Transformation in South African asset management - 27four

194

Transformation in South African asset management BEE . conomics ™ 1 7 s u st a i n a b l e d e v e l o p m e n t go als ( S D G s ) t o t r a n sf o r m o u r w o rl d 2020

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Transformation in South African asset management - 27four

Transformation in South African asset management

BEE.conomics™

17 sustainable development goals (SDGs) to transform our world

2020

2

3

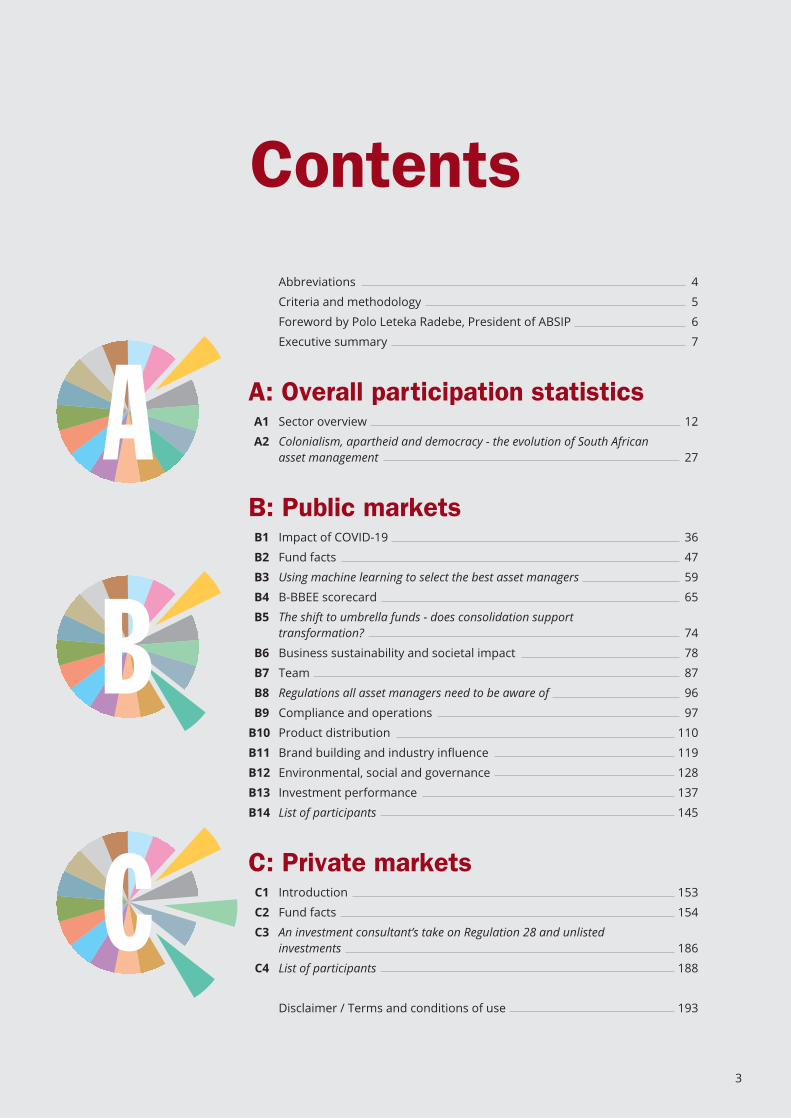

Contents

Abbreviations 4

Criteria and methodology 5

Foreword by Polo Leteka Radebe, President of ABSIP 6

Executive summary 7

A: Overall participation statisticsA1 Sector overview 12

A2 Colonialism, apartheid and democracy - the evolution of South Africanasset management 27

B: Public marketsB1 Impact of COVID-19 36

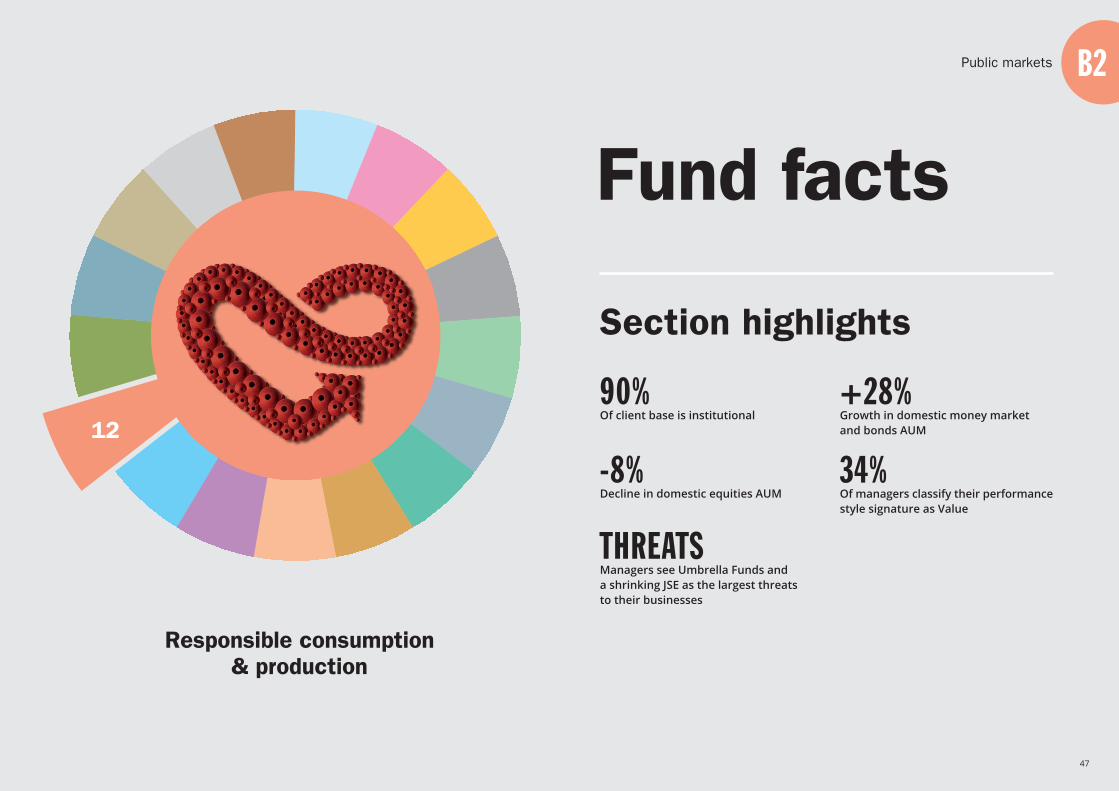

B2 Fund facts 47

B3 Using machine learning to select the best asset managers 59

B4 B-BBEE scorecard 65

B5 The shift to umbrella funds - does consolidation supporttransformation? 74

B6 Business sustainability and societal impact 78

B7 Team 87

B8 Regulations all asset managers need to be aware of 96

B9 Compliance and operations 97

B10 Product distribution 110

B11 Brand building and industry influence 119

B12 Environmental, social and governance 128

B13 Investment performance 137

B14 List of participants 145

C: Private marketsC1 Introduction 153

C2 Fund facts 154

C3 An investment consultant’s take on Regulation 28 and unlistedinvestments 186

C4 List of participants 188

Disclaimer / Terms and conditions of use 193

ABSIP Association of Black Securities and Investment Professionals

ASISA Association for Savings and Investment South Africa

AUM Assets Under Management

B-BBEE Broad-Based Black Economic Empowerment

CFA Chartered Financial Analyst

CIS Collective Investment Scheme

COFI Bill Conduct of Financial Institutions Bill

CRISA Code for Responsible Investing in South Africa

DFI Development Finance Institution

DTI Department of Trade and Industry

EAC Effective Annual Cost

EME Exempted Micro Enterprise

ESD Enterprise and Supplier Development

ESG Environmental, Social and Governance

FSC Amended Financial Services Sector Code of 2017

FSCA Financial Sector Conduct Authority

FSTC Financial Sector Transformation Council

GEPF Government Employees Pension Fund

GIPS Global Investment Performance Standards

GP General Partner

JSE Johannesburg Stock Exchange

LDI Liability Driven Investment

LISPs Linked Investment Services Providers

LP Limited Partner

LSM Living Standards Measure

NPAT Net Profit After Tax

PA Prudential Authority

PIC Public Investment Corporation

QSFI Qualifying Small Financial Institution

SARB South African Reserve Bank

SARS South African Revenue Services

SAVCA Southern Africa Venture Capital and Private Equity Association

SDGs Sustainable Development Goals

SED Socio-Economic Development

SOE State Owned Enterprise

TER Total Expense Ratio

TIC Total Investment Charge

UCITS Undertakings for Collective Investment in Transferable Securities

UN PRI United Nations Principles for Responsible Investment

4

Abbreviations

5

The survey has been designed with comparability toprevious years in mind. The report is also published

1 Questionnaire design Changing industry dynamics require an annual reassessment of therelevance of the questions asked.

2 Research content A key feature of the survey is the inclusion of research articles ofinterest and interviews with stakeholders.

3 Asset manager universe We cast our net wide to ensure that our universe is all-encompassing.

4 Invitation to participate Asset managers were invited to complete the online questionnaire on 2 June 2020.

5 Submission deadline The cut-off-date for participation was 14 July 2020.

6 Information collation Information submitted was cleaned, verified, collated and presentedin a visual format.

7 Commentary Statistics, facts and figures were interpreted, observations made andcommentary provided.

8 Publish The completed product is assembled for artwork, final editing and publication.

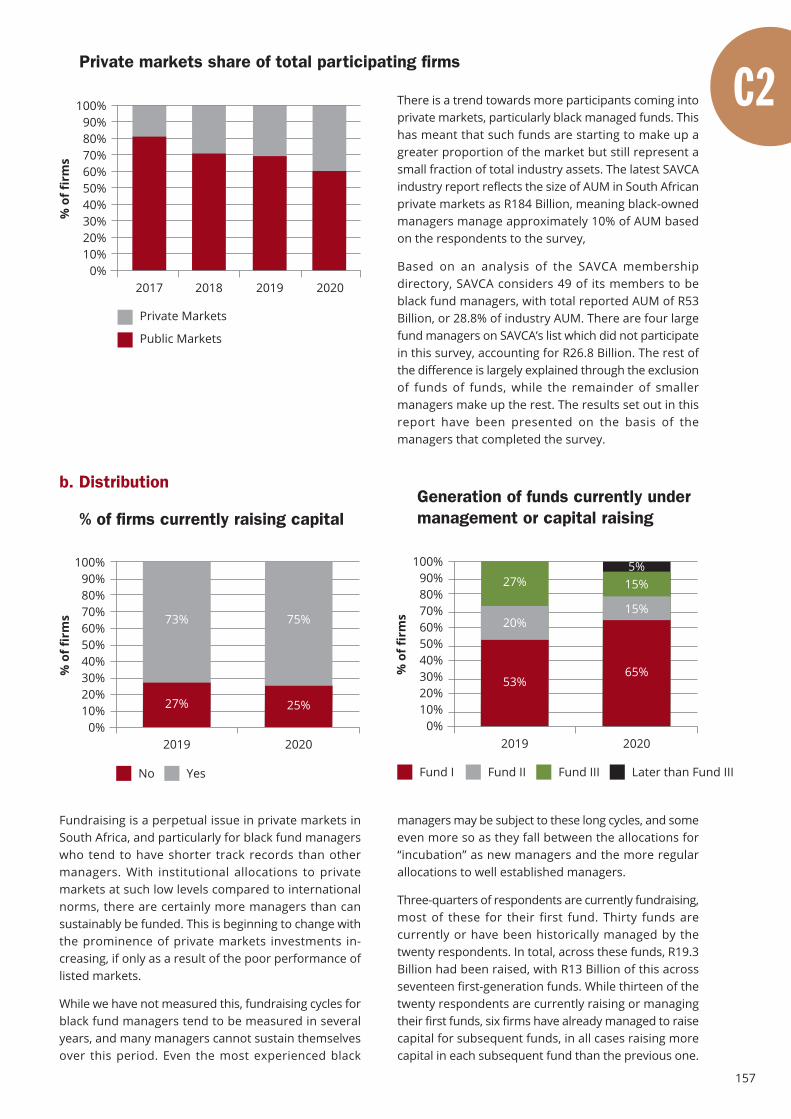

Criteria and methodologyPurpose of the survey

The purpose of this survey is to map the progress oftransformation in the South African asset managementsector and to showcase the universe of majority black-

Who would participate?

Asset managers which met the following criteria wereapproved for participation in the survey:

1. The company is at least 51% black-owned whereblack people hold at least 51% of the economicinterest and where black people hold at least 51%of exercisable voting rights.

2. At least 51% of the company’s board of directors areblack.

3. At least 51% of the company’s senior portfolio managers are black.

Research methodology

All data is presented as at 30 June 2020. The graphic below articulates the research process followed.

and made freely available for the benefit of all stake-holders across the savings and investments ecosystem.

4. The company is registered with the Financial SectorConduct Authority for the business that the companycarries out.

Random checks were conducted by 27four to verify thateach participant met the criteria. However, this was notindependently vetted. All information was voluntarilyprovided as is by participating firms.

owned, managed and controlled asset managers acrossboth public and private markets.

Forewordby Polo Leteka Radebe, President of ABSIP

6

The year 2020 is turning out to be a watershed momentfor the world at large and for South Africa in particular.As a country with a unique history premised on yearsof historical injustices and a unique transitional projectinto democratic rule, the South African story alwaysneeds to be narrated and articulated in a manner thatacknowledges the uniqueness of our society at large.

The rise and the spread of the coronavirus pandemichas forced a reset of what the world thought were therules of engagement and the ways of working and living.Similarly, in South Africa, it has forced us to confront somany of the fundamental fracture points inherent inour society that have become accepted rather thanchallenged. As a country that had a unique mission toproactively seek to heal and bridge the injustices of thepast and map a future of shared prosperity andsolidarity, South Africa by default had to come up withcreative and innovative ways of bridging its great socialdivides.

This is the basis of the various transformation initiativesand instruments that have been put in place over thepast 25 years. Key to these instruments is the regulatoryregime that seeks to provide guidance for various marketparticipants in various sectors on what needs to bedone in order to achieve meaningful transformation inthe various areas that they are in. The role of transfor-mation legislation in its various forms can therefore notbe over-emphasised in the South African context. Whatalso becomes very critical in relation to any form ofregulation and social leadership is the ability to monitorthe effectiveness of intervention instruments that havebeen proposed and implemented. To this end, the ideaof a policy barometer is an important concept for acountry like South Africa.

This is simply because whatever instruments of inter-vention are proposed and applied must be evaluatedagainst objective benchmarks that provide insights intothe effectiveness of such instruments in converging oursociety closer to shared characteristics rather thanamplifying our historic divides. In the financial servicessector, given its transversal and pervasive role acrossall sectors of our society and economy, it is even moreimportant to not only put transformation measures inplace but also to objectively assess and evaluate them.It is with this in mind that ABSIP is fully supportive ofthe 2020 Transformation in South African Asset Manage-ment Survey.

In our view, this survey serves as an important barometerthat enables us to track the performance and progressof transformation within the sector over a particularperiod of time. The reason why tracking and monitoringtransformation is quite important is that we all acknow-ledge that this sector is still dominated by a few marketparticipants who possess significant market power. Suchmarket power is amplified by the significant barriers ofaccess for incomers. The new and emerging players inthe asset management industry therefore need to beassisted in firstly understanding the market and alsoidentifying points of entry.

It is in a survey of this nature that we are able to identifywhether such initiatives exist and if so what theireffectiveness has been in ensuring that we open up thesector and create an ecosystem that is receptive to newentrants, and for black asset managers in particular, tobe able to succeed within the sector. As 27four Invest-ment Managers has conducted this BEE.conomicsTransformation in South African Asset ManagementSurvey for the past 12 years, it has become an importantreference point for deliberations around the table withinABSIP structures in analysing and understanding theasset management industry and what its ongoingchallenges are. It is with this in mind that we welcomethe 2020 survey which indicates to us that not only dowe still have a lot of work to do but also identifiesparticular areas of focus that must become the focusarea for ABSIP and the various role players in the assetmanagement sector going forward.

7

Executive summary1. Black-owned market share• As at 30 June 2020, total assets managed by black-

owned firms advanced to R668 Billion, an increase of15% from last year.

• There are 51 black-owned asset managers acrossboth the public and private markets (2019: 50).

• The universe of participants includes a small numberof very large firms and a long tail of medium andsmall-sized firms. Median asset manager AUM is R1.6Billion and mean AUM is R13.1 Billion.

• Black market share of the total estimated SouthAfrican savings and investment pool is 9%.

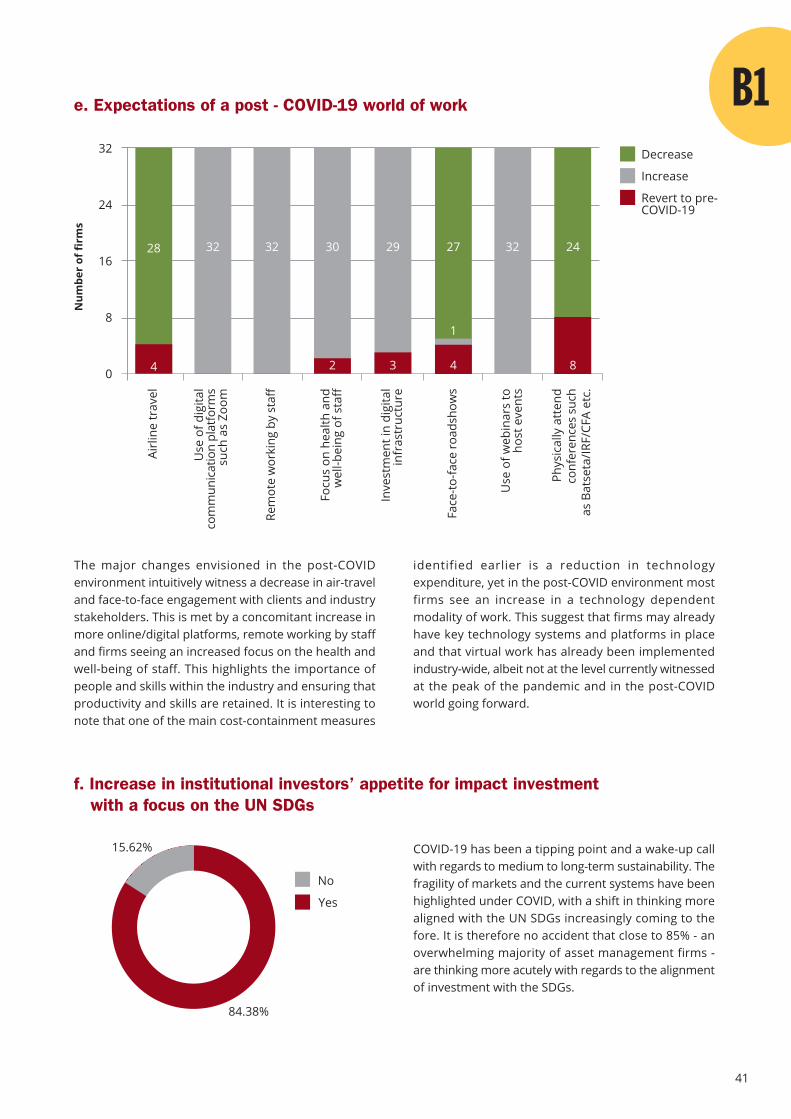

2. Impact of COVID-19• Around half of all participants expect COVID-19 to

have a negative impact on their bottom-line. Suchfirms have implemented a number of cost contain-ment measures which include reducing marketingbudgets, deferring or cancelling planned investments,placing freezes on new hires and taking bonus andsalary sacrifices.

• Only a handful of firms took advantage of governmentrelief measures such as tax deferral holidays.

• An overwhelming majority of firms envision a newworld of work with less air travel and an increase inremote working and use of technology-based commu-nication platforms.

• The pandemic has also brought impact investmentto the forefront as many debt and equity recoveryfunds have emerged to support businesses mitigatethe negative financial consequences inflicted by theeconomic slowdown.

3. Asset allocation trends andchanges in the demand side

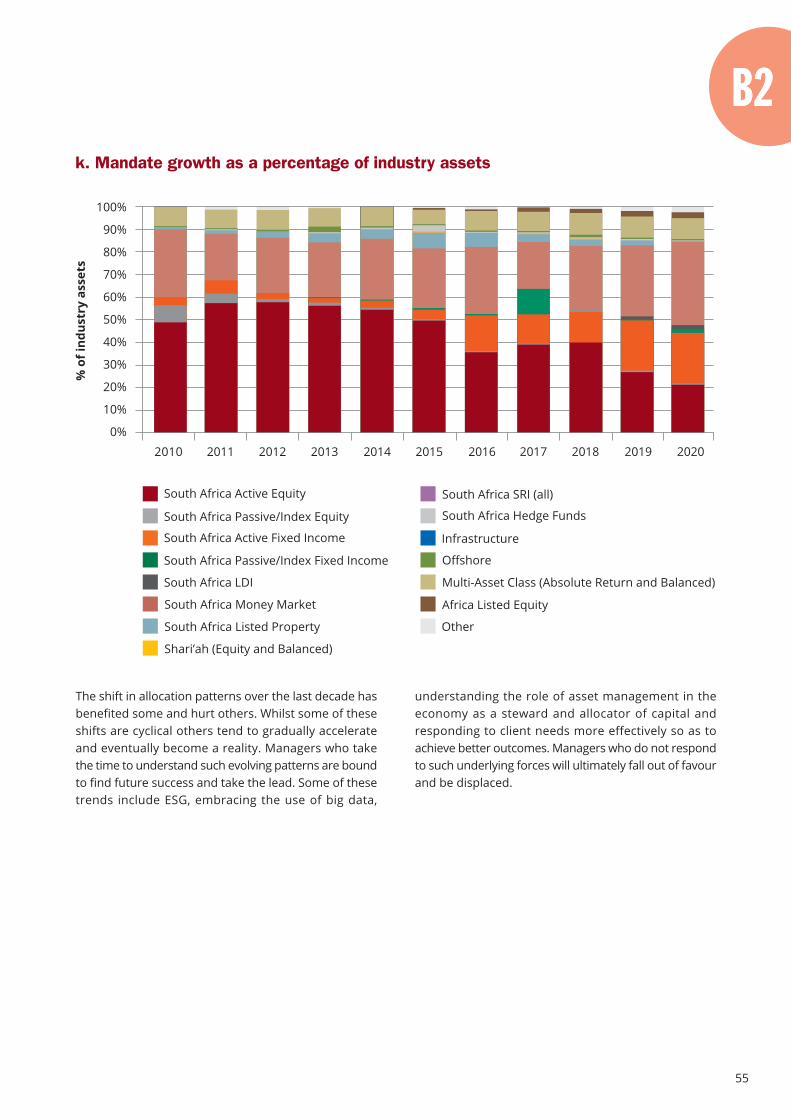

• Within public markets, just over 60% of industry assetsare currently invested in low risk money market andfixed income products. These are also low marginproducts and require significant scale to drive profit-ability. Domestic equities have progressively beenlosing market share over the past decade and nowmake up just 22% of AUM having made up 50% oftotal AUM in 2010. Exposure to domestic equities hasfallen sharply, a reflection of lacklustre performance,

low investor confidence and an economy on its knees.Outflows from domestic equities were equipoised byflows into domestic money market and fixed income,where the safety of real yields and low volatility wasfavoured by investors. The lion’s share of managersoperating in the public markets space are focused onthe management of specialist domestic equitymandates and have been the hardest hit by this shift.Managers with established fixed income and moneymarket offerings gained the most.

• Less than 2.5% of public markets AUM is managed inglobal mandates even though eleven firms have globalofferings. It is unfortunate that managers with globalofferings have not been able to build adequate scaleeven though institutions and individuals have takenfull advantage of the global exchange control allow-ance.

• The demand side in South Africa is changing, andinvestors have become much more discerning andless tolerant of lacklustre performance and high feesparticularly in the case of active fund management.Institutional investors are also searching for diversifiedsources of return that can match long-term liabilities,cushion portfolios from the shocks of market selloffs,meet developmental goals and deliver inflationbeating returns. Given these multiple objectives, wecan expect the industry to gradually adapt to suchpressures with more offerings emerging at oppositeends of the spectrum - costly high alpha alternativeswhere managers are paid for the delivery of long-term performance, and low-cost passive betasolutions.

4. Private markets, prescribedassets & change in regulations

• An already weak economy exacerbated by COVID-19has left government seeking a new narrative toaccelerate an economic recovery. As such, the ideaof using prescribed assets to help foster economicgrowth has resurfaced, packaged in the form of aninfrastructure fund to finance strategic projects bycombining capital from the public and private sectors,retirement funds, development finance institutionsand multilateral development banks. With expecta-tions of capital flows into real assets, the assetmanagement industry appears to be readying itself- new and existing firms are building capacity andskills to be able to manage such flows.

8

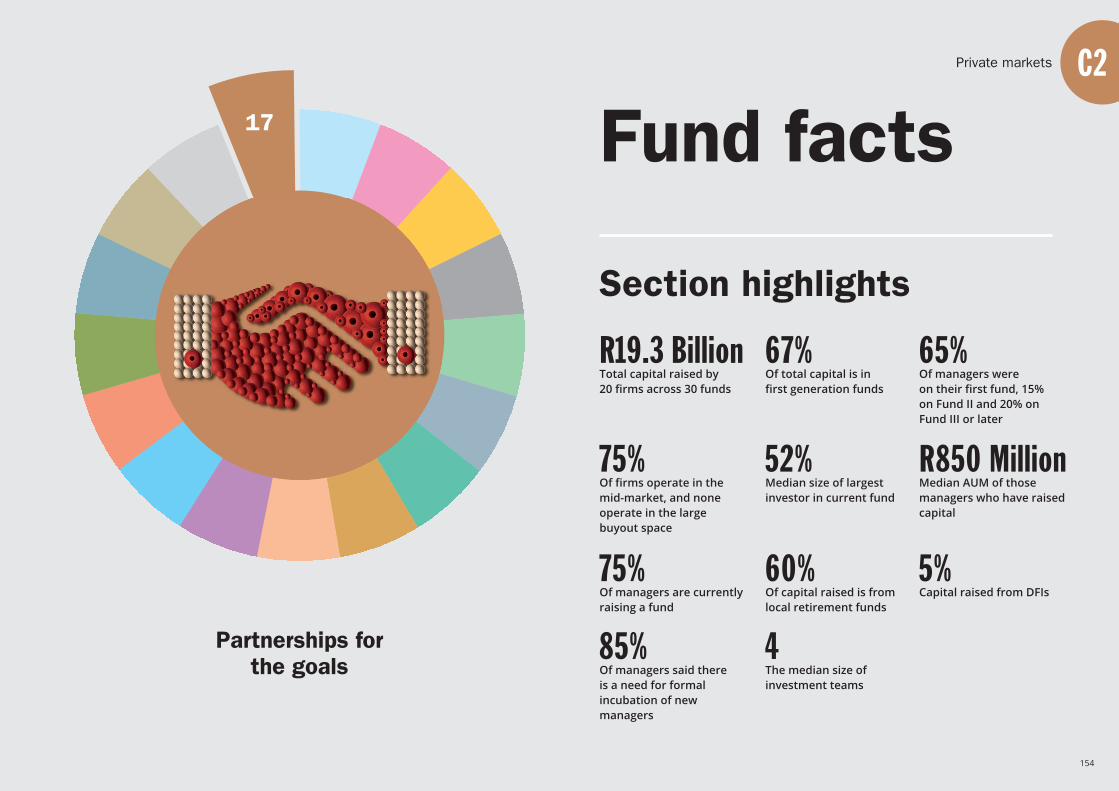

• Twenty private markets firms completed our surveythis year, which have raised a total of R19.3 Billionacross 30 funds, representing both an increase inparticipation and AUM from last year. While the overallasset size is encouraging, it is important to note thatthe universe of participating firms’ AUM is highlyskewed, with many managers currently at subscaleand continuing to experience challenges of longfundraising cycles.

• The resulting growth in appetite for impact investmentthrough unlisted assets may precipitate a change toRegulation 28 of the Pension Funds Act, whichcurrently caps private equity and hedge funds at 15%.Calls have been made by SAVCA to separate hedgefunds from private equity and gradually increase theprivate equity limit. The Minister of Finance haspublicly flirted with the idea of increasing the limitindicating that this is under review by the NationalTreasury. Similar calls have been made to amendCISCA to allow unit trusts to hold unlisted exposure.

5. Scale and distribution• There are now two firms who each manage more

than R100 Billion and collectively represent almosthalf (48%) of total assets. Breaking beyond the R15Billion mark appears to be the largest challenge formanagers. Most private market participants fall inthe <R1 Billion category.

• Ninety percent of public market asset managers’ assetbase is sourced from institutional investors such asretirement funds and are therefore concerned aboutthe consolidation of retirement funds under umbrellaarrangements. This apprehension is not without meritas argued in “The Shift to Umbrella Funds – DoesConsolidation Support Transformation?”.

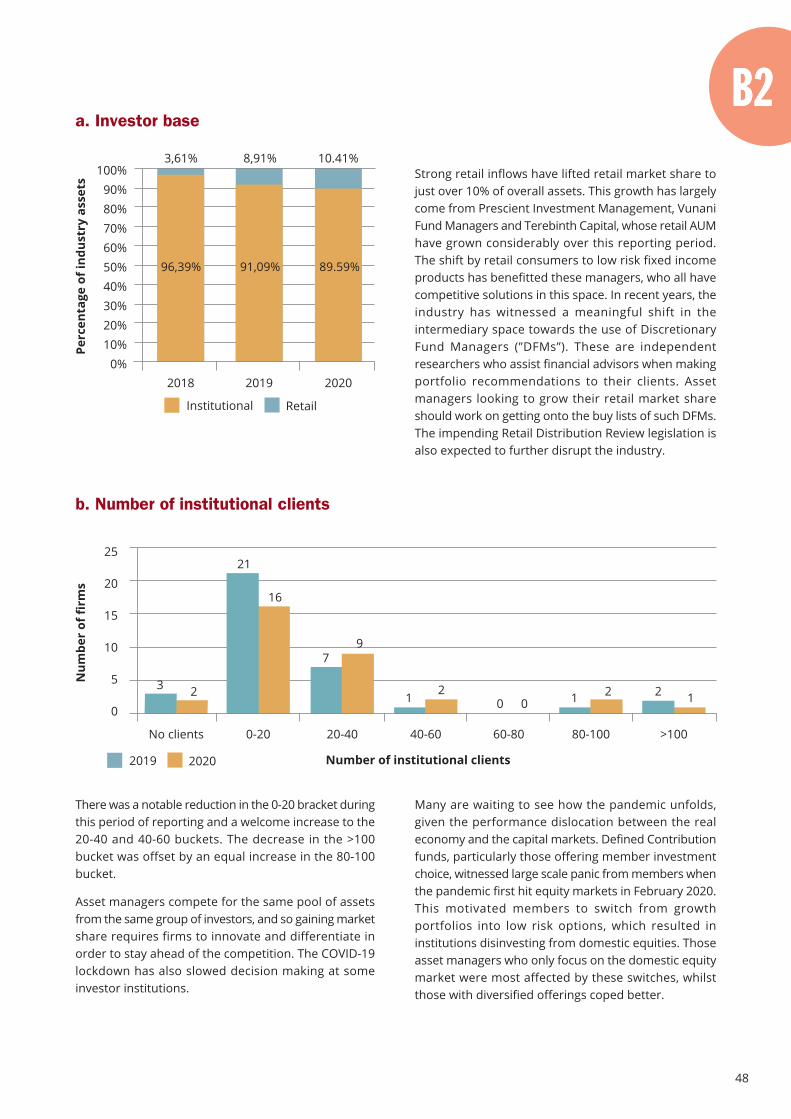

• Retail penetration appears to be lethargically prog-ressing with black-owned asset managers’ marketshare of the unit trust industry now at 9% representedby 25 firms managing 106 unit trust portfolios.

• Firms also envision a greater increase in mergers andacquisitions as companies harness skills, expertiseand resources together in a shift towards greatermarket consolidation.

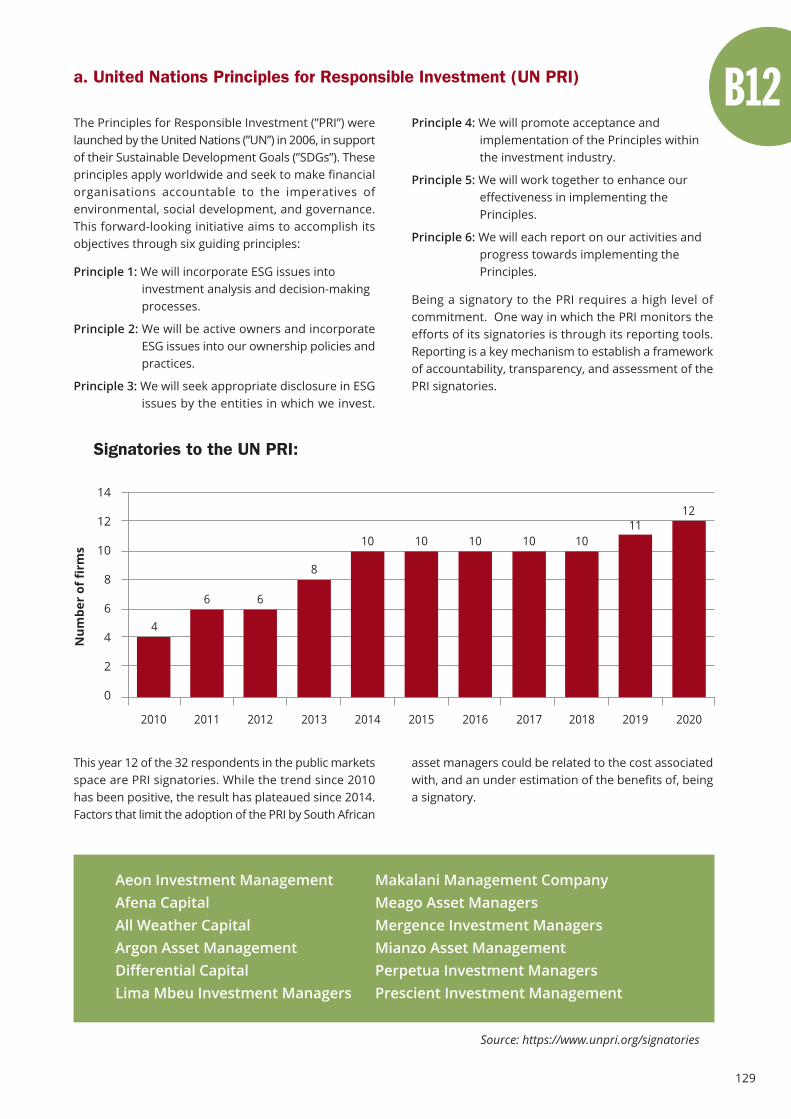

6. ESG• Twelve firms are signatories to the UN PRI.

• Ninety percent of all firms integrate ESG into theirinvestment processes and over two-thirds of publicmarkets managers acknowledge that ESG factorshave impacted the risk and return characteristics ofthe portfolios they manage.

• The overwhelming majority of firms agree that thepandemic has once again exposed the fragility of thefinancial markets and current economic systems andthat a shift of alignment to achieving the UN SDGs isbecoming urgent.

7. Socio-economic statistics• The revenue model of asset management is built for

scale, and so the increase in industry AUM did nottranslate into an increase in job creation. The industrycurrently employs a total of 638 people, marginallydown from last year.

• There was little movement in the demographiccomposition of asset manager teams since 2019.None of the managers’ teams are homogenous andpositively reflect both race and gender diversity.

• There was a marked improvement in the number offirms achieving profitability as 76% of all firms indica-ted that they are profitable up from 68% recorded inthe previous year.

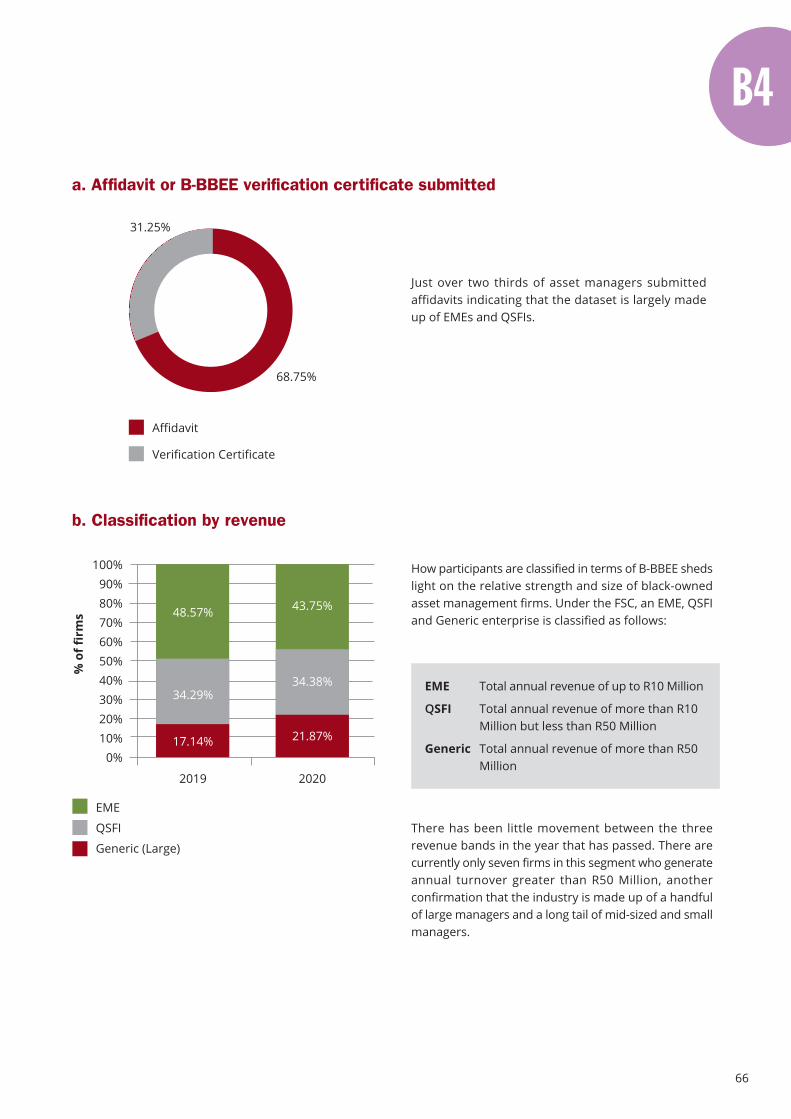

• There was overall improvement in the size of publicmarkets firms based on revenue as 44% (2019: 48%)are classified as EMEs, 34% (2019: 34%) as QSFIs and22% (2019: 17%) as large enterprises.

• Women representation at both ownership and direc-torship levels continue to disappoint relative to allother sectors within the economy (B-BBEE Commis-sion, 2020).

• Over half the universe of public markets managersprocure less than 20% of services from more than51% black-owned and / or 30% black women-ownedbusinesses suggesting that the industries from whichasset managers procure services from are largelyuntransformed.

• Going into 2021, transformation of the financial sectorwill be in the spotlight with new legislation focusedon achieving parity within the sector coming into play.Such legislation includes the Employment EquityAmendment Bill, currently in draft form, which willallow for the Minister of Employment and Labour toidentify sectoral numerical targets to ensure repre-sentation reflective of our demographics. We can alsoexpect to see the Conduct of Financial InstitutionsBill come into effect, and an updated iteration of theFinancial Sector Code gazetted.

9

10

17 sustainable developmentgoals (SDGs) to transform

our world

1. No poverty 2. Zero hunger 3. Good health& well-being

4. Quality education

7. Affordable& clean energy

8. Decent work &economic growth

9. Industry, innovation& infrastructure

10. Reducedinequalities

11. Sustainable cities& communities

12. Responsibleconsumption& production

13. Climate action 14. Life below water

5. Gender equality 6. Clean water& sanitation

15. Life on land 16. Peace, justice &strong institutions

17. Partnershipsfor the goals

Overallparticipationstatistics

11

12

SectoroverviewSection highlights

DECLINEDomestic equities have experiencedthe worst decline over the decade

51The number of black-owned assetmanagers across both public andprivate markets

R668 BillionTotal industry AUM

R1.6 BillionMedian asset manager AUM

R13.1 BillionMean asset manager AUM

8.8%Black market share of the total estimated South African savings and investment pool

8.7%Black market share of the unit trustindustry

10.5%Black market share of the privatemarkets industry

638The number of people employed in theindustry, down 4.5% from last year

76%The percentage of profitable firms

Decent work &economic growth

8

13

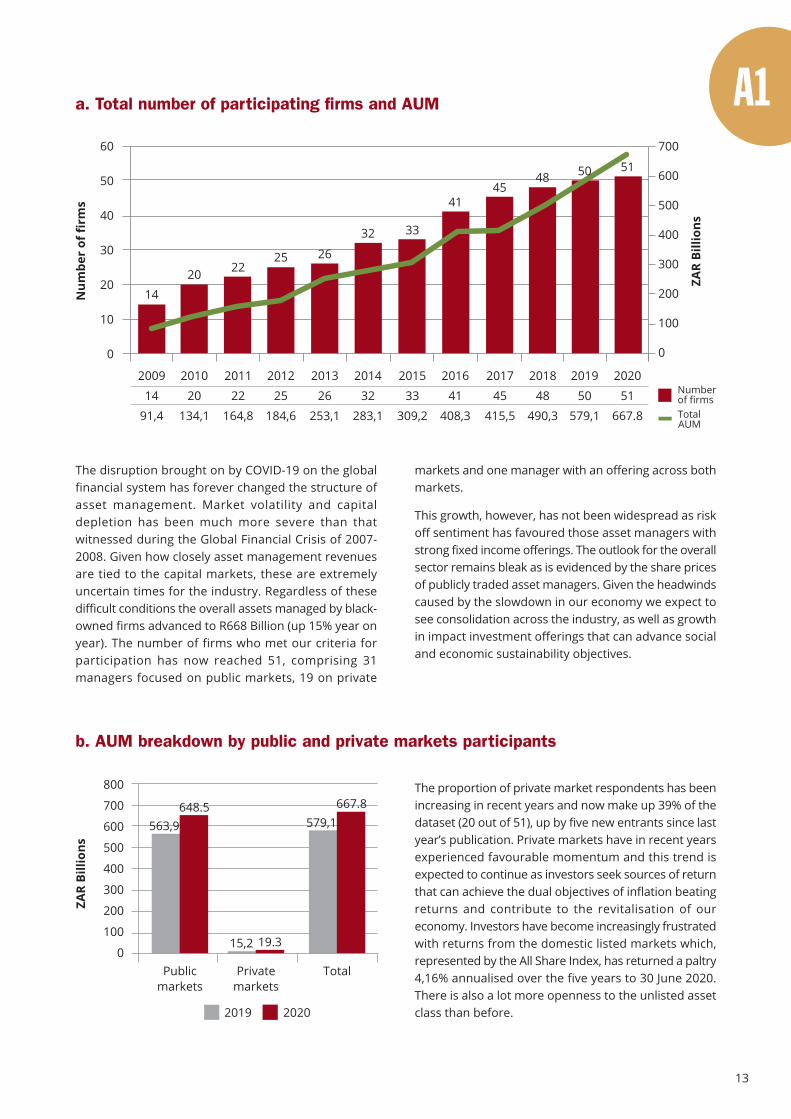

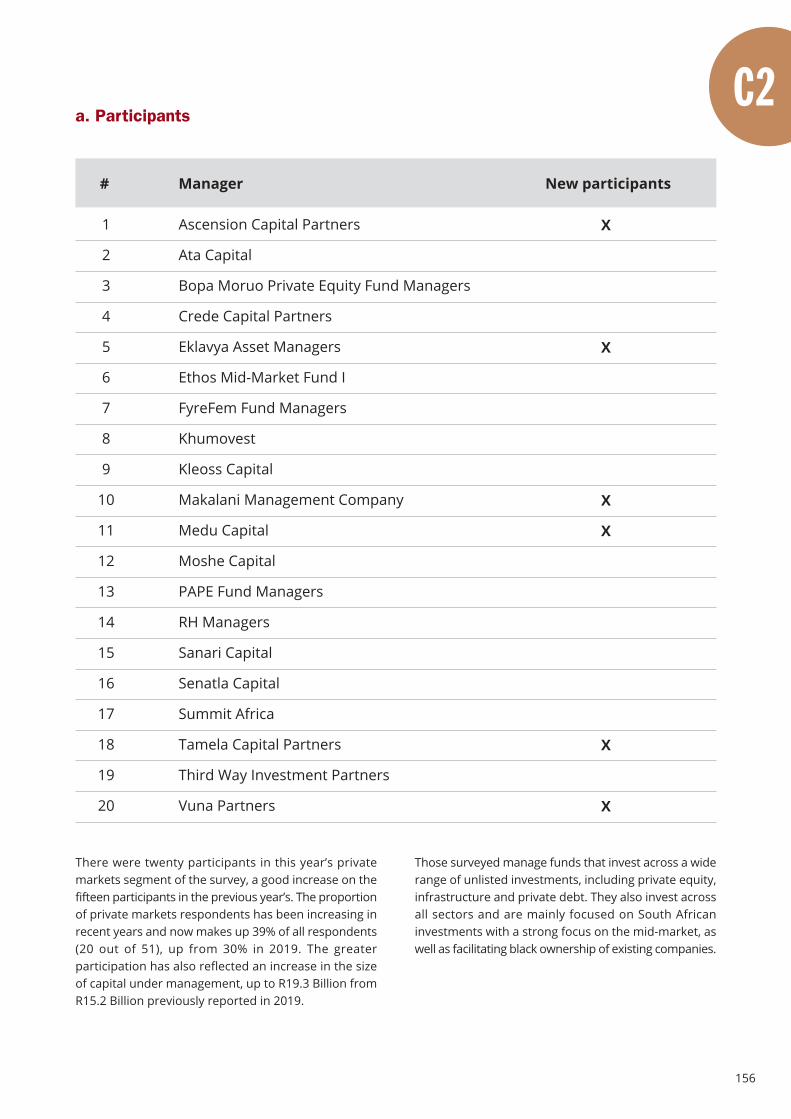

The proportion of private market respondents has beenincreasing in recent years and now make up 39% of thedataset (20 out of 51), up by five new entrants since lastyear’s publication. Private markets have in recent yearsexperienced favourable momentum and this trend isexpected to continue as investors seek sources of returnthat can achieve the dual objectives of inflation beatingreturns and contribute to the revitalisation of oureconomy. Investors have become increasingly frustratedwith returns from the domestic listed markets which,represented by the All Share Index, has returned a paltry4,16% annualised over the five years to 30 June 2020.There is also a lot more openness to the unlisted assetclass than before.

The disruption brought on by COVID-19 on the globalfinancial system has forever changed the structure ofasset management. Market volatility and capitaldepletion has been much more severe than thatwitnessed during the Global Financial Crisis of 2007-2008. Given how closely asset management revenuesare tied to the capital markets, these are extremelyuncertain times for the industry. Regardless of thesedifficult conditions the overall assets managed by black-owned firms advanced to R668 Billion (up 15% year onyear). The number of firms who met our criteria forparticipation has now reached 51, comprising 31managers focused on public markets, 19 on private

markets and one manager with an offering across bothmarkets.

This growth, however, has not been widespread as riskoff sentiment has favoured those asset managers withstrong fixed income offerings. The outlook for the overallsector remains bleak as is evidenced by the share pricesof publicly traded asset managers. Given the headwindscaused by the slowdown in our economy we expect tosee consolidation across the industry, as well as growthin impact investment offerings that can advance socialand economic sustainability objectives.

a. Total number of participating firms and AUM

Num

ber

of fi

rms

ZAR

Billi

ons

2018

48

490,3

60

50

40

30

20

10

0

700

600

500

400

300

200

100

0

2009

14

91,4

2010

20

134,1

2011

22

164,8

2012

25

184,6

2013

26

253,1

2014

32

283,1

2015

33

309,2

2016

41

408,3

2017

45

415,5

2019

50

579,1

2020

51

667.8

48

14

20 2225 26

32 33

4145

50 51

Numberof firmsTotalAUM

ZAR

Billi

ons

b. AUM breakdown by public and private markets participants

800

700

600

500

400

300

200

100

0Private

marketsPublic

marketsTotal

563,9

15,2

579,1648.5

19.3

667.8

2019 2020

14

Ascension Capital Partners

Eklavya Asset Managers

Idwala Capital

Makalani Management Company

Medu Capital

Tamela Capital Partners

Volantis Capital

Vuna Partners

2020 saw seven new participants join the survey withfive firms operating in private markets and two in publicmarkets. Makalani Management Company is not a newentrant to the survey. They previously only participatedunder public markets and now also participate underprivate markets. Idwala Capital and Tamela CapitalPartners are both re-entries to the survey havingpreviously participated in the 2018 edition. Buddingnew entrants Volantis Capital has come to market witha fixed income offering and Vuna Partners is a private

c. Exits and entrants to the survey

Entrants Public PrivateMarkets Markets

Acanthin

Black Mountain Investment Management

Convergence Partners Management

Differential Capital

Legacy Africa Fund Managers

Pan-African Asset Management

Exits Public PrivateMarkets Markets

equity manager focused on the mid-market sector.There were a total of six exits this year, five in publicmarkets and one in private markets. One of the six isno longer in operation. Reasons for non-participationinclude: missing the deadline to submit data, beingfocused on retail clients only, have experienced acontraction in AUM or not been successful in assetgathering, no longer meet the criteria for participationor find no value in participating.

15

d. Public markets participants

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

Prescient Investment Management

Vunani Fund Managers

Taquanta Asset Managers

Kagiso Asset Management

Makalani Management Company

Mergence Investment Managers

Argon Asset Management

Aeon Investment Management

Afena Capital

Meago Asset Managers

Sentio Capital Management

All Weather Capital

Prowess Investment Managers

Balondolozi Investment Services

Mianzo Asset Management

First Avenue Investment Management

Cachalia Capital

Perpetua Investment Managers

Benguela Global Fund Managers

Terebinth Capital

Fortitudine Vincimus Capital Advisors

Lodestar Fund Managers

Lunar Capital

MSM Property Fund

Independent Alternatives Investment Managers

Aluwani Capital Partners

Excelsia Capital

Value Capital Partners

Idwala Capital

Lima Mbeu Investment Managers

Ngwedi Investment Managers

Volantis Capital

21.84

20.95

20.77

18.59

15.89

15.76

15.26

15.16

14.67

14.30

13.01

12.17

11.59

10.22

9.92

9.42

8.14

7.75

7.36

7.25

5.92

5.50

5.46

4.91

4.91

4.58

4.17

4.00

2.92

2.81

1.92

1.03

R100 694.68

R42 158.65

R217 635.00

R30 291.88

R150.00

R32 592.97

R25 270.03

R12 377.62

R4 152.32

R7 935.00

R15 894.00

R8 029.00

R7 310.96

R5 454.00

R7 700.00

R5 646.76

R822.00

R9 678.57

R4 547.00

R7 163.20

R263.20

R904.00

R69.20

R268.68

R125.00

R87 421.26

R1 221.10

R5 480.02

R647.93

R532.85

R6 042.00

R0.00

38

33

39

47

8

48

30

8

12

12

20

13

14

16

14

6

3

26

16

6

3

2

2

2

3

34

10

16

2

6

10

4

Fund manager Years inoperation

AUM(ZAR Millions)

Total staffheadcount

Total R648 468.88 503

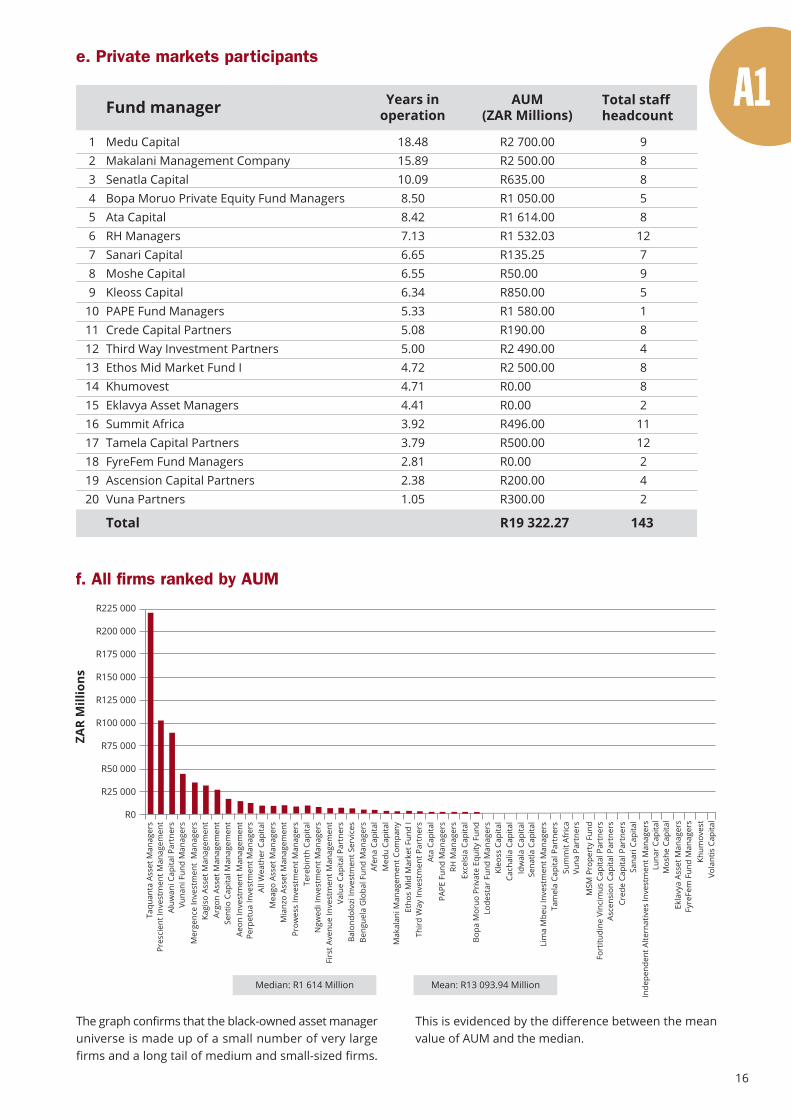

The graph confirms that the black-owned asset manageruniverse is made up of a small number of very largefirms and a long tail of medium and small-sized firms.

e. Private markets participants

123456789

1011121314151617181920

Medu CapitalMakalani Management CompanySenatla CapitalBopa Moruo Private Equity Fund ManagersAta CapitalRH ManagersSanari CapitalMoshe CapitalKleoss CapitalPAPE Fund ManagersCrede Capital PartnersThird Way Investment PartnersEthos Mid Market Fund IKhumovestEklavya Asset ManagersSummit AfricaTamela Capital PartnersFyreFem Fund ManagersAscension Capital PartnersVuna Partners

18.4815.8910.098.508.427.136.656.556.345.335.085.004.724.714.413.923.792.812.381.05

R2 700.00R2 500.00R635.00R1 050.00R1 614.00R1 532.03R135.25R50.00R850.00R1 580.00R190.00R2 490.00R2 500.00R0.00R0.00R496.00R500.00R0.00R200.00R300.00

98858

12795184882

1112242

Total R19 322.27 143

Fund manager Years inoperation

AUM(ZAR Millions)

Total staffheadcount

f. All firms ranked by AUM

ZAR

Mill

ions

R225 000

R200 000

R175 000

R150 000

R125 000

R100 000

R75 000

R50 000

R25 000

R0

Taqu

anta

Ass

et M

anag

ers

Pres

cien

t Inv

estm

ent M

anag

emen

tAl

uwan

i Cap

ital P

artn

ers

Vuna

ni F

und

Man

ager

sM

erge

nce

Inve

stm

ent

Man

ager

sKa

giso

Ass

et M

anag

emen

tAr

gon

Asse

t Man

agem

ent

Sent

io C

apita

l Man

agem

ent

Aeon

Inve

stm

ent M

anag

emen

tPe

rpet

ua In

vest

men

t Man

ager

sAl

l Wea

ther

Cap

ital

Mea

go A

sset

Man

ager

sM

ianz

o As

set M

anag

emen

tPr

owes

s In

vest

men

t Man

ager

sTe

rebi

nth

Capi

tal

Ngw

edi I

nves

tmen

t Man

ager

sFi

rst A

venu

e In

vest

men

t Man

agem

ent

Valu

e Ca

pita

l Par

tner

sBa

lond

oloz

i Inv

estm

ent S

ervi

ces

Beng

uela

Glo

bal F

und

Man

ager

sAf

ena

Capi

tal

Med

u Ca

pita

lM

akal

ani M

anag

emen

t Com

pany

Etho

s M

id M

arke

t Fun

d I

Thir

d W

ay In

vest

men

t Par

tner

sAt

a Ca

pita

lPA

PE F

und

Man

ager

sRH

Man

ager

sEx

cels

ia C

apita

lBo

pa M

oruo

Pri

vate

Equ

ity F

und

Lode

star

Fun

d M

anag

ers

Kleo

ss C

apita

lCa

chal

ia C

apita

lId

wal

a Ca

pita

lSe

natla

Cap

ital

Lim

a M

beu

Inve

stm

ent M

anag

ers

Tam

ela

Capi

tal P

artn

ers

Sum

mit

Afri

caVu

na P

artn

ers

MSM

Pro

pert

y Fu

ndFo

rtitu

dine

Vin

cim

us C

apita

l Par

tner

sAs

cens

ion

Capi

tal P

artn

ers

Cred

e Ca

pita

l Par

tner

sSa

nari

Cap

ital

Inde

pend

ent A

ltern

ativ

es In

vest

men

t Man

ager

sLu

nar

Capi

tal

Mos

he C

apita

lEk

lavy

a As

set M

anag

ers

Fyre

Fem

Fun

d M

anag

ers

Khum

oves

tVo

lant

is C

apita

l

Median: R1 614 Million Mean: R13 093.94 Million

This is evidenced by the difference between the meanvalue of AUM and the median.

16

17

This year, Prescient Investment Management joinsTaquanta Asset Managers in the plus R100 Billion club.Collectively the two managers represent almost half(48%) of total assets managed by all firms thatparticipated in the survey. Breaking beyond the R15

Billion mark appears to be the largest challenge formanagers. The majority of private market participantsfall in the <R1 Billion category. Little has changed fromprevious years as the data re-affirms the lopsidedtopography of this group of managers.

Concentration in the pool increased between 2019 and2020 with the top five and ten firms now representing72% and 86% of overall industry assets, respectively.The COVID-19 shock to the capital markets in Februarythis year resulted in members of retirement fundsswitching out of growth portfolios into low risk portfolios

heavily weighted to fixed income securities. Assetmanagers with established track records in fixed income,of which there are several in the top 10, were recipientsof this flow. In this light, the increase in concentrationlevels is not surprising.

g. Assets managed by firm size

>100bn

50 to 100bn

30 to 50bn

15 to 30bn

5 to 15bn

1 to 5bn

<1bn

Total AUM of firmin ZAR Billions

Number of firms

Total

1

1

2

4

5

10

18

1

1

2

3

6

11

21

1

1

2

4

6

11

23

1

2

2

3

9

13

20

2016201720182019

41454850

2

1

3

2

11

11

21

2020

51

h. Combined market share of top firms by AUM

% o

f ind

ustr

y as

sets

100%90%80%70%60%50%40%30%20%10%

0%

Top 5 Top 10

2014 2015 2016 2017 2018 2020

69,89%

88,01% 86,47%

68,59%76,83%

94,01%

74,21%

91,26%83,59%

64,96%

83,40%

67,04%

85.96%

71.95%

2019

18

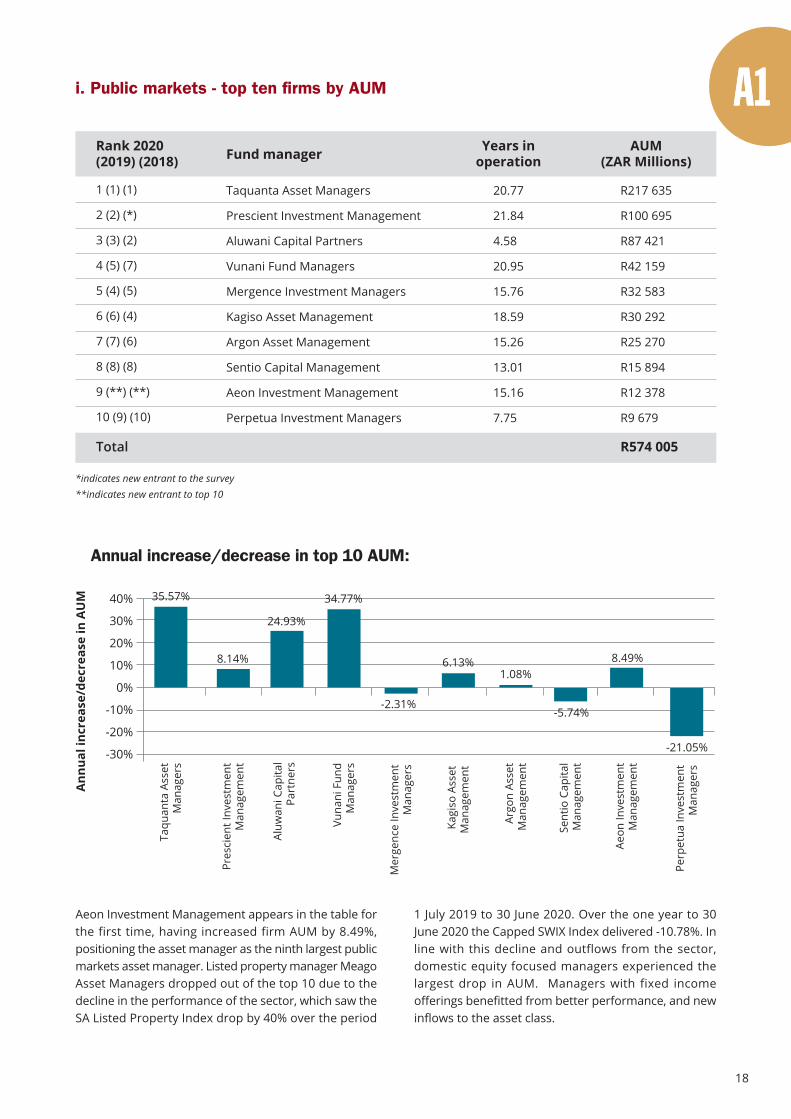

Aeon Investment Management appears in the table forthe first time, having increased firm AUM by 8.49%,positioning the asset manager as the ninth largest publicmarkets asset manager. Listed property manager MeagoAsset Managers dropped out of the top 10 due to thedecline in the performance of the sector, which saw theSA Listed Property Index drop by 40% over the period

1 July 2019 to 30 June 2020. Over the one year to 30June 2020 the Capped SWIX Index delivered -10.78%. Inline with this decline and outflows from the sector,domestic equity focused managers experienced thelargest drop in AUM. Managers with fixed incomeofferings benefitted from better performance, and newinflows to the asset class.

i. Public markets - top ten firms by AUM

R217 635

R100 695

R87 421

R42 159

R32 583

R30 292

R25 270

R15 894

R12 378

R9 679

AUM(ZAR Millions)

20.77

21.84

4.58

20.95

15.76

18.59

15.26

13.01

15.16

7.75

Taquanta Asset Managers

Prescient Investment Management

Aluwani Capital Partners

Vunani Fund Managers

Mergence Investment Managers

Kagiso Asset Management

Argon Asset Management

Sentio Capital Management

Aeon Investment Management

Perpetua Investment Managers

1 (1) (1)

2 (2) (*)

3 (3) (2)

4 (5) (7)

5 (4) (5)

6 (6) (4)

7 (7) (6)

8 (8) (8)

9 (**) (**)

10 (9) (10)

Years inoperationFund managerRank 2020

(2019) (2018)

R574 005Total

*indicates new entrant to the survey**indicates new entrant to top 10

Ann

ual i

ncre

ase/

decr

ease

in A

UM 40%

30%

20%

10%

0%

-10%

-20%

-30%

35.57%

8.14%

24.93%

34.77%

-2.31%

6.13%1.08%

-5.74%

8.49%

Annual increase/decrease in top 10 AUM:

Argo

n As

set

Man

agem

ent

Pres

cien

t Inv

estm

ent

Man

agem

ent

Kagi

so A

sset

Man

agem

ent

Mer

genc

e In

vest

men

tM

anag

ers

Sent

io C

apita

lM

anag

emen

t

Taqu

anta

Ass

etM

anag

ers

Aluw

ani C

apita

lPa

rtne

rs

Vuna

ni F

und

Man

ager

s

Aeon

Inve

stm

ent

Man

agem

ent

Perp

etua

Inve

stm

ent

Man

ager

s

-21.05%

19

j. Private markets - top ten firms by AUM

R2 700

R2 500

R2 500

R2 490

R1 614

R1 580

R1 532

R1 050

R850

R635

18.48

4.72

15.89

5.00

8.42

5.33

7.13

8.50

6.34

10.09

Medu Capital

Ethos Mid Market Fund I

Makalani Management Company

Third Way Investment Partners

Ata Capital

PAPE Fund Managers

RH Managers

Bopa Moruo Private Equity Fund Managers

Kleoss Capital

Senatla Capital

1(*)

2(2)

3(**)

4(3)

5(4)

6(5)

7(7)

8(6)

9(8)

10(9)

R17 451Total

AUM(ZAR Millions)

Years inoperationFund managerRank 2020 (2019)

Both Medu Capital and Makalani Management Companymake the top 10 this year with Summit Africa exitingthe top 10. Many of the firms are still raising capital forfund closure, whereas some have closed and begundeployment. Overall private market assets haveincreased from R15.2 Billion recorded last year to R19.3Billion this year - the top 10 account for 90% of thisfigure. This universe of managers include managersfocused on private equity, debt, and infrastructure.

As South Africa responds to its developmental needsthrough infrastructure investment, inviting blendedfinance and public private partnership opportunities,we expect this pool of managers to benefit from suchactivity. The biggest tailwind for the industry is theexpected increase in the retirement fund investmentlimit of 10% to private equity which we understand iscurrently under review by the National Treasury.

k. Black asset management market share of the overall savings pool in South Africa

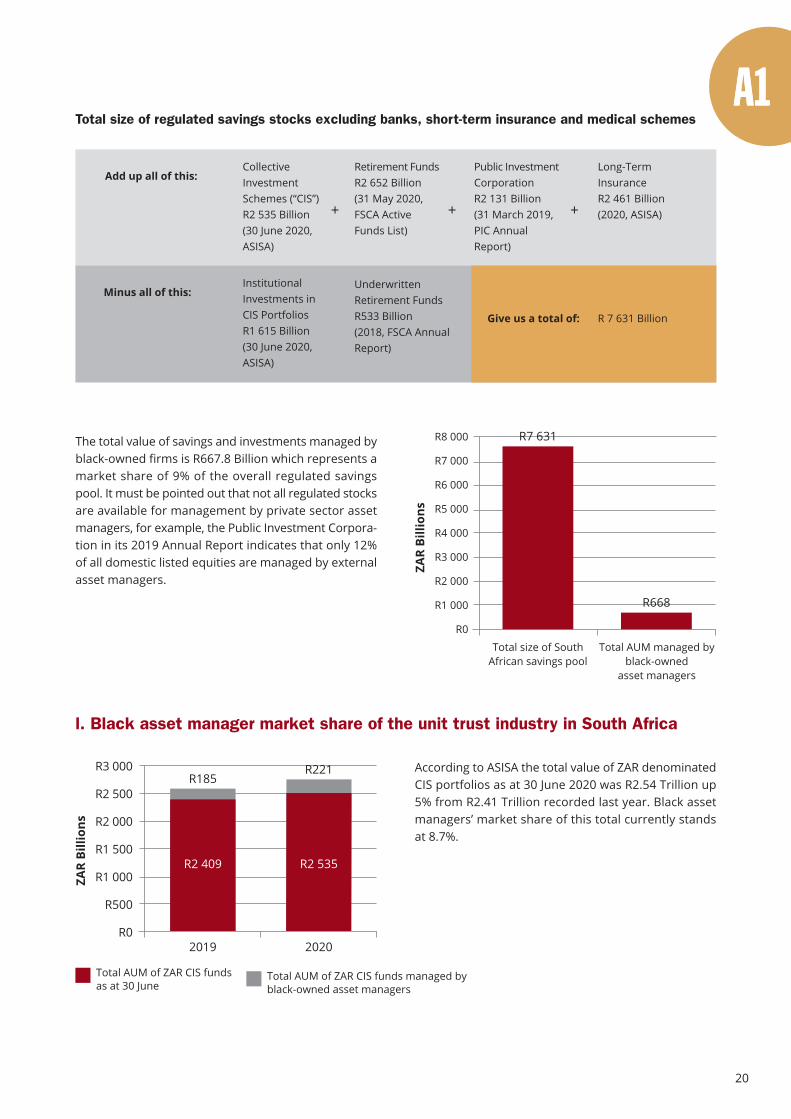

To calculate the total black market share of the regulatedsavings pool in South Africa we need to first calculatethe total size of regulated savings stocks. This calculationis provided next and excludes short-term insurance,medical schemes and banking stocks. It is important to

note that there is no official source for this statistic anddifferent figures have been quoted in the industry,varying from R6.5 Trillion to R8.5 Trillion. The valuesprovided are from a range of sources which report atdifferent times.

*indicates new entrant to the survey**indicates new entrant to top 10

20

The total value of savings and investments managed byblack-owned firms is R667.8 Billion which represents amarket share of 9% of the overall regulated savingspool. It must be pointed out that not all regulated stocksare available for management by private sector assetmanagers, for example, the Public Investment Corpora-tion in its 2019 Annual Report indicates that only 12%of all domestic listed equities are managed by externalasset managers.

According to ASISA the total value of ZAR denominatedCIS portfolios as at 30 June 2020 was R2.54 Trillion up5% from R2.41 Trillion recorded last year. Black assetmanagers’ market share of this total currently standsat 8.7%.

ZAR

Billi

ons

R8 000

R7 000

R6 000

R5 000

R4 000

R3 000

R2 000

R1 000

R0

Total size of SouthAfrican savings pool

R7 631

R668

Total AUM managed byblack-owned

asset managers

l. Black asset manager market share of the unit trust industry in South Africa

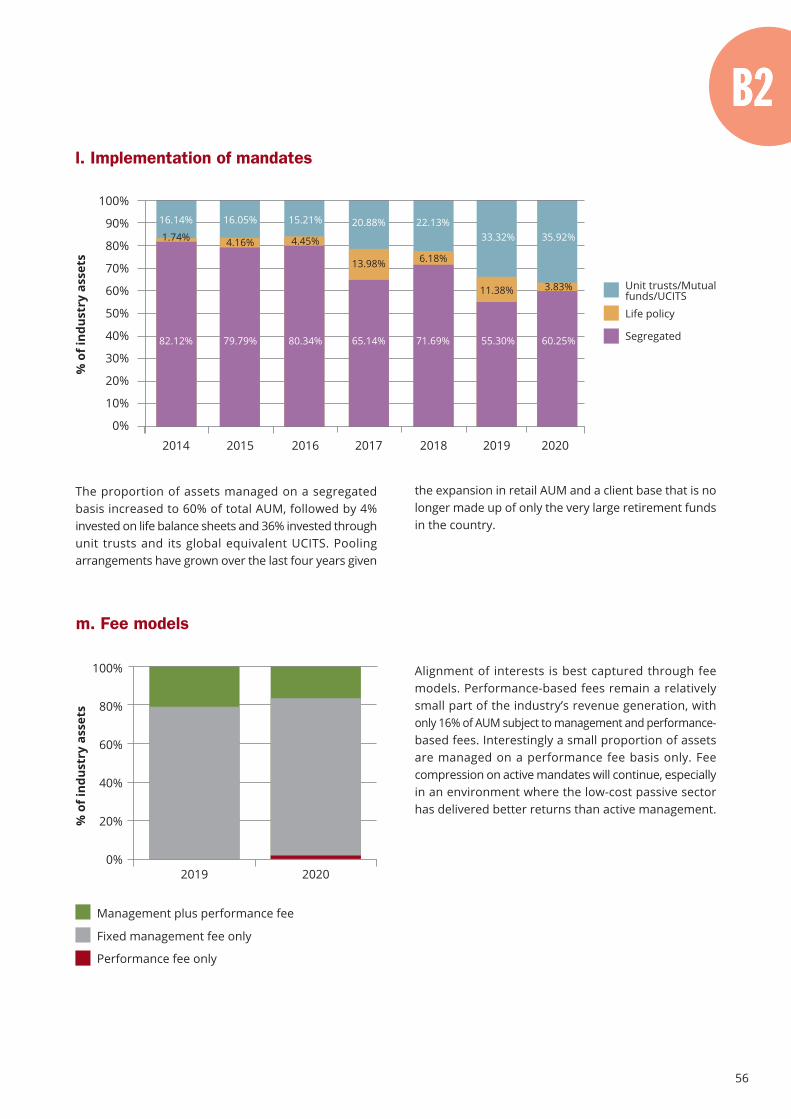

Total AUM of ZAR CIS funds managed byblack-owned asset managers

Total AUM of ZAR CIS fundsas at 30 June

ZAR

Billi

ons

R3 000

R2 500

R2 000

R1 500

R1 000

R500

R02019 2020

R2 409 R2 535

R185

Total size of regulated savings stocks excluding banks, short-term insurance and medical schemes

Minus all of this:InstitutionalInvestments inCIS PortfoliosR1 615 Billion(30 June 2020,ASISA)

UnderwrittenRetirement FundsR533 Billion(2018, FSCA AnnualReport)

Add up all of this:CollectiveInvestmentSchemes (“CIS”)R2 535 Billion(30 June 2020,ASISA)

Retirement FundsR2 652 Billion(31 May 2020,FSCA ActiveFunds List)

Public InvestmentCorporationR2 131 Billion(31 March 2019,PIC AnnualReport)

Long-TermInsuranceR2 461 Billion(2020, ASISA)+ + +

Give us a total of: R 7 631 Billion

R221

21

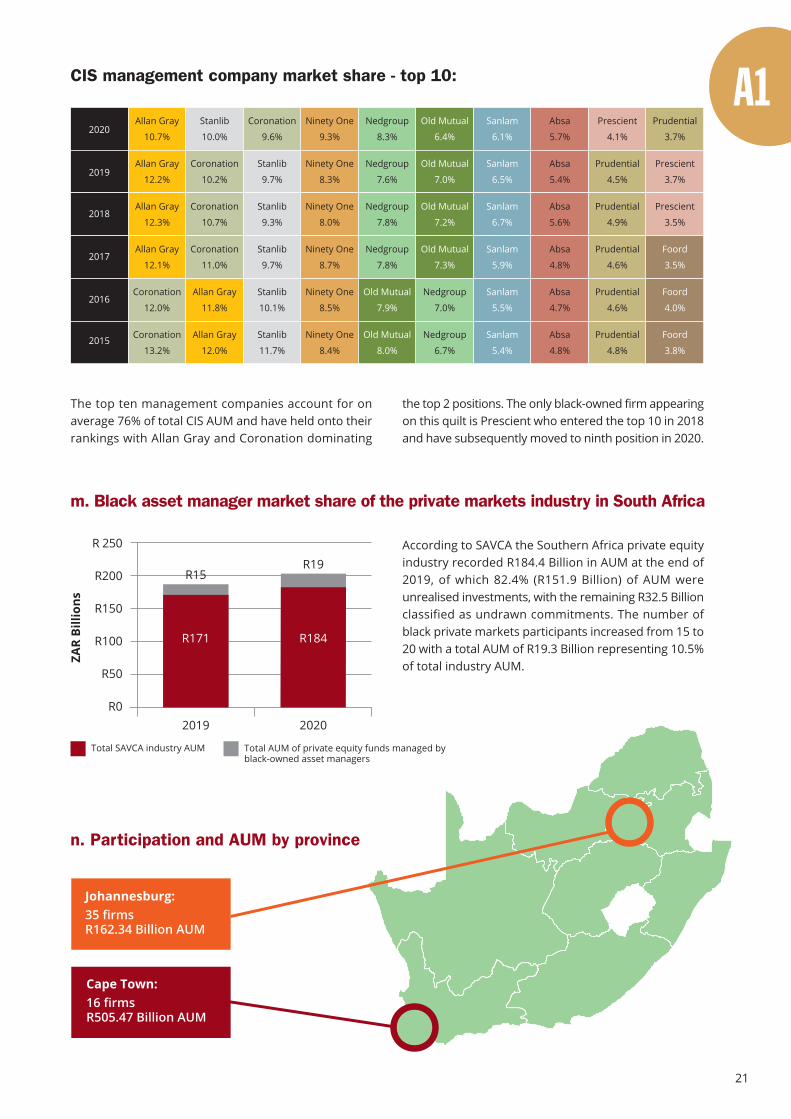

n. Participation and AUM by province

Cape Town:16 firmsR505.47 Billion AUM

Johannesburg:35 firmsR162.34 Billion AUM

According to SAVCA the Southern Africa private equityindustry recorded R184.4 Billion in AUM at the end of2019, of which 82.4% (R151.9 Billion) of AUM wereunrealised investments, with the remaining R32.5 Billionclassified as undrawn commitments. The number ofblack private markets participants increased from 15 to20 with a total AUM of R19.3 Billion representing 10.5%of total industry AUM.

The top ten management companies account for onaverage 76% of total CIS AUM and have held onto theirrankings with Allan Gray and Coronation dominating

2020

2019

2018

2017

2016

2015

Allan Gray

10.7%

Allan Gray

12.2%

Allan Gray

12.3%

Allan Gray

12.1%

Allan Gray

11.8%

Allan Gray

12.0%

Stanlib

10.0%

Stanlib

9.7%

Stanlib

9.7%

Stanlib

9.3%

Stanlib

10.1%

Stanlib

11.7%

Coronation

9.6%

Coronation

10.2%

Coronation

10.7%

Coronation

11.0%

Coronation

12.0%

Coronation

13.2%

Ninety One

9.3%

Ninety One

8.3%

Ninety One

8.0%

Ninety One

8.7%

Ninety One

8.5%

Ninety One

8.4%

Nedgroup

8.3%

Nedgroup

7.6%

Nedgroup

7.8%

Nedgroup

7.8%

Nedgroup

7.0%

Nedgroup

6.7%

Old Mutual

6.4%

Old Mutual

7.0%

Old Mutual

7.2%

Old Mutual

7.3%

Old Mutual

7.9%

Old Mutual

8.0%

Sanlam

6.1%

Sanlam

6.5%

Sanlam

6.7%

Sanlam

5.9%

Sanlam

5.5%

Sanlam

5.4%

Absa

5.7%

Absa

5.4%

Absa

5.6%

Absa

4.8%

Absa

4.7%

Absa

4.8%

Prescient

4.1%

Prescient

3.7%

Prescient

3.5%

Prudential

3.7%

Prudential

4.5%

Prudential

4.9%

Prudential

4.6%

Prudential

4.6%

Prudential

4.8%

Foord

3.5%

Foord

4.0%

Foord

3.8%

CIS management company market share - top 10:

m. Black asset manager market share of the private markets industry in South Africa

ZAR

Billi

ons

R 250

R200

R150

R100

R50

R0

Total AUM of private equity funds managed byblack-owned asset managers

Total SAVCA industry AUM

2019 2020

R171 R184

R15R19

the top 2 positions. The only black-owned firm appearingon this quilt is Prescient who entered the top 10 in 2018and have subsequently moved to ninth position in 2020.

22

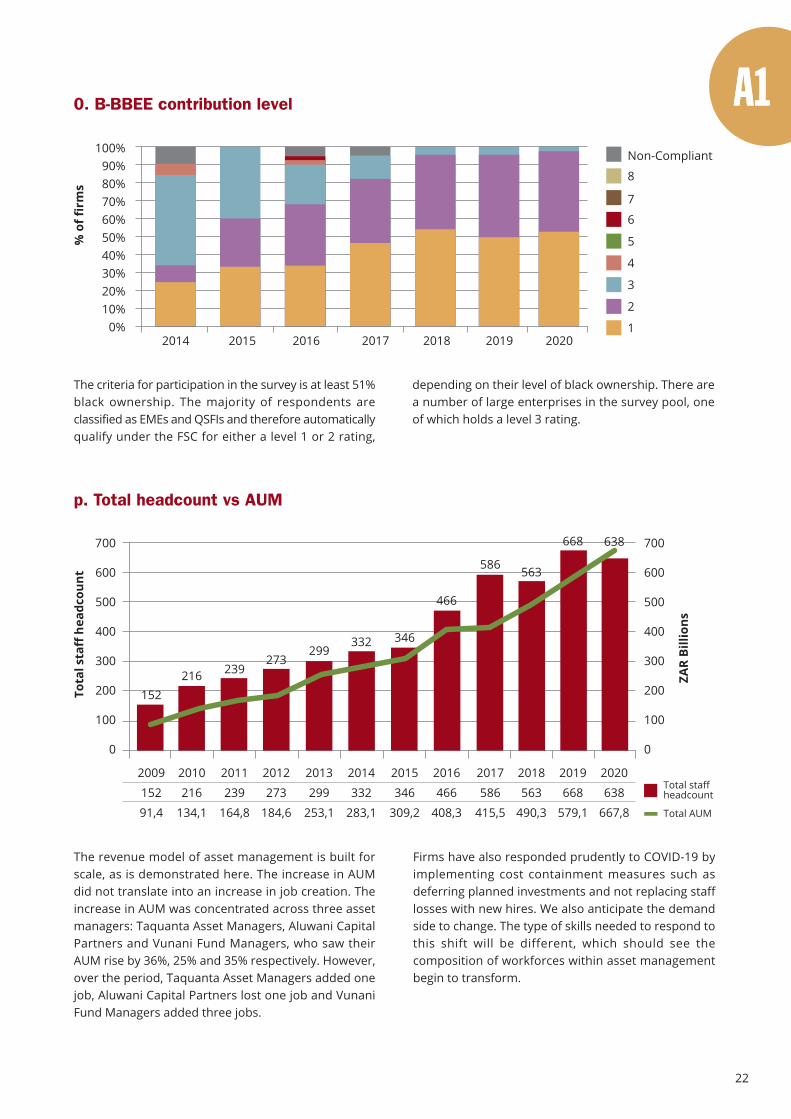

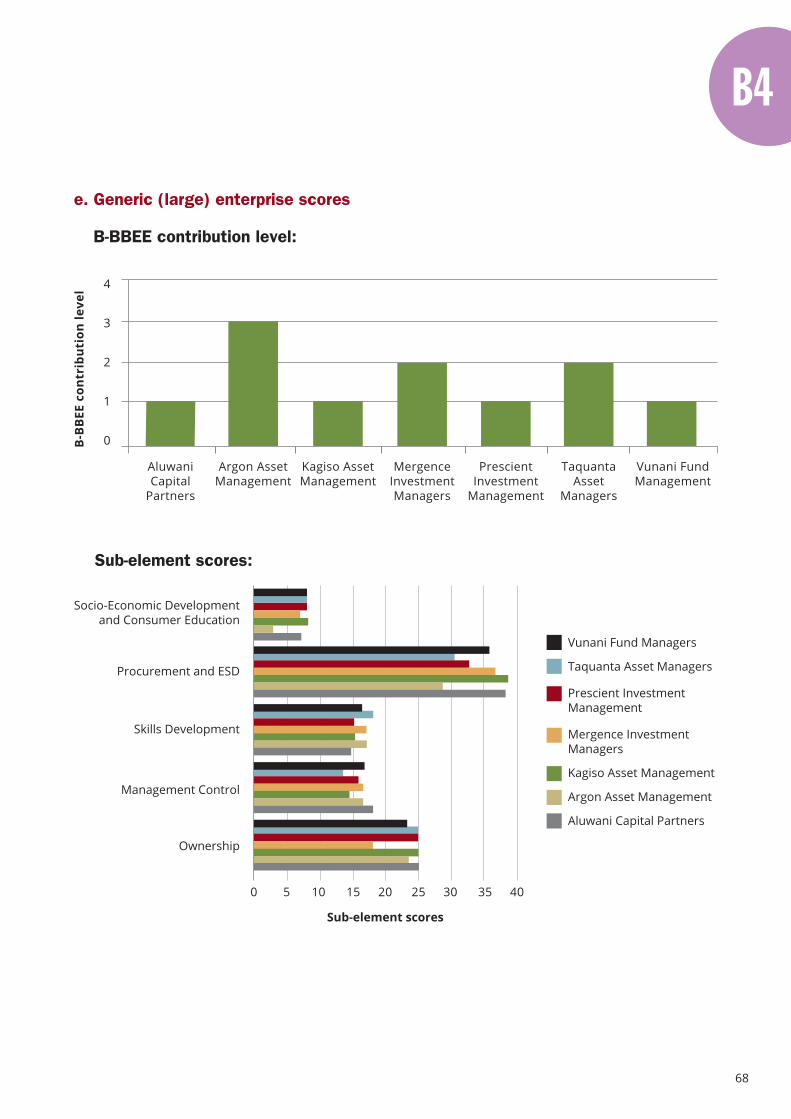

The criteria for participation in the survey is at least 51%black ownership. The majority of respondents areclassified as EMEs and QSFIs and therefore automaticallyqualify under the FSC for either a level 1 or 2 rating,

depending on their level of black ownership. There area number of large enterprises in the survey pool, oneof which holds a level 3 rating.

The revenue model of asset management is built forscale, as is demonstrated here. The increase in AUMdid not translate into an increase in job creation. Theincrease in AUM was concentrated across three assetmanagers: Taquanta Asset Managers, Aluwani CapitalPartners and Vunani Fund Managers, who saw theirAUM rise by 36%, 25% and 35% respectively. However,over the period, Taquanta Asset Managers added onejob, Aluwani Capital Partners lost one job and VunaniFund Managers added three jobs.

Firms have also responded prudently to COVID-19 byimplementing cost containment measures such asdeferring planned investments and not replacing stafflosses with new hires. We also anticipate the demandside to change. The type of skills needed to respond tothis shift will be different, which should see thecomposition of workforces within asset managementbegin to transform.

0. B-BBEE contribution level

% o

f fir

ms

Non-Compliant

8

7

6

5

4

3

2

12014 2015 2016 2017 2018 2019

100%90%80%70%60%50%40%30%20%10%

0%2020

Total staffheadcount

Total AUM

p. Total headcount vs AUM

Tota

l sta

ff h

eadc

ount

700

600

500

400

300

200

100

0

ZAR

Billi

ons

700

600

500

400

300

200

100

0

2009

152

91,4

2010

216

134,1

2011

239

164,8

2012

273

184,6

2013

299

253,1

2014

332

283,1

2015

346

309,2

2016

466

408,3

2017

586

415,5

2018

563

490,3

2019

668

579,1

2020

638

667,8

152216 239

273299

332 346

466

586 563

668 638

23

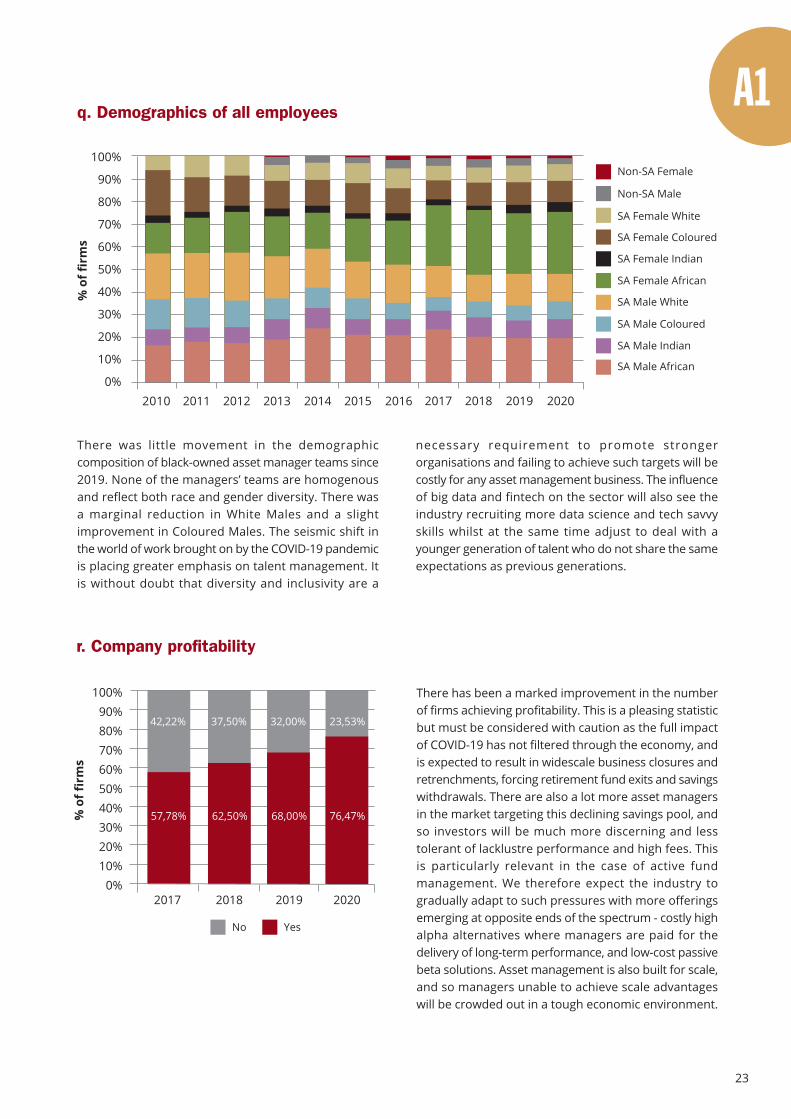

There was little movement in the demographiccomposition of black-owned asset manager teams since2019. None of the managers’ teams are homogenousand reflect both race and gender diversity. There wasa marginal reduction in White Males and a slightimprovement in Coloured Males. The seismic shift inthe world of work brought on by the COVID-19 pandemicis placing greater emphasis on talent management. Itis without doubt that diversity and inclusivity are a

necessary requirement to promote strongerorganisations and failing to achieve such targets will becostly for any asset management business. The influenceof big data and fintech on the sector will also see theindustry recruiting more data science and tech savvyskills whilst at the same time adjust to deal with ayounger generation of talent who do not share the sameexpectations as previous generations.

There has been a marked improvement in the numberof firms achieving profitability. This is a pleasing statisticbut must be considered with caution as the full impactof COVID-19 has not filtered through the economy, andis expected to result in widescale business closures andretrenchments, forcing retirement fund exits and savingswithdrawals. There are also a lot more asset managersin the market targeting this declining savings pool, andso investors will be much more discerning and lesstolerant of lacklustre performance and high fees. Thisis particularly relevant in the case of active fundmanagement. We therefore expect the industry togradually adapt to such pressures with more offeringsemerging at opposite ends of the spectrum - costly highalpha alternatives where managers are paid for thedelivery of long-term performance, and low-cost passivebeta solutions. Asset management is also built for scale,and so managers unable to achieve scale advantageswill be crowded out in a tough economic environment.

SA Male Indian

q. Demographics of all employees

% o

f fir

ms

Non-SA Male

SA Female White

SA Female Coloured

SA Female Indian

SA Female African

SA Male White

SA Male Coloured

Non-SA Female

SA Male African

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

r. Company profitability

% o

f fir

ms

100%90%80%70%60%50%40%30%20%10%

0%

YesNo

20182017 2019

62,50%

37,50%

57,78%

42,22%

68,00%

32,00%

76,47%

23,53%

2020

24

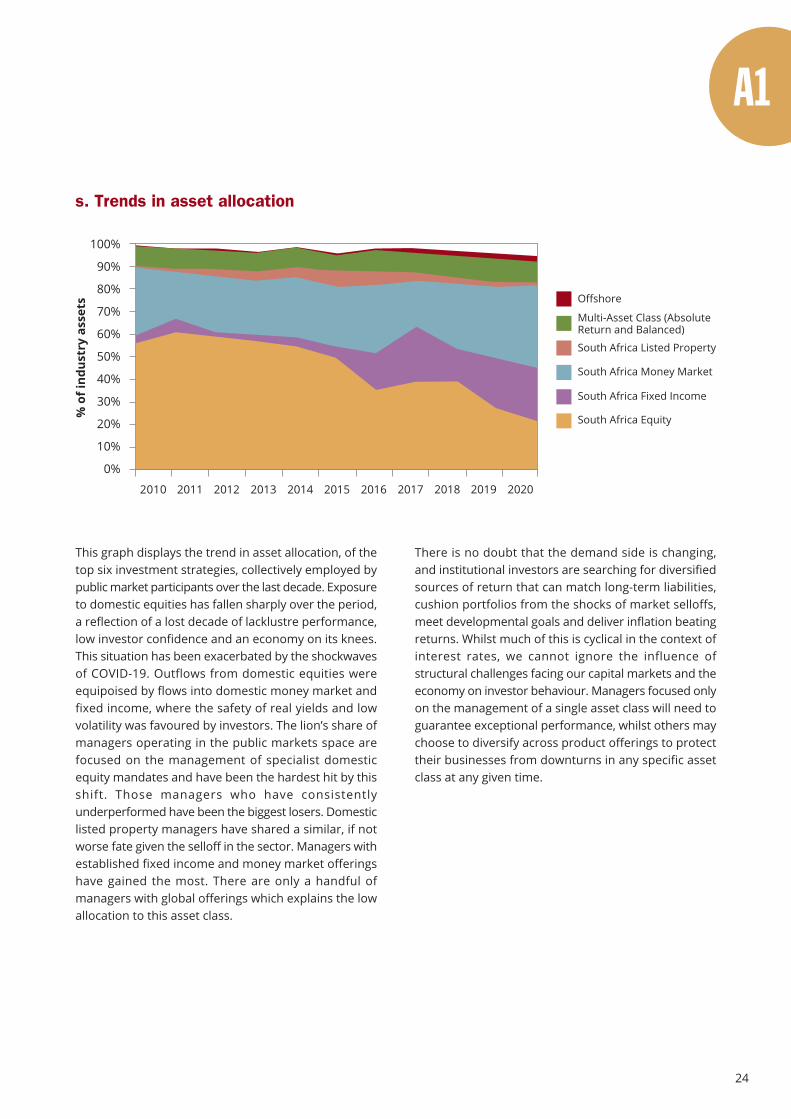

This graph displays the trend in asset allocation, of thetop six investment strategies, collectively employed bypublic market participants over the last decade. Exposureto domestic equities has fallen sharply over the period,a reflection of a lost decade of lacklustre performance,low investor confidence and an economy on its knees.This situation has been exacerbated by the shockwavesof COVID-19. Outflows from domestic equities wereequipoised by flows into domestic money market andfixed income, where the safety of real yields and lowvolatility was favoured by investors. The lion’s share ofmanagers operating in the public markets space arefocused on the management of specialist domesticequity mandates and have been the hardest hit by thisshift. Those managers who have consistentlyunderperformed have been the biggest losers. Domesticlisted property managers have shared a similar, if notworse fate given the selloff in the sector. Managers withestablished fixed income and money market offeringshave gained the most. There are only a handful ofmanagers with global offerings which explains the lowallocation to this asset class.

s. Trends in asset allocation

% o

f ind

ustr

y as

sets Offshore

Multi-Asset Class (AbsoluteReturn and Balanced)

South Africa Listed Property

South Africa Money Market

South Africa Fixed Income

South Africa Equity

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

There is no doubt that the demand side is changing,and institutional investors are searching for diversifiedsources of return that can match long-term liabilities,cushion portfolios from the shocks of market selloffs,meet developmental goals and deliver inflation beatingreturns. Whilst much of this is cyclical in the context ofinterest rates, we cannot ignore the influence ofstructural challenges facing our capital markets and theeconomy on investor behaviour. Managers focused onlyon the management of a single asset class will need toguarantee exceptional performance, whilst others maychoose to diversify across product offerings to protecttheir businesses from downturns in any specific assetclass at any given time.

25

26

Zero hunger

2

27

1. PwC, Africa Asset Management 20202. Alexander Forbes Manager Watch Annual Survey 2019

1845 - 1947: Era of colonisation

The institutionalisation of the savings and investmentssector began with the establishment of insurers andbanks in the 19th century, which saw the emergence ofthe bancassurance model. This model of crossshareholding between insurers and banks remainsprevalent today. For example, Sanlam and Absa sharea relationship, as do Old Mutual and Nedbank, Libertyand Standard Bank, and Momentum and FirstRand. Thebancassurance model also gave birth to the assetmanagement industry as these financial institutionsestablished investment management arms, to manage

Asset management plays a critical role in the functioningof the South African economy through the efficientmobilisation and allocation of savings. The sectorsupports financial market infrastructure and ensuresthe smooth functioning of the capital markets, abarometer of the health of an economy. The sector isalso a significant contributor to GDP. In fact, financialservices as a whole is the largest contributor to GDP, at22%1. The asset management industry is also well-regulated, thereby providing trust, confidence, andstability to the financial system.

South Africa’s status as the most mature financial marketin Africa is a culmination of its evolution from colonialism,through apartheid, and its eventual entry into the globalmarketplace following democracy in 1994. The structureand institutionalisation of the sector has largely beeninfluenced by the politics of the day. This review exploresthe periods before and after democracy and is sub-divided into distinct periods of political reign, control,and leadership.

life and other assets. According to Alexander Forbes2,as at the end of 2019, insurer owned asset managementfirms Old Mutual Investment Group, Sanlam InvestmentManagement, Stanlib Asset Management and MomentumAsset Managers are ranked one, five, six and thirteenby total assets under management respectively. On thisbasis, one could argue that South Africa has never reallyconceptualised a new economy and that the colonial orapartheid structure remains intact with a few companies,their subsidiaries, and associated companies dominatingthe sector.

We look at how each of these periods shaped SouthAfrican asset management and explore what lies ahead.

1845-1947 1948-1993 1994-2008 2009-todayANC rule

Golden period ofdemocracy

ANC rule

Period of politicaland economic crisis

Colonial rule

Period of Anglo BoerWars, British rule,

Union of SA

National Party rule

Period of apartheidbased on racial

segregation

Period before democracy Period after democracy

Colonialism, apartheid anddemocracy - the evolutionof South African assetmanagement

28

Nu

mb

er o

f m

emb

ers

18 000 000

16 000 000

14 000 000

12 000 000

10 000 000

8 000 000

6 000 000

4 000 000

2 000 000

0

Private sector members

Private sector assets

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

AU

M M

illi

on

s

R5 000 000

R4 500 000

R4 000 000

R3 500 000

R3 000 000

R2 500 000

R2 000 000

R1 500 000

R1 000 000

R500 000

0

GEPF and other SOEs members

GEPF and other SOEs assets

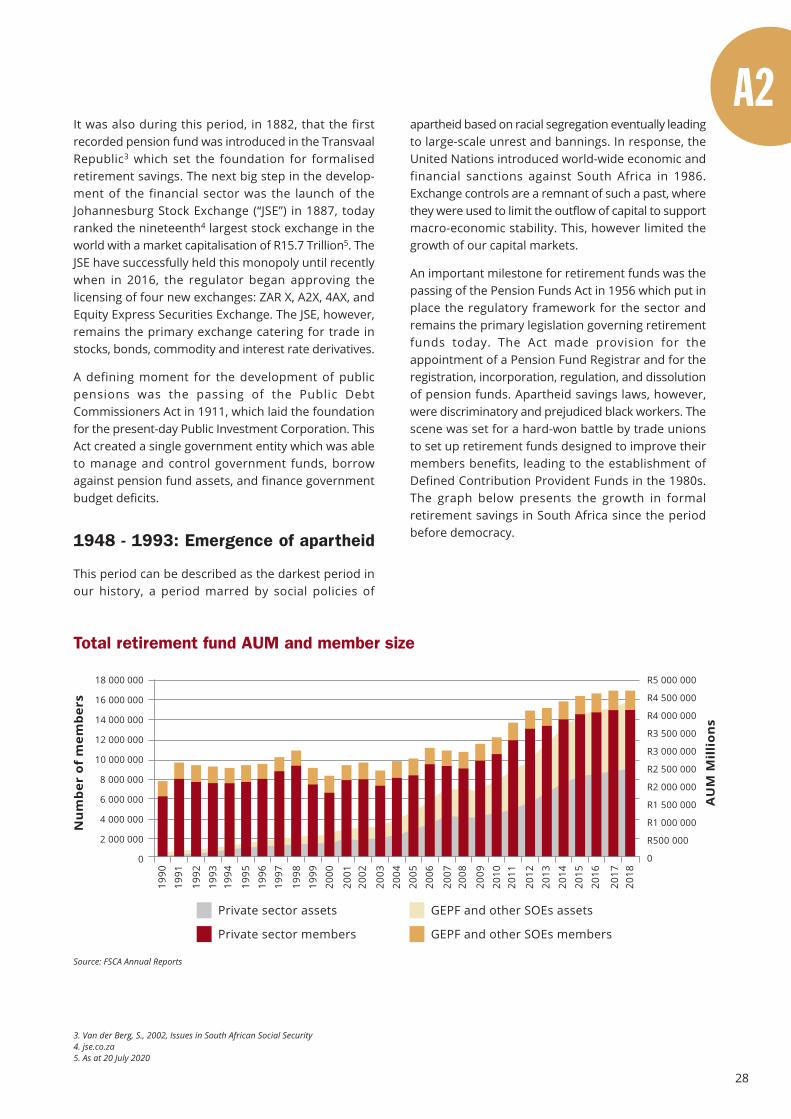

Total retirement fund AUM and member size

apartheid based on racial segregation eventually leadingto large-scale unrest and bannings. In response, theUnited Nations introduced world-wide economic andfinancial sanctions against South Africa in 1986.Exchange controls are a remnant of such a past, wherethey were used to limit the outflow of capital to supportmacro-economic stability. This, however limited thegrowth of our capital markets.

An important milestone for retirement funds was thepassing of the Pension Funds Act in 1956 which put inplace the regulatory framework for the sector andremains the primary legislation governing retirementfunds today. The Act made provision for theappointment of a Pension Fund Registrar and for theregistration, incorporation, regulation, and dissolutionof pension funds. Apartheid savings laws, however,were discriminatory and prejudiced black workers. Thescene was set for a hard-won battle by trade unionsto set up retirement funds designed to improve theirmembers benefits, leading to the establishment ofDefined Contribution Provident Funds in the 1980s.The graph below presents the growth in formalretirement savings in South Africa since the periodbefore democracy.

Source: FSCA Annual Reports

It was also during this period, in 1882, that the firstrecorded pension fund was introduced in the TransvaalRepublic3 which set the foundation for formalisedretirement savings. The next big step in the develop-ment of the financial sector was the launch of theJohannesburg Stock Exchange (“JSE”) in 1887, todayranked the nineteenth4 largest stock exchange in theworld with a market capitalisation of R15.7 Trillion5. TheJSE have successfully held this monopoly until recentlywhen in 2016, the regulator began approving thelicensing of four new exchanges: ZAR X, A2X, 4AX, andEquity Express Securities Exchange. The JSE, however,remains the primary exchange catering for trade instocks, bonds, commodity and interest rate derivatives.

A defining moment for the development of publicpensions was the passing of the Public DebtCommissioners Act in 1911, which laid the foundationfor the present-day Public Investment Corporation. ThisAct created a single government entity which was ableto manage and control government funds, borrowagainst pension fund assets, and finance governmentbudget deficits.

1948 - 1993: Emergence of apartheid

This period can be described as the darkest period inour history, a period marred by social policies of

3. Van der Berg, S., 2002, Issues in South African Social Security4. jse.co.za5. As at 20 July 2020

29

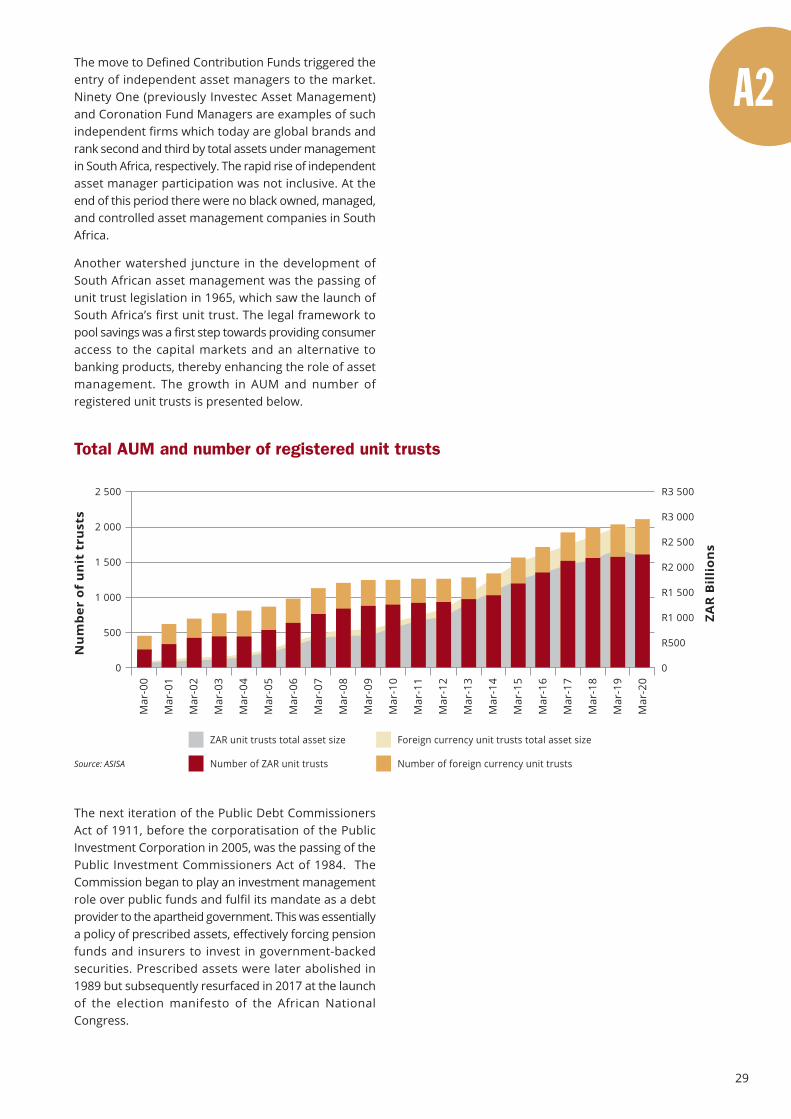

The move to Defined Contribution Funds triggered theentry of independent asset managers to the market.Ninety One (previously Investec Asset Management)and Coronation Fund Managers are examples of suchindependent firms which today are global brands andrank second and third by total assets under managementin South Africa, respectively. The rapid rise of independentasset manager participation was not inclusive. At theend of this period there were no black owned, managed,and controlled asset management companies in SouthAfrica.

Another watershed juncture in the development ofSouth African asset management was the passing ofunit trust legislation in 1965, which saw the launch ofSouth Africa’s first unit trust. The legal framework topool savings was a first step towards providing consumeraccess to the capital markets and an alternative tobanking products, thereby enhancing the role of assetmanagement. The growth in AUM and number ofregistered unit trusts is presented below.

The next iteration of the Public Debt CommissionersAct of 1911, before the corporatisation of the PublicInvestment Corporation in 2005, was the passing of thePublic Investment Commissioners Act of 1984. TheCommission began to play an investment managementrole over public funds and fulfil its mandate as a debtprovider to the apartheid government. This was essentiallya policy of prescribed assets, effectively forcing pensionfunds and insurers to invest in government-backedsecurities. Prescribed assets were later abolished in1989 but subsequently resurfaced in 2017 at the launchof the election manifesto of the African NationalCongress.

Nu

mb

er o

f u

nit

tru

sts

ZAR

Bil

lio

ns

Total AUM and number of registered unit trusts

2 500

2 000

1 500

1 000

500

0

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

R3 500

R3 000

R2 500

R2 000

R1 500

R1 000

R500

0

Number of ZAR unit trusts

ZAR unit trusts total asset size

Number of foreign currency unit trusts

Foreign currency unit trusts total asset size

Source: ASISA

30

In 1999 South Africa became a founding member of theG20. This has significance since subsequent regulatoryreforms introduced in the financial sector have beenpremised on G20 principles. Policymakers and regulatorshave often been criticised for being too focused onmeeting international standards without consideringimportant parochial features of the domestic economy.Putting it bluntly, the policies failed to transform thefinancial services industry to broaden the participationof black people in the sector. An example of South Africafulfilling its G20 commitments was when in 2015 hedgefunds which were previously unregulated, becameregulated under the Collective Investment SchemesControl Act (“CISCA”). Under the new legislation hedgefunds were required to be registered under CISCAapproved Hedge Fund Management Companies.However, the licensing approach was not supportive ofnew black entrants, inadvertently entrenching thedominant positioning of incumbents. This has beencorrected in subsequent legislation such as the InsuranceAct and the Draft Conduct of Financial Institutions Bill,where the regulator has adopted a more developmentalapproach and is explicitly supportive of transformationimperatives.

USD

ZAR

R 20

R18

R 16

R 14

R 12

R 10

R 8

R 6

R 4

R 2

R 0

ZAR

Mil

lio

ns

R60 000

R40 000

R20 000

R0

-R20 000

-R40 000

-R60 000

-R80 000

-100 000

Foreign participation in South African capital markets since democracy

Mar

94

Jan

95

Nov

95

Sep

96Ju

l 97

May

98

Mar

99

Jan

00

Nov

00

Sep

01

Jul 0

2

May

03

Mar

04

Jan

05

Nov

05

Sep

06

Jul 0

7

May

08

Mar

09

Jan

10

Nov

10

Sep

11Ju

l 12

May

13

Mar

14

Jan

15

Nov

15

Sep

16

Jul 1

7

May

18

Mar

19

Jan

20

Net foreign purchases of shares Net foreign purchases of bonds USDZAR

The historic Financial Sector Summit was held in 2002,where Nedlac social partners committed to thedevelopment of a Black Economic Empowerment (“BEE”)Charter for the financial services sector. The Charterwas signed in 2003 and came into effect in 2004. Thenext iteration of the Charter was the Financial SectorCode of 2012 followed by the Amended Financial SectorCode of 2017. The last iteration included a voluntary B-BBEE Scorecard for the Top 100 retirement funds, whichobliged them to report to the Financial Sector Transfor-mation Council (”FSTC”) on their preferential procurementactivities, on an annual basis. This was a significant winfor black owned asset management firms, furtheringrepresentation and ownership reflective of our demo-graphics across the industry. The current Code is underreview and it is expected that this dispensation willmove from voluntary to compulsory in the next iterationof the legislation. The illustration which follows showsa historic timeline of the evolution of the Financial SectorCode.

1994 – 2008: Democracy!

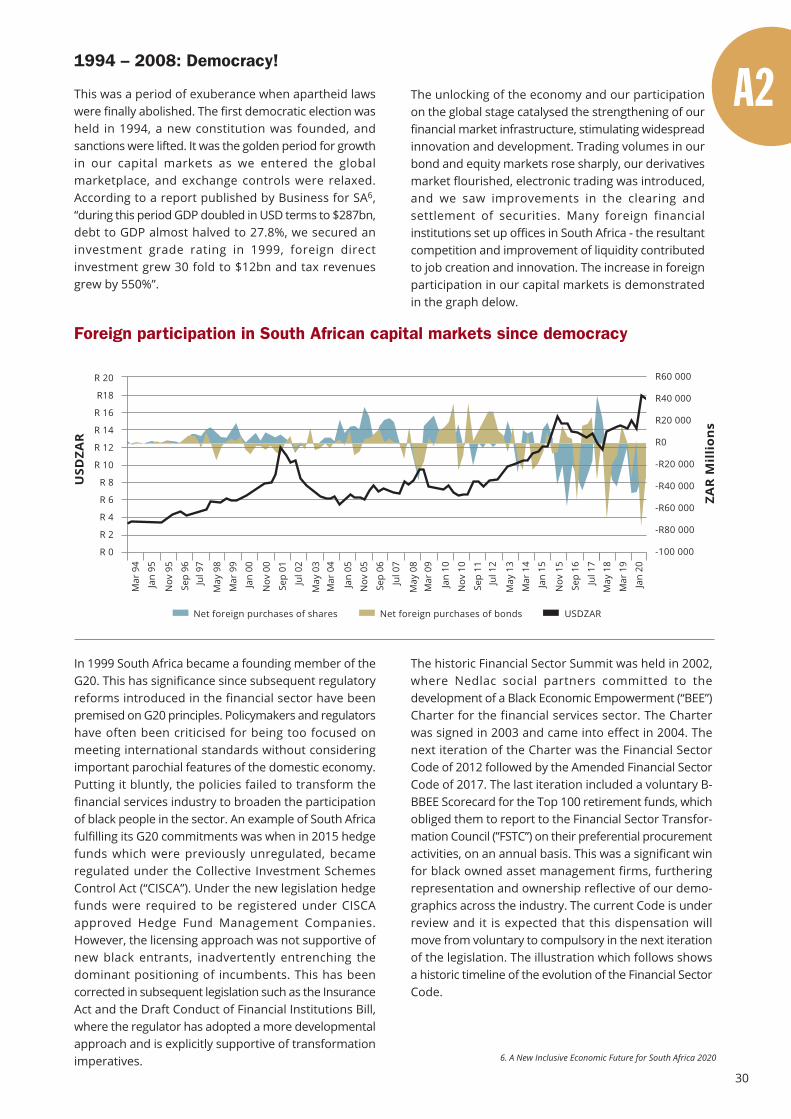

This was a period of exuberance when apartheid lawswere finally abolished. The first democratic election washeld in 1994, a new constitution was founded, andsanctions were lifted. It was the golden period for growthin our capital markets as we entered the globalmarketplace, and exchange controls were relaxed.According to a report published by Business for SA6,“during this period GDP doubled in USD terms to $287bn,debt to GDP almost halved to 27.8%, we secured aninvestment grade rating in 1999, foreign directinvestment grew 30 fold to $12bn and tax revenuesgrew by 550%”.

The unlocking of the economy and our participationon the global stage catalysed the strengthening of ourfinancial market infrastructure, stimulating widespreadinnovation and development. Trading volumes in ourbond and equity markets rose sharply, our derivativesmarket flourished, electronic trading was introduced,and we saw improvements in the clearing andsettlement of securities. Many foreign financialinstitutions set up offices in South Africa - the resultantcompetition and improvement of liquidity contributedto job creation and innovation. The increase in foreignparticipation in our capital markets is demonstratedin the graph delow.

6. A New Inclusive Economic Future for South Africa 2020

31

Another profound milestone for asset managementworldwide was the launch of the United NationsPrinciples for Responsible Investment (“PRI”) in April2006, an organisation dedicated to promote theincorporation of environmental, social, and corporategovernance factors (“ESG”) into investment decision-making. The Government Employees Pension Fund ofSouth Africa was a founding signatory to the PRI. Sincethen the PRI has grown to 3 2477signatories worldwiderepresenting over US$100 Trillion in assets undermanagement. Currently 61 South African institutions(asset managers and asset owners) are signatories tothe PRI.

2009 – today: Lost years

Following the global financial crisis of 2007-2008,regulators responded by revising regulations to streng-then the financial system and to protect consumers andeconomies. South Africa responded through the passingof the Financial Sector Regulation Act in 2017 givingeffect to what is referred to as the Twin Peaks systemof financial regulation. This regulation is aimed at makingthe sector safer and closing any regulatory gaps withinthe system. Under Twin Peaks, two new regulators cameinto operation: the Prudential Authority which is theregulator of financial institutions, and the FinancialSector Conduct Authority which regulates marketconduct with respect to ethics and transparency. Thereform process is ongoing with the next phase beingthe harmonisation of the legal landscape within whichfinancial institutions operate. The draft Conduct ofFinancial Institutions Bill published in December 2018represents this new legal framework. This Bill is alsobest placed to give legal effect to transformationrequirements in support of targets agreed through theFinancial Sector Transformation Council and specifiedin the Financial Sector Code.

History of the Financial Sector Code

2002 2003 2004 2007 2012 2013 2017 2019

Financial SectorSummit –

Nedlac – makecommitment to

the developmentof a BEE Charterfor the financialservices sector

Financial SectorCharter signed

B-BBEE Actgazetted

Financial SectorCharter– comes

into effect on 1 Jan2004

dti GenericCodes of Good

Practicegazetted –

superior legalstatus toCharters

Financial SectorCode gazetted– 26 Nov 2012

Revised dtiGeneric Codes of

Good Practicegazetted –

11 Oct 2013

Amended FinancialSector Code gazettedon 1 December 2017

Parliament holdspublic hearings on

transformation of thefinancial sector.

Standing Committeeon Finance (”SCOF”)

and the PortfolioCommittee on Tradeand Industry (”PCTI”)

release reporton financial sector

transformation whichis adopted byParliament

FSTC commencesreview of the

Amended FinancialSector Code. As

part of this reviewprocess all

recommendationsmade by SCOF andthe PCTI are being

taken intoconsideration

Ironically, just one year after the launch of the PRI, theglobal financial crisis laid bare the vulnerabilities of theglobal financial system.

Whilst much has been achieved since 1994, the extentto which economic growth has been shared equitablyamongst all South Africans has not been adequate forthe requirements of a stable, integrated, and prosperoussociety. Over the last decade rising levels of unemploy-ment, highly unequal distribution of income, and lowlevels of growth and investment have become deeplyentrenched. Our economy was also subjected to thelethal triple cocktail of greed, weak governance andinadequate oversight, overshadowed by state captureand malfeasance. South Africa subsequently lost itsinvestment grade rating and our fiscal position hasdeteriorated sharply, with debt to GDP expected toexceed 100% by 2023.

An already weak economic position has been exacer-bated by COVID-19, leaving government desperatelyseeking a new narrative to accelerate an economicrecovery. As such, the idea of using prescribed assetsto help foster economic growth has resurfaced, packagedin the form of an infrastructure fund to finance strategicprojects by combining capital from the public and private

7. unpri.org

32

The two-century long trajectory described here shedssome light on the way forward for the asset managementsector. The pendulum swing from prescribed to unpre-scribed, and back, reflects the changing social andeconomic dynamic in our country. These are tidal forces,to which the asset management industry must adapt,with transformation being a vital component.

There are a number of developing trends facing thesector - we list our top three which we anticipate willhave the most significant influence:

1 ESG will take centre stage. Both asset owners andpolicymakers will be uncompromising in their effortsto promote a more sustainable financial sector andeconomy. There will be a rise in demand for impactinvestment aligned to meeting UN SustainableDevelopment Goals, a collection of 17 global goalsdesigned to be a “blueprint to achieve a better andmore sustainable future for all”8. We will also see anincrease in public private partnerships and blendedfinance investments.

Ave

rage

nu

mbe

r of

sh

ares

Average number of listed shares per year excluding cash shells, trusts and ETFs Private Equity AUM

Private equity vs the JSE

ZAR

Bill

ion

s

700

600

500

400

300

200

100

0

200180160140120100806040200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

sectors, retirement funds, development financeinstitutions and multilateral development banks. Withexpectations of capital flows into real assets, the assetmanagement industry appears to be readying itself -new and existing firms are building capacity and skillsto be able to manage such flows. The COVID-19pandemic has also brought impact investment to theforefront with many new debt and equity funds poppingup to support businesses in their efforts to mitigate thenegative economic impact, whilst providing investorswith a competitive return.

The resulting growth in appetite for impact investmentthrough unlisted assets may precipitate a change to

Regulation 28 of the Pension Funds Act, which currentlycaps private equity and hedge funds at 15%. Calls havebeen made by the Southern African Venture Capitaland Private Equity Association to separate hedge fundsfrom private equity and gradually increase the privateequity limit. The Minister of Finance has publicly flirtedwith the idea of increasing the limit indicating that thisis under review by the National Treasury. Similarlycalls have been made to amend CISCA to allow unittrusts to hold unlisted exposure. The growth in privateequity and the decline in the listed markets is presentedin the graph below.

What then does the future hold for South African asset management?

2 The number of listings on the JSE will continue todecline as businesses seek alternative sources ofcapital through, for example, private equity. This willresult in concentrated listed markets offering limiteddiversification benefits, thus negatively impactingactive asset managers who are primarily focused onthe domestic equity markets. The rise in passiveinvesting is also expected to continue.

3 Transformation of the financial sector will be in thespotlight with new legislation focused on achievingreal parity within the sector coming into play. Suchlegislation includes the Employment EquityAmendment Bill, currently in draft form, which willallow for the Minister of Employment and Labour toidentify sectoral numerical targets to ensurerepresentation reflective of our demographics. Wecan also expect to see the Conduct of FinancialInstitutions Bill come into effect, and an updatediteration of the Financial Sector Code gazetted.

8. United Nations

33

34

Life on land

15

35

Publicmarkets

36

Impact ofCOVID-19

Section highlights

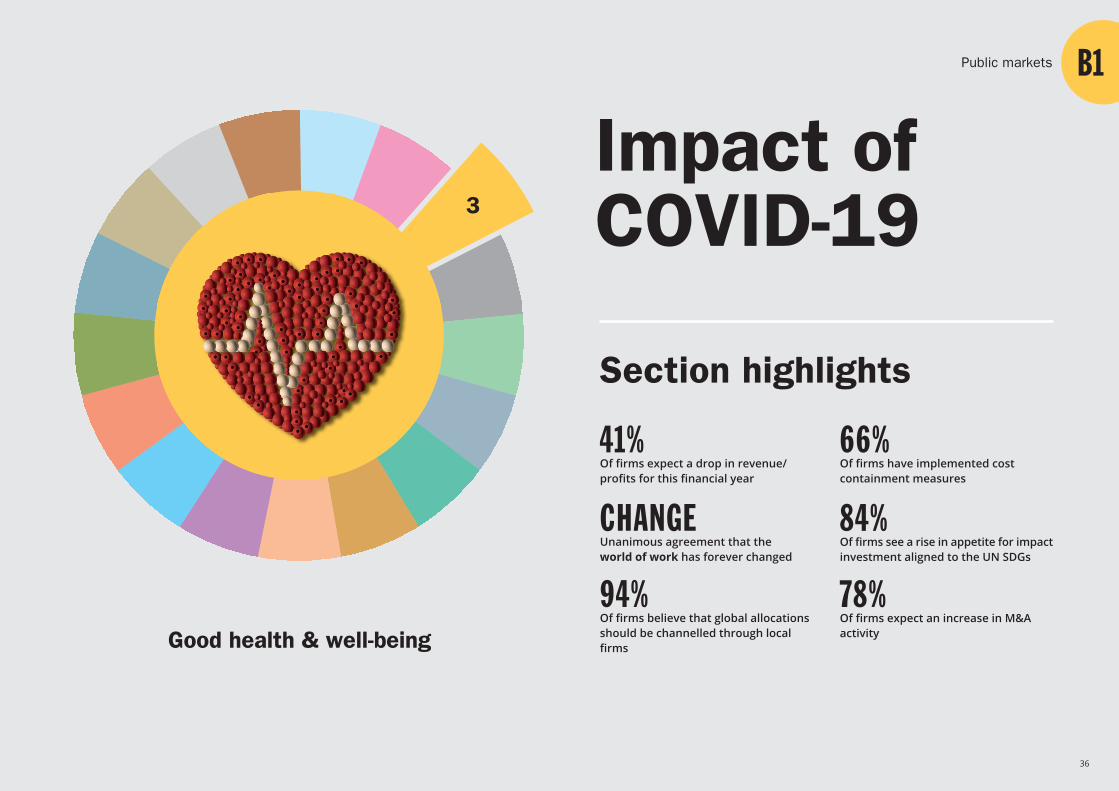

41%Of firms expect a drop in revenue/ profits for this financial year

CHANGEUnanimous agreement that theworld of work has forever changed

84%Of firms see a rise in appetite for impactinvestment aligned to the UN SDGs

94%Of firms believe that global allocations should be channelled through local firms

78%Of firms expect an increase in M&A activity

66%Of firms have implemented cost containment measures

Good health & well-being

Public markets

3

37

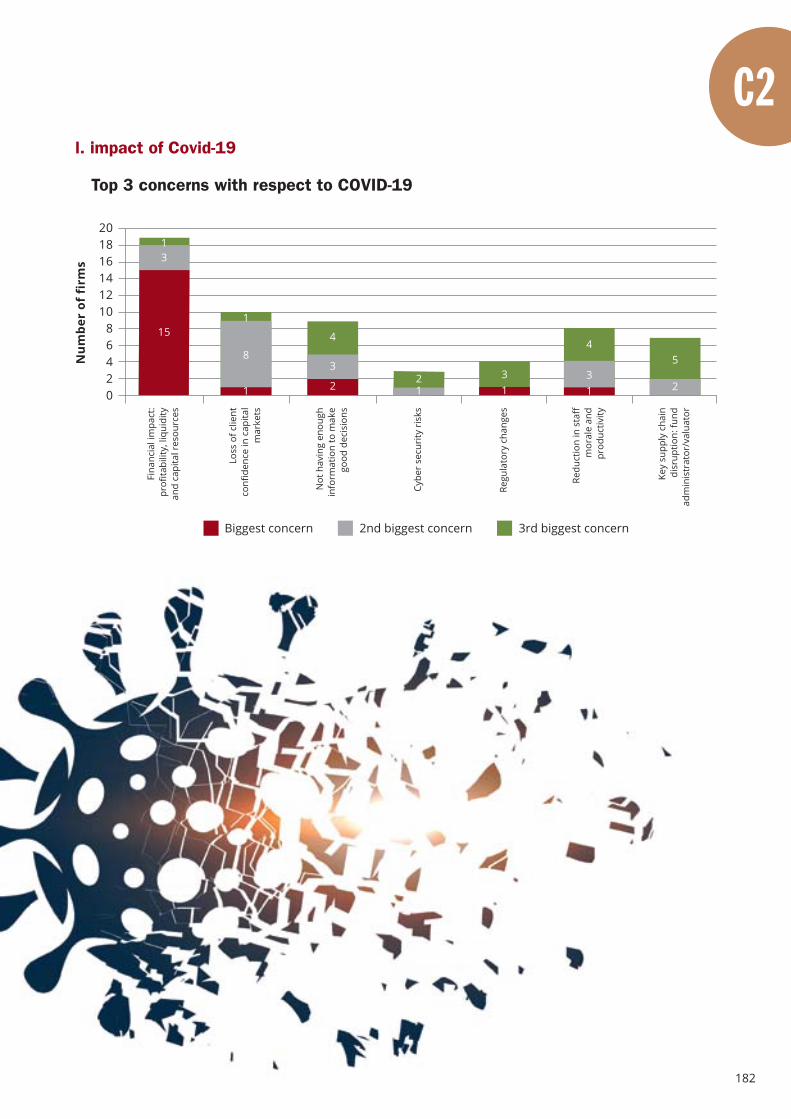

In the first week of January with South Africa continuingits sojourn into the New Dawn with a 20/20 vision ofgrowth and possibility, there was little anticipation ofwhat was to be in the coming months. COVID-19 hascome to the fore with dramatic economic and socialimplications - not only in South Africa, but across theglobe. The global pandemic has brought into questionpredicted trajectories for economic growth, employment,profitability, sustainable development and - vital within

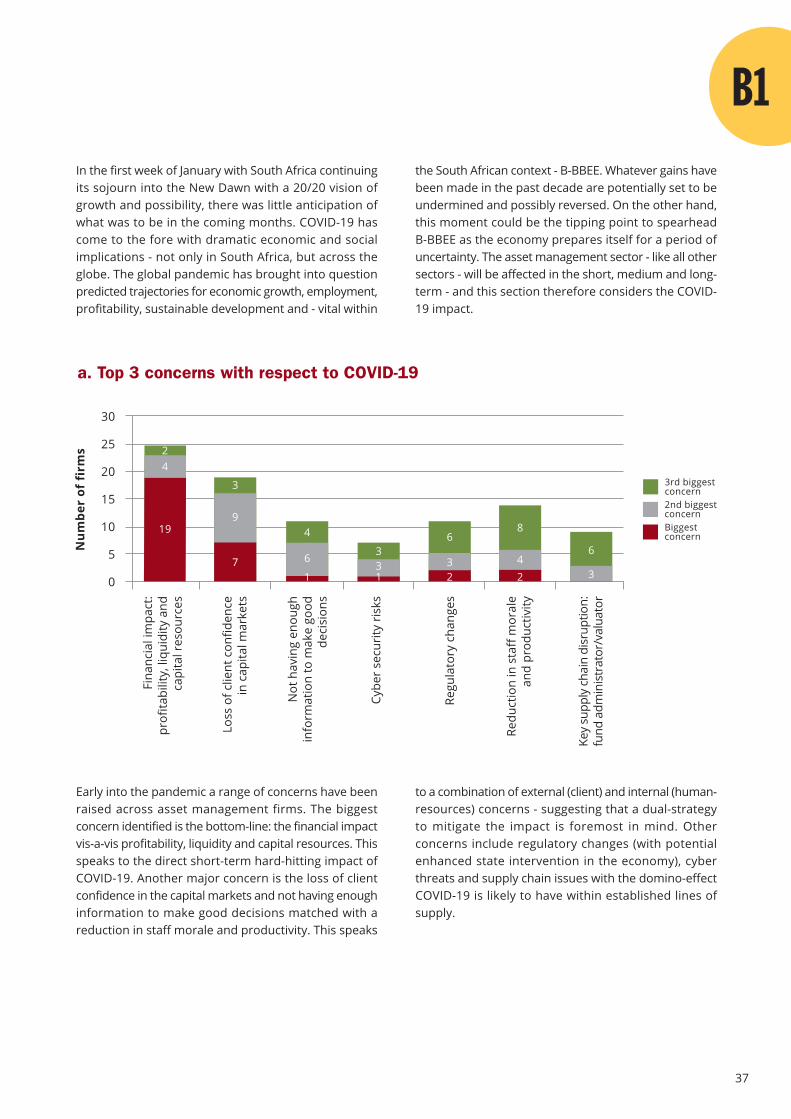

Early into the pandemic a range of concerns have beenraised across asset management firms. The biggestconcern identified is the bottom-line: the financial impactvis-a-vis profitability, liquidity and capital resources. Thisspeaks to the direct short-term hard-hitting impact ofCOVID-19. Another major concern is the loss of clientconfidence in the capital markets and not having enoughinformation to make good decisions matched with areduction in staff morale and productivity. This speaks

the South African context - B-BBEE. Whatever gains havebeen made in the past decade are potentially set to beundermined and possibly reversed. On the other hand,this moment could be the tipping point to spearheadB-BBEE as the economy prepares itself for a period ofuncertainty. The asset management sector - like all othersectors - will be affected in the short, medium and long-term - and this section therefore considers the COVID-19 impact.

to a combination of external (client) and internal (human-resources) concerns - suggesting that a dual-strategyto mitigate the impact is foremost in mind. Otherconcerns include regulatory changes (with potentialenhanced state intervention in the economy), cyberthreats and supply chain issues with the domino-effectCOVID-19 is likely to have within established lines ofsupply.

a. Top 3 concerns with respect to COVID-19

Num

ber

of f

irm

s

30

25

20

15

10

5

0

2nd biggestconcern

3rd biggestconcern

Regu

lato

ry c

hang

es

Fina

ncia

l im

pact

:pr

ofita

bilit

y, li

quid

ity a

ndca

pita

l res

ourc

es

Loss

of c

lient

con

fiden

cein

cap

ital m

arke

ts

Cybe

r se

curi

ty r

isks

Redu

ctio

n in

sta

ff m

oral

ean

d pr

oduc

tivity

Not

hav

ing

enou

ghin

form

atio

n to

mak

e go

odde

cisi

ons

Key

supp

ly c

hain

dis

rupt

ion:

fund

adm

inis

trat

or/v

alua

tor

Biggestconcern

24

19

3

9

7 6

4

1

331 2

6

3

8

42 3

6

38

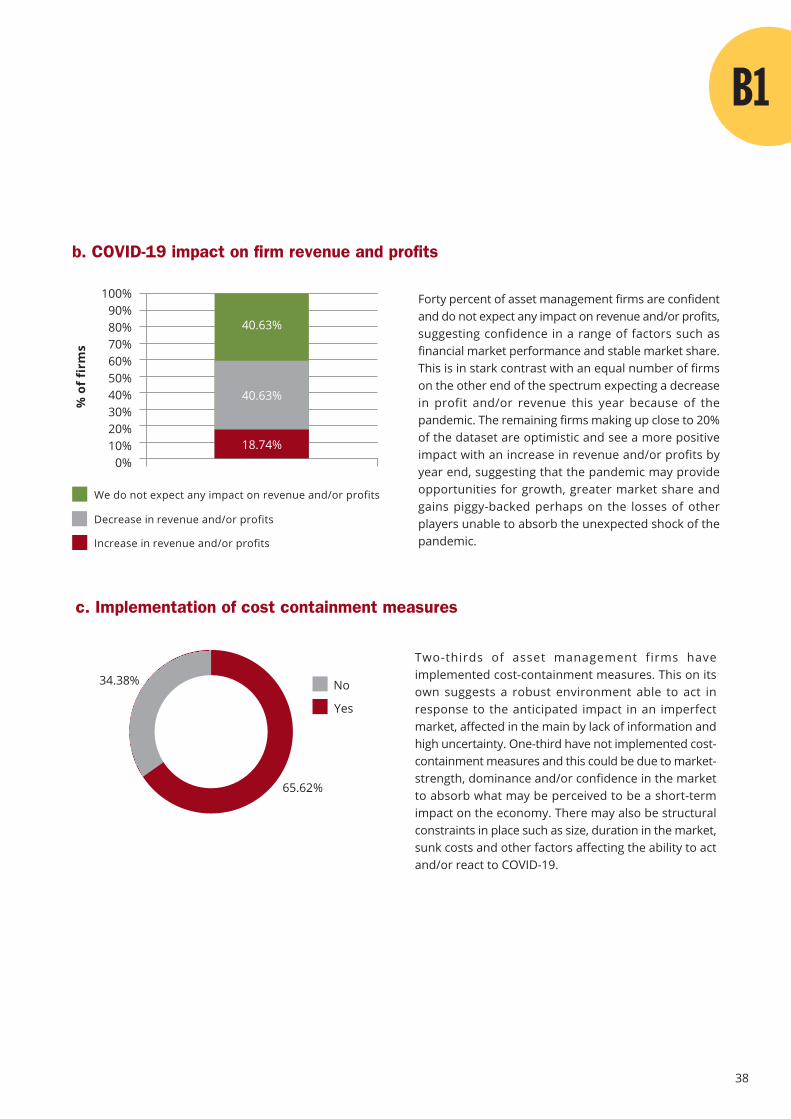

Forty percent of asset management firms are confidentand do not expect any impact on revenue and/or profits,suggesting confidence in a range of factors such asfinancial market performance and stable market share.This is in stark contrast with an equal number of firmson the other end of the spectrum expecting a decreasein profit and/or revenue this year because of thepandemic. The remaining firms making up close to 20%of the dataset are optimistic and see a more positiveimpact with an increase in revenue and/or profits byyear end, suggesting that the pandemic may provideopportunities for growth, greater market share andgains piggy-backed perhaps on the losses of otherplayers unable to absorb the unexpected shock of thepandemic.

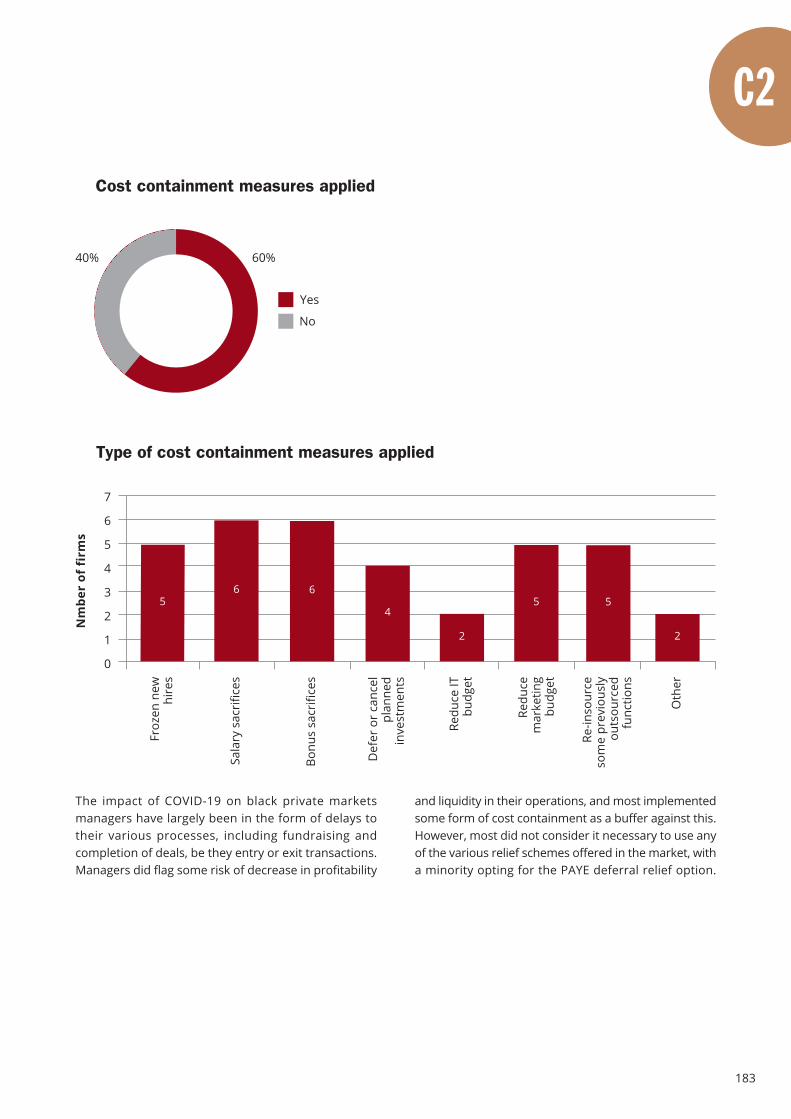

Two-thirds of asset management firms haveimplemented cost-containment measures. This on itsown suggests a robust environment able to act inresponse to the anticipated impact in an imperfectmarket, affected in the main by lack of information andhigh uncertainty. One-third have not implemented cost-containment measures and this could be due to market-strength, dominance and/or confidence in the marketto absorb what may be perceived to be a short-termimpact on the economy. There may also be structuralconstraints in place such as size, duration in the market,sunk costs and other factors affecting the ability to actand/or react to COVID-19.

b. COVID-19 impact on firm revenue and profits

100%90%80%70%60%50%40%30%20%10%

0%

We do not expect any impact on revenue and/or profits

Decrease in revenue and/or profits

Increase in revenue and/or profits

40.63%

40.63%

18.74%

34.38%

65.62%

Yes

No

c. Implementation of cost containment measures

% o

f fi

rms

39

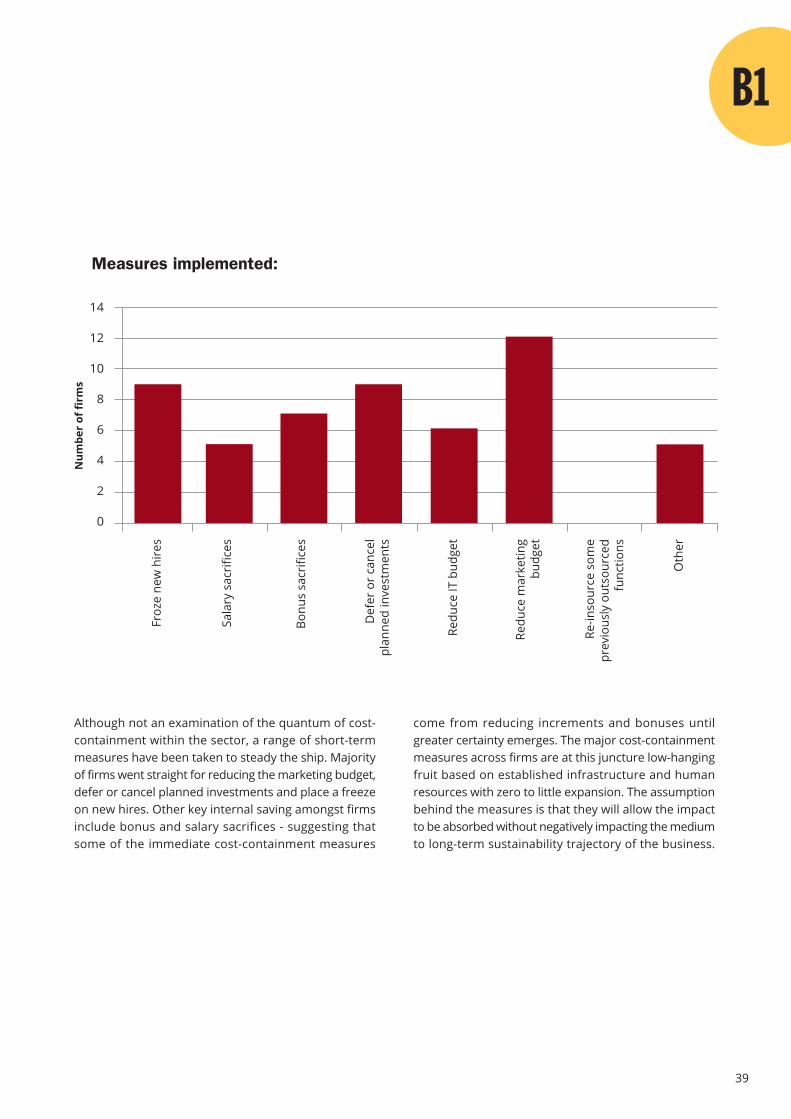

Although not an examination of the quantum of cost-containment within the sector, a range of short-termmeasures have been taken to steady the ship. Majorityof firms went straight for reducing the marketing budget,defer or cancel planned investments and place a freezeon new hires. Other key internal saving amongst firmsinclude bonus and salary sacrifices - suggesting thatsome of the immediate cost-containment measures

come from reducing increments and bonuses untilgreater certainty emerges. The major cost-containmentmeasures across firms are at this juncture low-hangingfruit based on established infrastructure and humanresources with zero to little expansion. The assumptionbehind the measures is that they will allow the impactto be absorbed without negatively impacting the mediumto long-term sustainability trajectory of the business.

Measures implemented:

Num

ber

of fi

rms

Froz

e ne

w h

ires

Sala

ry s

acri

fices

Bonu