5

Semen Indonesia Persero 4,567 10,625.0 21.4 17.2 10.2 11.7 10.0 -6.8 1.8 10.9

Taiwan Cement Corp 5,286 36.4 13.9 13.5 6.3 9.8 9.7 9.4 1.2 8.4

Siam Cement 18,598 486.0 10.9 10.4 2.1 9.2 8.8 -0.9 1.6 16.7

Asia Cement Corp (ACC) 3,173 27.6 14.7 14.0 2.8 13.3 13.9 18.3 0.7 4.8

India

UltraTech 17,241 4,110 39.5 30.7 24.4 17.7 15.4 17.0 3.5 11.9

Ambuja Cements 7,194 236 26.6 23.7 15.9 9.4 8.4 9.6 1.6 7.0

Shree Cement 8,588 16,096 33.2 28.6 19.8 17.9 15.9 16.4 4.5 17.2

ACC 4,427 1,545 28.3 24.2 20.9 13.0 11.5 10.3 2.7 12.0

Average - - 31.9 26.8 14.6 14.5 12.8 8.8 3.1 12.0

Source: Bloomberg, Nirnal Bang Institutional Equities Research

Institutional Equities

31 Cement Sector

We continue our negative view on the sector because of premium valuation commanded by cement companies though fundamentals are still far from improving (except for companies with EBITDA/EBITDAM correction, those moving from a lower base). The valuations are already factoring in the demand and the resultant earnings growth for the next two years. We have recommended to avoid companies with high debt, low on governance and premium valuations. We have Sell recommendation on JK Lakshmi Cement, Heidelberg Cement and India Cements sighting continuing margin pressure, higher debt (JKLC and ICEM), lack of cost efficiencies and higher valuations. We feel valuations are far stretched of Shree Cement and Dalmia Cement despite the challenges these companies are likely to counter in the next two years and hence have assigned a Sell rating. However, we prefer companies with cost efficiency, lower debt and better corporate governance. We have assigned a BUY rating on The Ramco Cements and JK Cement. In the small-cap space, we have a Buy recommendation on Sagar Cements. Among the large cap we have assigned ‘ACCUMULATE’ rating on Ultratech Cement. ACC and Ambuja continue to be in our dis-comfort zone due to structural weakness.

Key conclusions about cement sector for the next two years

Cement demand is likely to register high single-digit growth in the next two years (8% in FY19E/FY20E), expecting the current momentum to continue.

Eastern region to lead the growth pack, while revival in southern region will be the key positive. However, central region will be key beneficiary of demand-supply balance.

Demand to accelerate in the medium term till FY20, driven by numerous government-led initiatives.

We expect 30mtpa of capacity to be added till FY20E. However this is following 130mtpa added in the past five years (FY12-FY17). This implies the DD-SS gap to continue in the range of ~100mt-120mt.

Capacity utilisation will continue to remain at ~73%-75% at pan-India level in FY19E-FY20E. This implies the industry’s pricing power will not return in the next two years.

With active inter-regional movement and introduction of GST, the pressure on prices will continue.

Prices are expected to rise marginally by 2%, driven by northern and central regions; but high price volatility is a certainty. Supply discipline in southern region will keep prices elevated, albeit volatility in the region.

Pet coke and coal prices heading northward and will limit margins of cement companies.

Sell-off by debt-ridden players continues to drive deal activity in the sector, but no significant impact on prices likely.

Institutional Equities

32 Cement Sector

Annexure:

India has miles to go in terms of cement consumption

Low per-capita consumption leaves enough headroom for strong demand in India

Although India is the second-largest producer of cement and there is disconnect between GDP growth and cement output in recent years, the country has enough headroom to drive cement demand. This drive needs to be backed by prudent policy formulation and robust spending n by the state.

Exhibit 53: Main cement producers - G20 group

Country 2001 2007 2008 2009 2010 2011 2012 2013 2014 2015

China 661.0 1,361.2 1,388.4 1,644.0 1,881.9 2,063.2 2,137.0 2,359.0 2438.0 2,350.0

India

102.9 170.5 185.0 205.0 220.0 270.0 239.0 272.0 280.0 270.0

European Union e 225.6 269.1 250.8 209.0 192.1 191.6 170.5 157.5 165.8 172.0

USA

88.9 95.5 86.3 63.9 65.2 68.6 74.0 77.2 83.2 83.4

Brazil p 39.4 45.9 51.6 51.7 59.1 63.0 68.0 71.9 72.0 73.0

Turkey

30.0 49.3 51.4 54.0 62.7 63.4 63.8 70.8 72.6 72.8

Russian Federation p 28.7 59.9 53.5 44.3 50.4 56.1 53.0 55.6 68.4 69.0

Japan

79.5 71.4 67.6 59.6 56.6 56.4 59.3 61.7 61.9 59.5

Korea, Rep. of p 52.0 52.2 51.7 50.1 47.4 48.2 46.9 47.3 47.0 49.1

Saudi Arabia p 20.0 30.3 37.4 37.8 42.5 48.0 43.0 48.0 51.8 54.0

Indonesia p 31.1 35.0 38.5 36.9 39.5 45.2 53.5 52.0 54.2 54.4

Mexico p 33.2 38.8 37.1 35.1 34.5 35.4 36.8 37.0 39.4 40.0

Germany e 32.1 33.4 33.6 30.4 29.9 33.5 32.4 31.9 32.5 32.0

Italy

39.8 47.5 43.0 36.3 34.4 33.1 26.2 23.1 21.4 20.8

France 19.1 22.1 21.2 18.1 18.0 19.4 18.0 17.5 16.4 15.6

Canada

12.1 15.1 13.7 11.0 12.4 12.0 12.5 12.1 12.8 12.5

Argentina 5.5 9.6 9.7 9.4 10.4 11.6 10.7 11.9 11.8 12.2

South Africa p 8.4 13.7 13.4 11.8 10.9 11.2 13.8 14.9 13.8 14.0

Australia p 6.8 9.2 9.4 9.2 8.3 8.6 8.8 8.6 9.0 9.1

United Kingdom e 11.9 12.6 10.5 7.8 7.9 8.5 7.9 8.5 9.2 9.6

Notes: p: Preliminary - e: Estimate; Source: Cembureau

Even after seven decades of independence, and nearly two-and-a-half decades of globalisation, India is one of the lowest per capita consumer of cement, which clearly indicates that the space still requires sufficient infrastructure and housing push. Average consumption is just ~200kg/year compared to 1700 kg/year in China and 660kg/year in Vietnam (comparable developing economy). The global average consumption is far ahead at 580kg/year.

This leaves enough headroom for India’s cement demand to shore up on uptick in the economic cycle.

Exhibit 54: World cement production in 2015 by regions and main countries

Exhibit 55: Per capita cement consumption (kg)

Source: Cembureau Source: Cembureau, Company presentations

China , 57%Africa, 5%

USA, 2%

America (Excluding USA),

5%

Europe & Others, 8%

Asia (Excluding China & India),

17%

India , 7%

0

450

900

1,350

1,800