PENGARUH GENDER DAN PENGALAMAN AUDIT TERHADAP AUDIT JUDGMENT

Upload

khangminh22Category

view

3download

0

Audit PolicyVersion 7

Audit Policy, Ver. 7 Page 2 of 102

Charter for the Internal Audit Department

and

Audit Policy

Document Owner: Chief Audit Executive, Bandhan Bank Limited. Version History:

Version Author Recommended by Approved

by

Date of

Approval

Effective date

Version 1 Head Internal

Audit

Board of

Directors

July 10, 2015 July 10, 2015

Version 2 Head Internal

Audit

Audit Committee

of the Board

Board of

Directors

May 11, 2016 May 11, 2016

Version 3 Chief Audit

Executive

Audit Committee

of the Board

Board of

Directors

April 26, 2017 April 26, 2017

Version 4 Chief Audit

Executive

Audit Committee

of the Board

Board of

Directors

July 7, 2018 July 7, 2018

Version 5 Chief Audit

Executive

Audit Committee

of the Board

Board of

Directors

June 14, 2019 June 14, 2019

Version 6 Chief Audit

Executive

Audit Committee

of the Board

Board of

Directors

October 12,

2020

October 12,

2020

Version 7 Chief Audit

Executive

Audit Committee

of the Board

Board of

Directors

May 6, 2021 May 6, 2021

VALIDITY OF THE POLICY

This Audit Policy would be put into force after approval of the Board.

POLICY UPDATION

This documents and processes described herein are subject to review by Authorities from time to

time as per the need of the Bank for the effective functioning of Internal Audit.

The Policy shall be subjected to review at least once annually to keep it current with regulatory /

statutory and business requirements. Revisions other than as stated herein shall be done only in

case of any major regulatory / environment changes, which shall be placed for ratification before

the ACB / Board.

Audit Policy, Ver. 7 Page 3 of 102

Contents of the Document

Part – I ............................................................................................................................................. 6

Charter for the Internal Audit Department .................................................................................... 6 1 Introduction ............................................................................................................................. 7 2 Authority ................................................................................................................................. 7 3 Audit Department ................................................................................................................... 8 4 Roles & Responsibilities .......................................................................................................... 9

4.1 Senior Management 4.2 Chief Audit Executive or Head of Internal Audit ................................................................. 9 4.3 Heads of General Banking Audit verticals and Micro Banking Audit verticals ............. 10 4.4 Offsite Audit Head ................................................................................................................... 10 4.5 Information System (IS) Audit Head .................................................................................... 11 4.6 Head Concurrent Audit .......................................................................................................... 11 4.7 Team Leaders of Audit verticals ............................................................................................ 11 4.8 Cluster Audit Heads of Banking Unit audits ....................................................................... 11

5 Selection and Recruitment for IA Department ...................................................................... 12 5.1 Qualification and Experience Profile of the Internal Auditor ........................................... 12 5.2 Age Profile................................................................................................................................. 12 5.3 Rotation ..................................................................................................................................... 13

6 Code of Ethics for Internal Auditor ....................................................................................... 13 6.1 Integrity, Objectivity & Independence of Internal Auditor ............................................... 13 6.2 Confidentiality .......................................................................................................................... 14 6.3 Proficiency and Due Professional Care ................................................................................. 14

7 Duties of the Internal Auditor ............................................................................................... 16 8 Limitations ............................................................................................................................. 16

Part – II ......................................................................................................................................... 18

Audit Policy .................................................................................................................................. 18 Preamble ....................................................................................................................................... 19 1 Risk Governance Model - Three Lines of Defence ................................................................ 19

1.1 Independence............................................................................................................................ 20 1.2 Reporting Structure ................................................................................................................. 21 1.3 Risk Based Internal Audit (RBIA) .......................................................................................... 21 1.4 Expectation Setting .................................................................................................................. 22

2 Risk Assessment Framework ................................................................................................ 23 2.1 Identification of Audit Universe ............................................................................................ 23 2.2 Risk assessment methodology ............................................................................................... 25

3 Risk Matrix for the Bank ........................................................................................................ 26 3.1 Measurement of impact of risk parameters .......................................................................... 27 3.2 Control Risk evaluation for a business group ...................................................................... 28 3.3 Risk Profiling of Auditable Units:.......................................................................................... 30 3.4 Direction of Risk: ...................................................................................................................... 30

4 Audit Planning ...................................................................................................................... 31 4.1 Training Needs Assessment ................................................................................................... 31

Audit Policy, Ver. 7 Page 4 of 102

4.2 Frequency of audits ................................................................................................................. 32 4.3 Frequency of Risk Based Internal Audit ............................................................................... 32 4.4 Audit Scope and Coverage ..................................................................................................... 33 4.5 Audit Report ............................................................................................................................. 33

5 Issue Assessment Framework, Reporting and Communication ........................................... 34 5.1 Escalation Matrix ...................................................................................................................... 36

6 Audit Ratings (Other than BU) .............................................................................................. 37 7 Compliance Report / Issue tracking Standards .................................................................... 37 8 Other relevant features of the audit policy ........................................................................... 39 9 Audit of Banking Units (BU) ................................................................................................. 39 10 Offsite Audit .......................................................................................................................... 41 11 Snap / Special audit .............................................................................................................. 43 12 Concurrent Audit .................................................................................................................. 44 13 Audit of Head Office (HO) Departments / Products & Processes ....................................... 44 14 Credit Audit ........................................................................................................................... 44 15 Audit Committee of Executives (ACE) ................................................................................. 45

15.1 Constitution of Audit Committee of Executives (ACE): .................................................... 45 15.2 The functions of the proposed ACE are listed below ......................................................... 46

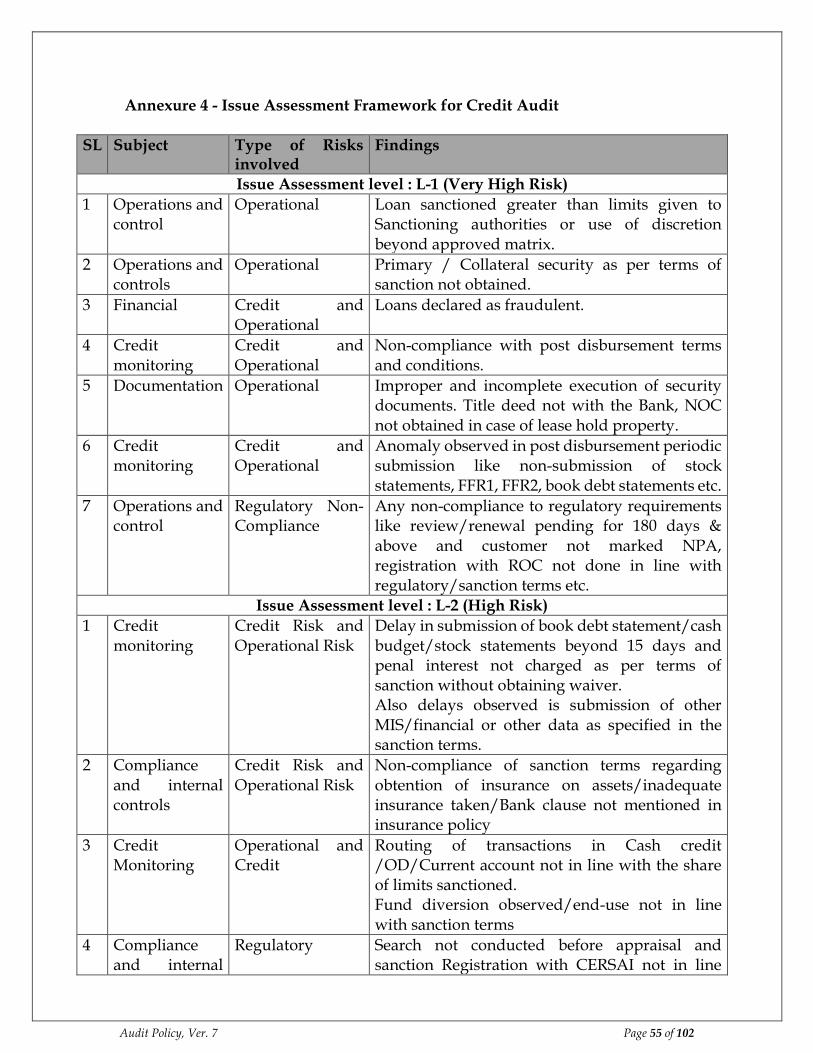

Annexure I - Issue Assessment Framework for Audit of Branches: ............................................ 47 Annexure 3 - Issue Assessment Framework for Audit of Small Enterprise Loans (SEL) ............ 53 Annexure 4 - Issue Assessment Framework for Credit Audit ..................................................... 55 Annexure 5 - Issue Assessment Framework for Audit of Housing Finance ................................ 57 Annexure 6 - Concurrent Audit ................................................................................................... 60

Part III ........................................................................................................................................... 68

Information System Audit Policy ................................................................................................. 68 Preamble ....................................................................................................................................... 69 1 IS Audit Policy ....................................................................................................................... 69

1.1 Definition ................................................................................................................................... 69 1.2 Mission Statement .................................................................................................................... 69 1.3 Aims/Goals of IS Audit Policy .............................................................................................. 70 1.4 Scope of IS Audit ...................................................................................................................... 70 1.5 Objectives .................................................................................................................................. 71 1.6 Independence............................................................................................................................ 71 1.7 Relationship with external IS Auditors ................................................................................. 71 1.8 Relationship with Internal Auditors ..................................................................................... 72 1.9 Coverage of Outsourced Services .......................................................................................... 72 1.10 Critical Success Factors............................................................................................................ 72

2 Authority ............................................................................................................................... 73 2.1 Right to Access Information ................................................................................................... 73 2.2 Scope or any limitations of scope .......................................................................................... 73 2.3 Functions to be audited ........................................................................................................... 73 2.4 Reporting relationship ............................................................................................................. 73 2.5 IS Audit Skills ........................................................................................................................... 74

3 Accountability ....................................................................................................................... 74 4 IS Audit Planning .................................................................................................................. 74

Audit Policy, Ver. 7 Page 5 of 102

4.1 Risk Based Audit Approach ................................................................................................... 74 4.2 Defining the IS Audit Universe .............................................................................................. 75 4.3 Information System Risk Assessment methodology .......................................................... 75

4.3.1 Identification of inherent risks in Information system units ..................................... 76 4.3.2 Measurement of impact of risk parameters .................................................................. 77 4.3.3 Control Risk evaluation and rating of an IS System ................................................... 77 4.3.4 Risk Matrix for the Information Systems of the Bank ................................................. 78 4.3.5 Risk Profiling of Auditable Units ................................................................................... 79

4.4 Scoping for IS Audit ................................................................................................................ 79 4.5 Documenting the Audit Plan.................................................................................................. 80

5 Issue Assessment Framework ............................................................................................... 80 6 Performance of Audit Work .................................................................................................. 82

6.1 Review of System Strategies ................................................................................................... 82 6.2 Review of system related policies /compliance .................................................................. 82 6.3 Organization and Administration ......................................................................................... 82 6.4 Review of system responsibilities of owners of business process ..................................... 83

6.4.1 Consideration of external factors ................................................................................... 83 6.4.2 Materiality ......................................................................................................................... 83

7 Frequency of Audit ................................................................................................................ 84 8 Compliance and Closure of Audit Report ............................................................................. 84 9 Audit Documentation ............................................................................................................ 85 10 Restriction of Scope ............................................................................................................... 85 IS Annexure – I: Audit Approach ................................................................................................. 86 IS Annexure – II: Audit Methodology .......................................................................................... 88 IS Annexure - III: AUDIT CONSIDERATIONS FOR IRREGULARITIES .................................... 91 IS Annexure – IV: AUDIT EVIDENCE/INFORMATION ........................................................... 92 IS Annexure – V - Issue Assessment Illustrations ........................................................................ 95 Glossary ...................................................................................................................................... 100

Audit Policy, Ver. 7 Page 6 of 102

Part – I

Charter for the Internal Audit Department

Audit Policy, Ver. 7 Page 7 of 102

1 Introduction

“The Charter for the Internal Audit Department” is approved by the Audit Committee of

the Board and it defines the Internal Audit Department’s purpose, authority, stature,

responsibility and position within the organization.

The Audit Policy is prepared based on reference and best practises on Standards of

Auditing issued by ICAI, Guidelines issued by Basel Committee and Banking

Supervision (BSBA), Institute of Internal Auditors (IIA) and International Standard for

professional practices from time to time.

2 Authority

The internal audit activity, with strict accountability for confidentiality and safeguarding

of records and information, should be authorized full, free, and unrestricted access to any

and all of records, physical properties, and personnel pertinent to carrying out any

engagement. All employees of the Bank are expected to assist the Internal Audit activity

in fulfilling its roles and responsibilities.

Following are the facilities which needs to be ensured by the Bank to the Internal Audit

function:

i) The Internal Audit Department in the Head Office shall be provided a separate sitting

arrangement and sufficient record room to keep their audit records and files safe and

intact along with separate sets of computers and its peripherals and other

communications facility.

Additionally, the Internal Audit Department shall be provided with an access to a

separate server space or file server in the Bank. The access to the server space or file

server should be provided to all members of the internal audit department. This

server or storage space should be a common drive where all audit reports, audit

evidences & correspondences should be stored for record purposes and ready

retrieval.

ii) The Internal Auditor should have full & free access to all departments and all the

records. The Internal Audit is free to review and critically appraise any activity of the

Departments/authorities, but their review and appraisal does not in any way relieve

Audit Policy, Ver. 7 Page 8 of 102

the Executives and Line supervisors of their responsibilities as internal audit is an

advisory function

iii) The usefulness of the internal audit will depend much on the co-operation and

working facilities provided to the department.

iv) Head of Internal Audit would have power to split the yearly programme as approved

by the Audit Committee into detailed quarterly programme / monthly programme.

All tours and contingency will be planned accordingly.

v) Internal Audit department should not be involved in any operational activities like

tendering, hiring, etc.

vi) Due to large number of Departments/ Disciplines, it will not be possible to audit all

the Departments/ Disciplines each year. Therefore, selection of the Departments/

disciplines for audit should be in line with the Risk Based Audit Plan, where

preference should be given to those Departments/Disciplines which have been

identified as high risk areas as per audit policy or which by nature of their activities

and as revealed by past experience, are more sensitive. The functions selected for this

purpose should include those where lapses and inadequacy of internal control may

result into considerable financial losses.

3 Audit Department

The Internal Audit Department will be an independent department. Neither the Chief

Audit Executive nor any Internal Auditors shall have any reporting relationship with the

business verticals, shall not assume operational responsibilities and shall not be given

any business targets. Persons transferred to or temporarily engaged by the Internal Audit

department should not be assigned to audits of activities which they previously

performed until a reasonable period of time has elapsed.

The Audit Policy of the Bank depicts the proposed organization chart showing internal

audit set-up, their locations and area of activities. Based on strength available, the

preference shall be given to plan audits with the internal team. In absence of required

manpower strength or the requisite skillsets, specific Internal Audits can be outsourced

by the CAE in consultation with the MD & CEO, subject to the ACB being assured that

Audit Policy, Ver. 7 Page 9 of 102

such expertise does not exist within the audit function of the bank. However, the

ownership of the audit reports in all such cases shall rest with regular functionaries of the

internal audit function.

4 Roles & Responsibilities

The Duties and responsibilities of various functionaries of the bank including the internal

audit department are as under:

4.1 Role of Senior Management

i) Senior management shall be responsible for developing an adequate, effective and

efficient internal control framework that identifies, measures, monitors and

controls all risks faced by the bank.

ii) It should maintain an organisational structure that clearly assigns responsibility,

authority and reporting relationships and ensures that delegated responsibilities

are effectively carried out.

iii) Senior Management should inform the internal audit function of new

developments, initiatives, projects, products and operational changes and ensure

that all associated risks, known and anticipated, are identified and communicated

at an early stage.

iv) Senior management should be accountable for ensuring that timely and

appropriate actions are taken on all internal audit findings and recommendations.

v) Senior management should ensure that the head of internal audit has the necessary

resources viz. staffs, financial tools and otherwise, available to carry out his or her

duties commensurate with the annual internal audit plan, scope and budget

approved by the audit committee, thereby enabling the auditors to carry out their

assignments with objectivity.

4.2 Chief Audit Executive or Head of Internal Audit

The Head of Internal Audit, as defined in the RBI circular, will be designated as Chief

Audit Executive of the bank.

Audit Policy, Ver. 7 Page 10 of 102

i) To update the Audit Policy from time to time and place the same before the ACB for

approval.

To update the Audit Manuals and Audit Department’s organization chart from time

to time and get the same approved by the competent authority.

ii) To timely inform the Management about the findings of all the Internal Audits

undertaken by internal auditors along with the compliances given by Head of the

auditee units.

iii) To investigate in the matters assigned by the Audit Committee from time to time.

iv) Finalize the Audit plan for the Bank as a whole and obtain the approval from the

ACB.

v) Timely submission of MIS and inform MD & CEO and the ACB on all the matters

pertaining to Internal Audit Department.

vi) Design appropriate training programme for the executives in internal audit.

vii) To arrange for periodical internal audit in accordance with the audit plan.

viii) To arrange for a special audit as and when required and also as per the direction of

the management.

ix) To ensure prompt disposal of audit observations.

x) To update the checklist for audit at regular intervals based on the experience gained

during audit as well as based on changes in regulatory requirements or operations.

4.3 Heads of General Banking Audit verticals and Micro Banking Audit verticals

They shall be responsible for the audit plan of their respective audit verticals and shall

ensure smooth functioning of the audits under their respective vertical.

4.4 Offsite Audit Head

Bank has established an Offsite Audit vertical, headed by Head-Offsite Audit, within the

Internal Audit Department for offsite monitoring of certain transactions/activities at

branches/offices/BUs. The tasks for offsite monitoring team would be added/modified

based on new issues arising and based on feedback from field auditors.

For carrying out these tasks the Team will be provided with read only access to the MIS-

Audit Policy, Ver. 7 Page 11 of 102

databases and other systems to enable them to query the required data using tools like

SQL, etc.

The Offsite Audit Team will support on-field branch banking auditors and Banking Unit

auditors with the necessary reports/ inputs that may be required.

4.5 Information System (IS) Audit Head

Bank has established an IS Audit vertical, headed by Head-IS Audit, within the Internal

Audit Department. The scope of IS Audit covers all information systems used by the bank

in related activities viz. system planning, organization, acquisition, implementation,

delivery and support to end-users. The scope also covers monitoring of implementation

in terms of its process effectiveness, input/output controls and accomplishments of

system goals. The IS Audit scope includes testing on the processes for planning and

organizing the information systems activities and the processes for monitoring those

activities

4.6 Head Concurrent Audit

The Head of Concurrent Audit, along with the CAE and Advisor Concurrent Audit, will

be responsible for satisfactory implementation of the Concurrent Audit system of the

Bank, including review and reporting of observations noted during the audit and their

timely compliance.

4.7 Team Leaders of Audit verticals

They shall be responsible for execution of the audits as per the allotted work in

accordance with the audit programme of their respective audit verticals.

4.8 Cluster Audit Heads of Banking Unit audits

They shall be responsible for execution of the audit plans in their BU audit clusters by

optimum utilization of allocated auditors to him/her. The utilities and responsibilities of

the subordinates should be communicated to the Team Leader of the BU audit verticals.

Audit Policy, Ver. 7 Page 12 of 102

5 Selection and Recruitment for IA Department

The Bank should have a well-defined HR policy, including the recruitment process and

the same should be applicable for the Internal Audit Department.

5.1 Qualification, Experience and Competence of the Internal Auditor

The qualification and experience requirements of the internal auditors for the department

should be well defined. Adequate number of resources of the Internal Audit Department

should be professionally competent, qualified and/or experienced bankers to ensure

effectiveness of the bank's internal audit function. The desired areas of knowledge and

experience shall include banking operations, accounting, information technology, data

analytics and forensic investigation, among others. Bank shall ensure that internal audit

function has the requisite skills to audit all areas of the bank. Given below are some

indicative qualifications / experience required:

5.2 Age Profile

A conscious effort needs to be made to maintain a proper mix of people in the

Professionally Qualified Persons Or

Chartered Accountant/Cost Accountant/ CISA/ DISA/ CAIIB/ MBA

Experienced Persons from the Department Or

i. Persons promoted under departmental promotion process or persons with experience and knowledge in respective domain ii. Persons with technical qualifications and having field experience.

IS Auditor Appropriate number of CISA qualified and remaining should have required skills, knowledge and expertise.

Offsite Auditor Persons with knowledge and experience in banking sector in addition to experience in database querying and analysis

Branch Auditor Persons promoted or transferred through departmental action having the requisite experience in Branch Banking operations.

BU Auditor Persons promoted or transferred through the departmental action having the requisite experience in Micro Banking operations.

Support Staff Graduates or Persons laterally hired or transferred through departmental action.

Audit Policy, Ver. 7 Page 13 of 102

department. A constant review should be done of the age profile of the internal auditors

to ensure that there are adequate numbers of fresh and young people willing to undertake

intensive travel.

Age limit for retired staff engaged as internal / concurrent auditors shall be capped at 70

years.

5.3 Rotation

The bank has a separate and independent Audit team and hence any staffs posted in

Audit team (career internal auditor or otherwise) shall work in the Department for a

minimum period of three years. Post that permanent staff within the Internal Audit

Department may be transferred to other departments. Transfer of any staff from Internal

Audit before the stipulated three years’ period would require exception approval from

the CAE or Head-HR.

Vacancies so created can be fill up by way of recruitment of suitable resources possessing

specialized knowledge useful for the audit function from within the bank or outside to

ensure continuity and adequate skills for the staff in Audit Function.

Similarly, the maximum period for which an external concurrent auditor shall be allowed

to continue with a branch/business unit shall not be more than three years.

6 Code of Ethics for Internal Auditor

There are certain moral principles which the Internal Auditors should follow. These are

illustrative and not exhaustive; these provide the basic guidelines to the Internal Auditors

with regard to the moral hazards and conflicts which they may face while carrying out

Internal Audit assignments.

6.1 Integrity, Objectivity & Independence of Internal Auditor

i) Internal Auditor shall have an obligation to exercise honesty, objectivity, and

diligence in performance of their duties and responsibilities.

ii) Internal Auditors holding the trust of the Bank, shall exhibit loyalty in all matters

pertaining to the affairs of the Bank.

Audit Policy, Ver. 7 Page 14 of 102

iii) Internal Auditors shall refrain from entering into any activity which may be in conflict

with the interest of the Bank.

iv) Internal Auditors shall not accept a fee or a gift from an employee, a Contractor or a

supplier.

v) Internal Auditor must be fair and must not allow prejudice or bias to override his

objectivity. She/he should maintain an impartial attitude. The internal auditor should

not, therefore, to the extent possible, undertake activities, which are or might appear

to be incompatible with her/his independence and objectivity. For example, to avoid

any conflict of interest, the internal auditor should not review an activity for which

she/he was previously responsible.

vi) Internal Auditor should immediately bring any actual or apparent conflict of interest

to the attention of the appropriate level of management so that necessary corrective

action may be taken.

6.2 Confidentiality

i) Internal Auditor shall be prudent in the use of information acquired in the course of

their duties. She/he shall not use confidential information for any personal reason or

in a manner which would be detrimental to the interest of the Bank.

ii) Internal Auditor should not disclose any such information to a third party, including

employees of the entity, without specific authority of management/ client or unless

there is a legal or a professional responsibility to do so.

6.3 Proficiency and Due Professional Care

i) Internal Auditor should exercise due professional care in carrying out the work

entrusted to him in terms of deciding on aspects such as the extent of work required

to achieve the objectives of the engagement, relative complexity and materiality of the

matters subjected to internal audit, assessment of risk management, control and

governance processes and cost benefit analysis. Due professional care, however,

neither implies nor guarantees infallibility, nor does it require the internal auditor to

go beyond the scope of his engagement.

Audit Policy, Ver. 7 Page 15 of 102

ii) Internal Auditor should have obtained required skills and competence through

general education, technical knowledge obtained through study and formal courses,

as are necessary for the purpose of discharging his responsibilities.

iii) Internal Auditor shall also have a continuing responsibility to maintain professional

knowledge and skills at a level required to ensure that the Bank receives the

advantage of competent professional service based on the latest developments in the

profession, the economy, the relevant industry and legislation.

iv) in cases of serious acts of omission or commission noticed in the working of bank's

own staff or retired staff, working as concurrent auditors, the accountability action

would be fixed as per the extant process of the bank.

v) Ensure adherence to various Standards of Practice issued by Institute of Chartered

Accountants of India such as:

a) SA 230, Audit Documentation: The record of audit procedures performed,

relevant audit evidence obtained, and conclusions the auditor reached (b) Audit

file: One or more folders or other storage media, in physical or electronic form,

containing the records that comprise the audit documentation for a specific

engagement

b) SA 320, Materiality in Planning and Performing an Audit: The concept of

materiality is applied by the auditor both in planning and performing the audit,

and in evaluating the effect of identified misstatements on the audit and of

uncorrected misstatements.

c) SA 315, Identifying and Assessing the Risks of Material Misstatement

through understanding the Entity and its environment: The objective of the

auditor is to identify and assess the risks of material misstatement, whether due

to fraud or error, at the financial statement and assertion levels, through

understanding the entity and its environment, including the entity’s internal

control, thereby providing a basis for designing and implementing responses to

the assessed risks of material misstatement. This will help the auditor to reduce

the risk of material misstatement to an acceptably low level.

Audit Policy, Ver. 7 Page 16 of 102

d) SA 500, Audit Evidence: Information used by the auditor in arriving at the

collusions on which the auditor’s opinion is based. Audit evidence includes

both information contained in the accounting records underlying the financial

statements and information obtained from other sources. The auditor shall

design and perform audit procedures that are appropriate in the circumstances

for the purpose of obtaining sufficient appropriate audit evidence.

e) SA 530, Audit Sampling: When designing an audit sample, the auditor shall

con-sider the purpose of the audit procedure and the characteristics of the

population from which the sample will be drawn. The auditor shall determine

a sample size sufficient to reduce sampling risk to an acceptably low level.

7 Duties of the Internal Auditor

Key objectives of the internal auditor can be summarized as:

i) To obtain sufficient appropriate audit evidence regarding compliance with the

provisions of those laws and regulations generally recognized to have a direct effect

on the determination of material amounts and disclosures in the financial statements.

ii) To perform specified audit procedures to help identify instances of non-compliance

with other laws and regulations that may have a significant impact on the functioning

of the entity.

iii) To respond appropriately to non-compliance or suspected non-compliance with laws

and regulations identified during the internal audit.

8 Limitations

Owing to the inherent limitations of an internal audit, there is an unavoidable risk that

some non-compliance with laws and regulations and consequential material

misstatements in the financial statements may not be detected, even though the internal

audit is properly planned and performed in accordance with the SIAs. In the context of

laws and regulations, the potential effects of inherent limitations on the internal auditor’s

ability to detect non-compliance are greater for such reasons as the following:

Audit Policy, Ver. 7 Page 17 of 102

a) There are many laws and regulations, relating principally to the operating aspects of

an entity that typically do not affect the financial statements and are not captured by

the entity’s information systems relevant to financial reporting.

b) Non-compliance may involve conduct designed to conceal it, such as collusion,

forgery, deliberate failure to record transactions, management override of controls or

intentional misrepresentations being made to the internal auditor.

Whether an act constitutes non-compliance is ultimately a matter for legal determination

by a court of law. Ordinarily, certain non-compliance is from the events and transactions

captured or reflected in the entity’s information systems relevant to financial reporting,

the less likely the internal auditor is to become aware of it or to recognize the non-

compliance.

Audit Policy, Ver. 7 Page 18 of 102

Part – II

Audit Policy

Audit Policy, Ver. 7 Page 19 of 102

Preamble

The role of internal audit is to provide independent assurance that an organization’s risk

management, governance and internal control processes are operating effectively. The

Bank will have a risk based Annual Internal Audit Plan, approved by the Audit

Committee of the Board. Relevant audits and reviews will be carried out by the Internal

Audit Department in accordance with the audit methodology defined in the Audit Policy.

Under risk-based internal audit, the focus is prioritization of audit areas and allocation

of audit resources in accordance with the risk assessment of all areas and functions of the

Bank. It is therefore essential for the Bank to have a well-defined policy, for undertaking

risk-based internal audit. The policy shall include the risk assessment methodology for

identifying the risk areas based on which the audit plan would be formulated. Risk based

policy to focus on frequency, prioritizing, extent of checking, risk-assessment/ profiling

of activities/ functions/ products and their updating, broadening the risk classifications

etc. during audit process.

This Audit Policy is formulated taking consideration of RBI requirements, best industry

practices and other factors as per the need of the Bank. It will come to effect immediately

on approval by the Board and will be in force until the same is revised.

1 Risk Governance Model - Three Lines of Defence

To manage different risks across various products and processes, the Bank has adopted

‘three lines of defence’ under Risk Governance model. The first line of defence role is the

line management, while second line of defence are the Risk Management, Compliance

and other Control Functions and Internal Audit Department (IAD) being the third line of

defence.

This model defines the following responsibilities at various levels:

i) FIRST LINE of DEFENCE: Primary accountability for identifying, assessing and

managing the various operational and compliance risks pertaining to their business

or area of operation (e.g. Branches, Treasury, Information Technology, etc.) rests with

Heads of Business Units and Departments.

Audit Policy, Ver. 7 Page 20 of 102

ii) SECOND LINE of DEFENCE: Risk Management, Compliance and other Control

Functions:

a) Have to coordinate, oversee and objectively challenge the execution of business

/ operations (keeping in mind the risk and control framework), management, etc.

b) Are independent of the management and personnel that originate or manage the

risk exposures

c) Have the power to escalate / veto high risk business activity

iii) THIRD LINE of DEFENCE: IAD is independent of both business and risk functions

and performs independent evaluation / assessments of the first two lines of defence.

IAD places reliance on review procedures conducted by the two lines of defence and

effectively uses the results in assessing and developing an audit approach which is a

judicious combination of various assurance practices that are in place. This approach

promotes the convergence between various monitoring, evaluation and assessment

procedures and aims at reducing redundancies (in terms of time, cost and effort).

1.1 Independence

The Internal Audit function shall be an independent function with ability to provide

independent assurance and consulting services designed to add value and improve the

Bank’s operations and also make appropriate recommendations for improving the

corporate governance, including ethics and values of the Bank. The Head of Internal

Audit shall be a Senior Executive having relevant experience with no operational or

business responsibilities, shall have the ability to exercise independent judgement and

shall be appointed for a reasonably long period, preferably for a period of three years.

The Board and Audit Committee of the Board shall be kept informed of any change in

Head of Internal Audit, as also reasons for the change in the incumbent. The name of

Head of Internal Audit and any change in incumbency shall be intimated to RBI, as &

when it takes place.

Audit Policy, Ver. 7 Page 21 of 102

1.2 Reporting Structure

The Chief Audit Executive (Head of Internal Audit) shall functionally report to the MD

& CEO of the bank. Audit Committee of Board shall meet the CAE (HIA) at least once in

a quarter, without the presence of the senior management, including the MD & CEO.

The ‘reviewing authority’ shall be with the ACB and the ‘accepting authority’ shall be

with the Board in matters of Performance Appraisal of the HIA.

All ACB directions will be monitored by the CAE.

Accordingly, the overall structure of the Internal Audit Department shall be as given

below:

1.3 Risk Based Internal Audit (RBIA)

RBI vide its circular no. DBS.CO.PP.BC.10/11.01.005/2002-03 dated December 27, 2002

provided a guidance note on Risk Based Internal Audit. RBI advised initiation of

Audit Policy, Ver. 7 Page 22 of 102

necessary steps to prepare a risk-based internal audit system in a phased manner,

keeping in view Bank’s risk management practices, business requirements, manpower

availability etc.

A sound internal audit function plays an important role in contributing to the

effectiveness of the internal control system. The audit function shall provide high quality

counsel to the management on the effectiveness of risk management and internal controls

including regulatory / statutory compliance by the bank.

1.4 Expectation Setting

This step facilitates the alignment of IAD resources with the Bank’s business objectives to

maximize the value delivered to business by IAD and hence it forms a key cornerstone of

IAD planning. This activity which requires extensive interaction between the IAD and

Top Management would be accomplished through workshops, facilitated sessions, one-

to-one interactions, or other forums considered appropriate by IAD.

The following are the key milestones of this activity:

i) Risk assessment: Risk Assessment is a critical and important part of Planning. It

includes the process of identifying the risks, assessing the risk, taking steps to

reduce the risks to acceptable levels, considering both probability and impact of

the risks. Risk Assessment allows the auditor to determine the scope of the audit

and nature, extent and timing of audit. Risk Assessment mainly implies Inherent

risk assessment, control risk assessment and the residual risk. The Auditor should

satisfy himself that the risk assessment procedure adequately covers the periodic

and timely assessment of all the risks.

ii) Prioritization of business objectives through identification of priority / focus

level of business areas: Priority should be given to the risk that has the potential

to cause significant impact and harm.

iii) Scope, coverage and management expectations from IAD: Coverage would

specify the extent of audit work to be conducted. Expectations of Management, is

the outcome of audit which would satisfy the objective and its requirement to all

Audit Policy, Ver. 7 Page 23 of 102

the stakeholders. In order that there is no confusion, the scope, coverage and

management expectation should be clearly defined and that should be integrated

as a part of the Planning exercise.

iv) Timelines with respect to completion and presentation of results to

management: Timeline is an essential milestone to measure the achievement of

objectives of audit. It defines the timeliness of delivery of required deliverables to

various stakeholders. Reports should be issued in a timely manner, to encourage

prompt corrective measures. When appropriate, the auditor should report

significant findings promptly to the concerned persons.

2 Risk Assessment Framework

The risk assessment framework would include the following:

i) Identification of Audit Universe

ii) Inherent Risk Assessment

iii) Control Risk Assessment

iv) Residual Risk Assessment.

All the activities will be reviewed annually along with the overall Policy.

2.1 Identification of Audit Universe

The first step in performing the risk assessment is to identify various business groups

and support functions within the Bank based on which the inherent risk profile would be

prepared and presented for each such groups. The groups shall be identified and updated

to remain aligned with the other prevailing frameworks for management oversight and

control of the business and operations. Thus the Audit Universe of the Bank, comprises

of the Business, Operation, Corporate Centre and other Support groups collectively

called “Business Groups”. Each Group is further broken up into auditable units/areas.

Based on the risk assessment process explained below, a risk matrix for the Bank,

comprising all the Business groups is drawn up. Further a risk matrix for each Business

Group comprising various auditable units/ areas, is also drawn up.

At the beginning of the year as a first step towards preparation of the RBAP (Risk Based

Audit Policy, Ver. 7 Page 24 of 102

Audit Plan), a list of all Business Groups and the auditable units/areas are drawn up.

This will consider and evaluate modifications during the financial year, required on

account of changes, if any in the control environment in the auditee units within the same

business / group.

The Audit Universe would cover the following units and activities:

• Branch Banking

• Micro Banking i.e., Banking Units (BUs)

• Central Processing Units (CPU) o Account Opening o Accounts Modification Unit o Collateral & Logistics Unit o Loan Processing Unit o Phone Banking Unit o Corporate Internet Banking Admin Function o EDC MID/TID processing o Aadhaar Enrolment and updation Operation

• Head Office Departments: (in alphabetical order) o Administration o Banking Operations & Customer Service o Business Intelligence Unit o Company Secretary o Compliance o Corporate Branding & Communication o Corporate Legal o Corporate Services o Finance & Accounts o Fraud containment and Monitoring Department o Human Resource o Information Security o Information Technology o Logistics & Purchase o Payments and Settlement system (as per NPCI guideline) o Retail Banking including Head, ZH, RH & CH o Risk o Third Party Products o Treasury o Vigilance o Wholesale Banking including the controlling offices at all places

• Products, Processes and Activities: o Outsourced Activities (including payment gateway service providers) o Following loan products at various Asset Centres:

Audit Policy, Ver. 7 Page 25 of 102

• Retail Assets (Housing Loans, Loans against Property, Personal Loans, Two wheeler Loans, Gold Loans etc.)

• Small Enterprises Loans (SEL) o SME Loans o Any other Loans & Advances (Funded or Non-funded) o Debit/ATM Cards and Credit cards o Merchant acquisition business o Forex & Trade Finance

2.2 Risk assessment methodology

The risk assessment process should, inter alia, include the following: -

Risk Assessment for Business Groups based in business model

i) Identification of inherent business risks in each Business Group in the bank;

ii) Evaluation of the effectiveness of the control systems for monitoring the inherent

risks of the business groups (`Control risk’);

iii) Drawing up a risk-matrix for taking into account both the factors viz., inherent and

control risks. As per illustrative risk-matrix above.

The steps to be followed is detailed hereunder:

i) The basis for determination of the inherent risk (high, medium, low) should be

clearly spelt out.

ii) The process of inherent risk assessment may make use of both quantitative and

qualitative approaches.

iii) Compare of the current residual risk of auditable units with that of the previous

audit to assess the effectiveness of the control environment and assess the direction

of risk.

While the quantum of credit, market, and operational risks could largely be determined

by quantitative assessment, a qualitative approach may be adopted for assessing the

regulatory and reputation risks in various business groups. In order to focus attention on

areas of greater risk to the bank, an activity-wise and location-wise identification of risk

Audit Policy, Ver. 7 Page 26 of 102

should be undertaken.

The risk assessment methodology will also include, inter alia, the following parameters:

• Previous internal audit reports and compliance

• Proposed changes in business lines or change in focus

• Significant change in management / key personnel

• Results of latest regulatory examination report

• Reports of external auditors

• Volume of business including quantum of cross selling and complexity of activities

• Substantial performance variations from the budget etc.

• Operational Risk, Credit and Market Risk parameters, like CTR/STR, NPA, etc.

• Number of Customer complaints

• Industry trends and other environmental factors

• Time elapsed since last audit

3 Risk Matrix for the Bank

Based on the Control Risk Score and the Inherent Risk Scores, a Risk Matrix for the Bank

is prepared comprising all Business Groups. Based on the Inherent Risk and Control Risk

for each group, the group will be placed in the Risk Matrix.

Inherent Risk

Inherent Business risks indicate the intrinsic risk in a particular area/activity of the Bank

and could be grouped into low, medium and high categories depending on the severity

of risk.

For ease of determination, all the primary risks will be grouped into six categories,

namely, credit risk, market risk, operation risk, regulatory risk, reputation risk, and

information technology risk. These may be further broken down into risk parameters as

under:

i) Operations Risk

a) Volume of transaction

b) Complexity

c) Documented process

d) Staff skills

ii) Market Risk

a) Risk from changes in

interest/exchange rates

b) Laid down system support

c) Availability of tools/models

Audit Policy, Ver. 7 Page 27 of 102

e) Frequent changes in process

f) System Support

d) Skill sets

iii) Reputation Risk

a) Impact of process on reputation of

Bank

b) Extent of customer interaction

c) Risk on account of outsourcing

d) Proper grievance handling

mechanism

iv) Credit Risk

a) Existence of proper credit appraisal

process

b) Complexity of products

c) Existence of strong Delegation of

Financial Power (DFP) System

d) Level of delinquencies

v) Regulatory Risk

a) Degree of regulation in process

b) Complexity of regulation

c) Existence of compliance risk

monitoring process

d) Regulatory findings

vi) IT Risk

e) Complexity of system

f) Vulnerability of system to cyber

attacks

g) Dependence on external vendor for

system support

h) Existence and effectiveness of

BCP/DRP

3.1 Measurement of impact of risk parameters

The risk parameters as defined above for all the primary risks are considered for arriving

at the score for Inherent Risk. A high, medium or low score is assigned to each parameter,

wherever applicable. Based on these scores for each risk parameter, an aggregate score

for that risk category is quantified and a score on the scale of 1 to 6 (High 5-6, Medium 3-

4 and Low 1-2) is awarded to each of the six primary risks listed above. Where a business

group is not exposed to a particular risk, a score of zero is given.

Thus the maximum Inherent Risk score would be 36 (aggregate of six primary risks) for

Audit Policy, Ver. 7 Page 28 of 102

any business group based on discussion and internal judgment, an inherent risk of up to

20% may be considered as “low”, between 21% to 50% may be considered as “medium”

and inherent risk greater than 50% may be considered as “high”.

3.2 Control Risk evaluation

The previous audit rating would indicate the level of control risk. Control risks arise out

of inadequate control systems, deficiencies/gaps or likely failures in the existing control

processes, incidents pointing to gaps in implementation of control processes etc. The

control risks could also be classified into low, medium and high categories. Control Risk

would be numerically indicated on a “0 to 100” scale, with a score of “0” being the ideal

score, which would indicate that the risks are fully covered by the existing controls.

In order to measure the extent to which the inherent risks are addressed by controls,

threshold limits i.e. three levels of threshold for measurement of Control Risk viz.,

“High”, “Medium” and “Low” have been defined. These would be expressed in terms of

percentage as under:

Control Risks Score

Low Less than 15%

Medium 15% to 30%

High Above 30%

The gaps observed in the control risks vis-à-vis, the inherent risks lead us to the residual

risk. The residual risks can be classified into Extremely High, Very High, High, Medium

and Low based on the following and accordingly fall in the respective cells in the Risk

Matrix (as under):

Risk Matrix

Inh

ere

nt

Bu

s

ines

s Ris

ks High “4” “2” “1”

Audit Policy, Ver. 7 Page 29 of 102

High Risk Very High Risk Extremely High Risk

Medium “7”

Medium Risk

“5”

High Risk

“3”

Very High Risk

Low “9”

Low Risk

“8”

Medium Risk

“6”

High Risk

Low Medium High

Control Risks

[ Inherent Risk: Low 0-7, Medium 8-18, High 19-36] Scale of 0 to 36 [ Control Risk: Low <15%, Medium 15%-30%, High >30%] Scale of 0 to 100

In the overall risk assessment both the inherent business risks and control risks should

be factored in. The overall risk assessment as reflected in each cell of the risk matrix is

explained below:

1 – Extremely High Risk – Both the inherent business risk and control risk are high which

makes this an Extremely High Risk area. This area would require immediate audit

attention, maximum allocation of audit resources besides ongoing monitoring by the

bank’s top management.

2 – Very High Risk- The business unit/area is perceived to have “high” inherent risk

coupled with medium control risk makes this a Very High Risk area

3 – Very High Risk – Although the inherent business risk is medium, this is a Very High

Risk area due to high control risk.

4 – High Risk- The business unit/area is perceived to have “high” inherent risk, but the

control risks as borne out by the previous audit ratings are weak (cells 4, 5, & 6).

5 – High Risk – Although the inherent business risk is medium this is a High Risk area

because of control risk also being medium.

6 – High Risk – Although the inherent business risk is low, due to high control risk this

becomes a High Risk area.

7 – Medium Risk – Although the control risk is low this is a Medium Risk area due to

Audit Policy, Ver. 7 Page 30 of 102

Medium inherent business risks.

8 – Medium Risk - The inherent business risk is low and the control risk is medium.

9 – Low Risk – Both the inherent business risk and control risk are low.

3.3 Risk Profiling of Auditable Units:

Where any Business group itself comprises of several independent auditable units with

different level of controls, like branch banking etc., the following approach will be taken:

A risk map of all the auditable units will be prepared taking the “inherent risk” of the

individual units to be the same as that of the group. The control risk of the individual

auditable units would be derived from the previous audit ratings as well as other factors

like any frauds detected etc.

3.4 Direction of Risk:

i) If the Current Control Risk Score is more than 3% of the previous Audit score, the

Direction of Risk would be considered as “Decreasing”

ii) If the Current Control Risk Score is in the range of +3% to – 3% of previous Audit

score, the Direction of Risk would be considered as “Stable”

iii) If the Current Control Risk Score is less than 3% of the previous Audit score, the

Direction of Risk would be considered as “Increasing”

In addition to the above, where the direction of risk is found to be increasing, the below

shall also be taken into consideration, for the limited purpose of deciding the frequency

of next audit, as under:

i) The difference in Control Risk score between previous audit and current audit is

greater than 5% but less than 10%, then 5% will be deducted from the current audit

score to arrive at the Control Risk score.

ii) The difference in Control Risk score between previous audit and current audit is

between 10% to 15%, then 7% will be deducted from the current audit score to arrive

at the Control Risk score.

Audit Policy, Ver. 7 Page 31 of 102

iii) The difference in Control Risk score between previous audit and current audit score

is more than 15%, then 10% will be deducted from the current audit to arrive at the

Control Risk score.

4 Audit Planning

An Audit plan defines the scope, coverage and resources, including time, required for

audit over a defined period. Adequate planning ensures that appropriate attention is

devoted to significant areas of audit, potential problems are identified, and that the skills

and time of the staff are appropriately utilised.

The Audit plan would be drawn up consistent with the goals and objectives of the

Internal Audit function as listed out in the Internal Audit charter as well as the goals and

objectives of the Bank.

All new branches shall be subjected to internal audit within six months of opening of the

branch.

A plan once prepared would be continuously reviewed by the IAD to identify any

modifications required to bring the same in line with the changes, if any, in the audit

environment. However, any major modification to the plan would be done in

consultation with the ACB.

4.1 Training Needs Assessment

At the beginning of every financial year, IAD shall examine and assess the training needs

of the internal auditors across all verticals, according to the skill-sets required to conduct

the audits of various entities - as per the approved Audit Plan. This shall be

communicated to the HR Department for arrangement of in-house, appropriate training

programmes or deputing the concerned auditor(s) to suitable institutes for imparting

relevant inputs.

The staffs in the Internal Audit department shall also appear for all mandatory and

functional e-learning courses hosted on the LMS from time to time. The current courses

relevant to audit team include KYC/AML, Operational Risk, Reading Financial

Statements, Fraud awareness etc.

Audit Policy, Ver. 7 Page 32 of 102

IAD will implement the process of rotation of auditors by transferring them to other

departments at regular intervals and fill up the gaps either by way of rotation or

recruitment of suitable resources from outside to ensure the quality of auditors.

4.2 Frequency of audits

The IAD carries out internal audits as a part of the overall audit assurance framework to

the Bank. The risk map of the auditable units so derived will decide the frequency of

audit of the respective units as under:

4.3 Frequency of Risk Based Internal Audit

Frequency of individual auditable unit would be based on the position of the individual

auditable unit in the Risk Matrix. All the auditable unit will be audited at least once in

two years.

Auditable units falling under cell “9” (i.e., Low Risk) would be audited once in two years.

Auditable units falling under cell “7 & 8” (i.e., Medium Risk) would be audited once in

eighteen months.

Auditable units falling under cell “4, 5 & 6” (i.e., High Risk) would be audited once in

twelve months.

Auditable units falling under cell “2 & 3” (i.e., Very High Risk) would be audited once in

nine months.

Auditable units falling under cell “1” (i.e., Extremely High Risk) would be audited once

in six months.

The above intervals between two internal audits is indicative and the interval is the outer

limit and the audit must be conducted within the quarter in which the audit becomes

due.

The internal audits of Bank Branches shall be conducted with an element of surprise; no

advance intimation shall be given to the branches. The audits may be conducted any time

within a period of three months prior to the outer limit.

Audit Policy, Ver. 7 Page 33 of 102

4.4 Audit Scope and Coverage

The scope of each audit shall be determined by respective Audit Team Lead and

approved by the Head of respective Audit vertical in consultation with the CAE.

However, at the minimum, the scope will cover the following areas:

i) Availability of approved product / process guidelines ii) The control environment in various areas iii) Data integrity, information security iv) Regulatory and Internal Compliance v) Adherence to KYC/AML Guidelines vi) Compliance with outsourcing guidelines vii) Customer Service Quality viii) Compliance to previous audit observations

The field work shall be conducted by the internal auditors at the branches (onsite) with

the audit checklist prepared by IAD. The audit checklist shall be revised by the audit

manager whenever there is any change in the underlying process and it shall be approved

by CAE.

4.5 Audit Report

At the end of the field work a draft report shall be prepared containing the executive

summary, the objective of the audit, the scope including limitations and exclusions,

sampling methodology (Annexure 7), audit rating and opinion. All the audit findings in

the audit reports shall be categorized and levelled as per the Issue Assessment

Framework. All the audit findings will be communicated to the respective groups and an

auditee response having the components- proposed actions, timelines for compliance and

responsibility will be obtained. The reports will be peer-reviewed, rated and circulated

as defined hereunder:

i) Bank Branches Report would be issued to the Branch Head and Cluster Head, copy

marked to the concerned controllers i.e. Regional Head, Head-Branch Banking.

ii) BUs (Refer Point No. 10 below for the defined process)

iii) Other reports: Rating would be done as per the Audit Policy; draft report would be

shared with the Head of the Department of the respective Department for

Audit Policy, Ver. 7 Page 34 of 102

management response. Final Report would be issued to the respective Department

Head.

iv) Sign-off, on the draft audit report from the respective auditee department, to be

obtained before release of the final report.

5 Issue Assessment Framework, Reporting and Communication

The process of issue assessment distinguishes between “Very High”, “High”, “Medium”

and “Low” Risk categorization of audit issues, where “Very High” is classified as “Level-

1” or L1, “High” as “Level-2” or L2, “Medium” as “Level-3” or L3 and “Low” as “Level-

4” or L4.

The categorization of issues as L1, L2, L3 or L4 is done on the basis of the estimated

likelihood and the potential impact of the control weakness as depicted hereunder:

Likelihood Impact

Less Likely Possible Most Likely

Very High L2 L1 L1

High L3 L2 L1

Medium L4 L3 L2

Low L4 L4 L3

The likelihood and the impact assessed would be broadly carried out taking into

consideration the following factors.

Likelihood:

Most Likely: Has happened in several instances or process gap exists.

Possible: Could happen in the foreseeable future.

Less Likely: Less likely to happen.

Impact:

The Impact assessment shall be based on various factors individually or in combination

of the below factors:

Audit Policy, Ver. 7 Page 35 of 102

Risk Customers Affected

Financial Impact

Brand & Reputation Impact

Systems / Services affected

Regulatory, Internal Policy and Legal implications

Information Security risk / System users impacted.

Very High

> 2% > Rs. 25 lacs

Coverage in high profile global/ national media which could lead to significant damage of brand

Poses any systemic risk. Critical business system / service is affected.

Non-compliance to regulatory guidelines / law having impact of possible penalty from regulatory / law enforcement bodies. Not complying with Statutory Audit or RBI Audit Observations

i) Potential loss of all information ii) > 5000 user affected. ii) Application Security testing / VAPT not conducted in case of public facing applications.

High 1 - 2% > Rs. 10 lacs and up to Rs. 25 lacs

Coverage in industry specific / local media which could lead to negative impact on brand

Poses any undefined or unexpected risks. Non- critical business systems / services are affected.

Non-compliance to regulatory guidelines / law not having direct impact of penalty. Non-Compliance of Bank’s Policy or PCMC approved process.

i) Potential loss of confidential information ii) 500-5000 users affected. iii) Application Security testing / VAPT not conducted in case of internal financial applications e.g. CBS, ITMS

Medium Up to 1%

> Rs. 5 lacs and up to Rs. 10 lacs

Negative Information limited to employees/ vendors

Only Support services are affected, but business can run as usual.

No violation of any regulatory gudelines / law. Partial non-compliance to the Policies / SOPs.

i) Potential loss of internal Information ii) < 500 users affected. iii) Application Security testing / VAPT not conducted in case of internal applications – non-financial but identified as critical e.g. AML, ALM.

Low No Customers affected

Upto Rs. 5 lacs

Negative Information in closed user group

No Systems / Services affected

No Implication i) Potential loss of public information ii) No users affected iii) Application Security testing / VAPT not conducted in case of non- critical internal applications.

Notwithstanding the above matrix for financial impact, instances of Revenue leakage shall be

classified based on the quantum of leakage / potential of leakage identified. Where gap is

identified in the process of recovery of revenue, which can potentially lead to a high revenue

leakage at bank level or quantum of leakage identified is Rs. 1 lac & above the same shall be

classified as Level 1, leakage below Rs. 1 lac and up to Rs. 10000, shall be classified as Level 2 and

any revenue leakage below Rs. 10000 shall be classified as L3 at a Unit level.

Audit Policy, Ver. 7 Page 36 of 102

Compliance to Audit Observation: Any submission of compliance to audit observation without

actual rectification of the audit observation is very high risk and shall be classified as Level 1

issue. Similarly repeat audit observation in more than 1 area coupled with an increased direction

of risk at the unit level shall be treated as Level 2 issue, where the direction of risk is stable the

same shall be classified as L3 issue and where the direction of Risk is decreasing the same shall

be classified as L4 issue.

The key findings of all the audit reports would be classified into four levels L1, L2, L3 &

L4, L1 being the highest level of importance.

While endeavour would be made to ensure that the audit issues would be classified as per the

framework, in the event the assessment framework requires any interpretation / clarity, the risk

can be upgraded /downgraded, as per direction of CAE.

Under the overall Issue Assessment Framework detailed above, an illustrative list of

specific audit issues identified at Branches, BUs, SEL, Credit Audit and HF (Housing

Finance Department) have been separately drawn up and the same is furnished in

Annexure 1 to 5 respectively.

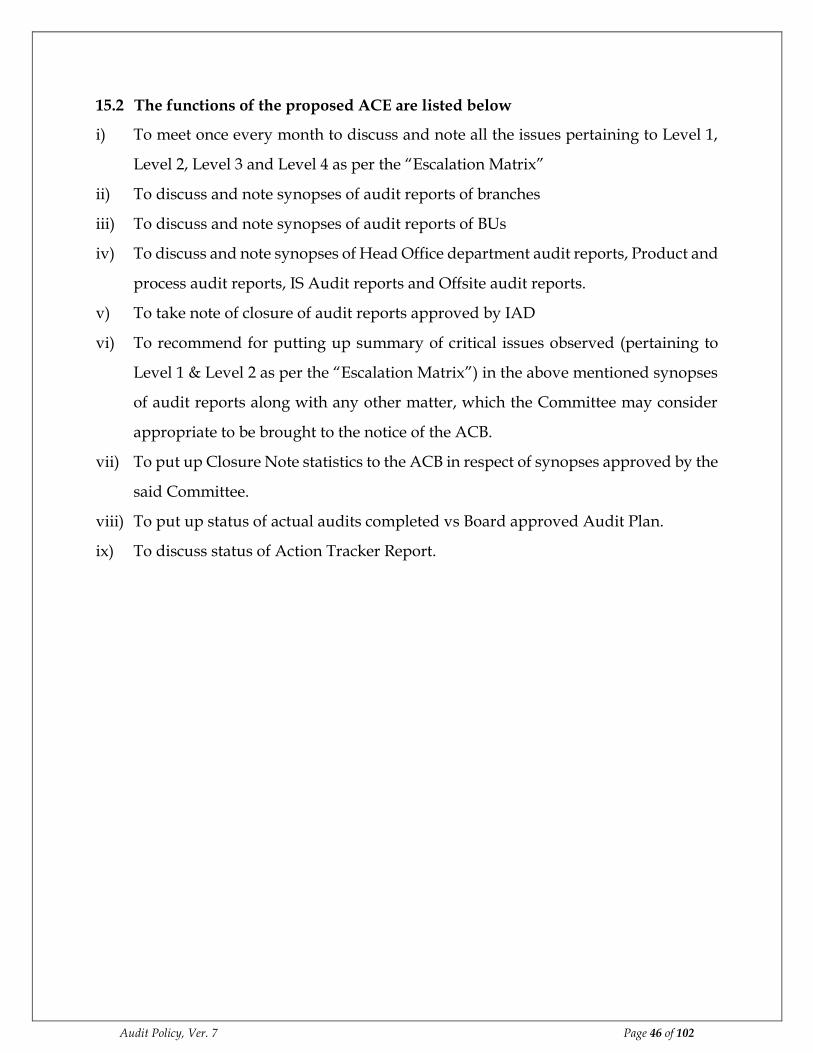

5.1 Escalation Matrix

In order to enable the Audit Committee of the Board /Management get a more business

/ function -wide view of processes across the Bank and the key findings noted thereof,

including effectiveness of audit thereof, the IAD at the end of the audit cycle or at other

periodic intervals (as directed by Top Management and the ACB) would present the

aggregated audit findings and would also present the key reports / dashboards to the

Top Management and the Audit Committee of the Board.

The individual audit observations would be presented as under:

• Level 1: To be reported to MD & CEO and all levels below

• Level 2: To be issued to Business/Department Head and all levels below

Audit Policy, Ver. 7 Page 37 of 102

• Level 3: To be issued to Deputy Business/Deputy Department Head all levels below

• Level 4: To be issued to respective Unit Head

All the issues pertaining to Level 1, Level 2, Level 3 and Level 4 will be put up to the

Audit Committee of Executives (ACE).

All the issues pertaining to Level 1 & 2 and the Minutes of meeting of the ACE will be

put up to the Audit Committee of Board at their next meeting.

A summary of the high risk issues will be placed to the Board on a half yearly basis.

Apart from the above escalations, if there are any serious regulatory and other violations,

instances of suspected fraud or malpractices, those will be escalated to MD, and Senior

Management within ten working days from the date of detection of such incidents.

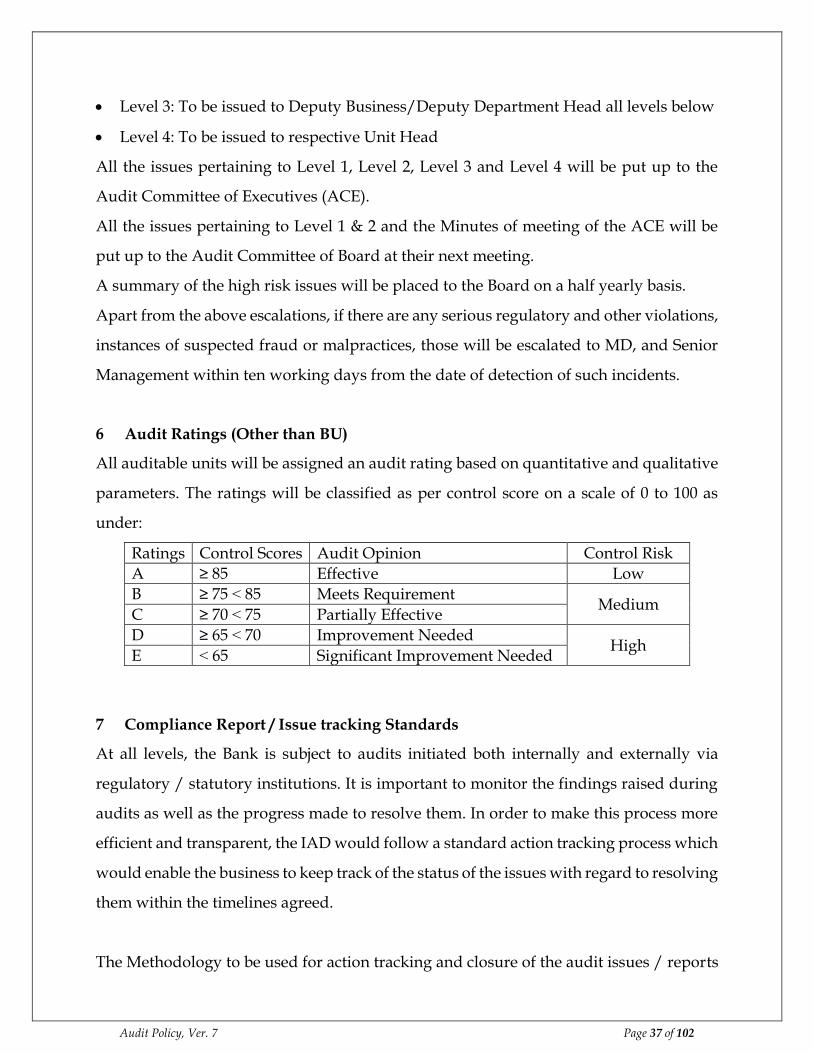

6 Audit Ratings (Other than BU)

All auditable units will be assigned an audit rating based on quantitative and qualitative

parameters. The ratings will be classified as per control score on a scale of 0 to 100 as

under:

Ratings Control Scores Audit Opinion Control Risk

A ≥ 85 Effective Low

B ≥ 75 ˂ 85 Meets Requirement Medium

C ≥ 70 ˂ 75 Partially Effective

D ≥ 65 ˂ 70 Improvement Needed High

E ˂ 65 Significant Improvement Needed

7 Compliance Report / Issue tracking Standards

At all levels, the Bank is subject to audits initiated both internally and externally via

regulatory / statutory institutions. It is important to monitor the findings raised during

audits as well as the progress made to resolve them. In order to make this process more

efficient and transparent, the IAD would follow a standard action tracking process which

would enable the business to keep track of the status of the issues with regard to resolving

them within the timelines agreed.

The Methodology to be used for action tracking and closure of the audit issues / reports

Audit Policy, Ver. 7 Page 38 of 102

would be as under:

Nature of the Audit Issue

Timelines for submission of the compliance by the Units

Timelines for IAD to assess the responses and consider closure of the issue.

Extremely High Risk / Very High Risk (L1)

15 working days 7 working days

High Risk (L2) 21 working days 7 working days

Medium Risk (L3) 30 working days 15 working days

Low Risk (L4) 30 working days 15 working days

i) The follow-up with auditee units would be undertaken on a regular basis, keeping

the H.O. Department / Competent Authority controlling the auditee units concerned

in the loop, to ensure closure of the audit issues within the stipulated time.

ii) The audit issues overdue for closure would be advised to H.O. Department /

Competent Authority controlling the auditee units concerned on monthly basis to

ensure closure of the issues at the earliest.

iii) The extension of timelines for closure of issues would be considered by the Internal

Audit Department based on the satisfactory recommendations received from the

Competent Authority controlling the auditee units concerned.

iv) The audit reports will need to be closed within an overall period of 45 days. The audit

reports would be considered for the closure after receipt of satisfactory compliances

of the audit issues. Issues where the concerned department has completed their

actionable shall be considered as satisfactory compliance for this purpose. Issues

where there is dependency on other departments / customers, shall be considered as

satisfactory compliance for the concerned department.

Audit reports, with any other open issues, would be considered for closure only in

exceptional cases with the approval of the Head of the Department. In such cases, the

overall resolution of the issue would be tracked centrally though ATR.

v) IAD will compile a report on issues pending for compliance on monthly basis and

present it to the Competent Authority controlling the auditee units concerned and on

quarterly basis to the ACB. The action tracking report will also provide information

Audit Policy, Ver. 7 Page 39 of 102

to Audit Committee of the Board, Senior Management and Line Management on the

status of overdue issues.

vi) Closure of Audit report at various levels would be based on Risk assessment which

would be based on the Audit Rating / Control Score as under:

Control Risk Audit Rating Control Score Closure Level

Low A >85% Team Leader / Vertical Head of the Audit Department at the level of AVP & above

Medium B & C 70 - 85% CAE

High D & E <70% CAE

vii) IAD will test the correctness of all compliances reported on a test check basis and a

report on the same will be placed to the ACB at half yearly intervals.

8 Other relevant features of the audit policy

While Risk Assessment Methodology, Audit Plan, Reporting, etc. have been enumerated

above, certain other features of the audit policy with regard to Information System Audit,

BU Audits, Snap/Special audits are furnished below.

9 Audit of Banking Units (BU)

There will be separate audit vertical as well as dedicated resources, having specific skill

sets, deployed to audit BUs. For better control, all BUs are to be divided into adequate

number of Audit Clusters by including a few Business Clusters in each Audit Cluster.

Each Audit Cluster is headed by an Audit Cluster-In Charge and there are internal

auditors in each Audit Cluster depending on the number of BUs of the respective Audit