Financial Audit

82

Financial Audit A mapping tool for ISSAI Implementation Draft Version 1 December 2012 iCAT

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Financial Audit

Financial Audit A mapping tool for ISSAI Implementation

Draft Version 1 December 2012

iCAT

iCAT:FinancialAudit

Howtoreadthisdocument

TheISSAIComplianceAssessmentTool(iCAT)isdetaileddrilleddowntool,basedentirelyontheISSAIsat

level2andlevel4oftheISSAIframework.ThistoolismeanttoassistSAIsinmappingtheircurrentaudit

practicestoISSAIrequirements,sothattheycanidentifytheirneedsforISSAIimplementation.

This document is divided into seven chapters. The first chapter explains briefly the ISSAIs, the ISSAI

framework and the format of the iCAT. The ISSAI requirements at level 2 of the ISSAI framework are

detailed in Chapter 2. This chapter needs to be readwithAnnexe1. Chapters 3 to 6 contain detailed

guidanceonhowtoassessthecurrentauditpracticeagainsteachISSAIrequirementforfinancialauditat

level 4 of the ISSAI framework. For the purpose of assessing current audit practice, the ISSAI

requirements at level 4 have been categorised as per the stages of a financial audit process. These

chaptersshouldbereadwithAnnexe2thatcontainsall ISSAIrequirementsat level4.Thelastchapter

providesguidanceonwritingareportbasedontheuseoftheiCAT.Thisreportwouldbenecessaryfor

theSAImanagementtoformulateitsstrategyforISSAIimplementation.

Thisisthefirstdraftversionoftheguidancedocument.Itisstillworkinprogress.Yourcomments,

suggestionsandfeedbackwillhelptheprojectteaminfurtherrefiningthistoolandmakingitmore

relevantandusefulforallstakeholders.

iCAT:FinancialAudit

TableofContent:

Chapter Topic Pageno.

1. ImplementingISSAIsandIntroductiontoISSAIComplianceAssessmentTools(iCATs)

4

2. UnderstandingthePrerequisitesforRobustAuditPractices–ISSAIsatlevel2andAscertainStatusonLevel2ISSAIRequirements

20

3. Pre-engagement

29

4. PlanninganAuditofFinancialStatement

44

5. Fieldwork

58

6. ConclusionandReporting

69

7. WritingtheISSAIComplianceAssessmentReport

80

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page4

Chapter1

ImplementingISSAIsandIntroductiontoISSAIComplianceAssessmentTools(iCATs)

Introduction

The International Organization of Supreme Audit Institutions (INTOSAI), the umbrella organization for

the external auditing community, has, since it was founded in 1953, developed and improved public

sectorauditingworldwide.Standards,guidelinesandbestpracticesaredevelopedundertheauspicesof

three of INTOSAI’s standing committees, the Professional Standards Committee (PSC), the Knowledge

SharingCommittee(KSC)andtheCapacityBuildingCommittee(CBC).Theadoptionofacomprehensive

setofInternationalStandardsforSupremeAuditInstitutions(ISSAIs)atthe2010INTOSAICongressgives

INTOSAImembers anupdated frameworkof international standards, guidelines andbestpractices for

public sector auditing. The standards are of significant value for member SAIs as well as providing a

commonframeofreferenceforpublicsectorauditing.In2010INTOSAIidentifiedtheimplementationof

theInternationalStandardsforSupremeAuditInstitutions(ISSAIs)frameworkasakeystrategicpriority

forthecomingyears.

In line with the Lima and Mexico Declarations and recognizing the independence of each individual

INTOSAI member to determine its own approach consistent with national legislation, through the

JohannesburgAccords theXX INCOSAI calledupon INTOSAImembers touse the ISSAI frameworkasa

common frameof reference. InadditionSAIswereencouraged to implement the ISSAIs inaccordance

with their mandate and national legislation and to measure their own performance and auditing

guidanceagainsttheISSAIs.

The implementation of the ISSAI framework is a demanding task that requires attention at global,regionalandcountrylevels.

The INTOSAI Strategic Plan and the ISSAI Rollout Model approved by INTOSAI Governing Board inOctober2011mandatedtheIDIto‘supportISSAIImplementation’.InkeepingwiththismandatetheIDIhas launched a comprehensive capacity development programme called the ISSAI ImplementationInitiative(3iprogramme).

InthischapterwewillprovidebriefinformationontheISSAIFramework,discussstrategicconsiderationsthat an SAI needs to think of in implementing ISSAIs, the process of ISSAI implementation and alsointroduceyoutotheISSAIComplianceAssessmentTool.Inthischapterwewillgetabriefoverviewof

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page5

theISSAIComplianceAssessmentTool(iCAT)intermsofitspurpose,formatandsomebroadprinciplesonhowtousethetool.

ISSAIFramework

INTOSAI issues two sets of professional standards: The International Standards of Supreme AuditInstitutions(ISSAIs)andtheINTOSAIGuidanceforGoodGovernance(INTOSAIGOV).

The ISSAIs and INTOSAI GOVs convey the generally recognized principles and shared professionalexperiencesoftheinternationalcommunityofSupremeAuditInstitutions.AllISSAIsandINTOSAIGOVsaredevelopedandmaintainedinaccordancewiththeDueProcessforINTOSAI’sProfessionalStandardsandissuedafteradecisionoffinalendorsementbyallSupremeAuditInstitutionsatINTO-SAI’scongress(INCOSAI).

TheISSAIsaimtosafeguardindependentandeffectiveauditingandsupportthemembersofINTOSAIinthedevelopmentoftheirownprofessionalapproachonthebasisoftheirspecificmandate.

TheISSAIsformahierarchyofofficialpronouncementswithfourlevels:

Level1-FoundingPrinciples(ISSAI1)

Level1oftheISSAIframeworkcontainsthefoundingprinciplesofINTOSAI.ISSAI1TheLimaDeclarationfrom1977callsfortheestablishmentofeffectiveSupremeAuditInstitutionsandprovideguide-linesonauditingprecepts.ThefullsetofISSAIsdrawandelaborateonthishistoricaldocument.

Level2-PrerequisitesfortheFunctioningofSupremeAuditInstitutions(ISSAIs10-99)

ThePrerequisitesfortheFunctioningofSupremeAudit InstitutionscontainINTOSAI’spronouncementson thenecessarypreconditions for theproper functioningandprofessional conductof SupremeAuditInstitutions. These include principles and guidance on independence, transparency and accountability,ethics and quality control. The prerequisites may concern the institution’s mandate and furtherlegislationaswellastheestablishedproceduresanddailypracticesoftheorganizationanditsstaff.Byissuing pronouncements on these generally accepted prerequisites, INTOSAI aims to advance soundprinciplesfortheeffectivefunctioningofpublicsectorauditingonaninternationallevel.2/2

Level3-FundamentalAuditingPrinciples(ISSAIs100-999)

The PSC Harmonisation Project is drafting new ISSAIs 100, 200, 300 and 400 on Level 3 of the ISSAIframework.Youcanreadmoreabouttheprojectatwww.psc-intosai.org

Level4-AuditingGuidelines(ISSAIs1000-5999)

TheAuditingGuidelines translate the fundamental auditing principles intomore specific, detailed andoperationalguidelinesthatcanbeusedonadailybasisintheconductofauditingtasks.ThepurposeoftheguidelinesistoprovideabasisforthestandardsandmanualsonpublicsectorauditingwhichmaybeappliedbytheindividualmembersofINTOSAI.Eachguidelinehasadefinedscopeofapplicationandmaybeadoptedinfulloradaptedasnecessarytoreflecttheindividualcircumstancesofthejurisdiction.Such

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page6

circumstancesmayincludethelegalmandateandfurtherstrategiesandcapacityoftheSupremeAuditInstitutionaswellas thespecificpurposeandcharacterof theauditassignments.Someof the level4guidelines include specific requirements related to authority. The General auditing guidelines (ISSAIs1000-4999)containtherecommendedrequirementsoffinancial,performanceandcomplianceauditingand provide further guidance to the auditor. They are developed and continuously updated byspecialized subcommitteesanddefine the internationally recognizedbest currentpracticewithin theirgeneral scope of application. The Guidelines on specific subjects (ISSAIs 5000-5999) pro-videsupplementary guidance on specific subjectmatters or other important issueswhichmay require thespecialattentionofSupremeAuditInstitutions.TheseguidelinesexpressthekeylessonsresultingfromthesharingofknowledgeandgoodpracticesamongINTOSAI’sexperts.

WhyshouldanSAIconsiderimplementingISSAIs?

Before any SAI takes on theonerous taskof implementing the ISSAIs, a question thatwould come to

mindis‘whatpossiblebenefitcantheSAIgetfromtakingonsuchaproject’.ItisimportantfortheSAI

topmanagementtoanswerthisquestionandbeconvincedabouttheanswerbeforeplungingintoISSAI

implementation.ThedraftCBCguidanceonImplementingtheISSAIs–StrategicConsiderationsliststhe

followingthreebenefits

Quality -Carryingoutaudits inaccordancewithglobally

accepted standardswill ensure a certain level of quality

andconsistencyinaudits.AllSAIsstrivetoearnthetrust

of citizens and stakeholders alike. Applying

internationally accepted standards in audits is one

important step in the direction of earning this trust. A

high-quality standard will reduce auditor’s risk. The

credibility of all audit organizations is built on the quality achieved in its audits. The use of globally

acceptedstandardswillsimplifybenchmarking,regionalqualityassuranceinitiativesandpeerreviewsas

wellasthesharingofexperiencesinotherways.Usingsimilarauditmethodsindifferentcountriescan

inspireorganizationstocontinuousimprovement.

Credibility - Using globally accepted standards will strengthen the credibility of both the audit

organizationanditsauditors.Externalstakeholderswillgainincreasedconfidenceandtrustinthework

of auditors using globally accepted standards. The results and conclusions of an audit conducted in

accordancewithgloballyacceptedstandardscanstandexternalscrutiny.Thetransparencyprovidedby

using standards well-known to audited organizations and other stakeholders also leads to increased

credibility of the audit results. Increase in credibilitywill help SAIs engagewith their stakeholders for

improvedinstitutionalframeworkandstrongerauditmandates.

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page7

Professionalism-Standardsformthebasisforprofessionalizationofauditorsandauditorganizationsby

providing a structured process for the audit work. Common standards can improve opportunities for

exchange of professional views and experiences across national and sector borders. Joint training

activitiesandsharingexperienceswillbeeasierifauditorsapplythesamesetofprofessionalstandards.

Globallyacceptedstandardsalsoprovideacommonlanguagebetweenpublicandprivatesectorauditors

in areas of similar responsibilities. Applying globally accepted standards will strengthen the audit

professioningeneral.

StrategicConsiderationsinImplementingISSAIs

If an SAI decides to implement ISSAIs, it is recommended that theymay like to thinkof the following

considerations

1. Implementing ISSAIs involves institutional, organisational and professional staff capacity

development – As you have seen above the ISSAI framework operates at both the SAI and the

individual audit level. As such it encompasses not only all functions in an SAI, but also covers the

institutionalframeworkwithinwhichtheSAIoperates.WhileconsideringISSAI implementationthe

SAImanagementwouldneed toput inplace strategies that coverall threeaspects. E.g. if theSAI

management is considering ISSAI compliance in its performance audit function, it would not be

enoughto justtrainSAIstaff inperformanceaudit ISSAIs.TheSAIwouldneedto lookat introduce

changesinitsperformanceauditpracticeatanorganisationallevel.Itwouldneedtoconsiderissues

like appropriatemandate, competent staff, ethical considerations, auditmethodology and quality

control.

2. ISSAI Implementation, Strategic Planning and SAI Capacity Development may not be different

process–WebelievethatimplementingISSAIs,developingandimplementingastrategytoachievea

vision and developing capacity of the SAI are all different aspects of one and same process. It is

important for the SAI leadership to understand and integrate these processes and not to start

separateprocessesthatmayleadtoduplication.

3. RoleofSAILeadership–SAIleadershipneedstoplayadefiningroleinimplementingISSAIs.Creating

a conducive culture and environment, formulating a strategy for implementation, engaging with

internal and external stakeholders and putting in place a robust monitoring and evaluation

mechanismaresomeofthekeyrolesforSAIleadership.

4. Leading and Managing change – One important aspect of ISSAI Implementation is change

management.Asdiscussedearlier,ISSAIimplementationwouldimplyarelookandpossiblechanges

inallareasoffunctioninginanSAI.Thiscancreateuncertainty,fearandresistanceinSAIstaff.The

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page8

SAImanagementandleadershipneedstocarefullyconsidertheimplicationsofchangeandthinkof

measure tomanagechange.Raisingawarenessof ISSAIs,adoptingaparticipatoryapproach to the

implementationprocess, creating champions for ISSAI implementation,providingopportunities for

acquiringrequiredknowledgeandskillscouldbesomeofthechangemanagementstrategiesthatan

SAIemploy.

5. SAI environment - Regardless of whether a SAI decides to implement the ISSAIs for financial,

compliance,orperformanceaudit,theorganisationneedstotakeintoconsiderationbothitsinternal

andexternalconditions.TheimportanceofdifferentconditionsmayvarydependingonwhatISSAIs

are being implemented. However, accounting and financial management systems, access to

necessaryinformation,relationstoparliamentandotherstakeholdersaswellasthecountry’saudit

culture are relevant to all audit tasks. These conditions may provide opportunities or limitations

whichwill influence the implementation of ISSAIs. If the SAI is considering introducing new audit

tasksinaccordancewiththeISSAIs,itisimportanttoensurethattheSAIhastherequiredmandate

and all legal prerequisites are in place. Furthermore, it is important to ensure that there is an

appropriateandfunctioningrecipientofauditresults.Introducingnewauditstandardsandpractices

willnotonlyaffecttheSAI,butalsotheauditedorganizationsandtheparliament.Itisthereforevery

important to consider when and how to communicate with external stakeholders to ensure a

smooth implementationprocess. Informingstakeholdersofthemotivesbehindandbenefitsofthe

introduction of new standards is very important in order to create a supportive environment for

auditsinaccordancewithISSAIs.

6. Stakeholder Expectations – In decidingon the implementationpath tobe followedan SAI should

ascertainandconsidertheexpectationsthatitsclientsandexternalstakeholdershave.

7. Impact of implementation - It is important to differentiate ISSAI requirements that will create a

paradigmshiftintheauditpractice,fromthosethatmightonlyinvolvechangesinsomeprocedures.

8. Resources required – If the ISSAIs are to be implemented and its requirements followed, an SAI

would require considerable resources in terms of funds, systems, people etc.While developing a

strategy the SAI should develop an implementationmatrix where it details its plan for putting in

placetherequiredresources.

ProcessofISSAIImplementation

In our view an ISSAI Implementation Process is the same as a strategic planning process.We would

recommendthefollowingstagesintheimplementationprocess

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page9

Assessing ComplianceNeeds

•ThefirststepforaSAIistoascertainISSAIrequirements,assessthestatusoftheSAIvisavistherequirements,thecausesfornoncomplianceandSAIneedsinordertobecompliant.TheendproductofthisstagewouldbeanISSAIComplianceAssessmentReport.

DevelopISSAIImplementation

Strategy

•BasedontheissuesandcausesidentifiedintheISSAIComplainceAssessmentreport,theSAImanagementshoulddetermineanimplementationstrategythatarticluatesitsvisionandgoalsforISSAIimplementationandthestrategythattheSAIwillemploytoreachthegoals.Abroadbasedparticipatoryapproachisrecommended.

ImplementStrategy

• TheSAIleadershipshouldputinplaceamechanismforimplementingitsstrategy.ItisadvisablethatthismechanismbeintegratedwiththelinefunctionoftheSAIandnotrunparalleltothesefucntions.TheSAIwouldberequiredtodothingsdifferentlyratherthatdifferentthiings.

MonitorandEvaluate&LessonsLearned

•TheSAIneedstohavearegualrmechanismformonitoringimplementationacitivtiesandmanagingimplementationrisks.TheSAIshouldalsoprovideforperiodicevaluationofitsISSAIimplementationefforts.ThelessonslearnedinimplementationwouldhelptheSAIinenhancingitsfutureimplementationefforts.

ReportonPerformance

•TheSAIshouldreportontheextentofitsachievementsinaoverallperformancereporttoitsstakeholders.

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page10

IntroductiontoISSAIComplianceAssessmentTool(iCAT)

Asmentionedintheprevioussection,thefirststepinimplementingISSAIsisassessingtheSAI’spresent

levelofcompliance.Thisisdonebycomparingitsauditpracticestotherequirementsrecommendedby

the ISSAIs. In order to assist the SAIs in assessing their complianceneeds the IDI has developed ISSAI

ComplianceAssessmentTools.AtoolsetoffouriCATshavebeendeveloped.Theyare

1. iCATforLevel2ISSAIs

2. iCATforLevel4FinancialAuditISSAIs

3. iCATforLevel4PerformanceAuditISSAIs

4. iCATforLevel4ComplianceAuditISSAIs

ThepurposeoftheiCATsistopresenttheISSAIrequirementsinasimpleformanddefineaprocessfor

assessingcompliance

iCATFormat

While the individual iCATsmayhave some variation in their formats, depending on the nature of the

level4ISSAIs,alltheiCATShavethefollowingcommoncomponents

ISSAIReference

ISSAIRequirement

StatusofCompliance

Mechanism/InstrumentofCompliance

Reasonsfornoncompliance

This columnreferences theISSAIrequirementtotheISSAI

This columncontains theISSAIrequirementinabriefform.

Three options areavailable for statusofcomplianceMet–Tobeselectedwhen therequirement isentirelymetPartially Met – Thisoption covers theentire gamut fromwhere the SAI hasjust startedimplementation ofthis requirement, ithas some elementsof compliance inplace, it has a largeextentofcompliancein place but is notentirelycomplaint,Not met – The SAI

Inthiscolumnthepersonconducting theiCAT shouldmention thespecificdocument,provision, systemthrough whichthe SAI complieswith the ISSAIrequirement. Thiscolumn will befilled inwhen thestatus ofcomplianceismetorpartiallymet

When the status ofcompliance is notmetor partially met, thereasons for noncompliance should berecorded here. Thiscolumnisimportantindetermining futureimplementationstrategy, which willinvolveaddressing thereasons for noncompliance

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page11

does not complywith therequirementatallNot applicable– Therequirement is notapplicable to the SAIdue the laws andregulations thatgovernit.

GuidingPrinciplesforconductinganiCAT

iCATisnotanevaluationtool–TheiCATsformulatedasapartofthe3iprogrammeaimtohelpSAIsin

understandingISSAIrequirementsandassessingtheirneedsforcomplyingwithISSAIs.TheiCATisthus

formulatedasaneedsassessmenttoolratherthananevaluationtool.

ScopeoftheiCAT-Asapartofthe3iprogrammefour iCATshasbeendeveloped.Level2 ISSAIs iCAT,

FinancialAudit Level4 iCAT,PerformanceAudit Level4 iCAT,ComplianceAudit Level4 iCAT.As faras

possible, it is better to conduct all four iCATs so that a consolidated strategy can be developed for

implementationofISSAIs.However,ifthatisnotfeasibleinanSAI,thenitisrecommendedthattheSAI

conductthelevel2iCATalongwiththelevelfouriCATofthechosenauditstream.Thisisbecause,the

compliancegapsidentifiedatauditlevel(level4)wouldinvariablyhavetheirreasonsattheinstitutional

level(level2).

WhocanconductaniCAT–IftheSAIhasadequatecapacityitcandecidetoconductitsowniCATs.An

SAImayalsoaskforexternalsupportinhelpingitconducttheiCAT.ItisenvisagedthatthepoolofISSAI

facilitatorscreatedasapartof the3iprogrammewillhelptheirownSAIs,aswellasotherSAIs in the

regionsconductiCATs.ForthepurposeofobjectivityanSAImayalsoexercisethechoiceofhavingthe

iCATconductedbyanexternalteamfromtheregion.

iCATteam-WhatevertheapproachtheSAIselects,itisrecommendedthattheiCATbeusedbyateam

andnotasingleperson.FormingacompetentandcredibleneedsiCATteamisthefirststeptobetaken.

The iCAT team should consist of at least one trained ISSAI facilitator. Team members must have

managerial backgrounds so that they have a good organisational overview and necessary influence in

subsequentimplementation.BesidesmemberswhohaveagoodunderstandingofSAIlevelissues(level

2ISSAIs),theteamshouldalsohavememberswhoarewellconversantwiththerelevantauditpractice

asdefinedintheISSAIsandasactuallypracticedintheSAI.

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page12

ParticipatoryApproach-Abroad-basedconsultativeprocessisrecommendedforconductingiCATs.Itis

importantfortheiCATteamtoconsultwithacrosssectionofSAIstaffacrossvariouslevels.Stafffrom

differentlevelsanddifferentareasoftheSAIshouldbeconsultedinthisprocessandtheirviewsshould

begivendueweightiniCAT.Externalstakeholders’viewsandneedsshouldalsobetakenintoaccount.

The involvement ranges from providing information or opinion to having an integral part on making

decisionsonneedsandpriorities.Themorepeoplefeeltheyareinvolved,thegreatertheownershipand

thuseffectivenessoftheresults.IftheSAImanagementisabletofacilitateownershipfortheprocessat

theiCATstageitself,thesubsequentstagesofdevelopingandimplementinganISSAIstrategywillhave

greateracceptanceintheSAI.

Top and senior management support – The success of the iCAT is highly dependent on the level of

commitmentathigh levels intheSAI.TheSAImanagementshould insistonknowingthesituationand

the needs as they are. The SAImanagement should also ensure that the iCAT team has the required

resourcestoconducttheiCAT.

Documentation – The iCAT team should systematically document all the working papers and the

evidencethat itgenerates infillingouttheiCATformat.Besideshelpingtheteaminlatercompilingits

ISSAIComplianceAssessmentReport,documentationwillalsobehelpfulinillustratingthefindingofthe

iCATtotheSAImanagementandhelpfutureiCATteamsinconductingsimilarexercises.

ProcessofconductinganiCAT

Planning the

iCAT–Likeany

other project,

conductinganiCATwouldrequireresourcesintermsoffinancialresources,infrastructure,time,people

etc.ItisrecommendedthattheiCATteamprepareanactionplandetailingthemilestones,theresource

requirementandtherisksattachedtotheachievementofeachmilestone.

Usevarietyofdatagathering tools– Inorder togatherdata to fill in the iCAT format the iCAT team

shoulduseavarietyofdatagatheringtoolslikefocusgroups,interviews,documentreview,surveyand

physical observation. It is important that the tool used is appropriate for gathering valid and relevant

information forassessing compliance. Forexample if the ISSAI facilitatorwants to check theextent to

whichapolicy isactually implemented, interviewingpeoplemaynotbeenough,he/shewouldhaveto

PlanningtheiCAT

Gatheringdatatofillintheformat

WritingISSAIComplianceAssessment

Report

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page13

review documentation supporting implementation. A table listing the pros and cons of each tool is

attachedasAnnexe1.

WritingtheISSAIComplianceAssessmentReport–TheendproductofaniCATistheISSAICompliance

assessment report. The format of this report and guiding principles while writing this report are

containedinthelastchapter.

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page14

Annexe1

ThefollowingfivetoolscanbeusedforgatheringdatatofilltheiCATformat.Theseare:

Document review: Process to gather/organise information contained in various documents to

achievepre-definedobjectives.

Interview: Data and information collection procedure in the form of a carefully planned set of

questionsthatisaskedthroughaconversationtoobtainin-depthideasandperceptionsonatopic

ofinterest

Focus group: Group of interacting individuals having some common interest or characteristics,

brought together by a facilitator, who uses the group and its interaction as a way to gain

informationaboutaspecificorfocusedissue.Discussionmethodcentresonkeylimitedquestions

Physical observation: Site visit by observers who record what they see/hear on site, using a

checklist

Survey: systematic process that uses standardised questionnaires to obtain information from a

largenumberofrespondents

Thisdocumentlistsvariousaspectsofthesetoolsinatable.

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page15

Tools Purpose Skillsrequired Target Whentoconduct

Howtoconduct/Steps

Strengths Limitations

Documen

tReview

• UnderstandfunctioningofSAI• UnderstandenvironmentalforcesinfluencinganSAI• Identifyareasoffocus• Identifyinformationtobegathered• Validategatheredinformation• Findweaknesses/theircauses

• Languageproficiency• Abilitytoassimilatelargeamountsofinformation• Speedreading• Structured/systematicapproach• Analysis,evaluation,synthesis• Subjectmatterknowledge• Writingskills

• Initialreview-attheverybeginningofplanning• Continuousprocessas/whenneed/opportunityarises

1. Input2. Proces

sing3. Outpu

t

• ProvidesoverviewofSAI,itsactivitiesandtheenvironmentinwhichitoperates.• Allowstoreducevolumeofinformationtobeprobed• Canbeacrediblesourceofinformation

• Timeconsuming• Difficulttofindaskilfulperson• Lackofrelevantwrittenmaterialsoravailabilityoftoomanydocuments• Documentsmaynotmatchwithactualsituation

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page16

Tools Purpose Skillsrequired Target Whentoconduct

Howtoconduct/Steps

Strengths Limitations

Interview

Toobtainviews/opinionsoftheintervieweeondevelopmentneedsoftheSAI,suchas;• Keyresultareas• Challengestobeaddressed• Capacitybuildingstrategies• Supportrequired• etc.

• Languagefluency• Listeningskills• Goodobservationskills• Discussionleadingskills• Timemanagementskills• Abilitytoremainneutral• Goodwritingskills• Abilitytotakenotesquickly• Analyticalandsynthesisingskills• Knowledgeandexperienceonthesubject

Dependsontheinterviewpurpose:• FromwithinSAI• Fromamongexternalstakeholders

• AfterobtaininganunderstandingoftheSAI• Aftersurvey/documentreview

1. Planning

2. Conducting

3. Concluding

4. Documenting

• Providesflexibilitytoexplorenewideas/issues• Facilitatesexpressionofdiverseopinions/ideas• Allowsrespondenttoelaborate• Allowsprobing/clarification• Facilitatescommonunderstanding• Providesopportunitytoobtainsensitive/confidentialinformation• Providesopportunitytoobtaininformationfromnon-verbalcommunication

• Notappropriateforquantitativedata• Riskofgatheringunreliableinformation• Informationprovidedmaynotberepresentative• Susceptibletointerviewerbias• Difficulttoprovefindings• Noteasytoquantify/analyseinformationgathered• Canbetime-consuming

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page17

Tools Purpose Skillsrequired Target Whentoconduct

Howtoconduct/Steps

Strengths Limitations

FocusG

roup

• Togainaninsightintocertainissuesthrougha‘groupthinking’process

Knowledge:

• Groupinteractionanddynamics• Topicsofdiscussion

Skills:

• Activelistening/effectivesummarising• Askingquestions• Givingfeedback• Observingbehaviours• Focusingattention• Leadingdiscussions• Stimulatingandsustaininginterest

Attitudes:

• Empathy• Acceptance• Flexibility• Notdogmatic,opinionated,rigid,orauthoritarian• Dealingwithanotherpersonathis/herpace• Objectivityandimpartiality• Freedominexpressingideasandopinions• Displayingfaithandtrustinthegroup

• Composedofpeoplewhohavesomethingincommononsomespecifiedcriteriaofinterest• LevelofhomogeneitydependsonpurposeofFG• Notmorethan12ifdiscussionsinplenary• Asmanyas30ifdiscussionswillbeheldinsub-groups

AtanystageoftheNAprocess:• beforeothertoolsareused• Inpreparationforothertools• Afterhavinggathereddata

BeforeFocusGroup:• Definepurpose• Specifyparticipants• Developquestions• Checkthesettings

During

Focus

Group:

• Settheenvironment• Setexpectations• Askquestionsandgetresponses• Encouragefullparticipation• Keepthegroupontrack• Summarizeandclosethesession

After

Focus

Group:

• Makeconclusi

• Groupthinkingprocesscanenrichideasofindividualparticipants/qualityofdiscussions.• Caninteractdirectlywithparticipants(allowclarification,follow-upquestions,probing)• Cangaininformationfromnon-verbalresponsestosupplementverbalresponses.• Veryflexible

• Difficulttobringeveryonetogether• Requiresfinancialandmaterialresources• Limitedabilitytogeneralisetolargerpopulations• Maybiasresultsbyprovidingcuesaboutwhattypesofresponsesaredesirable• Resultsmaybebiasedbydominant/opinionatedmember• Dataanalysisisoftencomplexandtime-consuming

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page18

Tools Purpose Skillsrequired Target Whentoconduct

Howtoconduct/Steps

Strengths Limitations

PhysicalObservatio

n

• Toverify/appraiseSAI’sinfrastructure,technologyandsupportservices• Tocheckexistenceofdocuments• Tohavemoreconfidence,accuracy,reliabilityandvalidityoftheresultsofpriorNAtoolsused

• Atleasttwoobserverstomaximiseobjectivity• Observersnotworkingatthesitetoensureimpartial/externalviewpoint• Experiencedobserversonthesubjecttoenhanceappraisalsandcredibility

• Physicalinfrastructure(premises,offices,facilities,utilities)• Peopleworkingonsite,theirinteraction,• Interpersonalrelations• Workclimate• Stakeholdersrelations

• Aspreliminarytaskbeforeinterviews/documentreviews• AsvalidatingtooltoconfirmresultsofpriorNAtools.

1. Planning

2. Conducting

3. Concluding

4. Documenting

• Revealsrealconditionsofnaturalsettings• Timesavingtool• Providesquickappraisaloftheconditions/thingsorpeople• Requiresnoexpertisewhenanalysingtheresults

• Notrelevantforgeneralisation• Observerbias• Mayaffectbehavioursandreducereliabilityofresults

iCAT:FinancialAudit

Chapter1:ImplementingISSAIsandIntroductiontoiCAT

Page19

Tools Purpose Skillsrequired Target Whentoconduct

Howtoconduct/Steps

Strengths Limitations

Survey

• ToobtainfeedbackonSAIenvironment• TogatherinformationonSAIstructures,operationalframeworks,andemployees

• Formulatingquestions• Analyticalskills• Abilitytosynthesize• Dataanalysisskills• Subjectmatterknowledge

Dependsonfocusarea:• ForHR:employeesatalllevels• Forexternalstakeholderrelations:externalstakeholders• Forauditmethodologyandstandards:fieldauditorsandsenior/middlemanagement• etc.

• AtthebeginningofNAtogainoverallunderstandingofSAI’soperations• Atalaterstagetofocusonspecificareas• Whereinformationisrequiredfromawiderangeofgeographicallydispersedemployees• Whenintentionistoarriveataggregatedquantifiedinformation

1. Developingthesurvey

2. Implementingthesurvey

3. Dataentry

4. Dataanalysis

5. Recordingresults

• Informationcanbeobtainedfromalargenumberofrespondents• Widerangeofinformationcanbecollectedatonetime• Consistencyofdata• Easytoadminister• Costeffective

• Dependentonrespondents’motivation,memory,abilitytorespondeffectively• Respondentsnotmotivatedtoaccuratelyanswer,butpresentthemselvesinfavourablelight• Doesn’tfacilitatein-depthexaminationofcauses• Errorsduetononresponsemayexist• Couldhavesubjectiveresponses• Canbetimeconsuming• Doesn’tallowprobingformoredetailedinformation

InthenextchapterwewilldiscussabouttheLevel2ISSAIrequirements.Theserequirementsarethebasicpre-requisitesforrobustauditpracticesintheSAI.

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page20

Chapter2

UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Introduction

As mentioned in the previous chapter the ISSAI framework is a very comprehensive framework thatarticulatesboth–thenatureofrobustauditpracticesinanSAIandthekeydriversat institutionalandSAI level that need to be in place for implementation of robust audit practices on a consistent basis.WhilethenatureandrequirementsforrobustauditpracticesareoutlinedinLevel3andLevel4ISSAIs,thekeydriversandprerequisitesforthesearehighlightedatlevel1andlevel2oftheISSAIFramework.

Assuchbeforegoingintothedetailsofimplementinglevel4ISSAIs,weneedtolookatthelevel2ISSAIsandunderstandtheir impactonLevel4 implementation issues.Forthepurposeofclarityandprocess,thischapterisdividedintotwoparts:

Part1–UnderstandingthePrerequisitesforRobustAuditPractices

Part2–AscertainstatusonLevel2Requirements.

Forunderstandingoflevel2ISSAIspart1canbeused.FromChapter3toChapter6level4iCATguidanceisdiscussed.Please consider that, status Level 2 requirementsof an SAIwill beascertainedonly afterchecking the Level 4 requirements (by following the guidance from Chapter 3 to 6). Though Level 2guidanceismentionedinChapter2,pleasecomebacktothischapteraftercompletingChapter3to6onLevel 4. At the endof the twoparts youwould be able to identify your SAIs needs regarding Level 2requirementsandalso link thegaps in Level2 requirements to thegaps in implementing level4 ISSAIrequirementswhichyouwillbeabletofindwhilegoingthroughChapter3to6.

Part1UnderstandingthePrerequisitesforRobustAuditPractices

Whatdoesa SAIneed forputting inplacewell functioningauditpractices that generatevalue for SAIstakeholders?AspertheISSAIsanSAIwould need the following fourprerequisites

These four prerequisites are the fourmain ISSAIs level2 ISSAIs thatwewilllook at.- ISSAI 10, 20, 30 and 40. Inrecent years SAIs have beenincreasingly expected to demonstratetheir own value and benefit to theirstakeholders. This has resulted in anumber of initiatives at the INTOSAI

ISSAILevel4RobustAuditPractices

ISSAI10Independence &LegalFramework

ISSAI30CodeofEthics

ISSAI20Accountability&TransparencyMechanisms

ISSAI40QualityControl

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page21

levelthathavecentredaroundtheSAIatastrategiclevel.Suchinitiativesinclude:

• Mexicodeclaration (now incorporated in ISSAI10withexamples in ISSAI11) – lookingat therolesandresponsibilitiesofSAIs

• PrinciplesofTransparencyandAccountabilityofSAI (ISSAI20andexamplesprovided in ISSAI21)– lookingat fundamental goodprinciplesofhowanSAI shouldperform its functionsandwhattypeoffunctionsitshouldperform.

• CodeofEthics(ISSAI30)–providingaframeworkforensuringSAIbehaveatthehighestlevelofcredibility

• Quality Assurance (ISSAI 40) looking at the critical ingredients required to make a SAI meetstandardsrequiredtoaddcredibilitytoanyresultsorreportspublishedbytheSAIs.

The above documents form the basis for level 2 of the ISSAI framework and the participant shouldfamiliarizethemselveswiththedocuments.

The level 2 framework is also supported by a number of other publications and initiatives aimed atsupportingSAIs.Someofthesethatareimportantfortheparticipantsinclude:

• IDICapacitybuildinginitiativesandframeworks-thisprovidesamechanismforassistingSAIinidentifyingtheirneedstoachievethedevelopmentsrequiredtoperformtheirtaskswithintheISSAIframework.

• SAIPerformanceManagementFramework–thisprovidesaframeworkforreportingtheresultsoftheSAIandmeasuringitsimprovementovertime.(version2.0ofthisdocumentisavailableonwww.idi.no)

• SAIvalueandbenefits–thiswasthetheme1paperfromINCOSAIXXanditsummarizesalltheaspectsofdemonstratinghowSAIcanshowtheirvaluetotheirstakeholders.ItisintendedthatthedocumentwouldbeincorporatedintotheISSAIframework.

Therearenumerousotherdocumentsavailablearoundthistopic;howevertheoneslistedaboveprovideasufficientoverview.

TheISSAIsatlevel2requirecapacitydevelopmentofanSAIinallthreeareas

1. InstitutionalCapacityDevelopment2. OrganisationalSystemsCapacityDevelopment3. ProfessionalStaffCapacityDevelopment

Institutional capacity of an SAI refers to the SAI having the appropriate Independence and LegalFramework,mandateandenvironmenttocarryoutitscorebusinessfunctionseffectively.OrganisationalCapacityreferstotheinternalsystemsandprocessofaSAIandprofessionalstaffcapacityreferstoSAIpeopleandtheirabilitytocarryouttheirrolesprofessionally.

In order to have robust audit practices as described by level 4 ISSAIs, a SAI would need all threecapacities – Independence and Legal Framework, appropriate internal processes and structures andsufficient number of qualified people. The IDI’s Capacity Building Framework shown explains therelationshipbetweentherequirementsoflevel2ISSAIsandthethreeaspectsofcapacitybuilding.

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page22

ThecapacitybuildingframeworkattemptstoshowapictureofboththecapacitiesthataSAImusthaveand the performance that the SAI must deliver to generate value for its stakeholders. For a SAI tocontribute to good governance, it needs to have required audit impact. In order to achieve the auditimpact the SAImust havehighquality audit outputs. These audit outputs are a result of robust auditpractices (ISSAI Level 4) or ‘SAI Core Processes’ as they are referred to in the capacity buildingframework. The key drivers of robust audit practices within the SAI are SAI Leadership and internalgovernance mechanism, SAI resources and SAI external stakeholder relations (Parliament, Executive,Media, Civil Society etc). It is the SAI leadership’s role to ensure that the governance mechanism(includingimplementationofcodeofethics),requiredresourcesandstakeholderrelationsareinplace.AcriticalfactoroutsidetheSAIthatcanhamperorhelptheSAI’sperformanceandeffectivenessistheSAI independenceandlegalframeworkandthegeneralpublicfinancialmanagementenvironmentthattheSAIoperatesin.

SAILeadershipdrivestheperformanceandcapacitybuildinginitiativesoftheSAI.TheleadersintheSAI

needtosetthetoneandtenorfordetermininghowthingswillbedoneintheSAI.TheSAIasawhole

also should set an example in good governance to be emulated by the audited entities. As such the

leadership should ensure good SAI governance in terms of its planning, code of ethics and conduct,

accountability&transparency,internalcontrolsandcontinuousimprovement.TheSAIleadershipwillbe

considerablyeffectiveinitsinternalgovernanceeffortsiftheyhaveinplacearobustandvibrantinternal

communicationmechanism.

ThiselementisthekeydrivertoensurethattheSAImakesthemostofwhatiswithinitscontrolthroughamongst others, effective strategic and operational planning. The category of managementarrangementshasbeenusedtoidentifythesekeydrivers.Thiselementthenbecomesthedriverfortheothersubelementsof:

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page23

• Humanresources• Supportstructuresandinfrastructure

These two elements are taken as sub elements of the leadership and internal governance. As oftendeficiencies or areas for improvement in these areas require senior management intervention, forexample,identifyingandrunningtrainingprograms.

SAICoreProcessesconsistof:

• Auditstandards(aselaboratedintheISSAIFramework)• Auditmanualsandguidance• Auditplansshorttermandlongterm• Audittoolssuchascomputerassistedaudittechniques• Qualityassurance

AlltheseaspectsareaimedatensuringthatprofessionalandconsistentauditproductsaredeliveredbySAIs on a sustainable basis. The critical aspects are to ensure that the processes and intentions arereflected in the practice of the SAI and are not simply documents produced but not followed by theauditors.

ExternalStakeholderscanbeseenfromtwodistinctperspectives,namely:

• Reportingtostakeholders• Communicationwithstakeholders

Reporting is often a combination of what is mandated and what may be good practice. This oftenincludesreportstoparliamentandtotheauditedentities.SAIareoftenalsoexpectedtoproducereportson their own performance. SAI annual report or equivalent provides an opportunity for the SAI todocumentitsachievementsaswellastheresultsfromtheauditsconducted.

IntermsofcommunicationwithstakeholdersSAIshaveaveryimportantroleindealingwithlegislatures,mediaandauditedentity.OftenenhancingtheprofileandimageoftheSAIcanimproveitseffectivenessincarryingoutitsauditsthroughimprovedcooperation.

ForexampleifanSAIwheretoconsiderimplementingLevel4ISSAIinPerformanceaudititwouldneedanappropriatemandatetodoso,strongsupporting institutionalstructures i.e.awell functioningPAC.Leadershipthatdrivestheimplementationprocessandputsinplacenecessarysystemsandstructurestoensure implementation, qualified people and adequate resources and good relations with importantstakeholders.

AssuchimplementingISSAIsandbuildingcapacityofaSAIareinactualfactoneandthesameprocess.!

Seeingthismatch,wehavetriedtocategorisetheISSAIrequirementsat level2intothefollowingfourcategoriesandsubcategories

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page24

The first category refers to the institutional capacityof the SAI anddescribes the requirementsunderISSAI10.ThesecondcategoryreferstotheorganizationalandprofessionalstaffcapacityoftheSAIthatisdrivenbySAIleadership.AcombinationofLevel2ISSAIrequirementsareplacedunderthiscategory.The third category refers to SAI coreprocesses,whichare theSAI level requirements specific toauditprocesses. The fourth category refers to external stakeholder relations both in terms of reportingrequirementsandcommunicatingwithstakeholdersforauditeffectivenessandimpact.

Thelevel2ISSAIrequirementsplacedunderthesefourcategoriescanbeseenintheexcelsheetcalledISSAILevel2Requirements.

Part2ofthischapterdescribestherequirementsandhowtoassessneedsrelatedtotherequirements.Whilewewould recommend that you read through thePart 2 now, the actual collectionof data andfillinginoftheformatshouldbedoneafteryouhavecompletedtheiCATformatforlevel4.

Independence&Legal

Framework

Leadership&InternalGovernance•Codeofethics•ManagementArrangements•Resources

SAICoreProcesses

ExternalStakeholderRelations•ReportingPractices•Communication

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page25

Part2–AscertainStatusonLevel2ISSAIRequirements

The ISSAI framework is a very comprehensive framework that articulates the nature of robust auditpractices inanSAIaswell as thekeydriversat institutionalandSAI level thatneed tobe inplace forimplementationofrobustauditpracticesonaconsistentbasis.ThenatureandrequirementsforrobustauditpracticesareoutlinedinLevel3andLevel4ISSAIs,andthekeydriversandprerequisitesforthesearehighlightedatlevel1andlevel2oftheISSAIFramework.

Inpart1wehavementionedthatbeforegoingintothedetailsofimplementinglevel4ISSAIs,weneedtolookatthelevel2ISSAIsandunderstandtheirimpactonLevel4implementationissues.FromChapter3 to Chapter 6 you will conduct the check for the Level 4 ISSAIs. You will ascertain the status ofcompliance at Level 4 in these four modules. You will also identify what are the reasons for non-complianceoftherequirementsatLevel4intheChapter3to6.

You will see that the reasons for non-compliance lies at the issues which actually the drivers orprerequisitesforLevel4ISSAIs.TheseareallhighlightedatLevel2ISSAIs.SoitisclearthatatLevel2onastrategiclevelSAIscantakemeasuresthatwouldsolvetheissuesofnon-complianceattheLevel4.InthischapteryouwilllookintothislinkagebetweenLevel2andLevel4ISSAIs,alsohowthegapsinLevel2requirements linedtothegaps in implementing level4 ISSAIrequirements.BasedonyoufindingsatLevel2andLevel4youwillwritetheISSAIComplianceAssessmentReport.

1. AscertainthestatusofLevel2ISSAIrequirements

Beforeascertainingthestatusoflevel2ISSAIrequirementsyouwouldhavedonethefollowingactivities:

• Understoodlevel2ISSAIrequirementsinChapter2• CompletedtheiCATformatforlevel4inChapter3toChapter6

OnthisbasiswewillnowproceedtodiscusshowtoidentifySAIneedsandascertainthestatusatlevel2.Thisstepintheprocesswillalsohelpyouinconsolidatingyourfindingsonlevel4ISSAIsparticularlythereasonfornon-compliancewhichisrelatedtotheLevel2ISSAIsandcreatethelinkagebetweenthetwolevelsofISSAIs.BasedonthiswewillpreparetheISSAIComplianceAssessmentReport.

4.1HowtocompletetheLevel2ISSAIRequirements

AswehavementionedinChapter2theiCATforLevel2containsalltherequirementsfromtheISSAI10-40.Alltheserequirementshavebeengroupedunderfollowingmajorcategories:

• Independenceandlegalframework• Leadershipandinternalgovernance

o Codeofethicso Managementarrangementso Resources

• SAIcoreprocesses

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page26

• ExternalStakeholdero Reportingpracticeso Communication

In the following sectionswewill discusshow the columnsof the individual ISSAI requirements canbefilledinstepbystep.

Step1-CompletingColumns5and6ofLevel2ISSAIrequirement

Aftercompletionoflevel4oftheiCAT:

• workshopshouldbeheldwithrelevantseniormanagementtodiscussthefindingsonlevel4• Thepurposeoftheworkshopisforseniormanagementtoassignlevel4findingstotheirspecific

requirementswithinthelevel2ISSAIrequirements.

When completing the level 2 ISSAI requirement the participant should understand the relationshipbetween levels2 and4of the ISSAI Framework. Level 2provides the strategicdirectionand level 4 isaimedatthedetailsofauditpracticeswhenimplementingthestrategicaspects.

Therearethreepossibleresultstobeenteredintocolumn4SAIStatus,namely:

1. Fullcompliance–wherelevel2andlevel4requirementsaremet2. Partial Compliance – where level 2 requirements aremet but the implementation on

level4hasnotbeenachieved.(exampleprovidedbelow)orwhererequirementsaremetat level 4 and not at level 2 (This is highly possible for instance Principle 8, ISSAI 20requires that “The SAI reports are available and understandable to the wide publicthroughvariousmeans(e.g.summaries,graphics,videopresentations,pressreleases)”.While,attheSAIleveltheremaynotbesucharequirement,somefieldofficesmaybringoutsummaryoftheirperformanceauditreportsandissuepressreleasesaftertablingofaPerformanceAuditReport and satisfy ISSAI 3100, Section35onmakingaudit reporteasilyaccessibletogeneralpublic).Anotherreal-lifeexamplethatwasquotedbyseveralparticipantsoniCATrelatingtodisclosureofthesourceofdataintheauditreportisthatwhile there isnosuchrequirement in their standards todisclosesourceofdata, ithasbeenfollowedintheperformanceauditengagementsreviewedbythem.

3. Noncompliance–whererequirementsonlevel2and4arenotmet

ExampleofPartialCompliance:

If the SAI has no individual declaration of interests for each audit, but the SAI has an organizationalpolicy.ThenthiswouldbereflectedintheiCATasfollows:

• Withincolumn4theSAIstatuswouldbepartiallyimplemented• Within column 5 the entry should be that there is a finding with regard to “no individual

declarationintheauditfiles”fortherequirementsunderISSAI30paragraph13.

Column6shouldbeusedtostatewhatactionneedstobetakenandwithinwhattimeframe.

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page27

Information gathered in Column 6 can then be used to complete the ISSAI Compliance AssessmentReport.

Step2-CompletingColumns3and4ofLevel2ISSAIrequirement

i. Independence and Legal Framework

ThissectionlargelydealswithISSAI10whichaspreviouslystatedlinkstotheMexicoDeclaration. TheISSAIrequirementscan largelybe linked inmost jurisdictionstotheenabling legislationoftheSAI (SAIlaw).Mostoftheaspectsshouldbereadilyidentifiablefromthelaw.FurtherenquiriesfromtheHeadoftheSAItoclarifyuncertaintiesmaybeuseful.

It is important tosimply identify theresponsibilitiesandnotnecessarily toassess the implementation.ForexampleifaSAIcan“selecttheauditissues”butinpracticeisnotdoingsothisshouldbeincludedincolumn4(SAIstatus)aspartiallycomplying.TheremaybereferencestotheSAIsinotherlegislation,forexample,relatingtotheSAIbudget(principle8ISSAI10).Intheseinstancestheparticipantmayneedtobeawareofsuchdocumentsandreferencethemincolumn3oftheiCAT.

ii. Leadership and Internal Governance

CodeofEthics

ThissectionlargelydealswiththeISSAI30CodeofEthics.InmanySAIsthisiscoveredthroughpoliciesattheentitylevelaswellasthroughdeclarationsmadeineachauditengagement.Theparticipantshouldobtainthesedocumentsandassesswhattypeofcomplianceisexpectedbythestaff(forexampleannualdeclarationsofincomeandassets).

If there is anabsenceof compliance tools suchasannualdeclarations thesewill behighlighted in thelevel4assessmentandwillbeincludedincolumns5and6oftheiCAT.

ManagementArrangements

This section takes fundamental aspects of the SAI leadership and internal arrangements at a strategiclevel.Thissectionwillgiverisetotheimportantelementsthatincludestrategicplanningandthereforeprioritization for future decisionmaking.Whatever the SAI is deciding to domust be communicatedthroughthisareaandthereforerepresentsafundamentalareawheremanyimprovementsatlevel4oftheframeworkwillbemanaged.

Thissectionshouldbecompletedthroughreviewsofstrategies,businessplansandotherkeystrategicdocumentationincludingperformancemanagementpolicies,qualityassurancepoliciesandrecruitmentplans.

Resources

This aspect of the internal governance and leadership follows directly from the managementarrangements.This is theassessmentof the requirementsof theSAIandshouldbe identified throughreviews and studies and be included in key policies and strategies. Therefore operational documentssuchasannualworkplansanddelegationsshouldbereviewed.

iCAT:FinancialAudit

Chapter2:UnderstandingthePrerequisitesforRobustAuditPractices–level2ISSAIsandAscertainStatusonLevel2ISSAIRequirements

Page28

Responses to this section should also relate to themanagement arrangementswhen considering thelevel 4 gaps. For example, issues regarding ISSAI 40 element 4 “ensuring staff have competencies tocarryouttheirwork”canbe linkedtothe itemunder managementarrangementsprinciple6 ISSAI20“the SAI measures the efficiency and effectiveness with which it uses its funds”. When completingcolumns5and6oftheiCATtheserelationshipswillbeanalyzedtoensurethattheactionplansareaspracticalaspossible.

iii. SAICoreProcesses

ThisareaoftheLevel2ISSAIrequirementsismainlyconcernedwiththeISSAI40QualityAssurance.Forthe SAI tomeet the requirements of level of the framework a numberof factors are required fromatechnicalperspective.Theseinclude:

• Auditreporting• Followuponauditfindings• Methodology• AuditingStandards

Alltheaboveneedtobeinplacetoensurethattheauditrisk(therisktheauditorreachesanincorrectconclusion)isminimized.Toassesstherequirements, itwillbeadvisabletoscheduleaninterviewwiththe person responsible for quality assurance and control in the SAI.Many of the practices should bedocumentedin instructionsthroughmanualsand/orcirculars.TheseshouldbeassessediftheyincludetheelementsstatedintheLevel2ISSAIRequirements.Ifthepracticeisstatedindocumentationandnotfollowed:atthisstagesimplystateundercolumn4thatthereispartialcompliance(tobeconsistentwiththe viewespousedat Step2 i. Independence and Legal Framework). When the level 4 assessment isundertakenthiswillidentifytheproblemoftheimplementation.

iv. ExternalStakeholder

ReportingPractices

This section lists all the reporting requirements identified in level 2 of the framework. There are 18requirements.ThisrepresentsalargeexpectationonSAIstoreportontheiractivitiesandresults.Manyof these reports can be included in a single SAI annual report for example. The participant shouldtherefore obtain all external correspondences that the SAI issues and assess them against the 18requirements.

ExternalStakeholderRelations

This section assesses the SAI relationship with its primary stakeholders. This can include: legislature,parliaments and special committees of parliament. The SAI may include this information in acommunicationstrategyandoftenhaveaspokespersonoranofficedirectly linkedto theHeadof theSAI.Itisadvisabletointerviewtherelevantpersonnelandobtainthenecessaryprotocols,strategiesandpolicies.Fromnextchapterguidanceonlevel4ISSAIsforFinancialaudit iselaborated.Guidancefor irststepofthe Financial audit process is Pre engagement and relevant ISSAIs is described in chapter 3.

iCAT:FinancialAudit

Chapter3:Preengagement

Page29

Chapter3

Pre-engagement

Introduction

ThischapterisrequiredtoensurethatthefacilitatoridentifiesthepreconditionsforenablingtheSAItoimplementlevel4ofISSAIframeworkoffinancialauditing.ItisimportantthatthefacilitatorunderstandstherequirementsexpectedwithinaSAIenvironmentbeforeconsideringanyspecificaudit.TheseaspectsincludefactorswhichrequiredecisionsthatareconsistentwithSAIpoliciesasdiscussedonlevel2.Inthischapterspecificreferencestopoliciesandareasforconsiderationarehighlightedfortheappropriatefoundationtobeputinplacebeforeanauditcommences.

Section1providesanoverviewofthefinancialauditprocessasisexplainedinthestandards.Section2highlightsalltheareaswheretherequirementswithintheiCATarecontained.Section3-6providesemphasistothemostimportantelementsofpre-engagement.

1. OverviewofthefinancialauditprocessandtheexpectationoftheISSAIfacilitator

1.1FinancialAuditProcess:

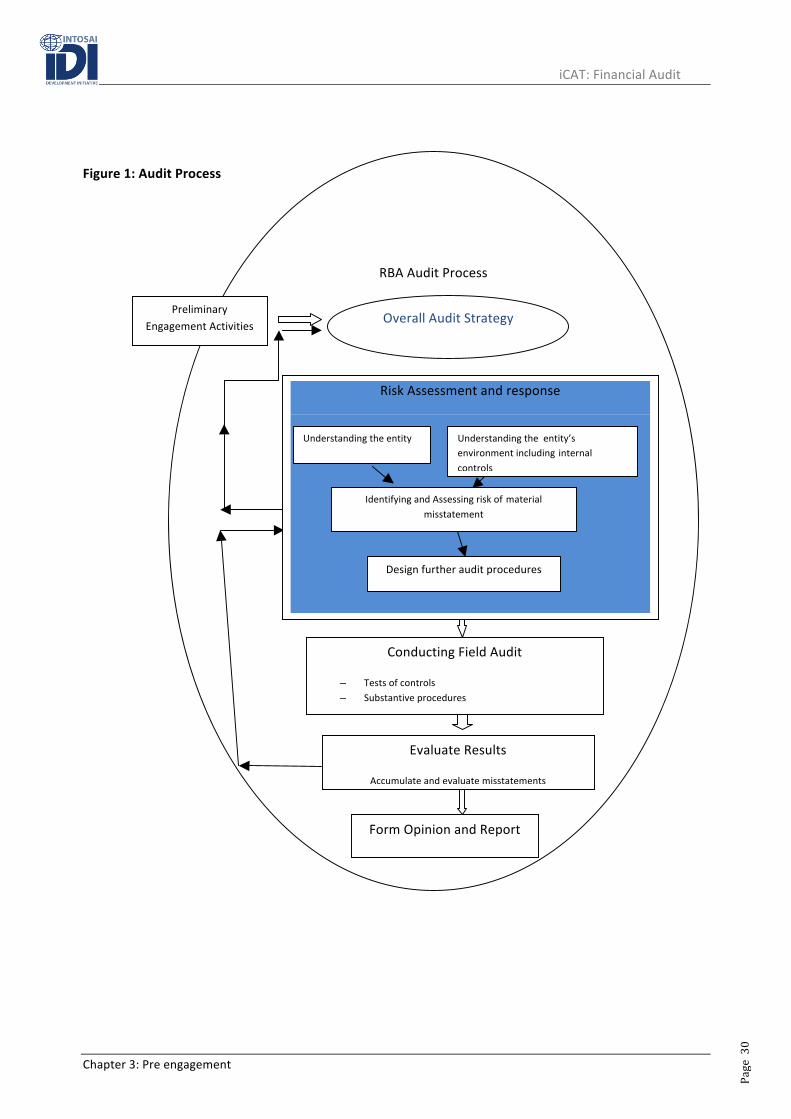

Figure1belowprovidesanunderstandingoftheauditprocess.Itisessentialtounderstandthattheauditprocessisnotsimplyaonewayprocessfromplanningthroughtoreporting.Reconsiderationofthecriticalaspectsoftheauditprocessiscontinuallyinneedofre-evaluation.Thisisreflectedinthefeedbackloopsinthefigurebelow.Forexample,whenevaluatingtheresultsfromtheauditfieldwork,theassumptionsmadeintheplanningregardingmaterialmisstatementmaybeincorrect.Inthissituationtheauditorisrequiredtoreflectthechangesintheplanningdocumentation.

iCAT:FinancialAudit

Chapter3:Preengagement

Page30

Figure1:AuditProcess

RBAAuditProcess

FormOpinionandReport

PreliminaryEngagementActivities

OverallAuditStrategy

RiskAssessmentandresponse

Designfurtherauditprocedures

IdentifyingandAssessingriskofmaterialmisstatement

Understandingtheentity’senvironmentincludinginternalcontrols

Understandingtheentity

ConductingFieldAudit

– Testsofcontrols– Substantiveprocedures

EvaluateResults

Accumulateandevaluatemisstatements

iCAT:FinancialAudit

Chapter3:Preengagement

Page31

1.2ExpectationsfromtheISSAIFacilitators

Table1belowprovidesanoverviewofwhattheISSAIfacilitatorisrequiredtodoateachstageoftheauditprocess.InadditiontotheexpectationsinTable1,theISSAIfacilitatorisrequiredtobefamiliarwiththeissuesdiscussedinlevel2oftheISSAIframeworkcoveredinChapter2.Forfinancialauditsomeoftheseissuesaregivenmoreemphasisasdiscussedintable2ofthismodule.

Atthisstage,theISSAIfacilitatorisexpectedtohaveaccesstoSAIfinancialauditseniormanagementandselectaminimumoftwoauditfilestosupporttheconclusionsdrawnfromthediscussionswithmanagement.

BeforelookingattheiCAT,thefacilitatorshouldunderstandtheauditingstandards.TheInternationalStandardsofSupremeAuditInstitutions(ISSAIs)forfinancialauditingarebasedontheprivatesectorInternationalStandardsonAuditing(ISA)issuedbytheInternationalFederationofAccountants(IFAC).TheISSAIsthereforecomprisesoftheentireISA.TheISAshaveaconsistentstructuresincludingrequirementsofthestandardsandthenreferencedtothisiswhatiscalledtheapplicationoftherequirements.Theapplicationiseffectivelyguidanceonunderstandingtherequirements.

TheISSAIsthenenhancestheISAwithspecificguidancefortheSAIenvironmentthroughtheuseofpracticenotes.Theseoftenprovideexamplesforthepublicsectorcontextorexplainsituationsinwhichthestandardsapply.

iCATcomprisesallrequirementsfrom36ISSAIs.InadditiontorequirementsfromInternationalStandardsonAuditing(ISAs)therequirementsfromthepracticenoteshavebeenadded.Altogether531requirementsareincludediniCAT.

InordertofacilitatetheuseofiCAT:

• Requirementshavebeensplitintoauditingphases:Pre-engagement,Planning,FieldworkandReportinganddescribedintherespectivemodulesofthecourse.Someoftheserequirementsflowthroughouttheauditprocessandthefacilitatorwillberequiredtounderstandthestartingpointoftherequirement.

• Whethertherequirementisimportantoninstitutionallevelorauditlevelhasalsobeenidentified.

• Documentsthatprovetheapplicationoftherequirementhavebeenoutlined,e.g.planningdocuments,workingpapers,auditreportetc.

iCAT:FinancialAudit

Chapter3:Preengagement

Page32

Table1:Overview–ActivitiesofISSAIFacilitator

AuditProcessReference

CoreTextmodule BriefDescription ISSAIreference ExplanationofISSAIFacilitatorknowledge

Preliminaryauditengagement

Chapter3 Thisstageoftheauditiswhereassessmentoftheauditrequirementsaremadeandtheauditteamcommunicateswiththeauditedentity

ISSAI1210 ThefacilitatorshouldunderstandtheSAIsstandardpracticeandassessifithasbeenappliedconsistently

OverallAuditStrategy

Chapter4 Togainahighlevelunderstandingoftheauditedentityandassessthemateriality.

ISSAI1300,1315and1320

ThefacilitatorshouldbeabletoidentifythedocumentationwithintheSAItorelatestotherequirementsoftheoverallauditstrategyandassesswhethertheelementsofthestrategyarecovered.

Riskassessmentandriskresponses

Chapter4 Theprocessinvolves:Understandingtheentityincludingitscontrolenvironment.Identifyingtheriskofmaterialmisstatementanddesigningfurtherauditproceduresforassessingtherisks.

ISSAI1200and1300series

TheISSAIfacilitatorisrequiredtounderstandtheSAImethodologyandhowitcoversthemainaspectsoftheauditplanningrequirements.AnassessmentofthemainelementsoftheSAIsprocessisthenassessedagainstauditfilestoseeiftheycontaintheinformationexpected.Assessmentoftheadequacyofthe

iCAT:FinancialAudit

Chapter3:Preengagement

Page33

AuditProcessReference

CoreTextmodule BriefDescription ISSAIreference ExplanationofISSAIFacilitatorknowledgeplanningconclusionsandthedesignofauditproceduresisbeyondthescopeofthefacilitator.

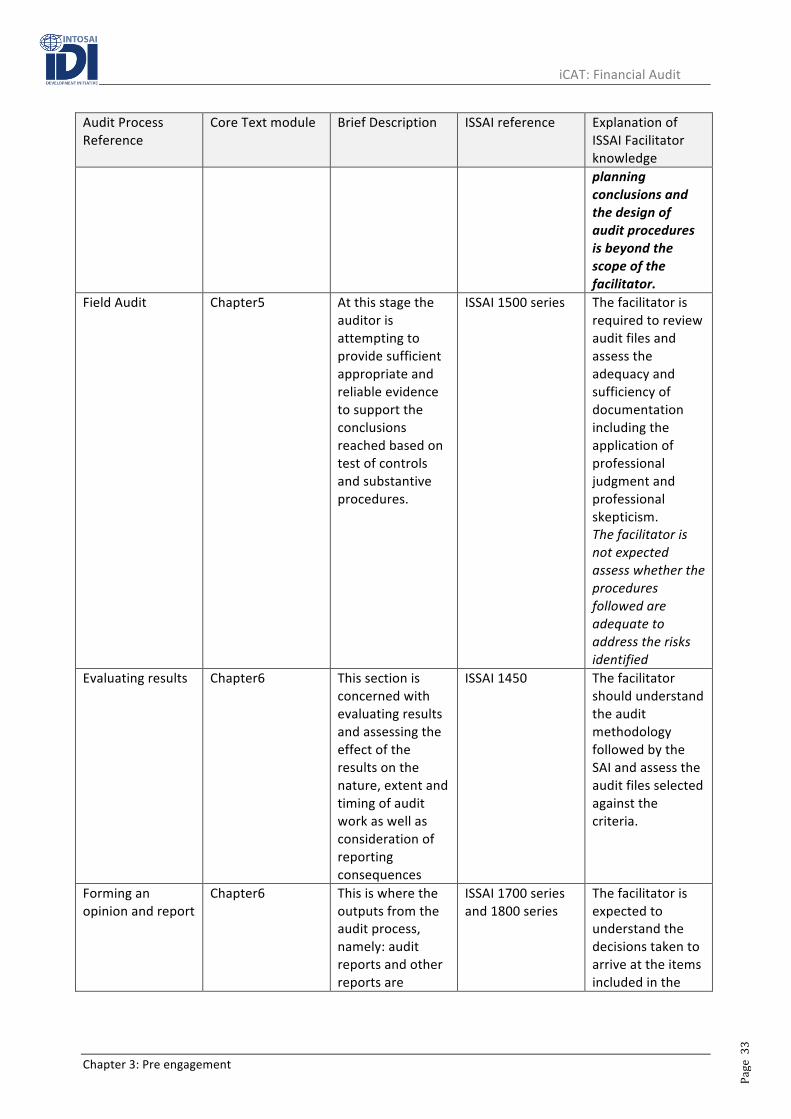

FieldAudit Chapter5 Atthisstagetheauditorisattemptingtoprovidesufficientappropriateandreliableevidencetosupporttheconclusionsreachedbasedontestofcontrolsandsubstantiveprocedures.

ISSAI1500series Thefacilitatorisrequiredtoreviewauditfilesandassesstheadequacyandsufficiencyofdocumentationincludingtheapplicationofprofessionaljudgmentandprofessionalskepticism.Thefacilitatorisnotexpectedassesswhethertheproceduresfollowedareadequatetoaddresstherisksidentified

Evaluatingresults Chapter6 Thissectionisconcernedwithevaluatingresultsandassessingtheeffectoftheresultsonthenature,extentandtimingofauditworkaswellasconsiderationofreportingconsequences

ISSAI1450 ThefacilitatorshouldunderstandtheauditmethodologyfollowedbytheSAIandassesstheauditfilesselectedagainstthecriteria.

Forminganopinionandreport

Chapter6 Thisiswheretheoutputsfromtheauditprocess,namely:auditreportsandotherreportsare

ISSAI1700seriesand1800series

Thefacilitatorisexpectedtounderstandthedecisionstakentoarriveattheitemsincludedinthe

iCAT:FinancialAudit

Chapter3:Preengagement

Page34

AuditProcessReference

CoreTextmodule BriefDescription ISSAIreference ExplanationofISSAIFacilitatorknowledge

produced reportandassessiftheyarecomplianttotherelevantstandardsandSAIpractice.

2. Institutionallevelconsiderationspriortoassessinganindividualaudit

Asthefacilitatoryouarealreadyfamiliarwiththelevel2considerationsoftheISSAIframework.Level2ISSAIsstateandexplainthebasicprerequisitesfortheproperfunctioningandprofessionalconductofSAIs.Thesearetheinstitutionallevelconsiderationsthatrequiredtobeanalyzedbeforeassessinganindividualauditprocess.

Thefocusshiftsslightlytoassessingtheseconsiderationsinthespecificcontextoffinancialauditing.Themainareaswheretheseconsiderationsarenecessaryarebroadlycoveredby:

2.1 Compliancetothelevel4financialauditISSAIs2.2 Assessmentoftheaccountingandlegalframeworkgoverningthefinancialstatementsin

yourjurisdiction2.3 ConsiderationoftheSAIbeforecommencingwithindividualaudits

2.1Compliancetothelevel4financialauditISSAIs

TheiCAThasidentifiedseveralreferencesforexampleISSAI1200.20wheretheuseofISAhastobecarefullyconsidered.Itstates“TheauditorshallnotrepresentcompliancewithISAsintheauditor’sreportunlesstheauditorhascompliedwiththerequirementsofthisISAandallotherISAsrelevanttotheaudit”.ThismeanstheSAIcannotdecidetofollowafewaspectsofISAanddepartfromothersandstillstatetheyarecomplyingwithISAsandthereforetheISSAIsforfinancialaudit.

Exampleswherethissituationwillneedtobeconsideredcouldincludethefollowingscenarios:

• WheretheSAIhasfundamentalcapacityrestrictionsinmeetingtheISSAIrequirementsfromcurrentresources

• Wherethestakeholderexpectationsortheauditingenvironmentdoesn’tprovideforfullISSAIimplementation

InthecaseofcapacityrestrictionstheSAIcanconsiderassessingthescopeoftheauditsandasstatedunderISSAI40(acceptanceandcontinuation)andshouldbringthistotheattentionoftheHeadofSAIoreventhelegislatureorbudgetauthority.TheSAIinthisregardshouldhaveanoverallplanthatwillbediscussedunderresourceconsiderationsbelow.

InthesituationwherefullISSAIimplementationmaybelimitedbytheenablingenvironment,forexample,wheretheaccountingframeworkisstillunderdevelopedorthescrutinyofthefinancialstatementsandauditreportishighlylimitedthereareseveralfactorsthattheSAIshouldconsider.

iCAT:FinancialAudit

Chapter3:Preengagement

Page35

FirstlytheSAIshouldassesswhataspectsoftheISSAIsarethemostrelevanttoimplementandbeginwiththese.InthisinstanceasstatedinISSAI1805.8theauditorcanconsidertheapplicabilityoftheISSAIs.IngeneraliftheinformationprovidedtousersisinsufficienttocovertheirneedsthentheSAIshouldidentifythedeficienciesandreportthemtotheappropriatestakeholders.

Secondly,SAIshouldassessoveralltheimportanceoftheISSAIsandidentifythekeyvaluetheISSAIswillprovideandfocusontheseareas.However,inthesesituationsitmaynotbepossiblefortheSAItostatethatitisauditingincompliancewiththeISSAIs.AstatementintheSAI’sstrategicdocumentationshouldreflectthisposition.TheSAIshouldrefertoISSAI1000.28forotheralternativesforcompliancetotheISSAIFramework.

InthespecificinstanceofthedeficiencyofthefinancialreportingframeworktheSAIshouldconsiderthesectionbelow.

2.2Assessmentoftheaccountingandlegalframeworkgoverningthefinancialstatementsinyourjurisdiction

TheISAsmakereferencetotheaccountingframeworkunderwhichthefinancialstatementsaremade.Therearetwoverypopularframeworksthatarewellestablishedintheinternationalcommunitynamely:

• InternationalFinancialReportingStandards(IFRS)• InternationalPublicSectorAccountingStandards(IPSAS)

TheseframeworksprovidecoveragefortherequirementsoftheISSAIs.Forexample,disclosuresinrelationtorelatedpartiesarecoveredbytheframeworks.Itisinthisregardthatthefinancialreportingframeworkneedstobecomprehensiveastoprovidetheusersofthestatementswiththerelevantinformationprovidedinasuitablyunderstandableformat.

Manyjurisdictionsareoperatingwithentitiesatdifferentlevelsofaccountingbases.ForexampleMinistriesmaybeoncashormodifiedcashbasiswhereascorporationscanbefullycomplianttoIFRS.TheIPSASexplainsthedifferentbasisofaccountingandprovidesforthemigrationfromfullcashtofullaccruals.ThefacilitatorcanobtainreviewtheIPSASandIFRSframeworksthroughthewebsitewww.ifac.org(publicsectorforIPSAS).

IftheaccountingframeworkislimitedorunderdevelopmentthefacilitatorshouldconsiderwhethertheSAIhasenquiredoftherelevantmanagementwhetherthefinancialstatementsaresufficienttomeettheuserrequirements(ISSAI1200practicenote5refers).

ManySAIsoperateinenvironmentswheretheaccountingframeworkisprescribedwithinthelegislationofthecountry.Inthesecasestheassessmentoftheapplicabilityoftheframeworkforusersshouldstillbeundertakenandrecommendationsmadetotherelevantstandardsetterse.g.MinistryofFinanceorAccountantGeneral.

iCAT:FinancialAudit

Chapter3:Preengagement

Page36

2.3ConsiderationoftheSAIbeforecommencingwithindividualaudits

WhenconsideringtheoverallfinancialauditstrategyfortheSAItherearemanyfactors.Thesefactorsneedtobeconsideredpriortoanyresourceallocationandassessmentofindividualauditstrategy.Manyoftheseaspectsarealsoreferredtoatlevel2oftheISSAIframeworkandarereflectedinSAIpolicyandprocedures;however,thereisaneedforsomeannualconsiderations.Table2belowissummaryofthetypeofconsiderationsaSAIshouldconsider.

Table2:SAIPrecondition

Considerations Decision Guidance ISSAIReferenceISSAIcompliancelevel4financial

Full/Partial TheSAIneedstodecideontheapplicabilityoftheframeworkandtheintentiontocomplywiththerequirements.Iftherearereasonsforelementsoftheframeworktobeomittedtheyshouldbestated.Thestatementofthebasisoftheopinionandanyoverallmodificationstotheauditreportsshouldbeprovided.

AllISSAIslevel4

AdequacyofFinancialReportingFramework

Adequate/Limited/Notapplicable

SAIshouldconsidercommunicatingitsconclusioniftheframeworkisnotadequatetotherelevantstandardsettingbodies.Inextremesituationsmodificationstotheauditreportsorspecialreportsshouldbeconsidered

ISSAI40underacceptanceandcontinuanceandISSAI1000(paragraphs43and44)

Auditresourcesrequiredinternally(ISSAI40acceptanceandcontinuation)

Adequate/inadequate

InthecaseofinadequateauditresourcestheSAIshouldconsidertheeffectonthescopeoftheauditoridentifyalternativeapproachestoobtainassurancee.g.contractingoutfunctionsThisisparticularlyimportantinthecaseofsmallSAIswhohavelimitedcapacityTheSAIisalsorequiredtohaveresponsesinplacetoanauditedentity,whichmaybepreventingtheSAIfromadequatelycarryingoutitsresponsibilities.AswithdrawalisnotusuallyanoptioninSAIenvironmentalternativesmeasuresmayneedtobesought.

iCAT:FinancialAudit

Chapter3:Preengagement

Page37

Considerations Decision Guidance ISSAIReferenceManagementofAuditresourcescontractedout

Appropriate/trainingorguidanceneeded

WhereotherauditorsoutsidetheSAIareemployedtoconductaudits,particularassessmentshouldbemadeoftheirprofessionalcompetenceandtheirunderstandingofthepublicsectorrequirements(aselaboratedinthepracticenotes)

ISSAI1600practicenote

UseofExperts(includinginternalauditors)

Required/Notrequired

Astrategicdecisionisrequiredtoassesstheneedforexpertsorothergovernmentalagencies(e.g.antimoneylaunderingagencies).Theauditstowhichtheyrelatedandthescopeofworkshouldbeunderstood.TheSAIshouldthenassesstheauditriskoverallandprioritizetheexpertsrequired.

ISSAI1610andISSAI1620

Specificcomplexitiesintheauditedentitiesthateffecttheindividualauditstrategies

Yes/No Thesecaninclude:• Serviceorganizations• Specificreporting

requirements• Highriskclients• Otheraudits/investigations

beingperformedbytheSAI• Relatedparties• Particularissuesinthepublic

intereste.g.highrankingofficialexpenses

• Consolidations• Restructuringofgovernment

organizations• Specificinstructionsfrom

legislature/thirdparties• Previousallegations

Alltheaboveshouldbeconsideredandtheeffectontheauditstrategiesandresourceallocationsshouldbestated.

ISSAI1402ISSAI1700ISSAI1300ISSAI1240ISSAI1550IISSAI1315ISSAI1600ISSAI1510ISSAI1210ISSAI1240

ReportsissuedotherthanthoseincompliancetoISSAI1700and1800series.

Yes/No IftheSAIintendstoissueotherauditreportsthatarenotinconformancetothestandards.ThentheSAIshouldstatethebasisandcriteriaforsuchreports.AnydiscussionofkeyauditthemesandthemethodtheSAIusestoincludetheseissuesinthereportshouldbeexplained.

ISSAI1700seriesand1800series

iCAT:FinancialAudit

Chapter3:Preengagement

Page38

Considerations Decision Guidance ISSAIReference

Qualitycontrolplan Yes/no Aqualitycontrolplanfortheyearshouldbeprovided

ISSAI40andISSAI1220

EvidenceofEthicalRequirementsinplacepriortothecommencementoftheaudits

Yes/no TheSAIshouldoperationalizetherequirementsofISSAI30toensureanannualprocessforethicalrequirementsisundertaken.

ISSAI30

3. QualityControl

ISSAI40principle1Leadershipstatesclearlytheimportanceofqualitycontrolasshownbelow:

An SAI should establish policies and procedures designed to promote an internal culturerecongnisingthatquality isessential inperformingallof itswork.SuchpoliciesandproceduresshouldbesetbytheHeadoftheSAI,whoretainsoverallresponsibilityforthesystemofqualitycontrol.

ThefacilitatorhasalreadyunderstoodtheroleoftheISSAI40onlevel2oftheISSAIFramework.AtthisstagetheSAIalsorequiresamechanismfortranslatingtheseinstitutionalrequirementsintotheindividualauditprocess.ISSAI1220providesforsuchalink.Itlooksatthequalitycontrolfunctionemployedattheauditlevel.Thequalitycontrolprocessisrelativelystraightforwardandiscapturedintheflowbelow.

1. Planning2. Conducting3. Monitoring

3.1PlanningQualityControlReview

AtthecommencementoftheauditcycletheSAIshouldbeawareoftheengagementqualitycontrolreviewsthatarerequiredtotakeplace.TheSAIshouldensurethattheengagementqualitycontrolreviewsinclude:

• AnylistedcompaniesauditedbytheSAI(ISSAI220.19)• OtherentitiesthattheSAIdeemsnecessaryduetothenatureoftheengagement.

ThecriteriatheSAIemploysforselectingtheauditstobequalitycontrolreviewedshouldbeexplicitlystatedandapprovedaspertheengagementqualitycontrolpolicy.Thecriteriacouldconsider:

• Auditswheremodifiedopinionswerepreviouslyissued• Auditswhichhaveahighpublicprofile• Auditswhichhaveallegationsrelatedtotheauditentity• Coveragetoincludeallengagementpartners

iCAT:FinancialAudit

Chapter3:Preengagement

Page39

ThequalitycontrolplanshouldbeapprovedandcommunicatedinlinewiththeSAIpoliciesandprocedures.ThecarryingoutoftheQAfunctioncaninvolveoutsideexpertise,adedicatedQAfunctionordelegationstospecificindividualsorcommittees.

3.2Conducting-EngagementPerformance

3.2.1Overview

Duringthefieldworktheengagementleadershalltakeresponsibility,amongotherthings,for:

a. thedirection,supervisionandperformanceoftheauditengagementincompliancewithprofessionalstandardsandapplicablelegalandregulatoryrequirements;andtheauditor’sreportbeingappropriateinthecircumstances;

b. reviewsbeingperformedinaccordancewiththefirm’sreviewpoliciesandprocedures;c. theengagementteamundertookappropriateconsultationondifficultorcontentiousmatters;d. determiningwhetherthereisaneedforanengagementqualityreviewandifsodetermined,

ensuringthatanengagementqualityassurancereviewerhasbeenappointed.

Wheredifferencesofopinionarisewithintheauditteamwiththoseconsultedand,whereapplicable,betweentheengagementleaderandtheengagementqualitycontrolreviewer,theauditteam,shouldfollowtheSAI’spoliciesandproceduresfordealingwithandresolvingdifferencesofopinion.

TheengagementleaderensuresreviewsareperformedinaccordancewiththeSAI’sreviewpoliciesandprocedureswhichshouldmeettherequirementsofISSAI40.(Ref:ISSAI1220paragraphs16andA.16toA.17,A.20andISSAI40-paragraphs32andA.34)

Theengagementleader/supervisorisresponsibleforensuringthatreviewsoftheworkingpapersarecarriedoutinordertobesatisfiedthattheydemonstratethatsufficientappropriateauditevidencehasbeenobtainedtosupportconclusionsreachedfortheauditor’sreporttobeissued.(Ref.ISSAI1220paragraphs17andA.18toA.20)

3.2.2ConsultationandDifferencesofOpinion

ISSAI1220givesresponsibilitytotheHeadoftheSAIforensuringthattheengagementteamundertakesappropriateconsultationondifficultorcontentiousmatters,andthattheconclusionsofconsultationsaredocumentedandimplemented.

Wheredifferencesofopinionarisewithintheengagementteam,withthoseconsultedand,whereapplicable,withintheSAI,theSAIshouldhavepoliciesandproceduresfordealingwithandresolvingdifferencesofopinion.

3.2.3EngagementQualityControlReview(EQCR)

EQCRistheobjectiveevaluationofthesignificantjudgmentsmadebytheauditteamandtheconclusionsreachedinformulatingtheindependentauditor’sreport.

Aspartofthesystemofqualitycontrol,ISSAI40statesthatanEQCRshouldbeperformedforallauditsmeetingtheagreedcriteria.Examples:

iCAT:FinancialAudit

Chapter3:Preengagement

Page40

• whereaqualifiedoradverseopinionisbeingproposedoranticipated;

• whereclientactivitiesareofspecialinteresttothegeneralpublicormedia;and

• whereclientsareconsideredasbeingofhigherauditrisk,forexampledueto:ahistoryofweakinternalsystemsofcontrol;orwherecomplexornovelaccountingissuesexist

ISSAI40requiresthatanEQCRisconductedinatimelymannersothatsignificantmattersareresolvedpriortotheopinionbeingissued.ThereforetheEQCRisperformedbeforetheissuingofthereport.

3.3. Monitoring

TheISSAI1220.32to1220.34explainsthatmonitoringisinrespectsoftwoelements:

• assessment,correctingandimprovinganyissueswithauditengagements• assessmentandimprovingthequalitycontrolprocessitself

AnyissueshighlightedarenotnecessarilydemonstratingfailuretomeetthestandardbutaremerelyaspectsthatrelatetooperationalaspectsoftheSAIsactivities.

4. Keyaspectsofauditevidenceincludinglinkagestoprofessionalskepticism

4.1OverviewTheISSAIfacilitatorhastobeawarethatthroughouttheauditprocesscertainrequirementsinregardtoauditevidencemustbekeptinmind.Thesearesummarizedinthetablebelow.

Table3:AspectsofAuditEvidence

Description ISSAIReference CommentUnderstandabilityofauditevidenceincludingsignificantprofessionaljudgment

ISSAI1230.8 Withintheapplicationtothestandardreferencesaremadetothepracticalitiesrelatedtoevidence.Clearlyauditorscannotrecordalldocumentationandjudgmentstaken.Theneedtorelatewhatisdocumentedtoassisttheusers(includingreviewersandfutureauditors)indischargingtheirfunctionsisthecriteria.

Typeofworkperformed,whoperformeditandwhoreviewedit

ISSAI1230.9 Ownershipandevidenceofreviewisessentialtotheauthorityoftheworkperformedandtoaccountabilityandresponsibilityfortheauditasawhole.

ConsiderationofSmallSAI

NotspecificallytoISSAIframework

Asdiscussedabovetheimplicationsontheauditscopeandcompliancetostandardshastobeconsidered.

Professionalskepticism

ISSAI1240.12 Thisisperhapsoneofthemostdifficultareasfacingtheauditors.Theabilitytodemonstrateskepticismwithintheauditevidencemaynotbestraightforward.Itmayrequireevidencethroughforexample,teammeetings.Considerationofallegationsandothersourcessuchaspress

iCAT:FinancialAudit

Chapter3:Preengagement

Page41

coverageshouldbeassessed.Seesection4.2belowforfurtherillustrationAcceptanceofdocumentationprovidedbytheauditedentityshouldbelinkedtotheinternalcontrolassessment.

SpecialconsiderationsinjudicialaspectsrelatingSAIfunctions

ISSAI1230PN15and16

InSAIswherethereisaresponsibilitybeyondfinancialreportingandexpressinganopiniontheSAImayhaveadditionalevidentialrequirements.Forexample,inpreparingdocumentationforimposingfinestheevidentialrequirementmaybestrongerthansimplyhighlightingthefinding.ThisshouldbereflectedinthepoliciesandproceduresoftheSAI.

4.2Skepticism

RecognizingThatManagementCanAlwaysCommitFraud

Managementisalwaysinapositiontooverrideotherwisegoodinternalcontrol.

Engagementteammembersaretosetasideanybeliefsthatmanagementandthosechargedwithgovernancearehonestandhaveintegrity,notwithstandingtheauditor’spastexperienceoftheirhonestyandintegrity.

AQuestioningMind Makecriticalassessmentsaboutthevalidityofauditevidenceobtained.

BeingAlert Doesauditevidencecontradictorbringintoquestionthereliabilityof:

•Documentsandresponsestoinquiries?

•Otherinformationobtainedfrommanagementandthosechargedwithgovernance?

BeingCareful Avoid:

•Overlookingunusualcircumstances.

•Over-generalizingwhendrawingconclusionsfromauditobservations.

•Usingfaultyassumptionsindeterminingthenature,timing,andextentoftheauditproceduresandevaluatingtheresultsthereof.

•Acceptinglessthanpersuasiveauditevidenceinabeliefthatmanagementandthosechargedwithgovernancearehonestandhaveintegrity.

•Acceptingrepresentationsfrommanagementasasubstituteforobtainingsufficientappropriateauditevidence.

iCAT:FinancialAudit

Chapter3:Preengagement

Page42

5. AuditCommunication

5.1OverviewIntheiCATthereareover70requirementswhereformalcommunicationisidentified.Thisthereforeemphasizestheimportanceplaceduponthiselementoftheaudit.

Thefacilitatorshouldappreciatetheimportanceoftheformalcommunicationwithmanagementandthosechargedwithgovernancerelatingtotheauditedentities.Inmanycasesthosechargedwithgovernancecanbeauditcommittees.Ininstanceswheretheauditorneedstocommunicatetothosechargedwithgovernance,includingonsensitivematters,thestandardhassomebroadinstructionsISSAI1260.29refers.

5.2 TypesandReasonsforFormalCommunication

StandardtemplatesandpoliciesandproceduresarerequiredtoensurethattheSAIcommunicatesinaconsistentandprofessionalmannerwithoutsideparties.

Table4belowprovidesexamplesofthetypesofformalcommunicationusedduringthecourseofanaudit:

Table4:TypesofCommunicationwithexternalstakeholders

TypeofCommunication Example ReferenceInformative Engagementletter ISSAI1210.16Clarification Furtherexplanationisrequiredontheaccounting

frameworkorsignificanttransactionsISSAI1210.18andISSAI1550.14

Representations Managementrepresentationlettersupportingthefinancialstatements.AnentireISSAIisconcernedwithmanagementrepresentations

ISSAI1580

Permission Insomeinstancestheauditormayrequirepermissionfromtheauditedentitytocontactthirdpartiesforconfirmations

ISSAI1501.11

Goingtoahigherauthority