WHAT DRIVES WORKING CAPITAL BEHAVIOUR OF INDIAN ...

17

WHAT DRIVES WORKING CAPITAL BEHAVIOUR OF INDIAN FMCG SECTOR? Dr. Vikas Bhargaw* Associate Professor, School of Commerce and Management, Om Sterling Global University, Hisar – 125001 (Haryana), India Dr. Reena Malik Assistant Professor, JCD Institute of Business Management, Sirsa – 125055 (Haryana), India ABSTRACT The present paper is an attempt to examine the determinants of working capital of Indian fast moving consumer goods (FMCG) companies for duration of nine years from 2010-11 to 2018- 19. The sample contains all eligible 52 FMCG firms listed in BSE-500 index. To carry out the study, six major variables namely size, sales growth, profitability, leverage, operating cycle and GDP growth have been used to explore their potential impact over the working capital behavior of the firms under study by applying descriptive statistics, Pearson coefficient of correlation and multiple linear regression techniques. The data firstly have been checked for non-existence of unit root by using Levin-Chin-Chu panel unit test. The descriptive parameters of the study show that the firms under study have their current assets exceeding their current liabilities. However, the leverage ratio is too high which is due to more use of non-current liabilities. The correlation analysis found operating cycle to be an important and prime factor having significant association with working capital behavior of sample companies. The variable-wise regression analysis holds firm size and leverage to have the negative relations whereas, corporate profitability and operating cycle are found to have positive association with the working capital ratio of sample companies. Keywords: Working Capital, Indian FMCG firms, BSE-500, Operating Cycle, Panel Unit Root Test Journal of Xi'an University of Architecture & Technology Volume XII, Issue V, 2020 ISSN No : 1006-7930 Page No: 2015

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of WHAT DRIVES WORKING CAPITAL BEHAVIOUR OF INDIAN ...

WHAT DRIVES WORKING CAPITAL BEHAVIOUR OF INDIAN FMCG

SECTOR?

Dr. Vikas Bhargaw*

Associate Professor,

School of Commerce and Management,

Om Sterling Global University,

Hisar – 125001 (Haryana), India

Dr. Reena Malik

Assistant Professor,

JCD Institute of Business Management,

Sirsa – 125055 (Haryana), India

ABSTRACT

The present paper is an attempt to examine the determinants of working capital of Indian fast

moving consumer goods (FMCG) companies for duration of nine years from 2010-11 to 2018-

19. The sample contains all eligible 52 FMCG firms listed in BSE-500 index. To carry out the

study, six major variables namely size, sales growth, profitability, leverage, operating cycle and

GDP growth have been used to explore their potential impact over the working capital behavior

of the firms under study by applying descriptive statistics, Pearson coefficient of correlation and

multiple linear regression techniques. The data firstly have been checked for non-existence of

unit root by using Levin-Chin-Chu panel unit test. The descriptive parameters of the study show

that the firms under study have their current assets exceeding their current liabilities. However,

the leverage ratio is too high which is due to more use of non-current liabilities. The correlation

analysis found operating cycle to be an important and prime factor having significant

association with working capital behavior of sample companies. The variable-wise regression

analysis holds firm size and leverage to have the negative relations whereas, corporate

profitability and operating cycle are found to have positive association with the working capital

ratio of sample companies.

Keywords: Working Capital, Indian FMCG firms, BSE-500, Operating Cycle, Panel Unit Root Test

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2015

1. Introduction

The corporate world is expected to see present and future financial requirements for all its stakeholders in

the business. It is largely, the corporate sector which provides growth and development to every kind of

economy. The concept of working capital in the world of corporate finance is also very important in this

direction. Every type of firm needs finance to carry out its operation. Working capital is one of the

sources of funds the firm can use to finance their day to day operation. Abor (2008) has also admitted that

in emerging economies, it is very imperious for corporate firms to be able to provide finance for their

various activities and move ahead overtime in order to support employment situation of an economy

along-with providing them dividends, profits and wages to households. The concept of working capital

holds a very important role in firm’s profitability, risk management and enhancement of the value of the

firm and it is very crucial element for each organization in order to survive in the market as well as to

maximize its wealth for its stakeholders. Rahman and Nasr (2007) have specifically mentioned the

importance of setting the optimal capital ratio to increase the firm’s value. A careful management of

short-term payment consideration along-with lower investment in liquid assets can enable a firm to

maximize its wealth. The importance of working capital is also supported by the argument that it

constitutes a larger part of total assets of a firm. The finance managers also devote much of their time to

manage the working capital required by the organization. The working capital also serves the role of risk

indicator for all its creditors. Smith (1980) states that working capital management is very important as it

not only affect the liquidity but also the profitability of the firm. The primary objective of this concept is

to safeguard the companies by providing sufficient liquidity to carry out its normal operations. The

availability of working capital prevents firms from inability to pay short-term liabilities as well as make

them stronger for adverse economic condition. However, unnecessary investment in working capital

imposes opportunity cost leading to decreased overall profitability. So, it is very important for the firms to

effectively manage its working capital. The appropriate and effective evaluation of the working capital

can be backed by identifying the underlying determinants to it that would help finance managers to

maintain the optimum level of investment in current assets. Strange but true, that a very little attention has

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2016

been given to identify the factors affecting working capital in the literature of finance (Deloof, 2003,

Nobanee et al. 2011). Further in India there is a lack of research in with regard to determinants of working

capital. The present study pays attention to enhance the body of knowledge by recognizing the significant

underlying factors, which affect working capital management in an emerging market like India. The rest

of the paper is organized as follows. Section 2 presents the literature review. Section 3 describes the

detailed research methodology adopted for the present study. Empirical results and discussion following

by conclusion are given in section 4 and 5 respectively.

2. Review of Literature

Since the beginning of this century, many studies have been conducted to investigate about the

determinants to working capital, especially in Asia pacific. In order to facilitate the foundation for

undertaking the present study, a brief literature survey has been carried out on the concept of working

capital. Following are the few prominent studies:

Pandey and Parera (1997) conducted a study on working capital management practices being followed by

Sri Lankan listed private sector companies and found that firms follow informal working capital policies.

Their study also revealed that the working capital of firms under study is largely influenced by the size of

the firms. Shin and Soenen (1998) investigated about the behavior of working capital by taking a large

sample of listed American companies for time duration of 20 years and found a negative association

between operating cycle and corporate profitability. Their study further analysed the association between

aggressive and conservative working capital practices and revealed that aggressive working capital

financing is balanced by following conservative working capital financing. Deloof (2003) also

investigated about the working capital behavior of Belgian firms by using correlation and regression

method the study found a significant negative relationship between operating income and the accounts

receivable period, inventories and accounts payable of sample firms. The study further revealed the

excess amount of cash as the part of working capital. The study suggested that managers can maximize

the wealth for their shareholders by dropping the accounts receivable period and inventories to a

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2017

reasonable minimum. Eljelly (2004) examined the association between profitability and liquidity as

measure of working capital by taking a sample of Saudi Arabian joint stock companies by using

correlation and regression analysis and found operating cycle being more important to be as a measure of

liquidity instead of current ratio that affects profitability. The study further supported the size of the firm

variable to have a significant impact on liquidity and working capital position of the sample firm.

Poutziouris et al. (2005) conducted empirical investigation on working capital management of UK’s 236

Small and Medium Enterprises and found a direct association between growth rate and practices of

working capital management. Their study supported that as companies grow their short-term finance

management practices also improve. Lazardidis and Tryfonidis (2006) investigated about the association

between profitability and working capital management in the Athens stock market listed 131 companies

during 2001-2004 and their study found a significant relationship between operational profit and the cash

conversion cycle. Moreover, their study suggested using right management policy for operating cycle in

order to generate more profits. Afza and Nazir (2009) conducted a study to explore the relationship

between profitability and working capital behaviour in Tehran stock exchange listed 208 companies

during 1998-2005 and found that managers following restrictive and conservative strategies have been

able to increase the value for their shareholders. Their study further revealed that while selecting an

investment portfolio, investors prefer firms having short term credit policies and comparatively lower

level of current liabilities. Gill et al. (2010) also investigated about the relationship between working

capital management and profitability by taking a data set of 3 years from 2005 to 2007 using a sample of

88 NYSE (New York Stock Exchange) listed American firms and found statistically significant

relationship between the cash conversion cycle and profitability, measured through gross operating profit.

Archavli et al. (2012) conducted the study to find empirical evidence for the effective working capital

management by using 211 Athens stock exchange listed Greek companies for a period of six years from

2005 to 2010 and reported significant negative correlations between the variables of working capital and

thus on the business performance. Afrifa (2015) investigated about the effect of working capital

management on the performance of 141 AIM (Alternative Investment Market) listed small and medium

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2018

enterprises during 2007-14 and revealed that inventory holding period, accounts receivable period and

accounts payable period are the most prominent factor affecting the working capital decision of sample

firms. Fatimatuzzahra and Kusumastuti (2017) also investigated about the factor responsible for working

capital decision of Indonesian listed firm during 2010-14 and found a significant association of firm size,

firm growth, cash flow, profitability, and GDP toward working capital. While the leverage and capital

expenditure shows insignificant effect. Nyeadi et al. (2018) empirically investigated about the

determinants of working capital by taking a sample of 28 listed firms in Ghana for a time period of 8

years from 2007 to 2014. Their study found profitability, age, and operating cycles as the factors having

positive association whereas, sales growth, GDP growth, and leverage as the factors having negative

association with the working capital decision. Nastiti et al. (2019) conducted a similar study by taking a

sample of 117 Indonesian stock exchange listed manufacturing firms for the years 2010–2017 and found

that sales growth and economic growth are the most prime factors affecting working capital decision.

However, the effects of these variables also depend upon the size of the firm as well as its tenure in terms

of years.

The above discussion on available worldwide literature reveals various factors such as firm size,

profitability, sales growth, operating cycle, leverage and growth in gross domestic product (GDP) etc. has

been found prominent to act as major determinants to working capital. However, their impacts have been

found contradictory among various studies. So there is still a need to discover more insights into it.

Further in India there is a lack of research in corporate sector with regard to determinants of working

capital. The fast moving consumer goods (FMCG) companies form a major segment of the Indian

corporate sector and also known as the backbone of Indian economy by playing a prime role in the growth

and development of the country. As far as the working capital decision is concerned, very few studies

have been undertaken over the Indian FMCG sector companies. So, a need for research in said sector on

this important topic of determinants of working capital is identified. In view of above, the present study is

an attempt to answer that what are the governing factors that affect the working capital decision of the

listed Indian FMCG firms.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2019

3. Research Methodology

3.1 Objective of the Study

The major objective of this study is to identify the variables that influence the working capital

requirements of the listed FMCG firms in India.

3.2 Variables and Hypotheses Development

In order to carry out the objective of the present study, it is required to identify some explanatory

independent variables which might have some influence over the working capital. For this, the selection

of appropriate dependent and independent (explanatory) variables is made on the basis of secondary

research on studies in the form of literature review of working capital. Based upon the literature survey,

the study uses the firm size, sales growth, profitability, leverage, operating cycle and GDP (Gross

Domestic Production) growth to be the independent variables explaining the working capital ratio. The

following table I describe the measurement of all the independent variables used for the purpose of

analysis.

Table I: List of Variables and their Measurement

S. No. Variable Type Measurement of the Variable

1 Working Capital

Ratio Dependent

It is calculated as (Current Assets - Current

Liabilities) / Total Assets

2 Size Independent A sum of Total Assets of the firm in a given year

3 Sales Growth Independent

It represents the annual percentage change in sales. It

is calculated as (Total Salest - Total Salest-1) / Total

Salest-1

4 Profitability Independent EBIT to Total Assets in a given year

5 Leverage Independent It is calculated as Total Debt / (Total Debt + Total

Equity)

6 Operating Cycle Independent

This is the sum of days in inventory and days in

accounts receivables. It is calculated as

Inventory Conversion Period (ICP) + Receivables

Conversion Period (RCP).

Where

ICP = (Average inventory/Annual Cost of goods sold)

* 365

RCP = (Average Accounts Receivables/Annuals

Sales) * 365

7 GDP Growth Independent This refers to the change in natural log of GDP

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2020

Following is the association brief of all the variables with working capital ratio along with their respective

hypotheses.

3.2.1. Firm Size: The argument that, large sized firms are expected to have a greater investment in

working capital due to their huge day-to-day operational needs signifies the positive association between

firm size and working capital ratio.

3.2.2. Sales Growth: The argument that, the cash basis sales leads to requirement of lesser amount of

working capital signifies the negative association between the sales growth and working capital ratio.

3.2.3. Profitability: The argument that, the more profitable firms employs its profits back in the business,

hence more working capital is required and thus signifies the positive association between profitability

and working capital ratio.

3.2.4. Leverage: The argument that, already levered firms are always very careful in managing their risk

and do so by keeping low investment on current asset signifies the negative association between leverage

and working capital ratio.

3.2.5. Operating Cycle: The argument that, longer the period of operating cycle of the firm would lead to

the higher working capital requirements signifies the positive association between operating cycle and

working capital ratio.

3.2.6. GDP Growth: The activities of the particular economy measured in terms of GDP (Gross Domestic

Production) certainly have an impact on the operations of the firm. For example, firm’s liquidity is

expected to increase during booming times and the vice versa during down times. This argument thus,

signifies the positive association between GDP growth and working capital requirements.

On the basis of above discussion the following hypotheses have been Formulated.

H1. Firm Size is positively related to working capital requirements

H2. Sale Growth is negatively related to working capital requirements

H3. Profitability is positively related to working capital requirements

H4. Leverage is negatively related to working capital requirements

H5. Operating Cycle correlates positively with working capital requirements

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2021

H6. Gross Domestic Product correlates positively with working capital requirements

3.3 Data Source and Sample Selection

The present empirical investigation has been done by taking a sample of FMCG companies, out of listed

companies in the BSE-500 index at Bombay Stock Exchange. All those FMCG companies were taken

into consideration for which required financial data was available. Further, only those companies have

been selected in the sample who comply all the listing regulation of Bombay Stock Exchange during the

period under study. Out of total 61 FMCG sector companies, 52 companies complied with this restriction,

hence form a final sample for the present study. The study has been covering a period of nine financial

years from 2010-11 to 2018-19. The complete list of companies is given in table II.

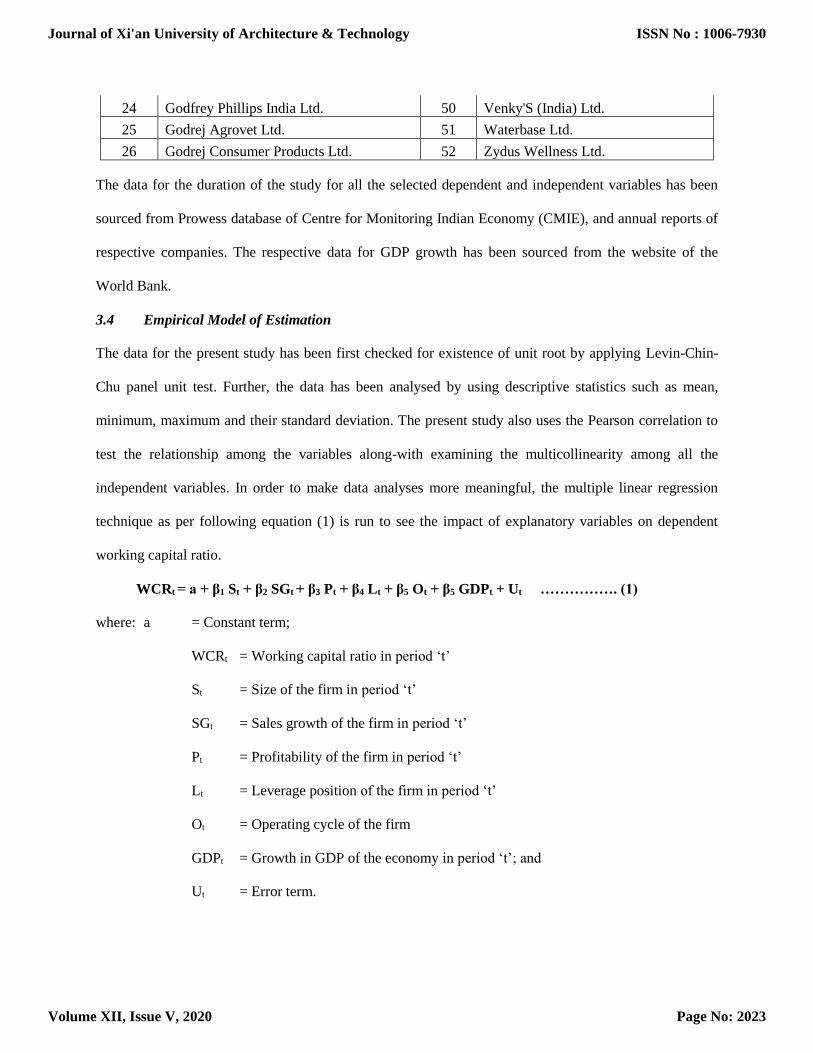

Table II: List of Sample Companies from Indian FMCG Sector

S. No. Name of the company S. No. Name of the company

1 A D F Foods Ltd. 27 Gujarat Ambuja Exports Ltd.

2 Advanced Enzyme Technologies Ltd. 28 Heritage Foods Ltd.

3 Agro Tech Foods Ltd. 29 Hindustan Unilever Ltd.

4 Associated Alcohols & Breweries Ltd. 30 I T C Ltd.

5 Avanti Feeds Ltd. 31 Jyothy Labs Ltd.

6 Bajaj Consumer Care Ltd. 32 K R B L Ltd.

7 Bajaj Hindusthan Sugar Ltd. 33 L T Foods Ltd.

8 Balrampur Chini Mills Ltd. 34 Marico Ltd.

9 Bombay Burmah Trdg. Corpn. Ltd. 35 Mcleod Russel India Ltd.

10 Britannia Industries Ltd. 36 Nath Bio-Genes (India) Ltd.

11 C C L Products (India) Ltd. 37 Nestle India Ltd.

12 Coastal Corporation Ltd. 38

Procter & Gamble Hygiene & Health

Care Ltd.

13 Colgate-Palmolive (India) Ltd. 39 Radico Khaitan Ltd.

14 D F M Foods Ltd. 40 Shree Renuka Sugars Ltd.

15 Dabur India Ltd. 41 Som Distilleries & Breweries Ltd.

16 Dalmia Bharat Sugar & Inds. Ltd. 42 Tasty Bite Eatables Ltd.

17 Dhampur Sugar Mills Ltd. 43 Tata Coffee Ltd.

18 Dwarikesh Sugar Inds. Ltd. 44 Tata Consumer Products Ltd.

19 E I D-Parry (India) Ltd. 45 Triveni Engineering & Inds. Ltd.

20 Emami Ltd. 46 United Breweries Ltd.

21 Eveready Industries (India) Ltd. 47 Uttam Sugar Mills Ltd.

22 G M Breweries Ltd. 48 V S T Industries Ltd.

23 Globus Spirits Ltd. 49 Vadilal Industries Ltd.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2022

24 Godfrey Phillips India Ltd. 50 Venky'S (India) Ltd.

25 Godrej Agrovet Ltd. 51 Waterbase Ltd.

26 Godrej Consumer Products Ltd. 52 Zydus Wellness Ltd.

The data for the duration of the study for all the selected dependent and independent variables has been

sourced from Prowess database of Centre for Monitoring Indian Economy (CMIE), and annual reports of

respective companies. The respective data for GDP growth has been sourced from the website of the

World Bank.

3.4 Empirical Model of Estimation

The data for the present study has been first checked for existence of unit root by applying Levin-Chin-

Chu panel unit test. Further, the data has been analysed by using descriptive statistics such as mean,

minimum, maximum and their standard deviation. The present study also uses the Pearson correlation to

test the relationship among the variables along-with examining the multicollinearity among all the

independent variables. In order to make data analyses more meaningful, the multiple linear regression

technique as per following equation (1) is run to see the impact of explanatory variables on dependent

working capital ratio.

WCRt = a + β1 St + β2 SGt + β3 Pt + β4 Lt + β5 Ot + β5 GDPt + Ut ……………. (1)

where: a = Constant term;

WCRt = Working capital ratio in period ‘t’

St = Size of the firm in period ‘t’

SGt = Sales growth of the firm in period ‘t’

Pt = Profitability of the firm in period ‘t’

Lt = Leverage position of the firm in period ‘t’

Ot = Operating cycle of the firm

GDPt = Growth in GDP of the economy in period ‘t’; and

Ut = Error term.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2023

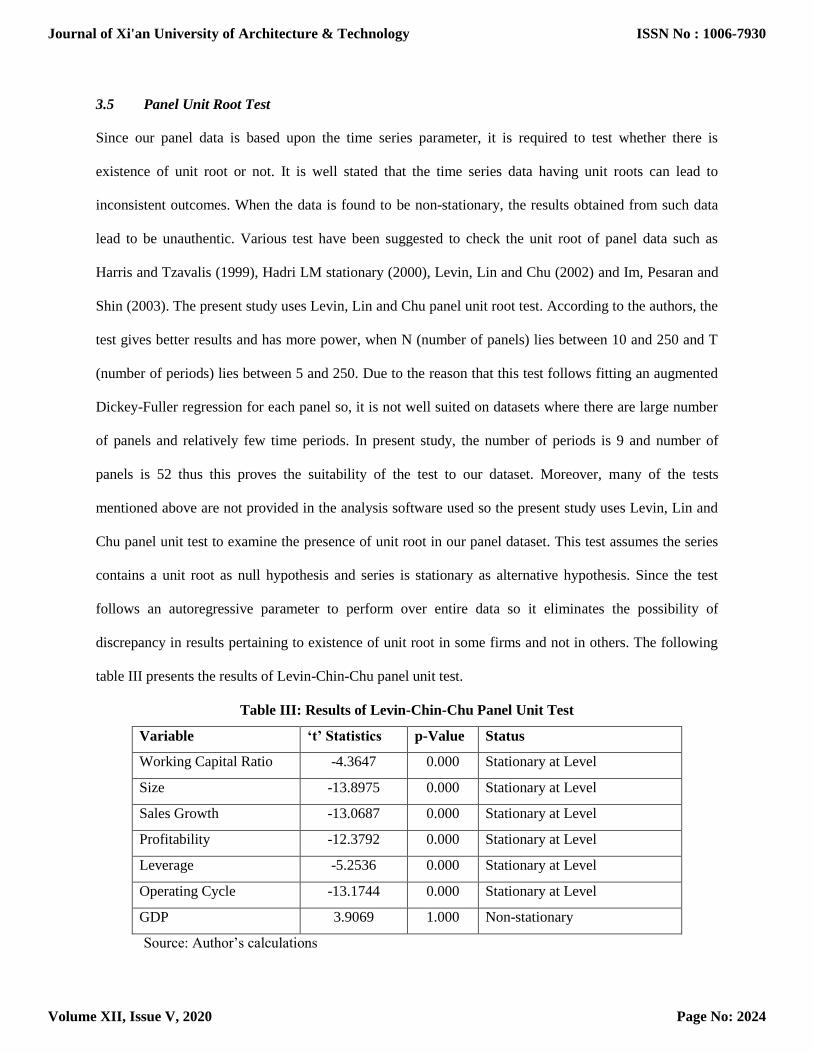

3.5 Panel Unit Root Test

Since our panel data is based upon the time series parameter, it is required to test whether there is

existence of unit root or not. It is well stated that the time series data having unit roots can lead to

inconsistent outcomes. When the data is found to be non-stationary, the results obtained from such data

lead to be unauthentic. Various test have been suggested to check the unit root of panel data such as

Harris and Tzavalis (1999), Hadri LM stationary (2000), Levin, Lin and Chu (2002) and Im, Pesaran and

Shin (2003). The present study uses Levin, Lin and Chu panel unit root test. According to the authors, the

test gives better results and has more power, when N (number of panels) lies between 10 and 250 and T

(number of periods) lies between 5 and 250. Due to the reason that this test follows fitting an augmented

Dickey-Fuller regression for each panel so, it is not well suited on datasets where there are large number

of panels and relatively few time periods. In present study, the number of periods is 9 and number of

panels is 52 thus this proves the suitability of the test to our dataset. Moreover, many of the tests

mentioned above are not provided in the analysis software used so the present study uses Levin, Lin and

Chu panel unit test to examine the presence of unit root in our panel dataset. This test assumes the series

contains a unit root as null hypothesis and series is stationary as alternative hypothesis. Since the test

follows an autoregressive parameter to perform over entire data so it eliminates the possibility of

discrepancy in results pertaining to existence of unit root in some firms and not in others. The following

table III presents the results of Levin-Chin-Chu panel unit test.

Table III: Results of Levin-Chin-Chu Panel Unit Test

Variable ‘t’ Statistics p-Value Status

Working Capital Ratio -4.3647 0.000 Stationary at Level

Size -13.8975 0.000 Stationary at Level

Sales Growth -13.0687 0.000 Stationary at Level

Profitability -12.3792 0.000 Stationary at Level

Leverage -5.2536 0.000 Stationary at Level

Operating Cycle -13.1744 0.000 Stationary at Level

GDP 3.9069 1.000 Non-stationary

Source: Author’s calculations

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2024

The table clearly reveals that the variables working capital ratio, size, sales growth, profitability, leverage

and operating cycle have been found stationary at level. Hence we accept the alternative hypothesis of

non-existence of unit root in the data pertaining to these variables. The only variable found to be non-

stationary is GDP. This variable presents the overall condition of entire economy and is affected by many

internal and external factors, which are difficult to measure. Moreover, the non-stationary variable can be

made stationary by differencing the series as prescribed by Johannes, Njong and Clement (2011). Thus

after differencing this GDP variable, the study obtains all the dataset to be stationary by rejecting the null

hypotheses mentioning presence of unit root and being non-stationary.

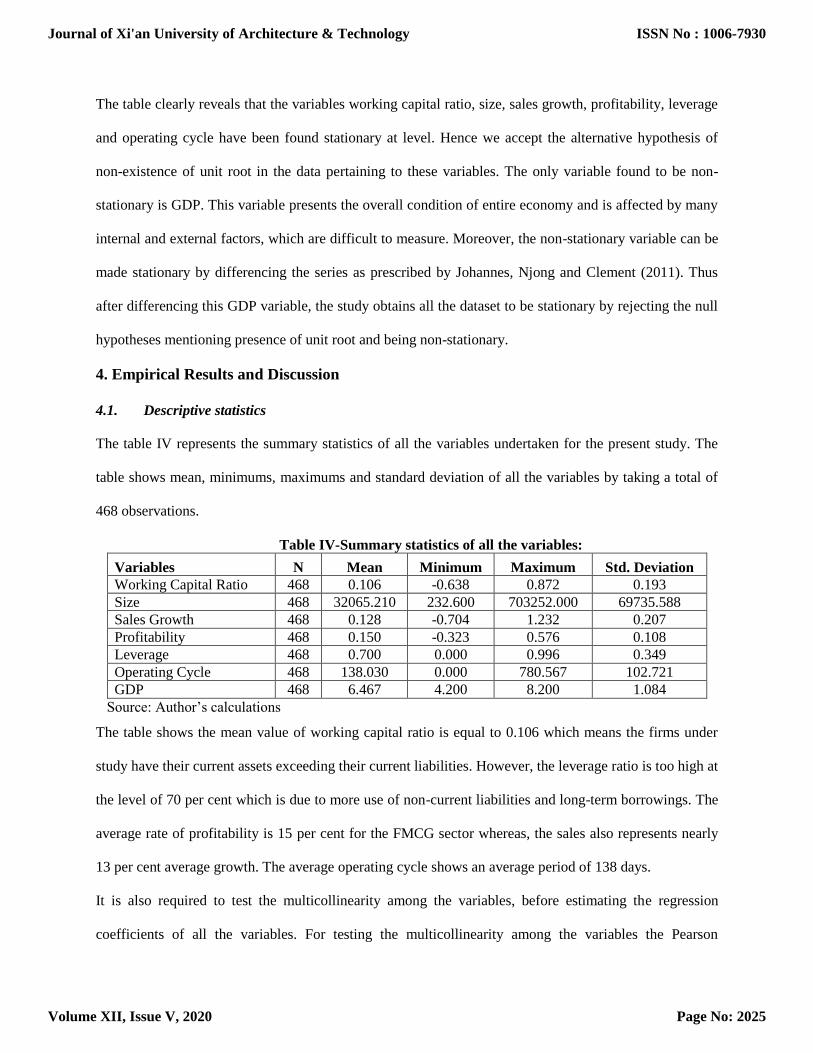

4. Empirical Results and Discussion

4.1. Descriptive statistics

The table IV represents the summary statistics of all the variables undertaken for the present study. The

table shows mean, minimums, maximums and standard deviation of all the variables by taking a total of

468 observations.

Table IV-Summary statistics of all the variables:

Variables N Mean Minimum Maximum Std. Deviation

Working Capital Ratio 468 0.106 -0.638 0.872 0.193

Size 468 32065.210 232.600 703252.000 69735.588

Sales Growth 468 0.128 -0.704 1.232 0.207

Profitability 468 0.150 -0.323 0.576 0.108

Leverage 468 0.700 0.000 0.996 0.349

Operating Cycle 468 138.030 0.000 780.567 102.721

GDP 468 6.467 4.200 8.200 1.084

Source: Author’s calculations

The table shows the mean value of working capital ratio is equal to 0.106 which means the firms under

study have their current assets exceeding their current liabilities. However, the leverage ratio is too high at

the level of 70 per cent which is due to more use of non-current liabilities and long-term borrowings. The

average rate of profitability is 15 per cent for the FMCG sector whereas, the sales also represents nearly

13 per cent average growth. The average operating cycle shows an average period of 138 days.

It is also required to test the multicollinearity among the variables, before estimating the regression

coefficients of all the variables. For testing the multicollinearity among the variables the Pearson

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2025

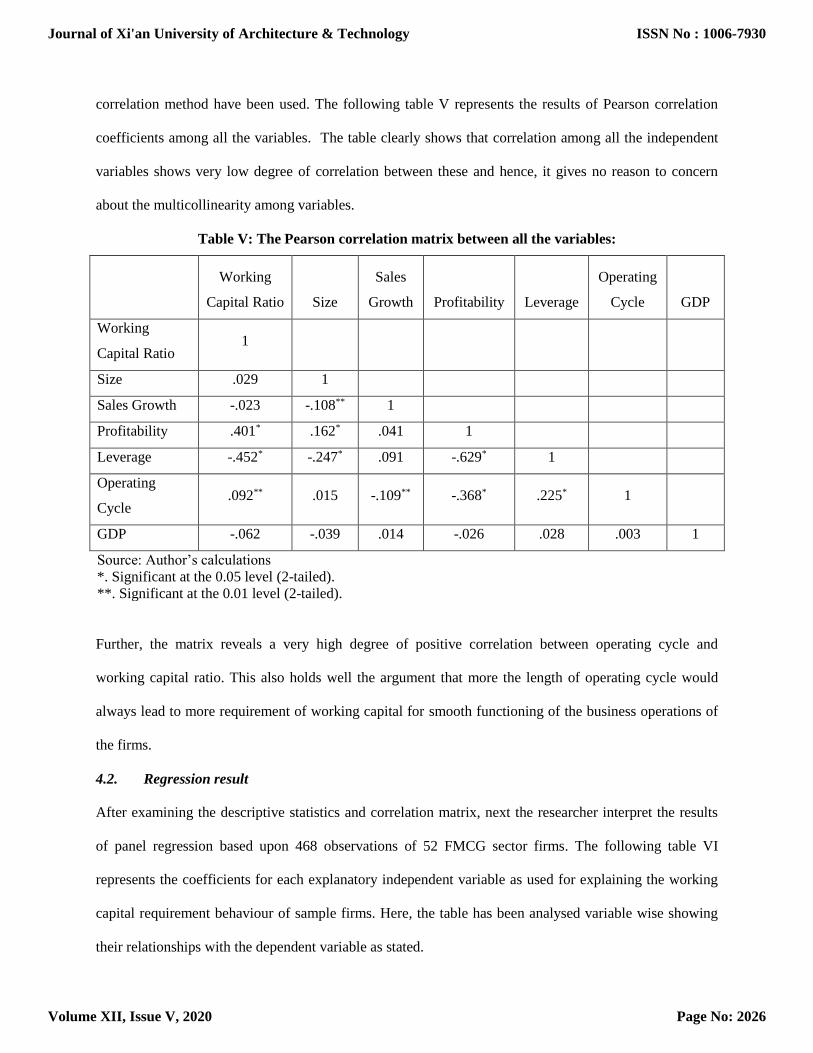

correlation method have been used. The following table V represents the results of Pearson correlation

coefficients among all the variables. The table clearly shows that correlation among all the independent

variables shows very low degree of correlation between these and hence, it gives no reason to concern

about the multicollinearity among variables.

Table V: The Pearson correlation matrix between all the variables:

Working

Capital Ratio Size

Sales

Growth Profitability Leverage

Operating

Cycle GDP

Working

Capital Ratio 1

Size .029 1

Sales Growth -.023 -.108** 1

Profitability .401* .162* .041 1

Leverage -.452* -.247* .091 -.629* 1

Operating

Cycle .092** .015 -.109** -.368* .225* 1

GDP -.062 -.039 .014 -.026 .028 .003 1

Source: Author’s calculations

*. Significant at the 0.05 level (2-tailed).

**. Significant at the 0.01 level (2-tailed).

Further, the matrix reveals a very high degree of positive correlation between operating cycle and

working capital ratio. This also holds well the argument that more the length of operating cycle would

always lead to more requirement of working capital for smooth functioning of the business operations of

the firms.

4.2. Regression result

After examining the descriptive statistics and correlation matrix, next the researcher interpret the results

of panel regression based upon 468 observations of 52 FMCG sector firms. The following table VI

represents the coefficients for each explanatory independent variable as used for explaining the working

capital requirement behaviour of sample firms. Here, the table has been analysed variable wise showing

their relationships with the dependent variable as stated.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2026

The coefficient of first explanatory variable i.e. size of the firms shows a statistically significant negative

relationship with working capital requirement of the firms. It means that larger the firm, lesser is the need

for working capital. So, the study rejects the null hypotheses (H1) that size of the firms is positively

related to working capital ratio. It may be due to the argument that larger firms are expected to have a

large number of supplier, supplying at more favorable terms to the companies hence less amount of

working capital is required. The second variable i.e. sales growth, surprisingly, has been found to have no

relationship with working capital ratio. So, the study rejects the null hypotheses (H2) that sales growth is

negatively related to working capital ratio. This may be due to cash sales policy of the Indian FMCG

firms which requires lesser necessity to hold working capital.

Table VI-Results of regression analysis

Model

Variables

Unstandardized

Coefficients

Standardized

Coefficients t Sig.

B Std. Error Beta

(Constant) 0.155 0.057 2.745 .006

Size -3.093 0.000 -0.112 -2.779 .006

Sales Growth 0.016 0.037 0.017 0.432 .666

Profitability 0.531 0.094 0.297 5.657 .000

Leverage -0.197 0.028 -0.357 -6.959 .000

Operating Cycle 0.001 0.000 0.286 6.795 .000

GDP -0.009 0.007 -0.050 -1.285 .200

a. Dependent Variable: Working Capital Ratio

b. Adjusted R2: 0.297

c. No. of firms: 52

d. No. of observations: 468

Source: Author’s calculations

The third independent variable, profitability, has been found to have a statistically significant positive

relation with regard to working capital requirements. So, the study rejects the null hypotheses (H3) that

profitability is positively related to working capital ratio. This may be due to the fact that firms having

higher profits are supposed to reinvest their money into their projects leading to availability of more

working capital. The next variable i.e. leverage, has been found to have a statistically significant negative

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2027

association with the working capital requirement. So, the study accepts the null hypotheses (H4) that

leverage is negatively related to working capital ratio. This may be due to fact that those companies which

are having higher leverage position try to reduce their risk by managing their working capital and keeping

low investment in current assets. The fifth variable, operating cycle, has been found to bear statistically

significant positive impact on the working capital requirement. So the study accepts the null hypotheses

(H5) that operating cycle is positively related to working capital ratio. With this result, the present study

supports the argument that longer operating cycle period takes necessitates higher amount of working

capital. The last independent variable i.e. GDP has been found having no relation with the requirement of

working capital of the Indian FMCG firms, thus, the study rejects the null hypotheses (H6) that GDP

growth is positively related to working capital ratio. Further, The coefficient of determination (R2) for

above regression model gives a value of 0.297 indicates that more than 29 per cent variation in working

capital is caused due to negative variation of size and leverage of the firms and positive variation in the

profitability and operating cycle of the Indian FMCG sector firms.

5. Conclusion

The present study has investigated about the determinants of working capital in the Indian FMCG sector

companies. To carry out the study, six major variables namely firm size, sales growth, profitability,

leverage, operating cycle and GDP growth have been identified and used to explore their potential impact

over the working capital ratio of the firms under study. The Levin, Lin and Chu panel unit root test clearly

reveals that all the explanatory independent variables except GDP growth have been found stationary at

level representing non-existence of unit root in the data pertaining to these variables. The descriptive

parameters of the study show that the firms under study have their current assets exceeding their current

liabilities. However, the leverage ratio is too high at the level of 70 per cent which is due to more use of

non-current liabilities and long-term borrowings. Further, the correlation analysis reveals a very high

degree of positive correlation between operating cycle and working capital ratio. This also holds well the

argument that more the length of operating cycle would always lead to more requirement of working

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2028

capital for smooth functioning of the business operations of the firms. The variable-wise regression

analysis holds firm size and leverage to have the negative relations with the working capital requirement

of the FMCG companies which means that large and more levered firms requires less working capital.

However, corporate profitability and operating cycle are found to have positive association with the

working capital ratio of companies, which proves the supposition that more profitable companies and

longer operating cycles lead to more requirement of working capital for smooth operation of the firms

under study. Finally, the study admits the firm size, leverage, profitability and operating cycle are the

most dominating factors in explaining the working capital requirement of Indian FMCG companies. The

major limitation of the study is that it has focused only on one corporate sector i.e. FMCG sector as well

as on one economy i.e. India. The study can be improved by using several economies and corporate

sectors to draw more comprehensive results. For future research, the researchers can develop a stronger

model by including several other macro-economic variables such as financial stability of the economy,

foreign direct investment, threats from terrorism and so on along with longer time duration. However, the

findings of the present study can help corporate sector and finance managers to anticipate and design their

working capital by estimating the impact of said factors over the day to day fund requirements of the

firms. The scholars working on this issue can also get an idea about the prevailing scenario in the field of

corporate finance.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2029

Bibliography

Abor, J. (2008). “Determinants of Capital Structure of Ghanaian Firms”. African Economic

Research Consortium, Research Paper No. 176.

Afrifa, G., Tauringana, V., and Tingbani, I. (2015). “Working capital management and

performance of listed SMEs”. Journal of Small Business & Entrepreneurship. Vol. 27. pp. 1-22.

Afza, T., and Nazir, M.S. (2007). “Is it Better to be Aggressive or Conservative in Managing

Working Capital?”. Journal of Quality and Technology Management. Vol. 3, pp. 11-21.

Archavli, E., Siriopoulos, C., and Arvanitis, S. (2012). “Determinants of Working Capital

Management”. SSRN Electronic Journal. Online available at 10.2139/ssrn.2179907.

Deloof, M. (2003). “Does Working Capital Management Affect Profitability of Belgian Firms?”

Journal of Business Finance & Accounting , Vol. 30, No. 3-4, pp. 573-588.

Eljelly, A.M. (2004). “Liquidity – profitability Trade off: An Empirical Investigation”. Journal

of Commerce and Management, Vol. 14, pp. 48-61.

Fatimatuzzahra, M., and Kusumastuti, R. (2017). “The Determinant of Working Capital

Management of Manufacturing Companies. MIMBAR, Jurnal Sosial dan Pembangunan. Vol. 32.

No. 2, pp. 276-281.

Gill, A., Bigger I.N., and Mathur, N. (2010). “The Relationship Between Working Capital

Management And Profitability: Evidence From The United States”. Business and Economics

Journal, Vol. 10, pp. 1-10.

Hadri, K. (2000). “Testing for stationarity in heterogeneous panels”. The Econometrics Journal,

Vol. 3, pp. 148–161.

Harris, R., and Tzavalis, E. (1999). “Inference for unit roots in dynamic panels where the time

dimension is fixed”. Journal of Econometrics, Vol. 91, No. 2, pp. 201-226.

Im, K.S., Pesaran, M.H., and Shin, Y. (2003). "Testing for unit roots in heterogeneous panels".

Journal of Econometrics, Elsevier, Vol. 115, No. 1, pp. 53-74.

Johannes, T.A., Njong, A.M., and Clement, N. (2011). “Financial development and economic

growth Cameroon, 1970–2005”. Journal of Economics and International Finance, Vol. 3, No. 6,

pp. 367–375.

Lazaridis, I., and Tryfonidis, D. (2006). “Relationship between working capital management and

profitability of listed companies in the Athens stock exchange”. Journal of Financial

Management and Analysis, Vol. 19, pp. 26-25.

Levin, A., Lin, C. F., and Chu, C. S. J. (2002). “Unit root tests in panel data: Asymptotic and

finite-sample properties”. Journal of Econometrics, Vol. 108, pp. 1–24.

Nastiti, P., Atahau, A., and Supramono, S. (2019). “The Determinants of Working Capital

Management: The Contextual Role of Enterprise Size and Enterprise Age”. Business,

Management and Education. Vol. 17, No. 2, pp. 94-110.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2030

Nobanee, H., Abdullatif, M., and Al-Hajjar, M. (2011). “Cash Conversion Cycle and Firm’s

Performance of Japanese Firms”. Asian Review of Accounting , Vol. 19, No. 2, pp. 147-156.

Nyeadi, J.D., Sarem Y.A., and Aawaar G. (2018). “Determinants of working capital requirement

in listed firms: Empirical evidence using a dynamic system GMM”, Cogent Economics &

Finance, Vol. 6, pp. 1-14.

Pandey, I.M., and Perera K.L.W. (1997). "Working Capital Management in Sri Lanka," IIMA

Working Papers WP1997-01-01_01425, Indian Institute of Management Ahmedabad, Research

and Publication Department.

Poutziouris, P., Michaelas, N., and Soufani, K. (2005). “Financial management on trade credit in

small – medium sized Enterprise:. European financial management Association ( EFMA).

Rahman, A., and Nasr, M. (2007). “Working capital management and profitability: Case of

Pakistani firms” (Unpublished Dissertation). COMSATS Institute, Pakistan.

Shin, H.H., and Soenen, L. (1998). "Efficiency of Working Capital Management and Corporate

Profitability". Financial Practice and Education, Vol.8, No. 2, pp. 37.

Smith, K. (1980). “Profitability versus liquidity tradeoffs in working capital management”. In

Readings on the management of working capital, St. Paul, MN: West Publishing Company, pp.

549-562.

Journal of Xi'an University of Architecture & Technology

Volume XII, Issue V, 2020

ISSN No : 1006-7930

Page No: 2031