A Kaleckian theory of tax inefficiency: How elite influence favours inefficient redistributive...

21

A Kaleckian theory of tax inefficiency: How elite influence favors inefficient redistributive mechanisms Kieran latty [email protected]

Transcript of A Kaleckian theory of tax inefficiency: How elite influence favours inefficient redistributive...

A Kaleckian theory of tax inefficiency:How elite influence favors inefficient redistributive

mechanisms

Kieran [email protected]

1.Introduction: Kalecki’s political economy of macroeconomic policy

2.Insights from optimal capital tax theory

3.Policy options

Kalecki’s political economy of macroeconomic policy

Seminar article ‘Political Aspects of Full Employment’ (1943) suggested that Keynesian macroeconomics was effective at securing high and stable growth and employment, but was difficult to implement due to business and elite opposition on the following grounds:

(i) ‘the dislike of Government interference in the problem of employment as such

(ii)the dislike of the direction of Government spending (public investment and subsidising consumption)

(iii)dislike of the social and political changes resulting from the maintenance of full employment’

(Kalecki 1943)

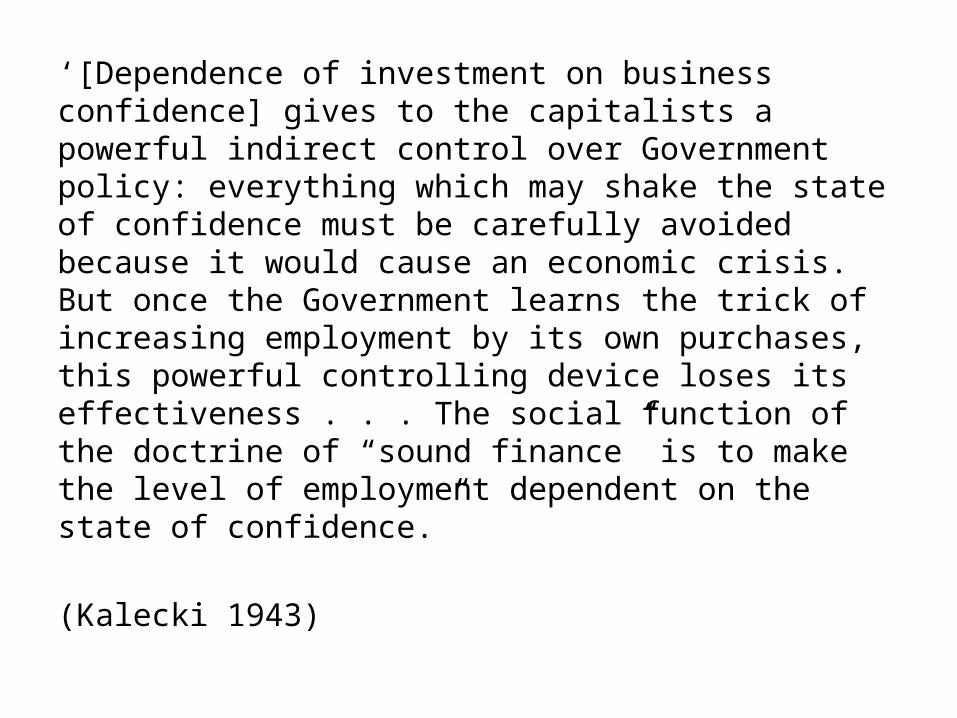

‘[Dependence of investment on business confidence] gives to the capitalists a powerful indirect control over Government policy: everything which may shake the state of confidence must be carefully avoided because it would cause an economic crisis. But once the Government learns the trick of increasing employment by its own purchases, this powerful controlling device loses its effectiveness . . . The social function of the doctrine of “sound finance” is to make the level of employment dependent on the state of confidence.”

(Kalecki 1943)

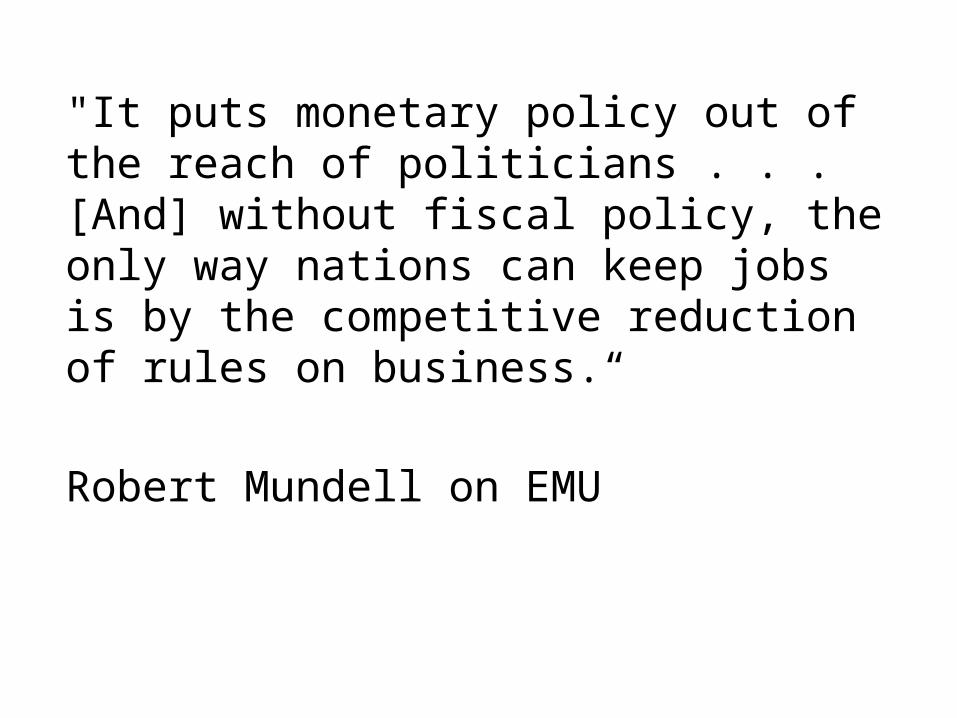

"It puts monetary policy out of the reach of politicians . . . [And] without fiscal policy, the only way nations can keep jobs is by the competitive reduction of rules on business.“

Robert Mundell on EMU

Kalecki and income distribution

Kalecki (1943) sees full employment as creating problems of control and discipline. But we can extend the analysis to include income distribution, which gives us a link with tax policy.

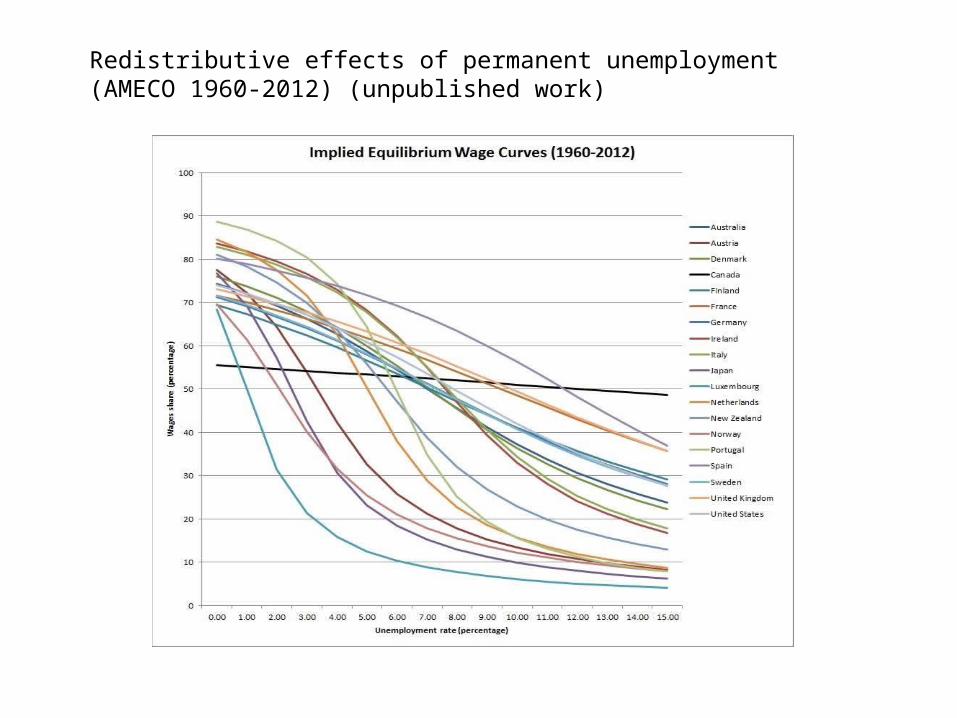

Kalecki got in wrong in regards to distributive effects of full employment (assuming full employment raised profits). We now know that the wage Phillips curve is more steep than the price Phillips curve, i.e. low unemployment has adverse effects on profit share.

See for example:

Redistributive effects of permanent unemployment (AMECO 1960-2012) (unpublished work)

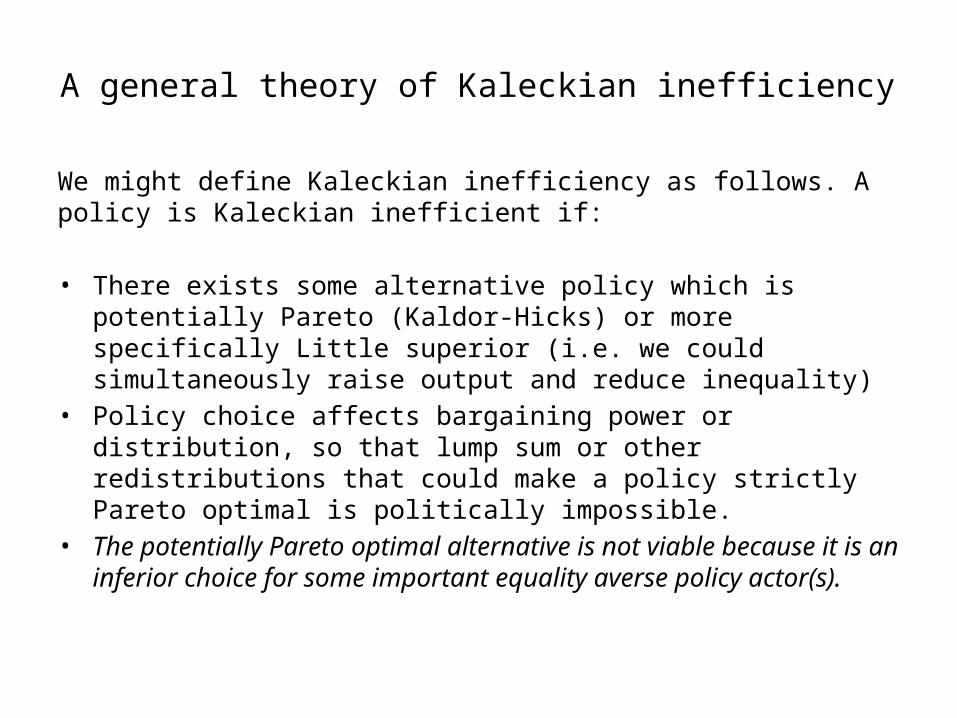

A general theory of Kaleckian inefficiency

We might define Kaleckian inefficiency as follows. A policy is Kaleckian inefficient if:

• There exists some alternative policy which is potentially Pareto (Kaldor-Hicks) or more specifically Little superior (i.e. we could simultaneously raise output and reduce inequality)

• Policy choice affects bargaining power or distribution, so that lump sum or other redistributions that could make a policy strictly Pareto optimal is politically impossible.

• The potentially Pareto optimal alternative is not viable because it is an inferior choice for some important equality averse policy actor(s).

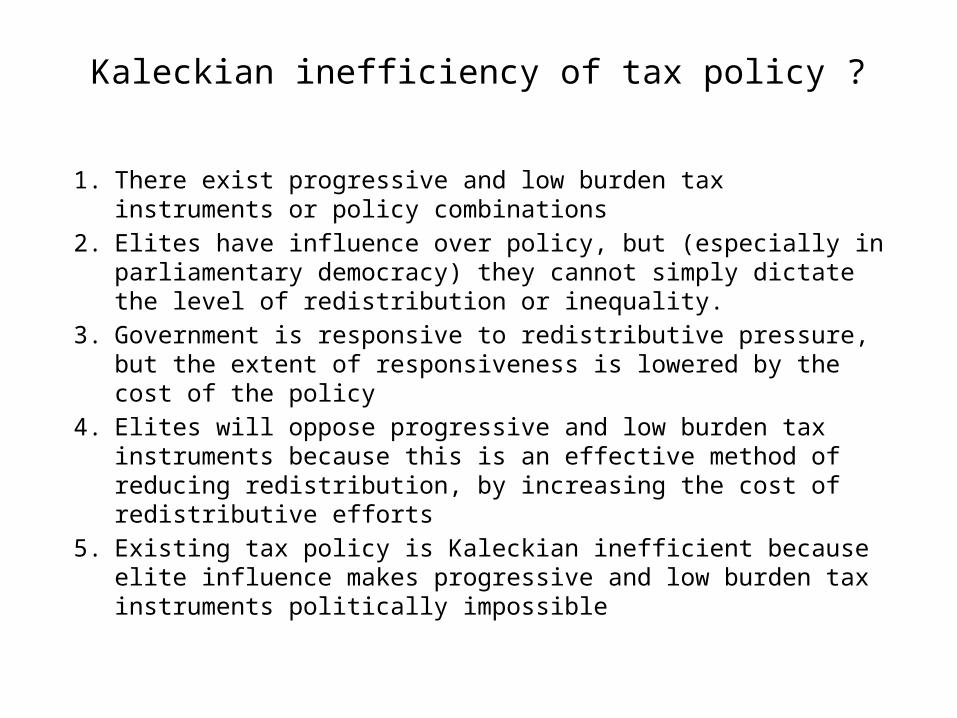

Kaleckian inefficiency of tax policy ?

1. There exist progressive and low burden tax instruments or policy combinations

2. Elites have influence over policy, but (especially in parliamentary democracy) they cannot simply dictate the level of redistribution or inequality.

3. Government is responsive to redistributive pressure, but the extent of responsiveness is lowered by the cost of the policy

4. Elites will oppose progressive and low burden tax instruments because this is an effective method of reducing redistribution, by increasing the cost of redistributive efforts

5. Existing tax policy is Kaleckian inefficient because elite influence makes progressive and low burden tax instruments politically impossible

Another way of looking at it

• Businesses which are unhappy with a policy can mount a ‘capital strike’ however they face a collective action problem. Reneging on the ‘strike’ is the best policy for individual firms

• However, if the progressive policy lowers the spread between marginal post-tax returns and the cost of capital, then it is individually optimal for firms to lower investment

• Progressive policies which have excess burden are not so scary for capital holders, because such polices automatically bring forward a reduction in investment without any coordination or collusion

• If governments has in its choice of permissible instruments low burden capital taxes, then even mild inequality aversion can lead to huge tax rates. Action to lower redistribution now needs to be in the form of coordinated political action.

Insights from the optimal capital tax literature

1. The ‘old’ view of capital taxation2. The case for positive capital taxation3. Progressive and low burden policy options

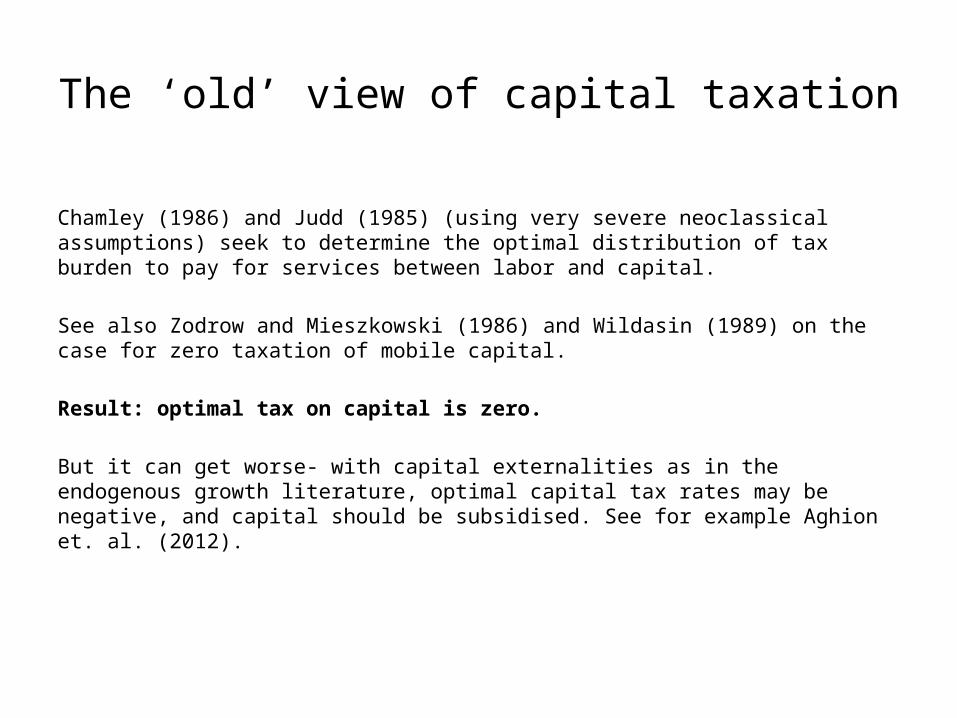

The ‘old’ view of capital taxation

Chamley (1986) and Judd (1985) (using very severe neoclassical assumptions) seek to determine the optimal distribution of tax burden to pay for services between labor and capital.

See also Zodrow and Mieszkowski (1986) and Wildasin (1989) on the case for zero taxation of mobile capital.

Result: optimal tax on capital is zero.

But it can get worse- with capital externalities as in the endogenous growth literature, optimal capital tax rates may be negative, and capital should be subsidised. See for example Aghion et. al. (2012).

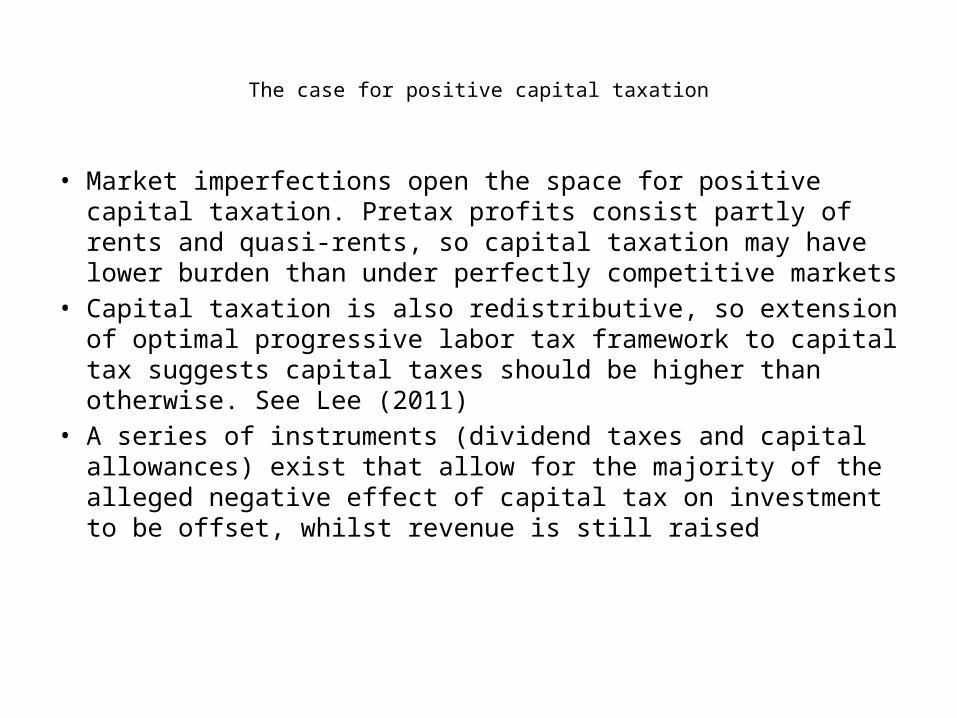

The case for positive capital taxation

• Market imperfections open the space for positive capital taxation. Pretax profits consist partly of rents and quasi-rents, so capital taxation may have lower burden than under perfectly competitive markets

• Capital taxation is also redistributive, so extension of optimal progressive labor tax framework to capital tax suggests capital taxes should be higher than otherwise. See Lee (2011)

• A series of instruments (dividend taxes and capital allowances) exist that allow for the majority of the alleged negative effect of capital tax on investment to be offset, whilst revenue is still raised

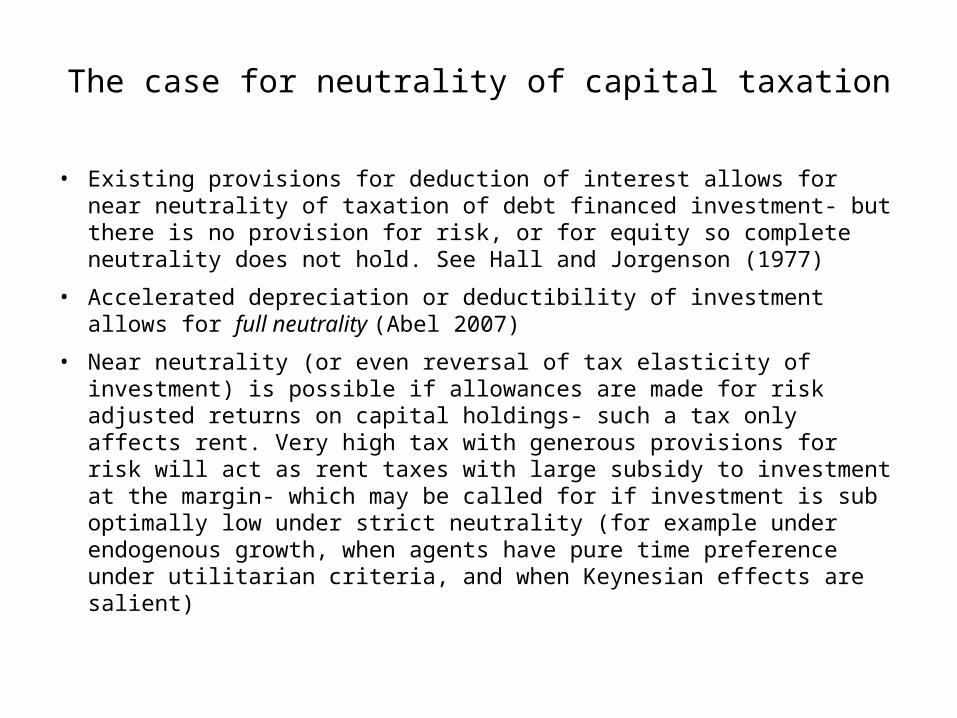

The case for neutrality of capital taxation

• Existing provisions for deduction of interest allows for near neutrality of taxation of debt financed investment- but there is no provision for risk, or for equity so complete neutrality does not hold. See Hall and Jorgenson (1977)

• Accelerated depreciation or deductibility of investment allows for full neutrality (Abel 2007)

• Near neutrality (or even reversal of tax elasticity of investment) is possible if allowances are made for risk adjusted returns on capital holdings- such a tax only affects rent. Very high tax with generous provisions for risk will act as rent taxes with large subsidy to investment at the margin- which may be called for if investment is sub optimally low under strict neutrality (for example under endogenous growth, when agents have pure time preference under utilitarian criteria, and when Keynesian effects are salient)

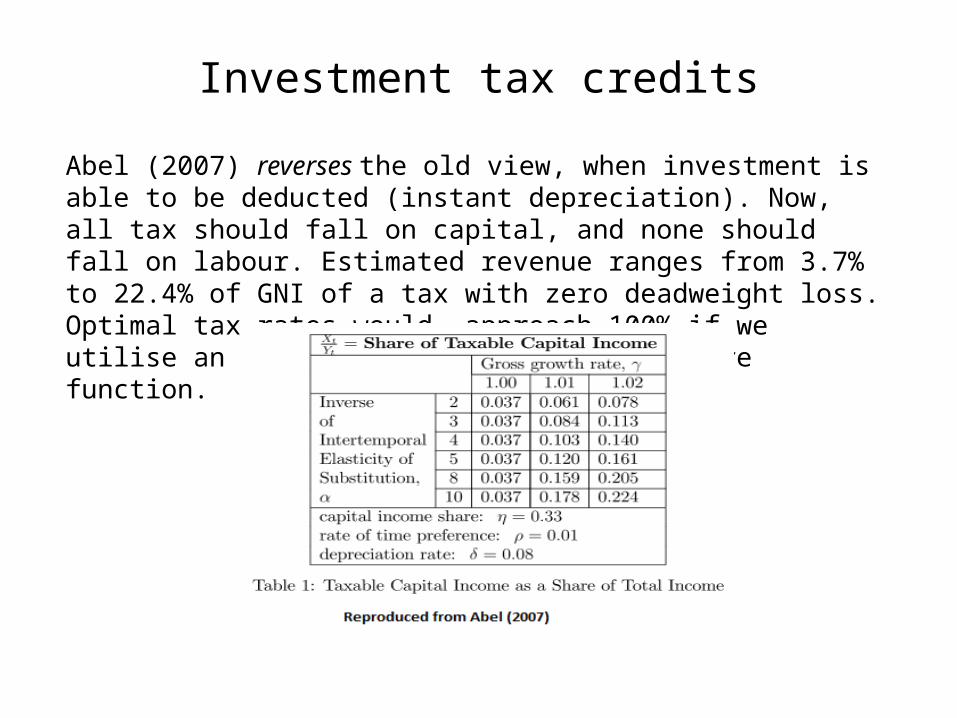

Investment tax creditsAbel (2007) reverses the old view, when investment is able to be deducted (instant depreciation). Now, all tax should fall on capital, and none should fall on labour. Estimated revenue ranges from 3.7% to 22.4% of GNI of a tax with zero deadweight loss. Optimal tax rates would approach 100% if we utilise an inequality averse social welfare function.

Super profits tax

A super profits tax is neutral for similar reasons that capital tax with instant depreciation is- whereas allowance for capital stock is made when invested under the ITC, it is deductible as a risk adjusted stream under a super profits tax (SPT)

Near neutrality (or even reversal of tax elasticity of investment) is possible if allowances are made for risk adjusted returns on capital holdings- such a tax only affects rent. Very high tax with generous provisions for risk will act as rent taxes with large subsidy to investment at the margin- which may be called for if investment is sub optimally low under strict neutrality (for example under endogenous growth, when agents have pure time preference under utilitarian criteria, and when Keynesian effects are salient)

Dividend taxesDividend taxation, like standard capital tax with investment credits, has zero near zero impact on investment (and may be positive if non permanent)

1. Marginal source of funds is retained profits, so equity is already trapped in the firm. Intertemporal choice of payout now, or invest and payout later is not affected by divided tax rate. See Stiglitz (1973) and Stiglitz (1976).

2. If the dividend tax is seen as temporary, investment rises as invest and payout later becomes preferred (declining dividend tax is equivalent to a negative interest rate). See Korinek and Stiglitz (2007); Stiglitz and Korinek (2008)

3. Empirical research suggests that dividend tax cuts increases dividend payouts and lower firm reinvestment rates. In general equilibrium we would then expect to see reduction in wages share and an excess increase in inequality if the elasticity of substitution between labour and capital is less than unit. Falling reinvestment rate is well correlated with falling wages share and rising inequality.

Other policy options (national level)• Capital controls , financial repression, and state development banks

can lower long term rates and reduce capital leakage, offsetting negative effects of capital taxation. Such an approach has been effective in accelerating capital deepening in for example China and South Korea. Under certain situations, such an approach may be self financing via higher savings (if the elasticity of marginal utility is high, or if it is high and relative income effects are salient), high growth and lower rates will both raise savings. (we can also get this result in habit formation models). Importantly, estimates of capital mobility suggest that mobility is still much lower than assumed in perfect mobility models. This lowers the DWL of capital taxation. Capital mobility is also clearly a policy modifiable variable. See the number of references on the ‘Feldstein-Horioka’ puzzle.

• Forms of cooperate financing and governance can affect the rate of firm reinvestment independently of capital tax changes. Use of bank and capital financing is associated with an increase in corporate reinvestment, as is general unimportance of equity finance and regulations limiting buybacks (See for example work by Lazonick and Hein)

• Industry policy and corporatist bargaining institutions may also have positive effects on investment that offset negative effects of corporate tax. (Henley and Tsakalatos 1997)

• Land value taxes target immovable land, and are therefore both progressive and feature low excess burden. See (OECD 2010; IMF 2013; Norregaard 2013; Arnott and Stiglitz 1975; Arnott and Stiglitz 1979)

• Inheritance taxes may have near zero effect on investment- especially if utility is derived directly from wealth hording independent of future consumption.

• Even distorting capital taxes which fund infrastructure or human capital formation can have net negative deadweight loss

Other policy options (national level)

International tax competition

• Reduction in tax competition and scope for avoidance will lower the negative impact of capital taxes on investment in each jurisdiction.

• This result may be one reason why tax competition is favored by elites. By increasing the excess burden of capital taxation, the rate is effectively lowered.

• Elites may face a ‘Jevon’s paradox’ whereby increased efficiency in taxation leads to greater tax rates

Summary

• Low burden capital tax instruments abound. A simultaneous increase in investment and reduction in inequality is economically feasible.

• Elites may, however especially dislike instruments which are egalitarian and ‘too’ efficient

• Existing policy is therefore ‘Kaleckian inefficient’

• Democratic reform (in the broadest sense) and mechanisms for limiting elite influence over policy instruments may be a precondition for more rational and egalitarian tax policy

• Optimal tax policy perhaps needs to be recast as a joint problem of economics and political economy