BAMBOO SPLITTING AND SLIVERING UNIT - CGSpace

25

INTERNATIONAL NETWORK FOR BAMBOO AND RATTAN (INBAR) TRANSFER OF TECHNOLOGY MODEL (TOTEM) BAMBOO SPLITTING AND SLIVERING UNIT by Indian Plywood Industries Research Institute (IPIRTI), P.B.No.2273, Tumkur Road, Bangalore, India.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of BAMBOO SPLITTING AND SLIVERING UNIT - CGSpace

INTERNATIONAL NETWORK FOR BAMBOO AND RATTAN(INBAR)

TRANSFER OF TECHNOLOGY MODEL (TOTEM)

BAMBOO SPLITTING AND SLIVERING UNIT

by

Indian Plywood Industries Research Institute (IPIRTI),P.B.No.2273, Tumkur Road,

Bangalore, India.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

2

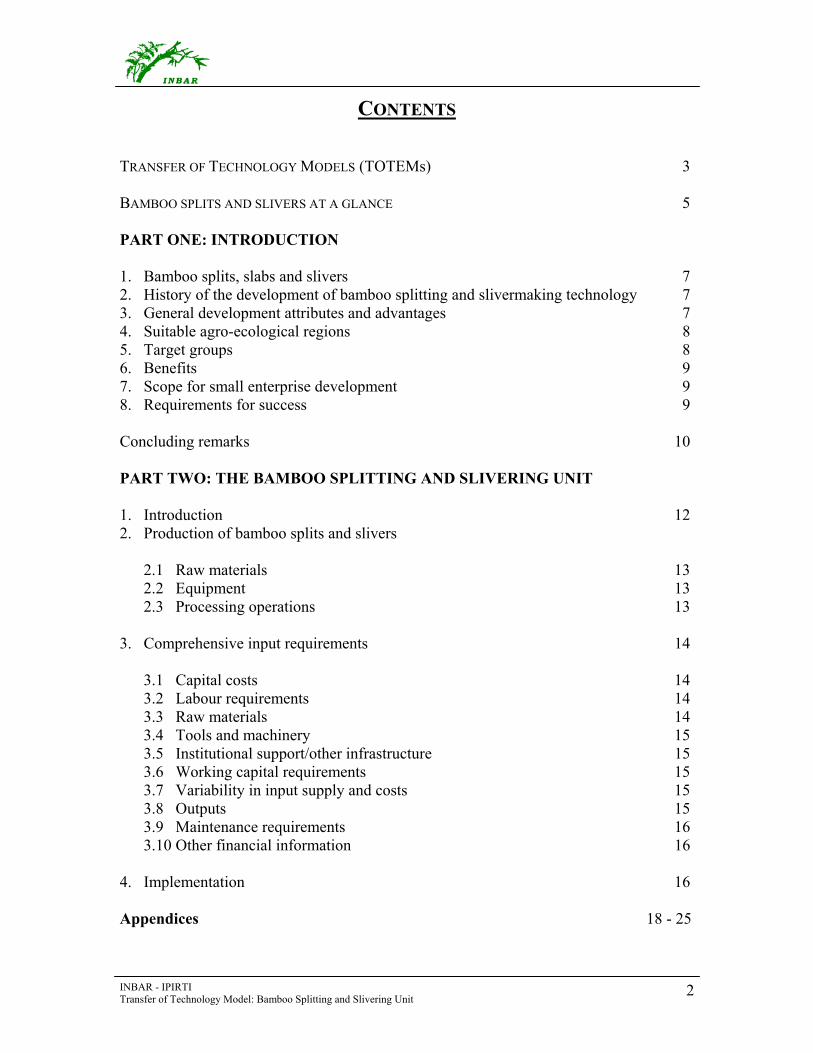

CONTENTS

TRANSFER OF TECHNOLOGY MODELS (TOTEMs) 3

BAMBOO SPLITS AND SLIVERS AT A GLANCE 5

PART ONE: INTRODUCTION

1. Bamboo splits, slabs and slivers 72. History of the development of bamboo splitting and slivermaking technology 73. General development attributes and advantages 74. Suitable agro-ecological regions 85. Target groups 86. Benefits 97. Scope for small enterprise development 98. Requirements for success 9

Concluding remarks 10

PART TWO: THE BAMBOO SPLITTING AND SLIVERING UNIT

1. Introduction 122. Production of bamboo splits and slivers

2.1 Raw materials 132.2 Equipment 132.3 Processing operations 13

3. Comprehensive input requirements 14

3.1 Capital costs 143.2 Labour requirements 143.3 Raw materials 143.4 Tools and machinery 153.5 Institutional support/other infrastructure 153.6 Working capital requirements 153.7 Variability in input supply and costs 153.8 Outputs 153.9 Maintenance requirements 163.10 Other financial information 16

4. Implementation 16

Appendices 18 - 25

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

3

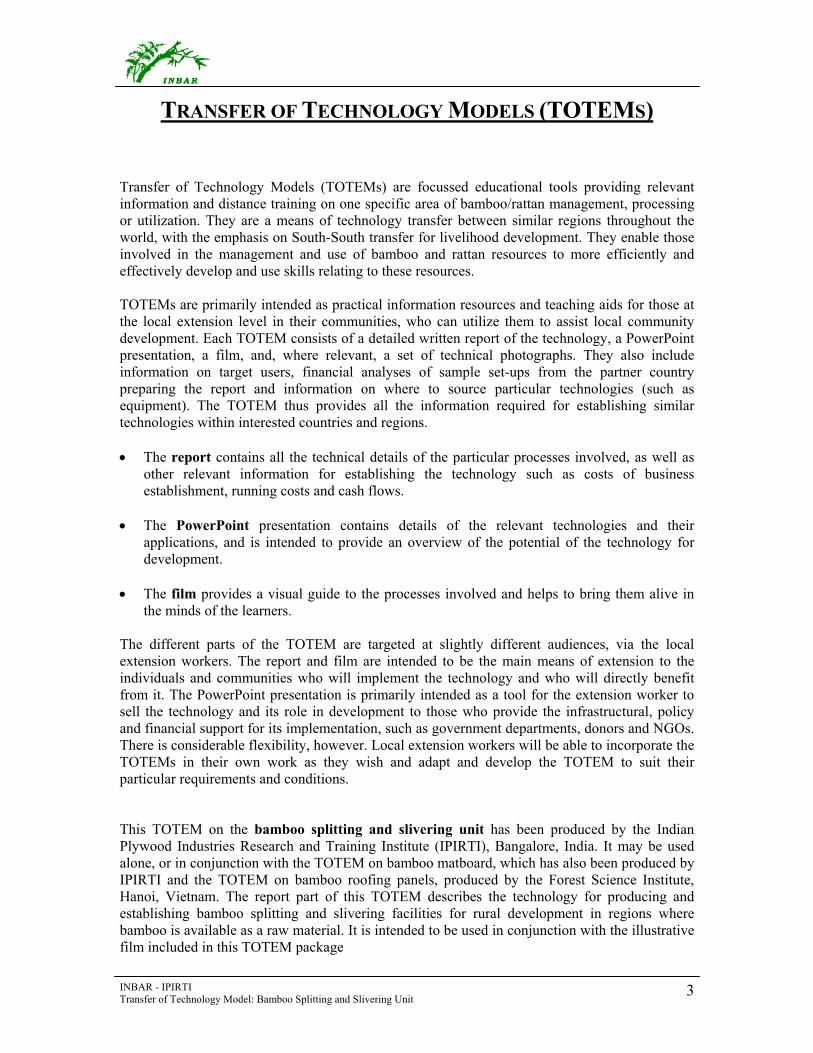

TRANSFER OF TECHNOLOGY MODELS (TOTEMS)

Transfer of Technology Models (TOTEMs) are focussed educational tools providing relevantinformation and distance training on one specific area of bamboo/rattan management, processingor utilization. They are a means of technology transfer between similar regions throughout theworld, with the emphasis on South-South transfer for livelihood development. They enable thoseinvolved in the management and use of bamboo and rattan resources to more efficiently andeffectively develop and use skills relating to these resources.

TOTEMs are primarily intended as practical information resources and teaching aids for those atthe local extension level in their communities, who can utilize them to assist local communitydevelopment. Each TOTEM consists of a detailed written report of the technology, a PowerPointpresentation, a film, and, where relevant, a set of technical photographs. They also includeinformation on target users, financial analyses of sample set-ups from the partner countrypreparing the report and information on where to source particular technologies (such asequipment). The TOTEM thus provides all the information required for establishing similartechnologies within interested countries and regions.

• The report contains all the technical details of the particular processes involved, as well asother relevant information for establishing the technology such as costs of businessestablishment, running costs and cash flows.

• The PowerPoint presentation contains details of the relevant technologies and theirapplications, and is intended to provide an overview of the potential of the technology fordevelopment.

• The film provides a visual guide to the processes involved and helps to bring them alive inthe minds of the learners.

The different parts of the TOTEM are targeted at slightly different audiences, via the localextension workers. The report and film are intended to be the main means of extension to theindividuals and communities who will implement the technology and who will directly benefitfrom it. The PowerPoint presentation is primarily intended as a tool for the extension worker tosell the technology and its role in development to those who provide the infrastructural, policyand financial support for its implementation, such as government departments, donors and NGOs.There is considerable flexibility, however. Local extension workers will be able to incorporate theTOTEMs in their own work as they wish and adapt and develop the TOTEM to suit theirparticular requirements and conditions.

This TOTEM on the bamboo splitting and slivering unit has been produced by the IndianPlywood Industries Research and Training Institute (IPIRTI), Bangalore, India. It may be usedalone, or in conjunction with the TOTEM on bamboo matboard, which has also been produced byIPIRTI and the TOTEM on bamboo roofing panels, produced by the Forest Science Institute,Hanoi, Vietnam. The report part of this TOTEM describes the technology for producing andestablishing bamboo splitting and slivering facilities for rural development in regions wherebamboo is available as a raw material. It is intended to be used in conjunction with the illustrativefilm included in this TOTEM package

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

4

The first part of the report introduces the technology, discusses its history, its developmentattributes, its benefits and it’s applicability. The second part of the report provides detailedinformation on the technical aspects of splitting and slivering bamboos. Appendixes I - IIIprovide full financial analyses for establishing and running a bamboo splitting and slivering unit.

This TOTEM is one of the first to be produced by INBAR/IPIRTI and your feedback is mostwelcome - kindly contact INBAR or IPIRTI with your comments or suggestions.

© International Network for Bamboo and Rattan 2001

Note 1: This TOTEM has been edited at INBAR and may differ slightly from the form in which it wasreceived from IPIRTI.

Note 2: All financial calculations are in Indian Rupees. At the time of writing 1 USD = 46 Rs.One lakh Rs = 100, 000 Rs.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

5

BAMBOO SPLITS AND SLIVERS AT-A-GLANCE

What are Bamboo Splits and Slivers?

Bamboo splits and slivers are longitudinal sections of a bamboo pole (culm). Splits are the fullthickness of the culm wall and have the green outer layer still attached. Slivers are thin, narrowsections of bamboo wood. They are the primary materials used for weaving a wide range ofproducts. On a small scale they may be used for handicraft items and objects of daily use. On alarge scale, one of the most useful products they can be woven into are the mats that are used toproduce bamboo matboard.

How are they produced?

Splits and slivers may be produced by hand splitting or mechanical splitting. Hand splitting issuitable for small-scale production and there is a wide range of tools available, both traditionaland modern. Automated splitting machines are more suitable for large-scale production of slivers.Fresh bamboo culms are passed through a series of machines that produce splits of successivelysmaller sizes until the desired size is reached.

What is the market for bamboo splits and slivers?

The market for bamboo splits is limited, because they are of limited use. However, bambooslivers are the primary raw material for mat making and the demand for mats is closely related tothe demand for matboard. Matboard is a versatile type of plywood and its markets are increasingrapidly. Often the splitting and slivering unit is established with very close linkages to thematboard factories and weaving facilities and weaving staff may be included in the unit. In someinstances the splitting and slivering unit may be a subsidiary part of the matboard factory.

What is the role of a bamboo splitting and slivering unit in ruraldevelopment?

The unit requires considerable supplies of raw bamboos, the management and harvesting ofwhich increases employment opportunities for farmers and foresters. Establishing new plantationswill benefit the environment and substituting bamboo for wood in products will help conservenatural forests. The unit offers employment opportunities for unskilled, semi-skilled andtechnically trained personnel for its operation and management. A large unit established withmat-weaving facilities included can provide employment for up to 400 people.

How do I establish a bamboo splitting and slivering unit?

A regular supply of raw bamboos, labour, electricity and an established market for the slivers, orthe mats if mat weaving is included in the unit, is required. A large bamboo splitting and sliveringunit with a production capacity of 1300 mats, 1.2 x 2.4 m per day, can be established forapproximately US $300, 000. Smaller facilities can be established for considerably less,depending on their size and intended production rates.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

6

PART ONE

INTRODUCTION

DEVELOPMENT ATTRIBUTES, TARGET GROUPS andBENEFITS of

BAMBOO SPLITTING AND SLIVERMAKING

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

7

1. Bamboo splits, slabs and slivers

Splits, slabs and slivers are longitudinal sections of a bamboo culm. Splits are producedwhen the culms are initially sectioned. They are the full thickness of the culm wall andhave the green outer layer still attached. The splits of larger culms are too coarse to beused for weaving or other uses, but those of small diameter culms may be utilised inspecific handicraft end-uses. Slabs are produced during an intermediary stage of thesplitting and slivering process. Slabs are thick sections of the culm wall but without thegreen epidermal layer and with the knots removed. These are not often used for products,but they find some uses; for example in China they are cut into short pieces and polishedand used to make seat covers for cars. Slivers are long, thin strips of bamboo, muchthinner than they are broad, that are the final product of this primary processing stage.Slivers are sufficiently pliable to be used for weaving a wide range of different productsincluding handicrafts and industrial uses such as mats for matboard production. They canbe produced in a wide range of different sizes.

Splits and slivers can be produced either by hand or by mechanical splitting machines.Hand splitting has been practiced for many generations in communities around the worldand there are many traditional and modern tools available. Hand splitting is suitable forsmall-scale production of splits and slivers but mechanical splitting in a splitting andslivering unit, as described in this TOTEM, is preferable for larger scale applications.

2. History of the development of bamboo splitting andslivermaking technology.

Mechanical splitting and slivermaking has been developed over the past few decades in anumber of countries, but most particularly in China where it is very widely practiced, andfrom where a wide range of relevant machines and equipment are available. Thetechnology has mostly been developed by private companies and research institutes. InIndia a unit for the primary processing of bamboo was established at IPIRTI, Bangaloreunder a project sponsored by the International Development Research Centre (IDRC),Canada in 1997 using machinery imported from Taiwan. The experience gained in theoperation of the unit has been made use of in the preparation of this technology transfermodel.

3. General development attributes and advantages

The main development attributes of the technology are as follows:

• Greater use of bamboo reduces dependence on wood-timber resources and henceincreases environmental protection and conservation.

• Rehabilitation of degraded forests and other waste lands through increased areas ofbamboo plantations.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

8

• Increased employment opportunities in bamboo growing for supply of raw materials,in running the unit, and in weaving the slivers into products.

• Greater income-generating opportunities for women, who are able to use the slivers athome to weave products.

• Permits the establishment of matboard production facilities with associated benefits(see matboard TOTEM).

The main advantages of the mechanical splitting and slivering unit over manual splittingare:

• The labour requirements are greatly reduced.• Efficient production of large numbers of slivers for weaving into mats and other

products.• Production of uniform slivers of a controllable size. The size of slivers produced can

be adjusted by changing the settings on the machines.• Removes drudgery in primary processing of bamboo and frees processors for more

lucrative weaving work.

4. Suitable agro-ecological regions

A splitting and slivering unit can be established almost anywhere that bamboos aregrown. This includes most tropical and sub-tropical regions of the world and manytemperate zones as well. However, the unit is best suited to the splitting of culms of largespecies that have long internodes such as Bambusa textilis, Melocanna baccifera andDendrocalamus brandisii and is ideally established in locations where supplies of thesetypes of bamboo are forthcoming. The unit is not suitable for areas in which only small,narrow-culmed bamboos are grown, such as higher altitude regions of the temperate andsub-tropical zones.

5. Target groups

There are two main target groups. The first are those who will be employed directly bythe unit. The establishment of the unit will provide employment opportunities for theunskilled, semi-skilled and technically trained personnel and the skills required can beacquired by men and women alike. The second group are the many small-scale weaverswho will be able to use the slivers produced by the unit to weave mats and other productsfor income generation. Many of these people are women who will be able to work athome, and who will have a regular source of income from the supply of mats to matboardfactories. The main by-product of the unit is the green epidermal layer of the culms, andthis can be used for weaving household utensils and handicrafts by local people.Additionally, bamboo cultivators and harvesters will benefit from the greater demands forbamboo culms. Establishing the unit as a cooperative venture within the community willalso benefit the community as a whole and lead to increased community prosperity.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

9

6. Benefits

The environmental benefits are considerable. The only raw material required for the splittingand slivering unit is good quality bamboo. Bamboos are fast growing giant grasses that canbe harvested annually. They are a versatile and renewable resource. Cultivation of bamboois also beneficial for soil conservation and afforestation activities and plantations areencouraged as part of social forestry programmes. Therefore bamboo and its products areconsidered as eco-friendly .The splitting and slivering unit consumes only a small quantityof water for the boiler and electrical energy requirements are not high.

As outlined in the previous section, the opportunities for employment of a range of people inthe rural areas are also very great, both in the unit itself and in related forward and backwardlinkages such as supply of raw materials and weaving of mats for matboard production.Particularly, the large-scale regular employment of weavers or craftspeople in the weavingsection of the unit will help them obtain financial security. It will create more economicactivities in the region and help improve the social and cultural conditions of thecommunities involved.

7. Scope for small enterprise development

The splitting and slivering unit is a means of mechanically producing slivers on a largescale for weaving. As an enterprise in itself it has great potential because the demand forwoven bamboo products is growing in most countries, and the potential for export is alsoincreasing. Additionally the unit may be established specifically to supply slivers forweaving into the mats that are the raw materials for matboard. Matboard is widely usedfor paneling, ceilings, cases, roofs, doors, furniture and household utensils and the marketfor these products is rapidly expanding.

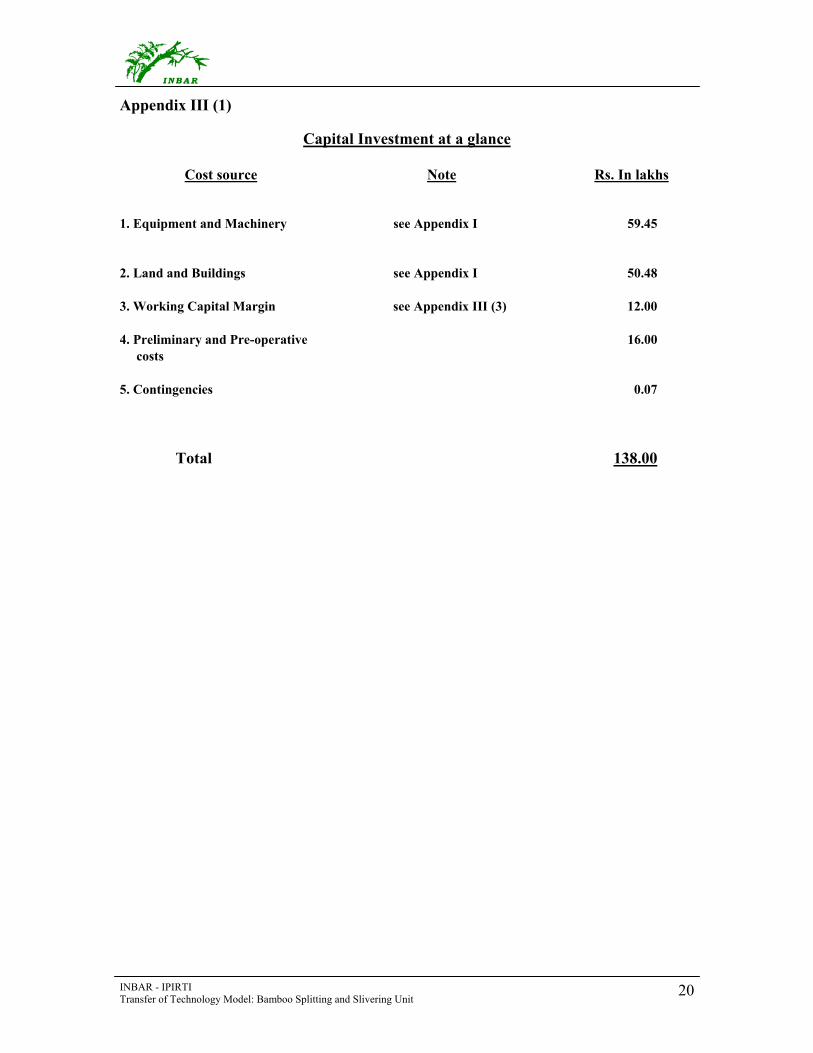

The establishment of a splitting and slivering unit requires an estimated capitalinvestment of approximately US$300, 000 (Appendices I and III (1)) and the runningcosts are shown in Appendix II and III (2). In India, the establishment of such a unitwould take place in the small-scale sector, and would thereby become eligible forincentives provided by the government for this sector. Similar incentives may beavailable in other countries - check with your local government office or businessadvisory centre for details.

8. Requirement for success

The essential requirements for a successful splitting and slivering unit are:

• Sustained supply of bamboos.• Sufficient capital available for initial investment in the unit.• Appropriate machinery and some technically trained personnel to manage and

maintain the unit.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

10

Concluding remarks

The bamboo splitting and slivering technology is a commercially and socially effectivemeans of providing large numbers of uniform slivers to the weaving industry and to thosethat use their products for further value addition processing. It permits and promotes thesustainable management of bamboo resources in the region, with consequent benefits ofenvironmental protection and conservation as a result of increased substitution of bamboofor wood-timber. It provides employment for local people in the unit itself. It supplies theraw materials to weavers, thus freeing them from the initial processing phase that theywould have otherwise have had to have done themselves and permits them to spend moretime on income generating activities. They are therefore able to be more productive, andable to increase their incomes.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

11

PART TWO

THE BAMBOO SPLITTING AND

SLIVERING UNIT

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

12

1. Introduction

Bamboo slivers are produced by the following basic steps:

• Harvesting bamboo culms and removing the tips• Cross-cutting culms into sections of a standard length• Longitudinal splitting of culms into splits• Removing the green epidermal layer and knots to produce slabs• Splitting the slabs into slivers

Although these processes have been done by hand for many generations, the mechanicalunit described in this TOTEM permits the efficient production of large numbers of splitsfor large-scale supply, generally to industrial processing plants.

2. Production of bamboo splits and slivers

2.1 Raw materials

The unit is preferably established near bamboo forest zones, so that bamboos areavailable to the unit in fresh green condition. Alternatively it may be possible to establishplantations specifically to supply the unit. The unit is best suited to the splitting of culmsof species that have long internodes that are the traditional source of slivers for weaving,such as Bambusa textilis and Melocanna baccifera, but can easily be used to split culmsof a wide range of species.

The ideal raw materials for mechanical processing are bamboos with the following physicalproperties.

• Lighter or less dense species, or species with density less than 1 g/cm3 .• Preferably straight with long internodes.• Medium culm wall thickness of 8-10 mm• Large inner diameter, preferably above 25 mm.

During the course of the IDRC sponsored project at IPIRTI, the following bamboo specieswere studied and found suitable for mechanical splitting and slivering:

1. Bambusa bambos (15-30 m height, 15-18 cms diameter, 20-40 cmsinternode length).

2. Bambusa nutans (6-15m height, 5-10 cm diameter, 25-45 cm internodelength).

3. Dendrocalamus brandisii (19-33 m height, 13-20 cm diameter, 30-38 cminternode length).

4. Dendrocalamus strictus (8-16m height, 2.5 to 8 cm diameter thick, up to 45cm internode length).

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

13

5. Melocanna baccifera (10-20m height, 3 to 7 cms diameter, 20-50 cmsinternode length).

After harvest they are transported as quickly as possible to the mechanical processing unitand care is taken to avoid damage to the culms in transit. The narrow portion at the tip of theculm is removed, leaving a culm of approximately uniform diameter throughout its length.The moisture content of freshly cut bamboo is about 50-60%. Dried bamboos are notsuitable for mechanical splitting as they are too brittle.

2.2 Equipment

The following pieces of equipment are required as the minimum to establish a splitting andslivering unit:

• Cross-cutting machine• Splitting machine• Knot removing and slab-making machine• Slivering machine

There are also a wide range of machines available that can process splits and slabs furtherduring the splitting process, but they are not essential and not listed here. Details of themachinery are listed in Appendix I.

2.3 Processing Operations

(i) Cross-cutting of Bamboo (Cross-cutting machine)

The first operation is crosscutting the bamboo culms. This involves cutting thebamboo culm into short, standard length sections to facilitate later processing. Themaximum length they can be cut into is usually about 2.4m but this depends on thespecifications of the machine used. Culms can be cut into shorter pieces butmaximum processing efficiency is achieved when the sections are as long aspossible.

(ii) Splitting of Bamboo (Splitting machine)

The next operation is splitting the bamboo to the required width of slivers, which formatboard is 15-20 mm. The splitting machine has a set of knives at one end,arranged radially on a mounting, and a pusher at the other end that pushes the culmsection through the knife set to split it. A range of knife sets are available, eachproducing different sizes of split and for culms of different diameters.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

14

(iii) Knot removing and slab making (Knot removing and slab making machine)

The splits are then passed through the knot removing and slab-making machine toproduce sections of bamboo of uniform thickness throughout their length. In thismachine the thickness of the split is reduced to 2.4mm, or multiples of 0.8 mmwhich is equivalent to the thickness of sliver. At this point the slab will cease to beinstantly recognisable as having originated from a bamboo culm. There is anothermachine available; the knot removing, width sizing and planing machine thatdresses the split to a perfect rectangular shape. However, this machine can bebypassed as it is expensive, non-essential and reduces the raw material recovery rate.

(iv) Sliver making (Slivering machine)

The slabs are finally processed through a sliver-making machine to produce 0.8mmthick slivers for weaving into mats.

3. Comprehensive input requirements

3.1 Capital costs

The capital cost of establishing a splitting and slivering unit with a capacity of 1300 mats(1.2m x 2.4m) per day (for 3 shifts) is estimated at 138 lakhs (USD $ 300, 000) (includingland and building) and details are given in Appendix I. The recurring costs of the project(Appendix II) are estimated on the following assumptions.

1. The unit will work 3 shifts of 8 hours per day for slab and sliver making activities.2. There are 300 working days per year.3. The unit will work to 50% of the installed capacity in year 1, 75% in year 2 and 100% in

year 3 onwards.

3.2 Labour requirements

The major labour force of the unit are the operators and the semi-skilled workers (35 nos.)who will be assisting the operators. If the unit is established to supply slivers for matboardproduction the labour force of 350 weavers can be considered as part of the unit’s labourforce.

3.3 Raw materials

The quantity of bamboo required for processing is 335 bamboo culms per day (at a rate of20 kg per culm).

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

15

3.4 Tools and Machinerys

The major machines used in the production of splits and slivers are:

• Cross cutting machine 1 No.• Splitting machine 1 No.• Slab making machine 3 Nos.• Sliver making machine 8 Nos.

The other ancillary machines/equipment needed for the unit are:

• Grinder 1 No.• Kilns (6x3x3 m) 2 Nos.• Boiler (capacity 300 kg/hr.) 1 No.• Air compressor 1 No.• Standby generator (50 KVA) 1 No.

The machinery manufacturers, suppliers and prices are given in Appendix IV.

3.5 Institutional Support /other infrastructure

The managerial, supervisory, technical and administrative staff required are listed inAppendix II, as are consumables such as electricity and water. A truck and jeep have beenincluded in the calculations, along with communication equipment (computer), officeequipment, furniture and fittings.

3.6 Working capital requirements

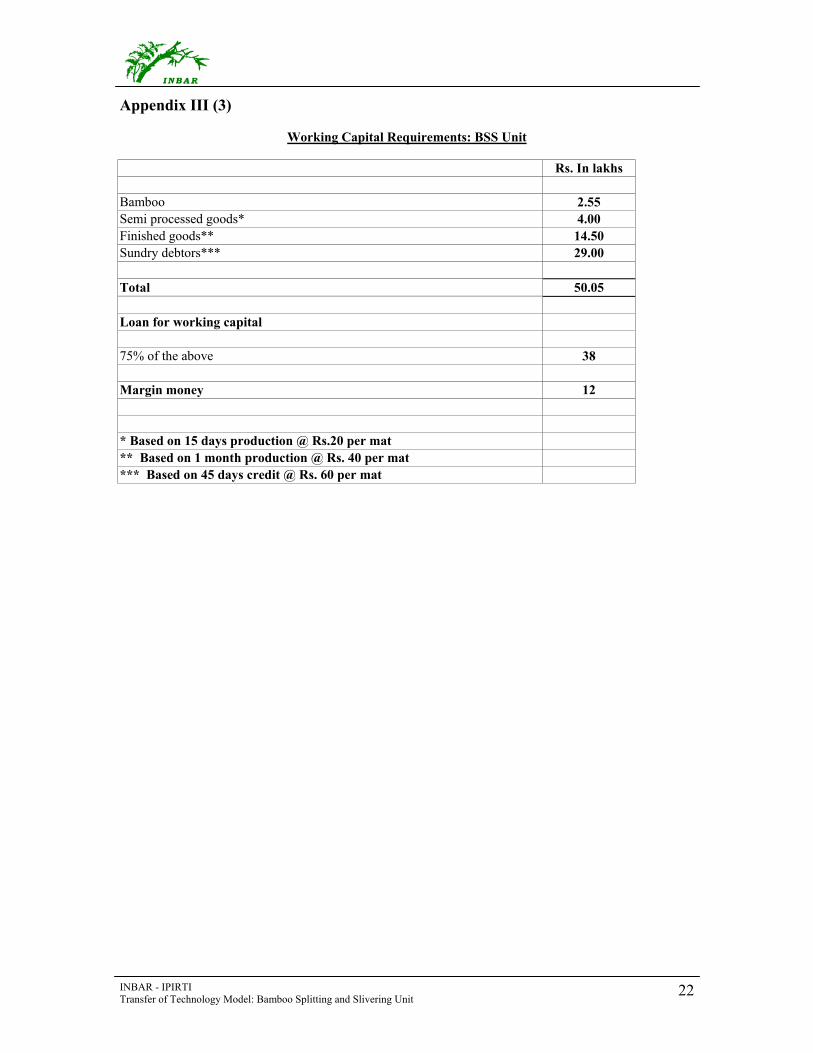

The working capital requirement for 3 months is Rs.50 lakhs and is shown in Appendix III(3).

3.7 Variability in input supplies and costs

The availability of bamboo and the cost of bamboo will fluctuate depending upon the localconditions and policies of the Government from time to time. However for calculationpurposes the price is fixed at Rs.10/- per bamboo culm (20 kg). Note that the variability insupply of raw materials could be avoided by the establishment by the splitting and sliveringunit of bamboo plantations dedicated to supplying the raw materials required.

3.8 Outputs

The bamboo splitting and slivering unit is usually expected to operate as an ancillary to abamboo matboard unit. The main out put of the unit would be 1300 mats (1.2m x 2.4m size)per day (for 3 shifts) and these are sold directly to the bamboo matboard factory. The mainby-product of the unit is 312 kg/day of the epidermal layer of bamboo, which can be utilisedfor making many handicraft items like baskets and speciality mats.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

16

3.9 Maintenance requirements

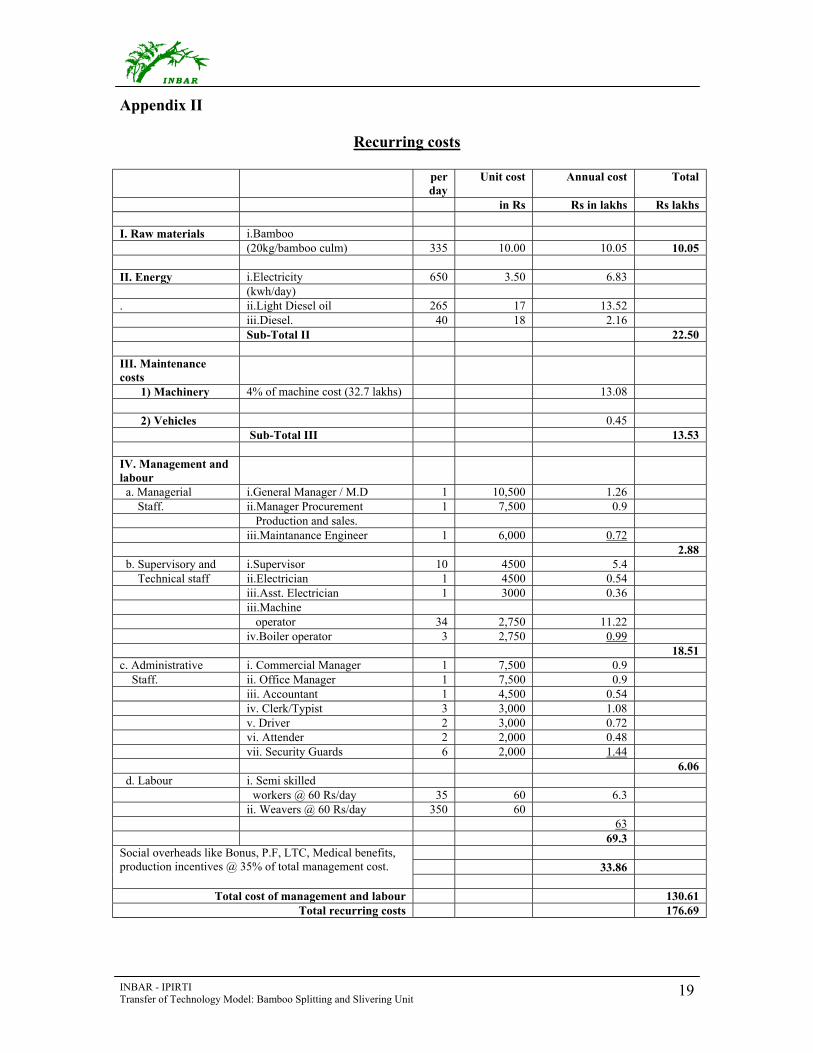

The maintenance requirement is divided into two groups, (i) maintenance of machines and(ii) maintenance of vehicles. Lubricating oil, emery paper, grinding wheels, saw blades,spare parts, bearings, etc. are included as machine maintenance and is estimated to beRs.13.08 lakhs per year and the vehicle maintenance is about Rs.0.45 lakhs per year.

3.10 Other financial information

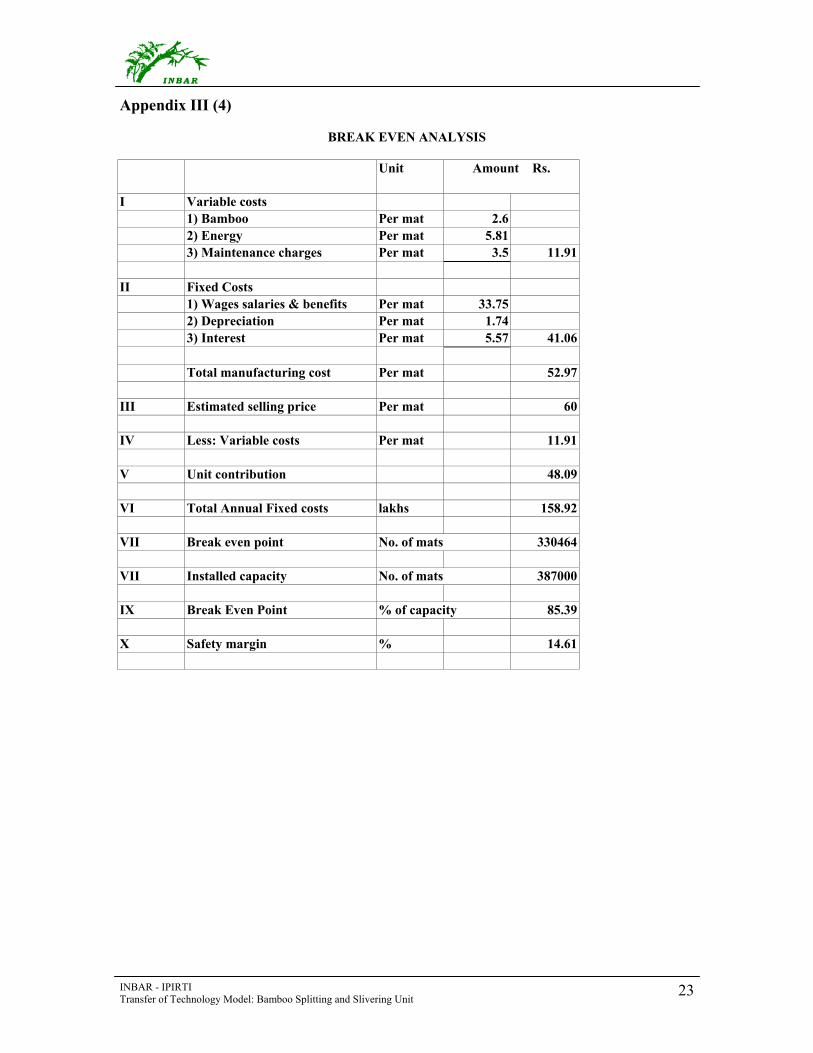

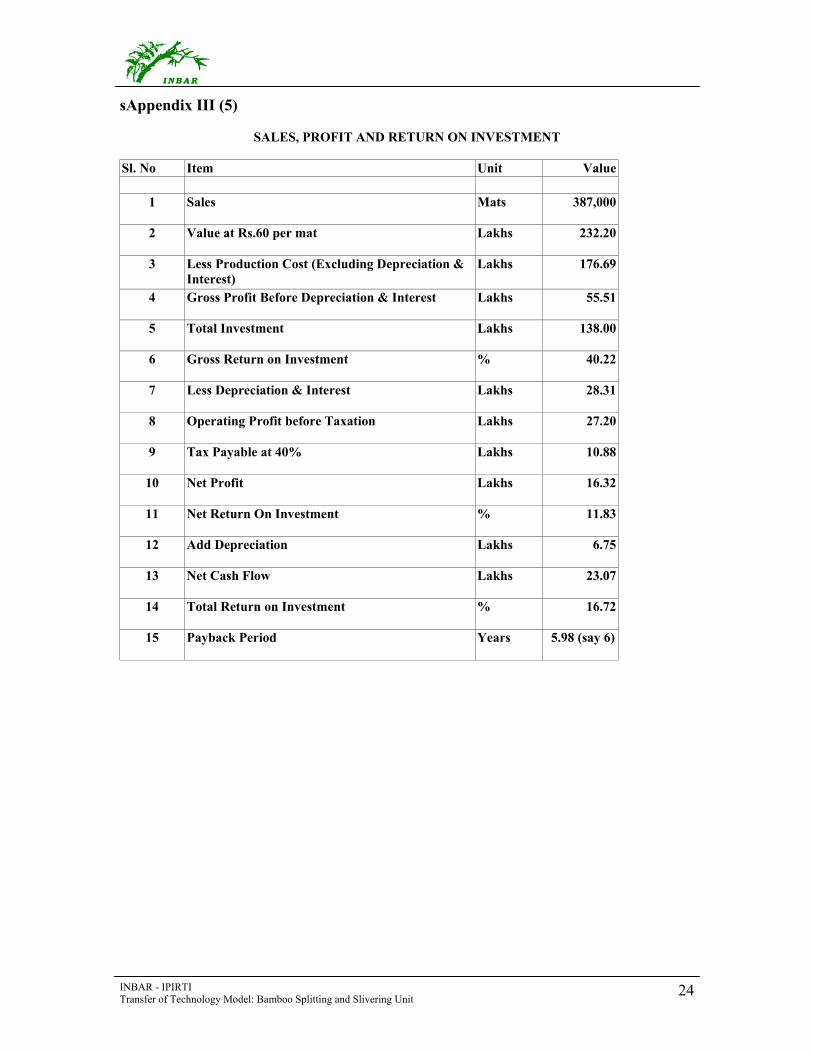

The break-even point of the unit is 83.7% of total capacity (Appendix III (4)) and thepayback period is calculated at 6.3 years (Appendix III (5)). A cash flow statement for 13years is shown in Appendix III (6).

4. Implementation

Policy aspect and successful use of the technology

The Government and local bodies wherever required will have to suitably modify or amendpolicies, regulations or laws etc., governing cultivation, growth and utilisation of bamboo inbamboo growing regions/countries with a view to set up BSS units for mechanical primaryprocessing of bamboo and the production of hand woven mats from the units as ancillary tobamboo matboard units.

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

17

APPENDICES

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

18

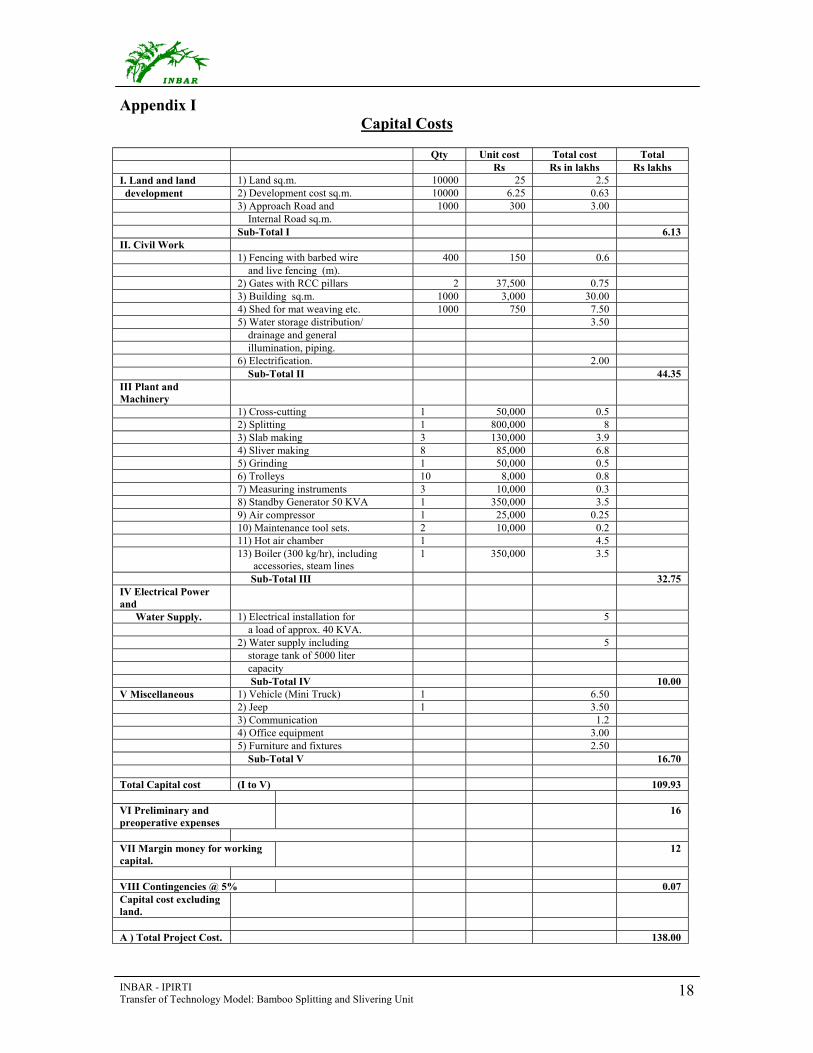

Appendix ICapital Costs

Qty Unit cost Total cost TotalRs Rs in lakhs Rs lakhs

I. Land and land 1) Land sq.m. 10000 25 2.5 development 2) Development cost sq.m. 10000 6.25 0.63

3) Approach Road and 1000 300 3.00 Internal Road sq.m.Sub-Total I 6.13

II. Civil Work1) Fencing with barbed wire 400 150 0.6 and live fencing (m).2) Gates with RCC pillars 2 37,500 0.753) Building sq.m. 1000 3,000 30.004) Shed for mat weaving etc. 1000 750 7.505) Water storage distribution/ 3.50 drainage and general illumination, piping.6) Electrification. 2.00 Sub-Total II 44.35

III Plant andMachinery

1) Cross-cutting 1 50,000 0.52) Splitting 1 800,000 83) Slab making 3 130,000 3.94) Sliver making 8 85,000 6.85) Grinding 1 50,000 0.56) Trolleys 10 8,000 0.87) Measuring instruments 3 10,000 0.38) Standby Generator 50 KVA 1 350,000 3.59) Air compressor 1 25,000 0.2510) Maintenance tool sets. 2 10,000 0.211) Hot air chamber 1 4.513) Boiler (300 kg/hr), including accessories, steam lines

1 350,000 3.5

Sub-Total III 32.75IV Electrical Powerand Water Supply. 1) Electrical installation for 5

a load of approx. 40 KVA.2) Water supply including 5 storage tank of 5000 liter capacity Sub-Total IV 10.00

V Miscellaneous 1) Vehicle (Mini Truck) 1 6.502) Jeep 1 3.503) Communication 1.24) Office equipment 3.005) Furniture and fixtures 2.50 Sub-Total V 16.70

Total Capital cost (I to V) 109.93

VI Preliminary andpreoperative expenses

16

VII Margin money for workingcapital.

12

VIII Contingencies @ 5% 0.07Capital cost excludingland.

A ) Total Project Cost. 138.00

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

19

Appendix II

Recurring costs

perday

Unit cost Annual cost Total

in Rs Rs in lakhs Rs lakhs

I. Raw materials i.Bamboo(20kg/bamboo culm) 335 10.00 10.05 10.05

II. Energy i.Electricity 650 3.50 6.83(kwh/day)

. ii.Light Diesel oil 265 17 13.52iii.Diesel. 40 18 2.16Sub-Total II 22.50

III. Maintenancecosts 1) Machinery 4% of machine cost (32.7 lakhs) 13.08

2) Vehicles 0.45 Sub-Total III 13.53

IV. Management andlabour a. Managerial i.General Manager / M.D 1 10,500 1.26 Staff. ii.Manager Procurement 1 7,500 0.9

Production and sales.iii.Maintanance Engineer 1 6,000 0.72

2.88 b. Supervisory and i.Supervisor 10 4500 5.4 Technical staff ii.Electrician 1 4500 0.54

iii.Asst. Electrician 1 3000 0.36iii.Machine operator 34 2,750 11.22iv.Boiler operator 3 2,750 0.99

18.51c. Administrative i. Commercial Manager 1 7,500 0.9 Staff. ii. Office Manager 1 7,500 0.9

iii. Accountant 1 4,500 0.54iv. Clerk/Typist 3 3,000 1.08v. Driver 2 3,000 0.72vi. Attender 2 2,000 0.48vii. Security Guards 6 2,000 1.44

6.06 d. Labour i. Semi skilled

workers @ 60 Rs/day 35 60 6.3ii. Weavers @ 60 Rs/day 350 60

6369.3

33.86Social overheads like Bonus, P.F, LTC, Medical benefits,production incentives @ 35% of total management cost.

Total cost of management and labour 130.61Total recurring costs 176.69

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

20

Appendix III (1)

Capital Investment at a glance

Cost source Note Rs. In lakhs

1. Equipment and Machinery see Appendix I 59.45

2. Land and Buildings see Appendix I 50.48

3. Working Capital Margin see Appendix III (3) 12.00

4. Preliminary and Pre-operative 16.00 costs

5. Contingencies 0.07

Total 138.00

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

21

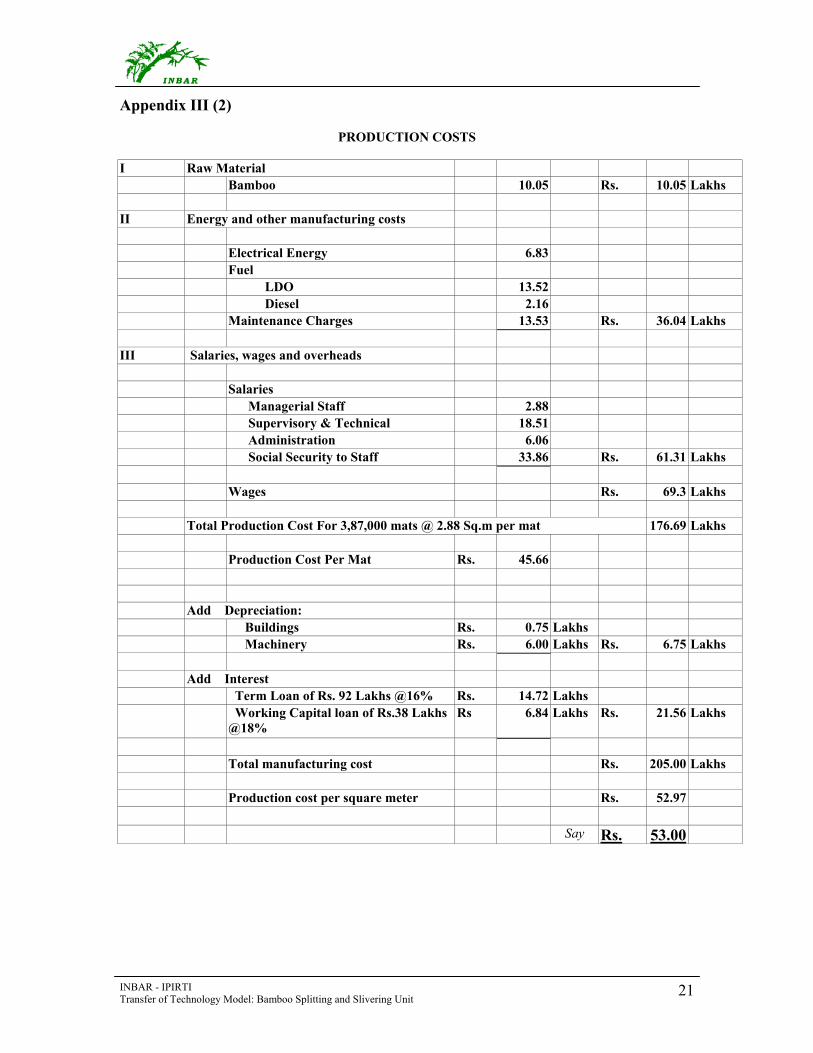

Appendix III (2)

PRODUCTION COSTS

I Raw MaterialBamboo 10.05 Rs. 10.05 Lakhs

II Energy and other manufacturing costs

Electrical Energy 6.83Fuel LDO 13.52 Diesel 2.16Maintenance Charges 13.53 Rs. 36.04 Lakhs

III Salaries, wages and overheads

Salaries Managerial Staff 2.88 Supervisory & Technical 18.51 Administration 6.06 Social Security to Staff 33.86 Rs. 61.31 Lakhs

Wages Rs. 69.3 Lakhs

Total Production Cost For 3,87,000 mats @ 2.88 Sq.m per mat 176.69 Lakhs

Production Cost Per Mat Rs. 45.66

Add Depreciation: Buildings Rs. 0.75 Lakhs Machinery Rs. 6.00 Lakhs Rs. 6.75 Lakhs

Add Interest Term Loan of Rs. 92 Lakhs @16% Rs. 14.72 Lakhs Working Capital loan of Rs.38 Lakhs@18%

Rs 6.84 Lakhs Rs. 21.56 Lakhs

Total manufacturing cost Rs. 205.00 Lakhs

Production cost per square meter Rs. 52.97

Say Rs. 53.00

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

22

Appendix III (3)

Working Capital Requirements: BSS Unit

Rs. In lakhs

Bamboo 2.55Semi processed goods* 4.00Finished goods** 14.50Sundry debtors*** 29.00

Total 50.05

Loan for working capital

75% of the above 38

Margin money 12

* Based on 15 days production @ Rs.20 per mat** Based on 1 month production @ Rs. 40 per mat*** Based on 45 days credit @ Rs. 60 per mat

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

23

Appendix III (4)

BREAK EVEN ANALYSIS

Unit Amount Rs.

I Variable costs1) Bamboo Per mat 2.62) Energy Per mat 5.813) Maintenance charges Per mat 3.5 11.91

II Fixed Costs1) Wages salaries & benefits Per mat 33.752) Depreciation Per mat 1.743) Interest Per mat 5.57 41.06

Total manufacturing cost Per mat 52.97

III Estimated selling price Per mat 60

IV Less: Variable costs Per mat 11.91

V Unit contribution 48.09

VI Total Annual Fixed costs lakhs 158.92

VII Break even point No. of mats 330464

VII Installed capacity No. of mats 387000

IX Break Even Point % of capacity 85.39

X Safety margin % 14.61

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

24

sAppendix III (5)

SALES, PROFIT AND RETURN ON INVESTMENT

Sl. No Item Unit Value

1 Sales Mats 387,000

2 Value at Rs.60 per mat Lakhs 232.20

3 Less Production Cost (Excluding Depreciation &Interest)

Lakhs 176.69

4 Gross Profit Before Depreciation & Interest Lakhs 55.51

5 Total Investment Lakhs 138.00

6 Gross Return on Investment % 40.22

7 Less Depreciation & Interest Lakhs 28.31

8 Operating Profit before Taxation Lakhs 27.20

9 Tax Payable at 40% Lakhs 10.88

10 Net Profit Lakhs 16.32

11 Net Return On Investment % 11.83

12 Add Depreciation Lakhs 6.75

13 Net Cash Flow Lakhs 23.07

14 Total Return on Investment % 16.72

15 Payback Period Years 5.98 (say 6)

INBAR - IPIRTITransfer of Technology Model: Bamboo Splitting and Slivering Unit

25

Appendix III (6)CASH FLOW STATEMENT FOR BSS UNIT

Rupees in Lakhs

Year 1 constr-uction period-

Total investment

Year 2(Ist year ofproduction)

Year 3(2nd year ofproduction)

Year 4(3rd year ofproduction)

Year 5(4th year ofproduction)

Year 6(5th year ofproduction)

Year 7(6th year ofproduction)

Year 8(7th year ofproduction)

Year 9(8th year ofproduction)

Year 10(9th year ofproduction)

Year 11(I0th year ofproduction)

Year 12(1Ith year ofproduction)

Year 13(I2th year ofproduction)

INCOME: Sale of Boards 174.05 232.20 232.20 232.20 232.20 232.20 232.20 232.20 232.20 232.20 232.20

Less: Production cost 88.35 132.53 176.69 176.69 176.69 176.69 176.69 176.69 176.69 176.69 176.69 176.69

Gross trading profit 27.75 41.52 55.51 55.51 55.51 55.51 55.51 55.51 55.51 55.51 55.51 55.51

Less: Interest charges 19.85 18.68 14.00 9.32 4.64 0.00 0.00 0.00 0.00 0.00 0.00

Less: Depreciation 3.38 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75

Profit before taxation 6.23 14.92 30.08 34.76 39.44 44.12 48.76 48.76 48.76 48.76 48.76 48.76

Less: Tax @ 40% 2.49 5.97 12.03 13.90 15.78 17.65 19.50 19.50 19.50 19.50 19.50 19.50Net profit -138 3.74 8.95 18.05 20.86 23.66 26.47 29.26 29.26 29.26 29.26 29.26 29.26Add: Depreciation 3.38 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75Positive cash flow 7.12 15.70 24.80 27.61 30.41 33.22 36.01 36.01 36.01 36.01 36.01 36.01Less: Loan repayments:

Term loan 18.00 18.00 18.00 18.00 20.00

Working capital 10.00 10.00 10.00 8.00

Net cash flow 7.12 -2.30 -3.20 -0.39 2.41 5.22 36.01 36.01 36.01 36.01 36.01 36.01Cumulative reserves / Surplus 7.12 4.82 1.62 1.23 3.64 8.86 44.87 80.88 116.89 152.90 188.91 224.92

IRR 10%

PV of Net profit (in lakhs) Rs. 140.14

NPV of Net Profit (Rs. In lakhs) Rs. 2.16

BC ratio (PV of net profits/ investment) 1.02

Term Loan 92 92.00 74.00 56.00 38.00 20.00

Working capital loan 19 28.50 38.00 28.00 18.00 8.00