IRS00134 Appendix B used in opposition to IRS motion for summary judgment

Upload

khangminh22Category

view

0download

0

North 40 Specific Plan DRAFT Last Modified: July 2, 2014

Appendix A Market Study and Business Opportunities Assessment

Appendix B Tree List

Appendix C Young Adult, Senior, and Empty Nester Design Summary

Appendix D Los Gatos Sustainability Plan

Appendix E Discretionary Approval Table

This Page Intentionally Left Blank

draft | May 2014

North 40 Specific Plan DRAFT Last Modified: July 2, 2014

Appendix A - Market Study and Business Opportunities Assessment

This Page Intentionally Left Blank

appendixA

draft | May 2014

1

M

arke

t Stu

dy &

Bus

ines

s O

ppor

tuni

ties

Ass

essm

ent

To

wn

of L

os G

atos

Sub

mitt

ed b

y B

AE

Urb

an E

cono

mic

s A

ugus

t 12,

201

1

bae

urba

n ec

onom

ics

Aug

ust 1

2, 2

011

Ms.

Jess

ica

von

Bor

ck

Econ

omic

Vita

lity

Man

ager

To

wn

of L

os G

atos

P.

O. B

ox 9

49

Los G

atos

, CA

950

31

Dea

r Ms.

Von

Bor

ck:

On

beha

lf of

BA

E U

rban

Eco

nom

ics,

Inc.

, we

are

plea

sed

to su

bmit

the

encl

osed

Nor

th 4

0 M

arke

t St

udy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

for t

he T

own

of L

os G

atos

pur

suan

t to

Purc

hase

Ord

er

Con

tract

#20

1103

17.

W

e ha

ve e

njoy

ed w

orki

ng w

ith y

ou a

nd y

our s

taff

col

leag

ues a

s wel

l as t

he N

orth

40

Adv

isor

y C

omm

ittee

, Pla

nnin

g C

omm

issi

on, a

nd T

own

Cou

ncil

on th

is e

xciti

ng o

ppor

tuni

ty to

enh

ance

the

Tow

n’s e

cono

mic

vita

lity

thro

ugh

the

deve

lopm

ent o

f the

Nor

th 4

0 Sp

ecifi

c Pl

an a

rea.

Si

ncer

ely,

Dav

id L

.R. S

hive

r R

aym

ond

Ken

nedy

Pr

inci

pal

Vic

e Pr

esid

ent

San

Fran

cisc

o Sa

cram

ento

Lo

s An

gele

s W

ashi

ngto

n D

C N

ew Y

ork

City

12

85 6

6th S

tree

t 80

3 2nd

Str

eet

5405

Wils

hire

Blv

d.

1346

U S

tree

t N

W

121

Wes

t 27

th S

tree

t Se

cond

Flo

or

Suit

e A

Suit

e 29

1 Su

ite

403

Suit

e 70

5 Em

eryv

ille,

CA

9460

8 D

avis

, CA

956

16

Los

Ange

les,

CA

9003

6 W

ashi

ngto

n, D

C 20

009

New

Yor

k, N

Y 10

001

510.

547.

9380

53

0.75

0.21

95

213.

471.

2666

20

2.58

8.89

45

212.

683.

4486

ww

w.b

ae1.

com

Ta

ble

of

Co

nte

nts

Ex

ecut

ive

Sum

mar

y ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..... 1

Site

Des

crip

tion

and

Loca

tion .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 1

Dem

ogra

phic

and

Eco

nom

ic O

verv

iew

.....

......

......

......

......

......

......

......

......

......

......

......

......

......

. 1

Ret

ail M

arke

t Ass

essm

ent ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

. 2

Off

ice

Mar

ket A

sses

smen

t ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 6

Hot

el M

arke

t Ass

essm

ent .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 7

Con

fere

nce/

Mee

ting

Spac

e M

arke

t Ass

essm

ent .

......

......

......

......

......

......

......

......

......

......

......

.... 8

Stra

tegi

es fo

r Nor

th 4

0 D

evel

opm

ent ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 8

Site

Des

crip

tion

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

. 13

Site

Loc

atio

n ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 15

Dem

ogra

phic

Ove

rvie

w ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 1

9

Def

initi

on o

f Ret

ail T

rade

Are

a vs

. Mar

ket A

rea .

......

......

......

......

......

......

......

......

......

......

......

. 19

Popu

latio

n an

d H

ouse

hold

Tre

nds .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

24

Hou

seho

ld C

hara

cter

istic

s ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

... 2

6 Em

ploy

men

t Tre

nds .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

... 2

8

Ret

ail M

arke

t Ass

essm

ent:

Exis

ting

Ret

ail R

eal E

stat

e C

ondi

tions

......

......

......

......

. 33

Ret

ail R

eal E

stat

e M

arke

t Con

ditio

ns ..

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

33

Ove

rvie

w o

f Los

Gat

os a

nd R

etai

l Tra

de A

rea

Ret

ail N

odes

.....

......

......

......

......

......

......

......

.. 34

Ret

ail M

arke

t Ass

essm

ent:

Sale

s an

d Le

akag

e A

naly

sis .

......

......

......

......

......

......

..... 4

5

Estim

ated

Ret

ail S

ales

in L

os G

atos

and

the

RTA

by

Maj

or R

etai

l Cat

egor

y ....

......

......

......

.. 45

R

etai

l Sal

es b

y M

ajor

Ret

ail C

ateg

ory

in L

os G

atos

, San

ta C

lara

Cou

nty,

and

Cal

iforn

ia ..

.. 49

Lo

s Gat

os T

axab

le R

etai

l Sal

es b

y D

istri

ct ...

......

......

......

......

......

......

......

......

......

......

......

......

.. 54

Le

akag

e an

d In

ject

ion

Ana

lysi

s for

Los

Gat

os a

nd th

e R

etai

l Tra

de A

rea

(RTA

) .....

......

......

. 59

Ret

ail M

arke

t Ass

essm

ent:

Sum

mar

y ...

......

......

......

......

......

......

......

......

......

......

......

.... 7

1

Exis

ting

Con

ditio

ns ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 71

Le

akag

e an

d In

ject

ion

Ana

lysi

s ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

74

Pote

ntia

l for

New

Ret

ail D

evel

opm

ent i

n Lo

s Gat

os ...

......

......

......

......

......

......

......

......

......

.....

75

Offi

ce M

arke

t Ass

essm

ent .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

77

Off

ice

Inve

ntor

y ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

77

Off

ice

Mar

ket T

rend

s ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 7

7 O

ffic

e Em

ploy

men

t Tre

nds .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 8

0 O

ffic

e D

eman

d A

naly

sis .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 82

Hot

el M

arke

t Ass

essm

ent ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

. 89

Exis

ting

Supp

ly ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 89

Pl

anne

d an

d Pr

opos

ed C

ompe

titio

n ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

. 91

Perf

orm

ance

Tre

nds .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

... 9

3

Mee

ting

Spac

e M

arke

t Ass

essm

ent .

......

......

......

......

......

......

......

......

......

......

......

......

... 97

Hot

el M

eetin

g Sp

ace .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 97

D

ay-U

se M

eetin

g Fa

cilit

ies .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 10

2 D

eman

d fr

om M

ajor

Em

ploy

ers .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

107

Opp

ortu

nitie

s &

Str

ateg

ies

for D

evel

opm

ent .

......

......

......

......

......

......

......

......

......

.... 1

09

Ove

rvie

w ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 1

09

Ret

ail D

evel

opm

ent O

ppor

tuni

ties .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

... 1

10

Ret

ail D

evel

opm

ent S

trate

gies

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.... 1

14

Off

ice

Dev

elop

men

t Opp

ortu

nitie

s ....

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

116

Hot

el D

evel

opm

ent O

ppor

tuni

ties .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

... 1

18

Con

fere

nce

and

Mee

ting

Spac

e D

evel

opm

ent O

ppor

tuni

ties .

......

......

......

......

......

......

......

.... 1

19

Prio

ritiz

ing

Opp

ortu

nitie

s ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.. 12

1

App

endi

ces .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..... 1

25

Ex

ec

uti

ve

Su

mm

ary

Site

Des

crip

tion

and

Loca

tion

The

Nor

th 4

0 si

te is

a h

ighl

y st

rate

gic

loca

tion

in th

e W

est V

alle

y fo

r new

com

mer

cial

de

velo

pmen

t:

− Th

e N

orth

40

site

is lo

cate

d at

the

inte

rsec

tion

of H

ighw

ays 8

5 an

d 17

, mak

ing

it a

high

ly v

isib

le a

nd d

esira

ble

loca

tion

for a

var

iety

of u

ses,

parti

cula

rly fo

r ret

ail,

hote

l, an

d m

eetin

g/co

nfer

ence

faci

litie

s.

− Th

e N

orth

40’

s loc

atio

n at

the

cros

sroa

ds o

f the

Wes

t Val

ley’

s fre

eway

syst

em m

akes

it

easi

ly a

cces

sibl

e to

man

y of

the

regi

on’s

maj

or h

ubs o

f act

ivity

, inc

ludi

ng m

ajor

em

ploy

ers s

uch

as A

pple

Com

pute

r, N

etfli

x, a

nd c

ultu

ral a

ttrac

tions

in d

ownt

own

San

Jose

. D

emog

raph

ic a

nd E

cono

mic

Ove

rvie

w

Whi

le L

os G

atos

itse

lf is

a sm

all c

omm

unity

, the

Tow

n an

d th

e Re

tail

Trad

e Ar

ea (R

TA) t

hat i

t is

situ

ated

in h

ave

a si

gnifi

cant

con

cent

ratio

n of

hig

h-in

com

e ho

useh

olds

and

hig

h ra

tes o

f ho

meo

wne

rshi

p th

at re

taile

rs a

nd h

otel

ope

rato

rs w

ill li

kely

find

attr

activ

e –d

espi

te m

odes

t fut

ure

popu

latio

n an

d ho

useh

old

grow

th:

−

The

Tow

n of

Los

Gat

os h

ad a

pop

ulat

ion

of 2

9,41

3 in

201

0 an

d ex

perie

nced

lim

ited

popu

latio

n or

hou

seho

ld g

row

th in

the

last

dec

ade.

− Lo

s Gat

os is

cha

ract

eriz

ed b

y re

lativ

ely

smal

l hou

seho

lds,

a hi

gh ra

te o

f hom

e ow

ners

hip,

and

hig

h in

com

es.

The

med

ian

hous

ehol

d si

ze fo

r Los

Gat

os w

as 2

.35

pers

ons p

er h

ouse

hold

in 2

010

com

pare

d to

the

Bay

Are

a av

erag

e ho

useh

old

size

of

2.69

. Th

e To

wn’

s med

ian

annu

al h

ouse

hold

inco

me

is o

ver $

115,

000,

sign

ifica

ntly

hi

gher

than

the

$79,

000

figur

e fo

r the

Bay

Are

a. A

ppro

xim

atel

y 63

per

cent

of

occu

pied

hou

sing

uni

ts a

re o

wne

r-oc

cupi

ed, i

n co

ntra

st to

just

ove

r 56

perc

ent f

or th

e B

ay A

rea.

− W

hile

not

at t

he le

vels

of t

he T

own,

the

Ret

ail T

rade

Are

a (R

TA) w

ith a

201

0 po

pula

tion

of 6

06,0

00 a

lso

has h

igh

inco

mes

and

hig

h ra

tes o

f hom

e ow

ners

hip.

The

m

edia

n ho

useh

old

inco

me

was

just

ove

r $94

,000

in 2

010.

The

RTA

’s h

omeo

wne

rshi

p ra

te w

as 6

1 pe

rcen

t of o

ccup

ied

hous

ing

units

. Th

e R

TA re

pres

ents

pop

ulat

ion

and

buyi

ng p

ower

with

in a

10

min

ute

driv

e of

the

Nor

th 4

0 si

te.

−

Bot

h Lo

s Gat

os a

nd th

e R

etai

l Tra

de A

rea

will

exp

erie

nce

mod

est p

opul

atio

n gr

owth

fr

om 2

010

to 2

020.

Bas

ed o

n th

e To

wn’

s rec

ently

ado

pted

Gen

eral

Pla

n, th

e To

wn

is

N

orth

For

ty S

peci

fic P

lan

Mar

ket S

tudy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

Pa

ge 1

of 1

50

slat

ed to

add

app

roxi

mat

ely

3,20

0 re

side

nts o

ver t

he d

ecad

e, b

ased

in p

art o

n th

e po

tent

ial f

or n

ew h

ousi

ng a

t the

Nor

th 4

0 si

te.

Futu

re re

side

ntia

l dev

elop

men

t op

portu

nitie

s in

the

Tow

n an

d th

e R

TA w

ill la

rgel

y be

infil

l on

site

s suc

h as

the

Nor

th 4

0.

D

espi

te a

com

mut

e pa

ttern

of m

ore

resi

dent

s com

mut

ing

out o

f the

RTA

than

oth

ers c

omm

utin

g in

, th

ere

are

near

ly 1

00,0

00 w

orke

rs c

omm

utin

g in

to th

e RT

A ev

ery

day

who

mos

t lik

ely

patr

oniz

e lo

cal r

etai

lers

and

serv

ice

prov

ider

s. T

he N

orth

40

site

ben

efits

from

the

prox

imity

of m

ajor

em

ploy

ers i

n th

e ad

jace

nt G

ood

Sam

arita

n H

ospi

tal a

nd o

ther

med

ical

faci

litie

s –th

ese

empl

oyee

s m

ay b

e ta

rget

mar

ket f

or n

ew re

tail:

− Lo

s Gat

os a

nd th

e R

TA fu

nctio

n as

a b

edro

om re

side

ntia

l com

mun

ity in

Sili

con

Val

ley

with

mor

e re

side

nts c

omm

utin

g ou

t eve

ry d

ay fo

r wor

k (1

86,9

00) t

han

com

mut

e in

(9

8,30

0).

− G

ood

Sam

arita

n ho

spita

l is t

wo

min

ute

driv

e fr

om th

e N

orth

40

site

, em

ploy

s 1,8

00

peop

le a

nd g

ener

ates

88,

000

patie

nt d

ays a

nnua

lly.

−

Col

umbi

a H

ealth

Car

e/M

issi

on O

aks H

ospi

tal i

s a th

ree

min

ute

driv

e fr

om th

e N

orth

40

and

em

ploy

s 2,0

00 p

eopl

e.

Ret

ail M

arke

t Ass

essm

ent

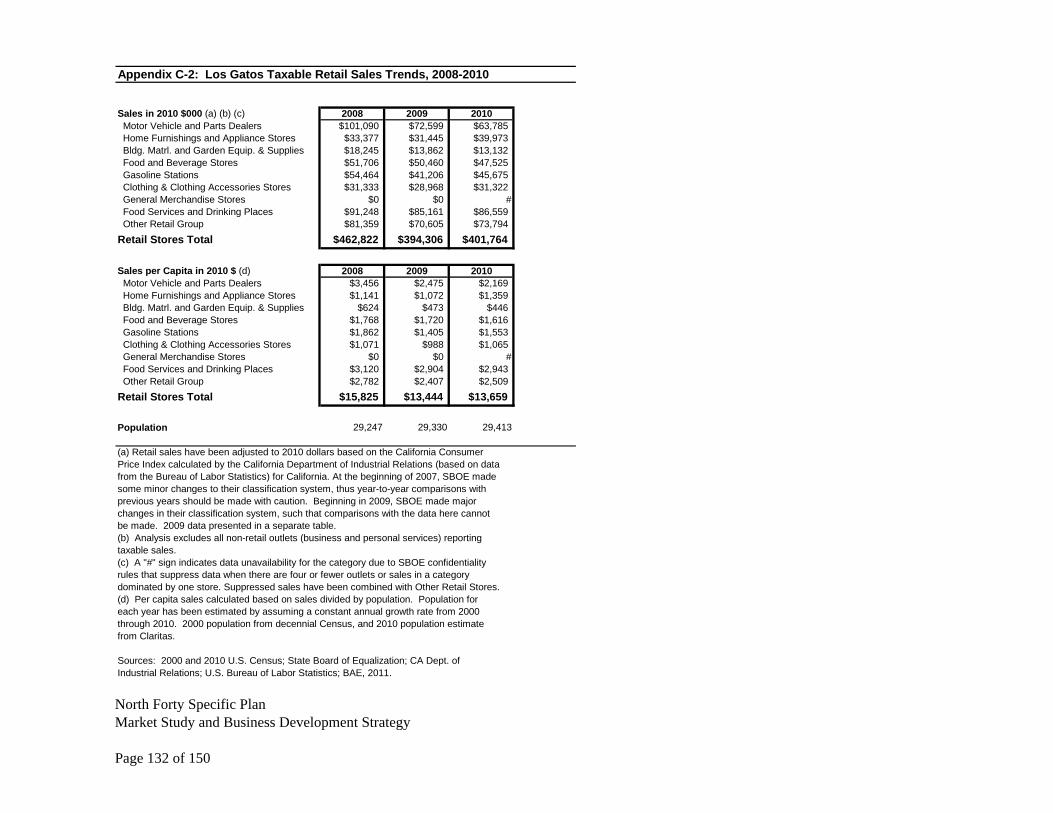

Los G

atos

has

a v

ery

stro

ng re

tail

sect

or w

ith a

div

erse

mix

of r

etai

lers

:

− R

etai

l sal

es fo

r the

Tow

n fo

r 200

8 ar

e es

timat

ed a

t app

roxi

mat

ely

$838

mill

ion.

Th

e th

ree

larg

est c

ateg

orie

s by

sale

s vol

ume

are

mot

or v

ehic

le a

nd p

arts

dea

lers

at

30 p

erce

nt, f

ood

and

beve

rage

stor

es a

t 23

perc

ent,

and

food

serv

ices

and

drin

king

pl

aces

at 1

5 pe

rcen

t. T

he p

ropo

rtion

of t

he T

own’

s tot

al re

tail

sale

s in

mot

or

vehi

cle

and

food

stor

e sa

les a

re v

ery

high

, alth

ough

mot

or v

ehic

le sa

les h

ave

decl

ined

sinc

e 20

08.

− O

n a

per c

apita

bas

is, r

etai

l sal

es in

Los

Gat

os a

re q

uite

hig

h, a

t $28

,653

ann

ually

co

mpa

red

to le

ss th

an $

14,0

00 a

nnua

lly fo

r the

RTA

; the

onl

y se

ctor

s lag

ging

the

RTA

in p

er c

apita

sale

s are

the

build

ing

mat

eria

ls g

roup

and

gen

eral

mer

chan

dise

st

ores

.

−

The

Tow

n is

unu

sual

in th

at it

als

o at

tract

s sho

pper

s for

eve

ryda

y ite

ms s

uch

as

groc

erie

s, du

e in

par

t to

the

loca

tion

of su

perm

arke

ts a

nd d

rugs

tore

s nea

r the

edg

es

of T

own

and

in p

art d

ue to

the

lack

of s

hopp

ing

in M

onte

Ser

eno,

Sar

atog

a an

d ot

her n

earb

y un

inco

rpor

ated

are

as.

Nor

th F

orty

Spe

cific

Pla

n M

arke

t Stu

dy a

nd B

usin

ess D

evel

opm

ent S

trate

gy

Page

2 o

f 150

−

Long

-term

dec

lines

in re

tail

sale

s in

Los G

atos

ove

r the

last

dec

ade

have

bee

n re

late

d la

rgel

y to

the

decl

ine

in th

e au

tom

otiv

e se

ctor

. In

201

0, ta

xabl

e m

otor

ve

hicl

e sa

les i

n th

e To

wn

wer

e on

ly 2

1 pe

rcen

t of 2

000

leve

ls a

fter a

djus

ting

for

infla

tion.

− W

ith it

s hig

h pe

r cap

ita sa

les l

evel

s, Lo

s Gat

os sh

ows i

njec

tions

of s

ales

in m

ost

maj

or re

tail

cate

gorie

s, in

dica

ting

attra

ctio

n of

shop

pers

from

out

side

the

Tow

n.

−

The

Tow

n is

unu

sual

in th

at it

als

o at

tract

s sho

pper

s for

eve

ryda

y ite

ms s

uch

as

groc

erie

s, du

e in

par

t to

the

loca

tion

of su

perm

arke

ts a

nd d

rugs

tore

s nea

r the

edg

es

of T

own

and

in p

art d

ue to

the

lack

of r

etai

l in

Mon

te S

eren

o, S

arat

oga

and

othe

r ne

arby

uni

ncor

pora

ted

area

s.

−

Inje

ctio

ns a

re a

lso

high

for m

otor

veh

icle

and

par

ts d

eale

rs a

nd fo

od se

rvic

es

(whi

ch in

clud

es re

stau

rant

s).

Two

cate

gorie

s, bu

ildin

g m

ater

ials

and

gen

eral

m

erch

andi

se st

ores

, sta

nd o

ut fo

r the

ir su

bsta

ntia

l lea

kage

s.

−

The

Tow

n’s p

rimar

y re

tail

area

s are

the

Dow

ntow

n, L

os G

atos

Bou

leva

rd a

nd th

e fo

ur n

eigh

borh

ood

cent

ers.

The

se a

reas

com

bine

d m

ake

up 5

9 pe

rcen

t of a

ll Lo

s G

atos

reta

il ou

tlets

but

gen

erat

e 88

per

cent

of t

he T

own’

s tax

able

reta

il sa

les.

Lo

s Gat

os’ D

ownt

own,

whi

le im

pact

ed b

y re

gion

al a

nd n

atio

nal e

cono

mic

tren

ds, h

as re

mai

ned

a st

rong

regi

onal

reta

il de

stin

atio

n, a

ttrac

ting

shop

pers

from

out

side

the

Tow

n.

−

Dow

ntow

n is

seen

as a

reta

il de

stin

atio

n, d

raw

ing

shop

pers

from

Los

Gat

os a

s wel

l as

oth

er n

earb

y co

mm

uniti

es.

Dow

ntow

n is

als

o a

tour

ist d

estin

atio

n, w

ith o

ut-o

f-to

wne

rs c

omin

g to

exp

erie

nce

the

smal

l tow

n an

d pe

dest

rian-

frie

ndly

am

bien

ce.

In

2010

, Dow

ntow

n Lo

s Gat

os g

ener

ated

app

roxi

mat

ely

$209

mill

ion

in ta

xabl

e re

tail

sale

s, or

ove

r 50

perc

ent o

f the

Tow

n’s t

otal

taxa

ble

reta

il sa

les,

conf

irmin

g its

si

gnifi

canc

e as

a sh

oppi

ng d

estin

atio

n an

d as

a ta

x ge

nera

tor f

or th

e To

wn.

− O

n an

infla

tion-

adju

sted

bas

is, t

his s

ales

leve

l has

dec

lined

from

taxa

ble

sale

s of

$225

mill

ion

in 2

008,

but

has

rebo

unde

d fr

om $

198

mill

ion

in 2

009.

Thi

s rec

ent

uptic

k is

due

in p

art t

o in

crea

sing

sale

s at t

he A

pple

Sto

re.

− Th

e D

ownt

own

Cor

e ar

ea a

ccou

nts f

or n

early

thre

e-qu

arte

rs o

f all

busi

ness

es in

the

Dow

ntow

n. T

he la

rges

t con

cent

ratio

ns a

re in

app

arel

, eat

ing

and

drin

king

, and

ot

her r

etai

l, w

hich

incl

udes

var

ious

type

s of s

peci

alty

reta

il ou

tlets

such

as s

porti

ng

good

s, to

y, a

nd b

ooks

/sta

tione

ry st

ores

. Th

e C

ore

is c

hara

cter

ized

by

smal

ler f

loor

pl

ates

, and

bec

ause

of t

he fo

rmul

a re

tail

ordi

nanc

e as

wel

l as t

he li

mite

d nu

mbe

r of

larg

er st

ore

spac

es a

vaila

ble,

the

Cor

e co

ntai

ns fe

w c

hain

reta

ilers

.

N

orth

For

ty S

peci

fic P

lan

Mar

ket S

tudy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

Pa

ge 3

of 1

50

−

Form

ula

reta

il, w

hile

rest

ricte

d in

the

Dow

ntow

n C

ore,

nev

erth

eles

s acc

ount

s for

a

sign

ifica

nt p

ropo

rtion

of t

axab

le re

tail

sale

s. In

201

0, st

ores

des

igna

ted

as fo

rmul

a re

tail

in th

e D

ownt

own

Cor

e pr

ovid

ed o

ver 3

0 pe

rcen

t of t

axab

le re

tail

sale

s in

the

area

, whi

le m

akin

g up

onl

y 11

per

cent

of t

he re

tail

outle

ts (e

xclu

ding

food

-rel

ated

re

tail

and

serv

ice

stat

ions

). E

xclu

ding

thes

e sa

me

outle

ts, (

not s

ubje

ct to

the

form

ula

reta

il or

dina

nce)

, for

mul

a re

taile

rs a

ccou

nt fo

r ove

r hal

f of t

he ta

xabl

e re

tail

sale

s in

the

Dow

ntow

n C

ore.

Lo

s Gat

os B

oule

vard

is a

mix

of c

omm

unity

shop

ping

cen

ters

anc

hore

d by

supe

rmar

kets

, aut

o de

aler

s and

rela

ted

busi

ness

es, a

nd fr

ee-s

tand

ing

reta

il ou

tlets

.

−

The

four

larg

er sh

oppi

ng c

ente

rs a

re a

ll an

chor

ed b

y su

perm

arke

ts, i

n a

clus

ter t

hat

serv

es L

os G

atos

and

nea

rby

area

s of C

ampb

ell a

nd S

an Jo

se.

The

high

pro

porti

on

of su

perm

arke

ts in

dica

tes t

he a

rea

is a

shop

ping

des

tinat

ion

for f

ood

item

s.

− Lo

s Gat

os B

oule

vard

had

taxa

ble

reta

il sa

les o

f app

roxi

mat

ely

$152

mill

ion

in

2010

, a st

eep

decl

ine

from

ear

lier y

ears

resu

lting

larg

ely

from

dec

reas

ing

sale

s in

the

auto

mot

ive

sect

or.

Th

e ne

ighb

orho

od c

ente

rs a

re la

rgel

y oc

cupi

ed b

y lo

cal-s

ervi

ng re

taile

rs p

rovi

ding

eve

ryda

y co

nven

ienc

e go

ods a

nd se

rvic

es.

−

Los G

atos

has

four

maj

or n

eigh

borh

ood

cent

ers:

Rin

cona

da C

ente

r, D

owni

ng

Cen

ter,

Wal

gree

ns S

quar

e, a

nd V

ason

a St

atio

n.

−

Thes

e ne

ighb

orho

od c

ente

rs a

re a

ll lo

cate

d at

or n

ear t

he T

own

boun

darie

s, th

us

attra

ctin

g sh

oppe

rs fr

om o

utsi

de th

e To

wn

sinc

e th

ey re

pres

ent t

he c

lose

st g

roce

ry

or d

rug

stor

e sh

oppi

ng.

Thes

e ce

nter

s com

bine

d ac

coun

ted

for a

muc

h sm

alle

r pr

opor

tion

of re

tail

sale

s tha

n D

ownt

own

or L

os G

atos

Bou

leva

rd.

Th

e Re

tail

Trad

e Ar

ea c

onta

ins a

larg

e m

ix a

nd v

arie

ty o

f reg

iona

l ret

ail s

hopp

ing

dest

inat

ions

w

hich

will

be

com

petit

ive

with

any

regi

on-s

ervi

ng re

tail

at th

e N

orth

40.

− Th

e R

TA’s

reta

il sa

les f

or 2

008

are

estim

ated

at a

ppro

xim

atel

y $8

.4 b

illio

n, a

bout

10

tim

es th

e sa

les i

n Lo

s Gat

os a

lone

. Th

e R

TA’s

leve

ls o

f per

cap

ita re

tail

sale

s ar

e on

ly a

bout

hal

f the

leve

ls fo

r the

Tow

n.

−

Leve

ls o

f lea

kage

s and

inje

ctio

ns a

ppea

r to

be m

uch

low

er o

n a

per c

apita

bas

is,

indi

catin

g a

rela

tive

bala

nce

betw

een

reta

il sa

les a

nd re

side

nt e

xpen

ditu

res i

n m

ost

cate

gorie

s.

Nor

th F

orty

Spe

cific

Pla

n M

arke

t Stu

dy a

nd B

usin

ess D

evel

opm

ent S

trate

gy

Page

4 o

f 150

The

Tow

n m

ay b

e ab

le to

enh

ance

its r

etai

l bas

e in

a ra

nge

of re

tail

type

s.

−

Alo

ng w

ith g

ener

al m

erch

andi

se st

ores

and

hom

e im

prov

emen

t cen

ters

, spe

cific

st

ore

type

s tha

t app

ear t

o be

lack

ing

in sa

les i

n th

e To

wn

incl

ude

appl

ianc

e st

ores

, an

d sp

ecia

lty fo

od st

ores

such

as m

eat m

arke

ts, f

ish

and

seaf

ood

mar

kets

, and

pr

oduc

e m

arke

ts.

The

sale

s inj

ectio

ns fo

r clo

thin

g an

d cl

othi

ng a

cces

sorie

s sto

res

refle

cts a

n ov

eral

l stre

ngth

, but

the

appa

rel s

tore

s in

the

Tow

n te

nd to

be

high

-end

st

ores

, not

nec

essa

rily

carr

ying

the

type

s of i

nexp

ensi

ve e

very

day

appa

rel m

ore

com

mon

ly fo

und

in m

any

gene

ral m

erch

andi

se st

ores

.

−

Giv

en th

e To

wn’

s alre

ady-

stro

ng a

ttrac

tion

as a

food

shop

ping

des

tinat

ion

and

dem

ogra

phic

pro

file,

the

lack

of s

peci

alty

food

stor

es m

ay a

lso

repr

esen

t an

oppo

rtuni

ty to

bro

aden

the

food

reta

iling

mix

and

enh

ance

the

Tow

n’s s

trong

po

sitio

n fo

r thi

s ret

ail c

ateg

ory.

− To

som

e ex

tent

, the

leak

age

of re

tail

sale

s in

certa

in c

ateg

orie

s dom

inat

ed b

y la

rge-

form

at st

ores

of 3

0,00

0 sq

uare

feet

or m

ore

refle

cts t

he T

own’

s des

ire to

reta

in a

sm

all-t

own

feel

, with

smal

ler s

hops

and

in th

e D

ownt

own

Cor

e, li

mite

d fo

rmul

a re

tail.

As a

resu

lt, th

ere

are

few

reta

il sp

aces

in L

os G

atos

of a

ppro

xim

atel

y 10

,000

squa

re fe

et o

r mor

e th

at a

re a

vaila

ble

to a

ccom

mod

ate

larg

er u

sers

such

as

appl

ianc

e st

ores

, hom

e im

prov

emen

t sto

res,

or g

ener

al m

erch

andi

se st

ores

. W

hile

th

e To

wn

will

und

oubt

edly

seek

to re

tain

its c

hara

cter

, app

ropr

iate

ly d

esig

ned

deve

lopm

ent a

t the

Nor

th 4

0 si

te m

ay p

rese

nt a

n op

portu

nity

to p

rovi

de re

tail

spac

e fo

r lar

ger u

sers

that

mig

ht c

ompl

emen

t the

exi

stin

g re

tail

mix

in L

os G

atos

an

d pr

ovid

e go

ods a

nd se

rvic

es th

at re

side

nts c

urre

ntly

seek

els

ewhe

re.

N

orth

For

ty S

peci

fic P

lan

Mar

ket S

tudy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

Pa

ge 5

of 1

50

Offi

ce M

arke

t Ass

essm

ent

Whi

le th

e Lo

s Gat

os o

ffice

mar

ket c

ompr

ises

a sm

all p

erce

ntag

e of

the

regi

onal

offi

ce m

arke

t it h

as

perf

orm

ed b

ette

r offi

ce sp

ace

in th

e M

arke

t Are

a an

d So

uth

Bay,

− Lo

s Gat

os c

urre

ntly

has

an

offic

e in

vent

ory

estim

ated

by

Cor

nish

and

Car

ey

Com

mer

cial

New

mar

k K

nigh

t Fra

nk to

be

appr

oxim

atel

y 1.

4 m

illio

n sq

uare

feet

, re

pres

entin

g ap

prox

imat

ely

2.2

of to

tal i

nven

tory

in th

e So

uth

Bay

.

− H

isto

rical

ly th

e Lo

s Gat

os o

ffic

e m

arke

t has

gen

eral

ly o

utpe

rfor

med

its M

arke

t Are

a an

d So

uth

Bay

ben

chm

arks

with

hig

her o

ccup

ancy

rate

s and

rent

s. T

he c

urre

nt

aver

age

full-

serv

ice

aski

ng re

nt in

Los

Gat

os is

$2.

58 p

er sq

uare

foot

com

pare

d to

$2

.39

for s

pace

in th

e M

arke

t Are

a an

d $2

.48

in th

e So

uth

Bay

as a

who

le.

Los G

atos

ha

s an

offic

e va

canc

y ra

te o

f 8.8

per

cent

com

pare

d to

9.3

per

cent

in th

e M

arke

t Are

a an

d 16

.6 p

erce

nt in

the

Sout

h B

ay.

The

Tow

n’s h

ighe

r lea

se ra

tes a

nd lo

wer

vac

ancy

ra

te in

dica

te th

at is

an

attra

ctiv

e an

d de

sira

ble

offic

e lo

catio

n.

−

Dur

ing

the

Gre

at R

eces

sion

Los

Gat

os re

nts w

ere

com

pres

sed

to n

ear t

he m

arke

t av

erag

e an

d ha

ve re

boun

ded

slig

htly

dur

ing

the

curr

ent r

ecov

ery.

Whi

le d

eman

d el

sew

here

in th

e So

uth

Bay

has

sign

ifica

ntly

stre

ngth

ened

, off

ice

dem

and

has n

ot fu

lly

reco

vere

d in

Los

Gat

os.

Dem

and

tend

s to

be d

riven

by

smal

ler u

sers

and

end

use

rs th

at

requ

ire la

rger

floo

r pla

tes s

uch

as N

etfli

x.

The

Nor

th 4

0 w

ould

be

an a

ttrac

tive

site

for o

ffice

and

em

ploy

men

t pro

ject

ions

supp

ort

cons

truc

tion

of o

ffice

spac

e, ta

king

into

acc

ount

exi

stin

g va

cant

spac

e an

d pl

anne

d an

d pr

opos

ed

proj

ects

.

− B

ased

upo

n em

ploy

men

t pro

ject

ions

pre

pare

d by

the

Ass

ocia

tion

of B

ay A

rea

Gov

ernm

ents

(AB

AG

), B

AE

estim

ates

that

the

Mar

ket A

rea

can

supp

ort a

n ad

ditio

nal

698,

000

to 9

57,0

00 fe

et o

f new

off

ice

spac

e be

twee

n 20

10 a

nd 2

030

afte

r acc

ount

ing

for p

lann

ed a

nd p

ropo

sed

proj

ects

, inc

ludi

ng th

e pr

opos

ed 5

50,0

00 sq

uare

foot

off

ice

use

at th

e A

lbrig

ht si

te in

Los

Gat

os.

− W

ith it

s stro

ng lo

catio

n, th

e N

orth

40

site

cou

ld c

aptu

re b

etw

een

70,0

00 a

nd 1

91,0

00

squa

re fe

et o

f thi

s tot

al n

et d

eman

d, a

pply

ing

a 10

and

20

perc

ent c

aptu

re ra

te.

−

Pote

ntia

l off

ice

prod

uct t

ypes

cou

ld in

clud

e la

rger

Cla

ss A

spac

e fo

r lar

ger u

sers

or a

n en

d us

er (1

00,0

00+

squa

re fe

et) o

r med

ical

off

ices

. A

noth

er p

oten

tial t

arge

t mar

ket

coul

d be

mul

titen

ant C

lass

B o

r A sp

ace

for s

tart-

ups,

smal

l ven

ture

s, an

d m

edic

al

offic

e th

at w

ould

find

the

who

le p

acka

ge o

f Nor

th 4

0 am

eniti

es h

ighl

y at

tract

ive

(e.g

., re

tail

and

hote

l/mee

ting

spac

e).

Nor

th F

orty

Spe

cific

Pla

n M

arke

t Stu

dy a

nd B

usin

ess D

evel

opm

ent S

trate

gy

Page

6 o

f 150

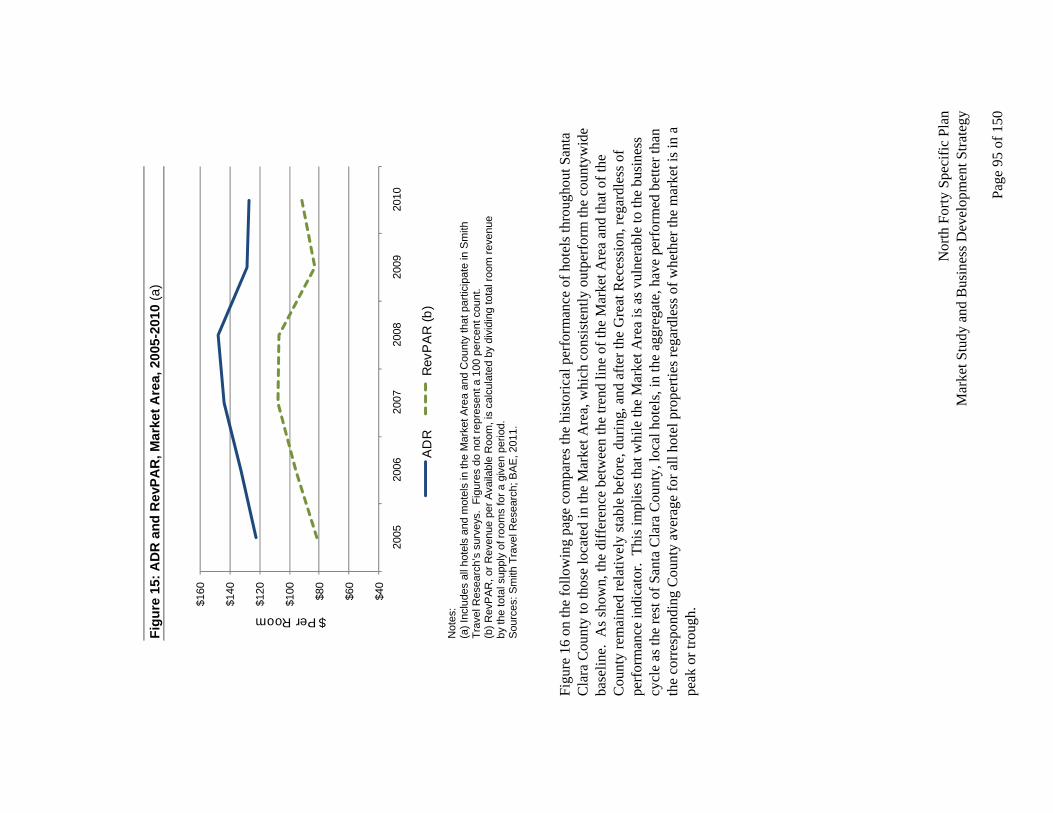

Hot

el M

arke

t Ass

essm

ent

Los G

atos

has

two

exis

ting

high

-end

full

serv

ice

hote

l pro

pert

ies.

The

per

form

ance

of h

otel

s with

in

the

Mar

ket A

rea

has f

ollo

wed

the

busi

ness

cyc

le b

ut h

as o

ut-p

erfo

rmed

its S

anta

Cla

ra C

ount

y be

nchm

ark.

− Th

e M

arke

t Are

a fo

r hot

els h

as a

n in

vent

ory

of a

lmos

t 2,0

00 ro

oms,

repr

esen

ting

7.6

perc

ent o

f the

tota

l roo

ms i

n Sa

nta

Cla

ra C

ount

y. O

ver 7

9 pe

rcen

t of t

hese

room

s in

the

Mar

ket A

rea

are

in p

rope

rties

con

side

red

as “

upsc

ale”

or b

ette

r by

Smith

Tra

vel

Res

earc

h (S

TR).

−

Los G

atos

is h

ome

to tw

o hi

gh-e

nd fu

ll se

rvic

e ho

tels

with

186

room

s, or

9%

of h

igh-

end

hote

l roo

ms i

n th

e M

arke

t Are

a.

−

Thro

ugho

ut th

e cu

rren

t bus

ines

s cyc

le, h

otel

pro

perti

es in

the

Mar

ket A

rea

have

co

nsis

tent

ly o

ut-p

erfo

rmed

thos

e in

oth

er p

arts

of S

anta

Cla

ra C

ount

y w

ith re

spec

t to

occu

panc

y le

vels

and

room

reve

nues

. O

ccup

ancy

in M

arke

t Are

a pr

oper

ties p

eake

d at

75

per

cent

in 2

007,

fell

to a

low

of 6

5 pe

rcen

t, an

d re

cove

red

to 7

2 pe

rcen

t as o

f the

en

d of

201

0. I

n co

ntra

st, p

rope

rties

in S

anta

Cla

ra C

ount

y ro

se to

a h

igh

of 7

0 pe

rcen

t in

200

7, d

ropp

ed to

a lo

w o

f 58

perc

ent i

n 20

09, a

nd ro

se b

ack

to 6

8 pe

rcen

t in

2010

.

−

Rev

enue

s in

the

Mar

ket A

rea

have

not

reco

vere

d as

stro

ngly

as o

ccup

ancy

: the

ave

rage

da

ily ra

te p

eake

d at

$14

8 in

200

8 an

d no

w st

ands

at $

127.

Rev

enue

per

ava

ilabl

e ro

om

also

follo

ws a

sim

ilar t

rend

. H

ighe

r occ

upan

cies

hav

e be

en a

chie

ved

by m

aint

aini

ng

com

petit

ive

room

rate

s. W

hile

a sm

all p

art o

f the

Mar

ket A

rea

and

Sant

a C

lara

hos

pita

lity

mar

ket,

Los G

atos

has

bee

n an

at

trac

tive

dest

inat

ion.

− In

terv

iew

s with

key

com

mun

ity a

nd b

usin

ess i

nfor

man

ts in

dica

te th

at L

os G

atos

’ ex

istin

g lo

dgin

g fa

cilit

ies a

nd o

vera

ll co

mm

unity

am

eniti

es c

ompl

emen

t the

mai

n de

man

d dr

iver

s for

ove

rnig

ht ro

om st

ays i

n Lo

s Gat

os, w

hich

incl

ude:

• B

usin

ess t

rave

l gen

erat

ed n

ot o

nly

by fi

rms l

ocat

ed in

Los

Gat

os, b

ut a

lso

thos

e lo

cate

d in

dow

ntow

n Sa

n Jo

se a

nd o

ther

are

as o

f cen

tral S

ilico

n V

alle

y; g

ener

al m

anag

ers o

f loc

al h

otel

s hav

e fo

und

cons

ider

able

succ

ess

mar

ketin

g to

hig

h-le

vel b

usin

ess t

rave

lers

, par

ticul

arly

thos

e w

ho tr

avel

w

ith th

eir s

pous

es;

• Le

isur

e tra

vel r

elat

ed to

shop

ping

and

din

ing

in d

ownt

own

Los G

atos

, as

wel

l as a

rea

win

erie

s; a

nd

• W

eddi

ngs a

nd o

ther

soci

al e

vent

s.

N

orth

For

ty S

peci

fic P

lan

Mar

ket S

tudy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

Pa

ge 7

of 1

50

New

hot

el c

onst

ruct

ion

is p

lann

ed in

Cup

ertin

o.

−

Two

plan

ned

and

prop

osed

hot

el p

roje

cts w

ould

add

as m

any

as 3

70 ro

oms t

o th

e M

arke

t Are

a w

ith a

t lea

st 1

23 ro

oms d

eem

ed u

psca

le o

r bet

ter.

The

se tw

o pr

ojec

ts a

re

loca

ted

at th

e no

rther

n en

d of

the

Mar

ket A

rea

in C

uper

tino.

Th

ere

are

oppo

rtun

ities

for n

ew h

otel

dev

elop

men

t at t

he N

orth

40

site

.

− Th

ere

is a

not

ewor

thy

lack

of n

atio

nal a

nd g

loba

l lux

ury

hote

l bra

nded

pro

perti

es in

Si

licon

Val

ley.

The

loca

tion

and

setti

ng o

f the

Nor

th 4

0 co

uple

d w

ith L

os G

atos

’ ric

h se

t of a

men

ities

may

be

attra

ctiv

e to

luxu

ry h

otel

iers

look

ing

for a

Sili

con

Val

ley

pres

ence

or t

o bo

utiq

ue o

pera

tors

/dev

elop

ers s

eeki

ng to

exp

and

in th

e M

arke

t Are

a.

−

One

dis

adva

ntag

e to

the

Nor

th 4

0 si

te fo

r glo

bal l

uxur

y br

ands

is it

s loc

atio

n ou

tsid

e a

maj

or b

usin

ess c

lust

er.

Con

fere

nce/

Mee

ting

Spac

e M

arke

t Ass

essm

ent

−

Ther

e is

a g

ener

al la

ck o

f mee

ting

and

conf

eren

ce sp

ace

that

can

acc

omm

odat

e m

ore

than

250

per

sons

in th

e M

arke

t Are

a.

−

Inte

rvie

ws w

ith k

ey in

form

ants

indi

cate

that

ther

e w

ould

be

loca

l sup

port

for n

ew,

stat

e-of

-the-

art m

eetin

g fa

cilit

ies w

ith a

cap

acity

of 2

50 to

500

per

sons

.

Stra

tegi

es fo

r Nor

th 4

0 D

evel

opm

ent

Dev

elop

ing

Use

s C

ompl

emen

tary

to D

ownt

own

Los

Gat

os

The

Gen

eral

Pla

n EI

R g

uida

nce

stat

es th

at n

ew d

evel

opm

ent a

t the

Nor

th 4

0 sh

ould

“co

mpl

emen

t an

d no

t com

pete

with

Los

Gat

os’ d

ownt

own

and

the

rest

of t

he c

omm

unity

.” B

AE

has f

orm

ulat

ed

seve

ral s

trate

gies

to h

onor

this

goa

l of c

ompl

emen

tary

reta

il de

velo

pmen

t: R

etai

l Stra

tegy

1: E

stab

lish

a cl

ear d

iffer

ence

in th

e sh

oppi

ng e

xper

ienc

e be

twee

n th

e D

ownt

own

and

Nor

th 4

0. T

he T

own’

s For

mul

a R

etai

l Ord

inan

ce h

elps

mai

ntai

n th

e do

wnt

own’

s sm

all-t

own

feel

and

a la

rge

pres

ence

of i

ndep

ende

nt re

taile

rs w

ith u

niqu

e pr

oduc

ts a

nd se

rvic

es a

nd

limits

the

num

ber o

f for

mul

a re

taile

rs su

ch a

s the

pre

sent

mix

of S

ur L

a Ta

ble,

App

le S

tore

, B

anan

a R

epub

lic, R

esto

ratio

n H

ardw

are,

and

the

Gap

am

ong

othe

rs.

The

Nor

th 4

0 ex

perie

nce

shou

ld b

e di

ffer

entia

ted

by a

focu

s on

form

ula

reta

il w

ith le

ss e

mph

asis

on

inde

pend

ent r

etai

lers

. A

ddin

g fo

rmul

a re

tail

to th

e To

wn-

wid

e in

vent

ory

of re

tail

prop

ertie

s wou

ld h

elp

Los G

atos

ca

ptur

e sa

les (

and

gene

rate

add

ition

al sa

les t

ax re

venu

e) fr

om T

own

resi

dent

s who

cur

rent

ly tr

avel

ou

tsid

e th

e to

wn

to sh

op a

t for

mul

a re

tail

outle

ts a

s wel

l as f

rom

shop

pers

who

wou

ld c

ome

from

ou

tsid

e Lo

s Gat

os.

Ther

e ar

e se

vera

l loc

al e

xam

ples

of d

ownt

owns

and

new

shop

ping

com

plex

es

com

plem

entin

g ea

ch o

ther

with

such

diff

eren

tiate

d sh

oppi

ng e

xper

ienc

es: D

ownt

own

and

Stan

ford

Nor

th F

orty

Spe

cific

Pla

n M

arke

t Stu

dy a

nd B

usin

ess D

evel

opm

ent S

trate

gy

Page

8 o

f 150

Shop

ping

Cen

ter i

n Pa

lo A

lto, a

nd E

lmw

ood/

Roc

krid

ge a

nd B

ay S

treet

in th

e in

ner E

ast B

ay

(Ber

kele

y, O

akla

nd, a

nd E

mer

yvill

e).

Ret

ail S

trat

egy

1.1:

For

mul

ate

a co

ordi

nate

d m

arke

t cam

paig

n fo

r bo

th th

e D

ownt

own

and

Nor

th 4

0 re

tail

deve

lopm

ent.

A c

oope

rativ

e m

arke

ting

effo

rt be

twee

n th

e To

wn

of L

os G

atos

, loc

al D

ownt

own

mer

chan

ts, a

nd th

e N

orth

40

deve

lope

r can

hel

p br

and

and

posi

tion

each

reta

il di

stric

t app

ropr

iate

ly to

rein

forc

e th

eir r

espe

ctiv

e co

re

stre

ngth

s and

cro

ss-m

arke

t eve

nts a

nd a

nnou

ncem

ents

–al

l to

rein

forc

e Lo

s Gat

os a

s a

shop

ping

des

tinat

ion.

R

etai

l Str

ateg

y 1.

2: C

ontin

ue a

nd E

nhan

ce D

ownt

own

Mer

chan

t Vita

lity

Prog

ram

s.

The

Tow

n of

Los

Gat

os p

rese

ntly

ope

rate

s sev

eral

pro

gram

s orie

nted

to b

usin

ess

deve

lopm

ent a

nd m

erch

ant a

ssis

tanc

e. T

hese

pro

gram

whi

ch in

clud

e bu

sine

ss w

orks

hops

in

par

tner

ship

with

the

Cha

mbe

r of C

omm

erce

and

Wes

t Val

ley

Col

lege

, men

torin

g se

rvic

es fo

r sm

all b

usin

esse

s, an

d m

arke

ting

even

ts, s

houl

d be

con

tinue

d an

d en

hanc

ed to

of

fer a

ssis

tanc

e to

mer

chan

ts d

ownt

own

to e

ffec

tivel

y m

arke

t to

new

shop

pers

bro

ught

in

by th

e N

orth

40.

R

etai

l Str

ateg

y 1.

3: R

einf

orce

the

Dow

ntow

n’s R

ole

as C

omm

unity

Hub

and

Soc

ial

Cen

ter.

By

cont

inui

ng to

pro

gram

Far

mer

s Mar

kets

, mus

ic a

nd a

rt fe

stiv

als,

and

spec

ial

even

ts, L

os G

atos

can

mai

ntai

n th

e D

ownt

own

as th

e To

wn’

s com

mun

ity h

ub.

With

its

dive

rse

set o

f bui

ldin

gs a

nd tr

aditi

onal

stre

et la

yout

the

Dow

ntow

n of

fers

an

auth

entic

sm

all d

ownt

own

expe

rienc

e th

at is

har

d fo

r a n

ew d

evel

opm

ent t

hat i

s pla

nned

at o

ne ti

me

to re

prod

uce

and

com

pete

with

. Th

e re

cent

repo

rted

purc

hase

of t

he L

os G

atos

The

ater

by

a lo

cal i

nves

tmen

t gro

up to

kee

p it

as a

smal

l mov

ie th

eate

r will

boo

st th

e To

wn’

s eff

orts

to

mai

ntai

n a

vita

l Dow

ntow

n.

R

etai

l Str

ateg

y 1.

4: B

rand

ing

and

Iden

tify

for

Los

Gat

os S

hopp

ing

Dis

tric

ts.

The

bran

ding

of t

he N

orth

40

for a

ny re

tail

use

shou

ld b

e ap

proa

ched

from

the

idea

that

stro

ng

iden

titie

s for

all

Los G

atos

’ sho

ppin

g di

stric

ts sh

ould

be

rein

forc

ed a

nd b

rand

ed to

off

er

Los G

atos

as a

who

le “

pack

age”

of s

hopp

ing

and

leis

ure

activ

ities

, inc

ludi

ng n

earb

y w

iner

ies.

Bra

ndin

g an

d id

entit

y sh

ould

be

acco

mpl

ishe

d in

par

t by

wel

l des

igne

d an

d co

nsis

tent

ly a

pplie

d w

ayfin

ding

and

sign

age

treat

men

ts th

at c

lear

ly id

entif

y w

here

one

is

with

in th

e To

wn.

For

new

shop

pers

com

ing

into

Los

Gat

os fo

r ret

ail a

t the

Nor

th 4

0, th

e N

orth

40

coul

d se

rve

as a

“ga

tew

ay”

to th

e To

wn

with

info

rmat

ion

kios

ks (b

oth

porta

ble/

seas

onal

and

per

man

ent).

R

etai

l Str

ateg

y 1.

5: Im

prov

e W

ay F

indi

ng a

nd P

ublic

Par

king

Sig

nage

. So

me

key

info

rman

ts re

porte

d th

at a

per

cept

ion

of la

ck o

f par

king

pre

sent

s a b

arrie

r to

loca

l res

iden

ts

patro

nizi

ng D

ownt

own

mer

chan

ts a

nd b

usin

esse

s. M

ost r

esid

ents

vis

it D

ownt

own

by c

ar

and

park

ing

whi

le a

dequ

ate

is so

met

imes

be

diff

icul

t to

find

or is

not

alw

ays i

n th

e m

ost

N

orth

For

ty S

peci

fic P

lan

Mar

ket S

tudy

and

Bus

ines

s Dev

elop

men

t Stra

tegy

Pa

ge 9

of 1

50

conv

enie

nt lo

catio

ns.

Inst

alla

tion

of b

ette

r d

irect

iona

l sig

nage

or e

lect

roni

c si

gns w

ith

avai

labl

e sp

aces

not

ed lo

ts c

ould

hel

p ov

erco

me

this

per

cept

ion.

R

etai