Delay and Capacity Trade-Offs in Mobile Ad Hoc Networks: A Global Perspective

Electronic copy available at: http://ssrn.com/abstract=1475380

1

Vertical divestitures through equity carve-outs and spin-offs: A product markets

perspective

Bharat A. Jaina, Omesh Kinib, *, Jaideep Shenoyc

a College of Business and Economics, Towson University, Towson, MD 21252 b Robinson College of Business, Georgia State University, Atlanta, GA 30302

c A.B. Freeman School of Business, Tulane University, New Orleans, LA 70118

_____________________________________________________________________________________

ABSTRACT

Using a product markets perspective to investigate the decision to vertically disintegrate, we find that vertical divestitures are more likely in response to positive industry demand shocks, favorable industry financing conditions, and lower parent firm relative productivity and are less likely when the potential for contracting problems is high. Conditional on vertical divestitures, equity carve-outs are more likely in environments in which relationship-specific investments are more prevalent and when the need for external funds is high, while spin-offs are more likely in larger industries and in industries that experience positive demand shocks. Our examinations of announcement-period wealth effects and changes in operating performance indicate that vertical divestitures are motivated by efficiency considerations. JEL classification: G34, L22, L25, D57 Keywords: Vertical divestitures, Equity carve-outs, Spin-offs, Product markets _____________________________________________________________________________________

☆We wish to thank Jayant R. Kale, Isabel Tkatch, Harold Mulherin, Vikram Nanda, Chip Ryan, Paul Spindt, and Sheri Tice for helpful comments. We are particularly thankful to Gordon Phillips (the referee) whose comments helped us significantly improve the paper. We thank Husayn Shahrur for providing us with a cleaned version of the Compustat data on the identity of key suppliers and customers and Ryan Williams for excellent research assistance. The usual disclaimer applies.

*Corresponding author. Robinson College of Business, Georgia State University, Atlanta, GA 30302,

USA. Tel. + 1-404-413-7343; Fax: + 1-404-413-7312. E-mail addresses: [email protected] (Bharat A. Jain), [email protected] (Omesh Kini), [email protected] (Jaideep Shenoy).

Electronic copy available at: http://ssrn.com/abstract=1475380

2

1. Introduction

Since the seminal work of Coase (1937), the extant literature on the structure of vertical

organizations has developed several theories to explain the determinants of the vertical boundaries of a

firm.1 On the one hand, this stream of literature has argued that common ownership over successive

stages of the production or distribution process can create value for the integrating firm through product

market considerations such as reduced transaction costs of negotiating with suppliers or customers and

improved incentives to make relationship-specific investments and facilitation of anti-competitive

strategies such as foreclosure, in which vertical integration is used to raise rival costs, or collusion, in

which vertical integration improves coordination between the integrated firm and its nonintegrated

rivals.2 On the other hand, researchers have suggested that higher organizational complexity and its

resultant negative impact on firm productivity as well as a greater need for external funds may cause

integrated firms to consider shrinking their boundaries.3

Given the trade-offs, value-maximizing managers contract the firm’s vertical boundary when the

potential benefits from product market considerations are dominated by the costs arising from higher

organizational complexity or a greater need for financing. Further, even when a firm decides to contract

its vertical boundary, the nature of the benefits and costs determines whether it chooses to partially or

fully disintegrate. While the causes and consequences of vertical integration are well studied, a paucity of

empirical evidence exists on vertical disintegration. In this paper, we examine whether product market

and financing considerations impact the probability of occurrence of vertical divestitures; the choice of

method of vertical divestitures, i.e., equity carve-outs versus spin-offs, conditional on vertical

1 See, for example, Stigler (1951), Perry (1989), Chen (2005), Joskow (2005), Sappington (2006), Lafontaine and Slade (2007), Eckbo and Thorburn (2008), Acemoglu, Johnson, and Mitton (2009), and Shenoy (2008) for extensive discussions on the economic forces behind vertical integration and disintegration. 2 Extensive research argues that vertical integration can lead to anti-competitive strategies such as foreclosure (e.g., Salinger, 1988; Hart and Tirole, 1990; and Ordover, Saloner, and Salop; 1990) or collusion (e.g., Chen, 2001; and Nocke and White, 2007). 3 Eckbo and Thorburn (2008), Rajan, Servaes, and Zingales (2000), and Burch and Nanda (2003) argue that higher organizational complexity can result in value destruction due to neglect of the firm’s core business, inefficient cross-subsidization, power plays of divisional managers, and poorly structured incentive compensation for divisional managers. Çolak and Whited (2007) and Lang, Poulsen, and Stulz (1995) indicate that financing considerations such as the need for capital influence divestiture decisions. Maksimovic and Phillips (2001, 2002) argue that industry demand shocks and low relative firm productivity cause industry players to reevaluate ownership of assets.

3

divestitures; the announcement-period wealth effects of vertical divestitures on the parent firm, parent and

subsidiary rival firms, supplier firms, and customer firms; and the changes in operating performance

around vertical divestitures.

Our analysis of the determinants of vertical divestitures reveals the following findings. First, the

probability of vertical divestitures increases with positive subsidiary industry demand shocks as well as

low parent firm relative productivity. These results are generally consistent with the neoclassical model of

firm organization proposed by Maksimovic and Phillips (2002). In addition, the probability of vertical

divestitures is lower if parent firms have more significant intra-firm vertical relations or if they belong to

industries containing a higher proportion of vertically integrated firms. Because high vertical relatedness

is indicative of contracting problems and the potential for holdup, our results suggest that vertical

divestitures are less likely in environments requiring investments in relationship specific assets to be

competitive. Finally, favorable industry financing conditions, particularly in subsidiary industries, instead

of parent firm internal financing constraints, are more likely to influence the vertical divestiture decision.

Conditional on vertical divestitures, our analysis of the choice of the method of vertical

divestitures provides insights on factors that explain partial vertical disintegrations via equity carve-outs

or complete vertical disintegrations via spin-offs. We find that partial divestitures through equity

carve-outs are more likely when relationship-specific investments in the subsidiary industry as measured

by its research and development (R&D) intensity are higher and in the presence of explicit product market

contractual agreements between the parent firm and the divested subsidiary after the divestiture. Because

R&D-intensive environments and the presence of product market agreements are likely to indicate

potential contracting problems, parents seem to foresee such problems and maintain an ownership stake in

the subsidiary through a carve-out. These results are consistent with Fee, Hadlock, and Thomas (2006),

who find that equity ownership in supplier firms by customer firms is beneficial when expropriation and

holdup problems are prevalent. In addition, we find that the probability of a vertical divestiture through a

carve-out is larger when the parent firm’s need for external funds is higher. Further, we find that complete

divestitures through spin-offs are more likely in larger industries and in industries that experience positive

4

demand shocks. These findings support Stigler (1951), who suggests that firms in larger industries and in

growing industries strive to capture benefits of specialization, which are maximized under complete

vertical separation. Finally, anti-competitive rationales such as collusion and foreclosure have no bearing

on the choice between equity carve-outs and spin-offs.

The undoing of the vertically integrated structure also enables us to evaluate the announcement-

period wealth effects of the parent firms, as well as related product market participants such as parent and

subsidiary rival firms, supplier firms, and customer firms. On the one hand, the wealth effects to parent

firms are likely to be positive because divestitures can enhance efficiency by decreasing organizational

complexity. On the other hand, negative parent firm wealth effects can occur because divestitures can

reduce efficiency by exacerbating the holdup problem and reducing the incentives to make relationship-

specific investments. The wealth effects to parent firms can also be negative due to a decreased ability to

either foreclose rival firms from critical inputs or collude with them after the divestiture. Further, the

effects to the parent firms are likely to spill over to all related product market participants [e.g., Eckbo

(1983) and Shenoy (2008) in the context of vertical takeovers].

For the full sample of vertical divestitures as well as for both the equity carve-out and spin-off

samples, we find significantly positive announcement-period abnormal returns to parent firms, parent

rival firms, and supplier firms and weakly positive abnormal returns to subsidiary rival firms and

customer firms. Taken together, the positive wealth effects to the parent firms, parent and subsidiary rival

firms, and supplier and customer firms are inconsistent with the foreclosure or collusion rationales. The

picture that emerges from our univariate wealth effects analysis is that vertical divestitures result in

efficiency gains to parent firms due to enhanced focus or specialization benefits and convey information

to parent and subsidiary rival firms that they too, can take advantage of these gains by changing their own

organizational structures. Furthermore, some of the resulting benefits accrue to supplier and customer

firms.

A potential problem with the above interpretation of our univariate results is that our hypotheses

are not mutually exclusive. We, therefore, design cross-sectional tests that enhance our ability to isolate

5

the impact of each potential economic determinant on wealth effects and on the changes in operating

performance around vertical divestitures. We find that the announcement-period wealth effects for parent

firms are higher when the pre-divestiture investments in relationship specific assets are lower. This result

indicates that the abnormal returns for parent firms are higher when the potential for ex post contractual

inefficiencies arising from the undoing of the integrated form is lower. Further, we show that the

announcement-period wealth effects for parent firms are larger if parent firms are less focused prior to the

divestiture. This result indicates that the abnormal returns for parent firms are larger if the potential for a

decrease in organizational complexity is higher. Our examination of changes in operating performance

around vertical divestiture events lends further support to efficiency considerations. Finally, the

determinants of the wealth effects to the rival firms, supplier firms, and customer firms yield further

corroborating evidence consistent with the efficiency-enhancing view and inconsistent with market

power-based rationales.

Our study makes the following contributions. First, it is the only study that we are aware of that

applies a product markets perspective to evaluate the decision to vertically disintegrate and the choice

between equity carve-outs versus spin-offs to conduct a vertical divestiture. Our analysis on determinants

of the vertical divestiture decision enables us to shed light on the extant theoretical and empirical

literature, which suggests that divestitures are optimal responses to industry demand shocks that results in

the transfer of ownership of assets to where they can be most productively deployed leading to efficiency

gains (e.g., Stigler, 1951; Maksimovic and Phillips, 2001, 2002; Chen, 2005; and Sappington, 2006).

Further, the modeling of the choice between carve-outs and spin-offs as alternative mechanisms in

vertical divestitures enables us to test if ownership through carve-outs is a choice made by firms to

mitigate contractual frictions or financial constraints. As such, our work also builds upon recent studies

showing that partial equity stakes in a vertical context are used to ease contracting and financing frictions

(e.g., Fee, Hadlock, and Thomas, 2006). Second, our study is also the first to examine the wealth effects

of vertical divestitures not only for parent firms, but also for parent and subsidiary rival firms, supplier

firms, and customer firms, thereby providing additional insights into the overall economic impact of

6

firms’ decisions to contract their vertical boundaries. Finally, our study complements the extant literature

on vertical integration by demonstrating that firms also shrink their boundaries for efficiency reasons and

that the original vertical integrated structure was not motivated by anti-competitive rationales such as

foreclosure or collusion (e.g., Eckbo, 1983; and Shenoy, 2008).

The remainder of the paper proceeds as follows. Section 2 provides a discussion of the factors

that can affect the vertical divestiture decision and the choice of method of vertical divestiture. In Section

3, we describe our data sources, sample selection criteria, and salient characteristics of our sample. We

present our univariate analysis followed by two-stage Heckman probit regressions in Section 4. In Section

5, we present our univariate and cross-sectional predictions and results regarding both

announcement-period wealth effects of vertical divestitures and changes in operating performance around

vertical divestitures. Finally, we summarize our results and conclude the paper in Section 6.

2. Vertical divestiture decisions: theoretical considerations and variable descriptions

Our analysis of the economics of vertical divestitures is conducted via a two-stage process

whereby in the first stage we examine factors influencing the vertical divestiture decision itself

(Subsection 2.1) and in the second stage, conditional on vertical divestitures; we evaluate the

determinants of the choice of method of vertical divestitures (Subsection 2.2). In these subsections, we

provide theoretical justifications for the selection of variables that are hypothesized to influence either the

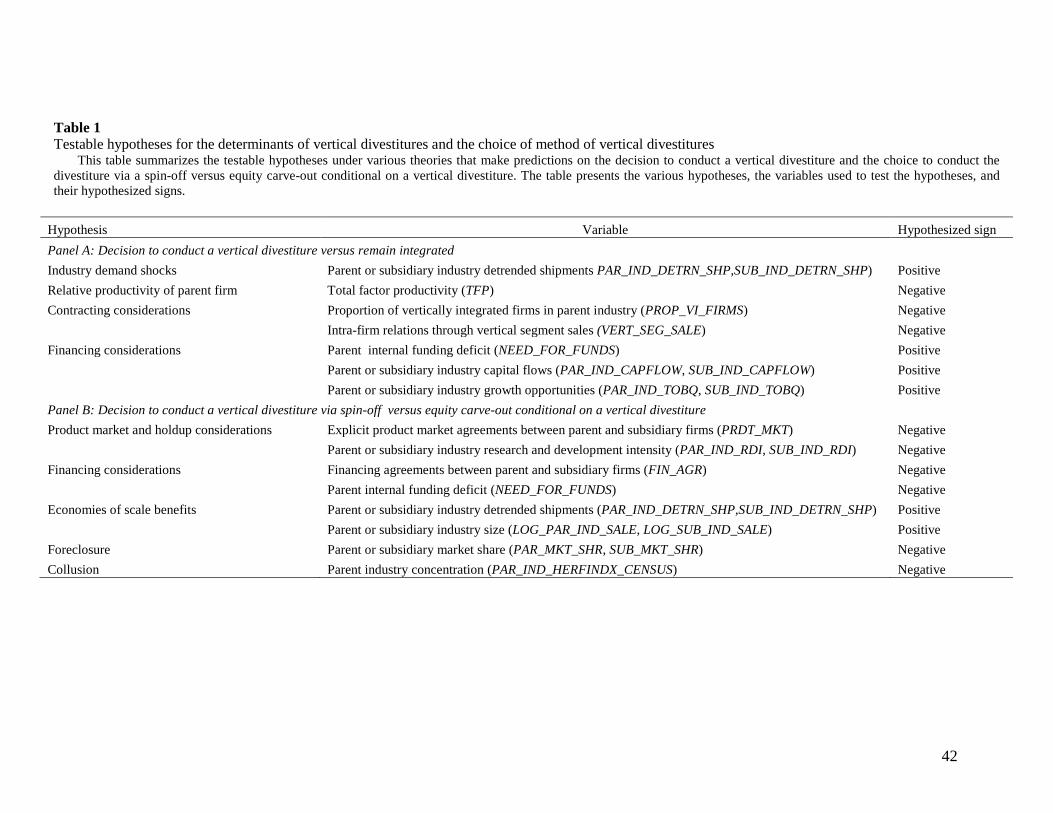

vertical divestiture decision or the method of divestiture. A summary of our hypotheses, variable names,

and predictions is provided in Table 1, and detailed variable descriptions and measurements are presented

in the Appendix.

[Insert Table 1 near here]

2.1. Factors influencing the vertical divestiture decision

In the discussion that follows, we provide the theoretical foundations for why industry demand

shocks, relative productivity of the parent, contracting considerations, and financing considerations can

impact the decision by firms to vertically divest.

2.1.1. Industry demand shocks and the decision to divest

7

Maksimovic and Phillips (2001, 2002) present a neoclassical model of firm organization that

provides predictions on factors that drive the sale of corporate assets. Assuming differential productivity

among industry firms, they argue that positive demand shocks to industries alter the value of the assets

causing less efficient producers to transfer assets if they are relatively more valuable to other more

efficient producers in the industry. As such, their model predicts that firms sell assets in their less

productive divisions in response to positive demand shocks to these divisions. In the context of vertical

divestitures, an alternative stream of literature has suggested that industry demand shocks reduce the

benefits of integration relative to separation and provide the impetus for vertically integrated firms to

divest either their upstream or downstream business to preserve the most efficient organizational form

(e.g., Stigler, 1951; Chen, 2005; and Sappington, 2006). The common thread in the literature is that

positive industry demand shocks trigger a change in organizational form.

Drawing on the above arguments, we hypothesize that parent (subsidiary) industry demand

shocks alter the extent of efficiency of the integrated structure and, therefore, influence the vertical

divestiture decision. Consistent with Maksimovic and Phillips (2002), we measure industry demand

shocks as the detrended value of the natural logarithm of parent (subsidiary) industry real sales,

PAR_IND_DETRN_SHP (SUB_IND_DETRN_SHP). We expect a positive relation between the measures

of demand shocks and the probability of a vertical divestiture.

2.1.2. Relative productivity of parent and the decision to divest

Firms are likely to be motivated to seek efficiency gains through a change in organizational form

when the current structure is not achieving competitive levels of productivity. As such, low or declining

firm productivity in an integrated structure is indicative of opportunities for efficiency improvement

under alternative organizational forms. Furthermore, Maksimovic and Phillips (2001) argue that firms sell

assets when they are less productive in comparison with their industry benchmarks when faced with

positive demand shocks. We posit that vertically integrated firms with productivity below benchmark

levels are likely to seek efficiency gains through divestitures. Consistent with Maksimovic and Phillips

(2001), we measure relative firm productivity as the total factor productivity of the parent firm, TFP,

8

computed on the basis of the methodology in Faleye, Mehrotra, and Morck (2006). We expect a negative

relation between total factor productivity and the probability of a vertical divestiture.

2.1.3. Contracting considerations and the decision to divest

It has been argued that vertical integration provides a solution to the holdup problem and allows

firms to undertake relationship specific investments (Coase, 1937; Klein, Crawford, and Alchian, 1978;

Williamson, 1971, 1979; Grossman and Hart, 1986; and Hart and Moore, 1990). Therefore, the vertical

divestiture decision is likely to be based on the economic trade-off between the potential efficiency gains

achieved through vertical separation and the likely increase in contractual inefficiencies when related

parties separate. We posit that in industries in which the need for and extent of investment in

relationship-specific assets is high, the potential for lower contracting costs in an integrated structure is

likely to dominate, thereby resulting in a lower probability of vertical divestiture. Furthermore, in such

industries, we would expect the extent of vertical relatedness among firms to be relatively high.

We consider two measures that capture the extent of vertical relatedness, one at the parent

industry level and the other at the parent firm level. The first measure is the proportion of vertically

integrated firms in the parent industry, PROP_VI_FIRMS. A higher proportion of vertically integrated

firms in the parent’s industry is indicative of an industry structure in which firms rely on investments in

relationship specific assets to secure a competitive advantage. As such, we would expect a negative

relation between the probability of vertical divestitures and the proportion of vertically integrated firms in

the parent industry. At the firm level, we measure the need for investments in relationship-specific assets

by assessing the extent of intra-firm relations through vertical segment sales, VERT_SEG_SALE. We

measure the extent of intra-firm relation by the proportion of the firm’s total sales accounted for by the

average vertically related secondary segment of the parent. A higher value of VERT_SEG_SALE implies

greater loss of contractual efficiencies in the event of a separation and, therefore, a lower likelihood of a

vertical divestiture.

2.1.4. Financing considerations and the decision to divest

9

The main premise behind the financing hypothesis is that firms divest assets when doing so

provides them with the cheapest source of funds (John and Ofek, 1995; and Lang, Poulsen, and Stulz,

1995). A vertically integrated firm could undertake a divestiture if it is capital-constrained and needs to

obtain financing to continue its operations or, alternatively, it could undertake a divestiture simply to take

advantage of favorable industry financing conditions. We use three variables to evaluate the impact of

financing considerations on the probability of vertical divestitures. Our first variable,

NEED_FOR_FUNDS, attempts to capture the extent of internal financing constraints faced by the

integrated firm. Our measure of need for funds is similar in spirit to Gomes and Phillips (2008) and

Maksimovic and Phillips (2008) and is measured as the difference between the firm's capital expenditures

and the sum of its operating income before depreciation and change in working capital. We expect a

positive relation between parent firm need for funds and the probability of a vertical divestiture.

The second variable is the extent of parent (subsidiary) industry capital flows,

PAR_IND_CAPFLOW (SUB_IND_CAPFLOW), and attempts to measure industry financing conditions. It

is measured as the ratio of the total debt and equity issuance in the parent (subsidiary) industry to industry

market capitalization. Our third financing variable measures the attractiveness of industry financing

conditions by assessing the attractiveness of industry valuations or the extent of industry growth

opportunities or both. Higher parent (subsidiary) industry valuations or growth prospects are likely to

increase the demand for capital from industry firms as well as the supply of external financing at

attractive terms. We measure parent (subsidiary) industry valuation or growth opportunities by the

industry Tobin’s q, PAR_IND_TOBQ (SUB_IND_TOBQ). We expect that the probability of a vertical

divestiture to be positively related to parent (subsidiary) industry capital flows and parent (subsidiary)

industry Tobin’s q.

2.2. Factors influencing the choice of method of divestitures conditional on vertical divestitures

Contingent on firms vertically divesting, we develop hypotheses that link product market and

holdup considerations, financial considerations, economies of scale benefits, and anti-competitive

10

rationales like foreclosure and collusion to the choice of method of vertical divestitures, i.e., spin-offs

versus equity carve-outs.

2.2.1. Product market and holdup considerations and the method of vertical divestitures

In the absence of complete vertical integration, extant research has argued that partial equity

ownership in vertically related businesses is a potential solution to the underinvestment problem in

relationship-specific assets (e.g., Aghion and Tirole, 1994; Dasgupta and Tao, 2000; and Harbaugh,

2001). Fee, Hadlock, and Thomas (2006) conclude that equity ownership by customers in suppliers is

beneficial when firms are concerned with expropriation and holdup problems arising from relationship-

specific investments.4

We argue that the presence of explicit long-term product market relations between the parent and

subsidiary after vertical divestitures is likely to indicate the potential for expropriation and holdup

problems. Therefore, the choice of divestiture method is likely to favor carve-outs rather than spin-offs.

We follow Allen and Phillips (2000) and treat buyer-supplier agreements, technology sharing and R&D

agreements, marketing and distribution agreements, and specialty services agreements between the parent

and subsidiary firms after the divestiture as explicit product market relations. Thus, the variable

PRDT_MKT takes on a value of one if explicit product market relations between parent and subsidiary

firm are maintained post-divestiture and is zero otherwise. We expect a negative relation between

PRDT_MKT and the probability of vertical divestitures through spin-offs.

As such, when vertical business relationships are characterized by the need for

investments in relationship-specific assets, equity carve-outs could be more advantageous relative to spin-

offs.

Recent research suggests that the need for investments in relationship-specific assets as well as

the potential for expropriation and holdup is greater in R&D-intensive environments (e.g., Allen and

Philips, 2000; and Fee, Hadlock, and Thomas, 2006). We, therefore, argue that vertical divestitures

through equity carve-outs are more likely when either the parent firm or its subsidiaries operate in high

4 Similarly, several studies show that equity ownership is beneficial when coupled with product market relations (e.g., Allen and Phillips, 2000; Gompers and Lerner, 2000; and Boone, 2003).

11

R&D-intensive industries. The parent (subsidiary) industry R&D intensity is measured by the variable

PAR_IND_RDI (SUB_IND_RDI). Thus, we expect a negative relation between parent (subsidiary)

industry R&D intensity and the probability of a vertical divestiture through a spin-off.

2.2.2. Financing considerations and method of vertical divestitures

We also examine how financing constraints of the parent influence the choice of method of

vertical divestiture. Fee, Hadlock, and Thomas (2006) find that the incidence of equity stakes is more

likely between buyer and supplier firms when financing constraints faced by the supplier firms are higher.

Other researchers argue that firms select carve-outs over spin-offs when they are motivated by a desire to

raise capital (e.g., Allen and McConnell, 1998; and Powers, 2001). We use two proxies to test the

financing hypothesis. First, we create a dichotomous variable FIN_AGR, which takes on the value of one

if the parent and subsidiary firms maintain financing agreements post-divestiture and equals zero

otherwise. If the presence of a financing agreement is indicative of financing constraints for the divested

firm, we expect a negative relation between the presence of financing agreements and the probability of

divestiture through spin-offs. Second, we include the parent firm’s need for external capital

(NEED_FOR_FUNDS). Because a higher value of NEED_FOR_FUNDS suggests that the needs of the

parent to raise external capital are greater, we expect a negative relation between NEED_FOR_FUNDS

and the probability of divestiture via spin-off.

2.2.3. Economies of scale benefits and method of vertical divestitures

Stigler (1951) argues that firms tend to vertically integrate their production if they operate in

industries that are either small or declining. In large or growing industries, however, upstream divisions of

some firms are disintegrated to take advantage of specialization and economies of scale and become

suppliers for the downstream industry. Thus, vertical integration is more likely in either nascent or

declining industries, while vertical disintegration is likely in either large or growing industries.

Subsequently, researchers have built on Stigler’s argument and developed theoretical models to show that

vertical divestitures result in efficiency gains (e.g., Chen, 2005; and Sappington, 2006).

12

Drawing on these studies, we hypothesize that industry shocks that signal a transition in the

industry growth phase influence the decision to conduct the vertical divestiture via spin-off or carve-out.

In particular, we argue that industry size and industry demand shocks signal the transition to a growth

phase. The stronger the magnitude of these shocks, the greater are the likely efficiency gains arising from

separation and consequently weaker the economic rationale for units to remain vertically integrated.

Further, because spin-offs represent a complete separation of vertically related businesses compared with

equity carve-outs in which the separation is partial, the opportunity to capture efficiency gains arising

from specialization are higher in the case of spin-offs.

Our measure of parent (subsidiary) industry demand shocks is PAR_IND_DETRN_SHP

(SUB_IND_DETRN_SHP). We compute parent (subsidiary) industry size as the natural logarithm of the

parent (subsidiary) industry real sales, LOG_PAR_IND_SALE (LOG_SUB_IND_SALE). We expect a

positive relation between the parent (subsidiary) industry size and industry demand shocks and the

probability of a vertical divestiture via spin-off.

2.2.4. Foreclosure and method of vertical divestitures

The foreclosure hypothesis suggests that vertical integration provides an opportunity for

integrated firms to raise the costs of their unintegrated rivals by denying or limiting access to inputs or

distribution outlets to their rivals (e.g., Salinger, 1988; Hart and Tirole, 1990; Ordover, Saloner, and

Salop, 1990; and Rey and Tirole, 2006). The potential for foreclosure benefits in a vertically integrated

structure, however, raises the question of whether vertical divestitures result in the erosion of these

benefits. If foreclosure benefits are high, then the integrated firms are more likely to seek vertical

divestitures through equity carve-outs, where they can continue to exert influence on the divested entity in

raising rival input prices in an attempt to preserve these benefits. Consistent with Shenoy (2008), who

argues that higher market shares of bidder and target firms in vertical takeovers increase the market power

of the integrated firm to foreclose on nonintegrated rivals, we include parent and subsidiary firm market

shares, PAR_MKT_SHR and SUB_MKT_SHR, respectively, as proxies for foreclosure benefits. We

13

expect a negative relation between parent (subsidiary) market share and the probability of a vertical

divestiture through a spin-off.

2.2.5. Collusion and method of vertical divestitures

The basic premise behind the collusion hypothesis is that the subsidiary of the integrated vertical

firm serves as a mechanism that facilitates the flow of information between the integrated firm and its

unintegrated rivals (e.g., Chen, 2001; and Nocke and White, 2007). This flow of information enables

better coordination between the integrated firm and its unintegrated rivals. Thus, vertical divestitures

reduce the ability of rival firms to collude because the divestiture of the input or distribution outlet

eliminates the coordination mechanism for collusion. Consequently, in environments in which

opportunities for collusion between integrated firms and their unintegrated rivals are high, we expect

partial divestures in the form of equity carve-outs instead of complete separation via spin-offs as

integrated firms attempt to retain control of their subsidiaries in an effort to continue to capture the

highest possible benefits from collusion. Because opportunities for collusion among rival firms are

typically higher in concentrated industries, we expect a negative relation between parent industry

concentration and the probability of a vertical divestiture through a spin-off. We follow the two-step

methodology outlined in Hoberg and Phillips (2009) to impute a Census-based Herfindahl index for the

parent industry, PAR_IND_HERFINDX_CENSUS.

2.2.6. Control factors influencing the method of vertical divestitures

In our multivariate tests, we include variables that potentially influence the choice of restructuring

through equity carve-outs versus spin-offs for all types of divestitures, and not just vertical divestitures, as

control variables. We, therefore, control for parent firm financing constraints (PAR_LEVER_PRE),

market conditions favoring equity issuances (SUB_FF_IND_RET and NUM_IPOSEO), and size of

subsidiary relative to parent (REL_SIZE) because the extant literature suggests that the economic forces

represented by these variables influence divestiture decisions (e.g., Allen, Lummer, McConnell, and

Reed, 1995; Hite and Owers, 1983; and Powers, 2001).

3. Data sources, sample selection, and salient characteristics of the sample

14

In this section, we describe the data sources and sample selection criteria used to identify our

sample of vertical divestitures and the control sample of vertically integrated firms. We also provide the

salient characteristics of our final sample of vertical divestitures.

3.1. Construction of initial sample of spin-offs and equity carve-outs

Our sample of divestitures includes both spin-offs and equity carve-outs over the period 1986 –

2005. Our initial sample of spin-offs is obtained from the Securities Data Company (SDC) Platinum

Mergers and Acquisitions database, and our equity carve-out sample is initially identified from SDC

Platinum’s New Issues database and from issues of Mergers and Acquisitions magazine. For each spin-off

and equity carve-out firm in our initial sample, we search for detailed transaction information on Factiva

and LexisNexis. We exclude spin-offs and carve-outs that are characterized by the following: (1) parent

firms are private firms, limited partnerships, financial firms, Real Estate Investment Trusts (REITs),

foreign firms, or joint ventures, (2) information on both the parent and subsidiary firm is unavailable on

Center for Research in Securities Prices (CRSP) immediately after the divestiture, (3) contemporaneous

announcements are made such as quarterly earnings; issues of equity, preferred stock, or warrants;

mergers and acquisitions; other asset sales; termination of technical agreements; share repurchases;

private placements; dividends; executive turnover; and work-force reduction, (4) parents firms

simultaneously announce an intent to divest multiple subsidiaries or split into multiple firms in the case of

spin-offs and to divest remaining ownership via a subsequent spin-off in the case of carve-outs, and (5)

proxy statements are unavailable. Finally, in the case of spin-offs, we retain only transactions that

represent pure spin-offs, which are defined as a tax-free distribution of 100% shares of the subsidiary and

which was 100% owned by the parent prior to the divestiture. As a result of all these restrictions, our final

sample consists of 161 spin-offs and 234 equity carve-out firms. For the identified spin-offs and equity

carve-outs, we hand-collect data on product market agreements and financial agreements from proxy

statements.

3.2. Sample of vertical divestitures through equity carve-outs and spin-offs

15

Prior research finds that firms change their industry classifications over time and recommend

using the historical Standard Industrial Classification (SIC) code instead of the current SIC code to

identify the primary industry classification of a firm (e.g., Kahle and Walkling, 1996). For each spin-off

and equity carve-out in our sample, we find the four-digit historical SIC code (Compustat data item 324)

of the parent and subsidiary for the calendar year following the announcement year of divestiture.

Because Compustat provides the historical SIC code only beginning 1987, for divestitures prior to 1987,

we use the four-digit SIC code of the segment with the highest sales during the announcement year using

Compustat segment data.

To identify vertical relations between the parent and subsidiary, we utilize the Use Table of the

benchmark input-output (IO) accounts for the US economy published by the Bureau of Economic

Analysis. We map the SIC codes of the parent and subsidiary to their respective IO codes by using the

SIC-IO concordance table developed by Fan and Lang (2000). Further, the 1997 benchmark input-output

accounts are based on the North American Industry Classification System (NAICS) instead of the SIC

system of industry classification. To tackle this issue, we first map the SIC codes to their respective

NAICS codes using the Bridge Tables provided by the Bureau of Census. We then find their respective

IO industries using the NAICS-IO concordance table provided under the 1997 benchmark input-output

accounts. Finally, because input-output relations between industries change over time, we use the 1987,

1992, and 1997 Use Tables for divestitures taking place during the periods 1986 – 1990, 1991 – 1997, and

1998 – 2005, respectively.

We then compute the vertical relatedness coefficient (VRC) between pairs of parent-subsidiary

industries. For every divestiture, we compute the dollar flow V1,PS (V1,SP) from the parent (subsidiary)

industry to the subsidiary (parent) industry for every dollar of the parent industry total output, and the

dollar flow V2,PS (V2,SP) from the parent (subsidiary) industry to the subsidiary (parent) industry for every

dollar of the subsidiary industry total output. Then, VRC is calculated as the maximum of the four

coefficients. We retain divestitures with a VRC of 1% or greater. Divestitures in which the parent and

16

subsidiary have the same four-digit SIC code are classified as horizontal divestitures and are not included

in our analysis. Our final sample consists of 46 vertical spin-offs and 65 vertical carve-outs.

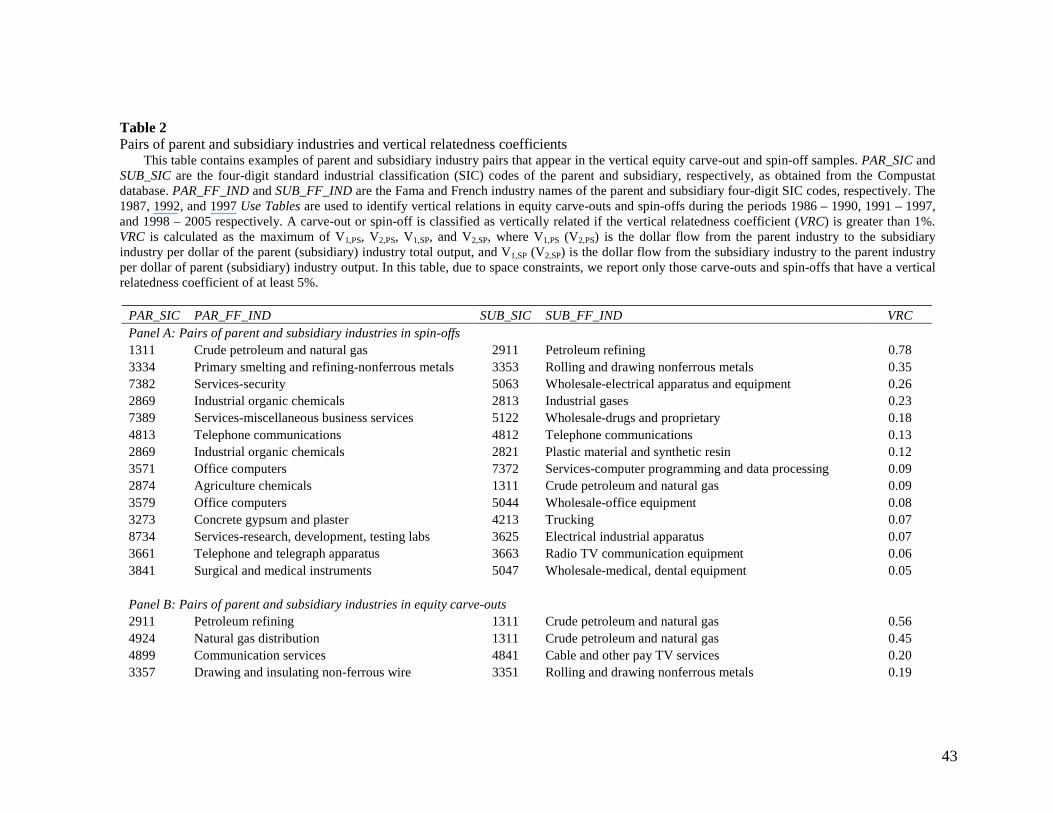

Table 2 presents the pairs of parent and subsidiary industries in spin-offs (Panel A) and equity

carve-outs (Panel B) in decreasing order of VRC. For purposes of brevity, we report only pairs of

industries in which the VRC is at least 5%. In both our spin-off and equity carve-out samples, the crude

petroleum and natural gas industry and the petroleum refining industry have the highest vertical linkages.

The VRC is different in the two samples for the same pair of industries only because the divestiture years

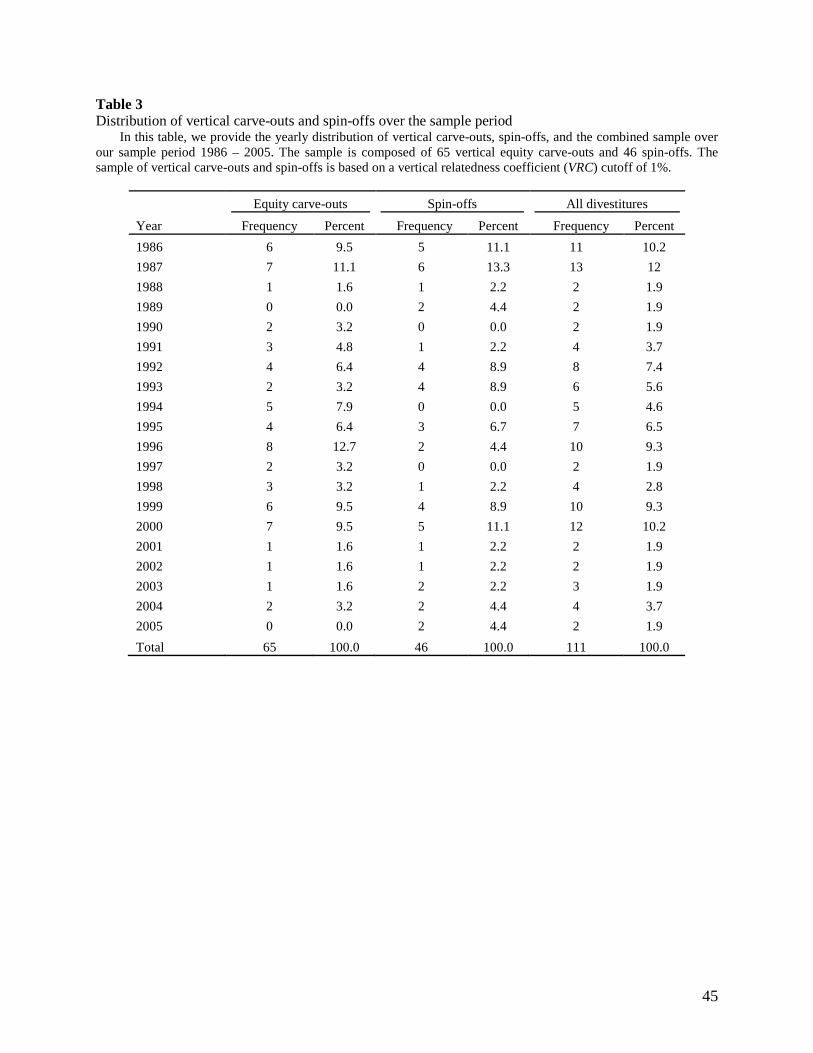

are not the same. Table 3 indicates that the yearly distribution of vertical divestitures appears to be similar

for equity carve-outs and spin-offs over our sample period 1986 – 2005.

[Insert Tables 2 and 3 near here]

3.3. Identification of rival, supplier, and customer firms in vertical divestitures

We identify parent (subsidiary) rivals as all firms on Compustat that have the same four-digit

primary SIC code as the parent (subsidiary) during the announcement year. We identify the customer

(supplier) firms for each vertical divestiture as follows. First, we identify the downstream and upstream

industry in the divestiture. Specifically, the downstream industry is the parent (subsidiary) industry if the

parent and subsidiary shared a backward (forward) vertical relation. The upstream industry is the

subsidiary (parent) industry if the parent and subsidiary shared a backward (forward) vertical relation.

The customer industry is the IO industry that purchases the highest proportion of its inputs from the

downstream industry provided it is greater than 1%. The supplier industry is the IO industry that is most

dependent on the upstream industry to sell its outputs provided it is greater than 1%. Finally, we identify

all firms on Compustat in the customer (supplier) IO industry during the divestiture announcement year.

3.4. Construction of control samples of vertically integrated firms

To model the decision to vertically divest, we identify four control samples of vertically

integrated firms. For this purpose, we use the Compustat segment tapes to first identify segment related

information reported by all US-based firms during our sample period 1986 – 2005. We exclude segments

that do not contain complete information on sales or SIC codes. We also eliminate firm-years with

17

missing firm assets or sales, in which the sum of segment sales is not within 5% of the total firm sales, the

sum of segment sales is less than $20 million, and any segment has a one-digit SIC code of six (financial

industry). Finally, because by definition vertically integrated firms involve at least two segments, we

retain only multi-segment firms.

We rely on extant literature to measure the extent of vertical relatedness in a multi-segment firm

(e.g., Fan and Lang, 2000; Acemoglu, Johnson, and Mitton, 2009; and Shenoy, 2009). Following Fan and

Lang (2000), we compute the extent of backward (forward) vertical relatedness between the primary

segment and all secondary segments of the firm. Similarly, following Acemoglu, Johnson, and Mitton

(2009), we compute the extent of backward (forward) vertical relatedness across all segments of the firm.

Then, a firm-year is treated as being vertically integrated when any of the above measures is greater than

1%. These sample selection criteria yield an initial sample of 10,874 vertically integrated firm-years.

Subsequently, we identify four different control samples of vertically integrated firms.

We construct Control Sample 1 by using our universe of all equity carve-outs and spin-offs to

delete firm-years that had any divestiture (vertical, horizontal, or conglomerate) during the observation

year. We also delete firm-years in which the number of reported segments increased (decreased) from the

previous year to the current year. This approach yields 6,038 firm-year observations. This is the most

general control sample to which we add further criteria to obtain the following three additional control

samples. Specifically, to create Control Sample 2, we retain a firm-year observation only if the firm

remains vertically integrated over a three-year period including the observation year (i.e., t, t-1, and t-2)

and the number of segments remains constant over this period. To construct Control Sample 3, we retain a

firm-year observation if the firm remains vertically integrated over a one-year window around each

observation year (i.e., t-1, t, and t+1) and the number of segments remains constant over this window.

Finally, to create Control Sample 4, we retain a firm-year observation only if the firm remains vertically

integrated over seven consecutive years and the number of segments remains constant over the seven-year

period. Control Sample 4 uses sample selection criteria similar to those in Çolak and Whited (2007).

4. Empirical analysis of vertical divestiture decisions

18

In this section, we empirically analyze vertical divestiture decisions to understand a firm’s

decision to dynamically set its boundaries over time.

4.1. Univariate analysis of the decision to vertically divest and the choice of method of divestiture

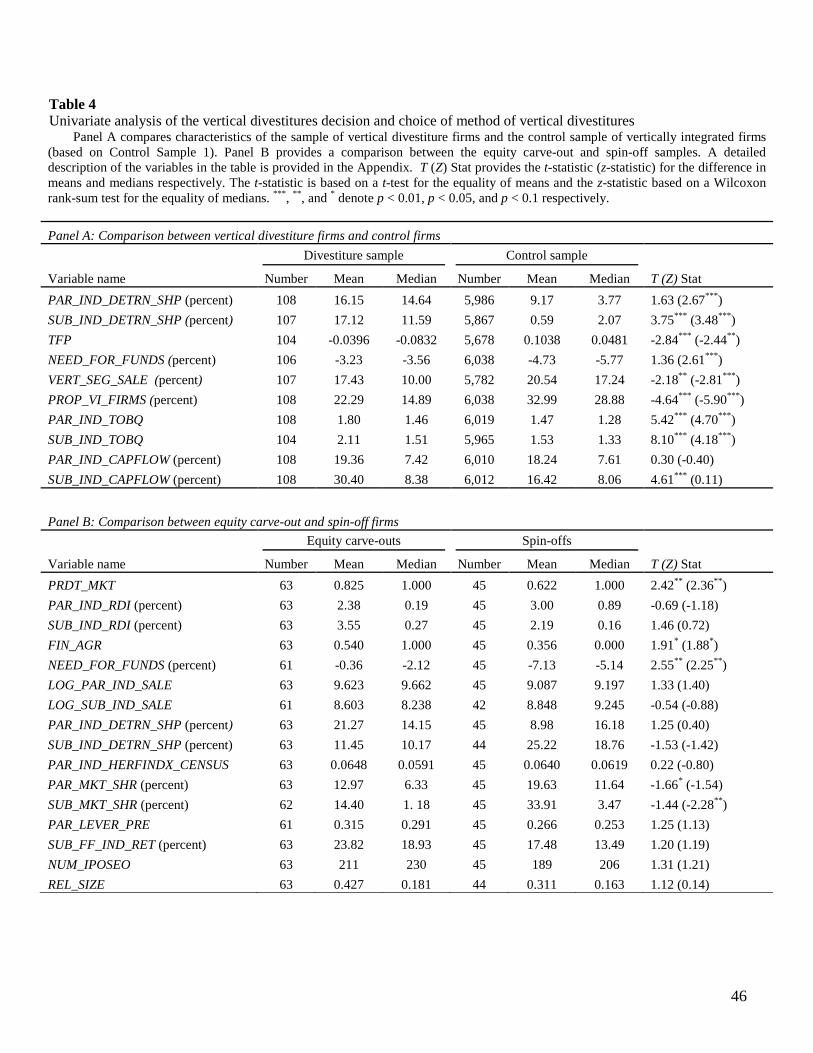

In Table 4, we present the results of our univariate analysis of the variables identified before as

factors that influence either the vertical divestiture decision (Panel A) or the choice of method of vertical

divestiture (Panel B). All variables are winsorized at their 1% and 99% values in our analysis. The

discussion below focuses on variables that are significantly different for either the divestiture decision or

method of divestiture decision. Comparing all vertical divestiture firms with control firms (Control

Sample 1), we find that the divestiture firms experience higher demand shocks to the subsidiary industry

(SUB_IND_DETRN_SHP), have lower total factor productivity (TFP), have lower intra-firm vertical

relatedness (VERT_SEG_ SALE), and belong to industries that have a smaller proportion of vertically

integrated firms (PROP_VI_FIRMS) and industries with attractive valuations or growth opportunities

(PAR_IND_TOBQ, SUB_IND_TOBQ). The above findings are invariant to the choice of control sample.

Comparing equity carve-out with spin-off firms, we find that carve-out firms have a higher incidence of

product market agreements (PRDT_MKT) and tighter financing constraints (NEED_FOR_FUNDS,

FIN_AGR). The above comparisons are statistically significant in the hypothesized direction.5

[Insert Table 4 near here]

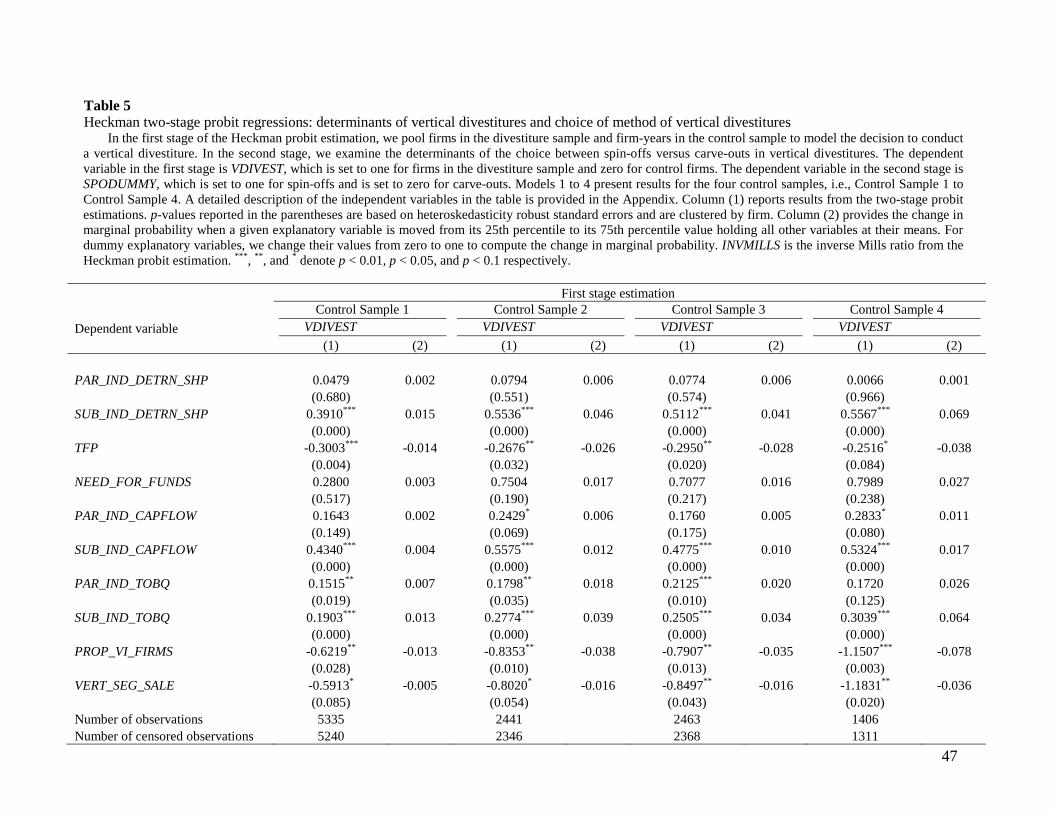

4.2. Two-stage probit selection model estimation results

We use a Heckman two-stage probit self-selection model (Heckprob command in STATA) to

estimate the determinants of the divestiture decision in the first stage and the choice between spin-offs

versus equity carve-outs in the second stage. The inverse Mills ratio (INVMILLS) from the first-stage

estimation is included as a control variable in the second stage to assess the prevalence of self-selection.

The dependent variable in the first stage (VDIVEST) is binary and takes on the value one if the firm

5 In results not reported in Table 4, we also attempt to ascertain whether funds raised in our 65 equity carve-out events are intended for use by the parent firm, subsidiary firm, or both. We find that in 19 (34.5%), 17 (31%), and 19 (34.5%) of the carve-out events, the capital raised at the divestiture is used solely by the parent firm, exclusively by the subsidiary firm, and by both the parent and subsidiary firms, respectively.

19

belongs to the vertical divestiture group and zero if it belongs to the control group of integrated firms.

Similarly, the dependent variable in the second stage (SPODUMMY) is a binary variable that takes on the

value one if the vertical divestiture is in the form of a spin-off and zero if it is through an equity carve-out.

We report results for the Heckman two-stage estimation for all four control samples in Table 5 to

demonstrate the robustness of our results. Because our results are qualitatively similar for all four models,

for purposes of brevity, the discussion of the results is based on the fourth model in Table 5, which was

estimated using the most restrictive control sample. We assess the economic significance of each variable

by computing the change in marginal probability as the value of each independent variable is varied from

its 25th to its 75th percentile value, keeping all other variables at their mean levels. For dummy

explanatory variables, we change their values from zero to one to assess their economic significance.

[Insert Table 5 near here]

We initially focus our discussion on the first-stage probit model to identify factors that influence

the vertical divestiture decision. As can be seen from Model 4 in Table 5, the marginal effect of

SUB_IND_DETRN_SHP is positive and significant, indicating that positive subsidiary industry demand

shocks increase the probability of vertical divestitures. In addition, we find that the marginal effect of

TFP is negative and significant, indicating a higher probability of vertical divestitures when parent firm

relative productivity is lower. Further, we find that the marginal effects of both PROP_VI_FIRMS and

VERT_SEG_SALE are negative and significant. Therefore, vertical divestitures are less likely in industries

with a high proportion of vertically integrated firms and when the parent has more significant intra-firm

vertical relatedness. These results support the argument that when the need for relationship-specific

investments is high, the probability of vertical divestitures is low as firms seek to preserve contractual

efficiency gains through the integrated structure. The results in Table 5 indicate that financing

considerations also influence the vertical divestiture decision. The marginal effects of

PAR_IND_CAPFLOW, SUB_IND_CAPFLOW, and SUB_IND_TOBQ are positive and significant.

However, the marginal effect of NEED_FOR_FUNDS, while positive, is not significant. Our results,

20

therefore, suggest that attractive industry financing conditions, particularly in subsidiary firm industries,

instead of parent firm internal financing constraints influence the vertical divestiture decision.

In addition, we find that when the subsidiary industry demand shock (SUB_IND_DETRN_SHP)

increases from its 25th to 75th percentile value, the probability of vertical divestiture goes up by 6.9%.

Similarly, as the parent firm total factor productivity (TFP) increases from its 25th to 75th percentile

value, the probability of a vertical divestiture declines by 3.8%. Further, as the proportion of vertically

integrated firms in the parent industry (PROP_VI_FIRMS) is varied from its 25th to 75th percentile value,

the probability of a vertical divestiture declines by 7.8%. Among financing considerations, the subsidiary

industry’s financing conditions (SUB_IND_TOBQ) is the most influential variable, causing the

probability of a vertical divestiture to increase by 6.4% when the subsidiary industry Tobin's q increases

from its 25th to 75th percentile value.

To identify the determinants of the choice of method of divestiture conditional on the vertical

divestiture decision, we analyze the results of the second stage of our probit analysis as reported in Table

5. We find that the marginal effects of PRDT_MKT and SUB_IND_RDI are negative and significant,

indicating that vertically integrated firms are likely to partially, not completely, separate to preserve

contractual efficiencies in environments in which the need for relationship-specific investments is greater.

In terms of economic significance, the results suggest that the probability of vertical divestitures via spin-

offs relative to carve-outs declines by 18.3% in the presence of product market contractual agreements

(PRDT_MKT). Similarly, the probability of a vertical divestiture via spin-offs relative to carve-outs

declines by 12.1% when the subsidiary industry R&D intensity (SUB_IND_RDI) is changed from its 25th

to 75th percentile value.

Further, as hypothesized, we find that the marginal effect of NEED_FOR_FUNDS is negative and

significant, indicating that the method of vertical divestiture is likely to be a carve-out instead of a

spin-off in the face of tighter financial constraints. The probability of a vertical divestiture via spin-offs

relative to carve-outs declines by 7.3% when the parent’s internal funding deficit (NEED_FOR_FUNDS)

is varied from its 25th to 75th percentile value. In addition, from our first- and second-stage analysis of

21

NEED_FOR_FUNDS, we can infer that while parent firm internal financing constraints do not influence

the vertical divestiture decision, they do affect the choice of method of divestiture. The marginal effect of

FIN_AGR is negative in all four models, but it is insignificant at conventional levels (p-values range from

0.11 to 0.12). The probability of vertical divestitures via spin-offs relative to carve-outs declines by 9.5%

in the presence of financial agreements (FIN_AGR).

We further find that the marginal effects of SUB_IND_DETRN_SHP and LOG_SUB_IND_SALE

are both positive and significant. The probability of vertical divestitures via spin-offs relative to

carve-outs increases by 9.9% (19.5%) when SUB_IND_DETRN_SHP (LOG_SUB_IND_SALE) increases

from its 25th to 75th percentile value. These results indicate that the higher the subsidiary industry sales

and demand shocks prior to the divestiture, the more likely that vertical divestitures occur through

spin-offs instead of carve-outs as firms strive to capture the benefits of specialization and economies of

scope, which are maximized under a complete vertical separation. While the marginal effect of

LOG_PAR_IND_SALE is negative and significant, the marginal effect of PAR_IND_DETRN_SHP is

insignificant. As such, we are unable to provide consistent evidence to indicate whether parent industry

demand conditions influence vertical divestitures of their subsidiary firms. We find the marginal effect of

PAR_IND_HERFINDX_CENSUS to be negative but insignificant, which is inconsistent with the

collusion hypothesis. Similarly, while the marginal effect of PAR_MKT_SHR and SUB_MKT_SHR are

both positive, only SUB_MKT_SHR is significant. These results do not support the foreclosure

hypothesis.

Several of the control variables are significantly related to the conditional choice of method of

vertical divestiture. The marginal effect of PAR_LEVER_PRE is negative and significant, further

indicating that parents with higher internal financing constraints prior to the divestiture are more likely to

vertically divest through a carve-out instead of a spin-off. Further, the marginal effect of REL_SIZE is

negative and significant, indicating that the larger the size of the subsidiary relative to the parent, the

more likely the vertical divestiture occurs through a carve-out. The marginal effects of

22

SUB_FF_IND_RET and NUM_IPOSEO are both negative as expected but insignificantly different from

zero.

5. Wealth effects and changes in operating performance

In this section, we examine the announcement-period wealth effects of vertical divestitures and

changes in operating performance around vertical divestitures in both univariate and cross-sectional

contexts. We design our cross-sectional tests in a manner that enhances our ability to discriminate

between non-mutually exclusive hypotheses.

5.1. Announcement-period wealth effects of vertical divestitures

In this subsection, we examine the announcement-period wealth effects of vertical divestitures on

parent firms, parent rivals firms, subsidiary rival firms, supplier firms, and customer firms.

5.1.1. Measurement of announcement-period wealth effects

Following Mulherin and Boone (2000), we use market-adjusted returns around the announcement

date to measure the wealth effects from the divestiture. Specifically, we calculate the cumulative

abnormal returns (CARs) over the event windows (0, +1), (-1, +1), (-2, +2), and (-5, +5) trading days

around the announcement date of each divestiture. For every vertical divestiture, we combine the parent

rivals, subsidiary rivals, supplier firms, and customer firms into separate equally weighted portfolios to

compute their portfolio returns. The equally weighted approach is used to account for the

contemporaneous cross-correlation in returns (Eckbo, 1983; Fee and Thomas, 2004; and Shahrur, 2005).

We calculate the market-adjusted returns to the parent rival, subsidiary rival, supplier, and customer

portfolios for the same event windows as for the parent firm.

5.1.2. Univariate results for the wealth effects of parent firms, rivals, suppliers, and customers

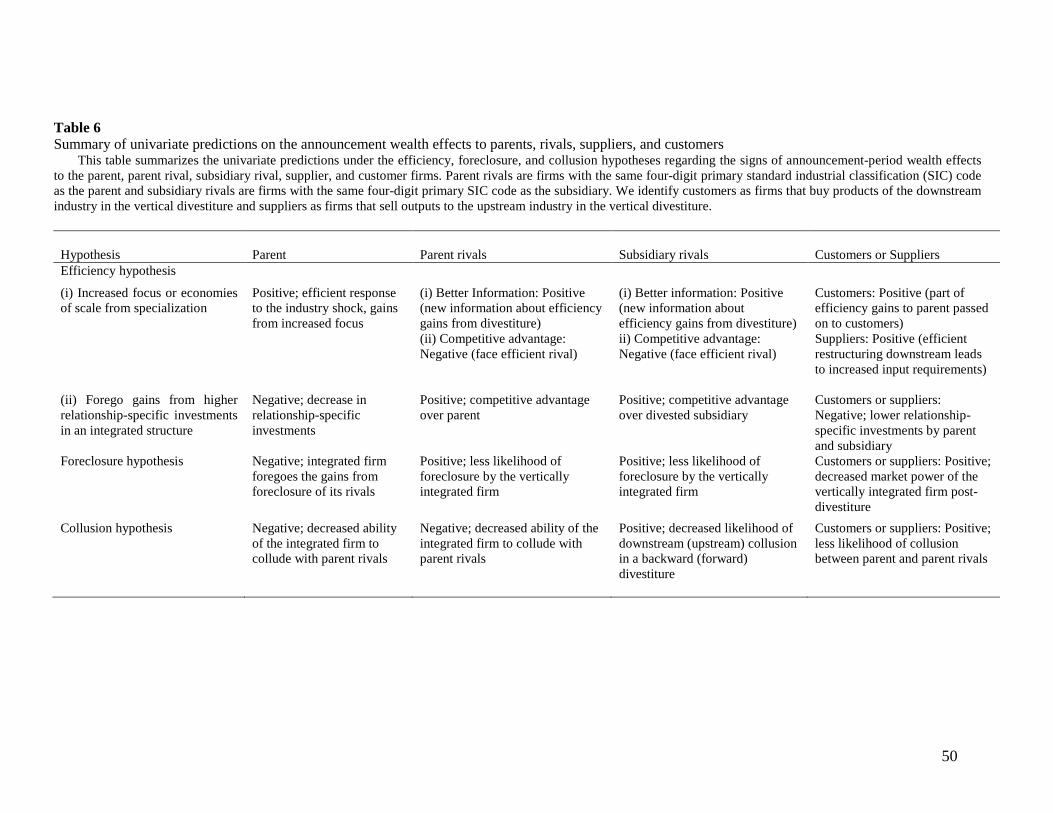

A summary of our predictions with brief explanations regarding the wealth effects of vertical

divestitures under the efficiency, collusion, and foreclosure hypotheses for parent firms, parent rival

firms, subsidiary rival firms, supplier firms, and customer firms is provided in Table 6. In Table 7, we

report the announcement-period wealth effects for all the above parties. The abnormal returns for parent

firms are reported in Panel A. For the full sample of vertical divestitures, we find that the mean abnormal

23

returns to parent firms are positive and significant for all four event windows examined. In addition, we

find that the mean wealth effects to parent firms are positive and significant in spin-offs for all windows,

and they are positive and significant in three of the four windows for equity carve-outs. For example, the

mean CAR is 2.68%, 1.63%, and 4.15% over the (0, +1) window for the parent firm in the full sample of

vertical divestitures, the subsample of vertical divestitures through equity carve-outs, and the subsample

of vertical divestitures through spin-offs, respectively.

[Insert Tables 6 and 7 near here]

Thus, it appears that the market assesses vertical divestitures to be value-creating events for

parent firms. The positive stock price reaction for parent firms is consistent with value creation due to

enhanced corporate focus or economies of specialization [see, e.g., Desai and Jain (1999) for spin-offs

and Vijh (2002) for carve-outs]. In a vertical divestiture there is likely to be underinvestment in

relationship-specific assets after the divestiture due to the higher potential for holdup, a lower probability

of collusion between the parent firm and its industry rivals, and a reduced ability to foreclose parent and

subsidiary rivals from inputs and outlets. All these effects would impact the stock price of the parent firm

negatively. The positive stock price reaction to parent firms is inconsistent with these explanations.

We report the abnormal returns to parent rival firms in Panel B. For the full sample of vertical

divestitures, we find that the mean abnormal returns for the parent rival firms are positive and significant

for all the event windows examined. In addition, we find that the mean wealth effects for parent rival

firms are also positive and significant in spin-offs for all the windows, and they are significantly positive

in equity carve-outs for three out of the four event windows. The positive parent rival abnormal returns

are consistent with the view that the divestiture announcement conveys better information to industry

participants about potential efficiency gains from restructuring (Eckbo, 1983, 1990; Rosengren and

Meehan, 1994; and Shenoy, 2008). They are inconsistent with the argument that a vertical divestiture

reduces the probability of collusion in the parent firm’s industry. These results, in conjunction with the

positive abnormal returns to the parent firm, are also inconsistent with the foreclosure argument.

24

The wealth effects for subsidiary rival firms are reported in Panel C. While the mean wealth

effects are positive, they tend to be insignificant. The abnormal returns are positive and significant for the

full sample of vertical divestitures and the sample of equity carve-outs only for the (-5, +5) window. The

positive, albeit generally insignificant, abnormal returns to subsidiary rival firms when viewed in

conjunction with the positive abnormal returns to parent rival firms are inconsistent with the collusion

hypothesis and when viewed in conjunction with the positive abnormal returns to the parent firm, they are

inconsistent with the foreclosure hypothesis.

Panel D contains the abnormal returns to customer firms, and Panel E contains the abnormal

returns to supplier firms. The mean abnormal returns to customers tend to be positive. They are, however,

insignificant in all the windows for the sample of equity carve-outs but significantly positive in the (0, +1)

and (-5, +5) windows for the full sample of vertical divestitures and the sample of spin-offs. The mean

abnormal returns to suppliers, however, are positive and statistically significant for all four event

windows in the overall sample. In addition, we observe a positive and significant wealth effect to supplier

firms in three of the four event windows in both subsamples of equity carve-outs and spin-offs. Again,

when viewed in conjunction with the positive wealth effects for parent firms and rival firms, the positive

wealth effects to the supplier and customer firms are consistent only with the efficiency hypothesis.6

5.1.3. Determinants of wealth effects for parent firms

However, because our hypotheses are not mutually exclusive, we design cross-sectional tests that allow us

to more cleanly disentangle all the economic forces at play.

We propose the cross-sectional regression model given by Equation (1) to examine the

determinants of the wealth effects to the parent firms in vertical divestitures. 6 The data on the customers (suppliers) are coarse because they are identified as all firms in the industry that is downstream (upstream) to the downstream (upstream) industry in the divestiture. As a robustness check, we identify actual key customers (suppliers) of the parent and subsidiary based on Financial Accounting Standards Board (FASB) No. 14 requirement for firms to report customers that account for at least 10% of sales (e.g., Fee and Thomas, 2004). We identify key customers (suppliers) for 23 (29) of the vertical divestitures in our sample. We find that key customers experience insignificant wealth effects and suppliers experience positive and statistically significant wealth effects. These results generally mirror our findings based on the industry level data. A bias of the 10% cutoff is that the data identify large customer firms. For example, we find that the median customer firm is about 14 times the size of the parent firm. The insignificant wealth effects to customers can at least partially be explained by this size differential.

25

)1(**__*_*8__*__*___*___*

___*__*__*_

111097

654

3210

εββββββββ

ββββ

++++++++

++++=

SPODUMMYMERGERPRELEVERPARSIZERELSHRMKTSUBSHRMKTPARCENSUSHERFINDXINDPARSHPDETRNINDSUB

SHPDETRNINDPARPREHERFINDXPARPRERDIPARCARPAR

In the model, the dependent variable PAR_CAR is the cumulative abnormal return to the parent

firm over the (-1, +1) day event window around the divestiture announcement date. The efficiency

hypothesis indicates that efficiency gains can come from enhanced corporate focus or economies of

specialization. We posit that the less focused the pre-divestiture parent firm, the greater the organizational

complexity and, hence, the higher the potential for gains from a divestiture. As a measure for

pre-divestiture corporate focus, we use the parent firm Herfindahl index, PAR_HERFINDX_PRE, and

expect it to be negatively related to PAR_CAR. Further, a source of efficiency gains from vertical

integration is the increase in relationship-specific investments due to the reduction in the severity of the

holdup problem. We use the pre-divestiture R&D intensity of the parent firm, PAR_RDI_PRE, as a proxy

for the extent of relationship-specific investments in the integrated structure (e.g., Levy, 1985; Armour

and Teece, 1980; and Boerner and Macher, 2001). We posit that if the pre-divestiture relationship-specific

investments are higher, the potential for ex post contracting problems after the divestiture is greater.

Therefore, we predict a negative relation between PAR_CAR and PAR_RDI_PRE. In addition, under the

efficiency umbrella, we include measures of parent and subsidiary industry demand shocks

(PAR_IND_DETRN_SHP and SUB_IND_DETRN_SHP). Maksimovic and Phillips (2001) argue that

positive industry demand shocks can lead to efficiency gains as firms are motivated to transfer ownership

of their less productive assets to industry players who can deploy them more productively. As such, we

expect parent and subsidiary industry demand shocks to be positively associated with wealth effects.

Under the collusion hypothesis, a vertical divestiture in a more concentrated industry results in

the parent firm potentially giving up a higher amount of the gains coming from colluding with its rivals.

Thus, we expect a negative relation between parent industry concentration,

PAR_IND_HERFINDX_CENSUS, and parent firm wealth effects. Under the foreclosure hypothesis, the

higher the market share of the parent and the subsidiary firms, the greater is the potential losses arising

26

from their inability to foreclose their rival firms after the vertical divestiture. We, therefore, expect a

negative relation between parent firm wealth effects with both the industry market share of the parent firm

(PAR_MKT_SHR) and industry market share of the subsidiary firm (SUB_MKT_SHR).

The remaining variables REL_SIZE, PAR_LEVER_PRE, MERGER, and SPODUMMY serve as

control variables in our regressions. Relative size of subsidiary to parent (REL_SIZE) is included in

accordance with Mulherin and Boone (2000), who find that the wealth effects for parent firms are

positively related to the relative size of the subsidiary to the parent. When PAR_LEVER_PRE is larger,

the market could be negatively surprised by the extent of the financial constraints faced by the parent and

react more negatively to the announcement. We include MERGER, which is an indicator variable that

equals one if either the parent or subsidiary became the target in an acquisition during the three years

subsequent to the announcement year, as an explanatory variable. If the divestiture wealth effects reflect

the expectation of the future acquisition premium paid by the acquirer, then we would find MERGER to

be positive.7

The cross-sectional results for the determinants of parent firm wealth effects in vertical

divestitures are reported in Table 8. Because the method of vertical divestiture (spin-off versus equity

carve-out) is a choice made by parent firm managers, we control for this choice by using a Heckman

treatment effect model. The first stage in the Heckman analysis is our model of choice of method of

vertical divestiture reported in Table 5. Thus, we report only the results from the second-stage parent

wealth effects regressions in Table 8.

To the extent that the parent wealth effects in a spin-off tend to be greater than those in

equity carve-outs, we also include the dummy variable SPODUMMY to capture any differential effect that

is not accounted for by all the other independent variables in the regression.

8

7 The results we report in Tables 8 and 9 are insensitive to the exclusion of MERGER from the regression specifications.

The p-values associated with all the reported coefficients are based

on heteroskedasticity robust standard errors and are clustered by parent firm.

8 Some variables in the first stage probit regression do not appear in the wealth effect regressions. To investigate if the excluded variables from the first stage make valid instruments, i.e., highly correlated with the choice of method of divestiture but uncorrelated with excess returns, we estimate a two-stage least squares (2SLS) model instead of a

27

[Insert Table 8 here]

In Model 1, we focus on the efficiency arguments by including PAR_RDI_PRE,

PAR_HERFINDX_PRE, PAR_IND_DETRN_SHP, and SUB_IND_DETRN_SHP as explanatory variables.

In Model 2, we focus on the anti-competitive hypotheses by including PAR_IND_HERFINDX_CENSUS,

PAR_MKT_SHR, and SUB_MKT_SHR as explanatory variables. Model 3 is the full specification and

includes all the independent variables. In both Models 1 and 3, we find that the relation between

PAR_CAR and PAR_RDI_PRE is significantly negative. This result indicates that the wealth effects on

announcement of vertical divestitures tend to be lower if the potential for ex post contractual

inefficiencies is higher. In addition, we find a significantly negative relation between PAR_CAR and

PAR_HERFINDX_PRE in both these models. This suggests that the wealth effects are higher when the

potential for an increase in focus as a result of the vertical divestiture is greater. Further, although the

coefficients of PAR_IND_DETRN_SHP and SUB_IND_DETRN_SHP are positively associated with

PAR_CAR, the results are not significant. In Models 2 and 3, we show a negative relation between the

wealth effects for parent firms and the industry concentration of the parent firm,

PAR_IND_HERFINDX_CENSUS. While the result is consistent with the collusion hypothesis, our earlier

analysis of determinants of choice of method of vertical divestitures revealed no evidence of collusion as

a factor.9 As such, we do not find consistent evidence in line with the collusion effect. The negative

coefficient of PAR_IND_HERFINDX_CENSUS is, however, indicative of vertical divestitures being more

beneficial in competitive industries as it allows the divested entities to more nimbly compete in their

industries.10

Heckman treatment model. We conduct relevance and validity tests on these instruments and find that they meet the exclusion restrictions. The results from the 2SLS model are similar to what we report here.

Finally, in the two models in Table 8 involving parent and subsidiary firm market shares, we

find that while the coefficient on the former is significantly positive, the coefficient on the latter is

unrelated to parent firm wealth effects. These results do not support the foreclosure hypothesis.

9 Also, in our analysis of the wealth effects of rival, supplier, and customer firms, we find no evidence to support the collusion hypothesis. 10 We thank the referee for this interpretation.

28

While the coefficient on PAR_LEVER_PRE is significantly negative in all three estimated

models, none of the remaining control variables is significant. The insignificant coefficient on the

SPODUMMY indicates that once we control for the determinants of parent wealth gains and self selection,

the method of divestiture has no impact on value creation in a vertical divestiture.

5.1.4. Determinants of wealth effects of parent and subsidiary firm rivals, suppliers, and customers

For completeness, we also examine the cross-sectional determinants of the announcement-period

wealth effects for the parent rivals, subsidiary rivals, suppliers, and customers.11

In the second set of specifications, we find a significantly negative relation between the wealth

gains to parent rival firms, subsidiary rival firms, and supplier firms and the pre-divestiture focus of the

parent firm. These results indicate that the announcement of the vertical divestiture provides information

to rival and supplier firms that they can also benefit from focus increasing restructuring activities.

Furthermore, we document that parent industry concentration has a significant negative relation with the

wealth effects for both subsidiary rival firms and supplier firms. It is, however, unrelated to the wealth

We estimate two

Heckman treatment effect regression specifications for each of these parties. In the first specification, we

include the abnormal returns to the parent firm in lieu of the efficiency variables. In the second regression

specification, we include the efficiency variables instead of the abnormal returns to the parent firm. In

both specifications, we include variables related to the foreclosure and collusion hypotheses. In the first

set of specifications, we find a significantly positive relation between the wealth effects to subsidiary rival

firms, supplier firms, and customer firms with the wealth effects to the parent firm. The relation between

the wealth effects to parent rival firms with the parent wealth effects is positive but statistically

insignificant. These results indicate that if more wealth is expected to be created for the parent firm from

the divestiture, then all the other parties along the supply chain are generally also better off. This evidence

can be consistent only with an efficiency-based explanation, where rival firms can restructure similarly,

and the resultant gains are passed along to suppliers and customers.

11 We do not report details of this analysis for purposes of brevity. The detailed results are available upon request.

29

effects for the parent rival firms and customer firms. These results are inconsistent with the collusion

hypothesis.

Finally, we find that the wealth effects to parent (subsidiary) rival firms are unrelated to the

market share of the subsidiary (parent) firm. We show a similar insignificant relation between parent

market share and both the customer firm and supplier firm wealth effects. These results are inconsistent

with the foreclosure hypothesis. We find a significantly positive relation between supplier firm wealth

effects and subsidiary market share and a significantly negative relation between customer firm wealth

effects and subsidiary market share. While the former result is consistent with the foreclosure hypothesis,

the latter result is inconsistent with this hypothesis. Hence, when we view the relation between the wealth

effects for all parties along the supply chain with parent and subsidiary market shares through one large

lens, the collective evidence does not support the foreclosure hypothesis. Overall, the cross-sectional

determinants of the wealth effects to the parent and subsidiary rivals, supplier firms, and customer firms

provide additional corroborating evidence in favor of the efficiency hypothesis.

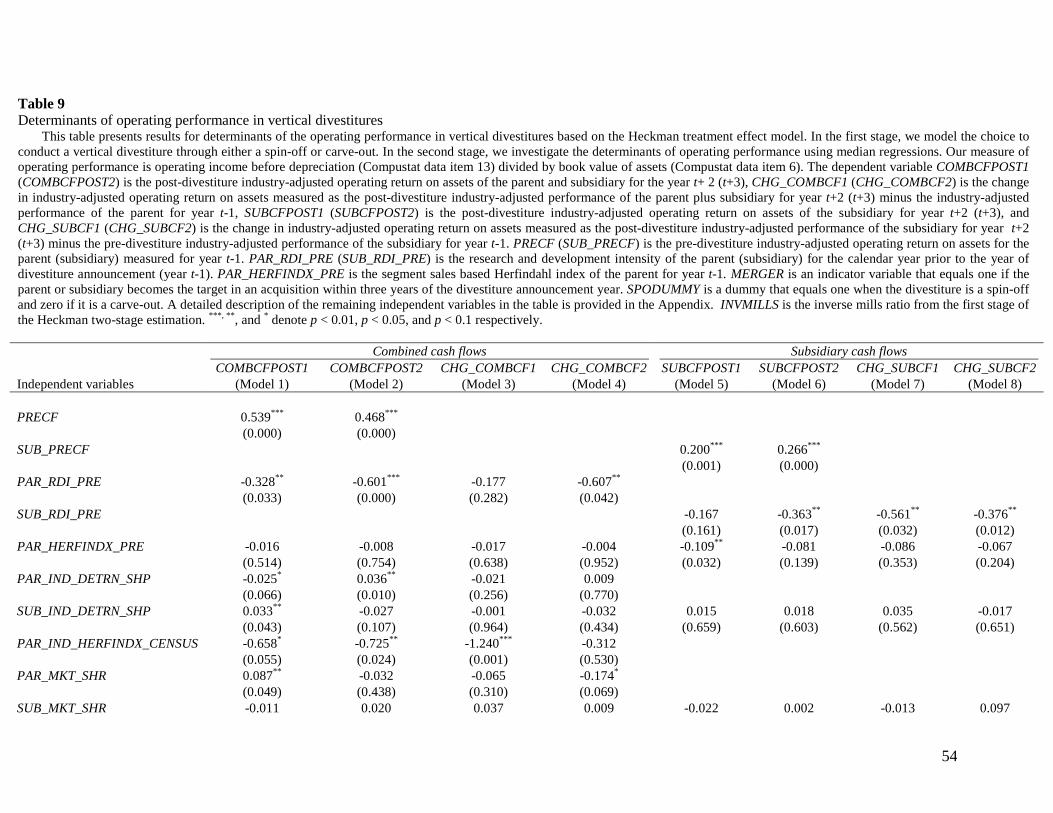

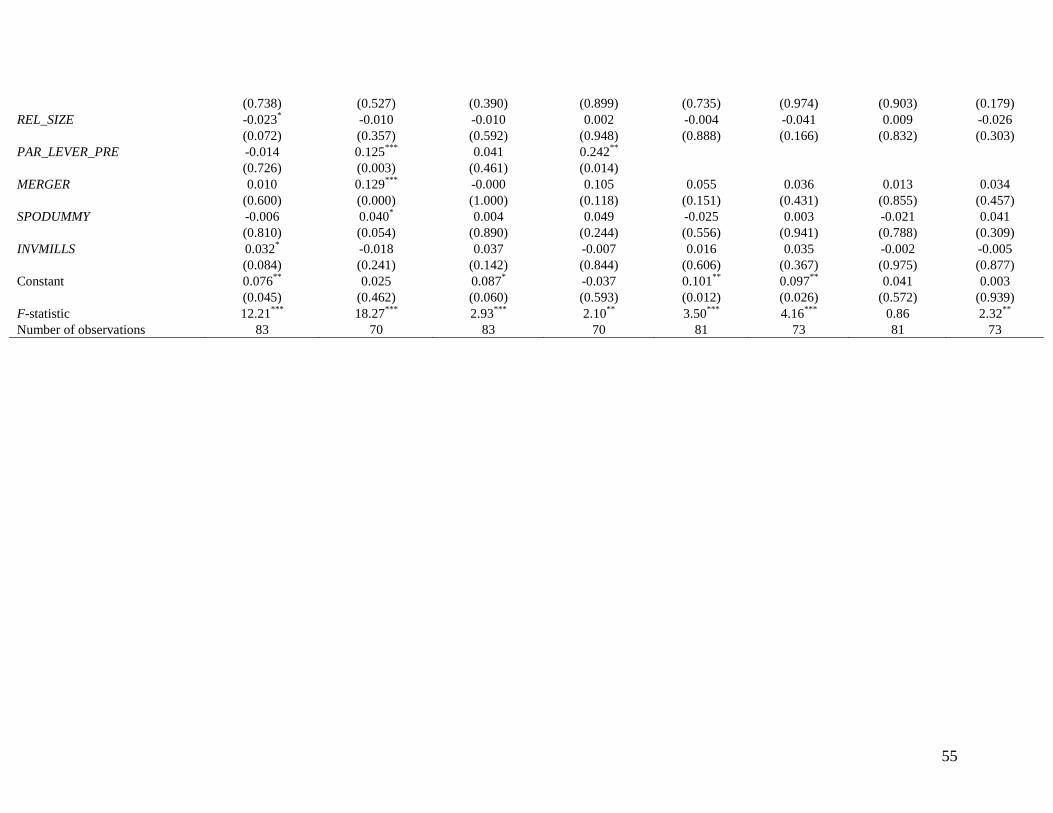

5.2. Determinants of changes in operating performance around vertical divestitures

In this subsection, we examine the determinants of changes in operating performance for our

sample of vertical divestiture firms. Our objective is to assess whether the potential for efficiency gains

from vertical divestitures arising as a result of improvement in focus, positive industry demand shocks,

and product market considerations are reflected in improvements in operating performance. We adopt the

widely used metric of operating cash flows deflated by total assets (Compustat data item 13 divided by

Compustat data item 6), also called operating return on assets, as our measure of operating performance

(e.g., Barber and Lyon, 1996; Daley, Mehrotra, and Sivakumar, 1997; and Jain and Kini, 1994). In

addition, we construct industry-adjusted operating performance measures by adjusting the pre- and post-

divestiture operating performance of sample firms by the median operating performance of all firms

(excluding the parent) that belong in the same two-digit SIC industry as the parent in the year under

consideration.

30

Because the divestitures can result in improvements in operating performance for either the

parent firm or subsidiary firm, or both, researchers have typically adopted a portfolio approach in which

the change in operating performance measure is constructed as the benchmark-adjusted post-divestiture

operating performance of the parent and subsidiary firms minus the benchmark-adjusted performance of

the parent firm in the pre-divestiture period (Daley, Mehrotra, and Sivakumar, 1997; and Desai and Jain,

1999).12

Our univariate analysis generally indicates an improvement in operating performance for the

combined parent and subsidiary firms. Specifically, the median change in industry-adjusted cash flows

from year t-1 to year t+2 (t+3) is 0.833% (1.404%), 1.549% (3.458%), and 0.204% (1.326%) for the

overall sample, spin-off subsample, and carve-out subsample, respectively. A consistent picture does not

emerge if we focus on changes in operating performance for subsidiary firms. The median change in the

industry-adjusted cash flows from year t-1 to year t+2 (t+3) is 0.163% (-0.312%), -2.03% (0.84%), and

0.826% (-1.388%) for the overall sample, spin-off subsample, and carve-out subsample, respectively.

Therefore, as a measure of pre-divestiture performance, we use the industry-adjusted operating

performance of the parent for year t-1, where year t is the divestiture year. For post-divestiture

performance we use the asset-weighted industry-adjusted operating performance of the parent and

divested subsidiary for years t+2 and t+3. We examine changes in operating performance over the (t-1,

t+2) and (t-1, t+3) windows. In addition, we investigate operating performance changes around vertical

divestitures pertaining solely to the divested subsidiary firms. We use Thompson One Banker database

and obtain the first annual report published by the subsidiary firms after the divestiture transaction. We

then use these annual reports to collect financial information on the divested entity for the calendar year

prior to the divestiture transaction (t-1).

In our cross-sectional regression analysis, we follow the extant literature and adopt two

alternative forms of expectation models to detect the change in operating performance around vertical

divestitures. The first model constructs the dependent variable as the change in benchmark-adjusted