Week 1 rights issues 2015AB

40

M.Sc. Finance, M.Sc. International Banking & Finance, M.Sc. Investment & Finance, M.Sc. International Accounting & Finance, M.Sc. in Quantitative Finance and the M.Sc. in Economics and Finance AG915: Advanced Corporate Finance & Applications AG917: Topics in Corporate Finance Raising Equity Capital and Rights Issues Dick Davies February 2015

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Week 1 rights issues 2015AB

M.Sc. Finance, M.Sc. International Banking & Finance, M.Sc. Investment & Finance, M.Sc. International

Accounting & Finance, M.Sc. in Quantitative Finance and the M.Sc. in Economics and Finance

AG915: Advanced Corporate Finance & ApplicationsAG917: Topics in Corporate Finance

Raising Equity Capital and Rights Issues

Dick DaviesFebruary 2015

2

Financing Decisions – Theoretical Frameworks

• Non-analytical (traditional approach)

• Perfectly competitive capital markets and Modigliani-Miller approach

• Relaxation of assumptions• Taxation• Imperfect information• Asymmetric information

• Behavioural approach.

3

Financing Decisions• Seasoned equity Issues• General cash offers• Rights issues• Open offers

• Dividend policy and valuation• Dividends and retention policy• Dividends and share repurchases

• Use of debt and gearing• Capital structure decisions• Different forms of debt

• Initial Public Offerings (IPOs)

4

Seasoned Equity Issues by Quoted Companies

• A seasoned equity offer is the sale of shares by a quoted company to raise additional equity capital.

• General cash offers: shares are usually sold by an investment bank on behalf of the company to investors.

• Rights issues – shares are offered to the company’s existing shareholders in proportion to their existing holdings, usually at a discount.

• Open offers - shares are offered to existing shareholders with an arrangement for those shares not taken up to be placed with institutional investors.

5

Seasoned Equity Issues in the USA• Seasoned equity issues in the USA generally involve the purchase of the additional shares to be issued by a company by investment banks for re-sale to investors.

• The investment banks are described as the underwriters and the process is often referred to as a purchase and sale.

• Underwriters buy the securities from the issuing company for sale at a fixed price, and the issuer is paid this price less a specified gross underwriting spread.

• The risk of not being to sell the issue at the agreed price is borne by the underwriter (more usually a syndicate of underwriters for large issues).

• The cost of an issue is around 5 per cent of the gross proceeds for the largest issues, and can be more than 10 per cent for small issues.

• Some issues are managed by investment banks on a Best Efforts basis – the underwriter does not guarantee to absorb any shares that cannot be sold

Issue costs and cost of capital – some illustrative arithmetic (1)• Assume that a company has 100 shares outstanding and these are selling at £5.00 and the company is expected to produce EPS of £0.60 and the company pays out of 100% earnings.

• The rate of return expected by investors is £0.60/£5.00= 0.12

• The company has an investment opportunity of £120 and can sell 30 shares to yield £4.00 per share net of issuing costs, a discount of 20 per cent to the current price

6

Issue costs and cost of capital – some illustrative arithmetic (2)• What is the minimum rate of return that must be earned on this additional capital to make the investment and financing worthwhile for existing shareholders?

• To continue to earn £0.60 per share will require an increment of earnings of 30 x £0.60 = £18

• The rate of return will have to be £18/£120 = 15 per cent

7150800

1202001

1201

discountimplicit for the compensate tohigher be tohas capital new on thereturn of rate the

1£11£

...

).(.

-d)(r r*

r x-d) (r*x

8

Pre-emptive Rights Issues• Companies in the UK are required by company law to

offer new issues of shares to existing shareholders, unless shareholders vote to give up the right to acquire shares.

• Rights issues in the UK are favoured by the body representing large institutional investors as well as being embodied in company law.

• Investors are offered the opportunity to buy shares in a new issues in proportion to their existing holdings – such issues are referred to as rights issues.

• Rights issues allow existing shareholders to maintain their proportionate ownership of the company following a new issue

• Rights issues imply that managers cannot arrange to sell shares to outsiders at a discount or to dilute the interests of existing shareholders.

9

Rights Issues and the Subscription Price• Rights issues are usually made at a discount –conventionally set at around 20 per cent or so of the pre-issue price, but discounts have been significantly higher as a result of the financial crisis

• Rights issues avoid the difficulties of setting a price for the sale of shares to new investors.

• As a transaction that is “internal” to the company and its shareholders the price at which rights issues are made is not a critical factor, but not entirely unimportant!.

• For a rights issue to be successful the market price must remain above the subscription price

10

Underwriting of Rights Issues in the UK(1)• Most rights issues are underwritten – for a fee an

investment bank agrees to purchase any shares that are not taken up by shareholders (under-written issues in the USA are referred to as insured issues.)

• It provides a guarantee that the company receives the funds being sought even if the share price falls below the subscription price – whether this is the result of – a general fall in the overall market leading to a fall in the price of issuing company’s shares along with other shares in the market

– the market revalues the company’s shares downward

11

Underwriting of Rights Issues in the UK(2)

• As the underwriter has access to non-public information relating to the company the involvement provides some re-assurance to investors that the company has no major problems yet to be revealed to investors – a certification function

• To what extent did Merrill Lynch, Goldman Sachs and UBS as the underwriters of the 2008 RBS issue lend credible certification of the state of the Bank?

• Goldman Sachs subsequently sold some of its shares in RBS – about 20 per cent of its overall investment

Lawsuits subsequent to RBS’s failure contend errors of omissions/commission in the rights issue prospectus include • The understatement of RBS exposure to credit derivatives

• The understatement of RBS’s short term funding requirements

• The failure to mention the delay in the payment for LaSalle to be made to ABN AMRO for the sale of its US investment bank

• No mention that its tier -1 capital had fallen to 3.6 per cent by the end of April 2008

• No recognition that AMN was overvalued on its books• Did not admit to its incomplete knowledge of its own financial

position

• Understated difficulties encountered in the integration of ABNSee Ian Fraser “Shredded: Inside the Bank that Broke Britain”

12

13

Underwriting of Rights Issues as a Put Option

• An under-writing agreement is equivalent to a put option – the issuing company acquires the right to sell any shares not taken up by the shareholders at a fixed price (the exercise price)

• • In the UK the cost of underwriting appeared to be too

standardised, leading to the suggestion that investment banks were engaged in implicit collusion

• A study by Marsh of the LBS found the value of the underwriting agreement as a put option was found to be a relatively small proportion of the underwriting fee

Estimated value

Underwriting fee

PUT OPTION DIAGRAM+

_ 13

14

Mechanics of Rights Issues

•The management of the firm must decide:– How much capital to raise (F).– The exercise or subscription price (the price existing shareholders must pay for new shares) (Ps), specified as the prevailing market price less the discount

•These decisions determine the number of shares to be issued and the terms of the issue.

res-issue shaber of preto the numw sharesatio of neN/N- the r ressed as Terms are

PFΔNbe issuedshares to Number of

d)(PPon priceSubscripti

s

s

exp

10

15

Fall in Share Price in Rights Issue• As rights issues are made at a discount the

proportionate increase in the number of shares is greater than the proportionate increase in the value of the company.

• This implies that the share price can be expected to fall as a result of the mechanical aspects of the issue – the expected price following this price adjustment is known as the theoretical ex-rights price (Px)

• This anticipated fall in share price is a mechanical adjustment, a nominal change, and does not imply a real fall in value.

000

PNPN

VF

NN s

16

Explaining the Theoretical Ex-Rights Price• It is assumed that the announcement of rights issue adds no new information.

• If the no new information is released the value of the firm prior to the issue is given by the pre-issue share price times the number of shares (Vo).

• The value of the firm increases by the by the injection of additional cash (F), given by ΔNPS

• The post-issue value of the firm is given by the initial value of the company plus the cash raised (V0 + F).

17

Calculating the Theoretical Ex-Rights Price and the Value of a Right

GainCapitalExpectedPPRV

PNN

NPNN

NNNFVP

sx

sx

)(

0

0

Ex-rights price

Value of a right

18

Rights – a negotiable instrument• Rights can be exercised or sold to other investors – the letter offering the rights is a negotiable instrument

• An investor in principle will be equally well off by exercising the rights or their sale.

• A right is a call option – it gives the holder the right but not the obligation to buy the additional shares.

19

Rights Issues and Shareholder Wealth

•The mechanical aspect of a rights issues should have neutral impact on a shareholder’s wealth

– A capital gain can be anticipated on the new shares purchased at a discount (Px > Ps)

– A capital loss can be anticipated on the original shares (P0 > Px)

– The impact of capital gains and losses for shareholders will be offsetting

w sharesGain on neingsitial holdLoss on inPPxNPPxN sxx

)( )( 0

20

A Rights Issue: Balmorals plcBalmorals is a well established company that has run into various difficulties in recent years. Its management has recently undertaken a review of its activities and has decided to proceed with a radical re-structuring of the business. To restore the company's financial stability it has been decided it will be necessary to raise £160 through a rights issue. After consulting its investment bankers the company is planning to make the rights issue at a discount of 20 per cent to the current market price of £5.00.The company has 100m shares outstanding.

21

Terms of Balmorals’ Rights IssueInitial Value of Equity = 100 m x £5.00 = £ £500mFunds required = F = £ 160mSubscription price = PS =£5.00 (1- 0.2) = £4.00 Number of new shares = F / PS =£160m / £4.00 = 40mTerms = New shares / Old Shares = 40 / 100 = 2 for 5

Ex-rights Price(Initial Value + New Funds) / Old shares + New shares = =£4.7143

Theoretical Value of right = Ex – rights Price - Subscription Price = £4.7143 – £ 4.00 = £ 0.7143

22

Shareholder Exercises the Rights:Neutral Impact on Wealth

Assume shareholder owns 10 shares:Exercise the right

Initial investment 10 x £ 5.00 = £50.00Purchase of four new shares = £16.00Overall Investment = £66.00Value of 14 Shares (at Px = £4.7143) = £66.00

23

Shareholder Sells the Rights:Neutral Impact on Wealth

Sells the rights

Initial investment 10 x £ 5.00 = £50.00Sells four rights@ £0.7143 = £ 2.8572Net investment = £50.00 - £ 2.8572 = £47.143

Value of ten share at Px = £ 4.7143 x 10 = £47.143

Pressure on RBS for an increase in equity capital

• Hector Sants, the chief executive of the FSA, told Fred Goodwin (CEO RBS) on April 9th 2008 that the RBS had to increase its capital

• This was reinforced by two other requirements – it should be in the form of a rights issue and should be as large as possible

• During the week beginning April 14 there was considerable speculation that RBS would be announcing a rights issue

• The Bank’s board agreed a £12 billion issue on April 20, on April 21 the Bank of England announced a £50bn scheme to allow banks in the UK to swap mortgage debt for government bonds to strengthen their financial positions, and on April 22 RBS announced the rights issue.

• RBS also announced at the same time that it write down assets by £5.9 bn share price fell by 4 per cent 24

Royal Bank of Scotland Rights Issue 2008 (1)

• The share price prior to the announcement was £3.58 and there were 10,094,241,000 shares outstanding, giving an overall equity value of £36.137bn

• It was decided to raise £12,246,020,924 (£12.246bn) at a subscription price of £2.00. This implied issuing shares new 426,010,123,600.2£

924,020,246,12£

25

Royal Bank of Scotland Rights Issue 2008 (2)

• The Bank had 10,094,241,000 shares outstanding – implying a ratio of “new” to “old” shares of

• In more manageable numbers this implies approximately 11 new shares for every 18 old shares

• To buy one new share requires one right – and shareholders were given 0.6065845 rights for each share that they already held

share old oneevery for shares new6065845293.0000,241,094,10426,010,123,6

26

Wealth impact of either investing in new shares or selling rights (RBS issue 2008)

Invest in Shares (through rights)Shareholder's initial investm ent 18 shares at 3.58 £64.44Subscription to rights 11 at £2.00 £22.00Revised investm ent £86.44Value of shares at Ex-rights price 29 at £2.98 £86.44Change in W ealth £0.00

Sell RightsShareholder's initial investm ent 18 shares at 3.58 £64.44Sell 11 rights at £0.98 £10.78Revised investm ent in shares £53.66Revised value of shares 18 shares at £2.98 £53.64Change in W ealth 0.02*

* rounding errorIn principle the shareholders do not gain or lose as a result of a rights issue

27

28

Deep Discount Issues• A deep discount issue implies setting a relatively low subscription price

• This reduces the probability of the share price falling below the (low) subscription price.

• The larger the discount the greater the incentive for a shareholder to subscribe to the issue or sell the rights – this is necessary to avoid the capital loss on existing holdings of shares

• With a deep discount it is not necessary to arrange underwriting.

29

Underwriting and Deep DiscountRights Issues

What are the disadvantages of deep discount issues that are not under-written ?

– Deep discount issues imply more dilution (a

greater fall in the share price and in EPS) – but this involves nominal rather than real changes.

– No certification by the under-writers

– Deep discount issues may be mis-interpreted as indicting • management’s fear that the share price

will fall• a failure to arrange underwriting

30

Market Reaction To Equity Issues:

• Event studies have been used to evaluate the market’s reaction to the announcement of equity issues.

• The studies have typically recorded a fall in share price of about 3 per cent or so.

• The fall in share price of this magnitude implies a fall in the value of a company’s equity equivalent to about one third of the funds being raised, given the size of a typical issue.

31

Equity Issues and Longer Term Returns• Some studies have documented underperformance over a three to five year period following the issue of equity – evidence that is inconsistent with efficient market theory.

• The results have been questioned on the basis that it is difficult to develop reliable estimates of expected returns and performance benchmarks.

• It has been suggested that underperformance stems from the type of companies engaged in new issues rather than the event of raising capital – non issuers with the same characteristics as issuers also seem to under-perform using the same benchmark.

Figure 23.7 Post-SEO Performance

Source: Adapted from A. Brav, C. Geczy, and P. Gompers, “Is the Abnormal Return Following Equity Issuances Anomalous,” Journal of Financial Economics 56 (2000): 209–249, Figure 3.

32

33

Explanation of Price Reaction (Non-rights issues) : Information Asymmetry & Adverse Selection

• Managers are better informed than investors.• Managers will not issue equity if shares are undervalued.

• Managers will issue equity if shares are overvalued– New issues are consequently assumed to signal

over valuation– Market adjusts downwards on the announcement of

a new issue.• Pre-issue shareholders benefit to the extent that the adjustment to the over-valuation is shared with the new investors

• US seasoned issues are associated with significant negative announcement returns.

• Analysis is more relevant for seasoned equity issues made to external investors than for rights issues made to existing shareholders

Information Asymmetry – Arithmetical Illustration

34

A company has 1000 shares outstanding selling at £6.00 but the management believe on the basis of their knowledge of the company and its prospects that shares are only worth £4.00., implying a true value of £4,000

When the market recognises its error and the share price falls to £4.00 the shareholders will suffer a capital loss of 33 1/3 per cent.

Assume the company can sell 500 shares at £6.00, prior to the market recognising its error – its assets will increase in value by £3000. – now assume the market again recognises its error

The share price will fall to (£4,000+ £3000)/(1000+500)=£4.67 – a smaller capital loss than in the absence of the share issue – the savings for the initial shareholders stems from a loss imposed on the new shareholders

35

Another Explanation of Price Reaction: Price Pressure Hypothesis “If the supply of shares increases and

demand is unchanged the market price must fall”??

No of Shares

D

P0

P1

N0 N1

Price

This implies that unless the investment value of the share has fallen the shares will be under-priced and offer investors the possibility of abnormal returns.

N*

36

Explanation of Price Reaction: Price Pressure Hypothesis (2)

No of Shares

D2

P0

P1

N0 N1

Time

Price Price

P2

D1

To avoid the outcome that abnormal returns can be earned indefinitely into the future the price pressure hypothesis generally assumes that the price will drift upwards with the passing of time, as demand becomes mores elastic.

P0

Abnormal returns?

Predictable increase?

37

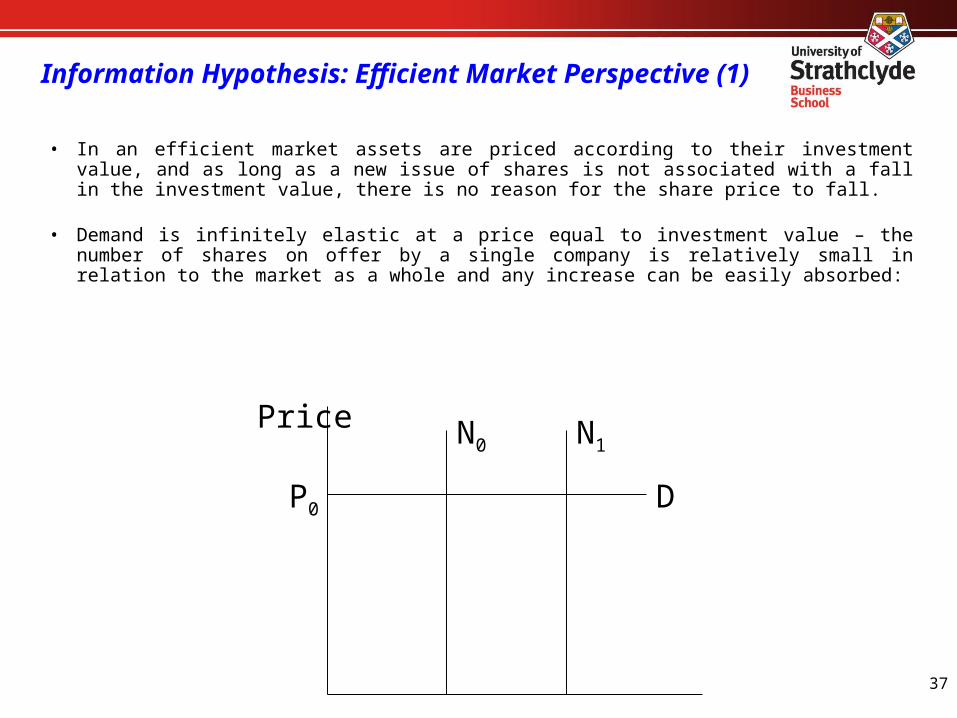

Information Hypothesis: Efficient Market Perspective (1)

P0

N0 N1

• In an efficient market assets are priced according to their investment value, and as long as a new issue of shares is not associated with a fall in the investment value, there is no reason for the share price to fall.

• Demand is infinitely elastic at a price equal to investment value – the number of shares on offer by a single company is relatively small in relation to the market as a whole and any increase can be easily absorbed:

Price

D

38

Information Hypothesis : Efficient Market Perspective (2)

P0

N0 N1

If adverse information is released at the time of the new issue there will be a downward revaluation of investment worth of the company’s shares – but this may be unavoidable

Price

D0

N

P1 D1

Information is criticalin explaining the market’sreaction – averages needto be treated carefully.

39

Price Pressure Hypothesis: Empirical Evidence

Change in Price

Size of Issue

0

A relationship between size of issue and price changes ??

The price pressure hypothesis implies the price fall will be related to the size of the issue – a downward sloping relationship

39

40

Information Hypothesis : Empirical Evidence

Change in Price

Size of Issue

0

No relationship between size of issue and price changes

• The information price pressure hypothesis implies the price fall will not be systematically related to the size of the issue•The evidence suggests no relationship – implicit support for the information hypothesis

40