US Natural Gas Export a sensible move? April presentation for the Oil and Gas Seminar at EUSP

18

US Natural Gas Export: a sensible move? Fabio Herrero presenting for the ENERPO Oil & Gas Seminar 2014 – Prof Maurizio Recordati

Transcript of US Natural Gas Export a sensible move? April presentation for the Oil and Gas Seminar at EUSP

US Natural Gas Export: a sensible move?

Fabio Herrero presenting for the ENERPO Oil & Gas Seminar 2014 – Prof Maurizio Recordati

Foreword + Contents 1 cubic meter = 35.3147 cubic foots 1 cubic foot = 0.0283168 cubic meters Shale gas is natural gas that is

found trapped within shale formations. Shale is a fine-grained, clastic sedimentary rock composed of mud that is a mix of flakes of clay minerals and tiny fragments of other minerals, especially quartz and calcite. Shale is characterized by breaks along thin laminae or parallel layering or bedding less than one centimeter in thickness, called fissility.

1. US is a net importer2. How much natural gas is the United States talking about exporting?3. Projected natural gas prices4. US shale gas and tight oil industry performance5. Conclusions6. References7. Author assessment

How much natural gas is the United States currently extracting?

US is a net importer

The United States is a natural gas importer, and has been for many years: in 2013 domestic production covered 89% of consumption. The EIA is forecasting that by 2017, the US will finally be able to meet their natural gas needs.

Canada is losing ground as a major player in North American natural gas production, the Conference Board of Canada said in a report Sept. 20. 2013. The report forecasts that production is expected to ratchet down over the next five years, led by declines in Alberta which is expected to slide by 20%.

Natural gas is the only fuel showing much growth in production between now and 2040

Natural gas is pretty much the only growth area, growing from 31% of total energy production in 2012 to 38% of total US energy production in 2040. Renewables are expected to grow from 11% to 12% of total US energy production (probably because the majority is hydroelectric, and this doesn’t grow much). All of the others fuels, including oil, are expected to shrink as percentages of total energy production between 2012 and 2040.

Mexico oil and gas production (conventional is in decline)

Excessive drawing down of amounts in storage

There is even discussion that at the low level in storage and current rates of production, it may not be possible to fully replace the natural gas in storage before next fall.

How much natural gas is the United States talking about exporting?

If we look at the applications for natural gas exports found on the Energy.Gov website, we find that applications for exports total 42 billion cubic feet a day, most of which has already been approved. This compares to US 2013 natural gas production of 67 billion cubic feet a day. In fact, if companies applying for exports build the facilities in, say, 3 years, and little additional natural gas production is ramped up, the US could be left with less than half of current natural gas production for our internal use. The already approved project represent over 60% of what it is currently produced.

How much are the United States’ own natural gas needs projected to grow by 2030?

If we believe the US Energy Information Administration, US natural gas needs are expected to grow by only 12% between 2013 and 2030. By 2040, natural gas consumption is expected to be 23% higher than in 2013. This is a little surprising for several reasons.

Why it is surprising?

For one, we are talking about scaling back coal use for making electricity, and we use almost as much coal as natural gas. Natural gas is an alternative to coal for this purpose.

Furthermore, the EIA expects US oil production to start dropping by 2020, my assessment here is that it means that more natural gas will be needed to substitute the oil.

The US currently use more oil than natural gas, so this change could in theory lead to a 100% or more increase in natural gas use, without even speaking about an eventual use of natural gas in transportation.

Many US nuclear plants in service will need to be replaced in the next 20 years. If the US substitute natural gas in this area as well, it would further send US natural gas usage up.

The EIA’s forecast of US natural gas needs definitely seem a little optimistic.

Projected natural gas prices

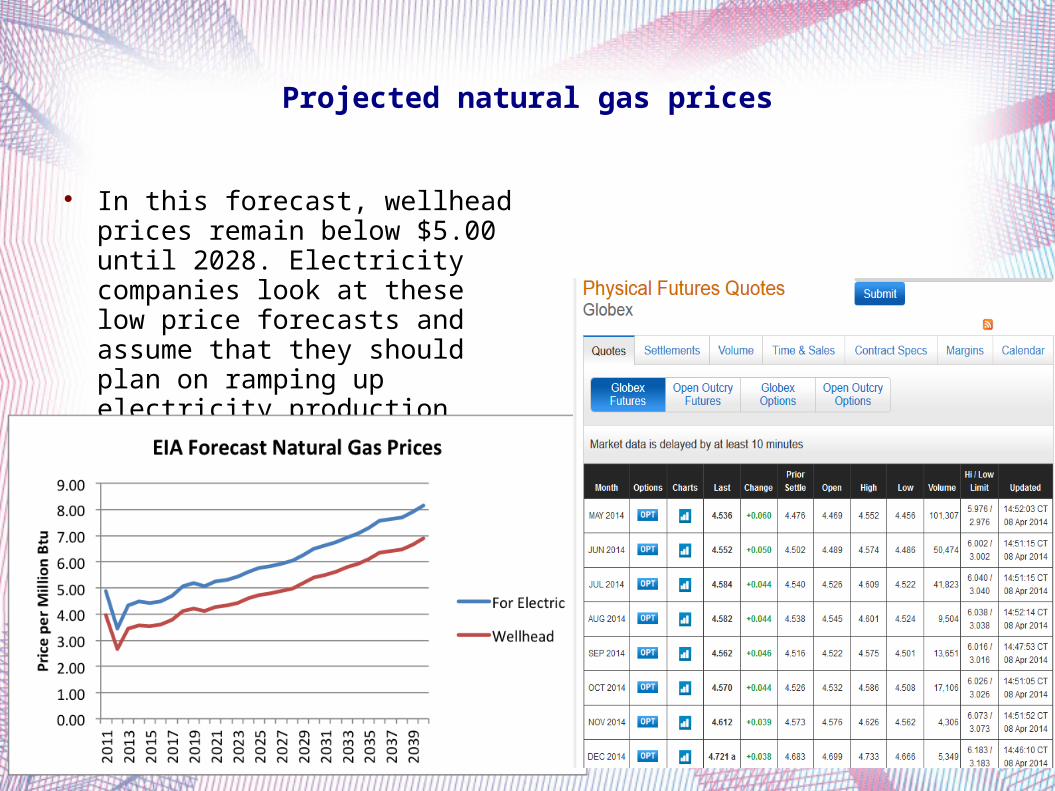

In this forecast, wellhead prices remain below $5.00 until 2028. Electricity companies look at these low price forecasts and assume that they should plan on ramping up electricity production from natural gas.

Natural Gas prices 1973 - 2013

Some considerations about the shale oil/gas

While drilling in Iraq could break even at about $20 a barrel. By contrast, the break-even price in U.S. shale is estimated at $60 to $80 a barrel, according to the IEA (Bloomberg 2014)

The output of shale wells drops faster, too, falling by 60 to 70 percent in the first year alone, according to Austin, Texas-based Drillinginfo Inc. Traditional wells take two years to fall by about 55 percent before flattening out. This forces companies to keep drilling new wells to make up for lost productivity (Bloomberg 2014)

Sandrea, Ivan, US shale gas and tight oil industry performance: challenges and opportunities, Oxfort Institute Energy Studies,

March 2014Financial problems of operators in US shale gas and tight oil plays might hold

production growth below current expectations, according to Sandrea. “What is not clear is if the industry (both large players and independents) can run a cash flow-positive business in both top-quality and in more marginal plays and whether the positive cash flow could be maintained when the industry scales up its operations.” Sandrea cites asset write-downs approaching $35B since the shale boom began among 15 of the main operators. “While most of the companies that have made write-downs are not quitting, many players in this industry have already noted that the revolution is not as technically and financially attractive as they expected. Sandrea also cites a recent analysis by Energy Aspects, a commodity research consultancy, showing 6 years of progressively worsening financial performance by 35 independent companies focused on shale gas and tight oil plays in the US. “This is despite showing production growth and shifting a large portion of their activity to oil since 2010, presumably to chase a higher-margin business,” he adds. Oil and gas production by the companies represented 40% of output in unconventional plays in last year’s third quarter. According to the Energy Aspects analysis, total capital expenditure nearly matches total revenue every year, and net cash flow is becoming negative as debt rises. Other financial indicators “add to concerns about the sustainability of the business,” Sandrea says. Still, shale-gas and tight-oil development remains “a fledgling industry” with hope for “a positive inflection point for cash flow and a full-cycle risk-adjusted return.” Some operators see that point as still 5 years away. Sandrea says “above-ground reasons” include the need to constantly acquire and drill leases, infrastructure needs, transportation costs, increasing costs to manage environmental considerations as operations grow, and “the fact that drilling and hydraulic fracturing costs respond to fluctuations in gas and oil prices as well as demand, leaving little excess profit for long.” Below ground, he says, rapid production declines and low recovery rates, remain problems in many plays and might worsen as operators move into increasingly challenging acreage. Unless financial performances improve, capital markets won’t support the continuous drilling needed to sustain production from unconventional resource plays, Sandrea suggests, asking, “Who can or will want to fund the drilling of millions of acres and hundreds of thousands of wells at an ongoing loss?” More likely, he says, “Parts of the industry will have to restructure and focus more rapidly on the most commercially sustainable areas of the plays, perhaps about 40% of the current acreage and resource estimates, possibly yielding a lower production growth in the US than is currently expected—but perhaps a more lasting one.”

Conclusions 1/2 The reason to exports gas is to increase the prices shale gas producers

can get for their gas. This comes partly by engineering higher US prices (by shipping an excessive portion overseas) and partly by trying to take advantage of higher prices in Europe and Japan.

Dumping huge amounts of natural gas on world export markets is likely to sink the selling price of natural gas overseas, just as dumping shale gas on US markets sank US natural gas prices here (and misled some people, by making it look as if shale gas production is cheap).

The amount of natural gas export capacity that is in the approval process is huge: 42 billion cubic feet per day. The European Union imports only about 30 billion cubic feet a day from all sources. This amount hasn’t increased since 2005, even though EU natural gas production has dropped. Japan’s imports amounted to 12 billion cubic feet of natural gas a day in 2012; China’s amounted to about 4 billion cubic feet.

The countries that are importing huge amounts of high-priced natural gas are not doing well financially. They aren’t going to be able to afford to import a whole lot more high-priced natural gas. In fact, a big part of the reason that they are not doing well financially is because they are paying so much for imported natural gas (and oil). If the US has to pay these high prices for natural gas the US won’t be doing very well financially either.

Conclusions 2/2 Another issue is that with shale gas, the US are the high cost producer. There is

a lot of natural gas production around the world, particularly in the Middle East, that is cheaper. If we add the high cost of shale gas to the high cost of shipping LNG long-distance across the Atlantic or Pacific, the US will most definitely be the high cost producer.

And there would seem to be great temptation to stir up trouble, to encourage Europe to buy our natural gas exports, rather than Russia’s. This whole narrative makes the US look more rich and powerful than it really is. The US can even pretend to offer help to the Ukraine. Reaéity is, Europe won't get its independence from Russia, but US consumers will pay more.

Last year the United States produced 24.28 trillion cubic feet of natural gas, an all-time record amount. However, the US still imported 2.5 tcf of gas (11 percent of total consumption). The trend in US gas production rates has leveled off and is likely to begin declining in just the next few years, just about the time new liquefied natural gas (LNG) export terminals will be ready for business.

Finally, an examination of previous government forecasts reveals that they invariably overestimate production.

Asked if Chenerie's terminal could rescue eastern European countries from their dependence on Russia, Mr Souki (The head of Cheniere Energy) said: “It’s flattering to be talked about like this, but it’s all nonsense. It’s so much nonsense that I can’t believe anybody really believes it.” (FT)

QuestionsQuestion 1: In light of this presentation, do you think that the US can become a major

exporter of LNG?Question 2Exporting domestic gas is advantageous from the point of view of the average

American?Question 3Does the shale gas revolution represents a massive misallocation of capital

due to the FED policies of QE (4T USD pumped in the Economy) and ZIRP (0% interest rates policy)?

We the People of America own our natural gas under our land and water and it won't just go the highest bidder to profit some multi-national oil company and banker investor/gas trader to fuel someone else while we pay higher prices at home as a result, right?