1998 SOUTHERN AFRICA ECONOMIC SUMMIT WINDHOEK ...

94

1998 SOUTHERN AFRICA ECONOMIC SUMMIT WINDHOEK, NAMIBIA 17-19 MAY Theme: “Priorities for Global Competitiveness in the 21st Century” Prepared by the SADC Finance and Investment Sector Co-ordinating Unit (FISCU) Department of Finance - South Africa

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 1998 SOUTHERN AFRICA ECONOMIC SUMMIT WINDHOEK ...

1998 SOUTHERN AFRICAECONOMIC SUMMITWINDHOEK, NAMIBIA 17-19 MAY

Theme:“Priorities for Global Competitiveness in the 21st Century”

Prepared by theSADC Finance and Investment Sector Co-ordinating Unit (FISCU)

Department of Finance - South Africa

2

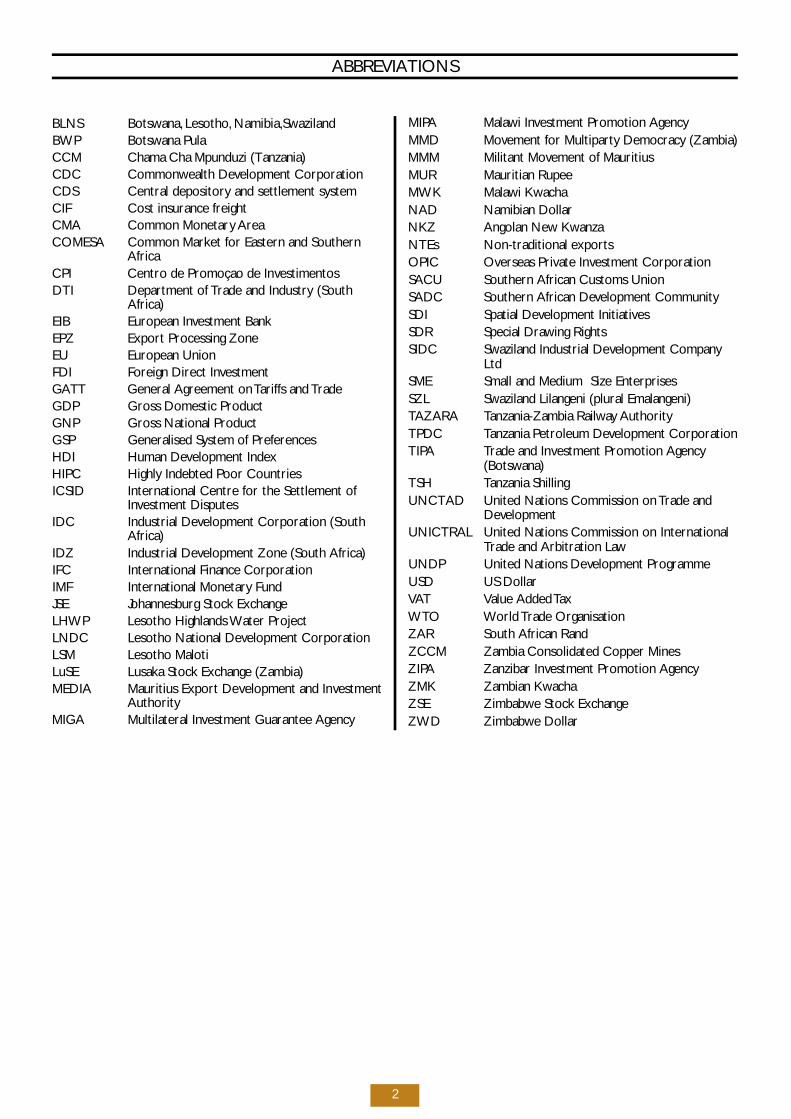

BLNS Botswana, Lesotho, Namibia,SwazilandBWP Botswana PulaCCM Chama Cha Mpunduzi (Tanzania)CDC Commonwealth Development CorporationCDS Central depository and settlement systemCIF Cost insurance freightCMA Common Monetary AreaCOMESA Common Market for Eastern and Southern

AfricaCPI Centro de Promoçao de InvestimentosDTI Department of Trade and Industry (South

Africa)EIB European Investment Bank EPZ Export Processing ZoneEU European UnionFDI Foreign Direct InvestmentGATT General Agreement on Tariffs and TradeGDP Gross Domestic ProductGNP Gross National ProductGSP Generalised System of PreferencesHDI Human Development IndexHIPC Highly Indebted Poor CountriesICSID International Centre for the Settlement of

Investment DisputesIDC Industrial Development Corporation (South

Africa)IDZ Industrial Development Zone (South Africa)IFC International Finance CorporationIMF International Monetary FundJSE Johannesburg Stock ExchangeLHWP Lesotho Highlands Water ProjectLNDC Lesotho National Development CorporationLSM Lesotho MalotiLuSE Lusaka Stock Exchange (Zambia)MEDIA Mauritius Export Development and Investment

AuthorityMIGA Multilateral Investment Guarantee Agency

MIPA Malawi Investment Promotion AgencyMMD Movement for Multiparty Democracy (Zambia)MMM Militant Movement of MauritiusMUR Mauritian RupeeMWK Malawi KwachaNAD Namibian DollarNKZ Angolan New KwanzaNTEs Non-traditional exportsOPIC Overseas Private Investment CorporationSACU Southern African Customs UnionSADC Southern African Development CommunitySDI Spatial Development InitiativesSDR Special Drawing RightsSIDC Swaziland Industrial Development Company

LtdSME Small and Medium Size EnterprisesSZL Swaziland Lilangeni (plural Emalangeni)TAZARA Tanzania-Zambia Railway AuthorityTPDC Tanzania Petroleum Development CorporationTIPA Trade and Investment Promotion Agency

(Botswana)TSH Tanzania ShillingUNCTAD United Nations Commission on Trade and

DevelopmentUNICTRAL United Nations Commission on International

Trade and Arbitration LawUNDP United Nations Development ProgrammeUSD US DollarVAT Value Added TaxWTO World Trade OrganisationZAR South African RandZCCM Zambia Consolidated Copper MinesZIPA Zanzibar Investment Promotion AgencyZMK Zambian KwachaZSE Zimbabwe Stock ExchangeZWD Zimbabwe Dollar

ABBREVIATIONS

3

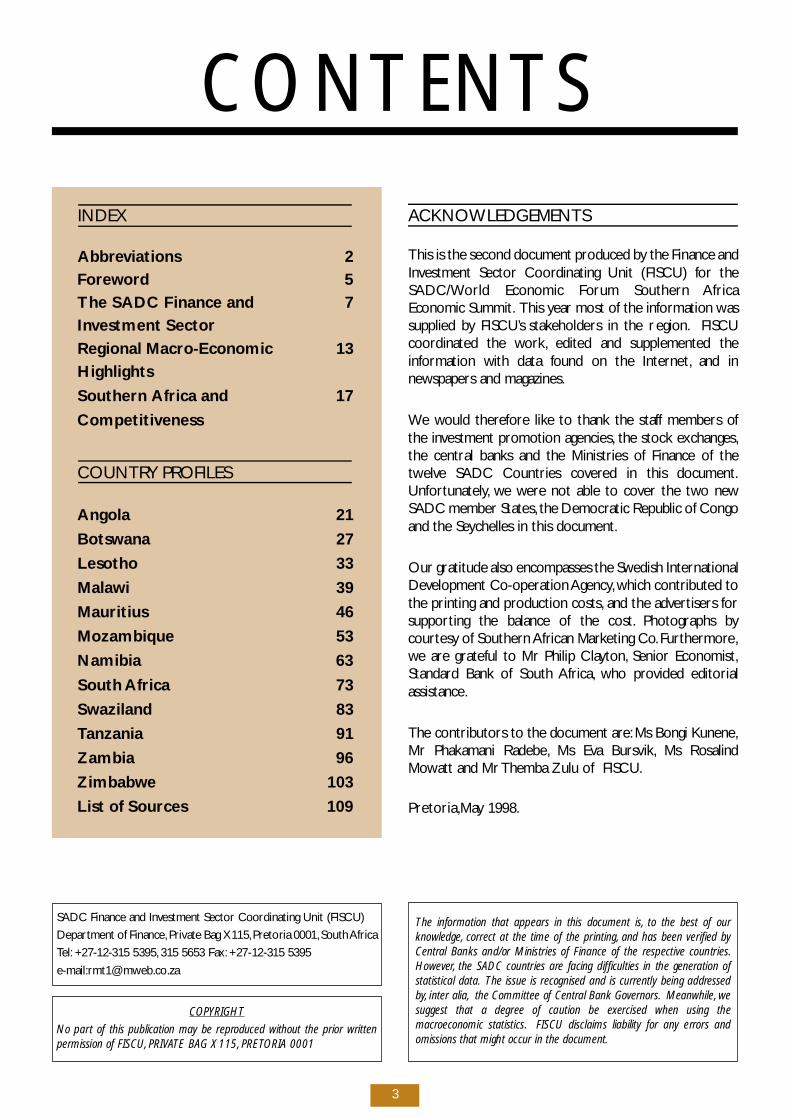

I N D E X

Abbreviations 2Foreword 5The SADC Finance and 7Investment SectorRegional Macro-Economic 13Highlights

Southern Africa and 17

Competitiveness

C O U N T RY PRO F I L E S

Angola 21

Botswana 27

Lesotho 33

Malawi 39

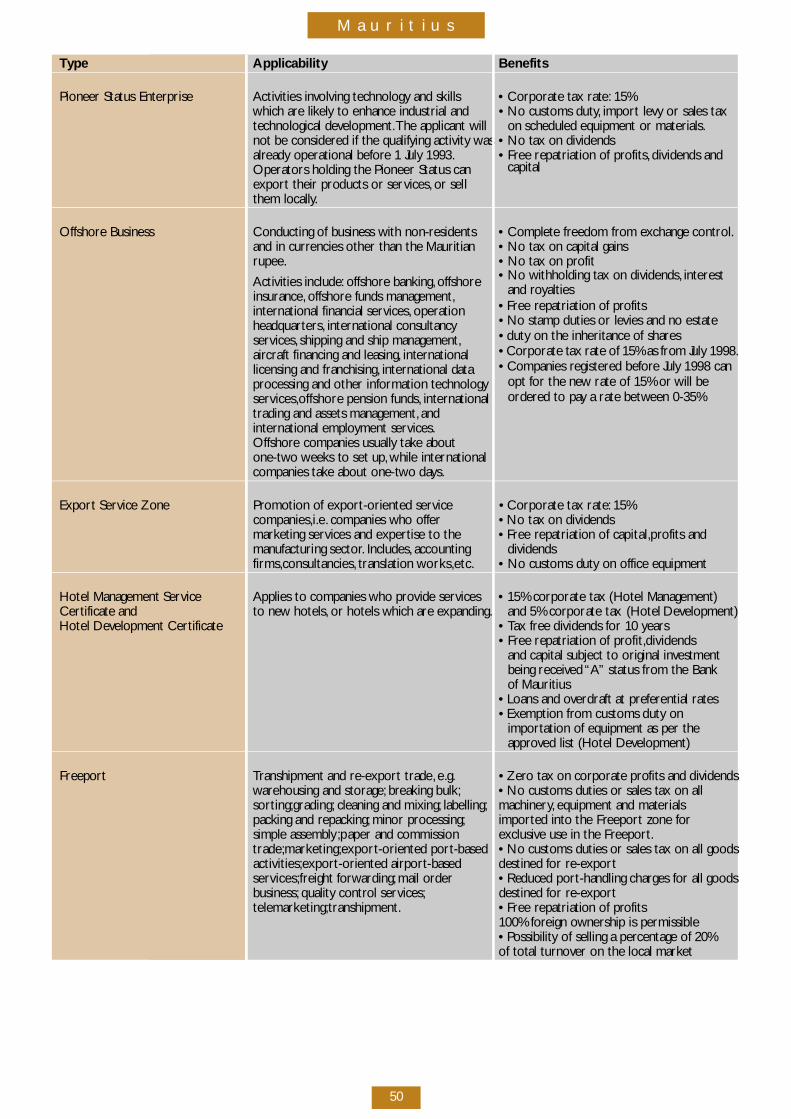

Mauritius 46

Mozambique 53

Namibia 63

South Africa 73

Swaziland 83

Tanzania 91

Zambia 96

Zimbabwe 103

List of Sources 109

AC K N OW L E D G E M E N T S

This is the second document produced by the Finance andI nvestment Sector Coordinating Unit (FISCU) for theS A D C / World Economic Forum Southern A f r i c aEconomic Summit. This year most of the information wassupplied by FISCU’s stakeholders in the re g i o n . F I S C Uc o o rdinated the wo r k , edited and supplemented thei n formation with data found on the Internet, and inn ew s p apers and magazines.

We would there fo re like to thank the staff members ofthe investment promotion agencies, the stock exchanges,the central banks and the Ministries of Finance of thet we l ve SADC Countries cove red in this document.U n fo rt u n a t e ly, we we re not able to cover the two newSADC member States, the Democratic Republic of Congoand the Seychelles in this document.

Our gratitude also encompasses the Swedish InternationalD evelopment Co-operation A g e n c y,which contributed tothe printing and production costs, and the adve rtisers fo rs u p p o rting the balance of the cost. P h o t o g r aphs byc o u rtesy of Southern African Marketing Co. F u rt h e r m o re,we are grateful to Mr Philip Clay t o n , Senior Economist,S t a n d a rd Bank of South A f r i c a , who provided editoriala s s i s t a n c e.

The contributors to the document are :Ms Bongi Ku n e n e,Mr Phakamani Radebe, Ms Eva Bursvik, Ms RosalindM owatt and Mr Themba Zulu of FISCU.

P re t o r i a ,M ay 1998.

CONTENTS

The information that appears in this document is, to the best of ourk n ow l e d ge, c o r rect at the time of the pri n t i n g , and has been veri fied byC e n t ral Banks and/or Ministries of Finance of the respective countri e s.H ow ev e r, the SADC countries are facing difficulties in the ge n e ration ofstatistical data. The issue is re c ognised and is currently being addre s s e dby, inter alia, the Committee of Central Bank Gov e r n o rs. M e a n w h i l e, w es u g gest that a degree of caution be exercised when using them a c roeconomic statistics. FISCU disclaims liability for any erro rs andomissions that might occur in the document.

SADC Finance and Investment Sector Coordinating Unit (FISCU)

D e p a rtment of Finance, Private Bag X115,P retoria 0001,South A f r i c a

Te l : +27-12-315 5395, 315 5653 Fax: +27-12-315 5395

e - m a i l :r m t 1 @ m we b. c o. z a

C O P Y R I G H T

No part of this publication may be re p roduced without the prior wri t t e npermission of FISCU, P R I VATE BAG X115, P R E TORIA 0001

5

The second publication of the Southern Africa EconomicSummit pre p a red by the Finance and Investment SectorC o o rdinating Unit (FISCU) takes place in the context ofsignificant regional and international political and financiald eve l o p m e n t s .Within SADC the political situation is stableand there is close collaboration by member-states to ensurethat peace holds in A n gola and the Democratic Republic ofthe Congo. M u l t i - p a rty democracy has become the norm inall SADC economies and the robustness of thesedemocracies is attested by the procedural elections to beheld in at least four SADC countries in 1998 and 1999. M o s tof the fo rthcoming elections will have internationalo b s e rvers and the presence of independent electoralcommissions ensure that the process is proper and fair. I nkeeping with mature democracies it is expected that thefo rthcoming elections will yield smooth succession andgovernment functions will not be disrupted in any way.

Significant economic policy changes within SADC haveo c c u rred over time as economies we re adjusting. T h o u g hadjustments we re a result of diffe rent circumstances thewhole region is benefiting from the positive contagion effe c t .Economic policy has become the focus of public debate asm a c ro-economic management issues are discussed with awide range of re l evant stakeholders such as labor, c o m m e rc eand industry, and non-government organizations. T h ecommitment of SADC governments to adhering to soundeconomic principles can not be questioned. As SADCeconomies continue to grow the debate is no longer onwhat economic systems to adopt but the focus has shifted toa point where the debate is on how to ensure that a marke tbased economic system embraces a wide majority in ord e rto add ress pove rty and other social backlogs. It is a concernof SADC citizens that the economic policy env i ronment isc o n d u c t i ve to attracting and keeping domestic, regional andfo reign inve s t o r s .

I n t e r n a t i o n a l ly the focus of multilateral deliberations havebeen on the Asian financial crisis which have outperfo r m e dp revious crises such as the Tu r key and Mexican crises of 1994re s p e c t i ve ly.The consequences of the Asian crisis continue toreverberate world-wide and the effect is transmitted ind eveloped economies through diminished demand of dollar-priced goods and serv i c e s , and through deleveraging infinancial marke t s . SADC economies have not been immu n eto the crisis.Asian countries import base metals and mineralsand other raw materials from the southern Africa re g i o n .Textiles and other labor intensive products from A s i acompete with textiles and other products produced by there g i o n . It is thus expected that the effect of the crisis will befelt in these sectors. In South A f r i c a , owing to the emergingm a r ket status accorded to the country, the impact felt in theEmerging Market Index (EMI) was easily and immediately fe l tin the first ro u n d .As a result of slower growth in Asia and itsimpact on world grow t h , SADC expects that the demand fo re x p o rted materials to decline and impact negative ly onregional export s . Notwithstanding the pessimistic outlookSADC economies are expected to grow faster than the re s tof Africa and other developing economies for the ye a r1 9 9 8 / 1 9 9 9 . It may be pre m a t u re to conclusive ly assess theimpact of the Asian crisis. H oweve r, c o m p a r a t i ve ly speaking,the effect on SADC seems to be minimal because theregional financial markets are not as globally integrated asthe financial markets in the rest of the wo r l d .

BONGI KUENE

D i rector (FISCU)

FOREWORD

7

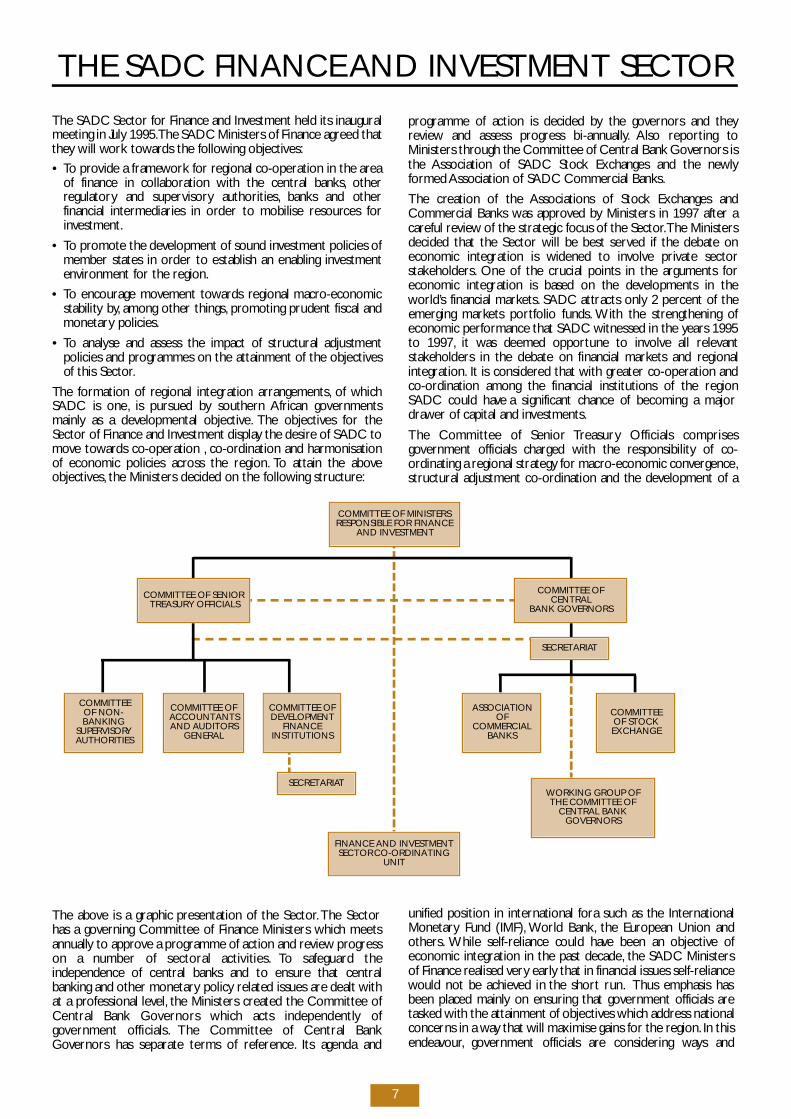

The SADC Sector for Finance and Investment held its inauguralmeeting in Ju ly 1995.The SADC Ministers of Finance agreed thatt h ey will work tow a rds the fo l l owing objective s :

• To provide a framework for regional co-operation in the are aof finance in collaboration with the central banks, o t h e rre g u l a t o ry and superv i s o ry authorities, banks and otherfinancial intermediaries in order to mobilise re s o u rces fo ri nve s t m e n t .

• To promote the development of sound investment policies ofmember states in order to establish an enabling inve s t m e n te nv i ronment for the re g i o n .

• To encourage movement tow a rds regional macro - e c o n o m i cstability by, among other things, p romoting prudent fiscal andm o n e t a ry policies.

• To analyse and assess the impact of structural adjustmentpolicies and programmes on the attainment of the objective sof this Sector.

The formation of regional integration arr a n g e m e n t s , of whichSADC is one, is pursued by southern African gove r n m e n t sm a i n ly as a developmental objective. The objectives for theSector of Finance and Investment display the desire of SADC tom ove tow a rds co-operation , c o - o rdination and harmonisationof economic policies across the re g i o n . To attain the aboveo b j e c t i ve s , the Ministers decided on the fo l l owing structure :

p rogramme of action is decided by the governors and theyrev i ew and assess pro g ress bi-annu a l ly. Also re p o rting toMinisters through the Committee of Central Bank Governors isthe Association of SADC Stock Exchanges and the new lyformed Association of SADC Commercial Banks.

The creation of the Associations of Stock Exchanges andC o m m e rcial Banks was ap p roved by Ministers in 1997 after ac a reful rev i ew of the strategic focus of the Sector.The Ministersdecided that the Sector will be best served if the debate oneconomic integration is widened to invo l ve private sectors t a ke h o l d e r s . One of the crucial points in the arguments fo reconomic integration is based on the developments in thewo r l d ’s financial marke t s . SADC attracts only 2 percent of theemerging markets port folio funds. With the strengthening ofeconomic performance that SADC witnessed in the years 1995to 1997, it was deemed opportune to invo l ve all re l ev a n ts t a keholders in the debate on financial markets and re g i o n a li n t e g r a t i o n . It is considered that with greater co-operation andc o - o rdination among the financial institutions of the re g i o nSADC could have a significant chance of becoming a majord r awer of capital and inve s t m e n t s .

The Committee of Senior Tre a s u ry Officials comprisesgovernment officials charged with the responsibility of co-o rdinating a regional strategy for macro-economic conve r g e n c e,structural adjustment co-ordination and the development of a

THE SADC FINANCE AND INVESTMENT SECTO R

The above is a graphic presentation of the Sector.The Sectorhas a governing Committee of Finance Ministers which meetsa n nu a l ly to ap p rove a programme of action and rev i ew pro g re s son a number of sectoral activities. To safe g u a rd theindependence of central banks and to ensure that centralbanking and other monetary policy related issues are dealt withat a pro fessional leve l , the Ministers created the Committee ofCentral Bank Governors which acts independently ofgovernment officials. The Committee of Central BankG overnors has separate terms of re fe re n c e. Its agenda and

COMMITTEE OF MINISTERSRESPONSIBLE FOR FINANCE

AND INVESTMENT

COMMITTEE OF SENIORTREASURY OFFICIALS

COMMITTEE OFCENTRAL

BANK GOVERNORS

COMMITTEE OF NON-BANKING

SUPERVISORYAUTHORITIES

COMMITTEE OFACCOUNTANTSAND AUDITORS

GENERAL

COMMITTEE OFDEVELOPMENT

FINANCEINSTITUTIONS

SECRETARIAT

ASSOCIATIONOF

COMMERCIAL BANKS

COMMITTEEOF STOCKEXCHANGE

WORKING GROUP OFTHE COMMITTEE OF

CENTRAL BANKGOVERNORS

FINANCE AND INVESTMENTSECTOR CO-ORDINATING

UNIT

SECRETARIAT

unified position in international fora such as the InternationalM o n e t a ry Fund (IMF), World Bank, the European Union ando t h e r s . While self-reliance could have been an objective ofeconomic integration in the past decade, the SADC Ministersof Finance realised ve ry early that in financial issues self-re l i a n c ewould not be achieved in the short run. Thus emphasis hasbeen placed mainly on ensuring that government officials aret a s ked with the attainment of objectives which add ress nationalconcerns in a way that will maximise gains for the re g i o n . In thise n d e avo u r, government officials are considering ways and

9

means that will have beneficial results in the spill over effects ofstructural adjustment pro c e s s e s , and in general, p romote soundm a c ro-economic management principles.

R e p o rting through the Committee of Tre a s u ry Officials are theCommittee of Accountants-Generals and A u d i t o r s - G e n e r a l s ,and the Committee of Non-Banking Superv i s o ry A u t h o r i t i e s .The Ministers realised that since trade integration effo rts arebeing seriously add ressed by the re g i o n , it would be prudent toe n s u re that institutional problems associated with macro -economic policy re form and financial infrastructure areattended to as a matter of urgency. Hence the invo l vement ofprivate and public sector pro fessionals such as the accountantsand auditors, and superv i s o ry authorities. The issue in thisre g a rd is that while SADC is developing region specific solutionsassociated with regional integration, it would be easy to losesight of integration as a tool for small open economies toexpand marke t s , but more import a n t ly, to take advantages ofglobalisation and international competitive n e s s .

A c c o rd i n g ly the regional accountants and auditors are taske dwith the responsibility to:

• determine the desirability and feasibility of harmonisings t a n d a rds within the re g i o n ;a n d

• determine what needs to be done at a pro fe s s i o n a l ,t e c h n i c a land political level to ensure that the private and public sectorsof the SADC region adhere to international standard s .

S i m i l a r ly, the regional superv i s o ry authorities are tasked with:

• obtaining an understanding of the nature, s t r u c t u re, p e r s o n sand institutions invo l ved in superv i s o ry activities in the re g i o n ;

• discussing the various cross border activities and superv i s o ryresponses that may be re q u i red as a re s u l t ;

• looking at the way fo r w a rd and considering a strategy inrelation to the establishment of a regional body,which may beprivate or public, charged with the responsibility for off-sitea n a lyses of adherence to prudential rules and regulations ona regional basis.

It is hoped that the invo l vement of various superv i s o ryauthorities in SADC fora will go a long way in the design ofefficient re g u l a t o ry systems, and as they will advise the Ministersand make recommendations on desirable changes, t h ey will addvalue tow a rds a solution to the negative perceptions on risk inS A D C.

The Finance and Investment Sector Co-ordinating Unit (FISCU)acts as a secretariat for the Ministers of Finance Committee.A ssuch it is responsible for the daily management of sectoriala c t i v i t i e s .The functions allocated to FISCU are dedicated to thes e rving of all sectorial committees and sub-committees. T h i si nvo l ves setting up the terms of re fe rence and determining awork plan and agenda for each sub-structure that is establishedin the support of sectorial objective s . FISCU also plays amonitoring role on all projects befo re submission to theM i n i s t e r s . Most of the projects undert a ken by the sector arefunded in collaboration with international co-operatingp a rt n e r s . FISCU is responsible for the identification of suitabledonors and partners for each pro j e c t , and negotiation offinancing pro p o s a l s .The process of identifying suitable part n e r sis critical to the success of each project as it identifies possibleconditionalities that the sector need to comply with andeliminates unnecessary processes and pro c e d u re s .The matchingof donors, p rojects and focus groups within the Sector re s u l t sin the signing of a memorandum of understanding (MOU) whichsets out the framework of the relationship between the Sectorand donors. FISCU pre p a res all the MOUs and where a pro j e c tre q u i res the services of consultants FISCU contracts a suitablyqualified candidate.

For the financial year 1998/99 FISCU’s key functions are :

• to produce a framework document that will be a composite

of policies and strategies that the sector needs to adopt tof u rther the aims of economic integration.

• to produce a Finance and Investment Protocol that will besubmitted to the Ministers for final ap p roval in June 1999.

• to produce a quart e r ly newsletter with information on theactivities of the sector.

• to identify suitable international co-operating partners for thes e c t o r ’s new activities.

• to produce a SADC macro-economic analysis document thatwill be used to inform current and potential regional andinternational investors of, amongst others, the inve s t m e n tclimate in each SADC economy, potential inve s t m e n to p p o rt u n i t i e s , and legal provisions for doing trade in SADC.This document will be available to participants at theSouthern Africa Economic Summit to be held on 17 - 19 May1998 in Namibia. It will also be available on Internet add re s s :w w w. f i n a n c e. gov. z a / S A D C.

• to work with the SADC stock exchanges in their pursuit ofharmonised policies and operations.

• to promote the establishment of effe c t i ve networks betwe e nSADC development finance institutions.

• to promote the adherence of SADC governments to prudentfiscal and monetary policies, t h rough inter alia, d evising anacceptable macro-economic convergence model.

• to promote effe c t i ve networking between non-bankingre g u l a t o ry agencies so as to devise a set of compatibleregional rules.

• to work with all re l evant stakeholders in the harmonisation ofpractices and standards in the accounting and auditingp ro fe s s i o n s .

• to provide input on regional dimensions in dialogue thatMinisters of Finance have with multilateral institutions such asthe IMF, World Bank, the Non Aligned Move m e n t ,C o m m o n wealth and others.

S E C TORAL AC T I V I T I E SIn a broad sense the Sector is add ressing various issues offinancial co-operation. In 1995 it was decided that financial co-operation will add ress the fo l l ow i n g :

• Financial re forms including the promotion of investment andtrade financing;

• The possibilities of establishing a regional finance andd evelopment mechanism with cognisance to the need for am o re balanced geographical pattern of inve s t m e n t ;

• Co-operation in the field of monetary matters such asm o n e t a ry policy, exchange rate policy, c u rrency conve rt i b i l i t y,fo reign exchange re s e rve management, fo reign debtmanagement and other issues related to the liberalisation offinancial marke t s ;

• The development of compatible rules and re g u l a t i o n sgoverning supervision of banks and other financial institutions;

• The development and strengthening of capital and moneym a r kets including national and regional stock exchanges;

• The development of human re s o u rce capacity in the areas offinance and inve s t m e n t ;

• The development of payment and clearance systems tofacilitate efficient cross border pay m e n t .

The Sector has three main themes and a number of pro j e c t sthat complement each other and add ress the adopted themes.

I . M AC RO-ECONOMIC MANAG E M E N TThe main thrust of this theme is to complement tradeintegration effo rts and to ensure that the political will that

10

c u rre n t ly exists in SADC governments is supported by soundeconomic management. In this context while the argument isdominated by trade liberalisation there is a realisation that non-tariff barriers affect trade, p roduction and inve s t m e n t . T h eMinisters of Trade and Industry are mainly concerned with thefirst two barr i e r s .The Ministers of Finance on the other handa re more concerned with ensuring that the gains from macro -economic re forms which counties have been undert a k i n gi n d i v i d u a l ly are regionalised by varying the intensity, scope andsequencing of economic policies.

H owever the Sector has had considerable difficulties inunderstanding the nature of the problems because of lack of anadequate database on which to base the analy s i s . In 1996 theCommittee of Governors ap p roved a project on thed evelopment of a statistical database with economic andfinancial info r m a t i o n . A re p o rt “Statistical tables and graphs fo rSADC countries” is produced bi-annu a l ly for presentation tothe meeting of SADC Central Bank Gove r n o r s . The ap p rove dstatistics appearing in this re p o rt are now available on In t e r n e t ,a dd re s s : w w w. s a d c b a n ke r s . o r g . The developments in thestatistical data base are discussed by senior officials from thecentral banks’ Departments of Research and Economics. T h elatest development concerns the proposed inclusion of fiscalstatistics to show the sources of government income anddistribution of government expenditure.

The statistics project is part of the Sector’s effo rts in thed evelopment of public confidence and information efficiency. I thas not been possible in the past to tackle governance issuesbecause the information base was ve ry narrow. T h ei m p rovements in the database will ensure that the sectore f fe c t i ve ly deals with macro-economic convergence issues anda c c o rd i n g ly adopts measurable indicators for conve r g e n c ec r i t e r i a .

An improvement in the management of SADC economies hasbeen characterised by the re m oval of exchange controls as partof economic re fo r m . H oweve r, the speed and effe c t i veness ofrelaxation of exchange controls have not been assessedre g i o n a l ly. The governors adopted a project looking at at h e o retical study on the macro-economic and re g u l a t o ryf r a m ework that should accompany the liberalisation ofexchange contro l s . The study noted that most SADCeconomies have already liberalised exchange controls on cert a i nc a t e gories of the current account, such as other export s ,i m p o rt s , s e rvices and income. A first objective for SADCeconomies should be to adopt A rticle VIII of the IMF’s A rt i c l e sof A g re e m e n t .Once this has been attained, f u rther relaxation onthe capital account are called fo r. G i ven the need for fo re i g ni nvestment in SADC countries it was recommended toMinisters that obstacles hindering inward financial flows shouldbe re c o n s i d e re d ,e s p e c i a l ly control restrictions on inward dire c ti nve s t m e n t , equity and port folio inve s t m e n t .

The consistency of the above conclusions we re echoed by theCommittee of Stock Exchanges in their recommendations toMinisters on harmonisation of economic activities withre fe rence to movement of capital flow s . South Africa acted onthese re c o m m e n d a t i o n s .The 1998/99 South African budget hasa l l owed a further relaxation of capital flows within SADC fro ma limit of ZAR50 million to ZAR250 million. L i kew i s einstitutional investors can now increase their fo reign curre n c yt r a n s fers from 2 percent to 10 percent of their previous ye a r ’snet inflow of funds.

The developments in SADC are happening in the context ofg l o b a l i s a t i o n , as a result of the expansion of internationally -d r i ven economic changes. It has thus been deemed useful toinclude cooperation in international negotiations with themultilateral institutions, e s p e c i a l ly in the development ofMultilateral Investment A g re e m e n t s , in the discussions of theMinisters of Finance. At present this debate is not we l la rticulated but it is clear that in the process of re-orientation of

the development strategy from a national strategy to a re g i o n a lo n e, it would be re l evant to assess the possibility ofs t rengthening the bargaining power of member countries. T h econcern is that as developments are instituted by the Wo r l dTrade Organisation (WTO ) , the Organisation for EconomicCo-operation and Development (OECD) and the UnitedNations Confe rence on Trade and Development (UNCTA D ) ,i tis almost impossible for developing countries to single-handedlyp o s i t i ve ly influence the outcomes for themselve s . Instead ofwaiting to respond to events once they are final it is perc e i ve dthat SADC Finance Ministers should collaborate with theirtrade counterparts for the fo r mulation of a coherent strategyon multilateral investment agreements for the benefit of there g i o n . It is envisaged that the issues arising out of this debatewill be codified to form a significant section of the pro p o s e dFinance and Investment pro t o c o l .

I I . FINANCIAL MANAG E M E N TMultilateral institutions have alw ays emphasised the import a n c eof good governance in any developing country. This in manyinstances has been used as a criteria for evaluating the level ofd evelopment finance flows that the developing countries get. I Nas much as good governance is part of the debate in SouthernA f r i c a , the SADC Ministers of Finance decided that financialmanagement as a theme would be one of the crucial areas thatSADC would be evaluated upon.A c c o rd i n g ly a programme thata dd ress this theme have been adopted. At the core of thisp rogramme is an attempt to add ress national problems in a waythat simu l t a n e o u s ly add resses regional needs.

Together with organisations, i n s t i t u t i o n s , and associations atinternational and regional leve l , the Finance and Inve s t m e n tSector Co-ordinating Unit (FISCU) is invo l ved in devising as t r a t e gy to add ress accounting and auditing matters within theSADC re g i o n .Among the regional bodies invo l ved are the Eastand Southern African Association of Accountants- General( E S A AG ) , the Eastern, Central and Southern African Fe d e r a t i o nof Accountants (ECSAFA ) , the Southern African Deve l o p m e n tC o m munity Organisation of Supreme Audit Institutions( S A D C O S A I ) .The World Bank and the Canadian InternationalD evelopment Agency are the two international partners whoseassistance has been sought to fund the activities of theseo r g a n i s a t i o n s .

At the core of the financial management agenda is the desire tobring about harmonisation of the accountancy and auditingp ro fessions on a regional basis.

The scope of the issues to be cove red in this programme cove r sa c c o u n t i n g , a u d i t i n g , government accountability, ethics andnorms of the pro fe s s i o n , m e rcantile law, and education andtraining of pro fessionals in the accounting and auditing fields. I twould be a futile exe rcise if SADC we re to attempt to conductthis work independent of the developments in the pro fe s s i o n sworld wide. For this reason the associations have had to bec o nversant with developments on improved financial re p o rt i n gbased on the adoption of international accounting and auditings t a n d a rds as pro mulgated by the International Federation ofAccountants (IFAC) and the International Accounting andS t a n d a rds Committee (IASC). E f fo rts by the governments withinSADC to improve accountability and there by prov i d eresponsible control of government finances will have the add e dbenefit of increasing investor confidence while complying withinternational standard s . F u rt h e r m o re ; with the inclusion ofAuditors-Generals in this initiative, c a re will be placed ons t rengthening their powers to enfo rce accountability andc o m p l i a n c e. While it is generally unquestioned in the privatesector that internal audit is a management tool that ensure sgood corporate gove r n a n c e, in the public sector the idea hasstill to be fully marke t e d . It is hoped that the commitment of theAuditors-Generals to this programme will re i n fo rce the

11

i m p o rtance of an effe c t i ve internal audit function withingove r n m e n t s .

An important element of financial management is cap a c i t ybuilding in the form of education and training at all leve l s .T h eSouth African Reserve Bank has been undertaking trainingcourses for central bank officials three times a ye a r.Collaboration with other regional and international institutionsthat provide macro-economic and financial management trainingis on-go i n g .S i m i l a r ly, in the accounting and auditing pro g r a m m ea crucial aspect will be the training and education ofp ro fessionals tasked with ap p lying harmonised standard s . T h es t a rting point would be comparability of standards in diffe re n tc o u n t r i e s . Once re c i p rocity and mutual recognition ofp ro fessions has been achieve d , t h e re could be greater mobilityof pro fessionals in the re g i o n .

While most of the work pertaining to financial management hasbeen undert a ken by the accounting and auditing institutions, t h eSADC central banks have collaborated in the area of re g u l a t i o nand superv i s i o n . This they have done as part of theirresponsibility for ensuring bank soundness. To avoid systemicrisks and as part of the agreement that central banks have withthe Bank of International Settlements (BIS), i n i t i a t i ves on thes u p e rvision of cro s s - b o rder activities are undert a ken toe n h a n c e :• the various principles, p h i l o s o p h i e s , ap p roaches and methods

u n d e r lying regulation and superv i s i o n ;

• the duties and responsibilities of the various players in there g u l a t i o n ,s u p e rvision and risk management of banks; a n d ,

• the basic principles and methods in the management andevaluation of diffe rent risks in banking.

Realising the importance of issues related to bankings o u n d n e s s , SADC central banks are ap p lying and designingregulations that are consistent with international standard s ,while compatible with local needs.

SADC non-banking superv i s o ry bodies are also in the pro c e s sof organising themselves into a regional body that will deal with:

• the question of re g u l a t o ry arbitrage;

• the effect of the demutualisation of South African mu t u a li n s u re r s ;

• the standard of regulation and the degree to which diffe re n c e sin the standards could affect future superv i s o ry activities; a n d ,

• the exchange of information relating to the fit and pro p e r n e s sof financial service institutions.

Financial management within SADC is also enhanced bye n s u r i n g ,w h e rever possible, that local initiatives are in line withinternational provisions as laid down by the InternationalOrganisation of Securities Commissions and the InternationalAssociation of Insurance Superv i s o r s .

I I I . FINANCIAL INFRASTRU C T U R EOne of the often neglected areas of finance in the past was thed evelopment of financial infrastructure.The SADC Central BankG overnors recognised this early in their discussions on financialc o - o p e r a t i o n . I n i t i a l ly, discussions centred on the legal systemsand frameworks within which central banks operate. T h i sculminated in a project document entitled SADC FinancialS y s t e m s : Po l i c i e s , S t r u c t u res and Marke t s . This documentcontains information on all SADC central banks, t h e i rgovernance and instruments. It is now available on Internet sitew w w. s a d c b a n ke r s . o r g . An independent opinion on thei n formation contained and the further use of this document isc u rre n t ly being sought from the International Monetary Fund( I M F ) .

In 1994 South Africa commenced with a project on thep ay m e n t s , clearing and settlement mechanisms. Among theo b j e c t i ves of the project was the need to reduce the settlementperiod between transaction and clearing in order to pro d u c ereal-time gross settlement. South Africa completed this pro j e c ts u c c e s s f u l ly in March 1998.When South Africa joined SADC,t h escope of the project was enlarged with the assistance of theWorld Bank to include other SADC member states.At countryl evel so far, the project has concentrated on info r m a t i o ngathering and stock-taking, d eveloping a vision and strategy, a n dconceptual design. The key issue in each country is that anefficient payment system must have the fo l l owing attributes asguiding principles: s p e e d , c e rt a i n t y, re l i a b i l i t y, s e c u r i t y,c o nvenience and fair costs. Some of the role players that havebeen invo l ved in each country have been banks, rural and urbane n d - u s e r s , s e rvice prov i d e r s , re g u l a t o ry bodies, and variousorgans of gove r n m e n t .

Much of the financial infrastructure is dependent on efficientc o m munication tools. This area is a subject of in-depthdiscussion by the Southern Africa Tr a n s p o rt andC o m munication Commission (SAT C C ) ,a SADC sector based inM o z a m b i q u e. H owever some crucial activities for the Financeand Investment Sector re ly on electronic communication in theform of e-mail connectivity via the internet. This has beena c h i eved for all SADC central banks. Plans to connect thed evelopment finance institutions and the investment pro m o t i o nagencies are on the card s .

The Ministers of Finance decided in Ju ly 1997 that the eightSADC stock exchanges should be an integral part of thediscussions on finance infrastructure. Issues of concern andmutual benefit that have been discussed so far include: t h eharmonisation of listing re q u i re m e n t s , dual listings and SADCd e p o s i t o ry re c e i p t s , c ross border inve s t m e n t , c e n t r a ldepositories and settlements. In less than a year some of therecommendations of the stock exchanges have developed intopolicy in some member states.

CHALLENGES AND CONSTRAINTS A selection of projects add ressing a number of Finance andI nvestment Sector themes presented above is not a completereflection of the scope of work that is being undert a ken tof u rther the objectives of the Sector within SADC. E ven with thes e l e c t i ve discussion of the projects it is clear that a lot of wo r kstill needs to be done to ensure that the interaction betwe e nthe Ministries of Finance, the central banks and financialinstitutions is such that a “ good result” is attained withoutdisrupting the marke t s . Also important is the need to ensurethat regional initiatives are congruent with internationald eve l o p m e n t s .

The future thus holds a number of challenges for the Sector,including the fo l l ow i n g :

• Political commitment;

• Institutional cap a c i t y ;

• Global trends and deve l o p m e n t s ;

• R e s o u rce constraints, a n d ;

• Relevance of regional economic blocs.

The Sector for Finance and Investment is re l a t i ve ly new in aSADC env i ronment yet its successes are discernible by theconsiderable level of government and private sectorcommitment and support in the development of its pro g r a m m eof action.The next challenge for the Sector will be the draftingof a Finance and Investment Protocol that will have the bro a drange of support from regional and international ro l e - p l aye r s .

13

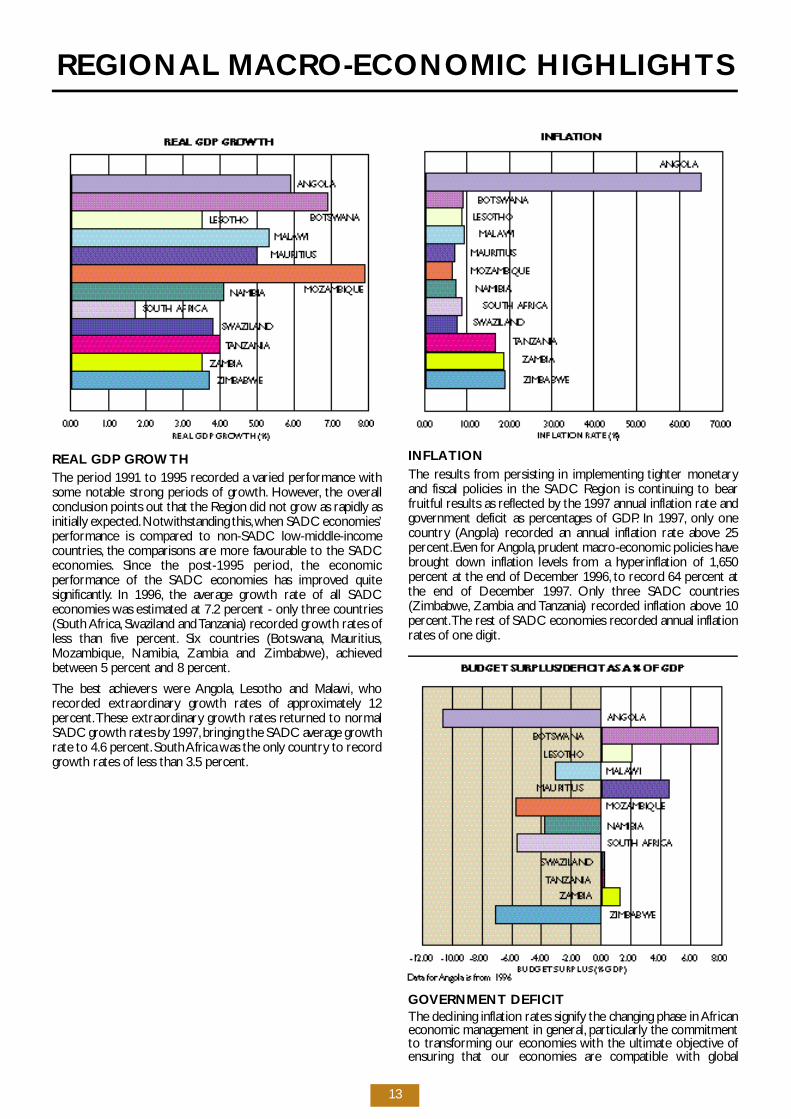

REAL GDP GROW T HThe period 1991 to 1995 re c o rded a varied performance withsome notable strong periods of grow t h . H oweve r, the ove r a l lconclusion points out that the Region did not grow as rap i d ly asi n i t i a l ly expected.Notwithstanding this,when SADC economies’p e r formance is compared to non-SADC low - m i dd l e - i n c o m ec o u n t r i e s , the comparisons are more favourable to the SADCe c o n o m i e s . Since the post-1995 period, the economicp e r formance of the SADC economies has improved quites i g n i f i c a n t ly. In 1996, the average growth rate of all SADCeconomies was estimated at 7.2 percent - only three countries(South A f r i c a , Swaziland and Tanzania) re c o rded growth rates ofless than five perc e n t . Six countries (Botsw a n a , M a u r i t i u s ,M o z a m b i q u e, N a m i b i a , Zambia and Zimbabwe ) , a c h i eve db e t ween 5 percent and 8 perc e n t .

The best achievers we re A n go l a , Lesotho and Malaw i , w h ore c o rded extraord i n a ry growth rates of ap p rox i m a t e ly 12p e rc e n t .These extraord i n a ry growth rates returned to normalSADC growth rates by 1997,bringing the SADC average grow t hrate to 4.6 perc e n t .South Africa was the only country to re c o rdg rowth rates of less than 3.5 perc e n t .

I N F L AT I O NThe results from persisting in implementing tighter monetaryand fiscal policies in the SADC Region is continuing to bearfruitful results as reflected by the 1997 annual inflation rate andgovernment deficit as percentages of GDP. In 1997, o n ly onec o u n t ry (Angola) re c o rded an annual inflation rate above 25p e rc e n t .E ven for A n go l a , prudent macro-economic policies haveb rought down inflation levels from a hyperinflation of 1,650p e rcent at the end of December 1996, to re c o rd 64 percent atthe end of December 1997. O n ly three SADC countries( Z i m b a b we, Zambia and Tanzania) re c o rded inflation above 10p e rc e n t .The rest of SADC economies re c o rded annual inflationrates of one digit.

G OVERNMENT DEFICITThe declining inflation rates signify the changing phase in A f r i c a neconomic management in general, p a rt i c u l a r ly the commitmentto transforming our economies with the ultimate objective ofensuring that our economies are compatible with global

REGIONAL MAC RO-ECONOMIC HIGHLIGHTS

15

d e m a n d s . The declining levels of SADC government deficitwhich accompany the falling inflation rates, bear testimony tothis commitment. In 1997, six SADC1 ) economies re f l e c t e dgovernment surpluses, with Botswana and Mauritius re c o rd i n ggovernment surpluses of 8 percent and 4.5 percent re s p e c t i ve ly.L e s o t h o, S w a z i l a n d , Tanzania and Zambia also re c o rd e dgovernment surpluses, while Malaw i , M o z a m b i q u e, N a m i b i a ,South Africa and Zimbabwe reflected government deficits.

1)1997 Government deficit data for A n gola not av a i l a b l e.

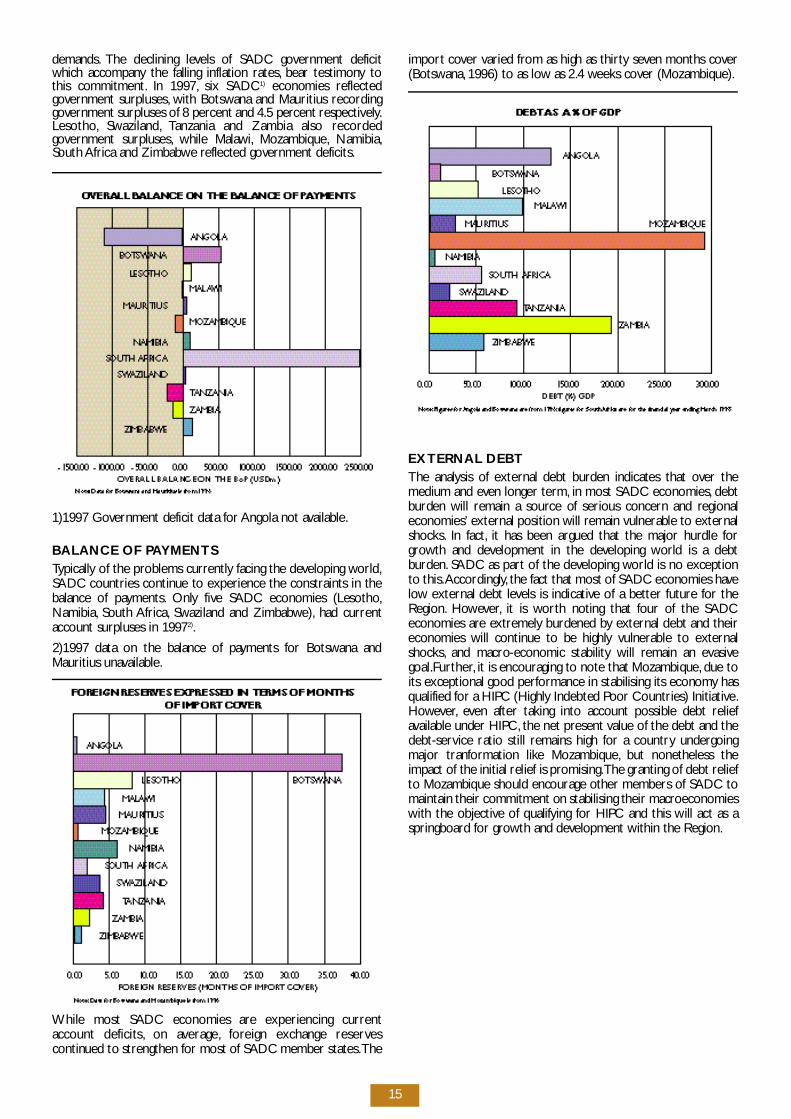

BALANCE OF PAY M E N T STy p i c a l ly of the problems curre n t ly facing the developing wo r l d ,SADC countries continue to experience the constraints in thebalance of pay m e n t s . O n ly five SADC economies (Lesotho,N a m i b i a , South A f r i c a , Swaziland and Zimbabwe ) , had curre n taccount surpluses in 19972 ).

2)1997 data on the balance of payments for Botswana andMauritius unav a i l a b l e.

While most SADC economies are experiencing curre n taccount deficits, on ave r a g e, fo reign exchange re s e rve sc o n t i nued to strengthen for most of SADC member states.T h e

i m p o rt cover varied from as high as thirty seven months cove r( B o t sw a n a , 1996) to as low as 2.4 weeks cover (Mozambique).

EXTERNAL DEBTThe analysis of external debt burden indicates that over themedium and even longer term, in most SADC economies, d e b tb u rden will remain a source of serious concern and re g i o n a leconomies’ external position will remain vulnerable to externals h o c k s . In fact, it has been argued that the major hurdle fo rg rowth and development in the developing world is a debtb u rd e n . SADC as part of the developing world is no exceptionto this.A c c o rd i n g ly, the fact that most of SADC economies havel ow external debt levels is indicative of a better future for theR e g i o n . H oweve r, it is wo rth noting that four of the SADCeconomies are extre m e ly burdened by external debt and theireconomies will continue to be highly vulnerable to externals h o c k s , and macro-economic stability will remain an ev a s i vego a l .F u rt h e r, it is encouraging to note that Mozambique, due toits exceptional good performance in stabilising its economy hasqualified for a HIPC (Highly Indebted Poor Countries) Initiative.H oweve r, even after taking into account possible debt re l i e favailable under HIPC, the net present value of the debt and thed e b t - s e rvice ratio still remains high for a country undergo i n gmajor tranformation like Mozambique, but nonetheless theimpact of the initial relief is pro m i s i n g .The granting of debt re l i e fto Mozambique should encourage other members of SADC tomaintain their commitment on stabilising their macro e c o n o m i e swith the objective of qualifying for HIPC and this will act as as p r i n g b o a rd for growth and development within the Region.

17

This ye a r ’s theme at the Southern African Economic Summit ofthe World Economic Fo r u m , is “Priorities for GlobalC o m p e t i t i veness in the 21st Century ” .O ver the past few ye a r s ,m a ny of the Southern African Development Commu n i t y(SADC) economies have moved aw ay from isolation andpatterns of low growth - South A f r i c a ’s ap a rtheid regime hasbeen dissolve d , dictatorships have been replaced bydemocracies and economic policy in general is moving rap i d lyt ow a rds free market principles. N ow, t h e re is an incre a s i n gamount of international attention being paid to Southern A f r i c a ,which is beginning to be seen as a region with enormousp o t e n t i a l .

In terms of competitive n e s s , h oweve r, S A D C, as a whole lagsbehind the developed wo r l d , as well as behind some of theother so-called “emerging markets” such as China, South EastA s i a , Latin America and Eastern Euro p e. H aving embraced thepolicy logic of the free market and its implications - minimisingstate intervention in the economy, l owering barriers to tradeand attracting fo reign inve s t m e n t , among others - the countriesof Southern Africa have no option but to accept the realities ofthe economic env i ronment in the 21st Century. Te c h n o l o gy isadvancing at a rapid rate, the volume of cro s s - b o rder cap i t a lf l ows is expanding, i nvestors are incre a s i n g ly looking outsidetheir traditional boundaries for new opportunities and neww ays of making money ; in short , the world is becoming smaller.On top of this, donor aid to developing countries is not asfo rthcoming as it used to be. To be players in the wo r l de c o n o my in the next century, the countries of Southern A f r i c awill need to become more competitive, and to develop somew ay of holding their own against the dominant fo rc e s .

The Africa Competitiveness ReportA f r i c a ’s entry into the world economy is evidenced by thep roduction (for the first time) of the Africa Competitive n e s sR e p o rt . Compiled for this ye a r ’s World Economic Forum (heldin Davo s , Switzerland in Janu a ry / Fe b r u a ry) the re p o rt looks at24 African countries and evaluates them in terms of theirc o m p e t i t i ve n e s s . Conclusions are based on a survey of A f r i c a nb u s i n e s s , as well as data collected from sources such as theWorld Bank, the International Monetary Fund, the UN, a n dAfrican ministries of finance and central statistical offices. A l lSADC countries, with the exception of the DemocraticRepublic of Congo and the Sey c h e l l e s ,a re included.

Topping the overall Competitiveness Index (calculated on thebasis of six indices - openness, gove r n m e n t , f i n a n c e, l a b o u r,i n f r a s t r u c t u re and institutions) is Mauritius. Other high-rankingSADC countries include Botswana (3), Namibia (4) and SouthAfrica (7). Swaziland (8), Lesotho (10), Zambia (12) and Ta n z a n i a(16) fall into the middle rankings, whilst Mozambique (18),Z i m b a b we (20), M a l aw i (21) and A n gola (23) are near thebottom of the table.

The re p o rt explains Mauritius’s and Botsw a n a ’s re l a t i ve ly highl evel of competitiveness in terms of the stability (both politicaland economic) of the countries, as well as we l l - m a n a g e deconomies and sound macroeconomic policies which have beenin place for some time. The re p o rt also found evidence of“ g e o g r aphic bunching”, i . e. countries in a certain geograp h i c a la rea tended to have similar rankings - this is most notable inrelation to the Southern African Customs Union countries. Ac o rrelation between competitiveness and human we l f a re was

also noted, suggesting that competitiveness could contribute tohigher levels of human deve l o p m e n t , and vice ve r s a .

Countries generally re g a rded as “ good re formers” (e. g .Mozambique) did not necessarily fare well in terms ofc o m p e t i t i ve n e s s , illustrating that real change does not take placeovernight and that time is needed to strengthen institutions,i n f r a s t r u c t u re and the economy in general. W h e re countriessuch as Mozambique did obtain high rankings was in terms oft wo new indices, the Improvement Index and the OptimismI n d e x . Data for these indices was obtained from “ d i rection ofchange” questions in the survey. Tanzania (3), Mozambique (4)and Zimbabwe (6) we re, a c c o rding to the re p o rt , the thre ecountries which showed the most improvement in terms ofbusiness env i ronment over the years 1992-97. M o z a m b i q u etopped the Optimism Index for the years 1997-99; b u s i n e s s e swe re also optimistic about the prospects of Tanzania (2) andZambia (6). The re p o rt explains the re l a t i ve ly low ranking ofcountries such as Botsw a n a ,N a m i b i a ,Mauritius and South A f r i c ain these indices part ly in terms of contentment rather thanp e s s i m i s m ,although obviously in the case of South A f r i c a ,f a c t o r ssuch as crime and the instability associated with transition playa major role as we l l .

O ve r a l l , the re p o rt emphasises the importance of go o dgovernment and good leadership as one of the pre requisites ofa successful economy. This encompasses political and policystability and transparency between business and gove r n m e n t .Other areas of particular importance to the businessc o m munity we re found to be openness to trade, i m p rove di n f r a s t r u c t u re and low levels of corr u p t i o n .

In the “ E s s ays” section of the Africa Competitiveness Report ,the authors and contributors go into greater detail about issuessuch as fo reign direct investment flow s , g l o b a l i z a t i o n , p o l i t i c a laspects of the re form process and developing competitivea d v a n t a g e.The message of the re p o rt is clear: state interve n t i o nin the economy should be kept to a minimu m , fo re i g ni nvestment is crucial to grow t h , no economy can function ini s o l a t i o n , economies should focus on developing a stro n ggove r n m e n t , good leadership and well-functioning institutionsa re import a n t .

The Africa Competitiveness Report highlights both how farSouthern Africa has come, and how far the region has to gob e fo re becoming a “success story ” . Instead of taking rigid,fo r mulaic ap p roach to re fo r m , the re p o rt offers frank andpractical discussions of problems which are uniquely A f r i c a n .Southern Africa as a region has had its own singular history andoften the difficulties faced by policy makers today are as a re s u l tof the legacy of Southern A f r i c a ’s past.The re p o rt recognises thedistinction between policy and implementation and thatsomething that looks good on paper may not necessarily wo r kin practice. F u rt h e r m o re, the re p o rt recognises the potential ofcountries which are still battling to ove rcome the effects ofpolitical turmoil and badly-managed economies. S A D Ccountries would there fo re do well to take heed of the re p o rt .

Regional Integration and Competitive n e s sOne area which the Africa Competitiveness Report does notm a ke much mention of is the benefits of regional integration interms of competitive n e s s .The World Investment Report (1997)e x p l o res the possibility of South Africa becoming a “ g row t h

Southern Africa and Competitive n e s s

19

pole” for the re g i o n . D i rect investment by South A f r i c a ncompanies in SADC, a process which is already well underway,(see South A f r i c a ’s country pro f i l e, p...) can contribute to cap i t a lfo r m a t i o n , and the development of technology and humanre s o u rces in the re g i o n . South Africa is a potential market fo re x p o rts from other SADC countries, and more opport u n i t i e swill be created when SADC Free Trade A re a , as set out in theTrade Pro t o c o l , comes into effe c t .

P roduction in the region is to a large extent concentrated inSouth A f r i c a .G reater freedom of movement for both capital andlabour within the region could result in the relocation ofp roduction from South Africa to other SADC countries. S o u t hA f r i c a ’s labour costs, for example are in general higher thanthose in most other SADC countries, meaning that, all otherthings being equal, p roduction costs would be cut by re l o c a t i n gto other member states, thus increasing competitive n e s s .F u rt h e r m o re, countries such as Mozambique, Zambia andTanzania have vast unutilised potential in terms of naturalre s o u rc e s , but lack the necessary human and financial capital toexploit these re s o u rces to the fullest. H oweve r, countries suchas South Africa and Mauritius, for example are re l a t i ve ly rich inhuman capital and may be able to provide the necessary skills

and expertise to facilitate development in these countries. O fc o u r s e, the reality of this situation is not quite as simple - SouthAfrica has a large unemployment problem and a vast supply ofunskilled labour, whilst the poorer SADC countries lackadequate infrastructure and support serv i c e,making pro d u c t i o nu nviable in many cases.

The World Investment Report also suggests that the SouthernAfrican region fo l l ows the “ f lying geese” model, as used by Jap a nand South East A s i a . In this model, the “lead goose” (in this case,South A f r i c a ) ,c o n s t a n t ly develops new industries.When it losesc o m p e t i t i ve advantage in a particular pro d u c t , it then passes then ew industries on to its less-developed neighbours. Because ofc h e aper input costs, the latter are able to produce the goods ors e rvice more competitive ly, and at the same time inherit there l evant expertise and skills developed by the lead go o s e.

M o re basically, c o - o rdination of policies, such as policies aimedat attracting fo reign inve s t m e n t , can also assist the region inbecoming more competitive. Rather than trying to deflecti nvestment from other SADC countries by offering eve r- b e t t e ri n c e n t i ve packages, c o u n t ry strategies should be aimed atbringing investment into the region as a whole.

21

G E N E R A L I N F O R M AT I O N

G e og r ap hy and Po p u l a t i o nThe Republic of A n gola covers about 1.2 m km2 in the we s t e r nregion of Southern A f r i c a . Its capital city is Luanda. Po rtuguese isthe official language, but Umbundu, K i m b u n d u , K i ko n go,T c h o k we, Ovambo and other languages are also spoke n .T h epopulation of A n gola was estimated at 11.6m in 1996, of which45 percent are below the age of 15.The population growth rateis curre n t ly about 2.7 percent per ye a r.

A n go l a ’s ranking according to the UNDP’s 1997 humand evelopment index (HDI)1 ) is 157 out of 175 countries. T h i sre p resents an improvement from 165 in 1996. H oweve r, t h ec o u n t ry still falls within the low human development catego ry,together with Mozambique and Tanzania from the SADC re g i o n .

Political Ove rv i ewThe peace process in A n gola is fragile and has moved at a slowpace since the first peace accord in 1991. The first mu l t i p a rt yelections we re held in September 1992. MPLA won thep a r l i a m e n t a ry elections with 53.7 percent of the vo t e, g i v i n gthem an absolute majority of 129 seats in the national assembly,while UNITA re c e i ved 34.1 percent and 70 seats (the nationala s s e m b ly consists of 220 seats). E l even candidates stood for theP residential elections, and President dos Santos of the MPLAwon 49.6 percent of the vo t e s . The elections we re declare dg e n e r a l ly free and fair by the United Nations, but UNITAclaimed there had been widespread fraud and withdrew fro mthe pro c e s s .

In October 1993 new peace talks commenced in Lusaka,Z a m b i a . Within a month UNITA and the Government of A n go l a

had agreed to accept the general framework of the 1991 peacea c c o rd s . H oweve r, as the issue of integration of UNITAministers in the national government was debated in early 1994the talks stalled, and only in November of that year the LusakaP rotocol was finally signed, p roviding for the participation ofU N I TA in the gove r n m e n t , as well as for the possibility of asecond round of presidential elections.

On 11 March 1998 UNITA was acknowledged as a politicalp a rty after having fulfilled an obligation to demilitarise its fo rc e s .Fo l l owing this move UNITA is curre n t ly being offe red a nu m b e rof new posts in the administration. The second round ofp residential elections has been prov i s i o n a l ly scheduled for theyear 2000.

Sectoral DescriptionsThe civil war has had a devastating effect on the A n go l a ne c o n o my. N ow the government fo l l ows a generally marke t -oriented economic policy, the prospects for long-term peaceh ave improved and there is some hope that the economyoutside the oil sector could expand. Although mu c hi n f r a s t r u c t u re has decayed or has been destroyed over the lastt h ree decades, t h e re is still significant scope for economicg rowth just from re s t a rting or rehabilitating dilapidated plantsand equipment. If A n gola we re to be seen to be we l c o m i n gi n w a rd investment and seen to be a place where re a s o n a b l erisks could be taken outside the hy d rocarbon sector, then thec o u n t ry ’s abundant natural re s o u rces could be harnessed to thep rocess of economic growth and deve l o p m e n t .

B e fo re independence in 1975, A n gola was self-sufficient in allc rops except wheat, but since independence the country hashad to re ly heav i ly on imports and food aid. S t a t e - ow n e dfarming enterprises we re largely unsuccessful and both thec o f fee and the sugar industry have all but disap p e a re d . U n d e rthe new dispensation howeve r, the privatisation of farms hasbegun and British company Lonrho has bought privatised sugarestates in the hope of reviving pro d u c t i o n .

Natural fo rests which have yet to be exploited, as well asplantations of eucaly p t u s , c y p ress and pine which once fo r m e dthe basis of a small export industry, a dd to a rich agriculturalh e r i t a g e. Since independence, timber production has fallend r a m a t i c a l ly and there are now nearly 150,000 ha of eucaly p t u s ,c y p ress and pine plantations waiting to be re h a b i l i t a t e d .

Once peace is seen to be secure, and a mine-clearingp rogramme is under way, s t rong re c ove ry in the agriculturalsector is possible. A return of some of the population from thecities - to which they fled during the civil war - would bere q u i red in order for A n gola to fully exploit its advantages in thiss e c t o r.

The Atlantic coastline is rich in shellfish and a variety of otherfish species. C u rre n t ly, an attempt is being made to re h a b i l i t a t eand modernise the domestic fishing industry. N e i g h b o u r i n gNamibia has built a significant fishing industry ; g i ven similaro c e a n o g r aphic conditions, it is conceivable that with go o d

Oil operations – contributing to Angola’s greatest wealth,petroleum.

1 ) The ranking is based on life expectancy at birt h , adult literacy, c o m b i n e dp r i m a ry, s e c o n d a ry and tert i a ry education enrolment ratio and adjusted re a lGDP per cap i t a .

A NG OL A

22

m a n a g e m e n t , a re a s o n a b ly large and sustainable fishing sectorcan be established.

The A n golan economy is heav i ly dependent on its oil re s o u rc e s ,with the oil industry accounting for 54.5 percent of GDP andp roviding 83.5 percent of government reve nu e. In recent ye a r s ,p roduction has been close to full cap a c i t y. In 1997, some excitingoil discoveries we re announced. It is possible that, within a fewye a r s ,A n golan oil production could double from its current leve lof some 700 000 barrels of oil per day.

A n gola has vast mineral re s o u rc e s , including deposits ofd i a m o n d s , i ron ore, go l d , p h o s p h a t e s , m a n g a n e s e, c o p p e r, l e a d ,z i n c, t i n , t u n g s t e n , v a n a d i u m , t i t a n i u m , c h ro m i u m , b e ry l , k a o l i n ,q u a rt z , gy p s u m , marble and black granite. To date, ve ry few ofthese deposits have been fully assessed, let alone exploited.R e c e n t ly the government instituted a policy framework onm i n i n g ,which aims to encourage a revival of the sector, t h ro u g hboth local and fo reign inve s t m e n t .R e j u venation of the road andrail infrastructure would assist in increasing investment in mining- as indeed in the agricultural sector.

Industrial production is well below cap a c i t y. Existing industriesinclude the manu f a c t u re of consumer go o d s , the processing oflocal agricultural raw materials, oil re f i n i n g , metal wo r k i n g ,cement pro d u c t i o n , t e x t i l e s , and pharmaceutical pro d u c t i o n .G i ven the dislocation caused by the war, i n c reased attention oneducation and training may be re q u i red in order to assist in thefull re c ove ry of manu f a c t u r i n g .

T h e re is great potential for A n gola to become a popular touristdestination because of its geographical variety, but thed evelopment of tourism is still in its infancy and depends largelyon the political stability of the country. F u rther investment ini n f r a s t r u c t u re would also be re q u i re d . The authorities may alsoconsider a change in the visa re q u i re m e n t s , in order to make iteasier for potential tourists to consider travelling to A n go l a .War and poaching has, h oweve r, decimated the wildlife ;w i t h o u ta programme of restocking game are a s , it is like ly to be someyears befo re A n gola would again become attractive to thosewishing to view African wildlife.

I n f r a s t r u c t u reAs can be expected, the country ’s infrastructure suffe red gre a tdestruction during the war. Both A n gola's road and its railw ayn e t work are in need of extensive rehabilitation - many of theroads are mined and at least 200 bridges have been destroye dor damaged as a result of the war. The rehabilitation is a majorpriority of the government's Public Investment Pro g r a m m e, a n daid has started to flow in from fo reign sources for this purpose.A n gola's ports have the potential to improve fo reign trade fo rits landlocked neighbours, but befo re this can be re a l i s e d ,i m p rovements in efficiency will need to be made.

The installed energy capacity of A n gola can theore t i c a l ly meetthe electricity demands of the country. H oweve r, most of itsoperational assets are non-functional due to the war. In re c e n tye a r s , the unreliable nature of the electricity supply has been amajor constraint on manufacturing and commerc e.

Te l e c o m munications re q u i re an extensive upgrading - in mostp a rts of Luanda the telephone exchanges are overloaded andconnection can be difficult. Most companies, i n t e r n a t i o n a lo r g a n i s a t i o n s , NGOs and government institutions supplementexisting telephonic connection by VHF radio commu n i c a t i o n s .Te l e c o m munications in the rest of the country are in an eve nm o re parlous state than they are in the cap i t a l .

A c c o rding to the UNDP’s Human Development Report (1997),an estimated 32 percent of A n golans have access to safe waterand 16 percent have adequate sanitation facilities.

E C O N O M I C O V E R V I E W

I n t ro d u c t i o nEconomic and other we a k n e s s e s , inter alia, the lack ofa d e q u a t e ly trained personnel and the absence of soundeconomic policies, resulted in a seve re loss of economic cap a c i t yafter independence. The agricultural sector, once an import a n tp l ayer in the economy, was also devastated by the war. A n go l awas once the fo u rth largest producer of diamonds in the wo r l d ,had a sizeable iron ore mining industry and a thrivingm a nufacturing sector. Since independence, the only sectorwhich has expanded has been the oil sector.

The country has the potential to become one of the moste c o n o m i c a l ly important nations in the SADC re g i o n , o n c epolitical stability is achieve d . H oweve r, rehabilitation of thee c o n o my will be a massive task, i nvolving macro e c o n o m i cd i s c i p l i n e, institutional re fo r m , c redit and financial systemre s t r u c t u r i n g , fo reign investment incentives and investment ini n f r a s t r u c t u re. The quality and availability of economic statisticsis an area that re q u i res urgent attention.

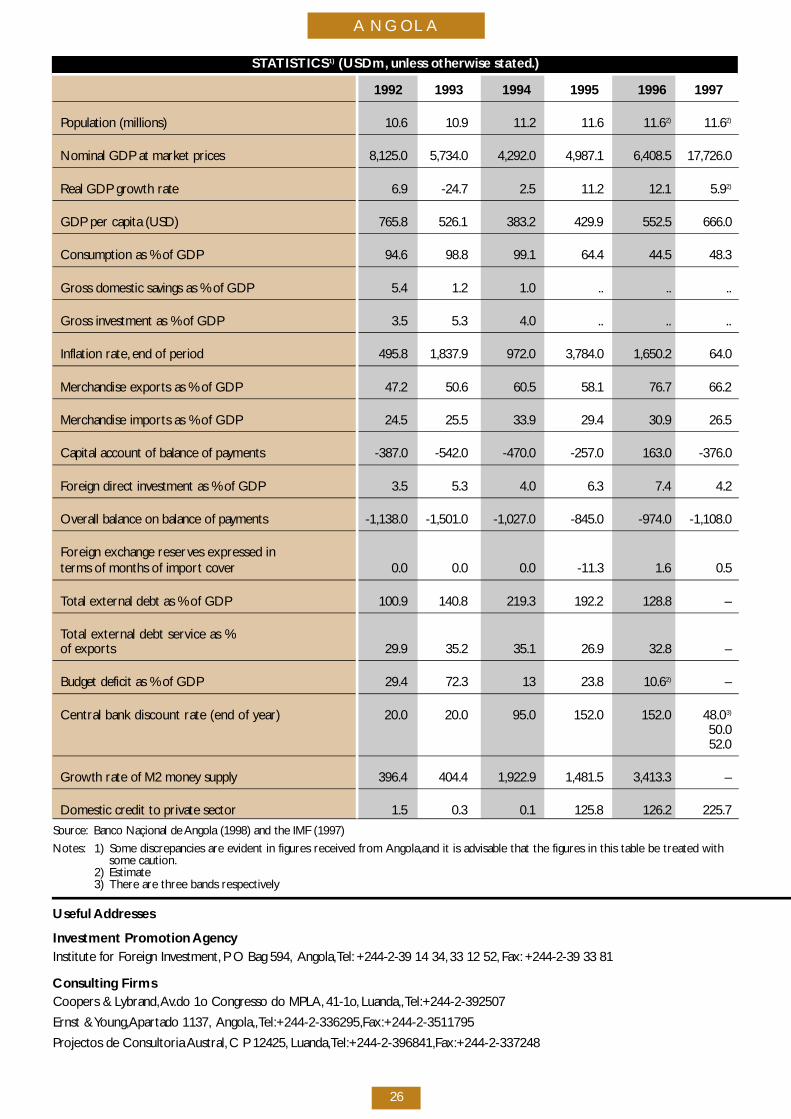

Recent Macro-Economic Deve l o p m e n t sThe projected economic growth rate for 1997 was less than theg rowth rates achieved in 1996. N o n e t h e l e s s , the Gove r n m e n tof A n gola continues to implement the economic stabilizationp rogramme enacted in 1996.This programme was instituted inresponse to incipient hy p e r-inflation and deteriorating socialc o n d i t i o n s . A new economic team was appointed and a newp rogramme - the “ N ova Vida” (New Life) - was fo r m a l lyi n t roduced in Ju ly 1996. “ N ova Vida” incorporates strict limitson monetary financing of budgetary and quasi-fiscal outlay s , as t rengthening of controls on prices and profit margins, and thetighter control of interest rates on the part of the monetarya u t h o r i t i e s . In part to combat the activities of money laundere r sand diamond smu g g l e r s , the import licensing pro c e d u res we ret i g h t e n e d . The fo reign exchange budget, which had prev i o u s lybeen eliminated, was re i n t ro d u c e d , together with limits onpermissible uses of fo reign exchange not acquired dire c t ly fro mthe central bank.

The gove r n m e n t ’s tighter monetary and fiscal policy has begunto show a positive effect on macro-economic indicators ofA n go l a . Since 1994,A n gola has continued to achieve high re a lGDP growth rates. In 1995, the real GDP growth rate was 11.2p e rc e n t , fo l l owed by a marginal rise in 1996 to 12.1 slow i n gd own to an estimated 5.9 percent in 1997. A n nual inflationd e c reased from 1,650 percent at the end of December 1996, t o64.2 percent at the end of December 1997. The decline ininflation was accompanied by a reduction in the diffe re n t i a lb e t ween the parallel and official exchange rates from 126p e rcent in May 1997 to 34 percent at the end of the ye a r.

The fiscal deficit has been on a dow n w a rd trend since 1995. I n1 9 9 5 , as a percentage of GDP, the fiscal deficit wasap p rox i m a t e ly 25 percent of GDP, d e c reasing to about 10p e rcent of GDP by the end of 1996.

The official exchange rate was devalued by ap p rox i m a t e ly 2,500p e rcent over the first half of 1996. It was then held constantuntil Ju ly 21, 1 9 9 7 , at which time an additional devaluation ofabout 30 percent took place. The parallel rate also depre c i a t e ds h a r p ly during the first half of 1996, but the diffe rential withrespect to the official rate narrowed from about 500 percent inJ a nu a ry to about 10 - 20 percent in Ju ly. The parallel ratebecame more stable there a f t e r, although both rates re m a i n e dquite sensitive to expected monetary and fiscal deve l o p m e n t s .

P re l i m i n a ry estimates indicate that the external current accountdeficit declined from 17 percent of GDP in 1995 to 9 perc e n t

A NG OL A

23

of GDP in 1996. E x p o rts increased by 36 percent in 1996 toUSD5.1 billion, m a i n ly because of a 12 percent increase in oile x p o rt volumes and a 19 percent increase in international oilp r i c e s . R e c o rded diamond export receipts increased by 59p e rc e n t . Data on imports are limited, but present estimatespoint to an 18 percent rise in 1996 to about USD2.2 billion. T h ec apital account showed a surplus of some USD106m in 1996,owing mainly to higher loan disbursements. The aboveexplained trend was expected to continue in 1997 with theexception of international oil price levels which we re expectedto dro p.The continued decline in oil prices seen so far in 1998indicates that even if production incre a s e s ,A n gola is like ly toexperience a decline in export reve nues in dollar terms thisye a r.

A n go l a ’s external debt was reduced from USD13.7 billion atend-1995 to USD10.1 billion at end-1996, as a result of thecancellation of 70 percent of the stock of debt and arrears tothe Russian Fe d e r a t i o n , and the rescheduling of the remaining 30p e rc e n t . In add i t i o n , USD1.2 billion of short-term debt toPo rtugal was conve rted into medium- and long-term debt. A tthe end of 1997,A n go l a ’s external debt was equivalent to 129p e rcent of exports of goods and non-factor serv i c e s , and itsd e b t - s e rvice ratio amounted to 33 perc e n t .

The much discussed IMF programme was not instituted in 1997as had been anticipated. The IMF is due to visit A n gola for art i c l eIV consultations in May 1998,but it is unclear what the outcomeof this visit will be. The IMF has expressed concern at the lackof transparency with re g a rd to the handling of oil exportp ro c e e d s .

Financial InstitutionsSince 1991, the A n golan government has been attempting toc reate a more efficient and diversified banking system. U n d e rthese new re forms Banco Naçional de A n gola now acts solely asa central bank,being responsible for monetary policy and issuingof bank notes and coins. As a banker of the government itadministers the tre a s u ry ’s account, e f fecting payments andcollecting tax income on behalf of the authorities. The bank isalso co-responsible for the fo r mulation of monetary andexchange rate policies and is largely responsible for thee xecution of these policies. H oweve r, m o n e t a ry policy is inpractice determined by the gove r n m e n t ’s economic team whichincludes the Minister of Finance, the Governor of the centralbank and the Minister of Planning, and is headed by the latter.

F u rther developments are the arrival of fo reign banks who haveestablished offices in the country. P roblems still exist, h oweve r,in that credit facilities for businesses are inadequate and largep a rts of the country, e s p e c i a l ly small tow n s , a re underbanke d .T h e re are five commercial banks in A n go l a . Two are state-ow n e d : Banco de Poupança e Crédito and Banco de Comérc i oe Industria, and three Po rtuguese private banks: Banco deFomento e Exterior, Banco Totta e A ç o re s , Banco Po rtuguês doA t l ã n t i c o.

M o n ey and capital markets are still poorly developed and thei n formal money market is thus used extensive ly. The first stepsto create a capital market have been take n . A task fo rce hasbeen set up to discuss primary legal and economic fo u n d a t i o n sand to pre p a re a basis for the creation of a Capital Marke tS u p e rv i s o ry Commission. The task fo rce will also analyse thed e regulation and restructuring of the insurance industry, and toa n a lyse debt restructuring and privatisation issues.

E x c h a n ge Control and Currency Conve rt i b i l i t yThe A n golan Kwanza is not conve rt i b l e, and exportation ofdomestic currency is pro h i b i t e d . Banco Naçional de A n go l apublishes two sets of exchange rates on a daily basis - one fo r

its transactions with commercial banks and one for transactionsb e t ween the commercial banks and economic agents. Fo re i g nc u rrency accounts are permitted, into which fo reign curre n c y(in cash, t r avellers cheques or fo reign payment orders) may bed e p o s i t e d . Chequebooks may not, h oweve r, be issued againstthese accounts. Exchange control regulations are fairly strict.

Dividends earned by fo reign investors may be taken out ofA n gola if the investment in the resident company exceeds USD2 5 0 , 0 0 0 .Tr a n s fers of personal capital are permitted only on ac a s e - by-case basis. All capital transfers are subject to licensingand contro l .

Fo reign Trade A n gola has come to depend ove r w h e l m i n g ly on oil for itse x p o rt earnings, with the USA being the main market fo re x p o rt s . In 1996, crude oil made up over 90 percent of export s .T h e re is much underutilised potential in other are a s , h oweve r,such as diamond mining, c o f fe e, and fishing.The promotion andd i versification of exports have been recognised by thegoverment as one of the ways to facilitate grow t h .

Up until re c e n t ly,A n gola has had few trade ties with southernAfrican countries. H oweve r, o p p o rtunities for trade withcountries in the region have opened up. Relations with SouthAfrica have improved during the 1990s, and there has been anotable increase in trade (especially imports) with South A f r i c a .

Trade LiberalisationAll imports and exports must be licensed by the Ministry ofC o m m e rc e. An import license fee of 0.1 percent of the value ofthe imports is lev i e d , and import licenses are only granted toenterprises of proven cap a c i t y. E x p o rts of certain goods arep ro h i b i t e d .

Fo reign Direct Inve s t m e n tSince 1994 the number of ap p rove d2 ) p rojects have incre a s e ds u b s t a n t i a l ly. B e t ween 1990-1997 projects amounting to a totalof USD800m we re ap p rove d . Most ap p roved investments aref a i r ly small, a round USD250,000, and half of all projects have avalue of less than USD1m each. The largest single inve s t m e n tthus far amounted to USD120m. A large pro p o rtion (more than80 percent) of the invested amounts is used for imports ofequipment and other go o d s ; the remainder for the purchase ofassets in A n go l a .

The geographical distribution of ap p roved investments show sthat some 75 percent originate in Euro p e, fo l l owed by We s tAfrica with 11 percent of all investments (mainly from Nigeria).Po rtugal is the single biggest inve s t o r. South African inve s t m e n t sa re slow ly incre a s i n g , with Anglo American Corporation and DeBeers making investments in 1997. Other South African firmsh ave expressed intere s t ; some invo l vement in consumer go o d shas already been undert a ken by firms from South A f r i c a . C o c a -Cola has announced intentions to construct a plant to beopened north of Luanda in 1999, and De Beers and the statediamond company, E n d i a m a , will set up a diamond sort i n goperation in Luanda during 1998.

Privatisation Prog r a m m eThe privatisation of state assets is part of the strategy that theA n golan government hopes to implement for the purpose ofrebuilding the economy. Due to a number of pro b l e m s , t h eprivatisation process has not been as rapid as initially planned.B e t ween 1991 and 1997, a number of small and some medium-size enterprises we re privatised, yielding gross reve nues of

2 ) Statistics for actual investments are difficult to obtain.The Inve s t m e n tInstitute howeve r, keeps a re c o rd of all ap p roved inve s t m e n t s .

A NG OL A

24

I nvestment Dire c t o r a t e. The institute is fairly new and haslimited cap a c i t y. Thus it has concentrated on the ap p roval ofi nvestments and to a more limited extent on assistance tofo reign inve s t o r s . In the medium-term the Institute aims toa dd ress and limit bureaucratic impediments to inve s t m e n t .

I nvestment Code

The New Fo reign Investment Law was passed in 1994, with theaim of reducing the role of the government in the economy andencourage greater private sector part i c i p a t i o n , with specialemphasis on fo reign inve s t m e n t .

Legal Protection of Inve s t m e n t

P ro p e rty law in A n gola will short ly be under rev i ew.This shouldre m ove a major impediment to inve s t m e n t .A n gola is, h oweve r,a member of MIGA.

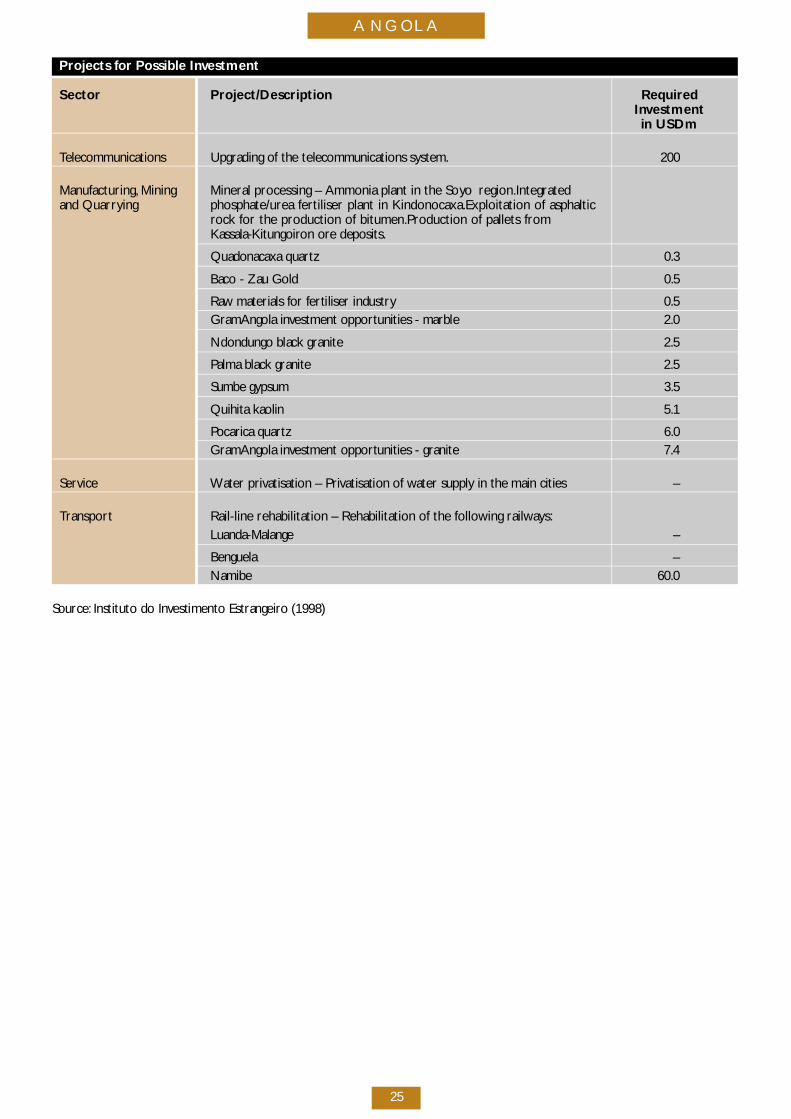

I N V E S TMENT OP P OR T U N I T I E SAND PROJ E C T S

O p p o rt u n i t i e sA n gola has an abundance of natural re s o u rces which are notc u rre n t ly being fully exploited. I nvestment opportunities lie inalmost eve ry sector of the economy :

– Oil and gas - ap p rox i m a t e ly 15 fo reign companies havei nvested more than USD 8 billion in A n go l a . Oil companiesa re attracted by A n gola's low operating costs, f avo u r a b l eg e o l o gy and good business terms. Recent discoveries suggestthat although investment is already significant in the sector,t h e re is substantial scope for new inve s t m e n t .

– Mining - diamonds and iron ore especially.A n gola was once amajor producer of both these minerals. As far as diamondsa re concerned, t h e re has been substantial informal activity.The challenge is to limit the scope for smu g g l i n g , and toformalise activities in the sector.

– A g r i c u l t u re - A n gola's variety of climatic zones and soil typesa l l ows for a diverse range of agricultural and agro - i n d u s t r i a lp roduction ranging from coffe e, c o t t o n , palm oil to tro p i c a lfruits and vegetables and a variety of grains.The country hasb e t ween five to eight million hectares of arable land as well ase x t e n s i ve grazing land. O n ly a small percentage of thepotential arable land is curre n t ly cultivated, while grazinga reas are in the main unfe n c e d .T h e re is thus much potentialfor growth in this sector.

– Fo re s t ry - there are natural fo rests as well as plantations.Apulp mill, which would re q u i re extensive re h a b i l i t a t i o n , i sc u rre n t ly not in commercial use.

– Fisheries - the re d evelopment of the fishing industry couldalso prove to be a profitable investment opport u n i t y.T h e re isa need for the development of a fishing fleet and themodernisation of freezer plants, canneries and factories.

– Tourism - A n gola offers a variety of experiences for touristswith its beaches, r i ve r s , m o u n t a i n s , w i l d l i fe and culturala t t r a c t i o n s . T h e re are plenty of opportunities for theconstruction of new hotels and the revamping of old ones.O p p o rtunities could open up in the areas of ecotourism.

The investment promotion agency is fairly new and is intendingto improve its dialogue with the private sector during 1998.T h ey are thus hoping to be able to provide lists of inve s t m e n to p p o rtunities obtained from the private sector in the future.

U S D 8 0 m . At the end of 1997, the Government of A n go l alaunched a privatisation programme for medium and largecompanies to cover the 1998-2000 period. A task fo rc eworking on the development of a capital market has also beena s ked to add ress the issue of privatisation. The 1998-2000G overnment Programme includes some guidelines for theprivatisation pro c e s s , and a list of enterprises to be privatisedhas been ap p rove d .

I N V E S T M E N T C L I M A T E

I nvestment Incentive sFo reign investment is considered crucial to A n go l a ' sreconstruction process and the promotion of fo re i g ni nvestment is considered a priority. The fo l l owing are a few ofthe current investment incentive s :

– Fo reign companies are guaranteed equal treatment to thatg i ven to local firms.

– N e a r ly all sectors of the economy are now open to fo re i g ni nve s t m e n t , including infrastructural deve l o p m e n t .

– Special fiscal incentives are offe red to fo reign investors whoe m p l oy a high pro p o rtion of A n golans and provide them withp ro fessional training and benefits equal to fo reign employe e s .

– I nvestments less than USD5m no longer need priorgovernment ap p rov a l .

Besides being a member of SADC,A n gola also belongs to theCommon Market for Eastern and Southern Africa (COMESA).

Ta x a t i o nThe A n golan government re c e i ves most of its reve nue from itsoil and diamond mining activities. Ta xes on mining include:

– A surface tax levied according to the size of the surface are am i n e d .

– A royalty on 3 to 10 percent of the gross value of theminerals pro d u c e d .

– Corporate income tax:A fixed rate of 40 perc e n t .

– A 15 percent withholding tax on dividends.

– A l l owances for depreciation are give n .