Minda Industries

45

Share price (%) 1 mth 3 mth 12 mth Absolute performance 0.3 20.6 1.8 Relative to Nifty (5.7) 8.6 (4.2) Shareholding Pattern (%) Mar-20 Sep-20 Promoter 70.8 70.9 Public 29.2 29.1 Scenario Analysis Bear case Base case Bull case Console Rev CAGR FY20- FY23 (%) 12.0 15.0 17.0 FY23E EBIDTA Margins (%) 12.0 12.6 13.0 FY23E EPS (Rs.) 12.6 15.3 17.4 Target P/E mutiple (x) 25 30 35 TP (Rs.) 315 460 610 1 Year Stock Price Performance Note: * CMP as on 10 November 2020 Multiple Growth Drivers Justify Premium Valuation Financial Summary Y/E Mar (Rs.mn) FY19 FY20E FY21E FY22E FY23E Net Sales 59,081 54,651 56,522 74,322 83,340 EBITDA 7,252 6,192 5,244 9,043 10,536 EBITDA margin (%) 12.3 11.3 9.3 12.2 12.6 EPS(Rs.) 10.9 6.3 2.1 11.5 15.3 RoE (%) 18.2 9.3 3.0 14.4 16.7 P/E (x) 31.1 54.0 161.8 29.5 22.1 Source: Company, RSec Research f Minda Industries Ltd. (MNDA) is well-diversified auto ancillary company in Indian auto component space with strong presence in lighting, switching, horn and light weight products segments for domestic as well as global original equipment manufacturers (OEMs). f MNDA enjoys leadership in 4W and 2W switches segment with 55% and 65% market share, respectively. It is also the leader in domestic horn segment with ~47% market share, while it has decent presence in lighting segment with ~22% market share. f Its core i.e. switches, lighting and acoustic businesses contribute 37%, 23%, 12% (combined 72%) to its consolidated revenue. Newer product lines comprising of alloy wheels, aluminium die casting, sensors/controllers, which account for the balance 28% of consolidated sales are the real growth drivers, going ahead. It has the largest installed 4W alloy wheel capacity in India and recently started production of 2W alloy wheels. f Newly launched products i.e. Advance Driver Assistance System (ADAS), airbags, filters, sensors and upcoming product lines would help MNDA to outperform the industry despite the current tough time. Incremental revenue from Harita Seating business, addition of sensor plant in FY21, filter business and 2W alloy wheel plant would help the company to improve its revenue over the next 2 years. f Presence across various key product segments of ancillary, new product addition, acquisition of new product segment and technological up-gradation justify premium valuation. ESG Analysis: While analyzing 20 key criteria under ESG Matrix, we have assigned an overall score of 65% to MNDA. Under “Environmental Head”, we have assigned 56% score, as it has sizable power generation through non-conventional (wind and solar) energy sources and various energy efficiency initiative. Under “Social Head”, we have assigned 66% score, as the company scores high on customer satisfaction, despite scoring low on gender diversity. Under “Governance Head”, the company scores fairly well (73%) across criteria (please refer to page no 4. for detailed ESG analysis). Outlook & Valuation Strong rebound in automobile production post a major slump would be key driver for earnings revival, in our view. Moreover higher content, value addition on the back of premiumization, entry into new high-margin segments would be key triggers for MNDA’s earnings and valuation re-rating, going forward. Its consolidated revenue is likely to clock 15% CAGR over FY20-FY23E, while its earnings would clock 35% CAGR over the same period. Considering the multiple positive triggers on revenue and margin front from long-term perspective, we expect the stock’s valuation to steadily move towards the industry’s peak multiple. In light of outperformance despite COVID-led uncertainty and faster-than-expected recovery of auto industry, we initiate coverage on MNDA with BUY and a 2-year Target Price of Rs460, valuing the stock at 30x FY23E EPS), which implies >35% upside from the current level. Head of Research: Mitul Shah Contact: (022) 4303 4628 / 9869253554 Email: [email protected] Research Associate: Sheryl Fernandes Contact: (022) 4303 4628 / 8879415031 Email: [email protected] Click Image for Video Presentation Minda Industries CMP (Rs)* 339 Upside/(Downside) (%) 36 Bloomberg Ticker MNDA IN Market Cap. (Rs bn) 92 Free Float (%) 29 Shares O/S (mn) 272 Automobile | India Institutional Equity Research Initiating Coverage | 11 November 2020 BUY Key Triggers Sustained outperformance with value addition and continued portfolio expansion Premiumization and favourable regulation to expand value-added product offerings Expected strong recovery in 2HFY21E and FY22E Expanding product portfolio and inorganic expansion Valuation expansion to continue for such conglomerates of key auto ancillary segments 2 Year Target Price: Rs.460 We have made changes to our Recommendation and Target Price. Please refer to Page no. 44 at the end of the report. 200 250 300 350 400 450 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Minda Industries

Share price (%) 1 mth 3 mth 12 mth

Absolute performance 0.3 20.6 1.8

Relative to Nifty (5.7) 8.6 (4.2)

Shareholding Pattern (%) Mar-20 Sep-20

Promoter 70.8 70.9

Public 29.2 29.1

Scenario Analysis Bear case

Base case

Bull case

Console Rev CAGR FY20-FY23 (%)

12.0 15.0 17.0

FY23E EBIDTA Margins (%) 12.0 12.6 13.0

FY23E EPS (Rs.) 12.6 15.3 17.4

Target P/E mutiple (x) 25 30 35

TP (Rs.) 315 460 610

1 Year Stock Price Performance

Note: * CMP as on 10 November 2020

Multiple Growth Drivers Justify Premium Valuation

Financial Summary Y/E Mar (Rs.mn)

FY19 FY20E FY21E FY22E FY23E

Net Sales 59,081 54,651 56,522 74,322 83,340EBITDA 7,252 6,192 5,244 9,043 10,536EBITDA margin (%) 12.3 11.3 9.3 12.2 12.6EPS(Rs.) 10.9 6.3 2.1 11.5 15.3RoE (%) 18.2 9.3 3.0 14.4 16.7P/E (x) 31.1 54.0 161.8 29.5 22.1Source: Company, RSec Research

f Minda Industries Ltd. (MNDA) is well-diversified auto ancillary company in Indian auto component space with strong presence in lighting, switching, horn and light weight products segments for domestic as well as global original equipment manufacturers (OEMs).

f MNDA enjoys leadership in 4W and 2W switches segment with 55% and 65% market share, respectively. It is also the leader in domestic horn segment with ~47% market share, while it has decent presence in lighting segment with ~22% market share.

f Its core i.e. switches, lighting and acoustic businesses contribute 37%, 23%, 12% (combined 72%) to its consolidated revenue. Newer product lines comprising of alloy wheels, aluminium die casting, sensors/controllers, which account for the balance 28% of consolidated sales are the real growth drivers, going ahead. It has the largest installed 4W alloy wheel capacity in India and recently started production of 2W alloy wheels.

f Newly launched products i.e. Advance Driver Assistance System (ADAS), airbags, filters, sensors and upcoming product lines would help MNDA to outperform the industry despite the current tough time. Incremental revenue from Harita Seating business, addition of sensor plant in FY21, filter business and 2W alloy wheel plant would help the company to improve its revenue over the next 2 years.

f Presence across various key product segments of ancillary, new product addition, acquisition of new product segment and technological up-gradation justify premium valuation.

ESG Analysis: While analyzing 20 key criteria under ESG Matrix, we have assigned an overall score of 65% to MNDA. Under “Environmental Head”, we have assigned 56% score, as it has sizable power generation through non-conventional (wind and solar) energy sources and various energy efficiency initiative. Under “Social Head”, we have assigned 66% score, as the company scores high on customer satisfaction, despite scoring low on gender diversity. Under “Governance Head”, the company scores fairly well (73%) across criteria (please refer to page no 4. for detailed ESG analysis).

Outlook & ValuationStrong rebound in automobile production post a major slump would be key driver for earnings revival, in our view. Moreover higher content, value addition on the back of premiumization, entry into new high-margin segments would be key triggers for MNDA’s earnings and valuation re-rating, going forward. Its consolidated revenue is likely to clock 15% CAGR over FY20-FY23E, while its earnings would clock 35% CAGR over the same period. Considering the multiple positive triggers on revenue and margin front from long-term perspective, we expect the stock’s valuation to steadily move towards the industry’s peak multiple. In light of outperformance despite COVID-led uncertainty and faster-than-expected recovery of auto industry, we initiate coverage on MNDA with BUY and a 2-year Target Price of Rs460, valuing the stock at 30x FY23E EPS), which implies >35% upside from the current level.

Head of Research: Mitul Shah

Contact: (022) 4303 4628 / 9869253554Email: [email protected]

Research Associate:Sheryl Fernandes

Contact: (022) 4303 4628 / 8879415031Email: [email protected]

Click Image for Video Presentation

Minda Industries CMP (Rs)* 339

Upside/(Downside) (%) 36

Bloomberg Ticker MNDA IN

Market Cap. (Rs bn) 92

Free Float (%) 29

Shares O/S (mn) 272

Automobile | India

Institutional Equity Research

Initiating Coverage | 11 November 2020

BUY

Key Triggers Sustained outperformance with value addition and continued portfolio expansion

Premiumization and favourable regulation to expand value-added product offerings

Expected strong recovery in 2HFY21E and FY22E

Expanding product portfolio and inorganic expansion

Valuation expansion to continue for such conglomerates of key auto ancillary segments

2 Year Target Price: Rs.460

We have made changes to our Recommendation and Target Price. Please refer to Page no. 44 at the end of the report.

200

250

300

350

400

450

Nov

-19

Dec

-19

Jan-

20

Feb

-20

Ma

r-20

Ap

r-20

Ma

y-20

Jun-

20

Jul-2

0

Aug

-20

Sep

-20

Oct

-20

Nov

-20

1

Our ThesisOur Thesis

Key Investment Theme

Key Sectoral Theme

f Domestic 2W & 4W Industry: After sharp plunge due to COVID-19, we expect domestic 2W and PV industry to record CAGR of 16% and 17% over FY21-FY23E, post recording decline of 12% and 7.5% YoY in FY21E, respectively.

f Premiumization & Favourable Regulation: Trend of higher sales of entry-level vehicles during the ongoing pandemic would reverse soon and trend of premiumization would reestablish across vehicle and component segments in terms of value addition. Further, the government regulation has been warranting many new components to be mandatorily fitted in the vehicles.

f Fuel Efficiency & Light Weighting: In order to meet the emission norms and have better fuel efficiency, every OEM is in the race of reducing overall weight of the vehicle by maximizing usage of light weight components.

f After Market Opportunities: In past few years, after market segment has witnessed strong traction for the branded components, particularly post GST implementation, which eliminated many small players from the system.

f Strong Outperformance vs. Industry: MNDA recorded 21% revenue CAGR as against domestic 2W and 4W industry growth of 2% and 1% over FY15-FY20. We expect similar outperformance to continue, going forward on account of value addition and increasing content per vehicle.

f Higher Content & New Products to Drive Profitability: Premiumization trend and favourable regulation would not only drive the revenue but also would expand margin due to entry into high-margin light weight components segment. This would drive 38% earning CAGR over FY21-FY23E.

f New Segment & Aftermarket Business: To mitigate the concentration risk, MNDA has entered into light weight components segment, which has been witnessing strong traction over the years. Further, it entered into new segment through acquisition (Harita Seating). With increasing focus, its aftermarket business is also expected to witness double-digit growth over next 2 years.

Key Risks

f Delayed economic recovery from COVID-led slowdown

f Delayed recovery of domestic and global PV/2W industry

f Pricing pressure from the OEMs

f Split in JVs and/or technology tie-ups with global partners

f Sharp rise in commodity prices

f Adverse government regulation

2

EPS & Target Price

Source: Company, RSec Research

Price Sensitivity AnalysisEPS (Rs) Growth (%) FWD P/E 27.5 30.0 32.5 35.0

FY17 (-3) 6.5 49.3 178 195 211 227

FY18 (-2) 10.7 65.2 29.9 295 322 348 375

FY19 (-1) 10.9 1.6 29.4 299 327 354 381

FY20E (Base Year) 6.3 -42.3 51.0 173 188 204 220

FY21E (Year 1) 2.1 -66.6 152.4 58 63 68 74

FY22E (Year 2) 11.5 447.6 27.8 316 345 374 403

FY23E (Year 3) 15.3 33.2 20.9 421 460 498 536

Source: Company, RSec Research

6.5

10.7 10.9

6.3

2.1

11.5

15.3

195

322 327

188

63

345

460

-

50

100

150

200

250

300

350

400

450

500

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY17 (-3) FY18 (-2) FY19 (-1) FY20E (Base Year)

FY21E (Year 1) FY22E (Year 2) FY23E (Year 3)

EPS (Rs) Target price

Scenario AnalysisRevenue & Margin Sensitivity on Consolidated Earnings

Bear case Base case Bull case

Console Rev CAGR FY20-FY23 (%) 12.0 15.0 17.0

FY23E EBIDTA Margins (%) 12.0 12.6 13.0

FY23E EPS (Rs.) 12.6 15.3 17.4

Source: Company, Rsec Research

Base Case Scenario: In Base Case scenario, we expect MNDA’s revenue to clock 15% CAGR over FY20-FY23E assuming marginally higher growth from new product segment, while FY23E EBITDA margin is pegged at 12.6%. Assigning 30x P/E multiple to its FY23E EPS of Rs15.32, we arrive at a Target Price of Rs460.

Bull Case Scenario: In Bull Case scenario, we expect MNDA’s revenue to clock 17% CAGR over FY20-FY23E with higher growth in OEM production and strong growth in its new product segments, while FY23E EBITDA margin is pegged at 13%. Assigning 35x P/E multiple to its FY23E EPS of Rs17.44, we arrive at a Fair Value of Rs610.

Bear Case Scenario: In Bear Case scenario, we expect MNDA’s revenue to clock 12% CAGR over FY20-FY23E with lower growth in OEM production and lower traction from new product segment, while FY23E EBITDA margin is pegged at 12%. Assigning 25x P/E multiple to its FY23E EPS of Rs12.6, we arrive at a Fair Value of Rs315, which is more or less around CMP, making risk reward favourable for the company.

Price Target Scenario

Target Price (Rs) FY23E EPS Down-Cycle Target Up-Cycle(Rs) Multiple Multiple Multiple

1 Yr Fwd P/E 25 30 35Bear case 12.61 315 378 441

Base case 15.32 383 460 536Bull case 17.44 436 523 610

Source: Company, Rsec Research

3

Key Criteria Score Risk Comments

Management Quality 7 Low The management is capable to manage tough situations across business segments; track record on guidance front has so far been fair

Promoter's Holding Pledge 9 Low Overall promoters’ holding is 71% with zero pledging

Board of Directors Profile 8 LowA perfect blend of experience, expertise and professionalism offers great comfort; MNDA’s total board strength is 7, consisting of 4 independent directors, 1 non-executive director and 2 executive directors

Industry Growth 8 Low Industry (2W and 4W) is expected to witness high double-digit growth over FY21-FY23E

Regulatory Environment / Risk 5 MediumDue to nature of business linked with the OEMs, MNDA has higher issue on environment and regulatory front; however, regulatory changes provide an opportunity for new products/content addition, which are beneficial from long-term perspective

Entry Barriers / Competition 6 Low Competition level is low due to entry barriers for high-quality products

New Business/Client Potential 8 Low The company has been consistently adding business segment as well as new clients; it has a decent potential of expansion through new products / clients

Business Diversification 7 LowBusiness is diversified into lighting, switch, acoustics, LMT and other segments (4W and 2W); it has also developed exports and aftermarket business along with OEM business

Market Share Potential 6 Low Over the years its market share improved gradually with likelihood of further market share gain, going forward

Margin Expansion Potential 7 Low Its margin is expected to contract by 200bps in FY21E and improve by 80bps and 40bps in FY22E and FY23E, respectively

Earning Growth 8 Low EPS is expected to clock 170% CAGR over FY21-23E compared to -33% CAGR over FY17-FY20

Balance Sheet Strength 6 Low Balance sheet is fair enough to manage the current challenging business situation despite some debt on book

Debt Profile 5 Medium Its Debt/Equity ratio is under control; net debt stood at ~Rs8bn as of Sept'20 end

FCF Generation/NWC 5 Medium FCF would remain negative for the next 2 years, while its FCF generation is seen at Rs2bn in FY23E

Dividend Policy 6 Low Though the company pays regular dividend, dividend yield is low; current dividend yield is 0.12%; average dividend payout ratio stood at ~8% over last 3 years

Total Score Out of 150 101

Average Score (%) 67% Low

Investment Decision Matrix (IDM)

4

Key Criteria Score Risk Comments

Environmental

Climate Change and Carbon Emission 3 HighAs MNDA is primarily into manufacturing of vehicle parts, it emits CO2 and creates air pollution, while the end-use of the finished products also emits huge CO2; however, the company has implemented several initiatives i.e. solar power/wind power across plants, which reduce CO2 emission by 65,928T; about 30% of power requirement is met through green/alternative energy

Air & Water Pollution 3 HighAs the company is in the business of manufacturing vehicle parts, it generates sizable pollution. To mitigate water and air pollution associated with its business, the company has waste and effluent treatment plants in place to reduce toxic /emission

Biodiversity 6 Low In its endeavour towards protecting biodiversity, MNDA planted 3,000 trees in FY20

Deforestation 5 MediumAs most of its plants are located in a remote industrial zone since many years, deforestation is not carried out in recent time; moreover it planted 3,000 trees in FY20; the company is constantly expanding its business across various locations including close to the forest areas, which may require deforestation in future

Energy Efficiency 6 LowMNDA has installed (1) 315 KWP solar plant and (2) transparent sheet on roof terrace of shop floor for optimum usage of sunlight during the day time; further, it plans to (1) replace diesel fired burners with PNG burners for powder coating; (2) replace old ACs with new inverter drive energy efficient ACs; and (3) install solar panel in 2022-23

Waste Management 6 LowIts business operations do not create any significant process waste; it recycles the reusable materials and responsibly discards non-usable materials as per applicable statutory provisions

Defence / Arms / Ammunition Exposure 10 Low No exposure to arms and ammunition space

Social

Customer Satisfaction 8 LowThe company is rated high on customer satisfaction in terms of quality, precision and technology; it received several awards from domestic and global OEMs; the company continues to be one of the most preferred auto ancillary suppliers for the OEMs

Data Protection & Privacy 8 Low The company maintains high level of data protection and privacy of customers’ data/details; it follows confidentiality policy

Gender & Diversity 8 Low Out of total 3,895 employees, ~1,050 are permanent women employees (~27%), which is one of the highest in the auto ancillary industry

Employee Engagement 7 LowThe company conducts various employee-engagement programmes i.e. safety training, skill up-gradation, and cultural activities to ensure an employee-friendly environment; it has recognized employee welfare association and union

Community Relations / Service 6 LowThe company is proactive in CSR activities to support community; it spent Rs30mn in FY20 towards CSR activities, which include education and vocational trainings

Human Rights 6 LowIt has proper human rights policy in place, which is applicable to all stakeholders and extended to all JV plants of the group; the stakeholders include: suppliers, contractors, consultants and outsourced employees besides employees and directors of the company

Labour Standard 3 HighThe company follows labour standards in terms of work place, facilities and employee benefits; though it has employee union at its plants, which is recognized by management but only ~4% of permanent employees are members of the recognized employee union, which is very low compared to peers

Environmental Social Governance Matrix (ESGM)

5

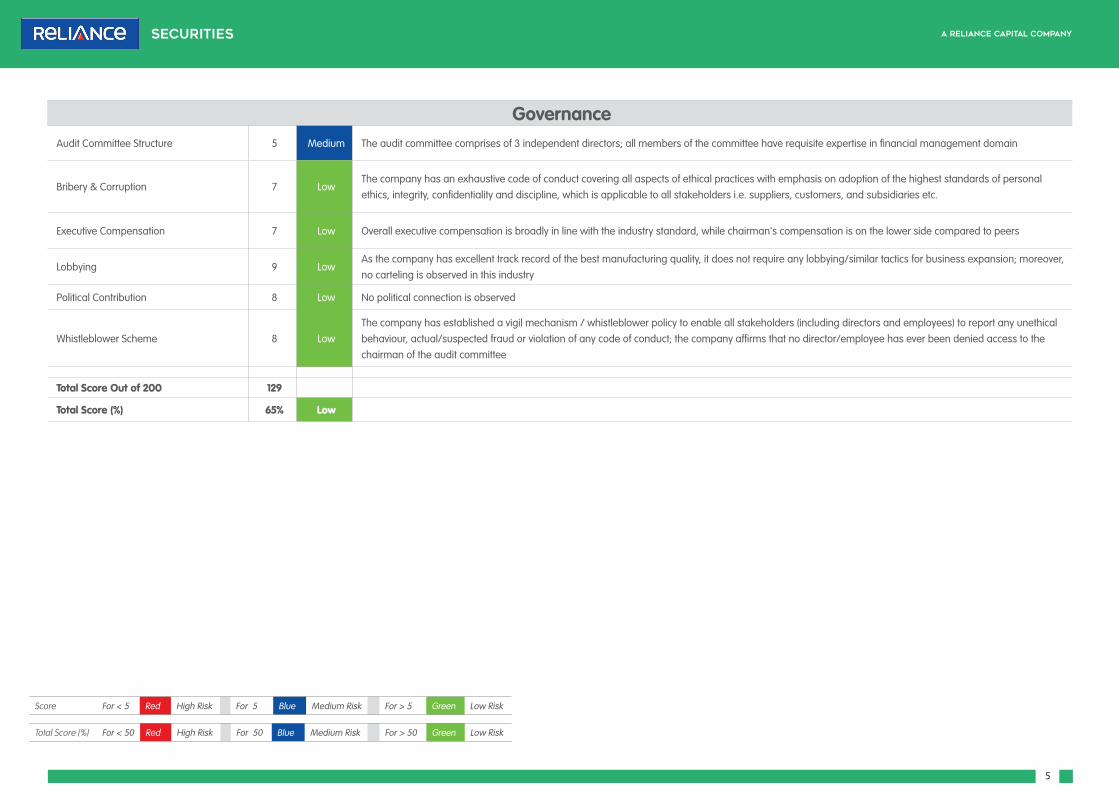

GovernanceAudit Committee Structure 5 Medium The audit committee comprises of 3 independent directors; all members of the committee have requisite expertise in financial management domain

Bribery & Corruption 7 LowThe company has an exhaustive code of conduct covering all aspects of ethical practices with emphasis on adoption of the highest standards of personal ethics, integrity, confidentiality and discipline, which is applicable to all stakeholders i.e. suppliers, customers, and subsidiaries etc.

Executive Compensation 7 Low Overall executive compensation is broadly in line with the industry standard, while chairman's compensation is on the lower side compared to peers

Lobbying 9 LowAs the company has excellent track record of the best manufacturing quality, it does not require any lobbying/similar tactics for business expansion; moreover, no carteling is observed in this industry

Political Contribution 8 Low No political connection is observed

Whistleblower Scheme 8 LowThe company has established a vigil mechanism / whistleblower policy to enable all stakeholders (including directors and employees) to report any unethical behaviour, actual/suspected fraud or violation of any code of conduct; the company affirms that no director/employee has ever been denied access to the chairman of the audit committee

Total Score Out of 200 129

Total Score (%) 65% Low

Score For < 5 Red High Risk For 5 Blue Medium Risk For > 5 Green Low Risk

Total Score (%) For < 50 Red High Risk For 50 Blue Medium Risk For > 50 Green Low Risk

6

Higher Automobile Production: Waning Impact of Covid-19 despite Rising Cases

As given in below table, deterioration due to COVID-led disruptions seems to be waning, as people have accepted it as routine phenomenon for the medium-term. It is visible from the fact that despite rising number of COVID-19 cases, monthly automobile vehicle production has been rising constantly, which almost reverted to pre-COVID-19 level in Aug’20. This also indicates that no further deterioration is expected, while other favourable economic factors like good monsoon, healthy agri output, higher MSP, strong rural economy, pent-up demand from urban markets and improving sentiment across regions would keep automobile volume momentum healthy, going forward.

New COVID cases per day in India

Source: World data

Monthly Production Trend - 2W

Source: SIAM

Monthly Production Trend - PV

Source: SIAM

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

(%)

2W (unit) MoM growth (RHS)

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

(%)

PV (unit) MoM growth (RHS)

7

Table of Key Fundamental Parameters

As indicated in above table, all fundamental factors relating to domestic industry would become favourable over next 2 years and would help MNDA in witnessing healthy earnings growth. This would transform into valuation expansion for the company, going forward.

Key Parameters (%) FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Overall Automobile Sales Growth 4.0 6.6 3.2 7.1 14.5 5.3 -17.7 -12.6 25.2 10.0

Consolidated Rev. Growth 27.3 30.8 13.2 34.0 32.0 32.2 -7.5 3.4 31.5 12.1

PV Production Growth -4.9 4.8 7.6 9.7 5.8 0.2 -14.8 -8.0 25.0 9.0

2W Production Growth 7.2 9.5 1.8 5.9 16.2 5.8 -14.1 -12.0 22.0 10.0

Ratio of Mini-car/PV 21.3 18.9 17.6 16.8 15.1 12.4 9.7 11.0 10.0 11.0

Ratio of SUV/PV 18.4 19.5 20.7 23.9 27.2 27.3 32.8 37.0 37.0 37.0

Ratio of 125CC+ Bikes to total 2W 12.0 13.0 14.0 15.0 15.0 15.0 14.0 14.0 14.0 14.0

LMT Rev. Contribution NA NA NA NA 13.1 15.0 14.0 15.4 15.6 16.0

Acoustic Rev. Contribution 21.0 27.0 22.0 18.2 15.0 12.0 12.0 9.7 9.7 9.5

Consolidated EBIDTA Margin 4.6 6.9 9.4 11.0 11.9 12.3 11.3 9.3 12.2 12.6

Aftermarket Rev. Growth 15.0 25.0 17.4 3.4 11.3 13.7 -2.6 -5.0 30.0 18.0

RoE 2.1 16.3 25.2 21.3 22.7 18.2 9.3 3.0 14.4 16.7

RoCE 2.7 11.4 15.2 14.0 14.9 11.8 6.6 3.9 9.8 11.3

No of Positive Fundamental Parameters out of 13 2 4 6 8 9 10 6 5 13 13

1 Yr Fwd P/E (x) 77.4 9.1 4.7 15.4 9.9 29.4 50.9 152.7 27.8 20.9

Source: Company, Rsec Research NA: Not Available

8

Key Takeaways of Management Commentary

f Whilst MNDA’s domestic and overseas plants are fully operational, they are operating at utilization level of ~75% currently.

f The company commissioned 2 lines of its new projects i.e. 2W alloy wheel and BS-VI sensor in 2QFY21 and is likely to commission another 2 lines by FY21-end. The management foresees promising growth opportunities from these two businesses, going forward.

f Post successful acquisition in Dec’19, Delvis was consolidated for the full quarter in 4QFY20. The company received new orders from Daimler and Audi for its Delvis operations.

f In terms of other businesses, the company has started supply of wheel speed sensor for its Korean customers.

f The final NCLT hearing on merger of Harita Seating Systems is scheduled to be held on 16th Nov, 2020. Whilst all requisite approvals are in place, the merger was delayed due to the COVID-19 pandemic.

f The company received its first order for electronic horn from M&M for PV division. In 2W lighting space, it received new orders from Royal Enfield, E-bikes, TVS, Bajaj and Honda.

f It incurred ~Rs7bn capex in FY20 and plans to spend ~Rs2.5bn routine capex and Rs1.2-1.5bn for subsidiary and associate companies taking overall capex and investment to <Rs5bn in FY21E.

9

Channel CheckIndian PV Companies Management Commentaries/ViewMaruti Suzuki According to the management, the company witnessed a strong start of the festival season led by Onam and Ganesh Chaturthi

in August and positive on coming festivals. However, demand sustainability will depend on overall economic recovery as well as improvement in COVID scenario. It expects some down-trading due to fall in income. In PV segment, lower-end models continued to see the strongest demand, which suggest higher demand from rural areas and middle-class families. The company expects better traction, going forward on the back of rising personal mobility led by the need for social distancing. Enquiry levels and bookings for ongoing festivals are healthy.

Tata Motors As per the management, this year demand (bookings) is going to be significantly higher than last year. And this would be true for the industry, indicating very strong festive demand to kick in. The second big growth driver would be personal mobility, with cars and two-wheelers having gone up in the priority of discretionary spending of people. This will remain a priority purchase for a lot of households. The company expects this to be a sustainable trend for at least a year or so. It has also taken certain proactive actions since two months in anticipation of supply constraints and expects to ramp-up capacity to meet the demand.

M&M With 2-week delay in festive season this year, the company is gearing up to build inventory to meet the festive demand. The company gained market share in LCV segment and it is positive on tractors, SUVs and LCVs, going ahead. The company sees decent positive traction for on going festive season.

Toyota The company stated that there might be a good demand during the festive season particularly from Tier-I-II cities.

Hyundai The company anticipates a positive outlook for the festive season and expects increased demand for personal mobility amid the COVID-19 pandemic to further enhance sale prospects for passenger vehicle industry. In order to cater to the expected increase in demand, the company is ramping up production.

2 Wheeler Cos

Bajaj Auto As the supply chain continues to remain very fragile, the focus is on ramping up capacity and meeting demand. Currently, demand stands at ~90% level as compared to the same period last year.

Hero MotoCorp The company stated that the inquiries and call trends are very encouraging and they are confident of a good festive season. It also stated that semi-urban and urban also are catching up and this wave of growth is not going to end. It further indicated that the positivity would continue, going forward.

HMSI The company expects demand to improve during upcoming festive period, which will support retail sales further. Along with the pent-up demand, the company is seeing new customers who are moving away from public transport to personal mobility. Launch of couple of new products and upgrades from BS-IV to BS-VI have been helping the company to gain additional traction.

Source: Company

10

Comparative AnalysisMinda Industries Minda Corporation Varroc Engineering Motherson sumi Systems

Business Minda Industries is a leading multi-product auto ancillary with a diversified presence across industry segments and products. It primarily caters to 2W and PV segments. Its major product include: Switching, Lighting, Acoustics and Light Weight Products.

Minda Corporation is a diversified automotive components maker catering all automobile segments. Its product portfolio includes: Safety, Security, Restraint Systems, Plastic Interior Systems and Driver Information & Telematics Systems for auto OEMs across the globe.

Varroc is a global Tier-I automotive component group. It designs, manufactures and supplies exterior lighting systems, plastic/ polymer components, electrical-electronics components and precision metallic components. It caters primarily to PVs, CVs and 2Ws with some presence in off-highway vehicle OEMs.

Motherson Sumi Systems is a specialised full-system solutions provider. It caters to a diverse range of customers in automotive industries across Asia, Europe, North America, South America, Australia and Africa. The company primarily caters to PV segment. It has a strong presence in wiring harnesses, mirrors and plastics comprising cockpits, bumpers, interior trim.

Manufacturing Facilities

It has 62 manufacturing facilities globally.

It has 28 manufacturing facilities in India and 2 manufacturing facilities in South-East Asia.

It has 16 global manufacturing facilities and 26 manufacturing facilities for India business.

It has 41 new plants (16 Greenfield and 25 Brownfield)

Annual Turnover

Rs72bn (Group turnover), while MNDA’s turnover is Rs54.6bn

Rs28bn Rs23bn Rs626bn

Key Clients Bajaj Auto, BMW, Daimler, Hero MotoCorp, Audi, Honda Motorcycle and Scooter India, Hyundai, M&M, Maruti Suzuki, Suzuki Motorcycle, TVS Motor, Tata Motors, Volkswagen, Yamaha Motor and Renault etc.

Ashok Leyland, Bajaj Auto, CNH, Daimler, Hero MotoCorp, Honda Motorcycle and Scooter India, Hyundai, M&M, Maruti Suzuki, Suzuki Motorcycle, TVS Motor, Tata Motors, VE Commercial Vehicles, Volkswagen and Yamaha Motor etc.

Bajaj Auto, Honda, Royal Enfield, Yamaha and M&M etc.

Audi, Mercedes Benz, Volkswagen, Ford, BMW, Maruti Suzuki, Renault, Daimler, Hyundai, GM and Paccar etc.

Revenue Break-up

Switch: 37%Lightings: 23%Acoustics: 12%LMT: 14%Others: 14%

Mechatronics: 46.4%Information & Connected Systems: 33.5%Plastics & Interiors:20.1%

Lightings; 60.4%Polymer: 15.7%Electrical: 12%Metallic: 16.9%Others: 5%

Modules & Polymer Products:55%Wiring Harness: 25.3%Vision System: 19.4%Others: 0.3%

Specialty The company is aggressively progressing in new segments of LMT, sensors and controllers.

The company is a specialist in Mechatronics segment with strong presence in domestic and global markets.

The company is a specialist in lighting system with strong presence in domestic and global markets.

The company is a specialist in plastics / polymers and mirror segment in global markets, while it is the leader with strong presence in wiring harness in domestic markets.

Management The management is very strong and capable to manage uncertain situation.

The management’s capability is not as high as Minda Industries and past track record of guidance is also not very impressive.

The management is better than the average but not as strong as Minda Industries.

The management is very strong and capable to manage uncertain situation.

Financials (Rs Mn) FY19 FY20 FY19 FY20 FY19 FY20 FY19 FY20

Minda Industries Minda corporation Varroc Eng Motherson sumiRevenue 59081 54651 30920 28131 120365 111219 635229 635368

EBITDA 7252 6192 3751 175 11810 9105 56817 54895

PBT 4,547 2,522 2361 -1544 5185 395 32003 21129

PAT 2856 1550 1692 -1998 4287 25 20981 12945

Adj PAT 2856 1647 1575.1 -42.8 4217 -8 16071 11677.5

Growth (%)Revenue 32.2% -7.5% 19.2% -9.0% 17.1% -7.6% 12.8% 0.0%

EBITDA 35.8% -14.6% 23.0% -95.3% 19.5% -22.9% 8.2% -3.4%

PBT 12.1% -44.5% 23.4% -165.4% 0.5% -92.4% -2.0% -34.0%

Adjusted PAT 1.6% -42.3% 9.2% -102.7% -6.3%s -100.2% -6.6% -27.3%

Margin (%)EBITDA Margin 12.3% 11.3% 12.1% 0.6% 9.8% 8.2% 8.9% 8.6%

NPM 4.8% 3.0% 5.1% -0.2% 3.5% 0.0% 2.5% 1.8%

Source: Company;RSec Research

11

Key ChartsExhibit 1: PV Volume growth vs. MNDA’s PV Revenue growth

Source: SIAM, RSec Research

Exhibit 2: 2W Volume growth vs. MNDA’s 2W Revenue growth

Source: SIAM, RSec Research

Exhibit 3:EBIDTA Margin Trend

Source: Company, RSec Research

Exhibit 4: Premium P/E Valuation to Continue

Source: Company, RSec Research

f PV segment is non-cyclical industry, which records growth during most fiscals.

f Long-term average industry growth is 11%.

f During positive economic situation, it records a decent double-digit growth of 12-25%, while during slowdown, it records either lower or flat growth except for 1-2 occasions.

f MNDA’s PV segmental revenue outperformed the industry by 18% over FY15-FY20.

f We expect the PV industry to witness strong bounce-back in FY22E and FY23E.

f 2W is non-cyclical industry, which records decent growth during most fiscals.

f Long-term average industry growth is 8.5%.

f During positive economic situation, it records a decent growth of 12-18%, while during slowdown, it records lower growth of 2-5% except for 1-2 occasions.

f MNDA’s 2W segmental revenue outperformed the industry by 12% over FY15-FY20.

f We expect 2W industry to witness strong bounce-back in FY22E and FY23E.

f MNDA’s EBIDTA margin has expanded gradually to double-digit over the years.

f The company has decent pricing power with higher focus on high-margin products.

f MNDA’s margin would expand on account of increasing contribution of new segments, majority of which enjoy higher margin.

f MNDA’s long-term average 1-year forward P/E was lower due to lower RoE, while its P/E would expand with increasing return from the high-margin segments.

f Higher earnings CAGR of 35% over FY21-FY23E justifies premium valuation.

f Continuous outperformance vs. the industry warrants valuation expansion.

Exhibit 5: Product-wise Revenue Break-up & Segmental Revenue Break-up

Source: Company

f MNDA has diversified its revenue segments across product categories i.e. Switches, Lights, Acoustics, Light Metal Products and other smaller segments.

f Balanced revenue across 2Ws and PVs also supports de-risking.

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000

30,00,000

35,00,000

40,00,000

45,00,000

2015 2016 2017 2018 2019 2020

PV (unit) YoY growth (RHS) MNDA PV Rev. growth (RHS)

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

50,00,000

1,00,00,000

1,50,00,000

2,00,00,000

2,50,00,000

3,00,00,000

2015 2016 2017 2018 2019 2020

2W (unit) YoY growth (RHS) MNDA 2W Rev. growth (RHS)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23

EBITDA (Rs Mn) EBITDA Margin (RHS)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

Date

May

-10Au

g-10

Nov-

10Fe

b-11

May

-11Au

g-11

Nov-

11Fe

b-12

May

-12Au

g-12

Nov-

12Fe

b-13

May

-13Au

g-13

Nov-

13Fe

b-14

May

-14Au

g-14

Nov-

14Fe

b-15

May

-15Au

g-15

Nov-

15Fe

b-16

May

-16Au

g-16

Nov-

16Fe

b-17

May

-17Au

g-17

Nov-

17Fe

b-18

May

-18Au

g-18

Nov-

18Fe

b-19

May

-19Au

g-19

Nov-

19Fe

b-20

May

-20

Close -Unit Curr 28x 15x 20x 25x 30x

12

Investment RationaleOur investment thesis is based on the following premises:

1. Strong Presence across Product Offerings with Sustained Segmental Leadership

2. Multiple Technological Tie ups & Strong R&D Capabilities

3. Strong Long-term Relationship with Major OEMs Bodes Well

4. Premiumization Trend & Favourable Regulatory Measures to Drive Growth

5. Rising Opportunities in High-margin New Product Segments

6. Continued Focus on Aftermarket

7. Successful Acquisition Strategy to Drive Revenue

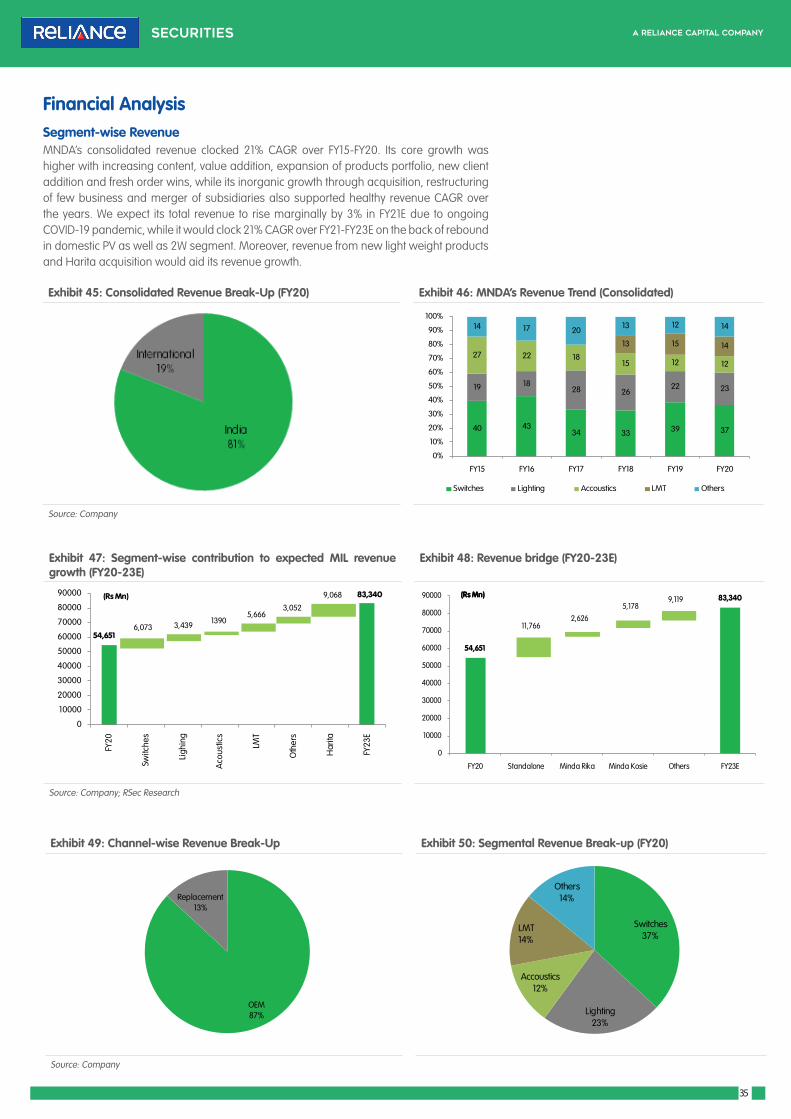

I. Strong Presence across Product Offerings with Sustained Segmental Leadership Minda Industries (MNDA) is a leading multi-products auto ancillary company with a diversified presence across industry segments. Over the years, it has demonstrated excellent foresight in entering into diverse product lines. It has evolved as a Tier-I supplier to various auto components with solutions for most major Indian OEMs across 4W and 2W segments.

It is the largest manufacturer of 2W switches, 4W switches and automotive horns and has the largest installed alloy wheel capacity in India. MNDA’s core businesses i.e. switches, lighting, acoustics form 37%, 23%, 12%, (combined ~72%) of its consolidated sales. It enjoys leadership position across segments with higher market share, which helped its outperformance vs. the industry over the years.

Exhibit 7: Product wise Revenue Break-up

Source: Company Source: Company

Exhibit 6: Consistent outperformance across segments vs. OEM industry led by higher content/vehicles

Source: Company

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

FY15 FY16 FY17 FY18 FY19 FY20

2W Production volume growth PV Production volume growth

MNDA 2W Rev. growth MNDA PV Rev. growth

13

Exhibit 9: Segment wise contribution to MIL revenue growth in FY15-20

Source: Company; RSec Research

Exhibit 10: MNDA: Among the top players in each segment (FY20)Component Segment Remarks

Switch 4W #1 player with 55% market share

2W #1 player with 65% market share

Horns 4W #1 player with 40% market share

2W #1 player with 47% market share

Lights 4W #3 player with 13% market share

2W #3 player with 27% market share

Air Bags 4W #2 player with 25% market share

Alloy Wheels 4W #1 player with 45% market share

Air Filters 4W #2 player

Source: Company

The company commands 55% and 65% market share in 4W and 2W switches, respectively, ~22% in lighting, ~47% in horns in domestic market. It has the largest installed 4W alloy wheel capacity in India. Its newer product lines i.e. alloy wheels, aluminium die casting, sensors/controllers, air bag, infotainment system (28% of consolidated sales) are the key growth drivers, going ahead. The company is largely a domestic-focused play with its India business accounting for ~81% of its consolidated revenue..

Exhibit 8: Product segment wise revenue break-up

Source: Company

11344 1475323042 20221

958311579

1299812570

6163

6706

70906558

3950

5856

88627651

2823

5812

70907651

0

10000

20000

30000

40000

50000

60000

70000

FY17 FY18 FY19 FY20

Switches Lighting Acoustic LMT Others

44,706

54,651

33,863

59,081

(Rs Mn)

22,320

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

FY15

Switc

hes

Light

ings

Acou

stics LM

T

Oth

ers

FY20

Switc

hes

Light

ings

Acou

stics LM

T

Oth

ers

FY23

E

11,293

8,329 5327,651 4,526

6,073 3,439 1,390

5,666 3,052

54,651

83,340(Rs Mn)

14

Exhibit 12: Group product portfolio - 4W

Source: Company

Exhibit 11: Group product portfolio - 2W

Source: Company

15

Exhibit 13: Product portfolio and clientele

Source: Company

16

Exhibit 15: Switch EBITDA and Margin Trend Exhibit 16: Key Clients (FY20)

Source: Company; RSec Research Source: Company

Switches: MNDA is the largest automotive switch player in India (4W and 2W) and the largest 2W switch manufacturer worldwide by volume. The segment is the company’s oldest and largest and contributes ~37% to its total revenue. Its 4W products include: switches for audio, cruise, door lamp, HVAC, power window, mirror, panel and lever combination etc. The 2W products include: switches for handlebar assemblies, CBS, off-road, noise suppressor caps and other customized switches.

The company serves the 4W segment through subsidiary i.e. Mindarika (MNDA has 51% stake, rest with Japanese partner Tokai Rika), while the 2W switch business is a standalone entity. It focuses on development of cost-effective and advanced solutions i.e. tactile switching technology, smart switch system, integrated blinker with hazard switching system, winker with flasher and engine stop with start. It has its own independent in-house R&D and also a design office in Japan to design and develop latest switching solutions. The company has 5 plants in India and 1 each in Indonesia and Vietnam. In addition to Mindarika, the company had another subsidiary i.e. Minda Auto Component (MACL), which was merged with the standalone business in FY20. However, the company has 2 other foreign subsidiaries in switching division i.e. (1) Minda Industries Vietnam Company Pvt. Ltd. (which caters to domestic customers in Vietnam and few other countries) and (2) PT Minda ASEAN Automotive, which caters to domestic customers including Yamaha, Toyota, Honda, Suzuki, Kawasaki and Nissan. Overall switch division exports to the USA, France, Italy, Austria and others countries, which accounts for ~6% of total switch sales.

Exhibit 14: Switch Revenue Trend

Source: Company; RSec Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

500

1000

1500

2000

2500

3000

3500

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Mn) EBITDA Margin (RHS)

-30.0%-20.0%-10.0%0.0%10.0%20.0%30.0%40.0%50.0%60.0%

0

5000

10000

15000

20000

25000

30000

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Revenue (Rs Mn) YoY growth (RHS)

40% 43% 34%

% of overall revenue

33% 39% 37% 32% 32% 32%46%

17

This business clocked ~17% revenue CAGR over FY14-FY20 outperforming the auto sales over the same period. Operating margin for the business has improved by 190bps from 8% % in FY14 to 9.9% in FY20. The growth in this segment is led by growth in auto production and higher premiumization. The company has been able to grow faster than the industry by taking advantage of technology evolution for ease of riding, e.g. climate control and transition from manual to automatic. The company has a strong relationship with at MSIL and Toyota in 4W and Bajaj Auto, TVS Motor and HMSI in the 2W space. Though the current uncertainty is expected to weigh on the near-term prospects for the switching division, we expect the company to return to positive growth territory and continue to grow faster than the industry in the forward years.

BS-VI transition – which has led to sizable increase in switching and sensor content – is expected to augment MNDA’s switching revenue over the medium-term despite current sluggish volume. MNDA’s content per vehicle ranges between Rs4,000-12,000/vehicle in 2W space and Rs445-1,40,800/vehicle in 4W space. While the overall demand could be impacted by several factors i.e. COVID-19 and overall slow pick up in the automotive market, MNDA will continue to inch up with its content per vehicle owing to BS-VI transition and safety norms.

We expect this segment to decline by 12% in FY21E and witness 21% CAGR over FY21-23E. We estimate its EBIDTA margin to improve by 260bps to 12.5% over FY20-FY23E.

Lighting: The lighting business is MNDA’s second oldest product segment, which contributed ~23% to its consolidated revenue in FY20. MNDA is India’s third largest automotive lighting player with ~13% market share in 4W space and ~27% market share in 2W space (overall market share of ~22%). It has a design centre in Taiwan and technical arrangement with AMS Company, Korea.

Acquisition of Rinder Group in Spain (2016) for €5mn benefitted the company significantly, as Rinder is the pioneer in technology relating to automotive LED lighting. Its expertise on the lighting front from design to aftermarket is backed by R&D facilities in India (for PV), Spain (for 2W) and Taiwan (including design centre). Whilst this segment witnessed strong organic growth, acquisition of Rinder pushed MNDA to a higher orbit (Minda-Rinder currently accounts for ~50% of overall lighting segment at the consolidated level. Acquisition of Rinder boosted MNDA’s competitiveness in the premium lighting space especially in LED lighting space given its technological support. In FY20, the company merged its Rinder business with the standalone entity. Acquisition of of Germany-based Delvis in 2019 is set to further complement MNDA’s competitiveness in lighting division particularly in PV headlamps with recent new annual orders of worth Rs1bn from 2 large OEMS. MNDA aims to leverage Delvis’ technological, design and R&D capabilities as well as its presence with global 4W OEMs like Volkswagen, Audi and Skoda. The content per vehicle for lighting ranges between

Exhibit 17: Lightings Revenue Trend

Source: Company; RSec Research

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

02000400060008000

1000012000140001600018000

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Revenue (Rs Mn) YoY growth (RHS) % of overall revenue

14% 19% 18% 28% 26% 22% 23% 20% 20% 20%

18

Exhibit 18: Lighthings EBITDA and Margin Trend Exhibit 19: Key Clients (FY20)

Source: Company; RSec Research Source: Company

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

200

400

600

800

1000

1200

1400

1600

1800

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Mn) EBITDA Margin (RHS)

Going forward, we expect the overall prospects of lighting division to remain strong due to increasing LED penetration and market share gain from the peers in non-LED segment. Currently, LED penetration stands at 30% in 4Ws and 45-50% in 2Ws, which we expect to reach to 75% in 4W and ~95% in 2W space over next 3-4 years. Given low heat emission and higher energy efficiency, LED lights have much longer life vs. the conventional halogen lamps, which has resulted in more vehicles getting equipped with LED lights. Moreover, the value of LED lighting is >2x compared to that of halogen, which indicates a sharp rise in content per vehicle. MNDA, with diversified presence in 2W/4W LED lighting space, stands to gain further market share, going forward. Recently, it has won new orders for supplying 2W headlamps to TVS’ (for Qute electric scooter) and LED headlamps for Honda’s Dio. Within 4W, it has secured large orders from Maruti and Toyota for supplying headlamps and tail lamps.

We expect this segment to clock 21% CAGR over FY21E-23E, post recording 14% decline in FY21E. We expect segmental EBIDTA margin to expand by 280bps to 10.5% over FY20-FY23E.

Acoustics: Acoustics i.e. automotive horns form ~12% of MNDA’s consolidated revenue. The company is India’s largest player in this segment (with 47% market share) and also the second largest player globally. It has strong in-house R&D capabilities developed with FIAMM, Italy. After acquiring Spain-based Clarton Horns in 2013, MNDA became the sec-ond largest global player. Clarton has the technology for electronic horns in Europe, which can be eventually introduced in India as well. It manufactures electronic automotive horns, trumpet horns and disc horns for PVs, 2Ws, CVs and other vehicles. Acquisition of Clarton Horns significantly expanded MNDA’s scale in the segment. Clarton chiefly serves leading European PV OEMs and contributes around two-third of current segmental revenues. The Indian acoustics business caters equally to PV and 2W segments.

Currently, MNDA has plants in Manesar and Pantnagar with installed capacity of 36mn and supplies to all major OEMs i.e. Maruti Suzuki, Bajaj Auto, TVS Motor, Royal Enfield, Ya-maha and M&M. Acoustics division has clocked 2% CAGR over FY17-20 despite flattish vol-ume recorded by the OEMs. However, revenue growth was impacted by muted demand in Europe owing to World harmonized Light-duty vehicles Test Procedure (WLTP) norms, which came into effect in 2018 and thus had an impact on MNDA’s acoustics division. Content in-crease in this segment is driven by shift from mechanical horns to electro-mechanical and electronic horns. Major global/domestic clients for the division include: BMW, Volkswagen, Daimler and Audi, Maruti Suzuki, Bajaj Auto, Tata Motors, Hyundai and Honda Motorcycles.

19

Exhibit 21: Acoustics EBITDA and Margin Trend Exhibit 22: Key Clients (FY20)

Source: Company; RSec Research Source: Company

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0

100

200

300

400

500

600

700

800

900

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Mn) EBITDA Margin (RHS)

Exhibit 20: Acoustics Revenue Trend

Source: Company; RSec Research

While the acoustics division would support MNDA’s overall performance in coming years in absolute terms, we expect the growth rate to be relatively slower largely on account of significant presence in slow-growing European markets.

We expect this segment to clock 20% CAGR over FY21E-23E, post recording 16% decline in FY21E. We expect EBIDTA margin to expand by 280bps to 10% over FY20-FY23E.

Sensors, Actuators & Controller (SAC): With the acquisition of iSYS, MNDA entered into controllers business, which comprises of body control for door closure, gate closure and pinch technology etc. Further, MNDA also has presence in controllers for CV segment (with acquired technology from KPIT), which will be used for application in the buses and cabs, where AIS 140 has become mandatory. Sensor content in a car is likely to rise rapidly, as the vehicles become more intelligent and autonomous. MNDA is one of the early entrants in this segment (started in 2005). It supplies start stop sensors, contact and non-contact type speed sensors, HID ballast, tyre pressure monitoring system (TPMS), electronic accelerator pedal module (EAPM), DC-DC converter, and head lamp leveling motors etc.

In order to enhance its expertise in this division, MNDA also entered into tie-up with US-based Sensata Technologies and telematics division of KPIT.

Sensors from Sensata: MNDA entered into an agreement with US-based Sensata Technologies in 2018 for high-end sensors for BS-VI vehicles. This includes acquisition of magnetic speed and position sensors and sharing of technology support for 5 years. Sensata is exposed to a wide range of sensors used in different industries and in the automotive business. It manufactures sensors for engines, transmission, tyre pressure monitoring, air conditioning and electronic stability. Whilst MNDA imports high-temperature sensors, high-end sensors for pressure, BS-VI compliant engine and crank sensors, it has also started manufacturing few sensors in India in its endeavour to localize sensor production to a greater extent.

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

0100020003000400050006000700080009000

FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Revenue (Rs Mn) YoY growth (RHS)% of overall revenue

22% 18% 15% 12% 12% 10%10% 10%

20

Controllers: MNDA acquired Germany-based iSYS RTS for €5mn (for 80% stake) in Jul’18, which specializes in electronic control units (ECUs) for automotive body and control systems and software components for automotive lighting, interior lighting, electrical drive ECUs, HMI and infotainment applications. MNDA plans to localize this technology and offer it to existing clients.

Telematics: MNDA has also acquired KPIT’s telematics hardware business for Rs250mn in Jan’19. The products included vehicle telematics system i.e. AIS 140, On Bus Integrated Telematics Systems OBITS, and products for school buses.

MNDA enjoys competitive advantage over global peers owing to cost advantage of (~20-25%) led by localization. The management targets to achieve market share in the excess of 30%. This segment contributed ~2% to total revenue in FY20. We estimate its share would jump to ~7% by FY23E. Segmental EBITDA margin is likely to be higher than the company’s average, which would positively impact its overall margin. The company expects addressable market size of controllers and sensors would be ~Rs10-15bn and targets to achieve ~30% market share, as the overall market is expected to reach ~Rs18-20bn over next 2 years. Currently, controller is imported into India in the absence of ability for manufacturing the same locally by any major auto ancillary company. MNDA sees an opportunity in controller manufacturing, which would be mutually helpful for both the OEMs and MNDA.

Infotainment Systems: In-vehicle infotainment systems are likely to see incremental demand led by premiumization, as the customers prefer mid-to-high-end variants over entry-level variants. Broadly, the penetration of infotainment system as OE fitment is ~100% in sedan and higher segment cars but significantly lower in entry level cars (20-30% only) and hatchback (~45%). Thus, we expect penetration of infotainment systems in the entry segment cars to rise to ~50% over the next few years with rising premiumization trend. These systems cost from ~Rs4k for entry models to ~Rs15k for higher-end models. It has a JV with Denso Ten of Japan, which is one of the key manufacturers of infotainment products. The JV has an integrated design, development and localized manufacturing plant of car infotainment systems with products i.e. audio visual navigation (AVN), display audio, CD tuner, rear view camera, speakers and antenna amplifier. These products are marketed by another JV i.e. Minda D-ten. MNDA has 2 JVs – manufacturing is done in a 49% JV (Denso-ten Minda) while marketing is done in 51% JV (Minda D-ten). Minda Onkyo is a 50% JV with Onkyo Japan, and supplies speakers to Denso-ten, aftermarkets and exports.

Light Metal Technology (LMT): Since FY19, MNDA started reporting LMT as an individual segment, as revenue/profitability of this segment started contributing meaningfully. MNDA entered into LMT business with 30:70 JV with Kosei aluminum in Dec’10. This subsidiary manufactures alloy wheels and precision aluminum die casting parts majorly for Toyota with no major contribution in overall segment. In 2011, MNDA established MJ casting for die casting components for the 2W OEMs i.e. HMSI, TVS Motor and Wabco India. MJ casting operates two plants in India (1 each in Hosur and Bawal). This business was merged with the standalone entity in FY20. In Feb’15, MNDA established a JV with Kosei Aluminum Co. and started alloy wheel manufacturing in May’16. Minda Kosei Aluminum wheels (MKAW) is the market leader in PV segment with 45% market share and supplies to the 4W OEMs i.e. MSIL, M&M, RNA, Nisaan and Honda cars etc. MNDA has also set up a plant for 2W alloy wheels in FY21 and expects a huge demand for the same (as import substitute) over next

Exhibit 23: LMT Revenue Trend

Source: Company; RSec Research

-40%-20%0%20%40%60%80%100%120%140%

0

2000

4000

6000

8000

10000

12000

14000

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Revenue (Rs Mn) YoY growth (RHS)

13% 15% 14% 15% 16% 16%

% of overall revenue

21

Exhibit 24: LMT EBITDA and Margin Trend Exhibit 25: Key Clients (FY20)

Source: Company; RSec Research Source: Company

The 2W industry is expected to grow in higher single-digit in the long-term, while premiumisation would lead to double digit growth for MNDA’s 2W business over next 3-4 years. Alloy wheel penetration currently stands at ~80%, which we expect to reach to 95% over next 2-3 years. While major chunk of 2W alloys are imported currently, MNDA sees huge potential for local manufacturing with a dedicated plant, which has already started production at the end of 2QFY21 with major customer being Bajaj Auto.

Overall LMT business contributed ~14% to MNDA’s consolidated revenue in FY20 with EBITDA margin of ~26.7% (the highest in MNDA’s business segments).

Other Products: We believe that focus on value creation within the business through technology led inorganic growth and systematic realignment of businesses has helped MNDA so far. We expect new products lines, which include: airbags, reverse parking assistance system (RPAS), filters and upcoming products of Harita Seating would help MNDA to improve its financials. We believe additional revenue from Harita Seating, addition of sensor plant in FY21, filter business and 2W alloy wheel plant would improve MNDA’s revenue further despite the current difficult times. Further, focus on EV has helped MNDA to secure orders for smart plugs i.e. chargers and DC/AC converters from 2W OEMs like TVS and Bajaj auto. We envisage MNDA would continue to deliver healthy growth even during the difficult times, as evolving technologies i.e. automated manual transmission (AMT), antilock braking systems (ABS), and electronic control units/sensors etc. are expected to witness higher demand.

Air filter/Canisters: MNDA’s 49% JV with Roki Compamy of Japan manufactures air filtration systems and carbon canisters. This product segment is likely to see a significant jump in demand under BS-VI regime, which came into effect from April’20. Activated carbon canisters are used to capture hydrocarbon vapor emissions from the fuel tank as a part of evaporative emission control system (EVAP). Roki is a leading manufacturer of automotive air intake systems, carbon canisters, and auto transmission fluid filters etc., and it supports the entity for all product design and development needs.

Toyoda GOSEI (TG Minda): Toyoda Gosei is a part of Toyoda Group and it is a Toyoda ancillary. Considering the Toyoda brand and quality, it has an excellent track record. TG Minda is into automotive safety system (airbags), fuel cap and weather-strips sealing parts and body ceiling parts. TG Minda is an associate company of MNDA with ~48% holding. This associate company started generating meaningful revenue from Jul’19 onwards, as the government made airbags mandatory from Jul’19. However, regulation was revised later to make only driver bag mandatory and not the co-passenger, which impacted the overall growth. Currently, it is supplying to the OEMs like Maruti Suzuki (~25% market share and supplying ~0.75mn airbags), Toyota and Honda Cars.

Minda TTE DAPS: MNDA entered into 50:50 JV with TT Electronics in FY17 to manufacture reverse parking assistance system (RPAS). The JV was expecting mandatory implementation of RPAS from Apr’18, which was eventually got implemented in July’19. Both JV partners have made investment of ~Rs350-400mn and expect revenue of Rs2.5bn in future with >15% RoCE. Currently, it has assembling facility in Manesar with import content to the tune of ~30%. Minda TTE DAPS currently supplying RPASs to Maruti Suzuki and M&M and target to achieve ~30% market share.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

500

1000

1500

2000

2500

3000

FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Mn) EBITDA Margin (RHS)

22

II. Multiple Technological Tie ups & Strong R&D CapabilitiesWe believe market leadership in key product offering on the back of investments in R&D would continue to help MNDA in coming period. The company has long-standing technical agreements with global players in several areas. Over the period of time, MNDA has explored inorganic route to gain and extend capabilities in diverse product offerings.

Leveraging its JVs and tie-ups with global players, MNDA has expanded product offerings in the technology-intensive segments i.e. infotainment systems, airbags, ADAS, alloy wheels, carbon canisters and sensors and controllers. We expect these faster growing segments to contribute 30% to MNDA’s PAT in FY23E compared to 15% in FY20. Safety norms introduced in 2019, which made RPAS and airbags mandatory for all PVs benefited Minda TTE and TG Minda, the leading suppliers of ADAS and airbags, respectively. MNDA’s JVs with Denso Ten and Onkyo will capitalize on rising demand for infotainment systems, which is largely met through CBU imports. Minda Kosei is the leader in alloy wheels, benefiting from rapidly rising penetration. Implementation of BS-VI emission norms from FY21 is boosting demand for carbon canisters made by ROKI Minda. MNDA has tied-up with SENSATA for sensors for BS-VI applications and has acquired iSys RTS, which develops ECUs for automobiles.

Exhibit 26: Minda has a leadership position in core product segments

Product segment Entity Technology tie-up Competitive scenario

2W switches Minda Industries Design centre in Japan 65% OEM market share in India

4W switches Minda Rika Tokai Rika is global leader in 4W switches 55% OEM market share in India

Horns Minda Industries, Clarton Horns FIAMM Italy is technology partner #1 player in India with 47% mkt share

2W Lighting Rinder Light Systems and Technical Centre (Spain) 27% market share in 2W lighting space

4W Lighting Minda Industries Technical license with AMS (Korea) #3 player behind Lumax and Fiem

Lighting Delvis Access to global lighting technology and deep R&D capabilities

Source: Company

Exhibit 27: Key technical agreements

Year Company Country Product area

1995 Tokai Rika Japan 4-W switches

2010 Emer Italy CNG kits

2010 Roki Co Japan Air filters

2011 Kyoraku Nagase Japan Blow moulding

2011 Toyoda Gosei Japan Safety system and hoses

2015 Kosei Japan Alloy wheels

2016 Onkyo Japan Infotainment

2017 Katolec Japan Printed circuit boards (PCB)

2017 TTE taiwan Driver Assistance Systems & Products (DAPS)

2018 Sensata Technologies USA High-end sensors for BS-VI

2019 Harita Seating Systems India Seating systems

2019 iSys RTS Germany Embedded software

2019 Delvis Germany Lightings

Source: Company

Strong R&D Capabilities: MNDA has limited exposure to engine and engine related parts in its product portfolio. The company makes CNG, LPG kits (alternate fuel systems), fuel hoses and fuel caps, which contribute ~5-10% to its consolidated revenues. To mitigate it, the company is proactively working on development of EV components i.e. battery management systems, on-board chargers, DC controllers and innovative technologies like wireless charging systems etc., which will open up new areas of possible revenue generation. MNDA has consistently demonstrated its focus on R&D as a means to be more self-reliant in areas of technology and product innovation. Its state-of-the-art Centre for Research, Engineering and Advance Technologies (CREAT) is a significant step in this direction. The centre works on embedded electronic products related to connected vehicles, telematics, ADAS, infotainment, EV technologies, controllers and sensors, advance lighting and others. It works for various areas like cockpit electronics and advanced technologies, body exterior and safety technologies, creative design and innovation and product assurance lab.

23

Exhibit 28: R&D expenses trend at MNDA

Source: Company; RSec Research

On the technology development front, it has in-house capabilities for electronics. Minda Katolec JV has set up plant in Pune as an Electronic Manufacturing Services (EMS). The company offers turnkey as well as job work solutions. The products manufactured include: Printed Circuit Boards (PCB) and Box Build Assemblies.

iSys RTS – incorporated in 2004 – develops and produces embedded systems and ECUs for automotive applications. It is engaged in engineering services, prototype development and series production in the field of automotive ECUs. Key customers for iSys are: Rolls Royce, BMW and Webasto etc. iSys’ products find their application in: (i) infotainment; (ii) body (door control) and interiors; (iii) EV applications; and (iv) ADAS and autonomous driving.

BS-VI transition, higher active safety features and rising share of hybrid/electric vehicles are expected to increase sensors and electronics content in vehicles rapidly. MNDA has already tied-up with technology leaders i.e. Sensata, and acquired ECU specialists i.e. iSYS and telematics hardware business from KPIT Engineering. We believe the future potential of this segment is high with competition mainly from the global players.

Localizations through Partnerships with Global Leaders: MNDA has been a pioneer in successfully forging partnership with global technology leaders for affordable localization of several components. This started with Tokai Rika, Japan for 4W switches in 1995 and expanded over 14 partnerships till date. Apart from providing technical support, the partners also help in providing latest solutions to meet the demand of the OEMs. MNDA provides a local understanding and operating environment to these partners, which include Toyota group companies. We believe that these tie-ups can potentially benefit MNDA, going forward.

Other Small Business: In addition to major revenue contribution from switches, horns, lighting, sensors electronics, infotainment and alloy wheels, MNDA has also invested in few more businesses i.e. Minda Kyoraku in blow moulding, MJ Casting in aluminium die casting, TG Rubber in fuel caps and Minda Storage Batteries. Cross-selling has helped MNDA to increase revenue of each of these businesses at a healthy pace

2.1%2.0%

1.7%

1.5% 1.5%

1.3%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0

100

200

300

400

500

600

700

800

900

1000

FY15 FY16 FY17 FY18 FY19 FY20

R&D Expense (Rs Mn) as % of revenue (RHS)

24

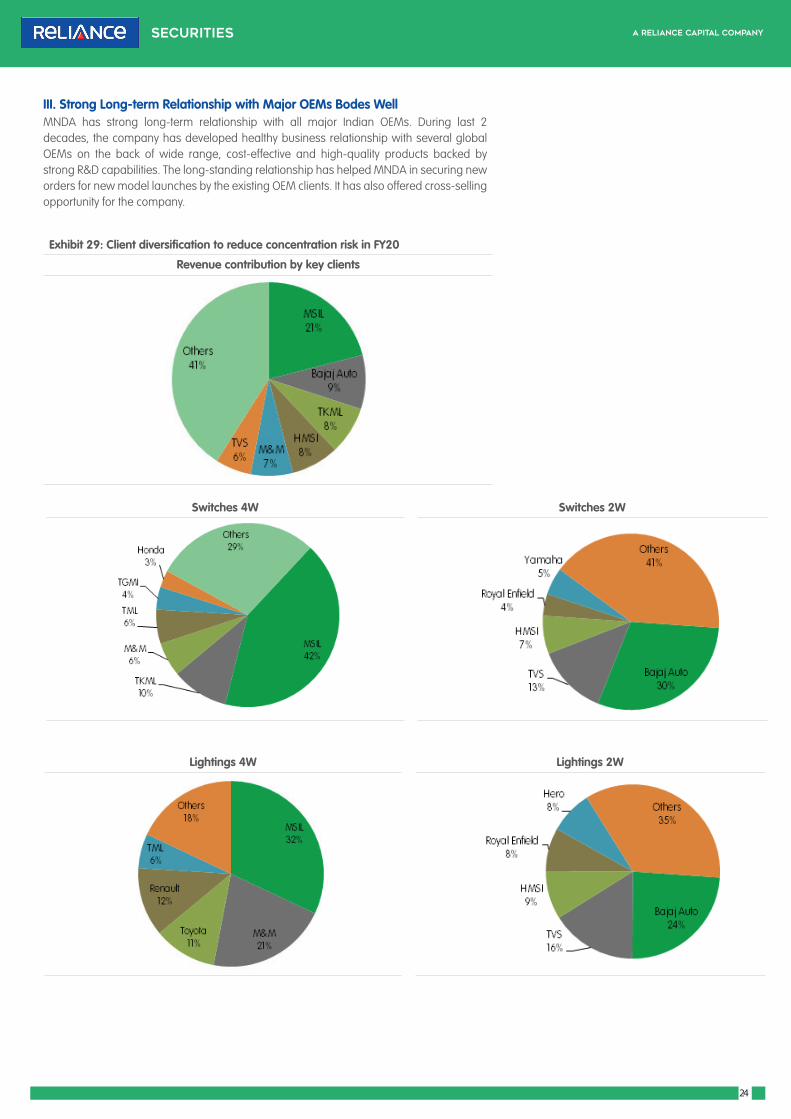

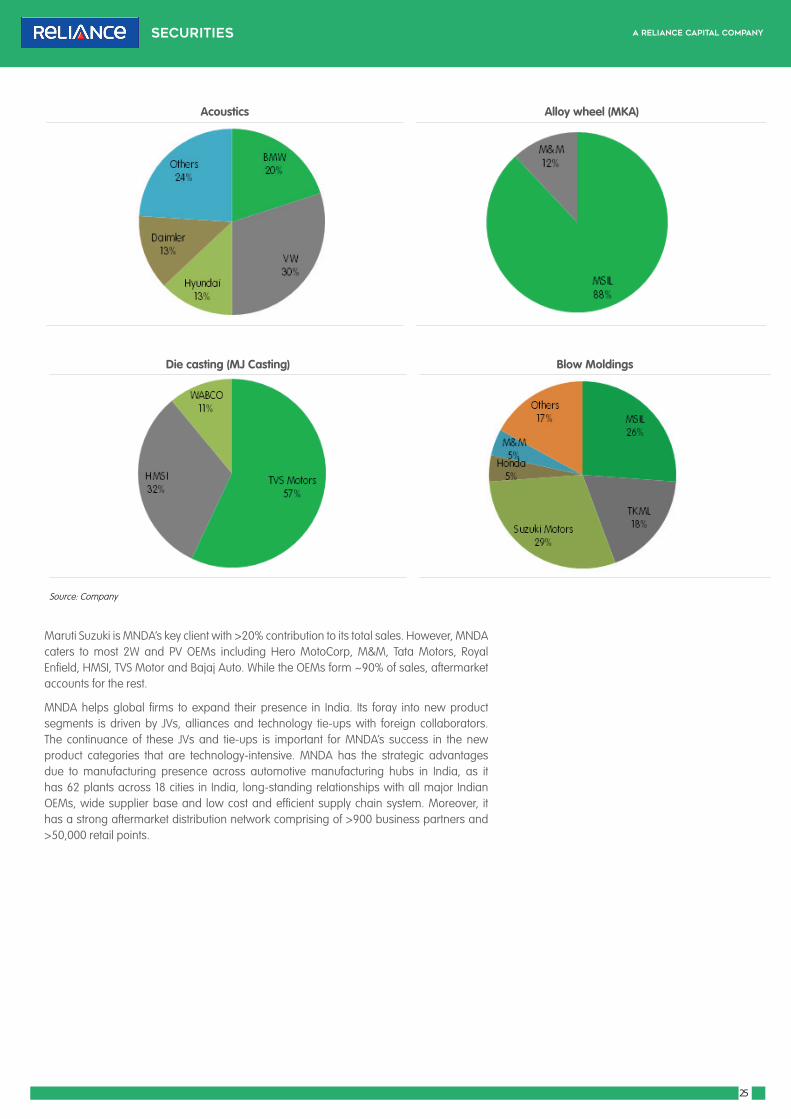

III. Strong Long-term Relationship with Major OEMs Bodes WellMNDA has strong long-term relationship with all major Indian OEMs. During last 2 decades, the company has developed healthy business relationship with several global OEMs on the back of wide range, cost-effective and high-quality products backed by strong R&D capabilities. The long-standing relationship has helped MNDA in securing new orders for new model launches by the existing OEM clients. It has also offered cross-selling opportunity for the company.

Exhibit 29: Client diversification to reduce concentration risk in FY20

Revenue contribution by key clients

Switches 4W Switches 2W

Lightings 4W Lightings 2W

25

Acoustics Alloy wheel (MKA)

Die casting (MJ Casting) Blow Moldings

Source: Company

Maruti Suzuki is MNDA’s key client with >20% contribution to its total sales. However, MNDA caters to most 2W and PV OEMs including Hero MotoCorp, M&M, Tata Motors, Royal Enfield, HMSI, TVS Motor and Bajaj Auto. While the OEMs form ~90% of sales, aftermarket accounts for the rest.

MNDA helps global firms to expand their presence in India. Its foray into new product segments is driven by JVs, alliances and technology tie-ups with foreign collaborators. The continuance of these JVs and tie-ups is important for MNDA’s success in the new product categories that are technology-intensive. MNDA has the strategic advantages due to manufacturing presence across automotive manufacturing hubs in India, as it has 62 plants across 18 cities in India, long-standing relationships with all major Indian OEMs, wide supplier base and low cost and efficient supply chain system. Moreover, it has a strong aftermarket distribution network comprising of >900 business partners and >50,000 retail points.

26

IV. Premiumization Trend & Regulatory Measures to Drive GrowthWith five chief product lines (switches, lighting, acoustics, light metal technology and others), MNDA has a widespread manufacturing units (62 plants in 7 countries), R&D centres (6 locations) and global sales presence. Its corporate structure is slightly complex, encompassing 16 direct subsidiaries, 12 step-down subsidiaries, 8 JVs, 2 associate companies as of FY20. In the second leg of its corporate history, MNDA has been ahead of the curve in identification of product segments that have attracted higher market attention. Accelerated adoption of some of these products (e.g. alloy wheels, LED lighting and infotainment systems etc.) coupled with up-gradation in purchase by the Indian consumers have helped the company in gaining positive traction across product offerings.

Exhibit 30: MNDA Average Kit Value for 2W Exhibit 31: MNDA Average Kit Value for 4W

Source: Company

Premiumization in Lighting through LED: Globally, growth in LED lighting in the PV space has outpaced growth of competing technologies i.e. halogen and xenon in the first half of the last decade (LED lighting clocked 15.7% CAGR over 2012-16 vs. flattish growth for halogen and xenon, as per Yole research). The technology gained prominence owing to its higher design flexibility and luminous efficacy as well as lower power consumption. Further, LED lights can last up to 50,000 hours (several times more than halogen and xenon lights). LED penetration remains skewed towards tail lamps on account of relatively lower ASPs. Looking ahead, we expect tighter regulatory requirement around fuel consumption/emission along with consumers’ preference for aesthetically appealing products to drive penetration of LED headlamps in coming years.

Exhibit 32: Rising Premiumisation in PVs with Higher SUV Contribution

Exhibit 33: UV’s to dominate fresh launches in CY20 & CY21

Source: SIAM Source: Company, autocar india

5,53,699 5,86,6767,61,972

9,22,322 9,41,461 9,42,922

26,01,11127,89,239

30,46,66732,88,581 33,77,436

27,75,081

21.3% 21.0%

25.0%28.0% 27.9%

34.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000

30,00,000

35,00,000

40,00,000

FY15 FY16 FY17 FY18 FY19 FY20

UV Volumes PV Volumes UV as a % of PV

OEM Model

Hyundai Tucson Facelift, New Creta

TML Tata HBX, Altroz EV, Gravitas

Nissan Nissan Magnite, Nissan Leaf

M&M New XUV 500, New Scorpio, eXUV300

Renault Kiger

MSIL Jimny, Brezza Petrol

Volkswagen T-Roc, Taigun

Kia Sonet

4572 51

62

6801

4308

2750

5209 57

66 6966

4664

3580

8387 92

75

11932

6137

4042

0

2000

4000

6000

8000

10000

12000

14000

MCC upto 110 cc

MCC upto 135 cc

MC>135 cc Scooters Mopeds

FY18 FY19 FY20

(Rs)

1989

3 3290

6

4406

4

7587

9

3378

2592

4 4359

6

5045

2

8093

4

3450

4454

5 5852

8

5838

9

1407

88

6873

0

20000

40000

60000

80000

100000

120000

140000

160000

Up to Rs. 2.2 Lacs

Rs. 2.21 - 4.5 Lacs

Rs. 4.5 - 8.3 Lacs >Rs 16 lacs Tractors

FY18 FY19 FY20

(Rs)

27

Despite increasing LED adoption, India remains behind the western markets in terms of overall penetration of ~40%. Domestic PV OEMs started introducing LED elements for headlamps in a meaningful manner only from 2014 with the pace of adoption increasing thereafter. Most PV launches (new launches or facelifts) over the past few years have incorporated LED content, while the trend is expected to continue amid the ongoing premiumization in automotive space.

For MNDA, LED lighting forms 40% of its 2W lighting business, while the share of LED is lower on the PV segment at ~25-30%, largely owing to price differential in these two segments (2W LED ASPs at ~Rs1000-2500, which can go as high as ~Rs15000 for 4W). LED lamps are priced at >2x their halogen counterparts. LED prices are expected to fall due to increasing volume, higher localization and increased competitive intensity. Moreover, this is a high-margin segment compared to the conventional halogen lighting. We expect the demand for LED lighting to form an important factor of MNDA’s premiumization play. Further, the technological edge provided by acquisition of Rinder and Delvis are expected to help MNDA in improving the share of LED lighting further. Increased preference for localized sourcing from by the domestic OEMs as a cost control measure during the ongoing industry downturn is a positive development for MNDA. On 2W front, adoption rate of LED lighting has increased post implementation of AHO regulations from 2017.

Moreover, premiumization trend has also led to increased usage of infotainment system with more added features, music system, other interior lightings and increased aesthetics. Consumers’ increasing preference for higher variants of vehicles is visible from the shift from entry level mini cars to compact/super compact cars over last 5 years. Kit value per vehicles is 30% higher in compact cars as against mini cars. This would drive the demand for higher component and value of kit per vehicle, which augurs well for MNDA.

Regulatory Factors as Kit Value Booster: Over last 5 years, the government has moved legislation in areas relating to crash tests (NCAP), braking (ABS/CBS), better on-road visibility (AHO), vehicular and pedestrian safety. Regulatory push and higher consumer awareness have led to the trend of gravitation towards safer vehicles.

Safety scores for Indian cars tested under the global NCAP crash procedures have improved significantly over the past decade. Component makers in areas of airbags, sensors, ABS/CBS and other electronics are set to benefit from realisation-led growth in this space in future. For MNDA, higher preference for safer 4W provides a huge opportunity in the form of higher demand on airbag and sensors/controllers front.

The 4W airbag industry in India is pegged at ~Rs25bn. Front airbags (mainly driver side airbag) had reached ~65% penetration, while other airbags (side, side torso, knees, curtain and rear etc.) are penetrated to the extent of ~10%. MNDA is well-placed in this space as one of the leading players, commanding ~25% market share. It serves the segment through its 48% JV with Toyoda Gosei i.e. TG Minda India and caters to Toyota Kirloskar and Maruti Suzuki among others.