Bahasa

Halaman

Hukum

Electronic copy available at: http://ssrn.com/abstract=1963023

Innovative Capacity and the Asset Growth Anomaly*

Praveen Kumara Dongmei Lib

Abstract

Innovative capacity (IC) is the ability of firms to produce and commercialize a sequence of

innovations. Expected returns need not fall following asset growth by high IC firms because

investment can generate new growth options. Using patent intensity based IC measures we

provide the first analysis of the effects of IC on financial markets' response to asset growth. We

find that the well-known negative relation between asset growth and subsequent excess returns

holds only for firms with high asset growth and low IC and does so in a stronger and more robust

fashion than reported earlier. However, high IC firms with high asset growth not only do not

suffer negative excess returns but actually earn significantly positive subsequent excess returns.

Moreover, and as predicted by a model of optimal dynamic investment with sequentially arising

growth options, changes in the market risk loadings of firms following asset growth episodes are

positively related to their IC. The innovative capacity of firms, therefore, appears to play an

important role in the dynamics between their asset growth and returns, and in driving their time-

varying market risk.

* We thank Jonathan Berk, Wayne Ferson, Michael Fishman, Paolo Fulghieri, Richard Green, Dirk Hackbarth, David Hirshleifer, Kewei Hou, Ravi Jagannathan, Dirk Jenter, Nisan Langberg, Michael Lemmon, Jeremy Stein, Sheridan Titman, and Jianfeng Yu for valuable discussions and comments. We also thank Lu Zhang for sharing the investment and profitability factors returns.

a C.T. Bauer College of Business, University of Houston, Houston, TX 77204. Email: [email protected] b Rady School of Management, University of California, San Diego, La Jolla, CA 92093. Email: [email protected]

Electronic copy available at: http://ssrn.com/abstract=1963023

Innovative Capacity and the Asset Growth Anomaly

January 2012

Abstract

Innovative capacity (IC) is the ability of firms to produce and commercialize a sequence of

innovations. Expected returns need not fall following asset growth by high IC firms because

investment can generate new growth options. Using patent intensity based IC measures we

provide the first analysis of the effects of IC on financial markets' response to asset growth. We

find that the well-known negative relation between asset growth and subsequent excess returns

holds only for firms with high asset growth and low IC and does so in a stronger and more robust

fashion than reported earlier. However, high IC firms with high asset growth not only do not

suffer negative excess returns but actually earn significantly positive subsequent excess returns.

Moreover, and as predicted by a model of optimal dynamic investment with sequentially arising

growth options, changes in the market risk loadings of firms following asset growth episodes are

positively related to their IC. The innovative capacity of firms, therefore, appears to play an

important role in the dynamics between their asset growth and returns, and in driving their time-

varying market risk.

Keywords: Innovative capacity; Asset growth; Excess returns; Risk dynamics; Patents

JEL classification codes: G12, G32, O31

1

1. Introduction

The effects of capital investment and asset growth on stock returns have important

implications for both asset pricing and corporate finance. Recently, a number of empirical

studies highlight a negative relation between firms’ asset growth and subsequent abnormal stock

returns ─ the “asset growth anomaly” (Titman, Wei, and Xie, 2004; Anderson and Garcia-Feijoo,

2006; Cooper, Gulen, and Schill, 2008).1 In particular, Titman et al. (2004) document a negative

relation between large increases in capital investment and subsequent benchmark-adjusted

returns, and Cooper et al. (2008) show that this relation extends to the growth in total assets.

The asset growth anomaly has generated both behavioral and risk-based explanations. For

example, Titman et al. (2004) argue that investors underreact to empire building by managers

and show that the negative relation between capital investment and subsequent abnormal returns

is stronger for firms with greater investment discretion (i.e., firms with higher cash flows and

lower debt ratios), while Cooper et al. (2008) suggest an overreaction to asset growth and

interpret the negative abnormal returns as a correction to the initial overreaction. On the other

hand, a variety of models in the literature predict a negative equilibrium relation between

investment and future returns. In particular, real options models (e.g., McDonald and Siegel,

1986; Majd and Pindyck, 1987; Carlson, Fisher, and Giammarino, 2006) predict a decline in

systematic risk following the exercise of risky growth options. From this perspective, the

observed relation between asset growth and subsequent returns is not an anomaly and indeed a

number of recent papers present direct evidence supportive of the risk-based explanations (see

Cooper and Priestly, 2011). These alternative interpretations of the data have profoundly

1 Other studies on the asset growth anomaly include Xing (2008), Li and Zhang (2010), Titman, Wei, and Xie (2011), Lam and Wei (2011), Stambaugh, Yu, and Yuan (2011), and Watanabe et al. (2011), among others.

2

different implications. In particular, a systematic negative bias in the market's capitalization of

asset growth should have a major impact on corporate investment and financial policies; it also

suggests formulation of trading strategies to exploit this market inefficiency.

In this paper, we present new evidence on the dynamics between asset growth and stock

returns by building on the notion of innovative capacity (IC), which is a measure of firms' ability

to generate multiple growth options ─ for example, through a sequence of innovations based on

their patent holdings. We motivate the role of IC by noting the potential heterogeneity in the

effects of asset growth across different IC firms. Specifically, asset growth of high IC firms is

more likely related to innovation activities, such as construction of long-range research facilities

and purchase of machinery/materials for use on current and future R&D projects, or acquisition

of patents, or development of knowledge absorption capacities. This type of asset growth tends

to generate new growth options and investment opportunities because innovations are often the

source of new ideas and opportunities (Schumpeter, 1942; Maclaurin, 1953). In contrast, the

asset growth of low IC firms is more likely to reflect capital expenditures in traditional industries

where investment converts growth options to assets-in-place and lowers risk.

To fix ideas, consider a firm that has developed an innovation ─ for example, a new

smart-phone operating system or a new class of drugs or a more powerful resonance imaging

system ─ that potentially opens long run economic opportunities through multiple improvements

(“new generations”) of the basic innovation and creation of ancillary and support industries.

However, these new growth opportunities arise only if the firm maintains a technological lead

over imitators or rival technologies, which requires an effective innovation generation

3

infrastructure and additional investments over time.2 High IC firms with low asset growth may

therefore obtain only the benefits of the initial innovation, but high IC firms with high asset

growth will have the opportunity to generate and exploit new growth opportunities.

In sum, from the real options viewpoint, the predicted effects of asset growth on

subsequent expected returns should differ according to firms’ IC. Specifically, if the asset growth

of low IC firms mainly converts growth options to assets-in-place, then it should reduce the risk

premium or expected returns. In contrast, if the rapid asset growth of high IC firms is a precursor

to the generation of future growth options, then the expected returns should not subsequently

decline and may even rise. Meanwhile, from the behavioral viewpoint, mispricing of asset

growth may differ across IC groups if there is a negative correlation between IC and investment

discretion, or if there is a negative correlation between IC and valuation uncertainty since

psychological biases appear to be stronger among firms that are harder to value (e.g., Daniel,

Hirshleifer, and Subrahmanyam, 1998; Kumar, 2009). Therefore, examining the effects of IC on

the relation between asset growth and subsequent returns is of substantial interest from both the

rational and behavioral perspectives.

Building on the large literature that uses patent holdings as a measure of firms’ inventive

activity and available growth options (e.g., Pakes, 1986; Griliches, Hall, and Pakes, 1991), we

use patent intensity based measures of IC (i.e., recent annual patents granted to a firm normalized

by various measures of assets) for this study. To our knowledge, this is the first study of the

2 For instance, when a firm builds a laboratory or invests in technological infrastructure to enhance knowledge absorption capacities (Cohen and Levinthal, 1990), the fixed cost is capitalized and reflected as asset growth; yet, the firm is not exercising a pure growth option, but is setting up a generator of future growth options.

4

effects of innovative capacity on the response of financial markets to investment and asset

growth. We summarize the results of our analysis as follows.

Firms’ innovative capacity plays an important role in the asset growth anomaly. While

we confirm the negative correlation between asset growth and subsequent abnormal returns for

the overall sample, we find that this anomaly holds only for the subset of firms that exhibit high

asset growth and have low IC; i.e., the asset growth anomaly is essentially restricted to firms that

have low innovative capacity and exhibit high asset growth. Indeed, the asset growth anomaly

for the low IC firms is stronger and more robust to risk-adjustment than has been reported in the

literature (e.g., Cooper et al., 2008). On the other hand, for high IC firms with rapid asset growth

not only is there no significantly negative relation with subsequent abnormal returns, but we find

significantly positive abnormal returns in the fourth and fifth year after the asset growth events.

These results, which are based on independent (double) sorts of IC measures and asset growth,

are robust to benchmarking with the Fama and French (1992, 1993) three-factor model, the

Carhart (1997) four-factor model, and the investment-based three-factor model of Chen, Novy-

Marx, and Zhang (2011).

The positive influence of IC on the post-asset growth abnormal returns is confirmed by

the Fama-MacBeth (1973) regressions. For example, in the year after investment, higher patent

intensity dilutes significantly the negative effects of asset growth on subsequent returns

controlling for firms’ characteristics. In sum, the stylized fact of a negative relation between

asset growth and subsequent abnormal stock returns ─ that we confirm for our overall sample ─

masks considerable heterogeneity in the data, with the innovative capacity of firms playing an

important role.

5

These results are of interest from both the behavioral and rational perspectives. From the

behavioral viewpoint, our analysis indicates that the market appears to have a persistent or

systematic mispricing problem in evaluating high asset growth by low IC firms. But since

Titman et al. (2004) argue that the asset growth anomaly is consistent with investors’

underreaction to managers’ empire building, a natural question is whether the low IC firms also

tend to have high investment discretion. However, our data refute this conjecture because we

find that on average the low IC firms with high asset growth have negative cash flows and their

leverage is also not appreciably lower than the sample average. Furthermore, our results also do

not support the hypothesis that the low IC firms are harder to arbitrage than, say, the high IC

firms. And, from the overreaction viewpoint of Cooper et al. (2008), our results imply that

investors overreact only to low IC firms with high asset growth but not to the other firms, while

they underreact to the positive growth implications of asset growth by high IC firms. In addition,

we find that valuation uncertainty measures, such as age and idiosyncratic volatility, do not differ

significantly between low and high IC firms.

However, the heterogeneity across IC groups with respect to the abnormal returns

following asset growth uncovered by our analysis is along the lines suggested by the real options

framework. In particular, the negative effects of asset growth on abnormal returns are diluted by

firms’ IC, and asset growth by high IC firms can eventually lead to positive abnormal returns. If

the abnormal returns following asset growth are caused by missing risk factors instead of

mispricing, then the evidence is consistent with the hypothesis that the effect of asset growth on

firms’ systematic risk varies with their IC. The delay in observing the positive abnormal returns

(subsequent to the asset growth events) for the high IC firms could be due to the time-to-build

effect (Kydland and Prescott, 1982) on the development of new growth options.

6

We therefore examine further the effects of innovative capacity on the firm risk premium

following asset growth both theoretically and empirically. We develop this intuition by

constructing a theoretical sequential real options model where the optimal dynamic investment

policy of firms generates a time-varying risk premium for firms that depends on their IC. Firms

initially invest to build their long run IC, and then optimally and sequentially exercise growth

options that arrive at random times. Higher IC firms have both a greater likelihood of developing

a sequence (“new generations”) of innovations and higher expected cash flow growth conditional

on realizing the innovations. Our model demonstrates that the post-investment drop in

equilibrium firm risk premium will be lower (or diluted) for firms with higher IC compared with

low IC firms, and forms the basis of our empirical test design.3 Empirically, we predict that the

change in firms’ market betas (following asset growth events) will be positively associated with

their innovative capacity.

We test this prediction by examining the changes in firms’ market betas subsequent to the

asset growth events using independent portfolio sorts based on the IC measures and asset growth.

Consistent with the prediction, when we examine the change in betas between the first and the

fourth year following high asset growth, we find that market betas decrease for low IC firms but

increase for high IC firms. When we compare the pre- and post-asset growth betas, we find that

while market betas increase after high asset growth for both the high and low IC firms, the

increase in betas is significantly greater for the high IC firms.

The increase in market betas (for both high and low IC firms) subsequent to asset growth

appears contrary to the prediction of a variety of models where firms' systematic market risk

3 We emphasize that we do not restrict the sign of the post-investment change in stock returns (it may still be negative for high IC firms, for example). Rather, the prediction is that the change will be positively related to the IC.

7

declines subsequent to investment (see Section 2) and does not appear to have been documented

in the empirical literature.4 More generally, our analysis adds to the extensive literature that

identifies a variety of causes for time-varying betas (or systematic market risk of firms) --- from

business cycle variables to changes in estimation risk based on firm-specific information.5 In

particular, our results indicate that firms' IC is an important characteristic in explaining the time-

variation in their betas that occur due to pro-cyclical asset growth.

Our framework may also help reconcile the negative relation between asset growth (AG)

and returns with the observed positive relation between significant R&D growth and returns.

Eberhart, Maxwell, and Siddique (2004) identify positive dynamics between significant R&D

growth and subsequent stock returns and offer investor under-reaction as a possible explanation.

However, our results indicate that the relation between AG and returns of high IC firms is

significantly different (up-to a change of sign) from the overall negative relation. Because

significant R&D growth is most likely to be associated with high IC firms, the negative (positive)

relation between AG (significant R&D growth) and returns are not inconsistent with equilibrium

risk premia and correct market assessment of the implications of investment.

Finally, our paper is also related to the literature that examines the effects of innovation

activity on firms' market valuation (Griliches, Hall, and Pakes, 1987, 1991; Hall, Jaffe, and

Trajtenberg, 2005) and typically finds a positive relation between IC indicators and market value.

4 Cooper and Priestly (2011) find that for value-weighted returns loadings of one of the five (non-traded) Chen, Ross, and Roll (1986) factors declines significantly after rapid asset growth, while the loading on unexpected inflation actually increases significantly. However, we obtain significant results on the dynamics of market beta changes, when sorted on firms’ IC, using value-weighted returns. Thus, it appears that the effects of asset growth on loadings on market risk are quite different from its effects on loadings on non-traded factors. 5 Ferson, Kandel, and Stambaugh (1987), Ferson and Harvey (1991), Ferson and Schadt (1996), Jagannathan and Wang (1996), and Lettau and Ludvigson (2001), among others, relate the time-variation in betas to business cycle related variables. And Kumar et al. (2008) show changes in the betas following release of firm-specific information that affects estimation risk.

8

In contrast, we analyze the implications of IC on the abnormal returns and market risk changes

subsequent to asset growth. Our analysis indicates that patent intensities do not by themselves

have a significant influence on stock returns; rather, innovative capacity influences the abnormal

returns and market risk changes subsequent to asset growth. Thus, our results introduce another

dimension, so to speak, in evaluating the effects of innovative activity on stock returns.

We organize the paper as follows. Section 2 develops the concept of innovative capacity

and motivates the empirical measures. Section 3 describes the data and the empirical framework.

Section 4 discusses the results on the relation between IC and excess returns subsequent to asset

growth. Section 5 describes the empirical test design regarding the effects of IC on the changes

in firms' risk factor loadings following asset growth and presents the results. Section 6

summarizes the results and concludes.

2. The Asset Growth Anomaly and Innovative Capacity: Motivation

2.1 The Asset Growth Anomaly

The “asset growth anomaly” refers to the negative relation between capital investment

(and more generally asset growth) and subsequent abnormal stock returns that has been

uncovered by a number of recent studies. For example, Titman et al. (2004) use Carhart’s (1997)

four-factor model and find negative benchmark-adjusted returns following increased capital

investments. Because they find that this effect is more pronounced for firms with greater

investment discretion (i.e., firms with higher cash flows and lower leverage, and when hostile

takeovers are less prevalent), they argue that their results are consistent with investors reacting

slowly (or underreacting) to overinvestment by empire building managers. And using standard

models of risk-adjustment, Cooper et al. (2008) document a significant negative correlation

9

between firms’ total asset growth and subsequent abnormal returns (alphas). They then argue that

investors overreact to asset growth so that the observed negative post-AG abnormal returns are a

correction for the initial overreaction.

On the other hand, a number of theoretical models in the literature predict a negative

relation between investment and subsequent returns.6 Real options models (such as, McDonald

and Siegel, 1986; Majd and Pindyck, 1987; Berk, Green, and Naik, 1999; and Carlson, Fisher,

and Giammarino, 2006) predict a decline in systematic risk following the exercise of risky

growth options. In a related vein, Berk, Green, and Naik (2004) present a model where

investment resolves uncertainty with an attendant decline in the risk premium. Similarly, optimal

dynamic investment based on the neoclassical q-theory may lead to a negative relation between

investment and future returns (Liu, Whited, and Zhang, 2009; Li and Zhang, 2010).

From an empirical perspective, Cooper and Priestly (2011) present evidence that is

consistent with the rational or risk-based explanations of the asset-growth anomaly.

Complementary evidence is provided by recent papers indicating that an investment factor, i.e.,

the return on a portfolio of low investment stocks over the return on a portfolio of high

investment stocks, can help explain cross-sectional returns (e.g., Xing, 2008; Chen et al., 2011).

But clearly there is substantial heterogeneity in the effects of asset growth across firms.

Introspection suggests that the implications of one-time additions to manufacturing capacity

versus those of acquisition of patents ─ both of which are examples of asset growth in

accounting terms ─ are substantially different in terms of generating future growth options and

investment opportunities. Consequently, there should be heterogeneity in the relation between

6 Cooper and Priestly (2011) provide a good summary of these models.

10

asset growth and subsequent returns across firms based on their capacity to generate future

growth options from asset growth. We now develop this intuition.

2.2 Innovative Capacity: Concept and Measures

The chain of innovations and growth opportunities starts with inventions or new ideas

that, when developed for economic and commercial purposes, become innovations. Innovations

not only lead to new technologies and economic opportunities through development of new

markets, but are also often the source of new ideas that result in a sequence of innovations --- a

process that is central to economic growth (Schumpeter, 1942; Maclaurin, 1953). Building on

this, the literature on research and economic growth has developed the notion of national

innovative capacity, i.e., the ability of a country (or a geographical region) to produce and

commercialize a flow of innovative technology over the long term (Furman, Porter, and Stern,

2000, and onwards).

But, so defined, the concept of innovative capacity (IC) is also an important financial

characteristic at the level of the firm. To fix ideas, consider the well-known decomposition of

firm value into value from assets-in-place and value from growth options (Myers, 1977). Ceteris

paribus, firms with higher IC should have a greater ability to generate multiple growth options

and, therefore, IC should be positively associated with market value. But IC also has important

dynamic implications related to capital investment and asset growth. This is because investment

by higher IC firms is more likely to generate subsequent growth options and risky investment

opportunities compared with low IC firms. In particular, while investment by a low IC firm may

reflect exercising a non-replaceable growth option, for a high IC firm the capital investment may

be a precursor to the generation of new growth options and hence higher expected returns.

11

While innovative capacity, as a concept, may have interesting implications, its empirical

content depends on finding appropriate proxies or measures. Since firms benefit economically

from inventions only if they are protected or patented, the number of patents held by a firm (the

patent counts) indicates its potential to generate growth options over time through a sequence of

innovations. There is a long standing literature that uses patents as measures of firms' inventive

activity and growth options (Griliches, 1990; Pakes, 1986). More recently, the literature on IC at

the national and geographical levels also gives prominence to patent output (Furman et al., 2000).

In a related vein, Cohen and Levinthal (1990) and a large literature thereafter argue that firms

can develop knowledge creation and absorptive capacities, i.e., their ability to recognize,

assimilate, and apply new information to commercial benefit, that is reflected in higher IC.

R&D investment is highly uncertain and is an input to innovation, while patents reflect

innovation output and future growth options directly. We, therefore, take the patent counts as the

principal building block of our measures for firm IC. In addition, we argue that for our study

patent holdings are more appropriate and accessible than their citations because our interest is in

the forward looking aspects of inventive activity, i.e., the expected generation of future growth

options based on the invention levels achieved by the firm at any given time, whereas future

citations are not fully observable to investors as it takes time for patents to be cited (Hall et al.,

2005). Furthermore, patent counts are actually highly correlated with future citations as shown in

Hirshleifer, Hsu, and Li (2011).

3. Data and Innovative Capacity Measures

3.1 Data and Measures

12

Our sample consists of firms at the intersection of Compustat, CRSP (Center for

Research in Security Prices), and the NBER patent database. We obtain accounting data from

Compustat and stock returns data from CRSP. All domestic common shares trading on NYSE,

AMEX, and NASDAQ with accounting and returns data available are included except financial

firms, which have four-digit standard industrial classification (SIC) codes between 6000 and

6999 (finance, insurance, and real estate sectors). Following Fama and French (1993), we

exclude closed-end funds, trusts, American Depository Receipts, Real Estate Investment Trusts,

units of beneficial interest, and firms with negative book value of equity. To mitigate backfilling

bias, we require firms to be listed on Compustat for at least two years.

Patent-related data are from the updated NBER patent database originally developed by

Hall, Jaffe, and Trajtenberg (2001).7 This database contains detailed information on all U.S.

patents granted by the U.S. Patent and Trademark Office (USPTO) between January 1976 and

December 2006: patent assignee names, firms’ Compustat-matched identifiers, the number of

citations received by each patent, the number of citations excluding self-citations received by

each patent, application dates, grant dates, and other details. Patents are included in the database

only if they are eventually granted by the USPTO by the end of 2006. The NBER patent database

contains two time placers for each patent: its application date and grant date. To prevent any

potential look-ahead bias, we choose the grant date as the effective date of each patent and

measure firm i’s innovation output in year t as the number of patents granted to firm i in year t

(“patent counts”).

7 The updated NBER patent database is available at https://sites.google.com/site/patentdataproject/Home/downloads.

13

We use three proxies for innovative capacity (IC): patent counts scaled by total assets

(CTA), patent counts scaled by year-end market equity (CTME), and patent counts scaled by

book equity (CTBE). We construct these three IC proxies for each year from 1976 to 2006. Since

we focus on the effect of IC on the asset growth anomaly, we compute asset growth for the same

sample period.

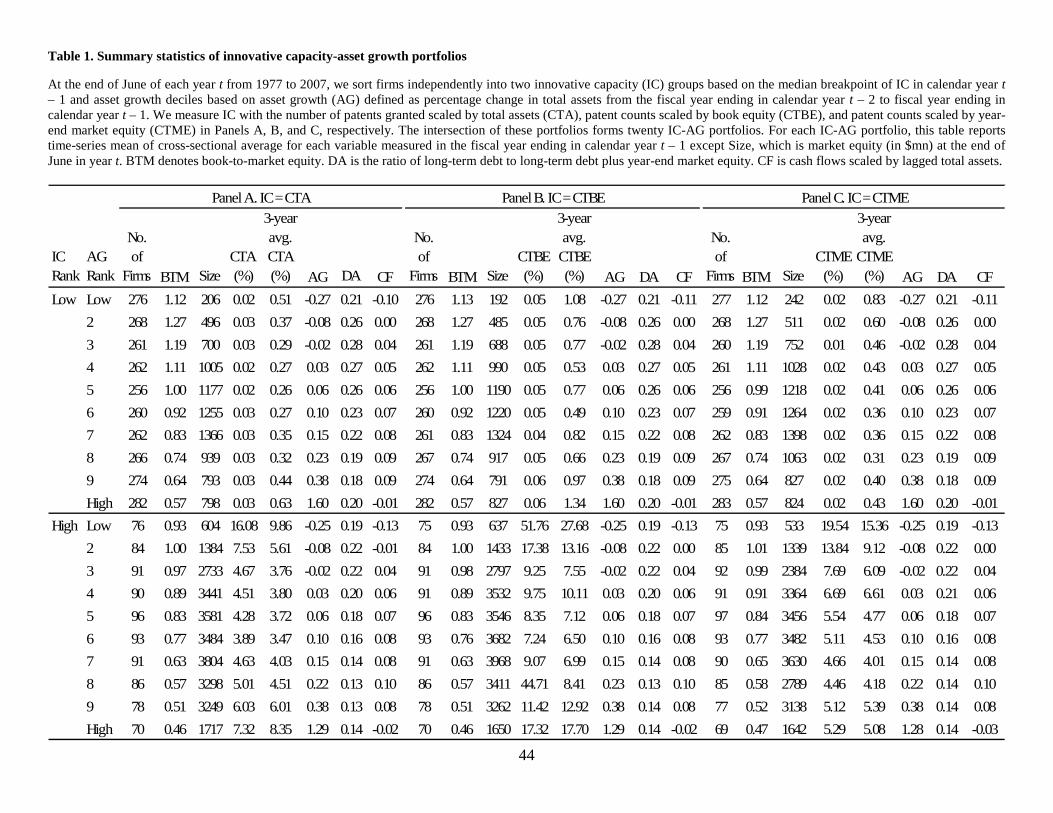

3.2 Summary Statistics

At the end of June of each year t from 1977 to 2007, we sort firms independently into two

IC groups (“Low” and “High”) based on the median breakpoint of the IC measures in calendar

year t – 1 and asset growth deciles based on asset growth (AG) defined as percentage change in

total assets (Compustat item AT) from the fiscal year ending in calendar year t – 2 to fiscal year

ending in calendar year t – 1. Firms with missing IC measure are assigned to the low IC group.

The intersection of these portfolios forms twenty IC-AG portfolios. For each IC-AG portfolio,

Table 1 reports the time-series means of the cross-sectional averages of the following variables:

number of firms, book-to-market equity (BTM), market equity (size), innovative capacity, three-

year average innovative capacity, asset growth, leverage (the long-term debt to assets ratio, DA)

and cash flow (CF). Leverage and cash flow are defined in the same way as Titman et al. (2004).

Specifically, leverage is the ratio of long-term debt to the sum of long-term debt and year-end

market value of equity. Cash flow, which is scaled by lagged total assets, is operating income

before depreciation minus interest expenses, taxes, preferred dividends, and common dividends.

All variables are measured in the fiscal year ending in calendar year t – 1 except size, which is

market equity (in millions) at the end of June in year t.

14

In Table 1, we measure IC with CTA, CTBE, and CTME in Panels A, B, and C,

respectively. Panel A shows that the average number of firms in the low IC group is much higher

than that in the high IC group. This is consistent with the inclusion of firms with missing IC in

the low IC group. In general, BTM decreases with asset growth in both low and high IC groups,

suggesting that high asset growth firms tend to be growth firms, while low asset growth firms

tend to be value firms. Furthermore, each AG portfolio in the low IC group has higher BTM than

its counterpart in the high IC group. This pattern supports our claim that IC is a proxy of growth

options. The average size of low IC firms is smaller than that of high IC firms; a contributing

factor here may be the high market valuations of hi-tech firms during the 1980s and 1990s.

Within both IC segments (low and high), the relation between AG and firm size appears to be

hump-shaped, i.e., firms in the middle AG deciles tend to be larger on average than firms in the

extreme (very low and very high) AG deciles.

Panel A shows that in the low IC group, the average CTA is very low and does not vary

much across the AG deciles, ranging from 0.02% to 0.03%. In the high IC group, the average

CTA is much higher and varies with AG in a U-shape, ranging from 16.08% for the lowest AG

portfolio to 4.28% for the middle AG portfolio to 7.32% for the highest AG portfolio. In addition,

the level of IC tends to be persistent as low IC firms also have low CTA averaged over the prior

three years. The spreads in asset growth across the AG deciles in both IC groups are wide and

similar: Asset growth ranges from –0.27 to 1.60 in the low IC group and from –0.25 to 1.29 in

the high IC group. We will comment on the leverage and cash flow patterns in Section 4.

The summary statistics based on the other two proxies of IC are very similar as reported

in Panels B and C. For example, the average number of firms in each IC-AG portfolio is almost

15

identical across the three proxies of IC. The other characteristics are also very close, such as

BTM, size, and asset growth, i.e., the three IC measures are highly correlated with each other. In

addition, we find the results reported in the next two sections are also very similar across the

three IC measures. For brevity, we only report results based on CTA in the rest of the paper.8

4. Innovative Capacity and the Asset Growth Anomaly

In this section, we use both portfolio sorts and Fama-MacBeth (1973) cross-sectional

regressions to study the impact of innovative capacity on the asset growth anomaly documented

in the literature (e.g., Cooper et al., 2008). As discussed in the introduction, we expect a weaker

AG effect among high IC firms since the asset growth of such firms may generate new

investment opportunities and growth options.

Total assets used in computing asset growth includes not only tangible assets (such as,

property, plant, and equipment) resulting from capitalization of traditional investment, but also

tangible assets resulting from certain types of R&D investment and intangible assets, such as

patents. In general, under current GAAP (generally accepted accounting principles), R&D

investment is immediately expensed and included in R&D expenditures (Compustat item XRD)

and, therefore, is excluded from total assets and asset growth. However, R&D investment that

has usage for future R&D projects, such as investment in building research facilities and

purchase of machinery and materials for use on current and future R&D projects, is capitalized

and included in total assets and asset growth. Similarly, the acquisition costs for patents are

included in intangible assets and are a part of total assets and asset growth. This type of

8 The results for the other two innovative capacity proxies are available upon request.

16

innovation-related asset growth facilitates the generation of new growth opportunities instead of

simply exercising pre-existing growth options.

However, existing studies on the asset growth anomaly do not disentangle different types

of asset growth based on whether it is caused by traditional capital investment, which tends to

reduce growth options and risks, or by innovation-related investment, which can generate new

options and increase risks. We now examine how this differentiation sheds light on the asset

growth anomaly. Although these innovation-related investments are included in total assets, they

are not reported separately in Compustat. Therefore, we use firms’ innovative capacity to

differentiate between these two types of asset growth.

4.1 Portfolio Sorts

4.1.1 One-way Sort on Asset Growth

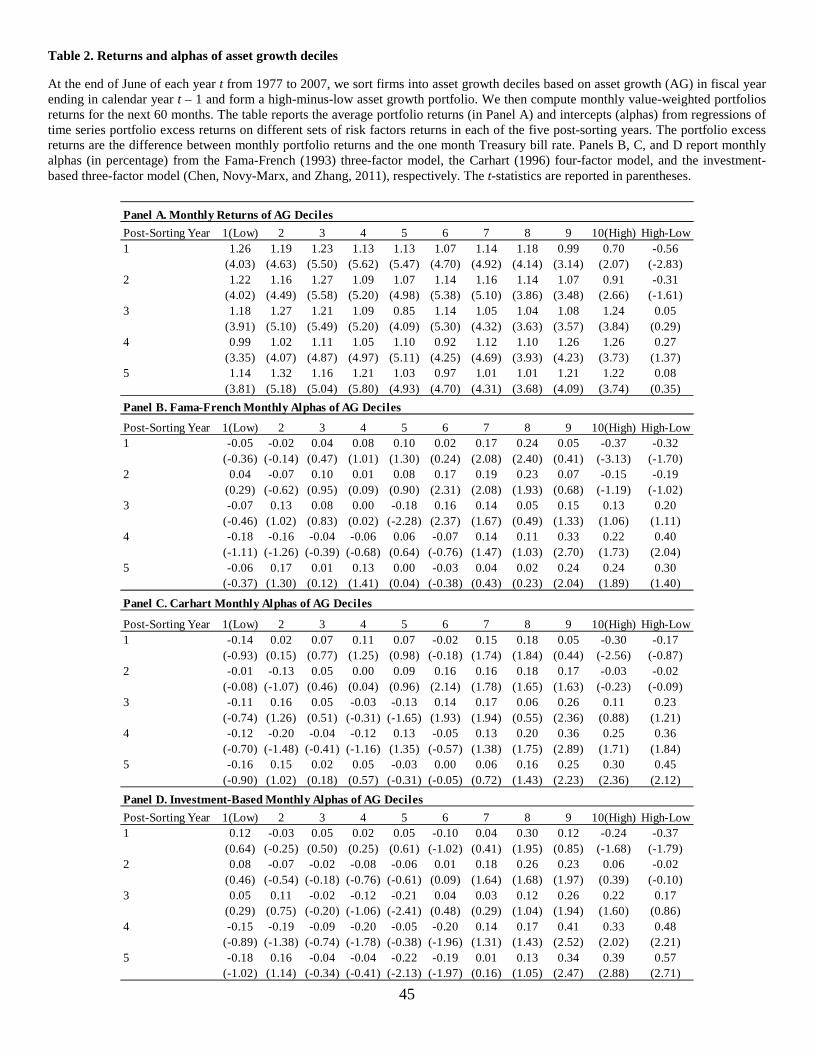

We first show in Table 2 the existence of the asset growth anomaly in our sample period

from July of 1977 to June of 2008, which is different from the sample period from 1968 to 2002

in Cooper et al. (2008). Following Cooper et al. (2008), we form asset growth deciles at the end

of June of each year t from 1977 to 2007 based on asset growth in fiscal year ending in calendar

year t – 1. We also form a high-minus-low AG portfolio, which buys firms in the highest AG

decile and sells firms in the lowest AG decile. We then hold these portfolios for the next 60

months and compute value-weighted monthly returns for each portfolio and report the time-

series mean and corresponding t-statistics (in parentheses) of these portfolios’ returns in Panel A

of Table 2.

We examine value-weighted portfolio returns for two main reasons. First, because all the

factors returns we use are value-weighted, using equal-weighted portfolio returns in the factor

17

regressions will induce a bias towards finding significant alphas. Second, we want to ensure that

our results are not driven by smaller firms that are likely to have higher patent intensity, i.e., we

want to ensure that the “innovative capacity effect” is not essentially a “small firm effect”.

Consistent with Cooper et al. (2008), we find a significantly negative relation between

AG and returns in the first post-sorting year. The value-weighted monthly average return of the

high-minus-low AG portfolio is –0.56% (t = –2.83) in the first post-sorting year. Cooper et al.

(2008) find a much larger return difference of –1.05% between the high and low AG deciles

using data from 1968 to 2002. However, our result is more consistent with Cooper and Priestley

(2011), who find a return difference of –0.46% using data from 1960 to 2009. In addition,

Cooper et al. (2008) find that the negative AG-return relation continues to be significant over the

second and third post-sorting years. But we find that this relation is insignificant over the second,

third, fourth, and fifth post-sorting years; these differences could also be due to the different

sample periods and the fact that high-tech firms become more prevalent after 1975.

We also compute risk-adjusted returns for these portfolios over the five post-sorting years

by regressing the time-series of portfolio excess returns on risk factor returns. The monthly

portfolio excess return is measured by the difference between the value-weighted portfolio return

and the one-month Treasury bill rate. We report the intercepts (alphas) from the Fama-French

(1993) three-factor model, the Carhart (1997) four-factor model, and the investment-based three-

factor model (Chen et al., 2011) in Panels B, C, and D of Table 2, respectively. The Fama-

French three-factor model contains the market factor (MKT), the size factor (SMB), and the

value factor (HML). The Carhart four-factor model contains the momentum factor (MOM) in

addition to the Fama-French three factors. The market factor is the return on the value-weighted

18

NYSE/AMEX/NASDAQ portfolio minus the one-month Treasury bill rate. The size factor and

the value factor are returns on the factor-mimicking portfolios associated with the documented

size effect and book-to-market effect (Fama and French, 1992). The momentum factor is return

on the factor-mimicking portfolio associated with the momentum effect (e.g., Jegadeesh and

Titman, 1993). The investment-based three-factor model contains the market factor, the

investment (INV) factor, and the return on equity (ROE) factor. The INV factor is the difference

between the return to a portfolio of low-investment stocks and the return to a portfolio of high-

investment stocks. The ROE factor is the difference between the return to a portfolio of stocks

with high ROE and the return to a portfolio of stocks with low ROE.9

Compared with Cooper et al. (2008) who focus on Fama-French alphas in the first post-

sorting year, we examine alphas from three different factor models over the five post-sorting

years. We find some interesting patterns over time. For example, the alphas of the high AG

portfolio and the high-minus-low AG portfolio become significantly positive in the fourth and/or

the fifth post-sorting years. We now discuss the results in more detail.

Panel B of Table 2 shows that the monthly Fama-French alpha for the high-minus-low

AG portfolio is negative and marginally significant in the first post-sorting year (–0.32%, t = –

1.70). However, it starts to weaken and turns to positive over the next four years. Specifically, it

becomes insignificant in the second post-sorting year (–0.19%, t = –1.02) and turns positive over

the next three years: 0.20% (t = 1.11), 0.40% (t = 2.04), and 0.30% (t = 1.40) for the third, fourth,

and fifth post-sorting years, respectively. This pattern is driven mainly by the high AG decile.

The monthly Fama-French alpha of the high AG decile is significantly negative in the first post-

9 We obtain Carhart’s (1997) four factors returns and the one-month Treasury bill rate from Kenneth French’s website: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/.

19

sorting year, –0.37% (t = –3.13). It increases over the next four years to 0.24% (t = 1.89) in the

fifth post-sorting year. In contrast, the Fama-French alpha of the low AG decile is always small

and insignificant over the five post-sorting years.

Panel C reports the monthly Carhart alphas for the AG portfolios over the five post-

sorting years. It shows a negative but insignificant Carhart alpha for the high-minus-low AG

portfolio in the first year (–0.17%, t = –0.87). In other words, the negative AG-return relation in

the full sample can be fully explained by the Carhart four-factor model during this sample period.

Furthermore, the Carhart alpha for the high-minus-low AG portfolio also increases over the next

four years to 0.45% (t = 2.12) in the fifth post-sorting year. Similar to the Fama-French alphas,

these patterns are also driven mainly by the high AG portfolio. For example, the Carhart alpha

for the high AG portfolio is significantly negative in the first year (–0.30%, t = –2.56) but

significantly positive in the fifth year (0.30%, t = 2.36). In contrast, the alphas for the low AG

portfolio are always small and insignificant.

In Panel D, we examine the explanatory power of the three-factor model motivated by the

investment-based asset pricing and find patterns similar to that of the other factor models. The

monthly alphas in the first post-sorting year are negative and marginally significant for the high

AG portfolio (–0.24%, t = –1.68) and the high-minus-low AG portfolio (–0.37%, t = –1.79). The

alphas also increase over time to 0.39% (t = 2.88) for the high AG portfolio and 0.57% (t = 2.71)

for the high-minus-low AG portfolio in the fifth post-sorting year. In fact, the alphas for the high

AG portfolio and the hedge portfolio become significantly positive as early as the fourth post-

sorting year: 0.33% (t = 2.02) and 0.48% (t = 2.21), respectively.

20

Overall, these results show a weakened asset growth anomaly in our sample period and

illustrate some new interesting dynamics of this anomaly over the five post-sorting years. We

now examine the interaction between the asset growth anomaly and firms’ innovative capacity.

For simplicity, we focus on risk-adjusted returns only.

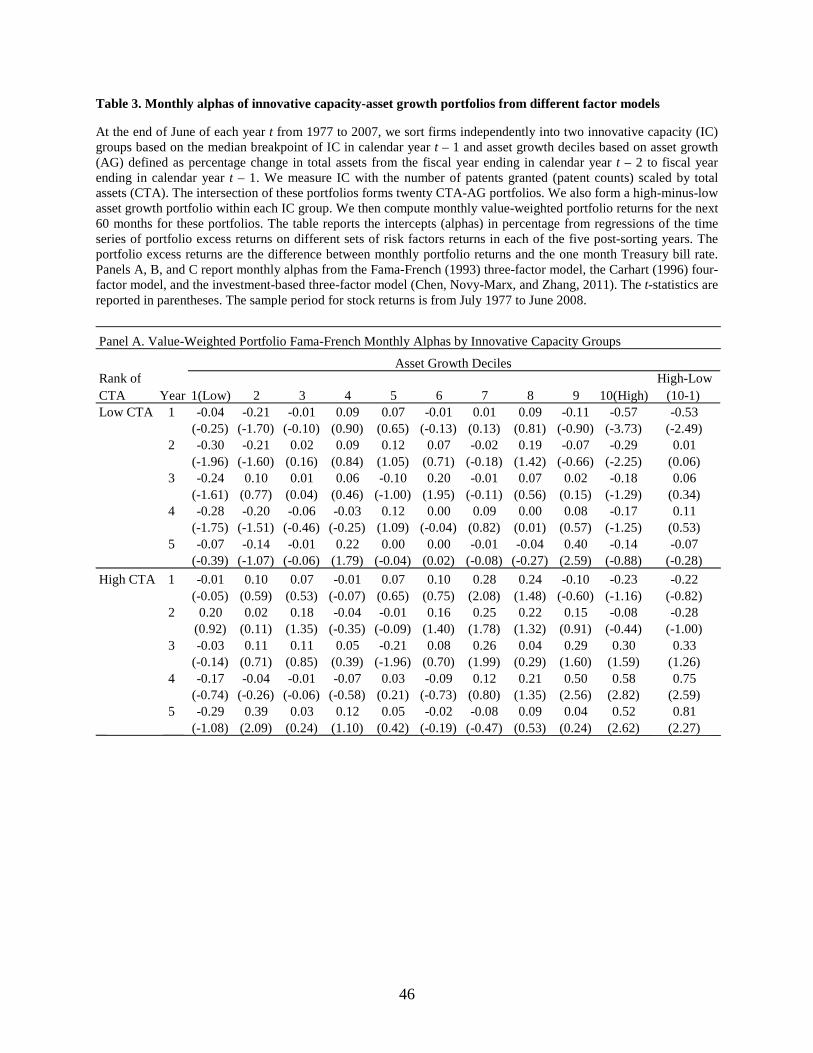

4.1.2 Double Sorts on Innovative Capacity and Asset Growth

In this subsection, we study the impact of innovative capacity on the asset growth

anomaly through independent double sorts on IC and AG. Table 3 reports the value-weighted

monthly alphas (in percentage) for the AG deciles across the IC groups formed in the same way

as in Table 1. Specifically, at the end of June of each year t from 1977 to 2007, we sort firms

independently into two IC groups (“Low” and “High”) based on the median breakpoint of

innovative capacity in year t – 1 and asset growth deciles based on asset growth in fiscal year

ending in calendar year t – 1. Firms with missing IC measures are assigned to the low IC group.

We measure IC with patent counts scaled by total assets in Table 3 since the other two measures

of innovative capacity generate very similar results. The intersection of these portfolios forms

twenty IC-AG portfolios. Furthermore, we create a high-minus-low AG portfolio within each IC

group. We then compute the monthly value-weighted portfolio returns for all these portfolios

over the next 60 months and regress the time-series of portfolio excess returns on different sets

of factor returns in each of the five post-sorting years. The monthly portfolio excess return is

measured by the difference between the value-weighted portfolio return and the one-month

Treasury bill rate. We report the intercepts (alphas) in percentage from the Fama-French model,

the Carhart model, and the investment-based factor model in each of the five post-sorting years

in Panels A, B, and C of Table 3, respectively.

21

We find a sharp contrast in the AG anomaly across the IC groups. Panel A shows that the

AG effect differs dramatically across the two IC groups. In the low IC group, the AG effect is

significantly negative in the first post-sorting year. However, in the high IC group, the AG effect

is insignificant in the first post-sorting year and significantly positive in the fourth and fifth post-

sorting years. Specifically, in the low IC group, the monthly Fama-French alpha of the high-

minus-low AG portfolio is significantly negative in the first post-sorting year, –0.53% (t = –2.49),

but is small and insignificant over the next four years. The pattern is similar for the high AG

portfolio in the low IC group. The monthly Fama-French alpha for the high AG, low IC portfolio

is –0.57% (t = –3.73) and –0.29% (t = –2.25) in the first and second years, respectively, but is

small and insignificant over the next three years.

By contrast, in the high IC group, the monthly Fama-French alphas for the high AG

portfolio and the high-minus-low AG portfolio are insignificant in the first three post-sorting

years, but are significantly positive in the fourth and the fifth years. For example, the alphas for

the high-minus-low AG portfolio are 0.75% (t = 2.59) and 0.81% (t = 2.27) in the fourth and the

fifth years, respectively. Similarly, the alphas for the high AG portfolio are 0.58% (t = 2.82) and

0.52% (t = 2.62) in the fourth and fifth years, respectively.

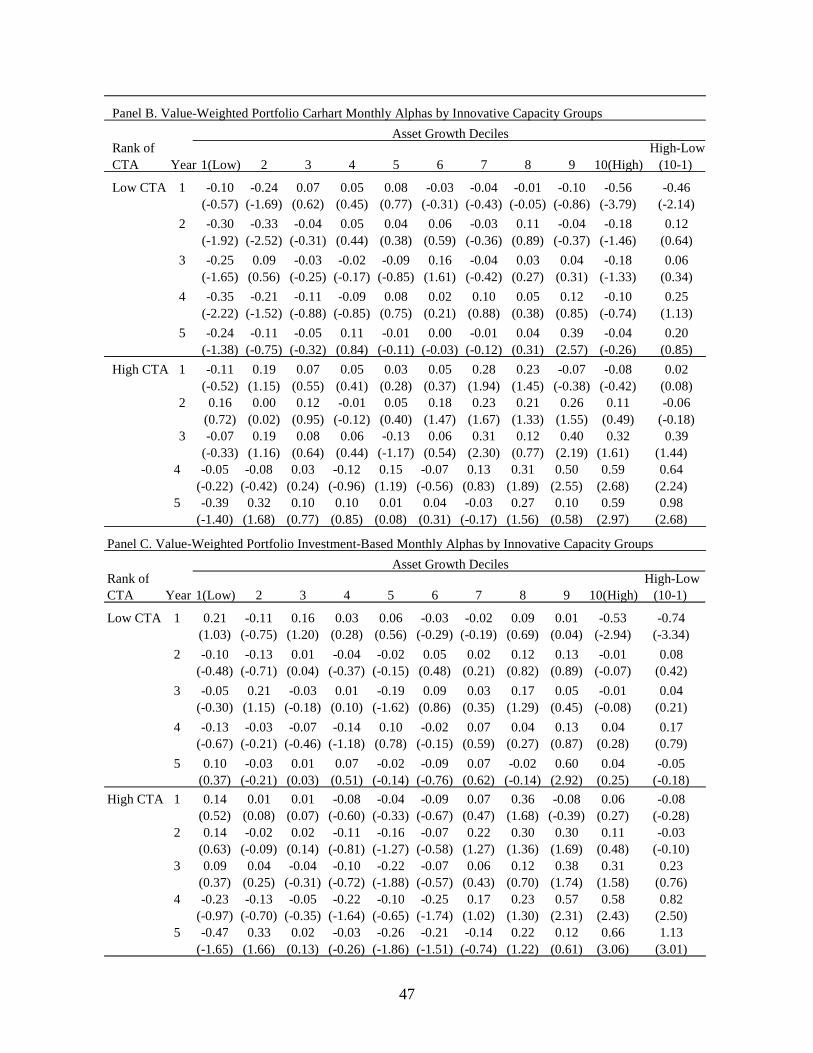

This striking contrast in the AG effect between the low IC group and the high IC group is

robust to alternative factor models as shown in Panels B and C. For both the Carhart four-factor

model and the investment-based three-factor model, we find a significantly negative alpha only

for the high AG portfolio and the high-minus-low AG portfolio created in the low IC group in

the first post-sorting year, but a significantly positive alpha for the high AG portfolio and the

hedge portfolio created in the high IC group in the fourth and fifth post-sorting years.

22

Specifically, Panel B shows that in the low IC group, the monthly Carhart alphas for the high AG

portfolio and the hedge portfolio are –0.56% (t = –3.79) and –0.46% (t = –2.14), respectively, in

the first year, but are insignificant over the next four years. However, in the high IC group, the

monthly Carhart alphas in the first year are only –0.08% (t = –0.42) for the high AG portfolio

and 0.02% (t = 0.08) for the hedge portfolio, but the alphas in the fourth and fifth years are 0.59%

(t = 2.68) and 0.59% (t = 2.97) for the high AG portfolio and 0.64 (t = 2.24) and 0.98% (t = 2.68)

for the hedge portfolio, respectively.

Similarly, Panel C shows that in the low IC group, the monthly alpha estimated from the

investment-based three-factor model is –0.53% (t = –2.94) for the high AG portfolio and –0.74%

(t = –3.34) for the hedge portfolio in the first year, but is small and insignificant in the next four

years for these portfolios, ranging from –0.05% to 0.17%. However, in the high IC group, the

corresponding monthly alpha is only 0.06% (t = 0.27) for the high AG portfolio and –0.08% (t =

–0.28) for the hedge portfolio in the first year, but is 0.58% (t = 2.43) and 0.66% (t = 3.06) for

the high AG portfolio in the fourth and fifth years, respectively, and are 0.82% (t = 2.50) and

1.13% (t = 3.01) for the hedge portfolio in the fourth and fifth years, respectively.

Furthermore, the negative AG effect among low IC firms is stronger and more robust to

risk adjustment than that in the full sample. Specifically, Table 3 shows that the monthly Fama-

French alpha, the Carhart alpha, and the investment-based alpha for the high-minus-low AG

portfolio formed in the low IC group are all significantly negative in the first year: –0.53% (t = –

2.49), –0.46% (t = –2.14), and –0.74% (t = –3.34), respectively. In contrast, Table 2 shows that

the counterparts of these alphas for the hedge portfolio formed in the full sample are smaller and

either marginally significant or insignificant: –0.32% (t = –1.70), –0.17% (t = –0.87), and –0.37%

23

(t = –1.79), respectively. Similarly, the negative alphas of the high AG portfolio formed in the

low IC group are also more robust than those of the high AG portfolio formed in the full sample.

The three corresponding alphas in the first year for the low IC, high AG portfolio are

significantly negative at the 1% level: –0.57% (t = –3.73), –0.56% (t = –3.79), and –0.53% (t = –

2.94), respectively. In comparison, these alphas for the high AG portfolio formed in the full

sample are much smaller: –0.37% (t = –3.13), –0.30% (t = –2.56), and –0.24% (t = –1.68),

respectively.

This conspicuous contrast between the low IC group and the high IC group and the

contrast between the low IC group and the full sample illustrated above cannot be attributed to

the difference in the AG spread. As shown in Table 1, the low IC group and the high IC group

have very similar average AG spread between the highest and the lowest AG deciles: 1.87 vs.

1.54. In unreported results, we find the average AG spread in the full sample is also similar

(1.82). In addition, the rank of asset growth tends to be persistent. For example, the average asset

growth of the highest AG decile continues to be higher than that of the lowest AG decile over the

next three (five) years for the low (high) IC group. Therefore, the positive AG effect in the high

IC group in the fourth and fifth post-sorting years cannot be explained by the asset growth over

the post-sorting years.

These results illustrate the important role of innovative capacity in understanding the

asset growth anomaly. They suggest that the negative asset growth effect documented in the

literature is mainly driven by low IC firms. Among high IC firms, the asset growth effect is

insignificant in the first post-sorting year and turns significantly positive in the fourth and the

fifth post-sorting years.

24

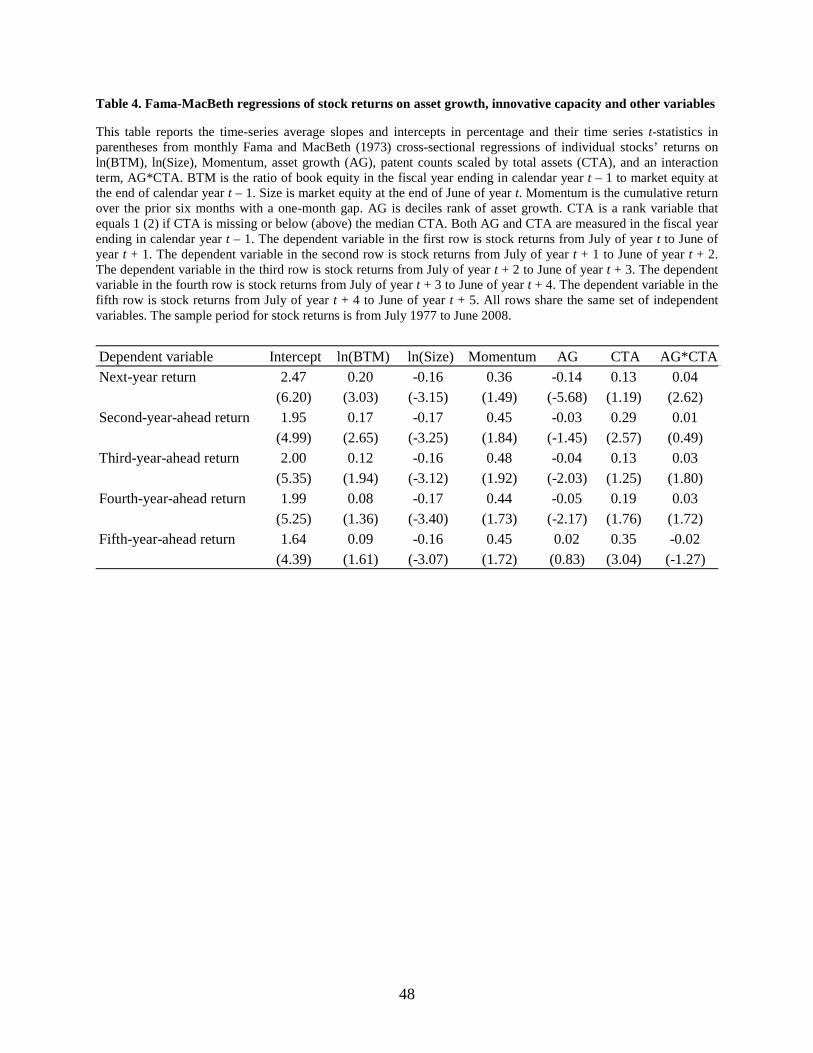

4.2 Fama-MacBeth Regressions

In this subsection, we examine the interaction effect between innovative capacity and the

asset growth effect using Fama-MacBeth (1973) cross-sectional regressions to control for other

characteristics that can predict returns and to ensure that the impact of innovative capacity on the

asset growth effect documented in Section 4.1.2 is robust.

The first row of Table 4 reports results from regressions with stock returns in the first

post-sorting year as the dependent variable. Specifically, for each month from July of year t to

June of year t + 1, we regress monthly returns of individual stocks on ln(BTM), ln(Size),

Momentum, asset growth (AG), patent counts scaled by total assets (CTA), and an interaction

term, AG*CTA, to capture the effect of innovative capacity on the asset growth effect.10 BTM is

the ratio of book equity in the fiscal year ending in calendar year t – 1 to market equity at the end

of calendar year t – 1. Size is market equity at the end of June of year t. Momentum is the

cumulative return over the prior six months with a one-month gap to reduce the effect of short-

term reversal. AG and CTA are measured in the fiscal year ending in calendar year t – 1. The

minimum six-month lag between stock returns and BTM and AG ensures the accounting

variables are fully observable. We winsorize all independent variables at the 1% and 99% levels

to reduce the impact of outliers.

The first row reports the time series average intercepts and slopes (in percentage) and

their time-series t-statistics (in parentheses) from the series of monthly cross-sectional

regressions. The slope on AG*CTA is significantly positive, 0.04% (t = 2.62). This implies a

10 We get similar results in the Fama-MacBeth regressions when we control for industry dummies based on Fama and French’s (1997) 48 industries.

25

weaker AG effect in firms with higher CTA, which is consistent with the findings in portfolio

sorts in the first post-sorting year. Consistent with the literature, the slope on ln(BTM) is

significantly positive, 0.20% (t = 3.03), and the slope on ln(Size) is significantly negative, –0.16%

(t = –3.15). The slope on Momentum is positive but insignificant, 0.36% (t = 1.49).

We also conduct monthly cross-sectional regressions of stock returns in the second post-

sorting year (July of year t + 1 to June of year t + 2) on the same set of independent variables

used in the first row. We report the time series average intercepts and slopes (in percentage) and

their time-series t-statistics (in parentheses) from these regressions in the second row. Similarly,

the dependent variables in the third to the fifth rows are stock returns in the third post-sorting

year (July of year t + 2 to June of year t + 3), the fourth post-sorting year (July of year t + 3 to

June of year t + 4), and the fifth post-sorting year (July of year t + 4 to June of year t + 5),

respectively. The independent variables in these rows are the same as those used in the first row.

The sample period for stock returns is from July 1977 to June 2008.

Consistent with the results from portfolio sorts, the slope on the interaction term,

AG*CTA, is significantly positive at the 10% level in the third and the fourth post-sorting years:

0.03% (t = 1.80) and 0.03% (t = 1.72), respectively. However, the slope on AG*CTA in the fifth

year is insignificant. The slight difference between portfolio sorts and Fama-MacBeth (FM)

regressions may be due to the fact that we impose a linear relation in regressions and that AG

and CTA could be highly correlated with the interaction term, AG*CTA.11 Furthermore,

portfolio sorts control for loading on risk factors, while Fama-MacBeth regressions control for

11 To reduce the high correlation between the interaction term and its component variables, we use decile rank of AG and a rank variable for CTA (2 for firms above the median CTA and 1 for the other firms) in the regressions instead of the original variables. The interaction term, AG*CTA, is also constructed from the decile rank of AG and the rank variable for CTA.

26

characteristics. Overall, these FM regressions results support the analysis from portfolio sorts

because they indicate that the effect of asset growth on subsequent stock returns is influenced by

firms’ innovative capacity in a statistically and economically significant manner, especially in

the first year after the asset growth event.

To summarize the results of this section, we find that firms’ innovative capacity plays a

substantial role in the asset growth anomaly. The significantly negative AG effect documented in

the literature exists only among low IC firms in the first post-sorting year. Furthermore, the

negative AG effect among low IC firms is stronger and more robust to risk adjustment than that

in the full sample. For example, the Carhart four-factor model can fully explain the negative AG

effect in the full sample, but not among the low IC firms. In contrast, the AG effect among high

IC firms is insignificant in the first post-sorting year and turns significantly positive in the fourth

and fifth post-sorting years. In addition, the Fama-MacBeth regressions also show a significant

positive interaction effect between asset growth and innovative capacity on subsequent stock

returns; these results reinforce the inference from the portfolio sorting analysis that higher IC

significantly weakens, and even over-turns, the asset growth anomaly.

4.3 Implications and Relation to the Literature

We now relate our results to some of the main mispricing explanations presented in the

literature for the asset growth anomaly, and to the seemingly related net operating assets

anomaly considered by Hirshleifer et al. (2002). We also develop further the implications of our

results for the real options viewpoint.

27

4.3.1 Innovative Capacity and Investment Discretion

As we noted before, Titman et al. (2004) find that the negative relation between high

capital investment and abnormal returns is stronger for firms that have greater investment

discretion, i.e., firms with higher cash flows and lower debt ratios. They then relate investment

discretion to the moral hazard for managerial empire building and suggest that the anomaly may

be due to investors’ slow reaction to the empire building implications of high investment. Prima

facie, the fact that the asset growth anomaly appears to hold only for low IC firms may not be

inconsistent with the empire building explanation if low IC firms are highly represented in the

category of high investment discretion firms (e.g., “cash cow” firms). However, returning to

Table 1, we do not find support for the conjecture that firms in the low IC/high asset growth (AG)

group are also high investment discretion firms. In fact, this group has negative cash flows on

average and the average debt ratio is also not significantly lower than those of the other groups.

It is possible, of course, that the patent-based IC measures are very effective in

discriminating between firms with value-destroying asset growth (i.e., the low IC firms) and

potentially value-enhancing asset growth (i.e., the high IC firms), and our results may indicate

slow investor reaction to the unproductive investment of the low IC firms. If this is the case, then

our analysis is still of substantial interest because it would indicate that patent intensity is a

significant predictor of investment efficiency.

We note that the underreaction to empire building only explains the negative effect of AG

on subsequent stock returns. But this viewpoint does not appear to explain our finding that there

are positive abnormal returns for the high IC firms following rapid asset growth.

28

4.3.2 Innovative Capacity and the Limits to Arbitrage

Another possible reason for the mispricing of asset growth only for the low IC firms

(following rapid asset growth) could be that these firms are harder to arbitrage compared to the

high IC firms; i.e., the limits to arbitrage emphasized, for example, by Shleifer and Vishny (1997)

apply especially to the low IC/high AG group. However, in untabulated results we find that low

and high IC firms both have very similar average idiosyncratic volatility, a major measure of

limits to arbitrage (Ali and Hwang, 2003; Lam and Wei, 2011).12 We also note that the low IC

firms are smaller than the high IC firms on average and this may be a factor that exacerbates the

limits to arbitrage for this group. However, Cooper et al. (2008) show that the significantly

negative AG effect is robust to size and exists in firm size groups. Furthermore, the short leg of

the trading strategy exploiting the AG anomaly is the high AG/low IC group. The average size of

this group is $798 million, which is not very small (although it is smaller than the high AG/high

IC group). In addition, we find a strong interaction effect of IC and AG on stock returns in the

Fama-MacBeth regressions controlling for size in Section 4.2.

Finally, our analysis also poses a challenge to the overreaction hypothesis of Cooper et al.

(2008). From this perspective, our results imply that investors overreact only to low IC firms

with high asset growth, but not to other firms. Furthermore, if the positive post-AG alphas for

high IC/high AG firms are due to mispricing, then this suggests that investors underreact to the

positive effects of high asset growth by the high IC firms and the positive alphas reflect the

correction for that underreaction.

12 Idiosyncratic volatility is also a popular measure of valuation uncertainty (e.g., Kumar, 2009). In addition, we also find the average firm age (another measure of valuation uncertainty) does not vary significantly between the IC groups. Therefore, this evidence suggests that the difference in the AG effect across the IC groups is not driven by valuation uncertainty.

29

4.3.3 Innovative Capacity and the Net Operating Assets Anomaly

Hirshleifer et al. (2002) find a significantly negative relation between net operating assets

(NOA) and future abnormal stock returns, and interpret this evidence as consistent with the view

that investors with limited attention overvalue firms with bloated balance sheets, i.e., with high

NOA. We also examine how innovative capacity interacts with the NOA anomaly. In unreported

results, we find that while the NOA anomaly exists in both low and high IC firms, it is more

robust in low IC firms. However, while seemingly related, a closer examination indicates that

asset growth and the NOA are conceptually quite different, and this may help explain the

different effects of IC on AG versus NOA. Specifically, as noted by Hirshleifer et al. (2002), the

NOA is a cumulative measure of the deviation between operating income (accounting value-

added) and free cash flow (cash value-added) scaled by lagged assets.13 Indeed, the NOA can be

expressed as the sum of cumulative operating accruals and cumulative investments. In contrast,

asset growth is a flow variable because it reflects change in assets scaled by lagged total assets.

4.3.4 Innovative Capacity and Time-Varying Firm Risk Premium

Our results are potentially consistent with a framework where there is time-varying risk

premium driven by investment and where the change in the risk premium is positively related to

firms’ IC. From this viewpoint, asset growth of low IC firms mainly converts growth options to

assets-in-place and thereby reduces the risk premium or expected returns; hence, we observe the

significantly negative alphas of the high-minus-low AG portfolio and the high AG portfolio 13 The NOA is computed as the difference between operating assets and operating liability scaled by lagged total assets, where operating assets is the difference between total assets and cash and short-term investments (Compustat

item CHE) and operating liabilities is total assets – debt in current liabilities (item DLC) − long-term debt (item

DLTT) – minority interest (item MIB) – preferred stock (item PSTK) – common equity (item CEQ).

30

formed in the low IC group. In contrast, asset growth of high IC firms is likely related to

innovation activities that can generate new growth options and therefore increases the risk

premium and expected returns. And due to time-to-build effects (Kydland and Prescott, 1982),

we start to observe the positive abnormal returns only in the fourth and fifth years after the asset

growth event; this is reflected in the significantly positive alphas of the high AG portfolio and

the hedge AG portfolio formed in the high IC group.

In sum, if the alphas following asset growth are caused by missing risk factors instead of

mispricing, as would be suggested by an equilibrium asset pricing model with time-varying firm

risk premium, then our evidence is consistent with the view that high IC firms generate growth

options after rapid asset growth, while the low IC firms exercise non-replaceable growth options.

We turn now to explicating and testing the empirical implications of such a framework.

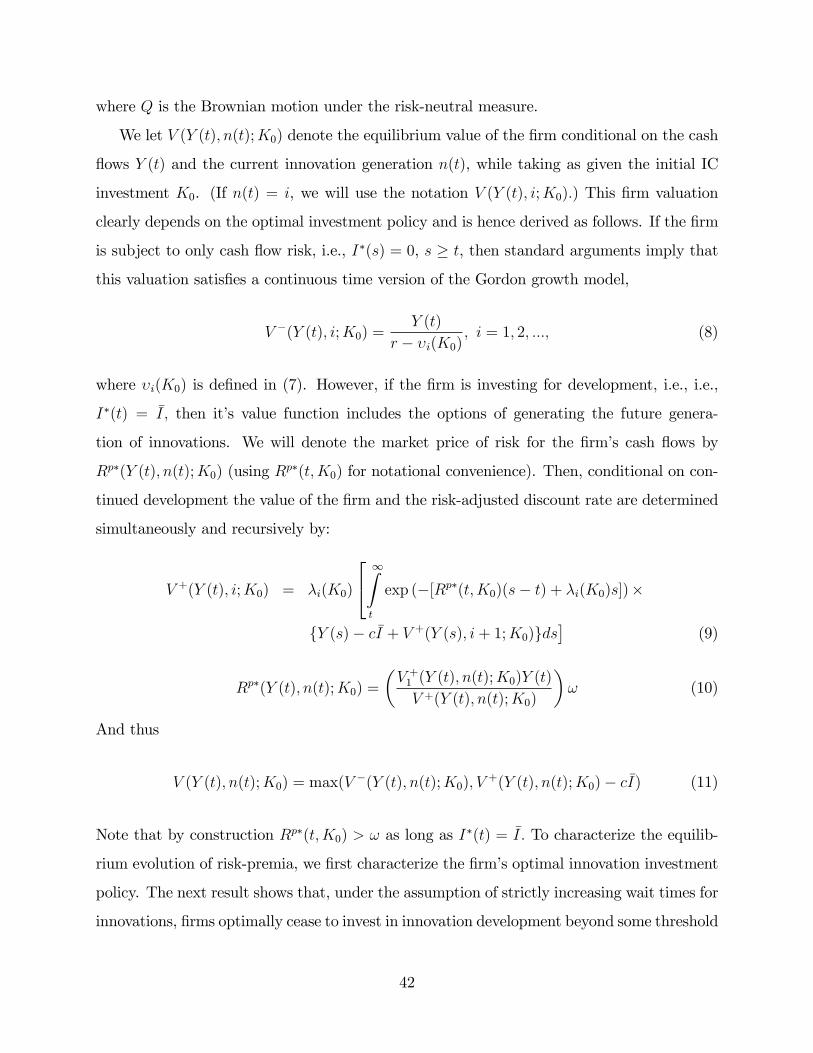

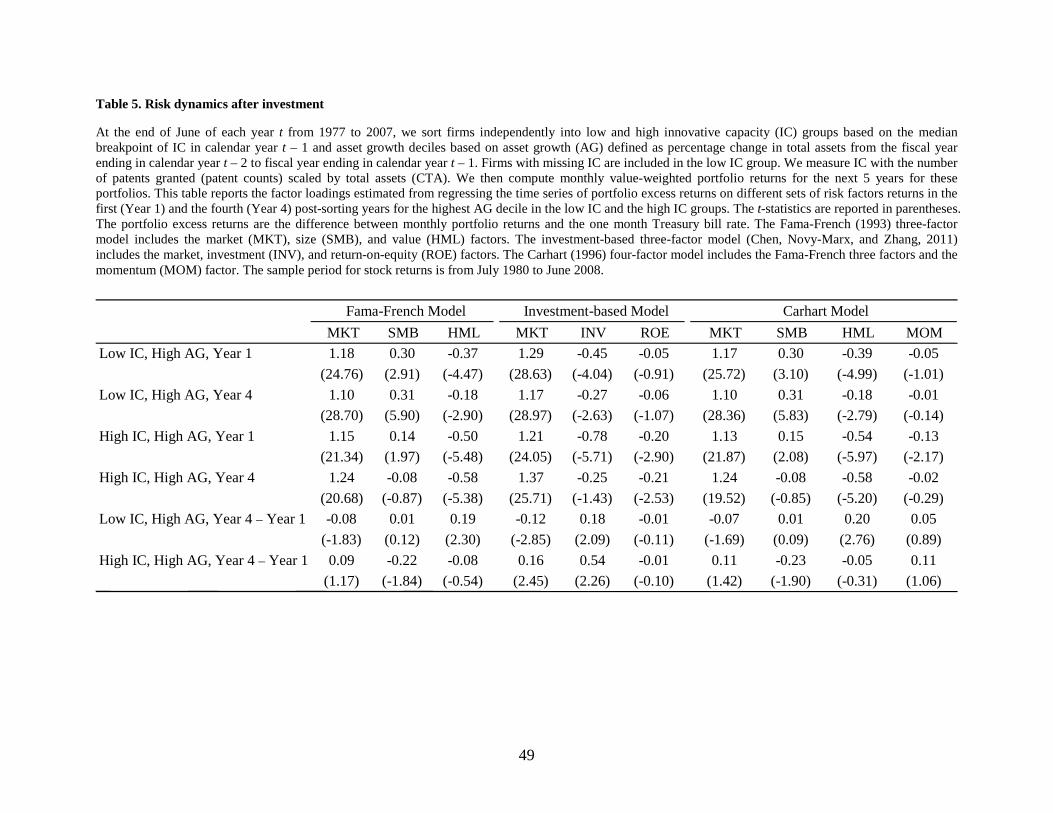

5. Innovative Capacity and Risk Dynamics

In this section, we further examine the hypothesis that asset growth in low IC firms tends

to exercise options and thereby reduce the risk premium, while asset growth in high IC firms

tends to generate new growth options and increase the risk premium. In Appendix A we present

a theoretical real options model where the optimal dynamic investment policy of firms generates

time-varying risk premium that depends on the firms’ IC. Firms with higher IC have both a

greater likelihood of developing new growth options and higher expected cash flow growth

conditional on realizing the innovations. In equilibrium, the change in firms’ market price for

risk subsequent to asset growth is positively associated with their IC (cf. Theorem 1).

To test this prediction, we examine the risk dynamics of the highest AG decile formed in

both IC groups. Specifically, we study the change in factor loadings between the first and the

31

fourth post-sorting years for the highest AG decile formed in the two IC groups. In addition, we

also study the change in factor loadings before and after high asset growth across the IC groups.

Our evidence supports the prediction of the equilibrium time-varying risk premium viewpoint.

In Table 5, we form the IC-AG portfolios using the method described in Section 4.1.2.

Specifically, at the end of June of each year t from 1977 to 2007, we sort firms independently

into low and high innovative capacity groups based on the median breakpoint of IC in calendar

year t – 1 and asset growth deciles based on asset growth in fiscal year ending in calendar year t

– 1. Firms with missing IC are included in the low IC group. We measure IC with the number of

patents granted (patent counts) scaled by total assets. We then compute monthly value-weighted

portfolio returns for the next five years for these portfolios. As shown in Table 3, the AG effect

in low IC firms is significantly negative only in the first post-sorting year, while the AG effect in

high IC firms is insignificant in the first post-sorting year and turns significantly positive as early

as the fourth post-sorting year. Furthermore, the AG effect is mainly driven by the highest AG

decile. Therefore, we only report the factor loadings in the first and the fourth post-sorting years

for the high AG and low IC portfolio (i.e., the highest AG decile formed in the low IC group)

and the high AG and high IC portfolio (i.e., the highest AG decile formed in the high IC group).

Table 5 reports the factor loadings along with changes in the factor loadings estimated

from regressing the time series of portfolio excess returns on different sets of risk factors returns

in the first (Year 1) and the fourth (Year 4) post-sorting years for the highest AG decile formed

in the low IC and the high IC groups. Similar to Tables 2 and 3, we estimate the factor loadings

from the Fama-French three-factor model, the investment-based three-factor model, and the

Carhart four-factor model. Since the fourth post-sorting year starts from 1980, the sample period

32

for stock returns is from July 1980 to June 2008 to ensure the same number of months for the

time series of Year 1 and Year 4 returns.

As there are still debates on whether the size (SMB), value (HML), momentum (MOM),

investment (INV), and profitability (ROE) factors capture systematic risk or mispricing, we

focus on the loading on the market (MKT) factor derived from general equilibrium models.

Furthermore, the investment-based factor model is motivated by the q-theory of investment and

contains an investment factor based on the change in net PPE (property, plant, and equipment)

plus change in inventory scaled by lagged total assets, which is a major component of asset

growth. This suggests that the investment-based model is the most appropriate benchmark in

examining the risk dynamics related to asset growth. However, for completeness, we also report

the loadings estimated from the other factor models.

Consistent with our conjecture that the effect of asset growth on options and risks for low

IC firms is different from that for high IC firms, we find that the loading on the market factor

decreases from Year 1 to Year 4 for the high AG and low IC portfolio, but increases for the high

AG and high IC portfolio. Specifically, for the high AG and low IC portfolio, the changes in

market risk estimated from the Fama-French model, the investment-based model, and the Carhart

model between Year 1 and Year 4 are negative: –0.08 (t = –1.83), –0.12 (t = –2.85), and –0.07 (t

= –1.69), respectively. In contrast, the counterparts of these changes in market risk for the high

AG and high IC portfolio are positive: 0.09 (t = 1.17), 0.16 (t = 2.45), and 0.11 (t = 1.42),

respectively.

33

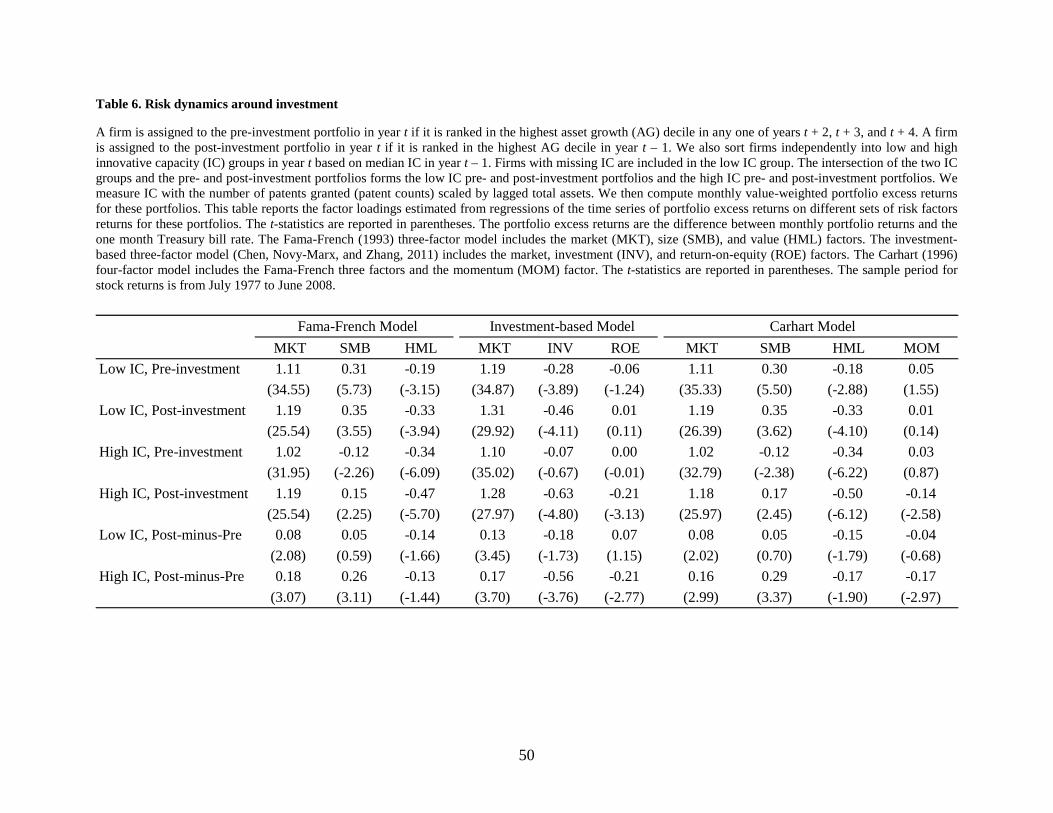

Following Cooper and Priestley (2011), we also examine the change in risk around

investment.14 We define the pre- and post-investment portfolios in the same way as in Cooper

and Priestley (2011). A firm is assigned to the pre-investment portfolio in year t if it is ranked in

the highest asset growth decile in any one of years t + 2, t + 3, and t + 4. Following Cooper and

Priestley (2011), we exclude firms in the top AG decile in year t + 1 from the pre-investment

portfolio due to investment planning (e.g., Lamont, 2000) or time to build (Kydland and Prescott,

1982). A firm is assigned to the post-investment portfolio in year t if it is ranked in the highest

AG decile in year t – 1.

Finally, we sort firms independently into the low and high IC groups in year t based on

the median IC in year t – 1. Firms with missing IC are included in the low IC group. The

intersection of the two IC groups and the pre- and post-investment portfolios forms the low IC

pre- and post-investment portfolios and the high IC pre- and post-investment portfolios. We

measure IC with the number of patents granted (patent counts) scaled by lagged total assets.15

We then compute monthly value-weighted portfolio excess returns for these portfolios.

Table 6 reports the factor loadings along with changes in the factor loadings estimated

from regressions of the time series of portfolio excess returns on different sets of risk factors

returns in the pre- and post-investment periods. The t-statistics are reported in parentheses. The

sample period for stock returns is from July 1977 to June 2008. As in Table 5, we report factor

14 This exercise is mainly for comparison purposes only. In general, this analysis may not capture fully the risk dynamics around investment because firms assigned to the pre-investment portfolio can be very different from firms assigned to the post-investment portfolio in the same year. Furthermore, Cooper and Priestley (2011) examine loadings on non-traded factors, while we focus on traded factors. 15 We scale patent counts by lagged total assets to avoid the confounding effect of asset growth in the same year on the IC measure.

34

loadings estimated from the Fama-French three-factor model, the investment-based three-factor

model, and the Carhart four-factor model; as before, we focus on the market factor loadings.

The results show that the market beta increases after high asset growth for both high IC

firms and low IC firms. However, the increase in the market beta for high IC firms is much

larger than that for the low IC firms. Specifically, the increases in the market betas estimated

from the Fama-French model, the investment-based model, and the Carhart model for the high

IC firms are 0.18 (t = 3.07), 0.17 (t = 3.70), and 0.16 (t = 2.99), respectively. In contrast, the

counterparts of these increases for low IC firms are only 0.08 (t = 2.08), 0.13 (t = 3.45), and 0.08

(t = 2.02), respectively. The increase in market risk after asset growth for the low IC firms may

be because firms assigned to the pre-investment portfolio can be very different from firms

assigned to the post-investment portfolio (based on the method in Cooper and Priestley (2011)).

In sum, the evidence presented in this Section illustrates the effect of innovative capacity

on firms’ risk dynamics. In addition, the results indicate that the decline in loadings on non-

traded factors following high asset growth documented in Cooper and Priestley (2011) may not

generalize to traded factors.

6. Summary and Conclusions

The negative relation between asset growth and subsequent benchmark-adjusted stock

returns attracts much attention because it has profound implications for both market efficiency

and corporate investment policy. In particular, it may indicate mispricing or biased capitalization

of investment by financial markets, or it may indicate an efficient response to lower expected

returns following the exercise of growth options.

35

We motivate and document the importance of firms' innovative capacity (IC) in

understanding the response of financial markets to asset growth. Theoretically, innovative

capacity, which is the ability of firms to produce and commercialize a sequence of innovations,

should influence the evolution of equilibrium expected returns following asset growth. In

particular, expected returns need not fall following asset growth by high IC firms because

investment can generate new growth options. More generally, we construct a sequential growth

options model that predicts a positive relation between the changes in firms' market price of risk

subsequent to asset growth and their IC.

Using patent intensity based measures of innovative capacity, we analyze the effects of

IC on financial markets' response to asset growth and find evidence consistent with the real

options viewpoint. We find that the negative relation between asset growth and subsequent

excess returns holds only for the subset of firms with high asset growth and low IC. High IC

firms with high asset growth rates not only do not suffer negative excess returns subsequent to

asset growth, they actually earn significantly positive subsequent excess returns. Moreover,

changes in the market risk loadings of firms following asset growth episodes are positively

related to their IC. The innovative capacity of firms, therefore, appears to play an important role

in the dynamics between asset growth and returns and in driving the time-variation in their

market risk.

36

References

Ali, A., L.S. Hwang, and M.A. Trombley, 2003. Arbitrage risk and the book-to-market anomaly. Journal of Financial Economics 69, 355-373.

Anderson, C., and L. Garcia-Feijoo, 2006. Empirical evidence on capital investment, growth

options, and security returns, Journal of Finance 61, 171-194.

Berk, J., R. Green, and V. Naik, 1999. Optimal investment, growth options, and security returns, Journal of Finance 54, 1513-1607.

Berk, J., R. Green, and V. Naik, 2004. Valuation and return dynamics of new ventures, Review of Financial Studies 17, 1-35.

Carlson, M., A. Fisher, and R. Giammarino, 2006. Corporate investment and asset price

dynamics: Implications for SEO event studies and long-run performance, Journal of Finance 61, 1009-1034.

Carhart, M., 1997. On persistence in mutual fund performance, Journal of Finance 52, 57-82. Chen, N.F., R. Roll, and S. Ross, 1986. Economic forces and the stock market, Journal of

Business 59, 383-403. Chen, L., R. Novy-Marx, and L. Zhang, 2011. An alternative three-factor model, Working Paper,

Ohio State University. Cohen, W., and D. Levinthal, 1990. Absorptive capacity: A new perspective on learning and

innovation, Administrative Science Quarterly 35, 128-152. Cooper, M., H. Gulen, M. Schill, 2008. Asset growth and the cross section of stock returns,

Journal of Finance 63, 1609-1651. Cooper, I., and R. Priestly, 2011. Real investment and risk dynamics, Journal of Financial

Economics 101, 182-205. Daniel, K., D. Hirshleifer, and A. Subrahmanyam, 1998, Investor psychology and investor

security market under- and overreactions, Journal of Finance 53, 1839-1886. Eberhart, A., W. Maxwell, and A. Siddique, 2004. An examination of long-term abnormal stock

returns and operating performance following R&D increases, Journal of Finance 59, 623-650. Fama, E., and K. French, 1992. The cross-section of expected stock returns, Journal of Finance

47, 427-465.

37

Fama, E., and K. French, 1993. Common risk factors in the returns on stocks and bonds, Journal of Financial Economics 33, 3-56.

Fama, E., and K. French, 1997. Industry costs of equity, Journal of Financial Economics 43,

153-193. Fama, E., and J. MacBeth, 1973. Risk, return and equilibrium: Empirical tests, Journal of

Political Economy 81, 43-66. Ferson, W., S. Kandel, and R. Stambaugh, 1987. Tests of asset pricing with time-varying

expected risk premiums and market betas, Journal of Finance 42, 201-220. Ferson, W., and C. Harvey, 1991. The variation of economic risk premiums, Journal of Political Economy 99, 385-415. Ferson,W., and R. Schadt, 1996. Measuring fund strategy and performance in changing

economic conditions, Journal of Finance 51, 425-461. Furman, J., M. Porter, and S. Stern, 2000. The determinants of national innovative capacity,