Trade Analysis of Retail and Service Industries in North Dakota for Planning Local Economic...

28

Agricultural Economics Report No. 363 October, 1996 TRADE ANALYSIS OF RETAIL AND SERVICE INDUSTRIES IN NORTH DAKOTA FOR PLANNING LOCAL ECONOMIC DEVELOPMENT Sanjib Bhuyan Quentin Burdick Center for Cooperatives * Department of Agricultural Economics North Dakota State University * Fargo, ND 58105-5636

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Trade Analysis of Retail and Service Industries in North Dakota for Planning Local Economic...

Agricultural Economics Report No. 363 October, 1996

TRADE ANALYSIS OF RETAIL AND SERVICE INDUSTRIES IN NORTHDAKOTA FOR PLANNING LOCAL ECONOMIC DEVELOPMENT

Sanjib Bhuyan

Quentin Burdick Center for Cooperatives * Department of Agricultural Economics North Dakota State University * Fargo, ND 58105-5636

TRADE ANALYSIS OF RETAIL AND SERVICE INDUSTRIES IN NORTH DAKOTA FOR

PLANNING LOCAL ECONOMIC DEVELOPMENT

Sanjib Bhuyan

Department of Agricultural EconomicsNorth Dakota State University

Fargo, ND 58105-5636

The analyses and views reported in this paper are those of the author. They are not necessarilyendorsed by the Department of Agriculture or by North Dakota State University.

North Dakota State University is committed to the policy that all persons shall have equal access toits programs, and employment without regard to race, color, creed, religion, national origin, sex,age, marital status, disability, public assistance status, veteran status, or sexual orientation.

Information on other titles in this series may be obtained from: Department of AgriculturalEconomics, North Dakota State University, P.O. Box 5636, Fargo, ND 58105. Telephone: 701-231-7441, Fax: 701-231-7400, or e-mail: [email protected].

Copyright © 1996 by Sanjib Bhuyan. All rights reserved. Readers may make verbatim copies ofthis document for non-commercial purposes by any means, provided that this copyright noticeappears on all such copies.

TRADE ANALYSIS OF RETAIL AND SERVICE INDUSTRIES IN NORTH DAKOTA FOR

PLANNING LOCAL ECONOMIC DEVELOPMENT

Sanjib Bhuyan

ABSTRACT

Trade analysis of retail and service sectors allows economic development practioners toevaluate the performance of these sectors in their respective communities. Estimation of marketpotential identifies specific business categories (e.g., computer stores) that have potential forfurther growth. Trade analysis of retail and service sectors in North Dakota shows that except ina few urban counties, such as Cass, Grand Forks, or Burleigh, these sectors were inefficient inretaining and attracting customer dollars. Market potential estimation of over 130 specificbusiness categories showed that a considerable number of business categories have potential forfurther growth, e.g., computer and software stores, used merchandise stores, and heavyconstruction equipment rental and leasing services.

Key words: trade analysis, market potential, economic development

PREFACE

Preparation of this report was funded by cooperative research agreement FMHA-94-57between the Rural Business and Cooperative Development Service, Rural Economic andCommunity Development, USDA, and the North Dakota State University AgriculturalExperiment Station. Dr. Randall Torgerson of the RBCS/RECD/USDA, served as liaison; andDr. David Cobia was the principal investigator. This report also contributes to NDSUAgricultural Experiment Station project 1394, titled “Strategies for Rural CooperativeDevelopment."

The study is based on secondary data collected from public domain sources. The authoris grateful to David Cobia, Larry Stearns, Dean Bangsund, Jay Leitch, Vidya Satyanarayana, andCole Gustafson for their comments on an earlier draft. However, any remaining errors are thesole responsibility of the author. Ms. Donna Adam is appreciated for her assistance in preparingthe printer-ready copy of this report.

TABLE OF CONTENTS

ABSTRACT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

HIGHLIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

BACKGROUND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

RETAIL AND SERVICE SECTOR PERFORMANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

MARKET POTENTIAL OF RETAIL AND SERVICE SECTOR INDUSTRIES. . . . . . . . . . . 7Retail Trade Industries. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Service Sector Industries. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

CONCLUSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

LIST OF TABLES

Table 1: Trade Performance of Retail and Service Sectors in North Dakota by County, 1992 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Table 2: Market Potential and Other Related Information on Retail Industries in North Dakota, 1992. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Table 3: Market Potential and Other Related Information on Service Industries in North Dakota, 1992. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

FIGURE

Figure 1: County Trade Pull Factors of Retail and Service Sectors, North Dakota, 1992. . . . . . 6

ii

ABSTRACT

Trade analysis of retail and service sectors allows economic development practioners toevaluate the performance of these sectors in their respective communities. Estimation of marketpotential identifies specific business categories (e.g., computer stores) that have potential forfurther growth. Trade analysis of retail and service sectors in North Dakota shows that except ina few urban counties, such as Cass, Grand Forks, or Burleigh, these sectors were inefficient inretaining and attracting customer dollars. Market potential estimation of over 130 specificbusiness categories showed that a considerable number of business categories have potential forfurther growth, e.g., computer and software stores, used merchandise stores, and heavyconstruction equipment rental and leasing services.

Key words: trade analysis, market potential, economic development

iii

HIGHLIGHTS

This study evaluates the performance of retail and service sectors in 53 North Dakotacounties and analyzes the availability and market potential of over 130 retail and service sectorbusinesses in the state. The analyses are conducted using central place theory-based regionaleconomics models and secondary data.

Trade analysis is an inexpensive and relatively simple way to assess the performance oflocal retail and service sector activities in terms of attracting customer dollars, market size, orgrowth potential of businesses. Knowledge of such information has proven useful in buildingawareness and support for local economic development activities (Harris and Shonkwiler, 1996). Trade analysis provides answers to questions such as ‘‘what is the level of goods and servicescurrently provided locally and what goods and services are imported from elsewhere?’’ Or ‘‘whatis the market size, in terms of sales dollars in a specific line of business?’’ And ‘‘given theexisting demand and competition, does his/her line of business have market or businesspotential?’’

Over the years, both the population and businesses have declined gradually in nearly allcounties in North Dakota--the exceptions are the relatively urban counties of Cass, Grand Forks,Burleigh, Ward, and Stutsman. The U.S. Small Business Administration (1995) reported thatduring 1991-92 business failure in the state was 16.4% compared to the national average of9.9%. In terms of population, while the U.S. population rose by 9.8% during 1980-92,population in North Dakota fell by 2.1%. A recent report by the U.S. Small BusinessAdministration (SBA, 1995) shows that retail sales in North Dakota (adjusted for inflation) fellabout 20 percent from 1980 to 1988. Such shrinkage in population and economic activity wassubstantially more severe in outlying rural areas and towns than in areas with relatively higherpopulation such as Cass County, which includes the City of Fargo.

The purpose of this paper is to (1) analyze the effectiveness of retail and service sectors inNorth Dakota counties in attracting potential consumer purchases and (2) to examine whichkinds of retail and service businesses have the potential for future growth in the state. Evaluationof retail and service sector performances in North Dakota shows that for most counties these twosectors were less successful in retaining and attracting customer purchases. Moreover, thesituation has deteriorated over the last decade for most rural counties in the state. Given such anoutcome, the past or ongoing economic development programs and strategies to improvebusiness environment and attract customers may not have been as desired. However, it is morethan likely that the situation would have been worse had no economic development programsbeen undertaken in these communities. Reevaluation of on-going economic developmentprograms and strategies may be required to improve the performance of retail and service tradesin those communities that did not perform well. Active cooperation among private businesses,potential entrepreneurs, or economic development agencies may also contribute towardsimproving retail and service sectors performances in North Dakota.

iv

Analysis of market potential of specific businesses in retail and service sectors has shownthat among the 130-plus business categories selected for this study, the following have highermarket potential in their respective sectors: in the service sector -- computer rent/lease andmaintenance services; public golf courses; and heavy construction equipment rental and leasingservices retail sector -- computer and software stores; catalog and mail-order houses; and usedmerchandise stores. These are some of the businesses that may be targeted by potentialentrepreneurs in North Dakota for opening new business ventures. However, before deciding toopen a new business venture, an entrepreneur must conduct a thorough feasibility study as a partof his/her business plan. For those interested in starting a new business in North Dakota, contactthe Department of Economic Development and Finance at (701) 221-5320 for information andassistance or regional economic development commissions for further information.

Research Associate, Quentin Burdick Center for Cooperatives, North Dakota State University,*

Fargo.

TRADE ANALYSIS OF RETAIL AND SERVICEINDUSTRIES IN NORTH DAKOTA FOR

PLANNING LOCAL ECONOMIC DEVELOPMENT

Sanjib Bhuyan*

BACKGROUND

It is common for economists and development planners to conduct applied research andextension education programs to help local economic development practioners evaluate theperformance of their local business sectors, e.g., retail sector. It is essential for the economicdevelopment practioners to know how effective the retail or service sectors in their communityare in attracting potential consumer purchases. This information is important, because if thesesectors are not performing well, local business and community leaders will need to reevaluatetheir on-going programs and strategies and start new ones to improve the performance of variouslocal businesses. Conversely, communities where these sectors are doing well may intensifytheir existing economic development strategy. Bringing such performance evaluations to a groupof citizens or decision-makers concerned with the economic future of a community has provenuseful in building awareness and support for local economic development activities (Harris andShonkwiler, 1996).

Trade analysis is a commonly used procedure to provide local economic developmentplanners and decision makers with information about current local retail and service sectoractivities (Shaffer, 1989; Ariyaratne and Darling, 1995). Trade analysis is an inexpensive andrelatively simple way to obtain information such as relative performance of differentcommunities in attracting customer dollars, market size, or performance of specific businesscategories. Economic development practioners face questions such as what is the level of goodsand services currently provided locally and what goods and services are imported fromelsewhere? A crucial question faced by any entrepreneur is what is the market size, in terms ofsales dollars, in his/her line of business? And given the existing demand and competition, doeshis/her line of business have market or business potential? Trade analysis tries to provideanswers to such questions.

Over the years, both population and businesses are declining gradually in nearly allcounties in North Dakota--the exceptions are the relatively urban counties of Cass, Grand Forks,Burleigh, Ward, and Stutsman. Declining population and businesses put financial stress on thesecommunities to provide and maintain services such as local credit, health services, garbagedisposal, grocery stores, and other retail and service related outlets. For instance, on averageNorth Dakota residents drive 68 miles to and from the closest hospital (Hamm et al., 1993). TheU.S. Small Business Administration (1995) reported that during 1991-92 business failure in thestate was 16.4% compared to the national average of 9.9%. In terms of population, while the

2

U.S. population rose by 9.8% during 1980-92, population in North Dakota fell by 2.1%. Arecent report by the U.S. Small Business Administration (SBA, 1995) shows that retail sales inNorth Dakota (adjusted for inflation) fell about 20% from 1980 to 1988. Such shrinkage inpopulation and economic activity was substantially more severe in outlying rural areas and townsthan in areas with relatively higher population such as Cass County, which includes the City ofFargo.

Economic development efforts in North Dakota are carried out by organizations such aslocal and regional economic development agencies (e.g., Traill County Economic DevelopmentCommission), by state government agencies (e.g., Department of Economic Development andFinance), and trade associations (e.g., North Dakota Association of Rural Electric Cooperatives). In some rural communities, cooperatives have taken direct action by entering into new venturesto keep small town businesses alive and well. For example, Farmers Union Oil Company inLidgerwood had taken over a lumber store and a grocery store which were closing, and recentlyreported a profit of over $12,000 in each operation (Miller, 1996).

Irrespective of the measures or strategies used by economic development planners andpractioners to retain local customers and attract outside customers, some communities may notbe able to make much progress. These communities may not be able to make strategicinvestment in commercial development, often a common way of attracting customers, sincemany small communities are usually unable to garner the financial strength necessary to makesuch investments. In some circumstances, those communities with poorly performing retailand/or service sectors may cooperate with adjacent communities with similar characteristics toprovide combined and stronger retail and service sectors offerings to their residents and outsideconsumers.

Another way of retaining local customer dollars is to provide locally the goods andservices that are in demand. Residents in Bonaparte, Iowa (population: 465) cooperated to invest$2,000 each to become partners in the local stores to save this hamlet from economic ruin. Withsimilar concerted efforts, some rural communities in North Dakota may also be able to maketheir economies more healthy. Potential entrepreneurs who may not have the financial strengthnecessary to open a new business may cooperate to open a new business venture as a cooperative. To survive in a competitive business environment, similar kinds of businesses in adjacent ruralcommunities may cooperate to combine resources to capture benefits a single business enterprisemay not realize if the tasks were undertaken individually (Bhuyan, 1996).

While the purpose of this paper is not to analyze customers’ shopping patterns or findingways to retain customer dollars locally, an attempt is made (1) to analyze the effectiveness ofretail and service sectors in North Dakota counties in attracting potential consumer purchases and(2) to examine which kinds of retail and service businesses have the potential for future growthin the state. Most of the past trade analysis for North Dakota focused on evaluating theperformance of the retail sector (Bangsund et al., 1991; Leistritz and Wanzek, 1993). A fewothers went further to evaluate trade performance of specific business categories, such as eating

3

and drinking places, automotive dealers, and drug stores (Bangsund et al., 1995). This study isbroader in scope as it estimates market potentials of over 130 retail and service businesscategories in addition to evaluating the trade performance of retail and service sectors in NorthDakota.

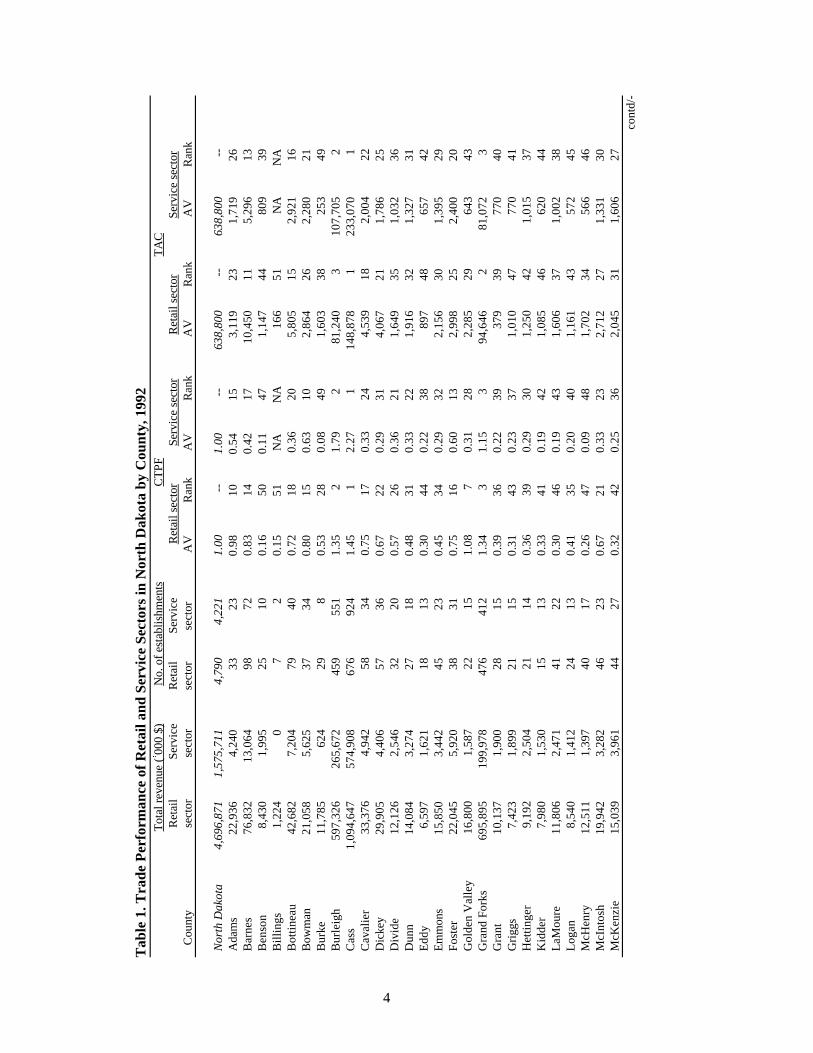

RETAIL AND SERVICE SECTOR PERFORMANCE

Evaluation of retail and service sectors performance at the county level is carried outusing County Trade Pull Factors (CTPF) and Trade Area Captures (TAC) for North Dakotacounties in 1992. The CTPF is a measure of relative performance of retail or service activities ina county compared to the respective state averages. It is computed by dividing the per capitacounty sales by per capita North Dakota sales for each sector, i.e., CTPF is the per capita retail orservice sales in each county relative to that of the state for the retail or service sector. Datasources were the 1990 Census of Population and Housing and the 1992 Economic Census, bothpublished by the U.S. Department of Commerce. Obviously, the pull factors for both retail andservice sectors at the state level are equal to 1.00. If a county has a CTPF value less than 1.00 in,for example, retail trade, then its retail trade is losing customers to other counties orcommunities; conversely, a CTPF value greater than 1.00 implies that the county attractscustomers from other communities or counties.

The purpose of estimating TAC is to measure how many customers are drawn to aparticular community to shop for specific products or services. TAC is one way of measuringmarket capture by existing establishments in retail or service sectors in a community/county. It iscomputed by multiplying the community/county population by its CTPF. Both CTPF and TACvalues are used to evaluate the performance of retail and service sectors in each county.

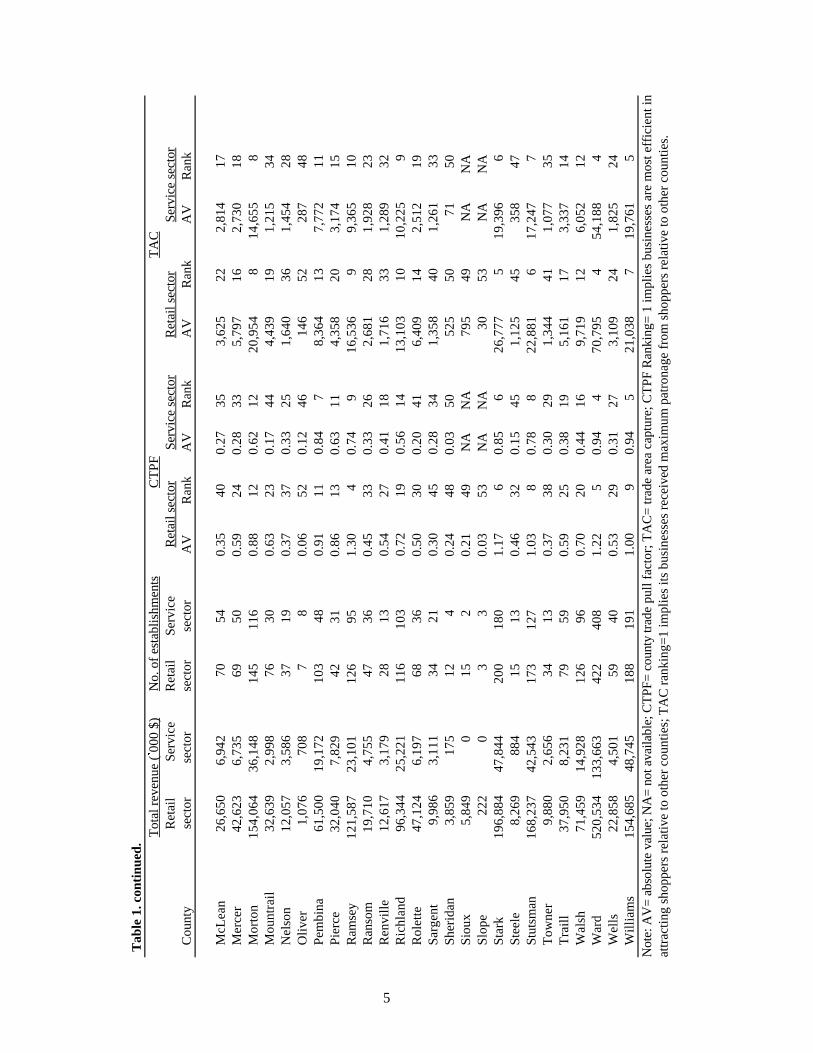

There were over 4,700 retail and 4,200 service establishments in North Dakota in 1992which grossed over $4.6 billion and $1.5 billion in sales, respectively (Table 1). Only 4 countiescrossed the half-billion dollar mark in retail sales (Cass, Grand Forks, Burleigh, and Wardcounties) and only one county reached this mark in service revenue (Cass County). Among 53counties, Slope County (population: 907) had the lowest retail sales, which amounted to$222,000, or a per capita yearly sale of only $244.76. Data on service revenue was not availablefor Billings, Sioux, and Slope counties. Over 45% of retail and over 57% of serviceestablishments were concentrated in the counties which have the major population centers inNorth Dakota: Cass, Grand Forks, Burleigh, Ward, and Stutsman. Each of the followingcounties reported less than 10 establishments in either retail or service sectors: Billings, Burke,Oliver, Sheridan, Sioux, and Slope.

4

Tab

le 1

. Tra

de P

erfo

rman

ce o

f Ret

ail a

nd S

ervi

ce S

ecto

rs in

Nor

th D

akot

a by

Cou

nty,

199

2T

otal

rev

enue

(&00

0 $

)N

o. o

f est

ablis

hmen

tsC

TP

FT

AC

Ret

ail

Ser

vice

Ret

ail

Ser

vice

Ret

ail s

ecto

rS

ervi

ce s

ecto

rR

etai

l sec

tor

Ser

vice

sec

tor

Cou

nty

sect

or

sect

orse

ctor

sect

orA

VR

ank

AV

Ran

kA

VR

ank

AV

Ran

k

No

rth

Da

kota

4,6

96

,87

11

,57

5,7

11

4,7

90

4,2

21

1.0

0--

1.0

0--

63

8,8

00

--6

38

,80

0--

Ada

ms

22

,93

64

,24

03

32

30

.98

10

0.5

41

53

,11

92

31

,71

92

6B

arn

es

76

,83

21

3,0

64

98

72

0.8

31

40

.42

17

10

,45

01

15

,29

61

3B

en

son

8,4

30

1,9

95

25

10

0.1

65

00

.11

47

1,1

47

44

80

9 3

9B

illin

gs

1,2

24

0 7

20

.15

51

NA

NA

16

65

1N

AN

AB

ott

ine

au

42

,68

27

,20

47

94

00

.72

18

0.3

62

05

,80

51

52

,92

11

6B

owm

an2

1,0

58

5,6

25

37

34

0.8

01

50

.63

10

2,8

64

26

2,2

80

21

Bu

rke

11

,78

56

24

29

80

.53

28

0.0

84

91

,60

33

82

53

49

Bu

rle

igh

59

7,3

26

26

5,6

72

45

95

51

1.3

52

1.7

92

81

,24

03

10

7,7

05

2C

ass

1,0

94

,64

75

74

,90

86

76

92

41

.45

12

.27

11

48

,87

81

23

3,0

70

1C

ava

lier

33

,37

64

,94

25

83

40

.75

17

0.3

32

44

,53

91

82

,00

42

2D

icke

y2

9,9

05

4,4

06

57

36

0.6

72

20

.29

31

4,0

67

21

1,7

86

25

Div

ide

12

,12

62

,54

6 3

22

00

.57

26

0.3

62

11

,64

93

51

,03

23

6D

un

n1

4,0

84

3,2

74

27

18

0.4

83

10

.33

22

1,9

16

32

1,3

27

31

Ed

dy

6,5

97

1,6

21

18

13

0.3

04

40

.22

38

89

74

86

57

42

Em

mon

s1

5,8

50

3,4

42

45

23

0.4

53

40

.29

32

2,1

56

30

1,3

95

29

Fo

ste

r2

2,0

45

5,9

20

38

31

0.7

51

60

.60

13

2,9

98

25

2,4

00

20

Go

lde

n V

alle

y1

6,8

00

1,5

87

22

15

1.0

87

0.3

12

82

,28

52

96

43

43

Gra

nd

Fo

rks

69

5,8

95

19

9,9

78

47

64

12

1.3

43

1.1

53

94

,64

62

81

,07

23

Gra

nt

10

,13

71

,90

02

81

50

.39

36

0.2

23

93

79

39

77

04

0G

riggs

7,4

23

1,8

99

21

15

0.3

14

30

.23

37

1,0

10

47

77

04

1H

ett

ing

er

9,1

92

2,5

04

21

14

0.3

63

90

.29

30

1,2

50

42

1,0

15

37

Kid

de

r7

,98

01

,53

01

51

30

.33

41

0.1

94

21

,08

54

66

20

44

La

Mo

ure

11

,80

62

,47

14

12

20

.30

46

0.1

94

31

,60

63

71

,00

23

8L

og

an

8,5

40

1,4

12

24

13

0.4

13

50

.20

40

1,1

61

43

57

24

5M

cHe

nry

12

,51

11

,39

74

01

70

.26

47

0.0

94

81

,70

23

45

66

46

McI

nto

sh1

9,9

42

3,2

82

46

23

0.6

72

10

.33

23

2,7

12

27

1,3

31

30

McK

en

zie

15

,03

93

,96

14

42

70

.32

42

0.2

53

62

,04

53

11

,60

62

7 con

td/-

5

T

able

1. c

ontin

ued. T

ota

l re

ven

ue

(&00

0 $

)N

o. o

f est

ablis

hmen

tsC

TP

FT

AC

Ret

ail

Ser

vice

Ret

ail

Ser

vice

Ret

ail s

ecto

rS

ervi

ce s

ecto

rR

etai

l sec

tor

Ser

vice

sec

tor

Cou

nty

sect

orse

ctor

sect

orse

ctor

AV

Ran

kA

VR

ank

AV

Ran

kA

VR

ank

McL

ea

n2

6,6

50

6,9

42

70

54

0.3

54

00

.27

35

3,6

25

22

2,8

14

17

Me

rce

r4

2,6

23

6,7

35

69

50

0.5

92

40

.28

33

5,7

97

16

2,7

30

18

Mo

rto

n1

54

,06

43

6,1

48

14

51

16

0.8

81

20

.62

12

20

,95

48

14

,65

58

Mo

un

tra

il3

2,6

39

2,9

98

76

30

0.6

32

30

.17

44

4,4

39

19

1,2

15

34

Ne

lso

n1

2,0

57

3,5

86

37

19

0.3

73

70

.33

25

1,6

40

36

1,4

54

28

Oliv

er

1,0

76

70

87

80

.06

52

0.1

24

61

46

52

28

74

8P

em

bin

a6

1,5

00

19

,17

21

03

48

0.9

11

10

.84

78

,36

41

37

,77

21

1P

ierc

e3

2,0

40

7,8

29

42

31

0.8

61

30

.63

11

4,3

58

20

3,1

74

15

Ram

sey

12

1,5

87

23

,10

11

26

95

1.3

04

0.7

49

16

,53

69

9,3

65

10

Ran

som

19

,71

04

,75

54

73

60

.45

33

0.3

32

62

,68

12

81

,92

82

3R

en

ville

12

,61

73

,17

92

81

30

.54

27

0.4

11

81

,71

63

31

,28

93

2R

ich

lan

d9

6,3

44

25

,22

11

16

10

30

.72

19

0.5

61

41

3,1

03

10

10

,22

59

Ro

lett

e 4

7,1

24

6,1

97

68

36

0.5

03

00

.20

41

6,4

09

14

2,5

12

19

Sa

rge

nt

9,9

86

3,1

11

34

21

0.3

04

50

.28

34

1,3

58

40

1,2

61

33

Sh

eri

da

n3

,85

91

75

12

40

.24

48

0.0

35

05

25

50

71

50

Sio

ux

5,8

49

01

52

0.2

14

9N

AN

A7

95

49

NA

NA

Slo

pe

22

20

33

0.0

35

3N

AN

A3

05

3N

AN

AS

tark

19

6,8

84

47

,84

42

00

18

01

.17

60

.85

62

6,7

77

51

9,3

96

6S

tee

le8

,26

98

84

15

13

0.4

63

20

.15

45

1,1

25

45

35

84

7S

tuts

man

16

8,2

37

42

,54

31

73

12

71

.03

80

.78

82

2,8

81

61

7,2

47

7T

ow

ne

r9

,88

02

,65

63

41

30

.37

38

0.3

02

91

,34

44

11

,07

73

5T

raill

37

,95

08

,23

17

95

90

.59

25

0.3

81

95

,16

11

73

,33

71

4W

als

h7

1,4

59

14

,92

81

26

96

0.7

02

00

.44

16

9,7

19

12

6,0

52

12

Wa

rd5

20

,53

41

33

,66

34

22

40

81

.22

50

.94

47

0,7

95

45

4,1

88

4W

ells

22

,85

84

,50

15

94

00

.53

29

0.3

12

73

,10

92

41

,82

52

4W

illia

ms

15

4,6

85

48

,74

51

88

19

11

.00

90

.94

52

1,0

38

71

9,7

61

5N

ote:

AV

= a

bsol

ute

valu

e; N

A=

not

ava

ilabl

e; C

TP

F=

cou

nty

trad

e pu

ll fa

ctor

; TA

C=

trad

e ar

ea c

aptu

re; C

TP

F R

anki

ng=

1 im

plie

s bu

sine

sses

are

mos

t effi

cien

t in

attr

actin

g sh

oppe

rs r

elat

ive

to o

ther

cou

ntie

s; T

AC

ran

king

=1

impl

ies

its b

usin

esse

s re

ceiv

ed m

axim

um p

atro

nage

from

sho

pper

s re

lativ

e to

oth

er c

ount

ies.

A D A M S0 .9 80 .5 4

B A R N E S0 .8 30 .4 2

B E N S O N0 .1 60 .1 1

B I L L I N G S0 .1 5N A

B O T T I N E A U0 .7 20 .3 6

B O W M A N0 .8 00 .6 3

B U R K E0 .5 30 .0 8

B U R L E I G H1 .3 51 .7 9 C A S S

1 .4 52 .2 7

C A V A L I E R0 .7 50 .3 3

D I C K E Y0 .6 70 .2 9

D I V I D E

0 .5 70 .3 6

D U N N

0 .4 80 .3 3

E D D Y0 .3 00 .2 2

E M M O N S0 .4 50 .2 9

F O S T E R0 .7 50 .6 0

G R A N D F O R K S1 .3 41 .1 5

G R A N T0 .3 90 .2 2

G R I G G S0 .3 10 .2 3

H E T T I N G E R0 .3 60 .2 9

K I D D E R0 .3 30 .1 9

L A M O U R E0 .3 00 .1 9

L O G A N0 .4 10 .2 0

M C H E N R Y0 .2 60 .0 9

M C I N T O S H0 .6 70 .3 3

M C K E N Z I E0 .3 20 .2 5 M C L E A N

0 .3 50 .2 7M E R C E R

0 .5 90 .2 8

M O R T O N0 .8 80 .6 2

M O U N T R A I L0 .6 30 .1 7

N E L S O N0 .3 70 .3 3

O L I V E R0 .0 60 .1 2

P E M B I N A0 .9 10 .8 4

P I E R C E0 .8 60 .6 3

R A M S E Y1 .3 00 .7 4

R A N S O M0 .4 50 .3 3

R E N V I L L E0 .5 4

0 .4 1

R I C H L A N D0 .7 20 .5 6

R O L E T T E0 .5 00 .2 0

S A R G E N T0 .3 00 .2 8

S H E R I D A N

0 .2 40 .0 3

S I O U X0 .2 1N A

S L O P E0 .0 3N A

S T A R K1 .1 70 .8 5

S T E E L E0 .4 60 .1 5

S T U T S M A N1 .0 30 .7 8

T O W N E R0 .3 70 .3 0

T R A I L L0 .5 90 .3 8

W A L S H0 .7 00 .4 4

W A R D

1 .2 20 .9 4

W E L L S0 .5 30 .3 1

W I L L I A M S

1 .0 00 .9 4

G O L D E NV A L L E Y

1 .0 80 .3 1

A D A M S0 .9 80 .5 4

B A R N E S0 .8 30 .4 2

B E N S O N0 .1 60 .1 1

B I L L I N G S0 .1 5N A

B O T T I N E A U0 .7 20 .3 6

B O W M A N0 .8 00 .6 3

B U R K E0 .5 30 .0 8

B U R L E I G H1 .3 51 .7 9 C A S S

1 .4 52 .2 7

C A V A L I E R0 .7 50 .3 3

D I C K E Y0 .6 70 .2 9

D I V I D E

0 .5 70 .3 6

D U N N

0 .4 80 .3 3

E D D Y0 .3 00 .2 2

E M M O N S0 .4 50 .2 9

F O S T E R0 .7 50 .6 0

G R A N D F O R K S1 .3 41 .1 5

G R A N T0 .3 90 .2 2

G R I G G S0 .3 10 .2 3

H E T T I N G E R0 .3 60 .2 9

K I D D E R0 .3 30 .1 9

L A M O U R E0 .3 00 .1 9

L O G A N0 .4 10 .2 0

M C H E N R Y0 .2 60 .0 9

M C I N T O S H0 .6 70 .3 3

M C K E N Z I E0 .3 20 .2 5 M C L E A N

0 .3 50 .2 7M E R C E R

0 .5 90 .2 8

M O R T O N0 .8 80 .6 2

M O U N T R A I L0 .6 30 .1 7

N E L S O N0 .3 70 .3 3

O L I V E R0 .0 60 .1 2

P E M B I N A0 .9 10 .8 4

P I E R C E0 .8 60 .6 3

R A M S E Y1 .3 00 .7 4

R A N S O M0 .4 50 .3 3

R E N V I L L E0 .5 4

0 .4 1

R I C H L A N D0 .7 20 .5 6

R O L E T T E0 .5 00 .2 0

S A R G E N T0 .3 00 .2 8

S H E R I D A N

0 .2 40 .0 3

S I O U X0 .2 1N A

S L O P E0 .0 3N A

S T A R K1 .1 70 .8 5

S T E E L E0 .4 60 .1 5

S T U T S M A N1 .0 30 .7 8

T O W N E R0 .3 70 .3 0

T R A I L L0 .5 90 .3 8

W A L S H0 .7 00 .4 4

W A R D

1 .2 20 .9 4

W E L L S0 .5 30 .3 1

W I L L I A M S

1 .0 00 .9 4

G O L D E NV A L L E Y

1 .0 80 .3 1

A D A M S0 .9 80 .5 4

B A R N E S0 .8 30 .4 2

B E N S O N0 .1 60 .1 1

B I L L I N G S0 .1 5N A

B O T T I N E A U0 .7 20 .3 6

B O W M A N0 .8 00 .6 3

B U R K E0 .5 30 .0 8

B U R L E I G H1 .3 51 .7 9 C A S S

1 .4 52 .2 7

C A V A L I E R0 .7 50 .3 3

D I C K E Y0 .6 70 .2 9

D I V I D E

0 .5 70 .3 6

D U N N

0 .4 80 .3 3

E D D Y0 .3 00 .2 2

E M M O N S0 .4 50 .2 9

F O S T E R0 .7 50 .6 0

G R A N D F O R K S1 .3 41 .1 5

G R A N T0 .3 90 .2 2

G R I G G S0 .3 10 .2 3

H E T T I N G E R0 .3 60 .2 9

K I D D E R0 .3 30 .1 9

L A M O U R E0 .3 00 .1 9

L O G A N0 .4 10 .2 0

M C H E N R Y0 .2 60 .0 9

M C I N T O S H0 .6 70 .3 3

M C K E N Z I E0 .3 20 .2 5 M C L E A N

0 .3 50 .2 7M E R C E R

0 .5 90 .2 8

M O R T O N0 .8 80 .6 2

M O U N T R A I L0 .6 30 .1 7

N E L S O N0 .3 70 .3 3

O L I V E R0 .0 60 .1 2

P E M B I N A0 .9 10 .8 4

P I E R C E0 .8 60 .6 3

R A M S E Y1 .3 00 .7 4

R A N S O M0 .4 50 .3 3

R E N V I L L E0 .5 4

0 .4 1

R I C H L A N D0 .7 20 .5 6

R O L E T T E0 .5 00 .2 0

S A R G E N T0 .3 00 .2 8

S H E R I D A N

0 .2 40 .0 3

S I O U X0 .2 1N A

S L O P E0 .0 3N A

S T A R K1 .1 70 .8 5

S T E E L E0 .4 60 .1 5

S T U T S M A N1 .0 30 .7 8

T O W N E R0 .3 70 .3 0

T R A I L L0 .5 90 .3 8

W A L S H0 .7 00 .4 4

W A R D

1 .2 20 .9 4

W E L L S0 .5 30 .3 1

W I L L I A M S

1 .0 00 .9 4

G O L D E NV A L L E Y

1 .0 80 .3 1

A D A M S0 .9 80 .5 4

B A R N E S0 .8 30 .4 2

B E N S O N0 .1 60 .1 1

B I L L I N G S0 .1 5N A

B O T T I N E A U0 .7 20 .3 6

B O W M A N0 .8 00 .6 3

B U R K E0 .5 30 .0 8

B U R L E I G H1 .3 51 .7 9 C A S S

1 .4 52 .2 7

C A V A L I E R0 .7 50 .3 3

D I C K E Y0 .6 70 .2 9

D I V I D E

0 .5 70 .3 6

D U N N

0 .4 80 .3 3

E D D Y0 .3 00 .2 2

E M M O N S0 .4 50 .2 9

F O S T E R0 .7 50 .6 0

G R A N D F O R K S1 .3 41 .1 5

G R A N T0 .3 90 .2 2

G R I G G S0 .3 10 .2 3

H E T T I N G E R0 .3 60 .2 9

K I D D E R0 .3 30 .1 9

L A M O U R E0 .3 00 .1 9

L O G A N0 .4 10 .2 0

M C H E N R Y0 .2 60 .0 9

M C I N T O S H0 .6 70 .3 3

M C K E N Z I E0 .3 20 .2 5 M C L E A N

0 .3 50 .2 7M E R C E R

0 .5 90 .2 8

M O R T O N0 .8 80 .6 2

M O U N T R A I L0 .6 30 .1 7

N E L S O N0 .3 70 .3 3

O L I V E R0 .0 60 .1 2

P E M B I N A0 .9 10 .8 4

P I E R C E0 .8 60 .6 3

R A M S E Y1 .3 00 .7 4

R A N S O M0 .4 50 .3 3

R E N V I L L E0 .5 4

0 .4 1

R I C H L A N D0 .7 20 .5 6

R O L E T T E0 .5 00 .2 0

S A R G E N T0 .3 00 .2 8

S H E R I D A N

0 .2 40 .0 3

S I O U X0 .2 1N A

S L O P E0 .0 3N A

S T A R K1 .1 70 .8 5

S T E E L E0 .4 60 .1 5

S T U T S M A N1 .0 30 .7 8

T O W N E R0 .3 70 .3 0

T R A I L L0 .5 90 .3 8

W A L S H0 .7 00 .4 4

W A R D

1 .2 20 .9 4

W E L L S0 .5 30 .3 1

W I L L I A M S

1 .0 00 .9 4

G O L D E NV A L L E Y

1 .0 80 .3 1

6

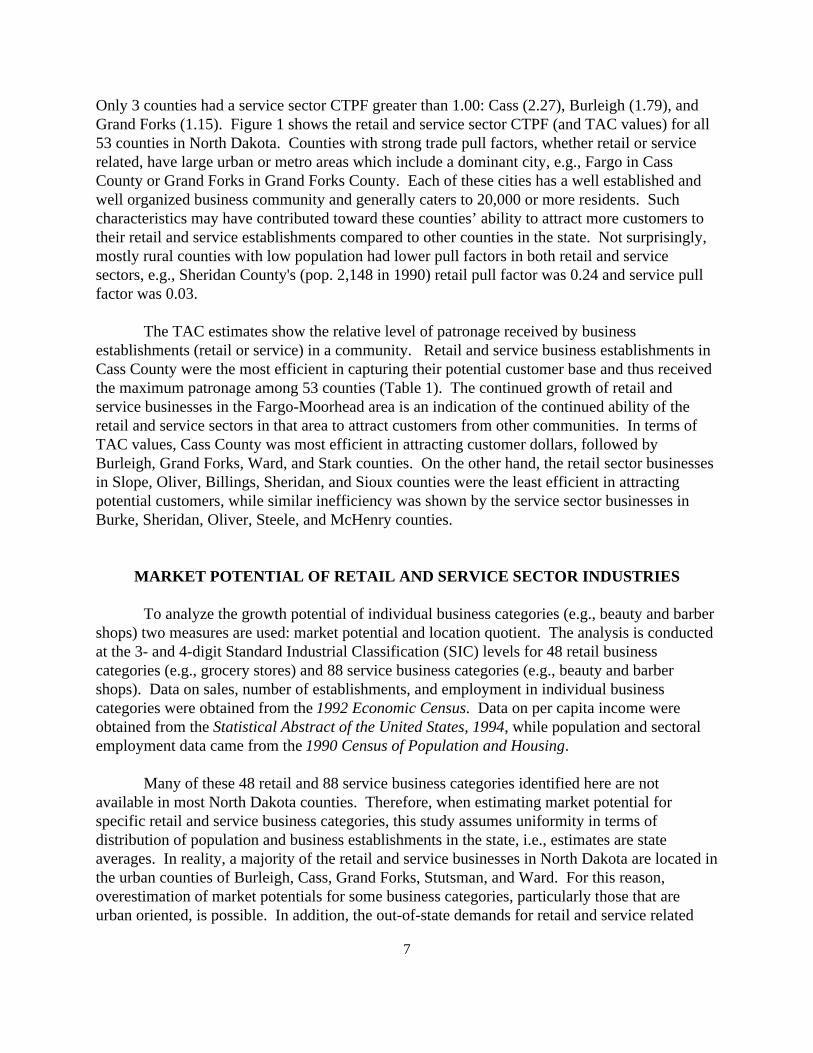

In terms of CTPF for the retail sector, 8 counties out of 53 had pull factors greater than 1.00:Burleigh (1.35), Cass (1.45), Golden Valley (1.08), Grand Forks (1.34), Ramsey (1.30), Stark (1.17),Stutsman (1.03), and Ward (1.22). Williams County had a pull factor equal to 1.00, closely followedby Adams County (0.98). The remaining 43 counties had retail pull factors less than 1.00. Thecounties that showed lowest retail pull factors include Benson (0.16), Billings (0.15), McHenry(0.26), Oliver (0.06), Sheridan (0.24), Sioux (0.21), and Slope (0.03). In a previous study whereCTPF for retail sectors in North Dakota counties were computed for 1980 and 1990, Bangsund etal. (1995) found that 13 counties out of 53 had CTPF values greater than 1.00 in 1980 while thatcount dropped to 10 in 1990. The only counties that had a retail CTPF of greater than 1.00 in 1980,1990, and 1992 were Burleigh, Cass, Golden Valley, Grand Forks, Ramsey, Stark, Stutsman, andWard. Among these, Burleigh, Cass, and Grand Forks counties were able to improve their abilityto attract customers, i.e., they showed an increase in the retail CTPF value. For example, the CTPFincreased from 1.10 in 1990 to 1.35 in 1992 for Burleigh County and from 1.20 to 1.45 for CassCounty during the same period. Therefore, the trend of urban counties pulling more and moredollars from non-urban counties is continuing. On the other hand, Golden Valley, Stark, andStutsman counties showed a slight decline in CTPF value from 1990, and Ramsey County’s retailCTPF value remained unchanged. Economic development agencies and public policy makers maywant to examine the factors responsible for declining business performance in the concerned NorthDakota counties/communities.

Figure 1: County Trade Pull Factors (CTPF) of Retail and Service Sectors, North Dakota, 1992 (CTPF values at top and bottom refer to the retail and the service sectors, respectively. NA = not available)

When it comes to the service industry, most North Dakota counties did not perform well.

7

Only 3 counties had a service sector CTPF greater than 1.00: Cass (2.27), Burleigh (1.79), andGrand Forks (1.15). Figure 1 shows the retail and service sector CTPF (and TAC values) for all53 counties in North Dakota. Counties with strong trade pull factors, whether retail or servicerelated, have large urban or metro areas which include a dominant city, e.g., Fargo in CassCounty or Grand Forks in Grand Forks County. Each of these cities has a well established andwell organized business community and generally caters to 20,000 or more residents. Suchcharacteristics may have contributed toward these counties’ ability to attract more customers totheir retail and service establishments compared to other counties in the state. Not surprisingly,mostly rural counties with low population had lower pull factors in both retail and servicesectors, e.g., Sheridan County's (pop. 2,148 in 1990) retail pull factor was 0.24 and service pullfactor was 0.03.

The TAC estimates show the relative level of patronage received by businessestablishments (retail or service) in a community. Retail and service business establishments inCass County were the most efficient in capturing their potential customer base and thus receivedthe maximum patronage among 53 counties (Table 1). The continued growth of retail andservice businesses in the Fargo-Moorhead area is an indication of the continued ability of theretail and service sectors in that area to attract customers from other communities. In terms ofTAC values, Cass County was most efficient in attracting customer dollars, followed byBurleigh, Grand Forks, Ward, and Stark counties. On the other hand, the retail sector businessesin Slope, Oliver, Billings, Sheridan, and Sioux counties were the least efficient in attractingpotential customers, while similar inefficiency was shown by the service sector businesses inBurke, Sheridan, Oliver, Steele, and McHenry counties.

MARKET POTENTIAL OF RETAIL AND SERVICE SECTOR INDUSTRIES

To analyze the growth potential of individual business categories (e.g., beauty and barbershops) two measures are used: market potential and location quotient. The analysis is conductedat the 3- and 4-digit Standard Industrial Classification (SIC) levels for 48 retail businesscategories (e.g., grocery stores) and 88 service business categories (e.g., beauty and barbershops). Data on sales, number of establishments, and employment in individual businesscategories were obtained from the 1992 Economic Census. Data on per capita income wereobtained from the Statistical Abstract of the United States, 1994, while population and sectoralemployment data came from the 1990 Census of Population and Housing.

Many of these 48 retail and 88 service business categories identified here are notavailable in most North Dakota counties. Therefore, when estimating market potential forspecific retail and service business categories, this study assumes uniformity in terms ofdistribution of population and business establishments in the state, i.e., estimates are stateaverages. In reality, a majority of the retail and service businesses in North Dakota are located inthe urban counties of Burleigh, Cass, Grand Forks, Stutsman, and Ward. For this reason,overestimation of market potentials for some business categories, particularly those that areurban oriented, is possible. In addition, the out-of-state demands for retail and service related

ETSx'Per capita salesx( Total populationND(per capita income in North Dakota(ND)

National per capita income.

ETSgas. serv. stn. '134,705,359249,908,000

( 638,800( 15,68818,177

' 0.53902( 638,800( 0.86307' 297,177 (000$).

xx ETS

ETSETS

ETS

x

8

(1)

(2)

goods and services from North Dakota establishments are assumed negligible relative to in-statedemands. Although a detailed feasibility study of a specific business is an effective countermeasure against such potential defects, it is beyond the scope of this study. Conducting such adetailed feasibility study would be a next step for a potential entrepreneur who is consideringopening a new business venture in a category that has business potential.

Market potential is the expected total sales of a commodity, a group of commodities, or aservice in a market for all firms (U.S. Department of Commerce, 1979). This definition isslightly modified to suit the needs of this study where the interest is to identify businesses thathave potential for further growth.

To identify businesses with market potential, the following steps are taken:

Step 1: Expected total sales (ETS) of business category x (e.g., gasoline service stations)in North Dakota in 1992 is estimated by

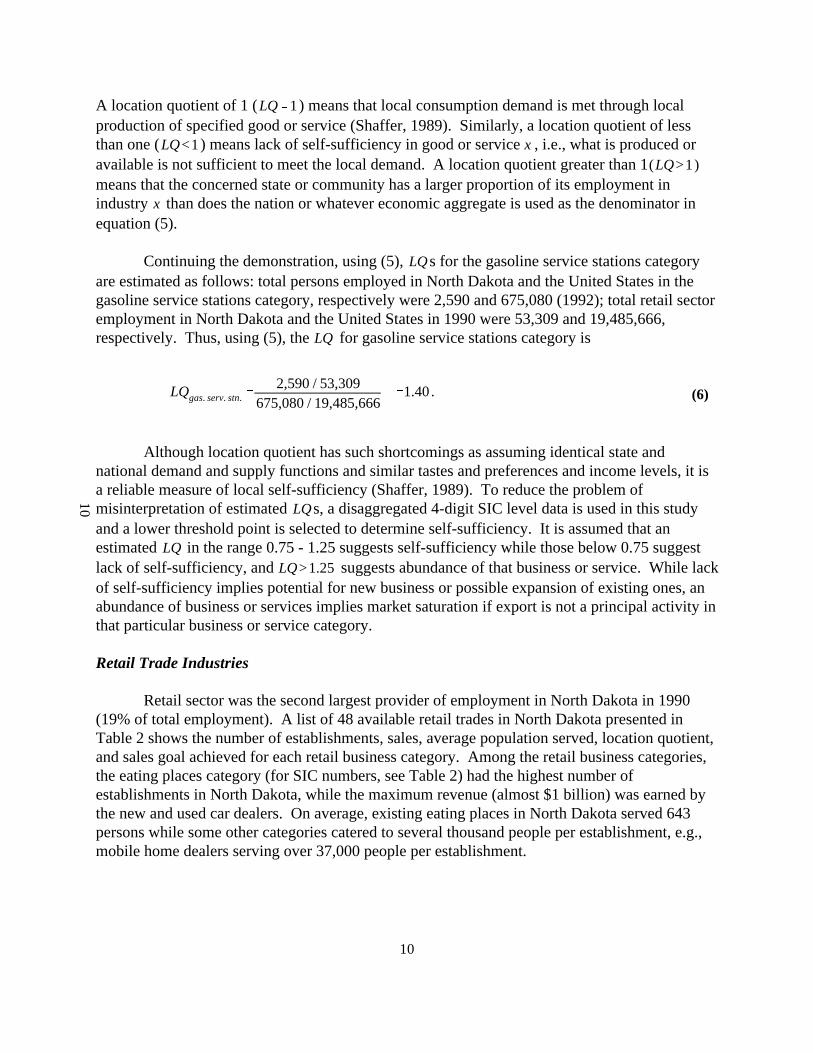

Per capita sales is the national average per capita sales in category and is obtained by dividingthe total national revenue in business by total U.S. population. is a demand relatedconcept. Although this measure ignores differences in state consumption patterns except foradjusting the level by relative state income, it does provide a readily calculated estimate ofmarket size (Shaffer, 1989).

Estimation of is demonstrated using the gasoline service stations category. Thenecessary data to compute are total U.S. revenue (1992) $134,705,359,000; total U.S.population (1990) 249,908,000; North Dakota population (1990) 638,800; per capita income inNorth Dakota and the United States (1992) $15,688 and $18,177, respectively. Then, the for gasoline service stations for 1992 is (rounded),

Step 2: The share of actual revenue to the expected total sales in 1992 is estimated for business. This share is termed %%sales goal achieved,&& and defined as

Sales goal achievedx'Actual total sales in1992x

ETSx in 1992,

Sales goal achievedgas. serv. stn. '297,177 (000$)439,968(000$)

( 100 '148.05%.

LQ for x'Percent of North Dakota employment in x

Percent of U.S. employment in x.

LQLQ

x

9

(3)

(4)

(5)

and expressed in percentage terms. Continuing the demonstration, using (3), it can be shown thatgasoline service station category exceeded expected sales in 1992, i.e.,

Step 3: All business categories are ranked in terms of their respective sales goal achieved inascending order, i.e., 1 being the business with the least amount of sales goal achieved. Based onsales goal achieved in 1992, the gasoline service stations category is ranked 39th out of the 46ranked retail trade categories in North Dakota.

Those businesses that either did or did not achieve their total sales potential in 1992 areidentified in Step 3. To identify the businesses that may have potential for further growth it isassumed that those businesses that have achieved 70% or more of their expected total sales havereached market saturation and, thus, have no further growth potential. On the other hand, thosebusinesses that have yet to reach at least 70% of their expected sales have unfulfilled demandand, thus, have potential for growth. A ranking of 1 in Step 3 thus implies a market potentialranking of 1, indicating the business category that has the highest market potential.

Location quotient is an additional measure used to supplement the above procedure fordetermining market potential. A common question faced by communities in both rural and urbanareas is what is the level of goods and services currently provided locally and what goods andservices are imported from elsewhere--location quotient ( ) provides an answer to suchquestions. thus is a measure of self-sufficiency of goods or services in a community(Shaffer, 1989). Location quotient is a commonly used tool to identify non-manufacturingindustries for industrial recruitment, which is a popular economic development strategy. Forexample, Doescher et al. (1986) used this tool to identify non-manufacturing industries forindustrial recruitment in Oklahoma.

Location quotient is defined as the ratio of the share of state employment in a particularbusiness category ( ) to the share of national employment in that category:

LQgas. serv. stn. '2,590 / 53,309

675,080 / 19,485,666'1.40.

LQ'1

LQ<1 x(LQ>1)

x

LQ

LQ

LQ

LQLQ>1.25

10

(6)

10

A location quotient of 1 ( ) means that local consumption demand is met through localproduction of specified good or service (Shaffer, 1989). Similarly, a location quotient of lessthan one ( ) means lack of self-sufficiency in good or service , i.e., what is produced oravailable is not sufficient to meet the local demand. A location quotient greater than 1means that the concerned state or community has a larger proportion of its employment inindustry than does the nation or whatever economic aggregate is used as the denominator inequation (5).

Continuing the demonstration, using (5), s for the gasoline service stations categoryare estimated as follows: total persons employed in North Dakota and the United States in thegasoline service stations category, respectively were 2,590 and 675,080 (1992); total retail sectoremployment in North Dakota and the United States in 1990 were 53,309 and 19,485,666,respectively. Thus, using (5), the for gasoline service stations category is

Although location quotient has such shortcomings as assuming identical state andnational demand and supply functions and similar tastes and preferences and income levels, it isa reliable measure of local self-sufficiency (Shaffer, 1989). To reduce the problem ofmisinterpretation of estimated s, a disaggregated 4-digit SIC level data is used in this studyand a lower threshold point is selected to determine self-sufficiency. It is assumed that anestimated in the range 0.75 - 1.25 suggests self-sufficiency while those below 0.75 suggestlack of self-sufficiency, and suggests abundance of that business or service. While lackof self-sufficiency implies potential for new business or possible expansion of existing ones, anabundance of business or services implies market saturation if export is not a principal activity inthat particular business or service category.

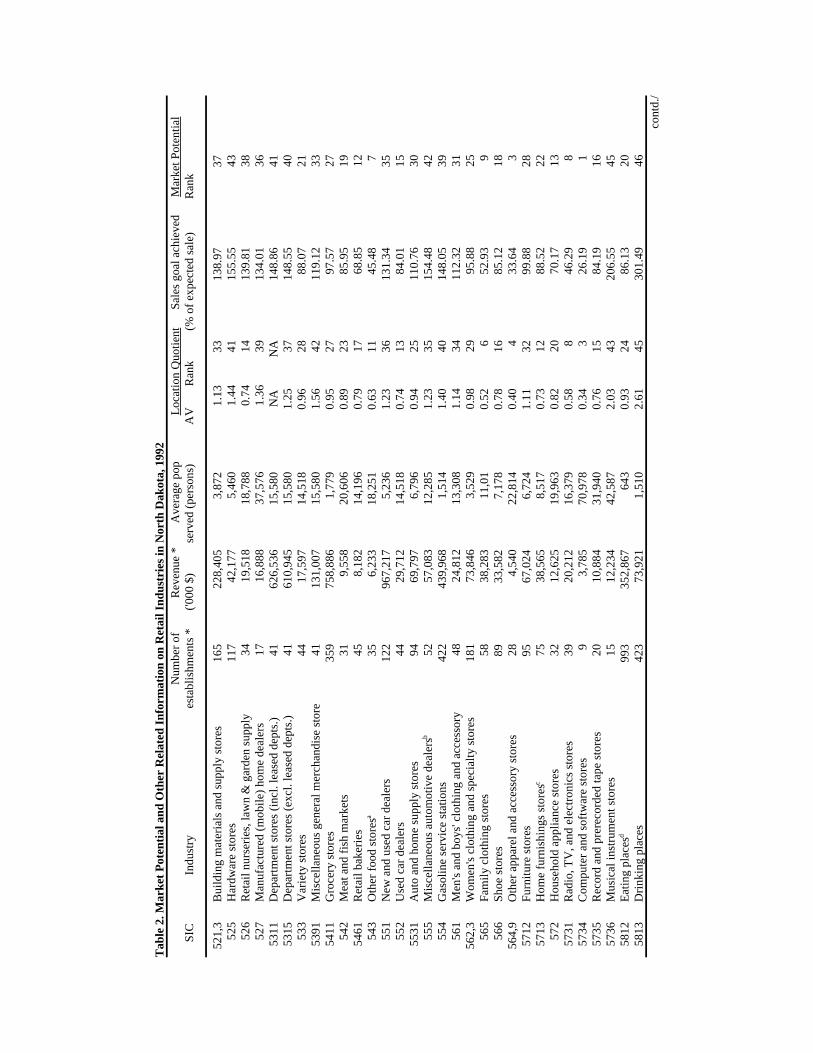

Retail Trade Industries

Retail sector was the second largest provider of employment in North Dakota in 1990(19% of total employment). A list of 48 available retail trades in North Dakota presented inTable 2 shows the number of establishments, sales, average population served, location quotient,and sales goal achieved for each retail business category. Among the retail business categories,the eating places category (for SIC numbers, see Table 2) had the highest number ofestablishments in North Dakota, while the maximum revenue (almost $1 billion) was earned bythe new and used car dealers. On average, existing eating places in North Dakota served 643persons while some other categories catered to several thousand people per establishment, e.g.,mobile home dealers serving over 37,000 people per establishment.

Tab

le 2

. Mar

ket P

oten

tial a

nd O

ther

Rel

ated

Info

rmat

ion

on R

etai

l Ind

ustr

ies

in N

orth

Dak

ota,

199

2

Num

ber

of

R

even

ue *

Ave

rage

pop

L

ocat

ion

Quo

tient

Sal

es g

oal a

chie

ved

M

arke

t Pot

entia

l

S

IC

In

du

stry

e

sta

blis

hm

en

ts *

('0

00

$)

se

rve

d (

pe

rso

ns)

AV

R

an

k

(

% o

f e

xpe

cte

d s

ale

)

Ra

nk

52

1,3

Bu

ildin

g m

ate

ria

ls a

nd

su

pp

ly s

tore

s1

65

22

8,4

05

3,8

72

1.1

33

31

38

.97

37

52

5H

ard

wa

re s

tore

s1

17

42

,17

75

,46

01

.44

41

15

5.5

54

35

26

Re

tail

nu

rse

rie

s, la

wn

& g

ard

en

su

pp

ly3

41

9,5

18

18

,78

80

.74

14

13

9.8

13

85

27

Ma

nu

fact

ure

d (

mo

bile

) h

om

e d

ea

lers

17

16

,88

83

7,5

76

1.3

63

91

34

.01

36

53

11

De

pa

rtm

en

t st

ore

s (i

ncl

. le

ase

d d

ep

ts.)

41

62

6,5

36

15

,58

0N

AN

A1

48

.86

41

53

15

De

pa

rtm

en

t st

ore

s (e

xcl.

lea

sed

de

pts

.)4

16

10

,94

51

5,5

80

1.2

53

71

48

.55

40

53

3V

ari

ety

sto

res

44

17

,59

71

4,5

18

0.9

62

88

8.0

72

15

39

1M

isce

llan

eo

us

ge

ne

ral m

erc

ha

nd

ise

sto

re4

11

31

,00

71

5,5

80

1.5

64

21

19

.12

33

54

11

Gro

cery

sto

res

35

97

58

,88

61

,77

90

.95

27

97

.57

27

54

2M

ea

t a

nd

fis

h m

ark

ets

31

9,5

58

20

,60

60

.89

23

85

.95

19

54

61

Re

tail

ba

keri

es

45

8,1

82

14

,19

60

.79

17

68

.85

12

54

3O

the

r fo

od

sto

res

35

6,2

33

18

,25

10

.63

11

45

.48

7a

55

1N

ew

an

d u

sed

ca

r d

ea

lers

12

29

67

,21

75

,23

61

.23

36

13

1.3

43

55

52

Use

d c

ar

de

ale

rs4

42

9,7

12

14

,51

80

.74

13

84

.01

15

55

31

Au

to a

nd

ho

me

su

pp

ly s

tore

s9

46

9,7

97

6,7

96

0.9

42

51

10

.76

30

55

5M

isce

llan

eo

us

au

tom

otiv

e d

ea

lers

52

57

,08

31

2,2

85

1.2

33

51

54

.48

42

b

55

4G

aso

line

se

rvic

e s

tatio

ns

42

24

39

,96

81

,51

41

.40

40

14

8.0

53

95

61

Me

n's

an

d b

oys

' clo

thin

g a

nd

acc

ess

ory

48

24

,81

21

3,3

08

1.1

43

41

12

.32

31

56

2,3

Wo

me

n's

clo

thin

g a

nd

sp

eci

alty

sto

res

18

17

3,8

46

3,5

29

0.9

82

99

5.8

82

55

65

Fa

mily

clo

thin

g s

tore

s5

83

8,2

83

11

,01

0.5

26

52

.93

95

66

Sh

oe

sto

res

89

33

,58

27

,17

80

.78

16

85

.12

18

56

4,9

Oth

er

ap

pa

rel a

nd

acc

ess

ory

sto

res

28

4,5

40

22

,81

40

.40

43

3.6

43

57

12

Fu

rnitu

re s

tore

s9

56

7,0

24

6,7

24

1.1

13

29

9.8

82

85

71

3H

om

e f

urn

ish

ing

s st

ore

s7

53

8,5

65

8,5

17

0.7

31

28

8.5

22

2c

57

2H

ou

seh

old

ap

plia

nce

sto

res

32

12

,62

51

9,9

63

0.8

22

07

0.1

71

35

73

1R

ad

io,

TV

, a

nd

ele

ctro

nic

s st

ore

s3

92

0,2

12

16

,37

90

.58

84

6.2

98

57

34

Co

mp

ute

r a

nd

so

ftw

are

sto

res

93

,78

57

0,9

78

0.3

43

26

.19

15

73

5R

eco

rd a

nd

pre

reco

rde

d t

ap

e s

tore

s2

01

0,8

84

31

,94

00

.76

15

84

.19

16

57

36

Mu

sica

l in

stru

me

nt

sto

res

15

12

,23

44

2,5

87

2.0

34

32

06

.55

45

58

12

Ea

ting

pla

ces

99

33

52

,86

76

43

0.9

32

48

6.1

32

0d

58

13

Dri

nki

ng

pla

ces

42

37

3,9

21

1,5

10

2.6

14

53

01

.49

46

con

td./

12

Tab

le 2

. con

tinue

d.N

umbe

r of

Rev

enue

*

Ave

rage

pop.

Loca

tion

Quo

tient

Sal

es g

oal a

chie

ved

Mar

ket P

oten

tial

SIC

In

du

stry

est

ab

lish

me

nts

*

(

'00

0 $

)

serv

ed

(p

ers

on

s)

AV

R

an

k

(

% o

f e

xpe

cte

d s

ale

)

R

an

k

59

11

Dru

g a

nd

pro

pri

eta

ry s

tore

s1

76

15

2,9

51

3,6

30

0.8

92

18

9.4

72

35

92

Liq

uo

r st

ore

s1

37

78

,01

84

,66

32

.10

44

17

4.0

44

45

93

Use

d m

erc

ha

nd

ise

sto

res

46

5,0

28

13

,88

70

.62

94

0.3

34

59

4M

isce

llan

eo

us

sho

pp

ing

go

od

s st

ore

s3

35

14

0,7

61

1,9

07

1.0

33

19

6.4

22

6e

59

42

Bo

ok

sto

res

25

10

,09

52

5,5

52

0.5

67

57

.09

11

59

44

Jew

elr

y st

ore

s6

82

8,4

50

9,3

94

0.8

92

19

2.1

02

45

94

3O

the

r m

isc

sho

pp

ing

go

od

s st

ore

s1

79

47

,71

03

,56

90

.94

26

72

.82

14

f

59

61

Ca

talo

g a

nd

ma

il-o

rde

r h

ou

ses

25

25

,03

62

5,5

52

0.4

25

32

.82

25

96

2A

uto

ma

tic m

erc

ha

nd

isin

g m

ach

ine

op

era

tor

11

5,9

91

58

,07

30

.24

14

2.9

06

59

63

Dir

ect

se

llin

g e

sta

blis

hm

en

ts4

12

7,8

49

15

,58

01

.01

30

12

4.1

23

4g

59

8F

ue

l de

ale

rs4

23

0,9

95

15

,21

00

.80

18

10

1.2

62

95

99

2F

lori

sts

89

14

,34

97

,17

81

.26

38

11

3.7

23

25

99

3T

ob

acc

o s

tore

s a

nd

sta

nd

s1

D6

38

,80

0N

AN

AN

AN

A5

99

4N

ew

s d

ea

lers

an

d n

ew

ssta

nd

s3

63

42

12

,93

8N

A2

40

.80

55

99

5O

ptic

al g

oo

ds

sto

re3

08

,97

02

1,2

93

0.8

01

98

4.6

01

75

99

9a

Pe

t sh

op

s1

23

,28

35

3,2

33

0.6

31

05

5.5

71

05

99

9b

Art

de

ale

rs2

D3

19

,40

0N

AN

AN

AN

AN

ote:

(i)

a= in

clud

es fr

uit a

nd v

eget

able

mar

kets

, can

dy a

nd c

onfe

ctio

nery

ven

dors

, dai

ry p

rodu

ct s

tore

s, a

nd m

isc.

food

sto

res;

b=

incl

udes

boa

t dea

lers

, RV

dea

lers

, and

mot

orcy

cle

deal

ers;

c=

incl

udes

SIC

571

3 (f

loor

cov

erin

g st

ores

),57

14 (

drap

ery,

cur

tain

, and

uph

olst

ery

stor

es),

and

571

9 (m

isc.

hom

e fu

rnis

hing

sto

res)

; d=

incl

udes

re

stau

rant

s, c

afet

eria

s, r

efre

shm

ent p

lace

s, a

nd o

ther

eat

ing

plac

es; e

= in

clud

es s

port

ing

good

s st

ore

and

bicy

cle

shop

s; f

= in

clud

es s

tore

sde

alin

g w

ith s

tatio

nery

, hob

by, t

oy a

nd g

ame,

gift

, nov

elty

and

sou

veni

r, lu

ggag

e an

d le

athe

r go

ods,

and

sew

ing

and

need

lew

ork;

g=

incl

udes

furn

iture

, hom

e fu

rnis

hing

, mob

ile fo

od s

ervi

ce, b

ooks

and

sta

tione

ry a

nd o

ther

; (ii)

Loc

atio

nqu

otie

nt o

r se

lf-su

ffici

ency

ran

king

= 1

bei

ng th

e le

ast s

elf-

suffi

cien

t ind

ustr

y/bu

sine

ss.

Tho

se r

anke

d 15

or

high

er a

re s

elf-

suffi

cien

t (i.e

., LQ

> 0

.75)

; (iii

) M

arke

t pot

entia

l ran

king

= 1

impl

ies

high

est m

arke

t pot

entia

l giv

en c

urre

nt n

umbe

ro

f e

sta

blis

hme

nts.

Tho

se r

anke

d hi

gher

tha

n 1

2 a

chie

ved

70

per

cent

or

mor

e of

the

ir m

arke

t po

tent

ial;

(iii)

* =

da

ta fr

om 1

99

2 E

con

om

ic C

en

sus

CD

RO

M,

Bur

eau

of C

ensu

s,

U.S

. D

ep

t. o

f Com

mer

ce;

(iv)

AV

= a

bsol

ute

valu

e, N

A=

info

rmat

ion

not a

vaila

ble

to p

rovi

de a

val

ue, D

= n

ot d

iscl

osed

.

13

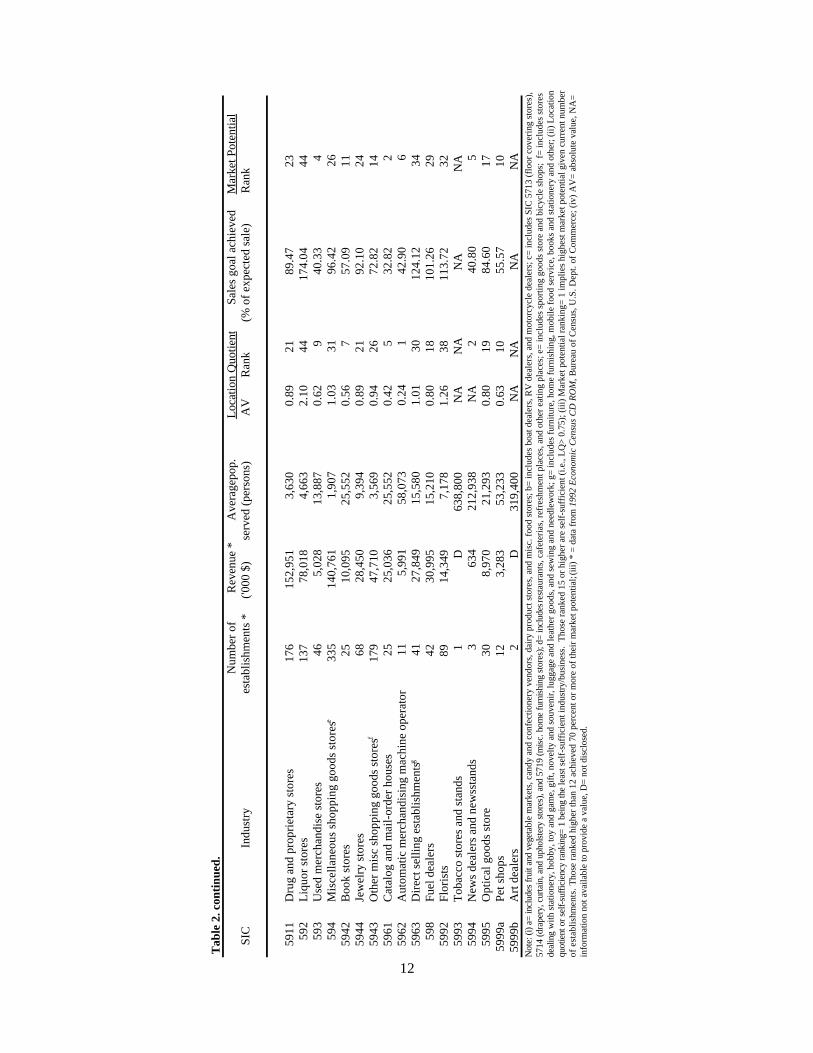

Location quotient or self-sufficiency estimation of retail business categories in NorthDakota ranged from 0.24 in the automatic merchandising machine operators category to 2.61 inthe drinking places category. Among the 48 retail business categories, the state is self-sufficientin those ranked 15 or higher, i.e., their estimated location quotient is greater than 0.75. Thefollowing businesses are ranked among the ten least self-sufficient businesses in North Dakota:news dealers and newsstands; computer and software stores; apparel and accessory stores;catalog and mail-order houses; family clothing stores; book stores; radio, TV, and electronicsstores; used merchandise stores; and pet shops. The existing business establishments in theseretail business categories were unable to fulfill the local/state demand for their respective serviceor merchandise. This also implies that to fulfill the local/state demand, these goods and serviceswere imported from out-of-state sources; customers of these businesses shopped away from thelocal stores.

In terms of the extent of sales goal achieved by the existing establishments andconsequent evaluation of market potential of individual business categories, those retailcategories ranked 12 or higher in Table 2 are considered lacking potential for further growthbecause they already achieved 70% or more of their sales goal. For those business categories forwhich market potential could not be estimated, a potential entrepreneur may conduct moredesegregated market research (e.g., city level) to study their respective business potential. Market potential rankings of retail businesses show that computer and software stores categoryhave the highest market potential in North Dakota, followed by catalog and mail-order houses. Itis likely that the ranking of the catalog and mail-order businesses could be either over- or under-estimated because this business caters to both out-of-state and in-state customers. Other retailbusinesses among the top 10 categories with high potential for future growth are apparel andaccessory stores; used merchandise stores; news dealers and newsstands; automaticmerchandising machine operators; food stores (other than grocery stores, meat and fish markets,and retail bakeries); radio, TV, and electronics stores; family clothing stores; and pet shops.

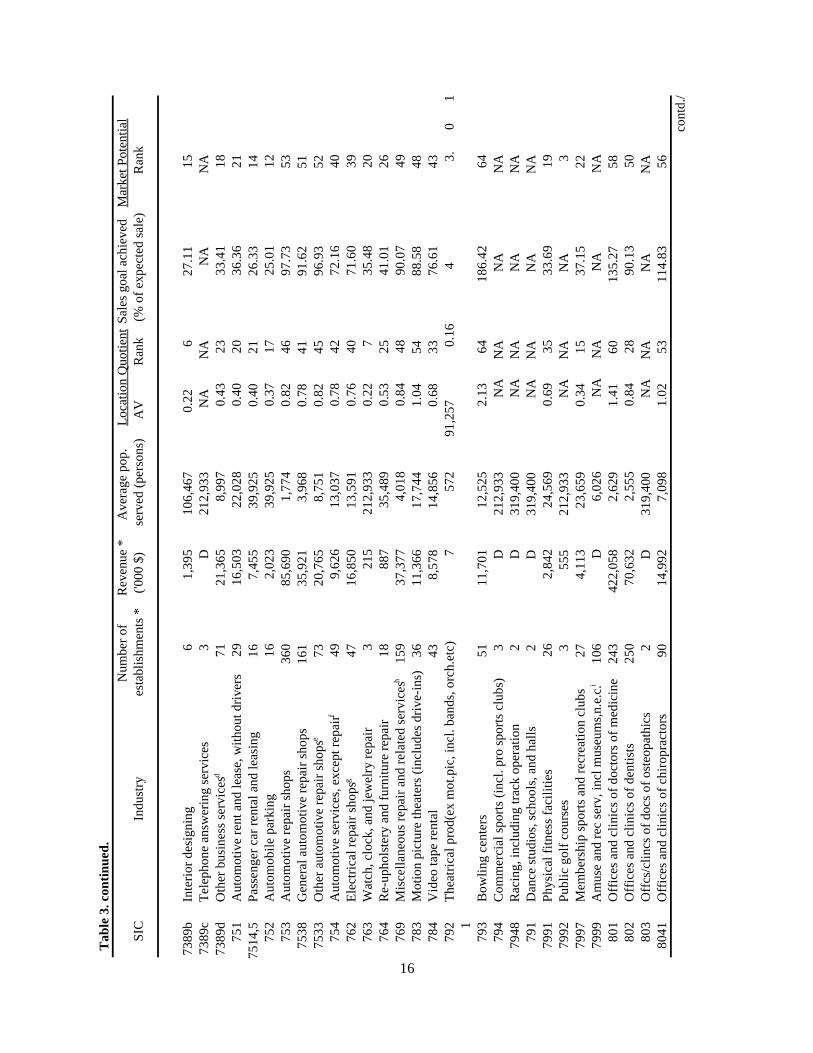

Service Sector Industries

The service sector was the largest employer in North Dakota in 1990 (35% of totalemployment), reflecting a pattern similar to the national average. A list of 88 service categoriesavailable in North Dakota is presented in Table 3. Among the service categories, the maximumnumber of establishments was reported by the beauty and barber shop category (total 369)followed closely by the automotive repair shops (total 360). In terms of earnings, the maximumearning was reported by offices and clinics of doctors of medicine (over $420 million). As in theretail sector, those ranked 38 and higher are considered self-sufficient because their locationquotient was 0.75 or higher. Self-sufficiency rankings show that computer rent/lease andmaintenance services were the least self-sufficient service category in North Dakota in 1992. This kind of service was imported from out-of-state sources to satisfy local or in-state demand.Other services that were identified as lacking self-sufficiency are camps and recreational vehicleparks; personal supply services such as employment agencies; theatrical production; heavy

14

construction equipment rental and leasing services; interior designing; watch, clock, and jewelryrepair services; commercial photography, art, and graphics services; photocopying andduplicating services; and advertising services.

In Table 3, businesses ranked 37 or higher achieved 70% or more of their marketpotential and are considered lacking further growth potential. Among the service businesses forwhich market potential rankings were obtained, computer lease/rent and maintenance servicestops the ranking, indicating it has the highest potential for further growth. Other businesscategories with higher market potentials are public golf courses; heavy construction equipmentrental and leasing; personnel supply services; photocopying and duplicating services; advertising;commercial photography, art and graphic services; computer programming and data processingservices; mailing, copying, photography, and steno services; and management and publicrelations services.

15

Tab

le 3

. Mar

ket P

oten

tial a

nd O

ther

Rel

ated

Info

rmat

ion

on S

ervi

ce In

dust

ries

in N

orth

Dak

ota,

199

2N

umbe

r of

Rev

enue

*

Ave

rage

pop

.

L

ocat

ion

Quo

tient

Sal

es g

oal a

chie

ved

Mar

ket P

oten

tial

SIC

In

dust

ryes

tabl

ishm

ents

*('0

00 $

)

ser

ved

(per

sons

)A

VR

ank

(% o

f exp

ecte

d sa

le)

Ran

k

70

11

aH

ote

ls

69

64

,50

89

,25

80

.86

49

52

.73

32

70

11

bM

ote

ls,

mo

tor

ho

tels

, a

nd

to

uri

st c

ou

rts

16

05

9,7

12

3,9

93

2.6

26

52

30

.60

66

70

2R

oo

min

g a

nd

bo

ard

ing

ho

use

s4

34

41

59

,70

00

.74

37

52

.93

33

70

3C

am

ps

an

d r

ecr

ea

tion

al v

eh

icle

pa

rks

12

1,0

71

53

,23

30

.15

22

8.2

81

67

21

La

un

dry

, cle

an

ing

, an

d g

arm

en

t se

rvic

es

11

92

9,6

35

5,3

68

0.7

63

97

8.3

74

57

22

Ph

oto

gra

ph

ic s

tud

ios,

po

rtra

it5

28

,15

31

2,2

85

0.7

53

81

15

.81

57

72

3,4

Be

au

ty a

nd

ba

rbe

r sh

op

s3

69

33

,27

01

,73

11

.40

59

14

5.7

56

07

25

Sh

oe

re

pa

ir s

ho

ps

an

d s

ho

e s

hin

e p

arl

or

10

85

76

3,8

80

1.6

46

21

40

.86

59

72

6F

un

era

l se

rvic

e a

nd

cre

ma

tori

es

68

23

,20

89

,39

41

.07

55

14

7.2

36

27

29

1T

ax

retu

rn p

rep

ara

tion

se

rvic

es

44

3,0

59

14

,51

80

.79

43

10

7.0

45

47

29

9M

isce

llan

eo

us

pe

rso

na

l se

rvic

es,

n.e

.c.

35

5,3

70

18

,25

10

.61

29

62

.65

37

a

72

99

aD

iet

an

d w

eig

ht

red

uci

ng

se

rvic

es

16

2,8

80

39

,92

50

.91

52

86

.34

46

73

1A

dve

rtis

ing

ag

en

cie

s &

se

rvic

es

(all

typ

es)

28

8,0

96

22

,81

40

.31

10

18

.86

77

32

Ad

just

me

nt,

co

llect

ion

, cre

dit

ag

en

cie

s3

19

,94

42

0,6

06

0.8

75

17

3.2

84

27

33

Ma

ilin

g, c

op

yin

g, p

ho

tog

rap

hy,

ste

no

. se

rv.

43

9,0

05

14

,85

60

.32

12

22

.26

10

73

31

Dir

ect

ma

il a

dve

rtis

ing

se

rvic

es

5D

12

7,7

60

NA

NA

NA

NA

73

34

Ph

oto

cop

yin

g a

nd

du

plic

atin

g s

erv

ice

s5

1,3

92

12

7,7

60

0.2

49

18

.21

67

33

5C

om

me

rcia

l ph

oto

gra

ph

y, a

rt,

an

d g

rap

hic

s1

62

,91

03

9,9

25

0.2

38

20

.32

87

33

8S

ecr

eta

ria

l an

d c

ou

rt r

ep

ort

ing

se

rvic

es

17

D3

7,5

76

NA

NA

NA

NA

73

42

Dis

infe

ctin

g a

nd

pe

st c

on

tro

l se

rvic

es

3D

21

2,9

33

NA

NA

NA

NA

73

49

Bu

ildin

g c

lea

nin

g a

nd

ma

inte

na

nce

se

rvic

es

12

9D

4,9

52

NA

NA

NA

NA

73

52

Me

dic

al e

qu

ipm

en

t re

nta

l an

d le

asi

ng

97

,35