Adoption trend for mobile banking in Urban Bangladesh

75

MOBILE BANKING IN URBAN BANGLADESH: ADOPTION SCENARIO AND CURRENT TRENDS

Transcript of Adoption trend for mobile banking in Urban Bangladesh

MOBILE BANKING IN URBAN

BANGLADESH: ADOPTION SCENARIO

AND CURRENT TRENDS

i | P a g e

ACKNOWLEDGEMENT

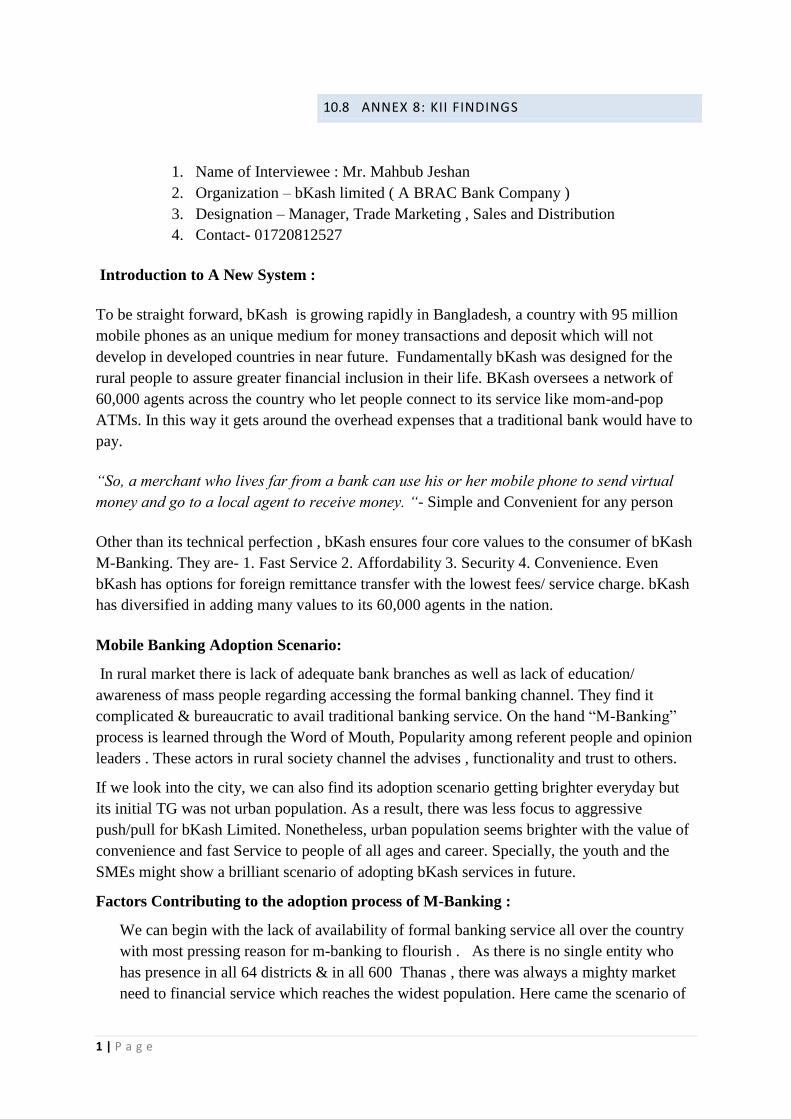

We would like to acknowledge to Mr Mahbub Jeshan, manager of trade marketing at Bkash

and Mr Shahedul Islam, Head of logistics of Dutch Bangla Bank Limited for providing us

with invaluable industry insight for the completion of the report. Finally, we express our

heartfelt gratitude to those who have cooperated with us in taking the surveys and helped us

complete the report through their encouragement.

ii | P a g e

CONTENTS

Acknowledgement ................................................................................................................................... i

1 Introduction ..................................................................................................................................... 0

Background ............................................................................................................................. 0 1.1

Issues ....................................................................................................................................... 1 1.2

Research question ................................................................................................................... 1 1.3

Objectives ............................................................................................................................... 2 1.4

1.4.1 Broad objective ................................................................................................................... 2

1.4.2 Specific objectives .............................................................................................................. 2

Hypotheses .............................................................................................................................. 2 1.5

Rationale ................................................................................................................................. 3 1.6

Scope ....................................................................................................................................... 3 1.7

Limitations .............................................................................................................................. 4 1.8

Contribution of the research .................................................................................................... 4 1.9

2 Literature Review ............................................................................................................................ 5

Adoption process: Diffusion of innovation theory .................................................................. 7 2.1

3 Research type .................................................................................................................................. 8

4 Research Method: ........................................................................................................................... 9

Sample size determination ...................................................................................................... 9 4.1

Questionnaire Development .................................................................................................. 10 4.2

4.2.1 Questionnaire Design ........................................................................................................ 10

4.2.2 Questionnaire validity ....................................................................................................... 10

4.2.3 Questionnaire reliability .................................................................................................... 11

Data Collection ..................................................................................................................... 11 4.3

4.3.1 Primary DataCollection ..................................................................................................... 11

4.3.2 Secondary Data ................................................................................................................. 14

5 findings ......................................................................................................................................... 14

adoption scenario .................................................................................................................. 14 5.1

5.1.1 adoption summary ............................................................................................................. 14

5.1.2 Identification variables ...................................................................................................... 14

5.1.3 Interpretation ..................................................................................................................... 15

5.1.4 frequencies ........................................................................................................................ 15

5.1.5 Adopter profile .................................................................................................................. 15

sample statistics .................................................................................................................... 16 5.2

iii | P a g e

5.2.1 Sample demography .......................................................................................................... 16

5.2.2 Access to supporting technology ...................................................................................... 17

5.2.3 Decision sources ............................................................................................................... 19

mean analysis ........................................................................................................................ 20 5.3

similarity test ......................................................................................................................... 21 5.4

Regression Analysis .............................................................................................................. 21 5.5

Hypothesis Testing ................................................................................................................ 24 5.6

5.6.1 Specific Objective 1: To identify the relations between consumer adoption of mobile

banking and user characteristics.. ................................................................................................. 25

5.6.2 Specific Objective 2: To analyze the perception of m-banking adopters regarding the

technology ..................................................................................................................................... 33

5.6.3 Specific Objective 3: To provide a holistic view on the industry trends. ......................... 36

Qualitative finding: industry trend ........................................................................................ 39 5.7

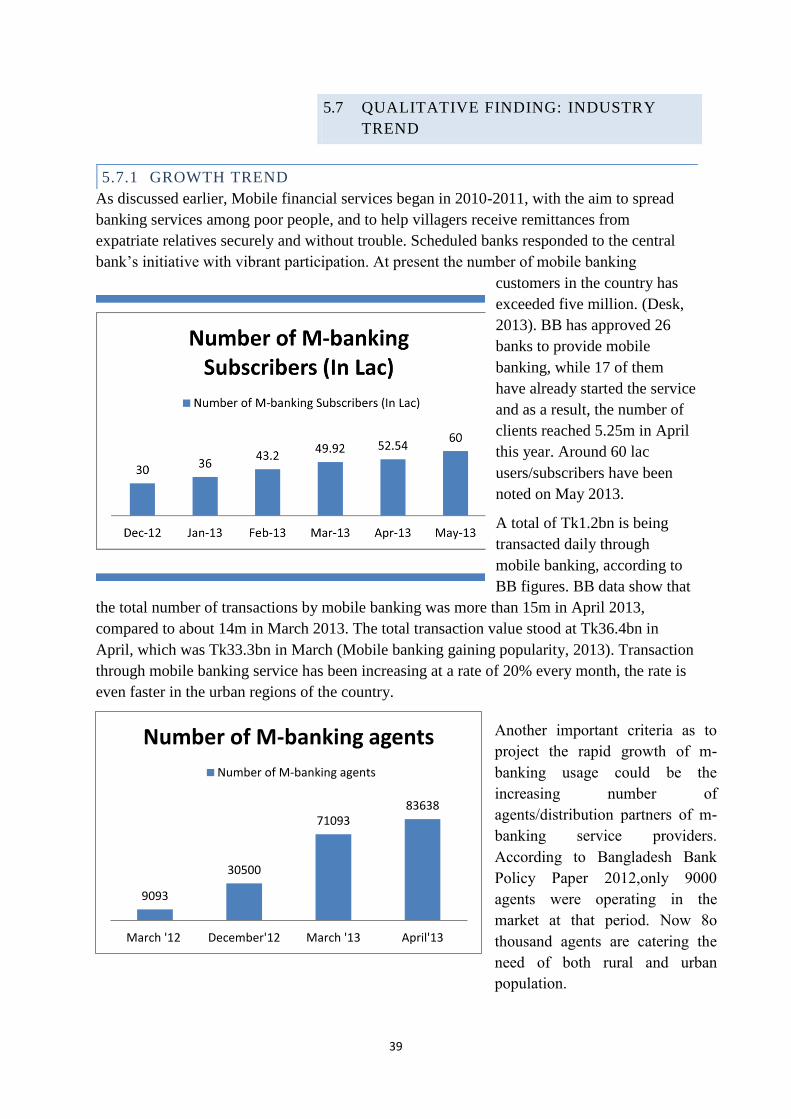

5.7.1 Growth trend ..................................................................................................................... 39

5.7.2 Market Players: ................................................................................................................. 40

6 recommendations .......................................................................................................................... 41

7 conclusion ..................................................................................................................................... 42

8 appendix ........................................................................................................................................ 43

Notes ..................................................................................................................................... 43 8.1

bibliography .......................................................................................................................... 44 8.2

9 Bibliography ................................................................................................................................. 44

10 Annexure ....................................................................................................................................... 45

Annex 1: Reliability Test ...................................................................................................... 45 10.1

Annex 2: Descriptive test ...................................................................................................... 47 10.2

10.2.1 Frequency ...................................................................................................................... 47

Annx 3: Similarity test .......................................................................................................... 57 10.3

Annex 4: Regression analysis ............................................................................................... 60 10.4

Annex 5: Correlation ............................................................................................................. 61 10.5

Annex 6: Schema .................................................................................................................. 62 10.6

Annex 7: Questionnaire ........................................................................................................ 63 10.7

Annex 8: KII Findings ............................................................................................................ 1 10.8

iv | P a g e

EXECUTIVE SUMMARY

Electronic banking, internet banking, mobile banking, SMS banking these are the buzzwords

of the global financial world. Bangladesh, the 60th

ranked (in terms of Nominal GDP figure,

World Bank 2012) low income democracy in the South Asia, is no stranger to these

phenomena. Mobile banking services in emerging economies like Bangladesh has the

potential to bring the unbanked potential under the banking sector. Mobile banking is

basically the provision of banking and financial services, such as cash-in, cash out, merchant

payment, utility payment, salary disbursement, foreign remittance, government allowance

disbursement, ATM money withdrawal through mobile technology devices. It is usually

operated through a collaboration of commercial banks and mobile service providers. Mobile

banking operations in Bangladesh started in 2011 and currently there are two major mobile

banking service providers in Bangladesh: Dutch Bangla Bank mobile banking and bKash, a

concern of BRAC Bank. Apart from them, 15 other banks are providing this service on a

small scale. At present the number of mobile banking customers in the country has exceeded

five million and 95% of the market share belongs to bKash (80% almost) and DBBL.

To detect the adoption pattern, consumers were grouped into 5 major categories in the

adoption process: Innovator, Early adopter, Early majority, Late majority and Laggards. The

scope of this research was Dhaka city only. Convenience issue apart, the diversified

population in the capital city accounts for 40% of the total urban population of the country.

To ensure a balanced reach in all areas of the city, the users are classified into three

categories according to the geographic location of their residents: Central Dhaka, Newly

developed areas and Outskirts. Although the primary target market for m-banking is rural

Bangladesh but they have a lower access to IT enabled services. Since the initial target

market is not absolutely ready, urban market-having greater technological accessibility rate

can be an effective niche to popularize m-banking. Moreover the m-banking service

providers have their strong customer base already (of other services like ATM, e-banking,

regular banking etc.) in urban areas which will work as a primary determinant behind

introduction of m-banking here. There is no elaborative research paper online as on this

arena. Thus the issues like urban scenario of mobile banking option, current market forces

etc. needed vital attentions as to bridge the research gap.

A survey questionnaire was designed addressing several factors in the process and quota

based sampling was done to derive responses from different areas of the city. At 95%

confidence interval sample size was determined 384 but budget and time constraints allowed

196 responses. That adjusts our confidence interval at 91.12% for a 10% precision level.

Majority of the respondents were male, 25-31 years old, Graduate/Postgraduate, central

Dhaka residents, private service holders, low mid to mid income non-adopters of mobile

banking.

The dominant adopter group is early adopter in urban m-banking market. Innovators or

current adopters cover1/4th

of the potential market share. This suggests that the market is still

in its premature stage in Bangladesh and response generation will take a long time.

Demographic factors do not seem to have much impact on the adoption process, but access to

v | P a g e

supporting technology and literacy level of these technologies tends to affect the adoption. In

general, adopters have a negative user experience with m-banking and they still perceive it to

be a low safety technology. Majority of the banked customers complained about the time

consumption of traditional banking mode and the adopters perceive m-banking to be low

time-consuming. This advantage apart, m-banking has not yet been able to extend its

potential contributions to the market. This might be due to lack of motivated efforts by the

banks in this regard. Bkash apart, no other bank considers this section as a strategic business

unit and seem to be introducing the service only as a response to Bangladesh bank‟s green

banking policy.

Targeted value proposition, increased promotion, channel improvement, strategic alliance

with telecommunication companies have been recommended based on the evidences

extracted from international and local market case studies. With the proper utilization of the

consumer market understanding, the Banks are expected to augment their services in m-

banking section and benefit all the stakeholders immensely.

1 INTRODUCTION

BACKGROUND 1.1

Technology is changing the way that consumers connect with banks and with each other

presenting new opportunities for the previously unbanked. The sector is hopping from one

technology to the next to widen its access in a cost-effective and green way. Electronic

banking, internet banking, mobile banking, SMS banking these are the buzzwords of the

global financial world. Bangladesh, the 60th

ranked (in terms of Nominal GDP figure, World

Bank 2012) low income democracy in the South Asia, is no stranger to these phenomena.

Bangladesh has 4 State Owned Commercial Banks, 30 Private commercial banks, 4

specialized banks, 9 Foreign Commercial Banks and 4 non-scheduled banks 1under the

authority of its central bank, Bangladesh Bank, for serving the financial purposes of its

current population of 150,493,658( World bank, 2011). These 47 banks operate in 7772

branches spread countrywide. The banking sector has been experiencing rapid changes

because of numerous digitalization oriented initiatives encouraged by the govt. All banks

now are computerized at least at head office level. If we go at branch level only; 19%

branches of NCBs, 38% branches of PCBs and97 % branches of FCBs are computerized. An

ITRC survey found that overall computer density in the banking sector is 1.64. Majority of

banks is planning to introduce ICT for integration of banking services and new ICT based

banking services.

Foreign commercial banks are playing the pioneer role in introducing modern financial

products and services. Private Commercial Banks have started to follow the same pattern. On

the other hand Nationalized Commercial Banks and the Specialized Banks (SBs) could not

yet show notable performance regarding the issues. But due to the demands of the time, they

are now taking initiatives to launch modern and innovative products and services. Currently

most of the banks in Bangladesh are providing electronic products and services to their

Customers‟ .We cannot say they are completely following electronic way.

While banking sector is getting all electronic and carbon-free2, the penetration rate of

telecommunication has increased exponentially. In between 2003-2008, the number of mobile

subscribers increased by 97.8% in the region (UNESCAP Statistics Division, 2011). 60% of

the total population now has access to mobile phones. This one device has shaped the

economic and social condition of the country and its population by adding various layers to

its services. Communication, business, social cohesion etc. are some of the opportunities this

sector and its services have facilitated over the years. The total impact of mobile

1 Non- scheduled banks are those banks which are not registered under schedule of RBI act, 19

2 According to the carbon-finance unit of world bank, the general term is applied to investments in GHG

emission reduction projects.

1

communications on Gross Domestic Product (GDP) has been, and continues to be, substantial

and it accounted for 2.1% of GDP in 2004 that increased up to 6.2%of GDP in 2007.

Rapid growth of mobile phone users and wider range of the coverage of Mobile Network

Operators (MNOs) have made their delivery channel an important tool‐of‐the‐trade for

extending banking services to the unbanked/banked population. To avail of this opportunity,

the banking sector has, under its umbrella of electronic-banking, introduced a new dimension

of services; mobile banking. The country now has 17 banks providing the mobile-banking

facilities both for the banked and unbanked population for ease of transaction and financial

inclusion.

ISSUES 1.2

Although millions of dollars have been spent on building mobile banking systems, reports on

mobile banking show that potential users may not be using the systems, despite their

availability. This is a recurring issue particularly for the low income, developing countries.

Beneath its shiny features, mobile banking is plagued with trust and security concern. The

half or uneducated Bangladeshis , even today, use mobile mainly as a communication tool

and are not very aware and/or interested in its value added services3. The urban population

has better access to amenities that facilitate adoption of latest technologies. However, if we

consider the standard of the amenities available in Bangladesh, we will not find anything

encouraging. But the country, like any other country cannot avoid the changes that are

turning the world upside down. As Bangladesh is slowly entering the field of advanced

banking technologies with its limited resources, it is becoming more important to actually

investigate and evaluate the real opportunities the sector and its services have given its still

developing population. Also, the fact that, only 36.17% (17 among 47) of the Banks have

invested in this technology, makes it clearer that thorough analysis of the potential consumer

market is essential to eradicate the uncertainties ( whether they will adopt or refuse) involved

for further investments.

RESEARCH QUESTION 1.3

The questions that stem from the context set above are:

Is the already facilitated urban Bangladesh ready to adopt (and thus become

customers from potential consumers) the advanced mobile banking technology?

3 According to a survey conducted by BIDS in 2009 on awareness of ICT in rural Bangladesh, 68% of the

respondents, most of which are women, do have own mobile phone. All of them use mobile phone mainly for communicating with friends and family members, the other uses include listening songs, watching videos, capturing picture, etc. Majority of the respondents are neither aware of nor use other mobile phone value-added services, such as money transfer, mobile banking, bill pay, internet browsing, medical and agriculture services etc.

2

What is the nature of the usage pattern for existing customers of mobile banking?

What are the current trends in the sector in terms of growth and competition?

OBJECTIVES 1.4

1.4.1 BROAD OBJECTIVE

To find out the adoption pattern of m-banking in Urban Bangladesh and analyze its current

trend in the growing banking sector.

1.4.2 SPECIFIC OBJECTIVES

To identify the relationship between consumer adoption of m-banking and user

characteristics.

To analyze the perception of m-banking adopters regarding the technology.

To provide a holistic view on the industry trends.

HYPOTHESES 1.5

1. There is no relationship between age and consumer‟s adoption of m-banking.

2. There is no relationship between income and consumer‟s adoption of m-banking

3. There is no relationship between gender and consumer‟s adoption of m-banking.

4. There is no relationship between occupation and consumer‟s adoption of m-banking.

5. There is no relationship between educational qualification and consumer‟s adoption of

m-banking

6. There is no relationship between residence and consumer‟s adoption of mobile

banking.

7. There is no relationship between level of literacy about mobile functions in learning

m-banking and consumer‟s adoption of m-banking.

8. There is no relationship between the amount of money transacted and usage of m-

banking

9. Consumer‟s adoption of m-banking is not influenced by the views of social

networking websites.

10. Consumer‟s adoption of mobile banking is not influenced by the decision of family

members and peers.

11. Frequency of computer usage in personal life does not affect consumer adoption m-

banking.

12. Frequency of computer usage in professional life does not affect consumer adoption

of m-banking.

13. Frequency of internet usage in personal life does not affect consumer‟s adoption of m-

banking.

3

14. Frequency of internet usage in professional life does not affect consumer‟s adoption

of m-banking.

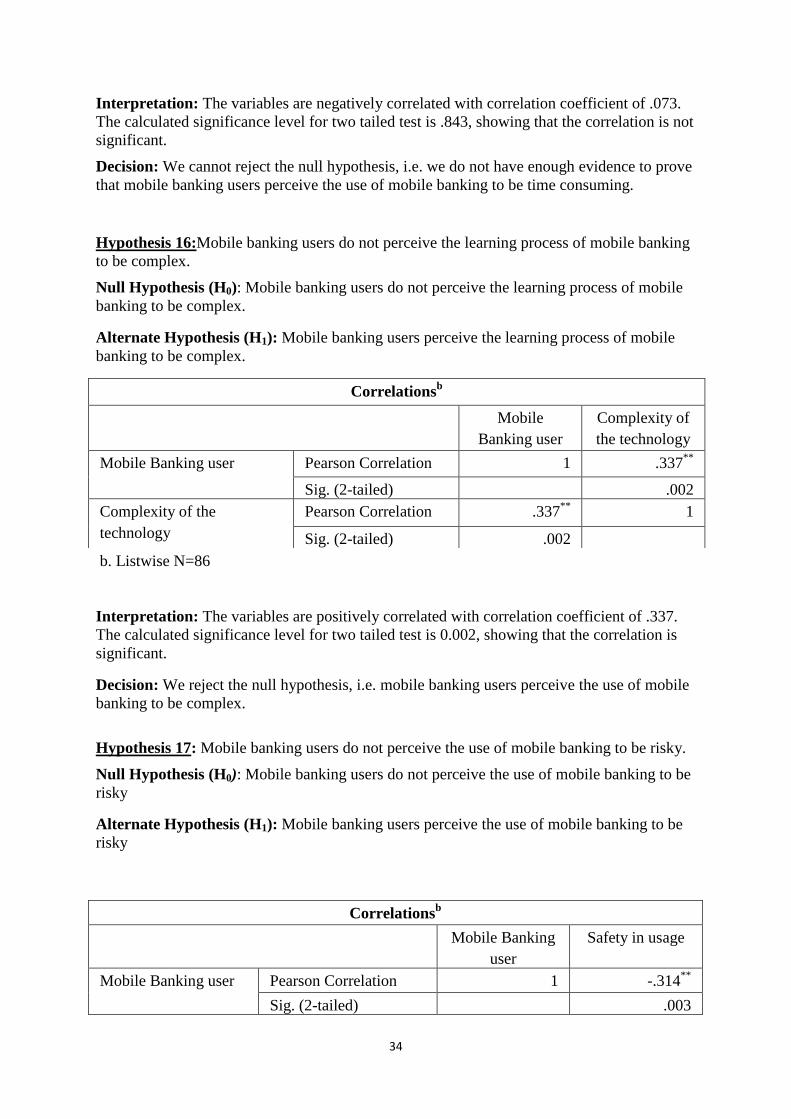

15. Mobile banking users do not perceive the use of mobile banking to be time

consuming.

16. Mobile banking users do not perceive the learning process of mobile banking to be

complex.

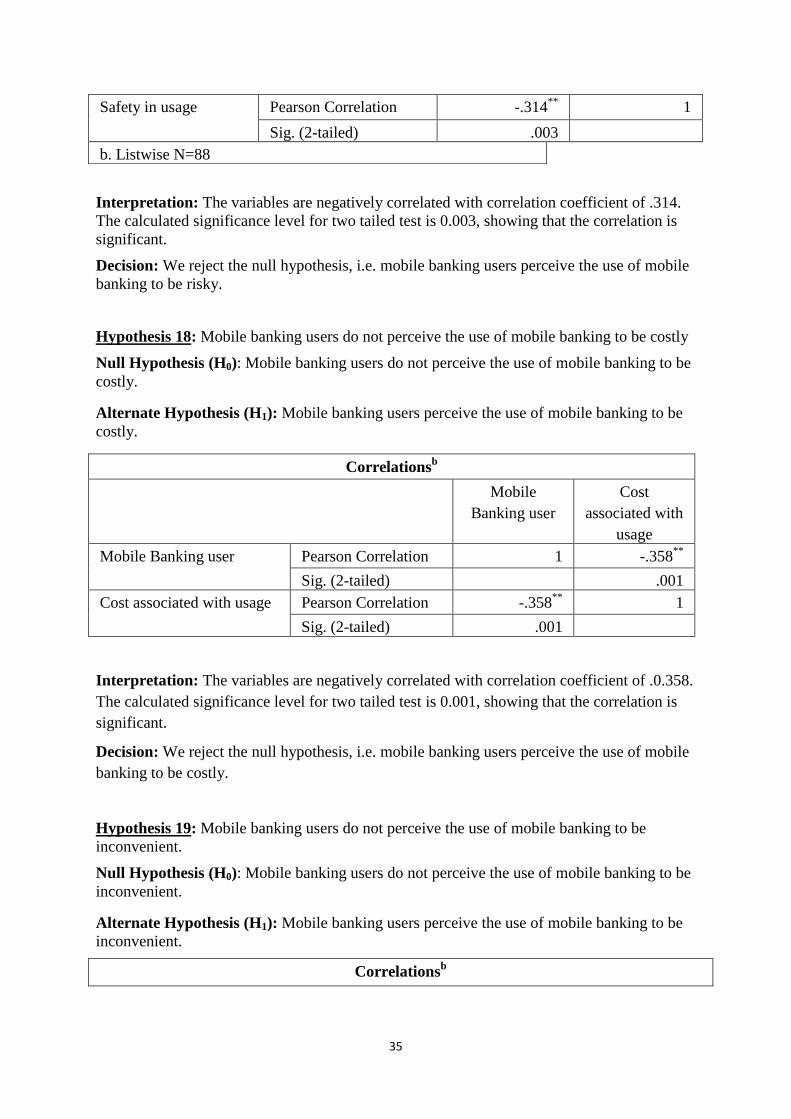

17. Mobile banking users do not perceive the use of mobile banking to be risky.

18. Mobile banking users do not perceive the use of mobile banking to be costly

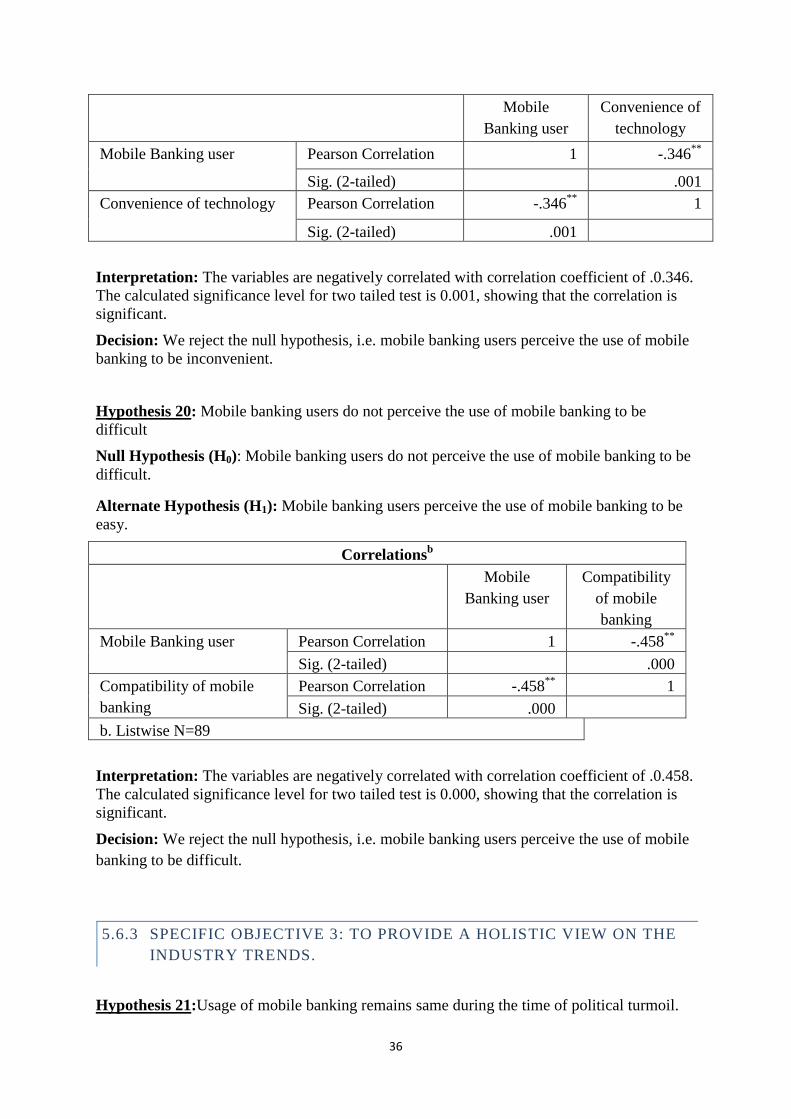

19. Mobile banking users do not perceive the use of mobile banking to be inconvenient.

20. Mobile banking users do not perceive the use of mobile banking to be difficult

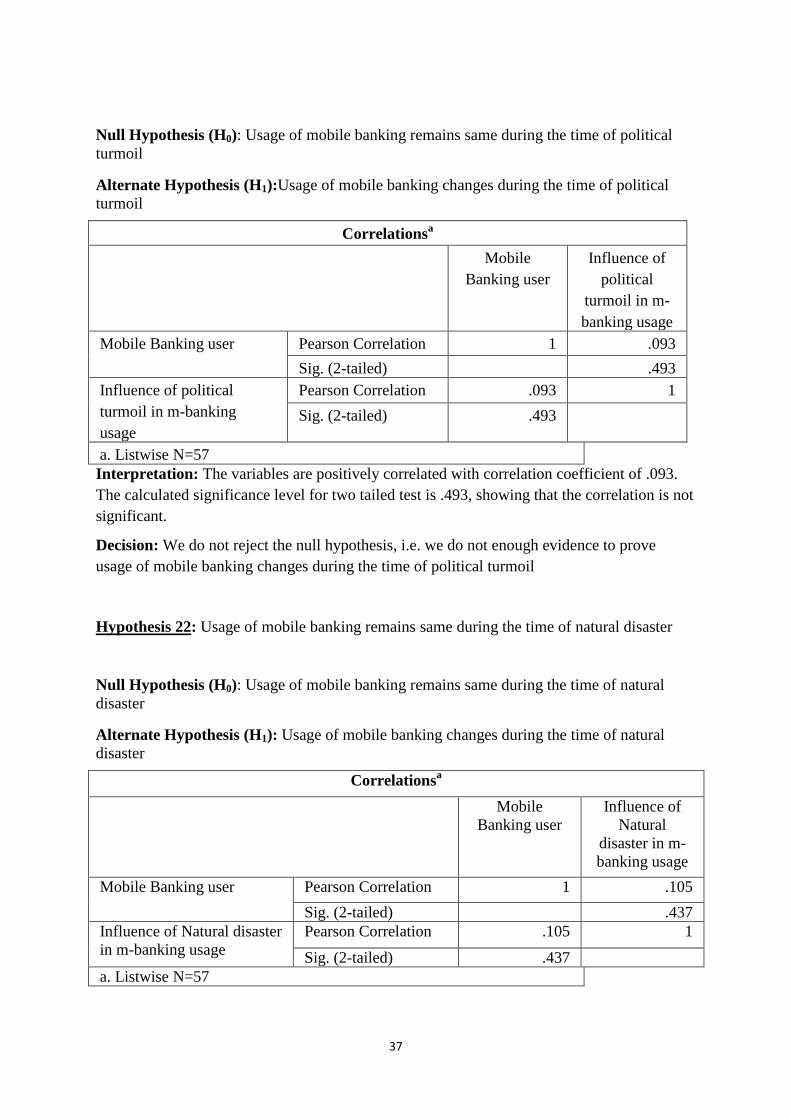

21. Usage of mobile banking remains same during the time of political turmoil.

22. Usage of mobile banking remains same during the time of natural disaster

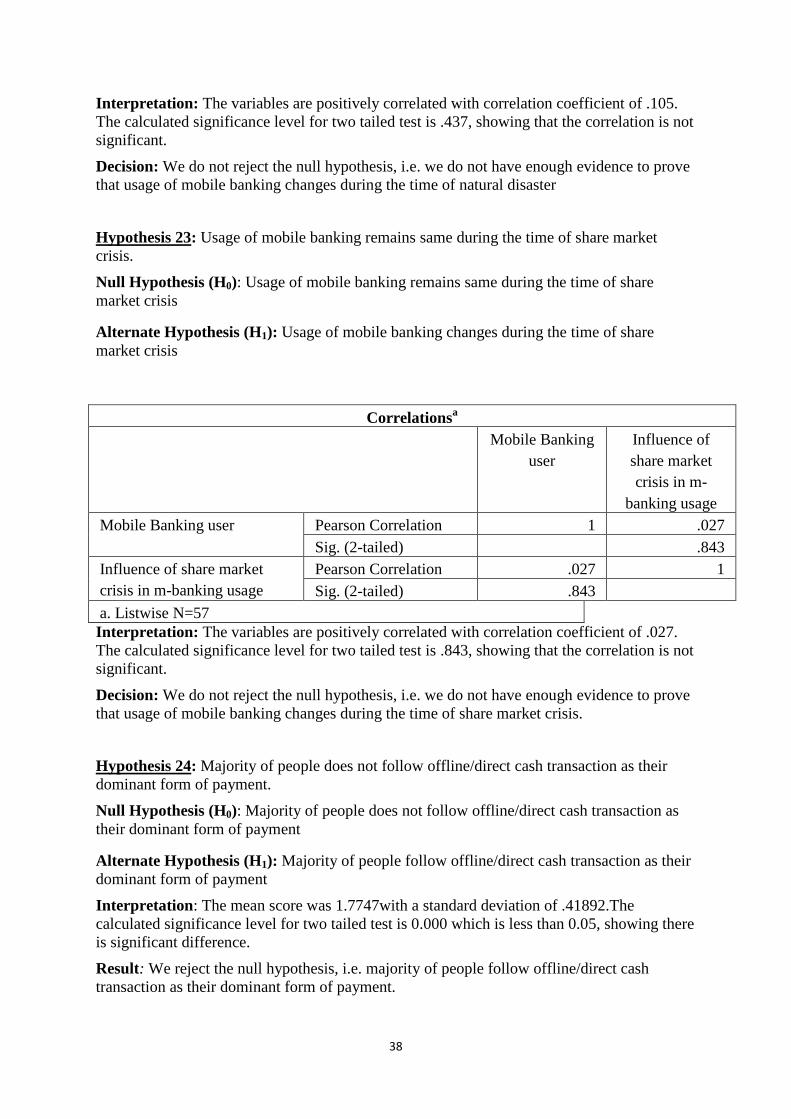

23. Usage of mobile banking remains same during the time of share market crisis.

24. Majority of people does not follow offline/direct cash transaction as their dominant

form of payment

RATIONALE 1.6

Mobile banking has been introduced in Bangladesh targeting rural people exclusively, with a

view to providing financial services to the unbanked communities efficiently and at an

affordable cost. However these rural communities are yet dependent on NGO loans and

Micro Finance Institutions. Since the initial target market is not absolutely ready, urban

market-having greater technological accessibility rate can be an effective niche to popularize

m-banking. Moreover the m-banking service providers have their strong customer base

already (of other services like ATM, e-banking, regular banking etc.) in urban areas which

will work as a primary determinant behind introduction of m-banking here. Hence, the

initiation of this research took place. Urban people usually have a very busy schedule which

does not allow them to waste time via traditional banking procedures. Added to that many of

their demographic segments are early innovators of any new technological advancement

introduced. On the other hand, unlike rural villagers the amount of money transected is much

higher by urban customers, so need for secured money transfer and mitigation of perceived

risk etc. are vital to adoption of mobile banking here. In a nutshell, mobile banking in Urban

Bangladesh is going to be a potential inclusion. But there is no elaborative research paper

online as on this arena. Thus the issues like urban scenario of mobile banking option, current

market forces and future prospect etc. need vital attentions as to bridge the research gap.

SCOPE 1.7

The research has been conducted on the mobile users of Dhaka city. Convenience issue apart,

the diversified population in the capital city accounts for 40% of the total urban population of

4

the country. To ensure a balanced reach in all areas of the city, the users are classified into

three categories according to the geographic location of their residents.

1. Central Dhaka (Gulshan, Banani, Dhanmondi, Mohammadpur etc.)

2. Recently developed areas (Uttara sector 11, JoarShaharaetc.)

3. Outskirts (Keraniganj, Luter Char etc.)

LIMITATIONS 1.8

Though, the area of the research is extensive, there are some constraints which have limited

the scope of the research:

Time constraint is the key limitation in this research.

This is accompanied by financial constraints which will limit the scope of the

research.

The absence of sufficient secondary data in this field resulted in the reliance of

primary data for drawing suitable conclusions.

The consistent objectivity of the parameters is dependent on individual respondents‟

perceptions.

Some of the respondents were not interested towards the filling of the questionnaire

resulting in biased opinion which has affected the outcome.

CONTRIBUTION OF THE RESEARCH 1.9

All the key stakeholders with regard to m-banking service provision will be benefitted by this

report. Given our report has explored multiple dimension of m-banking adoption practices

and its most recent market dynamics, it will factor into constructive contribution for the

concerned stakeholders mentioned below:

1. Bangladesh Bank: Since Mobile banking works as the most effective tool as to

propel the financial inclusion of the unbanked population of the country, BB has

always put a special focus on it. It has been developing Policy report on m-banking

from 2010, published annually- where growth prospect and risk scenario of m-

banking is discussed under the paradigm of only Key informant interviews with m-

banking service providers and Mobile network operators. Since our report has covered

an analysis (with primary data collected from field level consumer survey) on the

adoption pattern of current m-banking subscribers, BB will definitely be helped by

this.

2. M-bankers: Though 26 banks have been provided with the license as to carry on m-

banking, only 17 have adopted the alternative financial service delivery line. Again,

out of these 17 banks only two have 95% market share though almost all of them have

started simultaneously, first mover advantage did not come into play in this sector.

5

Moreover, except the two leading m-bankers (i.e. Bkash and DBBL) other banks have

not been making any substantial growth in their customer base though the market is

growing in every month, 12-15% growth in every month of 2013. Hence we can say

that most of the market players of m-banking service have failed to understand the

market dynamics, customers‟ adoption practices and urban trend in subscribing to m-

banking. Our report will most definitely help them tap the urban market with better

understanding of the market behavior.

3. MNO: Mobile network Operators play a vital role behind m-banking. Right now we

have 6 mobile network operators in the country (Robi,GP, Banglalink, Airtel ,

Citycell and Teletalk). Till now they have been working as partners of m-bankers as

to provide the network platform of the service. Now that government has introduced

payment gateway system4, all these MNOs might start their own m-banking systems

whereby no external partnership will be needed. If that comes into being, these MNOs

can analyze the urban market scenario with particular focus to the consumers‟

technology diffusion process.

2 LITERATURE REVIEW

For the past two decades, the banking sector has chosen several new service channels based

on the progress of information technology to respond to the changes in customer preferences

and needs. E-baking, m-banking, Automated Teller Machines etc. are few of these new

dimensions attached to banking sector jargons off late. Owing to Increasing competition

from non-banks and changes in demographic and social trends (Lederer, 2001); banks have

acknowledged the value to differentiate themselves from other financial institutions through

these avenues of new service distribution channels (Daniel, 1999) which is often termed as

virtual Banking. For example, E-banking has been continuously growing as a new industry

during the last decade, and now all banking transactions can be completed through internet

applications (Smith, 2008). With the success of e-banking technologies, m-banking ideas

have started taking pace in recent years, and the availability of a wider network of service

delivery has led to increasing adoption among consumers. M-banking, hence, is the most

innovative and user friendly addition to the list of convenient banking.(Servon, 2008)

Mobile Banking is a financial transaction conducted by logging on to a bank's website using a

cell phone, such as viewing account balances, making transfers between accounts, or paying

bills. This can be conducted through the internet browser on the phone, through a program

downloaded from the bank, or by text-message (SMS) (Karim, 2008). Mobile banking is an

application of m-commerce which enables customers to access bank accounts through mobile

devices to conduct and complete bank-related transactions such as balancing cheques,

checking account statuses, transferring money and selling stocks (hoan, 2010)defined mobile

banking as an innovative method for accessing banking services via a channel whereby the 4 The service that automates the payment transaction between the shopper and merchant. It is usually a third-

party service that is actually a system of computer processes that process, verify, and accept or decline credit card transactions on behalf of the merchant through secure Internet connections ( Bangladesh Bank, 2013)

6

customer interacts with a bank using a mobile device. Across the developing countries,

millions of people rely on informal economic activity and local level networks to earn their

living. Most of these populations are from bottom of pyramid and they don‟t have access to

basic financial services/banks as access to them is costly and very limited. However, the

outstanding growth of mobile sector worldwide has created a unique opportunity to provide

social and financial services over the mobile network to those grass root level people. With

over 4 billion mobile cellular subscriptions worldwide, mobile network has the ability to

immediately offer mobile banking to 61% of the world population (Sultana, 2009).

In Bangladesh, Mobile banking has been introduced by Dutch Bangla Bank Limited in 2011.

With the combination of two most recent technological advancements – internet and mobile

phone, mobile banking (mobile data service) was enabled and now such wireless internet

based commercial transaction is being performed by several banks here, bringing about a

paradigm shift in technology acceptance of even bottom of the pyramid population.

Following several years of deliberations and ad hoc permissions on Mobile Financial

Services, the Department of Currency Management and Payment Systems of Banglades

h Bank issued “Guidelines on Mobile Financial Services (MFS) for the Banks” on 22 Sept

ember 2011 which were subsequently amended on 20 December 2011. These guidelines

state that only a bank‐led model will be permitted. For Bangladesh Bank this means

that a customer‟s account, termed "Mobile Account", will rest with the bank and will

be accessible through the customer‟s mobile device. This mobile account will be a non‐

chequing account classified separately from a standard banking account.

It is believed that m-banking will provide another new channel for banking services,

especially in Bangladesh; because here more than 60% people own mobile phones but only

13% people have a bank account. (Ahmad, Laukkanen and Lauronen, 2005). In a

survey(stratified, SS-200) done in 2008 across the capital city Dhaka , showed that only

45.6% people of age between 20 to 35 years are currently using mobile service (Smith, 2008).

Hence Strategic implications and customer perception of m-banking services needs to be

explored with a focus on the consumer value creation and a better understanding about the

customer-perceived value of m-banking services.

Some demographic variables have interrelations which might have influence on the adoption

of mobile banking. As Lee (2009) stated that the cognitive propensity of individuals to risk-

differs across culture. This means that the customers‟ acceptance of mobile banking may be

influenced by cultural differences. For instance, mobile internet service has been quite

popular in Japan (over 60 million users in 2003) especially for those young and single (i.e.,

unmarried) consumers (Scornavacca and Barnes, 2004) But In many technologically

developed countries like Norway, m-banking is yet to be popularized. Although millions of

dollars have been spent on building mobile banking systems, reports on mobile banking show

that potential users may not be using the systems, despite their availability. Mobile banking

adoption has become such inconsistent because many people argue that internet and other

technology based transaction is not safe, not practical and would lead to fraud. On the other

hand a lot of people think it safer, flexible in time and can be done anywhere and anytime

(Chowdhury&Ahmmad 2011). Mattila (2010) in his research found that most of mobile

7

banking users have average age ranges from 23 years to 34 years. Similarly, Cheah et.al

(2011) found the age range of most of the mobile banking users is 20-25. In earlier studies in

this regard have provided interesting observations like , Wu and Wang (2005), in a study on

middle class populations, found that cost had minimal significant impact on the adoption of

mobile banking while perceived risk, compatibility and perceived usefulness have significant

influences. On the other hand Karnani (2009) argues that cost plays important role in

choosing mobile banking. Rotchanakitumanuai and Speece (2003) investigated why

corporate customers do not accept mobile banking, which can assist banks to implement this

self-service technology more efficiently. Many Thai banks are currently implementing

mobile banking. Banks that offer service via this channel claim that it reduces costs and

makes them more competitive (Servon, 2008). However, many corporate customers are not

highly enthusiastic about mobile banking. The interviews with Thai firms suggested that

security of the Internet is a major factor inhibiting wider adoption. Those already using

Internet banking seem to have more confidence that the system is reliable, whereas non-users

are much more service conscious, and do not trust financial transactions made via Internet

channels.

In line with the analysis above we can conclude that Bangladesh has high potential in terms

popularizing m-banking as the main stream banking process. Given the need to continue

to advance financial inclusion we can say that fully developed Mobile Financial Service

operations can reduce barriers of physical access and cost and over time enable a much

higher proportion of the population to use basic formal sector deposit and payment services.

Access into the formal system might eventually lead to product innovations in

insurance, credit, pensions and government payments that reach many millions of

Bangladeshis. Entry to the formal financial sector can lead to greater financial intermediation

and contribute to growth. But the adoption status of Mobile banking technology will depend

on Factors such as perceived usefulness (PU), perceived ease of use (PEOU), relative

advantages (RA) and personal innovativeness (PI) (Cheah et.al 2011) of the local

demography.

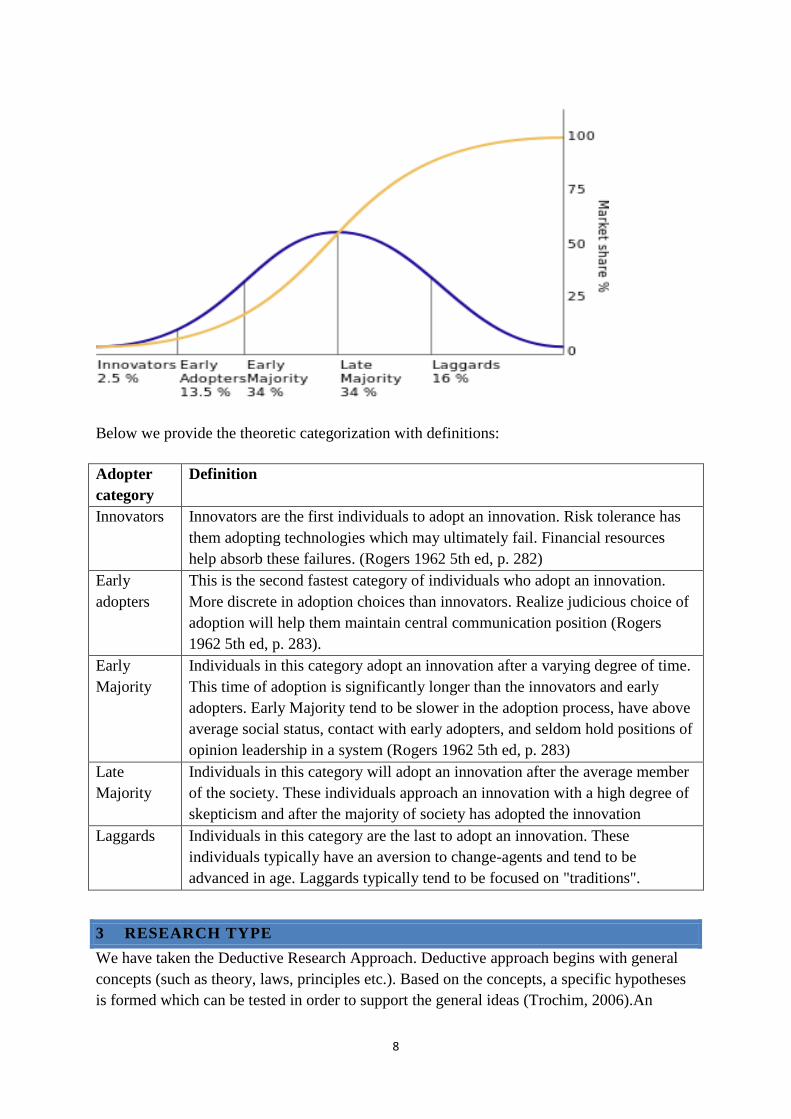

ADOPTION PROCESS: DIFFUSION OF 2.1

INNOVATION THEORY

In the book Diffusion of Innovations, Rogers suggests a total of five categories of adopters in

order to standardize the usage of adopter categories in diffusion research. The adoption of an

innovation follows an S curve when plotted over a length of time:

8

Below we provide the theoretic categorization with definitions:

Adopter

category

Definition

Innovators Innovators are the first individuals to adopt an innovation. Risk tolerance has

them adopting technologies which may ultimately fail. Financial resources

help absorb these failures. (Rogers 1962 5th ed, p. 282)

Early

adopters

This is the second fastest category of individuals who adopt an innovation.

More discrete in adoption choices than innovators. Realize judicious choice of

adoption will help them maintain central communication position (Rogers

1962 5th ed, p. 283).

Early

Majority

Individuals in this category adopt an innovation after a varying degree of time.

This time of adoption is significantly longer than the innovators and early

adopters. Early Majority tend to be slower in the adoption process, have above

average social status, contact with early adopters, and seldom hold positions of

opinion leadership in a system (Rogers 1962 5th ed, p. 283)

Late

Majority

Individuals in this category will adopt an innovation after the average member

of the society. These individuals approach an innovation with a high degree of

skepticism and after the majority of society has adopted the innovation

Laggards Individuals in this category are the last to adopt an innovation. These

individuals typically have an aversion to change-agents and tend to be

advanced in age. Laggards typically tend to be focused on "traditions".

3 RESEARCH TYPE

We have taken the Deductive Research Approach. Deductive approach begins with general

concepts (such as theory, laws, principles etc.). Based on the concepts, a specific hypotheses

is formed which can be tested in order to support the general ideas (Trochim, 2006).An

9

Inductive reasoning works the other way around, it works from observation (or observations)

toward generalizations and theories. Inductive can be seen as a theory developing through

interpreting collected data (Elo & Kyngas, 2008). We started off with the literature review

and formed hypotheses based on the current trends of mobile banking adoption in

Bangladesh. The existing research works explaining the demographic and social

characteristics of the mobile banking users were also taken into account from literature

review. Based on these we formed our research objectives and methodology

4 RESEARCH METHOD:

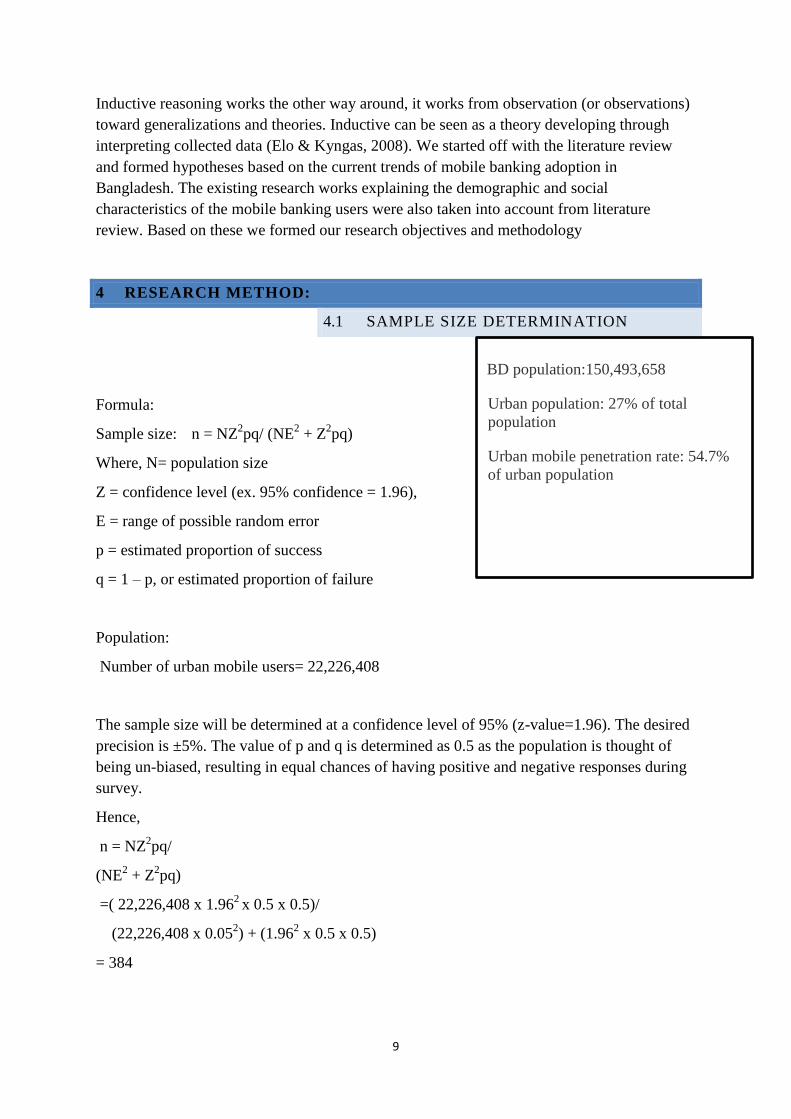

SAMPLE SIZE DETERMINATION 4.1

Formula:

Sample size: n = NZ2pq/ (NE

2 + Z

2pq)

Where, N= population size

Z = confidence level (ex. 95% confidence = 1.96),

E = range of possible random error

p = estimated proportion of success

q = 1 – p, or estimated proportion of failure

Population:

Number of urban mobile users= 22,226,408

The sample size will be determined at a confidence level of 95% (z-value=1.96). The desired

precision is ±5%. The value of p and q is determined as 0.5 as the population is thought of

being un-biased, resulting in equal chances of having positive and negative responses during

survey.

Hence,

n = NZ2pq/

(NE2 + Z

2pq)

=( 22,226,408 x 1.962 x 0.5 x 0.5)/

(22,226,408 x 0.052) + (1.96

2 x 0.5 x 0.5)

= 384

BD population:150,493,658

Urban population: 27% of total

population

Urban mobile penetration rate: 54.7%

of urban population

10

However, due to budget and time constraint, our survey was limited to 196 responses. That

adjusts our confidence interval at 91.12% for a 10% precision level.

QUESTIONNAIRE DEVELOPMENT 4.2

4.2.1 QUESTIONNAIRE DESIGN

Individual Questionnaire: Based on our cognitive understanding of the research topic

through secondary research and group study, we developed the questionnaire. Since our

survey respondents were to comprise urban population as majority, who usually maintain a

busy schedule; h/she would not get enough time to answer any descriptive question. We put

short multiple choice questions with ratings inscribed to most so that instead of random

answering, the respondents have to think and rate in a synchronized manner. Personal

questions like „household income‟ or „name of the bank respondent is having an account at‟

were put later in the questionnaire to ensure that it‟s not too early to have the real answer

before we establish a rapport with the test participant/respondent.

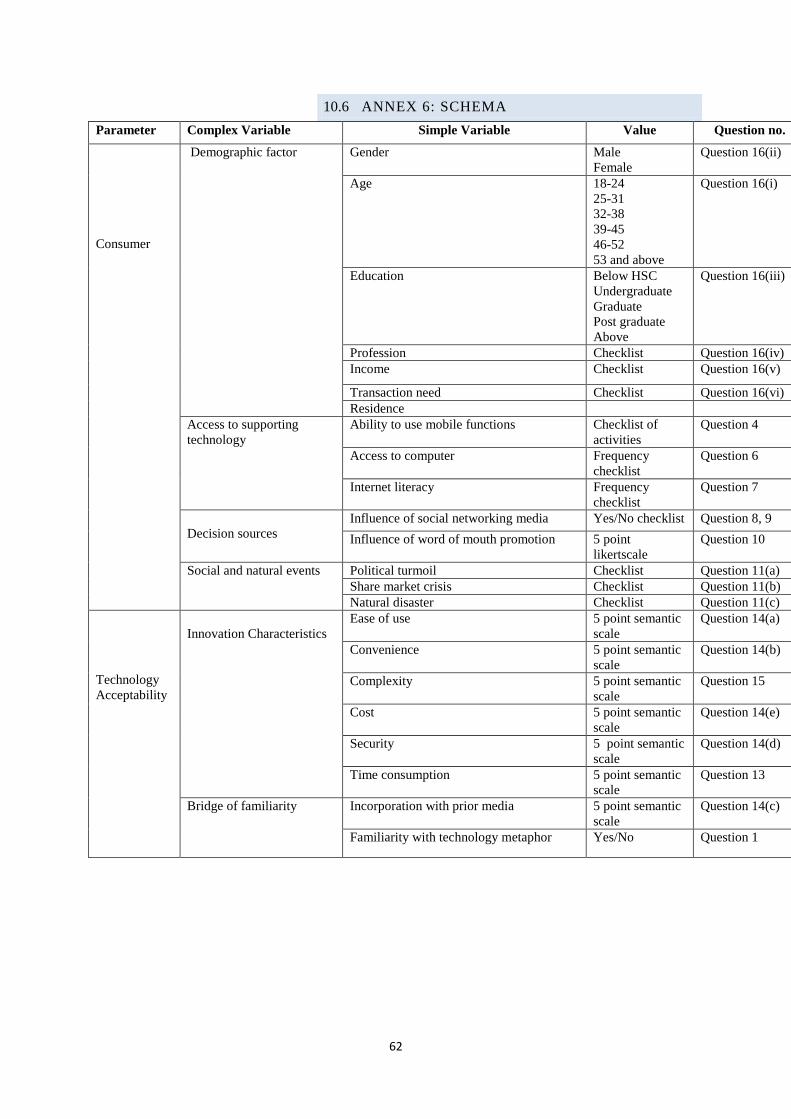

We have used a co-ordination schema of 2 parameters and 6 complex variables. The complex

variables were further expanded into 23 simple variables. The questions were formed in

accordance with the variables. Both likert scale and semantial scale format along with

multiple choice questions were designed in the questionnaire. The respondents were asked to

rate each of the variables relevant to the features of mobile banking on a scale of 1 – 5. The

questions were formed in a way so that a score of 1 on each of the questions denoted the

lowest value whereas a score of 5 denoted the highest. Both the co-ordination schema and

the questionnaire have been included in the appendix section.

KII Questionnaire: A short semi structured questionnaire was prepared for conducting Key

Informant interviews in Bkash and Dutch Bangla Bank Limited. Sensitive questions for the

company management were avoided. The questions specifically addressed the following

aspects to get a holistic scenario of the present scenario of mobile banking adoption in Urban

Bangladesh:

1. Characterization of mobile banking adoption in both rural (initial target) and urban

region at present.

2. Factors contributing to the growth of mobile banking usage in the urban regions.

3. Strengths and weaknesses towards the growth of mobile banking adoption in the

urban market.

4. Prospects of mobile banking in Urban Bangladesh in the coming years.

4.2.2 QUESTIONNAIRE VALIDITY

11

We have chosen face validity method to measure the validity of the variables for the research.

Face Validity implies that the items chosen to measure a variable are logically related to it.

From the literature reviews, we have logically chosen six complex variables to measure the

present mobile banking adoption scenario. The variables are demographic factors, access to

supporting technology, decision sources, impacts of social and natural events, innovation

characteristics and bridge of familiarity. All these variables are logically related to measure

consumer adoption of mobile banking. The service is considered to be effective if the

customers think it fulfills all their banking needs, it is secure, social environment supports the

use of mobile banking and the innovation characteristics are simple and convenient.

Under the 6 complex variables there are 23 simple variables to measure the consumer

adoption of mobile banking. Each of the questions designed are directly and logically related

to the objectives of our research. For example- to measure the influence of social norms on

his/her decision of mobile banking adoption we asked How much do you rely on family

members and peers when adopting new technologies? To measure the influence of

communication channels specifically the socialmedia we asked Influence of social

networking websites on you-and the respondents rated the statement on a scale of 1-5. All the

items chosen to ask the respondents are logically related to the simple variables, their

corresponding complex variable and lead to measure the mobile banking adoption scenario

among the urban consumers at present.

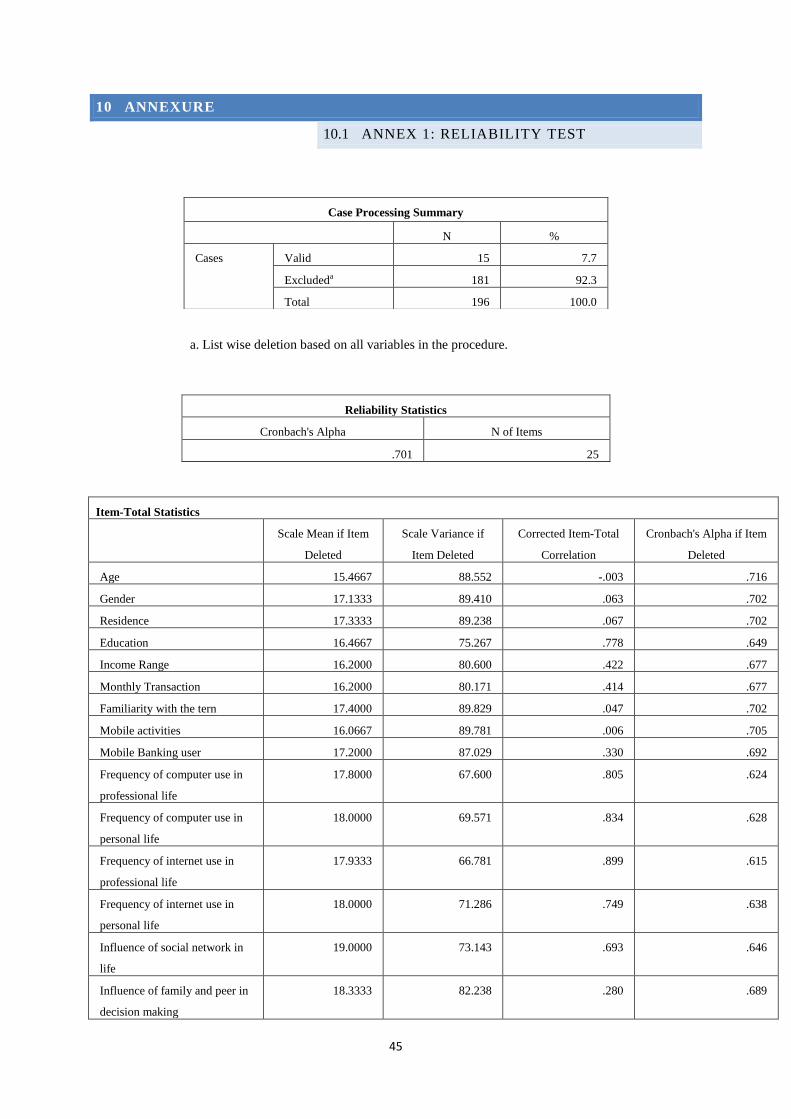

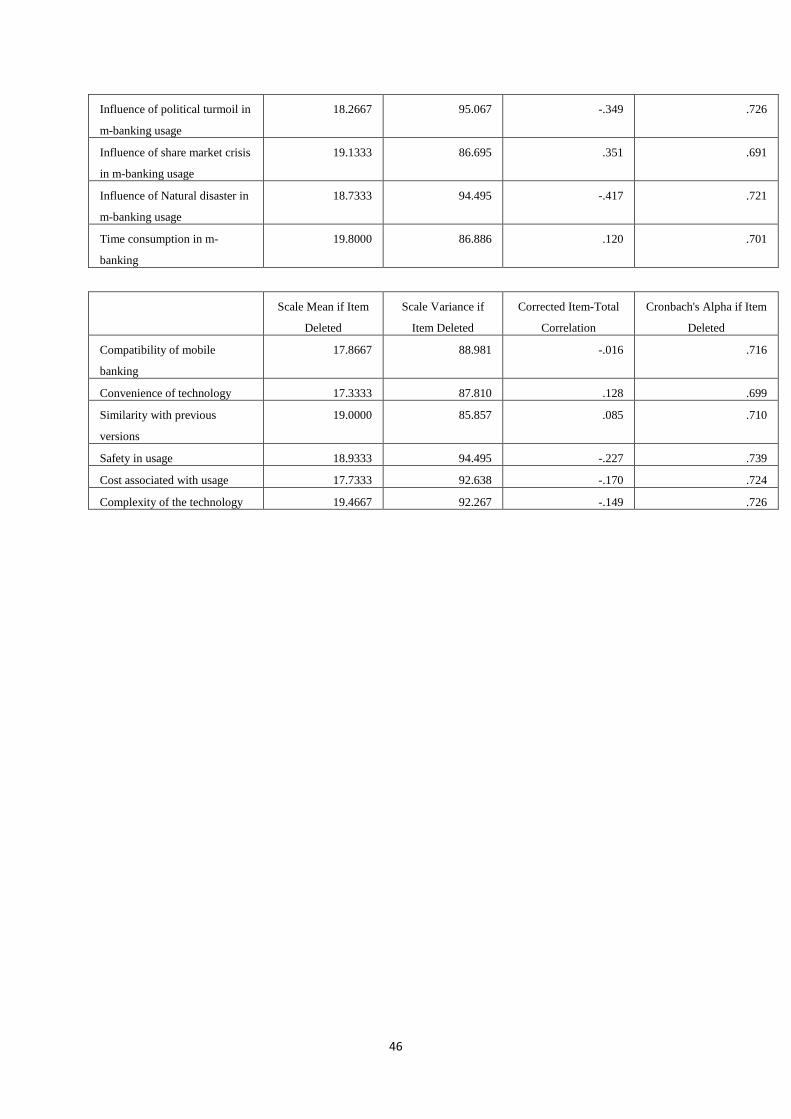

4.2.3 QUESTIONNAIRE RELIABILITY

If a measure, when applied repeatedly to the same object under constant conditions, produces

the same result each time, it is called reliable. There are few techniques to measure reliability.

Reliability test

The reliability of data was verified using both Alpha and Split Half Technique. The data was

found to be:

Reliability Statistics

Cronbach's Alpha N of Items

.701 25

A Cronbach‟s Alpha of 0.70 and above is considered to be reliable. Our Cronbach‟s Alpha

based on standardized items is 0.701, indicating the reliability of data.

DATA COLLECTION 4.3

4.3.1 PRIMARY DATACOLLECTION

Individual Survey: We have conducted 196 field individual surveys as to collect the

data. Urban development pattern has occurred in different parts of the city following

varied direction. From a broader spectrum we have divided the capital city with

12

regards to development trend, into 3 primary categories: 1. Central Dhaka 2. Out

Skirts 3.Recently Developed Areas. Depending on the development scenario (Road,

Infrastructure development, Socio economic change in the last decade etc.) adoption

of anything new will not be homogeneous in these areas. We used to quota sampling

to assign a fixed number of surveys for each of these locations thus ensuring

participation from among all the varied regions of the urban environment. Our survey

conduction was designed like this:

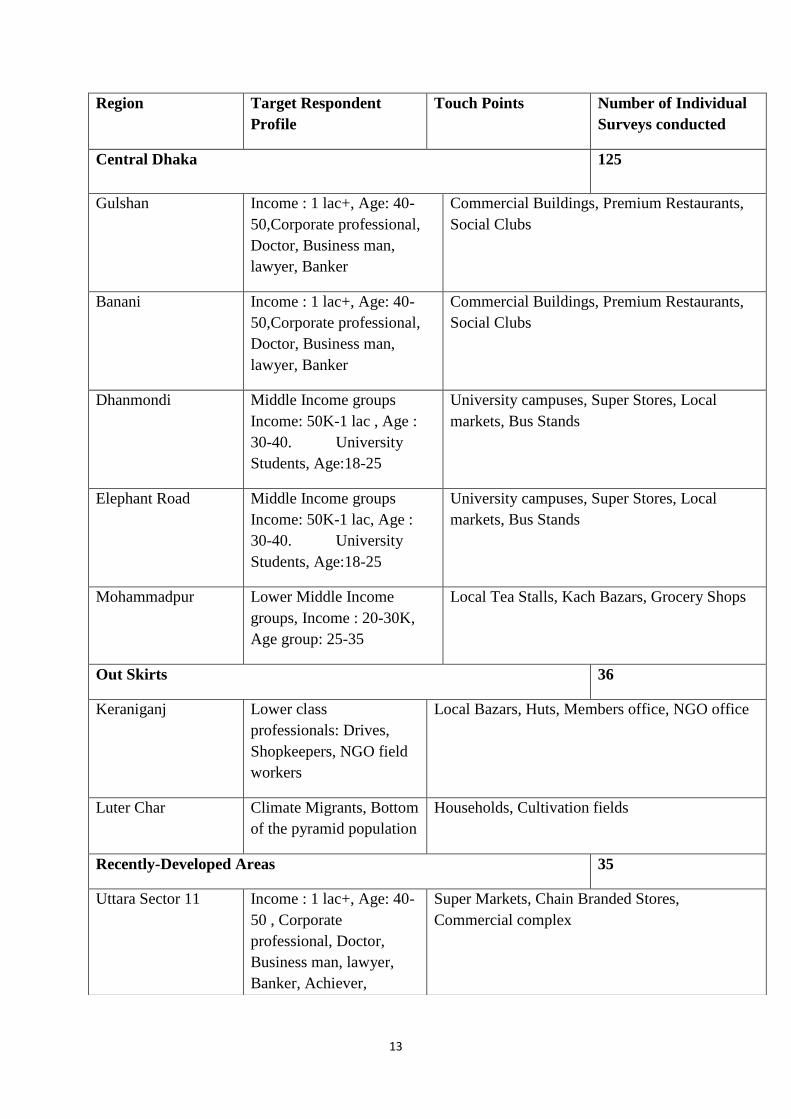

13

Region Target Respondent

Profile

Touch Points Number of Individual

Surveys conducted

Central Dhaka 125

Gulshan Income : 1 lac+, Age: 40-

50,Corporate professional,

Doctor, Business man,

lawyer, Banker

Commercial Buildings, Premium Restaurants,

Social Clubs

Banani Income : 1 lac+, Age: 40-

50,Corporate professional,

Doctor, Business man,

lawyer, Banker

Commercial Buildings, Premium Restaurants,

Social Clubs

Dhanmondi Middle Income groups

Income: 50K-1 lac , Age :

30-40. University

Students, Age:18-25

University campuses, Super Stores, Local

markets, Bus Stands

Elephant Road Middle Income groups

Income: 50K-1 lac, Age :

30-40. University

Students, Age:18-25

University campuses, Super Stores, Local

markets, Bus Stands

Mohammadpur Lower Middle Income

groups, Income : 20-30K,

Age group: 25-35

Local Tea Stalls, Kach Bazars, Grocery Shops

Out Skirts 36

Keraniganj Lower class

professionals: Drives,

Shopkeepers, NGO field

workers

Local Bazars, Huts, Members office, NGO office

Luter Char Climate Migrants, Bottom

of the pyramid population

Households, Cultivation fields

Recently-Developed Areas 35

Uttara Sector 11 Income : 1 lac+, Age: 40-

50 , Corporate

professional, Doctor,

Business man, lawyer,

Banker, Achiever,

Super Markets, Chain Branded Stores,

Commercial complex

14

4.3.2 Secondary Data

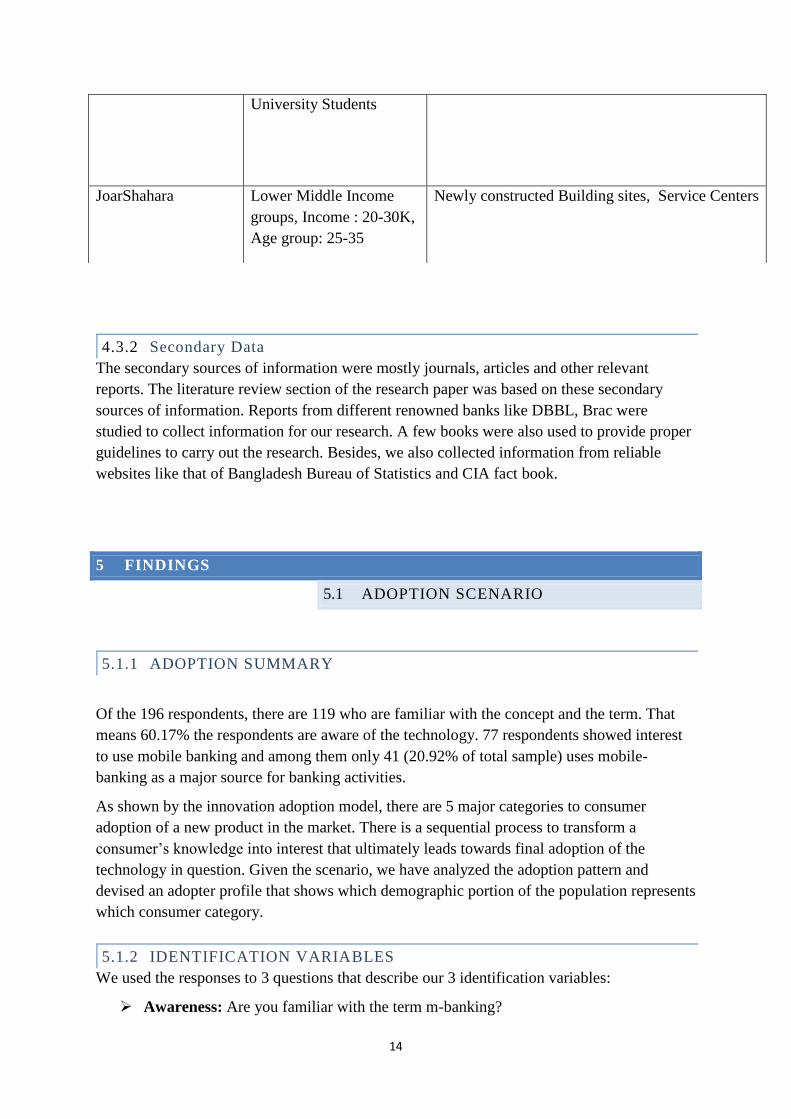

The secondary sources of information were mostly journals, articles and other relevant

reports. The literature review section of the research paper was based on these secondary

sources of information. Reports from different renowned banks like DBBL, Brac were

studied to collect information for our research. A few books were also used to provide proper

guidelines to carry out the research. Besides, we also collected information from reliable

websites like that of Bangladesh Bureau of Statistics and CIA fact book.

5 FINDINGS

ADOPTION SCENARIO 5.1

5.1.1 ADOPTION SUMMARY

Of the 196 respondents, there are 119 who are familiar with the concept and the term. That

means 60.17% the respondents are aware of the technology. 77 respondents showed interest

to use mobile banking and among them only 41 (20.92% of total sample) uses mobile-

banking as a major source for banking activities.

As shown by the innovation adoption model, there are 5 major categories to consumer

adoption of a new product in the market. There is a sequential process to transform a

consumer‟s knowledge into interest that ultimately leads towards final adoption of the

technology in question. Given the scenario, we have analyzed the adoption pattern and

devised an adopter profile that shows which demographic portion of the population represents

which consumer category.

5.1.2 IDENTIFICATION VARIABLES

We used the responses to 3 questions that describe our 3 identification variables:

Awareness: Are you familiar with the term m-banking?

University Students

JoarShahara Lower Middle Income

groups, Income : 20-30K,

Age group: 25-35

Newly constructed Building sites, Service Centers

15

Interest: Would be interested in m-banking?

Adoption: Do you use m-banking as a major source for your banking activities?

5.1.3 INTERPRETATION

As the definitions suggest:

We label a consumer as an innovator if he/she has responded positively to all 3

components.

We label a consumer as an early adopter if he/she has awareness and interest but has

not adopted the technology yet. We also label the consumers early adopters who has

adopted but show a negative interest for their risk-aversion nature.

A consumer is labeled as early majority if despite the lack of awareness, shows a

quick response to awareness and is interested to use the technology in the future.

A late majority member has awareness, still has no interest, which is indicator to slow

response to adoption process.

A laggard has neither of the components and is the last group in the society to accept

a new trend.

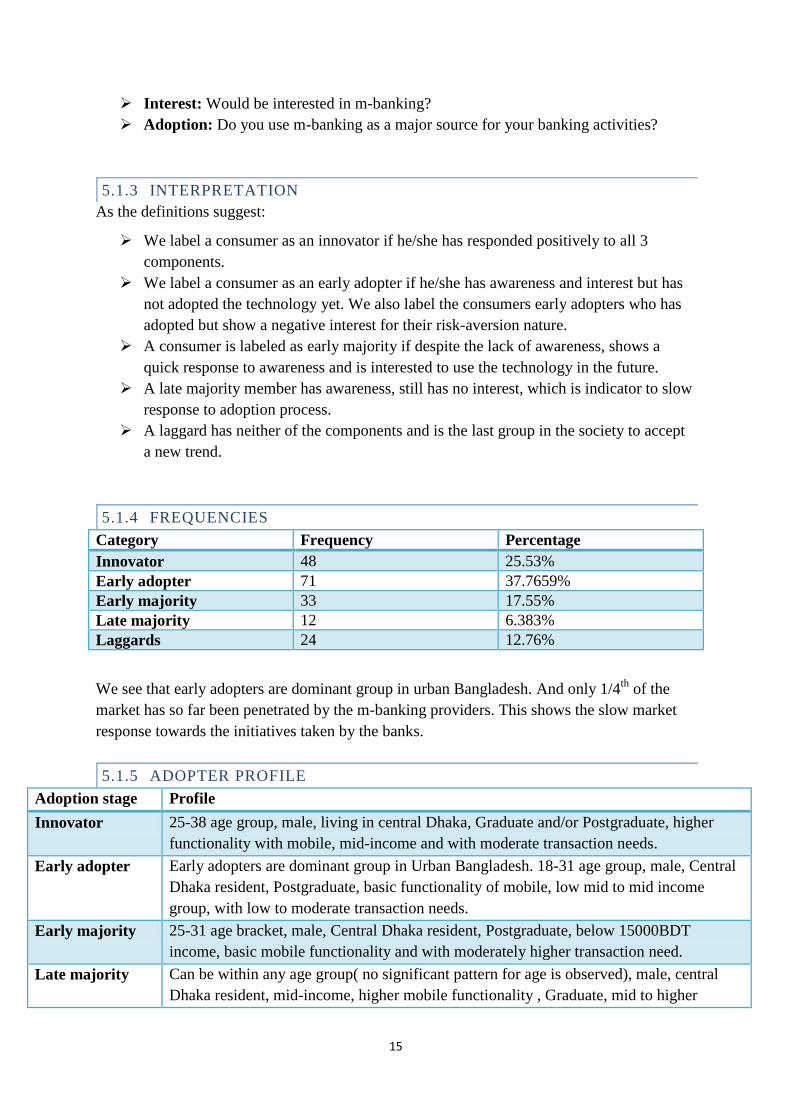

5.1.4 FREQUENCIES

Category Frequency Percentage

Innovator 48 25.53%

Early adopter 71 37.7659%

Early majority 33 17.55%

Late majority 12 6.383%

Laggards 24 12.76%

We see that early adopters are dominant group in urban Bangladesh. And only 1/4th

of the

market has so far been penetrated by the m-banking providers. This shows the slow market

response towards the initiatives taken by the banks.

5.1.5 ADOPTER PROFILE

Adoption stage Profile

Innovator 25-38 age group, male, living in central Dhaka, Graduate and/or Postgraduate, higher

functionality with mobile, mid-income and with moderate transaction needs.

Early adopter Early adopters are dominant group in Urban Bangladesh. 18-31 age group, male, Central

Dhaka resident, Postgraduate, basic functionality of mobile, low mid to mid income

group, with low to moderate transaction needs.

Early majority 25-31 age bracket, male, Central Dhaka resident, Postgraduate, below 15000BDT

income, basic mobile functionality and with moderately higher transaction need.

Late majority Can be within any age group( no significant pattern for age is observed), male, central

Dhaka resident, mid-income, higher mobile functionality , Graduate, mid to higher

16

income group.

Laggard 39 to 45 years old, male, outskirts resident, Undergraduate , low income, low transaction

need and with very basic mobile functionality.

SAMPLE STATISTICS 5.2

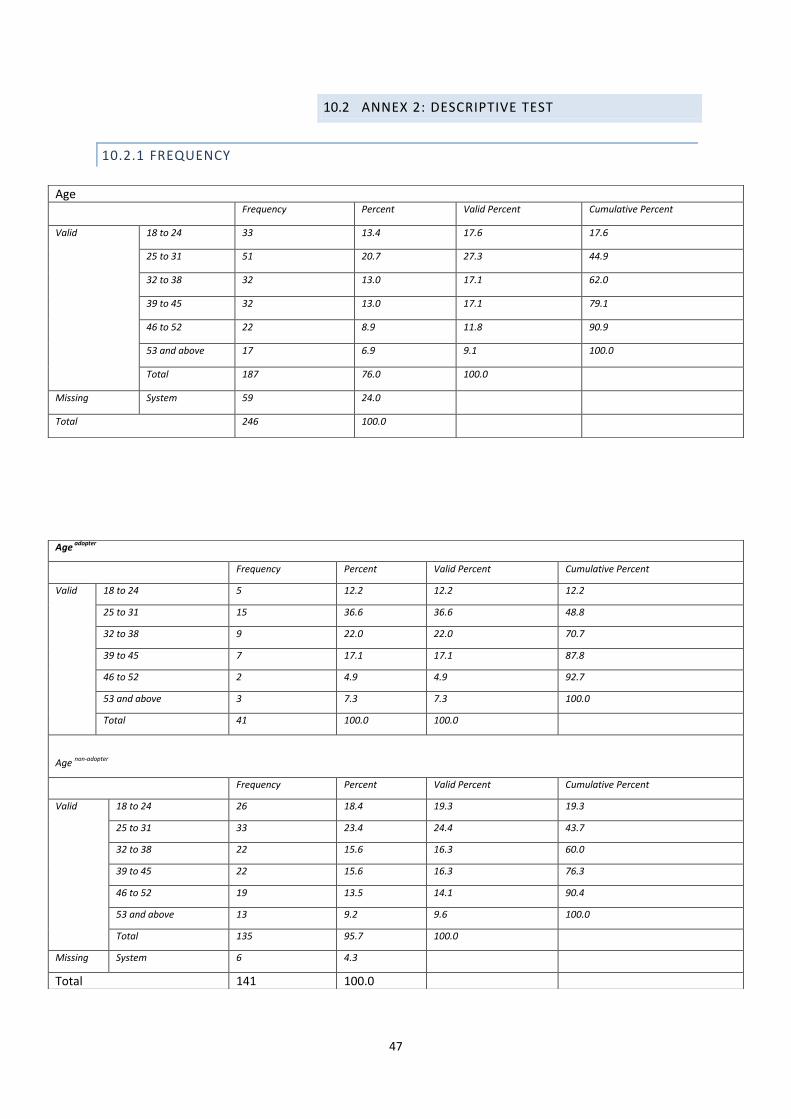

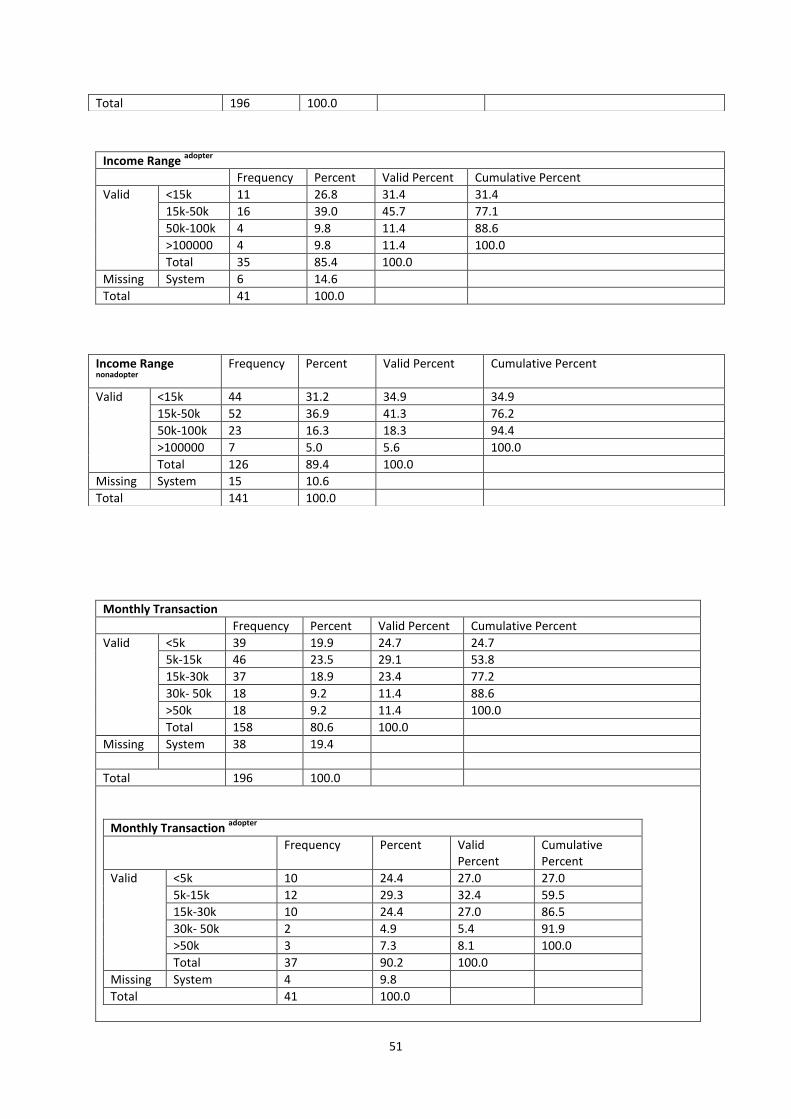

5.2.1 SAMPLE DEMOGRAPHY

1. Age

The lowest age group is 18 to 24, that includes 17.6% of the respondents. The analysis shows

that dominant age group here is 25 to 31 (27.3% of the respondents) while only 9.1%

respondents are from 53 and higher age group.

Age distribution of adopters and non-adopters:

Clearly the non-adopters outnumber the adopters of m-banking in all age groups. 36.6% of

the adopters are in 25-31 age group, while similarity in frequency is shown by 32-38 and 39-

45 age group.

2. Gender:

69.4% of the total 196 respondents are male, whereas about 29.6% of the respondents are

female. There were also two missing values contributing to the remaining 1 percent of the

respondents.

Gender distribution of adopters and non-adopters:

Male are the dominant m-banking adopters. Among the 41 respondents who are adopters,

around 68.3% are male and around 31.7 % are female.

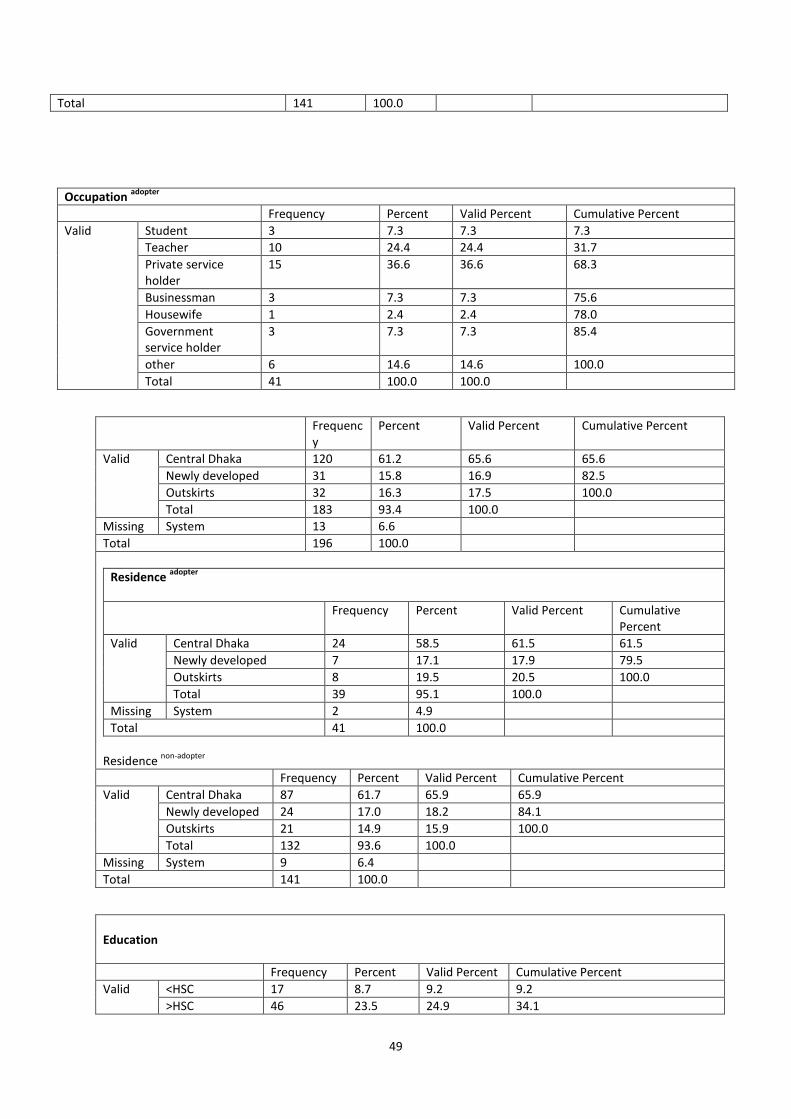

3. Occupation

Majority of our respondents were Private Service Holder which is about 21.4% of the total

respondents. The least number of respondents were housewives which comprises about 6.6%

of the total respondents. Teacher respondents were roughly around 15.8% whereas student

respondents were close around 14.3%

It can be clearly seen from the statistics above that among the 41 respondents who are the

adopters of mobile banking, about 36.6 % of the respondents are Private Service Holder and

the closest occupational group who are adopters are teachers who holds a handsome 24.4% of

17

the total respondents. The rest 39% of the adopters comprise of the remaining interviewed job

holder types such as Students (7.3%), Businessman (7.3%) and housewives being the least

with only 2.4% of the adopters.

Among the 141 respondents who were non-adopters, about 18.4% of the respondents were

private service holders, and the closest non-adopters‟ occupational group to the private

service holders are students who constitute about 17% of the total non-adopter group.

4. Residence:

61.2% of the total respondents are from central Dhaka. Among the 125 central Dhaka

residents, we find 21 as adopters, which is 16.8% of this segment. If we look into the 35

residents from newly developed regions in Dhaka, we can see that 20% of these respondents

are adopters and the adoption rate is slightly higher in outskirts (22.22% of the outskirts

residents).

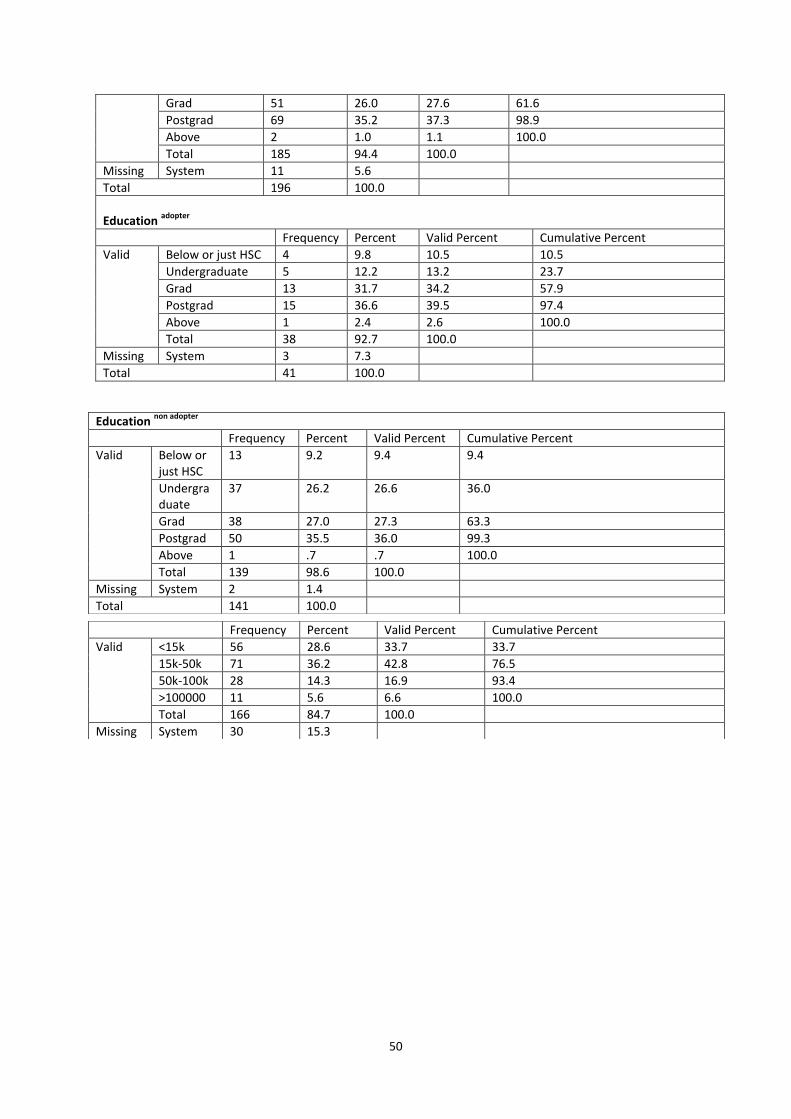

5. Education:

The adopters outnumber the non-adopter in most of the educational level. Undergraduates are

mostly non adopters with 26.6%. Among the adopters, postgraduates dominate the list with

39.5% followed by graduates, undergraduates and HSC degree holders.

6. Income:

There is no clear distinction as to who dominates the lists in case of income earned. The

income range 15k-50k encomprises majority of the adopters and non-adopters with 45.7%

and 41.3% respectively. They are followed by the income range less than 15K with 31.4% for

the adopters and 34.9% for the non-adopters. Income range 50-100k follows suit with

respondents having an income of 100000 and above are both the lowest number of adopters

and non-adopters.

7. Transaction amount:

The adopters outnumber the non-adopter in most of the transaction level. People transacting

money in the range less than 5k are mainly adopters with 27%. The non-adopters in this

range make up 25% of the respondents. The range 5K-15K dominates among both adopters

and non-adopters with 32.4% and 26.7% respectively. The range 30-0 K and above 50K is

dominated by the non-adopters with 13.8% and 12.9% respectively. This shows that mainly

people with low to moderate transaction need adopt mobile-banking for their banking

activities.

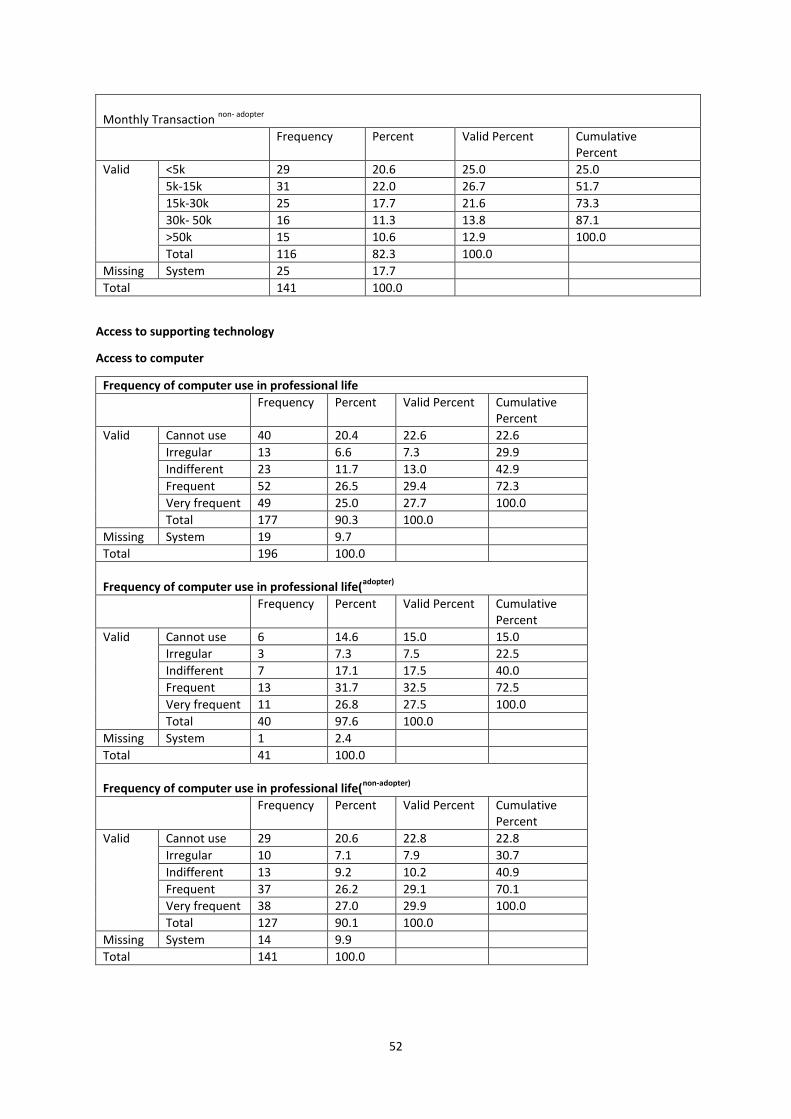

5.2.2 ACCESS TO SUPPORTING TECHNOLOGY

18

1. Access to computer

a) Frequency of computer usage in professional life:

Among the 141 non-adopters, there is also a very high percentage (about 26.2%) of people

use computer in their professional lives and about 27% use very frequently. But it can also be

mentioned that among the non-adopters, about 20.6% of them cannot use computer in their

professional lives.

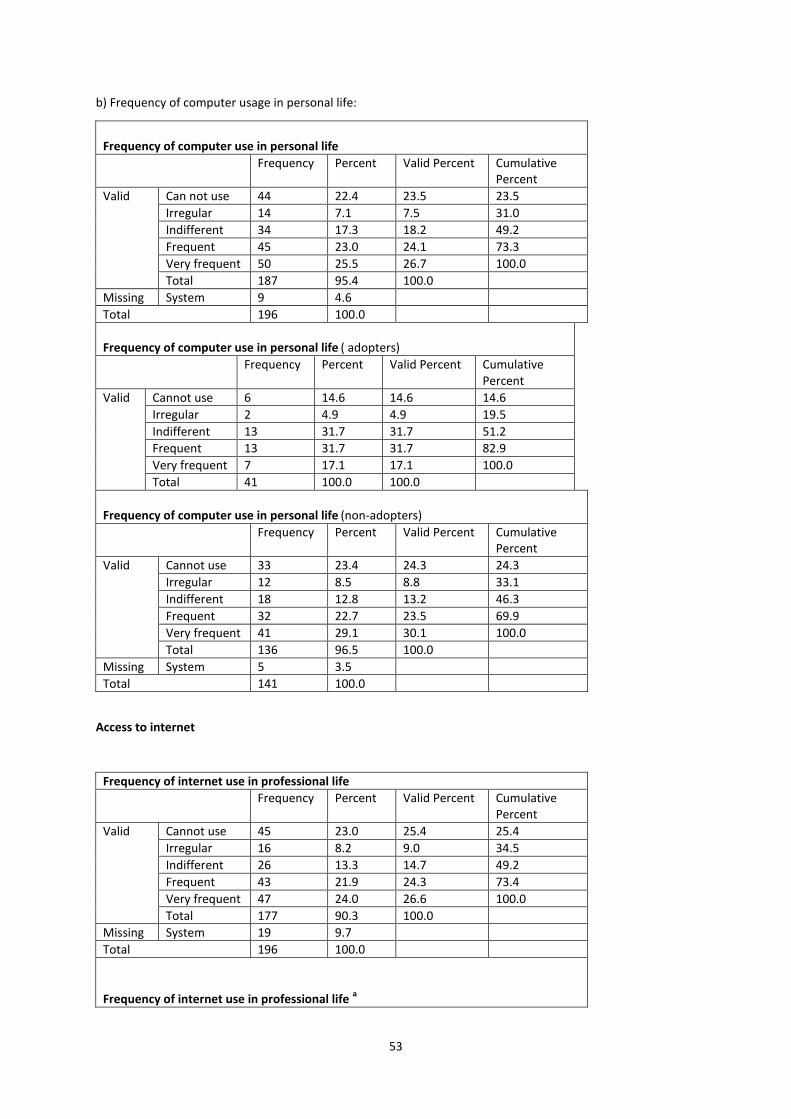

b) Frequency of computer usage in personal life:

Among the 196 respondents, about 22.4% respondents cannot use computer in their personal

lives whereas a high percentage of respondents (about 23%) use computer in their personal

lives frequently and about 25.5% use computer in their personal lives very frequently.

Among the 41 adopter respondents, around 31.7% respondents use computer frequently in

their personal lives and about 17.1% respondents use computer very frequently in their

personal lives. Only 14.6% of the respondents cannot use computer in their personal lives.

Among the 141 non-adopters, although about 22.7% of the respondents use computer in their

personal lives frequently and about 29.1% people very frequently, about 23.7% of the

respondents cannot use computer in their personal lives.

2. Access to internet

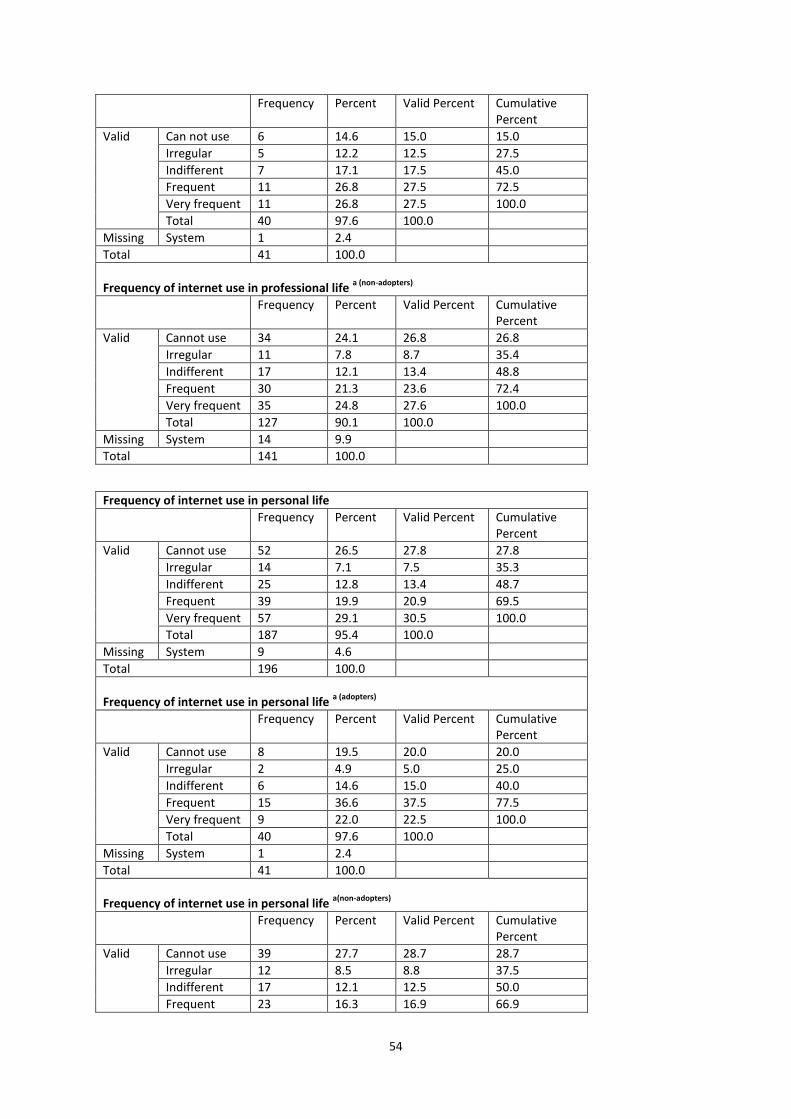

a) Frequency of internet usage in professional life:

Among the 196 respondents, about 23% respondents cannot use computer in their

professional lives whereas a high percentage of respondents (about 21.9%) use internet in

their professional lives frequently and about 24% use computer in their professional lives

very frequently.

Among the 41 adopters, around 26.8% respondents use internet frequently and 26.8% use

very frequently in their professional lives. A low percentage ( about 14.6%) of adopters

cannot use internet in their professional life.

b) Frequency of internet usage in personal life:

Among the 196 respondents, about 26.5% of the respondents replied that they cannot use

internet in their personal life. There is also a very high percentage of respondents, about

29.1% who use internet very frequently in their personal lives.

19

Among 41 adopter respondents, around 22% respondents use internet very frequently in their

personal lives and about 36.6% use internet frequently. There are also 19.5% adopter

respondents who cannot use internet in their personal lives.

Among the 141 non-adopters, although about 31.9% of the respondents use internet very

frequently in their personal lives, there are also 27.7% respondents who cannot use internet in

their personal lives.

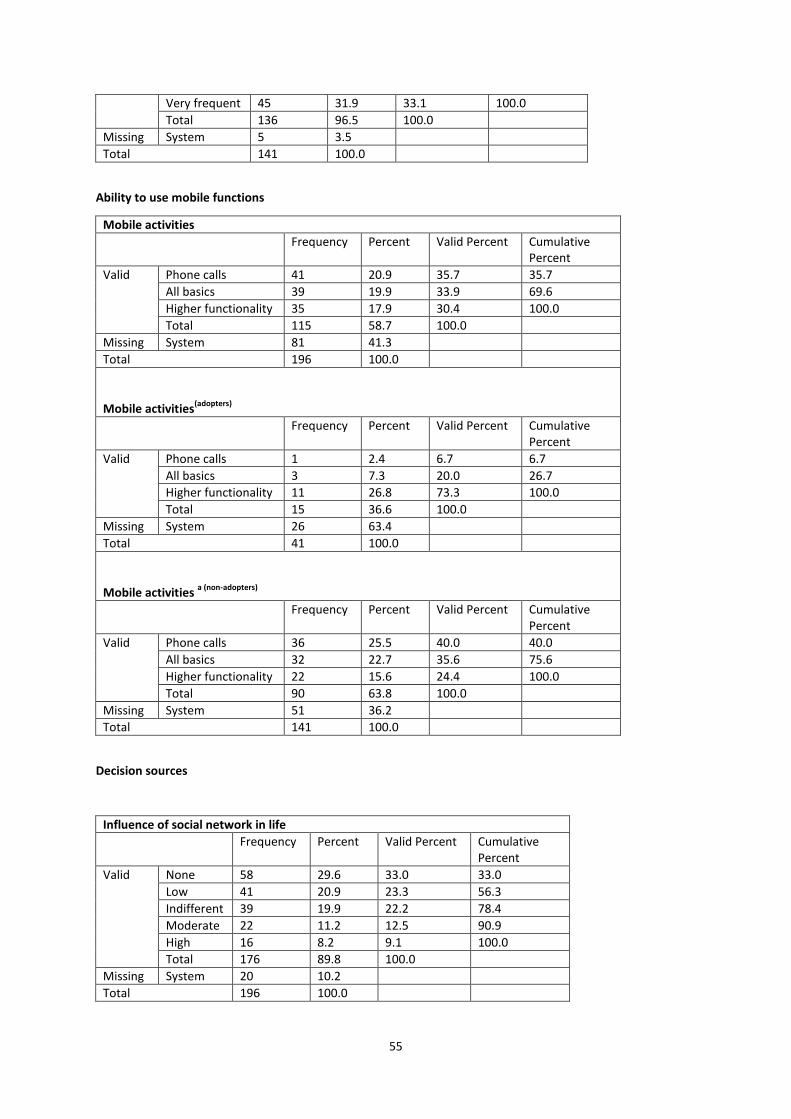

3. Ability to use mobile functions

Among the 196 respondents, although about 35.7% of the respondents replied that they can

only make phone calls through their mobile device, a high 30.4% replied that they can use all

the functionalities of a mobile device.

From the 41 respondents who are adopters, about 73.3 % replied that they can use all the

functionalities of mobile phone whereas about 20% replied that they can use all the basics of

mobile devices.

Among the received responses of non-adopters, about 40% of them can only use phone calls

through their phone device and a merely 24.4% only can use all the functions of a mobile

phone.

5.2.3 DECISION SOURCES

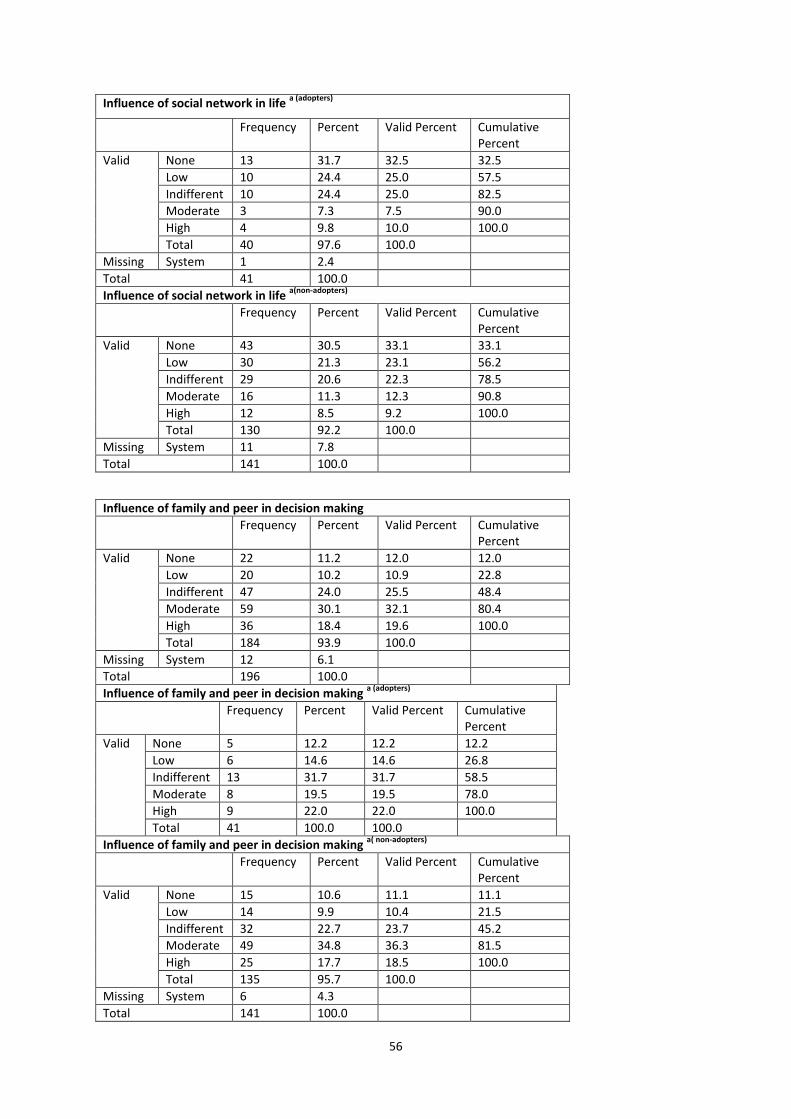

1. Influence of social network

Among the 196 respondents, about 29.6% replied that they were not at all influenced by

social networks, whereas only 8.2% of the respondents replied that they are highly influenced

by social networks.

Among the 41 adopters of mobile banking, a low 9.8% replied that they are highly influenced

by mobile banking and a very high figure of 31.4% respondents replied that they are not

influenced by social networking sites.

From the 141 non-adopter responses, 30.5% of them are not at all influenced by social

networking sites whereas only a mere 8.5% are highly influenced by social networking sites

2. Influence of family and peer in decision making

Among the 196 respondents, around 30.1% replied that they are moderately influenced by

family and peer in decision making and about 18.4% who are highly influenced by family

and peers.

20

Among the 41 adopters, around 31.7 replied that they are indifferent to the influence of

family and peer in decision making and only a mere percentage of 12.2% replied that they are

not at all influenced by family and peers.

Among the 141 non-adopters, around 34.8% replied that they are moderately influenced by

peer and family in decision making and only 17.7% replied that they are highly influenced by

family and peers.

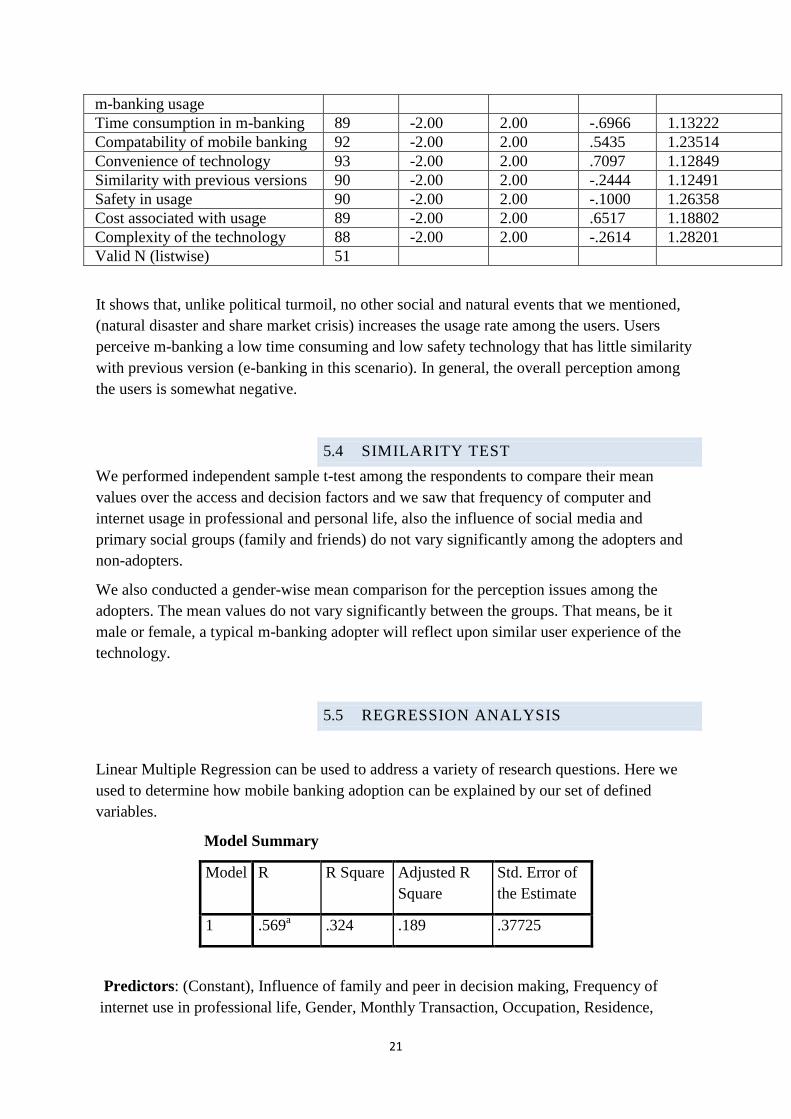

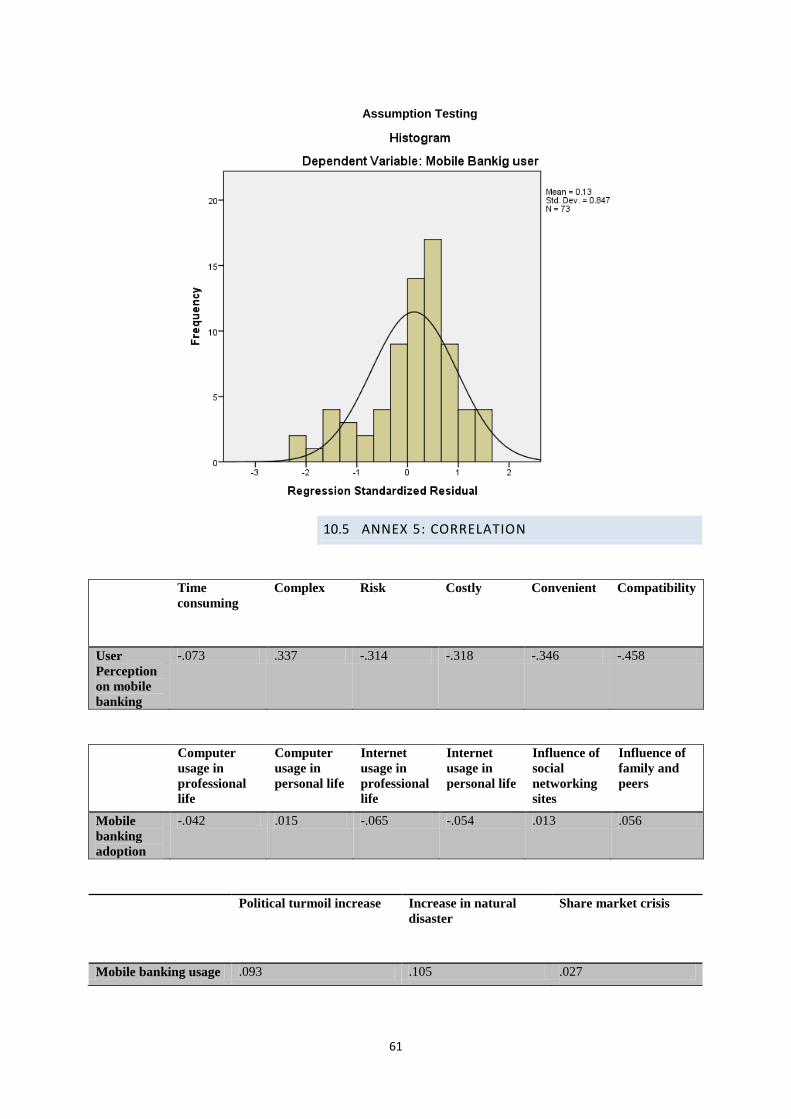

MEAN ANALYSIS 5.3

In order to find out the level of access to computer, internet and the influence of different

decision sources, we derived a 5-point scale where zero frequency was given a -2 value and

very high frequency was given a value of 2. Our mean analysis shows us:

N Minimum Maximum Mean Std. Deviation

Statistic Statistic Statistic Statistic Statistic

Frequency of computer use in

professional life

177 -2.00 2.00 .3220 1.51253

Frequency of computer use in

personal life

187 -2.00 2.00 .2299 1.51180

Frequency of internet use in

professional life

177 -2.00 2.00 .1751 1.54767

Frequency of internet use in

personal life

187 -2.00 2.00 .1872 1.61053

Influence of social network in

life

176 -2.00 2.00 -.5852 1.30651

Influence of family and peer in

decision making

184 -2.00 2.00 .3641 1.25145

Valid N (listwise) 160

While access to computer and internet both have a frequent direction among the respondents,

influence of social media as a decision source has a negative mean (low influence). Family

and peer is a viable decision source with a mean 0.3641, slightly higher than 0 (somewhat

rely on them).

Also, we calculate the mean values of the perception factors that were exclusive to the user:

N Minimum Maximum Mean Std. Deviation

Statistic Statistic Statistic Statistic Statistic

Influence of political turmoil in

m-banking usage

60 -1.00 1.00 .3167 .67627

Influence of share market crisis

in m-banking usage

59 -1.00 1.00 -.1695 .46060

Influence of Natural disaster in 60 -1.00 1.00 -.0333 .60971

21

m-banking usage

Time consumption in m-banking 89 -2.00 2.00 -.6966 1.13222

Compatability of mobile banking 92 -2.00 2.00 .5435 1.23514

Convenience of technology 93 -2.00 2.00 .7097 1.12849

Similarity with previous versions 90 -2.00 2.00 -.2444 1.12491

Safety in usage 90 -2.00 2.00 -.1000 1.26358

Cost associated with usage 89 -2.00 2.00 .6517 1.18802

Complexity of the technology 88 -2.00 2.00 -.2614 1.28201

Valid N (listwise) 51

It shows that, unlike political turmoil, no other social and natural events that we mentioned,

(natural disaster and share market crisis) increases the usage rate among the users. Users

perceive m-banking a low time consuming and low safety technology that has little similarity

with previous version (e-banking in this scenario). In general, the overall perception among

the users is somewhat negative.

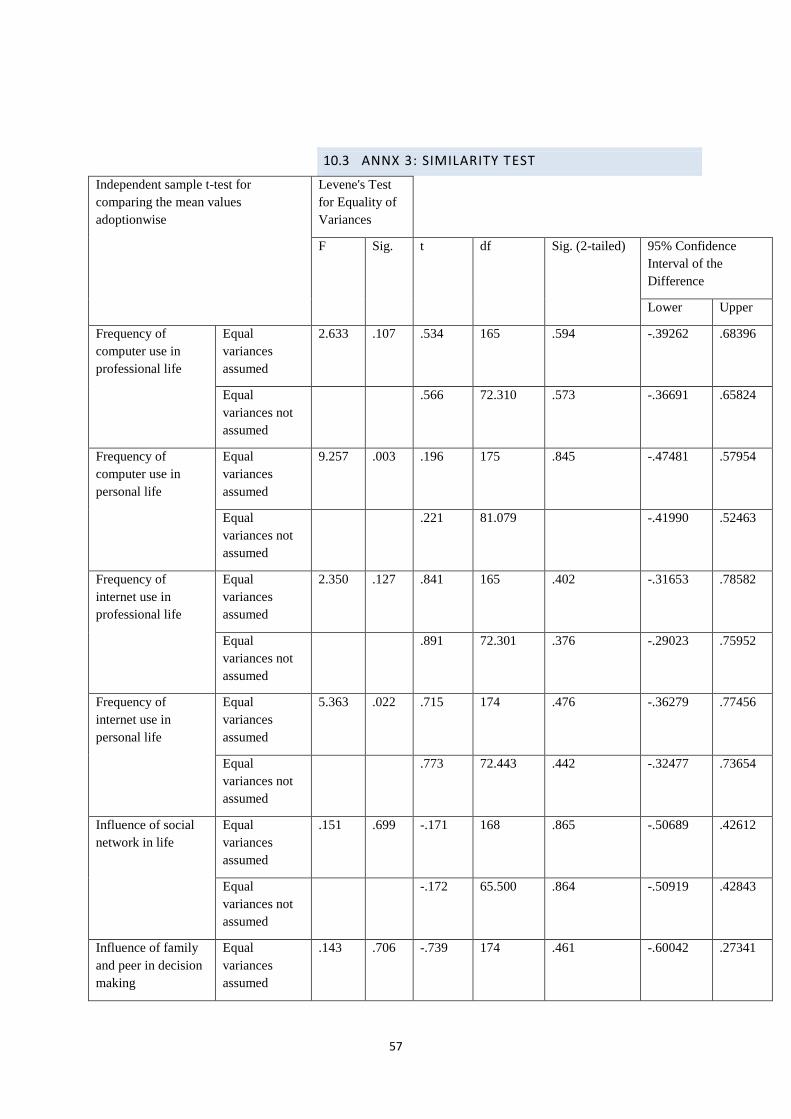

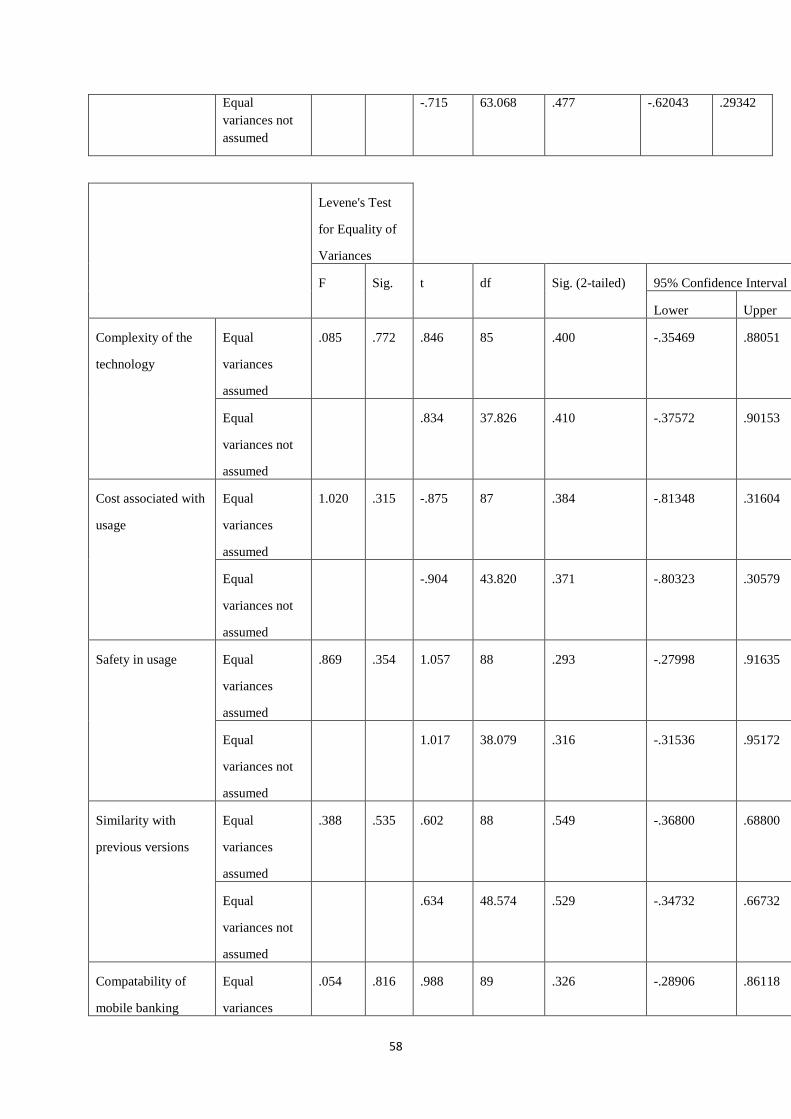

SIMILARITY TEST 5.4

We performed independent sample t-test among the respondents to compare their mean

values over the access and decision factors and we saw that frequency of computer and

internet usage in professional and personal life, also the influence of social media and

primary social groups (family and friends) do not vary significantly among the adopters and

non-adopters.

We also conducted a gender-wise mean comparison for the perception issues among the

adopters. The mean values do not vary significantly between the groups. That means, be it

male or female, a typical m-banking adopter will reflect upon similar user experience of the

technology.

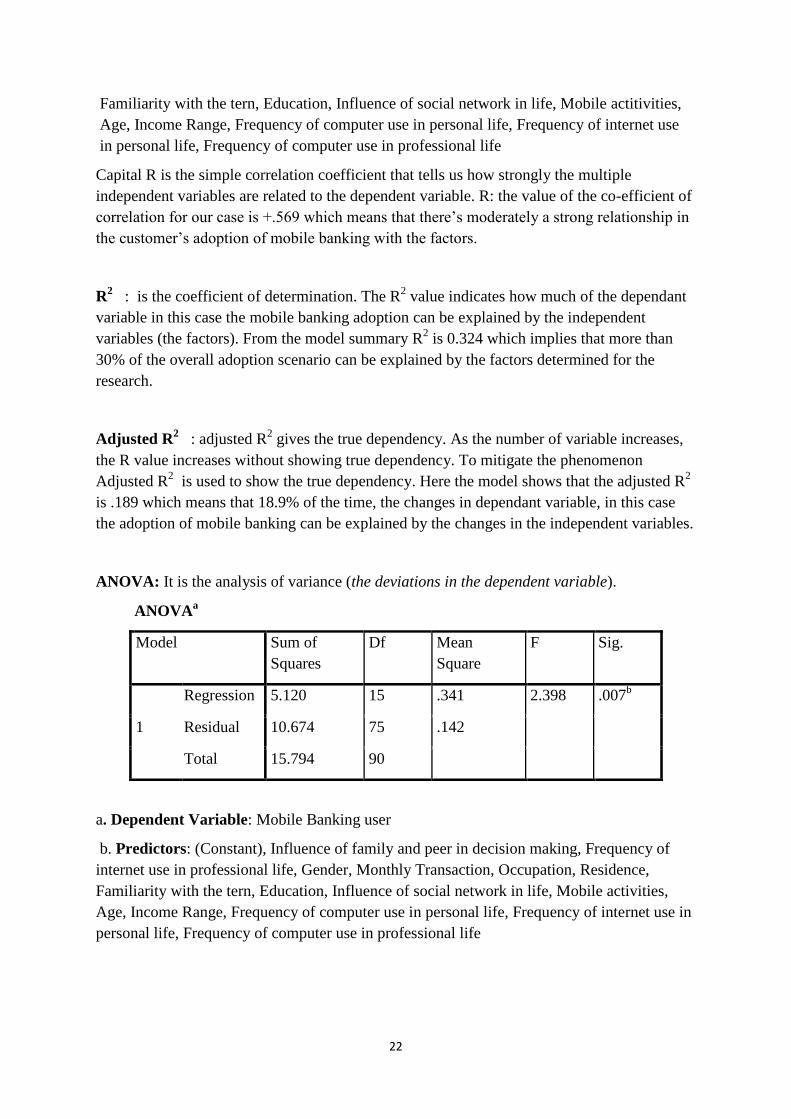

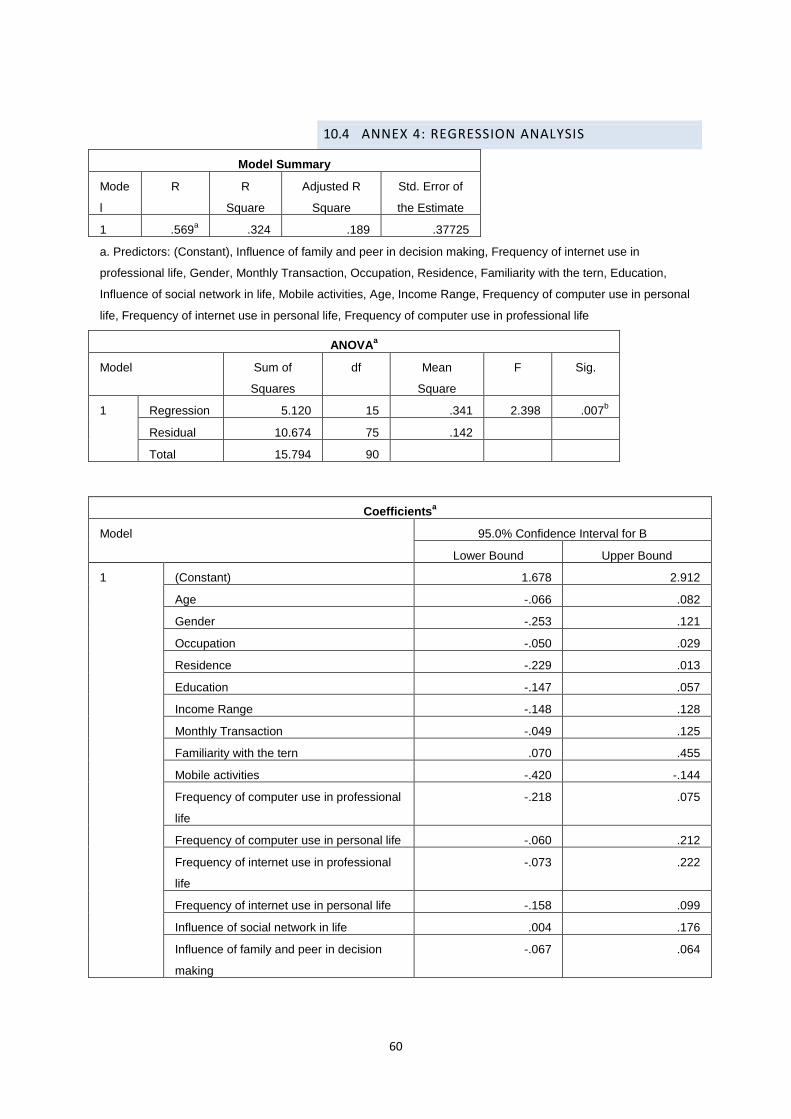

REGRESSION ANALYSIS 5.5

Linear Multiple Regression can be used to address a variety of research questions. Here we

used to determine how mobile banking adoption can be explained by our set of defined

variables.

Model Summary

Model R R Square Adjusted R

Square

Std. Error of

the Estimate

1 .569a .324 .189 .37725

Predictors: (Constant), Influence of family and peer in decision making, Frequency of

internet use in professional life, Gender, Monthly Transaction, Occupation, Residence,

22

Familiarity with the tern, Education, Influence of social network in life, Mobile actitivities,

Age, Income Range, Frequency of computer use in personal life, Frequency of internet use

in personal life, Frequency of computer use in professional life

Capital R is the simple correlation coefficient that tells us how strongly the multiple

independent variables are related to the dependent variable. R: the value of the co-efficient of

correlation for our case is +.569 which means that there‟s moderately a strong relationship in

the customer‟s adoption of mobile banking with the factors.

R2

: is the coefficient of determination. The R2 value indicates how much of the dependant

variable in this case the mobile banking adoption can be explained by the independent

variables (the factors). From the model summary R2 is 0.324 which implies that more than

30% of the overall adoption scenario can be explained by the factors determined for the

research.

Adjusted R2

: adjusted R2 gives the true dependency. As the number of variable increases,

the R value increases without showing true dependency. To mitigate the phenomenon

Adjusted R2

is used to show the true dependency. Here the model shows that the adjusted R2

is .189 which means that 18.9% of the time, the changes in dependant variable, in this case

the adoption of mobile banking can be explained by the changes in the independent variables.

ANOVA: It is the analysis of variance (the deviations in the dependent variable).

ANOVAa

Model Sum of

Squares

Df Mean

Square

F Sig.

1

Regression 5.120 15 .341 2.398 .007b

Residual 10.674 75 .142

Total 15.794 90

a. Dependent Variable: Mobile Banking user

b. Predictors: (Constant), Influence of family and peer in decision making, Frequency of

internet use in professional life, Gender, Monthly Transaction, Occupation, Residence,

Familiarity with the tern, Education, Influence of social network in life, Mobile activities,

Age, Income Range, Frequency of computer use in personal life, Frequency of internet use in

personal life, Frequency of computer use in professional life

23

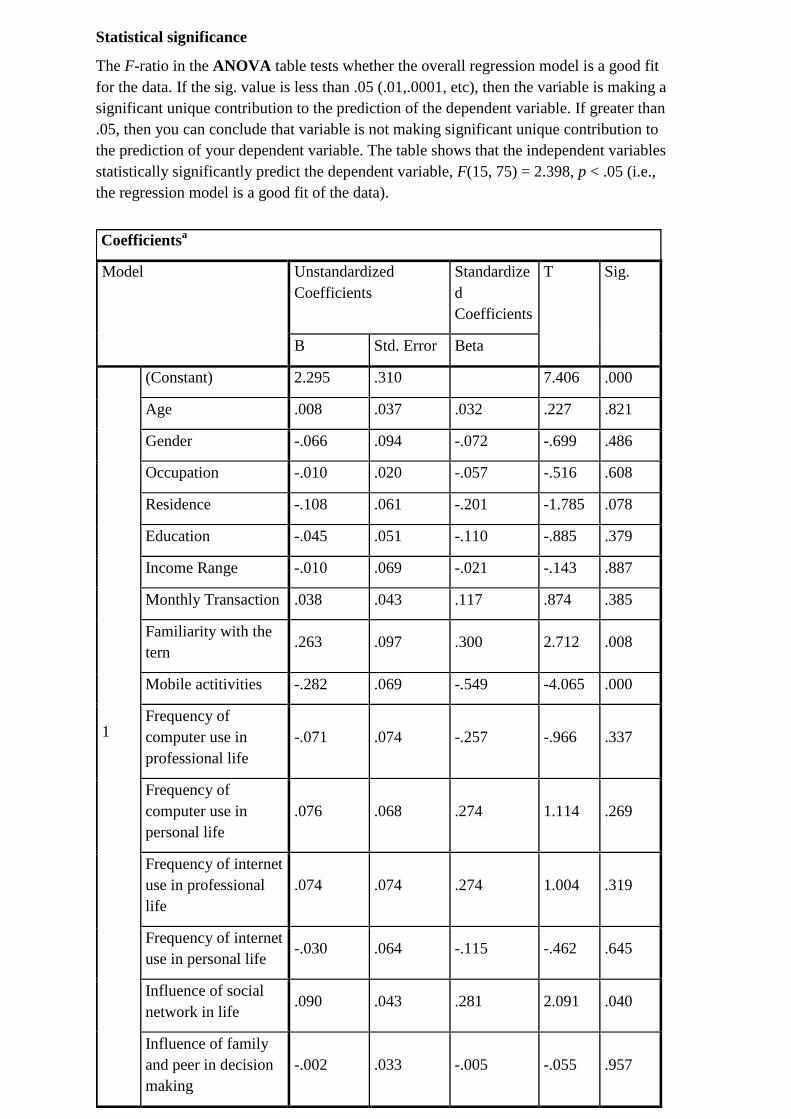

Statistical significance

The F-ratio in the ANOVA table tests whether the overall regression model is a good fit

for the data. If the sig. value is less than .05 (.01,.0001, etc), then the variable is making a

significant unique contribution to the prediction of the dependent variable. If greater than

.05, then you can conclude that variable is not making significant unique contribution to

the prediction of your dependent variable. The table shows that the independent variables

statistically significantly predict the dependent variable, F(15, 75) = 2.398, p < .05 (i.e.,

the regression model is a good fit of the data).

Coefficientsa

Model Unstandardized

Coefficients

Standardize

d

Coefficients

T Sig.

B Std. Error Beta

1

(Constant) 2.295 .310 7.406 .000

Age .008 .037 .032 .227 .821

Gender -.066 .094 -.072 -.699 .486

Occupation -.010 .020 -.057 -.516 .608

Residence -.108 .061 -.201 -1.785 .078

Education -.045 .051 -.110 -.885 .379

Income Range -.010 .069 -.021 -.143 .887

Monthly Transaction .038 .043 .117 .874 .385

Familiarity with the

tern .263 .097 .300 2.712 .008

Mobile actitivities -.282 .069 -.549 -4.065 .000

Frequency of

computer use in

professional life

-.071 .074 -.257 -.966 .337

Frequency of

computer use in

personal life

.076 .068 .274 1.114 .269

Frequency of internet

use in professional

life

.074 .074 .274 1.004 .319

Frequency of internet

use in personal life -.030 .064 -.115 -.462 .645

Influence of social

network in life .090 .043 .281 2.091 .040

Influence of family

and peer in decision

making

-.002 .033 -.005 -.055 .957

24

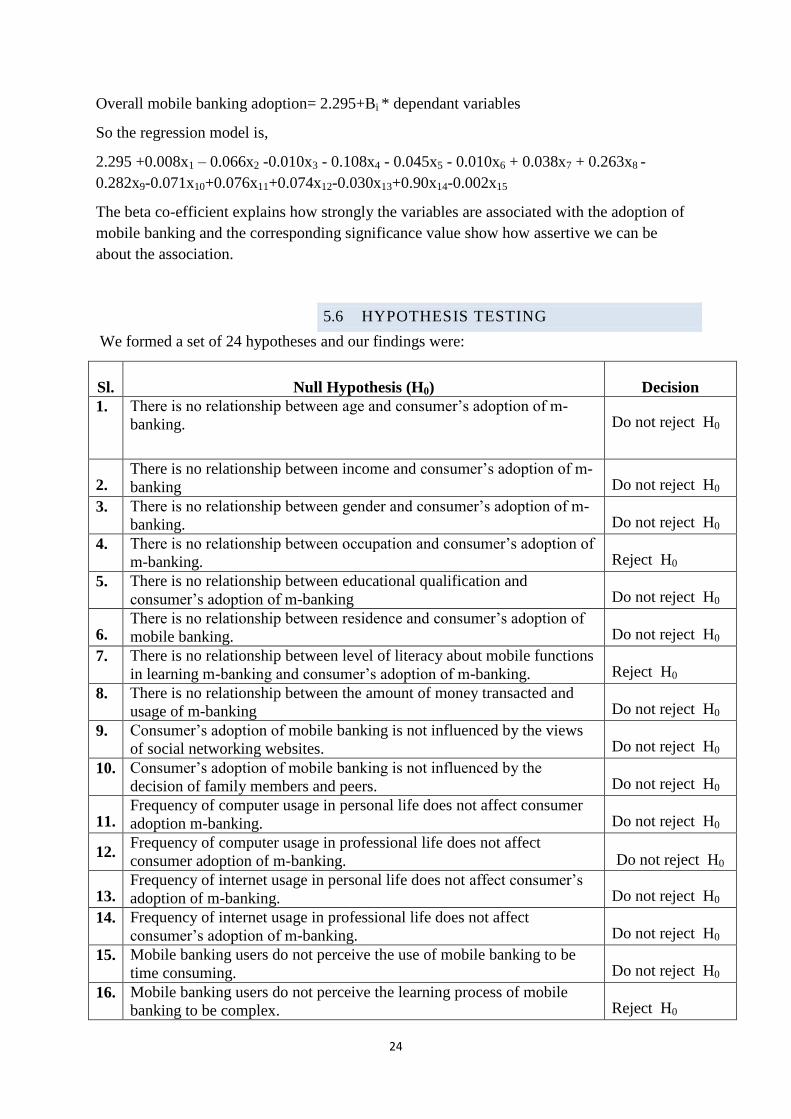

Overall mobile banking adoption= 2.295+Bi * dependant variables

So the regression model is,

2.295 +0.008x1 – 0.066x2 -0.010x3 - 0.108x4 - 0.045x5 - 0.010x6 + 0.038x7 + 0.263x8 -

0.282x9-0.071x10+0.076x11+0.074x12-0.030x13+0.90x14-0.002x15

The beta co-efficient explains how strongly the variables are associated with the adoption of

mobile banking and the corresponding significance value show how assertive we can be

about the association.

HYPOTHESIS TESTING 5.6

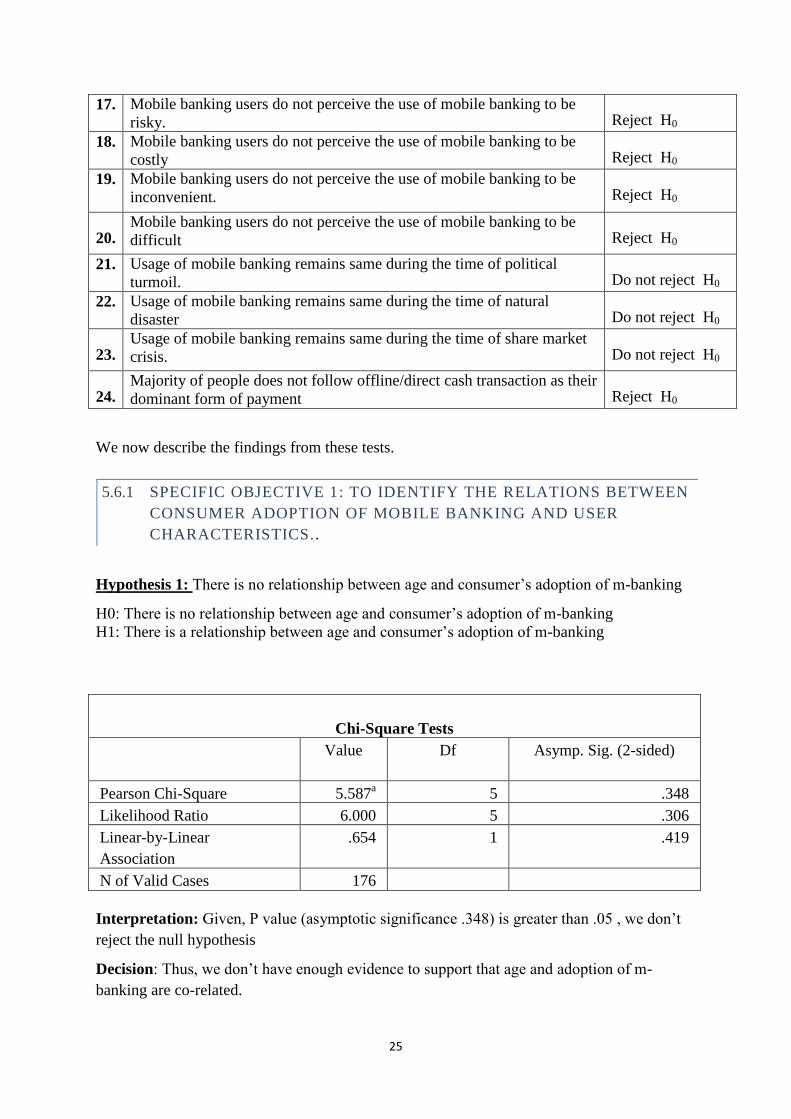

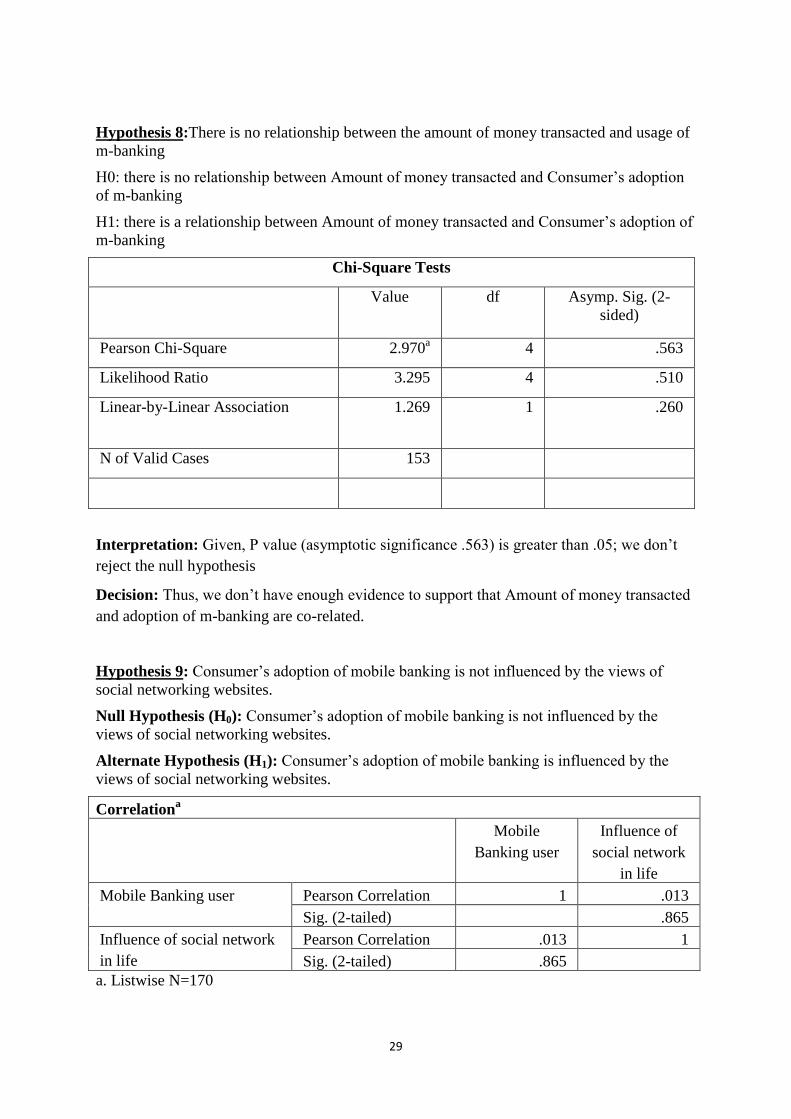

We formed a set of 24 hypotheses and our findings were:

Sl. Null Hypothesis (H0) Decision

1. There is no relationship between age and consumer‟s adoption of m-

banking. Do not reject H0

2. There is no relationship between income and consumer‟s adoption of m-

banking Do not reject H0

3. There is no relationship between gender and consumer‟s adoption of m-

banking. Do not reject H0

4. There is no relationship between occupation and consumer‟s adoption of

m-banking. Reject H0

5. There is no relationship between educational qualification and

consumer‟s adoption of m-banking Do not reject H0

6. There is no relationship between residence and consumer‟s adoption of

mobile banking. Do not reject H0

7. There is no relationship between level of literacy about mobile functions

in learning m-banking and consumer‟s adoption of m-banking. Reject H0

8. There is no relationship between the amount of money transacted and

usage of m-banking Do not reject H0

9. Consumer‟s adoption of mobile banking is not influenced by the views

of social networking websites. Do not reject H0

10. Consumer‟s adoption of mobile banking is not influenced by the

decision of family members and peers. Do not reject H0

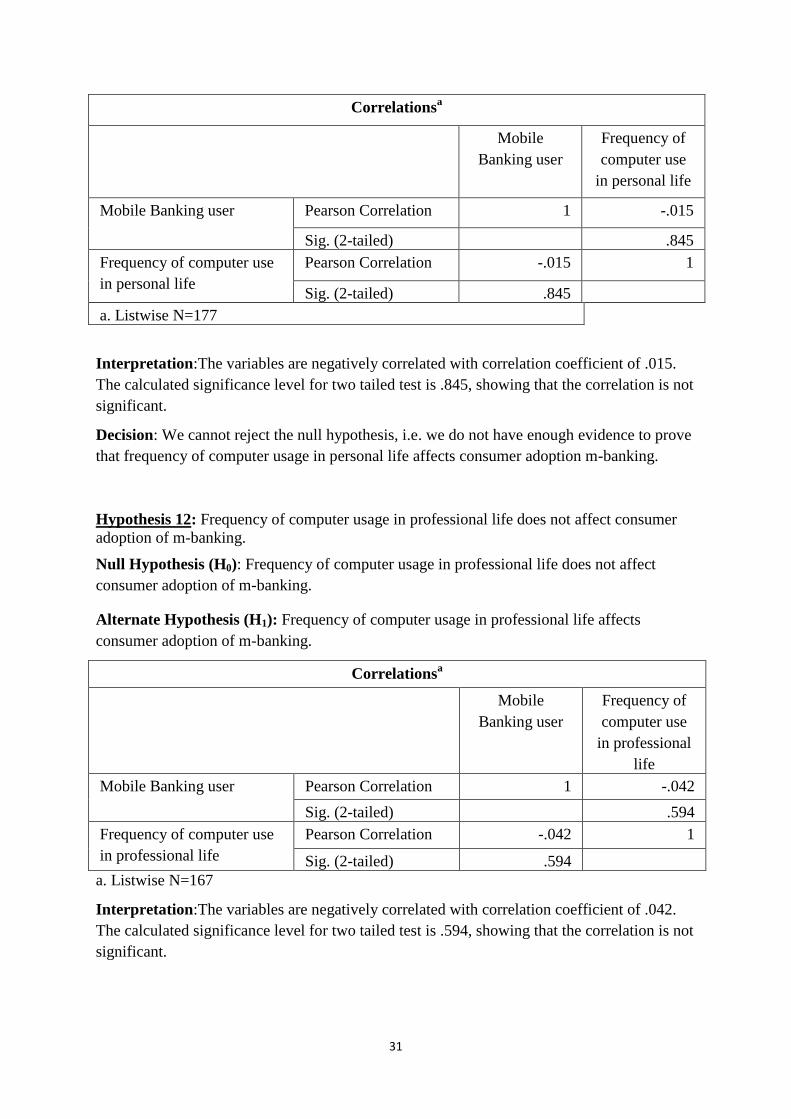

11. Frequency of computer usage in personal life does not affect consumer

adoption m-banking. Do not reject H0

12. Frequency of computer usage in professional life does not affect

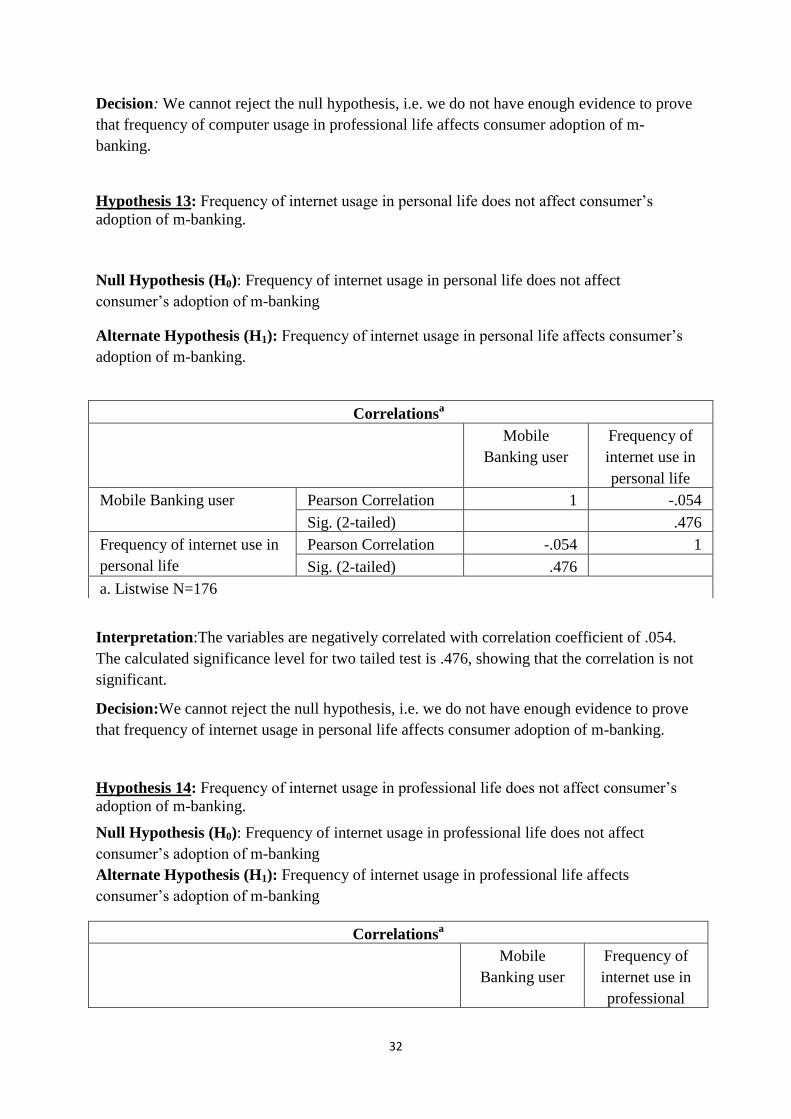

consumer adoption of m-banking. Do not reject H0

13. Frequency of internet usage in personal life does not affect consumer‟s

adoption of m-banking. Do not reject H0

14. Frequency of internet usage in professional life does not affect

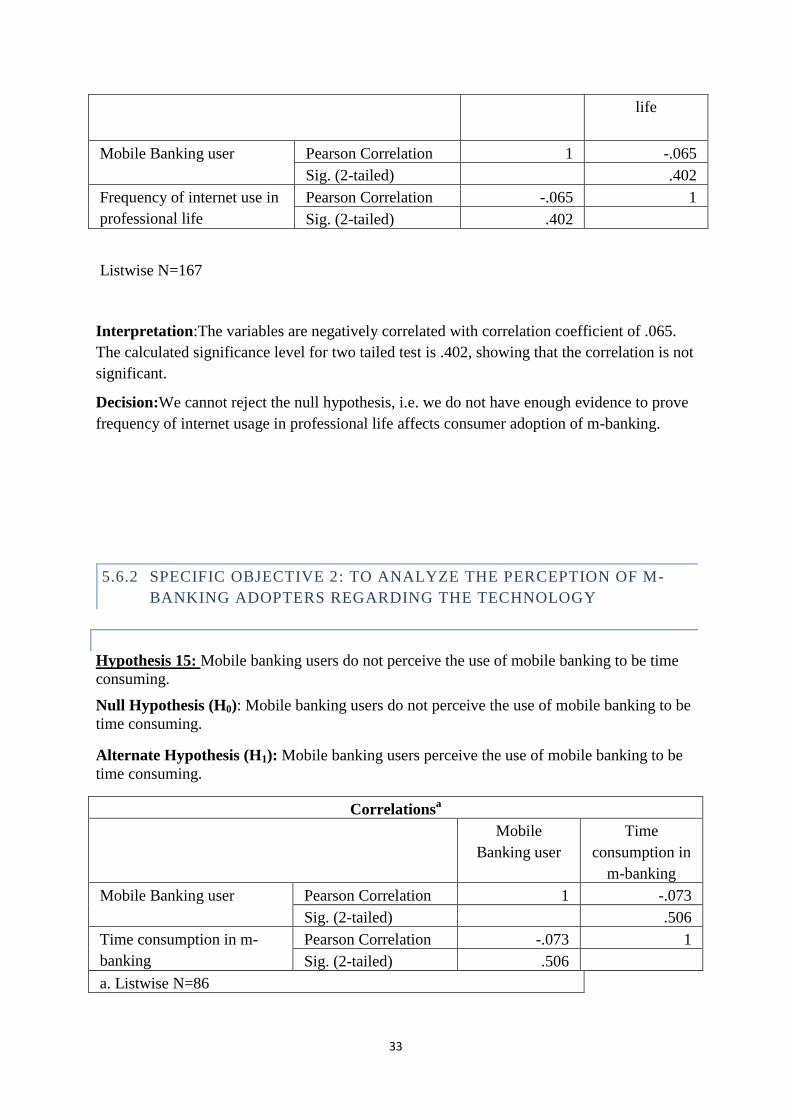

consumer‟s adoption of m-banking. Do not reject H0

15. Mobile banking users do not perceive the use of mobile banking to be

time consuming. Do not reject H0

16. Mobile banking users do not perceive the learning process of mobile

banking to be complex. Reject H0

25

17. Mobile banking users do not perceive the use of mobile banking to be

risky. Reject H0

18. Mobile banking users do not perceive the use of mobile banking to be

costly Reject H0

19. Mobile banking users do not perceive the use of mobile banking to be

inconvenient. Reject H0

20. Mobile banking users do not perceive the use of mobile banking to be

difficult Reject H0

21. Usage of mobile banking remains same during the time of political

turmoil. Do not reject H0

22. Usage of mobile banking remains same during the time of natural

disaster Do not reject H0

23. Usage of mobile banking remains same during the time of share market

crisis. Do not reject H0

24. Majority of people does not follow offline/direct cash transaction as their

dominant form of payment Reject H0

We now describe the findings from these tests.

5.6.1 SPECIFIC OBJECTIVE 1: TO IDENTIFY THE RELATIONS BETWEEN

CONSUMER ADOPTION OF MOBILE BANKING AND USER

CHARACTERISTICS..

Hypothesis 1: There is no relationship between age and consumer‟s adoption of m-banking

H0: There is no relationship between age and consumer‟s adoption of m-banking

H1: There is a relationship between age and consumer‟s adoption of m-banking

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 5.587a 5 .348

Likelihood Ratio 6.000 5 .306

Linear-by-Linear

Association

.654 1 .419

N of Valid Cases 176

Interpretation: Given, P value (asymptotic significance .348) is greater than .05 , we don‟t

reject the null hypothesis

Decision: Thus, we don‟t have enough evidence to support that age and adoption of m-

banking are co-related.

26

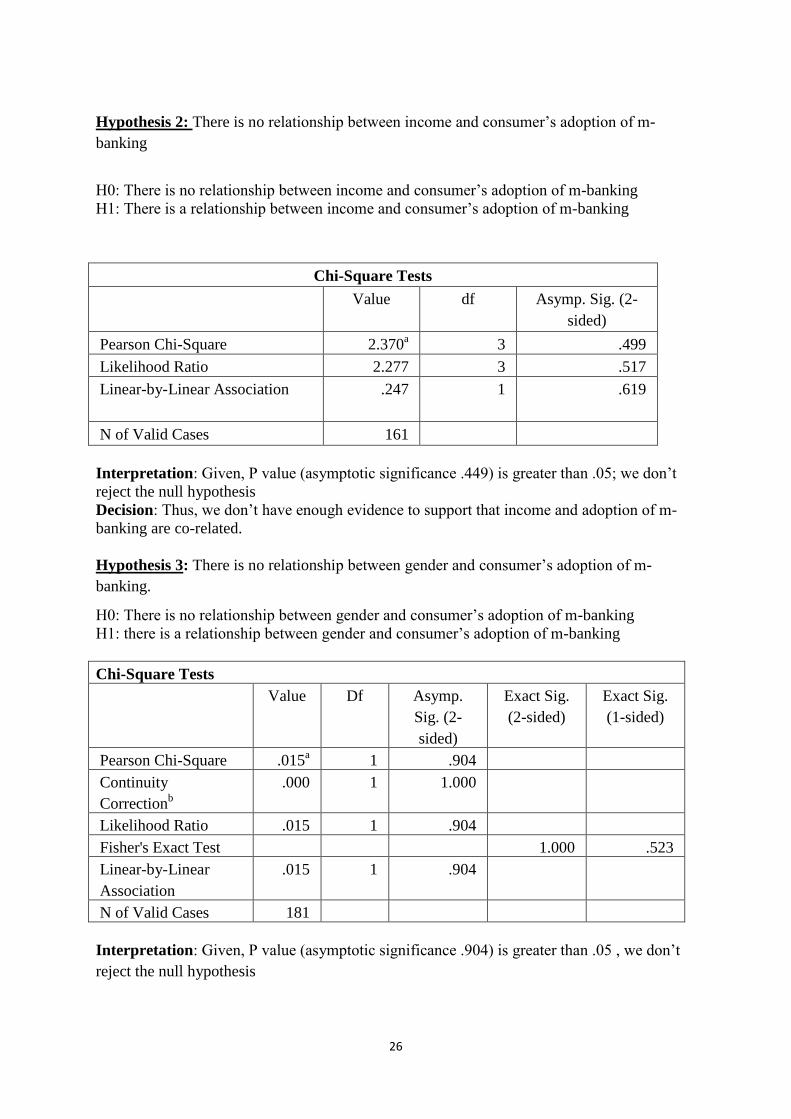

Hypothesis 2: There is no relationship between income and consumer‟s adoption of m-

banking

H0: There is no relationship between income and consumer‟s adoption of m-banking

H1: There is a relationship between income and consumer‟s adoption of m-banking

Chi-Square Tests

Value df Asymp. Sig. (2-

sided)

Pearson Chi-Square 2.370a 3 .499

Likelihood Ratio 2.277 3 .517

Linear-by-Linear Association .247 1 .619

N of Valid Cases 161

Interpretation: Given, P value (asymptotic significance .449) is greater than .05; we don‟t

reject the null hypothesis

Decision: Thus, we don‟t have enough evidence to support that income and adoption of m-

banking are co-related.

Hypothesis 3: There is no relationship between gender and consumer‟s adoption of m-

banking.

H0: There is no relationship between gender and consumer‟s adoption of m-banking

H1: there is a relationship between gender and consumer‟s adoption of m-banking

Chi-Square Tests

Value Df Asymp.

Sig. (2-

sided)

Exact Sig.

(2-sided)

Exact Sig.

(1-sided)

Pearson Chi-Square .015a 1 .904

Continuity

Correctionb

.000 1 1.000

Likelihood Ratio .015 1 .904

Fisher's Exact Test 1.000 .523

Linear-by-Linear

Association

.015 1 .904

N of Valid Cases 181

Interpretation: Given, P value (asymptotic significance .904) is greater than .05 , we don‟t

reject the null hypothesis

27

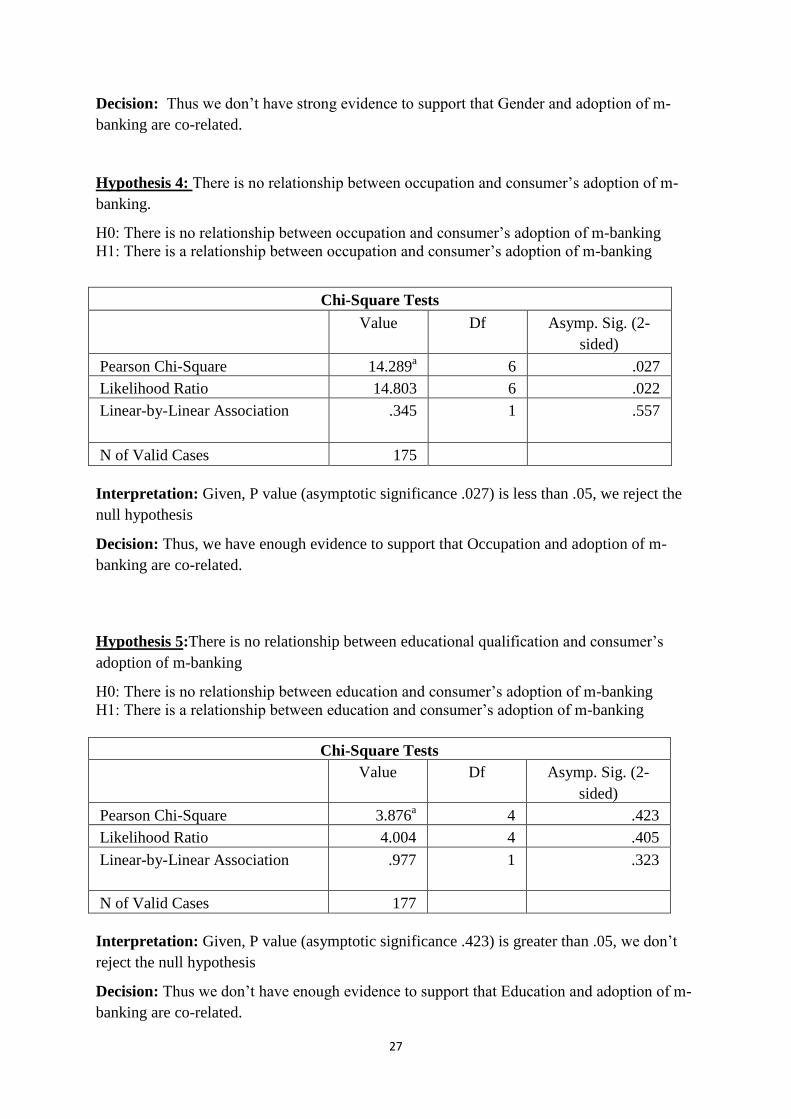

Decision: Thus we don‟t have strong evidence to support that Gender and adoption of m-

banking are co-related.

Hypothesis 4: There is no relationship between occupation and consumer‟s adoption of m-

banking.

H0: There is no relationship between occupation and consumer‟s adoption of m-banking

H1: There is a relationship between occupation and consumer‟s adoption of m-banking

Chi-Square Tests

Value Df Asymp. Sig. (2-

sided)

Pearson Chi-Square 14.289a 6 .027

Likelihood Ratio 14.803 6 .022

Linear-by-Linear Association .345 1 .557

N of Valid Cases 175

Interpretation: Given, P value (asymptotic significance .027) is less than .05, we reject the

null hypothesis

Decision: Thus, we have enough evidence to support that Occupation and adoption of m-

banking are co-related.

Hypothesis 5:There is no relationship between educational qualification and consumer‟s

adoption of m-banking

H0: There is no relationship between education and consumer‟s adoption of m-banking

H1: There is a relationship between education and consumer‟s adoption of m-banking

Chi-Square Tests

Value Df Asymp. Sig. (2-

sided)

Pearson Chi-Square 3.876a 4 .423

Likelihood Ratio 4.004 4 .405

Linear-by-Linear Association .977 1 .323

N of Valid Cases 177

Interpretation: Given, P value (asymptotic significance .423) is greater than .05, we don‟t

reject the null hypothesis

Decision: Thus we don‟t have enough evidence to support that Education and adoption of m-

banking are co-related.

28

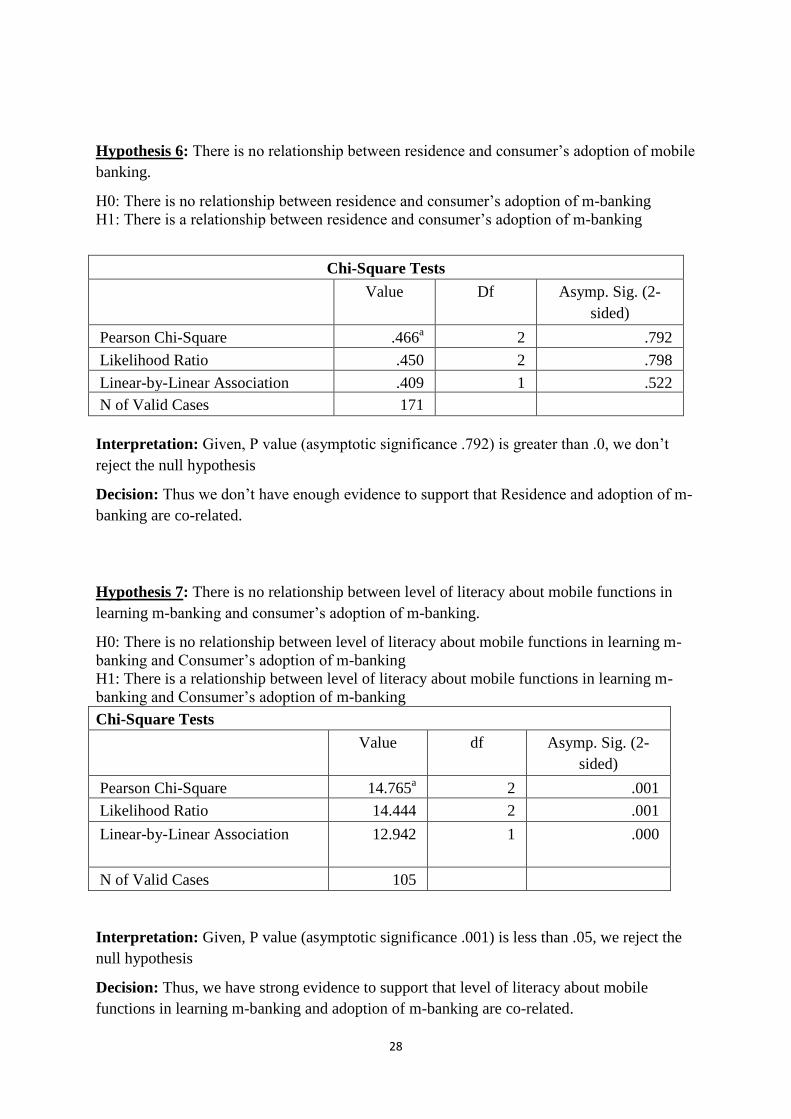

Hypothesis 6: There is no relationship between residence and consumer‟s adoption of mobile

banking.

H0: There is no relationship between residence and consumer‟s adoption of m-banking

H1: There is a relationship between residence and consumer‟s adoption of m-banking

Chi-Square Tests

Value Df Asymp. Sig. (2-

sided)

Pearson Chi-Square .466a 2 .792

Likelihood Ratio .450 2 .798

Linear-by-Linear Association .409 1 .522

N of Valid Cases 171

Interpretation: Given, P value (asymptotic significance .792) is greater than .0, we don‟t

reject the null hypothesis