transfer pricing study reports

73

TRANSFER PRICING STUDY REPORTS – WHY, WHAT AND HOW ?? For Suburban Study Circle Jointly with Technology Initiative Study Circle – BCAS By Naman Shrimal November 16, 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of transfer pricing study reports

TRANSFER PRICING

STUDY REPORTS –

WHY, WHAT AND HOW

??

For Suburban Study Circle Jointly

with Technology Initiative Study

Circle – BCAS

By Naman Shrimal

November 16, 2019

INDEX

2

© JSCO

Usage other than transfer pricing

Live search process – Prowess IQ

Various databases

Format of TP Study

Introduction

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

DISCLAIMER !!!

• No Acts & Rules

• No Case Laws

• Informal Workshop

• Outside the CA Cloak

• Do Not write anything

• No one right way

3

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

INTRODUCTION

Transfer Pricing4

NORMAL SCENARIO

5

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

MENTOS SCENARIO

6

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

TRANSFER PRICING

• Income tax is a tax on income.

• Income is net result of transaction entered Into

by a person/entity during the relevant period i.e

financial year. Every Transaction involves

transfer of goods, services to various user.

• When the Transfer of goods or services is in

between the group or where there is “ intra

group transaction” then the concept of transfer

pricing arises.

• A MNC Group may exploit the opportunity to

shrink the overall tax burden of the group

through either under-charging or over-charging

the transaction within the group7

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Multinational Group

• Country A(Tax Rate 30%)

Company

• Country B(TaxRate 15%)

Associated Enterprise

Sells @ Lower Price say

Rs.500

Actual Price Rs.700

Manufacturer of Goods

Tax loss of Host Country (Rs.700-

500)*30%= Rs 200*30% = Rs 60

Total Tax Saving of the Group Rs30 (60-30)

8

EXAMPLE

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

TRANSFER PRICING

DOCUMENTATION

STEPS9

© JSCO© JSCO

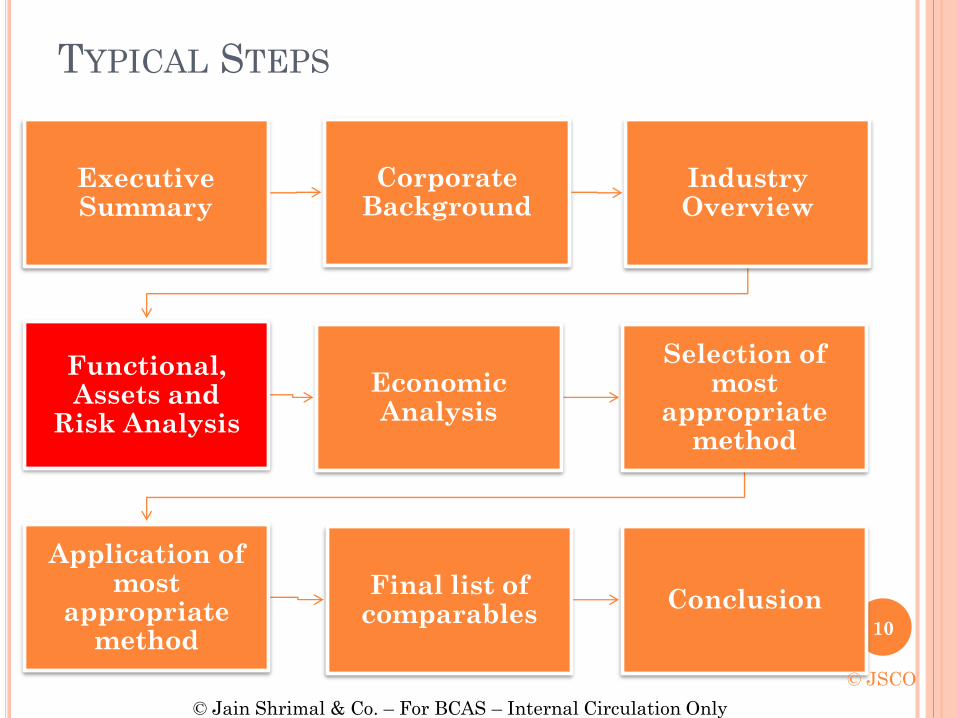

Executive Summary

Corporate Background

Industry Overview

Functional, Assets and

Risk Analysis

Economic Analysis

Selection of most

appropriate method

Application of most

appropriate method

Final list of comparables

Conclusion10

TYPICAL STEPS

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

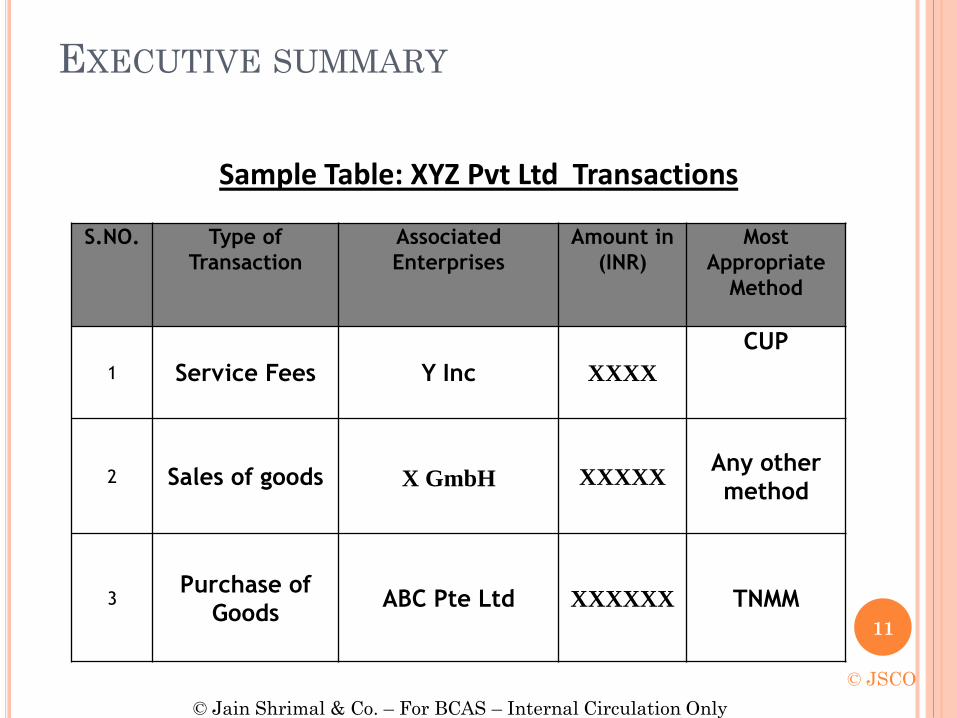

S.NO. Type of

Transaction

Associated

Enterprises

Amount in

(INR)

Most

Appropriate

Method

1 Service Fees Y Inc XXXX

CUP

2 Sales of goods X GmbH XXXXXAny other

method

3Purchase of

GoodsABC Pte Ltd XXXXXX TNMM

Sample Table: XYZ Pvt Ltd Transactions

11

EXECUTIVE SUMMARY

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Profile Of XYZ Pvt. Ltd.

One such family whose name emerges on the map of Rajasthan

is that of the XYZ. This family has been in business since 1880.

Mr. X, a visionary started the business of Handicrafts & carpets,

under the name & style of X & Co., which became known for its

Brass wares & carpets.

Profile Of ABC Pte Ltd.

ABC Pte Ltd. was originally incorporated as ABC Trading Ltd

in 1996. For the purpose of Trading of Handicrafts and Carpets.

The name of the company was then changed to ABC Ltd. The

Company is profitable company since its inception.

Profile of the Group

S. No. Name XYZ Pvt. Ltd.

1 ABC Ltd. 51.00

2 X GmbH 49.00

TOTAL 100.00

.

12

CORPORATE BACKGROUND

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

•IBEF

•Articles in Newspaper /General Journals

•Industrial Association Journals

•Industry bodies like CII, FICCI, ASSOCHAM

•Annual Reports of Similar listed companies

13

INDUSTRY OVERVIEW

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

• The functions, assets and risks analysis provides factual

foundation for establishing the transfer pricing methodology

consistent with the arm’s length standard set forth in the relevant

transfer pricing regulations contained in the Act and the Rules.

• A FAR analysis reviews the functions, assets and risks assumed by

the taxpayer and its AEs for the specific international transactions

under review. By providing a description of the functions and

assets and their location within a corporate group, the FAR

analysis provides the first step in evaluating the relative

contribution to profit of various related entities.

• FAR analysis helps in finding the comparables for benchmarking

the transactions.

14

FUNCTIONS, ASSETS AND RISK ANALYSIS

(FAR ANALYSIS)

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Functions Performed Assets held Risks assumed

• R&D

• Procurement of Raw

material

• Negotiation of prices

• Advertisement

activity

• Providing after sales

service• Warranty service

• Premises

• Equipments

• Machines

• Employee skill base

• Brand Names

• Trademarks

• Market Risk

• Inventory Risk

• Credit Risk

• Product Technology Risk

• Foreign Exchange Risk

• Personnel Risk

15

COMMONLY USED FUNCTIONS, ASSETS &

RISKS

Characterization

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

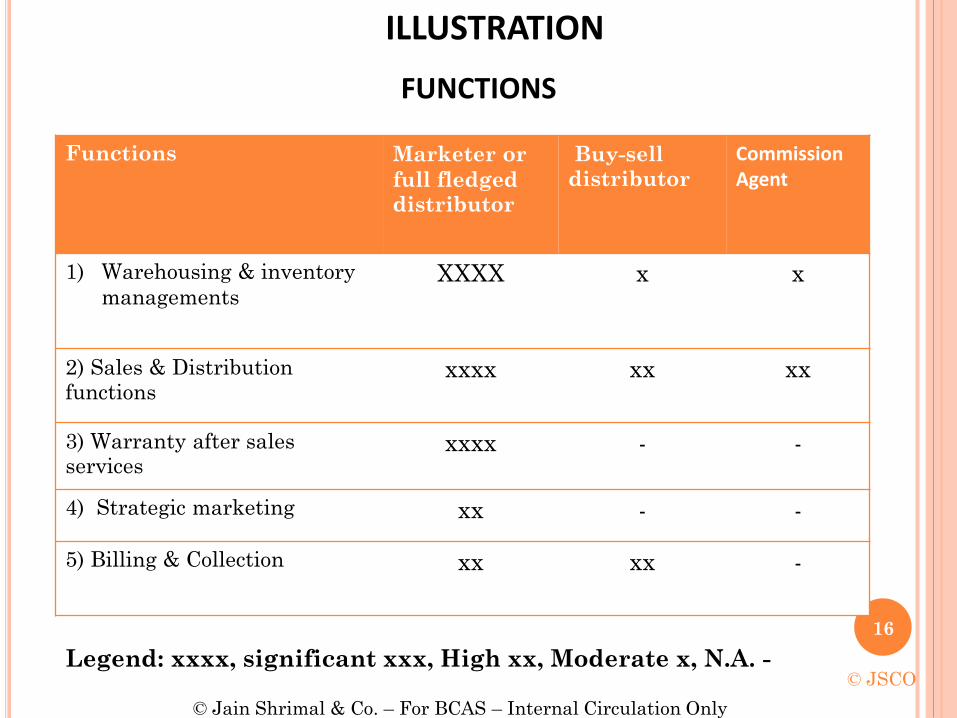

16

ILLUSTRATION

FUNCTIONS

Functions Marketer or

full fledged distributor

Buy-selldistributor

CommissionAgent

1) Warehousing & inventory

managements XXXX x x

2) Sales & Distribution functions

xxxx xx xx

3) Warranty after sales services

xxxx - -

4) Strategic marketing xx - -

5) Billing & Collection xx xx -

Legend: xxxx, significant xxx, High xx, Moderate x, N.A. -© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

17

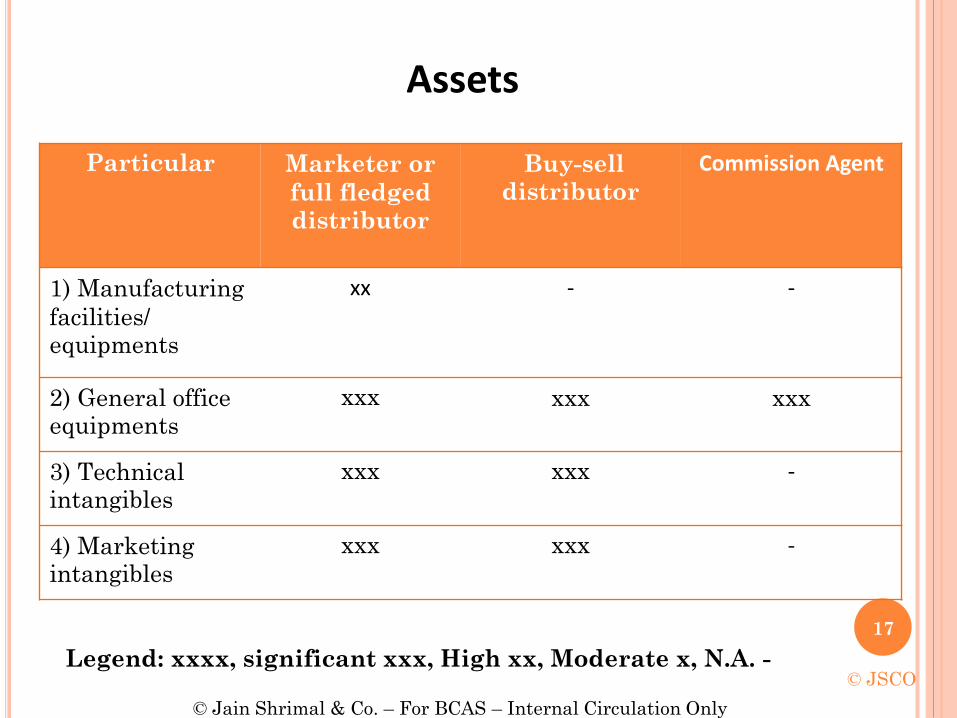

Assets

Particular Marketer or

full fledged distributor

Buy-selldistributor

Commission Agent

1) Manufacturing

facilities/ equipments

xx - -

2) General office equipments

xxx xxx xxx

3) Technical intangibles

xxx xxx -

4) Marketing intangibles

xxx xxx -

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Legend: xxxx, significant xxx, High xx, Moderate x, N.A. -

18

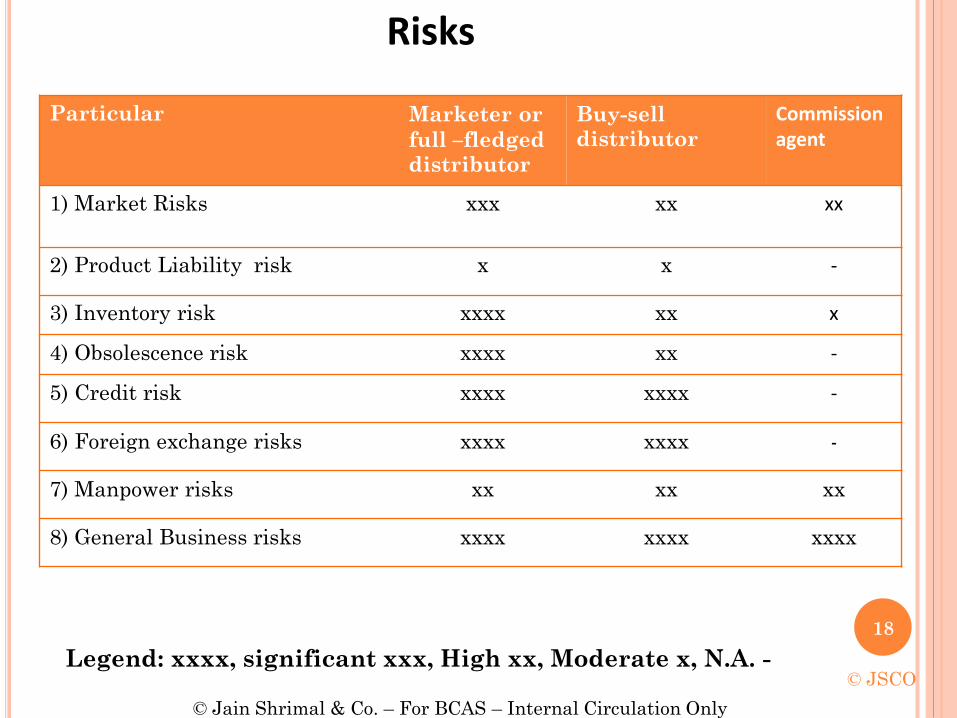

Risks

Particular Marketer or

full –fledged distributor

Buy-selldistributor

Commissionagent

1) Market Risks xxx xx xx

2) Product Liability risk x x -

3) Inventory risk xxxx xx x

4) Obsolescence risk xxxx xx -

5) Credit risk xxxx xxxx -

6) Foreign exchange risks xxxx xxxx -

7) Manpower risks xx xx xx

8) General Business risks xxxx xxxx xxxx

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Legend: xxxx, significant xxx, High xx, Moderate x, N.A. -

YOU FINALLY KNOW ABOUT YOURSELF

19

Selection of Tested Party Tested Party A participant to the international transaction with reference to whom the international transaction is tested

Factors for selection of tested party • Least complex FAR and does not own significant

intangibles

• Selected Transfer Pricing method can be applied in

most reliable manner

• Availability of reliable comparable data

• Requiring least adjustments

This analysis involves selection of tested enterprise , selecting the

most appropriate method, conducting a search for uncontrolled

comparables based on the selection of the most appropriate method,

selecting a measure of profitability (where appropriate) and finally

determining the arm’s length results

20

ECONOMIC ANALYSIS

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

The calculation of ALP has to be carried out by using the most

appropriate method. The most appropriate method must be selected

from the following methods:

• Comparable Uncontrolled Price Method (‘CUP’)

• Resale Price Method (‘RPM’)

• Cost Plus Method (‘CPM’)

• Profit Split Method (‘PSM’)

• Transactional Net Margin Method (‘TNMM’)

• Any Other Method

Some of the factors to take into account are:

• The availability, coverage and reliability of data necessary for the

application of the method;

• The extent to which reliable and accurate adjustments can be made to

account for differences, if any, between the international transaction

and the comparable uncontrolled transaction or between the

enterprises entering into such transactions; and

• The nature, extent and reliability of assumptions required to be made

in application of a method.

SELECTION OF MOST APPROPRIATE METHOD

21

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

• CUP has been defined as a price charged by an entity to

another independent entity in an uncontrolled

transaction.

• In this method, the price charged or paid in a

comparable uncontrolled transaction is identified and

adjusted to account for the differences between the

international transaction and the uncontrolled

transaction.

• This adjusted price is taken to be at arm’s length price

in relation to the international transaction between the

AEs.

• Formula can also be taken as Indicator

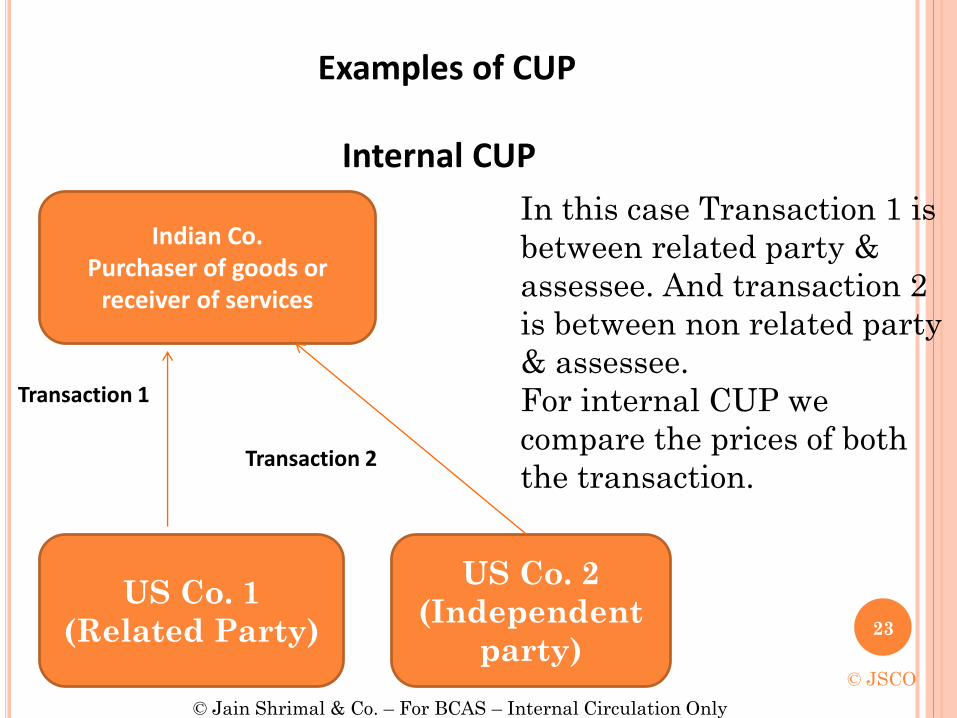

• There are two types of CUP

• Internal CUP

• External CUP 22

CUP

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

23

Examples of CUP

Internal CUP

Indian Co.Purchaser of goods or

receiver of services

US Co. 1

(Related Party)

US Co. 2

(Independent

party)

In this case Transaction 1 is

between related party &

assessee. And transaction 2

is between non related party

& assessee.

For internal CUP we

compare the prices of both

the transaction.

Transaction 1

Transaction 2

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

24

External CUP

Indian Co. 1

Purchaser US Co. 1 (Related party)

Seller

Indian Co. 2

Purchaser US Co. 2 (Unrelated party)

Seller

Transaction 1

Transaction 2

In this case transaction 1 is between Assesee

& related party. Similar transaction 2 is done

between co. which are not related.

Prices of both the transactions are compared

for using external CUP

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

25

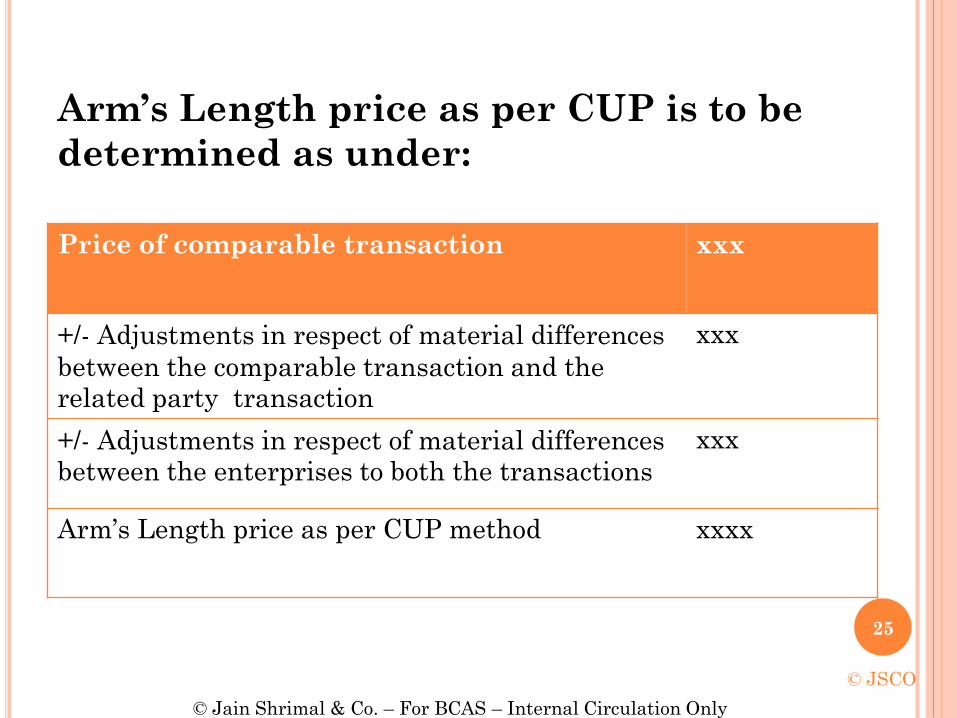

Arm’s Length price as per CUP is to be

determined as under:

Price of comparable transaction xxx

+/- Adjustments in respect of material differences

between the comparable transaction and the related party transaction

xxx

+/- Adjustments in respect of material differences between the enterprises to both the transactions

xxx

Arm’s Length price as per CUP method xxxx

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

26

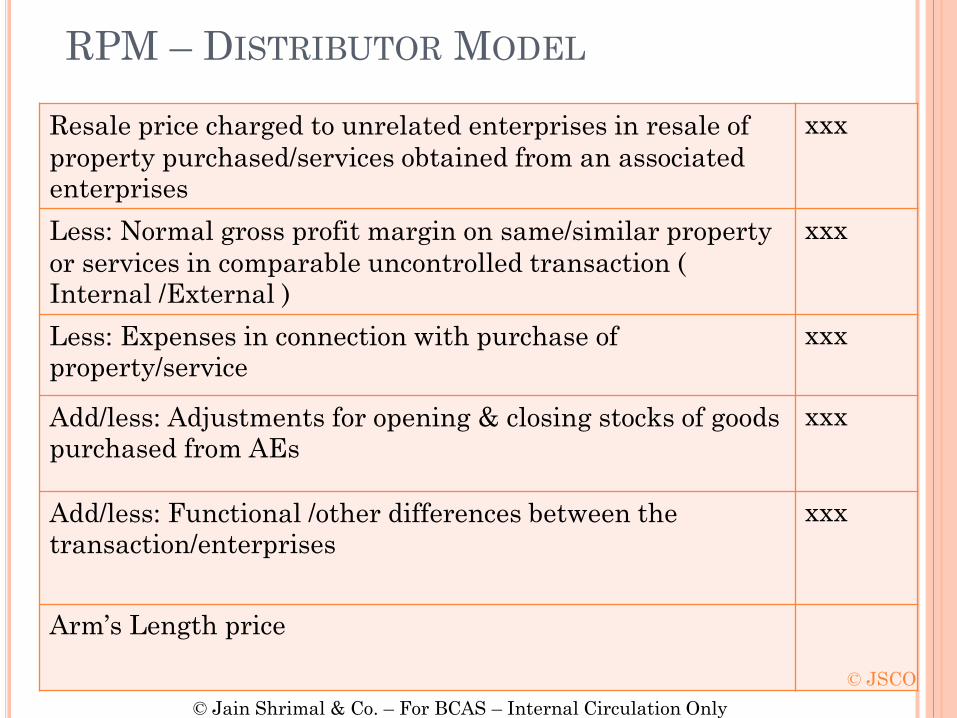

Resale price charged to unrelated enterprises in resale of

property purchased/services obtained from an associated enterprises

xxx

Less: Normal gross profit margin on same/similar property

or services in comparable uncontrolled transaction ( Internal /External )

xxx

Less: Expenses in connection with purchase of property/service

xxx

Add/less: Adjustments for opening & closing stocks of goods purchased from AEs

xxx

Add/less: Functional /other differences between the transaction/enterprises

xxx

Arm’s Length price

RPM – DISTRIBUTOR MODEL

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

27

Particulars

Direct & Indirect costs incurred by the enterprises in

respect of property transferred/services provided to AE

xx

Add: Gross profit { GP is taken which has taken in

similar unrelated party transaction}

xx

+/- Adjustment in GP is to be done {functional & other

differences between the transactions}

xx

Arm’s length price xx

In short ALP as per CPM = Direct costs +indirect costs + adjusted GP

margin

© JSCO

CPM – SUPPLIER MODEL

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

28

PSM

This method may be used in international transactioninvolving transfer of unique intangible or in multipletransactions amongst AEs, where transaction are so interrelated that they cannot be value separately for thepurpose of determining ALP of any one transaction.

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

TNMM

• Under this method, the net profit margin realized by an AE from

a transaction is computed in relation to a particular factor such

as cost incurred, sales, assets utilized, etc.

• The net profit margin realized by the assessee or an unrelated

enterprises from a comparable uncontrolled transaction is

computed having regard to the same factor & adjustments are

made to the net profit margin to take into account the

differences between the transactions & uncontrolled

transactions.

• The net profit margin realized by an AE is established in

conformity with net profit margin of the uncontrolled

transaction to arrive at the ALP.

© JSCO

29

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

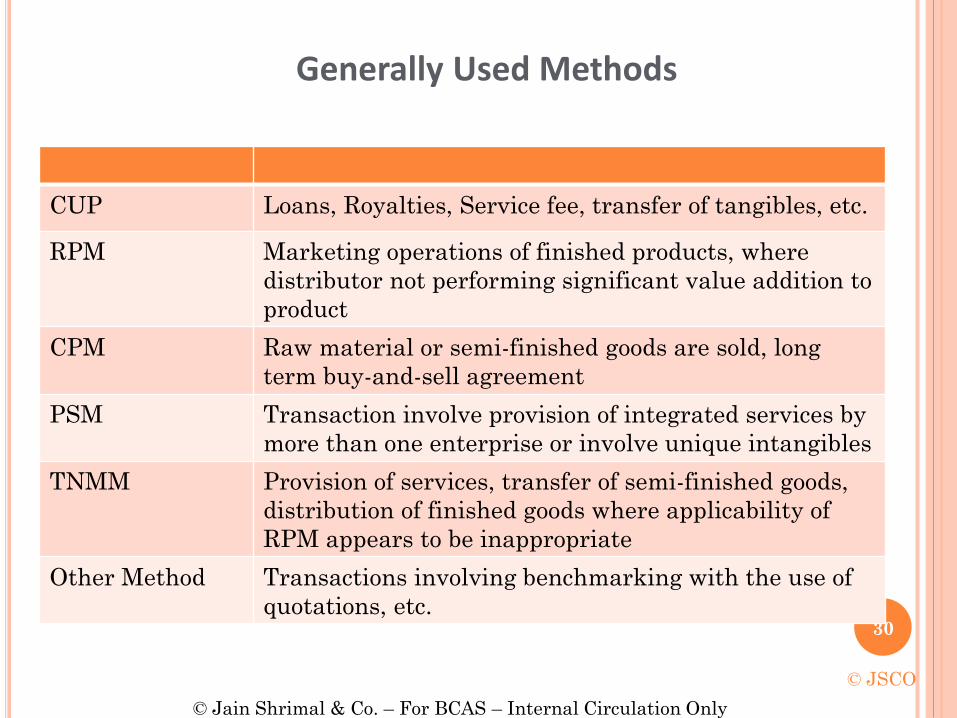

Generally Used Methods

© JSCO

30

CUP Loans, Royalties, Service fee, transfer of tangibles, etc.

RPM Marketing operations of finished products, where

distributor not performing significant value addition to

product

CPM Raw material or semi-finished goods are sold, long

term buy-and-sell agreement

PSM Transaction involve provision of integrated services by

more than one enterprise or involve unique intangibles

TNMM Provision of services, transfer of semi-finished goods,

distribution of finished goods where applicability of

RPM appears to be inappropriate

Other Method Transactions involving benchmarking with the use of

quotations, etc.

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

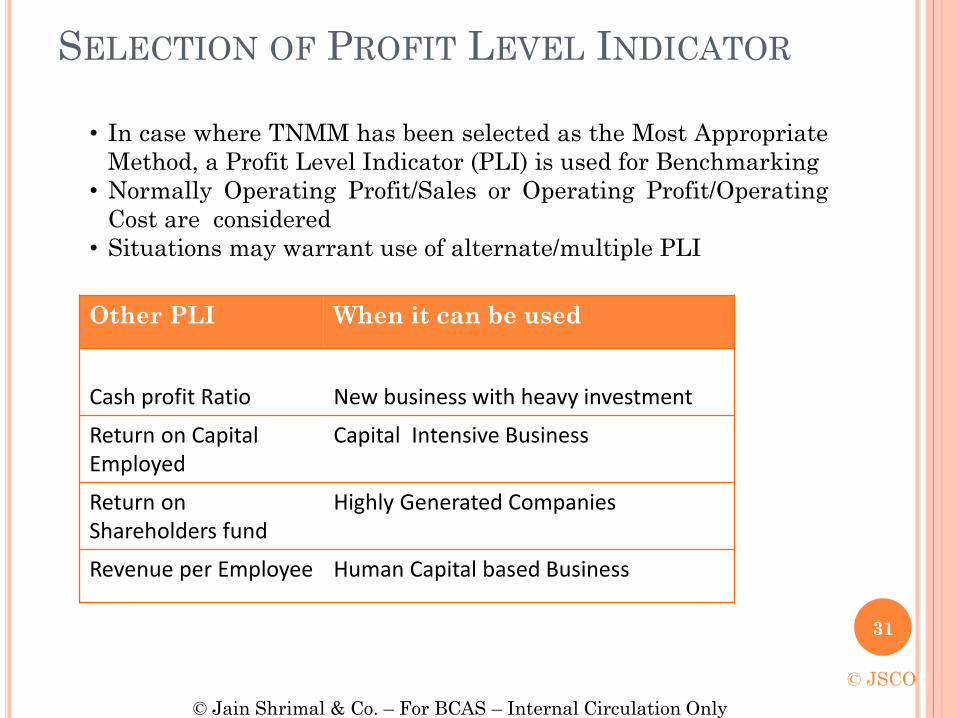

• In case where TNMM has been selected as the Most Appropriate

Method, a Profit Level Indicator (PLI) is used for Benchmarking

• Normally Operating Profit/Sales or Operating Profit/Operating

Cost are considered

• Situations may warrant use of alternate/multiple PLI

Other PLI When it can be used

Cash profit Ratio New business with heavy investment

Return on Capital Employed

Capital Intensive Business

Return on Shareholders fund

Highly Generated Companies

Revenue per Employee Human Capital based Business

SELECTION OF PROFIT LEVEL INDICATOR

31

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

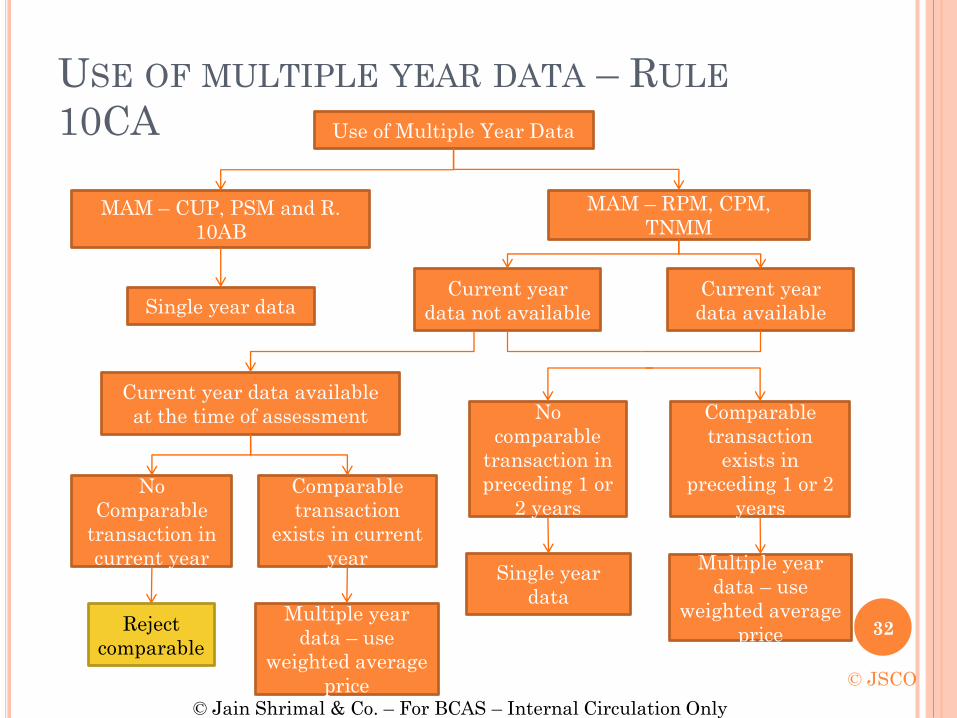

USE OF MULTIPLE YEAR DATA – RULE

10CA Use of Multiple Year Data

MAM – RPM, CPM,

TNMMMAM – CUP, PSM and R.

10AB

Single year dataCurrent year

data available

Current year

data not available

Comparable

transaction

exists in

preceding 1 or 2

years

No

comparable

transaction in

preceding 1 or

2 years

Single year

data

Multiple year

data – use

weighted average

price

Current year data available

at the time of assessment

No

Comparable

transaction in

current year

Comparable

transaction

exists in current

year

Reject

comparable

Multiple year

data – use

weighted average

price

32

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

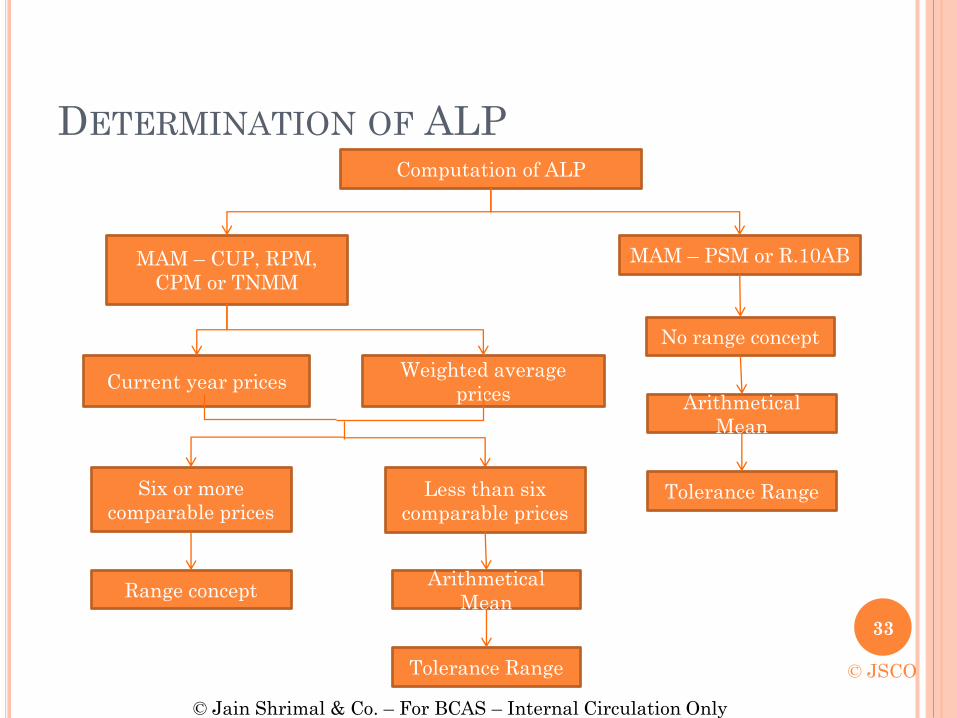

DETERMINATION OF ALPComputation of ALP

MAM – CUP, RPM,

CPM or TNMM

MAM – PSM or R.10AB

Current year pricesWeighted average

prices

Six or more

comparable pricesLess than six

comparable prices

No range concept

Arithmetical

Mean

Tolerance Range

Arithmetical

Mean

Tolerance Range

Range concept

33

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

CALCULATION OF RANGE

• Arrange prices in ascending order

• Find the price at 35th percentile & 65th percentile

➢ xth percentile is the value which is greater than or equal to

at least x% of the total values

➢ If x% of total values is a whole number, the average of that

value and its next value will be taken as the xth percentile

• Arm’s length range is between the prices at 35th and 65th

percentile

• If transaction price is between the arm’s length range, then

transaction price is considered to be at arm’s length

• If transaction price is outside the arm’s length range, then

median will be considered as the arm’s length price and

adjustment will be made

➢ Median is the central value (50th percentile) of the dataset 34

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

ANY OTHER METHOD

35

• CBDT vide notification no18/2012 dated 23May 2012

introduced a new method referred to as “other method” vide

10AB. As per the notification other method is applicable

from F.Y.2012-13.

• As per the rule 10AB, the other method for determination

of ALP of a transaction can be any method which takes into

account the price that has been charged or paid, for the

same or similar uncontrolled transaction, with or between

non AEs, under similar circumstances and after giving due

v]consideration to all the relevant facts.

• Between deep sea and devil !!!!

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

36

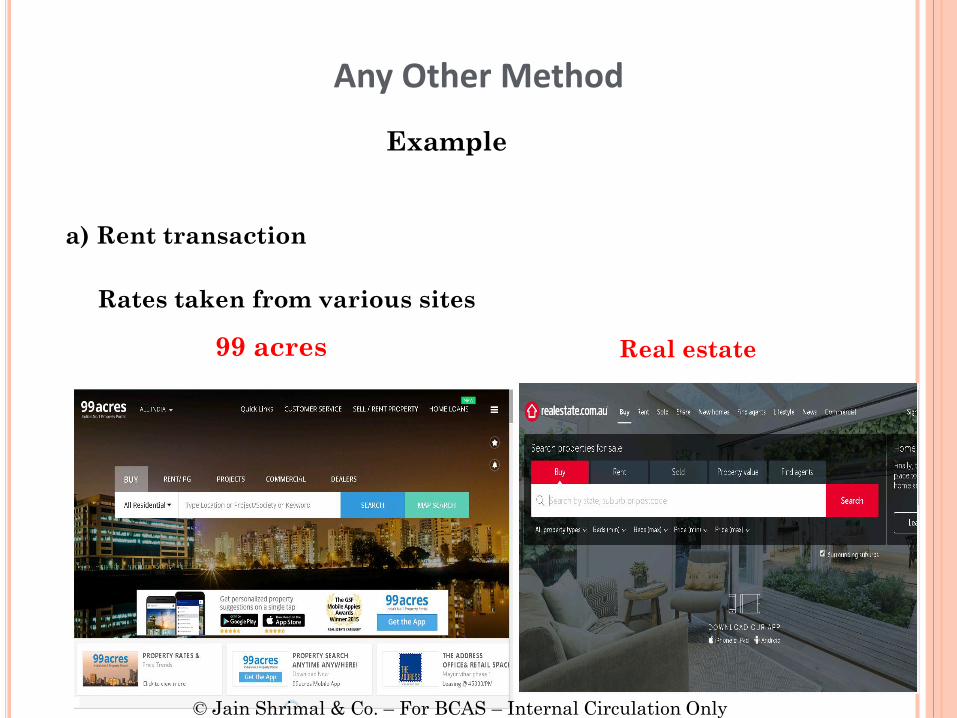

Any Other Method

Example

a) Rent transaction

99 acres Real estate

Rates taken from various sites

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

37

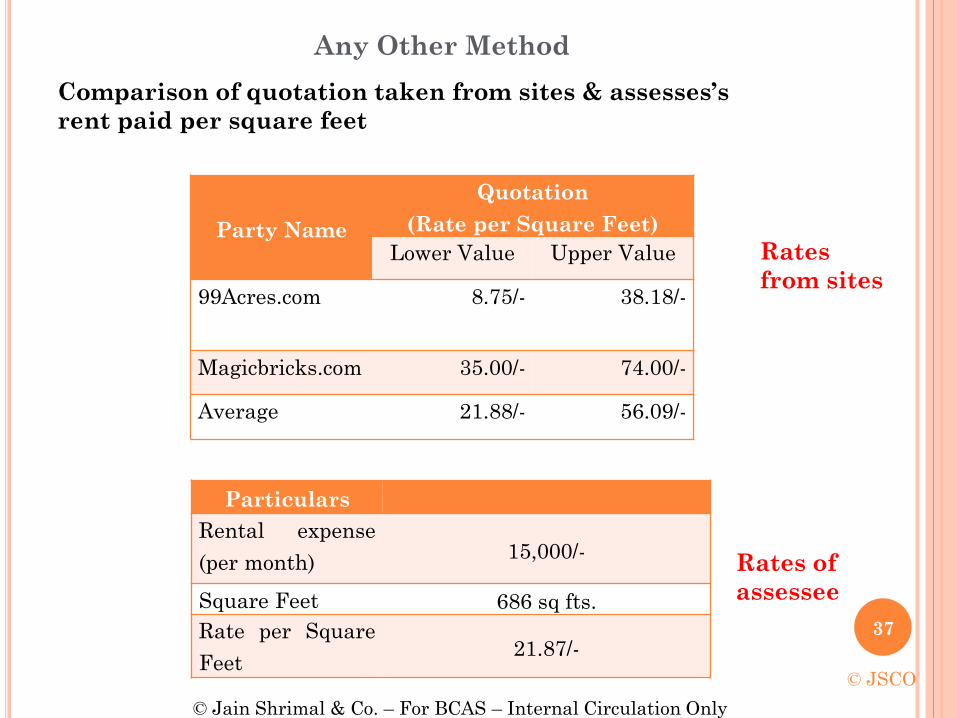

Any Other Method

Party Name

Quotation

(Rate per Square Feet)

Lower Value Upper Value

99Acres.com 8.75/- 38.18/-

Magicbricks.com 35.00/- 74.00/-

Average 21.88/- 56.09/-

Particulars

Rental expense

(per month)15,000/-

Square Feet 686 sq fts.

Rate per Square

Feet21.87/-

Comparison of quotation taken from sites & assesses’s

rent paid per square feet

Rates

from sites

Rates of

assessee

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

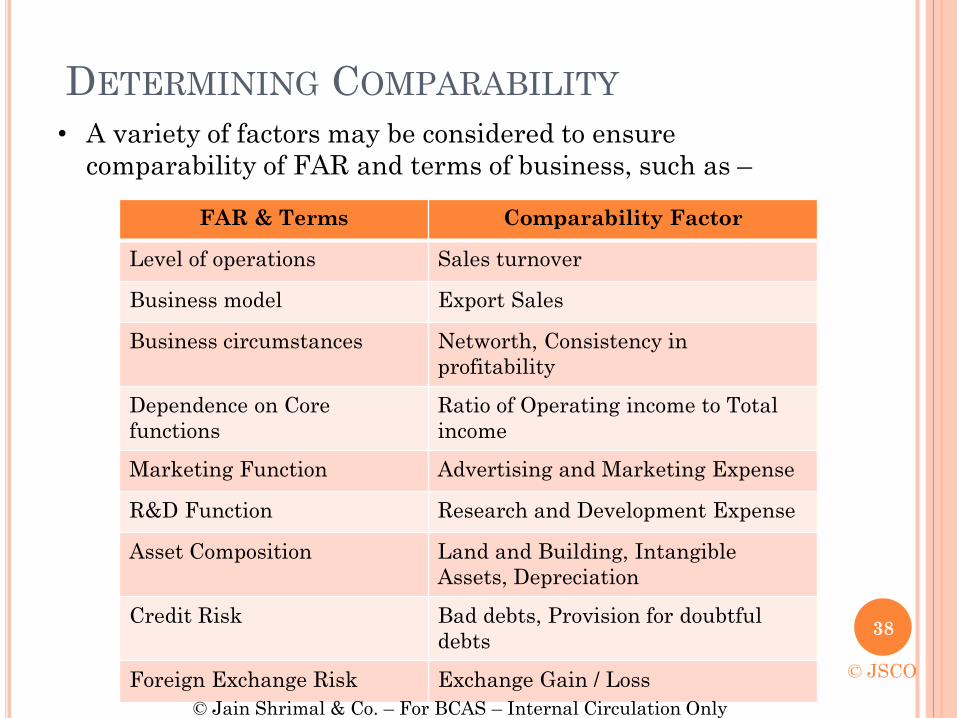

DETERMINING COMPARABILITY

• A variety of factors may be considered to ensure

comparability of FAR and terms of business, such as –

FAR & Terms Comparability Factor

Level of operations Sales turnover

Business model Export Sales

Business circumstances Networth, Consistency in

profitability

Dependence on Core

functions

Ratio of Operating income to Total

income

Marketing Function Advertising and Marketing Expense

R&D Function Research and Development Expense

Asset Composition Land and Building, Intangible

Assets, Depreciation

Credit Risk Bad debts, Provision for doubtful

debts

Foreign Exchange Risk Exchange Gain / Loss

38

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

COMPARABILITY ADJUSTMENTS

• Adjustments which can be made based on the information

available in the Financial Statements –

➢ Differences in FAR

➢ Idle Capacity

➢ Credit Period

➢ Working Capital

• It is important to demonstrate the need and basis of the

adjustments

39

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Report is being summarized. For eg.:

Based on the information, data and analysis contained in TP report, it

may be reasonably concluded that the analysis in TP report meets the

specified requirements and contains all of the principal documents

required to be maintained under the standards of the Indian transfer

pricing regulations. Accordingly, the Company has complied with the

provisions of Indian Transfer Pricing Regulations in respect of its all

specified domestic transactions.

CONCLUSION

40

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

INDIAN DATABASES

Types of Databases with description41

© JSCO

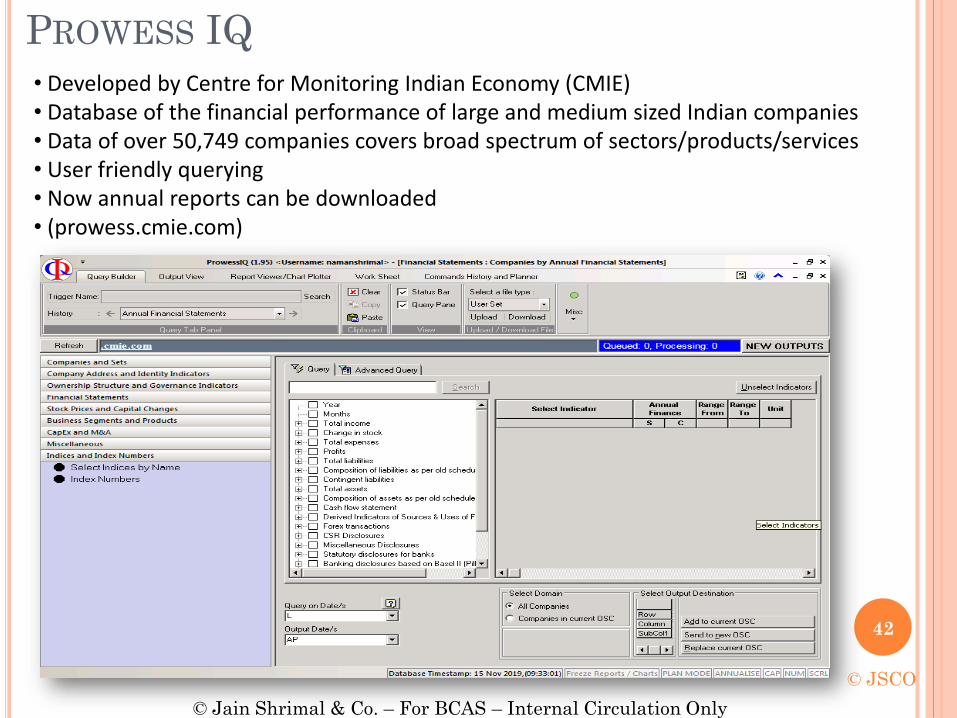

PROWESS IQ

• Developed by Centre for Monitoring Indian Economy (CMIE)• Database of the financial performance of large and medium sized Indian companies• Data of over 50,749 companies covers broad spectrum of sectors/products/services• User friendly querying• Now annual reports can be downloaded • (prowess.cmie.com)

42

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

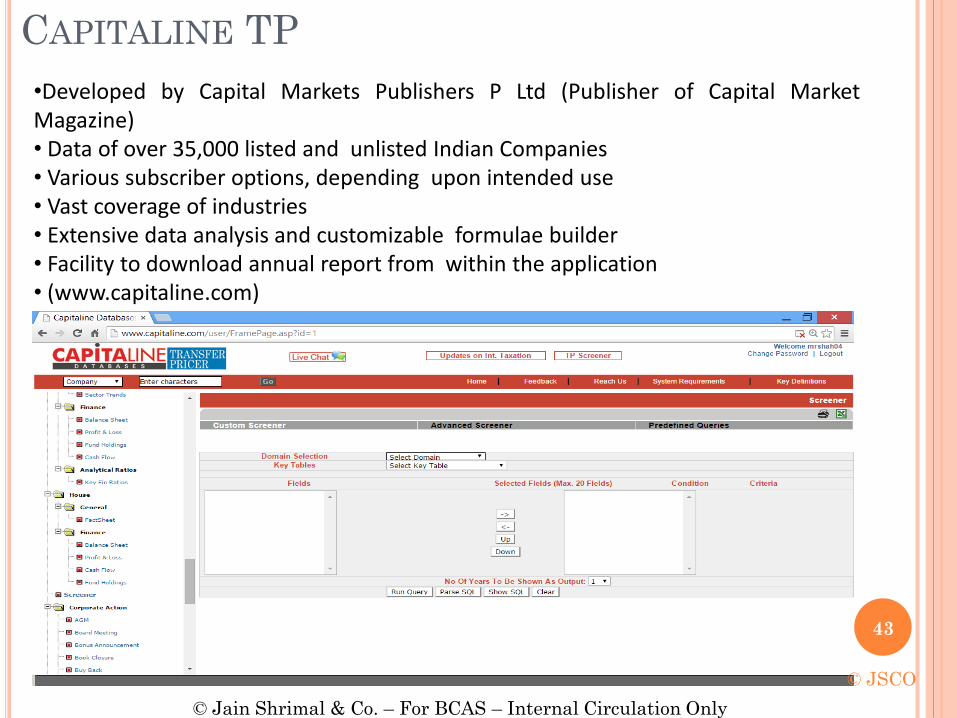

•Developed by Capital Markets Publishers P Ltd (Publisher of Capital MarketMagazine)• Data of over 35,000 listed and unlisted Indian Companies• Various subscriber options, depending upon intended use• Vast coverage of industries• Extensive data analysis and customizable formulae builder• Facility to download annual report from within the application• (www.capitaline.com)

CAPITALINE TP

43

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

ACE TP

•Developed by Accord InfoTech P Ltd

• Database of over 38,000 Indian Companies

• 1750 unique financial fields

• Specially developed with inputs from Transfer Pricing professionals

• User customizable formulae

• Varity of subscribing options available

• (www.acetp.com)

44

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

LIVE SEARCH

On the software –

Prowess IQ

45

© JSCO

HOW EFFECTIVE SEARCH IS CONDUCTED ??

46

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

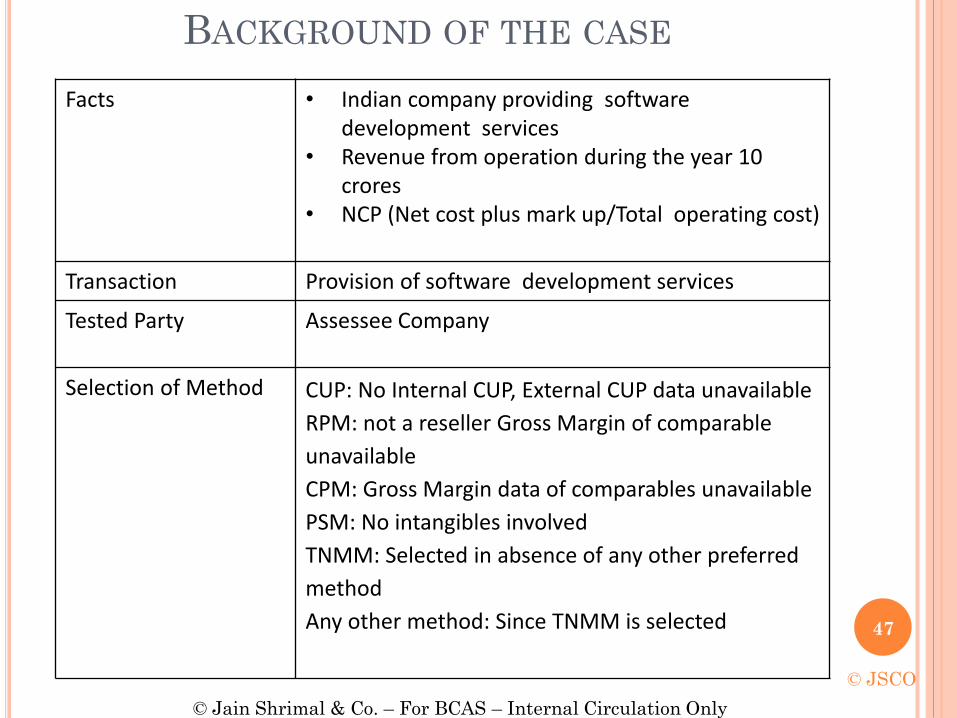

FAR

Analysis

Facts • Indian company providing software development services

• Revenue from operation during the year 10 crores

• NCP (Net cost plus mark up/Total operating cost)

Transaction Provision of software development services

Tested Party Assessee Company

Selection of Method CUP: No Internal CUP, External CUP data unavailable

RPM: not a reseller Gross Margin of comparable

unavailable

CPM: Gross Margin data of comparables unavailable

PSM: No intangibles involved

TNMM: Selected in absence of any other preferred

method

Any other method: Since TNMM is selected 47

BACKGROUND OF THE CASE

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

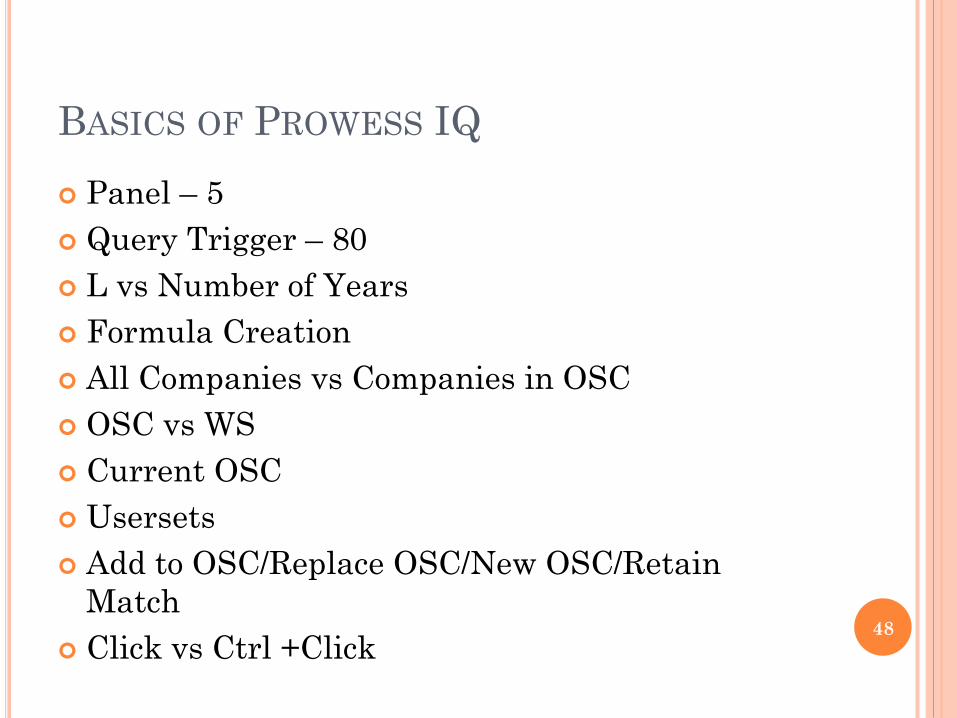

BASICS OF PROWESS IQ

Panel – 5

Query Trigger – 80

L vs Number of Years

Formula Creation

All Companies vs Companies in OSC

OSC vs WS

Current OSC

Usersets

Add to OSC/Replace OSC/New OSC/Retain

Match

Click vs Ctrl +Click 48

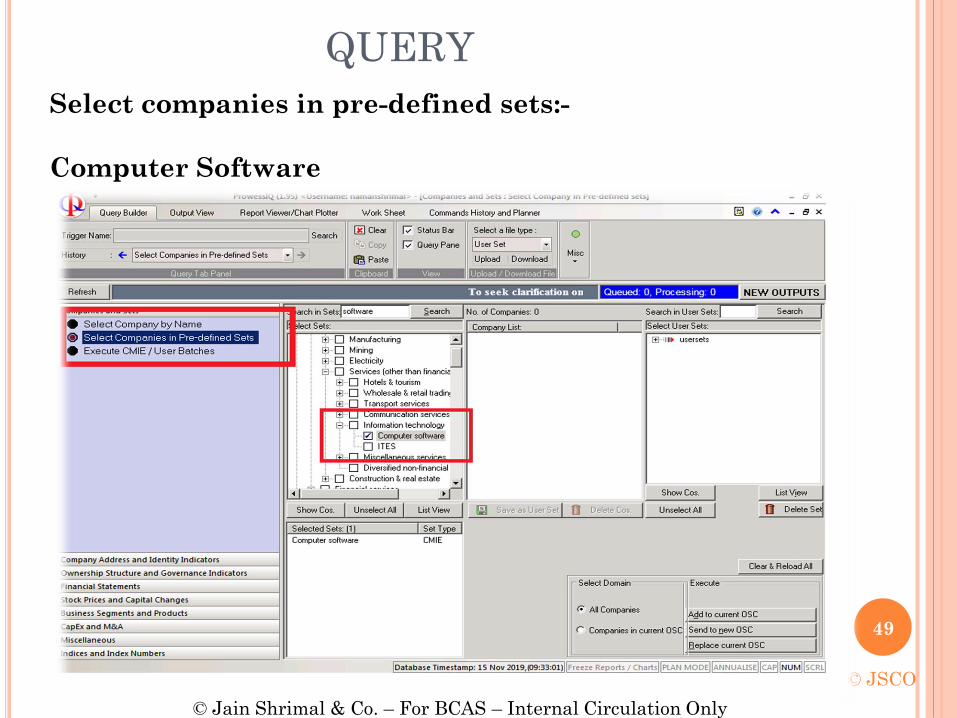

QUERY

Select companies in pre-defined sets:-

Computer Software

49

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

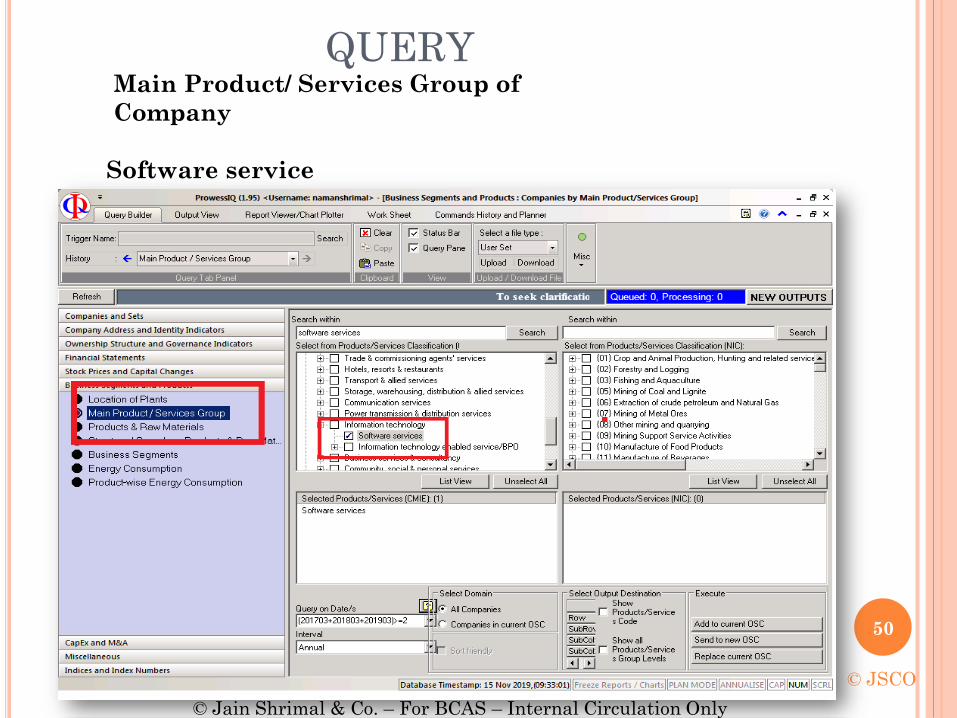

Main Product/ Services Group of

Company

Software service

QUERY

50

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

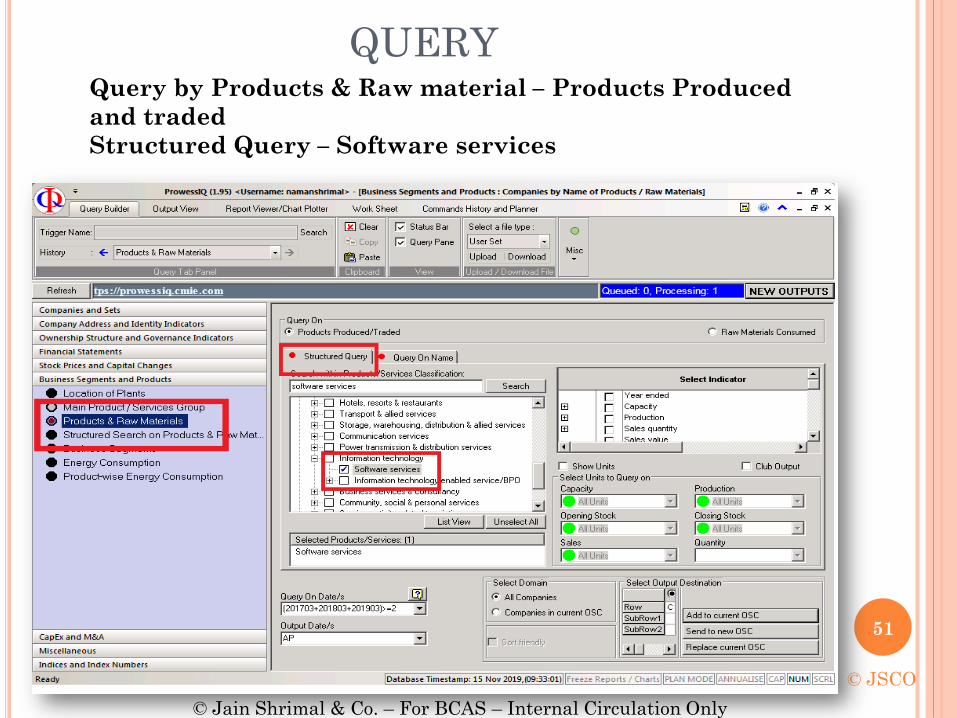

Query by Products & Raw material – Products Produced

and traded

Structured Query – Software services

QUERY

51

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Query by Products & Raw material – Products Produced and

traded

Query On Name – Software services ( Auto Search)

QUERY

52

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

53

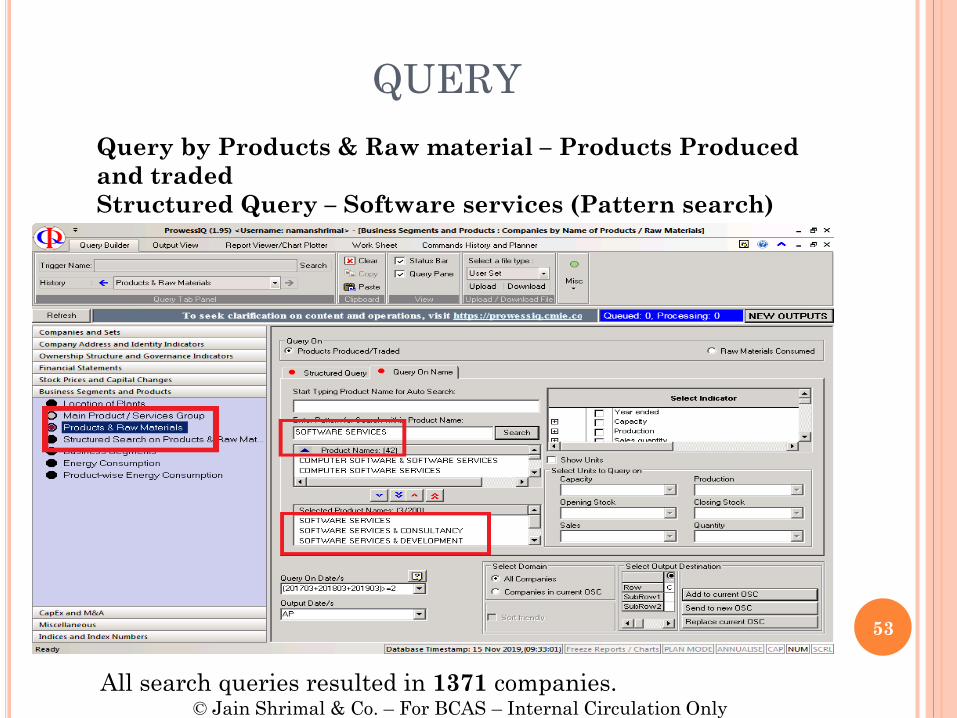

Query by Products & Raw material – Products Produced

and traded

Structured Query – Software services (Pattern search)

QUERY

All search queries resulted in 1371 companies. © Jain Shrimal & Co. – For BCAS – Internal Circulation Only

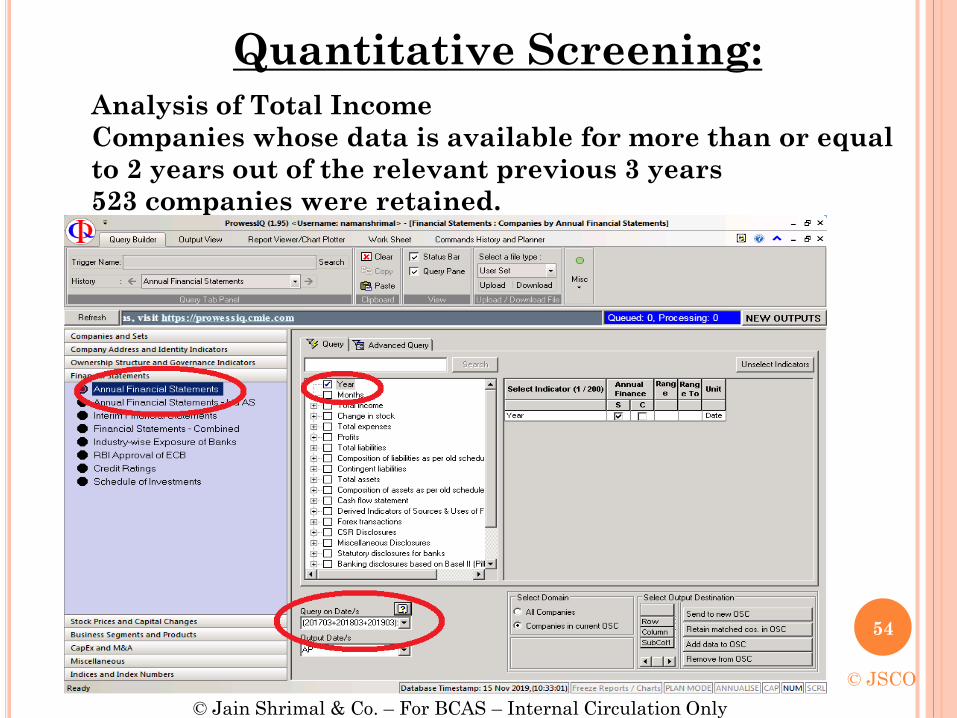

Quantitative Screening:

Analysis of Total Income

Companies whose data is available for more than or equal

to 2 years out of the relevant previous 3 years

523 companies were retained.

54

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

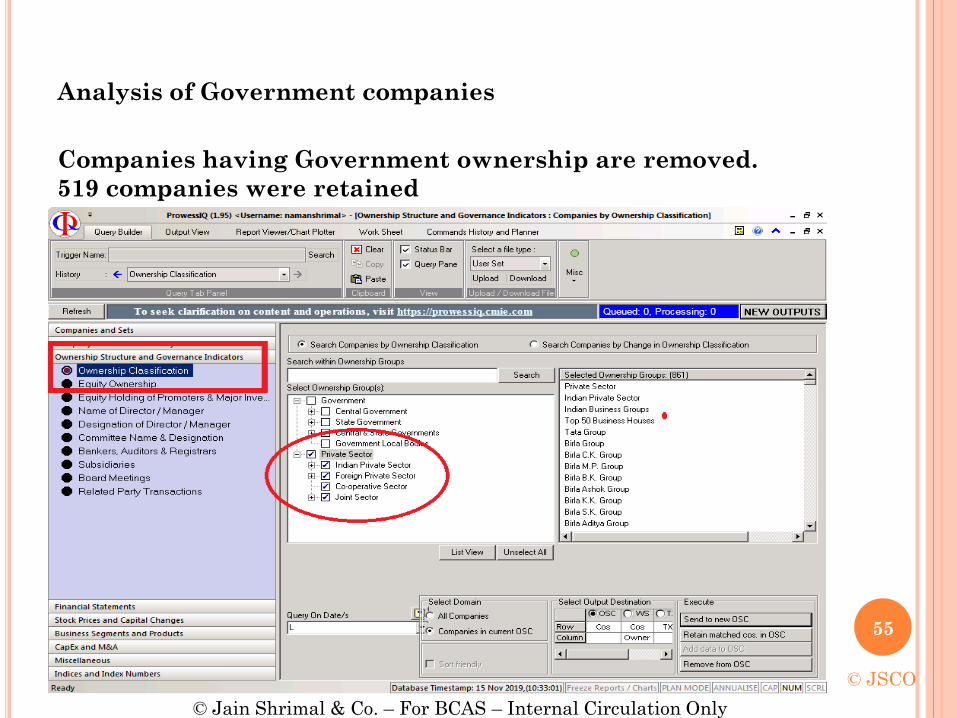

Analysis of Government companies

Companies having Government ownership are removed.

519 companies were retained

55

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

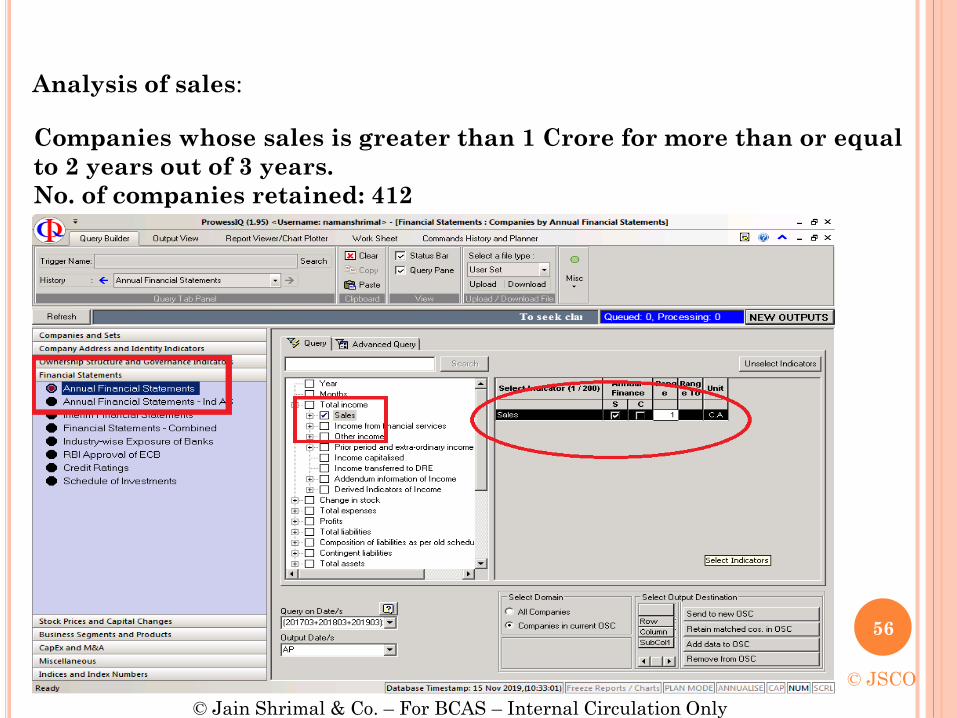

Analysis of sales:

Companies whose sales is greater than 1 Crore for more than or equal

to 2 years out of 3 years.

No. of companies retained: 412

56

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

57

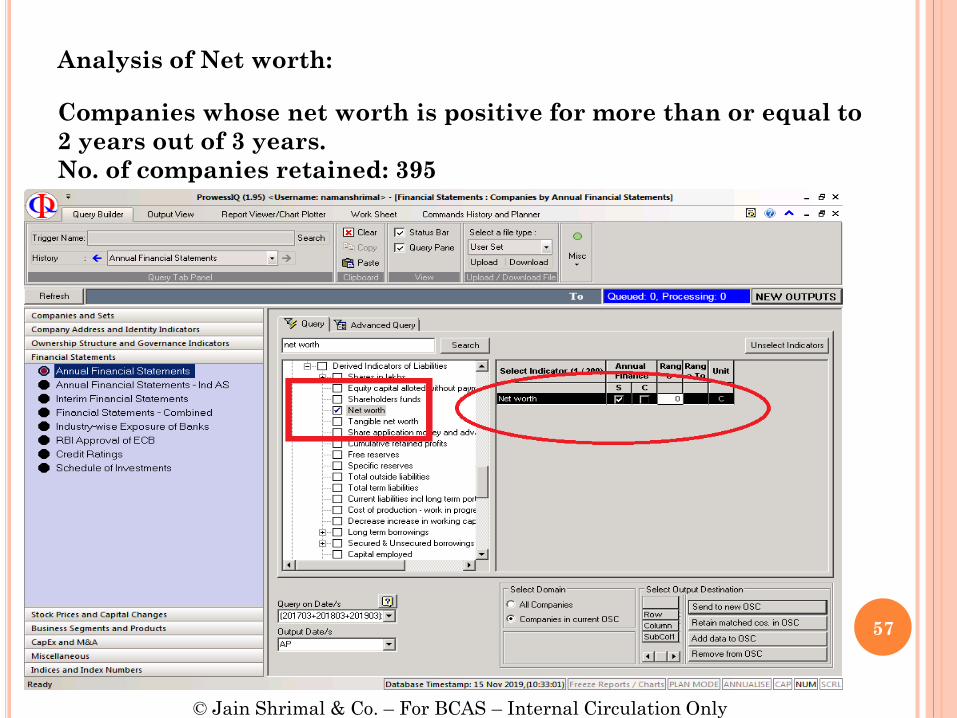

Analysis of Net worth:

Companies whose net worth is positive for more than or equal to

2 years out of 3 years.

No. of companies retained: 395

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

58

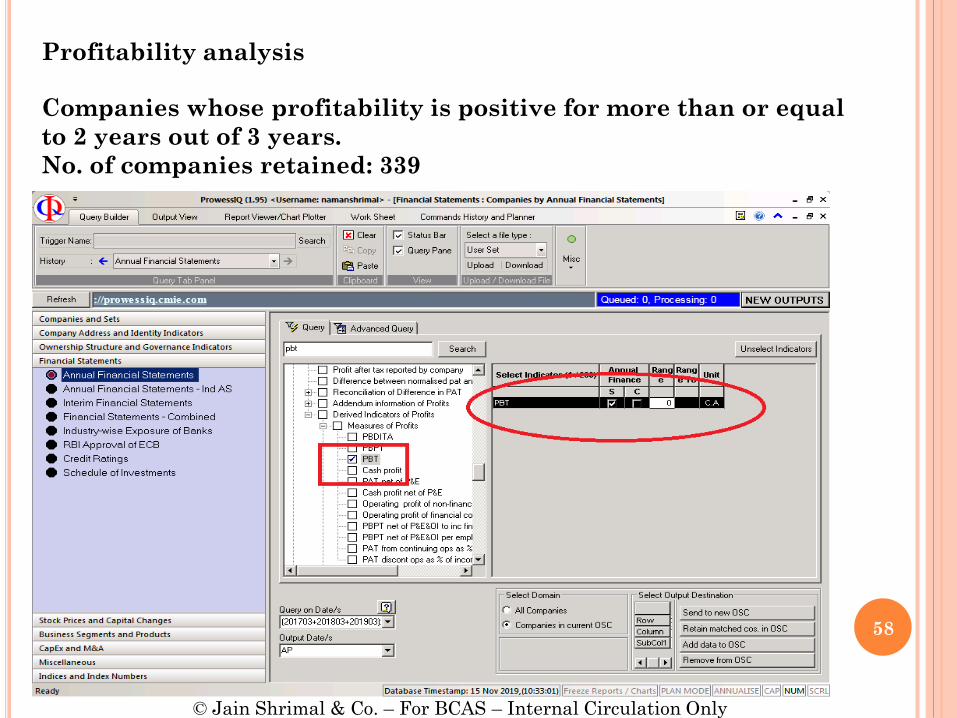

Profitability analysis

Companies whose profitability is positive for more than or equal

to 2 years out of 3 years.

No. of companies retained: 339

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

59

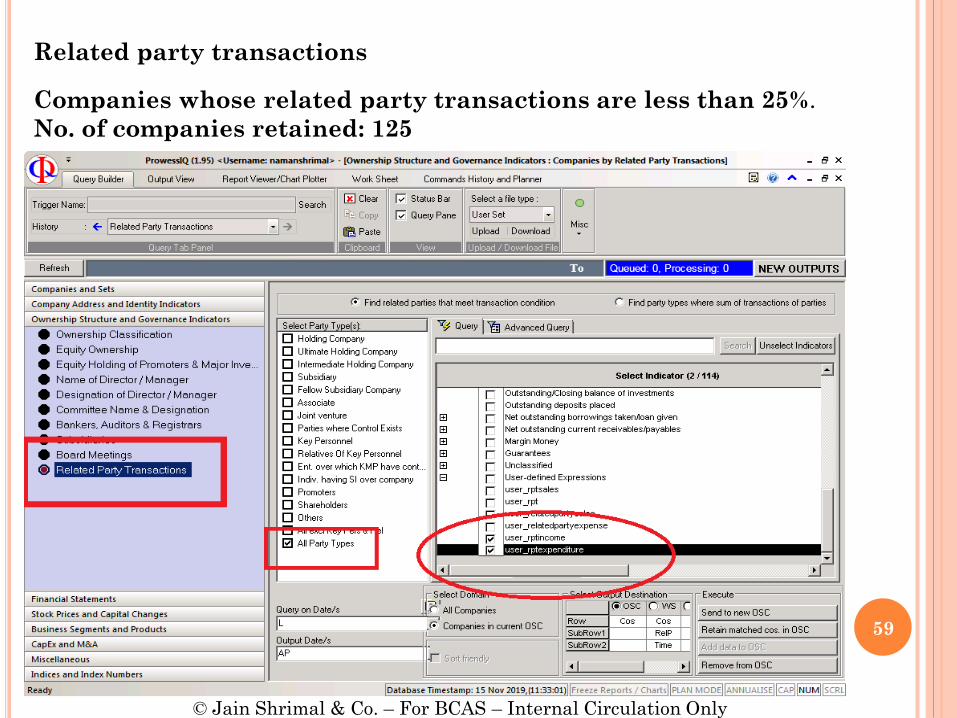

Related party transactions

Companies whose related party transactions are less than 25%.

No. of companies retained: 125

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

60

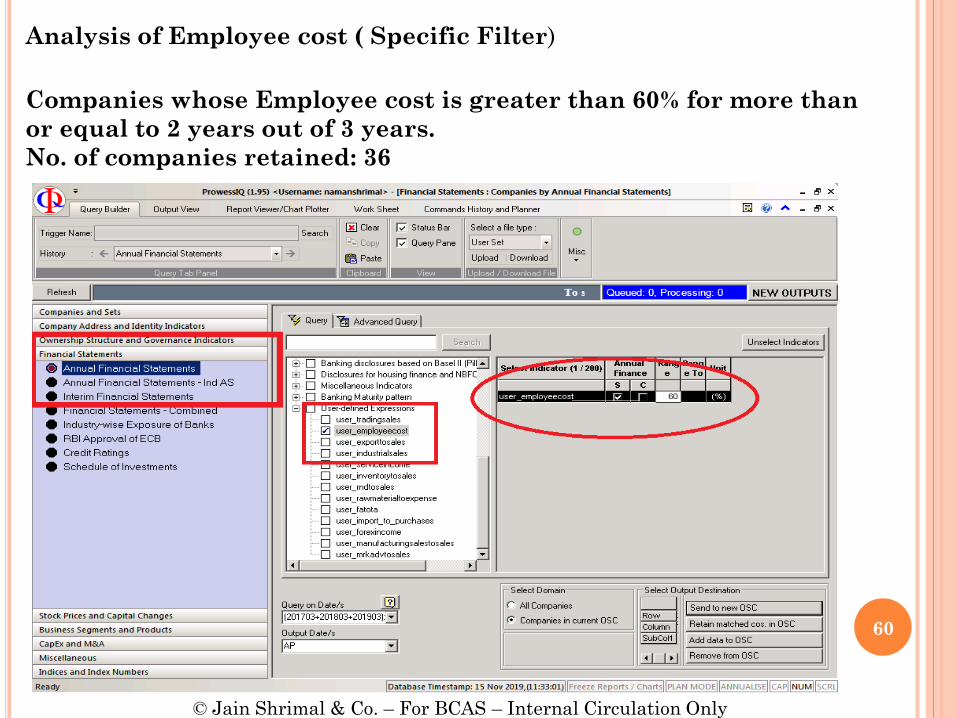

Analysis of Employee cost ( Specific Filter)

Companies whose Employee cost is greater than 60% for more than

or equal to 2 years out of 3 years.

No. of companies retained: 36

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

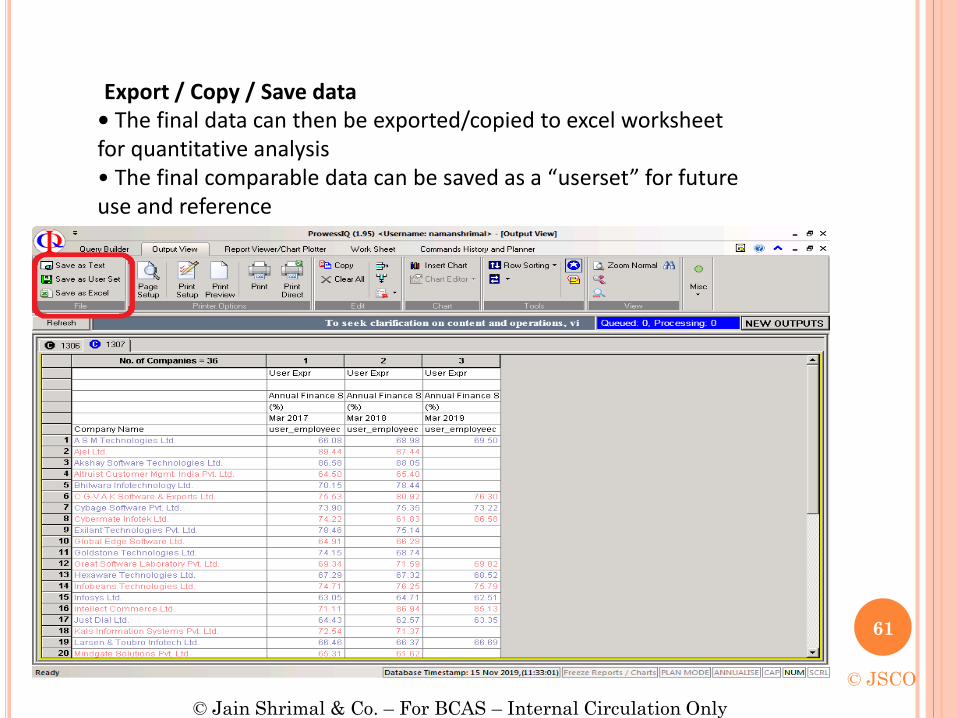

Export / Copy / Save data• The final data can then be exported/copied to excel worksheet for quantitative analysis• The final comparable data can be saved as a “userset” for future use and reference

61

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

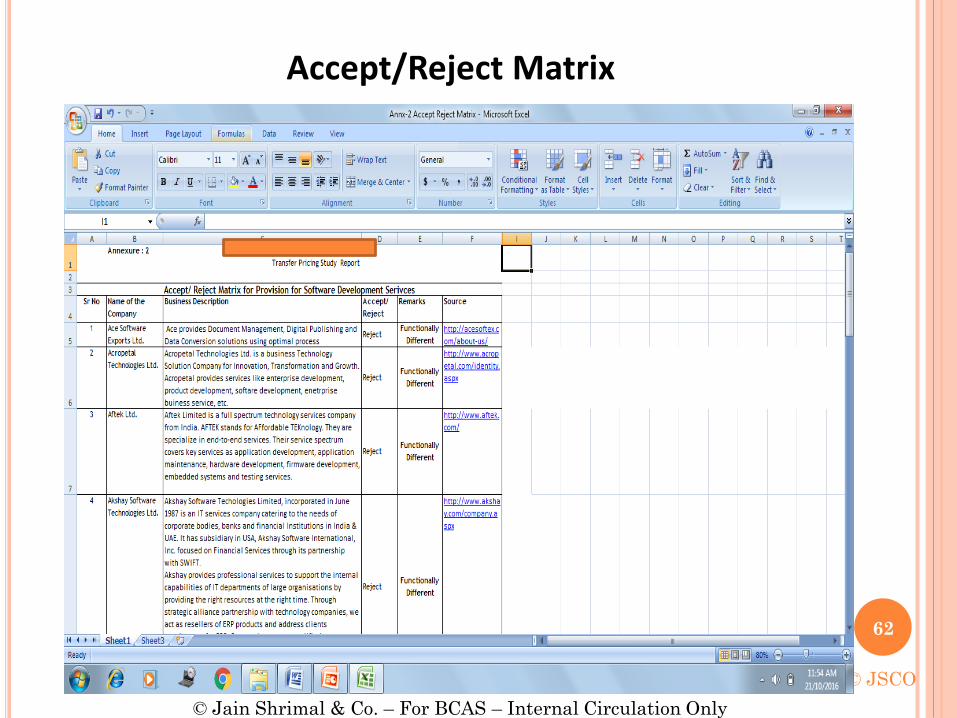

Accept/Reject Matrix

62

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

Criteria TotalCount

Companies removed

Search from Prowess:

No of companies resulted by keywords. 1371

Companies whose data is available for two or more years 523 848

Companies other than Government Companies519 4

Companies whose sales turnover is greater than 1 crore 412 107

Companies whose net worth is positive 395 17

Companies whose profit is greater than 0. 339 56

Companies whose related party transactions are less than 25% 125 214

Companies whose employee cost are greater than 60 %. 36 89

Comparable Companies selected 8 28

Summary

63

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

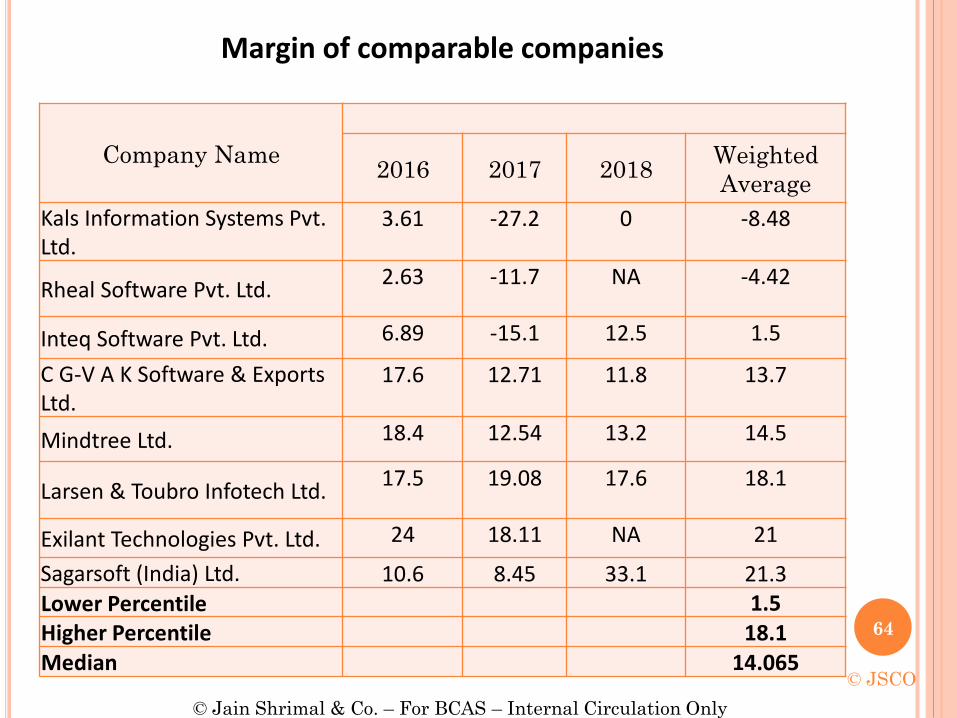

Margin of comparable companies

64

Company Name2016 2017 2018

Weighted

Average

Kals Information Systems Pvt. Ltd.

3.61 -27.2 0 -8.48

Rheal Software Pvt. Ltd.2.63 -11.7 NA -4.42

Inteq Software Pvt. Ltd. 6.89 -15.1 12.5 1.5

C G-V A K Software & Exports Ltd.

17.6 12.71 11.8 13.7

Mindtree Ltd. 18.4 12.54 13.2 14.5

Larsen & Toubro Infotech Ltd.17.5 19.08 17.6 18.1

Exilant Technologies Pvt. Ltd. 24 18.11 NA 21

Sagarsoft (India) Ltd. 10.6 8.45 33.1 21.3Lower Percentile 1.5Higher Percentile 18.1Median 14.065

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

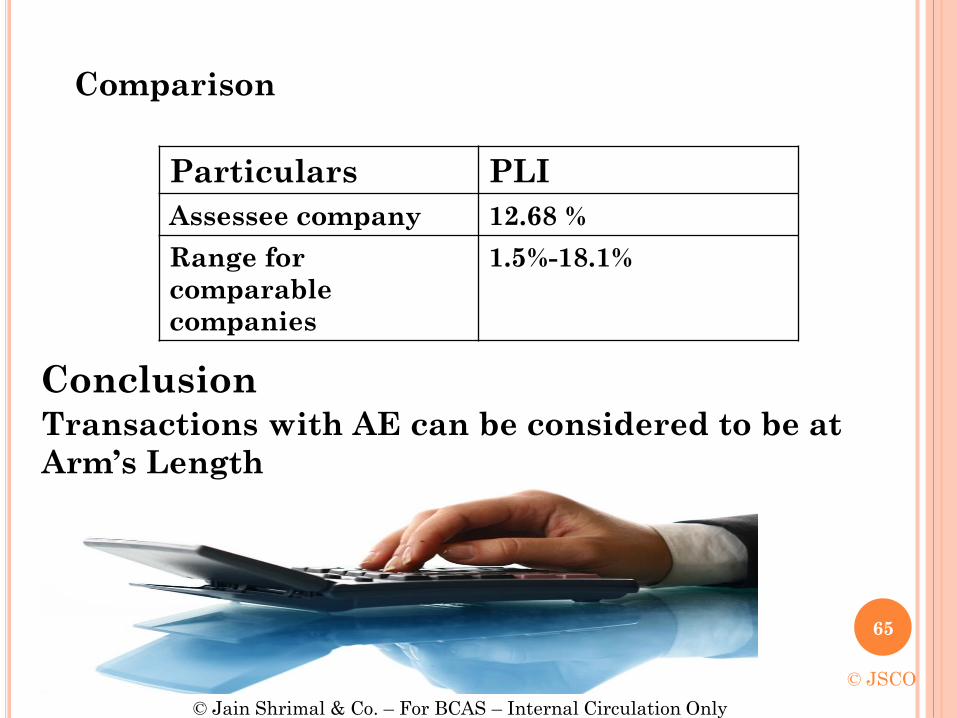

Comparison

Conclusion

Particulars PLI

Assessee company 12.68 %

Range for

comparable

companies

1.5%-18.1%

65

© JSCO

Transactions with AE can be considered to be at

Arm’s Length

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

OTHER USES OF TRANSFER

PRICING DATABASE

66

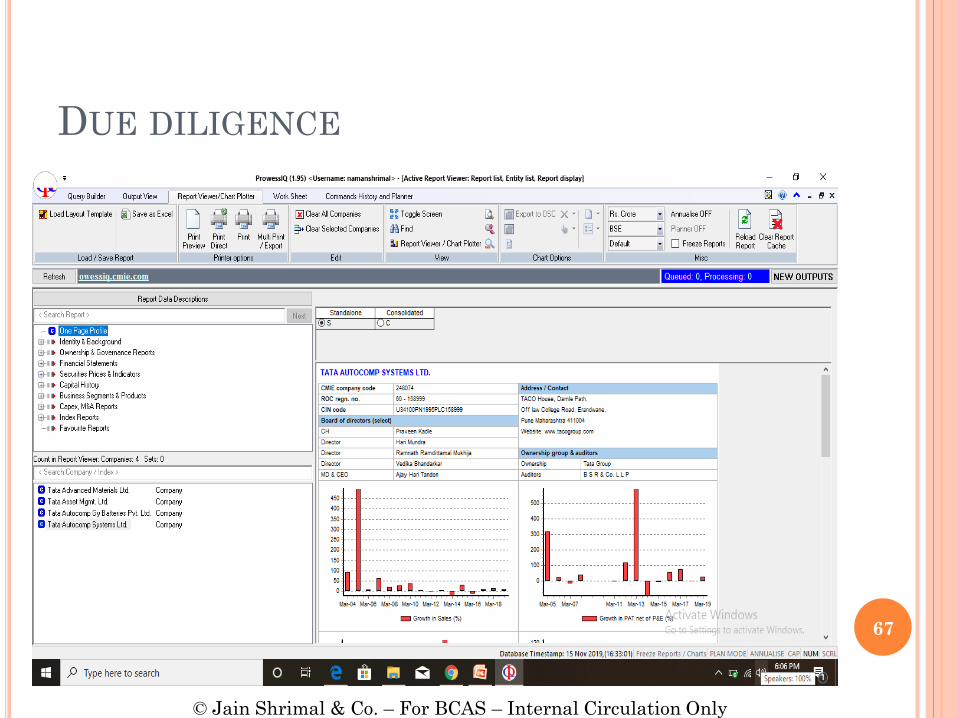

DUE DILIGENCE

67

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

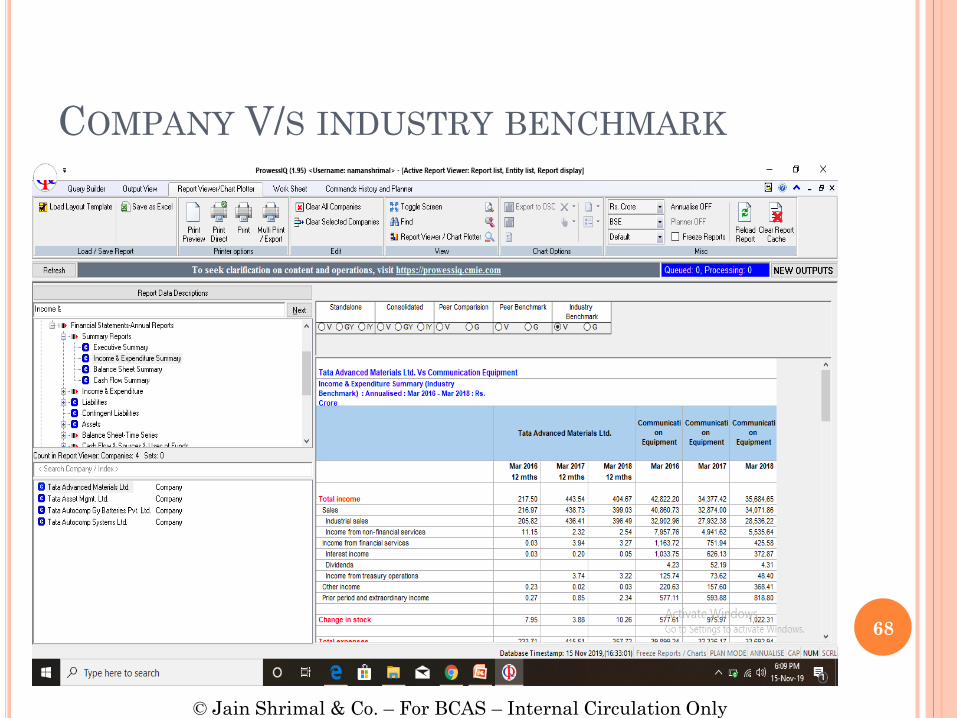

COMPANY V/S INDUSTRY BENCHMARK

68

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

PEER COMPARISON

69

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

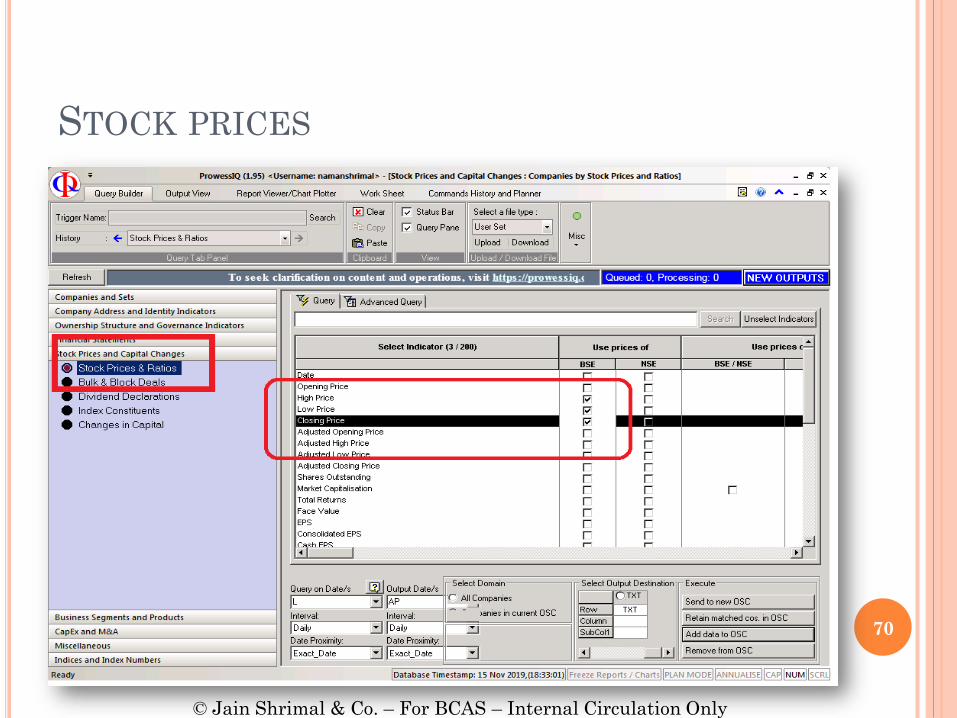

STOCK PRICES

70

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

TIPS FOR TP STUDY !!!!

• Be Creative (Do not just Copy Paste )

• Understand the working of databases – Use Multiple sources

• Do lot of Trial and Errors

• Stringent Qualitative Analysis

• Discussion with only Client’s accountant with not help –

Understand the Business – Step out of the Cabin

• Transaction-wise analysis vs Entity level analysis

• Identify alternative sources of information in public domain

• Make suitable adjustments, well backed by supporting

workings and bases

• Analyze implication of market conditions on business of the

Assessee

• Avoid cherry picking of comparables

• Document the whole process along with reasons

• ENJOY IT !!! 71

© JSCO

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

© Jain Shrimal & Co. – For BCAS – Internal Circulation Only

72

Naman Shrimal

+91 9636111444

Jain Shrimal & Co.

62, Gangwal Park,

M.D. Road – Jaipur -302004

www.jainshrimal.com

HAVE A NICE EVENING !!!!

73