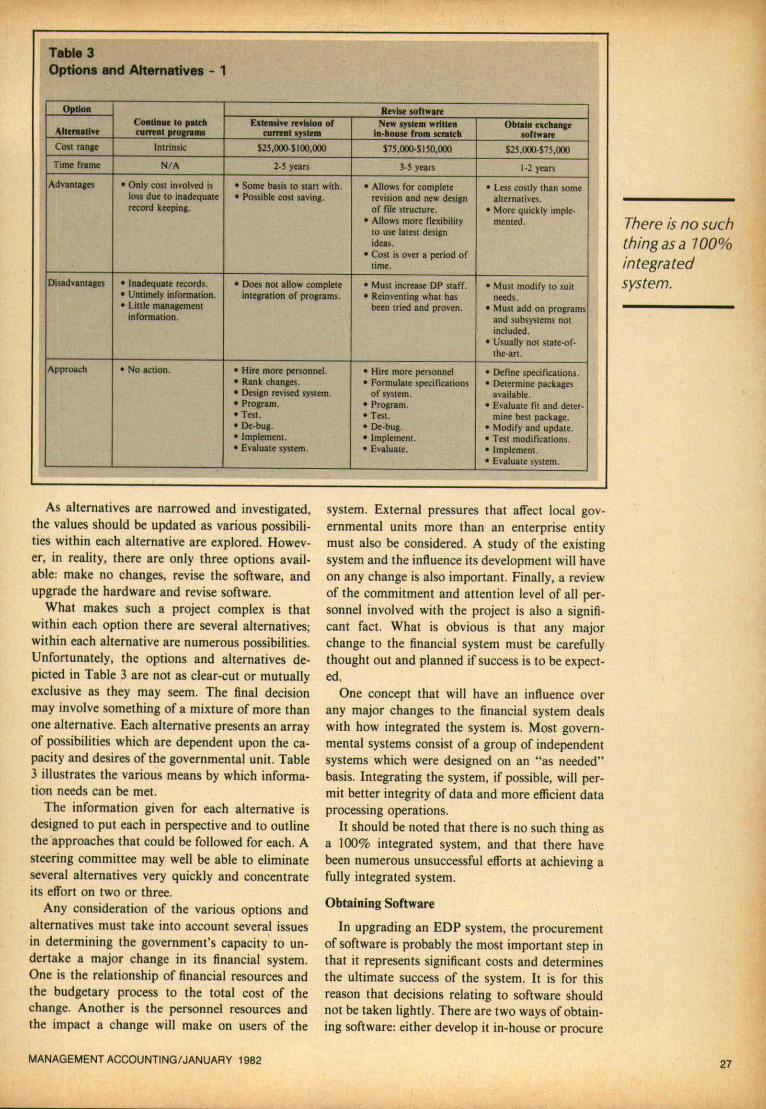

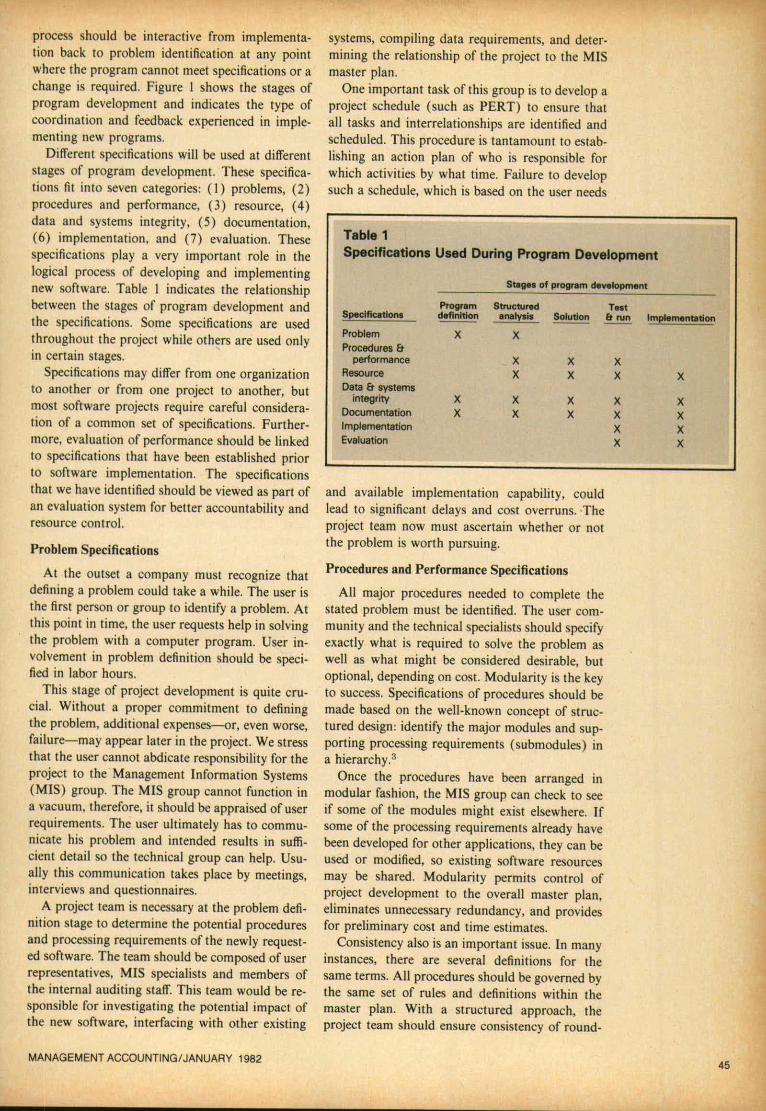

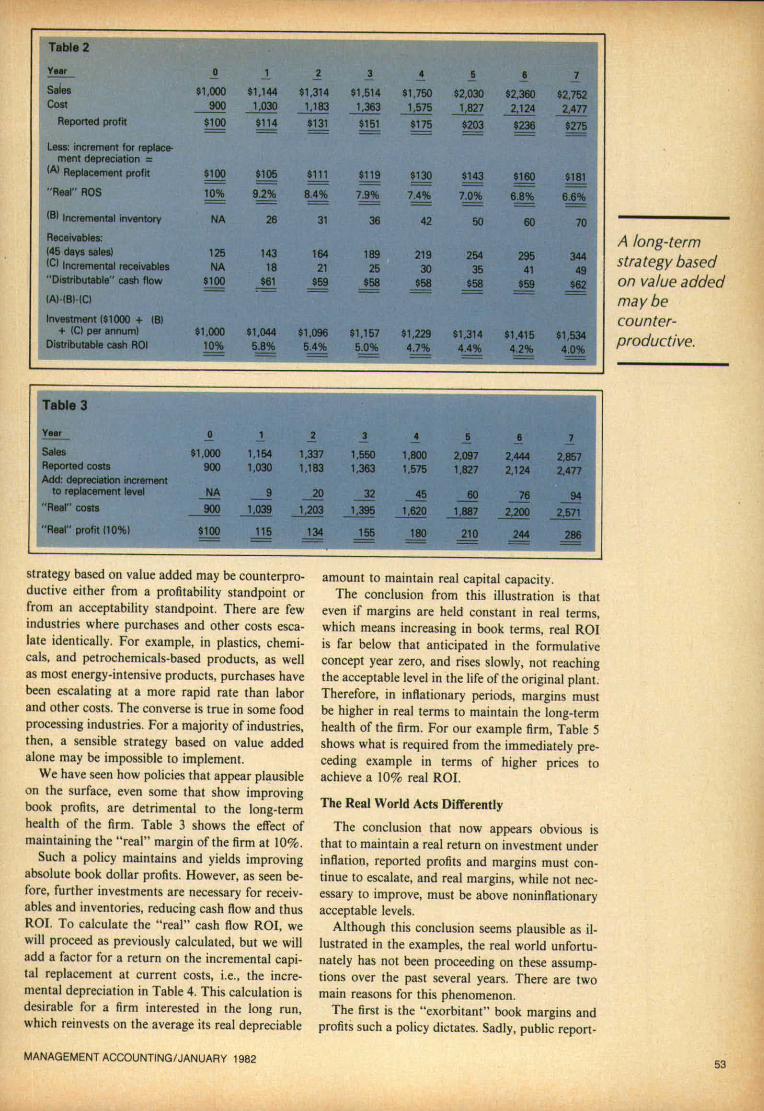

ALI ILN Ft - Strategic Finance

76

ALI ILN Ft 669L0 f N JjjgVNO 3AV VHVd LEq 1 ZzV.93H H MHo ZB /II 500 L) 3 N I9LESO

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ALI ILN Ft - Strategic Finance

ALI ILN Ft

6 6 9 L 0 f N JjjgVNO

3A V VH V d LE q1ZzV.93H H MHo

ZB /II 500 L) 3 N I9LESO

"I'm Convi*nced. OnlySoftware International'sFinancial PackagesMeet All OurRequire ments."

p . s

v .

Call OrWrite Today. -

Software International has sold more General Ledgersystems than all of its major competitors combined.

Elm Square. Andover, MA 01810 (617)475 -5040

The World Leader in Financial Management Software

General Ledger and Financial Reporting Accounts Receivable Accounts Payable Payroll/ PersonnelHuman Resources Fixed Asset Accounting Work Order Management Forecasting

Atlanta (404) 955 -3705 Columbus, OH (614) 773 -2167 Houston (713) 444 -3348 San Jose (408) 292 -9700Boston (617) 729 -8962 Dallas (214) 960 -0220 Los Angeles (213) 573 -0402 Montreal (514) 866 -5728Chicago (312) 298 -3500 Denver (303) 696 -8591 New York (914) 253 -8050 Toronto (416) 924 -1461

Vancouver(604)669 -6122OFFICES AROUND THE WORLD

D &B debunks Myth #1about information holdouts.

"When my clients areestablished businesses

and get allthe credit they need,

why talk toDun & Bradstreet ?"Don't kid yourself. Somebody's checking.

Dun & Bradstreet subscribers do,in fact, make inquiries on long -time cus-tomers. After all, credit policies changeand new credit managers take over.

Something else to keep in mind:those who supply products aren't the only

mes who request D &B Reports. Those who>rovide services, like banks and insurance,ompanies, do too.

When clients ask you, their accoun-nt, to respond to D &B's request forformation about their companies, it's ineir best interests for you to provide it.-cause many suppliers insist on a completed up -to -date D &B Report before talkingisiness. And a comprehensive report,-luding a financial statement, usually as-res the buyer of the best possible terms.

It is essential for America'sisinesses to have an easy- access, third -rty source for this information. That'siy they call on Dun & Bradstreet —over,000,000 inquiries a year from over,000 subscribers— rather than callingyour client or you directly. D &B acts

'ictly as an impartial gatherer of informa-n; we ourselves have no use for theormation per se.

The next time a D &B businessalyst contacts you, cooperate. You'll being your client a favor— because, in a,rld where 4 out of 10 business trans -:ions are done on credit, Dun & Bradstreetthe essential business.

Dun &BradstreetBBa company of

TheDun&BradstreetCorponition

InformationSystems

ManagementAccountingIssuns

MANAGEMENTACCOUNTING

How Weyerhaeuser Made Its MIS Work 16By Dennis Loewe

In the last five years Weyerhaeuser Co. decreased the size of its corporate consolidationsstaff while at the same time it increased the quality and quantity of corporate reporting.How did it achieve this high standard in productivity? It carefully planned its CorporateFinancial Information Systems with special attention given to four key elements: people,system design, software, and operating system.

Improving Financial Information Systems in Local Government 23By Thomas Newkirk

How can a municipal manager determine the best approach to addressing accounting andmanagement information needs? Generally, there are three phases that require the com-mitment and involvement of local officials —needs determination, acquisition and imple-mentation, and operation. It's also important to identify the potential problems when plan-ning to improve the current system.

A Personal Information System Checkup 29By Bradley M. Roof

When is the last time you took time to have a physical examination of your PERIS? If it hasbeen more than a year or two, perhaps your decisions are suffering as a result of thisneglect. PERIS, by the way, means Personal Information System and it includes all theprocesses through which you receive data for decision making. Analyzing your PERIS isimportant to prevent synthemombosis.

Training MIS Users Through Simulation 36By Warren A. DeBord and Jerry D. Siebel

The effectiveness of a true management information system stands and falls, ultimately,on the decision maker's ability to use the information effectively. That is why training usersto use MIS outputs effectively has been one of the most difficult phases of systemsdevelopment. Described here is a successful simulation program, designed to train dealer-ship personnel.

Certificate of Merit, 1980 -81

Find the Right Software Through SpecificationsBy Gary I. Green and Earl A. Wilcox

43

Programming projects typically run past deadlines and exceed budget, but they can becontrolled better by following specifications for development and implementation. Usergroups should be involved in determining these specifications, which fit into seven majorcategories. Here is how Motorola's Semiconductor Group learned from its mistakes.

Pricing Policies Under Inflation 51By William H. Hernandez

Today many firms are under pressure to increase prices for their products because ofincreased costs of manufacturing. But what pricing strategy should a firm adopt: absorbthe cost increase itself, pass through the cost increase and maintain dollar profitability,maintain percentage margins, maintain value added or maintain real margins? The key isfor a firm to assess the long -term strategic implications of its pricing actions.

MANAGEMENT ACCOUNTING /JANUARY 1982

Feature Playing the Consulting Game 56By Earl K. Littrell and Roy H. Glen

Knowing how to use such ploys as "water cooler," ''smoke screen,'' and "shield thyposterior" separates the winners from the losers in the great consulting game which annu-ally rages up and down thousands of corporate corridors. In self- defense, managementaccountants should learn the basic rules by heart.

Research NAA Research Committee Solicits Proposals 70

Researchers are invited to submit proposals on a number of management accountingtopics.

The Costs of Implementing FAS No. 33 71By Research Staff

The costs of reporting inflation adjusted figures have not been too burdensome, accordingto NAA survey of some New York area corporations.

Conference 3rd Annual Controllers' Conference 72

Controllers get the latest data on the economic environment —from mini - computers tomergers —at NAA special conference.

Departments President's Perspective third annual controllers' conference 4

Opinion a conversation with Paul Kolton 6Management Accounting Practices FASB on tax benefit sales 8Management Information Systems MIs Costs 10Letters to the Editor 12

Data Sheet one -third of major firms seek acquisitions 22People in the News 64

Small Business matching businesses with sources of capital 68

Future Assessing and evaluating the effectiveness of accountants has always been a difficult

Issues task. In discussing this issue in March, we delve into the academic deficiencies of entrylevel accountants, the acceptance of accountants by operating personnel, and the evalua-tion of cost accounting departments. In April, we explore the factors involved in the analy-sis of a company. Other future themes: government accounting, May, and budgeting, June.

Cover: "Cowboy hat" is a computer - generated image recorded with a Model 3000 ColorGraphic Recorder manufactured by Matrix Instruments, Inc., Northvale, N.J. Software by SASInstitute, Inc.

Views expressed herein are authors' and do not represent Association policy unless so stated.Reprints of any articles appearing in any issue of MANAGEMENT ACCOUNTING are available from SpecialOrder Department, NAA, 919 Third Ave., New York, N.Y. 10022.

MANAGEMENT ACCOUNTING /JANUARY 1982 3

PRESIDENT'S PERSPECTIVE

Controllers' Conference in Washington

Our Third Annual Controllers' Conference in Washington, D.C., Octo-ber 27 -29, featured outstanding speakers, good course materials, anda productive interchange of information — largely as a result of the rap-

port between the speakers and the audi-

ence.In a unique feature of the three -day con-

ference, in- depth, concurrent full -day work-shops were spent on the acquisition of amini - computer and corporate mergers andacquisitions. The first general session onWednesday was devoted to individual pre-sentations on the impact of inflation on in-ternal planning and control, managementand motivation of the financial manager,and controllership from the divisional con-troller's point of view. In the luncheon ad-dress, the head of an executive search firm

described the qualities that employers looked for in hiring financialexecutives. Three afternoon sessions were devoted to discussion ofthe FASB's foreign currency translation standard, and three sessionsto personal and estate planning, user - driven computer systems, andcorporate tax planning.

Thursday morning Lee B. Spencer, Jr., director of the Division ofCorporate Finance of the Securities and Exchange Commission, de-scribed the SEC's plans under the new administration. The tenor of hispresentation was that the SEC is seeking to streamline filing proce-dures in order to be more responsive to both the investor and thebusiness community and thus aid in the raising of capital. In the wrap -up session, four executives on a special outlook panel exchangedviews on current problems in the business world.

The response to this conference by the more than 100 controllersand financial executives attending was very affirmative. Some com-ments: "Most informative. Need more time on certain topics dis-cussed." "This is my first formal introduction to this subject [mergersIand it was well worth my time." "Well organized — excellent speakers.""Excellent. May I suggest covering in more detail the concern of ac-countants."

Because of the enthusiastic response to this conference, your Asso-ciation will hold the controllers' conference again this year. It also isconsidering the feasibility of presenting the conference at more thanone location to reach a larger audience. Special conferences like thisone demonstrate that the Association can attract member account-ants and other financial executives to educational meetings that arewell- organized, feature knowledgeable speakers, and cover specific,timely topics in depth. We intend to continue to hold such meetings.

EMIL SCHARFFPresident, 1981 -82

MANAGEMENTACCOUNTING

( ISSN 0025 -1690)

VOL. LXIII NO.7 JANUARY 1982

official publication of theNational Association of Accountants

Executive DirectorRobert L. Shultis

PUBLISHERJames D. Collier

EDITORErwin S. Koval

MANAGING EDITORRobert F. Randall

TECHNICAL EDITORMorris Gartenberg

PRODUCTION MANAGERStephen McCrea

FEATURE EDITORKathy Williams

CONTRIBUTING EDITORSLouis Bisgay, Israel Blumenfrucht, JamesBulloch, Earl K. Littrell, Stephen F. Piron,

Grover L. Porter, Jerold M. Weiss

ADVERTISING MANAGERWilliam L. Richardson

BUSINESS & CIRCULATIONMANAGER

Colin C. Campbell

EDITORIAL ASSISTANTSEllen Hannan DelgadoMadeline Krakowsky

ADVERTISING REPRESENTATIVESNew York 10022 —W L. Richardson, NAA,919 Third Ave.. (212) 754 -9896.

Chicago 60611 —James K. Millhouse. 919 N.Michigan Ave., (312) 642 -6625.

Oakland. Calif.. 94611— CoughlinlWheelerCo., 6211 LaSalle St., Suite 5. (415) 339-1914,

Pasadena, Calif. 91105 —Ken Jordan. JJH &S,119 W. Bellvue Dr., (213) 796 -9200.

MANAGEMENT ACCOUNTING (ISSN 0025 1690) is publishedmonthly by the National Association of Accountants. 919Thud Ave., New York. N Y . 10022. Pace 54 00 per copySubscription rates, per year nonmembers. S42.00Second class postage paid at New York, N. V.. and additionalmailing offices To ensure uninterrupted mail service. sendpresent address label and new address including ZIP numberto Membership Records Dept., NAA, 919 Third Ave., NewYork, N.Y., 10022. Allow six weeks for change. POSTMAS-TER. Send address changes 10 MANAGEMENT ACCOUNTING,919 Third Ave. New York. N Y 10022

Copyright Dc1982 by theNational Association of Accountants

4 MANAGEMENT ACCOUNTING /JANUARY 1982

Knowing what it's worthcan I e worth a last.

X i C A NW e w e re n ' t a ro u n d t o h e lp i n t r o d u c e P P R .A I S AL o t h e r b r ig h t i d ea s . Th e w o r ld ' s

t h e h g h t b u lb , B u t we d id h e lp w it h ' la r g es t a p p r a is a l f i r m c a n h e lp y o u ,th e s t r in g - t y p e l aw n t r im m e r a n d to o , w i t h p a t e n t s a n d m u ch m o r e .

WE KNOW VALUES.At l an t a • Ba lt im o r e Ba n g k o k • Ba t s e - D o r t o n • Bu f f a lo • Ch a r lo t t e • Ch ic a g o • C i n c i n n a t i • C l e v e l a n d • D a ll a s - D e n v e r - D e t r o i t • Ho n g Bo n g • Ho n o lu l u • Ho u s t o n • J a k a r t a

8a n s a e C it y • Lo nd o n • Lce An ge l as • Ma d rid • Ma nila • Mex ic o , D.r. - M1a ml • Milan • Milw wan k e e • Min n e a p o lis Mo n t r e a l • c a Or le a n s • Ae w 7 o r k - Pa s a da n a • P h ila d elp h ia • Pit ts tmr ghPort lan d • Pr inc e to n • Bo lli ng Me a dows • Ro me • S t . Lom a • Sa lt Lak e C ity • S an r r a n c i s o o • S e at t le • S in g a po r e - S p ok a n e • S ta m f or d • Ta m pa • T or o nt o • Van c ou v er - Wa sh in gt on , D. C.

OpinionRobert L. Shultis

Notes on a Conversationwith Paul Kolton of FASAC

Recently we enjoyed a long conversation withone of the individuals most involved on the ac-counting scene today —Paul Kolton, chairmanof the Financial Accounting Standards AdvisoryCouncil. Involved, yes, but decidedly not ahousehold name, even among those reason-ably well versed in matters of accounting. ( Nor,for that matter, is the Financial AccountingStandards Advisory Council ( FASAC) famil-iar.) We saw this as an opportunity to have Mr.Kolton explain to us a little about the workingsof the Council and something of his philosophyas well.

Question of BalanceOne problem constantly facing the Financial

Accounting Standards Board is obtaining bal-anced input from all its constituencies as re-gards accounting issues either on its agenda orpotentially on its agenda. Not that there is anydearth of responses to the FASB. Far from it!Every issue generates comments aplenty. Thekey word, however, is "balanced." Are all sec-tors being heard from, and are the many sidesof key questions being explored?

A major function of the Council, according toMr. Kolton, is to supply this balance —to offerthe Board an opportunity to hear reasoned dis-cussion of the important issues it faces. To useMr. Kolton's felicitous phrase, the Councilrepresents the Board's "constituency in micro-cosm." Its 40 members are drawn from indus-try, academia, public accounting, users of fi-nancial information, government, the securitiesindustry and the major professional accountingassociations. (We are privileged to representNAA's membership on the Council.)

The Council meets quarterly, with certain ap-pointed committees, such as the Small Busi-ness Advisory Committee, meeting betweentimes. The meeting discussions are wide rang-ing —both as to the agenda itself and as to the

individual items on the agenda. That the Coun-cil meetings stay on track and accomplish theirpurpose is due in large measure to Mr. Kolton'snot inconsiderable talents as meeting planner,organizer, and, if you will, orchestrator. To en-sure that divergent, but considered, viewpointsare heard, Mr. Kolton will frequently contacttwo or three Council members in advance to beprepared to present briefly their views on par-ticular agenda topics. Then general discussionby the whole group follows, and, subsequent tothe meeting, each member of Council receivesa post- meeting questionnaire that offers themember a further opportunity to comment.

A Full PlateThe agenda of a recent meeting of FASAC

included, among other items, a review of thelatest exposure draft of the FAS No. 8 revision,a discussion of the accounting implications ofthe Economic Recovery Tax Act of 1981, anupdate on FASB activities by Chairman DonKirk, an analysis of the data being reported un-der FAS No. 33, a discussion of the post -em-ployment benefits discussion memorandum,proposed activities within the small businesssector, and the 4 -3/5 -2 Board voting issue. Afull plate, by any definition, and one which af-fec *.s us all —as accountants, as business peo-ple, as citizens_

We asked Mr. Kolton what he felt was theprime purpose of the Council and whether theBoard itself found the deliberations of theCouncil of value. He said "yes," he was com-fortable and convinced that the Council's activi-ties were useful to the Board, citing the factthat the full Board nearly always attends andparticipates in Council discussions. He also hasobserved instances where the comments ofCouncil members are reflected in subsequentBoard discussions.

As for purpose, Mr. Kolton views the Councilas what its name implies —an advisory body —and therefore the Council is not asked to vote,pro or con, on the issues it deliberates. Rather,the Council helps to expose for the Board thewidely divergent ideas and subtleties inherentin nearly every key issue, both those that arenew and those that are being re- evaluated.

Council activities benefit the Board's constit-uencies as well, according to Mr. Kolton, byserving as an "early- warning system" of the im-plications and potential effects of major ac-counting issues before they become final. Fu-ture issues before the Board may well have aneven greater impact on business and the ac-counting profession, making the early- warningsystem even more vital to the standards - setting

process.► ►67

MANAGEMENT ACCOUNTING /JANUARY 1982

0 1 7 1 0 1 J i l 0 1 ' *1 •It's a hard look into your operations today for

better productivity tomorrow.The Citi of Tomorrow brings you

the latest electronic banking. And thepeople who can tell you how to use itbest: Citibankers.

Citibank's financial experts canhelp you take full advantage of newtechnological advances to make yourback office more productive.

They'll make sure your system istailored to your specific business needs.And at the other end, there will alwaysbe a team of Citibankers who knowyour business and can track down any

problem. These Citibankers can alsoshow you how electronic banking canstreamline your present back officeoperation. And they can advise you inother areas, including ways to utilizeyour banks more effectively.

The Citi of Tomorrow. Instead ofjust answers to problems, a strategy toavoid them,

Call Robert Mendes, VP, at (212)559-1980 for more details.

CIT/BAWO'GLOBAL ELECTRONIC BANKING

c 1981 Citibank. N.A Member FDIC The Gtr or Tomorrow and Global Electronic Bankinq are service marks of Citibank. N.A.

ManagementAccountingPracticesLouis Bisgay, Editor

FASB Proposes Accountingfor Purchase and Sale of Tax Benefits

In the wake of the Economic Recovery Tax Actof 1981, which allows a company to sell taxbenefits through a lease, the Financial Ac-counting Standards Board has proposed toclarify the accounting for both buyer and sellerof these benefits. The tax benefits that can beso transferred are credits such as the invest-ment tax credit and deductions under the ac-celerated cost recovery system (ACRS).

The Board had been asked to specify wheth-er or not transactions that are called leases butwhich, in substance, represent solely the pur-chase and sale of tax benefits, should be ac-counted for in accordance with FAS No. 13,"Accounting for Leases." It was the Board'stentative conclusion that such leases are notcovered by Statement No. 13 unless the trans-actions convey the right to use or share residu-al value of the property or involve financing ofthe property.

Under the proposed rules, the seller of taxcredits should account for the proceeds by itsusual method of accounting for those credits —flow through or deferral. The buyer would ac-count for the purchase of the credits as an in-vestment. The seller of deductions under theACRS treats the sales price as a reduction ofthe cost of the related property. The buyer ofACRS deductions would account for the netcost as an asset and amortize it over the leaseterm when tax savings exceed investment.Sellers and buyers of both tax credits andACRS deductions should allocate between thecomponents.

Other FASB Actions

The Board issued Interpretation No. 36, "Ac-counting for Exploratory Wells in Progress at

the End of a Period." It resolves the question ofwhen to charge or expense the costs of an ex-ploratory oil or gas well in progress at the endof a period that is determined to be a dry holebefore financial statements for that period areissued. The Interpretation clarifies that thecosts incurred through the end of the periodshould be expenses for that period.

According to a research report released bythe Board, more summary indicators of a com-pany's financial performance than just earningsper share increasingly should form the basis forcommunication with readers of financial state-ments. The study was undertaken by AssociateProfessor Paul Frishkoff of the University of Or-egon to provide an historical perspective and areport on the status of summary indicators infinancial reporting. Summary indicators are de-vices that condense information about a com-pany's performance or risk. The research re-port deals mainly with summary indicators offinancial performance and their uses. The re-port concludes with a suggestion that financialstatement readers should be educated awayfrom dependence on a single summary indica-tor.

SEC on Management's Discussion andAnalysis of Financial Condition

The Securities Exchange Commission's staffhas issued a release that sets forth its assess-ment of disclosures regarding management'sdiscussion and analysis of financial conditionand the results of operations that were con-tained in 1980 filings with the Commission. Thereview focused on changes in the disclosuresmandated by new requirements which were is-sued September 2, 1980. Included in the re-lease (No. 33 -6349) are examples of howsome companies provided disclosures dealingwith liquidity, the results of operations, and theimpact of inflation. The release makes clearthat the published examples were chosen sole-ly to illustrate particular points and do not nec-essarily suggest preference by the staff. Over-all, the staff indicates it was pleased with thequality of the presentations it reviewed.

Other SEC News

The Commission announced it was rescindingAccounting Series Release No. 261, which hadbeen issued in 1979 to provide guidance to oiland gas producers regarding the use of fullcost or successful efforts accounting pendingdevelopment by the Commission of reserve

► ►13

8 MANAGEMENT ACCOUNTING /JANUARY 1982

BIGGER ISN'TBETTERANYMOREO

Introducing the general ledger programthat gives you "big computer" capabilities at a

microcomputer price.

Built In Systen ; ;e e r i l y - -User Defined Account -- _ -=Structure —Standard Charts of AccountsFlexible Data -User DefixWAS is — -Complete G/L Rspdrts - -_ -_

Unlimited Financial ReportFormatsMull[ -Level Consolidations

Budget and Comparative � �=

Post Facto Payroll y

Big computergeneral ledger

The big computer program vs. AMI and the smallcomputer. Until now, if you wanted to buy a computersystem you had to choose between small computereconomies and big computer capabilities.

No more. Now you can have both in a sophisticatedgeneral ledger program from Accountants Micro-systems, Inc. A program that delivers big computercapabilities at a surprisingly affordable microcom-puter cost.

System flexibility. AMI s flexiblegeneral ledger pro-gram lets you meet the individual needs of even themost demanding clients. You can define client ac-count structure, data input, journal format, and finan-cial statements to meet your specific requirements.

Your choice of computer. No matter which micro-computer you like best, chances are its compatiblewith AMI. Ourgeneral ledger program will operate withover 80 different microcomputers .

Built In System SecurityUser Defined AccountStructureStandard Charts o f Accounts

Flexible Data Entry

User Def ined Journals

Complete G /L ReportsFx) 'CF61tiit bnt a ort

lQlftioBudget and Comparative_ReportsPost Facto Payroll

AMI Microcomputervs. general ledger.

written in plain. simple English. And a long -term com-mitment that we will be there if you ever have aquestion or a problem.

Other AMI products. General ledger is only one ofa complete line of quality microcomputer programsdesigned exclusively for the f inancial administrator.Each with big computer system capabilities. And asmall computer price. For more information, returnthis coupon, or call (206) 643 -2050.

I 'el l me more.I Narne

Firm

Ad d res s

State

More support longer. When you buy AMI's general L Eledger program, you get more than quality software. —You get quality support services. too. Like formalclassroom training. Comprehensive documentation

City

Zip Phone

ACCOUNTANTSMICROSYSTEMSINC.1404 1 ueethpIaceICFBellevue. WA 98007(206) 643 -2050

ManagementInformationSystemsStephen F. Piron, Editor

MIS Costs —You Can't Evaluate the CostUnless You Understand the Benefit

The MIS area continues to be brought intomore and more parts of the business. In thelast ten years, MIS has implemented a varietyof systems. Batch systems sped up the manualprocessing of day -to -day business transac-tions. On -line systems processed transactions,but also allowed quick access to information forthose who needed it. Decision - support systems(e.g., models) allowed analysis personnel andmanagement to review more alternatives be-fore making a decision. Executive informationsystems focused on giving executives specificinformation to meet specific managementneeds —as opposed to giving management re-ports containing only data which the batch andon -line systems processed.

Applied TechnologyThis growth in these various types of sys-

tems is a result of the successful application oftechnology to the expressed needs of busi-ness. Office automation is a good example oftechnology being applied to the needs of busi-ness. Storing characters magnetically and dis-playing them electronically, via word process-ing, has made secretaries more productive.Sending audio messages electronically, now inits infant stage, will make managers more pro-ductive. Connecting word processors to com-puters is allowing access to more data thanwas available to word processing users in thepast. The rate of applying technology to busi-ness processes will continue to grow, primarilybecause of the emphasis on productivity.

MIS Costs — Definition and EvaluationManagement has seen a continuing growth

in MIS costs over the last decade. To some,the growth in costs is alarming. To those, I

would suggest they look at how MIS costs aredefined in their organization. The definition ofMIS costs usually means those costs related tothe computer. With the advent of data process-ing, it meant the MIS budget: cost of computerequipment, programmers, analysts, and man-agers. These costs were measured as apercent to sales (as were other categories ofbusiness expenses). As technology changed —allowing a variety of computers to spread to de-partments outside of the MIS department —MIScosts, as viewed by management, took on acompany -wide scope as opposed to a MIS de-partment scope.

As the company incurred more and morecomputer costs, the total MIS costs and its as-sociated percent -to -sales figure rose. In manysituations where management received reportsof only these two number (i.e., total MIS costsand percent to sales), the growth of MIS wasmistakenly limited to a specific percent of salesgrowth rate.

In many cases, management was not awarethat demand for MIS equipment and serviceswithin the company continued to exceed de-mand (i.e., growth rate) for the companies'products. This demand occurred because ofbenefits achieved in areas of the company out-side of the MIS department, But if managementonly measured MIS costs on the basis of per -cent-to- sales, it was most likely not aware ofthe benefits which the company was achievingfrom this application of computer technology. Inthese cases, MIS Directors failed to educatemanagement as to the positive impact this ap-plied technology was having on the entire orga-nization. If this education had occurred, man-agement could have an opportunity to evaluatethe MIS costs on a company -wide benefit ba-sis, seeing more clearly the various productivityand decision- making benefits being experi-enced throughout the total organization.

MIS.- Costs or Investments in the Company'sFuture?

Today, MIS costs should be evaluated from abroader viewpoint. To some degree they arecosts to process volumes of business transac-tions. To another degree they are investmentsmade in the company's success or failure in thefuture. This latter viewpoint (i.e., as an invest-ment in the company's future) is very realistic.The success or failure of managements' deci-sions depends largely on the information avail-able (e.g., on the company, on the market-place, on competition). To an increasingdegree, this information is a result of a decisionto incur an MIS cost.

Today's technology can be employed to10,10-13

10 MANAGEMENT ACCOUNTING /JANUARY 1982

AtMSA,0 0

isaservice

John Imlay and MSA Customer Support Team specialists Betty Feezor, Larry Smart. and Fat Tinley.

Tlapos more than a corporatetlicy at MSA. Its some-

thing we all believe in. From topmanagement on down"

John Imlay believes in service.In the past decade, MSA has grownto become the acknowledged leaderin the independent software industry

The key? TotalsofttvaresupportforMSA customers.

Here's what this can meanto you.

Get advicefrom the experts

One of the best reasons to choosesoftware from MSA is the teambehind our systems. Your CustomerSupport Team includes softwareprofessionals who have specializedknowledge of different types of busi-ness and the operational require-ments of different industries.

Led by an MSA Account Man-ager, these people help plan your

new system and work with you on adetailed implementation schedule.

They help get your system upand running. On schedule. Work-ing smoothly.

The teambehind the team

Backing -up your Customer SupportTeam are hundreds of other MSApeople who work behind the scenesDevelopment, for example, is ahigh priority. Last year alone, wespent more than $17 million toenhance and improve our applica-tion packages. This investmentexceeds total revenues of many ofour key competitors.

Look for morethan just software

With more than 6800 of our sys-tems installed around the world,MSA software is user - proven and

software0

John P. Imlay,Jr.,Chairman MSA

highly refined.But we don't stop there. We

support every MSA software in-stallation with the most extensivecustomer support organization inthe industry.

And it's staffed with trainedspecialists who have only one full -time job —to be available and readyto help whenever you need them.

We follow upSoftware maintenance costs canamount to more than fifty percentof your data processing budget. Butyour MSA application package in-cludes a full year of support servicesat no charge. (After that, you cantake advantage of our on -goingsupport option.)

As part of our customer sup-port program, we keep track ofchanges in government regulations,accounting procedures, and tech-nological advances in the dataprocessing industry. And we re-spond with timely enhancementsand releases for your system.

Write or callFor more information on MSAsoftware systems (or software formicrocomputers from our Peach-tree Division), please write us onyour company letterhead. Orcall Robert Carpenter at (404)262 -2376. And be sure to includeinformation about your company'scomputer so that we can send youthe right information.

The Software CompanyManagement Science America, Inc.

3445 Peachtree Road, N.E.Atlanta, Georgia 30326

AT LAST. SOFTWARE THATCAN TAKE ON YOURTOUGHEST PROBLEMS.

, v0s,

Pr 'ferns you once dre de : Put off. Had a hard time.with once you got to them. Because they were compli-cated. Time - consuming. And they never got easier, justfarther and farther behind schedule. But now there is a

e of high quality, professionally developed microcom-pOter software that tackles the rough stuff for you. It'scalled Execuware'"

The programs are reliable. Thorough. Easy to under-stand. Quick. And flexible, so they can meet the needs of

y ` tyour business. They're the end - result of years of researchand evaluation.

The Execuware Financial Analysis Package can tell youwhen to lease or buy, as well as help you come to gripswith the cost recovery provisions of the Economic RecoveryTax Act of 1981. Execuware can help you minimize yourinventory carrying costs with our EOQ program – a uniqueaccurate inventory management tool. And our growing,hardworking line of executive software will soon be ableto solve other tough problems you face every day.

Ask to see Execuware in action at your nearest APPLET11

I or IBM personal computer dealer. Or returnthe coupon below and we II show you how to

II I I I I I I I I tackle those problems that always seem togive you a hard time.

EXECUWARE MICROCOMPUTER SOFTWARE FOR EXECUTIVES FROM AERONCA, INC.1M

_ _ - _

I'd like to know more about Execuware. Please send information about:( ) EOQ ( ) Financial Analysis Package( ) The location of an APPLE or IBM Dealer near me. !

Name !

! Company_ !

Title Telephone !

! Street !

city State Zip I! Mail to: Microcomputer Software Division of Aeronca, Inc. !

LP.O. Box 909, Pineville_N.C. 28124_(704) 525 -9881.

- - - - - - - - - - - - - - - - - - - -J

u 1981 Aeronca. Inc "Execuware" Is a Trademark of Aeronca, Inc.Apple" is the registered Trademark of Apple Computer, Inc.

LettersTO THE EDITOR

Where ZBB Really Started

In his October Opinion column, RobertL. Shultis states, "Zero -based budgeting

in its present form seemed to have givenbirth at Texas Instruments in the 1971annual budgeting process." Seemed tohave given birth is the proper term herebecause zero -based budgeting was actu-ally born in 1962. The place of birth wasthe U.S. Department of Agriculture.

Incidentally, zero -based budgetingfailed —it was considered a waste oftime and a source of frustration. Formore information, see Public BudgetingSystems by Robert D. Lee and RonaldW. Johnson.

Paull. RubackyFranklin Lakes. ?1'.J

Update on U.K. Accounting

In Mr. Schweikart's article (Aug.'81)on Consolidation of Foreign Subsidiar-ies in Management Accounting he stat-ed that "the U.K. is governed by aCompanies Act." Regrettably, in fact,since the enactment of the CompaniesAct 1948 there have been three furtherCompanies Acts as well as a host of oth-er secondary and primary legislationbearing on company behaviour. Workon the consolidation of the CompaniesActs is under way so there is a possibili-ty that the legislation will take the formof one mammoth Act in the foreseeablefuture.

More important., however, was hisomission of any reference to the work ofthe Accounting Standards Committeein the U_K. This committee was set upin 1970 with the object of developingdefinitive standards on financial report-ing, and has subsequently produced aseries of Statements of Standard Ac-counting Practice. Any accountant whoassociates his name with published ac-counts which do not conform to thesestandards can be asked by his profes-sional body to explain why he has notconformed, so that the increase in thedegree of standardization in publishedaccounts over the last ten years, has

been appreciable.Since the issue in 1975 of SSAP 10 on

Statements of source and application offunds, changes in financial position havehad to be disclosed and with the issue ofSSAP 16 in early 1980, larger entitieshave been required to produce, in addi-tion to accounts based on historicalcost, a profit and loss account and a bal-ance sheet based on current cost. Inthese organizations the requirement isdefinite and not merely a permission tovaILI fixed assets at appraisal value.

A. YoungDirector of Technical Services

The Institute of Cost andManagement Accountants

London, England

MANAGEMENTINFORMATIONSYSTEMS

10-4.4

varying degrees to gather, process,and make available information tomanagement. The degree to whichthis technology is employed is man-agement's decision. This decision, tobe a good one for the company, mustbe based on an understanding of thebenefits provided to the company.Understanding MIS costs requires acommitment of time: time spent bythe educator (the MIS Director) andtime spent by the learner (manage-ment who decides on MIS costs).How informed are you and your man-agement of the company's MIS bene-fits?

MANAGEMENTACCOUNTINGPRACTICES8 4 4

recognition accounting (RRA). Inas-much as the Commission no longer isworking to develop RRA for primaryfinancial statements and has no im-mediate plans for adopting a singleuniform method of accounting, thereasons for issuing ASR 261 no long-er exist. Henceforth, the SEC will relyon GAAP in accepting accountingchanges to or from the full cost meth-od or successful efforts method.

HIWTHENEW YORKflU 8

THE 1120BEFORE FAST -TAX, WE WERE

WASTING PROFESSIONAL TIME."If we made a change in one of our forty -

five subsidiaries, we had to manually adjust theconsolidated return and as many as 20 schedules.Now we make one entry, and FAST -TAX automaticallycarries it through.

"Loading the information is relatively simple, the serviceis smooth, and we like the finalproduct— a printed return andall its copies — ready to sign.

"With FAST -TAX, I can spend more time on research and additionalspecial projects. FAST -TAX proformas save our secretaries considerable timetyping and copying. We're able to keep our work at an even pace, so wesave on overtime and temporary help, as well.

"The FAST -TAX system has been a substantial benefit to theentire department." Robin Hatch, Tax Manager — Federal Tax Compliance

The New York Times Company

Tax management is essentially strategic thinking. There is asure way to conserve the unique energies it

requires while outpacing routine calculation and clearing each 1120hurdle with ease: Run with the processing leader ... FAST -TAX.

Start today: 214/934 -7000 (Ask for John Lewis.)

HST•Running ahead.

World Headquarters: 2395 Midway Road, Carrollton, Texas 75006 • Telex: 73 -0934

Proposals have been issued thatwould codify existing administrativepractices relative to pro forma finan-cial statements ( release 33 -6350) ,and exempt smaller registrants fromcertain reporting and other require-ments ( release 34- 18189) .

MAP Comment Letters Issued

The Management Accounting Prac-tices Committee sent a letter datedOctober 26 to the SEC regardingeight proposals in connection with itsintegrated disclosure project.

On October 26, another letter wasmailed to the AICPA on a proposed

Statement on Auditing Standards —"Supplementary Mineral Reserve In-formation."

FASB Proposes Rules forRelated Party Disclosures

The Financial Accounting StandardsBoard has issued a proposed state-ment which would establish require-ments for related party disclosures.The Board has been asked to provideguidance on disclosures of relatedparty transactions because generalaccounting or reporting guides for

► ► 15

MANAGEMENT ACCOUNTING /JANUARY 1982 13

TE GOLD in the 1120 goes to the taxmanager who protects the biggest

slice of corporate profits.He stays on top of the figs

one jump ahead in compliarfirm control of staffing and ncrunching, so that talented nfree to plan for tomorrow.

At FAST -TAX, we understarstrategy. Processing millionspages of returns a year, FAST -has become the prime EDP rsource to the nation's leadinCPA firms. And "class N' corpations have been running wus for years ... running ahea

1. A Quick Start. TheFAST -TAX management sys-tem is fully compatible withyour own established con-trols, standards, and routine!It harmonizes with the state -of- the -art methods of out-side professionals whoserve you.

FAST -TAX Proformas areautomatically pre - printedwith last year's dataand this year'srepetitive numbers.To get started, all ittakes is a copy of 1 U W

last year's financials.2. Endurance for

the long run. Fullcompliance with Federal andstate regulations is a given.The FAST -TAX management programs aredocumented up -to- the - minute at the begin-ning of each tax year — and updated, asneeded, all year long.

3. W inning comes down to "form ".Here's a sample: Single 1120 returns with all

applicable schedules and forms, fully cross -referenced ... ADR and non -ADR depreci-

ation, complete ... company or divisionalicluding easy -to- handle,ales, forms 1122 and 851Dss, NOL, tax liability, taxSKY at the consolidatedtax credit computations,861 -8, 1120F, 2952, and

printed work - papers forack -up ... proformas ...it returns ...4. You get speed ...

o- the -wire, you can relyhe same accuracy at the15th of September finishit you are guaranteed alllong.

S. ... And training.own local FAST -TAX rep - ntative will be with youthrough the day -to -day

,oblems and potential of)ur company's corporate< processing. Documen-

tation, working guides,seminars, bulletins.

The payoff: Finalreturns — exact

duplicates of Federaland state forms —

accurate, complete,ready to sign

and send.There's no other race

like the 1120. The startingline, the route, and the

N Tt1120.

rules keep changing. It can be painful togo it alone.

So run with the leader. Run ahead. WithFAST -TAX.

On your m ark . . . Get set . . .1- 214 - 934 -7000 ... (Ask for John Lewis.

r M / M T40T M _ (Computerized corporate tax processing ...

Running ahead.

MANAGEMENTACCOUNTINGPRACTICES

1344

such transactions do not exist now ingenerally accepted accounting princi-ples.

The requirements of the proposalare generally consistent with those inStatement on Auditing Standards(SAS) No. 6, "Related Party Trans-actions," issued by the AICPA. How-ever, authoritative auditing pro-nouncements are intended to directthe activities of auditors, not of report-ing enterprises.

The FASB proposal, Related PartyDisclosures, would require inclusionin the financial statements of disclo-sures of related party transactionsthat are necessary for users to under-stand the statements. However, dis-closures need not be made for trans-actions that are eliminated in thepreparation of consolidated or com-bined financial statements. The dis-closures should include the followingitems.

• The nature of the relationship (s)involved.

A description of the transactions,including those to which noamounts or nominal amounts wereascribed, for each period and suchother information deemed neces-sary to an understanding of the ef-fects of the transactions on the fi-nancial statements.

• The dollar amounts of transactionsfor each period and the effects ofany change in the terms fromthose used previously, if determin-able.

Amounts due from or to related par-ties at the most recent balancesheet date and, if not otherwise ap-parent, the terms and manner ofsettlement.

If an enterprise is controlled by an-other party, the nature of the controlrelationship should be disclosed inthe financial statements even thoughthere may have been no transactionsbetween them.

HOW THETELEX CORPORATIONRUNS 1120„ We produce separate

returns for each of our subsidiaries,spin off the state returns, and thenproduce the consolidated return for theparent company. Considering we file in virtuallyevery state, it's a job of unbelievable proportions.

"Running with FAST-TAX has cut the amount of time spenton routine work — typing, doing the math, checking the results,duplicating ... by 90% or more.

"The service is fantastic. The turnaround time is superior to othersystems. The quality of the f inal product has been superb. Andthe cost is so cheap, it's immaterial.

"When we started with FAST -TAX, it gave the guy who signs thisreturn the time for research and planning and making sure the returnis in compliance and to the best advantage o f my company„

David Gannon, Assistant Treasurer and Director or TaxesThe Telex Corporation

Tax management is essentially strategic thinking. There is asure way to conserve the unique energies it

requires while outpacing routine calculation and clearing each 1 120hurdle with ease: Run with the processing leader ... FAST -TAX.

Start today: 214/934 -7000 fAsk for John Lewis.)

miST44M.Running ahead.

World Headquarters: 2395 Midway Road, Carrollton, Texas 75006 • Telex: 73 -0934

FASB Proposes Aa Bond YieldsAs Substitute for Prime Rate inCertain EPS Computations

In place of using the prime interestrate as a benchmark for the "cashyield test" for convertible securities indetermining earnings per share, theFinancial Accounting StandardsBoard has issued a proposed state-ment that would substitute the aver-age double A ( "Aa ") corporate bondyield. The change potentially affectsall companies that issue convertiblesecurities.

The proposal, Determining Whether

a Convertible Security Is a CommonStock Equivalent, would rectify theproblem caused by using the volatileprime interest rate. The cash yieldtest uses the prime interest rate as asubstitute for a long -term rate in de-termining if, and to what extent, earn-ings per share should be diluted, orreduced, by the issuance of securitiesthat are convertible into the compa-ny's common stock.

Proposal would allow companies touse several sources to obtain quotesof bond yields, as long as the qualityof bonds included in the quote isequal to those rated Aa by Moody's orStandard & Poor.

MANAGEMENT ACCOUNTING /JANUARY 1982 15

Dennis Loewe is thecontroller of financial

services forWeyerhaeuser Co. inTacoma, Wash., and

also is serving asspecial program

manager forinformation systems.He is president of the

Mt. Rainier Chapterthrough which he

submitted this article.

How WeyerhaeuserMade Its MIS Work

The corporate financial managers agreed at the outset that if thecompany found the necessary technology, it would proceed in gradual hops—

and not attempt to make the great leap in a single bound.

By Dennis Loewe

During the last five years, Weyerhaeuser Compa-ny increased sales from $2.9 billion to $4.5 billionand increased assets from $3.7 billion to $5.2 bil-lion. At the same time our corporate consolida-tions staff decreased in size, while the quality andquantity of corporate reporting increased. By anystandards used to measure productivity we are ob-viously pleased with the results.

The key element in this success was implemen-tation of our Weyerhaeuser Financial InformationSystem ( WEYFIS). This effort involved muchmore than plugging in software to generate con-solidated reports. Several elements were present inevolving our current technical capabilities, but theconceptual design featured four key leveragepoints.

• People• System design• Software• Operating system

Ultimately the technical considerations leadingto software selection and choice of operating sys-tem provided us with the tools we required. Themost important contributions, however, weremade in the conceptual design stages and in the

selection of people who were to be directly in-volved. This approach involved corporate officersand key staff members. Their message was specificand in the longer term has proved durable: "Buildus a matrix to store financial data and we'll definethe reports as we need them." This approch re-sulted in the successful blending of many talentsto produce a rare accomplishment for a large mul-tinational firm —a system that satisfies a sophisti-cated user group.

People, Pencils and Perspiration

The most important ingredient in developingWEYFIS was people. Even the best designed sys-tem is doomed to failure if the people it is de-signed to serve do not have a proprietary interest.In Weyerhaeuser's case, the sponsors also com-prised the implementation team..

At the time we decided to search for computertechnology to aid our corporate reporting process,we were using a manual system. The preparationof the annual report to shareholders, 10 -K report,internal senior management reports, and respons-es to other regulatory agencies were all laborious-ly accomplished with pegstrips, pencils andperspiration. It was an extremely flexible systembecause human ingenuity provided the requiredsorts each step of the way. It was also an extreme-ly redundant process and response times were pre-

16 0025 - 1690/82/6307 - 0912/601.00/0 Copyright ©1982 by the National Association of Accountants

dictably slow. The human element, of course, in-troduced errors of its own, resulting in conflictingdata from the same source in some cases.

In 1973 the corporate controller approachedthe senior vice president of finance and planningwith a proposal that included these key points.

• We would search for technology that fit ourconceptual requirements. We would not com-puterize only to scrap the entire effort in two tofive years. This strategy translated into a singlewatchword — flexibility— flexibility in file struc-tures and data independence from reports. Ifsuitable technology could not be found in thecurrent state of the art, we would halt oursearch and gear up additional manpower forthe manual effort.

• Second, if we felt we were successful in locatingthe necessary technology, we would proceed ingradual hops during implementation and not at-tempt to make the great leap in a single bound.

A steering committee was formed at this junc-ture under the sponsorship of the senior vice pres-ident offinance and planning. It was comprised ofthe corporate controller, the assistant corporatecontroller, the manager of corporate informationsystems, our client services manager and the man-ager ofcorporate consolidations. The compositionof this committee demonstrates the commitment

that was made by the concerned parties. Two cor-porate officers represented the user group, two keyindividuals from corporate systems provided tech-nical support, and two managers directly involvedin corporate data collection and reporting repre-sented the guys in the trenches.

The committee was small enough to work effec-tively and one with necessary stature to call uponadditional resources when necessary. It was also agroup that embodied the necessary ingredient forsuccess; it contained the people with a proprietaryinterest in making the project succeed.

System Design— Flexibility

The major design aspect ofthe project was flexi-bility. Flexibility for us meant:

• Ease ofchanging our minds without significantchanges to the system or to the data base.

• Ease ofuse which would allow us to control thedata and the system, not vice versa, and to getat the data easily and in a variety ofways.

• Being able to expand, to be responsive to thegrowth of the company, for new acquisitionsand businesses, as well as growth in the volumeofline items that would be requested.

• Sharing the data files. We saw a real opportuni-ty to cut duplication in data handling and re-porting, thus enabling us to add new applica-tions without destroying the old and to be

MANAGEMENT ACCOUNTING /JANUARY 1982 17

Our shoppinglist of what wewanted out of

an M15 soundedlike the

impossibledream.

receptive to modifications in user requirements.In retrospect, this shopping list sounds like the

impossible dream. It surely contains some or all ofthe elements that EDP managers have been con-fronted with by clients who want implementationof their most critical system requirements. At thesame time we were dedicated to the principle thatif suitable technology could not be found, wewould not proceed.

This concept did not shift responsibility orpoint blame at the systems community if suitabletechnology could not be found. We jointly sharedin the conceptual design. Heavy user involvementduring the early stages made us a part of the proc-ess. As the first user in line and primary beneficia-ry of the proposed system, I was designated toprepare the functional flowcharts. Personally, Ican think of no better way to make the user a partof the process, to refine his thinking to specificsand to get him to share responsibility with theprogrammers for the work that lies ahead. It isreally not surprising that the finger pointing,which can result from an unsuccessful effort, canbe eliminated through a process such as this.

Software

Having developed the conceptual frameworkand prepared functional flowcharts, we now wereprepared to search for the required software. Itsoon became apparent that software could be ana-lyzed by grouping the available types into threebroad categories.

The first category contains what we call stan-dard business languages. This group includes CO-BOL and FORTRAN. These languages have thevirtue of being familiar and a known quantity.Their major and, fatal, shortcoming in our view isthe data dependency inherent in their use. Ourmajor objective was to achieve flexibility to thesystem, to make it responsive to a volatile environ-ment, to change the components within the database, to modify file structures, and to achieve rap-id response to ad hoc report writing. These lan-guages could not give us this flexibility, so wereeliminated.

That is not to say that standard languagesshould never be used given the current state of theart. Obviously, we continue to develop systems us-ing COBOL and FORTRAN. Their use should,however, fit the application. This criterion limitstheir use to relatively mature transactional sys-tems having fixed reporting requirements. Theymay also be used where front -end data base up-dates are mature and only a report generator isrequired to access the data for report writing.

These constraints did not suit our application,particularly because our controller specified thathe would not define end -use reports. They wouldevolve over time from the information needs ofthe corporation.

The second group of languages we designate ashigher level languages. This group includesMARK IV, ASI -ST and a few others. As opposedto languages that lie somewhere between standardbusiness languages and higher level languagessuch as Meta COBOL, Work Ten or Genasys,these higher level languages make a completebreak with COBOL.

With languages such as MARK IV it is possibleto produce object code directly. In fact, a singlepackage provides a procedural language, a filemanagement system and a report generator. Thesefeatures seemed to offer the potential tool we wereseeking. We probably could have stopped oursearch at this juncture, but we could not do sowithout some examination of data base manage-ment systems (DBMS), which is the third general

category.The data base management system category in-

cludes TOTAL and System 2000. Our studiesshowed them to be most effective when managingmany different data files. They allow files to beinterrelated through directories and allow ad hocreporting across data files. Clearly these capabili-ties would be desirable in a multi- faceted file sys-tem.

In our case we were seeking to build a new file,not interrelate existing files. At the same time wedid not want to preclude the use of a DBMS atsome future date. The resolution of the problemcentered on the answer to one question. Could webuild a system using higher level languages and inturn use them to build files for a DBMS at somefuture date, should our needs warrant the addi-tional cost? With the file management capabilitiesof the higher level languages we were given thetechnical assurances that this could indeed bedone. With this assurance we opted for the higherlanguage, and this choice had favorable impactson all aspects of systems development. .

Impact of Higher Level Languages

Too often in the past the user has become utter-ly frustrated with the demands and time delaysthat seem to be inherent in a COBOL -based envi-ronment. The situation gets so bad that the userdoes not articulate his full needs anymore. Theimpact on productivity of such a situation is pre-dictable. This was not the case in our selection ofMARK IV.

We found MARK IV provided an orderlystructure for the development process. The broadoutlines we had conceptualized could be accom-modated. We did not have to define report for-mats, input documents or program decisions aswould be done with COBOL. We developed broadconcepts such as input, edit, update and reportfunctions. File structures were developed to pro-vide maximum flexibility for updating and output-ting the data. Fields were arranged without regard

18 MANAGEMENT ACCOUNTING /JANUARY 1982

to complexity of hierarchial structure or recordsize. Newly defined files were structured from cur-rent input. Output reports could be written fromthese files with minimal changes.

Throughout development, which has virtuallynever ceased, modifications and enhancementshave continued. In conventional COBOL -basedsystems, changes ofthe magnitudes that we madehave entailed programming and cost considera-tions equal to the original system proposal. Thiswas not the case in using a high level language.

Ease of coding is a particularly productive useof programmer's time when higher level languagesare used. Although the system is extremely com-plex, it was largely accomplished by using a singleprogrammer dedicated full time. Though difficultto judge the effective leverage ratio, we estimatethat he accomplished the work of at least five CO-BOL programmers. Many of the accomplishmentssimply could not have been achieved without theuse of a higher level language.

Training time to being an individual up to speedin the use of higher language is similarly short-ened when compared to COBOL. In our case,training consisted of a formal two -week coursecoupled with 90 days ofon -site development helpfrom the software firm.

Another factor that contributed to the produc-tivity we have enjoyed is the continuity of onesenior programmer on the project. This continuityis attributable to two factors: job satisfaction frombeing involved in an exciting and highly visiblecorporate system and the opportunity to create,which cannot be matched in the more structuredenvironment of standard business languages.

Operating System

We cannot attribute all of our productivitygains to the use of higher level languages. Theselection of an appropriate operating system wasalso vital in obtaining maximum benefits, bothduring program development and subsequent sys-tem operation.

JCL, or job control language; is an industrystandard that is widely used to govern the proce-dural steps necessary to execute a job stream. Un-fortunately, JCL can carry some heavy productiv-ity losses with it. Because operating steps must beuniquely designed in series for each job, multipleJCL decks must be prepared to execute complexsystems that have numerous permutations andcombinations. In our case there are several hun-dred job streams that can be selected. In additionto the time required to set up the JCL decks, hu-man error in selecting and loading the proper JCLfor a particular run can occur.

Given the problems and frustrations of workingwith JCL, we selected an alternate operating sys-tem known as the Cambridge Monitor System(CMS). Basically, it is an English language ver-

sion of JCL and can be used to program jobstacks. For WEYFIS all operating systems aregoverned by CMS. We have been provided execu-tive routine (EXECS) which allow the user tospecify the system functions and reports which areto be generated from a production run. This isaccomplished by providing prompting routinesthat can be accessed through time - sharing. By re-sponding to simple questions on -line, the programroutines build the CMS commands necessary forexecution of a particular job. It is simply a shop-ping list approach that puts operation of the sys-tem in the hands of the user.

At the end of a terminal session the us& isasked if he wishes the job to be run on -line (at fullcost rates) or as an overnight batch job (at halfthe cost). Because these costs are directly ab-sorbed and budgeted by the user, job priorities canbe placed in their proper perspective. The choiceis clearly up to the user.

The elements just described lead up to systemsimplementation. Another tool that has had a highdegree of payout for us in the production stage isthe use of data transmission.

Benefits of Data Transmission

In the days of manual consolidations, all infor-mation was collected on hard copy. Receipt of in-formation was dependent on the mail. Since theconsolidation could not be completed until thelast unit was received, it was problematic as towhen earnings per share would be available. Withthe advent of a computerized process and the useof data transmissions, three improvements havebeen made in productivity:

1. The first, of course, has been the elimination ofmail delays and the inherent waste of time indata preparation and release of earnings.

2. The second is the syndication of key data prep-aration across our 400 reporting locations,rather than performing the entire task at head-quarters from hard copy.

3. The third is the ability of reporting units toprepare the data once in their general ledgers.The data is automatically translated into pre-scribed corporate formats, which discontinuesthe clerical task of manual data preparation.Computer transmissions have now freed gradu-ate accountants to perform the work for whichthey are qualified—data analysis —not "beancrunching."

Uses of WEYFIS

WEYFIS is a corporate financial data base. Inits first small hop it provided the means to consol-idate the company's financial statements. It pro-vided the necessary information for the annualreport, 10 -K report, internal senior managementreports and other regulatory reports. Since 1974

At the end of aterminalsession, the userhas the optionto run the jobon -line or as anovernightbatch.

MANAGEMENT ACCOUNTING /JANUARY 1982 19

ensuing applications have provided unit reportingcommunications, business segment reporting,business consolidations, and preparation of federaltax returns.

Other applications include internal and externalaudit support, staff and corporate analysis, corpo-rate earnings planning, corporate debt planning,corporate capital tracking and reporting, and ahost of related support activities.

While it may be useful to list the applicationsthat we have developed as general background in-formation, it is more important that they serve asevidence of what can be accomplished over timeusing the flexible file handling and reporting char-acteristics of a high level language.

In retrospect our computer development deci-sions have been based on the classical trade -offsbetween a labor- intensive solution versus a capi-tal- intensive solution. Both applications software

and operating software have been bound in histo-ry to run "efficiently" on a computer. That, inturn, has translated into using languages that areas close to machine language as possible. Whencomputer core size was the economic driver thatmade sense. Capital (the machine) was more ex-pensive than labor. Labor, in this case, refers tothe programmers who were required to writelengthy and inflexible programs that could be effi-ciently digested by machines. As the cost of mem-ory has dropped, the cost of labor has soared.Given this equation, -only tentative steps havebeen taken to give programmers more highlyleveraged languages with which to program.Because the skills of existing staffs must be reori-ented to take advantage of the new technologies,major resistence will likely be encountered. Thepayoff in real terms is, however, too large to beignored. ❑

PO MANAGEMENT ACCOUNTING /JANUARY 1982

YOURS IS ,

O

a50000

of any one of these outstanding accounting boo! PLUS�—�"no�stringsmembership in the book club that thousands of accountants and controllers

rely on for the best in professional reading and reference

The ACCOUNTANTS' and CONTROLLERS'BOOKCWB

No other purchase necessary at this time. And you may cancel yourmembership whenever you choose.

Yes, to welcome you to the Club, we're offering youyour choice of any one of these top cal ibre books.Books typical of those the C lub offers month aftermonth�—books�that�give�you�the�know�-how�you�needto make it to the top in profess ional st anding andincome.Join�the�ambitious�professionals�—join�the�Accoun-tants' and Controllers' Book Club and build a career -bui lding library of�outstanding�books�—top valuetitles at lowest possible prices?

Why YOU should join nowl•�BEST�AND�NEWEST�BOOKS�IN�YOUR�FIELD�—Books�are

selected from a wide range of publishers by expert editorsand consultants to give you continuing access to the best andlatest books in your field.

•�BIG�SAVINGS�—Build�your�library�and�save�money�too!�Sav-ings�ranging�up�to�30%�or�more�off�publishers'�list�prices�—usually 20%n to 25% .

•�BONUS�BOOKS�—You�will�immediately�begin�toparticipate in our Bonus Book Plan that allows yousavings of between 70% and 80%n off the publishers'pr i ce s of many p ro fe s s io nal a nd gene ra l int e re s tbooks!

•�CONVENIENCE� -10 � -12� times � a �y ea r�y ou� rec ei ve� the �ClubBull e tin FREE. It f ully de scri bes the Mai n Se lec ton and a l-te rnat e se le ct io ns . A da te d Re pl y Ca rd i s incl ud ed . If y ouwant� the �Main�Select ion,� you� s imply�do� nothi ng�—i t�wil l �beshipped�automatically. �If�you�want�an�alternate � selection�—orno�book�at�a ll �—you�simply� indicate �i t �on� the �Reply�Card�andreturn it by the date specified. You will have a t least 10 days todecide, If, because of la te delivery of the Bulle tin you receivea Main Selection you do not want, you may re turn it for creditat the Club's expense.

T AX IDEAS DES K BOOK By A. Iad aro la and S .C. L amb e rt , 582254 -7Pub. Pr., $34.95 Club Pr., $23.50

T HE BI G E IG HT : AN I NS I DE VIE W O F AMERI CA' S E IGHT MOS TP OWE RF UL AND INF L UENT IAL ACCOUNT I NG F IR MS By M. S te-vens, 582400 -0 Pub. Pr., $12.95 Club Pc, $10.9S

T AX HANDBO O K O N C OR P OR AT E DI S T R IBUT I O NS AND DI VI -DENDS By L.D. Cr umb le y an d D. Bra nd y, 58 23 74 -8 P ub . Pr., $27.95Club Pr., $19.95TAX S HELT ERS AND T AX -F REE INCOME F OR EVERYONE, 4/e ByW. C , Drollinger, 788 /669 Pub. Pr., $19.95 C lub Pr., $16.95

HANDBO OK OF MODER N ACC OUNT I NG By S . Da vid s o n and R . L.Weil, 154/513 Pub. Pr., $49.95 Club Pr., $37.50

F IELD AUDIT OR ' S MANUAL AND GUIDE By S . R . No v ak , 582093 -5Pub. Pr., $49.50 Club Pr., $38.95

T HE CP A E XAMINAT IO N T ex t , P r o b lems , an d S o lut io n s By A. N .Mo s ic h and E. J. La rs en , 434/352 P ub . P r., $31.50 Club P r. , S24.9S

CONT R OLLER 'S HANDBO OK E d it e d b y S . R . G o o d man a nd J . S .Reece, 787 /514 Pub. Pr., $35.00 Club Pr., $27.95

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -i McGraw -Hill Book Clubs 1 i

ACCOUNTANTS' and CONTROLLERS' BOOK CLUB � : +P.O. Box 582, Hi ght st o wn , New J er sey 0 85 20 nPl e ase e nro l l me as a membe r and s e nd me t he boo k i ndi c ate d bi l l i ng me 1

1 $3.95, pl us l o cal t ax , s hi ppi ng and handl i ng c h ar ge s . Me mbe r s hi p i s ac - 11 ce pte d by me as o utl i ned in the Cl ub pl an de sc r ibe d i n t hi s ad. 1

11 Write Code N of your $3.45 selection here: 1

If yo u want addit io nal se le ct io ns (at di sc ount Cl ub pr i ce s ), wri te bo ok co de 11 Ms here: 11 11 1i 11 Charge my Visa O MasterCard Exp. Date I1 I

Credit Card N 1I Signature 11 11 Name

' Address Apt. f II

1 City, State, Zip 1

iCo rpor at e Af fi li at io nThi s order subjec t to ac ceptanc e by McGraw-Hi ll. All pr i ces subjec t tochange wi t ho ut no t i c e . Of f e r goo d o nl y t o ne w me mbe r s. A s hi ppi ng and Ihandl i ng c har ge i s adde d t o al l s hi pme nt s. Or de r s f r om o ut s i de t he U.S. 1

i cannot be accepted. T44151 1L - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - J

Data SheetRobert F. Randall, Editor

One -Third of Major Firms SeekAcquisitions

More than one -third of the nation's 480 biggestindustrial companies are actively seeking ac-quisitions, according to the latest survey of theNational Association of Accountants_ Almosthalf of the corporations, 49 %, said they consid-er themselves vulnerable to a takeover; 44%of that number indicated they do not have aformalized plan to ward off a possible acquisi-tion. Some 44% of the companies surveyedbelieve that acquisitions and mergers amongthe biggest corporations have a beneficial im-pact on the nation's economy, while 17% saidthey had an adverse effect. The chief financialofficers of 154 of the 480 companies queriedresponded to the survey, a 32% response rate.

Conference Board Sees 7.8% Inflation

Good news for the new year according to theConference Board's panel of top -level financialexecutives: it projects that inflation will average7.8 % in 1982 and is expected to fall to 7.3 % in1983. The panel, however, foresees RealGross National Product as averaging only2.2% in 1982.

Italian Company Recasts FiguresInto U.S. GAAP Format

In a pioneering move designed to assist in itsexpansion abroad, the Montedison Group —world's eighth largest chemical company —hasrecast its 1980 financial statements in U.S.GAAP format. The Italian holding company,which had more than $8 billion in sales and aloss of $523 million in 1980, said its financialstatements were in substantial compliance withthe EEC 4th Directive and International ac-counting standards. Italian companies are at-tempting to bring their financial statements upto levels in the rest of the industrialized world,and Montedison is considered one of the lead-ers in this effort. In fact, shareholders appoint-

ed Price Waterhouse to certify consolidatedstatements for 1983 -85, a procedure not cur-rently required under Italian law. Professor PaulAron of the Graduate School of Business Ad-ministration of New York University advisedMontedison on the preparation of the state-ments.

`U.K. Auditors Slower than U.S. CPAs'

"On average, U.K. auditors take more thantwice as long as U.S. auditors and half as longagain as French auditors," writes David Fan-ning in the September 11 th issue of Accountan-cy Age. Basing his conclusions upon a randomsample of 200 companies quoted on the Lon-don Stock Exchange, he says the average timefrom between the date of the year end and thepublication of audited accounts is approximate-ly 122 days. He suggests the disparity might beexplained by the very different relationship be-tween British and American boards of directorsand their auditors. "British directors seem moreprepared to tolerate a reduced standard of per-formance than their American peers, it hasbeen argued, and the company /auditor rela-tionship is significantly different."

Bankers Support Economic Program

Others may be expressing doubts, but the na-tion's bankers support President Reagan'seconomic policies and overwhelmingly agreethat the Economic Recovery Tax Act will bene-fit their industry, according to a survey taken byDeloitte Haskins & Sells' Chicago office at theFifth Annual Conference for Bank Manage-ment. None of the bank managers felt the Pres-ident's current economic program would fail,but they believe the reduction in the rate of in-flation will be gradual. Nine in ten bankers feelinterest rates will decrease over the six -monthperiod from November to April; after that periodthe smaller banks believe rates will revert to anincrease later this year.

Business /Accounting Briefs

Peat Marwick International's revenues rosenearly 20% in the year ended June 30, 1981,and chargeable hours were up 8.2 %.... La-venthol & Horwath has merged with the Denverfirm of Stark, Hochstadt, Kark & Co.... Market-ing chiefs deemed a financial background mostimportant when asked which managementfunctions other than marketing they would rec-ommend, according to Weston Group, Inc.

22 MANAGEMENT ACCOUNTING /JANUARY 1982

ImprovingFinancial Information Systems

in Local Government

Many local government management information systems areobsolete systems which provide only basic accounting information

By Thomas E. Newkirk

Many of the fiscal problems in local governmentstoday can be attributed to inadequate financial in-formation systems. The problem is widespread,and is by no means limited to any one geographicarea. One major reason the problem is so commonis that current systems cannot sound early warn-ing signals. If New York City and Cleveland hadadequate information systems, they might havehad time to avert fiscal crises that faced them inthe Seventies.

A modern financial management informationsystem involves more than just collecting andprocessing information through a computer to as-sist in financial accounting and reporting. It isalso concerned with integrating the various localgovernment departments through an exchange ofinformation that will assist management in mak-ing decisions.

Over the last few years, it has become increas-ingly apparent that many local governments arequickly outgrowing their accounting and informa-tion systems. These systems have grown to becomplex and cumbersome, and directed toward

rather than vital management information.

basic accounting information rather than vitalmanagement information.

Growth as well as changes in local government,such as consolidation of services and the restruc-turing of departments, have placed additionalstrains on accounting systems. In recognition ofthese problems, management of local governmentmust determine the best approach to address itsaccounting and management information needs.

Generally, the task can be broken into threemajor phases: needs determination, acquisitionand implementation, and operation. They providea workable framework within which to considerthe development ofa financial management infor-mation system for a governmental unit.

1. Needs determination sets the basis for the en-tire development process. It involves identify-ing and responding to the needs ofall of thesystems's users — management, supervisory,and clerical personnel.

2. Acquisition and Implementation. Once theneeds have been determined, the actual devel-opment or acquisition of a system can occur.Implementation involves the process of install-

Thomas E. Newkirk is amanager at Wooden&Benson,CPAs,Baltimore, Md. A CPA,he holds a B.S. degreefrom the University ofMaryland. He submittedthis article through theBaltimore Chapter.

0025-1690/82/6307-1472/$01.00/0 Copyright © 1982 by the National Association of Accountants 23

Some needswill be criticallyimportant while

others willrepresent a'wish list'

ing and testing a system as well as assuring thattraining and documentation have been provid-ed. In addition, this phase requires manage-ment to be sensitive to potential personnelproblems brought about by organizationalchanges.

3. Operation is an evolutionary phase that in-volves ongoing training, operational responsi-bility, and future system improvements.

The success of the development of a financialmanagement information system is highly depen-dent upon the commitment and involvement bylocal officials to pull the three phases together.Without this commitment and involvement, theprocess can become fragmented, resulting in ei-ther an inadequate system or total failure.

The Determination Process

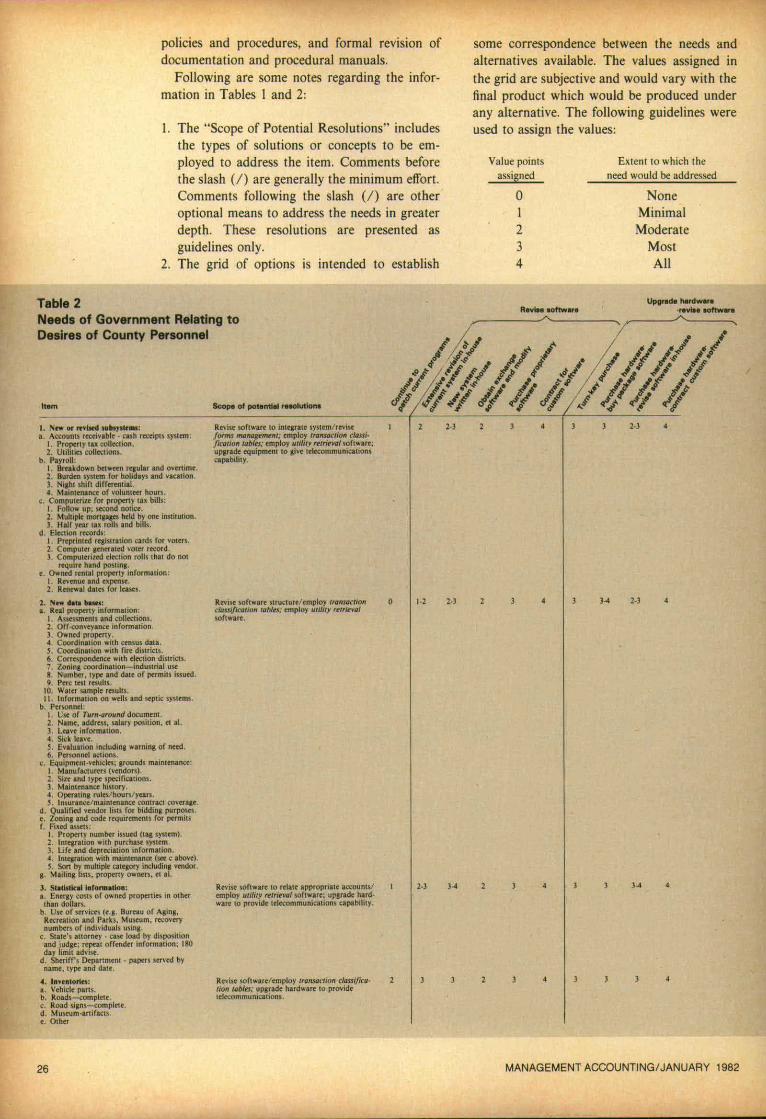

The first and probably most important step indeveloping a financial management informationsystem is to define the government's needs for in-formation. To facilitate this process, a steeringcommittee is formed representing user depart-ments of the government. The role of the steeringcommittee is to plan and implement the develop-ment process.

Specifically, in performing the needs determina-tion phase, the steering committee should:

• Review the existing system for elements thatcurrently meet the needs and those that do not.

• Analyze current and future needs.• Make a priority list.• Perform on -site visits of similar jurisdictions

and evaluate their systems.• Communicate the final needs assessment to

elected officials, management, and system staff.

The needs addressed are as diverse as the activi-ties within a government, but not all needs are ofequal stature or make the same demands. Somewill be critically important, while others will rep-resent a "wish list" from users. In addition to list-ing some of these problems and needs, we summa-rize here potential solutions and various optionsavailable to the governmental unit. Our purpose isto facilitate understanding of directions a steeringcommittee can take in implementing the develop-ment of a financial management information sys-

tem.

Problems Encountered

Typical problems in traditional government fi-nancial information systems exist because systemswere developed in response to increased transac-tion volume in subactivities of the accounting orbudget process. Examples of subactivities includepayroll preparation, check writing, grant report-ing, and capital project management. Additional

inefficiencies, which create delays in recordingand reporting, occur because systems are typicallyfragmented into numerous journals, registers andsubledgers, which must be posted or updated sep-arately and later reconciled.

The environment in which governments operatepresent factors that usually are not addressedwhen an information system is originally devel-oped, including: