TURKISH ENERGY TRANSITION AND CURRENT ...

68

Master in Global Energy Transition and Governance 2018-2019 TURKISH ENERGY TRANSITION AND CURRENT CHALLENGES Author: Cüneyt Taha Özkan Supervisor: Gilles Lepesant Abstract Turkish energy system has experienced a radical reform process starting from the 70’s in line with global trends mainly in developed countries. Turkish energy transition pathway consists of an extensive restructuring of the energy market and this fact led to serious changes in the roles of market actors. The major factors which leads to such a transition are the swiftly growing energy demand and the high rates of dependency on imported energy sources. Turkey has one of the fastest growing energy demand among IEA member states and import dependency ratio is close to 70% in primary energy sources. This paper tries to explain the factors inhibiting or accelerating the energy transition in Turkey while describing Turkish energy market reforms with a particular focus on the electricity market and on the issue of energy efficiency. It tries to explain the historical evolution of Turkish energy market and electricity market liberalization, taking into account the changes of roles of market players and other actors. illustrates the current situation and the evolution of Turkish renewable energy and energy efficiency policies and regulations which give direction to the Turkish clean energy transition process. Turkey has experienced a fast proliferation of renewable energy sources in mainly in electricity production thanks to those policies and regulations.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of TURKISH ENERGY TRANSITION AND CURRENT ...

Master in Global Energy Transition and Governance 2018-2019

TURKISH ENERGY

TRANSITION AND

CURRENT CHALLENGES

Author: Cüneyt Taha Özkan

Supervisor: Gilles Lepesant

Abstract Turkish energy system has experienced a radical reform process starting from the 70’s in line

with global trends mainly in developed countries. Turkish energy transition pathway consists of

an extensive restructuring of the energy market and this fact led to serious changes in the roles

of market actors. The major factors which leads to such a transition are the swiftly growing

energy demand and the high rates of dependency on imported energy sources. Turkey has one

of the fastest growing energy demand among IEA member states and import dependency ratio

is close to 70% in primary energy sources. This paper tries to explain the factors inhibiting or

accelerating the energy transition in Turkey while describing Turkish energy market reforms

with a particular focus on the electricity market and on the issue of energy efficiency. It tries to

explain the historical evolution of Turkish energy market and electricity market liberalization,

taking into account the changes of roles of market players and other actors. illustrates the current

situation and the evolution of Turkish renewable energy and energy efficiency policies and

regulations which give direction to the Turkish clean energy transition process. Turkey has

experienced a fast proliferation of renewable energy sources in mainly in electricity production

thanks to those policies and regulations.

Ek 1: Bursiyer ve Programa Ait Bilgi Formu

Adı-Soyadı Cüneyt Taha Özkan

Sözleşme No. TR2016/DG/04/A1-01/1098

Başvuru Yaptığı Sektör

(Kamu-Üniversite-Özel Sektör) Kamu

Başvuru Esnasında Bağlı Bulunulan Kurum Enerji Piyasaları İşletme A.Ş.

Başvuru Esnasında Bağlı Bulunulan Kurumdaki Unvan

Eğitim ve Araştırma Uzman Yardımcısı

Çalışma Alanı (AB Müktesebat Başlığı) Enerji

Öğrenim Görülen Ülke Fransa

Öğrenim Görülen Şehir Nice

Programın Öğretim Dili İngilizce

Üniversite Centre International de Formation Européenne

Fakülte -

Bölüm -

Program Adı Master in Global Energy Transition and Governance

Programın Başlangıç/Bitiş Tarihleri (PDS belgesindeki tarihler)

15.10.2018 / 26.06.2019

Öğrenim Süresi (ay) 9 months

Tez/Araştırma Çalışmasının Başlığı Türkiye Enerji Dönüşümü ve Mevcut Engeller

Danışmanının Adı/Soyadı Dr. Gilles Lepesant

Danışmanının E-posta Adres/leri [email protected]

NOT: Bu sayfa bilgisayar ortamında doldurulduktan sonra tez/araştırma raporu metnine ilgili sıra ile eklenmelidir.

Annex 1: Scholar and Programme Information Form

Name/Surname Cüneyt Taha Özkan

Contract No. TR2016/DG/04/A1-01/1098

Sector as of the Application Date

(Public Sector-University-Private Sector) Public

Institution as of the Application Date Enerji Piyasaları İşletme A.Ş.

Title as of the Application Date Research and Training Assistant Specialist

Field of Study (i.e. EU Acquis Chapter) Energy

Country of Host Institution France

City of Host Institution Nice

Language of the Programme English

Host Institution Centre International de Formation Européenne

Faculty -

Department -

Name of the Programme Master in Global Energy Transition and Governance

Start/End Dates of the Programme (as in the PDS) 15.10.2018 / 26.06.2019

Duration of the Programme (months) 9 months

Title of the Dissertation/ Research Study The Turkish Energy Transition and Current Challenges

Name of the Advisor Dr. Gilles Lepesant

E-mail/s of the Advisor [email protected]

NOT: Bu sayfa bilgisayar ortamında doldurulduktan sonra tez/araştırma raporu metnine ilgili sıra ile eklenmelidir.

1

Table of Contents

Table of Contents ......................................................................................................... 0

Abbreviations ............................................................................................................... 3

Introduction .................................................................................................................. 5

Chapter 1. Historical Evolution of Turkish Energy Market ......................................... 8

1.1 Market Reforms of 2001 .................................................................................. 12

1.1.1 Energy Market Regulatory Agency (EMRA) ........................................... 12

1.1.2 Unbundling of Activities ........................................................................... 13

1.1.3 Other Reforms ........................................................................................... 14

1.2 2004 Strategy Document .................................................................................. 16

1.3 Balancing & Settlement ................................................................................... 17

1.4 Tariff Structure ................................................................................................. 18

1.5 The new Electricity Market Law of 2013 ........................................................ 20

Chapter 2. Policies and Legislations on Renewable Energy and Energy Efficiency . 23

2.1 2004 Strategy Document .................................................................................. 23

2.2 2009 Strategy Paper ......................................................................................... 24

2.3 2014 National Renewable Energy Action Plan ................................................ 26

2.4 Legislations ...................................................................................................... 29

2.5 2005 Renewables Law ..................................................................................... 32

2.6 Amendments to Renewable Energy Law ......................................................... 33

2.7 Unlicensed Generation ..................................................................................... 36

2.8 Renewable Energy Resource Areas (YEKA) - Auction System for Renewables

.................................................................................................................................... 38

2.9 Other Legislations Promoting Energy Generation from Renewables .............. 40

2

2.10 Energy Efficiency Policies and Regulations .................................................. 40

Chapter 3. PESTLE Factors That Affect the Success of Renewable Energy Policies in

Turkey ............................................................................................................................. 44

3.1 Political ............................................................................................................ 44

3.1.1 The Coal Issue ........................................................................................... 44

3.2 Economic.......................................................................................................... 46

3.2.1 Increasing burden of feed-in tariff ............................................................ 46

3.2.2 Jobs and economic activity ....................................................................... 48

3.3. Social ............................................................................................................... 50

3.4 Technological ................................................................................................... 51

3.4.1 System Integration Challenges of Variable Renewable Energy Sources.. 51

3.5 Legal ................................................................................................................. 51

3.6 Environmental .................................................................................................. 53

Conclusion ................................................................................................................. 56

Bibliography ............................................................................................................... 58

Appendix .................................................................................................................... 60

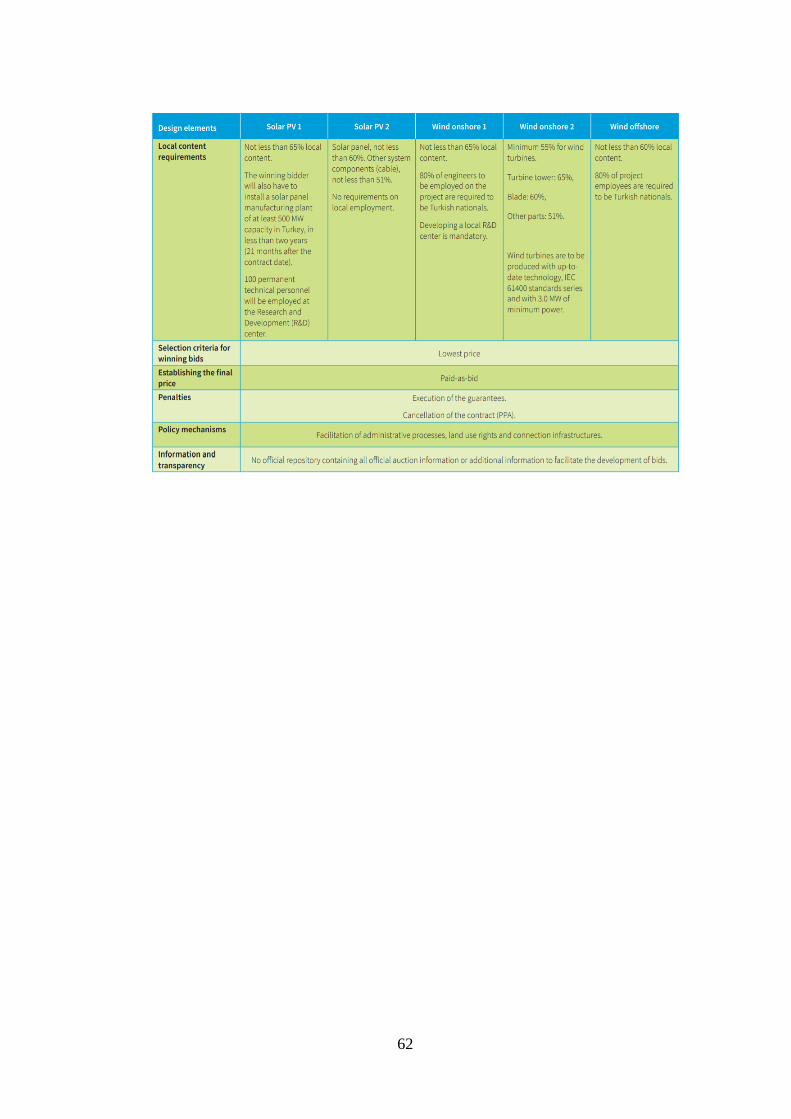

Table 2.3: Status of YEKA auction design elements, as of December 2018 (SHURA,

2018) ........................................................................................................................... 60

3

Abbreviations

BO Build-Operate

BOT Build-Operate-Transfer

BPM Balancing Power Market

DAM Day-Ahead Market

EBRD European Bank for Reconstruction and Development

EIE Electrical Power Resources Survey and Development Administration (under

MENR)

EML Electricity Market Law

EMRA/EPDK Energy Market Regulatory Authority - Enerji Piyasası Düzenleme Kurumu

ETS Emission Trading System

EPİAŞ Turkish Energy Exchange - Enerji Piyasaları İşletme Anonim Şirketi

EU European Union

EÜAŞ Electricity Generation Corporation - Elektrik Üretim Anonim Şirketi

FiT Feed-in Tariff

IEA International Energy Agency

IMF International Monetary Fund

IRENA International Renewable Energy Agency

MBI Market Based Instrument

MCP Market Clearing Price

MENR/ETKB Ministry of Energy and Natural Resources - Enerji ve Tabii Kaynaklar

Bakanlığı

MYTM National Load Dispatch Center - Milli Yük Tevzi Merkezi

NDC/INDC (Intended) Nationally Determined Contributions

4

NETA New Electricity Trading Arrangement

PESTLE Political, Economic, Social, Technological, Legal, Environmental

PMR Partnership for Market Readiness

PMUM Market Financial Settlement Center - Piyasa Mali Uzlaştırma Merkezi

PPA Power Purchase Agreement

PV Photovoltaic

REC Renewable Energy Certificate

REN21 Renewable Energy Policy Network for the 21st Century

RES Renewable Energy Source(s)

TBSR Transitional Balancing and Settlement Regulation

TEAŞ Turkish Electricity Generation and Transmission Company - Türkiye Elektrik

Üretim-İletim Anonim Şirketi

TEDAŞ Turkish Electricity Distribution Company - Türkiye Elektrik Dağıtım Anonim

Şirketi

TEİAŞ Turkish Electricity Generation Corporation - Türkiye Elektrik İletim Anonim

Şirketi

TEK Turkish Electricity Authority

TETAŞ Turkish Electricity Trading and Contracting Corporation - Türkiye Elektrik

Ticaret ve Taahhüt Anonim Şirketi

TOR Transfer of Operating Rights

UNFCCC United Nations Framework Convention on Climate Change

VRE Variable Renewable Energy (Wind and Solar)

YEKA Renewable Energy Resource Areas - Yenilenebilir Enerji Kaynak Alanları

YEKDEM Renewable Energy Resources Support Mechanism - Yenilenebilir Enerji

Kaynakları Destekleme Mekanizması

ABSTRACT

Turkish energy system has experienced a radical reform process starting from the 70’s in line

with global trends mainly in developed countries. Turkish energy transition pathway consists

of an extensive restructuring of the energy market and this fact led to serious changes in the

roles of market actors. The major factors which leads to such a transition are the swiftly

growing energy demand and the high rates of dependency on imported energy sources.

Turkey has one of the fastest growing energy demand among IEA member states and import

dependency ratio is close to 70% in primary energy sources. This paper tries to explain the

factors inhibiting or accelerating the energy transition in Turkey while describing Turkish

energy market reforms with a particular focus on the electricity market and on the issue of

energy efficiency. It tries to explain the historical evolution of Turkish energy market and

electricity market liberalization, taking into account the changes of roles of market players

and other actors, illustrates the current situation and the evolution of Turkish renewable

energy and energy efficiency policies and regulations which give direction to the Turkish

clean energy transition process. Turkey has experienced a fast proliferation of renewable

energy sources in mainly in electricity production thanks to those policies and regulations.

ÖZET

Türk enerji sistemi, 70'lerden başlayarak, özellikle gelişmiş ülkelerdeki küresel eğilimler

doğrultusunda radikal bir reform süreci yaşamıştır. Türkiye'nin enerji geçiş yolu, enerji

piyasasının kapsamlı bir şekilde yeniden yapılandırılmasından oluşmaktadır ve bu durum

piyasa aktörlerinin rollerinde ciddi değişikliklere yol açmıştır. Böyle bir geçişe yol açan

temel faktörler, hızla büyüyen enerji talebi ve ithal enerji kaynaklarına yüksek bağımlılık

oranlarıdır. Türkiye, IEA üyesi ülkeler arasında en hızlı büyüyen enerji talebinden birine

sahiptir ve birincil enerji kaynaklarında ithalat bağımlılığı oranı% 70'e yakındır. Bu çalışma,

Türkiye enerji piyasası reformlarını özellikle elektrik piyasasına ve enerji verimliliği

konusuna odaklanarak açıklarken, Türkiye'de enerji geçişini engelleyen veya hızlandıran

faktörleri açıklamaya çalışmaktadır. Piyasa oyuncularının ve diğer aktörlerin rollerindeki

değişiklikleri dikkate alarak, Türkiye enerji piyasasının ve elektrik piyasasının

serbestleştirilmesinin tarihsel gelişimini açıklamaya çalışmaktadır. Türkiye'nin temiz enerji

geçiş sürecine yön veren, Türkiye'nin yenilenebilir enerji ve enerji verimliliği politika ve

düzenlemelerinin mevcut durumunu ve gelişimini göstermektedir. Türkiye, bu politikalar ve

düzenlemeler sayesinde, esas olarak elektrik üretiminde yenilenebilir enerji kaynaklarının

hızla yayılmasını sağlamıştır.

5

Introduction

“Through a variety of interlinked measures, Turkey’s energy reforms have achieved

energy security for a fast-growing economy with rapidly increasing energy needs. These

measures include legislation regarding electricity, gas, renewable energy, and energy

efficiency; the establishment of an energy sector regulatory authority; energy price

reform; the creation of a functional electricity market and large-scale introduction of

natural gas; the restructuring of state-owned energy enterprises; and large-scale private

sector participation through privatization and new investment. As a result, (a) an

electricity market with over 800 participants has been developed, (b) from 2001 to 2014

over 30,000 megawatts (MW) of market-based, private-sector power generation capacity

was commissioned; and (c) investors took over the entire power distribution system

between 2008 and 2013.” (Dilli & Nyman, 2015)

“The Turkish energy sector reforms should be studied within the context of global

restructuring and energy market trends. Energy industry is global with increasing

interconnections of electricity and pipeline networks, increased trade of oil, products, and

natural gas (both in liquefied form as LNG and via pipelines); climate change is another

factor that brings countries together to focus on emissions from the energy industry.

Turkey is, in some ways, a leader and, in many other ways, a follower of sector trends.

As a country that is heavily dependent on energy imports but one that is also playing an

increasingly important role as a conduit between resource-rich regions of the Caspian and

Middle East and consumers in Europe and elsewhere, Turkey learned from the

experiences of others as the country restructured its energy sectors but also has a lot to

offer in lessons learned.” (Atiyas, Çetin, & Gülen, 2012)

As the quote above explains to some extent, Turkish energy system has experienced a

radical reform process starting from the 70’s in line with global trends mainly in

developed countries. Turkish energy transition pathway consists of an extensive

restructuring of the energy market and this fact led to serious changes in the roles of

market actors. The first step towards a modern Turkish energy market structure was the

market liberalization, which is followed by a transition from a fossil-based energy sources

to a system in which renewable energy sources constitutes a significant share in total

6

energy consumption of the country thanks to progressive energy policies and renewable

energy support mechanisms.

The major factors which leads to such a transition are the swiftly growing energy

demand and the high rates of dependency on imported energy sources. Turkey has one of

the fastest growing energy demand among IEA member states and import dependency

ratio is close to 70% in primary energy sources. “To meet this growing demand while

dealing with import dependency, Turkey decided to transform its energy markets and

started implementing major market reforms. The main objectives were to establish

financially viable, stable, transparent, and competitive markets under independent

regulation to ensure reliable and affordable energy supply to consumers in an

environmentally friendly manner. These objectives are based on several laws and

covering most aspects of the relevant European Union (EU) acquis. According to the

EU’s Turkey 2018 Progress Report “Turkey has continued to align with the EU acquis.

As regards the internal energy market, good progress was made on the electricity market

and good progress can be reported on renewable energy and energy efficiency.”

(Bayraktar, 2018)

This paper tries to explain the factors inhibiting or accelerating the energy transition

in Turkey while describing Turkish energy market reforms with a particular focus on the

electricity market and on the issue of energy efficiency. Although there are various

definitions of the term energy transition, it is defined as an irreversible and persistent

structural change in the energy system for the purpose of this study. Turkish energy

transition is examined in two dimensions; first the changes in electricity market structure

and second, the renewable energy and energy efficiency policies and regulations which

substantially reformed the energy system of the country.

The first chapter tries to explain the historical evolution of Turkish energy market and

electricity market liberalization, taking into account the changes of roles of market

players and other actors. It is not possible to understand Turkish energy transition

pathway without learning how the energy system evolved over time and which actors

took part in the transition.

The second chapter illustrates the current situation and the evolution of Turkish

renewable energy and energy efficiency policies and regulations which give direction to

7

the Turkish clean energy transition process. Turkey has experienced a fast proliferation

of renewable energy sources in mainly in electricity production thanks to those policies

and regulations.

However, future success of this transition depends on various factors. To be able to

map those factors that inhibit or accelerate the transition, PESTLE analysis method is

utilized in the third chapter. The PESTLE analysis is a useful and comprehensive tool to

illustrate political, economic, social, technological, legal and environmental factors that

may alter the future success of the energy transition in a country.

8

Chapter 1. Historical Evolution of Turkish Energy

Market

In the beginning of 1960’s, after the establishment of State Planning Organization,

five-year development plans are prepared for the period between 1963-67 and 1967-71.

It was determined in the first five-year development plan (1963-1967) and the second

five-year development plan (1967-1971) that the whole electricity generation,

distribution, transmission and trading activities would be under public authority control.

In accordance with those plans, national electricity monopoly company, TEK (Türkiye

Elektrik Kurumu - Turkish Electricity Authority) was established in 1970, with a

monopoly over all activities carried out in the electricity market. Ironically, in Turkish

language, the word “tek” can be translated into English as “only one, single”. The

establishment of TEK as a state-owned public company created the vertically integrated

structure in the Turkish electricity market. (Çetintaş & Bicil, 2015)

“Until the 1970s the system was fragmented. Except for some regional networks, the

transmission and distribution systems were not interconnected; instead they were owned

and operated by different public administrations, and all electrification programs were

carried by different public entities. Municipalities and private concessionary companies

had their own rights and responsibilities with respect to electricity generation,

transmission, distribution, and sales. Although there were several public organizations

dealing with electricity generation, transmission, and distribution, there was no central

planning.” (Dilli & Nyman, 2015)

There were several efforts to liberalize the energy market and to attract private capital

in 1980’s and 1990’s. It was partly a result of the transformation of the whole economy

from import substitution policy regime to the export-oriented and market-oriented

regime. Import substitution policy regime can be summarized as the heavy state

involvement in various economic activities, especially those which are considered of

strategic importance, such as energy and telecommunications. Another important driver

for these liberalization efforts was the need of huge investments to meet growing energy

demand. A prominent scholar in the field of energy economics in Turkey explained this

situation as the following: “In addition, there was a strong public finance reason for

9

privatization: throughout the 1990s Turkey experienced high public deficits and mounting

public debt. Forecasting high growth in electricity demand, and high investment

requirements to build the necessary generation capacity, Turkish governments wanted to

reduce the burden on the public budget by attracting private investment to the industry.”

(Atiyas et al., 2012)

To be able to attract private investments, three types of contracts between private

actors and the government were introduced: BO (Build-Operate), BOT (Build-Operate-

Transfer) and TOR (Transfer of Operating Rights). “In the 1980s and 1990s, attempts to

engage the private sector took the form of designing investment schemes such as BOT,

BO, and transfer of operating rights (TOR) contracts. The first law that established a legal

framework for private sector participation in the electricity industry was enacted in 1984

(Law No. 3096). This law introduced two types of contracts: BOT contracts for new

generation facilities and TOR for existing generation and distribution facilities. A BOT

was a concession through which a company would build and operate a generation plant

for 99 years (later reduced to 49 years) and then transfer the plant to the state at no cost.

A TOR was a lease-like arrangement under which the private company would operate

and, where necessary, rehabilitate a government-owned facility for a specified period of

time. The attractiveness of the BOT projects was enhanced in 1994 through Law No.

3996, which provided tax exemptions and authorized the treasury to grant guarantees. In

1997, the BO model was introduced through Law No. 4283. Investments under the BO

model were also eligible for treasury guarantees.” (Atiyas et al., 2012)

“Under the BOT model, companies were allowed to build and operate power plants,

selling their generation to the public utility (TEK and later TEAŞ and TEDAŞ) through a

combination of long-term power purchase agreements (PPAs) and “assignment” or

concession contracts between the Ministry of Energy and Natural Resources (MENR) and

the company. At the end of each contract, the plant was transferred to public ownership.

The terms and PPA price were determined in the main contract and TEAŞ had to sign the

PPA according to the main contract.” (Dilli & Nyman, 2015)

“As a result of BOT model implementation, 24 power plants were commissioned

between 1984 and 2001: 18 hydro, 2 wind, and 4 natural gas Combined Cycle Gas

Turbine. As shown in Figure 1.1, in 1994 BOT installed power was only 35 MW; most

10

of these plants were contracted and commissioned after 1994; and the total installed

power of these BOT plants reached 2,450 MW. Compared with the country’s energy

needs, as well as the government’s continuous efforts and ambitious expectations, this

outcome cannot be considered as satisfactory.” (Dilli & Nyman, 2015)

Figure 1.1 - Development of the BOT Plant Capacity 1984-2005

There were some structural problems regarding BO and BOT contracts that prevented

increased competition in the electricity market for several reasons. Firstly, some of those

contracts were awarded without a competitive procedure, there are some claims that some

of them were selected among bids from preselected companies. Another reason was the

fact that those contracts were designed so as to provide earlier cost recovery for investors,

this led to expensive electricity purchase by the state, especially for the first years of

contracts. Finally, those contracts included take-or-pay clauses which means that they did

not have to compete in the market, all commercial risks were taken by the state. State was

buying the electricity from those facilities with a fixed price; thus, it did not enhance cost

minimization. Private investors were competing for the market through the tenders

organized for BO, BOT and TOR contracts. (Atiyas et al., 2012)

Another type of private electricity generators at the time were autoproducers, which

were mainly industrial companies which need heat in their production processes, and the

electricity production is not the main objective. Before the liberalization period, there

were some state-owned industrial facilities (e.g. sugar factories) functioning as

cogeneration power plants. The government decided to incentivize autoproducers to

11

increase investments in electricity supply, their numbers and shares increased

significantly. New cogeneration plants were built mainly to generate electricity, and

autoproducer groups were formed. Autoproducer groups refer to industrial companies

coming together and establishing a generation company to meet their own electricity

needs, and selling excess energy to TEAŞ or TEDAŞ with a fixed price regardless of the

generation time. The growth of autoproducer power plant installed capacity at the time is

shown in Figure 1.2. (Dilli & Nyman, 2015)

Figure 1.2 Growth of Autoproducer Plant Installed Capacity, 1984–2001 (MW)

(Dilli & Nyman, 2015)

There had been an attempt to privatize TEK by selling ownership rights in 1994.

Constitutional Court intervened and cancelled relevant legislation since it was concerned

about foreign ownership of a strategic industry such as energy, and another concern was

the fact that there were no provisions preventing excess market power in forms of

monopolization and cartelization. (Atiyas et al., 2012)

The first unbundling of activities related to electricity system took place in 1993, when

the state monopoly, TEK was divided into two separate corporate entities: TEAŞ (Turkish

Electricity Generation and Transmission Company) and TEDAŞ (Turkish Electricity

Distribution Company). TEAŞ was responsible for electricity generation, transmission

and wholesale activities whereas TEDAŞ was in charge of electricity distribution.

However, both of these companies were publicly owned monopolies and this attempt did

12

not cause a change in the vertically integrated structure of the electricity sector in Turkey.

Electricity market structure of that period is illustrated in Figure 1.3 below.

Figure 1.3 Electricity Market Structure in 2000 (Dilli & Nyman, 2015)

1.1 Market Reforms of 2001

“Dissatisfaction with the BOT–BO model of private participation in electricity had

already led the bureaucracy to search for more competitive models of electricity supply.

A stabilization program supported by the IMF and the World Bank became instrumental

in pursuing a more fundamental restructuring of the electricity industry through the

adoption of the electricity market law (EML, Law No. 4628) in 2001. Electricity Market

Law envisaged a competitive market, liberalization of both supply and demand and the

creation of an independent regulatory authority.” (Atiyas et al., 2012)

1.1.1 Energy Market Regulatory Agency (EMRA)

One of the major reforms of 2001 EML was the establishment of the energy market

regulator. Electricity Market Regulatory Authority (EMRA) was the regulator of

electricity markets with wide powers to issue secondary legislation. After the enactment

of Gas Market Law in 2001 and Petroleum Market Law in 2003, the EMRA was also

given authority over the natural gas and oil industries. Its name was also changed to

Energy Market Regulatory Authority (EMRA).

13

The EML describes the EMRA as an ‘‘independent, administratively, and financially

autonomous public institution’’. It is governed by its own board which consists of nine

members and a president, appointed for 6 years by the Council of Ministers. The Board

members cannot hold jobs in the industry for 2 years after their term in office is

completed.

1.1.2 Unbundling of Activities

There is no doubt that another main pillar of the liberalization of the electricity market

is unbundling of activities, namely distribution, transmission, generation, trading and

supply. “Under the new regime, public assets were legally unbundled into separate public

companies: TEAŞ was separated into EÜAŞ, the Electricity Generation Corporation,

TEİAŞ, the Turkish Electricity Transmission Corporation, and TETAŞ, Turkish

Electricity Trading and Contracting Corporation, a wholesale trading company. It was

envisaged that assets owned by EÜAŞ and TEDAŞ would be privatized. Transmission

activities, on the other hand, would remain under public ownership. The primary task of

TETAŞ was to take over all energy sale and purchase agreement of TEDAŞ and TEAŞ,

including energy purchase and sales agreements entered into under BOT, BO, and TOR

contracts and also export and import contracts. Also, initially EÜAŞ would sell all the

electricity it has generated to TETAŞ. The idea was that the relatively expensive

electricity purchased through BOT, BO, and TOR contacts would be balanced by what

was perceived to be relatively cheap electricity purchased from EÜAŞ and the electricity

would be sold under a uniform price to TEDAŞ. Hence essentially, TETAŞ would work

under an average cost pricing scheme.” (Atiyas et al., 2012)

Electricity market structure changed after 2001 reforms, following the unbundling of

activities and new private actors emerged in the sector. Figure 1.4 from the World Bank

report illustrates the structure of the market at the time.

14

Figure 1.4 Electricity Market Structure After 2001 Electricity Market Law (Dilli &

Nyman, 2015)

1.1.3 Other Reforms

The market model introduced by the 2001 Electricity Market Law had two pillars, a

market for bilateral contracts and a balancing mechanism to provide real-time balance

between supply and demand of electricity. This system had many similarities with the

New Electricity Trading Arrangement (NETA) of England and Wales which was

introduced at the same year, 2001. (Atiyas et al., 2012)

The new Electricity Market Law of 2001 defined each activity regarding electricity

sector, namely generation, wholesale trade, transmission, distribution and retail supply to

final consumers. To be able to provide any of these activities required obtaining a licence

from the energy regulator, EMRA. On the supply side, it was carried out by state company

EÜAŞ, Electricity Generation Corporation, and some other private generators who

possess a generator licence issued by the regulator. Private generators also included

autoproducers, which generate electricity for their own use, and they were able to sell

generated surplus electricity to the market. Distribution companies were able to supply

electricity to final consumer provided that they were granted a retail licence by the

regulator. (Atiyas et al., 2012)

15

This new system liberalized the demand side of the electricity market as well, together

with the introduction of the concept “eligible consumer”. According to the provisions of

the Electricity Market Law, EMRA was assigned to determine a level of consumption

and consumers exceeding that level of annual consumption would be defined as “eligible

consumers” and they had the freedom to choose their electricity supplier. This eligibility

threshold was set to 9 million kWh per year, and it is being reduced gradually since then.

In 2019, the limit is reduced to 1600 kWh/year.

The privatization of generation and distribution assets was another crucial step for the

market liberalization. Electricity market law of 2001 mentioned privatization of state-

owned facilities and assets, but provisions including further details and a timetable was

provided with a strategy document issued in 2004. This document prioritized the

privatization of distribution companies over generation facilities, with the assumption that

private distributors would facilitate new entrants to generation side. (Atiyas et al., 2012)

Turkey was divided into 21 distribution regions, and 21 companies were founded for each

region, with a distribution licence issued by regulator (EMRA) for 49 years.

It was expected by policy makers that private distributors would reduce losses and

theft better than public authorities, as the theft and loss in suburbs of big cities and less

developed, socially frustrated regions were and still is a big problem.(Atiyas et al., 2012)

Loss and theft in distribution network is the amount of energy lost inside the grid due to

technical reasons, accompanied with the illegal withdrawal of energy from the grid

without paying for it. Izak Atiyas explained the causes as the following: “The fact that

loss ratios were highest in provinces that have suffered most from violence associated

with the Kurdish problem also suggests the presence of deeply rooted social factors. There

is anecdotal evidence that theft is also high in poorer districts and shanty towns in some

urban centers (most notably in Istanbul) and that in some cases industrialists engage in

large amounts of theft in areas where law enforcement is weak.”(Atiyas et al., 2012)

According to data published by EMRA for the year 2017, out of 21, 2 distribution regions

have the share of loss & theft over 50 per cent, and third highest has 25%. (EMRA, 2018)

16

1.2 2004 Strategy Document

The Strategy Document, which is issued for the implementation of Electricity Market

Law, introduced several types of transitional contracts between major actors of the

industry. One type being the contracts between EÜAŞ hydro power plants and TETAŞ,

the trading company. These contracts were used to balance TETAŞ wholesale electricity

prices that distributors have to pay, since TETAŞ was also buying expensive electricity

from private electricity generators. Other type of transitional contract was between

TETAŞ and distribution companies, which were to sell electricity purchased from EÜAŞ

and private generators. Another type being contracts between distributors and generators

for maximum 5 years period, and afterwards, they were meant to be replaced by market-

based contracts. The last type of transitional contracts was between distributors and

suppliers. (Atiyas et al., 2012)

The privatization process of distribution companies took more time than it was

expected. Strategy Document targeted to finish the privatization process until the end of

2006, whereas it was completed in 2013 with the transfer of ownership for 8 remaining

distribution companies. Among the reasons of this delay was the time needed to find the

appropriate legal form of ownership. TOR based share sale model was adopted for the

privatization of distribution companies. According to this model, the Privatization

Authority established 21 companies which have distribution and retail licences from

EMRA and these companies has the monopoly to operate distribution grids in their

respective regions. 100% share of those companies would be sold to private actors,

however, all of the existing assets and all new assets that will be created will stay under

the ownership of TEDAŞ, public distribution company. (Atiyas et al., 2012)

Huge difference of costs between distribution regions, mostly due to the varying shares

of loss & theft among regions, was dealt with a “price equalization scheme” which was

introduced with the strategy document mentioned above. This scheme is using cross-

subsidies to balance costs, regions which have low rates of losses are compensating for

the regions with high rates of loss & theft. It was preferred to direct subsidies as it does

not inflict extra burden to public budget directly. EMRA was given the authority to design

and publish the details of the scheme. This scheme was foreseen for a transitional period

17

at that time, which would end at 2010, but it is still in practice, current deadline is

announced as 2020. (Dilli & Nyman, 2015)

1.3 Balancing & Settlement

The first version of balancing and settlement mechanism was created in 2004, which

was called temporary at that time, since it was planned as the first step towards a more

complete wholesale market. Balancing markets are mechanisms to keep the balance of

electricity production and consumption at the same level all the time. Before the balancing

market started operations in 2006 balancing was held according to bid and offers proposed

by TETAŞ, the trading company and prices used for financial settlement of those

balancing measures were approved by EMRA, the regulator. (Dilli & Nyman, 2015) So

called “transitional Balancing and Settlement Regulation - TBSR” was introduced with

the basic principle that financial settlement of balancing transactions would be carried out

together with the settlement of bilateral contracts. Between 2006-09, the balancing

mechanism was more like a day-ahead scheduling mechanism rather than a day-ahead

market. Generators were submitting their hourly generation plans twice a month for the

next 15 days. Demand were being determined by the system operator, TEİAŞ, for every

hour of the next day. Financial settlement of balancing measures was done by Market

Financial Settlement Center at the end of each month. Settlement periods were not hourly,

it was calculated for night, peak and off-peak time periods of a day.

The functioning of the balancing mechanism changed with the adoption of the so-

called “final” version of the balancing and settlement mechanism in 2009, and day-ahead

planning was separated from the real-time balancing system. (Atiyas et al., 2012) Day-

ahead planning provides a daily electricity generation plan for each hour of the next day,

whereas real-time balancing is used to reestablish the balance when generation and

consumption is not at the same level at real time. Between 2009-11, generators were

submitting their bids every day for each hour of the next day, and demand was still being

determined for each hour by TEİAŞ National Load Dispatch Center. Marginal prices for

each hour were published one day before real time. Financial settlement of balancing

measures was done for each hour, at the end of each month. (Dilli & Nyman, 2015)

18

Day-ahead planning system used in this period served as a transition period to day-

ahead market which started operations in December 2011. The Day-Ahead Market

(DAM) is a marketplace where suppliers submit their offers for each hour of the next day

as the demand side of the market, and generators submit their bids for each hour of the

next day as the supply side of the market. The market clearing price, or the spot price, is

determined for each hour according to bids and offers of market participants. The system

operator is not acting as the demand side of the market according to estimations for the

next day’s consumption anymore. Rather, TEİAŞ operates the Balancing Power Market

(BPM) based on the bids submitted by generators one day before for real-time balancing

measures, i.e. up-regulations and down-regulations. During real time, when there is a

momentary imbalance between supply and demand, National Load Dispatch Center gives

instruction to some generators to increase or decrease their output.

In May 2009, another strategy paper called “Electricity Market and Supply Security

Strategy Document” was published. Regarding the further implementation of competitive

wholesale market mechanisms, this strategy document defined a road map for day-ahead

and balancing power markets. Furthermore, this document mentioned for the first time

the creation of an independent market operator as an electricity exchange. The paper also

set some target for renewables within the context of energy supply security. To decrease

dependency on costly natural gas, which was over 40% for the electricity generation at

that time, paper aimed to maximize the use of domestic sources such as hydro and lignite,

and to increase the share of renewables in electricity generation over 30% by 2023. (Dilli

& Nyman, 2015)

1.4 Tariff Structure

The Electricity Market Law of 2001 also defined tariffs that are regulated by EMRA,

such as tariffs concerning connection and use of transmission and distribution grids, retail

tariffs for non-eligible consumers and tariffs applied for the trading transactions of

TETAŞ, the wholesale trading public company. Table 1.1 summarizes the tariffs with

methodologies in regulation. Details of the tariff regulations has been subject to many

changes over time. (Atiyas et al., 2012)

Table 1.1 - Regulated Tariffs (Atiyas et al., 2012)

19

Tariff structure for distribution and retail

companies was created for a transition period

between 2006-2010, and cost-based tariffs

were intended for the period afterwards. As

Atiyas explains: “During the transition period

tariffs would entail various types of cross

subsidies across regions as well as consumer

groups, through the application of a price

equalization scheme. As a result, there was a

single national tariff structure uniform across

regions but differentiated according to

consumer groups. The price equalization

scheme was adopted to prevent large

variations in technical losses and theft across regions from resulting in large variations in

end-user tariffs.” (Atiyas et al., 2012) Price equalization scheme and cross-subsidies are

still in force, due to the fact that substantial difference in loss ratios between distribution

regions are still present.

End-user tariffs were meant to be regulated by EMRA, but for the transition period

(2006-2010), TEDAŞ, the distribution company, was offering a tariff and EMRA was

approving without making changes. The Electricity Market Law and Electricity Market

Regulation adopted by EMRA unbundled end-user tariff for electricity into following

components: retail sales, retail services, distribution, transmission and loss & theft. Retail

sales component were reflecting the overall average cost of a unit of energy to distribution

companies. Retail services and distribution components included the costs of services

plus investment requirements related to retail and distribution services, which is called

“revenue cap” model. (Atiyas et al., 2012)

Increased risk of power shortages and increased financial instability of state-owned

energy companies paved the way for a shift in a more cost-reflective tariff mechanism in

2008, when the price of electricity had increased by around 50%, the first massive

increase since 2003. The so called “automatic pricing mechanism” required quarterly

adjustment of the prices of EÜAŞ, TETAŞ, BOTAŞ (the national oil and natural gas

transmission company), and distribution companies. (Dilli & Nyman, 2015)

20

The current tariff structure causes some financial problems for private suppliers

offering energy to eligible consumers. For the private suppliers, the cost of buying

electricity in the spot market changes a lot due to fluctuating spot prices especially caused

by gas supply shortages and increasing costs of feed-in tariff. The increase in costs of

feed-in tariff was mainly caused by rapid growth in electricity generation from

renewables as well as serious devaluation of Turkish Lira in the past few years.

1.5 The new Electricity Market Law of 2013

The new Electricity Market Law (No. 6446) was enacted in 2013, repealing the EML

of 2001, other than the provisions related to the energy regulator, EMRA. The new law

made some significant changes on the electricity market structure, such as changing the

role of state-owned companies and legal unbundling of retail and distribution activities,

and the provisions regarding the establishment of an independent energy exchange,

EPİAŞ.

Before the new Electricity Market Law, distribution and retail supply activities were

carried out by distribution companies, but financial accounts were being held separately

(i.e. account unbundling). The new Law necessitated legal unbundling of those activities,

distribution companies were divided into “assigned supplier” companies and distributors.

Since then, distribution companies are responsible for the operation and maintenance of

the distribution grid in their region, whereas assigned supplier company is a retail

company with an obligation to act as “supplier of the last resort”. Supplier of the last

resort is obliged to procure electricity to non-eligible consumers and eligible consumers

who did not opt for switching their supplier. (Dilli & Nyman, 2015)

21

Figure 1.5 Role of EÜAŞ and TETAŞ before the 2013 Electricity Market Law (Dilli

& Nyman, 2015)

The new Law also

changed the roles of

EÜAŞ (public generation

company) and TETAŞ

(public wholesale trading

company). Before, EÜAŞ

was not allowed to make

new generation

investments with an

exception for the reasons

of supply security. Its role

was to own and operate

remaining state-owned

generation facilities,

mostly large hydro plants. It was only allowed to take over hydro plants built by State

Hydraulic Works, a public institution in charge of issues related to water. The new Law

removed all these restrictions from EÜAŞ and made the company an active player in the

market with the freedom to invest in new generation capacity. since then, EÜAŞ has equal

rights and responsibilities with private generators who possess generation licence from

the regulator. It is also allowed to have shares in a private generation company. (Dilli &

Nyman, 2015) Figure 1.6 shows the shares of each generator types regarding ownership

in total installed capacity in Turkey as of June 2019.

22

Figure 1.6 Shares of Generation Capacity by Ownership Type (Source: TEİAŞ)

Before 2013, Market Financial Settlement Center (PMUM), which was a department

under the roof of TEİAŞ, transmission and system operator, was responsible from

electricity market operations, e.g. day-ahead market since 2011. The new Law defined

market operation activities as “the operation of organized power markets and the financial

settlement of the transactions made in these markets.” A new licence type was introduced

for this specific activity which is called “market operation licence” and the Law ruled the

establishment of an independent company named EPİAŞ (Turkish Energy Exchange).

EPİAŞ was established in March 2015 and obtained market operations licence from the

regulator in September 2015.

Figure 1.7 - Final Electricity Market Structure (Dilli & Nyman, 2015)

23

Chapter 2. Policies and Legislations on Renewable

Energy and Energy Efficiency

2.1 2004 Strategy Document

The first strategy paper after the 2001 energy market liberalization reforms was

announced in 2004 with the name “Electricity Sector Reform and Privatization Strategy

Document”. The World Bank Report on Turkish energy transition explained the first

strategy document as the following: “The 2004 Strategy paper provided a roadmap for

the reform process and aimed to increase the confidence of market participants, especially

private parties who could potentially invest in Turkey.” (Dilli & Nyman, 2015) The report

also advocates that the Strategy Document was a crucial step towards liberalization

reform as it established the basis for privatization, the creation of the organized wholesale

market, and transitional measures that will be taken such as transitional contracts and the

role of public energy companies during transition. (Dilli & Nyman, 2015)

As it is explained shortly above, the 2004 Strategy Paper contained the principles of

privatization of public energy assets and entities such as distribution and generation. The

objective of the preparation of that document was stated as “ensuring adequate and

continuous supply of electricity at a low cost and to achieve the objective of integration

with EU acquis”. Based on this fact, we can argue that the target of being an EU member

was a major driver to energy market liberalization reforms and in general, the energy

transition in Turkey since the beginning.

The expected benefits from electricity market reforms were explained in the Strategy

Document as well. Those benefits are demonstrated below:

1. Reducing the costs by utilizing distribution and generation assets efficiently,

2. Enhancing electricity supply security and improving the quality of supply,

3. Preventing loss and theft, reducing the share of loss and theft to the average of

OECD countries,

4. Ensuring that necessary investments in renovation and expansion of the electricity

system are made by private sector without increasing the burden of public entities,

24

5. Reflecting the benefits of increased competition in electricity generation and trade

and increased service quality to final consumers.

2.2 2009 Strategy Paper

2004 Strategy Paper focused on privatization of assets and market liberalization, but

the reference to the renewables or energy efficiency is missing in the document, since it

was not among the priorities of the Turkish government and policy makers at that time.

Five years later, another Strategy Document named “Electricity Market and Security of

Supply Strategy Paper” was published in 2009, which set some targets for renewables in

Turkey for the first time. The share of renewable sources in electricity generation in

Turkey is targeted to reach 30% by 2023, 100th anniversary of the foundation of the

Republic of Turkey, and the target includes generation from large scale hydro dams. The

main objective of this Strategy Paper is to promote further utilization of domestic energy

sources such as lignite and renewables, and the share of almost completely imported

natural gas in electricity generation will be reduced below 30% by 2023, and this

reduction will be compensated with indigenous energy sources in order to enhance energy

supply security and to decrease the costs energy related imports.

Atiyas claims that the target for renewable electricity generation is rather realistic than

ambitious since the large-scale hydropower generation had around 25% share in total

electricity generation in 2010. (Atiyas et al., 2012) Figure 2.1 illustrates the shares of

hydropower and the whole renewables in electricity generation by 2009, the year when

the Strategy Paper was published. The graph shows that almost all electricity generation

from renewable sources came from hydropower plants until that date, and it supports the

argument that 30% share of renewable electricity was not an ambitious target. Even

though electricity demand has increased significantly after 2009 and the expansion of

hydropower generation met only a small percentage of that increase in demand, wind and

solar power as well as other renewable sources such as geothermal increased significantly

thanks to significantly reducing costs and renewables support mechanism (YEKDEM).

25

Figure 2.1 Shares of Renewables and Hydro in Electricity Generation in Turkey

(1970-2009) (Source: TEİAŞ)

The 2023 targets for each renewable source are specified as well by the 2009 Strategy

Document. For hydropower, the target is to utilize all technical and economic potential

in the country by the year 2023. The installed capacity of wind energy is targeted to be

increased to 20,000 MW (20 GW). Regarding geothermal, the whole potential capacity,

which is stated as 600 MW for electricity generation in the Paper, will be utilized. There

is no specific target for the share of solar energy in electricity generation, the target is

stated as “to ensure the utmost utilization of Turkey’s potential of solar power”.

Energy efficiency is also mentioned in the 2009 Strategy Paper. There is no specific

deadline or a numerical target in the Paper, but it provided commitment for the creation

of energy efficiency standards for electrical motors, air conditioners, electrical home

appliances and light bulbs that are being used in Turkey. It is also worth noting that the

Paper declares the intention of the government at that period to apply measures to ensure

energy efficiency in electricity consumption without compromising social and economic

development targets. The Paper also pledges that technical losses will be minimized in

electricity generation, transmission and distribution, and it commits the Ministry of

Energy and Natural Resources to create regulations concerning demand side

management, a topic which is still not properly addressed by the regulations yet.

26

2009 Strategy Paper declares targets for the shares other non-renewable sources in

electricity generation, e.g. reaching to a minimum 5% share from nuclear power plants

by 2020 and limiting the share of natural gas to 30%. It appears that the target for nuclear

will not be achieved as the commissioning of the first two reactor units of Akkuyu Nuclear

Power Plant is expected to be completed by 2023. (MENR, 2019)

2.3 2014 National Renewable Energy Action Plan

Another policy document regarding renewable energy is the “National Renewable

Energy Action Plan for Turkey” which was published in December 2014 in accordance

with the EU Directive 2009/28/EC, the so called “Renewable Energy Directive”. The

Directive obliged all Member States to prepare a National Renewable Energy Action Plan

for the period 2011-2020 with a projection to comply with the 2020 renewable energy

targets of the European Union. The action plans that are prepared by Member States

should establish specific targets so that EU will reach a 20% share of energy from

renewable sources by 2020 in electricity, heating and cooling sectors and 10% in transport

sector.

As it is explained in the “rationale” part of the Action Plan, Turkey, as a candidate

country, prepared its own National Renewable Energy Action Plan for the period 2013-

2023 to demonstrate its commitment to EU renewable energy targets and EU accession

process. The Action Plan was prepared by the Ministry of Energy and Natural Resources

and Directorate-General of Renewable Energy in collaboration with EBRD, European

Bank for Reconstruction and Development, and Deloitte, a giant transnational

consultancy firm, based on the methodology shared by the European Commission.

The Action Plan first explains existing renewable energy and energy efficiency

policies and legislations, then gives data and forecasts about expected energy demand and

generation in Turkey by 2023. The Action Plan is prepared in accordance with the existing

relevant policies and legislations, namely Strategy Documents and Strategic Plans of the

Ministry of Energy and Natural Resources.

Figure 2.2: Electricity generation and installed capacity from renewable sources:

2013 data and 2023 forecast (MENR, 2014)

27

Regarding targets for renewable share in electricity generation, Figure 2.2 from the

Action Plan shows the existing installed power capacity and electricity generation by

source in 2013, and specifies targets for each source and technology, which will lead to

accomplishment of the overall target for renewables. For solar power facilities, the target

for installed capacity is 5 GW and for electricity generation is 8 TWh for the target year,

2023, according to the Action Plan.

Figure 2.3: Electricity generation and installed capacity: 2013 data and 2023 forecast

(MENR, 2014)

28

The Figure 2.3 illustrates forecasted shares of each renewable technology in electricity

generation. As it may be observed, future forecasts for renewables goes beyond 2023

target and expected to increase to 38% thanks to further deployment of wind, solar and

biomass technologies in electricity sector. Another important fact the Figure 2.3 shows is

that the demand for electricity will almost double in 10 years. The Action Plan also

reveals the strategy of the Government to limit the share of natural gas in electricity

generation to 30% by 2023, which is also in line with the 2009 Strategy Paper.

Table 2.1: National target for 2023 and the expected progression of renewable

sources in the sectors of electricity, heating and cooling, and transportation (MENR,

2014)

Table 2.1 indicates 2023 renewable targets for each sector, namely heating & cooling,

transportation and electricity. According to the plan, the share for renewable sources in

total energy consumption will reach to 20.5% from 13,5 % 2013. according to this table,

provided the target for transportation (10%) will be achieved. Considering the fact that

total energy demand will increase more than double in the same time period, achieving

this target will require significant deployment of renewable sources not only in the

electricity sector, but also in transport and heating & cooling sectors.

The Action Plan also demonstrates numerous measures and actions that are already in

force or still under consideration in order to achieve indicated targets. Regarding the

implication of the feed-in tariff, the Plan underlines the deadline which is extended to

2020. The Action Plan does not indicate a specific support mechanism which will be

applied after 2020, but it mentions several options from a communication by the European

Commission with a title” Guidance for the Design of renewables support schemes”

published in November 5, 2013. The Action Plan acknowledges the need to reform

existing feed-in tariff mechanism to adapt falling costs of renewable technologies. The

alternative options to reform the feed-in mechanism consists of the creation of a

29

competitive allocation mechanisms, e.g. auctions, introduction of the feed-in premium

mechanism as a more market-based option and the introduction of a quota obligation

system, as it is explained in the Action Plan with reference to the aforementioned

Communication from the European Commission.

Competitive allocation mechanism option started being implemented with the

introduction of the auction system “Renewable Energy Resource Areas - YEKA” which

will be explained more in detail in the following sections. The second alternative, feed-in

premium system works as follows: the supported energy price is determined as the

wholesale market price plus a premium in feed-in premium systems, so this support

system has more interaction with the market compared to feed-in tariffs. It is still not

announced whether the feed-in premium system will be implemented or not in the post-

2020 period. The third option, quota system, is an obligation for energy suppliers to

procure a certain share of their overall consumption from renewable sources. Quota

obligation system took place in a primitive form in the first version of the Renewables

Law, but it was removed in a short period of time with an amendment. It is crucial to

design the system properly to avoid double compensation of renewable generators and to

prevent making the burden of the support system unbearable to energy suppliers and to

consumers if the quota system will be considered in the future.

2.4 Legislations

Renewable energy support mechanisms started being developed in Turkey in early

2000’s. One of the main drivers for policy makers at that time to introduce such support

mechanisms was Turkey’s accession process to the EU, which had a higher priority for

the Turkish government at that time. EU member states had already developed various

support mechanisms earlier, and EU had ambitious targets and goals for supporting

renewables, as it is the case for the time being. Another driver, especially for the second

part of that decade, was the issue of energy supply security, as Russians started cutting

natural gas supply to the Ukraine, and increase in oil prices at that time also contributed

to the decision to support renewables in Turkey in the beginning of 2000’s. (Atiyas et al.,

2012)

30

The first Electricity Market Law of 2001 mentioned for the first time “renewables”, it

consisted some provisions for EMRA to encourage renewable energy sources, but the law

did not introduce any incentives or support mechanisms, and it did not provide any clear

definition of renewables, i.e. it was not clear which sources and technologies were

considered as renewables. The Figure 2.4 illustrates a timeline for the milestone

developments and key legislative and regulative acts for renewables in Turkey for the

period 2001-2010. (Atiyas et al., 2012)

31

Figure 2.4 Legal and regulatory timeline for renewables (Atiyas et al., 2012)

A definition of renewables was introduced with an amendment in 2003 and it was

revised several times afterwards. Final definition includes wind, solar, geothermal,

biomass, biogas (including municipal waste), wave, tidal, pumped storage, run-of-the-

river hydro, and hydroelectric dams with less than 15 km2 of reservoir area.

32

First incentives to renewables were observed in 2003 with an amendment to the

Electricity Market Licencing Regulation. Those incentives included grid connection

priority to installations using renewable or domestic sources, significant reductions in

licencing fees, and even an obligation to retail suppliers to buy the electricity they procure

to non-eligible consumers from renewables unless there is a cheaper supply source. Later,

the strategy paper of 2004 assigned the Ministry of Energy and Natural Resources

(MENR) and State Planning Organization the responsibility to promote renewable energy

sources. (Atiyas et al., 2012)

2.5 2005 Renewables Law

The most important progress was made with the enactment of the Law on Utilization

of Renewable Energy Resources for Electricity Production No. 5346, which is known as

the Renewables Law, in 2005. The Law introduced a Feed-in Tariff (FiT) as a support

mechanism for renewables, similar to other legislations in the EU member states at that

time. The first version of the feed-in tariff was in the form of purchase obligation for all

retail suppliers. The support price was the average wholesale electricity price of the

previous year and it was limited between 5 to 5.5 €cent/kWh and according to Atiyas, it

was a fairly low price compared to other feed-in tariffs applied especially in Europe.

(Atiyas et al., 2012)

Renewable generators needed to obtain a certificate called “Renewable Energy

Source” from the regulator, in order to be able to benefit from the support mechanism.

This certificate might be confused with the tradable green certificates, or tracking

mechanisms such as guarantees of origin, but it is essentially different. Aforementioned

RES certificate is granted to renewable generators only once before they start operations,

and it is not connected to the amount of electricity being generated in that facility which

it was issued for.

Renewable generators had the opportunity to sell the electricity they produce in the

spot market or via bilateral contracts when the rates were higher. Renewable facilities

were also granted many exemptions from land use fees and 85% discount in state lands

for the first ten years of operation. (Atiyas et al., 2012)

33

Supported renewable generators were exempt from reserve capacity requirements,

which is a requirement for all electricity generators with more than 50 MW of installed

capacity. This reserve is being kept for ancillary services such as primary and secondary

frequency control which is needed for the operation of the transmission system. Since

renewable generation is intermittent, reserve capacity requirements could not be applied

to most renewable technologies with the exception of dam-type hydro power plants.

Retail suppliers had to purchase renewable generation equivalent to their market share

in the previous year. The first version of the Renewables Law even included a quota

system for retail suppliers, an obligation to meet at least 8% of their total supply from

renewables, but it was not implemented and removed with the first amendment in 2007.

Some strict rules and penalties were introduced in 2007 for developers who did not

comply with construction time limits and schedules. The main reason for this measure

was the existence of multiple applications for the same wind farm location. Those

penalties included nullification of the generation licence. (Atiyas et al., 2012)

2.6 Amendments to Renewable Energy Law

Renewable Energy Law was amended several times, but the most comprehensive

amendment passed from the Grand National Assembly of Turkey in December 2010 and

entered into force in January 2011. A new version of feed-in tariff (YEKDEM - the

Renewable Energy Resources Support Mechanism) and premiums were introduced with

the 2011 amendment. Renewable generation facilities were supported with different rates

for each technology, and a local content premium was introduced. Table 2.2 shows the

rates that are being applied since then. This new tariff is applied for renewable generation

facilities started operations between 2005 - 2015 and for the generation facilities started

operations later than that day, the President is authorized to decide the tariffs. The existing

rates are the same rates indicated in table X.X, with an exception for building integrated

photovoltaic installations (≤10kW for residential consumers) which receive national tariff

prices for electricity consumers as the supported generation price. The feed-in tariff may

be applied to an installation for 10 years from the first operation date.

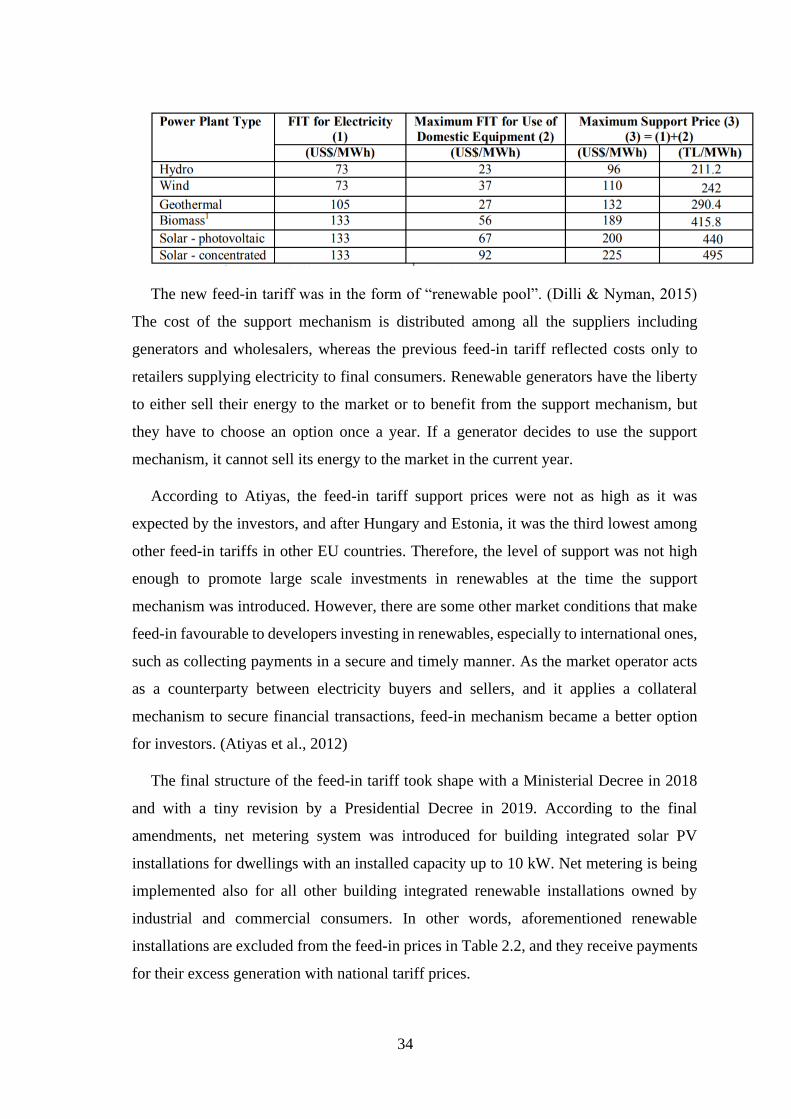

Table 2.2 - Feed-in tariff for renewables in Turkey (Gözen, 2014)

34

The new feed-in tariff was in the form of “renewable pool”. (Dilli & Nyman, 2015)

The cost of the support mechanism is distributed among all the suppliers including

generators and wholesalers, whereas the previous feed-in tariff reflected costs only to

retailers supplying electricity to final consumers. Renewable generators have the liberty

to either sell their energy to the market or to benefit from the support mechanism, but

they have to choose an option once a year. If a generator decides to use the support

mechanism, it cannot sell its energy to the market in the current year.

According to Atiyas, the feed-in tariff support prices were not as high as it was

expected by the investors, and after Hungary and Estonia, it was the third lowest among

other feed-in tariffs in other EU countries. Therefore, the level of support was not high

enough to promote large scale investments in renewables at the time the support

mechanism was introduced. However, there are some other market conditions that make

feed-in favourable to developers investing in renewables, especially to international ones,

such as collecting payments in a secure and timely manner. As the market operator acts

as a counterparty between electricity buyers and sellers, and it applies a collateral

mechanism to secure financial transactions, feed-in mechanism became a better option

for investors. (Atiyas et al., 2012)

The final structure of the feed-in tariff took shape with a Ministerial Decree in 2018

and with a tiny revision by a Presidential Decree in 2019. According to the final

amendments, net metering system was introduced for building integrated solar PV

installations for dwellings with an installed capacity up to 10 kW. Net metering is being

implemented also for all other building integrated renewable installations owned by

industrial and commercial consumers. In other words, aforementioned renewable

installations are excluded from the feed-in prices in Table 2.2, and they receive payments

for their excess generation with national tariff prices.

35

After 2011, renewable generators were exempted from the responsibility to carry the

real-time market risk when their predicted generation did not match with the realized

generation, i.e. real-time imbalance. The National Load Dispatch Center provided the

day-ahead supply predictions from renewable sources for each hour of the next day to the

day ahead market for each renewable installation. Any mismatch was handled via

ancillary services. (Atiyas et al., 2012) This rule was changed with an amendment in May

2016 and balancing requirements were introduced for licenced renewable generators.

Since then, all licenced renewable generators have to forecast for the next day and submit

their bids to the day ahead market. In case of a mismatch in real time, they have to pay

all the necessary fees in day-ahead market, and final settlement is being done at the end

of each month according to the feed-in tariff.

Another unique feature of the reformed feed-in tariff is the local content bonus.

Implementation regulation which was introduced after the 2011 amendment included

some requirements for developers to be able to benefit from the local content bonus

payment, such as compatibility with national and international standards. In June 2011, a

specific regulation regarding the local content bonus was issued by the regulator, EMRA.

This regulation put forward some extra technical standards for the parts being used in

solar facilities and a department under the roof of the Ministry of Energy, Electrical Power

Resources Survey and Development Administration (EIE), is authorized for the

supervision of technical requirements. (Atiyas et al., 2012)

2011 amendment to the Renewables Law introduced a limit (600 MW) for the total

capacity of licenced solar installations that could be deployed in Turkey. Smaller

(unlicensed) installations with less than a certain amount of installed capacity (currently

5 MW) were not included to this limitation. The final version of the law still has the same

limit for total solar capacity; however, this limit includes only solar facilities installed

until the end of 2013, and for newer ones, the government (President) is limit is authorized

to determine a limit. One may assert that this limitation on total solar capacity did not

pose an obstacle to the proliferation of solar PV generators in Turkey, as the total installed

capacity of licenced solar generators at the end of 2013 was at an insignificant level.

36

2.7 Unlicensed Generation

An amendment to the Electricity Market Law exempted from licencing obligation the

facilities utilizing renewable sources and smaller than 500 kW of installed capacity. The

term “unlicensed generation” was introduced first with the Energy Efficiency Law

enacted in 2007, and the initial threshold for the exemption from licencing was 200 kW.

Amendments to the Renewables Law in 2010 increased the threshold to 500 kW and

allowed unlicensed generators to sell their excess energy to assigned regional suppliers.

(Dilli & Nyman, 2015) The new Electricity Market of 2013 (No.6446) set the limit to 1

MW and authorized the government to increase the limit up to 5 MW. This limit is

increased to 5 MW with a presidential decree in May 2019. Isolated facilities, emergency

generators and micro-cogeneration facilities (less than 50 kW) are also included into the

“unlicensed” category.

Unlicensed generators can be private individuals who decide to invest in renewable

energy installations in their homes, farms etc. to meet their own energy consumption, and

they are allowed to inject their excess generation to the distribution grid. They were

included into the renewable support system and were enjoying feed-in tariff prices.

Private individuals and local businesses who opt for collectively investing in small scale

energy facilities, i.e. establishing energy communities or energy cooperatives are also

considered under the “unlicensed generation” as long as the installed capacity of those

energy facilities is within the given limits. Such small-scale energy facilities may include

rooftop solar PV installations, small wind turbines, micro-hydroelectric plants, municipal

waste plants and small biomass facilities. (Dilli & Nyman, 2015)

The main reason for the policy makers and legislators to introduce this concept was to

promote distributed power generation from renewables. In other words, the objective of

creating such a category within the renewable support system is to promote small scale

energy facilities to increase efficiency and the share of renewable sources, and to decrease

grid losses by promoting energy generation as close as possible to the location where it is

consumed.