BMI Kazakhstan Agribusiness Report Q4 2013

104

Q4 2013 www.businessmonitor.com KAZAKHSTAN AGRIBUSINESS REPORT INCLUDES 5-YEAR FORECASTS TO 2017 ISSN 2044-5717 Published by:Business Monitor International

Transcript of BMI Kazakhstan Agribusiness Report Q4 2013

Q4 2013www.businessmonitor.com

KAZAKHSTANAGRIBUSINESS REPORTINCLUDES 5-YEAR FORECASTS TO 2017

ISSN 2044-5717Published by:Business Monitor International

Kazakhstan Agribusiness ReportQ4 2013INCLUDES 5-YEAR FORECASTS TO 2017

Part of BMI’s Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: August 2013

Business Monitor InternationalSenator House85 Queen Victoria StreetLondonEC4V 4ABUnited KingdomTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.businessmonitor.com

© 2013 Business Monitor InternationalAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind asto the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View ............................................................................................................... 7

SWOT .................................................................................................................................. 10Agribusiness ........................................................................................................................................... 10

Industry Forecast .............................................................................................................. 12Dairy Outlook ......................................................................................................................................... 12

Table: Kazakhstan Milk Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table: Kazakhstan Cheese Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table: Kazakhstan Butter Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table: Kazakhstan Milk Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Table: Kazakhstan Cheese Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Table: Kazakhstan Butter Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Livestock Outlook .................................................................................................................................... 16Table: Kazakhstan Poultry Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Table: Kazakhstan Pork Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Table: Kazakhstan Beef & Veal Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Table: Kazakhstan Poultry Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Table: Kazakhstan Pork Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Table: Kazakhstan Beef & Veal Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Grains Outlook ....................................................................................................................................... 22Table: Kazakhstan Wheat Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Table: Kazakhstan Corn Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Table: Kazakhstan Barley Production & Consumption, 2012-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Table: Kazakhstan Wheat Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Table: Kazakhstan Corn Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Table: Kazakstan Barley Production & Consumption, 2007-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Commodities Price Analysis ............................................................................................. 31Monthly Grains Strategy ........................................................................................................................... 31

Table: Select Commodities - Performance & BMI Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Table: BMI Commodities Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Monthly Softs Strategy .............................................................................................................................. 41Table: Select Commodities - Performance & BMI Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Table: BMI Commodities Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Upstream Analysis ............................................................................................................ 51Europe GM Outlook ................................................................................................................................. 51

Europe Machinery Outlook ........................................................................................................................ 56

Europe Fertiliser Outlook ......................................................................................................................... 63

Downstream Analysis ....................................................................................................... 69Food ..................................................................................................................................................... 69

Food Consumption ................................................................................................................................. 69

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 4

Table: Food Consumption Indicators Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Canned Food ........................................................................................................................................ 71Table: Canned Food Value/Volume Sales Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Confectionery ........................................................................................................................................ 72Table: Confectionery Volume/Value Sales Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Processed Foods .................................................................................................................................... 75Table: Processed Meat Volume Sales, Production And Trade Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

Table: Frozen Fruits and Vegetables Volume Sales, Production And Trade Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

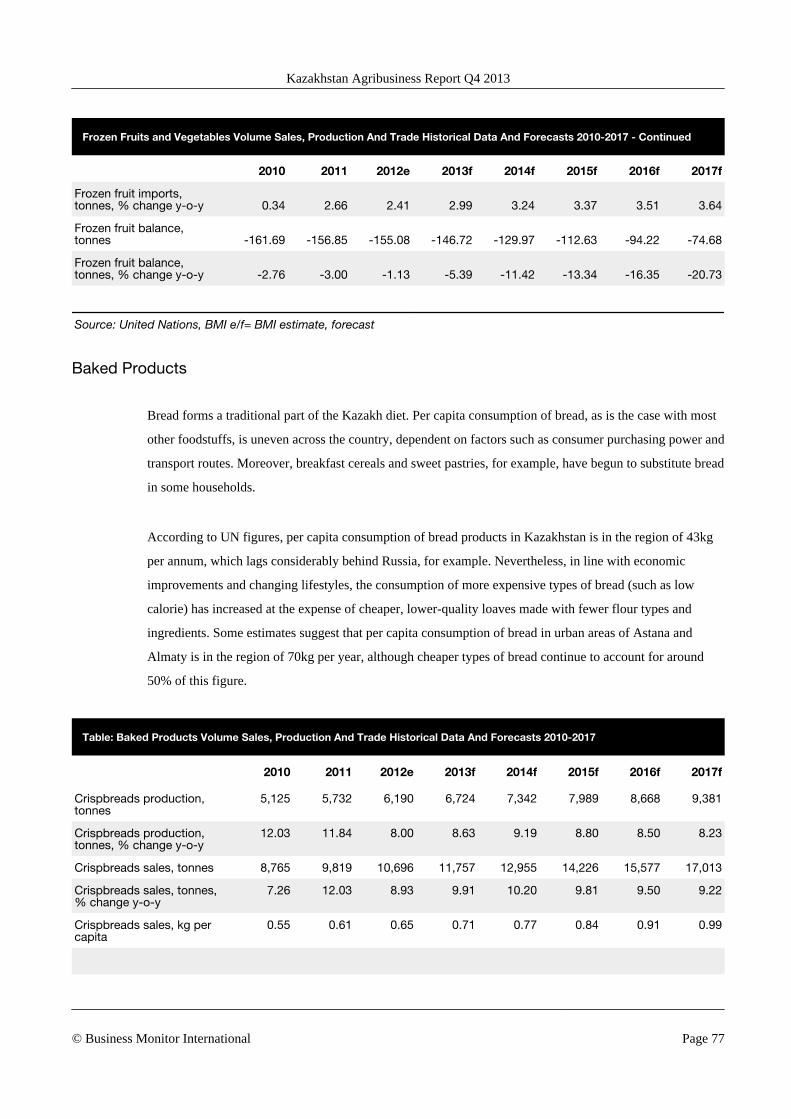

Baked Products ..................................................................................................................................... 77Table: Baked Products Volume Sales, Production And Trade Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Pasta ................................................................................................................................................... 78Table: Pasta Volume Sales, Production And Trade Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

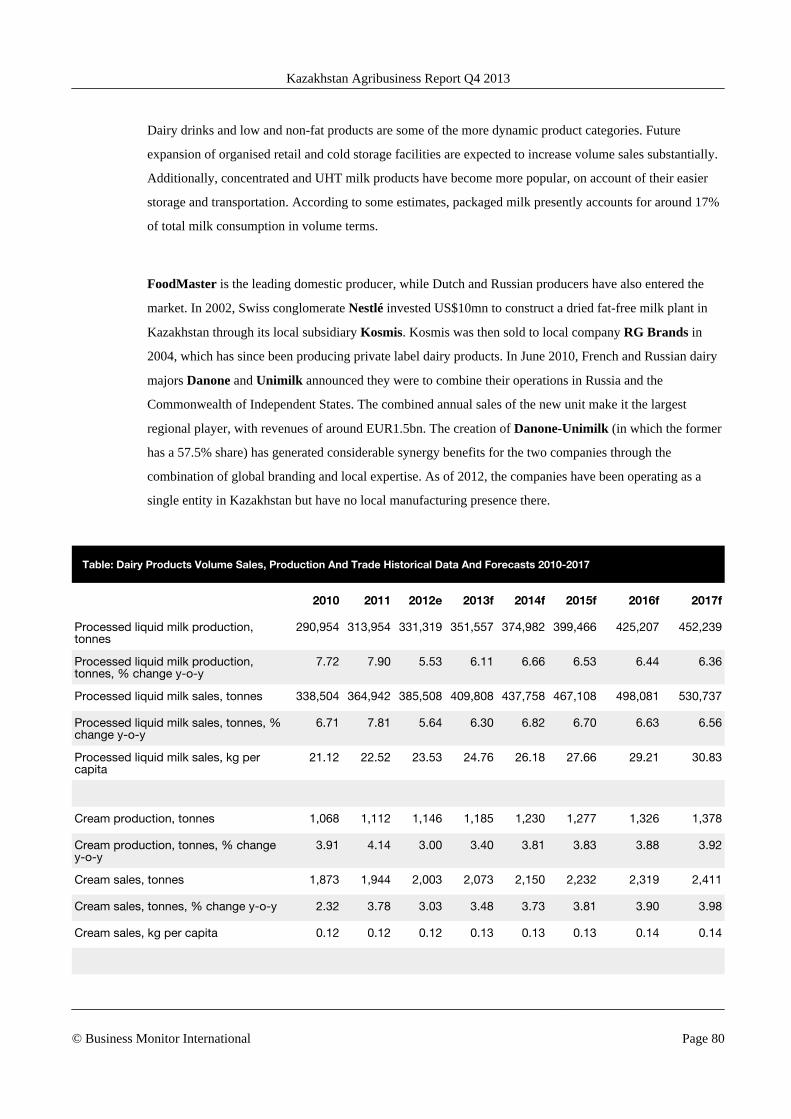

Dairy ................................................................................................................................................... 79Table: Dairy Products Volume Sales, Production And Trade Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Drink .................................................................................................................................................... 82

Alcoholic Drinks ................................................................................................................................... 82Table: Alcoholic Drinks Volume/Value Sales Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

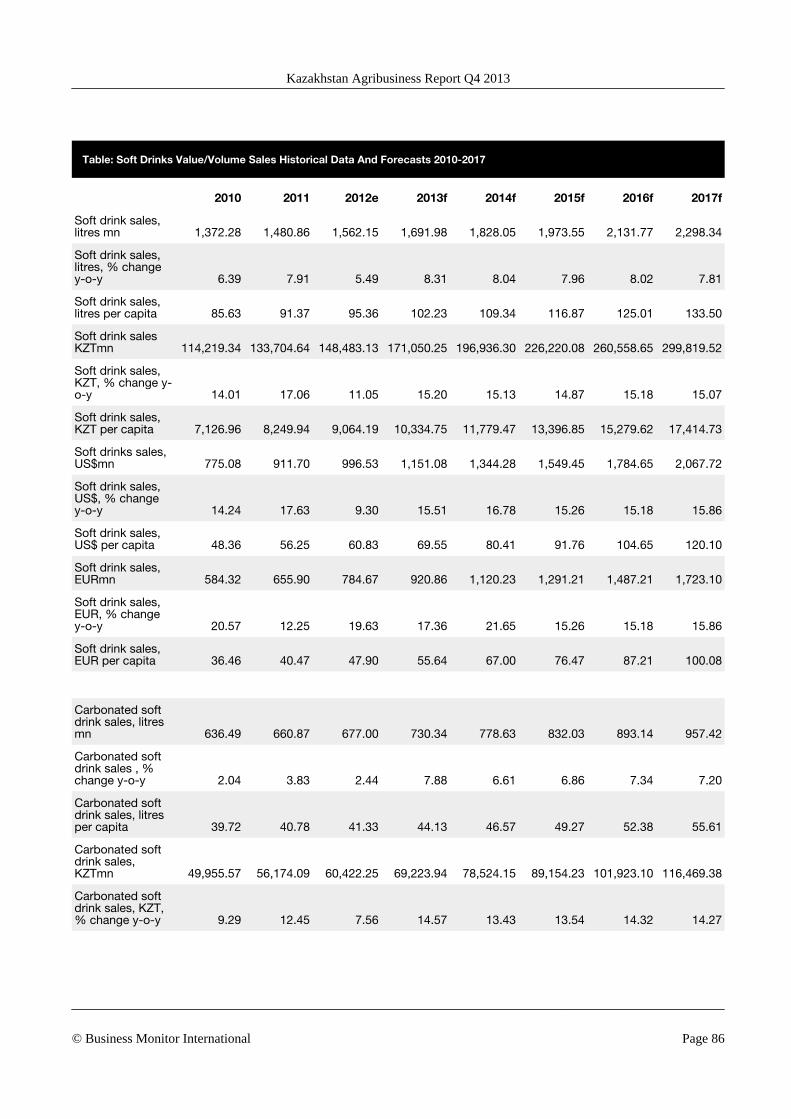

Soft Drinks .......................................................................................................................................... 85Table: Soft Drinks Value/Volume Sales Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

Hot Drinks ............................................................................................................................................ 89Table: Hot Drinks Volume/Value Sales Historical Data And Forecasts 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

Mass Grocery Retail ................................................................................................................................ 90

Regional Overview ............................................................................................................ 92Regional Overview - Europe ...................................................................................................................... 92

Table: EU Farm Size Statistics In 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Demographic Forecast ..................................................................................................... 98Table: Kazakhstan's Population By Age Group, 1990-2020 ('000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

Table: Kazakhstan's Population By Age Group, 1990-2020 (% of total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

Table: Kazakhstan's Key Population Ratios, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Table: Kazakhstan's Rural And Urban Population, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Methodology .................................................................................................................... 102

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 5

BMI Industry View

BMI View: We expect the Kazakh grain sector to outperform, especially as Kazakhstan sees more export

opportunities to Central Asia and China. We expect limited growth for the livestock and dairy sectors, as

export potential for both industries will remain limited. Only domestic demand, which we expect to be

strong, could partially encourage domestic production. That said, cheap imports from Russia could put

local growers at a disadvantage. We have not identified any major public company operating in the sector

that we would highlight.

Grains Taking Their Share

Kazakhstan - BMI Market Value By Commodity (% of total)

Note: The BMI Market Value is an addition of all domestically produced commodities' value (calculated

by multiplying the production with the international benchmark prices, converted in US$/tonne); f = forecast.

Source: BMI.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 7

Key Forecasts

■ Wheat production to 2016/17: -23.7% to 17.4mn tonnes. Efforts to diversify into oilseeds and otherfield crops and little potential for a repeat of the perfect conditions of 2011/12 will see production fallover our five-year forecast period.

■ Cheese consumption growth to 2017: 51.5% to 81,300 tonnes. This will come from increased demandfor value-added dairy products on the back of accelerating urbanisation and improvements ininfrastructure.

■ Beef production growth to 2016/17: 35.7% to 576,700 tonnes. The comprehensive overhaul of the beefherd continues apace as imported breeding stocks improve quality.

■ 2013 real GDP growth: 5.4%, up from 5.0% in 2012.

■ 2013 average consumer price inflation: 6.2% year-on-year (y-o-y), up from 5.1% y-o-y in 2012.

■ BMI universe agribusiness market value: 35.5% y-o-y decrease to US$6.9bn in 2012/13, forecast togrow on average 9.8% annually between 2011/12 and 2016/17.

Key Revisions To Our Forecasts

■ 2013/14 wheat production revised up from 16.0mn tonnes to 17.0mn tonnes on the back of the latestofficial estimates.

■ 2014 wheat consumption revised up from 6.9mn tonnes to 7.2mn tonnes as lower prices boost localdemand.

■ 2012/13 poultry production revised up from 120,000 tonnes to 125,000 tonnes as the impact of highergrain prices seems to be wearing off.

■ 2012/13 pork production revised down from 231,000 tonnes to 215,000 tonnes owing to lowerpreference among the local population and subdued prospects for exports in the short term.

■ 2012/13 poultry consumption revised up from 369,000 tonnes to 379,500 tonnes because of localpreference for the meat and its price competitiveness compared with other meats.

Industry Outlook

We believe Black Sea countries will see increased grain demand from Asia in the coming years after the

region was largely ignored for at least the past three seasons. Disappointing harvests in Asian countries'

traditional suppliers, mainly the US, Australia and India, partially account for this. In addition, rising middle

classes and changing dietary habits are increasingly putting strains on the region's grain production balance;

this will force Asian importers to look for increased volumes and lower prices for grain purchases in the

medium term.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 8

We believe Kazakhstan has the potential to improve the quality and efficiency of its meat output via a

strong increase in cattle imports. This supports our forecast for beef production to grow by 35.7% out to the

end of our forecast period, to 576,720 tonnes in 2017. In 2011, the Ministry of Agriculture announced a

plan for 'the development of beef export potential for Kazakhstan' to be implemented in two phases. The

first phase, covering 2011-2015, targets the rapid expansion of the number of high-yielding breeding cattle

in Kazakhstan. The second phase, from 2016-2020, would push for the development of beef export

potential.

The Board of the Eurasian Economic Commission has increased custom duties on several dairy products in

order to protect domestic dairy producers against cheap competition in a context of high domestic feed and

strong demand. The duties were raised on butter, cottage cheese and dairy spreads from 15% to 20%. For

other types of dairy products, such as grated and powdered cheese, including Schabziger, duties were raised

to 20%. Import duties on feta cheese made from cow milk were taken to 25% of their customs value

(against 15% currently).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 9

SWOT

Agribusiness

SWOT Analysis

Strengths ■ Kazakhstan has fertile soil and a strong agricultural tradition.

■ More than 70% of Kazakhstan's land area is occupied by agricultural crops and

animal husbandry.

■ The recent efforts from the government to develop the industry will very likely help to

boost production over the long term.

Weaknesses ■ Decades of collective and state farming with little incentive to maximise production

have left Kazakhstan's agriculture with poor yields by international standards.

■ Aging Soviet-era infrastructure increases costs and makes expansion into new areas

difficult.

■ Many farmers lack the skills to run a profitable business without government aid.

• Because the country is land-locked and transportation infrastructure is lacking,

shipping costs for grains to the export market make the crop uncompetitive

compared with other Black Sea region producers such as Russia and Ukraine.

Opportunities ■ Poor yields leave much room for increasing production through better farming

practices.

■ The government has invested heavily in the development of large and efficient

corporate farms, creating greater opportunity for further expansion.

■ Rising disposable incomes will enable domestic demand for food products to pick up.

• Because of recently tight grains markets by historical standards, export demand is

likely to be sufficient to encourage production growth in Kazakhstan.

Threats ■ The global recession hit Kazakhstan hard. We estimate GDP growth was only 1.2% in

2009, accompanied by a rapid fall in consumer expenditure. While GDP growth has

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 10

SWOT Analysis - Continued

since recovered, the eurozone crisis could continue to constrain the country's growth

and thus consumer demand.

■ The rural population is declining rapidly, with many young people heading for the

cities.

• Much of the country suffered from environmental degradation in Soviet times; if not

dealt with, this could threaten agricultural production in the future.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 11

Industry Forecast

Dairy Outlook

BMI Supply View: We forecast a 1.4% year-on-year (y-o-y) decline in milk production in 2012/13 to

4.9mn tonnes. This fall in production reflects damage to pastures due to the severe drought in summer 2012.

In the medium term, the country's output growth is likely to be limited, as 90% of dairy production comes

from the household sector, with most output for home consumption. Over the longer term, however, we are

positive about the government's recent plan for the development of large-scale modern dairy farms and its

significant investment in machinery for these farms. Therefore, we see plenty of room for growth coming

from the commercialisation of the sector and forecast milk production to rise 23.9% on the 2011/12 level to

6.1mn tonnes by 2016/17.

Less than 40% of milk produced in Kazakhstan is processed in formal dairy plants. This is because of the

uneven availability of fresh milk between summer and winter, the high cost of transportation, as well as the

poor quality of the milk produced in the country. Therefore, we maintain our view for cheese and butter

production to be subdued over our forecast period. We forecast cheese and butter production to come in at

24,090 and 18,060 tonnes respectively in 2012/13, reflecting increases of 9.0% and 14.0% y-o-y. Out to

2016/17, we expect cheese and butter production to remain low, at 30,600 and 23,650 tonnes respectively.

BMI Demand View: In 2013, we expect fluid milk consumption growth of 3.6% y-o-y to 4.9mn tonnes.

Even if demand is lower than domestic production, we see room for some imports because of the low

quality of domestic milk and the potential for spoilage. Out to 2017, we forecast milk consumption to grow

19.6% to 5.7mn tonnes, as a boost in production is likely to continue to increase milk demand.

However, we expect most dairy sector consumption growth to come from increased demand for processed

and higher-value dairy goods. This trend will be especially evident outside of Kazakhstan's major urban

centres, where underdeveloped infrastructure has to date impeded the distribution of perishable dairy items.

In line with this, we forecast cheese and butter consumption to grow 51.5% and 65.6% respectively to 2017.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 12

Table: Kazakhstan Milk Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Milk Production, '000 tonnes 2 4,919.2 4,850.2 5,303.9 5,554.9 5,815.9 6,096.9

Liquid Milk Consumption, '000 tonnes 1,3 4,761.6 4,930.5 5,136.2 5,339.1 5,526.0 5,694.5

Notes: e BMI estimates. f BMI forecasts. 1 Based on food supply data; estimated after 2005. Sources: 2 The Agency ofStatistics of the Republic of Kazakhstan, BMI; 3 FAO.

Table: Kazakhstan Cheese Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Cheese Production, '000 tonnes 1 22.1 24.1 25.8 27.3 29.0 30.6

Cheese Consumption, '000 tonnes 2 53.0 58.4 63.7 69.2 75.1 81.3

Notes: e BMI estimates. f BMI forecasts. Sources: 1 UN Industrial Commodity Statistics Database; 2 UN IndustrialCommodity Statistics Database, UN Comtrade, BMI calculation.

Table: Kazakhstan Butter Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Butter Production, '000 tonnes 1 15.8 18.1 20.2 22.7 24.9 23.7

Butter Consumption, '000 tonnes 2 38.3 43.0 47.9 53.0 58.5 64.3

Notes: e BMI estimates. f BMI forecasts. Sources: 1 UN Industrial Commodity Statistics Database; 2 UN IndustrialCommodity Statistics Database, UN Comtrade, BMI calculation.

More Protectionist Measures To Aid Competitiveness Of Sector

The Board of the Eurasian Economic Commission (EEC) announced recently it would increase custom

duties on several dairy products in order to protect domestic dairy producers against cheap competition in a

context of high domestic feed and strong demand. The duties were raised on butter, cottage cheese and dairy

spreads from 15% to 20%. For other types of dairy products, such as grated and powdered cheese, including

Schabziger, duties were raised to 20%. Import duties on feta cheese made from cow milk were taken to 25%

of their customs value (against 15% currently).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 13

The EEC was established upon the decision of the presidents of Russia, Belarus and Kazakhstan at the end

of 2011. It is a single permanent regulating body of the Customs Union and the Single Economic Space. We

believe the recent restrictions in dairy imports were linked to difficult operating environment for dairy

producers in all three countries and the aim to protect them against foreign competition, especially from

Western Europe. All three markets are not concentrated and particularly vulnerable to shocks, such as

soaring input costs in 2012.

Investment To Boost Production In Spite Of Remaining Challenges

The Kazakh government has announced that it wants to invest US$1.5bn in milk and meat production in the

coming years in order to address major challenges facing both sectors. After the dissolution of the Soviet

Union, Kazakhstan lost its major export markets for dairy products, which resulted in milk production

plummeting by 40.0% in four years. This also drastically cut herds; levels have not yet regained their 1992

levels.

Kazakhstan's dairy sector is inefficient and uncompetitive, which makes it unlikely to find other export

markets of the size of the former Soviet Union. The quality of milk is poor, and agricultural workers'

productivity is very low. This is partly because small farms account for 90% of production, and because

most of the output is directed at household consumption. Historically, there has been little incentive for

production to increase beyond that level, especially as levels of government support to the sector have been

very low.

Foot-And-Mouth A Constant Threat

In 2011, Kazakhstan was hit by a number of foot-and-mouth disease (FMD) outbreaks, showing that the

disease continues to pose a serious risk to the country's dairy and beef industries. The country was affected

by three consecutive disease outbreaks in two villages in Uralsk in north-west Kazakhstan and in the village

of Kurchumskiy in eastern Kazakhstan. That incident resulted in the destruction of 69 animals. While all

three outbreaks were contained, there remains the possibility of a wider epidemic, and we see this as posing

downside risk to our forecasts through our outlook period.

Throughout the summer of 2012, cases were reported in the east of the country. Out of 1,040 susceptible

cattle, 721 cases were reported. All affected animals were destroyed. The source of the outbreak has yet to

be determined.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 14

In June 2013, more cases were reported in the east of the country. According to the World Organisation for

Animal Health, a total of 2111 cattle were found susceptible to the FMD virus (serotype A), out of which 50

cases were reported. A total of 901 animals were destroyed.

Table: Kazakhstan Milk Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Milk Production, '000 tonnes 2 5,073.2 5,198.0 5,303.0 5,381.0 5,235.0 4,919.2

Liquid Milk Consumption, '000 tonnes 1,3 3,978.7 4,165.0 4,233.1 4,491.1 4,612.8 4,761.6

Notes: e BMI estimates. 1 Based on food supply data; estimated after 2005. Sources: 2 The Agency of Statistics of theRepublic of Kazakhstan, BMI; 3 FAO.

Table: Kazakhstan Cheese Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Cheese Production, '000 tonnes 1 19.4 17.7 18.1 18.8 20.0 22.1

Cheese Consumption, '000 tonnes 2 36.4 39.0 40.5 45.5 49.6 53.0

Notes: e BMI estimates. Sources: 1 UN Industrial Commodity Statistics Database; 2 UN Industrial Commodity StatisticsDatabase, UN Comtrade, BMI calculation.

Table: Kazakhstan Butter Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Butter Production, '000 tonnes 1 19.7 16.6 15.3 14.0 14.6 15.8

Butter Consumption, '000 tonnes 2 27.0 23.3 24.8 31.5 35.3 38.3

Notes: e BMI estimates. Sources: 1 UN Industrial Commodity Statistics Database; 2 UN Industrial Commodity StatisticsDatabase, UN Comtrade, BMI calculation.

Risks To Outlook

We see upside risks to our Kazakh fluid milk production forecasts. Our current growth projections assume a

similar level of commercialisation over the next five years as has occurred over our review period.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 15

However, a wider government push towards improved food security, coupled with increased private sector

investment in agriculture, could see this rate of commercialisation accelerate. This would translate into

greater efficiencies and higher output quality and could see our currently reasonably modest milk

production growth forecasts surpassed.

Another outbreak of foot-and-mouth disease hit Kazakh dairy herds again in 2013. It has been contained so

far. We see the possibility of a wider outbreak posing downside risk to our milk production forecasts.

Livestock Outlook

BMI Supply View: We have revised up our 2012/13 forecast for poultry production to 125,000 tonnes

(from 120,000 tonnes previously). Over the forecast period, poultry is expected to be the outperformer of

the livestock sector, with output increasing by 69.2% to reach 203,000 tonnes by 2016/17. The

government's subsidy programme, combined with an import tariff system and financial support for new

enterprises, will underpin this growth. We also highlight renewed private sector interest in the sector, which

is likely to enhance efficiency and quality of the industry over the medium term. The sector nevertheless

faces challenges, notably rising feed prices and a lack of expertise.

We have revised down our forecast for 2012/13 pork production and now expect output to stagnate at

215,000 tonnes. Similarly, beef production is projected to stagnate at 425,000 tonnes in 2012/13. Over our

forecast period, all sectors of Kazakhstan's livestock industry are forecast to experience solid growth.

Government investment, including initiatives to improve livestock farming standards and encourage greater

industry participation, is part of a wider plan to improve the country's food self-sufficiency. With meat

representing a large part of the traditional Kazakh diet, the livestock industry is set to be a major

beneficiary. A government drive to improve the country's bovine genetics by importing stock from the US

is likely to have a fairly powerful effect on beef production, helping it to expand by 35.7% over our forecast

period, reaching 576,700 tonnes in 2016/17.

BMI Demand View: As with production, demand across all Kazakh livestock sectors will be robust,

although poultry is set to be the outperformer. To 2017, poultry demand is forecast to increase by 43.6%,

while consumption of pork and beef will increase by 29.1% and 17.2% respectively. The outperformance of

poultry will be a product of its lower starting point - it is not as widely consumed as pork or beef - but will

also be a result of the increased presence of imported processed poultry goods on the local market. More

generally, livestock consumption will benefit from strong domestic production increases, which will help to

improve product affordability, as well as from Kazakhstan's healthy forecast economic growth outlook,

which will increase demand for processed livestock products.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 16

Table: Kazakhstan Poultry Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Poultry Production, '000 tonnes 1 120.0 125.0 125.0 146.0 171.0 203.0

Poultry Consumption, '000 tonnes 2 345.0 379.5 405.7 433.7 463.6 495.6

Notes: e BMI estimates. f BMI forecasts. Sources: 1 Official Statistics of Kazakhstan, USDA; 2 USDA.

Table: Kazakhstan Pork Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Pork Production, '000 tonnes 1 215.0 215.0 237.9 244.5 251.1 257.7

Pork Consumption, '000 tonnes 2 231.0 243.0 258.4 272.9 286.3 298.2

Notes: e BMI estimates. f BMI forecasts. Sources: 1 Official Statistics of Kazakhstan, USDA; 2 USDA.

Table: Kazakhstan Beef & Veal Production & Consumption, 2012-2017

2012e 2013f 2014f 2015f 2016f 2017f

Beef & Veal Production, '000 tonnes 1 425.0 425.0 450.0 508.6 542.6 576.7

Beef & Veal Consumption, '000 tonnes 454.0 454.0 474.9 495.0 514.1 531.9

Notes: e BMI estimates. f BMI forecasts. Sources: 1 Official Statistics of Kazakhstan, USDA.

Support To Beef Sector To Aid Export Capacity

We believe Kazakhstan has the potential to improve the quality and efficiency of its meat output via a

strong increase in cattle imports. This supports our forecast for beef production to grow by 35.7% out to the

end of our forecast period, to 576,720 tonnes in 2017. In 2011, the Ministry of Agriculture announced a

plan for 'the development of beef export potential for Kazakhstan' to be implemented in two phases. The

first phase, covering 2011-2015, targets the rapid expansion of the number of high-yielding breeding cattle

in Kazakhstan. The second phase, from 2016-2020, would push for the development of beef export

potential.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 17

Recovering Slowly

Kazakhstan - Cattle Numbers ('000 head)

Source: Kazakhstan Statistics Agency

The strategy has been so far a success, as it has encouraged a boom in import demand for better-quality

cattle. Cattle imports into Kazakhstan climbed from just 1,556 head in 2009 (worth US$6mn) to more than

16,713 head in 2012 (worth US$66mn). In 2012, Kazakhstan imported mostly from the United States and

the EU, while Canada and Australia took a smaller share of the country's purchases. Most of the imports

were of beef breeds (primarily Angus).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 18

Booming Imports

Kazakhstan - Cattle Imports (head)

Source: Kazakhstan Customs, USDA

We expect these trends to accelerate further in the coming years, as the Kazakh government announced in

February that large-scale subsidised imports of cattle will continue. The goal is to develop the country's

herds back to the level seen at the start of the 1990s, when the country still had the capacity to export beef.

For 2013, an import target of 21,000 head of cattle has been set. This compares with 16,713 imported in

2012, and 13,892 imported in 2011. In addition to cattle imports, the plan also outlines goals for increased

use of semen for in vitro fertilisation and increased use of transplanted bovine embryos. The subsidy for

breeding cattle was set at KZT235,000 (US$1,555) for cattle from Australia or North and South America,

and KZT154,000 (US$1,020) for cattle from Europe.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 19

Looking For US Heifers

Kazakhstan - Cattle Imports By Country (LHS) & Type (% of total, RHS)

Source: Kazakhstan Ministry of Agriculture, USDA

Government support, combined with renewed private interest in the sector, underpins our forecast for the

country's beef production deficit to narrow over the coming years and turn into a small surplus out to 2017.

That said, we still believe the government is being too optimistic in expecting a return to 1990s production

levels by 2020. We forecast beef production to reach 576,720 tonnes in 2017; the country produced

600,000-700,000 tonnes in the early 1990s, which allowed steady exports every year. We would revise up

our forecasts if we see clear signs that the country's booming cattle imports and improvements in

genetics aid production capacity over the medium term. Also, we would need to see better quality and safety

standards in place if the country wants to be a reliable export source for some markets.

Private Sector Interest Highlights Strong Growth Potential

In the Kazakh poultry sector, we believe the recent US$108mn investment by Israeli technology provider

MAD Corporation to build five large poultry farms in the north of the country will unleash growth

potential in the sector. This is in addition to strong government support for the industry. Even though the

sector has benefited from large feed subsidy programmes, poultry production is still hampered by a lack of

breeding material as well as the vulnerability of animals to disease, as well as the lack of high-quality

vaccines to treat them. We expect the project to improve poultry farming technology and quality. We also

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 20

believe these types of projects could attract other private companies to the country, boosting private

investment in the sector in the medium term.

As a result of these developments, we have revised up our forecasts for poultry production in Kazakhstan

out to 2016/17. We now forecast output to reach 203,000 tonnes out to 2016/17, as experts project annual

production of 50,000-70,000 tonnes from the new projects, with full capacity reached in four years.

Table: Kazakhstan Poultry Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Poultry Production, '000 tonnes 1 65.0 75.0 90.0 101.0 100.0 120.0

Poultry Consumption, '000 tonnes 2 209.0 206.0 199.0 225.0 278.0 345.0

Notes: e BMI estimates. Sources: 1 Official Statistics of Kazakhstan, USDA; 2 USDA.

Table: Kazakhstan Pork Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Pork Production, '000 tonnes 1 194.0 206.0 209.0 206.0 214.0 215.0

Pork Consumption, '000 tonnes 2 207.0 215.0 220.0 216.0 225.0 231.0

Notes: e BMI estimates. Sources: 1 Official Statistics of Kazakhstan, USDA; 2 USDA.

Table: Kazakhstan Beef & Veal Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012e

Beef & Veal Production, '000 tonnes 1 370.0 384.0 400.0 407.0 415.0 425.0

Beef & Veal Consumption, '000 tonnes 414.0 419.0 411.0 422.0 433.0 454.0

Notes: e BMI estimates. Sources: 1 Official Statistics of Kazakhstan, USDA.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 21

Risks To Outlook

The key risks to our outlook relate to production and are weighted to the downside. If oil prices remain

subdued, we expect ongoing government investment in economic diversification. Agriculture and livestock

are likely to be key beneficiaries of this diversification owing to the secondary government initiative of

improving food security. However, any sustained uptick in oil prices could undermine this drive. Such an

uptick would mean greater oil revenues to invest, but it would also mean far lower urgency in terms of the

need for diversification.

Another general downside risk relates to possible disease outbreaks, particularly an outbreak of bird flu in

the case of our optimistic poultry production forecast. Kazakhstan's poultry industry has been growing

strongly in recent years. However, it remains under-invested and, consequently, the impact of a disease

outbreak in what remains a relatively immature agricultural sub-sector could be pronounced. The outbreak

of foot-and-mouth disease in eastern Kazakhstan in July 2012 shows the disease remains a threat and poses

downside risk to our pork and beef forecasts.

Grains Outlook

BMI Supply View: We have revised up slightly our 2013/14 wheat production forecast to 17.0mn tonnes

(compared with a previous forecast of 16.0mn tonnes) on the back of the latest official estimates. This still

represents a significant 73.4% year-on-year (y-o-y) rebound, as weather conditions have improved. Even

though in 2013/14 the country is expected to plant the same area for wheat as in 2012/13, area harvested is

likely to be slightly higher, and yields are expected to recover strongly, boosting total wheat production

back to 2010 levels. We expect wheat production to increase gradually by an average of 5.0% annually over

the last three years of our forecast period, reaching 17.4mn tonnes in 2016/17, which is still below the

2011/12 level.

The barley crop is also forecast to recover strongly in 2013/14, by 40.0% to 2.1mn tonnes. This will come

from increased area dedicated to the crop at the expense of wheat as the government seeks to decrease its

dependence on wheat production and exports. Also, barley yields will most likely recover from their low in

2012/13, when the crop was affected by droughts to the same extent as the wheat crop was. We forecast

barley production to increase by an average of 2.0% annually over the last three years of our forecast

period, reaching 2.3mn tonnes in 2016/17.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 22

The corn crop, which is planted in spring, benefited from much milder weather and soil moisture conditions

in 2012/13, with rainfall starting again around the plantings period. As a result, and because of base effects,

we forecast output to drop slightly in 2013/14 to 480,000 tonnes. Out to 2016/17, we forecast corn

production to grow by 8.0% on the 2011/12 level to reach 510,000 tonnes.

BMI Demand View: Unlike neighbouring Ukraine, Kazakhstan did not impose a wheat export ban despite

suffering a similarly poor harvest as a result of drought. The higher average prices, which we expect to

continue in H113, will have the effect of encouraging exports and raising prices for domestic consumers.

We therefore forecast a moderate decline in wheat consumption in 2013, of 7.9% to 7.0mn tonnes, which is

still considerably higher than the 2011 figure of 6.2mn tonnes. Over our forecast period to 2017, we see

hardly any potential for additional growth in domestic wheat demand and forecast consumption to reach

7.5mn tonnes, a marginal increase on the 2012 figure.

Most of Kazakhstan's barley is used for feed for domestic livestock. Consumption has consequently shown

itself highly volatile to supply dynamics as farmers switch to other feed types when supply tightens and

prices rise. In 2013, we forecast barley consumption to fall 18.6% y-o-y to 1.5mn tonnes, as local barley

output will be severely restricted by the effects of drought. Kazakhstan has traditionally relied on domestic

supplies, only importing 55,000 tonnes of barley in 2010/11, another year that saw poor harvests. The corn

harvest has emerged relatively unscathed from the drought, and we expect most of the supply to be taken up

by domestic consumption as usual, with demand increasing 5.0% y-o-y to 498,100 tonnes in 2013. Out to

2017, we forecast barley and corn demand of 2.0mn tonnes and 822,300 tonnes respectively.

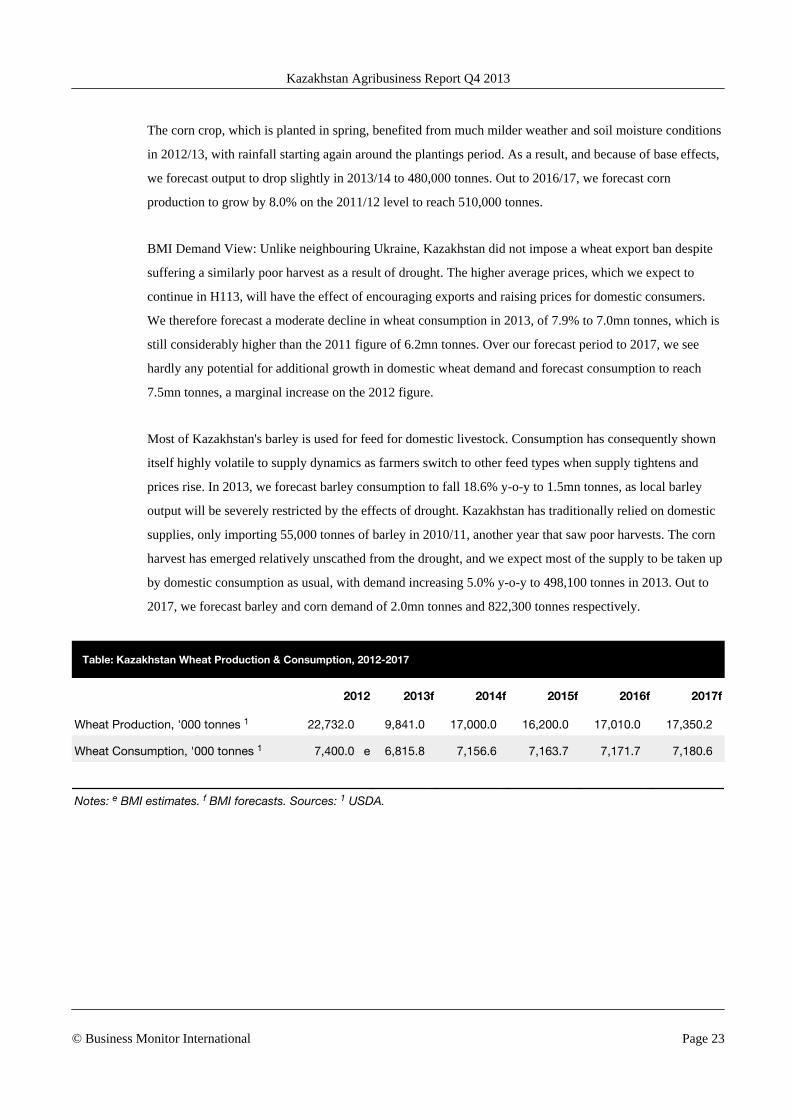

Table: Kazakhstan Wheat Production & Consumption, 2012-2017

2012 2013f 2014f 2015f 2016f 2017f

Wheat Production, '000 tonnes 1 22,732.0 9,841.0 17,000.0 16,200.0 17,010.0 17,350.2

Wheat Consumption, '000 tonnes 1 7,400.0 e 6,815.8 7,156.6 7,163.7 7,171.7 7,180.6

Notes: e BMI estimates. f BMI forecasts. Sources: 1 USDA.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 23

Table: Kazakhstan Corn Production & Consumption, 2012-2017

2012 2013f 2014f 2015f 2016f 2017f

Corn Production, '000 tonnes 1 482.0 500.0 480.0 490.0 500.0 510.0

Corn Consumption, '000 tonnes 1 475.0 e 498.8 514.1 601.5 703.7 823.3

Notes: e BMI estimates. f BMI forecasts. Sources: 1 USDA.

Table: Kazakhstan Barley Production & Consumption, 2012-2017

2012 2013f 2014f 2015f 2016f 2017f

Barley Production, '000 tonnes 1 2,593.0 1,500.0 2,096.0 2,148.4 2,202.1 2,257.2

Barley Consumption, '000 tonnes 1 1,825.0 e 1,485.1 1,793.4 1,861.8 1,918.3 1,976.4

Notes: e BMI estimates. f BMI forecasts. Sources: 1 USDA.

Export Potential Shifting East

We believe Black Sea countries will see increased grain demand from Asia in the coming years after the

region was largely ignored for at least the past three seasons. Disappointing harvests in Asian countries'

traditional suppliers, mainly the US, Australia and India, partially account for this. In addition, rising middle

classes and changing dietary habits are increasingly putting strains on the region's grain production balance;

this will force Asian importers to look for increased volumes and lower prices for grain purchases in the

medium term.

Thailand and the Philippines have already bought 200,000 tonnes of wheat from Black Sea countries in

recent months, and traders expect between 2.0mn and 2.5mn tonnes to flow into Asia in 2013/14. Thailand

bought Black Sea wheat for US$280-285/tonne, including cost and freight, while the Philippines purchased

wheat for US$282/tonne. India quoted about US$320-325/tonne for similar quantities. We see potential for

other large wheat importers in the region, such as Indonesia, China and Bangladesh, to turn to the Black Sea

region in the coming months, especially as we expect a bumper harvest in all the producing countries of the

region (we forecast a 41.4% year-on-year rebound in wheat production in Russia, Ukraine and Kazakhstan).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 24

Surging Import Demand

Select Asian Countries - Corn (LHS) & Wheat (RHS) Imports ('000 tonnes)

Source: USDA, BMI

More specifically, we see tremendous potential for China to increase its corn imports from Ukraine in the

coming years. A recent agreement between both governments could result in the delivery of 2mn-4mn

tonnes of corn from Ukraine to China for the 2013/14 season. As part of the agreement, Ukraine's State

Food Grain Corporation (GPZKU) obtained a US$1.5bn loan to finance improvements to the former Soviet

republic's agriculture. GPZKU will then export its grain output via Chinese operator China National

Machinery Complete Industry Engineering Corporation. Most of the grain shipped will be corn given

China's booming import demand for the feed. We believe this will come on the back of China's aim to

diversify away from the US as its major supplier for corn and soybean. As China has so far failed to develop

reliable supply agreements with Brazil and Argentina because of infrastructure and administrative

bottlenecks, Ukraine, which exported 12.9% of global corn in 2011/12, would be an efficient alternative.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 25

Asia Still Small Share Of Black Sea Exports

Ukraine (LHS) & Russia (RHS) - Wheat Exports By Region/Country (% of total)

Note: Ukraine exports are for 2011/12 season; Russian exports are for H113; Source: USDA, Sovecon

As a result of this emerging demand and significant long-term growth potential, we have seen tailored port

capacity coming online in the region. The plan by Russia's United Grain Company to develop a grain

terminal on Russia's Far East coast will serve that purpose. Russia is seeing grain shipments to Asia

expanding very fast (set to increase to about 1mn tonnes in 2012/13, compared with almost nothing in

2011/12) but is lacking the relevant infrastructure to keep up with demand. The development of shipping

capacity in Siberia and the Far East will make Russia even more competitive than it is currently on Asian

markets.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 26

Upside Potential For Far East Russian Ports

Port of Vostochny - Throughput ('000 tonnes) & Growth (% year-on-year)

e/f = BMI estimate/forecast. Source: Port Authority

Ukraine is pouring investment into its grain port terminal capacity in order to be better prepared for the

surge in demand from Asia. Recent financing projects aim to increase Illichivsk port's annual capacity from

30mn tonnes to 76mn tonnes. A new grain terminal was launched at the port of Odessa in April, with 11

reservoirs, a total capacity of 72,400 tonnes, brought online. The grain terminal will have a final annual

capacity of between 2mn and 3mn tonnes and will be one of the most advanced terminals in the Black Sea.

For Kazakhstan, transport subsidies support exports to Russian and Baltic ports, in turn directed to Asia,

mainly China. Approximately 160,000 tonnes of grain was shipped to China in 2011/12, compared with just

31,000 tonnes the year before. Also, Kazakhstan launched its own grain terminal in the Iranian port of

Amirabad (which it supplies from its port of Aktau). BMI believes that this will offer Kazakhstan the ability

to not only cater for Iranian demand, but also to Asia as grains will be shipped to Amirabad, freighted

through Iran and then shipped out to central and eastern Asia, via Iran's ports on the Persian Gulf.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 27

Booming Export Capacity

Black Sea Countries - Wheat Exports ('000 tonnes)

f = BMI forecast. Source: USDA, Sovecon

Only developed markets (and established grain importers) in Asia will resist the renewed attractiveness of

Black Sea grains. In fact, we expect Japan and South Korea to stay with their current traditional suppliers

(mainly the US), as they are far less price sensitive markets and more wary of the quality of imported

products. Also, volatility in export capacity could be an issue for these markets, as they import roughly the

same amount of grains every season and are looking for long-term supply agreements with exporters. This

will be less of a critical point for emerging grain importers in the region, as they are constantly looking for

the best bargain on global markets rather than long-term security of supply. Only India and China could be

exceptions to this rule.

Output Recovery, Diversification On The Cards

We forecast wheat production in Kazakhstan to recover by 73.4% in 2013/14 to 17.0mn tonnes thanks to

higher yields. The strong growth in output follows losses seen in 2012/13 as a result of severe droughts.

Area harvested is set to increase by about 7.2% in 2013/14, while yields are set to recover by more than

40%.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 28

Kazakhstan's objective to diversify away from wheat production is likely to push the country's corn and

barley production higher in 2013/14. The country has faced challenges in terms of getting wheat exports to

distant markets, and the government is pushing to increase domestic livestock and poultry production. The

area dedicated to feed crops and oilseeds is therefore likely to be prioritised at the expense of wheat. In

recent years, wheat planted area has represented 64% of all planted area in Kazakhstan, and 83% of grain

and pulse planted area. We believe the share allocated to wheat will decrease in the near term.

We expect an improvement in the grain production balance will benefit the country's exports in 2013/14.

Kazakh wheat exports remained particularly subdued in 2012/13, even below capacity. The US Department

of Agriculture estimates that the country exported about 6.5mn tonnes in 2012/13, while the production

balance stood at 3.0mn tonnes and stocks at a record of 11.8mn tonnes. Kazakh wheat prices were

supported by high prices in Russia, which saw wheat production almost halved owing to droughts in

2012/13. Kazakhstan also massively increased shipments to the region in order to fill the regional deficit,

which we see as temporary. In fact, we expect the country to boost exports to non-former Soviet Union

countries in 2013/14.

Overall, we see strong potential for growth in grain production and exports for Kazakhstan in the medium

term on the back of increased government support to the sector. In 2012, the Ministry of Agriculture

announced a number of programmes to support spring sowing and the 2013/14 crop production in general.

These included a KZT60bn (US$400mn) budgetary loan to major players in the sector, such as KazAgro

Holding. These funds will give preferential rates to farmers in order to support plantings as well as help

microcredit institutions propping up the sector. The ministry also launched a forward purchasing of wheat

and barley at a rate of KZT6,000/ha (US$40/ha), representing a total budget of KZT13bn (US$86mn). The

government also increasingly makes sure that relevant fuel, machinery, seeds and fertiliser supply are made

available to farmers.

Our outlook for grain prices will be supportive of increased plantings and investment in these crops in

Kazakhstan, as well as export demand, especially from Asia. We forecast wheat prices to remain

particularly elevated in the short term, while all grains are expected to trade at a premium compared with

their historical average in the coming years. Our strong forecasts for consumption growth in Asia, and the

country's development into these markets, will also boost revenues and investment in grain crops out to

2016/17.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 29

Table: Kazakhstan Wheat Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012

Wheat Production, '000 tonnes 1 13,460.5 16,466.9 12,538.2 17,051.0 9,638.0 22,732.0

Wheat Consumption, '000 tonnes 1 7,500.0 7,500.0 7,500.0 7,600.0 6,200.0 7,400.0 e

Notes: e BMI estimates. Sources: 1 USDA.

Table: Kazakhstan Corn Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012

Corn Production, '000 tonnes 1 414.0 421.0 420.0 470.8 462.0 482.0

Corn Consumption, '000 tonnes 1 425.0 425.0 425.0 425.0 450.0 475.0 e

Notes: e BMI estimates. Sources: 1 USDA.

Table: Kazakstan Barley Production & Consumption, 2007-2012

2007 2008 2009 2010 2011 2012

Barley Production, '000 tonnes 1 1,953.0 2,441.0 2,059.0 2,519.0 1,313.0 2,593.0

Barley Consumption, '000 tonnes 1 1,350.0 1,700.0 1,850.0 2,000.0 1,475.0 1,825.0 e

Notes: e BMI estimates. Sources: 1 USDA.

Risks To Outlook

The high prices Kazakh growers received for their wheat crop in 2012 may provide them with the capital to

make further investments, for instance, in improved mechanisation and storage. This represents an upside

risk to our forecasts. Drought, which in 2012 resulted in y-o-y falls in grains production of around 50%,

shows that the weather remains an ever-present risk to our forecasts.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 30

Commodities Price Analysis

Monthly Grains Strategy

■ Having declined steadily since Q412 in line with our view, we believe grain prices will find a base inQ413 as prices approach key support levels and planting prospects in the Southern Hemispheredeteriorate due to the lower prices.

■ Corn prices could stage a temporary recovery following recent weakness, as we believe the bulk of theprice declines are behind us. Corn (and to a lesser extent soybean) are expected to experience a period ofvolatile prices in the coming weeks leading up to the US harvest.

■ Wheat prices will remain supported owing to strong import demand from China and reduced plantingprospects in the Southern Hemisphere.

• Rice prices will face downside pressure in the coming months as the Thai government releases stockson the international market.

Grain Feels The Pain (weekly chart)

S&P GSCI Grains Index

Source: Bloomberg

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 31

Corn: Temporary Strength After Free Fall

Our view of corn prices breaking below multi-year support around USc650/bushel has played out, and we

now see prices forming a base around support at USc425/bushel in the coming weeks. Prices have collapsed

in recent weeks: the US harvest remains on track for a significant rebound in 2013/14 owing to better

weather, and key demand drivers such as the livestock sector remain comparatively subdued. We have also

revised our 2013 and 2014 price forecasts lower to USc600/bushel and USc525/bushel respectively. The

view for lower prices is premised on our forecasts for three consecutive large global surpluses starting in

2013/14 - of at least 10mn tonnes - before the market returns to deficit in 2016/17.

Betting The Farm

US Corn - Largest Planted Areas By Season Since 1926 (mn acres)

Note: Corn and soybean began sharing acreage in 1964. Sources: BMI, USDA, NASS

However, we believe the bulk of the price declines is behind us and see potential for corn to form a base

around the USc400-425/bushel level, which corresponds with technical support. The main reason is that we

expect the significant decline in prices to reduce corn plantings in South America, a key export hub that

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 32

experienced record plantings in 2012/13 on the back of high prices. Indeed, official forecasts are also for a

decline in the area dedicated to corn in 2013/14.

Mind The Gap

Front-Month CBOT Corn, USc/bushel (weekly chart)

Sources: BMI, Bloomberg

Rice: Signs Of Changes To Thai Policy

Supported by a price premium stemming from Thailand's rice pledging programme and tightness on the US

domestic market (which has a significant influence on CBOT rice prices), we believe front-month rice

prices will trade within their moderate channel uptrend (US$15.00/cwt and US$17.00/cwt) in the coming

months. We have slightly revised up our 2013 price forecast owing to the strength in prices since the

beginning of the year; we now expect rice to average US$15.00/cwt over the year (compared with US

$14.50/cwt previously).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 33

More Weakness Coming

Front-Month CBOT Rough Rice, US$/cwt (weekly chart)

Sources: BMI, Bloomberg

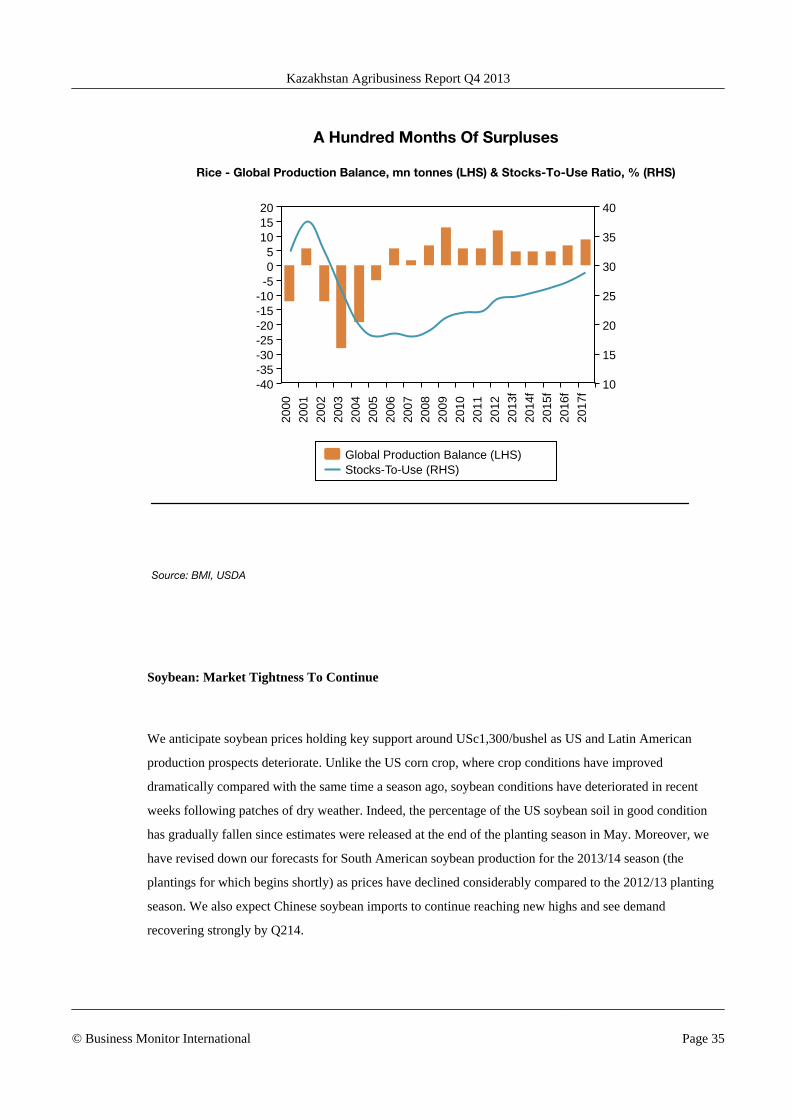

However, we continue to forecast lower average rice prices beyond 2013, as ample global supply is likely to

keep prices in check. The global market will record surpluses of around 5mn tonnes in 2012/13 and

2013/14, which will maintain the stocks-to-use ratio at a relatively elevated level. Prices are expected to

eventually head lower once Thailand releases its unsustainably high stocks on the market at a discounted

price. This will increase the availability of rice on the international market and push prices below multi-year

support, which comes in around US$15.00/cwt. As a result, we forecast prices to average lower in 2014, at

US$13.00/cwt.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 34

A Hundred Months Of Surpluses

Rice - Global Production Balance, mn tonnes (LHS) & Stocks-To-Use Ratio, % (RHS)

Global Production Balance (LHS)Stocks-To-Use (RHS)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

f

2014

f

2015

f

2016

f

2017

f

-40-35-30-25-20-15-10-505

101520

10

15

20

25

30

35

40

Source: BMI, USDA

Soybean: Market Tightness To Continue

We anticipate soybean prices holding key support around USc1,300/bushel as US and Latin American

production prospects deteriorate. Unlike the US corn crop, where crop conditions have improved

dramatically compared with the same time a season ago, soybean conditions have deteriorated in recent

weeks following patches of dry weather. Indeed, the percentage of the US soybean soil in good condition

has gradually fallen since estimates were released at the end of the planting season in May. Moreover, we

have revised down our forecasts for South American soybean production for the 2013/14 season (the

plantings for which begins shortly) as prices have declined considerably compared to the 2012/13 planting

season. We also expect Chinese soybean imports to continue reaching new highs and see demand

recovering strongly by Q214.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 35

Weaker Growth In 2013/14

Brazil & Argentina - Combined Annual Growth In Soybean Plantings (%)

Source: BMI, USDA

Overall, we believe the soybean market will remain one of the tightest in the grains complex, as it is

rebounding from a record 17mn tonne deficit during the 2011/12 season. Indeed, the soybean futures curve

is the only curve in the grains complex that is in backwardation. Therefore, soybean is the only grain for

which we forecast higher average prices in 2014 (USc1,450/bushel) than 2013 (USc1,400/bushel).

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 36

Weakness Won't Last

Front-Month CBOT Soybean, USc/bushel (weekly chart)

Source: BMI, Bloomberg

Wheat: Prices To Find Support

We have revised down our average annual wheat price forecasts. Wheat prices have fallen by almost 20%

since January, brought on by improving harvest prospects in major producers such as the EU, United States

and Black Sea region. Indeed, we forecast the global wheat market to rebound from a 35mn tonne deficit in

2012/13 to be essentially balanced in 2013/14. Consequently, we have revised our average price forecasts

lower and now see wheat averaging USc690/bushel in 2013 and USc650/bushel in 2014.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 37

Looking For Support

Front-Month CBOT Wheat, USc/bushel (weekly chart)

Sources: BMI, Bloomberg

Over the short term, however, we believe prices will remain supported around the USc600/bushel level as

more wheat is diverted to feed in the US and because Chinese imports are forecast to reach a multi-decade

high of 9mn tonnes in 2013/14. This would make China the world's largest wheat importer during the

season. Prices will also receive support as we are forecasting only a minor increase in Argentine production

for the 2013/14 season, mainly owing to better yields. Indeed, official forecasts see the area dedicated to

wheat in Argentina falling to its second lowest level in 40 seasons in 2013/14.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 38

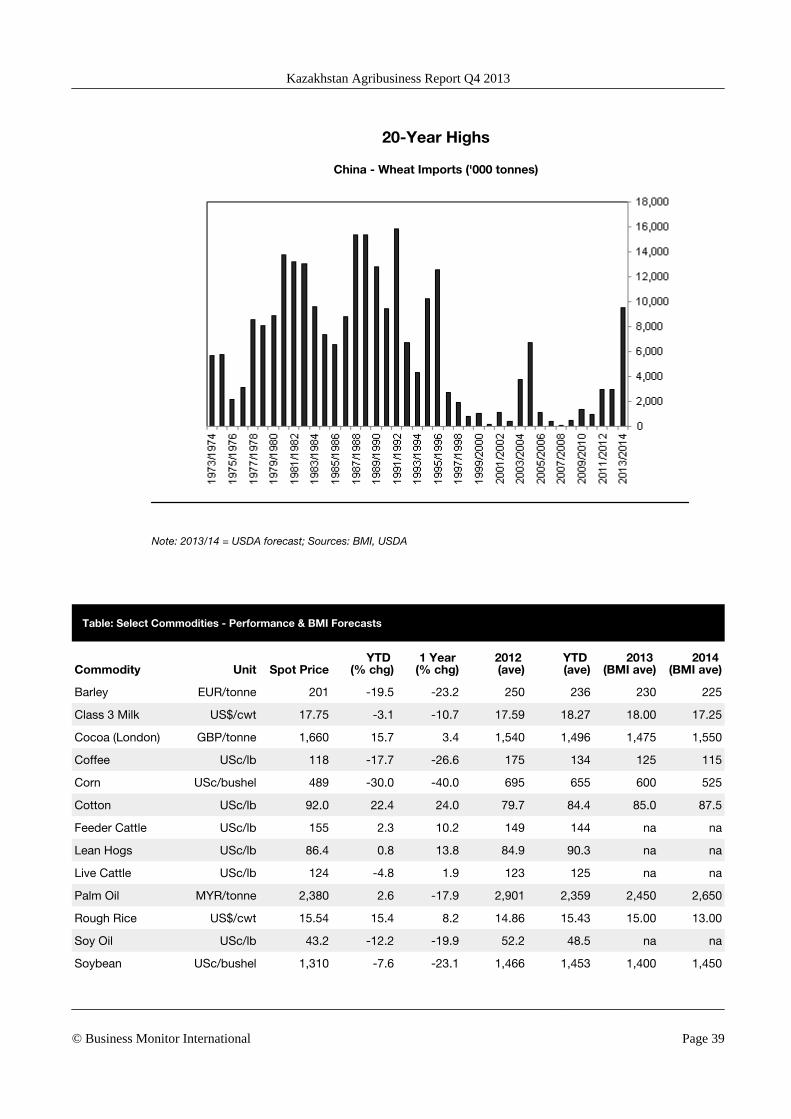

20-Year Highs

China - Wheat Imports ('000 tonnes)

Note: 2013/14 = USDA forecast; Sources: BMI, USDA

Table: Select Commodities - Performance & BMI Forecasts

Commodity Unit Spot PriceYTD

(% chg)1 Year

(% chg)2012 (ave)

YTD (ave)

2013 (BMI ave)

2014 (BMI ave)

Barley EUR/tonne 201 -19.5 -23.2 250 236 230 225

Class 3 Milk US$/cwt 17.75 -3.1 -10.7 17.59 18.27 18.00 17.25

Cocoa (London) GBP/tonne 1,660 15.7 3.4 1,540 1,496 1,475 1,550

Coffee USc/lb 118 -17.7 -26.6 175 134 125 115

Corn USc/bushel 489 -30.0 -40.0 695 655 600 525

Cotton USc/lb 92.0 22.4 24.0 79.7 84.4 85.0 87.5

Feeder Cattle USc/lb 155 2.3 10.2 149 144 na na

Lean Hogs USc/lb 86.4 0.8 13.8 84.9 90.3 na na

Live Cattle USc/lb 124 -4.8 1.9 123 125 na na

Palm Oil MYR/tonne 2,380 2.6 -17.9 2,901 2,359 2,450 2,650

Rough Rice US$/cwt 15.54 15.4 8.2 14.86 15.43 15.00 13.00

Soy Oil USc/lb 43.2 -12.2 -19.9 52.2 48.5 na na

Soybean USc/bushel 1,310 -7.6 -23.1 1,466 1,453 1,400 1,450

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 39

Select Commodities - Performance & BMI Forecasts - Continued

Commodity Unit Spot PriceYTD

(% chg)1 Year

(% chg)2012 (ave)

YTD (ave)

2013 (BMI ave)

2014 (BMI ave)

Soymeal US$/tonne 417 -1.0 -21.8 430 433 na na

Sugar #11 USc/lb 16.54 -15.2 -19.3 21.57 17.50 17.50 17.00

Wheat USc/bushel 636 -18.3 -27.7 751 702 690 650

Source: BMI, Bloomberg

Table: BMI Commodities Strategy

EntryDate

EntryLevel

Gain/(Loss) Rationale

AGRICULTURE

- - - - -

ENERGY

- - - - -

METALS

Bullish Platinum (spot) vsGold (spot)

29-May-201

3 1.055 5.89%Supply disruption in South Africa, growing autos use to supportplatinum prices. Bearish gold.

Note: Returns do not take into account roll yield, unless stated otherwise. Source: BMI, Bloomberg

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 40

Monthly Softs Strategy

■ In line with our view, softs have outperformed grains and industrial commodities since the start of theyear.

• We believe the softs index is close to a bottom, especially for sugar and coffee.

• Cotton and cocoa will remain the best supported among softs on the back of China's ongoingstockpiling policy (cotton) and subdued supply prospects in West Africa (cocoa).

• Despite little upside potential in the short term, palm oiI prices are likely to start to recover in 2014.

More Neutral On Softs Now

Select Commodities & Indices - Prices (rebased)

Note: 2 January 2013 = 100. Source: BMI, Bloomberg

Cocoa: Supply Risks Remaining

We expect cocoa prices to continue trading within the GBP1,400-1,700/tonne range in the coming months.

Concerns over delays to the coming West African crop, combined with quality issues, will prevent

significant declines in prices. Indeed, we have revised down our 2012/13 and 2013/14 cocoa supply

forecasts for Ghana, as poor rainfall has affected yields. However, we believe the recent rally in prices will

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 41

fade as new supply comes online. Despite strong European grindings in Q213, we believe any demand

recovery in Europe will be uneven in the short term given the high prices.

Range Trading

Front-Month LIFFE Cocoa, GBP/tonne (weekly)

Source: Bloomberg, BMI

We forecast small global cocoa deficits in the coming seasons, which will push cocoa prices higher in the

medium term. We are particularly cautious about supply prospects in West Africa, where ageing trees and

farmers, low efficiency and limited access to credit will restrict production growth. As a result, we forecast

cocoa prices to average GBP1,550/tonne in 2014.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 42

Picking Up

Europe - Year-On-Year Q2 Cocoa Grindings (% of previous year)

Source: BMI, European Cocoa Association

Coffee: Finding A Bottom Soon?

We expect coffee prices to remain weak in the coming months as ample global supply puts pressure on

prices. The supply problems in Central America related to coffee rust disease have had little impact on

prices so far, mainly because Colombia is projected to offset its neighbours' production drop. Although we

still expect a decline in 2013/14 production in Vietnam, concerns over a prolonged dry spell have now

eased.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 43

Little Support Before US$1 Level

Front-Month ICE Coffee (USc/lb, weekly) & RSI (below)

Source: Bloomberg, BMI

Prices could drift towards USc100/lb, a level we believe presents strong psychological support. Farmers in

major producers, including Brazil, Colombia, Vietnam and Indonesia, will consider hoarding in the face of

sharply declining profitability. Moreover, Brazil's soon-to-be-announced support programme for coffee

farmers is likely to include a subsidies scheme, which will limit the downside for prices. We forecast prices

to stabilise in the coming years, averaging USc115/bushel in 2014 and 2015 compared with USc125/bushel

in 2013.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 44

Downside Pressure For Sugar And Coffee

BRL/US$ Exchange Rate (weekly chart)

Source: Bloomberg, BMI

Cotton: Stable For Now

We expect cotton prices to respect current resistance at USc90.00/lb in the coming months, as the global

market remains well supplied. Net speculative long positions are still high by historical standards, which is

likely to limit upside risks for prices in the near term. Prices could make a decisive move above the

USc90.00/lb level towards the end of the year, when the market is likely to enter a supply trough after a

disappointing year in terms of output growth. We do not foresee a major change to China's stockpiling

policy before mid-2014 at least; this will maintain domestic prices at elevated levels and incentivise millers

to import significant volumes of cotton.

In the medium term, we expect the global market to record decreasing surpluses as relatively low prices

continue to discourage plantings and demand recovers at a stronger pace. We forecast cotton prices to

average USc85.00/lb in 2013 and USc87.50/lb in 2014.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 45

Resistance To Hold For Now

Front-Month ICE Cotton, USc/lb (daily) & RSI (below)

Source: Bloomberg, BMI

Palm Oil: Recovery In 2014

Although we continue to believe palm oil prices have bottomed, we see limited upside to prices in the

coming months given the lack of a significant fundamental upward catalyst. We continue to expect prices to

trade along support at MYR2,250/tonne. The demand picture has deteriorated in recent months, as the

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 46

depreciating Indian rupee is weighting on India's imports, which usually represent close to 20% of the

world's total trade. Meanwhile, Malaysia and Indonesia are now in the part of the season during which

yields peak, and when production is at its highest.

Weakness For Now

Three-Month Palm Oil (MYR/tonne, weekly)

Source: Bloomberg, BMI

Prices are expected to start to recover in 2014 as production growth slows and consumption maintains a

healthy growth rate. Palm oil remains competitive compared with other vegetable oils, as the palm oil/soy

oil and palm oil/soybean ratios are still low by historical standards. We see prices averaging MYR2,650/

tonne in 2014, compared with MYR2,450/tonne in 2013.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 47

Weak Rupee Weighting On Imports

India - Palm Oil Imports ('000 tonnes)

Source: BMI, India Solvent Association

Sugar: Bottoming Out

We maintain our view that sugar prices are close to bottoming out and are likely to show resilience over a

three-to-six-month horizon. Prices could face downward pressure in the very short term, as sugar prices

have recently regained competitiveness over ethanol prices in Brazil, which could prompt millers to turn

more cane into sugar. The continued weakness in the Brazilian real also poses downside risk to sugar

prices. However, unfavourable weather in June and July and the upcoming end of the harvest season in

Brazil suggest that supply will only tighten. The Brazilian sugarcane association Unica revised down its

production estimate for Brazil in April and could do so again in its next report in September. We forecast

the global surplus to significantly narrow in 2013/14, to 5mn tonnes, down 37.5% year-on-year. This will

help prices recover slightly in 2014 to average USc18.00/lb, compared with USc17.50/lb in 2013.

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 48

Reversal In Sight?

Front-Month ICE Sugar, USc/lb (weekly)

Source: Bloomberg, BMI

Table: Select Commodities - Performance & BMI Forecasts

Commodity Unit Spot PriceYTD

(% chg)1 Year

(% chg)2012 (ave)

YTD (ave)

2013 (BMI ave)

2014 (BMI ave)

Barley EUR/tonne 205 -17.7 -21.5 250 236 230 225

Class 3 Milk US$/cwt 17.55 -4.2 -11.7 17.59 18.27 18.00 17.25

Cocoa (London) GBP/tonne 1,654 15.3 3.1 1,540 1,496 1,475 1,550

Coffee USc/lb 115 -20.2 -28.5 175 134 125 115

Corn USc/bushel 483 -30.8 -41.9 695 654 600 525

Cotton USc/lb 86.7 16.3 14.3 79.7 84.4 85.0 87.5

Feeder Cattle USc/lb 155 2.7 11.2 149 144 na na

Lean Hogs USc/lb 86.9 1.3 14.6 84.9 90.3 na na

Live Cattle USc/lb 124 -4.5 3.7 123 125 na na

Palm Oil MYR/tonne 2,385 2.8 -17.7 2,901 2,359 2,450 2,650

Rough Rice US$/cwt 15.75 15.4 8.2 14.86 15.43 15.00 13.00

Soy Oil USc/lb 43.0 -12.6 -22.7 52.2 48.5 na na

Soybean USc/bushel 1,309 -7.7 -25.3 1,466 1,452 1,400 1,450

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 49

Select Commodities - Performance & BMI Forecasts - Continued

Commodity Unit Spot PriceYTD

(% chg)1 Year

(% chg)2012 (ave)

YTD (ave)

2013 (BMI ave)

2014 (BMI ave)

Soymeal US$/tonne 412 -2.0 -24.2 430 432 na na

Sugar #11 USc/lb 16.49 -15.5 -16.6 21.57 17.49 17.50 18.00

Wheat USc/bushel 635 -18.4 -29.5 751 702 690 650

Source: BMI, Bloomberg

Table: BMI Commodities Strategy

EntryDate

EntryLevel

Gain/(Loss) Rationale

AGRICULTURE

- - - - -

ENERGY

- - - - -

METALS

Bullish Platinum (spot) vsGold (spot)

29-May-201

3 1.055 5.47%Supply disruption in South Africa, growing autos use to supportplatinum prices. Bearish gold.

Note: Returns do not take into account roll yield, unless stated otherwise. Source: BMI, Bloomberg

Kazakhstan Agribusiness Report Q4 2013

© Business Monitor International Page 50

Upstream Analysis

Europe GM Outlook

BMI View: Europe is expected to remain the smallest region for genetically modified (GM) plantings in the

world, as there is still strong public opposition to GM products in the region's largest grain producers,

among them France. The EU's reliance on GM feed imports has pushed several retailers in the UK to step

back from their initial commitment to source non GM-fed poultry meat.

Strict regulations on production and the use of genetically modified (GM) food, as well as negative public

opinion, make the EU the smallest region for GM plantings in the world. GM plantings in the EU only

represent 0.6% of global GM plantings, while the US and South America represent 77.8%. Only two crops