BEPS Update

28

BEPS UPDATE

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of BEPS Update

BEPS UPDATE

What is BEPS?

Why BEPS?

Why is BEPS a

problem?

Why address BEPS now?

BEPS Action Plan

4 Key Questions

2

o BEPS occurs because under the existing rules MNEs are often able to artificially separate the allocation of their taxable profits from the jurisdictions in which these profits arise

o This can result in income not being taxed anywhere, and significantly reduces the corporate income tax paid by MNEs in the jurisdictions where they operate

What is BEPS ?

3 3

International Tax Principles: Out-of-date?

• Many developed in the 1920s

built on the assumption that profits are taxed in the other country;

less cross-border activity

bricks-and-mortar business models

• Changes to business models, e.g. globalisation of value chains, increasing importance of intangibles, “digital economy”

• Focus has historically been on the development of common standards to eliminate double taxation for cross border investments

– Model Tax convention

Why BEPS?

4

What’s the problem?

• It distorts competition

• It distorts investment decisions

• It is an issue of fairness

5

Why now?

6

Unprecedented Public Attention

Debate on BEPS issues has reached high political levels

Increased Media Attention

• Addressing Base Erosion and Profit Shifting

• Published on 12 February 2013

identifies main pressure areas leading to opportunities for BEPS

Notes the need for a holistic and coordinated approach

Calls for an Action Plan to tackle BEPS

The OECD Report: The Diagnosis Stage 1

Hybrid Mismatch Arrangements

Related party debt-financing

Digital economy Availability of preferential regimes

Anti-avoidance measures

Transfer pricing 7

The BEPS Action Plan Stage 2

BEPS Action Plan published in July 2013

15 Actions organised around three main pillars:

• The coherence of corporate tax at the international level

• A realignment of taxation and substance

• Transparency, coupled with certainty and predictability

It also calls for targeted work in the area of the digital economy, and for the development of a multilateral instrument to implement the measures developed under the action plan.

Endorsed by G20 Leaders (6 September 2013):

…“We fully endorse the ambitious and comprehensive Action Plan […] Profits should be taxed where economic activities deriving the profits are performed and where value is created. (…)

9

Structure – 15 Actions

10

Coherence

Hybrid Mismatch Arrangements (2)

Harmful Tax Practices (5)

Interest Deductions (4)

CFC Rules (3)

Substance

Preventing Tax Treaty Abuse (6)

Avoidance of PE Status (7)

TP Aspects of Intangibles (8)

TP/Risk and Capital (9)

TP/High Risk Transactions (10)

Transparency and Certainty

Methodologies and Data Analysis (11)

Disclosure Rules (12)

TP Documentation (13)

Dispute Resolution (14)

Digital Economy (1)

Multilateral Instrument (15)

OECD/G20 BEPS Project

• Associates

– participate on an equal footing with OECD countries

• Business and civil society

– invited to comment

• Engagement with Developing countries

11

• All 8 non-OECD G20 countries (Argentina, Brazil, China, India, Indonesia, Russia, Saudi Arabia and South Africa) and OECD Accession countries (Colombia and Latvia) are Associates in the BEPS Project

Engagement with Developing Countries

12

New structured dialogue process

A strategic dialogue meeting on engaging in BEPS Project was held on 11-12 December 2014 in Paris

13

An ambitious timeline - Deliverables

September 2014 September 2015 December 2015

Digital Economy Report

Hybrids Review of HTP

Regimes Preventing Treaty

Abuse Addressing TP

aspects of Intangibles (1)

Addressing TP documentation

Multilateral Instrument Report

CFC Rules Interest Deductibility Strategy: expansion of FHTP Addressing avoidance of PE

status Addressing TP aspects of

Intangibles (2) Addressing TP aspects of risks

and capital Addressing TP aspects of other

high risk transactions Report on Data and Economic

Analyses Mandatory Disclosure Rules Dispute Resolution

Addressing TP Interest Deductions

Revision of HTP Criteria

Multilateral Instrument

THE 2014 DELIVERABLES

14

• Explanatory Statement

• 3 Reports: – Final report on the Digital Economy (Action 1)

– Final report on the Feasibility of a Multilateral Instrument (Action 15)

– Interim report on harmful tax competition (Action 5)

• 4 Instruments: – Hybrid Mismatch Arrangements

– Treaty Abuse

– TP Intangibles

– TP Documentation and CBC template

15

The 2014 Deliverables

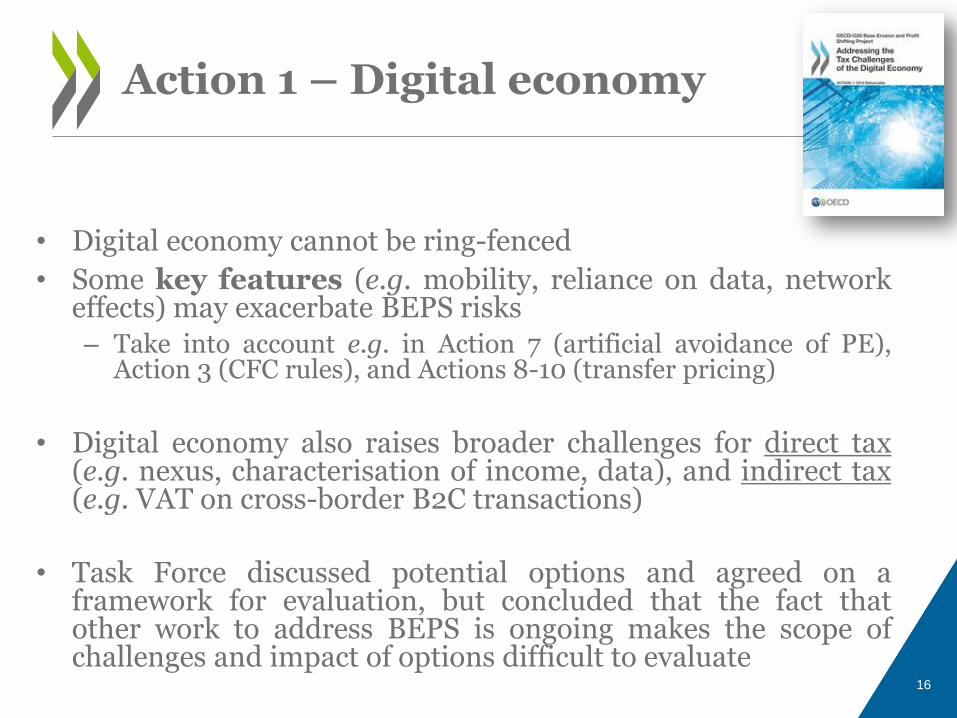

• Digital economy cannot be ring-fenced

• Some key features (e.g. mobility, reliance on data, network effects) may exacerbate BEPS risks – Take into account e.g. in Action 7 (artificial avoidance of PE),

Action 3 (CFC rules), and Actions 8-10 (transfer pricing)

• Digital economy also raises broader challenges for direct tax (e.g. nexus, characterisation of income, data), and indirect tax (e.g. VAT on cross-border B2C transactions)

• Task Force discussed potential options and agreed on a framework for evaluation, but concluded that the fact that other work to address BEPS is ongoing makes the scope of challenges and impact of options difficult to evaluate

Action 1 – Digital economy

16

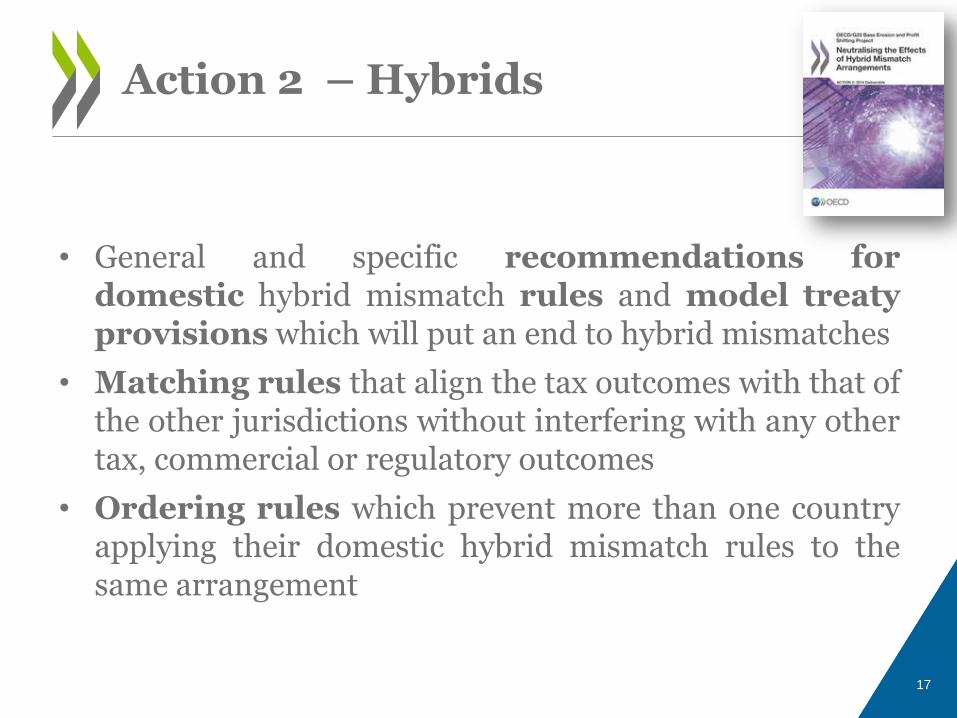

• General and specific recommendations for domestic hybrid mismatch rules and model treaty provisions which will put an end to hybrid mismatches

• Matching rules that align the tax outcomes with that of the other jurisdictions without interfering with any other tax, commercial or regulatory outcomes

• Ordering rules which prevent more than one country applying their domestic hybrid mismatch rules to the same arrangement

Action 2 – Hybrids

17

2014 Progress Report

• Agreement that preferential regimes need to require presence of substantial activity not to be considered harmful.

• Agreement that preferential regimes need to be transparent.

• Agreement reached on framework for compulsory spontaneous exchange on rulings related to preferential regimes.

Action 5 – Harmful tax practices

18

• Agreement that treaties should not be used to generate double non-taxation

• Agreement on a common minimum standard to tackle treaty abuse

• Work ongoing concerning technical details related to the drafting of the provisions

• Work ongoing on the impact of anti-abuse provisions on collective investment vehicles

Action 6 – Treaty Abuse

19

• Consensus was reached on treatment of corporate synergies, location savings and definition of intangibles

• Interim guidance on allocation of returns from intangibles

− legal ownership alone is not enough

− contributions to intangible value must be appropriately rewarded

• This action is closely related to the 2015 work on risks and re-characterisation of transactions so some sections are bracketed

Action 8 – Intangibles

20

• Agreement on standard TP documentation which includes a Master file, a Local file and a Country-by-Country reporting template

• Overview of where profits, sales, employees, and assets are located and where taxes are paid and accrued on a country-by-country basis

• Useful tool for risk assessment

• Ongoing work to ensure high confidentiality of information given to tax administration

• Ongoing work on scope and filing mechanism discussed at January 2015 CFA

• Post implementation review by 2020

Action 13 – TP Doc and CBC

21

• Based on precedents from various areas other than tax, a multilateral instrument to implement BEPS measures is feasible

• It is also desirable to ensure the sustainability of the consensual framework to eliminate double taxation

• Goal is to expedite and streamline the implementation of the measures developed to address BEPS

• Report recommends a multilateral instrument to be developed soon and to cover at least tax treaty measures related to BEPS

Action 15 – Multilateral Instrument

22

BEPS 2015 - WORK IN

PROGRESS

23

First steps towards implementation

24

1. mandate for the development of a

multilateral instrument

2. implementation package for country-by-

country reporting

3. Intellectual Property regimes

G20 Finance Ministers

Istanbul, 9-10 February

• 2014 deliverables further refined to address technical issues and consider interaction with the 2015 deliverables

• Work on 2015 deliverables ongoing

• Consultation with stakeholders will continue

• Engagement with developing countries will be strengthened

• Finalise the work by December 2015

2014 and 2015 Deliverables

25

CFC Rules Interest Deductibility Strategy on expansion of FHTP Addressing avoidance of PE status Addressing TP – Intangibles (Part 2) Addressing TP – risks and capital Addressing TP – other high risk

transactions Report on Data and Economic

Analyses Mandatory Disclosure Rules Dispute Resolution

Addressing TP Interest Deductions Revision of HTP Criteria Multilateral Instrument

2015

DISCUSSION

DRAFTS

26

• TP: risk, recharacterisation, special measures (actions 8, 9, 10)

• TP: use of profit splits (action 10)

• TP: commodity transactions (action 10)

• Low value-added services (action 10)

• Cost contribution arrangements (action 8)

27

Discussion drafts

Further Information

Website: www.oecd.org/tax/beps.htm

Contact: [email protected]

Tax email alerts: www.oecd.org/oecddirect