40098357.pdf - International Atomic Energy Agency

819

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 40098357.pdf - International Atomic Energy Agency

Programme - 21 February 2005

Chair: Vladimír Hecl, Energy Centre Bratislava 9.00-11.00 Session 1: RES Policies, strategies, political background

09:00 Vladimír Hecl, ECB, welcome speach , Slovakia

09:05 Zsolt Simon, Minister, Ministry of Agriculture SK, Development and recent changes in Biomass sector in Slovakia, Slovakia

09:15 Representative, Ministry of Economy SK, Renewable energy development and Slovak Energy Policy, Slovakia

09:25 Representative, EC Representative, EU Trends and position of European Commission,

09:35 Friedrich Rauter, Amt der NÖ Landesregierung, Renewable Energy in Lower Austria , Austria

09:45 Pavel Manchev, Eneffect Center for Energy Efficiency, Biomass situation in Bulgaria, Bulgaria

10:25 Jaroslav Jakubes, Enviros s.r.o., Biomass situation in Czech Republic, Czech Republic

10:35 Krzystof Gierulski, EC BREC, Biomass situation in Poland, Poland

10:45 Discussion

Chair : Fiona Santokie, Natsource Europe Ltd , UK

11.20-13.30 Session 2: Bioenergy markets, tools and influence factors

11:20 Fiona Santokie, Natsource Europe Ltd., Biomass international markets situation and development scenarios, United Kingdom

11 :40 Ján Ilavský, Finnish Forest Research Institute, Energy Wood Potential of Forests in the European Union, Finland

11:55 Alexandra Langenheld, Ministry of Environment DE, REFITs / service or contradiction?, Germany

12:10 Kees Kwant, SenterNovem, Green Certificates, a tool for market development, Netherlands

12:25 Helena Princová, Ministry of Environment SK, Kyoto flexible mechanisms - past and current situation, reaching the objective ?, Slovakia

12:40 Karol Dvorák, Regulatory Authority SK, Regulation framework for RES in Slovakia, Slovakia

12:55 Irena Plocková, Ministry of Industry and Trade CZ, Sustainable construction and renewable energy, the Czech Republic

13:10 Discussion

Chair : Karol Vinš, State Forests Company, SK

14.30-18.05 Session 3: Biomass fuels production and trading

14:30 Karol Vinš, State Forests Company SK, Biomass potential in Slovakia, processing of biomass fuels, Slovakia

14:45 Michael Wild, EBES, Biomass fuels trading, Austria

15:00 Jozef Mikulec, Slovnaft Vurup, Strategy for Production and Utilisation of Alternative Fuels, Must or Pain?, Slovakia

15:15 Roman Réh, Association of wood-processing industries, Utilization of biomass in woo-processing industry, Slovakia

15:30 Michael Golser, Holzforschunginstitute Austria, Production of wood pellets – R&D and standardisation , Austria

15:45 Wieslaw Denisiuk, POLBIOM- Ekolog, Straw heating technologies, Poland

16:00 Discussion

Chair : Jozef Víglaský, SK BIOM

16:35 Štefan Molnár, Renem, s.r.o., Production of bio-oils, situation in CEEC, Slovakia

16:50 Kent Nystrom, Swedish Bioenergy association SVEBIO, Biomass pellets markets, situation and development trends, Sweden

17:05 Marián Laššák, Doka Drevo, s.r.o., Biomass briquetts markets, situation and development trends,, Slovakia

17:20 Pentti Hakkila, VTT, Large scale woodchips production, Finland

17:35 Jozef Víglaský, SK BIOM, Energy crops utilisation and perspectives, Slovakia

17: 50 Discussion

Programme - 22 February 2005

Chair : Miroslav Mravec, Herz, SK 9.00-11.20 Parallel Session 4: Biomass firing technologies

09:00 Milan Novák, Thermo/solar Žiar, s.r.o., Biomass/solar installations, Slovakia

09:20 Claus Justsen, Justsen Energiteknik A/S, Technologies with installed capacity over 1 MW, Denmark

09:40 Miroslav Mravec, Herz, s.r.o., Technologies with installed capacity under 1 MW, Slovakia

10:00 Horst Jauschneg, Austrain Biomass Association, Development of the pellets market and of the pellets technologies, Austria

10:20 Ladislav Novák, TTS Eko Třebíč, Wood residues firing technologies, the Czech Republic

10:40 Ľubomír Šooš, Slovak Technical University, Biomass production technologies, Slovakia

11:00 Discussion

Chair : Pavel Manchev, EnEffect Consult, BG

9.00-11.20 Parallel Session 5: Municipal projects uptake

09:00 Martin Cahn, Energie Cites, Are European Cities going towards « greener « future, Belgium

09:20 Christian Aichernig, Repotec GmbH, biomass CHP Plant Gussing – Reliable solution for Fossil Free Municipality, Austria

09:40 Miroslava Knotková, City of Zlín, Realisation of Biomass projects in Zlin Region, the Czech Republic

10:00 Adam Gula, AGH-University of Science and Technology, Krakow, Project example in Poland, Poland

10:20 Kristina Dely, Delfy Bt. , Project example in Hungary, Hungary

10:40 Juraj Zamkovský, CEPA, Utilisation of biomass in small municipalities in Central Slovakia

11:00 Discussion

Chair : Pavol Švarc, Utilities Novaky. SK

11:40-13:20 Parallel Session 6: Biomass large and small CHP

11:40 Eloi Piel, EUROHEAT and Power, Opportunities for CHP/DH, EU

12:00 Pavol Švarc, Energy Utilities Nováky, Biomass/coal co-firing in Utilities, Slovakia

12:20 Matthias Lieblich, WIP Germany, Mini and Micro CHP technologies, Germany

12:40 Ján Gaduš, Slovak Agriculture University, Aplication of biogas in fuel cells, Slovakia

13:00 Ivan Ďuďák, Intech Ltd., Marketing of CHP technologies in Slovakia, Slovakia

13:20 Discussion

Chair : Representative of European Commission

11:40-13:20 Parallel Session 7: Environmental biomass technologies

11:40 Nominated representative, DG Enviro, European Commission, EC requirements related to legislation

12:00 Julius Bizoň, SES Tlmače, Ash processing and recycling, Slovakia

12:20 Jiří Balajka, ECOSYS, Exploitation of biomass within the emissions trading and JOINT IMPLEMENTATION, Slovakia

12:40 Jozef Šoltés, Slovak Energy Agency, Emissions metering methodology in Slovakia, Slovakia

13:00 Klaus Grepmeier, ZREU, European progress within environmental technologies, Germany

13:20 Discussion

Chair : Alexandra Amerstorfer, Kommunalkredit, Austria

14:40-16:40 Session 8: Biomass projects financing roundtable

14:40 Martin Kedro, SARC, R+D Programmes, Slovakia

14:50 Representative, European Commission, Energy Intelligent – Europe Programme

15:00 Alexandra Amerstorfer, Kommunalkredit Austria, Austrian JI/CDM Programme, Austria

15:10 Drahoslav Kvašovský, Slovak energy Agency, Structural funds, Slovakia

15:20 Dária Juhasová, Ministry of Economy SK, Interreg III C, Slovakia

15:30 Bronislava Herdová, ECB, Guarantee programmes, Slovakia

15:40 Marian Rutšek, EE TEK, Private financing, Slovakia

15:50 Vladimír Vacho, Dexia, Banking, Slovakia

16:00 Kristina Vilimaite, The Regional Environmental Centre for Central and Eastern Europe , Grants/foundations, Hungary

16:10 Discussion

16:30 End of conference, Vladimír Hecl, ECB

ADDRESS OF THE MINISTER OF AGRICULTURE OF THE SLOVAK REPUBLIC

Zsolt Simon Minister of Agriculture of the Slovak Republic Ministry of Agriculture of the Slovak Republic Phone: + 421 2 592 66 241 E-mail: [email protected] Ladies and Gentlemen!

I am very glad to be able to participate in the event starting today, the topic of which I consider to be of utmost importance. It is without doubt that the issue of sustainable development from the viewpoint of food and energy production draws the attention of all countries of the world. The speed of depletion of energy sources and the growing consumption of energies force people all over the world to seek solutions that would ensure high-quality life for the present and future generations, and, at the same time, sustainable development for our planet. That is why no country can act as if this problem did not concern it.

The Slovak Republic, of course, is not an exception in this regard. Our country is dependent on imports of primary energy sources, of which we import almost 90%. Domestic energy sources are limited to renewable sources and brown coal. In 2003, the Government of the Slovak Republic approved the “Concept of Utilisation of Renewable Energy Sources”. The sector of agriculture responded to the document by presenting a “Concept of Utilisation of Agricultural and Forestry Biomass for Energy Purposes” to the Government. After an inventory we arrived at a conclusion that the total energy potential was 63.4 PJ, of which 46 PJ was in agricultural biomass. In agriculture, this includes particularly straw, waste wood, excrement of livestock and green mass for the production of biogas, and growing of oil crops and cereals for production of biofuels. However, it needs to be said objectively that the energy potential mentioned can be used in the sector only to a limited extent. Our effort is to utilise it particularly in heat generation and in agricultural drying plants. However, we have a lot of work ahead of us to implement measures to ensure gradual replacement of a proportion of motor fuels with biofuels, to introduce generation of “green” electric power, and to increase heat generation in the municipal sector using biomass.

Several examples from Slovakia already indicate that this is possible. At Kysucký Lieskovec, they started production of wooden pallets; forestry organisations operate 14 boiler houses using forest dendromass; the greatest consumer of forest wood is a machinery manufacturer, the company of Stredoslovenské energetické strojárne Tlmače; agricultural biomass (straw, natural seeding of forest tree species) is used in heat generation at the agricultural cooperative of Liptovský Ondrej and that of Prašice; biogas is generated at the agricultural cooperative of Brezov, Agros Bátka, SPU Nitra, and it is about to be launched at the agricultural cooperative of Kapušany. Almost 100 tons of

production capacities for plant oil esters are ready and construction of a distillery for dry bioethanol is in preparation. These projects are waiting for adoption of the “National Programme for Biocomponent Production Support in the Slovak Republic and Its Application in Internal Market in Motor Fuels with Subsequent Use in Transportation”.

The main source of dendromass in Slovakia is the forestry, where portion of the wood unsuitable for use in wood processing industry can be utilised; but also the wood processing industry itself, which produces waste suitable for energy use. The total annual potential of Slovakia in production of forest dendromass suitable for energy use will reach approximately 1,810 thousand tons by 2010, which represents an energy equivalent of 16.9 PJ. The energy value of useful waste of wood processing industry represents 18.1 PJ (1,410 thousand tons of waste per annum). The largest concentrations of useful biomass from mechanical wood processing are in the districts of Čadca, Brezno, Lučenec and Svidník.

Promising sources of fuel biomass include the growths of fast-growing tree species (poplar, willow, locust, aspen, alder), annual and perennial energy crops. Energy crop growths may be established only on land unsuitable for classical agricultural and forestry production; on soils temporarily excluded from agricultural production, suitable only for non-food purposes; and also on devastated areas in industrial agglomerations.

On the basis of a zoning of land suitable for energy forests done in the years 2000 – 2001 in the Slovak Republic, locations were selected with the area of 8,400 ha in the forestry soil stock and 37,000 ha of agricultural lands, where for a very short, 3 – 5 years’ turnover, an average increment of about 10 tons of dry mass per year could be achieved. To verify the possibilities of production, experimental growths of cultivated poplars, willows and locust have been established, which confirm the realistic possibilities of utilisation of energy crop growths thus established.

In the state budget for 2005, the Rural Development Plan was allocated SKK 72,800 thousand for afforestation of agricultural land, which represents state budget funds for afforestation of 500 ha of agriculturally unused land in 2005. These funds can be used also for establishment of the so-called energy crop growths.

On the basis of a resolution of the Government of the Slovak Republic on the Concept presented by us, we are monitoring the present effect of the valid legislation on the support for use of renewable energy sources; jointly with the Ministry of Education, we are examining the possibilities of adding the issue of biomass to the existing public programmes of science and research in the field of energy; and last but not least we expect that the Higher Territorial Units will prepare their own energy concepts as requested by the Government. Our experts from the Technical and Testing Agricultural Institute at Rovinka and from the Forestry Research Institute at Zvolen are ready to provide consulting assistance in their preparation.

Ladies and Gentlemen, use of biomass and other renewable energy sources enables us to become more independent of energy imports, to reduce foreign currency expenditures due to growing energy prices, to reduce volumes of carbon dioxide emissions, to create new jobs, and to develop new technologies. We also

must not forget about rural development and landscape enhancement. At the presently changing Common Agricultural Policy of the countries of the European Union, production of biomass for energy purposes is a chance for our agriculture. However, it is a chance also for the Slovak technical intelligentsia to engage in solution of problems related to utilisation of biomass and renewable energy sources, and also a chance for the machinery industry to become involved in international cooperation in manufacture of necessary machines and installations. For the purpose of exchange of experience obtained in the field of utilisation of biomass in agriculture, we are presently preparing a trilateral special seminar with participation of leading experts from Austria, Hungary and Slovakia to be held this May.

Ladies and Gentlemen, it was not my intention to summarise and name all issues we have to solve, I rather wanted to suggest that the use of biomass and renewable energy sources is impossible without cooperation. Farmers and foresters cannot do without people from energy sector and it is not possible to progress without science and research and the entire process must also be supported by economic tools. In conclusion, let me express a wish that this conference show paths to solutions benefiting further progress in biomass use and thereby contribute to general development of the Slovak Republic.

Thank you for your attention.

RENEWABLE ENERGY IN LOWER AUSTRIA Dipl.Ing. Friedrich Rauter Head of Department of Environmental Technology Amt der Niederösterreichischen Landesregierung Landhausplatz 1, A 3109 Sankt Pölten, Austria Phone: 0043 2742 9005/14250 E-mail: [email protected] ABSTRACT The year 2004 was very successful for renewable energy in Lower Austria and more biomass district heating plants, biomass power plants, biogas plants and windmills were built then the years before. Renewable energy has become an important factor in energy supply. About 7% of electricity in Lower Austria is produced by wind, biomass and biogas. Investments of about 185 million Euros were effected by supports and are also important for the economy. There are 240 biomass district heating plants with 282 MW thermal output in operation. The fuel need of 1,4 million cubic meters wood and 15.000 tons straw per year safeguards jobs in rural areas. After the decision of the Ecological Electricity Act 2002 a biogas campaign started in Lower Austria. Biogas plants for renewable resources and agricultural products are supported by subsidies and regulated prices for renewable electricity which is fed into the national grid. There was also a considerable increase of windmills in the year 2004 and today 197 plants with 251 MW output are in operation.

121. 2. 2005

Renewable Energy in Lower Austria

Dipl.Ing. Friedrich RauterOffice of the Government of Lower AustriaDepartment of Environmental Technology

221. 2. 2005

Energy in Austria

natural gas18,7%

crude oil47,3%

district heating

3,1%

coal2,1%

renewable energy10,5%

electricity18,3%

Final energy consumption in Lower Austria 2002: 210.640 TJ

321. 2. 2005

Energy in Lower Austria

natural gas29,4%

crude oil25,8%

waste0,5%

wood14,6%

biogenous fuels7,1%

heat pump1,2%

wind,PV0,4%

hydropower21,1%

Energy production in Lower Austria 2002: 137.687 TJ

421. 2. 2005

Energy Plan of Lower Austria

• implementation of a comprehensive protection of climate and environment

• sparing use of resources• to ensure the basis for life and economy• to achieve a wide participation and cooperation

521. 2. 2005

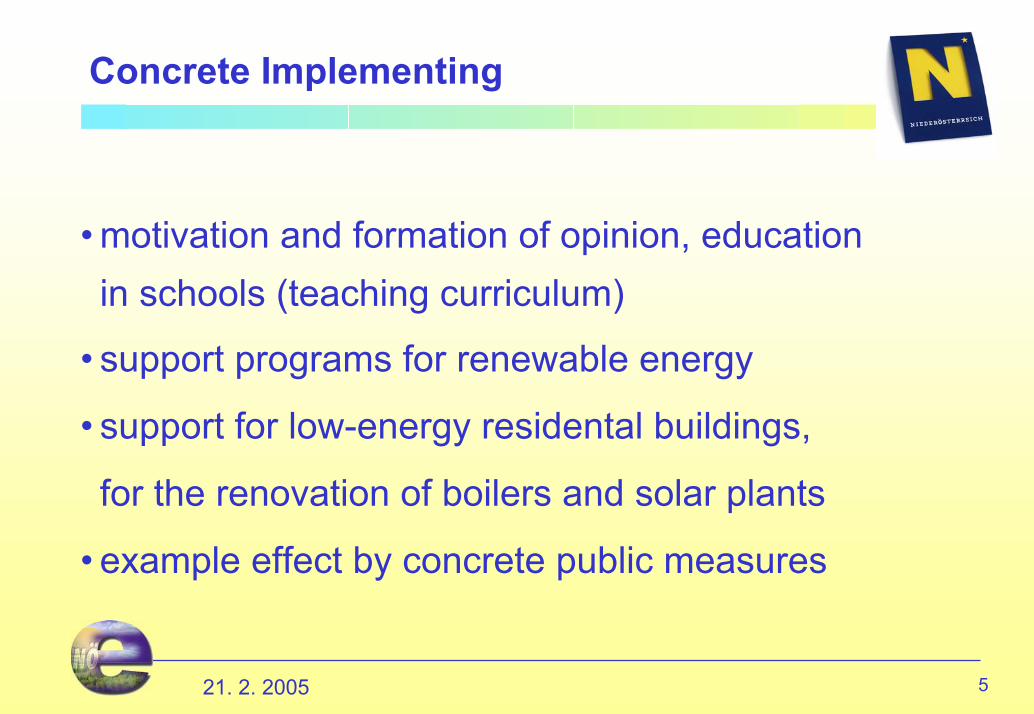

Concrete Implementing

• motivation and formation of opinion, educationin schools (teaching curriculum)

• support programs for renewable energy

• support for low-energy residental buildings,

for the renovation of boilers and solar plants

• example effect by concrete public measures

621. 2. 2005

Hydropower

• About 70% of the Austrian electricity consumption issupplied by hydropower.

• 394 small-scale hydropower plants supply about 4% of the demand of electricity in Lower Austria,the continuance is ensured by regulatedprices for feeding into the grid.

• The hydropower plants a the Danube providean essential share in the total productionof electricity in Austria.

721. 2. 2005

Energy from Biomass

• Support of numerous research and developmentprojects for the use of bioenergy (development ofboilers and etc.)

• Subsidies for the construction of municipal districtheating plants

• Subsidies for biomass boilers in residential buildings• Assured tariffs for electricity from biomass and

biogas• Subsidies for biomass power plants

821. 2. 2005

Support for Biomass

Success by a consistent support:

• Increasing share in electricity supply• Ensured income for the forestry and agriculture• Independence from imports• Technological progress for boilers and fuel technology• Export of combustion plants• Rising acceptance for the thermal use of biomass

921. 2. 2005

Support for Biomass

240 plants• 282 MW thermal output• 380 km pipelines• 1,4 million cubicmeters

fuel consumption• 680 GWh heat supply

Biomass district heatingplants:

1021. 2. 2005

Woodfired boilers in Austria

Small heating plants for woodchips and woodpellets from 1989 to 2003:a total of 49.158 plants

woodchips woodpellets

Annual increment

1121. 2. 2005

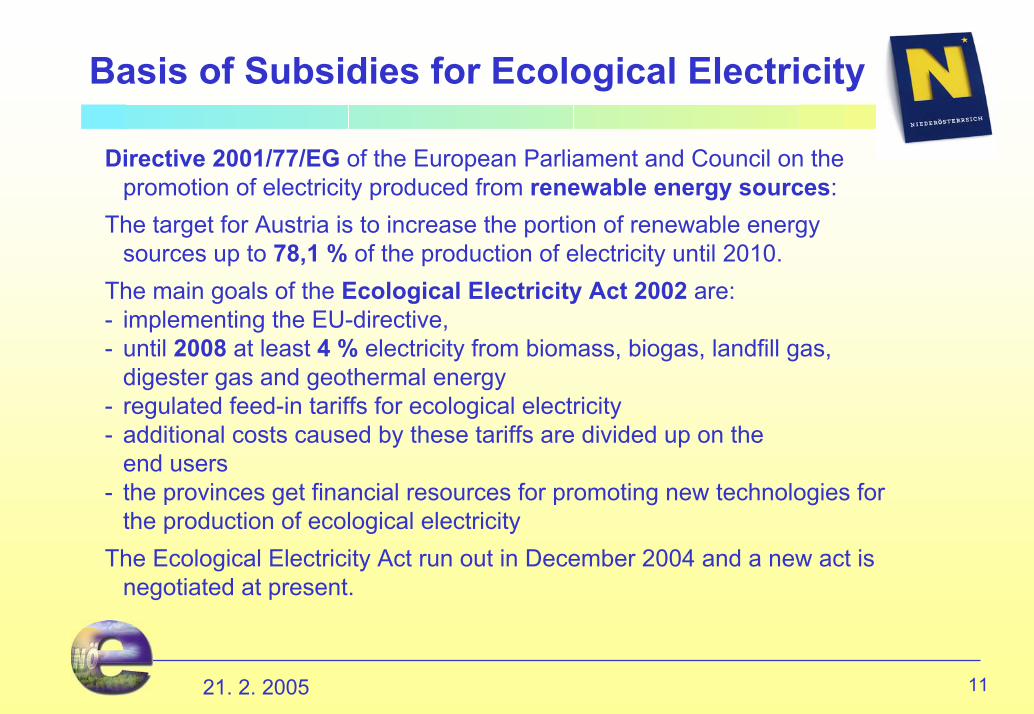

Basis of Subsidies for Ecological Electricity

Directive 2001/77/EG of the European Parliament and Council on thepromotion of electricity produced from renewable energy sources:

The target for Austria is to increase the portion of renewable energysources up to 78,1 % of the production of electricity until 2010.

The main goals of the Ecological Electricity Act 2002 are:- implementing the EU-directive,- until 2008 at least 4 % electricity from biomass, biogas, landfill gas,

digester gas and geothermal energy- regulated feed-in tariffs for ecological electricity- additional costs caused by these tariffs are divided up on the

end users- the provinces get financial resources for promoting new technologies for

the production of ecological electricityThe Ecological Electricity Act run out in December 2004 and a new act is

negotiated at present.

1221. 2. 2005

Electricity from Biomass

Present state in Lower Austria:

1 plant with 5 MW, commanded heat, in operation1 identical plant in construction1 plant with 2 MW, commanded by heat, in construction2 ORC plants (about 500 kW) in operation1 plant with biodiesel 1,3 MW in operation1 plant with 600 kW in test operationseveral small plants with biodiesel and vegetable oilSeveral plants with 5 MW and plants withwood-distilling are in planning.

by

1321. 2. 2005

Biogas Campaign in Lower Austria

Target: 1% electricity from biogas- information and advice- well-defined responsibility for advice, approval

and subsidisation- standardized approval procedures- clear and simply understandable guidelines for

subsidiesUp till now the biogas campaign is verysuccessful.There will be increases if the economic conditions will last.

1421. 2. 2005

Biogas Campaign in Lower Austria

End of December 2004 there were 32 biogas plants with a total electrical output of 9,15 MW in operation and 17 furtherplants are in construction. The target of 1% (about 15 MW) will be reached this year.

1521. 2. 2005

Support for Windmills

• In the nineties there were voluntaryagreements with the operators of the gridabout feed-in tariffs.

• Since 1999 there were legal regulations in the provinces about the obligation of theoperators of distribution networks to purchase electricity generated by wind.The feed-in tariffs were regulated by theprovinces and financed by price surchargesfor end users.There were also additional subsidies fromthe federal government.

• Since 2002 a federal regulation about theobligatory purchase of ecological electricitywith fixed tariffs took place.The provinces can allocate additional supports.

1621. 2. 2005

Windmills

• 197 windmills with a total electrical output of 251 MW (about 5 % of the consumption of electricity) are in operation in Lower Austria.

• There will be a continuous increase of wind turbines within the next years if the economic conditions will last.

1721. 2. 2005

Balance of Ecological Electricity

Biomass: 16 plants with 8,5 MWBiogas: 32 plants with 9.15 MWWind: 197 plants with 251 MWlandfill gasand digester gas: 7 plants with 1,5 MW

Biomass and biogas plants produce about 2% and windmills about 5% of the consumption of electricity in Lower Austria.

A further considerable increase can be awaitedwithin the next years.

1821. 2. 2005

Solar Energy

The use of direct solar energy for water heating has a long tradition in Lower Austria.Several years ago most facilities were built by self-constructiongroups.Today most solar plants are produced and put up by professionals. Within the last years a solid market was set up by specific support.There are several instruments for promoting solar plants for residentialbuildings as well as for trade.Solar plants also are important exportable goods.

1921. 2. 2005

Renewable Energy in Lower Austria

Thank You for Your Attention!

BIOMASS SITUATION IN THE CZECH REPUBLIC

Jaroslav Jakubes Senior Consultant ENVIROS, s.r.o., Na Rovnosti 1, 130 00 Praha 3, Czech Republic Phone: +420 284 007 493 E-mail: [email protected] ABSTRACT In the context of implementation of RES-E Directive 2001/77/EC, Czech Republic has adopted an indicative target for RES-E share in gross electricity consumption the level of 8% in 2010. In addition, an updated Energy Policy from 2004 sets indicative target for share of RES at the level of 15-16% TPES in 2030. Biomass is the renewable energy resource with key current share as well as with key potential contribution to meeting the indicative targets in the future. Although positively directed, the current development of the biomass utilisation in the Czech Republic is, however, a result of uncoordinated and often contradictory and contraproductive efforts. The maximal utilisation of biomass potential needs a quick adoption of new support schemes for both RES-electricity and RES-heat, coordinated approach with agricultural policies, support to project development, clear rules for investment support as well as stimulation of development of local biomass market.

International Slovak Biomass Forum, Bratislava 2005

International Slovak Biomass Forum, Bratislava 2005

International Slovak Biomass Forum, Bratislava 21.02.2005

Biomass Situationin the Czech Republic

Jaroslav Jakubes, ENVIROS, Prague

International Slovak Biomass Forum, Bratislava 2005

- Biomass Utilisation and Potential in the Czech Republic

- Current RES Support Policy in the Czech Republic

- Barriers and Constraints

- Outlook for RES Support Policy in the CR

- Conclusions

Contents of Presentation

International Slovak Biomass Forum, Bratislava 2005

Updated RES statistics for the Czech Republic 2003

0

5

10

15

20

25

30

35

40

PJ/

year

Hydro (excl.pumpedstorage)

Solid biomass Biodegradablepart of waste

Solar thermal Geothermal(heat pumps)Wind Liquid

biofuelsBiogas

Solar PV

Ministry of Industry and Trade - PHARE project - updated RES statistics since 2003- higher biomass consumption compared to previous data - especially in small sources

- Total consumption of primary RES in 2003:- approx. 49,2 PJ = 2,8% of TPES- lower share of hydro energy than in 2002- share of wind energy still negligible

Biomass + biogass:37,4 PJ of primary fuel => 29,6 PJ heat + 481 GWh electricity

International Slovak Biomass Forum, Bratislava 2005

Current utilisation of biomass in the Czech Republic - facts

• 2003: 29,6 PJ heat + 481 GWh electricity from biomass + biogas• > 35 thous. biomass boilers (< 50 kW) in family houses (woodchips,

log wood), smaller number of pellets boilers• Industry & commerce: approx. 80 biomass boilers >1 MW + approx.

30 waste wood boilers up to 3 MW in wood processing industry • > 25 small district heating systems with BM sources

(0,5 - 9 MW, woodchips, straw) installed in 1994 – 2003• Extensive RME (biodiesel) market - result of “Oleoprogram” (started

1992) - support for production capacities of RME + subsidies + tax. exempts - current prod. capacity approx. 75 000 t/year

• Energy crops – commercial production just in the beginning (approx. 1250 ha in 2004, growing tendency)

International Slovak Biomass Forum, Bratislava 2005

Biomass potentials in the Czech Republic

Type of Biomass (biofuel)Current utilisation

2003[PJ/year]

Available potentials 2010[PJ/year]

Firewood and waste wood, other solid biofuels 37,2

0,040,2

~ 02,66

~ 0Biogas 1,7 4,7 - 7 (21,8)TOTAL 41,8 72,4 – 121,6 (176,9)

32,8 - 39,3 *

Cereal straw 6 - 22,4Rapeseed straw 9,7 - 12,2Energy crops 6 - 22,5 (63)Biodiesel 4,2 - 9,2Bioethanol < 9

Source – potentials: National Energy Efficiency Study – Czech Republic 1999 (lower estimate), CZ BIOM 2002(higher estimate)* underestimated ???

International Slovak Biomass Forum, Bratislava 2005

RES support policy in the Czech Republic– current status

• Energy Act (458/2000) and Energy Management Act (406/2000)• Decrees - definition of RES (214/2001), buy-out of electricity from RES and

CHP (252/2001)• 2001 - 2005 Feed-in tariffs for RES electricity (incl. from biomass or biomass

co-firing with fossil fuels)• Integration of RES into local/regional energy plans• Continuation of updated National programme for promotion of EE and wider

use of RES: investment + non-investment support for RES projects (Czech Energy Agency, State Environmental Fund, Ministry of Agriculture)

– Investment subsidies for individual projects (BM boilers, CHP)– Production subsidies - energy crops, RME + bioethanol (non-food

agricultural production)• Continuation and update of framework measures – partially tax incentives,

Kyoto mechanisms (JI, ET)

International Slovak Biomass Forum, Bratislava 2005

0

0,5

1

1,5

2

2,5

3

2002 2003 2004 2005

CZK

/kW

h

0

2

4

6

8

10

€c/k

Wh

Solid biomass and biogas(installations until 2004)Biogas (installations after 2004)

Woodchips / sawdust co-firing

Wood waste / straw co-firing

Energy crops co-firing

Biomass-produced electricity supportProblems with large-scale co-firing

International Slovak Biomass Forum, Bratislava 2005

RES support mechanisms and relatedproblems

• Tax incentives:• reduced VAT rate (5% instead of 19%) for biomass-based

fuels and selected RES + RUE equipment• zero excise tax on biodiesel and bioethanol and• reduced VAT (5% instead of 19%) on heat from district heating

• Carbon/energy tax: several studies/analyses already done, introduction desirable but “wait for EU” position

• RES-E support scheme:• fixed feed-in tariffs since 2002 announced by ERO annually, • no long-term guarantee, • problems with large scale biomass co-firing, • new Renewable Energy Law more than 2 years under discussion with

no results

International Slovak Biomass Forum, Bratislava 2005

Barriers for wider use of biomass in the Czech Republic (1)

• Current biomass market = result of framework conditions, variousother factors, efforts and developments, very often unbalanced andcontraproductive => non-existence of stable biomass market with clear rules

• Energy policy - current targets for RES - non-binding, inconsistent, still missing framework support mechanism(s) – not only for RES-E but also for RES-heat ! Priority must be given to biomass incl. energy crops – necessary close coordination of Ministries of Industry and Agriculture

• Differences in individual country markets – not supportive to development - prices of briquettes, pellets - distortion given by low prices of competitive fuels (coal) and high prices of biofuels in neighbour countries (AT, DE) => export rather than local use of refined biofuels

International Slovak Biomass Forum, Bratislava 2005

Barriers for wider use of biomass in the Czech Republic (2)

• Information about realistic possibilities and potentials of BM oftenconfusing - contradictory information on pollution from BM combustion (dioxins), uncritical promotion of energy crops monocultures, etc..

• Most of larger biomass projects dependent on grant support: grant financing + pressure of technology suppliers => low economic efficiency of projects (oversized, inadequate technology, low connection rate)

• Low quality of project development (economic and technology asssessment, biomass logistics) => several examples of problematic projects

International Slovak Biomass Forum, Bratislava 2005

RES support policy in the Czech Republic– what next?

• New Renewable Energy Law under preparation since 2003 –now 2nd reading in the Parliament

- compliance with RES-E Directive 2001/77/EC and White Paper- indicative targets for RES and RES-E - 8% RES-E in 2010

(currently approx. 2.5 % RES, 2-4% RES-E) => very ambitioustarget

- priority on biomass – will be clear after adoption of implementingDecrees

- RES-E support - most probably „green bonus“ scheme (more/lessmodified current feed-in tariff scheme)

- BIG QUESTION - new support scheme for heat from RES – not found its way into current version of Renewable Energy Law proposal

International Slovak Biomass Forum, Bratislava 2005

Conclusions• Biomass – key contributor to meeting of RES indicative targets in the CR• Necessary new support schemes for RES-E and RES-heat – hopefully

during 2005• Necessary to balance support to co-firing of biomass• Financing support – rather soft loans than grant support• Necessary to support improvement of project development• Necessary to stimulate local solid biofuels market (wood pellets,

briquettes, woodchips) - biomass logistics / market information / fuelsexchange

• Need for initial support for increase of production capacities of refined biofuels (pellets)

• Necessary coordination of energy / agricultural / regional policies(support of non-food agricultural production – biofuels, energy crops)

International Slovak Biomass Forum, Bratislava 2005

Thank you for your attention

Contact:

Jaroslav JakubesEnviros, s.r.oNa Rovnosti 1130 00 Praha 3Czech Republic

tel.: +420 284 007 493fax: +420 284 861 245e-mail: [email protected]: www.enviros.cz

POTENTIAL AND TRADING OPPORTUNITIES FOR BIOMASS IN POLAND

Dr Magdalena Rogulska Deputy Director EC Baltic Renewable Energy Centre (EC BREC/IBMER) Centre of Excellence and Competence in Renewable Energy in Poland RECEPOL ul. Rakowiecka 32, Warsaw, Poland +48 22 8484832 Mr Krzysztof Gierulski Deputy Director EC Baltic Renewable Energy Centre (EC BREC/IBMER) Ul. Reduta Zbik 5, Gdansk, Poland +48 58 3016636 www.ecbrec.pl ABSTRACT Rural areas are a vital element in the Polish economy. Agricultural lands occupied about 60% of the Poland territory. Agriculture and forestry give only 4.8% of GDP but 27% of the employed in Poland work in agriculture (0.4% in forestry). Local renewable energy sources can play a significant role in the development of rural areas in Poland. Biomass energy has been recognised as a most promising and most important renewable energy source in near future for Polish conditions. The total technical potential for biomass resource has been calculated at 755 PJ. Largest resources relates to the agricultural residues, forestry residues and forestry fuel wood. Energy crops will play more important role in mid and long term perspective. The development of biomass technologies is the fastest growing RE branch in Poland. In the paper actual situation of biomass sector in Poland is presented as well as trends of development in short and mid term perspective.

BACKGROUND Rural areas are a vital element in the Polish economy. There are some regions where agriculture is still the major sector of the economy. The share of agriculture in GDP (including hunting and forestry) was 4.8% in 2001 with a continuous downward trend (in 1988, it was 11.8% as compared to 6.4% in 1994). Reduced share of agriculture in GDP results from declining prices and volume of agricultural output accompanied by the rapidly growing prices and output volume in other sectors of the economy, especially industry. The average employment in agriculture (including hunting and forestry) reaches almost 4 million people, i.e. 25.8% of the total labour force. Agriculture is the main source of income for 4 390

thousand people, i.e. over 11% of Poland's total population, including 27.4% of the rural population. Rural areas have a very high unemployment rate reaching even 50% in some places. Additionally, rural areas show a negative economic balance - a large part of agricultural incomes often outflow to urban areas, e.g. with expenses related to energy costs [1]. The Polish agricultural sector covers many farms which are considerably vary in terms of their organisation structure, type of ownership, farm size and output volume. Unpredictable weather conditions and fluctuating profitability of various production lines result in a lack of agricultural production stability. The agricultural production in Poland is not regulated with a quota regime and the producer bears the entire production risk, with only few crop deliveries based on supply contracts (made between a producer and food processing plants), e.g. sugar beets, rape seed, flower and vegetable seeds. Mixed type of farming with crop growing accompanied with animal production prevails in most farms in Poland and the majority of them lack clearly defined specialisation. In the group of bigger farms with the acreage of over 50 hectares, over 38% have plant production only, 17% - animal production and 45% of such farms are involved in mixed farming. Only in 16.2% of all farms there are no livestock. Of the total number of farms, 64% have cattle and over 50% keep pigs. Total crops area in 2000 year was 12.4 million ha. In total structure basic cereals occupied 8.8 million ha (71.0%), potatoes - 1.3 million hectares (10.1%) and industrial crops - 0.8 million ha (6.5%). Crop structure was slightly changing during the last decade. Except for cereals acreage of which increased from 59.9% in 1990 to 71.0% in 2000, area of other crop production was decreasing. In Poland animal production is rather traditional, in small scale requiring high labour inputs, in bigger scale - consuming a lot of energy. Yearly quantities of cattle and swine excrements in Poland, estimated on the basis of analysis of the actual state of animal production and Ministry of Agriculture and Rural Development forecasts equal approximately 38 million m3 of liquid manure and 51 million tons of dung per year. In connection with those data it is obvious that in the whole country activities tending towards proper animal wastes storage and management should be carried out. Rational management of agricultural wastes based on their proper removal from livestock buildings, storage and afterwards utilization have enormous meaning for natural environment. Moreover, development of the complementary sanitation systems in agriculture, including anaerobic wastes treatment installations, is necessary for solving problems in rural regions connected with three main types of organic pollution sources: human liquid and solid wastes, animal production wastes and wastes from small agro-food industry. Agriculture is this branch of the economy in which there are the most favourable conditions for practical realisation of the principles of sustainable development by way of production of wholesome food, by proper management of the environment and by implementation of technologies utilising renewable sources of energy. Conventional methods of cultivation are more and more often regarded as unfavourable to sustainable development. The progress of technology and intensification permit greater production but the costs, quality, waste and adverse effects on the environment are becoming a problem. On the other hand, agriculture

is a producer of a large volume of biomass which is generally not used as a source of income for farms. The creation of new jobs as well as the generation of additional income is one of the priorities of sustainable regional development. The utilisation of local sources of energy in order to satisfy local energy requirements makes the local market stronger and additional income supports the local community.

NATIONAL POLICY SUPPORTING BIOENERGY The problem of the renewable energy sources (RES), in that bioenergy, covers the issues that are traditionally within the scope of responsibilities of several ministries; thus the works on the documents referring to various aspects of RES utilisation were initiated in different institutions. The policy-making documents are of strategic nature and deal with specific areas of the country’s development. When talking of the important documents which touch upon RES development, the following should be mentioned: ‘National Development Plan’1, ‘Initiative, Development, Labour’2, ‘Development Plan of the Polish Rural areas 2004-2006’3, ‘National Environmental Policy for the period 2003-2006 with the 2007-2010 perspective’4.

One of the key strategic documents is the ‘National Development Plan 2004-2006’ which sets the strategic objective of creation of competitive economy based on knowledge and initiative, assuring long-term, sustainable development, employment-rate increase and ability to catch up with the EU economic and social standards both on regional and governmental level. The following objectives considered of prior importance in the document can contribute to the RES development: high level of environmental protection, increase of share of high value added sectors (e.g. biomass), support for all regions and social groups to participate in the development and modernisation processes. Structural transformations in agriculture and fisheries constitute one of the social and economic development axes of NDP. Financial resources to support the achievement of the objectives set in the document will be provided by the EU (structural funds and coherence funds) as well as by the national institutions (central budget, local governments’ budget and targeted funds). The Sectoral Operational Programme (SOP) The Restructuring and Modernisation of the Food Sector and Rural Development constitutes one of the elements of the social and economic development strategy defined in the National Development Plan.

1 The Council of the Ministers. 2003 ‘National Development Plan for the years 2004-2006’, 2 The Council of the Ministers. 2002. ‘Initiative, Development, Labour. Economy Strategy of the Coalition SLD-PSL’ 3 Ministry of Agriculture and Rural Development 2002. ‘Rural Areas Development Plan for Poland for the years 2004-2006’ 4 The Council of Ministers. 2002. ‘National Environmental Policy for the period 2003-2006 with the 2007-2010 perspective’

The following objectives have been defined in the SOP strategy: 1) enhancing the competitiveness of agriculture and the food economy, 2) sustainable development of rural areas. The above will be implemented within the three priorities of the programme: I. Supporting change and adjustment in agriculture. II. Sustainable development of rural areas. III. Development and adjustment to EU norms regarding to the processing of agricultural production. The SOP covers the years 2004-2006 and its implementation will be based on EU funds together with domestic funds (state budget, local government and support beneficiaries’ own funds). The Polish policy regarding renewable energy is guided by the accession to the EU and the adherence to the Kyoto Protocol. The end of 90-s is the period of increased political engagement in creating conditions for renewable energy development. In 2000, the Council of Ministers adopted the document ‘Development Strategy of Renewable Energy Sources‘, then it was endorsed by the Parliament in 2001. It is the first policy document relating to the whole renewable energy sector, pointing the basic goals and conditions for its development to 2020. It was elaborated in response to the EU White Paper ‘Energy for the future: Renewable Energy Sources’. The ‘Strategy’ calls for 7,5% contribution of renewable energy to the primarily energy of the balance in 2010 and 14% in 2020, as development targets for renewable. Such increase of renewable in the energy balance would require production of 340 PJ of ‘green energy’ in 2010, i.e. growth by 235 PJ compared with 1999, assuming the energy needs of Poland in 2010 at 4570 PJ. Such targets oblige the government to take actions to actively support renewable in Poland. The amounts are ambitious: in comparison to ca.2,5% share in 1999, it means triple increase in utilisation of energy produced from renewable sources during the coming ten years. The document ‘Environmental Policy for the period 2003-2006, with the 2007-2010 long-term perspective’, an up-dated version of the Second Environmental Policy, gives much attention to the RES use, in that bioenergy as well. The process of Poland’s accession to the EU and the transposition of the Polish legal system resulted in gradual adoption of the EU regulations in the field of the RES development to the Polish conditions, what has also significant impact on bioenergy sector. For example Directive 2001/80/EC on the limitation of emissions of certain pollutants into the air from large combustion plants is a strong driving force for development of co-firing biomass with coal at large scale in the country. BIOMASS POTENTIAL Poland posses large potential for the most kind of various bio-energy resources, but in the short period the most important are :

• wood from forests, tree cuttings, orchard waste and short rotation coppice;

• straw and other by-products and/or wastes from agricultural production; • liquid/solid manure used for methane fermentation; • oil seeds processed into esters used as bio diesel; • potatoes, cereals and other crops or wastes processed into ethanol.

Estimates of the present use of bioenergy are uncertain, because there is lacking statistics on that subject. Technical potential for biomass resources has been calculated at the level of over 755 PJ but Poland's geographical location as well as its diversified water and climate conditions may contribute to the growth of the potential of biomass allocated for energy purposes. Largest resources relates to the agricultural residues - basic cereals straw and hay c.12 mln t/year (195 PJ) [2], forestry residues 6-7 mln m3 and forestry fuel wood 2,5 mln m3 (41,6 PJ). Wood industry by-products, which equals ca. 8,3 mln m3 (58,1 PJ) are also potential resource for energy production. Diversification of regional economic development causes possibility for finding, relatively rich logging-residue and agricultural areas in Poland, where it might be supplied to the district heating systems. Table 1. Theoretical and technical energy potential of straw in Poland [2].

Type Total quantity(mln tons)

Utilisation factor

(%)

Quantity available for

energy purposes (mln ton)

Technical potential

(PJ)

Cereals straw 21,5 50 8,9 147 Rape straw 2,4 70 1,4 23

Hay 18,1 10 1,5 25 TOGETHER 11,8 mln t 195

The use of straw for energy was estimated on 40 ktons in 2001, or about 0.5 PJ. In 2002 there were about 65 small and medium scale (0,5 – 7 MWt) straw fired district heating plants, the first of which were implemented as demonstration projects in 1995. In addition there were perhaps 150 straw fired boilers in agricultural dwellings. It was estimated in Polish conditions that for every 1 MWt straw-fired district heating, it is needed employment of 3÷4 people [2]. Some results shows the costs of straw-fired small-scale district heating as the cheapest among the other sources of fuels, although the investment cost are relatively higher than natural-gas or fuel-oil. Utilisation of biogas in terms of digestion of liquid manure, sewage sludge and landfill gas production plays less important role than solid biofuels. Energy crops will play more important role in mid and long term perspective. Currently there has been several pilot and research short rotation coppice (SRC) plantations. Poland has not implemented internal governmental support system for energy crops, therefore further development is expected to be achieved by CAP regulations provided by the EU.

There are 2,3 Mha of unused land and about 645 thou. ha of contaminated agricultural land which may be withdrawn from agricultural use [1]. Using this area for short rotation coppice would result in c.424 PJ. Thus, the near term potential is much more greater than the present bioenergy use.

B io g a s5 %

O th e r e n e rg y c ro p s5 6 %

F o re s t re s id u e s &

w o o d w a s te1 3 %

S tra w , h a y2 6 %

Figure 1. Estimation of technical biomass potential in Poland, PJ (EC BREC/IBMER 2003) ENERGY CROPS Among energy crops tested in the country conditions are: short rotation coppice of willow (e.g. Salix viminalis), perennial grasses like Miscanthus s. giganteus, Miscanthus s sacchariflorus, artichoke, Rosa multiflori and Sida hermaphrodita. At present Salix Viminalis is most common energy crop. Total area currently cultivated is not exceeding 2000 ha. Willow plantations are used as biological sewage-treatment plants especially in rural regions. High annual growth of biomass indicates usefulness of those plantations for energy purposes. First trials showed that it is possible to gain 15-20 tons of dry matter per year from 1 hectare. Willow is also a good filter trapping toxic compounds from soil. These species however require special habitat conditions, mainly water and this fact must be taken into account while planning future energy plantations. Shortage of equipment for willow harvest on Polish market is another barrier for wider implementation. Pilot Salix plantations have been established and analysed by the Warmia-Mazury University in Olsztyn [3]. The pilot plants were established close to the University in Olsztyn (North-East) and second pilot plantations close to the Vistula river (North). Conducted tests included investigations of the yield mass in dependence on different factors (density of plants, cutting cycle, different clones). Usefulness of chosen perennial grasses of C-4 photosynthesis with a high biomass production also was tested in Polish conditions as potential raw material for energy production. Many species of potential energy grasses were analysed in the Institute of Growing and Acclimatisation of Plants and particularly by its Botanical Garden in

Bydgoszcz. Since 1971 there were collected over 400 species of grasses. The species included: Miscanthus giganteus, Miscanthus sacchariflorus, Miscanthus sinensis, Spartina pectinata (Praerie cordgras), Andropogon gerardi (big bluestem), Panicum virgatum (switchgrass), Arundo donax. The results of analysis had shown that amongst investigated species mainly Arundo donax and Miscanthus giganteus were interesting for energy purposes due to high yields [4]. Tolerant to heavy metals concentrations indicate that these species may be suitable for planting along the roadsides. Perspective breeding programs for 'alternative grasses' in Poland should cover: soil and climatic requirements, multiplication, agricultural methodology and technology of processing. LIQUID BIO-FUEL (RME, ETHANOL) Liquid biofuels, ethanol and biodiesel, have attracted huge interest in Poland and “hot” discussion from several years. Surplus production of ethanol stimulated the first experiments with using ethanol as an additive to gasoline in 1991. Raw materials include molasses and low quality grain, potatoes or other agricultural products. In 1997 ethanol additive to gasoline reached 100 ktons/a then dropped to c.50 ktons/a and remains stable until 2003. As concerning rape methyl ester (RME) Poland has only some small production on a pilot scale and some projects under development phase. A key driving force was the expectation that liquid biofuels can facilitate rural industrialization and reduce the high unemployment rates in rural regions. Act on Biofuels and Biocomponents was prepared in 2002 but since it was vetoed by the President the whole legislative procedure was undertaken which resulted in new proposal of the act (March 2003) adopted by Parliament in October 2003. However this version of Biofuel Act was also neglected, this time by Constitution Tribunal. So at that moment future of liquid biofuels in Poland is not clear.

BIOGAS National Sanitary Inspectorate in 1997 classified over 60% of the controlled rural water wells as polluted. Anaerobic digestion of animal manure is one of the options to minimise negative environmental impact of animal farms. The most responsible for water pollution in the rural areas in Poland is animal production and intensive fertilising. Until now, biogas plants in agriculture have been developed mainly to generate thermal energy only and, in some cases, to produce high quality fertiliser as a by-product. In the recent 20 years in Poland 10 biogas installations have been developed at individual farms. The majority of them are not working for both economic and technical reasons. Prospective investors has been discouraged by high investment costs and the lack of adequately proven technologies. However, there is a an interest in biogas production for energy at big industrial pig or cattle breeding farms and several, centralised co-fermentation biogas plants are being under development. The total biogas technical potential was estimated as 34 PJ in Poland [5]. Current utilisation of biogas is only around 1,5 PJ. The biggest is the technical potential of agricultural biogas. Landfill biogas also presents significant technical potential.

Poland has about 30 biogas systems in waste water treatment plants with an installed capacity of about 38,9 MW producing approximately 250 TJ heat and 72 GWh electricity. This equals together 1 PJ primary energy from municipal biogas.

15,2

11,5

4,6

1,7 0,9

02468

10121416

agriculturalbiogas

landfill biogas municipalbiogas

industrialbiogas

park greenwaste

PJ

Figure 2. Biogas potentials in Poland [5]

IMPLEMENTATION OF BIOENERGY TECHNOLOGIES The development of biomass technologies based on solid biofuels is the fastest growing RE branch in Poland. Successfully implemented several demonstration biomass DHP systems since 1990 pushed the market pressure causing great DHP operators interest in bioenergy. Wood-processing together with pulp and paper industry utilises majority of waste biomass since early 80’s so the sector development is at the advanced level. It may be predicted further intensive growth of production and import of domestic systems based on fuel wood and straw. The nearest bioenergy challenge is implementation of full chain biofuels production and larger scale biofuels market development. Further relevant renewable policy objectives improvement and solid biofuels market development should create basis for larger scale biomass electricity production and cogeneration in long term perspective. Development of liquid biofuels market waits on final political decisions. Detailed analysis of biomass market potential shows huge perspectives for bioenergy development in Poland. Solid-biofuels may play a very important role in the development of rural areas energy systems in short and mid-term. Elaboration of the renewable energy related policy within next years should be one of strongest factor in bioenergy development support. Current needs in short-term perspective in a field of solid biofuel utilisation include among other: prooven small-scale technology for domestic dwellings (<40 kW) from ecological and economical point of view, intensive district heating straw-fired technologies implementation (0,5–5MW), full chain equipment import or production (chippers, forwarders, transporters, containers handling and storage facilities) for forestry fuel production, elaboration and implementation of local forestry wood fuels production and supply demonstration projects, experience in planning, consulting and implementation of medium-scale projects.

Table 2. Biomass energy technologies implemented in Poland– state in 2002 (ECBREC & GUS, 2003)

Energy production per year* Type of installation

Power installed MW th/el Electricity

GWh Thermal

TJ CHP systems in pulp&paper and furniture industry

450 500 5000

Automatic wood-fired heating plants >500 kW

450 - 6750

Straw district heating plants >500 kW 90 - 920 Wood small and medium-scale boilers <500 kW

5 500 - 98800

Straw small and medium scale boilers <500 kW

23 - 230

Biogas plants (CHP and DH) 43 / 18 38 450 Landfill gas plants (CHP and DH) 19 / 7 22 200

In Poland the production of wood briquettes started in early 90’s, while production of wood pellets has started 3-4 years ago. At present on Polish market there are 15 producers of briquettes (in that one producer of straw briquettes) and 16 producers of pellets. Most of technologies of pellets/briquettes production is based in sawmills or manufactories consuming wood industry by-products. Wood briquettes (roughly estimated production - 65.000 t/year) are produced for Polish and EU market, while pellets are mainly exported to Germany, Denmark and Sweden. Data on production level has not been proved yet, as the market is in the initial phase however it can be estimated current production of pellets on c.130.000 t/year. BIOENERGY FINANCING Strong financial support for bioenergy at district heating sector and industrial projects has been developed in the last years. On average all investments in industrial and district heating applications have been supported with 30-50% investment subsidies. A rough estimate is that over 40 mln and 20 mln PLN as investment grants and soft loans subsidised bio-energy investments since 1990 mainly through national and bilateral financing. Some of the bioenergy industrial and district heating projects were funded through bilateral co-operation programmes with Sweden, Denmark, Finland and the Netherlands. EU structural funds and coherence funds are being expected to increase bioenergy applications especially in rural areas. There are also expectations that JI-projects (as Kyoto Protocol flexible mechanisms) will be a source of funding for bioenergy investments. Since 1995 several AIJ and JI pilot projects have been implemented in the country, notably

together with Norway, Canada, Finland and The Netherlands. Poland has signed MoU (Memorandum of Understanding) with Canada, Finland, The Netherlands and others are currently being under development. National guidelines for JI are being drafted, showing that 50-130 Mt CO2 equivalent may be available for the first commitment period. National priorities for JI are renewable energy (especially small- and medium-scale biomass district heating and wind), CHP, energy efficiency improvement and forestry activities. SUMMARY Taking into account analysis on both the utilization and technical potential of renewable energy sources in Poland one may state that, first of all, the use of biomass for heating sector and co-combustion in large plants will grow in the first phase, since it is a very cost-effective option. Also on the mid-term bioenergy production will play a crucial role in the development of renewable energy in Poland. It is expected that bioenergy will be the main contributor (more than wind and hydro) in green electricity target in Poland. Development of biofuels for transport sector depends on final political decisions. The only question – will be enough biomass available for fulfilling all targets in short term? The most important activities on bioenergy utilisation include elaboration of long-term strategy of bioenergy sector development in Poland. The main objective of it is an assessment of possible Polish input in development of biomass-energy technologies and technologies of production of liquid, solid and gaseous fuels as well as support to integration process of Polish agriculture with EU agriculture. Results should help reaching of quantities targets of RES share in energy balance, implementation of Kyoto protocol, improvement of energy security in enlarged European Union (EU25) and identify conditions for sustainable development of rural areas (in that assessment of external costs and benefits). These actions to be taken in the near future will enhance the development of bioenergy market in Poland although it is clear that through close regional co-operation, especially with neighbouring countries, a stronger synergic effect can be achieved through better transfer of experience/technology, development of common standards and financial frameworks for joint projects. Concluding it should be stated that despite major expectations (national RES Strategy for Poland) and forecasting for technical opportunities relating to bioenergy deployment in Poland (ECBREC, 2000) the sector faces difficulties in entering the market due to various imperfections of the legal/policy framework in Poland. Closer co-operation and joint research within the enlarged EU may help design solutions suitable for wider implementation of bioenergy in the region.

REFERENCES

[1] GUS – Central Statistical Office. Statistical Yearbook of Poland, Warszawa, 2003.

[2] GRZYBEK A., GRADZIUK P., KOWALCZYK K.. Straw-as a fuel, Warsaw POLBIOM, 2001.

[3] SZCZUKOWSKI S., BUDNY J., „Wierzba krzewiasta – roślina energetyczna. Poradnik” (Willow as an energy crop. Guideline), Olsztyn 2003.

[4] MAJTKOWSKI W. Perennial grass species as energy crops in Poland. Proceedings of the international conference “Renewable energy sources on the verge of the XXI century”. Warsaw 10-11th December 2001.

[5] ONISZK-POPŁAWSKA A. , ZOWSIK M., NOWAKOWSKI S. State of the art and perspectives for development of different biogas technologies in Poland. VIII Polish-Danish Workshop on Biomass for Energy, Starbienino, June 2003

ENERGY WOOD POTENTIAL OF FORESTS IN THE EUROPEAN UNION

Ján Ilavský, Timo Karjalainen, Antti Asikainen Finnish Forest Research Institute Joensuu Research Centre Yliopistokatu 6, 80101 Joensuu, Finland Tel.: +358 10 211 3296 E-mail: [email protected]

ABSTRACT The potential sources of forest fuels in 25 EU member countries are presented. Felling residues and stumps from current fellings as well as the roundwood balance between the net annual increment and current fellings were identified as potential energy wood resources. It was estimated that felling residues total 173 mill. m3

annually. Annually harvestable felling residues were estimated to be 63 mill. m3. In addition, about 9 mill. m3 stump wood from current fellings (out of 78 mill. m3 total potential) could be used for energy production. When 25 % of the roundwood balance, including above ground biomass, is directed to energy use, 64 mill. m3 of above ground biomass and about 4 mill. m3 of stump wood could be used for energy annually. Thus the available forest fuel totals about 140 mill. m3 per year, i.e. about 56 mill. owen dry tons of wood, which corresponds to about 280 TWh of energy or 24 Mtoe. This would be about 24% of the current use of renewables in EU25.

ISBF 2005, Bratislava, 21 – 22 February 2005

1

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Energy Wood Potential of Forests

in the European UnionJán Ilavský, Timo Karjalainen, Antti Asikainen

Finnish Forest Research Institute, Joensuu Research CentreYliopistokatu 6, 80101 Joensuu, Finland

Tel.: +358 10 211 3296, e-mail: [email protected]

ISBF 2005, Bratislava, 21 – 22 February 2005

2

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Contract from VTT Processes:results utilised in BioFuture project: Impact of increased use of bioenergy in Europe on forestand energy industries

Aim:estimation of energy wood potential in EU25, based on available statistics and reports reflecting the situation in late 1990’s - early 2000

ISBF 2005, Bratislava, 21 – 22 February 2005

3

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Gross Inland Consumption

Country group Country All fuels Renewables Biomass % of

renewables Finland 33.2 7.6 84Sweden 51.6 15.0 54Nordics

Total 84.8 22.6 Estonia 5.0 0.5 100Latvia 4.3 1.5 84Lithuania 8.2 0.7 96

Baltics

Total 17.5 2.7 Austria 30.3 6.7 45Czech Republic 41.0 0.7 74Hungary 25.1 0.4 95Poland 90.2 4.1 95Slovakia 18.5 0.7 41

C-E Europe

Total 205.1 12.6 France 262.3 18.6 65Germany 348.8 9.9 72Luxembourg 3.8 0.1

C-W Europe

Total 614.9 28.6 Belgium 55.6 0.8 88Denmark 19.9 2.2 82Ireland 14.4 0.3 67The Netherlands 77.6 1.6 94United Kingdom 232.5 2.7 85

N-W Europe

Total 400.0 7.6 Portugal 24.2 3.4 62Spain 126.3 8.3 50Iberia

Total 150.5 11.7 Cyprus 2.4 0.04 3Greece 28.9 1.3 77Italy 176.6 13.5 46Malta 0.9 - Slovenia 6.6 0.7 55

S & S-E Europe

Total 215.4 15.5 Grand total 1688.2 101.3

EU15•6% renewables•biomass 62% of the renewables

new member countries• 4.6% renewables•biomass 84% of the renewables

most of the biomass used for energy is wood

ISBF 2005, Bratislava, 21 – 22 February 2005

4

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Three parts of analysis:

3) Estimation of felling residues from forestsavailable for wood supply

1) Estimation of roundwood balance on forest available for wood supply, i.e. estimation of unutilised roundwood potential that could be used for energy purposes, but also for manufacturing conventional products in the forest based industries or not harvested

• Roundwood balance calculated as a difference between net annual increment and fellings

2) Roundwood and conventional fuelwood production

ISBF 2005, Bratislava, 21 – 22 February 2005

5

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Methods• background data

– data for net annual increment (NAI), fellings, and balance between NAI and fellings from the UN-ECE/FAO Forest Resources Assessment 2000 report (national data adjusted to fit internationally agreed terms and definitions)

– data for Cyprus from 1980’s – early 1990’s, for the other countries from mid 1990’s

– Estimation of roundwood and fuelwoodproduction based on the data from the Finnish Statistical Yearbooks 1999-2001 (FAOSTAT Forestry Data)

ISBF 2005, Bratislava, 21 – 22 February 2005

6

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Results on roundwood balance• standing volume (growing stock + dead

trees)18 140 million m3 (65% conif.)• growing stock 17 930 million m3

– 66% in five countries: France, Germany, Sweden, Finland and Poland

– 32% in Germany and France• forest resources increasing, since 1950

– forest cover +8%– average growing stock +10%– average net annual increment +25%

ISBF 2005, Bratislava, 21 – 22 February 2005

7

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

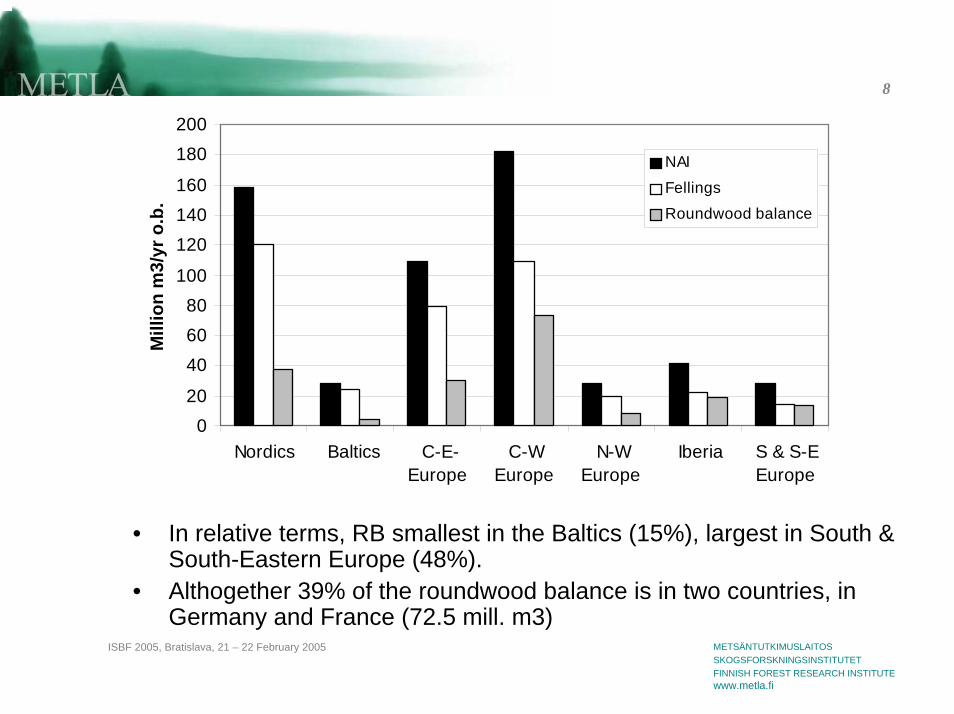

NAI Fellings Roundwood balance

Coniferous species dominated forests 384.9 277.1 107.8

Broadleaved species dominated forests 190.7 112.2 78.5

Total 575.6 389.3 186.3

Results on roundwood balance, continued

• fellings 68% of the NAI– 72% in conif.– 59% in broadl.

• roundwood balance 186 million m3/yr, i.e. unutilised increment 32% of the NAI

• more than 16% of the fellings used for energy production (industrial residues and recovered products)

•use of rounwood for energy purposes would depend of the prices for roundwood, wood-based products, energy

ISBF 2005, Bratislava, 21 – 22 February 2005

8

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

020

406080

100

120140160

180200

Nordics Baltics C-E-Europe

C-WEurope

N-WEurope

Iberia S & S-EEurope

Mill

ion

m3/

yr o

.b.

NAI

Fellings

Roundwood balance

• In relative terms, RB smallest in the Baltics (15%), largest in South & South-Eastern Europe (48%).

• Althogether 39% of the roundwood balance is in two countries, in Germany and France (72.5 mill. m3)

ISBF 2005, Bratislava, 21 – 22 February 2005

9

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Roundwood production (RP)

• wood over bark harvested from forests and used for commercial wood processing and fuelwood purposes during a year

• 368 million m3 per year in late 1990s (15% higher in 2000 than in 1997)– Approximately 69% softwood– Relative proportion of softwood logs 63% and hardwood logs

52%– 62% in Sweden, Finland, Germany and France

• Conventional fuelwood production – 48,4 million m3 per yearor – 13% of RP

ISBF 2005, Bratislava, 21 – 22 February 2005

10

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Estimation of felling residues from fellings of forests available for wood supply

Main sources of felling residues:

1. Residues from fellings of roundwood (branches, needles, tops, off cuts)

2. Potential residues from felling balance

3. Stumps and coarse roots

ISBF 2005, Bratislava, 21 – 22 February 2005

11

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Estimation of biomass components:

Roots estomation Roots estomation(Nordic and Baltic countries) (rest of Europe)

BROADLEAVED Group / 14.7%8.0%78.2% 12.1% 1.7%

67.7%

19.1%

19.3%

Stem+stembark Branches Needles

55% 24% 11%

TOTAL

SPRUCE Group

PINE Group 8%

Tops

2%

17.7% 4.6% 2%

Decayed stem

8% 100%

100%

100%

21.9%

19.8%

22.4%

ISBF 2005, Bratislava, 21 – 22 February 2005

12

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

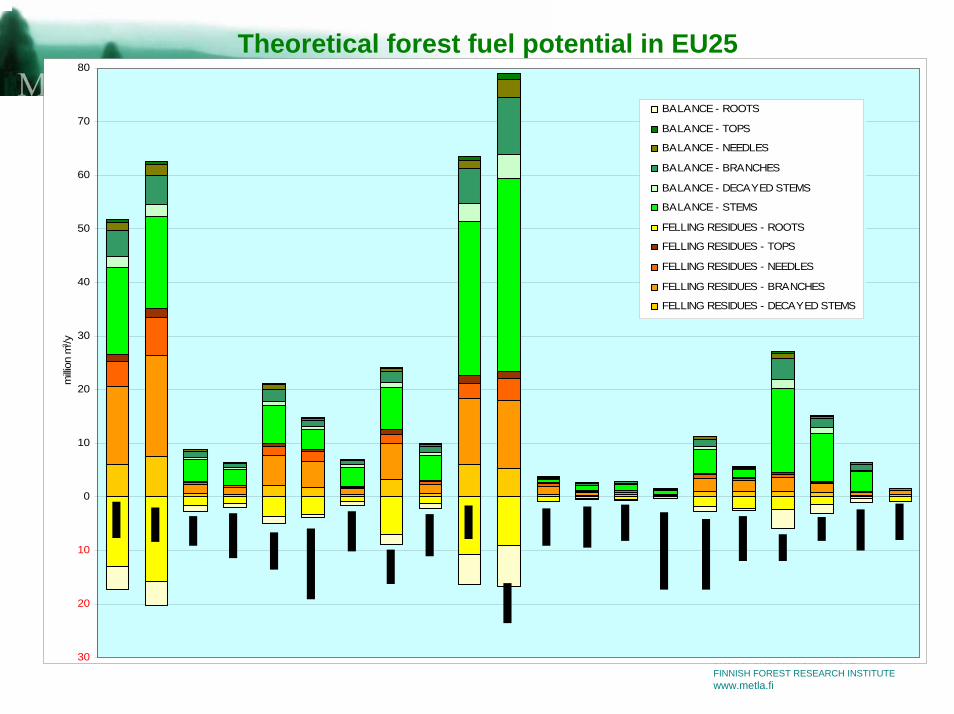

ResultsTheoretical forest fuel resources of EU25:logging residues + balance = 560 mill. m3 (+144%)

BIOMASSCOMPONENTS

ROOTS 78

BRANCHES 93,9

9,7

NEEDLES

TOPS

28,8

OFF CUTS 40,8

LOGGING RESIDUES

million m3/y

(STEM+STEMBARK) (389.3)

BIOMASSCOMPONENTS

BALANCE = NAI - FELLINGS

46

million m3/y

STEM+STEMBARK 186.3

ROOTS 37.7

13,6

4,8

NEEDLES

TOPS

OFF CUTS 20,3

BRANCHES

ISBF 2005, Bratislava, 21 – 22 February 2005

13

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Theoretical forest fuel potential in EU25

30

20

10

0

10

20

30

40

50

60

70

80m

illion

m3 /y

BALANCE - ROOTS

BALANCE - TOPS

BALANCE - NEEDLES

BALANCE - BRANCHES

BALANCE - DECAYED STEMS

BALANCE - STEMS

FELLING RESIDUES - ROOTS

FELLING RESIDUES - TOPS

FELLING RESIDUES - NEEDLES

FELLING RESIDUES - BRANCHES

FELLING RESIDUES - DECAYED STEMS

ISBF 2005, Bratislava, 21 – 22 February 2005

14

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Estimation of technically harvestableforest fuel potential

REDUCTION FACTORS:

1. On 75% of clearcut sites and on 45% of thinning sites, residues can be harvested

65% of residues from mechanized cutting are recoverable

50% of residues from manual cutting are recoverable

2. 20% of volume of roots from clearcuts are harvestable

3. 25% of volume of balance is harvestable(roots volume of balance is not taken under consideration)

ISBF 2005, Bratislava, 21 – 22 February 2005

15

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Volume of available forest fuels by country

Share of timber Share of Total felling AVAILABLE RESIDUES AVAILABLE RESIDUES FELLING RESIDUES BALANCEfrom clearcuts mechanization in residues OF FELLING OF BALANCE VOLUME OF ROOTS VOLUME OF ROOTS

Austria 18 % 30 % 10,1 2,9 2,7 0,2 0,1

Belgium (70% by default) 80 % 2,6 1,1 0,3 0,1 0,0

Cyprus

Czech Republic 83 % 10 % 8,9 3,2 1,5 0,5 0,1

Denmark 70 % 50 % 1,2 0,4 0,4 0,0 0,0

Estonia 73 % 55 % 1,6 0,6 0,0 0,1

Finland 79 % 97 % 26,7 11,4 6,3 1,8 0,6

France 76 % 40 % 22,6 8,6 10,2 1,6 0,9

Germany 5 % 35 % 23,4 6,0 13,9 0,1 0,1

Greece 6 % 0 %

Hungary 72 % 15% A.A. estimation 2,0 0,7 1,2 0,1 0,1

Ireland 82 % 95 % 1,3 0,6 0,4 0,1 0,0

Italy 20 % 2 % 2,9 0,7 3,1 0,1 0,1

Latvia 76 % 5 % 2,9 1,0 1,5 0,2 0,2

Lithuania 50 % 0 % 2,2 0,7 1,1 0,1 0,1

Luxembourg

Malta

The Netherlands 80 % 25 % 0,6 0,2 0,3 0,0 0,0

Poland 44 % 2,0% 12,5 3,6 2,9 0,6 0,2

Portugal (70% by default) (40% by default) 3,6 1,3 0,5 0,3 0,0

Slovakia 40,2% 0,7% 3,0 0,9 1,7 0,1 0,1

Slovenia 0 % 0,7% 1,1 0,3 1,3 0,0 0,0

Spain (70% by default) (40% by default) 4,4 1,6 5,7 0,3 0,5

Sw eden 70 % 98 % 35,2 15,0 6,9 2,2 0,6

United Kingdom (70% by default) 90 % 4,4 1,8 1,7 0,2 0,1

COUNTRY

TOTAL 173,2 62,6 63,5 9,0 3,8

% cutting % (mill. m3 /y) (mill. m3 /y) (mill. m3 /y) AVAILABLE (mill. m3 /y) AVAILABLE (mill. m3 /y)

ISBF 2005, Bratislava, 21 – 22 February 2005

16

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

Volume of technically available forest fuels in EU25:71.6 mill. m3 from felling residues + 67.3 mill m3 from balance = 138.9 mill. m3

= approximately 25% of the theoretical potential 560 mill. m3

TOTAL AVAILABLE AVAILABLE VOLUME OF ROOTS VOLUME OF ROOTSFELLING RESIDUES SHARE AVAILABLE AVAILABLE

RESIDUES OF FELLING OF BALANCE FROM FELLINGS FROM BALANCE(mill. m3 /y) (mill. m3 /y) (mill. m3 /y) (mill. m3 /y) (mill. m3 /y)

3,8173,2 62,6 63,5 9,0

above ground 36% ofresidues

25% of above ground balance

14% on top of above ground availablefelling residues

6% on top of above groundavailable balance

ISBF 2005, Bratislava, 21 – 22 February 2005

17

METSÄNTUTKIMUSLAITOSSKOGSFORSKNINGSINSTITUTETFINNISH FOREST RESEARCH INSTITUTEwww.metla.fi

The whole study is available in PDFformat at:

http://www.metla.fi/julkaisut/workingpapers/2004/mwp006.htm

Thank you for your attentionĎakujem za pozornosť

REFITS – AN INSTRUMENT FOR RENEWABLES’ MARKET LAUNCH BESIDES OTHERS

Alexandra Langenheld, Christof Stein Division “Solar energy, Biomass, Geothermal energy, market incentive pro-grammes for renewable energies” Federal Ministry for the Environment, Nature Conservation and Nuclear Safety, Alexanderplatz 6, 10178 Berlin, Germany +49 1888 305-3625 [email protected] ABSTRACT Achieving a sustainable energy supply requires the global turn of energy policy: Phasing out nuclear technology, cutting off the „oil-drip“ and replacing them by re-newable energies, economical use of energy and energy efficiency. To reach the German Federal Government’s goal of meeting 20 % of the needs of electricity by renewable energies until 2020 the increasing use of biomass – providing a reason-able mix of all lines of renewable energies – is an important premise in the future. Biomass is predicted to have a promising future because of its exceeding potential. It is the most multifaceted type of energy use requiring a well adapted and flexible raft of measures: Renewable Energy Sources Act, Market Incentive Programme and Ac-companying Ecological Research are the Federal Government’s instruments to sup-port biomass on its way to competitiveness on the energy market. INTRODUCTION Achieving a sustainable energy supply requires the global turn of energy policy: Phasing out nuclear technology, cutting off the „oil-drip“ and replacing them both by renewable energies instead of fossil resources, economical use of energy and en-ergy efficiency. To reach the Federal Government’s goal of meeting 20 % of the needs of electricity and 10 % of the needs of primary energy consumption by renewable energies until 2020 the increasing use of biomass – providing a reasonable mix of all lines of re-newable energies – is an important premise in the future. CONTENT 1. Energy policy and sustainability strategies 2. Challenges – Climate protection, economic efficiency and securing the energy

supply 3. Policy targets in the development of renewable energies – Where do we

stand?! 4. Biomass – The most multifaceted and oldest type of energy use 5. Political framework: Policy instruments for promoting renewable energies espe-

cially biomass – Renewable Energy Sources Act, Market Incentive Programme, Ecological Accompanying Research

6. Outlook – Market launch of biomass

ENERGY POLICY AND SUSTAINABILITY STRATEGIES Achieving a future-orientated energy supply is one of the Federal Government’s prime goals. In this, equal emphasis is laid on the following objectives: • conservation of the environment and resources, especially climate protection, • economic efficiency for producers and consumers and • securing the energy supply. Germany has initiated a new direction in energy policy. The key aspects are: • massive expansion of renewable energies, • marked improvements in energy efficiency and economical use of energy and • phasing out nuclear technology and its attendant risks. Additional information can be derived from the official website of the Federal Envi-ronment Ministry: http://www.bmu.de/de/800/js/base/ or the website especially for renewable energies: http://www.erneuerbare-energien.de/1024/. CHALLENGES …of climate protection On a worldwide basis, 70 % of the greenhouse effect is due to energy-induced CO2-emissions. In Germany the figure is as high as 88 %. Therefore Germany has under-taken to make a 21 % reduction in its emissions of the six greenhouse gases listed in the Kyoto Protocol from 1990 levels by 2008/ 12. Germany, along with the EU, advocates ambitious targets in the international nego-tiations that are starting on further development of the Kyoto targets after 2012 (sec-ond commitment period). Mentioned must be here the recently submitted special report of the WBGU (Scientific Advisory Council on Global Environmental Change) “Climate Protection Strategies for the 21st Century”. The Renewable Energy Sources Act is one of the most efficient instruments for cli-mate protection in Germany. In 2003 about 50 million tons of carbon dioxide have been saved by using renewable energies. But furthermore, there is a need to develop a new energy supply structure in view of climate protection. This is being done under the lead management of the Federal Chancellor’s Office as part of the First Progress Report on the Federal Government’s National Sustainability Strategy. …of economic efficiency Germany is faced with fundamental decisions with regard to energy policy. The age structure of the country’s power stations means that over the next 20 years it will be necessary to replace some 40,000 to 60,000 MW of electric power station capacity (about half of the existing power stations). This offers a real opportunity to achieve a structural change towards more decentral-ised energy supplies in an economically efficient way. Phasing out nuclear technol-ogy will support this necessary process of modernisation. …of securing the energy supply The task of further improving economic efficiency, improving the quality of life, as well as eliminating poverty around the world at the same time, requires reliable and