APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL ...

135

REVIEW REPORT [ ●] To The Shareholders of Huaxin Cement Co., Ltd. Introduction We have reviewed the accompanying interim financial statements of Huaxin Cement Co., Ltd. (the “Company”), which comprise the consolidated and Company’s balance sheets as at 30 June 2021, and the interim consolidated and Company’s income statements, the interim consolidated and Company’s cash flow statements, and the interim consolidated and Company’s statements of changes in shareholders’ equity for the six months ended 30 June 2021, and the notes to the financial statements. The management of the Company is responsible for the preparation and presentation of the interim financial statements in accordance with the China Accounting Standards for Business Enterprises issued by the Ministry of Finance of the People’s Republic of China. Our responsibility is to express a conclusion on these interim financial statements based on our review. Scope of Review We conducted our review in accordance with International Standard on Review Engagement 2410 “Review of Interim Financial Information Performed by the Independent Auditor of the Entity”. A review of the interim financial statements consists of making inquiries (primarily of persons responsible for financial and accounting matters), and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly we do not express an audit opinion. Conclusion Based on our review, nothing has come to our attention that causes us to believe that the accompanying interim financial information does not present fairly, in all material respects, the financial position of the consolidated and Company as at 30 June 2021, and of its financial performance and its cash flows for the six-month period then ended in accordance with China Accounting Standards for Business Enterprises. Deloitte Touche Tohmatsu CPALLP Shanghai, China Chinese Certified Public Accountant: Chinese Certified Public Accountant: [ ●] The review report and the accompanying consolidated interim financial statements are English translations of the Chinese review report and consolidated interim financial statements prepared under China Accounting Standards for Business Enterprises. These consolidated interim financial statements are not intended to present the financial position and results of operations and cash flows in accordance with accounting principles and practices generally accepted in other countries and jurisdictions. In case the English version does not conform to the Chinese version, the Chinese version prevails. THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2021 – IV-1 –

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL ...

REVIEW REPORT

[●]

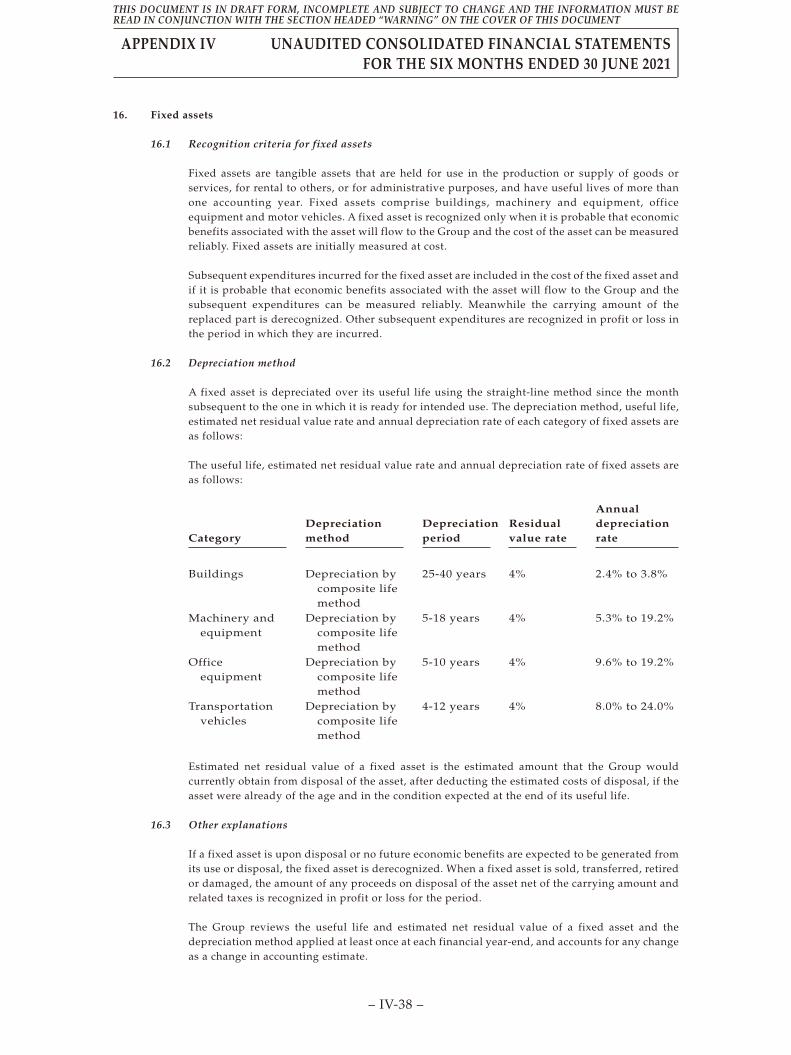

To The Shareholders of Huaxin Cement Co., Ltd.

Introduction

We have reviewed the accompanying interim financial statements of HuaxinCement Co., Ltd. (the “Company”), which comprise the consolidated and Company’sbalance sheets as at 30 June 2021, and the interim consolidated and Company’s incomestatements, the interim consolidated and Company’s cash flow statements, and theinterim consolidated and Company’s statements of changes in shareholders’ equity for thesix months ended 30 June 2021, and the notes to the financial statements. The managementof the Company is responsible for the preparation and presentation of the interimfinancial statements in accordance with the China Accounting Standards for BusinessEnterprises issued by the Ministry of Finance of the People’s Republic of China. Ourresponsibility is to express a conclusion on these interim financial statements based on ourreview.

Scope of Review

We conducted our review in accordance with International Standard on ReviewEngagement 2410 “Review of Interim Financial Information Performed by theIndependent Auditor of the Entity”. A review of the interim financial statements consistsof making inquiries (primarily of persons responsible for financial and accountingmatters), and applying analytical and other review procedures. A review is substantiallyless in scope than an audit conducted in accordance with International Standards onAuditing and consequently does not enable us to obtain assurance that we would becomeaware of all significant matters that might be identified in an audit. Accordingly we do notexpress an audit opinion.

Conclusion

Based on our review, nothing has come to our attention that causes us to believe thatthe accompanying interim financial information does not present fairly, in all materialrespects, the financial position of the consolidated and Company as at 30 June 2021, and ofits financial performance and its cash flows for the six-month period then ended inaccordance with China Accounting Standards for Business Enterprises.

Deloitte Touche Tohmatsu CPA LLPShanghai, China

Chinese Certified Public Accountant:

Chinese Certified Public Accountant:

[●]

The review report and the accompanying consolidated interim financial statements areEnglish translations of the Chinese review report and consolidated interim financial statementsprepared under China Accounting Standards for Business Enterprises. These consolidated interimfinancial statements are not intended to present the financial position and results of operationsand cash flows in accordance with accounting principles and practices generally accepted in othercountries and jurisdictions. In case the English version does not conform to the Chinese version,the Chinese version prevails.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-1 –

CONSOLIDATED BALANCE SHEETAs at 30 June 2021

RMB

Item NotesBalance at

30 June 2021

Balance at31 December

2020

Current AssetsCash and bank balances V(1) 7,429,933,411 8,641,612,847Held-for-trading financial assets V(2) – 1,004,581,752Notes receivable V(3) 124,033,871 79,939,117Accounts receivable V(4) 1,066,639,655 653,219,779Financing with receivables V(5) 937,354,912 1,020,306,419Prepayments V(6) 321,890,888 378,619,350Other receivables V(7) 371,520,100 375,253,958

Including: Interest receivable 79,399 641,915Inventories V(8) 2,898,132,495 2,349,156,189Other current assets V(9) 582,942,575 631,922,798

Total Current Assets 13,732,447,907 15,134,612,209

Non-current AssetsDebt investments 7,500,000 7,500,000Long-term receivables 34,638,462 29,141,216Long-term equity investments V(10) 593,779,530 512,281,201Other equity instrument investments V(11) 35,180,864 33,774,995Other non-current financial assets V(12) 28,086,810 32,827,254Fixed assets V(13) 19,481,730,637 19,185,630,257Construction in progress V(14) 4,070,807,952 3,104,429,340Right-of-use assets V(15) 189,547,925 –Intangible assets V(16) 4,505,047,843 4,267,008,181Development expenditure 6,991,441 2,050,090Goodwill V(17) 611,050,112 476,084,798Long-term prepaid expenses V(18) 333,510,201 363,760,774Deferred tax assets V(19) 431,550,520 437,800,338Other non-current assets 470,749,883 341,608,498

Total Non-current Assets 30,800,172,180 28,793,896,942

Total Assets 44,532,620,087 43,928,509,151

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-2 –

RMB

Item NotesBalance at

30 June 2021

Balance at31 December

2020

Current LiabilitiesShort-term borrowings V(21) 500,500,000 625,000,000Held-for-trading financial liabilities 3,587,852 –Notes payable V(22) 222,804,276 472,696,537Accounts payable V(23) 5,911,035,705 5,297,633,770Contract liabilities V(24) 669,790,684 830,492,042Employee benefits payable V(25) 320,633,241 529,877,921Taxes payable V(26) 978,007,767 1,186,166,143Other payables V(27) 938,759,531 786,246,239

Including: Interest payable 58,646,797 30,026,120Dividend payable 142,391,012 63,842,709

Non-current liabilities duewithin one year V(28) 2,147,153,103 1,874,484,159

Total Current Liabilities 11,692,272,159 11,602,596,811

Non-current LiabilitiesLong-term borrowings V(29) 3,511,168,528 3,504,279,973Bonds payable V(30) 1,925,779,933 1,943,763,447Lease liabilities V(31) 159,840,888 –Long-term payables V(32) 352,968,294 191,011,663Long-term employee benefits payable V(33) 57,260,817 127,205,104Provisions V(34) 225,803,850 233,393,286Deferred income V(35) 287,902,969 301,399,766Deferred tax liabilities V(19) 290,097,580 284,920,603

Total Non-current Liabilities 6,810,822,859 6,585,973,842

TOTAL LIABILITIES 18,503,095,018 18,188,570,653

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-3 –

RMB

Item NotesBalance at

30 June 2021

Balance at31 December

2020

Shareholders’ EquityShare capital V(36) 2,096,599,855 2,096,599,855Capital reserve V(37) 2,004,254,965 1,943,538,052Less: Treasury shares V(38) 610,051,971 610,051,971Other comprehensive income V(40) (310,345,610) (275,292,763)Surplus reserve V(39) 1,111,880,257 1,111,880,257Retained profits V(41) 19,480,480,298 19,304,701,887

Total equity attributableto shareholders of the Company 23,772,817,794 23,571,375,317

Minority interests 2,256,707,275 2,168,563,181

Total Shareholders’ Equity 26,029,525,069 25,739,938,498

TOTAL LIABILITIES ANDSHAREHOLDERS’ EQUITY 44,532,620,087 43,928,509,151

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-4 –

BALANCE SHEET OF THE COMPANY

As at 30 June 2021

RMB

Item NotesBalance at 30

June 2021

Balance at 31December

2020

Current AssetsCash and bank balances 3,798,083,283 4,650,418,319Held-for-trading financial assets – 1,004,581,752Notes receivable 500,000 100,000Accounts receivable XV(1) 859,343,209 545,749,566Financing with receivables 142,591,980 151,473,769Prepayments 190,920,146 226,396,232Other receivables XV(2) 4,998,140,893 4,396,614,326

Including:Interest receivable 449,563,031 –Inventories 500,267,408 320,998,776Non-current assets due within one year 1,580,000 1,580,000Other current assets 22,170,189 18,886,995

Total Current Assets 10,513,597,108 11,316,799,735

Non-current AssetsLong-term receivables 68,579,132 18,738,952Long-term equity investments XV(3) 11,613,708,765 11,119,516,523Other equity instrument investments 35,180,864 33,774,995Other non-current financial assets 28,086,810 32,827,254Fixed assets 424,590,637 437,139,833Construction in progress 275,355,289 209,773,010Right-of-use assets 64,602,155 –Intangible assets 39,424,810 40,397,874Long-term prepaid expenses 14,223,466 15,339,306Deferred tax assets 35,206,310 17,350,047

Total Non-current Assets 12,598,958,238 11,924,857,794

TOTAL ASSETS 23,112,555,346 23,241,657,529

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-5 –

RMB

Item NotesBalance at 30

June 2021

Balance at 31December

2020

Current LiabilitiesShort-term borrowings – 300,000,000Held-for-trading financial liabilities 3,587,852 –Notes payable – 24,246,455Accounts payable 401,350,111 410,565,470Contract liabilities 22,004,605 14,795,403Employee benefits payable 13,847,228 63,346,794Taxes payable 228,569,452 234,439,071Other payables 6,969,422,147 7,224,579,499Including: Interest payable 51,000,144 22,543,588

Dividend payable 44,488,081 23,821,382Non-current liabilities due

within one year 1,374,413,010 1,321,867,253

Total Current Liabilities 9,013,194,405 9,593,839,945

Non-current LiabilitiesLong-term borrowings 1,458,850,000 1,202,780,000Lease liabilities 48,686,086Long-term employee benefits payable 90,846,929 99,997,218Provisions 7,472,518 8,282,611Deferred income 10,639,500 12,085,332

Total Non-current Liabilities 1,616,495,033 1,323,145,161

TOTAL LIABILITIES 10,629,689,438 10,916,985,106

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-6 –

RMB

Item NotesBalance at 30

June 2021

Balance at 31December

2020

Owners’ (or Shareholders’) EquityPaid-up capital (or share capital) 2,096,599,855 2,096,599,855Capital reserve 2,402,598,249 2,341,881,336Less: Treasury shares 610,051,971 610,051,971Other comprehensive income 14,816,548 13,762,146Surplus reserve 1,111,880,257 1,111,880,257Retained profits 7,467,022,970 7,370,600,800

Total Owners’ (or Shareholders’) Equity 12,482,865,908 12,324,672,423

TOTAL LIABILITIES AND OWNERS’(OR SHAREHOLDERS’) EQUITY 23,112,555,346 23,241,657,529

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-7 –

CONSOLIDATED INCOME STATEMENTFor the period from 1 January 2021 to 30 June 2021

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

I. Total operating income 14,744,386,072 12,564,947,176Including: Operating income V(42) 14,744,386,072 12,564,947,176

II. Total operating costs 11,438,418,665 9,557,609,709Including: Operating costs V(42) 9,307,552,289 7,667,011,135

Taxes and levies V(43) 278,083,038 203,702,287Selling and distribution

expenses V(44) 1,048,956,699 862,846,359General and administrative

expenses V(45) 677,883,399 725,182,057Research and development

expense 23,001,179 8,441,524Financial expenses V(46) 102,942,061 90,426,347Including: Interest expenses 134,691,908 91,575,780

Interest income 54,748,194 26,422,427Add: Other income V(47) 112,778,854 106,085,591

Investment income V(48) 28,068,456 33,824,872Including: Income from

investments inassociates and jointventures 11,240,371 30,991,838

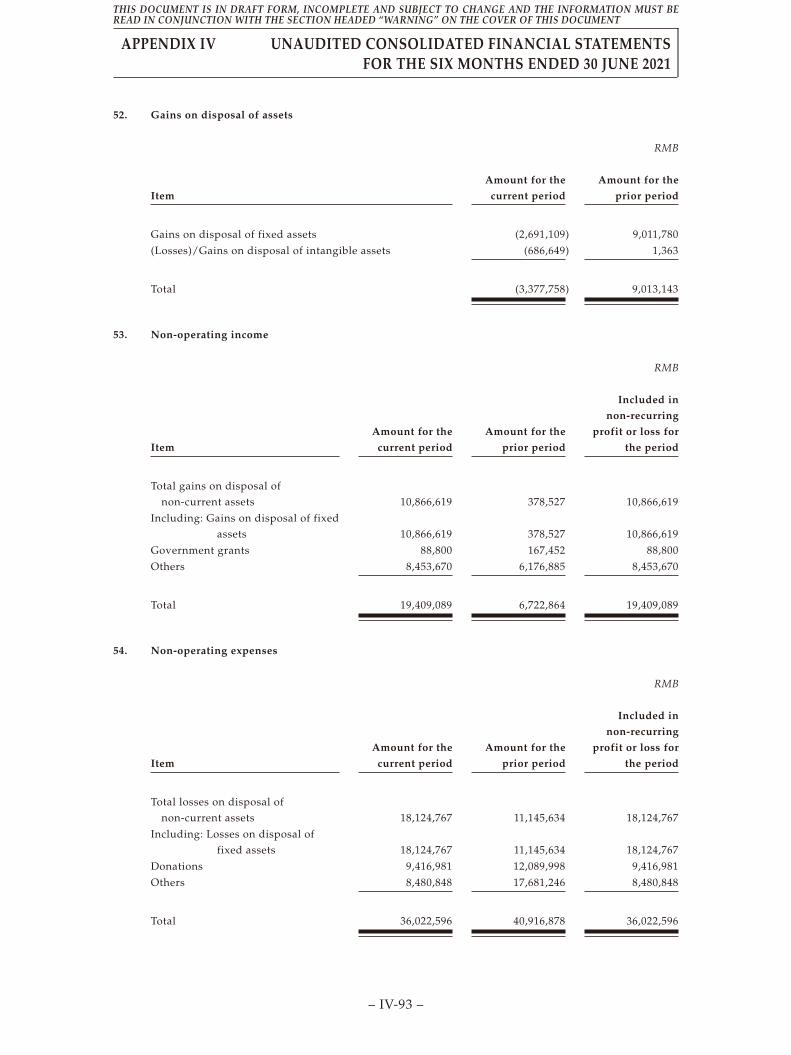

Losses on changes in fair value V(49) (12,910,048) (7,446,328)Impairment losses on credit V(50) (15,190,828) (27,159,259)Impairment losses on assets V(51) (21,803,772) (4,569,536)(Losses) Gains on disposal of

assets V(52) (3,377,758) 9,013,143

III. Operating profit 3,393,532,311 3,117,085,950Add: Non-operating income V(53) 19,409,089 6,722,864Less: Non-operating expenses V(54) 36,022,596 40,916,878

IV. Profit before tax 3,376,918,804 3,082,891,936Less: Income tax expenses V(55) 711,280,078 627,229,329

V. Net profit (loss) 2,665,638,726 2,455,662,607(i) Classified by the continuity of

operation1. Net profit from continuing

operations 2,665,638,726 2,455,662,6072. Net profit from discontinued

operations(ii) Classified by the ownership

1. Net profit attributable toshareholders of the Company 2,438,324,279 2,251,974,011

2. Profit or loss attributable tominority interests 227,314,447 203,688,596

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-8 –

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

VI. Other comprehensive income,net of tax (42,086,008) (64,615,963)

(i) Other comprehensive incomeattributable to owners of theCompany, net of tax (35,052,847) (56,167,300)1. Other comprehensive income

that cannot be reclassified toprofit or loss 1,054,402 (3,341,329)(1) Changes in

re-measurement ofdefined benefit plans

(2) Other comprehensiveincome that cannot bereclassified to profit orloss under the equitymethod

(3) Changes in fair value ofinvestments in otherequity instruments 1,054,402 (3,341,329)

2. Other comprehensive incomethat will be reclassified toprofit or loss (36,107,249) (52,825,971)(1) Other comprehensive

income that can bereclassified to profit orloss under the equitymethod

(2) Changes in the fair valueof other debtinvestments

(3) Amount of financialassets reclassified toother comprehensiveincome

(4) Provision for creditimpairment of otherdebt investments

(5) Reserve for cash flowhedges (36,107,249) (52,825,971)

(ii) Other comprehensive incomeattributable to minorityinterests, net of tax (7,033,161) (8,448,663)

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-9 –

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

VII. Total comprehensive income 2,623,552,718 2,391,046,644Total comprehensive income

attributable to owners of theCompany 2,403,271,432 2,195,806,711

Total comprehensive incomeattributable to minority interests 220,281,286 195,239,933

VIII. Earnings per share(i) Basic earnings per share (RMB) 1.18 1.08(ii) Diluted earnings per share (RMB) 1.18 1.08

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-10 –

INCOME STATEMENT OF THE COMPANYFor the period from 1 January 2021 to 30 June 2021

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

I. Operating income XV(4) 2,092,362,300 1,597,282,876Less: Operating costs XV(4) 1,898,769,539 1,398,379,989

Taxes and levies 4,585,329 7,879,108Selling and distribution

expenses 27,223,758 35,270,956General and administrative

expenses 131,017,453 171,142,944Research and development

expense 10,179,493 2,705,214Financial expenses 45,804,582 11,008,263Including: Interest expenses 115,741,796 104,943,099

Interest income 90,294,263 78,419,015Add: Other income 3,728,301 2,129,972

Investment income XV(5) 2,376,125,614 1,738,080,189Including: Income from

investments inassociates and jointventures 6,934,284 25,240,749

Income (loss) fromderecognition offinancial assetsmeasured atamortized cost

Net exposure hedging gains(losses)

Losses on changes in fair value (12,910,050) (7,446,328)Impairment gains (losses) on

credit 30,391 (1,377,388)Impairment losses on assets (316,939) (37,766)Gains on disposal of assets 348,827 58,295

II. Operating profit 2,341,788,290 1,702,303,376Add: Non-operating income 10,805,174 9,713Less: Non-operating expenses 1,142,300 7,056,418

III. Profit before tax 2,351,451,164 1,695,256,671Less: Income tax expenses (7,516,874) (11,412,381)

IV. Net profit 2,358,968,038 1,706,669,052(i) Net profit from continuing

operations 2,358,968,038 1,706,669,052(ii) Net profit from discontinued

operations

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-11 –

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

V. Other comprehensive income, net oftax 1,054,402 (3,341,329)

(i) Other comprehensive income thatcannot be reclassified to profit orloss 1,054,402 (3,341,329)1. Changes from re-measurement

of defined benefit plans2. Other comprehensive income

that cannot be reclassified toprofit or loss under theequity method

3. Changes in fair value ofinvestments in other equityinstruments 1,054,402 (3,341,329)

4. Changes in fair value of theenterprise’s credit risk

(ii) Other comprehensive income thatwill be reclassified to profit orloss – –1. Other comprehensive income

that can be reclassified toprofit or loss under theequity method

2. Changes in the fair value ofother debt investments

3. Amount of financial assetsreclassified to othercomprehensive income

4. Provision for creditimpairment of other debtinvestments

5. Reserve for cash flow hedges6. Exchange differences on

translation of financialstatements denominated inforeign currencies

7. Others

VI. Total comprehensive income 2,360,022,440 1,703,327,723

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-12 –

CONSOLIDATED CASH FLOW STATEMENT

For the period from 1 January 2021 to 30 June 2021

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

I. Cash Flows from Operating Activities:Cash receipts from the sale of goods

and the rendering of services 14,241,433,968 14,212,636,697Receipts of tax refunds 50,431,431 88,156,749Other cash receipts relating to

operating activities V(56)(1) 251,549,612 147,919,775

Sub-total of cash inflows fromoperating activities 14,543,415,011 14,448,713,221

Cash payments for goods purchasedand services received 8,438,918,378 7,835,803,386

Cash payments to and on behalf ofemployees 1,598,886,397 1,331,025,807

Payments of various types of taxes 1,874,457,133 1,449,767,278Other cash payments relating to

operating activities V(56)(2) 339,068,463 331,142,066

Sub-total of cash outflows fromoperating activities 12,251,330,371 10,947,738,537

Net Cash Flow from OperatingActivities V(57)(1) 2,292,084,640 3,500,974,684

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-13 –

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

II. Cash Flows from Investing Activities:Cash receipts from disposal and

recovery of investments 1,000,000,000 500,070,000Cash receipts from investment income 14,890,816 2,518,544Net cash received from disposal of

fixed assets, intangible assets andother long-term assets 19,214,294 4,383,289

Net cash receipts from disposal ofsubsidiaries and other businessunits 22,000 –

Other cash receipts relating toinvesting activities V(56)(3) 5,602,256 40,918,268

Sub-total of cash inflows frominvesting activities 1,039,729,366 547,890,101

Cash payments to acquire or constructfixed assets, intangible assets andother long-term assets 1,863,103,382 1,819,958,508

Cash payments to acquire investments 70,000,000 528,304,258Net cash payments for acquisition of

subsidiaries and other businessunits V(57)(2) 231,262,607 7,100,000

Other cash payments relating toinvesting activities V(56)(4) – 654,896,092

Sub-total of cash outflows frominvesting activities 2,164,365,989 3,010,258,858

Net Cash Flow used in InvestingActivities (1,124,636,623) (2,462,368,757)

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-14 –

RMB

Item Notes

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

III. Cash Flows from Financing Activities:Cash receipts from capital

contributions 2,000,000 106,160,000Cash receipts from borrowings 757,500,000 2,238,224,814Other cash receipts relating to

financing activities – –

Sub-total of cash inflows fromfinancing activities 759,500,000 2,344,384,814

Cash repayments of borrowings 692,294,746 640,007,835Cash payments for distribution of

dividends or profits or settlement ofinterest expenses 2,365,422,870 128,544,252

Other cash payments relating tofinancing activities V(56)(5) 50,146,934 180,865,306

Sub-total of cash outflows fromfinancing activities 3,107,864,550 949,417,393

Net Cash Flow (used in) fromFinancing Activities (2,348,364,550) 1,394,967,421

IV. Effect of Foreign Exchange RateChanges on Cash and CashEquivalents (12,737,649) (3,338,154)

V. Net (Decrease) Increase in Cash andCash Equivalents (1,193,654,182) 2,430,235,194

Add: Opening balance of cash andcash equivalents 8,420,246,369 4,918,296,452

VI. Closing Balance of Cash and CashEquivalents V(57)(3) 7,226,592,187 7,348,531,646

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-15 –

CASH FLOW STATEMENT OF THE COMPANY

For the period from 1 January 2021 to 30 June 2021

RMB

Item NOTES

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

I. Cash Flows from Operating Activities:Cash receipts from the sale of goods

and the rendering of services 1,642,363,399 1,775,804,019Receipts of tax refunds 2,844,644 –Other cash receipts relating to

operating activities 639,550,893 900,405,421

Sub-total of cash inflows fromoperating activities 2,284,758,936 2,676,209,440

Cash payments for goods purchasedand services received 1,820,506,301 1,654,513,295

Cash payments to and on behalf ofemployees 176,051,844 368,233,167

Payments of various types of taxes 75,687,605 26,785,929Other cash payments relating to

operating activities 273,355,468 489,199,630

Sub-total of cash outflows fromoperating activities 2,345,601,218 2,538,732,021

Net Cash Flow (used in)/fromOperating Activities (60,842,282) 137,477,419

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-16 –

RMB

Item NOTES

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

II. Cash Flows from Investing Activities:Cash receipts from disposal and

recovery of investments 1,000,000,000 500,000,000Cash receipts from investment income 1,919,628,299 1,404,208,431Net cash received from disposal of

fixed assets, intangible assets andother long-term assets 16,019,269 2,042,758

Other cash receipts relating toinvesting activities 1,563,347,992 84,297,793

Sub-total of cash inflows frominvesting activities 4,498,995,560 1,990,548,982

Cash payments to acquire or constructfixed assets, intangible assets andother long-term assets 24,761,597 60,147,680

Cash payments to acquire investments – 500,000,000Net cash payments for acquisition of

subsidiaries and other businessunits 487,000,000 600,000,000

Other cash payments relating toinvesting activities 1,613,252,566 –

Sub-total of cash outflows frominvesting activities 2,125,014,163 1,160,147,680

Net Cash Flow from InvestingActivities 2,373,981,397 830,401,302

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-17 –

RMB

Item NOTES

For the sixmonths ended

30 June 2021

For the sixmonths ended

30 June 2020

III. Cash Flows from Financing Activities:Cash receipts from borrowings 400,000,000 900,000,000Other cash receipts relating to

financing activities – 5,657,201,026

Sub-total of cash inflows fromfinancing activities 400,000,000 6,557,201,026

Cash repayments of borrowings 403,652,662 534,705,887Cash payments for distribution of

dividends or profits or settlement ofinterest expenses 2,259,013,377 25,573,619

Other cash payments relating tofinancing activities 894,143,889 5,767,658,206

Sub-total of cash outflows fromfinancing activities 3,556,809,928 6,327,937,712

Net Cash Flow (used in)/fromFinancing Activities (3,156,809,928) 229,263,314

IV. Effect of Foreign Exchange RateChanges on Cash and CashEquivalents (2,362,015) (779,349)

V. Net (Decrease) Increase in Cash andCash Equivalents (846,032,828) 1,196,362,686

Add: Opening balance of cash andcash equivalents 4,624,314,323 3,141,838,852

VI. Closing Balance of Cash and CashEquivalents 3,778,281,495 4,338,201,538

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-18 –

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

For the period from 1 January 2021 to 30 June 2021

RMB

For the six months ended 30 June 2021

Attributable to owners of the parent Company

Item Share capitalCapitalreserve

Less:Treasury

share

OtherComprehensive

incomeSurplusreserve

Retainedprofits Sub-total

Minorityinterests

Totalowners’

equity

Balance at 31 December2020 2,096,599,855 1,943,538,052 610,051,971 (275,292,763) 1,111,880,257 19,304,701,887 23,571,375,317 2,168,563,181 25,739,938,498

Balance at 1 January 2021 2,096,599,855 1,943,538,052 610,051,971 (275,292,763) 1,111,880,257 19,304,701,887 23,571,375,317 2,168,563,181 25,739,938,498Changes in the period – 60,716,913 – (35,052,847) – 175,778,411 201,442,477 88,144,094 289,586,571(i) Total comprehensive

income – – – (35,052,847) – 2,438,324,279 2,403,271,432 220,281,286 2,623,552,718(ii) Owners’ contributions

and reduction incapital – 60,716,913 – – – – 60,716,913 2,000,000 62,716,913

1. Ordinary sharescontributed byowners – – – – – – – 2,000,000 2,000,000

2. Capital contributionfrom holders ofother equityinstruments – – – – – – – – –

3. Share-basedpaymentrecognized inowners’ equity – 60,458,955 – – – – 60,458,955 – 60,458,955

4. Others – 257,958 – – – – 257,958 – 257,958(iii) Profit distribution – – – – – (2,262,545,868) (2,262,545,868) (134,137,192) (2,396,683,060)

1. Withdrawl othersurplus reserve – – – – – – – – –

2. Transfer to generalrisk reserve – – – – – – – – –

3. Distribution toowners (orshareholders) – – – – – (2,262,545,868) (2,262,545,868) (134,137,192) (2,396,683,060)

4. Others – – – – – – – – –(iv) Transfers within

owners’ equity – – – – – – – – –(v) Special reserve – – – – – – – – –(vi) Others – – – – – – – – –

Balance at 30 June 2021 2,096,599,855 2,004,254,965 610,051,971 (310,345,610) 1,111,880,257 19,480,480,298 23,772,817,794 2,256,707,275 26,029,525,069

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-19 –

RMB

For the six months ended 30 June 2020

Attributable to shareholders of the Company

ITEM Share capitalCapitalreserve

Less:Treasury

share

Othercomprehensive

incomeSurplusreserve

Retainedprofits Sub-total

Minorityinterests

Totalshareholders’

equity

Balance at 31 December2019 2,096,599,855 1,913,438,767 – (17,416,212) 1,111,880,257 16,204,540,023 21,309,042,690 2,058,640,055 23,367,682,745

Balance at 1 January 2020 2,096,599,855 1,913,438,767 – (17,416,212) 1,111,880,257 16,204,540,023 21,309,042,690 2,058,640,055 23,367,682,745Changes in the period – 1,403,795 122,533,983 (56,167,300) – (284,911,814) (462,209,302) 169,326,327 (292,882,975)(i) Total comprehensive

income – – – (56,167,300) – 2,251,974,011 2,195,806,711 195,239,933 2,391,046,644(ii) Owners’ contributions

and reduction incapital – 1,403,795 122,533,983 – – – (121,130,188) 106,160,000 (14,970,188)1. Ordinary shares

contributed byowners – – 122,533,983 – – – (122,533,983) 106,160,000 (16,373,983)

2. Capital contributionfrom holders ofother equityinstruments – – – – – – – – –

3. Share-basedpaymentrecognized inowners’ equity – – – – – – – – –

4. Others – 1,403,795 – – – – 1,403,795 – 1,403,795(iii) Profit distribution – – – – – (2,536,885,825) (2,536,885,825) (132,073,606) (2,668,959,431)

1. Withdrawl othersurplus reserve – – – – – – – – –

2. Transfer to generalrisk reserve – – – – – – – – –

3. Distribution toowners (orshareholders) – – – – – (2,536,885,825) (2,536,885,825) (132,073,606) (2,668,959,431)

4. Others – – – – – – – – –(iv) Transfers within

owners’ equity – – – – – – – – –(v) Special reserve – – – – – – – – –(vi) Others – – – – – – – – –

Balance at 30 June 2020 2,096,599,855 1,914,842,562 122,533,983 (73,583,512) 1,111,880,257 15,919,628,209 20,846,833,388 2,227,966,382 23,074,799,770

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-20 –

THE COMPANY’S STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

For the period from 1 January 2021 to 30 June 2021

RMB

For the six months ended 30 June 2021

Item Share capitalCapitalreserve

Less:Treasury

share

Othercomprehensive

incomeSurplusreserve

Retainedprofits

Totalshareholders’

equity

I. Balance at 31 December 2020 2,096,599,855 2,341,881,336 610,051,971 13,762,146 1,111,880,257 7,370,600,800 12,324,672,423II. Balance at 1 January 2021 2,096,599,855 2,341,881,336 610,051,971 13,762,146 1,111,880,257 7,370,600,800 12,324,672,423III. Changes in the period – 60,716,913 – 1,054,402 – 96,422,170 158,193,485

(i) Total comprehensive income – – – 1,054,402 – 2,358,968,038 2,360,022,440(ii) Owners’ contributions and

reduction in capital – 60,716,913 – – – – 60,716,9131. Ordinary shares contributed

by owners – 60,458,955 – – – – 60,458,9552. Capital contribution from

holders of other equityinstruments – 257,958 – – – – 257,958

3. Share-based paymentrecognized in owners’equity – – – – – –

4. Others – – – – – –(iii) Profit distribution – – – – – (2,262,545,868) (2,262,545,868)

1. Transfer to surplus reserve – – – – – – –2. Distribution to owners

(shareholders) – – – – – (2,262,545,868) (2,262,545,868)3. Others – – – – – – –

(iv) Transfers within owners’ equity – – – – – – –1. Capitalization of capital

reserve – – – – – – –2. Capitalization of surplus

reserve – – – – – – –3. Loss offset by surplus

reserve – – – – – – –4. Retained earnings carried

forward from changes indefined benefit plans – – – – – – –

5. Retained earnings carriedforward from othercomprehensive income – – – – – – –

6. Others – – – – – – –(v) Special reserve – – – – – – –(vi) Others – – – – – – –

IV. Balance at 30 June 2021 2,096,599,855 2,402,598,249 610,051,971 14,816,548 1,111,880,257 7,467,022,970 12,482,865,908

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-21 –

RMB

For the six months ended 30 June 2020

Item Share capitalCapitalreserve

Less:Treasury

share

Othercomprehensive

incomeSurplusreserve

Retainedprofits

Totalshareholders’

equity

I. Balance at 31 December 2020 2,096,599,855 2,311,782,051 – 17,103,476 1,111,880,257 6,745,724,011 12,283,089,650Add: Changes in accounting

policies – – – – – – –Corrections of prior period

errors – – – – – – –Others – – – – – – –

II. Balance at 1 January 2021 2,096,599,855 2,311,782,051 – 17,103,476 1,111,880,257 6,745,724,011 12,283,089,650III. Changes in the period – 1,403,795 122,533,983 (3,341,329) – (830,216,773) (954,688,290)

(i) Total comprehensive income – – – (3,341,329) – 1,706,669,052 1,703,327,723(ii) Owners’ contributions and

reduction in capital – 1,403,795 122,533,983 – – – (121,130,188)1. Ordinary shares contributed

by owners – – 122,533,983 – – – (122,533,983)2. Capital contribution

received from noncontrolling interests – – – – – – –

3. Capital contribution fromShare-based payment – – – – – – –

4. Others – 1,403,795 – – – – 1,403,795(iii) Profit distribution – – – – – (2,536,885,825) (2,536,885,825)

1. Transfer to surplus reserve – – – – – –2. Distribution to owners

(shareholders) – – – – – (2,536,885,825) (2,536,885,825)3. Others – – – – – – –

(iv) Transfers within owners’ equity – – – – – – –1. Capitalization of capital

reserve – – – – – – –2. Capitalization of surplus

reserve – – – – – – –3. Loss offset by surplus

reserve – – – – – – –4. Retained earnings carried

forward from changes indefined benefit plans – – – – – – –

5. Retained earnings carriedforward from othercomprehensive income – – – – – – –

6. Others – – – – – – –(v) Special reserve – – – – – – –(vi) Others – – – – – – –

IV. Balance at 30 June 2021 2,096,599,855 2,313,185,846 122,533,983 13,762,147 1,111,880,257 5,915,507,238 11,328,401,360

Mr. Li YeqingLegal representative

Mr. Chen QianPrincipal in charge of accounting

Mr. Wu XinHead of accounting department

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-22 –

NOTES TO THE FINANCIAL STATEMENTSFor the period from 1 January 2021 to 30 June 2021

I. BASIC INFORMATION ABOUT THE COMPANY

1. Company profile

Huaxin Cement Co., Ltd. (the “Company”) is a limited company established in the People’s Republic ofChina (the “PRC”). In 1994, as approved by Hubei Provincial People’s Government, the Company’sshares were listed on the Shanghai Stock Exchange. In 2006, as approved by the Ministry of Commerce* ofthe PRC, the legal status of the Company was changed to a foreign-invested limited company. In April2019, based on its total share capital of 1,497,571,325 shares at the end of 2018, the Company allottedshares from its capital reserve or surplus reserve at 4 shares for every 10 shares, amounting toRMB599,028,530. As a result, the total shares of the Company increased to 2,096,599,855, including1,361,879,855 RMB ordinary shares (A shares) and 734,720,000 RMB foreign shares (“B shares”), both ofwhich are issued domestically.

The Company and its subsidiaries (collectively referred to as the “Group”) are principally engaged inmanufacturing and sales of cement, concrete, clinker, aggregate and other construction materials. Theaddress of the Company’s registered office is No. 600, East Daqi Avenue, Huangshi City, Hubei Provinceand the office address of the headquarter is Huaxin Plaza, No. 426 Gaoxin Avenue, Donghu NewTechnology Development District, Wuhan City, Hubei Province.

The Company’s and consolidated financial statements were authorized for issue by the Company’s Boardof Directors on 28 August 2021.

2. Scope of consolidated financial statements

Principal subsidiaries included in the scope of consolidation are listed in Note VII “Equity Interests inOther Entities”. For the detailed changes in the scope of the consolidated financial statements in thecurrent year, are included in Note VII “Changes in Scope of Consolidation”.

II. BASIS OF PREPARATION OF FINANCIAL STATEMENTS

1. Basis of Preparation

The Group adopts China Accounting Standard for Business Enterprises and relevant regulations issuedby the Ministry of Finance. In addition, the Group also discloses financial information in accordance withthe Preparation Convention of Information Disclosure by Companies Offering Securities to the PublicNo.15 - General Rules on Financial Reporting (Revised in 2014).

2. Going concern

The Group assessed its ability to continue as a going concern for the 12 months from 30 June 2021 and didnot notice any events or circumstances that may cast significant doubt upon its ability to continue as agoing concern. Therefore, the financial statements have been prepared on a going concern basis.

3. Basis of accounting and principle of measurement

The accrual basis of accounting has been adopted. Except for certain financial instruments which aremeasured at fair value, the Group adopts the historical cost as the principle of measurement in thefinancial statements. Where assets are impaired, provisions for asset impairment are made in accordancewith relevant requirements.

Where the historical cost is adopted as the measurement basis, assets are recorded at the amount of cashand cash equivalents paid or the fair value of the consideration given to acquire them at the time of theiracquisition. Liabilities are recorded at the amount of proceeds or assets received or the contractualamounts for assuming the present obligation, or, at the amounts of cash and cash equivalents expected tobe paid to settle the liabilities in the normal course of business.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-23 –

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderlytransaction between market participants at the measurement date. Regardless of whether that price isdirectly observable or estimated using another valuation technique, fair value for measurement anddisclosure purposes in these financial statements is determined on such a basis.

In the measurement of non-financial assets at fair value, market participants’ ability to best utilize suchassets to generate most economic benefits, or the ability to sell such assets to other market participantswho are able to best utilize the assets to generate economic benefits is taken into account.

For financial assets which are transacted at fair value on initial recognition, and a valuation techniqueinvolving unobservable input is used in subsequent measurement, the valuation technique is calibratedso that at initial recognition the results of the valuation technique equal the transaction price.

Fair value measurements are categorized into Level 1, 2 or 3 based on the degree to which the inputs tothe fair value measurements are observable and the significance of the inputs to the fair valuemeasurement in its entirety:

• Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilitiesthat the entity can access at the measurement date;

• Level 2 inputs are inputs, other than inputs within Level 1, that are observable for the asset orliability , either directly or indirectly; and

• Level 3 inputs are unobservable inputs for the asset or liability.

III. SIGNIFICANT ACCOUNTING POLICIES AND ACCOUNTING ESTIMATES

Tips on specific accounting policies and accounting estimates:

The Group determines specific accounting policies and accounting estimates based on actual businessoperation characteristics, including provision of expected credit loss for receivables (Note III(10)), thedepreciation of fixed assets and the amortization of intangible assets (Note III (16), (19)) and the timepoint of time of revenue recognition(Note III (26)) etc.

The key judgement made by the Group in determining significant accounting policies are detailed inNote III (31).

1. Statement of compliance with the CASBEs

The financial statements of the Group have been prepared in accordance with China AccountingStandards for Business Enterprises (“CASBEs”), and present truly and completely, the Group’sconsolidated and the Company’s financial position as at 30 June 2021, and consolidated and theCompany’s results of operations, changes in shareholders’ equity and cash flows for the six monthsended 30 June 2021.

2. Accounting period

The Group has adopted the calendar year as its accounting year, i.e. from 1 January to 31 December. Thefinancial statement covers the period from 1 January 2021 to 30 June 2021.

3. Operating cycle

An operating cycle refers to the period since an enterprise purchases assets for processing purpose till therealization of those assets in cash or cash equivalents. The Group’s operating cycle is 12 months.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-24 –

4. Functional currency

Renminbi (“RMB”) is the currency of the primary economic environment in which the Company and itsdomestic subsidiaries operate. Therefore, the Company and its domestic subsidiaries choose RMB astheir functional currency. The Company’s foreign subsidiaries, namely, Huaxin Gayur (Sogd) CementLLC, Huaxin Yovon Cement LLC, Cambodian Cement Chakrey Ting Factory Co., Ltd.,Yuzhno-Kyrgyzskyi Cement CJSC, Huaxin Cement Dzizak Co., Ltd. and Maweni Limestone Ltddetermine TJS, TJS, USD, SOM, UZS and shilling as their functional currencies based on the currency ofthe primary economic environment in which they operate. The Company adopts RMB to present itsfinancial statements.

5. The accounting treatment of business combinations involving enterprises under common control andbusiness combinations not involving enterprises under common control

Business combinations are classified into business combinations involving enterprises under commoncontrol and business combinations not involving enterprises under common control. The Group has onlybusiness combinations not involving enterprises under common control.

5.1 Business combinations not involving enterprises under common control and goodwill

A business combination not involving enterprises under common control is a businesscombination in which all of the combining enterprises are not ultimately controlled by the sameparty or parties before and after the combination.

The cost of combination is the aggregate of the fair values, at the acquisition date, of the assetsgiven, liabilities incurred or assumed, and equity securities issued by the acquirer in exchange forcontrol of the acquiree. The intermediary expenses incurred by the acquirer in respect ofreviewing, legal services, valuation and consultancy services, etc. and other associatedadministrative expenses attributable to the business combination are recognized in profit or losswhen they are incurred.

The acquiree’s identifiable assets, liabilities and contingent liabilities, acquired by the acquirer ina business combination, that meet the recognition criteria shall be measured at fair value at theacquisition date.

Where the cost of combination exceeds the acquirer ’s interest in the fair value of the acquiree’sidentifiable net assets, the difference is treated as an asset and recognized as goodwill, which ismeasured at cost on initial recognition. Where the cost of combination is less than the acquirer ’sinterest in the fair value of the acquiree’s identifiable net assets, the acquirer firstly reassesses themeasurement of the fair value of the acquiree’s identifiable assets, liabilities and contingentliabilities and measurement of the cost of combination. If after that reassessment, the cost ofcombination is still less than the acquirer ’s interest in the fair value of the acquiree’s identifiablenet assets, the acquirer recognizes the remaining difference immediately in profit or loss for thecurrent period.

Goodwill arising on a business combination is measured at cost less accumulated impairmentlosses, and is presented separately in the consolidated financial statements.

6. Preparation of consolidated financial statements

The scope of consolidated financial statements is determined on the basis of control. Control is the powerover the investee, exposures or rights to variable returns from its involvement with the investee, and theability to use its power over the investee to affect the amount of the investor ’s returns. The Groupreassesses whether or not it controls an investee if facts and circumstances indicate that there are changesof the above elements of the definition of control.

Consolidation of a subsidiary begins when the Group obtains control over the subsidiary and ceaseswhen the Group loses control of the subsidiary.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-25 –

For a subsidiary disposed of by the Group, the operating results and cash flows before the date ofdisposal (the date when control is lost) are included in the consolidated income statement andconsolidated cash flow statement, as appropriate.

For a subsidiary acquired through a business combination not involving enterprises under commoncontrol, the operating results and cash flows from the acquisition date (the date when control is obtained)are included in the consolidated income statement and consolidated cash flow statement, as appropriate.

The significant accounting policies and accounting periods adopted by the subsidiaries are determinedbased on the uniform accounting policies and accounting periods set out by the Company.

The portion of subsidiaries’ equity that is not attributable to the Company is treated as minority interestsand presented as “minority interests” in the consolidated balance sheet within shareholders’ equity. Theportion of net profits or losses of subsidiaries and other comprehensive income for the periodattributable to minority interests is presented as “Profit or loss attributable to minority interests” in theconsolidated income statement below the “Net profit” and “Other comprehensive income attributable tominority interests, net of tax” in the consolidated income statement below the “Other comprehensiveincome, net of tax” line item.

When the amount of loss for the period attributable to the minority shareholders of a subsidiary exceedsthe opening balance of the minority shareholders’ portion of the owners’ equity of the subsidiary, theexcess amount are still allocated against minority interests.

All significant balances of receivables and payables, transactions and unrealized profits within the groupare offset when the consolidated financial statements are prepared. The unrealized internal transactiongains and losses arising from the sale of assets by the Company to its subsidiaries shall fully offset the netprofits attributable to the shareholders of the parent company; the unrealized internal transaction gainsand losses arising from the sale of assets by the subsidiaries to the Company shall be proportionally offsetbetween the net profits attributable to the shareholders of the parent company and the gains and losses ofminority shareholders based on distribution ratio of the Company to its subsidiaries. The unrealizedinternal transaction gains and losses arising from the sale of assets between subsidiaries shall be offset bythe distribution proportion of the parent company to the subsidiaries of the seller between the net profitsattributable to the shareholders of the parent company and the gains and losses of minority shareholders.

If the identification of the same transaction with the Group as the accounting entity and the Company orsubsidiary as the accounting entity is different, the transaction shall be adjusted from the perspective ofthe Group.

7. Classification of joint venture arrangement and accounting treatment of joint venture

A joint venture arrangement is divided into joint operation and joint venture. The classification isdetermined according to the rights and obligations of the parties to the joint venture arrangement byconsidering the structure, legal form and contractual terms of the arrangement. Joint operation means ajoint venture arrangement in which the assets and liabilities related to the arrangement are enjoyed bythe joint venture party. A joint venture is an arrangement in which the parties are entitled only to the netassets of the arrangement.

The Group’s investment in the joint venture shall be accounted by the equity method. For details, seeNote (3) “15.3.2 Long-term Equity Investment as measured by the Equity Method.”

8. Cash and cash equivalents

Cash comprises cash on hand and deposits that can be readily withdrawn on demand. Cash equivalentsare the Group’s short-term, highly liquid investments that are readily convertible to known amounts ofcash and which are subject to an insignificant risk of changes in value. Restricted bank deposits are notregarded as cash or cash equivalents in the preparation of cash flow statements.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-26 –

9. Translation of transactions and financial statements denominated in foreign currencies

9.1 Transactions denominated in foreign currencies

A foreign currency transaction is translated into RMB, on initial recognition, by applying the spotexchange rate on the date of the transaction.

At the balance sheet date, foreign currency monetary items are translated into RMB using the spotexchange rates at the balance sheet date. Exchange differences arising from the differencesbetween the spot exchange rates prevailing at the balance sheet date and those on initialrecognition or at the previous balance sheet date are recognized in profit or loss for the period,except that exchange differences related to a specific-purpose borrowing denominated in foreigncurrency that qualify for capitalization are capitalized as part of the cost of the qualifying assetduring the capitalization period.

Foreign currency non-monetary items measured at historical cost are translated into functionalcurrency at the spot exchange rates on the dates of the transactions and the amounts in functionalcurrency remain unchanged.

9.2 Translation of financial statements denominated in foreign currencies

For the purpose of preparing the consolidated financial statements, financial statements of aforeign operation are translated from the foreign currency into RMB using the following method:assets and liabilities on the balance sheet are translated at the spot exchange rate prevailing at thebalance sheet date; shareholders’ equity items are translated at the spot exchange rates at thedates on which such items arose; all items in the income statement as well as items reflecting thedistribution of profits are translated at the spot exchange rates on the dates of the transactions.The difference between the translated assets and the aggregate of liabilities and shareholders’equity items is recognized as other comprehensive income and included in shareholders’ equity.

Cash flows arising from a transaction in foreign currency and the cash flows of a foreignsubsidiary are translated at the spot exchange rate on the date of the cash flows. The effect ofexchange rate changes on cash and cash equivalents is regarded as a reconciling item andpresented separately in the cash flow statement as “Effect of exchange rate changes on cash andcash equivalents”.

The opening balances and the comparative figures of previous year are presented at the translatedamounts in the previous year ’s financial statements.

10. Financial instruments

Financial assets and financial liabilities are recognized when the Group becomes a party to thecontractual provisions of the instrument.

For regular way purchase or sale of financial assets, assets to be received or liabilities to be assumed arerecognized on the trade date, or assets already sold are derecognized on the trade date.

Financial assets and financial liabilities are initially measured at fair value. For financial assets andfinancial liabilities at fair value through profit or loss, transaction costs are immediately recognized inprofit or loss. For other financial assets and financial liabilities, transaction costs are recognized in theirinitially recognized amounts. When the Group initially recognizes accounts receivable without asignificant financing component or without considering a significant financing component in thecontract of 1 year or less in accordance with the CASBEs No.14-Revenue (the “revenue standard”), theaccounts receivable are initially measured at the transaction price defined in the revenue standard.

The effective interest method is a method of calculating the amortized cost of a financial asset or afinancial liability and of allocating the interest income or interest expense over the relevant period.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-27 –

The effective interest rate is the rate that exactly discounts estimated future cash flows through theexpected life of the financial asset or financial liability to the carrying amount of a financial asset or to theamortized cost of a financial liability. When calculating the effective interest rate, the Group estimatesfuture cash flows by considering all the contractual terms of the financial asset or financial liability (forexample, early repayment, extension, call option or other similar options) but does not consider theexpected credit losses.

The amortized cost of a financial asset or a financial liability is the amount of a financial asset or afinancial liability measured at initial recognition minus principal repayment, plus or minus cumulativeamortization of any difference between that initial amount and the maturity amount using the effectiveinterest method, adjusted from any cumulative loss allowance (only applicable to financial assets).

10.1 Classification, recognition and measurement of financial assets

Subsequent to initial recognition, the Group’s financial assets of various categories aresubsequently measured at amortized cost, at fair value through other comprehensive income or atfair value through profit or loss, respectively.

If contractual terms of the financial asset give rise on specified dates to cash flows that are solelypayments of principal and interest on the principal amount outstanding, and the financial asset isheld within a business model whose objective is to collect contractual cash flows, such asset isclassified as subsequently measured at amortized cost, which include cash and bank balances,notes receivable, accounts receivable, other receivables, debt investments, and long-termreceivables etc.

Financial assets that meet the following conditions are classified as at fair value through othercomprehensive income (“FVTOCI”): and the contractual terms of the financial asset give rise onspecified dates to cash flows that are solely payments of principal and interest on the principalamount outstanding and the financial asset is held within a business model whose objective isachieved by both collecting contractual cash flows and selling the financial assets. Financialassets subsequently measured at FVTOCI include Notes receivable classified as at FVTOCI uponacquisition which are presented as financing with receivables.

On initial recognition, the Group may irrevocably designate an equity instrument, as financialassets at FVTOCI on an individual basis, if that equity instrument is neither held for trading norcontingent consideration recognized through business combination not involving enterprisesunder common control. Such financial assets at FVTOCI are presented as other equity instrumentinvestments.

A financial asset is classified as held-for-trading if one of the following conditions is satisfied:

• It has been acquired principally for the purpose of selling in the near term; or

• On initial recognition, it is part of a portfolio of identified financial instruments that theGroup manages together and there is objective evidence that the Group has a recent actualpattern of short-term profit-taking.

• It is a derivative that is not designated as a financial guarantee contract and effective as ahedging instrument.

Financial assets that do not meet the conditions of being classified as financial assets at amortizedcost or financial assets at FVTCOI are classified as financial assets at FVTPL. Such financial assetsmainly include money market funds and stock investments in the secondary market, etc.

The financial assets at FVTPL are presented as held-for-trading financial assets and those dueafter one year from the balance sheet date (or with no fixed term) and expected to be held for morethan one year are presented as other non-current financial assets.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-28 –

10.1.1 Financial assets measured at amortized cost

The financial assets measured at amortized cost are subsequently measured at amortizedcost using the effective interest method. Gain or loss arising from impairment orderecognition is recognized in profit or loss.

The Group recognizes interest income from financial assets classified as financial assets atamortized cost using the effective interest method. The Group calculates and recognizesinterest income through account balance of financial assets multiplying effective interest,except for the following circumstances:

• For purchased or originated credit-impaired financial assets, the Group calculatesand recognizes its interest income based on amortized cost of the financial assetand the effective interest through credit adjustment since initial recognition.

• For purchased or originated financial assets without credit impairment incurredwhile with credit impairment incurred in subsequent periods, the Groupcalculates and recognizes its interest income based on amortized cost of thefinancial asset and the effective interest in subsequent periods. If the credit risk ofthe financial asset is reduced during subsequent periods and credit impairmentdoes not exist, and the improvement can be related to an event occurring afterapplication of aforesaid provisions, the Group shall calculate and recognizeinterest income through account balance of financial assets multiplying effectiveinterest.

10.1.2 Financial assets classified as at fair value through other comprehensive income (FVTOCI)

Impairment losses or gains related to financial assets at FVTOCI, interest incomemeasured using effective interest method are recognized into profit or loss for the currentperiod, except for the above circumstances, changes in fair value of the financial assets areincluded in other comprehensive income. Amounts charged to profit or loss for everyperiod equal to the amount charged to profit or loss as it is measured at amortized costs.When the financial asset is derecognized, the cumulative gains or losses previouslyrecognized in other comprehensive income shall be removed from other comprehensiveincome and recognized in profit or loss.

10.1.3 Financial assets designated as at fair value through other comprehensive income

Subsequent to the designation of non-trading equity investments to financial assets atFVTOCI, the changes in fair value of such financial asset is recognized in othercomprehensive income. Upon derecognition of the financial asset, the cumulative gains orlosses previously recognized in other comprehensive income are transferred and includedin retained earnings. During the period in which the Group holds the non-trading equityinstrument, revenue from dividends is recognized in profit or loss for the current periodwhen (1) the Group has established the right of collecting dividends; (2) it is probable thatthe associated economic benefits will flow to the Group; and (3) the amount of dividendscan be measured reliably.

10.1.4 Financial assets at fair value through profit or loss (“FVTPL”)

Financial assets at FVTPL are subsequently measured at fair value. Any gains or lossesarising from changes in the fair value and any dividend or interest income earned on thefinancial assets are recognized in profit or loss.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-29 –

10.2 Impairment of financial instruments

The Group recognizes loss allowance for financial assets classified as at amortized cost andfinancial assets at FVOCI based on ECL.

The Group measures loss allowance for notes receivable and accounts receivable arising fromtransactions regulated by the revenue standard based on the amount of lifetime ECL.

For other financial instruments, except for the purchased or originated credit-impaired financialassets, at each balance sheet date, the Group assesses changes in credit risk of relevant financialinstruments since initial recognition. If the credit risk of the above financial instruments hasincreased significantly since initial recognition, the Group measures loss allowance based on theamount of lifetime ECL; if credit risk of the financial instrument has not increased significantlysince initial recognition, the Group recognizes loss allowance based on 12-month ECL of thefinancial instrument. Increase in or reversal of credit loss allowance is included in profit or loss asloss/gain on impairment, except for financial assets classified as at fair value through othercomprehensive income. The Group recognizes credit loss allowance for financial assets atFVTOCI in other comprehensive income and recognizes loss/gain on impairment in profit or lossfor the period, without reducing the carrying amount of the financial assets presented in thebalance sheet.

The Group measured loss allowance at the full lifetime ECL of the financial instruments in theprior accounting period, while as at the balance sheet date for the current period, for the abovefinancial instruments, due to failure to qualify as significant increase in credit risk since initialrecognition, the Group measures loss allowance for the financial instrument at 12-month ECL atthe balance sheet date for the current period. Relevant reversal of loss allowance is included inprofit or loss as gain on impairment.

10.2.1 Significant increase in credit risk

In assessing whether the credit risk has increased significantly since initial recognition,the Group compares the risk of a default occurring on the financial instrument as at thebalance sheet date with the risk of a default occurring on the financial instrument as at thedate of initial recognition.

In particular, the following information is taken into account when assessing whethercredit risk has increased significantly:

(1) Existing or forecast adverse changes in business, financial or economic conditionsthat are expected to cause a significant change in the borrower’s ability to meet itsdebt obligations;

(2) An actual or expected significant change in the operating results of the borrower;

(3) An actual or expected significant adverse change in the regulatory, economic, ortechnological environment of the borrower;

(4) Significant changes in the value of the collateral supporting the obligation or in thequality of third-party guarantees, which are expected to reduce the borrower’seconomic incentive to make scheduled contractual payments or to otherwise havean effect on the probability of a default occurring;

(5) Significant changes that are expected to reduce the borrower’s economic incentiveto make scheduled contractual payments;

(6) Expected changes in the loan documentation including an expected breach ofcontract that may lead to covenant waivers or amendments, interest rate step-ups,requiring additional collateral or guarantees, or other changes to the contractualframework of the instrument;

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-30 –

(7) Significant changes in the expected performance and behavior of the borrower;

(8) Changes in the Group’s credit management approach in relation to the financialinstrument.

Irrespective of whether the credit risk has increased significantly after the aboveassessment, taking into account the characteristics of the industries and the contractualstipulations, the Group considers that when the contractual payment for the financialinstruments is overdue for 180 (inclusive) days, it indicates that the credit risk on thefinancial instruments has increased significantly.

The Group assumes that the credit risk on a financial instrument has not increasedsignificantly since initial recognition if the financial instrument is determined to havelower credit risk at the balance sheet date. A financial instrument is determined to havelower credit risk if: i) it has a lower risk of default, ii) the borrower has a strong capacity tomeet its contractual cash flow obligations in the near term and iii) adverse changes ineconomic and business conditions in the longer term may, but will not necessarily, reducethe ability of the borrower to fulfil its contractual cash flow obligations.

10.2.2 Credit-impaired financial asset

A financial asset is credit-impaired when one or more events that have a detrimentalimpact on the estimated future cash flows of that financial asset have occurred. Evidencethat a financial asset is credit-impaired includes observable data about the followingevents:

(1) significant financial difficulty of the issuer or the borrower;

(2) a breach of contract by the debtor, such as a default or delinquency in interest orprincipal payments;

(3) the lender(s) of the borrower, for economic or contractual reasons relating to theborrower’s financial difficulty, having granted to the borrower a concession(s) thatthe lender(s) would not otherwise consider;

(4) it is becoming probable that the borrower will enter bankruptcy or other financialreorganization.

Based on the Group’s internal credit risk management, if the information acquiredinternally or externally indicates that the debtor of the financial instrument is not able torepay the creditor (including the Group) in full regardless of any guarantees obtained, theGroup believes that the default has occurred.

10.2.3 Determination of expected credit loss

The Group recognizes the credit loss on other receivables, contract assets, long-termreceivables and debt investments as well as credit-impaired accounts receivable, etc. on anindividual basis, and the remaining accounts receivable with impairment matrix on acollective basis. The Group classifies the remaining accounts receivable into differentgroups based on different types.

The Group determines expected credit losses of relevant financial instruments using thefollowing methods:

• For a financial asset, the credit loss is the present value of difference between thecontractual cash flow receivable and the expected cash flows to be received.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT

APPENDIX IV UNAUDITED CONSOLIDATED FINANCIAL STATEMENTSFOR THE SIX MONTHS ENDED 30 JUNE 2021

– IV-31 –

• For credit-impaired financial assets other than the purchased or originatedcredit-impaired financial assets at the balance sheet date, credit loss is thedifference between the account balance of financial assets and the present value ofexpected future cash flows discounted at original effective interest rate.

The Group’s measurement of ECL of financial instruments reflects factors includingunbiased probability weighted average amount recognized by assessing a series ofpossible results, time value of money, reasonable and supportable information related tohistorical events, current condition and forecast of future economic position that isavailable without undue cost or effort at the balance sheet date.

10.2.4 Write-off of financial assets

The Group shall directly reduce the account balance of a financial asset when the Grouphas no reasonable expectations of recovering a financial asset in its entirety or a portionthereof. A write-off constitutes a derecognition event.

10.3 Transfer of financial assets

The Group derecognizes a financial asset if one of the following conditions is satisfied: (1) thecontractual rights to the cash flows from the financial asset expire; (2) the financial asset has beentransferred and substantially all the risks and rewards of ownership of the financial asset istransferred to the transferee, or (3) The financial asset has been transferred. Although the Groupneither transfers nor retains almost all the risks and rewards of the ownership of the financialasset, it does not retain control over the financial asset.

For a transfer of a financial asset in its entirety that satisfies the derecognition criteria, thedifference between (1) the carrying amount of the financial asset transferred at the derecognitiondate; and (2) the sum of the consideration received from the transfer of financial assets and anycumulative gain or loss allocated to the part derecognized which has been previously recognizedin other comprehensive income, is recognized in profit or loss. If the financial assets transferredby the Group are designated as equity instrument investments at fair value through othercomprehensive income that are not held for trading, the cumulative gains or losses previouslyrecognized in other comprehensive income are transferred out and included in retained earnings.