An Overview on Service Tax in India

49

An Overview on

-

Upload

adityabirla -

Category

Documents

-

view

4 -

download

0

Transcript of An Overview on Service Tax in India

An Overview on

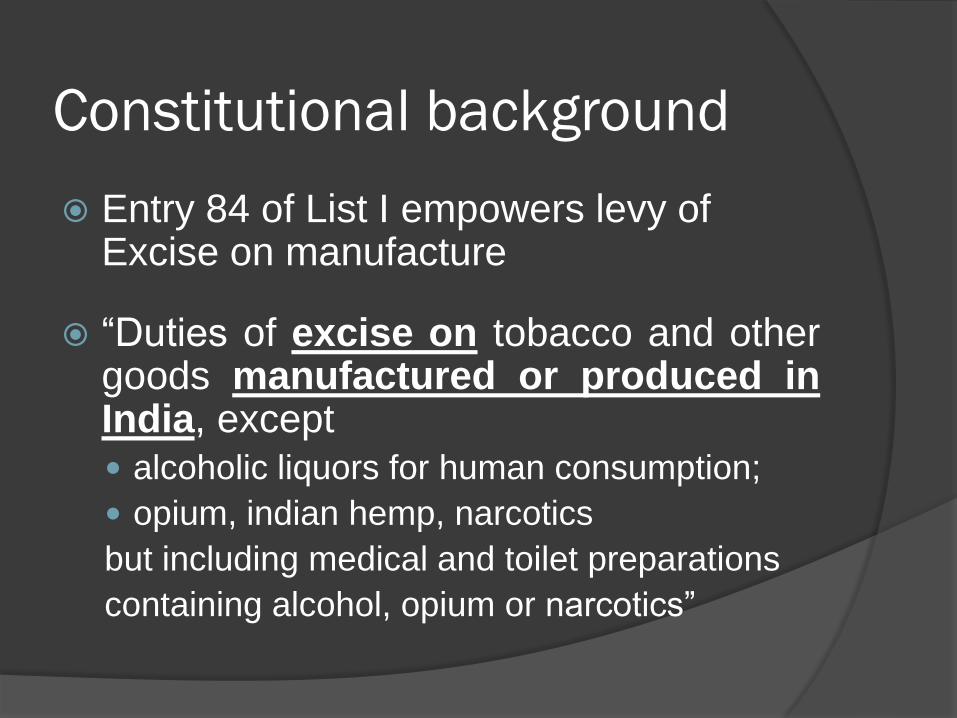

Constitutional background

Entry 84 of List I empowers levy of Excise on manufacture

“Duties of excise on tobacco and othergoods manufactured or produced inIndia, except

alcoholic liquors for human consumption;

opium, indian hemp, narcotics

but including medical and toilet preparations

containing alcohol, opium or narcotics”

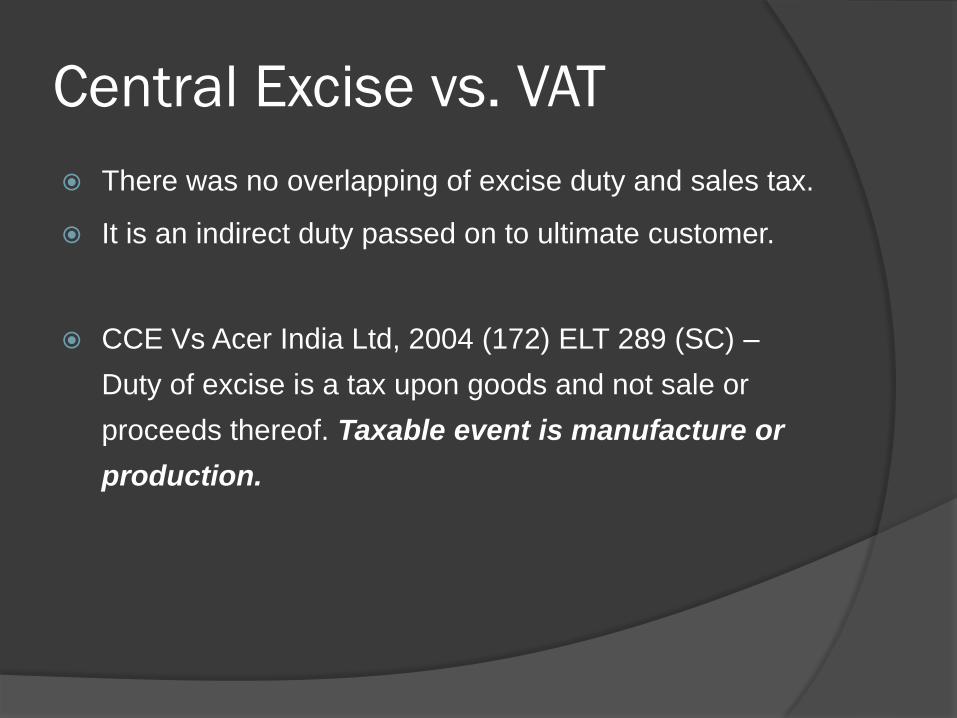

Central Excise vs. VAT

There was no overlapping of excise duty and sales tax.

It is an indirect duty passed on to ultimate customer.

CCE Vs Acer India Ltd, 2004 (172) ELT 289 (SC) –

Duty of excise is a tax upon goods and not sale or

proceeds thereof. Taxable event is manufacture or

production.

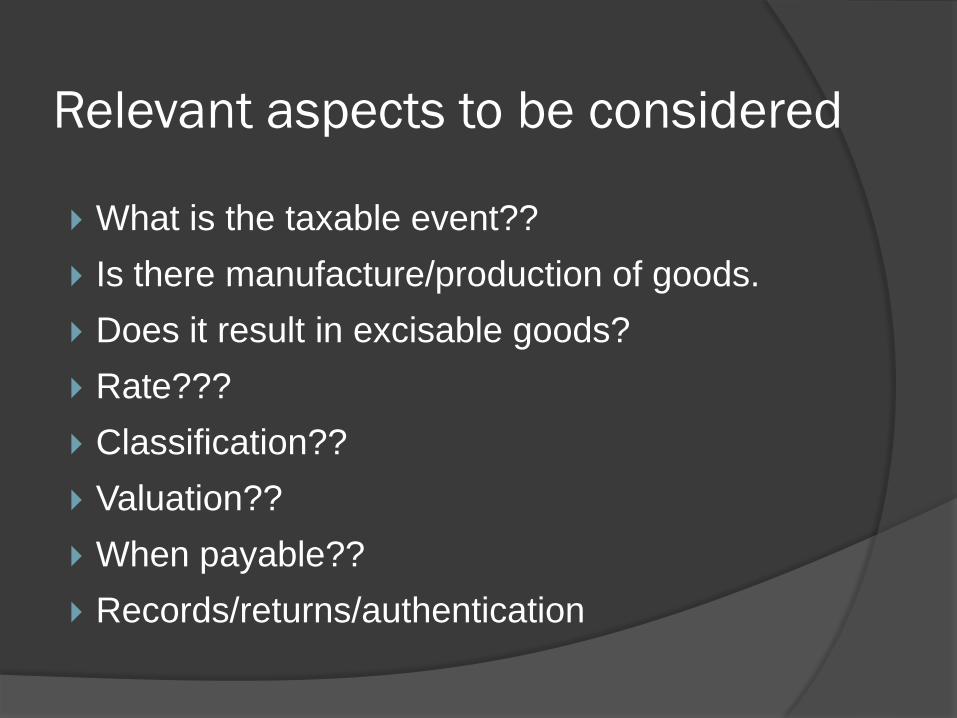

Relevant aspects to be considered

What is the taxable event??

Is there manufacture/production of goods.

Does it result in excisable goods?

Rate???

Classification??

Valuation??

When payable??

Records/returns/authentication

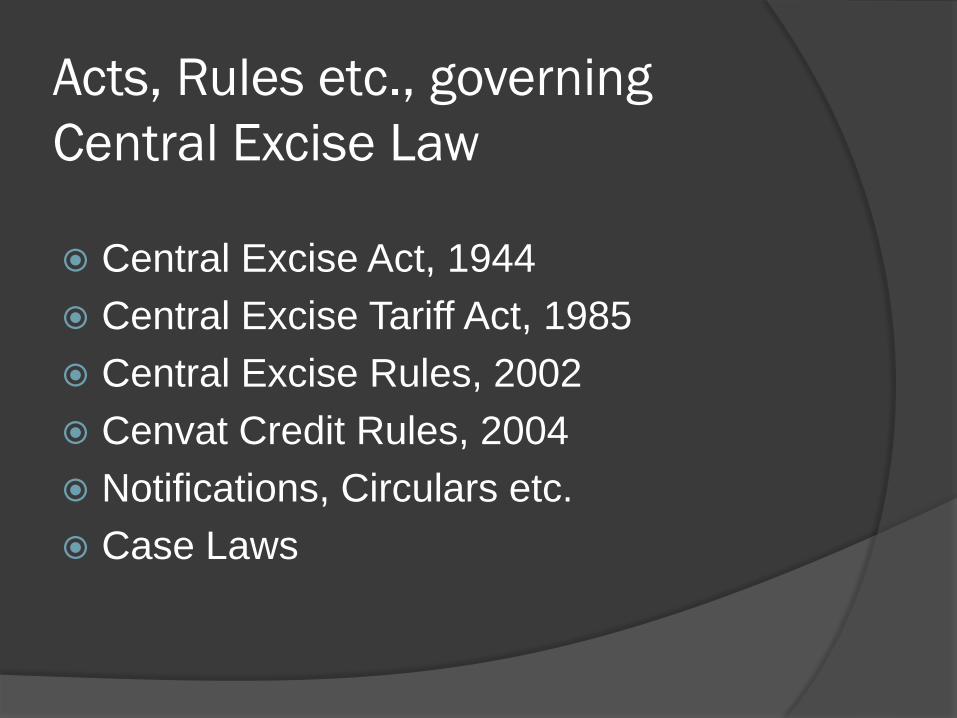

Acts, Rules etc., governing

Central Excise Law

Central Excise Act, 1944

Central Excise Tariff Act, 1985

Central Excise Rules, 2002

Cenvat Credit Rules, 2004

Notifications, Circulars etc.

Case Laws

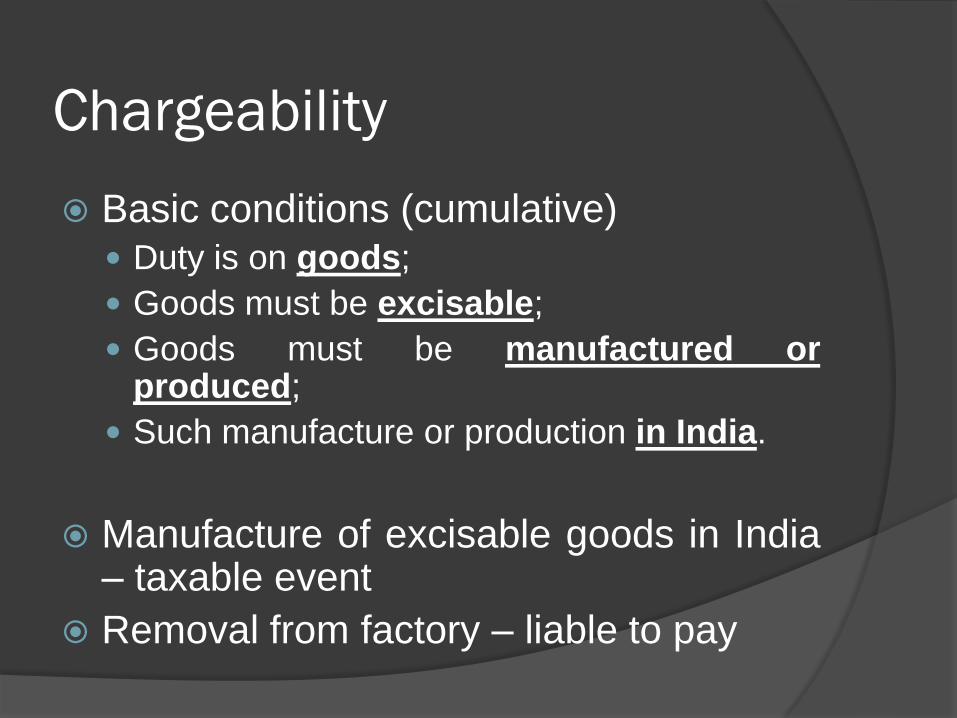

Chargeability

Section 3 – charging section

Somaiya Organics Ltd Vs State of UP,2001 (130) ELT 3 (SC) – the wordcollection in Art.265 would meanphysical realization of tax, which islevied or imposed. Levy and collect arenot synonymous terms.

Levy means charging or impositionof tax, collect means physicalrealization.

Chargeability

Basic conditions (cumulative)

Duty is on goods;

Goods must be excisable;

Goods must be manufactured orproduced;

Such manufacture or production in India.

Manufacture of excisable goods in India– taxable event

Removal from factory – liable to pay

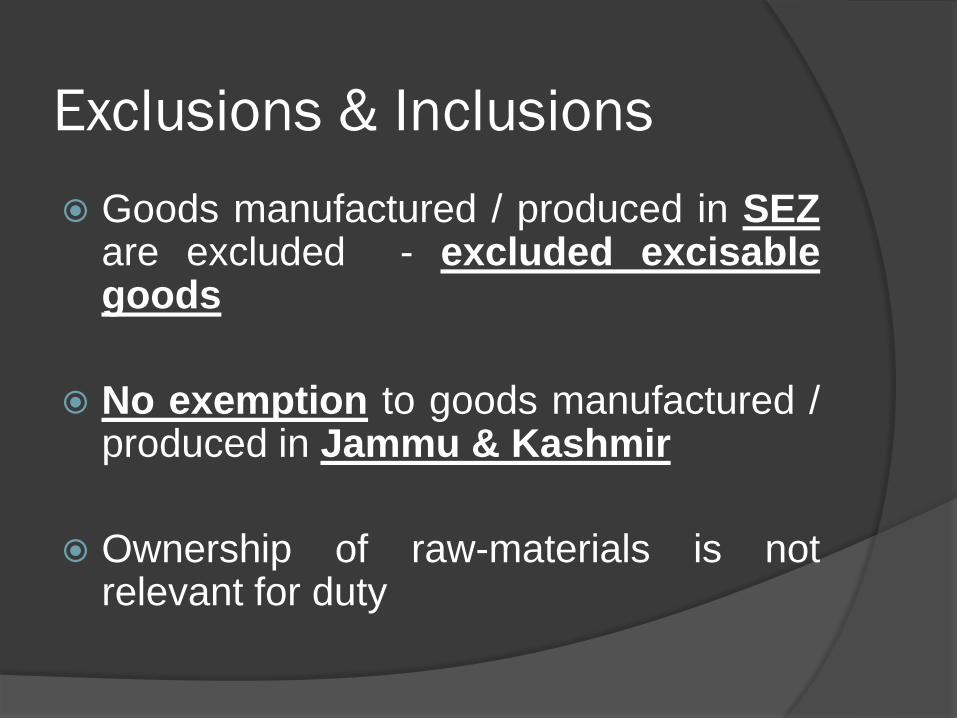

Exclusions & Inclusions

Goods manufactured / produced in SEZare excluded - excluded excisablegoods

No exemption to goods manufactured /produced in Jammu & Kashmir

Ownership of raw-materials is notrelevant for duty

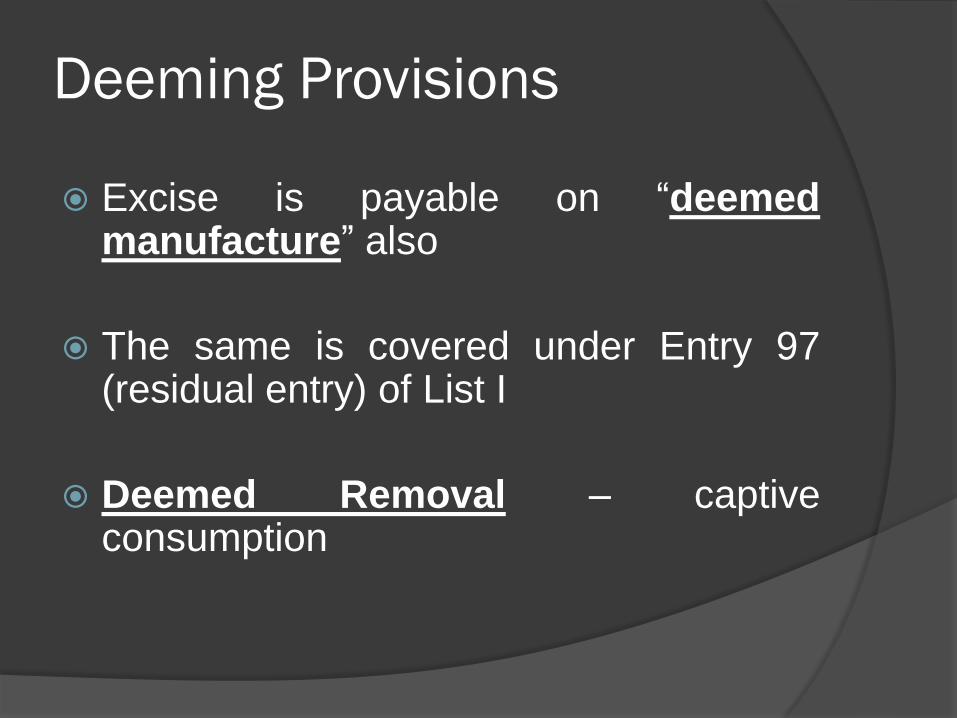

Deeming Provisions

Excise is payable on “deemedmanufacture” also

The same is covered under Entry 97(residual entry) of List I

Deemed Removal – captiveconsumption

Person liable to pay excise duty

Generally – Manufacturer / Producer ofexcisable goods

Exceptions

Goods stored in warehouse – person whostores goods;

Molasses produced in Khandasari sugarfactory – producer who procures for use inmanufacture of any commodity.

Rate of Duty The general excise duty rate is 12%

Education Cess @ 2%

Secondary and Higher Education Cess @1%

Effective rate is 12.36%

Duty payable is as applicable at the timeof removal i.e., clearance from factory

Duty payable even when not collected(Sec. 3)

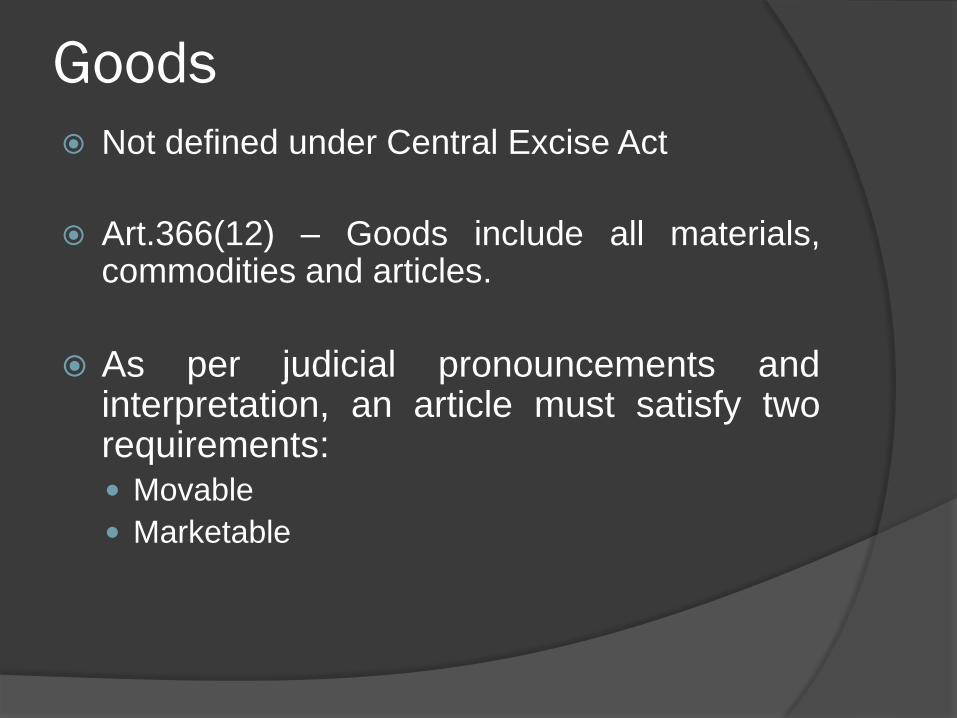

Goods

Not defined under Central Excise Act

Art.366(12) – Goods include all materials,commodities and articles.

As per judicial pronouncements andinterpretation, an article must satisfy tworequirements: Movable

Marketable

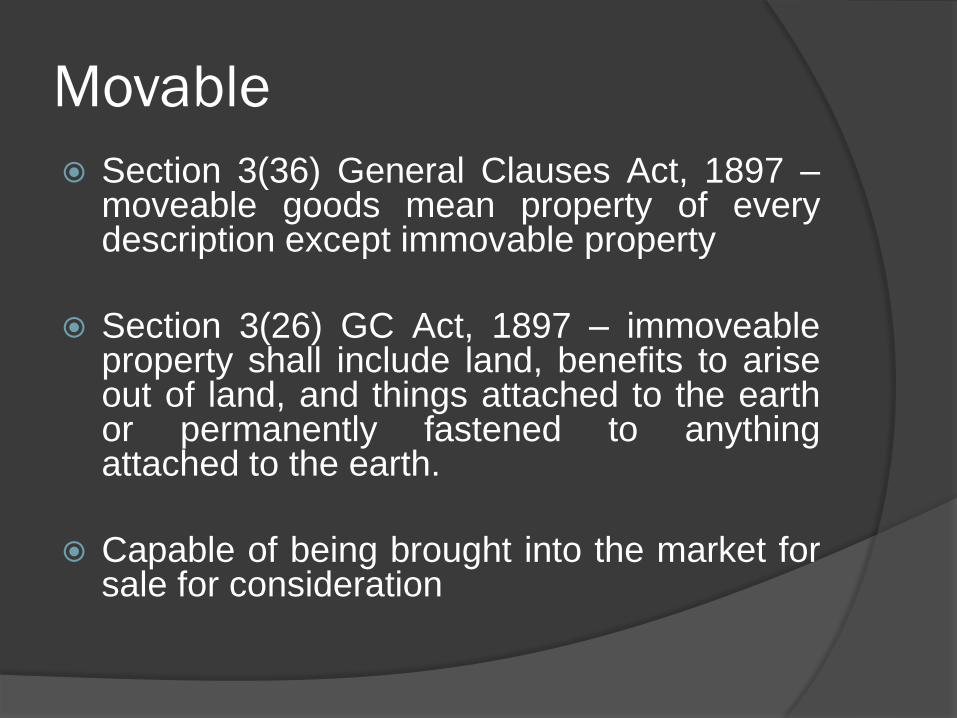

Movable

Section 3(36) General Clauses Act, 1897 –moveable goods mean property of everydescription except immovable property

Section 3(26) GC Act, 1897 – immoveableproperty shall include land, benefits to ariseout of land, and things attached to the earthor permanently fastened to anythingattached to the earth.

Capable of being brought into the market forsale for consideration

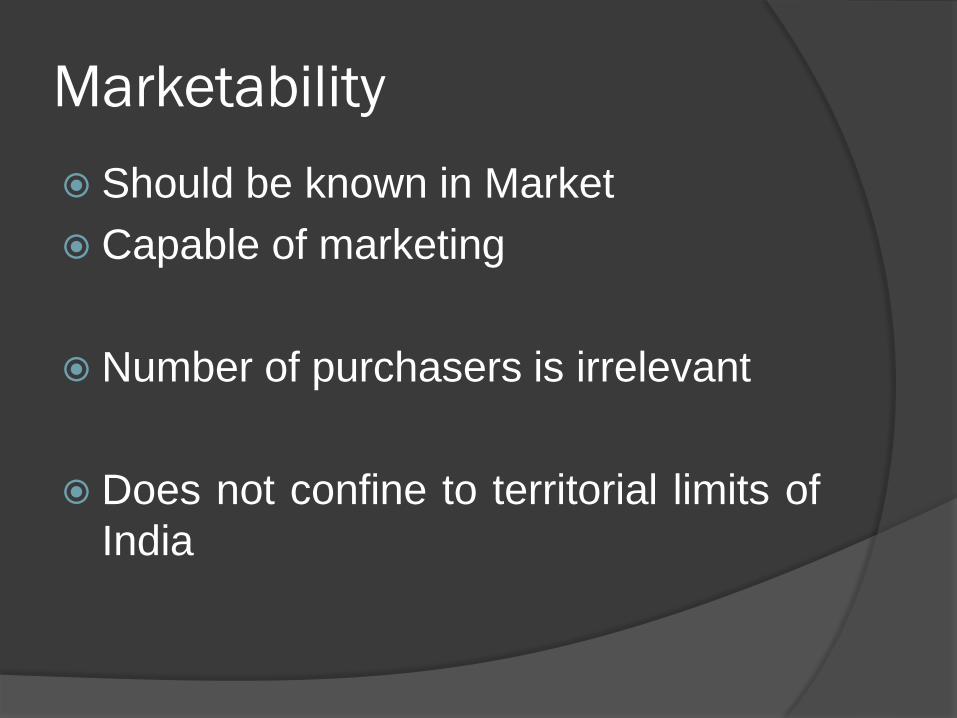

Marketability

Should be known in Market

Capable of marketing

Number of purchasers is irrelevant

Does not confine to territorial limits of

India

Excisable Goods

Section 2(d) of CE Act – it means goodsspecified in the First and SecondSchedules to the CE Tariff Act, 1985 asbeing subject to a duty of excise andincludes salt.

Explanation – Goods include any article,material or substance which is capableof being bought and sold for aconsideration and such goods shall bedeemed to be marketable.

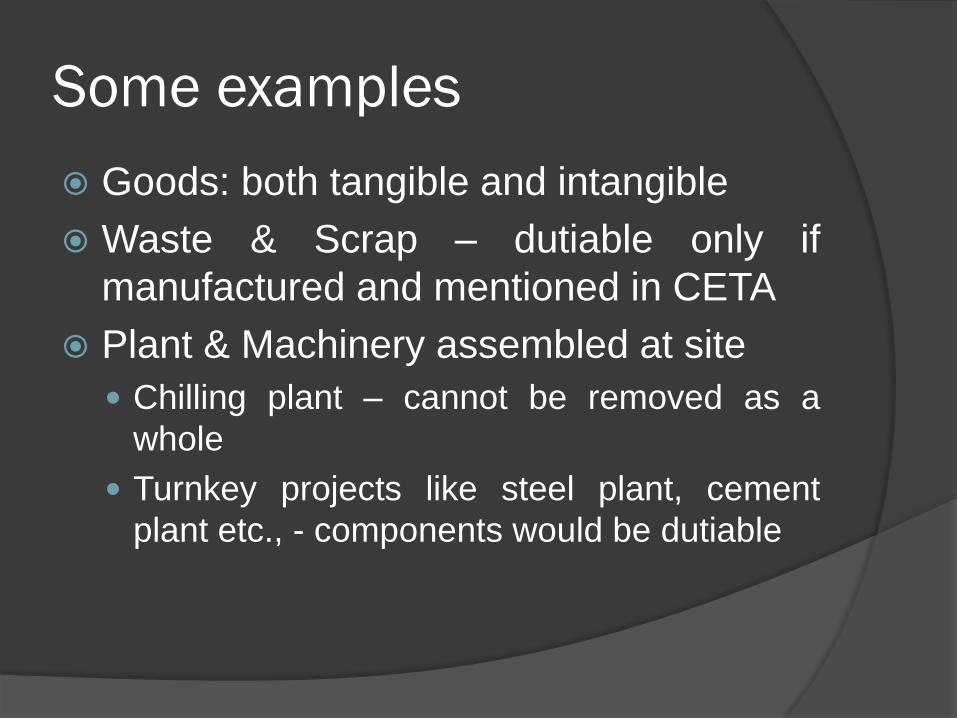

Some examples

Goods: both tangible and intangible

Waste & Scrap – dutiable only if

manufactured and mentioned in CETA

Plant & Machinery assembled at site

Chilling plant – cannot be removed as a

whole

Turnkey projects like steel plant, cement

plant etc., - components would be dutiable

Case for Deemed Removal

Assessee imported various parts andcomponents for testing equipment. The testingequipment was manufactured and captivelyused.

Assessee claimed that goods were not takenout of premises.

Since there is no removal of goods, duty is notpayable.

Apex Court held that “it is a case of deemedremoval and hence duty to be paid”

Manufacture

“Manufacture” includes any process, -

◦ i) incidental or ancillary to the completion of a

manufactured product;

◦ ii) which is specified in relation to any goods in the

Section or Chapter notes of the First Schedule to the

Central Excise Tariff Act, 1985 (5 of 1986) as amounting to

manufacture; or

Manufacture

◦ iii) which, in relation to the goods specified in the Third Schedule,

involves packing or repacking of such goods in a unit container or

labelling or re-labelling of containers including the declaration or

alteration of retail sale price on it or adoption of any other

treatment on the goods to render the product marketable to the

consumer

and the word “manufacturer” shall be construed accordingly and shall

include not only a person who employs hired labour in the production

or manufacture of excisable goods, but also any person who engages in

their production or manufacture on his own account;

Manufacture

Definition starts with the word “includes”

3 limbs in the definition

2nd and 3rd limb – “Deemed manufacture”

Manufacture

Taxable event for central excise duty is

manufacture or production in India.

„Manufacture‟ can be

(a) as defined by Court or

(b) Deemed manufacture.

Manufacture

As defined by Courts

„Manufacture‟ takes place only when the

process results in a commercially

different article or commodity

manufacture means bringing into

existence a new substance. A new and

different article must emerge having a

distinctive name, character or use.

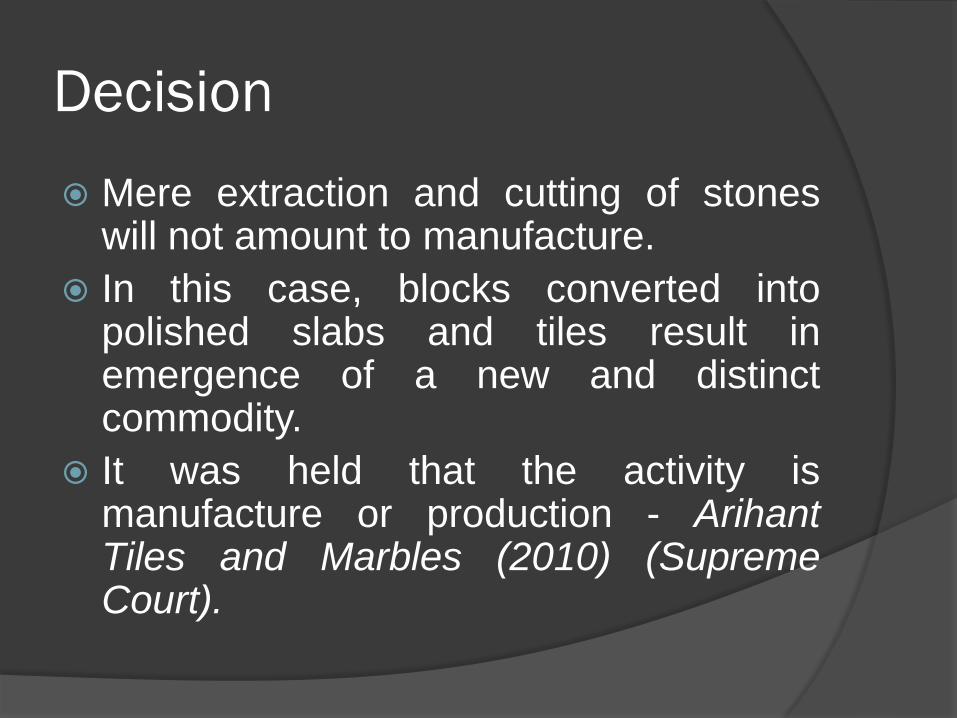

Case Study - Manufacture

Assessee was engaged in business of

polished slabs and tiles.

Assessee was getting raw material

marble blocks from mine owners and

processed it by various activities.

Assessee contended that the activity is

not „manufacture‟.

Decision

Mere extraction and cutting of stoneswill not amount to manufacture.

In this case, blocks converted intopolished slabs and tiles result inemergence of a new and distinctcommodity.

It was held that the activity ismanufacture or production - ArihantTiles and Marbles (2010) (SupremeCourt).

Deemed Manufacture

Deemed manufacture is a process as

specified in CETA.

Over 35 processes have been specified

Repacking, relabeling, putting or altering

MRP

Deemed Manufacture

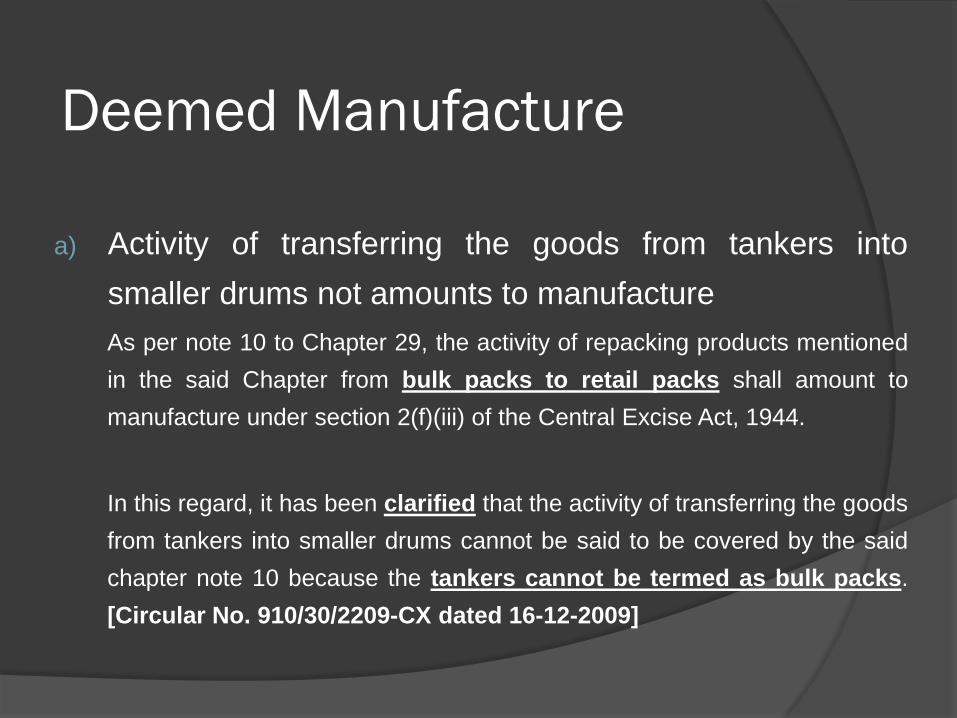

a) Activity of transferring the goods from tankers into

smaller drums not amounts to manufacture

As per note 10 to Chapter 29, the activity of repacking products mentioned

in the said Chapter from bulk packs to retail packs shall amount to

manufacture under section 2(f)(iii) of the Central Excise Act, 1944.

In this regard, it has been clarified that the activity of transferring the goods

from tankers into smaller drums cannot be said to be covered by the said

chapter note 10 because the tankers cannot be termed as bulk packs.

[Circular No. 910/30/2209-CX dated 16-12-2009]

Instances of Processes not amounting to Manufacture:

Final Products Product /

Process/Activity

Citation

Aluminium Cutting, drilling and

punching of aluminium

section

CCE Vs. Ajit India Pvt. Ltd.

2000 (119) ELT 274 (S.C.)

Aluminium cans (torch

bodies)

Aluminium slugs converted

to intermediate product

Union Carbide India Ltd. Vs.

CCE 1986 (24) ELT 169

(S.C); Geep Industrial

Syndicate Ltd. Vs. CG 1987

(31) ELT 865 (S.C)

Butter Stirring of cream State of Tamil Nadu Vs.

Bharat Diary Farm 1992

(61) ELT 25 (Mad.)

BOPP Films Winding, slitting and packing CC&CE Vs. Crown Tapes

Pvt. Ltd. 2009 (233) ELT

357 (Tri. Ahmd)

Cable Joining Kits Putting together different

duty paid items not

manufacture

XI Telecom Ltd. Vs. CCE

1999 (105) ELT 263 (A.P.)

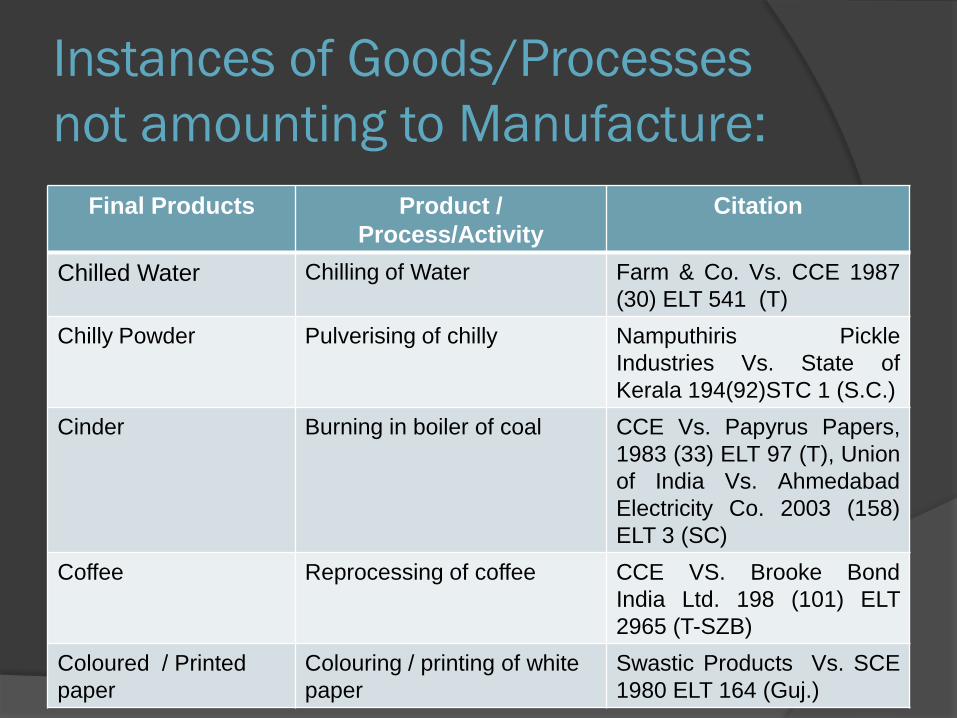

Instances of Goods/Processes

not amounting to Manufacture:

Final Products Product /

Process/Activity

Citation

Chilled Water Chilling of Water Farm & Co. Vs. CCE 1987

(30) ELT 541 (T)

Chilly Powder Pulverising of chilly Namputhiris Pickle

Industries Vs. State of

Kerala 194(92)STC 1 (S.C.)

Cinder Burning in boiler of coal CCE Vs. Papyrus Papers,

1983 (33) ELT 97 (T), Union

of India Vs. Ahmedabad

Electricity Co. 2003 (158)

ELT 3 (SC)

Coffee Reprocessing of coffee CCE VS. Brooke Bond

India Ltd. 198 (101) ELT

2965 (T-SZB)

Coloured / Printed

paper

Colouring / printing of white

paper

Swastic Products Vs. SCE

1980 ELT 164 (Guj.)

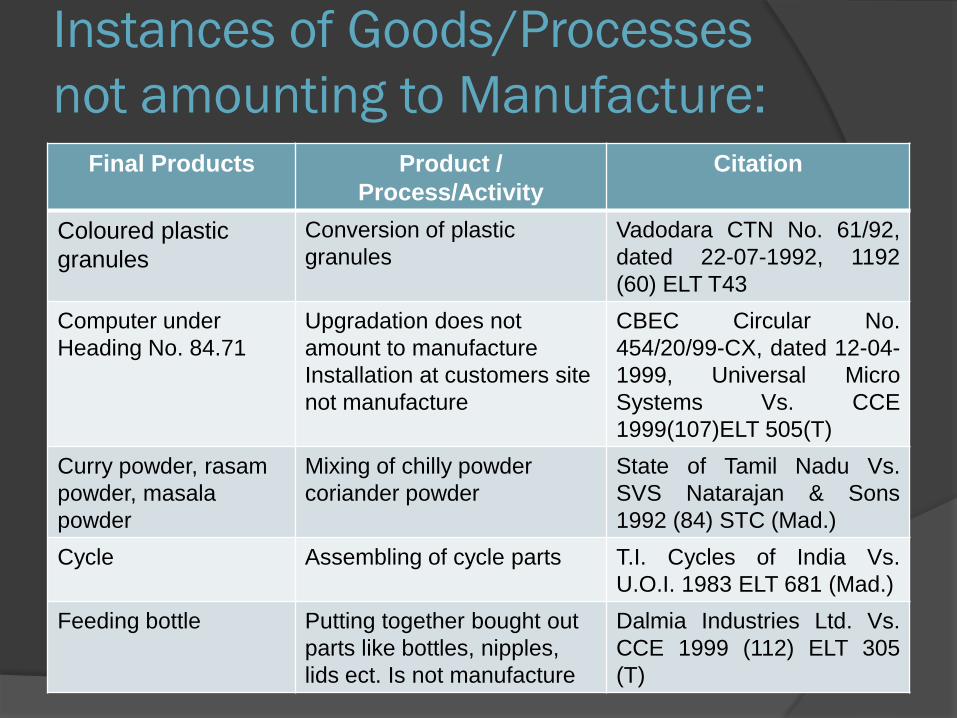

Instances of Goods/Processes

not amounting to Manufacture:Final Products Product /

Process/Activity

Citation

Coloured plastic

granules

Conversion of plastic

granules

Vadodara CTN No. 61/92,

dated 22-07-1992, 1192

(60) ELT T43

Computer under

Heading No. 84.71

Upgradation does not

amount to manufacture

Installation at customers site

not manufacture

CBEC Circular No.

454/20/99-CX, dated 12-04-

1999, Universal Micro

Systems Vs. CCE

1999(107)ELT 505(T)

Curry powder, rasam

powder, masala

powder

Mixing of chilly powder

coriander powder

State of Tamil Nadu Vs.

SVS Natarajan & Sons

1992 (84) STC (Mad.)

Cycle Assembling of cycle parts T.I. Cycles of India Vs.

U.O.I. 1983 ELT 681 (Mad.)

Feeding bottle Putting together bought out

parts like bottles, nipples,

lids ect. Is not manufacture

Dalmia Industries Ltd. Vs.

CCE 1999 (112) ELT 305

(T)

Instances of Goods/Processes

not amounting to Manufacture:Final Products Product / Process/Activity Citation

Filler wire Straightening and cutting into

required sizes of wires

(stainless steel)

D&H Sechron Electrodes Pvt.

Ltd. Vs. CCE 1990 (40) ELT

401 (T)

Furniture (for

resale)

Polishing / colouring of old

furniture

CST Vs. Musarafalli Kutbuddin

35 STC 503 (Bom.) CST Vs.

Habib Kasambai 35 STC 560

(Bom.)

Garland /

bouquets

Preparation of flowers Sudhir Ch. Mukherjee Vs. Addl.

Commissioner of CT 1976 (37)

STC 554 (Cal.)

Ingots / billets Recycling of aluminium waste Salco Extrusions P. Ltd. Vs.

CCE 1984 (16) ELT 356 (T)

Jelly (stone) (See

contra decision

under Table

below)

Breaking of boulders Reliable Rock Builders Vs.

State of Karnataka, 49 STC 110

(Kant); Kher Stone Crushers

Vs. G.M. District Industries

Centre, 1992 (62) ELT 586

(M.P.)

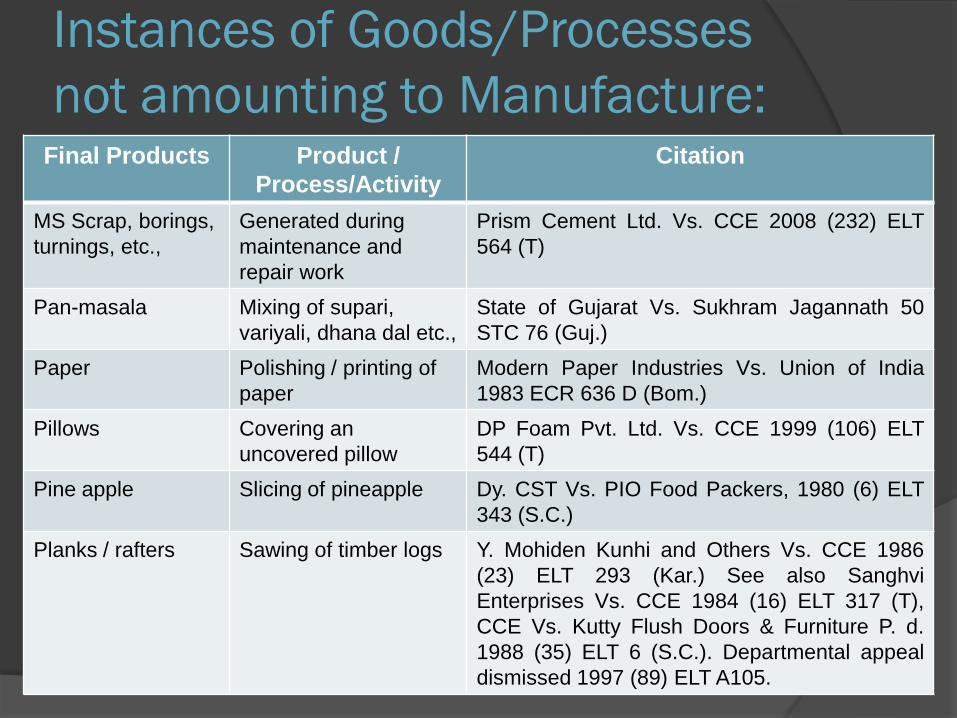

Instances of Goods/Processes

not amounting to Manufacture:Final Products Product /

Process/Activity

Citation

MS Scrap, borings,

turnings, etc.,

Generated during

maintenance and

repair work

Prism Cement Ltd. Vs. CCE 2008 (232) ELT

564 (T)

Pan-masala Mixing of supari,

variyali, dhana dal etc.,

State of Gujarat Vs. Sukhram Jagannath 50

STC 76 (Guj.)

Paper Polishing / printing of

paper

Modern Paper Industries Vs. Union of India

1983 ECR 636 D (Bom.)

Pillows Covering an

uncovered pillow

DP Foam Pvt. Ltd. Vs. CCE 1999 (106) ELT

544 (T)

Pine apple Slicing of pineapple Dy. CST Vs. PIO Food Packers, 1980 (6) ELT

343 (S.C.)

Planks / rafters Sawing of timber logs Y. Mohiden Kunhi and Others Vs. CCE 1986

(23) ELT 293 (Kar.) See also Sanghvi

Enterprises Vs. CCE 1984 (16) ELT 317 (T),

CCE Vs. Kutty Flush Doors & Furniture P. d.

1988 (35) ELT 6 (S.C.). Departmental appeal

dismissed 1997 (89) ELT A105.

Instances of Goods/Processes

not amounting to Manufacture:Final Products Product /

Process/Activity

Citation

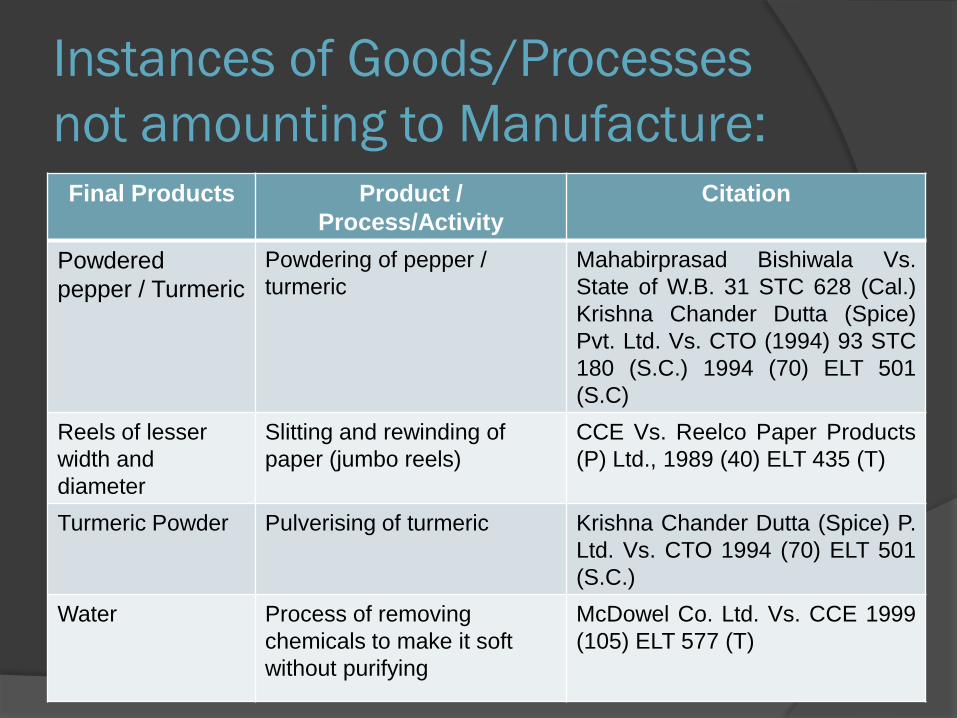

Powdered

pepper / Turmeric

Powdering of pepper /

turmeric

Mahabirprasad Bishiwala Vs.

State of W.B. 31 STC 628 (Cal.)

Krishna Chander Dutta (Spice)

Pvt. Ltd. Vs. CTO (1994) 93 STC

180 (S.C.) 1994 (70) ELT 501

(S.C)

Reels of lesser

width and

diameter

Slitting and rewinding of

paper (jumbo reels)

CCE Vs. Reelco Paper Products

(P) Ltd., 1989 (40) ELT 435 (T)

Turmeric Powder Pulverising of turmeric Krishna Chander Dutta (Spice) P.

Ltd. Vs. CTO 1994 (70) ELT 501

(S.C.)

Water Process of removing

chemicals to make it soft

without purifying

McDowel Co. Ltd. Vs. CCE 1999

(105) ELT 577 (T)

Instances of Processes amounting to Manufacture:Final

Products

Product / Process/Activity Citation

Audio

Cassettes

Recording of audio cassettes

amounts to manufacture as

pre-recorded cassette is

distinct

Gramophone Co. Ltd. Vs. CC 1999 (114)

ELT 770 (SC)

Bagasse Crushing of sugarcane Deccan Sugar and Abkhari Company

Vs. Union of India, 1986 (26) ELT 209

(Mad.)

Bed Sheets,

bed spreads

and table

cloths

Cutting, hemming and

stitching of running cloth

Kapri International Vs. CCE 1986 (23)

ELT 538 (T)

Biris Rolling of Tobacco Y. Tirupathy Rao Vs. CCE 1983 ELT

2346 (AP)

Brass Mixing of copper & Zinc Khandelwal Metal & Engg. V. Union of

India 1983 ELT 292 (Del.) (affirmed in

1985(20)ELT 222 (S.C.)

Brass tubes

new

Marking and remarking of

tubes of brass out of old brass

tubes

Multi. Metal Ltd. Vs. CCE 1995 (75) ELT

938 (T) affirmed by the Supreme Court

in 1995 (78) ELT A31

Instances of Goods/Processes

amounting to Manufacture:Final

Products

Product / Process/Activity Citation

Bright bars Drawing of round bars Veekayan Industries Vs. CCE 1985

(21) ELT 596 (T)

Camphor

Cubes

Conversion of camphor

granules

Om Prakash Gupta Vs. CTO 38 STC

73 (Cal.)

Canned Foods Canning of vegetable

products

Ramnagar Cane & Sugar Co. Vs.

Union of India, 1983 ELT 6 (Raj.)

Chappals Assembly of rubber sole &

rubber strap mouldings

Achamma Sebastian Vs. State of

Kerala, 1967 (20) STC 483 (Ker.)

Cinema Wall

paper

Printing of paper CCE Vs. Sudhakar Litho Printers, 1988

(36) ELT 346 (T)

Circles Rolling & billets of copper Union of India Vs. Ramlal, 1978 ELT

(J389) (SC)

Coconut fiber Conversion of coconut husk DCST Vs. Coco fibers, 1991 (53) ELT

515 (SC)

Instances of Goods/Processes

amounting to Manufacture:Final

Products

Product / Process/Activity Citation

Computers Assembly of computer from

duty paid parts amounts to

manufacture

Sheth Computers Pvt. Ltd. Vs. CCE

2000 (121) ELT 738 (T)

Dyed &

printed cloth

Dyeing & printing of grey cloth Lal Woolen and Silk Mills P. Ltd. Vs.

CCE 1999(108) ELT 7 (S.C)

Evacuated

Bottles

Empty bottles cleaned,

siliconized, evacuated sealed

and sterlised to make a new

product

Shri Krishna Keshav Laboratories

Ltd. Vs. CCE 1999 (105) ELT 117 (T)

Fruit Drink Conversion of fruit pulp to ready

made drink

Godrej Foods Ltd. Vs. CCE 2000

(122) ELT 231 (T)

Ghee Boiling of butter Motilal Ramchandra Oswal Vs. State

of Bombay 3 STC 140 (Bom.)

Glass Moulds Grinding polishing of glass

blanks-opthalmic

Forbes Gokak Ltd., Vs. Collector of

C.Ex., 2003 (153) ELT 24 (SC)

Instances of Processes amounting to Manufacture:

Final

Products

Product / Process/Activity Citation

Gittis,

ballast

Crushing of stone boulders Kher Stone Crusher Vs. G.M. Dist.

Industries Centre 1992 (61) ELT 587

(MP-FB); Contra Reliable Rock Builders

Vs. State of Karnataka, 1982 (49) STC

110 (Kar.)

Ground

black

pepper

Grinding of black pepper CCE Vs. Herbal Isolates (P) Ltd. 1994

(74) ELT 929(T)

Hair Oil Addition of perfume to hair oil CCE Vs. Zandu Pharmaceuticals Works

Ltd, 2006 (204) ELT 18 (SC)

Ingots Melting of scrap Iron Rangoon Meal & Refining Com Vs.

State of Tamil Nadu 47 STC 60 (Mad.)

Jewellery Conversion of Crude diamonds Bapalal & Co. Vs. Government of India,

1981 ELT 587 (Mad.)

Masala

Powser

Prepared by grinding and

mixing of various spices and

condiments in certain proportion

– After grinding and mixing,

integredients

AP Products Vs. State of Andhra

Pradesh, 2007 (214) ELT 485 (SC)

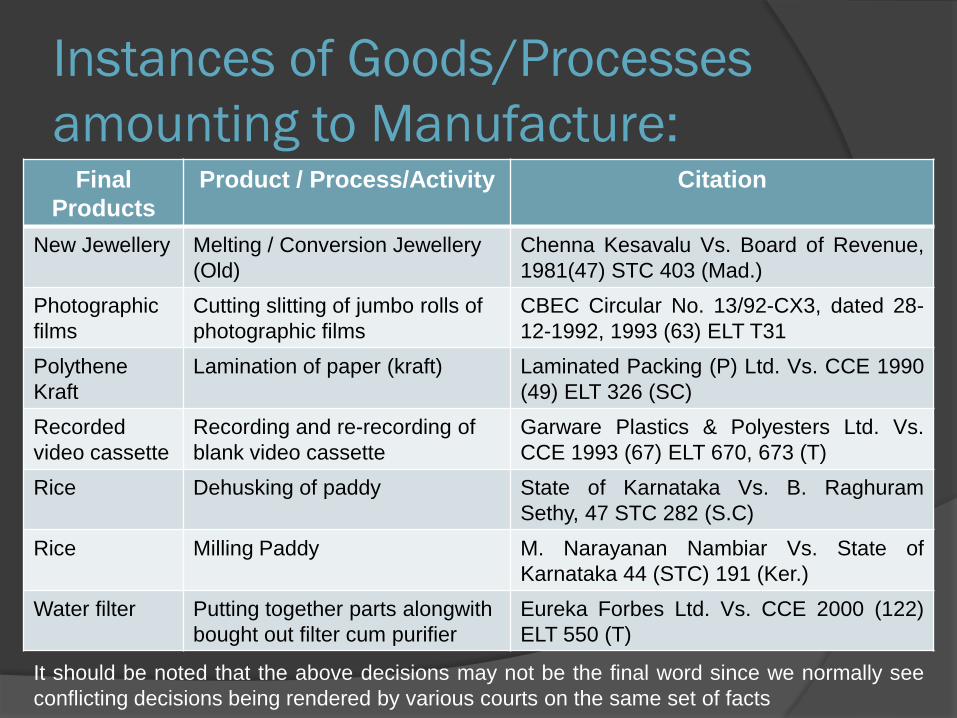

Instances of Goods/Processes

amounting to Manufacture:Final

Products

Product / Process/Activity Citation

New Jewellery Melting / Conversion Jewellery

(Old)

Chenna Kesavalu Vs. Board of Revenue,

1981(47) STC 403 (Mad.)

Photographic

films

Cutting slitting of jumbo rolls of

photographic films

CBEC Circular No. 13/92-CX3, dated 28-

12-1992, 1993 (63) ELT T31

Polythene

Kraft

Lamination of paper (kraft) Laminated Packing (P) Ltd. Vs. CCE 1990

(49) ELT 326 (SC)

Recorded

video cassette

Recording and re-recording of

blank video cassette

Garware Plastics & Polyesters Ltd. Vs.

CCE 1993 (67) ELT 670, 673 (T)

Rice Dehusking of paddy State of Karnataka Vs. B. Raghuram

Sethy, 47 STC 282 (S.C)

Rice Milling Paddy M. Narayanan Nambiar Vs. State of

Karnataka 44 (STC) 191 (Ker.)

Water filter Putting together parts alongwith

bought out filter cum purifier

Eureka Forbes Ltd. Vs. CCE 2000 (122)

ELT 550 (T)

It should be noted that the above decisions may not be the final word since we normally see

conflicting decisions being rendered by various courts on the same set of facts

Manufacture

Whether that something else is a

different commercial commodity having

its distinct character, use and name and

is commercially known as such, is an

important consideration in determining

whether there is a manufacture.

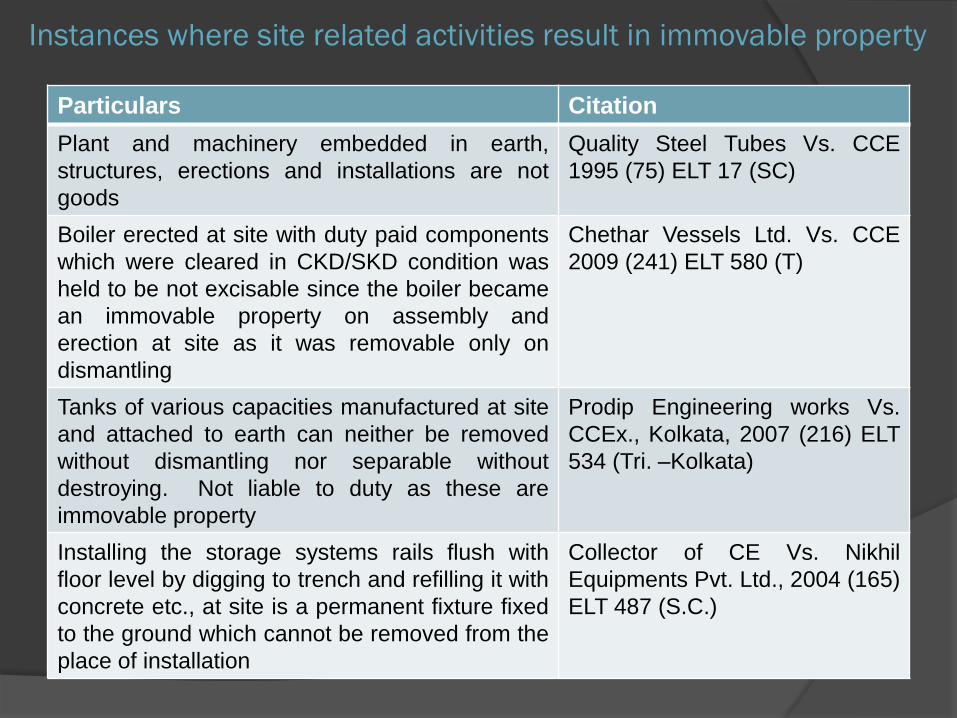

Instances where site related activities result in immovable property

Particulars Citation

Plant and machinery embedded in earth,

structures, erections and installations are not

goods

Quality Steel Tubes Vs. CCE

1995 (75) ELT 17 (SC)

Boiler erected at site with duty paid components

which were cleared in CKD/SKD condition was

held to be not excisable since the boiler became

an immovable property on assembly and

erection at site as it was removable only on

dismantling

Chethar Vessels Ltd. Vs. CCE

2009 (241) ELT 580 (T)

Tanks of various capacities manufactured at site

and attached to earth can neither be removed

without dismantling nor separable without

destroying. Not liable to duty as these are

immovable property

Prodip Engineering works Vs.

CCEx., Kolkata, 2007 (216) ELT

534 (Tri. –Kolkata)

Installing the storage systems rails flush with

floor level by digging to trench and refilling it with

concrete etc., at site is a permanent fixture fixed

to the ground which cannot be removed from the

place of installation

Collector of CE Vs. Nikhil

Equipments Pvt. Ltd., 2004 (165)

ELT 487 (S.C.)

Instances where site related activities result in

excisable goods and not immovable propertyParticulars Citation

UPS is goods and not an immovable property National Radio & Electronics

Co. Ltd. Vs. CCE 1995 (76)

ELT 436 (T)

RCC Poles erected for electricity purposes

are goods

APSEB Vs. CCE, 1994 (70)

ELT 3 (SC)

Machines first assembled and then affixed to

ground are goods

Wandleside National

Conductors Ltd. Vs. CCE,

1996 (84) ELT 419 (T)

D.G. set assembled at site is goods and

marketable as such, hence the same is

excisable. The D.G. set is assembled and

bolted to the concrete platform so that its

operation is vibration free. The D.G. set could

be easily unbolted and bought and sold.

Therefore, D.G. Set assembled at site cannot

be held to be immovable property. They are

goods and are marketable.

Cheran Spinners Ltd. Vs. CC

Ex. Coimbatore, 2008 (231)

ELT 315 (Tri. – Chennai)

Manufacturer

Person carrying activity of manufacture

i.e, who actually brings new and

identifiable product into existence or

undertakes process as defined in

„deemed manufacture‟.

Job Worker

Brand name owner is not

„manufacturer‟.

Registration Registration is mandatory for

manufacturer or producer of excisable

goods;

Dealer who issues cenvatable invoice.

A unit whose turnover crossed limit of

Rs. 90 lacs shall submit declaration to

the department.

Upon reaching turnover of Rs. 150 lacs,

registration needs to be done.

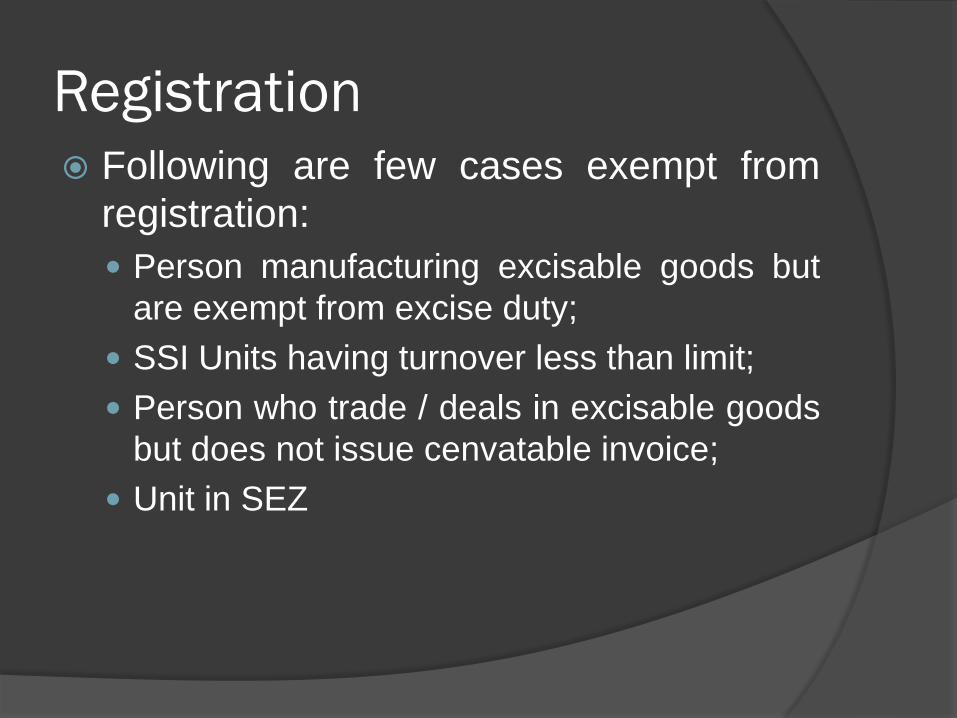

Registration Following are few cases exempt from

registration:

Person manufacturing excisable goods but

are exempt from excise duty;

SSI Units having turnover less than limit;

Person who trade / deals in excisable goods

but does not issue cenvatable invoice;

Unit in SEZ

Registration

Registration under central excise has to

be applied for each premises (factory).

Registration number is 15digit code and

is PAN based. First ten digits is PAN

number. Next 2 digits is XM in case of

manufacturer or XD in case of dealer.

Last 3 digits will be 001, 002, 003 etc.

Small Scale Industry (SSI) Unit whose trunover is less than Rs. 400

lacs are eligible for SSI.

SSI Unit whose turnover in the previousyear is Rs. 400 lacs or less, can claimexemption for turnover upto Rs. 150lacs.

If an assessee who is not willing to takethe exemption of SSI, he has to informin writing to Asst Commissioner. Theoption once availed cannot bewithdrawn.

Small Scale Industry (SSI) Cenvat Credit

On inputs or input services not to be

claimed; and

On capital goods permissible during

exemption period, but not to utilise.

Where a manufacturer has more than

one factory, turnover of all factories to

be clubbed for calculation of Rs. 150 or

Rs. 400 lacs.

Small Scale Industry (SSI) Following Turnover to be excluded while

computing Rs. 400 lacs:

Export turnover;

Turnover of non-excisable goods;

Intermediary products;

Captive consumption.

Payments

Monthly payments to be made on or

before 5th of the following month. In case

of e-payment, due date is 6th.

For the month of March, the due date is

31st March.

SSI units has to pay duty on quarterly

basis by 5th (6th in case of e-payment) of

the month following quarter.

Returns

Monthly returns to be filed on or before

10th of the following month.

In case of SSI, quarterly returns to be

filed on or before 10th of the next month

of the quarter.