Why don't you cut your coat according to your cloth?

19

1 Why don’t you cut your coat according to your cloth? – factors influencing budget overruns in Danish Municipalities after amalgamation By Kurt Houlberg ([email protected] ) and Lene Holm Pedersen ([email protected] ). AKF: Danish Institute of Governmental Studies Paper presented at the XIX Nordiske Kommunalforskerkonference 2010 in Odense 25.-27. of november 2010 Work in progress – please do not quote without permission of the authors! Dansk abstract: Hvilke forhold har betydning for om de danske kommuner sætter tæring efter næring? Det spørgsmål er centralt efter at krisen for alvor er begyndt at kradse i de danske kommuner. I paperet analyseres det hvilke forhold der påvirker budgetoverskridelserne i de danske kommuner i 2008 og 2009. Abstract: In the years after the local government reform (2007) the budget overruns have been rising in the Danish municipalities. A pooled regression analysis shows that this is explained by several factors. The contextual conditions matter as budgets are easier to manage, if they are large. But changes in the population and the socio-demographic needs make budget overruns more frequent. However, external factor are only part of the story. Budget making is nested in policy making. Councils which have a higher degree of consensus have lower budget overruns. If decisions in the council are taken in unanimity it may be easier to take the unpopular decisions necessary when budget overruns are threatening. More complex amalgamation continues to have an impact on overruns also in 2009. However, the financial management tools which have been the recommended recipe for better steering does not seem to have an impact. Budgetary factor such as the changes in the budget, the budgeted operating surplus and the budget culture continues to have a large impact on overruns. As such the budget overruns in the municipalities are not just due to external factors. The financial management is nested in the decision making in the local policy making and administration.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Why don't you cut your coat according to your cloth?

1

Why don’t you cut your coat according to your cloth?

– factors influencing budget overruns in Danish Municipalities after amalgamation

By Kurt Houlberg ([email protected]) and Lene Holm Pedersen ([email protected]).

AKF: Danish Institute of Governmental Studies

Paper presented at the XIX Nordiske Kommunalforskerkonference 2010 in Odense 25.-27. of november

2010

Work in progress – please do not quote without permission of the authors!

Dansk abstract: Hvilke forhold har betydning for om de danske kommuner sætter tæring efter næring? Det spørgsmål er centralt efter at krisen for alvor er begyndt at kradse i de danske kommuner. I paperet analyseres det hvilke forhold der påvirker budgetoverskridelserne i de danske kommuner i 2008 og 2009. Abstract: In the years after the local government reform (2007) the budget overruns have been rising in the Danish municipalities. A pooled regression analysis shows that this is explained by several factors. The contextual conditions matter as budgets are easier to manage, if they are large. But changes in the population and the socio-demographic needs make budget overruns more frequent. However, external factor are only part of the story. Budget making is nested in policy making. Councils which have a higher degree of consensus have lower budget overruns. If decisions in the council are taken in unanimity it may be easier to take the unpopular decisions necessary when budget overruns are threatening. More complex amalgamation continues to have an impact on overruns also in 2009. However, the financial management tools which have been the recommended recipe for better steering does not seem to have an impact. Budgetary factor such as the changes in the budget, the budgeted operating surplus and the budget culture continues to have a large impact on overruns. As such the budget overruns in the municipalities are not just due to external factors. The financial management is nested in the decision making in the local policy making and administration.

2

1. Introduction

What makes it so difficult to cut one‟s coat according to one‟s cloth? That is a central

question for the Danish municipalities, as they have been facing increasing budget overruns

in recent years (Houlberg & Jensen, 2010). Factors such as financial crisis, socio-

demographic changes and reform of the equalisation system are seen as important drivers of

the problems of gaining budgetary stability, but the discussion on the reasons and

responsibilities remain inconclusive. There is a considerable element of blame avoidance in

the debate. On one hand, the national politicians have an interest in presenting economic

instability and budget deficits in the municipalities as being due to insufficient financial

management in the municipalities. On the other hand, the municipalities have an interest in

presenting budget overruns as being due to external factors beyond their control – and their

possibilities for taking action as being severely restricted by central regulations and

expectations on service delivery. Therefore, it is highly relevant to analyse what factors

influence budget overruns?

Budget overruns are the primary dependent variable in the analysis. A budget overrun is an

unexpected cost incurred in excess of a budgeted amount due to an under-estimation of the

actual cost during budgeting. As such it is an indicator of instability in the financial

management of the municipality. There are, however, several other frequently applied

indicators of overspending and economic instability. Firstly, budget deficits denote the

difference between revenue and spending plus interest payment on the debt. However, the

municipal budgets do not have to balance. In fact, they mostly have a surplus in order to

finance interest on debt. The advantage of focusing on budget overruns rather than budget

deficits is that it makes it possible to exclude the analysis of the development in municipal

revenue and direct attention to factors influencing spending in the municipalities. This is

highly relevant as we are primarily interested in the financial management of the

municipalities rather than factors causing decreases in municipal revenue. Second, the

growth in public expenditures is an important indicator of the development in the economy.

However, the growth is mainly a problem if it is not matched by equivalent growth in the

revenues. Furthermore, growth in expenditures may in itself be a factor, which influences

budgetary overruns, as large growth in expenditures may make the budget less manageable.

In sum, focusing on budget overruns increases the focus on the financial management,

however, other indicators such as the growth in the expenditures are highly relevant in order

to get a more encompassing picture of the development in economy of the municipalities.

Several factors may influence the development in the economy in general and budget

overruns more specifically. Firstly, the external conditions in the environment matter. If the

demography and the socio-economic needs are changing, budgets become less manageable.

However, external factors may not be the whole story. The political life in the local councils

may also matter. Attention has previously been drawn to the importance of political

ideology, the political life in the local councils, such as the fractionalisation and broadness

of the coalitions and the importance of the political business cycle (Blom-Hansen, 2002;

Serritzlew, 2005). However, the political factors may have a more indirect influence on the

financial management in the municipalities. The municipalities are not mainly arenas of

3

large ideological conflict in contrast the local councillors are very closely involved in the

administration (Berg, 2004; Berg and Kjær, 2007). Therefore, it is relevant to analyse how

financial management instruments, which have been recommended in the last decade

influence budget deficits. Among these management by objectives, decentralisation, cross-

sectoral coordination and increased documentation stand out as some of the most central

recommendation. However, it is also evident that budgetary factors matter. For instance it

may be easier to balance larger budgets and budgets containing large amounts of slack

(Blom Hansen 2002, Serritzlew 2005).

In sum the analysis focus on how political factors, recommendations for financial

management, budgetary factors and contextual factors influence budget overruns.

2. Explanatory factors

2.1 Political factors

A long range of political factors in the local councils may influence budget overruns. In the

following the importance of political ideology, absolute majorities, party fractionalisation,

political consensus and the political business cycle are discussed.

As the political ideologies vary in their views on the role of the public sector in the

economy, and as left wing parties traditionally have been favouring larger public

expenditures than right wing governments the link between political ideology and public

expenditures is much discussed. In analysis of the municipalities this is often investigated

by analysing the correlation between bourgeois mayors and increases in expenditures and

budget overruns (Blom-Hansen, ibid.; Serritzlew, ibid.). However, it may not just be the

political ideologies and the colour of the mayor which matter. The ability to make political

decisions in the councils is influenced by the level of conflict and the ability to reach

political compromises. The composition of the council may matter. Compromises may be

more essential and require better coordination if there is a large number of parties. An index

of fractionalisation has been developed which measure how divided the council is. It takes a

high value if the council consists of many small parties, but a low value if the council

consists of few large parties (Rae, 1967; Serritzlew, 2005: 421). Thus, party

fractionalisation and ideological dispersion is expected to correlate with high budget

overruns, where as having a bourgeois mayor is expected to give lower budget overruns.

Even if the councils can make decisions based on a simple majority, the norm to a large

extent is that the largest possible unanimity should be formed behind as many decisions as

possible (Berg and Kjær, 2007: 14). Thus, it is possible to talk about a norm of consensus

which has been established along with the principles on majority decision making, which

have been established in the Danish municipalities. Even in municipalities where there is an

absolute majority, an effort is generally made to establish the largest possible unanimity

behind the decisions made in the council (Berg and Kjær, 2007: 111). Research also shows

that broad coalitions are very common in the municipalities. In other words, more parties

4

than required forms a majority between the choice of mayor (Skjæveland et al., 2007: 216).

Furthermore, the coalitions are also often broad in an ideological sense, as they in some

cases encompass right and left wing parties at the same time. This can for instance be the

Liberal Party and the Social Democrats at the same time – something which would be

highly unlikely at the national level. The possible consequences of the norm of consensus

have been discussed. On one hand it has been criticized for having a negative impact on the

possibility of undertaking major reforms and political changes. As many actors have to

agree, status quo and stability is seen as the most likely political consequence (Berg and

Kjær, 2007: Kap. 8; Hansen, 2008). Furthermore, the division of powers may make it

difficult to hold the politicians accountable. It all political parties agree on the major

decisions in the council, who are the voters then to hold responsible? (Mouritzen, 2001:

372). In addition, it has been argued that consensus may have a negative impact on citizen

involvement. If the norm of consensus makes the debate between the political parties

disappear, the votes may lose interest in participation in local policy making (Hansen,

2008). But even if the norm of consensus in this way could have negative impacts on local

democracy, it may be very crucial to the possibility of exercising political leadership and a

norm on consensus may facilitate political decisions also when they may turn out to be

unpopular in the electorate (Berg and Kjær, 2007: Kap 8). Hence, political consensus is

expected to have a positive impact on the ability to keep the budget.

Political business Cycle and year specific effects

Politicians seeking re-election and conceptualizing voters as myopic with a decaying

memory may have incentives to create local electoral cycles expanding services for the

citizens in election years and contracting in mid election years (Alesina 1989; Houlberg

2007; Geys 2007; Serritzlew 2005). Empirically studies of Danish municipalities prior to

the 2007-reform has testified, that budget overruns are systematically larger in election

years (Houlberg 1999; Houlberg 2007; Serritzlew 2005; KREVI 2008). There is no reason

to belive, that this tradition hasn‟t been prolonged into the era of the new municipalities.

Hence, budgetoverruns are expected to be larger in the election year 2009.

2.2 Recommendations for financial management

Budget overruns indicate that the financial management of the municipalities has not been

successful. Therefore, it is also relevant to analyse if some of the policy recommendations

which have been marketed in the municipalities in the last decades seem to improve the

financial management. In the following, management by objective, decentralisation, cross

sectoral policymaking and documentation is presented as some of the central

recommendations for financial management. Firstly, management by objectives has been a

central element on the reform agenda in the municipalities. Where budget frames draw less

attention to what goals are accomplished, the management by objectives is promoted as a

means to draw attention to the content of the policy. It is seen as means to make it subject to

discussion in the council how political ideas should be transformed into political priorities

in the budget for instance in the form of what types and level of public services the

municipality should supply and what the quality of the services should be. Management by

objectives implies that objectives are set hierarchically for sectors as well as the specific

5

institutions and that the objectives have budgetary consequences. Second, economic

decentralization to the service producing units – such as schools, kindergardens and care-

centres – has also been part of the recommendations in the NPM era. Economic

decentralisation should facilitate innovation and adjustment to local needs. Thus it is

recommended that leadership as well as economic responsibilities are decentralised.

Thirdly, cross-sectoral policy-making is recommended as a means to increase the

coordination around the budget. The sectoral committee structure leads to development of

sectoral preferences among the councillors (See Bækgaard, 2010). This as well as the

sectoral organisation of the administration has been seen as a hinderance to coordinated

policy making. Hence, direction models where the administrative directors in the

administration do not have specific sector responsibilities have been promoted. Therefore,

municipalities which have a higher degree of cross sectoral policy making may have lower

budget overruns.

2.3 Budgetary factors and tractability

Vulnerability of the budget

Larger budget are less vulnerable to changes in the environment in the budget year than

smaller budgets (Houlberg 1999; Blom-Hansen 2009, Serritzlew 2005), and consequently

larger municipalities and municipalities with a high level of expenditure per capita are

assumed to have lesser budget overruns. Empirically this has been verified for Danish

Municipalities prior to the 2007-reform (ibid.), and the same is expected to be the case after

the reform.

Lax budgets

Growing budgets are easier to keep than declining ones (Houlberg 1999; Blom-Hansen

2009). A growing budget can be considered more lax and tractable (Serritzlew 2005) and

thereby inducing less budget overrunning. On the other hand budget reductions are more

likely to lead to budget overruns. This effect is found in earlier studies (Houlberg 1999;

Blom-Hansen 2009; Serritzlew 2005) and also in the first year after the local government

reform (KREVI 2009b: 36), and the same is expected to be the case in the second year after

the reform.

Besides changes in the expenditure budget from previous year the budget can be more or

less lax with regard to budgeted operating surplus, ie. the difference between operating

revenue and operating expenditures. If municipalities are ambitious in respects of capital

investments or strengthening liquid assets they may budget with a large operating surplus,

hereby demanding a bigger effort to keep the budget and realizing the budgeted surplus.

Conversely a municipality budgeting a smaller operating surplus or even planning a budget

deficit may find it easier to keep the budget than the more surplus ambitious municipality. A

budget not overrun in other words is not only an indicator of good financial management,

but can also be seen as a result of modest budget ambitions regarding the operating surplus.

A better understanding of the nature of budget overruns involves differentiation between

service areas as some service areas are more tractable than others because of differences in

6

state regulation, concentration of benefits, distribution of cost and the homogeneity and

organizational potentials of the users and personnel of the service areas (Serritzlew 2005).

This however is beyond the scope of this paper, as the chief aim is to study the effect of

contextual, political and budgetary factors on total budget overrun.

Budget culture

Budget institutions and norms for financial management and steering of expenditures are

locally rooted, sanctioned and developed. Some municipalities have strong emphasis on

keeping the budgets and have institutionalized routines for compensating cuts elsewhere in

the budget when supplementary appropriations are given, while others have a more lax view

on supplementary appropriations and budget overruns (Houlberg 1999). Consequently some

municipalities have tradition for overrunning their budget, others not. This cultural

autocorrelation or cultural path dependency is expressed in a high correlation between

budget overruns in one year and another. This was the case in the old municipalities

(Houlberg 1999; Houlberg 2007; Blom-Hansen 2009) as well as in the new municipalities

(Houlberg & Jensen 2009). Also the culture of operating surpluses has been transformed

from the old to the new municipalities (KREVI 2009a: 35)

Amalgamations and tractability

Research shows that municipal amalgamations give rise to common-pool problems and that

the old municipalities may try to spent as much money as possible before closing time

(Blom-Hansen, 2010; Hansen, 2009). Danish Municipalities facing amalgamation January

in the last year prior to The Local Goverment Reform of 2007 were exploiting the common-

pool and behaving opportunistic by overrunning their budgets on both current expenditures

and - in particular - capital expenditures (Blom-Hansen, 2010) as well as by reducing their

short term net assets (Hansen 2009). Adding to this, the merging municipalities in the

process of harmonizing policies post-reform have increased expenditures relative to the

non-merging municipalities (Hansen 2009) and have experienced significantly larger budget

overruns in the first year after amalgamating (KREVI 2009b). The difficulties keeping the

budgets may be due to direct costs of amalgamation relating to infrastructure, ICT,

personnel etc. or due to the unavoidable first-year turbulence relating to implementation of a

new organisation, new financial structure, new budgetary processes and instruments for

financial management as well as discretionary elements in budgeting new tasks under

uncertain conditions (KREVI 2009b). We expect budget overruns will be larger in more

complex amalgamation. Amalgamations are seen as more complex if there are many

municipalities participating and if the municipalities are largely similar in size. In other

words, big brother amalgamations may be more simple if smaller municipalities are being

assimilated by a dominant organisation, than if municipalities of a more equal size are to

find a new administrative equilibrium.

2.4 Contextual factors

The fiscal environment of municipalities affects the policy. In the literature of public

budgeting it is a widespread assumption that stable environments and stable growth

facilitates incremental changes in the budget independently of changes in demography and

7

needs, while a turbulent environment and austerity to a larger extent links expenditure

changes and resource allocation to changes in the environment (fx Mouritzen 1991:410-430;

Jørgensen & Mouritzen 2002; Serritzlew 2003).

Previous analysis shows that the size, distribution and growth of the budget are affected, but

not determined by factors external to the councils (Boyne 1996; Wildawsky and Leiden

1997). Even if the external environment is influential, the budget is at the heart of political

decision-making and it is the product of interplay and bargaining between politicians,

bureaucrats, citizens and interest groups etc. The budget institutions are nested in political

institutions (Blom-Hansen 2002: 100), and the setting of balance between net and gross

appropriations, allowance of reallocation between wages and other current expenditure or

transferring appropriations between years are decided upon in the local councils.

Adaption to changing demographic or socio-economic conditions not only passes new

demands to the making of the budget but also to financial management after the budget has

been approved. A deteriorating fiscal environment makes it harder to keep the budget

(Houlberg 1999; Blom-Hansen 2009, Serritzlew 2005), whether the changes are related to

scarcer resources or growing needs. Drop in revenues or expanding needs induces shocks to

the municipal economy (Rattsø & Tovmo 1998, Poterba 1994), calling for policy changes

and challenging financial management and the keeping of the budget. A changing

population size induces turbulence and may make it harder to keep the budget, no matter if

the population is growing or declining. A growing population demands adaption of capacity

and services to expanding needs while a declining population decreases total revenue and

calls for reductions in capacity and expenditures. Changes in demographic or socio-

economic composition of the population and/or revenue base resulting in growing

expenditure needs or declining revenues per capita also challenges the keeping of the

books. This for instance could be the result of an aging population. Earlier studies have

entailed needs related to changes in the size of population groups sensible to economic

fluctuations like unemployed or recipients of social benefits (Houlberg 1999; Blom-Hansen

2009) and found that changes in these subgroups significantly contributes to budget

overruns.

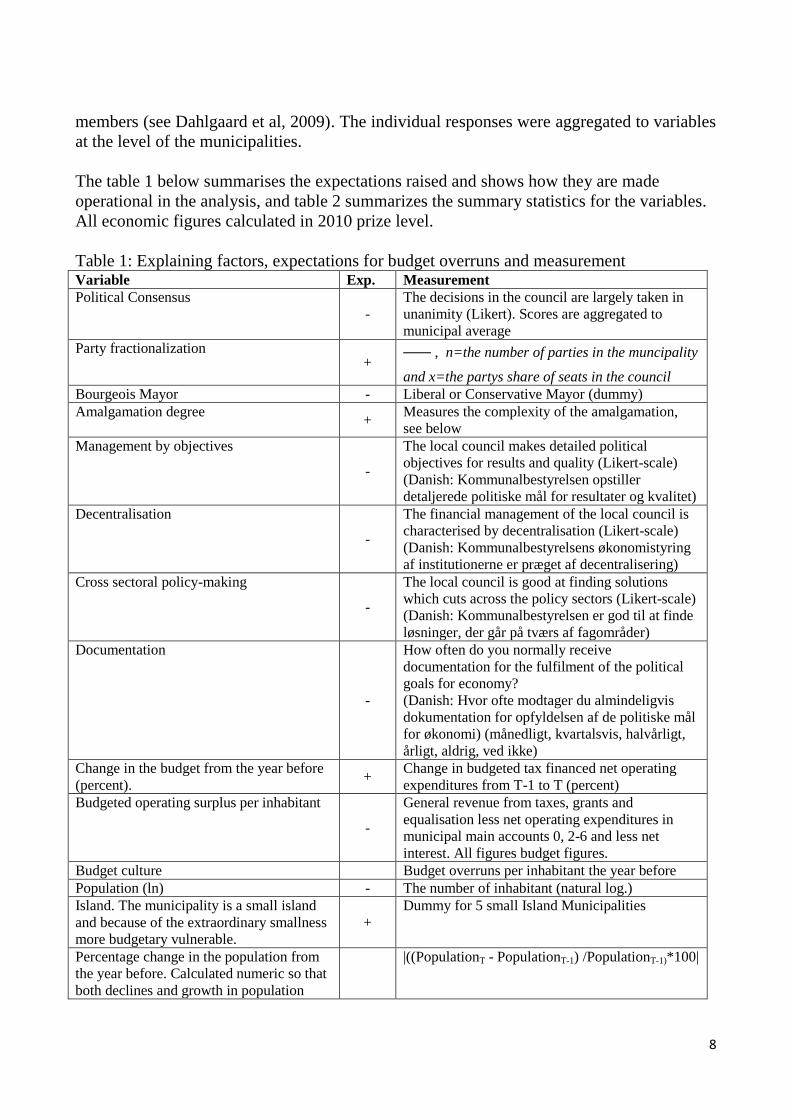

3. Method and data

Data on contextual and budgetary factors are based on publicly available municipal register

data from Statistics Denmark (www.statistikbanken.dk) and the Ministry of the Interior and

Health (Indenrigs- og Socialministeriet 2009). All operationalizations of revenues and

expenditures are done according to accounts in the municipal accounting system (Indenrigs-

og Socialministeriet 2010). Changes in needs are calculated on basis of the official

criterions and weights in the equalization system for Danish municipalities. Weights in the

2010 equalisation system are used for all. Data on political consensus and financial

management tools were collected in March 2009 as part of a broader research project on

role perception among local councillors in all 98 Danish municipalities. The individual-level

data were collected through an email-based questionnaire among all sitting municipal

councillors. The response rate was 53% which amounts to approximately 1,336 council

8

members (see Dahlgaard et al, 2009). The individual responses were aggregated to variables

at the level of the municipalities.

The table 1 below summarises the expectations raised and shows how they are made

operational in the analysis, and table 2 summarizes the summary statistics for the variables.

All economic figures calculated in 2010 prize level.

Table 1: Explaining factors, expectations for budget overruns and measurement Variable Exp. Measurement

Political Consensus

-

The decisions in the council are largely taken in

unanimity (Likert). Scores are aggregated to

municipal average

Party fractionalization +

, n=the number of parties in the muncipality

and x=the partys share of seats in the council

Bourgeois Mayor - Liberal or Conservative Mayor (dummy)

Amalgamation degree +

Measures the complexity of the amalgamation,

see below

Management by objectives

-

The local council makes detailed political

objectives for results and quality (Likert-scale)

(Danish: Kommunalbestyrelsen opstiller

detaljerede politiske mål for resultater og kvalitet)

Decentralisation

-

The financial management of the local council is

characterised by decentralisation (Likert-scale)

(Danish: Kommunalbestyrelsens økonomistyring

af institutionerne er præget af decentralisering)

Cross sectoral policy-making

-

The local council is good at finding solutions

which cuts across the policy sectors (Likert-scale)

(Danish: Kommunalbestyrelsen er god til at finde

løsninger, der går på tværs af fagområder)

Documentation

-

How often do you normally receive

documentation for the fulfilment of the political

goals for economy?

(Danish: Hvor ofte modtager du almindeligvis

dokumentation for opfyldelsen af de politiske mål

for økonomi) (månedligt, kvartalsvis, halvårligt,

årligt, aldrig, ved ikke)

Change in the budget from the year before

(percent). +

Change in budgeted tax financed net operating

expenditures from T-1 to T (percent)

Budgeted operating surplus per inhabitant

-

General revenue from taxes, grants and

equalisation less net operating expenditures in

municipal main accounts 0, 2-6 and less net

interest. All figures budget figures.

Budget culture Budget overruns per inhabitant the year before

Population (ln) - The number of inhabitant (natural log.)

Island. The municipality is a small island

and because of the extraordinary smallness

more budgetary vulnerable.

+

Dummy for 5 small Island Municipalities

Percentage change in the population from

the year before. Calculated numeric so that

both declines and growth in population

|((PopulationT - PopulationT-1) /PopulationT-1)*100|

9

assumes positive values

Change in demographic needs per

inhabitant in budget year +

Demographic needs per inhabitant in Year T+1

less demographic needs per inhabitant in Year T.

All years calculated on basis of criterions and

weights in the 2010 equalisation system.

Change in Socioeconomic needs per

inhabitant in budget year +

Socioeconomic needs per inhabitant in Year T+1

less Socioeconomic needs per inhabitant in Year

T. All years calculated on basis of criterions and

weights in the 2010 equalisation system.

Change in general revenue during the

budget year

Change in taxes and grants per inhabitant from

budget to final accounts in year T

Election Year

The year 2009 as dummy (reference category

2008)

Table 2 Summary Statistics for the variables

N Minimum Maximum Mean

Std.

Deviation

Budget overrun per capita 196 -1126 3733 1155.08 960.665

Population (ln) 196 7.585 13.177 10.64256 .783661

Small Island Municipality 196 0 1 .05 .221

Δ Population |percent| 196 .0 7.8 .640 .6942

Δ Socioeconomic needs 196 -3532.4 2234.9 -74.626 473.9382

Δ Demographic needs 196 -1591.8 931.1 13.074 284.4728

Δ General revenue during the

budget year 196 -818.0 2201.0 391.546 264.5786

2009 (ref. = 2008) 196 0 1 .50 .501

Consensus 196 1.50 4.55 3.2923 .73232

Party fractionalization 196 1.9200 5.6500 3.363061 .6676901

Liberal/Conservative Mayor 196 0 1 .49 .501

Amalgamation degree 196 1.0000 5.5300 2.207245 1.1777378

Amalgamation degree * 2009 196 .00 5.53 1.1036 1.38483

Management by objectives 196 2.8 4.5 3.661 .3223

Decentralisation 196 2.7 4.8 3.848 .3960

Cross-sectoral policy-making 196 2.00 4.17 3.1134 .45492

Documentation frequency 196 1.0 2.8 1.759 .4023

Δ Budget 196 -4.8 19.1 1.954 2.0452

Budgeted operating surplus 196 -7889.3 3914.7 1306.736 1116.5029

Budget culture (Budget overrunt-1) 196 -1930.8 6422.4 707.068 1056.5981

Budget overruns are measured as the difference between tax financed net operating

expenditures in the final accounts and the originally approved budgets, calculated per

10

inhabitant1. Capital expenditures are excluded as well as operating expenditures for service

areas fully financed by users. These user financed service areas - municipal supply

companies, sewage and renovation – are treated separately in the municipal budgets and are

not allowed to be financed by taxes. The operating expenditures are calculated net to cover

only the part of expenditures to be financed by the municipality itself. I.e. conditional

grants, user fees and payments from other municipalities are subtracted.

Amalgamation degree measures the complexity of the municipal amalgamation. It is an

expression of the number and the degree of equal size between the populations in a

municipal amalgamation. Thus the measure is suited to distinguish between amalgamations

where there are several municipalities, but which vary in complexity. In other words, if a

large municipality takes in three small municipalities in a „big brother‟ amalgamation this is

seen as less complex than a „quadruplet‟ amalgamation of four municipalities of equal size.

The measurement is 1/the sum of the old municipality‟s part of the new municipality

squared and hence parallel to the measurement of party fractionalisation. Thus it can be

interpreted as the effective number of municipalities in an amalgamation.i Other measure of

amalgamation are if the municipality is amalgamated (measured as a dummy), the number

of municipalities in a municipality, or the size of the change can be measured as the number

of inhabitants in the old municipality compared to the number of inhabitants in the new

municipality (Dahlgaard et al., 2009).

1 The figures are not adjusted for eventual changes in municipal tasks stemming from national legislation after the budget was approved.

11

4. Results and discussion

The results are presented in Table 3.

Table 3 Regression Analysis of budget overruns for tax financed net operating expenditures per

capita 2008 og 2009 (2010 prices). Unstandardized coefficients (pooled OLS regression)

Model 1

Con-

textual

factors

Model 2

+

political

factors

&

amalaga

mation

Model 3

+

financial

manage

ment

tools

Model 4

+ lax

budget

Model 5

+

budget-

culture

Constant 3478 *** 3840 *** 989 1528 -770

Contextual factors:

Population (ln) -244 ** -374 *** -276 *** -338 *** -159

Small Island Municipality -340 -531 -301 -216 112

Δ Population |percent| 209 ** 232 *** 198 ** 225 *** 79.9

Δ Socioeconomic needs .130 .243 * .283 ** .403 *** .372 ***

Δ Demographic needs .801 *** .108 .105 -.205 -.238

Δ General revenue in budget year .418 * .121 .080 .003 .070

Political factors:

2009 (ref. = 2008) 1185 *** 1220 *** 1354 *** 1322 ***

Consensus -84.0 -163 * -173 ** -93.6

Party fractionalization 109 91.0 86.5 67.9

Bourgeois Mayor -186 -185 -159 19.5

Amalgamation:

Amalgamation degree 346 *** 380 *** 404 *** 315 ***

Amalgamation degree * 2009 -194 * -204 ** -202 ** -207 **

Financial management tools

Management by objectives 407 ** 207 227

Decentralisation 132 123 170

Cross sectoral policy-making 86.5 211 207

Documentation frequency -110 -22.4 10.8

Budgetary factors:

Δ Budget -11.9 -108 ***

Budgeted operating surplus .236 *** .213 ***

Budget culture (Budget overrunt-1) .418 ***

N 194 194 194 194 194

R2 (adj.) 0.101 0.312 0.319 0.376 0.511

Significance: * = 0.10 ** = 0.05 ***= 0.01 Two outliers excluded. VIF (Variance Inflation Factor) in model 2-5 is 5.4 and 6.1 for 2009 and Amalgamation degree*2009 respectively. In model 3-5 VIF for Population (ln) is 2.5-2.7 and 2.5-2.6 for Amalgamation degree. For all other variables VIF < 2.2.

The results presented above show that contextual factors, characteristics of the budget as

well as political factors have an impact on the budget overruns.

12

4.1. Political factors

The political business cycle

With so far only one post-reform election hold, no final conclusions on electoral cycles for

the new municipalities can be made, but in order to catch a potential election year effect a

dummy for the election year 2009 is included in the analysis. The results show that budget

overruns were significantly larger in the election year. This supports the theory on political

business cycles. Politicians do seem to be more likely to spend excess amounts of money in

election years. Empirical research indicate that political business cycles affected budget

overruns in the years prior to the reform (Serritzlew, 2005). This analysis adds to this result

by finding the same to be the case after the reform. However, the specific year 2009 also

captures the financial crises affecting the municipal economy with full strength in 2009.

Therefore, indicators of economic crises such as unemployment have been tested in the

analysis. These showed to have an explanatory power, however, treating the election year as

a dummy proved to have the larger explanatory power. This indicates that the budget

overruns in 2009 primarily are of political origin and theoretically related to opportunistic

behaviour of politicians seeking re-election.

Ideology and the level of conflict and cooperation

The political orientation of the mayor as being more or less left wing has previously been

found to have an impact on budget growth (Blom-Hansen, 2002). However, in this analysis

having a bourgeois mayor does have a negative impact on budget overruns, but it remains

insignificant. Budget growth and budget overruns are essentially different. The reason is

probably that ideology is more linked to budget growth as the right wing traditionally have

had a priority for lower taxes, where as better public service and hence a larger public sector

has been the priority of the left wing. In contrast, budget overruns are more linked to the

financial management of the municipalities. In other words, ideology may influence if the

budgets are expanding, but if they are kept is a different matter.

The level of conflict may not just be due to ideological differences in the council. It is also

likely to be influenced by the composition of the councils. Compromise will be more

essential and require better coordination and more consensus building, if there is a large

number of parties in the council. This has previously been measured employing Rae‟s index

of fractionalization (Rae, 1967, see Serritzlev, 2005). However, political differences should

also be taken into account as many parties which are close ideologically, may be more likely

to reach political agreement (Serritzlev, ibid.). Therefore a measure of ideological

dispersion from the position of the mayor was tested, but ideological polarization do not

correlate with budget overruns. In line with the argument above, a higher degree of party

fragmentalisation was expected to have a negative impact on budget overruns, as a more

fragmented council would make decision making more difficult. However, this does not

seem to be the case. The reason for this could be that the impact of fragmentalisation can

run in two ways. In some incidences a low fragmentation may invoke a decision making

capability, which can be used to reduce budget overruns, but in other cases low

fragmentation may indicate that there is a stable majority which may induce a reliance on

13

own authority, which again may lower the agility towards punishment from the electorate.

Furthermore, taking unpopular decisions may also be more difficult. In situations where

budget has been passed by a very stable majority – the opposition are less responsible for

the problems arising and more likely to benefit politically from budget overruns. Hence, the

opposition in situations with a stable majority has less incentive to work to reduce the

benefits. The latter is supported by the result in model 4 (see table 3), which show that

consensus lowers the budget overruns. This indicate that it is not so much the formal party

fractionalisation which matter in the council, but the degree to which it has been possible to

build a political consensus in the councils where decisions largely are taken in unanimity.

The reason may be that a large degree of consensus makes it easier for the councils to take

unpopular decisions, which may be required in order bring potential budget overruns under

control.

This result is highly interesting. Local politics have long been seen as synonymous with

political consensus and the norm does seem to be supported also by the formal rules in the

committee governance form (Berg and Kjær, 2007). The local councils are organised in

several committees and the members of the committees are divided between the political

parties according to the principle of proportionality. This secures a broad political

representation and a protection of the minority. Furthermore, the administrative

responsibility is divided so that the committees have the decision responsibility in their area,

where as the mayor has the responsibility for the daily administration (Berg, 2004). Thus the

council members share the responsibility for administering a sector area with members of

the council from different parties. This promotes the sense of team work and reduces the

importance of ideological differences in the council. However, it also leads to sectoral

preferences of the committee members and hence may make it more difficult to make cross

sectoral compromises (Bækgaard, 2010). It has been contested if the effects of political

consensus are negative or positive. It has been indicated that the impacts on democracy in

terms of accountability and citizen engagement are negative, however, it has all been

proposed that consensus in the councils constitutes a form of political capital which the

mayor may exploit in order to exercise an effective leadership (Berg and Kjær, 2007). The

result here indicates that consensus does indeed have a positive impact on decision making

in times of rapid economic changes in the municipal budgets. In this situation the need for

taking unpopular decisions and to make cuts are evidently high. Consensus facilitates this.

4.2 Amalgamation and budgetary tractability

The results show that more complex amalgamations have larger budget overruns than less

complex amalgamations. The explanation for this may be found in the political life of the

councils as well as in the administrative life of the amalgamated municipalities. Considering

the role of the councillors it may be more difficult to adjust to changes in the economic

situation, if the councillors see themselves as representatives of their old municipalities,

This may make it difficult to make cuts or postpone expenditures which are benefitting their

former constituencies, This is likely to be the case as they often depend on the electorate in

these areas for renomination and reelection. In the new amalgamated municipalities new

cleavages may emerge along the fault-lines of the old-municipalities (tjek Bækgaard, 2010),

14

and this is more likely to be the case if units of equal size with each their centers are

merging, than if a big-brother is coopting smaller units, as the pendling patterns towards the

larger city makes it a less contestable center. Considering the administrative side of the

amalgamation more complex mergers may be less manageable, as loyalties to former

leaders may make the organisations less manageable. Furthermore, it may be more difficult

to make the right guess on what the expenditures of the new municipalities will be, if

different levels of service between units of equal size are being harmonised, rather than if

small units with different levels of service are being incorporated in a larger unit.

Fortunately, the effect of amalgamation seems to be diminishing as the interaction term

between amalgamation and 2009 is negative (see model 2, table 3).

The analysis of amalgamation was extended by employing different measures of

amalgamation such a dummy variable for amalgamation, measures on the number of

municipalities in the amalgamation and measures based on the number of inhabitants in the

old municipalities. The results show that the dummy variable was not significant. However,

the amalgamation degrees as well as a variable simply counting the number of

municipalities in the amalgamation are significant. This indicates that it does not per se

make a difference if the municipality is amalgamated or not, what matters seem to be the

complexity of the amalgamation. The more complex amalgamations are the more likely

budget overruns are.

The result adds to existing analysis on the relationship between amalgamations and

budgetary spending. They show that the municipalities facing amalgamations increase their

spending before closing time, as they know that deficits will be shared between the

members of the new municipality after the amalgamation. In other words, there are common

pool problems in amalgamation situations, and the costs should be taking into consideration,

when deciding to make amalgamations (Blom-Hansen, 2010; Welling, 2010). In addition,

the present results show that there are costs associated with amalgamation also not just

before closing time, but certainly also after as the budget overruns are higher in

municipalities with a high degree of amalgamation.

4.3 Procedural instruments for financial management

The analysis shows that management by objectives, financial decentralisation to the service

producing institutions, cross-sectoral policy making as well as frequency of documentation

for the fulfilment of political objectives for the economy does not influence budget

overruns, when the budgeted operating surplus is taken into account (see model 4, table 3).

This may seem surprising, as these management instruments have been recommended to the

municipalities in the last decades. One reason may of course be that these management tools

do not have a significant impact on budget overruns. Another explanation for this may be

methodological. The result is based on survey data, where the responses of the individual

council members are aggregated to the level of the municipality. One problem with this

method is that the council members – when they answer the survey – do not operate on a

scale, which places their responses in comparison with other municipalities. They answer if

they see the level of management by objectives as being very detailed, but this is not

15

necessarily seen in comparison to the level of detail in the other municipalities – indeed the

council members may not have a large insight in what the situation is in other municipalities

than their own. In contrast, they may see the level of detail in comparison to what it has

been previously. Thus, an analysis which also applies data based on observable

characteristics could be preferable.

4.4 Budgetary factors and tractability

Not surprisingly, the results show that having a lax budget has a substantial negative impact

on budget overruns (see table 3, model 4). This is quite straightforward as there is a larger

buffer for unforeseen expenses if the resources in the budget are slack, and hence budget

overruns are less frequent. As such lax budgeting may be a sign of an unambitious financial

management practise. Alternatively it can be a sign of a budget which have been

„massaged‟. In order to make the budget break even the councils may be tempted to include

unrealistic savings in the budget. For instance, it can simply be stated that increasing levels

of contracting out will cause unrealistically large savings.

Essentially, it reduces the part of the budget which is subject to political decision making,

and the citizens may face a situation where they pay high taxes but the service levels

guaranteed in the budget are low. However, lax budgeting may also occur

Between model 3 and 4 the explanatory power of the model raises from 0.319 to 0.376.

Thus the differences in the budgeted surplus explain quite a large degree of the variance in

budget overruns in the municipalities. This indicates that budget overruns is only an

indicator of economic problems in the municipalities. In fact, the municipalities which

appear to have a healthy economy due to not having budget overruns may in fact just have a

slack budgeting and a financial management which is less ambitious.

As such the budget culture explains a large proportion of the budget overruns in the

municipalities. In line with previous research budget culture is measured as the budget

overruns in the previous year (Houlberg, 1999; Blom-Hansen, 2002). If the budget is

overrun one year, it is much more likely to be overrun the following year as well.

Subsequent budget overruns are seen as an indicator of the present of a budget culture. In

other words, it indicates that budget overruns are seen as something which can happen in

subsequent year without action being taken. This may be due to the existence of a particular

culture where budget overruns are seen as accepted and appropriate. However, an

alternative explanation could be that external factors cause subsequent budget overruns. The

introduction of this variable increases the explanatory power of the model substantially (see

model 5, table 3).

The result – once again - shows that the informal institutions surrounding the budgeting

process and budget overruns are very important to the financial management in the

municipalities. In some municipalities it may be accepted to operate with slack budgets,

which make budget overruns less frequent. Similarly, repeatedly budget overruns seem to be

accepted in some municipalities. It is evident that if informal institutions develop which

16

regard this kind of financial management as appropriate, then it may financial management

difficult in the municipalities in the longer run.

5.0 Conclusion

This paper shows that external conditions in the form of changes in the demography and the

socio-demographic needs of the municipalities are important drivers of budget overruns. But

even if the external conditions are influential the budget and the financial management of

the budget are nested in the political and administrative life in the councils.

The decision making in the councils does influence budget overruns through the norm of

consensus. If the councils take the major part of their decisions in unanimity they are also

more able to make the unpopular decisions required to avoid budget overruns. The norm of

consensus is an integrated part of the committee system in the Danish municipalities. The

mayors‟ ability to built consensus in the councils have been seen as a way to accumulate

political capital and decision making power. As such consensus is an indicator of an

effective political leadership and apparently this political capital can be used to control

budget overruns in the municipalities.

Amalgamations continue to influence budget overruns in the municipalities. In the last year

before closing time the amalgamation lead to budget overruns due to common-pool

problems (Welling-Hansen, 2009). However, the analysis here shows that the

amalgamations continue to influence budget overruns also in 2009. Evidently, this is not

due to common pool problems as the new municipalities are not about to close. In contrast,

the analysis shows that budget overruns are larger the more complex the amalgamations are.

Hence, budget overruns after amalgamation seem to be due to intractability. The more

complex amalgamations, the more difficult it is to integrate the book keeping of the old

municipalities.

Over the years management by objectives, decentralisation of the budget to the institutional

level, cross sectoral policymaking and documentation of the economic results have been

recommended as a means to improve the financial management of the municipalities.

However, the analysis here shows that these instruments do not have any significant impact

on budget overruns, when their measurement is based on individual survey data.

Budgetary factor also matter. Lax budgeting does make budget overruns less frequent.

However, this is not necessarily positive as it is a sign of a less ambitious financial

management. In addition, budget overruns are more frequent if budget overruns occurred in

the year before. This indicates a budget culture where budget overruns are not sanctioned or

prevented the following year. In addition, changes in the budgets make overruns more

likely. As such, the decision-making in the councils may also have an indirect effect on

budget overruns as the councillors may have an influence on the tractability of the budget

and certainly also on to what extent lax budgeting and budget overruns are accepted.

17

Literature:

Alesina, Alberto (1989): Politics and business cycles in industrial democracies. Economic

Policy, 4(1) 1989.

Berg, R. (2004). Kommunale styreformer - erfaringer fra ind- og udland. Politologiske

Skrifter 5, 1-35.

Berg, Rikke & Ulrik Kjær (2007): Lokalt politisk lederskab. Odense: Syddansk

Universitetsforlag.

Bhatti, Y., A. L. Olsen, and L. H. Pedersen (2009). The effects of administrative

professionals on contracting out. Governance 22 (1), 121-137.

Blom-Hansen, Jens (2010): Municipal Amalgamations and Common Pool Problems: The

Danish Local Government Reform in 2007, in Scandinavian Political Studies, 33 (1): 51-73

Blom-Hansen, J. & J. Elklit & S. Serritzlew (eds.) (2006): Kommunalreformens

konsekvenser. København: Academica.

Blom-Hansen, J., Serritzlew, S. 2008, Budgetlægning i kommuner og regioner, i

Christiansen, P.M. (red.) Budgetlægning og offentlige udgifter, Systime Academic, Århus, s.

79-108.

Blom-Hansen, J., Monkerud, L.C., Sørensen, R. 2006, "Do parties matter for local revenue

policies? A comparison of Denmark and Norway", European Journal of Political Research,

vol. 45, s. 445-465.

Blom-Hansen, Jens (2002): Budget Procedures and the Size of the Budget: Evidence from

Danish Local Government. Scandinavian Political Studies, 25(1): 85-106.

Boyne, George A. (2004): Explaining Public Sector Performance: Does Management

Matter? Public Policy and Administration, 19 (4): 100-117

Boyne, George A. (1996): Constraints, Choices and Public policies. London: JAI Press.

Bækgaard, M. (2010): Committee bias in legislatures with a high degree of party cohesion:

Evidence from the Danish municipalities, in European Journal of Political Research

Cole, M. (2002). The role(s) of county councillors: An evaluation. Local Government

Studies, 28(4), 22–46.

Egner, Bjorn, Heinelt, & Hubert (2008). Explaining the differences in the role of councils:

an analysis based on a survey of mayors. Local Government Studies, 34(4), 529–544.

18

Geys, Benny (2007): Government weakness and Electoral Cycles in Local Public Debt:

Evidence from Flemish Municipalities. Local Government Studies, 33(2), 237-251

Frandsen, A. G. (2003). Deltagelse ved kommunalvalg. In U. Kjær and P. E. Mouritzen

(Eds.), Kommunestørrelse og lokalt demokrati, pp. 109- 126. Odense: Syddansk

Universitetsforlag.

Hansen, Karin (2008): “Nye veje” I den kommunale styring? Valg af politisk organiserings-

og styringsform i de nye kommuner. I: Nye kommuner i støbeskeen. Hansen, Karin et.al.

Handelshøjskolens Forlag 2008.

Hansen, Sune Welling (2009): Towards Genesis or the Grave. Financial Effects of Local

Government Mergers. Ph.d.-afhandling. Institut for Statskundskab, Syddansk Universitet,

Odense.

Houlberg, Kurt (1999): Budgetoverskridelsernes anatomi. En analyse af forskelle i danske

kommuners overholdelse af budgetterne. Nordisk Administrativt Tidsskrift, 3/1999/200-

232.

Houlberg, Kurt (2007): The Fine Art of Creating Local Political Business Cycles - The case

of Danish Municipalities 1989 - 2005 (revised). Den XVI Nordiske

Kommunalforskerkonference, Göteborg, Sverige 23.- 25. november 2007.

Houlberg, Kurt & K.B. Jensen (2010): Kommunernes økonomiske situation og

udgiftspolitiske prioriteringer. København: AKF.

Indenrigs- og Socialministeriet (2009): Kommunal udligning og generelle tilskud 2010.

København: Indenrigs- og Socialministeriet juni 2009.

Indenrigs- og Sundhedsministeriet (2010): Budget - og regnskabssystem for kommuner.

København: Indenrigs- og Sundhedsministeriet.

http://www.budregn.im.dk/im/site.aspx?p=2895, accessed 12. september 2010.

KREVI (2008b): Struktur i styringen – strukturelle forklaringer på kommunernes

økonomistyring 1996-2005. Århus: Det Kommunale og Regionale Evalueringsinstitut

KREVI (2009a): Kommunernes økonomi efter kommunalreformen. Driftsresultat og

finansiel egenkapital. NIRAS Konsulenterne for KREVI. Århus: Det Kommunale og

Regionale Evalueringsinstitut

19

KREVI (2009b): Kommunernes økonomi efter kommunalreformen. Budgetoverholdelse og

administrative udgifter. NIRAS Konsulenterne for KREVI. Århus: Det Kommunale og

Regionale Evalueringsinstitut

Lassen, D. D. and S. Serritzlew (2008). Political centralization and local democracy:

Evidence from large-scale municipal reform. Working Paper. Department of Economics.

University of Copenhagen, 1-44.

Martinussen, P. (2004). Majority rule in consensual democracies: Explaining political

influence in norwegian local councils. Local Government Studies, 30(3), 303.

Mouritzen, Poul Erik and James H. Svara (2002): Leadership at the Apex – Politicians and

administrators in Western local governments. University of Pittsburgh Press

Mouritzen, Poul Erik (2001): Er udvalgsstyret den rigtige styreform? I: Rolf Norstrand og

Niels Groes: Kommunestyrets fremtid. Akf 2001.

Rattsø, Jørn & Per Tovmo (1998): Local Government Responses to Shocks in Denmark.

Finansministeriet: Kommunal budgetoversigt. København: Finansministeriet.

Serritzlew, S. (2003). Shaping local councillor preferences: Party politics, committee

structure and social background. Scandinavian Political Studies 26 (4), 327-348.

Serritzlew, Søren (2003): Inkrementalisme og normer i budgetlægningen. Nordisk

Administrativt Tidsskrift, 84(3):308-335

Serritzlew, Søren (2005): Breaking Budgets: An Empirical Examination of Danish

Municipalities. Financial Accountability & Management, 21(4):413-435.

Skjæveland, A., S. Serritzlew, and J. E. N. S. Blom-Hansen (2007).Theories of coalition

formation: An empirical test using data from Danish local government. European Journal of

Political Research 46 (5), 721-745.

Wildawsky, A. & N. Caiden (1997): The New Politics of the Budgetary Process. New York:

Longman i See Asmus Olsen forthcoming for a research note on the measurement of amalgamation