VECTUS INDUSTRIES LIMITED

442

DRAFT RED HERRING PROSPECTUS Dated June 16, 2018 Please read Section 32 of the Companies Act, 2013 (The Draft Red Herring Prospectus will be updated upon filing with the RoC) Book Built Offer VECTUS INDUSTRIES LIMITED Our Company was incorporated as “Vectus Industries Limited” at Gwalior, pursuant to a certificate of incorporation dated August 30, 2007 issued by the RoC, upon the conversion of “M/s. Vector Polymers”, a partnership firm, into a public limited company, in accordance with the provisions of Part IX of the Companies Act, 1956. Our Company received a certificate of commencement of business on July 14, 2008 from the RoC. For further details of change in the name and Registered Office of our Company, see “History and Certain Corporate Matters” on page 140. Registered Office: 262, Jiwaji Nagar, Thatipur, Gwalior 474 011, Madhya Pradesh; Tel: +91 751 243 2428; Fax: +91 751 223 2402 Corporate Office: A-36, Sector 83, Noida 201 305, Uttar Pradesh; Tel: +91 120 475 3200; Fax: +91 120 475 3285 Contact Person: Mahipal Singh, Company Secretary and Compliance Officer; Tel: +91 120 475 3205; Fax: +91 120 475 3285; E-mail: [email protected]; Website: www.vectus.in Corporate Identity Number: U25202MP2007PLC019781 OUR PROMOTERS: ASHISH BAHETI AND ATUL LADHA INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (“EQUITY SHARES”) OF VECTUS INDUSTRIES LIMITED (“OUR COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (“OFFER PRICE”) AGGREGATING UP TO ₹ [●] MILLION, COMPRISING A FRESH ISSUE OF UP TO [●] EQUITY SHARES AGGREGATING UP TO ₹ 850.00 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO 3,898,575 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION, COMPRISING UP TO 657,341 EQUITY SHARES BY ASHISH BAHETI AND UP TO 394,405 EQUITY SHARES BY ATUL LADHA (TOGETHER, THE “PROMOTER SELLING SHAREHOLDERS”) AND UP TO 2,846,829 EQUITY SHARES BY LATINIA LIMITED (THE “INVESTOR SELLING SHAREHOLDER”) (THE INVESTOR SELLING SHAREHOLDER AND THE PROMOTER SELLING SHAREHOLDERS ARE COLLECTIVELY, THE “SELLING SHAREHOLDERS”) (THE “OFFER FOR SALE”, AND TOGETHER WITH THE FRESH ISSUE, THE “OFFER”). THE OFFER WILL CONSTITUTE [●]% OF OUR POST-OFFER PAID-UP EQUITY SHARE CAPITAL. THE FACE VALUE OF EACH EQUITY SHARE IS ₹10 EACH. THE OFFER PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDERS IN CONSULTATION WITH THE BRLMS AND WILL BE ADVERTISED IN [●] EDITIONS OF [●] (A WIDELY CIRCULATED ENGLISH NATIONAL DAILY NEWSPAPER) AND [●] EDITIONS OF [●] (A WIDELY CIRCULATED HINDI NATIONAL DAILY NEWSPAPER, HINDI ALSO BEING THE REGIONAL LANGUAGE OF MADHYA PRADESH WHERE OUR REGISTERED OFFICE IS LOCATED), EACH WITH WIDE CIRCULATION AT LEAST FIVE WORKING DAYS PRIOR TO THE BID/OFFER OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”, TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR UPLOADING ON THEIR RESPECTIVE WEBSITES. In case of any revision to the Price Band, the Bid/Offer Period will be extended by at least three additional Working Days after such revision of the Price Band, subject to the total Bid/ Offer Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the website of the BRLMs and at the terminals of the Syndicate Members and by intimation to the Designated Intermediaries. This Offer is being made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”) read with Regulation 41 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”). This Offer is being made through the Book Building Process in accordance with Regulation 26(1) of the SEBI ICDR Regulations wherein not more than 50% of the Offer shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (the “QIB Portion”), provided that our Company and the Selling Shareholders in consultation with the BRLMs may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis. One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid Bids being received from the domestic Mutual Funds at or above the Anchor Investor Allocation Price. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received from them at or above the Offer Price. All Bidders, other than Anchor Investors, are mandatorily required to participate in the Offer through the Application Supported by Blocked Amount (“ASBA”) process by providing details of their respective bank accounts which will be blocked by the Self Certified Syndicate Banks (“SCSBs”). Anchor Investors are not permitted to participate in the Anchor Investor Portion through the ASBA Process. For details, see “Offer Procedure” on page 373. RISK IN RELATION TO THE FIRST OFFER This being the first public issue of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹ 10 and the Floor Price is [●] times the face value and the Cap Price is [●] times the face value. The Offer Price (determined and justified by our Company and Selling Shareholders in consultation with the BRLMs as stated in “Basis for Offer Price” on page 82) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 16. ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, the Selling Shareholders severally and not jointly accept responsibility that this Draft Red Herring Prospectus contains all information about them as Selling Shareholders in the context of the Offer for Sale and further severally assume responsibility for statements in relation to them included in this Draft Red Herring Prospectus and the Equity Shares offered by them in the Offer and that such statements are true and correct in all material respects and not misleading in any material respect. LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus until the Bid/ Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 435. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER Edelweiss Financial Services Limited 14th Floor, Edelweiss House Off CST Road, Kalina Mumbai 400 098 Maharashtra Tel: +91 22 4009 4400 Fax: +91 22 4086 3610 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.edelweissfin.com Contact Person: Shubham Mehta / Ashish Gupta SEBI Registration No.: INM0000010650 ICICI Securities Limited ICICI Centre, H.T. Parekh Marg Churchgate Mumbai 400 020 Maharashtra Tel: +91 22 2288 2460 Fax: +91 22 2282 6580 E-mail: [email protected] Investor grievance E- mail:[email protected] Website: www.icicisecurities.com Contact Person: Suyash Jain SEBI Registration No.: INM000011179 IDFC Bank Limited Naman Chambers, C – 32, G Block Bandra Kurla Complex Bandra (E), Mumbai 400 051 Maharashtra Tel: +91 22 7132 5500 Fax: +91 22 4222 2088 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.idfcbank.com Contact Person: Akshay Bhandari SEBI Registration No.:MB/INM000012250 Karvy Computershare Private Limited Karvy Selenium, Tower B Plot Nos. 31 - 32, Gachibowli Financial District, Nanakramguda Hyderabad 500 032 Telangana Tel: +91 40 6716 2222 Fax: +91 40 2343 1551 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.karisma.karvy.com Contact Person: Muralikrishna M SEBI Registration No.: INR000000221 BID/OFFER PROGRAMME BID/OFFER OPENS ON [●]* BID/OFFER CLOSES ON [●]** * Our Company and the Selling Shareholders may, in consultation with the BRLMs, consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor Bid/Offer Period shall be one Working Day prior to the Bid/Offer Opening Date. ** Our Company and the Selling Shareholders may, in consultation with the BRLMs, consider closing the Bid/Offer Period for QIBs one Working Day prior to the Bid/Offer Closing Date in accordance with the SEBI ICDR Regulations.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of VECTUS INDUSTRIES LIMITED

DRAFT RED HERRING PROSPECTUS Dated June 16, 2018

Please read Section 32 of the Companies Act, 2013 (The Draft Red Herring Prospectus will be updated upon filing with the RoC)

Book Built Offer

VECTUS INDUSTRIES LIMITED

Our Company was incorporated as “Vectus Industries Limited” at Gwalior, pursuant to a certificate of incorporation dated August 30, 2007 issued by the RoC, upon the conversion of “M/s. Vector Polymers”, a partnership firm, into a public limited company, in accordance with the provisions of Part IX of the Companies Act, 1956. Our Company received a certificate of commencement of business on July 14, 2008 from the RoC. For further details of change in the name and Registered Office of our Company, see “History and Certain Corporate Matters” on page 140.

Registered Office: 262, Jiwaji Nagar, Thatipur, Gwalior 474 011, Madhya Pradesh; Tel: +91 751 243 2428; Fax: +91 751 223 2402 Corporate Office: A-36, Sector 83, Noida 201 305, Uttar Pradesh; Tel: +91 120 475 3200; Fax: +91 120 475 3285

Contact Person: Mahipal Singh, Company Secretary and Compliance Officer; Tel: +91 120 475 3205; Fax: +91 120 475 3285; E-mail: [email protected]; Website: www.vectus.in Corporate Identity Number: U25202MP2007PLC019781

OUR PROMOTERS: ASHISH BAHETI AND ATUL LADHA INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (“EQUITY SHARES”) OF VECTUS INDUSTRIES LIMITED (“OUR COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (“OFFER PRICE”) AGGREGATING UP TO ₹ [●] MILLION, COMPRISING A FRESH ISSUE OF UP TO [●] EQUITY SHARES AGGREGATING UP TO ₹ 850.00 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO 3,898,575 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION, COMPRISING UP TO 657,341 EQUITY SHARES BY ASHISH BAHETI AND UP TO 394,405 EQUITY SHARES BY ATUL LADHA (TOGETHER, THE “PROMOTER SELLING SHAREHOLDERS”) AND UP TO 2,846,829 EQUITY SHARES BY LATINIA LIMITED (THE “INVESTOR SELLING SHAREHOLDER”) (THE INVESTOR SELLING SHAREHOLDER AND THE PROMOTER SELLING SHAREHOLDERS ARE COLLECTIVELY, THE “SELLING SHAREHOLDERS”) (THE “OFFER FOR SALE”, AND TOGETHER WITH THE FRESH ISSUE, THE “OFFER”). THE OFFER WILL CONSTITUTE [●]% OF OUR POST-OFFER PAID-UP EQUITY SHARE CAPITAL. THE FACE VALUE OF EACH EQUITY SHARE IS ₹10 EACH. THE OFFER PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDERS IN CONSULTATION WITH THE BRLMS AND WILL BE ADVERTISED IN [●] EDITIONS OF [●] (A WIDELY CIRCULATED ENGLISH NATIONAL DAILY NEWSPAPER) AND [●] EDITIONS OF [●] (A WIDELY CIRCULATED HINDI NATIONAL DAILY NEWSPAPER, HINDI ALSO BEING THE REGIONAL LANGUAGE OF MADHYA PRADESH WHERE OUR REGISTERED OFFICE IS LOCATED), EACH WITH WIDE CIRCULATION AT LEAST FIVE WORKING DAYS PRIOR TO THE BID/OFFER OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”, TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR UPLOADING ON THEIR RESPECTIVE WEBSITES. In case of any revision to the Price Band, the Bid/Offer Period will be extended by at least three additional Working Days after such revision of the Price Band, subject to the total Bid/ Offer Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the website of the BRLMs and at the terminals of the Syndicate Members and by intimation to the Designated Intermediaries. This Offer is being made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”) read with Regulation 41 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”). This Offer is being made through the Book Building Process in accordance with Regulation 26(1) of the SEBI ICDR Regulations wherein not more than 50% of the Offer shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (the “QIB Portion”), provided that our Company and the Selling Shareholders in consultation with the BRLMs may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis. One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid Bids being received from the domestic Mutual Funds at or above the Anchor Investor Allocation Price. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received from them at or above the Offer Price. All Bidders, other than Anchor Investors, are mandatorily required to participate in the Offer through the Application Supported by Blocked Amount (“ASBA”) process by providing details of their respective bank accounts which will be blocked by the Self Certified Syndicate Banks (“SCSBs”). Anchor Investors are not permitted to participate in the Anchor Investor Portion through the ASBA Process. For details, see “Offer Procedure” on page 373.

RISK IN RELATION TO THE FIRST OFFER This being the first public issue of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹ 10 and the Floor Price is [●] times the face value and the Cap Price is [●] times the face value. The Offer Price (determined and justified by our Company and Selling Shareholders in consultation with the BRLMs as stated in “Basis for Offer Price” on page 82) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 16.

ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, the Selling Shareholders severally and not jointly accept responsibility that this Draft Red Herring Prospectus contains all information about them as Selling Shareholders in the context of the Offer for Sale and further severally assume responsibility for statements in relation to them included in this Draft Red Herring Prospectus and the Equity Shares offered by them in the Offer and that such statements are true and correct in all material respects and not misleading in any material respect.

LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus until the Bid/ Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 435.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER

Edelweiss Financial Services Limited 14th Floor, Edelweiss House Off CST Road, Kalina Mumbai 400 098 Maharashtra Tel: +91 22 4009 4400 Fax: +91 22 4086 3610 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.edelweissfin.com Contact Person: Shubham Mehta / Ashish Gupta SEBI Registration No.: INM0000010650

ICICI Securities Limited ICICI Centre, H.T. Parekh Marg Churchgate Mumbai 400 020 Maharashtra Tel: +91 22 2288 2460 Fax: +91 22 2282 6580 E-mail: [email protected] Investor grievance E-mail:[email protected] Website: www.icicisecurities.com Contact Person: Suyash Jain SEBI Registration No.: INM000011179

IDFC Bank Limited Naman Chambers, C – 32, G Block Bandra Kurla Complex Bandra (E), Mumbai 400 051 Maharashtra Tel: +91 22 7132 5500 Fax: +91 22 4222 2088 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.idfcbank.com Contact Person: Akshay Bhandari SEBI Registration No.:MB/INM000012250

Karvy Computershare Private Limited Karvy Selenium, Tower B Plot Nos. 31 - 32, Gachibowli Financial District, Nanakramguda Hyderabad 500 032 Telangana Tel: +91 40 6716 2222 Fax: +91 40 2343 1551 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.karisma.karvy.com Contact Person: Muralikrishna M SEBI Registration No.: INR000000221

BID/OFFER PROGRAMME BID/OFFER OPENS ON [●]* BID/OFFER CLOSES ON [●]** * Our Company and the Selling Shareholders may, in consultation with the BRLMs, consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor

Bid/Offer Period shall be one Working Day prior to the Bid/Offer Opening Date. ** Our Company and the Selling Shareholders may, in consultation with the BRLMs, consider closing the Bid/Offer Period for QIBs one Working Day prior to the Bid/Offer Closing Date in accordance

with the SEBI ICDR Regulations.

TABLE OF CONTENTS

SECTION I: GENERAL ........................................................................................................................................................... 1

DEFINITIONS AND ABBREVIATIONS ............................................................................................................................. 1 PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA ........................................................................ 13 FORWARD-LOOKING STATEMENTS ............................................................................................................................ 15

SECTION II: RISK FACTORS ............................................................................................................................................. 16

SECTION III: INTRODUCTION.......................................................................................................................................... 39

SUMMARY OF INDUSTRY ............................................................................................................................................... 39 SUMMARY OF OUR BUSINESS ....................................................................................................................................... 44 SUMMARY OF FINANCIAL INFORMATION ................................................................................................................. 48 THE OFFER ......................................................................................................................................................................... 55 GENERAL INFORMATION ............................................................................................................................................... 57 CAPITAL STRUCTURE...................................................................................................................................................... 65 OBJECTS OF THE OFFER .................................................................................................................................................. 76 BASIS FOR OFFER PRICE ................................................................................................................................................. 82 STATEMENT OF TAX BENEFITS..................................................................................................................................... 85

SECTION IV: ABOUT OUR COMPANY ............................................................................................................................ 90

INDUSTRY OVERVIEW .................................................................................................................................................... 90 OUR BUSINESS ................................................................................................................................................................ 121 REGULATIONS AND POLICIES ..................................................................................................................................... 137 HISTORY AND CERTAIN CORPORATE MATTERS .................................................................................................... 140 OUR MANAGEMENT ...................................................................................................................................................... 147 OUR PROMOTERS AND PROMOTER GROUP ............................................................................................................. 163 OUR GROUP COMPANIES .............................................................................................................................................. 167 DIVIDEND POLICY .......................................................................................................................................................... 172 RELATED PARTY TRANSACTIONS ............................................................................................................................. 173

SECTION V: FINANCIAL INFORMATION .................................................................................................................... 174

FINANCIAL STATEMENTS ............................................................................................................................................ 174 FINANCIAL INDEBTEDNESS......................................................................................................................................... 322 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.................................................................................................................................................................... 325

SECTION VI: LEGAL AND OTHER INFORMATION .................................................................................................. 347

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ......................................................................... 347 GOVERNMENT AND OTHER APPROVALS ................................................................................................................. 350 OTHER REGULATORY AND STATUTORY DISCLOSURES ...................................................................................... 352

SECTION VII: OFFER INFORMATION .......................................................................................................................... 367

TERMS OF THE OFFER ................................................................................................................................................... 367 OFFER STRUCTURE ........................................................................................................................................................ 371 OFFER PROCEDURE ....................................................................................................................................................... 373 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES .................................................................... 414

SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION ................................................................. 415

SECTION IX: OTHER INFORMATION ........................................................................................................................... 435

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ............................................................................ 435 DECLARATION ................................................................................................................................................................ 437

1

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

This Draft Red Herring Prospectus uses certain definitions and abbreviations which, unless the context otherwise indicates or implies, or unless otherwise specified, shall have the meaning as provided below. References to any legislation, act, regulation, rules, guidelines or policies shall be to such legislation, act or regulation, as amended from time to time and any reference to a statutory provision shall include any subordinate legislation made from time to time under that provision.

The words and expressions used in this Draft Red Herring Prospectus but not defined herein, shall have, to the extent applicable, the meanings ascribed to such terms under the Companies Act, the SEBI ICDR Regulations, the SCRA, the Depositories Act or the rules and regulations made thereunder.

Notwithstanding the foregoing, terms used in “Statement of Tax Benefits”, “Financial Statements”, “Main Provisions of Articles of Association”, “Outstanding Litigation and Material Developments”, “Regulations and Policies” and “Offer Procedure – Part B” on pages 85, 174, 415, 347, 137 and 382, respectively, shall have the meaning ascribed to such terms in these respective sections.

General Terms

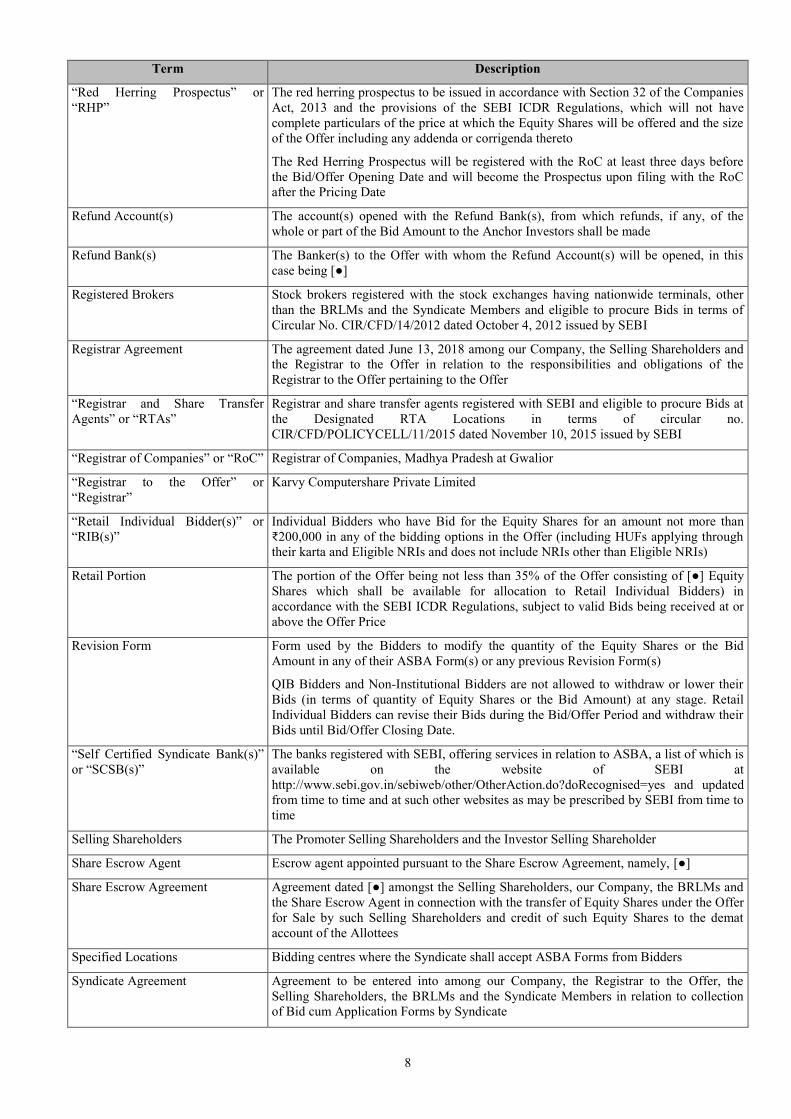

Term Description

“our Company”, “the Company” or “the Issuer”

Vectus Industries Limited, a company incorporated under the Companies Act, 1956 and having its registered office at 262, Jiwaji Nagar, Thatipur, Gwalior 474 011, Madhya Pradesh

“we”, “us”, or “our” Unless the context otherwise indicates or implies, our Company together with its Subsidiaries, on a consolidated basis

Company Related Terms

Term Description

“Articles of Association” or “AoA” Articles of Association of our Company, as amended

Audit Committee The audit committee of the board of directors, as described in “Our Management” on page 147

“Auditors” or “Statutory Auditors” Statutory auditors of our Company, namely, Walker Chandiok & Co LLP, Chartered Accountants

“Board” or “Board of Directors” Board of directors of our Company or a duly constituted committee thereof

CCDs Compulsorily convertible debentures of our Company, with a face value of ` 1,000 each and bearing zero coupon rate

Chief Financial Officer Chief financial officer of our Company

Corporate Office A-36, Sector 83, Noida 201 305, Uttar Pradesh

Corporate Social Responsibility Committee

The corporate social responsibility committee of our Board, as described in “Our Management” on page 147

Director(s) Director(s) on the Board

Equity Shares Equity shares of our Company of face value of ₹10 each

ESOP 2018 Vectus Industries Limited Employee Stock Option Plan 2018

Executive Directors Executive Directors of our Company

Group Companies Companies which are covered under the applicable accounting standards and other companies as considered material by our Board. For details, see “Our Group Companies” on page 167

IPO Committee The IPO Committee of our Board, constituted to facilitate the process of the Offer, as described in “Our Management” on page 147

Independent Directors Independent directors on our Board, and eligible to be appointed as independent directors under the provisions of the Companies Act and the SEBI Listing Regulations. For details of the Independent Directors, see “Our Management” on page 147

2

Term Description

Investment Agreement Investment Agreement dated June 12, 2014, as amended on June 18, 2015 and May 30, 2018, amongst the Company, Promoters, Sarika Baheti, Ashish Baheti (HUF), Pure Ganga Water Systems Private Limited, Misha Baheti, Divian Baheti, Sunita Ladha, Shanti Devi Ladha, Atul Ladha and Sons (HUF), Shivangi Polymers Private Limited, G.D. Ladha, Manorama Ladha and Latinia Limited. For details, see “History and Certain Corporate Matters” on page 140

Key Management Personnel Key management personnel of our Company in terms of Regulation 2(1)(s) of the SEBI ICDR Regulations, the Companies Act, 2013 and as disclosed in “Our Management” on page 147

“Memorandum of Association” or “MoA”

Memorandum of Association of our Company, as amended

Nomination and Remuneration Committee

The nomination and remuneration committee of our Board, as described in “Our Management” on page 147

Promoter Group The persons and entities constituting the promoter group of our Company in terms of Regulation 2(1)(zb) of the SEBI ICDR Regulations. For details see “Our Promoter and Promoter Group” on page 163

Promoters The promoters of our Company namely, Ashish Baheti and Atul Ladha. For details, see “Our Promoter and Promoter Group” on page 163

Registered Office Registered office of our Company located at 262, Jiwaji Nagar, Thatipur, Gwalior 474 011, Madhya Pradesh

“Registrar of Companies” or “RoC” Registrar of Companies, Madhya Pradesh at Gwalior

Restated Consolidated Financial Information

The restated consolidated financial information of our Company, which comprises the restated consolidated statement of assets and liabilities, the restated consolidated statement of profit and loss (including other comprehensive income), the restated consolidated statement of changes in equity and the restated consolidated statement of cash flow as at and for the financial years ended March 31, 2018, March 31, 2017, March 31, 2016, March 31, 2015 and March 31, 2014, together with the annexures and notes thereto (presented in accordance with Ind AS), prepared in terms of the requirements of Section 26 of Part I of Chapter III of the Companies Act, 2013, as amended read with the SEBI ICDR Regulations as amended from time to time in pursuance of provisions of SEBI Act, 1992.

The restated consolidated financial information as at and for each of the years ended March 31, 2016, March 31, 2015 and March 31, 2014 are referred to as “the Proforma Ind AS Restated Consolidated Financial Information” as per the Guidance Note on Reports in Company Prospectuses (Revised 2016) issued by the Institute of Chartered Accountants of India

Restated Financial Statements Collectively, the Restated Consolidated Financial Information and the Restated Standalone Financial Information

Restated Standalone Financial Information

The restated standalone financial information of our Company, which comprises the restated standalone statement of assets and liabilities, the restated standalone statement of profit and loss (including other comprehensive income), the restated standalone statement of changes in equity and the restated standalone statement of cash flow as at and for the financial years ended March 31, 2018, March 31, 2017, March 31 2016, March 31, 2015 and March 31, 2014, together with the annexures and notes thereto (presented in accordance with Ind AS) prepared in terms of the requirements of Section 26 of Part I of Chapter III of the Companies Act, 2013, as amended read with the SEBI ICDR Regulations as amended from time to time in pursuance of provisions of SEBI Act, 1992.

The restated standalone financial information as at and for each of the years ended 31 March 2016, 31 March 2015 and 31 March 2014 are referred to as “the Proforma Ind AS Restated Standalone Financial Information” as per the Guidance Note on Reports in Company Prospectuses (Revised 2016) issued by the Institute of Chartered Accountants of India

3

Term Description

Scheme I Scheme of amalgamation between Sintir Plast Containers Private Limited and our Company approved by the High Court of Madhya Pradesh vide its order dated November 1, 2013

Scheme II Scheme of amalgamation between Baheti Rotoplast Private Limited and our Company approved by the High Court of Delhi and the High Court of Madhya Pradesh vide their respective orders dated January 28, 2014 and March 11, 2014

Scheme III Scheme of amalgamation between Waterwell Containers Private Limited and our Company approved by the National Company Law Tribunal, Ahmedabad Bench, vide its order dated December 15, 2017

Shareholders Equity shareholders of our Company, from time to time

Stakeholders’ Relationship Committee

The stakeholders’ relationship committee of our Board as described in “Our Management” on page 147

Subsidiaries Subsidiaries of our Company, namely, Gangotri Polymers Private Limited, Sunrise Tanks Private Limited and Vectus Containers Private Limited. For details, see “History and Certain Corporate Matters” on page 140

Offer Related Terms

Term Description

Acknowledgement Slip The slip or document issued by a Designated Intermediary to a Bidder as proof of registration of the Bid cum Application Form

“Allot”, “Allotment” or “Allotted” Unless the context otherwise requires, allotment of Equity Shares pursuant to the Fresh Issue and transfer of Equity Shares offered by the Selling Shareholders pursuant to the Offer for Sale to the successful Bidders

Allotment Advice Note or advice or intimation of Allotment sent to the Bidders who have been or are to be Allotted the Equity Shares after the Basis of Allotment has been approved by the Designated Stock Exchange

Allottee A successful Bidder to whom the Equity Shares are Allotted

Anchor Investor A Qualified Institutional Buyer, applying under the Anchor Investor Portion in accordance with the requirements specified in the SEBI ICDR Regulations and the Red Herring Prospectus

Anchor Investor Allocation Price The price at which Equity Shares will be allocated to Anchor Investors in terms of the Red Herring Prospectus, which will be decided by our Company and the Selling Shareholders, in consultation with the BRLMs during the Anchor Investor Bid/Offer Period

Anchor Investor Application Form The form used by an Anchor Investor to make a Bid in the Anchor Investor Portion and which will be considered as an application for Allotment in terms of the Red Herring Prospectus and Prospectus

Anchor Investor Bid/Offer Period The day, being one Working Day prior to the Bid/Offer Opening Date, on which Bids by Anchor Investors shall be submitted, prior to and after which the BRLMs will not accept any bids from Anchor investors, and allocation to Anchor Investors shall be completed

Anchor Investor Offer Price Final price at which the Equity Shares will be issued and Allotted to Anchor Investors in terms of the Red Herring Prospectus and the Prospectus, which price will be equal to or higher than the Offer Price but not higher than the Cap Price. The Anchor Investor Offer Price will be decided by our Company and the Selling Shareholders, in consultation with the BRLMs

4

Term Description

Anchor Investor Portion Up to 60% of the QIB Portion which may be allocated by our Company and the Selling Shareholders in consultation with the BRLMs, to Anchor Investors on a discretionary basis, in accordance with the SEBI ICDR Regulations.

One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price

Application Supported by Blocked Amount or ASBA

An application, whether physical or electronic, used by ASBA Bidders to make a Bid and authorize an SCSB to block the Bid Amount in the ASBA Account

ASBA Account A bank account maintained with an SCSB and specified in the ASBA Form submitted by Bidders for blocking the Bid Amount mentioned in the ASBA Form

ASBA Bidders All Bidders except Anchor Investors

ASBA Form An application form, whether physical or electronic, used by ASBA Bidders which will be considered as the application for Allotment in terms of the Red Herring Prospectus and the Prospectus

Banker(s) to the Offer Collectively, the Escrow Collection Bank(s), Refund Bank(s) and Public Offer Account Bank(s)

Basis of Allotment Basis on which Equity Shares will be Allotted to successful Bidders under the Offer and which is described in “Offer Procedure” on page 373

Bid An indication to make an offer during the Bid/Offer Period by an ASBA Bidder pursuant to submission of the ASBA Form, or during the Anchor Investor Bid/Offer Period by an Anchor Investor pursuant to submission of the Anchor Investor Application Form, to subscribe to or purchase the Equity Shares of our Company at a price within the Price Band, including all revisions and modifications thereto as permitted under the SEBI ICDR Regulations. The term “Bidding” shall be construed accordingly

Bid Amount The highest value of optional Bids indicated in the Bid cum Application Form and payable by the Bidder or blocked in the ASBA Account of the Bidder, as the case may be, upon submission of the Bid

Bid cum Application Form The Anchor Investor Application Form or the ASBA Form, as the context requires

Bid Lot [●] Equity Shares

Bid/Offer Closing Date Except in relation to any Bids received from the Anchor Investors, the date after which the Designated Intermediaries will not accept any Bids, being [●], which shall be published in [●] editions of [●] (a widely circulated English national daily newspaper), [●] editions of [●] (a widely circulated Hindi national daily newspaper, Hindi also being the regional language of Madhya Pradesh, where our Registered Office is located). In case of any revisions, the extended Bid/Offer Closing Date shall also be notified on the websites and terminals of the Syndicate Members, as required under the SEBI ICDR Regulations. Our Company and the Selling Shareholders may, in consultation with the BRLMs, consider closing the Bid/Offer Period for the QIB Category one Working Day prior to the Bid/Offer Closing Date in accordance with the SEBI ICDR Regulations

Bid/Offer Opening Date Except in relation to any Bids received from the Anchor Investors, the date on which the Designated Intermediaries shall start accepting Bids, being [●], which shall be published in [●] editions of [●] (a widely circulated English national daily newspaper), [●] editions of [●] (a widely circulated Hindi national daily newspaper, Hindi also being the regional language of Madhya Pradesh, where our Registered Office is located)

Bid/Offer Period Except in relation to Anchor Investors, the period between the Bid/Offer Opening Date and the Bid/Offer Closing Date, inclusive of both days, during which prospective Bidders can submit their Bids, including any revisions thereof

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring Prospectus and the Bid cum Application Form and unless otherwise stated or implied, includes an Anchor Investor

5

Term Description

Bidding Centers Centers at which at the Designated Intermediaries shall accept the ASBA Forms, i.e, Designated SCSB Branches for SCSBs, Specified Locations for Syndicate, Broker Centres for Registered Brokers, Designated RTA Locations for RTAs and Designated CDP Locations for CDPs

Book Building Process Book building process, as provided in Schedule XI of the SEBI ICDR Regulations, in terms of which the Offer is being made

Book Running Lead Managers or BRLMs

The book running lead managers to the Offer namely, Edelweiss Financial Services Limited, ICICI Securities Limited and IDFC Bank Limited

Broker Centres Broker centres notified by the Stock Exchanges where Bidders can submit the ASBA Forms to a Registered Broker

The details of such Broker Centres, along with the names and contact details of the Registered Broker are available on the respective websites of the Stock Exchanges (www.bseindia.com and www.nseindia.com)

“CAN” or “Confirmation of Allocation Note”

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who have been allocated the Equity Shares, after the Anchor Investor Bid/Offer Period

Cap Price The higher end of the Price Band, above which the Offer Price and the Anchor Investor Offer Price will not be finalised and above which no Bids will be accepted

Cash Escrow Agreement Agreement dated [] entered into by our Company, the Selling Shareholders, the Registrar to the Offer, the BRLMs, the Syndicate Members, the Bankers to the Offer for collection of the Bid Amounts from Anchor Investors, transfer of funds to the Public Offer Account and where applicable, refunds of the amounts collected from Bidders, on the terms and conditions thereof

Client ID Client identification number maintained with one of the Depositories in relation to demat account

“Collecting Depository Participant” or “CDP”

A depository participant as defined under the Depositories Act, 1996, registered with SEBI and who is eligible to procure Bids at the Designated CDP Locations in terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Cut-off Price Offer Price, finalised by our Company and the Selling Shareholders, in consultation with the BRLMs

Only Retail Individual Bidders are entitled to Bid at the Cut-off Price. QIBs and Non-Institutional Bidders are not entitled to Bid at the Cut-off Price

Demographic Details Details of the Bidders including the Bidder’s address, name of the Bidder’s father/husband, investor status, occupation and bank account details

Designated CDP Locations Such locations of the CDPs where Bidders can submit the ASBA Forms. The details of such Designated CDP Locations, along with names and contact details of the Collecting Depository Participants eligible to accept ASBA Forms are available on the respective websites of the Stock Exchanges (www.bseindia.com and www.nseindia.com)

Designated Date The date on which funds are transferred from the Escrow Account and the amounts blocked by the SCSBs are transferred from the ASBA Accounts, as the case may be, to the Public Offer Account or the Refund Account, as appropriate, after filing of the Prospectus with the RoC

Designated Intermediaries Syndicate, sub-syndicate/agents, SCSBs, Registered Brokers, CDPs and RTAs, who are authorized to collect ASBA Forms from the ASBA Bidders, in relation to the Offer

Designated RTA Locations Such locations of the RTAs where Bidders can submit the ASBA Forms to RTAs.

The details of such Designated RTA Locations, along with names and contact details of the RTAs eligible to accept ASBA Forms are available on the respective websites of the Stock Exchanges (www.bseindia.com and www.nseindia.com)

6

Term Description

Designated SCSB Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which is available on the website of SEBI at http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes

Intermediaries or at such other website as may be prescribed by SEBI from time to time

Designated Stock Exchange [●]

“Draft Red Herring Prospectus” or “DRHP”

This draft red herring prospectus dated June 16, 2018 issued in accordance with the SEBI ICDR Regulations, which does not contain complete particulars of the price at which the Equity Shares will be Allotted and the size of the Offer

Edelweiss Edelweiss Financial Services Limited

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an offer or invitation under the Offer and in relation to whom the ASBA Form and the Red Herring Prospectus will constitute an invitation to subscribe to or to purchase the Equity Shares

Escrow Account Account opened with the Escrow Collection Bank(s) and in whose favour the Anchor Investors will transfer money through direct credit/NEFT/RTGS/NACH in respect of the Bid Amount when submitting a Bid

Escrow Collection Bank(s) Banks which are clearing members and registered with SEBI as bankers to an issue and with whom the Escrow Accounts will be opened, in this case being [●]

First Bidder Bidder whose name shall be mentioned in the Bid cum Application Form or the Revision Form and in case of joint Bids, whose name shall also appear as the first holder of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, subject to any revision thereto, at or above which the Offer Price and the Anchor Investor Offer Price will be finalised and below which no Bids will be accepted

Fresh Issue The fresh issue of up to [●] Equity Shares aggregating up to ₹ 850.00 million by our Company

“General Information Document” or “GID”

The General Information Document for investing in public issues, prepared and issued in accordance with the circular (CIR/CFD/DIL/12/2013) dated October 23, 2013 notified by SEBI, suitably modified and and updated pursuant to, inter alia, the circular (CIR/CFD/POLICYCELL/11/2015) dated November 10, 2015 and (SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January 21, 2016 notified by SEBI and included in “Offer Procedure” on page 373

ICICI Securities ICICI Securities Limited

IDFC IDFC Bank Limited

Investor Selling Shareholder Latinia Limited

Maximum RIB Allottees Maximum number of RIBs who can be allotted the minimum Bid Lot. This is computed by dividing the total number of Equity Shares available for Allotment to RIBs by the minimum Bid Lot

Mutual Fund Portion 5% of the QIB Portion (excluding the Anchor Investor Portion), or [●] Equity Shares which shall be available for allocation to Mutual Funds only on a proportionate basis, subject to valid Bids being received at or above the Offer Price

Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996

Net Proceeds Proceeds of the Fresh Issue less our Company’s share of the Offer related expenses. For further information about use of the Offer Proceeds and the Offer related expenses, see “Objects of the Offer” on page 76

Net QIB Portion The portion of the QIB Portion less the number of Equity Shares Allotted to the Anchor Investors

“Non-Institutional Bidder” or “NIBs”

All Bidders that are not QIBs or Retail Individual Bidders and who have Bid for Equity Shares for an amount more than ₹ 200,000 (but not including NRIs other than Eligible NRIs)

7

Term Description

Non-Institutional Portion The portion of the Offer being not less than 15% of the Offer consisting of [●] Equity Shares which shall be available for allocation on a proportionate basis to Non-Institutional Bidders, subject to valid Bids being received at or above the Offer Price

Non-Resident A person resident outside India, as defined under FEMA and includes NRIs, FPIs and FVCIs

Offer The public issue of up to [●] Equity Shares of face value of ₹10 each for cash at a price of ₹ [●] each, aggregating up to ₹ [●] million comprising the Fresh Issue and the Offer for Sale

Offer Agreement The agreement dated June 16, 2018 amongst our Company, the Selling Shareholders and the BRLMs, pursuant to which certain arrangements are agreed to in relation to the Offer

Offer for Sale The offer for sale of up to 3,898,575 Equity Shares by Selling Shareholders at the Offer Price aggregating up to ₹ [●] million in terms of the Red Herring Prospectus

Offer Price The final price at which Equity Shares will be Allotted to successful Bidders, other than Anchor Investors. Equity Shares will be Allotted to Anchor Investors at the Anchor Investor Offer Price in terms of the Red Herring Prospectus. The Offer Price will be decided by our Company and the Selling Shareholders, in consultation with the BRLMs on the Pricing Date, in accordance with the Book-Building Process and in terms of the Red Herring Prospectus

Offer Proceeds The proceeds of the Fresh Issue which shall be available to our Company and the proceeds of the Offer for Sale which shall be available to the Selling Shareholders. For further information about use of the Offer Proceeds, see the section titled “Objects of the Offer” on page 76

Price Band Price band of a minimum price of ₹ [●] per Equity Share (Floor Price) and the maximum price of ₹ [●] per Equity Share (Cap Price) including any revisions thereof. The Price Band and the minimum Bid Lot for the Offer will be decided by our Company and the Selling Shareholders in consultation with the BRLMs, and will be advertised, in [●] editions of the [●] (a widely circulated English national daily newspaper) and [●] editions of [●] (a widely circulated Hindi national daily newspaper, Hindi also being the regional language of Madhya Pradesh where our Registered Office is located), at least five Working Days prior to the Bid/Offer Opening Date, with the relevant financial ratios calculated at the Floor Price and at the Cap Price, and shall be made available to the Stock Exchanges for the purpose of uploading on their respective websites

Pricing Date The date on which our Company and the Selling Shareholders in consultation with the BRLMs, will finalise the Offer Price

Promoter Selling Shareholders Ashish Baheti and Atul Ladha

Prospectus The Prospectus to be filed with the RoC after the Pricing Date in accordance with Section 26 of the Companies Act, 2013, and the SEBI ICDR Regulations containing, inter alia, the Offer Price that is determined at the end of the Book Building Process, the size of the Offer and certain other information, including any addenda or corrigenda thereto

Public Offer Account Bank account to be opened with the Public Offer Account Bank under Section 40(3) of the Companies Act, 2013, to receive monies from the Escrow Account and ASBA Accounts on the Designated Date

Public Offer Account Bank The bank with which the Public Offer Account is opened for collection of Bid Amounts from Escrow Account and ASBA Account on the Designated Date, in this case being [●]

“QIB Category” or “QIB Portion” The portion of the Offer (including the Anchor Investor Portion) being not more than 50% of the Offer consisting of [●] Equity Shares which shall be Allotted to QIBs (including Anchor Investors)

“Qualified Institutional Buyers” or “QIBs” or “QIB Bidders”

Qualified institutional buyers as defined under Regulation 2(1)(zd) of the SEBI ICDR Regulations

8

Term Description

“Red Herring Prospectus” or “RHP”

The red herring prospectus to be issued in accordance with Section 32 of the Companies Act, 2013 and the provisions of the SEBI ICDR Regulations, which will not have complete particulars of the price at which the Equity Shares will be offered and the size of the Offer including any addenda or corrigenda thereto

The Red Herring Prospectus will be registered with the RoC at least three days before the Bid/Offer Opening Date and will become the Prospectus upon filing with the RoC after the Pricing Date

Refund Account(s) The account(s) opened with the Refund Bank(s), from which refunds, if any, of the whole or part of the Bid Amount to the Anchor Investors shall be made

Refund Bank(s) The Banker(s) to the Offer with whom the Refund Account(s) will be opened, in this case being [●]

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other than the BRLMs and the Syndicate Members and eligible to procure Bids in terms of Circular No. CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI

Registrar Agreement The agreement dated June 13, 2018 among our Company, the Selling Shareholders and the Registrar to the Offer in relation to the responsibilities and obligations of the Registrar to the Offer pertaining to the Offer

“Registrar and Share Transfer Agents” or “RTAs”

Registrar and share transfer agents registered with SEBI and eligible to procure Bids at the Designated RTA Locations in terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

“Registrar of Companies” or “RoC” Registrar of Companies, Madhya Pradesh at Gwalior

“Registrar to the Offer” or “Registrar”

Karvy Computershare Private Limited

“Retail Individual Bidder(s)” or “RIB(s)”

Individual Bidders who have Bid for the Equity Shares for an amount not more than ₹200,000 in any of the bidding options in the Offer (including HUFs applying through their karta and Eligible NRIs and does not include NRIs other than Eligible NRIs)

Retail Portion The portion of the Offer being not less than 35% of the Offer consisting of [●] Equity Shares which shall be available for allocation to Retail Individual Bidders) in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price

Revision Form Form used by the Bidders to modify the quantity of the Equity Shares or the Bid Amount in any of their ASBA Form(s) or any previous Revision Form(s)

QIB Bidders and Non-Institutional Bidders are not allowed to withdraw or lower their Bids (in terms of quantity of Equity Shares or the Bid Amount) at any stage. Retail Individual Bidders can revise their Bids during the Bid/Offer Period and withdraw their Bids until Bid/Offer Closing Date.

“Self Certified Syndicate Bank(s)” or “SCSB(s)”

The banks registered with SEBI, offering services in relation to ASBA, a list of which is available on the website of SEBI at http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes and updated from time to time and at such other websites as may be prescribed by SEBI from time to time

Selling Shareholders The Promoter Selling Shareholders and the Investor Selling Shareholder

Share Escrow Agent Escrow agent appointed pursuant to the Share Escrow Agreement, namely, [●]

Share Escrow Agreement Agreement dated [●] amongst the Selling Shareholders, our Company, the BRLMs and the Share Escrow Agent in connection with the transfer of Equity Shares under the Offer for Sale by such Selling Shareholders and credit of such Equity Shares to the demat account of the Allottees

Specified Locations Bidding centres where the Syndicate shall accept ASBA Forms from Bidders

Syndicate Agreement Agreement to be entered into among our Company, the Registrar to the Offer, the Selling Shareholders, the BRLMs and the Syndicate Members in relation to collection of Bid cum Application Forms by Syndicate

9

Term Description

Syndicate Members Intermediaries registered with SEBI who are permitted to carry out activities as an underwriter, namely, [●]

Syndicate The BRLMs and the Syndicate Members

Underwriters [●]

Underwriting Agreement The agreement among the Underwriters, our Company and the Selling Shareholders to be entered into on or after the Pricing Date

Working Day All days, other than second and fourth Saturday of a month, Sunday or a public holiday, on which commercial banks in Mumbai are open for business; provided however, with reference to (a) announcement of Price Band; and (b) Bid/Offer Period, “Working Day” shall mean all days, excluding all Saturdays, Sundays and public holidays, on which commercial banks in Mumbai are open for business; (c) the time period between the Bid/Offer Closing Date and the listing of the Equity Shares on the Stock Exchanges, “Working Day” shall mean all trading days of Stock Exchanges, excluding Sundays and bank holidays, as per the SEBI Circular SEBI/HO/CFD/DIL/CIR/P/2016/26 dated January 21, 2016

Technical / Industry Related Terms / Conventional and General Terms / Abbreviations

Term Description

“₹”, “Rs.”, “Rupees” or “INR” Indian Rupees

Adjusted Revenue Sale of our products before discounts, rebates and various promotional schemes, net of excise duty. For details see “Management’s Discussion and Analysis Of Financial Condition and Results Of Operations – Details of Adjusted Revenue” on page 339

AGM Annual general meeting

AIF Alternative Investment Fund as defined in and registered with SEBI under the Securities and Exchange Board of India (Alternative Investments Funds) Regulations, 2012

Air Act Air (Prevention and Control of Pollution) Act, 1981

AMRUT Atal Mission for Rejuvenation and Urban Transformation.

“AS” or “Accounting Standards” Accounting Standards issued by the Institute of Chartered Accountants of India

“Bn” or “bn” Billion

BSE BSE Limited

CAGR Compound Annual Growth Rate, which is computed by dividing the value of an investment at the year-end by its value at the beginning of that period, raise the result to the power of one divided by the period length, and subtract one from the subsequent result : ((End Value/Start Value)^(1/Periods) -1

Category I FPI(s) FPIs who are registered as “Category I foreign portfolio investors” under the SEBI FPI Regulations

Category II FPI(s) FPIs who are registered as “Category II foreign portfolio investors” under the SEBI FPI Regulations

Category III FPI(s) FPIs who are registered as “Category III foreign portfolio investors” under the SEBI FPI Regulations

CDSL Central Depository Services (India) Limited

Companies Act Companies Act, 1956 and the Companies Act, 2013, as applicable

Companies Act, 1956 Companies Act, 1956 (without reference to the provisions thereof that have ceased to have effect upon notification of the sections of the Companies Act, 2013) along with the relevant rules made thereunder

Companies Act, 2013 Companies Act, 2013, to the extent in force pursuant to the notification of the Notified Sections, along with the relevant rules, regulations, clarifications, circulars and notifications issued thereunder

10

Term Description

CPVC Chlorinated poly vinyl chloride

creditor days Creditor days is computed by dividing the amount of Trade payables as at the year-end divided by total value of adjusted revenue : (Trade payables/Adjusted revenue) X 365

“CRISIL” or “CRISIL Research” CRISIL Limited

CY Calendar Year

debtors days Debtors days is computed by dividing the amount of Trade receivables as at the year-end divided by total value of adjusted revenue : (Trade receivables/Adjusted revenue) X 365

Depositories NSDL and CDSL

Depositories Act Depositories Act, 1996

DIN Director Identification Number

Dealers and distributors Active dealers and distributors with whom we conducted business in the relevant fiscal year

DP ID Depository Participant’s Identification

“DP” or “Depository Participant” A depository participant as defined under the Depositories Act

EBITDA Earnings before Interest, Taxes, Depreciation and Amortization, which is calculated by adding finance cost and depreciation and amortization expense to Profit before exceptional items less other income

EGM Extraordinary General Meeting

Environment Protection Act The Environment Protection Act, 1986

EPS Earnings per Share

Factories Act Factories Act, 1948

FDI Foreign Direct Investment

FEMA Foreign Exchange Management Act, 1999, read with rules and regulations thereunder

FEMA Regulations Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2017

“Financial Year”, “Fiscal”, “fiscal”, “Fiscal Year” or “FY”

Unless stated otherwise, the period of 12 months ending March 31 of that particular year

FIPB The erstwhile Foreign Investment Promotion Board

FPI(s) Foreign Portfolio Investors as defined under the SEBI FPI Regulations

FVCI Foreign Venture Capital Investors as defined and registered under the SEBI FVCI Regulations

GDP Gross domestic product

“GoI” or “Government” Government of India

Gross Margin on Adjusted Revenue Adjusted revenue less Cost of material consumed less Purchase of traded goods less changes in inventory of finished goods, work in progress, traded goods and stores and spares.

GST Goods and services tax

Hazardous Waste Rules Hazardous and Other Wastes (Management and Transboundary Movement) Rules, 2016

ICAI The Institute of Chartered Accountants of India

IMF International Monetary Fund

“Income Tax Act” or “IT Act” Income Tax Act, 1961

Ind AS Indian Accounting Standards as referred to in and notified by the Ind AS Rules

Ind AS Rules The Companies (Indian Accounting Standard) Rules, 2015

India Republic of India

11

Term Description

Indian GAAP Generally Accepted Accounting Principles in India

inventory days Inventory days is computed by dividing the amount of closing Inventory by total value of adjusted revenue : Inventories/Adjusted Revenue X 365

IPO Initial public offering

IRDAI Insurance Regulatory and Development Authority of India

IST Indian Standard Time

JNNURM Jawaharlal Nehru National Urban Renewal Mission

MCLR Marginal cost of funds based lending rate

MCA Ministry of Corporate Affairs, Government of India

“Mn” or “mn” Million

MT Metric Tonne

“N.A.” or “NA” Not Applicable

NACH National Automated Clearing House

NAV Net Asset Value

NEFT National Electronic Fund Transfer

No. Number

Notified Sections The sections of the Companies Act, 2013 that were notified by the Ministry of Corporate Affairs, Government of India

NR Non-resident

NRE Account Non Resident External Account

NRI A person resident outside India, who is a citizen of India as defined under the Foreign Exchange Management (Deposit) Regulations, 2016 or an ‘Overseas Citizen of India’ cardholder within the meaning of Section 7(A) of the Citizenship Act, 1955

NRO Account Non Resident Ordinary Account

NSDL National Securities Depository Limited

NSE National Stock Exchange of India Limited

“OCB” or “Overseas Corporate Body”

A company, partnership, society or other corporate body owned directly or indirectly to the extent of at least 60% by NRIs including overseas trusts, in which not less than 60% of beneficial interest is irrevocably held by NRIs directly or indirectly and which was in existence on October 3, 2003 and immediately before such date had taken benefits under the general permission granted to OCBs under FEMA. OCBs are not allowed to invest in the Offer

p.a. Per annum

P/E Ratio Price/Earnings Ratio

PAN Permanent Account Number

PVC Poly vinyl chloride

PE Polyethylene

PPR Polypropylene Random Copolymer

RBI Reserve Bank of India

Regulation S Regulation S under the U.S. Securities Act

RTGS Real Time Gross Settlement

SCRA Securities Contracts (Regulation) Act, 1956

SCRR Securities Contracts (Regulation) Rules, 1957

12

Term Description

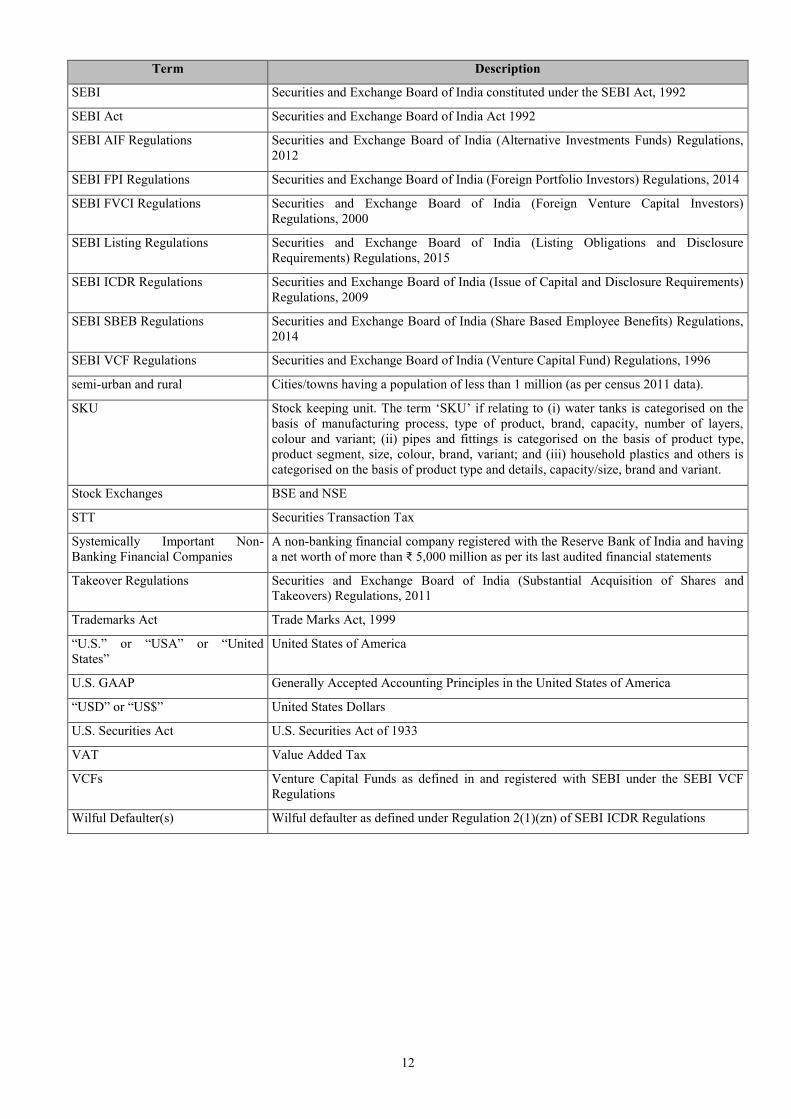

SEBI Securities and Exchange Board of India constituted under the SEBI Act, 1992

SEBI Act Securities and Exchange Board of India Act 1992

SEBI AIF Regulations Securities and Exchange Board of India (Alternative Investments Funds) Regulations, 2012

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2014

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investors) Regulations, 2000

SEBI Listing Regulations Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009

SEBI SBEB Regulations Securities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014

SEBI VCF Regulations Securities and Exchange Board of India (Venture Capital Fund) Regulations, 1996

semi-urban and rural Cities/towns having a population of less than 1 million (as per census 2011 data).

SKU Stock keeping unit. The term ‘SKU’ if relating to (i) water tanks is categorised on the basis of manufacturing process, type of product, brand, capacity, number of layers, colour and variant; (ii) pipes and fittings is categorised on the basis of product type, product segment, size, colour, brand, variant; and (iii) household plastics and others is categorised on the basis of product type and details, capacity/size, brand and variant.

Stock Exchanges BSE and NSE

STT Securities Transaction Tax

Systemically Important Non-Banking Financial Companies

A non-banking financial company registered with the Reserve Bank of India and having a net worth of more than ₹ 5,000 million as per its last audited financial statements

Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011

Trademarks Act Trade Marks Act, 1999

“U.S.” or “USA” or “United States”

United States of America

U.S. GAAP Generally Accepted Accounting Principles in the United States of America

“USD” or “US$” United States Dollars

U.S. Securities Act U.S. Securities Act of 1933

VAT Value Added Tax

VCFs Venture Capital Funds as defined in and registered with SEBI under the SEBI VCF Regulations

Wilful Defaulter(s) Wilful defaulter as defined under Regulation 2(1)(zn) of SEBI ICDR Regulations

13

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

Certain Conventions

All references to “India” contained in this Draft Red Herring Prospectus are to the Republic of India.

Unless stated otherwise, all references to page numbers in this Draft Red Herring Prospectus are to the page numbers of this Draft Red Herring Prospectus.

Financial Data

Unless stated otherwise, the financial information in this Draft Red Herring Prospectus is derived from our Restated Financial Statements. Certain additional financial information pertaining to our Group Companies is derived from their respective financial statements. The Restated Financial Statements included in this Draft Red Herring Prospectus are as at and for the Fiscals ended March 31, 2018, March 31, 2017, March 31, 2016, March 31, 2015 and March 31, 2014 and have been prepared in accordance with the Companies Act, Ind AS and have been restated in accordance with the SEBI ICDR Regulations and the guidance notes issued by ICAI. For further information, see “Financial Information” on page 174.

In this Draft Red Herring Prospectus, any discrepancies in any table between the total and the sums of the amounts listed are due to rounding off. All figures in decimals have been rounded off to the second decimal and all percentage figures have been rounded off to two decimal places.

Our Company’s financial year commences on April 1 and ends on March 31 of the next year. Accordingly, all references to a particular financial year, unless stated otherwise, are to the 12 month period ended on March 31 of that year. Unless stated otherwise, or the context requires otherwise, all references to a “year” in this Draft Red Herring Prospectus are to a calendar year.

There are significant differences between Ind AS, U.S. GAAP and IFRS. Our Company does not provide reconciliation of its financial information to IFRS or U.S. GAAP. Our Company has not attempted to explain those differences or quantify their impact on the financial data included in this Draft Red Herring Prospectus and it is urged that you consult your own advisors regarding such differences and their impact on our financial data. Accordingly, the degree to which the financial information included in this Draft Red Herring Prospectus will provide meaningful information is entirely dependent on the reader’s level of familiarity with Indian accounting policies and practices, the Companies Act, the Ind AS and the SEBI ICDR Regulations. Any reliance by persons not familiar with Indian accounting policies and practices on the financial disclosures presented in this Draft Red Herring Prospectus should accordingly be limited.

Unless the context otherwise indicates, any percentage amounts, as set forth in “Risk Factors”, “Our Business” and “Management’s Discussion and Analysis of Financial Conditional and Results of Operations” on pages 16, 121 and 325, respectively, and elsewhere in this Draft Red Herring Prospectus have been calculated on the basis of our Restated Financial Statements.

Currency and Units of Presentation

All references to:

“Rupees” or “₹” or “INR” or “Rs.” are to Indian Rupee, the official currency of the Republic of India; and

“USD” or “US$” are to United States Dollar, the official currency of the United States.

Our Company has presented certain numerical information in this Draft Red Herring Prospectus in “million” units. One million represents 1,000,000 and one billion represents 1,000,000,000.

Exchange Rates

This Draft Red Herring Prospectus contains conversion of certain other currency amounts into Indian Rupees. These conversions should not be construed as a representation that these currency amounts could have been, or can be converted into Indian Rupees, at any particular rate or at all.

The following table sets forth, for the periods indicated, information with respect to the exchange rate between the Rupee and the US$ (in Rupees per US$):

(Amount in ₹, unless otherwise specified) Currency As on March 31,

2018* As on March 31, 2017 As on March 31, 2016 As on March 31, 2015 As on March 31,

2014** 1 US$ 64.45 64.84 66.33 62.59 60.09

Source: RBI Reference Rate

14

* Exchange rate as on March 28, 2018, as RBI reference rate is not available for March 31, 2018, March 30, 2018 and March 29, 2018 being a Saturday and public holidays, respectively.

** Exchange rate as on March 28, 2014, as RBI Reference Rate is not available for March 31, 2014, March 30, 2014 and March 29, 2014 being a public holiday, a Sunday and a Saturday, respectively.

Industry and Market Data

Unless stated otherwise, industry and market data used in this Draft Red Herring Prospectus has been obtained or derived from the report titled “Assessment of the plastic tanks, plastic pipes and household & other plastic products industries” dated June 13, 2018 prepared by CRISIL Research (“CRISIL Report”). The CRISIL Report has been prepared at the request of our Company. In relation to the CRISIL Report, please see below the disclaimer specified in their consent letter dated June 13, 2018 issued to our Company:

“CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this report (Report) based on the Information obtained by CRISIL from sources which it considers reliable (Data). However, CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / Report and is not responsible for any errors or omissions or for the results obtained from the use of Data / Report. This Report is not a recommendation to invest / disinvest in any entity covered in the Report and no part of this Report should be construed as an expert advice or investment advice or any form of investment banking within the meaning of any law or regulation. CRISIL especially states that it has no liability whatsoever to the subscribers / users / transmitters/ distributors of this Report. Without limiting the generality of the foregoing, nothing in the Report is to be construed as CRISIL providing or intending to provide any services in jurisdictions where CRISIL does not have the necessary permission and/or registration to carry out its business activities in this regard. Vectus Industries Limited will be responsible for ensuring compliances and consequences of non-compliances for use of the Report or part thereof outside India. CRISIL Research operates independently of, and does not have access to information obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Ltd (CRIS), which may, in their regular operations, obtain information of a confidential nature. The views expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No part of this Report may be published/reproduced in any form without CRISIL’s prior written approval.”

All financial information in relation to the Company specified in the CRISIL Report, relates to the financial information of the Company prepared in accordance with Indian GAAP for the relevant period specified therein, and may not be comparable to our Restated Financial Statements contained in this Draft Red Herring Prospectus.

Industry publications generally state that the information contained in such publications has been obtained from publicly available documents from various sources believed to be reliable but their accuracy and completeness are not guaranteed and their reliability cannot be assured. Accordingly, no investment decisions should be based on such information. Although we believe the industry and market data used in this Draft Red Herring Prospectus is reliable, it has not been independently verified by us, the Selling Shareholders or the BRLMs or any of their affiliates or advisors. The data used in these sources may have been re-classified by us for the purposes of presentation. Data from these sources may also not be comparable. Such data involves risk, uncertainties and assumptions, and is subject to change based on various factors. Accordingly, investment decisions should not be based solely on such information. For details in relation to the risks involving the Report, see “Risk Factors”on page 16.

The extent to which the market and industry data used in this Draft Red Herring Prospectus is meaningful depends on the reader’s familiarity with and understanding of the methodologies used in compiling such data. There are no standard data gathering methodologies in the industry in which business of our Company is conducted, and methodologies and assumptions may vary widely among different industry sources.