2012 Annual Results

29

2012 Annual Results 18 March 2013

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2012 Annual Results

2012 Annual Results

18 March 2013

Content

ANNUAL RESULTS

BUSINESS REVIEW

PROSPECTS

2

Majestic City, Foshan

ANNUAL RESULTS

3

Glorious International, Xiamen

08 09 10 11 12

5,190 7,646

12,671

15,464

18,722

08 09 10 11 12

19,836

39,278 46,650

51,332

64,581

4

Unit 2012 2011

(Restated) Change

Turnover HK$ Million 64,580.7 51,332.3 25.8%

Turnover(including share of turnover of JCEs)

HK$ Million 77,907.9 57,723.3 35.0%

Gross Profit HK$ Million 24,725.2 20,672.2 19.6%

Net Profit HK$ Million 18,722.2 15,464.1 21.1%

Gross Margin Percentage % 38.3 40.3 - 2 ppts

Net Profit Margin Percentage % 29.0 30.1 -1.1 ppts

EPS HK cents 229.0 189.0 21.2%

DPS HK cents 41 33 24.2%

Turnover (HK$ mn)

Net Profit (HK$ mn)

Dividend payout ratio

Financial Summary

66 94

155

189 229

13 20 27 33 41

20% 21%

17% 17% 18%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

2008 2009 2010 2011 2012

EPS (HK cents) DPS (HK cents) Payout ratio

08 09 10 11 12

33.56 42.61

55.56

71.62

87.22

Financial Summary (cont’d)

5

Unit 31/12/2012 31/12/2011 (Restated)

Change

Cash on Hand HK$ Million 40,932 19,197 113.2%

L/T Debt HK$ Million 53,243 32,803 62.3%

Shareholders' Equity

HK$ Million 87,244 71,617 21.8%

Net Gearing (%) Percentage % 20.5 32.7 -12.2 ppts

Liabilities/Assets (%)

Percentage % 61.9 59.1 2.8 ppts

ROE(%) Percentage % 23.6 24.3 -0.7 ppts

ROA(%) Percentage % 9.2 9.1 0.1 ppts

ROE (%)

ROA(%)

Shareholder’s Equity (HK$ bn)

6.9

7.7

9.2 9.1 9.2

08 09 10 11 12

17.3

20.1

25.8 24.3 23.6

08 09 10 11 12

Pearl River Delta 17.3%

Yangtze River Delta

21.9% Bohai Rim

22.1%

Northern Region 10.4%

Western Region 24.2%

HK & Macau 4.1%

Pearl River Delta

15.5% Yangtze River Delta

20.0%

Bohai Rim 22.0%

Northern Region 16.3%

Western Region 23.0%

HK & Macau 3.2%

6

Turnover (HK$ million) Profit (HK$ million)

2012 2011

(Restated) Change 2012

2011 (Restated)

Change

Property Development

61,407 49,432 24.2% 25,152 20,025 25.6%

Property Investment

585 373 56.8% 4,147 3,331 24.5%

Others 2,589 1,527 69.5% 136 186 -26.8%

Total 64,581 51,332 25.8% 29,435 23,542 25.0%

Property Development Turnover by Region

Total Property Turnover: HK$ 61,407 million

Property Development Operating Profit by Region

Property Development Operating Profit: HK$ 22,510 million

Segment Results Highlights

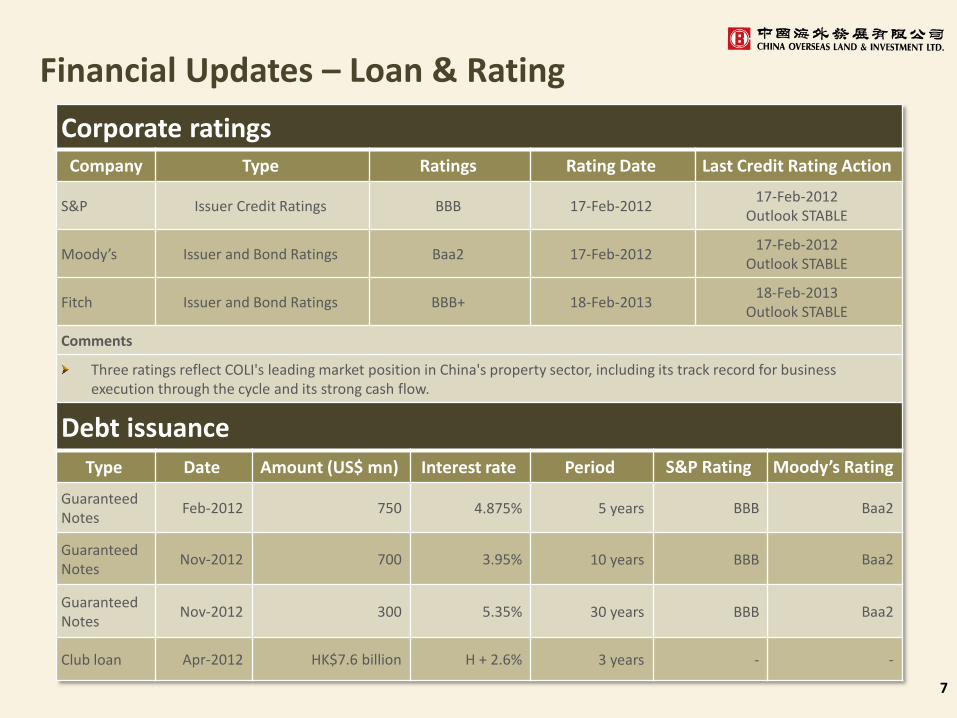

Financial Updates – Loan & Rating

7

Corporate ratings Company Type Ratings Rating Date Last Credit Rating Action

S&P Issuer Credit Ratings BBB 17-Feb-2012 17-Feb-2012

Outlook STABLE

Moody’s Issuer and Bond Ratings Baa2 17-Feb-2012 17-Feb-2012

Outlook STABLE

Fitch Issuer and Bond Ratings BBB+ 18-Feb-2013 18-Feb-2013

Outlook STABLE

Comments

Three ratings reflect COLI's leading market position in China's property sector, including its track record for business execution through the cycle and its strong cash flow.

Debt issuance Type Date Amount (US$ mn) Interest rate Period S&P Rating Moody’s Rating

Guaranteed Notes

Feb-2012 750 4.875% 5 years BBB Baa2

Guaranteed Notes

Nov-2012 700 3.95% 10 years BBB Baa2

Guaranteed Notes

Nov-2012 300 5.35% 30 years BBB Baa2

Club loan Apr-2012 HK$7.6 billion H + 2.6% 3 years - -

Financial Updates –Debt Structure

8

Interest bearing debts by currency

Debt maturity profile *

$HK mn Within 1

year 1-5

years 5-10 years

10+ years

Bank borrowings

5,546 32,095 - -

bonds - 5,787 13,060 2,301

Subtotal 5,546 37,882 13,060 2,301

Percentage 9% 91%

Amount(HK$ billion)

Cash 40.93

Unused credit facilities 8.22

Total 49.15

Net gearing 20.5%

13.7%

36.8%

49.5%

RMB US$ HK$

The Investment Property

The investment property

9

Major Occupied Investment Property

City Name of the project Usage GFA(000㎡)

Beijing China Overseas Plaza Office 139

China Overseas Property Building Office 24 China Overseas Property Plaza Office 82

Chengdu China Overseas International Center phase 1&2 Office 201

China Overseas Building Office 35

Hong Kong China Overseas Building Office 19.5

Horae Plaza Shopping mall 3.6 Union Plaza Shopping mall 6.2

Macau La Cite Shopping mall 4.2

The Fact of COLI’s Investment Property in 2012 (ex COGO)

Total Attributable Investment Property GFA (mn sq.m.) 2.4

The Number of Cities Entered 9

The Number of Unipark Shopping Malls 5

Total Rental Income(HKD mn) 585 22%

53%

25%

Investment property GFA by progress

Investment property GFAleased out

Investment propertylandbank under construction

Investment propertylandbank to be developped

Shopping mall Office

19% 7%

30%

6%

36%

2%

Investment Property landbank GFA by Region

Pearl River Delta

Yangtze River Delta

Bohai Rim

Northern Region

Western Region

HK& Macau

BUSINESS REVIEW

Property Sales

Landbank

Xue Fu Road, Kunming

10

18.14%

23.47%

19.11%

17.21%

15.62%

6.45%

Pearl River Delta

Yangtze River Delta

Bohai Rim

Northern Region

Western Region

HK & Macau

2012 Property Sales

11

Property sales sold by region

202.3

261.7

213.1 191.9

174.2

72.0

145.6

175.0

204.4

158.2 163.5

24.3 38.9% 49.6%

4.3% 21.3% 6.6%

196.3%

0%

50%

100%

150%

200%

250%

0

40

80

120

160

200

240

280

Pearl RiverDelta

Yangtze RiverDelta

Bohai Rim NorthernRegion

WesternRegion

HK & Macau

2012 Sales value (HK$'00mn) 2011 Sales value (HK$'00mn) YoY

Property sales in value

137.04 125.05

140.02

184.37

136.48

6.18

92.39 80.14

97.12

159.5

127.43

1.62

48.3% 56.0% 44.2%

15.6% 7.1%

281.5%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

0

20

40

60

80

100

120

140

160

180

200

Pearl RiverDelta

Yangtze RiverDelta

Bohai Rim NorthernRegion

WesternRegion

HK & Macau

2012 Sales GFA(‘000 Sq.m.) 2011 Sales GFA(‘000 Sq.m.) YoY

Property sales in GFA

18.79%

17.15%

19.20% 25.29%

18.72%

0.85%

Pearl River Delta

Yangtze River Delta

Bohai Rim

Northern Region

Western Region

HK & Macau

Property sales GFA by region

For 2012, the property contracted sales amounted to HK$ 104.7 billion and the contracted GFA reached 6.8 million square meters.

As at the end of 2012, the property subscription sales amounted to HK$ 6.79 billion and the subscription GFA reached 0.49 million square meters.

2013 Property Sales Updates

12

From Jan-13’ to Feb-13’, the total property contracted sales amounted to HK$25.5 billion and the total contracted GFA reached 1.6 million square. As at the end of February 2013, the property subscription sales amounted to HK$6.8 billion and the subscription GFA reached 377,500 square meters.

Region Contracted GFA

(‘0000sq.m.) Contracted amount

(HK$’00mn) Subscription GFA*

(‘0000sq.m.) Subscription amount*

(HK$’00mn)

Pearl River Delta 55.30 78.19 13.41 20.44

Yangtze River Delta 34.59 72.06 5.53 15.29

Bohai Rim 24.35 43.96 5.85 13.75

Northern Region 18.75 18.78 7.03 9.12

Western Region 26.08 32.64 5.93 9.40

HK & Macau 0.56 9.21 - -

Total 159.63 254.84 37.75 68.00

*As at the end of February 2013

Pearl River Delta, 24.3%

Yangtze River Delta, 45.8%

Bohai Rim, 9.5%

Northern Region, 6.4%

Western Region, 7.4%

HK & Macau, 6.6%

Pearl River Delta, 31.5%

Yangtze River Delta,

40.9%

Bohai Rim, 4.5%

Northern Region, 11.3%

Western Region, 11.5%

HK & Macau,

0.3%

New Land Acquisition in 2012

13

2 projects in 1st tier cities with attributable GFA of 300,703 m2 . 18 projects in 2nd tier cities with attributable GFA of 6.3 mn m2 .

* Exchange rate of Hongkong dollar to RMB is 0.812.

No. City Name of Project Attributable

Interest Land Area

(m2) Total GFA

(m2) Attributable

GFA (m2) Land Cost (RMB mn)

1 Foshan Nanhai District Guicheng Project

100% 199,471.70 731,481.00 731,481.00 1,456.30

2 Hongkong Ap Lei Chau Project 100% 3,050.00 21,350.00 21,350.00 2,060.86*

3 Chengdu Chengnan New District Project

100% 102,309.27 590,034.00 590,034.00 1,676.75

4 Tianjin Hexi District Project 100% 79,955.70 300,000.00 300,000.00 2,970.00

5 Kunming Wuhua District Project 100% 38,973.53 171,484.00 171,484.00 636.00

6 Yantai Gaoxin District Project 100% 74,203.00 207,515.00 207,515.00 270.70

7 Dalian Ganjingzi District Project 100% 99,000.00 216,930.00 216,930.00 648.35

8 Hangzhou Jianggan District Project 100% 84,255.00 422,656.00 422,656.00 5,588.00

9 Shenyang Huanggu District Project 100% 23,101.10 101,834.00 101,834.00 202.17

10 Shenzhen Bao'an District Project 100% 151,787.21 279,353.00 279,353.00 2,000.00

11 Wuhan Hangyang District Project 100% 48,765.00 209,853.00 209,853.00 966.00

12 Hangzhou Xihu District Project 100% 73,321.00 202,713.00 202,713.00 1,321.78

13 Xiamen Jimei District Project 51% 78,760.02 254,700.00 129,897.00 308.14

14 Suzhou Gusu District Project 100% 133,910.70 434,344.00 434,344.00 1,990.00

15 Qingdao Shibei District Project 100% 74,005.70 221,700.00 221,700.00 872.38

16 Suzhou Yuan District Project 100% 121,747.69 284,077.00 284,077.00 837.00

17 Foshan Nanhai Gaoxin District C project

100% 112,291.00 619,279.00 619,279.00 2,840.00

18 Suzhou Wuzhong District G-103 Project

100% 126,911.80 339,819.00 339,819.00 890.00

19 Ningbo Yinzhou New City No.11 South project

100% 186,211.00 507,945.00 507,945.00 1,787.63

20 Ningbo Yinzhou New City No.11 North project

100% 192,471.00 525,021.00 525,021.00 1,847.72

Subtotal: 2,004,501.42 6,642,088.00 6,517,285.00 31,169.78

New land acquisition of COGO : 1,204,068.58 3,679,017.00 3,407,568.36 4,489.42

Total: 3,208,570.00 10,321,105.00 9,924,853.36 35,659.20

Total GFA by region

Total land cost by region

New Land Acquisition in 2013

14

No. City Name of Project Attributable Interest Land Area

(m2) Total GFA

(m2) Attributable GFA (m2)

Land Cost (RMB mn)

1 Kunming Guandu District Project 65% 172,634.96 377,061.00 245,089.65 504.95

2 Beijing Shijingshan District Project 100% 38,097.08 159,648.00 159,648.00 2,018.00

3 Nanjing Jiangning District Project 100% 234,058.70 931,382.00 931,382.00 2,806.00

Subtotal: 444,790.74 1,468,091.00 1,336,119.65 5,328.95

New land acquisition of COGO : 427,543.99 1,459,175.07 1,293,790.27 2,164.12

Total: 872,334.73 2,927,266.07 2,629,909.92 7,493.07

Jiangangshan project, Baoan District Shenzhen

Project Completed in 2012

15

A total of 28 projects and 12 JV projects were completed in 2012.

Total Gross Floor Area (GFA) completed was 4.9 and 2.1 million m2 respectively.

About 82.3% and 67.8% of the total saleable GFA m2 completed was sold by 31 December 2012.

COLI projects completion

City Project Name GFA Completion (‘000m2 )

Beijing

The Metropolis(中海城) 72.3

Residence Nine(九号公馆) 178.3

Walden Pond Villa Phase 4(瓦尔登湖四期) 20.2

Suli Manner(苏黎世家) 66.8

Laogucheng(老古城) 193.5

Jinan International Community (国际社区) 457.4

Shenyang COLI City(中海城) 493.3

La Cite(寰宇天下) 378.3

Dalian Violet Palace(中海紫御观邸) 94.9

Qingdao International Community(国际社区) 219.8

Changchun

Rayal Court(紫御华府) 151.2

International Community(国际社区) 20.4

The Arch(凯旋门) 123.7

Suzhou International Community(国际社区) 346.5

Lohas Island(独墅岛二期) 130.4

Nanchang Sunrise Manor(中海朝阳郡) 58.4

Nanjing The Phoenix(凤凰熙岸) 130.8

Shenzhen Olympic City(康城国际花园) 15.2

Foshan Golden Sand Coast(中海金沙湾中区) 192.3

Zhongshan Dragon Bay phase 1 (龙湾花园一期) 77.5

Xiamen La cite(寰宇天下) 68.6

Changsha International Community(国际社区) 309.8

Xi'an International Community(国际社区) 304.9 Qianjiang new city project, Hangzhou

Pearl River Delta,

6 Yangtze River

Delta, 8

Bohai Rim, 8

Northern Region,

9

Western Region,

9

16

City Project Name GFA Completion (‘000 m2 )

Chengdu

One Villa South(中海城南官邸) 50.7

International Community(国际社区) 120.9

One City South(城南一号) 53.8

Majestic City(中海锦城) 462.6

Zhuhai Silver Bay(银海湾二期) 69.7

Subtotal: 4,862.3

COLI JV projects completion

City Project Name GFA Completion (‘000 m2 )

Tianjin Peaceland Cove(北宁湾) 336.3

Jinan Dragon Manor Phase 2(奥龙观邸二期) 55.3

Shenyang International Community(国际社区) 206.3

Qingdao Violet Palace(紫御观邸) 250.9

Suzhou Gusu Mansion(姑苏公馆一期) 49.0

Ningbo The Dynasty phase 1 (九唐华府一期) 46.1

Hangzhou La Cite(寰宇天下) 164.9

The Tudor(篁外山庄二期) 84.3

Xi'an Greenwood Cove(碧林湾) 244.4

Chongqing

The Throne(紫御江山) 124.2

La Cite(寰宇天下) 282.0

International Community(国际社区) 262.9

Subtotal: 2,106.6

Total: 6,968.9

Project completion by region

No. of Project completion by region

Project Completed in 2012

Pearl River Delta 11% Yangtze River

Delta 14%

Bohai Rim 20%

Northern Region

28%

Western Region

27%

Property Unbooked, Sales Presold & Booked GFA & Amount*

17

112 173 171

267

131 215

152 225

266

379 455

713

418

614

303

478

GFA('0000sq.m.) Amount(HK$'00mn) GFA('0000sq.m.) Amount(HK$'00mn) GFA('0000sq.m.) Amount(HK$'00mn) GFA('0000sq.m.) Amount(HK$'00mn)

JV 688

2011 Unbooked Sales 2012 Property Sales 2012 Booked Property Sales Presold Property

378 552 626 980 549 829 455 703

*Note: Excluding COGO’s property sales.

18

Current Landbank

18

Qingdao

Cities with COLI & COGO

Cities with COLI

COLI landbank by region

Total landbank by city tiers

Bohai

Rim

Yangtze River

Delta

Pearl River

Delta

Western

Region

Northern

Region

Shenzhen

Macau

Zhuhai

Hongkong Zhongshan

Guangzhou Foshan

Nanchang

Changsha

Xi’an

Chengdu

Chongqing

Shanghai

Ningbo

Hangzhou

Suzhou

Beijing

Tianjin

Jinan

Dalian

Shenyang

Changchun

Xiamen

Wuhan

HK&Macau

Yantai Qingdao

Nanjing

Kunming

Region No. City GFA

('000 m2) % Tier

Northern Region

4 Changchun 1,422 3.9% 2

5 Shenyang 5,116 14.0% 2

6 Dalian 608 1.6% 2

7 Qingdao 1,927 5.3% 2

8 Yantai 486 1.3% 2

Subtotal 9,559 26.1%

Region No. City GFA

('000 m2) % Tier

Bohai Rim

1 Beijing 437 1.2% 1

1 Tianjin 810 2.2% 2

3 Jinan 2,515 6.9% 2

Subtotal 3,762 10.3%

Region No. City GFA

('000 m2) % Tier

Yangtze River Delta

9 Shanghai 701 1.9% 1

10 Suzhou 2,407 6.6% 2

11 Nanjing 1,914 5.2% 2

12 Ningbo 1,428 3.9% 2

13 Hangzhou 1,739 4.8% 2

14 Nanchang 438 1.2% 2

Subtotal 8,627 23.6%

Region No. City GFA

('000 m2) % Tier

Pearl River Delta

15 Shenzhen 512 1.4% 1

16 Guangzhou 1,373 3.8% 1

17 Zhongshan 431 1.2% 2

18 Foshan 2,306 6.3% 2

19 Zhuhai 1,332 3.6% 2

20 Changsha 1,020 2.8% 2

21 Xiamen 399 1.1% 2

Subtotal 7,373 20.2%

Region No. City GFA

('000 m2) % Tier

Western Region

23 Chengdu 1,316 3.6% 2

24 Chongqing 3,210 8.8% 2

25 Xi'an 1,386 3.8% 2

26 Kunming 611 1.6%

Subtotal 6,523 17.8%

Region No. City GFA

('000 m2) % Tier

HK & Macau

27 Hongkong 70 0.2% 1

28 Macau 112 0.3% 1

Subtotal 182 0.5%

No. City GFA

('000 m2) % Tier

22 Wuhan 545 1.5% 2

Total Landbank (mn m²)

Att. Landbank (mn m²)

COLI (Incl. COGO) 47.16 41.98

COLI (EX. COGO) 36.57 32.91

COGO 10.59 9.07

8.8%

91.2%

1st tier cities('000sq.m)

2nd tier cities('000sq.m)

20.2%

23.6%

10.3%

26.1%

17.8%

1.5% 0.5%

Pearl River Delta Yangtze River Delta

Bohai Rim Northern Region

Western Region Wuhan

HK & Macau

PROSPECT

19

Qianjiang new city project, Hangzhou

Market Segment

20

Tier-1 Cities

Beijing, Shanghai, Guangzhou, Shenzhen

Cities COLI developed. Cities COLI would enter.

Cities COGO developed. Cities COGO would enter

COLI continues to focus on property market in tier-1 &2 cities.

COGO continues to develop in tier-3 cities with business potentiality.

The number of tier-1 &2 cities is more than 50. In light of current expansion pace, COLI should have ample development space.

Note: 4 national municipalities, 285 prefecture-level cities, and 369 county-level cities for a total amount of 658 cities in China.

Opportunities and Challenges Opportunities Challenges

Tier 1 in Mainland

Fast pace of economic development creates strong demand from first- home buyers

The upgrade of the service industry attracts a large number of talents with strong affordability

The risk associated with huge amount of individual project investments

Industry consolidation in the property market will accelerate, and the market share of top developers will increase

Risk from tightening policies

Tier 2 in Mainland

The acceleration of new urbanization and regional integration bring opportunities

Upgraded industry and population migration will create more demand and investment

Intensified market competition

Risk from inventory oversupply

Hong Kong & Macau

Scarcity of supply, strong affordability, and low interest-rate environment

High development cost with policy uncertainty

21

Strategies

22

Marketing

Investment

Financing

Operational

Stick to Marketing Segmentation Strategy towards various regions and product lines, leveraging market acumen to artfully schedule and organize new launches.

Ensure solid liquidity fundamentals and maintain sound liabilities structure, with net gearing level consistently below 40%.

Land replenishment will be focused on primary locations and strictly in line with cash collection and financial resources on hand.

Further strengthen control and management in every steps of the whole value chain to proactively enhance operational efficiency and effectiveness.

COLI

23

2013 Guidance 2012 Actual

Net profit growth Over 20% 21.1%

Project Completion (million Sq.m. ) 9.0 7.0

New Project Commencement (million Sq.m. )

10.8 9.7

Property Sales (HK$ billion ) 100(Contracted sales amount) 111.5

New Land Acquisition (million Sq.m. ) 8.0 6.6

Total Capex (HK$ billion) 102 65.0

- Outstanding Land Payment (HK$ billion)

22 5.7

- New Land Acquisition (HK$ billion)

30 21.5

- Projects Construction (HK$ billion)

50 37.8

Guidance for 2013

Property Completion Estimate by Region in 2013

24

Region GFA Completion

(‘000 m2)

Pearl River Delta * 2,054.6

Yangtze River Delta 1,815.1

Northern Region 2,890.4

Bohai Rim 770.0

Western Region 1,445.4

HK & Macau 37.6

Total 9,013.1

*Note: Including Zhuhai & Wuhan

Property completion by region in 2013

Pearl River Delta 23%

Yangtze River Delta 20%

Northern Region

32%

Bohai Rim 9%

Western Region

16%

HK & Macau 0%

Subsidiary of China State Construction Engineering Corporation(CSCEC), the largest construction conglomerate in China. CSCEC hold 53.2% of total shares. Incorporated in Hong Kong in 1979. listed on the Stock Exchange of Hong Kong Limited in August 1992. It was the first Chinese enterprise to acquire the listing status by its own local business or assets located in Hong Kong. On 10 December 2007, it became a constituent stock of the Hang Seng Index. Market value rank the first in mainland property sector. The first mainland property company awarded Standard & poors’ BBB rating and Moody’s Baa2 rating. Selected as one of the constituent of Standard & Poor's Global Property 40 Index

Appendix 1: Shareholding Structure

100%

53.0%

100%

53.2%

38%

Appendix 1: Corporate Profile

Macau

Zhuhai Hongkong

Zhongshan

Guangzhou Foshan

Nanchang

Changsha

Xi’an

Chengdu

Chongqing

Shanghai

Ningbo Hangzhou

Suzhou

Nanjing Hefei

Nanning

Guilin

Yinchuan

Hohhot

Beijing

Tianjin

Jinan

Dalian

Yantai

Qingdao

Shenyang

Changchun Jilin

Xiamen

Lanzhou

Wuhan

Ganzhou

Yangzhou

Kunming

Nantong

Changzhou

Yancheng Cities with COLI & COGO

Cities with COGO

Cities with COLI

Bohai

Rim

Yangtze River

Delta

Pearl

River

Delta

Western

Region

Northern

Region

Milestone

In 1995, the layout of the domestic market in tier 1 cities completed, established business in Beijing, Shanghai, Guangzhou, Shenzhen and HK

In 1992, listed on the Stock Exchange of Hong Kong Limited . It was the first Chinese enterprise to acquire listing status by its own local business or assets located in Hong Kong.

In 1988, the group invested in real estate projects in Shenzhen, started to enter China real estate industry.

Incorporated in Hong Kong in 1979.

In 2005, the first mainland property company awarded Standard & Poors’ BBB rating and Moody’s Baa2 rating, which is the highest rating in the industry.

In 2003, the land development became the majority source of profits for the group.

In 2000, Chengdu company established, starting to enter 2 tier cities.

After 1997 financial crisis, the group transferred its business to domestic market.

In 2012, the sales exceed 100 billion HKD,market capitalization exceed 180 billion HKD.

In 2008, city entries reached 20, the group has gradually developed into a trans-regional, first-class China property development enterprise and a national property brand.

On 10 December 2007, it became a constituent stock of the Hang Seng Index, with market capitalization over 160 billion HKD.

Footprints 1984 1988 1992 1993 1995 2000 2002 2003 2004 2005 2006 2007

Hongkong Shenzhen Shanghai Guangzhou Beijing Chengdu Changchun Zhongshan Xi'an Nanjing Macau Suzhou Foshan Ningbo Chongqing Hangzhou Zhuhai Qingdao Dalian Shenyang Tianjin

Cont’d 2008 2010 2011 2012 2013

Jinan Hohhot Guilin Yinchuan Changsha Jilin Yantai Nanchang Hefei Nanning Xiamen Lanzhou Wuhan Ganzhou Yangzhou Kunming Nantong Changzhou Yancheng

Thank you!

Q & A

Jiangangshan project, Shenzhen Acquired in Nov. 2012

Disclaimer

These materials have been prepared by China Overseas Land and Investment Ltd. (“COLI” or the “Company”) solely for information use during its presentation may not be reproduced or redistributed to any other person without the permissions from COLI. By attending this presentation, you are agreeing to be bound by the foregoing restrictions.

It is not the intention to provide, and you may not rely on these materials as providing, a complete or comprehensive analysis of the company’s financial or trading position or prospects. The information and opinions in these materials are provided as at the date of this presentation and are subject to change without notice. None of the Company nor any of its respective affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of these materials.

The information in this material contains certain forward-looking statements. These include statements regarding outlook on future development schedules, business plans and expectations of capital expenditures.

These statements are based on current expectations that involve a number of risks and uncertainties which could cause actual results to differ from those anticipated by the Company.

The materials and information in the presentations and other documents are for informational purposes only, and are not an offer or solicitation for the purchases or sale of any securities or financial instruments or to provide any investment service or investment advice.