Transfer Pricing in the Context of Strategic Congruence - DiVA ...

64

Transfer Pricing in the Context of Strategic Congruence Master’s Thesis 30 credits Department of Business Studies Uppsala University Spring Semester of 2017 Date of Submission: 2017-05-30 My Eliasson Adam Mankowski Supervisors: Fredrik Nilsson Shruti Kashyap

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Transfer Pricing in the Context of Strategic Congruence - DiVA ...

Transfer Pricing in the Context of Strategic Congruence

Master’s Thesis 30 credits Department of Business Studies Uppsala University Spring Semester of 2017

Date of Submission: 2017-05-30

My Eliasson Adam Mankowski Supervisors: Fredrik Nilsson Shruti Kashyap

I

Abstract The most common approach towards transfer pricing has been purely economic or with focus on tax regulations. However, transfer pricing has developed to become a component of organizational strategy. This indicates a growing focus on transfer pricing from a managerial perspective. A well-functioning transfer pricing structure can enable increased operational efficiency. The purpose of this paper is to explain the alignment between transfer pricing methods and strategy. The alignment between corporate levels and divisions enhances a corporation’s possibility to obtain strategic congruence, and thereby competitive advantage to become a stronger player on the market. The research is conducted as a multi-level case study with both qualitative and quantitative data collection. The result stresses that the case firms transfer pricing design is based on managerial objectives, and uses market-based and negotiated transfer price policies. The result finds that the methods and the strategy are partly aligned, which contributes to the corporation’s overall performance. Although, due to the levels different perceptions of profit maximization some sub-optimization occurs.

Keywords: Transfer Price, Strategy, Strategic Congruence, Operational Efficiency, Managerial Objectives

II

Acknowledgment We would like to sincerely thank our supervisors Fredrik Nilsson and Shruti Kashyap for their contributions with guidance and valuable advice. Also, we appreciate the enthusiasm and the support from our seminar group. This thesis would not be possible without the case firm’s willingness to provide us with access into their organization. This paper was achievable due to their encouragement and co-operation.

_______________ _______________

My Eliasson Adam Mankowski

Uppsala, 2017-05-30 Uppsala, 2017-05-30

III

Table of Contents

1 INTRODUCTION 11.1 PROBLEM DISCUSSION 21.2 AIM AND RESEARCH QUESTIONS 31.3 CONTRIBUTIONS 32 THEORY 42.1 OBJECTIVES OF TRANSFER PRICING 42.2 TRANSFER PRICING METHODS 52.2.1 COST-BASED 52.2.2 MARKET-BASED 62.2.3 NEGOTIATED 62.2.4 MANDATORY AND NON-MANDATORY AGREEMENTS 62.3 OPPORTUNISTIC BEHAVIOR AND FAIRNESS 72.4 STRATEGIC CONGRUENCE AND TRANSFER PRICING 82.4.1 STRATEGIC DIMENSIONS 82.4.2 CORPORATE LEVEL STRATEGY 102.4.3 BUSINESS LEVEL STRATEGY 122.4.4 FUNCTIONAL LEVEL STRATEGY 122.4.5 STRATEGIC INTERRELATIONS 132.5 SUMMARY THEORY 143 METHODOLOGY 153.1 RESEARCH DESIGN 153.1.1 CASE STUDY DESIGN 153.1.2 THE CASE SELECTION 163.1.3 LIMITATIONS 173.2 DATA COLLECTION 173.2.1 INTERVIEWS 183.2.2 QUESTIONNAIRES 193.2.3 ANNUAL REPORTS 193.2.4 THE RESPONDENTS 193.2.5 CONFIDENTIALITY 203.3 OPERATIONALIZATION 203.3.1 INTERVIEWS 213.3.2 QUESTIONNAIRES 223.3.3 ANNUAL REPORTS 223.4 ANALYTICAL APPROACH 224 EMPIRICAL RESULTS 244.1 OBJECTIVES OF TRANSFER PRICING 244.2 TRANSFER PRICING METHODS 254.3 OPPORTUNISTIC BEHAVIOR AND FAIRNESS 264.4 STRATEGIC CONGRUENCE AND TRANSFER PRICING 274.4.1 STRATEGIC DIMENSIONS 284.4.2 CORPORATE LEVEL STRATEGY 284.4.3 BUSINESS LEVEL STRATEGY 294.4.4 FUNCTIONAL LEVEL STRATEGY 295 ANALYSIS 31

IV

5.1 OBJECTIVES OF TRANSFER PRICING 315.2 TRANSFER PRICING METHOD 325.3 OPPORTUNISTIC BEHAVIOR AND FAIRNESS 335.4 STRATEGY AND TRANSFER PRICING 345.4.1 STRATEGIC DIMENSIONS 345.4.2 CORPORATE LEVEL STRATEGY 355.4.3 BUSINESS LEVEL STRATEGY 365.4.4 FUNCTIONAL LEVEL STRATEGY 375.5 DOES THE CASE FIRM HAVE STRATEGIC CONGRUENCE? 386 CONCLUSION 416.1 FUTURE RESEARCH 42REFERENCES 43APPENDIX 47

V

List of Figures and Tables Figure1:Themandatoryandnon-mandatoryagreementseffectsontransferpricingpolicies...............................7Figure2:Managersanalyticalplanemodel(MAP)........................................................................................................................9Figure3:CorporateLevelStrategiesbasedonPorter(1987)................................................................................................10Figure4:Acorporation’sstrategiccongruenceanditsalignmenttotransferpricingmethodsbasedonthehypotheses......................................................................................................................................................................................................13Figure5:Theselectedcasefirm’sstructure....................................................................................................................................16Figure6:Thedatagatheringprocessthroughouttheorganization...................................................................................18Table1:Operationalizationoftheinterviews...............................................................................................................................21Figure7:Themanagerialstructureinthecasefirm..................................................................................................................24Figure8:Thecasefirm’sstrategiccongruence.............................................................................................................................38

VI

Abbreviation List Business Unit 1 BU1 Business Unit 2 BU2 Business Unit Purchasing Manager BUPM Chief Executive Officers - Seller 1 CEO-S1 Chief Executive Officers - Seller 2 CEO-S2 Chief Operating Officer- Seller 1 COO-S1 Corporate Category Manager CCM Corporate Purchasing Manager CPM Manager’s Analytical Plane MAP Region 1 R1 Region 2 R2 Region 3 R3 Regional Purchasing Manager RPM Regional Purchasing Manager - Region 1 RPM-R1 Regional Purchasing Manager - Region 2 RPM-R2 Regional Purchasing Manager - Region 3 RPM-R3 Seller 1 S1 Seller 2 S2

1

1 Introduction Transfer pricing, which can be defined as an internal trade within a corporate group where different divisions supply each other with resources, have been a reoccurring issue in the academic world since the end of the 19th century (Eccles, 1985). Earlier transfer pricing research has mainly been economic and analyzed from technical or mathematical approaches (Eccles, 1985, 1983; Arvidsson, 1972). From a more practical point, the transfer price has been used as an accounting tool or as compliance for tax regulations (e.g. Bartelsman and Beetsma, 2003; Clausing, 2003; Elitzur and Mintz, 1996; Grubert and Mutti, 1991). An additional approach to transfer pricing is the managerial perspective, which is the focus of this paper and is characterized by taking social relationships between units into account (Martini, 2008; Eccles and White, 1988; Eccles 1985). Thus, the managerial aspect handles the issues of the management’s decision-making in a transfer pricing situation by taking the entire corporation’s interest into consideration (Lantz et al., 2002). Earlier research conducted from the managerial perspective implies that the best transfer pricing solution depends on various variables such as corporate objectives and organizational structures, therefore there is no general solution regarding this issue (Borkowski, 1990; Spicer, 1988; Eccles, 1985). The managerial view can be considered an important aspect for corporations to deal with regarding the transfer pricing methods, as its co-ordination affects the achievement of operational efficiency (Martini, 2008). The co-ordination in a corporation is dependent on strategies, and in turn strategies can be considered to have an impact on transfer pricing methods, which affects the corporate performance (Eccles, 1985). Most corporate groups are divided into multiple strategical levels (Nilsson and Rapp, 2005). Consequently, the corporate management cannot treat the transfer pricing policies as an isolated issue and solely handle it in one single unit. Rather, transfer pricing is affected by the relationships between the levels and the divisions’ impact on each other (Eccles and White, 1988). Research has found that the role of transfer pricing has developed into a component of organizational strategy (Merchant and Van der Stede, 2007; Cravens, 1997). Eccles (1983) adds to this by stressing, “Effective management of transfer pricing requires policies and organizational characteristics that are consistent with strategy” (p.161). A corporation can be divided into three organizational levels; the corporate level, the business level and the functional level (Nilsson and Rapp, 2005). The corporate level outlines a firm's overall goals and strategic aims, while the business level determines their individual strategies to achieve the corporate goals. At the functional level, the strategies are carried out and enable the business units to attain their goals (Ibid). If the strategies at the three levels are aligned, the corporation can achieve strategic congruence and obtain a competitive advantage on the market (Nilsson and Rapp, 2005). The importance of alignment for a corporation lies in the aim to reach operational efficiency and thereby optimize the corporation’s results (Martini, 2008). Therefore, to successfully implement strategies the managers should work towards the same goals (Jannesson et al., 2014). On the other hand, if divisions work towards different directions, strategic congruence

2

is not achieved and it rather creates inefficiencies for the corporation (Nilsson and Rapp, 2005; Lantz et al., 2002). This indicates a sub-optimization because the corporation fails to achieve the best possible co-ordination between the levels. The sub-optimization can evolve to units feeling mistreated over other divisions taking advantage of their resources and expertise, which revolves the issues of fairness (Eccles, 1983).

1.1 Problem Discussion

The root of the dilemma can be found in the notion that there is no universal way of solving the transfer pricing problem (Borkowski, 1990; Spicer, 1988; Eccles, 1985). This suggests that each organization have their own solution for the transfer pricing issue based on surrounding variables (Eccles, 1985). Eccles (1983) contributes to this with some well-chosen words to account for in the following research, stating, “Although no simple solution to the transfer pricing problem exists, it can be effectively managed” (p.161). This implies a contingency approach toward the issue (Cravens, 1997). The introduction explained that a managerial approach to transfer pricing methods could enhance the operational efficiency (Martini, 2008). However, a managerial perspective makes transfer pricing an issue for interpretations with a lack of definitive findings (Eccles, 1985). The latter is related to the contextual impact on transfer pricing, and the imperative adaption to changing circumstances (Ibid). Considering that the transfer price is based on relations between levels and units, the study takes all organizational levels in a corporation into consideration and is, therefore, a multi-level study. It is difficult to construct a narrow and delimited problem in a multi-level study, instead, one must contemplate the complexity of different levels and units that affect each other (Kozlowski and Klein, 2000). Additionally, because the solutions of transfer pricing depend on interactions and various variables, there are few theoretical models. This paper uses one of the models presented by Eccles (1985), which combines transfer pricing methods with strategic dimensions. Eccles (1985) model does not take the different strategic levels into consideration, and therefore is limited to fully recognize the interplay between strategies used throughout the different organizational levels. In order to better understand the strategic choices of a corporation, the model is researched in the context of strategic congruence to understand if the corporate level, the business level, and the functional level are aligned (cf. Nilsson and Rapp, 2005). Taking the strategic congruence into account, the academic literature allows a different viewpoint regarding the relationship between transfer pricing and strategy. One of the issues with transfer pricing is that it may create friction between organizational levels due to inefficiencies of strategic co-ordination (Eccles, 1985). This can result in that the corporation might find themselves to become a weaker player on the market (Nilsson and Rapp, 2005).

3

1.2 Aim and Research Questions

The aim of this paper is to explain how transfer pricing methods align to strategy and put it into the context of strategic congruence through a multi-level case study. The knowledge about aligned strategies and methods may benefit the corporation by increased competitive advantage and avoidance of sub-optimization of resources. The research question is therefore formulated as following: How is the transfer pricing structure designed and used throughout the case firm?

1.3 Contributions

The discussion above provides an understanding of the width and complexity of implementing an efficient transfer pricing structure. As there are a variety of broad studies conducted on the matter of transfer pricing (e.g. Adams and Drtina, 2008; Cravens, 1997; Eccles, 1985, 1983; Hirshleifer, 1956), Lantz et al. (2002) suggest that by gathering deeper transfer pricing knowledge through cases, it will be easier to compare and develop the research area. This paper conducts a case study, which contributes with explanations of given transfer pricing decisions and how they are affected by interdivisional relationships and strategic alignment. Considering that the case study has a multi-level approach, this paper may contribute to explain the deviating perceptions in the strategic co-ordination, which interfere with the strategic congruence. The research of this paper should consider the surrounding setting and interpreted it into the existing theoretical knowledge. The paper contributes with practical implications by highlighting the factors that enhance the alignment and operational efficiencies, respectively factors that hamper the alignment by creating inefficiencies of co-ordination as well as sub-optimizations.

4

2 Theory The theory section, initially, presents the objectives of transfer pricing from a financial perspective and a managerial perspective. Next, different transfer pricing methods are described. To reflect over these methods, opportunistic behavior and fairness are included. Further, the paper presents a section of the interrelation between transfer pricing and strategic congruence.

2.1 Objectives of Transfer Pricing

The planning of transfer prices derives from a firm’s different objectives, also knowable as goals (Martini, 2008). The objectives are fundamental for determining a firm’s strategy and thereby the process of creating policies and performance evaluation. Martini (2008) stresses that the objectives of transfer pricing can be divided into two categories; financial transfer pricing and managerial transfer pricing. Financial transfer pricing is a centralized decision-making tool that focuses on profit allocation through minimizing tax burdens and distribution of profits to minority shareholders. Managerial transfer pricing, on the other hand, focuses on optimal internal co-ordination disregarding profit allocation, which equals pre-tax profit (Martini, 2008). A managerial transfer pricing policy implies that the subsidiaries determines both the price and the trade, but do not consider minority shares or taxes. A managerial transfer pricing is based on decentralized decision-making, meaning that the unit with the largest amount of information is the most suitable to make decisions (Martini, 2008). A synonym to managerial transfer pricing is operational efficiency, which aims to align the objectives of the business and the employees into a cohesive system. The alignment of transfer pricing can be considered as a mechanism to reach corporate objectives, and thus strategic congruence throughout the firm (Nilsson and Rapp, 2005; Cravens, 1997). Development of objectives from a managerial transfer pricing perspective enables the transfer price policy to become an internal co-ordination component of corporate strategy, which is in line with the strategic concepts of Nilsson and Rapp (2005). The managerial perspective primarily takes effectiveness into account and puts the traditional view of transfer pricing as an accounting tool as a secondary consideration (Cravens, 1997). The strategy effectiveness can be assessed through measuring to which extent the objectives are met (Nilsson and Rapp, 2005), and transfer-pricing policies can be created based on those results (Cravens, 1997). Financial transfer pricing and managerial transfer pricing can be integrated to attain the optimal trade-off to reach profit maximization. Martini (2008) find that firms using either integrated transfer pricing, which is a combination of both the financial and managerial transfer pricing or solely managerial transfer pricing perform better than the ones only using financial transfer pricing. From a management perspective, both financial and non-financial objectives should be applied to make sure resources are used efficient (Kald et al., 2000).

5

2.2 Transfer Pricing Methods

Early economics and accounting literature argue that in perfectly competitive markets, marginal cost-based transfer pricing allows for profit optimization (Hirshleifer, 1956). However, the model does not discuss how the optimal equilibrium is to be reached through a managerial perspective (Martini, 2008; Arvidsson, 1972). Further, Arvidsson (1972) argues that decision-making of transfer pricing policies has a bounded rationality because of the lack of information and complex goal structures. Eccles (1985) found that transfer pricing is rarely used as a mechanism to allocate resources within a firm, but rather motivate managers to increase the value of internal assets on the vertical levels. As transfer pricing has been modeled through an economic perspective and with mathematical techniques, there are additionally two important aspects to consider. The first one is the general behavior of the managers in a decision-making situation, and the second considers the reactions between the managers in different divisions (Arvidsson, 1972). The managers determine the transfer pricing policies in a firm, and their valuation becomes the social relationship in the exchange (Eccles and White, 1988). Therefore, transfer pricing has little, or nothing, in common with resource allocation, which negates the traditional economic conception of how corporations use transfer pricing (Ibid). Eccles (1983) states that “Often a company will use several transfer pricing policies depending on the strategy of the groups, business units, and products involved” (p.151). Borkowski (1990), Spicer (1988), and Eccles (1985) acknowledge that it does not exist a single correct method of transfer pricing, in line with contingency theory. However, there are three generally accepted transfer pricing methods within the literature, which are; cost-based, market-based, and negotiated pricing (Cravens, 1997). Additionally, Arvidsson (1972) found that the cost-based method and the market-based method are the most commonly used transfer pricing methods, and negotiation between the divisions of the transfer price was less common and only used as a complement to other methods.

2.2.1 Cost-Based

In most cases, markets are imperfectly competitive, and then the market price most likely will be greater than the marginal cost (Eccles, 1983). When this is the case, the marginal cost is not applicable as a transfer pricing policy. In the case of no existence of an external market or information about the external market, neither marginal cost nor market-based cost can be used. In these situations, the cost of producing a product may be applied, called cost-based transfer pricing, and implies that the division which sells the final product to a third part recognize the full profit. The cost-based method maximizes the earnings of a division and can lead to a sub-optimizing of the firm's overall outcome if the profits are not properly allocated (Eccles, 1985). Eccles (1983) raises the problem of the final product not being priced aggressively enough when using the cost-based method, resulting in loss of market shares or profits.

6

2.2.2 Market-Based

A market-based method links the cost of internal transfers with the price of the external market as one common approach. This is typically justified when the market has perfect competition, however, Arya and Mittendorf (2008) finds that market-based transfer price can also be justified in imperfect competition. The market-based method contributes to a firm's competitive advantage because the corporate level is compelled to drive down the product's market price, which translates to an aggressive production approach (Arya and Mittendorf, 2008). Therefore, the market-based transfer price may contribute to the firm’s competitiveness (Arvidsson, 1972). In contrast, Eccles (1983) stresses that the market-based method makes the final product become uncompetitive because each division will earn its individual profit by the percentage on percentage effect, and may contribute to making the final product more expensive. Further, due to factors as; hard to define market price, lack of market information, specialized products, or a difference between internal and external products, a market-based method may be impossible to apply (Vaysman, 1996). The divisions involved in the exchange can argue the market-based price to be untrue, and therefore affect the perceptions of the division's performance and the understanding of its contribution to the overall corporate profit (Eccles, 1983).

2.2.3 Negotiated

Negotiated prices allow the involved entities to discuss and settle at a price (Cravens, 1997). Vaysman (1996) explain that negotiated prices are established by using a foundation of both market-based and cost-based pricing. Adams and Drtina (2008) develops these thoughts by suggesting that negotiated transfer prices will be lower than the market price but higher than the cost of the product or service. This lead to the seller and the buyer dividing the result between them, which puts the selling part in a position where their investments bring less profit than initially was expected (Adams and Drtina, 2008). Furthermore, in an organization with a high degree of centralization, negotiated based transfer pricing can be used as a tool to minimize resistance between the involved units. Eccles (1985) stresses that specific unit’s discussion skills may be an issue that arises through a negotiated transfer pricing method. Since some negotiators are more successful, it might result in sub-optimization of the whole corporate group’s profit.

2.2.4 Mandatory and Non-Mandatory Agreements

The use of mandatory and non-mandatory agreements depends on the corporate group's level of vertical integration (Eccles, 1985). Eccles (1985) suggests that a corporation with a high degree of vertical integration implements a mandatory transfer pricing system. Figure 1 shows the relationships between the different trading options, based on the degree of vertical integration.

7

Figure 1: The mandatory and non-mandatory agreements effects on transfer pricing policies Source: Modified version of Eccles (1985)

Based on figure 1, Eccles (1985) suggest that if the vertical integration is high and the corporate units are not active on both the external and the internal market, it should implement a mandatory cost-based transfer price. If the units are selling substantial amounts to both internal and external customers, Eccles (1985) stresses the transfer price to be market-based. In a firm with less vertical integration, the individual units can decide independently from the corporate management with which suppliers to conduct their trades, Eccles (1985) mean that they, therefore, have exchange autonomy. A result of this is the manager in the individual business units to have a direct responsibility for the unit’s result, and the corporate management has a limited participation in the purchasing negotiations between the units (Eccles, 1985).

2.3 Opportunistic Behavior and Fairness

Langfield-Smith (1997) finds managers’ perceptions to be an influence that impact firm’s strategic change. The issue of deviating perceptions can create a variation of managerial approaches concerning the application of transfer pricing. For a firm to implement strategies, manager’s behavior must pull towards the same direction (Jannesson et al., 2014). Thus, firms’ face the risk of internal actors trying to maximize their own profits simultaneously, which increases the possibility of divisions sub-optimizing their aggregated contribution to the firm (Lantz et al., 2002). Because of agents’ acting in self-interest, the firms require an organizational structure that contributes to the firm’s objectives (Jensen and Meckling, 1992). Fonvielle and Carr (2001) find that units within a firm may have difficulties to see the contribution of its specific performance to the achievement for the total firm. This creates an unwillingness to share resources and information within a firm. Furthermore, Eccles (1983) have raised the issue of that managers do not always feel fairly treated due to how the transfer

8

pricing structures are set up. Occasionally internally traded products and services are difficult to measure, and the misperception of the value creation may generate friction between the entities (Merchant and Van der Stede, 2007).

2.4 Strategic Congruence and Transfer Pricing

An important factor to achieve strategic congruence, and competitive advantage, is the relationship between a firm's strategy and its external and internal environment (Nilsson and Rapp, 2005). In the result of Eccles (1983) research, transfer-pricing systems are tools to generate information and control for strategy implementation in a firm’s different levels. Cravens (1997) contribute to the understanding that transfer pricing is an important element of a firm's strategy rather than only an instrument for tax-allocation. Both Meer-Kooistra (1994) and Arvidsson (1972) stresses the close connections between transfer pricing and the co-ordination in the firm, and Govindarajan (1988) add to the latter through stating, “Matching administrative mechanisms with strategy is likely to be associated with superior performance” (p.829). Strategic congruence implies that the co-ordination of strategies at different levels can build competitive strength. Nilsson and Rapp (2005) highlight the common business logic as an advantage of co-ordinating strategy at all organizational levels, which consists of the corporate level, the business level, and the functional level. In a corporation, the transfer-pricing policies are active in-between the different levels and therefore aim to achieve strategic congruence. If there is an absence of strategic congruence, the outcome could sub-optimize the aggregated contribution to the overall performance (Nilsson and Rapp, 2005).

2.4.1 Strategic Dimensions

Eccles (1983) has developed a model of organizational structures, based on strategic dimensions and their most suitable type of transfer pricing methods. The model is called manager’s analytical plane (MAP). The organizational structure is analyzed from two strategic dimensions, namely diversification and vertical integration. More specific, diversification regards a firm's spread within different business areas, while the grade of vertical integration depends on the extent a firm owns the different steps in its supply chain. Vertical integration is a fundamental part in understanding the evaluation of a unit's earnings. By understanding the level of these two dimensions, Eccles (1983) MAP model, which is presented in figure 2, provides four organizational categorizations; collective organization, cooperative organization, competitive organization, and collaborative organization.

9

Figure 2: Managers analytical plane model (MAP) Source: Eccles (1985)

The first category is the collective organization, which has a low degree of diversification and a low degree of vertical integration. As the name suggest, the organization works as a collective and does not have a proper managerial hierarchy, and therefore have no need for any transfer pricing policies (Eccles, 1985). Second, a co-operative organization is characterized by low diversification and a high degree of vertical integration. This type of organization has the same strategy for all divisions, leading to that each division has a specific role to fulfill to reach the corporation's main goals. Further, co-operative organizations have an apparent vertical hierarchy and a centralized decision-making process of interdependent factors. The underlying thought of the performance in the organization is to bring value both for one's own divisions as well as for the corporate group. In contrast, a competitive organization has a decentralized decision-making process, with both high degree of diversification and low vertical integration. The competitive organization lack consideration for other units within the same corporate group, and the corporation's overall results. The decentralization of the competitive organization leads to the different divisions working considerably freely and is not directly affected by other divisions actions. At last, the fourth organizational category is the collaborative organization, which has both high diversification and high vertical integration. The collaborative organization is a mix of organizational structures, as it combines the high vertical integration from the co-operative organization, and the high diversification from the competitive organization. This puts pressure on individual profit centers to co-operate with the corporation's business units. The corporate strategy, therefore, blends a general strategy with the individual division’s

10

strategies. A result of this is that the managers can not solely focus on financial measurement systems when considering the development of the business (Eccles, 1985, 1983). Considering collective organizations, Eccles (1985) stresses that high involvement of the management in the operation influences the choice of transfer pricing policies. Eccles (1985) strategic dimensions have similar criteria to Porters (1987) corporate level strategy, which is also based on the degree of diversification but focuses on synergy potential instead of vertical integration.

2.4.2 Corporate Level Strategy

The leading objectives and goals of a corporation are what define the corporate strategy (Nilsson and Rapp, 2005; Hofer and Schendel, 1978). At the corporate level, Porter (1987) combine the synergy potential of business units with the degree of diversification. By doing so Porter (1987) developed four different corporate categories which are; portfolio management, restructuring, transfer of skills, and activity sharing, as shown in figure 3.

Figure 3: Corporate Level Strategies based on Porter (1987) Source: Nilsson and Rapp (2005)

In the model of Porter (1987), portfolio management identifies by a high degree of diversification between business units in the firm. Corporations that applies this strategy acquires undervalued businesses that function as independent organizations. In comparison to Eccles (1983), firms of the competitive or the collaborative type have a high degree of diversification. However, the two types differ in degree of vertical integration. The portfolio management has independent functioning units, like a competitive firm which has low vertical integration. The common denominator between a portfolio management strategy and the competitive organization is the broad range of products and services that are not sharing

11

production processes and materials in their production. Furthermore, financial measurements are the executive manager’s main tool to measure the performance of a specific unit. According to Eccles (1985), the competitive firm’s preferable transfer pricing policy is the market-based, and have the same relationship to the corporation's units as to the external market. However, the common transfer pricing between units, rather is the negotiation, because of the decentralized bottom-up relation. This result in the separate units trying to maximize their own profit, even though it is at the expense of the whole corporation. Additional, in comparison to the portfolio activity, firms with a restructuring strategy has a lower degree of diversification, but still possesses considerable higher diversification than firms with the transfer of skills or activity sharing strategy (Porter, 1987). In difference to the portfolio management and restructuring strategy, transfer of skills focus on synergy potential rather than the degree of diversification (Porter, 1987). The main aim of the transfer of skills strategy is to combine skills between the divisions. A transfer of skills strategy is often applied by firm’s active within one industry and has a long-term perspective on investments (Nilsson and Rapp, 2005). The difference between the transfer of skills and the activity sharing strategy should do with the activity sharing strategy’s greater focus on sharing the actual working processes rather than just skills. Therefore, the management always tries to maximize the synergy potential as well as the co-operation between units (Porter, 1987), and the co-ordination of the transfer of skills strategy enables cost-efficiency. If this is the case, the management is less likely to practice market-based transfer pricing. Instead, a firm with synergy strategy focuses its organization towards being co-operative. Like the competitive firm, the co-operative firm also uses negotiated transfer pricing policies. Although, the difference is that the co-operative firm focuses on the maximization of corporate objectives, and the top management has a larger influence in everyday functions, through a centralized decision-making process (Porter, 1987). The actions of the business units are determined by top managers, which lead to the notion that a co-operative firm uses various forms of cost-based transfer pricing. At last, the collaborative firm is a combination of a competitive and a co-operative organization, implying it is a hybrid of portfolio management and activity sharing strategies. Hence, the collaborative organization has a complex transfer pricing structure, which makes management process important in the decision-making of policies. Therefore, the collaborative firm tries to hybrid the different transfer pricing strategies of various organizational structures. To summarize at the corporate level, this paper, hypothetically assumes, that a firm with a portfolio management strategy and a competitive structure, likely has a market-based transfer price policy or a negotiated transfer price policy with a focus on maximization of unit’s result. Also, a firm with an activity sharing strategy and a cooperative structure likely has a cost-based transfer price policy or negotiated transfer price policy with a focus on maximization of the whole firm’s result.

12

2.4.3 Business Level Strategy

The business units of a corporation are the actors that compete directly in the external market (Nilsson and Rapp, 2005). Therefore, the business units outline their own strategic goals. Although, the overall corporation’s strategic aims should still align to the objectives (Ibid). Porter (1980) develop the business level typology strategies by identifying three strategic types; differentiation, cost-leadership, and focusing. The three typologies by Porter (1980) divide strategy by defining their different ways to position the business units and compete on the market. Differentiation intends to give the customers the values that they ask for, and then charged a higher price for the extra features (Porter, 1980). Also, factors such as sharing activities can enable an increased differentiation and create a possibility to charge premium prices (Nilsson and Rapp, 2005), which indicates cost-based transfer pricing policies. A cost-leadership strategy focuses on lowering the production costs as much possible, which is often obtained by implementing highly standardized products (Porter, 1980). Additionally, a cost-leadership strategy aims to have the lowest price on the market and therefore applies a market-based transfer pricing policy. Nilsson and Rapp (2005) emphasize effectiveness as key features of cost-leadership. Arya and Mittendorf (2008) mean that a market-based price may contribute to an aggressive production approach, and drive down the product's market price. The focusing strategy can be seen as a subcategory of both the differentiation and cost leadership strategies (Porter, 1980). To summarize at the business level, this paper, hypothetically assumes, that a firm with a cost-leadership strategy, likely has a market-based transfer price policy or a negotiated transfer price policy with a focus on maximization of unit’s result. Also, a firm with a differentiation strategy likely has a cost-based transfer price policy or negotiated transfer price policy with a focus on maximization of the whole firm’s result.

2.4.4 Functional Level Strategy

A functional strategy enables subsidiaries and divisions within a firm to achieve their goals (Nilsson and Rapp, 2005). The functional unit operates individually to manage the goals provided by the business unit (Ibid). To provide a working strategy at the functional level, the managers need to allocate and maintain a competitive advantage within their unit. To manage the identification of competitive advantage, Ward et al. (1996) stress the necessity of units understanding for the organizational structure, competitive strategy, manufacturing strategy, and environmental knowledge. Like the business level, the functional level can focus its strategies towards cost-minimizing or product differentiation (Hayes and Wheelwright, 1979). Alignment of strategy between the levels implies that strategic congruence and superior performance is more likely achieved if both business level and functional level simultaneously execute a differentiation strategy, alternatively a cost-minimizing strategy. The co-ordination of the business strategy and the functional strategy is necessary to align the goals of both levels (Nilsson and Rapp, 2005). The functional level executes transfer-pricing policies, therefore it has a significant impact on the efficiency of the strategies. Thus, understanding the processes in a corporation is crucial regarding the coherence of strategies

13

and if the transfer pricing policies are efficient enough to fulfill the corporate group’s strategic goals. To summarize at the functional level, this paper, hypothetically assumes, that a firm with a cost-minimizing strategy, likely has a market-based transfer price policy or a negotiated transfer price policy with a focus on maximization of unit’s result. Also, a firm with a differentiation strategy likely has a cost-based transfer price policy or negotiated transfer price policy with a focus on maximization of the whole firm’s result.

2.4.5 Strategic Interrelations

As mentioned, each corporate level has an individual approach to strategy. To achieve strategic congruence the strategies should be aligned (Nilsson and Rapp, 2005). The paper uses Porter’s (1987, 1980) and Hayes and Wheelwright’s (1979) strategy models to define each levels approach, and combines them with the transfer pricing methods presented by Eccles (1983). As illustrated in figure 4, strategic congruence is possible when portfolio management is combined with cost-leadership and cost-minimizing production. Based on the papers hypotheses, when trying to achieve strategic congruence, the corporate group most likely has a market-based, a negotiated transfer pricing structure, or both. Also, as described in figure 4, strategic congruence can be achieved when an activity sharing strategy is combined with differentiation and customized production. When applying this strategic approach throughout the corporation, the organization is likely having a cost-based and/or a negotiated transfer pricing structure. The strategic interrelations in figure 4 are based on the hypotheses from the different organizational levels.

Figure 4: A corporation’s strategic congruence and its alignment to transfer pricing methods based on the hypotheses

14

An aligned strategic approach throughout a corporation contributes to enhanced competitive advantage. If the strategy between levels is misaligned, it may hamper the corporation’s possibilities to become a strong competitor in the external market (Nilsson and Rapp, 2005). Nilsson (2002) point out that even though strategic congruence is difficult to obtain, it is still possible for the corporation to have a competitive advantage. Although, Nilsson (2002) then stresses the importance of the balance between the business units need of control and the corporations integrated control.

2.5 Summary Theory

Martini (2008) suggests that financial transfer pricing primarily focuses on profit allocation, while managerial transfer pricing focuses on operational strategy. By elaborating the managerial perspective, the theory section stresses the perception of opportunistic behavior and fairness. Hence, in transfer pricing structures, manager and subordinates perception is a common issue that will affect the firm's profit maximization. Eccles (1985) suggests that the organization structure of a corporation can be located based on the blend between diversification and the vertical integration. These two parameters relate to the strategic ideas provided by Porter (1987, 1980) and Hayes and Wheelwright (1979) considering strategy formulation on the corporate, the business level and the functional level. The study provided by Nilsson and Rapp (2005) illustrates the critical relations to align the strategic models for a corporation to obtain a competitive advantage. By combining transfer pricing theory with the different organizational levels strategies, figure 4 illustrates potential possibilities to gain strategic congruence. A corporation that manages to achieve strategic congruence can resourcefully maximize their operations and obtain a competitive advantage, thereby they become a strong player on the external market. However, when a corporation fails to achieve strategic congruence, the risk of sub-optimization of the aggregated contribution increases.

15

3 Methodology The methodology section presents the research design and continues a description of the data collection methods. This chapter also discusses the operationalization and the analytical approach of this thesis.

3.1 Research Design

To examine the transfer pricing structures and the strategies in a corporation this study has a research design suited for a case study. Saunders et al. (2016) define a case study as “Research strategy that involves the empirical investigation of a particular contemporary phenomenon within its real-life context, using multiple sources of evidence” (p. 711). The case study is used to explore a complex phenomenon and the dynamic of the context through observations. Another important aspect of a case study is its explanatory approach to interactions within a firm. The case study is conducted through a mixed data collection, which includes both qualitative and quantitative data. The use of both qualitative and quantitative data provides the study with the possibility to obtain various data and information. More specifically, interviews and annual reports contribute to carrying out an in-depth study and triangulates to the empirical result with data collected through questionnaires to obtain a broader opinion on the researched subject.

3.1.1 Case Study Design

A research question, starting with a how, invites to an explanatory study (Saunders et al, 2016; Yin, 2003). Yin (2003) finds an explanatory study to deal with operational links rather than with incidents, which is in line with the case firm. The approach to the theoretical aspects is deductive because the study uses the theory to formulate hypotheses (Ibid), which are analyzed based on the observations from the case firm. The case study can be characterized as multi-level due to the vertical focus throughout the firm, which is in line with Kozlowski and Klein (2000). To research the strategic congruence, a multi-level study needs to link the empirical data with the theory. Kozlowski and Klein (2000) define a multi-level study to be designed as a bridge between macro and micro perspectives and specifying relationships of a different phenomenon in the analysis. More specifically, Kozlowski and Klein (2000) refer to the relationship between, for example, organizations and individuals, or organizations and groups. This study finds the linkages by identifying the different organizational levels strategic approaches, its alignment to the transfer pricing methods, and explores the strategic congruence between the levels to determine its degree of alignment. To perform a multi-level study, it is especially important to specify the linkage between the different levels (Kozlowski and Klein, 2000). Even though this study integrates quantitative data, the multiple-level case study cannot be statistically generalized because the study does not present a result representative of the population (Gibbert et al., 2008). However, Gibbert et al. (2008) stress that a case study is a subject of analytical generalizability. The analytical approach can be generalized from the collected empirical data to the theory (Gibbert et al., 2008). Halkier

16

(2011) describes analytical generalization as typically bound to the context. The case study may be looked upon as a complex phenomenon, as its operative procedure and social interactions attempt to obtain analytical generalizability to conceptualize through a practical theoretical approach. Additionally, Halkier (2011) mean that it is a situation characterized by duality because it integrates the recognizably of both specific processes and relationships.

3.1.2 The Case Selection

The examined case is selected based on either being an extreme and unique example or as a representative and more general (Saunders et al, 2016; Silverman, 2005; Yin, 2003). The case firm in this study is representative and focuses on everyday conditions and circumstances. Moreover, the case firm is a publicly listed corporation, and operates within the construction and civil engineering industry, more specifically it supplies infrastructure, commercial buildings, and housings. The chosen industry fits into the requirements of similar processes with competing firms to the same kind of operations, as the industry follows standards and manufacturing processes that are well tested (KPMG, 2016; Dubois and Gadde, 2000). Yin (2003) explains that when the aspect of representativeness is considered, the research should be able to better develop the existing theoretical knowledge, as it can be applied to the surrounding settings. The corporate organization is divided into business units and subsidiaries. Each business unit is further divided into regions, where each region has several ongoing projects. The structure of the researched units of the corporation is shown in figure 5. From a transfer pricing point of view, the different projects in business unit 1 (BU1) are considered as the buyers. The subsidiaries, which are present in business unit 2 (BU2), functions as sellers because they provide the different projects with products and services.

Figure 5: The selected case firm’s structure

17

3.1.3 Limitations

The paper is limited in that it does not consider corporate interrelations regarding production units such as infrastructure or commercial buildings that could help in further developing the knowledge about the transfer pricing structure within the corporation. As such it is limited to focus on the housing production within the three largest regions the corporation operates within. Real estate construction is one of the case firm’s main expertise areas, where they focus on producing and developing housing projects. Even though, the limitation focuses on a specific product in specific geographical areas, the usage of transfer pricing can be representative for the whole organization. This is possible as the researched subsidiaries found in BU2 are used throughout the whole corporate group.

3.2 Data Collection

The study aims to research the transfer pricing structure and the strategic congruence throughout a corporation. Therefore, data from the organizational levels is collected, more precisely at the corporate level, the business level, and the functional level. The data collection consists of various sources, including interviews, questionnaires, and annual reports, which implies that the case study procures both qualitative and quantitative data. The interplay between the methods is significant to obtain a broader collection of information and to achieve a triangulation from various sources (Corbin and Strauss, 2008). The use of both qualitative and quantitative data collection approaches enabled the different types of data collection to counterbalance for each other’s limitations (Silverman, 2005). The mix of data collection provides a correct image of the organization as it contributes to an in-depth approach though the interviews and the annual reports, and provides descriptive statistics through a questionnaire to obtain a more informative opinion (Ibid). At the corporate level, the data consist of interviews and supporting documentation through annual reports, as described in the data gathering process model (Figure 6). The data collection at the corporate level is conducted with persons at the central management, meaning that the aim at the corporate level is to collect, understand and interpret the case firm’s core purpose of transfer pricing policies and strategies. While the corporate level sets policies and strategies, the business level and the functional level are the ones to implement them into the operations. At the business level, the data is collected from both business units. More specifically, from two sellers and three geographical regions, which specifies on the housing industry. Data from the subsidiaries was collected from senior managers that have an insight over the operation in all three geographical regions. At the functional level, questionnaires are conducted to capture the usage, design, and integration of transfer pricing.

18

Figure 6: The data gathering process throughout the organization

The intention of the interplay of methods is to create a triangulation of information, as a ground of validation assessment (Svensson and Starrin, 1996). At the corporate level, the comparison of formal documentation and interviews with strategically positioned employees provides a foundation to validate the collected data. The questionnaires collected at the functional level provides data to obtain the perception of the transfer pricing structure. The triangulation of sources works as a complementary method for a more valid result, but also as an approach to capture a complete picture and a contextual portrayal. Furthermore, the mix of methods can find notable differences within the same case, which might have been neglected in the use of a single method (Jick, 1979).

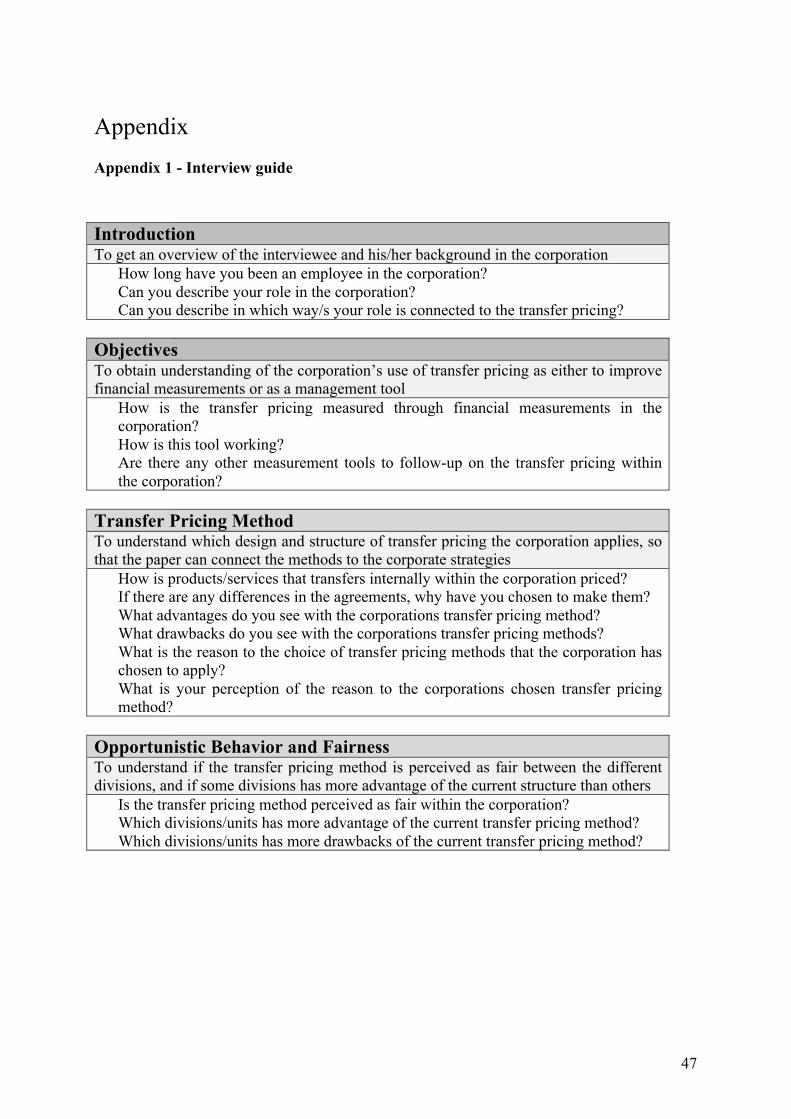

3.2.1 Interviews

The study’s main source of data collection is interviews. The interviews are conducted in a semi-structured way to increase the understanding of the case firm’s transfer pricing design and its usage. The questions are formulated in an interview-guide (Appendix 1), based on the study's theory. The semi-structured interviews aim to give the interviewee enough space to introduce their perception and ideas of the prevailing situation in the case firm (Flick, 2002). The openness in the interviews contributes to capture contextual information and to avoid preconceived concept (Ibid). The reliability of the data collection increases when the context is understood and interpreted (Svensson and Starrin, 1996). It also creates a possibility for the interviewee to bring up subjects that the researchers might have missed out on when designing the interview-guide, and therefore benefits the capturing of the whole picture. In comparison to the questionnaires, which are restricted by researches biased interpretation, the semi-structured interview highlights the interviewee’s viewpoint (Saunders et al., 2016). An issue that may arise from interviews as data collection is the possibility that the interviewees drift away from the subject (Ibid). To prevent this, the interviewees have access to the interview-guide during the interview, which helps in leading the respondent back to answering the research questions (Flick, 2002). Being aware of this problem, the researchers minimized the guidance of the questions in the interview and only intervened when the interviewee is off track on the topic. The strive to minimize the guidance refers to the avoidance of questions that encourage or prompts the desired answers or to not include

19

questions that provide the interviewee with alternatives. In this study, nine interviews have been conducted (Appendix 2). All interviews were constructed in a semi-structured way and were based on the same interview guide. The interviews ranged timewise from the longest at 81 minutes to the shortest at 44 minutes. The choice of interview length is based on having enough time to conduct an in-depth semi-structured interview to obtain data to answer the paper's research question (Saunders et al., 2016).

3.2.2 Questionnaires

The case firm has a comprehensive amount of simultaneously ongoing projects, which are all involved and affected by the transfer pricing policies. The questionnaires are conducted to capture the broad use and understanding of the transfer pricing policies. Furthermore, the questionnaires contribute with more data to find out how the transfer pricing methods are perceived and used at the functional level. The questionnaire (Appendix 3) consists of 16 questions and targets Foremen, Construction Engineers, Site Managers, and Project Managers. The questionnaire was sent out online to 127 suitable candidates that are affected by the transfer pricing policies. In total, 60 questionnaires were answered, which is equivalent to a response rate of 47 percent (Appendix 4). The online method is used to increase the effectiveness of sending out the questionnaire, sending out reminders, as well as it allows obtaining answers directly (Fink, 2009).

3.2.3 Annual Reports

To ensure the research validity, this paper triangulates the collected data from the interviews and the questionnaires with secondary data. The main sources of the secondary data are annual reports. The annual reports are publicly published and can be found on the case firm’s webpage. Additionally, the annual reports describe the corporation's formal approach towards goals and strategies. The use of secondary data provides a comparative ground to examine the representativeness from the interviews and questionnaires (Saunders et al, 2016).

3.2.4 The Respondents

Interviews at the corporate level are held with managers who are directly connected to the purchasing strategies within the case firm, and should, therefore, possess large knowledge of the transfer pricing procedures. The Corporate Purchasing Manager (CPM) has at the corporate level a functional responsibility for everything related to purchases. The Corporate Category Manager (CCM) acts supporting to the operational divisions on a strategic and organizational level but is little involved in direct operative issues. Considering the two sellers in this case study, the CCM is the contract manager for them both. At the business level, the study has targeted the persons in the case firm with the greatest experience of internal trade to capture the needed data. Three interviews have been conducted with respondents from the selling units. The Chief Executive Officer of Seller 1 (CEO-S1) gets in touch with the subject of transfer pricing every day, due to the involvement in the

20

unit’s strategic trades. The Chief of Operation Officer of Seller 1 (COO-S1) works with sales and project development issues within the subsidiary and has participated in the design and formulation of the internal agreements between the subsidiary and the buying units. The Chief Executive Officer of Seller 2 (CEO-S2) manages the subsidiary with the largest amount of internal sales within the corporation and therefore has a daily involvement in the procurements. At the buying units, four interviews have been conducted. The Business Unit Purchasing Manager (BUPM) mainly focuses on developing a central organization of purchases within the buying business unit. The Regional Purchasing Managers (RPM) for Region 1 (R1), Region 2 (R2), and Region 3 (R3) purpose is to be a supporting function for the individual purchasers within the region's projects. Furthermore, each of the units consists of several projects at the functional level, which are executing the transfer pricing policies. At the functional level the questionnaires have been targeting the respondents from the projects with leading roles on the construction sights, and continually trade and co-operate with the selling units. From 60 responses, the distribution results in 41.7 percent (25) answers from Foremen, 25 percent (15) answers from Construction Engineers, 25 percent (15) answers from Site Managers, and 8.3 percent (5) answers from Project Managers.

3.2.5 Confidentiality

Based on the case firm’s request, this paper provides the researched corporation with confidentiality. This regards the corporation's full name, the name of the subsidiaries, the name of the divisions, as well as the identity of the interviewed persons. The argument is that the case firm wants to minimize the risk of third parties to gain knowledge and insights of their strategic work. This results in a limited traceability of the data. The confidentiality approach can be beneficial for the paper because it increases the participants’ trust towards the researchers, and thus minimizing threats regarding the reliability (Saunders et al., 2016). The aim is therefore to gain a higher trust between the participants and the researchers, which could improve the collaboration and information exchange.

3.3 Operationalization

The collected data is analyzed based on the theory after each interview been individually processed. The questions in the interview-guide and the questions in the questionnaire are designed to complement each other. This should provide a solid foundation for the analysis regarding the theoretical hypotheses considering the alignment of strategic dimensions and the transfer pricing policies. Continuing, the analysis of the three organizational levels are viewed from a theoretical perspective of strategic congruence. The analysis then focuses on if the transfer pricing policies are aligned and if the strategy is congruent throughout the case firm’s different organizational levels. Additionally, the focus on alignment enables the study to highlight the factors that enhance and hamper the prevailing transfer pricing structure.

21

3.3.1 Interviews

The interview-guide is divided into several categories based on the theory, in order to gather information connected to them (Appendix 1). Flick (2002) implies that a consistent use of the same interview-guide in a study increases the comparability of the collected data, which contributes to distinguishing contextual factors and variances. Each category has been conceptualized by a defined aim, which has been used as a foundation to formulate questions (Table 1). Furthermore, the questions are formulated to obtain answers that contribute to the conclusion of the researched aim

Category Aim

Introduction To get an overview of the interviewee and its background in the corporation.

Objectives To obtain understanding of the corporation’s use of transfer pricing as either to improve financial measurements or as a management tool.

Transfer Pricing Method

To understand which design and structure of transfer pricing the corporation applies so the paper can connect the methods to the corporate strategies.

Opportunistic Behavior and Fairness

To understand if the transfer pricing method is perceived as fair between the different divisions, and if some divisions has more advantage of the current structure than others.

Organizational Structure

Aim to investigate the structure and degree of control within and between the corporation’s different levels to get an understanding of the corporation’s degree of decentralization or centralization.

Strategy To investigate the co-ordination of strategy on the different levels in the corporation and connect it to the transfer pricing methods.

Strategy: Corporate Level

To understand the degree of diversification in the corporation, if the corporation possesses synergies, and the degree of vertical integration.

Strategy: Business Level

To understand the business units’ approach to cost leadership and differentiation strategies.

Strategy: Functional Level

To understand if the projects approach to cost minimizing and differentiation strategies.

Table 1: Operationalization of the interviews

22

3.3.2 Questionnaires

The questions in the questionnaire are formulated based on the study’s theory, similarly to the interviews, to anchor reliability through consistent information. Most of the questions have a closed design, where the respondent received a question and five answering options to rank their answer as ‘totally agree’, ‘agree to large extent’, ‘agree to small extent’, ‘disagree’, and ‘do not know’. The two last questions have an open design, which allows the respondents to express their opinions freely. The closed-design of questions has been proven to generate a higher frequency of respondents, because of its ease to answer the questions (Fink, 2009). Additionally, the closed-designed questions enable the researchers to effectively enter and categorize data (Ibid). Open-ended questions provide the respondent with an opportunity to further develop a topic while contributing with explanatory and comprehensive answers. This means that open-ended questions are more exposed to interpretations and analysis (Saunders et al., 2016). The closed method does not give the respondent the same opportunity to express their own ideas, as the use of semi-structured interviews or open-ended questions do (Fink, 2009; Saunders et al., 2016). The questionnaire is designed so each question must be answered before the form can be submitted. This approach contributes to a higher degree of fully completed questionnaires. The respondents to the questionnaire have the option to answer, ‘do not know’, and thereby they are not forced to take a position in the questions. There is a risk that the respondents use the option ‘do not know’ when they have low ambitions to answer the questionnaire.

3.3.3 Annual Reports

The annual reports are viewed upon as a formal source of information from the case firm. The annual reports are formulated at the corporate level, and therefore contribute to interpreting the case firm’s overall objectives and approach to strategy. The annual reports have been used as a tool of information to establish a foundation of terms used in the interviews, the empirical result and the analysis. Also, the annual reports provide the empirical result with a frame of formal values. The annual reports are a source to obtain additional information for the interpretation of the corporate level.

3.4 Analytical Approach

Considering the mix of qualitative and quantitative data collection, the greatest obstacle to analyze the data is to correctly interpret and connect the information. This is what Saunders et al. (2016) call researchers error and researchers bias. By having clear communication with the participants regarding the findings, both problems should be minimized and thus give the research a higher reliability. The interviews have been recorded and transcribed to facilitate the analysis and the control of the data that is used in the paper, however, the transcriptions

23

are excluded from the appendix due to the confidentiality of the case firm. To analyze the data, a coding system by color marking has been used. Coding the data enables to link the answers from the interviews to the theory. Since the study uses semi-structured interviews, the questions have been freely answered by the interviewees and therefore occasionally affected other subjects than the category discussed. The coding system contributed to linking several questions to a specific subject. The empirical result is structured based on the outline found in the theory chapter and separated into sections where the findings are summarized. All statements presented in both the empirical results and the analysis is referred to the interviewed person who made the comment. Regarding the questionnaires, the results are presented in Appendix 5, however, excluding the answers from the open-ended questions due to the confidentiality. Although, selected citations from the respondents that contribute to the paper and maintain the confidentiality are presented in the empirical results. The references from the annual reports fall under confidentiality since the case firm has required being anonymous, which limits the full disclosure of information. The anonymity should, however, enhance the trust between the researchers and the case firm to minimize biased and incorrect answers from the participants. To conduct the analysis, the theory is used to interpret the collected empirical data through three theoretical hypotheses.

24

4 Empirical Results The following chapter presents the information gathered through the data collection from interviews, questionnaires, and annual reports. The section begins with objectives of transfer pricing, continues with the transfer pricing methods, then the reflections of opportunistic behavior and fairness, and at last the strategy. Note that the strategy section is divided into strategic congruence, strategic dimensions, and strategic approach based on the corporate levels, the business units, and the projects. To better understand the managerial structure in the corporation, figure 7 provides an overview of the interviewed respondents.

Figure 7: The managerial structure in the case firm

4.1 Objectives of Transfer Pricing

The corporate group is a publicly listed organization, and the study uses the information from the annual reports of 2016 and 2015 to complement with formal information that the corporation has provided their shareholders. The annual reports describe that the organization's goals are divided into both financial and non-financial. Regarding the financial objectives, the case firm strives to become the most profitable organization in the construction industry. The corporation has targeted specific measurements such as the return on equity, solidity and dividend policy to enable a common profit. All the interviews confirm that the sellers and regions have individual result requirements to meet. The RPMs explain that the measurements the projects must meet are grounded in financial results. The CEO-S1 elaborate the financial objectives through specifying them as returns on investments, operating capital and profitability. Furthermore, the CEO-S1 clarify that no non-financial measurement exists. However, the transfer pricing structure fulfills additional purposes, such as securing construction times and production capacity (CEO-S1). Furthermore, the transfer pricing

25

structure and the internal relationships contribute to a good understanding of the project's requirements on quality and certifications. From a managerial perspective, the COO-S1 identifies the values as administrative conditions and penalty clauses. Due to quality issues, that mainly exists in S1, the projects face delays of constructions timeline, which becomes an economical issue. Therefore, the central agreements have penalty clauses to secure the quality of the products and services (COO-S1). The CPM stresses the importance of quality and customer value, especially when the production supply chain is owned by the corporation. The CCM adds delivery measurement and damage investigations as subcategories to the quality aspect. Today there is no standardized measurement or template to use, and there is no documentation of these matters. The monitoring and feedback are therefore of importance, as there are factors except for the price level that affects the profitability (CCM).

4.2 Transfer Pricing Methods

According to the CCM, the contracts regarding internal transactions are designed to serve as agreements for several years and works as terms of collaboration. In addition, the different parties negotiate and discuss price revisions every year. When the price revision occurs, both the buyers and the sellers are responsible for finding the current level of the market price. The CPM, the CCM, the CEO-S1, the COO-S1 and the CEO-S2 agrees that the corporate transfer price method of internal transactions is market-based pricing. To achieve a market-based price, the CPM stresses the significance of commercial elasticity between the buyer and the seller. Although, the CPM adds that the balance of market price is difficult to obtain, and there continuously is a discussion about the accurate market price level. The CPM and the CCM stress the importance for the selling units to have an active role in both the internal and the external market. The internal seller must prove its competitiveness through having both internal and external customers that buy to an equal or a higher price level relative to the internal customer (CCM, CEO-S2), both of the sellers fulfills this criterion. (CEO-S1, CEO-S2, COO-S1). The turnover for S1 and S2 is approximately divided into 60 percent sales to the internal customers, and 40 percent sales to the external market. Additionally, the CEO-S1 states that the credibility of the organization towards the external customers is an important aspect to maintaining their current market shares, which contributes to justifying the price level. Even though the internal transfers are based on the market price, the RPMs indicates that it is not always the case. Although, the RPM-R1 stresses that prices from competitors cannot be directly compared, notion must be taken to additional factors, such as turnover discounts and internal profit interest rates. Furthermore, another aspect of the transfer pricing methods is the notion of whether using internal suppliers is mandatory or non-mandatory. In this case study, the CCM describes that it is optional for the internal buyers to use S1 in their projects, but it is mandatory for them to use S2. The framework of these agreements is built upon past events. The reliability is higher for S2 to deliver what is agreed upon, while S1 does not manage to meet the internal buyers’

26

requirements and volumes (CCM). The units are obliged to buy from S2, which means that S2 has an exclusive right in the corporation, but also the pressure to deliver to all projects. Therefore, the CEO-S2 means that the corporation’s units are prioritized customers in comparison to external buyers. Additionally, the CPM states that there must be an understanding for the financial game in the corporation to understand the transfer pricing structure. The profits in the projects are less likely to be allocated to the parent firm than it is from the sellers. Thus, the corporate management prefers that some units gain a larger profit than others. A risk of this setup is that the internal suppliers become too comfortable in their position, leading to decreasing the efficiency of the price elasticity between buyer and seller (CEO-S1, RPM-R2).

4.3 Opportunistic Behavior and Fairness

At the corporate management level, the view of the internal trade and transfer pricing is that it overall works great. Although, the CPM mean that people usually tend to find things to complain about, and therefore the perception of the transfer pricing can be different in the different regions and projects. The CCM mention that the project managers often try to maximize their project’s result through buying cheaper products from external actors, in that case, the corporation loses an internal affair, meaning that the projects save some costs, but the corporations lose profit. The CEO-S1 find transfer pricing to generally be a complicated issue that generates friction. More specifically, the internal buyers experience the external customers to get more attention from the sellers, and therefore lack focus from the sellers on problems concerning the corporation’s projects. The CEO-S1 experience that the subsidiary is handled fairly and is given the opportunity to have competitive prices, and rather the subsidiary gets neglected in administrative issues. The CEO-S2 means that their internal customers believe that the seller’s prices are high and stresses it to be an inherent problem when trading with internally owned subsidiaries, creating jealousy of who earns the most profit. As mentioned above, the corporate group has a variety of predetermined suppliers to buy from. The RPMs explains that this results in managers from the projects feeling mistreated as they are not free to minimize the project costs as they please, this is of importance for the projects have the possibility to earn a bonus based on the project's results. Additionally, the COO-S1 and the CEO-S2 mentioned a market analysis of customer satisfaction with both internal customers and external customers. The analysis for both sellers has shown a significantly higher positive grade from external customers than given by the internal customers. The CEO-S2 states that considering the external perception, the subsidiary has a top of the line performance. However, the internal grade is only half as good compared to the external grad, even though it is the same sales personnel and the same products. The managers of the projects mean that the mandatory agreements hamper the possibility to put pressure on the sellers in comparison to external suppliers, which increases their chances to earn their bonus. The issue is linked to the sellers taking the projects orders for granted and a lazy attitude from them considering the customer service. Thus, the sellers do not work to achieve internal customer satisfaction.

27

A respondent from the projects reflected as following the transfer pricing structure, “It is making us less sharp and competitive. Mechanically and far from competitive pricing. Perhaps positive for the group, but negative for the projects. We are getting weaker on the external market. Suppliers do not have to be equally efficient internally and need not to deliver the same quality, time or price as they would need in an external market.” Additionally, some respondents indicate that they have difficulties to understand who is supposed to earn money, the project or the subsidiaries. Also, the projects have to suffer in order for the corporations win, and they could do their own procurements with external customers but then the corporation would suffer. According to one respondent, the feeling of ‘us and them’ is apparent for operating in the same corporation, and therefore the organization lacks in co-operation.

4.4 Strategic Congruence and Transfer Pricing

According to the CPM, the COO-S1, and the CEO-S2, the business units in the corporation are aligned towards the same ambitions. The CPM and the CEO-S2 recognize the corporate culture to have strong core values throughout the firm. According to the BUPM and the COO-S1, the core values may be a reason for the customer’s choice to trade with the case firm. The transparency in the corporation can be found in the core values, which according to CEO-S1 contributes to similar working processes throughout the organization. The CEO-S2 stresses that the core values are implemented from top management all the way to its units, subsidiaries, regions, and projects. Although, the CEO-S1 points out that the corporation has partly grown through acquisitions, and have therefore sometimes difficulties to find common value denominators. The CEO-S1 highlights the risk of the units and the subsidiaries becoming more independent, which would lower the advantage of the internal supply chain, and affect the corporation’s competitive advantage. Furthermore, the corporation has a strong entrepreneurial spirit at all levels and a far-reaching decentralization. Therefore, an important aspect is the combination of decentralization and maintaining the totality in the overall organization (CEO-S1). The corporation is structured so the projects fight for its individual profit, which raises the issue of sub-optimizing, rather than have the overall corporation's perspective. A respondent at the functional level states “I have trust for the internal subsidiaries, and maybe the projects do not gain that much in terms of price when we trade, but the corporation makes a profit and that is the most important.” However, other managers from project level additionally mention that “The transfer pricing structure should make everything easier, but that is not the reality,” and “The transfer pricing is a good thought, but it does not work. Today the problem is larger with our internal suppliers than they are with our external suppliers.” Additionally, when the respondents in the projects were asked if the co-operation worked well between the business units and the subsidiaries, the answers were fragmented. While 26.7 percent thought the co-operation to a large extent worked well, 31.7 percent thought that it only worked to a small extent.

28

4.4.1 Strategic Dimensions