Bahasa

Halaman

Hukum

Masaryk University

Faculty of Economics and Administration

MASTER’S THESIS

Brno, 2019 Madhuparna DATTA

Masaryk University

Faculty of Economics and Administration

Field of study: Public Economics and Administration

PUBLIC SECTOR ENTERPRISES IN INDIAN ECONOMY:

CHALLENGES FACED AND MAJOR REASONS FOR FAILURE

Master’s Thesis

Thesis Supervisor: Author:

Mgr. Martin GUZI, Ph.D Madhuparna DATTA, BA (Hons)

Brno, 2019

MASARYK UNIVERSITY

Faculty of Economics and Administration

MASTER’S THESIS DESCRIPTION

Academic year: 2018/2019

Student: Madhuparna Datta, BA

Field of Study: Public Economics and Administration (Eng.)

Title of the thesis/dissertation: Public Sector Enterprises in Indian Economy: Challenges Faced & Ma-

jor Reasons for Failure

Title of the thesis in English: Public Sector Enterprises in Indian Economy: Challenges Faced & Ma-

jor Reasons for Failure

Thesis objective, procedure and methods used: Thesis will study Public Sector Enterprises (PSE) in India - their growth,

performance, challenges and issues being faced. Thesis will examine the reasons why many of these PSEs fail in their endeavour leading to insolvency or closure. We will bring evidence from several case- studies of loss-making PSEs in India operating in different sectors.

Extent of graphics-related work:

Extent of thesis without supplements:

Literature:

According to thesis supervisor’s instructions

60 – 80 pages

MILLWARD, Robert. Private and public enterprise in Europe : energy,

telecommunications and transport, 1830-1990. 1st ed. Cambridge:

Cambridge University Press, 2005. xix, 351. ISBN 0521835240. Privatization of public enterprises in Latin Amerika. Edited by

William P. Glade. San Francisco: International Center for

Economic Growth, 1991. 150 s. ISBN 1558151281.

Thesis supervisor: Mgr. Martin Guzi, Ph.D.

Thesis supervisor’s department: Department of Public Economics

Thesis assignment date: 2017/11/16

The deadline for the submission of Master’s thesis and uploading it into IS can be found in the academic year calendar. In Brno, date: 2019/05/04

Name and sur name o f t he author : Madhuparna DATTA

Master’s t hes is t it le: Public Sector Enterprises in Indian Economy: Challenges

Faced and Major Reasons for Failure

Depar tment : Department of Public Economics

Master’s t hes is super viso r : Mgr. Martin Guzi, Ph.D.

Master’s t hes is dat e: 2019

Abstract

The goal of the thesis is to understand and examine the major reasons for failure of many

public sector enterprises in India, leading to insolvency or closure. It also brings evidence

from several case-studies of loss making public entities which are operating in different

sectors of Indian economy.

The first part of the thesis concentrates on examining the major reasons for their failure and

the second part takes up case-studies, using the Altman Z-Score model, to predict bankruptcy

of the sample entities. The result shows that eight of the top ten loss making public entities

were facing financial distress and would require corrective actions to help improve their

performance. The study covers the period 2013-2017. My thesis contributes to the literature

by enlarging its scope to include other critical sectors of the Indian economy, such as

telecommunication, mining, services and transportation in addition to manufacturing.

Keywords:

India, Public Sector Enterprises, Performance, Altman Z-score, Financial Distress, Failure

Declaration

I certify that I have written the Master’s Thesis “Public Sector Enterprises in Indian

Economy: Challenges Faced and Major Reasons for Failure” by myself under the supervision

of Mgr. Martin Guzi, Ph.D. and I have listed all the literature and other specialist sources in

accordance with legal regulations, Masaryk University internal regulations, and the internal

procedural deeds of Masaryk University and the Faculty of Economics and Administration.

In Brno .......................................... ...................................................

Madhuparna Datta, BA (Hons)

Acknowledgement

I would like to acknowledge the time and effort dedicated by my thesis supervisor

Martin Guzi from Masaryk University. I would like to thank him for his valuable guidance

and support. I would also like to thank my family for their constant encouragement and

support.

TABLE OF CONTENTS

INTRODUCTION ........................................................................................................ 7

1. THEORIES OF THE STATE-OWNED FIRM.......................................................... 9

1.1 Property Rights Approach ................................................................................ 11

1.2 Transaction Cost Theory ................................................................................... 11

1.3 Agency Theory ................................................................................................. 12

1.4 Resource-based View ....................................................................................... 12

1.5 Summary .......................................................................................................... 13

2. PUBLIC SECTOR ENTERPRISES IN INDIA ....................................................... 14

2.1 Evolution and Characteristics of PSEs in India ................................................. 14

2.2 Performance Indictors of PSEs in India............................................................. 17

2.3 Summary .......................................................................................................... 19

3. THE FAILURE OF PUBLIC SECTOR ENTERPRISES ........................................ 20

3.1 Reasons for Failures ......................................................................................... 20

Soft Budget Constraint ........................................................................................... 20

Corporate Governance Challenges......................................................................... 21

Competition ............................................................................................................ 22

Capacity Under-Utilization .................................................................................... 23

Political Interference and Lack of Autonomy .......................................................... 23

3.2 Summary .......................................................................................................... 25

4. SCREENING FOR BANKRUPTCY RISK............................................................. 26

4.1 Altman Z-Score Model ..................................................................................... 26

4.2 Empirical Studies on Financial Distress of PSEs in India .................................. 27

4.3 Summary .......................................................................................................... 28

5. RESEARCH METHODOLOGY ............................................................................ 29

5.1 Profiles of Top 8 Loss Making PSEs in Study Sample ...................................... 29

5.2 Data Collection ................................................................................................. 31

5.3 Model Specification.......................................................................................... 31

6. PRESENTATION AND DISCUSSION OF RESULTS .......................................... 34

7. REFORMS FOR RESTRUCTURING PUBLIC SECTOR ...................................... 41

7.1 Strategies to Reform the Underperforming PSEs .............................................. 41

7.2 Government Policy for Revival of Sick PSEs ................................................... 41

CONCLUSION .......................................................................................................... 44

LIST OF LITERATURE ............................................................................................ 46

LIST OF TABLES ...................................................................................................... 55

LIST OF FIGURES .................................................................................................... 56

LIST OF ABBREVIATIONS ..................................................................................... 57

LIST OF APPENDICES ............................................................................................. 58

7

INTRODUCTION

The International Monetary Fund defines public sector enterprises as firms that are

owned and/or controlled by the government/state which implies that organisations that are

minority owned by the government can also be referred to as public sector enterprises

(Lienert, 2009). According to Bajo, Zuber, and Primorac (2018), public sector enterprises can

be in the form of joint stock companies or limited liability companies. Typically, state-owned

firms are large and operate in key sectors of the economy. Mallya (1971) describes public

sector enterprises in India as autonomous or semi-autonomous entities that are owned and

managed by the government. These entities participate in industrial and commercial activities.

The role of the public sector enterprises is critical to the economy. These entities

operate in areas that require long gestation periods and huge investments. They contribute

substantially to the total output. Thus, the financial wellbeing of these firms incessantly

affects the overall performance of the economy. Public Sector Enterprises (PSEs) were

formed in India, like in most other countries, to accelerate economic and social development.

The other major reasons for their formation include social welfare, employment generation,

income generation, import substitution, and regional development (Delhi Univ., Study

Material).

Over the years, governments across the globe have introduced reforms in the

management and operations of public sector enterprises. Some authors found that the

government run entities are less efficient and often a drain to public resources as they lacked

profit motive. In the late 1970s and throughout the 1980s there was a growing concern in

India about the performance of PSEs (Bhoothalingam, 1993; Marathe, 1989; Mujamdar,

1998). In the early 1990s, the Indian government introduced the Public Enterprises Reform

Process based on different policies. These policies include the New Industrial Policy,

Empowerment of Enterprises Policy, and Privatization (Khanna, 2012). The reforms entailed

liberalisation, disinvestment, measures for improving performance, downsizing, restructuring

and revival, autonomy to large enterprises, professionalism, and shutting-down of loss-

making PSEs (Chittedi and Singh, 2012).

The Indian government premised that these reforms would result in the public sector

enterprises becoming more efficient and productive. However, despite the reforms introduced

by the government, the firms are still facing challenges which affect their financial wellbeing

8

and sustainability (Deloitte, 2011). Given the importance of the PSEs in India, it is necessary

to determine the financial health and solvency of these entities. The consequences of failure

are not only felt by the government but also by the other stakeholders such as suppliers,

employees, and customers. Therefore, being able to accurately predict the bankruptcy of a

firm is important. The aim of the thesis is to understand the challenges and major reasons for

failure of PSEs in India. Additionally, the thesis will use a methodology to predict financial-

distress/insolvency of selected PSEs.

The thesis is divided in to eight chapters including introduction. The introduction

highlights the research problem and the significance of this thesis. Chapter one presents a

summary of the theory of state-owned firms and provides rationale for the formation and

importance of PSEs. Chapter two summarises background information on PSEs in India. This

includes the evolution, growth and performance of PSEs over the years. Chapter three

discusses the challenges faced by PSEs and examines the major reasons for their failure.

Chapter four highlights the financial distress and use of the Altman Z-score for

predicting bankruptcy of PSEs. Chapter five presents the research methodology to help

evaluate the financial health of selected PSEs in India. Chapter six summarizes the findings

and results of the thesis along with analysis. Chapter seven discusses the government policies

and reform measures for under-performing PSEs, and thereafter it ends with the conclusion.

9

1. THEORIES OF THE STATE-OWNED FIRM

This chapter highlights the theory that provides the basis for the formation and the

continued operations of PSEs. It also provides the argument for PSEs to be evaluated in a

similar manner as used for private entities.

In many countries, especially developing countries like India, the public sector firms

are formed for strategic purposes such as providing support to sectors that are important for

the development of the nation or for the control of the country’s natural resources (Shleifer,

1998). There are several differences between public sector firms and private firms. Grout and

Stevens (2003) identified the main difference between the two categories of firms as being

their objectives. The primary objective of private enterprises is to maximise profits of the

shareholder, whereas the main objective of public enterprises is to balance the interests of the

stakeholders and enhance social welfare.

Jakob (2017) further states that the state-owned firms differ from private enterprises in

terms of financing, liquidation management and compensation. In public enterprises, the state

provides the capital and most of the financial needs of the firm. Private enterprises typically

raise their capital from the shareholders. The government provides stability to public firms

and also subsidies in situations where their sources of income are not adequate to cover their

costs. In liquidation, private sector firms have to be declared bankrupt or acquired when

insolvent. Whereas, in case of insolvency of PSEs, the government first examines the strategic

importance of the enterprise to national economy and seeks ways to bail it out by providing

public funds (Peng, Bruton, Stan and Huang, 2016). The management of private companies is

strictly left to the managers who typically determine the strategies and policies for survival

and growth. Whereas in the case of the state-owned firms, the strategy and policy decisions

are taken by the government and those responsible to the parliament. Here the managers are

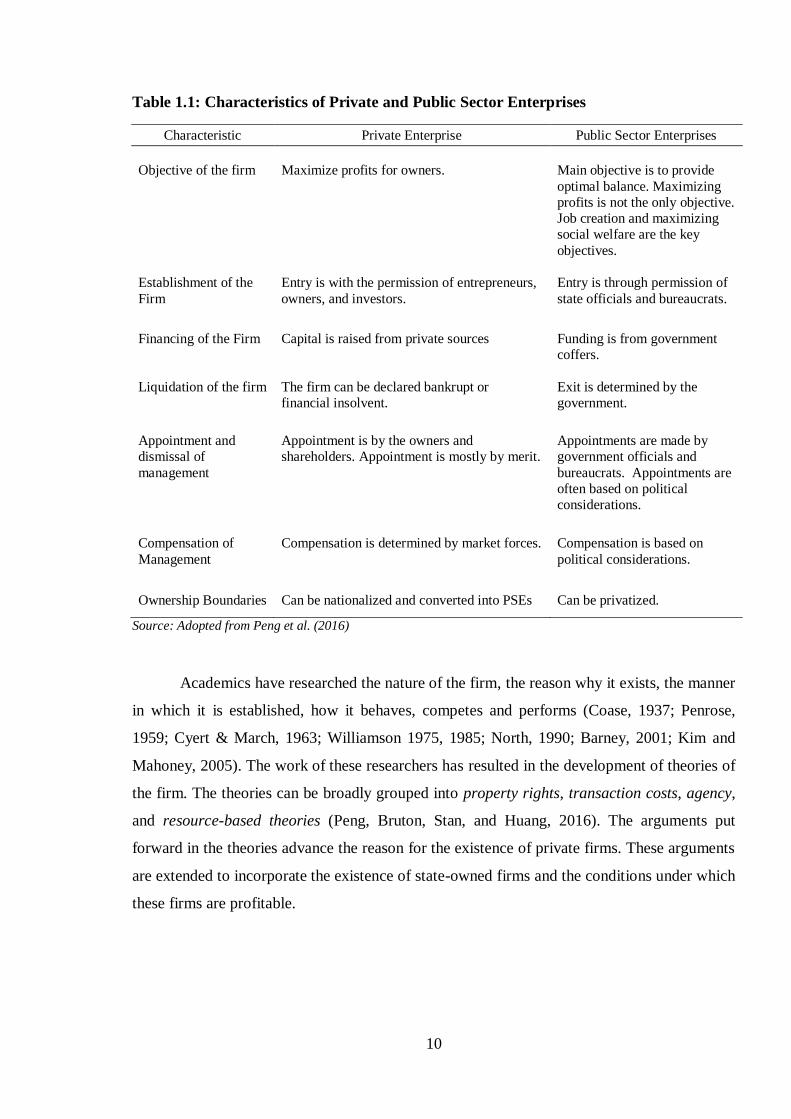

responsible for daily operations. The Table 1.1 below summarises the characteristics of

private firms versus the public sector enterprises.

10

Table 1.1: Characteristics of Private and Public Sector Enterprises

Characteristic Private Enterprise Public Sector Enterprises

Objective of the firm

Maximize profits for owners.

Main objective is to provide

optimal balance. Maximizing

profits is not the only objective.

Job creation and maximizing

social welfare are the key

objectives.

Establishment of the

Firm

Entry is with the permission of entrepreneurs,

owners, and investors.

Entry is through permission of

state officials and bureaucrats.

Financing of the Firm

Capital is raised from private sources

Funding is from government

coffers.

Liquidation of the firm

The firm can be declared bankrupt or

financial insolvent.

Exit is determined by the

government.

Appointment and

dismissal of

management

Appointment is by the owners and

shareholders. Appointment is mostly by merit.

Appointments are made by

government officials and

bureaucrats. Appointments are

often based on political

considerations.

Compensation of

Management

Compensation is determined by market forces. Compensation is based on

political considerations.

Ownership Boundaries

Can be nationalized and converted into PSEs

Can be privatized.

Source: Adopted from Peng et al. (2016)

Academics have researched the nature of the firm, the reason why it exists, the manner

in which it is established, how it behaves, competes and performs (Coase, 1937; Penrose,

1959; Cyert & March, 1963; Williamson 1975, 1985; North, 1990; Barney, 2001; Kim and

Mahoney, 2005). The work of these researchers has resulted in the development of theories of

the firm. The theories can be broadly grouped into property rights, transaction costs, agency,

and resource-based theories (Peng, Bruton, Stan, and Huang, 2016). The arguments put

forward in the theories advance the reason for the existence of private firms. These arguments

are extended to incorporate the existence of state-owned firms and the conditions under which

these firms are profitable.

11

1.1 Property Rights Approach

Karl Marx expressed that private ownership is a sin as capitalism contributed to the

greed of private owners who exploit their employees to maximize their profits (Peng et al.,

2016). According to Marx, the solution is to convert private property into public entities. In

this way the PSEs would create a new set of property rights (Monteiro and Zylbersztajn,

2012). There are three types of property rights:

(i) The right to generate income from the property. The owners of the firm are the citizens

and the income generated is given to them. For example the National Copper Corporation of

Chile which is the biggest firm in Chile generates approximately $ 7 billion per year. All

excess profits are paid to the state (Codelco, 2018). Similarly, in India, the Oil and Natural

Gas Corporation generates approximately $2.8 billion per annum with a significant amount of

the profits remitted to the exchequer (Republic of India, 2018).

(ii) The right to control and use the property. This dimension entails the fact that bureaucracy

determines how the organisation will be financed, appoint the managers, and also set their

compensation level.

(iii) The right to transfer or sale of property. The PSEs are owned and managed by the

government of India. The rights to control and use property and the right to transfer property

are maintained by the central government of India. This right is seen in divestment scheme

where the government has sold its stake in PSEs like, Bharat Aluminium Company,

Hindustan Zinc, and Indian Petrochemicals Corporation Limited.

1.2 Transaction Cost Theory

A key question of the transaction cost theory is to examine the purpose that the firms

serve. Therefore, by extension, the question becomes why do PSEs exist? The transaction cost

theory stipulates that the firm exists to economise on transaction costs efficiently. Extending

this logic it can be argued that PSEs, despite their challenges, exist to economize on

transaction costs in an effective manner in the market place (Peng et al., 2016). Williamson

(1975) indicates that in most countries around the world, it is market failure that results in the

formation of public firms. In countries that have severe market failure, the only viable firms

are the public firms (Rajan, 2010). Despite their numerous challenges one of the main benefits

of PSEs is to reduce transaction costs in economies that are suffering from severe market

12

failures. The textile industry is an example of a scenario in which the public sector enterprises

act as cost minimisers. Over the last few decades, the government of India has streamlined the

operations of textile PSEs resulting in firms exhibiting high levels of efficiency (Sen and

Kayal, 2017).

1.3 Agency Theory

The government is the defacto owner and the employees are the agents. This gives

rise to the conflict of interests between principals and agents that is at the heart of the agency

theory put forward by Jensen and Meckling (1976). There is a new nexus of contracts that

have replaced the previous nexus of contracts between principals and agents of private firms

and between owners and agents in the public sector (Wright et al., 2005). In private

companies the primary objective of the firm is to maximise financial performance.

Consequently, the focus is on aligning the interest of the management and those of the

owners. In public entities there is no diversification in ownership but there is diversification in

management. This makes the process of monitoring, control, and accountability beyond the

normal corporate governance template (World Bank, 2016). Additionally, the agency problem

in PSEs is more pronounced due to the fact that the PSEs are managed by several government

entities including the administrative ministry, the ministry of finance, the department of

enterprises, and the parliament. Approval for various projects undertaken by the PSEs needs

to be submitted by the cabinet committee. All these layers of management complicate the

governance structure and create complex agency relationships.

1.4 Resource based View

The Resource Based theory maintains that firms have to be competitive as they have

to develop the rare, valuable, and hard to imitate resources and abilities (Barney, 2001). A key

assumption of this theory is that firms operate in competitive markets. In a bid to extend the

resource based theory of the firm, numerous scholars have pointed out that the PSEs have a

stream of non-market based resources and capabilities that arise out of the political and

bureaucratic association of these firms (Oliver and Holzinger, 2008; Lux, Crook, and Woehr,

2011; Li, Peng, and Macaulay, 2013). The scholars argue that the political influences are

resources and capabilities that contribute significantly to the performance of the PSEs. Li, He,

Lan, and Yu (2012) maintain that all firms, regardless of their ownership, value political

connections and influence.

13

When competing with foreign and private entities, PSEs can leverage their political

resources. The political ties are thought to be rare, valuable, and hard to imitate (Xia. Ma, Lu,

and Yi, 2014). Subramanian (2016) established that state-owned firms in India have greater

advantages than private entities as the government creates conditions suitable for monopoly

rather than competitive markets. Additionally, the firms have access to unrestricted flow of

capital generated from the taxpayers.

1.5 Summary

Liberalisation, globalisation, and economic structural changes across the globe have

resulted in the expansion of the private sector and decline of the public sector. However, the

PSEs play an important role in the development of countries. Their contribution to the

nation’s wellbeing has resulted in reviewing the role of these entities. It has become clear that

PSEs need to be managed efficiently and effectively. Various theories have been adopted so

that they can be applied to the public sector.

14

2. PUBLIC SECTOR ENTERPRISES IN INDIA

This chapter aims to highlight the evolution and growth of PSEs in India, the role they

play in the economy and their performance over the last decade.

2.1 Evolution and Characteristics of PSEs in India

At independence (1947), India was a backward and an underdeveloped country. It had

a weak industrial base, low level of savings and investment and high unemployment rate. The

economy needed a big push which could not come from the private sector, as they lacked

funds and did not have the ability to take risks for large and long gestation investments

(Gupta, 1975). So, the government took initiative through public sector to become self-reliant

and overcome economic and social backwardness.

The PSEs in India emerged from the government’s efforts to transform the country

into an industrial based economy. The industrialization was meant to ensure that the country

was able to produce goods and services for mass consumption and raw materials needed in the

manufacturing sector (Mallay, 1971). Thus, the PSEs played an important role in the

development of the Indian industry. As laid down by the government, the characteristics and

objectives of the PSEs in India are mentioned below:

Characteristics of PSEs

- Owned, managed and controlled by the Government

- Welfare oriented

- Funded by the Government

- Meant for public utility services

- Responsible to the Parliament (DPE Report, 2010)

Objectives of PSEs

As stated in the Industrial Policy Resolution of 1956, the PSEs need to achieve the following

objectives:

- To achieve economic development by creating and expanding infrastructure

- To generate financial resources for development

- To promote redistribution of income and wealth

- To create employment opportunities

- To promote balanced regional growth

15

- To accelerate the expansion of small-scale/ancillary industries

- To encourage export promotion and import substitution

(Delhi Univ., Study Material)

In India, PSEs are owned by either the union government of India or the state

government or both. The law requires that the majority-owner (with 51% stake or higher)

should be a government entity. The PSEs are required to produce goods and services for the

government and/or citizens. The PSEs in India are present in the major sectors such as -

Petroleum, Mining, Metals & Steel, Heavy Engineering, Transportation, Banking, Insurance,

Power generation and transmission, Nuclear energy, Fertilizers & Chemicals, Aviation

industry, Warehouse and Public distribution, Shipping and Trading, Telecommunication, and

Consultancy services.

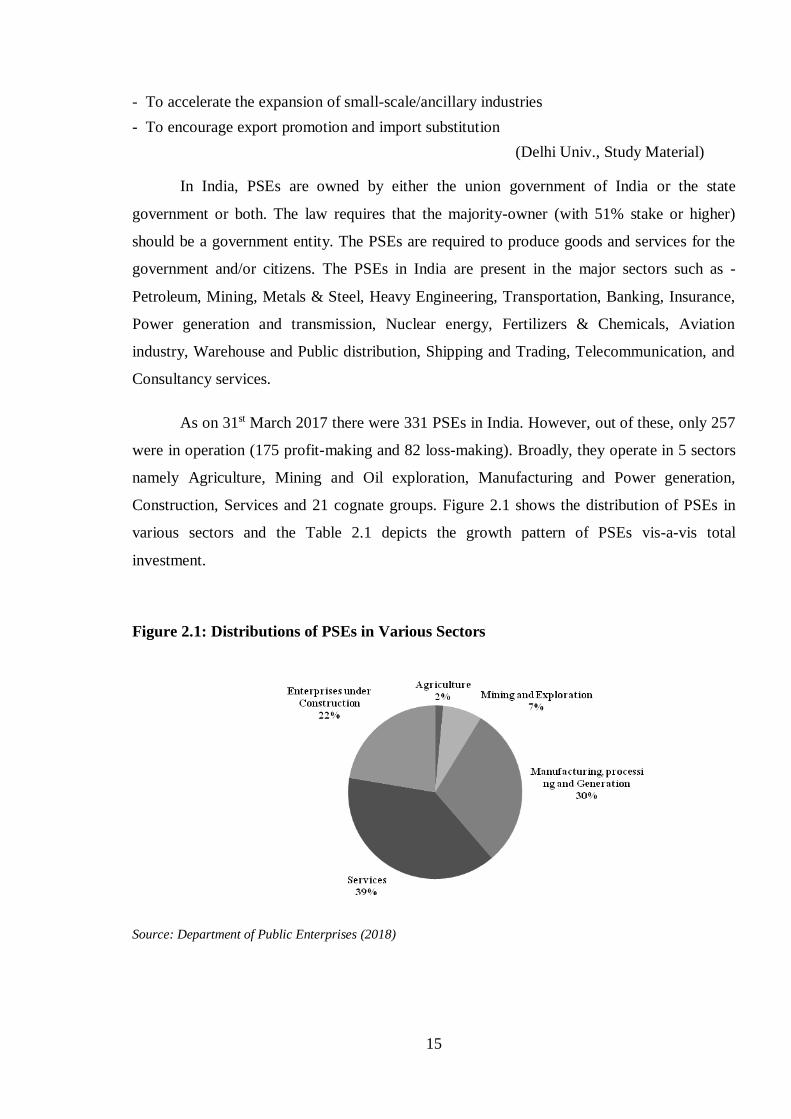

As on 31st March 2017 there were 331 PSEs in India. However, out of these, only 257

were in operation (175 profit-making and 82 loss-making). Broadly, they operate in 5 sectors

namely Agriculture, Mining and Oil exploration, Manufacturing and Power generation,

Construction, Services and 21 cognate groups. Figure 2.1 shows the distribution of PSEs in

various sectors and the Table 2.1 depicts the growth pattern of PSEs vis-a-vis total

investment.

Figure 2.1: Distributions of PSEs in Various Sectors

Source: Department of Public Enterprises (2018)

16

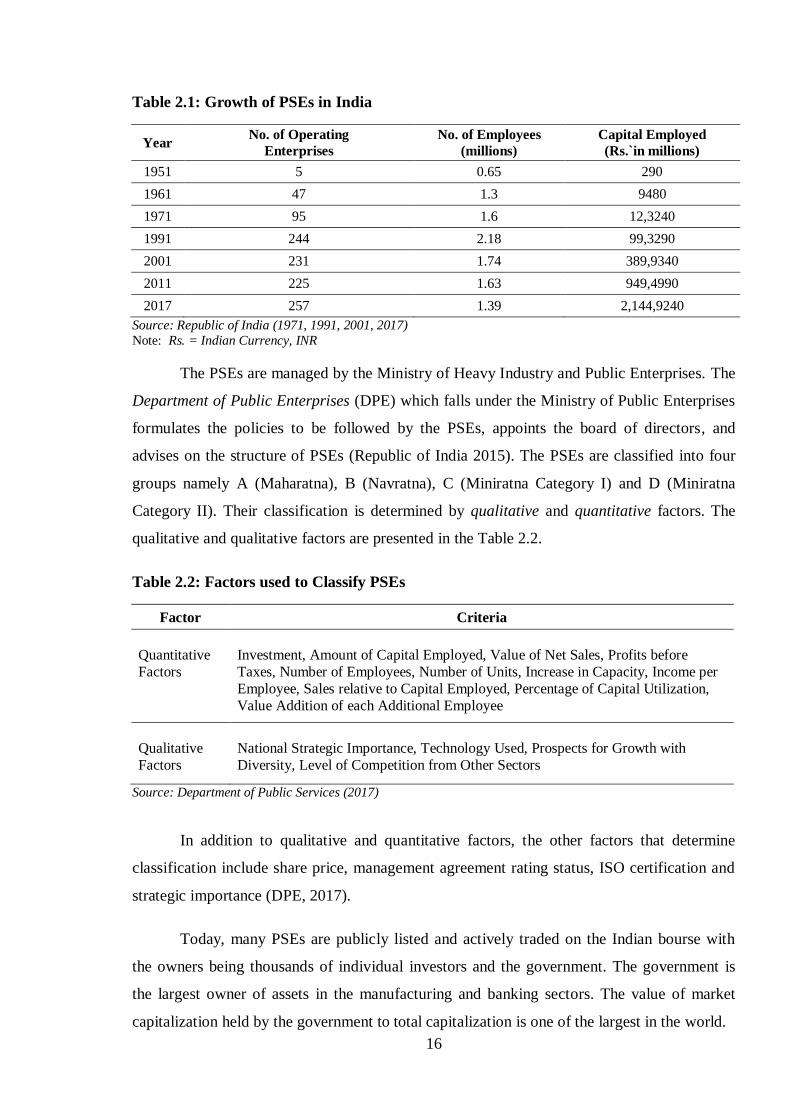

Table 2.1: Growth of PSEs in India

Year No. of Operating

Enterprises

No. of Employees

(millions)

Capital Employed

(Rs.`in millions)

1951 5 0.65 290

1961 47 1.3 9480

1971 95 1.6 12,3240

1991 244 2.18 99,3290

2001 231 1.74 389,9340

2011 225 1.63 949,4990

2017 257 1.39 2,144,9240

Source: Republic of India (1971, 1991, 2001, 2017)

Note: Rs. = Indian Currency, INR

The PSEs are managed by the Ministry of Heavy Industry and Public Enterprises. The

Department of Public Enterprises (DPE) which falls under the Ministry of Public Enterprises

formulates the policies to be followed by the PSEs, appoints the board of directors, and

advises on the structure of PSEs (Republic of India 2015). The PSEs are classified into four

groups namely A (Maharatna), B (Navratna), C (Miniratna Category I) and D (Miniratna

Category II). Their classification is determined by qualitative and quantitative factors. The

qualitative and qualitative factors are presented in the Table 2.2.

Table 2.2: Factors used to Classify PSEs

Factor Criteria

Quantitative

Factors

Investment, Amount of Capital Employed, Value of Net Sales, Profits before

Taxes, Number of Employees, Number of Units, Increase in Capacity, Income per

Employee, Sales relative to Capital Employed, Percentage of Capital Utilization,

Value Addition of each Additional Employee

Qualitative

Factors

National Strategic Importance, Technology Used, Prospects for Growth with

Diversity, Level of Competition from Other Sectors

Source: Department of Public Services (2017)

In addition to qualitative and quantitative factors, the other factors that determine

classification include share price, management agreement rating status, ISO certification and

strategic importance (DPE, 2017).

Today, many PSEs are publicly listed and actively traded on the Indian bourse with

the owners being thousands of individual investors and the government. The government is

the largest owner of assets in the manufacturing and banking sectors. The value of market

capitalization held by the government to total capitalization is one of the largest in the world.

17

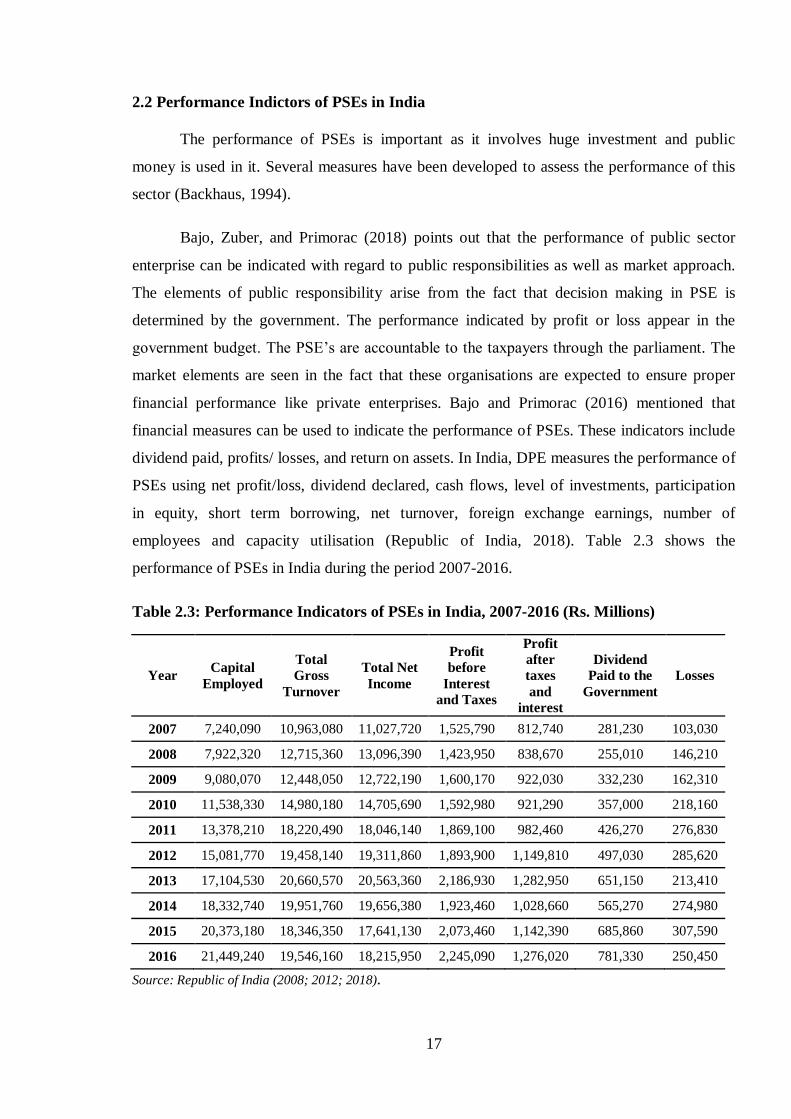

2.2 Performance Indictors of PSEs in India

The performance of PSEs is important as it involves huge investment and public

money is used in it. Several measures have been developed to assess the performance of this

sector (Backhaus, 1994).

Bajo, Zuber, and Primorac (2018) points out that the performance of public sector

enterprise can be indicated with regard to public responsibilities as well as market approach.

The elements of public responsibility arise from the fact that decision making in PSE is

determined by the government. The performance indicated by profit or loss appear in the

government budget. The PSE’s are accountable to the taxpayers through the parliament. The

market elements are seen in the fact that these organisations are expected to ensure proper

financial performance like private enterprises. Bajo and Primorac (2016) mentioned that

financial measures can be used to indicate the performance of PSEs. These indicators include

dividend paid, profits/ losses, and return on assets. In India, DPE measures the performance of

PSEs using net profit/loss, dividend declared, cash flows, level of investments, participation

in equity, short term borrowing, net turnover, foreign exchange earnings, number of

employees and capacity utilisation (Republic of India, 2018). Table 2.3 shows the

performance of PSEs in India during the period 2007-2016.

Table 2.3: Performance Indicators of PSEs in India, 2007-2016 (Rs. Millions)

Year Capital

Employed

Total

Gross

Turnover

Total Net

Income

Profit

before

Interest

and Taxes

Profit

after

taxes

and

interest

Dividend

Paid to the

Government

Losses

2007 7,240,090 10,963,080 11,027,720 1,525,790 812,740 281,230 103,030

2008 7,922,320 12,715,360 13,096,390 1,423,950 838,670 255,010 146,210

2009 9,080,070 12,448,050 12,722,190 1,600,170 922,030 332,230 162,310

2010 11,538,330 14,980,180 14,705,690 1,592,980 921,290 357,000 218,160

2011 13,378,210 18,220,490 18,046,140 1,869,100 982,460 426,270 276,830

2012 15,081,770 19,458,140 19,311,860 1,893,900 1,149,810 497,030 285,620

2013 17,104,530 20,660,570 20,563,360 2,186,930 1,282,950 651,150 213,410

2014 18,332,740 19,951,760 19,656,380 1,923,460 1,028,660 565,270 274,980

2015 20,373,180 18,346,350 17,641,130 2,073,460 1,142,390 685,860 307,590

2016 21,449,240 19,546,160 18,215,950 2,245,090 1,276,020 781,330 250,450

Source: Republic of India (2008; 2012; 2018).

18

The total capital employed during the fiscal year 2007-08 was Rs. 7,240,090 million

which increased steadily and was Rs. 21,449,240 million in 2016-17. This represents a growth

of 196.26 % over the last ten years. The largest share of capital employed by firms was in the

Service sector 47.4%, followed by Power 28.7%, Mining sector 14.7% and Agriculture 9.2%

(Republic of India, 2018). The total net income in 2007 was Rs. 11,027,720 million. The

amount has been increasing steadily and reached Rs. 18,215,950 million in 2016, representing

a growth of 65.18 % under the review period. Similarly, the amount of dividend paid out has

been growing steadily from Rs. 281,230 million in 2007 to Rs. 781,330 million in 2016,

representing a growth of 177.83%.

Cumulatively, the data in Table 2.3 shows that the PSEs have been profitable.

However, there are some public firms which realised significant losses. The loss realised from

the loss making PSEs was Rs. 250,450 million in the fiscal year 2016, which was a decline of

18.58% from that realised in 2015. Although the amount of loss decreased, the number of

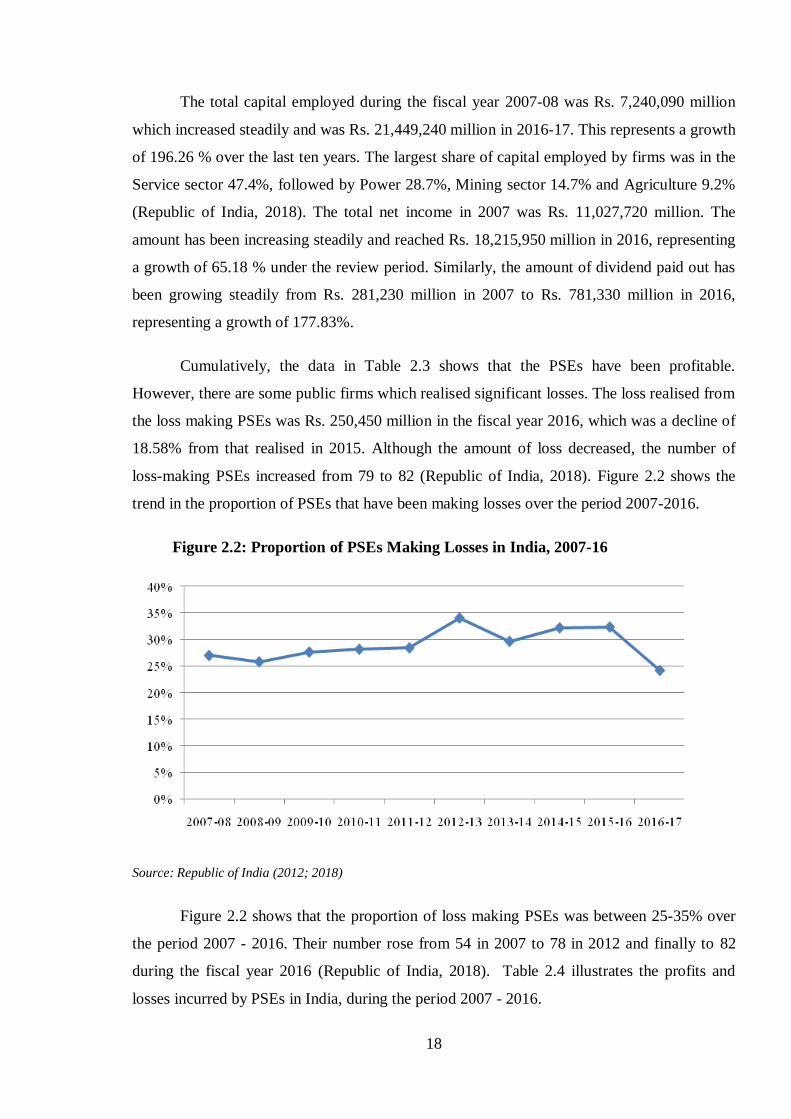

loss-making PSEs increased from 79 to 82 (Republic of India, 2018). Figure 2.2 shows the

trend in the proportion of PSEs that have been making losses over the period 2007-2016.

Figure 2.2: Proportion of PSEs Making Losses in India, 2007-16

Source: Republic of India (2012; 2018)

Figure 2.2 shows that the proportion of loss making PSEs was between 25-35% over

the period 2007 - 2016. Their number rose from 54 in 2007 to 78 in 2012 and finally to 82

during the fiscal year 2016 (Republic of India, 2018). Table 2.4 illustrates the profits and

losses incurred by PSEs in India, during the period 2007 - 2016.

19

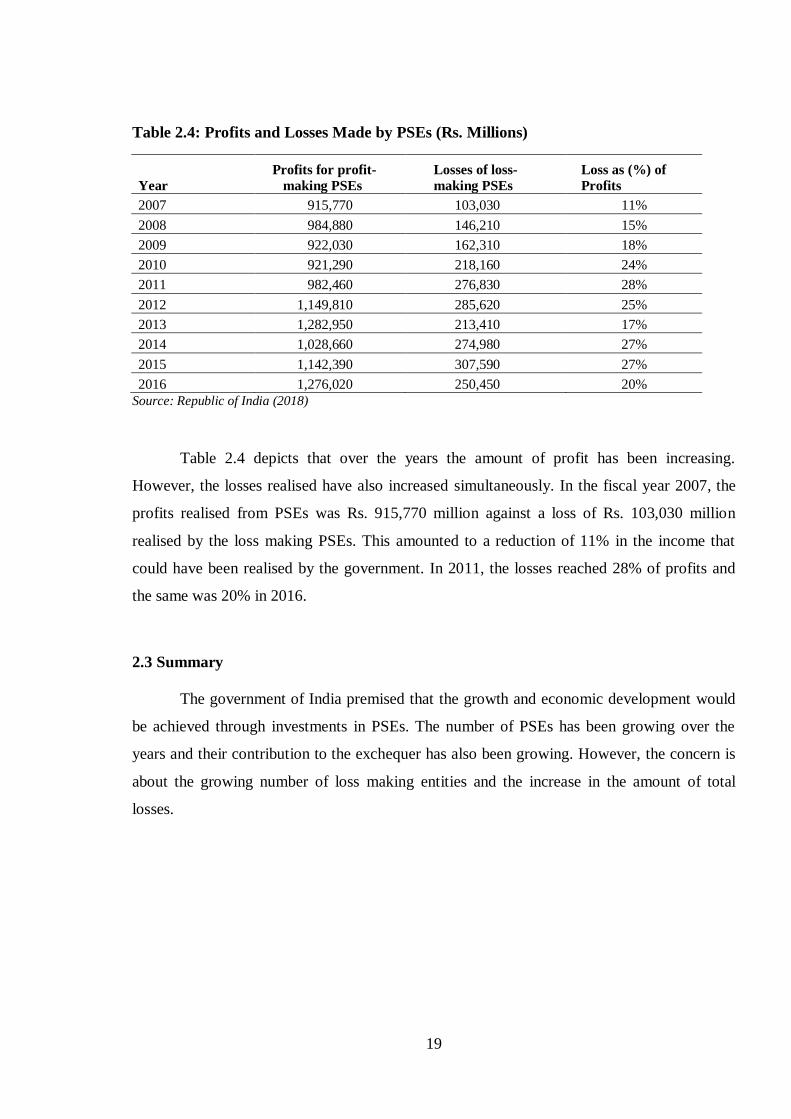

Table 2.4: Profits and Losses Made by PSEs (Rs. Millions)

Year

Profits for profit-

making PSEs

Losses of loss-

making PSEs

Loss as (%) of

Profits

2007 915,770 103,030 11%

2008 984,880 146,210 15%

2009 922,030 162,310 18%

2010 921,290 218,160 24%

2011 982,460 276,830 28%

2012 1,149,810 285,620 25%

2013 1,282,950 213,410 17%

2014 1,028,660 274,980 27%

2015 1,142,390 307,590 27%

2016 1,276,020 250,450 20%

Source: Republic of India (2018)

Table 2.4 depicts that over the years the amount of profit has been increasing.

However, the losses realised have also increased simultaneously. In the fiscal year 2007, the

profits realised from PSEs was Rs. 915,770 million against a loss of Rs. 103,030 million

realised by the loss making PSEs. This amounted to a reduction of 11% in the income that

could have been realised by the government. In 2011, the losses reached 28% of profits and

the same was 20% in 2016.

2.3 Summary

The government of India premised that the growth and economic development would

be achieved through investments in PSEs. The number of PSEs has been growing over the

years and their contribution to the exchequer has also been growing. However, the concern is

about the growing number of loss making entities and the increase in the amount of total

losses.

20

3. THE FAILURE OF PUBLIC SECTOR ENTERPRISES

This chapter focuses on the challenges faced by public sector enterprises in India and

the major reasons for their failure which lead to insolvency or closure.

3.1 Reasons for Failures

In most countries, PSEs are formed to stimulate economic and social development

(Ogohi, 2014). However, increasing evidence suggests that a number of these enterprises

either do not achieve the economic and social development targets set for them or do not

perform their functions and/or often require continued taxpayers’ support in order to continue

operation (World Bank, 2016). This has led the academics to question the viability of state-

owned corporations, probing the reasons why so many of these firms fail to sustain and

deliver services for which they were formed (Shleifer, 1998; Linert, 2009; Mayar-Abuja,

2011; Jakob, 2017). The annual published reports of the Department of Public Sector

Enterprises (DPE) shows that a significant number of PSEs in India have been making losses

over the years. The loss making PSEs which have received government bail outs are Air

India, State Bank of India, Dena Bank, Allahabad Bank (Tripathy, 2018). Additionally, the

review indicates that the number of loss making PSEs have been increasing over the years

(Republic of India 2008; 2012; 2018). According to Mukher (2019) the failures can be

attributed to various issues/challenges. Some of the major reasons are discussed in the

following sections.

Soft Budget Constraint

Goldeng, Grunfeld, and Benito (2008) expressed that many state owned firms suffer

from soft-budget constraint. Soft-budget constraint occurs because the government can give

various forms of financial and non-financial support to the PSEs. This results in the distortion

of the incentive structure, as the PSEs have other sources of support besides profit. The long-

term existence of the PSEs is not determined by the level of profits. Mukher (2019) identified

the lack of importance of profit motive as one of the main reasons of failure of key PSEs, such

as Solar Energy Corporation of India, Gujarati State Financial Corporation, and Water

Infrastructure Limited. Bhardwaj (2013) argues that the PSEs are not driven by profit motive

alone, but are formed to enhance the welfare of the citizens. The PSEs such as Water

21

Infrastructure Limited and Solar Energy Corporation provide essential services to the citizens

and facilitate manufacturing. Additionally, the Gujarati State Financial Corporation was

providing loans to firms which the mainstream financial sector had considered too risky to

finance (Bhardwaj, 2013). The soft budget constraint also alters the risk taking behaviour of

PSEs. Chattopadhyay (2011) observed that PSEs in India are prone to positive risk aversion.

Corporate Governance Challenges

Mukher (2019) also identified the lack of proper and professional management. The

management was found not to have the necessary educational and technical competencies

necessary to conduct their job function. Mukher (2019) attributed the lack of competencies of

the management to the way in which appointments were made. In private entities,

appointment of directors and management of the firm is based on educational attainment,

technical qualification, and individual performance at their previous jobs. However, Mukher

(2019) indicated that the appointment of directors and senior officers in PSEs was based on

political affiliation and cronyism which meant that the management, officials, and board of

directors did not have sufficient competencies to run the enterprises successfully. The PSEs

also face governance challenges arising from multiple principals, low levels of transparency

and accountability, and weak protection of minority shareholders (World Bank, 2014).

In 1948, the Indian Telephone Industry (ITL) was established as a Central PSE that

manufactured telecommunication equipments. By 2009, ITL had been privatised following a

number of years of continuous loss making. Subramania (2010) highlighted that the failure of

ITL was attributed to the high fixed costs that led to piling up of losses. The main fixed cost

was associated with overstaffing. The management of the firm was unable to take remedial

actions to mitigate the losses due to government policies. Government policy was to create

jobs. Therefore, reducing the labour force would have gone against government’s objectives.

Subramania (2010) concluded that government policies, although well intentioned and well

thought out, had sometimes constrained and weakened the performance of PSEs in India.

Mishra (2017) identified the incompetence of the board of directors of the PSEs, such

as Scooters India Ltd, Bharat Dynamics Ltd, Garden Reach Shipbuilders and Engineers Ltd,

Mazagon Dock Shipbuilders Ltd, Mishra Dhatu Nigam Ltd, Indian Railway Catering and

Tourism Corporation Ltd, RITES Ltd. The board of directors lacked professionalism and

efficiency needed for effectively managing these entities.

22

The corporate remuneration structure is designed to reward the efforts of the

management. Private sector employees’ income is determined by the level of profits and

growth dynamics of the firm. This rule does not apply to PSEs, where the pay structure is

designed based on the objective of ensuring social equality. Thus, the pay does not always

reward for good performance. As pay and performance are not always related, there is often

no structure in the corporate governance for monitoring of the enterprise’s performance.

Competition

Mayer-Ahuja (2011), found that PSEs in India were not geared up for changes in the

business environment. Citing the case of ITL, Maye-Ahuja (2011) argued that such PSEs

were formed at independence (1947) when these entities had a monopoly. Post 1991, with

economic liberalization in India, the new industrial policy 1991 adopted ‘de-reservation’ that

allowed the entry of private sector in the activities reserved for public sector. Thus, the PSEs

had to face competition from both, domestic private companies and the large multi-national

corporations. The burden of bureaucratic imperatives and inability to compete has led to the

collapse of several PSEs over the past few decades (DPE Reports, 2010 and 2017).

During the period 2000 - 2010, the revenue of some PSEs declined significantly (like

ONGC, ITI Ltd., MSTC Ltd., Mazgaon Dock Ltd., etc.) and some PSEs suffered heavy

financial losses (like BSNL, MTNL, Air India, Hindustan Photo Films, HMT, and IDPL)

leading to their insolvency/failure (Cromptroller and Auditor General of India, 2013). This

compelled the government to re-examine their case and take actions like winding up of non-

core and continuously loss making enterprises. This led to either their closure or privatisation.

In coming fiscal years, 2019-20 and 2020-21, Air India is projected to post losses of

approximately $1.5 – $2 billion (Center for Asia Pacific Aviation, 2018). This loss will be

funded by the taxpayers, in addition to bail-outs of $ 4 billion which have been provided to

the national carrier since 2012 (The Economic Times, 2018). The losses have been attributed

to the fact that the airline has lost its market share over the years to local and international

airline companies (The Economic Times, 2018).

23

Capacity Under-Utilization

Singh (2012) asserts that capacity under-utilisation is a serious problem that the PSEs

face in India. The firms were found to lack definable production targets, proper planning and

control and measures to identify future needs. This meant that the firms were unable to make

use of their fixed assets. This made them non-viable. Thus, leading to their

insolvency/collapse. Further, Singh (2012) indicated that the pricing policy was also

responsible for the failure of public firms. The government had not specified the rate of return

to be obtained from different undertakings. This was partly attributed to the entities being

expected to fulfil socio-economic objectives as well as poor planning.

Political Interference and Lack of Autonomy

Singh (2016b) found that political interference adversely affected the performance,

viability, and growth of public firms in India. Politicians particularly those from the ruling

party influenced the location, employment, and production of the firms. The politicians did

not take into consideration the feasibility, viability, and costs of their proposals. This led to

wastage of resources and improper actualisation of state firms. Additionally, Singh (2016b)

found that projects carried out by PSEs were often completed late. The delay in completion of

projects led to cost over-run which resulted in loss of money by the respective firms.

Chari and Gupta (2008), Ghosh (2009), and Jain (2016) observed that political factors

were the key factors in delaying the disinvestment from loss making PSEs. The political

factors were also responsible for the failure of PSEs to introduce reforms and reinvention. Jain

(2016) further argued that the challenges faced by the PSEs can also be attributed to the

ideologies of the political parties in power.

Research by Tiwari (2016) confirms the arguments of Jain (2016). Tiwari (2016)

showed that during the period 1999-2004 when the National Democratic Alliance (NDA), a

right-leaning political party was in power, more than 15 PSEs including Videsh Sanchar

Nigam Ltd, Bharat Aluminium Company Ltd, CMC Ltd and Hindustan Zinc were reformed

and privatised. When the United Progressive Alliance (UPA) came into power, the policy

took a back seat and only minority stake sales were undertaken. Again, since 2014, with NDA

in power the focus is on reforms and disinvestment of loss making PSEs.

24

Bloated Work Force and Corruption

The employment rate in the PSEs has been growing significantly over the years.

Between the 1970s and 1980s, the level of employment grew from 0.7 million to 2.24 million

constituting a 220% growth rate. The large labour force and over-staffing created a wage bill

that was not sustainable. Thus, the government introduced voluntary retirement schemes to

reduce the number of employees. The PSEs Survey in 2016-17 indicated that there are 1.13

million employees. However, Kapur (2019) indicates that although the number of employees

has decreased significantly, the relative wages and emoluments under the PSEs has more than

doubled. This has continued to constrain the performance of the PSEs. Further, Kapur (2019)

indicates that employment was based on cronyism and political influence that resulted in

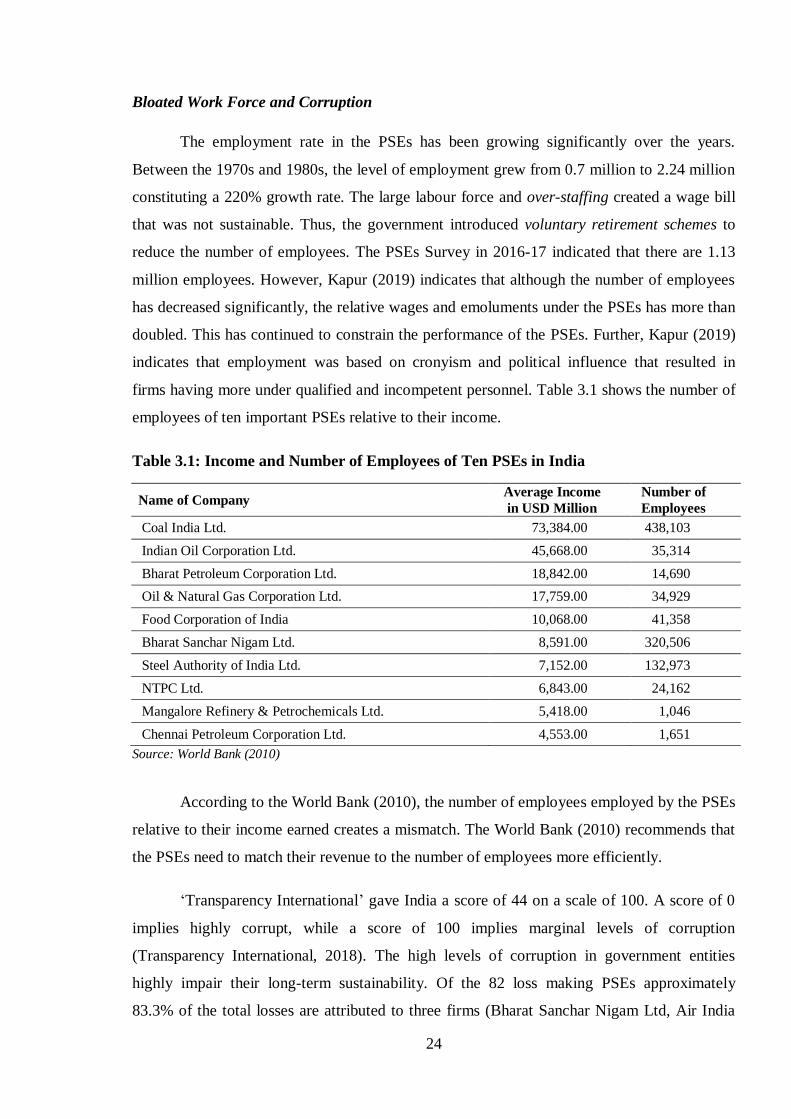

firms having more under qualified and incompetent personnel. Table 3.1 shows the number of

employees of ten important PSEs relative to their income.

Table 3.1: Income and Number of Employees of Ten PSEs in India

Name of Company Average Income

in USD Million

Number of

Employees

Coal India Ltd. 73,384.00 438,103

Indian Oil Corporation Ltd. 45,668.00 35,314

Bharat Petroleum Corporation Ltd. 18,842.00 14,690

Oil & Natural Gas Corporation Ltd. 17,759.00 34,929

Food Corporation of India 10,068.00 41,358

Bharat Sanchar Nigam Ltd. 8,591.00 320,506

Steel Authority of India Ltd. 7,152.00 132,973

NTPC Ltd. 6,843.00 24,162

Mangalore Refinery & Petrochemicals Ltd. 5,418.00 1,046

Chennai Petroleum Corporation Ltd. 4,553.00 1,651

Source: World Bank (2010)

According to the World Bank (2010), the number of employees employed by the PSEs

relative to their income earned creates a mismatch. The World Bank (2010) recommends that

the PSEs need to match their revenue to the number of employees more efficiently.

‘Transparency International’ gave India a score of 44 on a scale of 100. A score of 0

implies highly corrupt, while a score of 100 implies marginal levels of corruption

(Transparency International, 2018). The high levels of corruption in government entities

highly impair their long-term sustainability. Of the 82 loss making PSEs approximately

83.3% of the total losses are attributed to three firms (Bharat Sanchar Nigam Ltd, Air India

25

Ltd, and Mahanagar Telephone Nigam Ltd). The firms had been slated for divestment and/or

closure but remain open due to political interference and corruption in the government.

3.2 Summary

Unlike private entities which pursue profit motive, PSEs have both profit and social

welfare motives. The facts provided in this chapter show that capacity under-utilization,

competition, corporate governance challenges, political interference, and man-management

are the major challenges and reasons for their failure.

26

4. SCREENING FOR BANKRUPTCY RISK

Financial distress refers to the condition in which a firm is unable to meet its financial

obligations. This chapter highlights the method for evaluating financial distress of an entity.

4.1 Altman Z-Score Model

Outecheva (2007) indicates that financial distress of firms is characterised by four

stages: deterioration of performance, failure, insolvency and default. Firm decline and

deterioration affect the income and profitability of the firm, while insolvency and default

affect the liquidity position of the firm. Outecheva (2007) indicates a firm can be in financial

distress without defaulting on payments to creditors. However, default and eventual

bankruptcy cannot occur without the firm first experiencing financial distress.

The idea that financial ratios could be used to predict financial distress was first

postulated by Beaver (1966). He calculated financial ratios of firms that had failed and those

which were still in operation to prove his hypothesis. Beaver (1966), concluded that the ratio

of cash flow to total debt was the single most significant predictor of financial distress prior to

five years of the firm going bankruptcy. The model developed by Beaver (1966) was

univariate. Thus, the combined effect of all the financial ratios or variables could not be

identified in the estimation process. This was a significant shortcoming that affected the

results. These errors were corrected by the use of a multivariate model.

Altman (1968) developed the discriminant function referred to as the Z-score model,

using information from public entities that had been classified according to industry and size.

The model was designed to give predictive power, two years before bankruptcy. The model is

based on the multivariate discriminant analysis. This process uses data from multivariate

independent variables such as ratios and combines them into one score. This is then applied to

the classification of observation into either a-priori groups or mutually exclusive groups

(Altman, 1968). The Altman Z-score model consists of a linear equation consisting of four to

five commonly used financial ratios and weighted coefficients. The aim of the Altman Z-

score model is to assess the financial health of a company and to predict the probability that

the company will collapse within a period of two years.

27

Using Multiple Discriminant Analysis, Edward Altman combined a set of 5 financial

ratios to come up with the Altman Z-Score Formula, as given below:

Where denotes working capital to total assets, retained earnings to total assets,

earnings before interest and taxes to total assets, market value of equity to total

liabilities and sales to total assets (Altman, 2000). The zones of discrimination are set as

follows:

Z >= 3.0 - Safe zone

1.81 < Z < 3.0 - Grey zone

Z <= 1.81 - Distress zone

A study conducted by Heine (2000) covering various sample periods, over a period of

thirty years and based on 120 firms established that the Altman Z-score model retained its

reported high accuracy and was a robust estimator.

4.2 Empirical Studies on Financial Distress of PSEs in India

Pardeshi and Thorat (2013) analyzed the financial performance and efficiency of

selected PSEs in India. The study used the Altman Z-Score model to assess the financial

health of firms, such as Oil and Natural Gas Corporation Ltd (ONGC), Steel Authority of

India Ltd (SAIL), NTPC Ltd (NTPC), Bharat Electronics Ltd (BEL) and Rashtriya Chemical

and Fertilizers Ltd (RCF). The authors collected data from individual firms and used it to

evaluate their financial performance in comparison with the industry average. The study

established that ONGC, BEL and RCF were operating in the grey zone. SAIL and NTPC

were found to be operating in the distress zone. However, the study suffered from various

limitations, such as it was confined to PSEs operating in the manufacturing sector and

covered only three years.

Kumari (2013) evaluated the financial wellbeing of the Metal and Minerals Trading

Corporation of India (MMTC) using the Altman Z-Score model, covering the period 2007-

2012. The study found that the profit and investment position of the firm was very good. But

the financial assets held by it were found to be relatively low. The Z-score values showed that

the firm was in good financial health. However, the chances of bankruptcy were quite high.

28

Vijaya and Seethamma (2016) assessed the financial health of selected Indian PSEs.

The authors focused on National Thermal Power Corporation, Steel Authority Limited and

Oil and Natural Gas Commission during the period 1997-2015. The study established that the

liquidity and profit earning capacity of the firms was good and the firms were in good

financial condition. But the study focused only on three PSEs. My thesis contributes to this

literature by increasing the sample size of the study.

Batth, Nayak, and Pasumarti (2018) evaluated the financial performance and solvency

of ten public sector enterprises listed as Maharatna (large PSEs with financial autonomy and

operating in core sectors), during the period 2011-2016. The Maharatna classification was

introduced as a means of enabling PSEs to grow their operations and to become major

players, both in India and globally. The authors found that nine of the ten PSEs showed poor

financial health and only one firm reflected a healthy financial position.

Pandit and Verma (2019) examined the eight loss-making PSEs from the

manufacturing sector, listed on the Bombay Stock Exchange, for financial distress. The study

focused on the period 2011-2017. The study used the data collected from their annual

financial reports. The authors established that four of the companies were financially

distressed. Three were in the grey zone and one was financially healthy. Their study was

limited to manufacturing firms. My thesis further contributes by enlarging its scope to include

other critical sectors of the Indian economy, such as telecommunication, mining, services and

transportation in addition to manufacturing.

4.3 Summary

The Altman Z-score model provides effective variables that can be used to assess and

predict the financial distress of an enterprise. The Altman Z-score model is used in the

literature to evaluate the risk of bankruptcy of the selected PSEs.

29

5. RESEARCH METHODOLOGY

This chapter describes the methodology to be used to fulfil the objective of the thesis.

The sections below present the research design, data collection procedure and data analysis

for the thesis.

In the thesis, the Altman Z-score model has been used to evaluate and predict

bankruptcy for the selected PSEs in India. Similar to the approach used by Mamo (2011) and

Kipruto (2013), my thesis used the descriptive research design. The descriptive research

design is a scientific approach which entails observing and describing the behaviour of the

phenomenon under study (Shuttleworth, 2018).

For the thesis, the estimation sample comprises of the top eight loss making PSEs,

selected from diverse sectors of Indian economy and covers five financial years from 2013 to

2017. The selected loss making PSEs are reputed large enterprises in their respective sectors.

The author collected the financial data from their annual audited reports. A brief profile of

these sample PSEs is mentioned in the next section.

5.1 Profiles of Top 8 Loss Making PSEs in Study Sample

Bharat Sanchar Nigam Ltd. (BSNL): Bharat Sanchar Nigam Ltd. (Limited), founded in the

year 2000 through the merger of the Central Government Departments of Telecoms and

Telecoms Operation. It is one of the largest PSEs in India. The main function of BSNL is to

provide telecom services. The key objective of the firm is to bridge the digital divide between

the rural-urban areas (BSNL, 2019). In 2000, BSNL controlled over 60% of the fixed-

telephony and broadband market in India. Over the years, BSNL faced major challenges

including loss of customers to competitors, reduction in service offerings, underutilisation of

its infrastructure, surplus staff and low telecom traffic (Singh & Chawla, 2012). These

challenges are associated with the free market environment and competition in the telecom

sector.

Air India Ltd. (AIL): Air India, under aviation sector, was founded in 1932 (erstwhile known

as Tata Airlines). It was converted into a public limited company and renamed Air India. In

1953, the government of India acquired the majority stake of the airline (AIL, 2019). Over the

30

years, the firm has accumulated a debt of Rs. 460,000 million (Karnik, 2017). The funds were

used for expansion projects as well as to sustain its operations. In addition to debt, the firm

faces challenges of high oil prices and competition from private airline companies, both

domestic and international. Over the years, the market share of AIL has been falling.

Currently, the firm only controls 14% of the Indian market.

Mahanagar Telephone Nigam Ltd. (MTNL): The Company provides telecommunications

services in the metro cities of Mumbai and New Delhi in India (MTNL, 2018). Until 1992,

MTNL was the only telecommunications provider in Mumbai and New Delhi. Following the

liberalisation programme which was introduced by the government (1991), the firm has faced

increased competition. The firm’s shares are currently listed on the Bombay Stock Exchange,

the London Stock Exchange and the New York Stock Exchange (MTNL, 2018). In 2009, the

firm reported that it controlled 71% and 60% of the fixed telecommunication market in

Mumbai and New Delhi respectively and 17% of the mobile telephone market in both the

cities. By 2017, MTNL controlled less than 1% of the fixed and mobile phone markets in both

the cities (Khanna, 2017). According to Khanna (2017), the firm is unable to perform well as

it has a huge debt portfolio, is over staffed, has obsolete technology and has underutilized

capacity.

Brahmaputra Crackers & Polymer Ltd. (BCPL): The PSE was formed in 1985 with an aim

of bringing socioeconomic development in the North-East region of India. This PSE is a

dominant player in the production of petrochemicals. Over the past few years, the firm has

been posting poor performance due to a decline in the demand for its products. The decline

in demand has resulted in the under utilization of the firm’s capacity/facilities (Karmakar,

2018).

Steel Authority of India Ltd. (SAIL): The company was incorporated in 1973 and is a major

player in the steel sector. Currently, the firm produces 14.38 million metric tons of steel. This

makes it one of the largest steel producers in the world (SAIL, 2018). The company hopes to

increase its production capacity to 50 million tonnes by the year 2025 (SAIL, 2018). In 2017,

the firm announced that it was facing challenges, including decreased demand for steel and

market competition in the steel sector. This resulted in the firm being unable to optimise the

use of its assets and constrained its ability to be profitable (Singh, 2017).

Rashtriya Ispat Nigam Ltd. (RINL): Rashtriya Ispat Nigam Ltd is a steel producer. The firm

produces 7.3 million tonnes of steel in a year (RINL, 2012). The firm started its operation in

31

the 1980s. During the initial periods, the company suffered huge losses. The government took

over the firm in 2010 due to the huge losses it was accruing. However, in 2011 it registered an

impressive profit. The firm was able to grow its profits by 200% in the year 2014 (RINL,

2015). The firm posted losses of Rs. 12,360 million in 2016-17 and Rs. 13,690 million in

2017-18 (RINL, 2018). In a bid to improve performance, the firm has undertaken capacity

expansion program and modernization projects (RINL, 2018).

Western Coalfields Ltd. (WCL): Western Coalfields Ltd came into operations in 1956. It is a

subsidiary of Coal India Limited. The firm is engaged in the mining and production of coal

(WCL, 2019). The firm’s output increased over the years but the high cost of operations

diminished the margins (Arya, 2017). The firm also had to deal with corruption within the

organisation. The officers of the firm have been convicted of stealing money from the firm,

supplying adulterated coal and overcharging clients (The Economic Times, 2014).

State Trading Corporation of India Ltd. (STCL): The main business of the STCL is the

export of various products such as tea, rice, sugar, coffee, extractions, textiles, construction

materials, processed foods, castor oil, pharmaceuticals, consumer goods, leather ware,

engineering goods, chemicals, jewellery and clothing. The firm also imports goods such as

precious metals, edible oils, minerals, petrochemicals, fertilisers and metal ores (Bloomberg,

2019). In 2018, the firm reported revenue of Rs. 16,226 million compared to a loss of Rs. 22,

368 million. The losses were attributed to high operating costs (Bloomberg, 2019).

5.2 Data Collection

The estimation sample comprises the selected eight loss making PSEs and covers five

financial years, spanning over 2013-2017. I collected the financial data from their annual

audited reports.

5.3 Model Specification

Data analysis involves the systematic processing of the collected data, using statistical

methods, through the evaluation, transformation, and modelling of data in order to obtain

useful and meaningful information for decision making. The data was analysed using

Microsoft Excel and applying the Altman Z-Score Formula introduced in chapter 4.

32

Where denotes working capital to total assets ratio, retained earnings to total

assets ratio, earnings before interest and taxes (EBIT) to total assets ratio, market value

of equity to total liabilities ratio, and sales to total assets ratio (Altman, 1968). The

financial ratios have been explained below.

- Working Capital to Total Assets Ratio is used to indicate the net liquid assets of the firm

relative to the total capitalization. The liquid assets are the difference between the current

assets and the current liabilities. A firm that has continuous operating losses will have

reducing current assets relative to its total assets (Brown, 2019).

- Retained Earnings to Total Assets Ratio is used to measure the percentage of the total

assets owned by the firm that are financed by the retained earnings. This ratio indicates the

degree to which the firm is retaining its profits and using this retained funds to finance the

acquisition of assets instead of paying dividends (Brown, 2019). There is no right level of

the retained earnings to total assets ratio. Comparison can be made using the industry

average.

- Earnings before Interest and Tax (EBIT) to Total Assets Ratio indicates the degree to

which the firm’s profitability is generated using the firm’s assets. It shows how effectively

the firm is using its assets to generate income. EBIT is used instead of the net profits to

keep the focus on the operating income without the effect of tax and financing obligations.

This allows for comparison with similar firms (Brown, 2019).

- Book Value of Equity to Total Liabilities Ratio shows the extent to which the firm’s asset

reduce in value before the liabilities exceed the assets and the firm is declared insolvent

(Altman, 1968).

- Sales to Total Assets Ratio shows the sales generating capability of the assets held by the

firm. The ratio indicates the measures put in place by management to handle competitive

conditions. According to Heine (2000), this indicator is the most important as it is the least

33

significant ratio individually. Among all the ratios, this is often ranked second due to its

contribution to the overall discriminating ability of the model.

5.4 Summary

In my thesis, the Altman Z-score model has been used to evaluate and predict

bankruptcy in selected PSEs in India. The estimation sample comprises of the top 8 loss

making PSEs selected from diverse sectors of Indian economy and covers five financial years

from 2013 to 2017.

34

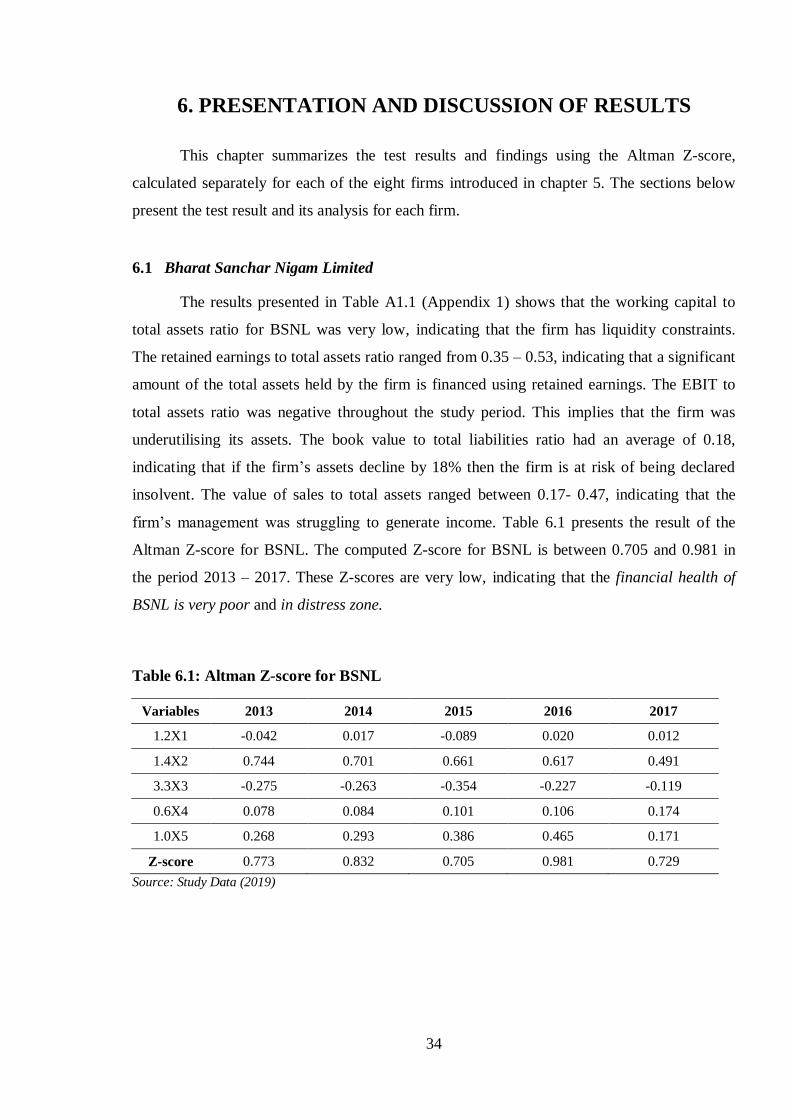

6. PRESENTATION AND DISCUSSION OF RESULTS

This chapter summarizes the test results and findings using the Altman Z-score,

calculated separately for each of the eight firms introduced in chapter 5. The sections below

present the test result and its analysis for each firm.

6.1 Bharat Sanchar Nigam Limited

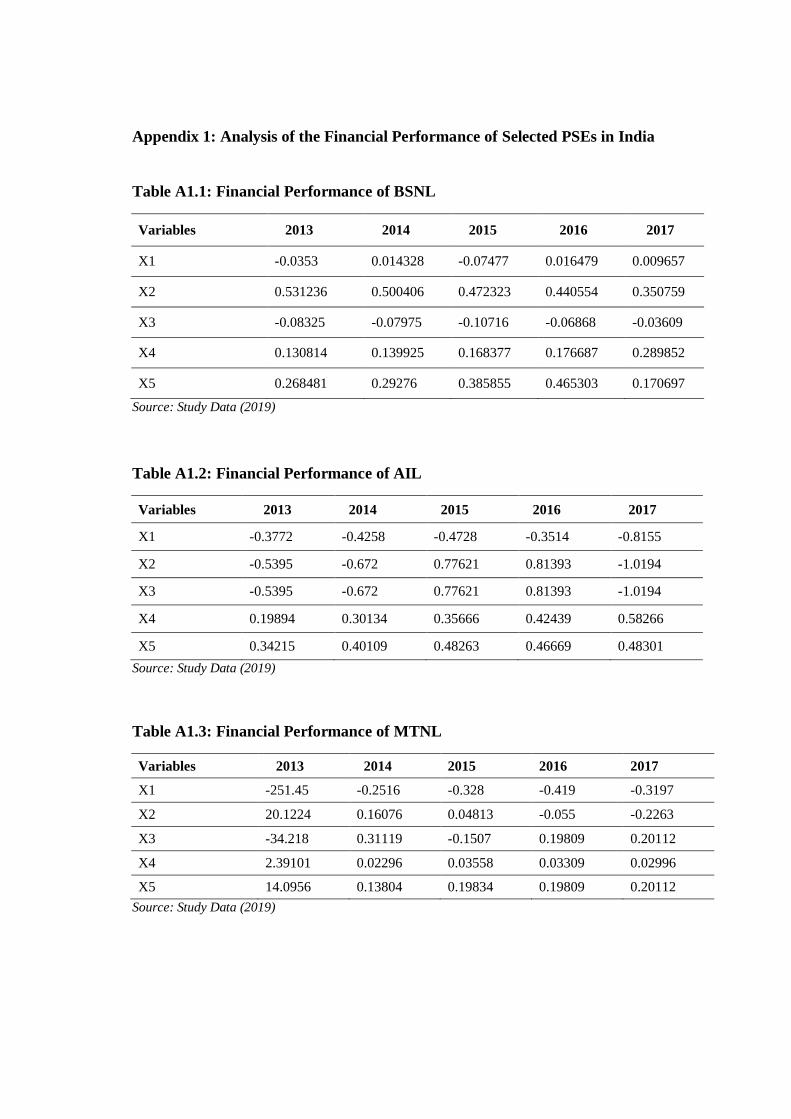

The results presented in Table A1.1 (Appendix 1) shows that the working capital to

total assets ratio for BSNL was very low, indicating that the firm has liquidity constraints.

The retained earnings to total assets ratio ranged from 0.35 – 0.53, indicating that a significant

amount of the total assets held by the firm is financed using retained earnings. The EBIT to

total assets ratio was negative throughout the study period. This implies that the firm was

underutilising its assets. The book value to total liabilities ratio had an average of 0.18,

indicating that if the firm’s assets decline by 18% then the firm is at risk of being declared

insolvent. The value of sales to total assets ranged between 0.17- 0.47, indicating that the

firm’s management was struggling to generate income. Table 6.1 presents the result of the

Altman Z-score for BSNL. The computed Z-score for BSNL is between 0.705 and 0.981 in

the period 2013 – 2017. These Z-scores are very low, indicating that the financial health of

BSNL is very poor and in distress zone.

Table 6.1: Altman Z-score for BSNL

Variables 2013 2014 2015 2016 2017

1.2X1 -0.042 0.017 -0.089 0.020 0.012

1.4X2 0.744 0.701 0.661 0.617 0.491

3.3X3 -0.275 -0.263 -0.354 -0.227 -0.119

0.6X4 0.078 0.084 0.101 0.106 0.174

1.0X5 0.268 0.293 0.386 0.465 0.171

Z-score 0.773 0.832 0.705 0.981 0.729

Source: Study Data (2019)

35

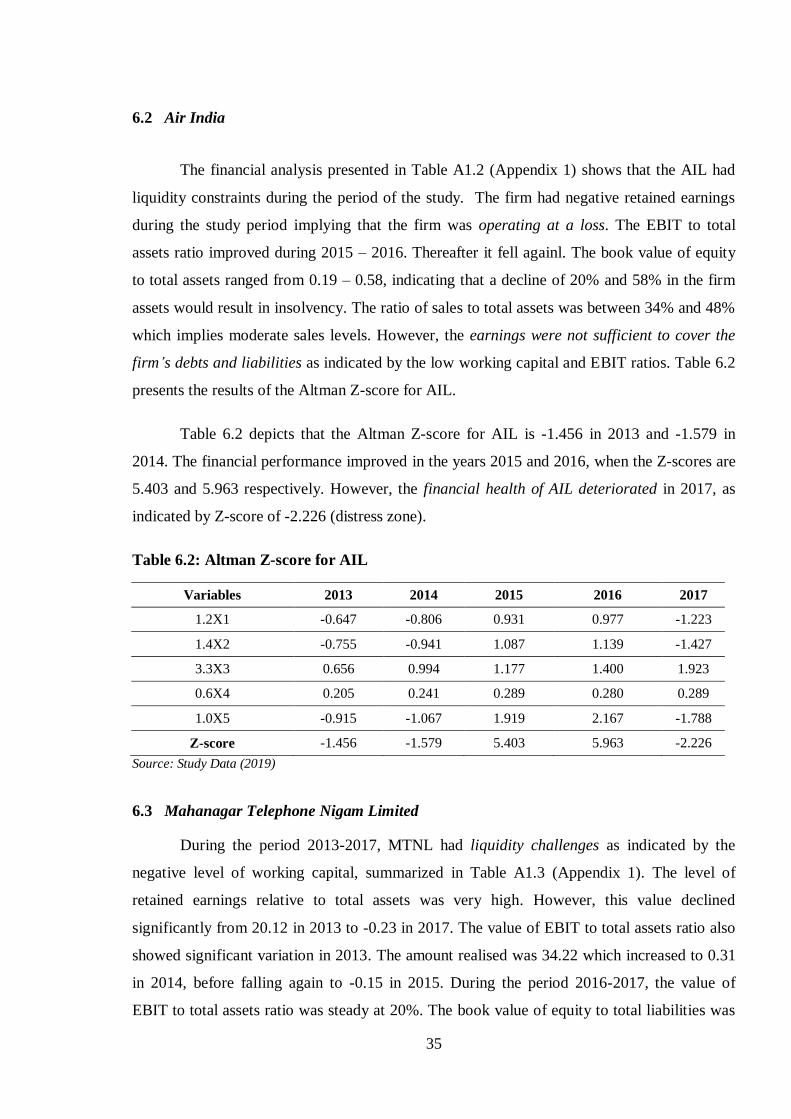

6.2 Air India

The financial analysis presented in Table A1.2 (Appendix 1) shows that the AIL had

liquidity constraints during the period of the study. The firm had negative retained earnings

during the study period implying that the firm was operating at a loss. The EBIT to total

assets ratio improved during 2015 – 2016. Thereafter it fell againl. The book value of equity

to total assets ranged from 0.19 – 0.58, indicating that a decline of 20% and 58% in the firm

assets would result in insolvency. The ratio of sales to total assets was between 34% and 48%

which implies moderate sales levels. However, the earnings were not sufficient to cover the

firm’s debts and liabilities as indicated by the low working capital and EBIT ratios. Table 6.2

presents the results of the Altman Z-score for AIL.

Table 6.2 depicts that the Altman Z-score for AIL is -1.456 in 2013 and -1.579 in

2014. The financial performance improved in the years 2015 and 2016, when the Z-scores are

5.403 and 5.963 respectively. However, the financial health of AIL deteriorated in 2017, as

indicated by Z-score of -2.226 (distress zone).

Table 6.2: Altman Z-score for AIL

Variables 2013 2014 2015 2016 2017

1.2X1 -0.647 -0.806 0.931 0.977 -1.223

1.4X2 -0.755 -0.941 1.087 1.139 -1.427

3.3X3 0.656 0.994 1.177 1.400 1.923

0.6X4 0.205 0.241 0.289 0.280 0.289

1.0X5 -0.915 -1.067 1.919 2.167 -1.788

Z-score -1.456 -1.579 5.403 5.963 -2.226

Source: Study Data (2019)

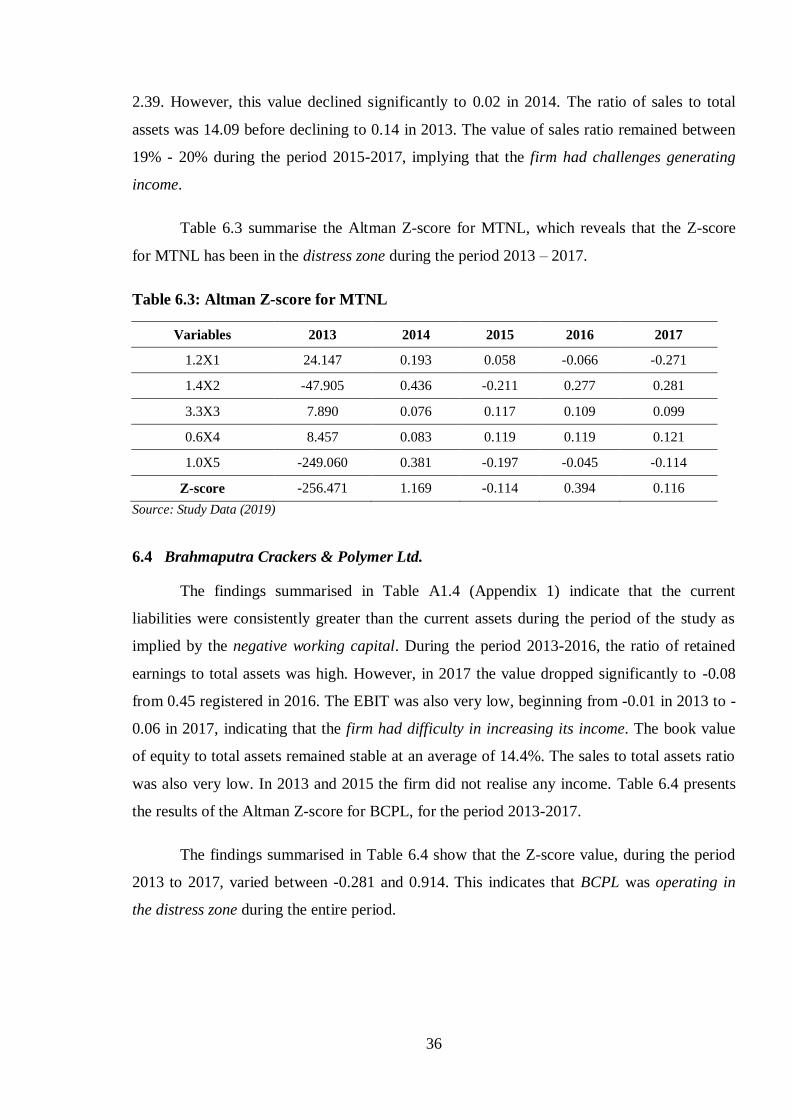

6.3 Mahanagar Telephone Nigam Limited

During the period 2013-2017, MTNL had liquidity challenges as indicated by the

negative level of working capital, summarized in Table A1.3 (Appendix 1). The level of

retained earnings relative to total assets was very high. However, this value declined

significantly from 20.12 in 2013 to -0.23 in 2017. The value of EBIT to total assets ratio also

showed significant variation in 2013. The amount realised was 34.22 which increased to 0.31

in 2014, before falling again to -0.15 in 2015. During the period 2016-2017, the value of

EBIT to total assets ratio was steady at 20%. The book value of equity to total liabilities was

36

2.39. However, this value declined significantly to 0.02 in 2014. The ratio of sales to total

assets was 14.09 before declining to 0.14 in 2013. The value of sales ratio remained between

19% - 20% during the period 2015-2017, implying that the firm had challenges generating

income.

Table 6.3 summarise the Altman Z-score for MTNL, which reveals that the Z-score

for MTNL has been in the distress zone during the period 2013 – 2017.

Table 6.3: Altman Z-score for MTNL

Variables 2013 2014 2015 2016 2017

1.2X1 24.147 0.193 0.058 -0.066 -0.271

1.4X2 -47.905 0.436 -0.211 0.277 0.281

3.3X3 7.890 0.076 0.117 0.109 0.099

0.6X4 8.457 0.083 0.119 0.119 0.121

1.0X5 -249.060 0.381 -0.197 -0.045 -0.114

Z-score -256.471 1.169 -0.114 0.394 0.116

Source: Study Data (2019)

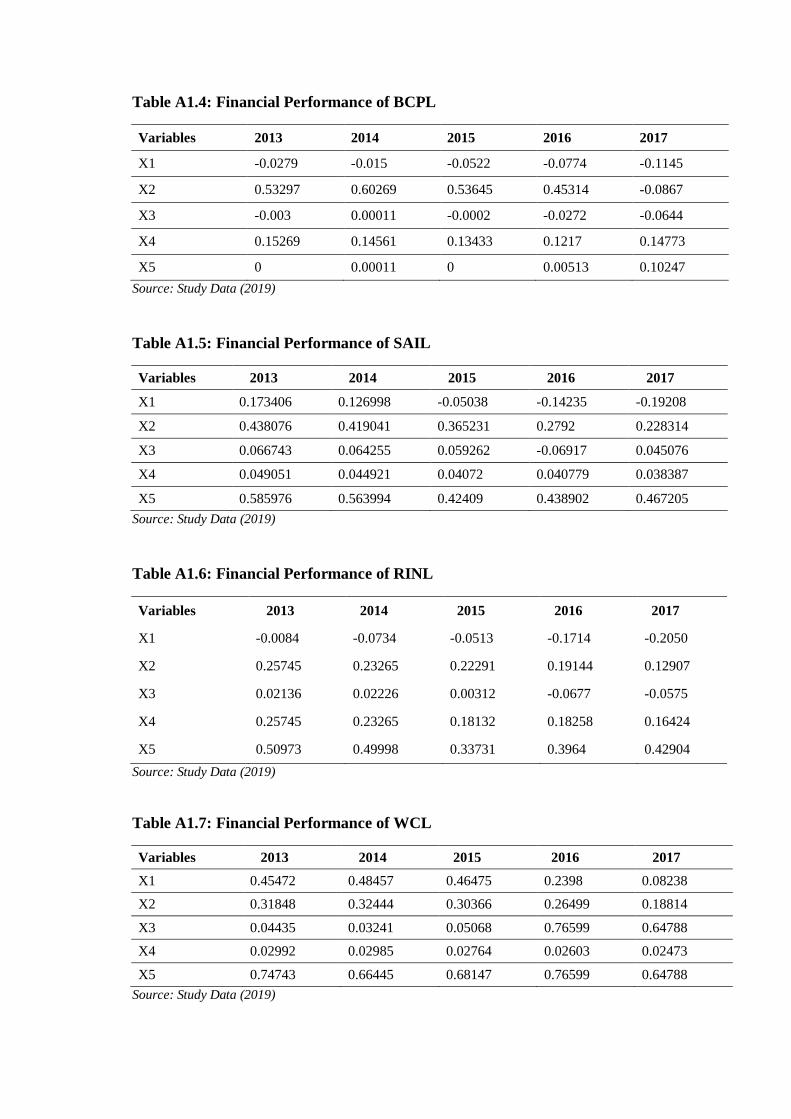

6.4 Brahmaputra Crackers & Polymer Ltd.

The findings summarised in Table A1.4 (Appendix 1) indicate that the current

liabilities were consistently greater than the current assets during the period of the study as

implied by the negative working capital. During the period 2013-2016, the ratio of retained

earnings to total assets was high. However, in 2017 the value dropped significantly to -0.08

from 0.45 registered in 2016. The EBIT was also very low, beginning from -0.01 in 2013 to -

0.06 in 2017, indicating that the firm had difficulty in increasing its income. The book value

of equity to total assets remained stable at an average of 14.4%. The sales to total assets ratio

was also very low. In 2013 and 2015 the firm did not realise any income. Table 6.4 presents

the results of the Altman Z-score for BCPL, for the period 2013-2017.

The findings summarised in Table 6.4 show that the Z-score value, during the period

2013 to 2017, varied between -0.281 and 0.914. This indicates that BCPL was operating in

the distress zone during the entire period.

37

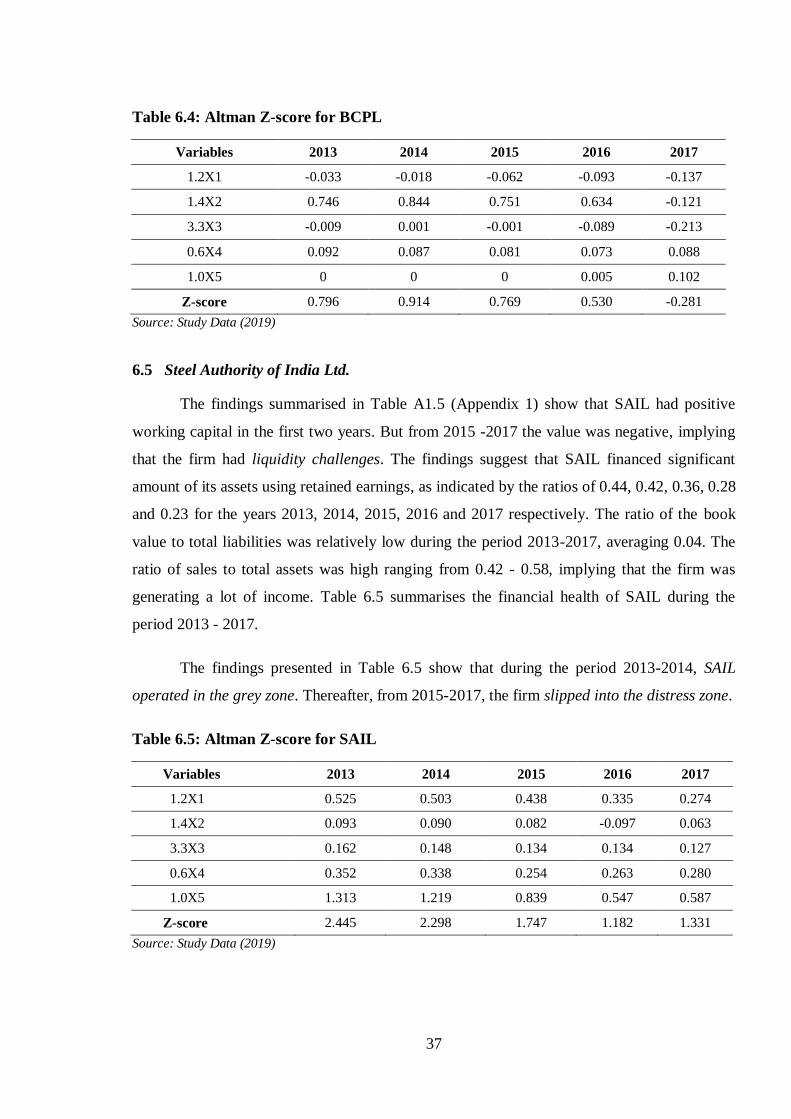

Table 6.4: Altman Z-score for BCPL

Variables 2013 2014 2015 2016 2017

1.2X1 -0.033 -0.018 -0.062 -0.093 -0.137

1.4X2 0.746 0.844 0.751 0.634 -0.121

3.3X3 -0.009 0.001 -0.001 -0.089 -0.213

0.6X4 0.092 0.087 0.081 0.073 0.088

1.0X5 0 0 0 0.005 0.102

Z-score 0.796 0.914 0.769 0.530 -0.281

Source: Study Data (2019)

6.5 Steel Authority of India Ltd.

The findings summarised in Table A1.5 (Appendix 1) show that SAIL had positive

working capital in the first two years. But from 2015 -2017 the value was negative, implying

that the firm had liquidity challenges. The findings suggest that SAIL financed significant

amount of its assets using retained earnings, as indicated by the ratios of 0.44, 0.42, 0.36, 0.28

and 0.23 for the years 2013, 2014, 2015, 2016 and 2017 respectively. The ratio of the book

value to total liabilities was relatively low during the period 2013-2017, averaging 0.04. The

ratio of sales to total assets was high ranging from 0.42 - 0.58, implying that the firm was

generating a lot of income. Table 6.5 summarises the financial health of SAIL during the

period 2013 - 2017.

The findings presented in Table 6.5 show that during the period 2013-2014, SAIL

operated in the grey zone. Thereafter, from 2015-2017, the firm slipped into the distress zone.

Table 6.5: Altman Z-score for SAIL

Variables 2013 2014 2015 2016 2017

1.2X1 0.525 0.503 0.438 0.335 0.274

1.4X2 0.093 0.090 0.082 -0.097 0.063

3.3X3 0.162 0.148 0.134 0.134 0.127

0.6X4 0.352 0.338 0.254 0.263 0.280

1.0X5 1.313 1.219 0.839 0.547 0.587

Z-score 2.445 2.298 1.747 1.182 1.331

Source: Study Data (2019)

38

6.6 Rashtriya Ispat Nigam Ltd.

The financial analysis presented in Table A1.6 (Appendix 1) shows that RINL had a

negative working capital throughout the study period. This indicates that the firm was unable

to meet its current liabilities when it was due. The findings indicate that on average 20.67%

of assets were financed using retained earnings, during the period 2013-2017. The ratio of

EBIT to total assets was very low ranging from -0.02 to -0.06. During this period the ratio of

sales to total assets ranged from 0.03 - 0.51, implying that the value of expenses incurred by

the firm was high relative to income resulting in low EBIT. Table 6.6 presents the results of

the Altman Z-score for RINL, during the fiscal year 2013 - 2017.

In 2013 and 2014, RINL had a Z-score of 2.531 and 2.292 respectively, which means

it was operating in the grey zone, likely to be bankrupt within 2 years. Test result shows,

during the period 2015-2017, the firm slipped into distress zone with Z-scores dipping below

1.81.

Table 6.6: Altman Z-score for RINL

Variables 2013 2014 2015 2016 2017

1.2X1 0.309 0.279 0.267 0.229 0.155

1.4X2 0.030 0.031 0.004 -0.095 -0.080

3.3X3 0.849 0.768 0.598 0.602 0.542

0.6X4 0.306 0.300 0.202 0.238 0.257

1.0X5 1.037 0.914 0.693 0.531 0.460

Z-score 2.531 2.292 1.764 1.505 1.334

Source: Study Data (2019)

6.7 Western Coalfields Ltd.

The findings summarised in Table A1.7 (Appendix 1) show that WCL had high

liquidity during the period 2013-2015, as implied by ratios of 0.45, 0.48 and 0.46 respectively.

It further deteriorated to 0.24 in 2016. This was followed by a decline to 0.08 in 2017,

indicating that the firm’s liquidity position was deteriorating in the study period. The findings

suggest that the firm financed approximately 27% of its assets using retained earnings. The

ratio of EBIT to total assets was low, ranging between 0.04 and 0.05, during 2013 - 2015.

Thereafter the value increased to 0.76 and 0.65 in 2016 and 2017 respectively. This implies

that the management tried to enhance revenue and/or reduce costs. The book value to total

39

liabilities was stable at approximately 0.03 during the study period. The ratio of sales to total

assets ranged between was 0.65 and 0.76, during 2013 – 2017.

The results presented in Table 6.7 show that WCL was in grey zone during the period

2013-2015 as implied by Z-score values being above 1.81. Thereafter, during 2016 – 2017,

with Z-score value being above 3.0, indicating the firm was in safe zone.

Table 6.7: Altman Z-score for WCL

Variables 2013 2014 2015 2016 2017

1.2X1 0.546 0.581 0.558 0.288 0.099

1.4X2 0.446 0.454 0.425 0.371 0.263

3.3X3 0.146 0.107 0.167 2.527 2.138

0.6X4 0.018 0.018 0.016 0.016 0.015

1.0X5 0.747 0.664 0.681 0.766 0.648

Z-score 1.903 1.824 1.847 3.968 3.163

Source: Study Data (2019)

6.8 State Trading Corporation of India Ltd.

The financial analysis presented in Table A1.8 (Appendix 1) shows that STCL had

liquidity challenges as implied by negative working capital. The firm also had negative

retained earnings. The negative EBIT to total assets ratio suggests that the firm had negative

income during the period 2013-2016. During the same period the level of sales relative to

total assets was high, ranging between 1.88 and 4.73. These findings imply that the expenses

were significantly higher than the income, resulting in poor liquidity and retained earnings.

Table 6.8 summarises the findings of the Altman Z-score test conducted on the

financial results of STCL. It shows that STCL with Z-score value of 2.484 in 2013 was in the

grey zone. But during 2014-2016, the Z-score indicates financial distress.

Table 6.8: Altman Z-score for STCL

Variables 2013 2014 2015 2016 2017

1.2X1 -0.604 -1.008 -0.786 -0.968 -1.260

1.4X2 -0.682 -1.419 -0.789 -0.948 -1.405

3.3X3 -0.546 -0.914 -0.888 -1.026 20.533

0.6X4 0.005 0.006 0.005 0.004 0.005

1.0X5 4.311 4.726 3.152 2.235 1.885

Z-score 2.484 1.391 0.694 -0.703 19.758

Source: Study Data (2019)

40

6.9 Summary:

The Altman Z-score model is useful to help assess and predict bankruptcy in advance

for a company, so that it can take corrective measures in time for improvement. Applying

Altman Z-score model for the selected 8 loss making PSEs, the test results established that

during the period 2013 – 2017 these PSEs were either in the grey zone or in the financial

distress zone.

41

7. REFORMS FOR RESTRUCTURING PUBLIC SECTOR

In India, the growing number of PSEs facing financial distress is a major concern as it