• CERTIFIED FINANCIAL PLANNER - Google Groups

81

•CERTIFIED FINANCIAL PLANNER 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of • CERTIFIED FINANCIAL PLANNER - Google Groups

• CERTIFIED FINANCIAL PLANNER

1

•• RETIREMENT PLANNING AND RETIREMENT PLANNING AND

EMPLOYEE BENEFITSEMPLOYEE BENEFITS

2

Defined contribution plans

• Nature of Defined contribution plans

• The benefits to be received at the time of

retirement are not fixed.

• The amount received depends upon the

earnings of the investment.

• There is no element of surety with this method.

• This is beneficial to the employer.

• If there is inadequate earning then the

employee gets to enjoy a lesser amount of

benefit.

• There is direct relation between the amount

contributed and amount received as benefit.3

Defined contribution plans

• Provident fund

• Employee’s Pension Scheme1995

• Employee’s Deposit Linked Insurance

Scheme1976

• Public Provident Fund

4

• Provident Fund Act

5

Income tax treatment of PF

6

Particulars SPF RPF URPF PPF

Employee’s Contribution

Deduction u/s 80C is available from the gross total income subject to thelimit specified therein

Deduction u/s 80C is available from the gross totalincome subject tothe limit specified therein

No deductionu/s 80C is available

Deduction u/s 80Cis available from the gross total income subject to the limit specified therein

Employer’scontribution

Fully exempt from tax

Exempt upto 12%of salary, excessis included in gross salary

Not exempt butalso not taxable every year

Not applicable asthere is only assesses own contribution

Interest on PF

Fully exempt from tax

Exempt u/s 10 up to 9.5%p.a. interest credited in excess is includedin gross salary

Not exempt but also not taxable every year

Fully exempt

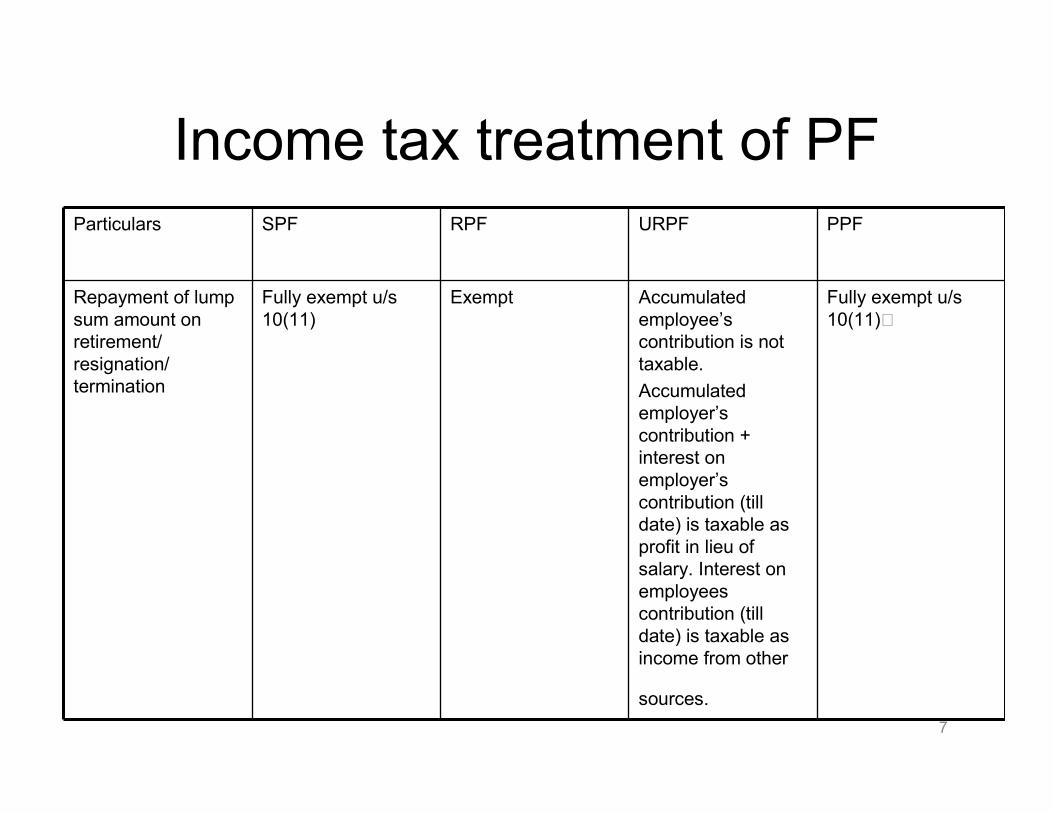

Income tax treatment of PF

Particulars SPF RPF URPF PPF

Repayment of lump

sum amount on

retirement/

resignation/

termination

Fully exempt u/s

10(11)

Exempt Accumulated

employee’s

contribution is not

taxable.

Accumulated

employer’s

contribution +

interest on

employer’s

contribution (till

date) is taxable as

profit in lieu of

salary. Interest on

employees

contribution (till

date) is taxable as

income from other

sources.

Fully exempt u/s

10(11)

7

Provident Fund

• Statutory provident fund

– This fund is set up under the provisions of the

provident fund Act, 1925.

– It is maintained by government and semi

government organizations, local

authorities,railways, universities and recognized

educational institutions.

– Have to Subscribe after completed continuous

Service of 1 year.

8

Provident Fund

• Recognized provident fund

– It is governed by employee’s provident fund

and miscellaneous provision act, 1952.

–Any organization employing 20 or more

employees are under obligation to register

itself under PF Act, 1952 and start a PF

scheme after three years of its

establishment.

9

Provident Fund

– They can even start before 3 years and with less

than 20 employees if wish so.

– They have two options:

• Either to join govt. scheme run by provident

fund commissioner u/PF Act, 1952; or

• They may start a PF scheme of their own and

get it approved by provident fund commissioner

and commissioner of Income tax.

•

10

Provident Fund

11

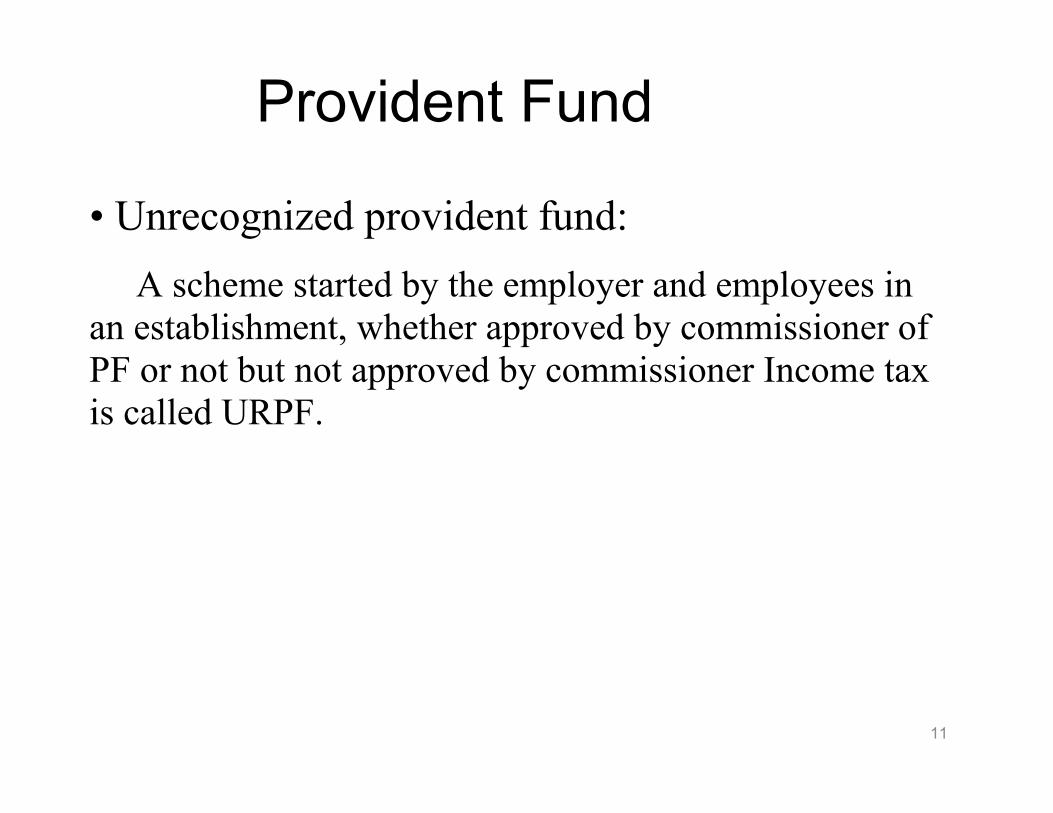

• Unrecognized provident fund:

A scheme started by the employer and employees in

an establishment, whether approved by commissioner of

PF or not but not approved by commissioner Income tax

is called URPF.

Employees’ provident fund

• Employee’s provident fund organization– The scheme extend to whole of India except the state of J & K.

– It applies to every establishment which is a factory engage din any industry specified, in which 20 or more persons are employed and to any other establishment employing 20 more persons or class of such establishment which the central govt. may notify.

– With the 2 months notice central govt. may notify any any establishment to be covered under the Act even employing less than 20 peoples.

12

Employees’ provident fund

– Even where it appears to the central provident

fund commissioner, either on an application made

to him or own his own, that the employer and the

majority of employees in relation to any

establishment have agreed that the provision of

this act should be made applicable to the

establishment then this act will be applicable here.

– If the no. of persons in an establishment falls

below twenty, still the act shall continue to apply.

13

Employees’ provident fund

• Investment norms:– Employer’s contribution to the fund shall be 12% of the basic wages, dearness allowance payable to each of the employee.

– The rate of contribution is 10% in following cases

• Any covered establishment with less than 20 employees.

• Any sick industrial company

• Any establishment where, any financial year losses are equal to exceeding it’s net worth

• Establishments engaged in manufacturing of beedi,jute, coir etc.

14

Employees’ provident fund

15

Exercise

• Mahesh is working for a pvt ltd company,

his basic salary is Rs.5000 per month

and he gets the da of 15% of the basic,

calculate his PF contribution per month.

The employer is giving the interest of

12% per annum. Calculate his total

Return.

16

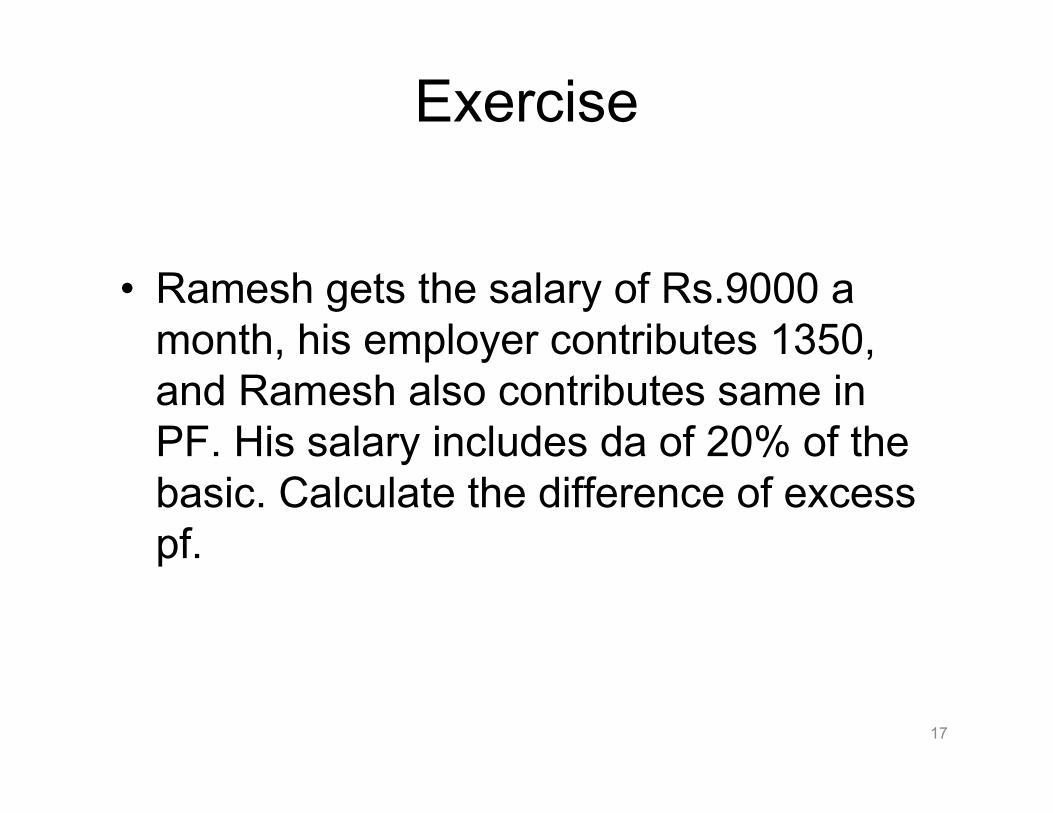

Exercise

• Ramesh gets the salary of Rs.9000 a

month, his employer contributes 1350,

and Ramesh also contributes same in

PF. His salary includes da of 20% of the

basic. Calculate the difference of excess

pf.

17

Employee’s Pension

Scheme,1995

• EPS-95 came into effect from 16.11.95.

• It has replaced the erstwhile family pension scheme, 1971.

• The scheme was compulsorily applicable to all new members of provident fund and the existing members who were contributing to to employee’s family pension-1971.

• Contributions: out of employers’ 12% contribution to provident fund, 8.33% goes to EPS. The central govt contributes 1.16% on wage at the end of the year.

18

Employee’s Pension

Scheme,1995• Benefits :

– Pension for life to the member, on superannuation/ retirement and

invalidation.

– Commutation of pension up to 1/3rd of pension amount.

– Superannuation / retirement pension will be available on –

– Minimum 10 year of eligible service and

– Attaining the age of 58 years.

– On ceasing employment earlier than 58 years, pension may be availed

by member but not before 50 years of age.

– No such eligibility applicable in case of death or disablement of the

member ( membership with one contribution is enough in such cases).

19

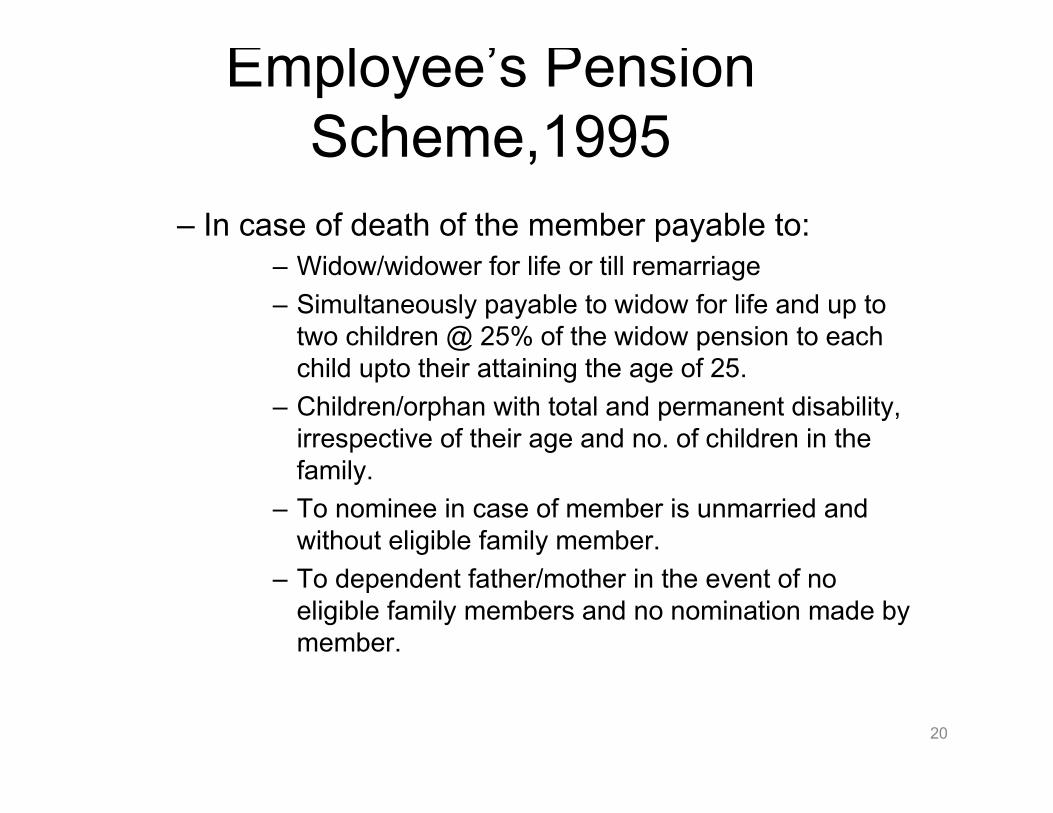

Employee’s Pension

Scheme,1995

– In case of death of the member payable to:

– Widow/widower for life or till remarriage

– Simultaneously payable to widow for life and up to

two children @ 25% of the widow pension to each

child upto their attaining the age of 25.

– Children/orphan with total and permanent disability,

irrespective of their age and no. of children in the

family.

– To nominee in case of member is unmarried and

without eligible family member.

– To dependent father/mother in the event of no

eligible family members and no nomination made by

member.

20

Employee’s deposit linked insurance scheme 1976

• It is to provide life insurance benefits to

employees of establishments who are

covered under employees’ provident

fund scheme 1952.

• This is a life insurance type of policy

providing term cover only so long as the

employee is member of employee

provident fund.

21

Employee’s deposit linked insurance scheme

1976

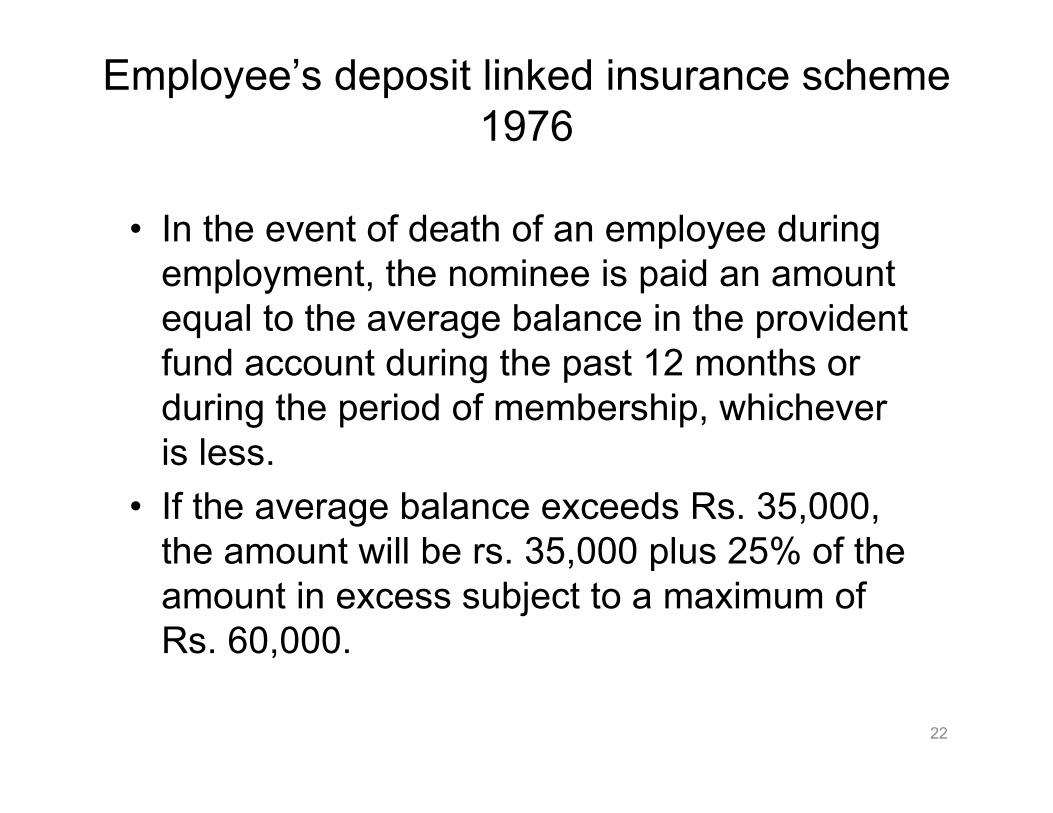

• In the event of death of an employee during

employment, the nominee is paid an amount

equal to the average balance in the provident

fund account during the past 12 months or

during the period of membership, whichever

is less.

• If the average balance exceeds Rs. 35,000,

the amount will be rs. 35,000 plus 25% of the

amount in excess subject to a maximum of

Rs. 60,000.

22

Employee’s deposit linked

insurance scheme 1976

• Illustration:

• An employee having the average

balance in his PF a/c amounting to Rs.

85000 dies, his nominee will get.

•

• 35000 + 12500 ( 25% of 50000) =

47500

23

Employee’s deposit linked

insurance scheme 1976

• Another employee having an average

balance of Rs. 2,00,000 dies. Under

EDLI scheme his nominee will get.

• Total cover amount:

• 35,000 + 41,250 =

76,250.

• But will receive only Rs. 60,000.

24

EDLI

• Contributions

– .5% of the salary of employee

– .01% administrative expense

– Upto maximum salary of 6500

25

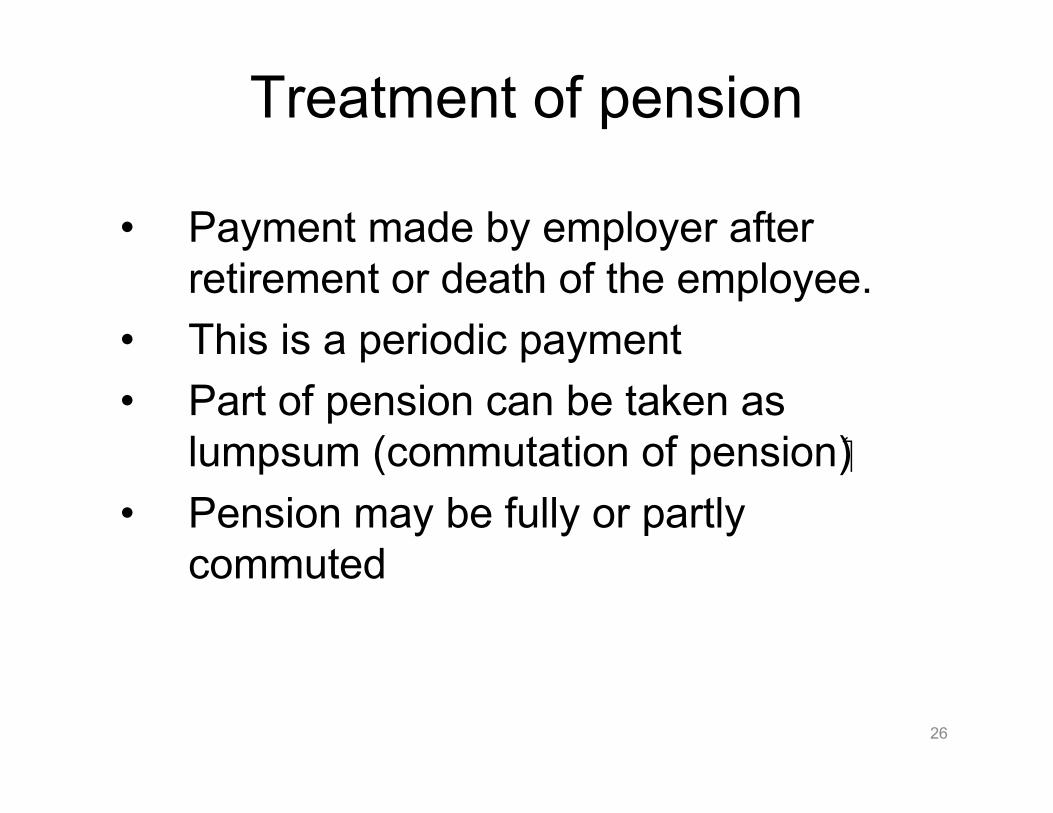

Treatment of pension

• Payment made by employer after

retirement or death of the employee.

• This is a periodic payment

• Part of pension can be taken as

lumpsum (commutation of pension)K

• Pension may be fully or partly

commuted

26

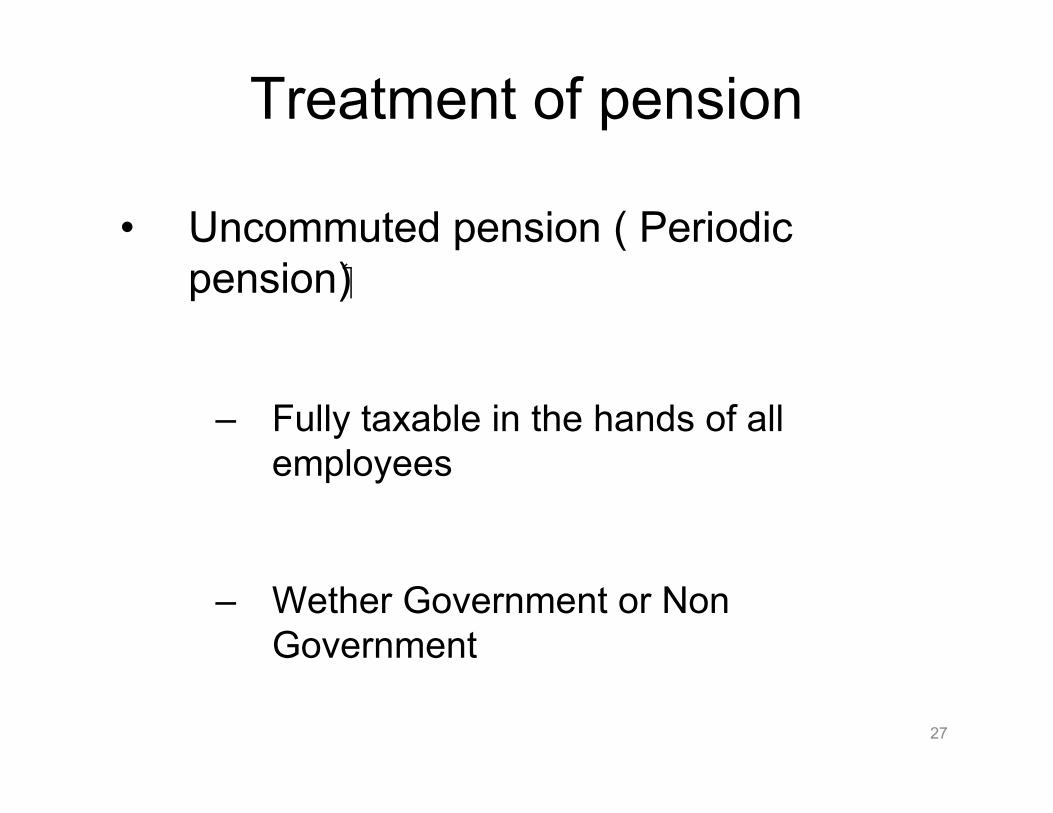

Treatment of pension

• Uncommuted pension ( Periodic

pension)K

– Fully taxable in the hands of all

employees

– Wether Government or Non

Government

27

Treatment of pension

• Commuted pension:

– Exemption u/s 10(10A)K

Govt. Employees, employees of local authorities

and employees of statutory corporations

Any other employee

Fully exempt a) If gratuity is not received Commuted value of

half of pension which he is normally entitled to

receive

b) If gratuity is also received Commuted value of

1/3rd of pension which he is normallly entitled to

receive

28

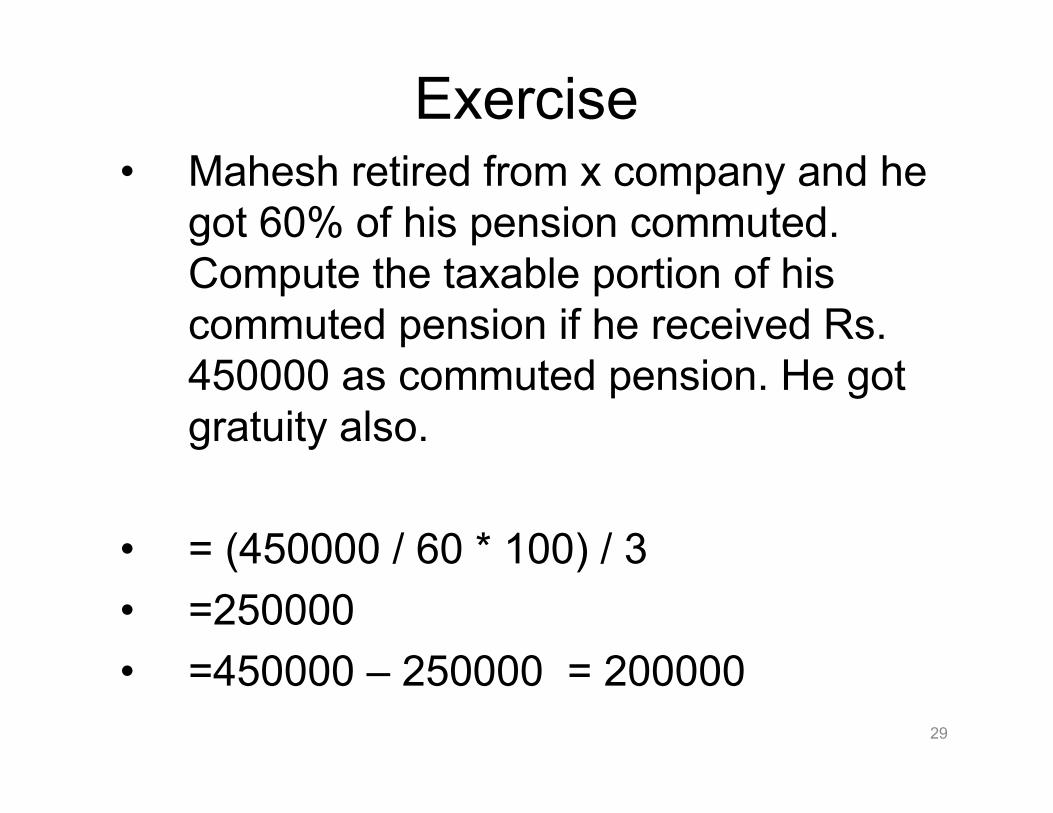

Exercise• Mahesh retired from x company and he

got 60% of his pension commuted.

Compute the taxable portion of his

commuted pension if he received Rs.

450000 as commuted pension. He got

gratuity also.

• = (450000 / 60 * 100) / 3

• =250000

• =450000 – 250000 = 200000

29

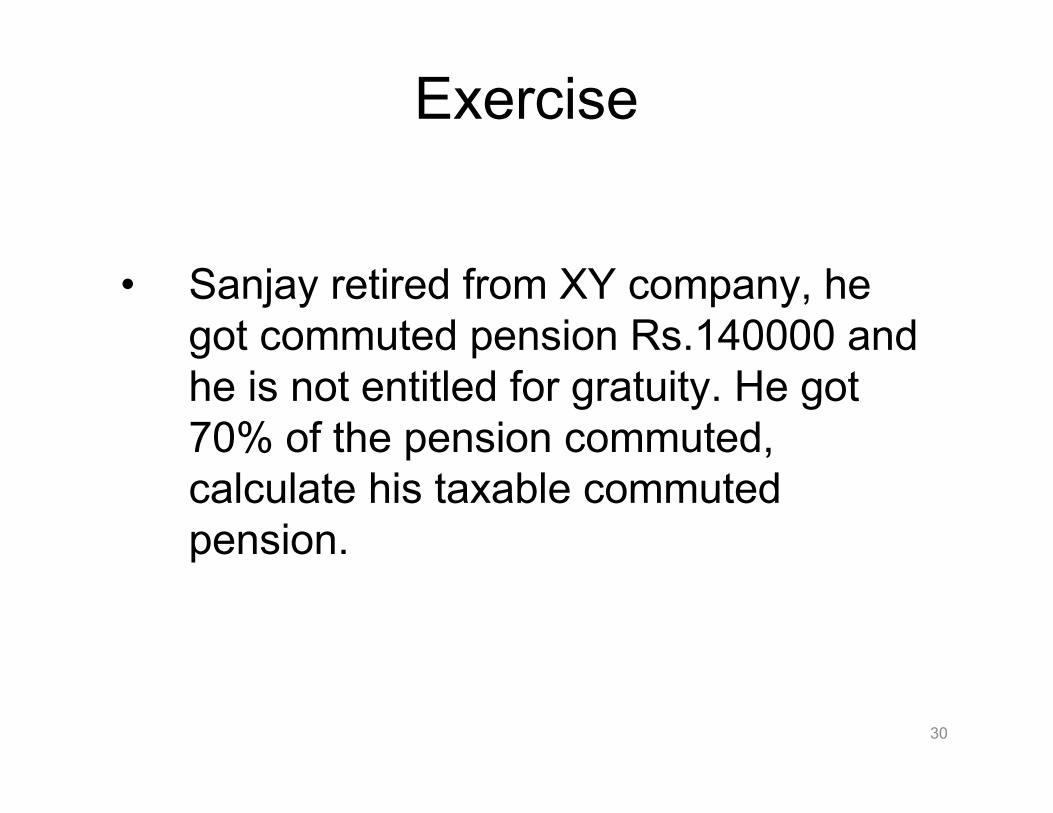

Exercise

• Sanjay retired from XY company, he

got commuted pension Rs.140000 and

he is not entitled for gratuity. He got

70% of the pension commuted,

calculate his taxable commuted

pension.

30

Exercise

• Jay gets Rs.9000 as basic and 20% of basic

as da,

• Calculate his pf value if he contributes at

month end.

• Calculate the amount that goes in EPS for

the first month

• Calculate the employee deposit linked

insurance part with administrative charges for

the first month

31

Solution

32

salary Total value EPS ded.

1 10800 1296 1296 396.36 1692.36 Rs.1,692.36 899.64 125.28 1024.92

2 10800 1296 1296 396.36 1692.36 Rs.3,545.49 899.64 125.28

3 10800 1296 1296 396.36 1692.36 Rs.5,574.68 899.64 125.28

4 10800 1296 1296 396.36 1692.36 Rs.7,796.63 899.64 125.28

5 10800 1296 1296 396.36 1692.36 Rs.10,229.67 899.64 125.28

6 10800 1296 1296 396.36 1692.36 Rs.12,893.85 899.64 125.28

7 10800 1296 1296 396.36 1692.36 Rs.15,811.12 899.64 125.28

8 10800 1296 1296 396.36 1692.36 Rs.19,005.54 899.64 125.28

9 10800 1296 1296 396.36 1692.36 Rs.22,503.43 899.64 125.28

10 10800 1296 1296 396.36 1692.36 Rs.26,333.61 899.64 125.28

Sr

No

Employee

contribution

Employers

contribution

Employers

real contri in PF

Total contri.

in PF

Govt

contribution

Total EPS

for 1st year

EDLI

salary

10800 54 10.8 64.8

Employers

contribution

Exercise

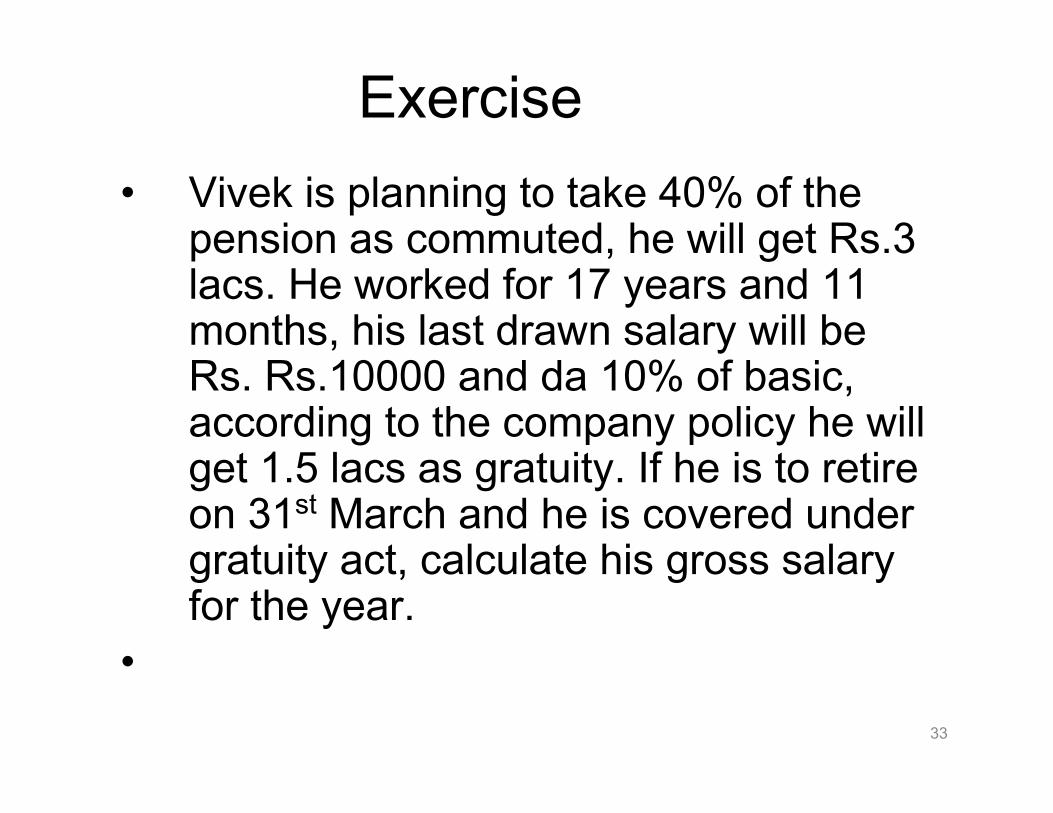

• Vivek is planning to take 40% of the pension as commuted, he will get Rs.3 lacs. He worked for 17 years and 11 months, his last drawn salary will be Rs. Rs.10000 and da 10% of basic, according to the company policy he will get 1.5 lacs as gratuity. If he is to retire on 31st March and he is covered under gratuity act, calculate his gross salary for the year.

•

33

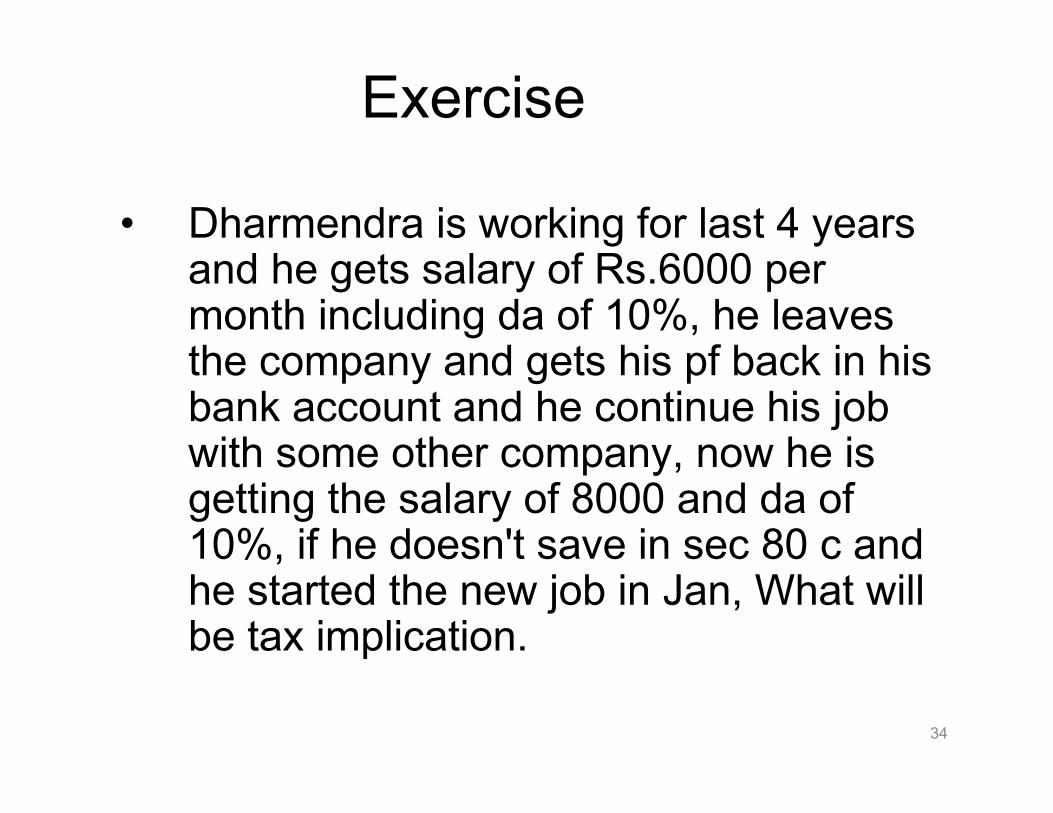

Exercise

• Dharmendra is working for last 4 years and he gets salary of Rs.6000 per month including da of 10%, he leaves the company and gets his pf back in his bank account and he continue his job with some other company, now he is getting the salary of 8000 and da of 10%, if he doesn't save in sec 80 c and he started the new job in Jan, What will be tax implication.

34

Exercise

• Suresh is contributing in an URP, his

salary is 5000 a month and da is 10%

of salary, if he works for 12 years

calculate his annual gross salary and

also calculate his taxable part of pf at

the end of 12 years.

35

Exercise

• A retired from his job w.e.f. 1-4-2007. He had joined the service

on 1-1-1980. He gets an increment in his basic salary amounting

to Rs. 500 every year on January 1. At the time of his retirement

he was getting a basic salary of Rs. 5,000 pm. He was also

entitled to dearness allowance @ 10% of basic salary and a

commission on turnover @1% of total sales achieved by him. His

turnover for the 12 months ending on 31-3-2007 was Rs.

4,00,000, spread evenly over the year. He received a sum of Rs.

1,60,000 as gratuity, calculate gratuity exemption amount. He is

not covered under gratuity act, also calculate his taxable salary

for the previous year

36

Retirement income stream

• Employer pension schemes

– Pension offered by insurance

companies

– Pension offered by mutual funds

– Provident fund

– Gratuity

– Employee pension scheme

37

Retirement income streams

• Rental income

• Dividend income

• Ineterest income

• Professional income

38

Retirement income stream

• Government employee's pension

– Related to final salary

– Linked with consumer price index

– Spouse and children pension after death

– In general calculated as 1/66th of average final

salary for each year of pensionable service

– Upto 40% can be commuted

– Commuted part is added after 15 years if he

survives

39

Retirement income stream

• Employee's pension scheme 1995

– Administered centrally by Employee's

provident fund organisation (EPFO)

– 1/70th of pensionable salary and

pensionable service (contribution

years)

– Pensionable salary - 6500 or higher

on which contribution was made

– Upto 1/3rd can be commuted

40

Retirement income streams

• Other income schemes– Fixed deposit:

• Bank fixed deposit– Most popular avenue for parking the retirement fund by retiree.

– They are safe up to Rs. 1,00,000 under guaranteed deposit insurance scheme.

– Liquidity

– Deduction u/s 80C of the IT Act for term deposit for a fixed period not less than 5 years with a scheduled bank.

• Company fixed deposit– Attractive due to falling interest rate of commercial bank.

–

41

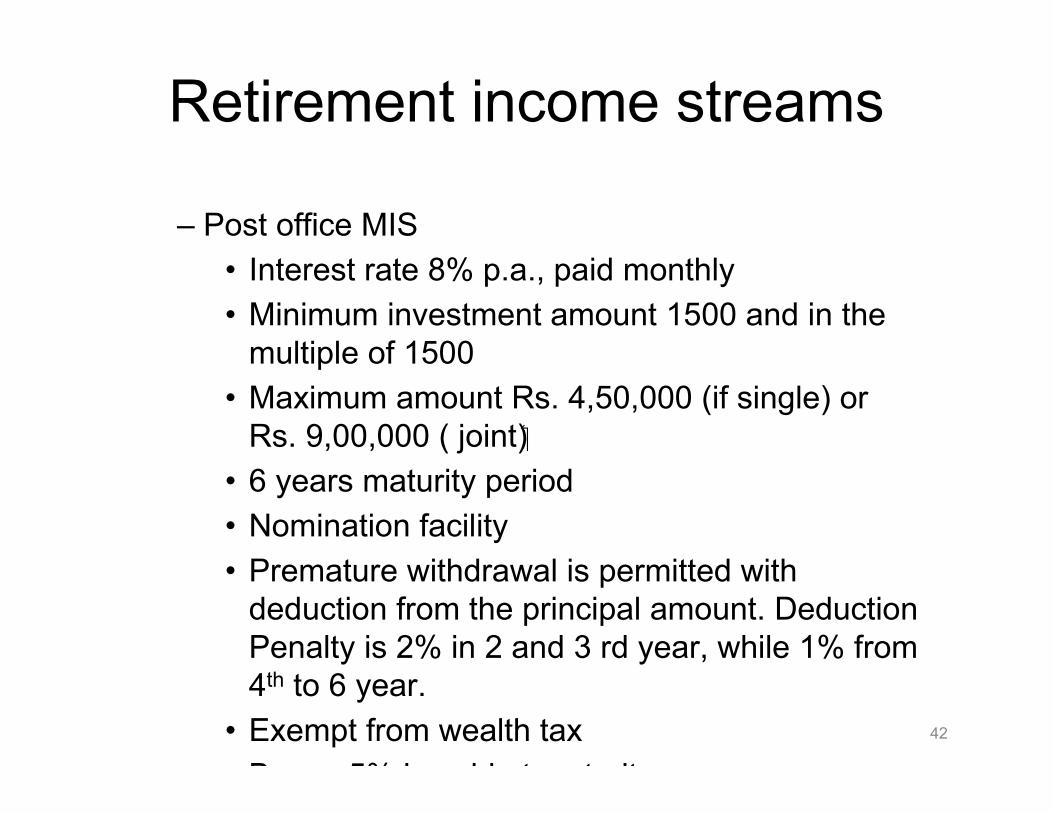

Retirement income streams

– Post office MIS

• Interest rate 8% p.a., paid monthly

• Minimum investment amount 1500 and in the

multiple of 1500

• Maximum amount Rs. 4,50,000 (if single) or

Rs. 9,00,000 ( joint)K

• 6 years maturity period

• Nomination facility

• Premature withdrawal is permitted with

deduction from the principal amount. Deduction

Penalty is 2% in 2 and 3 rd year, while 1% from

4th to 6 year.

• Exempt from wealth tax

• Bonus 5% is paid at maturity.

42

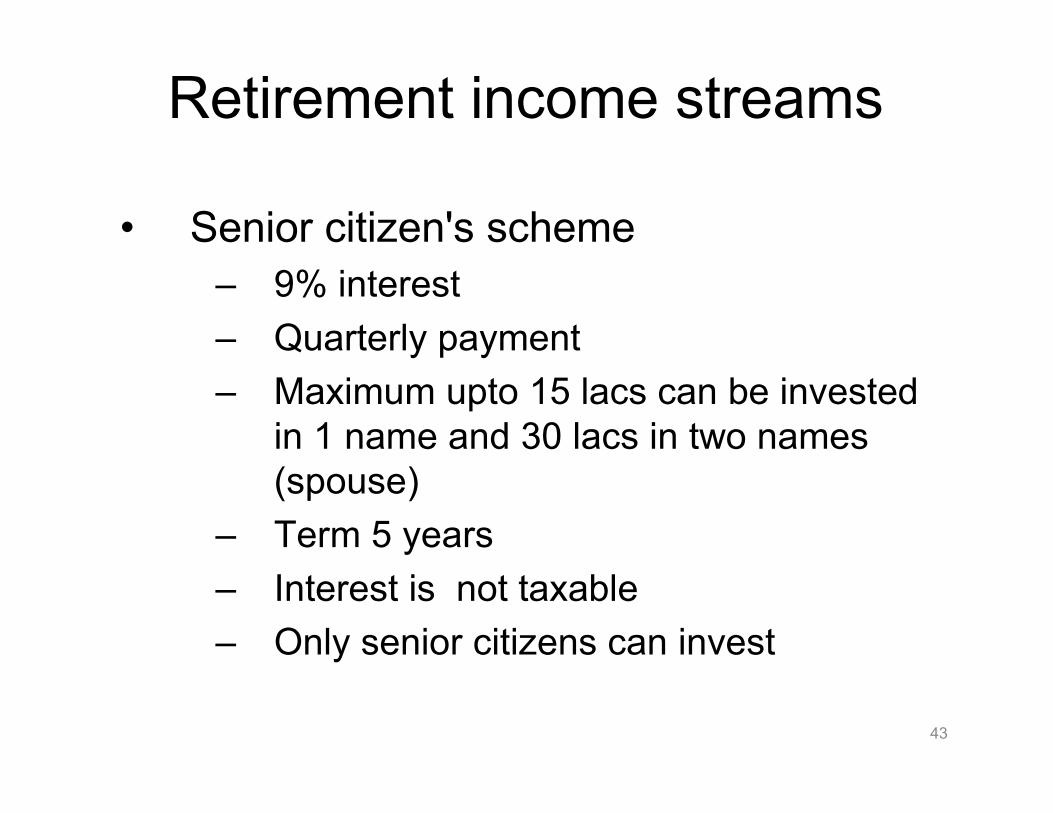

Retirement income streams

• Senior citizen's scheme

– 9% interest

– Quarterly payment

– Maximum upto 15 lacs can be invested

in 1 name and 30 lacs in two names

(spouse)

– Term 5 years

– Interest is not taxable

– Only senior citizens can invest

43

Retirement income streams

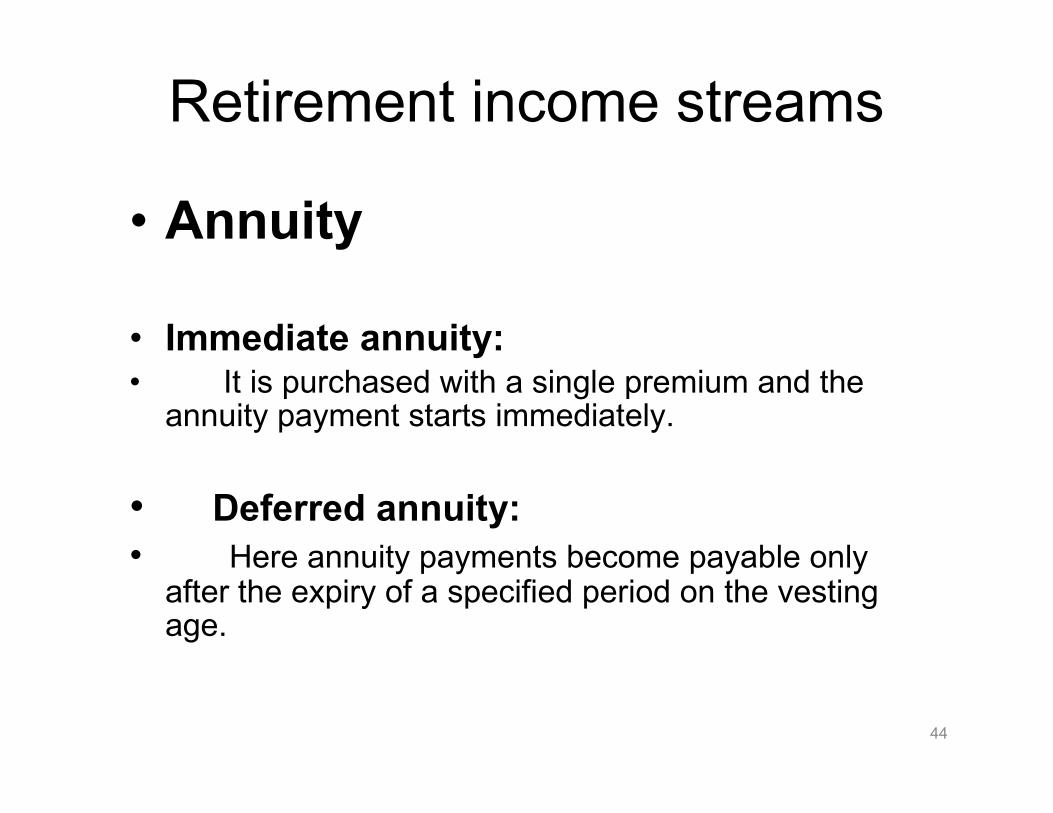

• Annuity

• Immediate annuity: • It is purchased with a single premium and the

annuity payment starts immediately.

• Deferred annuity:

• Here annuity payments become payable only after the expiry of a specified period on the vesting age.

44

Retirement income streams

• Deferred annuity can be:

• deferred immediate annuity

• deferred annuity due

• For example: in case of a deferred annuity certain due of Rs. 10000 pa for 5 years with a deferment period of 2 years which was purchased on 1st of Nov. 2004:-

• The deferment period being 2 years, the annuity shall vest for payment after 2 years I.e. on 1st Nov. 2006. That date is called vesting date.

• It is being annuity due the first payment of 10000 will be made in advance on the vesting date itself i.e. 1st of Nov. 2006

• It then being an immediate annuity, the 1st annual payment of Rs. 10000 will be made at the end of one year from the vesting date i.e 1st of Nov. 2007

•

45

Retirement income streams

• Annuity certain

• Here fixed annuity instalments are payable for a specified certain period.

• Life annuity

• Payment is till death

• Joint life annuity

– Payment till the death of last survivor

• Perpetual annuity

• Payment is for ever

46

Retirement income streams

• Life annuity with return of purchase

price

– Payment till death and nominee gets

the purchase price

• Joint life annuity with return of

purchase price

– Payment till the death of last survivor

and nominee gets the purchase price

after death

• Increasing annuity

– Payment increases every year 47

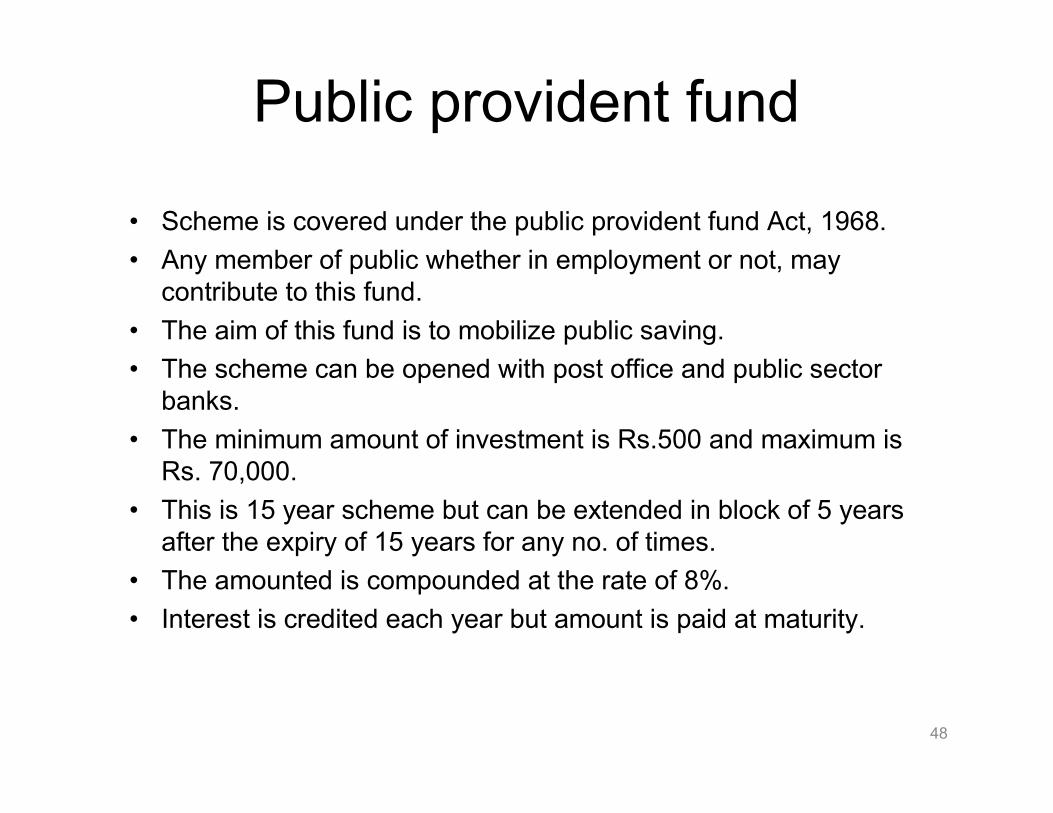

Public provident fund

• Scheme is covered under the public provident fund Act, 1968.

• Any member of public whether in employment or not, may

contribute to this fund.

• The aim of this fund is to mobilize public saving.

• The scheme can be opened with post office and public sector

banks.

• The minimum amount of investment is Rs.500 and maximum is

Rs. 70,000.

• This is 15 year scheme but can be extended in block of 5 years

after the expiry of 15 years for any no. of times.

• The amounted is compounded at the rate of 8%.

• Interest is credited each year but amount is paid at maturity.

48

Public provident fund

• Only one account can be opened by an individual on his behalf.

• Maximum contribution on self account + minor account = Rs.

70,000.

• A subscriber can take a loan from the fund. The first loan can be

taken in the third year of opening the account. If the a/c is

opened during the year 97-98, the first loan can be raised during

the year 99-00. The amount of loan will be restricted to 25% of

the balance including interest for the year 97-98 in the a/c as on

31-3-1998.

• Only one withdrawal can be made during anyone year. First

withdrawal can be made after the expiry of 5 years from the end

of the year in which the initial subscription was made.

49

Public provident fund

• Amount of withdrawal will be limited to 50% of the balance at

credit at the end of 4th year immediately preceding the year in

which the amount is withdrawn or at the end of preceding year

whichever is lower.

• Subscription to PPF qualify for deduction under section 80C.

• Interest credited to fund is totally exempt from income tax.

50

Exercise

• Ravi invested in a pension plan which

will give him Rs. 5 lacs on 60th year

and then it will increase by 5% per

annum for next 25 years. He is 45

now and how much he should

contribute per month to achieve this if

pre and post retirement inflation is 4%

and return is 12%.

51

Exercise

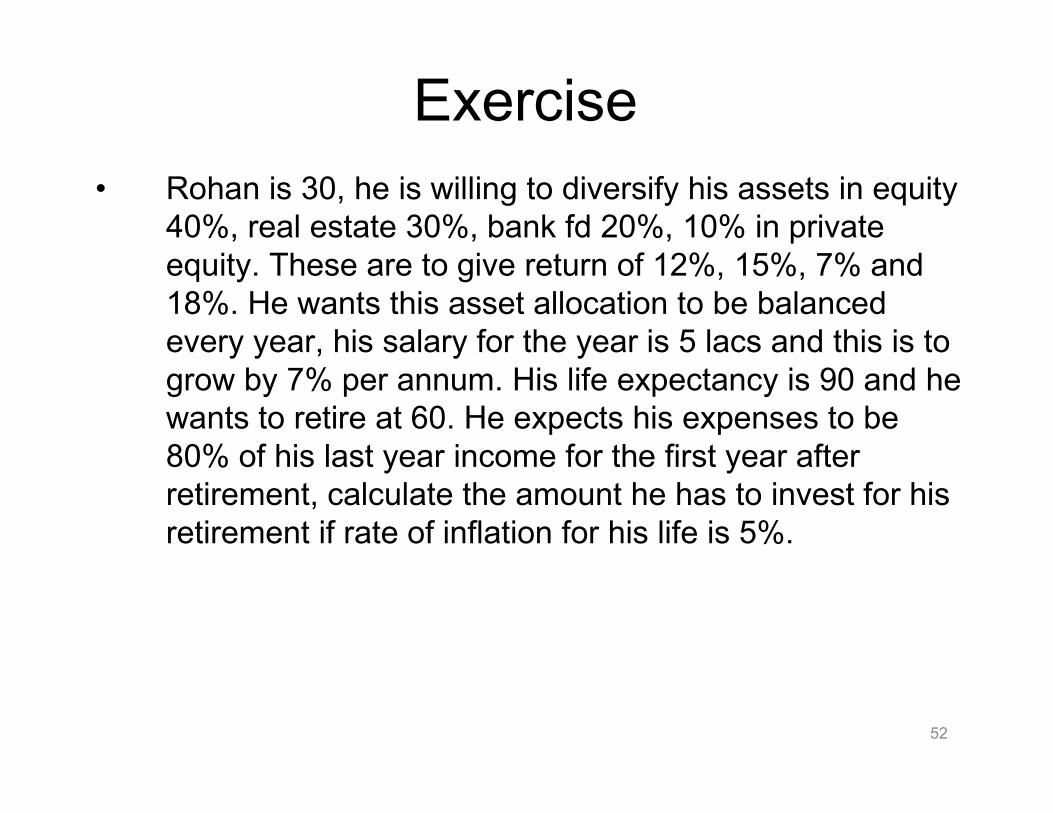

• Rohan is 30, he is willing to diversify his assets in equity

40%, real estate 30%, bank fd 20%, 10% in private

equity. These are to give return of 12%, 15%, 7% and

18%. He wants this asset allocation to be balanced

every year, his salary for the year is 5 lacs and this is to

grow by 7% per annum. His life expectancy is 90 and he

wants to retire at 60. He expects his expenses to be

80% of his last year income for the first year after

retirement, calculate the amount he has to invest for his

retirement if rate of inflation for his life is 5%.

52

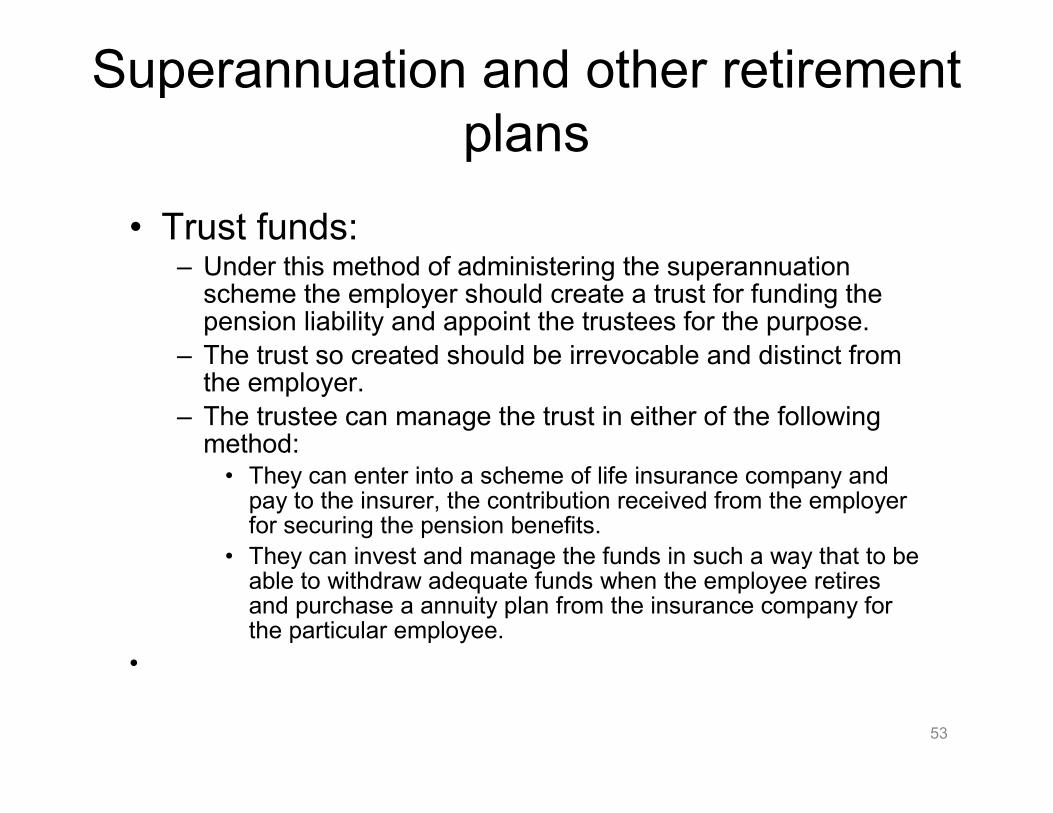

Superannuation and other retirement

plans

• Trust funds:– Under this method of administering the superannuation scheme the employer should create a trust for funding the pension liability and appoint the trustees for the purpose.

– The trust so created should be irrevocable and distinct from the employer.

– The trustee can manage the trust in either of the following method:• They can enter into a scheme of life insurance company and pay to the insurer, the contribution received from the employer for securing the pension benefits.

• They can invest and manage the funds in such a way that to be able to withdraw adequate funds when the employee retires and purchase a annuity plan from the insurance company for the particular employee.

•

53

Superannuation and other retirement

plans

• Approved superannuation funds:

• Employers contribution to

superannuation funds when approved

by income tax commissioner to be

treated as business expenses thus

reducing his income tax liability.

54

Superannuation and other retirement

plans

• Rules for getting the a superannuation fund

approved under income tax act, 1961:

– In order that a superannuation fund may receive

and retain approval as defined under the act,the

fund shall be established under an irrevocable

trust in connection with a trade or undertaking

carried on in India and not less than 90% of the

employees shall be employed in India.

– The fund should have its sole purpose of providing

annuities, pension to the employees working in

India.

55

Superannuation and other retirement

plans

• Income tax benefits for approved superannuation funds:

• Any payment made from an approved superannuation fund in

case of death of the beneficiary, commutation of annuity on his

retirement at specified age, on his becoming incapacitated prior

to such retirement, shall not be included in computing the total

income of a previous year of any person.

• Contribution of the employers’ under the approved

superannuation fund is allowed as deduction from business

income

• Employees contribution is also eligible for income tax deduction

u/s 80 C.

56

Superannuation and other retirement

plans

• Pension plans of insurance

57

Group life and Health

insurance

• Group insurance

– Contracts: it is a way providing protection against the

financial losses caused by the contingencies like death,

disability, or retirement to a changing group of individuals

who are associated with policyholder (employer) by some

common relationship other than the group formed for the

purpose of obtaining the insurance cover. All the members of

the group are covered by a single contract with an insurer

regardless of past history of health.

58

Group life and Health

insurance

• Characteristics:

• It follows a very simple underwriting procedure. It is granted

within certain parameters without medical examination and

other forms of insurability.

• Here a master policy is issued and the group receive an

individual certificate of insurance to serve as evidence of

their coverage under master policy.

• It is of low cost as the cost of underwriting,

administering,selling and servicing is low compared to

individual insurance policy.

59

Group life and Health

insurance

• Premiums are charged on year to year basis and

increased accordingly as the age of the group

increased and are also subject to experience

rating.

• It is a continuous contract. As new persons enter

into the organization are covered under the

scheme and exiting one result in termination of

cover.

60

Group life and Health

insurance

• Eligibility• The group should be formed for mutual continuing interest other than

for obtaining insurance

• There has to be steady flow of new entrants and retirement of old

persons to ensure predicted mortality experience. Disproportionate

number of aging lives will result in adverse selection.

• The amount of group life insurance is usually related to individual’s

earnings or job classification.

• There has to high participation in group plans to avoid risk selection

against insurer.

• Efficient administration of group plan made it a low cost plan.

61

Group life and Health

insurance

• Underwriting:• Successful underwriting seeks to achieve the same goal as

individual underwriting; to assess risk accurately and equitably

and to calculate premium to pay for the coverage. Favourable

experience may result in reduction of premium amount and vice

versa. Following factors receives more emphasis;

– Stability: stability of group and steady flow of new entrant

joining the group receives favourable consideration by the

underwriter.

– Size: a very large and reasonably large group not only

decreases the risk by spreading it but also decrease the

administrative cost.

– Occupation: nature of business is most important factor in

assessing the risk and the application of premium rates.

• 62

Group life and Health

insurance

• ‘Simple insurability condition’ differ from group to

group.

– If it is an employer-employee group (conventional group):

the employee should not absent from duty on the coverage

on the ground of sickness.

– Other than employer-employee group (non conventional

group): member has to give a simple declaration of good

health.

–

63

Group life and Health

insurance

• Group life insurance plans

– Majority of group life plans are term insurance

plans and the coverage and premiums are

renewable yearly.

– Evidence of insurability need not to be produced

again for the already covered employees.

– Insurer charged the renewal premium on the basis

of group’s existing distribution of age.

– Benefits of plan are payable only in the event of

death, no survival benefits.

64

Group life and Health

insurance

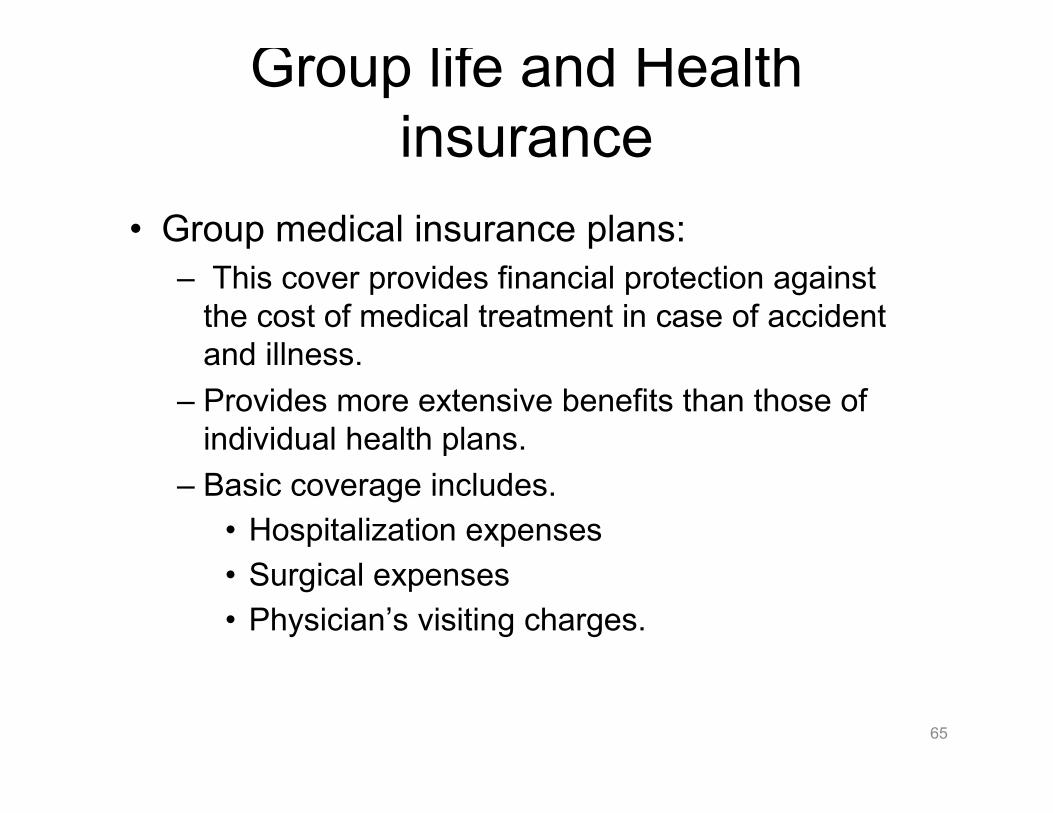

• Group medical insurance plans:

– This cover provides financial protection against

the cost of medical treatment in case of accident

and illness.

– Provides more extensive benefits than those of

individual health plans.

– Basic coverage includes.

• Hospitalization expenses

• Surgical expenses

• Physician’s visiting charges.

65

Group life and Health

insurance

– There are some additional benefits available under

the plans

• Cost of prescribed drugs

• Vision care

• Domiciliary health care

• X ray and laboratory services

66

Group life and Health

insurance

• Group managed care plans:

–Where physicians and hospitals are

grouped together in a business

arrangement and provide managed health

care plans to their subscribers.

– Instead of subscriber being reimbursed he

is provided with cash less hospital facility.

67

Group life and Health

insurance

• Group disability income plan– This cover is designed to provide an individual with specified amount of periodic income in the event that a person can’t work due to disabling illness or accident.

– The cover is provided for disabilities resulting from occupational / non occupational accident or accident and sickness.

– Disability is defined as the insured person must be unable to perform any job for which he or she is reasonably suited by reason of education,trainingor experience.

68

Group life and Health

insurance

–Group disability income plans specify benefits in terms of percentage of individual earning. It may be from 50% to 100% of regular salary as per terms of policy.

–Benefits generally varies from 13 weeks to disabled person’s age up to maximum of 65 years.

–This coverage is usually discontinued after the employee resigns or is terminated from the active work.

69

Post retirement counseling

• Investment risk and constraints• The variation of return from the expected rate of return is called

investment risk. There are three main reasons of investment risk; inflation, interest rate risk and the market rate risk.

• Investment portfolio evaluation– A client portfolio may consist of various financial assets.

Which is to be re-evaluated in the light of present life cycle stage and the time left for reaching the goal. A retired clients’ portfolio may be changed to income producing assets with minimum investment risk. Liquidity is another factor which is to be considered in case of retiree.

70

Post retirement counseling

• Risk tolerance and attitude to equities

• Risk tolerance may be defined, as the amount

of risk the client is ready to bear to achieve an

additional unit of return. In this the client’s risk

will be higher.

• Risk tolerant clients portfolio consist of mainly

equities, equity related mutual funds, unit linked

plans, variable annuities, real estates and long

term deposits.

• Risk averse people want to optimize return on

their portfolio with minimum risk. Therefore they

invest in diversified securities ranging from

higher risk to lower risk.71

Post retirement counseling

• Client’s

–Health

– Interests

–Hobbies

–Home

–Vacations

–Gifting

72

Pension Sector Reforms

• Need for reforms

–Demographic trends

–Coverage of population, organized,

unorganized, employment trends

–Un-funded pension liabilities

–Deficiencies in existing schemes

73

Pension Sector Reforms

• Demographic trends:

– Advanced medical science, urbanization, better

hygienic environment and other social changes

have improved life expectancy.

– Problem of ageing is increasing.

– Joint family system has almost disappeared with

changing value system.

– Elderly in India are retired without accumulating

enough for their post retirement period.

74

Pension Sector Reforms

– Post retirement life span is increasing, posing serious threat, in case if it is not properly planned and funded adequately.

– Fertility rate is decreasing, can disturb the working population ratio with non working population.

– India is undergoing the demographic transition that have been experienced in other parts of the industrial world.

– India’s preparedness on this front is very bleak and the chances of being affected by it are quiet certain. Thus it can hugely damage our social and financial structure.

75

Pension Sector Reforms

• Coverage of population: • On the basis of coverage of population under

social security schemes providing retirement

and old age benefits can be divided into three

categories-

– Employees working in government and public sector

or private sector organization.

– Others working in the un-organized sector and self

employed professional.

– Those doing petty jobs and living below poverty line.

76

Pension Sector Reforms

• Coverage of organized and unorganized sectors:

• Central and state govt. employees are entitled to non contributory indexed linked pension with defined death benefit and survivors benefits, mandatory provident fund (DC), gratuity.

• New pension scheme applicable to new entrant of central govt.( excluding armed forces) and railway services from 1st January 2004.

• Employees of PSUs, banks and insurance companies(public sector). These are currently in lieu of employers contribution to the provident fund.

• Employee provident fund organization (EPFO), managing mandatory savings DC scheme ( EPF), a DB pension scheme (EPS), EDLI

77

Pension Sector Reforms

• Employment trends:

–Urbanization and employment opportunities

• Economic globalization has created

better employment opportunities for the

skilled youth in urban areas but has

disturbed the demographic balance of

the cities.

78

Pension Sector Reforms

• Un-funded pension liabilities:

–Un funded pension schemes are now

considered by the government as great

burden and find it very difficult to carry on.

Therefore it has introduced the new

pension scheme applicable from 1st Jan.

2004. Falling interest rate and rising salary

has made the scheme virtually impossible

to run without causing burden to the

exchequers.

79

Pension Sector Reforms

• Deficiencies in existing schemes:– Low coverage, only about 12% of work force is covered.

– Under performance of provident fund scheme.

– Investment restrictions, mostly in govt. and public sector bonds.

– Administrative difficulty due to lack of professionalism.

– Underdeveloped private annuity market.

– Increase in informal workforce, majority of whom are not covered under employee benefit scheme.

80

Old age social and income security

81