CIN Company Name Investor First Name Investor Middle Name ...

Upload

independentCategory

view

1download

0

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

VINGROUP JOINT STOCK COMPANY

Investor Presentation April 2014

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

Table of contents

2

A. Introduction to Vingroup 6 - 12

B. Business Strategy 10 - 12

C. Key Investment Highlights 13 - 22

D. Business Overview 23 - 24

E. Financial Overview – VAS 25 - 32

F. Financial Overview – IFRS 33 - 39

G. Appendix – Vincom Retail 40 - 42

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

A. Introduction to Vingroup

3

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

History of Vingroup

Synergies with large land bank owned by Vinpearl

Lowered overall cost of funding for the Group

Critical mass and diversified business model and

revenue streams

Economies of scale

Membership program integration across all consumer

segments

Expanded operations into consumer focused industry

sectors such as hospitality and leisure

362 379435

2009 2010 2011 Jan-12

1,001 1,237

1,680

2,641

3,585

2009 2010 2011 2012 2013

Total Assets US$ mn

Established in 2001

Listed on the HOSE in Jan 2008

Opened the first resort, Vinpearl Resort Nha Trang in 2003

Opened Vinpearl Land in 2006 and Vinpearl Luxury Nha Trang,

Vinpearl Golf Club - Nha Trang, Vinpearl Luxury Danang in 2011

Established in May 2002

Listed on the HOSE in 2007

Opened the first commercial building Vincom Center Ba Trieu in 2004

Launched over 8,000 apartments at Royal City, Times City in 2010

and 2011

“Made a conscious decision to focus on the core business in Vietnamese

real estate” – McKinsey (2012)

1. Financials are prepared under VAS; Based on exchange rate of US$1 = VND21,135

2. Total assets from 2009-2011 contains only Vincom’s total assets. 2012 includes Vinpearl and Vincom’s total assets

Total Assets US$ mn

4

Vincom – Leadership in Residential, Commercial and Retail

Vinpearl – Leadership in Hospitality

Transformational Merger in 2011 to form Vingroup

Summary Financials(1)

Merger with

Vincom to form

Vingroup

(US$mn) 2010 2011 2012 2013

Revenue 183 109 374 870

EBITDA 152 84 185 550

Total Assets (2) 1,237 1,680 2,641 3,585

Cash + Cash

Equivalents + Short-

term investments

258 256 259 617

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 5

Integrated Platform Focused on the Vietnamese Urban Consumer

Uniquely positioned to benefit from Vietnam’s consumption growth

Source: Economist Intelligence Unit as of 31 December 2013

1. Total Consumer Spending equals Consumer Expenditure on Housing, on Tourism, on Hospital and others

Consumer Expenditure

on Housing

(US$ Bn)

Consumer Expenditure

on Tourism

(US$ Bn)

Consumer Expenditure

on Hospital

(US$ Bn)

Total Consumer

Spending (1)

(US$ Bn)

6.98.0

9.410.9

12.213.6

15.3

10 11 12 13E 14E 15E 16E

6.67.3

8.39.4

10.311.3

12.4

10 11 12 13E 14E 15E 16E

3.94.6

5.46.4

7.38.3

9.6

10 11 12 13E 14E 15E 16E

68.978.9

91.6104.9

115.6127.7

142.1

10 11 12 13E 14E 15E 16E

Largest Developer In Vietnam

Premium Brand Recognition

Diversified Sector Exposure

Develop, Manage and

Operate Commercial

and High-end

Residential and Mixed-

Use Properties

Residential and

Commercial

Manage and Operate

High-end Retail

Properties

Retail Properties

Develop, Manage, and

Operate Premium

Tourism, Hospitality

Properties

Manage and Operate

Entertainment Services

Hospitality and

Entertainment

Manage and Operate

a High-end and High-

quality Hospital

Hospital

Quality Formal

Education from

Kindergarten to High

School

Education

Own International &

Domestic retail brands;

Retail and

Lifestyle

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 6

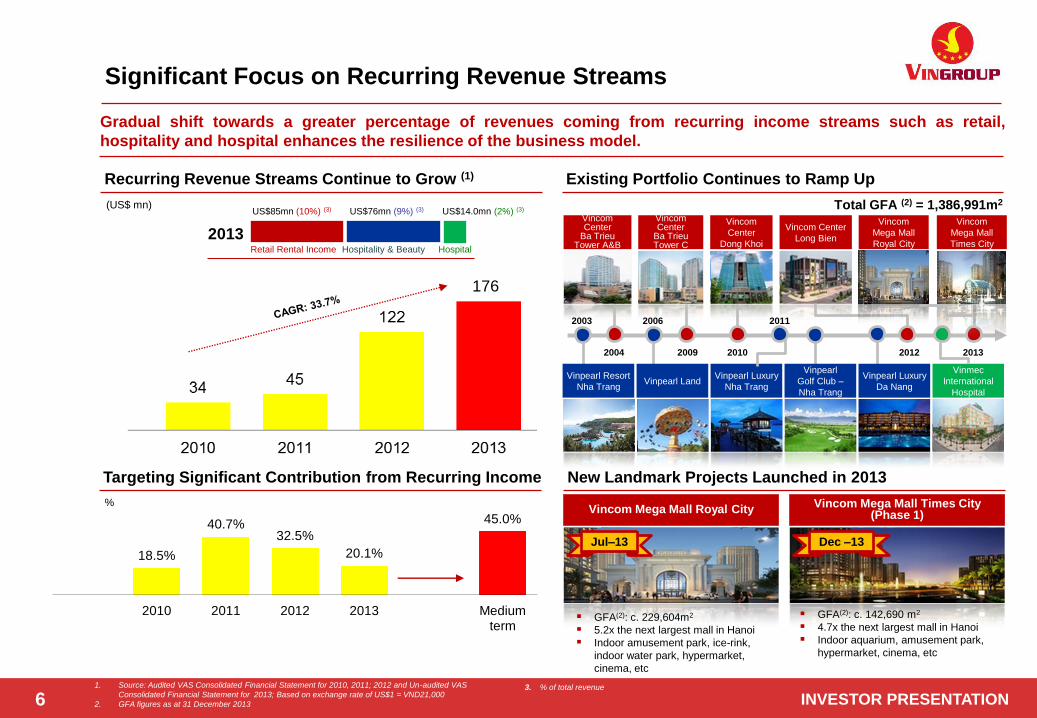

Significant Focus on Recurring Revenue Streams

Gradual shift towards a greater percentage of revenues coming from recurring income streams such as retail,

hospitality and hospital enhances the resilience of the business model.

1. Source: Audited VAS Consolidated Financial Statement for 2010, 2011; 2012 and Un-audited VAS

Consolidated Financial Statement for 2013; Based on exchange rate of US$1 = VND21,000

2. GFA figures as at 31 December 2013

(US$ mn)

Recurring Revenue Streams Continue to Grow (1)

%

Targeting Significant Contribution from Recurring Income

Existing Portfolio Continues to Ramp Up

New Landmark Projects Launched in 2013

2013

US$85mn (10%) (3) US$76mn (9%) (3) US$14.0mn (2%) (3)

Retail Rental Income Hospitality & Beauty Hospital

Vincom Mega Mall Royal City Vincom Mega Mall Times City

(Phase 1)

GFA(2): c. 229,604m2

5.2x the next largest mall in Hanoi

Indoor amusement park, ice-rink,

indoor water park, hypermarket,

cinema, etc

GFA(2): c. 142,690 m2

4.7x the next largest mall in Hanoi

Indoor aquarium, amusement park,

hypermarket, cinema, etc

Total GFA (2) = 1,386,991m2

Jul–13 Dec –13

2004 2009 2010 2012 2013

Vinpearl Resort

Nha Trang Vinpearl Land

Vinpearl Luxury

Nha Trang

Vinpearl

Golf Club –

Nha Trang

Vinpearl Luxury

Da Nang

Vinmec

International

Hospital

2003 2006 2011

Vincom Center

Ba Trieu Tower A&B

Vincom Center

Ba Trieu Tower C

Vincom

Center

Dong Khoi

Vincom Center

Long Bien

Vincom

Mega Mall

Royal City

Vincom

Mega Mall

Times City

176

3. % of total revenue

18.5%

40.7% 32.5%

20.1%

45.0%

2010 2011 2012 2013 Medium term

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 7

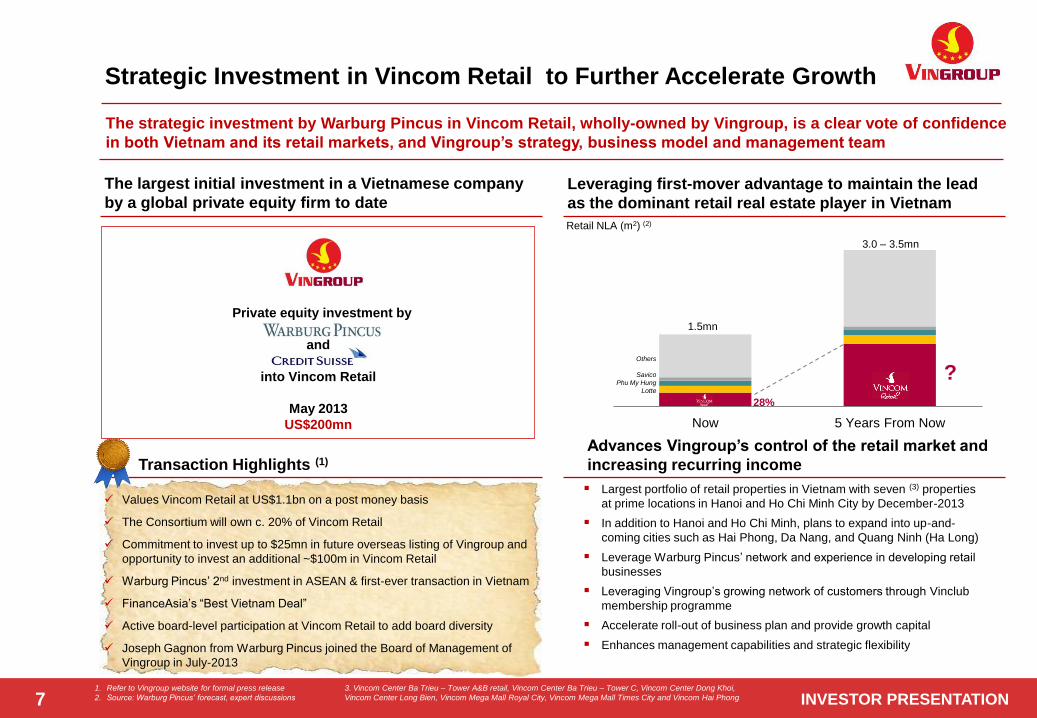

Strategic Investment in Vincom Retail to Further Accelerate Growth

The strategic investment by Warburg Pincus in Vincom Retail, wholly-owned by Vingroup, is a clear vote of confidence

in both Vietnam and its retail markets, and Vingroup’s strategy, business model and management team

1. Refer to Vingroup website for formal press release

2. Source: Warburg Pincus’ forecast, expert discussions

Private equity investment by

and

into Vincom Retail

May 2013

US$200mn

Largest portfolio of retail properties in Vietnam with seven (3) properties

at prime locations in Hanoi and Ho Chi Minh City by December-2013

In addition to Hanoi and Ho Chi Minh, plans to expand into up-and-

coming cities such as Hai Phong, Da Nang, and Quang Ninh (Ha Long)

Leverage Warburg Pincus’ network and experience in developing retail

businesses

Leveraging Vingroup’s growing network of customers through Vinclub

membership programme

Accelerate roll-out of business plan and provide growth capital

Enhances management capabilities and strategic flexibility

Advances Vingroup’s control of the retail market and

increasing recurring income

Values Vincom Retail at US$1.1bn on a post money basis

The Consortium will own c. 20% of Vincom Retail

Commitment to invest up to $25mn in future overseas listing of Vingroup and

opportunity to invest an additional ~$100m in Vincom Retail

Warburg Pincus’ 2nd investment in ASEAN & first-ever transaction in Vietnam

FinanceAsia’s “Best Vietnam Deal”

Active board-level participation at Vincom Retail to add board diversity

Joseph Gagnon from Warburg Pincus joined the Board of Management of

Vingroup in July-2013

The largest initial investment in a Vietnamese company

by a global private equity firm to date

Leveraging first-mover advantage to maintain the lead

as the dominant retail real estate player in Vietnam

Transaction Highlights (1)

Now 5 Years From Now

Others

Savico

Phu My Hung

Lotte

?

1.5mn

28%

Retail NLA (m2) (2)

3.0 – 3.5mn

3. Vincom Center Ba Trieu – Tower A&B retail, Vincom Center Ba Trieu – Tower C, Vincom Center Dong Khoi,

Vincom Center Long Bien, Vincom Mega Mall Royal City, Vincom Mega Mall Times City and Vincom Hai Phong

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 8

Residential Cash Flows Are Resilient & Locked In

Continue to ramp up our major development projects, with a substantial amount of presales locked in with cash

deposits on hand.

Vin

ho

me

s

Ro

ya

l C

ity

Total GFA: 1.207mn m2 (54% residential)

3,697/4,518 (82%) units sold and leased; of

which, 788 units delivered

Total contract value: US$539mn, received

US$468mn

90 149 65 255

694

361 290

78 71

434 244

873

605

(US$mn)

Resilient Apartment and Villa Sales with Upside to Come

2009 2010 2011 2012 2013

Major Projects To Be Handed Over This Year (1)

Vinhomes Riverside

Vinhomes Times City

Vinhomes Royal City

Vin

ho

me

sT

ime

s C

ity

Total GFA: 2.176mn m2 (64% residential)

Phase 1: 3,152/4,254 (74%) units sold; of

which, 2,419 units delivered

Total contract value: US$399mn, received

US$392mn

Vin

ho

me

s

Riv

ers

ide

Total GFA: 1.193mn m2 (56% residential)

Total contract value with 5 sub-developers

and a wholesaler: US$772mn, received

US$581mn

Promising Pipeline of New Projects (2)

1. As at 31 December 2013

2. These projects are undergoing an approval process as a result of which the components and GFA are subject to change

Vincom Projects Vinpearl Projects

Vin

co

m

Hai P

ho

ng

High-end retail, office & residential and

parking complex

Total GFA: c.144,730m2 (56% residential)

Expected start: 2Q – 2014

Expected completion: 1Q – 2015

Vin

co

m

Vil

lag

e 2

Mixed-use project adjacent to Vinhomes

Riverside in Long Bien, Hanoi

Total GFA: c. 596,523m2 (79% residential)

Expected start: 1Q – 2014

Expected completion: 4Q – 2016

56

Ng

uye

n

Ch

i T

ha

nh

Mixed-use residential, retail, office and

school

Total GFA(3): 226,382m2 (49% residential)

Expected start: 1Q– 2014

Expected completion: 1Q – 2017

Large scale resort development includes

hotel, golf course, villas, entertainment,…

Total GFA: 597,446m2

Started : 4Q– 2013

Expected completion: Oct 2014 (phase 1)

Vin

pe

arl

P

hu

Qu

oc

Unrecognized

revenue as at

31 Dec 2013

Progress

payment for

un-recognized

revenue

Vin

co

m

Cen

ter

Ha L

on

g Mixed-use site, a total land area of 1.6ha, 5

storey-mall with 1 basement

Total GFA(3): 43,589m2

Started: Oct 2013

Expected completion: Oct 2014

Pro

jec

t T

ho

ma

s Mixed-use project in Binh Thanh District, Ho

Chi Minh City

Site area: c. 355,000m2

Expected start: 3Q – 2014

Expected completion: 3Q – 2019

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

Understanding the Land Acquisition & Purchase Process

Understanding the development and presale process is a crucial part of appreciating Vingroup’s locked-in revenue streams.

Delivery Presales (1) Land Acquisition

1. Obtaining approval-in-principle

Acquire an “approval-in-principle”

from the local people’s committee

Indicates the approval of a

specific project

2. Investment Registration

Certificate

Can be obtained once “approval-

in-principle” received

After the investment certificate

obtained, a developer may

proceed to:

o Get approval on the land

clearance plan

o Commence the land

clearance process

o Start construction of the project

o Obtain the land use right

certificate for the project

First Stage of Presale

Via Loan Agreements

The Group offers

buyers option to sign

a loan agreement

presale

Loan principal

expected to be

applied to initial

installments due

under a sale and

purchase agreement

(SPA)

Typically loan

amount is 20-40% of

the purchase price

18 months at

~2% interest

Second Stage of

Presale – conversion

to SPA

When foundation

work or first floor area

is complete –

buyer has 15 days to

confirm purchase

On confirmation and

signing of SPA - loan

principal applied to

the deposit and

installments under the

SPA

Delivery of property

upon completion

Buyer has to pay

the remaining ~30%

of contract value

upon delivery

depending on SPA

Revenue can be

recognized by the

Group for sale

of property

Property is delivered

to buyer and removed

from inventory

Stage 1 – Loan

Agreements

Stage 2 – Sale &

Purchase Contract

Stage 3 –

Apportioned

Pre-sales Before

Completion

Third Stage –

Installments

Subsequent

installment

payments made –

depending on SPA

terms

Installment

payments of 10-20%

are made in varying

stages depending on

SPA

1. Vietnamese law requires the completion of either the foundation of a building or its 1st floor area for a sale and purchase agreement to be signed.

Hence all sales prior to this completion are made in Stage 1 by loan agreement, upon completion they are converted to SPAs under Stage 2 9

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

B. Business Strategy

10

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 11

What Differentiates Vingroup?

These elements provide competitive

advantages for Vingroup

Strong brand equity

attracts premium

tenants & clienteles

Pricing premium for

new projects focused

on the high / middle

class Vietnamese

consumer

Significant growth

potential in hospital,

retail, leisure,

education and

residential sectors

Fully leveraged to ride

expansion of upper /

middle class

Higher % of recurring

revenues over time

Asset sales allow

recycling of capital

into more consumer

driven business

segments

Realize synergies

between Vingroup’s

consumer focused

segments

Able to target different

tiers of high value

consumers through

differentiated

membership

Largest Developer in

Vietnam with Premium

Brand Name

Fully Integrated Real

Estate Owner &

Developer with Exposure

to Key Consumer

Segments

Unique Vingroup

Membership Platform

that Strategically Unites

Target High Value

Consumers

Capital Recycling Model

That has been

Successfully

Demonstrated

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 12

Business Strategies Are Reinforcing

Leverage on expertise and experience in identifying and securing

prime sites

Target the mid to high-end markets

Deliver on the need for high-quality retail and residential

space through mixed use developments which increases

its appeal

Develop high-quality resorts and villas

Capture the segment of increasing domestic

household wealth

Attract more international tourists

Develop a substantial portfolio of commercial buildings

(including office, retail and resort properties)

Provides a source of stable, recurring income

Potential for capital gains

Target the growing disposable income of upper and middle

class consumers by delivering on their various needs

Develop internal capabilities to enhance

efficiency and support its portfolio of prime

commercial investment properties

Sales and Leasing

Project management

Property management

Commence large-scale projects near

high-growth areas

Expansion into the upper mid-end segment

Expand addressable market by providing

more affordable units

Stable & Defensive Two pronged approach

Develop properties for sale

Operate properties for stable, recurring

income

Pre-sales reduces the need to raise capital

Focus on High-quality, Large-scale Mixed Use Developments

in Prime Locations and Further Expand into Selected

Strategic Cities

Grow Recurring Revenues Across Consumer Segments

and Enhance Inventory Property Turnover

Further Develop in-house Sales

and Leasing, Project Management

and Property Management

Capabilities Diversify and Enhance Property Income

Stream

1 2

3 4

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

C. Key Investment Highlights

13

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 14

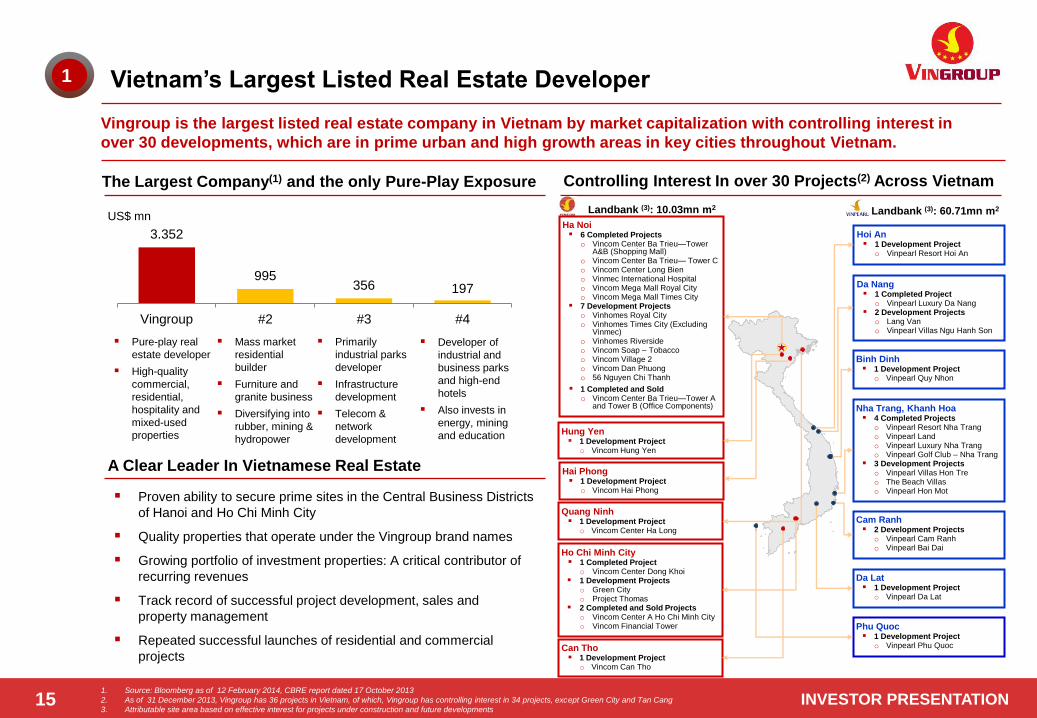

1 Vietnam’s Largest Listed Real Estate Developer

2 Capital Efficient Real Estate Platform with Track Record of Successful Asset

Disposals

3 One of the Largest Landbank in Prime Locations Across Vietnam

5 Proven Track Record of Access to Capital Markets

6 Highly Experienced Management and Good Corporate Governance

4 Well-recognized Premium Brand Names in Vietnam

Investment Highlights

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 15

Vietnam’s Largest Listed Real Estate Developer

1. Source: Bloomberg as of 12 February 2014, CBRE report dated 17 October 2013

2. As of 31 December 2013, Vingroup has 36 projects in Vietnam, of which, Vingroup has controlling interest in 34 projects, except Green City and Tan Cang

3. Attributable site area based on effective interest for projects under construction and future developments

Vingroup is the largest listed real estate company in Vietnam by market capitalization with controlling interest in

over 30 developments, which are in prime urban and high growth areas in key cities throughout Vietnam.

Proven ability to secure prime sites in the Central Business Districts

of Hanoi and Ho Chi Minh City

Quality properties that operate under the Vingroup brand names

Growing portfolio of investment properties: A critical contributor of

recurring revenues

Track record of successful project development, sales and

property management

Repeated successful launches of residential and commercial

projects

1

Controlling Interest In over 30 Projects(2) Across Vietnam The Largest Company(1) and the only Pure-Play Exposure

A Clear Leader In Vietnamese Real Estate

US$ mn

Pure-play real

estate developer

High-quality

commercial,

residential,

hospitality and

mixed-used

properties

Mass market

residential

builder

Furniture and

granite business

Diversifying into

rubber, mining &

hydropower

Primarily

industrial parks

developer

Infrastructure

development

Telecom &

network

development

Developer of

industrial and

business parks

and high-end

hotels

Also invests in

energy, mining

and education

3.352

995 356 197

Vingroup #2 #3 #4

Cam Ranh 2 Development Projects

o Vinpearl Cam Ranh o Vinpearl Bai Dai

Da Nang 1 Completed Project

o Vinpearl Luxury Da Nang 2 Development Projects

o Lang Van o Vinpearl Villas Ngu Hanh Son

Hoi An 1 Development Project

o Vinpearl Resort Hoi An

Nha Trang, Khanh Hoa 4 Completed Projects

o Vinpearl Resort Nha Trang o Vinpearl Land o Vinpearl Luxury Nha Trang o Vinpearl Golf Club – Nha Trang

3 Development Projects o Vinpearl Villas Hon Tre o The Beach Villas o Vinpearl Hon Mot

Da Lat 1 Development Project

o Vinpearl Da Lat

Hai Phong 1 Development Project

o Vincom Hai Phong

Hung Yen 1 Development Project

o Vincom Hung Yen

Ho Chi Minh City 1 Completed Project

o Vincom Center Dong Khoi 1 Development Projects

o Green City o Project Thomas

2 Completed and Sold Projects o Vincom Center A Ho Chi Minh City o Vincom Financial Tower

Ha Noi 6 Completed Projects

o Vincom Center Ba Trieu—Tower A&B (Shopping Mall)

o Vincom Center Ba Trieu— Tower C o Vincom Center Long Bien o Vinmec International Hospital o Vincom Mega Mall Royal City o Vincom Mega Mall Times City

7 Development Projects o Vinhomes Royal City o Vinhomes Times City (Excluding

Vinmec) o Vinhomes Riverside o Vincom Soap – Tobacco o Vincom Village 2 o Vincom Dan Phuong o 56 Nguyen Chi Thanh

1 Completed and Sold o Vincom Center Ba Trieu—Tower A

and Tower B (Office Components)

Landbank (3): 10.03mn m2 Landbank (3): 60.71mn m2

Binh Dinh 1 Development Project

o Vinpearl Quy Nhon

Quang Ninh 1 Development Project

o Vincom Center Ha Long

Can Tho 1 Development Project

o Vincom Can Tho

Phu Quoc 1 Development Project

o Vinpearl Phu Quoc

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

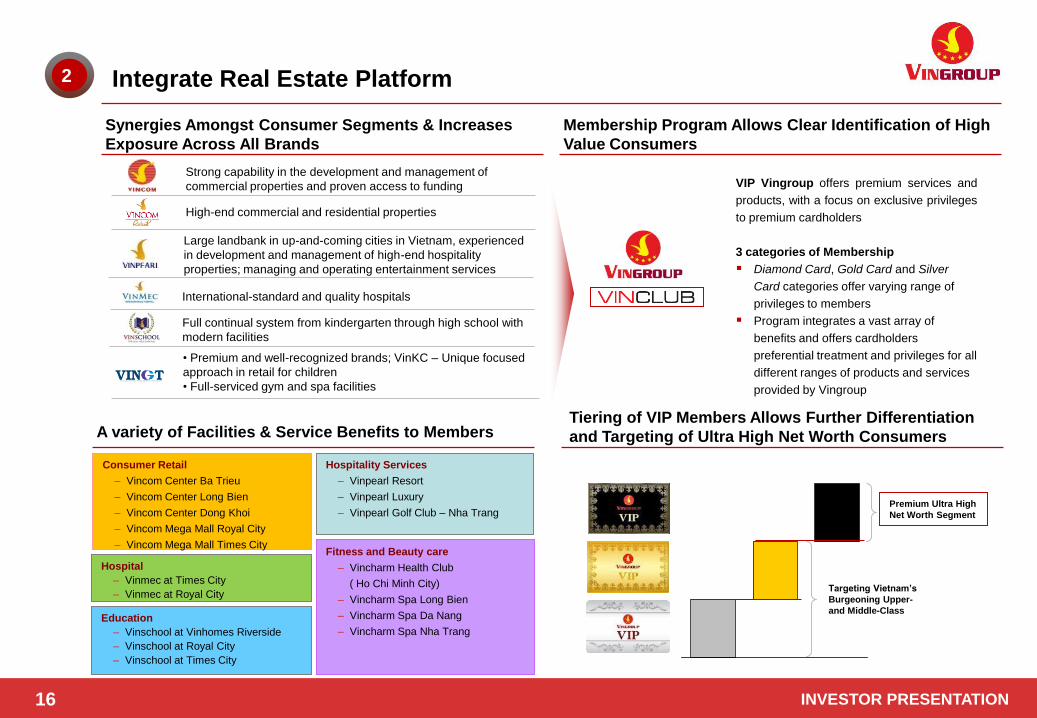

• Premium and well-recognized brands; VinKC – Unique focused

approach in retail for children

• Full-serviced gym and spa facilities

16

Targeting Vietnam’s

Burgeoning Upper-

and Middle-Class

Premium Ultra High

Net Worth Segment

Fitness and Beauty care

– Vincharm Health Club

( Ho Chi Minh City)

– Vincharm Spa Long Bien

– Vincharm Spa Da Nang

– Vincharm Spa Nha Trang

Hospital

– Vinmec at Times City

– Vinmec at Royal City

Hospitality Services

– Vinpearl Resort

– Vinpearl Luxury

– Vinpearl Golf Club – Nha Trang

Consumer Retail

– Vincom Center Ba Trieu

– Vincom Center Long Bien

– Vincom Center Dong Khoi

– Vincom Mega Mall Royal City

– Vincom Mega Mall Times City

Integrate Real Estate Platform

VIP Vingroup offers premium services and

products, with a focus on exclusive privileges

to premium cardholders

3 categories of Membership

Diamond Card, Gold Card and Silver

Card categories offer varying range of

privileges to members

Program integrates a vast array of

benefits and offers cardholders

preferential treatment and privileges for all

different ranges of products and services

provided by Vingroup

2

Synergies Amongst Consumer Segments & Increases

Exposure Across All Brands

Membership Program Allows Clear Identification of High

Value Consumers

A variety of Facilities & Service Benefits to Members Tiering of VIP Members Allows Further Differentiation

and Targeting of Ultra High Net Worth Consumers

Education

– Vinschool at Vinhomes Riverside

– Vinschool at Royal City

– Vinschool at Times City

Strong capability in the development and management of

commercial properties and proven access to funding

Large landbank in up-and-coming cities in Vietnam, experienced

in development and management of high-end hospitality

properties; managing and operating entertainment services

International-standard and quality hospitals

Full continual system from kindergarten through high school with

modern facilities

High-end commercial and residential properties

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 17

Capital Efficient Business Model (Cont’)

Demonstrated ability to create onshore liquidity by monetizing assets even in unfavorable conditions

1. By GFA as of 31 December 2013

2. Long-term operating lease with Vicentra, total cash was received as of 31 July 2013

Recycling of capital into consumer growth segments that are more defensible and higher yielding

2

Sale Price US$24.5mn US$51.1mn US$63.5mn US$471.6mn US$237.4mn

Profit %(3) 170% 100% 960% 129% 238%

Holding

period

(years)

2 0 (4) 8 1 3

Area Sold 22,480 m2 31,300 m2 24,059 m2 98,057 m2 77,694 m2

Acquirer

Integrated Development Model

Royal City

Residential GFA

54% (1)

Residential segment

presales used to fund

development of both the

residential and

commercial components

Commercial and

others’ GFA

46% (1)

Recurring

revenue

becomes a

larger

component of

total project

revenues

over time

Recycle Capital through Opportunistic Disposals

Vincom Center

Ba Trieu – Tower

A (office

component)

Vincom

Financial Tower

(office)

Vincom Center

Ba Trieu

–Tower B

(office

component)

Vincom Center A

HCMC

(shopping mall,

hotel)

Vincom Center

Dong Khoi

(office

component)(2)

2006 2010 2012 2013 2013

Retail

properties Hospitality,

Tourism and

Entertainment

Leading Retail Brands

• Fitness & Beauty care

International

Hospital

High quality

education

systems

Residential &

Commercial

3. % profit denotes the profit achieved from the sale, by comparing the sale price

with the construction cost, taking into account depreciation, of the assets

4. Vincom Financial Tower was sold upon construction completion

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 1. andbank and GFA as at 31 December 2013

1. Subject to change as projects are in planning phase

(million sqm)

Vincom Projects Vinpearl Projects

(million sqm)

Total GFA: 24,464,965m2 (2)(3)

One of the Largest Landbanks in Prime Locations Across

Vietnam Effective Landbank Breakdown by Construction Status (1) GFA Breakdown by Type (1)(2)

Planned GFA Breakdown by Construction Status (1)(2)

10.03 million sqm 60.71 million sqm

14.00 million sqm 9.38 million sqm

3

Land banking Strategy

70.74 million square metres of effective landbank is

sufficient for the next 10 years of deployment

Seek to acquire land adjacent to existing mixed-use

projects to benefit from economies of scale and increase

the critical mass of existing projects

Only look for land at prime locations in major cities

Proactive in infrastructure development to support

accessibility of own projects

0,05 1,878,02

3,77

21.51

39.2

Completed Underconstruction

Development Completed Underconstruction

Development

Villa

53%

Others

16%

Hospital and school

4%

Hotel

5%

Retail and Office ( 2)

9%

Apartment

13%

0,83

4,13

9,87

0,251,60

7,78

Completed Under construction Development Completed Under construction Development

3. GFA includes completed, under construction and development projects

18

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 19

Well-recognized Premium Brand Names in Vietnam

1. n February 2013, Vingroup transferred 100% interest in Vincom Center A Ho Chi Minh City to a real-estate investment company.

As at 31 May 2013, the cash proceeds have been received in full

4

Best Villa Development (Vietnam) for Vinhomes

Riverside

– South East Asia Property Awards 2012

Secured 2 (1) out of the 20 Golden Sites in Vietnam

Vingroup develops its commercial, retail, residential

and mixed-use properties under the Vincom brand

name

Demonstrated ability to sell residential and commercial

real estate even in difficult times in 2010 and 2011

Proven execution skills: Completion of large scale

projects under CBRE’s estimation of construction time

Recognized for quality of service

Successful in identifying and developing premium

hospitality projects

Hosted large national and international events e.g. Miss

Vietnam World 2008, Miss Universe 2010 and Miss

Earth 2010

World-class hospitals

International standard facility equipped with modern

test, diagnostic and operating facilities

Provides modern fitness and spa facilities operated by

professional fitness, beauty care and therapy

specialists to support other Vingroup brands

Best Retail Developer in Vietnam

– Euromoney Real Estate Awards 2012

Best Mixed-use Development (Asia) for Vinhomes

Riverside

– Asia Pacific Property Awards 2013

Best Developer (Vietnam)

– South East Asia Property Awards 2012

Vietnamese Golden Star Award

Strong Brands Across Segments

Numerous Awards from independent media is a

testimony of the Group’s brand name

Educational philosophy behind Vinschool focuses on

the overall development of students from an early

stage in order to develop and shape the future

generations of Vietnam and instill knowledge and

health and life skills

Full continual system from kindergarten through high

school with modern facilities

International Shopping Centre 2013 for Vincom

Center A HCMC

─ Global RLI Awards 2013

Best Condominium Development (Vietnam) for

Royal City

– South East Asia Property Awards 2013

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 20

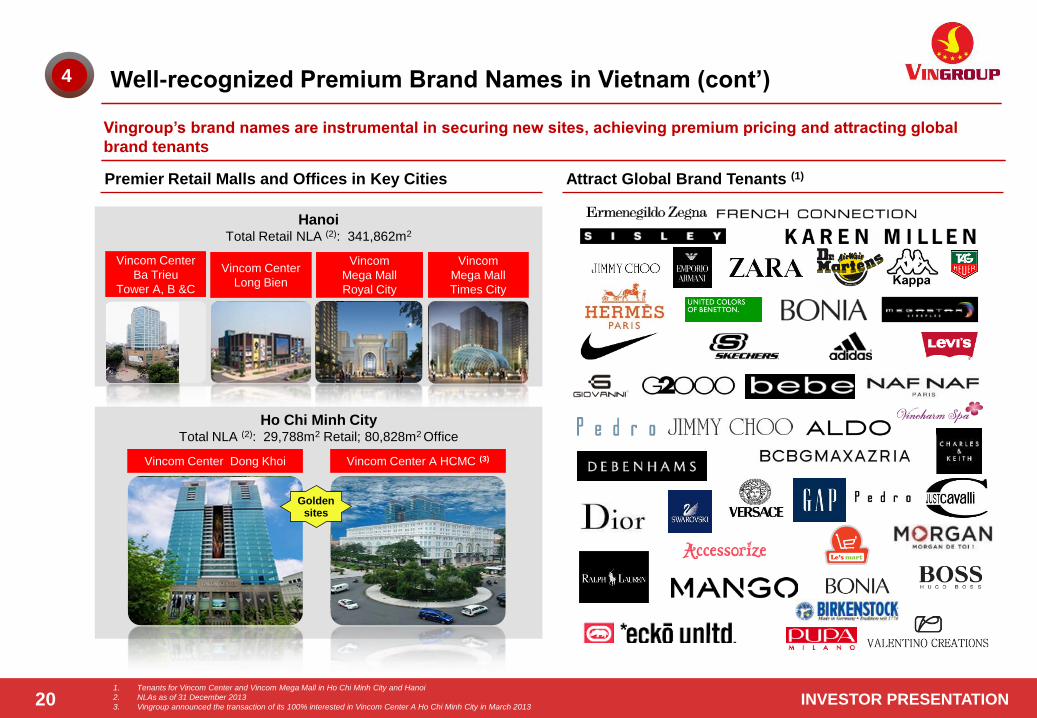

Well-recognized Premium Brand Names in Vietnam (cont’) 4

Vingroup’s brand names are instrumental in securing new sites, achieving premium pricing and attracting global

brand tenants

1. Tenants for Vincom Center and Vincom Mega Mall in Ho Chi Minh City and Hanoi

2. NLAs as of 31 December 2013

3. Vingroup announced the transaction of its 100% interested in Vincom Center A Ho Chi Minh City in March 2013

Premier Retail Malls and Offices in Key Cities Attract Global Brand Tenants (1)

Ho Chi Minh City Total NLA (2): 29,788m2 Retail; 80,828m2 Office

Vincom Center Dong Khoi Vincom Center A HCMC (3)

Golden sites

Hanoi Total Retail NLA (2): 341,862m2

Vincom

Mega Mall

Times City

Vincom Center

Ba Trieu

Tower A, B &C

Vincom Center

Long Bien

Vincom

Mega Mall

Royal City

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 21

Track Record in Accessing Capital Markets

Holistic cooperation with local banks, including facilitation

of mortgage financings for customers and transactional

banking services at Vingroup commercial properties

Good relationship with all leading domestic banks with

repeat loan and bond issuance

Cash & short term investments sufficient to cover any

near term debt maturities independent of any new capital

raising

Vingroup has a pioneering track record of success in the international capital markets, having raised more than

US$1 billion since 2009 through 6 major transactions

Strong cash balance maintained to service working

capital and interest payments

Demonstrated ability to create onshore liquidity through

capital recycling of non-core assets

Strong control over capital expenditures allow flexibility

around liquidity management

5

Private Equity

Investment by

into Vincom Retail

May 2013

US$200mn(1)

Best Capital Markets

Deal 2012

Convertible Bonds

Mar & Jul 2012

US$300mn

Best Vietnam Deal 2012

Best Vietnam Deal 2012

Unsecured Loans

January 2013

US$100mn

Convertible Bonds

Nov 2009

US$100mn

Debt and equity-linked

Deal of the year 2010

International

Syndicated Loan

October 2013

US$150mn

RegS/144A

International Senior

Unsecured Notes

October 2013

US$200mn

Best Vietnam Deal 2013 2013 Real-estate Deal of

the Year

Vietnam Capital

Markets Deal 2013

Best Vietnam Deal 2013

Best Vietnam Deal 2013

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 22

Experienced Management Team, Good Corporate Governance and

Strong Sponsor

Ms Mai Huong Noi

Board member and Deputy CEO

23 years in industry

8 years with Vingroup

Ms Vu Tuyet Hang

Vice Chairwoman & Deputy CEO

11 years in industry

9 years with Vingroup

Mr. Pham Nhat Vuong

Chairman of the Board of Management Holds a Bachelors Degree in Geological Economic Engineering

Long track record as an entrepreneur both in and out of Vietnam, founded Technocom Limited Company in Ukraine, which was sold to

Nestle S.A. in 2010

Established Vinpearl in 2001 and Vincom in 2002

Major shareholder of Vingroup

Mr Dang Thanh Thuy

Deputy General Director of

Vingroup JSC and General

Director of Vinpearl

18 years in industry

11 years with Vinpearl

Ms Tran Thi Khanh Van

Chief Accountant

23 years in industry

7 years with Vinpearl

Ms Nguyen Thi Huyen Tran

Deputy General Director

18 years with Vinpearl

Professor Do Tat Cuong

Acting CEO

41 years in industry

4 years with Vinmec

Mr Nguyen Manh Duc

Chief Accountant

14 years in industry

3 years with Vinmec

Ms Le Thuy Anh

COO

15 years in industry

3 years with Vinmec

Mr Pham Van Khuong

Deputy General Director

Over 29 years in industry

11 years with Vingroup

Ms Nguyen Dieu Linh

Vice Chairwoman & Deputy CEO

14 years in industry

9 years with Vingroup

6

Ms. Pham Thuy Hang

Vice Chairwoman

Ms. Nguyen Dieu Linh

Vice Chairwoman cum Deputy CEO

Ms. Mai Huong Noi

Vice Chairwoman cum Deputy CEO

Ms. Pham Thu Huong

Vice Chairwoman

Ms. Vu Tuyet Hang

Vice Chairwoman cum Deputy CEO

Mr. Marc Villers Townsend (1)

Independent Member

Mr. Ling Chung Yee Roy (3)

Independent Member

Ms. Le Thi Thu Thuy

Vice Chairwoman

Mr. Le Khac Hiep

Vice Chairman

Mr. Joseph Gagnon (2)

Independent Member

Board of Management

Key Executives

1. Mr. Marc Villers Townsend is the Managing Director of CBRE Vietnam (Ho Chi Minh City)

2. Mr. Joseph Gagnon is a Managing Director from Warburg Pincus

3. Mr. Ling Chung Yee Roy is the Managing Director of RL Capital Management

Ms Duong Thi Mai Hoa

CEO

Over 20 years in industry

Recently joined Vingroup

Ms Le Thi Thu Thuy

Vice Chairwoman

14 years in industry

6 years with Vingroup

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

D. Business Overview

23

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 24

Description Effective

Ownership (1) Occupancy rate (1)

Start date of

Construction/Operation GFA breakdown (m2)

Vincom Center Ba

Trieu - Tower A&B

Retail, office, in Hanoi

Office: Tower A was sold to BIDV in 2006; Tower B was

sold to Techcombank in Q1/2012

99.16% Office – Sold

Retail – 99% 2003 - Nov 2004 Retail: 27,103; Parking: 7,089

Vincom Center Ba

Trieu - Tower C Retail, residential, in Hanoi

Residential: 208 high-end apartments have been sold in

2009

99.16% Residential – Sold

Retail – 96% 2008 - Aug 2009 Apartments: 29,646; Retail: 15,386;

Parking: 7,253

Vincom Center

Dong Khoi Retail, office and apartments on one of the 20 “Golden

Sites”, in Ho Chi Minh City

99.16% Retail – 90% Jul 2008 - Apr 2010 Apartments: 16,463; Retail: 50,784; Office:

78,463; Parking: 32,214

Vincom Center Long

Bien

Vincom Mega Mall

Royal City

Retail, in Hanoi

Retail, amusement park and entertainment services,

in Hanoi

99.16%

99.16%

Retail - 87%

Retail – 95% (2)

May 2011 - Dec 2011

Jan 2010 – July 2013

Retail & Parking: 45,448

Retail and amusement park: 229,604;

Parking: 208,209

Vincom Mega Mall

Times City Retail, amusement park and entertainment services,

in Hanoi 88.47% Retail – 92% (3) Feb 2011 - Dec 2013 Retail and amusement park (phase 1): 222,471;

Parking: 348,410

Description Effective

Ownership (1)

Site Area

(sqm)

Start date of

Construction/Operation Components

Vinpearl Resort

Nha Trang An international 5 star hotel in Vinpearl Nha Trang

complex of hotel, resort, tourism, and recreation on Hon

Tre Island.

100.00% 1,327,037 Jul 2002 - Dec 2003 Hotel: 485 rooms

Restaurant & bars; Meeting facilities and fitness

center.

Vinpearl Land Hospitality and recreational complex built on an area

consists of many modern and unique large-scale

recreational facilities

100.00% 1,610,875 Nov 2005 - Aug 2006 Provides a variety of indoor and outdoor games,

a water park, an aquarium, a food village, a

shopping street, 1,350 seat event hall and 5,056

seat amphitheater.

Vinpearl Luxury

Nha Trang A luxurious resort located on Hon Tre Island 100.00% 151,363 Apr 2008 - May 2011 84 luxury hotel villas comprised of 18 Beach

Front Villas, 20 Hill-top Suites, 15 Grand Hill-top

Suites, 24 Pool Villas, 6 Pool-side Villas and 1

Presidential Suite.

Vinpearl Golf Club

- Nha Trang Vinperal Golf Club - Nha Trang is an 18 hole, par 71

championship golf course, located on Hon Tre Island

100.00% 684,819 Nov 2008 - May 2011 Golf course: 18 holes

Vinpearl Luxury

Da Nang Vinpearl Luxury Da Nang is situated on the most beautiful

beachfront site on the famous Son Tra Dien Ngoc beach

100.00% 155,087 Nov 2009 - Jul 2011 200 hotel rooms; 39 luxury villas

Others: 2 restaurants, 4 bars, business center

and meeting facilities.

Description Effective

Ownership (1) Facilities

Vinmec International

Hospital International General Hospital

Start date of Construction/Operation: Feb 2011/07 Jan

2012

88.59% International five-star hotel –hospital at Times City, Hanoi.

Total GFA of 77,459sqm

Vinschool High quality schools in urban areas

1st kindergarten school open in June 2013 at Vinhomes

Riverside

100.00% Vinschool currently has 3 facilities in Hanoi: Vinschool Times City, Vinschool Vinhomes Riverside,

Vinschool Royal City

Operational Properties

1. As of 31 December 2013

2. Retail at 2 underground floors B1, B2

3. Retail at underground floor B1

Golden site

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

E. Financial Overview – VAS

25

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 26

(VNDbn)

As of 31 December 2013, Vingroup has VND13,047 billion cash and cash equivalents and short term investment which

is adequate to cover the near term debt maturities.

Source: VAS Consolidated FS for 9M 2013

Debt Maturity

Source: VAS Consolidated Financial Statement for 2013

1. There is a high possibility that bonds are converted to equity. Yield to maturity is 1.4% to 1.14%, lower than 5.5% coupon at time of issuance

2,250

6,050 6,217

6,246

369

527

4,231

982

107

35

Less Than 1 Year 1-3 Years 3-5 Years More Than 5 Years

Corporate Bonds Convertible Bonds Convertible loan Long-Term Borrowings Short Term Borrowings

3,023

10,808

13,445

107

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 27

Debt Mix Analysis

Total: VND27,276 Bn (US$1.29Bn)

Diversified Funding Sources (1)

Notes: Based on an exchange rate of US$1=VND21,135

1. As of 31 December 2013

Debt Breakdown (1)

By Currency

By Interest Rate

Bank Loans 20,8%

Domestic Bonds 37,6%

Convertible Bonds 22,8%

International Bonds 15,4%

Others 3,4%

VND 47% USD

53%

Float 59%

Fixed 42%

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

152

84

185

550 82,7% 77,2%

49,4% 63,3%

Dec-10 Dec-11 Dec-12 Dec-13

EBITDA

34 45 122 176 149

65

252

694

Dec-10 Dec-11 Dec-12 Dec-13

Sale of inventory properties Recurring income

(In US$m)

Note: (1) EBITDA excludes valuation gains / losses of investment property and investment

property under construction.

(2) Margins greater than 100% primarily due to share of profits / losses of associates and

other operating income resulting from disposition of interest in associates / joint ventures

and gain from disposal of investment properties and other assets.

(In US$m)

Note: (1) Margins greater than 100% primarily due to valuation gains / losses of investment

property and investment property under construction.

(2) Includes profit after tax of discontinued operations.

(In US$m) (In US$m)

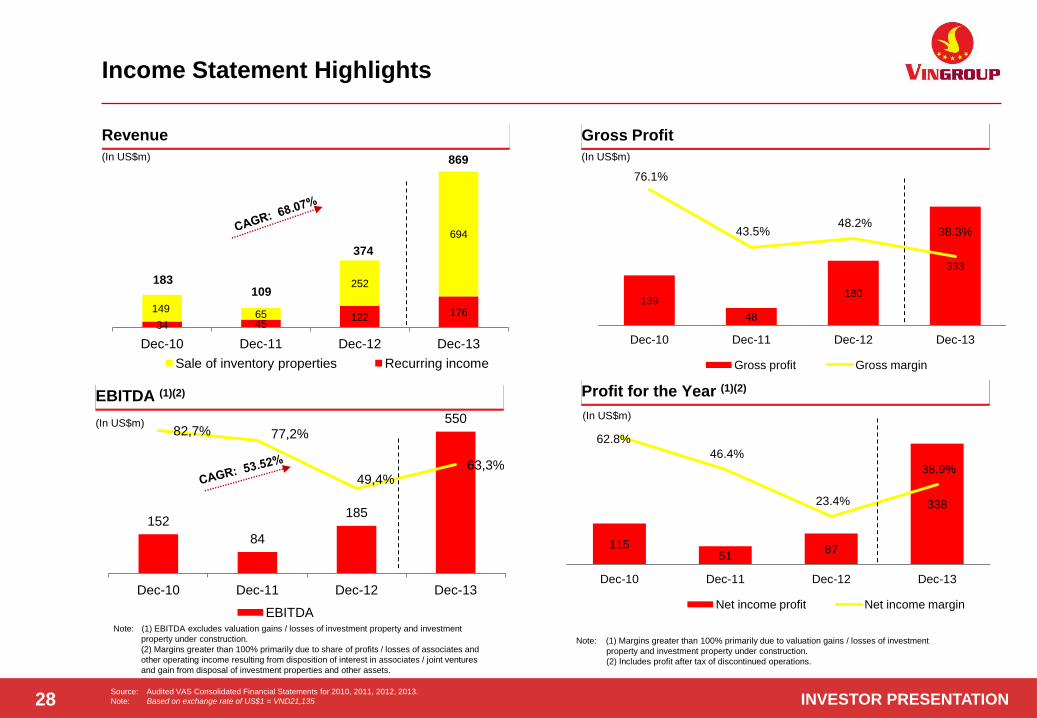

Source: Audited VAS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135 28

Income Statement Highlights

Revenue

EBITDA (1)(2)

Gross Profit

Profit for the Year (1)(2)

869

139

48

180

333

76.1%

43.5% 48.2%

38.3%

Dec-10 Dec-11 Dec-12 Dec-13

Gross profit Gross margin

374

109 183

115 51

87

338

62.8%

46.4%

23.4%

38.9%

–

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

Dec-10 Dec-11 Dec-12 Dec-13

Net income profit Net income margin

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

NA NA

7

13

2010 2011 2012 2013

NA NA

57

76

2010 2011 2012 2013

148

65

252

694

2010 2011 2012 2013

34

45

59

85

2010 2011 2012 2013

183

109

374

869

2010 2011 2012 2013

(In US$m)

Total Revenue

(In US$m)

((In US$m)

(In US$m)

(In US$m)

Rental Sale of Inventory Properties

Hospitality and Beauty Care Hospital

Source: Audited VAS Consolidated Financial Statements for 2010, 2011, 2012, 2013

Notes: Based on exchange rate of US$1 = VND21,135 29

Revenue Performance

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

(In US$m)

(In US$m)

(In US$m)

30

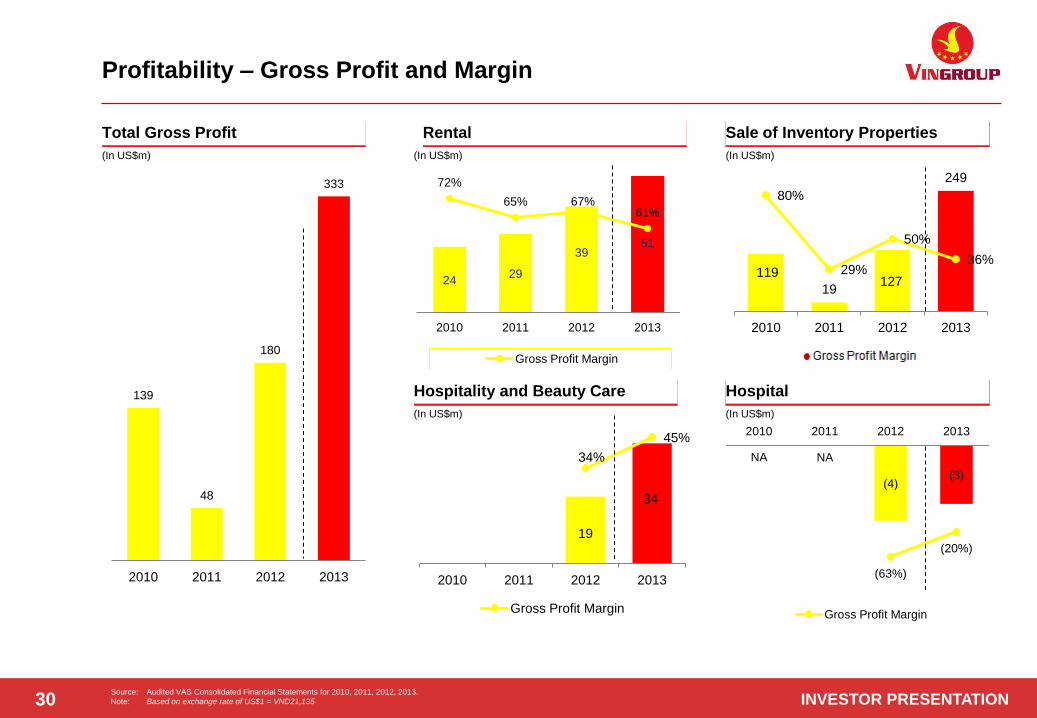

Profitability – Gross Profit and Margin

Total Gross Profit Rental Sale of Inventory Properties

Source: Audited VAS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135

Hospitality and Beauty Care Hospital

(In US$m) (In US$m)

139

48

180

333

2010 2011 2012 2013

24 29

39 51

72%

65% 67% 61%

2010 2011 2012 2013

Gross Profit Margin

NA NA

(4) (3)

(63%)

(20%)

2010 2011 2012 2013

Gross Profit Margin

19

34

34%

45%

0 0,05 0,1 0,15 0,2 0,25 0,3 0,35 0,4 0,45 0,5

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013

Gross Profit Margin

119

19 127

249

80%

29%

50%

36%

0%

20%

40%

60%

80%

100%

-

50

100

150

200

250

300

2010 2011 2012 2013

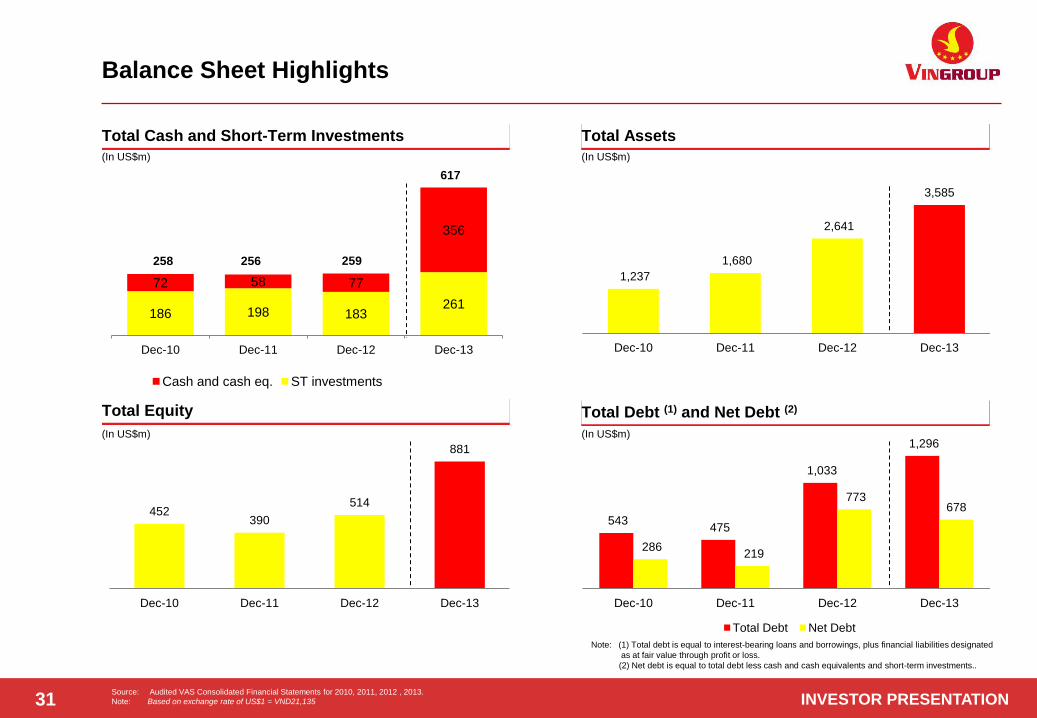

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

186 198 183 261

72 58 77

356

Dec-10 Dec-11 Dec-12 Dec-13

Cash and cash eq. ST investments

258

(In US$m) (In US$m)

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities designated

as at fair value through profit or loss.

(2) Net debt is equal to total debt less cash and cash equivalents and short-term investments..

(In US$m) (In US$m)

31 Source: Audited VAS Consolidated Financial Statements for 2010, 2011, 2012 , 2013.

Note: Based on exchange rate of US$1 = VND21,135

Balance Sheet Highlights

Total Cash and Short-Term Investments

Total Equity

Total Assets

Total Debt (1) and Net Debt (2)

617

259 256

1,237

1,680

2,641

3,585

Dec-10 Dec-11 Dec-12 Dec-13

452 390

514

881

Dec-10 Dec-11 Dec-12 Dec-13

543 475

1,033

1,296

286 219

773 678

Dec-10 Dec-11 Dec-12 Dec-13

Total Debt Net Debt

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

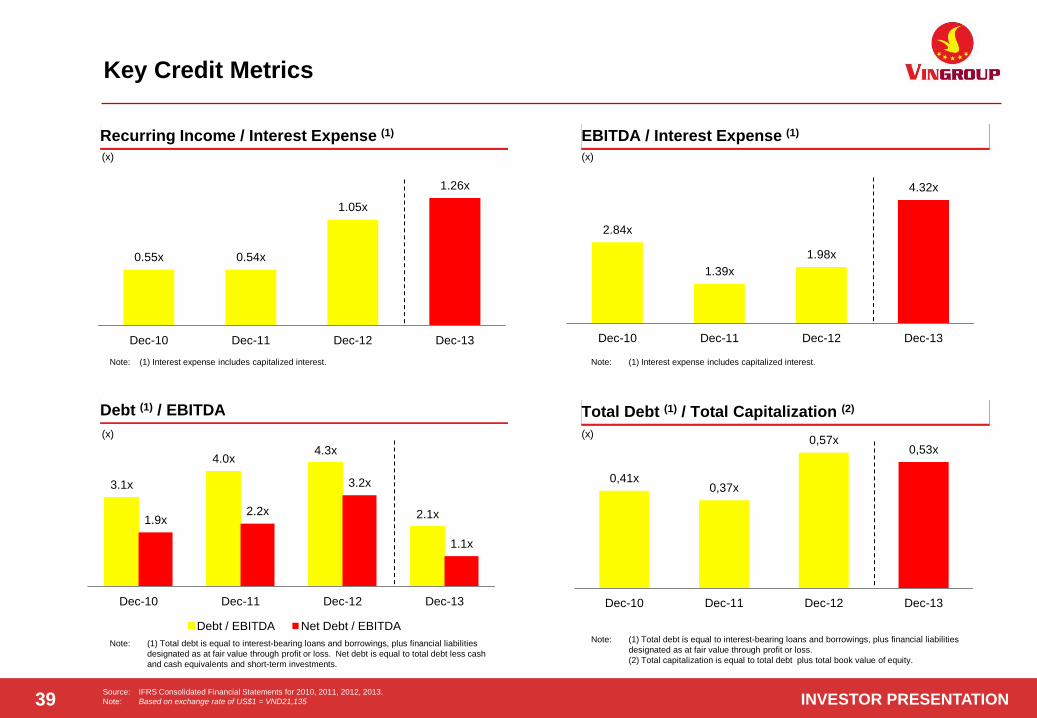

Recurring Income / Interest Expense (1)

Debt (1) / EBITDA

EBITDA / Interest Expense (1)

Total Debt (1) / Total Capitalization (2)

Note: (1) Interest expense includes capitalized interest.

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities

designated as at fair value through profit or loss. Net debt is equal to total debt less cash

and cash equivalents and short-term investments.

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities

designated as at fair value through profit or loss.

(2) Total capitalization is equal to total debt plus total book value of equity.

32 Source: Audited VAS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135

Note: (1) Interest expense includes capitalized interest.

Key Credit Metrics

(x) (x)

(x) (x)

0.57x 0.54

1.04x

1.26x

Dec-10 Dec-11 Dec-12 Dec-13

2.53x

1.04x

1.58x

3.93x

Dec-10 Dec-11 Dec-12 Dec-13

3.6x

5.6x 5.6x

2.4x 1.9x

2.6x

4.2x

1.2x

Dec-10 Dec-11 Dec-12 Dec-13

Debt / EBITDA Net Debt / EBITDA

0.55x 0.55x

0.67x 0.59x

Dec-10 Dec-11 Dec-12 Dec-13

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

F. Financial Overview - IFRS

33

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 34

(US$mn)

As of 31 December 2013, Vingroup has USD 616 million cash and cash equivalents and short term investment which is

adequate to cover the near term debt maturities.

Source: VAS Consolidated FS for 9M 2013

Debt Maturity

Source: IFRS Consolidated Financial Statement for 2013

1. There is a high possibility that bonds are converted to equity. Yield to maturity is 1.4% to 1.14%, lower than 5.5% coupon at time of issuance

106

283 284

222

17

25

17

193

46

5

Less than 1 year 1-3 years 3-5 years More than 5 years

Corporate bonds Convertible bond Convertible loan Long-term borrowings Short-term debts

5

141

501

552

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

176 117

232

604

97.0% 105.7%

75.5% 69.5%

Dec-10 Dec-11 Dec-12 Dec-13

EBITDA EBITDA margin

34 45 122 176 148 65

185

694

Dec-10 Dec-11 Dec-12 Dec-13

Recurring income Sales of Inventory Properties

182 110

307

869

(In US$m)

Note: (1) EBITDA excludes valuation gains / losses of investment property and investment

property under construction.

(2) Margins greater than 100% primarily due to share of profits / losses of associates and

other operating income resulting from disposition of interest in associates / joint ventures

and gain from disposal of investment properties and other assets.

(In US$m)

Note: (1) Margins greater than 100% primarily due to valuation gains / losses of investment

property and investment property under construction.

(2) Includes profit after tax of discontinued operations.

(In US$m) (In US$m)

Source: IFRS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135 35

Income Statement Highlights

Revenue

EBITDA (1)(2)

Gross Profit

Profit for the Year (1)(2)

73.1%

48.6% 41.6% 39.5%

Dec-10 Dec-11 Dec-12 Dec-13

Gross profit Gross margin

133

54

128

343

260

137 149

289

142.8%

123.9%

48.4% 33.3%

Dec-10 Dec-11 Dec-12 Dec-13

Net income profit Net income margin

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

182

110

307

869

2010 2011 2012 2013

NA NA

7

14

2010 2011 2012 2013

NA NA

57

76

2010 2011 2012 2013

148

65

252

694

2010 2011 2012 2013

34

45

59

85

2010 2011 2012 2013

(In US$m)

Total Revenue

(In US$m)

((In US$m)

(In US$m)

(In US$m)

Rental Sale of Inventory Properties

Hospitality and Beauty Care Hospital

Source: IFRS Consolidated Financial Statements for 2010, 2011, 2012, 2013

Notes: Based on exchange rate of US$1 = VND21,135

Revenue Performance

36

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

(In US$m)

(In US$m)

(In US$m)

37

Profitability – Gross Profit and Margin

Total Gross Profit Rental Sale of Inventory Properties

Source: IFRS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135

Hospitality and Beauty Care Hospital

(In US$m) (In US$m)

NA NA

(4) (3)

(63%)

(21%)

2010 2011 2012 2013

Gross Profit Margin

133

54

128

343

2010 2011 2012 2013

27 35

46 63

79% 77% 79% 74%

2010 2011 2012 2013

Gross Profit Margin

19

35

34%

46%

2010 2011 2012 2013

Gross Profit Margin

106

19

67

249 72%

29%

36% 36%

-

50

100

150

200

250

300

2010 2011 2012 2013

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

(In US$m) (In US$m)

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities designated

as at fair value through profit or loss.

(2) Net debt is equal to total debt less cash and cash equivalents and short-term investments..

(In US$m) (In US$m)

38 Source: IFRS Consolidated Financial Statements for 2010, 2011, 2012 , 2013.

Note: Based on exchange rate of US$1 = VND21,135

Balance Sheet Highlights

Total Cash and Short-Term Investments

Total Equity

Total Assets

Total Debt (1) and Net Debt (2)

139 156 181 260

71 58 77

356

Dec-10 Dec-11 Dec-12 Dec-13

Cash and cash eq. ST investments

210 214 258

616

1,720

2,454

3,325

4,056

Dec-10 Dec-11 Dec-12 Dec-13

792 790 771

1,103

Dec-10 Dec-11 Dec-12 Dec-13

556 472

1,005

1,268

346 258

747 652

Dec-10 Dec-11 Dec-12 Dec-13

Total Debt Net Debt

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

Recurring Income / Interest Expense (1)

Debt (1) / EBITDA

EBITDA / Interest Expense (1)

Total Debt (1) / Total Capitalization (2)

Note: (1) Interest expense includes capitalized interest.

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities

designated as at fair value through profit or loss. Net debt is equal to total debt less cash

and cash equivalents and short-term investments.

Note: (1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities

designated as at fair value through profit or loss.

(2) Total capitalization is equal to total debt plus total book value of equity.

39 Source: IFRS Consolidated Financial Statements for 2010, 2011, 2012, 2013.

Note: Based on exchange rate of US$1 = VND21,135

Note: (1) Interest expense includes capitalized interest.

Key Credit Metrics

(x) (x)

(x) (x)

0.55x 0.54x

1.05x

1.26x

Dec-10 Dec-11 Dec-12 Dec-13

2.84x

1.39x

1.98x

4.32x

Dec-10 Dec-11 Dec-12 Dec-13

3.1x

4.0x 4.3x

2.1x 1.9x

2.2x

3.2x

1.1x

Dec-10 Dec-11 Dec-12 Dec-13

Debt / EBITDA Net Debt / EBITDA

0,41x 0,37x

0,57x 0,53x

Dec-10 Dec-11 Dec-12 Dec-13

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

G. Appendix – Vincom Retail

40

RATINGS UPDATE PRESENTATION 41

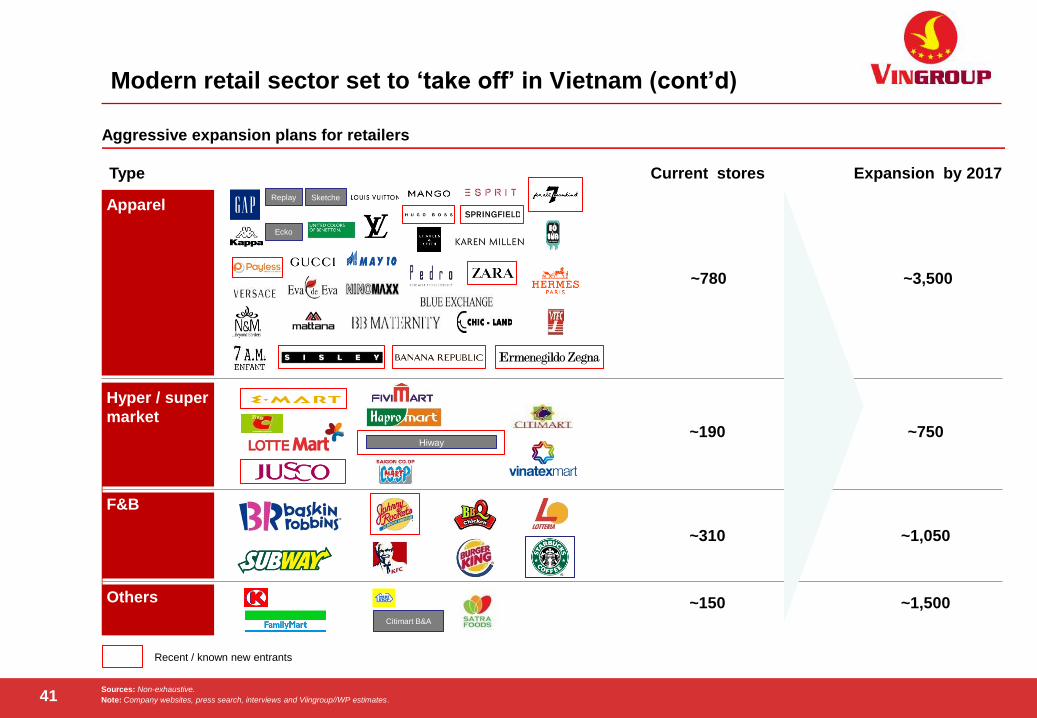

Modern retail sector set to ‘take off’ in Vietnam (cont’d)

Sources: Non-exhaustive.

Note: Company websites, press search, interviews and Viingroup//WP estimates.

Aggressive expansion plans for retailers

Type

F&B

Expansion by 2017

Replay Sketche

Ecko

Citimart B&A

~3,500

~750

~1,050

~1,500

Hiway

~780

~190

~310

~150

Current stores

Others

Apparel

Hyper / super

market

Recent / known new entrants

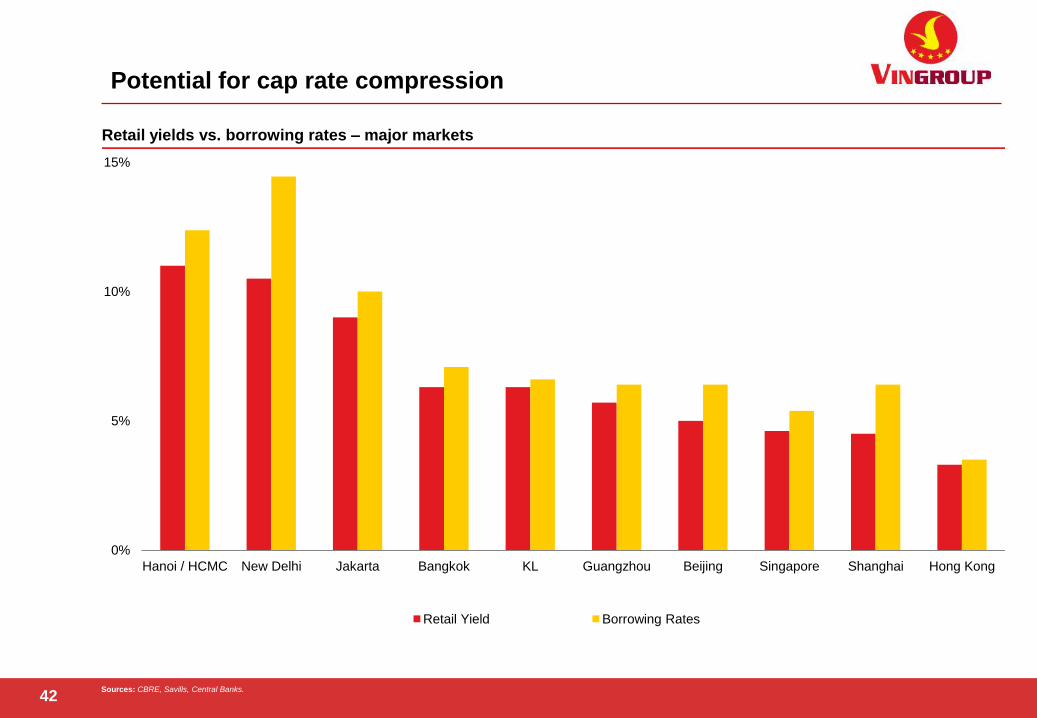

RATINGS UPDATE PRESENTATION 42

Potential for cap rate compression

Sources: CBRE, Savills, Central Banks.

Retail yields vs. borrowing rates – major markets

0%

5%

10%

15%

Hanoi / HCMC New Delhi Jakarta Bangkok KL Guangzhou Beijing Singapore Shanghai Hong Kong

Retail Yield Borrowing Rates

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION 43

This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future performance,

outcomes, and results may differ materially from those expressed in forward-looking statements as a result of a number of

risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry

and economic conditions, interest rate trends, cost of capital and capital availability, cost of construction, availability of real

estate properties and land, competition from other companies and venues for the sale/distribution of goods and services, shifts

in customer demands, customers and partners, changes in operation expenses, including employee wages, benefits and

training, governmental and public policy changes and the continued availability of financing in the amounts and the terms

necessary to support future business. You are cautioned not to place undue reliance on these forward-looking statements,

which are based on current view of management on future events.

Disclaimer

INVESTOR PRESENTATION INVESTOR PRESENTATION INVESTOR PRESENTATION

Vingroup JSC

Vingroup Office Tower, Vinhomes Riverside Eco-Urban Area

Long Bien District, Hanoi, Vietnam

Tel: +84 (4) 3974 9999 ext. 926

Fax: +84 (4) 3974 8888

Website: http://www.vingroup.net

E-mail: [email protected]

Investor Relations Department

Copyright © 2022 FDOKUMEN