Update of Market Analysis Study for the Richland Wye Area

75

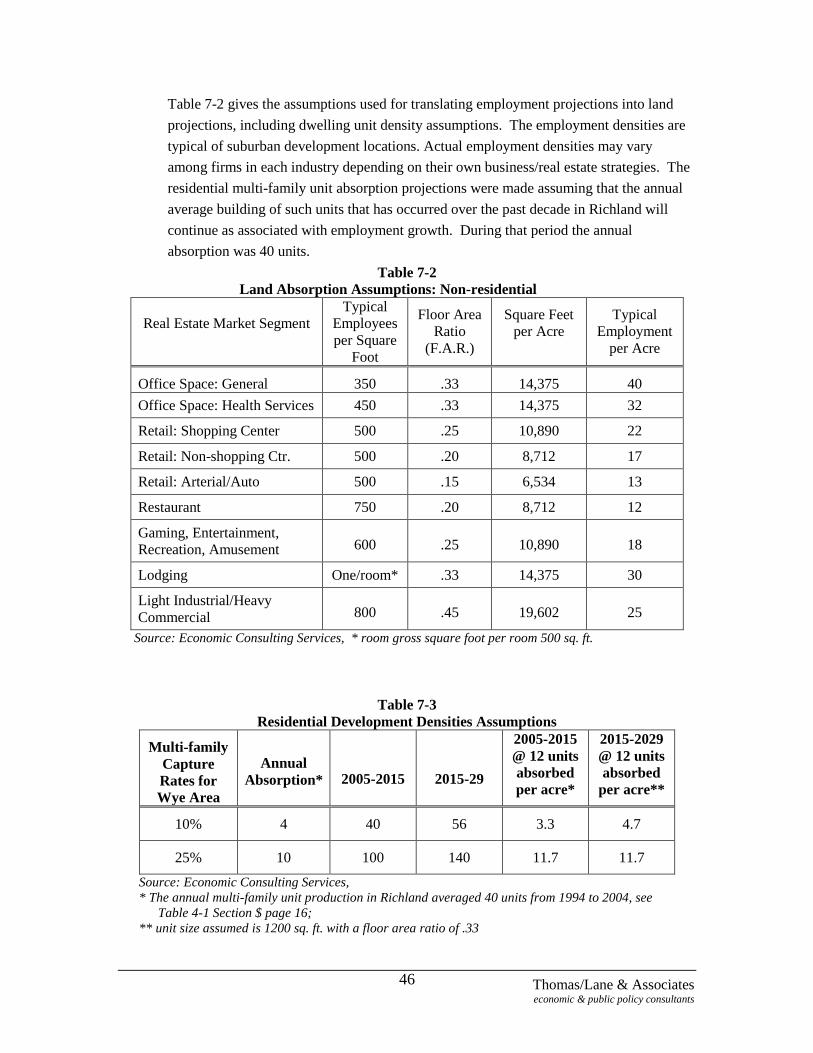

Thomas/Lane & Associates economic & public policy consultants 1 Update of Market Analysis Study for the Richland Wye Area City of Richland, Washington 1. Introduction 1.1 Objectives This updated Master Plan is designed to shape the future development of the Wye area. The Richland Wye area is a 350-acre mixed-use area bounded on the north by the Columbia River, on the west by the SR 240, on the south by SR 240 and the Tapteal commercial development, and on the east by Columbia Park and the City of Kennewick. The purpose of this Report is to update the short ―market assessment‖ section of the original Master Plan and provide a current market assessment of the Richland Wye area. The report provides a general economic and real estate guide that can be used in planning the future development of the Richland Wye area. This section of the overall masterplan report does not provide detailed development plans for individual parcels or sites, but defines the market parameters, which should guide the future development potentials of these parcels and sites. Within these defined parameters, the report offers some general recommendations for actions that the City of Richland can take to enhance the Wye area‘s future development potential. The goals of the market assessment are: Provide an overview of the Richland-Pasco-Kennewick MSA‘s economy. Assess the City of Richland‘s economic and fiscal status within the context of the Benton County and MSA economies. Describe the major attributes, ownership patterns and locational characteristics of the Wye area‘s real estate market. Provide generalized projections of likely future growth in the City of Richland and the Wye area. Present a discussion of the alternative development potentials and strategies for the Wye area.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Update of Market Analysis Study for the Richland Wye Area

Thomas/Lane & Associates economic & public policy consultants

1

Update of Market Analysis Study for the Richland Wye Area

City of Richland, Washington

1. Introduction

1.1 Objectives

This updated Master Plan is designed to shape the future development of the Wye

area. The Richland Wye area is a 350-acre mixed-use area bounded on the north

by the Columbia River, on the west by the SR 240, on the south by SR 240 and

the Tapteal commercial development, and on the east by Columbia Park and the

City of Kennewick. The purpose of this Report is to update the short ―market

assessment‖ section of the original Master Plan and provide a current market

assessment of the Richland Wye area.

The report provides a general economic and real estate guide that can be used in

planning the future development of the Richland Wye area. This section of the

overall masterplan report does not provide detailed development plans for

individual parcels or sites, but defines the market parameters, which should guide

the future development potentials of these parcels and sites. Within these defined

parameters, the report offers some general recommendations for actions that the

City of Richland can take to enhance the Wye area‘s future development

potential.

The goals of the market assessment are:

Provide an overview of the Richland-Pasco-Kennewick MSA‘s economy.

Assess the City of Richland‘s economic and fiscal status within the

context of the Benton County and MSA economies.

Describe the major attributes, ownership patterns and locational

characteristics of the Wye area‘s real estate market.

Provide generalized projections of likely future growth in the City of

Richland and the Wye area.

Present a discussion of the alternative development potentials and

strategies for the Wye area.

Thomas/Lane & Associates economic & public policy consultants

2

1.2 Methods

The method of analysis used in this report consists of two parts: (a) establishing a

realistic analysis of Richland‘s past and future major economic development

trends, and (b) identifying the real estate absorption implications of these trends

for the Wye area.

The report uses shift-share and regression (time series) analysis to identify the

extent to which Richland‘s economy has grown because it (a) partook in the

overall growth of all industries in Washington State, (b) enjoyed an above-

average concentration of economic activity that happened to be growing across

the state, (c) participated in the competitively driven growth resulting from the

location of economic activity in the State, or (d) all – or parts – of each the above.

Traditional shift-share analysis is modified to include an analysis of the

occupational make-up of Richland‘s work force. Many industries have both a

high-tech and low-tech component. For a city such as Richland, with its high-end

work force, the inclusion of occupational data is vitally important.

The second part of our approach uses real estate market analysis to identify

potential absorption of land in the Wye area, including the strategic implications

of such factors as infrastructure requirements, likely build-out schedules and

creation of development institutions and authorities (such as a redevelopment

agency).

The amount and kind of real estate developments that will be exerting a demand

for space in the future is determined by projecting the numbers of employees by

industry and occupation. Different industries and occupations within industries

obviously require different types of real estate development.

1.3 Limits

This section of the report is of a type sometimes referred to as a ―high altitude

reconnaissance‖ study. It proceeds from the view of an airplane flying over

Richland at an altitude of about 25,000 feet – low enough to make out the

significant, broad outlines of Richland and the Wye area‘s economic and real

estate markets. This level of analysis is appropriate to updating the overall Wye

Area Master Plan. To get down to detailed planning of specific parcels or sites

Thomas/Lane & Associates economic & public policy consultants

3

however will require much more detailed analysis than are contained in this

section of the report but may be addressed within other sections.

Finally, this section assumes:

The U.S. economy will continue to exhibit moderate real economic growth

with relatively low levels of inflation. The Federal Reserve will continue

to slowly increase interest rates, and both budget and trade deficits –

although continuing to be large – will be brought under control.

The U.S. will engage in no new wars or suffer major terrorist attacks.

The long-term relationship between the economies of the U.S. and the

State of Washington will remain essentially the same as they have been for

the past quarter of a century.

The long-term trend toward integration and globalization of the world‘s

economies will continue, although probably at a somewhat slower pace

then was true during the last decade.

Thomas/Lane & Associates economic & public policy consultants

4

2. Overview of the Richland-Pasco-Kennewick MSA’s Economy

2.1 The MSA Compared to the State’s Economy

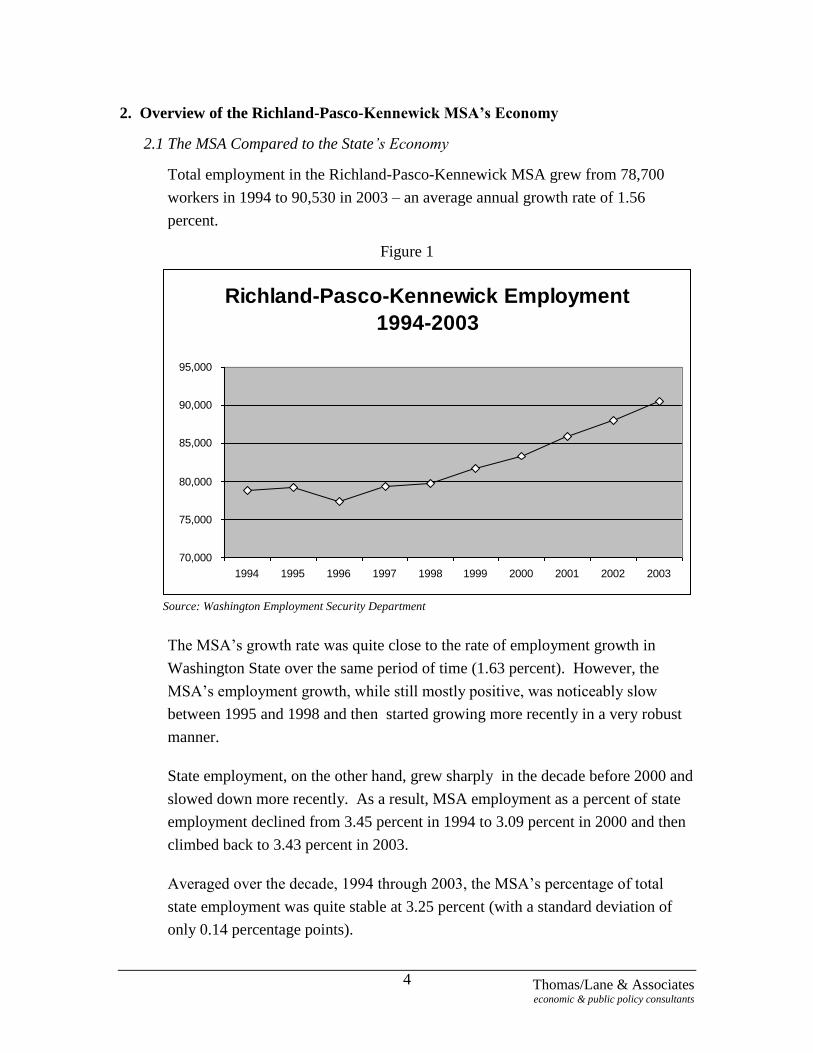

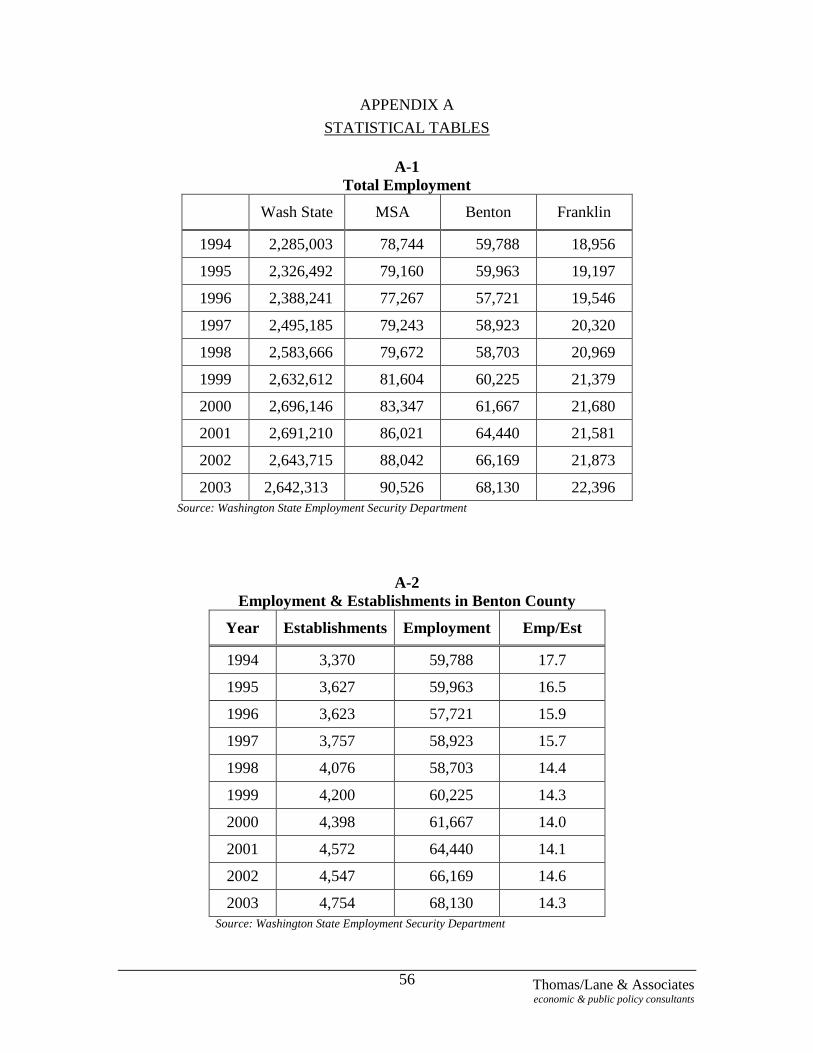

Total employment in the Richland-Pasco-Kennewick MSA grew from 78,700

workers in 1994 to 90,530 in 2003 – an average annual growth rate of 1.56

percent.

Figure 1

Richland-Pasco-Kennewick Employment

1994-2003

70,000

75,000

80,000

85,000

90,000

95,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: Washington Employment Security Department

The MSA‘s growth rate was quite close to the rate of employment growth in

Washington State over the same period of time (1.63 percent). However, the

MSA‘s employment growth, while still mostly positive, was noticeably slow

between 1995 and 1998 and then started growing more recently in a very robust

manner.

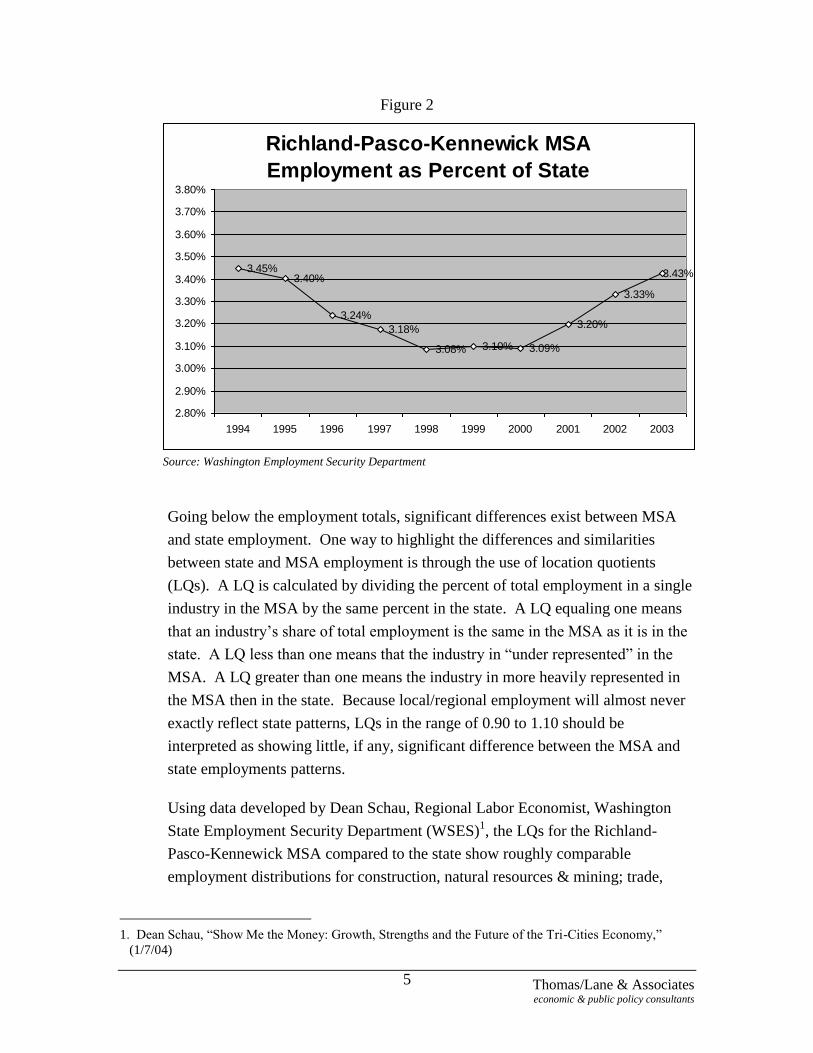

State employment, on the other hand, grew sharply in the decade before 2000 and

slowed down more recently. As a result, MSA employment as a percent of state

employment declined from 3.45 percent in 1994 to 3.09 percent in 2000 and then

climbed back to 3.43 percent in 2003.

Averaged over the decade, 1994 through 2003, the MSA‘s percentage of total

state employment was quite stable at 3.25 percent (with a standard deviation of

only 0.14 percentage points).

Thomas/Lane & Associates economic & public policy consultants

5

Figure 2

Richland-Pasco-Kennewick MSA

Employment as Percent of State

3.45%3.40%

3.24%

3.18%

3.08% 3.10% 3.09%

3.20%

3.33%

3.43%

2.80%

2.90%

3.00%

3.10%

3.20%

3.30%

3.40%

3.50%

3.60%

3.70%

3.80%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: Washington Employment Security Department

Going below the employment totals, significant differences exist between MSA

and state employment. One way to highlight the differences and similarities

between state and MSA employment is through the use of location quotients

(LQs). A LQ is calculated by dividing the percent of total employment in a single

industry in the MSA by the same percent in the state. A LQ equaling one means

that an industry‘s share of total employment is the same in the MSA as it is in the

state. A LQ less than one means that the industry in ―under represented‖ in the

MSA. A LQ greater than one means the industry in more heavily represented in

the MSA then in the state. Because local/regional employment will almost never

exactly reflect state patterns, LQs in the range of 0.90 to 1.10 should be

interpreted as showing little, if any, significant difference between the MSA and

state employments patterns.

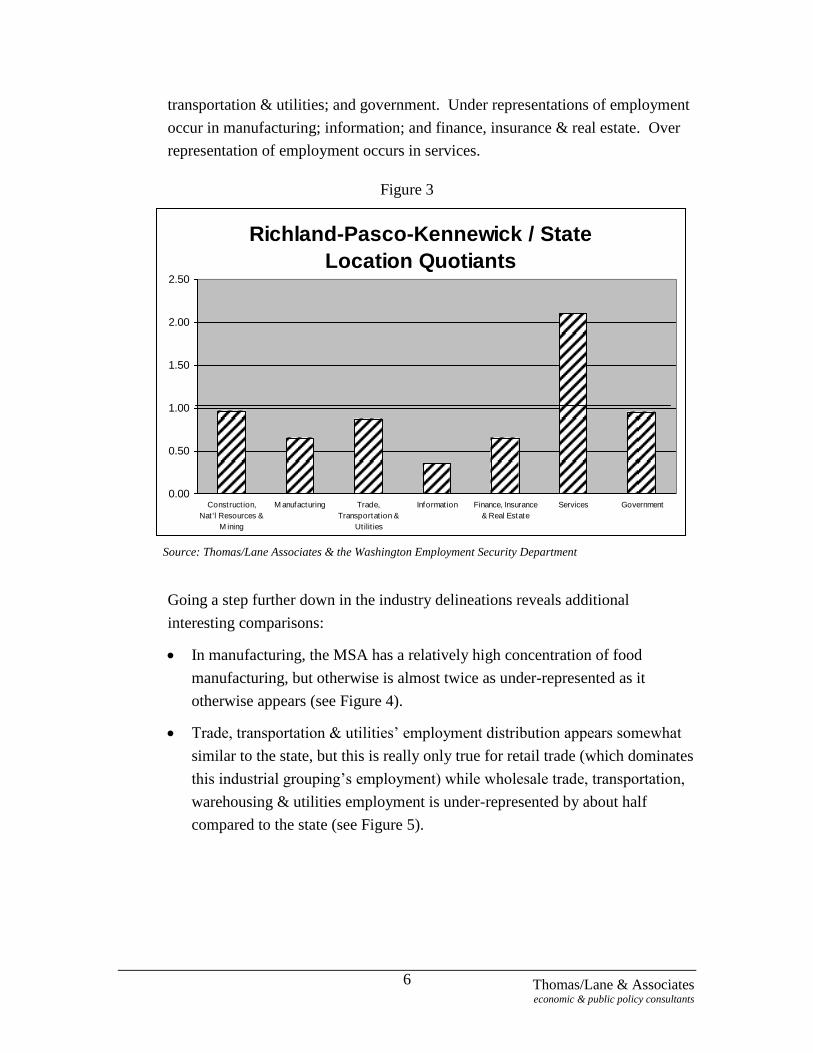

Using data developed by Dean Schau, Regional Labor Economist, Washington

State Employment Security Department (WSES)1, the LQs for the Richland-

Pasco-Kennewick MSA compared to the state show roughly comparable

employment distributions for construction, natural resources & mining; trade,

1. Dean Schau, ―Show Me the Money: Growth, Strengths and the Future of the Tri-Cities Economy,‖

(1/7/04)

Thomas/Lane & Associates economic & public policy consultants

6

transportation & utilities; and government. Under representations of employment

occur in manufacturing; information; and finance, insurance & real estate. Over

representation of employment occurs in services.

Figure 3

Richland-Pasco-Kennewick / State

Location Quotiants

0.00

0.50

1.00

1.50

2.00

2.50

Construct ion,

Nat 'l Resources &

M ining

M anufacturing Trade,

Transportat ion &

Utilit ies

Information Finance, Insurance

& Real Estate

Services Government

Source: Thomas/Lane Associates & the Washington Employment Security Department

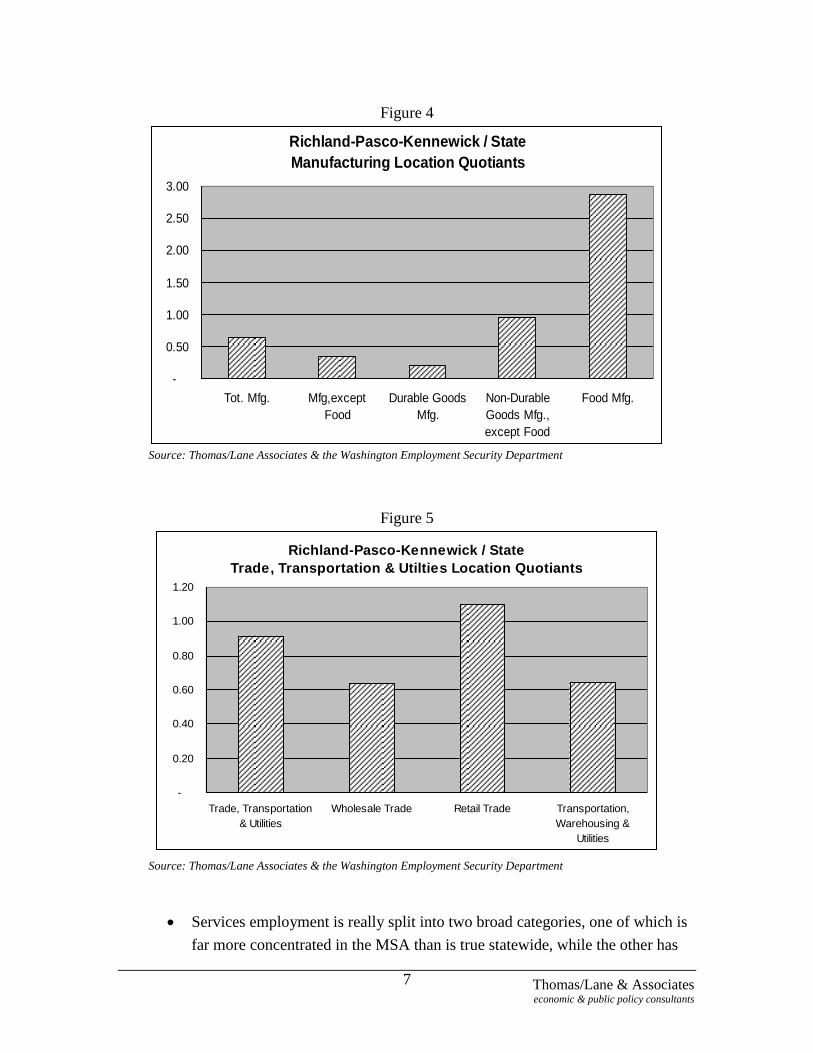

Going a step further down in the industry delineations reveals additional

interesting comparisons:

In manufacturing, the MSA has a relatively high concentration of food

manufacturing, but otherwise is almost twice as under-represented as it

otherwise appears (see Figure 4).

Trade, transportation & utilities‘ employment distribution appears somewhat

similar to the state, but this is really only true for retail trade (which dominates

this industrial grouping‘s employment) while wholesale trade, transportation,

warehousing & utilities employment is under-represented by about half

compared to the state (see Figure 5).

Thomas/Lane & Associates economic & public policy consultants

7

Figure 4

Richland-Pasco-Kennewick / State

Manufacturing Location Quotiants

-

0.50

1.00

1.50

2.00

2.50

3.00

Tot. Mfg. Mfg,except

Food

Durable Goods

Mfg.

Non-Durable

Goods Mfg.,

except Food

Food Mfg.

Source: Thomas/Lane Associates & the Washington Employment Security Department

Figure 5

Richland-Pasco-Kennewick / State

Trade, Transportation & Utilties Location Quotiants

-

0.20

0.40

0.60

0.80

1.00

1.20

Trade, Transportation

& Utilities

Wholesale Trade Retail Trade Transportation,

Warehousing &

Utilities

Source: Thomas/Lane Associates & the Washington Employment Security Department

Services employment is really split into two broad categories, one of which is

far more concentrated in the MSA than is true statewide, while the other has

Thomas/Lane & Associates economic & public policy consultants

8

roughly the same relative concentration. The category that is two to three

times more concentrated consists of two industry classifications: professional,

scientific & technical services (which, in the MSA, contains Pacific Northwest

National Laboratory ) and waste & remediation services (Fluor & Bechtel)

which are closely tied to the nuclear cleanup efforts at Hanford.

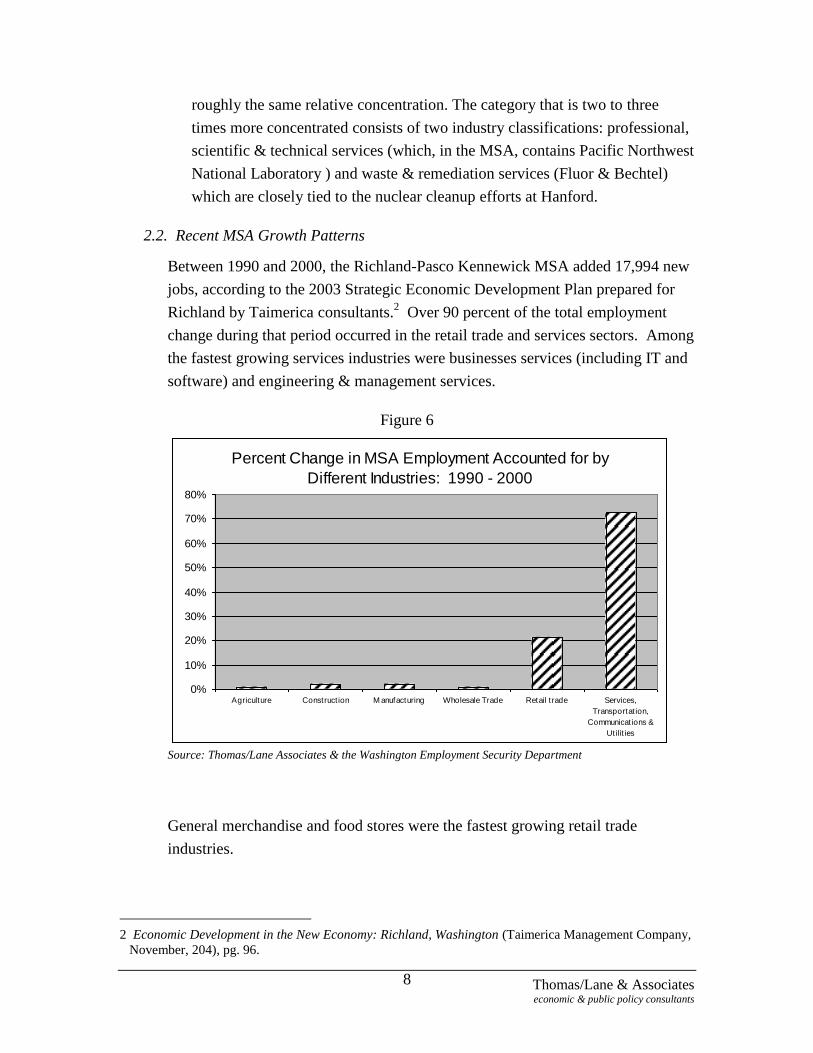

2.2. Recent MSA Growth Patterns

Between 1990 and 2000, the Richland-Pasco Kennewick MSA added 17,994 new

jobs, according to the 2003 Strategic Economic Development Plan prepared for

Richland by Taimerica consultants.2 Over 90 percent of the total employment

change during that period occurred in the retail trade and services sectors. Among

the fastest growing services industries were businesses services (including IT and

software) and engineering & management services.

Figure 6

Percent Change in MSA Employment Accounted for by

Different Industries: 1990 - 2000

0%

10%

20%

30%

40%

50%

60%

70%

80%

Agriculture Construct ion M anufacturing Wholesale Trade Retail t rade Services,

Transportat ion,

Communicat ions &

Utilit ies

Source: Thomas/Lane Associates & the Washington Employment Security Department

General merchandise and food stores were the fastest growing retail trade

industries.

2 Economic Development in the New Economy: Richland, Washington (Taimerica Management Company,

November, 204), pg. 96.

Thomas/Lane & Associates economic & public policy consultants

9

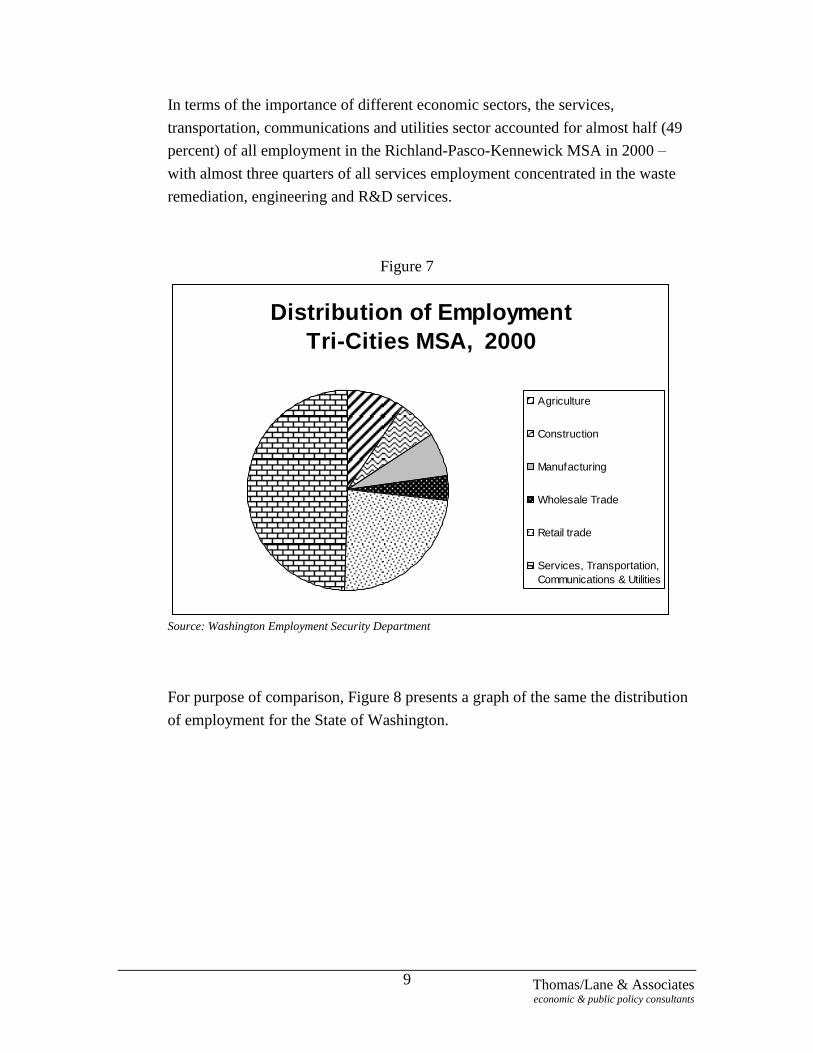

In terms of the importance of different economic sectors, the services,

transportation, communications and utilities sector accounted for almost half (49

percent) of all employment in the Richland-Pasco-Kennewick MSA in 2000 –

with almost three quarters of all services employment concentrated in the waste

remediation, engineering and R&D services.

Figure 7

Distribution of Employment

Tri-Cities MSA, 2000

Agriculture

Construction

Manufacturing

Wholesale Trade

Retail trade

Services, Transportation,

Communications & Utilities

Source: Washington Employment Security Department

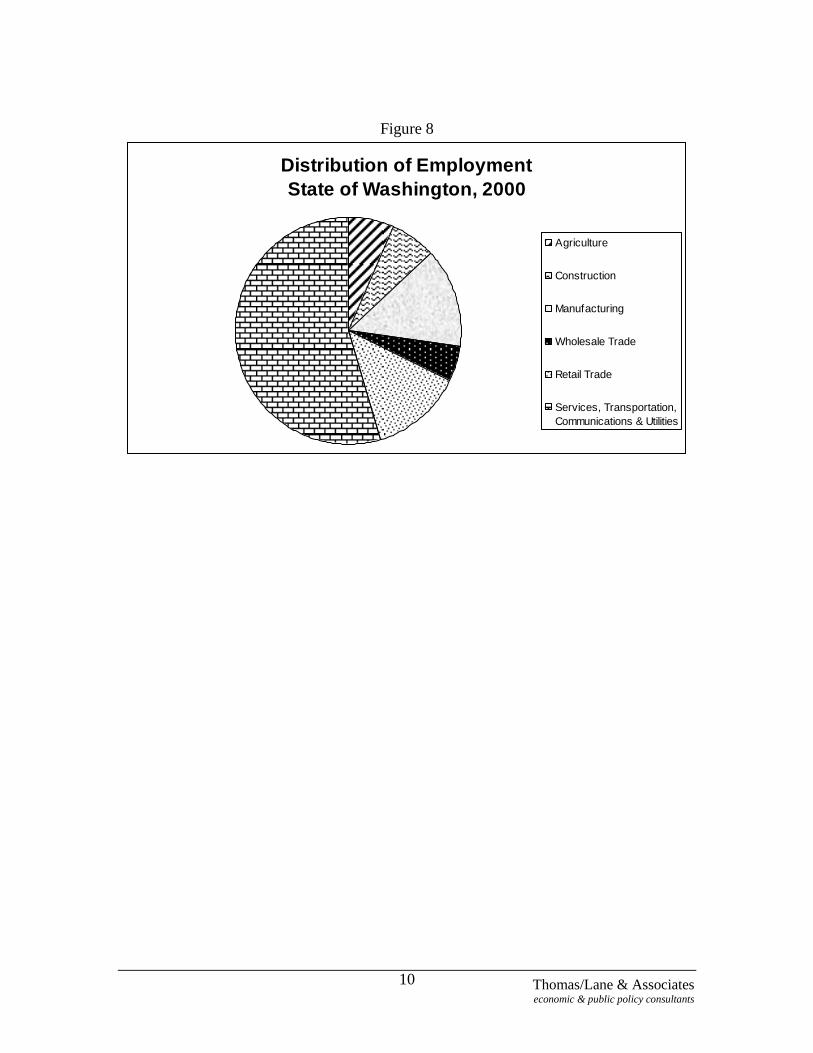

For purpose of comparison, Figure 8 presents a graph of the same the distribution

of employment for the State of Washington.

Thomas/Lane & Associates economic & public policy consultants

10

Figure 8

Distribution of Employment

State of Washington, 2000

Agriculture

Construction

Manufacturing

Wholesale Trade

Retail Trade

Services, Transportation,

Communications & Utilities

Thomas/Lane & Associates economic & public policy consultants

11

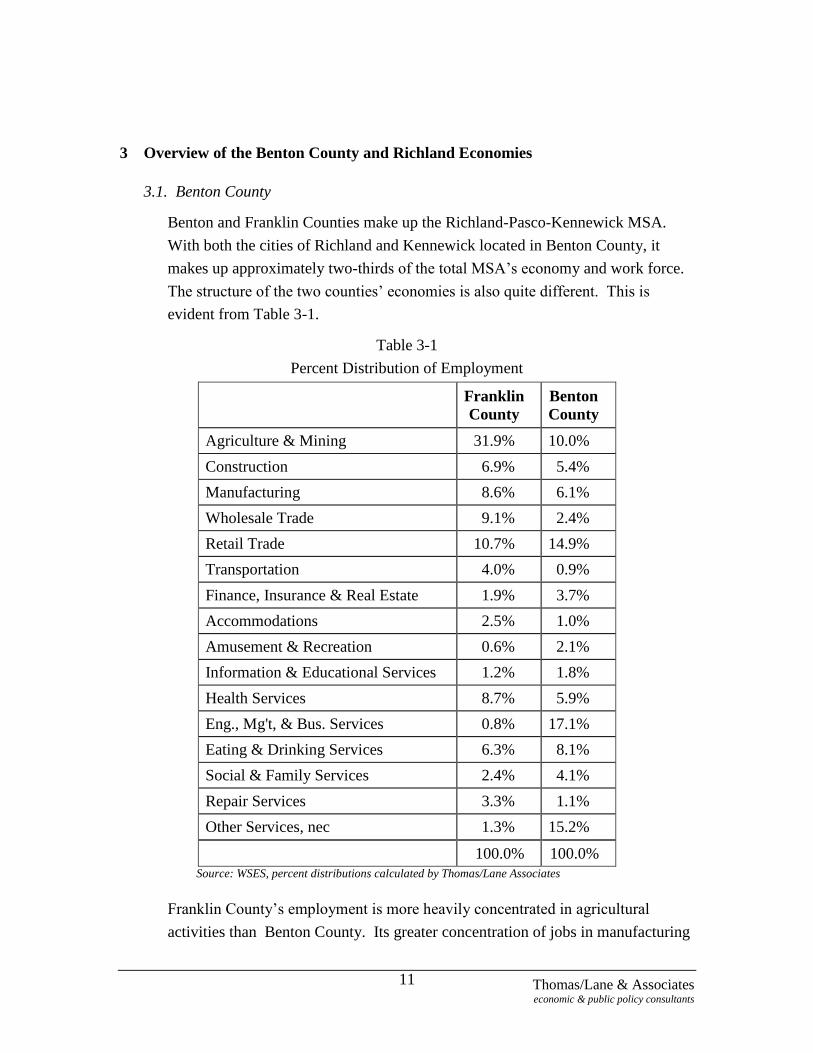

3 Overview of the Benton County and Richland Economies

3.1. Benton County

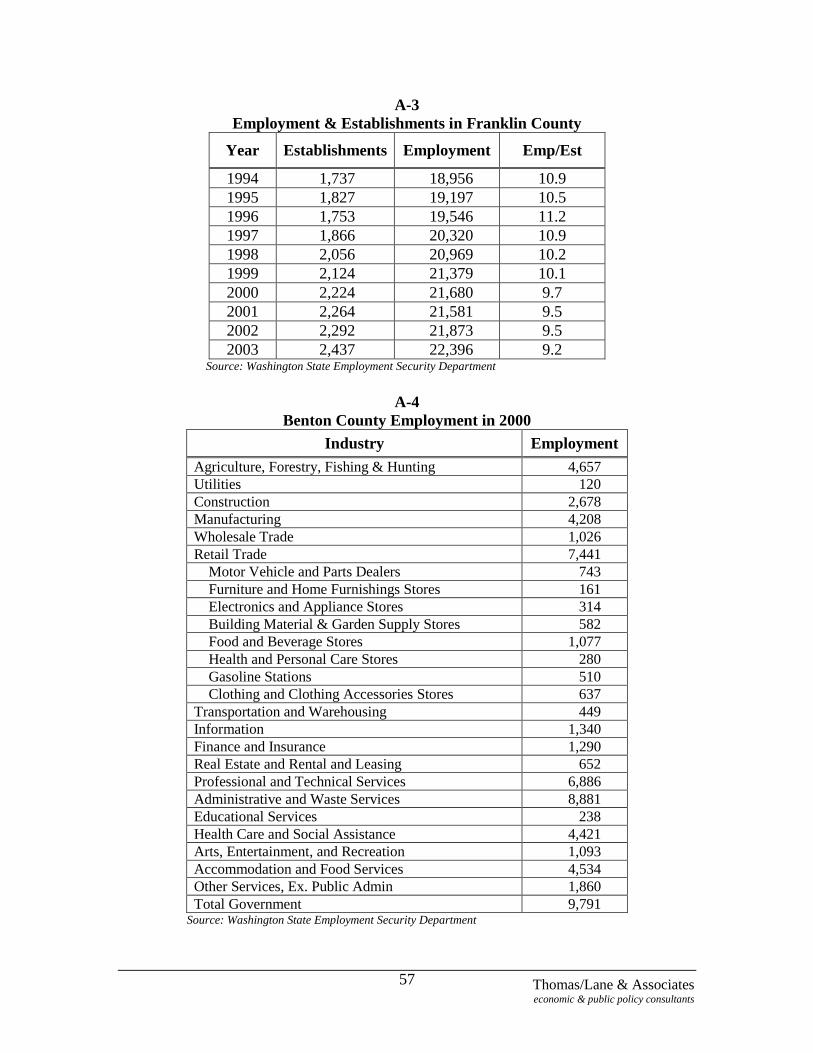

Benton and Franklin Counties make up the Richland-Pasco-Kennewick MSA.

With both the cities of Richland and Kennewick located in Benton County, it

makes up approximately two-thirds of the total MSA‘s economy and work force.

The structure of the two counties‘ economies is also quite different. This is

evident from Table 3-1.

Table 3-1

Percent Distribution of Employment

Franklin

County

Benton

County

Agriculture & Mining 31.9% 10.0%

Construction 6.9% 5.4%

Manufacturing 8.6% 6.1%

Wholesale Trade 9.1% 2.4%

Retail Trade 10.7% 14.9%

Transportation 4.0% 0.9%

Finance, Insurance & Real Estate 1.9% 3.7%

Accommodations 2.5% 1.0%

Amusement & Recreation 0.6% 2.1%

Information & Educational Services 1.2% 1.8%

Health Services 8.7% 5.9%

Eng., Mg't, & Bus. Services 0.8% 17.1%

Eating & Drinking Services 6.3% 8.1%

Social & Family Services 2.4% 4.1%

Repair Services 3.3% 1.1%

Other Services, nec 1.3% 15.2%

100.0% 100.0%

Source: WSES, percent distributions calculated by Thomas/Lane Associates

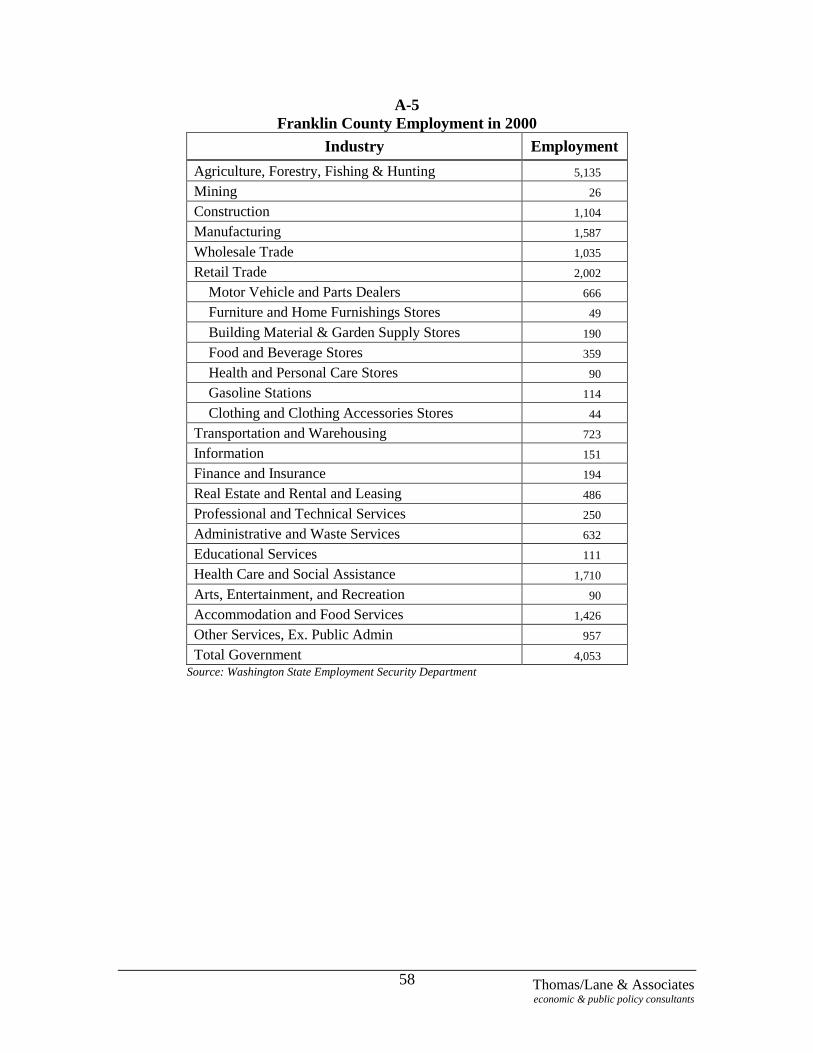

Franklin County‘s employment is more heavily concentrated in agricultural

activities than Benton County. Its greater concentration of jobs in manufacturing

Thomas/Lane & Associates economic & public policy consultants

12

and transportation are primarily in food processing and related activities – which

are related to the county‘s agricultural base. Franklin County also has a small

concentration of employment in health services.

Benton County‘s most notable concentration of employees is in engineering,

management and business services, which includes both the scientific and

technical work taking place at PNNL and in ―other services,‖ which includes the

waste & remediation services being done by Fluor, CH2Mhill, Bechtel, and

others.

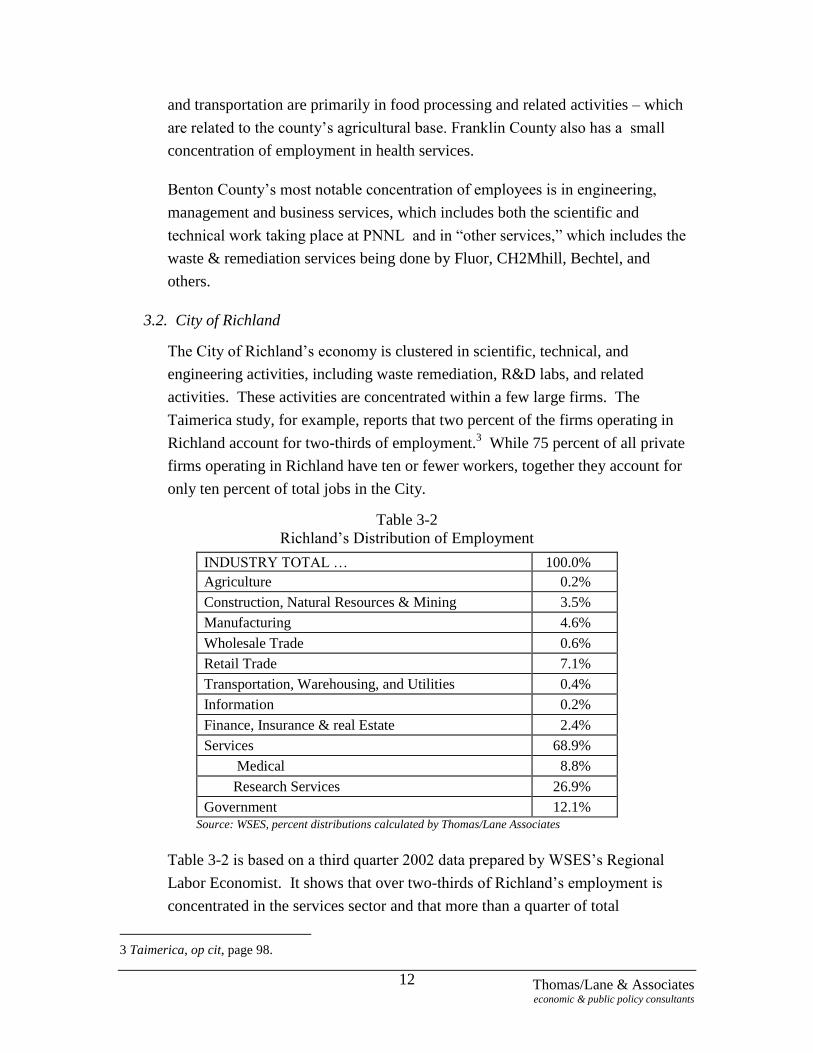

3.2. City of Richland

The City of Richland‘s economy is clustered in scientific, technical, and

engineering activities, including waste remediation, R&D labs, and related

activities. These activities are concentrated within a few large firms. The

Taimerica study, for example, reports that two percent of the firms operating in

Richland account for two-thirds of employment.3 While 75 percent of all private

firms operating in Richland have ten or fewer workers, together they account for

only ten percent of total jobs in the City.

Table 3-2

Richland‘s Distribution of Employment

INDUSTRY TOTAL … 100.0%

Agriculture 0.2%

Construction, Natural Resources & Mining 3.5%

Manufacturing 4.6%

Wholesale Trade 0.6%

Retail Trade 7.1%

Transportation, Warehousing, and Utilities 0.4%

Information 0.2%

Finance, Insurance & real Estate 2.4%

Services 68.9%

Medical 8.8%

Research Services 26.9%

Government 12.1% Source: WSES, percent distributions calculated by Thomas/Lane Associates

Table 3-2 is based on a third quarter 2002 data prepared by WSES‘s Regional

Labor Economist. It shows that over two-thirds of Richland‘s employment is

concentrated in the services sector and that more than a quarter of total

3 Taimerica, op cit, page 98.

Thomas/Lane & Associates economic & public policy consultants

13

employment is engaged in some type of research activity – including professional,

scientific & technical services and waste treatment and remediation services. The

next largest economic sector is government, which includes the federal

Department of Energy, the Richland School District and WSU-TC, as well as

ongoing state, county and local public administration services. Retail trade

accounts for just over seven percent of total employment.

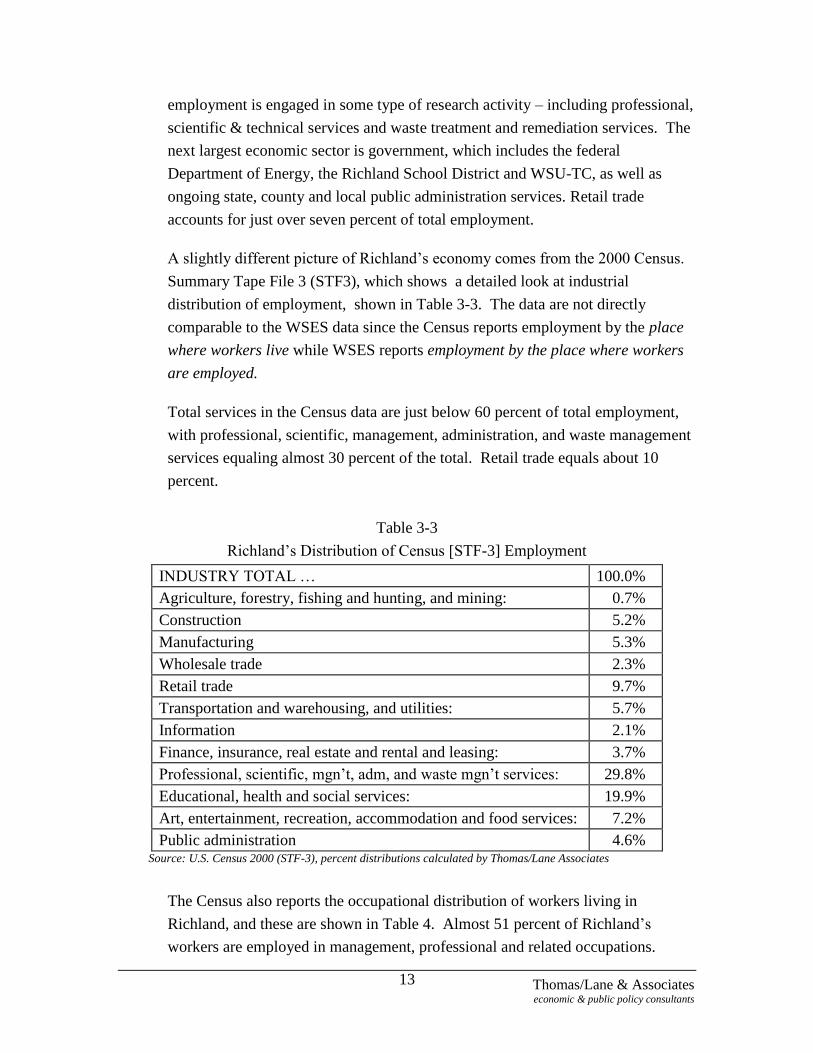

A slightly different picture of Richland‘s economy comes from the 2000 Census.

Summary Tape File 3 (STF3), which shows a detailed look at industrial

distribution of employment, shown in Table 3-3. The data are not directly

comparable to the WSES data since the Census reports employment by the place

where workers live while WSES reports employment by the place where workers

are employed.

Total services in the Census data are just below 60 percent of total employment,

with professional, scientific, management, administration, and waste management

services equaling almost 30 percent of the total. Retail trade equals about 10

percent.

Table 3-3

Richland‘s Distribution of Census [STF-3] Employment

INDUSTRY TOTAL … 100.0%

Agriculture, forestry, fishing and hunting, and mining: 0.7%

Construction 5.2%

Manufacturing 5.3%

Wholesale trade 2.3%

Retail trade 9.7%

Transportation and warehousing, and utilities: 5.7%

Information 2.1%

Finance, insurance, real estate and rental and leasing: 3.7%

Professional, scientific, mgn‘t, adm, and waste mgn‘t services: 29.8%

Educational, health and social services: 19.9%

Art, entertainment, recreation, accommodation and food services: 7.2%

Public administration 4.6% Source: U.S. Census 2000 (STF-3), percent distributions calculated by Thomas/Lane Associates

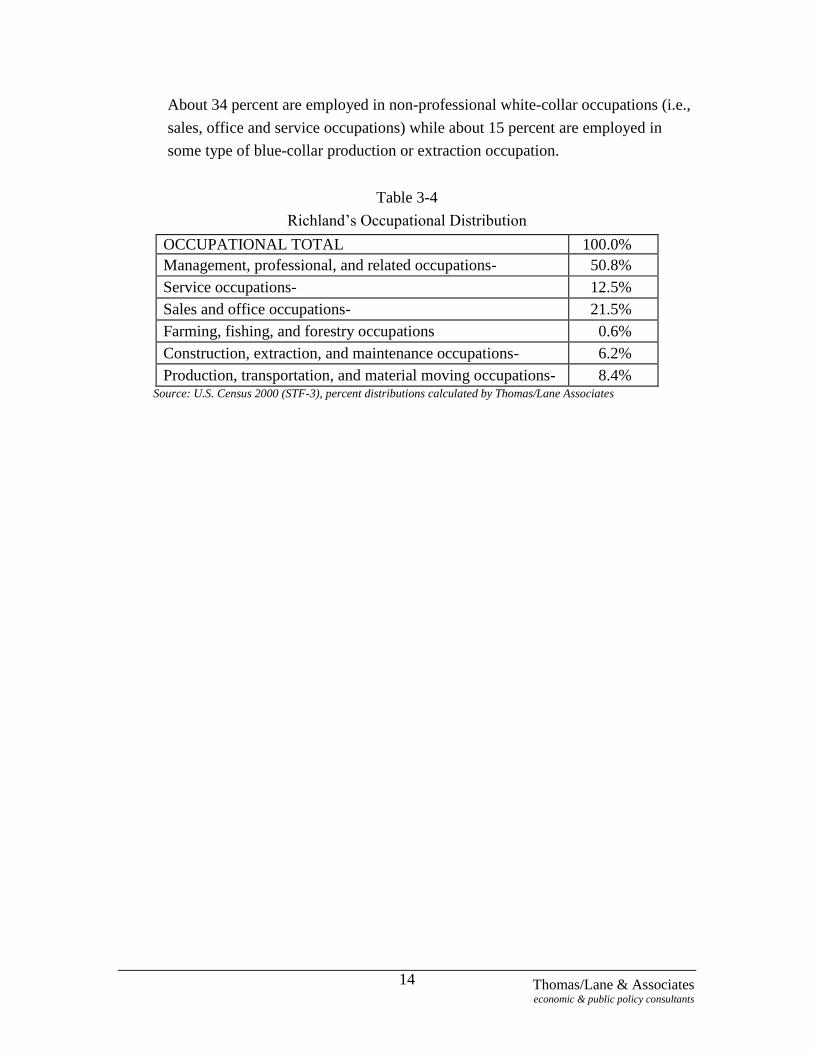

The Census also reports the occupational distribution of workers living in

Richland, and these are shown in Table 4. Almost 51 percent of Richland‘s

workers are employed in management, professional and related occupations.

Thomas/Lane & Associates economic & public policy consultants

14

About 34 percent are employed in non-professional white-collar occupations (i.e.,

sales, office and service occupations) while about 15 percent are employed in

some type of blue-collar production or extraction occupation.

Table 3-4

Richland‘s Occupational Distribution

OCCUPATIONAL TOTAL 100.0%

Management, professional, and related occupations- 50.8%

Service occupations- 12.5%

Sales and office occupations- 21.5%

Farming, fishing, and forestry occupations 0.6%

Construction, extraction, and maintenance occupations- 6.2%

Production, transportation, and material moving occupations- 8.4% Source: U.S. Census 2000 (STF-3), percent distributions calculated by Thomas/Lane Associates

Thomas/Lane & Associates economic & public policy consultants

15

4. Overview of the Local Real Estate Market

4.1. Specialization Within the Tri-Cities Market Area

The Tri-Cities real estate market area is self-contained and somewhat specialized.

It is isolated within Southeastern Washington, and it is not a part of, or even near,

another large concentration of competitive urban real estate. This attribute gives

the Tri-Cities real estate market its self-contained character.

Businesses would choose the Tri-Cities market as a location for one of several

general reasons:

to be located near to the Hanford complex or the labor force that has been

attracted to it,

to take advantage of opportunities provided by the growing, processing and

production of the region‘s agriculture/viniculture,

to locate warehouse/distribution/production facilities central to the Pacific

Northwest‘s economy with relatively easy access to the northern Rockies,

eastern Washington/Oregon, and inland British Columbia (via US 395, I-90 &

I-82), and

to serve the existing and expected population and businesses in the Tri-Cities

area.

Industrial and business parks associated with the Hanford complex of scientific-

industrial facilities dominate the Richland portion of the Tri-Cities area. Richland,

and to a lesser extent Pasco and Kennewick, offer a range of price levels for

newer and older residential areas, including the recently developed Columbia

Point mixed-use area. Much of Pasco‘s real estate is used for the storage,

processing, and manufacturing of agricultural and other resource-based products.

Kennewick is the location of a regional shopping mall that is surrounded by many

other freestanding retail buildings and strip-shopping centers. In addition,

Kennewick also provides a location for significant ―suburban style‖ quality office

space that is near its retail concentrations.

Thomas/Lane & Associates economic & public policy consultants

16

All three of the Tri-Cities communities have older downtown areas that are

diffuse and struggling. Richland has a long linear downtown/central business

district composed of three parts: (1) an ―uptown‖ area located near an old strip

shopping center of the same name left over from the post-war new town period

that also includes retail activity located in several smaller, but newer shopping

centers along George Washington Blvd; (2) a recently revitalized ―downtown‖

area; and (3) a ―central business district‖ that includes the city and federal

government complex along with a concentration of medical facilities around the

Kadlec Medical Center.

All three of the communities also have concentrations of suburban type retail

shopping centers adjacent to I-182. Recent developments in the newly developing

suburban portion of Pasco, the Queensgate area of south Richland, and southern

suburban areas of Kennewick are rapidly adding significant retail space. Pasco

also has a small but emerging business park area proximate to the airport.

Washington State University‘s Tri-Cities campus is located in north Richland near

PNNL and the Hanford contractors. Columbia Basin Community College is

located near the airport in Pasco.

Also near the Pasco airport is a 1960‘s-era hotel complex that in the past served as

the main regional convention center. A major outdoor event and recreation

complex is located in close proximity to the newer suburban areas in Pasco.

A recently completed convention center complex in Kennewick is expected to

attract major meetings. Kennewick also has a multi-events arena near the new

convention center, its airport and regional mall. Long linear shoreline parks and

recreation spaces in Richland, Kennewick and Pasco along the Columbia River

are a major regional recreational resource featuring the river shoreline.

The federal government has plans to (a) lower the flood control levee along the

Columbia River in the Wye area and (b) revitalize that stretch of shoreline for

open space, park, and recreational uses.

Freeways link the three Tri-Cities communities. These freeways also divide,

separate, and (to some extent) isolate portions of each community‘s real estate

markets. Two freeways run north-south through the Tri-Cities area. The US-395

corridor connects older areas of Pasco and Kennewick. The I-182 freeway

corridor links newer areas of all three communities. The Wye area is located near

Thomas/Lane & Associates economic & public policy consultants

17

the I-182 corridor and adjacent to SR-240, which is a main east-west connector

through Kennewick and Richland. A major widening of SR-240 and rebuilding

of the bridges over the Yakima River between Richland and Kennewick is

currently under construction. This re-alignment and reconfiguration of the SR-

240 freeway in the area will provide better access to the Richland Wye area.

While each community has an airport with significant land around it for

development, only the airport in Pasco has scheduled interregional service.

Pasco‘s industrial areas make the most use of the Columbia River for

transportation/shipping.

4.2. Overall Growth in the Tri-Cities Area

No publicly available consolidated data tracking the absorption of

commercial/industrial real estate for the Tri-Cities could be found. Table 4-1

illustrates the general trends in multi-family and non-residential construction

activity using building permit data obtained from the City of Richland.

The pattern for both multi-family and non-residential construction activity is one

of wide variation from year to year. This pattern is consistent with the cyclical

nature of the regional economy in the Tri-Cities. During the past five years there

has been a noted increase in non-residential activity. Due to rising household

incomes and lower interest rates, multi-family construction appears to have

slowed relative to the single-family construction.

In addition to the general specialization of economic and real estate activity

within the Tri-Cities metropolitan area, there is a noticeable degree of real estate

specialization among the typical segments of the local real estate market. Much of

the development in place has occurred in an era of post-war land-use planning.

This has tended to separate uses. There are also some emerging trends, which are

discussed below. An understanding of these market trends is useful for defining

the opportunities (and challenges) for the future development of the Wye area.

To develop successfully, the Wye area will have to compete with, and be competitive to,

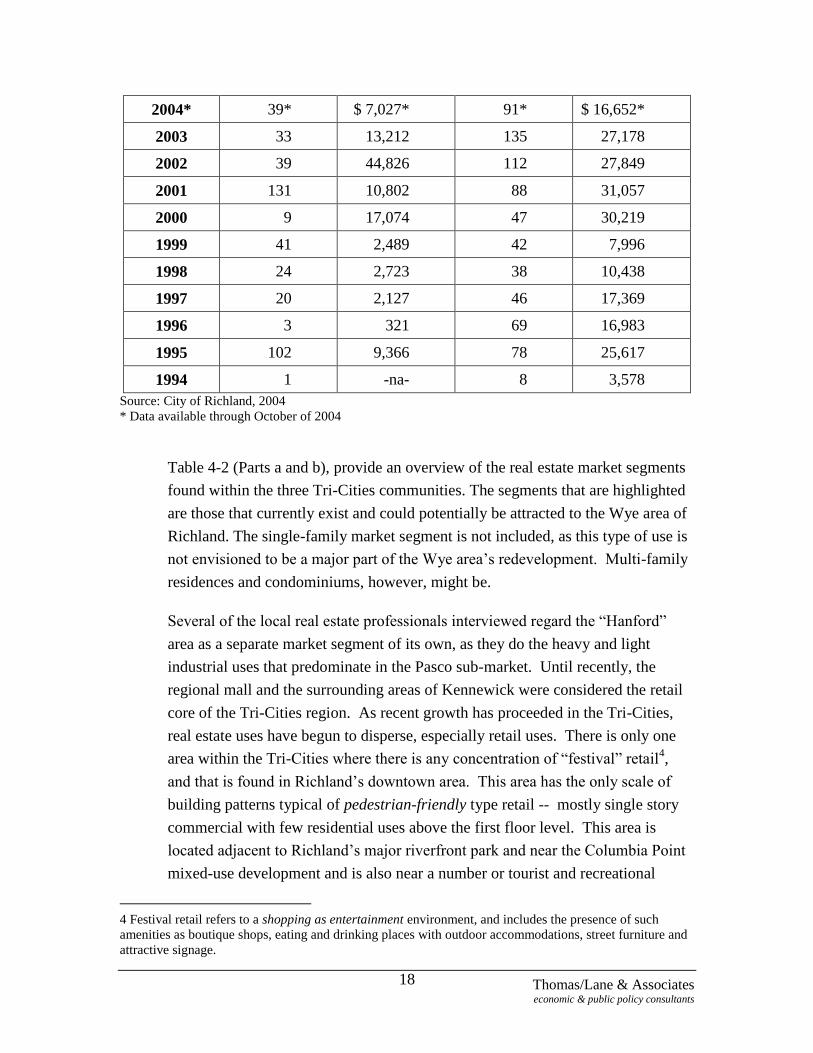

other parts of the Tri-Cities regional real estate market.Table 4-1

Richland Building Permit Data: 1994-2004.

Year Multi-family

Units

Value of Multi-

Family Permits

(000’)

New

Construction

Permits Non-

Residential

Value of New

Non-residential

Building

Permits

(000’s)

Thomas/Lane & Associates economic & public policy consultants

18

2004* 39* $ 7,027* 91* $ 16,652*

2003 33 13,212 135 27,178

2002 39 44,826 112 27,849

2001 131 10,802 88 31,057

2000 9 17,074 47 30,219

1999 41 2,489 42 7,996

1998 24 2,723 38 10,438

1997 20 2,127 46 17,369

1996 3 321 69 16,983

1995 102 9,366 78 25,617

1994 1 -na- 8 3,578

Source: City of Richland, 2004

* Data available through October of 2004

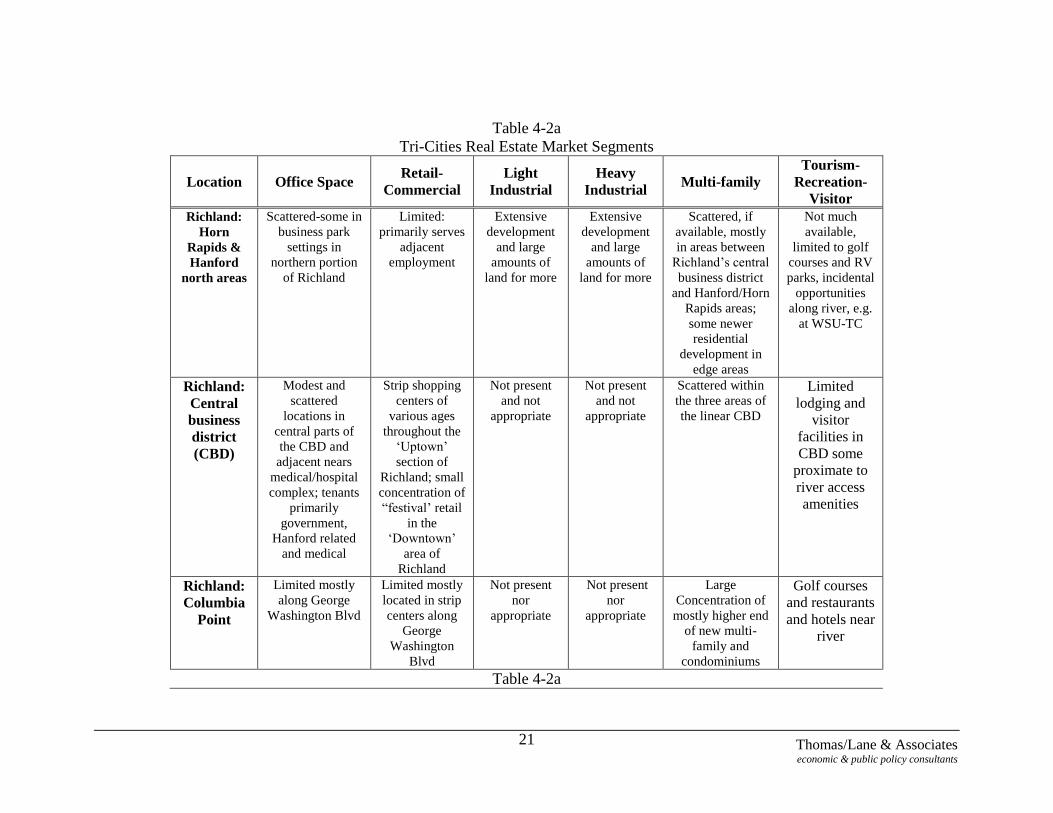

Table 4-2 (Parts a and b), provide an overview of the real estate market segments

found within the three Tri-Cities communities. The segments that are highlighted

are those that currently exist and could potentially be attracted to the Wye area of

Richland. The single-family market segment is not included, as this type of use is

not envisioned to be a major part of the Wye area‘s redevelopment. Multi-family

residences and condominiums, however, might be.

Several of the local real estate professionals interviewed regard the ―Hanford‖

area as a separate market segment of its own, as they do the heavy and light

industrial uses that predominate in the Pasco sub-market. Until recently, the

regional mall and the surrounding areas of Kennewick were considered the retail

core of the Tri-Cities region. As recent growth has proceeded in the Tri-Cities,

real estate uses have begun to disperse, especially retail uses. There is only one

area within the Tri-Cities where there is any concentration of ―festival‖ retail4,

and that is found in Richland‘s downtown area. This area has the only scale of

building patterns typical of pedestrian-friendly type retail -- mostly single story

commercial with few residential uses above the first floor level. This area is

located adjacent to Richland‘s major riverfront park and near the Columbia Point

mixed-use development and is also near a number or tourist and recreational

4 Festival retail refers to a shopping as entertainment environment, and includes the presence of such

amenities as boutique shops, eating and drinking places with outdoor accommodations, street furniture and

attractive signage.

Thomas/Lane & Associates economic & public policy consultants

19

attractions. Other recreational, tourist and public assembly attractions are either

located on the river shoreline or in public buildings in Pasco and Kennewick.

Tables 4-2a and 4-2b summarize the location of real estate uses that are currently

available and could compete with sites in the Wye are:

4.3. Real Estate Market Attributes

There are a number of attributes of the overall Tri-Cities real estate market that

will affect the potential of the Wye area‘s redevelopment potential. The

following is a listing of overall factors that affect real estate in most of the sub-

markets and locations within the Tri-Cities, including Richland.

Land availability – A striking characteristic of the Tri-Cities, especially the

areas south of the Columbia River (Richland and Kennewick), is that there are

literally thousands of acres of raw vacant land available. While the abundance

of land at relatively low prices is a good for attracting firms from outside the

area, it does not lead to dense development or to building for speculative or

rental markets. Such abundance of cheap developable land makes the

redevelopment of previously developed areas relatively expensive because of

the relocation, demolition, infrastructure replacement costs involved.

Land ownership patterns – The overwhelming amount of available land is

held for sale by public entities including the Ports of Kennewick and Benton,

the Kennewick Irrigation District, and the City of Richland. The development

incentives for these public owners are not the same as those for private

landowners.

Owner/users and commercial condominiums – in smaller metropolitan areas,

office development is an emerging trend. In addition, there has been a noted

dispersion of office industries throughout the State of Washington relative to

larger metropolitan areas. Other than the real estate sub-market associated

with Hanford, most private development occurs in small separated office

buildings in Richland and Kennewick. There is a large concentration of free-

standing owner-occupied, low density, high quality office buildings near

Columbia Center Mall; a small concentration near the Pasco airport, and a

scattering of small office buildings (plus a few multi-story office buildings) in

north Richland and along Jadwin Way and George Washington Boulevard in

downtown Richland. Government agencies, Hanford-related tenants, and

Thomas/Lane & Associates economic & public policy consultants

20

medical organizations occupy many of the buildings in this latter portion of

the market. A noticeable portion of these smaller and higher quality buildings

are condominiums.

Thomas/Lane & Associates economic & public policy consultants

21

Table 4-2a

Tri-Cities Real Estate Market Segments

Location

Office Space Retail-

Commercial

Light

Industrial

Heavy

Industrial

Multi-family

Tourism-

Recreation-

Visitor

Richland:

Horn

Rapids &

Hanford

north areas

Scattered-some in

business park

settings in

northern portion

of Richland

Limited:

primarily serves

adjacent

employment

Extensive

development

and large

amounts of

land for more

Extensive

development

and large

amounts of

land for more

Scattered, if

available, mostly

in areas between

Richland‘s central

business district

and Hanford/Horn

Rapids areas;

some newer

residential

development in

edge areas

Not much

available,

limited to golf

courses and RV

parks, incidental

opportunities

along river, e.g.

at WSU-TC

Richland:

Central

business

district

(CBD)

Modest and

scattered

locations in

central parts of

the CBD and

adjacent nears

medical/hospital

complex; tenants

primarily

government,

Hanford related

and medical

Strip shopping

centers of

various ages

throughout the

‗Uptown‘

section of

Richland; small

concentration of

―festival‘ retail

in the

‗Downtown‘

area of

Richland

Not present

and not

appropriate

Not present

and not

appropriate

Scattered within

the three areas of

the linear CBD

Limited

lodging and

visitor

facilities in

CBD some

proximate to

river access

amenities

Richland:

Columbia

Point

Limited mostly

along George

Washington Blvd

Limited mostly

located in strip

centers along

George

Washington

Blvd

Not present

nor

appropriate

Not present

nor

appropriate

Large

Concentration of

mostly higher end

of new multi-

family and

condominiums

Golf courses

and restaurants

and hotels near

river

Table 4-2a

Thomas/Lane & Associates economic & public policy consultants

22

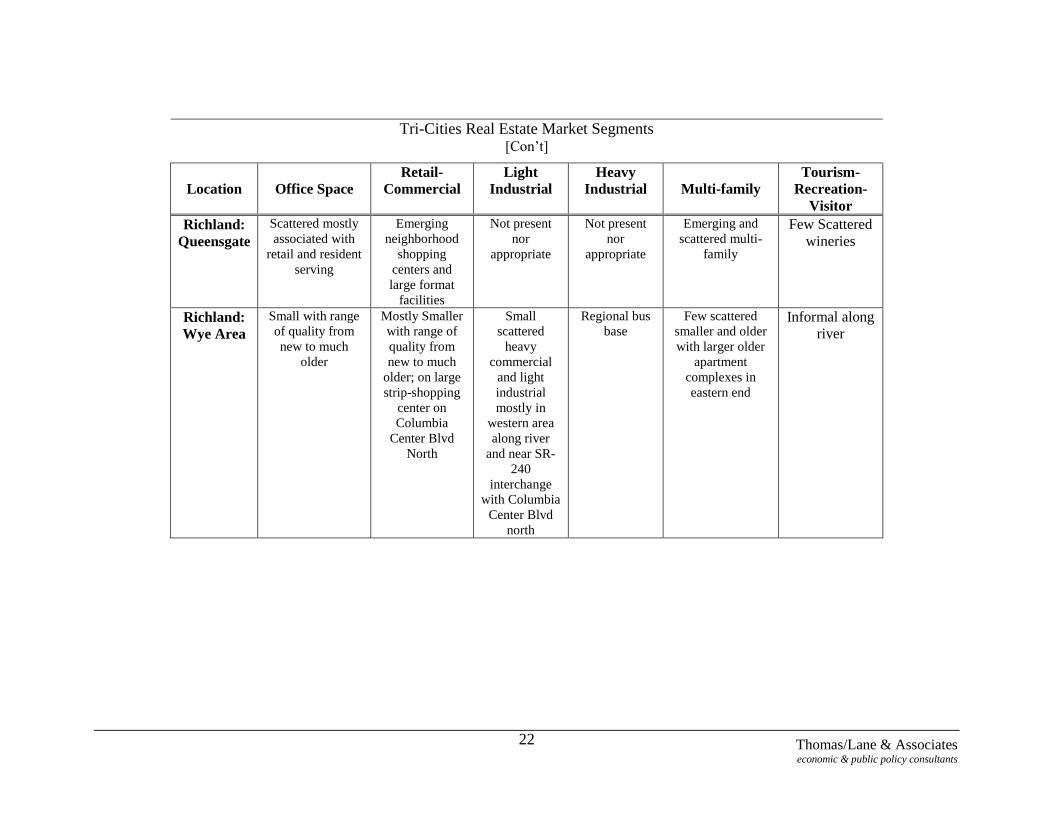

Tri-Cities Real Estate Market Segments [Con‘t]

Location

Office Space

Retail-

Commercial

Light

Industrial

Heavy

Industrial

Multi-family

Tourism-

Recreation-

Visitor

Richland:

Queensgate

Scattered mostly

associated with

retail and resident

serving

Emerging

neighborhood

shopping

centers and

large format

facilities

Not present

nor

appropriate

Not present

nor

appropriate

Emerging and

scattered multi-

family

Few Scattered

wineries

Richland:

Wye Area

Small with range

of quality from

new to much

older

Mostly Smaller

with range of

quality from

new to much

older; on large

strip-shopping

center on

Columbia

Center Blvd

North

Small

scattered

heavy

commercial

and light

industrial

mostly in

western area

along river

and near SR-

240

interchange

with Columbia

Center Blvd

north

Regional bus

base

Few scattered

smaller and older

with larger older

apartment

complexes in

eastern end

Informal along

river

Thomas/Lane & Associates economic & public policy consultants

23

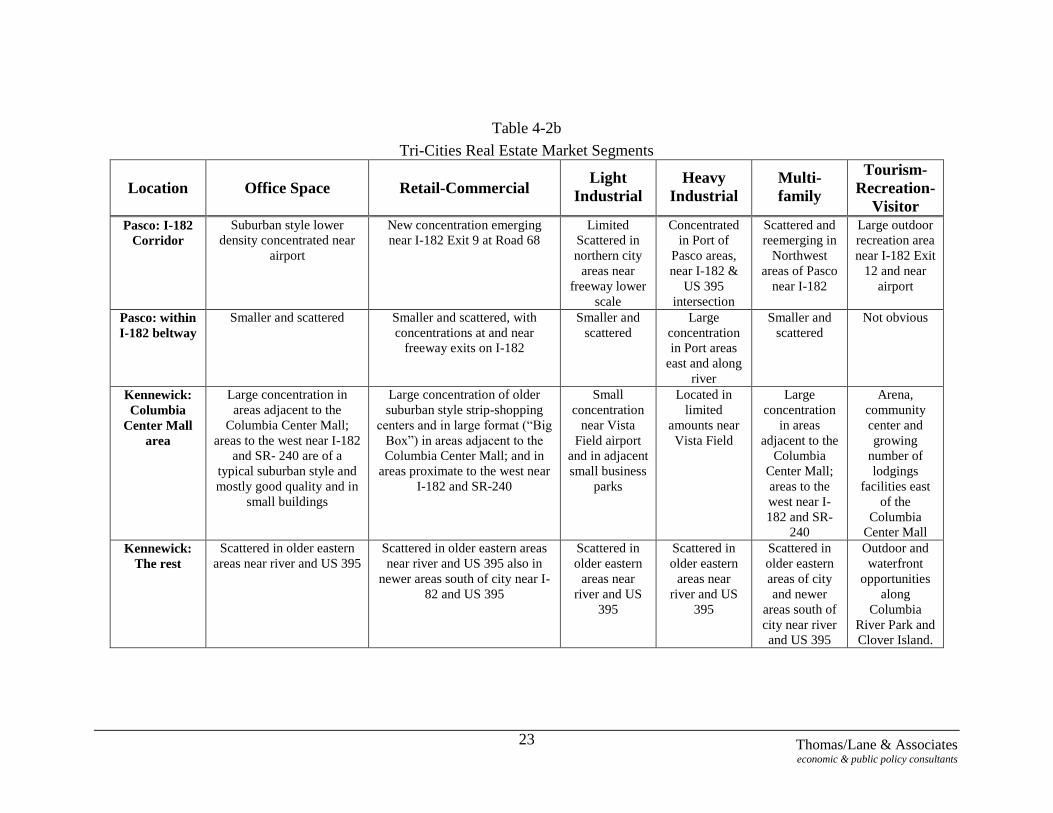

Table 4-2b

Tri-Cities Real Estate Market Segments

Location

Office Space

Retail-Commercial Light

Industrial

Heavy

Industrial

Multi-

family

Tourism-

Recreation-

Visitor

Pasco: I-182

Corridor

Suburban style lower

density concentrated near

airport

New concentration emerging

near I-182 Exit 9 at Road 68

Limited

Scattered in

northern city

areas near

freeway lower

scale

Concentrated

in Port of

Pasco areas,

near I-182 &

US 395

intersection

Scattered and

reemerging in

Northwest

areas of Pasco

near I-182

Large outdoor

recreation area

near I-182 Exit

12 and near

airport

Pasco: within

I-182 beltway

Smaller and scattered Smaller and scattered, with

concentrations at and near

freeway exits on I-182

Smaller and

scattered

Large

concentration

in Port areas

east and along

river

Smaller and

scattered

Not obvious

Kennewick:

Columbia

Center Mall

area

Large concentration in

areas adjacent to the

Columbia Center Mall;

areas to the west near I-182

and SR- 240 are of a

typical suburban style and

mostly good quality and in

small buildings

Large concentration of older

suburban style strip-shopping

centers and in large format (―Big

Box‖) in areas adjacent to the

Columbia Center Mall; and in

areas proximate to the west near

I-182 and SR-240

Small

concentration

near Vista

Field airport

and in adjacent

small business

parks

Located in

limited

amounts near

Vista Field

Large

concentration

in areas

adjacent to the

Columbia

Center Mall;

areas to the

west near I-

182 and SR-

240

Arena,

community

center and

growing

number of

lodgings

facilities east

of the

Columbia

Center Mall

Kennewick:

The rest

Scattered in older eastern

areas near river and US 395

Scattered in older eastern areas

near river and US 395 also in

newer areas south of city near I-

82 and US 395

Scattered in

older eastern

areas near

river and US

395

Scattered in

older eastern

areas near

river and US

395

Scattered in

older eastern

areas of city

and newer

areas south of

city near river

and US 395

Outdoor and

waterfront

opportunities

along

Columbia

River Park and

Clover Island.

Thomas/Lane & Associates economic & public policy consultants

24

Development climate – Recent years have produced a sustained positive development

climate propelled both by Hanford-related activities and the growth in the rest of the local

economy. The cyclical experiences of the past, as well as the size of the regional market,

have produced a gradual and incremental patterns in most real estate market segments.

These patterns featurer the predominance of owner-users, shopping centers being an

exception.

Columbia Center Mall and environs – A significant portion of the Tri-Cities non-

industrial real estate activity occurs in areas around the Columbia Center mall. Some real

estate planning and business professionals consider the Wye to be part of this market area

because of its physical proximity.

Geographically and from the perspective of transportation infrastructure, the Columbia

Center mall area is centrally located and accessible from most areas within the Tri-Cities

MSA. In some ways it functions as the central business district of the region (i.e., the

region‘s concentration of retail, office, recreation, tourist and commercial activity);

however unlike most central business districts, it is not an area of dense development.

Instead, it has a suburban horizontal character.

Often surrounding most central business districts there is an area of general-purpose real

estate occupied by businesses needing to be close to the central business district, but that

do not have to be in the higher priced buildings where their clients/customers are located.

The Wye area has the potential to draw these types of businesses.

The environs near the Columbia Center regional mall have attracted many retail

establishments that want to be close to a regional mall, but not in them. The relatively

newer (past twenty years) ―Big Box‖ or large format freestanding retailers have been

attracted to this portion of the Tri-Cities. As the Tri-Cities grows, this type of retail will

want to disperse to locations close to freeway exits. The Queensgate area in south

Richland, the Clearwater and Southridge areas in Kennewick, and the Road 68 area in

Pasco are locations that will compete for the types of retail currently in the Columbia

Center mall area.

Speculative/rental/lease – Large business and office park developments have not been

prevalent as a real estate pattern in the Tri-Cities. The exception is the Hanford area in

north Richland. Real estate developers tend to make a significant portion of their profit

Thomas/Lane & Associates economic & public policy consultants

25

by buying land, securing needed permits, building facilities, leasing-up and then selling

their projects to long-term institutional investors. In a market with lower priced and

abundant land this process tends to be more difficult; and speculative developers

interested in selling to institutional investors are rare.

Land prices and rents levels – Interviews with real estate professionals and published

reports indicate that commercial land at well located sites in the areas around the Wye

area sell for $2.50 to $6.00 per square foot. The land in the Port of Kennewick‘s

Spaulding Business Park goes at $2.75 to $3.25 per sq. foot. Office and better

commercial building space rents at up to $20.00 per square foot in the Gage Blvd area

west of the regional mall. Less desirable/locations and older buildings draw $8.00 to

$16.50 per square foot.

The re-development of the Wye area will by necessity fit into, and to some degree be framed

by, these overall regional real estate market patterns.

Thomas/Lane & Associates economic & public policy consultants

26

5. Real Estate & Location Analysis of the Richland Wye Area

5.1. Current Land/Real Estate Uses in Wye Area

Current land/real estate uses within the Wye area are a combination of single family

residences, multi-family apartment complexes, vacant land, local and regional retail, heavy

industrial (the Benton-Franklin Transit bus base), light industrial, small offices, public

waterfront/park recreational, and heavy commercial. This latter category, a type of

commercial real estate that typically does not have customers or clients visit the business,

tends to emphasize the repair and servicing of small, high valued equipment and machinery.

This type of real estate typically does not need the amenities of shopping centers or business

parks. Parking for trucks and service vehicles is desired, but large amounts of landscaping

and higher quality signature buildings are not. Heavy commercial uses are attracted to areas

adjacent to CBD‘s. Heavy commercial is a notable current use among the businesses in the

Wye area of Richland.

There is significant vacant land that is ready for development within the Wye area. The Port

of Kennewick has developed the 30-acre Spaulding Business Park, and is seeking to sell

parcels for development. There is a large, vacant, and presumably buildable lot — the site of

a former drive-in theater — along Columbia Park Trail immediately to the northeast of

Spaulding Business Park, on the east side of Georgia Avenue across from the marina

containing the Columbia River Journeys jet boats. Removal of some of the more seriously

deteriorated buildings and clean up of outside storage would produce more vacant space. In

addition, there are some smaller vacant sites within the area. Significant public ownership

exists in addition to the roadways, utilities corridors and port‘s holdings. The regional Benton

Franklin transit system has their major facility there. The area along the Columbia River

contains a shoreline area, a flood protection levee and City parklands, and there may be some

parcels available as a result of the freeway reconfiguration and new interchange that would

be owned by the State.

5.2. Physical Description

The following are key physical characteristics of the Wye area.

The area generally slopes to the north from the south affording views to the river and

north beyond the river to West Pasco, as well as to the east and also toward Saddle

Thomas/Lane & Associates economic & public policy consultants

27

Mountain. Sites at the top of the hill and near the freeway have views back across the

freeway and up the hill to the Columbia Center Mall area.

Much of the Wye area does not have significant tree coverage.

There are two major arterials: the east-west Columbia Park Trail Boulevard and North

Columbia Center Way along with Steptoe Boulevard, South of Columbia Park Trail

leading to the Tapteal Development.

A major exit/entrance to the SR-240 freeway exists central in the site at North Columbia

Center Way. The configuration of this interchange will be altered significantly as a result

of the proposed widening of the freeway.

Columbia River Park (a large regional park recreational facility) and the City of

Kennewick form the Wye area‘s boundary on the east side. The SR-240 freeway forms

the area‘s boundary on the south and west, while the Columbia River delineates the

area‘s northern boundary. Residential and public ownerships bound the Wye area on the

east.

Interviews with public officials reflected that there may be some concerns about

contaminated soils issues though the area since has been used as storage for autos and

parts as well as commercial/ industrial vehicle and machinery repair services.

Access to the rest of the MSA via SR-240 is easy from the south side of the Wye area and

access to SR-240 is also relatively easy from the west end.

There is a small boat launching and marina facility on the river near Bateman Island and

Columbia Park Marina.

Other than these attributes there are no other apparent or outstanding features that are

obvious.

5.3. Ownership Patterns

There are several key property owners, who are either owner-users or who have acquired

land for future or potential development or redevelopment. Owner-users include: Port of

Kennewick, the Benton-Franklin Transit System, the City of Richland, U.S Army Corps of

Engineers, State of Washington, and many local businesses and residents.

Properties that could be developed quickly are: the Port of Kennewick‘s Spaulding Business

park, the owners(s) of the vacant ―drive-in‖ theater site, two individual property owners who

own a large strip shopping center (Columbia Center North) and major parking areas plus

parcels in the southeastern corner of the Wye area along Fowler Avenue east of the North

Thomas/Lane & Associates economic & public policy consultants

28

Columbia Center Way. There is a large linear site on the south (Tapteal) side of the SR-240

freeway owned by the Robert Young Company. While this prime site is considered part of

the Wye Master Plan area, it is physically and functionally separated, and is not included in

our analysis.

In short, there is private sector interest in redevelopment. Once sites are assembled, the

challenge of development will be less daunting to them.

5.4. Locational Attributes

The Wye area has several strategic locational characteristics that provide potential developers

and businesses with important real estate advantages. These characteristics include:

A central location within the Tri-Cities MSA at the intersection of a major freeway

corridor. Several existing businesses in the Wye area stated that their location choice was

based on being able to get to all parts of the Tri-Cities MSA quickly and easily.

Proximity and sight lines to the Columbia Center Mall and the large concentration of the

retail commercial and other real estate attractions in that area. Some regional real estate

professionals and businesses in the Wye area consider that proximity a significant asset

for locating in the Wye area.

Visibility from the SR-240 freeway is a positive for businesses that need to draw support

from passing traffic. This attribute could also be an attractive feature for a firm that

wants its corporate image announced and visible to the region‘s residents and businesses.

Close proximity to the river is a positive business amenity, as well as a potential

recreation asset. It contributes value to both residential and non-residential real estate

within the Wye area.

The Wye area is adjacent to one of the last stretches of unimproved shoreline on the

Columbia River. The City of Richland and the U.S. Corps of Engineers plan to make it

more accessible as a recreational attraction by lowering the levee along that stretch of the

river. This should also add value to the real estate in the Wye area.

Relatively easy and quick access to the Port of Benton‘s Richland airport, Kennewick‘s

Vista Field airport and the scheduled air service at the Pasco airport is another potential

valuable locational attribute for sites within the Wye area.

Thomas/Lane & Associates economic & public policy consultants

29

However there are several locational aspects of the Wye area that provide a challenge for

development and redevelopment. These include:

The Wye area‘s close association with the regional mall is tenuous, particularly if the

regional mall has problems like other malls around the country with maintaining

competitive retail strength within a region in the face of new forms of dispersed retail,

especially large format retail. This could also be a challenge if the trend of moving

resident-serving retail to outlying locations within the region continues. If the future

development of the Wye area is less oriented to retail development, its association to the

mall is less of a potential problem.

Separation from the main areas of Richland by the Yakima River delta and I-182 plus

separation from the rest of the MSA by the SR-240 freeway and the Columbia River limit

the practical access to the Wye area to only a few points.

The current image presented to the traffic on SR-240 and historic reputation of the Wye

area (as being low income, low amenity and crime ridden) present challenges for some

types of future development. The location of a concentration of new auto dealers‘ sales,

service and storage lots along the southern and freeway visible edge of the Spaulding

Business Park cuts both ways. It is a strong identification and reinforces the area as a

retail site. It may not add much to enhancing a higher quality mixed-use ‗urban village‘

image for the area however. Some of this ambiguity could be managed by site and

amenity design and separation from the north sloped portion of the business park.

The word ―challenge‖ was selected advisedly in the above list since none of the

disadvantages are crucial to all types of real estate development and none of the locational

disadvantages seem insurmountable.

5.5. Reasons Current Uses Located in the Richland Wye Area

Interviews with current businesses in the Wye area produced a range of responses to

questions about why they were located there and/or why they stayed. The reasons included:

Central location within the Tri-Cities regional market.

Location near the mall reinforced their retail reputation and destination.

Proximity to and identification with the river and territorial views, recreation and regional

attraction of the Columbia River and its outdoor, open space and recreational facilities.

Thomas/Lane & Associates economic & public policy consultants

30

Cheaper land and buildings.

As one might expect, the businesses and property owners interviewed that were located in the

Wye Area had a better opinion of it than almost everyone else. They thought reports of

crime and drug problems were overstated. They pointed to the restaurants and retail stores

located in the Wye area and their ability to attract customers from throughout the Tri-Cities

MSA. They also pointed to the draw of the marina, boat launch, fishing and recreation

facilities as a strong positive that counters any of the negative historical images; and said that

when freeway construction displaced businesses, most desired to stay in the area. In

addition, they pointed to the presence of a number of well-kept owner-occupied single-family

commercial buildings that are sprinkled throughout the area. They also remarked favorably

about the small but cohesive community nature of the area.

The following are potentials that form a firm basis for development and redevelopment in the

Wye area:

Significant planned and proposed public and private projects in the master plan area.

Significant number of property owners who have major amounts of property assembled.

Basic real estate locational advantages within the Tri-cites regional market.

Existing and planned infrastructure improvements.

Existing viable, though small, businesses.

Significant areas that could change, i.e., older and modest single family and commercial

buildings, and underutilized sites and buildings.

5.6. Challenges, Opportunities and Uncertainties for Wye Master Plan Area

If no concerted action, other than the enforcement of the City‘s zoning and land use

regulations and planned public infrastructure improvements occur, the Wye will continue to

provide an area for low-income housing, and a place for less expensive and convenient

locations for smaller businesses. Market forces will eventually fill in the land that is

currently available. This process will probably be slow, given the nature of the overall real

estate development patterns in the region. However, there are enough large to medium sized

parcels in the Wye area that it would not take very long to have a major transformation occur.

Should the City of Richland decide to put forth a major redevelopment effort for the Wye

area, there are some short term and less expensive activities that can and should be

undertaken, including:

Thomas/Lane & Associates economic & public policy consultants

31

Identification and organization of the key property owners in the Wye master plan area.

Examination of state laws and application of public-private financing mechanisms for

redevelopment and blighted area actions, such as the Community Renewal Act‘s

mandates, local improvement district, and potential of a public development authority as

a vehicle for redevelopment.

Complete information and data gathering to reduce areas of uncertainties related to

physical site and infrastructure improvement, as well as design and costing of appropriate

infrastructure improvements for the Wye area.

Segmentation of the Wye area into parts that could provide a sharper focus for specific

appropriate real estate market segments and/or implementation actions.

Organize and staff multi-year, multi-jurisdiction, multi-constituent planning process for

the area to assure continuity.

Assure periodic constructive input from the local real estate development, marketing and

property management sector, periodically revisiting the Wye area‘s zoning and regulatory

approach and leaving sufficient flexibility to address unforeseen opportunities that may

arise.

Develop an information campaign to counter any lingering ―image‖ problems for the

area.

Develop a specific and explicit redevelopment strategy that identifies:

o Who will have what redevelopment responsibilities,

o What long term and short term actions and projects will be undertaken,

o Why that set of actions will result in redevelopment, i.e., be clear about the strategy

being followed that makes realistic economic and real estate sense,

o How will each component of the strategy be implemented, what are the action steps,

what are the sources and uses of funds,

o Set priorities for the sub-parts within the Wye master planning area for action, and

o Establish a reasonable phasing and monitoring process.

o Opportunities to determine if the water, sewer, storm or street capacity can handle

build out of redevelopment, and who will pay?

A range of redevelopment strategies for the Wye master planning area is discussed below.

5.7. Potential Land Uses/Real Estate Segments Appropriate for the Wye Master Plan Area

Thomas/Lane & Associates economic & public policy consultants

32

Heavy industrial uses, extensive processing, and storage uses and single family detached real

estate and market segments were not considered for the Wye area. Heavy industrial uses

usually require rail or marine transportation facilities, large amounts of outside storage, ‗lay-

down‘ areas, and often produce a whole range of ‗spillover‘ effects (dust, noise, smells, etc)

that are incompatible with existing or proposed and uses at the site.

Single-family residential development could be an appropriate land use at the site, but the

elimination of many current uses, rationalizing land ownership, and elimination of blighted

conditions would be necessary. In addition, there are many better locations in the region for

such uses. Multi-family and condominium residential uses could be developed in portions of

the Wye area if they were appropriately separated from non-residential uses. Reflecting the

high average age of workers employed at Hanford-related facilities, there may be a strong

―empty nester‖ market for mid-rise waterfront condos, similar to the type of development

that exists in the Columbia Point area.

Overall market assessment:

There is potentially a large amount of real estate development that could be

accommodated in the Wye area immediately, located in vacant and under-utilized areas

and eventually through redevelopment.

The Wye area will increasingly have to compete with other areas of the regional real

estate market to attract tenants.

The Wye area‘s advantages are: (1) proximity to and views of the river, (2) proximity to

other regional economic engines (Kennewick‘s mall, retail, office, and recreational

assets), (3) access to regionally important transportation networks, (4) significant existing

vacant and assembled land, (5) viable businesses already there, and (6) public agency

interest in its development and redevelopment.

Retail market assessment:

Neighborhood shopping centers – There already is a large concentration of retail

establishments south of the site. There are not large concentrations of residents nearby

and the Wye area is not centrally or conveniently located within an established or

emerging neighborhood. Eventually, should large amounts of condominiums and multi-

family residential units be developed in the Wye area, there could be some demand for

convenience and neighborhood retail.

Thomas/Lane & Associates economic & public policy consultants

33

Community shopping centers – There are better-located existing competitive locations

that are approximate to emerging and established concentrations of population within the

region.

Regional shopping centers - There is an established regional mall very close by. Some

portions of the Wye area, primarily the relatively flat southern portion adjacent to and

visible from SR-240 and the mall areas, could attract large format region serving retail

establishments, but the trend is for such large format retailers to disperse closer to new

and growing portions of the region.

Retailers with a need for large outside storage and display areas, e.g., auto sales, RV,

truck dealers new and used – There are appropriate sites on the relatively flat southern

portion adjacent to and visible from SR-240 and the mall areas that could attract such

region serving retail establishments. Separating such uses from the other types of uses

would be important.

Restaurants, entertainment facilities, lodging (short and long stay), recreational facilities

and specialty retail uses that complement and support them could be attracted to sites

near to, or visible from, the river, especially when the levee‘s height is reduced and park,

open space and recreation improvements are provided.

―Festival‖ retail – There is very little of this type of pedestrian oriented retail in the Tri-

Cities. There are almost no existing environments that could evolve into this type of use.

However if a modest size ―urban village‖ project were to develop in the Wye area‘ then

such ―festival‖ retail could be a part of it. This seems like a fairly long-term prospect and

would require dramatic change in the underlying development climate and parameters in

the Tri-Cities area.

Commercial market assessment:

Offices, small office parks, medium density office buildings; free standing, owner-user,

or multi-tenant development -- The river views, open space, recreational amenities,

integration with residential uses and proximity to existing similar developments up the

hill in the areas around the mall are reasons to believe that the Wye area could attract this

type of real estate market segment. The Brashears office building proposed at the

Columbia Park Trail Boulevard entrance to the Spaulding Business Park is a signal

project, and could demonstrate this market segment as a viable use here.

Heavy Commercial – This use is already a viable use in this area. The Lincare Medical

Products Company, electrical contractors, and professional services engineering and

Thomas/Lane & Associates economic & public policy consultants

34

surveying firms are examples. The Wye area‘s central location in the region is a strong

locational attraction for this type of use.

Medical/dental offices and labs would be a type of office use that could be attracted to

this area once appropriate amenities are present.

Thomas/Lane & Associates economic & public policy consultants

35

Business Park market assessment

Typically, business parks are oriented to different types of activities: office types, light

industrial types and hybrid types – a few of which are found within the Tri-Cities market.

Unless a major effort is made to assemble a large percentage of land in the Wye area, the

potential for business parks will produce relatively smaller versions, which, may be

appropriate to the size of the Tri-Cities market area.

Multi-family and condominium market assessment

Once the open space, recreational, park and waterfront amenities are in place, the Wye

area will be a very attractive location.

Thomas/Lane & Associates economic & public policy consultants

36

6. Projections of Future Growth in Richland

6.1. Projected Employment Growth

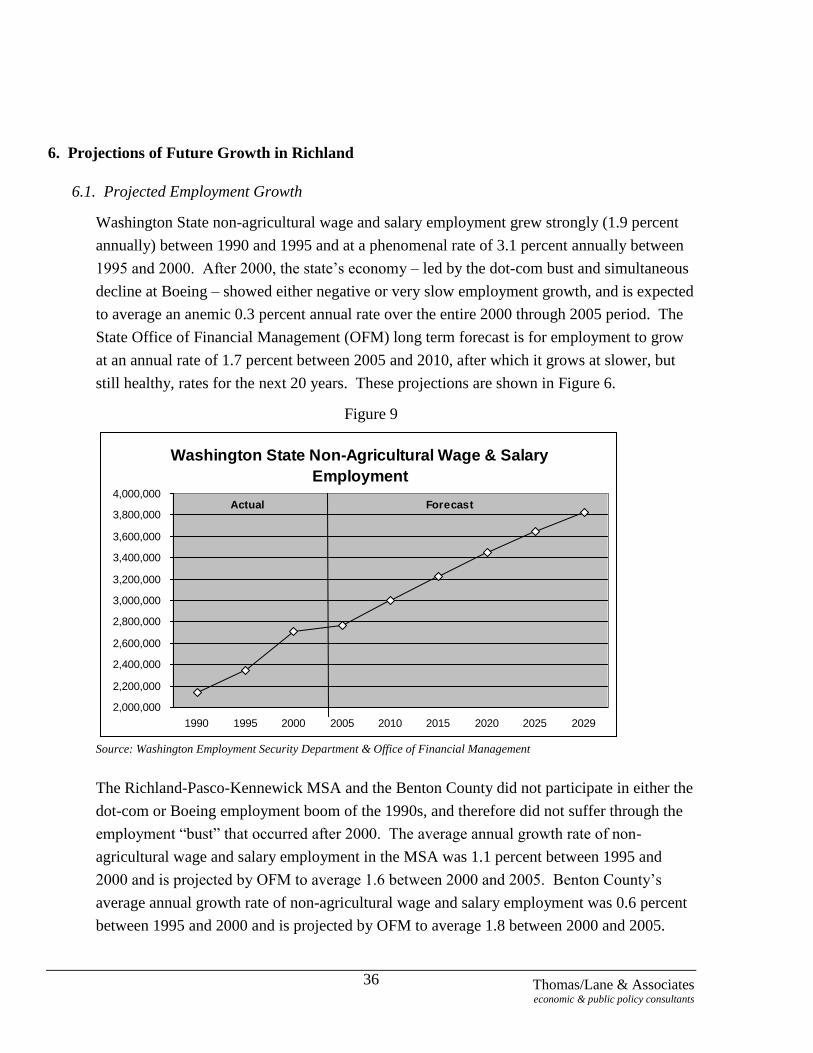

Washington State non-agricultural wage and salary employment grew strongly (1.9 percent

annually) between 1990 and 1995 and at a phenomenal rate of 3.1 percent annually between

1995 and 2000. After 2000, the state‘s economy – led by the dot-com bust and simultaneous

decline at Boeing – showed either negative or very slow employment growth, and is expected

to average an anemic 0.3 percent annual rate over the entire 2000 through 2005 period. The

State Office of Financial Management (OFM) long term forecast is for employment to grow

at an annual rate of 1.7 percent between 2005 and 2010, after which it grows at slower, but

still healthy, rates for the next 20 years. These projections are shown in Figure 6.

Figure 9

Washington State Non-Agricultural Wage & Salary

Employment

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

3,600,000

3,800,000

4,000,000

1990 1995 2000 2005 2010 2015 2020 2025 2029

Actual Forecast

Source: Washington Employment Security Department & Office of Financial Management

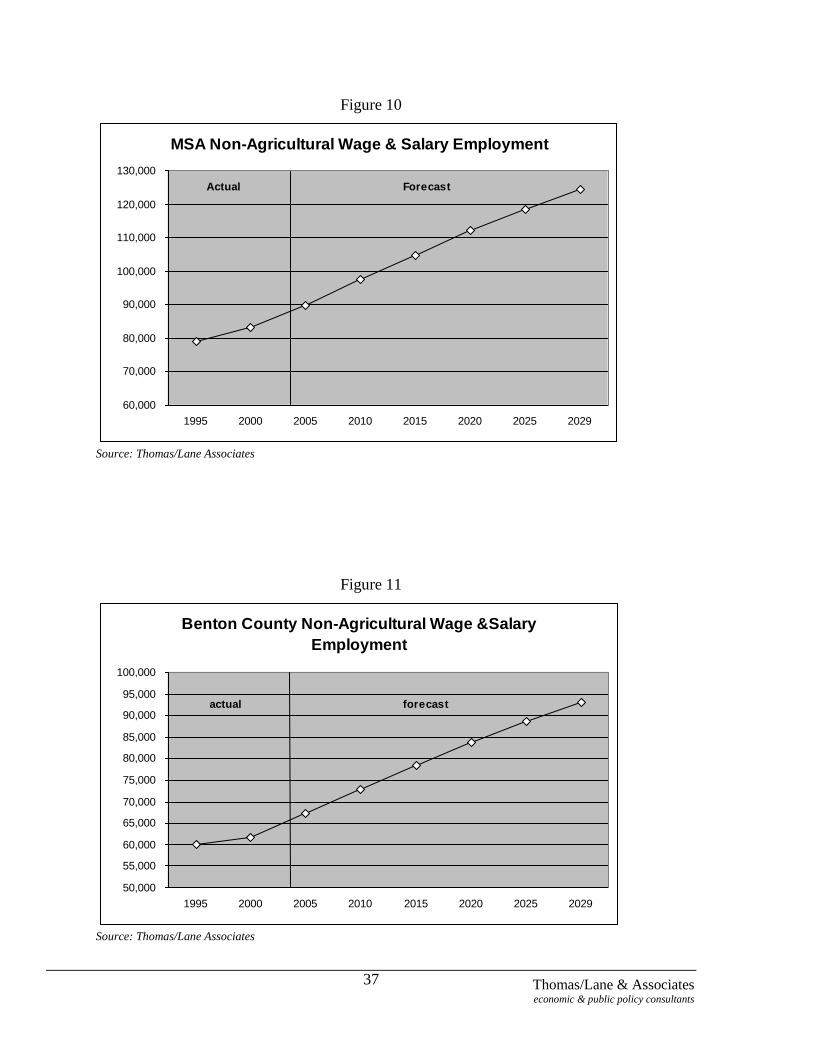

The Richland-Pasco-Kennewick MSA and the Benton County did not participate in either the

dot-com or Boeing employment boom of the 1990s, and therefore did not suffer through the

employment ―bust‖ that occurred after 2000. The average annual growth rate of non-

agricultural wage and salary employment in the MSA was 1.1 percent between 1995 and

2000 and is projected by OFM to average 1.6 between 2000 and 2005. Benton County‘s

average annual growth rate of non-agricultural wage and salary employment was 0.6 percent

between 1995 and 2000 and is projected by OFM to average 1.8 between 2000 and 2005.

Thomas/Lane & Associates economic & public policy consultants

37

Figure 10

MSA Non-Agricultural Wage & Salary Employment

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

1995 2000 2005 2010 2015 2020 2025 2029

Actual Forecast

Source: Thomas/Lane Associates

Figure 11

Benton County Non-Agricultural Wage &Salary

Employment

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

90,000

95,000

100,000

1995 2000 2005 2010 2015 2020 2025 2029

actual forecast

Source: Thomas/Lane Associates

Thomas/Lane & Associates economic & public policy consultants

38

Richland‘s growth of non-agricultural wage and salary employment is projected to closely

track Benton County patterns. Employment increased by 800 net new jobs between 1995

and 2000 – an average annual growth rate of 0.6 percent – and is projected to increase by just

over 2,600 net new jobs between 2000 and 2005 – an average annual growth rate of 1.8

percent. By 2029, non-agricultural wage and salary employment in the City of Richland is

expected to grow from its 2000 level of 28,900 to 43,600.

Figure 12

Richland Non-Agricultural Wage & Salary

Employment

20,000

25,000

30,000

35,000

40,000

45,000

1995 2000 2005 2010 2015 2020 2025 2029

actual forecast

Source: Thomas/Lane Associates

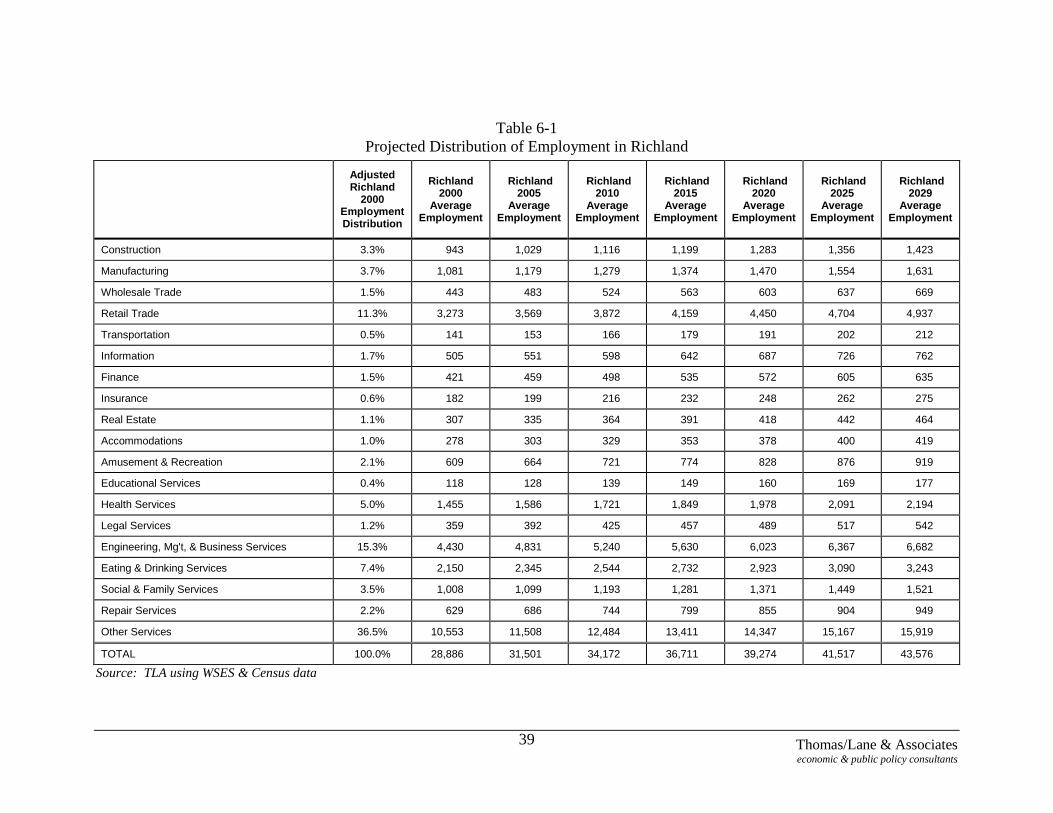

6.2. Distribution of Employment by Industry

The distribution of Richland‘s non-agricultural wage and salary workforce is based on its

adjusted percentage distribution by North American Industrial Classification System

(NAICS) industry codes for 2000. The ―adjustment‖ to the actual 2000 distributions reflects

both a time trending of industry patterns and weighting for different occupational

distributions in Richland and all of Benton County. The resulting distribution of

employment, by industry and by 5-year increment, is shown in Table 6-1.

Thomas/Lane & Associates economic & public policy consultants

39

Table 6-1

Projected Distribution of Employment in Richland

Adjusted Richland

2000 Employment Distribution

Richland 2000

Average Employment

Richland 2005

Average Employment

Richland 2010

Average Employment

Richland 2015

Average Employment

Richland 2020

Average Employment

Richland 2025

Average Employment

Richland 2029

Average Employment

Construction 3.3% 943 1,029 1,116 1,199 1,283 1,356 1,423

Manufacturing 3.7% 1,081 1,179 1,279 1,374 1,470 1,554 1,631

Wholesale Trade 1.5% 443 483 524 563 603 637 669

Retail Trade 11.3% 3,273 3,569 3,872 4,159 4,450 4,704 4,937

Transportation 0.5% 141 153 166 179 191 202 212

Information 1.7% 505 551 598 642 687 726 762

Finance 1.5% 421 459 498 535 572 605 635

Insurance 0.6% 182 199 216 232 248 262 275

Real Estate 1.1% 307 335 364 391 418 442 464

Accommodations 1.0% 278 303 329 353 378 400 419

Amusement & Recreation 2.1% 609 664 721 774 828 876 919

Educational Services 0.4% 118 128 139 149 160 169 177

Health Services 5.0% 1,455 1,586 1,721 1,849 1,978 2,091 2,194

Legal Services 1.2% 359 392 425 457 489 517 542

Engineering, Mg't, & Business Services 15.3% 4,430 4,831 5,240 5,630 6,023 6,367 6,682

Eating & Drinking Services 7.4% 2,150 2,345 2,544 2,732 2,923 3,090 3,243

Social & Family Services 3.5% 1,008 1,099 1,193 1,281 1,371 1,449 1,521

Repair Services 2.2% 629 686 744 799 855 904 949

Other Services 36.5% 10,553 11,508 12,484 13,411 14,347 15,167 15,919

TOTAL 100.0% 28,886 31,501 34,172 36,711 39,274 41,517 43,576

Source: TLA using WSES & Census data

Thomas/Lane & Associates economic & public policy consultants

40

Engineering, Management & Business Services employment is projected to

continue to grow even though there will be a workforce reduction after the

Hanford waste treatment (vitrification) plant is completed. As reported in The

Impact of the Waste Treatment Plant on the Hanford Communities report, the

annual peak of about 4,500 jobs over the eleven-year life of the project will be in

addition to the expected growth of almost 15,000 net new jobs in the Richland-

Pasco-Kennewick MSA projected to occur under a baseline – no vitrification

plant – scenario. Given the occupational and industrial composition of Richland‘s

economy, a significant number of those jobs will be in the Engineering,

Management and Business Services sector – particularly in the engineering and

scientific R&D industries.5

Other Services, is a catchall category. However much of its expected growth is

expected to occur in services associated with the aging of the Richland-Pasco-

Kennewick MSA‘s population.

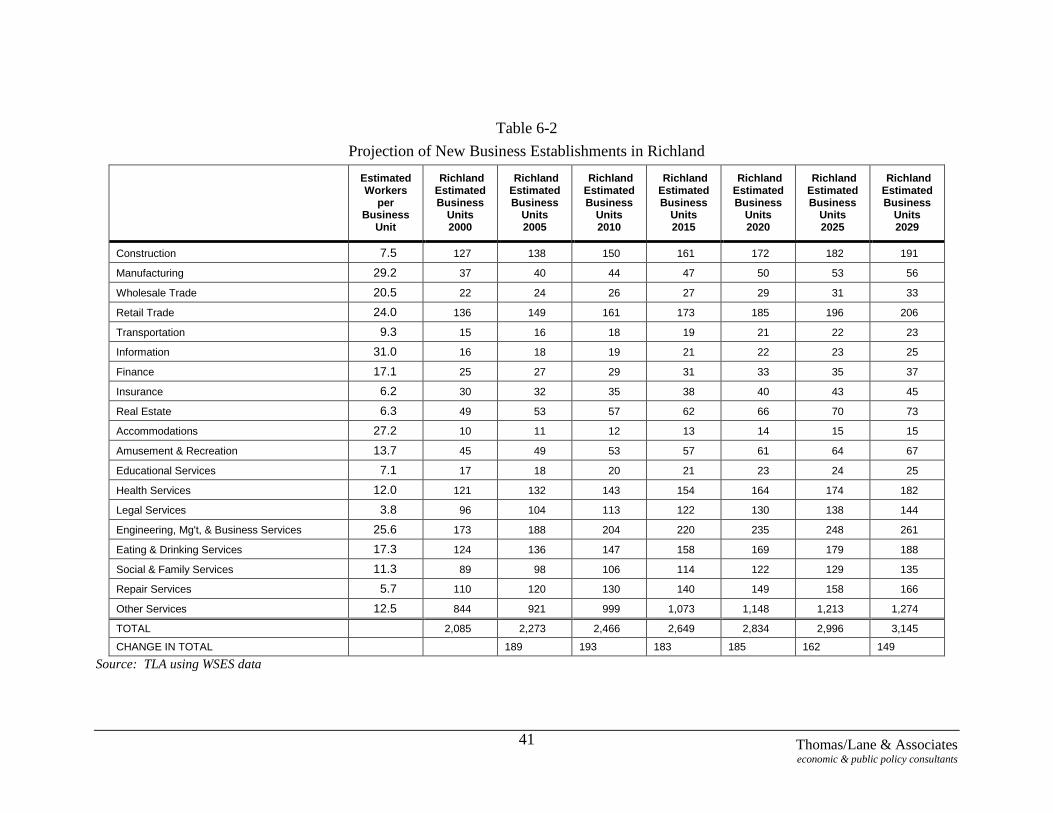

6.3. New Business Establishments by Industry

The number of new business establishments in Richland was projected by

dividing each industry‘s employment by the average number of workers per

establishment reported by WSES. These projections are shown in Table 6-6, on

the following page.

Between 2000 and 2020, Richland is projected to have between 180 and 190 net

new business establishments every five years, with this number falling to a level

of 150 land 160 net new business establishments for each five-year period

thereafter.

The industries with the most number of net new firms are projected to be

engineering, management and business services; retail trade; and eating and

drinking places.

5 Perteet Engineering, Thomas/Lane & Associates, and SCM Consultants, The Impact of the Waste

Treatment Plant Project on the Hanford Communities (The Hanford Communities, October, 201), pg3-3.

Thomas/Lane & Associates economic & public policy consultants

41

Table 6-2

Projection of New Business Establishments in Richland

Estimated Workers

per Business

Unit

Richland Estimated Business

Units 2000

Richland Estimated Business

Units 2005

Richland Estimated Business

Units 2010

Richland Estimated Business

Units 2015

Richland Estimated Business

Units 2020

Richland Estimated Business

Units 2025

Richland Estimated Business

Units 2029

Construction 7.5 127 138 150 161 172 182 191

Manufacturing 29.2 37 40 44 47 50 53 56

Wholesale Trade 20.5 22 24 26 27 29 31 33

Retail Trade 24.0 136 149 161 173 185 196 206

Transportation 9.3 15 16 18 19 21 22 23

Information 31.0 16 18 19 21 22 23 25

Finance 17.1 25 27 29 31 33 35 37

Insurance 6.2 30 32 35 38 40 43 45

Real Estate 6.3 49 53 57 62 66 70 73

Accommodations 27.2 10 11 12 13 14 15 15

Amusement & Recreation 13.7 45 49 53 57 61 64 67

Educational Services 7.1 17 18 20 21 23 24 25

Health Services 12.0 121 132 143 154 164 174 182

Legal Services 3.8 96 104 113 122 130 138 144

Engineering, Mg't, & Business Services 25.6 173 188 204 220 235 248 261

Eating & Drinking Services 17.3 124 136 147 158 169 179 188

Social & Family Services 11.3 89 98 106 114 122 129 135

Repair Services 5.7 110 120 130 140 149 158 166

Other Services 12.5 844 921 999 1,073 1,148 1,213 1,274

TOTAL 2,085 2,273 2,466 2,649 2,834 2,996 3,145

CHANGE IN TOTAL 189 193 183 185 162 149

Source: TLA using WSES data

Thomas/Lane & Associates economic & public policy consultants

42

7. Future Land Use Demand in the Richland Wye Area

7.1 Current Absorption Patterns

In recent years, the Wye area has seen the establishment of the Spaulding

Business Park by the Port of Kennewick and a limited number of other new

developments. Several of the businesses displaced by WSDOT‘s reconfiguration

of the SR-240 interchange have chosen to stay in the area and developed new

buildings. There are newer mixed use or small office buildings. There have been

several businesses that have purchased sites in the Fowler Avenue portion of the

Wye area near the Columbia Center Way North and SR-240 interchange. Some

churning of tenants has occurred at the Colombia Center North shopping center.

A mixed general tenant office building is proposed for site at the entrance to the

Spaulding Business Park. Most of these uses are light industrial/heavy

commercial uses, regionally focused specialty retail, or small professional office

uses.

7.2. Future Development Potential

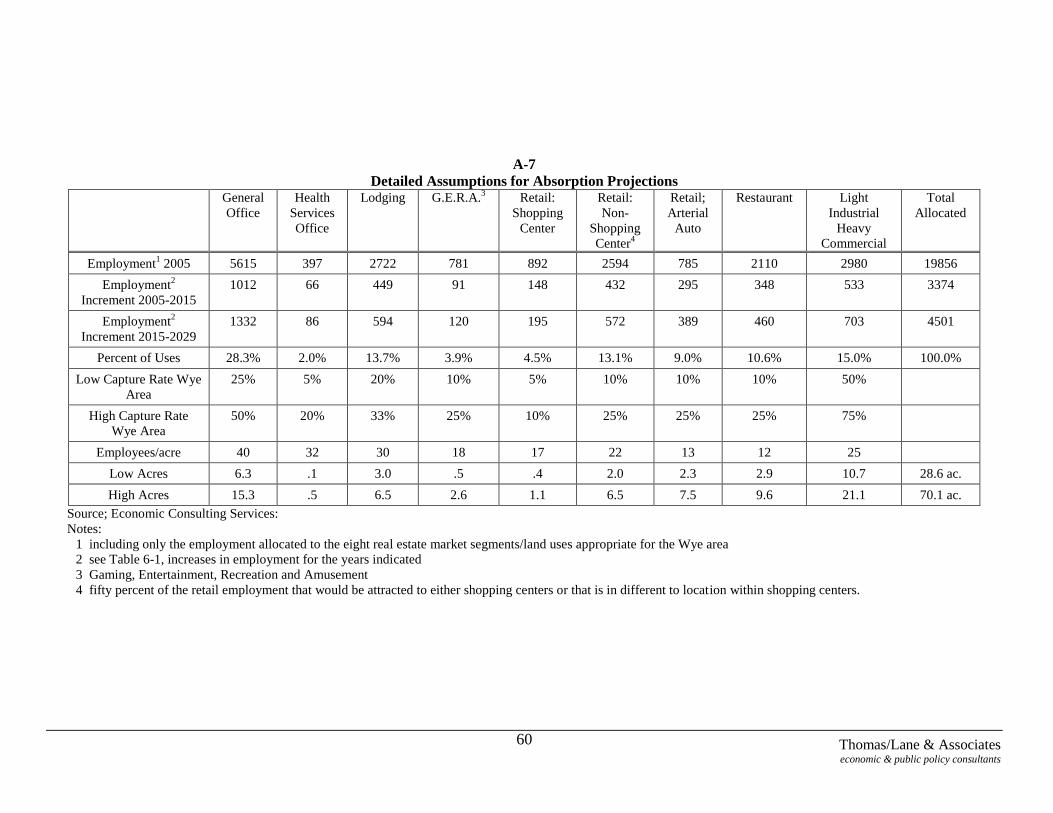

A multi-stepped process was followed to obtain projections of future growth that

are realistic for the Wye area. First, data on 22 occupational categories and 164

industrial (the new NAICS industrial) categories of employment were examined

and separated in eight real estate market segments that were appropriate for the

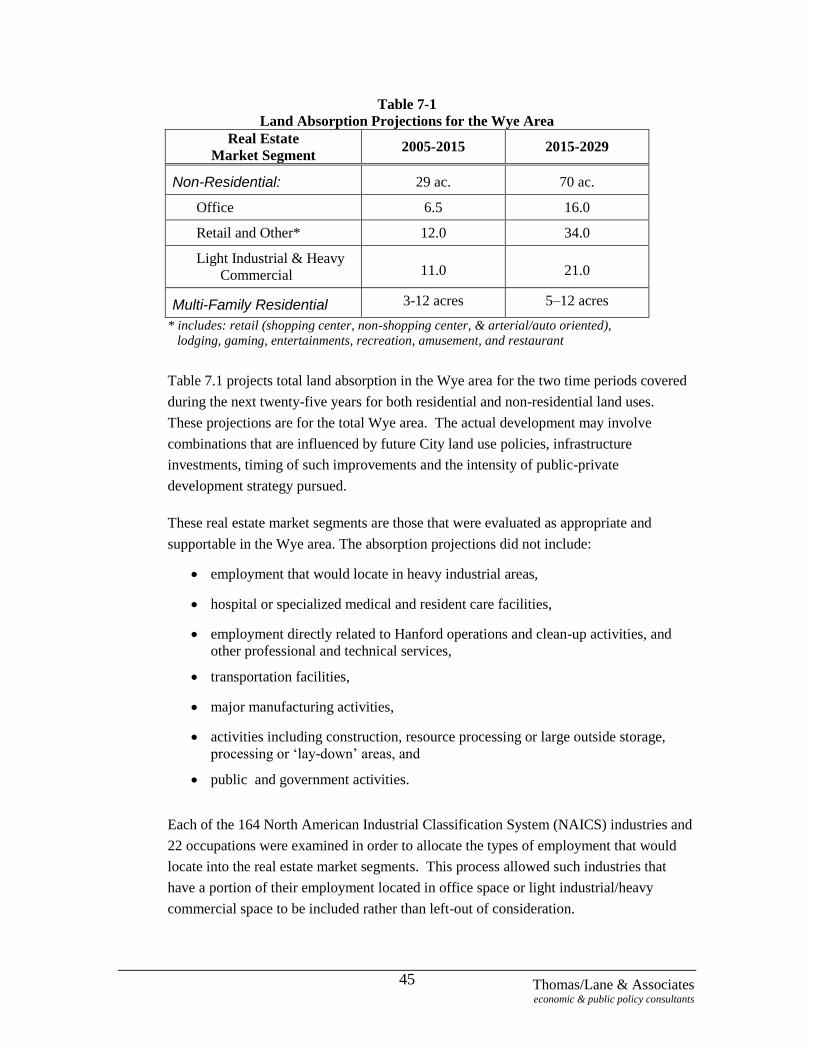

Wye area of Richland. Secondly, the employment projections for Richland