A REPORT ON Working Capital Management in SMIIEL (a unit of Motherson Sumi System Limited), noida...

134

A REPORT ON WORKING CAPITAL MANAGEMENT IN SMIIEL (A UNIT OF MOTHERSON SUMI SYSTEM LIMITED), NOIDA SECTOR 59 By Aarti Agarwal MBA II semester FMS-WISDOM Banasthali University 2014 Submitted To Submitted to MOTHERSON SUMI SYSTEM LIMITED MBA DEPARTMENT NAME OF MENTOR NAME FACULTY:- DIVYA MEHTA 1

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of A REPORT ON Working Capital Management in SMIIEL (a unit of Motherson Sumi System Limited), noida...

A REPORT

ON

WORKING CAPITAL MANAGEMENT IN SMIIEL (A UNITOF MOTHERSON SUMI SYSTEM LIMITED), NOIDA

SECTOR 59

By

Aarti Agarwal

MBA II semester

FMS-WISDOM

Banasthali University2014

Submitted To Submitted to

MOTHERSON SUMI SYSTEM LIMITED MBADEPARTMENT

NAME OF MENTOR NAME FACULTY:-

DIVYA MEHTA

1

2

TABLE OF CONTENTS

Acknowledgement

List of illustrations

Abstract

1. Introduction

1.1 Significance of topic, About

company

1.2 Objectives & Limitations

1.3 IMPORTANCE OF WORKING CAPITAL

RATIOS

2. Literature Review

3. Methodology

4. Analysis of Data / Finding

5. Conclusion & Recommendations.

3

Bibliography

Abstract

For increasing shareholder's wealth a firm has to

analyze the effect of fixed assets and current assets

on its return and risk. Working Capital Management is

related with the Management of current assets. The

Management of current assets is different from fixed

assets on the basis of the following points:

1. Current assets are for short period while fixed

assets are for more than one year.

2. The large holdings of current assets, especially

cash, strengthens liquidity position but also

reduces overall profitability, and to maintain an

optimum level of liquidity and profitability, risk

4

return trade off is involved in holding current

assets.

3. Only Current Assets can be adjusted with sales

fluctuating in the short run. Thus, the firm has

greater degree of flexibility in managing current

Assets. The management of Current Assets helps

affirm in building a good market reputation

regarding its business and economic condition.

Working capital may be regarded as the life blood of

business. Working capital is of major importance to

internal and external analysis because of its close

relationship with the current day-to-day operations of

a business. Every business needs funds for two

purposes:-

A. Long term funds are required to create production

facilities through purchase of fixed assets such as

plants, machineries, lands, buildings, etc.

5

B. Short term funds are required for the purchase of

raw materials, payment of wages, and other day-to-day

expenses. . It is otherwise known as revolving or

circulating capital

It is nothing but the difference between current assets

and current liabilities. i.e.

Working Capital = Current Assets – Current Liabilities.

6

Acknowledgement

I am grateful for the assistance of several

people who have contributed their ideas and valuable

suggestion for the fulfillment of this report. In this

context, I would like to thanks Mr. ………… (HOD),

Lecturers , College Name for helping me to give a

final structure of this report.

I would like to give my special thanks to Mr.

………………….. (Sales Manager), SMIIEL for providing me the

official help and mental support for the completion of

this report.

I would once again offer my sincere thanks to all

the office members for their help, without their

willingness and co-operation , nothing would have been

completed.

7

(Aarti )

INTRODUCTION

Working capital is the life blood and nerve centre of a

business. Just as circulation of blood is essential in the

human body for maintaining life, working capital is very

essential to maintain the smooth running of a business. No

business can run successfully without an adequate amount of

working capital.

Working capital refers to that part of firm’s capital which

is required for financing short term or current assets such

as cash, marketable securities, debtors, and inv entories.

8

In other words working capital is the amount of funds

necessary to cover the cost of operating the enterprise.

Meaning:

Working capital means the funds (i.e.; capital) available

and used for day to day operations (i.e.; working) of an

enterprise. It consists broadly of that portion of assets of

a business which are used in or related to its current

operations. It refers to funds which are used during an

accounting period to generate a current income of a type

which is consistent with major purpose of a firm existence.

Definition

Roland Berger Strategy Consultants study on working capital

management: Optimizing current assets helps tap into cash

potential and build buffers against insolvency

Our study entitled "Working capital – Cash for

recovery" looks at 216 European companies with total

sales of EUR 3,700 billion and total EBIT of EUR 422

billion

9

Presently, the insolvency risk is increasing as higher

cash requirements coincide with reduced cash supply and

high financing costs

Internal sources of finance are becoming more

interesting: one of the main lever is tapping into the

cash potential in working capital

The companies surveyed had a combined potential of EUR

353 billion in Q1 2009, roughly one third more than in

2008

Relative to tied-up working capital, utilities and

engineered products companies have the greatest cash

reserves hidden in their working capital

In the current economic situation, companies are facing a

higher risk of insolvency. On the one hand, they need more

cash; on the other, lenders are more tightfisted than usual

and the financing costs are higher. In its study entitled

"Working capital – Cash for recovery", Roland Berger

Strategy Consultants has analyzed 216 European companies by

taking a close look at their internal sources of finance.

10

The result? At the moment, releasing the cash reserves

hidden in working capital offers the greatest potential for

improving liquidity. According to the Roland Berger experts,

the companies surveyed had a total cash potential of EUR 353

billion. This turned out to be especially true for utilities

and engineered products companies.

"In the current recession, working capital is emerging as a

key source of internal finance," says Roland Schwientek,

Partner at Roland Berger's Operations Strategy Competence

Center. Increased cash requirements and a reduced cash

supply with higher financing costs combine to increase the

likelihood of insolvency. In their study called "Working

capital – Cash for recovery", the experts highlight

alternative sources of internal finance: "As some

traditional sources of cash have dried up, the most

promising solution is to tap into the liquidity potential

hidden in working capital," says Schwientek. According to

the experts, internal finance based on optimized working

capital is much more effective than external finance. Even

11

small improvements in receivables, inventories and payables

can generate significant reductions in external finance

requirements.

Survey of 216 European companies

The survey was based on an analysis of 216 European

companies from key industry sectors, such as automotive,

chemicals & oil, consumer goods & retail and

pharmaceuticals. The companies surveyed achieved combined

sales of EUR 3,700 billion and total EBIT of EUR 422 billion

or some 30% of the gross domestic product generated by the

EU25.

According to the Roland Berger experts, the companies

surveyed had total cash potential of EUR 353 billion in the

first quarter of 2009. The previous study conducted in 2004

had revealed no more than EUR 193 billion. Despite the

financial crisis, the cash potential was also up a full 32%

year on year. At 41%, payables offer the greatest potential,

followed by receivables (37%) and inventories (22%).

12

Significant differences between industries

In terms of working capital tied up, utilities and

engineered products companies have the greatest potential.

Average net working capital days are the lowest in

telecommunications and the highest in the airline industry.

The mining and automotive industries are leaders in

receivables management, while the construction and

telecommunications sectors come out on top in inventory

management. The telecommunications, construction and utility

industries lead the way in payables management.

Success factors for sustainability

There are a number of success factors that help ensure the

sustainable success of working capital projects. Roland

Berger offers a comprehensive toolset (Cash Navigator,

"Bible of Levers" toolbox, EVA/cash calculator, customer

risk and value flow analysis) designed to improve working

capital management. "In times of crisis, when we are facing

a significantly higher risk of insolvency, companies should

have a very clear idea of their potential – and use it.13

Nobody can afford to leave billions of euros idle in their

working capital," stresses Roland Berger expert Schwientek

in pointing out the need for effective working capital

management.

14

Objectives of working capital:

Every business needs some amount of working capital. It

is needed for following purposes-

For the purchase of raw materials, components and

spares.

To pay wages and salaries.

To incur day to day expenses and overhead costs such as

fuel, power, and office expenses etc.

To provide credit facilities to customers etc.

Factors that determine working capital:

The working capital requirement of a concern depend upon a

large number of factors such as

? Size of business

? Nature of character of business.

? Seasonal variations working capital cycle

? Operating efficiency

15

? Profit level.

? Other factors.

16

Sources of working capital:

The working capital requirements should be met both from

short term as well as long term sources of funds.

? Financing of working capital through short term sources of

funds has the benefits of lower cost and establishing close

relationship with banks.

? Financing of working capital through long term sources

provides the benefits of reduces risk and increases

liquidity.

Types of working capital:

Working capital can be divided into two categories-

Permanent working capital:

It refers to that minimum amount of investment in all

current assets which is required at all times to carry

out minimum level of business activities.

Temporary working capital:17

The amount of such working capital keeps on fluctuating

from time to time on the basis of business activities.

Advantages of working capital:

• It helps the business concern in maintaining the goodwill.

• It can arrange loans from banks and others on easy and

favorable terms.

• It enables a concern to face business crisis in

emergencies such as depression.

• It creates an environment of security, confidence, and

over all efficiency in a business.

• It helps in maintaining solvency of the business.

Disadvantages of working capital:

• Rate of return on investments also fall with the shortage

of working capital.

18

• Excess working capital may result into over all

inefficiency in organization.

• Excess working capital means idle funds which earn no

profits.

• Inadequate working capital cannot pay its short term

liabilities in time.

19

1.1 COMPANY PROFILESMIIEL (a unit of Motherson Sumi Systems Ltd.)

Located in Noida, India, SMIIEL (a unit of Motherson SumiSystems Ltd.) is a

commercial Tool Room supplying to a wide spectrum ofindustries. SMIEL-TD develops

small to medium size molds for a wide range of applicationswhich include, wiring

harness components, automotive applications, white goods,medical and electrical

equipment.

Product & Services of the company includes productdesigning, tool designing, tool

manufacturing, specialisation in high precision injectionmolding tools and press

stamping tools

Motherson Sumi Systems Limited is the flagship company of

the Samvardhana Motherson Group and was established in 1986.

It is a joint venture between Samvardhana Motherson Group

and Sumitomo Wiring Systems (Japan). SMIIEL is a focused,

dynamic and progressive company providing customers with

innovative and value-added products, services and solutions.

20

SMIIEL facility in Noida Sector 59

The Company is listed at the stock exchanges since 1993. The

acquisition of mirror business from Visiocorp (now renamed

as Samvardhana Motherson Reflectec) and Peguform (now named

Samvardhana Motherson Peguform) has helped SMIIEL evolve as

one of the world’s leading manufacturers of automotive rear

view mirrors and a leading manufacturers of instrument

panels, bumpers and door trims in Europe.

The company is one of the leading manufacturers of

automotive wiring harnesses and mirrors for passenger cars

in India. It is also a leading supplier of plastic

components and modules to the automotive industry. Over the

years SMIIEL has collaborated with global technology leaders

21

and has further leveraged its competency in existing areas

to create products fulfilling the technical needs of its

customers. SMIIEL and its joint ventures have invested in

state-of-the-art technologies and infrastructure to ensure

superior efficiencies & total customer satisfaction.

SMIIEL is strengthening its position as a globally preferred

solutions provider by offering end-to-end solutions

encompassing designing from basic data to prototyping,

tooling, moulding, assembly and integrated modules. The

ability to provide this end-to-end solution in each product

category and combine these solutions in the form of full

system solutions has enabled the Company to evolve as a

preferred supplier. These solutions are supported by the

flexibility to supply from any of the alternative

manufacturing bases and logistic models best suited to

customer requirements. .

SMIIEL has developed a network of manufacturing bases,

design centers, logistics centers, marketing support and

sourcing hubs across a diversified geographical base. SMIIEL

has presence in 25 countries which includes India (Noida ,

22

Gurgaon, Manesar, Faridabad , Pune, Bengaluru, Chennai,

Kandla, Pathredi, Tapukara, Lucknow & Puducherry), UAE., Sri

Lanka, Singapore, China, South Korea, Japan, Germany, UK.,

Czech Republic, Austria, Hungary, Italy, Spain, France,

Ireland, U.S.A, Mexico, South Africa, Australia, Mauritius,

Brazil, Portugal, Slovakia and Thailand to provide timely

and quality delivery to its customers worldwide. SMIIEL has

manufacturing bases across six continents - Asia, Europe,

North America, South America, Africa & Australia to support

its customers. SMIIEL’s diverse global customer base

comprises of almost all leading automobile manufacturers

globally.

The Samvardhana Motherson Group is a focused, dynamic and

progressive Group providing customers with value added

products, services and innovative solutions.

The Group has core competencies in manufacturing of

Electrical Distribution Systems (EDS), automotive rearview

mirrors and polymer processing. These competencies are

supported by specialization in engineering & design,

23

information technology, tool manufacturing and metal

machining.

Product Range

It has been SMIIEL’s endeavour to constantly add new

products in its product line with the objective of emerging

as a single-service interface for multiple customer needs.

The Company has collaborated with technology leaders in

their respective fields to bring relevant technologies for

the products required by its customers. SMIIEL’s diversity

of product range coupled with the depth within each product

portfolio, has helped the company garner leadership in its

area of operations.

The product range of the company along with its

subsidiaries and joint ventures includes:

Automotive Rear View Mirrors

Wiring Harnesses

Wires Grommets

24

Wiring Harness

Components

Seals

Tubes

Fuse Boxes

Injection Moulded Products

Blow Moulded Products

Liquid Silicone Rubber Moulded Components

Injection Moulding Tools

Extruded Rubber Products

Precision Machined Metal Components

Modules

IP/ Cockpit

Door Trims

Bumpers

Air intake

manifolds

Air filter

systems

HVAC Systems

Waste Recycling System

SMIIEL Wiring Harness Division

The wiring harness division of SMIIEL is one of the

25

largest manufacturers of wiring harnesses in India,

serving the entire cross-section of the automotive

industry. SMIIEL also supplies wiring harnesses to

Material Handling, Earth Moving and Farm Equipment, White

Goods & Electronics, Elevators, Office Automation and

Medical Equipment industries.

The Samvardhana Motherson Group is a focused, dynamic and

progressive Group providing customers with value added

products, services and innovative solutions.

The Group has a diversified product range to serve multiple

industries, with automotive industry being the main industry

served.

The Group business portfolio comprises electrical

distribution systems (wiring harnesses), automotive rearview

mirrors, polymer processing, injection moulding tools,

elastomer processing, modules and systems, machined metal

products, cutting tools, IT services, engineering & design,

CAE services, vehicle air conditioning systems, lighting

26

systems, cabins for off-highway vehicles, cutting tools and

thin film coating metals.

The Group has invested in technologies that provide

manufacturing support, including compressors, paint coating

equipment, auxiliary equipment for injection moulding

machines and automotive manufacturing engineering services.

Key Facts

One of the largest manufacturers of exterior rearview

mirrors in the world

One of the largest manufacturers of IP modules, door trims

and bumpers in Europe

One of the largest manufacturers in India for:

Wiring harnesses and rearview mirrors for passenger cars

Moulded components and modules

Cabins for large size dump trucks

Gear cutting tools.

27

CBN & PCD cutting tools.

Plastic air intake manifold.

Presence in 25 countries across the globe.

Group Turnover USD 5.4 billion approx. ( 2012-13)

Joint ventures in key technology areas.

Over 62, 000 qualified professionals.

28

History

1975

Motherson was founded

1977

First Cable factory started

1983

Technical agreement with Tokai

Electric Co. (Now Sumitomo Wiring

Systems - Japan) for Wiring Harness

1986

JV with Sumitomo Wiring

Systems Japan

1989

Injection Moulding

1992

Cutting Tool Manufacturing

29

1994

Tool Room for small and Medium

sized Moulds (upto 650 Tons)

1995

Cockpit Assemblies

Automotive Mirrors

1997

Blow Moulding

1998

Rubber Injection Moulding

1999

First Overseas office

established (Austria)

2000

IT and Design Company

Representetive Office at Singapore

2001

Liquid Silicon Rubber Injection

moulding

30

Machined Metal Components

2002

Wiring Harness manufacturing

at Sharjah

Design Centre at Ireland

2003

Offices in USA & UK established

Tool Room at Sharjah

2004

European Headquaters at Germany

Sheet Metal Die Design

2005

Injection Moulding & metal

Machining in Germany

JVs for

o Environment Management Systems

o Automotive Manufacturing

Engineering

Plastic Moulding & Metal Machining

at Germany

31

PVC Tube Manufacturing

2006

Wiring Harness Manufacturing in UK

Bus Airconditioning Systems

Auxiliary Equipment for Injection

moulding machines

Cabins for off road vehicles in

India

2007

Rubber parts Manufacturing

in Australia

JVs for

o HVAC Systems, Meterclusters,

Body Control Modules &

Compressors

o Bimetal BandSaws

o Thin Film coating metals

2008

JV for Lighting Systems, Pedal Box

Assembly & Air Intake manifolds

32

JV for Precision machined metal

components

2009

Visiocorp becomes a part of

Samvardhana Motherson Group and

renamed Samvardhana Motherson

Reflectec (SMR)

Gear cutting tool manufacturing

through a new venture Motherson

Advanced Tooling Solutions

Polymer Compounding

2010

JV for HVAC Systems for commercial

vehicles & Off highway vehicles

JV for Gear Cutting Tools

Freezers & Retail Refrigeration

2011

Peguform becomes a part of

Samvardhana Motherson Group

JV with Vacuform 2000 (Pty) Limited

for thermo formed polyethylene

33

components and blow moulded

components for automotive and other

applications.

2012

JV with Sintermetal S.A. to produce

sintered parts for suspension and

powertrain.

34

1.2 OBJECTIVES OF THE STUDY

The study areas for this Project include various

functions of Finance department. The main objectives

for the project are as follows:

To analyze the Working Capital of the Company and

also analyze its various determinants in the

Company.

To measure the size of Working Capital in a Power

Generating Company,

To determine the efficiency of Working Capital and

measure the Operational Efficiency of the Company.

35

LIMITATIONS OF THE STUDY

As each project has its own limits, I also face certain

constraints during my project. I tried my best to

overcome these limits but still certain boundaries

cannot be broken. Limitations of report are:

Before coming to this organization I had very

little knowledge of working capital management.

Though I have gone through extensive study, I must

admit that I had tried my best to give expert

comments on the topic.

Eight Weeks time was not sufficient to understand

the topic to the expertise level or I can say to

understand the topic in a comprehensive manner.

Hence this research report has a time constraint

with it.

The data, on which the whole report is based, is

comparison of three years i.e. 2010, 2011 and 2012

36

as it is difficult to compare lot of data in short

span of time.

This project report has been completed keeping in

mind the pocket limit.

The survey has been carried out in the corporate

office itself and not the manufacturing plants. So

the information about the inventory may be exact

or may be having some differences with actual

figures.

As information on core working capital is hard to

get and difficult to explain, it is based just on

the minimum inventory level. It might leave the

reader with his/her doubts.

Most of the report is based on the Secondary data using

financial ratios but still, one doubt give rise to some

other doubt, which is actually a major constraint in

every research project.

37

1.3 IMPORTANCE OF WORKING CAPITAL RATIOS

Ratio analysis can be used by financial executives to

check upon the efficiency with which working capital is

being used in the enterprise. The following are the

important ratios to measure the efficiency of working

capital. The following, easily calculated, ratios are

important measures of working capital utilization.

Formulae Result Interpretation

Stock

Turnove

r

(in

days)

Average

Stock *

365/

Cost of

Goods Sold

= x

days

On average, you turn over

the value of your entire

stock every x days. You may

need to break this down into

product groups for effective

stock management.

Obsolete stock, slow moving

lines will extend overall

38

stock turnover days. Faster

production, fewer product

lines, just in time ordering

will reduce average days.

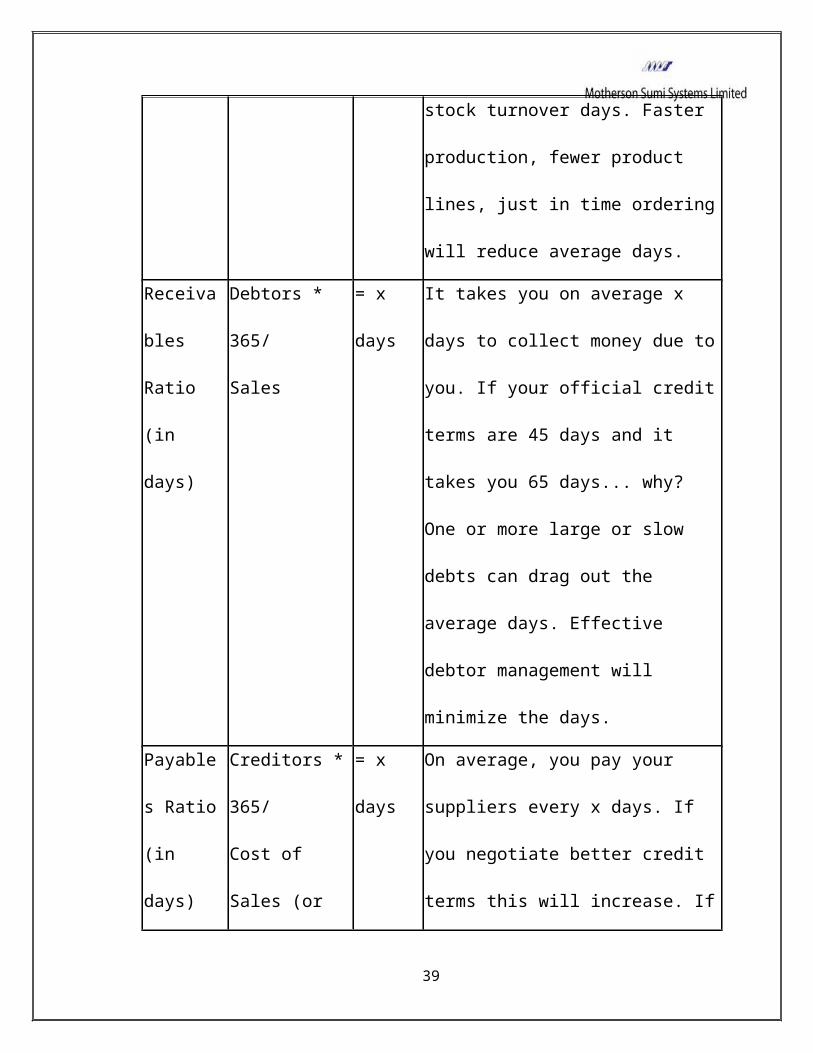

Receiva

bles

Ratio

(in

days)

Debtors *

365/

Sales

= x

days

It takes you on average x

days to collect money due to

you. If your official credit

terms are 45 days and it

takes you 65 days... why?

One or more large or slow

debts can drag out the

average days. Effective

debtor management will

minimize the days.

Payable

s Ratio

(in

days)

Creditors *

365/

Cost of

Sales (or

= x

days

On average, you pay your

suppliers every x days. If

you negotiate better credit

terms this will increase. If

39

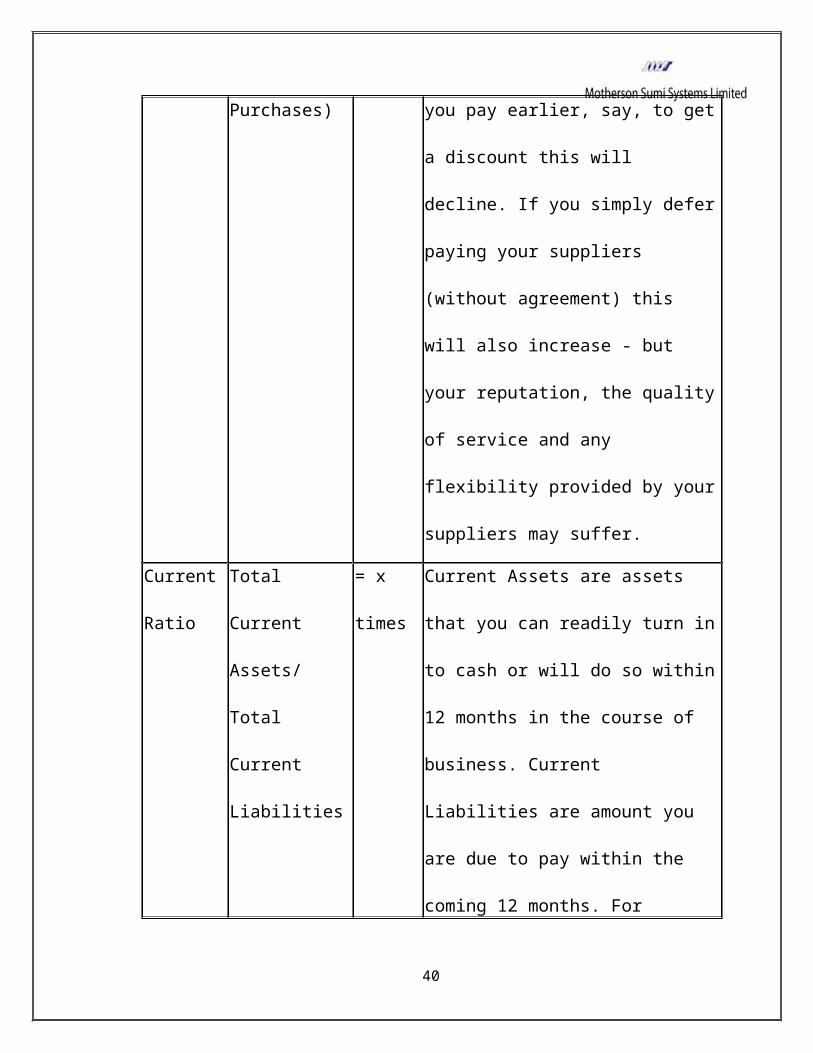

Purchases) you pay earlier, say, to get

a discount this will

decline. If you simply defer

paying your suppliers

(without agreement) this

will also increase - but

your reputation, the quality

of service and any

flexibility provided by your

suppliers may suffer.

Current

Ratio

Total

Current

Assets/

Total

Current

Liabilities

= x

times

Current Assets are assets

that you can readily turn in

to cash or will do so within

12 months in the course of

business. Current

Liabilities are amount you

are due to pay within the

coming 12 months. For

40

example, 1.5 times means

that you should be able to

lay your hands on $1.50 for

every $1.00 you owe. Less

than 1 times e.g. 0.75 means

that you could have

liquidity problems and be

under pressure to generate

sufficient cash to meet

oncoming demands.

Quick

Ratio

(Total

Current

Assets -

Inventory)/

Total

Current

Liabilities

= x

times

Similar to the Current Ratio

but takes account of the

fact that it may take time

to convert inventory into

cash.

Working (Inventory As % A high percentage means that

41

Capital

Ratio

+

Receivables

-

Payables)/

Sales

Sales working capital needs are

high relative to your sales.

LITERATURE REVIEWRELATIONSHIP B/W PERMANENT AND TEMPORARY WORKING CAPITAL

42

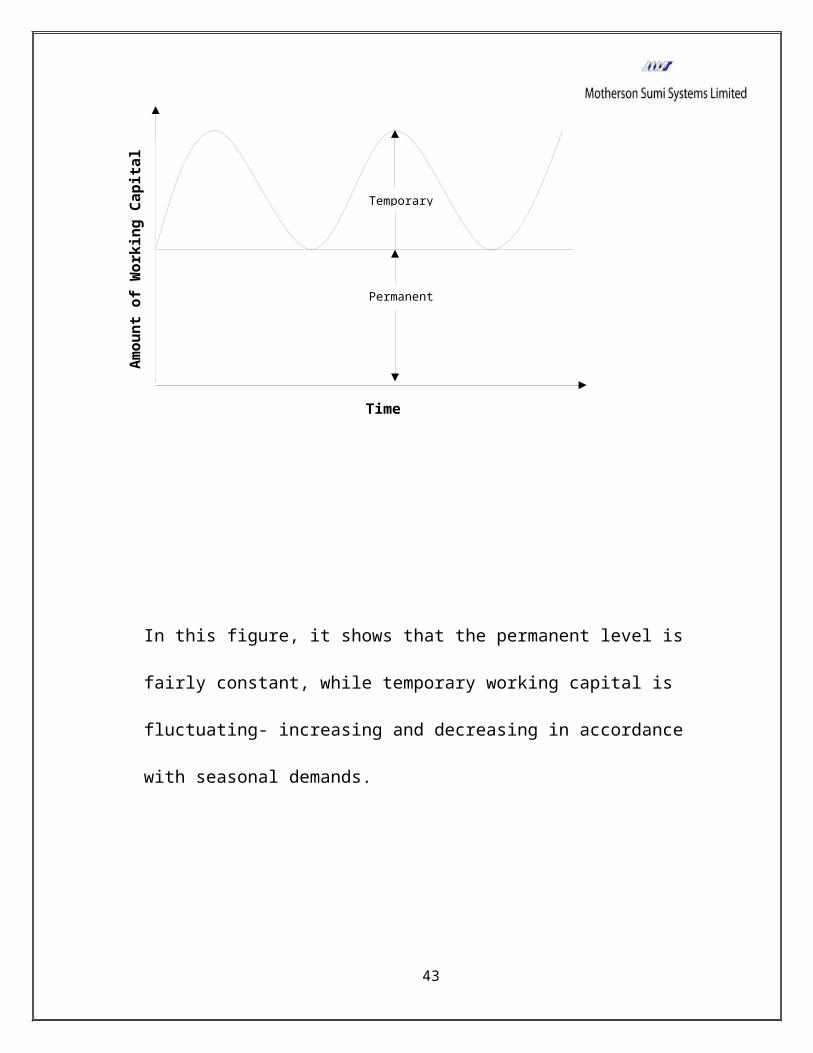

Permanent and Temporary Working Capital

In this figure, it shows that the permanent level is

fairly constant, while temporary working capital is

fluctuating- increasing and decreasing in accordance

with seasonal demands.

43

Temporary

Permanent

Amou

nt o

f Work

ing

Capita

l

Time

Temporary

Permanent

Tim

e

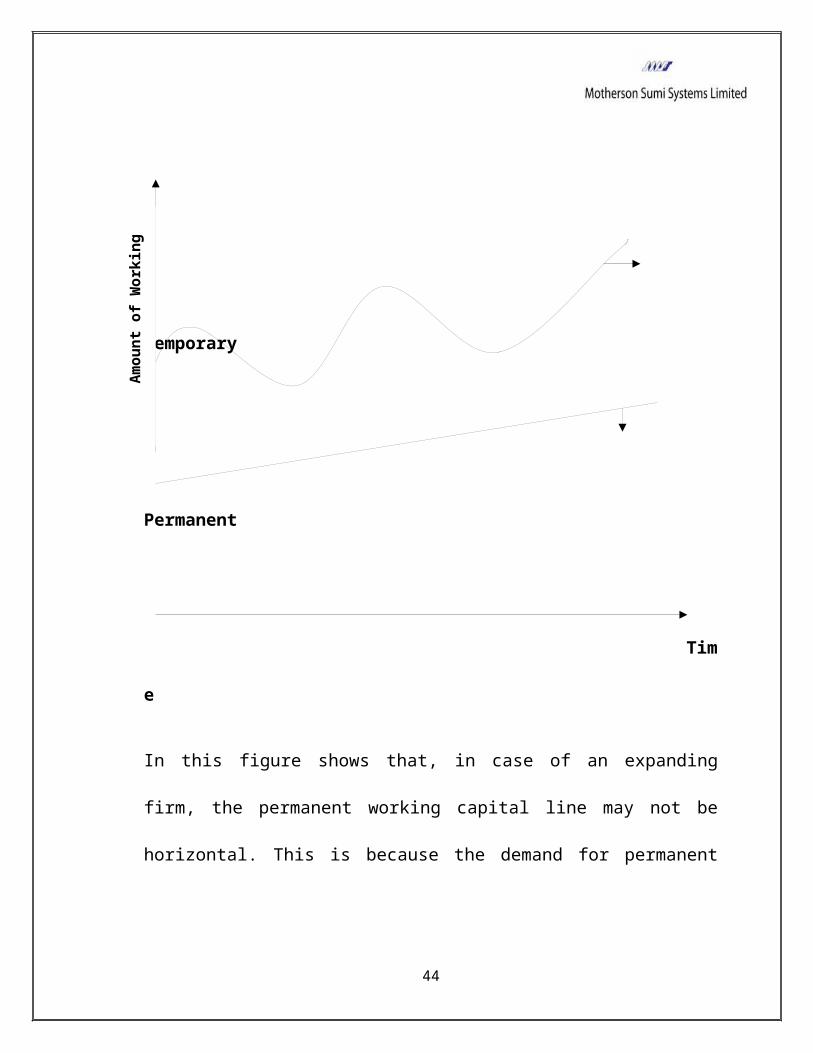

In this figure shows that, in case of an expanding

firm, the permanent working capital line may not be

horizontal. This is because the demand for permanent

44

Amou

nt o

f Work

ing

Capi

tal

current assets might be increasing or decreasing to

support a rising level of activity.

COMPONENTS OF WORKING CAPITAL

There are two components of working capital:

Current Assets: Current assets are those assets which

can be converted into cash in the normal course of

business within a short period say a maximum of one

year. They are also called floating or circulating

assets because they cannot be put to constant use. The

list of current assets is:

1. Cash in hand & Bank balances.

2. Bills Receivables.

3. Sundry Debtors.

4. Short term loans and advances.

5. Inventories of stocks

6. Prepaid expenses.

7. Accrued income.

45

Current Liabilities: Current Liabilities are those

liabilities which are intended to be paid in the

ordinary course of business within a short period of

normally one accounting year out of the current assets

or the income of the business. Example of current

liabilities is:

1. Bills Payable.

2. Sundry creditors or Accounts payable.

3. Accrued or outstanding Expenses.

4. Short term loans and advances and deposits.

5. Bank overdraft.

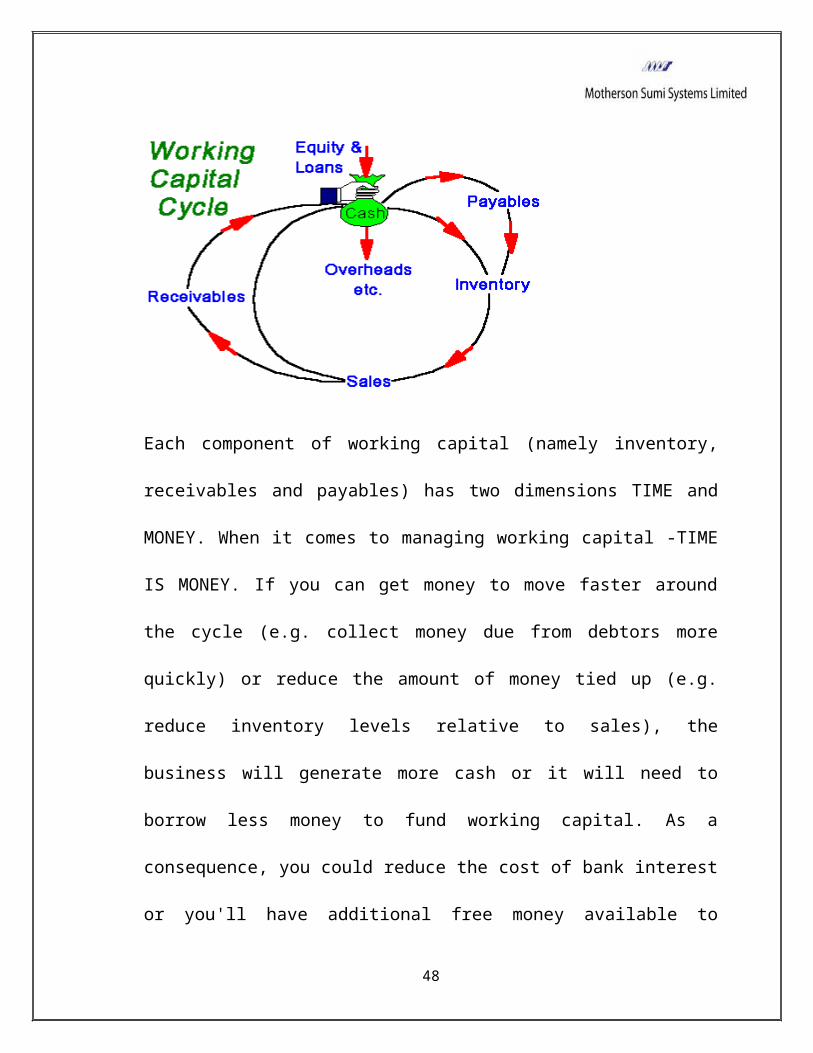

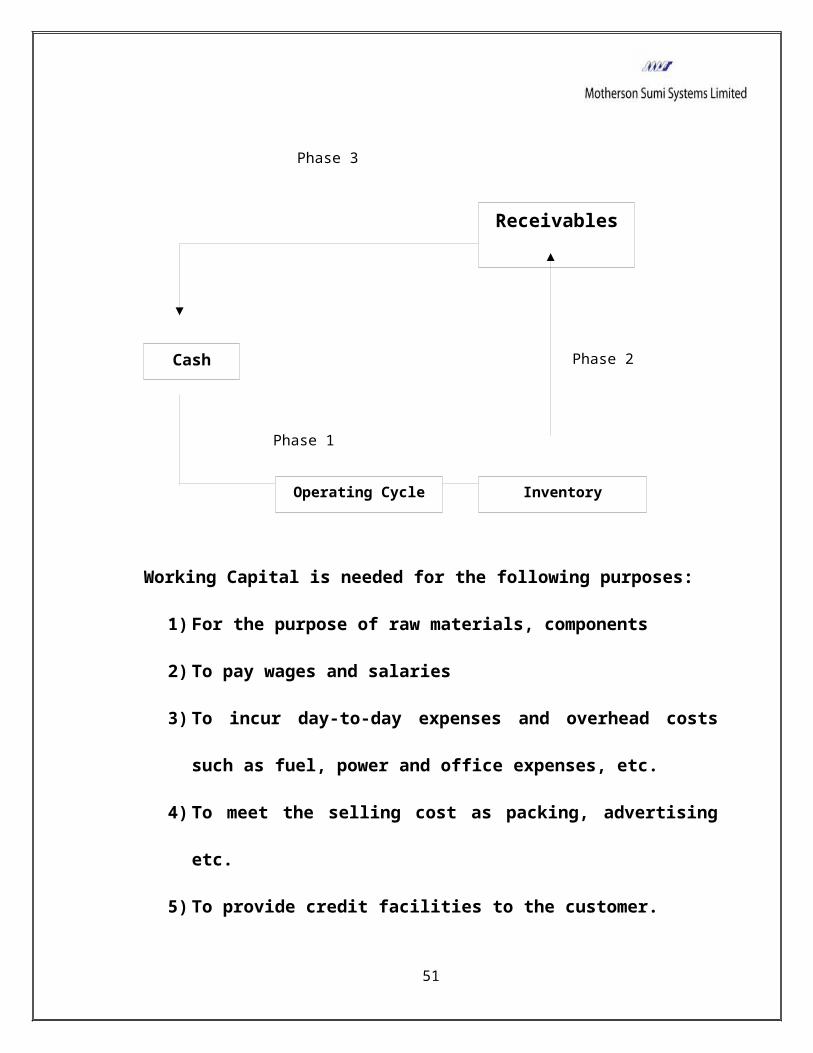

WORKING CAPITAL CYCLE

Cash flows in a cycle into, around and out of a

business. It is the business's life blood and every

manager's primary task is to help keep it flowing and

to use the cash flow to generate profits. If a business

is operating profitably, then it should, in theory,

46

generate cash surpluses. If it doesn't generate

surpluses, the business will eventually run out of cash

and expire.

The faster a business expands the more cash it will

need for working capital and investment. The cheapest

and best sources of cash exist as working capital right

within business. Good management of working capital

will generate cash will help to improve profits and

reduce risks. Bear in mind that the cost of providing

credit to customers and holding stocks can represent a

substantial proportion of a company's total profits.

There are two elements in the business cycle that

absorb cash - Inventory (stocks and work-in-progress)

and Receivables (debtors owing you money). The main

sources of cash are Payables (your creditors) and

Equity and Loans.

47

Each component of working capital (namely inventory,

receivables and payables) has two dimensions TIME and

MONEY. When it comes to managing working capital -TIME

IS MONEY. If you can get money to move faster around

the cycle (e.g. collect money due from debtors more

quickly) or reduce the amount of money tied up (e.g.

reduce inventory levels relative to sales), the

business will generate more cash or it will need to

borrow less money to fund working capital. As a

consequence, you could reduce the cost of bank interest

or you'll have additional free money available to

48

support additional sales growth or investment.

Similarly, if you can negotiate improved terms with

suppliers e.g. get longer credit or an increased credit

limit; you effectively create free finance to help fund

future sales.

More businesses fail for lack of cash than for want of

profit.

Need for Working Capital

A successful sales program is necessary for earning

profits by any business enterprise. However sales do

not convert into cash instantly; there is invariably a

time lag between the sale of goods and receipts of

cash.

A sufficient amount of working capital is necessary to

sustain sales activity. Technically this is referred to

as the operating or cash cycle.

49

The operating cycle can be said to at the heart of the

need for working capital.

50

Working Capital is needed for the following purposes:

1) For the purpose of raw materials, components

2) To pay wages and salaries

3) To incur day-to-day expenses and overhead costs

such as fuel, power and office expenses, etc.

4) To meet the selling cost as packing, advertising

etc.

5) To provide credit facilities to the customer.

51

Cash

Receivables

Inventory

Phase 1

Phase 2

Phase 3

Operating Cycle

6) To maintain the inventories of raw material, work-

in-progress and finished goods.

52

DETERMINANTS OF WORKING CAPITAL

General nature of business

The working capital requirements of an enterprise are

basically related to the conduct of the business. The

public utilities have certain features which have a

bearing on their working capital needs. The two

relevant features are:

1. The cash nature of the business that is cash

sales.

2. Sale of services rather than commodities.

At the other extreme are trading and financial

enterprises. The nature of their business is such that

they have to maintain a sufficient amount of cash,

inventories and book debts. The proportion of current

assets to total assets measures the relative

requirements of working capital of various industries.

Production Cycle

53

The term production cycle or manufacturing cycle refers

to time involved in the manufacture of goods. It covers

the time span between the procurement of raw materials

and the completion of the manufacturing process leading

to the production of finished goods. Funds have to be

necessarily tied up during the process manufacturing

necessitating enhanced working capital. In other words,

there is some time gap before raw material converts to

finished goods. To sustain such activities the need for

working capital is obvious. The longer the times span

(i.e. the production cycle), the larger will be the

tied up funds and, therefore, the larger is the working

capital needed and vice versa.

Business Cycle

The working capital requirements are also determined by

the nature of the business cycle. Business fluctuations

leading to cyclical and seasonal changes that, in turn,

cause a shift in the working capital position,

54

particularly for temporary working capital

requirements. The variations in business conditions may

be in two directions:-

1. Upswing phase when boom conditions prevail.

2. Downswing phase when economic activity is marked

by decline.

During the upswing of business activity, the need for

working capital is likely to grow to cover the lag

between increased sales and receipt of cash as well as

to finance purchases of additional material to cater to

the expansion of the level of activity. Additional

funds may be required to invest in plant and machinery

to meet the increased demand. The downswing phase of

business cycle has exactly an opposite effect on the

level of working capital requirement. The need for

working capital in recessionary conditions is bound to

decline. Thus business fluctuations influence the size

of working capital mainly through the effect on

55

inventories. The response of inventory to business

cycles is mild or violent according to nature of the

business policy.

Production Policy

In the case of certain business the demand for products

is seasonal, the production policy followed in such

case have two options open to such steady enterprises

are :-

Either they confine their production only to periods

when goods are purchased or they follow a steady

production policy throughout the year and produce goods

at a level to meet the peak demand. Working capital

planning has to incorporate this pattern of

requirements of funds when production and seasonal

sales are steady. The nature of some products may be

such that accumulation of inventories may create a

special risk and cost problems. For them, a production

policy in tune with the changing demands may be

56

preferable. Therefore, production policies have to be

formulated on the basis of individual setting of each

enterprise and the magnitude and dimension of the

working capital problems will accordingly vary.

Credit Policy

The credit policy influences the requirement of working

capital in two ways:-

1. Through credit terms granted by the company to its

customers/ buyers of goods.

2. Credit terms available to the company from its

creditors.

The credit terms granted to customers have a bearing on

the magnitude of working capital by determining the

level of book debts. The credit sales result in higher

book debts (receivables). Higher book debts mean more

working capital. The working capital requirements of a

business are, thus affected by the terms of purchase

57

and sale, and the role given to credit by a company in

its dealings with creditors and debtors.

The prevailing trade practices as well as changing

economic conditions affect credit terms fixed by an

enterprise. Adoption of rationalized credit policies

are a significant factor in determining the working

capital needs of an enterprise. A company that operates

in a highly competitive market to win and retain

customers may be forced to offer generous credit terms

to them. The investment in book debts will consequently

be of a higher order, necessitating large working

capital in another way. The degree of competition is,

therefore, an important factor influencing working

capital requirements.

Growth and Expansion

As a company grows its logical to expect that a larger

amount of working capital is required. It is difficult

to determine precisely the relationship between the

58

growth in volume of business of a company and the

increase in its working capital. The composition of

working capital in a growing company also shifts with

economic circumstances and corporate practices. The

critical fact, however, is that the need for planning

of working capital is, therefore, a continuing

necessity for a growing concern.

Vagaries in the Availability of Raw Material

There may be some materials, which cannot be procured

easily either because of their sources, are few or they

are irregular. To sustain smooth production, therefore,

the company might be compelled to purchase and stock

them far in excess of genuine production needs. This

will result in an excessive inventory of such

materials. Procurement of some essential raw materials

is difficult because of their sporadic supply. This

happens very often with raw materials that are in short

supply and are controlled to ensure equitable

59

distribution. The buyer has in such cases very limited

options as to the quantum and timing of procurement. It

may so happen that a bulk consignment may be available

but the company may be short of funds, while when

surplus funds are available the commodities may be in

short supply. This element of uncertainty would lead to

a relatively high level of working capital.

Profit Level

The level of profits earned differs from enterprise to

enterprise. The nature of the product, hold on the

market, quality of management and monopoly power would

by and large determine the profit earned by a company.

It can be generalized that a company dealing in a high

quality product, having a good marketing arrangement

and enjoying monopoly power in the market, is likely to

earn high profits and vice versa. Higher profit margin

would improve the prospects of generating more internal

funds thereby contributing to the working capital pool.

60

The net profit is a source of working capital to the

extent that it has been earned in cash. In practice,

the net cash inflows from operations cannot be

considered as cash available for use at the end of cash

cycle. Even as a company’s operations are in progress,

cash is used for augmenting stock, book debts and fixed

assets. It must, therefore be seen that cash generation

has been used for furthering the interest of the

enterprise. The availability of internal funds for

working capital requirements is determined not merely

by the profit margin but also by the manner of

appropriating profits. The availability of such funds

would depend upon the profits appropriations for

taxation, dividend, reserves and depreciations.

Level of taxes

The first appropriation out of profit is payment or

provision for tax. The amount of taxes to be paid is

determined by prevailing tax regulations. The

61

management has no discretion in this respect. Very

often taxes have to be paid in advance on the basis of

the profit of proceeding year. Tax liability is, in a

sense, short – term liability payable in cash. An

adequate provision for tax payments is, therefore an

important aspect of working capital planning. If tax

liability increases, it leads to an increase in the

requirement of working capital and vice versa. The

service of tax experts can be availed of to take

advantage of the various concessions and incentive

through avoidance as opposed to evasion of taxes. Tax

planning can, therefore, be said to be an integral part

of working capital planning.

Dividend Policy

Another appropriation out of profits that has a bearing

on working capital is dividend payment. The payment of

dividend consumes cash resources and thereby, affects

working capital to that extent. If the company does not

62

pay dividend but retains the profits, working capital

increases. A company should retain profits to preserve

cash resources and, at the same time, it must pay

dividends to satisfy the expectations of investors.

When profits are relatively small, the choice is

between retention and payment. There are wide

variations in industry practices as regards the

interrelationship between working capital requirements

and dividend payment. In some cases, shortage of

working capital has been a powerful reason for reducing

or even skipping dividends in cash. There are

occasions, on the other hand, when dividend payments

are continued in spite of inadequate earnings in a

particular year because of sound liquidity. Dividend

policy is thus, a significant element in determining

the level of working capital in an organization.

Depreciation Policy

63

Depreciation policy also exerts an influence on the

quantum of working capital. Depreciation charges do not

involve any cash outflows. The effect of depreciation

policy on working capital is, therefore, indirect.

Depreciation affects the tax liability and retention of

profits. Depreciation is allowable expenditure in

calculating net profits. Enhanced rates of depreciation

lower the profits and, therefore, the tax liability

and, thus more cash profits. Higher depreciation also

means lower disposable profits and, therefore, a

smaller dividend payment. Thus cash is preserved. If

current capital expenditure falls short of the

depreciation provision, the working capital position is

strengthened and there may be no need for short-term

borrowing. If on the other hand, the current capital

expenditure exceeds the depreciation provision; either

outside borrowing will have to be adapted to prevent

the working capital position from being adversely

64

affected. It is in these ways that depreciation policy

is relevant to the planning of working capital.

Price Level Changes

Changes in the price level also affect the requirements

of working capital. Rising prices necessitate the use

of more funds for maintaining an existing level of

activity. For the same level of current assets higher

cash outlay are required. The effect of rising prices

is that a higher amount of working capital is needed.

The implications of changing price levels on working

capital position vary from company to company depending

on the nature of its operations, it’s standing in the

market and other relevant considerations.

Operating Efficiency

The operating efficiency of the management is also an

important determinant of the level of working capital.

65

The management can contribute to a sound working

capital position through operating efficiency. Although

the management cannot control the rise in prices, it

can ensure the efficient utilization of resources by

eliminating waste, improving coordination, and a fuller

utilization of existing resources, and so on.

Efficiency of operations accelerates the pace of cash

cycle and improves the working capital turnover. It

releases the pressure on working capital by improving

profitability and improving the internal generation of

funds.

66

FACTORS AFFECTING WORKING CAPITAL MANAGEMENT

1) Nature and Size of Business:

The requirement of working capital of a firm is widely

related to the nature and size of business unit. For

example, trading and financial firms require a large

amount of investment in working capital but a

significantly smaller amount of investment in fixed

assets. Similarly, a service oriented firm, e.g.

transport or electricity generation, needs a modest

working capital requirement since it has a very short

operating cycle and sales are made on cash basis.

Moreover, the size of the firm is also important factor

because, smaller firm needs smaller amount of working

capital on the basis of its production activities and

vice-versa.

2) Length of Production cycle: The time taken to

convert raw material into finished product is

known as the production cycle. The level of

67

working capital depends upon the production cycle.

Longer the production cycle, more will be the need

for working funds in order to finance the current

assets during the prolonged manufacturing cycle

and vice-versa.

3) Seasonal Operation: If a firm is operating in

goods and services having seasonal fluctuation in

demand, then the working capital requirement will

also fluctuate with every change. In cold drink

factory, the demand will certainly be high during

summer season and therefore, more working capital

is required to maintain higher production.

4) Market Competitiveness: The market

competitiveness has an important bearing on the

working capital needs of a firm. In view of the

competitive conditions prevailing in the market,

the firm may have to offer liberal credit firm to

the customer resulting in hire debtors.

68

5) Credit Policy: The credit policy means the

totality of terms and conditions on which goods

are sold and purchased. A firm has to interact

with two types of credit policies at a time. For

example, a firm might be purchasing goods and

services on credit terms but selling goods only

for cash. The working capital requirement of this

firm will be lower than that of a firm which is

purchasing cash but has to sell on credit basis.

6) Supply Conditions: The time taken by supplier of

raw materials, goods etc after placing an order,

also determines the working capital requirements.

A goods a received as soon as or in a short period

after placing an order, then the purchaser will

not like to maintain a high level of inventory of

that goods and vice-versa.

7) Growth and Diversification of Business: Growth

and Diversification of business call for larger

69

volume of working fund. The need of increased

working capital does not follow the growth of

business operations but precedes it. Working

capital needs is in fact assessed in advance in

reference to the business plan.

8) Other Factors: For example, banking relation,

price level changes, operating efficiency,

taxation policy, dividend policy etc. also

influence the requirement of working capital.

IMPORTANCE OF ADEQUATE WORKING CAPITAL

1) Solvency of the Business: Adequate working capital

helps in maintaining solvency of the business by

providing uninterrupted flow of production.

2) Goodwill: Sufficient working capital enables a

business concern to make prompt payments and hence

helps in creating and maintaining goodwill.

3) Easy Loans: A concern having adequate working

capital, high solvency and goods credit standing

70

can arrange loans from banks and other financial

institutions on easy and favourable terms.

4) Cash Discount: Adequate working capital also

enables a concern to avail cash discounts on the

purchases and hence it reduces the cost.

5) Regular supply of raw material: Sufficient working

capital ensures regular supply of raw materials

and continuous production.

6) Ability to face crises: Adequate working capital

enables a concern to face business crises in

emergencies, such as, depression because during

such period, generally, there is much pressure on

working capital.

7) High morale: Adequacy of working capital creates

and environment of security, confidence, high

morale and creates overall efficiency in a

business.

IMPACT/HARM OF REDUNDANT OR EXCESSIVE WORKING CAPITAL

71

* Excessive WC means idle funds, which earn no profits

for the business, cannot earn proper rate of return on

its investment.

* When there is a redundant WC, it may lead to

unnecessary purchasing and accumulation of inventories

causing more chances if theft, waste and losses.

* Excessive WC implies excessive debtors and defective

credit policy, which may cause higher incidences of bad

debts.

* It may result into overall inefficiency in the

organizations.

* When there is excessive WC relation with banks and

other financial institutions may not be maintained.

* The redundant WC gives rise to speculative

transaction.

72

* Due to low rate of return on investments the value of

shares may also fall.

* In case of redundant WC there is always a chance of

financing long terms assets from short terms funds,

which is very harmful in long run for any organization.

DANGER OF SHORT OR INADEQUATE WORKING CAPITAL

*A concern, which had inadequate WC, cannot pay its

short-term liabilities in time. Thus it will lose its

reputation and should be not be able to get good credit

facilities.

* It cannot buy its requirements in bulk and cannot

avail discounts. It stagnates growth.

73

* It becomes difficult for the firms to exploit

favourable market conditions and undertake profitable

projects due to non-availability of WC funds.

* The firm cannot pay day-to-day expenses of its

operations and its credit inefficiencies, increases

cost and reduces the profits of the business.

* It becomes impossible to utilize efficiently the

fixed assets due to non-availability of liquid funds

thus, the firm’s profitability would deteriorate.

* The rate of return on investments also falls with the

shortage of WC.

* Operating inefficiency creeps in and it will become

difficult to implement operating plans and achieve the

firms profit targets.

74

FACTORS REQUIRING CONSIDERATION WHILE ESTIMATING

WORKING CAPITAL

The average credit period expected to be allowed

by suppliers.

Total costs incurred on material, wages.

The length of time for which raw material are to

remain in stores before they are issued for

production.

The length of the production cycle (or) work in

progress.

The length of sales cycle during which finished

goods are to be kept waiting for sales.

The average period of credit allowed to customers.

The amount of cash required to make advance

payment.

75

RESEARCH METHODOLOGY

The study is conducted based on secondary data sources.

Secondary sources of data mainly include annual reports

of SMIIEL. Statement of changes in working capital for

the past 5 years is done using the data taken from

these financial reports. Similarly time series analysis

of operating cycle and calculations of ratios is done.

Apart from this, the website of SMIIEL. is referred

to know the services, services facilities, network etc.

Industry analysis is done based on the information

76

gathered from newspapers and websites of Indian steel

ministry & other sector related websites.

WORKING CAPITAL ANALYSIS

The basic goal of Working Capital Management is to

manage the current assets and current liabilities of a

firm in such a way that the level of Working Capital is

77

neither inadequate nor excessive as both the situations

are bad for any firm. There should be no shortage of

funds and also no working capital should be idle.

Working Capital Management policies have a great impact

on the profitability, liquidity and structural health

of the firm. So working capital management can be seen

as three dimensional in nature as it is concerned with-

1. Formulation of Policies with reference to

profitability, liquidity and risk.

2. Decisions about the composition and level of

current assets.

3. Decisions about the composition and level of

current liabilities

Working Capital Analysis: Adequate amount of working

capital is very much essential for the smooth running

of any business. It directly affects the liquidity

positions of the firm. Hence it is necessary to

78

evaluate the efficiency with which the working capital

is employed in the business. This can be achieved by

carrying out the Working Capital Analysis.

The analysis of working capital can be conducted

through a number of devices such as:

1. Ratio Analysis

2. Funds Flow Analysis

3. Budgeting

Ratio Analysis: A ratio is a simple arithmetical

expression one number to another. The technique of

ratio analysis can be employed for measuring short-term

liquidity or working capital position of a firm. The

following ratios can be calculated for the purpose of

(a) Liquidity Ratios and (b) Current Assets movements

Ratios

79

Fund Flow Analysis: Fund flow analysis is a technical

device designated to study the sources from which

additional funds were derived and the use to which

these sources were put. The fund flow analysis consists

of (a) Preparing schedule of changes of working capital

and (b) Statement of sources and application of funds.

It is an effective management tool to study the changes

in financial position (working capital) business

enterprise between beginning and ending of the

financial dates.

Working Capital Budget: A budget is a financial or

quantitative expression of business plans and policies

to be pursued in the future time period. Working

Capital budget as a part of the total budgeting process

of a business is prepared estimating future long term

and short term working capital needs and sources to

finance them, and then comparing the budgeted figures

with actual performance for calculating the variances,

80

if any, so that corrective actions may be taken in

future. The objective of working capital budget is to

ensure availability of funds as and when needed, and to

ensure effective utilization of these resources.

Analysis of Short Term Financial Position of the Firm

(Ratio Analysis):

1. Liquidity Ratio: Liquidity refers to the ability of

a firm to meet its current obligations as and when

these become due. The short-term obligations are

met by realizing amount from current, floating or

circulating assts. The

current assets should either be liquid or near about

liquidity. These should

be convertible in cash for paying obligations of

short-term nature. The sufficiency or insufficiency of

current assets should be assessed by comparing

them with short-term liabilities. If current assets can

pay off the current81

liabilities then the liquidity position is

satisfactory. On the other hand, if the

current liabilities cannot be met out of the current

assets, then the liquidity

position is bad. To measure the liquidity of a firm,

the following ratios can be

calculated:

a) Current Ratio

b) Quick Ratio

c) Absolute Liquid Ratio

2. Efficiency Ratio or Current Asset Movement Ratio:

Funds are invested in various assets in business to

make sales and earn profits. The efficiency with which

assets are managed directly affects- the volume of

82

sales. The better the management of assets, larger is

the amount of sales and profits. Current assets

movement ratios measure the efficiency with which a

firm manages its resources. These ratios are called

turnover ratios because they indicate the speed with

which assets are converted or turned over into sales.

Depending upon the purpose, a number of turnover ratios

can be calculated. Some are -

a) Working capital Turnover Ratio

b) Debtors Turnover Ratio

c) Average Collection Period

83

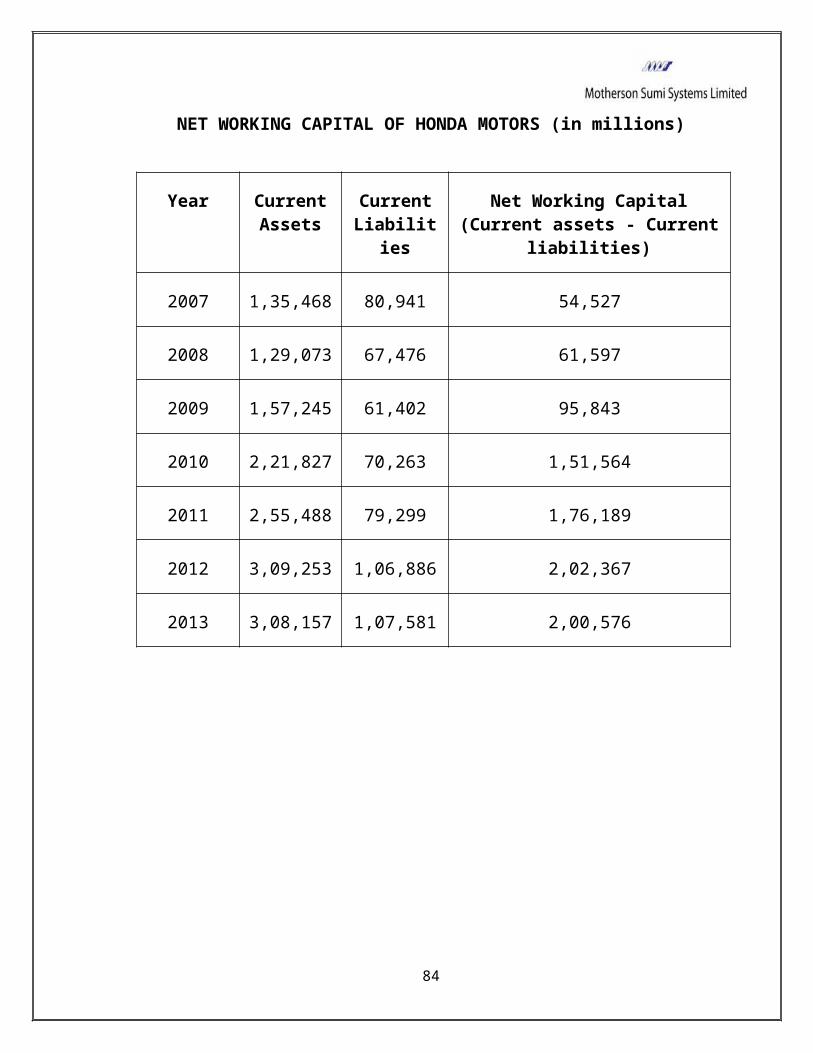

NET WORKING CAPITAL OF HONDA MOTORS (in millions)

Year CurrentAssets

CurrentLiabilit

ies

Net Working Capital(Current assets - Current

liabilities)

2007 1,35,468 80,941 54,527

2008 1,29,073 67,476 61,597

2009 1,57,245 61,402 95,843

2010 2,21,827 70,263 1,51,564

2011 2,55,488 79,299 1,76,189

2012 3,09,253 1,06,886 2,02,367

2013 3,08,157 1,07,581 2,00,576

84

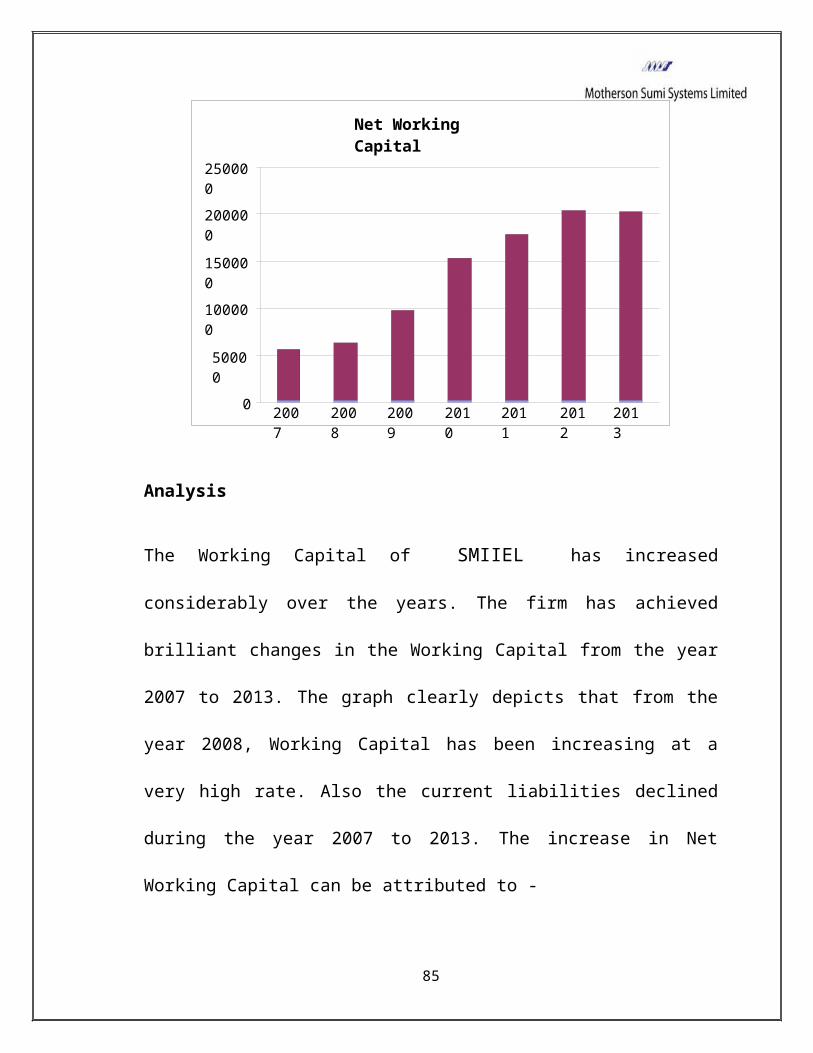

Net Working Capital

2007

2008

2009

2010

2011

2012

2013

0

50000

100000

150000

200000

250000

Analysis

The Working Capital of SMIIEL has increased

considerably over the years. The firm has achieved

brilliant changes in the Working Capital from the year

2007 to 2013. The graph clearly depicts that from the

year 2008, Working Capital has been increasing at a

very high rate. Also the current liabilities declined

during the year 2007 to 2013. The increase in Net

Working Capital can be attributed to -

85

Increase in inventory such as Components and Spare

Parts, Fuel Oil, Stock of Coal, Chemical and

Consumables etc.

Increase in cash and bank balance (which include

increase in current account and term deposit

account)

Overall increase in Debtors

Increase in loan and advances

86

CURRENT RATIO

Current Ratio is a measure of general liquidity and it

is most widely used to make the analysis of short term

financial position or liquidity of a firm. I shows the

ability of a firm to meet its short term obligations.

Current ratio is given by

Current Ratio = Current Assets/Current Liabilities

Current Assets include cash, marketable securities,

bill receivables, sundry datas, inventories and work in

progress. Current liabilities include outstanding

expenses, bills payable, dividend payable etc.

A relatively high current ratio is an indication that

the firm is liquid and has the ability to pay its

current obligations in time. On the other hand, a low

current ration represents that the liquidity position

of the firm is not good and the firm shall not be able

to pay its current liabilities in time. A Ratio equal87

or near to the Rule of Thumb of 2:1 that is current

assets double the current liabilities is considered to

be satisfactory.

88

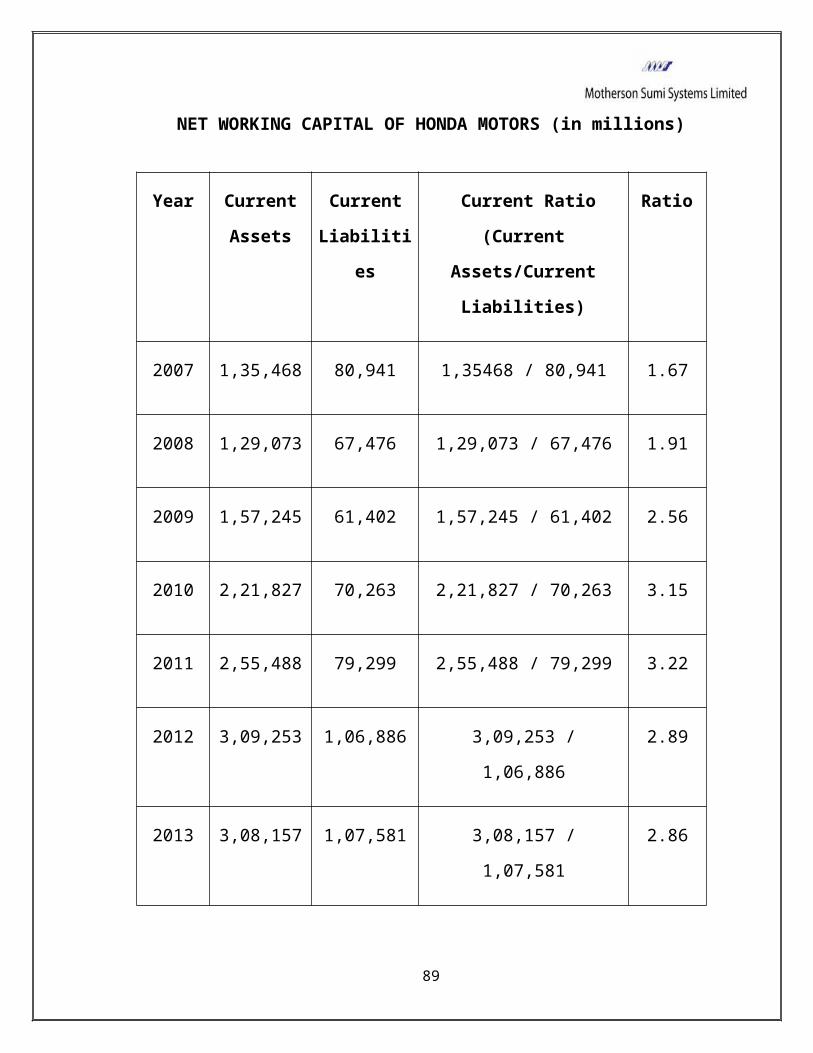

NET WORKING CAPITAL OF HONDA MOTORS (in millions)

Year Current

Assets

Current

Liabiliti

es

Current Ratio

(Current

Assets/Current

Liabilities)

Ratio

2007 1,35,468 80,941 1,35468 / 80,941 1.67

2008 1,29,073 67,476 1,29,073 / 67,476 1.91

2009 1,57,245 61,402 1,57,245 / 61,402 2.56

2010 2,21,827 70,263 2,21,827 / 70,263 3.15

2011 2,55,488 79,299 2,55,488 / 79,299 3.22

2012 3,09,253 1,06,886 3,09,253 /

1,06,886

2.89

2013 3,08,157 1,07,581 3,08,157 /

1,07,581

2.86

89

Current Ratio

2013

2012

2011

2010

2009

2008

2007

0

0.5

1

1.5

2

2.5

3

3.5

Analysis:

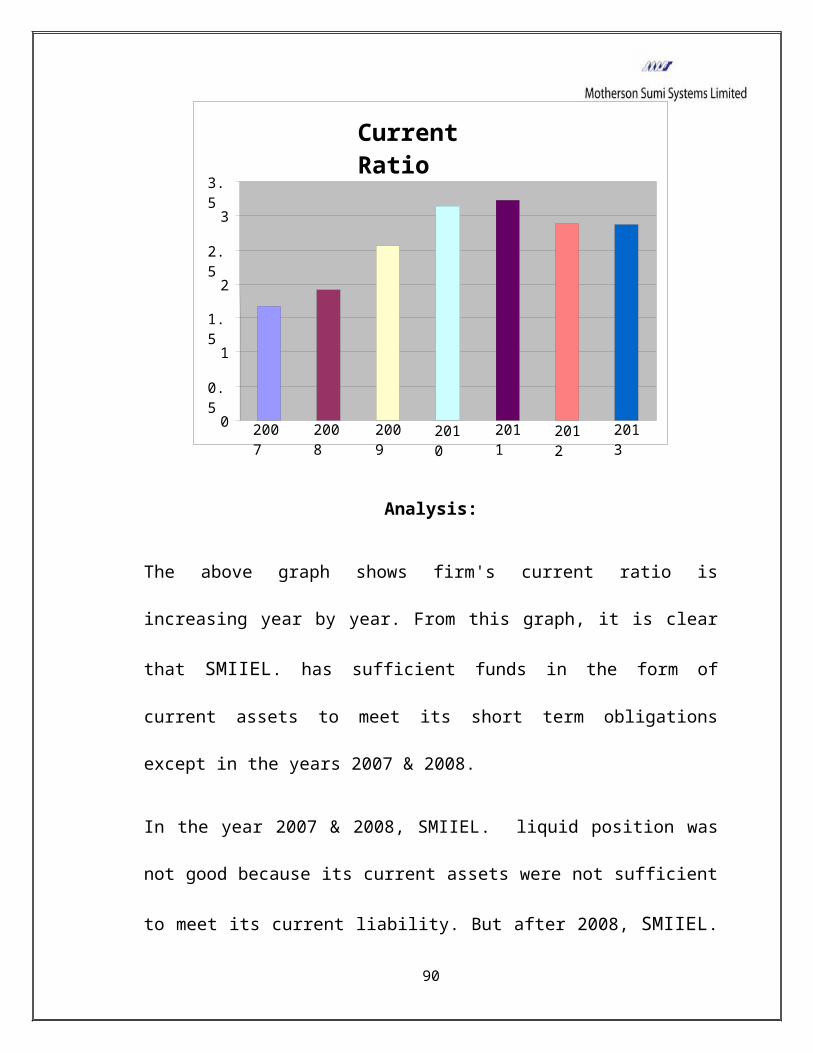

The above graph shows firm's current ratio is

increasing year by year. From this graph, it is clear

that SMIIEL. has sufficient funds in the form of

current assets to meet its short term obligations

except in the years 2007 & 2008.

In the year 2007 & 2008, SMIIEL. liquid position was

not good because its current assets were not sufficient

to meet its current liability. But after 2008, SMIIEL.

90

position got stronger to meet its current obligation.

The reason for increase in current ratio is increase in

current assets. The current asset is increasing every

year at a higher rate after 2008. The reasons are:

1) Increase in Fuel Oil, Spare Parts and Naphtha in

inventory.

2) Increase in unsecured debts and other debts in

sundry debtors.

3) Increase in Cash balance of Term Deposit account

of the firm..

4) Increase the advances and deposits with customer

in loan & advances.

5) Increase in creditors both for capital expenditure

and for goods & services.

6) Increase in Bond and term loan in current

liability.

91

92

QUICK RATIO:

Quick Ratio is a more rigorous test of liquidity than

current ratio. Quick Ratio may be defined as the

relationship between Quick/Liquid assets and Current or

Liquid liabilities. An asset is set to be liquid, if it

can be converted into cash within a short period

without loss of value. It measures the firm's capacity

to pay off the current obligations immediately.

Quick Ratio = Quick Assets/Current Liabilities

Quick Assets includes marketable securities, cash in

hand, cash in bank and debtors. As a Rule of

Thumb, ratio 1:1 is considered satisfactory. It is

generally thought that if quick assets are equal to

current liabilities, then the concern may be able

to meet its short term obligations. However, a firm

having high quick ratio may not have a

93

satisfactory liquidity position, if it has slow paying

debtors.

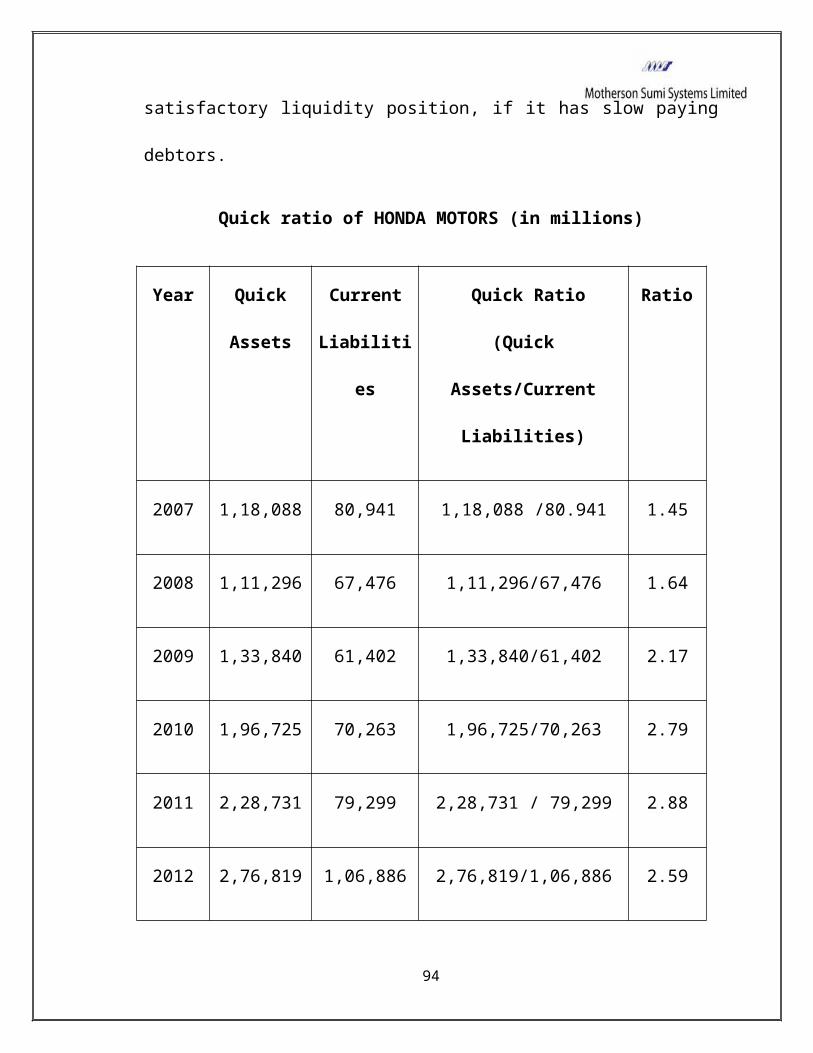

Quick ratio of HONDA MOTORS (in millions)

Year Quick

Assets

Current

Liabiliti

es

Quick Ratio

(Quick

Assets/Current

Liabilities)

Ratio

2007 1,18,088 80,941 1,18,088 /80.941 1.45

2008 1,11,296 67,476 1,11,296/67,476 1.64

2009 1,33,840 61,402 1,33,840/61,402 2.17

2010 1,96,725 70,263 1,96,725/70,263 2.79

2011 2,28,731 79,299 2,28,731 / 79,299 2.88

2012 2,76,819 1,06,886 2,76,819/1,06,886 2.59

94

Quick Ratio

2013

2012

2011

2010

2009

2008

2007

0

0.5

1

1.5

2

2.5

3

3.5

2013 2,74,680 1,07,581 2,74,680/1,07,581 2.55

Analysis:

From this graph, it is seen that the firm’s quick ratio

is very sound. From the beginning i.e. 2007 to 2013,

SMIIEL. has a good liquidity position. In the year

2009 and 2010, it is very high which is 2.8 and 2.88,

95

but after that it has decreased, the reason for which

are:

Increase in Cash & Bank balance of SMIIEL.

Increase in Loan & Advances

Overall there is increase in debtors

Overall there is increase in current liabilities

96

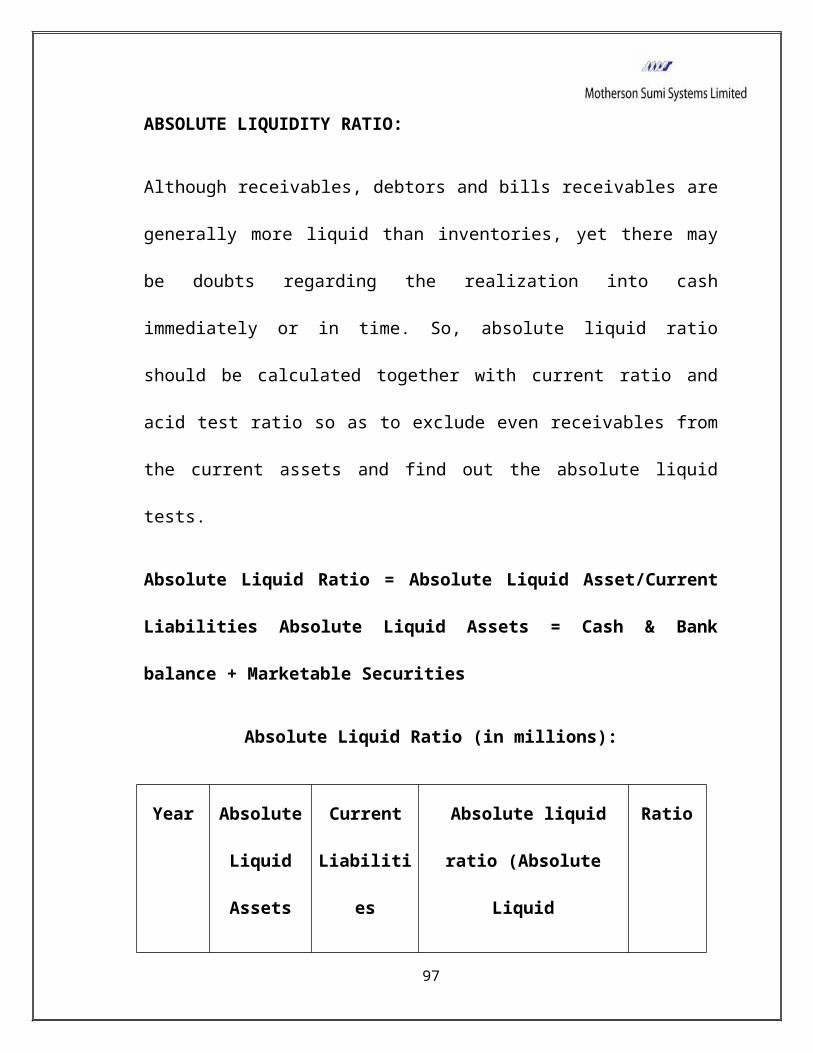

ABSOLUTE LIQUIDITY RATIO:

Although receivables, debtors and bills receivables are

generally more liquid than inventories, yet there may

be doubts regarding the realization into cash

immediately or in time. So, absolute liquid ratio

should be calculated together with current ratio and

acid test ratio so as to exclude even receivables from

the current assets and find out the absolute liquid

tests.

Absolute Liquid Ratio = Absolute Liquid Asset/Current

Liabilities Absolute Liquid Assets = Cash & Bank

balance + Marketable Securities

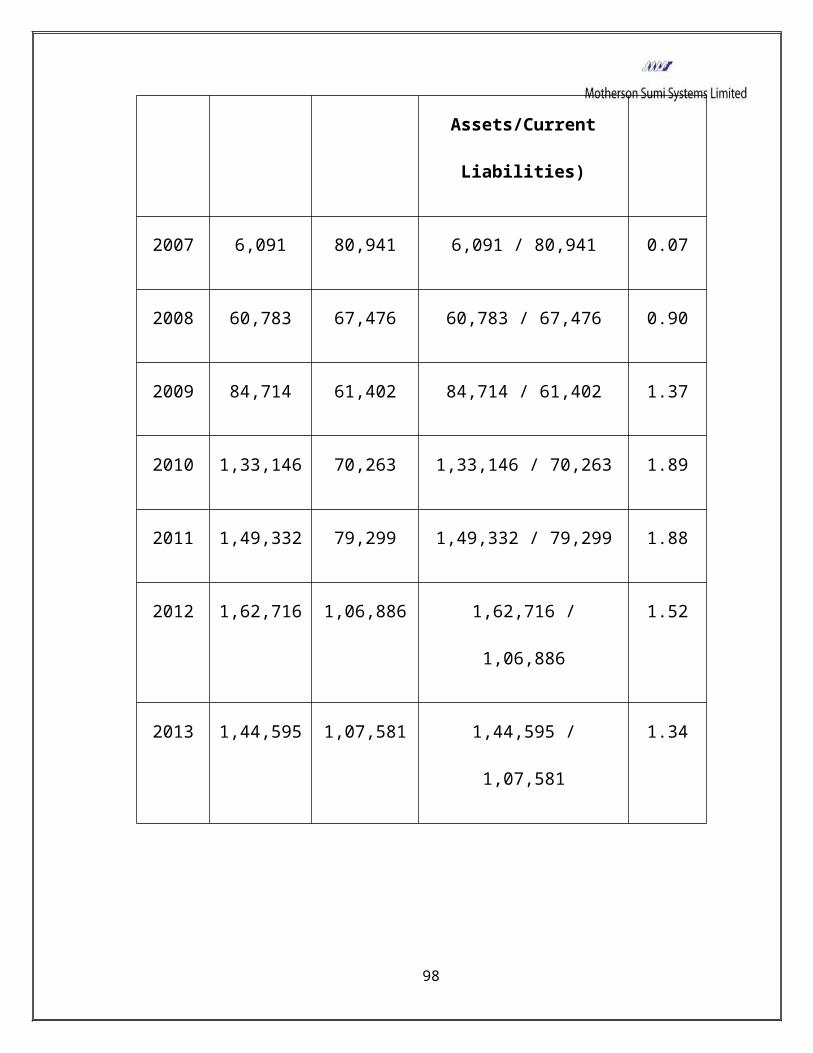

Absolute Liquid Ratio (in millions):

Year Absolute

Liquid

Assets

Current

Liabiliti

es

Absolute liquid

ratio (Absolute

Liquid

Ratio

97

Assets/Current

Liabilities)

2007 6,091 80,941 6,091 / 80,941 0.07

2008 60,783 67,476 60,783 / 67,476 0.90

2009 84,714 61,402 84,714 / 61,402 1.37

2010 1,33,146 70,263 1,33,146 / 70,263 1.89

2011 1,49,332 79,299 1,49,332 / 79,299 1.88

2012 1,62,716 1,06,886 1,62,716 /

1,06,886

1.52

2013 1,44,595 1,07,581 1,44,595 /

1,07,581

1.34

98

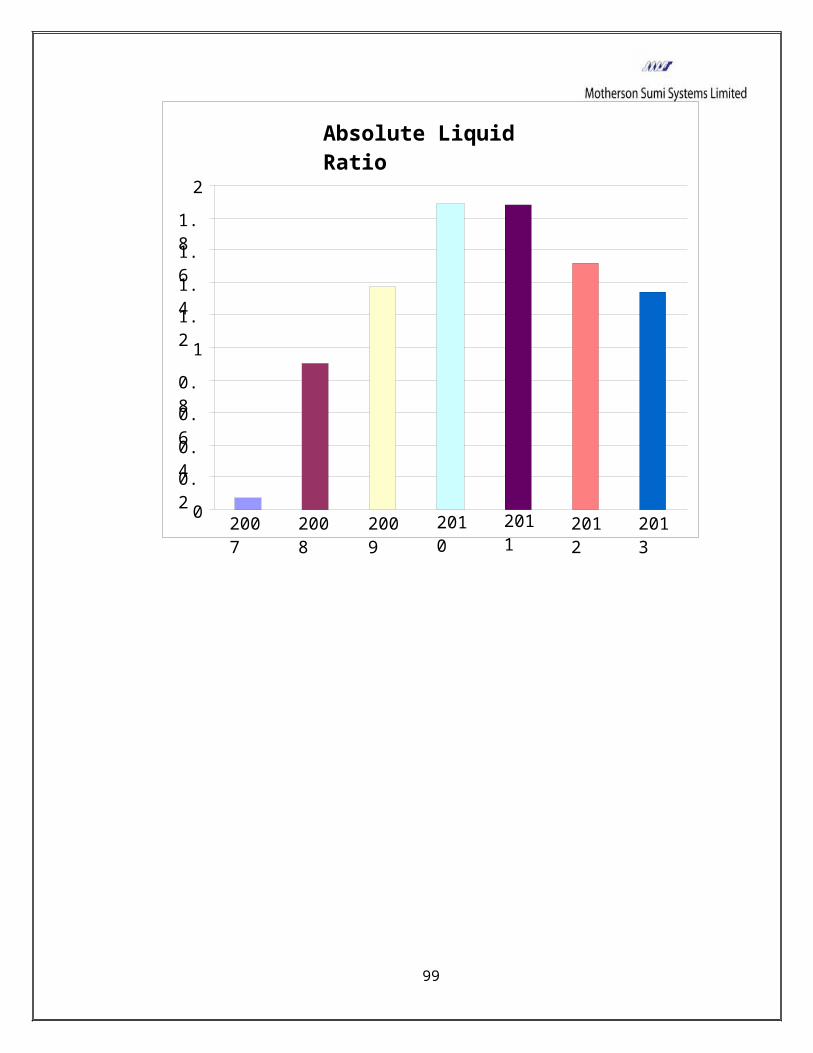

Absolute Liquid Ratio

2013

2012

2011

2010

2009

2008

2007

00.2

0.4

0.6

0.8

11.2

1.4

1.6

1.8

2

99

Analysis:

From this graph, it is seen that the firm has

sufficient cash balance to meet its current obligations

except in the year 2007. In the year 2007, the firm's

ratio was 0.07 which was very low. In 2010 & 2011,

after that the firm has achieved a very strong cash

balance to meet its obligations but we can see that the

ratio decreased in 2012 & 2013. The main reason for

this decrease can be attributed to increase in cash &

bank balance at a very high rate with a subsequent

increase in current liabilities.

100

101

CURRENT WORKING CAPITAL TURN-OVER RATIO:

Working Capital Turn-Over ratio indicates the pace of

utilization of Net Working Capital. This ratio measures

the efficiency with which the Working capital is used

by the firm. A high ratio indicates efficient

utilization of working capital and a low ratio

indicates otherwise. But a very high WCTR is not good

situation for any firm.

WCTR = Net Sales/Net Working Capital

DEBTOR TURN-OVER RATIO

Debtor turnover ratio indicates the pace of debt

collection of firm. A high debtor turnover ratio

indicates the efficient management of debtor or more

liquidity is the debtor. Similarly low debtor's

turnover ratio implies inefficient management of debtor

and less liquidity debtor. There is no rule of thumb

102

for an ideal debtor turnover ratio. It varies from firm

to firm.

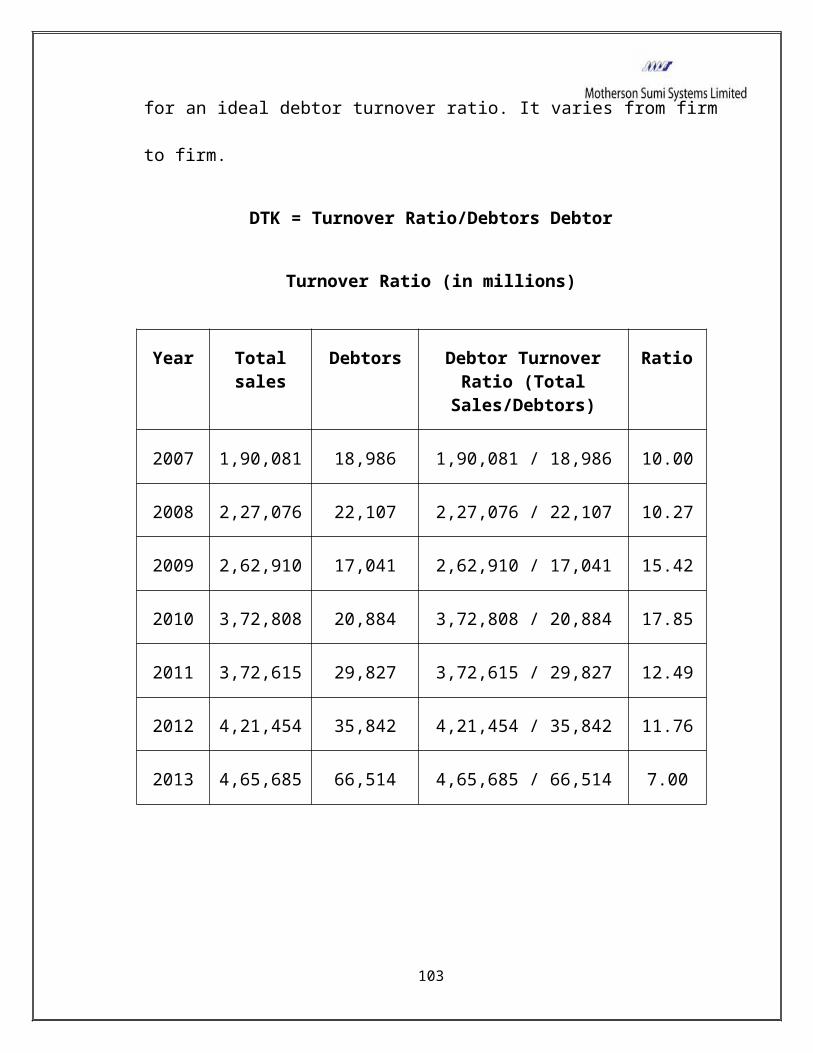

DTK = Turnover Ratio/Debtors Debtor

Turnover Ratio (in millions)

Year Totalsales

Debtors Debtor TurnoverRatio (Total

Sales/Debtors)

Ratio

2007 1,90,081 18,986 1,90,081 / 18,986 10.00

2008 2,27,076 22,107 2,27,076 / 22,107 10.27

2009 2,62,910 17,041 2,62,910 / 17,041 15.42

2010 3,72,808 20,884 3,72,808 / 20,884 17.85

2011 3,72,615 29,827 3,72,615 / 29,827 12.49

2012 4,21,454 35,842 4,21,454 / 35,842 11.76

2013 4,65,685 66,514 4,65,685 / 66,514 7.00

103

Debtor Turnover Ratio

2013

2012

2011

2010

2009

2008

2007

0246810

12

14

16

18

20

Analysis :

It is seen from the graph that the debtor turnover

ratio of the firm has grown in the period from 2007 to

2010. It shows the firms efficient management of debts.

The reasons for increase in debtor turnover ratio is-

1) Increase in Sales activity

2) Liberal Credit Policy by the firm

104

But after that firm's debtor turnover ratio has

declined. The reasons for the same could be -

1) Increase in sales at a lower rate

2) Restricted Credit Policy by the firm

105

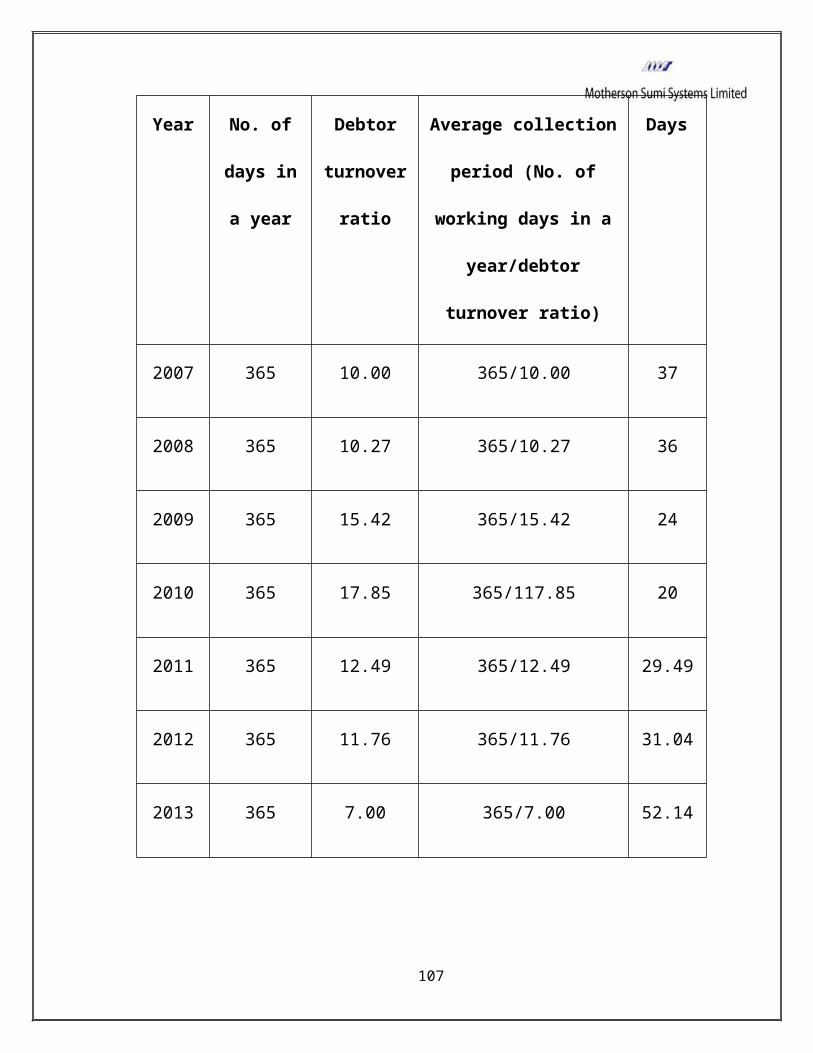

AVERAGE COLLECTION PERIOD

Average collection period represents the average number

of days, the firm has to wait before its receivable are

converted in to cash. It measures the quality of

debtor. Generally shorter the average collection period

the better is quality of debtor. Similarly the higher

collection period implies inefficient collection

performance which in turn adversely affects the

liquidity or short term paying capacity of the firms

out of its current liability.

Also, longer the average collection period, there are

more chances of bad debt. Though there is no rule of

thumb for the average collection period, it is

generally given 2 to 3 months. It also varies from firm

to firm.

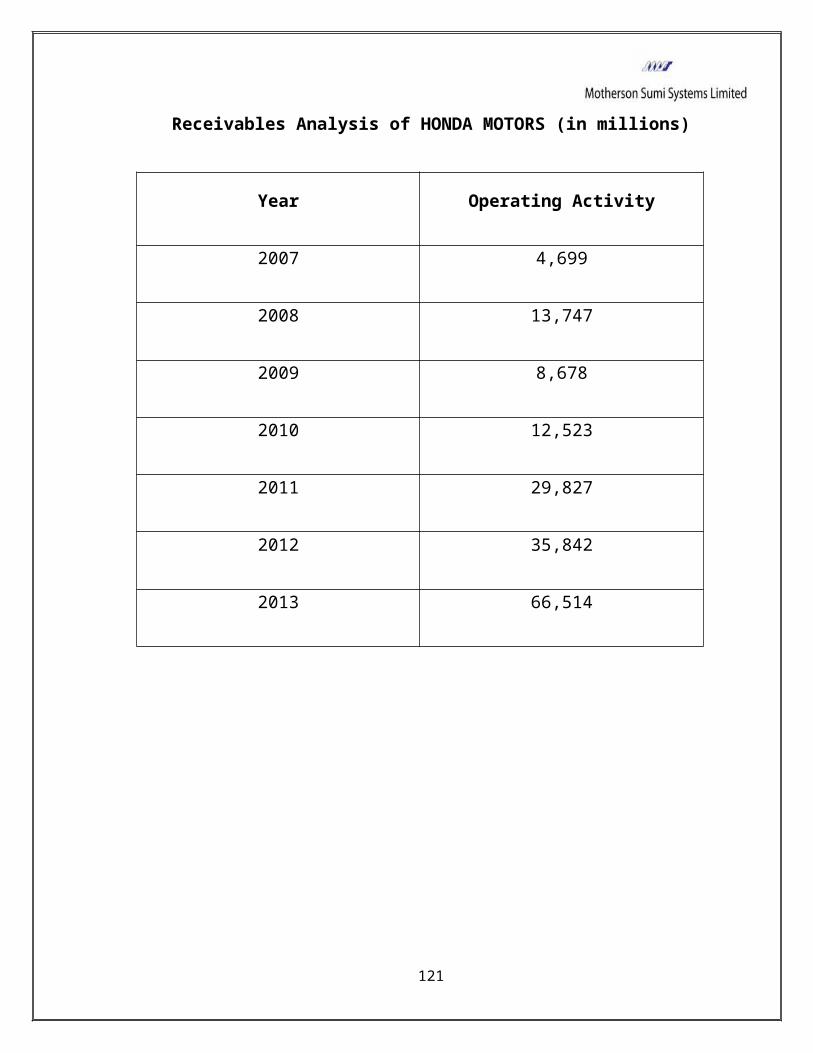

Average Collection Period of HONDA MOTORS (in millions)

106

Year No. of

days in

a year

Debtor

turnover

ratio

Average collection

period (No. of

working days in a

year/debtor

turnover ratio)

Days

2007 365 10.00 365/10.00 37

2008 365 10.27 365/10.27 36

2009 365 15.42 365/15.42 24

2010 365 17.85 365/117.85 20

2011 365 12.49 365/12.49 29.49

2012 365 11.76 365/11.76 31.04

2013 365 7.00 365/7.00 52.14

107

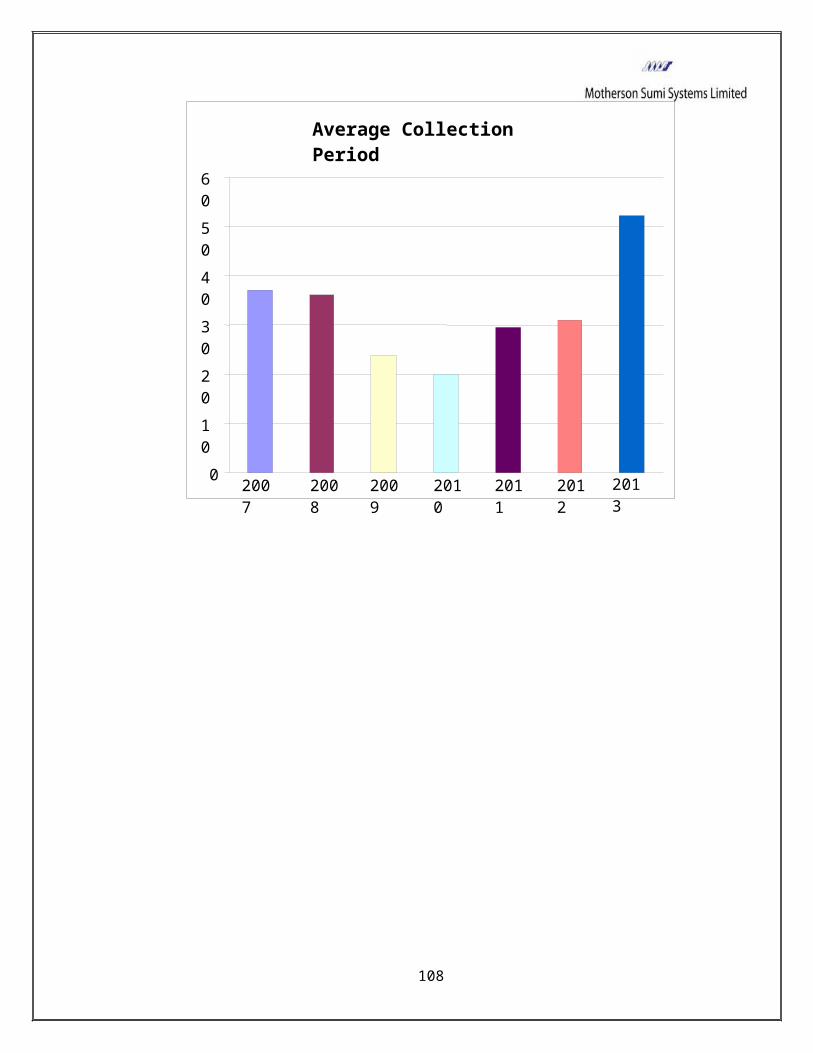

Average Collection Period

2013

2012

2011

2010

2009

2008

2007

0

10

20

30

40

50

60

108

Analysis

As it is seen that the firm has restricted the credit

policy, by which its average collection period has

declined from the year 2007 to 2010. But after that it

has increased due to liberal credit policy. SMIIEL. is

focusing 100% payment and also giving incentive to

debtor in form of 2% discount on the billing. It is

allowing 2 months credit to its debtor.

109

RECEIVABLES MANAGEMENT

Receivables constitute a significant part of current

asset of the firm. Receivable represent amount owed to

the firm as a result of sale of goods or service in the

ordinary course of business. These are the claim of the

firm against its customer. This receivable is known as

trade credit or trade receivable. It is an investment

because it blocks some portion of firm's funds. The

purpose of maintaining or investing in receivables is

to meet competition and to increase the sales and

profit. Receivable management is the process of making

decision relating to investment in trade debtors.

Factors Influencing Receivable:

1. Credit Policy: A firm with aggressive credit

policy will have a low size of receivable while a

firm has liberal credit policy will higher size

receivable.

110

2. Term of Credit : If the term of credit period

is allowed more, then the receivable will be more.

While credit period is short, then the size of

receivable will be less.

3. Expansion Plan: When firm enter into a new

market for expansion of its business, it gives

credit facility to attract its customer by which

receivables get increased.

111

Tools of Receivable Management:

Receivable management consists of various factors such

as -

1. Forming Credit Policy

2. Executing Credit Policy

3. Formulating & Executing Collection Policy

Forming Credit Policy:

A suitable credit policy is essential for efficient

management of receivables. A optimum credit policy is

the one which maximizes value of the firm. A credit

policy is related to decisions such as credit standard,

length of standard, length of credit period, cash

discount and discount period etc.

(a) Credit Standards:

112

Credit standards are the criteria which a firm follows

in selecting customer for the purpose of credit

extension. By liberalizing credit policy the volume of

sales will get increased which result into increase the

profit. It also increases the volume of sales which

enhance the risk of bad debts and delayed receipt. On

the other hand, a tight credit policy will decrease the

volume of sales which result in decrease in the chances

of bad debt loses.

113

(b) Credit Period:

Credit period refers to the time period allowed to the

customer for making the payment. There is no binding on

fixing the terms of credit. It varies from firm to firm

depending on its objective. A firm lengthens its credit

period will block more money which ultimately involves

more debt collection cost and more bad debt losses. The

firm may tighten its credit period; if its customers

are defaulting too frequently and bad debt losses are

building up.

(c) Discount period:

The collection of receivables is influenced by the

period allowed for availing discount. It is the

additional period allowed for the customer- to avail

discount and make payment.

(d) Cash Discount:

114

It is a reduction of payment offered to customers to

induce them to repay credit obligations within a

specific period of time which will be less than normal

credit period. It is given to speed up the collection

of receivables.

115

Executing Credit Policy:

(a) Collecting Credit Information

It refers to the collection of information about

customers regarding their financial position for giving

credit. This information helps in improving the quality

of receivable which ultimately reduces the chances of

bad debt losses. This information can be collected from

financial statement, credit rating agencies, backs etc.

(b) Credit Analysis

Credit analysis is the determination of the degree of

risk associated with the

account, the capacity of the customer to borrow and its

ability and

willingness to pay the credit amount. At the time of

credit analysis the

manager keeps in various factors like Character,

116

Capacity, Capital, Condition

and Collateral.

c) Credit Decision

Credit decision is taken by the manager by matching the

creditworthiness of the customer with the credit

standard of the firm.

117

Collect Policy:

Collection refers to obtaining payment of past due

account. A good collection policy accelerates the

collection from slow payer and reduces the bad debt

losses. It keeps the debtor alert and urges them to pay

their dues promptly. The collection policy is either

strict or lenient. A strict collection policy enables

early collection and reduces bad debt losses but it

reduces the volume of sales and increases the

collection cost. A lenient policy increases the bad

debt losses and increase debt collection period. The

credit manager makes or frames some collection effort

for collecting the credit amount from customers. Some

are -

a) Sending a letter informing the customer regarding

the past due status that are overdue.

b) Making a telephone call to the customer.

118

c) Employing a collection agency

d) Taking a legal action against the customer

The firms need to continuously monitor and control its

receivable to ensure the success of collection efforts.

There are two methods for evaluating the management of

receivable. Such are -

119

(a) Average Collection Period:

It represents the average number of days for which a

firm has to wait before its receivable is converted

into cash. It measures the quality of debtor. Generally