Masaryk UniversityFaculty of Economics and Administration

70

Masaryk UniversityFaculty of Economics and Administration Faculty of Economics and Administration Field of study: Accounting Financial reporting for non-current and current assets under national GAAP and global IFRS for SME. Evidence from Belarus Master’s Thesis Supervisor: Author: Ing. Oleksandra LEMESHKO Mikhail BALYKA Brno, 2019

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Masaryk UniversityFaculty of Economics and Administration

Masaryk UniversityFaculty of Economics and Administration

Faculty of Economics and Administration

Field of study: Accounting

Financial reporting for non-current and current assets under national

GAAP and global IFRS for SME. Evidence from Belarus

Master’s Thesis

Supervisor: Author: Ing. Oleksandra LEMESHKO Mikhail BALYKA

Brno, 2019

2

3

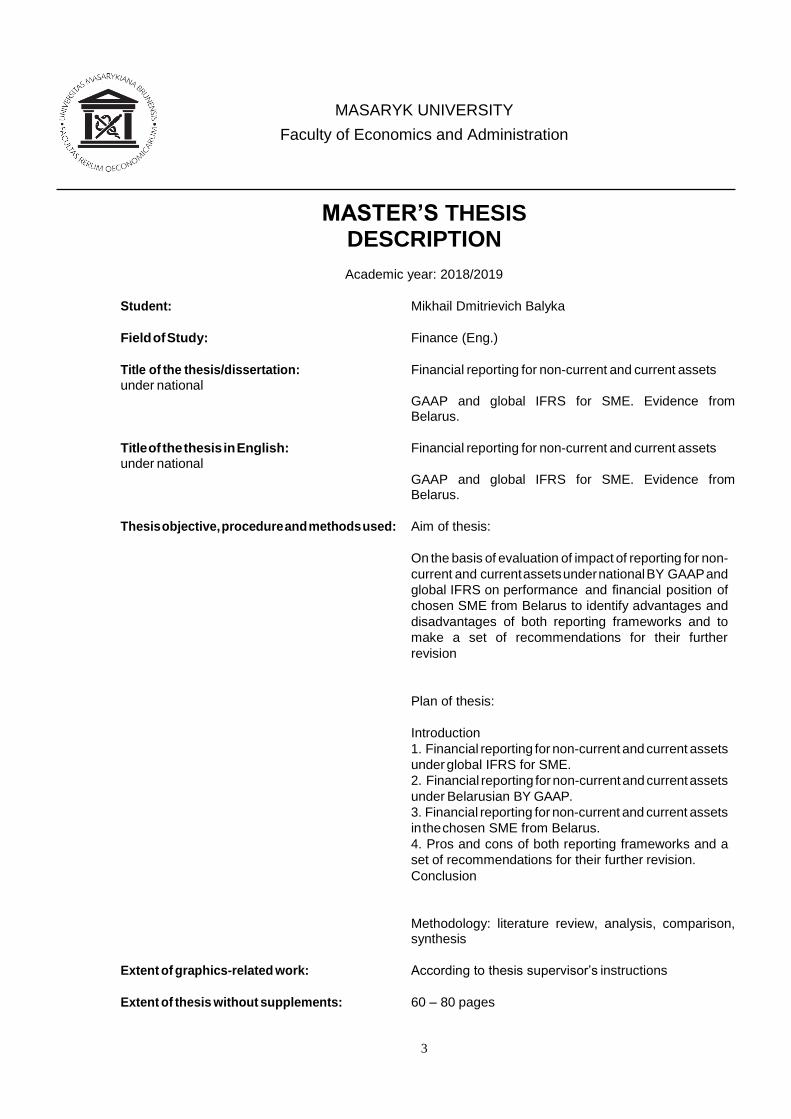

MASARYK UNIVERSITY

Faculty of Economics and Administration

MASTER’S THESIS DESCRIPTION

Academic year: 2018/2019

Student: Mikhail Dmitrievich Balyka

Field of Study: Finance (Eng.)

Title of the thesis/dissertation: Financial reporting for non-current and current assets under national

GAAP and global IFRS for SME. Evidence from Belarus.

Title of the thesis in English: Financial reporting for non-current and current assets under national

GAAP and global IFRS for SME. Evidence from Belarus.

Thesis objective, procedure and methods used: Aim of thesis:

On the basis of evaluation of impact of reporting for non-

current and current assets under national BY GAAP and

global IFRS on performance and financial position of

chosen SME from Belarus to identify advantages and

disadvantages of both reporting frameworks and to

make a set of recommendations for their further

revision

Plan of thesis:

Introduction

1. Financial reporting for non-current and current assets

under global IFRS for SME.

2. Financial reporting for non-current and current assets

under Belarusian BY GAAP.

3. Financial reporting for non-current and current assets

in the chosen SME from Belarus.

4. Pros and cons of both reporting frameworks and a

set of recommendations for their further revision.

Conclusion

Methodology: literature review, analysis, comparison, synthesis

Extent of graphics-related work: According to thesis supervisor’s instructions

Extent of thesis without supplements: 60 – 80 pages

4

Literature: Accounting and reporting Act of July 12th 2013 57-Z. :

Ministry of Finance of the Republic of Belarus, 2013.

Decree of the Ministry of Finance of the Republic of Belarus of April 12th 2012 №25 "Concerning approval of the instruction on intangible assets accounting". 2012.

Decree of the Ministry of Finance of the Republic of

Belarus of April 30th 2012 №26 "Concerning approval

of the instruction on PPE accounting". 2012.

Decree of the Ministry of Finance of the Republic of

Belarus of November 12th 2010 133 ”Concerning

approval of the instruction on inventory accounting”.

2010.

Decree of the Ministry of Finance of the Republic of

Belarus of September 30th 2011 No.102 ”Concerning

approval of the instruction on revenues and expenses

accounting”. 2011.

IFRS Manual of accounting (global edition) two-

volume set. 2016. ISBN 978-0-7545-5439-4.

International financial reporting standard for small and

medium-sized entities (IFRS for SMEs). London:

International Accounting Standards Board, 2009. 230

s. ISBN 9781907026171.

Thesis supervisor: Ing. Oleksandra Lemeshko

Thesis supervisor’s department: Faculty of Economics and Administration

Thesis assignment date: 2018/04/22

The deadline for the submission of Master’s thesis and uploading it into IS can be found in the academic year calendar.

In Brno, date: 2019/05/07

5

6

Name and surname of the author : Mikhail Balyka

Master’s thesis t i t le: Financial reporting for non-current and current

assets under national GAAP and global IFRS for

SME. Evidence from Belarus

Department : Finance

Master’s thesis supervisor: Ing. Oleksandra Lemeshko

Master’s thesis date : 2019

Annotation

The goal of the submitted thesis: “Financial reporting for non-current and current assets under

national BY GAAP and global IFRS. Evidence from Belarus” to identify advantages and

disadvantages of both reporting frameworks and to make a set of recommendations for their further

revision on the basis of evaluation of impact of reporting for non-current and current assets under

national BY GAAP and global IFRS on performance and financial position of chosen SME from

Belarus.

Keywords

Belarus, property plant and equipment, intangible assets, inventories, comparison, IFRS, IAS16,

IAS38, IAS 2

7

8

Declaration

„I certify that I have written the Master’s Thesis ‘Financial reporting for non-current and current

assets under national GAAP and global IFRS for SME. Evidence from Belarus’ by myself under

the supervision of Oleksandra Lemeshko and I have listed all the literary and other specialist

sources in accordance with legal regulations, Masaryk University internal regulations, and the

internal procedural deeds of Masaryk University and the Faculty of Economics and

Administration.“

Brno,

Author’s s ignature

9

Table of contents

INTRODUCTION ......................................................................................................................... 11

CHAPTER I. COMPARISON OF THE REPORTING UNDER INTERNATIONAL

FINANCIAL REPORTING STANDARDS AND BELARUSIAN GENERALLY ACCEPTED

ACCOUNTING PRINCIPLES ..................................................................................................... 13

1.1 Property, plant and equipment ................................................................................................. 14

1.1.1 Recognition and measurement ...................................................................................... 14

1.1.2 Subsequent measurement .............................................................................................. 15

1.1.2.1 Depreciation............................................................................................................ 15

1.1.2.2 Revaluation ............................................................................................................. 17

1.1.2.2 Impairment ............................................................................................................. 19

1.1.2.3 Modernization, reconstruction, repair .................................................................... 22

1.1.3 Derecognition and disposal ........................................................................................... 23

1.2 Intangible assets ....................................................................................................................... 23

1.2.1 Recognition and measurement ...................................................................................... 23

1.2.2 Subsequent measurement .............................................................................................. 26

1.2.2.1 Amortisation ........................................................................................................... 26

1.2.2.2 Revaluation ............................................................................................................. 29

1.2.2.3 Impairment ............................................................................................................. 30

1.2.3 Goodwill ........................................................................................................................ 31

1.2.4 Derecognition and disposal ........................................................................................... 32

1.3 Inventories ............................................................................................................................... 32

1.3.1 Recognition and measurement ...................................................................................... 32

CHAPTER II. EVALUATION OF THE IMPLEMENTAION OF INTERNATIONAL

FINANCIAL REPORTING STANDARDS AND ITS IMPACT ON FINANCIAL REPORTING

OF BEK-EXPERT ......................................................................................................................... 39

2.1 Company profile ...................................................................................................................... 39

2.2 Methodology ............................................................................................................................ 40

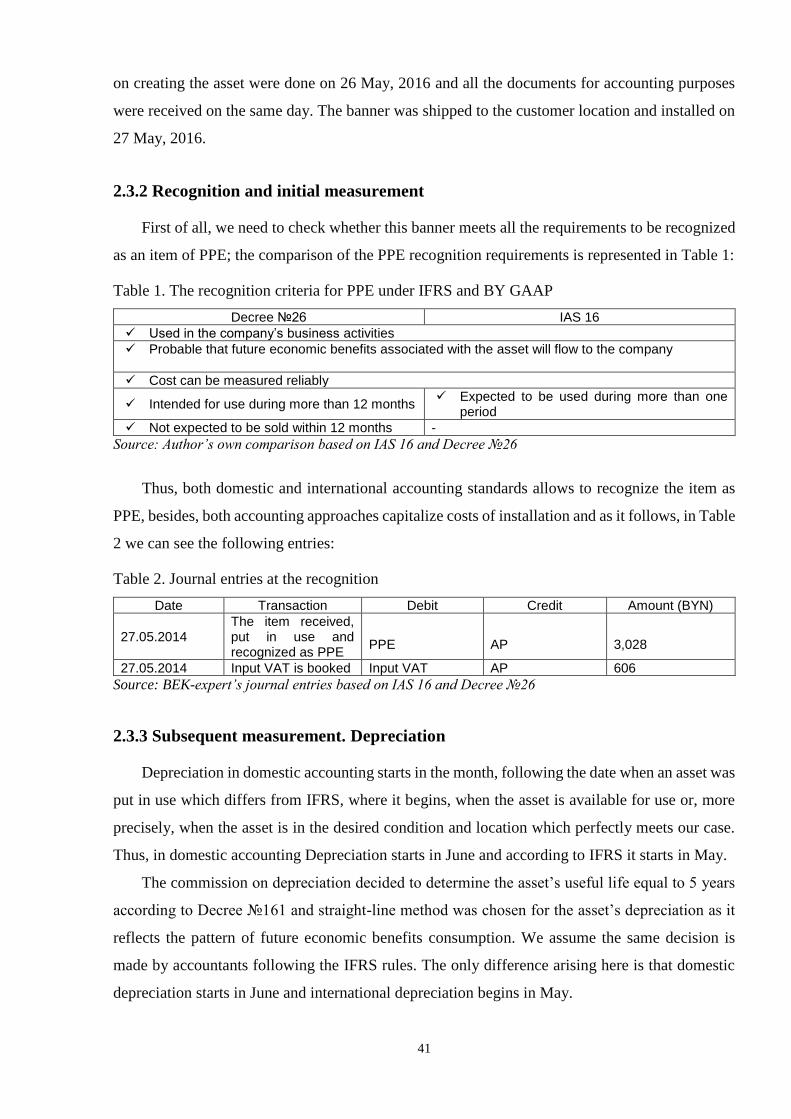

2.3 Case study I: Acquisition of PPE. Depreciation charge. Repairment costs ............................ 40

2.3.1 Case summary ............................................................................................................... 40

2.3.2 Recognition and initial measurement ............................................................................ 41

2.3.3 Subsequent measurement. Depreciation ....................................................................... 41

2.3.4 Repairment costs ........................................................................................................... 42

2.3.5 Useful life review under IFRS ...................................................................................... 43

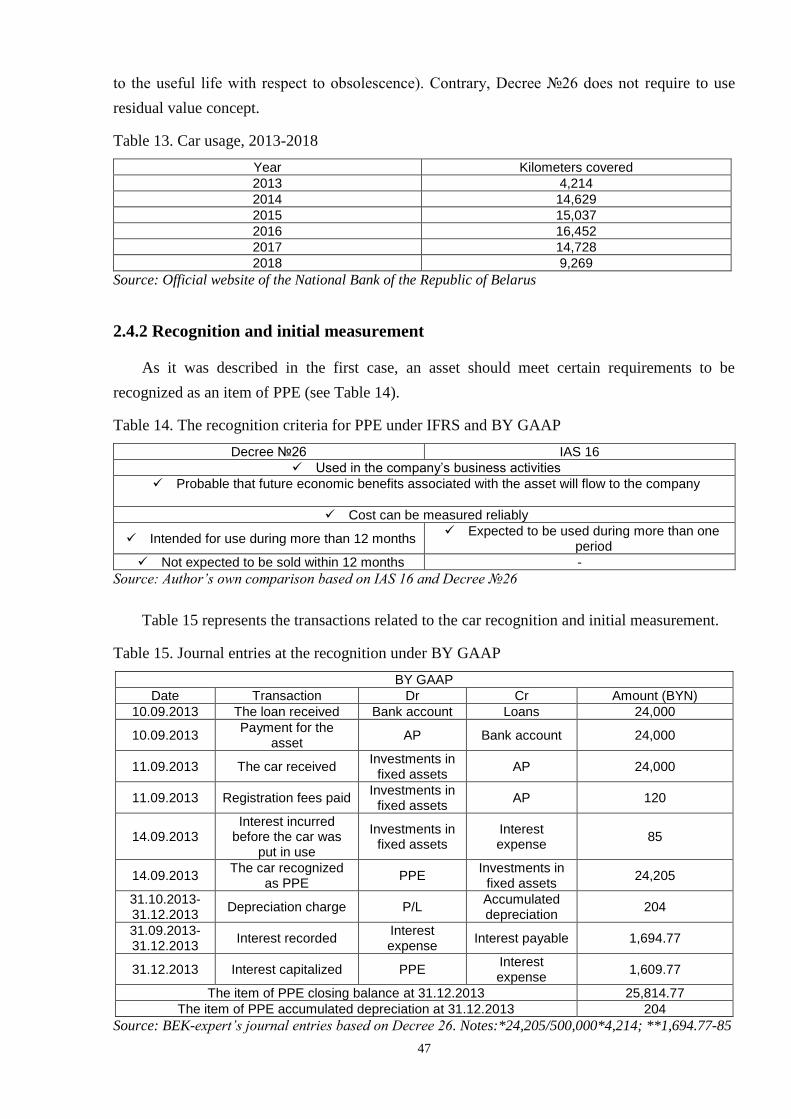

2.4 Case study II: Acquisition of PPE. Borrowing costs ............................................................... 46

10

2.4.1 Case summary ............................................................................................................... 46

2.4.2 Recognition and initial measurement ............................................................................ 47

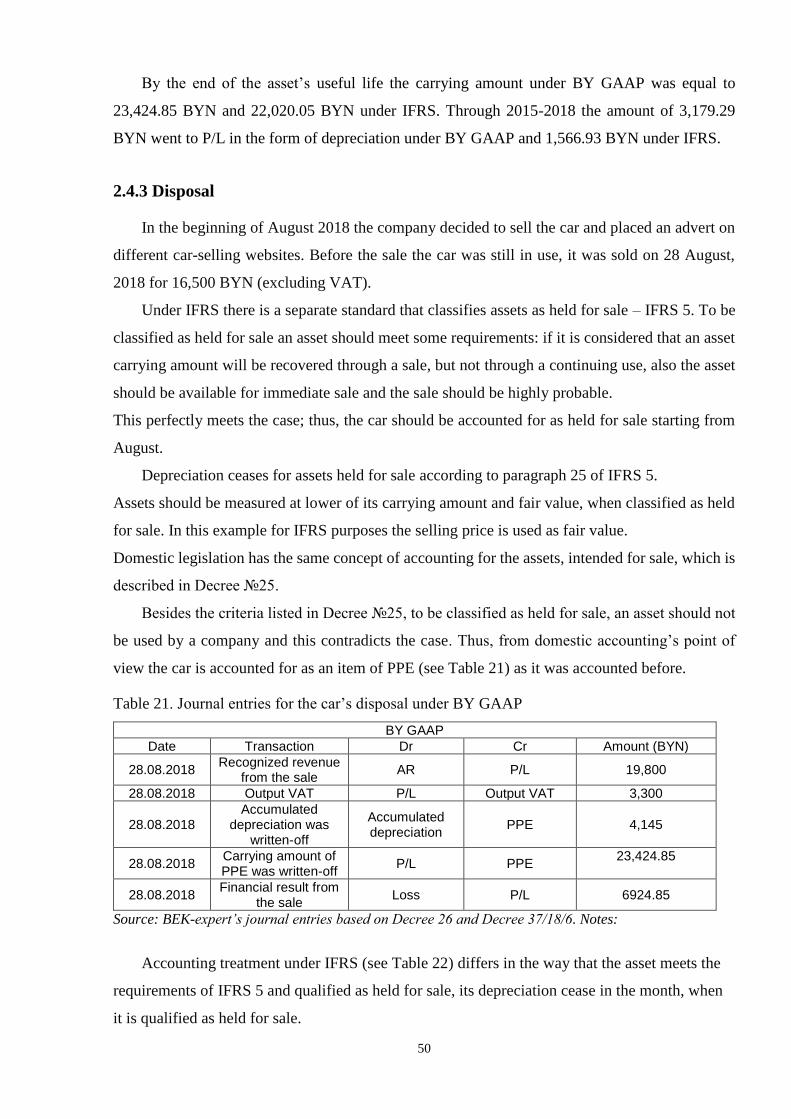

2.4.3 Disposal ......................................................................................................................... 50

2.5 Case study III: Acquisition of PPE. Precious metals............................................................... 51

2.5.1 Case summary ............................................................................................................... 51

2.5.1 Precious metals treatment.............................................................................................. 52

2.6 Case study IV: Acquisition of IA. Recognition criteria ......................................................... 57

2.6.1 Case summary ............................................................................................................... 57

2.6.2 Recognition ................................................................................................................... 57

2.6 Case study V: Acquisition of inventories. Net realisable value ............................................. 59

2.6.1 Case summary ............................................................................................................... 59

2.6.1 Recognition ................................................................................................................... 59

2.6.2 Measurement of inventories. Cost of purchase ............................................................. 59

2.6.3 Net realisable value ....................................................................................................... 60

Recommendations for BY GAAP ................................................................................................. 62

Conclusion ..................................................................................................................................... 64

List of literature ............................................................................................................................. 66

List of tables .................................................................................................................................. 68

List of abbreviations ...................................................................................................................... 70

11

INTRODUCTION

Since independence, Belarus has been harmonizing the national accounting and auditing

system with international standards. During these 25 years different stages of accounting

development has been passed through: in the beginning the accounting system was extremely strict

and facilitated the needs of tax authorities. This set a stamp upon accountants’ perception of actions

the can take within the scope of their professional area. The next stage in the development of

accounting system was related to the creation of the union with Russia and, as a result, convergence

with Russian accounting system. The present stage characterized with a movement of accounting

system towards the international practice.

As of today, International Financial Reporting Standards (hereinafter – IFRS) in Belarus are

required by domestic public companies (i.e. all listed companies and financial institutions).

For all the other companies national standards are used. And the first problem here is that

officially there is the only body which sets accounting standards: Ministry of Finance, but in fact

there could be different bodies.

And this is the issue because sometimes clashes between different legal acts appear for the

same transactions and in that case we need to use the one which was issued later. To find solutions

on these issues we will observe, compare and analyze Belarusian accounting standards and IFRS.

Importance of the topic chosen is confirmed by the fact that Belarus, being a European

country, should not stay on the sideline from the global development trends in financial reporting.

Like many countries in the world, Belarus is involved in the harmonization of the national

accounting system in accordance with IFRS.

The importance of IFRS in modern financial relations is that the use of such standards

contributes to that companies become opened to the world investment market, thus, obtaining

loans in foreign banks, and attract investments from foreign companies. These areas are very

relevant for our country.

The goal of the diploma thesis is to identify advantages and disadvantages of both global full

IFRS (also IFRS for SMEs) and Generally Accepted Accounting Principles (hereinafter – BY

GAAP) reporting frameworks and to make a set of recommendations for their further revision on

the basis of evaluation of impact of reporting for non-current and current assets under national BY

GAAP and global IFRS on performance and financial position of chosen SME from Belarus.

The aim of the diploma thesis is accomplished within the following structure of thesis. Thesis

comprises two parts:

12

- the first one is a theoretical review and comparison of accounting standards for property,

plant and equipment (hereinafter – PPE), intangible assets (hereinafter – IA) and inventories, using

domestic legislation acts, international accounting standards and articles on its application;

-the second part is the implementation of the results made on the basis of the theoretical review

using the examples from the business activity of the Belarusian company, BEK-expert, in 2012-

2018.

Based on the analysis performed one general conclusion can be made: National accounting

and reporting standards are highly harmonized with IFRS. On the other hand, BY GAAP is more

rule-based, while IFRS is more judgement based. Although, Accounting and reporting Act of July

12th 2013 57-Z declares the priority of economic substance, but in reality, BY GAAP are more

focused on legal form, accounting procedures and documentation requirements and, to a lesser

extent, the economic substance of operations.

Methodology used in the work: literature and legislation review in the theoretical part

comparative analysis (в практике) of impact of IFRS based reporting and BY GAAP based

reporting on financial performance and position of the chosen company.

Based on the conducted study it is recommended to continue gradual harmonization with IFRS

while avoiding complete adoption. That is fair value concept should be introduced in a separate

document as it is done in IFRS 13; depreciation approach should be reviewed for the assets retired

from the active use; recognition criteria for intangible assets should be changed; the concept of net

realizable value for inventories should be implemented.

13

CHAPTER I. COMPARISON OF THE REPORTING UNDER

INTERNATIONAL FINANCIAL REPORTING STANDARDS

AND BELARUSIAN GENERALLY ACCEPTED ACCOUNTING

PRINCIPLES

Belarus is continuing the convergence of the national accounting and auditing system with

international standards. Accounting and reporting act, which establishes a multi-level accounting

system was adopted, as well as the Act on Auditing.

The introductory period (1990-1994) was characterized by the development of national

approaches of the accounting standards in connection with the state formation.

The accounting methodology was actually tailored to the needs of the tax system. The

composition of the costs included in the cost of production (work delivery, service rendering) was

strictly regulated.

The core stage (1995 - 1998) began with the entry into legal force of the laws on accounting

and auditing. This stage was characterized by the emergence of a new level of regulation in

connection with the introduction of the concept of an accounting policy of the organization, as

well as a steady trend towards strengthening the fiscal function of accounting.

The system development stage (1999 - 2008) was associated with the need to unify the

legislations of Belarus and Russia in connection with the conclusion of the Treaty on the creation

of the Union State of Russia and Belarus. This event determined a significant impact of the Russian

accounting practice on the development of accounting in our country. There is a new type of

accounting – tax accounting. As a result, the fiscal accounting function has been decreased. At this

stage, two sets of accounting documents were adopted (for banks and for the corporate sector) and

a system of audit rules.

At the present stage (2009 - present), measures are being implemented for the adoption of

International Financial Reporting Standards (hereinafter – IFRS) in the territory of the Republic

of Belarus, enshrined in a number of policy documents. Our country has ratified three international

agreements, having committed to unify the rules of accounting for financial market participants.

Currently, the first and the main task is to introduce IFRS as technical regulatory legal acts.

The second task is the development of a system of national standards. The third task is to organize

certification with the subsequent issuance of certificates of professional accountants.

14

1.1 Property, plant and equipment

1.1.1 Recognition and measurement

According to Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012

№26 "Concerning approval of the instruction on PPE accounting" (hereinafter referred to as

Decree №26) assets are recognized as PPE if:

assets are intended for using in a company’s business activity (i.e. production, work

delivery, rendering of services, administrative needs or assignment for temporary use;

it is assumed that a company will receive economic benefits associated with the usage of

an asset;

the cost of an asset can be measured reliably.

assets are intended for use within more than 12 months;

a company doesn’t expect these assets to be sold within 12 months from the date of

acquisition;

All these requirements are mentioned on IAS 16 except the last one.

In Belarus PPE that are expected to be sold should be transferred to another account “Fixed

assets held for sale”.

Also, a company may define in its accounting policy a minimum threshold (amount of money)

for assets that are assumed to be recognized as PPE.

According to Decree №26 an item of PPE initially should be recorded at cost. The cost of

acquired PPE is the sum of actual:

cost of acquisition, included:

contractual value of PPE;

customs fees and duties;

loans interest;

freight insurance;

cost of services related to bringing an asset to “ready-for-use” condition;

other costs directly associated with acquisition, delivery, installation and assembly.

In addition to this in IAS 16 there is one more criterion:

the initial estimate of cost of dismantling and removing an item of fixed assets and restoration of

the area occupied by it an obligation for which a company assumes either when an asset is

15

acquired, or because of its use over a certain period for purposes other than the production of

inventories during that period1.

In Belarus this is not obligatory - a company has the right to include this estimated cost. For

this purpose, a provision should be created.

The initial cost of self-constructed assets is determined in the amount of actual direct and

variable indirect costs incurred during its construction2.

The cost of assets which were an owner’s capital contribution is determined based on an

estimate of their value made in accordance with the law.

The cost of donated assets is determined based on their fair value as of the recognition date.

If PPE was acquired in exchange for a non-monetary asset or combinations of monetary and

non-monetary assets its cost is measured as a value of these non-monetary assets according to

Decree №26 and as a fair value according to IAS16.

The cost of PPE identified during assets reconciliation is determined on the date of the

recognition based on documents confirming the price of similar assets (price lists, catalogs and

others), or based on valuation reports made by persons conducting valuation activities.

1.1.2 Subsequent measurement

1.1.2.1 Depreciation

In IFRS, depreciation of fixed assets is not described under a separate document and included

in IAS 16 and IAS 38. But for understanding of approaches we should also address to some other

standards of IFRS.

Determination of a depreciable item in IAS 16 based on the idea of recognizing an asset,

primarily as controlled by the company and bringing her economic benefits over a period of time.

Pursuant to paragraph 55 of IAS 16 depreciation begins when it is available for use, but not

when it is put for use as it is stated in Belarusian standard.

IFRS requires that the depreciable amount of an asset should be mandatory allocated on a

systematic basis over its useful life3. Hence, if an asset works and participates in a flow of

economic benefits, non-depreciation, as it is allowed by Belarusian legislation, is prohibited4.

1 Paragraph 16 of IAS 16 “Property, plant and equipment” of June 30th, 2014; paragraph 17.10 of IFRS for SMEs,

IASB, ed. 2015 2 Paragraph 10 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №26

"Concerning approval of the instruction on PPE accounting", paragraph 22 of of IAS 16 “Property, plant and

equipment” of June 30th, 2014 3 Paragraph 50 of IAS 16 “Property, plant and equipment” of June 30th, 2014; paragraph 17.16 of IFRS for SMEs,

IASB, ed. 2015 4 Resolution of the Council of Ministers of Belarus №802 ”On depreciation non-charging of PPE and intangible

assets in 2018 and further years” as of October 30, 2017

16

Depreciable amount is the cost of an asset less its residual value and as it was mentioned above

it should be allocated over an asset’s useful life. According to paragraph 51 of IAS 16 residual

value should be restated in the end of each financial year if an entity’s current expectations differ

from the previous evaluations. Using of a residual value is not a requirement but a recommendation

due to Belarusian accounting standards5.

Paragraph 55 of IAS 16 emphasizes that depreciation does not cease when an asset becomes

idle or retired from active use unless it is fully depreciated, except in the case when it is already

fully depreciated. Unlike Belarusian standards, IAS does not require to change source of

depreciation during repair, idle time, etc.

Useful life of an asset is determined in terms of expected utility of the asset and it is a matter

of professional judgement based on the entity’s experience with similar assets.

As an analogue of this rule in Belarusian accounting, to some extent, is considered a work of

a depreciation commission that is created to define an asset’s useful life. Initially the commission

should determine so called standard operation time using the Decree of the Ministry of Economics

as of 30.09.2011 №161 “On determining PPE’s standard operation time” (hereinafter Decree

№161). This document represents a list of tables with number of years assigned against each group

of assets. With the reference to this table the commission then define an asset’s useful life within

the prescribed range:

for buildings – 0.8-1.2 of the standard operation time;

for machines, mechanisms and equipment – 0.5-1.5 of the standard operation time;

computers – 0.5-1.5 of the standard operation time;

transport vehicles – 0.5-1.5 of the standard operation time6.

IAS 16 declares that the depreciation method used should reflect the scheme in which an asset’s

expected future economic benefits will be consumed. Herewith, p. 62 of IAS 16 offers to use the

straight-line method, the diminishing balance method and the units of production method.

National accounting standard disclose two additional methods – sum of years’ digits and

inversed sum of years’ digits methods.

The first method is an accelerated method that allows to depreciate and quickly replace an

asset which wears very fast and thus loses its productivity efficiency in the first years. Under this

method, a depreciation expense is computed by dividing the remaining useful life of an asset by

the sum of the useful life years’ digits and multiplying it by the carrying amount.

5 Paragraph 7-1 of Decree of the Ministry of Economics, Ministry of Finance, Ministry of Architecture № 37/18/6

“On depreciation of PPE and amortization of intagible assets” 6 Appendix 3 to Decree of the Ministry of Economics as of 30.09.2011 №161 “On determining PPE’s standard

operation time”

17

The inverse method of the sum digits is to determine the annual amount of depreciation based

on the depreciable amount of assets and the ratio, in the numerator of which is the difference

between the useful life and the number of years remaining until the end of the useful life, increased

by 1, and in the denominator - sum of numbers of years of useful life. At its core, the inverse

method of a slow depreciation, which in the first years of use of an item of fixed assets makes it

possible to charge minimum depreciation amounts with a gradual increase in subsequent years.

Upon that, the method applied is a subject to review at least each financial year-end7. If a

significant change is found in the expected consumption pattern of future economic benefits

embodied in the asset, this method should be adjusted to reflect this change. Such an adjustment

is should be accounted for as a change in an accounting estimate according to IAS 88.

Note that this does not mean that a company can change the depreciation method in order to affect

its financial results, as it is allowed in paragraph 46 of Decree № 37/18/6 “On depreciation of PPE

and amortization of intangible assets”.

According to this clause an entity has the right to change a depreciation method the straight-

line method in case of unforeseen changes in production conditions sales of goods, products,

services that causes losses.

In paragraph 43 of IAS 16, each component of an item of fixed assets, the cost of which is

significant compared to the total cost of the item, should be necessarily depreciated separately. In

Belarus, it is also possible to depreciate different parts of the same item at different useful lives.

Thus, in accordance with paragraph 6 of Decree №26, in the case if an item has several parts

with different useful lives, each such part is accounted for as an independent inventory item. But

in IFRS in books it is recognized as a unit item, not as separate ones.

Pursuant to Decree №26 an asset’s cost is not subject to change, except of the following cases:

revaluation of PPE;

impairment of PPE;

reconstruction (modernization, restoration) of PPE.

1.1.2.2 Revaluation

IFRS provide for two models of PPE carrying after its recognition: cost model and revaluation

model. According to the first model an entity’s PPE should be carried at its cost less depreciation

and impairment, but the second model requires to use a fair value instead of a cost9. Fair value is

7 Paragraph 61 of IAS 16 “Property, plant and equipment” of June 30th, 2014; paragraph 17.19 of IFRS for SMEs,

IASB, ed. 2015 8 Paragraph 32 of IAS 8 “Accounting Policies, Changes in Accounting Estimates and Errors” as of October 31st,

2018; paragraph 10.15 of IFRS for SMEs, IASB, ed. 2015 9 Paragraph 28 of IAS 16 “Property, plant and equipment” of June 30th, 2014; paragraph 17.15 of IFRS for SMEs,

IASB, ed. 2015

18

a market-based measurement that takes into account a market participant’s ability to generate

economic benefits by using the asset in its highest and best use. The highest and best use is

determined from the perspective of market participants that would be acquiring the asset, but the

starting point is the asset’s current use. It is presumed the current use is the asset’s highest

and best use, unless market or other factors suggest that a different use would be result in a

higher value10.

Contrary to IAS 16, Decree №26 does not allow an entity to choose either the cost or

revaluation model for carrying of PPE after a recognition11. According to Decree №26 it is

compulsory to revaluate the following classes of PPE: buildings, pipelines, electrical transmission

lines. It has to be done in case if a November’s inflation rate reaches the level of 100% to the last

mandatory revaluation date (last time it happened in January 2014)12. The current inflation rate

according to Statistics Committee is 57,8%13, which means that entities are not obliged to make a

revaluation, but they are eligible to make it on a voluntary basis – for the all entity’s PPEs or just

for a chosen group.

Under Presidential Decree №622 the following methods are used in the revaluation of an

organization’s property:

direct appraisal - recalculation of the value of PPE into prices for January 1 of the year

following the reporting year using documents prepared by an entity itself, or an entity

engaged in appraisal activities;

recalculation of foreign currency - restatement of the value of property in foreign currency

at the official rate of the National Bank as of December 31 of the reporting year;

index method - revaluation by the index method involves the calculation of the revalued

amount by multiplying the cost of the property recorded before the revaluation by the rate

of change in the value of PPE that is published by the National Statistical Committee of

the Republic of Belarus each January following the reporting date.

IAS16 allows using the following two methods for revaluation methods:

index method

write-off method.

Depending on the method chosen, the calculation and the reflection of the revaluation will

10 Paragraph 29 of IFRS 13 “Fair value measurement” of December 12th, 2013; paragraph 2.34 of IFRS for SMEs,

IASB, ed. 2015 11 Paragraph 10 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №26

"Concerning approval of the instruction on PPE accounting" 12 Paragraph 1.1.1 of Decree of the President of the Republic of Belarus of October 20th, 2006 №. 622 “Concerning

revaluation of fixed assets” 13 http://www.belstat.gov.by/ofitsialnaya-statistika/makroekonomika-i-okruzhayushchaya-sreda/tseny/operativnaya-

informatsiya_4/ob-urovne-inflyatsii/ob-urovne-inflyatsii-v-noyabre-2018-g-k-date-provedeniya-posledney-

pereotsenki/

19

differ.

Index method - according to it, the amount of accumulated depreciation (3) is recalculated in

proportion (1) to the change in the gross carrying amount of an asset (2), so that the carrying

amount after revaluation equals the revalued amount. This method is often used when an asset is

revalued using an index in order to determine its depreciable recoverable amount.

The following formulas are used:

𝐼𝑟 =𝐹𝑎𝑖𝑟 𝑣𝑎𝑙𝑢𝑒

𝐶𝑎𝑟𝑟𝑦𝑖𝑛𝑔 𝑎𝑚𝑜𝑢𝑛𝑡 (1)

𝐶𝑜𝑠𝑡𝑟 = 𝐶𝑜𝑠𝑡 × 𝐼𝑟 (2)

𝐴𝑐𝑐𝑢𝑚. 𝑑𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛𝑟 = 𝐴𝑐𝑐𝑢𝑚. 𝑑𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛 × 𝐼𝑟 (3)

Write-off method - its peculiarity is that it provides for the elimination of the accumulated

depreciation. The value of an asset obtained after this is revalued in such a way to make it equal

to the fair value. In other words, the cost becomes equal to the fair value, and the accumulated

depreciation becomes equal to zero. Mostly this method is used for revaluation of buildings.

IAS 16 does not require to involve a professional appraiser. The standard does not contain a

requirement for professional appraisal performed by an independent company or for engaging a

professional value for this purpose, although in practice entities often use professional appraisal

services14.

Revaluation frequency is not prescribed by IAS 16. The only requirement is that revaluations

should be made with sufficient regularity to ensure that the carrying amount does not differ

materially from the fair value at the end of the reporting period15.

The date of any voluntary revaluation in Belarus is only January 1 of the year following the

reporting year. A revaluation that is made in accounting more than once a year or on a different

reporting date contradicts the law16.

1.1.2.2 Impairment

Based on the concept of prudence in the process of accounting and the preparation of financial

statements, it is necessary to ensure that assets and revenues of an entity should not be

overestimated. To comply with this requirement in accordance with Decree № 26, an entity may,

based on a decision of its manager, reflect in books at the end of the reporting period the amount

of impairment of fixed assets. It must be equal to the amount of the excess of the carrying amount

14 E&Y LLP, Wiley,2016. International GAAP2016 under IFRS,p.1298 15 Paragraph 31 of IAS 16 “Property, plant and equipment” of June 30th, 2014;paragraph 17.15B of IFRS for SMEs,

IASB, ed. 2015 16 Paragraph 1.2 of Decree of the President of the Republic of Belarus of October 20th, 2006 №. 622 “Concerning

revaluation of fixed assets”

20

of an asset over its recoverable amount. This requires the availability of documentary evidence of

indication of impairment of the fixed asset and the possibility of reliable measurement of the

amount of impairment17.

Hence, recognition of impairment is a right in the Republic of Belarus, and not an obligation

for entities. This is a much more liberal approach than in IFRS, where testing of certain assets for

impairment is mandatory, and if there are relevant indicators, items should be accounted for at cost

less accumulated depreciation and accumulated impairment losses18.

In particular, paragraph 9 of IAS 36 "Impairment of Assets" (hereinafter - IAS 36) states that the

organization should assess at the end of each reporting period whether there are any indications of

impairment of assets. If any indication exists, the entity should estimate the asset's recoverable

amount.

In turn, in accordance with paragraph 63 of IAS 16, an entity applies IAS 36 to determine

whether an impairment has occurred with an item of PPE. This standard explains how an entity

analyzes the carrying amount of its assets, how it determines the recoverable amount of an asset

and when it recognizes or reverses impairment losses.

Based on the paragraph 16 of Decree № 26, and paragraph 12 of Decree №25 “On Accounting

of Investment Real Estate”, an entity should specify in its accounting policy whether it will apply

the procedure for impairment of assets. If impairment of assets is foreseen, then the accounting

policy should also disclose the procedure for determining of the discount rate.

International framework offers different ways for determining of discount rate if it is not

available at market. For instance, an entity could use its WACC, incremental borrowing rate or

other market rates19. Conversely, Decree №26 offers just one approach: using of key rate set by

the National Bank.

According to p. 16 of Decree № 26 the following indications should be considered in assessing

whether there is impairment (for the period from the beginning of the year to the reporting date):

a significant (more than 20%) decrease in the current market value of an asset;

significant changes in the technological, market, economic environment in which an entity

operates;

increase in market interest rates;

a significant change in the use of the asset;

physical damage;

17 Paragraph 16 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №26

"Concerning approval of the instruction on PPE accounting"; paragraph 17.24 of IFRS for SMEs, IASB, ed. 2015 18 Paragraph 30 of IAS 16 “Property, plant and equipment” of June 30th, 2014; "; paragraph 17.24 of IFRS for

SMEs, IASB, ed. 2015 19 Paragraph 57 of IAS 36 “Impairment of assets” of May 29th, 2013

21

other signs of impairment of the asset.

Notably, that these indications are almost the same we those described by p.12 IAS 36, but do

not include the indicator, when net assets of the company higher than market capitalization.

Obviously, it was missed because there are no capital markets in Belarus and only some companies

who are listed in foreign exchanges.

And the last indicator presented in this list makes a room for an accountant’s professional

judgement such as;

asset is idle, part of a restructuring or held for disposal;

worse economic performance than expected;

for investments in subsidiaries, joint ventures or associates, the carrying amount is higher

than the carrying amount of the investee's assets, or a dividend exceeds the total

comprehensive income of the investee, that were mentioned in IAS 36.

Decree № 26 does not specify which documents should confirm the presence of these

indications and how to evaluate the possibility of reliable assessment of the amount of impairment.

Apparently, the first issue should be enshrined in an accounting policy, and the second should be

determined by the professional judgment of an accountant.

A decrease in the current market value of an asset can be confirmed by the results of an

independent or internal assessment20.

Significant changes in the technological, market, economic environment in which the

organization operates, as well as the method of using the asset can be confirmed by referring to

business plans, production programs, management accounting data, decisions of the board of

directors etc.

If there are signs of impairment of the asset, its recoverable amount at the end of the reporting

period should be determined. It is the higher of the fair value of the asset, less the estimated costs

directly attributable to its sale, and the value in use of the asset21.

Value in use is the present (discounted) value of future cash flows from the use of the asset

and its disposal at the end of the useful life. It is calculated by multiplying the discounting rate and

the amount of future cash flows from the use of the asset. At the same time, future cash flows are

determined for the period not more than 5 years. The principle of calculating of value in use is the

same for IFRS and national accounting standards.

20 Paragraphs 5,8 of Decree of the President of the Republic of Belarus as of 13.10.2006 № 615 "On valuation

activity in the Republic of Belarus". 21 PwC LLP, Global Accounting services, 2016.Manual of accounting: IFRS 2017,p. 137, ISBN 978-0-7545-5439-4

22

1.1.2.3 Modernization, reconstruction, repair

Investments in the reconstruction, modernization or restoration of PPE are widely distributed

in a business practice of entities. The procedure for accounting and reporting of these capital

investments raises many questions both within the framework of Belarusian accounting standards,

and in the preparation of financial statements under IFRS.

IAS 16 does not describe specific criteria for qualifying costs associated with existing assets,

as capitalization costs for reconstruction, modernization or restoration. The concept of

reconstruction in IFRS does not exist as well.

Companies should be guided by the general rules for capitalizing expenses related

to fixed assets22, as well as requirements for the measuring of subsequent costs included in IAS

16. Thus, an entity should not recognize in the book value of PPE costs of day-to-day maintenance

of facilities, including the cost of repairs and routine maintenance23. However, in some cases,

subsequent costs associated with an asset might be capitalized, in particular, the cost of regularly

replacing parts of an asset, as well as the cost of regular major technical inspections necessary to

continue its operation. Moreover, the subsequent costs capitalization is possible only if the general

criteria for their recognition in the book value of the asset are met24:

likelihood of obtaining (increasing) future economic benefits associated with the item;

the possibility of a reliable measurement of the cost of the item.

The decision on whether costs met the capitalization criteria or not relates to the professional

judgment of an accountant, which can be based on information received from technical specialists,

calculations of the financial and economic departments regarding the economic efficiency of

investments made etc.

In contrast with international accounting rules Belarusian accounting legislation has a clearer line

regarding the concepts of such costs.

Indeed, the appendix №5 to the Decree №37/18/6 “On depreciation of PPE and amortization of

intangible assets” provides the following definitions:

repair - a set of actions which is intended to restore the correct functioning or operability

of an item (or its parts with bringing the item into compliance with the requirements defined

by technical regulatory legal acts) as well as to prevent their further intensive wear and

tear;

modernization - a set of works to improve the item by replacing its structural elements and

22 Paragraph 4.3 of “Conceptual Framework for financial reporting” issued by IASB, March 2018 23 Paragraph 12 of IAS 16 “Property, plant and equipment” of June 30th, 2014; "; paragraph 17.15 of IFRS for

SMEs, IASB, ed. 2015 24 Paragraphs 7, 13, 14 of IAS 16 “Property, plant and equipment” of June 30th, 2014

23

systems with more efficient ones, leading to an increase in the technical level and economic

characteristics of the item.

In accordance with paragraph 20 of the Decree № 26, actual costs associated with the

reconstruction (modernization, restoration) of PPE, and other similar works are included in its

costs.

Hence, we can find the main difference in two approaches: IFRS allows in some circumstances

to capitalize costs related to repair of an asset whereas national BY GAAP prohibit it and capitalize

only those costs, which improve the characteristics of the asset.

1.1.3 Derecognition and disposal

In IAS16 derecognition of an item takes place when:

it is disposed;

no future economic benefits are expected from its use.

Gain or loss arising from derecognition of an item of PPE is included in profit or loss at the

time of derecognition of the item.

If PPE that is to be derecognized contains precious metals, then they must be collected and

recognized in the manner prescribed by Decree № 34 “Concerning use of precious metals and

stones”.

Thus, the value of PPE containing precious metals (precious stones), during its transfer or sale

must not be lower than the cost of the precious metals (precious stones) contained in it, calculated

at prices of the first day of month when these assets were derecognized.

When an asset is disposed the value of precious metals it contains should be recognized as a

current asset and a profit from this disposal is recognized as well. Afterwards precious metals

should be sold to the state25.

Accumulated depreciation is eliminated against an asset’s cost and if there is revalue surplus

it should go to retained earnings – these principles are the same for both IFRS and Belarusian BY

GAAP.

1.2 Intangible assets

1.2.1 Recognition and measurement

The procedure of recognition of intangible assets in entities is determined by the Decree of the

Ministry of Finance of the Republic of Belarus of April 30th, 2012 №25 " Concerning approval of

25 Paragraphs 71,75 of Decree № 34 “Concerning use of precious metals and stones” of March 15 th, 2004.

24

the instruction on intangible assets accounting" (hereinafter referred to as Decree №26). For

accounting purposes assets are recognized as intangible assets by a company if they do not have a

physical form and when certain criteria are met:

they must be identifiable, i.e. separable from other assets of an entity;

it is assumed that a company will receive economic benefits associated with the usage of

an asset and is able to block access of others to these benefits;

cost of an asset can be measured reliably;

assets over a period of more than 12 months;

an entity does not expect assets to be sold within 12 months from the date of the acquisition.

All these requirements except the last two we can find in IAS 38 “Intangible assets”. The list

of items that can be accounted as intangible assets of an entity in accordance with the Belarusian

legislation differs from that under IFRS. According to IAS 38, these include trademarks, brand

names, software, licenses and franchises, copyrights, patents and other industrial property rights,

service and maintenance rights, recipes, formulas etc.

In Decree № 25 trademarks, trade names are excluded from the list of possible items of

intangible assets.

IAS 38 applies for costs incurred on advertising, development training, and start-up research

expenses. Assets obtained under a finance lease agreement may also be intangible if the terms for

acquisition were more favorable than market terms. These items are also not mentioned as possible

intangible assets in Decree № 25. Such a restriction of the range of assets that may be considered

as intangible may lead to an underestimation of value of assets of an enterprise as when it is sold

to external investors26.

Also, Belarusian standard requires an entity that created an item of intangible assets to have

documents confirming the ownership (patents, certificates)27, while IAS 38 (paragraph 13) states

that legal enforceability of the right is an optional condition for control28.

In practice, these documents become the main obstacle to the reliable accounting of the main

part of intangible assets - intellectual property rights. Because all the documents noted in the decree

except just one (brand registration certificate) are not right stating documents. As a result, there

may be errors in accounting for intangible assets, its amortization, tax calculation, nullity of license

agreements and alienation of property rights.

From the standpoint of accounting, the main problem that one has to face in practice is a legal

paperwork related to confirmation of existence of an asset itself. To properly qualify these

26 Zubkov A.S., 2017 Changing the value of intangible assets. Glavnaya kniga, 24, p. 5 27 Paragraph 9 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №25

"Concerning approval of the instruction on intangible assets accounting" 28 Paragraph 13 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.16 IFRS for SMEs, IASB, ed. 2015

25

documents, you must have sufficient legal knowledge in the field of copyright and patent law. The

lack of this knowledge among practicing accountants causes difficulties in deciding on the

allocation of costs for the acquisition of an asset that does not have a tangible form29.

Contrary to Belarussian accounting, the structure of costs that can be allocated to intangible

assets on its initial measurement depends on the method of acquisition of intangible assets.

Unlike this rule, Decree №25 states that an intangible asset should be measured at its cost on

initial recognition i.e.:

acquisition cost of intangible assets;

customs fees and duties;

interest on loans and borrowings;

the cost of the services of other persons related to bringing intangible assets into a condition

suitable for use;

other costs directly related to the acquisition of intangible assets and bringing them into a

condition suitable for use30.

All these costs are similar to those mentioned in IAS 38 for separate acquisition cases. In

addition to it, acquisitions can be made through business combinations, government grants,

exchange of assets or internal generation. When an item acquired as a result of a business

combination or an asset exchange, it is measured at fair value. When an item of intangible assets

was internally generated an entity needs to assess whether the item meets the requirements for

recognition by classifying the process of its generation into two phases31:

research;

development.

Research refers to planned work aimed at obtaining new scientific and technical knowledge,

activities on application of the results, as well as the search for alternative materials, devices,

products, processes, systems, services, etc.

Costs incurred at the research phase are not capitalized but are recognized as expenses during

the period in which they were incurred, because at the research phase a company cannot

demonstrate assurance in receiving future economic benefits32.

Development - the application of research results in manufacturing engineering, new or

significantly improved materials, products, etc. before the start of their commercial production.

The costs incurring at the development stage are associated with the design, construction and

29 Zubkov A.S., 2017 Changing the value of intangible assets. Glavnaya kniga, 24, p. 5 30 Paragraph 13 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №25

"Concerning approval of the instruction on intangible assets accounting" 31 Paragraph 52 of IAS 38 “Intangible assets” of May 12th, 2014;paragraph 18.14 IFRS for SMEs, IASB, ed. 2015 32 Paragraph 54 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.15 IFRS for SMEs, IASB, ed. 2015

26

testing of experimental samples of products, which, due to their scale, are not suitable for

commercial use. These costs may be considered as components of the value of intangible assets

when the following conditions are met33:

the creation of an intangible asset is technically feasible, an entity plans to complete the

development phase and has resources for this;

created asset can be used by an entity or be sold;

there is a rationale for how the company will receive economic benefits from an asset;

the cost of creating an asset during the development phase can be reliably measured.

All costs incurred prior to the fulfillment of the above conditions and written off for the

expenses of the period cannot be recovered and included in the value of an asset.

1.2.2 Subsequent measurement

1.2.2.1 Amortisation

In IAS 38 useful life is generally defined in the same way as the useful life of PPE in IAS 16.

Under IAS 38, the useful life is:

the period during which an asset is expected to be available for use by an entity; or

the number of units of production or similar units that an entity expects to receive from the

use of an asset.

In accordance with IAS 38, when assessing the useful life of an intangible asset, many factors

should be taken into account, among which are:

the expected use of an asset by a company;

typical asset life cycle for an asset and publicly available information on estimates of useful

lives of similar assets that are operated in the same way;

technical, technological, commercial and other types of asset obsolescence;

the stability of the industry in which the asset is involved, and changes in market demand

for products or services produced using the asset;

expected actions of competitors (including potential competitors);

the period of control over an asset, legal or other restrictions on the use of the asset;

dependence of the useful life of a relevant asset on the useful life of the other assets of an

entity.

As already noted, IAS 38 does not provide any mandatory requirements regarding useful usage

of intangible assets for more than 12 months. This is due to the fact that the use of such intangible

33 Paragraph 57 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.17 IFRS for SMEs, IASB, ed. 2015

27

assets such as new technologies and software may be short due to their rapid obsolescence. The

maximum useful life is also not limited.

IAS 38 regulates the regular revision of the useful life of intangible assets at least once at the

end of each reporting year34.

This international standard provides several methods for the amortisation of intangible assets.

Method that is used must comply with the scheme of obtaining economic benefits from the item

of intangible assets. IAS 38 recommends the following methods for the depreciation of intangible

assets:

straight-line method;

diminishing balance method;

units of production method.

The listed methods do not differ from the depreciation methods for fixed assets, therefore, they

do not require separate clarification.

For intangible assets with an indefinite useful life amortisation is not charged. Goodwill is also

not amortised when purchase price of the acquisition exceeds the fair value of the assets and

liabilities acquired.

IAS 38 necessitate to revise the method of amortisation of intangible assets at least once at the

end of each fiscal year. If there has been a significant change in the pattern of economic benefits

from an asset, the amortisation method needs to be changed.

Depreciable amount under IAS 38 is equal to the original (or revalued) value of an item,

reduced by its residual value. Residual value is defined in IAS 38 as the estimated amount that an

entity would have received from the disposal of an asset after deducting the estimated costs of

disposal.

Residual value of an intangible asset under IAS 38 differs from zero only if an entity intends

to sell an asset at the end of its useful life. Residual value should be reviewed at least at the end

of each fiscal year35.

Amortisation should begin from the moment when an intangible asset becomes available for

use, i.e. when its location and condition provide the possibility of its use in accordance with the

intentions of the management of a company. Amortisation should cease at the earlier of the two

dates:

the date when the asset is classified as held for sale (or included in a disposal group

classified as held for sale) in accordance with IFRS 5;

at the date of its derecognition.

34 Paragraph104 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.21 IFRS for SMEs, IASB, ed. 2015 35 Paragraph102 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.20 IFRS for SMEs, IASB, ed. 2015

28

Decree № 37/18/6, in contrast to IAS 38 for intangible assets, establishes a useful life of at

least 12 months. At the same time, contrary to this international standard, the Belarusian regulation

does not require an annual check on the useful life of intangible assets, but it can be reviewed if

an asset’s functioning is prolonged or resumed36. The factors that should be taken into account in

Decree № 37/18/6 when assessing the useful life of intangible assets are not clearly described as

it done in IAS 38. According to the Belarusian act, the useful life of these assets is determined

based on the following:

expected physical wear and tear, depending on conditions of production: operating mode

(number of shifts), environmental impact;

obsolescence as a result of increase in efficiency of newly introduced similar assets;

restrictions on the use of an asset.

The decision is made by the depreciation commission based on the specified conditions,

reproduction needs, approved business plans, plans for technological renewal and restructuring of

production, established competitiveness of goods, products, works, services. Obviously, the list of

factors listed in IAS 38 is much wider than that presented in Decree № 37/18/6.

Moreover, the Decree put limits on maximum useful life duration of different groups of

assets37:

intellectual property designations – up to 40 years;

for industrial property rights – up to 20 years;

other intangible assets – up to 10 years.

The methods of amortisation calculation of intangible assets correspond to the methods

prescribed by IAS 38. Unlike the international standard, the Decree does not require to revise the

method of amortisation of intangible assets.

The procedure for evaluation of the depreciable amount of intangible assets in domestic and

international standards is somewhat different. Decree № 37/18/6 does not include residual value

(which is used in IAS 38) when calculating the depreciable amount. In this regard, the amount of

amortisation of intangible assets calculated in accordance with Belarusian accounting standard

may be higher than the amount of amortisation defined in accordance with IAS 38.

There is no indefinite useful life duration mentioned in Decree № 37/18/6, which means that

every item of intangible asset should be amortised all other conditions being equal.

In IFRS and national accounting standards, the dates of beginning and cease of the amortization

36 Paragraph 24 of Decree of the Ministry of Economics, Ministry of Finance, Ministry of Architecture № 37/18/6

“On depreciation of PPE and amortization of intagible assets” 37 Paragraph 20 of Decree of the Ministry of Economics, Ministry of Finance, Ministry of Architecture № 37/18/6

“On depreciation of PPE and amortization of intagible assets”

29

of intangible assets do not coincide. In contrast to IAS 38 for Decree № 37/18/6, amortisation

starts on the 1st day of the month following the month when these assets are booked (and not from

the moment when these intangible assets become available for use). Amortisation of intangible

assets according to Decree № 37/18/6 cease from the 1st day of the month following the month of

full amortisation or derecognition of these assets from accounting (and not earlier than two dates:

a) on the date of classification of these assets as held for sale or b) on the date of their derecognition

- as provided for by IAS 38).

1.2.2.2 Revaluation

According to paragraph 17 of Decree №25, cost of intangible assets is not subject to change,

except for cases established by law. Decree № 25 discloses one of the cases of change in the initial

value of these assets, namely, their revaluation at the current market value when it can be reliably

measured from the active market data of these assets.

To carry out revaluation of intangible assets in Belarus in practice is hard if not impossible

due to immaturity of the market for the vast majority of intangible assets. The reasons for this lie

in some types of intangible assets, and in the insufficiency of the number of producers for these

types of assets. Intangible assets items such as copyright, as well as items of industrial property

law (inventions, industrial designs, production secrets, etc.), The results of scientific and technical

activities have unique characteristics, are made in single copies and can not be repeated in other

assets of this type. The market for these assets is represented by single copies of the product and

operates in the absence of competition or slight competition. Thus, pricing of assets of this type

can not be of a market nature, where the ratio of supply and demand is crucial38.

Some types of intangible assets, such as computer software and databases, are represented on

the market by several development companies. However, at present, the market for each type of

software is controlled by certain companies. Prices in such conditions are not determined by the

influence of market factors but are set by developers on a cost basis and are often tied to the dollar

(euro) rate. Therefore, their value remains relatively stable and changes mainly with the change in

the exchange rate of the national currency. As a result, the revaluation of intangible assets at market

value is also virtually impossible.

Similar to IAS 16, IAS 38 allows companies to use to model after recognition39:

cost model;

revaluation model.

38 Zubkov A.S., 2017 Changing the value of intangible assets. Glavnaya kniga, 24, p. 5 39 Paragraph 74 of IAS 38 “Intangible assets” of May 12th, 2014

30

If revaluation model is chosen, an asset should be carried at a revalued amount, which is fair

value less any accumulated amortisation and impairment loss. The frequency is not prescribed, but

it is required to perform revaluations that by the end of reporting year an asset carrying amount

would not differ materially from its fair value40. Belarusian standard allows to revalue assets just

once per year.

1.2.2.3 Impairment

Based on the principle of prudence41 in the process of accounting and the preparation of

financial statements it is necessary to ensure that the accounting estimate of the assets and income

of an organization is not overstated.

In order to comply with this requirement under BY GAAP, an organization is entitled, on the

basis of a decision of its manager, to recognize at the end of the reporting period the amount of

impairment of intangible assets42. It must be equal to the amount of the excess of the residual value

of the asset over its recoverable amount. This requires the availability of documentary evidence of

indicators of impairment of the asset and the ability to reliably determine the amount of the

impairment.

Thus, recognition of impairment is a right in the Republic of Belarus, and not an obligation

for organizations. This is a much more liberal approach than in International Financial Reporting

Standards, where testing certain assets for impairment is mandatory, and if there are relevant

indicators, PPE and intangible assets, should be accounted for at cost less accumulated

depreciation impairment losses.

In particular, paragraph 9 of IAS 36 specifies that an entity should assess at the end of each

reporting period whether there are any signs of impairment of assets. If any such indication

exists, the entity must estimate the asset's recoverable amount.

Regardless of whether there are any indications of impairment, the entity also43:

tests an intangible asset with an indefinite useful life or an intangible asset that is not yet

ready for use for impairment annually by comparing its book value with the recoverable

amount.

This impairment test may be carried out at any time during the annual period, provided that it is

held at the same time every year. Various intangible assets can be tested for impairment at different

40 Paragraph 75 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 18.21 IFRS for SMEs, IASB, ed. 2015 41 Paragraph 2.16 of “Conceptual Framework for financial reporting” issued by IASB, March 2018; section 3,

paragraph 8 of “Accounting and reporting Act” of July 12th 2013 57-Z 42 Paragraph 18 of Decree of the Ministry of Finance of the Republic of Belarus of April 30th, 2012 №25

"Concerning approval of the instruction on intangible assets accounting" 43 Paragraph 10 of IAS 36 “Impairment of assets” of May 29th, 2013; paragraph 27.7 IFRS for SMEs, IASB, ed.

2015

31

times. However, if such an intangible asset was initially recognized during the current annual

period, then it should be tested for impairment before the end of the current annual period;

tests goodwill acquired in a business combination for impairment annually.

In IAS 36, it is noted that the ability of an intangible asset to produce future economic benefits

in an amount sufficient to recover its carrying amount is usually subject to greater uncertainty

before the asset is started to be used than after the start of its use. Therefore, IAS 36 prescribes that

an entity should conduct an impairment test at least once a year for the carrying amount of an

intangible asset that is not yet ready for use44.

A company under IFRS framework should test an intangible asset with an indefinite useful life

for impairment by comparing its recoverable amount with its book value annually, as well as every

time when there are indications of a possible impairment of the intangible asset45.

Under BY GAAP an entity should specify in its accounting policy whether it will apply the

asset depreciation procedure. If impairment of assets is foreseen, then the accounting policy should

also indicate the procedure for determining the discount rate.

If there are indications of impairment, a recoverable amount of an item of intangible assets at

the end of the reporting period is determined as the higher of the current market value of the item

less the estimated costs directly related to its sell and the value in use.

The calculation of value in use is similar to that, described in the chapter 1.1.2.2, hence, there

is no need for the further clarification.

1.2.3 Goodwill

Belarusian legislation did not define goodwill before January 1st, 2015, when National

Standard №46 “Consolidated financial statement” (hereinafter - Standard №46) was implemented.

In the previous years accountants did not have the opportunity to recognize goodwill as a separate

item of financial statement.

This standard defines goodwill as an asset arising at the date of acquisition in the amount of

excess of investments of a parent company in the authorized capital of a subsidiary or associated

company over the value of the share capital of a subsidiary or associated company owned by the

parent company46.

According to paragraph 13 of Standard №46, goodwill is included in the consolidated

statement as an item of fixed assets.

44 Paragraph 11 of IAS 36 “Impairment of assets” of May 29th, 2013; paragraph 27.10 IFRS for SMEs, IASB, ed.

2015 45 Paragraph 108 of IAS 38 “Intangible assets” of May 12th, 2014; paragraph 27.9 IFRS for SMEs, IASB, ed. 2015 46 Paragraph 2 of National Standard №46 issued by the Ministry of Finance of the Republic of Belarus of June 30th,

2014

32

Under IFRS there are two standards that define the treatment of goodwill. IFRS 3 “Business

combinations” defines goodwill as an asset representing the future economic benefits arising

from other assets acquired in a business combination that are not individually identified and

separately recognized47. This standard sets out the principles on the recognition and measurement

of assets and liabilities acquired through a business combination and the determination of

goodwill. It requires an acquirer to recognize goodwill as the difference between:

the aggregate of: the consideration transferred measured in accordance with this IFRS,

which generally requires acquisition‑date fair value; the amount of any non‑controlling

interest in the acquire measured in accordance with this IFRS; and in a business

combination achieved in stages, the acquisition‑date fair value of the acquirer’s previously

held equity interest in the acquiree.

the net of the acquisition‑date amounts of the identify able assets acquired and the

liabilities assumed measured in accordance with this IFRS.

1.2.4 Derecognition and disposal

According to paragraph 112 of IAS 38 an intangible asset should be derecognized in two

cases: on its disposal or when the future economic benefits from the use of an asset are not expected

anymore.

As for Decree № 25 – it does not provide the clear situations as it is done in IAS 38, but it

establishes forms of different source documents that should be used when an item of intangible

assets is disposed, swelled or donated. Thus, it is put an emphasis on the documentation, but not

on disclosure or providing a guideline for accountants.

As a result, we can imagine a situation when an entity under IFRS should derecognize an asset

because it does not provide the company with economic benefits whereas under BY GAAP is not

required to derecognize the asset because expectation of economic benefits is an initial recognition

criterion, but it does note arise from the absence of this criteria in the future that an entity must

derecognize such a type of assets.

1.3 Inventories

1.3.1 Recognition and measurement

Inventories are a critical component of the accounting records of commercial organizations

engaged in the production and sale of products. Their assessment as an element of the

47 Appendix A to IFRS 3 “Business combinations” of October 22nd, 2018

33

organization’s current assets is taken into account when determining its solvency. The higher the

estimate of inventories recognized in a balance sheet asset, the higher a current liquidity ratio,

which is calculated as the ratio of the entity’s current assets to its current liabilities. The greater its

value, the more solvent in the eyes of stockholders is the reporting entity.

On the other hand, the accounting methodology for assessing a company’s inventories has an

impact on the users' impression of the profitability of a business entity. From this point of view,

the cost of inventories is the capitalized expenses of the entity, which form the financial result of

the reporting period at the time of their decapitalization, that is, the write-off when sales are

booked.

The change in the value of the financial result (profit or loss), that is visible to users of

financial reports, forms the opinion of the users on the profitability of the entity. After all,

profitability indicators are calculated by comparing the amount of profit with a number of

indicators: WACC, costs, revenue, equity and others.

The volume of capitalization and decapitalization of costs for the purchase (creation) of an

entity’s inventories depends on the methods of allocating costs, which are determined by its

accounting policy regarding the accounting of the entity’s inventories48.

In formulating its main objective, IAS 2 indicates that the main issue in inventory accounting

is to determine the amount of costs to be recognized as an asset and transferred to the next reporting

periods before recognizing the corresponding revenue. This means that eventually, the meaning of

all accounting methodologies in the field of inventory accounting is to distribute the costs incurred

by an entity for the purchase (creation) of stocks between the balance sheet (capitalized part that

does not decrease the profit of the reporting period) and the profit and loss statement (the

decapitalized part, which forms the profit of the reporting period). This decision determines the

values of analytical indicators to assess profitability and solvency.

An important point in applying the requirements of IAS 2 is to determine its scope. First of all,

IAS 2 defines the concept of inventories. According to IAS 2, stocks are defined as assets49:

intended for sale during the main activity of the company;

created in the course of production for sale during the main activity of the company;

representing raw materials or materials intended for use in the production process or in the

rendering of services.

Compliance with at least one of the criteria, mentioned above, allows the relevant asset to be

classified as inventories.

48 Bancevich E.E., 2014 Inventories in IFRS. Ilex, 35, p.8 49 Paragraph 6 of IAS 2 “Inventories” of December 18th, 2003; paragraph 13.1 IFRS for SMEs, IASB, ed. 2015

34

IAS 2 states that inventories acquired also include items purchased for resale. These include,

for example, goods purchased by a retailer, or land and other property held for resale. Inventories

also include work in progress, produced by an entity, raw materials and materials intended for

further use in the production process. In service companies, inventory includes the cost of unsold

services, that is, those for which the entity has not yet recognized the related revenue.

Along with the special definition of the term “inventories”, IAS 2 separately introduces two

concepts: “net realisable value” and “fair value”.

According to IAS 2, the net realisable value of inventories is the estimated selling price in the

normal course of business less selling costs50.

The fair value of inventories is the amount by which an asset can be exchanged, or an

obligation settled when a transaction is made between well-informed, willing to make such a

transaction and independent from each other parties.

Two separate definitions of these concepts in the text of IAS 2 indicates that the net realisable

value of inventories may not be equal to their fair value less costs to sell. The fact is that the net

realisable value is related to the net amount that an entity expects to receive from the sale of stocks

in the course of normal activities, that is, is determined by management decisions of a particular

company. The fair value of inventories reflects the amount for which it is theoretically possible to

exchange similar stocks in a transaction between well-informed, willing buyers and sellers in the

market to make such a deal.

IAS 2 establishes a general rule that an entity’s inventories should be booked at the lower of

two values: cost and net realisable value51. According to IAS 2, the cost of inventories includes all

the acquisition costs, processing and other costs incurred in order to bring the stocks to their current

condition and place. Thus, the idea of determining the cost is to calculate the full

amount of costs incurred to purchase or produce an item of assets, attributable to inventories. The

cost of an entity’s acquisition of inventory in IAS 2 may include their purchase price, import

customs duties and other taxes (except those that are later refunded to companies by tax authorities,

such as VAT in domestic taxation practices), as well as the costs of transportation, processing and

other costs directly related to the acquisition of the item.

Defining the accounting treatment for the cost of inventory conversion, IAS 2 sets the rules

for capitalization and decapitalization of fixed and variable, direct and indirect costs associated

with the production and processing of stocks.

According to IAS 2, fixed overhead production costs are those indirect production costs that

remain relatively constant regardless of the volume of production, such as depreciation and