adaptive risk management in mining project development: a ...

288

ADAPTIVE RISK MANAGEMENT IN MINING PROJECT DEVELOPMENT: A FLEXIBLE APPROACH TO IMPROVE RISK RESPONSE by Craig Matthew Rice B.Eng, Mechanical Engineering, University of Victoria, 2004 M.Eng, Civil Engineering, The University of British Columbia, 2009 A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF Doctor of Philosophy in THE FACULTY OF GRADUATE AND POSTDOCTORAL STUDIES (Mining Engineering) THE UNIVERSITY OF BRITISH COLUMBIA (Vancouver) October 2021 © Craig Matthew Rice, 2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of adaptive risk management in mining project development: a ...

ADAPTIVE RISK MANAGEMENT IN MINING PROJECT DEVELOPMENT:

A FLEXIBLE APPROACH TO IMPROVE RISK RESPONSE

by

Craig Matthew Rice

B.Eng, Mechanical Engineering, University of Victoria, 2004

M.Eng, Civil Engineering, The University of British Columbia, 2009

A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

Doctor of Philosophy

in

THE FACULTY OF GRADUATE AND POSTDOCTORAL STUDIES

(Mining Engineering)

THE UNIVERSITY OF BRITISH COLUMBIA

(Vancouver)

October 2021

© Craig Matthew Rice, 2021

ii

The following individuals certify that they have read, and recommend to the Faculty of Graduate and Postdoctoral Studies for acceptance, the dissertation entitled:

Adaptive Risk Management in Mining Project Development: A Flexible Approach to Improve Risk Response

submitted by Craig Rice in partial fulfillment of the requirements for

the degree of Doctor of Philosophy

in Mining Engineering Examining Committee:

W. Scott Dunbar, Professor, Department Head, Norman B. Keevil Institute of Mining Engineering, UBC Supervisor

Franco Oboni, PhD, President, Oboni Riskope Associates Inc. Supervisory Committee Member

Omar Swei, Assistant Professor, Department of Civil Engineering, UBC Supervisory Committee Member

Sheryl Staub-French, Professor, Department of Civil Engineering, UBC University Examiner

John Steen, Associate Professor, Norman B. Keevil Institute of Mining Engineering, UBC University Examiner

iii

Abstract

Capital project development is the mechanism through which mining companies turn promising

orebodies into profitable mines. However, broad-scale project success is elusive, with projects

frequently exceeding approved cost and schedule estimates. Researchers and mining

professionals have pointed to project risk management as a way to improve project success.

Despite mature project risk management practices and widespread adoption, projects still

repeatedly fail. This is due partly to the current risk management paradigm of prediction and

advanced planning, with risks frequently materializing differently than predicted. One method of

addressing uncertainty underlying project risks is by embracing flexibility and using an adaptive

management approach to risk response. This dissertation demonstrates how adaptive project risk

management can preserve project value and reduce time to resolve risks.

This dissertation first establishes the state of project risk management practices in mining

through an exploratory survey of industry practitioners. The survey fills a literature gap by

documenting the methods currently used and attitudes towards them. Next, the adaptive project

risk management framework is proposed, describing a structured, iterative process to pursue

multiple competing response alternatives in parallel. The framework also details how

experimentation, observation, and learning support the adaptive process. A continuous

discounted cash flow model and stochastic simulation address uncertain elements of both the risk

and the risk response alternatives. The system model provides insight into the effects of different

risk responses and the value gained through the adaptive approach.

iv

The adaptive framework and system model are explored through two case studies. The first case

involved multiple adaptive iterations and demonstrates how the adaptive process gathers and

models new information using Bayesian inference while pursuing and dynamically tracking

multiple risk response alternatives. The second case study shows how experiments and pilot tests

can be used to learn more about the risk and viability of risk responses. These cases demonstrate

that an adaptive approach can increase project value, reduce the duration of resolving risks, and

potentially limit downside risk compared to a non-adaptive response. The methods proposed in

this dissertation give decision-makers the tools to manage project risks more effectively and

improve risk management outcomes.

v

Lay Summary

Successfully building new mines is vital to mining companies, but mine construction frequently

goes over budget and schedule. Ineffective risk management is suggested as one of the reasons

for this widespread underperformance. Improved risk management techniques that embrace

flexibility, learning, and adapting to changing information may improve mine construction

budget, schedule, and overall performance.

This research includes three parts aimed at improving risk response decision-making in mining

capital projects. The first part includes a survey of project risk management methods used in

industry and the perceptions of these methods. The second part includes the development of a

process and quantitative tools to value an adaptive approach to risk response. The third part

validates the process and tools through two case studies involving unexpected project risks

during mine design and construction. The results show that an adaptive approach can increase

project value while decreasing the time required to resolve risks.

vi

Preface

This dissertation is the original work of the author, Craig Rice. The research idea was generated

through practical work in project development in the mining sector. The research program,

including the methodology, data analysis, and writing this dissertation, was designed and

completed by the author. The research was supervised by Dr. W. Scott Dunbar at the Norman B.

Keevil Institute of Mining Engineering at the University of British Columbia.

The survey on project risk management in the mining industry presented in Chapter 3 was

conducted under UBC Behavioural Research Ethics Board certificate H18-03272. The case study

interviews that provided data for the Meadowbank case study presented in Chapter 7 were

conducted under UBC Behavioural Research Ethics Board certificate H18-03278.

A preliminary and summary presentation of the adaptive project risk management framework

presented in this dissertation, primarily in Chapter 4, was published in the conference

proceedings of the Risk and Resilience Mining Solutions 2016 conference, held in Vancouver,

BC, in November 2016. This paper was co-authored with Dr. Dunbar. I was the lead researcher

and first author and was responsible for structuring, researching, and writing the article. Dr.

Dunbar reviewed the paper, provided insight and guidance, and contributed to manuscript edits.

vii

Table of Contents

Abstract ......................................................................................................................................... iii

Lay Summary .................................................................................................................................v

Preface ........................................................................................................................................... vi

Table of Contents ........................................................................................................................ vii

List of Tables .............................................................................................................................. xiv

List of Figures ............................................................................................................................. xvi

List of Abbreviations ................................................................................................................. xix

Acknowledgements .................................................................................................................... xxi

Dedication ................................................................................................................................. xxiii

Chapter 1: Framing the Research Opportunity .........................................................................1

1.1 Introduction ..................................................................................................................... 1

1.2 Research Motivation ....................................................................................................... 6

1.3 Research Questions ......................................................................................................... 7

1.4 Methodology ................................................................................................................... 9

1.5 Contribution and Significance ...................................................................................... 11

1.6 Dissertation Structure.................................................................................................... 12

Chapter 2: Literature Review .....................................................................................................14

2.1 Introduction to the Literature Review ........................................................................... 14

2.2 Capital Projects in the Mining Industry ........................................................................ 16

2.3 The Risk Concept .......................................................................................................... 18

2.4 Project Risk Management ............................................................................................. 23

viii

2.5 Managing Uncertainty and Flexibility in Projects ........................................................ 27

2.6 Synthesis of the Literature ............................................................................................ 30

Chapter 3: Survey on Project Risk Management in the Mining Industry .............................32

3.1 Survey Objectives ......................................................................................................... 32

3.2 Survey Design and Methodology.................................................................................. 33

3.3 Multiple Choice Results and Analysis .......................................................................... 34

3.3.1 Respondent Profiles: Survey Section 1 ..................................................................... 35

3.3.2 Exposure to Project Risk Management: Survey Section 2 ....................................... 37

3.3.3 Definitions of Risk: Survey Section 3 ...................................................................... 39

3.3.4 Use and Perception of Risk Management Tools: Survey Section 4 ......................... 42

3.3.5 The Risk Concept and New Perspectives on Risk: Survey Section 5....................... 47

3.4 Open-Ended Results and Analysis: Survey Section 6 .................................................. 52

3.4.1 Strengths of Project Risk Management..................................................................... 53

3.4.1.1 Theme #1 (T1): Building Risk Awareness ....................................................... 54

3.4.1.2 Theme #2 (T2): Better Understanding Risks .................................................... 54

3.4.1.3 Theme #3 (T3): A Platform for Action ............................................................. 55

3.4.1.4 Theme #4 (T4): Improving Project Outcomes .................................................. 55

3.4.2 Weaknesses, Challenges, and Improvements ........................................................... 56

3.4.2.1 Theme #1 (T1): Improving Risk Assessment Accuracy and Completeness..... 58

3.4.2.2 Theme #2 (T2): Gaining Management Support and Effective Participation .... 59

3.4.2.3 Theme #3 (T3): Improving Risk Management Follow-Through ...................... 60

3.4.2.4 Theme #4 (T4): Improving Risk Management Knowledge and Training ........ 61

3.4.2.5 Theme #5 (T5): Fit for Purpose and Consistent Application ............................ 61

ix

3.4.2.6 Theme #6 (T6): Moving from Compliance to Value-Add................................ 62

3.4.2.7 Theme #7 (T7): Clarifying Tools, Methods, and Systems................................ 63

3.4.2.8 Theme #8 (T8): Quality Assurance and Continual Improvement .................... 63

3.5 Conclusion .................................................................................................................... 64

Chapter 4: The Adaptive Project Risk Management Framework ..........................................67

4.1 Introduction ................................................................................................................... 67

4.2 Literature Review.......................................................................................................... 68

4.2.1 Foundations of Adaptive Management ..................................................................... 68

4.2.2 Adaptive Risk Management ...................................................................................... 71

4.2.3 Other Applications of Adaptivity in Project Management ....................................... 74

4.2.4 Discussion of the Literature ...................................................................................... 76

4.3 Defining the Adaptive Project Risk Management Concept .......................................... 77

4.3.1 Clarifying the Requirements of Adaptive Project Risk Management ...................... 77

4.3.2 The Motivation for Adaptive Project Risk Management .......................................... 78

4.3.3 Integrating the New Risk Perspectives ..................................................................... 81

4.3.4 Risk Archetypes for Adaptive Project Risk Management ........................................ 82

4.4 The Adaptive Risk Management Process ..................................................................... 83

4.4.1 Step 1: Risk Emergence ............................................................................................ 86

4.4.2 Step 2: Characterize the Risk .................................................................................... 87

4.4.3 Step 3: Define the Decision Space ............................................................................ 88

4.4.4 Step 4: Frame the Design Alternatives ..................................................................... 89

4.4.5 Step 5: Align the Decision Space and the Design Alternatives ................................ 91

4.4.6 Step 6: Develop and Run the System Model ............................................................ 92

x

4.4.7 Step 7: Execute the Workplan for the Current Iteration ........................................... 95

4.4.8 Step 8: Evaluate Results of the Current Iteration...................................................... 96

4.5 Conclusion .................................................................................................................... 97

Chapter 5: Adaptive System Model and Stochastic Simulation ..............................................98

5.1 Introduction ................................................................................................................... 98

5.2 Literature Review.......................................................................................................... 99

5.2.1 Continuous Cash Flow Models for Capital Investment ............................................ 99

5.2.2 Capital Investment Evaluation in Mining ............................................................... 100

5.3 Model Structure .......................................................................................................... 103

5.3.1 Continuous Cash Flow Profiles .............................................................................. 109

5.3.2 Net Present Value Expressions ............................................................................... 110

5.4 Stochastic Simulation Description .............................................................................. 114

5.4.1 Alternative Selection Uncertainty Model ............................................................... 115

5.4.2 Work Package Variable Distributions .................................................................... 116

5.4.3 Simulation Algorithm ............................................................................................. 118

5.5 Interpreting Simulation Results and Outputs .............................................................. 119

5.6 Conclusion .................................................................................................................. 124

Chapter 6: Exploring the Adaptive Process and Model .........................................................126

6.1 Case Study Introduction and Overview ...................................................................... 126

6.1.1 MineCo and the Arsenic Orebody Surprise ............................................................ 126

6.1.2 Case Study Motivation and Methodology .............................................................. 128

6.2 Framing the Adaptive Process .................................................................................... 129

6.2.1 Risk Emergence: Drill Results show Arsenic in the Orebody ................................ 129

xi

6.2.2 Characterizing the Risk ........................................................................................... 129

6.2.3 Defining the Risk Management Decision Space .................................................... 130

6.2.4 Framing the Design Alternatives ............................................................................ 131

6.2.5 Aligning the Decisions Space and Design Alternatives ......................................... 133

6.3 Stochastic Model Structure ......................................................................................... 134

6.3.1 Planning the Adaptive Iterations ............................................................................. 134

6.3.2 Scenarios and Design Alternatives ......................................................................... 136

6.3.3 Work Packages, Model Variables, and Distributions ............................................. 142

6.3.4 Arsenic Concentration Uncertainty Model ............................................................. 146

6.4 Simulation Results ...................................................................................................... 150

6.4.1 First Adaptive Iteration ........................................................................................... 150

6.4.2 Second Adaptive Iteration....................................................................................... 155

6.4.3 Third Adaptive Iteration ......................................................................................... 163

6.5 Discussion and Conclusion ......................................................................................... 169

6.5.1 Case Study Insights on the Adaptive Process ......................................................... 169

6.5.2 Effects of Varying Model Parameters/Inputs ......................................................... 171

6.5.3 Limitations of Analysis ........................................................................................... 174

Chapter 7: The Meadowbank SAG Mill ..................................................................................175

7.1 Introduction to the Case Study .................................................................................... 175

7.1.1 Overview of Meadowbank Gold Mine ................................................................... 175

7.1.2 Starting up the Meadowbank SAG Mill ................................................................. 178

7.1.3 Case Study Motivation and Methodology .............................................................. 182

7.2 Framing the Adaptive Process .................................................................................... 183

xii

7.2.1 Risk Emergence: SAG Mill Underperformance ..................................................... 184

7.2.2 Characterizing the Risk ........................................................................................... 184

7.2.3 Defining the Risk Management Decision Space .................................................... 185

7.2.4 Framing the Design Alternatives ............................................................................ 186

7.2.5 Aligning the Decision Space and the Design Alternatives ..................................... 187

7.3 Stochastic Model Structure ......................................................................................... 188

7.3.1 Scenarios and Design Alternatives ......................................................................... 188

7.3.2 Work Packages and Model Variables ..................................................................... 191

7.3.3 Design Alternative Uncertainty Modelling ............................................................. 193

7.4 Simulation Results ...................................................................................................... 195

7.4.1 Retrospective Analysis............................................................................................ 195

7.4.2 Prospective Analysis ............................................................................................... 198

7.4.3 Value of Information in Tests and Pilots ................................................................ 202

7.5 Case Study Conclusion ............................................................................................... 208

7.5.1 Discussion of Results .............................................................................................. 208

7.5.2 Limitations of Analysis ........................................................................................... 210

Chapter 8: Conclusion ...............................................................................................................211

8.1 Conclusion .................................................................................................................. 211

8.2 Contribution and Significance .................................................................................... 213

8.3 Limitations and Future Work ...................................................................................... 217

References ...................................................................................................................................221

Appendices ..................................................................................................................................236

Appendix A Survey Documentation ....................................................................................... 236

xiii

A.1 Survey Questions and Summarized Responses ...................................................... 236

Appendix B System Model Appendices ................................................................................. 249

B.1 Continuous Cash Flow Profiles .............................................................................. 249

Appendix C Case Study Documentation ................................................................................ 253

C.1 Scenario Activity Diagrams .................................................................................... 253

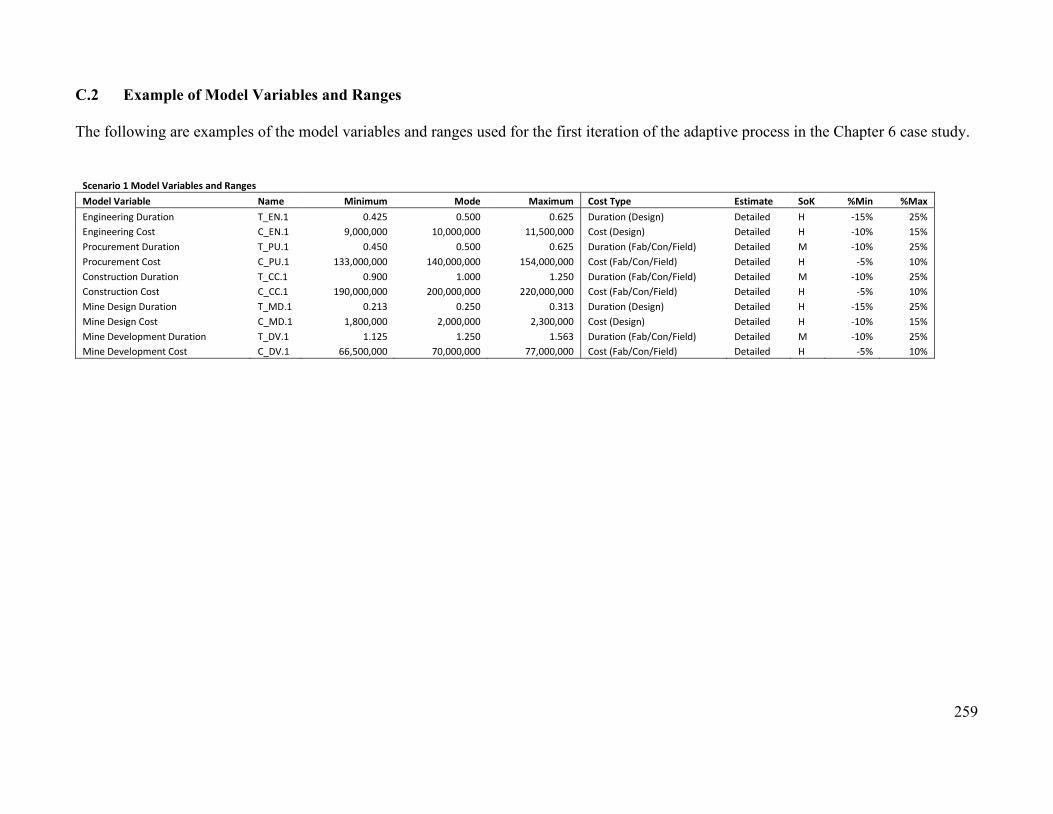

C.2 Example of Model Variables and Ranges ............................................................... 259

xiv

List of Tables

Table 3.1 Level and area of survey respondent education ............................................................ 36

Table 3.2 Type of company and typical role/position .................................................................. 37

Table 3.3 Crosstab of risk knowledge and risk management training/education ......................... 38

Table 3.4: Level of knowledge of company documentation on project risk management ........... 39

Table 3.5: Definitions of risk and strength of belief in definition ................................................ 41

Table 3.6: Views on the nature of risks in project management ................................................... 42

Table 3.7: Belief in project risk assessment effectiveness ............................................................ 43

Table 3.8 Use of project risk management tools and methods ..................................................... 44

Table 3.9 Perceived effectiveness of project risk management tools and methods ...................... 44

Table 3.10 Use of probability modelling techniques in project risk assessments ........................ 45

Table 3.11 Perceptions of effectiveness of probability modelling techniques ............................. 46

Table 3.12 Perceptions on the effectiveness of risk ranking and prioritization methods ............. 47

Table 3.13 Perceptions on unexpected and unforeseen risks ........................................................ 48

Table 3.14 Definition of uncertainty in project risk management ................................................ 49

Table 3.15 Definition of probability in project risk management ................................................ 50

Table 3.16 Perceptions on including strength of knowledge in risk assessments ........................ 52

Table 3.17 Survey response topics grouped by major theme (question Q6.1) ............................. 53

Table 3.18 Survey response topics grouped by major theme (questions Q6.2, Q6.3, Q6.4) ........ 57

Table 5.1 Example work package and model variables .............................................................. 109

Table 6.1 Work packages, cash flow profile shapes, and model variable distributions. ............ 143

Table 6.2 Strength of Knowledge (SoK) assessments and variable uncertainty ranges ............. 146

Table 6.3 Prior, likelihood, and posterior distributions of arsenic concentration, Iterations 1-3 149

xv

Table 6.4 ENPV for all modelled scenarios, Iteration 1 ............................................................. 151

Table 6.5 NPV Value at Risk and Gain (VaR/VaG) for (α=.05), Iteration 1 ............................. 153

Table 6.6 Expected critical path durations for all scenarios, Iteration 1 ..................................... 154

Table 6.7 Updated probabilities for alternative selection, Iteration 2. ........................................ 158

Table 6.8 ENPV for all modelled scenarios; Iteration 2 ............................................................. 159

Table 6.9 NPV Value at Risk and Gain (VaR/VaG) for (α=.05), Iteration 2 ............................. 161

Table 6.10 Expected critical path durations for all scenarios, Iteration 2................................... 162

Table 6.11 Updated probabilities for alternative selection, Iteration 3....................................... 164

Table 6.12 ENPV for all modelled scenarios; Iteration 3 ........................................................... 165

Table 6.13 Expected critical path durations for all scenarios, Iteration 3................................... 168

Table 7.1 Work packages and model variables .......................................................................... 191

Table 7.2 Summary results of the retrospective analysis ............................................................ 196

Table 7.3 Summary results of the prospective analysis .............................................................. 199

Table 7.4 NPV VaR and VaG for prospective analysis (α=.05) ................................................. 200

Table 7.5 Probabilistic ENPV for value of information alternatives .......................................... 206

Table 7.6 Expected Value of Perfect Information (EVPI) stochastic model results ................. 207

xvi

List of Figures

Figure 2.1 Structure of Literature Review Groups and Subgroups .............................................. 15

Figure 4.1 Diagram of the General Adaptive Management Process based on Holling (1978),

Walters & Hillborn (1978), Walters (1986) .................................................................................. 69

Figure 4.2 Example activity diagram of non-adaptive and adaptive risk responses ..................... 80

Figure 4.3 Process diagram of the Adaptive Project Risk Management process ......................... 84

Figure 5.1 Example decision tree for the adaptive system model. ............................................. 106

Figure 5.2 Example activity diagram for Scenario 1 - Wait for Permitting Decision ................ 107

Figure 5.3 Example activity diagram for Scenario 2 - Pursue Alternative 1 .............................. 107

Figure 5.4 Example activity diagram for Scenario 3 - Pursue Alternative 2 .............................. 108

Figure 5.5 Example activity diagram for Scenario 4 - Adaptive Response ................................ 108

Figure 5.6 Example CDF showing first order stochastic dominance. ........................................ 120

Figure 5.7 Example CDF showing second order stochastic dominance. .................................... 121

Figure 5.8 Example CDF showing VaR(α) and VaG(α) where α=0.10 ..................................... 123

Figure 6.1 Activity diagrams for the baseline project plan and risk resolution alternatives ...... 134

Figure 6.2 Structure of Iterative Adaptive Process ..................................................................... 135

Figure 6.3 Decision tree for all case study scenarios .................................................................. 137

Figure 6.4 Activity diagram for Scenario 1 ................................................................................ 138

Figure 6.5 Activity diagram for Scenario 2, Iteration 1 .............................................................. 138

Figure 6.6 Activity diagram for Scenario 3A, Iteration 1 ........................................................... 139

Figure 6.7 Activity diagram for Scenario 3B, Iteration 1 ........................................................... 140

Figure 6.8 Activity diagram for Scenario 3C, Iteration 1 ........................................................... 140

Figure 6.9 Activity diagram for Scenario 4, Iteration 1 .............................................................. 141

xvii

Figure 6.10 Activity diagram for Scenario 4, Iteration 2 ............................................................ 142

Figure 6.11 Activity diagram for Scenario 4, Iteration 3 ............................................................ 142

Figure 6.12 Posterior PDF of arsenic concentration, Iteration 1. ............................................... 148

Figure 6.13 Posterior CDF of arsenic concentration, Iteration 1. ............................................... 148

Figure 6.14 NPV box-whisker plot, Iteration 1 .......................................................................... 152

Figure 6.15 NPV cumulative distribution function, Iteration 1 .................................................. 152

Figure 6.16 Critical path cumulative distribution function (descending), Iteration 1 ................ 155

Figure 6.17 Probability density function of arsenic concentration in orebody, Iteration 2. ....... 157

Figure 6.18 Cumulative distribution function of arsenic concentration in orebody, Iteration 2. 157

Figure 6.19 NPV box-whisker plot, Iteration 2 .......................................................................... 160

Figure 6.20 NPV cumulative distribution, Iteration 2 ................................................................ 160

Figure 6.21 Critical path cumulative distribution function (descending), Iteration 2 ................ 162

Figure 6.22 PDF of arsenic concentration in orebody, Iteration 3.............................................. 164

Figure 6.23 CDF of arsenic concentration in orebody, Iteration 3 ............................................. 164

Figure 6.24 NPV box-whisker plot, Iteration 3 .......................................................................... 167

Figure 6.25 NPV cumulative distribution function, Iteration 3 .................................................. 167

Figure 6.26 Critical path cumulative distribution function (descending), Iteration 3 ................ 168

Figure 7.1 Location of Meadowbank and other Agnico Eagle properties in Nunavut ............... 176

Figure 7.2 Meadowbank process flow diagram without secondary crusher ............................... 179

Figure 7.3 Chronology of events for the Meadowbank case study ............................................. 180

Figure 7.4 Meadowbank process flow diagram with permanent secondary crusher. ................. 181

Figure 7.5 Activity diagram for Scenario 1: Base Plan .............................................................. 188

Figure 7.6 Activity diagram for Scenario 2: Actual Events ........................................................ 189

xviii

Figure 7.7 Activity diagram for Scenario 3: Adaptive Response ............................................... 190

Figure 7.8 Activity diagram for Scenario 4: Prospective Response ........................................... 190

Figure 7.9 Probability mass function of operating modifications resolving the risk. ................. 195

Figure 7.10 NPV box whisker plot of the retrospective analysis ............................................... 196

Figure 7.11 NPV cumulative distribution function of the retrospective analysis ....................... 197

Figure 7.12 Critical Path cumulative distribution function (descending) for the retrospective

analysis ........................................................................................................................................ 198

Figure 7.13 NPV box whisker plot of the prospective analysis .................................................. 199

Figure 7.14 NPV cumulative distribution function of the prospective analysis ......................... 200

Figure 7.15 Critical Path cumulative distribution function (descending) for the prospective

analysis ........................................................................................................................................ 201

Figure 7.16 Value of information decision tree with no test information available ................... 203

Figure 7.17 Value of information decision tree with test information available ........................ 203

Figure 7.18 Activity diagram for value of information scenario V1 (SV1) ............................... 204

Figure 7.19 Activity diagram for value of information scenario V2 (SV2) ............................... 205

xix

List of Abbreviations

AACEI: Association for the Advancement of Cost Engineering International

C$: Canadian Dollar

CAPEX: Capital Expenditure

CDF: Cumulative Distribution Function

CIM: Canadian Institute of Mining, Metallurgy, and Petroleum

CP: Critical Path

CPM: Critical Path Method

DCF: Discounted Cash Flow

ENPV: Expected Net Present Value

EVPI: Expected Value of Perfect Information

FEL: Front End Loading

FCF: Free Cash Flow

FOSD: First Order Stochastic Dominance

ISO: International Organization for Standardization

LOM: Life of Mine

NAV: Net Asset Value of Mining Operations

NI 43-101: National Instrument 43-101 (Standards of Disclosure for Mineral Projects)

NPV: Net Present Value

NPV: Net Present Value

NRCAN: Natural Resources Canada

OPEX: Operating Expenditure

xx

PDF: Probability Density Function

PERT: Program Evaluation and Review Technique

PFD: Process Flow Diagram

PMF: Probability Mass Function

PMI: Project Management Institute

RADR: Risk-Adjusted Discount Rate

RO: Real Options Analysis/Valuation

SAG Mill: Semi-Autogenous Grinding Mill

SD: Stochastic Dominance

SOSD: Second Order Stochastic Dominance

SRA: Society for Risk Analysis

TPD/tpd: Tonnes per Day

US$: United States Dollar

VaG: Value at Gain

VaR: Value at Risk

VoI: Value of Information

WACC: Weighted Average Cost of Capital

xxi

Acknowledgements

Many people have supported and encouraged me during my time as a PhD student. Dr. Scott

Dunbar supervised my work, provided guidance and mentorship, and helped navigate the

complexities of my PhD research. During my studies, his patience and calm advice provided

reassurance at times it was most needed. I enjoyed our blue-sky discussions on the mining

industry and the possibilities for the future of mining. I would also like to thank the other

members of my committee, Dr. Franco Oboni and Dr. Omar Swei, for their support. Dr. Oboni

offered wisdom and insights that helped me see my work through a practical lens. I am

especially thankful for his willingness to participate as a non-faculty committee member. Dr.

Swei introduced me to many concepts and ideas in design flexibility and decision analysis that

have led to a greater appreciation and understanding of these areas, as well as a deep curiosity

towards applying these concepts in my professional work. I would also like to thank Dr. Thomas

Froese for contributing as a committee member before leaving the University of British

Columbia.

I am sincerely grateful to Agnico Eagle Mines for giving permission to use Meadowbank Gold

Mine as a case study for my research and for providing access to their data and personnel. I owe

particular thanks to Pathies Nawej Muteb, Meadowbank Process Plant General Superintendent,

for the time and effort on the phone and over email as I interviewed him for the case study. I

would not have been able to complete this research without his assistance.

Midway through my PhD program, I left a full-time job to start my own consulting company and

began travelling the world helping clients plan and manage mining projects. This challenged my

xxii

ability to balance work, life, and study but added layers to my learning as I discovered new areas

both professionally and academically and explored their intersection. I am thankful to the clients

who have given me the opportunity to work with them; they have granted me great latitude to

investigate new ideas and approaches in mining project development.

My parents, Jack and Karin Rice, have always been supportive of my educational pursuits. I am

thankful that they embraced and fostered my curiosity as a child, answered my endless questions,

and gave me Lego every year for my birthday. I wouldn’t have become an engineer without

them. Thanks are also due to my sister, Sonia, for her thoughtfulness and constant support over

the years.

Lastly, I must thank Saffrina. I could not have done any of this without her enduring kindness,

care, and encouragement. We met shortly after I started my PhD; since then, we’ve gotten

married, started a family, and moved to the country. We’ve done a lot in a short time, and I’ve

enjoyed every bit of it. I’m looking forward to more adventures together.

xxiii

Dedication

For Saffrina, Georgia, and Jack. Stay curious.

xxiv

Billy’s been through a lot of storms, though, and he’s probably brought her around earlier in the evening, maybe even before talking to Barrie. Either way, it’s a significant moment; it means they’ve stopped steaming home and are simply trying to survive. In a sense, Billy’s no longer at the helm, the conditions are, and all he can do is react. If danger can be seen in terms of a narrowing range of choices, Billy Tyne’s choices have just ratcheted down a notch. A week ago he could have headed in early. A day ago he could have run north like Johnston. An hour ago he could have radioed to see if there were any other vessels around. Now the electrical noise has made the VHF practically useless, and the single sideband only works for long range. These aren’t mistakes so much as an inability to see into the future. No one, not even the Weather Service, knows for sure what a storm’s going to do.

- Sebastian Junger, The Perfect Storm.

1

Chapter 1: Framing the Research Opportunity

1.1 Introduction

The mining industry makes a significant contribution to economies and societies worldwide.

Mining provides the raw material inputs for countless other industries, from rare-earth metals for

high-technology devices to crop nutrients for agriculture. It provides jobs and economic

development in countries and communities where mines are located and provides service and

support employment internationally. There are few areas of industry and society that are not

touched and improved by the mining sector.

A strong mining industry requires substantial capital investment to develop mining assets and

infrastructure capable of mining and extracting valuable metals and minerals. Before a metal or

mineral deposit becomes an operating mine, it becomes a project that is studied, designed,

planned, and constructed over several years through a capital project development process.

Project development is one of the critical mechanisms through which mining companies

implement growth and development strategies. These projects can range from small maintenance

and sustaining capital projects to several billion-dollar mega projects. Effective capital project

development is critical for mining companies to execute their strategic growth plans.

Despite being a large, global, and mature industry, and despite centuries of experience

developing mining projects, project success – simply defined as implementing the planned scope

within the approved planned budget and schedule – is elusive. Studies and surveys have shown

that project failure is the rule, not the exception. One study across industrial sectors, including

mining, showed that 65% of capital megaprojects fail to achieve their cost and schedule

2

estimates (Merrow, 2011), while another demonstrated that 45% of large engineering projects

fail to meet objectives (Miller & Lessard, 2001). Mining projects seem to align with the broad

studies of industrial projects (Bertisen & Davis, 2008; Ernst and Young, 2017b; Kuvshinikov et

al., 2017).

Explanations for project failures largely fall into two broad categories: shortcomings in the

techniques and methods for managing projects (Lawrence & Scanlan, 2007; Miller & Lessard,

2001; T. Williams, 2005), and a broad failure in preparing realistic cost and schedule estimates

(Flyvbjerg, 2008). A subset of those who attribute project failure to ineffective project

management methods suggest that common methods and tools for managing risks in projects -

described further in Chapter 2 - are ineffective and contribute to project failure (Ward &

Chapman, 2003). The literature presented in Chapter 2 of this dissertation suggests many areas

for improvement for project risk management. One of those areas is managing emerging,

unforeseen, and unexpected risks - risks typically characterized by high uncertainty, low

information, and poor knowledge. Paradoxically, while project risk management is premised on

managing uncertain events and their outcomes, there is little appreciation or understanding of

managing uncertainty in risk response. Classical project risk management methods focus on

advanced prediction, planning, and control, establishing a number of possible risk response

actions to be implemented when the risk occurs. However, if the risk emerges differently than

predicted or unforeseen risks emerge, pre-planned responses may not be suitable. In these cases,

a flexible risk response system that offers multiple alternatives for project decision-makers can

provide value by resolving risks quickly and minimizing their impact to project value.

3

The value and benefit of a flexible approach to risk response when unexpected risks emerge can

be illustrated through two examples. Copper Mountain Mining Company developed and

commissioned the new processing plant at their namesake Copper Mountain Mine in Princeton,

BC, in May 2011. Immediately following commissioning and ramp-up of the mine, a consistent

production shortfall was noticed, with the processing plant unable to meet design capacity. The

problem was diagnosed as a SAG Mill that could not achieve production throughput and target

grind size despite running at nearly 100% full motor power (Rose et al., 2015). Copper Mountain

tested various operational improvements without significant effect while also performing

additional hardness tests on a wide selection of ore samples and undertaking additional SAG Mill

throughput modelling. In December 2014, they commissioned a new permanent crusher to

resolve the SAG Mill throughput. Implementing a response to resolve this risk took Copper

Mountain over 2.5 years. While they followed a longer resolution path to ensure technical

accuracy underlying the decision process and contain costs, significant value was lost due to the

extended period of lower production. Taking a flexible and adaptive approach to managing this

risk that recognizes the uncertainty in risk response effectiveness may have resulted in a faster

risk resolution. Pursuing multiple resolution alternatives in parallel may have resulted in faster

risk resolution and less loss in value.

The second example is in a Goldcorp project at the Red Lake Complex in Red Lake, ON, to

develop a six-kilometre underground haulage drift tunnel connecting the Cochenour mine to the

Campbell processing plant facilities. When the tunnel was approximately 70% complete, the

project team unexpectedly encountered a talc-chlorite schist section in the tunnel routing (Moore,

2014). Unlike the hard basalt host rock present for most of the tunnel development, the talc

section was very soft and less stable. The development and ground support mechanisms used for

4

the previous sections of the tunnel weren’t suitable and needed to be redesigned, and Goldcorp

was unsure whether the ore-transport rail system they had designed would work in this section.

In addition, it was not possible to tell how much of the tunnel routing was through this talc zone.

In light of these uncertainties, Goldcorp investigated various design alternatives for the ore

transportation, tested additional ground support mechanisms, and modified the development

methods to account for softer and less stable material, all while gathering new information about

the characteristics and extent of the talc zone material. While this approach did not follow the

formal adaptive process introduced in this dissertation, it demonstrates the benefit of following a

flexible approach to risks response in light of high uncertainties. The impact on the haulage drift

project cost and schedule was reduced by taking this approach.

The critical consideration in the adaptive approach to risk management investigated in this

research is recognizing the uncertainty in risk response effectiveness and how management

should structure their approach to risk response to address and manage that uncertainty.

Addressing and managing uncertainty in the risk response stage of risk management – when the

threat or hazard underlying the risk has occurred, and the impacts must be mitigated – is an area

of project risk management that is less explored in academic research than the risk management

areas of risk identification, assessment, and analysis.

This research program focuses on exploring and testing the integration of adaptive management

methods into project risk management. Adaptive management is an approach to management

decisions and actions that recognizes the value in learning, observing, and adjusting responses

based on new information. It is a structured, formal, and iterative process that uses a system

model to predict the effects of management actions that can be updated with new information as

5

it becomes available. Project decision-makers can pursue multiple risk resolution options in

parallel when the best response alternative is not apparent and use new information to update the

model iteratively until the best alternative is identified. The framework and model introduced in

this dissertation integrate adaptive management with classical risk assessment processes and use

a stochastic continuous discounted cash flow model to support risk resolution decisions. The

stochastic simulation models the value of pursuing an adaptive response through a time-cost

trade-off that aims to accelerate project risk resolution and achieve commercial production of the

mine faster. The research also considers new perspectives on risk, a different definition and

concept of risk that considers the information and knowledge that underlies the risk assessment

approach. While the research questions are described in more detail later in this chapter, they can

be summarized as follows: How can adaptive management methods be used to manage mining

project risks? What quantitative tools can support decision-making in an adaptive project risk

management framework? Will new perspectives on risk and uncertainty improve risk

characterization and analysis in the adaptive management approach?

The research approach is a mixed-methods program consisting of fours parts:

1. Surveying mining industry stakeholders to determine current practices and perspectives

on project risk management.

2. Developing a framework for the adaptive project risk management process.

3. Developing stochastic models to structure the adaptive processes and assess the value

gained by pursuing an adaptive response to project risks.

4. Investigating case studies to explore the application of the framework and stochastic

model to different situations in project risk management.

6

The expected result of the research is a preliminary adaptive project risk management system

that provides a structured format to better characterize, analyze, and manage emerging and

unforeseen risk in mining projects. This research is intended to generate evidence that this

approach to project risk management can reduce the potentially negative consequences of risks

in mining projects and improve project and asset value for mining companies.

1.2 Research Motivation

The motivation for this research comes from recognizing the need for improved project risk

management tools that focus on implementing risk responses that will help project teams manage

surprises that arise during mining project planning and execution. The classical project risk

management paradigm focuses on identification, analysis, and response planning, with a much

lesser focus on managing and controlling risks when and if they materialize, especially those not

predicted as part of a risk assessment exercise. Although the efforts on risk analysis and planning

are admirable and necessary, a more significant effort to implement risk management actions

throughout project execution is needed. This research aims to specifically improve the risk

response portion of the overall project risk management approach.

The practical necessity for this is apparent: projects continue to go over budget and over

schedule with such frequency that it has been termed the “iron law of megaprojects”: over

budget, over time, over and over again (Flyvbjerg, 2014). While there are many reasons for

project failure, the inadequacies of risk management is certainly one. If the risk management

tools being used are not improving project success, then perhaps the tools are incorrect, or they

are being applied incorrectly. The evidence of project success – or lack thereof – rightfully raises

the question about whether the things we are doing are helping decrease risk and the negative

7

impacts of hazards/threats? Improper tools may harm projects and increase risk by giving project

teams an unwarranted sense of confidence and reassurance that they have adequately “de-risked”

their project.

Both the literature and trends in project performance indicate that improved approaches are

needed. However, while advances in academic research have been promising and show potential

to benefit industrial projects, acceptance of these approaches in practical settings is often slow or

non-existent. This is unfortunate and highlights an unnecessary gap between academic research

and its practical application. This research intends to help bridge that gap; to provide both a

practical and academic contribution to improving project risk management practices.

1.3 Research Questions

The research program investigated whether an alternative approach to project risk management

that embraces flexibility through adaptive risk management can improve project success by more

effectively managing emerging, unexpected, and unforeseen risks. This approach is achieved by

uniting three distinct but related areas: adaptive risk management, economic modelling of mining

capital projects, and new perspectives on risk.

Classical project risk management has a heavy focus on advanced prediction and planning

responses to known risks. This works well for the subset of risks that are known and identifiable.

However, unforeseeable and unexpected risks require a different approach. Augmenting classical

project risk management methods with adaptive management will help manage uncertainty and

improve knowledge through experimenting, learning, and adapting as the risk characteristics

8

become better understood. Building on the concepts of adaptive risk management, the first

research question asks:

Question 1: How can adaptive management methods be incorporated into project

risk management to give flexibility in identifying and developing management

alternatives for emerging or unforeseen risks with high uncertainties?

In an adaptive project risk management framework, project managers can pursue multiple

parallel risk response alternatives. Though there is an increased cost to pursuing an adaptive

approach, the expectation is that the adaptive response will reduce time to resolve the risk and

reduce the time to production. Thus, the value is created through a time-cost trade-off. The

question of how much value is created through the adaptive approach – and the maximum

amount that decision-maker should be willing to pay to pursue the adaptive response – is a key

concern. Quantitative tools can provide insight to whether it is worth pursuing an adaptive

response, leading to the second research question:

Question 2: What quantitative tools or methods will allow project teams to assess

the value of pursuing an adaptive risk response through multiple iterations of the

adaptive process?

A concept that helps better incorporate elements of learning and information in the adaptive

project risk management process is an expanded definition of risk called the new perspectives on

risk. The new perspectives on risk include assessments of uncertainty and knowledge in risk

analysis to provide more information to risk analysts and decision-makers. This research will

9

provide insight into understanding if adopting these new perspectives on risk will improve

project risk management outcomes. Thus, the third and final research question is:

Question 3: Can adopting new perspectives on risk allow better understanding,

assessment, and management of capital project risks?

1.4 Methodology

The research methodology includes a survey to establish the current state of project risk

management in the mining industry, developing an adaptive risk management framework and

modelling tools, and validating the tools through two case studies. The following paragraphs

describe the methodology for the research program.

The research began with a literature review spanning many different fields: risk analysis, risk

management, adaptive management, decision analysis, project management, construction

management, and mining project development. The search delved into the specifics of risk,

including foundations such as definitions and concepts and adjacent ideas such as complexity,

ambiguity, and resilience. The literature review also highlighted a research gap on the use and

perceptions of risk management tools in mining project development.

The first step of the research was a survey on project risk management in the mining industry.

The purpose of the survey is to establish current practices, acceptance, and perception of project

risk management and to elicit opinions on the strengths and weaknesses of project risk

management methods. This survey fills a research gap and can be used as a platform for further

research into the efficacy and value of project risk management programs in the mining industry.

10

The survey is exploratory and is not testing any specific hypotheses or correlations between risk

management perceptions, behaviours, and outcomes. Further research may consider comparing

the use of risk management tools and project success or further testing the preliminary insights

gained from this survey. The structure and format of the survey are detailed in Chapter 3.

A conceptual framework and detailed process for Adaptive Project Risk Management was

developed that considers existing theory and frameworks for project risk management and

adaptive risk management. The framework can be understood as applying adaptive management

philosophies and processes to project risk management, with additional processes for modelling

and valuing the benefits of the adaptive response.

A general system model for valuing and supporting decisions in the adaptive project risk

management framework is presented. A specific system model for each risk scenario being

managed will need to be developed based on the decision structure, possible risk resolution

alternatives, and potential for experimentation, learning, and observations. Since each system

model is bespoke to the risk scenario, a general model is outlined in Chapter 5 that details the

structure, format, and algorithm behind the model and simulation tools.

The framework and model were applied to two case studies. The first was a constructed “toy

problem” case study. This case study shows how the adaptive approach can be used in a

multiple-iteration risk situation where new information acquired during the adaptive iteration is

included in the model through Bayesian updating. The second case study was an industry case

study with Agnico Eagle Mines and the Meadowbank Complex using actual project data,

analyzing a risk scenario through a single-iteration adaptive approach. Case studies were selected

11

as the most appropriate methodology for empirically testing the adaptive framework and system

model. The case studies are exploratory in nature, intended to test and validate the approach and

answer the question of how risk management outcomes have been improved through applying

the adaptive project risk management approach.

1.5 Contribution and Significance

This research into adaptive project risk management will contribute to both the scholarly body of

knowledge and the applied practice of project risk management. There is a research gap in the

project risk management literature on how to manage unforeseen and unforeseeable risks

characterized by high uncertainty. Similarly, there is little academic research that establishes and

discusses the project risk management methods used in the mining industry. This dissertation

addresses the research opportunity to extend the understanding of project risk management in the

mining industry, integrate adaptive risk management into capital project risk methods, and

provide modelling tools to value pursuing an adaptive risk response.

My research aims to contribute in the following ways:

• Identifying what project risk management tools are used in the mining industry, the

perceptions and attitudes towards these tools, and the strengths, weaknesses, challenges,

and potential improvements for project risk management methods.

• Applying adaptive management frameworks and methods to capital project development.

This research will propose a framework for adaptive project risk management that can

manage risks characterized by high uncertainty.

12

• Providing quantitative tools to quickly model the value of multiple competing risk

resolution alternatives to determine if the best alternative is available and quantify the

value of pursuing an adaptive response to risk.

• As a whole, this research will provide techniques to improve risk management outcomes

in mining projects and increase project value by proposing a flexible and adaptive

approach to risk response that minimizes time to risk resolution.

1.6 Dissertation Structure

This dissertation is organized into the following eight chapters:

Chapter 1 - Framing the Research Opportunity: This chapter introduces the motivation,

research questions, methodology, and significance and contribution of the research.

Chapter 2 - Literature Review: This chapter reviews the scholarly work related to mining

capital projects, the risk concept and project risk management, new approaches to managing risk

and uncertainty in projects, and flexibility in engineering design and projects. The chapter

concludes with a synthesis of the various topics and shows how the research presented in this

dissertation addresses and extends the literature.

Chapter 3 - Survey on Project Risk Management in Mining: This chapter presents the results

of a survey designed to determine the level of acceptance, application, and perceived

effectiveness in project risk management tools in the mining industry, as well as perceptions on

new perspectives on risk and uncertainty.

13

Chapter 4 - Framework for Adaptive Project Risk Management: This chapter contains the

development of the adaptive project risk management framework, which is an extension and

combination of processes used in adaptive management, risk analysis, and project management.

Chapter 5 – Adaptive System Model: This chapter includes a description of the stochastic

model structure and approach to developing unique models for specific risk scenarios. The model

provides decision support by simulating the value of pursuing an adaptive risk response.

Chapter 6 – Exploring the Adaptive Process and Model: This chapter includes a constructed

“toy problem” case study that was developed to explore the adaptive framework and model.

Chapter 7 – The Meadowbank SAG Mill: This chapter is a case study of the Meadowbank

mine SAG Mill start-up and demonstrates how the adaptive process could be applied to a real

scenario faced by a mining company to resolve a project risk.

Chapter 8 - Conclusion: This chapter includes a summary and synthesis of the discussion, key

insights, contribution, and significance of the research. It also includes limitations and presents

areas for future research in adaptive project risk management.

14

Chapter 2: Literature Review

2.1 Introduction to the Literature Review

The literature review focuses on three areas related to this research program; the first area of the

literature review is the focus of this chapter. It includes mining capital projects, the evolution of

project risk management, shortcomings of the classical approaches to project risk management,

and recent advances to improve risk and uncertainty management in projects. The second area of

the literature review is included in Chapter 4 and gives the relevant background for the proposed

adaptive project risk management framework. It explores the theory and history of adaptive

management and adaptive risk management and how it can be positioned as an additional

approach to improve project risk management. The third area of the literature review is included

in Chapter 5 and provides background for the proposed adaptive system model. It focuses on

capital project economic appraisal and evaluation, documenting how mining and capital

infrastructure projects are appraised using various methods.

This research is intended to extend the body of work in each of these three areas of focus. It will

improve the approach to managing project risks by providing a framework and tools to manage

specific project risks. It extends the literature in adaptive management by applying it to the

mining sector and a project risk management context. Finally, it extends the literature in capital

project appraisal by using economic modelling tools to inform risk analysis and decision-making

by quantifying the value of pursuing adaptivity in risk response through a time-cost tradeoff.

The literature review began with a broad search covering project risk management and mine

project development, then narrowing the range until the key literature areas were understood and

15

the research questions were formed. Following the definition of the research questions, the

literature review was focused and deepened around the research program. As the research

includes both an academic and applied focus, the literature review includes academic journals,

high-quality industry journals and conference proceedings focused on project risk management

and mining. While the academic literature provided theoretical perspectives on project risk

management in mining, the industry publications provided a practical view on the same topics.

The areas of literature studied were categorized into four primary groups with sixteen subgroups,

as shown in Figure 2.1. These primary groups included: project risk management, risk and

uncertainty, adaptive management, and modelling and valuing adaptivity.

Figure 2.1 Structure of Literature Review Groups and Subgroups

16

2.2 Capital Projects in the Mining Industry

Effective capital project development is a necessary skill for mining companies to be successful.

Capital projects are the vehicle through which metal and mineral assets are turned into producing

mines capable of generating free cash flow. Mining is a capital-intensive industry, and access to

and allocation of capital to pursue strategic growth initiatives are issues of significant concern for

mining companies (Ernst and Young, 2021). Efficiently allocating this capital to development

projects and managing projects well is critical for mine operators to achieve expected returns.

The need for effective project management is significant: the major project inventory for mining

projects in Canada lists 120 projects representing C$82B in capital costs for projects currently

under construction or planned between 2020-2030 (Natural Resources Canada, 2020). Of these

120 projects, 29 have capital budgets larger than C$1B. Despite the need and desire for

successfully implemented projects, broad-scale project success is elusive. Industry reports and

studies point to projects routinely going over budget and schedule. A study on the bias and error

in capital cost estimating in mining projects founds that mining project costs on average exceed

Feasibility Study estimates by 14%, and approximately half of all projects in the sample

exceeded the expected 15% accuracy range of the Feasibility Study cost estimate (Bertisen &

Davis, 2008). Global consulting firm McKinsey found that 80% of mining projects are late and

over budget by an average of 43% (Kuvshinikov et al., 2017), while Ernst & Young (2017b)

found that 62% of projects within their study group had a cost over-run. Mining industry

executives have identified effective capital project development as one of mining companies' top

risks (Ernst and Young, 2017a). More rigorous industry studies show that 65% of industrial

megaprojects fail to meet objectives (Merrow, 2011). Mining projects are large, technologically

challenging, and complex endeavours and share characteristics with other types of megaprojects.

17

Megaproject development has even been identified as the primary delivery model for mining

assets (Flyvbjerg, 2014). Mining companies have a significant interest in improving capital

project performance to deliver expected returns on investment and to justify project funding

decisions.

To combat poor project performance, mining companies invest heavily in exploration and front-

end planning and studying of projects before committing to a full-funding decision and

constructing the mine (Cooper & O’Shea, 2015; Galloway, 2004). Significant time, resources,

and capital are invested in exploration programs to reduce geological uncertainty and better

define the mineral resource. In parallel with exploration efforts, the project will progress through

stages of study with progressively more detailed designs and analyses before committing to full

project funding. This staged development method is typically called Front-End Loading (FEL)

process. It reduces technical uncertainty, improves schedule and cost predictability, and raises

confidence in the eventual investment decision (Jergeas, 2008; Kühn & Visser, 2014; T.

Williams et al., 2019). Before execution, the final stage is to complete a Feasibility Study, which

includes full-scale scoping, project execution planning, and preparing cost and schedule

estimates with the detail necessary to request project funding. This rigorous process of Front-

End-Loading is intended to improve project definition and reduce the risk of project

underperformance.

However, some question the full effectiveness of Front-End Loading as a method to reduce

project risks. Some industry and academic researchers suggest that the rigorous process that is

inflexible to change creates blinders for project team members and limits their view of the risk

landscape (Rolstadas et al., 2011). Others question the motivation and performance of the people

18

involved during these initial study stages, suggesting that initial estimates of project scope,

schedule, and cost are subject to political influences. In the early stages of project study and

planning, those responsible for preparing the cost and benefit projections for the project are those

who are most interested and personally invested in seeing it get approved. Through both strategic

misrepresentation (“deception”) and optimism bias (“delusion”), initial project cost and schedule

estimates often present a more palatable depiction of the project than will play out in reality

(Flyvbjerg, 2006).

In addition to questions about the Front-End Loading process and the motivations of project

promoters, a growing body of research is investigating the link between uncertainty, risk, and

project performance. The belief is that improved project risk management shows promise for

improving project success. However, one of the critical challenges in implementing effective risk

management programs is defining risk and the corresponding methods to assess, analyze, and

plan risk responses (Kaplan, 1997). There are many different conceptual frameworks and

definitions of risk, and these concepts and definitions must be explored before discussing

methods to improve project risk management.

2.3 The Risk Concept

One of the central challenges with implementing effective project risk management lies with the

many diverging definitions, concepts, and opinions about risk and uncertainty. In one of the

earlier works attempting to clarify this issue, risk was defined as a situation where the outcome

was uncertain, but the probabilities could be accurately calculated, while uncertainty was a

situation where the probabilities were unknown due to lack of information (Knight, 1921). This

definition has been disputed, with the two concepts described by Knight as “risk” and

19

“uncertainty” now more widely understood as aleatory and epistemic uncertainty (Paté-Cornell,

1996). Reconciling these two types of uncertainty into a single probabilistic measure suitable for

risk analysis has been challenging, as aleatory uncertainty is often expressed through classical

statistical approaches (e.g., the variance of a parameter), while epistemic uncertainty is often

expressed through expert judgement and more subjective approaches (e.g., range of possible

underlying models). Bayesian theories of probability have been suggested as a way to combine

expert opinion and statistical information in technical risk analyses (Apostolakis, 1990).

Cohesive definitions of the concept of risk are no easier to find. In one of the seminal works

defining risk and risk analysis, Kaplan and Garrick (1981) define risk as the triplet of a scenario

or event, the probability of that scenario or event occurring, and the consequences of that

scenario. Risk is then the set of triplets of possible scenarios with their corresponding

probabilities and outcomes, expressed as the following:

{ }, , 1, 2, ,i i iR s p x i N= = (1)

where:

is is scenario or event i,

ip is the probability of scenario i occurring, and

ix is the consequences of scenario i.

This definition essentially asks the questions: What could go wrong? What is the probability it

will go wrong? If it does go wrong, what are the consequences? Kaplan and Garrick (1981) also

define the relationship between hazard and risk, stating that hazard is a source of danger or

potential unwanted events, while risk includes the probability of converting that hazard into

negative consequences.

20

While the Kaplan and Garrick definition of risk is still the cornerstone of risk definitions in

project risk management, guidelines and standards have taken a more general view on risk. The

Project Management Institute (PMI) (2017) defines project risk as “an uncertain event or

condition, that if it occurs, has a positive or negative effect on one or more project deliverables.”

The Association for Advancement in Cost Engineering International (AACEI) (2015) includes a

more detailed and nuanced explanation of risk. Recognizing the definitional debate, they include

considerable discussion around the many ways to understand and analyze project risks. However,

they still approach the definition of risk in as simple and inclusive a way as possible, defining

risk as “An uncertain event or condition that could affect a project objective or business goal.”

In an effort to craft a definition that is universally applicable to any situation involving risk and

risk management, the International Organization for Standardization (ISO) defines risk as “the

effect of uncertainty on objectives” (International Organization for Standardization 2018 [ISO],

2018). The ISO definition – a generalized but virtually identical definition to both the AACEI

and PMI definition of project risk – has its supporters and detractors. Some feel that the process

has created a more unified language around risk, albeit with compromise and essential trade-offs

required for building consensus and standardization (Purdy, 2010). Others find it incomplete,

lacking clarity, and too vague to be truly useful (Aven, 2011; Leitch, 2010). Engineers Canada,

the national assembly of provincial engineering licensing organizations and accreditor of