IFRS UPDATE - Deloitte

70

IFRS UPDATE Topics October 2020

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of IFRS UPDATE - Deloitte

IFRS UPDATETopics

October 2020

2© Deloitte

Welcome

3© Deloitte

Information relatingto credit points

4

In hour perspective you can yield 1 hour for your

certification.

If you require a certification please contact Silvia Ebeloe ([email protected])

after the event.

However, it is important to point out that it is always the auditor's own responsibility to assess whether the completed

continuing education professional content is in accordance with section 4 of the Auditors Act and rules issued in

pursuance thereof.

Learning credit points

5© Deloitte

IFRS 16 – current status 6

IASB - What's new for 2020 and subsequent years 18

ESEF - European Single Electronic Format 28

Climate change - Impact on Financial Statements 34

Corporate Governance 38

IFRS in focus 47

Enforcement outlook 2020 53

Trends in Financial Reporting 55

Contents

6© Deloitte

IFRS 16 – current status

7© Deloitte

Lease Accounting Background

Initial implementation focused on stakeholder communication

Focus on data collection, impact calculation and stakeholder communication

Choice of system:

• Some large/complex organizations implemented dedicated lease systems

• Large and medium-sized companies implemented temporary systems or Excel models

Challenges to processes

• Many companies did not align processes after implementation

• Key symptom: Reconciliation between expected calculated payments and actuals payments increases over time

• Consequence: Increased workload before reporting

8© Deloitte

Lease Accounting BackgroundThe 3 enablers in Finance – Processes, Systems and People

What enables

FinancePROCESS & POLICY

ORGANIZATION & PEOPLE

INFORMATION & SYSTEMS

Policies

Organization Structure

Service Delivery Model

Talent & Business

Partnering

Architecture

Analytics

Small/medium-sized companies Large companies

What enables

FinancePROCESS & POLICY

ORGANIZATION & PEOPLE

INFORMATION & SYSTEMS

Policies

Organization Structure

Service Delivery Model

Talent & Business

Partnering

Architecture

Analytics

ProcessManagement

Controls & Compliance

Applications

What enables

FinancePROCESS & POLICY

ORGANIZATION & PEOPLE

INFORMATION & SYSTEMS

Policies

Organization Structure

Service Delivery Model

Talent & Business

Partnering

Architecture

Analytics

What enables

FinancePROCESS & POLICY

ORGANIZATION & PEOPLE

INFORMATION & SYSTEMS

Policies

Organization Structure

Service Delivery Model

Talent & Business

Partnering

Architecture

ProcessManagement

Controls & Compliance

Applications

Analytics

9© Deloitte

Lease Accounting

Designing effective processes

Design objective: design clear processes that ensure high data quality with efficient use of resources.

Responsibility for contract data Decentralized

(countries/regions)Centralized

(Group functions)

Overall designIntegrated in existing

processesSeparate sub-

process

ReconciliationYearlyMonthly

AccountingAdjustment to

consolidation systemLocal postings to

ERP

Deloitte general observations

Flow-charts, activity descriptions, risk and control matrices are created to ensure transparency though the contract lifecycle and reporting

Design considerations

10© Deloitte

Lease Accounting

Designing effective processes

Lease system

External

vendors

ERP

• Incorrect invoices due to billing mistake or indexation error• Invoices incorrect for modified or terminated leases

• Lease expenses not booked or accrued for and accruals not processed correctly• Lease GL coding not followed (e.g. low value)• Lease expense not split correctly (variable or service component)

• Leases entered incorrectly and contracts not identified (contract data incomplete)• Impact of non-standard leases which generate differences• Supporting master data such as indexation rates not entered correctly

Examples of risks

11© Deloitte

Benefits of dedicated lease system

Lease Accounting

Increased relevance of dedicated lease systems

The number of companies realizing the effort required to maintain temporary systems or Excel models is higher than

expected.

Prices have been adjusted during the last 12-18 months, increasing the relevance

for Danish companies in general.Cost decrease Realizing benefits

Data quality

Contract managementSupport clear delegation of roles and responsibilities on

contract level

Reporting

Reduces the inhered risk of maintaining and consolidating various excel sheets

Lease systems support improvement of data quality by providing “one source of truth” for contract data.

Systems can automate journal creations for posting to ERP or consolidation system

Possibility of attaching contracts and having notifications e.g. when extension options must be evaluated

Systems have dashboard functionalities to provide transparency across the lease portfolio

12© Deloitte

Overview of Selected Vendors

Vendor Nordic references (examples)

FE Boarding

13© Deloitte

Lease contracts and the specific circumstances of the Covid-19 pandemic Accounting for rent concessions

Change in payments

(rent concessions)

Accounting depends on whether:

The lessee was entitled to the economic relief (due to contractual arrangement or jurisdictional laws)

The relief was given or negotiated outside the original agreement.

Lease modificationIf no change in scope (assets leased or duration of the lease term), remeasure lease liability using a revised

discount rate & adjust asset

Variable (negative) rent(Practical expedient)

Recognize through P&L in the period incurred

Lessee

If relief is received from another party than the lessor, such as government, account for the subsidies as a government grant (IAS 20).

• If provided through the lessor, assess, whether the lessor is acting as an agent or providing the rent concessions themselves.

14© Deloitte

Lease contracts and the specific circumstances of the Covid-19 pandemic

Accounting for rent concessions - cont.

Change in payments

(rent concessions)

The practical expedient applies to rent concessions directly related to COVID-19 and only, if

• Total payments on the lease are diminished or stay the same, and

• Concession impacts payments due before 30 June 2021, and

• Other terms of the contract are not impacted.

Practical expedient Recognize through P&L in the period incurred.

Disclose that the practical expedient has been applied (and nature of contracts to which applied), and the

amount recognized in P&L

Lessee

15© Deloitte

Lease contracts and the specific circumstances of the Covid-19 pandemic

Applying the practical expedient for rent concessions

Change in payments

(rent concessions)

How to apply the practical expedient

Forgiveness or waiver of lease payments

• Account for as a variable lease payment (recognize through P&L in the period incurred)

• De-recognize the part of the lease liability that has been extinguished.

A change in lease payments that reduces payments in one period but proportionally increases payments in another

• No change to the overall consideration for the lease• Only the timing of individual payments changes• Continue to recognize interest on the liability• Reduce the liability for payments made to the lessor

Lease payments are reduced in one period but increased by a lower amount in a later period

• Incorporates both forgiveness and deferral of payments

• Immediate accounting for the variable payments

• Liability impacted only when payments are made

Lessee

16© Deloitte

Lease contracts and the specific circumstances of the Covid-19 pandemic

Transitional provisions for rent concessions

Change in payments

(rent concessions)

Transitional provisions

• Apply for annual reporting periods beginning on or after 1 June 2020. Earlier application is permitted, including in interim reports and in financial statements not yet authorisedfor issue at 28 May 2020.

• To be applied retrospectively

• Any difference arising on initial application recognized in the opening balance of retained earnings (or other component of equity, as appropriate) at the beginning of the annual reporting period of first-time application.

• Not required to disclose information required by IAS 8:28(f) (amount of the adjustment for each line item affected or effect on EPS)

Endorsed in EU 9th October 2020

Lessee

17© Deloitte

Lease contracts and the specific circumstances of the Covid-19 pandemic

Lease contracts and the specific circumstances of the Covid-19 pandemic Lessor

COVID-19 may impact the collectability of lease payments:

• If the lessor estimates that the lease income may not be collectable, can income still continue to be recognized?

• IFRS 16 does not include requirements to assess the probability for receiving payment.

• The lease receivables are subject to impairment testing under IFRS 9.

Finance leases

• IFRS 9 applies.

• Consider if lease modification changes the classification of the contract

If so, then account for as a new contract from the effective date of the modification

Operating leases

• Account for as a new contract from the effective date of the modification

Lease modifications

18© Deloitte

IASB – What’s new for 2020 and subsequent years

19© Deloitte

Overview

New and Amended Standards 2020 and Subsequent Years

Status: 12.10.2020 Endorsed

Amendments to

References to the

Conceptual

Framework in IFRS

Standards

IFRS 3

Definition of a

Business

IAS 1/IAS 8

Definition of

Material

IFRS 9/IAS 39/

IFRS 7

Interest Rate

Benchmark

Reform – Phase 1

IFRS 16

Covid-19-

Related Rent

Concessions

IFRS 9/IAS 39/ IFRS 7/ IFRS 4/IFRS

16

Interest Rate Benchmark Reform

– Phase 2

IFRS 3

References to the Conceptual

Framework

IAS 37

Onerous Contracts – Costs of

Fulfilling a Contract

IAS 16

PP&E: Proceeds before

Intended Use

AIP 2018-2020

IFRS 1, IFRS 9, IFRS 16, IAS 41

IFRS 17

Including Amendments to IFRS 17

IAS 1

Classification of Liabilities as

Current or Non-current including

Deferral of Effective Date

2020 2021 2022 20231.1. 1.6. 1.1. 1.1. 1.1.

20© Deloitte

Areas of IAS 1 impacted:

• Statement of financial performance (income statement)

• Statement of financial position (balance sheet)

• Statement of cash flow

• The notes:

• Unusual income and expenses

• Management Performance Measures (MPMs)

Current status and overview

Exposure Draft - General Presentation and Disclosures

OBJECTIVETo improve how information is communicated in the financial statements, with a focus on information included in the statement of profit or loss.

2015 2016-2019 Q4 2019 Q1-Q3 2020 Q4 2020

Agenda Consultationidentified the project

as a priority

Board discussion to develop Exposure

Draft

Exposure Draftpublished for public

comment

Comment period(ended 30

September)

Board starts redeliberations

Better Communication in Financial Reporting

Financial statements Outside the financial

statements

Content

Delivery

Primary

Financial

Statements

Disclosure

Initiative

Management

Commentary

IFRS Taxonomy

21© Deloitte

Statement of financial performance (income statement)

Exposure Draft - General Presentation and Disclosures

Subtotals in the statement of profit or loss

Revenue X

Other income X

Operating expenses X

Operating profit or loss X

Share of profit or loss of integral associates and joint ventures X

Operating profit or loss and income and expenses from integral associates and joint ventures X

Share of profit or loss of non-integral associates and joint ventures X

Dividend income X

Profit or loss before financing and income tax X

Expenses from financing activities (X)

Unwinding of discount on pension liabilities and provisions (X)

Profit or loss before tax X

Income tax (X)

Profit or loss for the year X

Operating

Integral associates

and joint ventures

Investing

Financing

Key changes in the profit or loss statement would include:

• Income and expenses would have to be categorized as operating,

investing, financing activities.

• Income and expenses from the main business activities are classified as

operating (which can be more than one activity) and will for some

industries include investing or financing, e.g. banks and property

investing.

• An entity would have to provide three additional mandatory subtotals

• Entities would be required to present their analysis of operating

expenses using the method (by nature or by function) that provides the

most useful information in the face of the statement of profit or loss.

• FX gains or losses shall be classified within the same category as income

or expenses giving rise to gain or loss.

• Result of designated hedge instruments and result of derivatives used

for risk management purpose (where hedge accounting is not applied –

economic hedge) shall be classified within the same category that is

affected by the risk so hedged or managed.

• Result of derivatives not used for risk management purpose and result

of economic hedges that cannot be allocated without involvement of

undue cost shall be included in the investing category.

22© Deloitte

Statement of cash flows (IAS 7)

Exposure Draft - General Presentation and Disclosures

Statement of cash flows

Operating profit X

Adjustment for:Depreciation

X

[…]

Income taxes paid (X)

Net cash from operating activities X

Acquisition of integral joint venture X (X)

Acquisition of non-integral associate Y (X)

Dividends received from integral associate A X

Dividends received from non-integral associate B X

Purchase of property, plant and equipment (X)

[…]

Net cash used in investing activities (X)

Dividends paid (X)

[…]

Net cash used in financing activities (X)

Net increase in cash an cash equivalents X

Consistent starting point for indirect method for operating cash flows

Separate presentation of cash flows from integral and non-integral associates and joint

ventures within invesing cash flows

Elimination of classification options for interest and dividends

23© Deloitte

Statement of financial performance (income statement)

Exposure Draft - General Presentation and Disclosures

Inve

stin

g ca

tego

ryFi

nan

cin

gca

tego

ry

Enable comparison of entities´performance before

their financing decisions.

Income and expenses on liabilities arising from financing activities

Interest income and expenses on other liabilities

Income and expenses from cash & cash equivalents

Objective is to communicate information about

returns from investment separately

Income and expenses from investments

Incremental expenses incurred generating income and investments from

investments

Objective Includes:

24© Deloitte

Classification of foreign exchange differences and of fair value gains and losses on derivatives and hedging instruments

Exposure Draft - General Presentation and Disclosures

Classify FX differences in the same category as income or expense giving rise to gain or

loss

• Exchange differences related to financing

activities

• Exchange differences on cash and cash

equivalents

Financing category

Exchange differences on investments Investing category

All other exchange differences Operating category

Used for risk

management

Designated as a

hedging

instrument

Not designated

as a hedging

instrument

Not used for risk management

Include in the category affected by the risk the

entity intends to manage, except when it would

involve grossing up gains and losses – then

include in the investing category

DerivativesNon-derivative

financial instruments

Classify as above except

when it would involve undue

costs or effort – then include

in the investing category

Include in the investing

category

Apply Board´s

definitions for

categories

Derivatives & Risk Management – P&L classificationFX gains or losses– P&L classification

25© Deloitte

Unusual income and expenses

Exposure Draft - General Presentation and Disclosures

In the notes to the financial statements, an entity would have to disclose and explain unusual items (i.e. income and expenses with limited predictive value) in a single note.

Definition

Disclosures

• Income and expenses with limited predictive value

• Income and expenses have limited predictive value when it is reasonable to expect that income or expenses that are similar in type and amount will

not arise for several future annual reporting periods

• Income and expenses from the recurring remeasurement of items measured at a current value would not normally be classified as unusual.

Amount & narrative

description

Amount disaggregated by:

• Line items presented in statement of profit or loss; and

• Line items disclosed in analysis of operating expenses by nature, if the entity analyses expenses by function in the

statement of profit or loss

26© Deloitte

Unusual income and expenses - examples

Exposure Draft - General Presentation and Disclosures

Past periods (not a decisive factor)

Reporting period Expectations for future periods

0

0

0

0 0

2,400 2,500

2,500

2,500

0 0 0 0 0

0 0 02,700 2,600

350 500 400 550 500 400 300 350

Unusual

Unusual

Not Unusual

Income/expense in reporting period:

27© Deloitte

Management performance measures (MPMs)

Exposure Draft - General Presentation and Disclosures

Information that constitutes management performance measures (MPMs):

• would be defined, and

• entities would be required to disclose all MPMs used in a single note to the financial statements, accompanied by disclosures aimed at enhancing their transparency.

Definition

Disclosures

Subtotals of income and expenses that:

• Are used in public communications outside financial statements

• Complement totals or subtotals specified by IFRS Standards

• Communicate management´s view of an aspect of an entity´s financial performance

Amount & narrative

description

Including:

• Reconciliation between the MPM and the most directly comparable total or subtotal specified by IFRS Standards; and

• Income tax effects and effects on non-controlling interests

28© Deloitte

ESEF

European Single Electronic Format

29© Deloitte

ESEF – European Single Electronic FormatNew reporting requirements for listed entities

ESEF is the product of the European Securities and Markets Authority’s (ESMA) development of regulatory technical standard (RTS) as to how this electronic reporting format would work.

• New reporting requirements apply to entities whose capital or debt is listed on a European regulated market. • The previous PDF format file will no longer comply with the requirements and new audit requirements of the electronic format are introduced.

Second key date

First key date

Annotation/Tagging

Preparation

3.

4.

1.

2.

• Consolidated IFRS statements will be digitally tagged using iXBRL

• iXBRL tagging will follow the published ESEF taxonomy

Periods beginning on or after 1 January 2020

• Entire AFR to be prepared in XHTML

• Primary consolidated financial statements to tagged in iXBRL(voluntary extended tagging of notes, etc. possible)

Periods beginning on or after 1 January 2022

• Entire AFRs to be prepared in XHTML

• Primary consolidated financial statements and the full set of disclosures and policies to tagged in iXBRL

• Issuers will prepare their entire Annual Financial Reports (AFRs) in XHTML format

30© Deloitte

ESEF – European Single Electronic FormatDefinition of key terms

XBRL• Another markup language, this time used for expressing

semantic meaning required for business reporting.• ESEF XBRL taxonomy defines the reporting concepts required

in ESEF compliant IFRS consolidated financial statements.

iXBRL • A mechanism for embedding XBRL tags into XHTML documents to make it machine readable.

• iXBRL tagged XHTML financial statements are commonly referred to as the “machine readable layer” in the context of ESEF.

XHTML• A markup language used to structure data within documents for presentation. An extension to HTML.

• Financial Statements will be prepared in XHTML, which is commonly referred to as the “human readable layer” in the context of ESEF

ESEF taxonomy• There is a specific XBRL taxonomy required for

ESEF tagging.• Based on IFRS taxonomy

31© Deloitte

ESEF – European Single Electronic FormatFiling process in Denmark

Current

Process

Future

Process

Annual report approved at

oard meeting

Annual reportapproved at general

assembly

Conversion to PDFConversion

to XBRL

Key steps

in annual reporting

process

Annual Report

preparation

Close and

ConsolidationDesign, review and sign-off

The conversion to xHTML/iXBRL has to be done before the board meeting, as tagging must be approved by

the Board.

Conversion to

‘DBA tagging’

xHTML/

iXBRL

conversion

The annual report - in xHTML and iXBRL format -has to be reported to the Danish FSA immediately

after approval by the Board.

As a consequence of the new requirements, a need for two

supplementary taggings occurs, (Danish FSA based on ESEF

taxonomy and DBA based on a DBA taxonomy)

Deadline for reporting to the Danish Business Authorities

(DBA)

32© Deloitte

ESEF – European Single Electronic FormatReporting – what changes?

For periods beginning on or after 1 January 2020, entities with debt or equity listed on a European regulated market will be required to prepare their AFR in accordance with ESEF (xHTML). Entities

who prepare consolidated financial statements in accordance with IFRS will have to XBRL-tag the primary financial statements within the xHTML-file (iXBRL).

Area of change Impact on management

AFR to be prepared and filed using the XHTML format and iXBRL tagging

• Understand the ESEF, XHTML and iXBRL requirements and develop processes and controls to prepare and authorise the ESEF filing

• If necessary, identify appropriate software or third parties to assist with the preparation of the filing

• Prepare or arrange to be prepared, the ESEF filings when the relevant financial statements have been audited and approved

Primary financial statements in the AFR to be tagged in iXBRL using the ESEF taxonomy

• Prepare initial mappings from the taxonomy to the primary financial statements, along with any voluntary tagging

• Identify requirements for any extensions and where to anchor them

• Consider preparing and tagging 2019 financial statements as a readiness exercise

• Involve the auditor in the process and make sure to include in the processes and time schedule, that the auditors has to conclude on the XBRL-tagging in the auditor’s report

33© Deloitte

ESEF – European Single Electronic FormatWhat to do now?

Step 2Step 1 Step 3 Step 4 Step 5

Identify and select software tool and/or an outsourcing partner

Review Tagging Accuracy before year-end and agree with your auditor

Incorporate relevant

internal controls in the

financial closing

process

Report the updated

Financial Closing process

to the audit committee

before year-end

Consider long-term

impact

34© Deloitte

Climate Change

Impact on Financial Statements

35© Deloitte

Climate Change – Impact on Financial StatementsImpact on narrative reporting and disclosure

Investors are concerned that companies do not disclose enough information about climate change and their strategy for handling the challenge.

Companies should address, and report on, the effects of climate change as they have a responsibility to consider their impact on the environment and the likely consequences of any business decisions in the long term.

From 2020, Danish companies in reporting class C (large) and D are required to disclose their principal risks and uncertainties arising in connection with the entity’s operations, including climate-related issues when they are material to the entity.

In the UK, the Financial Reporting Labs report, Climate-related corporate reporting, highlights examples of current best practice and is structured using the Taskforce on Climate-related Financial Disclosures (TCFD)’s core elements

The non-financial reporting regulations require Public Interest Entities (PIEs) with more than 500 employees within all EU member states to disclose information relating to environmental matters.

Information should include: • description of the principal risks

relating to environmental matters

• policies on environmental matters, due diligence over those policies and outcomes of the policies

Management’s review Taskforce on Climate-related Financial Disclosures

Non-financial reporting regulations (EU member states)

Examples of good disclosure

For examples of good climate change disclosures, we refer to:• The European Lab’s interactive

digital report that can be accessed here.

• Deloitte UK publication Annual report insights 2019: Surveying FTSE reporting, the TCFD 2019 Status Report, the TCFD Good Practice Handbook published by CDSB and SASB, and the FRC Financial Reporting Lab report: Climate-related corporate reporting.

36© Deloitte

Climate Change – Impact on Financial Statements

Dealing with uncertainties

It is necessary for companies to make assumptions about the impact of climate change when preparing cash flow projections that underpin measurement and recognition in the financial statements, including in the following areas:

The assumptions should be consistent with:

Forecasts of future availability of taxable profits in assessing recoverability of deferred tax assets

Going concern assessment over a period of at least 12 months from the date of signing the financial statements

Cash flow forecasts for determining value-in-use to assess impairments of assets and cash-generating units (CGUs)

Commitments made by the entity to investors and other stakeholders

Regulations and other commitments made by governments of jurisdictions in which the entity operates

Risk management, strategy and business model disclosure

37© Deloitte

Climate Change – Impact on Financial StatementsProvisions, contingencies and onerous contracts

The pace and severity of climate change, as well as accompanying government policy, may impact the recognition, measurement and disclosure of provisions, contingencies and onerous contracts.

Onerous contractsExisting contracts

may become onerous due to the cost of fulfilling a

contract increasing or due to the benefits from fulfilling the

contract decreasing.

TimingThe timing of when an asset may need

to be decommissioned

may change, accelerating the

required cash outflows for asset

retirement obligations.

New obligationsNew provisions may need to be

recognised due to new obligations or

due to existing obligations now

being considered probable.

DisclosureNew contingencies

may need to be disclosed for

possible obligations, or due

to existing contingencies

previously considered remote becoming possible.

AssumptionsCash flows and

discount rates used in measuring

provisions need to take into account

the risks and uncertainties of

climate change and accompanying

regulations.

38© Deloitte

Corporate Governance

39© Deloitte

ESG in the Context of Financial Reporting

Definition of ESGs and ESG metrics

Definition of ESGs and ESG metrics

ESG generally means a broad set of environmental, social and corporate governance considerations that may impact an entity´s ability to execute its business strategy and create value over the long-term.

While ESG factors are at times non-financial, how an entity manages them undoubtedly have measurably financial consequences. Hence, the ESG Reporting Guide provides suggested ESG metrics to consider such as:

Environmental (E) Social (S) Corporate Governance (G)

Energy usage

Energy mix

Water usage

Environmental operations

Climate oversight

Climate Risk Mitigation

CEO Pay Ratio

Gender Pay Ratio

Employee Turnover

Gender Diversity

Injury Rate

Board Diversity

Data Privacy

Ethics and Anti-Corruption

Disclosure practices

External Assurance

40© Deloitte

Engage investors, customers and employees in the effort

Manage and measure ESG performance according to well-defined KPIs

Assign resources to address material ESG issues to assist with ESG strategy

Align ESG with the core strategy, products/services, and operations of the company

ESG in the Context of Financial ReportingESG management framework

ESG management framework

The right management approach to ESG is still somewhat undetermined, but there is a process taking root. An influential Thompson Reuters blogpost argued for the following procedures:

3

4

1

2

41© Deloitte

The Audit Committee role related to ESG reportingAudit Committees face front-line sustainability risks

The increased focus on ESG has reinforced the critical importance of credible, reliable, transparent disclosure regarding how an entity drives its strategy over the long term

• Audit committees are not expected to be experts in specific ESG issues, but they are ideally situated in organisations to proactively engage with management in appropriate

discussion and advise how information is presented to investors.

• Audit committees can be most effective in this role if they begin by asking the right probing questions and knowing where to turn to find the information.

• As an important component of an effective governance structure, external assurance also plays an important role in helping organisations bring rigor and discipline in their

reporting of ESG issues.

Investors focus on enterprise risk

to the benefit of the wider stakeholders

by seeking insights into financial impact of climate and other ESG

risks

42© Deloitte

Preparing for Mandatory Remuneration Reports for 2020The Danish Business Authority (DBA) recommends using ‘granted pay’ as primary reporting

Content of the remuneration report for 2020

Explanation of how total remuneration complies with the

policy, including how it contributes to the entity’s long-term performance

Information on how the performance criteria were applied

Relative proportion of fixed and variable remuneration

Annual change in remuneration over a six-year period for each director

compared to entity performance and average employee remuneration (on

FTE basis), excluding directors

For each individual director, total remuneration broken down by

component

43© Deloitte

Practical Examples of Remuneration ReportsWhat to include and how to present the information, including a statement by the board of directors and in the independent auditor’s report

ALK 2019 ChemoMetec 2019/20

Novo Nordisk 2019

Ørsted 2019

Vestas 2019

44© Deloitte

The Independent Auditors’ Report on Remuneration ReportsBoards should plan for the appropriate level of assurance on remuneration reports to add value to shareholders

Possible options for levels of assurance from the independent auditor

2

3

4

5

Reasonable assurance on

Manage-ment’s compliance with section 139b(3)

Consistency check as part of

audit

Limited assurance

report

Audit opinion of certain numbers

1

No assurance, but a statutory

statement

45© Deloitte

Remuneration ReportingAt Deloitte, we guide clients on strategy, design, committee work, policy, implementation, communication and reporting

RemunerationDesign

RemunerationCommittee

RemunerationPolicy

Implementation& Communication

RemunerationReporting

RemunerationStrategy

New remuneration

program

46© Deloitte

New Draft Danish Recommendations on Corporate GovernanceSignificant proposed changes expected to be effective from 2021

New elements focus on sustainability, social responsibility, overall purpose of the entity, tax and diversity policies as well as board and management evaluations

Extended policy relating to corporate social responsibility, including sustainability and social responsibility, which should be made available on the entity´s website.

New recommendation that the Board of Directors approves a tax policy and makes it available on the entity's website.

New recommendation that the Board of Directors consider to the entity's overall objective which is also to be disclosed in the management’s review of the annual report.

New policy on diversity in the entity to be disclosed in the management’s review of the annual report.

Increased focus on importance of evaluation of the Board of Directors and the Executive Management, and the value of involvement of external support.

47© Deloitte

IFRS in focus

48© Deloitte

COVID-19 and its Impact on Financial ReportingIAS 2 - Valuation of inventories

Some entities with inventories that are seasonal or are subject to expiration have to assess whether a write-down for obsolescence or slow-moving inventories may be necessary as a result of a slower sales pace.

Write down for obsolescence

Other entities may have to assess whether a decline in their future estimated selling price is expected, which may require a write-down in the cost of inventory which are measured at the lower of their cost and net realizable value (NRV).

As a result of the pandemic, the NRV of an item of inventory may fall below its cost, e.g. a decline in selling prices or an increase in the estimate of costs to complete and market the inventories.

Manufacturing entities may have to reassess their practices for fixed overhead cost absorption if production volumes become abnormally low during the year as a result of plant closures or lower demand for their products.

The COVID-19 pandemic may affect manufacturing entities which may result in an abnormal reduction of an entity’s production levels. In such circumstances, an entity should not increase the amount of fixed overhead costs allocated to each inventory item. Rather, the unallocated fixed overhead costs are recognized in profit or loss in the period in which they are incurred.

Net realizable value

Overhead costs

49© Deloitte

COVID-19 and its Impact on Financial ReportingFinancial instruments – allowance for expected credit losses (ECL)

IFRS 9 (in general)

Applying IFRS 9 Financial Instruments, an entity should measure ECL in a way that reflects:

The impact of COVID-19 on ECL will be particularly challenging and significant for banks and other lending businesses. The effect could also be significant for non-financial corporates.

Reasonable and supportable information that is available without undue cost or effort at the reporting date about past events, current

conditions and forecasts of future economic conditions

An unbiased and probability-weighted amount that is determined by evaluating a range of possible outcomes;

The time value of money;

50© Deloitte

COVID-19 and its Impact on Financial ReportingFinancial instruments – allowance for expected credit losses (ECL)

COVID-19 will require entities to

revisit the provision matrix approach

and consider these 4 areas

Operational disruption introduces uncertainty as to whether the full amount will be recovered and this uncertainty is required to be reflected in the ECL measurement.

Uncertainties

An entity may already be observing the default of debtors and will need to determine the impact that these observations have on expectations of recoveries and future default of other debtors.

Default of debtors

Loss rates may need to be applied to individual receivables or sub-portfolios of receivables if the

receivables in the overall portfolio no longer exhibit similar credit risk characteristics.

Portfolio approach

Reconsider previous credit loss expectations if these are based on unadjusted historical experience that is

not reflective of the current market conditions.

Unadjusted historical experience

Trade receivables and contract assets

51© Deloitte

COVID-19 and its Impact on Financial Reporting

Revenue from contracts with customers

Factors to consider as a result of COVID-19 when assessing revenue from contracts with customers:

the time value of money; and

Business disruptions associated with the COVID-19 pandemic may prevent an entity from entering into customer agreements by using its normal business practices.

Entities may need to develop additional procedures to properly assess the collectability of its customer arrangements and consider changes in estimates related to variable consideration.

Variable consideration

Update the estimated transaction price if expecting

• an increase in product returns, • decreased usage of goods or services or royalties• to potentially pay contractual penalties

Recognition of revenue

• If not able to fulfil the stand-ready obligation due to government-mandated shutdowns, you may need to cease recognising revenue until being able to perform.

Contract enforceability

• You may not be able to obtain the signatures you normally obtain when entering into a contract and thus a contract with enforceable rights and obligations between you and the customer.

Collectability

• Evaluate whether those circumstances result in a determination that it is no longer probable that the customer has the ability to pay, resulting in no revenue recognition under IFRS 15.

Factors to consider

52© Deloitte

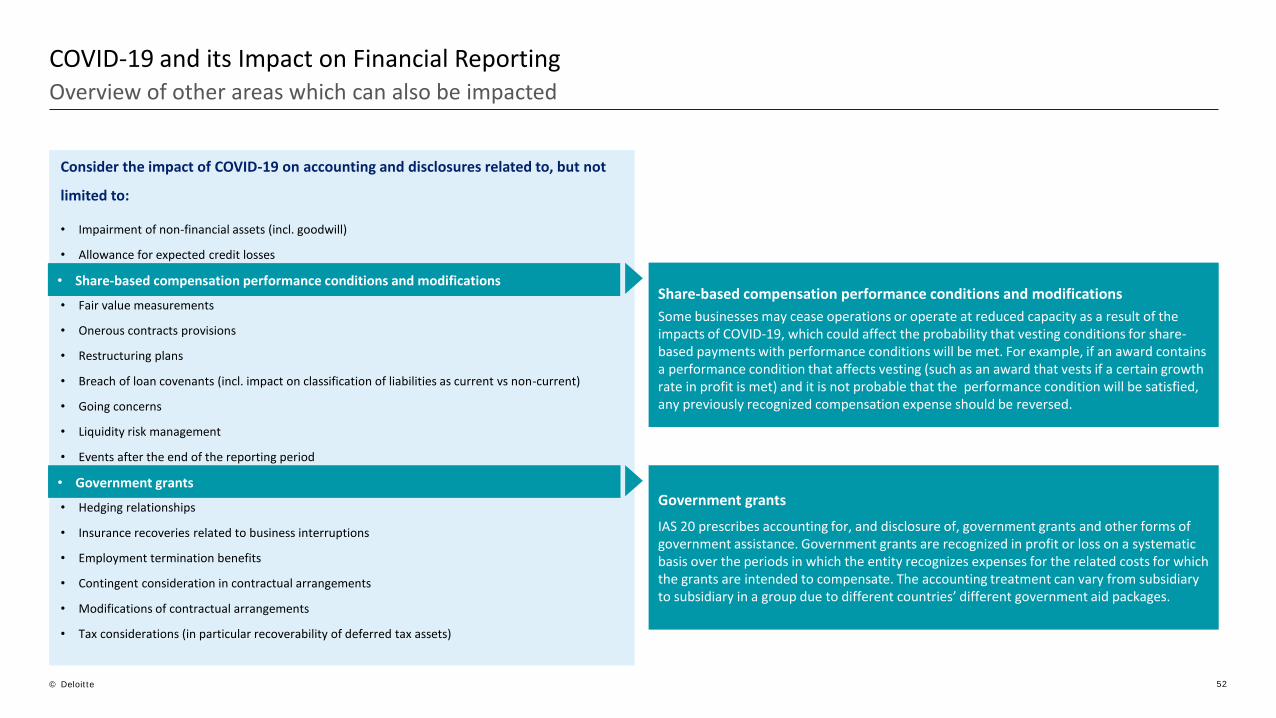

Consider the impact of COVID-19 on accounting and disclosures related to, but not

limited to:

• Impairment of non-financial assets (incl. goodwill)

• Allowance for expected credit losses

• Fair value measurements

• Onerous contracts provisions

• Restructuring plans

• Breach of loan covenants (incl. impact on classification of liabilities as current vs non-current)

• Going concerns

• Liquidity risk management

• Events after the end of the reporting period

• Government grants

• Hedging relationships

• Insurance recoveries related to business interruptions

• Employment termination benefits

• Contingent consideration in contractual arrangements

• Modifications of contractual arrangements

• Tax considerations (in particular recoverability of deferred tax assets)

• Share-based compensation performance conditions and modifications

COVID-19 and its Impact on Financial ReportingOverview of other areas which can also be impacted

• Government grants

Share-based compensation performance conditions and modifications

Some businesses may cease operations or operate at reduced capacity as a result of the impacts of COVID-19, which could affect the probability that vesting conditions for share-based payments with performance conditions will be met. For example, if an award contains a performance condition that affects vesting (such as an award that vests if a certain growth rate in profit is met) and it is not probable that the performance condition will be satisfied, any previously recognized compensation expense should be reversed.

Government grants

IAS 20 prescribes accounting for, and disclosure of, government grants and other forms of government assistance. Government grants are recognized in profit or loss on a systematic basis over the periods in which the entity recognizes expenses for the related costs for which the grants are intended to compensate. The accounting treatment can vary from subsidiary to subsidiary in a group due to different countries’ different government aid packages.

53© Deloitte

Enforcement Outlook 2020

54© Deloitte

ESMA Enforcement Priorities for 2020Deloitte expectation – final publication outstanding

Based on experience from prior years, ESMA will most likely focus on

• Economic, market (e.g. COVID-19) or industry conditions

• Application of new IFRSs that might have lead to diversity in practice

• Significant level of judgement required applying IFRSs

• Topics identified through EU enforcement work

• Important topics at EU level

• NFI information

• Areas, where disclosure improvements is warranted

European Common Enforcement Priorities

published

Experience from prior years shows that ESMA starts planning in early summer through collection of input

from EU enforcers and any market information about topics that could be relevant.

Autumn (end of October) 2020Early summer 2020

55© Deloitte

Trends in Financial Reporting

56© Deloitte

Trends in Financial ReportingLatest trends and insights in financial reporting from Denmark

01Climate and sustainabilityIncorporating environmental data and strategy in the management report as well as sustainability throughout the annual report.

02Remuneration policy & reportingInclude information regarding remuneration reports and policies on the entity´s website or in the annual report. Preferably only a link to the website to reduce the size of the annual report.

Location of alternative reportsInclude a short summary for alternative reports such as CSR, diversity and sustainability in the management report and link it to the entity´s website.

03

04

05

06

Description of work in the different committees of the board of directorsGiving information about the number of meetings and members´ participation to become more transparent.

Inclusion of non-financial informationEnsure a link between financial and non-financial information (NFI) and inclusion of non-financial information in the business model within the annual report.

Expectations for the futureClear description of the expectations for the coming years kept to a relevant level with focus on significant risks and business model.

57© Deloitte

Trends in Financial Reporting Latest trends and insights in financial reporting from Denmark – cont.

07

08Focus on materialityLeaving out irrelevant information and explaining why it is left out. 09

10Introduction page with groupingIntroduction page in the annual report with grouping of notes to provide an overview of the developments, graphic illustrations and significant key figures.

Annual report preparation effectivenessAn efficient closing process transforms the resource intensive process of preparing the annual report to a smooth and efficient process leaving room for the finance team to take on other value adding projects.

IFRS 16 disclosuresDescription of IFRS 16 in the summary of significant accounting policies and notes including its impact, preferably on one page to improve transparency for the user and give a clear understanding of its effects.

Introduction

What should companies do?

Regulators expectations

Taskforce on Climate-related Financial

Disclosures (TCFD) recommendations

Governance

Types of climate change risk

Risk management and strategy

Metrics and targets

Impact on the financial statements

Impact on narrative reporting

Where to find examples of good disclosure

Contacts

Appendix – Climate Change FAQ

Introduction

As the world looks for pathways to an economic recovery from the impact of the

COVID-19 pandemic, action on climate change is emerging as a centrepiece of the

strategies being explored. Governments and businesses are looking into how they

can stimulate a sustainable economic recovery through accelerated

decarbonisation and growing a more inclusive, low-carbon economy.

The COVID-19 pandemic will continue to have dramatic effects across societies and

on the global economy for years to come. At the same time, we know that climate

change is also likely to drive some of the most profound and persistent changes to

business in our lifetimes. Impacts on products and services, supply chains, loss of

asset values and market dislocation are already being caused by more frequent

and severe climate-related events. These effects are now compounded by the

accelerating pace of policy and regulatory change, as humanity recognises the

challenge we face and the drastic and rapid actions we must all take in order to

protect our planet and our own livelihoods.

A growing number of scientific projections detail not only potential average

increases in global temperatures, but also the consequences, such as rising sea

levels and more frequent extreme weather events. Economic forecasts are also

increasingly reflecting these impacts, including related factors such as carbon

pricing initiatives and changing demand for fossil fuels and renewable energy. It is

critical to recognise that the past is no longer a predictor of the future.

A closer look Climate change - from a Danish perspective

For more information, please see the website

of Deloitte UK:

https://www.deloitte.co.uk/climatechange/

Investors, regulators and other business stakeholders are increasingly demanding

better disclosures on climate change matters and challenging companies that are

not factoring the effects of climate change into their critical accounting judgements.

Revenues, costs and asset lives could be impacted, and companies will need to

reassess their future cash flow forecasts and related management judgements

relating to impairment, asset retirement obligations, provisions and going concern.

In February 2020, the Danish parliament announced its proposal for a climate law,

including the legally binding climate targets for Denmark to reduce its greenhouse

gas emissions in 2030 by 70 percent compared to the level in 1990 and its

commitment to reach climate neutrality by 2050.

The proposal is ambitious and has already given rise to debate. The original

timetable for parliamentarian negotiations is delayed and the proposal has only

been discussed at the first reading.

Investors are challenging companies that are not factoring the effects of the Paris

Climate Agreement into their critical accounting judgements and are not disclosing

comprehensively these judgements, assumptions, sensitivities and uncertainties.

For example:

Climate Action 100+, a global investor initiative, is actively targeting the world’s

largest corporate greenhouse gas emitters to ensure that they take necessary

action on climate change. Climate Action 100+ involves over 370 investors

collectively representing $35 trillion in assets.

The Institutional Investors Group on Climate Change (IIGCC) published a

discussion paper, Voting for better climate risk reporting: the role of auditors and

audit committees, which emphasises the powerful levers that shareholders have

to hold boards and auditors to account for inadequate climate risk reporting.

What should companies do?

Regulators expectations

In response to reporting on climate, ESMA, in its Common Enforcement Priorities 2019, has drawn issuers’ attention to various

guidelines on climate, noting that they are useful in helping companies provide relevant information to explain the financial

consequences of climate change. In the UK, the regulator FRC (the Financial Reporting Council) issued a statement saying:

The FRC went on to say that they expect companies to disclose:

how climate change has been taken into account in assessing the resilience of the business model, its risks, uncertainties and

viability in the immediate and longer term; and

the current or future impacts of climate change on their financial position, for example in the valuation of assets, assumptions used

in impairment testing, depreciation rates, decommissioning, restoration and other similar liabilities and financial risk disclosures.

For Danish companies in reporting class C (large) and D, existing reporting obligations are included in section 99a (sustainability

report) of the Danish Financial Statements Act.

TCFD adoption

Assess readiness to make disclosures in line with those recommended by TCFD

Narrative reporting

Ensure that climate change disclosures in narrative reports are clear, balanced and meaningful

Financial statements

Reassess assumptions used in cash flow projections that underpin recognition and measurement

Provide transparent disclosures of the underlying assumptions used in the preparation of the financial statements

Metrics and targets

Set metrics and targets to address climate change effectively

Risk assessment and strategy

Assess climate change risk and opportunities and their implications on the business model

Governance

Bring climate change onto the board agenda Develop processes for considering the impact of climate change

“The Boards of UK companies have a responsibility to consider their impact on the environment and the likely consequences of any

business decisions in the long-term. They should therefore address, and where relevant report on, the effects of climate change (both direct

and indirect).”

In June 2019, the FSR - Danish Auditors published, in collaboration with CFA Society Denmark and Nasdaq – with assistance from ESG

Research – 15 suggestions about standardised ESG key figures for the annual report. The publication presents a standardised overview

of ESG key figures that can be published in the annual report together with the financial main and key figures. The objective of the ESG

key figure overview is to harmonise and standardise the basic ESG key figures, mainly for the benefit of analysts and investors.

The FRC’s Financial Reporting Lab (the Lab) published a report in October 2019, Climate-related corporate reporting, which aims to

reflect the views of investors on existing reporting by companies and to help companies move towards more effective and

comprehensive reporting. Structured around the TCFD framework, the Lab’s report sets out challenging questions for boards to ask

themselves and examples of good practice.

In its Annual Review of Corporate Reporting, and in an open letter to all Audit Committee Chairs and Finance Directors, the FRC has

further emphasised their expectation that boards address and report on the effects of climate change. The FRC has stated:

Taskforce on Climate-related Financial Disclosures (TCFD) recommendations

The TCFD was established by the Financial Stability Board to identify the information needed by investors, lenders, and credit and

insurance underwriters to assess and price appropriately climate-related risks and opportunities. It developed a framework to

facilitate voluntary, consistent climate-related financial disclosures, building on existing disclosure regimes.

The TCFD’s core recommendations are universally applicable to organisations across sectors and jurisdictions. They are structured

around core elements of how organisations operate: Governance; Strategy; Risk Management; and Metrics and Targets, and include

11 detailed recommended disclosures. The TCFD has also produced general and sector-specific guidance, and a technical supplement

on scenario analysis.

The TCFD recommendations are gaining momentum and have become the generally accepted framework for businesses to explain

their approach to climate change-related risk. Since their release in June 2017, the recommendations have received public support

from over 800 organisations. They include investors, banks and other financial institutions that are responsible for more than US$ 100

trillion in assets. The recommendations have been galvanising conversations about the impact of climate change on business.

In its May meeting 2020, the IASB amongst other discussed what guidance should be included in the revised Practice Statement 1

Management Commentary on risk that an entity faces, one of these risks being climate-related risks.

The European Commission (EC) has published new guidelines on reporting climate change-related information integrating the

recommendations of TCFD. ESMA, in its Common Enforcement Priorities 2019, draws issuers’ attention to these guidelines, noting that

they are useful in helping companies provide relevant information to explain the financial consequences of climate change.

The European Corporate Reporting Lab @ EFRAG (EU Lab) as its first project was investigating how to improve climate-related

reporting. The work resulted in a report and two supplements analysing reporting practices on climate-related disclosures and

scenario analysis derived from review of 149 companies and dialogues with stakeholders. This resulted in the identification of 58

examples of good reporting practices selected from 30 companies. The report also highlights areas for improvement and articulates

preparers' and users' perspectives on climate-related reporting. The European Lab’s environmental-friendly interactive digital report

can be accessed here.

The Financial Reporting Lab in the UK issued a report on climate change which sets out the questions boards should ask themselves

when considering the adequacy of their reporting in relation to TCFD.

For further information, please refer to the IFRS in Focus — Task Force on Climate-related Financial Disclosures issues its final report.

Governance

“In times of uncertainty, investors and other stakeholders expect greater transparency of the risks to which companies are exposed and

the actions they are taking to mitigate the impact of those uncertainties. The FRC expects companies to think beyond the period covered

by their viability statement and identify those keys risks that challenge their business models in the medium to longer term and have a

particular focus on environmental issues.”

The TCFD recommends that companies disclose the organisation's governance around climate-related risks and opportunities by

describing:

the board’s oversight of climate-related risks and opportunities; and

management’s role in assessing and managing climate-related risks and opportunities.

At its 2019 annual meeting, the World Economic Forum (WEF) published guidance for boards: How to Set Up Effective Climate

Governance on Corporate Boards: Guiding principles and questions.

Types of climate change risk

The TCFD recommendations divided climate change risks into two categories: physical risks and transition risks.

Physical risks

Physical risks are associated with disruption to business activities from climate change. Physical risks can be acute, one-off disruptions

such as from extreme weather events and they can also be chronic – gradual changes that have a more lasting impact e.g. due to

changing rain patterns, rising mean temperatures and sea levels, or prolonged periods of heat or drought.

Impacts from climate change-related events can be widespread across a company’s operations, with significant financial

consequences. Climate change can affect a business’s facilities, operations, supply and distribution chains, employees and customers.

Risks to businesses include:

Reduced revenue and/or increased operating costs arising from supply chain interruptions, reduced production capacity or impact

on the workforce.

Increased capital expenditure to protect operations and supply chains, or repair damage caused by climate change-related events.

Increased financial risk through higher cost of capital or cost of insurance in high-risk locations.

Write-offs and early retirement of existing assets.

Transition risks

Transition risks arise from moving to a low-carbon economy, i.e. how governments and business stakeholders respond to the global

commitment to limit the global temperature increase to 1.5-2°C.

Transition risks consist of policy and legal risks, technology risks, market risks and reputation risks as a result of transitioning to a

lower-carbon economy.

Policy and legal risks – Policy actions by governments may tighten regulation, cap the use of resources, or introduce carbon taxes.

These can all reduce demand for products and services, or increase operating costs. An increase in climate-related litigation claims

heightens legal risks.

Technology risks – New technologies that support the transition to a lower-carbon economy can impact the demand for existing

products. Furthermore, the cost of researching and developing alternative technologies can be high. Unsuccessful innovations may

have to be written off.

Market risks – Consumers are increasingly looking for low-carbon products and services, such as food, clothing, energy and travel. This

can lead to reduced demand for existing products and services as ‘green’ products become more attractive. Changing markets and

availability of resources can also lead to increased costs of raw materials and production.

Reputation risks - Risks connected to society’s trust in business are increasing. Stakeholders have higher expectations of how

businesses are responding to climate change issues.

Risk management and strategy

TCFD recommends that companies disclose how the organisation identifies, assesses, and manages climate-related risks, by

describing:

the organisation’s processes for identifying and assessing climate-related risks;

the organisation’s processes for managing climate-related risks; and

how processes for identifying and assessing, and managing climate-related risks are integrated into the organisation’s

overall risk management.

TCFD recommends that companies disclose the actual and potential impacts of climate-related risks and opportunities on the

organisation's businesses, strategy, and financial planning where such information is material, by describing:

the climate-related risks and opportunities the organisation has identified over the short, medium, and long term;

the impact of climate-related risks and opportunities on the organisation’s businesses, strategy, and financial planning;

and

the resilience of the organisation’s strategy, taking into consideration different climate-related scenarios, including a 2°C

or lower scenario.

When assessing climate change risk, it is important to appreciate that no company is immune. Every company will be affected. Risks

may lie outside of the immediately consolidated boundary and it is necessary to consider a company’s supply/value chain and its

business model. It is also necessary to consider multiple layers of uncertainty and long-term horizons. This starts from understanding

the scientific facts and the impacts that physical risks could have on the business, and how these might translate into policy or

regulatory changes.

Factors that may significantly affect a company’s specific exposure to climate change risk include:

Geography and jurisdiction of operations.

Life cycle of operations, including life of infrastructure etc.

Specific business model and business practices.

Societal/Political instability arising from the cumulative impact of multiple physical risk impacts.

Macroeconomic impacts arising from the cumulative impact of multiple physical and transition risk impacts.

The following resources may be helpful when assessing your company’s climate change risk:

European Environment Agency, Climate Change, Impacts And Vulnerability in Europe 2016 (2017)

Taskforce for Climate-related Financial Disclosures, Final Report (2017) and 2019 Status Report (2019)

World Economic Forum Strategic Intelligence

Metrics and targets

In order to address climate change effectively, companies should adopt metrics and targets as part of their wider risk management

and strategy development. They provide a common language for articulating the threats that exist to the business arising from climate

change.

While many frameworks and metrics are used to report climate-related financial information, two are widely accepted and broadly

aligned with the TCFD recommendations, as follows.

The Carbon Disclosure Standards Board (CDSB) Framework provides guidance, principles and content elements (i.e. requirements)

on reporting to investors in a mainstream filing about climate, natural capital and other environmental issues. Although it takes a

less prescriptive approach to the disclosure of indicators and other metrics, the CDSB Framework achieves nearly full alignment

across the TCFD’s 11 recommended disclosures, and signposts the TCFD’s recommended disclosures.

The Sustainability Accounting Standards Board (SASB) Standards are designed for reporting to investors on financially material

environmental, social and governance issues through metrics and disclosures for 77 industries. The SASB Standards are well-

aligned overall with the TCFD recommendations. They are also complementary with the TCFD’s Governance, Strategy and Risk

Management core elements.

SASB and CDSB have produced the TCFD Implementation Guide demonstrating how the two bodies’ guidance can be used to make the

11 recommended disclosures of the TCFD.

The level of vulnerability and existing capability to deal with climate change will vary from business to business. Each company needs

to focus on the most important risks for its circumstances. Where practical, seeking subject matter expertise in relation to a specific

risk can help companies to determine the correct metrics and targets and also challenge underlying assumptions.

Companies may also set targets that are aligned to the goals of the Paris Agreement, for example through the Science Based Targets

initiative. Its website includes helpful guidance on how to go about setting targets to drive change.

TCFD recommends that companies disclose the metrics and targets used to assess and manage relevant climate-related risks

and opportunities where such information is material, by:

disclosing the metrics used by the organisation to assess climate-related risks and opportunities in line with its strategy

and risk management process;

disclosing Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks; and

describing the targets used by the organisation to manage climate-related risks and opportunities and performance

against targets.

Impact on the financial statements

To a greater or lesser extent, the risks and uncertainties arising from climate change are likely to have an impact on the financial

statements of all companies.

Dealing with uncertainty

There is significant uncertainty around by how much the global temperature will increase, what the impact of different climate change

scenarios on a company’s business might be, and how these factors may result in changes to cash flow projections or to the level of

risk associated with achieving those cash flows.

It is therefore necessary for companies to make assumptions about the impact of climate change when preparing cash flow

projections that underpin measurement and recognition in the financial statements, including in the following areas:

Cash flow forecasts for determining value-in-use to assess impairments of assets, cash-generating units (CGUs) and goodwill.

Forecasts of future availability of taxable profits in assessing recoverability of deferred tax assets.

Going concern assessment over a period of at least 12 months from the date of signing the financial statements.

The assumptions should be consistent with:

risk management, strategy and business model disclosure;

commitments made by the company to investors and other stakeholders; and

commitments made by governments of jurisdictions in which the company operates, e.g., the Danish Climate Act proposing legally

binding climate targets for reducing greenhouse gas emissions in 2030 by 70 percent compared to the level in 1990 and to reach

climate neutrality by 2050 in accordance with the 2016 Paris Agreement.

In line with investor and regulatory demand for transparency, disclosures of assumptions made in the preparation of the financial

statements should be clear, balanced and meaningful.

Going concern assessment

All companies are required to make a rigorous assessment of whether a company is a going concern when preparing financial

statements. The period of assessment will be determined by the directors. Whilst this should cover a period of at least 12 months

from the approval of the financial statements, it could be significantly longer. This is because in making their assessment, directors

should consider all available information about the future at the date they approve the financial statements, such as the information

from budgets and forecasts.

Impairment of non-financial assets

The uncertainties in relation to climate change may result in changes to management’s cash flow projections or to the level of risk

associated with achieving those cash flows, in which case they form part of a value-in-use assessment. For instance:

Revenue streams and growth forecasts may need to change to reflect changing customer preferences, technology and market

trends.

Increased cost of resources and production, costs of compliance with new policies or legislation or rising cost of insurance may

need to be factored in.

Availability of finance and net impact of availability of insurance on cost of finance should be considered.

A company should consider the following with regard to value-in-use calculations:

Incorporation of changes

expected to occur beyond

the period covered by

financial budgets and

forecasts

If management’s best estimate is that a climate change-related event will affect cash flows beyond the forecast or

budget period, it would be inappropriate to exclude this from a value-in-use calculation by simply extrapolating

budgeted or forecast cash flows using an expected rate of general economic growth. Instead, the extrapolation

of budgeted or forecast cash flows should be modified to incorporate the anticipated timing, profile and

magnitude of the effect of climate change.

Incorporation of expected

changes in consumer

behaviour into estimates

of future cash flows

Management’s best estimate of any forecast changes in consumer behaviour expected to result in (positive or

negative) changes in either the volume or price of future sales should be included in a value-in-use calculation

(e.g., a decreased demand for products with an environmental impact). The same approach should be applied to

expected changes in the behaviour of a company’s suppliers, who may themselves react to changing

expectations of society, resulting in changes to a company’s cost base.

Incorporation of expected

government action into

estimates of future cash

flows

Judgement will be required in determining when expected government action, such as a levy on greenhouse gas

emissions, should be factored into cash flow forecasts. However, it is not appropriate to wait for the enactment

of a change before it is incorporated into an estimate of future cash flows. If management’s best estimate is that,

whilst the exact nature or form of the government legislative or regulatory action is not certain, there will

nonetheless be an effect on the company’s cash flows, then the expected changes in cash flows should be

included in a value-in-use calculation.

Consideration of

restructuring or capital

expenditure plans

Determining whether a change in the scope or manner of operations due to climate-related factors meets the

definition of a restructuring to be excluded from a value-in-use calculation will require judgement. In applying

that judgement it will often be necessary to consider whether either the output or the process of producing that

output will change significantly (indicating a material change that is excluded until the company is committed), or

whether the change is a refinement to that output or process (indicating that the change does not meet the

definition of a restructuring) and should be included.

Expenditure on

maintaining and

improving assets

If an asset is expected to be replaced due to climate-related factors by an asset that does not significantly

change the manner of operations, but instead is a technological upgrade fulfilling the same function, then the

expenditure on the replacement (and resultant continuation of cash inflows) should be included in a value-in-use

calculation. Conversely, if the replacement asset enhances the economic output of the asset or cash-generating

unit, the expenditure on the replacement (and resultant continuation of cash inflows) should not be included in a

value-in-use calculation.

Disclosure of climate as a

key assumption

When climate change is a significant factor in a value-in-use calculation, the key assumptions applied together

with a description of management’s approach to determining the value assigned to each key assumption should

be disclosed. When relevant, this disclosure should provide an explanation of not only the key assumption, but

also of its forecast effects on the company’s future cash flows.

In the UK, the FRC’s Thematic Review on Impairment of Non-Financial Assets, published in October 2019, stated that:

Log into or subscribe to the Deloitte Accounting Research Tool (DART) for further guidance and examples of climate change-related

impairment considerations.

Useful lives of assets

Climate change-related factors may indicate that an asset could become physically unavailable or commercially obsolete earlier than

previously expected. Furthermore, the expected timing of the replacement of existing assets may be accelerated. Such factors should

be incorporated into a review of an asset’s useful economic life.

“… when preparing impairment related disclosures in 2019 accounts… companies for whom climate change and environmental impact

are significant will explain how such factors, specific to the company’s industry and value chain, have been taken into account in assessing

medium and long term growth potential, costs and licence to operate.”

Provisions, contingencies and onerous contracts

The pace and severity of climate change, as well as accompanying government policy and regulatory measures, may impact the

recognition, measurement and disclosure of provisions, contingencies and onerous contracts.

New provisions may need to be recognised due to new obligations (for example, fines levied for polluting activities or for failing to

meet climate-related targets), or due to existing obligations now being considered probable.

The timing of when an asset may need to be decommissioned may change, accelerating the required cash outflows for asset

retirement obligations.

New contingencies may need to be disclosed for possible obligations, or due to existing contingencies previously considered

remote becoming possible.

Cash flows and discount rates used in measuring provisions need to take into account the risks and uncertainties of climate change

and accompanying regulations.

Existing contracts may become onerous contracts due to the cost of fulfilling a contract increasing – for example, due to an increase

in the cost of energy or water – or due to the benefits from fulfilling the contract decreasing.

Assumptions underlying asset retirement obligations is a particular area of investor focus. Transparent disclosures of the key

assumptions applied should be included in the financial statements. In addition, sufficient information should be disclosed to help

users understand the level of sensitivity of asset retirement obligations to changes in the key assumptions used. For example, such

disclosures might include sensitivity analysis as to the timing of the asset retirement obligations.

Key judgements and estimates disclosures

If assumptions related to the impact of climate change have a significant risk of resulting in a material adjustment to the carrying

amounts of assets and liabilities within the next financial year, then disclosures about the nature of the assumptions should be

provided.

In addition, sufficient information should be disclosed to help users understand the level of sensitivity of assets and liabilities to

changes in the assumptions used. Sensitivity analysis provides an important insight when the level of uncertainty is high and factors

affecting it are complex. A wider range of reasonably possible outcomes may be relevant in some cases when performing sensitivity

analysis and those need to be disclosed and explained. One approach to explaining the possible impact of uncertainty would be to

disclose the results of scenario testing, including qualitative and quantitative information about the potential effects of different

scenarios, if possible. Alternatively, the disclosures could be provided in narrative form, explaining the potential impact of a different

outcome occurring.

Estimates where the risk of material adjustment is not significant within the next year should not be included in the IAS 1 key estimates

disclosure to avoid obscuring key messages about those items that are in scope. However, disclosure may nevertheless be necessary

for an understanding of the financial statements (see below).

For further guidance refer to our IFRS in Focus Spotlight on key judgements and estimates disclosures.

Information that is relevant to understanding the financial statements

If investors could reasonably expect that climate change-related risks will have significant impact on the company and this would

qualitatively influence investors’ decisions, then management should clearly disclose information about the climate change

assumptions that they have made (if not disclosed elsewhere), including disclosures around the sensitivity of those assumptions. This

is to enable users to understand the basis of forecasts on which the financial statements are prepared. This may mean that disclosure

is provided even if the effects of climate change on the company may only be experienced in the medium to longer term.

Impairment of financial assets

Climate-related events, such as floods and hurricanes, can impact the creditworthiness of borrowers due to business interruption,

impacts on economic strength, asset values and unemployment. Policy and regulatory changes put in place to combat climate change

could also result in a rapid deterioration of credit quality in sectors and/or countries affected, particularly if policy changes are radical

or quickly implemented. In addition, lenders could also suffer increased credit losses through exposure to assets that become