AccountAble Handbook FCRA 2010

87

Foreign Contribution (Regulation) Act, 2010 Foreign Contribution (Regulation) Rules, 2011 ❈ ❈ ❈ Sanjay Agarwal B.Com. (Hons.), FCA Context, Concepts and Practice ACCOUNTABLE HANDBOOK FCRA 2010

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of AccountAble Handbook FCRA 2010

Foreign Contribution (Regulation) Act, 2010Foreign Contribution (Regulation) Rules, 2011

! ! !

Sanjay AgarwalB.Com. (Hons.), FCA

Context, Concepts and Practice

ACCOUNTABLE HANDBOOK

FCRA 2010

2 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Published by AccountAid India55-B, Pocket C, Siddharth Extension, New Delhi – 110014, IndiaPhone No.: +91-11-2634 3128Email: [email protected] Edition: June 2002Reprint: April 2004Second Edition: September 2012Third Edition: June 2021Copyright © Sanjay Agarwal

All rights reserved. Without limiting the rights under copyright reserved above, no part of this publication may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording or otherwise), without the prior written permission of the copyright owner of this book.The law in this book has been updated till 30-Jun-2021.Printed and bound in India.

Due care and diligence have been taken while editing and printing this book. Neither the author nor the publisher of the book holds any responsibility for any mistake that may have inadvertently crept in. The publisher shall not be liable for any direct, consequential, or incidental damages arising out of the use of this book.

Price: `1,400/-FCRA 2010: Context, Concepts and PracticeISBN13: 978-81-910854-2-6 (Hardback)ISBN13: 978-81-910854-3-3 (eBook)

Cover Picture: iStockphoto.com/DolasQuickBooks is a registered Trademark of Intuit Inc. Excel is registered Trademark of Microsoft Corporation. Tally is a Trademark of Tally Solutions Pvt. Ltd. AccountAid, AccountAble, and AuditAble are Trademarks of AccountAid India.Printed at:PRINTWORKS, C-94, Okhla Industrial Area Phase I, Okhla, New Delhi - 110020

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 3

Dedicated to the memory of

my father, who taught me the value of

contemplation and moderation

and

my mother,who showed me how !abda can sometimes be

more reliable than anum"na.

! ! !

Contents at a Glance

Foreword 31

Preface to the Third Edition 33

Preface to the Second Edition 35

Preface to the First Edition 37

Acknowledgements 39

Guide to using this book 41

Abbreviations 43

Figures and tables 48

I. Context 49

II. Concepts 81

III. Practice 190

IV. Filing 279

V. Appendices 370

VI. Current Act and Rules 421

VII. 1976 Act and Rules 477

VIII. Selected Noti#cations, Notices, Guidelines, Charters, etc. 489

IX. Online Resources 530

X. References and Case Law 531

XI. Index 538

6 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Detailed Table of Contents

Foreword 31Preface to the Third Edition 33Preface to the Second Edition 35Preface to the First Edition 37Acknowledgements 39Guide to Using this Book 41About Online Resources 41About Footnotes 41Looking up Author References 41Locating Case Law 41Using the Index 41Section and Rule References 42Abbreviations 43Figures & Tables 48

I. Context 491. Introduction 50Box: What is FCRA? 50Numbers and Trends 52The next Decade 52Box: Poverty and Charity 53Overview of the Chapters 54

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 7

I. Context 54II. Concepts 54III. Practice 55IV. Filing 55Appendices 55

2. The History of FCRA 56Cold War and Elections 56Box: The 1976 Act 57Passing of the 1976 Act 57Box: National Interest 58Kudal Commission 58Box: The 1984 Change 58Work in Progress 59Box: NGOs, Emergency and FCRA 59The New FCRA of 2010 60Box: The 2010 Act 60The New India and FCRA 60Box: The 2020 Changes 60Cultural Globalization 62Religious Evangelism 62International Environment 63The Globalization of FCRA 64Group A: Political Funding: Complete ban; NPO Funding: Restricted 64Group B: Political Funding: Complete ban; NPO Funding: Less restricted or unrestricted 65Group C: Political Funding: Partial ban; NPO Funding: Less restricted or unrestricted 66

3. The Politics of FCRA 67The Political in FCRA 68Box: Those who Dig Holes for Others… 70The Political in Practice 70Organizations of a Political Nature 71INSAF in Courts 71Reading the INSAF Judgment 73National Interest 74Interests of the State 74Court-side View 75NGOs and Politics 76Inquisition, FCRA and Dharma 79Box: The Nationalization of Charity 78

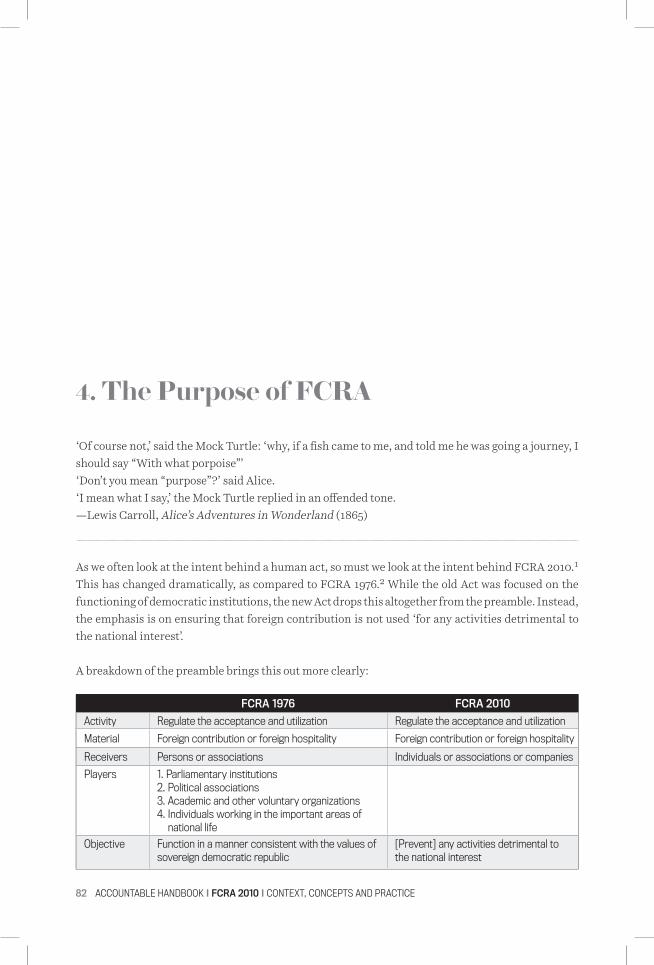

II. Concepts 814. The Purpose of FCRA 82

8 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Box: The Great Wall of China 83Box: Raising the Drawbridge 84Jurisdiction 85Repeal of FCRA 1976 85

5. Foreign Contribution 87De#ning Foreign Contribution 87Commercial Receipts 88Box: Loans from Foreign Sources 88Payments to For-Pro#ts 88A. For Products 89B. For Services 89C. Subsidy 90Impact Investments 90Conclusion 91What’s Covered 92A. Articles 92Box: Awards & Prizes 92B. Currency 93C. Securities 96And What’s Not… 96Scholarships & Stipend 98A. Scholarship 98B. Stipend 99C. Payment of a like nature 99D. Fellowships 100E. Fellowship or Fees? 100

6. Donors 102Foreign Source 102Primary Foreign Source 102Box: Colors of Xenophobia 1031. Individuals 1032. Government 1063. International Agencies 1064. Non-pro#t organizations 1075. Business Organizations 110A. Foreign Company 110Box: Neither Here nor There 110B. Subsidiary 112I. Foreign Subsidiaries only? 114Box: Foreign Control, Subsidiaries and MNCs 114II. Subsidiaries Excluded by 2016 Change? 115C. Registered O$ce 116D. Corporation 116

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 9

E. Foreign MNC 116Box: Group Companies 116F. Company under Foreign Control 117Secondary Foreign Source 117Foreign Source or Not 117Interest on FCRA Bank Balance 118Other Interest 118Giving Portals 119Box: Other Income 119Non-foreign sources 119Indian Sources 120Becoming Indian 120Exempt Sources 120‘Prohibited’ Sources 120Donors in Prior Reference Category 120Due Diligence 121

7. Receivers 122A. Prohibited 123Exceptions 123Box: Identifying Journalists 124Media 124Print Media 124Electronic Media 124Social Media 126Coverage and Content 126Bureaucrats 127Public Servants 128Judiciary 130Politicians 130Legislature 130Box: Electoral Trust Donations 130Election Candidates 131Political Parties 132Quasi-political Organizations 132Identifying Quasi-political Organizations 132Restriction on the Organization 133Forms of Organization 134B. Exempt 134 Three Conditions for Exemption 1341. Set up by the Government 1342. Wholly Owned by the Government 1363. Compulsory CAG Audit 136 Who is Exempt? 137A. Autonomous Bodies or Societies 137

10 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

B. Government Companies 138C. Public Sector Undertakings 138D. Legislative Bodies 141E. Municipalities 142F. Panchayats 142G. Central Government 143Other Exempt Organizations 143Implications of FCRA Exemption 144C. Regulated 145NPOs/NGOs 146Box: Section 8 Company 146Form of NPO/NGO 146Sec. 8/25 Companies 147Associations 147Objectives of the NGO 148Other Areas 154Service Delivery, Civil Rights or Research? 155Box: Crowdfunding Platforms 156Corporate Foundations 157Electoral Trusts 158Charitable Individuals 159Charitable HUF 159Charitable Business 160D. Permitted 160Private Individuals 160Remittances from Relatives 160Businesses 163CSR, B-Corps and Social Businesses 163Cooperative Societies 164Producer Companies 164SHGs/Mahila Mandals/CBOs 166Liaison O$ce 166Branch O$ce 168Nominal Branch O$ce 168

8. Foreign Hospitality 169Universities 170Approval 170

9. Prohibitions, Penalties and Compounding 171A. Prohibitions 171i. Giving to Unregistered Persons 171ii. Regranting or Passing on FC to Others 171iii. Using for Other Purposes 172iv. Political Activities 172

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 11

v. News Media 172vi. Speculative Activities 172vii. Administrative Expenses 172Box: Salary and Other Dirty Words 173B. Penalties 174i. Unlawful acceptance of Foreign Contribution or Hospitality 174ii. Regranting of Foreign Contribution 174iii. Misuse of Foreign Contribution 174iv. Defaults in Documentation/Intimation 174v. Banking-related O%ences 174vi. Miscellaneous O%ences/Events 175C. Compounding 175Filing the Application 176D. Penal Action 177i. Suspension 177Box: Which Bank Account? 178ii. Freezing of Prior-permission 178iii. Cancellation 178Box: Coup de grâce for Charity? 179Grounds for Cancellation 179E. Surrender 180Box: Charity: Instant Relief or Slow Release? 180Complications 181F. Custody and Management 181Defunct Organizations 181Funds in FCRA Bank 182

10. Investigation, Prosecution & Appeal 183Inspection 184Asking for Information or Documents 184Powers of Investigation 184Seizure 1851. Accounts and Records 1852. Foreign Contribution 185Inventory/Disposal 186Adjudication 186Con#scation 186Jurisdiction 186Appeals 187Con#scation Orders 187Orders Appealable in High Court 187Non-appealable Orders 188Revision of Orders 188Applying for Revision 188Relief 188

12 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

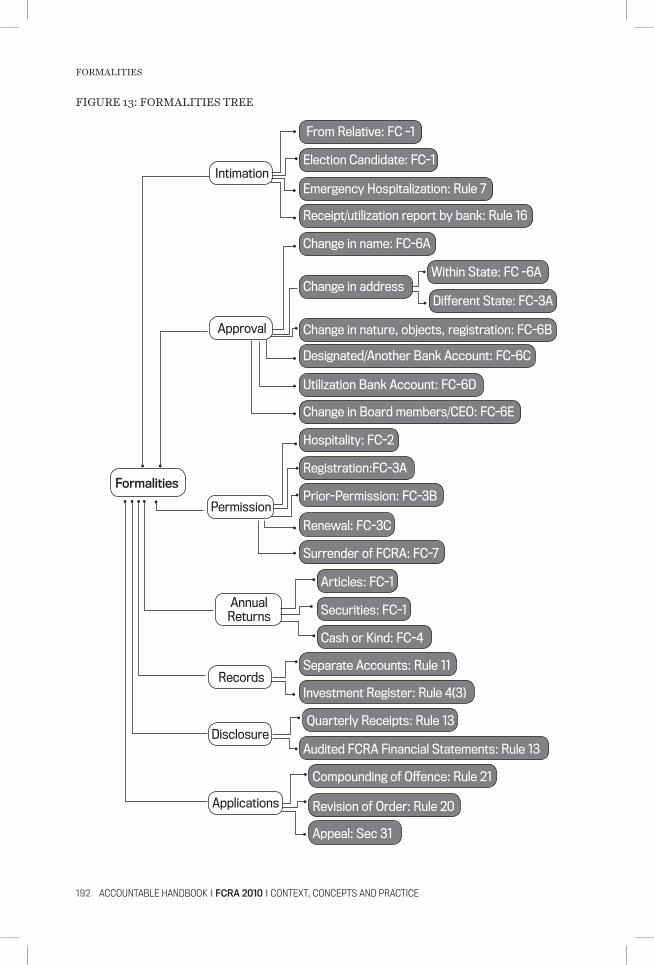

III. Practice 19011. Formalities 191Darpan ID 191A. Intimations 193i. Gift from Relative: FC-1 193ii. Receipt by Election Candidate: FC-1 193iii. Emergency Medical Aid 193iv. Reports by Bank 194a. Receipt/Utilization without Permission 194b. Receipts/Utilization by a person with FCRA 194B. Registration/Permissions 194i. FCRA Registration 194ii. FCRA Prior Permission 195iii. FCRA Renewal 195iv. Foreign Hospitality 195C. Approvals 195i. Opening or Changing Designated Bank Account 195ii. Opening or Changing Another Bank Account 196iii. Opening a Utilization Account 196iv. Change in Name or Address 196v. Change in Nature, Objects or Registration 196v. Change in Board Members or Key Functionaries 197D. Annual Returns 197i. Receipt of Material/Securities: FC-1 198ii. Receipt of Foreign Contribution: FC-4 198

12. Prior-permission, Registration and Renewal 199A. FCRA Prior-Permission 199Grounds for Denial 200Copy of Order 202Time Limit 202Old Permission – FCRA 1976 202Proxy Permission: FC-10 204Secondary Transfers 204B. FCRA Registration 204Track Record 204Cooling-o% Period 206C. FCRA Renewal 206Due Date 206Extension 207Delayed Application 207No Application 207Delayed Approval 208Fees 208Box: Rebirth and Renewal 208

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 13

13. Banking, Accounts and Records 210A. Bank Accounts 210i. Designated FCRA Bank Account 210Cut-o% Date 211Using the Account 211ii. Additional Bank Accounts 212Conditions 212iii. Permitted Deposits 214RBI Purpose Code 214Bank Charges 215Exchange Rate 215iv. Cash Withdrawals 215B. Account Books 215Heads of Account 217C. Records 218i. Fixed Assets Register 218ii. Ownership of Assets 218iii. Physical Veri#cation Records 219ii. Salary Register 219iii. Investment Register 220iv. Stock Register 220v. Distribution Register 221vi. Program Registers 221

14. Public Disclosure 222A. Publishing Quarterly Details 222Contribution in Kind 222Box: Restoring Public Trust 223Own Website 223On FCRA Site 224B. Publishing FCRA Audited Financials 224i. FCRA Balance Sheet 224ii. FCRA Income & Expenditure Account 225iii. FCRA Receipts & Payments Account 225

15. CSR and FCRA 227Companies as ‘Foreign Source’ 227Box: The Politics of Change 228Confusion Compounded 229Foreign Company – Indian Source? 229CSR Foundations 229Items Covered 229Case Studies 230Precautions 230a. For NGOs 230

14 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

b. For Companies 230c. For Banks 231

16. Impact Investing & Social Stock Exchange 232a. Impact Investment Instruments 232Instruments 232For-pro#t or Not-for-pro#t? 233Business Transactions 233Pro#t or Impact? 233Caveat Investors 234b. Social Stock Exchange 235Untangling SOSTEX & FCRA 239

17. Monitoring and Enforcement 240a. Monitoring 240Intelligence Bureau 240PFMS 241Tax Returns 241Data Analysis 241Whistle-blowers and Activists 241FCRA Questionnaire 242b. Enforcement 242Scrutiny of Records 242Site Visits/Audits 242Prior Reference Category (Donor Watchlist) 242Show-cause Notice 243Compounding Fees 243Suspension 243Cancellation 244Punishment 245

18. Myths and Mysteries of FCRA 247A. Registration, Permission, Approvals 247FCRA applies only to NGOs... 247FCRA Grants to Individuals 248Businesspeople/Professionals 248Shadow-lending 248Advances 248Reimbursement 248How Much 249Unused prior-permission 249Churches and Ashrams 249Commissioned News Stories 250Advertisement Campaign 250FEMA and FCRA 250

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 15

B. Fund-raising 250Foreigners in India 250Dollar donations are foreign contribution? 250Rupee donations are not foreign contribution. 251Foreign Company can be an Indian source... 251UN Bodies 251Consultancy Contracts 251FCRA Interest 251Anonymous Donations 251Sharing Bank Account Numbers 252Online Fund-raising 252Crowdfunding 252Catalogues & Souvenirs 252Religious Books 252Souvenir Advertisements 253NRI donations 253Charity Events 253Art Sale 254Raising funds abroad 254Consultancy Income 255Income from FCRA Projects 255Sale of Publications 256Hire Charges 256Sta% Recoveries 256Guest recoveries 256Recoveries from Bene#ciaries 257C. Receipts and Utilization 257When do FC Funds become Indian 257Converting FC Funds 257Re-purposing FC Funds 257Endowment or Corpus 258Endowment Investments 258Endowment Income 258Bi-lateral funds 258Unrestricted FC funds 258Unrestricted FC funds – under Prior Permission 259Program Salaries are not administrative expenses... 259Programs Outside India 259Mixing of FC and non-FC 259D. Transfers, Sub-granting or Regranting 259Box: NGO Networks & FCRA 260Payments to For-Pro#ts 260Program vs. Services 260Service Contracts with Foreign NGOs 261Service Contracts with Domestic NGOs 261

16 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Regranting to Exempt Entities 261Crowdfunding Platforms 262Placing Personnel in India 262Assets created out of FC 262Conversion of Organization Form 262Mergers & Takeovers 263Making Direct Disbursals 263O%-shore Banking 264O%-shore Granting 264Reimbursements 264Advances 264Direct Implementation 265Utilization by Proxy 265E. Other Issues 266Expenditure on Fixed Assets 266Personal Gifts 266Old items in FC-1 and FC-4 266Micro-Credit 266Change of Bank Account Number 267Loans between FC and Indian 268Grant Refund or Transfer 268Sale of Fixed Assets 268Separate Books 269Consolidated Accounts 269Non-cash Grants in FC-4 269Second or Subsequent Recipient 269Opening Branch Abroad 269Foreign Volunteers 270

19. Checklists 271A. Govt. Servants, Politicians, Political Parties 271B. Journalists, Public Servants 272C. Ordinary Individuals 272D. Foreigners and PIOs 272E. Donor Agencies 273F. CSR Companies 274G. NGOs/Charities 274H. For-pro#t Companies with Programs 277I. Individuals with a Program 277J. Bankers 277K. Auditors 278

IV. Filing 27920. Filing Annual Return in FC-1 280Form FC-1 for NGOs: Articles 280

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 17

Receipt of Articles 281Valuing the Articles? 281Use of Articles 281Review and Submission 281Form FC-1 for NGOs: Securities 281Receipt of Securities 282Valuing the Securities? 282Mode of Utilization/Disposal 282Review and Submission 282Form FC-1 for Indian Citizens and Resident Foreigners 282Relative 283For Remittances 283For Articles 283For Securities 284Submitting the form 284Form FC-1 for Election Candidates 284Submitting the form 285

21. Filling up form FC-2 for Foreign Hospitality 286Applicability 286Member of Legislature 286O$ce-bearer of a political party 287Judge 288Government Servant 288Employee of Government Organization 288Public Servant 289Filling up the Form 290Details of Applicant 290Forwarding Details and Status 290Saving the Form 290Details of Hospitality 290Details of Host 291Hospitality Availed 291Hospitality Denied 291Attachments 291Filing 291

22. Form FC-3A for Registration 292Old Applications 292Eligibility 292Filling the Form 293Association Details 294Details of Applicant 294Details of Registration 294Aims and Objects 294

18 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Executive Committee 294Chief Functionary 295Relationship with Other Board Members 296Occupation 296Other details 296Nationality, Aadhaar and PAN 296Government O$cers 297Foreigners, PIOs, and NRIs 297Aadhaar and PAN 297EC Details and Others 297Conviction or Prosecution 298Misuse of Funds 298FCRA Prohibition 298Other NGOs 299Details of the Case 299Branch, Unit or Associate of Another Organization 299Adverse FCRA Orders 299Bank Details 300Other Details 300Past Prior-permissions 300Funds without Prior-permission? 300Past Applications for Registration 300Past Applications for Prior-permission 300Close Links with Other Organizations 301Cancelled Registration 301Upload Documents 301Filing the Form 302Status of Application 302Secondary Submissions 302

23. Form FC-3B for Prior Permission 303Old Applications 303Eligibility 303Filling the Form 305Association Details 305Details of Applicant 305Details of Registration 305Aims and Objects 305Executive Committee 306Chief Functionary 307Relationship with Other Board Members 307Occupation 307Other details 307Nationality, Aadhaar and PAN 308Government O$cers 308

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 19

Foreigners, PIOs, and NRIs 308Aadhaar and PAN 308EC Details and Others 308Conviction or Prosecution 309Misuse of Funds 310FCRA Prohibition 310Other NGOs 310Details of the Case 310Branch, Unit or Associate of Another Organization 310Adverse FCRA Orders 310Bank Details 311Other Details 311Past Prior-permissions 311Funds without Prior-permission? 311Past Applications for Registration 312Past Applications for Prior-permission 312Close Links with Other Organizations 312310 Registration 312Donor Commitment 312Donor Details 313Institutional Donors 313Multiple Donors 314Upload Documents 314Filing the Form 314Status of Application 315Secondary Submissions 315

24. Form FC-3C for Renewal 316Old Applications 316Due Date 316Preparatory Steps 316Delayed Filing 317Filling the Form 317Association Details 317Details of Applicant 317Details of Registration 317Aims and Objects 318Executive Committee 318Adding Members or Updating Details 319Chief Functionary 320Relationship with Other Board Members 320Occupation 320Other details 320Nationality, Aadhaar and PAN 320Government O$cers 321

20 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Foreigners, PIOs and NRIs 321Aadhaar and PAN 321E%ective Date and Reasons 322EC Details and Others 322Conviction or Prosecution 322Misuse of Funds 322FCRA Prohibition 322Other NGOs 323Details of the Case 323Branch, Unit or Associate of Another Organization 323Adverse FCRA Orders 324Bank Details 324Designated Account with SBI 324Utilization Accounts 324Other Details 324Past Prior-permissions 324Funds without Prior-permission 325Past Applications for Registration 325Past Applications for Prior-permission 325Close Links with Other Organizations 325Upload Documents 326Filing the Form 326Status of Application 326Secondary Submissions 327

25. Filling up FC-4 328Due Date 328Unable to #le? 329Filling up the Form 329Welcome Screen 329Section 2: Details of Receipt of Foreign Contribution. 330(i): Summary of Foreign Contribution. 330(ii): Details of Foreign Contribution Received 332Section 3: Details of Utilization of Foreign Contribution. 334(a) Project-wise Utilization 334Details of Utilization of FC 335Administrative Expenses 335Number of Foreigners 336(b) Purchase of Fixed Assets 336(c) Transfers to Other NGOs 336(d) Total Utilization in the Year 338Section 4: Unutilized Foreign Contribution. 338(i) FC Invested in Term Deposits 338(i) FC in form of cash or bank balances 3385. Foreigners 338

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 21

6: Unutilized Land & Buildings 3387: Details of FCRA Bank Accounts. 3398. Questions 3399. Audited Financial Statements 340i. FCRA Financial Statements 340ii. Audit Certi#cate 341Additional Tests by Auditors 341Management Letter 342Upload Documents 342Review and Submission 342Revision 343

26. Form FC-6A for Changes in Name, Address etc. 344Due Date 344Intimation or Approval? 344Processing Time 344Filling the Form 344Association Details 344Change of Organization’s Name 344Documents Needed 344Change of Address within State 345Documents Needed 345Communication Details 345Upload Documents 345Filing the Form 345

27. Form FC-6B for Changes in Nature, Objects, etc. 346Due Date 346Intimation or Approval? 346Processing Time 346Filling the Form 346Association Details 347Nature, Aims, Objects and Registration on Record 347a. Change in Nature 347Documents Needed 347b. Change in Aims and Objects 347Documents Needed 348c. Change in Registration 348Documents Needed 348Communication Details 348Save the form 348Upload Documents 348Preview 349Filing the Form 34928. Form FC-6C for Designated/Another FCRA Account 350

22 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

I. Due Date 3511. Intimation or Approval? 3512. Processing Time 351II. Filling Up the Form 3521. Association Details 3522. Present Designated Bank Account Details 3523. Intimated Designated FCRA Account? 3524. SBI NDMB Bank Account Details 3525. Communication Details 3526. Another Bank Account Details 3527. Another Bank Account as per Records 3538. Intimate or Change Another FCRA Account? 3539. Adding Details of Another Bank Account 35310. Documents Needed 353III. Filing the Form Online 3531. Preview 3532. Common Errors 354a. Yes or No? 355b. Old Designated as SBI Designated 355c. SBI NDMB as Another Account 355d. SBI NDMB as Designated and as Another 355e. City and State in SBI Designated Account Screen 3553. Filing 3554. Resubmission 3565. Correction after Approval 356

29. Filing Form FC-6D for Utilization Account 357Due Date 357Intimation or Approval? 358Processing Time 358Filling the Form 358Association Details 358Present Utilization Bank Account Details 358Adding New Utilization Bank Account 358Closing or Changing Utilization Bank Account 358Documents Needed 358Communication Details 359Filing the Form 3594. Resubmission 3595. Correction after Approval 359

30. Form FC-6E for Key Functionaries 360Due Date 360Change in Details 360Intimation or Approval? 360

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 23

Processing Time 360Form Pending for Approval 361Corrections 361Filling the Form 361Darpan Details 361Association Details 361Existing Key Functionaries 361Change in Key Members 361Communication Details 362Changes in Key Functionaries 362Adding Members or Updating Details 362Chief Functionary 363Relationship with Other Board Members 363Occupation 363Other details 363Nationality, Aadhaar and PAN 364Government O$cers 364Foreigners, PIOs and NRIs 364Aadhaar and PAN 364E%ective Date and Reasons 364Upload Documents 364Filing the Form 365Clari#cations 365Key Functionary A$davit 365Purpose of the A$davit 365Which Violations 366Implications for Key Functionaries 366How 366Who are Covered? 366When 366Di$culties 367

31. Form FC-7 for Surrender of FCRA 368Due Date 368Intimation or Application? 368Processing Time 368The Last Temptation 368Filling the Form 369Con#rmation Screen 369Association Details 369Bank Accounts 369Upload Documents 369Filing the Form 369

V. Appendices 370

24 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

1. Change of Forms 371Current Forms (online) 3712. Intimation of Emergency Medical Aid 3723. Donor’s Commitment Letter 3734. Undertaking from Employee 3745. Undertaking from an FCRA-Exempt Entity 3756. Undertaking from Grantee 3767. Key Functionary A!davit 3778. CSR Questionnaire 3789. Calculating and Reporting Administrative Expenses 379Box: The Reason for Capping 379a. Research 380b. Training 380Box: Research: Academic or Subversive? 381c. Welfare-Oriented? 382Box: Welfare vs. Rights 383d. The Six Step Solution 383e. Disclosure in Accounts 38610. Standalone FCRA Financial Statements 387Balance Sheet 387Income and Expenditure Account 388Receipts and Payments Account 389Notes to Balance Sheet and Income & Expenditure Account 390Notes to the Financial Statements 39211. Columnar Domestic and FCRA Financial Statements 393Balance Sheet 393Income & Expenditure Account 394Receipt & Payment Account 395Schedule 1: Fixed Assets and Depreciation 396Schedule 2: Income & Expenditure Matrix 397Schedule 3: Reserves & Surplus 399Schedule 4: Unspent Grant Balances 399Schedule 4A: Unspent Grant Balances (Funder–wise) 399Schedule 5: Current Assets, Loans and Advances 399Schedule 6: Current Liabilities and Provisions 400Schedule 7: Signi#cant Accounting Policies & Notes to Accounts 40012. CA Certi"cate 40213. Management Letter 40314. FATF Compliance Checklist 405Guidelines 405Non-compliance 40715. Contacting FCRA Department 408Visiting Hours 408Postal Address 408Phone/Email 408

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 25

Organization Structure 40816. Penalties Ready Reckoner 409i. Unlawful acceptance of Foreign Contribution or Hospitality 409a. Foreign Contribution Accepted by Prohibited Person 409b. Foreign Contribution Accepted on behalf of Prohibited Person 409c. Foreign Contribution Delivered to Prohibited Person 410d. Foreign Contribution Provided to a Di%erent Person 410e. Foreign Contribution Given to Another for Delivery to Prohibited Person 410f. Delegate Accepts Gift without Following Government Rules 410g. Foreign Contribution Accepted without Registration or Permission 410h. Foreign Hospitality Accepted by Prohibited Person 412i. Foreign Contribution Delivered to Another by Prohibited Person 412j. Foreign Contribution Accepted during Suspension 412ii. Unlawful Transfer of Foreign Contribution 412a. FC-registered Organization Transfers FC to Unregistered Organization 412b. FC-registered Organization Transfers FC to Another Organization 412iii. Misuse of Foreign Contribution 413a. Inactive or Defunct 413b. Engaged in Disqualifying Activities 414c. Against Public Interest 414d. Used for Speculative Purposes 414e. Used for Other Purposes 414f. Overshooting Administrative Expenses Limit 414iv. Defaults in Documentation/Intimation 414a. False Statement for Registration/Renewal 414b. Fraud/Concealment for getting Registration/Permission 414c. False A$davit 415d. Foreign Hospitality not Reported 415e. Foreign contribution not Reported 416f. False Intimation of Foreign Contribution 416g. Not #ling FC-1 or FC-4 416h. Not applying for Renewal in Time 416j. Records or Accounts not kept Properly 416v. Banking-related O%ences 416a. Fresh Foreign Contribution not Deposited in Designated Account 416b. Foreign Contribution Deposited in non-FCRA Account 417c. Local Contribution Deposited in FCRA Account 418d. Transaction in FCRA account not Reported by Bank 418e. Receipt or Utilization by Unregistered Person not Reported by Bank 418vi. Miscellaneous O%ences/Events 418a. Violation of FCRA Provisions by Registered Person 418b. Violation of FCRA Provisions/Rules/Order/Conditions by Registered Person 418c. Contravention of FCRA Provision by Person under Prior-permission 418d. Possible Contravention of FCRA 419e. Contravention of FCRA 419

26 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

f. Violation of FCRA Provisions/Rules 419g. Surrendering FCRA Registration 420

VI. Current Act and Rules 4211. Foreign Contribution Regulation Act, 2010 422

Chapter I: Preliminary 4221. Short title, extent, application and commencement. 4222. De#nitions. 422

Chapter II: Regulation of Foreign Contribution and Foreign Hospitality 4243. Prohibition to accept foreign contribution. 4244. Persons to whom section 3 shall not apply. 4255. Procedure to notify an organization of a political nature. 4256. Restriction on acceptance of foreign hospitality. 4267. Prohibition to transfer foreign contribution to other person. 4268. Restriction to utilize foreign contribution for administrative purpose. 4269. Power of Central Government to prohibit receipt of foreign contribution, etc.,

in certain cases. 42610. Power to prohibit payment of currency received in contravention of the Act. 427

Chapter III: Registration 42711. Registration of certain persons with Central Government. 42712. Grant of certi#cate of registration. 42812A. Power of Central Government to require Aadhaar number, etc.,

as identi#cation document. 42913. Suspension of certi#cate. 42914. Cancellation of certi#cate. 42914A. Surrender of certi#cate. 43015. Management of foreign contribution of person whose certi#cate has

been cancelled [or surrendered]. 43016. Renewal of certi#cate. 430

Chapter IV: Accounts, Intimation, Audit and Disposal of Assets, etc. 43017. Foreign contribution through scheduled bank. 43018. Intimation. 43119. Maintenance of accounts. 43120. Audit of accounts. 43121. Intimation by candidate for election. 43222. Disposal of assets created out of foreign contribution. 432

Chapter V: Inspection, Search and Seizure 43223. Inspection of accounts or records. 43224. Seizure of accounts or records. 43225. Seizure of article or currency or security received in contravention of the Act. 432

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 27

26. Disposal of seized article or currency or security. 43327. Seizure to be made in accordance with Act. 433

Chapter VI: Adjudication 43328. Con#scation of article or currency or security obtained in contravention

of the Act. 43329. Adjudication of con#scation. 43330. Procedure for con#scation. 433

Chapter VII: Appeal and Revision 43331. Appeal. 43332. Revision of orders by Central Government. 434

Chapter VIII: O#ences and Penalties 43433. Making of false statement, declaration or delivering false accounts. 43434. Penalty for article or currency or security obtained in contravention

of section 10. 43435. Punishment for contravention of any provision of the Act. 43436. Power to impose additional #ne where article or currency or security is not

available for con#scation. 43537. Penalty for o%ences where no separate punishment has been provided. 43538. Prohibition of acceptance of foreign contribution. 43539. O%ences by companies. 43540. Bar on prosecution of o%ences under the Act. 43541. Composition of certain o%ences. 435

Chapter IX: Miscellaneous 43642. Power to call for information or document. 43643. Investigation into cases under the Act. 43644. Returns by prescribed authority to Central Government. 43645. Protection of action taken in good faith. 43646. Power of Central Government to give directions. 43647. Delegation of powers. 43648. Power to make rules. 43649. Orders and rules to be laid before Parliament. 43750. Power to exempt in certain cases. 43851. Act not to apply to certain Government transactions. 43852. Application of other laws not barred. 43853. Power to remove di$culties. 43854. Repeal and saving. 4382. Foreign Contribution (Regulation) Rules, 2011 4391. Short title and commencement 4392. De#nitions. 4393. Guidelines for declaration of an organization to be of a political nature,

not being a political party. 439

28 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

4. Speculative activities. 4395. Administrative expenses. 4406. Intimation of receiving foreign contribution from relatives. 4406A. When articles gifted for personal use do not amount to foreign contribution. 4407. Receiving foreign hospitality by speci#ed categories of persons. 4408. Action in respect of article, currency or security received in contravention

of the Act. 4419. Application for obtaining ‘registration’ or ‘prior permission’ to receive foreign

contribution. 4419A. Permission for receipt of foreign contribution in application for obtaining

prior permission. 44310. Validity of certi#cate. 44411. Maintenance of accounts. 44412. Renewal of registration certi#cate. 44413. Declaration of receipt of foreign contribution. 44414. Extent of amount that can be utilized in case of suspension of the certi#cate

of registration. 44515. Custody of foreign contribution in respect of a person whose certi#cate has

been cancelled. 44615A. Voluntary surrender of certi#cate. 44616. Reporting by banks of receipt of foreign contribution. 44617. Intimation of foreign contribution by the recipient. 44617A. Change of designated bank account, name, address, aims, objectives or key

members of the association 44618. Foreign contribution received by a candidate for election. 44819. Limit to which a judicial o$cer, not below the rank of an Assistant Sessions

Judge may make adjudication or order con#scation. 44820. Revision. 44821. Compounding of o%ence. 44822. Returns by the Investigating Agency to the Central Government. 44823. Authority to whom an application or intimation to be sent. 448Form FC-1 450Form FC-2 453Form FC-3A 455Form FC-3B 458Form FC-3C 461Form FC-4 465Form FC-6A 469Form FC-6B 470Form FC-6C 471Form FC-6D 472Form FC-6E 473Form FC-7 4743. Foreign Contribution (Acceptance or Retention of Gifts or Presentations)

Rules, 2012 475

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 29

VII. 1976 Act and Rules 477The Foreign Contribution (Regulation) Act, 1976 478The Foreign Contribution (Regulation) Rules, 1976 487

VIII. Selected Noti!cations, Notices, Guidelines, Charters, etc. 4891. Gazette Noti"cations 490Exemption for Government Bodies: 30-Jan-2020 490Exemption for Government Bodies: 1-Jul-2011 490Compounding Fees: 5-Jun-2018 490Modi#cation of Compounding Fees Noti#cation: 27-Jul-2018 492Compounding Fees: 16-Jun-2016 492Management of FCRA Assets: 5-Nov-2018 493Sanctioning Authorities: 27-Oct-2011 493Investigating Agencies: 27-Oct-2011 493FCRA Promulgation: 29-Apr-2011 494MHA OCI Rules: 4-March-2021 494

2. Public Notices 496Extension of Date for Opening SBI NDMB Account 496Procedure for Opening SBI NDMB Account 496Registration Validity Extended till 30-Sep-21 498Registration Validity Extended till 31-May-21 498Extension of Last Date for #ling FC-4 for FY 19-20 499Updating Board Changes 499Payments Above Rs. 20,000 500Uploading Quarterly Details 500Comments on Draft Amendment – De#nition of Foreign Source 501

3. Guidelines 502SOP for SBI NDMB Account 502FCRA Frequently Asked Questions 503Introduction to FCRA, 2010 503Key De#nitions and Concepts under FCRA, 2010 504A. Foreign Contribution 504B. Foreign Source 506C. Other Key De#nitions and Concepts 507Registration and Prior Permission 507A. Eligibility 507B. Executive Committee 509C. How to apply 509D. Filling of online form 510E. Required documents 510F. Payment of fee 511G. Status of Online Form 511Acceptance and Utilization of Foreign Contribution 511

30 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

A. Acceptance 511B. Administrative Expenses 512C. Utilization of funds 512Transfer of Foreign Contribution 513Maintenance of Accounts 513Filing of Annual Returns 513Banks and Banking related issues 513Change in Name, Address, Objectives, FC Account details etc. 514Renewal of registration. 514O%ences and Penalties and Compounding of certain o%ences. 515Suspension, Cancellation and Surrender of Registration. 516A. Suspension/Cancellation 516B. Surrender 516Foreign Hospitality 516FCRA Dos 517FCRA Don’ts 518Compliance with the Amended Act FCRA 2010 and FCRR 2011 520Approving Foreign Hospitality Applications 521

4. FCRA Charters 524A. Charter for NGOs Applying for Prior-Permission or Registration 524Annexure: Good practice Guidelines to the Non-Pro#t Organizations (NPOs) to ensure compliance with FATF requirements. 525B. Charter for NGOs with Prior-Permission or Registration 525Annexure: Good Practice Guidelines to the NPOs to ensure compliance with FATF requirements. 527C. FCRA Charter for Chartered Accountants 527D. FCRA Charter for Banks 528

IX. Online Resources 5301. Non-foreign Sources 5302. Banned Sources 5303. Organizations of a Political Nature 5304. Gazette noti#cations 5305. Public Notices 5306. Parliamentary Debates: 1967-2020 5307. Parliamentary Report: 2008 5308. Table of Contents (Searchable) 5309. Index (Searchable) 530

X. References and Case Law 531References 531Case Law 536

XI. Index 538

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 31

Foreword

Mark Sidel

Sanjay Agarwal’s books on the FCRA have long been our best guides and analyses of this complex Indian legislation and the practice surrounding it. For two decades practitioners, policymakers, activists, academics and perhaps even some regulators, in India and abroad, have relied on Sri Agarwal’s successive volumes on the FCRA to understand how the Act, the Rules under it, and implementation are changing and developing. The predecessor volumes have been widely cited around the world in analyses of the FCRA in India and this volume will continue to be relied upon and cited in many countries as NGOs, donors, policymakers, academics and many others seek to understand the FCRA.

This new edition of FCRA 2010: Context, Concepts and Practice (2021 Edition) continues to set the standard in this #eld. It is a comprehensive volume, covering the history and policy behind the FCRA, the speci#cs of the legislation and rules, and a full guide to FCRA practice and implementation. As philanthropy has changed, this volume has kept pace, now including expanded sections on FCRA and corporate social responsibility (CSR), impact investing, and other important areas.

There are some inaccuracies and myths in our understanding of the origins and history of the FCRA, and this volume seeks to correct those. There is signi#cant misunderstanding, in India and abroad, of a number of aspects of FCRA practice and implementation, and this volume helps a wide array of readers to understand what FCRA and its Rules and implementation really means, and how to comply with FCRA better.

32 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

This volume is important in another way. India was among the #rst countries to develop a broad and comprehensive Act in seeking to restrict the &ow of foreign contributions to India. Now, almost #ve decades later, India is far from the only country with such legislation in place. In the Asia-Paci#c region alone, we have recent moves to adopt legislation restricting foreign funding elsewhere in South Asia and in East and Southeast Asia as well. Among the most prominent examples is China, where the Overseas NGO Law (formally the Law of the People’s Republic of China on the Management of the Activities of Overseas NGOs within Mainland China), enacted in 2016 and e%ective in January 2017, also adopted a comprehensive, securitized approach to restricting, controlling and monitoring funding and activities by overseas NGOs, foundations, think tanks and other nonpro#ts in China.

What India began in restricting foreign funding in the 1970s has now spread across the globe, though often in di%erent forms than India enacted or has amended over the decades. Some may view being a pioneer in this area as perhaps a dubious honor, but it is a reality that we should acknowledge.

At the same time, there are some aspects of the Indian experience that are not often found in other parts of the Asia-Paci#c region, or other parts of the world, in which foreign funding laws have been enacted. For me one important example of the Indian experience that is not always found elsewhere is the continuing role of the Indian courts in reviewing the government’s practices in implementing the FCRA and, at times, the Act and its Rules themselves.

That review function, while formally available to courts in some other countries where foreign funding laws are in place, has been exercised more vigorously and robustly in India than in many other jurisdictions. That includes the recent INSAF case, which is discussed in detail in this volume. While some may have wished that courts in India might take a stronger position on aspects of FCRA and its implementation, the fact that judicial review is possible and is actually undertaken distinguishes India from some other jurisdictions, including, of course, China

I commend this exceptional volume to practitioners, policymakers, activists, analysts, academics and anyone else who seeks to understand this important area of law and its practice and implementation. I speak as someone who has studied foreign funding restrictions for many years across the Asia-Paci#c region and beyond, and who has long relied on Sri Agarwal’s #ne work as a guide to and analysis of the complexities of FCRA. We are in his debt for this #ne work.

Mark SidelDoyle-Bascom Professor of Law and Public A%airsUniversity of Wisconsin-MadisonConsultant (Asia), International Center for Not-for-Pro#t Law (ICNL)

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 33

Preface to the Third Edition

Western philanthropy is purposive at heart - it seeks to change nations across the world into better ones. Some nations happily acquiesce in this global project, while others do not. Indian society, through the agency of its government, seeks to resist this attempt at improvement. The result of this con&ict is re&ected in FCRA, which creates a refereed space where the two forces of modernity and tradition, change and resistance, can come to an understanding. The ‘regulation’ in Foreign Contribution (Regulation) Act (FCRA) is, therefore, somewhat like a gas valve. If it is tightened too much, the &ame of innovation and improvement will go out. If it is left untended, con&agration might result.

FCRA is not a new law, but it was rejuvenated in 2010, when the previous version was replaced with new one. At that time, there was trepidation about how FCRA 2010 will a%ect NGOs in India. This has been replaced by despondency. The Government is determined to bring NGOs to heel, and where better to aim than at foreign contribution, their Achilles’ heel. The focus of regulation remains on NGOs whose activities involve policy work, advocacy, human rights, or environment, though other cultural or religious issues also surface from time to time. Unfortunately, none of these terms are de#ned clearly. As a colleague once remarked, FCRA is quite ambiguous, and it is easy for people to trip up unintentionally. Therefore, NGOs need to develop a better understanding of FCRA to continue working with foreign donors while remaining within the law.

Due to the frequent changes in rules since 2015, and now major ones in the law as well, the second

34 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

edition had become quite outdated. There is also new understanding and several new developments, which called for revision. All the FCRA forms are now online, with major changes in the manner these should be #lled up. Bulk of the book has therefore been re-written. Like the ship of Theseus, there is probably very little here from the #rst edition, though signi#cant parts of the second edition still remain.

Additions include a new chapter on CSR and another on Impact Investing. Two chapters have been added on the political and enforcement aspects of FCRA. The existing treatment on Investigation and Prosecution has been expanded, largely because of a more active stance of FCRA Department. Some new issues such as crowd funding, Social Stock Exchange (SOSTEX), crypto-currencies, and grants to business entities are discussed in detail. Some of the material (such as parliamentary debates and reports) has been expanded but moved online. Also available online now are lists of exempt foreign sources, organizations noti#ed as political, and many gazette noti#cations related to FCRA. The chapter on statistics related to FCRA has been compressed into one short para.

The root cause of organized philanthropy in India appearing to be dominated by foreign money is the much more liberal taxation treatment for charitable donations in Western countries, which allows money to be spent abroad. As compared to this, the Income Tax Department restricts all spending to India. A recommendation to allow charitable spending abroad made in National Policy for Voluntary Sector 2007, was shot down by the Department, which is often at loggerheads with NPOs on this issue (Agarwal 2012). Deductions for domestic charity remain niggardly and the regime increasingly punitive. This puts organized domestic charity at a disadvantage.

The good news is that domestic philanthropy is surging despite all this, with much useful work being done by new money in IT and start-ups as well as by young Indians with disposable incomes. CSR is stabilizing as well as showing signs of maturity. A Social Stock Exchange (SOSTEX) is coming up and will allow NGOs to tap into India’s booming economy as well as experiment with new approaches. What’s more, domestic philanthropy is likely to be less problematic as it is rooted in and backed by domestic sentiments. A time may therefore come in the next decade or two when NGOs will not have to worry so much about compliance with FCRA.

30-Jun-2021 Sanjay Agarwal

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 35

Preface to the Second Edition

A law that places restraints on charity sounds like bad policy. Yet that is precisely what the FCRA does. It forces NGOs and others in India to get Government permission before accepting foreign donations. This sounds bureaucratic and [presumptive]. As a result, a large part of enforcement resources goes into frisking the innocent – while creating an illusion of great activity. Due to this, the FCRA Department is left with little time or resources to understand the sector or focus on organizations that misuse funds.

Is FCRA bad policy? A signi#cant part of the foreign donations enters India avowedly to improve Indian culture, society and religion. There is another component which attempts to promote legislation for a better society. However, as Ms. Pushpa Sundar has shown the impact of foreign contribution is mixed (even though it is bene#cial overall) (Sundar 2010). The Government, therefore, believes that it must be regulated.

This book is an attempt to understand and explain the controversial Foreign Contribution (Regulation) Act 2010. This replaces an earlier law passed in 1976. Early indications are that FCRA 2010 will be enforced more strictly than FCRA 1976. The Department is being strengthened by adding more people. Critical processes are being computerized. There is also a perceptible change in tone - FCRA is not being viewed as an enabling legislation by the Department. Another critical change is the introduction of compounding fees. This has made it simpler for the Department to penalize a larger number of o%ences, without getting into time-consuming court cases.

36 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

The #rst edition of this book was widely appreciated, partly perhaps because it was the only book available on FCRA at the time. People also liked its relatively simple language and emphasis on practical application. The present edition is markedly di%erent due to several reasons. Firstly, FCRA 2010 is more complex than FCRA 1976. Secondly, the NPO programs have evolved. Thirdly, we now understand much more about FCRA than we did earlier. As a result, the book has been completely restructured. While the #rst edition focused on formalities, this one gives considerable attention to interpretation as well. This required many section references and explanations. Most of these are technical and would tend to clutter up the book for a general reader. These have all been moved to the end.

It is, therefore, hoped that this edition will be useful both to NGOs and donor Agencies, as well as to the accounting and legal professionals. As CSR grows over the next few years, the book will also be of interest to foreign MNCs and Corporate Foundations in India – many of them will #nd FCRA to be a legal mine#eld in working with Indian NGOs.

14-Nov-2012

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 37

Preface to the First Edition

Foreign Contribution (Regulation) Act, 1976 is a curious piece of legislation. The Act has only 31 sections: a very short and simple piece of law by any standard. It has also been amended only once in the last 26 years. Very few cases have gone to court under FCRA.

The Act was essentially designed to prevent &ow of foreign funds to political parties in India. It was brought in after a big controversy erupted in 1967 over the possible use of foreign funds in parliamentary elections. By 2002, there were similar laws operating in many countries across the world, including USA, UK, France, Japan, Germany, Canada, Russia, Malaysia, and Spain.

In 1984, the law was amended to regulate &ow of funds to charitable organizations more closely, based on the Government’s perception that some of these organizations may be used to channelize funds to political parties. This has resulted in a lot of paperwork and confusion for non-pro#ts working in India. Re&ecting this confusion, one of our #rst issues on FCRA was titled ‘Mysteries of FCRA’!

With time, the mysteries have reduced somewhat. The FCRA Department has also adapted a citizen’s charter and has tried to streamline its working. However, much remains to be done.

One peculiar implication of the 1984 amendment has been that FCRA is now commonly perceived as a law focusing on the NGOs. While this was not the intention of the law, this is what may have happened, given the fact that most of the time FCRA Department is dealing with NGOs.1

1There are about 40,000 NGOs with FCRA registration. Of these at least 20,000 are active.

38 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

The present handbook is designed primarily for use by NGOs, who often #nd themselves on the receiving end, so far as FCRA is concerned (no pun intended). Similarly, consultants and auditors, who must advise NGOs on FCRA, would also #nd the book useful. Some sections would be of interest to grant-making Agencies working in India, who sometimes #nd that their programs and projects fall foul of FCRA provisions.

Many Agencies located abroad are not aware that such a law exists, and therefore, sometimes #nd it di$cult to understand why their projects are delayed. This handbook may help give them an overview.

30-Jun-2002

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 39

Acknowledgements

The third edition took several years in writing and re-writing. Several persons provided valuable support in researching the data, proo#ng the manuscript, and tracking down references.

Notable was the hard work put in by a youthful team of Bhawna Malik, Kuldeep Sharma, Rahul Talan, Roshan Yadav, Sanchit Agarwal and Samrat Bhatt who crunched the unwieldy FCRA databases, digging out numbers and nuggets of gold. Dinesh Gautam painstakingly trawled the internet, compiling FCRA data, locating Gazette noti#cations and helping build the appendices. Later Bhawna and Rahul diligently tracked down references, spelling and grammatical errors. Samrat Bhatt and Roshan Yadav meticulously read through many court judgments, helping summarize them. Chetan Agarwal, Kuldeep, Rahul and Samrat pored over the printer’s proofs for many days, relentlessly pursuing errors, both big and small. Chetan also helped build the index.

Dr. Lalit Kumar, who headed Voluntary Action Cell of the erstwhile Planning Commission for many years, was generous as ever, helping make invaluable connections and valuable corrections in the book. Despite a hectic schedule, Biraj Patnaik made time to carefully read through parts of the manuscript, o%ering thoughtful comments and encouragement. Prof. Jane Schukoske helped re#ne the three chapters in Context section, steering me away from treacherous terrain. I am particularly grateful to her for the gift of Prof. Inderjeet Parmar’s book, among many others. Tirthankar Roy also read through the tricky Context section, o%ering feedback and sensible advice.

Also in order, is a word of appreciation for Prof. Mark Sidel, who has helped improve my understanding

40 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

of NGO regulation across the world in so many unobtrusive ways over the years. He was also kind enough to share extremely perceptive comments, provide additional references on regulation of philanthropy in China and Vietnam and write a generous foreword. I am forever indebted to him for his support and encouragement. I must also acknowledge Dipankar Mazumdar (1961-2018), friend, mentor and colleague, who shared freely his learning, vision and wisdom with me, and contributed a great many of the insights about NGOs found in this book.

Aditya Agarwal patiently read through the manuscript while handling almost the entire workload of our #rm for several weeks as I struggled with the #nal version of this book. Renu Agarwal’s help in locating and reading through Parliamentary debates, references, updating citations, building the index and her encouragement as I recovered from the #rst two abortive attempts at revising this edition was invaluable. Her unstinting support in this and other book projects is like an ever-present glow of sunshine in my life.

Still, several errors probably remain, due to my ignorance or oversight. I will be grateful if my learned colleagues and practitioners point these out for correction in future editions.

Angshuman and Moushumi De designed the cover and completed the layout, working under an impossible timeline. I would also like to thank the team at PRINTWORKS for helping meet a sti% deadline despite the Covid pandemic in printing this publication.

I would also like to thank each one of the hundreds of NGO functionaries, auditors, CSR practitioners and grant-makers who have generously shared their knowledge and di$culties with me during workshops, webinars, through email, over phone and in personal meetings. Bulk of this book is made of the nectar I have gathered from them.

Finally, I must thank our client foundations, for good-naturedly bearing with delays, while I worked on this book, sometimes ignoring their pressing needs.

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 41

Guide to using this book

ABOUT ONLINE RESOURCESMany noti#cations, orders, reports and other lists have been moved online to a dedicated website www.fcra2010.in, to reduce the size and price of this volume. These can be viewed and downloaded free of cost.

ABOUT FOOTNOTESFootnotes provide additional comment or reference to sections, noti#cations, etc. Unlike the second edition, these are given on the same page for ease of reference. In some cases, footnotes contain links to additional material such as FCRA FAQ, given at the end of the book in a separate section.

LOOKING UP AUTHOR REFERENCESWhere another author or publication has been referred in the book, the reference is given in the main text itself in brackets:

(Parmar 2012, p.257, 264)

These usually provide the name of the author or title of the book or article, along with year of publication. Reference to page numbers is also given, where relevant. If you want to read more or check up on a reference, you will #nd the publication and author details in section X: References. The list is sorted alphabetically.

LOCATING CASE LAWCase law references are given in the main text in brackets:

(AVARD vs. UoI 1990)

These provide shortened title of the case along with year when the judgment was given. If you want to locate the full case reference, you will #nd it in section X: Case Law. The list is sorted alphabetically. The full judgment is usually available on the internet – IndianKanoon.org is a good resource. Alternatively, you can locate it on the particular court’s website.

USING THE INDEXThe index is designed to help locate material on particular topics or keywords. It is sorted alphabetically. Page references are given against each topic or sub-topic. Sub-topics are indented under the main entry for that topic. In some cases, keywords or topics are further sub-classi#ed a second time. These are indented a second time.

42 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

A

Aadhaar, of bene#ciaries, 406Aadhaar, recti#cation of, 309n20, 321n21accelerator grant, 236-7accounting, 215-8

chart of, 217-8computerized, 215-8cost centers, 215-8groups, 215-8manual, 215-8

address

Where the index entry refers to a footnote, the reference is to a page number followed by the footnote number. For example, 309n20 refers to footnote 20 on page 309.

If a topic or keyword is repeated on multiple pages, then all the page numbers are listed against the main topic or keyword. In some cases, there is a cross-reference to the main entry for that topic:

prior reference category. See donor watchlist

The cross-reference may be to sub-topics under the main topic:

#xed assets. See under records: #xed assets

Some topics are indexed twice (or even thrice) to help locate an issue from di%erent perspective. For example, there is an entry for ‘online fundraising’ under myths as well as directly under online fundraising.

Topics related to #lling of forms are mostly indexed under the form itself. For example ‘donors - project details’ will be found under main entry ‘form FC-4’.

SECTION AND RULE REFERENCES

Section and rule numbers refer to Foreign Contribution (Regulation) Act, 2010 and Foreign Contribution (Regulation) Rules, 2011, unless speci#ed otherwise.

advertisement, payment for, 253a$davit, 365

board members, personal liability of, 366implications of, 366notarizing, 366purpose of, 365-6stamp paper, 366violations to be reported, 366when needed, 366-7who should submit, 366worries about, 367

aid. See foreign aid

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 43

AbbreviationsAbbreviation TermA/c Account AIIMS All India Institute of Medical Science AOF Account Opening FormATM Automated Teller Machine AVARD Association of Voluntary Agencies for Rural Development

B-Corps Bene#t Corporation BJD Biju Janata DalBJP Bharatiya Janata Party

CA Chartered AccountantCAG Comptroller and Auditor General of India CASS Computer Assisted Scrutiny System CBDT Central Board of Direct TaxesCBI Central Bureau of Investigation CBO Community Based OrganizationCCD Compulsorily Convertible Debentures CCPS Compulsorily Convertible Preference Shares CDs Compact Disk CEO Chief Executive O$cer CFO Chief Financial O$cer CIA Central Intelligence Agency

44 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

CIC Chief Information Commissioner CIDA Canadian International Development Agency COO Chief Operating O$cerCPC Code of Civil Procedure 1908CPCB Central Pollution Control BoardCPSMS Central Plan Scheme Monitoring System CREES Cultural, Religious, Economic, Environmental, Social CrPC Code of Criminal Procedure CSIR Council of Scienti#c & Industrial Research CSR Corporate Social Responsibility CWT Commissioner of Wealth Tax

DFID Department for International Development DHE Department of Higher Education DOPT Department of Personnel and TrainingDWCD Department of Women and Child Development

EC Election Commission

FAQ Frequently Asked Questions FATF Financial Action Task Force FC Foreign ContributionFC-GPR Foreign Currency-Gross Provisional Return FC-TRS Foreign Currency Transfer FCDO The Foreign & Commonwealth Development O$ce FCRA Foreign Contribution Regulation ActFCRR Foreign Contribution Regulation Rules FD Fixed Deposits FDI Foreign Direct Investment FEMA Foreign Exchange Management Act FII Foreign Institutional Investors FMRRS Financial Management Research and Resource Society FRRO Foreigners Regional Registration O$cer

GB Governing BodyGDP Gross Domestic ProductGOI Government of IndiaGovt. Government GST Goods and Services Tax

HC High Court

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 45

HDFC Housing Development Finance Corporation HR Human Resource HUF Hindu Undivided Family

IB Intelligence BureauICAI Institute of Chartered Accountants of India ICICI Industrial Credit and Investment Corporation of India ID Identity Documents IFSC Indian Financial System Code IGP Income Generating ProjectIIM Indian Institutes of Management IISC Indian Institute of Science IIT Indian Institutes of Technology IMF International Monetary Fund INGO International Non-Governmental OrganizationINSAF Indian Social Action ForumIPAI Institute of Public Auditors of India IPC Indian Penal CodeIRS Internal Revenue Service ITR Income Tax Return

JJB Juvenile Justice Boards JP Jai Prakash NarayanJPG/JPEG Joint Photographic Experts Group

KYC Know Your Customer

MACS Mutually Aided Cooperative SocietiesMCA Ministry of Corporate A%airs MD Managing Director MHA Ministry of Home A%airsMHRD Ministry of Human Resource Development MLA Member of the Legislative AssemblyMNC Multi-National Companies MP Member of Parliament

NABARD National Bank for Agricultural and Rural Development NAV Net Assets Value NBFC Non-Banking Finance Companies NCPCR National Commission for Protection of Child Rights NDA National Democratic Alliance

46 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

NDDB National Dairy Development BoardNDMA National Disaster Management Authority NDMB New Delhi Main Branch NDRF National Disaster Response Force NGO Non-Government Organization(used interchangeably with NPO)NLU National Law Universities Non FCRA Non Foreign Contribution Regulation ActNon-FD Non Fixed Deposits Non-FC Non Foreign Contribution NPO Not-For-Pro#t Organization (used interchangeably with NGO)NRI Non Resident Indian NSDF National Skill Development Fund

OCI Overseas Citizens of India OECD Organization for Economic Co-operation and Development

PAN Permanent Account Number PDF Portable Documents Format PFMS Public Financial Management SystemPIN Postal Index Number PIO Persons of Indian Origin PM CARES Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund PMLA The Prevention of Money Laundering ActPMNRF Prime Minister’s National Relief Fund PRBA Press and Registration of Books Act, 1867

RBI Reserve Bank of IndiaRJD Rashtriya Janata DalRTI Right to Information

SBI State Bank of India SCPCR State Commission for Protection of Child Rights Sec. Section SHGs Self Help Groups SHO Station House O$cer SIB Social Investment BondsSIDA Swedish International Development Cooperation AgencySMS Short Message Service SOP Standard Operating Procedure SOSTEX Social Stock Exchange STD Subscriber Trunk Dialing

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 47

TISS Tata Institute of Social Sciences TRP Television Rating PointTVC Town Vending Committees

UDIN Unique Document Identi#cation Number UGC University Grants Commission UK United KingdomUN United Nations UNDP United Nations Development ProgrammeUNGA United Nations General Assembly UNO United Nations OrganizationUSA United States of America USAID United States Agency for International Development UT Union Territory VMC Vigilance & Monitoring CommitteeZCZP Zero Coupon Zero Principal Bonds

48 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

Figures and Tables

Figure 1: Key Attributes of Foreign Contribution 91Figure 2: Foreign Sources 104Figure 3: Indians - Subcategories 105Figure 4: Indian Subsidiary of Foreign Company 112Figure 5: Primary and Secondary Sources 118Figure 6: Receivers 122Figure 7: Media 123Figure 8: Exempt Entities - Attributes 137Figure 9: Associations 147Figure 10: Program Attributes 149Figure 11: Types of Education 152Figure 12: Losing FCRA Registration 182Figure 13: Formalities Tree 192Figure 14: Manual Accounting 216Figure 15: Computerized Accounting 217Figure 16: SOSTEX - Mutual Fund 236Figure 17: SOSTEX – CSR Escrow 237Figure 18: SOSTEX – Social Impact Bonds 238Figure 19: SOSTEX – Pay-for-Success Through Lending Partner 239Figure 20: O%-shore Granting 265

Table 1: SHGs, Mahila Mandals, CBO - Stages 166Table 2: Universities 170Table 3: Compoundable O%ences 175Table 4: Permitted Deposits 214Table 5: Impact Investments & FCRA 234Table 6: Charity Events 253Table 7: Income from Art Sale 254Table 8: Using Unrestricted Funds 258

I. CONTEXTThings fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world, The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;The best lack all conviction, while the worst

Are full of passionate intensity.

W B Yeats, The Second Coming (1921)

50 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

1. Introduction

‘Yes, I did’, said Alice: ‘several thousand, I should think.’ ‘Four thousand two hundred and seven, that’s the exact number’, the King said, referring to his book.… —Lewis Carroll, Through the Looking Glass (1871)

The six decades from 1860s to 1920s of money-making on an industrial scale in the US were followed by the foundation-based philanthropy of the 1930s, arising perhaps out of remorse at capitalist excesses. These foundations gathered knowledge, expertise and reach to become powerful arbiters of national destinies. It has been argued that the foundations achieved this pre-eminent status by building knowledge networks, which bestowed ‘prestige on insiders’ and anointed selected approaches to development. This pattern has continued in the 21st century with tech billionaires setting up new foundations, leaving the old-money foundations dwarfed in terms of money power, even though they are unable to match the organization, dynamism and experience of the older foundations (Parmar 2012, p.257, 264).

Inter-state aid has long been accepted as a diplomatic tool to in&uence foreign policies of nations. It is always a mix of benevolence and realpolitik — sometimes the former serving merely as a patina to cover the grossness of leaden politics underneath. David Engerman has argued that Indian policies from the early 1960s to the late 1970s were deeply a%ected by the ‘Development Politics’ entrenched in American and Soviet aid, which served mainly to further the politics of the respective home governments, while claiming to advance the interests of the poorer nations. In his view, this ‘Janus-

WHAT IS FCRA?Called Foreign Contribution (Regulation) Act, this law was first passed by the Parliament in 1976. It applies to all of India and to all Indians, no matter where they live. The law is designed to make sure that foreign aid does not overly influence government policies, media, or social discourse. Accordingly, the law prohibits some from accepting any charitable contribution at all, while others are allowed to accept these only after some screening.

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 51

faced’ development politics was reborn as ‘development aid’ in the ’90s but became even ‘more corrosive than constructive of state power’, with ‘NGOs taking on tasks that were once the primary responsibility of states’. He concludes that ultimately this ‘disrupted domestic policies in relatively stable and institutionalized states like India’ (Engerman 2018).

As Western economies have grown rich on capital, innovation and trade, helped by diplomatic support from trade missions, and international travel became easier, a new source of charity emerged: institutionalized philanthropy, powered by charitable contributions of hundreds of thousands of individual donors in the West. This democratization of philanthropy has its own dynamics, feeding on stories of extreme penury and imposing unrealistic timetables of change and amelioration, to raise su$cient funds for an ever-expanding list of causes.

There’s a parallel to the transition from individual, personalized charity of past centuries to more purposive organized philanthropy. This is found in the way business has changed from individual or family-run enterprises to corporate entities which span continents. And just as the modern multinational corporations exercise enormous in&uence over the way we work and live, the modern international NGOs have come to in&uence the way we think and relate with our communities and the State. These in&uences, even with the best intentions, cannot always be aligned to the interests of the people whose lives they seek to improve through changes in thinking, cultural practices, as well as policies and politics of nations, considering especially the vast geographic and cultural distances across which the in&uence must travel. This dissonance lies at the heart of the contest between the new philanthropists and the newly philanthropized.

Be that as it may, there is evidence all-around of how modernity arising in the West, and carried overseas by philanthropic dollars, has changed our lives, often for the better. Programs such as micro-credit, watershed management, rainwater harvesting, solar energy, pollution control were all initially visualized and #nanced with foreign contribution. Ideas and institutions such as the powerful Chipko movement, the successful Dairy Cooperatives such as Amul, the idyllic Delhi University as well as the old reliable Doordarshan channel, owe part of their success to overseas support (Sundar 2010, p.115) (Staples 1992, p.31,36) (Shitak 2011, p.2). Improvements in the condition of undertrial prisoners and that of our jails as well as the clampdown on third-degree torture have also bene#ted from foreign funding. Foreign donors have also been able to build and sustain networks of NGOs working in remote and inaccessible areas where modern city dwellers would shudder to spend a night. Often these NGOs are the only brush with modernity that a villager in Chamoli or Mayurbhanj would ever have. These NGOs are an enormous source of strength to the communities which surround them, a crystallization of the romantic Bollywood staple in 1960s of a young handsome engineer or doctor who devoted his life to improving the lot of a village.

The increasingly important role of NGOs in India has led to increased demands for more regulation, since need for regulation is directly proportionate to the perceived importance of an institution. This development is not necessarily perverse — the corporate sector has bene#ted immensely from increased regulation in terms of increased public trust and access to resources. However, if regulations are not designed and implemented properly, these can create unintended consequences. This is the central challenge that FCRA must deal with.

52 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE

NUMBERS AND TRENDSThere was a time not long ago when most did not even know how much foreign contribution was coming into India each year. While this has changed enormously in terms of awareness, the total #gure remains elusive for several reasons. Part of the problem lies in how the basis of calculating and reporting foreign contribution has continued changing over the years. This edition therefore does away with the micro analysis of numbers — there are other and better sources of such data.

However, four points are in order. Firstly, the total amount of fresh foreign contribution has remained essentially static over the last several years at around Rs. 17,000 crores, or just about one percent of the annual tax revenue of the Government of India. This makes it easier for the Government to deal with NGOs, unlike Bangladesh and Philippines where NGOs contribute to a large part of the national budget. Also consider the fact that the foreign exchange brought in by NGOs is just about 4% of the annual FDI &ows (Rs. 3,68,520 crore in 2019). This means that the Government has little interest in the foreign exchange that NGOs bring in.

Secondly, the number of active NGOs has remained hovering around 20,000 for more than a decade. This is based on the number of NGOs who #le their returns annually. This has been so, despite the widely publicized crackdown on NGOs. The primary reason for this is that most of the twenty thousand NGOs who lost their licenses in the last decade were already inactive and were not #ling their annual returns. However, what is less well known is that about 2,000 active NGOs could not get their FCRA licenses renewed in 2016 for a variety of reasons, including activism. This problem is likely to be repeated in the second round of renewals in 2021, probably with more devastating impact, as a deeper scrutiny is now mandated. Given that getting and holding FCRA registration is now an onerous task, it is unlikely that this number will increase signi#cantly in the next one decade. It will probably gradually decline.

Thirdly, there is no evidence that the Government is singling out faith-based groups for punitive action under FCRA, even though they receive bulk of the foreign contribution. Rather it is NGOs with a more ‘political’ voice who are facing increased scrutiny and administrative action. This includes NGOs working on human rights, environment and policy matters. This trend is also likely to continue.

Fourthly, FCRA regulates foreign contributions for organized charity but does not restrict or monitor charitable contributions made directly to bene#ciaries themselves (individual-to-individual charity or organization-to-individual charity). This segment could develop signi#cantly as crowd funding platforms grow and could emerge as a counter to the restrictions on organized social work.

THE NEXT DECADEWill FCRA regulations be eased at any time in near future? This is quite unlikely for several reasons, irrespective of the political ideology which happens to be in power.

Firstly, political parties seek an accommodation with NGOs only when they are out of power. Once a party gains power, the very NGOs which may have been sympathetic to its rise, are seen as irritants. Periods of absolute majority for a party in Parliament are also the periods when NGOs have faced the maximum number of restrictions.

INTRODUCTION

ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE 53

Secondly, given the overall political environment, NGOs are unlikely to garner more support among the vocal middle classes in the near future. This also means less favorable treatment by popular press and media, which is driven mainly by TRPs and thus merely reinforces our favorite prejudices.

Thirdly, NGOs are likely to remain unwilling to make new alliances or friends in the corporate sector or among religious charities. This will continue to a%ect their ability to develop new sources of strength or ideas for improved and balanced regulation.

While FCRA is unlikely to be eased, there are chances that it will be made stronger in future, especially regarding monitoring and enforcement. The stage for this has already been set. Many NGOs are likely to lose their FCRA license or surrender it. Many others are now hesitant to get into

POVERTY AND CHARITYPoverty and property have lived side-by-side in India for thousands of years, with daan and tyag serving as a footbridge between the two. According to tradition, an impoverished Sudama, hesitantly approached his batchmate, royal Sri Krishna, not knowing the kind of reception he will get. As it turned out, Sri Krishna embraced him and his gift with grace and made sure Sudama was never poor again. The story of another batchmate, the learned Dronacharya did not go so well. Pushed to despair, unable to provide even a glass of milk to his son Ashwatthama, he approached King Drupad who greeted him with scorn. Hot with shame and a burning desire for revenge, Dronacharya schooled a batch of warriors, who got him half of Drupad’s kingdom in war as guru dakshina. This in turn led to another war, the famous Mahabharat. Renunciation was the chosen path for Prince Siddhartha, better known as Mahatma Buddh, and for Emperor Ashok, who gave up lordship over South Asia for a life of frugality and meditation. In more recent times, we have Mahatma Gandhi, who gave up the robes of an English barrister to trudge around India on foot, wearing but half-a-dhoti around his middle.This juxtaposition of poverty and wealth was not always visible to the rest of the world. Europe was fascinated with the riches of the princes and kings and later the splendor of the Mughal court, giving it the oft-quoted label of ‘Golden Bird’. These travelers and merchants did not mention that these riches were mostly with a privileged few and that the rest of India lived in thatched huts, sometimes unable to get two square meals a day. This distorted perception of India is what attracted East India companies to our shores, fleecing the princes and the traders, and thus universalizing poverty within India.For India, the rise of private philanthropy after end of the Second World War (and coincidentally of colonization as well) appears to have been triggered by two factors: first was the British familiarity and empathy, as well as, hopefully, a sense of guilt; the second was arrival of the American tourist, newly enriched by the emergence of US as the predominant economic power. India, equanimous in penury and plenty, has never tried to push its poverty out of sight through vagrancy laws or dwelling permits as some cities in the West and East do. This poverty, on stark display in the capitals and megalopolises of the India, and the indi!erence with which Indians look at it, is shocking for the average Westerner, who see this as an opportunity to be good Samaritans.In general, the modern West is much accustomed to purposeful giving, as distinct from daan or giving (Daan and Other Giving Traditions in India, p.14). This propensity to ‘give with a purpose’ is what has been leveraged by modern fund-raising organizations, which roll up every penny and dollar together to deliver a huge punch at poverty and other ills -- as perceived by them.

54 ACCOUNTABLE HANDBOOK I FCRA 2010 I CONTEXT, CONCEPTS AND PRACTICE