Understanding the outcomes of local investments: the Lloyds Banking Group community fund

24

July 2013 Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Transcript of Understanding the outcomes of local investments: the Lloyds Banking Group community fund

July 2013

Understanding the outcomes of local investments:

The Lloyds Banking Group Community Fund

Understanding the outcomes of

local investments: The Lloyds

Banking Group Community Fund

Authors: Rosemary Maguire, Joanna Allan

nef consulting limited

nef (new economics foundation)

3 Jonathan Street

London SE11 5NH

www.nef-consulting.co.uk

Tel: 020 7820 6304

nef consulting is a social enterprise foundedand owned by nef (the new economicsfoundation) to help public, private and thirdsector organisations put its ideas into action.

© 2013 nef consulting

No part of this publication may be reproduced, stored in a retrieval

system or transmitted in any form or by any means, electronic,

mechanical or photocopying, recording or otherwise for commercial

purposes without the prior permission of the publisher.

nef consulting 2

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

nef consulting 3

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Executive Summary 4

1. Introduction 6

2. The Lloyds Banking Group Community Fund 2012: 8

what we learned

3. Looking forward to 2013 investments: 16

what could the Lloyds Banking Community Fund achieve this year?

Contents

Executive summary

The Lloyds Banking Group Community Fund was set up in 2012 with the aim of

unlocking the potential of young people by supporting UK communities at the

grass roots level. In 2013 the fund has been extended to cover 400 local

communities, and its scope extended to ‘unlock(ing) the potential of

communities and the people in them’. Nominated projects are selected by

Lloyds Banking Group staff, then local communities are invited to vote for their

preferred local project.

The purpose of this research is to review the achievements of the 2012 funding

and consider the potential value to communities benefitting from the 2013

funding. It has been informed by primary research with funded projects and

Lloyds Banking Group staff, and a literature review of the impact of community

investments.

The Lloyds Banking Group Community Fund 2012: what we learned

Those supported by the Community Fund used the investment in three main

ways: directly delivering activities to young people and their families; purchasing

or replacing equipment and facilities used to deliver activities; and supporting

the strategic development of the organisation.

The following results were reported for the organisations and wider community:

� 96% stated that they had been able to grow the support base for their

organisation.

� 88% of those surveyed stated that they had been able to make links with new

people or organisations within the community.

� 79% of those surveyed felt that applying for the funding had helped them to

develop new project ideas

� 88% felt that there was an increase in new people taking part in activities in

their area.

� 71% felt that there was an increase in the links between different

organisations and groups

Feedback from all organisations that were funded was positive; they

appreciated the ease of the process, the support and media opportunities.

Organisations that were successful in receiving the funding worked extremely

hard to generate awareness of their work in their local communities, developing

clear messages and new approaches to increasing their support base.

This research found that the initial pilot of this programme has been successful

in testing an approach to funding, engaging and supporting community

organisations and growing awareness about their work. The funding has

supported local activity which people care about, and in many cases has been

invested in projects which will sustain beyond the duration of the funded activity.

The fund has helped to bring people together and in many cases has helped to

bring forward activity which may have struggled to find funding. The challenge

for the Lloyds Banking Group Community Fund team will be to gather

longitudinal data from the one year evaluation which helps them to understand

longer term gains from the funding.

nef consulting 4

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Looking forward to 2013 investments: what could the Lloyds Banking

Community Fund achieve this year?

The aspirations for Lloyds Banking Group colleagues for this year’s funding fall

into four main areas: taking the opportunity to help more people in local areas;

supporting groups to communicate their work locally; creating a positive link

between customers and the bank; and understanding the tangible changes from

the successful projects.

The literature review which formed part of this research found that key to

creating lasting change is to invest in activities which help to build the capacity

of organisations to generate further income and to understand how investing in

organisations that support individuals to make change in their lives can be

scaled up to achieve wider changes.

Overall, the aspirations for this year’s funding appear to build on what was

observed through the projects funded in 2012, and the results of the literature

review. There is a desire to fund activities which grow local organisations and

create better ties between the Lloyds Banking Group and the local communities

it serves. There is also a desire to better understand and evidence how change

happens, so that the growth of the fund can be effectively evaluated.

This piece of research is a starting point for Lloyds Banking Group to better

understand how its investments are creating change for communities, long after

the donations are made. Lloyds Banking Group is moving past the premise that

the act of giving alone can create change, and is using the data it collects from

projects and after projects have finished, to start to scrutinise the impact that it

is able to create through the programme. By taking the step of publicising an

assessment of how it performed in 2012, Lloyds Banking Group has set a

benchmark of the changes that the programme made through its pilot phase,

and can look forward to seeing if those changes can be replicated as the

programme is rolled out to further communities.

The learning gained from the 2012 and 2013 investments can be used more

widely within the Lloyds Banking Group to understand how community activities

can bridge the link between local branches, customers and community

organisations. A greater understanding of this relationship and its potential to

deliver local impact could help to align core business activities more closely to

communities’ needs, supporting them better through all of the work that Lloyds

Banking Group does.

nef consulting 5

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

1. Introduction

The Lloyds Banking Group Community Fund was set up in 2012 with the aim of

unlocking the potential of young people by supporting UK communities at the

grass roots level. Funding was offered to local organisations in the 66

communities along the Olympic Torch relay route. The projects were initially

nominated by Lloyds Banking Group colleagues, with shortlisted organisations

then taking part in a public vote for the funding. 132 organisations received

£5000 in 2012, using the funds to support local projects for young people.

In 2013 the fund has been extended to cover 400 local communities, and the

scope of the funding has been extended to ‘unlocking the potential of

communities and the people in them’. Projects in each area have been

nominated by Lloyds Banking Group colleagues and four have been shortlisted

for awards. The public in the participating communities will be invited to vote for

their preferred projects in September 2013; the two highest scoring projects will

receive £3000 and the remaining two will receive £300.

The research

The purpose of this research is to review the achievements of the 2012 funding

and to consider the potential value to communities benefitting from the 2013

funding. The research considered the high level achievements of the projects

funded in 2012, building on existing internal reviews and evaluations. It also

reviewed the aspirations for the 2013 funding from those involved in the Fund,

set within a wider understanding of the benefits of community investments.

The first stage of the research involved a literature review of existing

programme documentation, telephone interviews with Lloyds Banking Group

Community Fund staff and representatives of projects funded in 2012. An

electronic survey was also sent to a sample of the projects which were funded

in 2012. 25 organisations responded to this survey (out of a total of 132). The

locations of the respondents can be seen in Figure 1.

Figure 1: Map of respondents to survey

nef consulting 6

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

For the second phase of the research, a rapid literature review was undertaken

to assess current views on the benefits of community investment. The findings

were analysed in within the context of the results of the first phase of the

research.

This report contains the findings of this research. The report is structured as

follows:

� Chapter 2 looks at lessons drawn from the 2012 funding, based on the survey

findings. The research considers the experiences of both the organisations

and the communities in which they are based.

� Chapter 3 looks forward to the potential outcomes for the 2013 investments,

taking the views of Lloyds Banking Group staff and setting these within the

context of our understanding of the power of community investments, as

documented in current literature.

nef consulting 7

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

2.The Lloyds Banking Group Community Fund 2012: what

we learned

In 2012, 836 organisations applied to the Lloyds Banking Group Community

Fund. Of these organisations, 62% were registered charities, 24% were not for

profit organisations (e.g. sports clubs), 6% were schools and 8% were

companies or other organisations. Two projects were selected in each of the 66

locations which were part of the Olympic Torch Route.

Understanding communities

In order to contextualise our understanding of the changes experienced by

communities, we first asked those participating in the survey what they consider

to be their “community”. 72% of those who responded to the survey had a

geographical understanding of their community. This area ranged in size from a

village to a county. 24% of respondents stated that their community was a

specific group of people, those with a particular need, rather than geographically

based. 8% of respondents did not provide a definition.

What was the funding used for?

Those supported by the Community Fund used the investment in three main

ways (some projects used the funding in more than one way, therefore

percentages do not add up to 100):

� Directly delivering activities to young people and their families. This

included grants for travel to youth camps, training courses for local

swimmers, support through hospices for ill children and their families,

providing hardship funds so that other children can access activities and

supporting young people with autism to develop their mobile communications

in everyday life. 56% of projects used the funding in this way.

Definitions of community

“Our village, the farming community surrounding it and the neighbouringvillages and local small rural town.”

“Individuals who live in the local area and interact together and work togetheras a community.”

“Anybody willing to travel to use our service so they may not live locally butwe get to know them. They are local to us because they have a child withDown syndrome.”

“To define local community is to work together to enhance the lives of those inthe community itself. In Northern Ireland this can be made more difficultbecause of cultural differences. [Our project] strive[s] to bring communitiestogether especially those with Special needs which is the aim of ourClub/Project.”

“The "local community" is made up from people living in our local area, whointeract and support each other.”

nef consulting 8

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

� Purchasing or replacing equipment and facilities used to deliver

activities. This included developing a picnic area, contributing towards new

changing facilities, purchasing of camping equipment and providing all

weather surfaces for therapy centres. 40% of projects used the funding in this

way.

� Supporting the strategic development of the organisation. One

organisation used the funding to employ a specialist to evaluate their services

and produce a medium and long-term strategy for their future development.

� 8% of projects did not state how they used the funding.

The organisations were asked the extent to which they were able to bring in

additional community resources to support the delivery of the projects, for

example using community land and facilities. 64% of those surveyed stated that

they had been able to bring in community resources to an extent, with 24%

stating that this was to a great extent.

88% of the projects involved people participating in the activities who had not

participated in those kinds of activities before. In addition, in 63% of cases, the

activities were also organised and delivered by people who had not been

involved in activities before. 100% of those surveyed felt that the project would

increase the chance of people getting involved in future activities.

In some cases, organisations reported that the funding had been a “lifeline” and

had enabled them to continue delivering support to local people. Whilst any

funding and supportive activity should create positive benefits to those

individuals it targets, there is a question as to the sustainability of the outcomes

for the organisation. Both staff at Lloyds Banking Group and those projects

interviewed for this research stressed the importance of the fund not being used

nef consulting 9

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Different uses of funding

“The funding was used to support girls going to a large camp withinternational visitors. The girls were given a grant towards the cost whichincluded travel. The girls had many opportunities at camp which willcontribute to greater personal development in non-educational areas. Theyalso supported other girls with more fund raising to help cover costs.”

“The funds were used to improve the facilities and purchase or renew boxingequipment.”

“To replace ageing tents that were no longer fit for purpose. We were havingproblems equipping the young people for expeditions, and were concernedthat they would begin to form negative opinions about the Unit based on thecondition of the equipment.”

“To develop a picnic area with regard to encouraging wildlife that can be usedfor the school and other groups.”

“Provision of play and leisure activities for disabled young people aged 5-18years old. To enable them to have fun with their friends in a supportive andsave environment - helping them to be active, valued members of a fullyinclusive community.”

to fill emergency funding gaps and instead used as a way of investing in a

sustainable change. Those organisations consulted who used the funding to

invest in development and assets may reap longer term benefits from the fund.

nef consulting 10

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Case study: Thurso Players

Thurso Players were recommended for the funding by someone in an

amateur dramatics society. They are a drama club based at The Mill Theatre,

Thurso, Caithness in the far north of Scotland. The club includes junior, youth

and adult sections and puts on a number of productions each year, in some

cases written, produced and directed by members of the youth and junior

groups. This helps to provide entertainment and leisure activity for local

people, especially in the winter months.

Most of their fundraising for the year is generated through the annual

pantomime, which covers the cost of running the theatre and productions for

the rest of the year. Due to their remote location, they have fewer funding

opportunities than those based in the cities, but are able to gather good

support from the local community. These community assets help the Thurso

Players continue their work, but gaining additional funding or resources to

develop their work can be challenging. “There is no buffer of money.”

The nearest large town with a professional theatre to Thurso is Inverness, a

two hour journey away. The drama club finds it hard to access coaching and

professional support to help their youth and junior sections develop their

skills, and to research and share information about new approaches to

developing their theatrical and performance techniques.

The funding received from Lloyds Banking Group Community Fund has been

used to bring professional prosthetics staff to the theatre to run a training

session on make-up and prosthetics. This has been used by youth members

to run their latest version of Roald Dahl’s The Witches. The club also took a

group of junior members to Inverness to see a play, to observe how other

people put on their productions.

The second part of the funding has been used to purchase a smart TV which

can be used by members to screen and share their internet research into new

productions and theatre techniques. Previously videos were viewed on a

mobile ‘phone or laptop. It has also been used to screen the rehearsals so

that the junior members can observe their performance from the audience’s

perspective.

According to the Chairman of Thurso Players, they have “invested in things

that can reap benefits for years to come… we are investing in our own future

and ability to deliver.” He feels that they would not have been able to invest in

this development without the fund as they had not managed to access this

kind of funding previously. In addition, participating in the process created a

“buzz” amongst the juniors, as they were asked to help develop ideas of how

best to spend the money.

nef consulting 11

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Changes for the organisations

The aim of the fund was to be able to support organisations at grass roots level

of communities. In addition to directly supporting organisations with financial

resources, it was anticipated that participating in the application and voting

process would also have indirect benefits for those involved.

Those interviewed for this research expressed a great deal of enthusiasm for

participating in the voting process. They felt that it encouraged them to be more

creative in the ways in which they communicated their work to the local

community, that being part of a process under the Lloyds Banking Group name

gave them credibility to address local organisations and that it also helped them

to clarify their description of their work. One member of staff at the Lloyds

Banking Group felt that this was a crucial part of the process: understanding

and defining their USP (unique selling point). This is seen as a way of leaving

an indirect legacy from the funding; building the capacity of the organisations to

continue to raise awareness and access resources.

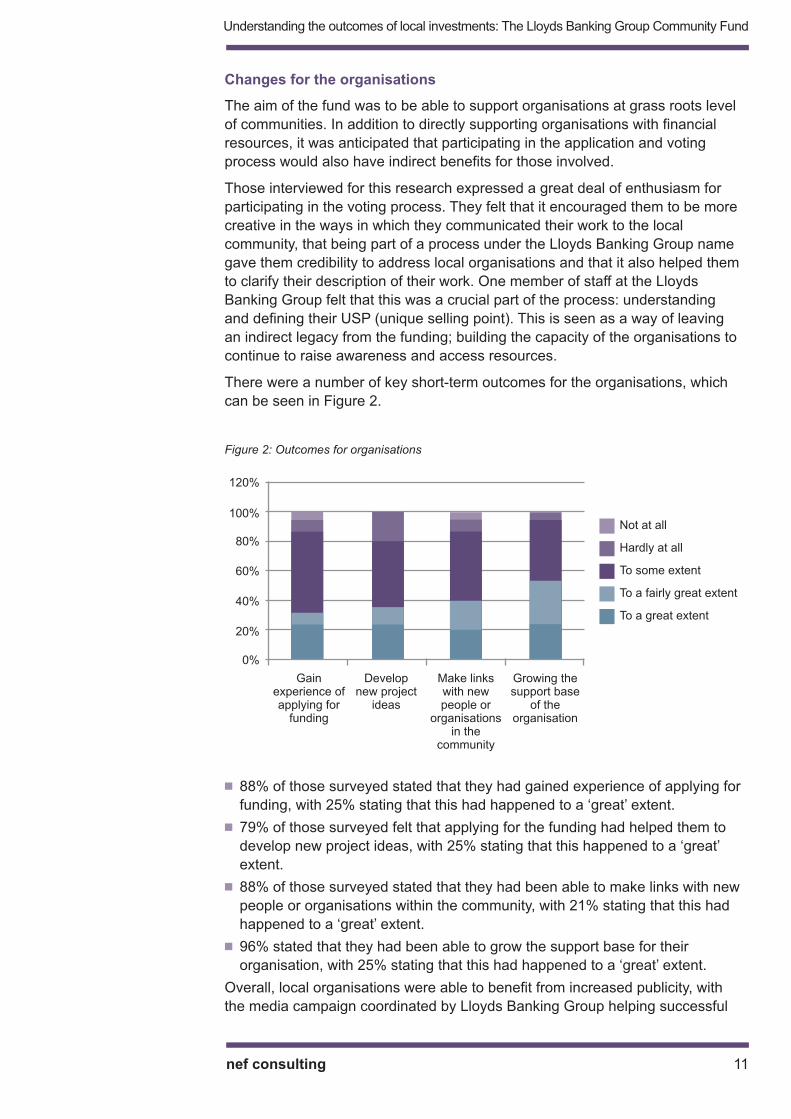

There were a number of key short-term outcomes for the organisations, which

can be seen in Figure 2.

Figure 2: Outcomes for organisations

� 88% of those surveyed stated that they had gained experience of applying for

funding, with 25% stating that this had happened to a ‘great’ extent.

� 79% of those surveyed felt that applying for the funding had helped them to

develop new project ideas, with 25% stating that this happened to a ‘great’

extent.

� 88% of those surveyed stated that they had been able to make links with new

people or organisations within the community, with 21% stating that this had

happened to a ‘great’ extent.

� 96% stated that they had been able to grow the support base for their

organisation, with 25% stating that this had happened to a ‘great’ extent.

Overall, local organisations were able to benefit from increased publicity, with

the media campaign coordinated by Lloyds Banking Group helping successful

120%

100%

80%

60%

40%

20%

0%

Gainexperience ofapplying for

funding

Developnew project

ideas

Make linkswith newpeople or

organisationsin the

community

Growing thesupport base

of theorganisation

Not at all

Hardly at all

To some extent

To a fairly great extent

To a great extent

organisations to further raise their profile within the local press. Organisations

were able to access funding which helped them to deliver their activities, and in

a number of cases, free up resources from fundraising to deliver activities.

Changes for the local area

In addition to the direct benefits of investments for the organisations and those

supported, there are wider benefits to the local area. Those consulted as part of

the research had varying definitions of their community, and therefore the

effects will vary from place to place, dependent on the size and makeup of the

perceived community, and level of interaction with the organisation. The results

nef consulting 12

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Case study: Calderdale SmartMove

Calderdale SmartMove is a registered charity that assists homeless and

vulnerably housed people to find accommodation in Calderdale. They support

individuals to find safe and secure accommodation using a support worker

and mentor model. They work with people for up to 15 months.

The people they work with tend to have a number of challenges they need to

overcome to make the transition to stable accommodation. These include

debt, drug misuse, domestic violence and learning difficulties. Calderdale

SmartMove helps them to find social housing or private rented

accommodation, supporting them to navigate the housing and support

systems.

For those moving into a new property, they often have nothing to take with

them. Calderdale SmartMove has found that for many, moving into a

completely empty property and with no personal possessions can cause

negative outcomes, such as depression.

The Lloyds Banking Group Community Fund was used to provide starter

packs for around 200 people moving into new accommodation. The packs

included food and hygiene products to help settling into a new home. As one

staff member stated “It’s not much but at least it’s something.” The idea is to

provide people with something tangible to start to build their home with.

People they support are “delighted” that they can help to find a property, the

home packs are the “icing on the cake”.

Calderdale SmartMove has been involved in a similar type of fundraising

initiative before, when they were nominated for the local authority Charity of

The Year award. The Finance Director of Calderdale SmartMove felt that both

campaigns involved a significant amount of work. Through local campaigning

they won 3500 votes which involved marketing and gaining media exposure.

He felt this experience gave them the impetus to share their message with

new people. An example of this was giving a talk at the team meeting at a

local call centre. Approximately 500 people attended the meeting and were

able to find out more about what they do. Since this meeting, the staff at the

call centre have continued to offer donations from their fundraising activities.

Almost more important to Calderdale SmartMove than the money was that

they could use the Lloyds Banking Group name. They were able to say they

were a community champion for Lloyds in Yorkshire and Humberside, which

helped raise their credibility with funders.

nef consulting 13

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

presented below are the perceptions of the representatives of funded

organisations.

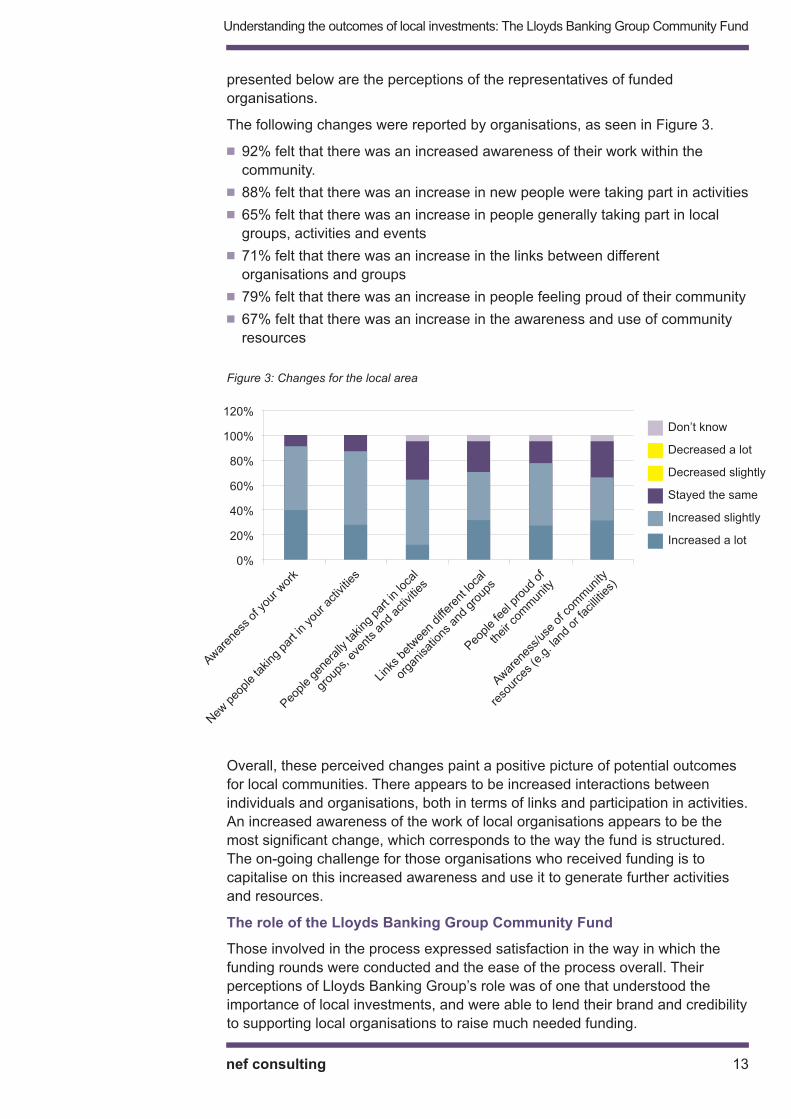

The following changes were reported by organisations, as seen in Figure 3.

� 92% felt that there was an increased awareness of their work within the

community.

� 88% felt that there was an increase in new people were taking part in activities

� 65% felt that there was an increase in people generally taking part in local

groups, activities and events

� 71% felt that there was an increase in the links between different

organisations and groups

� 79% felt that there was an increase in people feeling proud of their community

� 67% felt that there was an increase in the awareness and use of community

resources

Figure 3: Changes for the local area

Overall, these perceived changes paint a positive picture of potential outcomes

for local communities. There appears to be increased interactions between

individuals and organisations, both in terms of links and participation in activities.

An increased awareness of the work of local organisations appears to be the

most significant change, which corresponds to the way the fund is structured.

The on-going challenge for those organisations who received funding is to

capitalise on this increased awareness and use it to generate further activities

and resources.

The role of the Lloyds Banking Group Community Fund

Those involved in the process expressed satisfaction in the way in which the

funding rounds were conducted and the ease of the process overall. Their

perceptions of Lloyds Banking Group’s role was of one that understood the

importance of local investments, and were able to lend their brand and credibility

to supporting local organisations to raise much needed funding.

Decreased a lot

Don’t know

120%

100%

80%

60%

40%

20%

0%

Decreased slightly

Stayed the same

Increased slightly

Increased a lot

Awar

enes

s of

you

r wor

k

New

peo

ple

taking

par

t in

your

activities

Peo

ple

gene

rally

taking

par

t in

loca

l

grou

ps, e

vent

s an

d ac

tivities

Link

s be

twee

n diffe

rent

loca

l

orga

nisa

tions

and

gro

ups

Peo

ple

feel p

roud

of

their c

omm

unity

Awar

enes

s/us

e of

com

mun

ity

reso

urce

s (e

.g. lan

d or

facillitie

s)

57%

4%4% 9%

26%

nef consulting 14

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

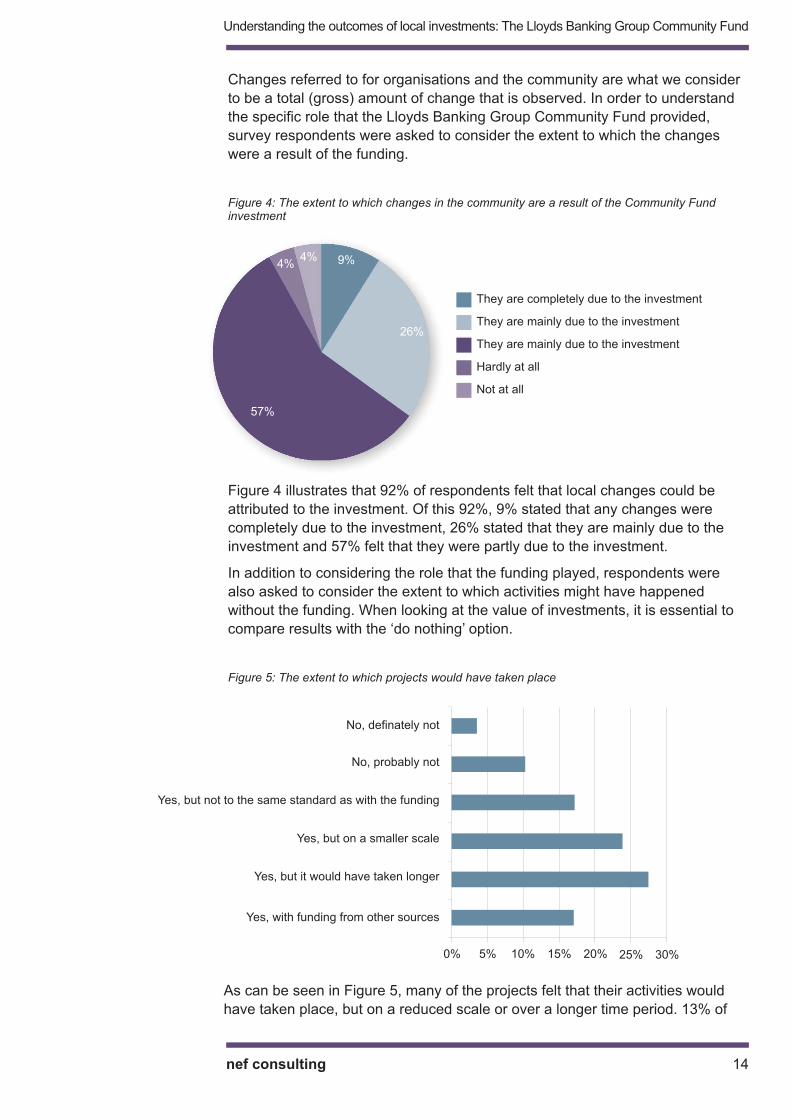

Changes referred to for organisations and the community are what we consider

to be a total (gross) amount of change that is observed. In order to understand

the specific role that the Lloyds Banking Group Community Fund provided,

survey respondents were asked to consider the extent to which the changes

were a result of the funding.

Figure 4: The extent to which changes in the community are a result of the Community Fundinvestment

Figure 4 illustrates that 92% of respondents felt that local changes could be

attributed to the investment. Of this 92%, 9% stated that any changes were

completely due to the investment, 26% stated that they are mainly due to the

investment and 57% felt that they were partly due to the investment.

In addition to considering the role that the funding played, respondents were

also asked to consider the extent to which activities might have happened

without the funding. When looking at the value of investments, it is essential to

compare results with the ‘do nothing’ option.

Figure 5: The extent to which projects would have taken place

As can be seen in Figure 5, many of the projects felt that their activities would

have taken place, but on a reduced scale or over a longer time period. 13% of

30%25%20%15%10%5%0%

No, definately not

No, probably not

Yes, but not to the same standard as with the funding

Yes, but on a smaller scale

Yes, but it would have taken longer

Yes, with funding from other sources

They are completely due to the investment

They are mainly due to the investment

They are mainly due to the investment

Hardly at all

Not at all

nef consulting 15

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Summary of findings

The Lloyds Banking Group Community Fund offered some exciting opportunities

to local organisations in 2012. Feedback from all organisations that were funded

was positive; they appreciated the ease of the process, the support and media

opportunities. Organisations that were successful in receiving the funding

worked extremely hard to generate awareness in their local communities about

their work, developing clear messages and new approaches to increasing their

support base.

The funding has supported local activity which people care about, and in many

cases has been invested in projects which will sustain beyond the duration of the

Olympics. The fund has helped to bring people together and in many cases has

helped to bring forward activity which may have struggled to find funding. The

challenge for the Lloyds Banking Group Community Fund team will be to gather

longitudinal data from the one year evaluation which helps them to understand

longer term gains from the funding. The above stories and survey results show

that the initial pilot of this programme has been successful in testing an

approach to funding, engaging and supporting community organisations and

growing awareness about their work.

Case study: DASH

DASH is a local charity in Ceredigion which provides respite weekends for

disabled children in their county. They are commissioned by the local

authority to deliver 10 of these weekends per year, and each year they seek

additional funding for a further two weekends.

The children and young people that attend the weekends have high support

needs and require 24 hour care from staff. The breaks are intended to benefit

children and young people, giving them a chance to develop their confidence,

independence and social skills. It also provides a break for carers and other

members of the family.

The funding provided by the Lloyds Banking Group Community Fund

provided two weekends away; six children attended each weekend.

Previously the organisation had raised funds from multiple sources, which

was time consuming for the staff. Fundraising has become harder in recent

years, with increased competition for resources.

The fundraiser found the voting to be a very interesting process. They had to

think outside the box and it resulted in a successful team effort; bringing

together all members at the Olympic event in Aberystwth. They felt that the

collective approach helped them to be successful; they had to “get out and

about” and make a lot of effort.

respondents felt that their project would not have taken place. When analysing

this information alongside the qualitative interview feedback, it is clear that

although many organisations feel that their activities may have happened

anyway, the speed at which they were able to obtain funding helped to reduce

the need to spend staff time sourcing funding. In addition, the added value of the

marketing and press coverage may create more sustainable outcomes than if

resources had been accessed through other means.

3. Looking forward to 2013 investments: what could the

Lloyds Banking Community Fund achieve this year?

In 2013, the fund has expanded to cover 400 communities across the UK.

Following from the areas and projects in 2012, each area is now more clearly

defined along local authority boundaries. The fund has also expanded its remit,

moving from a youth focus to all areas of the community.

The nominations and shortlist activities have been completed and the public

vote will commence in September 2013. From the applications which have been

shortlisted, we know:

� 95% of organisations are within five miles of their local Lloyds Banking Group

branch

� 79% of projects aim to support young people

� 57% of projects aim to support families

� 46% of projects aim to support those with special needs

� 36% of organisations want to grow and existing project; 21% want to develop

a new project

� 32% of projects offer a way of bringing people together; 18% offer skills and

training; 18% want to offer a community event

Lloyds Banking Group Community Fund: staff aspirations

The aspirations of Lloyds Banking Group colleagues for this year’s fund ranged

depending on their role in the organisation. Their responses fell into four broad

areas:

� The opportunity to help more people in local areas: the scaling up of the

Community Fund increases the potential numbers of people supported,

opening up the funding to around 1600 organisations. A number of members

of staff felt that this was a great opportunity to achieve small incremental

changes across a large group of people, which cumulatively may result in a

wider impact.

� Supporting groups to communicate their work locally: staff held high

aspirations for not only supporting organisations to increase their

communications, but also being able to share best practice in how to do this.

There was a keen emphasis on building the capacity of organisations to raise

their profile locally.

� Creating a positive link between customers and the bank. The Community

Fund is one of a number of activities that Lloyds Banking Group uses to

engage their customers and communities outside of the commercial services

it delivers. The Community Fund offers a way of creating a positive local

dialogue with customers and staff expressed an interest in maximising this

opportunity.

� Understanding the tangible changes from the successful projects. Staff felt

that in 2012 the investments resulted in exciting and positive projects, which

helped local people. There is a desire in the 2013 funding to gain a greater

appreciation of what this means in the longer term, something which will be

questioned in subsequent evaluation activities.

nef consulting 16

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Community investment in focus: what can be achieved with small

investments?

In considering community investment, we first make the distinction between

individual and community outcomes. An individual outcome is something that

changes in the life of an individual, which is often intended to help to improve

their life. This change can be achieved by accessing one to one support,

participating in group activities or receiving goods. Community outcomes are

broader and cover the changes experienced by a number of people, usually

intended to improve their lives. Achieving community outcomes is harder, as

people individually may need different support to achieve the change, and there

may be structural barriers in place which stop the community collectively to

move forward.

Collectively, lots of individual changes can result in a large total amount of

change. This is, however, most often evidenced and expressed at the individual

level.

We make this distinction to help understand the context in which a programme

like the Lloyds Banking Group Community Fund can offer support, and the way

in which it chooses to invest its funds. The remainder of this chapter looks at

current thinking on how to maximise the benefits of small investments, and

understand the change that results.

Small grants, big difference: making an impact with small investments

As Brick et al. have highlighted, “[s]mall sums, carefully targeted, have achieved

tangible change.” Much of the literature argues that small grants, especially

when unrestricted, can cover costs that charities might otherwise struggle to

pay.1 The capacity-building2 of staff, volunteers and even beneficiaries is one

such activity, which funders often overlook, but which nevertheless can increase

a charity’s ability to improve its efficiency, manage its resources better,

strengthen its resilience and achieve success in its goals.3 Using findings from a

Lloyds Banking Group TSB Foundation Scotland evaluation, Reid and Gibb

(2004) find that funding capacity building for small third sector organisations can

empower the latter to best achieve its goals, or enable an organisation to take

full advantage of opportunities for growth and development, whilst maintaining

its sustainability and autonomy.4 Whilst small grants can’t be considered a

replacement for long-term funding, there is no doubt that they can make a large

impact when used to build capacity.

Small grants to small charities have been proven by researchers, time and time

again, to work effectively as a “seed fund” to draw in further donations.5 Brick,

Kail, Järvinen and Fiennes (2009: 4) find that smaller grants hold huge potential

for attracting other funders, whilst, through a controlled experiment, List and

Lucking-Reiley (2002: 218) found that the use of seed-funding by a charity can,

in the case of public donations, “sharply increas[e] the participation rate of

donors and the average gift size received from participating donors.”

Similarly, according to The Funding Network’s (TFN) 10th anniversary impact

report (2012: 3), 62% of its funded projects report that initial TFN funding has

enabled them to leverage additional funding from other sources. A charity

funded by TFN explains, “TFN gave us the funds to grow, to believe in what we

were doing and to achieve enough to impress other donors.”6 Similarly, the

nef consulting 17

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

voting approach used by Lloyds Banking Group can significantly raise the profile

of grantees, increasing their credibility in the eyes of other potential funders and

awarding them a competitive edge.

As well as drawing in additional money, seed funding has other positive benefits

for small charities. It often acts as a source for new relationships (business

partners, other charities, corporate contacts), new trustees and volunteers, and

the securing of publicity and awards.7 It is also used to pilot new ideas, which

can then be scaled-up with other funding should they prove feasible.8

As Ludlow (2010) highlights, small grants can be harnessed to buy assets.

Small grants can be used by charities to purchase, for example, equipment

without which they would not be able to deliver the service or the change they

need. Small capital investments can therefore build the capacity of a charity to

achieve its mission in the longer term.9

Small grants can be harnessed to leverage a huge impact for individuals. Small

grants to individuals and families are seen by many donors as “one of the most

direct and effective ways of making a real difference in people’s lives.”10

Whereas there is little in the literature to support the idea that helping a single

individual can create structural-level change or an impact across a whole

community,11 there is no doubt that using small grants to create change for one

person can be situated on a longer pathway to change for community-level or

wider outcomes.

Large national and international charities provide further examples of how small

investments to make significant changes for individuals can be situated

amongst a programme of broader activities to achieve structural change. Plan

UK allows donors to contribute small amounts of funding to sponsor specific

children. Individual changes for these children are linked to wider policy,

advocacy and campaigning efforts, which – when combined – can feasibly aim

to create structural change.12 The key to ensuring that an investment in a single

individual has a wider societal impact is to situate that change along a pathway,

which can be articulated through a Theory of Change.

As the Centre for Theory of Change asserts, the Theory of Change approach

hinges upon defining all of the necessary conditions for bringing about a given

long-term goal.13 nef argues that the Theory of Change approach allows its

users an “intimate understanding of how an intervention creates an impact on

the lives of those affected”.14 By using such an approach, funded organisations

can be supported to understand how they achieve their goals. This may require

additional support to funded organisations, but would increase the information

available to Lloyds Banking Group as to how the investments create change.

Small levels of investment at different stages of the change process, such as

investing in training to build the capacity of community volunteers, can

contribute to higher-level impacts.15 The same can be said for an Assets-Based

approach, in which people and communities (and their respective human and

material assets) form the basis of a plan for change. Such an approach involves

the co-production of services, in which service-users are seen as assets in

themselves, and professionals and service-users work together to achieve their

common goal. As nef and NESTA highlight, “[w]here activities are co-produced

in this way, both services and neighbourhoods become far more effective

agents of change.”16

nef consulting 18

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

Corporate giving in context

The research findings above show that the key to creating lasting change is to

invest in activities which help to build the capacity of organisations to generate

further income and to understand how investing in organisations that create

individual change can be scaled up to achieve wider changes. In addition to

considering the ways in which small grants can be catalysts, we also consider

how corporate donors can maximise the links that they make between their core

business and their community activities.

Lloyds Banking Group has a number of community programmes, including the

Community Fund, which link their branches, staff and local communities. The

staff in branches are the Group’s strongest link to local communities, and this

programme is an example of how colleagues’ skills and local knowledge can be

used to better support their communities. At nef consulting, we see this

programme as part of a journey for corporate organisations like Lloyds Banking

Group; to consider how they can constantly improve their knowledge of, and

links to, local communities, bridging any gaps between specific community

activities and the products and services they offer to customers in those

communities.

The Lloyds Banking Group Community Fund has so far harnessed some of the

assets that are available to maximise the link between the organisation and the

community: the use of colleagues to recommend groups to be funded and

support the administration of the application process; local campaigns

supported by the central Community Fund team; local organisations and their

support networks using their skills and connections to raise awareness about

local causes; and a collective celebration of those who are successful.

In line with the aspirations of Lloyds Banking Group colleagues, we would echo

a desire to better understand how the engagement between the bank, its

customers and local organisations is working in practice, building on the links

established through the Community Fund and other activities. Understanding

how the 2013 funding creates change could help Lloyds Banking Group and its

local branches to better understand the needs of local communities and develop

and diversity the ways in which local branches can better support their

communities. This may in turn lead to a better business offer at a local level.

Understanding the impact of 2013 investments

Researchers and practitioners agree that measuring and demonstrating impact

is a key stage of the grant-making process. It can strengthen a funder’s future

programme-planning efforts, help to showcase the achievements of a

programme and makes a funder more transparent in the public’s eyes. The

nature of the Lloyds Banking Group Community Fund means that it invests

according to the priorities defined by local communities. Understanding the

common and collective impact of the investments can therefore be challenging.

There are three key areas of measurement which need to be undertaken to

effectively articulate the impact of an investment: the change that happens; the

attribution (how much credit you can take for any change); and an appreciation

of what might have happened anyway (the deadweight).

The Community Fund team could use the findings from this research and on-

nef consulting 19

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

going evaluation activities to map out common outcomes which may be

experienced by most, if not all projects, which would help to collect and collate

more in-depth data on the changes that are experienced at a local level. Any

outcomes that are selected should be verified with representatives of the

projects, to check that they are commonly understood and expressed in a way

which is meaningful for them. These outcomes could be measured through the

post-project evaluation forms, and consistent data could be gathered at the

national level. It’s important to stress that this data needs to go beyond what

has been gathered to date, moving from “what happened?” to “what changed?”

Any updates to evaluation processes should also include gathering data on

attribution (the role of the fund) and deadweight (what might have happened

anyway). This needs to be reported alongside outcome findings, to ensure an

accurate portrayal of impact is made.

The upcoming voting and awards rounds offer Lloyds Banking Group the

opportunity to put in place monitoring and evaluation requirements that can help

to capture some of this impact, in a way which is proportional to the amount

funded. This will help with any future review of the success of the funding.

Conclusions from the research

Overall, the aspirations for this year’s funding appear to build on what was

observed through the projects funded in 2012. There is a desire to fund

activities which grow local organisations and create better ties between the

Lloyds Banking Group and the local communities it serves. There is also a

desire to better understand and evidence how change happens, so that the

growth of the fund can be effectively evaluated. There are challenges ahead for

consistently measuring the impact of the projects, but there is a keen desire

within Lloyds Banking Group to put this in place and fully understand whether

the Community Fund represents a good business decision to help link the bank

and its local communities.

The Lloyds Banking Group is not alone in the banking sector for offering support

to communities. A number of other banking institutions offer similar local

investments to charities, reflecting the priorities of customers and staff. These

include the Nationwide Big Local Scheme, Santander Community Plus and the

Cooperative Membership Community Fund. However, this piece of research is a

starting point for Lloyds Banking Group to better understand how its

investments are creating change for communities, long after the donations are

made. Lloyds Banking Group is moving past the premise that the act of giving

alone can create change, and is using the data it collects from projects and after

projects have finished, to start to scrutinise the impact that it is able to create

through the programme. By taking the step of publicising an assessment of how

it performed in 2012, Lloyds Banking Group has set a benchmark of the

changes that the programme made through its pilot phase, and can look forward

to seeing if those changes can be replicated as the programme is rolled out to

further communities. It also offers the Community Fund a way of seeking

feedback on how it is measuring its impact, which can be used to inform future

measurements of success of the 2013 funding.

Our final thoughts rest upon how the potential success of this fund can be used

more widely within the Lloyds Banking Group to understand how community

nef consulting 20

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

activities can bridge the link between local branches, customers and community

organisations. A greater understanding of this relationship and its potential to

deliver local impact could help to align core business activities more closely to

communities’ needs, supporting them better through all of the work that Lloyds

Banking Group does. The analysis of this year’s performance and evaluation

activities should be used to inform the measurement of impact of the 2013

investments.

We look forward to seeing the results of the upcoming funding rounds, and the

resulting changes for local communities in the coming year.

nef consulting 21

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

1 B. Brick, A. Kail, J. Järvinen and T. Fiennes (2009), Lessons from funders

and charities, p.4.

2 Capacity-building here is understood as activities that improve charity

effectiveness. The Foundation Centre provides a bibliography of

resources to evidence the impact of capacity-building activities on its

website, available at

http://foundationcenter.org/getstarted/topical/capacity.html

3 A. Sherman (no date available), “Multiplying Effective Charity”, American

Outlook, available at http://www.americanoutlook.org/multiplying-effective-

charity.html.

4 M. Reid and K. Gibb, ‘Capacity building’ in the third sector and the use ofindependent consultants: evidence from Scotland, A paper presented at

the International Society for Third Sector Research 6th International

Conference, Ryerson University, Toronto, July 11-14 2004.

5 See J. List and D. Lucking-Reiley (2002), “The effects of seed money and

refunds on charitable giving: experimental evidence from a university

capital campaign”, The Journal of Political Economy, 110:1. The Funding

Network (2012), 10th Anniversary Impact Report, B. Brick, A. Kail, J.

Järvinen and T. Fiennes (2009), op.cit., and J. Andreoni, A. Payne and S.

Smith, (2013), Do grants to charities crowd out their income? Evidencefrom the UK, Bristol: The Centre for Market and Public Organisation.

6 The Funding Network (2012), op.cit., p.15.

7 The Funding Network (2012), op.cit., p.10

8 M. Hulme (no date), National Council for Voluntary Organisations (NCVO),

Making a Big Difference with Small Grants: Paper for the VSSNConference, p.1. B. Brick, A. Kail, J. Järvinen and T. Fiennes (2009),

op.cit, pp.11-12. J. Andreoni, A. Payne and S. Smith (2013), op.cit, p.3.

9 Joe Ludlow (2010), Capitalising the Voluntary and Community Sector: AReview, London: NCVO Funding Commission, pp.1-32.

10 The Silver Lady Fund, quote from case study of individual and family

support grants issued by the Fund, available at

http://www.silverladyfund.org/activities.htm.

11 As Tris Lumley notes (“Why charities must use impact to understand

beneficiaries”, The Guardian, 18 June 2013, available at

http://www.theguardian.com/voluntary-sector-

network/2013/jun/18/charities-impact-measurement), charities have been

criticized for claiming to have achieved high-impact social change through

activities that are solely focused on individuals.

12 This example is based on Plan UK’s “Because I am a Girl” Campaign. For

more information visit http://www.plan-uk.org/what-we-

do/campaigns/because-i-am-a-girl/.

13 The Centre for Theory of Change, “How Does Theory of Change Work?”,

available at http://www.theoryofchange.org/what-is-theory-of-change/how-

does-theory-of-change-work/#1.

14 New Economics Foundation, “Creating a Theory of Change Masterclass”,

available at http://www.nef-consulting.co.uk/sroicfx/sroi-masterclass/sroi-

theory-of-change-masterclass/.

nef consulting 22

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

15 For more on the Assets-Based Approach see Tara O’Leary, Ingrid Burkett

and Kate Braithwaite (2011), Appreciating Assets, Dunfermline: Carnegie

UK Trust, available at http://www.iacdglobal.org/publications-and-

resources/IACD-Publications/appreciating-assets.

16 nef and NESTA (2010), Right Here, Right Now: Taking co-production intothe mainstream, London: NESTA, p.3. See also nef (2008), Co-production: A Manifesto for growing the core economy, London: nef.

nef consulting 23

Understanding the outcomes of local investments: The Lloyds Banking Group Community Fund

nef consulting is a social enterprise founded and owned by the think tank nef

(the new economics foundation) to help public, private and third sector

organisations put its ideas into action. We are recognised experts in Social

Return On Investment (SROI) and well-being measurement. By adapting and

applying nef’s tools to prove and improve true social, economic and

environmental impact, nef consulting’s work places people and the planet at

the heart of organisational decision-making. To find out more about nef

consulting visit www.nef-consulting.co.uk.