US International Trade Commission - Agoa.info

405

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of US International Trade Commission - Agoa.info

U.S. International Trade Commission

Robert A. RogowskyDirector of Operations

COMMISSIONERS

Address all communications toSecretary to the Commission

United States International Trade CommissionWashington, DC 20436

Deanna Tanner Okun, Vice ChairmanStephen Koplan, Chairman

Marcia E. MillerJennifer A. HillmanCharlotte R. LaneDaniel R. Pearson

Robert B. KoopmanDirector of Economics

OMB No.: 3117--0188

12/04

ITC READER SATISFACTION SURVEYU.S. Trade and Investment with Sub-Saharan Africa

Fifth Annual Report

The U.S. International Trade Commission (USITC) is interested in your voluntary com-ments (burden less than 10 minutes) to help assess the value and quality of our reports, and to assistin improving future products. Please return survey by facsimile (202-205-2340) or by mail to theUSITC, or visit the USITC Internet home page(http://reportweb.usitc.gov/reader_survey/readersurvey.html) to electronically submit a Web version ofthe survey.

(Please print; responses below not for attribution):

Your name and title:

Organization (if applicable):

Which format is most useful to you? - CD-ROM - Hardcopy - USITC Internet site

Circle your assessment of each factor below: SA = strongly agree, A = agree, N = no opinion,D = disagree, or SD = strongly disagree.

Value of this report:" Statistical data are useful SA A N D SD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . ." Other non-numerical facts are useful SA A N D SD. . . . . . . . . . . . . . . . . . . ." Analysis augments statistical data/other facts SA A N D SD. . . . . . . . . . . ." Relevant topic(s)/subject matter SA A N D SD. . . . . . . . . . . . . . . . . . . . . . . ." Primary or leading source of information on this subject SA A N D SD. .

Quality of this report:" Clearly written SA A N D SD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ." Key issues are addressed SA A N D SD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ." Charts and graphs aid understanding SA A N D SD. . . . . . . . . . . . . . . . . . ." References cite pertinent sources SA A N D SD. . . . . . . . . . . . . . . . . . . . . . .

Other preferred source of information on this subject:

Specify chapters, sections, or topics in report that are most useful:

Identify any type of additional information that should have been included in report:

Suggestions for improving report:

Please update your mailing and electronic addresses below (voluntary)-

Mailing address:

City, state, and zip code:

E-mail address:

UNITED STATESINTERNATIONAL TRADE COMMISSION

WASHINGTON, DC 20436

OFFICIAL BUSINESSPENALTY FOR PRIVATE, USE $300

FOLD

NO POSTAGENECESSARY

IF MAILEDIN THE

UNITED STATES

BUSINESS REPLY MAILFIRST CLASS PERMIT NO. 12840 WASHINGTON, DC

POSTAGE WILL BE PAID BY ADDRESSEE

U.S INTERNATIONAL TRADE COMMISSION500 E STREET, SW.WASHINGTON, DC 20277--2840

ATTN:OFFICE OF ECONOMICSU.S. Trade and Investment with Sub-SaharanAfrica—Fifth Annual Report

U.S. International Trade CommissionWashington, DC 20436

December 2004

www.usitc.gov

Publication 3741

U.S. Trade and Investment WithSub-Saharan Africa

Fifth Annual ReportInvestigation No. 332-415

This report was principally prepared by

Arona Butcher, Chief, Country and Regional Analysis Division

Nannette Christ, Project LeaderLaura Polly, Deputy Project Leader

Office of EconomicsEdward Wilson, William Greene, and Selamawit Legesse

Office of IndustriesLaura Bloodgood, Cynthia Foreso, Alfred Forstall, John Fry, Amanda Horan,

Eric Land, Christopher Mapes, and Laura Rodriguez

Office of InvestigationsAndrew Rylyk and Barbara Bryan

Office of Information ServicesPatricia Augustine, Barbara Bobbitt, Patricia Holland, and Peggy Verdine

Student InternsKieshan Edwards, Joshua Finfrock, Melissa Ginsberg, Rebecca Havey, Kelly Kowalczyk,

Richard Qualters, Rikki Roullier, Danielle Rust, Jonathan Miner, Katherine Nunley,and Shakira Van Savage

Office of Pubishing

ReviewersCatherine DeFilippoDonnette Rimmer

Supporting assistance was provided by:Cecelia Allen, Office of Economics

Patricia Thomas, Office of Economics

i

EXECUTIVE SUMMARY

This report is the fifth in a 5-year series documenting U.S.-sub-Saharan Africa (SSA)trade and investment flows. The U.S. International Trade Commission (Commission orUSITC) compiled this report at the request of the United States Trade Representative(USTR). In a letter dated April 12, 2000,1 the USTR asked the Commission to submit areport that provides: an analysis of U.S.-SSA merchandise trade and services flows;country-by-country profiles of the economies of each SSA country, includinginformation on major trading partners and a summary of the trade and investmentclimates in each SSA country; a summary of U.S. foreign and total direct investmentand portfolio investment in SSA; information on SSA privatization efforts; updates onprogress in regional integration inSSA, including statistics onU.S. tradewith themajorregional groupings; and a summary of multilateral and U.S. bilateral assistance toSSA countries.

In a supplemental letter dated July 10, 2002, the USTR requested that the Commissionprovide the following additional information: the value ofU.S. imports from SSAunderthe African Growth and Opportunity Act (AGOA) including its Generalized System ofPreferences (GSP) provisions, by beneficiary country and major product categories;information on investment developments related to AGOA; a description and analysisof major SSA export sectors; expanded information on regional integration in SSA,including information on the Communauté Economique et Monétaire de l’AfriqueCentrale (CEMAC); a description of major U.S. trade capacity-building initiativesrelated to SSA; and a description of major non-U.S. trade preference programs forSSA countries.

The U.S.-SSA trade data included in this report generally cover full year 2003,depending on data availability. When possible, data for Africa are provided whenSSA data are not available. In cases where it is useful to show a trend, data for 1999through 2003 are provided. In addition, when possible, up-to-date developments ineconomic, social, trade, and commercial policies are included for the period January2004 through June 2004. Data sources include the U.S. Department ofCommerce, theEconomist Intelligence Unit, the World Bank, the United Nations, and industry-specificdata sources. In addition to the above-mentioned sources, qualitative discussions alsorely on articles sourced from databases such as All Africa and Newsedge.

U.S.-Sub-Saharan Africa Trade

S In 2003, U.S.-SSA merchandise trade rose to $32.1 billion, from $24.1 billionin 2002. This was a result of an increase in both U.S. exports to and U.S.

1 Copies of the request letters are in app. A.

ii

imports from the region. U.S. exports to SSA increased by 13.1 percent in2003 to approximately $6.7 billion, from $5.9 billion in 2002. Similarly, U.S.imports from SSA increased by 39.9 percent to approximately $25.5 billion in2003 from $18.2 billion in 2002.

S The increase in U.S. exports to SSA was attributed primarily to increasedexports of transportation equipment, agricultural products, and electronicproducts and increased exports to Ethiopia, South Africa, and EquatorialGuinea. The increase in U.S. imports from SSA was largely because of anincrease in energy-related products from Nigeria. Nonenergy-relatedimports increased by 20.0 percent to $7.8 billion in 2003.

S In 2002, the United States recorded a $2.2-billion surplus in services tradewith Africa. The primary U.S. cross-border service exports to Africa includedtourism and passenger transport, business services, education, and freighttransport and port services. U.S. service imports from Africa were mainly inthe tourism, passenger transport, business services, and freight transportsectors.

Foreign Direct Investment in Sub-Saharan Africa

S In 2003, SSA received $8.5 billion in new foreign direct investment (FDI), or6.3 percent of global foreign investment flows to developing countries.Political crises, poor weather conditions, and the HIV/AIDS pandemiccontinued to affect the investment climate.

S Net inward portfolio equity flows to SSA totaled $500 million in 2003. As inprior years, South Africa accounted for virtually all foreign portfolioinvestment flows to SSA in 2003.

S U.S. net direct investment flows to Africa totaled $1.4 billion in 2003,representing less than 1 percent of total U.S. direct investment abroad.Equatorial Guinea and Nigeria attracted the largest amounts of U.S. FDIflows, with $823 million and $340 million, respectively. Of the nonpetroleumexporting countries, South Africa and Cameroon attracted the largestamounts of U.S. FDI, with $89 million and $73 million, respectively.

S Reflecting the historically higher level of investment by European countries,many European countries have concluded a number of bilateral investmentagreements with SSA countries.

S Given the important role of investment in long-term economic development, anumber of international investment initiatives focusing on SSA have emerged.Such initiatives include an effort by Standard & Poor’s, working with theUnited Nations Development Programme (UNDP), to secure long-termsovereign ratings2 for SSA countries.

2 “A sovereign credit rating provides [general credit worthiness] as it signifies a country’s overallability to provide a secure investment environment.” Reem Heakal, “What is a Corporate Credit Rating,”found at Internet address http://www.investopedia.com, retrieved Oct. 7, 2004.

iii

African Growth and Opportunity Act

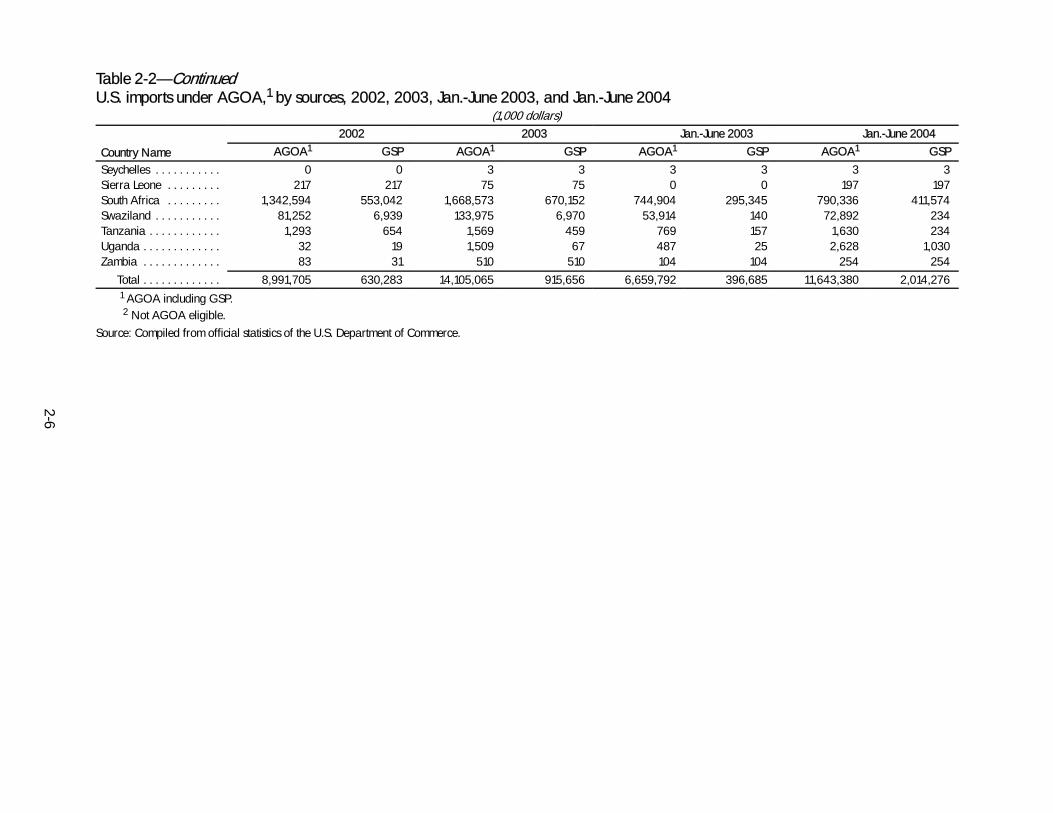

S Total U.S. imports from SSA countries eligible for AGOA benefits (includingGSP provisions) totaled almost $14.1 billion in 2003, an increase of 36.3percent from $9.0 billion in 2002. The largest share of U.S. imports underAGOA came from Nigeria (66.3 percent), followed by South Africa (11.8percent) and Gabon (8.3 percent). Other major suppliers included Lesotho,Republic of the Congo, Madagascar, and Kenya.

S U.S. purchases of energy-related products in 2003 represented 79.5 percentof total AGOA imports in 2003, up from their 75.9-percent share in 2002.Significant value increases were recorded, however, for textiles and apparel,which accounted for 8.5 percent of the total in 2003, down from an8.9-percent share in2002, and transportation equipment, which representeda 5.2-percent share in 2003, compared with a 6.1-percent share in 2002.

S AGOA III amended the textile provisions of AGOA to clarify language in theprior legislation and to expand and extend a number of provisions to provideAGOA countries with additional sourcing flexibility. The extension of the leastdeveloped beneficiary country third-country fabric provision was viewed bymany as the most important feature of AGOA III, as this provision had beenscheduled to expire.

S In anticipation of the AGOA III legislation and its subsequent passage in July2004, AGOA-eligible SSA countries continued to receive investmentsupported, in part, by their access to trade preferences under the AGOAprogram.

S Although a substantial portion of investments continued to target the apparelsector, increased investment has also occurred in the textile, mining, andmotor vehicle industries. Investment patterns also highlight the extension ofAGOA-related investment into small- and medium-sized businesses andefficiency-enhancing technology investment.

Regional Integration

S In 2003, the nine regional organizations in SSA continued to focus efforts onpromoting economic and monetary integration. They also worked towardpolicy harmonization in the telecommunications, transportation, andagricultural sectors. In addition to common investment policies, the regionalorganizations also continued to work toward eliminating regional tariffs inorder to increase intra-SSA trade. Moreover, the creation of exportprocessing zones has encouraged diversification from agricultural toindustrial production. The nine regional organizations are:

- the Economic Community of West African States (ECOWAS);

- the Union Economique et Monétaire Ouest Africaine (UEMOA);

- the Common Market for Eastern and Southern Africa (COMESA);

iv

- the Southern African Development Community (SADC);

- the Southern African Customs Union (SACU);

- the East African Community (EAC);

- the Intergovernmental Authority on Development (IGAD);

- the Indian Ocean Commission (IOC);

- the Communauté Economique et Monétaire de l’Afrique Centrale(CEMAC).

S Regional organizations continued to work toward increased economicintegration, although progress has been slow. ECOWAS continued efforts toestablish a customs union by 2007. In addition, ECOWAS and UEMOAbegan coordinating monetary union efforts. COMESA continued to expandtrade opportunities by launching FTA discussions with the EU. SADC workedtoward establishing regulations, such as single-digit inflation requirements,that would foster more stable integration. The United States and SACUcontinued FTA negotiations, as SACU has continued to expand its list ofpotential FTA partners. The EAC committed to establishment of a commonexternal tariff bySeptember 2004. IGAD focused on food and security issues;and IOC focused on transportation and communication issues. A regionalpassport scheme for CEMAC was implemented in early 2003, and CEMACinaugurated a new stock exchange in mid-2003.

S Current African Union3 (AU) policies focus on economic and exportdiversification. The AU is also seeking todevelop anAfrican CommonMarket.Other AU policies promote peace, economic stability, and regional securityas part of the AU’s poverty reduction efforts.

Multilateral and U.S. Bilateral Assistance

S In 2003, the World Bank lending commitments to SSA totaled $3.7 billion. Ofthe total funding, over 21 percent ($811 million) was for human development(primarily HIV/AIDS-related initiatives), 15 percent was for social protection,and 11 percent was for education. The International Finance Corporation(IFC) committed $164 million to support the expansion of SSA banks andfinancial institutions in FY 2004. Likewise, the World Bank’s MultilateralInvestment Guarantee Agency (MIGA) issued investment guarantees orcoverage for nine projects in Africa totaling $953 million.

S In 2003, the African Development Bank (AfDB) Group approved 16 newprojects and programs with a combined value of $465.1 million. The AfDBalso signed 118 loan and grant agreements valued at $2.6 billion. TheInternational Monetary Fund (IMF) committed $1.9 billion in grants to 23 SSAcountries. In FY 2003, the IMF approved Poverty Reduction and Growth

3 The AU is a successor to the Organization of African Unity.

v

S Facility arrangements for the Democratic Republic of Congo, The Gambia,Senegal, and Uganda.

S Export-Import Bank (Ex-Im Bank) provided loan guarantees and insurance toSSA totaling $572 million. As of September 2003, Ex-Im Bank’s totalexposure in SSA was $3.6 billion. Democratic Republic of the Congoaccounted for 24 percent, Nigeria made up 23 percent, and South Africarepresented 16 percent of total regional Ex-Im Bank exposure. U.S. Trade andDevelopment Agency (TDA) obligations in SSA decreased to $5.9 million inFY 2003 from $9.9 million in FY 2002. TDA’s SSA funding accounted for 11.2percent of all TDA funding in 2003. Overseas Private Investment Corporation(OPIC) invested $384 million in FY 2003. The United States Agency forInternational Development’s (USAID) Development Assistance and otherEconomic Assistance Program obligation for SSA totaled $1.4 billion in FY2003 compared to $1.1 billion in FY 2002. USAID continued to supportseveral programs that started in 2002 including the Initiative to End Hunger inAfrica, the African Education Initiative, and the Anti-Corruption Initiative.

U.S. Trade Capacity-Building Initiatives

S U.S. government agencies continued to fund and implement a broad range oftrade capacity-building initiatives in SSA. SSA received $132.7 million in FY2003, representing 17.4 percent of total U.S. funding for tradecapacity-building initiatives. The level was a 19.3-percent increase over FY2002.

S Numerous individual countries received less direct trade capacity-buildingfunding in FY 2003 as funding increasingly targeted regional organizationsin SSA such as COMESA and SACU. The percent share of the top five fundingrecipients declined from 54.1 percent in FY 1999 to 32.1 percent in FY 2003.

S The primary funding categories were “Human Resources and LaborStandards,” which accounted for 29 percent of FY 2003 total SSA funding,followed by “Trade Facilitation” and “Trade-related Agriculture,” whichaccounted for 25 percent and 15 percent, respectively. The subcategory“Export Promotion” accounted for 32 percent of “Trade Facilitation.”

Industry Sector Profiles

The six industry sectorsdiscussedbeloware:agriculture, fisheries,and forest products;chemicals; petroleum and energy-related products; minerals and metals; textiles andapparel; and certain transportation equipment. These sectors account for the majoritems traded between the United States and SSA. Figure ES-1 provides an overview ofU.S. trade and FDI positions in these sectors.

Agriculture, Petroleum, &Fisheries, and Energy-related Minerals and Textiles and Certain TransportForest Products Chemicals Products Metals Apparel Equipment

S Côte d’lvoire, South S South Africa, S Nigeria, Angola S South Africa S Lesotho, South S South AfricaAfrica, Madagascar Equatorial Guinea Africa, Mauritius

Madagascar, KenyaS Cocoa beans, S Methanol, certain S Crude petroleum S Plantinum-group S Woven cotton S Passenger vehiclesvanilla beans, organic chemicals, metals, diamonds pants/shorts, cottontobacco, coffee, natural rubber topsbeans, cocoa pasteS South Africa, S South Africa S Nigeria, Gabon S South Africa S Lesotho, S South AfricaCôte d’lvoire, Malawi Madagascar, Kenya

Mauritius, SouthAfrica, Swaziland

S Citrus, tobacco, cane S Silicon, titanium S Crude petroleum S Ferroalloys, S Woven cotton S Passenger vehiclessugar, cocoa powder, dioxide pigments, aluminum products pants/shorts, cottonmacadamia nuts car tires topsS Nigeria, South S South Africa S South Africa, S South Africa S South Africa, S South Africa,Africa, Ethiopia Nigeria Equatorial Guinea, Ghana, Nigeria Nigeria

Angola, NigeriaS Cereals S Fertilizers, misc. S Refined petroleum S Precious metals S Used clothing S Passenger vehicles

medicaments, productsisocyanates

S South Africa S South Africa S Equatorial Guinea, S Ghana, Zambia, S Not available S South AfricaChad, Gabon, KenyaNigeria

Figure ES-1SSA sector profiles summary data, 2003

Source: Data compiled from official statistics of the U.S. Department of Commerce (tade data) and Bureau of Economic Analysis (investment data).

Primary Sources

Primary Products

Primary Sources

Primary Products

Primary Markets

Primary Products

Primary FDICountries

U.S

.Exp

orts

AG

OA

Impo

rtsU

.S.I

mpo

rts

0

U.S. importsAGOA importsU.S. exportsU.S. FDI position

Million dollars

NA131

198

17,6

74

11,2

24

4,75

4

2,99

6

vi

2,000

4,000

6,000

8,000

10,00012,000

14,00016,000

18,000

1981,23

5

2741,

277

598

177

343

717

492

166

11,2

24

413

269

47

11,2

24

1,55

2

1,20

2

742

716

412

vii

Agriculture, Fisheries, and Forest ProductsS SSA represents a relatively small market for U.S. exports of agriculture,

fisheries, and forest products, totaling $1.2 billion, or approximately 1 percentof total U.S. sector exports in 2003. Sector exports to SSA increased by 17percent in 2003 compared with 2002. Primary SSA markets for such exportscontinued to be Nigeria (27 percent of the total value), South Africa (20percent), and Ethiopia (13 percent). Cereals such as nondurum wheat andmilled rice accounted for approximately 54 percent of total U.S. sectorexports to SSA in 2003. Food shortages throughout SSA account for theincreasing demand for U.S. cereal exports.

S U.S. sector imports from SSA totaled $1.3 billion in 2003, up by 30 percentfrom the previous year. SSA accounted for about 1 percent of total U.S. sectorimports in 2003, the same share as the previous year. The high price of cocoaduring most of 2003 was the primary contributor to the increase in importvalue. In 2003, the top five import commodities accounted for 57 percent oftotal U.S. sector imports from SSA, and included cocoa beans, vanilla beans,tobacco, coffee beans, and cocoa paste.

S In 2003, the value of U.S. sector imports from SSA under AGOA (includingGSP) was $274 million, representing an increase of 13 percent over theprevious year. Such imports accounted for about 2 percent of total AGOAimports and 21 percent of total sector imports from SSA in 2003. South Africa,Côte d’Ivoire, and Malawi supplied 85 percent of all AGOA imports fromSSA in 2003, up from 82 percent in 2002. Principal products included freshcitrus, unmanufactured tobacco, raw cane sugar, cocoa powder, andmacadamia nuts.

S This sector accounts for a relatively minor share of the total U.S. FDI in theregion in 2003. U.S. FDI in the SSA food sector increased by one-third in2003, reaching $198 million. South Africa continued to be the primary SSAlocation for U.S. sector FDI in the region.

ChemicalsS The South African chemical industry accounts for approximately 77 percent

of SSA chemical production. This industry remains among the largestmanufacturing sectors of the South African economy, maintaining its5-percent share of gross domestic product. The sector is essentially composedof producers of petrochemical products produced in the four petroleumrefineries, producers of agricultural chemicals, pharmaceuticalmanufacturers, and various small firms producing chemical products for thedomestic/regional market.

S The most significant development in the SSA chemical industry during2003-04 was the development of SSA pharmaceutical production capacityalong with the ability to produce active pharmaceutical ingredients (APIs) foruse in generic pharmaceutical products. Aspen Pharmacare, the largestpharmaceutical manufacturer in Africa, received clearance from SouthAfrica’s Competition Commission to vertically integrate using the recently

viii

purchased Fine ChemicalsCorp. facility.Aspen releaseda statement assuringthe public that they would be using the plant to produce APIs, such as theretrovirals that treat HIV/AIDS.

S U.S. chemical sector imports from SSA reached $598 million in 2003, up byone-third from the previous year. U.S. sector imports from SSA accounted forless than 1 percent of total U.S. imports in 2003. Principal SSA sourcesincluded South Africa (58 percent of the total) and Equatorial Guinea (23percent), with Liberia accounting for 9 percent. The three largest U.S. sectorimports from SSA in 2003 were methanol; organic chemicals used asfeedstocks for producing chemical intermediates and chemical products,including unsaturated acyclic hydrocarbons; and natural rubber. In 2003,U.S. chemical sector imports under AGOA (including GSP) totaled $177million, an increase of 30 percent over 2002. These imports representedapproximately 30 percent of total U.S. imports of these products from theSSA. Nearlyall the U.S. chemical imports underAGOA(including GSP) camefrom South Africa.

S In 2003, U.S. chemical sector exports to SSA totaled $717million, an increaseof nearly 3 percent compared with 2002. SSA accounted for less than 1percent of total U.S. sector exports in 2003. The top three SSA markets forU.S. chemical exports in 2003 were South Africa, which accounted for 62percent of U.S. chemical exports, followed by Nigeria (8 percent) and Kenya(5 percent). These shares were similar to those in 2002. The United Statesexported a diverse selection of chemical items to SSA in 2003; the leadingexport items – fertilizers, other nonspecified medicaments, and isocyanates –each only accounted for 4 to 5 percent of total U.S. sector exports to SSA.

S The U.S. FDI position in the chemicals sector increased by 11 percent to $492million in 2003. South Africa accounted for 91 percent of the total.

Petroleum and Energy-Related ProductsS Crude petroleum in Nigeria and Angola, and coal in South Africa continue to

be the primary petroleum and energy-related products produced in SSA.Nigeria and Angola are the region’s first- and second-largest producers ofcrude petroleum, respectively. Coal continues tobe the primary fuel producedand consumed in South Africa and is its largest source of foreign exchange.South Africa accounts for about 4 percent of the world’s recoverable reservesof coal and is the second-largest net exporter of coal to the world market.

S Crude petroleum is the primary export product from SSA. In 2003, the UnitedStates was the primary market for SSA exports of petroleum andenergy-related products, while the EU accounted for most of the remainder.Refined petroleum products are the major products imported into the SSAregion, followed by crude petroleum; the United States and Western Europeare major sources of SSA imports of refined petroleum products.

S Nigeria, one of the world’s leading exporters of crude petroleum, has thepotential to increase its production of crude petroleum significantly in the nextfew years as recent discoveries come onstream. Several joint ventures

ix

between the Nigerian government and multinational petroleum companiesare expected to yield additional production of crude petroleum and naturalgas. In addition, recent discoveries of crude petroleum in Angola arebecoming attractive to the world’s leading production companies.

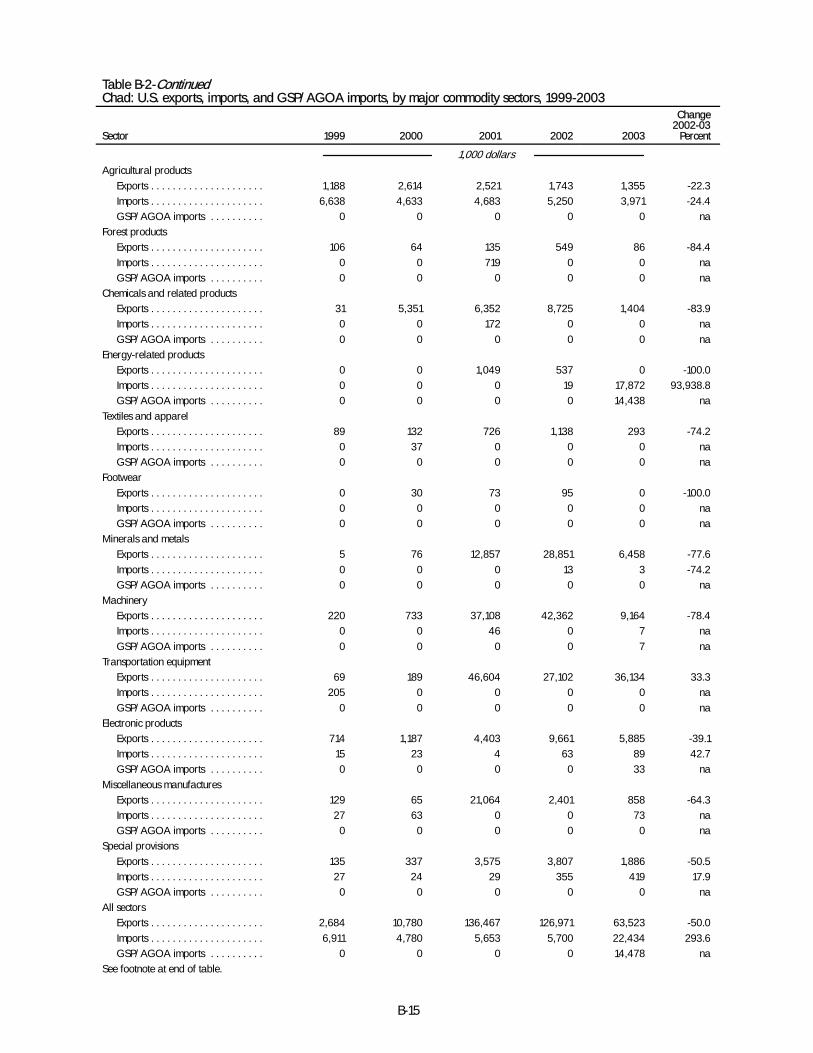

S The U.S. FDI position in the SSA mining sector (the most comparable sector topetroleum and energy-related products) increased by 20 percent to $4.8billion in2003. Equatorial Guinea, Chad, Gabon, and Nigeria accounted for83 percent of the regional total.

Minerals and MetalsS The minerals and metals sector remains a dominant sector for many SSA

countries. Prices for severalminerals andmetals continued to recover from theextreme lows during 1997 to early 2003, reflecting declining inventoriesarising from a combination of worldwide production shutdowns and risingconsumption. These price increases contributed to the improving economiesofthe SSA metal-producing countries and attracted additional internationalinvestment interest.

S In 2003, the U.S. minerals and metals trade deficit with SSA increased by 12percent, to $2.7 billion, with U.S. imports increasing by 11 percent, to $3.0billion. Sixty-eight percent of U.S. imports from SSA in 2003 wereplatinum-group metals (PGMs), which were almost all from South Africa, anddiamonds, mostly from South Africa, Democratic Republic of the Congo(DROC), and Angola. U.S. imports of iron and steel products also increased,reflecting the continued growth in the iron and steel industries in South Africa,Tanzania, and neighboring countries. AGOA imports (including GSP) totaled$413 million in 2003, up by 11 percent from the previous year. Imports underAGOA accounted for 14 percent of total sector imports from SSA in 2003. Thebulk was supplied by South Africa (96 percent) and Namibia (under 4percent), with iron and steel products, primarily ferroalloys, accounting for59 percent, and aluminum products increasing by 16 percent by value to 21percent of the total.

S The U.S. Clean Diamond Trade Act and the United Nation’s KimberleyProcess Certification Scheme (KPCS) continued to affect diamond trade. TheCentral African Republic joined the 61 member-countries of the KPCS inAugust 2003. DROC was suspended by the United Nations from world tradein diamonds in July 2004. Separately, DeBeers pled guilty to price fixing inU.S. District Court and agreed to pay $10 million to settle a 10-year-oldindictment. This settlement should allow DeBeers to re-establish a directmarketing presence in the United States.

S U.S. sector exports to the region increased marginally (up by 1 percent) to$269 million in 2003, but increased markedly to Equatorial Guinea, Angola,and South Africa. Many countries recorded double-digit declines, largely asa result of economic and political instability. Chad recorded the largestdecline, at $22 million. In the iron and steel sector, exports of oil and gastubular and ancillary products declined the most in value, reflecting less

x

exploration drilling. U.S. exports of structural commodities (steel structures,towers, and masts; and lime and cement products) registered the largestincrease, and were largely to support the oil and gas recovery and refiningfacilities.

S The South African President signed the Broad-Based Black Empowerment Actinto law in January 2004. Coupled with other laws (Mineral Law, Money Bill,Health and Safety Act) passed within the last few years that were intended torestructure the country, it has caused significant valuation and financial riskissues, delaying mine investment in South Africa. To counteract these effects, aBeneficiation Bill has been proposed that aims to promote South Africa’sminerals industry by giving South Africans the opportunity to own basic formsof gold (e.g., bullion), diamonds, and PGMs. This bill is expected to stimulatedownstream processing and fabrication of these basic forms in South Africaby providing producer incentives for locally-manufactured products. SouthAfrican investment in newly committed SouthAfricanmineral-relatedprojectsincreased by 29 percent in 2003, but exploratory investment decreased by 10percent. Eighty-eight percent of exploratory investment, or approximately$2.3 billion, was earmarked for primary mineral production.

S The U.S. FDI position in the SSA primary and fabricated metals sectordecreased by 30 percent to $47 million in 2003. Ghana was the leadingrecipient of U.S. FDI in the region.

Textiles and ApparelS SSA production and exports of textiles and apparel continue to be

concentrated in Mauritius, South Africa, Lesotho, Madagascar, and Kenya.Other countries such as Ethiopia, Ghana, Tanzania, and Swaziland areincreasing activity in the sector, owing to factors such as SSA governmentinitiatives, increased foreign investment, intra-SSA country partnerships, andtrade preferences such as AGOA. The AGOA program has stimulatednumerous foreign investment projects in several SSA textile-producingcountries. Most of the investment has come from Asian sources.

S U.S. sector imports from SSA rose by 37 percent in 2003, reaching $1.6billion. SSA represented 2 percent of total U.S. sector imports. Principal SSAsuppliers included Lesotho, South Africa, Mauritius, Madagascar, andKenya. Primary items included cotton pants and cotton tops. U.S. sectorimports under AGOA totaled $1.2 billion in 2003, up by 50 percent over the2002 level and representing just over three-fourths of total U.S. sector importsfrom SSA and 9 percent of total imports under AGOA. Principal AGOAsuppliers included Lesotho, Madagascar, Kenya, Mauritius, South Africa,and Swaziland.

S The growth of the textile and apparel industries in SSA countries continues tobe constrained by widespread shortages of raw materials and textile inputs,high production costs relative to Asian suppliers, obsolete equipment, andcapacity underutilization. The influx of used clothing and inexpensivesmuggled goods that compete with local production is also a factor in

xi

numerous countries. In addition, the export competitiveness of SSA countriesin the global textile and apparel market has been hampered by high taxes,utility and input costs, and for some SSA countries, currency appreciation. Thecontinued strength of the South African rand (to which the currencies ofSwaziland and Lesotho are pegged) relative to the U.S. dollar weakened thecompetitiveness of textile and apparel exports from these countries in 2003.

S U.S. sector exports to SSA in 2003 rose by 5 percent to $131 million. Suchexports accounted for a negligible share of the U.S. sector total. Primary SSAmarkets included South Africa, Ghana, and Nigeria; used clothing was by farthe major export item.

Certain Transportation EquipmentS South Africa is the dominant producer of, and market for, motor vehicles and

motor-vehicle parts in the SSA region, accounting for 95 percent of SSAmotor vehicle production and 60 percent of motor vehicle sales in 2003. Theautomotive industry in South Africa accounts for nearly 6 percent of thecountry’s gross domestic product, is the largest manufacturer, and is thelargest manufacturing exporter.

S U.S. imports of certain transportation equipment from SSA reached $742million in2003, an increase of $182million, or33percent. SSA accounted forless than 1 percent of the value of total U.S. sector imports in2003. Virtually allU.S. sector imports from SSA in 2003 were supplied by South Africa, withpassenger cars accounting for 84 percent of sector imports from SouthAfrica. Leading components imported from South Africa in 2003 includedroad wheels, miscellaneous auto parts, and miscellaneous engine parts. U.S.transportation equipment imports underAGOA (including GSP) increased by34 percent in 2003, reaching $716 million; the majority of such imports werefrom South Africa. In 2003, imports under AGOA accounted for 97 percentof total U.S. sector imports from SSA.

S In 2003, U.S. transportation equipment exports to SSA reached $412 million,up by 36 percent from the previous year. South Africa accounted fortwo-thirds of U.S. sector exports to SSA, and SSA accounted for less than 1percent of the value of total U.S. sector exports in 2003.

S The U.S. FDI position in the SSA transportation equipment sector decreasedby13 percent to $343 million in 2003. South Africa was the primary location forU.S. FDI in the region.

Country Profiles

S In 2003, SSA’s average GDP growth rate was 3.6 percent, up from 3.2percent in2002. The increasewasattributed to higher investment levels, risingglobal commodity prices, increased agricultural production, and increasing

xii

regional stability stemming from negotiations launched by the regionalorganizations to reduce civil unrest. The HIV/AIDS pandemic, however,continued to curb economic development formany SSA countries by loweringproductivity, inhibiting investment, and increasing social costs.

S Additional barriers to economic growth for many countries in SSA includedlower than expected economic growth in the EU, a major trading partner forSSA countries; a slowdown in tourism for many countries that are seeking todiversify into this sector; and large current account deficits.

S SSA countries’ efforts to increase their level of integration into the globaltrading economy continued to be hampered by a number of obstacles. Inaddition to social and political conflict, inadequate infrastructure, such asdilapidated road networks, congested ports, inefficient customs services, andprohibitively expensive air transport, hampered the national andinternational transport of merchandise. Many SSA countries continued todepend heavily on exports of primary commodity products, such aspetroleum, minerals, and agricultural products.

S For many SSA countries, economic development continued to be hindered bysocial unrest. For example, in 2003, Burundi, Central African Republic, Côted’Ivoire, Democratic Republic of the Congo, Guinea-Bissau, Republic of theCongo, Somalia, and Zimbabwe experienced social and political instabilitythat undermined economic development efforts. The political and socialinstability stemming from government land redistribution and economicpolicies in Zimbabwe resulted in another year of negative economic growth.

S For many other SSA countries, however, economic development continued tofocus on attempts to diversify the economy. For example, initiatives in Angola,Gabon, Nigeria, and São Tomé and Principe focus on diversifying within andaway from the petroleum and energy-related sector; Botswana’s ExportDevelopment and Investment Authority announced plans to encouragenontraditional products such as textiles and apparel, light manufacturing,and tourism; Kenya experienced some success in efforts to encouragediversification into horticultural products; Madagascar, Mauritius, and SãoTomé and Principe are using export processing zones to encouragediversification into aquaculture and tourism (Madagascar), lightmanufacturing and information and communication technology (Mauritius),and fishing (São Tomé and Principe); and Namibia has experienced initialsuccess in promoting local fish processing.

S Several SSA countries established policies that countered the general trendtoward trade liberalization in SSA. For example, trade barriers increasedwhen Angola required that all trade pass through government-controlledposts; Nigeria banned the import of more than 40 products, including certaintextiles, men’s footwear, soap, furniture, assembled bicycles, toothpaste,certain plastic products, vegetable oil, and certain meat products; theGovernment of Zambia increased the number of products subject to qualitymonitoring from 12 to 24, including bottled water, varnishes, hair oils andcreams, asbestos, and glycerine; and Zimbabwe announced an alternatemethod for calculating import duties,which is expected to increase theappliedduties on inputs used by the manufacturing and mining industries.

xiii

S Given the importance of inadequate infrastructure in hindering trade andinvestment, many SSA countries increased efforts to improve transportationinfrastructure. The instability in Côte d’Ivoire had a significant impact on tradein western Africa, further highlighting the general vulnerability of many SSAcountries to limited transport options. Examples of such infrastructure effortsinclude: construction of the Cotonou (Benin) fishing port, construction of theBurkina Faso-Ghana railway, Cameroon’s oil platform repair yardconstruction, Cape Verde’s port expansion, the Mali-Niger railwayextension, the Dubai Port (Djibouti) expansion, port and railway linking andexpansion in Kenya, rehabilitation of the Beira and Nacala ports inMozambique, development of the Walvis Bay Corridor and port in Namibia,and modernization of the port in Senegal.

S Although privatization efforts continued in many SSA countries, progress hasbeen hampered by the lack of transparency and corruption (Angola,Cameroon, Comoros, and Guinea), lack of interested parties (Angola,Cameroon, Gabon, and Guinea), and political resistance or social instability(Ethiopia, Guinea, Mauritius, South Africa, Tanzania, Togo, and Zambia).

S In an effort to increase investment, many SSA countries have pursuedregulatory reform. For example, Botswana passed initiatives to encouragejoint ventures between foreign investors and domestic partners; The Gambiapassed the Money Laundering Bill to improve the transparency of financialinstitutions; Ghana introduced the Foreign Exchange Bill, the Long-TermSavings Bill, the Credit Union Bill, and the Insurance Bill aimed at attractingforeign investment in the financial sector; Kenya passed the Anti-Corruptionand Economic Crimes Bill in mid-2003; Namibia’s new mining policyincreased security of tenure for holders of mining rights and created astandard licensing scheme; and in late 2003, Republic of the Congo adopteda bill that streamlines licensing procedures and reduces the state’s equityshare in mining companies.

xv

TABLE OF CONTENTS

PageExecutive Summary i. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

List of Abbreviations and Acronyms xxv. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Introduction xxvii. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Purpose and organization of the report xxvii. . . . . . . . . . . . . . . . . . . . . . . .Approach xxviii. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Scope of the report xxix. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chapter 1. U.S. trade and investment with sub-Saharan Africa 1-1. . . . . . . . . .U.S. merchandise trade 1-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

U.S. merchandise exports 1-3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .U.S. merchandise imports 1-5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Merchandise trade balance 1-11. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

U.S.-Africa services trade 1-14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Foreign investment in sub-Saharan Africa 1-20. . . . . . . . . . . . . . . . . . . . . .

Global investment in sub-Saharan Africa 1-20. . . . . . . . . . . . . . . . . . . .U.S. investment in sub-Saharan Africa 1-21. . . . . . . . . . . . . . . . . . . . . .Investment by country and by sector 1-21. . . . . . . . . . . . . . . . . . . . . . . .Investment agreements between sub-Saharan African countries

and foreign investment partners 1-24. . . . . . . . . . . . . . . . . . . . . . . .International investment initiatives focused on sub-Saharan

Africa 1-26. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chapter 2. AGOA-related imports and investment 2-1. . . . . . . . . . . . . . . . . . .African Growth and Opportunity Act 2-1. . . . . . . . . . . . . . . . . . . . . . . . .

AGOA Forum 2-3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .U.S. imports under AGOA 2-4. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .AGOA-related investment 2-8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chapter 3. Regional integration in sub-Saharan Africa 3-1. . . . . . . . . . . . . . . .Regional integration in 2003 3-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Economic Community of West African States 3-5. . . . . . . . . . . . . . . . . . .Union Economique et Monétaire Ouest Africaine 3-7. . . . . . . . . . . . . . . .Common Market for Eastern and Southern Africa 3-9. . . . . . . . . . . . . . . .Southern African Development Community 3-11. . . . . . . . . . . . . . . . . . . . .Southern African Customs Union 3-13. . . . . . . . . . . . . . . . . . . . . . . . . . . . .East African Community 3-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xvi

TABLE OF CONTENTS—ContinuedPage

Chapter 3. Regional integration in sub-Saharan Africa–ContinuedIntergovernmental Authority on Development 3-17. . . . . . . . . . . . . . . . . . .Indian Ocean Commission 3-19. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Communauté Economique et Monétaire de l’Afrique Centrale 3-21. . . . . .

Chapter 4. Multilateral assistance, U.S. bilateral assistance, and othertrade-related initiatives 4-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Sources of multilateral assistance to sub-Saharan Africa 4-1. . . . . . . . . .The World Bank Group 4-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

The World Bank/International Development Association 4-1. . . . .Multilateral Investment Guarantee Agency 4-8. . . . . . . . . . . . . . . .International Finance Corporation 4-9. . . . . . . . . . . . . . . . . . . . . . .

The African Development Bank Group 4-11. . . . . . . . . . . . . . . . . . . . . . . .International Monetary Fund 4-12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .New Partnership for African Development 4-14. . . . . . . . . . . . . . . . . . . . .Trade capacity-building initiatives of U.S. government agencies 4-17. . . . .

Country coverage 4-17. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Types of trade capacity-building initiatives 4-18. . . . . . . . . . . . . . . . . . .

The Export-Import Bank of the United States 4-31. . . . . . . . . . . . . . . . . . . .U.S. Trade and Development Agency 4-31. . . . . . . . . . . . . . . . . . . . . . . . .Overseas Private Investment Corporation 4-34. . . . . . . . . . . . . . . . . . . . . .U.S. Agency for International Development 4-35. . . . . . . . . . . . . . . . . . . . .

Chapter 5. Industry sector profiles 5-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Agricultural, fisheries, and forest products 5-3. . . . . . . . . . . . . . . . . . . . .

Overview 5-3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-7. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-7. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-7. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chemicals 5-11. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Overview 5-11. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-14. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-14. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-14. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xvii

TABLE OF CONTENTS—ContinuedPage

Chapter 5. Industry sector profiles–ContinuedPetroleum and energy-related products 5-17. . . . . . . . . . . . . . . . . . . . . . . .

Overview 5-17. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-18. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-20. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-20. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-20. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Minerals and metals 5-23. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Overview 5-23. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-25. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-27. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-27. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-27. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-29. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Textiles and apparel 5-33. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Overview 5-33. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-35. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-37. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-37. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-37. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-38. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Certain transportation equipment 5-41. . . . . . . . . . . . . . . . . . . . . . . . . . . .

Overview 5-41. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Trade 5-43. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Key U.S. import developments 5-45. . . . . . . . . . . . . . . . . . . . . . . . . .Key AGOA trade developments 5-45. . . . . . . . . . . . . . . . . . . . . . . .Key U.S. export developments 5-45. . . . . . . . . . . . . . . . . . . . . . . . . .

Investment 5-46. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chapter 6. Country profiles 6-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Regional overview 6-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tariff structure 6-3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Technical notes 6-5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Profiles of 48 sub-Saharan African countries 6-9. . . . . . . . . . . . . . . . . . .

Angola 6-9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Benin 6-11. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Botswana 6-13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xviii

TABLE OF CONTENTS—ContinuedPage

Chapter 6. Country profiles–ContinuedProfiles of 48 sub-Saharan African countries—Continued

Burkina Faso 6-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Burundi 6-17. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Cameroon 6-19. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Cape Verde 6-21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Central African Republic 6-23. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chad 6-25. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Comoros 6-27. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Côte d’Ivoire 6-29. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Democratic Republic of the Congo 6-31. . . . . . . . . . . . . . . . . . . . . . . . . .Djibouti 6-33. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Equatorial Guinea 6-35. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Eritrea 6-37. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ethiopia 6-39. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Gabon 6-41. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .The Gambia 6-43. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ghana 6-45. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Guinea 6-47. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Guinea-Bissau 6-49. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Kenya 6-51. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Lesotho 6-53. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Liberia 6-55. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Madagascar 6-57. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Malawi 6-59. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mali 6-61. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mauritania 6-63. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mauritius 6-65. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mozambique 6-67. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Namibia 6-69. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Niger 6-71. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Nigeria 6-73. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Republic of the Congo 6-77. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Rwanda 6-79. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .São Tomé and Principe 6-81. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Senegal 6-83. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Seychelles 6-85. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sierra Leone 6-87. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xix

TABLE OF CONTENTS—Continued

PageChapter 6. Country profiles–Continued

Profiles of 48 sub-Saharan African countries—ContinuedSomalia 6-89. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .South Africa 6-91. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sudan 6-95. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Swaziland 6-97. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tanzania 6-99. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Togo 6-101. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Uganda 6-103. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Zambia 6-105. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Zimbabwe 6-107. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Primary nongovernment sources for country profiles 6-109. . . . . . . . . . . .

AppendicesA. Request letters from the U.S. Trade Representative A-1. . . . . . . . . . . . . . .B. Trade data B-1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

FiguresES-1. SSA sector profiles summary data, 2003 vi. . . . . . . . . . . . . . . . . . . . . . .1. Map of sub-Saharan Africa xxx. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-1. U.S. trade with sub-Saharan Africa, 1999-2003 1-2. . . . . . . . . . . . . . . . . .1-2. U.S. nonenergy-related trade with sub-Saharan Africa,

1999-2003 1-4. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-3. U.S. exports to sub-Saharan Africa by trading partners,

by shares, 2003 1-4. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-4. U.S. exports to sub-Saharan Africa by commodity sectors,

by shares, 2003 1-6. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-5. U.S. exports to sub-Saharan Africa: Annual growth rate, by

commodity sectors, 2002-03 1-6. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-6. U.S. imports from sub-Saharan Africa by trading partners,

by shares, 2003 1-10. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-7. U.S. imports from sub-Saharan Africa by commodity sectors,

by shares, 2003 1-10. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-8. U.S. imports from sub-Saharan Africa: Annual growth rate,

by commodity, 2002-03 1-14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-9. U.S. cross-border trade in services with Africa: Exports, imports,

and trade balance, 1999-2002 1-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-1. U.S. trade capacity-building initiatives, by funding categories and

subcategories, FY 2003 4-20. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-1. Gross national income per capita, 2002 6-4. . . . . . . . . . . . . . . . . . . . . . .

xx

TABLE OF CONTENTS—ContinuedPage

Boxes1-1. Services trade in sub-Saharan Africa, selected investments 1-17. . . . . . . . .4-1. USAID and trade capacity-building initiatives 4-29. . . . . . . . . . . . . . . . . . .

Tables1-1. Sub-Saharan Africa: U.S. exports of domestic merchandise, imports for

consumption, and merchandise trade balance, by major commoditysectors, 1999-2003 1-7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-2. Sub-Saharan Africa: U.S. exports by major commodity items,1999-2003 1-8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-3. Sub-Saharan Africa: U.S. imports by major commodity items,1999-2003 1-12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-4. Total Africa and South Africa: U.S. cross-border services exports,1997 and 2002 1-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-5. Total Africa and South Africa: U.S. cross-border services imports,1997 and 2002 1-19. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-6. Global investment flows to sub-Saharan Africa and developingcountries, 1999-2003 1-21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1-7. U.S. direct investment abroad: Capital flows, 1999-2003 1-22. . . . . . . . . .1-8. U.S. direct investment position on a historical cost basis,

1999-2003 1-22. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-9. Bilateral investment treaties with sub-Saharan Africa, by selected

investment partner country, 2004 1-25. . . . . . . . . . . . . . . . . . . . . . . . . .2-1. Sub-Saharan African countries designated as beneficiary countries of

AGOA as of December 31, 2003 2-2. . . . . . . . . . . . . . . . . . . . . . . . . .2-2. U.S. imports under AGOA, by sources, 2002, 2003, Jan.-June 2003,

and Jan.-June 2004 2-5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-3. Major U.S. imports under AGOA, by major commodity sectors, 2002,

2003, Jan.-June 2003, and Jan.-June 2004 2-7. . . . . . . . . . . . . . . . . .2-4. Leading U.S. imports under AGOA, by HTS descriptions, 2002, 2003,

Jan.-June 2003, and Jan.-June 2004 2-9. . . . . . . . . . . . . . . . . . . . . . . .2-5. Selected examples of recent AGOA-related investment and events,

2003 to mid-2004 2-12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-1. Summary of general developments in multilateral and U.S. bilateral

assistance for sub-Saharan Africa, 2003 4-2. . . . . . . . . . . . . . . . . . . .4-2. World Bank/IDA: Eligible borrowers in sub-Saharan Africa (37) 4-3. . . .4-3. World Bank (IDA and IBRD) lending commitments in sub-Saharan Africa,

by theme and sector, average FY 1998-99 and FY 2000-03 4-5. . . . . .

xxi

TABLE OF CONTENTS—ContinuedPage

Tables–Continued4-4. World Bank projects approved in sub-Saharan Africa, FY 2003 4-6. . . .4-5. Sub-Saharan African MIGA members and countries in the process

of fulfilling membership requirements, 2003 4-9. . . . . . . . . . . . . . . . . .4-6. MIGA guarantees issued in sub-Saharan Africa, FY 2003 4-10. . . . . . . . .4-7. Total ADF and AfDB projects and programs approved during 2003,

by country 4-13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-8. U.S. support for building trade capacity, by geographic region,

FY 1999-FY 2003 4-18. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-9. Trade capacity-building initiatives, leading sub-Saharan African

country recipients, FY 1999-FY 2003 4-19. . . . . . . . . . . . . . . . . . . . . . . .4-10. Examples of trade capacity-building initiatives in sub-Saharan Africa,

FY 2003 4-21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-11. Sub-Saharan Africa: Export-Import Bank exposure, authorizations,

and availability for further support as of December 14, 2003 4-32. . . .4-12. U.S. Trade and Development Agency funds obligated for program

activities in Africa, FY 2003 4-33. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4-13. Sub-Saharan Africa: Selected OPIC investment projects, 2003 4-35. . . . . .4-14. USAID funds allocated for sub-Saharan Africa, by major

project categories, FY 2003 4-37. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-1. Aggregate governance index, selected sub-Saharan African countries,

1996 and 2002 6-3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-2. Tariffs in sub-Saharan African countries, various years 6-6. . . . . . . . . . .B-1. U.S. exports, imports, and trade balance, with sub-Saharan Africa,

by trading partners, 1999-2003 B-3. . . . . . . . . . . . . . . . . . . . . . . . . . .B-2. U.S. exports, imports, and GSP/AGOA imports, by major commodity

sectors, 1999-2003 B-7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Angola B-7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Benin B-8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Botswana B-9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Burkina Faso B-10. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Burundi B-11. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Cameroon B-12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Cape Verde B-13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Central African Republic B-14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chad B-15. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Comoros B-16. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Côte d’Ivoire B-17. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xxii

TABLE OF CONTENTS—Continued

PageTables–Continued

Democratic Republic of the Congo B-18. . . . . . . . . . . . . . . . . . . . . . . . . .Djibouti B-19. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Equatorial Guinea B-20. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Eritrea B-21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ethiopia B-22. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Gabon B-23. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .The Gambia B-24. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ghana B-25. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Guinea B-26. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Guinea-Bissau B-27. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Kenya B-28. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Lesotho B-29. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Liberia B-30. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Madagascar B-31. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Malawi B-32. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mali B-33. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mauritania B-34. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mauritius B-35. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mozambique B-36. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Namibia B-37. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Niger B-38. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Nigeria B-39. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Republic of the Congo B-40. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Rwanda B-41. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .São Tomé and Principe B-42. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Senegal B-43. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Seychelles B-44. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sierra Leone B-45. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Somalia B-46. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .South Africa B-47. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sudan B-48. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Swaziland B-49. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tanzania B-50. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Togo B-51. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xxiii

TABLE OF CONTENTS—ContinuedPage

Tables–ContinuedUganda B-52. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Zambia B-53. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Zimbabwe B-54. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B-3. Leading changes in sectoral trade, by sectors, 1999 and 2003 B-55. . . . .Angola B-55. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Côte d’Ivoire B-56. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Equatorial Guinea B-57. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Gabon B-58. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ghana B-59. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Kenya B-60. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Mauritius B-61. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Nigeria B-62. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Republic of the Congo B-63. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .South Africa B-64. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B-4. U.S. imports under AGOA and GSP, 2002, 2003, Jan.-June 2003,and Jan.-June 2004 B-65. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

xxv

List of Abbreviations and Acronyms

ADB Asian Development BankADF African Development FundAfDB African Development BankAGOA African Growth and Opportunity ActATIA African Trade Insurance AgencyATRIP African Trade and Investment Policy ProgramAU African UnionBEA Bureau of Economic Analysis (U.S. Department of Commerce)BIT Bilateral investment treatyCACEU Central African Customs and Economic UnionCEMAC Communauté Economique et Monétaire de l’Afrique CentraleCFA Communauté Financière AfricaineCMA Common Monetary AreaCOMESA Common Market for Eastern and Southern AfricaDROC Democratic Republic of the CongoEAC East African CommunityECOWAS Economic Community of West African StatesEU European UnionEx-Im Bank Export-Import Bank of the United StatesFDI Foreign direct investmentFTA Free trade agreement or free trade areaGATT General Agreement on Tariffs and TradeGDP Gross domestic productGSM Global system for mobile communicationsGSP U.S. Generalized System of PreferencesHIPC Heavily Indebted Poor CountriesHTS Harmonized Tariff ScheduleIBRD International Bank for Reconstruction and DevelopmentIDA International Development AssociationIFC International Finance CorporationIGAD Intergovernmental Authority on DevelopmentIMF International Monetary FundIOC Indian Ocean CommissionJSE Johannesburg Stock ExchangeLDBC Least developed beneficiary countryMOU Memorandum of UnderstandingMIGA Multilateral Investment Guarantee AgencyNEPAD New Partnership for African DevelopmentNGO Nongovernmental organizationNTF Nigerian Trust FundOAU Organization of African UnityOPIC Overseas Private Investment Corporation

xxvi

List of Abbreviations and Acronyms-Cont.

PRGF Poverty Reduction and Growth FacilityPRSC Poverty Reduction Support CreditPRSP Poverty Reduction Strategy PaperROC Republic of the CongoSACU Southern African Customs UnionSADC Southern African Development CommunitySDR Special Drawing RightsSSA Sub-Saharan AfricaTDA U.S. Trade and Development AgencyTRIPS Agreement on Trade-Related Aspects of Intellectual

Property RightsUDEAC L’Union Douanière Et EconomiqueUEMOA Union Economique Et Monétaire Ouest AfricaineUN United NationsUNCTAD United Nations Conference on Trade and DevelopmentUNDP United Nations Development ProgrammeUNECA United Nations Economic Commission for AfricaUNIDO United Nations Industrial Development OrganizationURA Uruguay Round AgreementsUSAID U.S. Agency for International DevelopmentUSDA U.S. Department of AgricultureUSDOC U.S. Department of CommerceUSITC U.S. International Trade CommissionUSTR United States Trade RepresentativeWIPO World Intellectual Property OrganizationWTO World Trade Organization

xxvii

INTRODUCTION

Purpose and Organization of the Report

This is the fifth report in a 5-year series documenting U.S.-sub-Saharan Africa (SSA)trade and investment flows.1 In a letter dated April 12, 2000,2 the United States TradeRepresentative (USTR) asked the United States International Trade Commission(Commission or USITC) to submit, annually for 5 years, a report that provides:

S an analysis of U.S.-SSA merchandise trade and services trade flows;

S country-by-country profiles of the economies of each SSA country, includinginformation on major trading partners, and a summary of the trade andinvestment climates in each;

S a summaryofU.S. foreignand total direct investment and portfolio investmentin SSA;

S information on SSA privatization efforts;

S updates on progress in regional integration in SSA, including statistics onU.S.trade with the major regional groupings; and

S a summary of multilateral and U.S. bilateral assistance to SSA countries.

In a supplementary letter dated July 10, 2002,3USTR asked the Commission to providethe following additional information:

S the value of U.S. imports from SSA under the African Growth andOpportunity Act (AGOA), including the Generalized System of Preferences(GSP) provisions, by beneficiary country and major product categories;

S information on investment developments related to AGOA;

S a description and analysis of major SSA export sectors;

1 In a letter dated June 5, 1996, the USTR asked the Commission to submit, annually for 5 years, thespecified report. A first series of reports resulted from section 134 of the Uruguay Round Agreements Act(URAA), which directed the President to develop a comprehensive trade and development policy for thecountries of Africa, and to report to the Congress annually for 5 years on the steps taken to carry out thatmandate. The Statement of Administrative Action approved by the Congress in the URAA broadlyoutlined the Administration’s plans for this work, and the assistance needed from the Commission for thePresident to fulfill this assignment. The series consisted of five reports, produced over the period1995–1999. See USITC, U.S.–Africa Trade Flows and Effects of the Uruguay Round Agreements and U.S.Trade and Development Policy, Fifth Annual Report, USITC pub. 3250, Oct. 1999.

2 Copy of the request letter is in app. A3 Copy of the supplemental letter is in app. A.

xxviii

S expanded information on regional integration in SSA, including informationon the Communauté Economique et Monétaire de l’Afrique Centrale(CEMAC);

S a description of major U.S. trade capacity-building initiatives related to SSA;and

S a description of major non-U.S. trade preference programs for SSAcountries.

The request letter acknowledged that the information included in the USITC reportswould be useful in USTR’s work and in meeting additional reporting requirementsstemming from AGOA.

This report contains six chapters and two appendices. Chapter 1 presents informationon U.S. merchandise and services trade with SSA. The services trade analysis includesinformation on cross-border and affiliate transactions. Chapter 1 also addressesforeign investment (direct and portfolio investment) in the SSA region. Chapter 2presents information on AGOA-related imports and investment. Chapter 3 updatesthe coverage of integration initiatives in the SSA region provided in the previous seriesofUSITC reports.4 Chapter4 is a compilationof informationonmultilateral assistance,U.S. bilateral assistance, and other trade-related initiatives related to the SSA regionin 2003. Chapter 5 contains a description and analysis of major SSA export sectors:agriculture, fisheries, and forest products; chemicals; petroleum and energy-relatedproducts; minerals and metals; textiles and apparel; and certain transportationequipment. These profiles present information on production, trade, and investment.Chapter 6 contains country profiles for each of the 48 countries of SSA including basiceconomic data as well as an update of economic, trade, and investment andprivatization events for each country. The formal request letter and supplemental letterfrom the USTR to the Commission for this study are included in appendix A. Relevantstatistics on U.S.-SSA trade are in appendix B.

Approach

The data included in this report generally cover either calendar or fiscal year (FY)2003, depending on data availability. In cases where it is useful to show a trend, datafor 1999 through 2003 are provided. Developments in economic, trade, andcommercial policies cover the period from January 2003 through mid-2004, wherepossible.

4 In addition, the previous series of five reports included information on progress on regionalintegration in SSA. See, for example, USITC, U.S.–Africa Trade Flows and Effects of the Uruguay RoundAgreements and U.S. Trade and Development Policy, Fifth Annual Report, USITC pub. 3250, Oct. 1999,pp. 2–22 through 2–34.

xxix

Online webpages dedicated to U.S.-SSA trade data are available at the USITCwebsitehttp://reportweb.usitc.gov/africa. These tablesprovideyear-to-datestatisticsthat update the information contained in certain tables of this report. The website isautomatically updated with quarterly data as they become available from the U.S.Department of Commerce (USDOC).

Various sources were used to compile the data in this report. Annual data on the valueof U.S. exports to and imports from SSA were obtained from the USDOC. Unlessotherwise indicated, “AGOA” trade data reported in this publication includes tradeunder AGOA’s GSP provisions. Data on U.S. investment flows to SSA were obtainedfrom USDOC and the U.S. Department of the Treasury. Information on majordevelopments in the WTO likely affecting U.S.-SSA trade flows was collected from theWTO and other public data sources. Information onU.S. trade and economic activitiespotentially affecting U.S.-SSA trade and investment flows was collected from USDOC;the U.S. Departments of State, Treasury, and Agriculture; the U.S. Agency forInternational Development; the Export-Import Bank of the United States; the OverseasPrivate Insurance Corporation; the U.S. Trade and Development Agency; and otherrelevant U.S. agencies.

Data on trade and economic policy changes in countries in SSA, as well as informationon multilateral project lending, were obtained from USDOC, the U.S. Department ofState, the World Bank, the African Development Bank, the International MonetaryFund, and the Economist Intelligence Unit. In addition, U.S. embassies in the SSAregion provided important trade and investment information.

Scope of the Report

As requested by USTR, the 48 countries that form the SSA region are covered by thisreport. Figure 1 shows the 48 countries in SSA covered in this investigation. Thecountries are:

Angola MadagascarBenin MalawiBotswana MaliBurkina Faso MauritaniaBurundi MauritiusCameroon MozambiqueCape Verde NamibiaCentral African Republic NigerChad NigeriaComoros Republic of the CongoCôte d’Ivoire RwandaDemocratic Republic of the Congo São Tomé and PrincipeDjibouti Senegal

Figure 1Map of sub-Saharan Africa

Angola

Zambia

Eritrea

Ethiopia

Kenya

Tanzania

Democratic Republicof the Congo

Somalia

Sudan

Niger

ChadMali

Mauritania

The GambiaGuinea-Bissau

Guinea

Liberia

Côted’Ivoire

Cape Verde

Ghana

Benin

Togo

Sierra LeoneNigeria

Burkina Faso Cameroon

CentralAfrican Republic

Rwanda

Burundi

UgandaGabon

Madagascar

Namibia Botswana

South Africa

Zimbabwe

Mozambique

Malawi

Swaziland

Lesotho

Djibouti

Mauritius

Comoros

Senegal

São Tomé &Principe

EquatorialGuinea

Republic of the Congo Seychelles