Vol. 1 - World Bank Documents

183

RESTRiCTED CA4 Vol. 1 This report wos prepored for use within the Bank and its affiliated organizalions. | They do not accept responsibility for its accuracy or completeness. The report may l not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION CURREN T ECONOMIC POSITION AND PROSPECTS OF GUYANA (in two volumes) r-\-, r- m VOLUME I ! MAIN REPORT i l -, ; '. Lu . October 1, 1970 Central America and Caribbean Departmnent Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

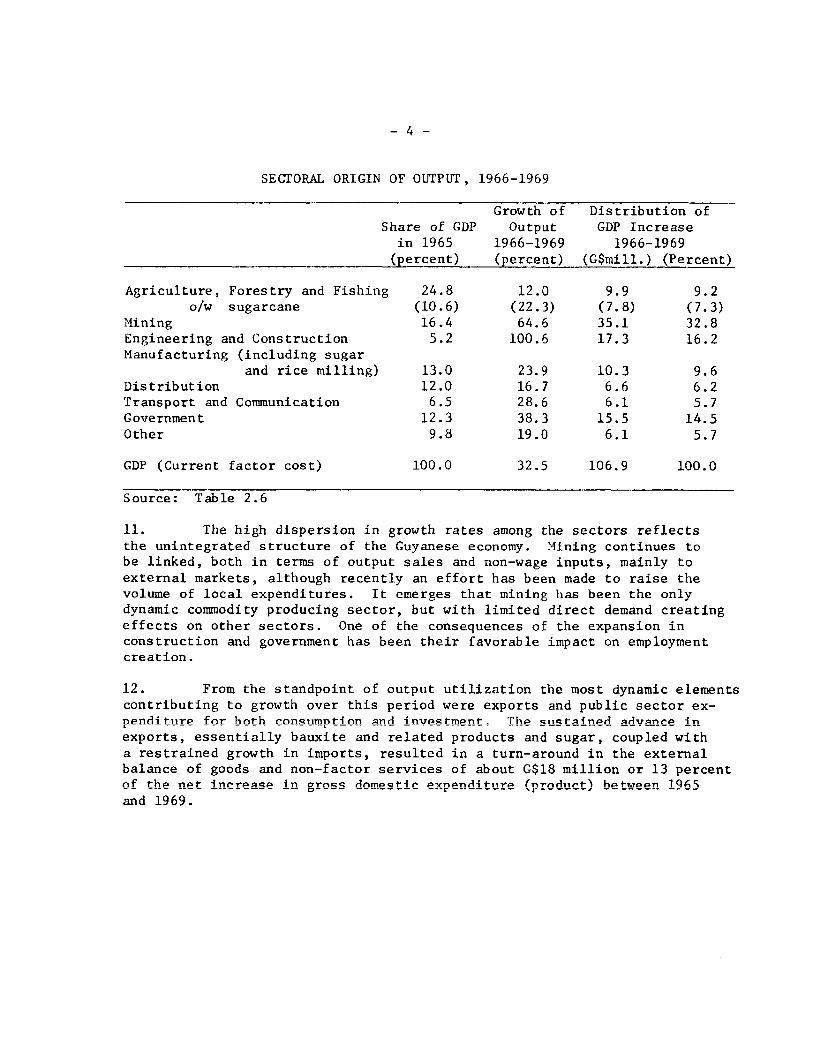

1 -

download

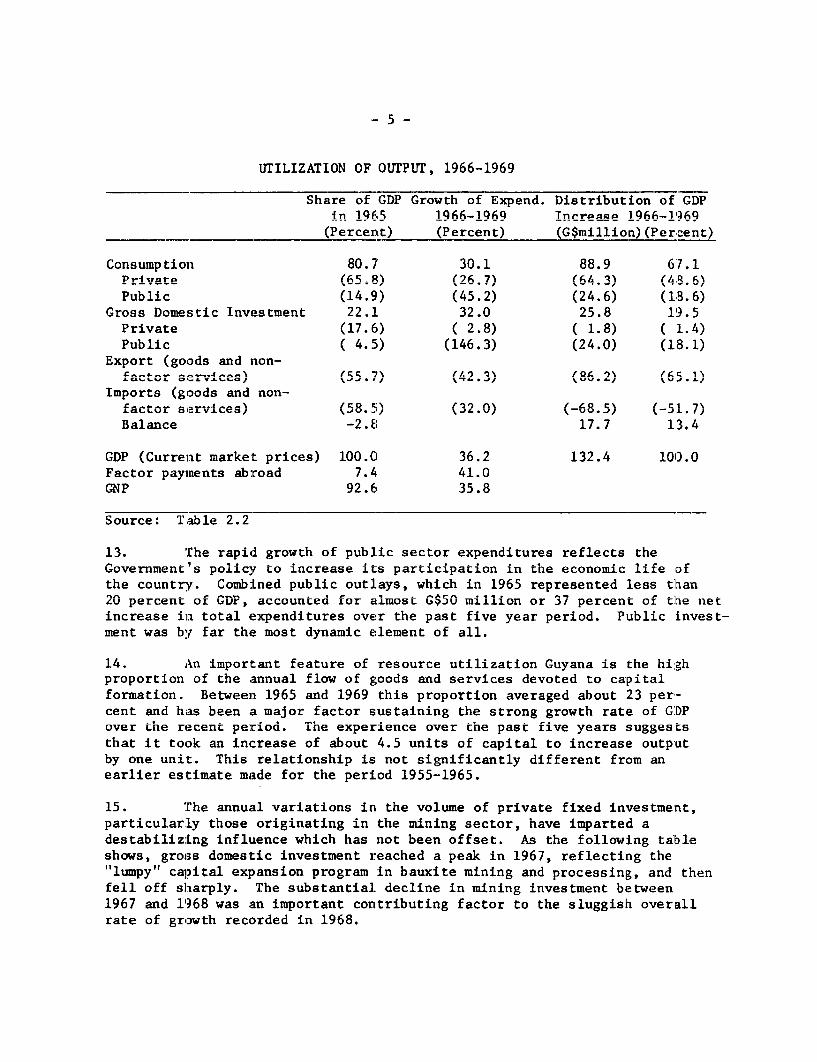

0

Transcript of Vol. 1 - World Bank Documents

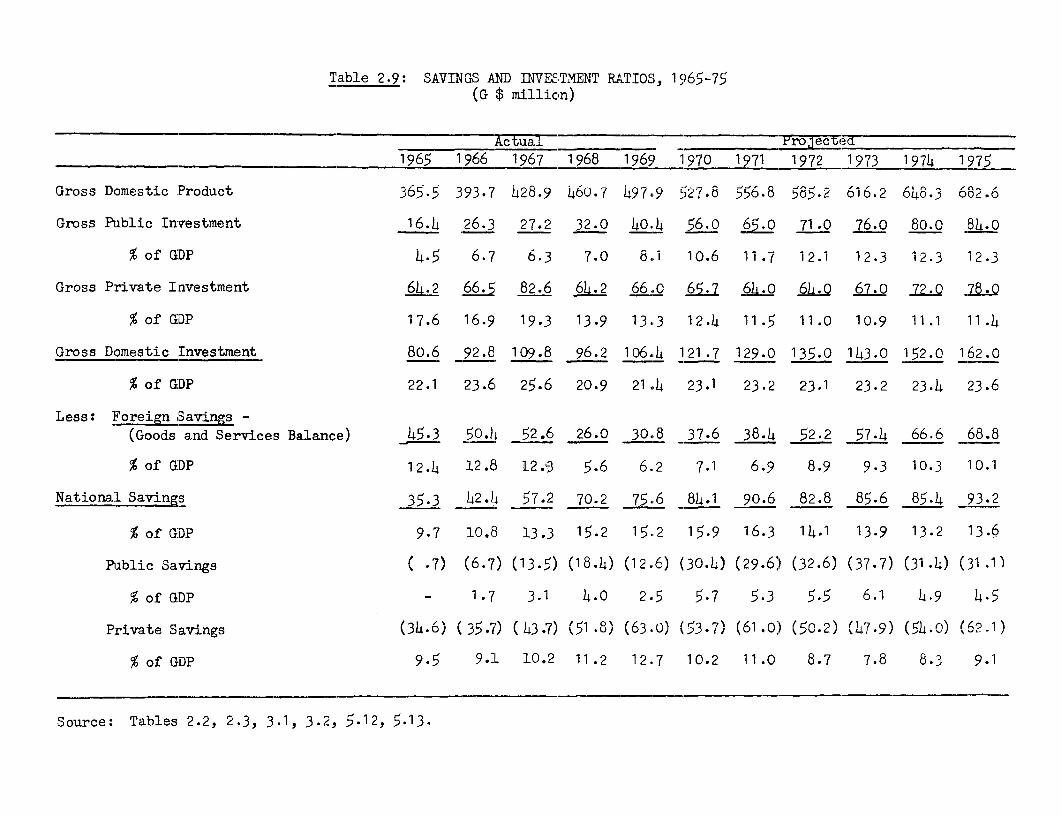

RESTRiCTED

CA4Vol. 1

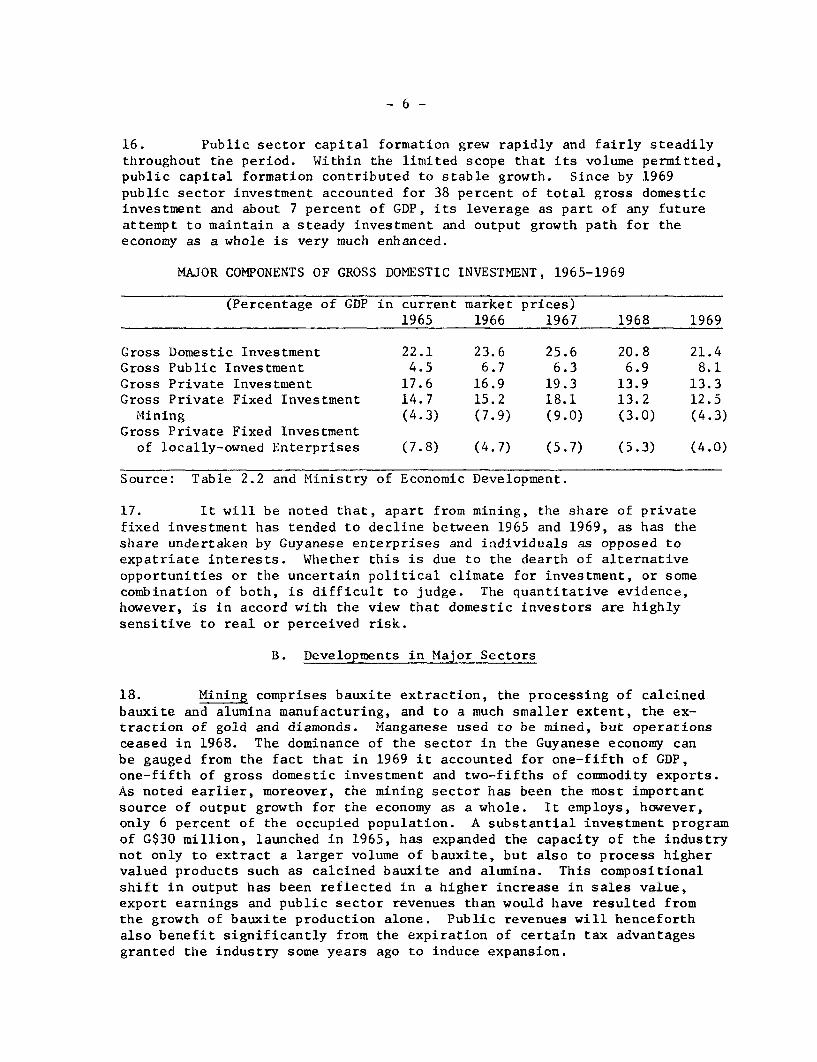

This report wos prepored for use within the Bank and its affiliated organizalions. |They do not accept responsibility for its accuracy or completeness. The report may lnot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

CURREN T ECONOMIC POSITION

AND PROSPECTS

OF

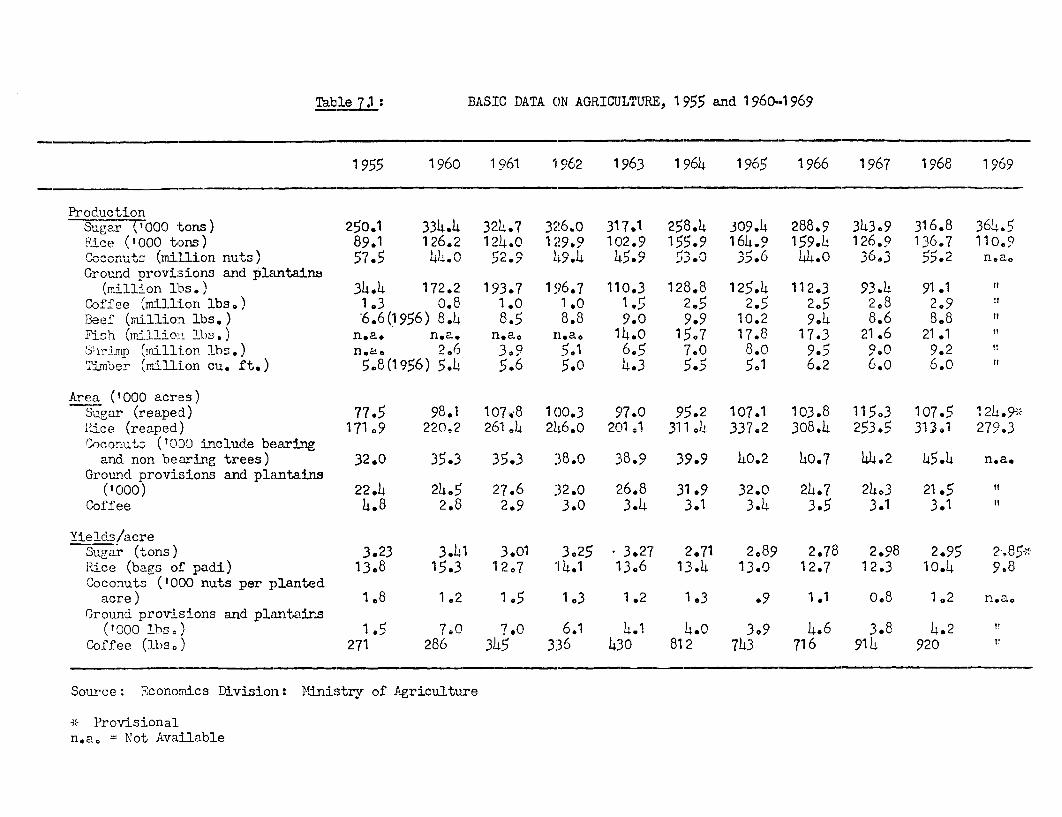

GUYANA

(in two volumes)

r-\-, r- mVOLUME I !

MAIN REPORT i l -, ; '.

Lu .

October 1, 1970

Central America and Caribbean Departmnent

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

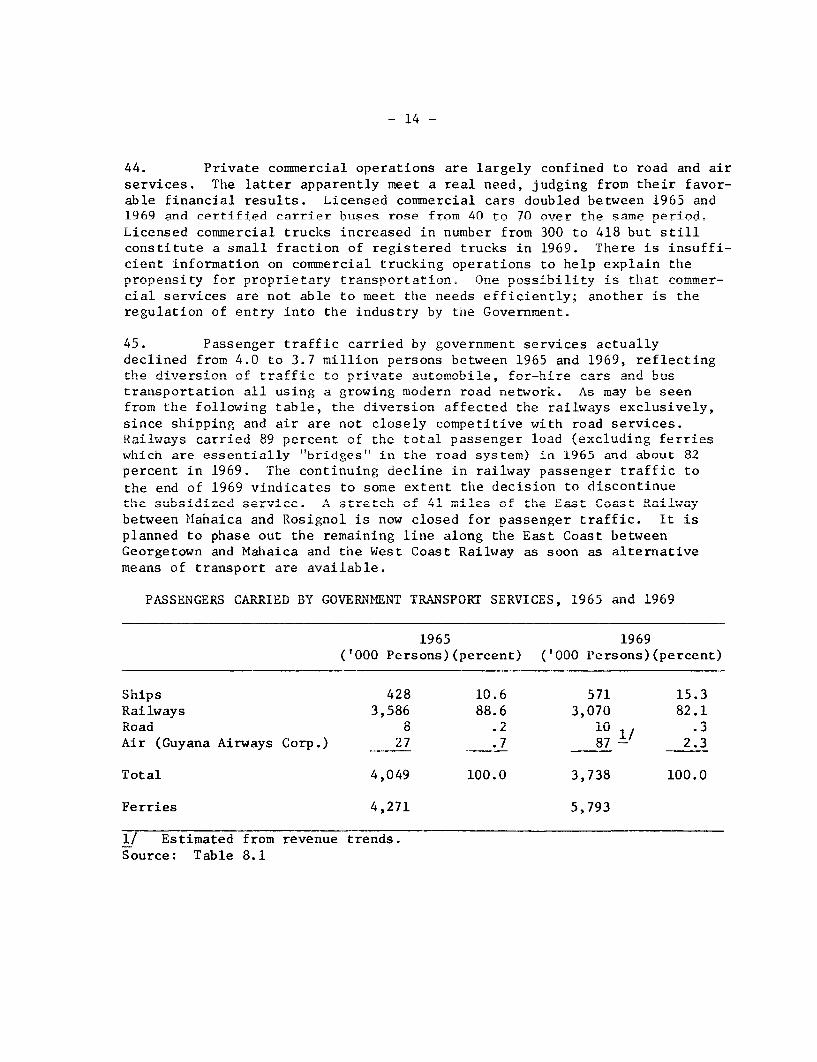

iscl

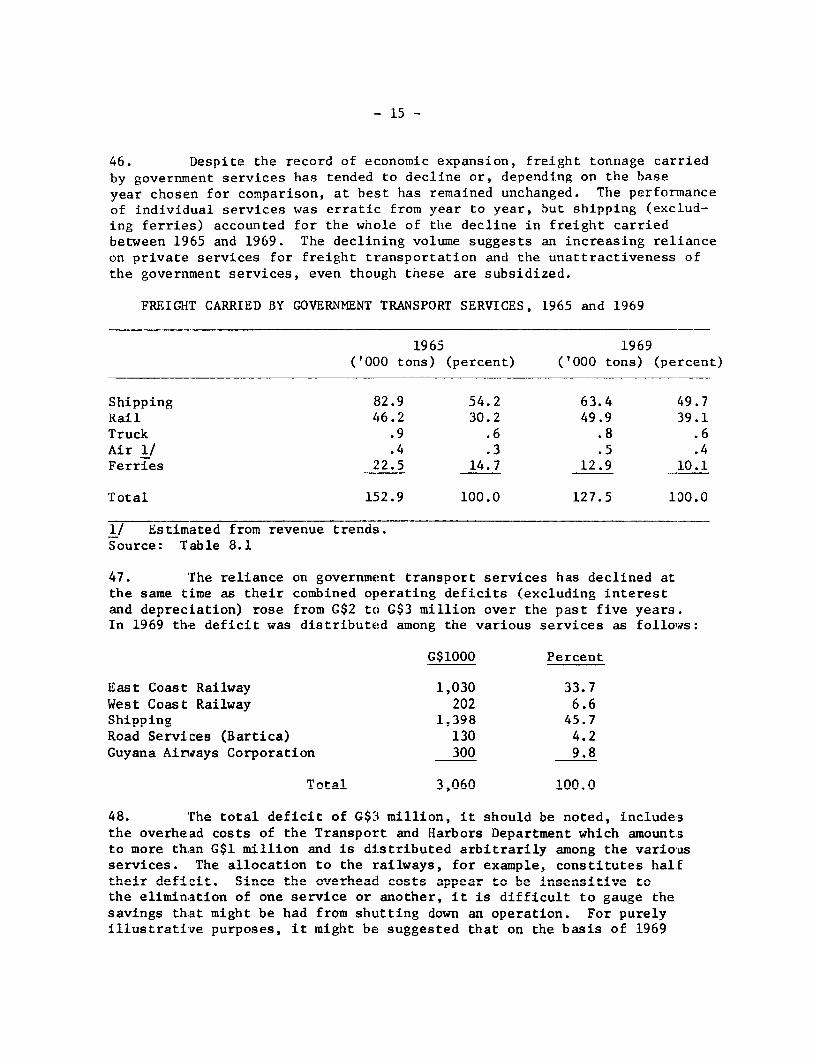

osur

e A

utho

rized

Pub

lic D

iscl

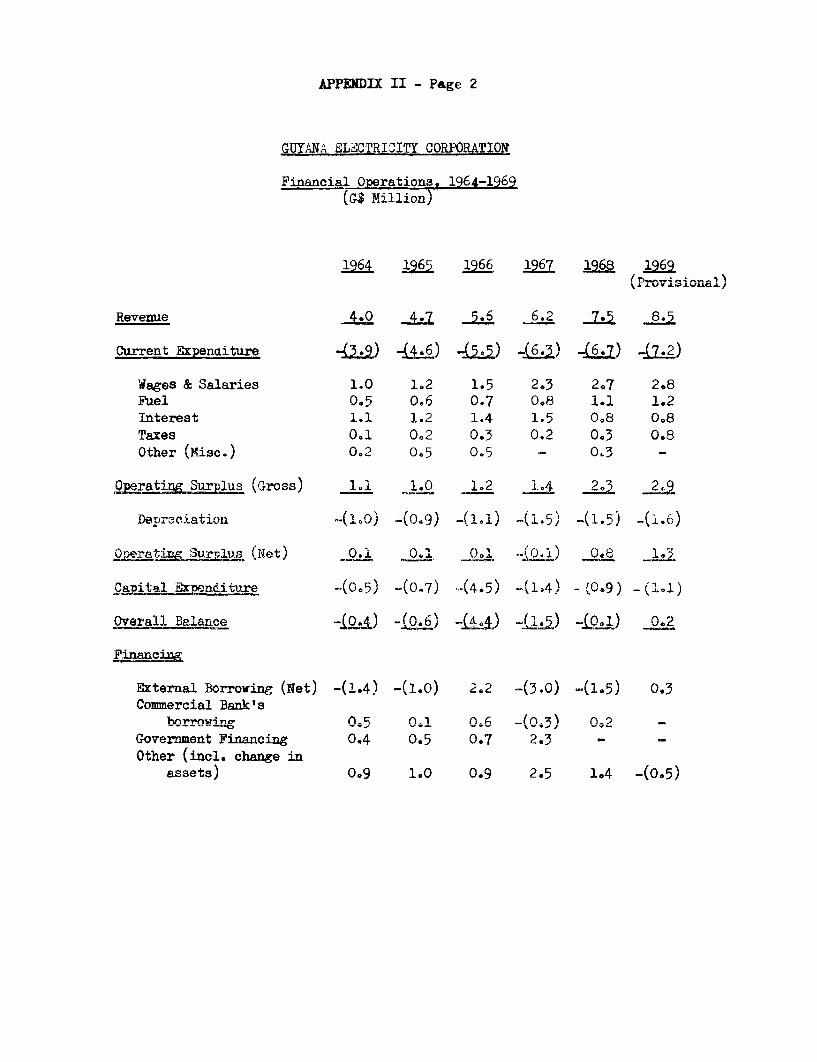

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

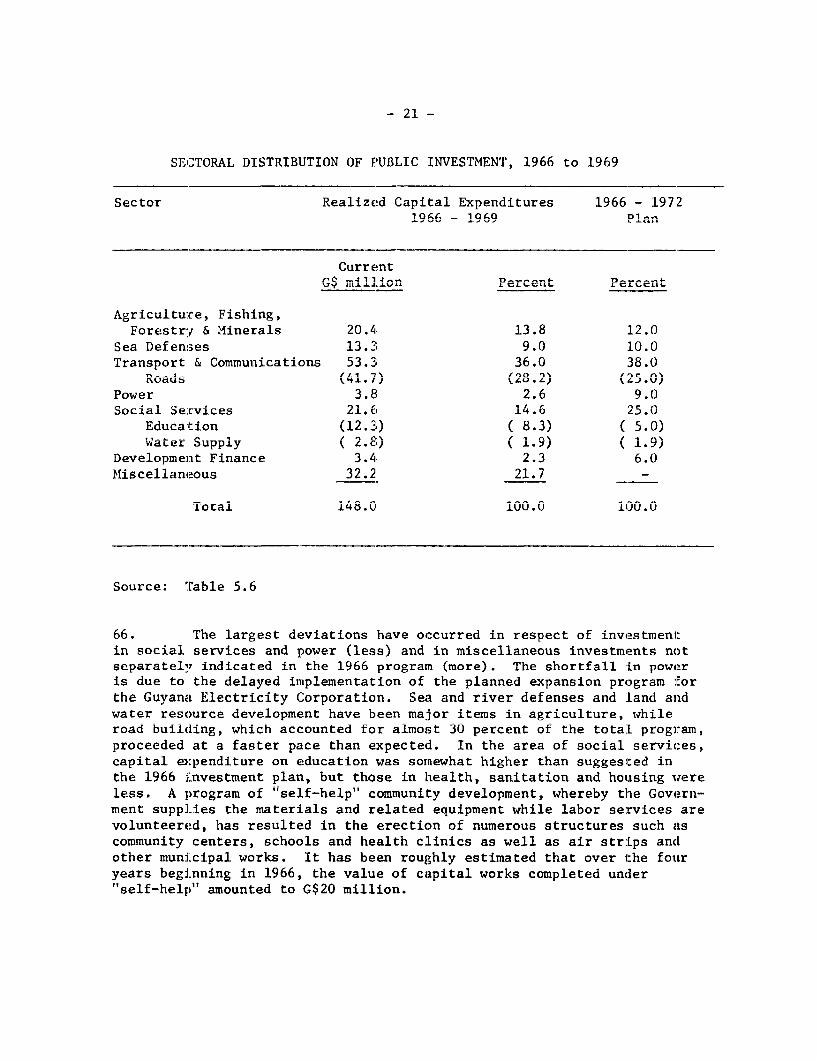

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

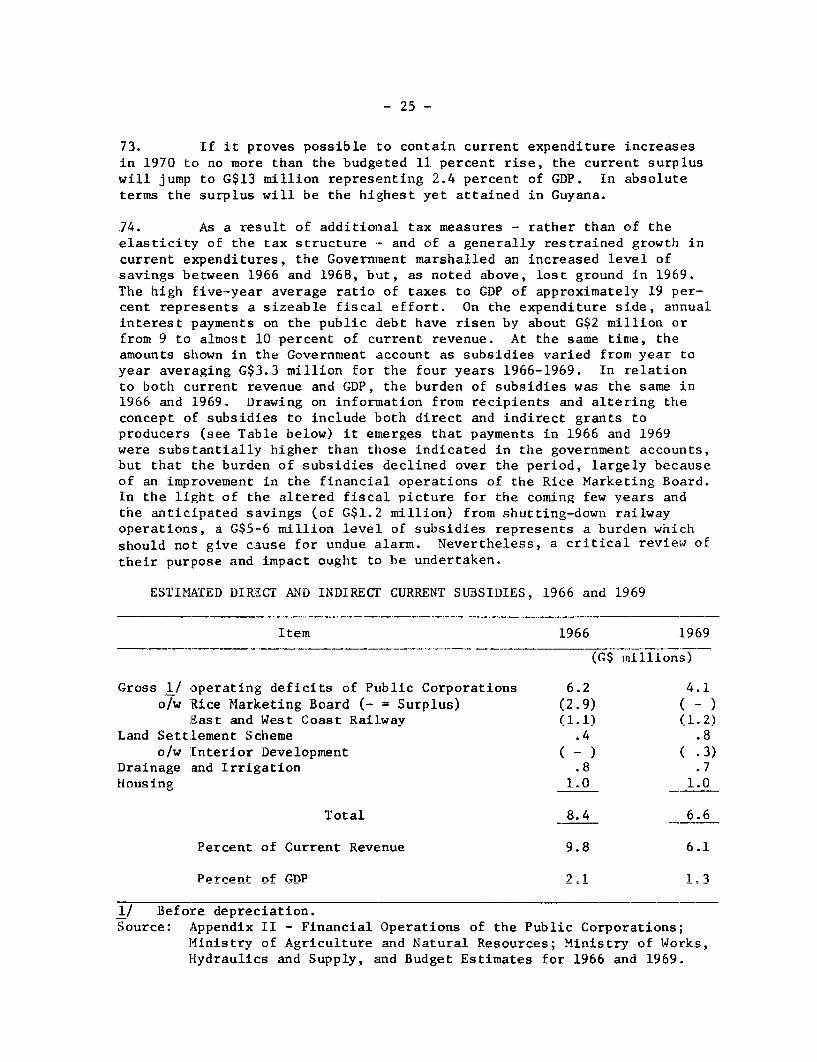

osur

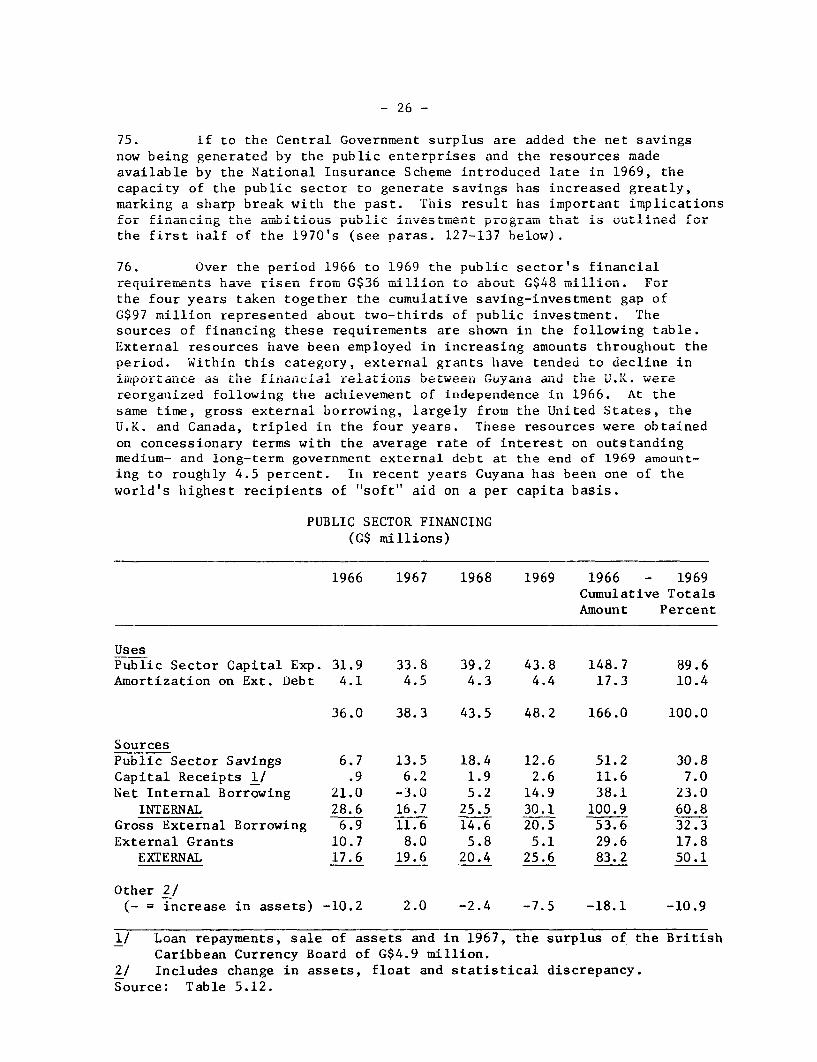

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

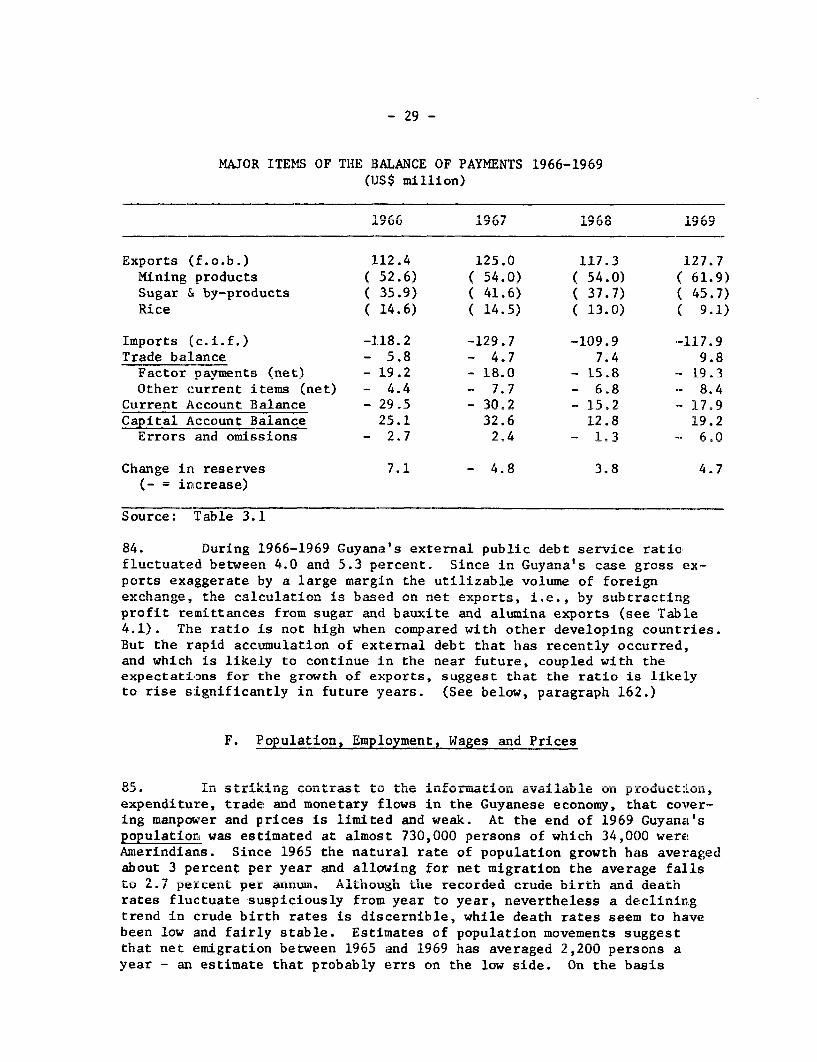

rized

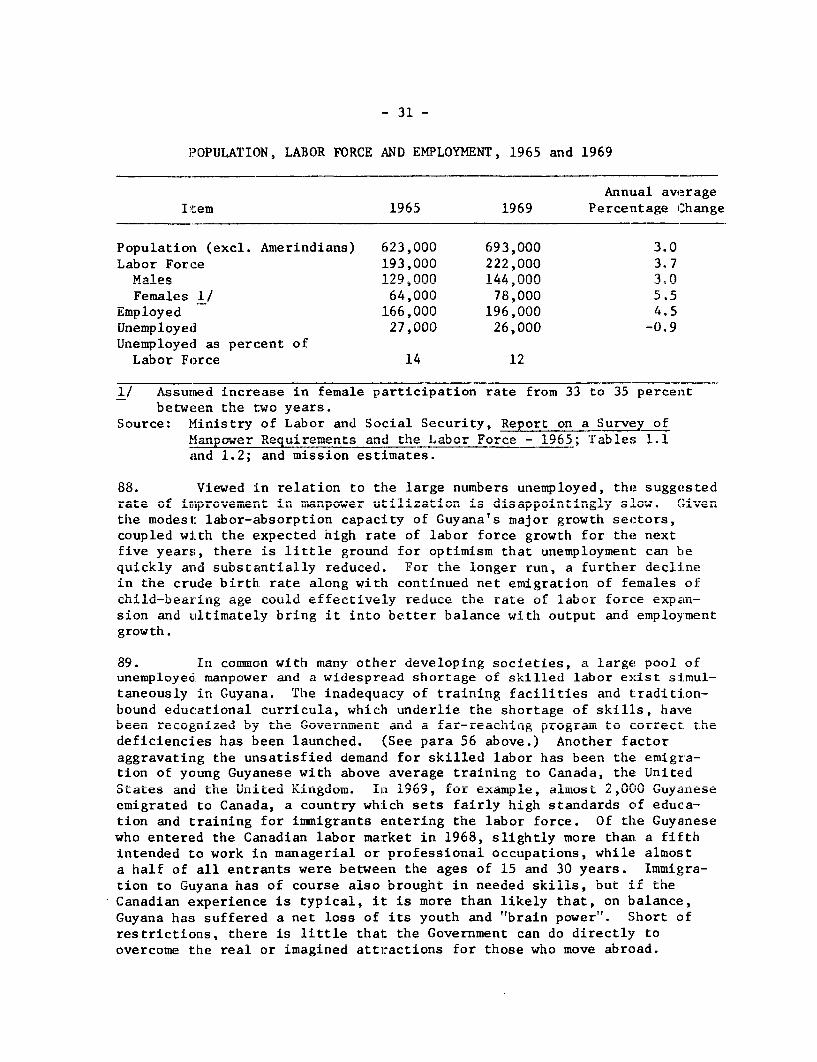

Pub

lic D

iscl

osur

e A

utho

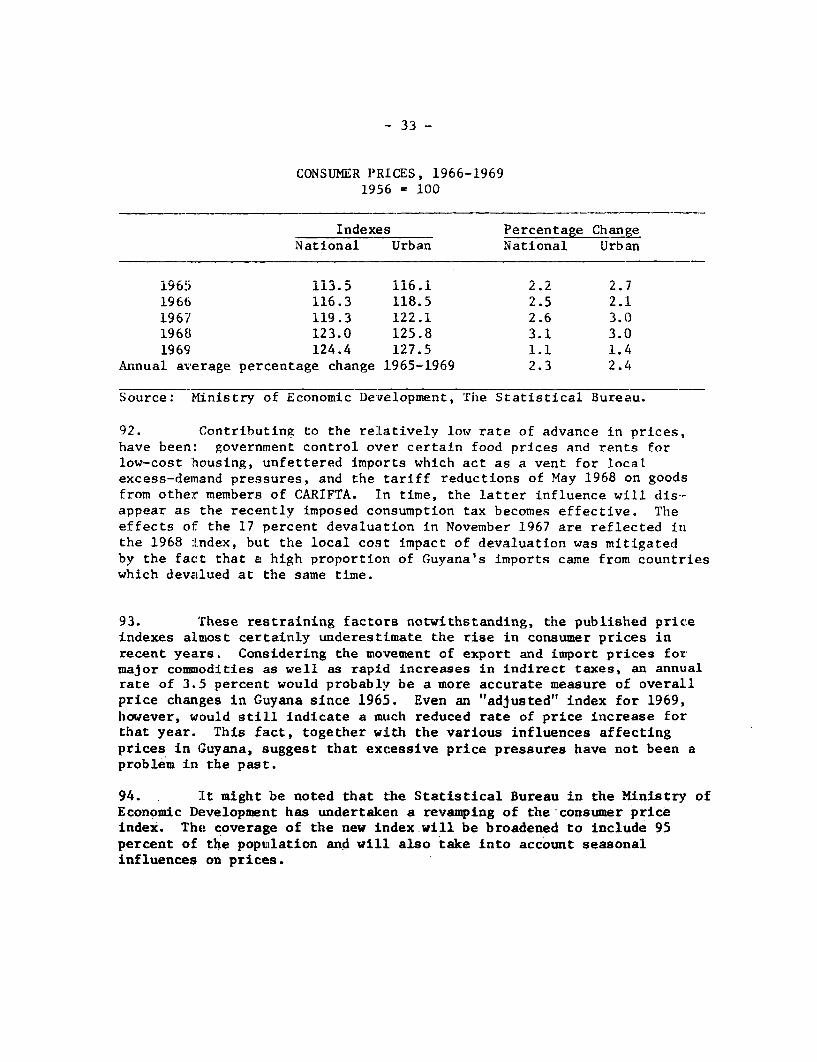

rized

Pub

lic D

iscl

osur

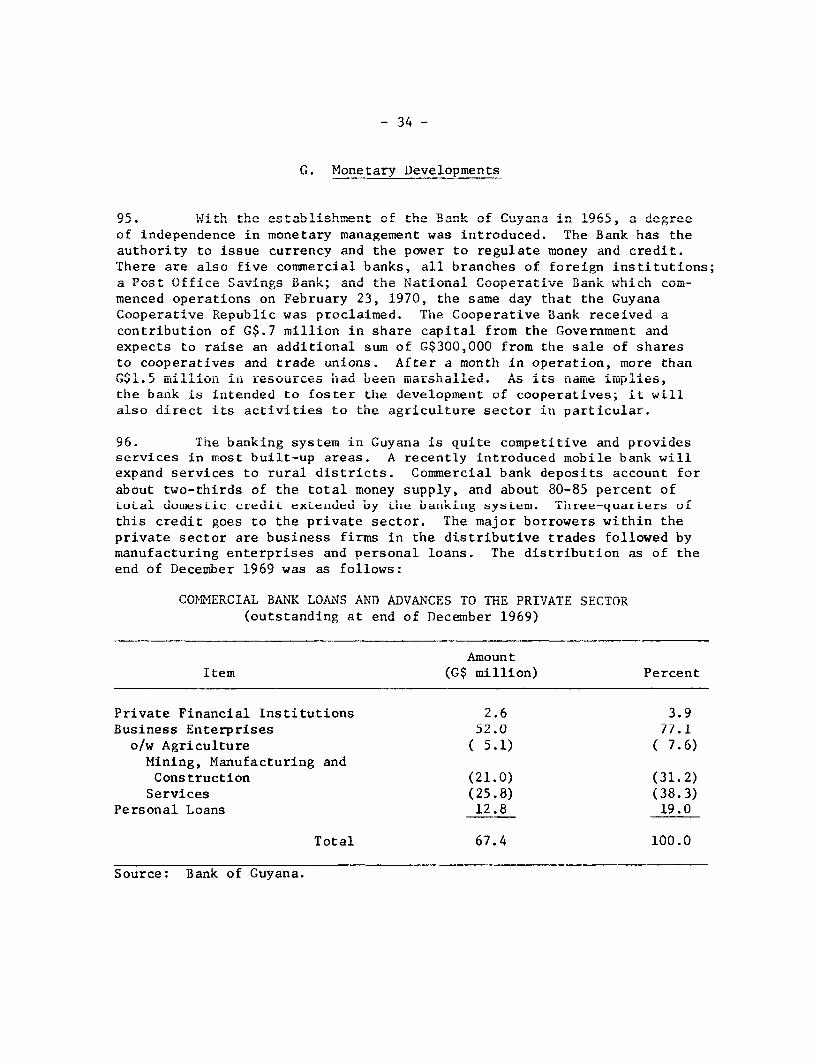

e A

utho

rized

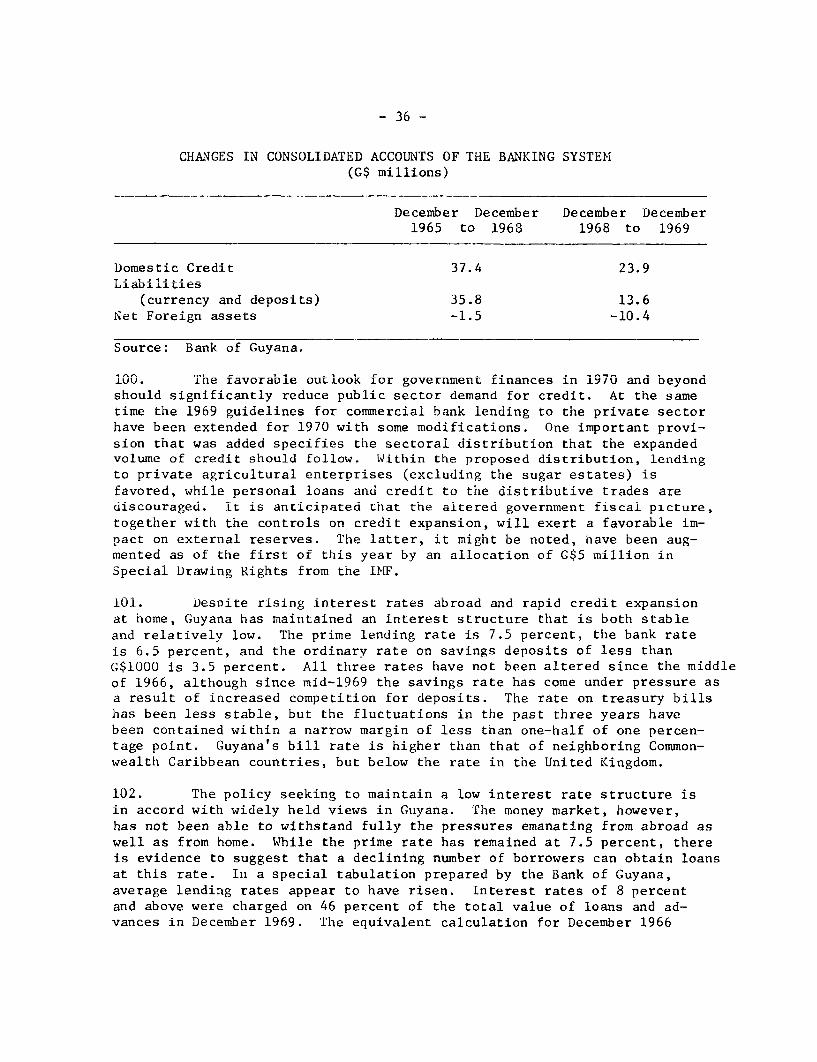

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

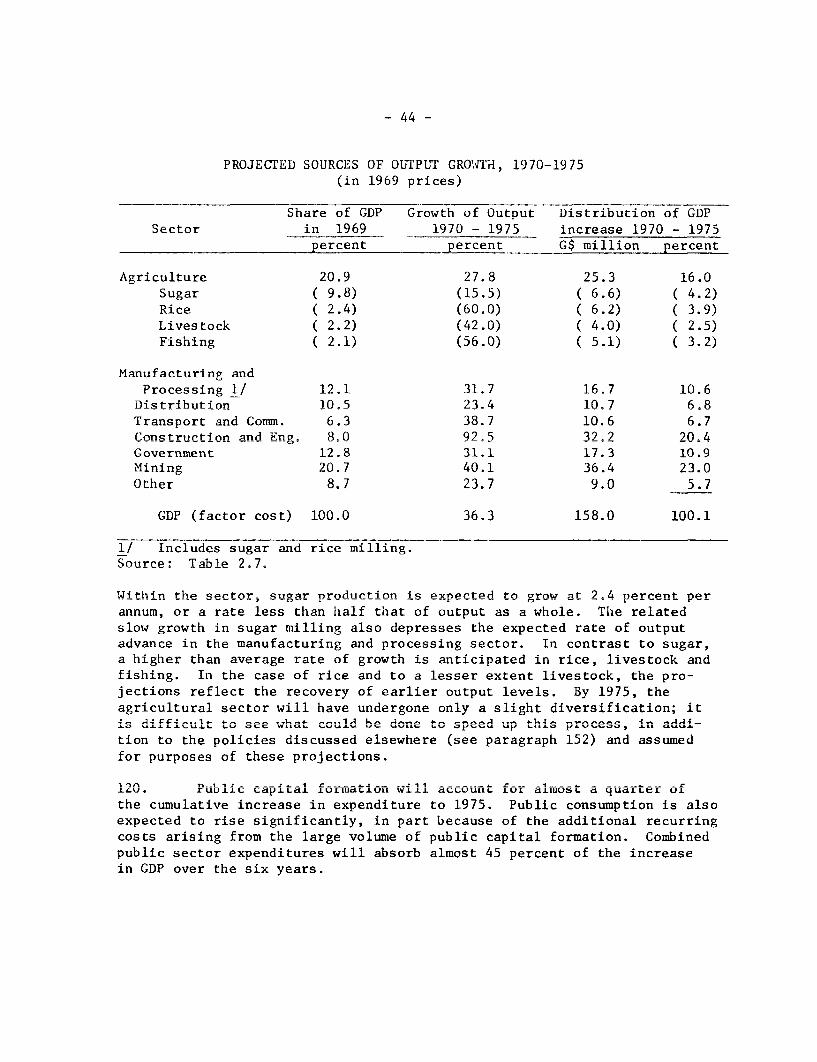

rized

Pub

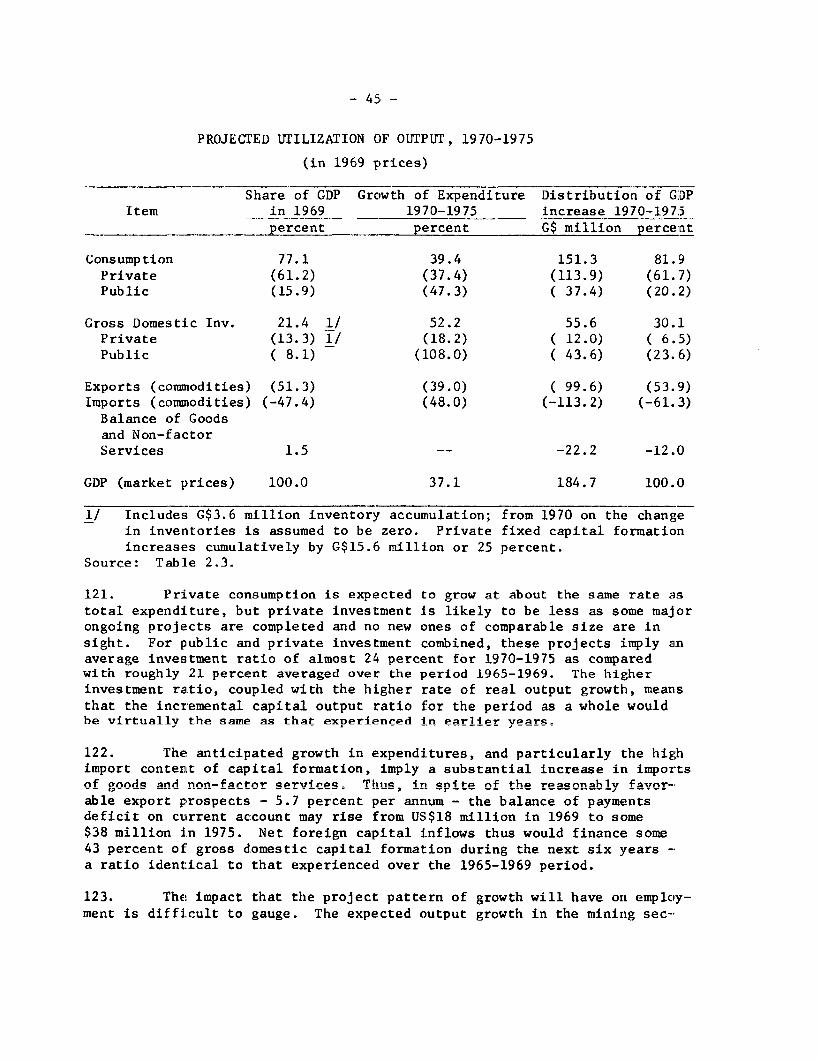

lic D

iscl

osur

e A

utho

rized

Pub

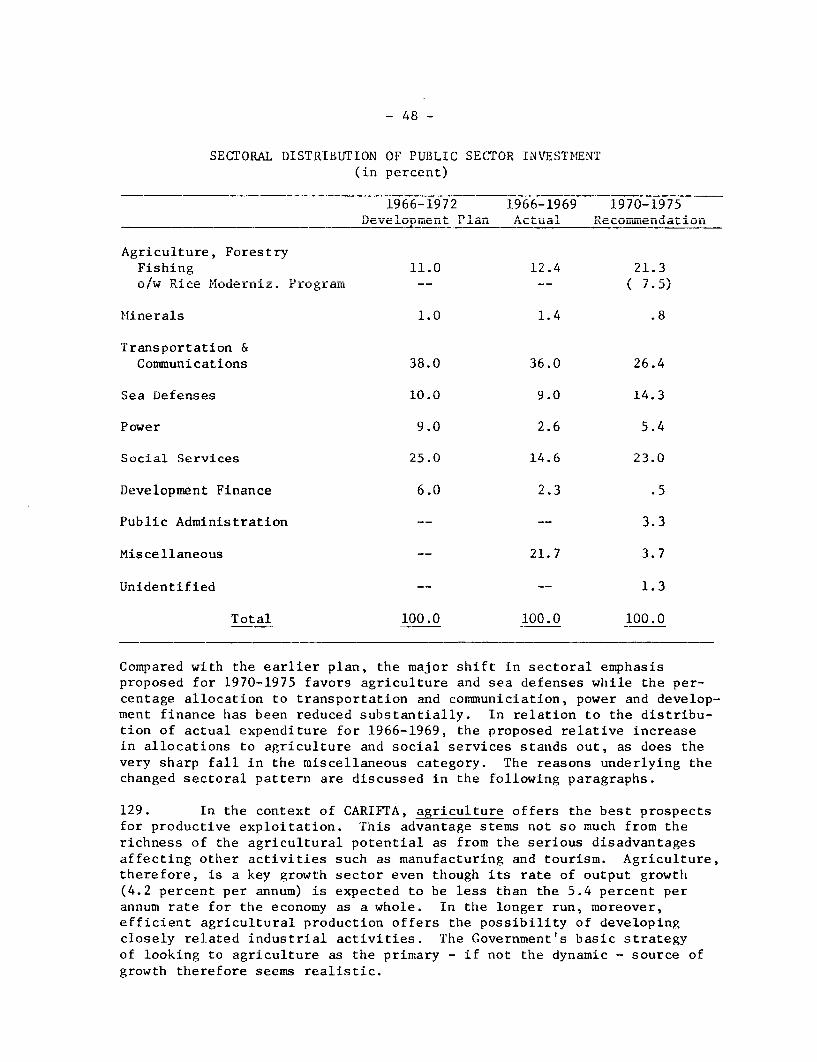

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

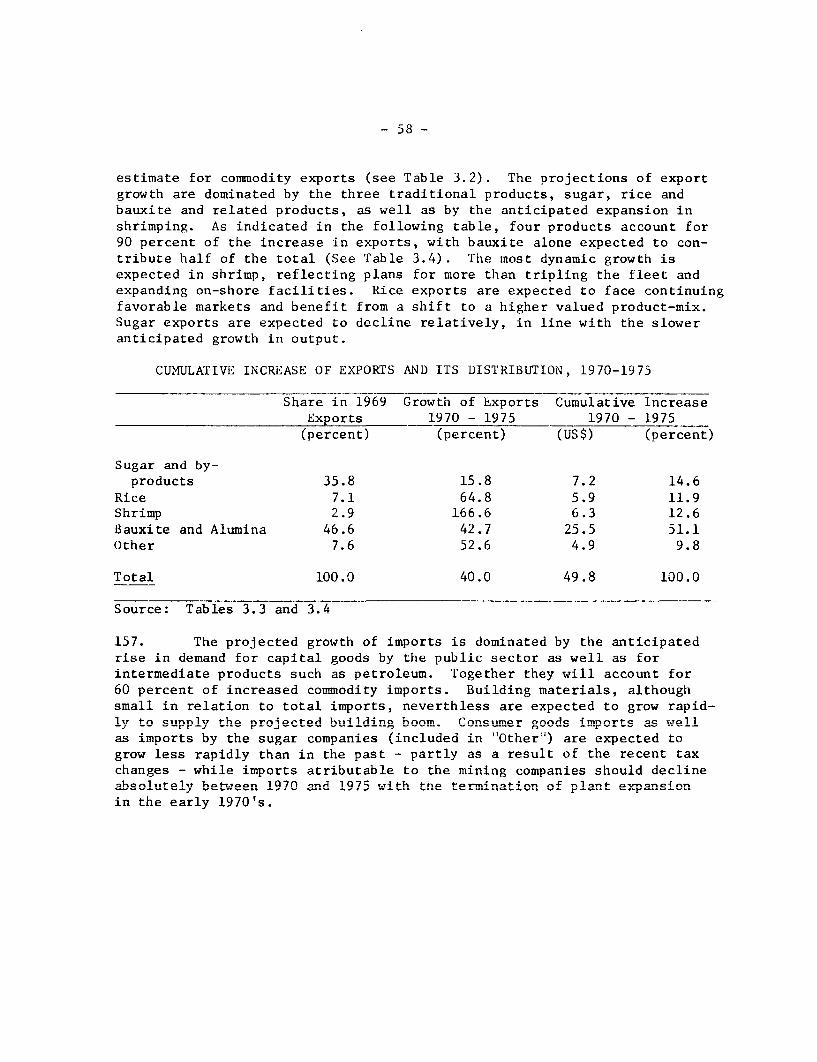

lic D

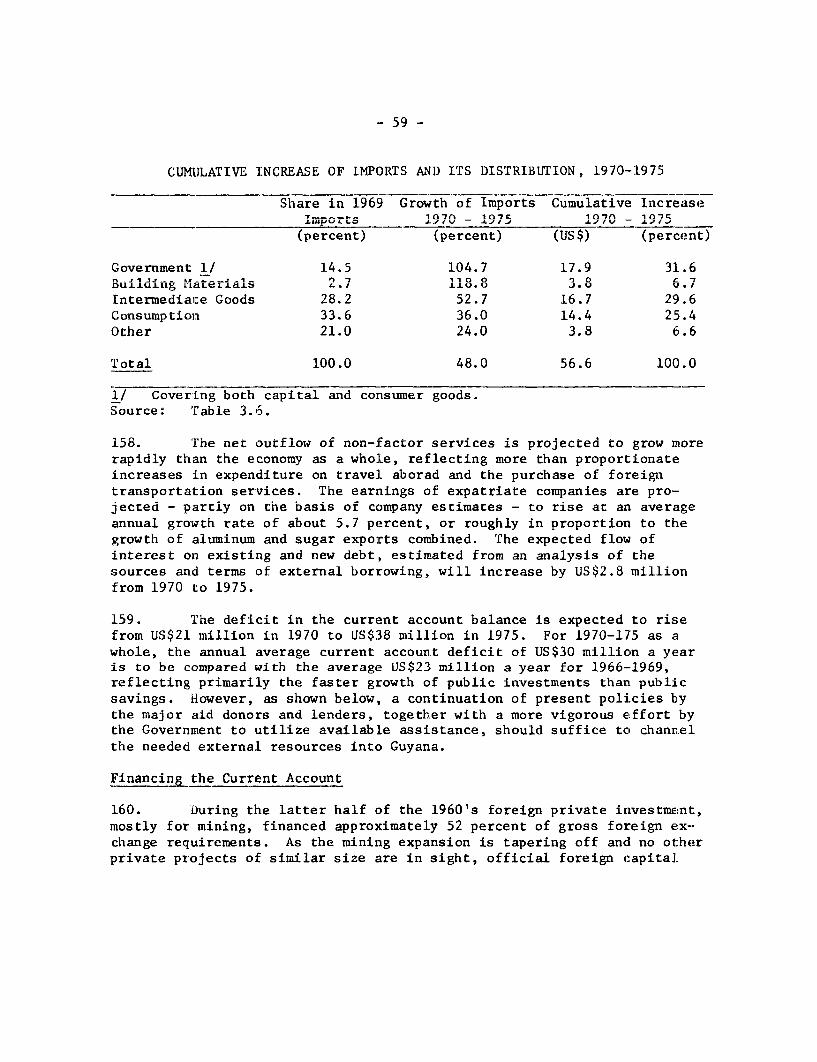

iscl

osur

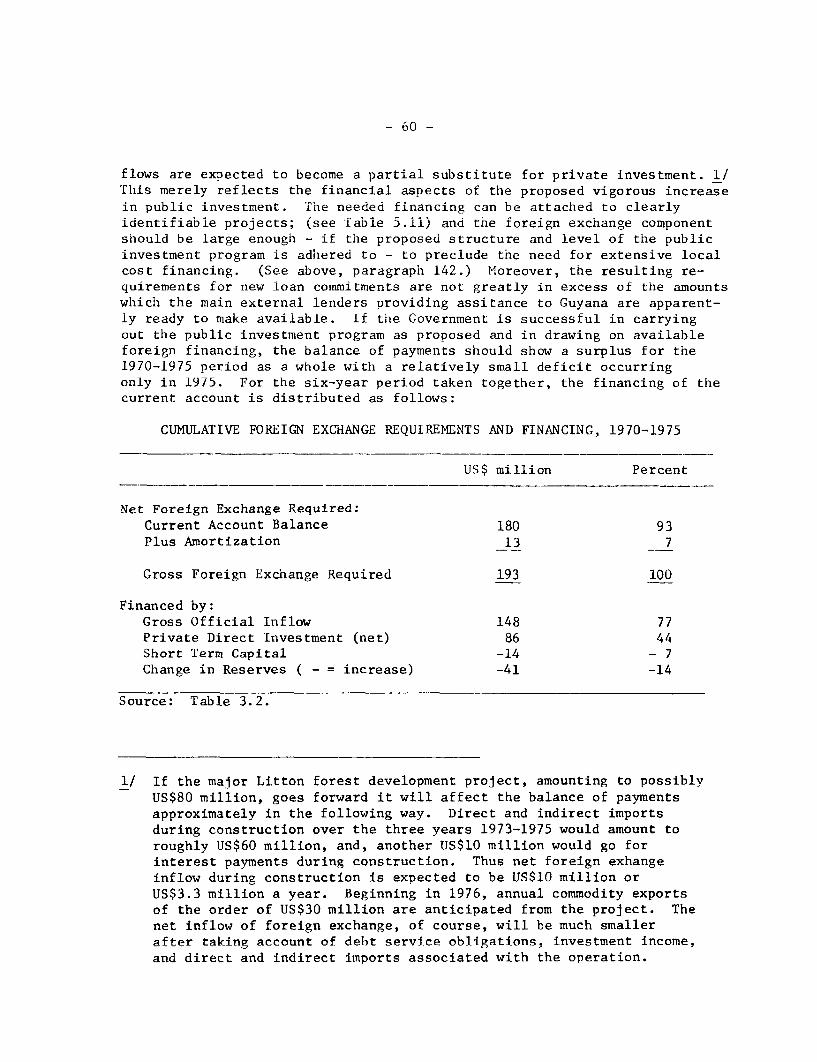

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CJRRENCY EQUIVALENTS

1 Guyanese Dollar (G$) = US$0n50*US$1 = G$2000

* New rate effective since devaluation ofNovember 1967 (old rate was G$1 = US$0-R:

US$1 = G$1071)

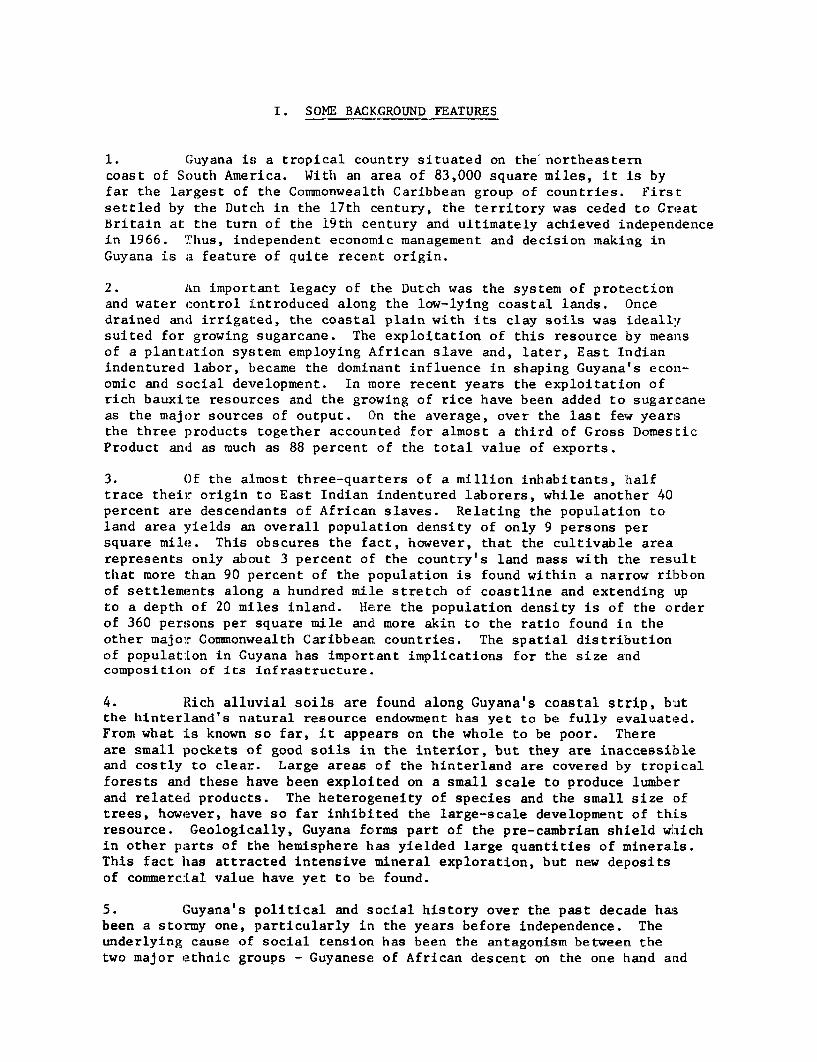

GUYANAS5~~~~~~ll.~"p '

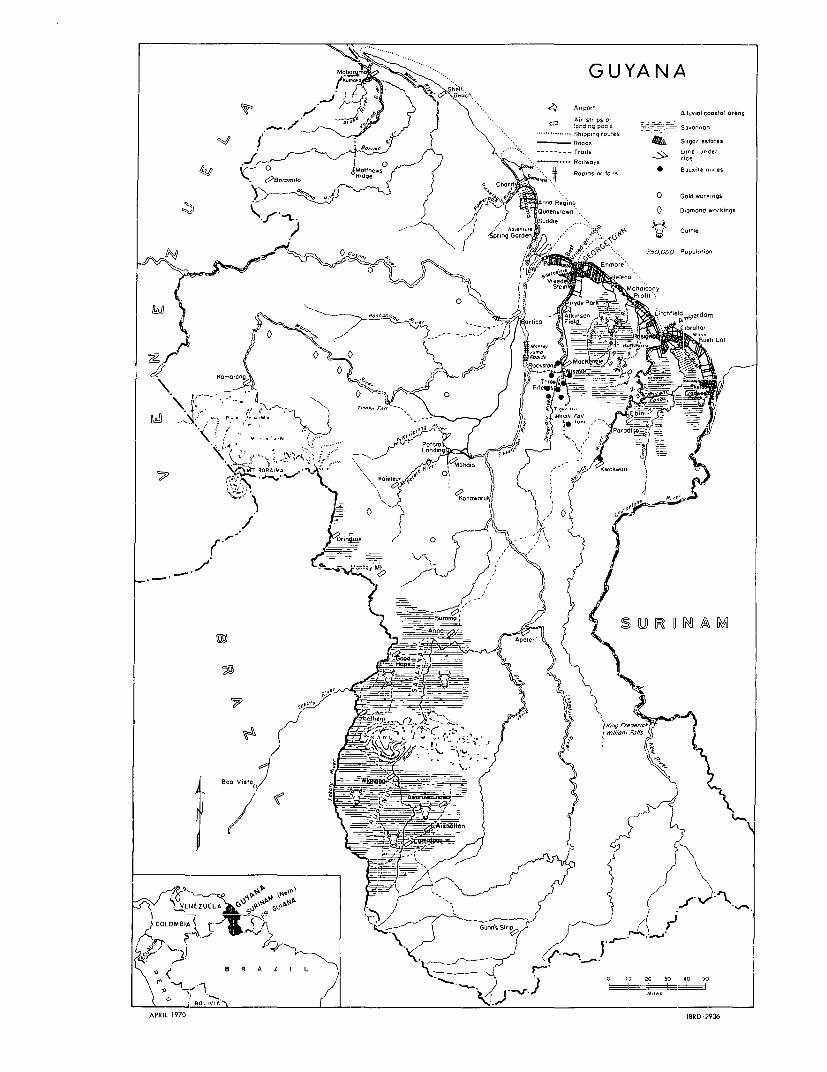

| Mc.bor~~'½ iI2 ->, .... GUY N A5

S,nu i7 ;y It . 4 d Alluviol costal oreas

* . Shi~~~~~~~~~~~~1ppin,g rodes

Roads A Sugar tstates

Bui,irrJ . 4 > Trgils .- L--,d -nder

| D ROp,dS O8c cml s o Ridge < / taC clwcR s * Wlpuxite mines

| , alaen,tO Redgie ° char ~ GSold wortirrgs

0 0r-em- d O.rkiegs

|drie Garde : Cattle

0

0 P.,

,~~~~~~~u.,* ~~~~~~~~~~~~~~~~~' E~ ~ ~ b,l.

r- 50 uaOt Fa

S Potoro ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~~~~ o

xi -~~~~~~~~~~~,

. . .M. .......

I~ ~ ~ ~ ~ , 08 77 _n 1

\ DCU| WS t CI ,¢

- A=. R

Boa Vista. -t----=

/~~~~I~ ~~~l I L , t)1y" 1\1 X-1 C 1l~ ~ ~ ~ ~~~~~~ ~ ~~~~~~~~~ ~ -l Sane' StriA S\

X oOMBID A |t

t 9 ( B R A Z _

APRIL 1970 IBRD-2936

TABLE OF CONTENTS

P age No.

BASIC DATA

SUMMARY AND CONCLUSIONS ............................. i v

I. SOME BACKGROUND FEATURES ..... ....................... 1

II. RECENT ECONOMIC DEVELOPMENTS ........................ 3

A. Output and Expenditure. 3B. Developments in Major Sectors ................... 6

Mining ........................................ 6

Agriculture, Fishing and Forestry .... ......... 8Manufacturing ....... .......................... 11Transportation ...... .......................... 13Communications ...... .......................... 16

Social Services ............................... 17

Health, Education, Water Supply, Sanitation . 17Housing ..................................... 19

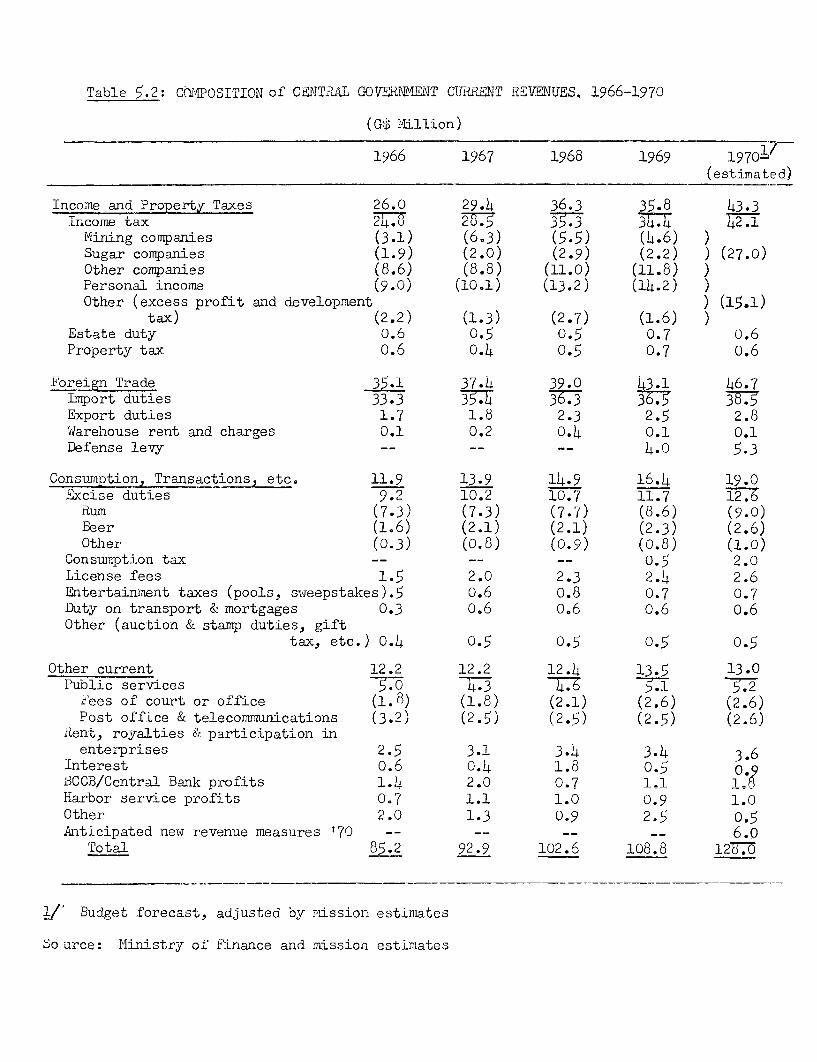

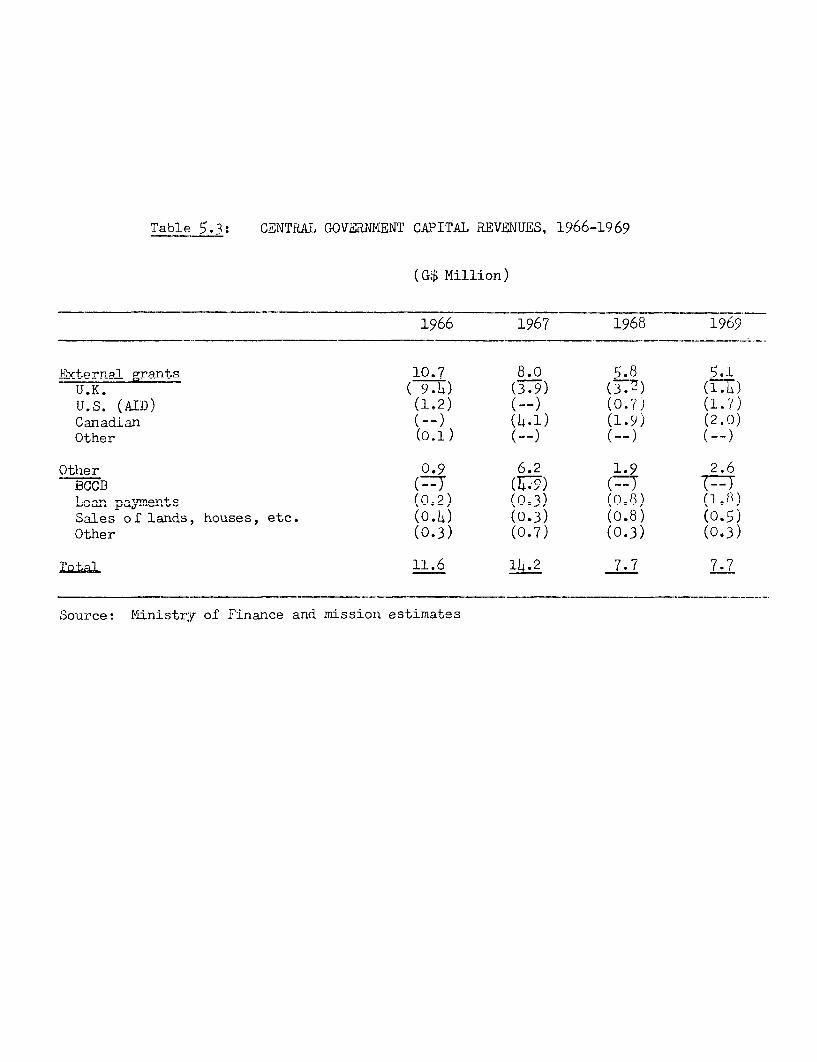

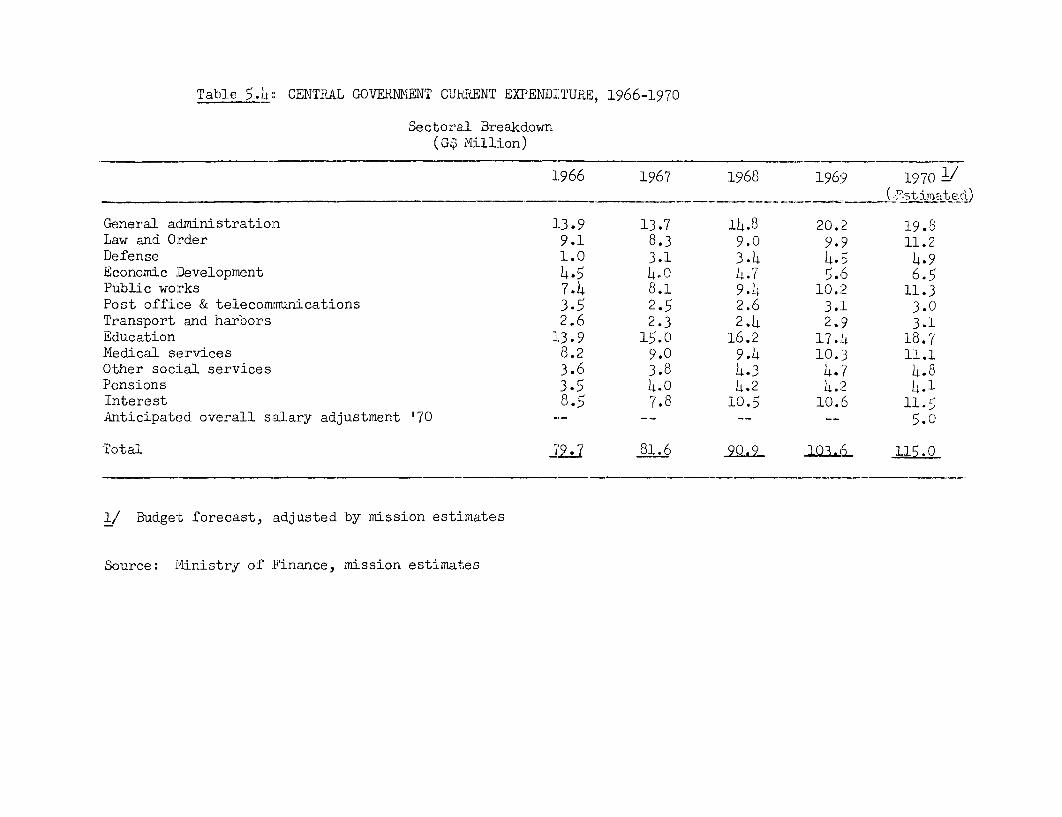

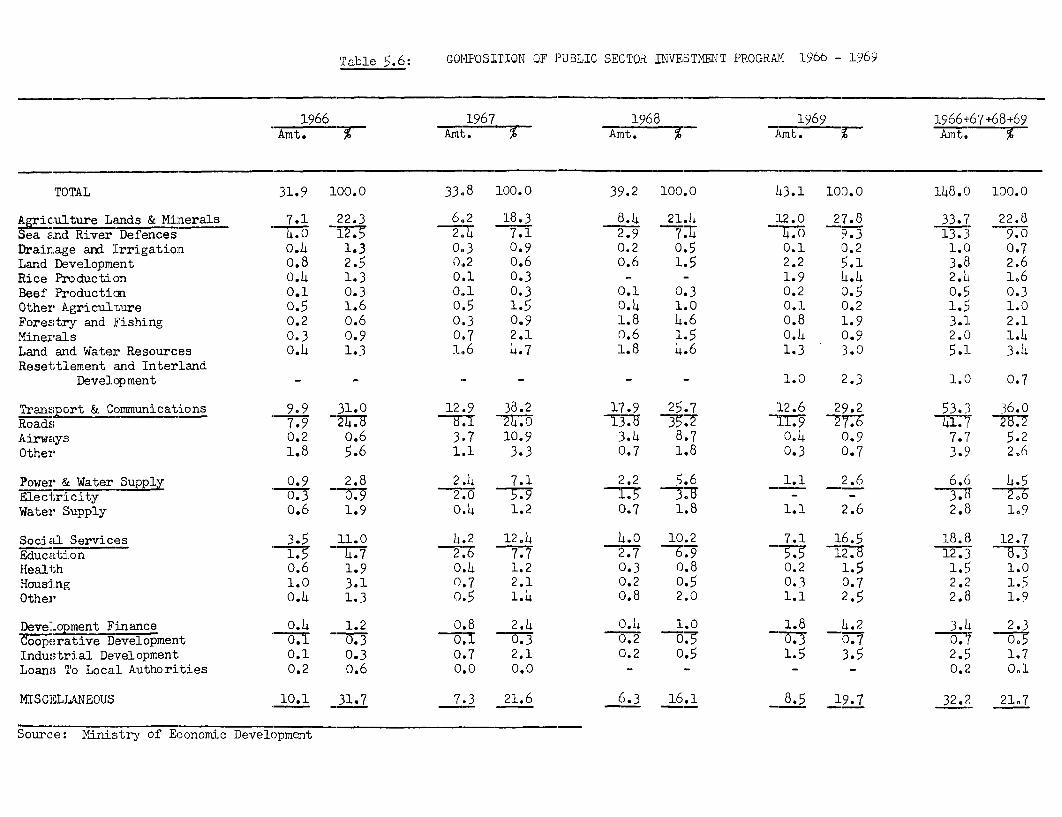

C. Public Sector Investment ....................... 20D. Public Finances ................................ 22E. Balance of Payments ............................ 28

F. Population, Employment, Wages and Prices ....... 29G. Monetary Developments .......................... 34

III. DEVELOPMENT PROSPECTS ............................... 38

A. Introduction ................................... 38

B. New Development Parameters ..................... 39

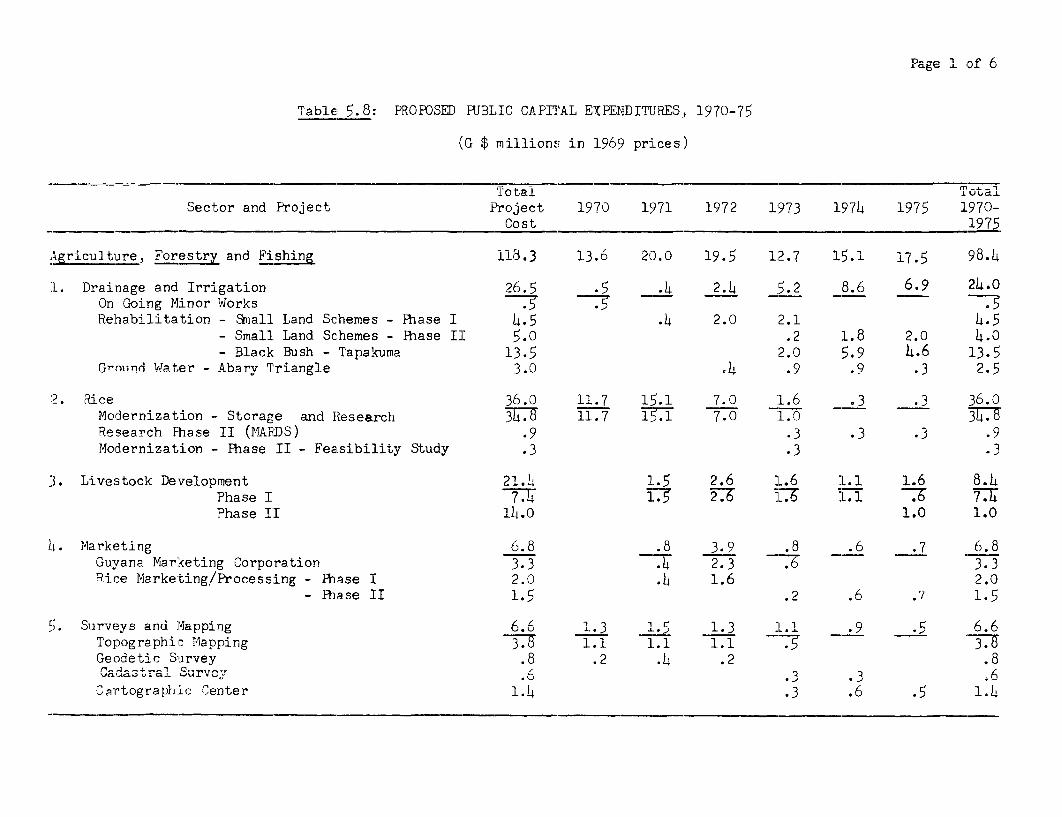

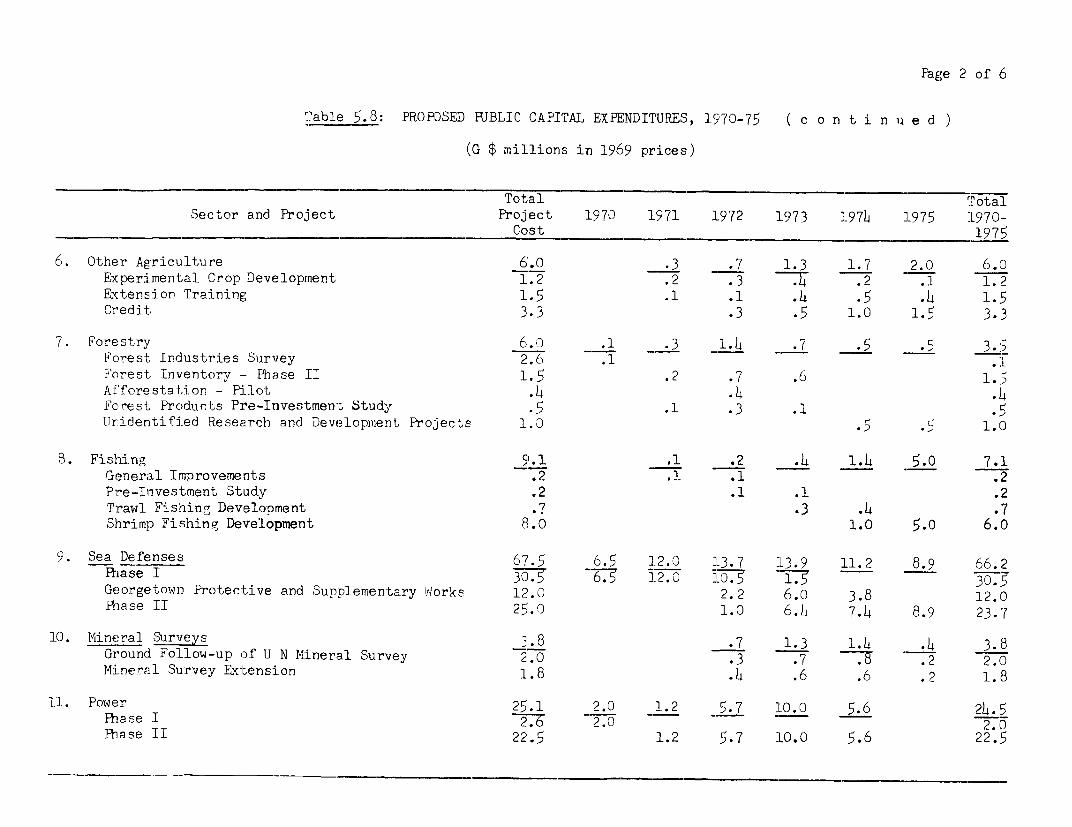

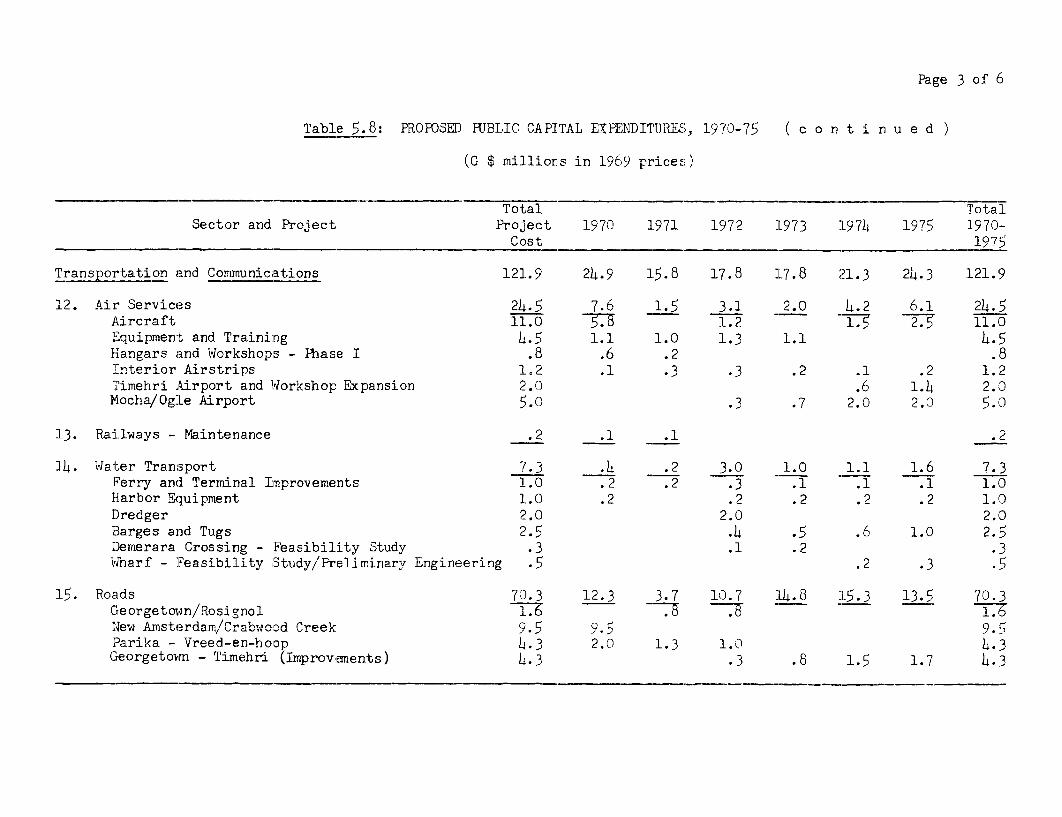

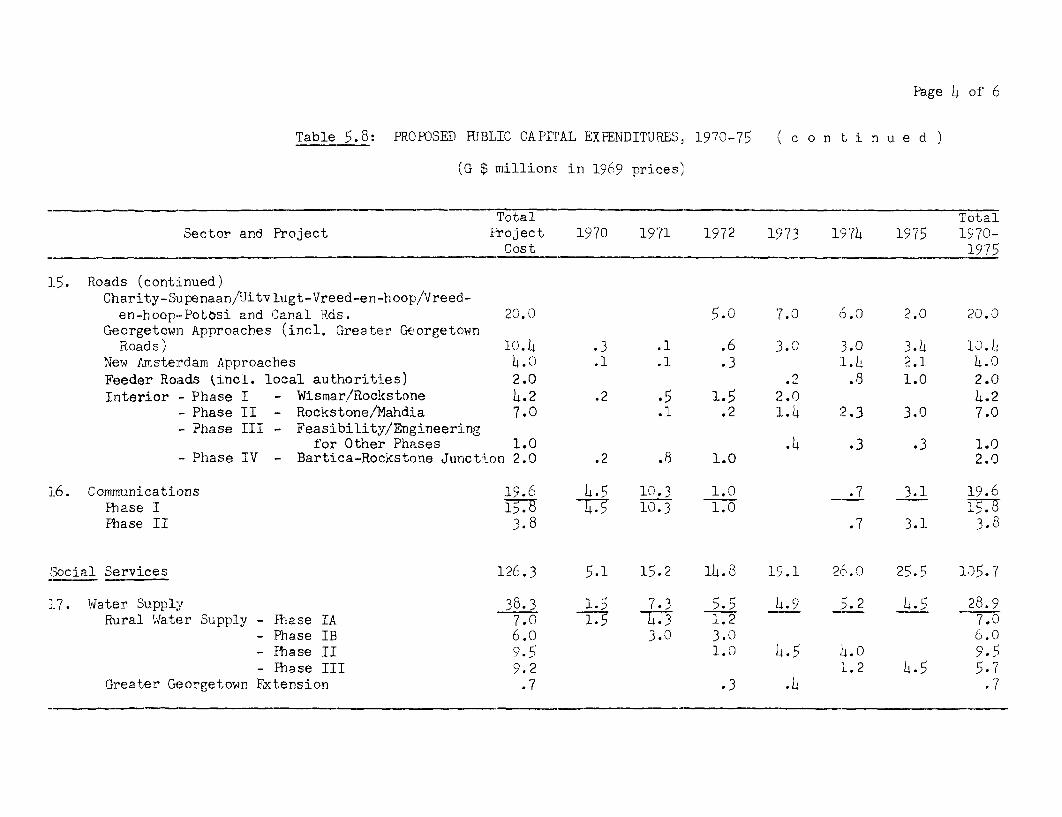

C. Prospects and Sources of Growth, 1970-1975 ..... 42D. Proposed Public Investment Program .... ......... 46E. Financing the Proposed Public Capital Expenditures 50F. Some Outstanding Policy Issues .... ............. 53

IV. THE EXTERNAL SECTOR: POLICIES AND PROSPECTS .57

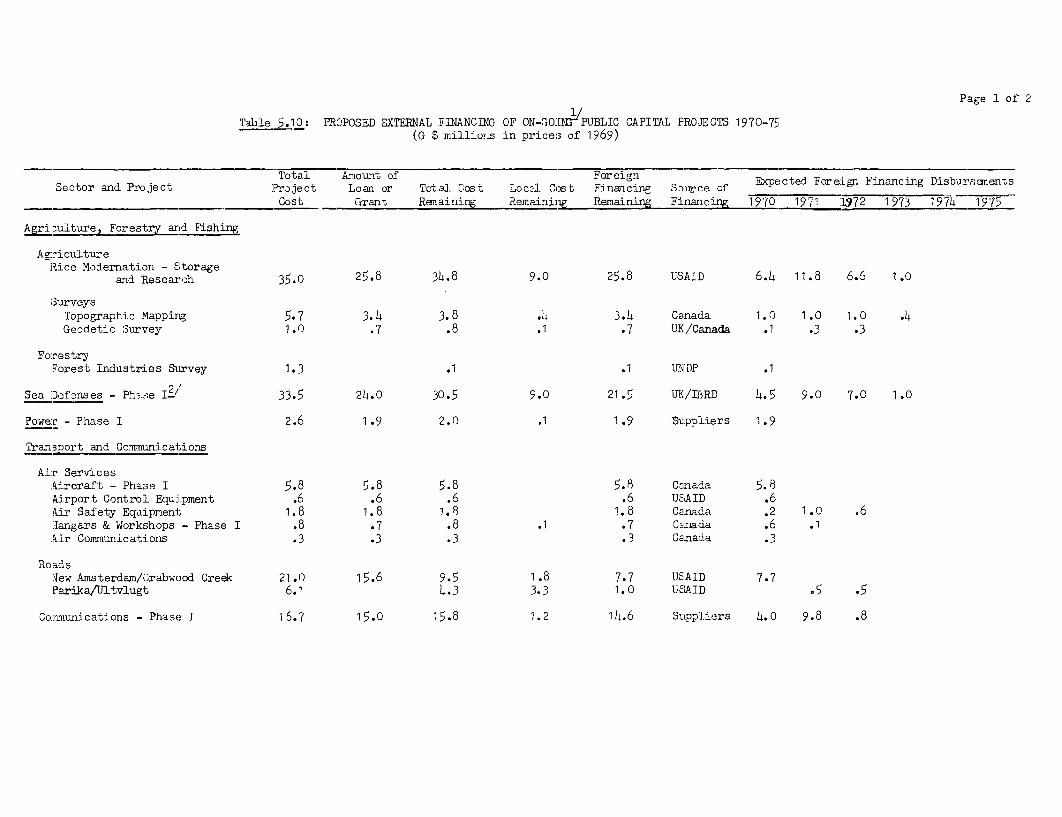

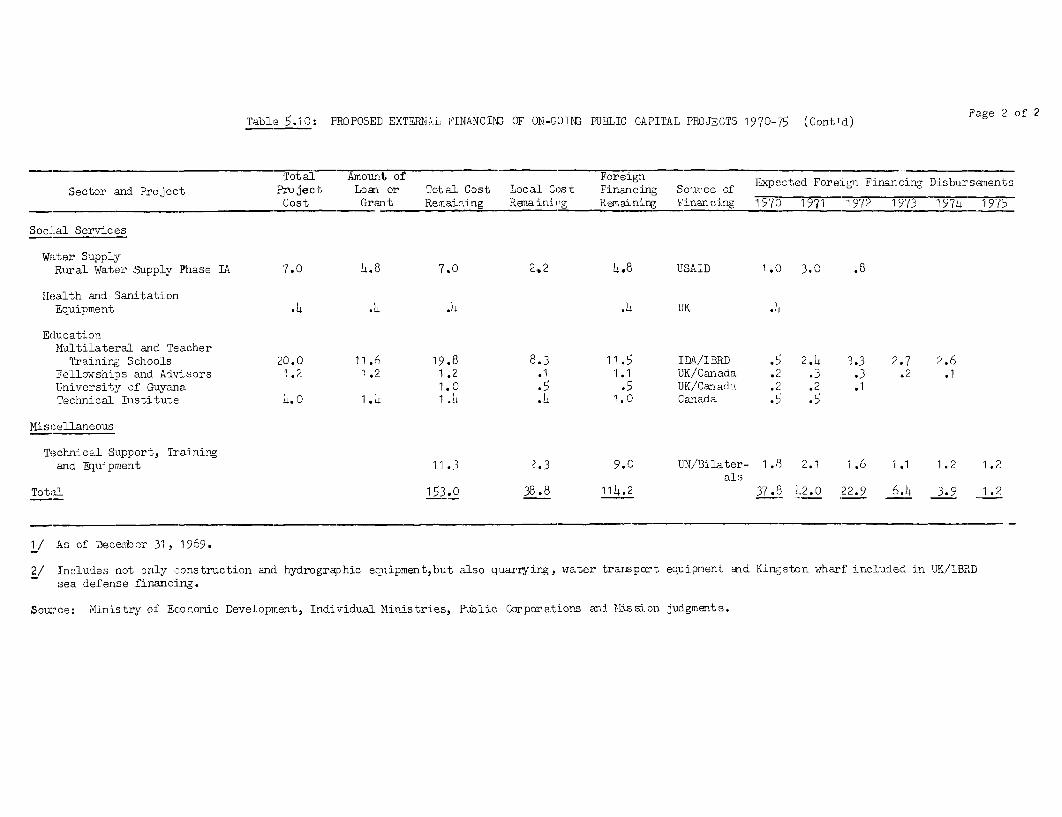

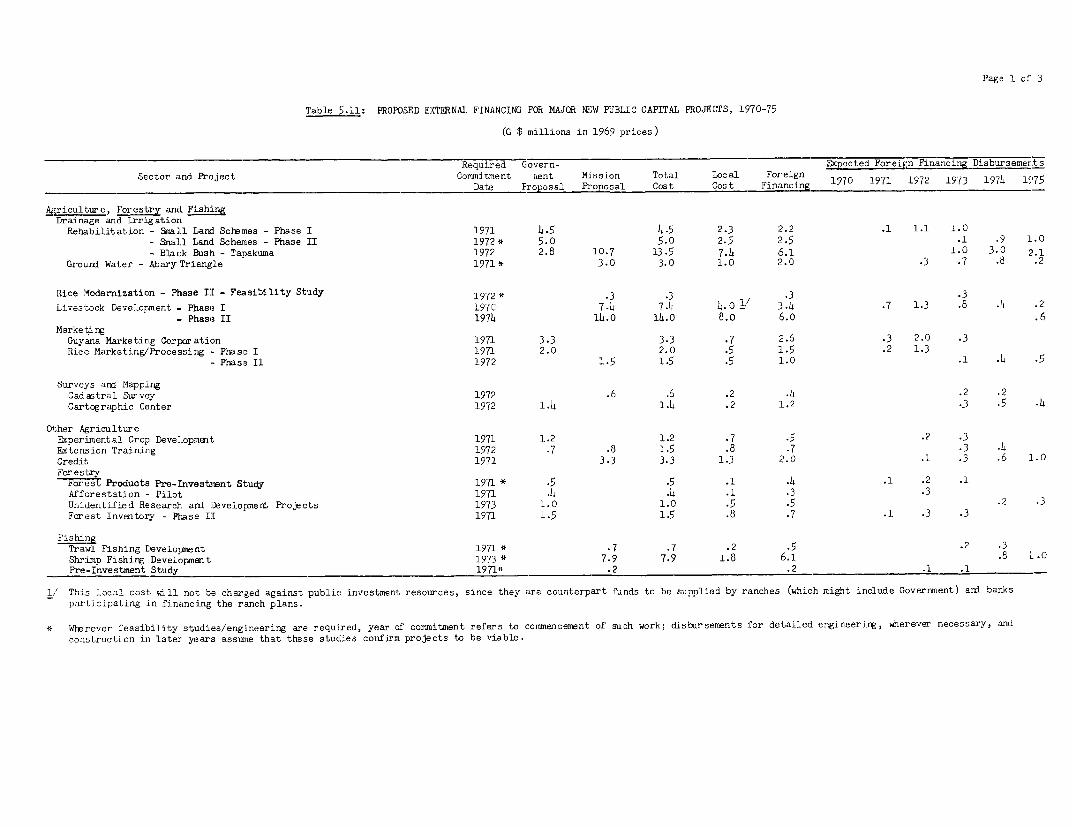

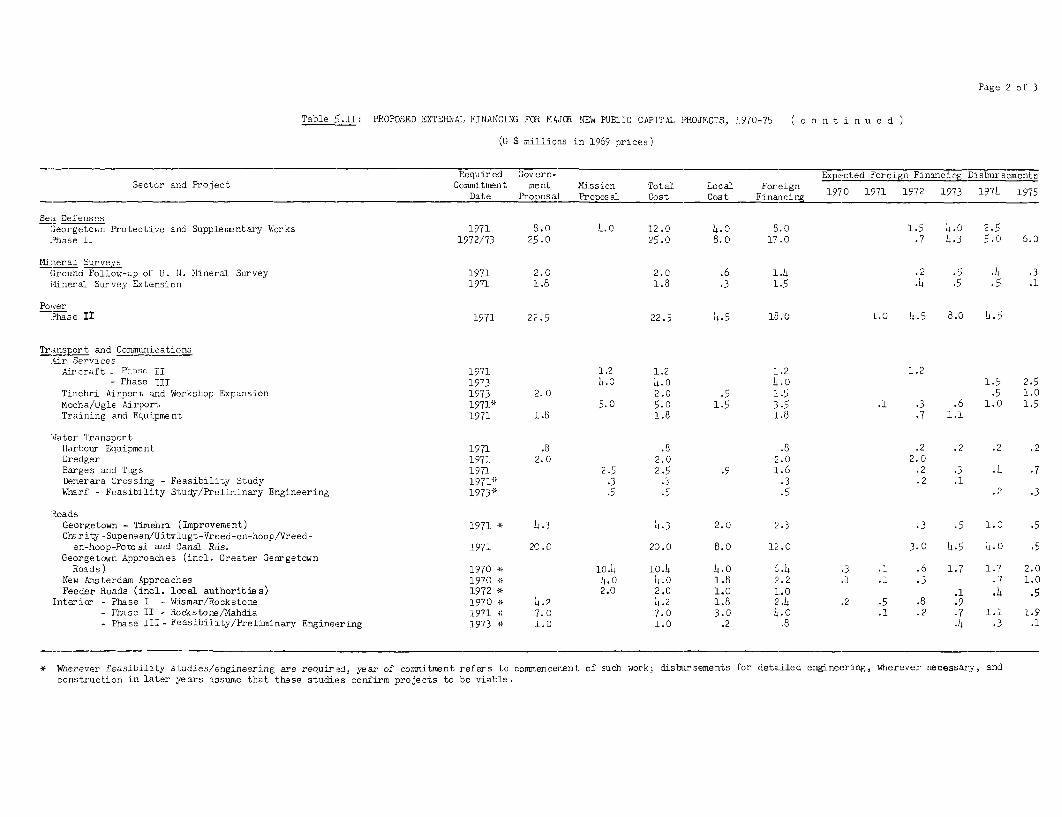

APPENDIX I Project Composition of Proposed Public Investment

Program, 1970-1975

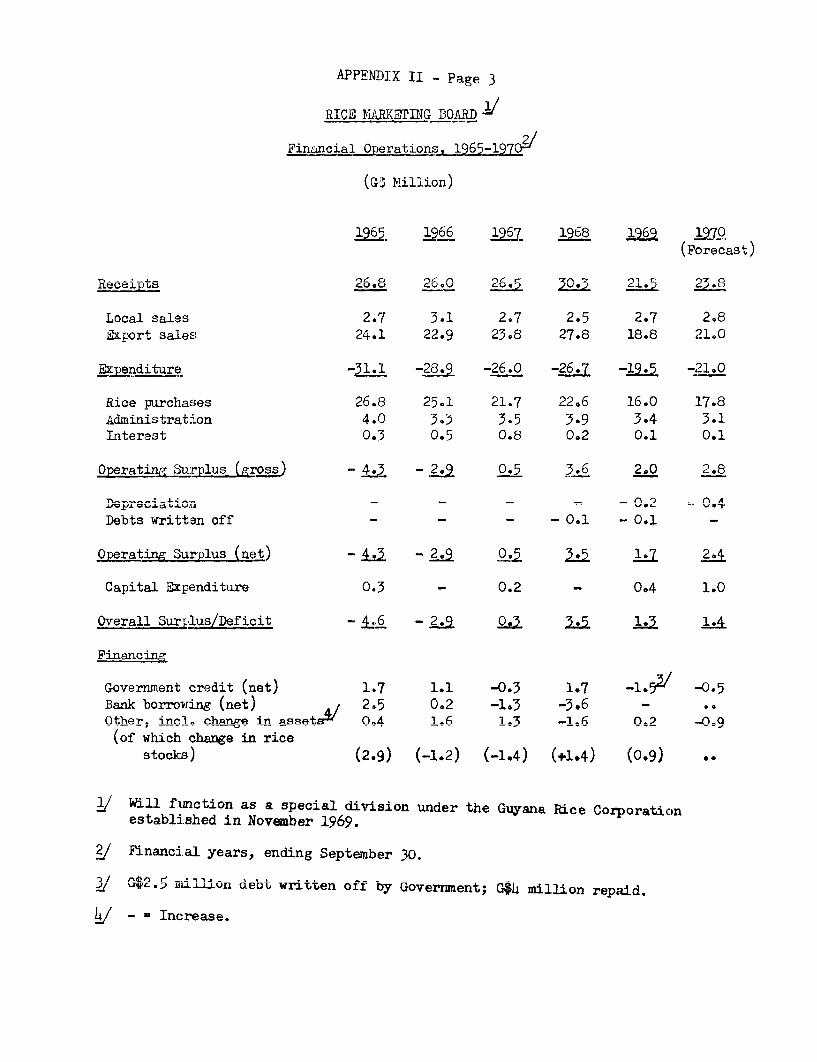

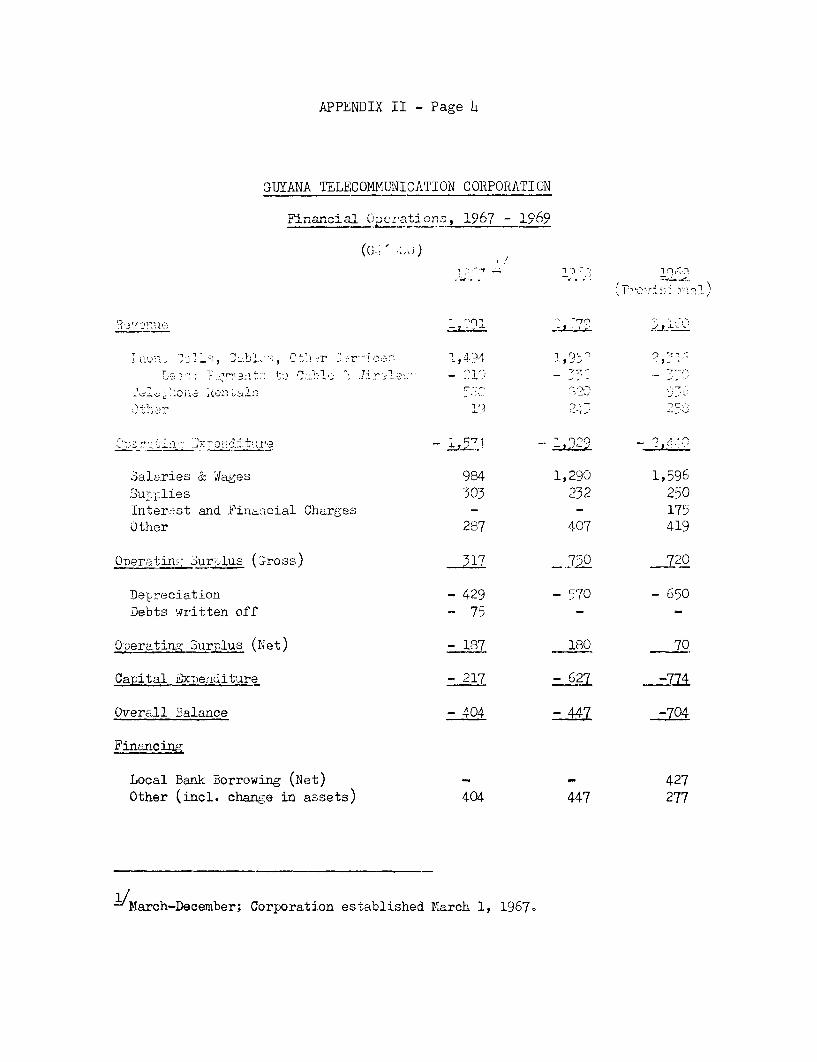

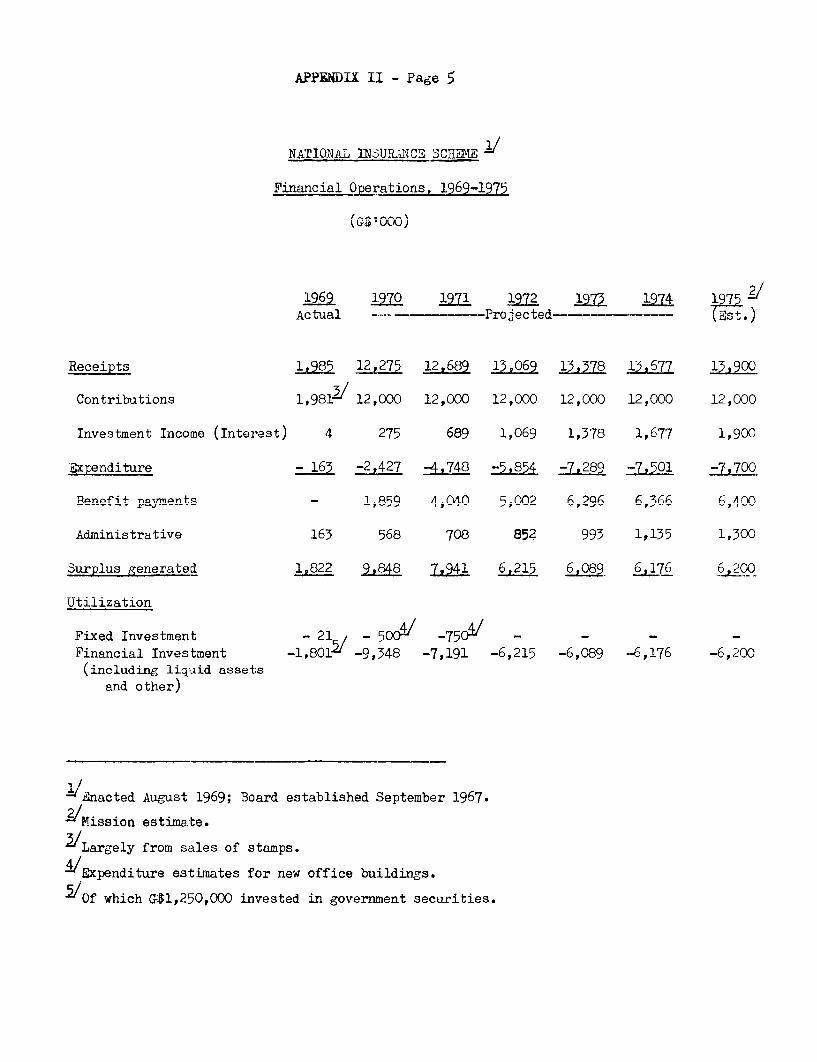

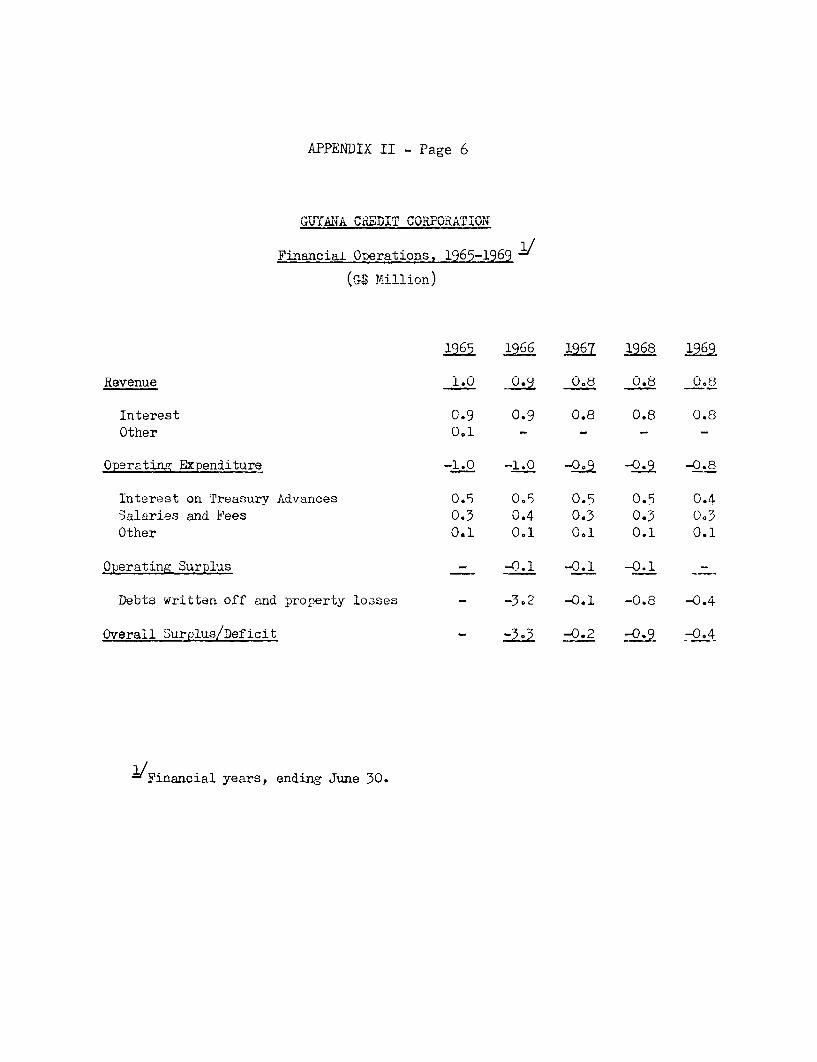

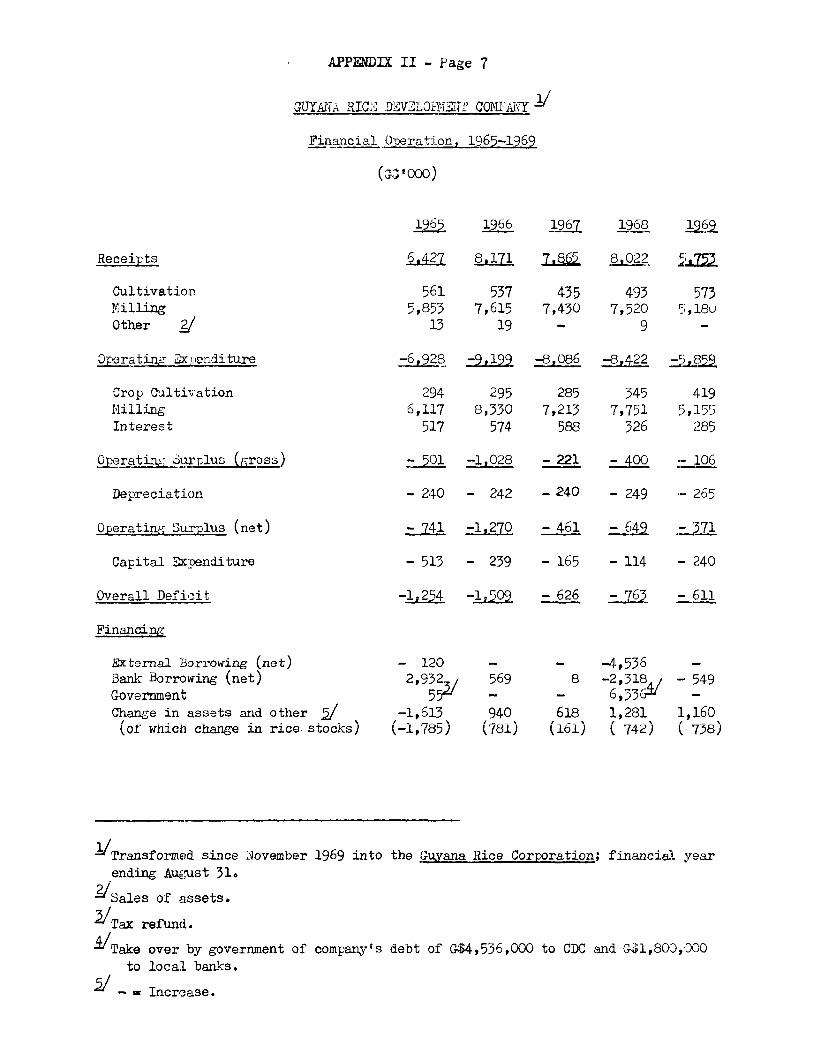

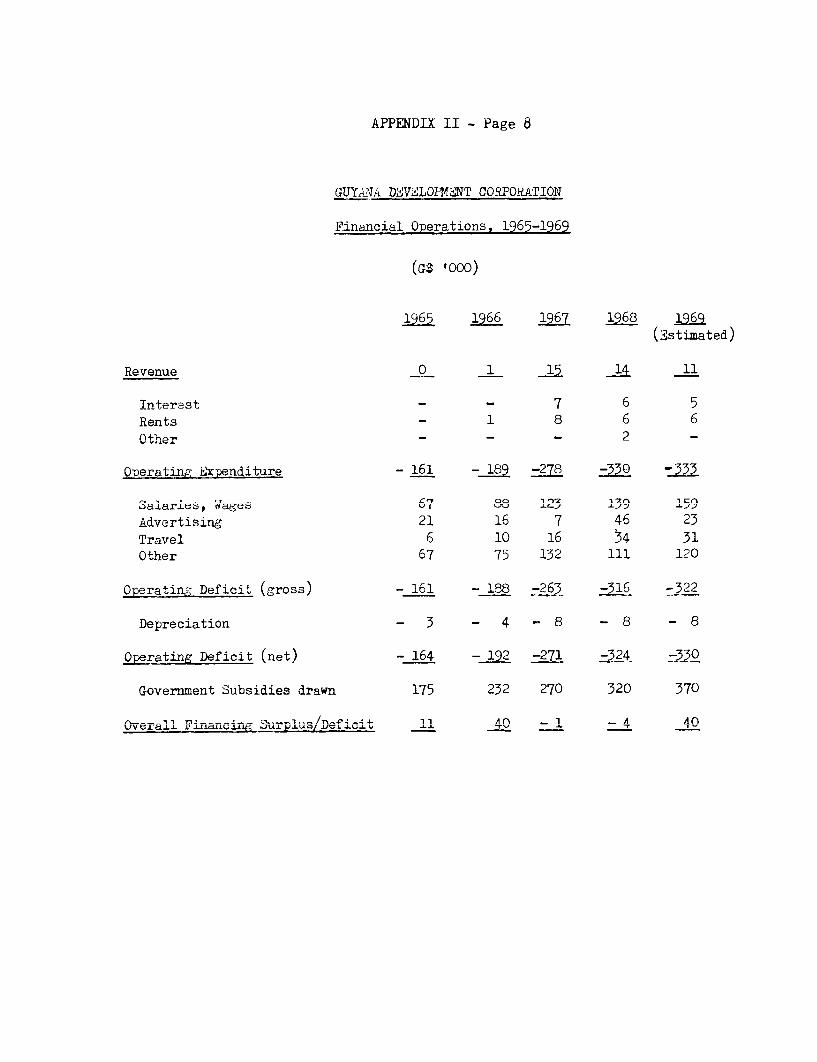

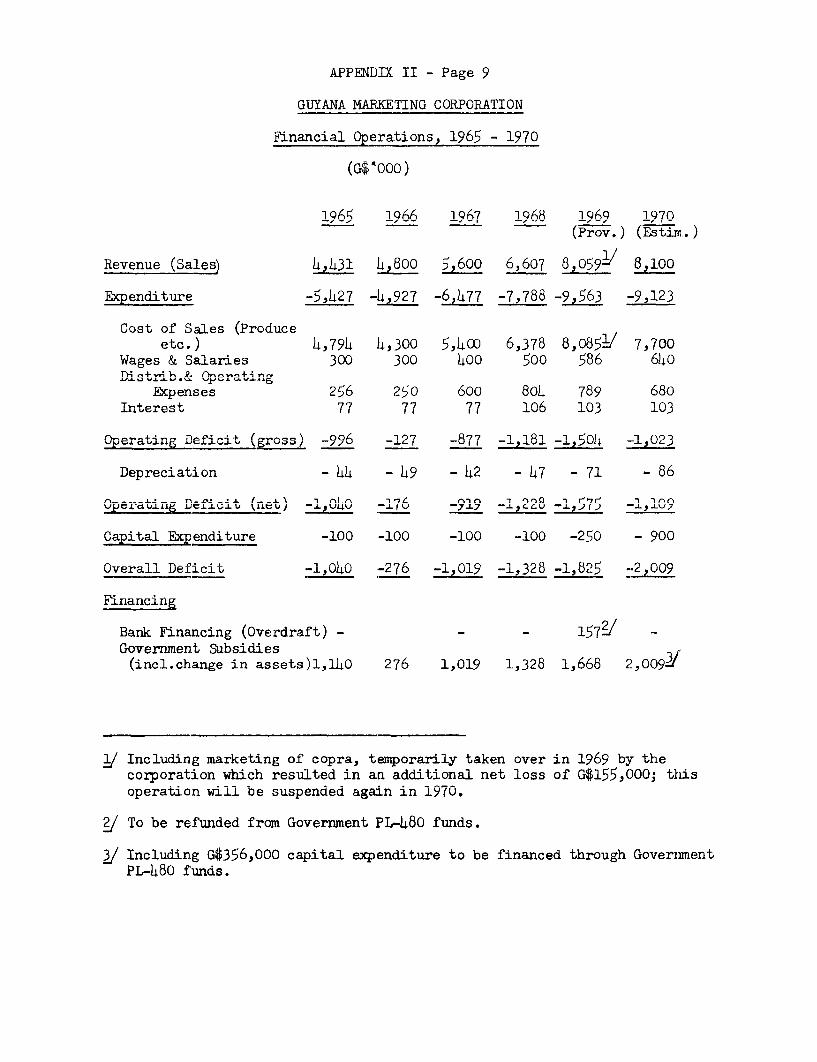

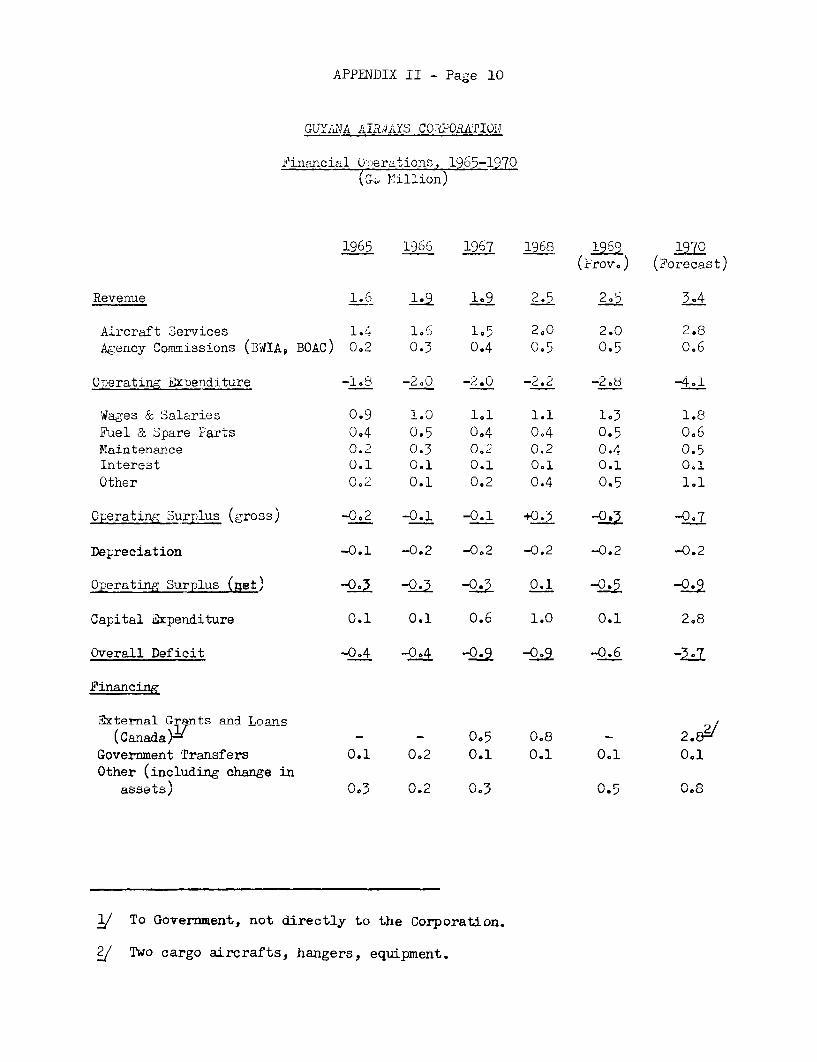

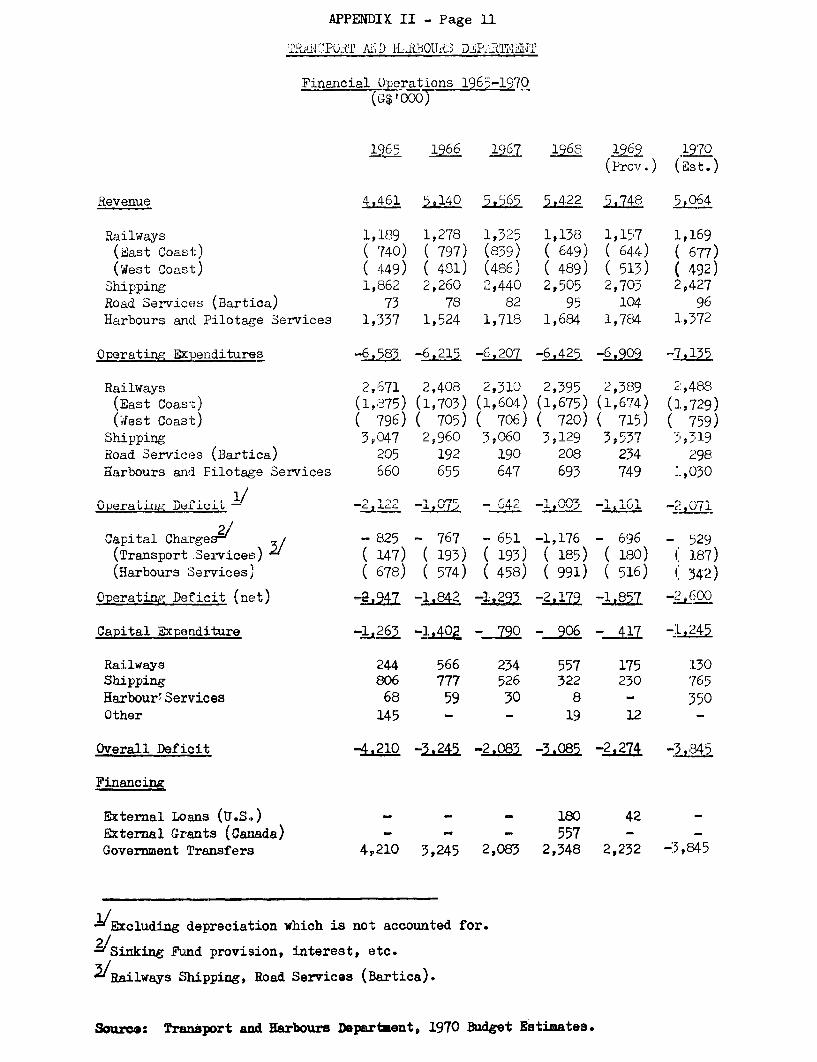

APPENDIX II Financial Operations of the Public Corporations

STATISTICAL APPENDIX

This report is the result of an economic mission which visited Guyana early

in 1970. The mission was composed of: Sidney E. Chernick, Chief of Mis-

sion; J. Hanns Pichler, Chief Economist; W.T. McGrath, General Economist;

Adi J. Davar, Public Investment Analyst (part-time); R.D. Crotty, Consultant -

Agricultural Economist; Merril Roberts, Consultant - Transportation Economist;

Mrs. Lourdes G. de Vera, Secretary. The mission benefited greatly from the

work of an International Monetary Fund mission which was visiting Guyana

concurrently.

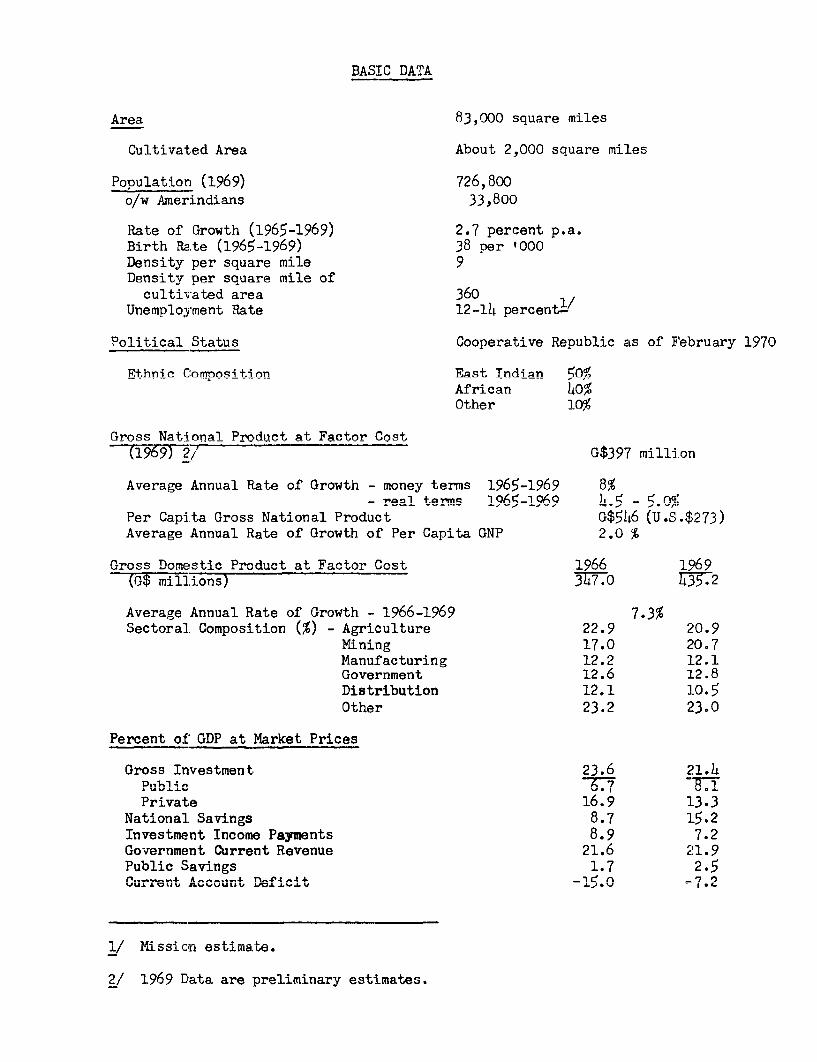

BASIC DATA

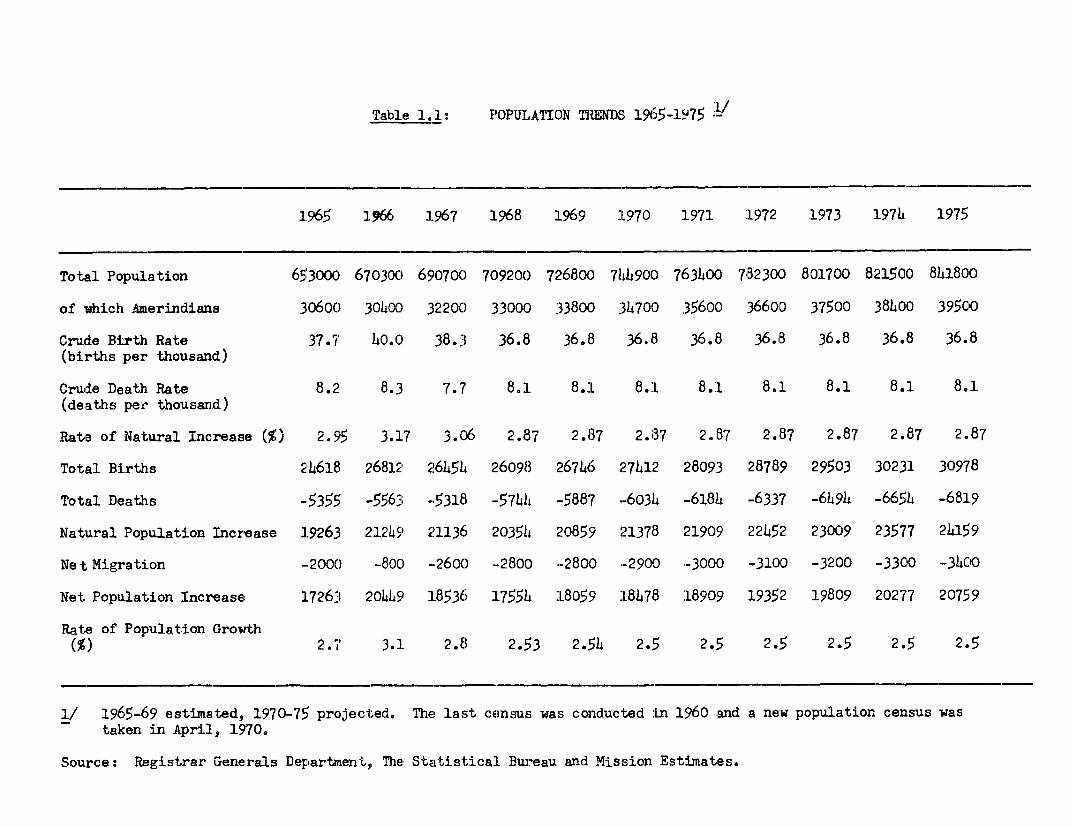

Area 83,000 square miles

Cultivat.ed Area About 2,000 square miles

Population (1969) 726,800o/w Amerindians 33,800

Rate of Growth (1965-1969) 2.7 percent p.a.Birth Rate (1965-1969) 38 Der '000Density per square mile 9Density Der sauare mile of

cultivated area 360Unemnlovment Rate 12-lLt percentlY

Pol i ti cal Status Coonerative Republic as of February 1970

Et.hnic Comnosi tion East Tndian qoa,African 0Other 109

Gross Nati.onal Prniduct at Factor Cost(1969)27- G$397 million

Average Annual Rate of Growth - money terms 1965-1969 8%l-rea -mn 1965-1969 ) _ 5. nq

Per Capita Gross National Product G$546 (U.S.$273)Average Annual Rate of Growth of Per Ca-it-a r-NP 2.0

Gross Dome!stic Product at Factor Cost 96l6(G$ millions) 377.0 735.2

Average Annual Rate of Growth - 1966-1969 7.3%Sectoral. r-coMposition (%) A- raculture 22.9 ... 20.9

Mining 17.0 20.7Manufacturing 12.2 12.1Government 12.6 12.8Distribution 12.1 10=5Other 23.2 23.0

Percent of' GD? at Market Prices

Gross Investment, 23.6 21.4

Private 16.9 13.3Nat+onal S-4- R 7 1 1f 9

Investment Income Payments 8.9 7.2G-overni,cot Current R. -J - LJP evenue 2.1.6 21 .9Public Savings 1.7 2.5CAU LI .k L L J. . U_LJur..rent Account ='L -,fif -. = 7.02

1/ us9i nj estimatUe.

2/ i969 Dlata are preliminary estimates.

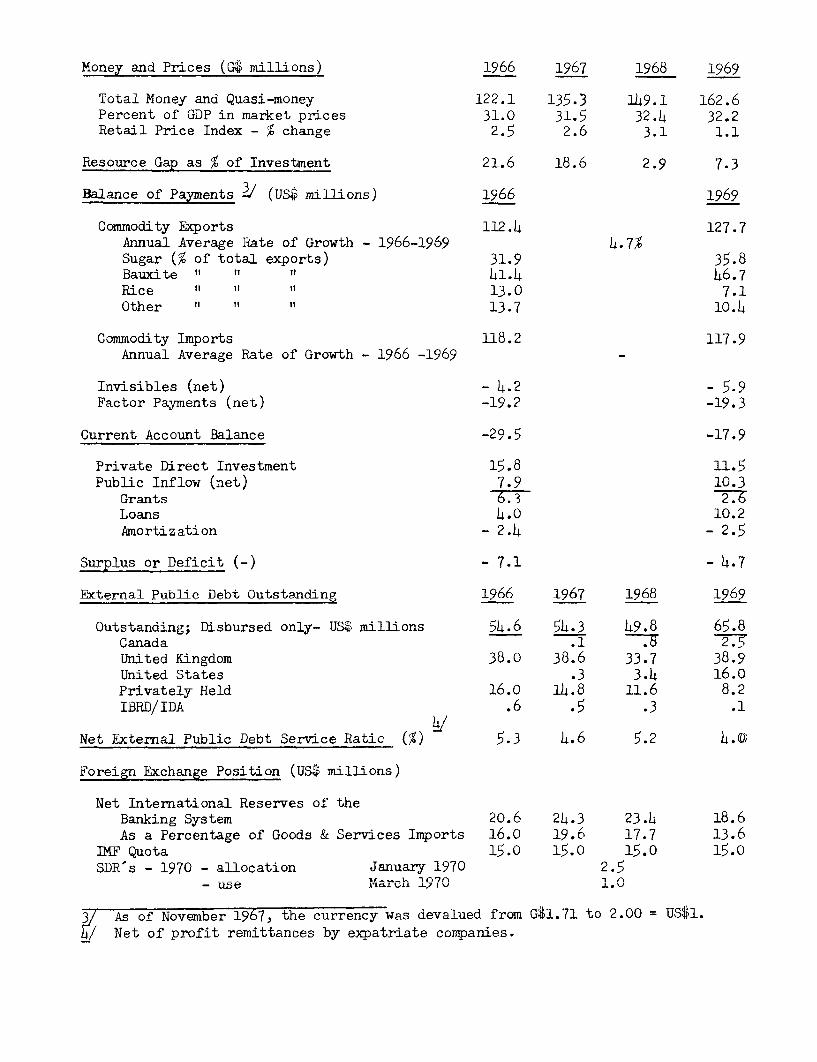

Money and Prices (G(P millions) 1966 1967 1968 1969

Total Money and Quasi-money 122.1 135.3 149.1 162.6Percent of GDP in market prices 31.0 31.5 32.4 32.2Retail Price Index - % change 2.5 2.6 3.1 1.1

Resource Gap as % of Investment 21.6 18.6 2.9 7.3

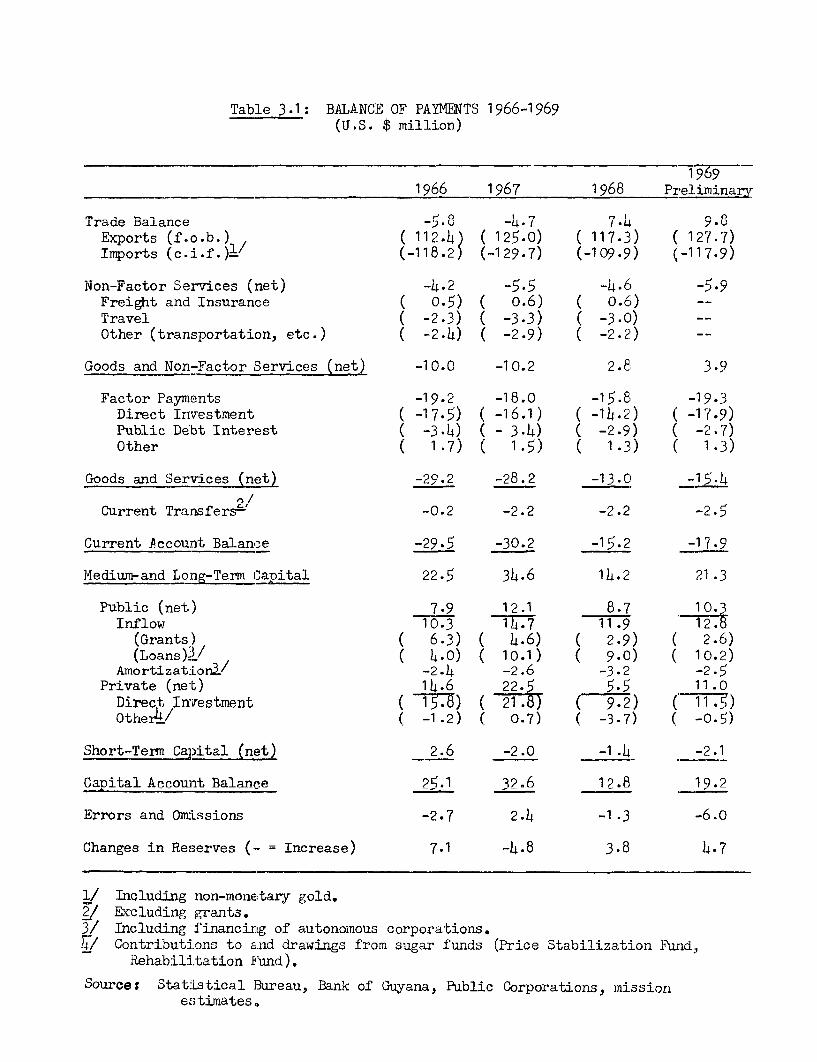

Balance of Payments dJ (US,$ millions) 1966 1969

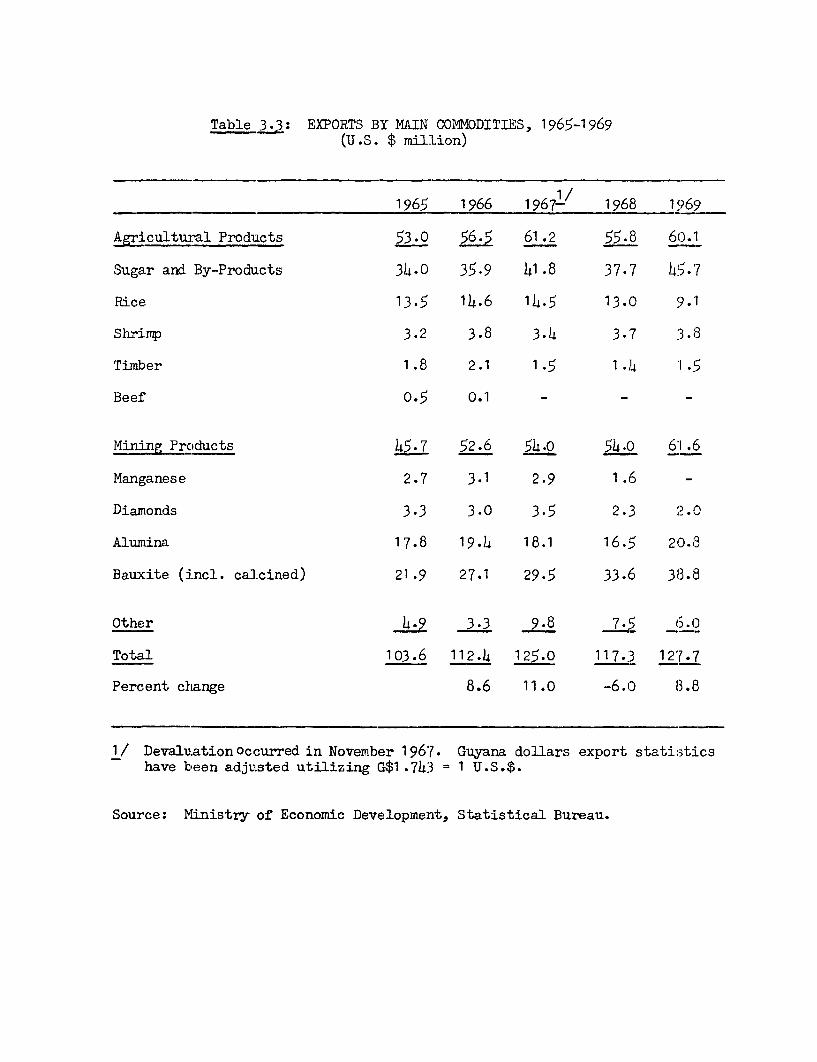

Commodity Exports 112.4 127.7Annual Average Rate of Growth - 1966-1969 4.7%Sugar (% of total exports) 31.9 35.8Bauxite " " f 41.h 46.7Rice if it Et 13.0 7.1Other it tt it 13.7 10.4

Commodity Imports 118.2 117.9Annual Average Rate of Growth - 1966 -1969

Invisibles (net) - 4.2 - 5.9Factor Payments (net) -19.2 -19.3

Current Account Balance -29.5 -17.9

Private Direct Investment 15.8 11.5Public Inflow (net) 7.9 10.3

Grants 6.3 2.6Loans 4.0 10.2Amortization - 2.4 - 2.5

Surplus or Deficit -) - 7.1 - 4 *.7

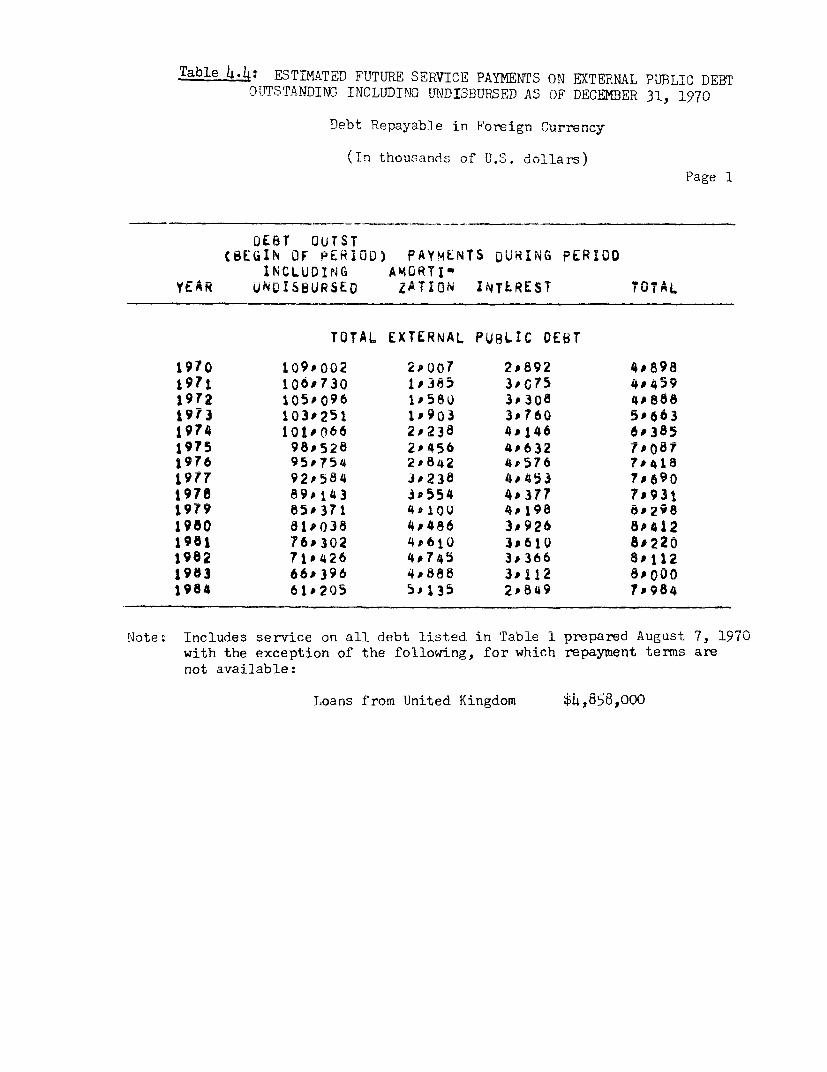

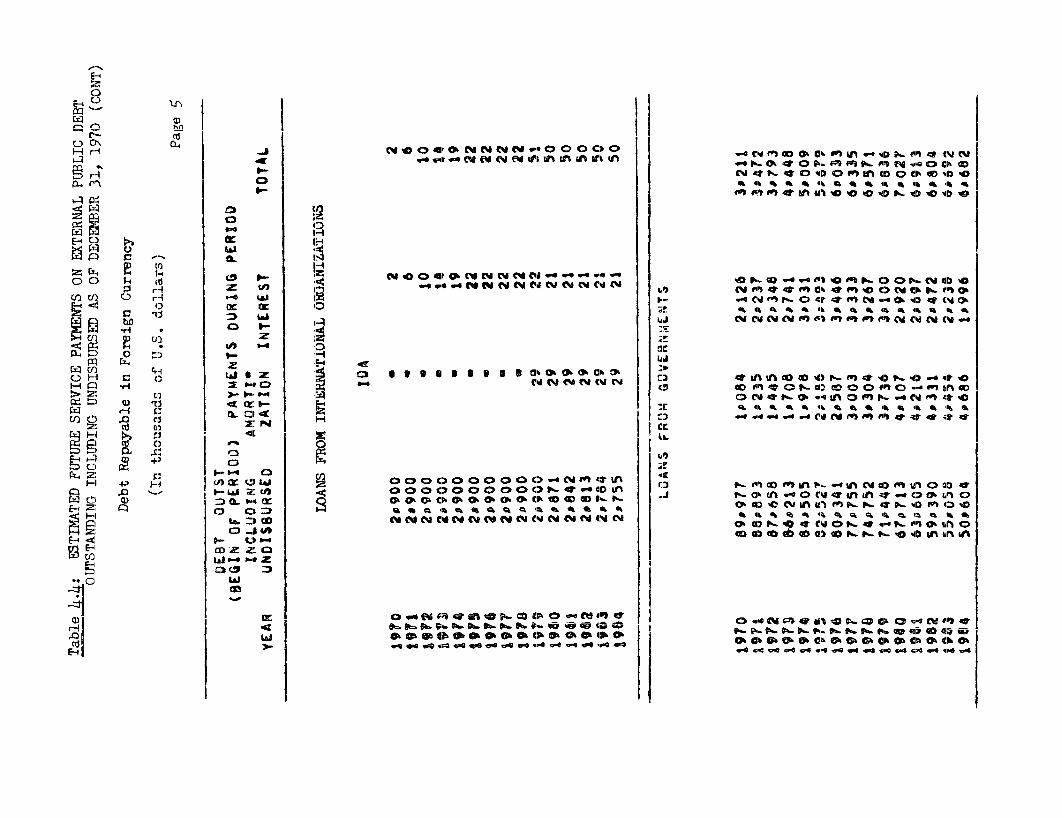

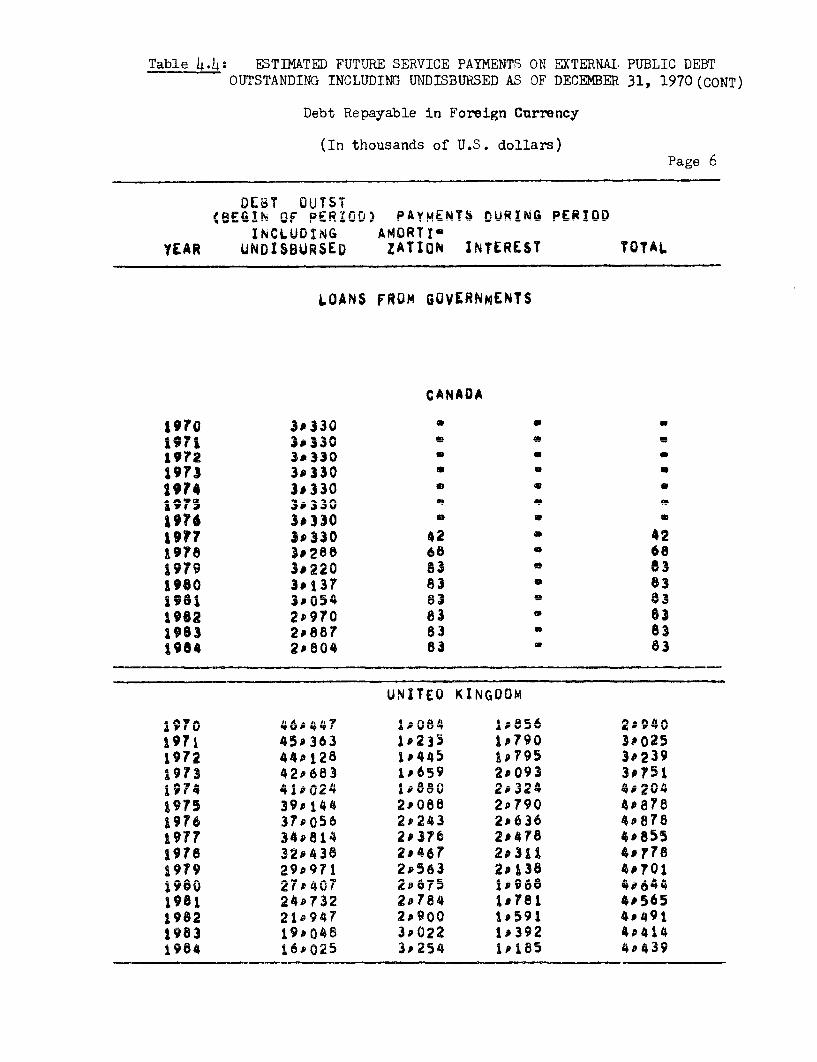

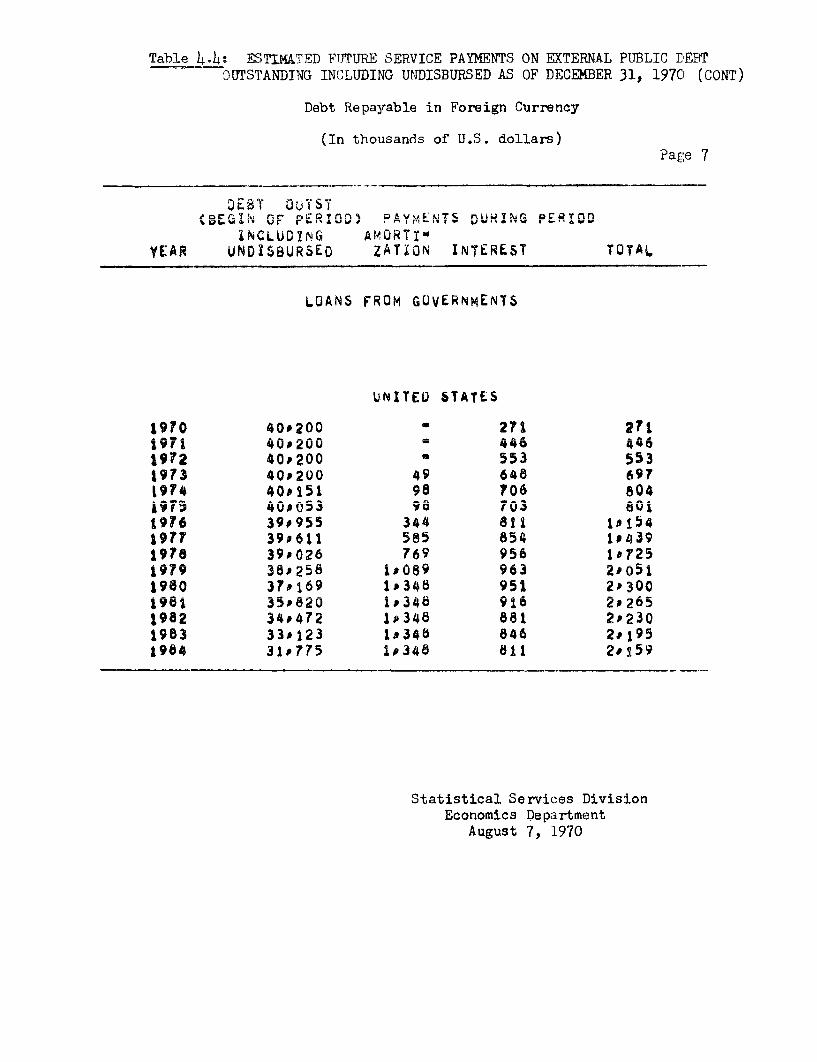

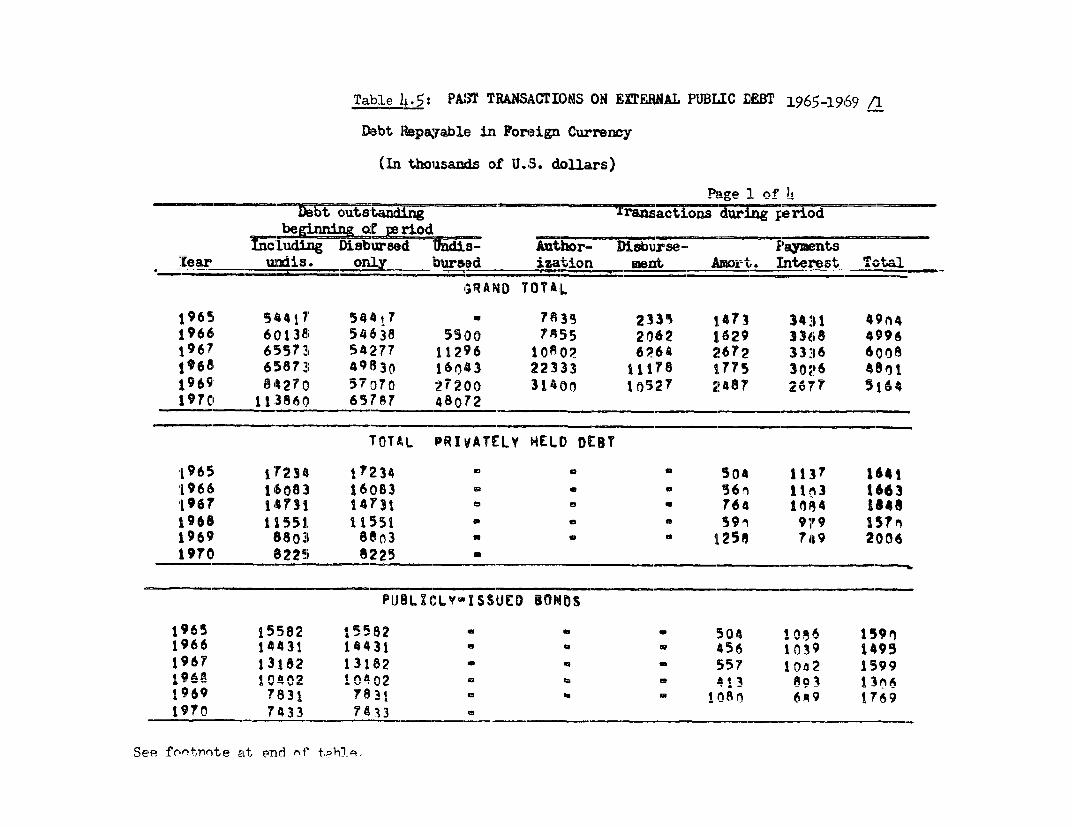

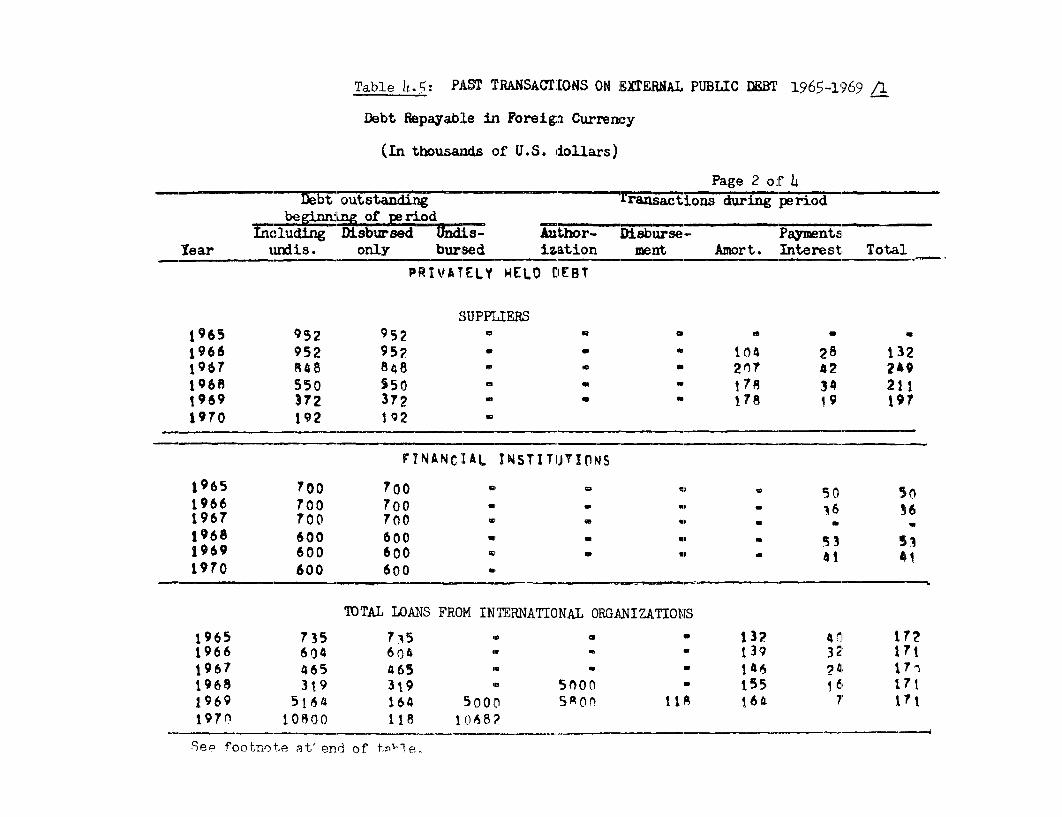

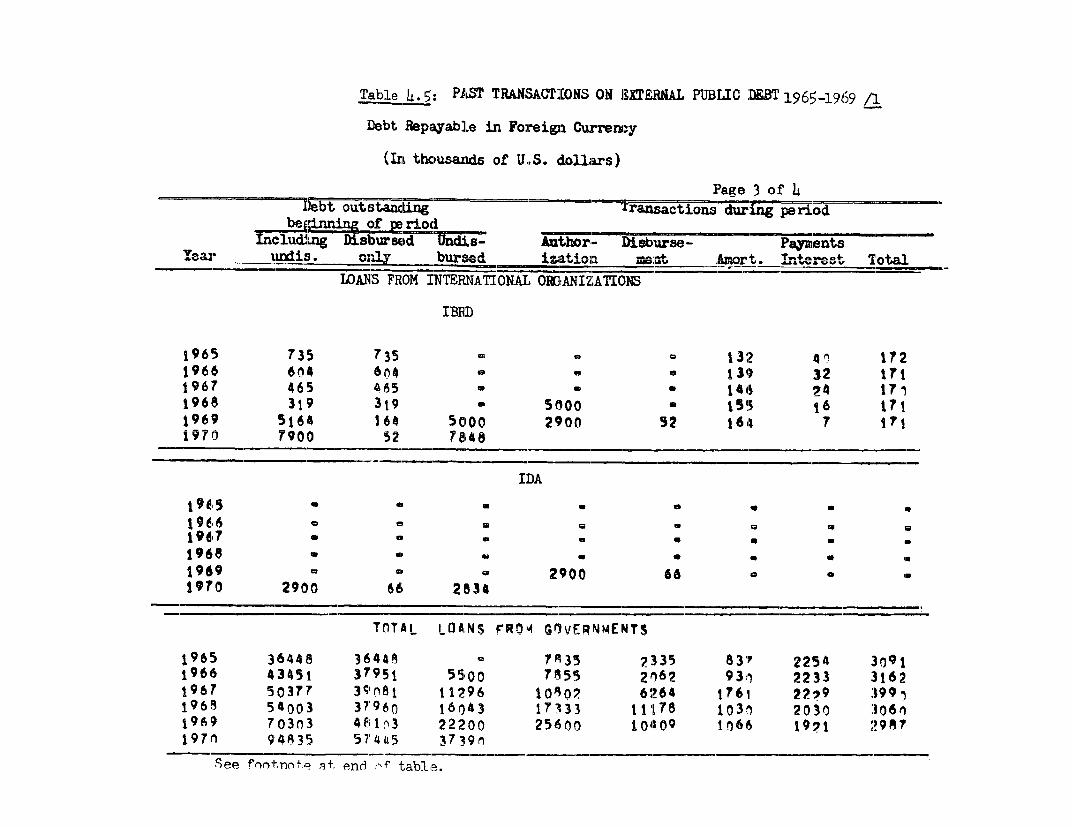

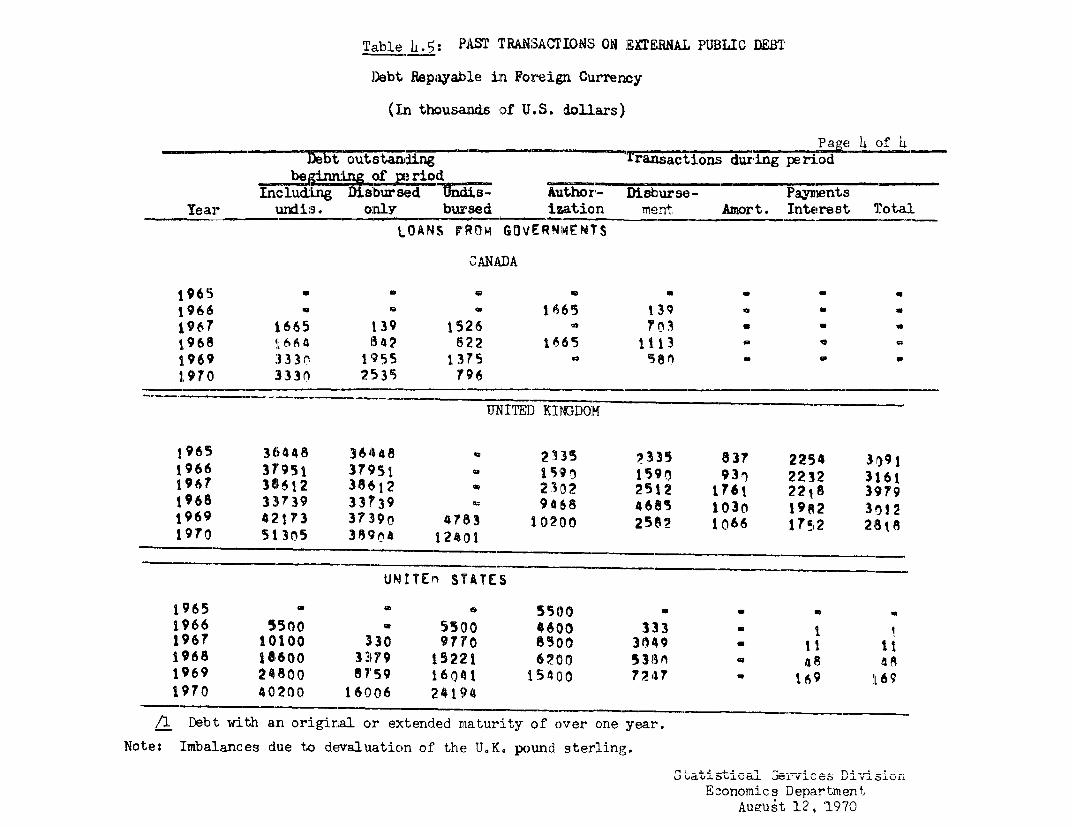

External Publie. Debt Ouitstanding 1966 1967 1968 1969

Oustanding; TisbhirqPt onlv- IT5S$ millionn 5h6 5L h J,9.8 65.8Canada .1. 27UTnited Kingdom 35=o 386 33.7 38=9United States .3 3.4 16.0Pt-j,trivatelyvr T-leld 1A6 1JA.8 11.6 8.2IBRD/IDA .6 .5 .3 .1

Net External Public Debt Service Ratic (X) 5.3 4.6 5.2 4.0

Foreign Exchange Position (US$ millions)

Net International Reserves of theBarll-4 ng Systemr,n A 2, .3 2. 1 AAs a Percentage of Goods & Services Imports 16.0 19.6 17.7 13.6

QrE uota 15, .0 15,,. 0 -L,.0 1.oSDR' s - 1970 - allocation January 1970 2.5

- use J-l-u± V. V

oAs f November 1967, the currency was devalued frm G-$1.71 to 2.00 - US$1.Net of profit remittances by expatriate companies.

Standn-by Agreemeints:

Fiebruary 13, l967 - r-ebruary 12, 1968 US 7.5 mi.February 15, 1968 - February 14, 1969 Us$ .0 m.March 29, 1969 - March 28, 1970 US$ 4.0 m.April 6, 1970 - April 5, 1971 Us$ 3. m.

International Relations

Member of CARIFTAMember of Commonwealth and Siterling BlocNot a member of OAS or IDB

SUMMARY AND CONCLUSIONS

1. Guyana is a n.. 4 st.all county w-aih, about th ree-quarters oi- a m4lLiUonpersons inhabiting a land mass roughly equivalent to that of the UnitedrA.rLgoUru. IL achLiLeveu LLs inUepenudence fLror Britain iLn 1D966 after a periodof internal strife between the two major ethnic groups -- the descendZntsof. £.4ast Indian iLnd.enturedU ULab'orers comprisLng abJout .0J percent andu thLeidescendants of African slaves representing about 40 percent of the popula-tiLno. Saocieal tensiLons hnave 'lebee relieved 'in recent years. nouniuary disputeswith Surinam and Venezuela have added to a climate of more than normal.uncertairLty in Guyana, but recently signed accords promise an alleviationof tensions.

2. The Government is reshaping the form and content of economicpolicy because of its concern with the high and seemingly intractablelevel of unemployment (12-14 percent of the labor force), particularlyamong urtban residents. It is also motivated by the desire for greaterequity and wider participation in economic activity among Guyanese. OnFebruary 23, 1970, Guyana proclaimed itself a Cooperative Republic toemphasize its political and economic independence in achieving its economicand social goals and to stress the importance attached to the cooperat:iveform of e!conomic organization as an instrument of development. In partic-ular, the Government plans to use the cooperative as a spearhead tor theaccelerated development of certain regions in the interior, another objec-tive ofi policy that has come strongly to the forefront in recent years.

3. Guyana's known resources are modest; the hinterland is stillbeing explored. About 90 percent of the population is concentrated in thenarrow ccoastal plain comprising less than 5 percent of the area of thecountry. Most of the coastal area is below sea level. Economic activrityis similarly concentrated on three basic commodities -- bauxite andrelated products, sugar and rice. They account for roughly a third o0( GDPand about: 90 percent of the value of commodity exports. On this narrowproductive base and despite poor rice crops, real output in Guyana hasgrown at an estimated rate of 4.7 percent per annum since 1965 or about2 percent in per capita terms. By 1969 gross national product per capitawas about: G$550 or US$275.

4. A substantial share -- about 21 percent of the annual flow ofresources since 1965 -- has gone for fixed capital formation. This reflects,in turn, a sizeable expansion in plant capacity in mining and a growingannual volume of public capital formation undertaken within a set ofguidelines provided by the Guyana Development Programme 1966-1972. Publicinvestment has focused on roads, sea and river defenses, agriculture andeducation. Except for 1969, annual expenditures roughly conformed withthe Development Programme. The sectoral distribution, however, did notaccord with the Plan in all respects. Especially noteworthy was a largerthan anti.cipated expenditure on numerous small "miscellaneous" projecl:s.Capital l-ormation in the agricultural sector in the 1960's was about 1L5percent of the total, but with the exception of sugarcane, the response interms of increased production has been poor compared with other sectorsof the economy. In large measure the low rate of return can be traced tothe rice industry where existing resources and opportunities have been

- ii -

inefficiently used. Investment in transportation, essentially road build-ing, has aiqo been large. However. the new canacitv created hag not hbenfully utilized because government transport services have been given in-adpeutArp furnds fnr apnital PeqTipment and hnve experienned organizaionnaland managerial difficulties. At the same time, the Government's regulatorypolicy, particlrly.q1- in repcznrt of connimrrinl t-rucikincg, has- discoragedqC&,

private entrepreneurs from expanding their operations.

5. A generally rising level of public savings financed about one-third of ptbhlir rcaitl - -xpnnditiire reflecting a strong fisca1 offcort- with

an average ratio of taxes to GNP of 19 percent. Another fifth came fromnet borrowing largely from the banking system.. Guyana also absorbed agrowing volume of external financing, with loans on concessionary termsbecoming more important thasn grants. Indeed, nn a pnr capni4f bass4 r- i..n,n

is one of the highest recipients in the world of "soft aid". Externalresources covered roughly half of total financi-al requi ------ t- for -ublicinvestment, but even so the official capital inflow was still less thanwhat aid don.ors were apparently Aea-y to pAovde. Given t act that aid

was largely tied to procurement in the donor countries and tied also tothe f4nancing of specific projects, Cuyan-'s failu-r to d-ra fully nn

-I'. A -LaI.I - .k -yL.LL'. -jJA.iJ , UaU- - _t.A .L_. '0

available external resources was largely due to deficiencies in its capacity'lo prepare and _ im1plement project's suitable for foreign fina-nci-ng.LU pA ofa C Cht _LIj _. CI L I. _A _J _'.. _O _ _I t.C . C v. _ vk £ _ _ A v. C.L~L A .A.IIah . L _1IaAV. Des>pite a greatly ±LALIkJLUVtU LLCU" LJCL.LCaLs uCLWrcCL v.LvJ aL- A.V.J

there was a surplus in the balance of payments in only one of the fouryears and netL. lUosses of fCoreiIgn e.hcil Lange reserve amounted LLiht. LU U$. r.± Il ion.

These losses stemmed in part from the excessive demand for foreign exchangeinduced by a too rapid expansion of private credit and, in particular,by substantial public borrowing from the banking system to finance publicinvestments. The producti-ve capacity of the Guyanese ecULUny is s-uchthat any sizeable borrowing from the banking system is immediately reflectedin an increased volume of imports and an enhanced burden of adjustment forthe balance of payments.

7. Looking ahead to the mid-1970's, the factors of limited provenresources and a small internal market (to be enlarged by CARIFTA, which how-ever, is not expected to be fully effective until after 1975) give the Govern-ment few options with respect to its development strategy. Guyana-s economyis likely to remain tied to the fortunes of the three traditional products forthis period, although there are promising prospects in shrimping and forestproducts. In the expectation that growth in bauxite mining, aluminaprocessing, particularly calcined bauxite production, and exports will besustained; that rice production will respond to a reorientation of govern-ment policy to recover former levels and possibly show a gain in productivity;and that sugar production and exports will continue to advance but at apace less rapid than in recent past years - it should be possible to raisethe real rate of output growth to over 5 percent per year. Combined with alower anticipated annual rate of population growth of 2.5 percent, real percapita output should advance at the reasonably satisfactory rate of almost3 percent. However, the prospects for rapid employment-creation in thenear future are not greatly encouraging. The idea that Guyana might

- iii -

encourage sellecti4ve i, .ig-titon of exarened mi..ers fro.. the m'ore der.sely

populated Caribbean islands should, therefore, be carefully considered inI. CJuiaLUI Lu LLL .CJ UOjJC Lvy=W: vLU CIlpIyLLICILL .LLL .AA>u4 LUL >.

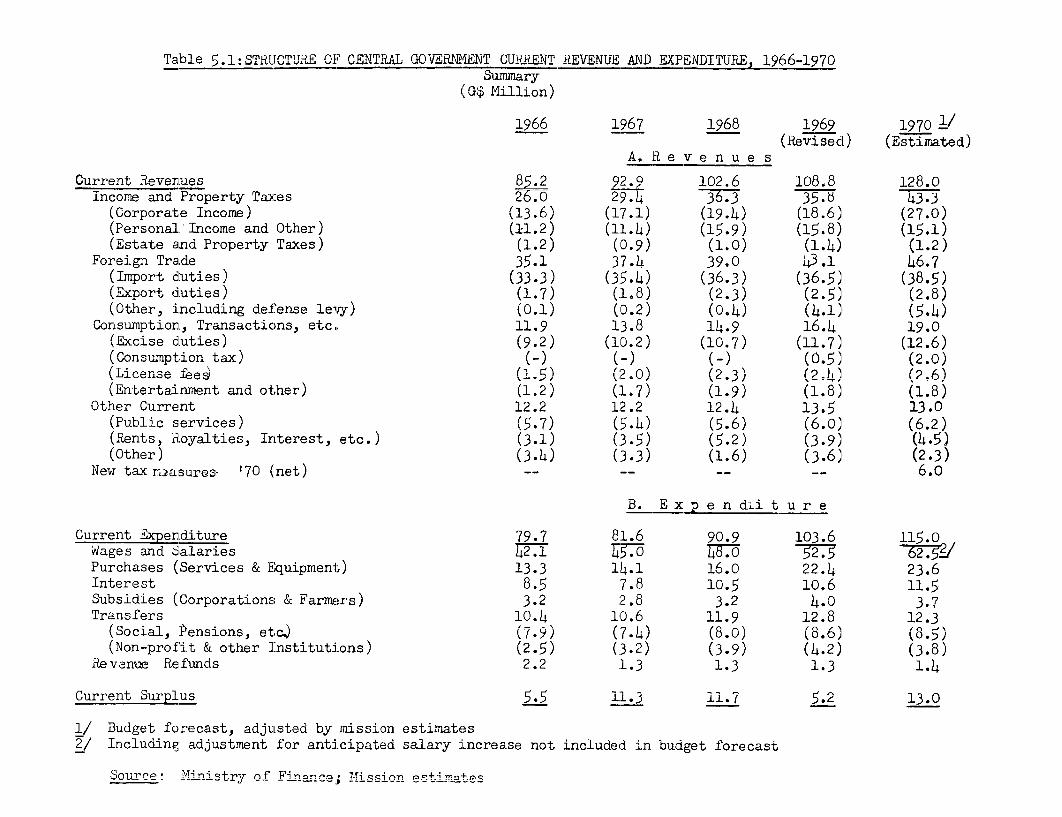

U. The Governu.ent Lis now prepariLng a co,.prehensive uevelopmuent planfor the 1970's, which is to include an enhanced economic role for coopera-tives as well as a WuclI expandedU diU'rect goverr[enit partiLcLpat'lon 'inproductive activities. The mission has outlined a public investment programto 1975 wnich, it is hoped, will assist the Government in formuiating itsown longer-range plan; however, it does not take account of the far reachingchanges in economic organization whicn tne Government seeks to incroduce.The public investment program proposed in this report is viewed as a keyelement in the future of the economy and calls for a doubling in tne annuairate of expenditure by 1975. The higher rate of public capital formationwill thus take up the anticipated slack in private investment faced withlimited opportunitiespand an uncertain investment climate. The broad stra-tegy is to expand ituimodernize the basic infrastructure in those sectorswith the greatest productive or cost-saving potential (agriculture, fishing,power, communications and air transport) and at the same time to augmentsignificantly the stock of capital in education, health, sanitationand housing. Although financial resource and administrative capacityconstraints inevitably limit what can be done in pursuit of these objectives,they do not seem so severe as to preclude such an ambitious program. Indeed,one of the assumptions underlying the mission's approach in formulating theproposed program for 19/U-1975 rests on the expectation that, over the nextfew years, there will be a sharp upward shift in the level of public savingsgiving Guyana access to a greater volume of domestic financial resourcesfrom this source than it has ever marshalled in the past. The CentralGovernment's current surplus should rise sharply as a result of new taxmeasures introduced in the 1970 Budget and the termination of tax conces-sions granted in the mid 1960's. At the same time, the newly establishedNational Insurance Scheme should contribute substantially to a much higherlevel of public savings, averaging 5.3 percent of CDP a year. At thislevel, it should be unnecessary to borrow from the banking system, thusavoiding potentially deleterious consequences for the balance of payments.The issue of additional fiscal measures is not likely to arise before 1973.

9. The projections have assumed that central government expenditureswill grow at the annual rate of about 7 percent in real terms. The under-lying expectation is that the Government will exercise restraint andintroduce economies in spending. It should be borne in mind, however,that at the margin, where capital projects promise less than a reasonablerate of return, a more efficient use of resources would be to substitutenon-capital development expenditures so as to enhance the efficientutilization of capital already in place. This might include, for example,expanded extension services in agriculture, improvement in the "quality"of teaching in schools and the "quality" of services in hospitals andclinics. The consequence of such a substitution would be reflected in areduced level of public savings. A possible side benefit of such expen-ditures would arise to the extent that professionally trained Guyaneseare dissuaded from emigrating abroad by the provision of more attractivework opportunities at home.

- iv -

10. A second assumDtion is the continued willin2ness of the Govern-ment, already in receipt of a high level of per capita aid, to draw uponthe sizeable volume of external financial resources (of the order ofG$50-60 million annually) that bilateral aid donors and internationalagencieA are annarentlv ready to provide. Thus, aLmost 60 npercent ofgross capital requirements are expected to be financed from abroad,essentiallv from the United States; the United KinainTcom CGanaid and the

IBRD/IDA. On this basis, the financing plan shows a surplus in everyyear excepting 1974 and 1975 when modest cieficits appear. Covering these

deficits will require additional fiscal measures if the high levels ofpubhl ic investment ar to he maint2inedL

11. Theprop d propo program of public capital expenditure should raisethe share of public capital formation in GDP to an annual average of12 percent for the next six years as m--posed to about 7 percent for the

latter half of the 1960's. Compared with the earlier 1966-1972 Plan,,.b44~~~4- 4., ~~~~ ~ ~ 4 aA far 1O~7 7O1Q1 l" - -- --- -.* 1- e m4_to; :|4r shA' i_ s e torAl - emp 4i popo ise fo 1 90 vn_1 GX1-{n _6-_

culture, including livestock development, forestry and fishing and seaAeflpenses, wh1-ile the percentage allocations to transportation anA omluiUCI CIL~~~Ct~~ , WLL~L.C ILiL CL at.jaLIJL L~..JL .taLIL LU LAILIU

cation, power and development finance have been reduced. Within the trans-portation sector, the come 1-ti4 of -a m

4ar r-ad bulldingprorarm -is in

sight and the mission has recommended that increased emphasis be given toat airnd water transport, m.odes which seem. to bDe particularly -ie t A

Guyana's needs. In comparison with the actual distribution of publicinve beti ween 4. 'd a--A 1.,2 the- p------- pA or.,. a------ -11 - - lL

relative shares to agriculture and the social services such as health andaitatiLoL hoL u[ UCbL UdevCelopJr,,CLLL L anIU rUral. water uLpAly. The

miscellaneous category of expenditure has been sharply reduced.

12. On the basis of information presently available, the publicL[LV1t4bL&i1t4LLL PLU5LWL dl UUL-JA-ICU U LLIUILL.Lbb~LULL Llab dabi6LCULL=L CL .LLW CLUIULU1II.LU

priority to hinterland development. The vision of extensive agriculturalsettlements anu massive natural resource exploitation is, wLth few excep-tions, not supported by hard analysis of economic feasibility. Indeed,interior agricultural developinent on a large scale wouldu ave to contendwith such powerful negative economic factors as relatively poor soils,high land preparation costs, additional requirements for economic andsocial infrastructure and high cost transportation. Continued explorationand experimentation would seem for now to be the appropriate focus ofpolicy. Any project which comes forward should of course be judged onits merits, but it is the mission's impression that there are better pros-pects for agricultural investment in other areas of Guyana closer to thecoast where there is no shortage of good land near commercial markets; whatare needed are capital and skills to develop it more productively. Inrecognition of the strong non-economic motives for interior development,however, the mission has included modest public capital outlays in theproposed investment program for on-going pilot agricultural settlementprojects such as that at Mathews Ridge, continued resource explorationsand some further work on the road to link Georgetown with the Brazilianborder.

13. The outlook for manufacturing or industrial development is notencouragingR; Guyana's comparative advantage lies rather in natural resourcedevelopment. Theres is the possibility of some major resource-based invest-ments (e.g. in forestry), although such developments cannot be expected tomake more than a minor direct contribution towards resolving the problemof unemployment. In this respect, there is the longer-term prospect thatsome lines of primary production will support resource transformationactivities which are more labor-intensive.

14. The deveLopment targets proposed for the period 1970-1975 arechallenging ones indeed. Their achievement depends on stimulating an in-creased generation of income in agriculture, fishing and forestry, possiblywithin the context of the expandecl market offered by CARIFTA. In thisrespect the private sector could be expected to play a crucial role. Italso depends on the Government's development effort within the public sectorwhich the experience of the last five years would judge to have been com-mendable. Economic "management" fIor the next few years must include thevigorous pursuit of certain measures among which the following are mostimportant:

a) the strengthening of the project preparation, coordinationand execution functions of the public sector;

b) the improvement of tax administration and collection;

c) the exploitation of agricultural resources includingfishing and forestry and in particular: leaving the sugarproducing sector undisturbed since it enjoys a comparativeadvantage in world markets; reorienting policy in riceproduction to favor increasing investment only where therate of return promises to be high and stimulating the moreefficient utilization of existing resources through a betterrice growing technology, an improved water control systemand the rational pricing of water, liberalizing and ration-alizing the land market, the provision of credit, a revisedprice structure to encourage the production and timelydelivery of higher quality grades and facilitating thedevelopment of efficient marketing services.

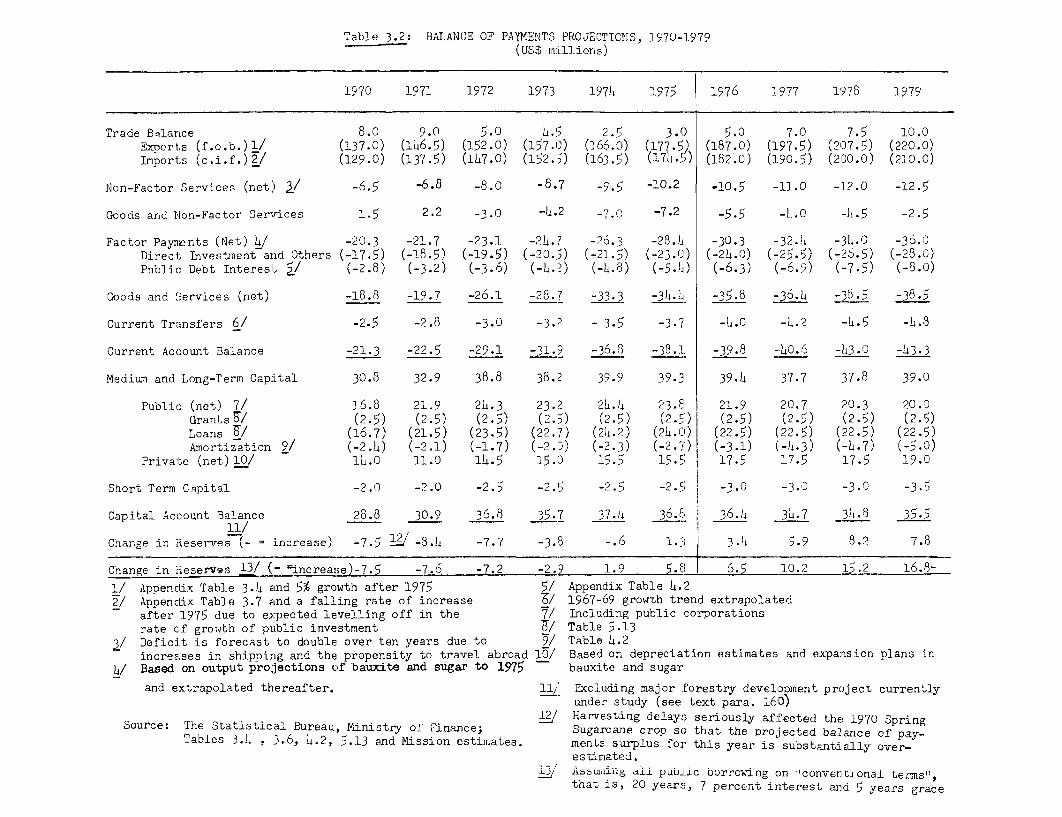

15. The balance of payments projections, including an expectedsustained growth in traditional exnorts and a much larger growth in imrortsinduced by the enlarged volume of public investment, should produce a sur-plus in all but the last year of the period. This outcome hinges onsuccessfully carrying out the public investment program as proposed and.in drawing nn Available foreign financino. But the he2v incre2sed hnr'row-ing over the coming six years, assuming a continuation of the presentmix of foreign assistanre, will hp reflerted in agrowing debpht- corl7it ratio

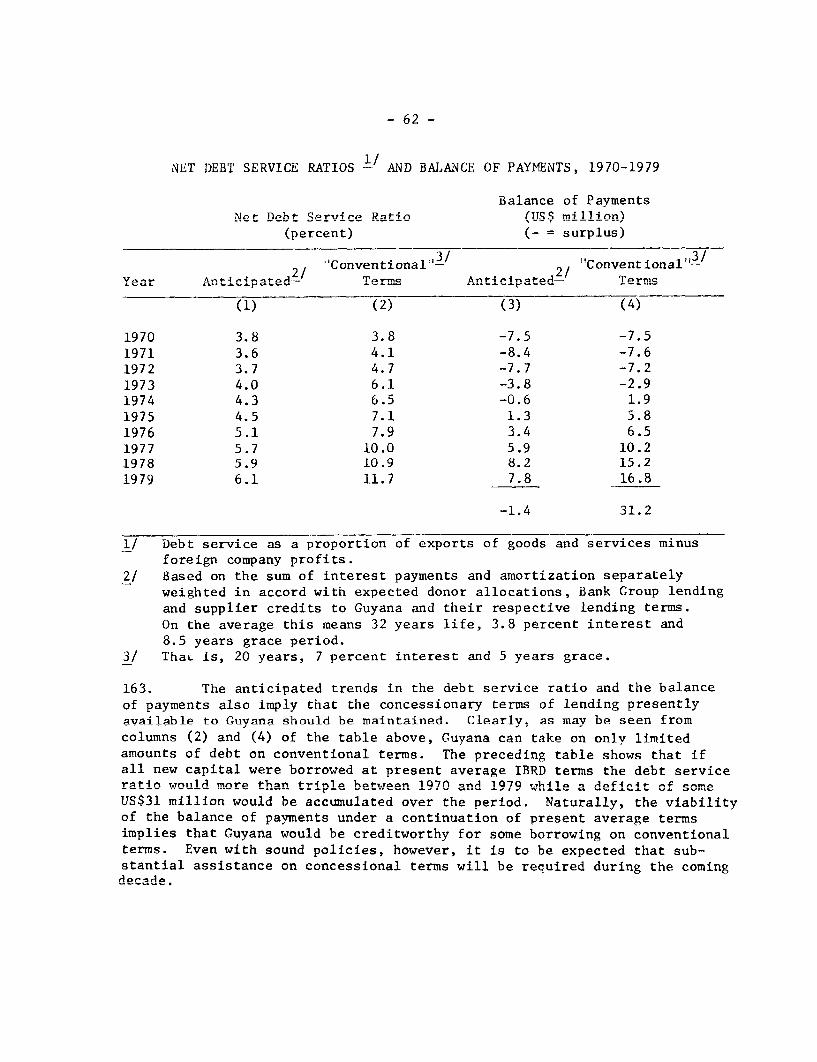

rising from 3.8 percent in 1970 to 4.5 percent in 1975 and 6.1 percent in1979. If external borrowina were aed to hb bad on "coAnventional

terms" (i.e. 20 year life, 7 percent interest and a 5 year grace periocd) thedeb t s e rvi c e ram-tio-n wuld - 1 - ti -ple~ bt- .7 en 19?70 ta nd 19)79 Q veni it-I sondll

policies, substantial assistance on concessional terms will be requirecl duringthe cof..ing decade to help Guy-aa achleve its --s.o.J. and social goals

I. SOME BACKGROUND FEATURES

i. ,Guyana is a tropical country situated on the northeasterncoast of South America. With an area of 83,000 square miles, it is byfar the largest of the Commonwealth Caribbean group of countries. Firstsettled by the Dutch in the 17th century, the territory was ceded to GreatBritain at the turn of the l9th century and ultimately achieved independencein 1966. Thus, inclependent economic management and decision making inGuyana is a feature of quite recent origin.

2. An important legacy of the Dutch was the system of protectionand water control introduced along the low-lying coastal lands. Oncedrained and irrigated, the coastal plain with its clay soils was ideallysuited for growing sugarcane. The exploitation of this resource by meansof a plantation system employing African slave and, later, East Indianindentured labor, became the dominant influence in shaping Guyana's econ-omic and social development. In more recent years the exploitation ofrich bauxite resources and the growing of rice have been added to sugarcaneas the major sources of output. On the average, over the last few yearsthe three products together accounted for almost a third of Gross DomesticProduct and as much as 88 percent of the total value of exports.

3. Of the almost three-quarters of a million inhabitants, halftrace their origin to East Indian indentured laborers, while another 40percent are descendants of African slaves. Relating the population toland area yields an overall population density of only 9 persons persquare mile. This obscures the fact, however, that the cultivable arearepresents only about 3 percent of the country's land mass with the resultthat more than 90 percent of the population is found within a narrow ribbonof settlements along a hundred mile stretch of coastline and extending upto a depth of 20 miles inland. Here the population density is of the orderof 360 persons per square mile and more akin to the ratio found in theother major Commonwealth Caribbean countries. The spatial distributionof population in Guyana has important implications for the size andcomposition of its infrastructure.

4. Rich alluvial soils are found along Guyana's coastal strip, butthe hinterLand's natural resource endowment has yet to be fully evaluated.From what is known so far, it appears on the whole to be poor. T'hereare small P3ockets of good soils in the interior, but they are inaccessiibleand costly to clear. Large areas of the hinterland are covered by tropicalforests and these have been exploited on a small scale to produce lumberand related products. The heterogeneity of species and the small size oftrees, however, have so far inhibited the large-scale development of thisresource. Geologically, Guyana forms part of the pre-cambrian shield whichin other parts of the hemisphere has yielded large quantities of minerals.This fact has attracted intensive mineral exploration, but new depositsof commerc:Lal value have yet to be found.

5. Guyana's Dolitical and social history over the nast decade hasbeen a stormy one, particularly in the years before independence. Theunderlving cause of social tension has been the antagonism between thetwo major ethnic groups - Guyanese of African descent on the one hand and

-2-

those of East Indian -orign onl -he otmr. A somewhat --reter measure ofstability has been achieved in the last few years since the People'sNlational Congress Party has grown to do.inate the L1.f.4- -ta - - -cen a to

form the Government either through coalitions or on its own. The woundsopened b-.y overt, - hnost4144-ies in the early 1960's have been gra lly b,-.-,14

There remains, nevertheless, an undercurrent of antagonism between theracial groups wLL.i.ch ILL continues . to affect locall investrvent aversely. T1his

influence on the investment climate, however, is probably outweighed atpresent bly thI'e enhanced dAegree ofll politi*4call stabl-tfwic Gyaa a

k-'1.

COCLA I.. LILC CIkL1~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1[t.CU UC5J. CC Lii pLIL.L L .Lt.at 0 5..aLitt4. Ly WLL.L 54L1 ania LLa~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~.LJ.6L ~~ ,WI L4 c G ya a '

achieved in recent years.

6. Another factor affecting the course of Guyana's economic develop-tenLt hIas beten tLLhe dispute over bLoundarite wit WI_ - and V CLenez a. Of

the two, the dispute with Venezuela has been the more troublesome. Asidefrom Ithe LICreLaSed diplomatic activity engendUered by the boundary issue,Guyana's reaction has been to channel a larger volume of resources to itsarmed forces and to push for a fastler pace of inLteriOr Settle emelnt thancould be justified on economic grounds alone. 1/ The very recent attenua-tion of the dispute is likely to have a salutory economic impact on tneinvestment climate and in preventing the diversion of scarce resourcesaway from pressing aevelopment needs.

7. Guyana became a Cooperative Republic on February 23, i970. Thedeclaration of a republic is intended to emphasize the country's statusof political independence and the concomitant need for it to work out itsown destiny without reliance on external assistance. The choice of theepithet "CooDerative" reflects the Government's disenchantment with privateenterpreneurship as the instrument of social and economic development, andits opting for cooperation as a supplementary, if not a substitute torce.This new policy thrust is motivated in part by an estimated 12-14 percentunemployment rate concentrated in urban areas, in part by the philosophydescribed by the Guyanese in such terms as "self-help" and "small man"participation in the economic life of the country and in part by the desireto develop the interior of Guyana. Indeed, cooperatives are expected toform a major third sector in the economy in addition to public and privateactivity.

8. Development efforts in Guyana thus must overcome the currentchallenges of a limited range of natural resources, a potential threat ofinundation by the sea, internal social tensions and the restoration ofrelations with some of its neighbors. Yet one cannot escape the impressionof a strong determination among Guyanese in all walks of life to meet thesechallenges and so secure a faster rate of social and economic progress.

1/ Recently an agreement with Surinam for Renewed "economic cooperation"has been signed. An agreement with Venezuela, calling for a twelveyear "moratorium" on claims to the disputed area, was signed on June 18,1970. The protocol incorporating the agreement with Venezuela is sub-iect to parliamentary ratification in both countries.

II. RECENT ECONOMIC DEVELOPMENTS

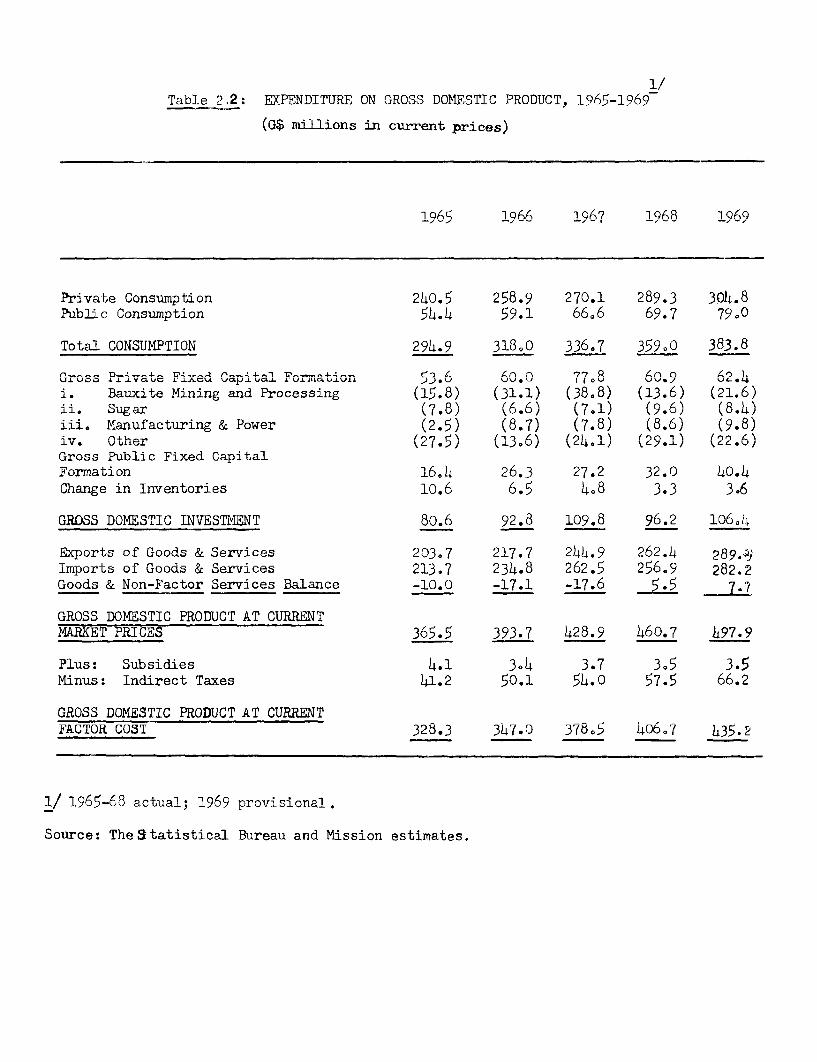

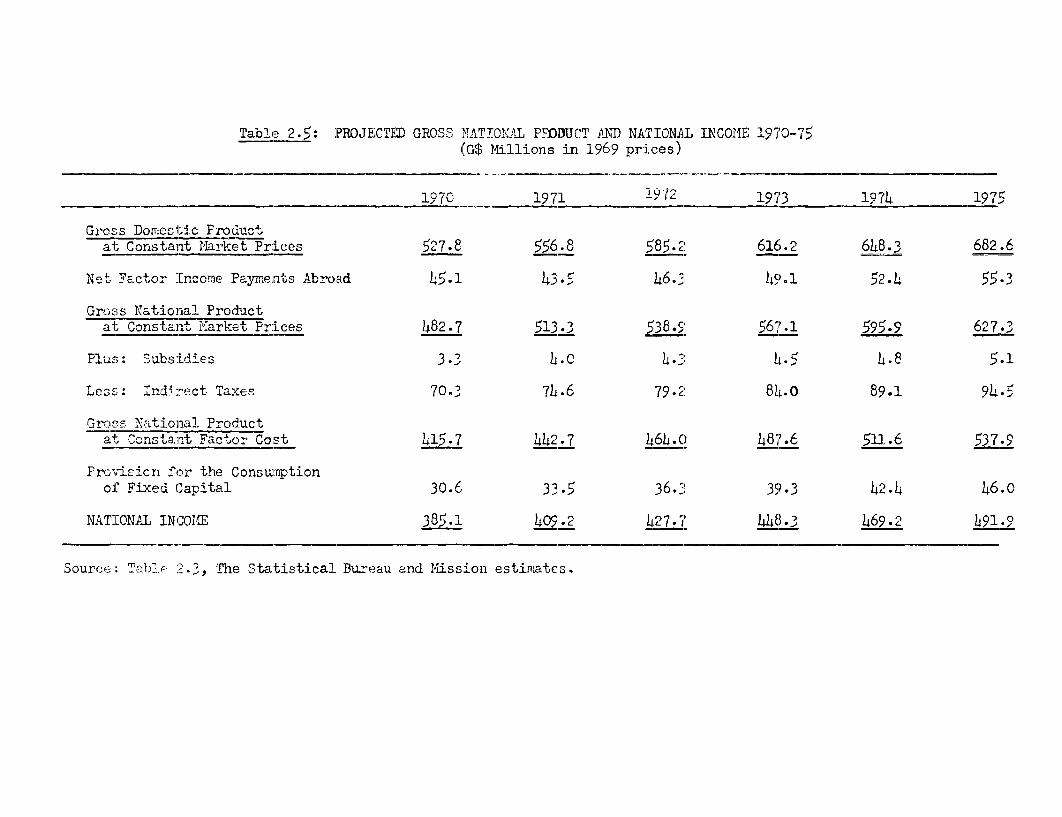

A. Output and Expenditure

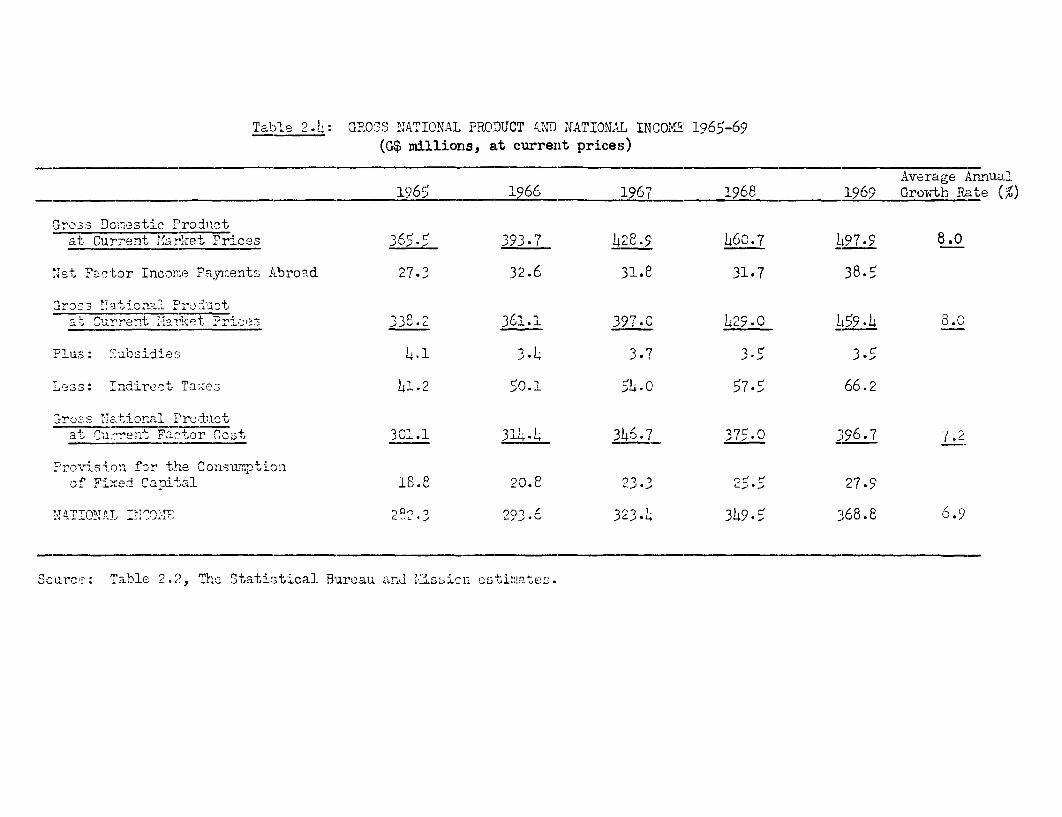

9. An approximate estimate puts annual average GDP growth in realterms since 1965 at 4.5 - 5 percent, which is reasonably satisfactory whencompared with the longer-term trend rate of growth of somewhat less than4.5 percent since the mid-fifties. 1/ Further, allowing for the net annualincrease in population of 2.7 percent, real per capita output advanced atan annual average rate of about 2 percent over the past four years. Bythe end of 1969, per capita GNP (at factor cost) amounted to G$546 orUS$273 million; the equivalent values in terms of national income percapita were G$507 or US$254.

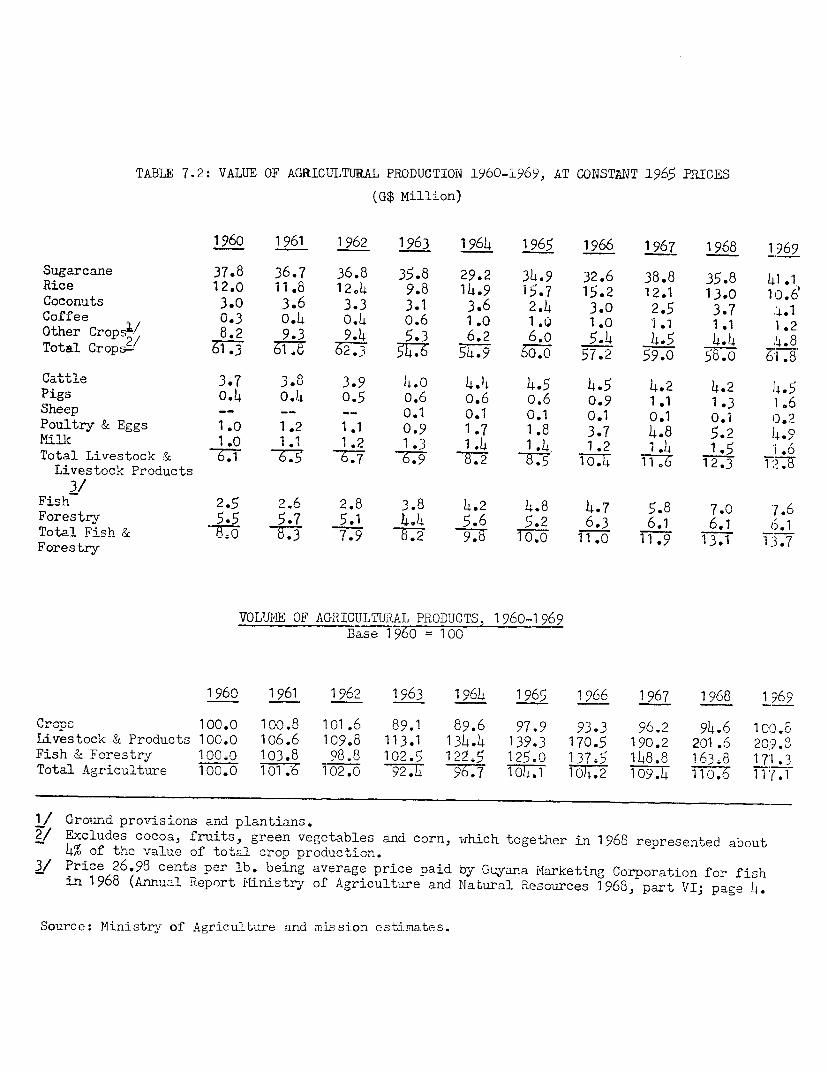

10. The improvement in the overall growth in output, however, hasbeen narrowly based on mining, engineering and construction. These sectors,which accounted for about one-fifth of value-added in 1965, grew much morerapidly than output as a whole. Of the G$106 million absolute increasein GDP (at current factor cost) between 1965 and 1969, G$52 million, oralmost half, was contributed by mining and construction. Most disappointingwas the performance in agriculture, forestry and fishing which in 1965represented a quarter of total GDP. Since that year, value-addedc grew byonly 12 percent and the sector contributed less than 10 percent of the netincrease in GDP recorded over the five year period. Wlat is more, noneof the major products of this primary producing sector displayed a rate ofgrowth which could be described as "dynamic". As for Guyana's two stapleagricultural crops, sugarcane production advanced modestly while the valueof rice output actually declined.

1/ The estimate of real output growth for 1965-1969 is derived from arough measure of price changes in aggregate GDP. Since officialprice deflators for the national accounts are not available forthis period, the subsequent discussion is in terms of data incurrent prices.

- 4 -

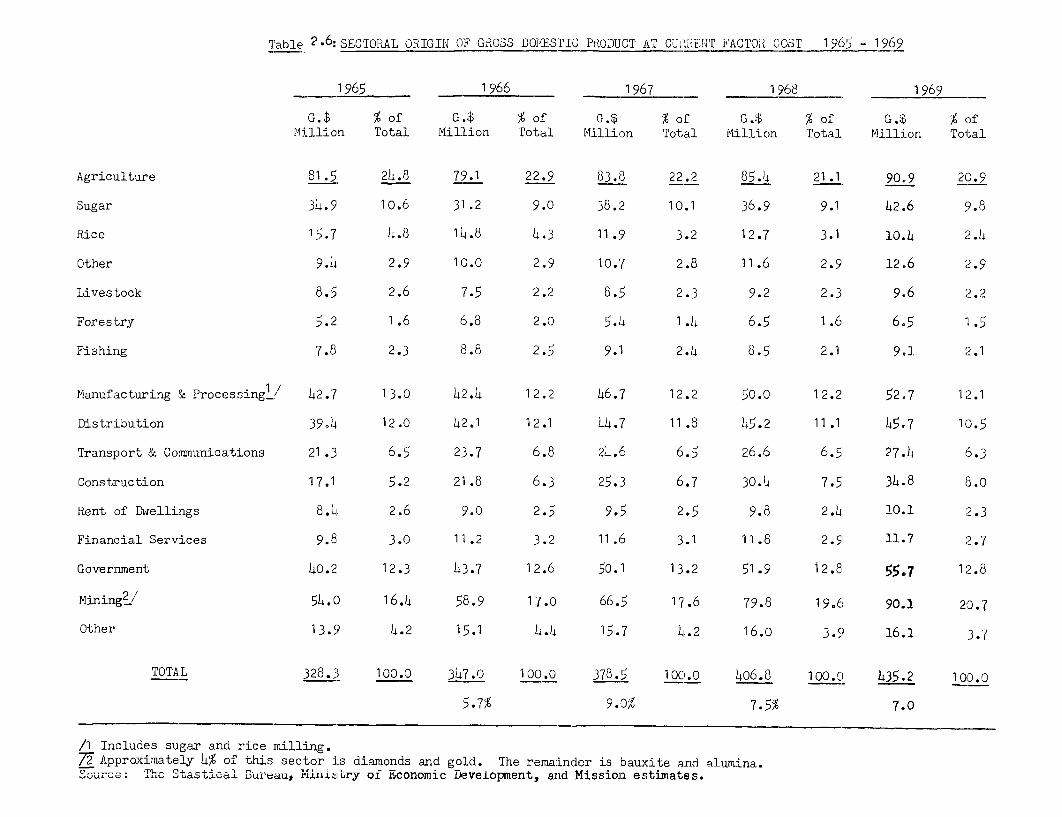

SECTORAL ORIGIN OF OUTPUT, 1966-1969

Growth of Distribution ofShare of GDP Output GDP Increase

in 1965 1966-1969 1966-1969(percent) (percent) (G$mill.) (Percent)

Agriculture, Forestry and Fishing 24.8 12.0 9.9 9.2o/w sugarcane (10.6) (22.3) (7.8) (7.3)

Mining 16.4 64.6 35.1 32.8Engineering and Construction 5.2 100.6 17.3 16.2Manufacturing (including sugar

and rice milling) 13.0 23.9 10.3 9.6Distribution 12.0 16.7 6.6 6.2Transport and Communication 6.5 28.6 6.1 5.7Government 12.3 38.3 15.5 14.5Other 9.8 19.0 6.1 5.7

GDP (Current factor cost) 100.0 32.5 106.9 100.0

Source: Table 2.6

11. The high dispersion in growth rates among the sectors reflectsthe unintegrated structure of the Guyanese economy. Mining continues tobe linked, both in terms of output sales and non-wage inputs, mainly toexternal markets, although recently an effort has been made to raise thevolume of local expenditures. It emerges that mining has been the onlydynamic commodity producing sector, but with limited direct demand creatingeffects on other sectors. One of the conseauences of the expansion inconstruction and government has been their favorable impact on employmentcreation.

12. From the standnoint of outntut utilization the most dynamic elementscontributing to growth over this period were exports and public sector ex-nenditure for hoth consu-mption and invePtmPnt= The s,istainpeid dvanncP in

exports, essentially bauxite and related products and sugar, coupled witha restrained growth in iTmnorts- rPesui1te-d in a tiirn-arnind in the evti-ernalbalance of goods and non-factor services of about G$18 million or 13 percentof the net increase in gross domestic xnpenditu,re (prnoduct) bhetween 1965

and 1969.

- 5 -

UTILIZATION OF OUTPUT, 1966-1969

Share of GDP Growth of Expend. Distribution of GDPin 1965 1966-1969 Tnrren-c 1966-19469

(Percent) (Percent) (G$million)(Percent)

Consumptioll 80.7 30.1 88.9 67.1Private (65.8) (26-7) (64.3) (4.B.6)Public (14.9) (45.2) (24.6) (18.6)

Gross Domestic Investment 22.1 32.0 25.8 19.5Private (17.6) ( 2.8) ( 1.8) ( 1.4)Pu b ic A. 4.) (146A.3)AN t (24. (J 1 .1)

Export (goods and non-factor s;rvices) (5.7) * (Q42 ( ) (65.1)

Imports (goods and non-factor sirvices\ (58o.5 (3.0 (=6.5)o (-51.-7\LA.L.L L ~ LVA..U %1.JJ.'/ V.S.~ / \ UV a# .A.f

Balance -2.8 17.7 13.4

GDP (Current market prices) 100.0 36.2 132.4 100.0-? L 1.1 Aractor pa-yirLents aubroad 7.4- '+.L.0

GNP 92.6 35.8

Source: Table 2.2

13. The rapid growth of public sector expenditures reflects theGovernment's policy to increase it:s participation in the economic life Dfthe country. Combined public outlays, which in 1965 represented less than20 percent of GDr, accounted for almost G$50 million or 37 percent of tLhe nerincrease in total expenditures over the past five year period. Public invest-ment was by far the most dynamic element of all.

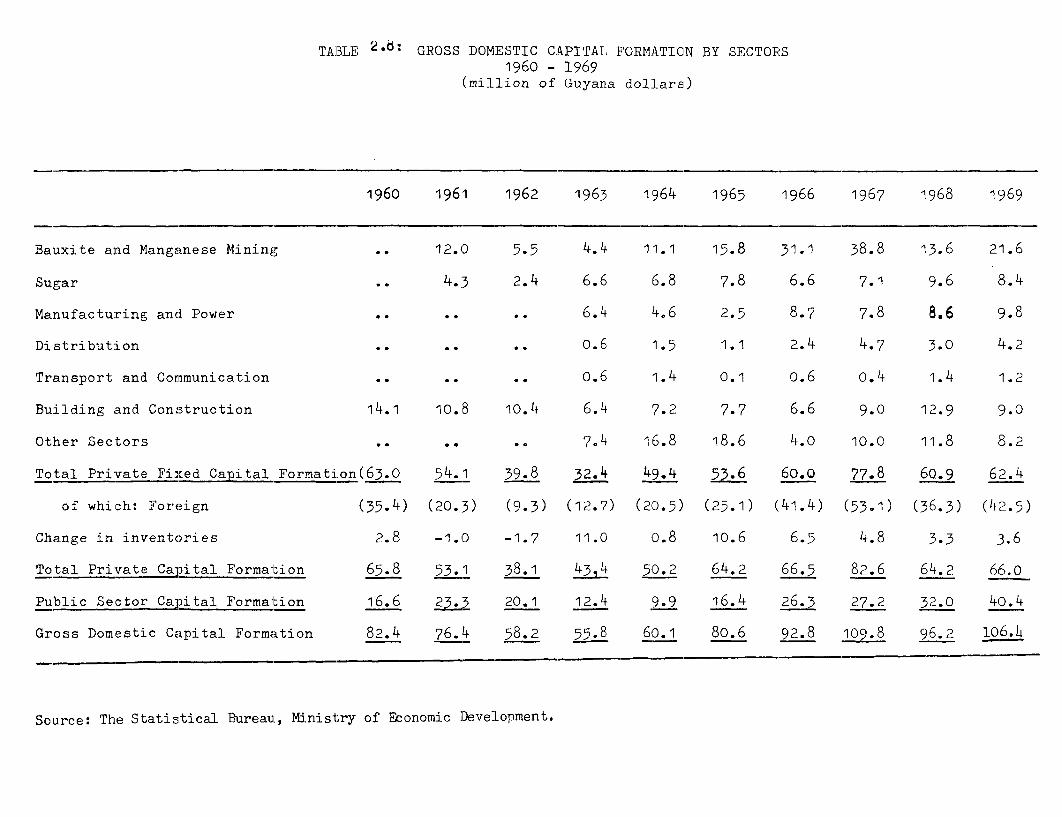

14. An important feature of resource utilization Guyana is the highproportion of the annual flow of goods and services devoted to capitalformation. Between 1965 and 1969 this proportion averaged about 23 per-cent and has been a major factor sustaining the strong growth rate of GDPover the recent period. The experience over tne past five years suggeststhat it took an increase of about 4.5 units of capital to increase outputby one unit. This relationship is not significantly different from anearlier esitimate made for the period 1955-1965.

15. Che annual variations in the volume of private fixed investment,particularly those originating in the mining sector, have imparted adestabilizing influence which has not been offset. As the following tableshows, gross domestic investment reached a peak in 1967, reflecting the"lumpy" capital expansion program in bauxite mining and processing, and thenfell off sharply. The substantial decline in mining investment between1967 and 1968 was an important contributing factor to the sluggish overallrate of growth recorded in 1968.

- 6 -

16. Public sector capital formation grew rapidly and fairly steadilythroughout the period. Within the limited scope that its volume permitted,public capital formation contributed to stable growth. Since by 1969public sector investment accounted for 38 percent of total gross domesticinvestment and about 7 percent of GDP, its leverage as part of any futureattempt to maintain a steady investment and output growth path for theeconomy as a whole is very much enhanced.

MAJOR COMPONENTS OF GROSS DOMESTIC INVESTMENT, 1965-1969

(Percentage of GDP in current market prices)1965 1966 1967 1968 1969

Gross Domestic Investment 22.1 23.6 25.6 20.8 21.4Gross Public Investment 4.5 6.7 6.3 6.9 8.1Gross Private Investment 17.6 16.9 19.3 13.9 13.3Gross Private Fixed Investment 14.7 15.2 18.1 13.2 12.5

;4ining (4.3) (7.9) (9.0) (3.0) (4.3)Gross Private Fixed Investment

of locally-owned Enterprises (7.8) (4.7) (5.7) (5.3) (4.0)

Source: Table 2.2 and Ministry of Economic Development.

17. It will be noted that, apart from mining, the share of privatefixed investment has tended to decline between 1965 and 1969, as has theshare undertaken by Guyanese enterprises and individuals as opposed toexpatriate interests. Whether this is due to the dearth of alternativeopportunities or the uncertain political climate for investment, or somecombination of both, is difficult to judge. The quantitative evidence,however, is in accord with the view that domestic investors are highlysensitive to real or perceived risk.

B. Developments in Major Sectors

18. Mining comprises bauxite extraction, the processing or caicinedbauxite and alumina manufacturing, and to a much smaller extent, the ex-traction of gold and diamonds. Manganese used to be mined, but operationsceased in 1968. The dominance of the sector in the Guyanese economy canbe gauged from the fact that in 1969 it accounted for one-fifth of GDP,one-fifth of gross domestic investment and two-fifths of commodity exports.As noted earlier, moreover, the mining sector has been the most importantsource of output growth for the economy as a whole. It employs, however,only 6 percent of the occupied population. A substantial investment programof G$30 million, launched in 1965, has expanded the capacity of the industrynot only to extract a larger volume of bauxite, but also to process highervalued products such as calcined bauxite and alumina. This compositionalshift in output has been reflected in a higher increase in sales value,export earnings and public sector revenues than would have resulted fromthe growth of bauxite production alone. Public revenues will henceforthalso benefit significantly from the expiration of certain tax advantagesgranted the industry some years ago to induce expansion.

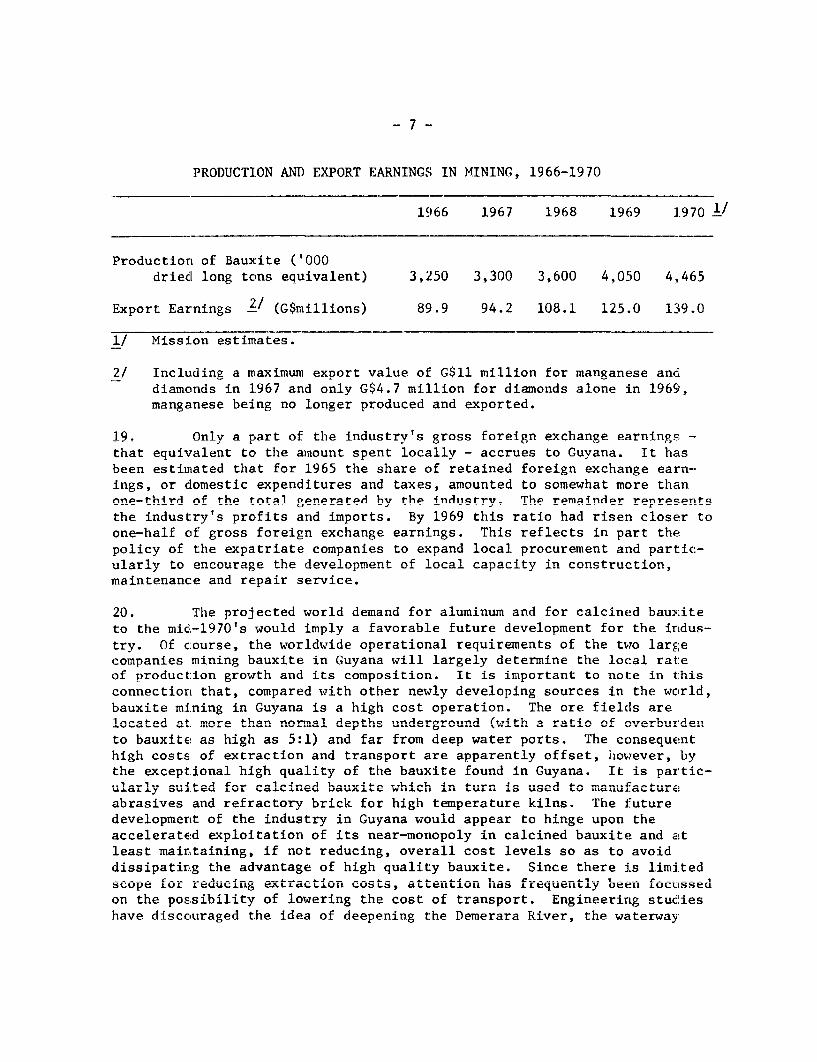

PRODUCTION AND EXPORT EARNINGS IN MINING, 1966-1970

1966 1967 1968 1969 J.970 1/

Production of Bauxite ('000driedl long tons equivalent) 3,250 3,300 3,600 4,050 4,465

Export Earnings 21 (G$millions) 89.9 94.2 108.1 125.0 139.0

1/ Mission estimates.

2/ Including a maximum export value of G$11 million for manganese anddiamonds in 1967 and only G$4.7 million for diamonds alone in 1969,man2anese being no longer produced and exported.

19. Only a nart of the industrv's gross foreign exchange earning5; -

that equivalent to the amount spent locally - accrues to Guyana. It hasbeen estimated that for 1965 the share of retained foreign exchange earn-

ings, or domestic expenditures and taxes, amounted to somewhat more thanone-third of the t:otal generated by the indt,strv. The remainder represents

the industry's profits and imports. By 1969 this ratio had risen closer toone-h:alf ,if grossc: foreign exrchancrg earnincgs This reflects in npart thE!

policy of the expatriate companies to expand local procurement and part:ic-ularly to encourage the development of lnocl rcapaity in cnnQtruc1tion,maintenanc:e and repair service.

20. The projected world demand for aluminum and for calcined bauxiteto the midA-197n's wo,.1r in.? a favorabl fuit-ure deverloment. fo-r t-he 4rAt uc-

try. Of course, the worldwide operational requirements of the two largec44, pan-4- mininf 4., in h1uya- -1l 1 rgely Aotorn.oin h the loc31 r-te

of production growth and its composition. It is important to note in thisconnection that, compared W.t-ith nf-otr new.,lxt Adevrolorpng sources in theo vcarAld

bauxite mining in Guyana is a high cost operation. The ore fields arelocated at. more than nortaal depths underground (with a ratio of overburdeno

to bauxite as high as 5:1) and far from deep water ports. The consequenthigh, cost-s, of extraction and transport are apparently offset, 'ho-wever, bythe exceptional high quality of the bauxite found in Guyana. It is partic-ularly suited 4or calcined bauxite which in turn is useA to manufactureabrasives and refractory brick for high temperature kilns. The futuredevelopment of the industry in Guana would appear to hinge upon theaccelerated exploitation of its near-monopoly in calcined bauxite and a!t

dissipating the advantage of high quality bauxite. Since there is limitedscope for reducing exLtractdLon costS, attention h'Ias f'requently been focussedon the possibility of lowering the cost of transport. Engineering studieshave uiscciuraged the idea of deepening the Demerara River, the waterway

-8-

used to transport mining supplies, bauxite and related products of DEMBA,±'one of the two bauxite interests in Guyana. On the other hand, proposalshave been made to dredge the bars at the mouth and up to 24 miles inland ofthe Berbice River. If this were feasible, transport costs on the exportsof the other bauxite interest, Reynolds Guyana Mines Ltd., would be reducedsignificantly. It could, in turn, contribute in an important way to thecontinued growth of the mining industry.

21. The search for new deposits of minerals other than bauxite hiasbeen intense, but much detailed ground survey work remains to be done toconfirm the existence of commercially exploitable deposits. The UNDP hassponsored aerial geophysical and mineral surveys covering part of thecountry, wqhile private U.S. and Canadian companies have explored variousareas for uranium and gold in particular. The UNDP supported surveys arelikely to continue in collaboration with the Guyana Geological Survey.

22. Agriculture, including fishing and forestrv, accounts for abouta fifth of GDP, provides about half of the country's exports, and engagesabout a third of the labor force. Sugarcane in turn accounts for nearlyhalf of agricultural output and employs about one-third of the agriculturalwork force. Rice is the second most important agricultural product.

23. The volume of agricultural production increased about 1.5 per-cent per annum during the 1960's compared with an annual growth rate ofpopulation of almost 3 percent and about 4.5 percent for GDP in realterms. This slow advance in agricultural output was due mainly to thefailure of crop production. Sugarcane output, after a serious setback inthe mid-1960's due to civil strife, has been expanding fairly rapidlysince then. Rice production in contrast suffered little during the periodof unrest, but has declined seriously during recent, more settled years.The poor performance of rice production occurred despite a heavy investmentin the industry. The decline of both acreage and yields in recent yearsmay be attributed to policies regarding land settlement, tenure and titletransfer arrangements, water pricing and other matters affecting agricul-tural development (see paragraphs 45-64 in Annex I).

1/ The Demerarn Rauxite Gnomnpny Ltd - incornorated in Guyana, is awholly-owned subsidiary of the Aluminium Company of Canada, Ltd.

-9-

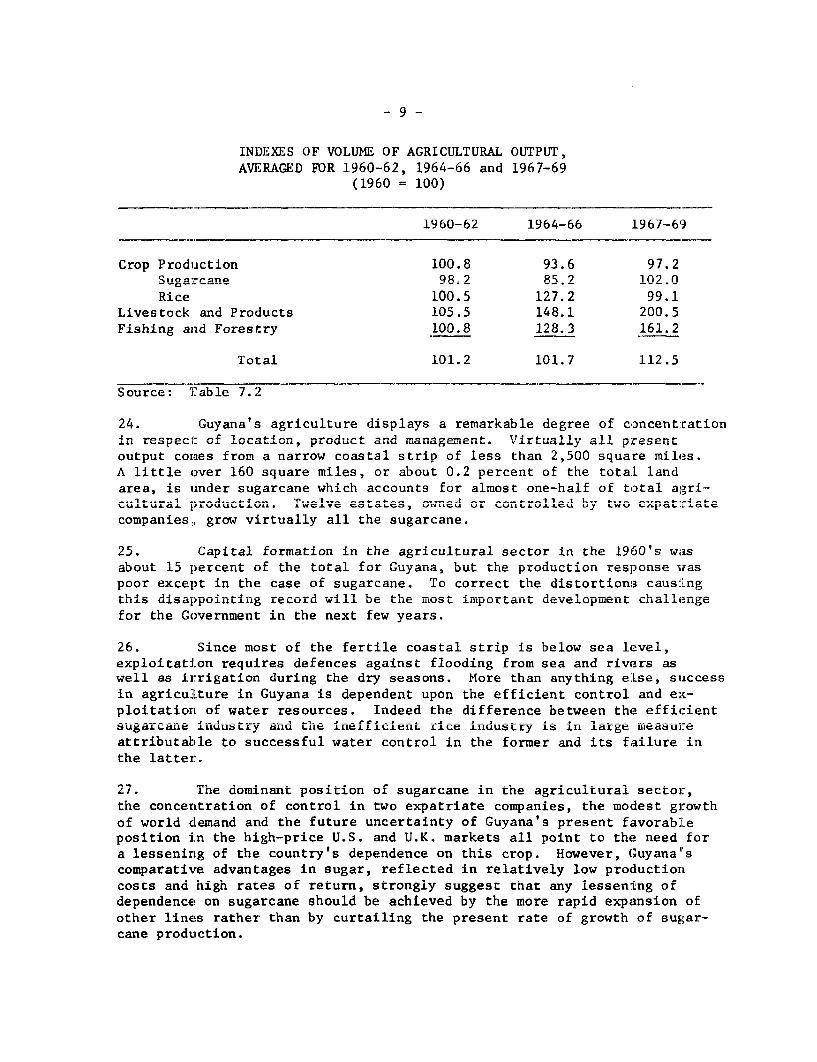

INDEXES OF VOLUME OF AGRICULTURAL OUTPUT,AVERAGED FOR 1960-62, 1964-66 and 1967-69

(1960 = 100)

1960-62 1964-66 1967-69

Crop Production 100.8 93.6 97.2Sugarcane 9.2 85.2 1020

Rice 100.5 127.2 99.1Livestock and Products 105.5 148.1 200.5Fishing and Forestry 100.8 128.3 161.2

Total 101.2 101.7 112.5

Source: Table 7.2

24. Guyana's agriculture displays a remarkable degree of concentrationin .-espect of location, proluct anu m..anage.ent. L.Viually a.. presentoutput comaes from a narrow coastal strip of less than 2,500 square miles.A littl- e over 160 square .M,i"es, or about 0.2 percent of the total land,Li. A. -L.LL± ~L .LVVJ 3M 0~ ILL. ctu ~JL aLJJU '..' %.1 UJ. LLL ~ tJI0. .L LLU

area, is inder sugarcane which accounts for almost one-half of total agri-cu'ltural productior.. "we've estates, ownedI or contro'lledI by Iwo expatriateu.LU04.jA. u U -.L'JL 4.6 ~ JVA~U L.L L A.LLU 'J W J i.p L 0L

companies, grow virtually all the sugarcane.

25. Capital formation in the agricultural sector in the 1960's wasaboutL 1 percent of thLle Loa Lfor Guyana, bUut the production response waspoor except in the case of sugarcane. To correct the distortions caus:LngL' ' disappointin ULU Wg reor Uw LL' t IhUe L ±II[IUtLdltL UeveUopurLLL e Lit ch tllen

for the Government: in the next few years.

26. Since most of the fertile coastal strip is below sea level,exploitation requires defences against flooding from sea and rivers aswell as irrigation during the dry seasons. More than anything else, successI_ ___ I n/ J__ .__ _ __ __ --- _ t_ _ros _ sl __ __ ____' __ .___-Iii agricuJLturte n1 GuyanLa is duepe LnUdentL upon thIe efLLIcIenL cO nLrol anIU --;L-

ploitatiorn of water resources. Indeed the difference between the efficientsugarcaLne industry and the inefficient rice industry is in large measureattributable to successful water control in the former and its failure inthe latter.

27. The dominant position of sugarcane in tne agricuiturai sector,the concerntration of control in two expatriate companies, the modest growthof world demand and the future uncertainty of Guyana's present favorableposition in the high-price U.S. and U.K. markets all point to the need fora lessening of the country's dependence on this crop. However, (;uyana'scomparative advantages in sugar, reflected in relatively low productioncosts and high rates of return, strongly suggest that any lessening ofdependence! on sugarcane should be achieved by the more rapid expansion ofother lines rather than by curtailing the present rate of growth of sugar-cane production.

- 10 -

28. The problems confronting the rice industry are deep-rooted andcomplex. They essentially stem from the inefficient use of existingresources and opportunities rather than from a dearth of these. Many ofthe occupants of government settlement lands were selected without regardto their aptitude or interest in farming. Moreover, rent controls militateagainst an efficient allocation and optimum use of land among growers. Therecovery from rice-growers of only a small proportion of the cost of watercontrol (irrigation and drainage) deprives the controlling authority ofthe resources necessarv to fulfill its functions effectively. At the sametime, an inappropriate price for an input as important as water leadsto its uneconomic use by rice farmers. Inadequate water control in turnhinders the introduction of a better technology, based on fertilizerand higher yielding varieties, which tends to be profitable only undergood growing conditions.

29. The average price obtained by Guyana for its rice exports hasdepended upon the distribution of sales as between markets under bilateralagreements with generally favorable price terms and "free markets" whereaverage prices are lower. For example, exports to CARIFTA markets in 1968were 58,000 tons at an average price of roughly US$23 per ton higher thanGuyana realized in "free markets". The value of this concession to Guyanain that year was, therefore, about US$1.3 million. Until 1966, Guyanarealized a higher price for its rice exports than the world average. Withthe loss of the Cuban market in 1965 and a simultaneous substantial in-crease in domestic production a larger volume of sales was shifted to"free markets" and the average export price dropped below the averagefor other exporting countries. An important factor influencing the loweraverage export price obtained in "free markets" is the relatively lowquality of Guyana's rice. The aspect of quality also poses some threat toGuyana's favorable position in CARIFTA markets. The adoption of policies,including improved differential price incentives covering rice grades andthe timing of delivery, to improve the quality of rice Rrown in Guyana, isan urgent requirement if rice exports are to be expanded and average pricesraised. At the present time, rice-growers are paid a price which on theaverage reflects the value of their product on the marginal "free market".An improvement in rice qualitv which is reflected in higher "free market"prices and is achived at a cost less than the increased value of the rice,would mAke nossihbl a higher nrice tn growers.

30. Little ciir'cs has been achipvpd so far in devlnoping crOpSother than sugarcane and rice. This has been largely due to the technicaldifficulty of growing such crops on the tiifficul t, frnequently water-loggedcoastal clays and, to an important extent, to the prevalence of praediallarcen.y.

31. PCrtl a npArndutin 4-n th) manctnl bah ore for lhon hfnninawrn

mainly by an inadequate institutional framework. Herds, for the mostpart s..all anA generally owned by rice f-r..ers, are grazed cnn.nunally onpastures which are badly overstocked. There is little incentive for the

- 11 -

individual owner to follow accepted husbandry practices in breeding, indisease and parasite control, and in nutrition. Any attempt by such smallindividual cattleowners to limit numbers in line with available grazingwould benefit them little, since it would merely leave more grazing forthe cattle of other owners. Development is further hampered by prevalentlarceny of stock and, where pastures are individually held, by trespass.

32. Although DoultrV Droduction has exnanded, neither it nor Digproduction can make a larger contribution to the economy until domesticsources of feedstuffs are more abundantlv available. But there are diffi-cult technological and economic problems involved in increasing the localproduction of feedstuffs.

33. Forests; which cover 80 nercent of the countrv; provide the basisfor only 1.5 percent of the GDP. Stands of the more valuable species, suchas cyreenheart tiutd for lmnbher are nearlv exhaniqtec1 in the a.rCe;qih1e

areas because of intensive selective exploitation. Continued exploitationrequires depner, more roRtlv penetration of the i,1n0le The eat-;h1iqhmPntof a proposed pulping plant and the perfection of a process of timber-imnregnation Qhnlld make it feasih1e to expnlnit- wider rance of encriesand could radically alter the economics of forest exploitation in Guyana.

34. Guyana's participation in the shrimping industry, which hasdeveloped I anidly Nff tha northeast oanst of onilth Amperica in recent years,has for the most part been confined to the provision of on-shore facilitiesfor foreign-otm.ed shri.mping trawlers. Such expansion of Guyana's fishingfleet as has occurred has been almost entirely for shrimping and with theva-st majorlt- of the vessels foreign-o .ed. The trawl fsigidsrhas been largely neglected.

35. Among the remaining producing sectors, manufacturing (includingsugar and ri.ce processing) is the most .mportar.t, L o- u g ar.o n d -

12 percent to GDP in 1969. l/ Sugar and rice milling accounted for about43 percent of this totlal. Wi.h1 t*h exc n of rm, .luber anA some drugand related products, most of the remainder is destined for the localm.arket. Thse smlall s-ize of: the local market coupled wid- relatirvely low-

fll*Lr'~ .. .L1 A .L 04( '4. a & "I .J.'0L . mA L . '.Jj . -LU WL LII A L L1. L~ 4.'.JW

per capita levels of income have inhibited the development of manufacture£or UllomesLtLc consumpUtionJ cI1U a'gvenI vuyoana' 'ULocat I, rsource elnlUoWmUeiIt

and the industrial heritage of the colonial period, the possibilities ofmanufLacturing Lfor export h1ave Ueeni even Luore unfavorable.

1/ This figure also includes the value-added of private power generationwhich, although not shown separately in the official accounts, isknown to be less than 1.5 percent of total output and represents aneven smaller share of private fixed capital formation.

36. The target set out in the Guyana Development Program 1966-1972was to double industrial production over the plan period. Il fact thegrowth in output between 1966 and 1969 for the sector as a whole was only12.6 percent - mucn less than the growLh In total output and far Oelow theplanned rate of expansion. Sugar and rice milling advanced more rapidlythan the remainder of the sector.

37. The level of fixed capital formation in manufacturing rose fromG$8.7 million in 1966 to G$9.8 million in 1969 or an increase of 11 percentover the period, thus according with the output experience. A decilne inthe industry's level of fixed investment is expected for 1970, reflectingthe completion of two fairly large enterprises last year.

38. The growth in manufacturing output and investment, sluggish as itwas, owes something to the Government's continuing efforts to promoteindustrial development thirough special incentive measures. These includeincome tax holidays for up to 10 years; accelerated depreciation of invest-ment; and duty free imports of raw materials, building materials andmachinery. These policies, as well as other promotional measures suclh asthe establishment of industrial parks, are the responsibility of the GuyanaDevelopment Corporation. From its inception in 1964 through 1969, appli-cations received by the GDC for concessions in manufacturing involved aplanned capital expenditure of G$36 million, about a third of this totalhaving been registered in 1969 in lumbering. It was also expected that,as a direct consequence of the planned capital expenditures, some 2,800new jobs would be created. Within the limited scope for industrial devel-opment, the GDC seems to have performed a useful promotional role.

39. The GDC also administers the Private Investment Fund establishedin late 1966 with the participation of the USAID which supplied the equiva-lent of half the total fund of G$6 million, while the Government was tofurnish the other half over a five-year period. The PIF lends up toG$425,000 at 7.5 percent interest per annum for 10 years, and is intendedto support the establishment and expansion of industries. By the end of1969, G$3.4 million had been provided in credits; about a third of thiswas for fishing and shrimping. Until 1969, the purposes of the Fund werenot being fully realized. The difficulty stemmed from the fact thatconditions offered by the PIF were hardly distinguishable from thoseprovided by the commercial banks, which are the commissioned agents ofthe Fund. Since the banks were required to apply traditional criteria inevaluating applications for credit and accept the risk on all loans made,they frequently chose to provide financial support from their own resourcesrather than drawing from the PIF. A further drawback is the requirementthat imports of equipment financed by PIF loans be procured only in theUnited States. With the increased upward pressure on interest rates andthe credit restraints imposed on commercial banks in 1969 (see paras. 98and 103 below). the concessionary terms of PIF funds were more sharnlvrevealed and the rate of lending from the Fund increased.

- 13 -

40. The advent of CARIFTA will raise the effective size of Guyana'smarket almost five-fold. At the same time there will be an attenpt toharmonize industrial incentives granted by the various member countries.Inter-country competition in the past has frequently led to excessiveconcessions. Even when these new favorable features are added to theGovernment's direct promotional efforts, the near-term prospects for rapidgrowth in industrial production are not encouraging. For the lorLger termthere is the more hopeful prospect that some lines of primary productionwill support resource transformation activities in canning, tanning andleather, glass fabrication (using the extensive deposits of white silicasands), pulp and paper and processed lumber products. But these possibil-ities are still on the horizon.

41. Apart from limitations of market, management skills and naturalresources hampering industrial development, the private sector as a wholeseems to lack dynamism. The explanation in part is related to the uncer--tain climate faced by those ethnic groups which generate a good part ofprivate sector savings available for investment. The Government's newstress on cooperatives, and its insistence on eauity participation in sometypes of enterprise, are factors which for the time being contribute tco anunsettled private investment climate.

42. The structure of Guvana's transDortation svstem reflects thedominance in the economy of bauxite, sugar and rice. In respect of allthree commodities. transportation is an especiallv intimate component ofthe production process and the resulting pattern of traffic flows arerelatively simnle. The countrv's settlement natterns; whereby built-unareas are concentrated along the coast and major rivers, also makes forsimnp]e lovisitiral reqnirements Finally, the water nrientatinn o!f theeconomy, wthereby all the major rivers flow into the Atlantic and lowelevatinns enahle navigable canals to be cut readily, cnsnat-itutsc -nimportant transportation element. Despite the large area, these influetncesareatlv simnlifv the transnnrt nrnhlem in Giuyana

43. An imnnnrtant fenature nf trnsnport- nrganiztfion in Guyana is the

responsibility assumed by producing companies (as distinguished fromtranspnro tatin ram,n

4aCa -a4 onnrnf- l - 1

4n- a 1 nF4taivly ; ponpart on Aof

r--F Wr--^ ~s rr -na vt...LJ nat6 .. -tS-- .

the countiy's transportation infrastructure and operating requirements.This helps. ea,lain the relatively smhall contri'Dution of aabout. 6 percentthat the transport and communications sector proper makes to GDP. Manyimportarnt transportratio4 n operfatlor,s a aeoA..n-te- by na- transr

prises. This condition extends beyond the three major commodity producingareas to include some of the larger wholesale an.d retail merchan.:ts as wrellUas the Guyana Marketing Corporation. The appropriation of much of thetrar.sportation market in thils wtay hLas restrained th_efull d 3evelopment cic.. . G Aa.JLLCL±ULL nalt nc .. ,n Ln.La Wa tia .caLLJ. c -LaI .L UL. U L~.LIjJ L .~I A.

a commercial carrier system. Additional inhibiting factors are the furnish-ing of sub' est;c for t s ation services Uy LLIt L,OVeXLlnIULIL WU a reg.-

latory policy effected largely in the form of control over entry to theIndustry.

- 14 -

44. Private commercial operations are largely confined to road and airservices. The latter annarentlv meet a real need iijudging from their favor-able financial results. Licensed commercial cars doubled between 1965 and1969 and rertified cirrier husies rose from 40 to 70 over the same neriod.Licensed commercial trucks increased in number from 300 to 418 but stillconstitute 2 small1 fraction of regmistered triuck irn 1969. There is insinuffi-cient information on commercial trucking operations to help explain thenronpenitv for nronrietnrv trannportation. One posslbility is t-hat commer-cial services are not able to meet the needs efficiently; another is theregulation of entry into the industry by the Govern ment.

45. Passenger traffic carried by government services actually

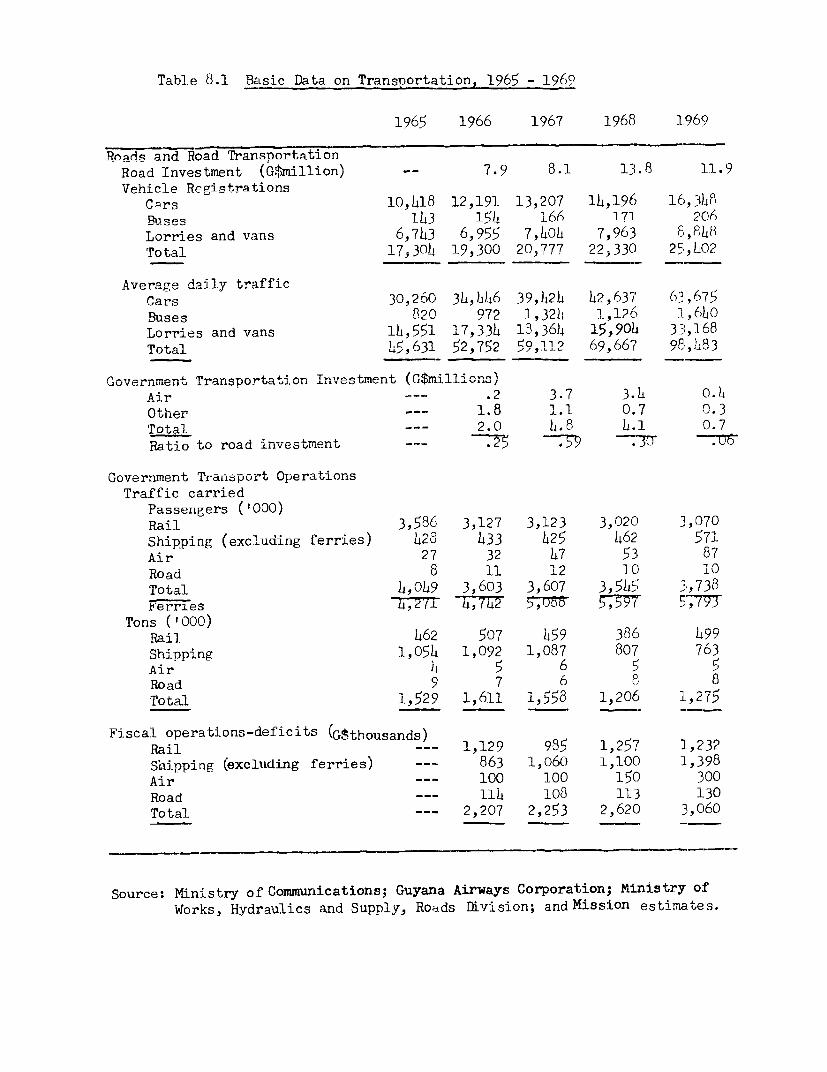

declined from 4.0 to 3.7 million persons between 1965 and 1969, reflectingthe diversion of traffic to private au,tonMr..i 1, for-hire cars and bustransportation all using a growing modern road network. As may be seenfrom the following table, the diversion affected the railways exclusively,since shipping and air are not closely competitive with road services.Ra41 -- -ca 4rriA 89 percent of the total -assenoer load (excluding ferries

which are essentially "bridges" in the road system) in 1965 and about 82percent in 1969. The cotinu-4g Adeclin in rai-a passenger traffic to

the end of 1969 vindicates to some extent tihe decision to discontinue"le subsidized servlice. A stretch oft 41 .ies or t1he 'as, Coast Railwaybetween Mahaica and Rosignol is now closed for passenger traffic. It ispLanned 'Lo phase out theU LL LV=1iLaAAI.LkLr, -LL1t.LU±J1k L1t- Fd- L Un lnaogL Uthe ELtWbe en

Georgetown and Mahaica and the West Coast Railway as soon as alternativerImeans of traLLsport are availauLe.

PASSENGERS CARRIED BY GOSVTER1ENT T1RAN SPOR SER-VICES, 1965 and 1969

1965 1969('000 Persons)(percent) ('000 Persons)(percent)

Ships 428 10.6 571 IRailways 3,586 88.6 3,070 82.1Road 8 .2 1U 1/ *3Air (Guyana Airways Corp.) 27 .7 87 - 2.3

Total 4,049 100.0 3,738 100.0

Ferries 4,271 5,793

1/ Estimated from revenue trends.Source: Table 8.1

- 15 -

46. Despite the record of economic expansion, freight tonnage carriedby government services has tended to decline or, depending on the baseyear chosen for comparison, at best has remained unchanged. The pertormanceof individual services was erratic from year to year, but shipping (exclud-ing ferries) accounted for the whole of the decline in freight carriedbetween 1965 and 1969. The declining volume suggests an increasing relianceon private services for freight transportation and the unattractiveness ofthe government services, even though these are subsidized.

FREIGHLT CARRIED BY GOVERNMENT TRANSPORT SERVICES, 1965 and 1969

1965 1096.L 9U.J .L 9UJ~

('000 tons) (percent) ('000 tons) (percent)

Shipping 82.9 54.2 63.4 49.7Rail 46.2 30.2 49.9 39.1Truck .9 .6 .8 .6Air l/ .4 .3 .5 .4Ferries 22.5 14.7 12.9 10.1

Total 152.9 100.0 127.5 1100.0

1/ Estimated from revenue trends.Source: Table 8.1

47. The reliance on government transport services has declined atthe same time as their combined operating deficits (excluding interestand depreciation) rose from G$2 to G$3 million over the past five years.In 1969 the deficit was distributed amonR the various services as follows:

G$1000 Percent

East Coast Railway 1,030 33.7West Coast Railway 202 6.6Shipping 1,398 45.7Road Services (Bartica) 130 4.2Guvana Airwavq CAnrnoranti r00 Q-R

Total 3,060 100.0

48- rhe torita! dfic-it of r$3q mnillionn, it shouild be- not-edr, inc-luds

the overhead costs of the Transport and Harbors Department which amountsto more than G'$ million and is distributed a.-bitrarily among the variousservices. The allocation to the railways, for example, constitutes halftheir deficit. Since the ovemrhead costs appear to be insensitive tothe elimination of one service or another; it is difficult to gauge thesavings that mlg.1 ht- be 0 ha from shutting down ar. operation. Ivor purelyillustrative purposes, it might be suggested that on the basis of 1969

operations and taking into account the surpluses generated by the ferries(G$ .350 Jrillion) and harbor services (G$l million) abandonLng the operationsof the Transport and liarbors Department would yield gross savings of G$1.7m illion 'or tiLe GoverLmfent.

49. With growing deficits in the face of declining logisticai res-ponsibility, government transport services appear to drain rather thannourish the econormLy. Specifically, government transport managementis weak, rates are generally high and operating costs appear excessive incomparison with those incurred by private services.

50. While there is no measure of traffic carried in non-governmentaloperations, indirect evidence permits a rough estimate of the role ofgovernment services. Compared with the tonnage generated by the majormining and agricultural activities, government freight traffic is minuscule.Considering the requirements ot manutacturing, however, crude estimatesindicate that government tonnage may comprise not more than 20 percent ofthe total. The passenger carrying role of public services is stronger.Similar estimates suggest that government services supply roughly 40 per-cent of total passenger travel.

51. The Government has not explicitly enunciated a transport policy,crucial as it is for investment guidelines and management effectiveness.There hlas been a strong propensity for the government to operate transportservices in all modes over and above the provision of infrastructure thatthe public sector normallv undertakes. Over the 1966 to 1969 period,government capital expenditures on transport amounted to G$53 millionor 36 percent of total capital outlays. Of this sum, much the largestshare - G$42 million - for road construction and improvement was primarilydesigned to link the major centers of population and the producing areasof the country. Less than G$10 million were devoted to the various trans-port services, mostly the airwavs while the railways, soon to be abandoned,received only a small amount. Capital expenditures on othertransport operations appear to have been inordinately small in relation tothe volume of services performed, and the need to at least maintain capitalintact. This helps explain the operating deficiencies in road services andshipping.

52. Internal communications, comprising telephonic, telegraphic andradio transmission, have been badly neglected in Guyana. The capacity ofthe telephone system has long since been exhausted, leaving a growingunsatisfied demand and an overloaded system that is prone to frequentmalfunctioning. Besides the diseconomies that the scarcitv of telephoneservice has induced, it has also turned this instrument of communicationinto a highly-valued symbol of social status. The Guyana TelecommunicationCorporation, organized in March 1967 as an autonomous public enterprise,operates 18 exchanges throughout the country and provides service to 7,000telephone subscribers at rates established in 1960. There is thus one

- 17 -

telephone per 100 persons or 1.7 per 100 persons if phone extensions arealso considered. Communications with interior settlements are based onan antiquated manually operated Mlorse Code system and a network of highfrequency radio stations. Capital expenditure in these services haveaveraged only G$5 million a year since 1967. A large part of this sumwas devoted to introducing a limited telex system in Georgetown.

53. In sharp contrast to the deficient internal system, externalcommunicat:ions are highly developed. Through the Cable and Wire:Less Com-pany, Guyana is tied into the world-wide communications network. Plansfor expancling and modernizing the internal communications system wereprepared in 1966 and 1967, but are only now beginning to be implemented.The program calls for a capital expenditure of G$17 million over the nextthree years and will add eight telephone exchanges in the major areas ofsettlement: and upgrade the interior communications system. The bulk ofthe financing requirements will be provided by suppliers of equipment,while the small remainder will be self-generated by the Corporation, whichin 1968 and 1969 recorded a small net operating surplus. (See AppendixII - Financial Opetrations of the public Corporations.)

54. The above review of recent nerformance in transport and communi-cations reveals some serious deficiencies in the Government's serviceoperations; regulatory measures and capital expenditure nrogram. Whatappears tco be required is a thorough critical review of all facets ofgovernment: transport onerations and nolicies. A ma'or obiective would beto redefine operational criteria - to continue to operate subsidized trans-nort qervices only where thi4 meets clear Peonomir or socril niirnpoePSuch a review is almost certain to reveal the need for organizationalreform, improved management derisinn makinga hbtter information anid aninvestment: program based on a considered strategy for the sector as awhol, andri wahirch fits well into the overa1l deveopment fram.ework.

55. In the various social services, - health, education, .wtater supplyand sanitaLtion - little or no improvement over the past five years hashpen evident Rouighly a third of eurrerlt gouprnmpnt pYnPnditi1rPcs is srpnt

on these services, largely on education. But since 1966 the growth inthpir nllrirntinn has been Iess rnnid than total ouInitlays= rnnitnl epndrBi-

ture averaiged only G$5.5 million a year, and of this sum the constructionof tHo Tln.7aiorya4 tx, n^f 2117o,,no MhQanvoAf tQtrz:t4!2ol OIIoMV Tn vie- f tho

backlog of needs and the increasing demands emanating from population andincome gro,wth, the star.ardA of social -4rvices, with tho psie4l excet 4.on

of education, has remained unchanged, and it is even doubtful whether t:hecapital st-cl, 4-i ths4 sect-r has been .aintained 4ntact.

56 The 1-literscy rate in. Guyana (83 pcent as of '1960) is c.LpauaL±vc-

ly high, reflecting the ready availability of basic education, even thoughd4eficicencies in -ibe quallifcations of teachers, -le existence of all-ageUA .J J. A IL LAJ ~ I L .Ld.L JI.. L±JL & L .I L LiiL LLL J. LL L~ LI . L

schools as departments of primary schools, limited access to secondaryschiooJLs andU overcrLowdUi[ng in priL ,ary schLoUUl aLe pLUr.iLnetIL Lt&LU. Be:cause

- 18 -

the present curricula bear only a remote relation to the economic and socialdevelopment needs of the country, the Government in January 1968 launchedi a

major program to restructure and expand the educational system. It isess-tially a4 a t the wrnAinal elimlnatinn of all-age schnoolc an t-h

creation of a comprehensive system of education at the secondary level.T+- 4s anticipated that by. 19a73 tnher ba4 fo-r -.. Ii n aFwFa;eTt *1 -. EO aL L..L -J L~ ---OI * vy Mt . i LI _S L <>7>v;-Litv2L UL - A J '. 6. z

have been laid. An IBRD/IDA loan is helping to finance the program whilethe United Kinbdom.l and Canad-a -4e aiti at the- level ofuniversity

education.

57. The improvement in health standards that occurred in the 1950'sandIU thI.e Lirst LLa.LL oLf L.Lie 19U60's was largely related to the eradi.ationof malaria. Crude death rates were reduced sharply by almost one half, while

lnifLarit mortalityy £ e±.L LJ3 5JJ percentL. Sma uLa.Ller auu± ddiL tional. JAL V t rulmn t s took

place in the past five years:

CHANGES IN HEALTH STANDARDS AND SERVICES, 1965 AND 1969

1965 1969

Crude death rate (per 1000) 8.2 8.1

Infant 11ortality rate (per 1000) 48 , 40Doctors (per 10,000) 2.3 -! 2.1General Hospital beds (per 1000) 3.2 3.0

1/ 1967.Source: Ministry of Health; United Nations, compendium of Social

Statistics 1967; and World Health Organization, FourthReport on the World Health Situation, April 1970.

The crude death rate has remained stable at its already low level whileinfant mortality continued to decline. The 1969 infant mortality rate islow in comparison with the average for Latin American countries, but isnevertheless onsidered by the G.vanese authorities to be unacceptably highand susceptible to further reduction. The shortage of doctors and generalhosnital hbds onntinuips to he acute; while the incidence of endemic diseases

has remained high. The control of typhoid in recent years has much improved,but there ic alwas t-hp thrpat nf a fulllcale enidpmic of this and otherwater-borne diseases so long as present low standards of sanitation in bothurban and rural areas persist. Of growina rnncern is the hioh incidenee of

malnutrition, particularly among children in rural areas. Nutritionaldeficiencies were the indicated cause of almr.st 30 percent of Ad.aths recorded

in the under five age group. A Ministry of Health sample survey in 1969found that 62 percer.t of the children under five years were suffering f-omvarying degrees of protein malnutrition.

- 19 -

58. A serious handicap in dealing with health issues has been theabsence of information and the consequent formulation of policy on thebasis of imperfect knowledge. While certain problem areas such asmalnutrition can be readily defined, their magnitude and the appropriatecorrective or preventive measures required can only be guessed. A pre-investment study of all facets of health, especially the provision ofservices outside the main centers of Georgetown and New Amsterdam, isbadly needed.

59. Since many of the endemic diseases in Guyana are water-borne.their control and eventual eradication are related to water supply andsanitation. Outside of Georgetown water sunnlv is limited- and. where itexists in rural areas, is often polluted. Approximately 30 percent ofthe rural notable water sunnlv is nrovided and maintained hv the SugarIndustries Labor Welfare Fund Committee, while 60 percent comes from theMinistryv nf nf WnorkR 1 Hvdr1r:lircz nnd S,innIv Thp Mini;trv -npndc nhni,rG$800,000 a year on both current and capital account and includes an elementnf suhbsid:lzat-inn s.inre rural water userq contrihbut-e little tow,.ards thecost. This sum has not permitted services to be maintained properly let

alone expanded, and as aresult…prcpt onum.to. <fle. Further-more, it is estimated that consumer waste together with leakages from the-n-tiquated system. produce losses of about two-thirds of the total outp:tof the rural water system.

60. If anything, sanitation facilities are even more inadequate andthe problem of sew:erage dlsposal in Georgetow has becom--e acute. nly13 perceni: of the population live in houses connected to a sewerage system.Poor disposal fac.lities lncludingope roadside drains frequently res;;lt

A. .JtJt tL&J9~o .3 tO. L. .j i.t O *lt..tS tA L,JCL* tjtO,i tA.M L.110 I.3. £ 9 AL&L..Ly LOC5UALL

in the contamination of potable water supplies.