Worldwide Market Forecast

186

Worldwide Market Forecast 2020-2040 March 2021 Japan Aircraft Development Corporation

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Worldwide Market Forecast

Worldwide Market Forecast 2020-2040

Worldwide Market Forecast

2020-2040

March 2021

Japan Aircraft Development Corporation

Worldwide Market Forecast 2020-2040

Worldwide Market Forecast 2020-2040

Preface

The aircraft industry is knowledge intensive and has a great ripple effect on industries, making it

effective in advancing the structure of industry as a whole. Accordingly, in Japan, which aims to

become a scientific powerhouse, many efforts have been made for the development and advancement

of the aircraft industry as an essential industry.

It is believed that ongoing information collection and analysis of the world’s commercial aircraft

markets are vital to the further development of Japan’s aircraft industry. Therefore, Japan Aircraft

Development Corporation (JADC) collects and investigates information on the commercial aircraft

markets of the world, including air transportation, aircraft, airlines, and aircraft manufacturers,

forecasting demand for air passengers, air cargo, and aircraft, based on the analysis.

This document, which summarizes our forecasts, is intended to be provided to all parties concerned

as well as to the public through our website (http://www.jadc.jp/en/).

Since 2020, the world has been in disruption caused by the COVID-19 and been forced to fight

against it with no preventive medicine or a cure. And the countries have been striving to prevent and

control infection by severely restricting the movement of people. As a result, demand for both air

passenger transportation and aircraft dropped significantly, causing both airlines and aircraft

manufacturers to face a painful struggle.

At the end of 2020, however, the long-awaited vaccine became available and started to be given

first to medical personnel who are constantly exposed to the virus and others who are at high risk for

infection. Since then, not only the effect of infection prevention, but also the effect of psychological

stability started to be heard, showing the first glimmer of hope that the pandemic will subside.

Looking back in history, airlines around the world have been thrown into disruption and suffered

losses due to terrorism, diseases, and so on in the past. But each time they faced such difficulties, air

transportation demand has always recovered in a curve that converges to the long-term forecast growth

curve made before the disruption occurred within several years of the elimination of the cause.

In this document, for the short term, the time when air transportation demand will start to pick up

is estimated based on the progress of vaccinations and the time when the demand for aircraft will

rebound is also estimated in light of past epidemics or pandemics. While, for the long term, demand

for air transportation and aircraft are estimated on forecasted data such as the GDP data with the impact

of the COVID-19 based on the analysis on actual data for the past 20 years. And this document also

attempts to sort out factors that may be related to the possibility that the world and air transportation

market will have a different character and scale than before after the recovery from pandemic.

March 2021

Japan Aircraft Development Corporation

YGR-5113

Worldwide Market Forecast 2020-2040

Worldwide Market Forecast 2020-2040

Table of Contents

1. Overview ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 1

2. Introduction ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 5

3. Summary of the Airline Industry ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 7

3.3 Until COVID-19 Calms Down ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 19

3.4 After COVID-19 Calms Down ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 27

4. Passenger Aircraft Demand Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 33

5. Air Passenger Demand Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 57

6. Factors Related to Air Transportation ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 83

7. Freighter Aircraft Demand Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 103

8. Air Cargo Traffic Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 111

9. Regional Overview ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 115

10. Airplane Sales Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 155

11. Aero Engine Sales Forecast ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 161

12. Methodology ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 163

Appendix A Definition of Airplane Segments ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 165

Appendix B Definition of Aero Engine Segments ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 166

Appendix C Air Passenger Traffic ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 167

Appendix D Air Cargo Traffic ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 168

Appendix E Airplane Demand ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 169

Appendix F Evaluation of Secondary Demand ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 171

Appendix G Trends in Cargo Transportation Result of Major Airlines ꞏꞏꞏꞏꞏꞏꞏꞏꞏ 172

Appendix H Approach to Successfully Putting SAF on Track ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 174

Glossary of Terms ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 176

Abbreviations ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 177

Reference Materials ꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏꞏ 179

The content pertaining to the impact of COVID-19 is mainly explained in sections 3.3

and 3.4.

Worldwide Market Forecast 2020-2040

Worldwide Market Forecast 2020-2040

1

1. Overview

Long-term forecasts for the demand in the commercial aircraft market provide useful

information for market risk assessment and examination, medium- to long-term business

planning, and product strategy development, to be carried out in the course of conducting

commercial aircraft business. JADC forecasted demand for air passengers, air cargo, aircraft

(passenger jets, passenger turboprops, and cargo jets), and aircraft engines for the 21 years

from 2020 to 2040 using the 2019 level as the baseline, based on our analysis of the data for

the past 20 years.

In 2020, the COVID-19 pandemic brought serious damage to the world economy including the

air transportation sector. This impact is expected to gradually wane over the next several years.

Although airlines around the world have been thrown into disruption due to terrorism, diseases,

and so on in the past, air transportation demand recovered within several years of the

elimination of the cause in a curve that converges to the long-term forecast growth curve made

before the disruption occurred. In this forecast, the impact of the COVID-19 pandemic on air

transportation and aircraft demand has been estimated in the “With” and “Post” COVID-19

period. (Related Part: 3.3 to 3.4)

The world economic growth rate (GDP) in the forecast period is expected to be 2.47% on an

annual average.

(In our forecast we used the GDP data, which strongly influences on air transportation demand, as of the end of 2020 that

takes into account the impact of COVID-19. Thereafter, the IMF, the OECD, and other institutions presented forecasts for a

faster and higher level of recovery by taking into account the effect of the spread of vaccinations. If such forecasts are correct,

air transportation and aircraft demand can be expected to shift to a higher level than our forecast.)

2019 actual 2040 forecast Growth Rate Sales (2019 US$billion)

World Economic Growrh Rate (GDP) 2.47%p.a.

Passenger Demand (RPK :×109 passenger km) 8,486 17,847 3.6%p.a.

Passenger Jet Airplane Fleet 24,015 * 38,868 2.3%p.a.

New Passenger Jet Airplane Deliveries 33,494 5,160

Cargo Demand (RTK :×109 ton km) 253 524 3.5%p.a.

Jet Freighter Fleet 2,023 * 3,041 2.0%p.a.

New Jet Freighter Deliveries 736 225

Total New Jet Airplane Deliveries 34,230 5,385

Passenger Turboprop Airplane Fleet 3,583 * 4,160 0.7%p.a.

New Passenger Turboprop Airplane Deliveries 3,311 73

New Engine Deliveries 82,871 1,213

(*:This data is based on the database of Cirium. )

Worldwide Market Forecast 2020-2040

2

Revenue Passenger Kilometers (RPK) will increase 2.1 times from 8.49 × 1012 passenger km

in 2019 to 17.8 × 1012 passenger km by 2040, with an annual average growth rate of 3.6%

during that period.

(In addition to the already declining growth rate in the Middle East region, in which long-distance routes are mainly operated

[set to an equivalent of 3.1% on an annual average], China is predicted to transit from the fast growing model of developing

country type to the slow growing model of developed country type as a result of an increase in income in the country during

the forecast period [set to an equivalent of 4.5% on an annual average].)

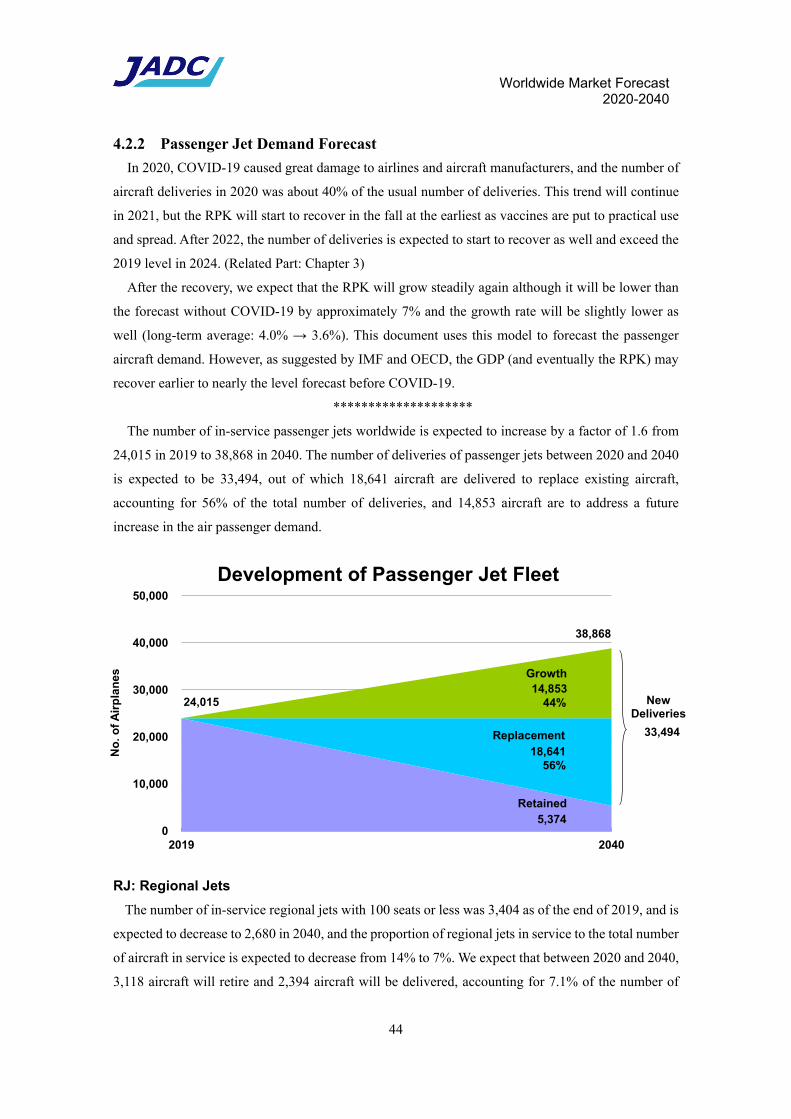

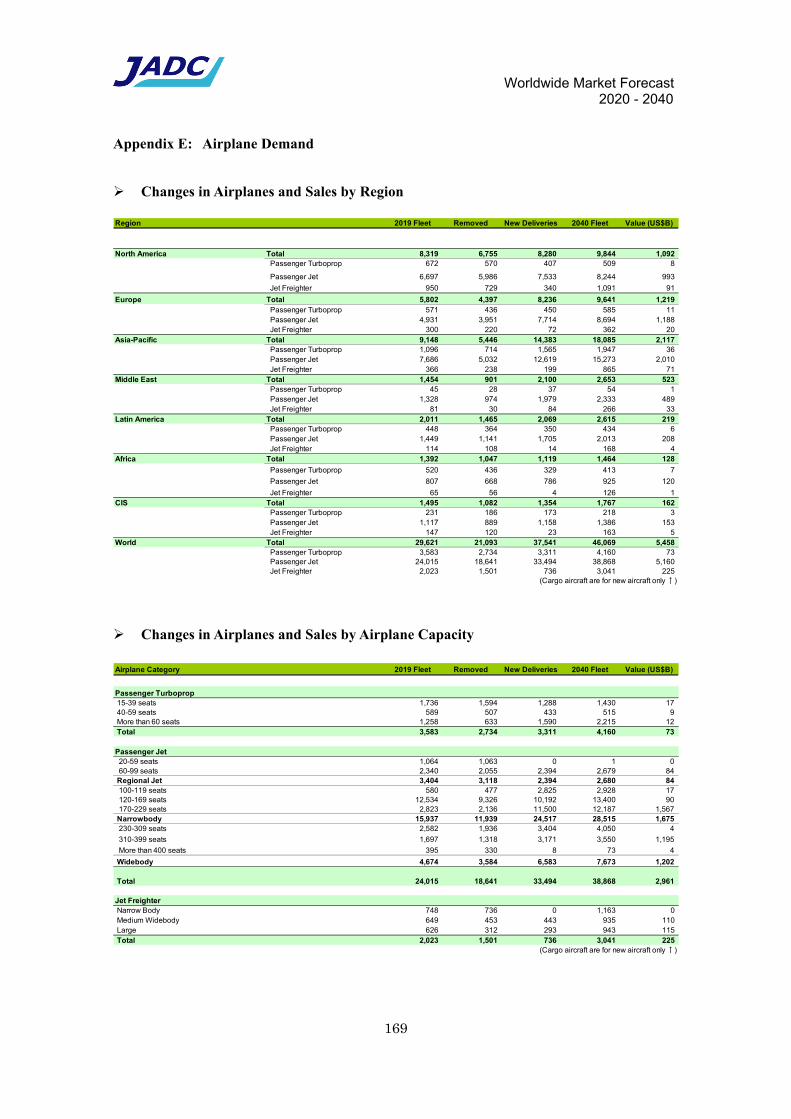

The number of passenger jets in service will increase from 24,015 at the end of 2019 to 38,868

by the end of 2040. The number of new airplanes to be delivered in the next 20 years will be

33,494, with sales of 5.16 trillion dollars (based on the prices listed in the 2019 catalog). The

highest number of new airplanes to be delivered will be the 170 to 229 seat class aircraft, with

11,500 airplanes. By region, North America (23%), Europe (23%), and China (16%) are the

top delivery locations, accounting for 62% of the total airplanes delivered in the world.

The number of passenger turboprops in service will increase from 3,583 in 2019 to 4,160 by

2040. The number of new airplanes to be delivered will be 3,311, with sales of 73 billion dollars

(based on the prices listed in the 2019 catalog). The highest number of new airplanes to be

delivered will be the 60 to 79 seat class aircraft, with 1,206 airplanes. There will be no

particular regions with a high number of airplanes to be delivered, showing a tendency of being

purchased evenly from all over the world, but there will be high demand for new airplanes in

the Southeast Asia (505 airplanes) and South Asia (564 airplanes) regions.

Air Cargo Demand (RTK) will increase 2.1 times from 253 × 109 ton km in 2019 to 524 × 109

ton km by 2040, with an annual average growth rate of 3.5% during that period.

The number of cargo jets in service will increase from 2,023 in 2019 to 3,041 in 2040. The

demand for newly built airplanes will be 736 airplanes (In addition, 1,783 planes will be

converted from passenger jets.), with sales of 225 billion dollars (based on the prices listed in

the 2019 catalog). The breakdown of demand for newly built airplanes will be 293 large jets

and 443 medium wide body jets.

The world engine demand (including spares) will be 82,871 units, amounting to 1.21 trillion

dollars (based on the market price in 2019). The breakdown of the demand is 75,583 jet engines,

with sales of 1.20 trillion dollars, and 7,288 turboprop engines, with sales of 16.1 billion dollars.

Worldwide Market Forecast 2020-2040

3

WorldNew Deliveries

Economy (GDP) 2.47% 37,541

Pax. Traffic (RPK) 3.6% Sales

Cargo Traffic (RTK) 3.3% (2019US$B)

Airline Fleet 2.1% 5,458

Growth Rate

North AmericaNew Deliveries

Economy (GDP) 1.8% 8,280

Pax. Traffic (RPK) 3.0% Sales

Cargo Traffic (RTK) 2.4% (2019US$B)

Airline Fleet 0.8% 1,092

Growth Rate

EuropeNew Deliveries

Economy (GDP) 1.2% 8,236

Pax. Traffic (RPK) 3.5% Sales

Cargo Traffic (RTK) 2.9% (2019US$B)

Airline Fleet 2.4% 1,219

Growth Rate

Asia-PacificNew Deliveries

Economy (GDP) 3.6% 14,383

Pax. Traffic (RPK) 4.5% Sales

Cargo Traffic (RTK) 3.8% (2019US$B)

Airline Fleet 3.3% 2,117

Growth Rate

Latin AmericaNew Deliveries

Economy (GDP) 2.4% 2,069

Pax. Traffic (RPK) 2.7% Sales

Cargo Traffic (RTK) 1.9% (2019US$B)

Airline Fleet 1.3% 219

Growth Rate

Middle EastNew Deliveries

Economy (GDP) 2.1% 2,100

Pax. Traffic (RPK) 3.1% Sales

Cargo Traffic (RTK) 4.4% (2019US$B)

Airline Fleet 2.9% 523

Growth Rate

CISNew Deliveries

Economy (GDP) 1.6% 13,540

Pax. Traffic (RPK) 1.7% Sales

Cargo Traffic (RTK) 3.5% (2019US$B)

Airline Fleet 0.8% 162

Growth Rate

AfricaNew Deliveries

Economy (GDP) 2.8% 1,119

Pax. Traffic (RPK) 2.7% Sales

Cargo Traffic (RTK) 3.6% (2019US$B)

Airline Fleet 0.2% 128

Growth Rate

( Airline Fleet, New Deliveries and Sales in the above graph are the sum of that for passenger jets, passenger turboprops and jet freighters.)

(The terms and abbreviations used in this document are listed on page 176 and subsequent pages.)

Worldwide Market Forecast 2020-2040

4

Intentionally Blank

Worldwide Market Forecast 2020-2040

5

2. Introduction

The development of an airplane takes nearly 10 years from the planning stage to the delivery of the

first airplane, costs some billions of dollars in development costs, and takes years to recover the

investment. Once developed, the airplane will then continue to be produced for several decades

including the development of derived types. And once delivered, the aircraft will be in service as a

long-lasting product, for a decade in a short lifecycle or for over 40 years in a long lifecycle. For this

reason, the aircraft industry is said to be an industry with high business risk.

The airlines to purchase and operate aircrafts are subject to the impact of the economic situation

and social conditions at that time, such as deregulation, privatization, competition with new entrants

such as low cost carriers (LCC), and soaring fuel costs. In order to minimize the business and market

risks in such a business environment, it is important to continue to observe and analyze the trends in

the economic and social environments surrounding the aircraft industry and airlines.

JADC has continued to collect, investigate, and analyze information on the world’s commercial

aircraft markets, including aircraft, air transportation, and airlines and has been forecasting the long-

term demand for air transportation and aircraft since the latter half of the 1970s in order to support for

Japan’s aircraft industry and all other parties concerned to plan long-term product strategies and to

develop long-term business plans.

This edition of "Worldwide Market Forecast," which is a long-term forecast of JADC, covers air

passenger transportation and air cargo transportation in the forecast period of 2020 to 2040, setting

2019 as the baseline for the report, and forecasts the demand for passenger turboprops with 15 or more

seats, passenger jets with 20 or more seats, cargo jets, and aircraft engines. This report is intended to

make the results of our forecast available to the public.

Factors Considered in Demand Forecast

Alternative Means of Transport

Airlines’ Strategies

Aircraft

Air Policy

Environment

Business Models

Travel/Tourism Trend

Economic Trend

Route Network

Oil Price

Infrastructure

Demographics

Long-term Demand Forecast

Worldwide Market Forecast 2020-2040

6

Intentionally Blank

Worldwide Market Forecast 2020-2040

7

3. Summary of the Airline Industry

3.1 Summary of the Airline Business

Global Situation

In 2020, the entire world was affected by COVID-19.

We were required to maintain our economic activities while preventing the spread of infection

without preventive medicine or a cure, so our lives and production activities were subject to various

restrictions. As a result, the world’s real GDP growth rate in 2020 is estimated to be −4.3% (IBRD) to

−3.5% (IMF). On the contrary, the world’s real GDP growth rate in 2021 is expected to be 4.0%

(IBRD) to 5.5% (IMF). Although different organizations give different forecasts, the world’s real GDP

in 2021 is expected to grow and recover to the 2019 level, nearly making up for the economic

shrinkage in 2020. The growth rate is expected to be 3.7% (OECD) to 4.2% (IMF) in 2022, and then,

decrease gradually from 2021 to 2040, averaging 2.87% (IHS). After 2021, if the conditions permit,

the world economy is expected to recover rapidly although it depends on the progress of vaccination.

The airline business experienced a more drastic shrinkage than the overall economy. RPK, which

indicates the actual transportation volume, dropped in 2020 by as much as 66% (IATA) relative to

2019, and is expected to remain around 50% (IATA, Nov. 2020) in 2021.

Generally, an increase or decrease in air transportation demand has a clear correlation with the

increase or decrease in economic activities, based on which various demands are forecast. To prevent

the spread of COVID-19 infection, however, epidemic control measures were implemented. As a result,

immigration on international flights was prohibited or, even if permitted, required self-isolation for a

certain period after arrival and other unusual burdens were imposed, which became a decisive factor

that strongly suppressed the transportation demand. As for domestic flights, although such

immigration restrictions were not imposed, we were requested to refrain from traveling between

different regions and many worried about the health condition of the passengers sitting next to them,

which eventually caused the RPK to fall. In the fight against the invisible virus and people’s anxiety

about it, the RPK fell drastically in 2020, completely separated from its normal correlation with the

GDP and other economic indicators.

The RPK and revenue of the airline business disappeared due to this pandemic, and we were forced

to wait for about two years until collective immunity was reached. During this period, financing is a

matter of life and death to airlines, which are currently making every effort to overcome it, going so

far as to sell their aircraft, postpone or cancel the delivery of aircraft they ordered, and lay off their

employees. Also, aircraft manufacturers, which should be thought of as airlines’ counterparts, are

forced to reschedule their delivery or significantly reduce their production. Amid such a situation, the

first emergency use of the long-awaited vaccines started in December 2020, about one year after the

emergence of COVID-19. Although there are concerns about things such as there being a short supply,

Worldwide Market Forecast 2020-2040

8

the vaccines are expected to be a trump card against COVID-19, and the diffusion of vaccines has

been incorporated into each institution’s GDP forecast. We expect that if vaccination proceeds

smoothly, the RPK of domestic and regional flights in major developed countries will start to recover

in 2021, and the revenue, including that from some international flights, will recover considerably in

2022.

Current Situation of the Airline Business

With regard to the global air transportation demand in 2020, IATA (Nov. 2020) estimates that the

passenger transportation volume (RPK) and operating profit will drop by 66.3% and 338%,

respectively, compared to the previous year. Then, looking at the financial results for 2020, the total

sales of all the airlines in the world is 328 billion dollars, smaller than the previous year by 60.9%,

and the net profit is 118.5 billion dollars, suffering a record deficit. In this situation, the revenue from

passengers dropped by 68.8% compared to the previous year but the revenue from cargo transportation

rose by 14.9%, resulting in a decrease in the total revenue by 56.8%.

The unit price of fuel dropped by 43%, but the passenger yield also dropped by 8.0% compared to

the previous year. Despite such a drastic drop in the RPK, the passenger load factor was maintained at

65.5%, but because of a significant shortage in cargo transportation capacity (lower hold in passenger

flights) due to a significant decrease in passenger flights, the cargo yield recorded a significant increase

by 30% compared to the previous year.

The net profit to sales ratio was significantly negative in every region.

Trends in Air Passenger Transportation Volume (RPK) and Sales Profit

Operating profit (× 109 dollars)

RPK (× 1012 passenger km)

Operating profit

Worldwide Market Forecast 2020-2040

9

According to the Ministry of Land, Infrastructure, Transport and Tourism (Nov. 2020), the year-to

date RPK of Japanese airlines in 2021 dropped by 55.4% for domestic flights and 78.9% for

international flights from the previous year. If limited to the period after the declaration of a state of

emergency in April, the RPK dropped by 68.9% for domestic flights and 95.8% for international

flights.

Net Profit to Sales Ratio of Airlines

Ne

t p

rofi

t to

sa

les

ra

tio

(%

)

Africa Asia Pacific Middle East Central andSouth America

North America Europe

Worldwide Market Forecast 2020-2040

10

3.2 Aircraft Orders and Deliveries

As of the end of 2019, 24,015 passenger jets, 3,583 passenger turboprops, and 2,023 cargo jets were

in service in the world.

As of the end of 2020, according to the database, 18,317 passenger jets, 2,773 passenger turboprops,

and 2,117 cargo jets were in service, however in actual, many of them were stationed on the ground

due to COVID-19 and there were many surplus aircraft, greatly affecting aircraft orders and deliveries.

The number of passenger planes in storage that can possibly be returned to service was 3,314 at the

end of 2019 and increased to 9,403 at the end of 2020.

Order Situation

The annual number of orders*4 for variants for passenger jets*3, cargo jets, etc. were 570 in 2020

and dropped by 1,002 compared to the previous year. In addition to the decrease in the number of

orders due to the suspension of delivery of the 737MAX beginning in 2019 (the number of orders

dropped by 741 compared to 2018, out of which 553 aircraft were 737MAX), COVID-19 dictated the

order situation in 2020.

Among the aircraft ordered, 77 aircraft are wide body jets (the number of orders for wide body jets

accounts for 14% of the total number of orders in 2020, dropping by 314 compared to 2019), 489

aircraft are narrow body jets (the number of orders for narrow body jets accounts for 86% of the total

number of orders in 2020, dropping by 484 compared to 2019), and 4 aircraft are regional jets (the

number of orders for regional jets accounts for 0.7% of the total number of orders in 2020, dropping

Trends in Orders*2 for Jets*1 No. of orders

Source: Airbus, Boeing, Bombardier, Embraer, Cirium, JADC (Some estimates are included.)

Other

Embraer

Bombardier

Boeing

Airbus

*1) Passenger planes (including combi and quick-change) and its variants (cargo, military, etc.)

*2) Net orders. Canceled orders have been subtracted from the number of orders in the year when each order was placed.

Worldwide Market Forecast 2020-2040

11

by 183 compared to 2019). Among the wide body jets ordered, the number of orders for variants for

cargo jets etc.*5 in 2020 is 23 (dropped by 5), and the number of orders for major passenger turboprops

in 2020 is 5 (dropped by 74).

(*3: Including combi aircraft and quick change aircraft)

(*4: Actual number of aircraft orders, which is obtained by subtracting

the number of canceled orders from the nominal number of orders)

(*5: Including cargo jets, VIP aircraft, and aerial refueling aircraft)

Delivery Situation

The annual number of deliveries of jets in 2020 is 821, decreasing from 1,377 in the previous year

by 556. The numbers of deliveries of jets by Airbus and Boeing decreased by 297 and 223, respectively.

The decrease in the number of deliveries by Boeing is partly attributable to the suspension of

delivery of the 737MAX from March 2019, but the delivery of the 737MAX was resumed in December

2020, since which 43 737-series aircraft have been delivered in total (of which 27 aircraft are

737MAX). During this period, Airbus delivered 446 A320-series aircraft (642 aircraft in 2019). With

regard to cargo jets*2, 46 aircraft were delivered in 2020 (52 aircraft in 2019). With regard to major

passenger turboprops, 32 aircraft were delivered in 2020 (89 aircraft in 2019).

(*2: Newly build wide body cargo aircraft. The number is out of the number of jets delivered.)

Trends in Deliveries of Jets*1

*1: Passenger planes (including combi and quick-change) and its variants (cargo, military, etc.)

Other

Embraer

Bombardier

Boeing

Airbus

No. of deliveries

Worldwide Market Forecast 2020-2040

12

Backlog Situation

The number of backlogs for passenger aircraft and cargo aircraft began increasing in 2005, when

the crude oil (fuel) price began skyrocketing. The number of orders for energy-efficient new aircraft

rose beyond the production capacity and the number of backlogs continued to rise year by year until

2013 and 2014 which were said to be a bubble in the aircraft manufacturing industry. After 2015, when

the crude oil price dropped sharply, the number of orders decreased and became almost the same as

the number of deliveries, bringing the number of backlogs into a stable state. At the end of 2019, the

total number of backlogs for passenger jets and variants such as cargo jets, etc. is 14,525.

When the COVID-19 pandemic began in 2020, the transportation demand dropped rapidly and the

financial health of airlines deteriorated rapidly, resulting in the cancellation of some aircraft orders.

The total number of backlogs for passenger jets and variants such as cargo jets, etc. as of the end of

2020 was 13,450, dropping by 1,075 from the end of the previous year, but no noticeable changes were

seen in the backlogs share by region.

Worldwide Market Forecast 2020-2040

13

(In this chart, the backlogs in the Middle-East before 2007 is included in “Other.”

Asian-Pacific

North America

Other

Middle-East

Europe

Number of Backlogs by Region (Cumulative) (No. of backlogs)

Number of Backlogs by Region

Share of Backlogs by Region

Other

Middle East

Asia Pacific

North America

Europe

(No. of backlogs) Europe

North America

Asia Pacific

Middle East

Other

Other

Middle East

Asia Pacific

North America

Europe

Worldwide Market Forecast 2020-2040

14

Looking at the distribution of firm orders (backlogs) for passenger jets, there is a characteristic

tendency that the delivery of ordered aircraft is postponed.

Distribution of firm orders for passenger jets (RJ + NJ + WJ): At the end of 2019, orders for

more than 1,500 aircraft were secured for the next year's scheduled delivery, and from the next year

onward, the number of confirmed orders gradually decreased while leaving room for sales activities.

In 2020, however, only 42% of aircraft scheduled to be delivered as of the end of 2019 were delivered.

In addition, the number of firm orders for delivery in 2021 or later dropped below 1,100 per year.

In the chart, this decrease in the number of firm orders appears as the postponement of deliveries,

and the annual number of firm orders increases from 2025 to 2027 by nearly 300, and after that, over

120 aircraft are scheduled to be delivered every year until 2034, showing the trend that deliveries are

postponed but are not easily canceled. In a similar trend, there are many cases where an order is

maintained but the delivery date is left open, and as a result, the number of such ‘open’ orders at the

end of 2020 increases by approximately 400 from the previous year.

The total number of firm orders after 2020 is 9,813 as of the end of 2019 (including 273 planes

whose delivery date is undetermined), but as of the end of 2020, it decreases to 9,398 (including 703

planes delivered in actual in 2020 and 644 planes whose delivery date is undetermined).

Distribution of firm orders for Widebody Jets (WJ): With regard to wide body jets, the number

of planes scheduled to be delivered in 2020 was 307 as of the end of 2019, but that of delivered in

actual was 142 (46%). The number of planes scheduled to be delivered for 2021 to 2022 decreases to

around 160. The chart shows that this decrease appears as the postponement of deliveries to 2023 and

subsequent years, and the number of planes scheduled to be delivered in each year for 2023 to 2025 is

nearly 200, which is larger than that for 2019. After that, the number of firm orders in each year

decreases and returns to almost the same level as 2019 in 2027.

The total number of firm orders for 2020 to 2039 is 1,538 (including 99 planes whose delivery date

is undetermined) as of the end of 2019, but has decreased to 1,450 (including 142 planes delivered in

actual in 2020 and 147 planes whose delivery date is undetermined) as of the end of 2020.

While 142 planes delivered in actual in 2020, 167 planes are scheduled to be delivered in 2021 and

152 planes scheduled in 2022. These are nearly the same as the number of aircraft delivered in 2020

and is considered to be a feasible level reached as a result of coordination between airlines and

manufacturers.

Distribution of firm orders for Narrowbody Jets (NJ): The number of planes scheduled to be

delivered in 2020 was originally 1,135, but 474 planes (42%) were delivered in actual.

The numbers of planes scheduled to be delivered for 2021 to 2023 decrease but the chart shows that

this decrease appears as the postponement of deliveries to 2024 and subsequent years.

Worldwide Market Forecast 2020-2040

15

Distribution of Firm Orders for Passenger Jets (RJ + NJ + WJ)

Planned year of delivery

Distribution of Firm Orders for Widebody Jets (WJ)

Distribution of Firm Orders for Narrowbody Jets (NJ)

No. of firm orders/year

No. of firm orders/year

No. of firm orders/year

This indicates the sum of the number of deliveries in 2020 and the number of backlogs for 2020. D

eliv

ery

da

te

un

dete

rmin

ed

Result for 2020

De

live

ry d

ate

u

nde

term

ined

D

eliv

ery

da

te

un

dete

rmin

ed

Result for 2020

Planned year of delivery

Planned year of delivery

Worldwide Market Forecast 2020-2040

16

The numbers of planes scheduled to be delivered for 2025 to 2027 are larger than that originally

scheduled during this period by 200 to 300 in each year, and this trend continues until around 2035*.

(*: The increase in the number of planes scheduled from 2030 to 2035 is mainly

contributed by airlines in Southeast Asia and India.)

The total number of confirmed orders since 2020 is 7,703 as of the end of 2019 (included 166 planes

whose the delivery date is undecided), but has decreased to 7,492 as of the end of 2020 (including 474

planes delivered in actual in 2020 and 342 whose delivery date is undecided).

The number of narrow body jets scheduled to be delivered in 2021 is 764, which is 290 more planes

than that of delivered in actual in 2020, a 1.6-fold increase. However, the RPK just started to recover

in 2021, and airlines will probably be struggling with severe financial hardship. Therefore, there is

some doubt about whether or not the delivery of this number of narrow body jets is feasible.

Negotiations between airlines and manufacturers are probably ongoing.

The planned monthly productions of Airbus and Boeing aircraft for 2021 and 2022 are shown in the

next section. For wide body jets, the planned annual production for 2021 and 2022 is 168 each year,

which is almost consistent with the numbers of wide body jets scheduled to be delivered in 2021 and

2022 (167 to 152). For narrow body jets, the planned production for 2021 is 720*1, which is almost

consistent with the number of scheduled to be delivered in 2021 (764). Both companies plan to

increase the production of narrow body jets in 2022, and the planned annual production is 1,080

planes*1, which is larger than 814 planes scheduled to be delivered for the year. And the number is

close to the number of firm orders for 2022 as of the end of 2019, i.e., before the emergence of COVID-

19*2. (*1: In addition to this, shipments of 737 MAX in stock will be added.) (*2: Related Page: P. 50)

2021 2022

Airbus Boeing Monthly

production (total)

Annual production

Airbus Boeing Monthly

production (total)

Annual production

Widebody Jet 2+5 2+5 14 168 2+5 2+5 14 168

Narrowbody Jet 5+40 15 ? 60 720 14+45 31 90 1080

(This table is an excerpt from the table below.)

Production Situation

As shown in the section describing the delivery situation, passenger plane manufacturers had been

increasing their production capacity year by year since 2005. For example, in 2019, Airbus and Boeing

planned to produce 50 to 60 planes to accommodate the orders for A320- and 737-series narrow body

jets. However, the delivery of the 737MAX was suspended in 2019, after which the numbers of planes

produced and delivered decreased remarkably. In addition, in 2020, the air transportation demand

dropped rapidly due to the COVID-19 pandemic, dealing significant damage to airlines that resulted

in financial difficulties that threatened their existence. As a result, many deliveries have been

postponed, and aircraft manufacturers have been forced to reschedule their production plans and have

Worldwide Market Forecast 2020-2040

17

announced that they will reduce the production of each model.

No. of deliveries

made in 1st half

Nominal monthly production Nominal monthly production

2018 2019 2020 2021 2022

Q1 Q2 Q3 Q4 No. of

deliveries made

Q1 Q2 Q3 Q4 No. of

deliveries made

Q1 Q2 Q3 Q4 No. of

deliveries made

Q1 Q2 Q3 Q4 Plan Q1 Q2 Q3 Q4 Plan

737 (NG+MAX)

52 580 52 40 127 34 Production increased from

a single-digit figure.

Target: 31 aircraft per month by Q1

9 Production of MAX resumed on May 27. 43

767 14 16 30 3 3

777&777X 4.5 48 4.5 45 10 16 (5) 26 2 2

787 14 145 14 157 36 17 (10) 53 6 → 5 5

A220 33 48 11 27 (4) 38 4 5 14

A319 8 6

157

289 (40)

3

40

43

45

45 A320 417 430 256

A321 201 206 187

A330 49 53 5 14 (2) 19 2 2

A350 93 112 23 36 (5) 59 5 5

737MAX: The monthly production was originally 52. The service and delivery were suspended in

March 2019. After April 2019, the shipment of the 737MAX was suspended but 40 aircraft were

produced per month to maintain the supply chain. The production of the 737MAX was suspended

in January 2020, and then resumed production in May and delivery in December. While

producing new 737MAX aircraft, Boeing will accelerate the modification and delivery of about

400 backlogged 737MAX aircraft produced in 2019, which, however, is expected to take about

two years. In 2021, Boeing will gradually accelerate its production, aiming to achieve a monthly

production of 31 aircraft by Q1 2022. For the 737MAX10, the Entry Into Service (EIS) is

scheduled in 2023 after countermeasures for the accident have been incorporated.

787: Due to the trade conflict between the United States and China, a reduction in production had been

planned before the COVID-19 pandemic, and was reduced further after COVID-19 started

spreading. In 2020, 787s were found to have manufacturing defects in their horizontal stabilizer

and fuselage. To address them, the delivery of 787s was suspended in November 2020 but

resumed in March 2021.

Old plan: Monthly production 12 (current) → 10 (late 2020) → 10 to 8 (2021) → 7 (2022)

New plan: Monthly production 6 (late 2020) → 5 (2021) → 5 (2022)

777X: The EIS was rescheduled from 2020 to late 2023 mainly because of a delay in engine

development, the rapidly decreasing demand for aircraft due to the COVID-19 pandemic, and the

increasingly stringent certification requirements and engineering changes after the 737MAX

accident. (For this reason, a delay of more than one year is expected in the delivery of some firm

orders, and as a result, the right of cancellation arises on the ordering party side.) Including the

production of 777 cargo aircraft, the monthly production of 777s and 777Xs will be reduced to 2

by the end of 2021.

No. of deliveries made in 2nd half (nominal monthly production)

Worldwide Market Forecast 2020-2040

18

A320 series: The target monthly production of A320 series aircraft (A319, A320, and A321) was

originally 60, but was decreased to 40 in 2020. Airbus plans to accelerate production after Q3

2021 and increase the monthly production to 45 in 2022.

A330: Airbus originally planned to produce 40 A330neo aircraft in 2020 (equivalent to a monthly

production of 3.3 aircraft), but delivered only 19 aircraft. Airbus decided to reduce the monthly

production to 2 after Q3 2020.

A350: Airbus originally planned to produce 9 or 10 A350XWB aircraft per month but decided to

reduce the monthly production to 5 after Q3 2020.

********************

The chart below shows the number of deliveries, planned production, backlogs for each year, and

forecasts of wide body jets.

We expect that the number of deliveries of wide body jets will start to recover in 2023 after

decreasing due to the COVID-19 pandemic. However, since a delay is expected in the recovery of the

GDP (or the RPK), the number of deliveries of wide body jets will probably remain below the level

before the COVID-19 pandemic for the time being, and be an average of around 300 per year until

around 2030. (Related Part: 4.2.2)

0

100

200

300

400

500

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

unit/year Delivery of Widebody Jets(Actual & Forecast)Backlog(End of 2019)Backlog(End of 2020)Delivered+Planned

Forecast(JADC)Forecast(averaged)

Worldwide Market Forecast 2020-2040

19

3.3 Until COVID-19 Calms Down

Airlines in the world have so far experienced disruptions such as terrorism and the pandemic, but

after the cause of each disruption was eliminated, the transportation demand recovered and returned

to the growth curve, predicted before the disruption, within several years. This section estimates the

path to overcoming COVID-19 and the influence of COVID-19, focusing on things that can be

determined from actual data.

Current Situation

Since the emergence of COVID-19, our world has been forced to fight against it without preventive

medicine or a cure. To block the spread of infection, each country is restricting movement of people,

and the demand for transportation, especially transportation on international flights, disappeared,

depriving airlines of a large part of their profits. Even in this situation, airlines are forced to spend a

lot of money every month and securing enough operating capital is a vital challenge to them. They are

making every effort to address this situation, such as getting loans from financial institutions, selling

their aircraft to get cash, laying off their employees, and trying to postpone payments for their ordered

aircraft by postponing the delivery of them. Amid this situation, the first emergency use of the long-

awaited vaccines started in some countries in December 2020. However, the vaccine production

capacity is still insufficient, and it probably will not be until late 2021 at the earliest that the air

transportation demand will recover after collective immunity is established in each country.

Cost Structure

According to Airlines for America (A4A), the operating expenses of American airlines in Q4 2019

directly related to flights include fuel expenses (18%), transportation-related expenses (13%), and

landing fees (2%). With no flights, these expenses, or 33% of the total expenses, may be unnecessary,

but the reality is that 67%*1 of the total expenses remain, so airlines are trying to cut these remaining

expenses by laying off employees and reducing the number of new hires.

(*1: Labor expenses account for 33% out of the 67%.)

The expenses necessary to own aircraft (e.g., depreciation expenses, lease expenses) account for

7%. In addition, not only that, if an ordered aircraft is delivered, the airline is required to spend billions

of yen*2 to receive it. (*2: For small narrow body jets)

Recovery of Demands and Orders

Currently, the delivery of many new aircraft has been postponed, and manufacturers have decided

to reduce production. The number of planes delivered in 2020 is in the 40% range of originally planned.

The demand for new aircraft depends on the balance between the increase in number of passenger

planes required to address a growing transportation demand and the decrease in number of planes in

service due to retirement of them. Currently, however, because of the influence of COVID-19, the

Worldwide Market Forecast 2020-2040

20

transportation demand has disappeared and airlines are forced to reduce their flights and leave many

of their aircraft on the ground. Because airlines have many surplus aircraft, there is no demand for

new aircraft. After that, the recovery of demand for new planes follows the recovery of transportation

demand (RPK), but the delivery of planes already ordered will be resumed first, and the new orders

will be made after the financial condition of airlines is further improved.

Past Epidemics

In the past 20 years, we have experienced two world-wide epidemics, SARS (in 2003) and Pandemic

H1N1 2009 (in 2009). The following looks back over these epidemics.

SARS (2003):

Name: Severe acute respiratory syndrome (SARS)

Symptoms: Severe atypical pneumonia

An outbreak is likely to occur with close contact with infected people.

Cause: Novel coronavirus (SARS-CoV)

Emergence: November 16, 2002 (Guangdong province, China)

Termination: On July 5, 2003, the WHO declared that SARS was under control.

Affected areas: 8,096 cases in 32 regions and countries (774 deaths)

(Excerpt from an article of the National Institute of Infectious Diseases (NIID))

https://www.niid.go.jp/niid/ja/kansennohanashi/414-sars-intro.html

-6

-4

-2

0

2

4

6

8

-60

-40

-20

0

20

40

60

80

1996 2001 2006 2011 2016

Operating Profit

Net Profit

RPK

Order

RPK, Profit, Ordersat the previous epidemicsProfit

(×10 9 US$ )PPK ( ×10 12 )

Orders ( ×10 3 )

Source : IATA, ICAO, Airbus, Boeing, Bombardier, Embraer

Skyrocketing Fuel Prices

European Debt Crisis911 SARS Financial Crisis

2009H1N1

Resuming Orders

(2005)

RPK initial Recovery

(2004)

Resuming Orders

(2011)

RPK initial Recovery

(2010)

after Pandemic 2009H1N1after SARS

Worldwide Market Forecast 2020-2040

21

SARS emerged before the wounds inflicted by the 9/11 attack was healed, and made the process of

RPK recovery from the incident prolonged.

The termination of SARS itself was declared in summer 2003. In the RPK recovery process after

the termination, the RPK dropped to 87% of its expected value*1 in 2003, but increased to 95% in

2004, showing a remarkable initial recovery. Furthermore, (despite the rocketing rise in the fuel price,)

the RPK continued a gradual recovery until 2007, eventually to 98.7% of the expected value*2.

In this recovery process, the airline business moved back into the black (although the surplus was

small) in terms of operating profit in 2004, and in 2006, moved back into the black in terms of net

profit. During this period, orders recovered drastically*3 in 2005 and returned to the level before the

9/11 attack.

(*1: The growth curve of the RPK through 1999 was extrapolated based on the average growth

rate from 1999 to 2019.)

(*2: After 2008, the RPK dropped again due to the disruption caused by the Global Financial

Crisis.)

(*3: It is natural that the return to profitability led to the recovery of orders, but in addition, it

became clear that crude oil prices began to rise in 2005, and airlines with sufficient sales

and financial resources seemed to have begun to order new models with excellent fuel

efficiency.)

H1N1 (2009)

Name: Pandemic (H1N1) 2009

Symptoms: Sore throat, soaring fever, cough, runny nose, fatigue, etc. H1N1 cannot be

distinguished from seasonal flu. The fatality rate in Mexico was 0.4 to 0.5%, which

is higher than the 0.05% of seasonal flu, and is almost the same as that of Asian flu.

More than half of those who died from H1N1 had underlying diseases, such as

asthma, diabetes, heart diseases, and diminished immune systems.

Cause: Novel influenza (Influenza A (H1N1) pdm: AH1pdm)

Emergence: April 12, 2009 (reported in Mexico)

Termination: In Japan, the H1N1 epidemic ended in March 2010.

(Excerpt from an article of the National Institute of Infectious Diseases (NIID))

https://idsc.niid.go.jp/iasr/30/356/tpc356-j.html etc.

The H1N1 influenza epidemic occurred during the process of recovery from the disruption due to

global financial crisis in 2008, and airlines were influenced by the H1N1, the financial crisis and the

skyrocketing fuel prices at the same time.

Worldwide Market Forecast 2020-2040

22

The H1N1 epidemic itself ended in spring 2010. Comparing the subsequent RPK recovery process

with the expected RPK value for each year, the RPK bottomed out at 87% of the expected value in

2009 but saw an initial recovery from 2010 to 2011, recovering to 90.6% and 92.4% respectively of

the expected values. During this period, the fuel prices stayed high, which affected the recovery of the

RPK. However, the RPK continued a gradual recovery until 2014 and eventually reached 95.7% of

the expected value.

In the recovery process, the airline business moved back into the black in terms of operating profit

in 2010, and orders began recovering in 2010 and, in 2011, returned to the level before the H1N1

epidemic and financial crisis.

Recovery from COVID-19

From these two cases, the recovery pattern can be read as follows:

- An epidemic having calmed down, the RPK immediately begins recovering and the ‘initial recovery’

ends by the end of the following year.

In the case of SARS, the RPK recovered to 95% of the expected value.

- Following the initial recovery, the RPK continues a gradual recovery for about three years. In the

case of SARS, the RPK recovered to 99% of the expected value.

- The airline business moves into the black in terms of operating profit after the initial recovery of the

RPK, and in the following year, moves into the black in terms of net profit and sees a recovery in

new aircraft orders.

Based on the above, the process of recovery from COVID-19 can be presumed as follows:

- Vaccines, the trump card against COVID-19, were developed speedily thanks to the efforts of those

involved, and the emergency use of some vaccines was started at the end of 2020. However, it will

probably take at least the full 2021 to spread vaccines and establish collective immunity on a

regional scale even in areas with fast progress such as developed countries. In developed countries,

the recovery of domestic and regional flights will proceed during this period, and after that, the

recovery of international flights between the vaccinated developed countries, such as Atlantic routes,

will take place. We expect that the demand for international flights will begin recovery when each

country relaxes its epidemic controls by confirming the level of collective immunity in destination

countries. However, it will take a long time for vaccinations to spread in developing countries, and

it will take another two or three years for the RPK to recover completely all over the world.

- The RPK will begin to recover in Q3 or Q4 2021 with the start of vaccination, but the RPK for the

full year 2021 will be still low as it lacks the contribution before Q3*1. The initial recovery is

expected to take place from 2022 and 2023, mainly in domestic and regional flights*2. It will be

Worldwide Market Forecast 2020-2040

23

around 2022 that the operating balance and financial power of airlines begin recovery and the

number of deliveries of backlogs starts to increase.

(*1: The RPK is expected to be 50% of the 2019 level. [IATA])

(*2: The RPK for 2022 is expected to be 75 to 80% of the 2019 level. [JADC. See the next section.])

- New orders for passenger planes are expected to resume in 2023, the year following the return of

airlines to profitability due to the initial recovery of RPK.

0

5,000

10,000

15,000

20,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

RPK(×10 9) Recovery of RPK from COVID‐19 (projection)

RPK(Actual Value)RPK(Forecast : Standard Model)RPK(Expected in the past) Projected deficit due to COVID‐19

Worldwide Market Forecast 2020-2040

24

RPK Recovery Models

Forecasts from 2021 to 2023

(JADC)

NA: North America, WE: Western Europe, EE: Eastern Europe, ME: Middle East

JA: Japan, OC: Oceania, NE: Northeast Asia, SE: Southeast Asia, AF: Africa

RPK (by route, compared to the same month of 2019)

Europe – Other regions Vaccination rate

RPK (by route, compared to the same month of 2019)

North America – Other regions

RPK (by route, compared to the same month of 2019)

China – Other regions

Results from January to December 2020 (IATA)

Within Europe North America (Atlantic route)

Vaccination rate

Within North America

Europe (Atlantic route)

Within China

Worldwide Market Forecast 2020-2040

25

Some of the RPK recovery models used for the analysis in the previous section are shown here.

Even in developed countries that are leading the way in securing vaccines, the vaccination to the

general public of the working-age generation, who are the main passengers of airlines, are expected to

be started after 2021Q2 at the earliest, since many countries give priority of vaccination for medical

personnel and the elderly. Therefore, we expect that the recovery of RPK resulting from vaccinations

will not proceed satisfactorily in the first half of 2021 but will be proceed in the last half of 2021.

Collective immunity is said to begin when the vaccination rate reaches about 70% of the population

of each country. In addition, at that situation, when you get on board a domestic flight, passengers

sitting next to you are highly likely to have been vaccinated. You will regain trust in your immunity

and have high expectations for the collective immunity of the general public and the health of their

neighbors, and use airlines on the sense of security. As a result, the RPK of domestic flights in

developed countries and flights within Europe is expected to rapidly recover especially from Q4 in

2021 or Q1 2022 at the latest. Likewise, international flights between developed countries will recover

about one quarter behind domestic flights and the RPK is expected to reach the normal level for most

of 2022 although this depends on the situation in destination countries.

On the other hand, vaccine acquisition is slow* and the number of infected patients has not

decreased in developing countries and such regions. To these countries, prevention measures by

vaccinated countries will be maintained to restrict traffic. As a result, the recovery of the RPK of

international flights with these countries will be slow. Hopefully, these countries will also obtain

sufficient vaccines in a few years as vaccine production including licensed production increases

around the world.

(* Emerging countries may experience more delays in vaccine acquisition due to lack of their purchasing power and

production power. In addition, if the duration of the antibody by the vaccine is not long, the vaccine will be procured

repeatedly for developed countries to make subsequent rounds of inoculation, and will be in short supply for developing

countries to procure. If the world must deal with new variants, the same thing may happen although this should be

addressed through production increase.)

The chart below shows the actual RPK of domestic flights. Although the RPK dropped below 20%

in each country when the pandemic started, the RPKs of domestic flights have often recovered to 40

to 60% of the normal level even before vaccinations spread, particularly in countries with large land

areas where airplane transportation is essential to living, indicating that the demand for transport is

solid.

Worldwide Market Forecast 2020-2040

26

In this document, the global RPK is expected to recover to 45 to 50% of the 2019 RPK in 2021,

75 to 80% in 2022 (start of the initial recovery) ,based on the assumed recovery models and the

composition ratio of each route in the global RPK at normal times. If vaccinations proceed smoothly,

the global RPK will recover to 90 to 95% in 2023 (completion of initial recovery), hopefully

exceeding 100% in 2024.

Maintenance of Airlines’ Transportation Capacity

Influenced by COVID-19, the airline industry has been suffering hardship for more than one year,

continuously facing financial difficulties. In response to this situation, airlines have reduced the

number of aircraft and cut their workforce. Airlines cut their workforce little by little through attrition

or early retirement, avoiding large-scale downsizing. Many airlines used government subsidy

programs to keep their employees, but some airlines and airport companies have announced that they

will start large-scale downsizing if such government subsidy programs are terminated*1.

(*1: Around fall 2020, some airlines announced that they decided to cut their workforce by 20% or so.)

Therefore, in 2020, airlines had almost the same numbers of aircraft and employees as in 2019, and

only the demand for passenger transportation dropped, but in 2021, airlines may be forced to dispose

of some aircraft and cut their workforce, resulting in a potential decrease in their available

transportation capacity, or ASK.

In the latter half of 2021, the RPK of domestic flights in developed countries is expected to begin

recovering, but if there is a delay in airlines recruiting staff, the ASK, which decreased temporarily

due to the reduced numbers of aircraft and employees, will probably be used up, resulting in a slight

delay in the recovery of the RPK to the 2019 level.

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12

% 国内線RPKの推移 (対2019年同月比:2020年1~12月)

China

Russia

Brazil

Japan

India

United States

Australia

Within Europe

Source:IATA

Trends in RPK of Domestic Flights (compared to the same month of 2019: January to December 2020)

Worldwide Market Forecast 2020-2040

27

3.4 After COVID-19 Calms Down

The world economy and airline business will fully recover when COVID-19 becomes preventable

and curable. However, COVID-19 forced us to restrict the movement of people and impose constraints

on our industrial and economic activities, and therefore, caused the greatest loss since the Great

Depression to our economic activities and lives. The impact of COVID-19 on the GDP and RPK is

expected to remain for a while. The following attempts to estimate the impact of COVID-19 on the

GDP and RPK based on currently available information.

Impact of COVID-19 on the GDP and RPK

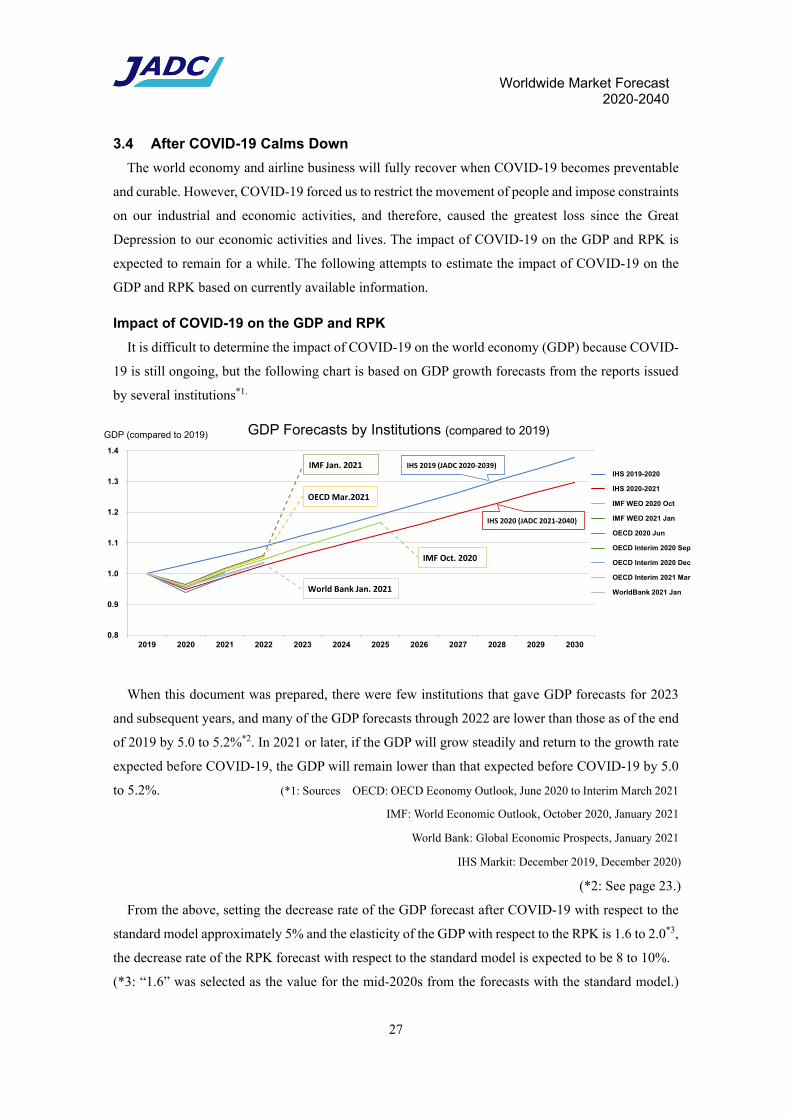

It is difficult to determine the impact of COVID-19 on the world economy (GDP) because COVID-

19 is still ongoing, but the following chart is based on GDP growth forecasts from the reports issued

by several institutions*1.

When this document was prepared, there were few institutions that gave GDP forecasts for 2023

and subsequent years, and many of the GDP forecasts through 2022 are lower than those as of the end

of 2019 by 5.0 to 5.2%*2. In 2021 or later, if the GDP will grow steadily and return to the growth rate

expected before COVID-19, the GDP will remain lower than that expected before COVID-19 by 5.0

to 5.2%. (*1: Sources OECD: OECD Economy Outlook, June 2020 to Interim March 2021

IMF: World Economic Outlook, October 2020, January 2021

World Bank: Global Economic Prospects, January 2021

IHS Markit: December 2019, December 2020)

(*2: See page 23.)

From the above, setting the decrease rate of the GDP forecast after COVID-19 with respect to the

standard model approximately 5% and the elasticity of the GDP with respect to the RPK is 1.6 to 2.0*3,

the decrease rate of the RPK forecast with respect to the standard model is expected to be 8 to 10%.

(*3: “1.6” was selected as the value for the mid-2020s from the forecasts with the standard model.)

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP(2019年⽐) 各機関によるGDP予測 (2019年⽐)

IHS 2019-2020

IHS 2020-2021

IMF WEO 2020 Oct

IMF WEO 2021 Jan

OECD 2020 Jun

OECD Interim 2020 Sep

OECD Interim 2020 Dec

OECD Interim 2021 Mar

WorldBank 2021 JanWorld Bank Jan. 2021

OECD Mar.2021

IMF Jan. 2021

IMF Oct. 2020

IHS 2019 (JADC 2020‐2039)

IHS 2020 (JADC 2021‐2040)

GDP Forecasts by Institutions (compared to 2019) GDP (compared to 2019)

Worldwide Market Forecast 2020-2040

28

“2.0” was selected as a representative value from the results of analysis of actual RPK, GDP, and

yield values.)

Assuming that the RPK will be lower than the standard model by 8 to 10% at the end of the gradual

recovery and grow at the same rate as the standard model, or 4.0% per year, this decrease is equivalent

to the growth for 2 to 2.5 years. It can be seen that the subsequent RPK will be delayed by about 2 to

3 years from the standard model.

0

5,000

10,000

15,000

20,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

RPK(×10 9) Recovery of RPK from COVID‐19 (projection)

RPK(Actual Value)RPK(Forecast : Standard Model)RPK(Post COVID‐19 : ‐7% estimated line) Projected deficit due to COVID‐19

Asymptotic Recovery completion

Equivalent to a delay of 2 to 3 years ( shift to right )

Initial Recovery completion

The recovery of the RPK and the number of aircraft deliveries after COVID-

19 forecast by JADC are based on the information available as of the time of

editing. JADC plans to prepare an updated version for the next fiscal year with

new input information, such as the latest GDP forecasts.

Worldwide Market Forecast 2020-2040

29

Estimation of the Number of Aircraft Deliveries

If the RPK grows 2 or 3 years behind the standard model as mentioned above, the number of

deliveries, which depends on the RPK, will grow 2 or 3 years behind the standard model as well, and

some expected deliveries will be postponed for 2 or 3 years and not done within the forecast period.

The table below estimates how the number of deliveries within the forecast period changes by using

this method on the standard model*4. (*4: Based on the data as of the end of 2019)

Number of Deliveries within the Forecast Period (2020-2039)

NJ (Narrowbody Jet)

Standard model (without COVID-19)

One-year delay

Two-year delay

Three-year delay

WJ (Widebody Jet)

Standard model

(without COVID-19)

NJ 24,989

WJ 7,808

Total 32,797

One-year delay

NJ 23,890

WJ 7,354

Total 31,244

Two-year delay

NJ 23,890 NJ 22,776

WJ 6,898 WJ 6,898

Total 30,788 Total 29,674

Three-year delay

NJ 22,776 NJ 21,663

WJ 6,438 WJ 6,438

Total 29,214 Total 28,101

The recovery of the passenger transportation demand relies fundamentally on the establishment of

collective immunity by the spread of vaccinations, which have been started in some countries. Each

country will speed up vaccinations, and as vaccinations proceed, the RPK will recover for domestic

flights, regional flights, and then international flights between vaccinated developed countries. As a

result, the RPK is expected to see an initial recovery from 2022 to 2023, then transit to gradual recovery.

In 2020 and in 2021, only the already scheduled firm orders will be received by airlines, but in 2022

and later, it is expected that the number of planes received will increase due to the recovery of

operating profit. In addition, demand for short- and medium-range narrow-body jets is expected to

begin to recover ahead of demand for long-range wide-body jets.

Separate from the method used in the previous section, the table below was obtained by directly

calculating the number of deliveries within the forecast period with new data*5, such as GDP forecasts

that take the impact of COVID-19 into consideration.

(*5: Based on the data as of the end of 2020)

Worldwide Market Forecast 2020-2040

30

Number of Deliveries within the Forecast Period (2020-2039)

YGR-5111 (2021)

NJ (Narrowbody Jet)

Standard model (without

COVID-19)

One-year delay Two-year delay (resumption of

delivery in 2022)

Three-year delay

(resumption of delivery in 2023)

WJ (Widebody Jet)

Standard model

(without COVID-19)

NJ 24,989

WJ 7,808

Total 32,797

One-year delay

Two-year delay (resumption of

delivery in 2022)

NJ 23,469

WJ 6,425

Total 29,894

Three-year delay (resumption of

delivery in 2023)

NJ 23,469 NJ 22,794 WJ 6,200 WJ 6,200 Total 29,669 Total 28,994

The area in dark green in this table, (resumption of delivery of NJ2022 and WJ2023) will be

explained in Chapter 4.

(Although the term “resumption” is used here, the delivery of backlogs will be carried out in 2020 and 2021 as well.)

In the calculation for this table and Chapter 4, the GDP data from IHS Markit (Dec. 2020) among

the reports listed on page 21 were used. Then, in spring 2021, IMF (Oct. 2020, Jan. 2021) and OECD

(Mar. 2021) suggested the possibility that the global GDP may recover earlier to a higher level (see

the graph on page 21). Since the detailed GDP data for each country are unavailable, JADC cannot

use that data in its calculations, but if the GDP recovers as suggested by IMF and OECD, the

transportation demand, or the RPK, is expected to be at a higher level after the gradual recovery period

(after 2025), and in addition, the aircraft demand is expected to be higher as well.

However, since COVID-19 caused serious financial damage to airlines, there may be a delay in the

recovery of their purchasing power. Also, the RPK of domestic flights is relatively small, accounting

for only about one-third of the global RPK, and therefore, the recovery of the RPK of international

flights is considered important for the full recovery of the financial power of the airline business.

Therefore, hopefully, we expect that the distribution of vaccines will be accelerated throughout the

world with the enhancement of vaccine production by countries capable of producing vaccines and

the framework like the COVAX Facility*, and it will lead to the recovery of the demand for

international flights. If the Southeast Asian countries and Central and South American countries fall

behind in vaccinations and international flights to these countries stand idle, the recovery of the RPK

of international flights will be greatly affected. In addition, in any region, suppressing the number of

infections is effective in reducing the possibility of the emergence of new variants.

(*: COVID-19 Vaccines Global Access Facility)

Worldwide Market Forecast 2020-2040

31

Other Factors

The table below shows the COVID-19-related factors that are likely to affect air transportation

demand and aircraft demand.

Factors that Affect Airlines and Aircraft Demand during and after COVID-19

Factor Key points Related

Part

Basic premise Establishment and diffusion of vaccines and treatments

Progress of vaccination delay or increase in production, handling of variants, antibody duration, procurement power of each country (purchasing power and international coordination) 3.3

Social changes

Epidemic control (immigration and movement restrictions) Shrinkage and recovery of GDP Changes in relationships between countries (triggered by COVID-19)

Termination timing and scope of epidemic control (directly related to the RPK of international flights) Period and progress of recovery (strongly related to RPK and GDP) Reconstruction of supply chain Changes in the movement of people and cargo

–

New way of doing things

Utilization of non-face-to-face media and remote media

Does such media partially replace air transportation and decrease the demand for transportation?

Video conferencing (substitute for conventional meetings: useful for remote persons and urgent meetings Does business traffic demand decrease?)

VR (virtual reality) (substitute for conventional sightseeing trip: inexpensive and easy Does consumer traffic demand decrease?)

Can such media be used as new media to attract customers and increase traffic demand?

VR (development of libraries: We can preview the proposed travel plan as if we actually visited each location.)

–

Hygiene measures

Hygiene, disinfection, elimination of anxiety

(acceleration of recovery of the RPK of domestic flights)

For Passengers: Vaccination, personal devices (masks, etc.)

For Airlines and airports: Disinfection of cabin equipment and airport facilities Screening by symptoms, such as fever Vaccine passport

–

Airlines Measures for survival

(securing operating capital)

Increase of debt, support from the government Airlines will have a large debt when they resume

flights and may refrain from placing new orders. –

(reduction of expenses)

Decrease of airplanes: Cancellation of orders, Retirement of airplanes

Downsizing: Layoff/dismissal Airlines may need to limit their transportation after

resuming flights, which could cause a delay in the recovery of their operating profit.

–

Environmental measures

Commencement of CO2 emissions regulations

Reduction of fuel consumption, driver to boost the demand to renew old models

5.3.1

The factors in the colored areas in this table have been reflected in this forecast calculation, or their

impact has been estimated.

In this forecast, the most reliable result is shown in the range that can be predicted quantitatively at

present, but the long-term recovery level of the RPK could be affected depending on the degree of

realization of each factor.

Worldwide Market Forecast 2020-2040

32

Intentionally Blank

Worldwide Market Forecast 2020-2040

33

4. Passenger Aircraft Demand Forecast

Chapter 4 describes the forecast of the number of passenger aircraft using the standard model.

The forecast of transportation demand (RPK), which is the basis for the number of aircraft

forecast, is presented in Chapter 5.

4.1 Number of Aircraft in Service

4.1.1 Income Level and Number of Aircraft in Service

In 1998, 15,820 passenger aircraft* were in service worldwide, and in 2018, 26,365 passenger

aircraft were in service, which means that the number of passenger aircraft in service increased by

10,545, or 1.67-fold, in 20 years.

(*: Total number of passenger jets and passenger turboprops. For passenger aircraft only.)

The number of passenger aircraft in service is increasing as transportation and travel demands

increase with the growing economy and increasing income. There is a positive correlation between the

number of aircraft in service per million people and the GDP per capita although it varies depending

on the land area and the degree of development of the ground transportation network.

Also, since it is known that in countries and regions with a GDP per capita of less than 10,000

dollars travel demand increases sharply as income increases, we expect that not only in China, which

has been growing remarkably, but also in Southeast Asian and South Asian countries, air transportation

demand will grow at a high rate, causing passenger aircraft demand to increase depending on the

population of each region.

(AF: Africa, CH: China, CI: CIS, EE: Eastern Europe, JA: Japan, LA: Latin America,

ME: Middle East, NA: North America, NE: Northeast Asia, OC: Oceania, SE: Southeast Asia,

SW: South Asia, WE: Western Europe)

For passenger jets in service only. Sources: IHS, Cirium

Trends in the Number of Passenger Aircraft (Jet + TP) per Million People (1996-2018)

Num

ber

of p

asse

nger

ai

rcra

ft in

ser

vice

pe

r m

illio

n pe

ople

Worldwide Market Forecast 2020-2040

34

4.1.2 Distribution of ASK by Route Distance

Airlines select suitable aircraft according to the distance of each route. According to the distribution

of ASK by route distance for regular non-stop flight routes, aircraft are operated as follows:

- Most turboprop aircraft are used for routes with a distance of 1,000 km or less, and the largest

number of turboprop aircraft are used for routes with a distance of 400 to 600 km.

- Regional jets are used mainly for routes with a distance of 400 to 1,500 km in all regions except

North America, but are used for routes with a distance of up to 2,000 km in North America, which

is a leading market.

- Narrow-body aircraft are operated on routes between 400 and 4,000 km. They are mainly used for

routes with a distance of 900 to 2,000 km. On routes up to 3,500 km, narrow-body aircraft provide

90% of the total ASK, and on routes up to 4,500 km, 98% of the total ASK. In all, narrow-body

aircraft provide 52% of the total ASK worldwide.

- Wide body jets are used for a wide range of route distances, but mainly for routes with a distance

of 5,500 to 10,000 km. Wide body jets supplied for routes with a distance of 4,500 to 13,000 km

account for 78% of the total ASK of wide body jets.

0

200

400

600

800

1000

1200

1400

(×109)

Distribution of ASK (Available Seat Kilometers) by Route Distance

Regional jet

ASK (× 109)

Turboprop

Regional jet

Narrow body jet

Wide body jet

Short range

Medium range

Long range

Source: Data by OAG as of September 2019

Non-stop route distance (km)

Worldwide Market Forecast 2020-2040

35

4.1.3 Distribution of ASK by Number of Seats

The distribution of ASK by number of seats in different route distances is as follows:

- For routes with a distance of 1 to 1,000 km, the bars for turboprop aircraft and regional jets with 40

to 99 seats are slightly higher than the other bars, and the bars for narrow body jets with 120 to 169

seats (e.g., A320, 737-700/800) are noticeably higher, showing that aircraft with 120 to 169 seats

are the mainstream.

- For routes with a distance of 1,000 to 2,000 km, aircraft with 120 to 169 seats are the most

commonly used as well. In addition, narrow body jets with 170 to 229 seats (e.g., A321, 737-900ER,

757) and wide body jets with 230 to 399 seats are also in service.

- For routes with a distance of 2,000 to 4,500 km, aircraft with 120 to 169 seats are the mainstream.

In addition, narrow body jets with 170 to 229 seats and wide body jets with 230 to 399 seats (e.g.,

A330, 767/787) are also in service. In this range of distances, due to the longer distances compared

to routes with a distance of 1,000 to 2,000 km, relatively large aircraft, such as narrow body jets

with 170 to 229 seats and wide body jets with 230 to 399 seats, are increasing.

- For routes with a distance of 4,500 km or more, the number of aircraft with 310 to 399 seats (e.g.,

A340, 777) is largest, followed by aircraft with 230 to 309 seats (e.g., A330, 787), aircraft with 500

to 800 seats (A380), and aircraft with 400 to 499 seats (747). In recent years, the number of aircraft

with 400 to 499 seats is decreasing due to the decreasing number of 747 aircraft.

1-1000

1001-2000

2001-4500

4501-

0

200

400

600

800

1000

1200

1400

1600

1800

2000

001-019

020-039 040-

059060-079 080-

099 100-119 120-

169 170-229 230-

309 310-399 400-

499 500-800

Distribution of ASK by Number of Seats – Global Total Annual ASK (× 109)

Regional jets and turboprop aircraft

Route distance (km)

Source: Data by OAG as of September 2019

Narrow body jets

Wide body jets

Number of seats (seats)

Worldwide Market Forecast 2020-2040

36

4.1.4 Increase in the Average Number of Seats (Adoption of Larger Aircraft with

More Seats)

Comparison of the relationship between the number of takeoffs and landings and the number of

passengers at the world’s top 50 airports between 2007 and 2019 shows that the number of takeoffs

and landings did not increase or decrease significantly but the number of passengers increased. The

average number of passengers per takeoff and landing in 2007 was 98, but it increased to 134 in 2019

by 37%. During this period, the world’s annual load factor increased from 76.1% to 81.9% by 5.8%.

Even with this in mind, the average number of seats per aircraft has increased, indicating that airlines

are working to increase the number of seats (increase the density) or increase the aircraft size to address

the increasing number of passengers.

The average number of seats per aircraft decreased until the mid-2000s because of the emergence

of regional jets, the adoption of twin-engine aircraft, which can be used for long-range flights, and

increased use of small aircraft in high frequency. After that, however, the average number of seats per

aircraft started to increase around 2004 first for routes with a distance of 2,000 km or less, due to the

rise of LCCs (high-density seat arrangement), the restricted number of takeoff-and-landing slots at

airports (difficulty in increasing flights), and the mergers of airlines which lead the reduction of