Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic...

29

1 Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic panel threshold models 8-19-2015-d Walid Mensi, Shawkat Hammoudeh, Seong-Min Yoon * and Duc Khuong Nguyen Abstract This study investigates the asymmetric linkages between the five BRICS countries’ stock markets and three country risk ratings (financial, economic and political risk) in the presence of major global economic and financial factors. Using the dynamic panel threshold models, we find evidence of asymmetry in most cases. However, the significance and the signs of the effects of these risk ratings on the BRICS market returns differ across the lower and upper regimes. Furthermore, improvements in the global stock, WTI and gold markets enhance the BRICS stock market performance. Increases in implied volatility indices lead to drops in the BRICS markets. JEL classification: G14; G15 Keywords: BRICS, country risk ratings, global factors, regime-switching, dynamic panel threshold model. * Yoon: Corresponding author, Department of Economics, Pusan National University, Jangjeon2-Dong, Geumjeong-Gu, Busan 609-735, Korea. Tel: +82-51-510-2557; E-mail: [email protected]. IPAG Business School, Paris, France. Mensi: Department of Finance and Accounting, University of Tunis El Manar, Tunis, Tunisia. Email: [email protected]. Hammoudeh: Lebow College of Business, Drexel University, Philadelphia, United States. E-mail: [email protected]. IPAG Business School, Paris, France. Nguyen: IPAG Lab, IPAG Business School, Paris, France. E-mail: [email protected]. The third author (S.-M. Yoon) is grateful for financial support from the National Research Foundation of Korea in a grant funded by the Korean Government (NRF-2013S1A5B6053791). All authors thank MSCI for providing us with the data for the BRICS stock markets.

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic...

1

Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic panel threshold models

8-19-2015-d

Walid Mensi, Shawkat Hammoudeh, Seong-Min Yoon* and Duc Khuong Nguyen

Abstract

This study investigates the asymmetric linkages between the five BRICS countries’ stock markets and three

country risk ratings (financial, economic and political risk) in the presence of major global economic and financial

factors. Using the dynamic panel threshold models, we find evidence of asymmetry in most cases. However, the

significance and the signs of the effects of these risk ratings on the BRICS market returns differ across the lower

and upper regimes. Furthermore, improvements in the global stock, WTI and gold markets enhance the BRICS

stock market performance. Increases in implied volatility indices lead to drops in the BRICS markets.

JEL classification: G14; G15

Keywords: BRICS, country risk ratings, global factors, regime-switching, dynamic panel threshold model.

* Yoon: Corresponding author, Department of Economics, Pusan National University, Jangjeon2-Dong, Geumjeong-Gu, Busan 609-735, Korea. Tel: +82-51-510-2557; E-mail: [email protected]. IPAG Business School, Paris, France. Mensi: Department of Finance and Accounting, University of Tunis El Manar, Tunis, Tunisia. Email: [email protected]. Hammoudeh: Lebow College of Business, Drexel University, Philadelphia, United States. E-mail: [email protected]. IPAG Business School, Paris, France. Nguyen: IPAG Lab, IPAG Business School, Paris, France. E-mail: [email protected]. The third author (S.-M. Yoon) is grateful for financial support from the National Research Foundation of Korea in a grant funded by the Korean Government (NRF-2013S1A5B6053791). All authors thank MSCI for providing us with the data for the BRICS stock markets.

1

Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic panel threshold models

Abstract

This study investigates the asymmetric linkages between the five BRICS countries’ stock markets and three

country risk ratings (financial, economic and political risk) in the presence of major global economic and

financial factors. Using the dynamic panel threshold models, we find evidence of asymmetry in most cases.

However, the significance and the signs of the effects of these risk ratings on the BRICS market returns differ

across the lower and upper regimes. Furthermore, improvements in the global stock, WTI and gold markets

enhance the BRICS stock market performance. Increases in implied volatility indices lead to drops in the

BRICS markets.

JEL classification: G14; G15

Keywords: BRICS, country risk ratings, global factors, regime-switching, dynamic panel threshold model.

2

1. Introduction

Brazil, Russia, India, China, and South Africa (BRICS thereafter) are the world’s most

important emerging economies. They have experienced spectacular economic growth and hold

a strong future promise owing to their large size, government stability, and financial and

economic ability to pay their obligations to creditors and investors. Enhanced by globalization

of world trade and financial liberalization, the stock markets of these countries have become

increasingly more integrated with those of the most developed economies by means of trade

and investment. The BRICS have cooperated among themselves in different economic sectors

such as energy, food and technologies. Additionally, they have reformed their respective

financial institutions and are working on creating new international institutions that may

augment or even replace the IMF and the World Bank such as the Asian

Infrastructure Investment Bank (AIIB) and New Development Bank (NDB) with headquarters

in Shanghai by 2016.1

Given their reasonable risks and opportunities, this group provides channels to investors

and traders to diversify their portfolios within a global financial framework. The BRICS stock

markets are consequently influenced by their own country risks (Hammoudeh et al., 2013) and

by global factors (Mensi et al., 2014).2 The successive series of major global and regional

financial crises in the last two decades have raised the concerns of international investors and

rating agencies, which have a strong bearing to individual BRICS country risks.

Due to the BRICS’s relevance to international financial markets, their country risk

ratings and their three own risk components (financial, economic and political risk factors)

have been closely watched by investors, policymakers, regulatory institutions and international

organizations, particularly in the wake of the recent global financial crisis and the euro-zone

3

debt crisis. More specifically, the BRICS’s risk ratings have several important implications for

the financial stability and the performance (capitalization) of their stock markets as well as for

their financial dependence on international stock markets and the world economy. Additionally,

country risk factors work in combination with the major global factors to influence stock prices.

For instance, oil price shocks and the U.S. economic policy uncertainty are found to be

interrelated and affect stock returns in many countries (Kang and Ratti, 2013).

Recently, the finance literature has increasingly shown more interest in the relationship

between country risks, global factors and the performance of stock markets. For instance, Erb

et al. (1995) suggest that country credit ratings help discriminate between high-expected-return

and low-expected-return countries. Diamonte et al. (1996) provide evidence that political risk

factors have a significant impact on emerging and developed stock markets. Kaminsky and

Schmukler (2001) examine the effects of sovereign ratings and outlook changes on the

instability of emerging financial markets. Among the BRICS stock markets, Hammoudeh et al.

(2013) indicate that only the Chinese stock market is sensitive to all own country risk factors

and global factors including the world’s major stock and oil markets. Additionally, the Brazilian

market shows special sensitivity to both economic and financial risk factors, while the Russian

and Chinese markets hold strong sensitivity to political risk factors. Furthermore, India

demonstrates special sensitivity to higher oil prices. As for the sensitivity of global factors, the

oil price is more sensitive to economic than financial risk factors, while the S&P 500 reverses

this relationship. Sari et al. (2013) provide evidence of a long-run relationship between

Turkey's risk ratings and its stock market movements. Turkey's three economic, financial, and

political risk ratings components are found to be the forcing variables of movements in its stock

market in the long-run. However, in the short-run only the reduced political and financial risk

ratings components have positive and significant impact on the Turkish market movements.

4

Liu et al. (2013) show that the long-run and short-run relationships between the stock market

and the three risk ratings factors of each BRICS country respond asymmetrically and at

different speeds to shocks for this group of the emerging stock markets, depending on the

direction of the shock.

In this study, we investigate how country risk ratings (i.e., financial risk, economic risk

and political risk) and important global financial and economic factors influence the

performance of the BRICS stock markets. Our paper is motivated by the fact that the fast-

growing BRICS are the major recipients of global investment flows and are among the main

global consumers of commodities (Mensi et al., 2014). Therefore, changes in both risk ratings

and major global financial and economic factors could be channels through which fluctuations

in the world’s credit, economic and financial conditions are transmitted to the BRICS stock

markets. Moreover, the global market actors such as investors, regulatory bodies, rating

agencies, banks, and trade partners are interested in the impact of changes in country risk

ratings on these five important emerging countries. Such interest enables this important group

of countries to offer several favorable opportunities including high returns, wide liquidity and

portfolio risk diversification to global investors who seek to reduce risk by integrating the

BRICS stocks in their portfolios.

In this light, the present paper attempts to address the following unanswered questions.

Do significant relationships exist between the stock markets of the BRICS and their

corresponding country risk ratings? Are these relationships symmetric or asymmetric under

different market conditions? Do influential global financial and economic factors related to oil

prices, global risks and uncertainty impact the BRICS markets? Providing answers to these

questions is important to our understanding of how the global stock markets, the major financial

and economic variables and country risk ratings contribute to a better understanding of the

5

movements of the BRICS stock markets.

We address these issues by using a dynamic panel threshold model which is designed to

examine the regime-switching behavior of the relationships between the BRICS stock markets

and country risk ratings through the estimation of the endogenous threshold parameter values.

Thus, this approach allows the stock market indices to switch between regimes over-time,

estimates asymmetric effects of the dependent variables across the BRICS markets and under

different regimes, and properly tests for the threshold effect. Another interesting feature of this

modeling approach is that it does not suffer from the generated regressors problem and the

resulting estimation and inference complexities, especially those inherent in dynamic panels

(Dang et al., 2012).Overall, this dynamic panel threshold model is particularly important and

relevant for the interactive relationships between country risk ratings and market returns in the

BRICS countries given the recent major crises that had plagued the world’s markets and

economies.

The results from our dynamic panel threshold model over the monthly period from

January 1995 to August 2013 show evidence of significant asymmetric relationships between

political risk ratings and the BRICS stock market returns when the threshold variables such as

WTI oil prices, and gold prices are used. The financial risk ratings have an asymmetric impact

on the BRICS market returns for the benchmark specification (i.e., the one-period lagged stock

return is used as a threshold variable). This impact is positive and statistically significant for

the upper regime, indicating that high risk ratings (i.e., low financial risk) improve the

performance of the BRICS markets, while it is negative for the lower regime. No significant

effect from economic risk ratings on stock returns is found, except for the benchmark

specification under the upper regime where an increase in the economic risk ratings decreases

the BRICS stock returns as well as when the USEPUI, WTI and WORLD threshold variables

6

are used. On the other hand, our results show small significant short-run effects of country risk

ratings on the BRICS stock returns. On the whole, the signs of the effects of the three risk

ratings on the BRICS market returns differ across the lower and upper regimes. We also

estimate the symmetric non-threshold dynamic panel models for the purpose of comparison,

but the latter does not reveal accurately links between country risk ratings and the BRICS

market returns.

Among the global factors, the implied volatility index is found to significantly decrease

the BRICS market returns, regardless of the considered transition variables. In contrast,

increases in the world equity market return, and the gold and WTI oil market returns have a

positive effect on the BRICS stock markets, which generally underscores the positive

responsiveness of the BRICS markets to the global financial and business cycles. Finally, the

St. Louis Fed’s financial stress index and the U.S. economic policy uncertainty index have no

statistically significant impacts on the BRICS markets.

The remainder of this article is organized as follows. Section 2 discusses the

methodology. Section 3 describes the data and descriptive statistics, while Section 4 presents

and discusses the results. Finally, Section 5 concludes.

2. Dynamic Panel Threshold Model

We use the dynamic panel threshold model, which contains the lagged dependent

variable 𝑦𝑦𝑖𝑖,𝑡𝑡−1, to examine the effects of country risk ratings and global factors on the BRICS

market returns. The empirical specification takes the following form:

𝑦𝑦𝑖𝑖,𝑡𝑡 = 𝜇𝜇𝑖𝑖 + 𝜙𝜙𝑦𝑦𝑖𝑖,𝑡𝑡−1 + 𝛼𝛼′𝑥𝑥𝑖𝑖,𝑡𝑡 + ∑ �𝛽𝛽1′𝑧𝑧𝑖𝑖,𝑡𝑡𝑗𝑗 𝐼𝐼�𝑞𝑞𝑖𝑖,𝑡𝑡 ≤ 𝛾𝛾𝑗𝑗� + 𝛽𝛽2′𝑧𝑧𝑖𝑖,𝑡𝑡

𝑗𝑗 𝐼𝐼�𝛾𝛾𝑗𝑗 < 𝑞𝑞𝑖𝑖,𝑡𝑡��𝑗𝑗 + 𝜀𝜀𝑖𝑖,𝑡𝑡, (1)

where the dependent variable 𝑦𝑦𝑖𝑖,𝑡𝑡 represents the stock returns which are computed as the

7

difference in the logarithm between two consecutive index prices. 𝑞𝑞𝑖𝑖,𝑡𝑡 is the threshold variable

being greater or less than the unknown threshold level 𝛾𝛾𝑗𝑗. 𝜇𝜇𝑖𝑖 denotes the country-specific fixed

effect. 𝜀𝜀𝑖𝑖,𝑡𝑡~𝑖𝑖𝑖𝑖𝑖𝑖(0,𝜎𝜎2)is the error term. 𝐼𝐼(. )is the indicator function representing the regime

defined by the threshold variable 𝑞𝑞𝑖𝑖,𝑡𝑡 and the unknown threshold level 𝛾𝛾𝑗𝑗. The coefficients 𝛽𝛽1′

and 𝛽𝛽2′ are the slope parameters associated with two different regimes. 𝑧𝑧𝑖𝑖,𝑡𝑡𝑗𝑗 is the jth regime-

dependent regressor (𝑗𝑗 = 𝑃𝑃𝑃𝑃,𝐹𝐹𝑃𝑃,𝐸𝐸𝑃𝑃) where 𝑃𝑃𝑃𝑃 , 𝐹𝐹𝑃𝑃 and 𝐸𝐸𝑃𝑃 denote the political, financial

and economic risk ratings, respectively. The subscript 𝑖𝑖 represents each of the five individual

BRICS countries.

The use of the first lag of the dependent variable, 𝑦𝑦𝑖𝑖,𝑡𝑡−1, is important not only because it

accounts for the dynamics of stock returns over time but also because it works as a proxy for

possible omitted variables (Bittencourt, 2011). 𝑥𝑥𝑖𝑖,𝑡𝑡 refers to a vector of control variables which

are uncorrelated with the error term. This vector includes 𝑆𝑆𝑆𝑆𝑃𝑃𝐸𝐸𝑆𝑆𝑆𝑆𝑡𝑡 (the St. Louis Fed’s

financial stress index FSI), 𝑉𝑉𝐼𝐼𝑉𝑉𝑡𝑡 (the stock market uncertainty index which is the Chicago

Board Options Exchange’s market volatility index), 𝑈𝑈𝑆𝑆𝐸𝐸𝑃𝑃𝑈𝑈𝐼𝐼𝑡𝑡 (the U.S. economic policy

uncertainty index), 𝑊𝑊𝑆𝑆𝐼𝐼𝑡𝑡 (the WTI spot price FOB in dollars per barrel), 𝐺𝐺𝐺𝐺𝐺𝐺𝐺𝐺𝑡𝑡 (the gold price

in dollars per troy ounce), and 𝑊𝑊𝐺𝐺𝑃𝑃𝐺𝐺𝐺𝐺𝑡𝑡 (the MSCI global equity index).

The sample observations are divided into two regimes (i.e., high and low regimes)

depending on whether the threshold variable 𝑞𝑞𝑖𝑖,𝑡𝑡 is smaller or larger than the unknown

threshold 𝛾𝛾𝑗𝑗 as indicated above. In order to estimate the above dynamic panel equation, a two-

step procedure is followed. First, the optimal threshold level must be identified according to

the approach developed by Hansen (1999). We apply the bootstrap-based procedure to test the

null hypothesis of no threshold effect (one regime) against the alternative hypothesis of a

threshold effect (two regimes) by extending the Hansen (1999) procedure.3 Second, when this

8

threshold parameter is estimated, one can return to the initial stage of estimation of the whole

model. The nonlinear dynamic panel data model in this paper includes a lagged dependent

variable as explanatory variable and also contains unobserved panel-level, fixed or random

effects. By construction, the unobserved panel-level effects are correlated with the lagged

dependent variables, making the standard estimators inconsistent. We will use the

corrected least square dummy variable (LSDVC) estimation method of Kiviet (1995, 1999),

because is known to derive consistent estimators of the unknown parameters as in our case.4

3. Data and Preliminary Analysis

3.1. Data Description

This study employs monthly data for the five stock market indices and the three country

risk ratings (FR, ER and PR) of the BRICS countries as well as for the six global financial and

risk factors over the period from January 1995 to August 2013. The stock market indices of

those five BRICS countries are Brazil’s BOVESPA, China’s Shanghai SEA index, India’s BSE

(100) NATIONAL, Russia’s RTS index, and South Africa’s FTSE/JSE ALL SHARE

(JSEOVER). The six global financial and risk factors include the U.S. equity VIX, the MSCI

world index, the West Texas Intermediate (WTI), the world gold price, the U.S. economic

policy uncertainty and the St. Louis Fed’s financial stress index (FSI).

9

Table 1. BRICS Stock Markets’ Financial Development Indicators

Market capitaliza-tion (% GDP)

Listed companies

Value traded (US$)

Turnover ratio (%)

2000 2012 2000 2012 2000 2012 2000 2012

Brazil 35.079 54.595

459 353

1,0128E+11 8,3453E+11

44.606 67.881

Russia 14.987 43.412 249 276 2,0312E+10 7,3224E+11 36.557 87.639

India 31.192 68.596 5937 5191 5,0981E+11 6,2248E+11 306.499 54.634

China 48.478 44.941 1086 2494 7,2154E+11 5,8265E+12 158.285 164.440

South Africa 154,241 160,148 616 348 7,7494E+12 3,11778E+13 33.157 54.925

Notes: Market capitalization is the share price times the number of shares outstanding. Listed domestic companies are the domestically incorporated companies listed on the country’s stock exchanges at the end of the year. Stocks traded refer to the total value of shares traded during the period. Turnover ratio which is a measure of market liquidity is the total value of shares traded during the period divided by the average market capitalization for the period. Average market capitalization is calculated as the average of the end-of-period values for the current period and the previous period. Source: World Bank (World Development Indicators).

Table 2. Financial, Economic and Political Risk Rating Components and Their Corresponding Risk Points Financial Risk Rating Economic Risk Rating Political Risk Rating

Component Points (max.) Component Points

(max.) Component Points (max.)

Foreign Debt % GDP 10 GDP per Head 5 Government Stability 12 Foreign Debt Service % XGS 10 Real GDP Growth 10 Socioeconomic Conditions 12 Current Account % XGS 15 Annual Inflation Rate 10 Investment Profile 12 Net International Liquidity 5 Budget Balance % GDP 10 Internal Conflict 12 Exchange Rate Stability 10 Current Account % GDP 15 External Conflict 12 Corruption 6 Military in Politics 6 Religious Tensions 6 Law and Order 6 Ethnic Tensions 6 Democratic Accountability 6 Bureaucracy Quality 4 Total 50 50 100

Notes: XGS denotes exports of goods and services. A political (economic or financial) risk rating of 0.0% to 49.9% (0.0% to 24.5%) indicates a very high risk; 50.0% to 59.9% (25.0% to 29.9%) high risk; 60.0% to 69.9% (30.0% to 34.9%) moderate risk; 70.0% to 79.9% (35.0% to 39.9%) low risk; and 80.0% (40.0%) or more very low risk. A political risk rating can be compensated for by better financial and/or economic risk ratings and vice versa. For further details on the range of risk rating subcomponents and the range of their risk points, see https://www.prsgroup.com/.

Table 1 shows some major financial indicators of the five BRICS stock markets. While

Brazil, Russia, India, and South Africa experienced a fast increase in stock market size relative

to economy as measured by the market capitalization to GDP ratio between 2000 and 2012.

10

Whereas, China realized a slight decline from 48.48% (2000) to 44.94%. In view of the

elevation in the turnover ratio, all markets experienced an increase in liquidity, except India

whose liquidity level decreased from 306.50% (2000) to only 54.63% (2012). China’s stock

market was the most liquid market in 2012.

The economic, financial and political risk ratings represent the three major measures of

country risks, computed from 22 variables and developed by the ICRG rating system. Each risk

component is measured by a scoring index (see Table 2). As shown in this table, the political

risk index is based on 100 points, while financial and economic risk factors have 50 points

each. The financial risk rating measures the country’s ability to service its financial obligations.

The economic risk rating measures a country’s current economic strengths and weaknesses and

gives an assessment of the country’s ability to finance its official, commercial, and trade debt

obligations. Finally, the political risk rating measures the political stability of a country, which

is the ability and willingness of a country to service its financial obligations.5

The global stock market is represented by the MSCI world index which covers 1,612

large and middle sized firms measured by capitalization across 23 developed market countries.

It captures approximately 85% of the free float-adjusted market capitalization in each country.

Also, the data include two major global commodity markets. The first is the West Texas

Intermediate (WTI) oil price which serves as the benchmark price for the United States and gl

obal oil markets for the light and sweet crude. The WTI crude oil, whose price is expressed in

U.S. dollars per barrel, is among the most traded oil on the world markets, and thus is

influenced by macro-financial variables (Choi and Hammoudeh, 2010).The second is the gold

market whose prices are expressed in U.S. dollars per ounce. Gold is one of the most important

precious metals and can serve as a hedge against stocks on average and also a safe haven during

extreme stock market movements (Baur and Lucey, 2010; Baur and McDermott, 2010, among

11

others). The BRICS economies include the world’s major consumers of oil and gold

commodities (e.g., China and India) but also large global commodity producers. More precisely,

South Africa is indeed known as one of the world's largest producers of some strategic

commodities including gold, platinum, and chrome, and Russia remains one of the top oil

producers, with an average daily production of 10.5 million bbl/d in 2013.

The influential global economic and financial factors include, among others, the implied

volatility of the U.S. equity market (Chicago Board Options Exchange market volatility index

- VIX), the US economic policy uncertainty index (USEPUI), and the St. Louis Fed’s financial

stress index (STRESS).6 These factors are expected to provide further understanding about ho

w the BRICS stock markets react to global market news and fluctuations. For instance, both

STRESS and VIX play an important role in asset allocation and portfolio strategies (e.g., Hood

and Malik, 2013; Balcilar et al., 2014; Mensi et al., 2014).

The data on the country risk ratings for the BRICS countries, the world stock market

index, oil prices, and gold prices are sourced from the ICRG database, the MSCI database, the

Energy Information Administration (EIA), and the World Gold Council (WGC), respectively.

The data of VIX, USEPUI, and STRESS come from Datastream International, the economic

policy uncertainty website, and the Federal Reserve Bank of St. Louis, respectively. Our study

period is marked by a number of extreme international economic, social, and political events

such as the 1997-1998 Asian financial crisis, the 1998 Russian crisis, the 1998-1999 Brazilian

crisis, the 2001 dot-com bubble, the September 11, 2001 terrorist attack, the Lehman Brothers

collapse on September 15, 2008, the 2008-2009 global financial crisis, the Arab Spring since

the end of 2010, and the 2009-2012 Euro zone debt crisis.

All stock market indices are denominated in U.S. dollars in order to eliminate the local

inflation and national exchange rate fluctuations. We compute the stock returns by taking the

12

difference in the logarithm between two consecutive prices. Similarly, for all the explanatory

variables, we consider the logarithmic changes in those variables.

3.2. Statistical and Stochastic Properties of Data

Table 3 shows the descriptive statistics of the stock markets and three risk rating indices

for the BRICS countries. The five countries are ranked according to the mean of their financial,

economic and political risk ratings where the higher the rank implies the lower the risk. The

statistics indicate that the BRICS countries form a heterogeneous group in terms of risk

assessment, despite their similarities. Specifically, Brazil’s BOVESPA index has the highest

return mean and volatility, while China’s Shanghai SEA index provides the lowest return mean

and volatility. As for country risk ratings, India has the lowest mean risk ratings in the political

and economic risk categories, and hence is ranked last. South Africa presents the highest

political risk ratings and is ranked first, followed by Brazil, China and Russia. China has the

highest financial and economic risk ratings, underlying this country’s ability to pay its

obligations. In contrast, Brazil has the lowest financial risk factors, suggesting the highest

fragility of its financial system relative to that in the other countries. Overall, we find moderate

levels of political risk for the five countries, while their financial and economic risks range

from low to moderate level.

The summary statistics for the global economic and financial factors in Table 4 show

that these variables deviate from the Gaussian distribution, in view of the Jarque-Bera test. The

STRESS, VIX and USEPUI variables are skewed to the right, while the remaining global

factors are skewed to the left.

Table 3. Summary Statistics of Stock Market and Risk Rating Indices

Statistics Brazil Russia India China South Africa

13

Stock market index Mean 1625.3999 542.0679 243.8656 45.2865 309.4244 Std. dev. 1168.2186 389.1174 160.3649 20.6782 150.6882 Skewness 0.7329*** 0.6639*** 0.6708*** 0.1579 0.4613*** Kurtosis (excess) -0.9078*** -0.5362 -0.9862*** -0.9613*** -1.2881*** Jarque-Bera (JB) 27.7456*** 19.1372*** 25.8778*** 9.5556*** 23.4292*** Political risk Mean 66.3326 61.4643 60.5156 66.1629 68.6920 Std. dev. 2.4126 5.8588 3.4222 3.3498 3.4769 Skewness -0.2511 -1.1094*** -0.2477 -0.3957** 0.5185*** Kurtosis (excess) -0.6688** 0.8768*** -0.6295* -1.1487*** -0.3395 Jarque-Bera (JB) 6.5284** 53.1249*** 5.9883 * 18.1610*** 11.1109*** Rank 2 4 5 3 1 Financial risk Mean 34.7455 39.4754 41.0759 45.1674 38.1763 Std. dev. 4.9951 6.7002 2.8409 3.1223 2.0589 Skewness -0.1986 -0.8379*** -0.3521** -1.2486*** -0.6106*** Kurtosis (excess) -0.5252 -0.6037* -1.2594*** 0.5321 0.0054 Jarque-Bera (JB) 4.0471 29.6133*** 19.4329*** 60.8479*** 13.9176*** Rank 5 3 2 1 4 Economic risk Mean 34.8578 37.1098 34.1264 39.4551 35.3820 Std. dev. 3.0271 6.8279 1.6235 1.7822 2.0384 Skewness -0.6283*** -1.1471*** -0.3756** -1.6155*** -0.6568*** Kurtosis (excess) 0.3811 0.5666* -0.4918 5.1551*** 0.0899 Jarque-Bera (JB) 16.0924*** 52.1207*** 7.5239** 345.4694*** 16.1828*** Rank 4 2 5 1 3 Notes: The data for the country risk ratings are obtained from the ICRG database, while the data of stock market indexes are from the MSCI database and denominated in U.S. dollars. The Jarque-Bera (JB) test corresponds to the statistic for the null hypothesis of normality in the sample return distributions. The five BRICS countries are ranked according to the mean of their political, financial and economic risk ratings. The rank numbers is function of the risk ratings mean. ***, **, * indicate a rejection of the null hypothesis at the 1%, 5% and10% significance levels, respectively.

Table 4. Summary Statistics of Control Variables

Statistics STRESS VIX USEPUI WTI GOLD WORLD Mean 0.0210 21.3132 106.3554 50.3006 663.6594 1121.2800 Std. dev. 1.0239 8.0280 37.8167 31.0466 462.6638 246.0984 Skewness 2.8017*** 1.5311*** 1.0110*** 0.5996*** 1.1298*** -0.0256 Kurtosis (excess) 11.0340*** 3.7320*** 0.2674 -0.8823*** -0.0879 -0.7722** Jarque-Bera (JB) 1429.39*** 217.51*** 38.82*** 20.69*** 47.72*** 5.59*

Note: See the notes of Table 3.

14

Table 5. Panel Unit Root Tests

Stock index Political risk Financial risk Economic risk Panel A. Series in level

Levin-Lin-Chu test 0.3533 -0.2116 -0.9798 -1.0862 Im, Pesaran and Shin test 0.3431 -2.3474*** -2.2564** -4.0911*** Breitung test -1.1311 -1.9483** -1.2562 -1.8751**

Panel B. Series in logarithm Levin-Lin-Chu test 0.1979 -0.1878 -0.8941 -1.2972* Im, Pesaran and Shin test 0.6326 -2.3923*** -2.4339*** -4.3289*** Breitung test -1.1334 -1.9703** -1.2107 -1.7286**

Panel C. Logarithmic changes Levin-Lin-Chu test -22.5710*** -24.9940*** -22.8563*** -23.3459*** Im, Pesaran and Shin test -22.8526*** -23.6524*** -23.3253*** -24.2980*** Breitung test -13.8738*** -25.4398*** -21.5248*** -24.3668***

Notes: This table presents the empirical statistics of the panel unit roots.***, **, and * indicate the rejection of the null hypothesis of a unit root at the 1%, 5% and 10% significance levels, respectively. The length of lags in the tests is chosen by SIC (Schwarz information criterion).

On the other hand, we examined the stationarity of the variables as the panels under

consideration. To do this, we employ three popular panel unit root tests (i.e., Breitung, LLC

and IPS), developed by Breitung (2000), Levin, Lin and Chu (2002), and Im, Pesaran and Shin

(2003), respectively. Table 5 presents the results of the estimation of these tests which provide

evidence that the null hypothesis of the panel unit root is strongly rejected for all the logarithmic

differences of the series under consideration. This indicates that the series differences are

stationary at the 1% level. Thus, the empirical model can be regressed.

4. Empirical Results

4.1. Threshold Variable Detection

Using the bootstrap-based procedure, Table 6 reports the results of identifying the

threshold values for each threshold variable. However, we show that all control variables

(Returns of STOCK index (t-1), STRESS, VIX, USEPUI, WTI, GOLD and WORLD index)

15

present a threshold effect as they present at least one significant threshold parameter. More

precisely, the first lagged BRICS stock index presents three significant threshold parameters

for the three break variables (political risk, financial risk and economic risk factors). As for

STRESS, the VIX, USEPUI, and WORLD threshold variables have a switching- regime for

both political risk and financial risk break variables, while the GOLD and WTI variables give

one significant threshold parameter for political risk. When we consider the implied volatility

(VIX) as the threshold variable, we find based on the bootstrap-based regime test statistic a

significant threshold level for the political and financial risk break variables, documenting the

presence of regime-switching. The estimated threshold parameter is equal to 40 for the PR

variable and 33.56 for the FR variable. This result implies that the effect of the rate of change

of the political and financial risk ratings on the BRICS stock returns depends on the rate of

change of these threshold variables. To sum up, the result indicates the presence of different

regimes and nonlinear behaviors, so that the regime-switching dynamic panel model emerges

as a more appropriate testing approach.

16

Table 6. Results of the Estimation of the Threshold Level

Regime dependent variables Threshold values F-statistics p-values Threshold variable = Returns of STOCK index (t-1)) Rate of change of Political Risk (t) -0.3445*** 33.1573 0.005 Rate of change of Financial Risk (t) 0.0842** 16.3970 0.021 Rate of change of Economic Risk (t) 0.3112*** 16.3801 0.001 Threshold variable = STRESS Rate of change of Political Risk (t) 0.3860*** 17.4953 0.009 Rate of change of Financial Risk (t) 0.8470*** 14.0279 0.004 Rate of change of Economic Risk (t) 0.1490 6.1905 0.525 Threshold variable = VIX Rate of change of Political Risk (t) 40.0000** 22.4455 0.043 Rate of change of Financial Risk (t) 33.5600* 11.1317 0.090 Rate of change of Economic Risk (t) 27.8800 8.0178 0.157 Threshold variable =USEPUI Rate of change of Political Risk (t) 75.8551*** 19.9367 0.001 Rate of change of Financial Risk (t) 66.0005* 16.5500 0.098 Rate of change of Economic Risk (t) 67.5329 5.0875 0.574 Threshold variable = WTI Rate of change of Political Risk (t) 15.0300*** 50.0579 0.002 Rate of change of Financial Risk (t) 14.9100 6.2758 0.389 Rate of change of Economic Risk (t) 14.1700 18.6379 0.122 Threshold variable = GOLD Rate of change of Political Risk (t) 273.0000* 17.0749 0.099 Rate of change of Financial Risk (t) 347.2000 4.6852 0.387 Rate of change of Economic Risk (t) 287.0500 3.4762 0.844 Threshold variable = WORLD Rate of change of Political Risk (t) 1335.0690*** 18.0170 0.007 Rate of change of Financial Risk (t) 1338.5000** 15.6891 0.034 Rate of change of Economic Risk (t) 669.3170 3.6857 0.729 Notes: The threshold values are identified by using the Hansen (1999) approach. The p-values are calculated using 1,000 bootstrap replications. The asterisks ***, **, * indicate rejection of null hypothesis (no threshold variable) at the 1%, 5%, 10% significance levels, respectively.

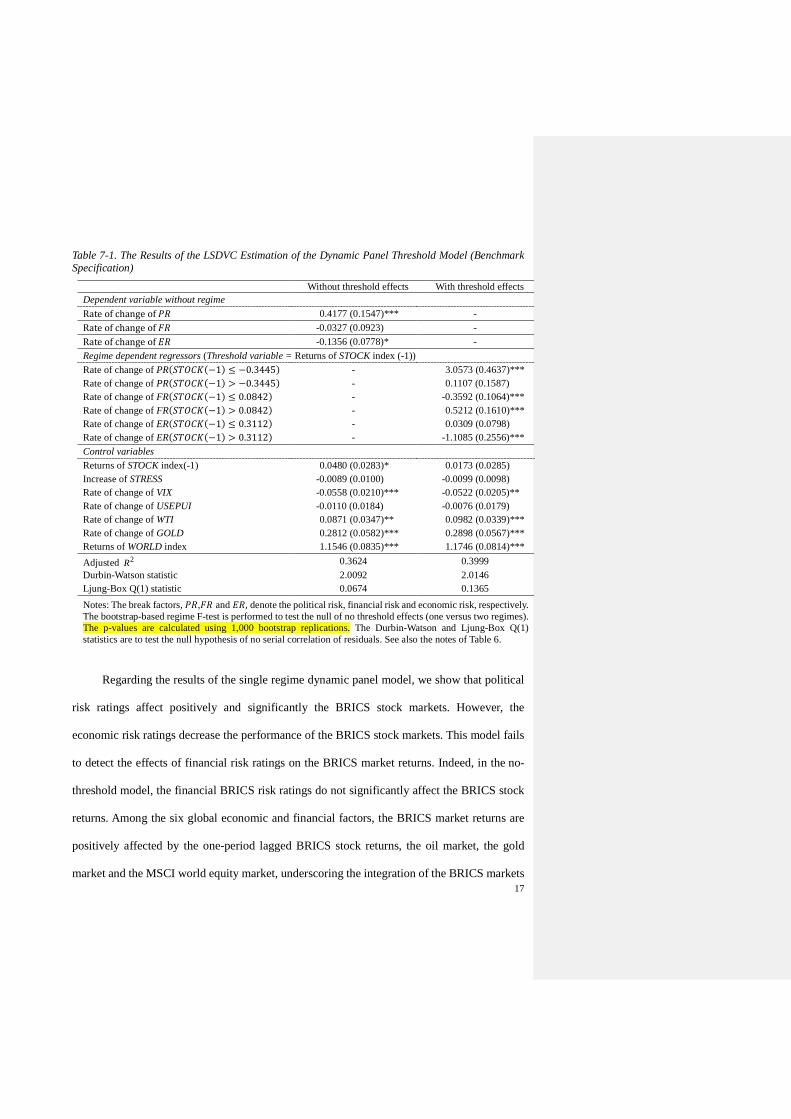

4.2. Regression Results for the Non-threshold Dynamic Panel Model and Basic Specification

Table 7-1 reports the estimated results from the two-step LSDVC estimation of the

symmetric, non-threshold (one regime) model as well as the threshold model for the one-period

lagged BRICS return threshold variable as the benchmark specification. As shown in the last

row of this table, the Durbin-Watson and Ljung-Box Q(1) statistics show that we do not reject

the null of no autocorrelation in the estimated models, meaning that the models are not

misspecified. Thus, the LSDVC estimation method produces consistent results of the

estimation.

17

Table 7-1. The Results of the LSDVC Estimation of the Dynamic Panel Threshold Model (Benchmark Specification)

Without threshold effects With threshold effects Dependent variable without regime Rate of change of 𝑃𝑃𝑃𝑃 0.4177 (0.1547)*** - Rate of change of 𝐹𝐹𝑃𝑃 -0.0327 (0.0923) - Rate of change of 𝐸𝐸𝑃𝑃 -0.1356 (0.0778)* - Regime dependent regressors (Threshold variable = Returns of STOCK index (-1)) Rate of change of PR(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) ≤ −0.3445) - 3.0573 (0.4637)*** Rate of change of PR(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) > −0.3445) - 0.1107 (0.1587) Rate of change of FR(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) ≤ 0.0842) - -0.3592 (0.1064)*** Rate of change of FR(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) > 0.0842) - 0.5212 (0.1610)*** Rate of change of ER(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) ≤ 0.3112) - 0.0309 (0.0798) Rate of change of ER(𝑆𝑆𝑆𝑆𝐺𝐺𝑆𝑆𝑆𝑆(−1) > 0.3112) - -1.1085 (0.2556)*** Control variables Returns of STOCK index(-1) 0.0480 (0.0283)* 0.0173 (0.0285) Increase of STRESS -0.0089 (0.0100) -0.0099 (0.0098) Rate of change of VIX -0.0558 (0.0210)*** -0.0522 (0.0205)** Rate of change of USEPUI -0.0110 (0.0184) -0.0076 (0.0179) Rate of change of WTI 0.0871 (0.0347)** 0.0982 (0.0339)*** Rate of change of GOLD 0.2812 (0.0582)*** 0.2898 (0.0567)*** Returns of WORLD index 1.1546 (0.0835)*** 1.1746 (0.0814)*** Adjusted 2R 0.3624 0.3999 Durbin-Watson statistic 2.0092 2.0146 Ljung-Box Q(1) statistic 0.0674 0.1365 Notes: The break factors, 𝑃𝑃𝑃𝑃,𝐹𝐹𝑃𝑃 and 𝐸𝐸𝑃𝑃, denote the political risk, financial risk and economic risk, respectively. The bootstrap-based regime F-test is performed to test the null of no threshold effects (one versus two regimes). The p-values are calculated using 1,000 bootstrap replications. The Durbin-Watson and Ljung-Box Q(1) statistics are to test the null hypothesis of no serial correlation of residuals. See also the notes of Table 6.

Regarding the results of the single regime dynamic panel model, we show that political

risk ratings affect positively and significantly the BRICS stock markets. However, the

economic risk ratings decrease the performance of the BRICS stock markets. This model fails

to detect the effects of financial risk ratings on the BRICS market returns. Indeed, in the no-

threshold model, the financial BRICS risk ratings do not significantly affect the BRICS stock

returns. Among the six global economic and financial factors, the BRICS market returns are

positively affected by the one-period lagged BRICS stock returns, the oil market, the gold

market and the MSCI world equity market, underscoring the integration of the BRICS markets

18

with these markets as a result of globalization and financialization reforms. The dependence

on the gold market can be explained by the fact that China and India are the world’ largest gold

buyers. In addition, South Africa and Russia are the world's largest producer of some strategic

commodities (e.g., gold, platinum, and chrome) and petroleum producer respectively.

Additionally, changes in the implied volatility index affect statistically and negatively the

performance of the BRICS markets, indicating that the BRICS market returns decrease as the

VIX increases. Mensi et al. (2014) also show that the BRICS stock markets exhibit dependence

with the changes in the CBOE volatility index.

Turning now to the benchmark specification, the results of the estimation of the threshold

dynamic panel model in the presence of the one lag stock returns serving as the threshold

variable are given in the last column of Table 7-1. The threshold parameter is statistically

significant at different levels for the three break variables (i.e., 𝑃𝑃𝑃𝑃, 𝐹𝐹𝑃𝑃 and 𝐸𝐸𝑃𝑃). We find an

insignificant effect between the first lag BRICS stock returns and the performance of the

BRICS stock markets, suggesting no evidence of short-run asymmetry between the past and

the current BRICS stock returns. Furthermore, the economic risk ratings affect negatively the

BRICS stock market performance for the high regime, indicating that an increase in the

economic risk ratings (i.e., a decrease in the risk level) leads to a decrease in the stock market

returns, which ever estimator is applied. Conversely, the political risk ratings influence

positively the BRICS stock markets for only the low regime, suggesting that low political risk

leads to an improvement in the performance of these emerging stock markets. Financial risk

has a significant impact on the BRICS stock markets for both regimes, indicating the

importance of the financial risk level for these stock markets. As for the control variables in

the benchmark model, we find that risk factors measured by the U.S. VIX influence negatively

the BRICS stock markets, implying that increases in these risk factors in the United States drive

19

down the BRICS stock returns, which is the case of the reaction of United States’ market to the

VIX. In contrast, a rise in both gold and oil returns as well as the MSCI world index improves

the BRICS emerging stock returns, signifying the importance of these commodities and the

global stock index as indicators of the relevance of the good health of world’s financial system

to the BRICS markets. Finally, the financial stress index and the U.S. economic uncertainty

policy index (USEPUI) have no significant impact on the stock market performance for both

models with and without threshold effects.

4.3. Regression Results for Alternative Specifications

Table 7-2 reports the results of the estimation of the threshold model for each of the six

global economic and financial risk factors (STRESS, VIX, USEPUI, WTI, GOLD and

WORLD) as alternative models, respectively. It is worth noting that the sample is classified

into the lower regime when the value of the transition variable is less than or equal to the

estimated threshold level, and the upper regime when the value of the transition variable is

greater than the estimated threshold level. The inspection of the Durbin-Watson and Ljung-Box

Q(1) statistics which are reported in these tables shows that all the seven models are not

misspecified since we do not reject the null of no autocorrelation in the estimated models. The

LSDVC estimation method thus produces consistent results of the estimation, regardless of the

threshold variables.

20

Table 7-2. Estimation of the LSDVC Estimation of the Dynamic Panel Threshold Model with Threshold Effects (Alternative Specifications)

Threshold variable STRESS VIX USEPUI Regime dependent regressors Rate of change of PR ( 0.3860)STRESS ≤ 0.5016 (0.2097)** - - Rate of change of PR ( 0.3860)STRESS > 0.2171 (0.2274) - - Rate of change of PR ( 40.0000)VIX ≤ - 0.1792 (0.1619) - Rate of change of PR ( 40.0000)VIX > - 2.1215 (0.5147)*** - Rate of change of PR ( 75.8551)USEPUI ≤ - - -0.4427 (0.2911) Rate of change of PR ( 75.8551)USEPUI > - - 0.7868 (0.1795)*** Rate of change of FR ( 0.8470)STRESS ≤ 0.1159 (0.1011) - - Rate of change of FR ( 0.8470)STRESS > -0.6873 (0.2056)*** - - Rate of change of FR ( 33.5600)VIX ≤ - -0.1085 (0.0949) - Rate of change of FR ( 33.5600)VIX > - 0.3174 (0.3362) - Rate of change of FR ( 66.0005)USEPUI ≤ - - -0.9520 (0.2730)*** Rate of change of FR ( 66.0005)USEPUI > - - 0.0934 (0.0984) Rate of change of ER -0.0401 (0.0825) -0.1161 (0.0772) -0.1950 (0.0790)** Control variables Returns of STOCK index (-1) 0.0549 (0.0283)* 0.0236 (0.0287) 0.0401 (0.0279) Increase of STRESS -0.0170 (0.0103)* -0.0065 (0.0102) -0.0079 (0.0099) Rate of change of VIX -0.0548 (0.0210)*** -0.0533 (0.0209)** -0.0494 (0.0208)** Rate of change of USEPUI -0.0060 (0.0184) -0.0105 (0.0182) -0.0123 (0.0182) Rate of change of WTI 0.0910 (0.0347)*** 0.0974 (0.0347)*** 0.0828 (0.0343)** Rate of change of GOLD 0.2718 (0.0581)*** 0.2901 (0.0577)*** 0.2870 (0.0575)*** Returns of WORLD index 1.1536 (0.0834)*** 1.1699 (0.0831)*** 1.1657 (0.0826)*** Adjusted 2R 0.3695 0.3742 0.3784 Durbin-Watson statistic 2.0026 1.9898 2.0110 Ljung-Box Q(1) statistic 0.0244 0.0035 0.0831 Note: See the notes of Tables 6 and 7-1.

21

Table 7-2. (continued)

Threshold variable WTI GOLD WORLD Regime dependent regressors Rate of change of PR ( 15.0300)WTI ≤ 3.3485 (0.6924)*** - - Rate of change of PR ( 15.0300)WTI > 0.2718 (0.1573)* - - Rate of change of PR ( 273.0000)GOLD ≤ - -0.6290 (0.3047)** - Rate of change of PR ( 273.0000)GOLD > - 0.7809 (0.1791)*** - Rate of change of PR ( 1335.0690)WORLD ≤ - - 0.2400 (0.1597) Rate of change of PR ( 1335.0690)WORLD > - - 2.2855 (0.5213)*** Rate of change of PR - - Rate of change of FR ( 1338.5000)WORLD ≤ - - -0.1148 (0.0947) Rate of change of FR ( 1338.5000)WORLD > - - 1.0239 (0.3297)*** Rate of change of FR -0.0716 (0.0921) -0.0568 (0.0921) - Rate of change of ER -0.1327 (0.0773)* -0.1129 (0.0776) -0.1369 (0.0770)* Control variables Returns of STOCK index (-1) 0.0495 (0.0281)* 0.0388 (0.0282) 0.0516 (0.0279)* Increase of STRESS -0.0086 (0.0099) -0.0080 (0.0100) -0.0090 (0.0099) Rate of change of VIX -0.0555 (0.0209)*** -0.0553 (0.0209)*** -0.0597 (0.0208)*** Rate of change of USEPUI -0.0109 (0.0182) -0.0101 (0.0183) -0.0117 (0.0182) Rate of change of WTI 0.0775 (0.0345)** 0.0936 (0.0346)*** 0.0867 (0.0343)** Rate of change of GOLD 0.2831 (0.0578)*** 0.2924 (0.0579)*** 0.3068 (0.0577)*** Returns of WORLD index 1.1698 (0.0830)*** 1.1634 (0.0831)*** 1.1400 (0.0826)*** Durbin-Watson statistic 2.0136 2.0180 2.0157 Adjusted 2R 0.3731 0.3711 0.3778 Note: see the notes of Tables 6 and 7-1.

22

The second column of Table 7-2 reports the estimate results for the dynamic panel

threshold model under changes in the financial stress threshold variable (STRESS). As reported

in this column, we find evidence of two regimes for the PR and FR variables. The results exhibit

evidence of asymmetry for political and financial risk ratings. More precisely, the political risk

ratings have a significant positive effect on the BRICS stock markets in low regime and an

insignificant effect under the high regime. This result is similar to those obtained in the

benchmark model. Moreover, financial risk ratings have a negative impact on the BRICS

markets in the high regime. This result also means that high foreign debt, current account,

international liquidity and exchange rate stability lead to a change in the performance of the

BRICS stock markets which are negative for the high regime. The obtained results show that

the international investors and financial institutions should consider the political and financial

risk variables when dealing with the BRICS countries. This result is in line with those of

Hammoudeh et al. (2013). As for economic risk ratings, these risks have no significant impact

on the BRICS stock markets.

The third column of Table 7-2 presents the results of the estimation when the changes in

the implied volatility (VIX) are considered as the threshold variable. The political risk ratings

have a positive and significant effect on the BRICS markets only for the high regime,

underscoring the importance of political stability during turbulent times. This means that

having a good governance in government stability, and improvements in socioeconomic

conditions, investment profile, internal and external conflict, corruption, military politics,

religious tensions, law and order, democratic accountability and bureaucracy quality enhance

the value of political risk and as a result elevates the performance of the BRICS markets. As

found in the dynamic panel model without a threshold parameter, we fail to provide evidence

between the BRICS markets and the financial risk ratings. Furthermore, economic risk ratings

23

have no significant impact on the BRICS equity markets.

The fourth column of Table 7-2 presents the results of the estimation under the USEPUI

threshold variable. The bootstrap-based testing procedure for the presence of a threshold effect

shows evidence under the low and high regimes for the break variables political risk and

financial risk. The political risk and financial risk threshold parameters reach 75.85 and 66.00,

respectively, suggesting evidence of the presence of low and high regimes (i.e., a regime-

switching behavior). Importantly, political risk ratings affect positively the BRICS stock

markets for the high regime. This suggests that having a good government stability, favorable

socioeconomic conditions, no internal and external conflicts, a control over corruption, etc.,

constitutes a good economic environment and is a signal for more investing, because it leads

to an improvement in the stock market performance. The investment position should be "long"

to benefit from a stock price increase. On the other hand, financial risk ratings impact

negatively the BRICS markets for the low regime. This indicates that an increase in the

financial risk index (or reduced financial risk rating) is associated with higher returns in this

regime. This converse movement states that these emerging stock markets are sensitive to

severe conditions. To sum up, both financial and political risk ratings are based on variables

that reflect crucial fundamentals about a BRICS country which international or local investors

should consider while making international investment decisions.

The results of the estimation for the WTI, gold and MSCI World index threshold

variables are reported in the last three columns of Table 7-2 (continued), respectively. Taking

a closer look at the estimated results of estimation under these threshold variables, political risk

ratings affect positively the BRICS markets under both the low (negatively for the case of gold

and insignificant for the case of world stock index) and high regimes when the WTI and gold

threshold variables are considered. These results imply strong evidence of an asymmetric

24

relationship between political risk ratings and the performance of the BRICS stock markets.

Financial risk ratings are positively linked to the BRICS markets under the high regime for the

world index threshold variable. Economic risk ratings are negatively related to the performance

of those markets, with the exception for the gold threshold variable.

As for the global factors, we find similar results as reported in Table 7-1. As mentioned

above for the benchmark model, nearly the same global factors affect significantly the BRICS

markets for the alternative specifications. In fact, the VIX variable affects negatively the

performance of the stock markets, while an increase in the returns of the global stock market,

WTI and the gold asset leads to an improvement in the BRICS stock markets. This result is

consistent with the benchmark specification.

The global stock index, WTI oil price and the gold price returns affect positively the

BRICS stock market performance, again highlighting the importance of these assets,

particularly the WTI and gold price, in explaining the movements of the BRICS markets under

extreme conditions. The negative relationships between the risk factor (i.e., implied volatility)

and the BRICS stock returns document that an increase in the policy uncertainty leads to a drop

in the stock markets and may inhibit investors from investing in markets with the high potential.

Generally, the financial stress index and the U.S. economic policy uncertainty index are not

significantly related to the performance of those emerging markets.

In sum, we find that the estimates of the coefficients of the three risk ratings for the

threshold model are much more significant and greater in absolute values than the non-

threshold model. This result suggests that employing the non-threshold technique

underestimate the impacts of country risk ratings on the BRICS stock market returns, and

therefore it could lead to mistaken conclusions.

25

5. Conclusions

With globalization and financial integration, the fast growing emerging countries seem

to provide international investors with better investment and risk diversification opportunities,

owing to their high returns having low correlations with returns in developed markets. However,

the reality suggests that the increased dependence of the BRICS markets and economies with

external market conditions, which is characterized by a rapid growth in international lending,

foreign direct investment and capital flow mobility, may increase the risk exposure of lenders

and investors. The country risk analysis has thus become extremely important for international

creditors and investors seeking to invest in emerging countries, particularly the BRICS

countries which are among the most prominent and liberalized markets within the emerging

markets universe.

In this paper, we investigate the asymmetric relationships between the three major

components of the country risks (financial risk, economic risk and political risk ratings) and

the BRICS stock market returns, while accounting for the presence of the influential global

economic and financial factors including the implied volatility of the U.S. equity market, the

U.S. economic uncertainty policy index, the St. Louis Fed’s financial stress index, the WTI

crude oil prices, the world gold prices, and the global stock market. Our empirical framework

relies on the use of the dynamic panel threshold model which accounts for the possibilities of

regime switching, attempting to test the non-uniform links between exogenous and endogenous

variables.

Our empirical evidence for the monthly data spanning the period from January 1995to

August 2013 reveals that the effects of one lag BRICS returns are significant when one regime

panel model as well as STRESS, WTI and WORLD threshold variables are used, but

26

insignificant for the other considered scenarios because the one lag BRICS returns do not

explain the current returns. On the other hand, we show significant and positive relationships

between the political risk ratings and the BRICS stock market returns for almost all

specification cases. As for the financial risk rating, its relationship with the BRICS stock

market is sensitive to the threshold variables. The economic risk ratings significantly and

negatively influence the BRICS stock markets for the benchmark specification in the case of

the upper regime. However, the economic risk ratings are insignificant when STRESS, VIX

and Gold threshold variables are used. Among the global financial and economic risk factors,

the implied volatility index (VIX) variable affects negatively the BRICS stock return.

Interestingly, increases in the global MSCI world index, the WTI oil price and gold price

returns have a positive effect on the BRICS markets, underscoring the important role of the

gold asset as a hedge or a safe haven in extreme stock market movements for the BRICS.

Finally, the U.S. economic policy uncertainty index (USEPUI) and the financial stress index

(STRESS) have no statistically significant impact on the BRICS stock markets. These findings

are useful for domestic and foreign investors, international organizations and ratings agencies.

References

Arellano, M. and S. Bond, “Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations,” Review of Economic Studies 58 (1991):277–97.

Arellano, M. and O. Bover, “Another Look at the Instrumental Variable Estimation of Error-Components Models,” Journal of Econometrics 68 (1995):29–51.

Balcilar, M., R. Demirer, and S. Hammoudeh, “What Drives Herding in Oil-Rich, Developing Stock Markets? Relative Roles of Own Volatility and Global Factors,” North American Journal of Economics and Finance 29 (2014):418–40.

Baur, D. and B. Lucey, “Is Gold a Hedge or Safe Haven? An Analysis of Stocks Bonds and Gold,” Financial Review 45 (2010):217–29.

Baur, D. and T. K. McDermott, “Is Gold a Safe Haven? International Evidence,” Journal of Banking and Finance 34 (2010):1886–98.

Bittencourt, M., “Inflation and Financial Development: Evidence from Brazil,” Economic Modelling 28 (2011):91–99.

27

Blundell, R. and S. Bond, “Initial Conditions and Moment Restrictions in Dynamic Panel Data Models,” Journal of Econometrics 87 (1998):115–43.

Breitung, J., “The Local Power of Some Unit Root Tests for Panel Data,” in H. Baltagi, T. B. Fomby, and R. C. Hill (eds.), Nonstationary Panels, Panel Cointegration, and Dynamic Panels (Advances in Econometrics, Volume 15), Amsterdam: Emerald Group Publishing Limited (2001):161–77.

Bun, M. J. G. and J. F. Kiviet, “The Effects of Dynamic Feedbacks on LS and MM Estimator Accuracy in Panel Data Models,” Journal of Econometrics 132 (2006):409–44.

Caner, M. and B. E. Hansen, “Instrumental Variable Estimation of a Threshold Model,” Economic Theory 20 (2004):813–43.

Choi, K. and S. Hammoudeh, “Volatility Behavior of Oil, Industrial Commodity and Stock Markets in a Regime-Switching Environment,” Energy Policy 38 (2010):4388–99.

Dang, V. A., M. Kim, and Y. Shin, “Asymmetric Capital Structure Adjustments: New Evidence from Dynamic Panel Threshold Models,” Journal of Empirical Finance 19 (2012):465–82.

Erb, C. B.,C. R. Harvey, and T. E. Viskanta, “Country Risk and Global Equity Selection,” Journal of Portfolio Management 21 (1995):74–83.

Hammoudeh, S., R. Sari, M. Uzunkaya, and T. Liu, “The Dynamics of BRICS's Country Risk Ratings and Domestic Stock Markets, U.S. Stock Market and Oil Price,” Mathematics and Computers in Simulation 94 (2013):277–94.

Hansen, B. E., “Threshold Effects in Non-Dynamic Panels: Estimation, Testing, and Inference,” Journal of Econometrics 93 (1999):345–68.

Hood, M. and F. Malik, “Is Gold the Best Hedge and a Safe Haven under Changing Stock Market Volatility?” Review of Financial Economics 22 (2013):47–52.

Im, K. S., M. H. Pesaran, and Y. Shin, “Testing for Unit Roots in Heterogeneous Panels,” Journal of Econometrics 115 (2003):53–74.

Judson, R. A. and A. L. Owen, “Estimating Dynamic Panel Data Models: A Guide for Macroecono-mists,” Economics Letters 65 (1999):9–15.

Kaminsky, G. and S. Schmukler, “Emerging Markets Instability: Do Sovereign Ratings Affect Country Risk and Stock Returns?” World Bank Policy Research Working Paper 2678 (2001).

Kang, W. and R. A. Ratti, “Oil Shocks, Policy Uncertainty and Stock Market Return,” Journal of International Financial Markets, Institutions & Money 26 (2013):305–18.

Kiviet, J. F., “On Bias, Inconsistency, and Efficiency of Various Estimators in Dynamic Panel Data Models, Journal of Econometrics 68 (1995): 53–78.

Kiviet, J. F., “Expectation of Expansions for Estimators in a Dynamic Panel Data Model; Some Results for Weakly Exogenous Regressors,” in C. Hsiao, K. Lahiri, L.-F. Lee, and M. H. Pesaran (eds.), Analysis of Panel Data and Limited Dependent Variables, Cambridge: Cambridge University Press (1999):199–225.

Levin, A., C.-F. Lin, and C.-S. J. Chu, “Unit Root Tests in Panel Data: Asymptotic and Finite Sample Properties,” Journal of Econometrics 108 (2002):1–24.

Liu,T., S. Hammoudeh, and M. A. Thompson, “A Momentum Threshold Model of Stock Prices and Country Risk Ratings: Evidence from BRICS Countries,” Journal of International Financial Markets, Institutions and Money 27 (2013):99–112.

MacKinnon, J. G., “Critical Values for Cointegration Tests,” in R. F. Engle and C. W. J. Granger (eds.), Long-Run Economic Relationships: Readings in Cointegration, New York: Oxford University Press (1991):266–76.

Mensi, W., S. Hammoudeh, J. C. Reboredo, and D.K. Nguyen, “Do Global Factors Impact BRICS Stock Markets? A Quantile Regression Approach,” Emerging Markets Review 19 (2014):1–17.

Omay, T. and E. Ö. Kan, “Re-Examining the Threshold Effects in the Inflation-Growth Nexus with Cross-Sectionally Dependent Non-Linear Panel: Evidence from Six Industrialized Economies,” Economic Modelling 27 (2010):996–1005.

Reboredo, J. C., “Is Gold a Safe Haven or a Hedge for the US Dollar? Implications for Risk Management,” Journal of Banking and Finance 37 (2013):2665–76.

Roodman, D. A., “Note on the Theme of Too Many Instruments,” Oxford Bulletin of Economics and

Commented [H1]: Seong-Min, this reference is not

cited in the paper

28

Statistics 71 (2009):135–58. Sari, R., M. Uzunkaya, and S. Hammoudeh, “The Relationship between Disaggregated Country Credit

Risk Ratings and an Emerging Stock Market’s Movements: An ARDL Approach,” Emerging Markets Finance and Trade 49 (2013):4–16.

Notes 1http://online.wsj.com/articles/brics-to-open-development-bank-by-2016-as-alternative-to-imf-1404888422. 2 The country risk ratings values are computed by commercial agencies including, among others, Bank of America’s World Information Services, Institutional Investor, Economist Intelligence Unit, Moody’s, Standard and Poor’s Rating Group, Euromoney, International Country Risk Guide (ICRG), Fitch IBCA, Business Environment Risk Intelligence S.A., S.J. Rundt & Associates, and Control Risks Group. The country risk ratings measure the ability and willingness of countries to service their financial obligations to their foreign creditors and investors. Risk rating agencies provide qualitative and quantitative country risk ratings which combine information from economic, financial and political risk ratings to obtain a composite country risk rating. 3See Dang et al. (2012) for further discussions. 4We can consider two estimation methods for dynamic panel models: the generalized method of moments (GMM) and LSDVC. In the case of small time-series and large cross-section panel data, the GMM estimators are con-sistent (see Anderson and Hsiao, 1982; Arellano and Bond, 1991; Blundell and Bond, 1998). But in the case of large time-series and small cross-section panel data as is our case, the GMM estimators may be inconsistent. In that case, the bias-corrected LSDV (LSDVC) estimator is consistent and more efficient than the instruments var-iable estimators and GMM estimators (see Kiviet, 1995, 1999; Bun and Kiviet, 2006). Monte Carlo evidence by Judson and Owen (1999) strongly supports LSDVC when the cross-section is small as is in our panel data. A complication of GMM estimators is that the instruments may be weak (Arellano and Bond, 1991; Blundell and Bond, 1998; Kiviet, 1995). But it is not necessary to consider this weak instrument problem, if we use the LSDVC estimator which assumes weak erogeneity. 5The composite risk accounts for 50% of the political risk rating and 25% of each of the financial and economic risk ratings. Specifically, the weighted composite country risk index is the total points from the three indices divided by two. It lies between zero and 100 and is also broken into categories from “Very Low Risk” (from 80 to 100 points) to “Very High Risk” (between zero and 49.9 points). This means the higher the index, the lower the risk. 6See http://www.policyuncertainty.com/ for details about the construction of the U.S. policy uncertainty index. As to the STRESS, it measures the degree of financial stress in the U.S. financial markets and is constructed from 18 weekly data series: seven interest rate series, six yield spreads and five other indicators. Each of these variables captures some aspect of financial stress. Accordingly, as the level of financial stress in the economy changes, the data series are likely to move together.