Cement Sector- Initiating Coverage-10 May 2017.pdf

60

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Cement Sector- Initiating Coverage-10 May 2017.pdf

Institutional Equities

This page has been intentionally left blank

Institutional Equities

Cement Sector

Initi

atin

g C

over

age

South India – On Course To Realise Its True Potential India’s southern region has some highly developed states with vast potential for cement demand, given the favourable demographics and income levels. During FY06-FY10, cement demand growth in this region had been higher than the all India average on account of higher government spending and robust housing and commercial segments. However, over the past five to six years, demand in the region witnessed considerable contraction as government spending dried up, political scenario worsened and the housing segment across the country weakened. Over the past 12-18 months, we have started witnessing a decent recovery in cement demand driven by higher spending in bifurcated states of Andhra Pradesh and Telangana and central government-sponsored low-cost housing programme in Tamil Nadu and Karnataka. We are quite upbeat about the demand prospects in the southern region and believe that cement prices will also remain elevated despite low capacity utilisation level. The combination of factors like: 1) Higher-than-industry volume growth, 2) Better pricing environment, and 3) Efficient operations will likely result in much better profitability for cement players. We initiate coverage on Dalmia Bharat (DBL) and Sagar Cements (SCL) with a Buy rating and Accumulate rating on The Ramco Cements (TRCL) to play this upcycle in the southern region. We believe these companies, despite the recent run-up in their share prices, still offer significant upside potential. Common investment thesis among these companies is efficient plant operations (resulting in very high EBITDA/mt), massive operating leverage (capacity utilisation less than 60%), higher-than-industry volume growth (FY16-FY19E volume CAGR of 8%-15%) and stable cement prices in its markets (prices in the southern region have been relatively stable at higher levels compared to other regions). The stocks under our coverage provide 10%-20% upside potential and have possibility of further earnings upgrade if demand growth turns out to be better-than-expected, leading to faster realisation of operating leverage. Key risks to our positive call include government intervention in cement prices, lower demand growth leading to increased competition and an adverse political scenario.

Demand is improving at the margin while supply dries up: After years of sluggishness, the southern region showed some green shoots of demand growth in FY17. For the region as a whole, volume growth in FY17 was in excess of 5% whereas some of the listed companies witnessed volume growth in high-teens. This volume growth can be partly attributed to a combination of weak base of the previous year and increased government spending on sectors like irrigation and housing. We believe this demand growth is sustainable as the momentum for key demand drivers of cement has just started and it is likely to continue, given the intention of various state governments to increase spending on capex coupled with growth-oriented schemes driven by the central government. We expect the southern region as a whole to grow at higher-than-all India average for the next couple of years whereas incremental supply in the region will be minimal.

Cement prices stable and costs under control: Cement prices in the southern region have been higher than the all India average for the past two to three years. Despite lower capacity utilisation level of the industry, pricing resilience has been quite remarkable in this region which has helped the industry to survive the excess supply situation. Since the middle of 2014, prices in the southern region have been higher by at least 15% compared to the all India average. Key reasons for higher prices include lower blending, higher input costs compared to players in the northern region and higher lead distance in certain cases.

We have Buy rating on DBL and SCL and Accumulate rating on TRCL: We initiate coverage on three companies with Buy rating on DBL and SCL with up to 18% upside, and Accumulate rating on TRCL.

Mangesh Bhadang Research Analyst [email protected] +91-22-3926 8172

View: POSITIVE Recommendation summary

Company Rating TP (Rs) Upside (%)

DBL Buy 2,806 17%

TRCL Accumulate 775 10%

SCL Buy 951 18%

Source: Nirmal Bang Institutional Equities Research

Market-cap CMP Target Up/ EV/E (x) P/B (x) RoE (%)

Company Rating Rsbn US$mn (Rs) price down(%) FY18E FY19E FY18E FY19E FY18E FY19E

Dalmia Bharat Buy 215 3,311 2,406 2,806 17% 12.2 10.2 4.2 3.5 15.4 17.6

Sagar cement Buy 17 259 806 951 18% 11.5 8.6 1.9 1.7 8.6 12.5

The Ramco Cements Accumulate 169 2,596 706 775 10% 11.9 10.8 3.9 3.3 17.0 17.0

Source: Company, Nirmal Bang Institutional Equities Research

10 May 2017

Institutional Equities

4 Cement Sector

Table of Content

Summary of stock recommendations…………………………………………………...…………..….…05

Demand growth in southern region to be superior compared with the rest of India…….……..…….08

Pricing environment is stable with reduced volatility…………………………………………….………13

Supply outlook………..…………………………………………………………..………...………….……15

Profitability snapshot of southern players……………………………………………….………..……...16

Snapshot of key states with possible demand potential………………………………………………..19

Companies

Dalmia Bharat ……………………………………………………………………….…………..….………27

Sagar cement ………………………………………………………..…………...…….…………………..39

The Ramco Cements……………………………………..……………………...…….…………………..51

Institutional Equities

5 Cement Sector

Summary of stock recommendations

Dalmia Bharat - The best growth story in cement space (Rating: Buy, CMP: Rs2,406, TP: Rs 2,806, Upside: 17%)

DBL, according to us, is probably the best and successful growth story in the cement space in India. From a capacity of mere 1.2mnmt in FY06, DBL has been able to grow 20.0x to a 25mnmt company by FY16, placing it among the top four cement companies in India. Now that a significant scale has been achieved through inorganic and organic routes, we expect the company to report much higher volume growth for the next few years along with increased market share. Apart from this, DBL has been able to achieve growth while focusing on improving efficiency as well. DBL boasts of significantly lower operating costs which help it to generate one of the highest EBITDA/mt among peers. DBL has various firsts to its credit like being the largest slag cement company in India, having one of the lowest electricity consumption patterns in the country, having one of the lowest carbon footprints in the world and a much higher cement-to-clinker ratio among peers. Given the scope for much higher volume growth, presence in regions where cement prices have been favourable and stable and also completion of a major capex programme, DBL is all set to achieve superior earnings growth driven by the excellence exhibited in the past in capex as well as opex. Moreover corporate restructuring - which is on the verge of completion - will create a pure play cement company, unlike a holding company in the past, which will further help shore up its financials and achieve better valuation multiples given its size. We have factored in 12.7%/20.6%/75.6% CAGR in sales, EBITDA and net profit over FY16-FY19E, respectively.

We initiate coverage on DBL with a Buy rating and a target price of Rs2,806. We believe DBL offers huge operating leverage as its plants currently operate at ~55% of their capacity. This operating leverage coupled with cost leadership and a presence in regions where pricing is in favour, like southern and north-east regions, makes DBL an exciting play in the cement space. We have valued the company based on the average of EV/EBITDA and EV/mt multiple. Our target multiple for EV/EBITDA calculation is 12.0x which is in line with the multiples we have assigned to other companies like ACC and Ambuja Cements. Our target price based on this method comes out to Rs2,806, up 17% from the current market price.

Exhibit 1: Earnings-based valuation Exhibit 2: Asset-based valuation

Particulars (Rsmn)

FY19E EBITDA 27,682

Target multiple (x) 12.0

Enterprise value 3,32,180

Net debt 40,685

Equity value 2,91,495

No. of shares (mn) 88.8

Value per share (Rs) 3,283

Particulars (Rsmn)

FY19E capacity (mnmt) 25.0

Target multiple (US$) 150.0

Enterprise value 2,47,500

Net debt 40,685

Equity value 2,06,815

No. of shares (mn) 88.8

Value per share (Rs) 2,329

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 3: Target price of Rs2,806, up 17% from the current market price

Particulars (Rs)

Value based on earnings multiple 3,283

Value based on asset valuation 2,329

Average value per share 2,806

Target price 2,806

CMP (Rs) 2,406

Upside (%) 17%

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

6 Cement Sector

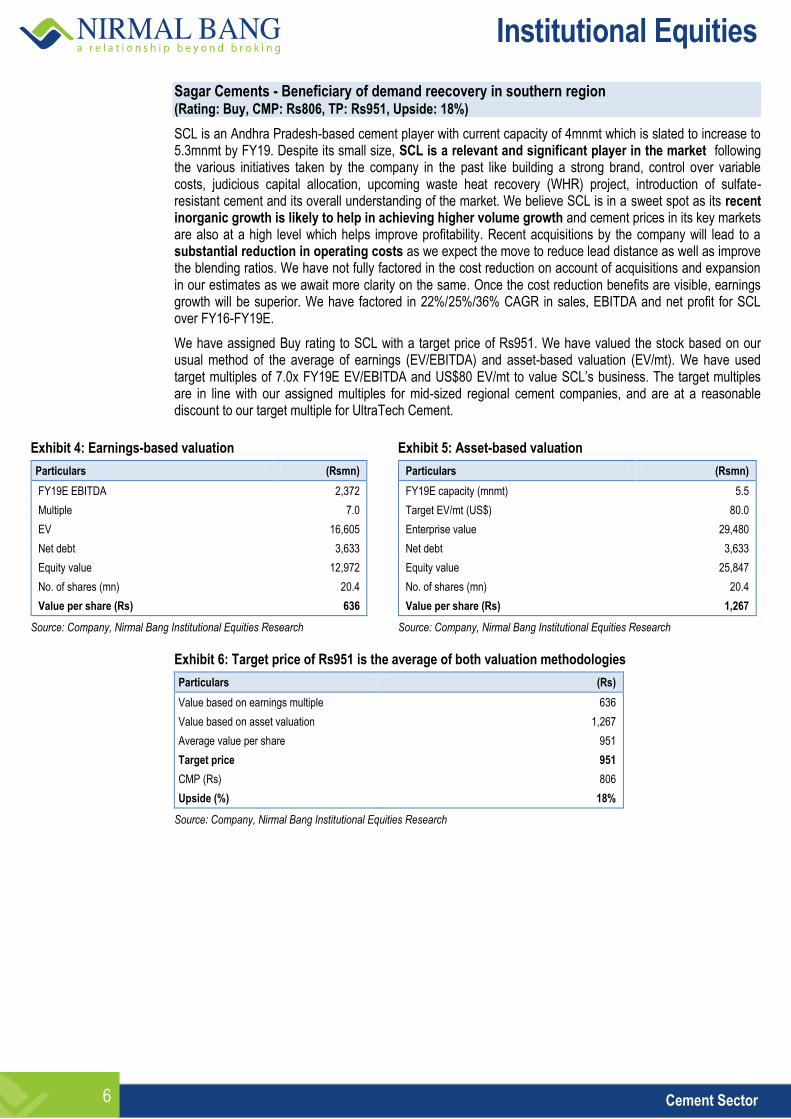

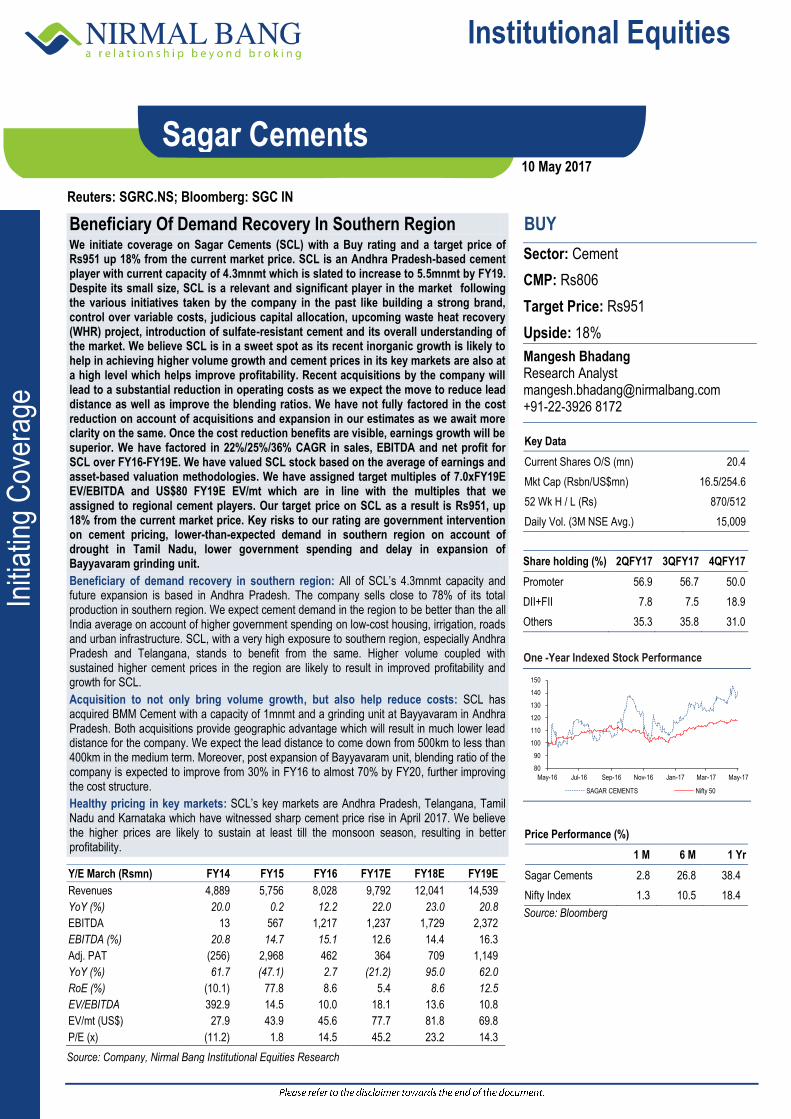

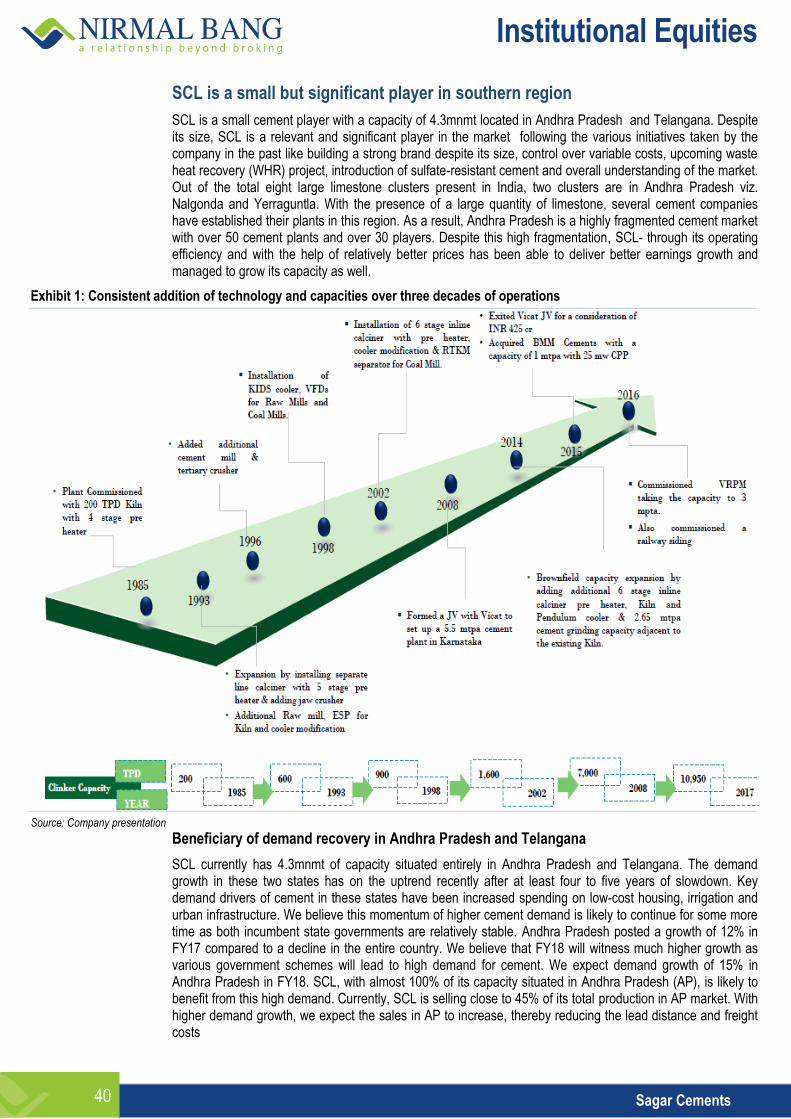

Sagar Cements - Beneficiary of demand reecovery in southern region (Rating: Buy, CMP: Rs806, TP: Rs951, Upside: 18%)

SCL is an Andhra Pradesh-based cement player with current capacity of 4mnmt which is slated to increase to 5.3mnmt by FY19. Despite its small size, SCL is a relevant and significant player in the market following the various initiatives taken by the company in the past like building a strong brand, control over variable costs, judicious capital allocation, upcoming waste heat recovery (WHR) project, introduction of sulfate-resistant cement and its overall understanding of the market. We believe SCL is in a sweet spot as its recent inorganic growth is likely to help in achieving higher volume growth and cement prices in its key markets are also at a high level which helps improve profitability. Recent acquisitions by the company will lead to a substantial reduction in operating costs as we expect the move to reduce lead distance as well as improve the blending ratios. We have not fully factored in the cost reduction on account of acquisitions and expansion in our estimates as we await more clarity on the same. Once the cost reduction benefits are visible, earnings growth will be superior. We have factored in 22%/25%/36% CAGR in sales, EBITDA and net profit for SCL over FY16-FY19E.

We have assigned Buy rating to SCL with a target price of Rs951. We have valued the stock based on our usual method of the average of earnings (EV/EBITDA) and asset-based valuation (EV/mt). We have used target multiples of 7.0x FY19E EV/EBITDA and US$80 EV/mt to value SCL’s business. The target multiples are in line with our assigned multiples for mid-sized regional cement companies, and are at a reasonable discount to our target multiple for UltraTech Cement.

Exhibit 4: Earnings-based valuation Exhibit 5: Asset-based valuation

Particulars (Rsmn)

FY19E EBITDA 2,372

Multiple 7.0

EV 16,605

Net debt 3,633

Equity value 12,972

No. of shares (mn) 20.4

Value per share (Rs) 636

Particulars (Rsmn)

FY19E capacity (mnmt) 5.5

Target EV/mt (US$) 80.0

Enterprise value 29,480

Net debt 3,633

Equity value 25,847

No. of shares (mn) 20.4

Value per share (Rs) 1,267

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 6: Target price of Rs951 is the average of both valuation methodologies

Particulars (Rs)

Value based on earnings multiple 636

Value based on asset valuation 1,267

Average value per share 951

Target price 951

CMP (Rs) 806

Upside (%) 18%

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

7 Cement Sector

The Ramco Cements - Best in class profitability awaiting operating leverage (Rating:Buy, CMP: Rs706, TP:Rs775, Upside: 10%)

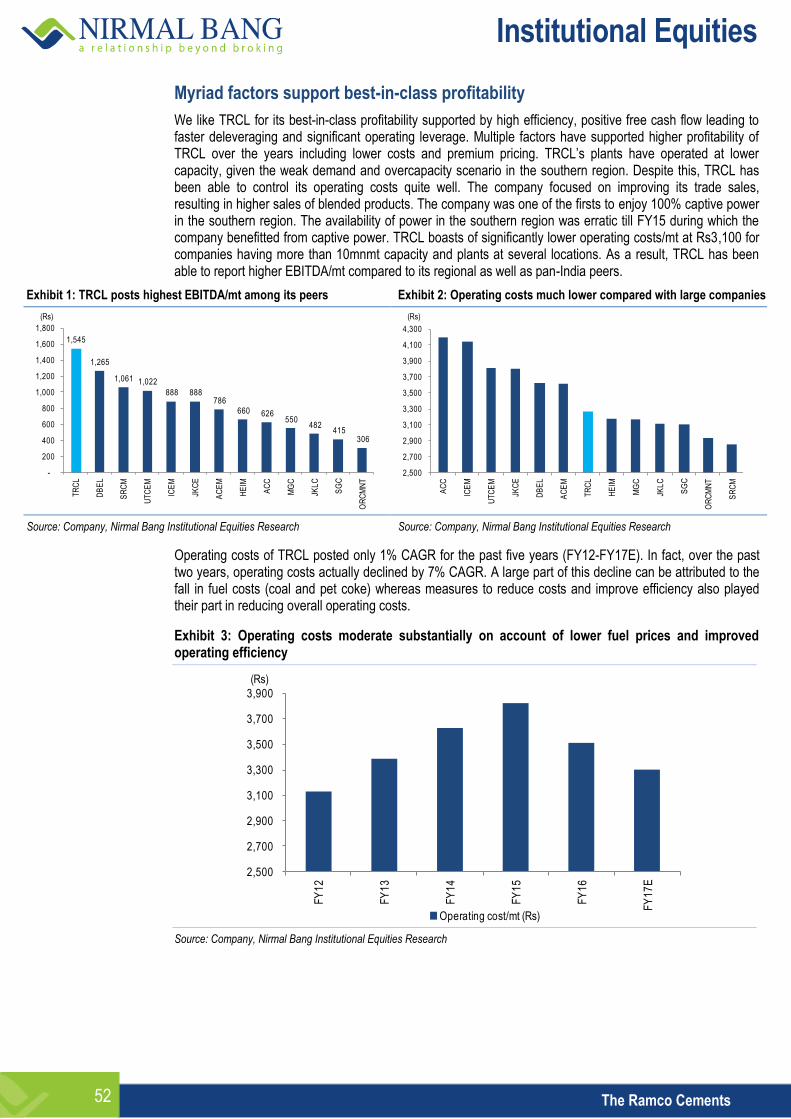

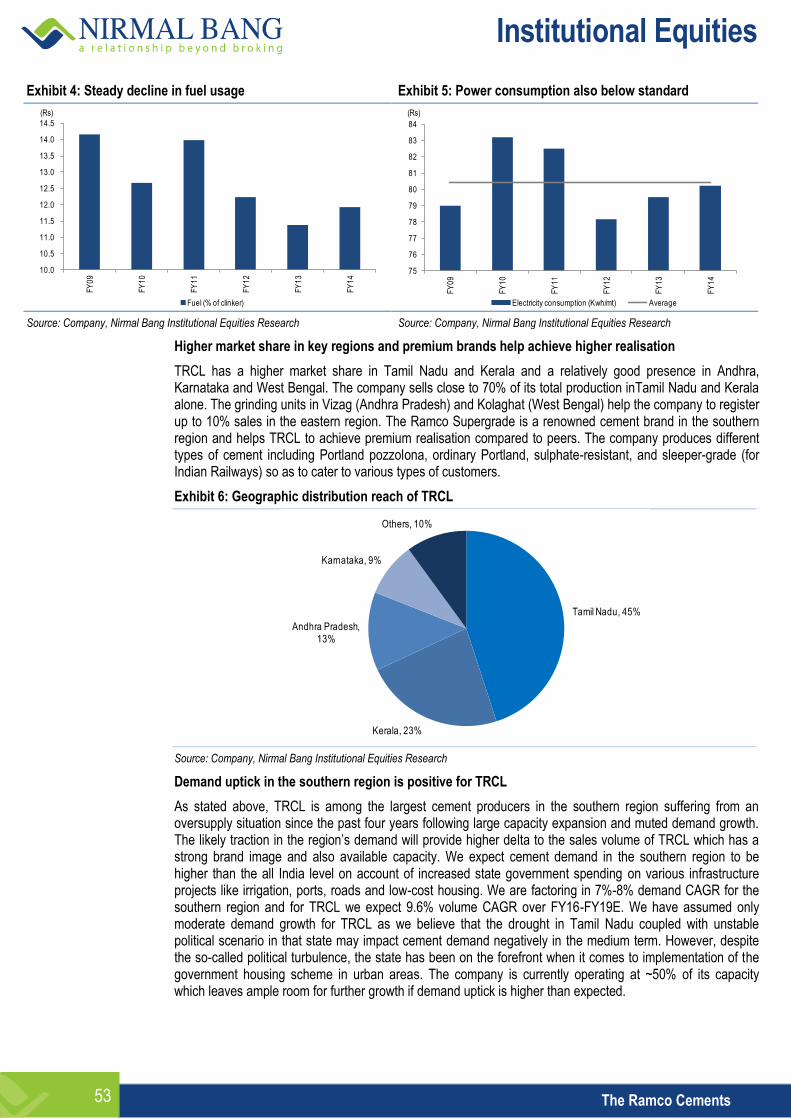

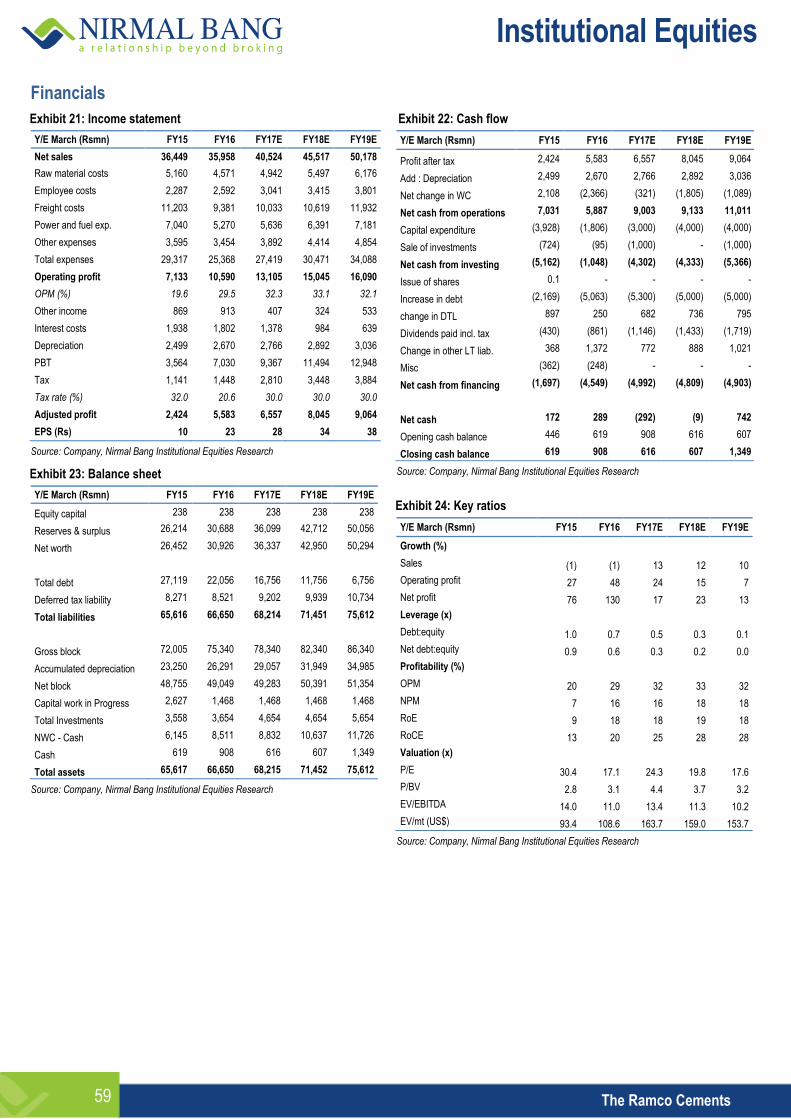

We like The Ramco Cements limited (TRCL) as it has several advantages in the southern region like (1) Cost efficiency (100% captive power plant and lower operating costs) and premium product pricing, resulting in superior profitability, (2) beneficiary of demand uptick in the southern region (strong brand image, large market share in Tamil Nadu and Kerala), (3) Completion of major capex, and robust operating cash flow expected to deleverage the balance sheet and improve return ratios, and (4) elevated but justified valuations given the return ratios. TRCL is highly efficient in its operations, as despite running on lower utilizations the company has been able to control its costs well. The company has been reporting higher EBITDA/mt compared to most other cement companies in India for the past few quarters. This best in class profitability is awaiting operating leverage to open up as the current utilization of the company is only 50% which leaves ample scope for further volume growth. We are building in sales/EBITDA/PAT CAGR of 11%/15%/17.5% over FY16-19E respectively. The revenue growth will be driven by 9.6% volume CAGR and a mere 2% pricing CAGR. Lower pricing growth in our assumption corresponds to already higher prices in its key regions. After declining in 9MFY17, we expect operating costs to increase by ~4% in FY18 and FY19. This will translate to higher EBITDA/mt for TRCL compared to other companies. Key downside risks to our call include government intervention in cement pricing, severe draught in Tamil Nadu impacting volumes for the company and increase in input costs.

We have assigned an accumulate rating on TRCL with a target price of Rs775. We have valued the stock based on our usual method of average of earnings based valuation (EV/EBITDA) and asset based valuation (EV/MT). We have used target multiples of 12.0x FY19 EV/EBITDA and US$160 EV/mt to value the business. The target multiples are slightly higher than our assigned multiples for mid-sized cement companies on account of better return profile and huge operating leverage. We believe TRCL is a must have stock in portfolio on account of credible management and best in class profitability.

Exhibit 7: Earnings-based valuation Exhibit 8: Asset-based valuation

Particulars (Rsmn)

FY19E EBIDTA 16,090

Multiple 12.0

EV 1,93,078

Net debt 2,312

Equity value 1,90,766

No. of shares (mn) 238.1

Value per share (Rs) 801

Particulars (Rsmn)

FY19E capacity (mnmt) 16.5

Target EV/mt (US$) 160.0

Enterprise value 1,80,730

Net debt 2,312

Equity value 1,78,418

No. of shares (mn) 238.1

Value per share (Rs) 749

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 9: Target price of Rs775 is the average of both valuation methodologies

Particulars (Rs)

Value based on earnings multiple 801

Value based on asset valuation 749

Average value per share 775

Target price 775

CMP (Rs) 706

Downside 10%

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

8 Cement Sector

Demand growth in southern region to be superior compared with the rest of India

Recent trends suggest that demand is improving at the margin

FY17 was a weak year for the cement sector with demand contraction of 1.3% YoY for the industry. However, amidst this dismal performance from the industry, the southern region stood out with better volume as well as prices. After years of sluggishness, the southern region showed some green shoots of demand growth in FY17. As per the quarterly volume data of four predominant south-based cement companies, volume growth for these companies was in high teens compared to volume contraction reported in the past. Even for the region as a whole, volume growth in FY17 was in excess of 5%. This volume growth can be partly attributed to the combination of weak base of last year and increased government spending on sectors like irrigation and housing. We believe this demand growth is sustainable as the momentum for key demand drivers of cement has just started and it is likely to continue given the intention of various state governments to increase capex coupled with growth-oriented schemes driven by the central government. We expect the southern region as a whole to grow at higher-than-all India average for the next couple of years.

Exhibit 10: Volume growth of south-based companies in high-teens for the past few quarters

Note: Data pertains to 4 south-based companies like India Cements, The Ramco Cements, Orient Cements and Sagar Cements; Source: Company, Nirmal Bang Institutional Equities Research

For the purpose of understanding how cement demand can shape up in this region, we have looked at long-term demand trends. The pattern of demand growth in this region can be classified into three phases.

The first phase is the years FY08-FY10 wherein demand growth was in high single digits. This time period coincides with the booming cement markets in the country where the real estate boom coupled with higher government spending and better rural income post MNREGA was driving demand growth. Moreover, during this period, housing schemes like India Awas Yojna was being implemented in full flow by Andhra Pradesh under its then chief minister, Mr. Y.S.R. Reddy.

Exhibit 11: Three phases of demand growth in the southern region

Source: Cement Manufacturers Association or CMA, Company, Nirmal Bang Institutional Equities Research

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

1QF

Y15

2QF

Y15

3QF

Y15

4QF

Y15

1QF

Y16

2QF

Y16

3QF

Y16

4QF

Y16

1QF

Y17

2QF

Y17

3QF

Y17

Aggregate volume growth of south based companies (% YoY)

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

E

FY18

E

FY19

E

Cement Demand Growth in South (% YoY)

High Growth period driven by higher government spending

for housing schemes and

booming real estate markets

Extremely weak period for cement demand with lack of government spending, weak or stagnant real estate market. Andhra Pradesh saw a huge

decline in cement demand during this period (accentuated by state bifurcation) with contraction

in demand for 6 years in a row.

Early signs of demand improvement in place with

recovery in Andhra Pradesh

and Telangana. Karnataka and Tamilnadu demand to revive

soon

Institutional Equities

9 Cement Sector

The next phase of depression lasted for a prolonged period from FY11 to FY16. This time period was characterised by the drop in government expenditure on account of high fiscal deficit and slowdown in property markets across India as the interest rate cycle reversed. Cement demand contracted in four out of six years during this phase. This prolonged demand compression is likely to be followed by volume growth over FY17-FY19E, in our view. We expect the southern region to deliver higher-than-industry demand growth on the back of increased activity in irrigation and housing segments.

Higher spending in irrigation and housing sector to be key drivers

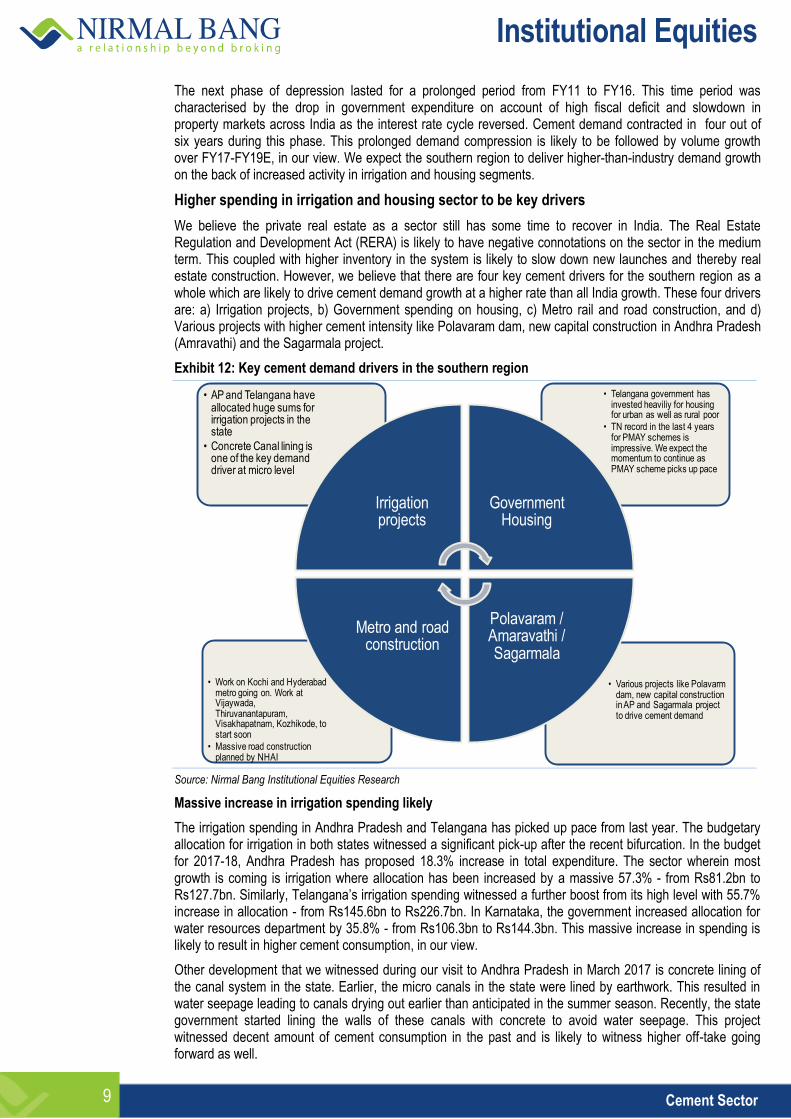

We believe the private real estate as a sector still has some time to recover in India. The Real Estate Regulation and Development Act (RERA) is likely to have negative connotations on the sector in the medium term. This coupled with higher inventory in the system is likely to slow down new launches and thereby real estate construction. However, we believe that there are four key cement drivers for the southern region as a whole which are likely to drive cement demand growth at a higher rate than all India growth. These four drivers are: a) Irrigation projects, b) Government spending on housing, c) Metro rail and road construction, and d) Various projects with higher cement intensity like Polavaram dam, new capital construction in Andhra Pradesh (Amravathi) and the Sagarmala project.

Exhibit 12: Key cement demand drivers in the southern region

Source: Nirmal Bang Institutional Equities Research

Massive increase in irrigation spending likely

The irrigation spending in Andhra Pradesh and Telangana has picked up pace from last year. The budgetary allocation for irrigation in both states witnessed a significant pick-up after the recent bifurcation. In the budget for 2017-18, Andhra Pradesh has proposed 18.3% increase in total expenditure. The sector wherein most growth is coming is irrigation where allocation has been increased by a massive 57.3% - from Rs81.2bn to Rs127.7bn. Similarly, Telangana’s irrigation spending witnessed a further boost from its high level with 55.7% increase in allocation - from Rs145.6bn to Rs226.7bn. In Karnataka, the government increased allocation for water resources department by 35.8% - from Rs106.3bn to Rs144.3bn. This massive increase in spending is likely to result in higher cement consumption, in our view.

Other development that we witnessed during our visit to Andhra Pradesh in March 2017 is concrete lining of the canal system in the state. Earlier, the micro canals in the state were lined by earthwork. This resulted in water seepage leading to canals drying out earlier than anticipated in the summer season. Recently, the state government started lining the walls of these canals with concrete to avoid water seepage. This project witnessed decent amount of cement consumption in the past and is likely to witness higher off-take going forward as well.

• Various projects like Polavarmdam, new capital construction in AP and Sagarmala project to drive cement demand

• Work on Kochi and Hyderabad metro going on. Work at Vijaywada, Thiruvanantapuram, Visakhapatnam, Kozhikode, to start soon

• Massive road construction planned by NHAI

• Telangana government has invested heaviliy for housing for urban as well as rural poor

• TN record in the last 4 years for PMAY schemes is impressive. We expect the momentum to continue as PMAY scheme picks up pace

• AP and Telangana have allocated huge sums for irrigation projects in the state

• Concrete Canal lining is one of the key demand driver at micro level

Irrigation projects

Government Housing

Polavaram / Amaravathi / Sagarmala

Metro and road construction

Institutional Equities

10 Cement Sector

Exhibit 13: Massive increase in budgetary allocation for irrigation in the southern states

State 2015-16 2016-17 2017-18 Growth

Key proposals Actual Revised Budgeted YoY %

Andhra Pradesh

45.5 81.2 127.7 57.3% Polavaram project is estimated to receive Rs72.51bn. This is more than a 100% increase as compared to the revised estimate for 2016-17.

Telangana 95.4 145.6 226.7 55.7% The government aims to provide irrigation to 10mn acres in the state.

Karnataka 81.6 106.3 144.3 35.8% Rs30bn is estimated to be spent on 21 different projects. This includes development of canal in the Cauvery basin.

Source: State budget documents, Nirmal Bang Institutional Equities Research

State-sponsored housing project is another important cement demand driver

Affordable housing segment in India is in vogue these days on account of the government’s ‘Housing For All’ initiative. Under this scheme, the central government provides assistance to individuals in terms of interest subsidy or direct benefit of upto Rs1.5lakh depending on the type of house constructed. Moreover, key highlight of state budgets of southern states was higher expenditure allocated for the housing schemes making use of some the central government’s flagship projects. In the past, schemes like Indira Awas Yojna and Rajiv Awas Yojna were implemented spiritedly in southern states. In fact, data on state-sponsored housing in urban areas indicates that southern states were leaders in the implementation of these schemes. In our recent report on affordable housing, we have mentioned that some of the beneficiaries of this scheme are likely to be southern states like Tamil Nadu, Andhra Pradesh and Karnataka. In the near term, various southern states are likely to up their spending on housing schemes using the incentives provided by the central government.

Tamil Nadu will be an important state to watch out as the government has come up with a slew of measures for the affordable housing segment. The state government has earmarked considerable funds for different programmes to provide housing facilities in rural and urban areas. It has launched a mission for housing the poor last year by dovetailing funds from many schemes to pursue this. It continues to strive for creating ‘hut-free’ villages and ‘slum-free’ cities in Tamil Nadu. Under the Pradhan Mantri Awas Yojana (PMAY), the government in Tamil Nadu will construct 1,76,000 houses in 2017-18 at a unit cost of Rs1,70,000. Of this, the central government’s contribution will be Rs72,000 per house while the state government will contribute Rs98,000. Roughly Rs17.5bn has been budgeted for the same. Apart from this, 20,000 houses will be constructed in 2017-18 under the Chief Minister’s Solar Powered Green House Scheme.

In Telangana, the government is providing two-bedroom houses for the poor. To encourage the implementation of Two-bedroom Housing Scheme, the government is providing sand free of cost. In addition, the government has entered into a pact with 31 cement companies to provide cement at Rs230 per bag as opposed to the market rate of Rs320 per bag. The contractors are slowly taking up the projects and progress has been satisfactory till date.

Update on Polavaram project

Indira Sagar (Polavaram) project is located on Godavari river near Ramayyapet village of Polavaram Mandal in West Godavari district of Andhra Pradesh. The project is multipurpose major terminal reservoir project on Godavari river for development of irrigation, hydropower and drinking water facilities to East Godavari, Vishakhapatnam, West Godavari and Krishna districts of Andhra Pradesh. The project will provide irrigation to 2,91,000 hectares(CCA) and hydropower with installed capacity of 960MW apart from 23.44tmc (663.7mcm) drinking and industrial water supply to Vishakhapatnam township and steel plant and diversion of 80tmc waters to Krishna rriv. The ultimate irrigation potential of the project is 436,800 ha and annual power generation will be 2369.43mn units. In addition, 540 villages will also be provided with drinking water facilities in the command area. The project implements Godavari-Krishna link under interlinking of rivers project. The project envisages transfer of 80tmc of surplus Godavari water to Krishna river which will be shared between Andhra Pradesh (AP), Karnataka and Maharashtra in the proportion of 45tmc by AP and 35tmc by Karnataka and Maharashtra as per the decision of the GWDT Award.

Institutional Equities

11 Cement Sector

Exhibit 14: 2BHK houses constructed by the government in Siddipet district of Telangana

Source: The Hindu newspaper

In Andhra Pradesh, the government has planned to build 1,10,000 houses in FY18 under the affordable housing project scheme. A sum of Rs14.6bn has been allocated for housing under the Pradhan Mantri Awas Yojana (PMAY) and NTR Rural Housing schemes in the state.

Karnataka also has massive plans for housing in the state. In the budget for 2017-18, the state government has allocated a large sum to build 7,00,000 houses out of which 6,00,000 houses will be built in rural areas. Even if the government achieves half of the state’s target, the resultant cement consumption can be huge.

Exhibit 15: Number of houses built under PMAY-U during FY14-FY17 (X)

Note: The data pertains to aggregate houses constructed in the past four years; Source: Ministry website, Nirmal Bang Institutional Equities Research

Exhibit 16: Number of houses sanctioned for construction under PMAY-Urban scheme as of April 2017 (X)

Source: Press Information Bureau, GoI, Nirmal Bang Institutional Equities Research

-

50,000

1,00,000

1,50,000

2,00,000

2,50,000

Ta

milN

ad

u

Ma

dh

ya

Pra

de

sh

An

dh

ra

Pra

de

sh

Ka

rna

taka

We

st B

en

ga

l

Gu

jara

t

Ma

ha

rash

tra

Bih

ar

Te

lan

ga

na

Jha

rkh

an

d

Oris

sa

Trip

ura

Pu

nja

b

Ra

jast

ha

n

Ch

ha

ttis

ga

rh

Ke

rala

Ass

am

Utt

ar P

rad

esh

Na

ga

lan

d

Miz

ora

m

Oth

ers

0

50,000

100,000

150,000

200,000

250,000

300,000

Ma

dh

ya

Pra

de

sh

Ta

mil

Na

du

An

dh

ra

Pra

de

sh

Gu

jara

t

Ka

rna

taka

We

st B

en

ga

l

Ma

ha

rash

tra

Bih

ar

Te

lan

ga

na

Jha

rkh

an

d

Od

ish

a

Trip

ura

Pu

nja

b

Ra

jast

ha

n

Ch

att

isg

arh

Ke

rala

Ass

am

Utt

ar

Pra

de

sh

Oth

ers

Southern states (including Maharashtra)

account for 43% of houses sanctioned under PMAY Urban scheme.

Institutional Equities

12 Cement Sector

Possibility of higher cement despatches from the southern region to other regions

On account of the presence of limestone clusters in the southern region, this region has generally been a net exporter of cement to nearby regions. States like Maharashtra, Odisha and West Bengal are the recipients of cement on account of either scarcity of limestone in these states or easy logistics because of proximity. While the eastern region witnessed good demand growth in the past, Maharashtra, which is a key state for volume growth of companies in the southern region, has witnessed subdued demand in the past year or so. With the uptick in urban infrastructure, metro rail-related work, increased road construction and railway station redevelopment, we expect cement demand in the state to improve which may increase the inter-state export of cement between Andhra Pradesh and Maharashtra.

Moreover, the government in its report on ‘Sagarmala’ had conducted origin-destination analysis for various classes of goods. For cement, the report indicated possible opportunity of 9mnmt-10mnmt of cement being moved through the coastal route by 2025. Out of that, roughly 5.5mnmt-6.0mnmt cement is expected to be despatched from Andhra Pradesh. With better development of coastal infrastructure, we expect higher amount of cement being despatched from states like Andhra and Karnataka, thereby improving the utilisation of existing capacities. Exhibit 17: Huge opportunity for coastal movement of cement in the southern region

Source: Sagarmala report by the Ministry of Shipping

Exhibit 18: Current inter-state flow of cement in India

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

13 Cement Sector

Pricing environment is stable with reduced volatility

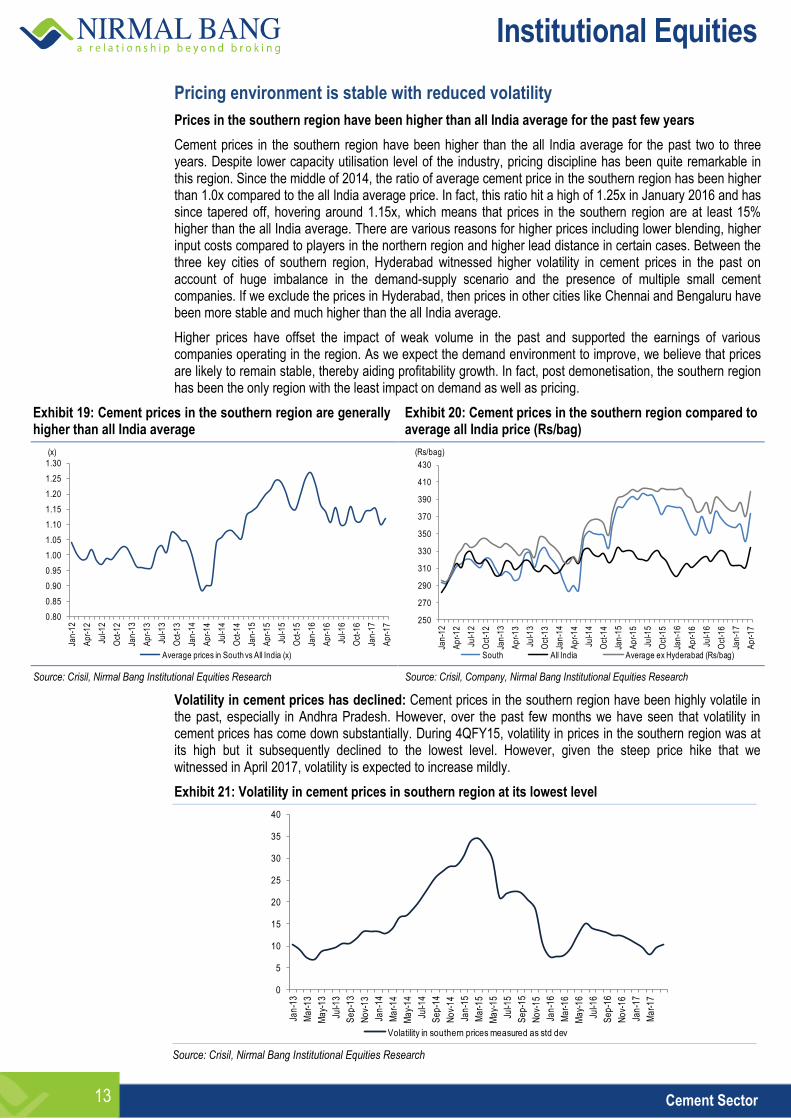

Prices in the southern region have been higher than all India average for the past few years

Cement prices in the southern region have been higher than the all India average for the past two to three years. Despite lower capacity utilisation level of the industry, pricing discipline has been quite remarkable in this region. Since the middle of 2014, the ratio of average cement price in the southern region has been higher than 1.0x compared to the all India average price. In fact, this ratio hit a high of 1.25x in January 2016 and has since tapered off, hovering around 1.15x, which means that prices in the southern region are at least 15% higher than the all India average. There are various reasons for higher prices including lower blending, higher input costs compared to players in the northern region and higher lead distance in certain cases. Between the three key cities of southern region, Hyderabad witnessed higher volatility in cement prices in the past on account of huge imbalance in the demand-supply scenario and the presence of multiple small cement companies. If we exclude the prices in Hyderabad, then prices in other cities like Chennai and Bengaluru have been more stable and much higher than the all India average.

Higher prices have offset the impact of weak volume in the past and supported the earnings of various companies operating in the region. As we expect the demand environment to improve, we believe that prices are likely to remain stable, thereby aiding profitability growth. In fact, post demonetisation, the southern region has been the only region with the least impact on demand as well as pricing.

Exhibit 19: Cement prices in the southern region are generally higher than all India average

Exhibit 20: Cement prices in the southern region compared to average all India price (Rs/bag)

Source: Crisil, Nirmal Bang Institutional Equities Research Source: Crisil, Company, Nirmal Bang Institutional Equities Research

Volatility in cement prices has declined: Cement prices in the southern region have been highly volatile in the past, especially in Andhra Pradesh. However, over the past few months we have seen that volatility in cement prices has come down substantially. During 4QFY15, volatility in prices in the southern region was at its high but it subsequently declined to the lowest level. However, given the steep price hike that we witnessed in April 2017, volatility is expected to increase mildly.

Exhibit 21: Volatility in cement prices in southern region at its lowest level

Source: Crisil, Nirmal Bang Institutional Equities Research

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Jan

-12

Ap

r-1

2

Jul-1

2

Oct

-12

Jan

-13

Ap

r-1

3

Jul-1

3

Oct

-13

Jan

-14

Ap

r-1

4

Jul-1

4

Oct

-14

Jan

-15

Ap

r-1

5

Jul-1

5

Oct

-15

Jan

-16

Ap

r-1

6

Jul-1

6

Oct

-16

Jan

-17

Ap

r-1

7

Average prices in South vs All India (x)

(x)

250

270

290

310

330

350

370

390

410

430

Jan

-12

Ap

r-1

2

Jul-1

2

Oct

-12

Jan

-13

Ap

r-1

3

Jul-1

3

Oct

-13

Jan

-14

Ap

r-1

4

Jul-1

4

Oct

-14

Jan

-15

Ap

r-1

5

Jul-1

5

Oct

-15

Jan

-16

Ap

r-1

6

Jul-1

6

Oct

-16

Jan

-17

Ap

r-1

7

South All India Average ex Hyderabad (Rs/bag)

(Rs/bag)

0

5

10

15

20

25

30

35

40

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-1

3

Se

p-1

3

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-1

4

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-1

5

Se

p-1

5

No

v-1

5

Jan

-16

Ma

r-1

6

Ma

y-1

6

Jul-1

6

Se

p-1

6

No

v-1

6

Jan

-17

Ma

r-1

7

Volatility in southern prices measured as std dev

Institutional Equities

14 Cement Sector

Southern region witnessed strong MoM price hike in April 2017 after weakness for a couple of months

Cement prices in the southern region witnessed a big MoM advance after relatively weak prices for the past two months. Dealers in Chennai stated that the price hike was notified to them at short notice. Prices in Chennai rose by around Rs20-Rs30 per bag while Hyderabad showed an uptick of Rs35-Rs40 per bag. However, the sharpest rise in this region was witnessed in Bengaluru where prices rose by Rs40-Rs50 per bag. Dealers indicated a fall in demand from the beginning of the current month, but were not sure whether it could be attributed to the hike. Dealers expect the demand to improve slightly, but remain unsure about future price prospects and whether the hiked prices can sustain. Some dealers also indicated that uncertainty coupled with lack of construction activity during the monsoon season will make it very tough to sustain the hiked prices. Some regions also saw follow-on pricing hikes in the second week of April 2017 as well.

Protest from CREDAI on higher cement prices

The Confederation of Real Estate Developers’ Association of India (CREDAI), which is an apex body of real estate developers in India, has protested against this massive price hike undertaken by cement companies. This body has been vocal in the past with respect to arbitrary cement price hikes undertaken by companies. In fact, on various occasions its members have even boycotted buying cement of premium brands to protest against the price hike.

CREDAI stated it has received numerous complaints and protest mails from its members across India about cement companies hugely jacking up prices of cement, thus negatively affecting the deliverability of affordable housing projects. Cement prices have witnessed a sudden jump of 20% to 40% in a short span of two months across India, while there are reports that cost of production of cement has not changed much. While the government laid emphasis on the housing industry and recognised its need, especially the affordable housing segment, by awarding it infrastructure status, this unjust price rise may increase construction costs which will have to be passed on to the consumers. CREDAI has regularly requested the central government for its swift intervention to put an end to the collusive practices in the industry and rein in price hikes so that it may contribute to the government’s goal of ‘Housing for All’ by 2022.

Here is the verbatim account of what the CREDAI president stated:

“We are pained by the complaints of unjustifiable and collusive jacking up of cement prices by cement manufacturers across India which have a potential to create unnecessary roadblocks and impediments in achieving the goals of Housing For All by 2022 envisioned by our Prime Minister. On earlier occasions too the Competition Commision of India has pulled up cement manufacturers for collusive pricing and imposed hefty fines on them. It is estimated that Rs100 rise in cement per bag results in increase in construction cost by at least Rs50 per square foot in the entire project. We are in talks with other affected parties like Builder’s Association of India as well as National Highway Builder’s Federation for possible joint action against this artificial price rise.”

Where do we think cement prices can go from here?

While the comments made by the property developer’s body are a threat to higher cement prices, we believe that historical instances like this have not yielded much result in favour of developers. We expect some correction in cement prices in the near term as the hike in April 2017 has been too steep. However, we believe that cement prices in the southern region will be resilient and that cement companies will pass on the increased cost burden to consumers by way of higher prices. We do not have pricing estimates for individual cities, but for companies in our coverage we have factored in 3%-6% increase in realisation from a low base.

More recently, a group of ministers (GOM) constituted by the Andhra Pradesh government, held talks with the cement companies to look into the steep price hike taken by the companies in the month of April. The construction industry already reeling under the pressure of low demand has alleged that the cement companies have created artificial scarcity in the market by deliberately stopping production intermittently. We expect the pricing in the southern region to be stable in the near-medium term as we expect some uncertainty on back of GST implementation etc.

Institutional Equities

15 Cement Sector

Supply outlook

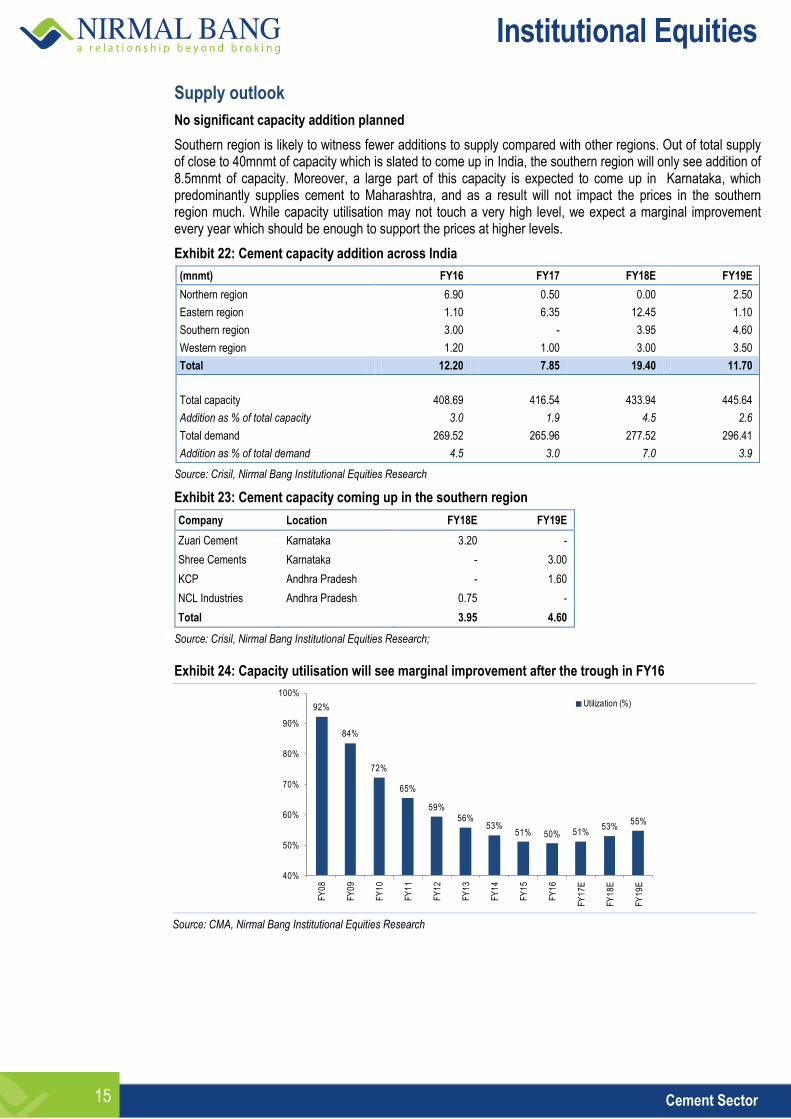

No significant capacity addition planned

Southern region is likely to witness fewer additions to supply compared with other regions. Out of total supply of close to 40mnmt of capacity which is slated to come up in India, the southern region will only see addition of 8.5mnmt of capacity. Moreover, a large part of this capacity is expected to come up in Karnataka, which predominantly supplies cement to Maharashtra, and as a result will not impact the prices in the southern region much. While capacity utilisation may not touch a very high level, we expect a marginal improvement every year which should be enough to support the prices at higher levels.

Exhibit 22: Cement capacity addition across India

(mnmt) FY16 FY17 FY18E FY19E

Northern region 6.90 0.50 0.00 2.50

Eastern region 1.10 6.35 12.45 1.10

Southern region 3.00 - 3.95 4.60

Western region 1.20 1.00 3.00 3.50

Total 12.20 7.85 19.40 11.70

Total capacity 408.69 416.54 433.94 445.64

Addition as % of total capacity 3.0 1.9 4.5 2.6

Total demand 269.52 265.96 277.52 296.41

Addition as % of total demand 4.5 3.0 7.0 3.9

Source: Crisil, Nirmal Bang Institutional Equities Research

Exhibit 23: Cement capacity coming up in the southern region

Company Location FY18E FY19E

Zuari Cement Karnataka 3.20 -

Shree Cements Karnataka - 3.00

KCP Andhra Pradesh - 1.60

NCL Industries Andhra Pradesh 0.75 -

Total

3.95 4.60

Source: Crisil, Nirmal Bang Institutional Equities Research; Exhibit 24: Capacity utilisation will see marginal improvement after the trough in FY16

Source: CMA, Nirmal Bang Institutional Equities Research

92%

84%

72%

65%

59%56%

53%51% 50% 51%

53%55%

40%

50%

60%

70%

80%

90%

100%

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

E

FY

18

E

FY

19

E

Utilization (%)

Institutional Equities

16 Cement Sector

Profitability snapshot of southern players

Exhibit 25: Financial and valuation snapshot

Market-cap CMP Target Up/ EV/E (x) P/B (x) RoE (%)

Company Rating Rsbn US$mn (Rs) price down(%) FY18E FY19E FY18E FY19E FY18E FY19E

Dalmia Bharat Buy 215 3,311 2,406 2,806 17% 12.2 10.2 4.2 3.5 15.4 17.6

Sagar cement Buy 17 259 806 951 18% 11.5 8.6 1.9 1.7 8.6 12.5

The Ramco Cements Accumulate 169 2,596 705 775 10% 11.9 10.8 3.9 3.3 17.0 17.0

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Exhibit 26: EBITDA/mt of southern players has been generally higher in recent quarters . . .

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 27: . . . so has been the volume growth

Source: Company, Nirmal Bang Institutional Equities Research;

0

200

400

600

800

1,000

1,200

1,400

TRCL DBEL SRCM UTCEM JKCE ICEM ACEM HEIM SGC ACC JKLC PRSC MGC

Southern players exhibited higher

EBITDA/mt in 3QFY17 on account of better

(EBITDA/mt (Rs))

22.1 21.6 20.0 20.0

5.9 4.6 4.0

0.5

(1.6) (1.7)(3.7) (4.5)

(8.8) (9.2)(11.1)

-15

-10

-5

0

5

10

15

20

25

TR

CL

ICE

M

OR

CM

NT

DB

EL

MG

C

SR

CM

JKL

C

SG

C

PR

SC

UT

CE

M

HE

IM

JKC

E

AC

EM

AC

C

BC

OR

P

Volume growth (y-y %)

(YoY %)

Institutional Equities

17 Cement Sector

Exhibit 28: Lower RoE for southern companies is a result of lower capacity utilisation

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 29: ROE expected to shoot up in the coming years Exhibit 30: With a favourable demand scenario, operating profit margins to go up

Source: Crisil, Nirmal Bang Institutional Equities Research Source: Crisil, Company, Nirmal Bang Institutional Equities Research

Exhibit 31: Snapshot of the EBITDA growth Exhibit 32: Free cash flow profile looks promising for Ramco

and Dalmia

Source: Crisil, Nirmal Bang Institutional Equities Research Source: Crisil, Company, Nirmal Bang Institutional Equities Research

0

5

10

15

20

25

Shr

ee C

emen

t

Ram

co C

cem

ent

Ultr

atec

h

JK C

emen

t

JK L

aksh

mi

Cem

ent

Hei

delb

erg

Cem

ent

AC

C

Dal

mia

Cem

ent

San

ghi C

emen

t

Man

gala

m C

emen

t

KC

P L

td

Orie

nt C

emen

t

Birl

a C

orp

Am

buja

Sag

ar C

emen

t

Indi

a C

emen

t

Lower utilization levels have resulted in lower ROE for the south based companies with the exception of Ramco which has a superior EBITDA despite weak utilisations

(%)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

TRCL DBEL SGC

ROE %

FY17E FY18E FY19E

0%

5%

10%

15%

20%

25%

30%

35%

TRCL DBEL SGC

OPM%

FY17E FY18E FY19E

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

TRCL DBEL SGC

EBITDA growth %

FY17E FY18E FY19E (2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

TRCL DBEL SGC

FCF

FY17E FY18E FY19E

Institutional Equities

18 Cement Sector

Exhibit 33: Our estimate vs consensus

(Rsmn) Our estimates Consensus estimates Deviation (%)

TRCL FY18E FY19E FY18E FY19E FY18E FY19E

Sales 45,517 50,178 44,618 49,566 2.0 1.2

EBITDA 15,045 16,090 13,015 14,548 15.6 10.6

PAT 8,045 9,064 7,542 8,811 6.7 2.9

DBL FY18E FY19E FY18E FY19E FY18E FY19E

Sales 82,829 92,052 84,383 96,138 (1.8) (4.3)

EBITDA 23,519 27,682 21,283 25,106 10.5 10.3

PAT 7,141 10,327 5,341 8,204 33.7 25.9

SCL FY18E FY19E FY18E FY19E FY18E FY19E

Sales 12,041 14,539 10,790 14,173 11.6 2.6

EBITDA 1,729 2,372 1,907 2,666 (9.3) (11.0)

PAT 709 1,149 642 1,133 10.5 1.4

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

19 Cement Sector

Snapshot of key states with possible demand potential

Andhra Pradesh - Largest producer of cement in India

Andhra Pradesh (AP) is the eighth-largest state in India covering an area of about 1,63,000sqkm. On its formation in 2014, Telangana became the newest state in India, making it the 12th-largest state in the country. The states of AP and Telangana account for the country’s largest reserves of limestone. The states together are home to about 40 cement plants out of the total 209 in the country. The AP-Telangana region is also home to Nalgonda cluster- one of the seven cement clusters in India. The states have an installed capacity of 60.2mnmt (15% of India’s total cement capacity) and demand of 16.7mnmt. As a result of this, Andhra Pradesh and Telangana are cement-surplus states exporting it to other states and surrounding markets. Major urban demand within these states comes from cities like Hyderabad, Warangal, Vizag and Vijaywada.

Exhibit 34: Consistently high growth in GSDP post 2013

Source: Government websites, Nirmal Bang Institutional Equities Research

Government spending

The common theme between the budgets of these two states has been increased spending on irrigation, which augurs well for increased cement consumption. Budgetary allocation for irrigation in Andhra Pradesh has been increased by 57% from the revised estimate of 2015-16 whereas the same in case of Telangana has been increased by a massive 169%. Spending on rural development is also higher, which will help rural income and in turn boost rural demand for cement.

The gross state domestic product (GSDP) of Andhra Pradesh for 2016-17 is estimated at Rs6.03trn, which is 13.2% higher than the estimate for 2015-16. Total expenditure for 2017-18 is estimated at Rs1,570bn, a 18.3% increase over the revised estimate of 2016-17. Departments of rural development, irrigation and health welfare witnessed increase in allocation for 2016-17. On the other hand, the department of municipal administration witnessed a 21.8% decrease in allocation for 2016-17. Irrigation allocation to the department of major and minor irrigation increased 57.3% for 2017-18, over the budget estimate of 2016-17. We expect these measures to positively contribute to higher cement demand.

The GSDP of Telangana for 2016-17 is estimated at Rs5.83trn, which is 15% higher than the revised estimate for 2015-16. Total expenditure for 2016-17 is estimated at Rs1,304bn, a 30.3% increase over the revised estimate of 2015-16. A sum of Rs241.3bn is expected to be spent on irrigation in the state, which is a massive increase of 169% over 2015-16. Moreover, 0.2mn two bed-room houses are budgeted to be built for eligible poor people. Mission Bhagirath scheme to provide drinking water supply to all houses in the state has also been allocated a significant sum. All these measures are expected to prop up cement demand in the state.

Exhibit 35: Andhra Pradesh state budget highlights

Andhra Pradesh (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Total expenditure 1356.0 1327.0 (2.2) 1569.0 18.3

Revenue deficit (48.7) (46.0) - (4.2) -

Fiscal deficit (205.0) (191.6) - (230.5) -

Primary deficit (82.4) (69.6) - (82.7) -

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

1,000

2,000

3,000

4,000

5,000

6,000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Nominal GSDP (INR mn) (LHS) GSDP growth (RHS)

(Rsmn)

Institutional Equities

20 Cement Sector

Exhibit 36: Telangana state budget highlights

Telangana (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Total expenditure 1304.0 1121.0 (14.0) 1496.0 33.4

Revenue deficit 37.2 2.0 - 45.7 -

as a % of GSDP 0.6 0.0 - 0.6 -

Fiscal deficit (234.7) (218.9) - (261.0) -

as a % of GSDP (3.5) (3.4) - 3.5 -

Primary deficit (157.6) (141.9) - (149.6) -

as a % of GSDP (2.3) (2.2) - (2.0) -

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Exhibit 37: Andhra Pradesh expenditure details

Andhra Pradesh (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Capital expenditure 215.2 204.6 (4.9) 310.9 52.0

Revenue expenditure 1141.7 1123.1 (1.6) 1259.1 12.1

Total expenditure 1356.9 1327.6 (2.2) 1570.0 18.3

Debt + interest 178.1 177.6 (0.3) 227.9 28.3

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Exhibit 38: Telangana expenditure details

Telangana (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Capital expenditure 332.1 253.2 (23.8) 411.3 62.5

Revenue expenditure 972.1 868.7 (10.6) 1085.1 24.9

Total expenditure 1304.2 1121.9 (14.0) 1496.5 (33.4)

Debt + interest 108.6 108.6 0.0 158.0 45.5

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Exhibit 39: Increased allocation for irrigation, panchayat raj and rural development

Andhra Pradesh (Rsbn) Department

2016-17 budgeted

2016-17 revised

Change (%)

Comments

Rural development 114.72 145.31 26.7 Under National RURBAN Mission, six clusters (Alur, Nandalur, Cheepurupalli, Sompet, Nujendla and Chendarlapadu) have been selected. Rs5.02bn has been allocated under Pradhan Mantri Gram Sadak Yojana.

Water resources (Irrigation)

81.2 127.7 57.3 Polavaram project is estimated to receive Rs72.51bn. This is more than a 100% increase as compared to the revised estimate in 2016-17. Under the scheme NTR Jala Sri, 120,000 new bore wells have been sanctioned. Rs440mn has been allocated in this regard.

Panchayat raj 56.96 66.1 16 Rs65.62bn has been allocated for MGNREGS.

Urban development 66.61 52.07 (21.8) Rs10.61bn has been allocated for capital development operations.

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Exhibit 40: Substantial increase in spending on irrigation in Telangana

Telangana (Rsbn) Department

2016-17 revised

2017-18 budgeted

Change (%)

Comments

Irrigation 145.6 226.7 55.7 The government aims to provide irrigation to 10mn people in the state. Manair River Front Project will be implemented at an estimated cost of Rs 5.06bn. A provision of Rs1.93bn has been proposed for the project in the budget.

Social welfare 68.9 103.8 50.6

It is proposed to procure and distribute 8.4mn sheep to 4,00,000 Yadava community families in the state over the next two years. Under the scheme, it is proposed to distribute 20 female and one male sheep to each eligible family enrolled under a Sheep Development Cooperative Society at 75% subsidy.

Rural development 63.5 74.4 17.3 Rs30bn is budgeted to be spent under MNREGA.

Panchayat raj 39.91 72.8 82.4 Current projects to convert WBM roads to BT roads, and maintenance of BT roads will be continued.

Source: State budget documents; PRS India, Nirmal Bang Institutional Equities Research

Institutional Equities

21 Cement Sector

Demand-supply scenario

Andhra Pradesh and Telangana together have been the largest producers of cement in India. With the abundance of limestone, AP and Telangana have been cement-surplus states for a long time. Over the past15 years, cement capacity in these states has gone up from 6.8mnmt in 2000 to 37.8mnmt in 2016. However, capacity utilisation in the southern region as a whole has been languishing at 55.4% since FY15. We expect no major capex in Andhra Pradesh in the next three years.

Exhibit 41: AP-Telangana region is a cement-surplus region due to the presence of Nalgonda cluster

Source: CMA, Nirmal Bang Institutional Equities Research

Exhibit 42: Cement demand growth has fallen behind GDSP growth for some time now

Source: CMA, Government websites, Nirmal Bang Institutional Equities Research

Exhibit 43: Per capita cement consumption has started to pick up once again

Source: Government websites,, Nirmal Bang Institutional Equities Research

0

10

20

30

40

50

60

70

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

E

Capacity Demand

(million metric ton)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Cement demand growth Nominal GSDP growth

0

50

100

150

200

250

300

65,000,000

70,000,000

75,000,000

80,000,000

85,000,000

90,000,000

95,000,000

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

E

Population (LHS) Per capita cement (in kg) (RHS)

(kg)

Institutional Equities

22 Cement Sector

Exhibit 44: Major cement brands

Installed capacity (mt) Brand

India Cements 7.09 Coromandel King-Sankar Sakthi- Raasi Gold

Penna Cement 6.5 Penna Power, Penna Premium

UltraTech Cement 5.6 UltraTech

Jaiprakash 5 Jaypee Cement

Source: Nirmal Bang Institutional Equities Research

Tamil Nadu- Large number of players in a competitive market

In the 2017-18 budget, Tamil Nadu government has formulated five priority missions - namely, water resource management, poverty reduction, housing for poor, skill building and clean Tamil Nadu. The budget has laid down a strong foundation for cement demand in the coming financial year. The government has decided to rejuvenate Kudiramamath, a programme to maintain and manage water bodies within the state. As Tamil Nadu is a water-deficit state, the government has increased the allocation to Rs3bn in 2017-18. The government has also proposed to take over irrigation, ground water recharge and other drinking supply projects in the state through an approval of Rs2.5bn. The total allocation for the water resources department is Rs48bn, up 41% from the revised estimate of 2016-17. Under the highways department, the state has allocated a total of Rs100bn. In addition to this, the government has allotted Rs37bn for the Chennai metro rail project.

Exhibit 45: GSDP has grown consistently at a CAGR of 9% since FY06

Source: Government websites, Nirmal Bang Institutional Equities Research

Exhibit 46: Cement capacity has far exceeded the state’s demand since FY09

Source: CMA, Nirmal Bang Institutional Equities Research

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

2,000

4,000

6,000

8,000

10,000

12,000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Nominal GSDP (Rsmn) (LHS) GSDP growth (RHS)

(Rsmn)

0

5

10

15

20

25

30

35

40

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

E

Capacity Demand

(million metric ton)

Institutional Equities

23 Cement Sector

Exhibit 47: Per capita cement consumption is expected to pick up after a flattish trend

Source: Government websites, Nirmal Bang Institutional Equities Research

Exhibit 48: Cement demand growth has lagged GSDP growth for a while now

Source: Government websites, CMA, Nirmal Bang Institutional Equities Research

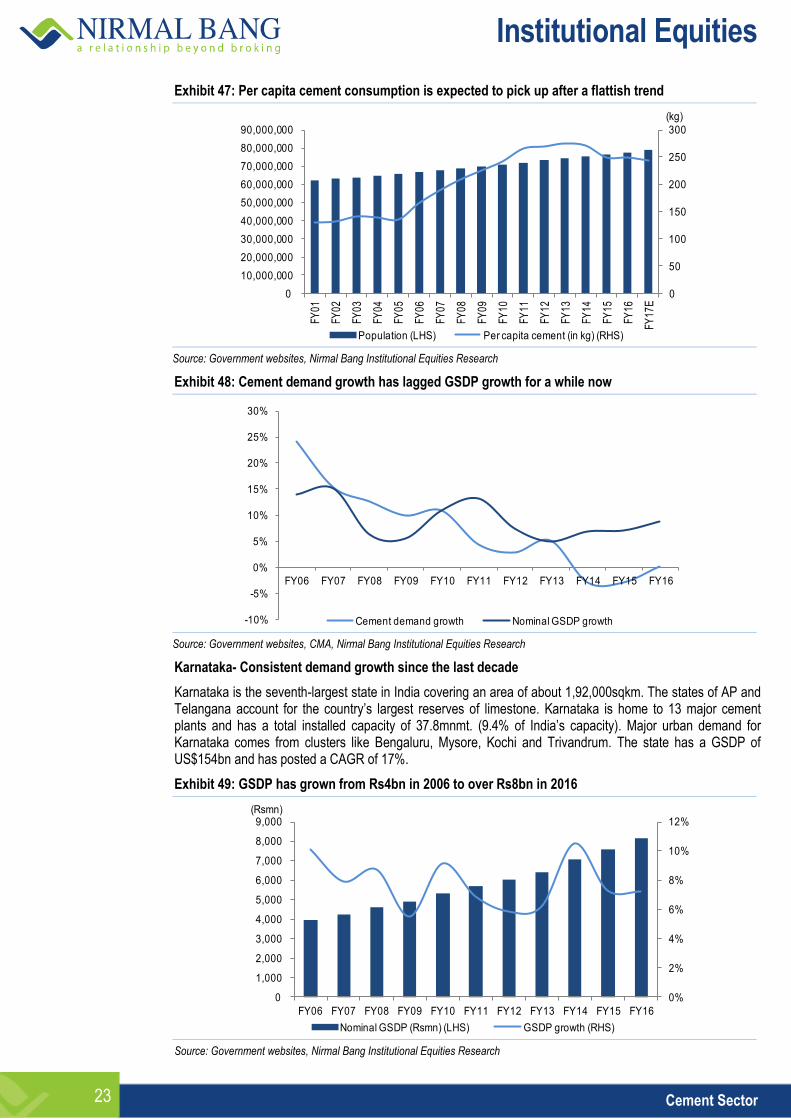

Karnataka- Consistent demand growth since the last decade

Karnataka is the seventh-largest state in India covering an area of about 1,92,000sqkm. The states of AP and Telangana account for the country’s largest reserves of limestone. Karnataka is home to 13 major cement plants and has a total installed capacity of 37.8mnmt. (9.4% of India’s capacity). Major urban demand for Karnataka comes from clusters like Bengaluru, Mysore, Kochi and Trivandrum. The state has a GSDP of US$154bn and has posted a CAGR of 17%.

Exhibit 49: GSDP has grown from Rs4bn in 2006 to over Rs8bn in 2016

Source: Government websites, Nirmal Bang Institutional Equities Research

0

50

100

150

200

250

300

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

E

Population (LHS) Per capita cement (in kg) (RHS)

(kg)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Cement demand growth Nominal GSDP growth

0%

2%

4%

6%

8%

10%

12%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Nominal GSDP (Rsmn) (LHS) GSDP growth (RHS)

(Rsmn)

Institutional Equities

24 Cement Sector

Government spending

Exhibit 50: Karnataka state budget highlights

Karnataka (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Total expenditure 1,634.0 1,644.0 0.6 1,865.0 13.4

Revenue deficit 5.2 10.6 - 1.4 -

as a % of GSDP 0.1 0.1 - 0.0 -

Fiscal deficit (256.6) (241.5) - (333.6) -

as a % of GSDP (2.3) (2.2) - (2.6) -

Primary deficit (129.9) (118.6) - (192.0) -

as a % of GSDP 1.2 (1.1) - (1.5) -

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

Exhibit 51: Karnataka expenditure details

Karnataka (Rsbn)

2016-17 budgeted

2016-17 revised

Change (%)

2017-18 budgeted

Change (%)

Capital expenditure 331.8 326.7 (1.5) 418.1 27.9

Revenue expenditure 1302.4 1318.1 1.2 1447.6 9.8

Total expenditure 1634.2 1644.8 0.6 1865.6 13.4

Debt + interest 200.5 200.8 0.2 226.9 13.0

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

Exhibit 52: Increased allocation for irrigation, urban & rural development and social welfare

Karnataka (Rsbn) Department

2016-17 budgeted

2016-17 revised

Change (%)

Comments

Irrigation 113.89 106.32 -6.6 Rs30bn is estimated to be spent on 21 different projects. This includes development of canal in the Cauvery basin at a cost of Rs5.1bn.

Urban development 110.29 105.62 -4.2 Bengaluru metro rail work for the line between Silk Board to K. R. Puram will be commenced at a cost of Rs42bn.

Rural development 127.61 127.44 -0.1 Rs22bn has been allocated for the Rural Water Supply Scheme. Rs 15.85bn will be provided for ensuring rural sanitation and creating an open defecation-free state.

Social welfare 91.1 92.58 1.6 Rs3bn has been allocated to distribute buffalo-cow or sheep/goat to 100,000 SC/ST families. Rs1bn has been allocated for LPG connections to SC/ST families living below the poverty line.

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

Exhibit 53: FY10 saw a spurt in capacity which is expected to be above demand for years to come

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

0

5

10

15

20

25

30

35

40

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

E

Capacity Demand

(million metric ton)

Institutional Equities

25 Cement Sector

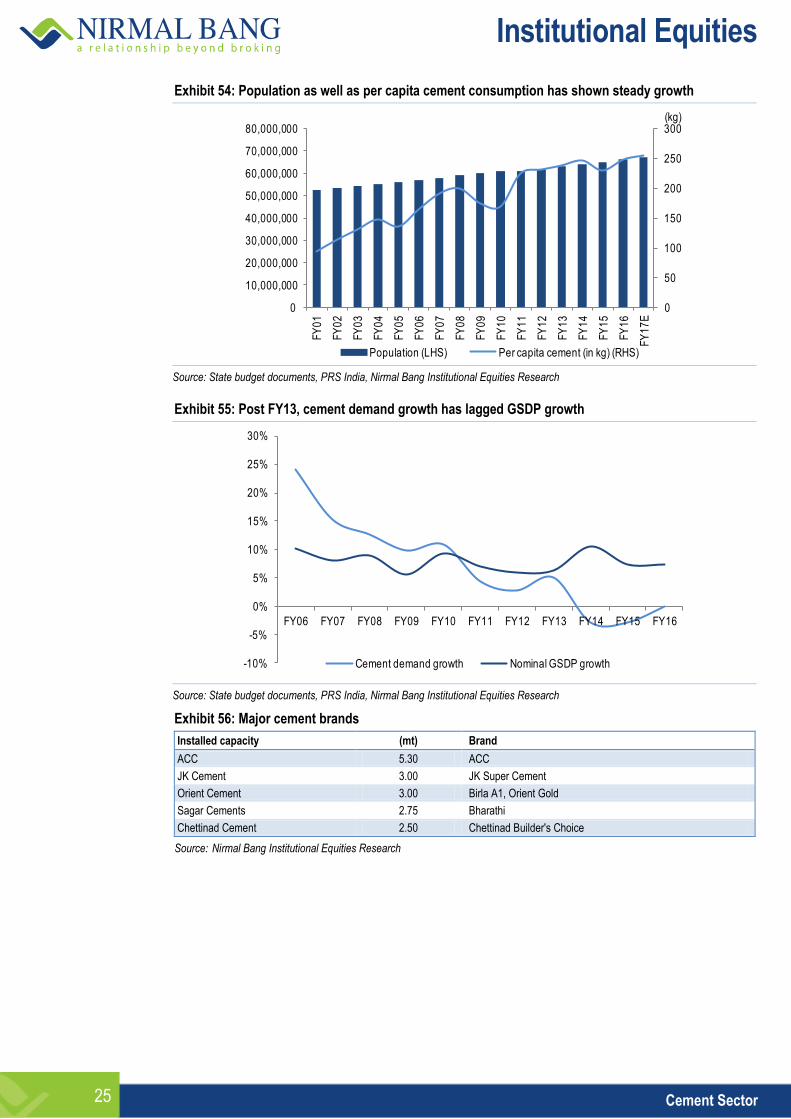

Exhibit 54: Population as well as per capita cement consumption has shown steady growth

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

Exhibit 55: Post FY13, cement demand growth has lagged GSDP growth

Source: State budget documents, PRS India, Nirmal Bang Institutional Equities Research

Exhibit 56: Major cement brands

Installed capacity (mt) Brand

ACC 5.30 ACC

JK Cement 3.00 JK Super Cement

Orient Cement 3.00 Birla A1, Orient Gold

Sagar Cements 2.75 Bharathi

Chettinad Cement 2.50 Chettinad Builder's Choice

Source: Nirmal Bang Institutional Equities Research

0

50

100

150

200

250

300

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

E

Population (LHS) Per capita cement (in kg) (RHS)

(kg)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Cement demand growth Nominal GSDP growth

Institutional Equities

26 Cement Sector

This page has been intentionally left blank

Institutional Equities

Initi

atin

g C

over

age

Reuters: DALA.BO; Bloomberg: DBEL IN

Dalmia Bharat

The Best Growth Story In Cement Space We initiate coverage on Dalmia Bharat (DBL) with a Buy rating and a target price of Rs2,806,up 17% from the current market price. DBL, according to us, is probably the best and successful growth story in the cement space in India. From a capacity of merely 1.2mnmt in FY06, DBL has been able to grow to a 25mnmt company by FY16, placing it among the top four cement companies in India. Now that a significant scale has been achieved through inorganic and organic routes, we expect the company to report much higher volume growth for the next few years along with increased market share. Apart from this, DBL has been able to achieve growth while focusing on improving efficiency as well. DBL boasts of significantly lower operating costs which help it to generate one of the highest EBITDA/mt among peers. DBL has various firsts to its credit like being the largest slag cement company in India, having one of the lowest electricity consumption patterns in the country, having one of the lowest carbon footprints in the world and a much higher cement-to-clinker ratio among peers. Given the scope for much higher volume growth, presence in regions where cement prices have been favourable and stable and completion of a major capex programme, DBL is all set to achieve superior earnings growth driven by the excellence exhibited in the past in capex as well as opex. Moreover corporate restructuring - which is on the verge of completion - will create a pure play cement company unlike a holding company in the past, which will further help shore up its financials and achieve better valuation multiples given its size. We have factored in 12.7%/20.6%/75.6% CAGR in sales, EBITDA and net profit over FY16-FY19E, respectively. We have valued DBL stock based on our usual method of the average of earnings and asset-based valuation. Our target multiples for DBL at 12.0x FY19E EV/EBITDA and US$150 FY19E EV/mt are higher than that of some pan-India players like ACC and Ambuja Cements but lower compared with UltraTech Cement. We believe that given the vast earnings potential and aggressive management approach, the higher multiples are justified. Our target price on the DBL stock is Rs2,806, up 17% from the current market price. Key risks to our call include demand slowdown in DBL’s key markets affecting the pricing and aggressive acquisition in future leading to strain on its balance sheet. Excellence in opex and capex to generate best return ratios in the industry: DBL has reduced its operating costs by 24% over the past few years on account of higher blending, increased usage of alternate fuel and higher production from its new and modern plants. The cost at which DBL has acquired capacity or has grown organically averages close to US$90/mt compared to much higher replacement cost. This trait of excellence in opex as well as capex is likely to generate much higher return ratios for DBL as its assets start operating close to their optimum capacity. Restructuring complete, pure play cement company to have much higher multiples: As DBL has grown its cement business through acquisitions right from 2006, the erstwhile corporate structure of the company had its cement business under various subsidiaries and associate companies along with other businesses not related to cement. Over the years and through a series of measures, DBL developed a much leaner structure and is now a large pure play cement company with huge operating leverage.

BUY

Sector: Cement

CMP: Rs2,406

Target Price: Rs2,806

Upside: 17%

Mangesh Bhadang Research Analyst [email protected] +91-22-3926 8172

Key Data

Current Shares O/S (mn) 89.0

Mkt Cap (Rsbn/US$mn) 214.1/3.3

52 Wk H / L (Rs) 2,422/813

Daily Vol. (3M NSE Avg.) 311,413

Share holding (%) 2QFY17 3QFY17 4QFY17

Promoter 57.4 57.3 57.8

DII+FII 13.3 13.8 13.4

Others 29.3 28.9 28.8

One -Year Indexed Stock Performance

Price Performance (%)

1 M 6 M 1 Yr

Dalmia Bharat 11.3 20.7 186.6

Nifty Index 1.3 10.5 18.4

Source: Bloomberg

Y/E March (Rsmn) FY14 FY15 FY16 FY17E FY18E FY19E

Revenues 30,158 35,141 64,380 73,140 82,829 92,052

YoY (%) 8.1 16.5 83.2 13.6 13.2 11.1

EBITDA 4,640 5,999 15,773 19,511 23,519 27,682

EBITDA (%) (26.5) 29.3 162.9 23.7 20.5 17.7

Adj. PAT (84) 30 1,908 3,800 7,141 10,327

YoY (%) - - - 99.2 87.9 44.6

EPS (Rs) (1) 0 21 43 80 116

RoE (%) 0 0 5 9 15 18

EV/EBITDA 13.73 19.3 10.9 13.9 11.2 9.2

EV/mt (US$) 53.41 73.9 105.3 167.0 162.5 156.5

P/E (x) - - 57.3 56.2 29.9 20.6

Source: Company, Nirmal Bang Institutional Equities Research

7090

110130150170190210230250270290310

May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17

DALMIA BHARAT LT Nifty 50

10 May 2017

Institutional Equities

28 Dalmia Bharat

The best growth story in the cement space

DBL is probably the best growth story in the cement space in India. From mere 1.2mnmt capacity in FY06, DBL currently has 25mnmt capacity, placing it among the top four players in the cement industry in India. DBL has pursued aggressive brownfield and greenfield /organic and inorganic capacity expansions along with focus on regions where it can attain a higher market share. Barring UltraTech Cement, none of the cement companies in India have been able to mirror the performance of DBL. While higher leverage was a cause for concern to DBL some time back, the focus on improving efficiency and controlled capital costs of acquisitions helped the company to achieve excellence in capex as well as opex.

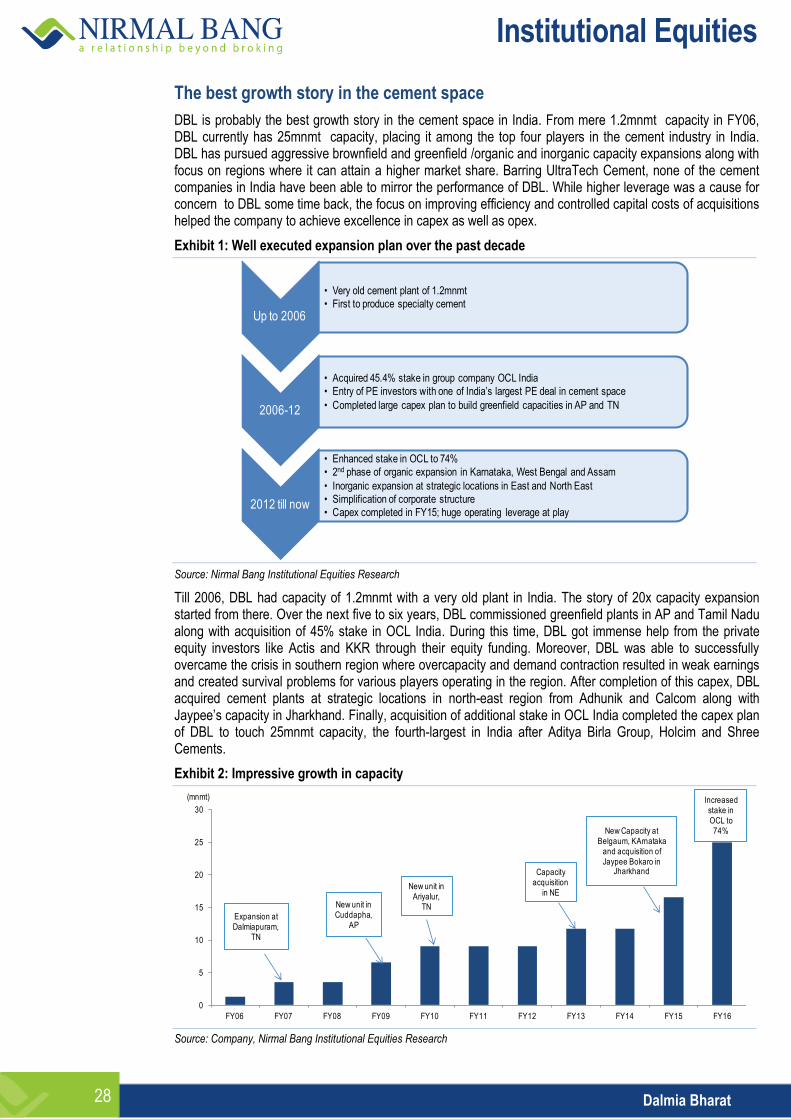

Exhibit 1: Well executed expansion plan over the past decade

Source: Nirmal Bang Institutional Equities Research

Till 2006, DBL had capacity of 1.2mnmt with a very old plant in India. The story of 20x capacity expansion started from there. Over the next five to six years, DBL commissioned greenfield plants in AP and Tamil Nadu along with acquisition of 45% stake in OCL India. During this time, DBL got immense help from the private equity investors like Actis and KKR through their equity funding. Moreover, DBL was able to successfully overcame the crisis in southern region where overcapacity and demand contraction resulted in weak earnings and created survival problems for various players operating in the region. After completion of this capex, DBL acquired cement plants at strategic locations in north-east region from Adhunik and Calcom along with Jaypee’s capacity in Jharkhand. Finally, acquisition of additional stake in OCL India completed the capex plan of DBL to touch 25mnmt capacity, the fourth-largest in India after Aditya Birla Group, Holcim and Shree Cements.

Exhibit 2: Impressive growth in capacity

Source: Company, Nirmal Bang Institutional Equities Research

Up to 2006

• Very old cement plant of 1.2mnmt

• First to produce specialty cement

2006-12

• Acquired 45.4% stake in group company OCL India

• Entry of PE investors with one of India’s largest PE deal in cement space

• Completed large capex plan to build greenfield capacities in AP and TN

2012 till now

• Enhanced stake in OCL to 74%

• 2nd phase of organic expansion in Karnataka, West Bengal and Assam

• Inorganic expansion at strategic locations in East and North East

• Simplification of corporate structure

• Capex completed in FY15; huge operating leverage at play

0

5

10

15

20

25

30

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Expansion at Dalmiapuram,

TN

New unit in Cuddapha,

AP

New unit in Ariyalur,

TN

Capacity acquisition

in NE

New Capacity atBelgaum, KArnataka

and acquisition of Jaypee Bokaro in

Jharkhand

Increased stake in OCL to74%

(mnmt)

Institutional Equities

29 Dalmia Bharat

Excellence in both opex and capex

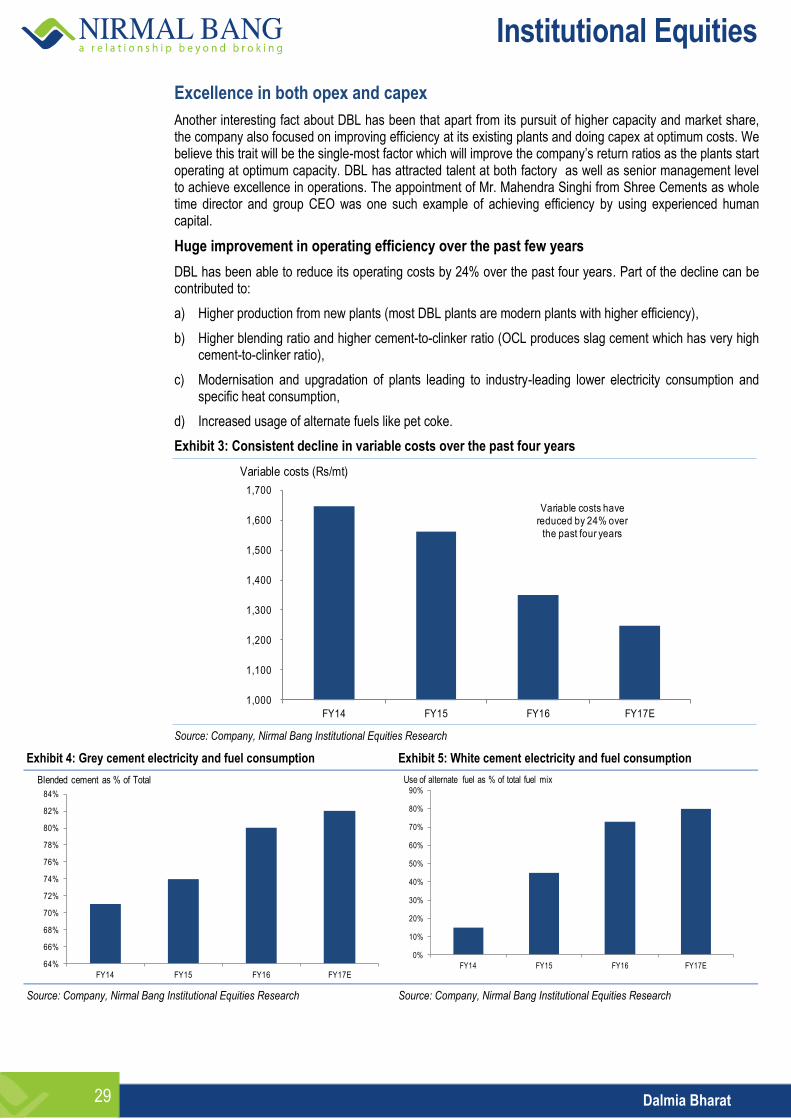

Another interesting fact about DBL has been that apart from its pursuit of higher capacity and market share, the company also focused on improving efficiency at its existing plants and doing capex at optimum costs. We believe this trait will be the single-most factor which will improve the company’s return ratios as the plants start operating at optimum capacity. DBL has attracted talent at both factory as well as senior management level to achieve excellence in operations. The appointment of Mr. Mahendra Singhi from Shree Cements as whole time director and group CEO was one such example of achieving efficiency by using experienced human capital.

Huge improvement in operating efficiency over the past few years

DBL has been able to reduce its operating costs by 24% over the past four years. Part of the decline can be contributed to:

a) Higher production from new plants (most DBL plants are modern plants with higher efficiency),

b) Higher blending ratio and higher cement-to-clinker ratio (OCL produces slag cement which has very high cement-to-clinker ratio),

c) Modernisation and upgradation of plants leading to industry-leading lower electricity consumption and specific heat consumption,

d) Increased usage of alternate fuels like pet coke.

Exhibit 3: Consistent decline in variable costs over the past four years

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 4: Grey cement electricity and fuel consumption Exhibit 5: White cement electricity and fuel consumption

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

FY14 FY15 FY16 FY17E

Variable costs (Rs/mt)

Variable costs have reduced by 24% over

the past four years

64%

66%

68%

70%

72%

74%

76%

78%

80%

82%

84%

FY14 FY15 FY16 FY17E

Blended cement as % of Total

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

FY14 FY15 FY16 FY17E

Use of alternate fuel as % of total fuel mix

Institutional Equities

30 Dalmia Bharat